ENHANCING LOCAL GOVERNMENT REVENUE THROUGH VARIOUS SOURCES Revenue.pdf · ENHANCING LOCAL...

37

ENHANCING LOCAL GOVERNMENT REVENUE THROUGH VARIOUS SOURCES Disediakan oleh:- Lifred Wong Pengarah Jabatan Penilaian Dewan Bandaraya Kota Kinabalu KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 1

-

Upload

truongthuy -

Category

Documents

-

view

215 -

download

0

Transcript of ENHANCING LOCAL GOVERNMENT REVENUE THROUGH VARIOUS SOURCES Revenue.pdf · ENHANCING LOCAL...

ENHANCING LOCAL

GOVERNMENT REVENUE

THROUGH VARIOUS

SOURCESDisediakan oleh:-

Lifred WongPengarah Jabatan Penilaian

Dewan Bandaraya Kota Kinabalu

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 1

CONTENTS

1.0 INTRODUCTION

2.0 SOURCE OF REVENUE

3.0 CHALLENGES

4.0 POSSIBLE WAYS OF IMPROVING COLLECTION

5.0 POTENTIAL SOURCES OF FUNDS

6.0 CONCLUSION

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014

2

1.0 INTRODUCTION• All local authorities have to operate within the

scope of its legislations and relatedregulations.

• They have to provide a host of useful servicesto their respective area.

• The difference lies in the ability to renderthese services effectively.

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 3

• Generally, local authorities that are betterequipped financially tend to “deliver” moreeffectively and efficiently.

• Today, with society’s changing needs anddemands local governments performancehave been put under greater scrutiny.

• It has to fulfill not only the mandatoryfunctions but to carry out its discretionaryservices within the constraining financial andpersonnel environment.

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 4

• Therefore to the Local Authorities, there is thenagging question of how can they improvethemselves, especially financially to cope withincreasing demands, and become the prime-mover of development.

• Certainly apart from financial constraints LocalGovernment also beset with other problemsparticularly the lack of skilled manpower andprevailing archaic laws.

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 5

THE PROBLEM

• The major constraint facing local Authorities in performing their role effectively seems to be their weak financial position

• Expenditure often exceed their income, or in other words the fiscal needs outrun fiscal capacity.

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 6

2.0 SOURCE OF REVENUE – IN LINE WITH

THE PROVISIONS OUTLINED BY PREVAILING LEGISLATION

Land Based• The single largest source of revenue generated is from

Property Rates imposed– Part X LGO 1961 (Section 72- 88)

• Cesses– Part XI LGO 1961 (Section 89-89A)

• Contribution In Lieu Of Rates– Section 56 LGO 1961 & Article 156 Federal Constitution

Part XII

• Recovery of rates and other amounts due– Part XII LGO 1961 (Section 90-98)

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 7

Is a tax for general upkeep of a system of LocalGovernment which brings indivisible benefits such ashealth and sanitation, construction and operation ofcommunity facilities, public cleaning services, etc. to allresidents.

Non-Land Based

• Other Sources of Local Authority revenue derived from• License & permit fees

• Compounds & Fines

• Rentals

• Various fees

• Earnings from investments

• Interest on moneys invested

• Other Income that is not rates

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 8

• Part VI LGO 1961 (Section 50-52A)

• Various Bylaws

• Section 61 LGO 1961 – fees

• Various Government Grants

• Power to raise loans (Section 58 LGO 1961)

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 9

Licenses & Permits• Advertisement• Hotel & Rest House• Pub & Bar Lounge• Entertainment Place• Petroleum• Restaurants• Coffee Shop• Coffee House• Canteens• Side Stalls• Bakery Shop• Food Factory – Big• Food Factory – Small• Drinks Factory – Big• Drinks Factory - Small

• Ice Factory

• Scrap Materials

• Offensive Trade

• Lottery

• Slot Machine

• Beauty Saloon

• Walkways & Lobby Permit

• Water Vending Machine Permit

• Dobby

• Massage Parlour

• Dog Registration & Control

• Tamu

• Market Stalls

• Hawkers

• Night MarketKONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 10

Compounds And Fees

• Compound• Notice of Demand• Building & Development Plan Fee• Parking Fee• Bus Terminal Fee• Endorsement Fee• Registration of Contractor Fee• Earthwork Fee• Capital Development Fee• Payment In Lieu Of Parking Bay

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 11

Rentals And Interest

• Community Halls• Market Cold Room• Rentals out of council’s properties• Stall• Kiosk• Interest on Current & Fixed Deposit• Dividend• Carwash Rental• Furniture & Equipment's• Land• Markets

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 12

3.0 CHALLENGES

• A compounding problem is the substantial sums of arrears of rates

• Outdated Valuation List

–Unreliable records and information

• Vacant land

• Unoccupied property

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 13

• Insufficient collection officers

– To trace errant property owner

• Compound Arrears

• Arrears of Various fees

• Arrears of Rentals

• Inefficient and weak administration

• Data and records are not computerized

• Lack of commitment among the staff

TIME FOR CHANGE

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 14

Generally, recovering of revenue involves:-

• People / Staff

• Equipments / Computer

• Processes

- Procedure

- Control

- Convenient way of paying – Various options

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 15

Usual approach

• Incentive – for those who pay early

• Penalty – for those who pay late

• Legal actions – for defaulter

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 16

4.0 POSSIBLE WAYS OF IMPROVING COLLECTION

• Taking aggressive legal action on defaulters

• Amending the relevant legislation or Bylaws to allows easy and efficient way of recouping arrears• Winding up – company RM30,000 and above

• Fix a limit where it is easy to Local Authorities to auction property

• Link up with passport renewal section for overseas owner

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 17

• To carry out Revaluation based on the Legal Provision

• To have adequate relevant staffs to discharge collection function

• Computerized the processes and relevant accounts

• Adopting high-commitment work system &reward those higher performers

• Accountability and discipline

• Convenient and various modes of payment

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 18

• Training and awareness programs

• Inclusion of Section 160 and 161 of the LGO 1970 into LGO,1961 & KKCE 1996

–Onus is on owner to notify Local Authorities when there is a transfer – it will be very helpful for property that yet to obtain individual title deed.

• Online network with Registration Department

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 19

5.0 POTENTIAL SOURCES OF FUNDS

Possible avenues available for local authorities toincrease their revenues which can be justified asfalling within the laws of the Ordinance.

• Rezoning of existing area

• e.g Residential to commercial• Higher assessment rates

• Urban Renewal Scheme

• Direct involvement – profit to local authorities

• Through property rates

• Providing facilities with competitive fees and charges(user-charges)

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 20

• Property Development

• Retaining it for long term return

• Development charge -- Planning Ordinance

• As a result of local plan or alteration of local plan effectsa change of use density, plot ration or floor area inrespect of any land so as to enhance the value of theland – development charge shall be levied.

• Ensuring all rateable properties are assessed accordingly.

• Involvement in a variety of business and economicactivities – through local authority investmentarm/company. - e.g. DBKK Holdings Sdn Bhd

• Investment of Funds – S54 LGO 1961

• With reputable funds and finance company

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 21

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014

22

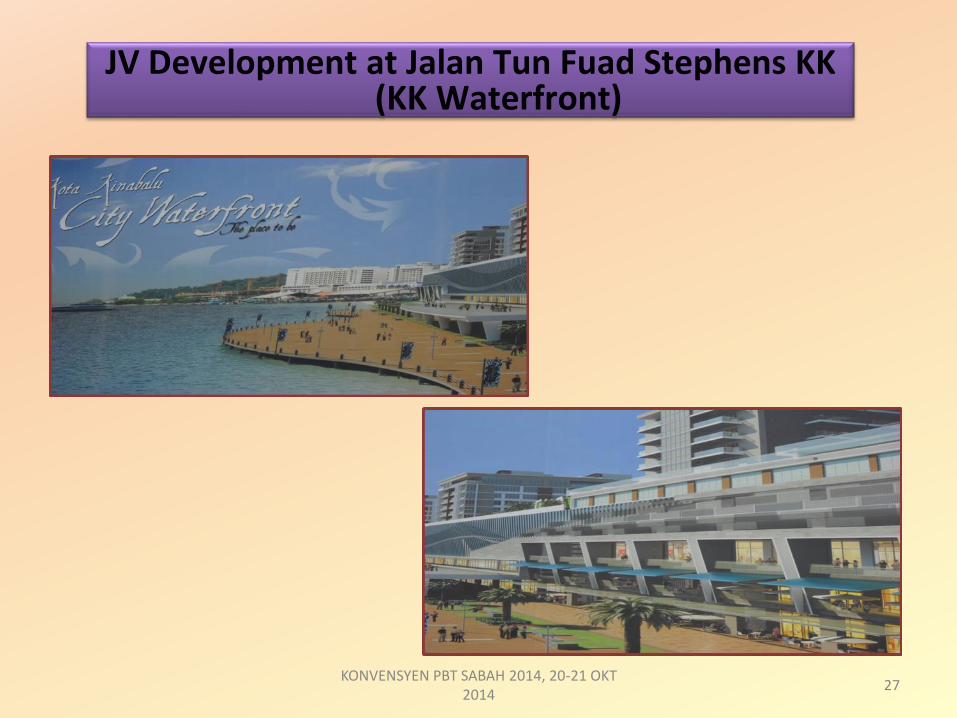

DBKK HOLDINGS SDN. BHD(527782-T)

Joint Venture Development

Projects

Management and Operations

Kota Kinabalu Water Front

Development

Mixed Commercial

Development cum Bus Transit

Facilities

City Bus Terminal North,

Inanam (CBTN)

Management and operation

of DBKK Car Parks

Monitoring of concessions

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014

23

Open Cafe, Jln Jati, KK

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014

24

Medan Seri Selera Kg Air , SEDCO COMPLEX

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014

25

City Bus Terminal North, Inanam(CBTN)

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014

26

Operations of DBKK Car Parks

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014

27

JV Development at Jalan Tun Fuad Stephens KK (KK Waterfront)

Community Participation and Involvement• Should allow the community which it serves the

opportunity to participate

• Through the process of involvement an awareness iscreated of the local authority, its functions and its role inthe community

• Through time, pride for the local authority can be instilledand this is important for the concept of image building of alocal authority

• Community participation and involvement if properlycarried out can result in reduced expenditure

• Through the voluntary organisations, and residents’associations the people can be mobilised to help their localauthorities in aspects such as• Beautification

• Maintaining cleanliness & disposal of household refuse, etc.KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 28

• Reduce operating cost in provision of suchservices --- actual savings which represents aform of revenue to the local authorities

• This approach if properly planned and nurturedwill benefit both the community and localauthorities.

• Need to impart leadership skill where necessary

• Volunteerism

smart partnership

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 29

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014

30

Assessment Booth

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014

31

Parking Booth

6. CONCLUSION• The need to increase revenue of local authorities

does not depend entirely on finding new sourcesof revenue.

• Local authorities have to relook and improve thefollowing areas:• Staffing

• Right value

• Motivated

• Processes

• System adopted• Manual

• ComputerisedKONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 32

• All these will entail among others local authoritiesto :

• Improve financial management system

• Straighten their records for rates collection andrecovery of accumulated arrears

• Carry out revaluation every 4 years with continuousupdating of current lists to incorporate any changes inproperties within the local authority area

• Computerise the processes

• Review outdated rates imposed on property

• Impose competitive user-chargers for servicesrendered

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 33

• To further enhance the local authorities revenue,there are few potential sources that can beconsidered especially those that are falling within thelaws of the ordinance.

• In addition, reduction of expenses throughparticipation and involvement of the community isalso worth to be pursued

• Smart partnership with private sector especially willbe another mean of enhancing local authoritiesrevenue

• With the nation’s objective of a developed nation inthe year 2020, it is imperative that local authoritiesbe innovative and dynamic so as to take advantage ofany opportunities arising for resource mobilisation.

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 34

• In a nutshell, there is a potential of enhancingrevenue of local authorities. Perhaps there isalready local authorities that are moving in thejourney towards financial sustainable andautonomous. Therefore, there should be afinance strategic plan that prioritise theinitiatives and actions that can be carried foreach local authorities based on theircapabilities. Certainly, greater impact of suchinitiatives and actions need the backing of thegovernment.

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 35

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 36

Tak Faham. Terangkan… (Bukan Ketawakan)

Tak Betul. Nasihatkan…. (Bukan Diumpatkan)

Tak Tahu. Tunjukkan…… (Bukan Dimarahkan)

Tak Jelas. Jelaskan…….. (Bukan Dirumitkan)

Tak Mampu. Usahakan…. (Bukan Dimanjakan)

KONVENSYEN PBT SABAH 2014, 20-21 OKT 2014 37