Semiotics of brand equity george rossolatos brand equity,semiotics

ENTERTAINMENTNovember 2010

2

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

ENTERTAINMENT November 2010

3

Advantage India - capital

Advantage

India

Improving

entertainment

infrastructure

Increasing investments by the private sector and foreign media and entertainment (M&E) majors have enhanced India‘s

entertainment infrastructure such as new multiplexes and digitization of TV distribution and theatre infrastructure.

High

production

volumes

• Producing more than 1,000 films

annually, India is the largest

producer of films in the world.

• There are more than 500 TV

channels in the country, requiring

30 hours of fresh programming per

week.

Large and under

penetrated

consumer

base

• In 2008, there were as many as 3.3 billion

theatre admissions in India.

• With the TV segment reaching as many as

134 million households in the country,

India is one of the largest TV markets in

the world.

Favourable

demographics

• India is among the world‘s youngest nations, as more than 52 per cent of its one billion-plus population is less than 25 years of age.

• This age group, with increasing disposable income levels, has given impetus to the entertainment industry.

Liberal

government

policies

Digital

revolution

• Digitisation and technological advancements

across the value chain are improving the quality

of content and reach, and also leading to new

business models. For example rural DTH

penetration is three times higher than in urban

areas, with digital TV penetration rate of 34% in

rural areas as compared to 12% in urban areas

Sources: ―Indian entertainment down South: from script to screen,‖ Ernst & Young, 2009; EY M&E NewsReel, Ernst & Young, 2009; ―India to have

100-mn cable homes this year,‖ Business Standard¸ 4 January 2010; ―Tune-in to India‘s entertainment economy: From emerging to surging,‖ Ernst &

Young, 2008; ―Tune into emerging entertainment markets- spotlight on BRIC,‖ Ernst & Young, 2010; ―Rural India's swift digital TV embrace,‖

Business Standard, 4 December 2010.

• A liberalised foreign investment regime

and other regulatory initiatives are

resulting in a conducive business

environment for Indian M&E.

• FDI upto 100 per cent is allowed in film

and advertising, TV broadcasting (except

news) and 26 per cent in newspaper

publishing.

• Migration from fixed to revenue sharing

license fee regime in radio segment and

roll out of digital cable will provide

further impetus to industry‘s growth.

Entertainment November 2010

ADVANTAGE INDIA

4

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

ENTERTAINMENT November 2010

5

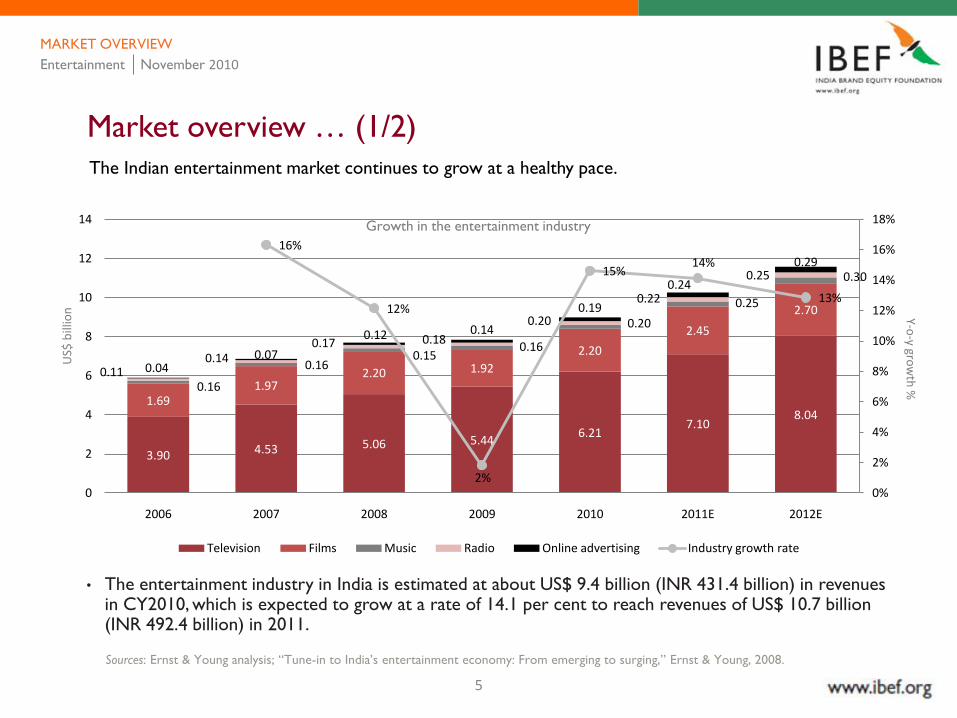

Market overview … (1/2)

The Indian entertainment market continues to grow at a healthy pace.

• The entertainment industry in India is estimated at about US$ 9.4 billion (INR 431.4 billion) in revenues in CY2010, which is expected to grow at a rate of 14.1 per cent to reach revenues of US$ 10.7 billion (INR 492.4 billion) in 2011.

Sources: Ernst & Young analysis; ―Tune-in to India‘s entertainment economy: From emerging to surging,‖ Ernst & Young, 2008.

MARKET OVERVIEW

Growth in the entertainment industry

3.90 4.53 5.06 5.446.21

7.108.04

1.691.97

2.20 1.92

2.20

2.45

2.70

0.16

0.160.15

0.16

0.20

0.25

0.30

0.110.14

0.17 0.18

0.20

0.22

0.25

0.040.07

0.12 0.14

0.19

0.24

0.29

16%

12%

2%

15%14%

13%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

2

4

6

8

10

12

14

2006 2007 2008 2009 2010 2011E 2012E

Television Films Music Radio Online advertising Industry growth rate

Entertainment November 2010U

S$ b

illio

n Y-o-y gro

wth

%

6

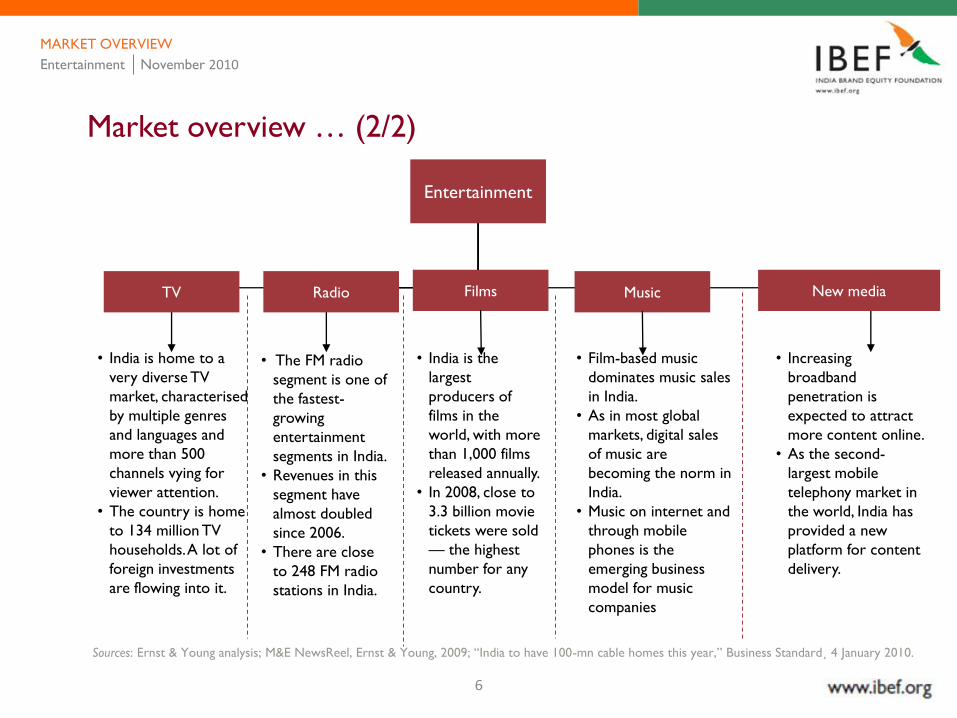

Entertainment

• The FM radio

segment is one of

the fastest-

growing

entertainment

segments in India.

• Revenues in this

segment have

almost doubled

since 2006.

• There are close

to 248 FM radio

stations in India.

• India is home to a

very diverse TV

market, characterised

by multiple genres

and languages and

more than 500

channels vying for

viewer attention.

• The country is home

to 134 million TV

households. A lot of

foreign investments

are flowing into it.

• Film-based music

dominates music sales

in India.

• As in most global

markets, digital sales

of music are

becoming the norm in

India.

• Music on internet and

through mobile

phones is the

emerging business

model for music

companies

• Increasing

broadband

penetration is

expected to attract

more content online.

• As the second-

largest mobile

telephony market in

the world, India has

provided a new

platform for content

delivery.

• India is the

largest

producers of

films in the

world, with more

than 1,000 films

released annually.

• In 2008, close to

3.3 billion movie

tickets were sold

— the highest

number for any

country.

Films New media

Sources: Ernst & Young analysis; M&E NewsReel, Ernst & Young, 2009; ―India to have 100-mn cable homes this year,‖ Business Standard¸ 4 January 2010.

Market overview … (2/2)

RadioTV Music

MARKET OVERVIEW

Entertainment November 2010

7

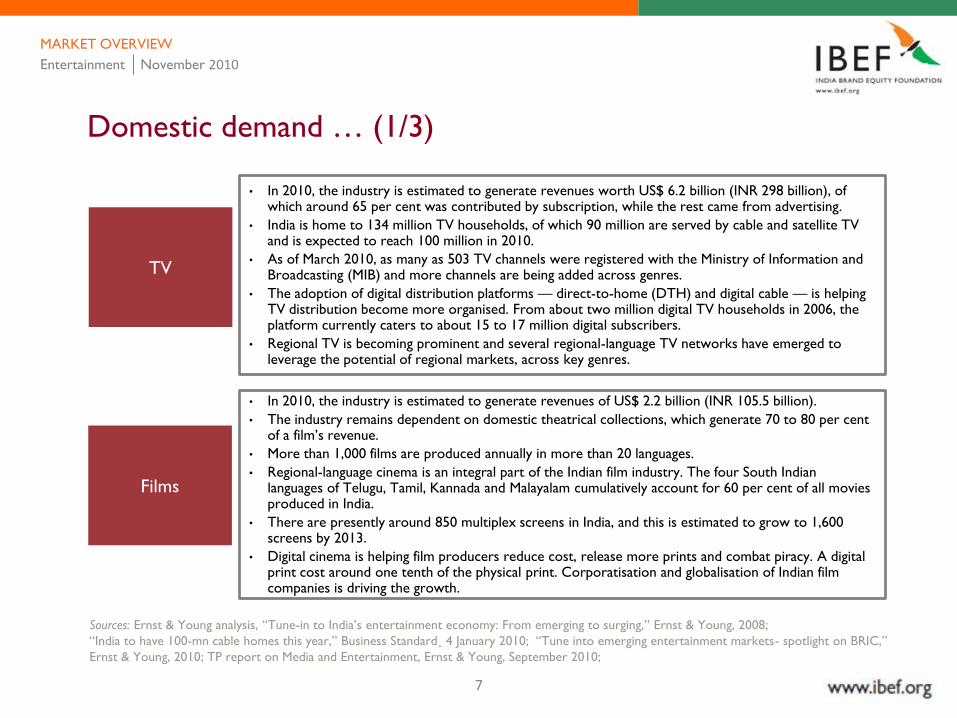

TV

Films

• In 2010, the industry is estimated to generate revenues worth US$ 6.2 billion (INR 298 billion), of which around 65 per cent was contributed by subscription, while the rest came from advertising.

• India is home to 134 million TV households, of which 90 million are served by cable and satellite TV and is expected to reach 100 million in 2010.

• As of March 2010, as many as 503 TV channels were registered with the Ministry of Information and Broadcasting (MIB) and more channels are being added across genres.

• The adoption of digital distribution platforms — direct-to-home (DTH) and digital cable — is helping TV distribution become more organised. From about two million digital TV households in 2006, the platform currently caters to about 15 to 17 million digital subscribers.

• Regional TV is becoming prominent and several regional-language TV networks have emerged to leverage the potential of regional markets, across key genres.

• In 2010, the industry is estimated to generate revenues of US$ 2.2 billion (INR 105.5 billion).

• The industry remains dependent on domestic theatrical collections, which generate 70 to 80 per cent of a film‘s revenue.

• More than 1,000 films are produced annually in more than 20 languages.

• Regional-language cinema is an integral part of the Indian film industry. The four South Indian languages of Telugu, Tamil, Kannada and Malayalam cumulatively account for 60 per cent of all movies produced in India.

• There are presently around 850 multiplex screens in India, and this is estimated to grow to 1,600 screens by 2013.

• Digital cinema is helping film producers reduce cost, release more prints and combat piracy. A digital print cost around one tenth of the physical print. Corporatisation and globalisation of Indian film companies is driving the growth.

Domestic demand … (1/3)

Sources: Ernst & Young analysis, ―Tune-in to India‘s entertainment economy: From emerging to surging,‖ Ernst & Young, 2008;

―India to have 100-mn cable homes this year,‖ Business Standard¸ 4 January 2010; ―Tune into emerging entertainment markets- spotlight on BRIC,‖

Ernst & Young, 2010; TP report on Media and Entertainment, Ernst & Young, September 2010;

MARKET OVERVIEW

Entertainment November 2010

8

Music

• The music industry is estimated to generate revenues of US$ 0.20 billion (INR 9.4 billion) in 2010.

• Distribution via digital formats on the Internet and through mobile phones is the emerging business model for music companies.

• Music sold via mobiles as ringtones, caller-back ringtones (CBRTs) and downloads of complete songs contribute 25 to 35 per cent of music companies‘ revenues.

• Business models built around mobile music such as track downloads and on-demand streaming are expected to emerge in the near future and gain further impetus with the rollout of 3G services.

• Music sales in physical formats are affected and music companies are repositioning their products to counter this decline by introducing low-cost, MP3-based compact discs (CDs) for low-end customers and premium packaged CDs for high-end customers. It is also being sold on memory cards and pen drives.

• By December 2011, the industry is expected to generate revenues of US$ 0.26 billion (INR 12.1 billion), exhibiting growth of 26.8 per cent over 2010.

Domestic demand … (2/3)

Radio

• In 2010, the industry has been estimated at US$ 0.20 billion (INR 9.4 billion), GoI-controlled All India Radio (AIR) and 37 private FM radio companies that operate close to 248 FM radio stations in India cater to this segment.

• The yet-to-be-launched Phase-III FM radio licensing policy is likely to give further impetus to the FM radio industry and open up licences for close to 700 stations and raise the FDI limit from current 20 per cent to 26 per cent.

• There is a growing advertiser interest in radio amongst the country level and the local advertisers.

• International radio players such as Radio Netherlands Worldwide (RNW) and BBC have made content-syndication deals with FM radio stations in India.

Sources: Ernst & Young analysis; ―Tune-in to India‘s entertainment economy: From emerging to surging,‖ Ernst & Young, 2008.

―FM-III 1st phase to auction 160 stations,‖ The Financial Express website, http://www.financialexpress.com/news/fmiii-1st-phase-to-auction-160-

stations/674181/, accessed 11 November 2010; ―Tune into emerging entertainment markets- spotlight on BRIC,‖ Ernst & Young, 2010;

MARKET OVERVIEW

Entertainment November 2010

9

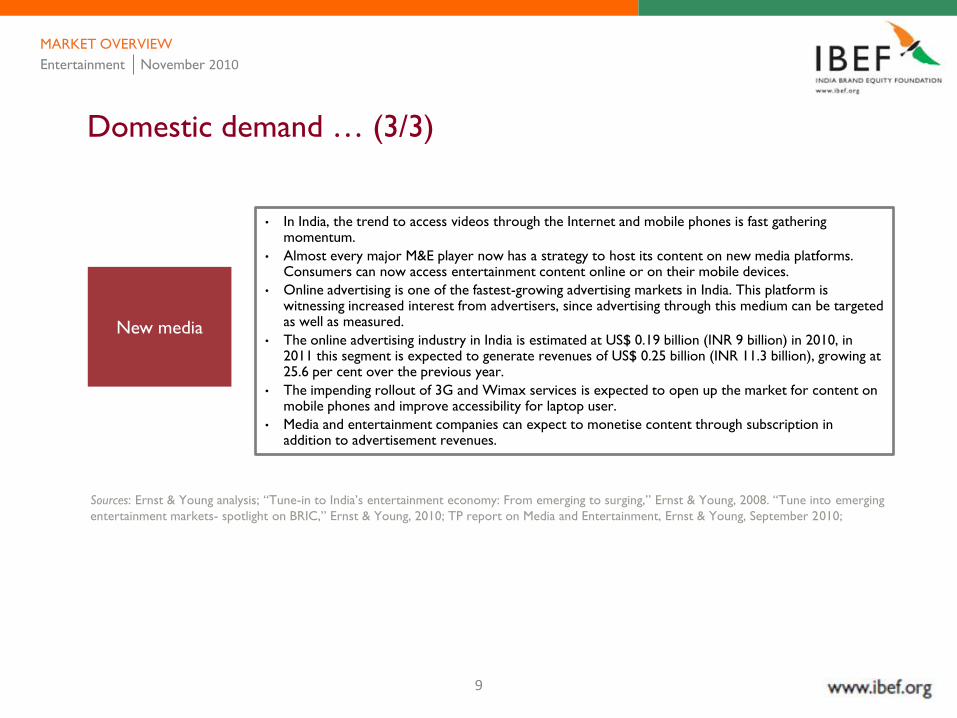

New media

• In India, the trend to access videos through the Internet and mobile phones is fast gathering momentum.

• Almost every major M&E player now has a strategy to host its content on new media platforms. Consumers can now access entertainment content online or on their mobile devices.

• Online advertising is one of the fastest-growing advertising markets in India. This platform is witnessing increased interest from advertisers, since advertising through this medium can be targeted as well as measured.

• The online advertising industry in India is estimated at US$ 0.19 billion (INR 9 billion) in 2010, in 2011 this segment is expected to generate revenues of US$ 0.25 billion (INR 11.3 billion), growing at 25.6 per cent over the previous year.

• The impending rollout of 3G and Wimax services is expected to open up the market for content on mobile phones and improve accessibility for laptop user.

• Media and entertainment companies can expect to monetise content through subscription in addition to advertisement revenues.

Domestic demand … (3/3)

Sources: Ernst & Young analysis; ―Tune-in to India‘s entertainment economy: From emerging to surging,‖ Ernst & Young, 2008. ―Tune into emerging

entertainment markets- spotlight on BRIC,‖ Ernst & Young, 2010; TP report on Media and Entertainment, Ernst & Young, September 2010;

MARKET OVERVIEW

Entertainment November 2010

10

• Indian films are increasingly gaining popularity among international audiences. Indian producers are releasing more prints to reach wider international audiences. As a result, collection from the overseas market is improving. The recent Hindi blockbuster, 3 Idiots, was released with an unprecedented 344 prints.

• Many Indian TV channels are available overseas on major TV distribution platforms.

International demand

Sources: Ernst & Young analysis; ―3 Idiots makes b‘wood history, ―Business Standard, 5 January 2010.

MARKET OVERVIEW

Entertainment November 2010

11

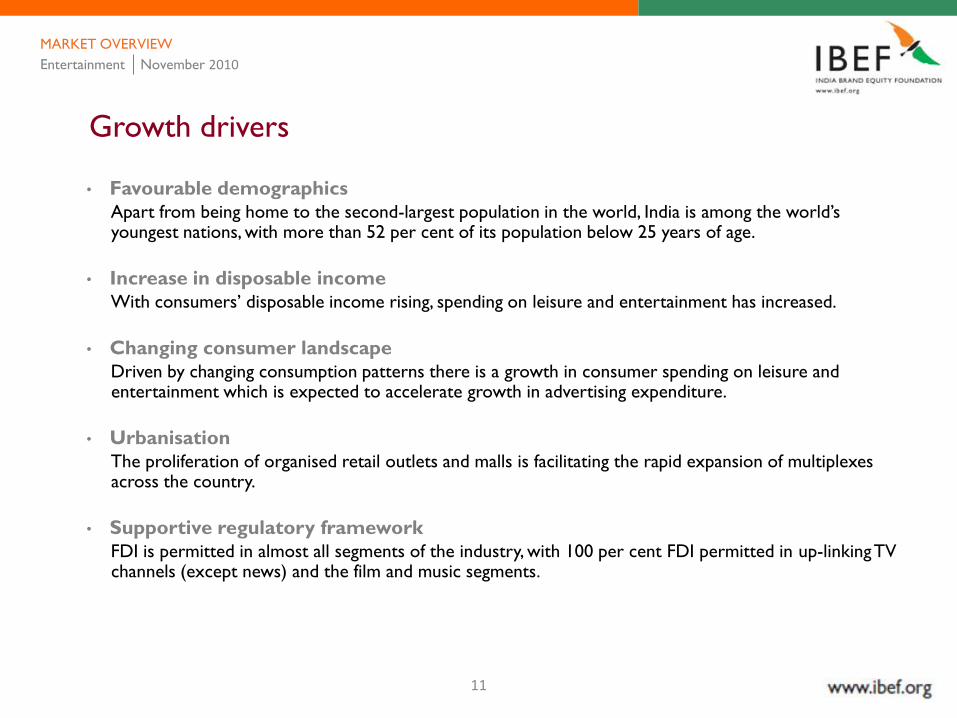

Growth drivers

• Favourable demographics

Apart from being home to the second-largest population in the world, India is among the world‘s youngest nations, with more than 52 per cent of its population below 25 years of age.

• Increase in disposable income

With consumers‘ disposable income rising, spending on leisure and entertainment has increased.

• Changing consumer landscape

Driven by changing consumption patterns there is a growth in consumer spending on leisure and entertainment which is expected to accelerate growth in advertising expenditure.

• Urbanisation

The proliferation of organised retail outlets and malls is facilitating the rapid expansion of multiplexes across the country.

• Supportive regulatory framework

FDI is permitted in almost all segments of the industry, with 100 per cent FDI permitted in up-linking TV channels (except news) and the film and music segments.

MARKET OVERVIEW

Entertainment November 2010

12

Growth drivers

Sources: ―Tune-in to India‘s entertainment economy: From emerging to surging,‖ Ernst & Young, 2008; ―India‘s digital revolution: impact on film

and television sectors,‖ Ernst & Young, 2007; ―Tune into emerging entertainment markets- spotlight on BRIC,‖ Ernst & Young, 2010; TP report

on Media and Entertainment, Ernst & Young, September 2010;

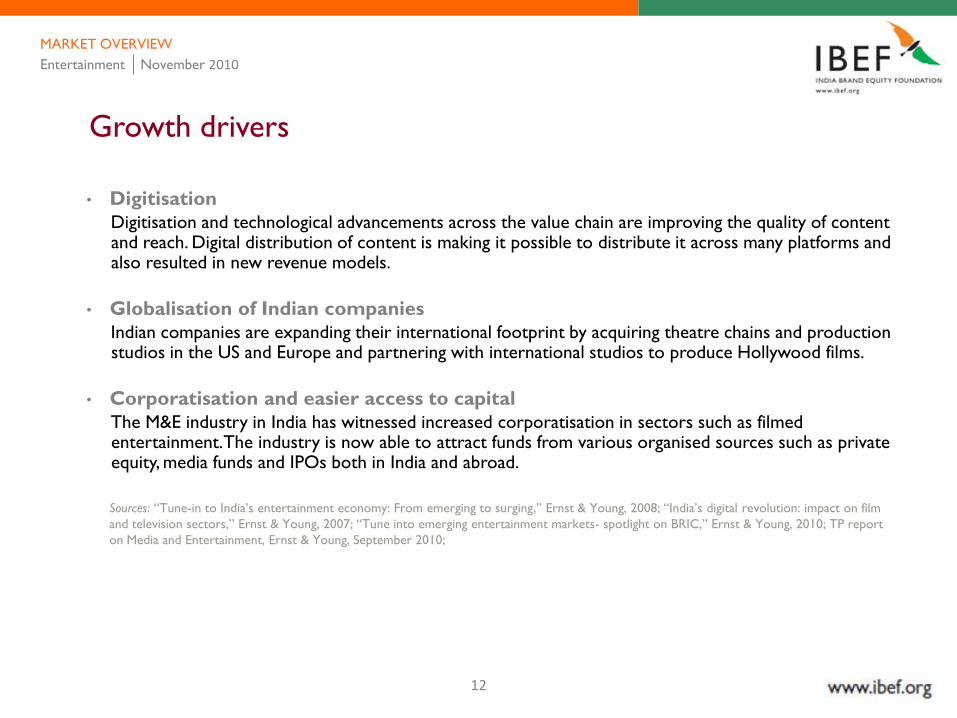

• Digitisation

Digitisation and technological advancements across the value chain are improving the quality of content and reach. Digital distribution of content is making it possible to distribute it across many platforms and also resulted in new revenue models.

• Globalisation of Indian companies

Indian companies are expanding their international footprint by acquiring theatre chains and production studios in the US and Europe and partnering with international studios to produce Hollywood films.

• Corporatisation and easier access to capital

The M&E industry in India has witnessed increased corporatisation in sectors such as filmed entertainment. The industry is now able to attract funds from various organised sources such as private equity, media funds and IPOs both in India and abroad.

MARKET OVERVIEW

Entertainment November 2010

13

Key trends

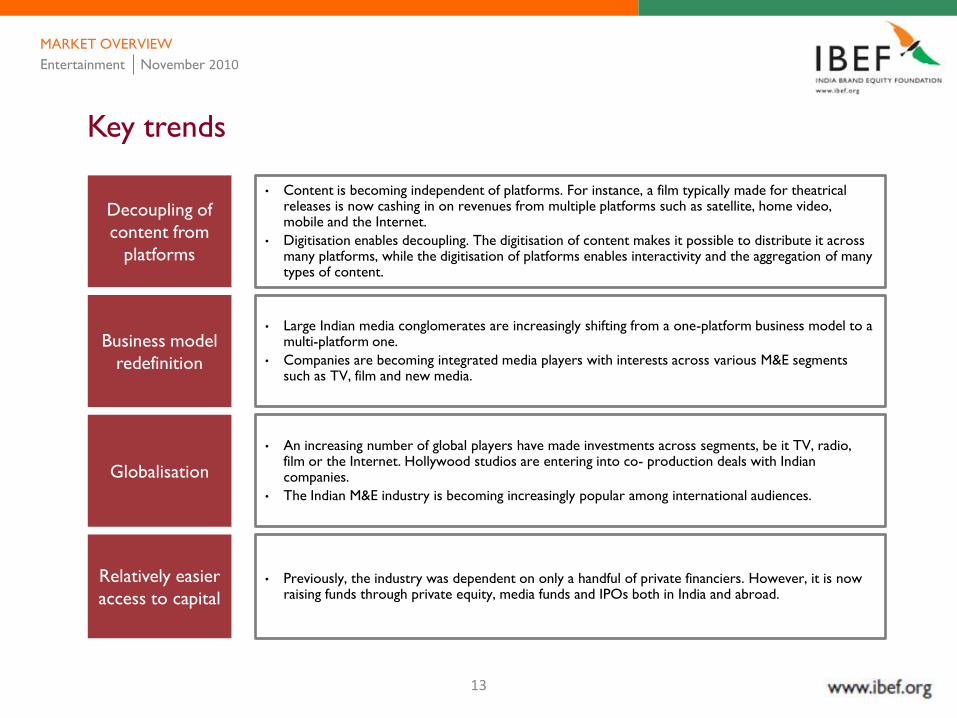

Decoupling of

content from

platforms

Business model

redefinition

• Content is becoming independent of platforms. For instance, a film typically made for theatrical releases is now cashing in on revenues from multiple platforms such as satellite, home video, mobile and the Internet.

• Digitisation enables decoupling. The digitisation of content makes it possible to distribute it across many platforms, while the digitisation of platforms enables interactivity and the aggregation of many types of content.

• Large Indian media conglomerates are increasingly shifting from a one-platform business model to a multi-platform one.

• Companies are becoming integrated media players with interests across various M&E segments such as TV, film and new media.

Globalisation

• An increasing number of global players have made investments across segments, be it TV, radio, film or the Internet. Hollywood studios are entering into co- production deals with Indian companies.

• The Indian M&E industry is becoming increasingly popular among international audiences.

Relatively easier

access to capital• Previously, the industry was dependent on only a handful of private financiers. However, it is now

raising funds through private equity, media funds and IPOs both in India and abroad.

MARKET OVERVIEW

Entertainment November 2010

14

Key trends

Regionalisation

• Media companies are innovating content to suit changing consumption preferences of small town India as regionalisation is becoming a significant factors driving growth with growing increase in literacy, consumption and disposable incomes in tier 2 & 3 cities.

• Demand for regional content is growing, advertisers are also increasing focus on rural markets. National broadcasters are adding regional channels to their portfolios, regional cinema is growing and international film studios are tapping regional markets in India.

Sources: ―Tune-in to India‘s entertainment economy: From emerging to surging,‖ Ernst & Young, 2008; ―What‘s next? for Indian media and

entertainment,‖ Ernst & Young, 2009; ―Tune into emerging entertainment markets- spotlight on BRIC,‖ Ernst & Young, 2010; TP report on Media

and Entertainment, Ernst & Young, September 2010;

MARKET OVERVIEW

Changing

consumer

preferences

• Consumer preferences are shifting towards international programming formats. There is an opportunity for global production houses to localise their content for the Indian audiences.

• There is a demand for youth oriented content and niche and regional content. Reality shows are also gaining popularity among the viewers.

Entertainment November 2010

15

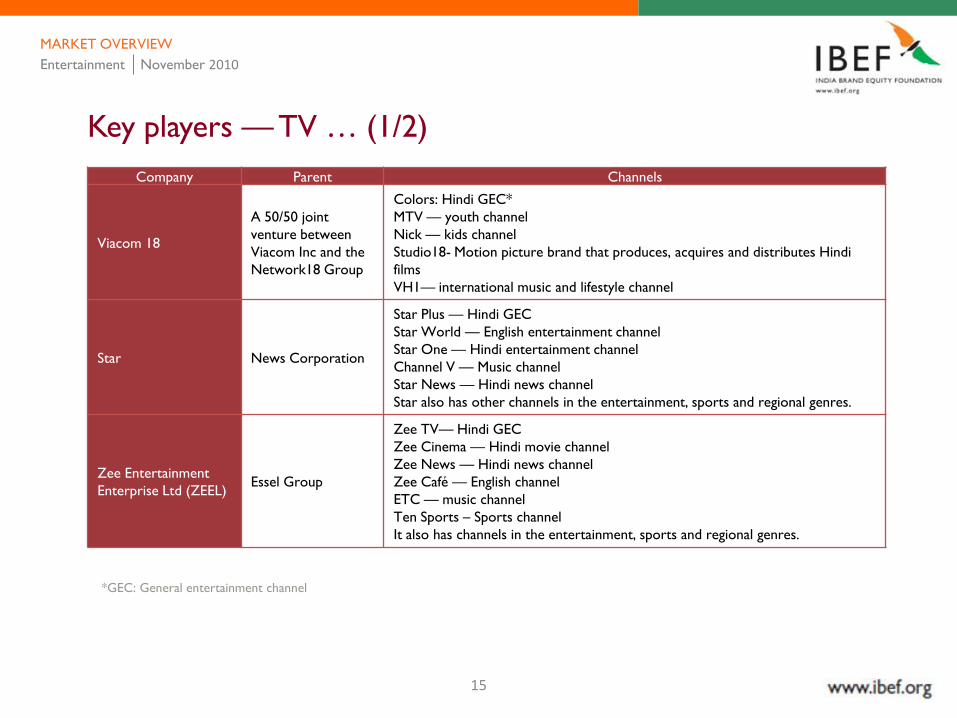

Key players — TV … (1/2)

Company Parent Channels

Viacom 18

A 50/50 joint

venture between

Viacom Inc and the

Network18 Group

Colors: Hindi GEC*

MTV — youth channel

Nick — kids channel

Studio18- Motion picture brand that produces, acquires and distributes Hindi

films

VH1— international music and lifestyle channel

Star News Corporation

Star Plus — Hindi GEC

Star World — English entertainment channel

Star One — Hindi entertainment channel

Channel V — Music channel

Star News — Hindi news channel

Star also has other channels in the entertainment, sports and regional genres.

Zee Entertainment

Enterprise Ltd (ZEEL)Essel Group

Zee TV— Hindi GEC

Zee Cinema — Hindi movie channel

Zee News — Hindi news channel

Zee Café — English channel

ETC — music channel

Ten Sports – Sports channel

It also has channels in the entertainment, sports and regional genres.

MARKET OVERVIEW

*GEC: General entertainment channel

Entertainment November 2010

16

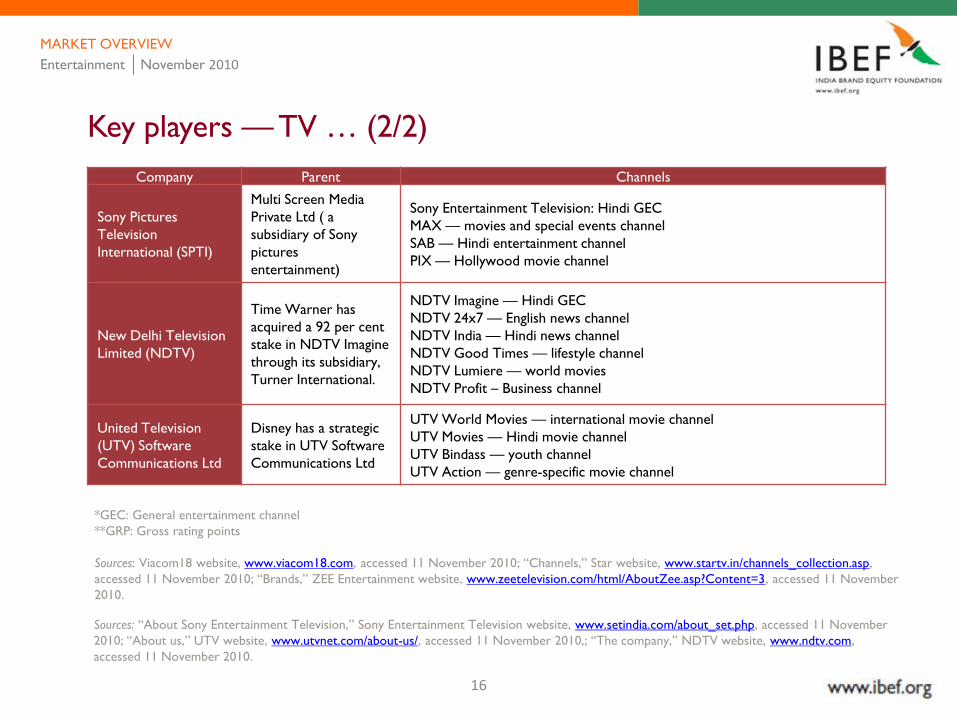

Key players — TV … (2/2)

Company Parent Channels

Sony Pictures

Television

International (SPTI)

Multi Screen Media

Private Ltd ( a

subsidiary of Sony

pictures

entertainment)

Sony Entertainment Television: Hindi GEC

MAX — movies and special events channel

SAB — Hindi entertainment channel

PIX — Hollywood movie channel

New Delhi Television

Limited (NDTV)

Time Warner has

acquired a 92 per cent

stake in NDTV Imagine

through its subsidiary,

Turner International.

NDTV Imagine — Hindi GEC

NDTV 24x7 — English news channel

NDTV India — Hindi news channel

NDTV Good Times — lifestyle channel

NDTV Lumiere — world movies

NDTV Profit – Business channel

United Television

(UTV) Software

Communications Ltd

Disney has a strategic

stake in UTV Software

Communications Ltd

UTV World Movies — international movie channel

UTV Movies — Hindi movie channel

UTV Bindass — youth channel

UTV Action — genre-specific movie channel

Sources: ―About Sony Entertainment Television,‖ Sony Entertainment Television website, www.setindia.com/about_set.php, accessed 11 November

2010; ―About us,‖ UTV website, www.utvnet.com/about-us/, accessed 11 November 2010,; ―The company,‖ NDTV website, www.ndtv.com,

accessed 11 November 2010.

MARKET OVERVIEW

*GEC: General entertainment channel

**GRP: Gross rating points

Sources: Viacom18 website, www.viacom18.com, accessed 11 November 2010; ―Channels,‖ Star website, www.startv.in/channels_collection.asp,

accessed 11 November 2010; ―Brands,‖ ZEE Entertainment website, www.zeetelevision.com/html/AboutZee.asp?Content=3, accessed 11 November

2010.

Entertainment November 2010

17

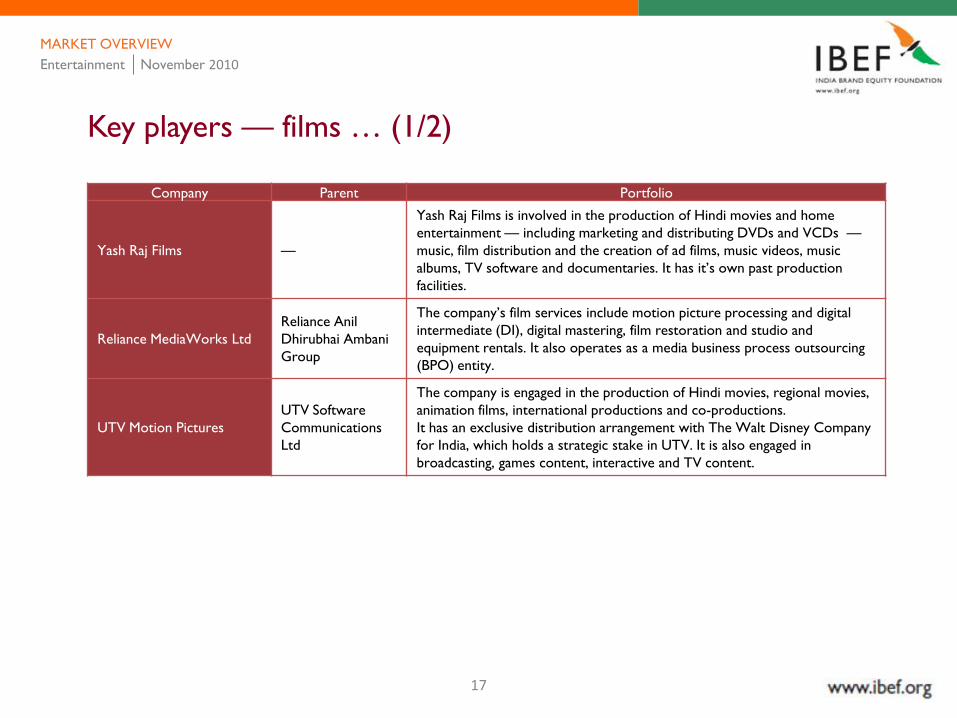

Key players — films … (1/2)

Company Parent Portfolio

Yash Raj Films —

Yash Raj Films is involved in the production of Hindi movies and home

entertainment — including marketing and distributing DVDs and VCDs —

music, film distribution and the creation of ad films, music videos, music

albums, TV software and documentaries. It has it‘s own past production

facilities.

Reliance MediaWorks Ltd

Reliance Anil

Dhirubhai Ambani

Group

The company‘s film services include motion picture processing and digital

intermediate (DI), digital mastering, film restoration and studio and

equipment rentals. It also operates as a media business process outsourcing

(BPO) entity.

UTV Motion Pictures

UTV Software

Communications

Ltd

The company is engaged in the production of Hindi movies, regional movies,

animation films, international productions and co-productions.

It has an exclusive distribution arrangement with The Walt Disney Company

for India, which holds a strategic stake in UTV. It is also engaged in

broadcasting, games content, interactive and TV content.

MARKET OVERVIEW

Entertainment November 2010

18

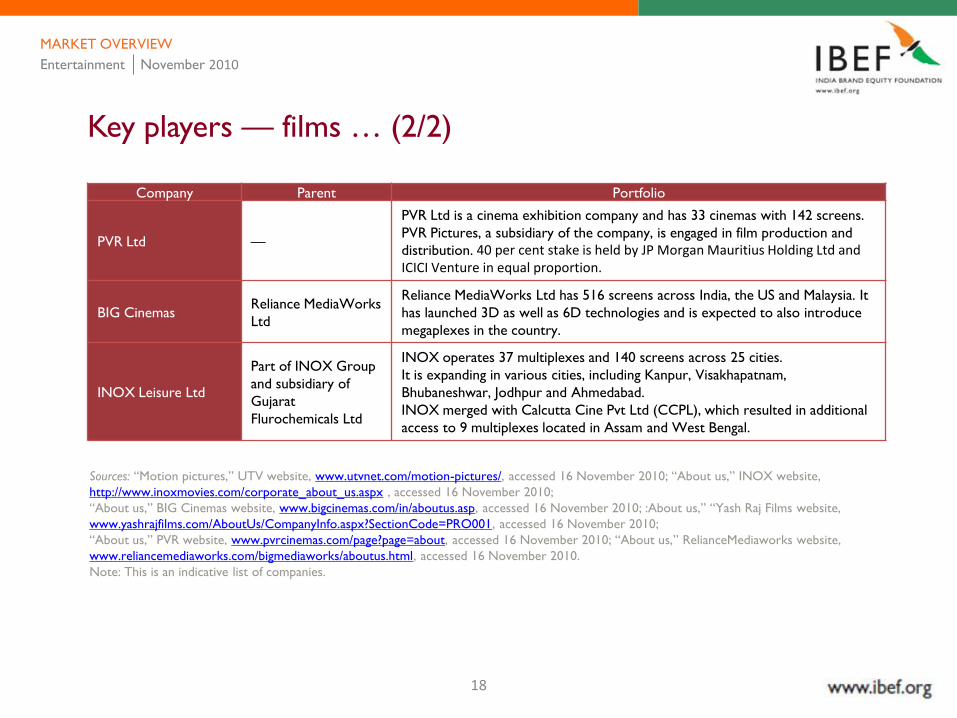

Key players — films … (2/2)

Company Parent Portfolio

PVR Ltd —

PVR Ltd is a cinema exhibition company and has 33 cinemas with 142 screens.

PVR Pictures, a subsidiary of the company, is engaged in film production and

distribution. 40 per cent stake is held by JP Morgan Mauritius Holding Ltd and ICICI Venture in equal proportion.

BIG CinemasReliance MediaWorks

Ltd

Reliance MediaWorks Ltd has 516 screens across India, the US and Malaysia. It

has launched 3D as well as 6D technologies and is expected to also introduce

megaplexes in the country.

INOX Leisure Ltd

Part of INOX Group

and subsidiary of

Gujarat

Flurochemicals Ltd

INOX operates 37 multiplexes and 140 screens across 25 cities.

It is expanding in various cities, including Kanpur, Visakhapatnam,

Bhubaneshwar, Jodhpur and Ahmedabad.

INOX merged with Calcutta Cine Pvt Ltd (CCPL), which resulted in additional

access to 9 multiplexes located in Assam and West Bengal.

Sources: ―Motion pictures,‖ UTV website, www.utvnet.com/motion-pictures/, accessed 16 November 2010; ―About us,‖ INOX website,

http://www.inoxmovies.com/corporate_about_us.aspx , accessed 16 November 2010;

―About us,‖ BIG Cinemas website, www.bigcinemas.com/in/aboutus.asp, accessed 16 November 2010; :About us,‖ ―Yash Raj Films website,

www.yashrajfilms.com/AboutUs/CompanyInfo.aspx?SectionCode=PRO001, accessed 16 November 2010;

―About us,‖ PVR website, www.pvrcinemas.com/page?page=about, accessed 16 November 2010; ―About us,‖ RelianceMediaworks website,

www.reliancemediaworks.com/bigmediaworks/aboutus.html, accessed 16 November 2010.

Note: This is an indicative list of companies.

MARKET OVERVIEW

Entertainment November 2010

19

Company Parent company Major brands

Entertainment Network

(India) Limited (ENIL)

Bennett, Coleman & Company

Ltd (BCCL) and Times

Infotainment Media Ltd

Radio Mirchi has a presence in 32 cities across India, including

Mumbai, Delhi, Kolkata, Chennai, Pune, Indore, Ahmedabad,

Bengaluru, Hyderabad, Jaipur, Patna and Jalandhar.

Big FM Reliance Media World LtdBIG FM has a 45-station network covering 45 cities, 1,000 towns and

50,000 villages.

South Asia FM Ltd

(SAFL)Sun TV Network

Suryan FM has a presence in seven cities in Tamil Nadu, while Red

FM has a presence across 37 cities in the country.

Key players — radio

Sources: ―About us,‖ ENIL website, www.enil.co.in/profile.html, accessed 16 November 2010;

―FM Radio,‖ SUN TV Network website, www.sunnetwork.org/FM/default.htm, accessed 16 November 2010;

―About us,‖ BIG 92.7 FM website, www.big927fm.com/Content.php?Id=3, accessed 16 November 2010.

MARKET OVERVIEW

Entertainment November 2010

20

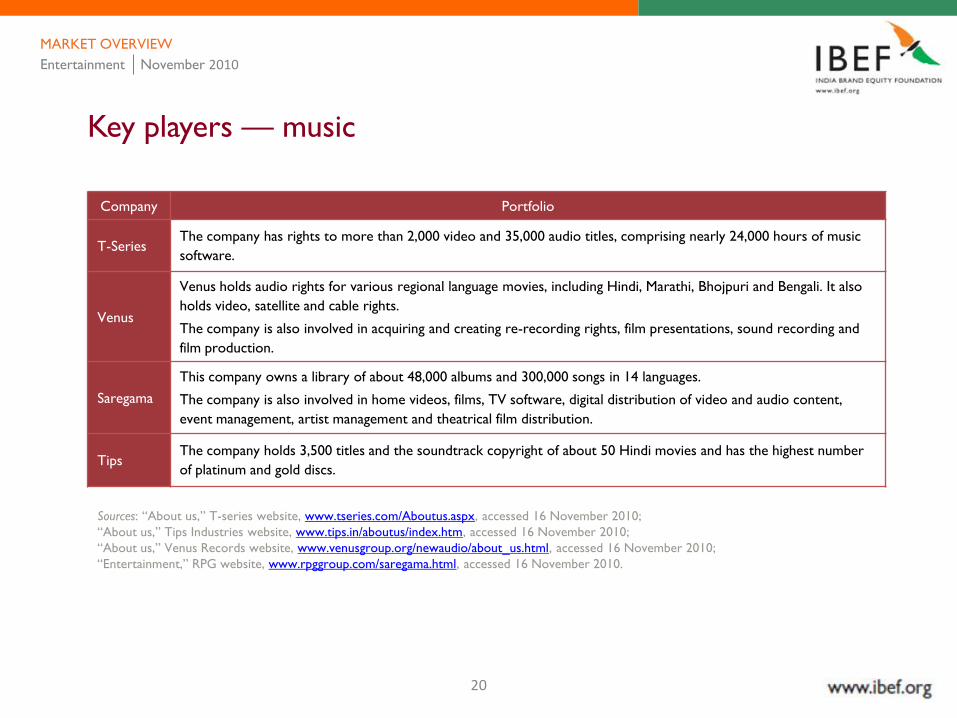

Key players — music

Company Portfolio

T-SeriesThe company has rights to more than 2,000 video and 35,000 audio titles, comprising nearly 24,000 hours of music

software.

Venus

Venus holds audio rights for various regional language movies, including Hindi, Marathi, Bhojpuri and Bengali. It also

holds video, satellite and cable rights.

The company is also involved in acquiring and creating re-recording rights, film presentations, sound recording and

film production.

Saregama

This company owns a library of about 48,000 albums and 300,000 songs in 14 languages.

The company is also involved in home videos, films, TV software, digital distribution of video and audio content,

event management, artist management and theatrical film distribution.

TipsThe company holds 3,500 titles and the soundtrack copyright of about 50 Hindi movies and has the highest number

of platinum and gold discs.

Sources: ―About us,‖ T-series website, www.tseries.com/Aboutus.aspx, accessed 16 November 2010;

―About us,‖ Tips Industries website, www.tips.in/aboutus/index.htm, accessed 16 November 2010;

―About us,‖ Venus Records website, www.venusgroup.org/newaudio/about_us.html, accessed 16 November 2010;

―Entertainment,‖ RPG website, www.rpggroup.com/saregama.html, accessed 16 November 2010.

MARKET OVERVIEW

Entertainment November 2010

21

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

ENTERTAINMENT November 2010

22

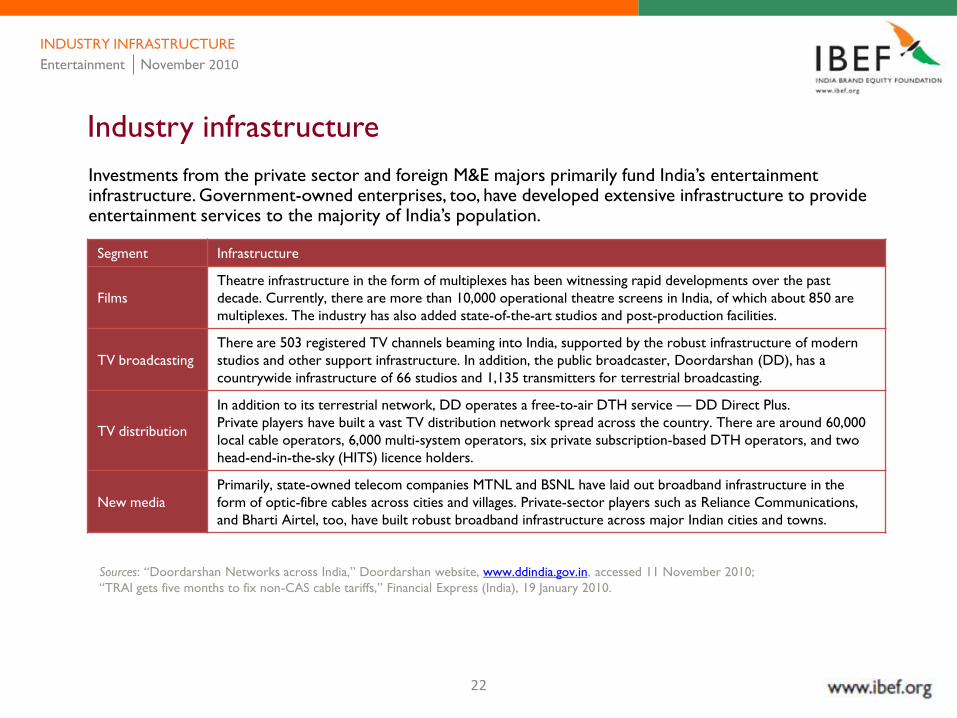

Industry infrastructure

Segment Infrastructure

Films

Theatre infrastructure in the form of multiplexes has been witnessing rapid developments over the past

decade. Currently, there are more than 10,000 operational theatre screens in India, of which about 850 are

multiplexes. The industry has also added state-of-the-art studios and post-production facilities.

TV broadcasting

There are 503 registered TV channels beaming into India, supported by the robust infrastructure of modern

studios and other support infrastructure. In addition, the public broadcaster, Doordarshan (DD), has a

countrywide infrastructure of 66 studios and 1,135 transmitters for terrestrial broadcasting.

TV distribution

In addition to its terrestrial network, DD operates a free-to-air DTH service — DD Direct Plus.

Private players have built a vast TV distribution network spread across the country. There are around 60,000

local cable operators, 6,000 multi-system operators, six private subscription-based DTH operators, and two

head-end-in-the-sky (HITS) licence holders.

New media

Primarily, state-owned telecom companies MTNL and BSNL have laid out broadband infrastructure in the

form of optic-fibre cables across cities and villages. Private-sector players such as Reliance Communications,

and Bharti Airtel, too, have built robust broadband infrastructure across major Indian cities and towns.

Sources: ―Doordarshan Networks across India,‖ Doordarshan website, www.ddindia.gov.in, accessed 11 November 2010;

―TRAI gets five months to fix non-CAS cable tariffs,‖ Financial Express (India), 19 January 2010.

Investments from the private sector and foreign M&E majors primarily fund India‘s entertainment infrastructure. Government-owned enterprises, too, have developed extensive infrastructure to provide entertainment services to the majority of India‘s population.

INDUSTRY INFRASTRUCTURE

Entertainment November 2010

23

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

ENTERTAINMENT November 2010

24

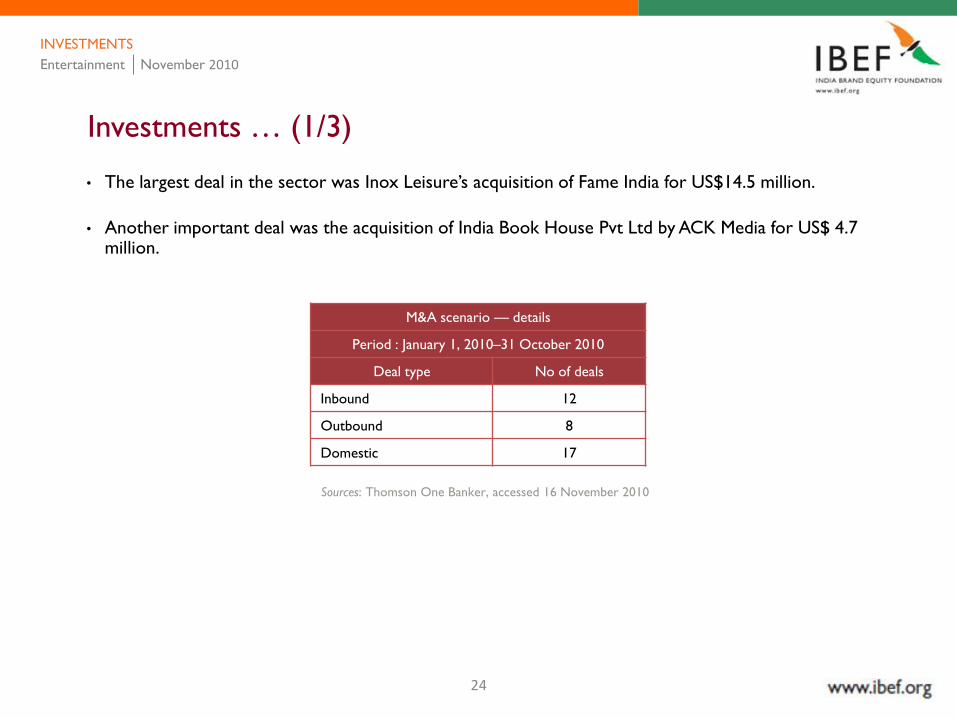

• The largest deal in the sector was Inox Leisure‘s acquisition of Fame India for US$14.5 million.

• Another important deal was the acquisition of India Book House Pvt Ltd by ACK Media for US$ 4.7 million.

M&A scenario — details

Period : January 1, 2010–31 October 2010

Deal type No of deals

Inbound 12

Outbound 8

Domestic 17

Sources: Thomson One Banker, accessed 16 November 2010

Investments … (1/3)

INVESTMENTS

Entertainment November 2010

25

DealDeal

typeAnnounce date

Announced

deal value

(US$ million)

Target nameTarget

country Acquirer

Acquirer

country

Domestic ACQ October 15, 2010 40.01Mid-Day Multimedia

Ltd-PrintIndia Jagran Prakashan Ltd India

Domestic ACQ September 22, 2010 NA INX Media Pvt Ltd IndiaZee Entertainment

EnterprisesIndia

Inbound ACQ September 7, 2010 NAAsianet Satellite

Commun LtdIndia

SIDOFI

CommunicationsMauritius

Inbound ACQ August 8, 2010 21.76Getit Infoservices Pvt

LtdIndia

Astro All Asia

Networks PLCMalaysia

Domestic ACQ July 30, 2010 NAReal Global

BroadcastingIndia

Alva Brothers

EntertainmentIndia

Domestic ACQ July 30, 2010 NA Miditech Pvt Ltd IndiaAlva Brothers

EntertainmentIndia

Inbound ACQ July 26, 2010 NATurmeric Vision Pvt

LtdIndia

Astro All Asia

Networks PLCMalaysia

Domestic ACQ June 16, 2010 NA Bloomberg UTV India Reliance Capital Ltd India

Inbound ACQ June 16, 2010 4.71Amar Chitra Katha

MediaIndia Investor Group

United

Kingdom

Outbound ACQ June 10, 2010 NA PostClick AustraliaKomli Media India Pvt

LtdIndia

Outbound ACQ May 7, 2010 NA IM Global LLCUnited

StatesReliance Big Ent Pvt Ltd India

Source: Thomson One Banker, accessed 16 November 2010;

Note: ACQ:Acquisition; PE: Private equity

Investments (Major acquisitions) … (2/3)

INVESTMENTS

Entertainment November 2010

26

DealDeal

typeAnnounce date

Announced

deal value

(US$ million)

Target nameTarget

country Acquirer

Acquirer

country

Outbound ACQ April 6, 2010 NACodemasters

Software Co Ltd

United

KingdomReliance Big Ent Pvt Ltd India

Domestic ACQ March 24, 2010 NAIndia Book House

Pvt LtdIndia Amar Chitra Katha Media India

Domestic ACQ February 5, 2010 2.75 Fame India Ltd India Inox Leisure Ltd India

Domestic ACQ February 3, 2010 14.46 Fame India Ltd India Inox Leisure Ltd India

Domestic ACQ January 28, 2010 16.43Maya Entertainment

LtdIndia Aptech Ltd India

Domestic ACQ January 20, 2010 NANext Gen Publishing

LtdIndia

Shapoorji Pallonji & Co

LtdIndia

Outbound ACQ January 18, 2010 44.15Taj Television Ltd

Mauritius

Utd Arab

Em

Zee Entertainment

EnterprisesIndia

Outbound ACQ January 7, 2010 NA i lab(UK)LtdUnited

KingdomReliance MediaWorks Ltd India

Source: Thomson One Banker, accessed 16 November 2010;

Note: ACQ:Acquisition; PE: Private equity

Investments (Major acquisitions) … (3/3)

INVESTMENTS

Entertainment November 2010

27

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

ENTERTAINMENT November 2010

28

Policy and regulatory frameworkTV

• In 2004, the Telecom Regulatory Authority of India (TRAI) was appointed as a regulator for the TV industry.

• Up to100 per cent FDI is permitted in TV channels.

• The foreign investment limit in the direct-to-home (DTH) business is 49 per cent, of which the FDI component limit is 20 per cent. The cable networks business has a 49 per cent foreign investment limit.

• TRAI has proposed to raise the FDI limit from 49 per cent to 74 per cent for DTH and national and state level MSOs. The regulatory body also recommended an FDI cap of 74 per cent on IPTV and mobile TV. There is no foreign investment policy on mobile TV at present.

• The rollout of DTH TV licenses and GoI-mandated digital conditional access systems (CAS) initiated the digitisation process. The recently announced Headend-in-the-Sky (HITS) policy which has 74 per cent FDI limit and a concessional customs duty of 5 per cent on importing digital headend equipment is expected to give further impetus to the digitisation process.

• To promote digitisation, the GoI is considering a conditional hike in foreign investment limits for those TV distributors who digitise their networks.

• TRAI has proposed four phase digitisation of cable TV networks by December 2013 and lifting the cap on the number of satellite-based TV channels intended for down-linking or up-linking from India.

Sources: ―Tune-in to India‘s entertainment economy: From emerging to surging,‖ Ernst & Young, 2008; ―The Telecommunication (broadcasting

and cable) services tariff order 2004 [1 of 2004]‖, TRAI, 15 January 2004; ―Cabinet approves policy to digitise cable TV operations,‖ Mint, 13

November 2009. ―Tune into emerging entertainment markets- spotlight on BRIC,‖ Ernst & Young, 2010; EY M&E Newsreel, August 2010, EY

M&E Newsreel, September 2010.

POLICY AND REGULATORY FRAMEWORK

Entertainment November 2010

29

Policy and regulatory frameworkFilms

• In 2000, the GoI granted industry status to the Indian film industry and permitted FDI of up to 100 per cent in film-related activities.

• Various state governments have also provided entertainment tax exemptions to multiplexes.

• In the Union Budget 2010–11, the GoI announced a rationalisation in the customs duty structure for the import of cinematographic films by charging customs duty only on the actual cost of the film and not on the value of the content.

Radio• Following the opening of FM radio broadcasting to private players in March 2000, the rollout of the

second phase of the FM radio licencing policy in 2005 provided a thrust to the sector.

• In radio companies, FDI is limited to 20 per cent of the company‘s paid-up equity capital. With the FM phase 3 policy this limit will be raised to 26 per cent. An increase in foreign investment limits is expected to attract additional growth capital for the industry.

• Political advertisements are now allowed on FM radio stations in India.

• In April 2010, The Cabinet Committee on Infrastructure approved the MIB‘s proposal on the All India Radio (AIR) and Doordarshan‘s digitisation of transmitters and studios, setting aside US$ 191.7 million and US$ 129.2 million, respectively, for the purpose.Sources: ―Tune-in to India‘s entertainment economy: From emerging to surging,‖ Ernst & Young, 2008; ―The Telecommunication (broadcasting and

cable) services tariff order 2004 [1 of 2004]‖, TRAI, 15 January 2004; ―Cabinet approves policy to digitise cable TV operations,‖ Mint, 13 November

2009; ―FM-III 1st phase to auction 160 stations,‖ The Financial Express website, http://www.financialexpress.com/news/fmiii-1st-phase-to-auction-

160-stations/674181/, accessed 11 November 2010; ―Tune into emerging entertainment markets- spotlight on BRIC,‖ Ernst & Young, 2010.

POLICY AND REGULATORY FRAMEWORK

Entertainment November 2010

30

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

ENTERTAINMENT November 2010

31

Opportunities … (1/3)

OPPORTUNITIES

Investment in regional markets

Alliances and partnerships

Development of content for a specific target

audience

Entertainment November 2010

• Rising affluence levels have directly led to increasing levels of consumption across semi-urban and rural towns. According to a study by Ernst & Young, non-metro and semi-urban towns constituted more than 70 per cent of the total consumption market of 100 cities mapped. In addition, the growth rate of consumer expenditure in these regional markets was higher than the metros.

• As the demand for regional content is growing, entertainment companies, both Indian and international are expected to focus on penetrating these regional markets, which hold the possibility of high returns.

• Entertainment companies are expected to form partnerships or alliances across content creation, distribution or sales to de-risk their businesses and optimise resources. The number of content-sharing alliances with domestic as well as foreign players has been increasing.

• Global studios have entered the Indian film industry to co-produce Indian and international films. Indian companies are also partnering with global studios for doing visual effect and post production work.

• Consumer preferences are shifting towards international programming formats. There is an opportunity for global production houses to localise their content for the Indian audiences.

• Entertainment companies will have to generate content that appeals to specific target audiences. More content is expected to be generated for youth and emerging niche audiences. Reality shows are making a headway and there is an opportunity as the new formats have helped TV companies earn revenue from mobile VAS services such as audience votes.

• Companies will have to understand consumer preferences to develop content and subscription models that can help them acquire and retain the right consumers.

32

Opportunities … (2/3)

OPPORTUNITIES

Investment in new media

New business and

revenue models

Entertainment November 2010

• India has witnessed significant growth in mobile penetration. In 2010 the number of mobile subscribers have crossed the 500-million mark and internet and broadband penetration is increasing.

• New formats for entertainment such as computers, mobiles and other handheld devices are likely to be the most significant channels, as digital media has the highest visible return on investment. The launch of 3G and WiMax is expected to throw open myriad opportunities in value added services segment.

• New media investments are becoming critical for certain sectors such as music and publishing. Entertainment companies will have to develop a focused new media strategy to monetise their content better. Traditional entertainment companies could also consider diversifying their risk by entering the new media segment. For instance, broadcasters could venture into mobile and Internet services. Traditional film production houses could increase revenues from their content libraries by going online.

• With the emergence of new media, Indian media conglomerates are moving from being a one-platform business to being a multi-platform one and are becoming integrated media players with interests across various M&E segments such as TV, film and new media.

• Opportunities exist to tap consumers horizontally across the different strata of the society and vertically, diversifying into various businesses. Companies are also moving toward different revenue models. For instance, gaming companies, which till the 1990s focused on video gaming alone, are moving to online versions.

33

Opportunities … (3/3)

OPPORTUNITIES

IP protection and monetisation

Digitisation

Sources: EY analysis; ―Tune-in to India‘s entertainment economy: From emerging to surging,‖ Ernst & Young, 2008; ―What‘s next? for Indian media

and entertainment,‖ Ernst & Young, 2008. ―Tune into emerging entertainment markets- spotlight on BRIC,‖ Ernst & Young, 2010; TP report on

Media and Entertainment, Ernst & Young, September 2010;

Media wise spend

Entertainment November 2010

• Entertainment companies will try to protect and monetise their intellectual property (IP). For instance, content producers and broadcasters can jointly own content and explore ways to tap revenues from different streams.

• Alternatively, broadcasters whose content reaches vast audiences in various countries would ensure effective monetisation of these rights.

• The industry is adopting digital technologies to overcome distribution inefficiencies, reduce the cost of distribution and curb piracy.

• There are around 35 million digital TV households currently, growing from around 17 million households in 2009. With local cable operators (LCOs) and multi-system operators (MSOs) going digital and the advent of DTH and Internet Protocol Television (IPTV), companies are likely to be witness vast opportunities in the long run through value-added services provided on these digital media. Companies will have to digitise their content and become digitally enabled to fully leverage such opportunities.

• With the introduction of HITS it will lead to enormous cost savings and elimination of digital head-end across locations.

• Indian M&E market mirrors the global M&E market, with more than 70 per cent of the share contributed by television and print media. However, the share of other segments such as radio (2 per cent), internet, music(1 per cent) and out-of-home media is significantly less than their share in global M&E market. This indicates an attractive growth opportunity for players in the market to tap the emerging segments as the consumer spending on media increases.

34

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

ENTERTAINMENT November 2010

35

Industry associations

Indian Motion Picture Producers' Association

‗IMPPA HOUSE‘

Dr Ambedkar Road, Bandra (West),

Mumbai – 400 050, INDIA

Phone: 91 22 2648 6344/45/1760

Fax: 91 22 2648 0757

The Film & Television Producers Guild Of India Ltd

G-1, Morya House, Veera Indl. Estate,

Off Oshiwara Link Road, Andheri (W),

Mumbai – 400 053, INDIA

Tel: 91 22 56910662, 91-22 26733065

Fax: 91 22 5691 0661

INDUSTRY ASSOCIATIONS

Entertainment November 2010

36

Note

Wherever applicable, numbers in the report have been rounded off to the nearest whole number.

Conversion rate used: US$ 1= INR 48

NOTE

Entertainment November 2010

37

India Brand Equity Foundation (―IBEF‖) engaged Ernst &

Young Pvt Ltd to prepare this presentation and the same

has been prepared by Ernst & Young in consultation with

IBEF.

All rights reserved. All copyright in this presentation and

related works is solely and exclusively owned by IBEF. The

same may not be reproduced, wholly or in part in any

material form (including photocopying or storing it in any

medium by electronic means and whether or not

transiently or incidentally to some other use of this

presentation), modified or in any manner communicated

to any third party except with the written approval of

IBEF.

This presentation is for information purposes only. While

due care has been taken during the compilation of this

presentation to ensure that the information is accurate to

the best of Ernst & Young and IBEF‘s knowledge and belief,

the content is not to be construed in any manner

whatsoever as a substitute for professional advice.

Ernst & Young and IBEF neither recommend nor endorse

any specific products or services that may have been

mentioned in this presentation and nor do they assume

any liability or responsibility for the outcome of decisions

taken as a result of any reliance placed on this

presentation.

Neither Ernst & Young nor IBEF shall be liable for any

direct or indirect damages that may arise due to any act

or omission on the part of the user due to any reliance

placed or guidance taken from any portion of this

presentation.

DISCLAIMER

ENTERTAINMENT November 2010