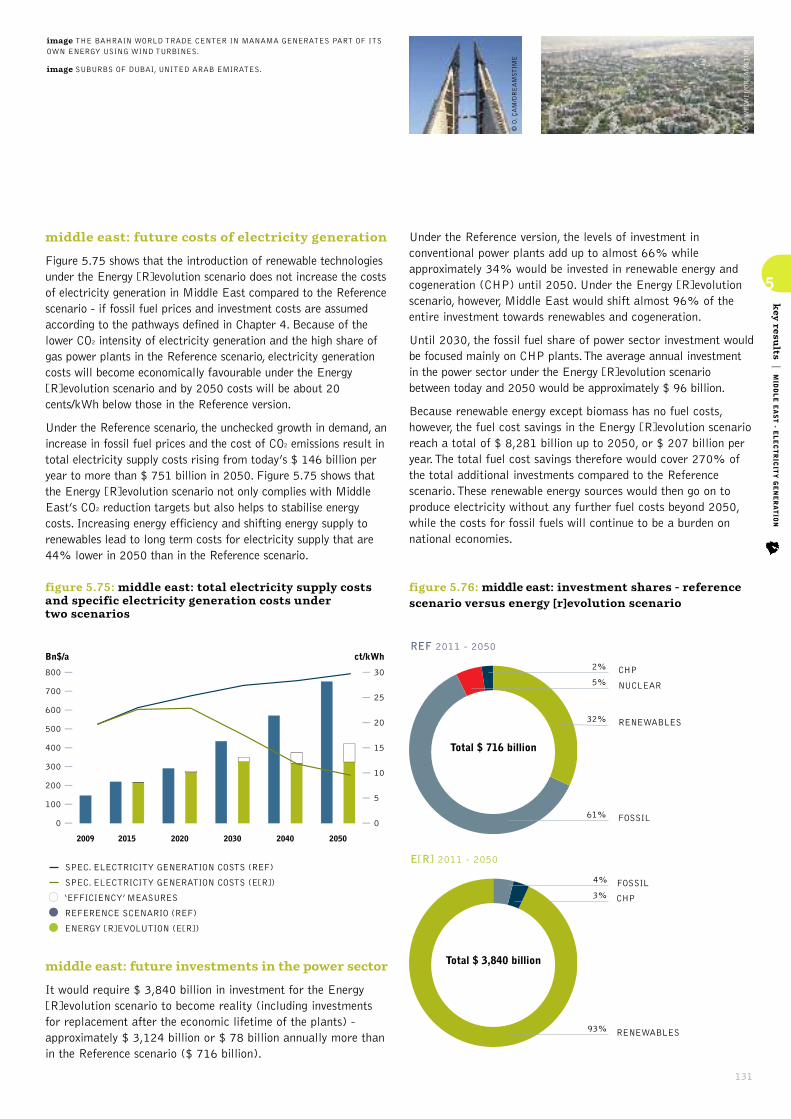

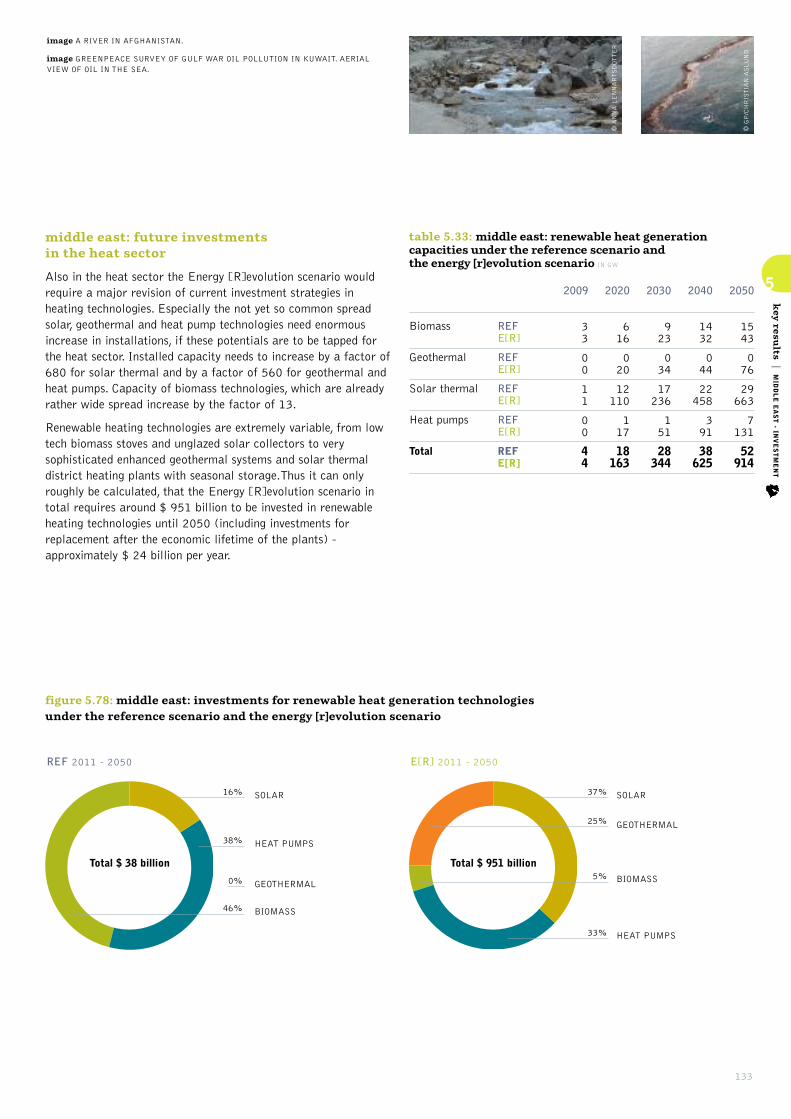

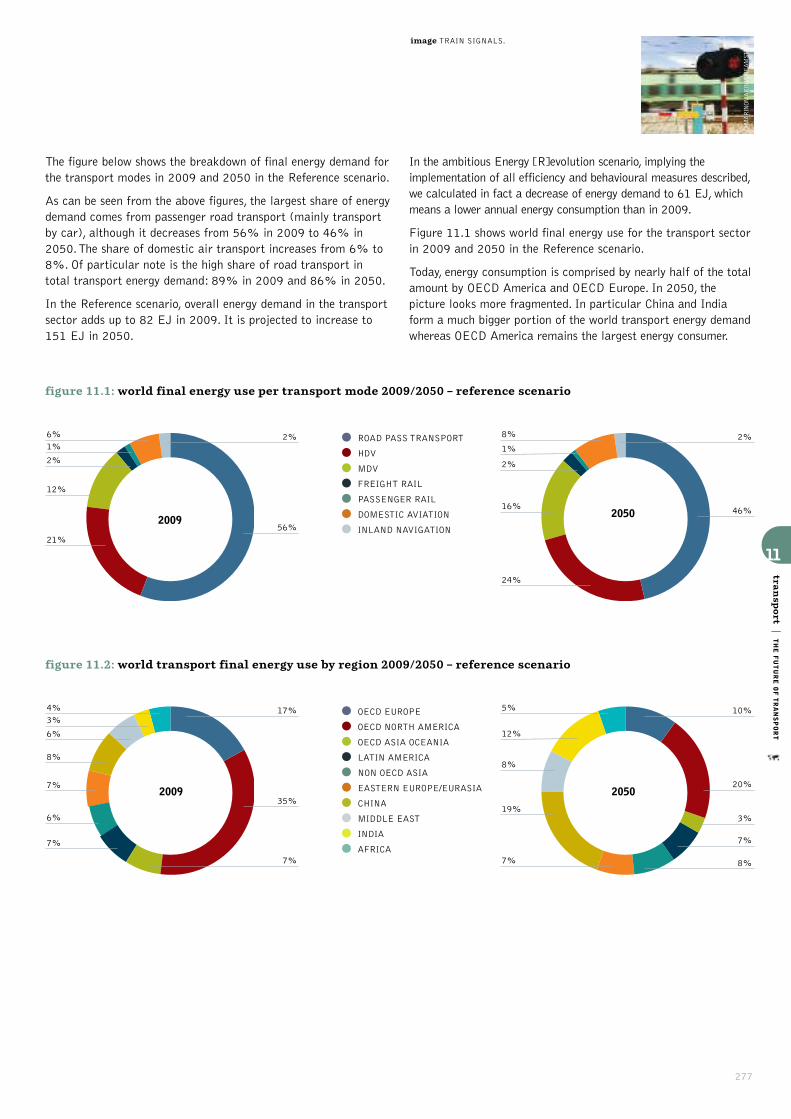

Energy Revolution 2012

340

report 4th edition 2012 world energy scenario energy [r]evolution A SUSTAINABLE WORLD ENERGY OUTLOOK EUROPEAN RENEWABLE ENERGY COUNCIL

-

Upload

greenpeace-international -

Category

Documents

-

view

271 -

download

6

description

Greenpeace, EREC and GWEC present the Energy Revolution Scenario

Transcript of Energy Revolution 2012

report 4th edition 2012 world energy scenario

energy[r]evolutionA SUSTAINABLE WORLD ENERGY OUTLOOK

EUROPEAN RENEWABLE ENERGY COUNCIL

image A WOMAN CARRIES HER DAUGHTER AS SHE WALKS THROUGH A FLOODED STREET NEAR BANGPA-IN INDUSTRIAL PARK IN AYUTTHAYA, THAILAND. OVER SEVEN MAJORINDUSTRIAL PARKS IN BANGKOK AND THOUSANDS OF FACTORIES HAVE BEEN CLOSED IN THE CENTRAL THAI PROVINCE OF AYUTTHAYA AND NONTHABURI WITH MILLIONS OFTONNES OF RICE DAMAGED. THAILAND IS EXPERIENCING THE WORST FLOODING IN OVER 50 YEARS WHICH HAS AFFECTED MORE THAN NINE MILLION PEOPLE.

partners

Greenpeace International,European Renewable Energy Council (EREC),Global Wind Energy Council(GWEC)

date July 2012

isbn 978-90-73361-92-8

project manager & lead author Sven Teske,Greenpeace International

EREC Josche Muth

Greenpeace InternationalSven Teske

GWEC Steve Sawyer

research & co-authors Overall modelling: DLR, Institute of Technical Thermodynamics,Department of Systems Analysis andTechnology Assessment, Stuttgart,Germany: Dr. Thomas Pregger, Dr. Sonja Simon, Dr. Tobias Naegler,Marlene O’Sullivan

“will we look into the eyes of our children and confessthat we had the opportunity,but lacked the courage?that we had the technology,but lacked the vision?”

2

© ATHIT PERAWONGMETHA/GREENPEACE

Transport: DLR, Institute of VehicleConcepts, Stuttgart, Germany: Dr. Stephan Schmid, JohannesPagenkopf, Benjamin FrieskeEfficiency: Utrecht University, The Netherlands: Wina Graus,Katerina KermeliFossil Fuel Resource Assessment:Ludwig-Bölkow Systemtechnik,Munich, Germany; Dr. Werner Zittel

Employment: Institute forSustainable Futures, University ofTechnology, Sydney: Jay Rutovitzand Steve HarrisGrid and rural electrificationtechnology: energynautics GmbH,Langen/Germany; Dr. ThomasAckermann, Rena Ruwahata, Nils Martensen

editor Alexandra Dawe, Rebecca Short, Crispin Aubrey(basic document).

design & layout onehemisphere,Sweden, www.onehemisphere.se

[email protected]@erec.org

Revised version of 21st June 2012,with new foreword, new maps, REN 21 Renewable energy marketanalysis 2011 and edits.

for further information about the global, regional and national scenarios please visit the Energy [R]evolution website: www.energyblueprint.info/Published by Greenpeace International, EREC and GWEC. (GPI reference number JN 330). Printed on 100% post consumer recycled chlorine-free paper.

3

4

image LA DEHESA 50 MW PARABOLIC SOLAR THERMAL POWER PLANT. A WATER RESERVOIR AT LA DEHESA SOLAR POWER PLANT. LA DEHESA, 50 MW PARABOLIC THROUGHSOLAR THERMAL POWER PLANT WITH MOLTEN SALTS STORAGE. COMPLETED IN FEBRUARY 2011, IT IS LOCATED IN LA GAROVILLA AND IT IS OWNED BY RENOVABLES SAMCA.WITH AN ANNUAL PRODUCTION OF 160 MILLION KWH, LA DEHESA WILL BE ABLE TO COVER THE ELECTRICITY NEEDS OF MORE THAN 45,000 HOMES, PREVENTING THE EMISSIONOF 160,000 TONNES OF CARBON. THE 220 H PLANT HAS 225,792 MIRRORS ARRANGED IN ROWS AND 672 SOLAR COLLECTORS WHICH OCCUPY A TOTAL LENGTH OF 100KM. BADAJOZ.

The Global Energy[R]evolution seriespresents us with acompelling vision of anenergy future for asustainable world. Thescenarios proposed bythe Energy [R]evolutionhave gained a reputationfor the insight andexplanations theyprovide decision makers.

This fourth editioncarries on this tradition,by outlining an updatedand well-articulatedpathway to achieve thetransition to a globalsustainable energyfuture. The InternationalRenewable Energy Agency(IRENA) welcomes therecognition of the centralrole that renewableenergy will play in thisnew energy paradigm.

contents at a glance

foreword

foreword 4

introduction 12

executive summary 14

climate & energy policy 19

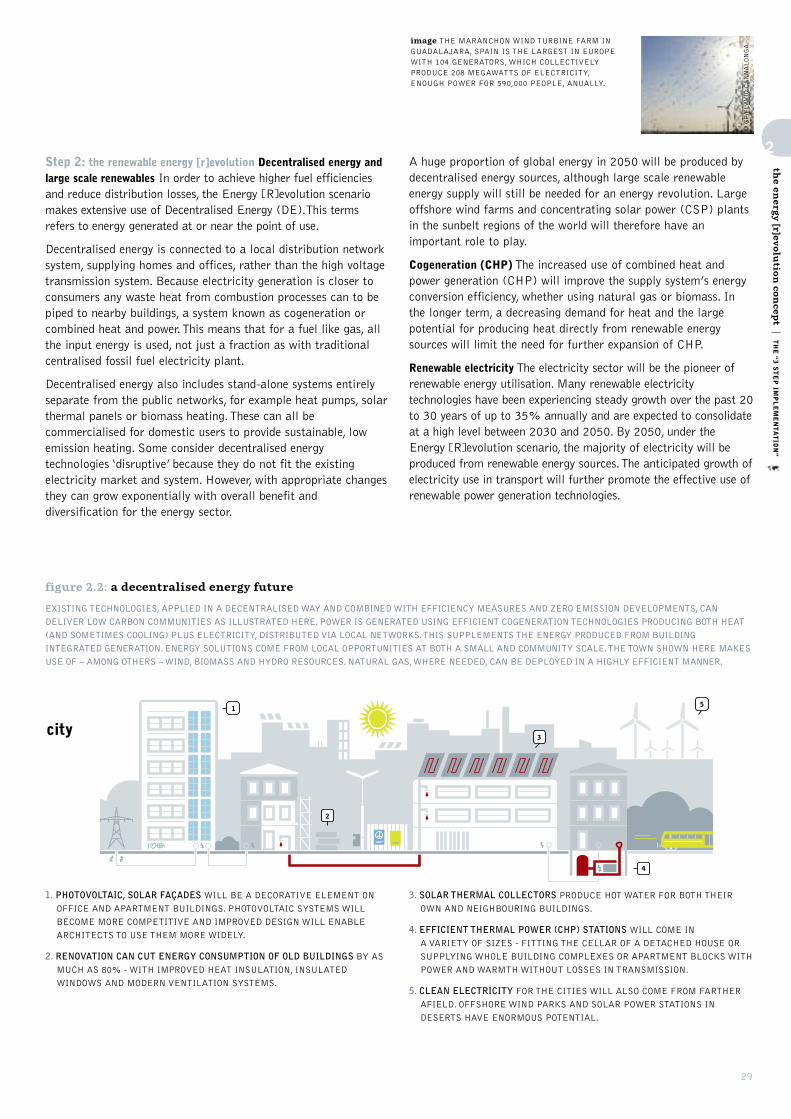

the energy [r]evolution concept 26

implementing the energy [r]evolution 48

scenarios for a futureenergy supply 54

1

2

3

4

5

© MARKEL REDONDO/GREENPEACE

Achieving this transition relies on addressing key energy issues suchas access to modern energy services, security of supply and thesustainability of the energy mix. Environmental degradation,increasing energy demand, and unsustainable resource use arecritical challenges that must be addressed. Renewable energy willplay an essential role in advancing sustainable development byimproving the access of millions to energy, whilst helping ensureenergy security, and mitigating the existential risk of climate changeby reducing emissions.

The benefits associated with renewable energy are influencing howcountries meet their energy needs, the increase in policies andinvestment globally attests to this. This growth in the uptake ofrenewable energy - the “Silent Revolution” - is playing out across theglobe: over the last decade 430,000 MW of renewable energycapacity has been installed, with global total investment reaching arecord $ 257 billion in 2011, a year in which renewable energybecame a trillion dollar industry, and the cost of modern renewableenergy technologies continued to fall.

Accelerating the “Silent Revolution” globally requires greaterlevels of commitment and cooperation to develop enabling policy,combined with practical business solutions. To enable this, policymakers, scientists and businesses require access to up-to-date,relevant and reliable data. Scenarios are a helpful aid for decisionmaking, by mapping out the complex issues and information thatmust be considered. Through its investigation of issues surroundingthe future of energy, the Global Energy [R]evolution 2012 makesan invaluable contribution to informing global decisions-makers.

The Global Energy [R]evolution publication provides an importantcomplement to IRENA’s efforts to provide knowledge and know-how,and to facilitate the flow of information encouraging the deploymentof renewables. Therefore, it is with pleasure that IRENA welcomesthis fourth edition of the Global Energy [R]evolution scenario, andthe contribution the European Renewable Energy Council andGreenpeace have made to the vital debate on transitioning the worldto a more secure and sustainable energy future.

Adnan Z. AminDIRECTOR-GENERAL

INTERNATIONAL RENEWABLE ENERGY AGENCY

JULY 2012

5

6

energy technologies 231

energy efficiency - more with less 260

transport 275

glossary & appendix 291

key results energy[r]evolution scenario 74

employment projections 188

7

8

9

10

11

12

the silent revolution – past & current market developments 198

energy resources andsecurity of supply 208

6

WORLD ENERGY [R]EVOLUTIONA SUSTAINABLE WORLD ENERGY OUTLOOK

foreword 4

introduction 12

executive summary 14

climate and energy policy 19

1.1 the UNFCCC and the kyoto protocol 201.2 international energy policy 201.3 renewable energy targets1.4 policy changes in the energy sector 211.4.1 the most effective way to implement

the energy [r]evolution: feed-in laws 211.4.2 bankable renewable energy support schemes 231.5 ftsm: special feed in law proposal

for developing countries 241.5.1 the feed-in tariff support mechanicsm 24

the energy [r]evolution concept 26

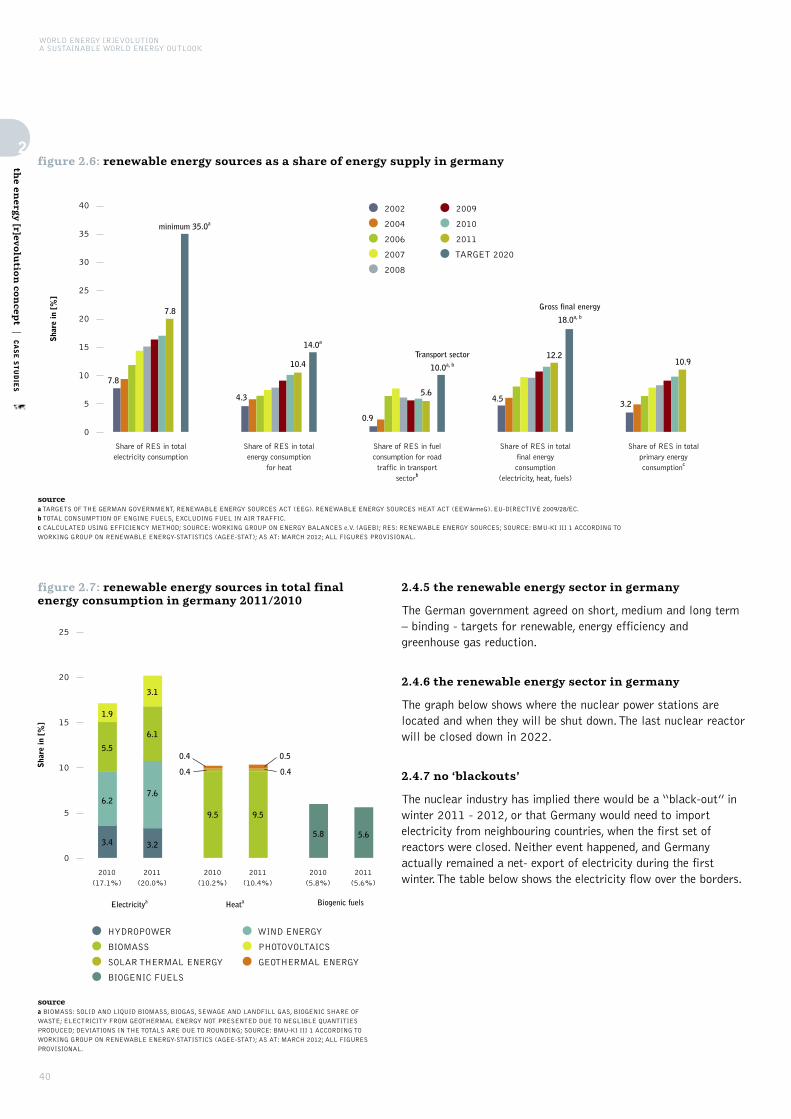

2.1 key principles 272.2 the “3 step implementation” 282.3 the new electricity grid 322.3.1 hybrid systems 332.3.2 smart grids 342.3.3 the super grid 362.3.4 baseload blocks progress 362.4 case study: a year after the german

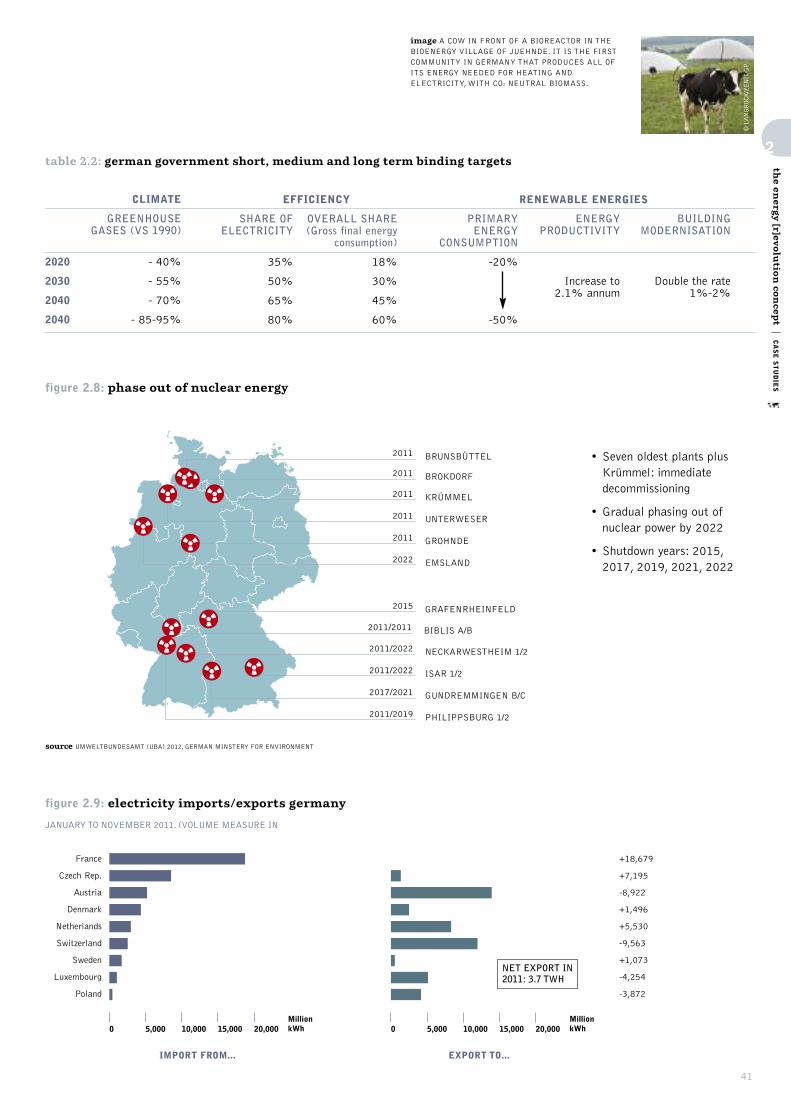

nuclear phase out 392.4.1 target and method 392.4.2 carbon dioxide emissions trends 392.4.3 shortfall from first round of closures 392.4.4 the renewable energy sector in germany 392.5 case study: providing smart energy to

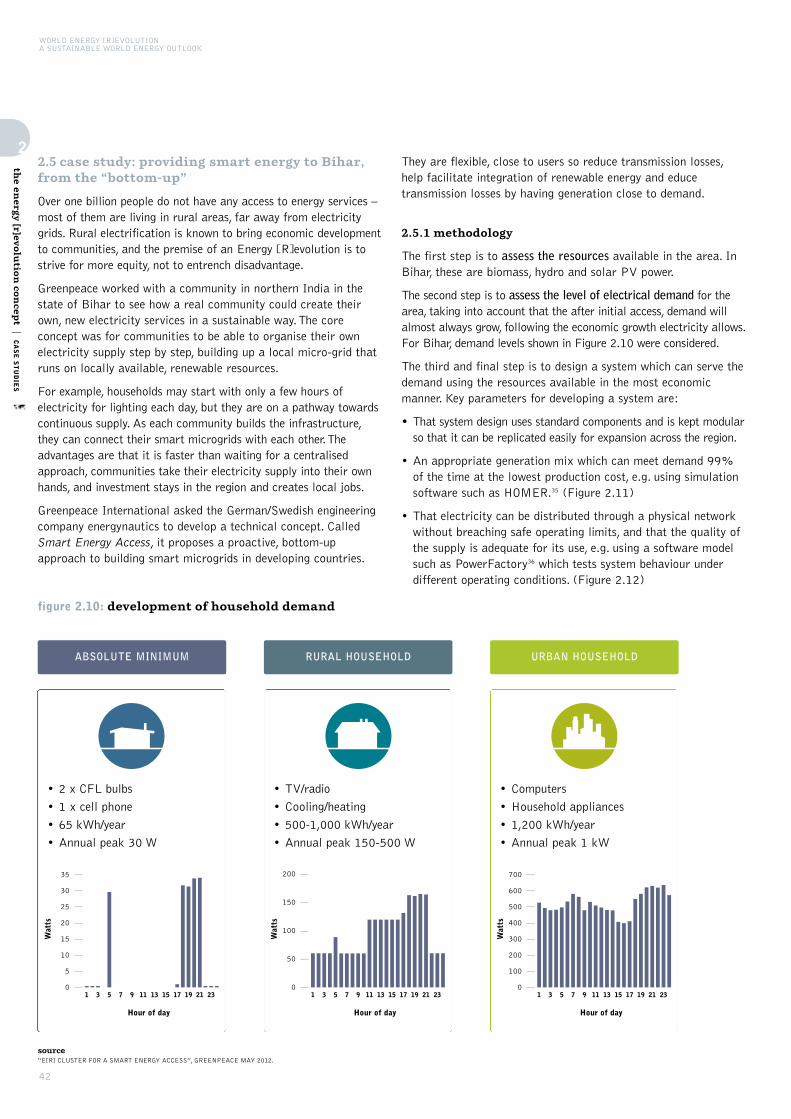

Bihar from the “bottom-up” 422.5.1 methodology 422.5.2 implementation 442.5.3 lessons from the study 442.6 greenpeace proposal to support a

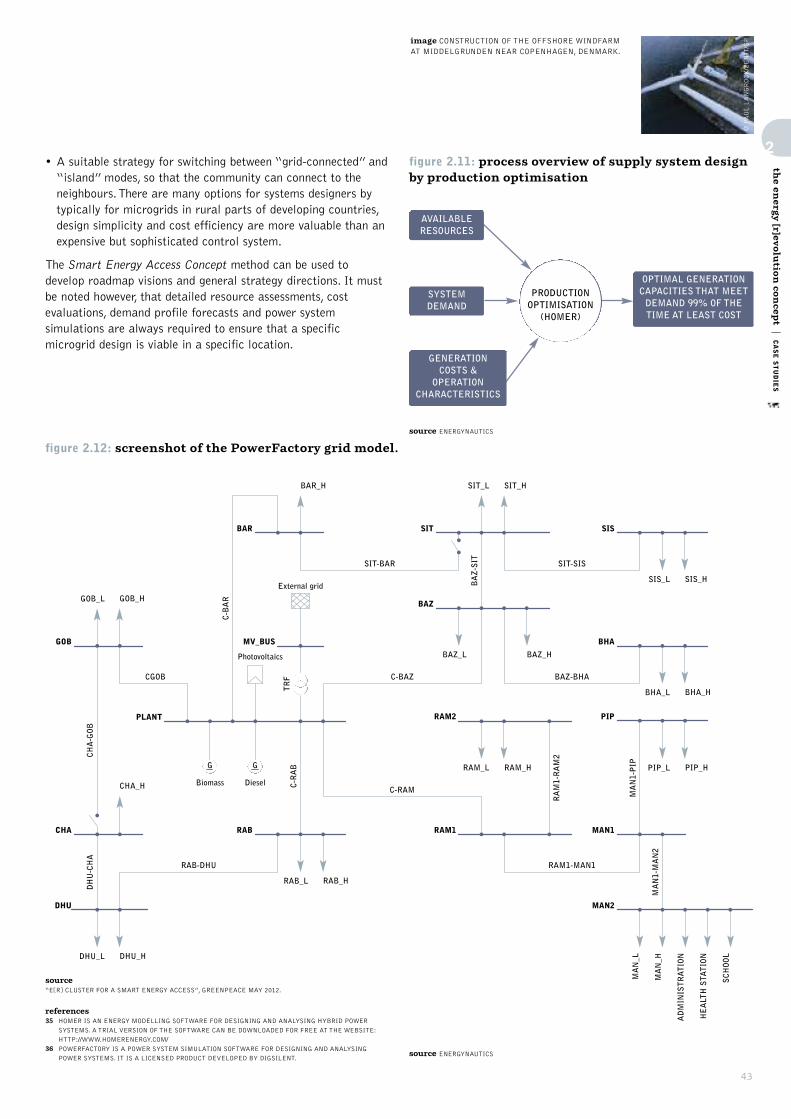

renewable energy cluster 452.6.1 a rural feed-in tariff for bihar 462.7 energy [r]evolution cluster jobs 46

implementing the energy [r]evolution 48

3.1 renewable energy project planning basics 503.2 renewable energy financing basics 503.2.1 overcoming barriers to finance and investment

for renewable energy 523.2.2 how to overcome investment barriers

for renewable energy 53

scenarios for a future energy supply 54

4.1 scenario background 574.1.1 energy efficiency study for industry,

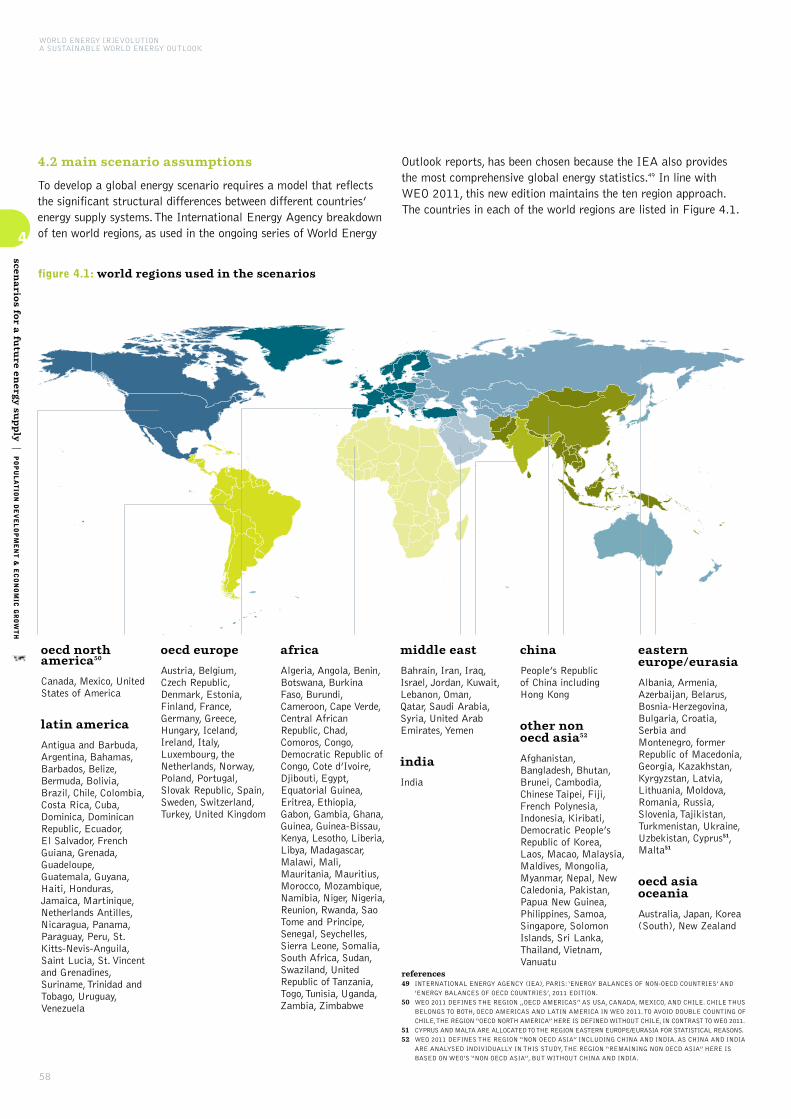

households and services 574.1.2 the future for transport 574.1.3 fossil fuel assessment report 574.1.4 status and future projections for renewable

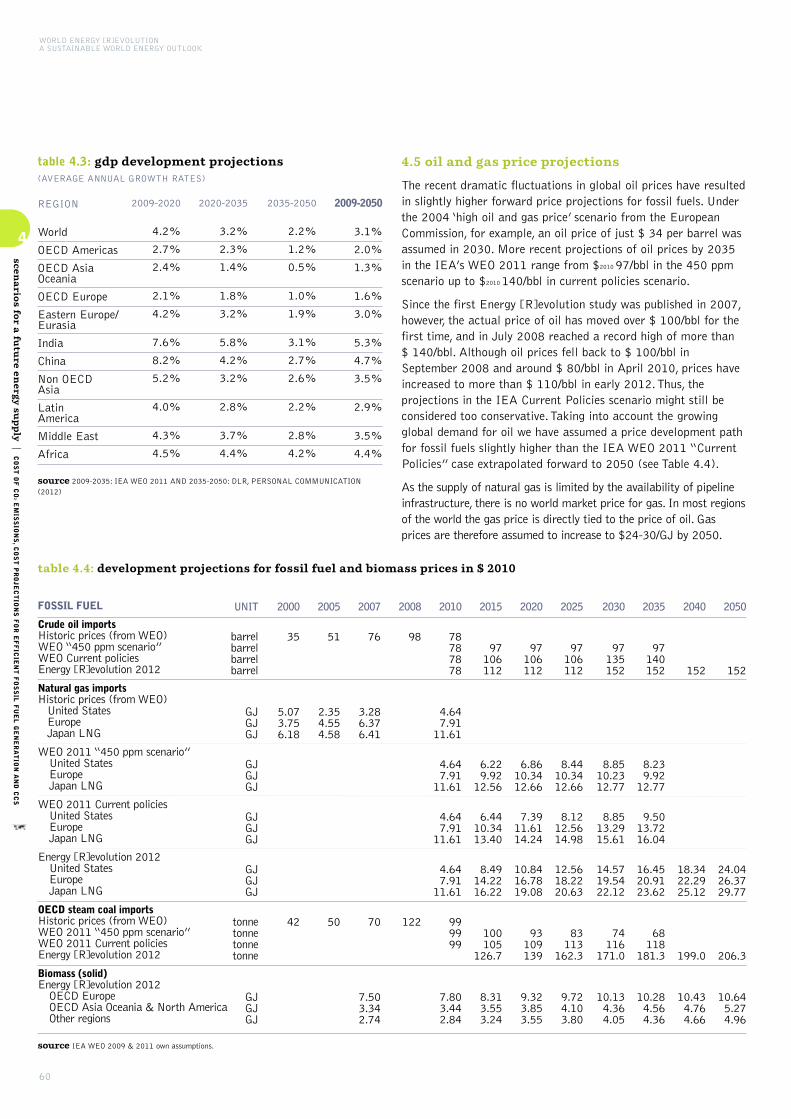

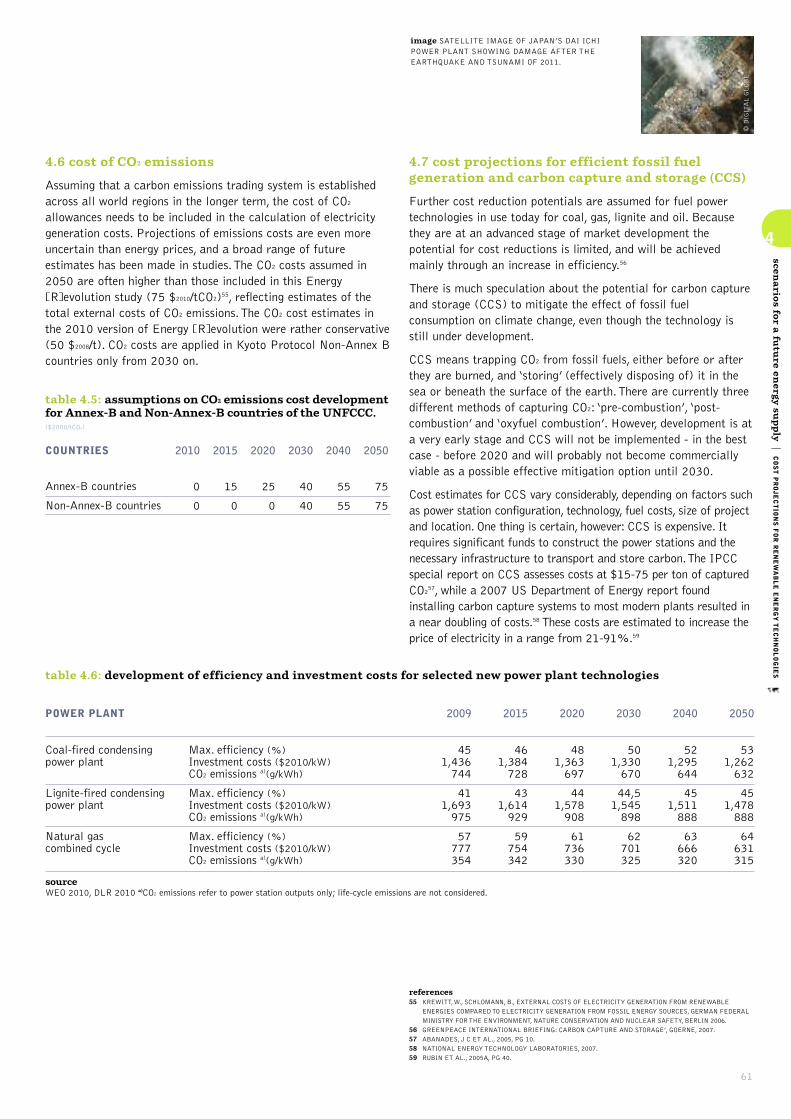

heating technologies 574.2 main scenario assumptions 584.3 population development 594.4 economic growth 594.5 oil and gas price projections 604.6 cost of CO2 emissions 614.7 cost projections for efficient fossil fuel generation

and carbon capture and storage (CCS) 614.8 cost projections for renewable

energy technologies 624.8.1 photovoltaics (pv) 634.8.2 concentrating solar power (csp) 634.8.3 wind power 644.8.4 biomass 644.8.5 geothermal 654.8.6 ocean energy 654.8.7 hydro power 664.8.8 summary of renewable energy cost development 664.9 cost projections for renewable

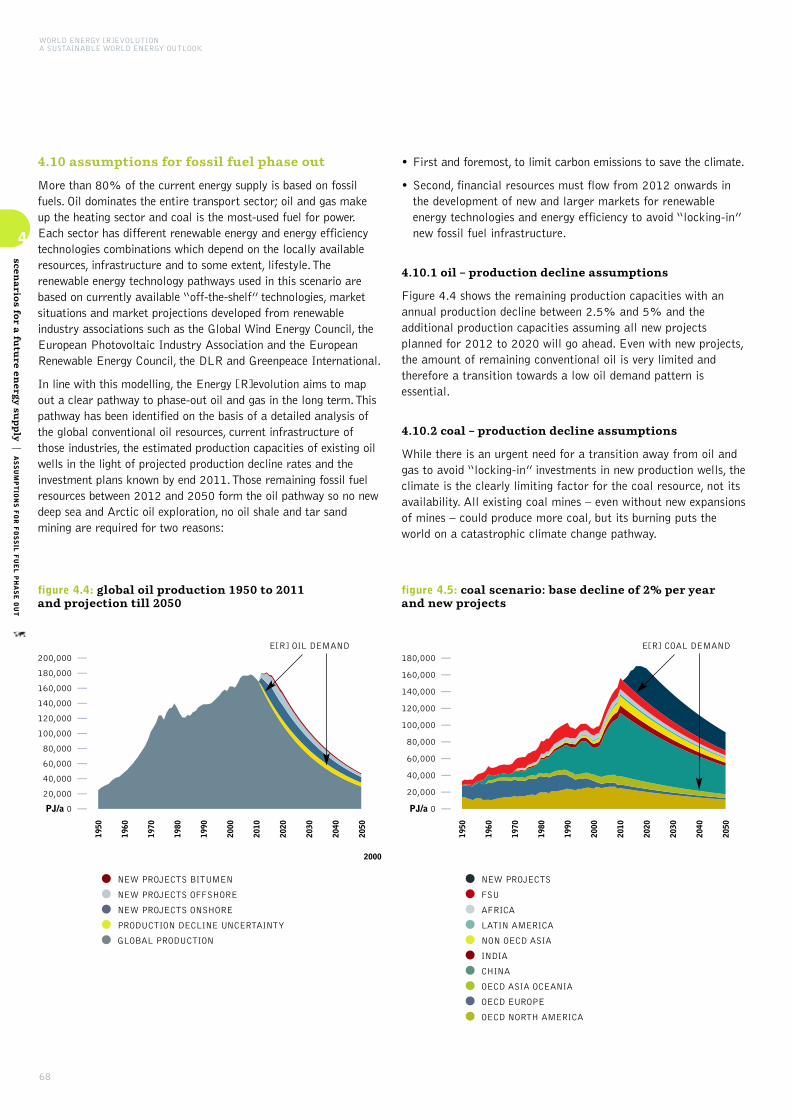

heating technologies 674.9.1 solar thermal technologies 674.9.2 deep geothermal applications 674.9.3 heat pumps 674.9.3 biomass applications 674.10 assumptions for fossil fuel phase out 684.10.1 oil - production decline assumptions 684.10.2 coal - production decline assumptions 684.11 review: greenpeace scenario

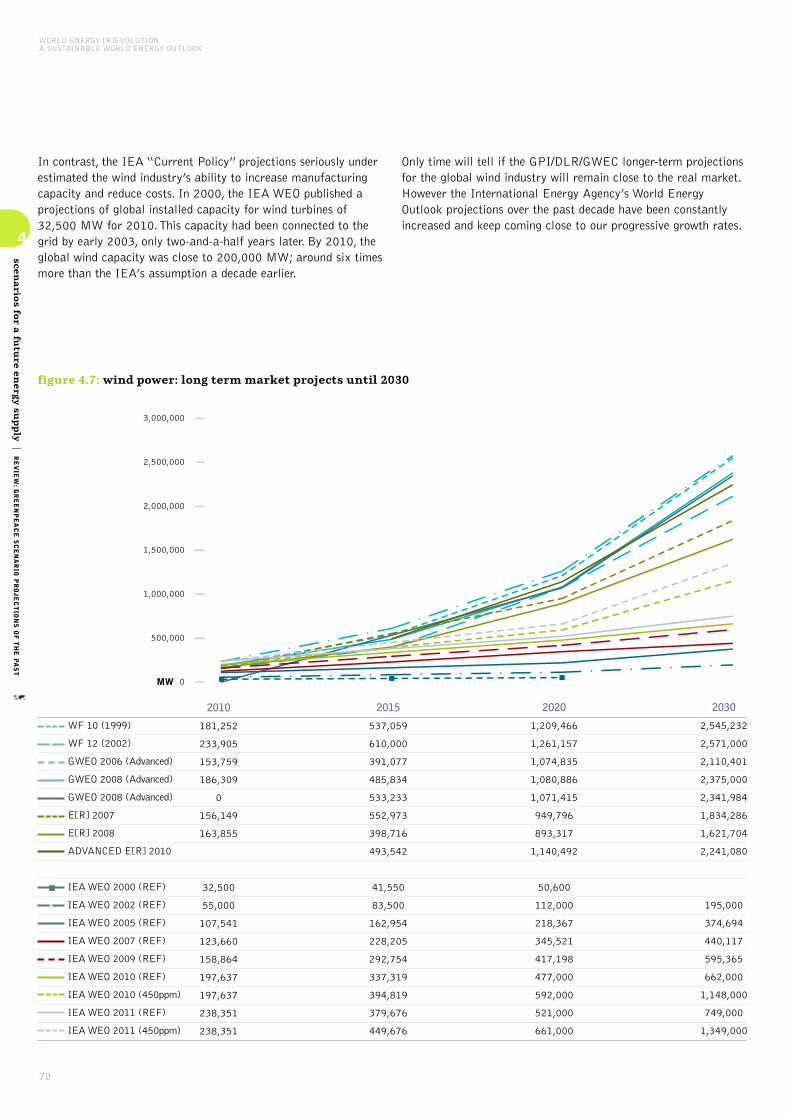

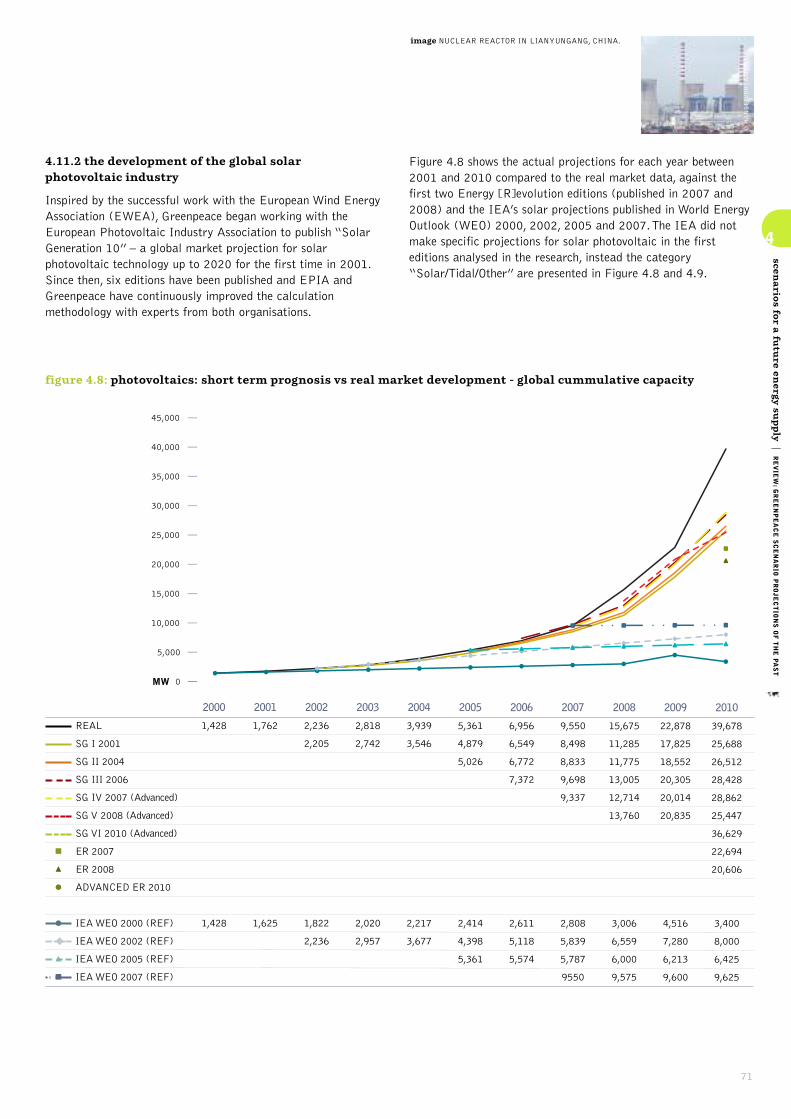

projections of the past 694.11.1 the development of the global wind industry 694.11.2 the development of the global

solar photovoltaic industry 714.12 how does the energy [r]evolution scenario

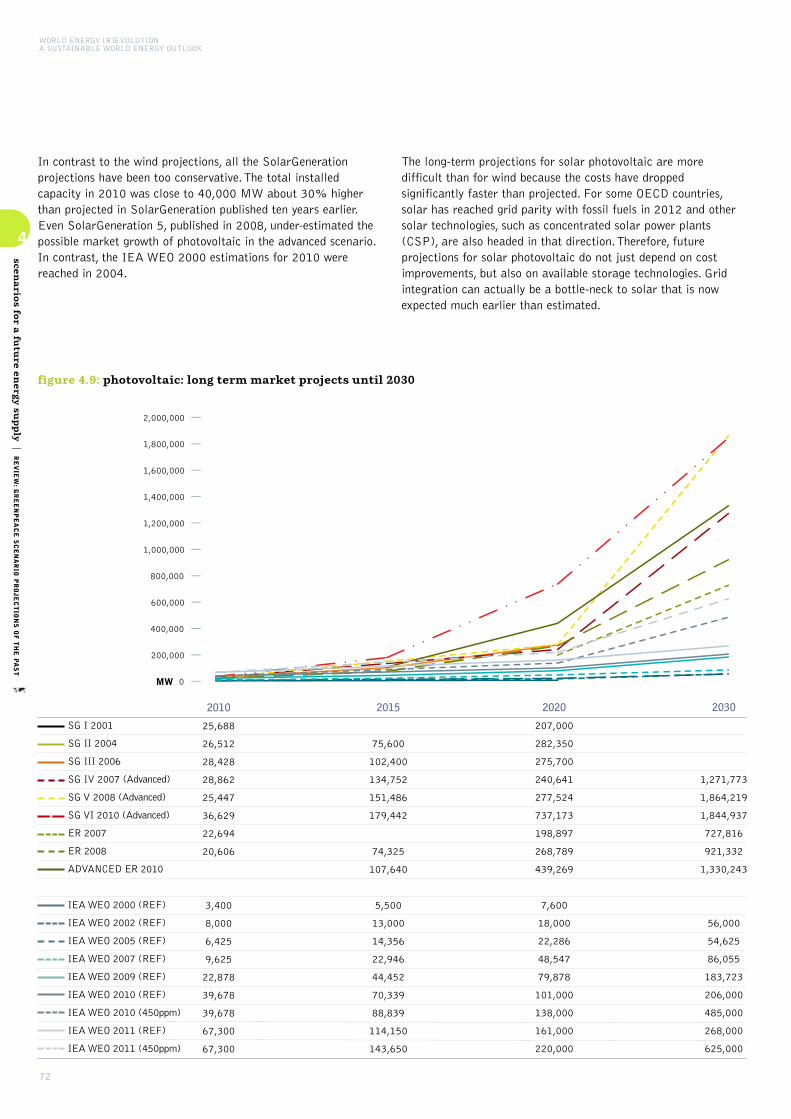

compare to other scenarios 73

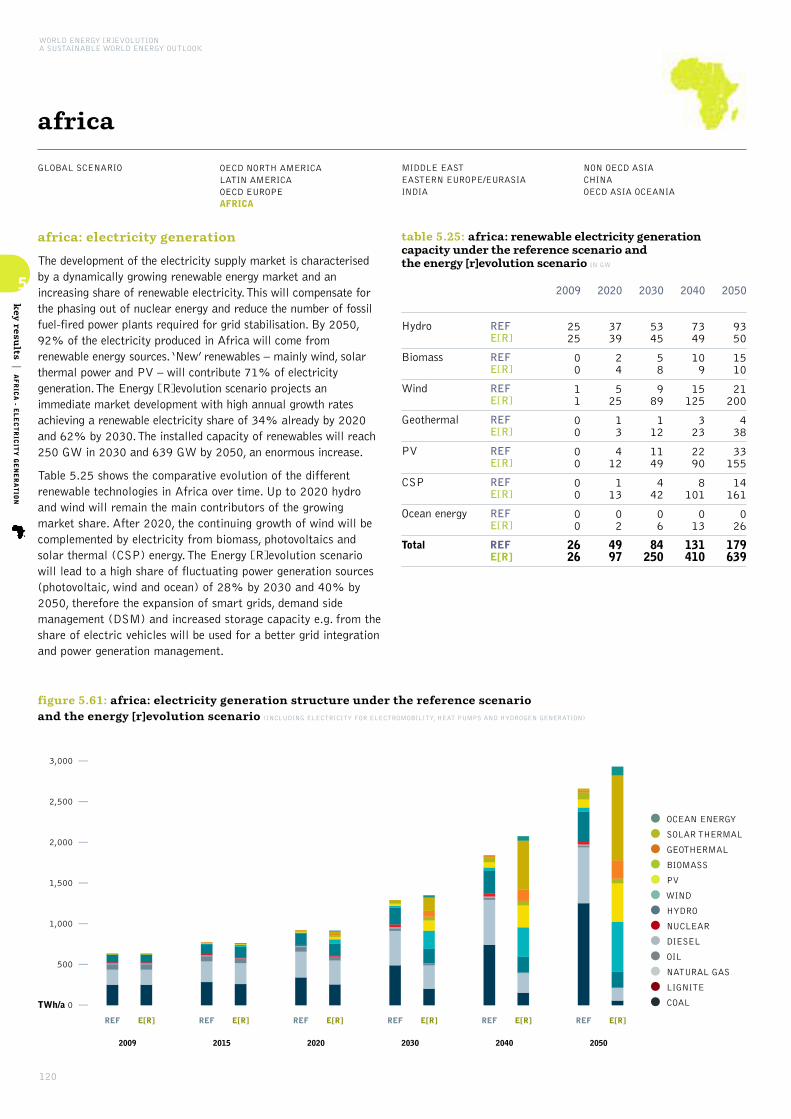

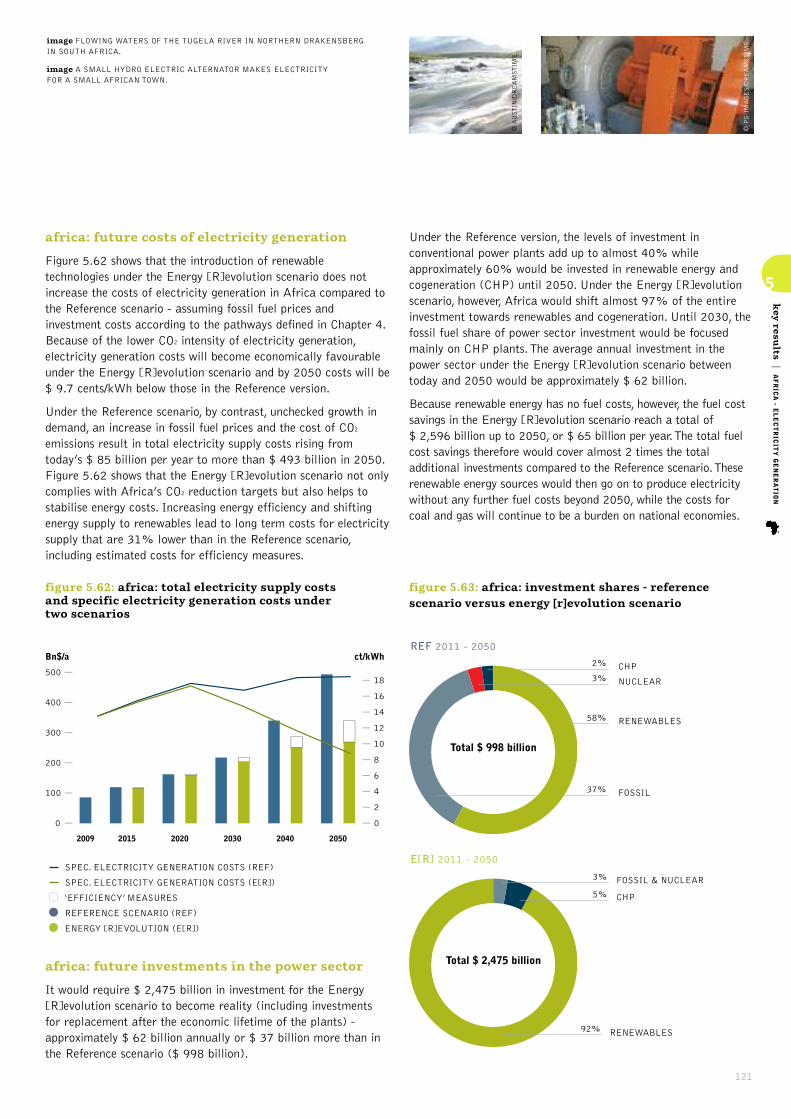

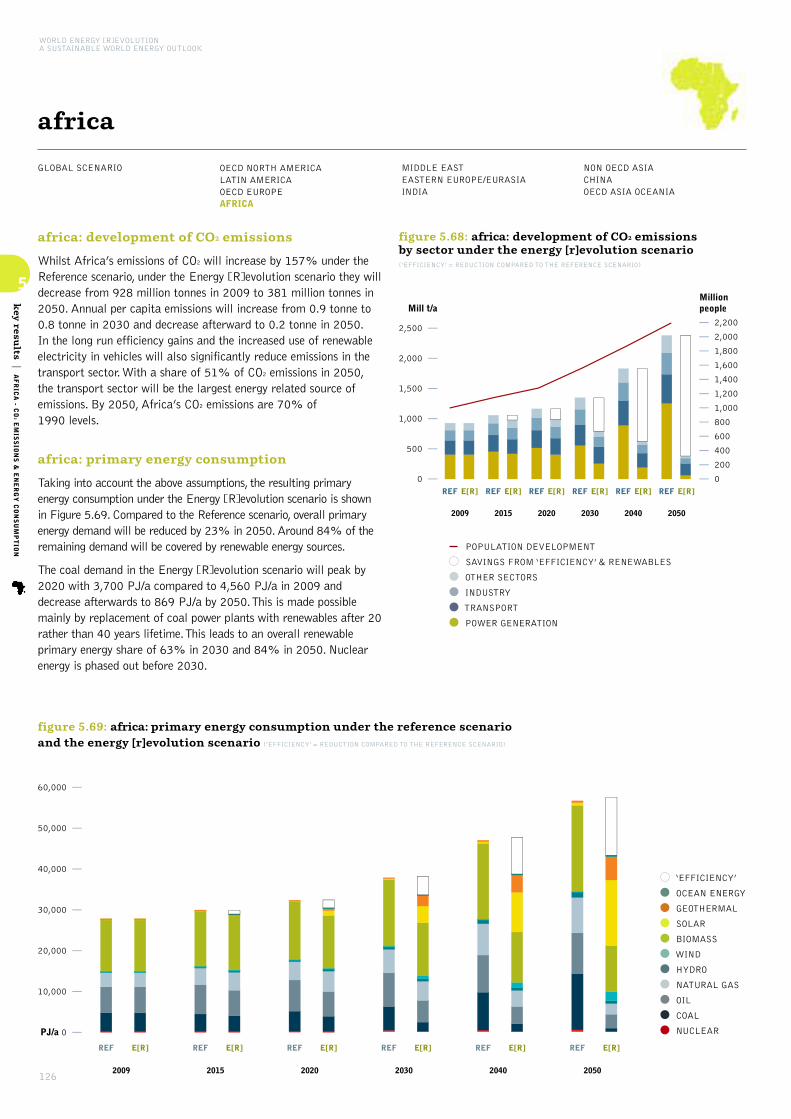

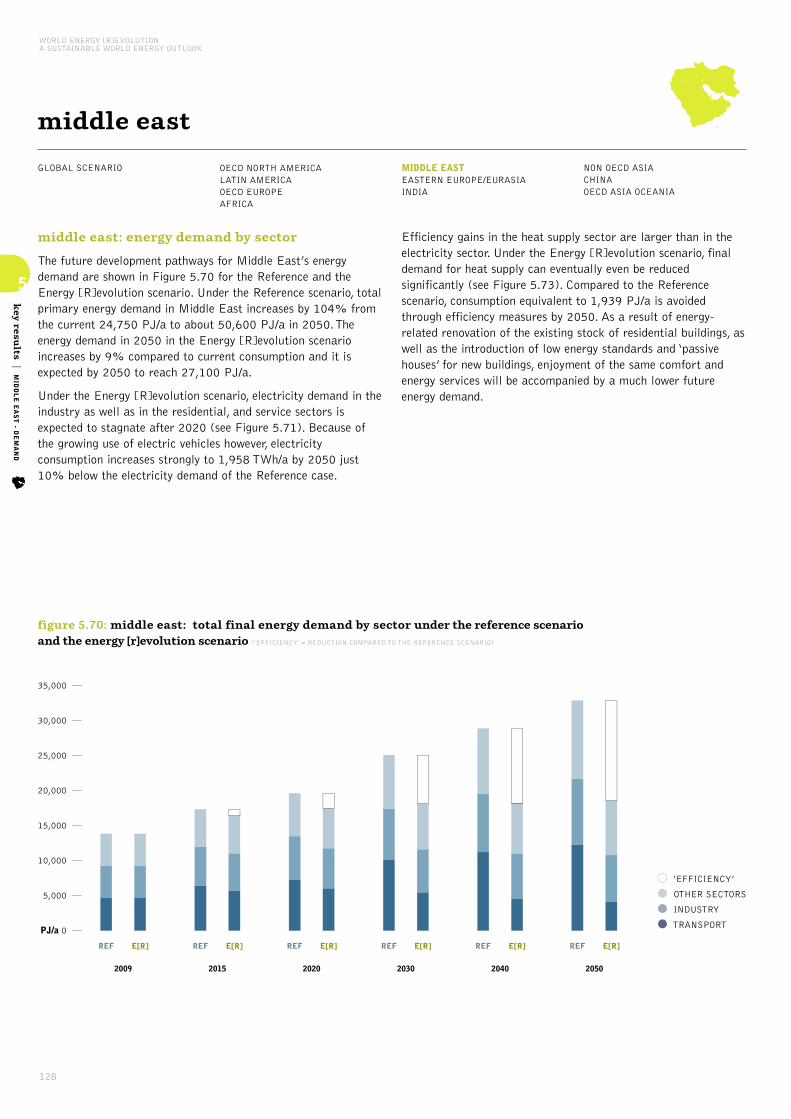

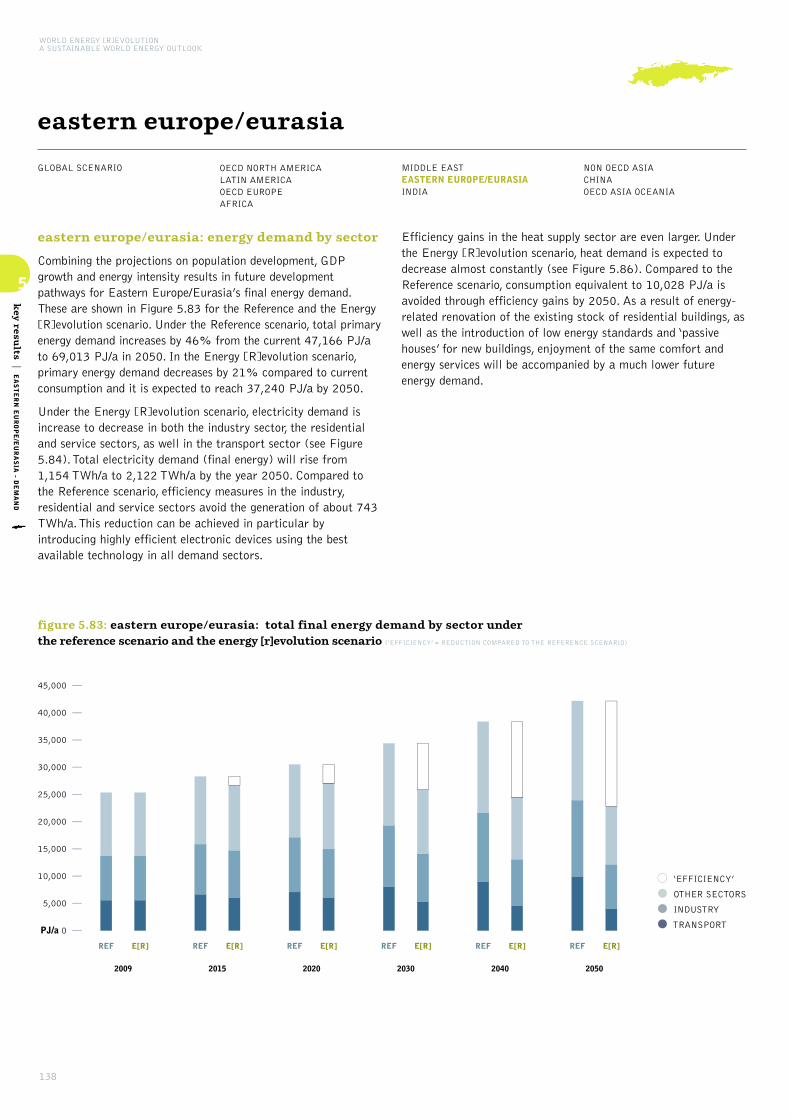

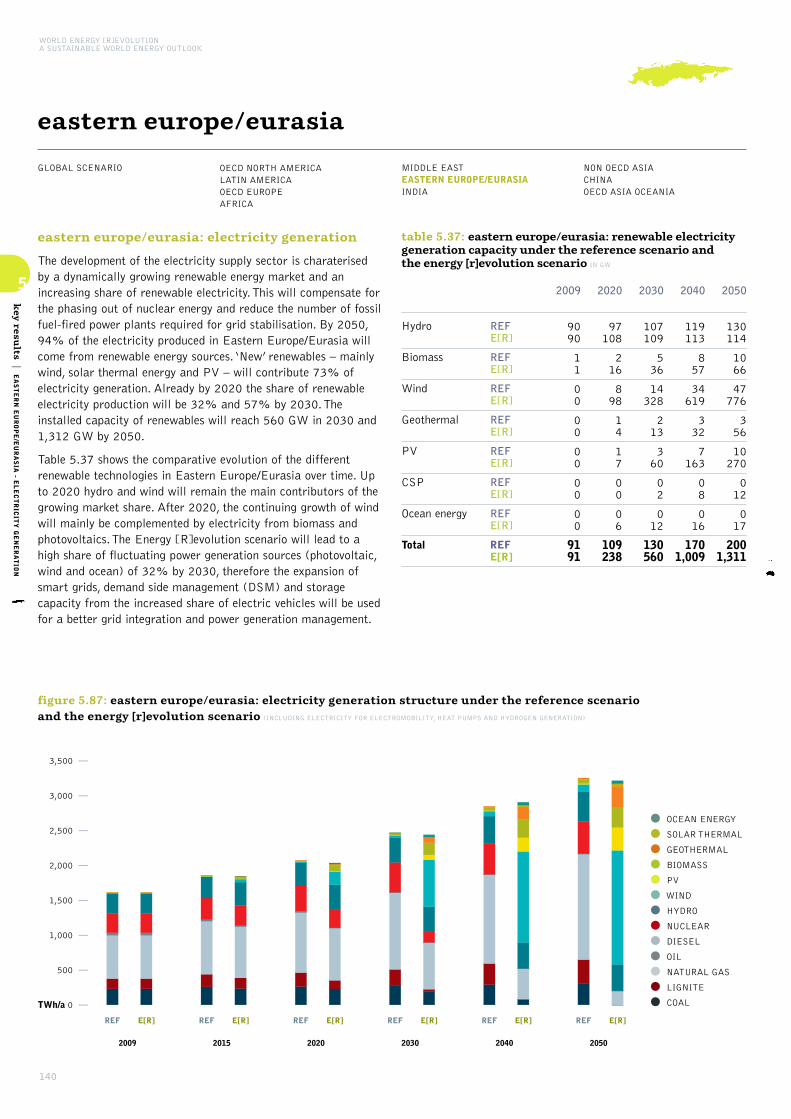

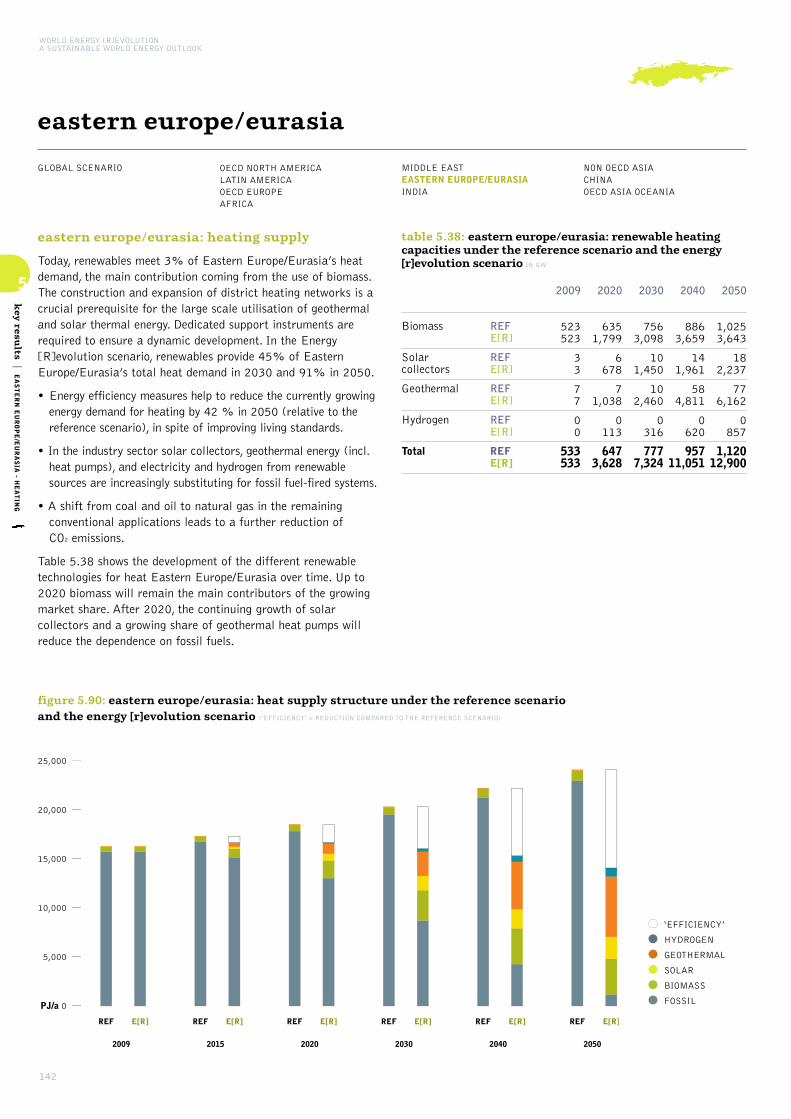

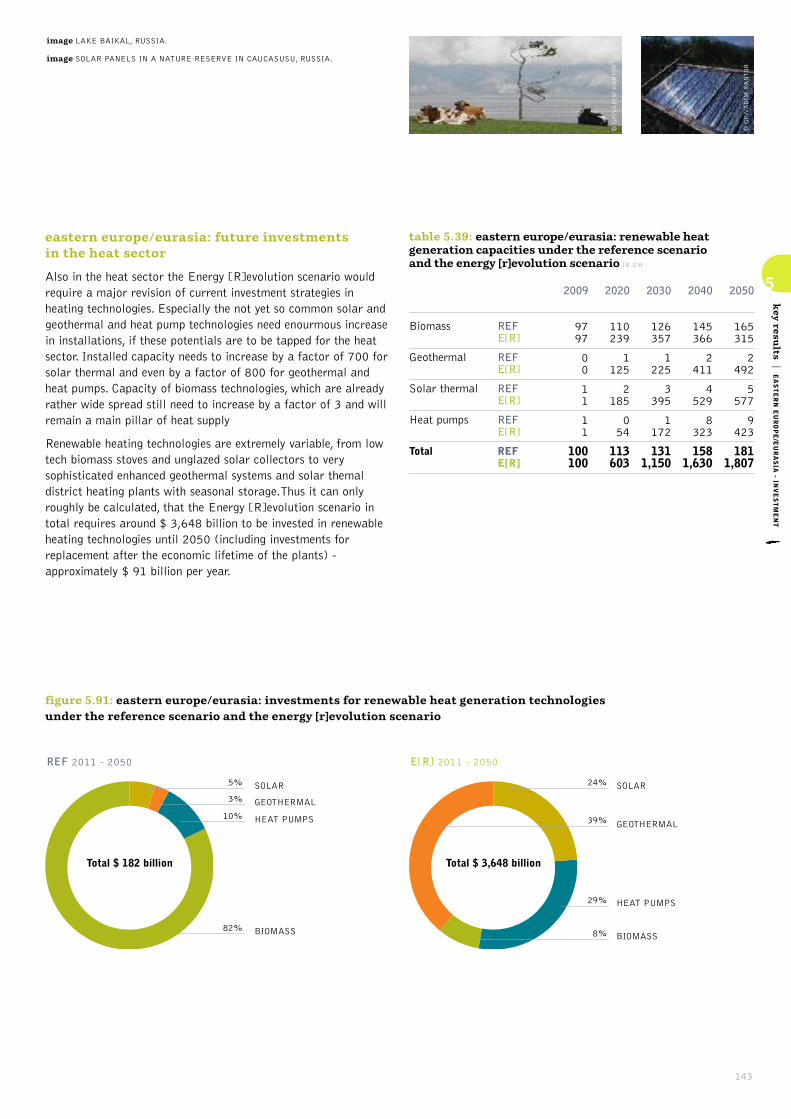

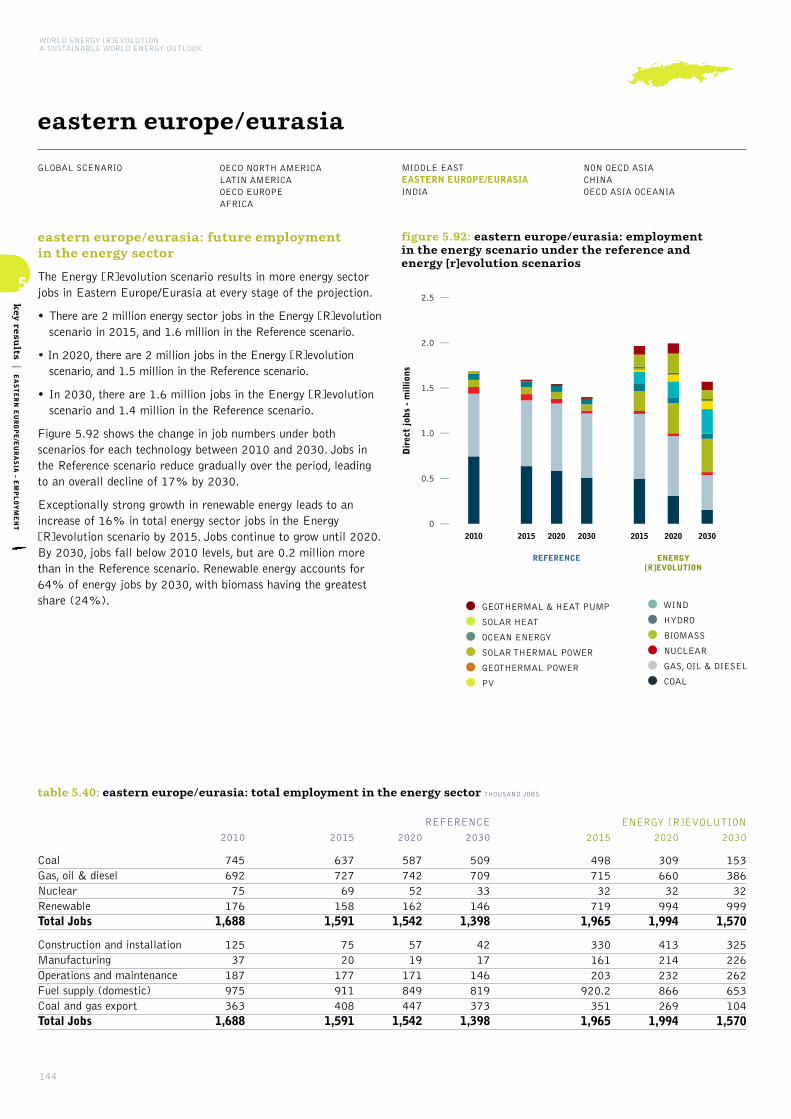

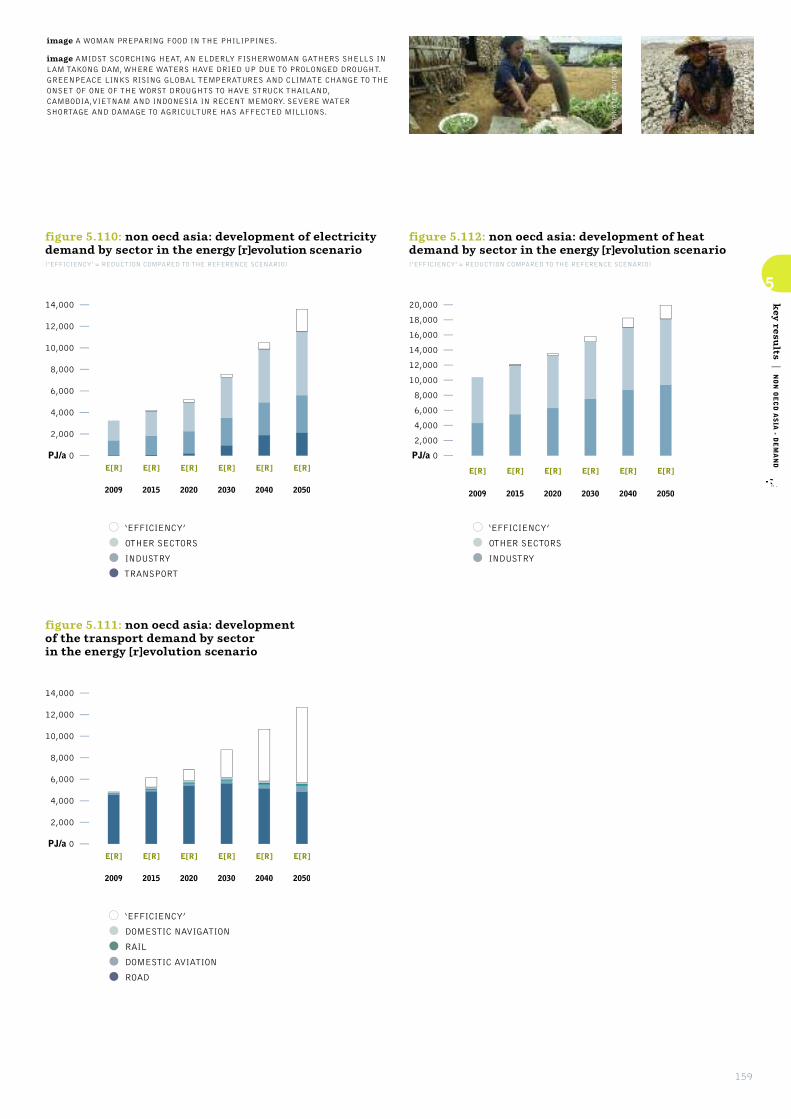

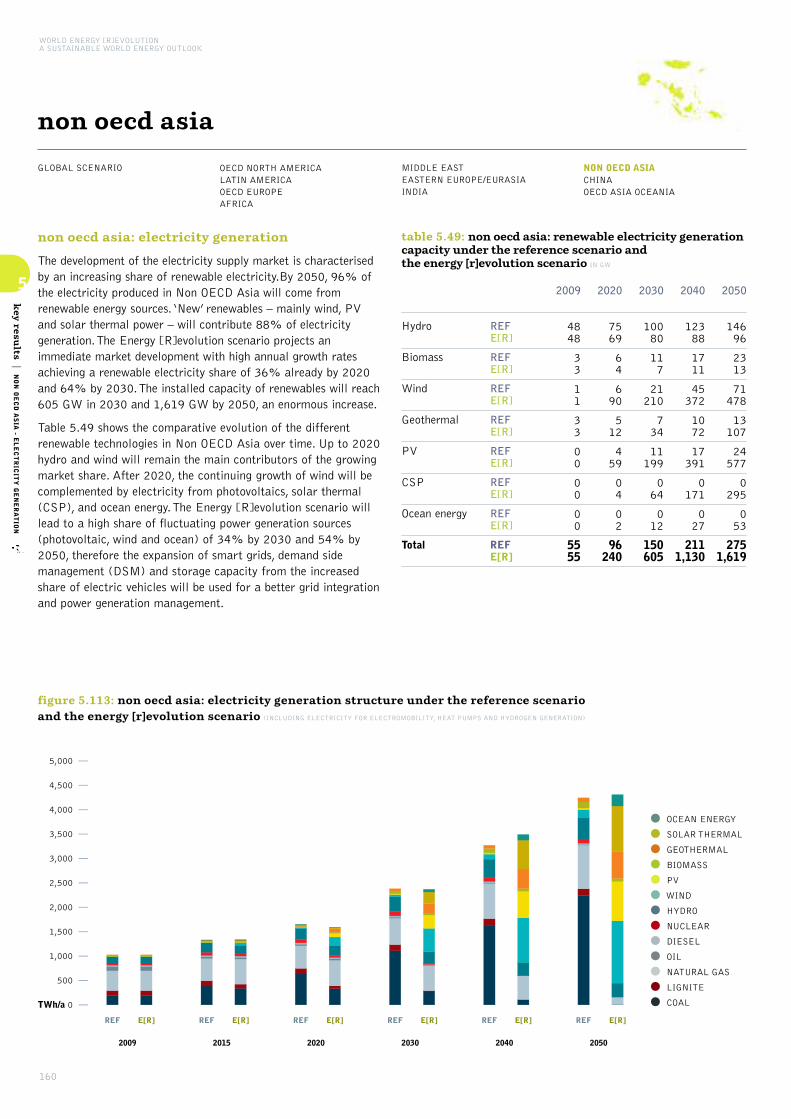

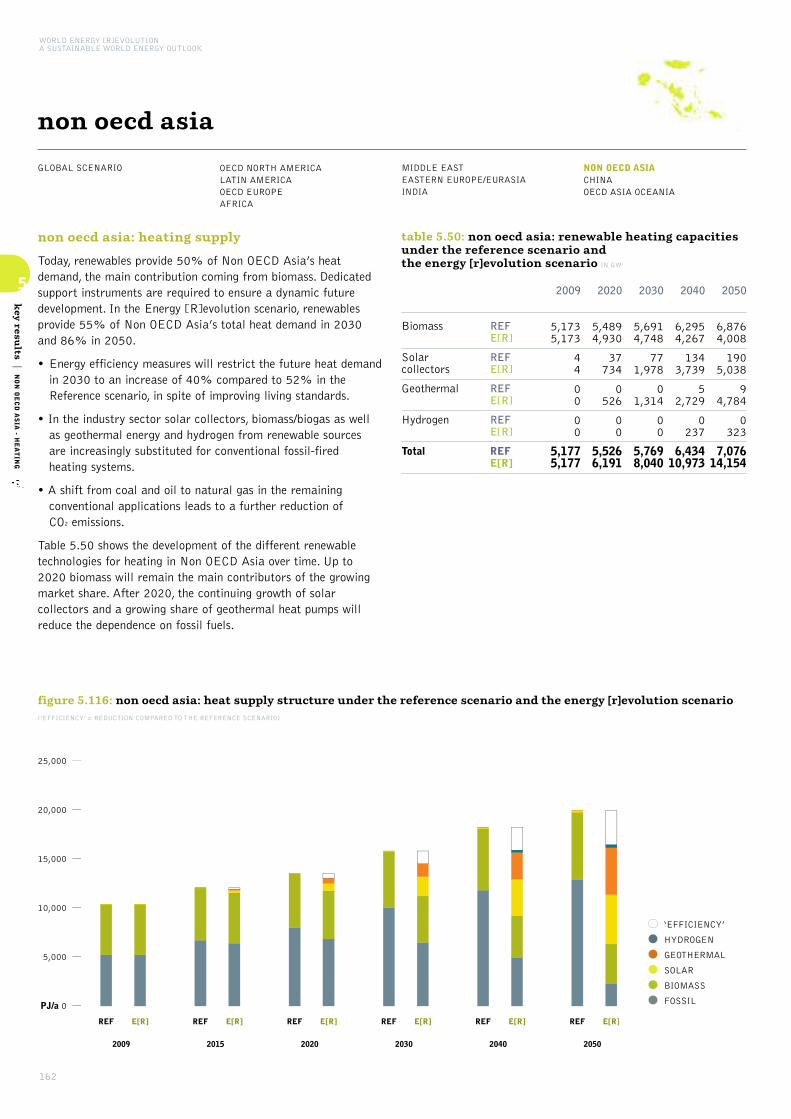

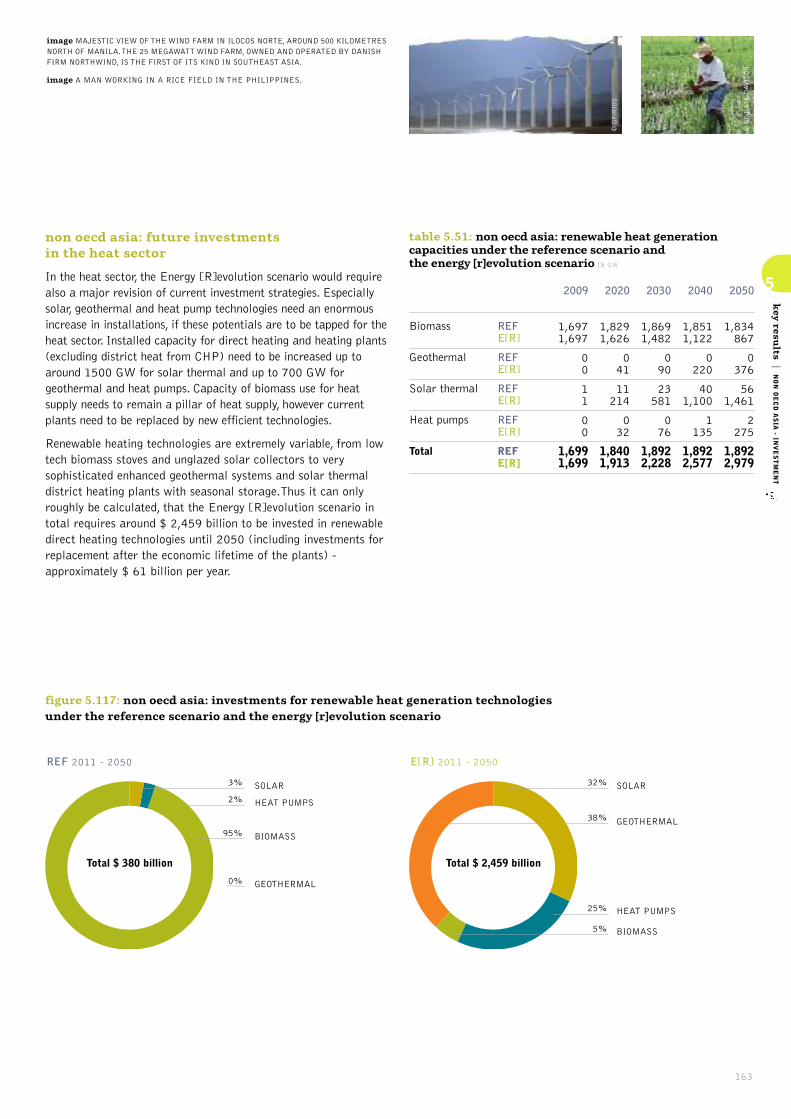

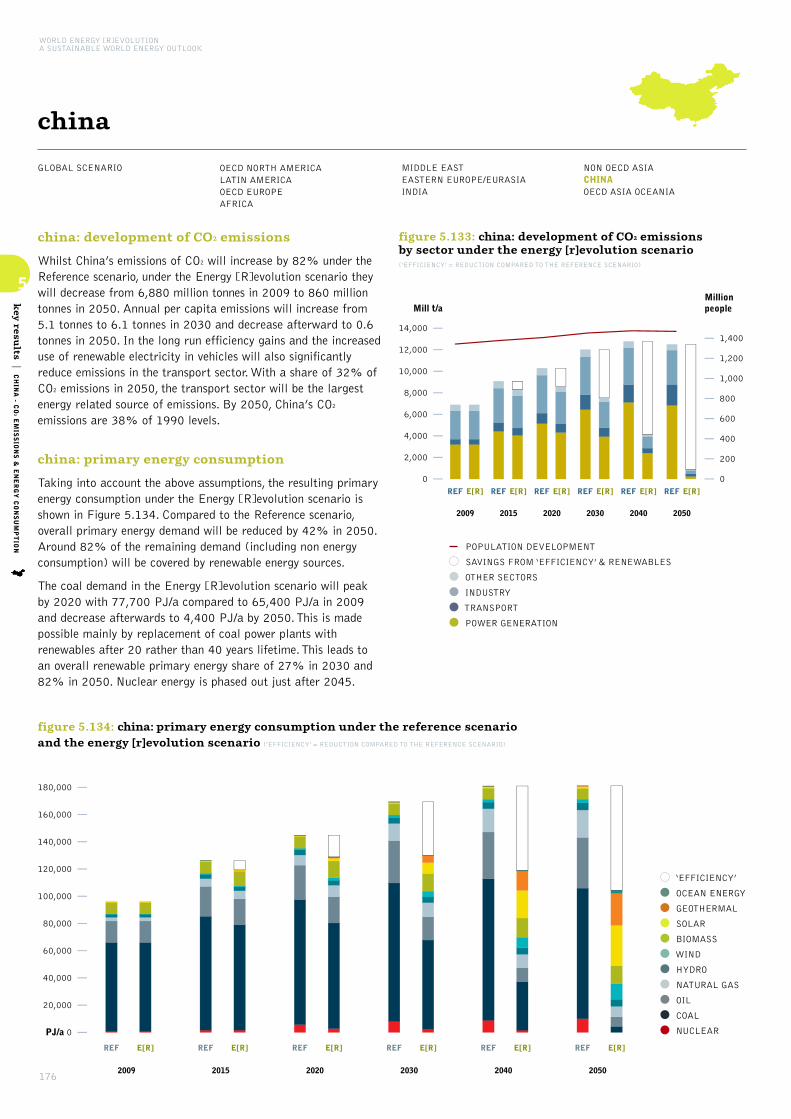

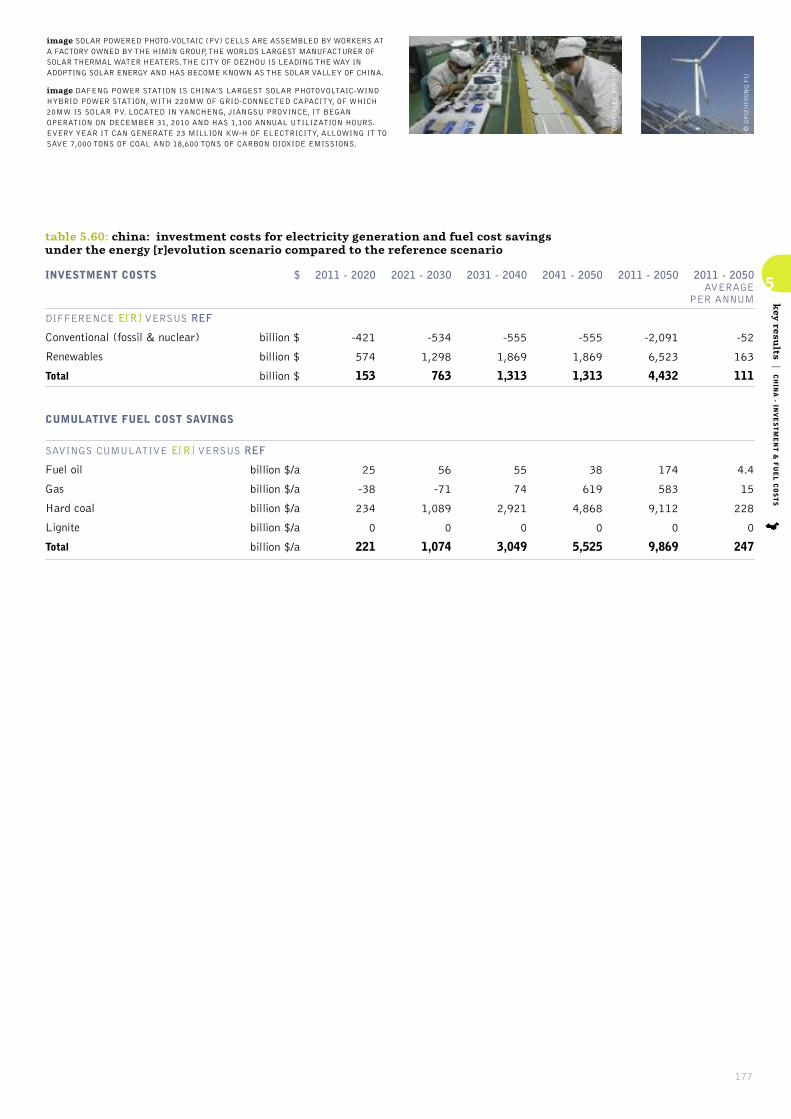

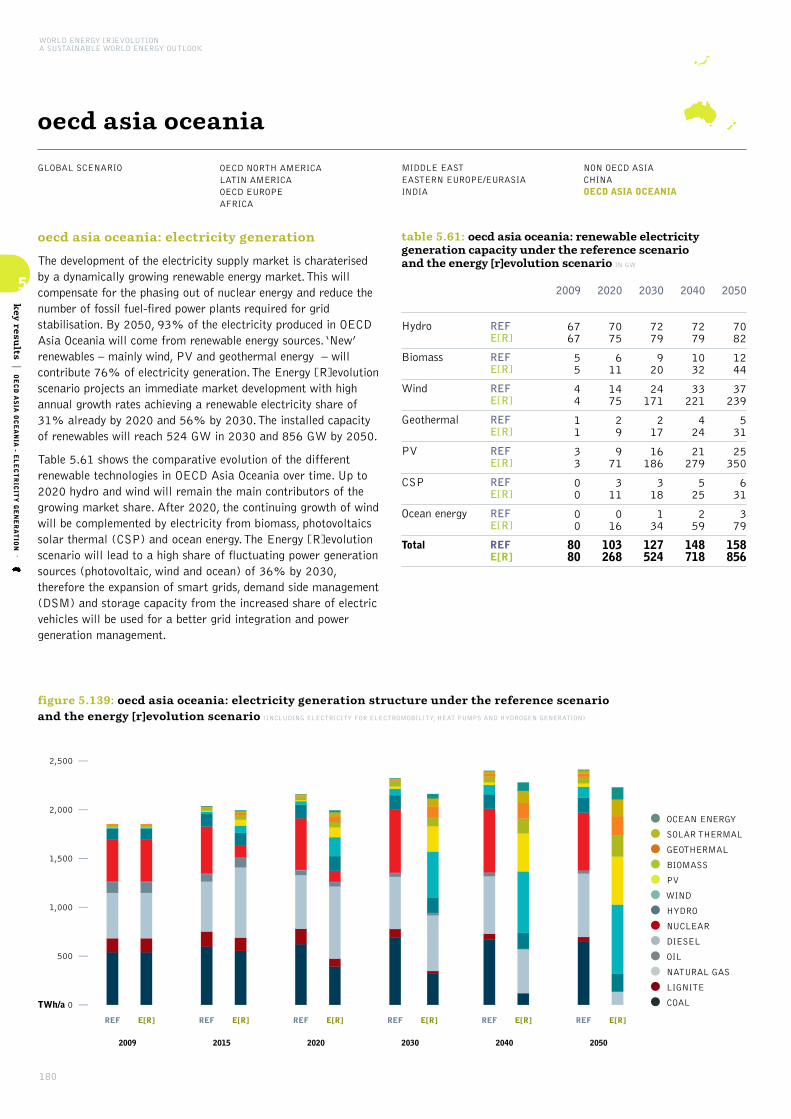

key results of energy [r]evolution scenario 74global scenario 75oecd north america 88latin america 98oecd europe 108africa 118middle east 128eastern europe/eurasia 138india 148non oecd asia 158china 168oecd asia oceania 178

contents

1

2

3

4

5

7

© GP/PETER CATON

image A WOMAN IN FRONT OF HER FLOODEDHOUSE IN SATJELLIA ISLAND. DUE TO THEREMOTENESS OF THE SUNDARBANS ISLANDS,SOLAR PANELS ARE USED BY MANY VILLAGERS. AS A HIGH TIDE INVADES THE ISLAND, PEOPLEREMAIN ISOLATED SURROUNDED BY THE FLOODS.

employment projections 188

6.1 methodology and assumptions 1896.2 employment factors 1906.3 regional adjustments 1916.3.1 regional job multipliers 1916.3.2 local employment factors 1916.3.3 local manufacturing and fuel production 1916.3.4 learning adjustments or ‘decline factors’ 1916.4 fossil fuels and nuclear energy - employment,

investment, and capacities 1936.4.1 employment in coal 1936.4.2 employment in gas, oil & diesel 1936.4.3 employment in nuclear energy 1936.5 employment in renewable energy technologies 1946.5.1 employment in wind energy 1946.5.2 employment in biomass 1946.5.3 employment in geothermal power 1956.5.1 employment in wave & tidal power 1956.5.2 employment in solar photovoltaics 1966.5.3 employment in solar thermal power 1966.6 employment in the renewable heating sector 1976.6.1 employment in solar heating 1976.6.2 employment in geothermal and heat pump heating 1976.6.2 employment in biomass heat 197

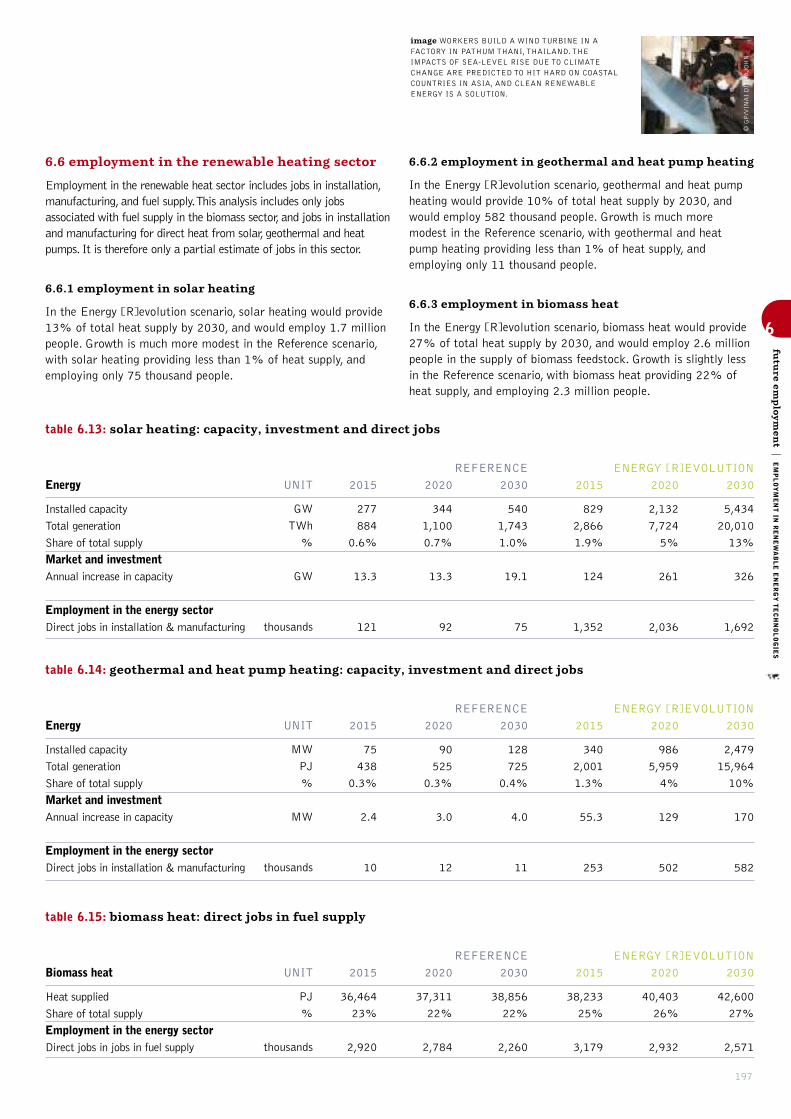

the silent revolution – past and current market developments 198

7.1 power plant markets in the us, europe and china 2007.2 the global market shares in the power plant

market: renewables gaining ground 202

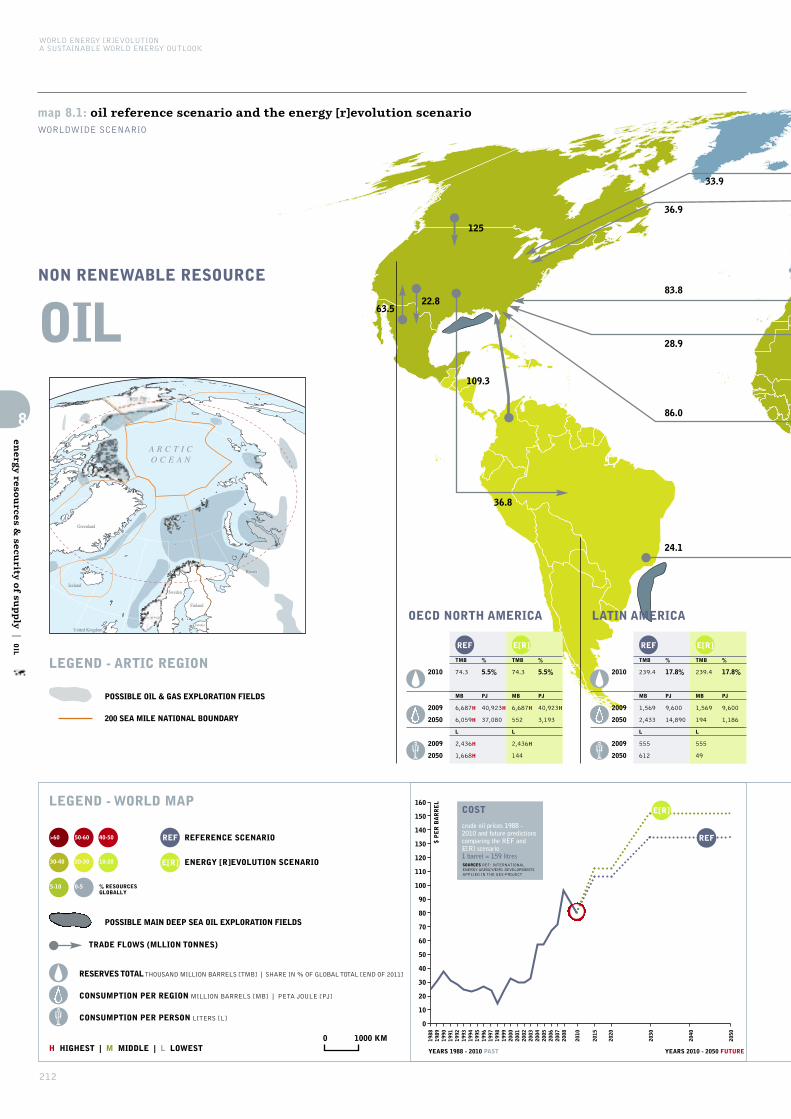

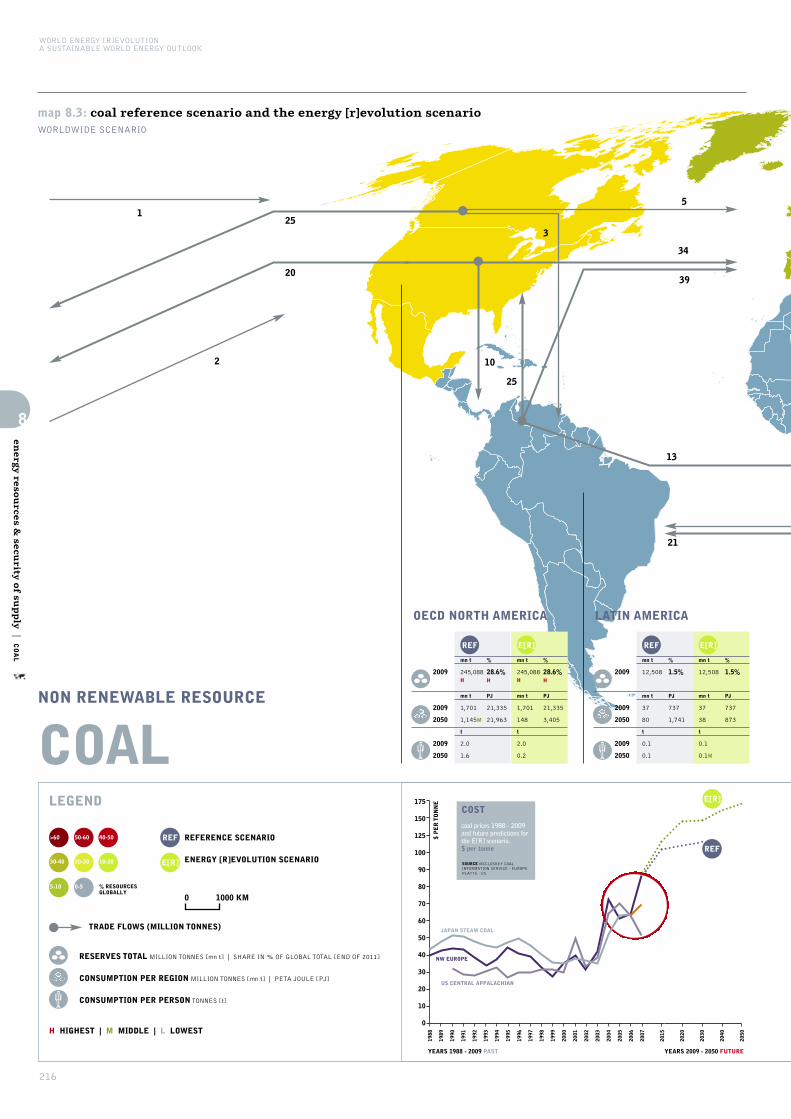

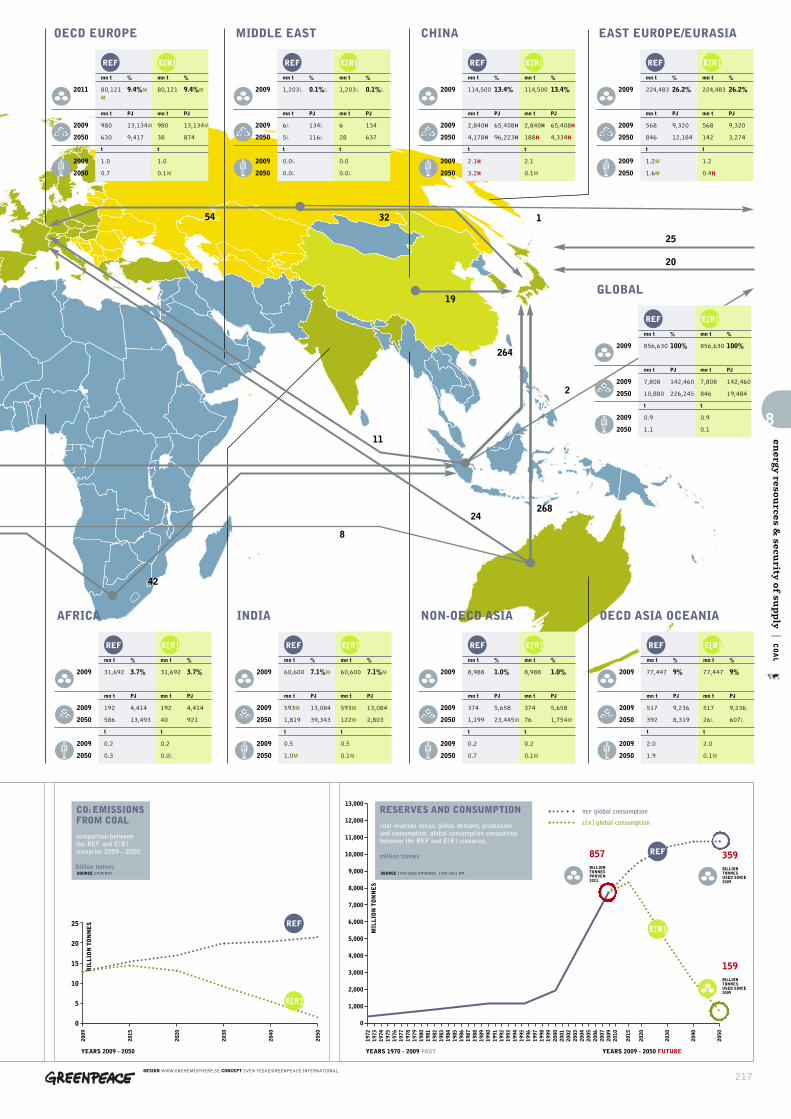

energy resources and security of supply 208

8.1 oil 2108.1.1 the reserves chaoas 2108.1.2 non-conventional oil reserves 2118.2 gas 2118.2.1 shale gas 2118.3 coal 2118.4 nuclear 2208.5 renewable energy 2218.6 biomass in the 2012 energy [r]evolution 2288.6.1 how much biomass 229

energy technologies 231

9.1 fossil fuel technologies 2319.1.1 coal combustion technologies 2319.1.2 gas combustion technologies 2319.1.3 carbon reduction technologies 231

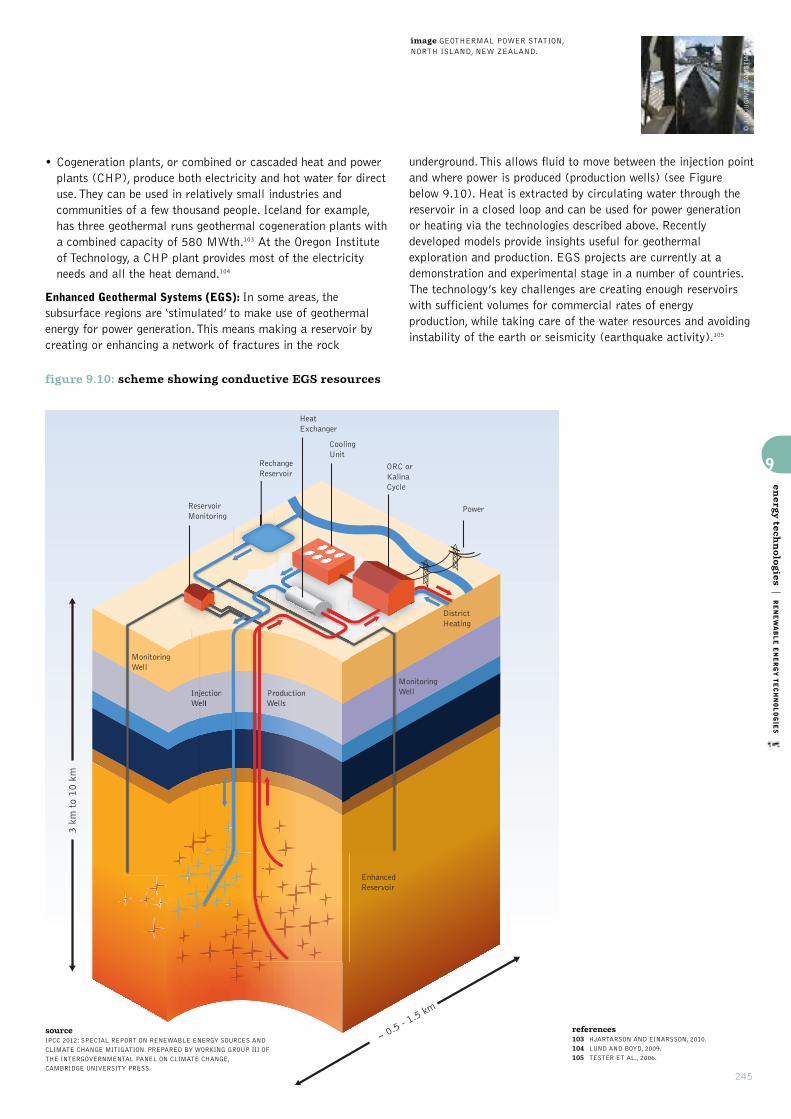

9.1.4 carbon dioxide storage 2329.1.5 carbon storage and climate change targets 2329.2 nuclear technologies 2349.2.1 nuclear reactor designs: evolution and safety issues 2349.3 renewable energy technologies 2359.3.1 solar power (photovoltaics) 2359.3.2 concentrating solar power (CSP) 2379.3.3 wind power 2399.3.4 biomass energy 2399.3.5 geothermal energy 2439.3.6 hydro power 2459.3.7 ocean energy 2489.3.8 renewable heating and cooling technologies 2519.3.9 geothermal, hydrothermal and aerothermal energy 2549.3.10 biomass heating technologies 2579.3.11 storage technologies 258

energy efficiency - more with less 260

10.1 methodology for the energy demand projections 26110.2 efficiency in industry 26310.2.1 energy demand reference scenario: industry 26310.3 low energy demand scenario: industry 26410.4 results for industry: efficiency pathway for

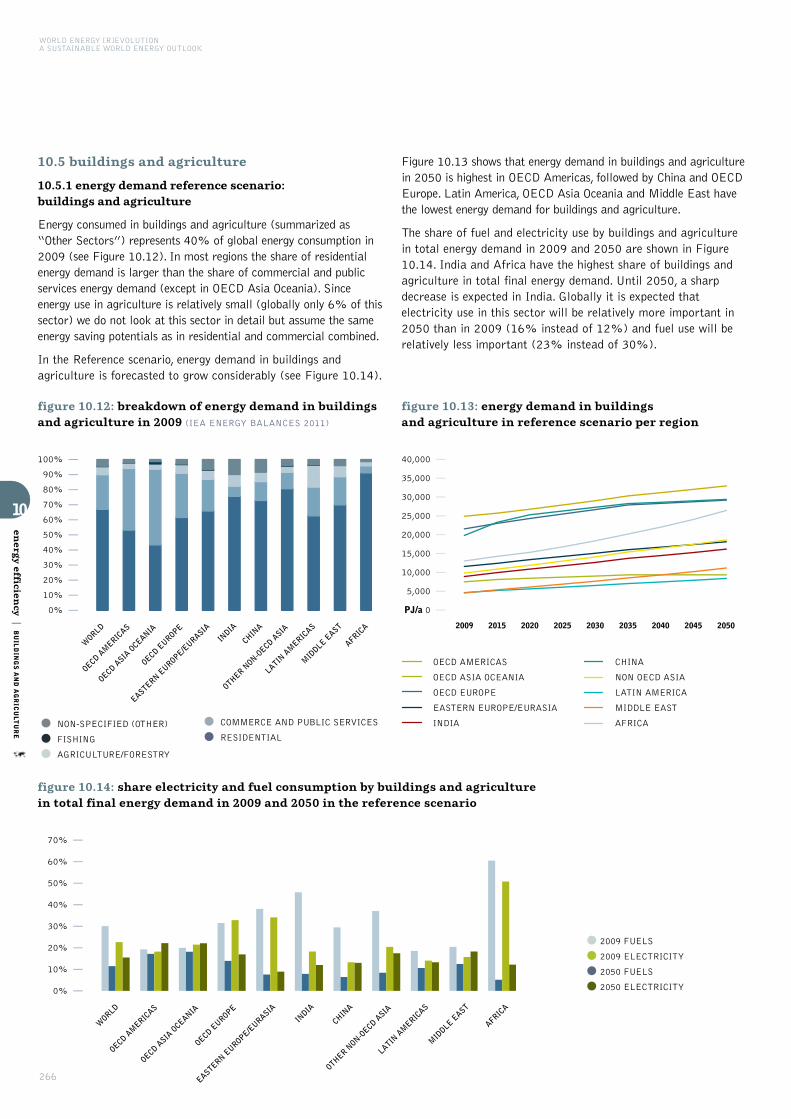

the energy [r]evolution 26510.5 buildings and agriculture 26611.5.1 energy demand reference scenario:

buildings and agriculture 26611.5.2 fuel and heat use 26711.5.3 electricity use 26810.6 the standard household concept 27010.7 low energy demand scenario:

buildings and agriculture 27210.8 results for building and agriculture:

the efficiency pathway for the energy [r]evolution 272

transport 275

11.1 the future of the transport sector in the energy[r]evolution scenario 276

11.2 technical and behavioural measures to reduce transport energy consumption 278

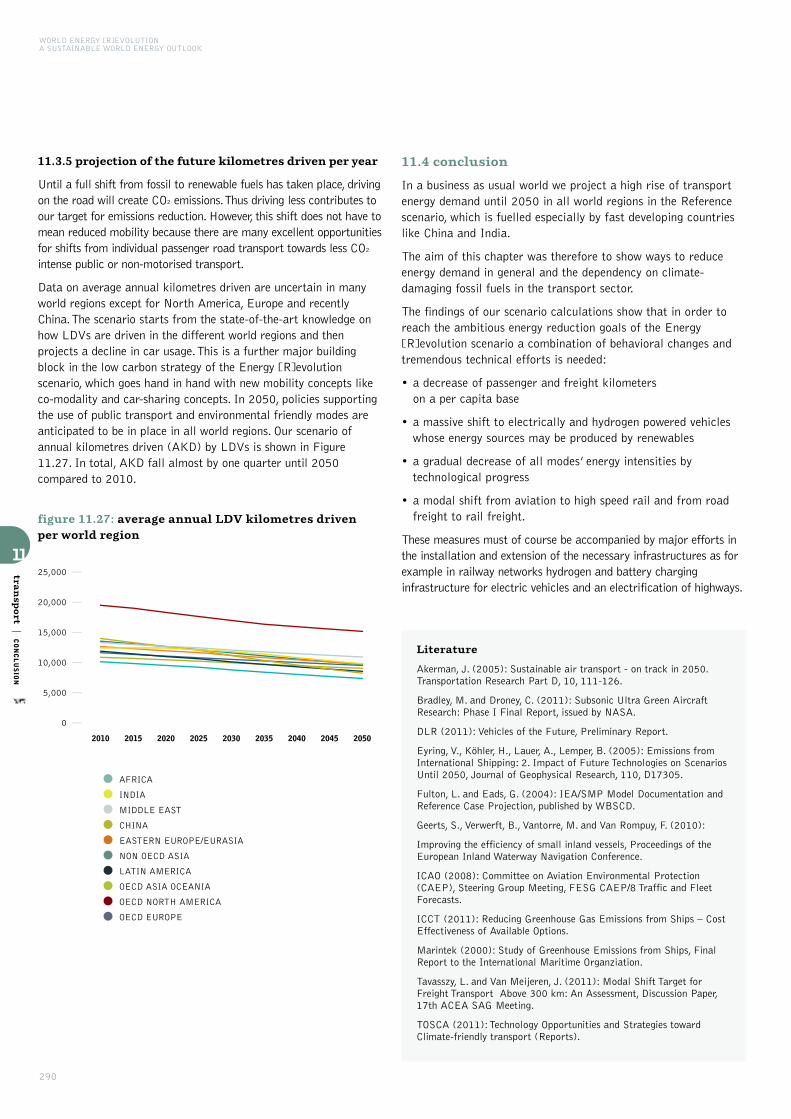

11.2.1 step 1: reduction of transport demand 27811.2.2 step 2: changes in transport mode 27911.2.3 step 3: efficiency improvements 28211.3 projection of the future LDV market 28811.3.1 projection of the future technology mix 28811.3.2 projection of the future vehicle segment split 28811.3.3 projection of the future switch to alternative fuels 28911.3.4 projection of the future global vehicle stock develoment 28911.3.5 projection of the future kilometres driven per year 29011.4 conclusion 290

glossary & appendix 291

12.1 glossary of commonly used terms and abbreviations 29212.2 definition of sectors 292scenario results data 293

6

7

8

9

10

11

12

8

WORLD ENERGY [R]EVOLUTIONA SUSTAINABLE WORLD ENERGY OUTLOOK

figure 1.1 ftsm scheme 25

figure 2.1 centralised generation systems waste more than two thirds of their original energy input 28

figure 2.2 a decentralised energy future 29figure 2.3 the smart-grid vision for the energy [r]evolution 35figure 2.4 a typical load curve throughout europe, shows

electricity use peaking and falling on a daily basis 37figure 2.5 the evolving approach to grids 37figure 2.6 renewable energy sources as a share of

energy supply in germany 40figure 2.7 renewable energy sources in total final energy

consumption in germany 2011/2010 40figure 2.8 phase out of nuclear energy 41figure 2.9 electricity imports/exports germany 41figure 2.10 development of household demand 42figure 2.11 process overview of supply system design by

production optimitsation 43figure 2.12 screenshot of PowerFactory grid model 43

figure 3.1 return characteristics of renewable energies 50figure 3.2 overview risk factors for renewable energy projects 51figure 3.3 investment stages of renewable energy projects 51figure 3.4 key barriers to renewable energy investment 53

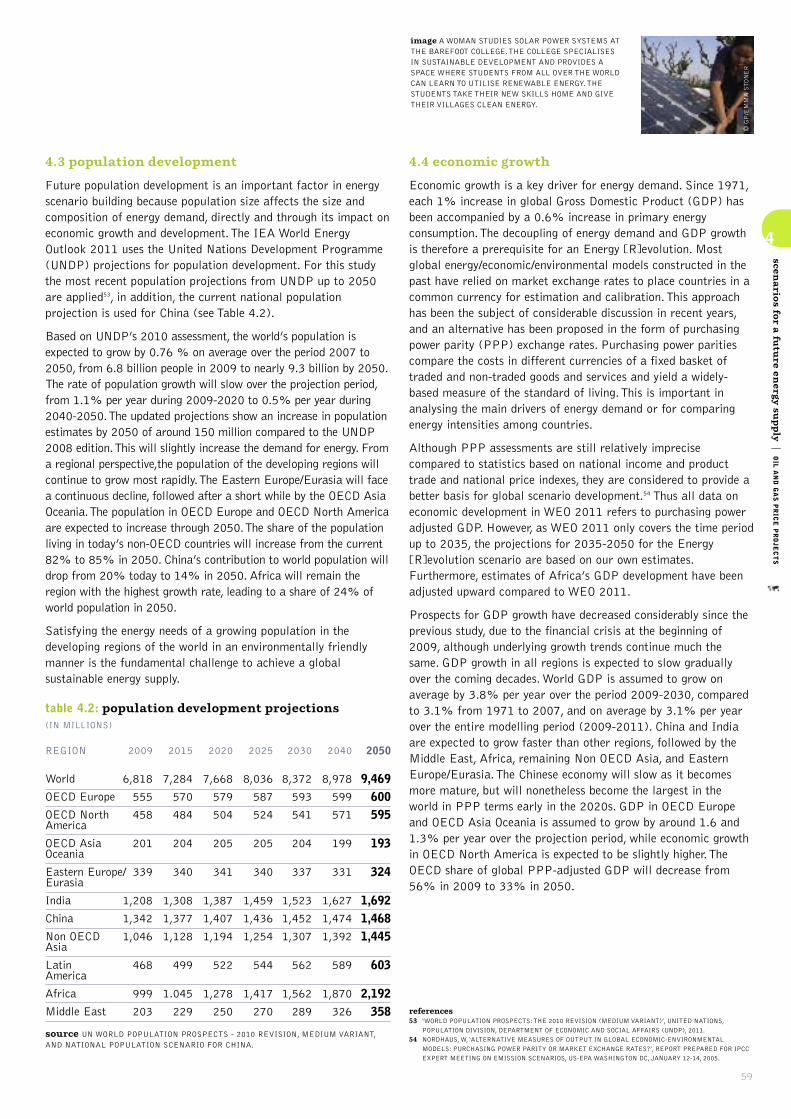

figure 4.1 world regions used in the scenarios 58figure 4.2 future development of investment costs for

renewable energy technologies 66figure 4.3 expected development of electricity generation

costs from fossil fuel and renewable options 66figure 4.4 global oil production 1950 to 2011 and

projection till 2050 68figure 4.5 coal scenario: base decline of 2% per year

and new projects 68figure 4.6 wind power: short term prognosis vs real market

development - global cummulative capacity 69figure 4.7 wind power: long term market projects until 2030 70figure 4.8 photovoltaic: short term prognosis vs real market

development - global cummulative capacity 71figure 4.9 photovoltaic: long term market projects until 2030 72

figure 5.1 global: final energy intensity under reference scenario and the energy energy [r]evolution scenario 75

figure 5.2 global: total final energy demand under the reference scenario and the energy energy [r]evolution scenario 76

figure 5.3 global: development of electricity demand by sector in the energy [r]evolution scenario 77

figure 5.4 global: development of the transport demand by sector in the energy [r]evolution scenario 77

figure 5.5 global: development of heat demand by sector in the energy [r]evolution scenario 77

figure 5.6 global: electricity generation structure under the reference scenario and the energy [r]evolution scenario 78

figure 5.7 global: total electricity supply costs & specific electricity generation costs under two scenarios 79

figure 5.8 global: investment shares - reference scenario versus energy [r]evolution scenario 80

figure 5.9 global: change in cumulative power plant investment 80figure 5.10 global: heat supply structure under the reference

scenario and the energy [r]evolution scenario 81figure 5.11 global: investments for renewable heat generation

technologies under the reference scenario and the energy [r]evolution scenario 82

figure 5.12a global: employment in the energy scenario under the reference scenario and the energy [r]evolution scenarios 82

figure 5.12b global: proportion of fossil fuel and renewable employment at 2010 and 2030 84

figure 5.13 global: final energy consumption for transport under the reference scenario and the energy [r]evolution scenario 85

figure 5.14 global: primary energy consumption under the reference scenario and the energy [r]evolution scenario 86

figure 5.15 global: regional breakdown of CO2 emissions in the energy [r]evolution in 2050 87

figure 5.16 global: development of CO2 emissions by sectorunder the energy [r]evolution scenarios 87

figure 5.17 global: CO2 emissions by sector in the energy [r]evolution in 2050 87

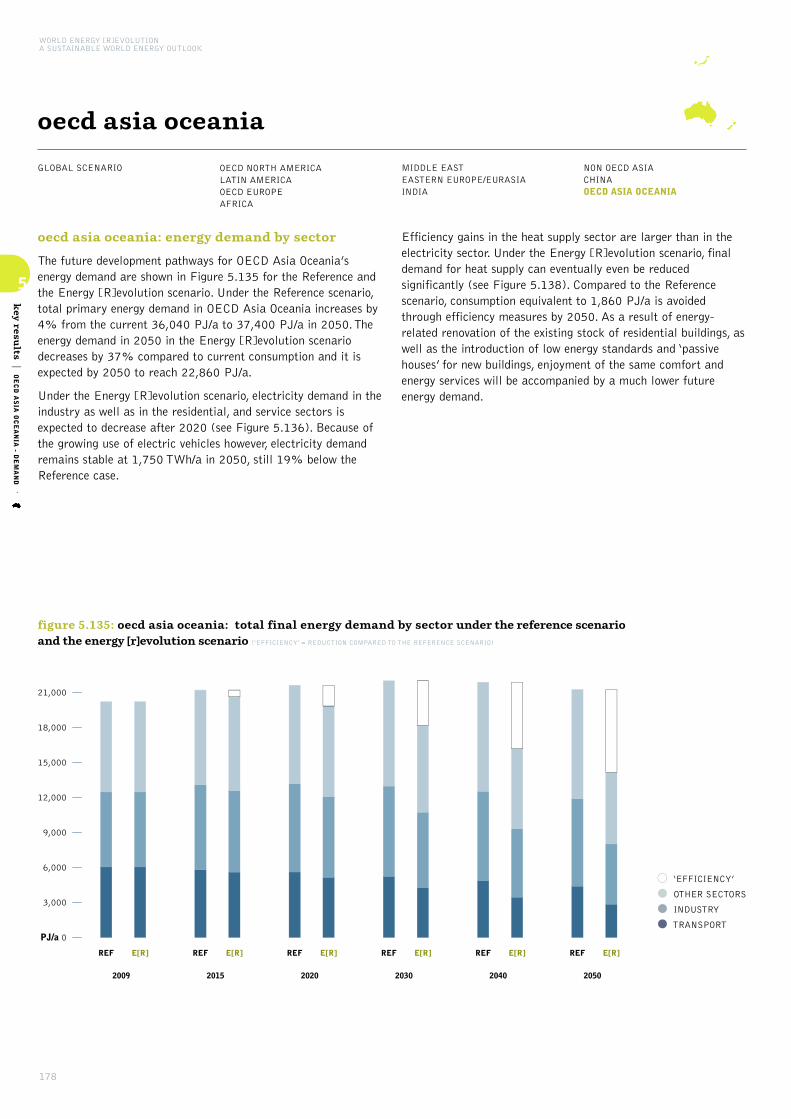

figures 5.18-5.30 north america 88figures 5.31-5.43 latin america 98figures 5.44-5.56 oecd europe 108figures 5.57-5.69 africa 118figures 5.70-5.82 middle east 128figures 5.83-5.96 eastern europe/eurasia 138figures 5.96-5.108 india 148figures 5.109-5.121 non oecd asia 158figures 5.122-5.134 china 168figures 5.135-5.147 oecd asia oceania 178

figure 6.1 proportion of fossil fuel and renewable employment at 2010 and 2030 192

figure 7.1 global power plant market 1970-2010 199figure 7.2 global power plant market 1970-2010, excl china 200figure 7.3 usa: annual power plant market 1970-2010 200figure 7.4 europe (eu 27): annual power plant market

1970-2010 201figure 7.5 china: annual power plant market 1970-2010 201figure 7.6 power plant market shares 1970-2010 203figure 7.7 historic developments of the global

power plant market, by technology 204figure 7.8 global power plant market in 2011 207figure 7.9 global power plant market by region 207

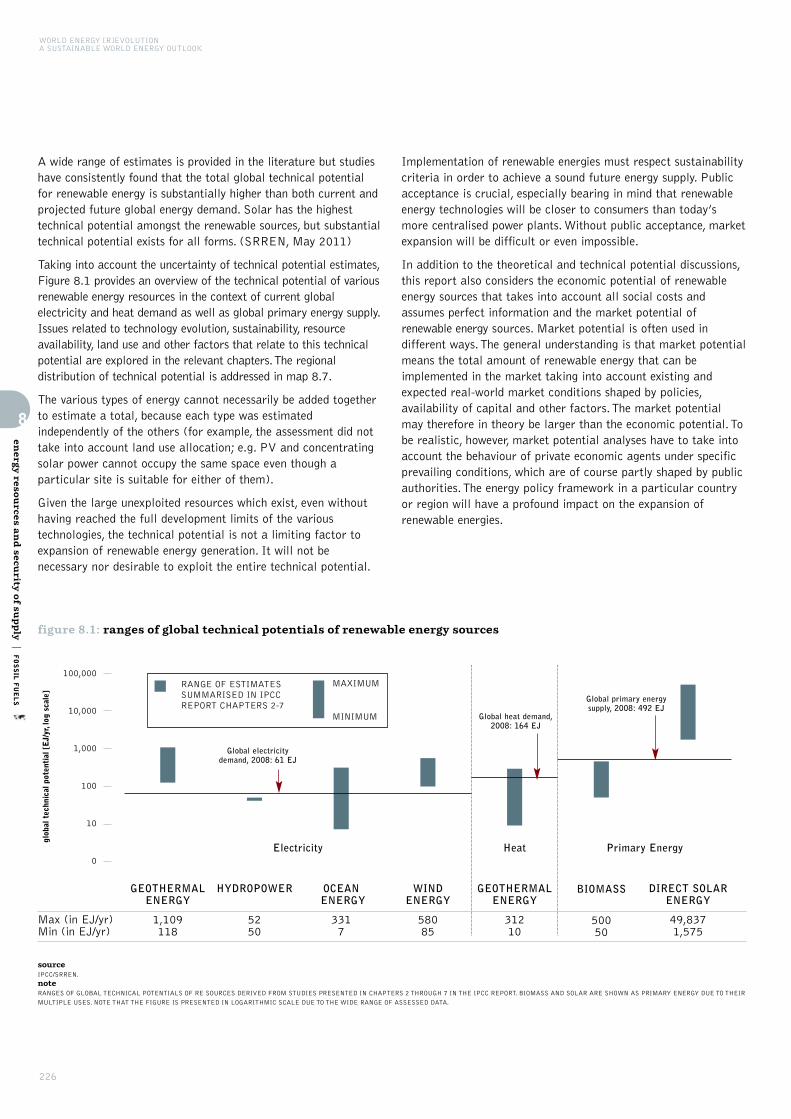

figure 8.1 ranges of global technical potentials of renewable energy sources 226

figure 9.1 example of the photovoltaic effect 235figure 9.2 photovoltaic technology 235figure 9.3 csp technologies: parabolic trough, central

receiver/solar tower and parabolic dish 238figure 9.4 early wind turbine designs, including horizontal

and vertical axis turbines 239

list of figures

1

2

3

4

5

6

7

8

9

9

© ANTHONY UPTON 2003

image NORTH HOYLE WIND FARM, UK’S FIRST WIND FARM IN THE IRISH SEA WHICHWILL SUPPLY 50,000 HOMES WITH POWER.

figure 9.5 basic components of a modern horizontal axis wind turbine with a gear box 240

figure 9.6 growth in size of typical commercial wind turbines 240figure 9.7 biogas technology 242figure 9.8 geothermal energy 243figure 9.9 schematic diagram of a geothermal condensing

steam power plant and a binary cycle power plant 244figure 9.10 scheme showing conductive EGS resources 245figure 9.11 run-of-river hydropower plant 246figure 9.12 typical hydropower plant with resevoir 246figure 9.13 typical pumped storage project 247figure 9.14 typical in-stream hydropower project using

existing facilities 247figure 9.15 wave energy technologies: classification based

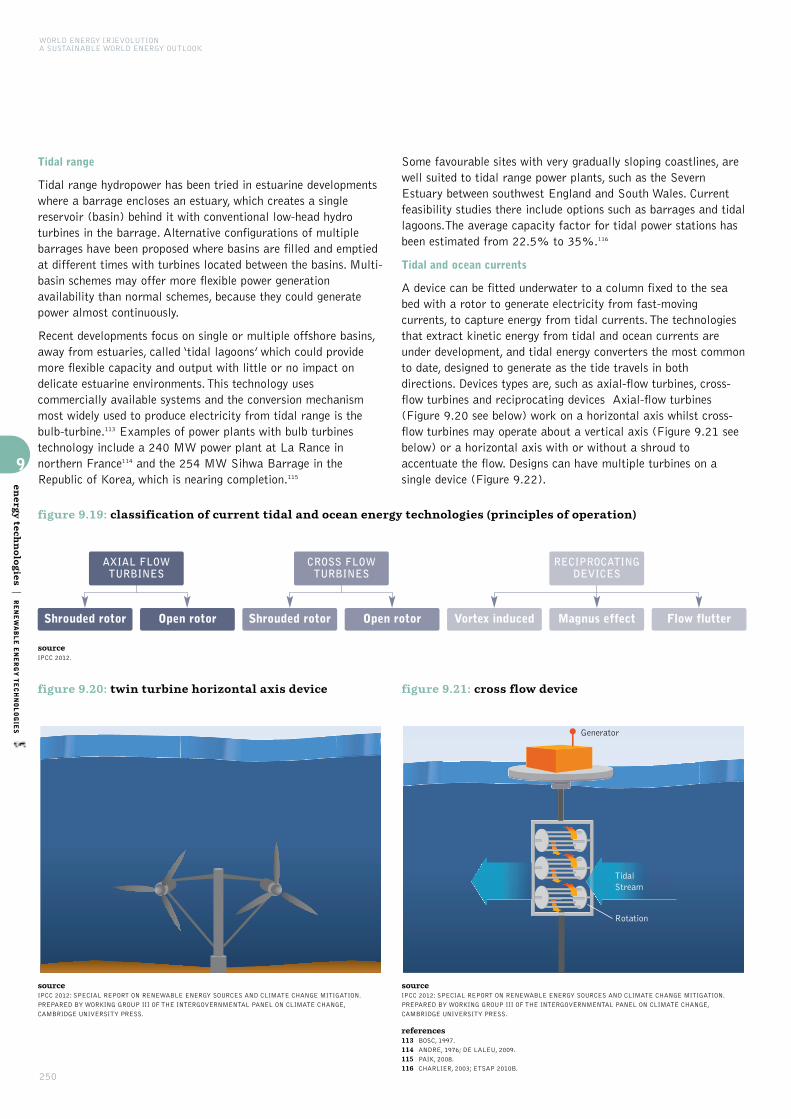

on principles of operation 248figure 9.16 oscillating water columns 249figure 9.17 oscillating body systems 249figure 9.18 overtopping devices 249figure 9.19 classification of current tidal and ocean energy

technologies (principles of operation) 250figure 9.20 twin turbine horizontal axis device 250figure 9.21 cross flow device 250figure 9.22 vertical axis device 251figure 9.23 natural flow systems vs. forced circulation systems 252figure 9.24 examples for heat pump systems 255figure 9.25 overview storage capacity of different energy

storage systems 259figure 9.26 renewable (power) (to) methane - renewable gas 259

figure 10.1 final energy demand (PJ) in reference scenario per sector worldwide 261

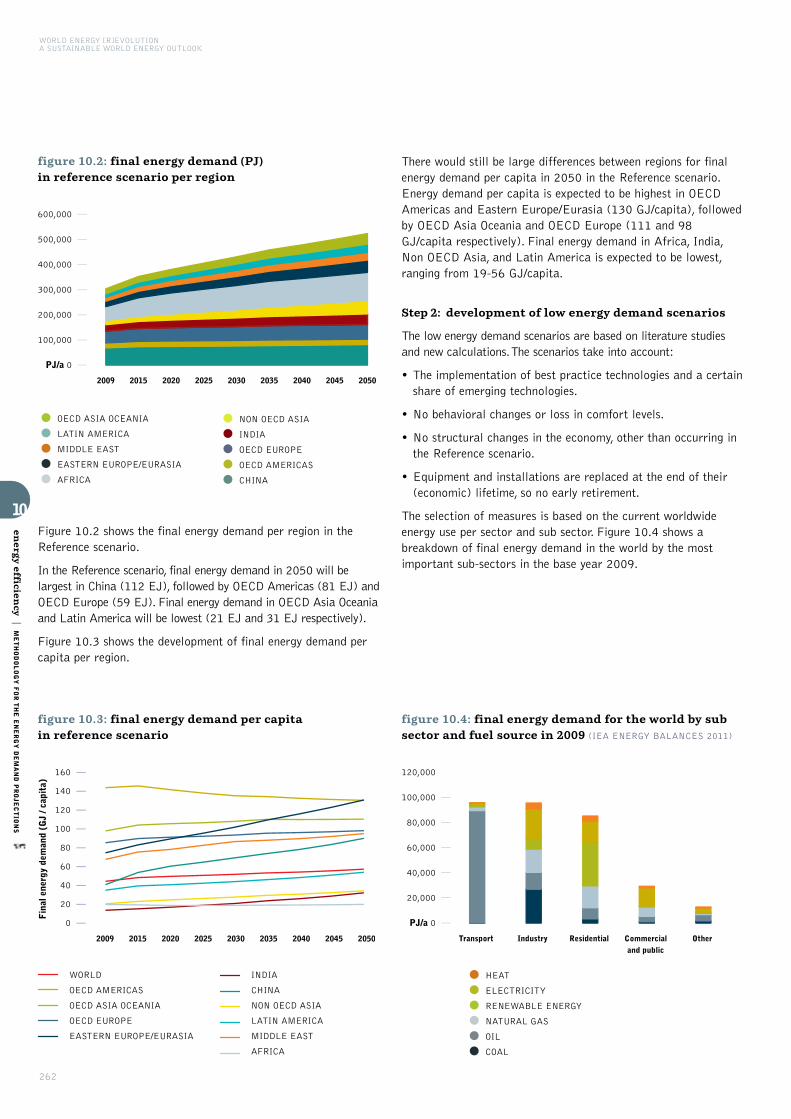

figure 10.2 final energy demand (PJ) in reference scenario per region 262

figure 10.3 final energy demand per capita in reference scenario 262

figure 10.4 final energy demand for the world by sub sector and fuel source in 2009 262

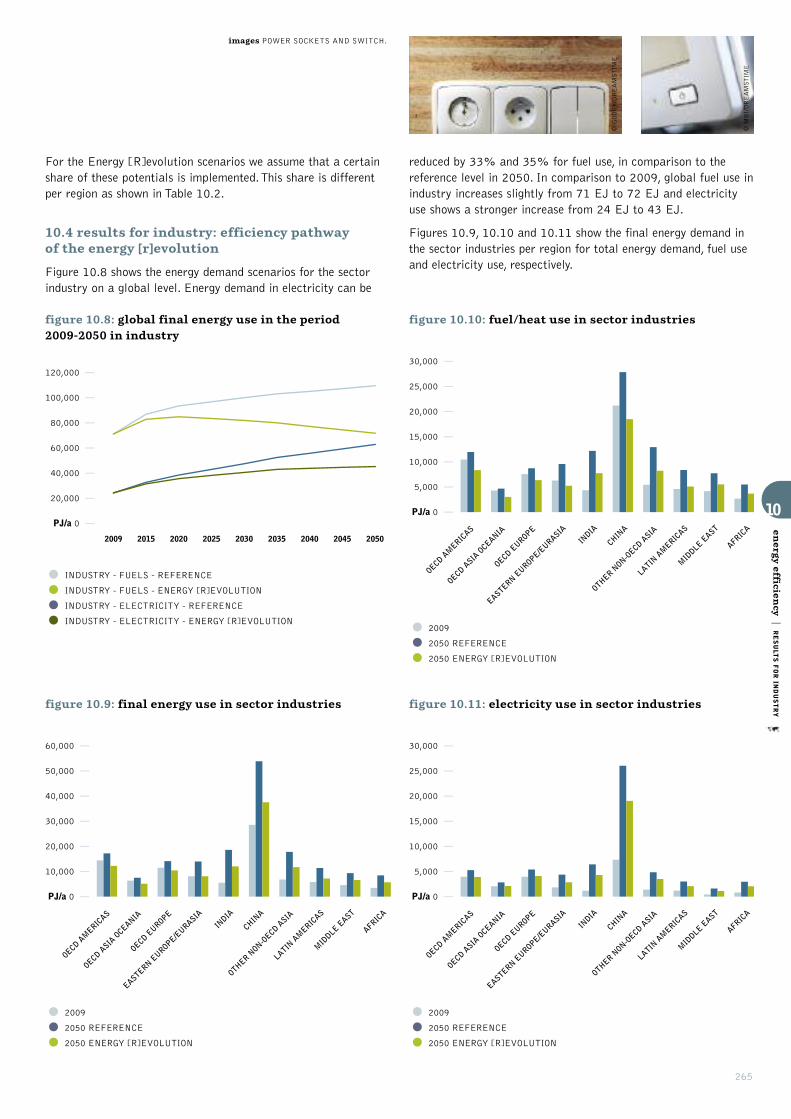

figure 10.5 projection of industrial energy demand in period 2009-2050 per region 263

figure 10.6 share of industry in total final energy demand per region in 2009 and 2050 263

figure 10.7 breakdown of final energy consumption in 2009 by sub sector for industry 263

figure 10.8 global final energy use in the period 2009-2050in industry 265

figure 10.9 final energy use in sector industries 265figure 10.10 fuel/heat use in sector industries 265figure 10.11 electricity use in sector industries 265figure 10.12 breakdown of energy demand in buildings and

agriculture in 2009 266figure 10.13 energy demand in buildings and agriculture in

reference scenario per region 266figure 10.14 share electricity and fuel consumption by

buildings and agriculture in total final energydemand in 2009 and 2050 in the reference scenario 266

figure 10.15 breakdown of final energy demand in buildings in 2009 for electricity and fuels/heat in ‘others’ 267

figure 10.16 breakdown of fuel and heat use in ‘others’ in 2009 267figure 10.17 elements of new building design that can

substantially reduce energy use 268figure 10.18 breakdown of electricity use by sub sector

in sector ‘others’ in 2009 269figure 10.19 efficiency in households - electricity demand

per capita 270

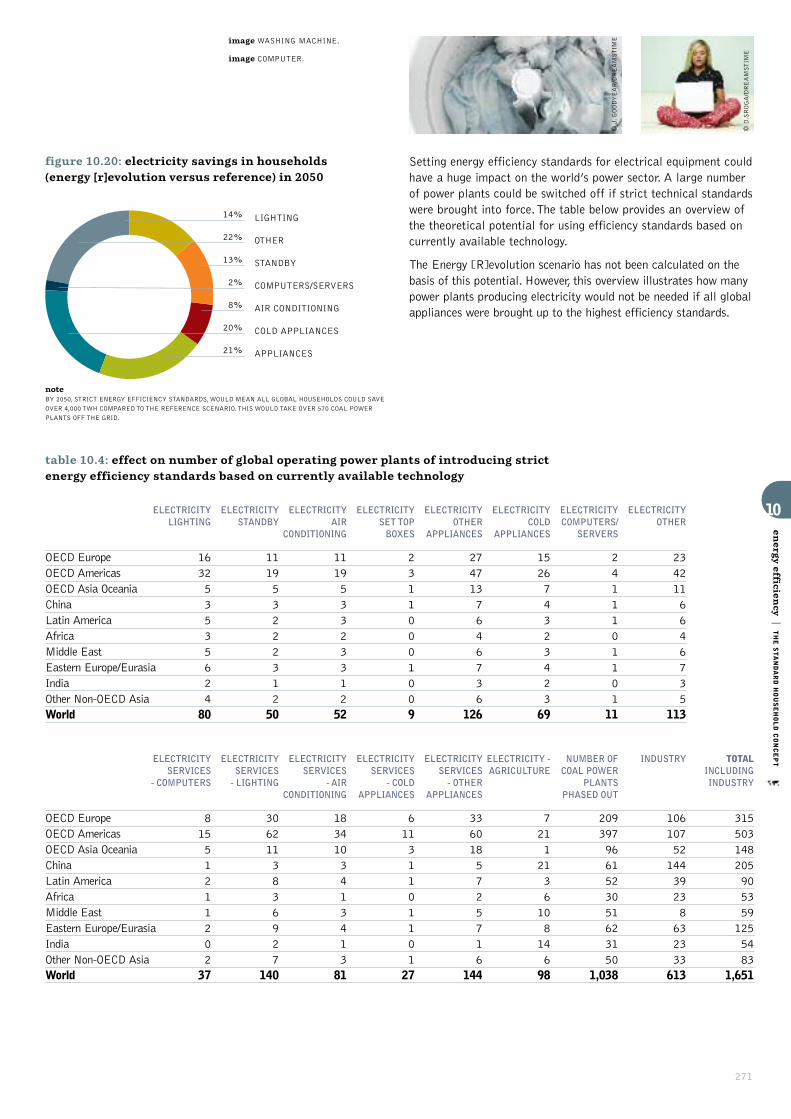

figure 10.20 electricity savings in households (E[R] vs. Ref) in 2050 271

figure 10.21 breakdown of energy savings in BLUE Map scenario for sector ‘others’ 272

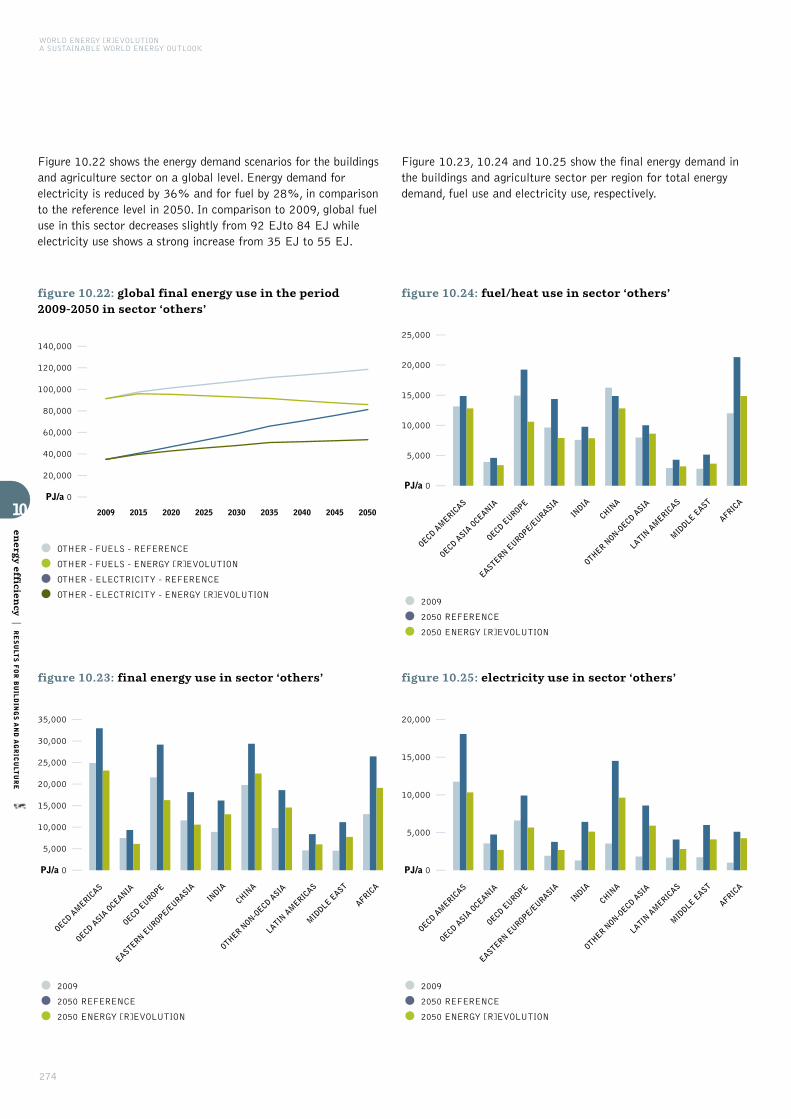

figure 10.22 global final energy use in the period 2009-2050 in sector ‘others’ 274

figure 10.23 final energy use i sector ‘others’ 274figure 10.24 fuel/heat use in sector ‘others’ 274figure 10.25 electricity use in sector ‘others’ 274

figure 11.1 world final energy use per transport mode2009/2050 - reference scenario 277

figure 11.2 world transport final energy use by region 2009/2050 - reference scenario 277

figure 11.3 world average (stock-weighted) passenger transport energy intensity for 2009 and 2050 279

figure 11.4 aviation passenger-km in the reference and energy [r]evolution scenarios 280

figure 11.5 rail passenger-km in the reference and energy [r]evolution scenarios 280

figure 11.6 passenger-km over time in the reference scenario 280figure 11.7 passenger-km over time in the energy

[r]evolution scenario 280figure 11.8 world average (stock-weighted) freight transport

energy intensities for 2005 and 2050 281figure 11.9 tonne-km over time in the reference scenario 281figure 11.10 tonne-km over time in the energy

[r]evolution scenario 281figure 11.11 energy intensities (Mj/p-km) for air transport

in the energy [r]evolution scenario 282figure 11.12 fuel share of electric and diesel rail traction for

passenger transport 283figure 11.13 fuel share of electric and diesel rail traction for

freight transport 283figure 11.14 energy intensities for passenger rail transport

in the energy [r]evolution scenario 284figure 11.15 energy intensities for freight rail transport

in the energy [r]evolution scenario 284figure 11.16 HDV operating fully electrically under a catenary 284figure 11.17 fuel share of medium duty vehicles (global average)

by transport performance (ton-km) 285figure 11.18 fuel share of heavy duty vehicles (global average)

by transport performance (ton-km) 285figure 11.19 specific energy consumption of HDV and MDV in

litres of gasoline equivalent per 100 tkm in 2050 285figure 11.20 energy intensities for freight rail transport in

the energy [r]evolution scenario 287figure 11.21 LDV occupancy rates in 2009 and in the

energy [r]evolution 2050 287figure 11.22 sales share of conventional ICE, autonomous

hybrid and grid-connectable vehicles in 2050 288figure 11.23 vehicle sales by segment in 2009 and 2050 in the

energy [r]evolution scenario 288figure 11.24 fuel split in vehicle sales for 2050 energy

[r]evolution by world region 289figure 11.25 development of the global LDV stock

under the reference scenario 289figure 11.26 development of the global LDV stock

under the energy [r]evolution scenario 289figure 11.26 average annual LDV kilometres driven per

world region 290

10

11

10

WORLD ENERGY [R]EVOLUTIONA SUSTAINABLE WORLD ENERGY OUTLOOK

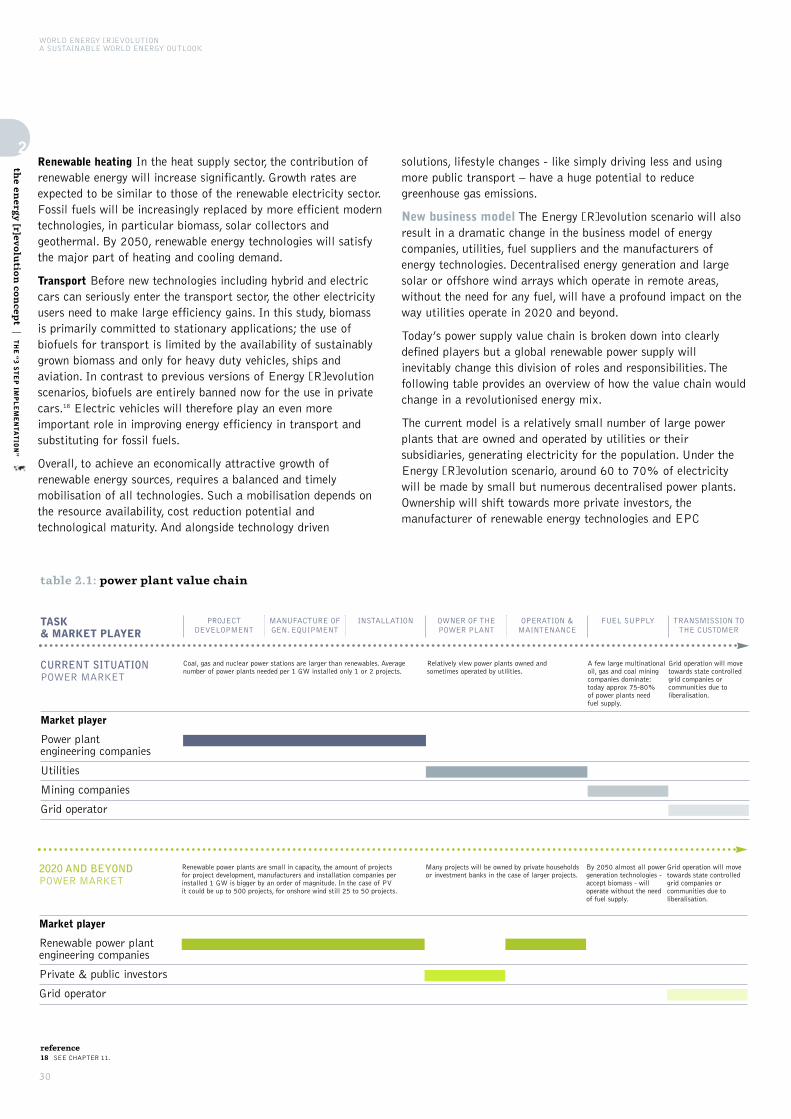

table 2.1 power plant value chain 30table 2.2 german government short, medium and

long term binding targets 41table 2.3 key results for energy [r]evolution village cluster 45table 2.4 village cluster demand overview 47

table 3.1 how does the current renewable energy market work in practice? 49

table 3.2 categorisation of barriers to renewable energy investment 52

table 4.1 assumed average growth rates and annual market volumes by renwable technologies 65

table 4.2 population development projections 59table 4.3 gdp development projections 60table 4.4 development projections for fossil fuel and

biomass prices in $ 2010 60table 4.5 assumptions on CO2 emissions cost development

for Annex-B and Non-Annex-B countries of the UNFCCC 61

table 4.6 development of efficiency and investment costs for selected new power plant technologies 61

table 4.7 photovoltaics (pv) cost assumptions 63table 4.8 concentrating solar power (csp) cost assumptions 63table 4.9 wind power cost assumptions 64table 4.10 biomass cost assumptions 64table 4.11 geothermal cost assumptions 65table 4.12 ocean energy cost assumptions 65table 4.13 hydro power cost assumptions 66table 4.14 overview over expected investment costs for

pathways for heating technologies 67table 4.15 overview of key parameter of the illustrative

scenarios based on assumptions that are exogenous to the models respective endogenous model results 73

table 5.1 global: renewable electricity generation capacity under the reference scenario and the energy [r]evolution scenario 78

table 5.2 global: investment costs for electricity generation and fuel cost savings under the energy [r]evolution scenario compared to the reference scenario 80

table 5.3 global: renewable heating capacities under the reference scenario and the energy [r]evolution scenario 81

table 5.4 global: renewable heat generation capacities under the reference scenario and the energy[r]evolution scenario 82

table 5.5 global: total employment in the energy sector 84table 5.6 global: transport energy demand by mode

under the reference scenario and the energy [r]evolution scenario 85

tables 5.7-5.12 north america 90figures 5.13-5.18 latin america 100figures 5.19-5.24 oecd europe 110figures 5.25-5.30 africa 120figures 5.31-5.36 middle east 130figures 5.37-5.42 eastern europe/eurasia 140figures 5.43-5.48 india 150figures 5.49-5.54 non oecd asia 160figures 5.55-5.60 china 170figures 5.61-5.66 oecd asia oceania 180

table 6.1 methodology overview 189table 6.2 summary of employment factors used in global

analysis in 2012 190table 6.3 employment factors used for coal fuel supply 191table 6.4 regional multipliers 191table 6.5 total global employment 192table 6.6 fossil fuels and nuclear energy: capacity,

investment and direct jobs 193table 6.7 wind energy: capacity, investment and

direct jobs 194table 6.8 biomass: capacity, investment and direct jobs 194table 6.9 geothermal power: capacity, investment and

direct jobs 195table 6.10 wave and tidal power: capacity, investment

and direct jobs 195table 6.11 solar photovoltaics: capacity, investment and

direct jobs 196table 6.12 solar thermal power: capacity, investment

and direct jobs 196table 6.13 solar heating: capacity, investment

and direct jobs 197table 6.14 geothermal and heat pump heating: capacity,

investment and direct jobs 197table 6.15 biomass heat: direct jobs in fuel supply 197

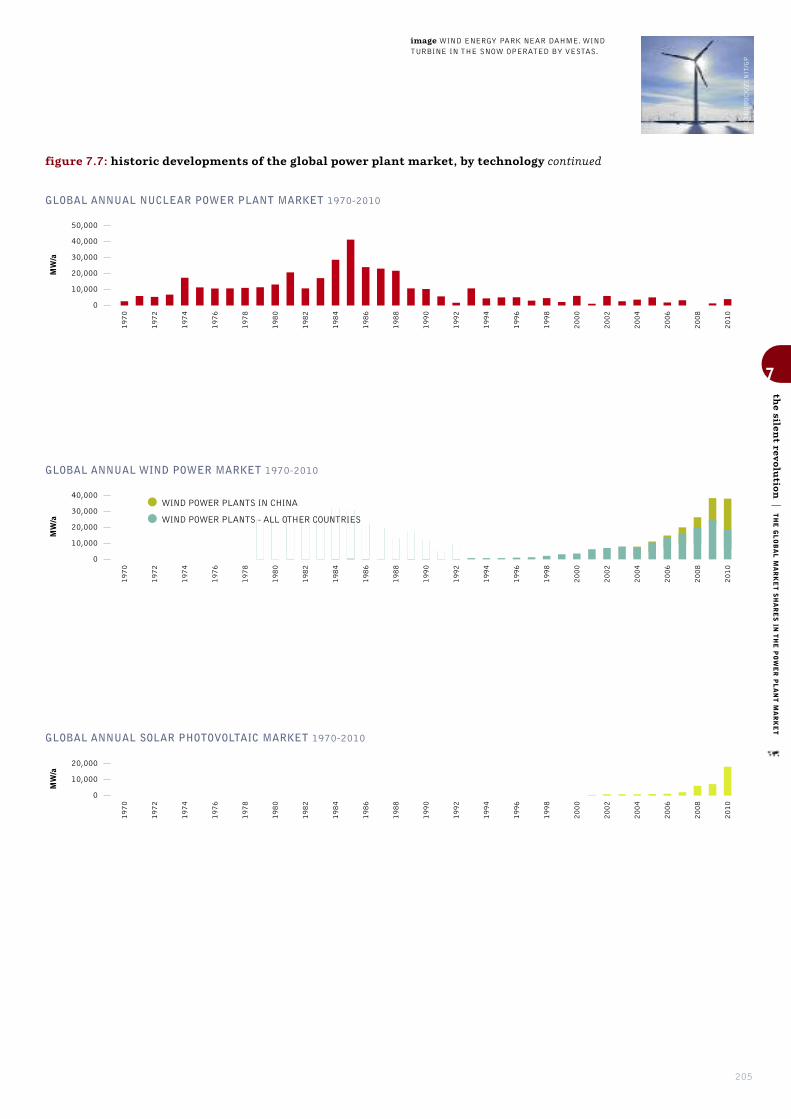

table 7.1 overview global renewable energy market 2011 207

table 8.1 global occurances of fossil and nuclear sources 209table 8.2 overview of the resulting emissions if all fossil

fuel resources were burned 210table 8.3 assumption on fossil fuel use in the

energy [r]evolution scenario 220table 8.4 renwable energy theoretical potential 221

list of tables

2

3

4

5

6

7

8

11

© GP/WILL ROSE

image A YOUNG INDIGENOUS NENET BOY PRACTICESWITH HIS REINDEER LASSO ROPE. THE INDIGENOUSNENETS PEOPLE MOVE EVERY 3 OR 4 DAYS SO THATTHEIR REINDEER DO NOT OVER GRAZE THE GROUNDAND THEY DO NOT OVER FISH THE LAKES. THE YAMALPENINSULA IS UNDER HEAVY THREAT FROM GLOBALWARMING AS TEMPERATURES INCREASE AND RUSSIASANCIENT PERMAFROST MELTS.

table 9.1 typical type and size of applications per market segment 236

table 10.1 reduction of energy use in comparison to the reference scenario per sector in 2050 264

table 10.2 share of technical potentials implemented in the energy [r]evolution scenario 264

table 10.3 reference and best practice electricity use by ‘wet appliances’ 269

table 10.4 effect on number of global operating power plants of introducing strict energy efficiency standards based on currently available technology 271

table 10.5 annual reduction of energy demand in ‘others’ sector in energy [r]evolution scenario in comparison to the corresponding reference scenario 272

table 10.6 global final energy consumption for sector ‘others’ (EJ) in 2030 and 2050 273

table 10.7 global final energy consumption for sector ‘others’ (EJ) in 2030 and 2050in underlying baseline scenarios 273

table 11.1 selection of measure and indicators 278table 11.2 LDV passenger-km per capita 278table 11.3 air traffic substitution potential of high

speed rail (HSR) 279table 11.4 modal shift of HDV tonne-km to freight rail

in 2050 281table 11.5 the world average energy intensities for MDV

and HDV in 2009 and 2050 energy [r]evolution 285table 11.6 technical efficiency potential for world

passenger transport 287table 11.7 technical efficiency potential for world

freight transport 287

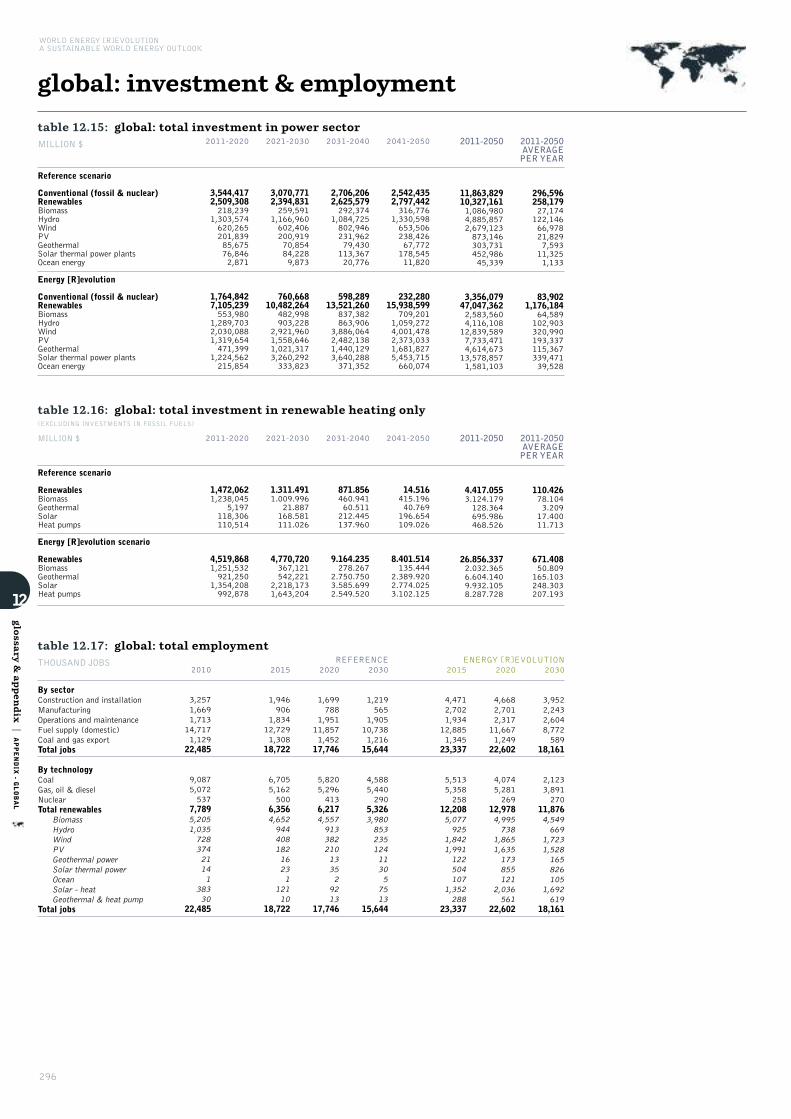

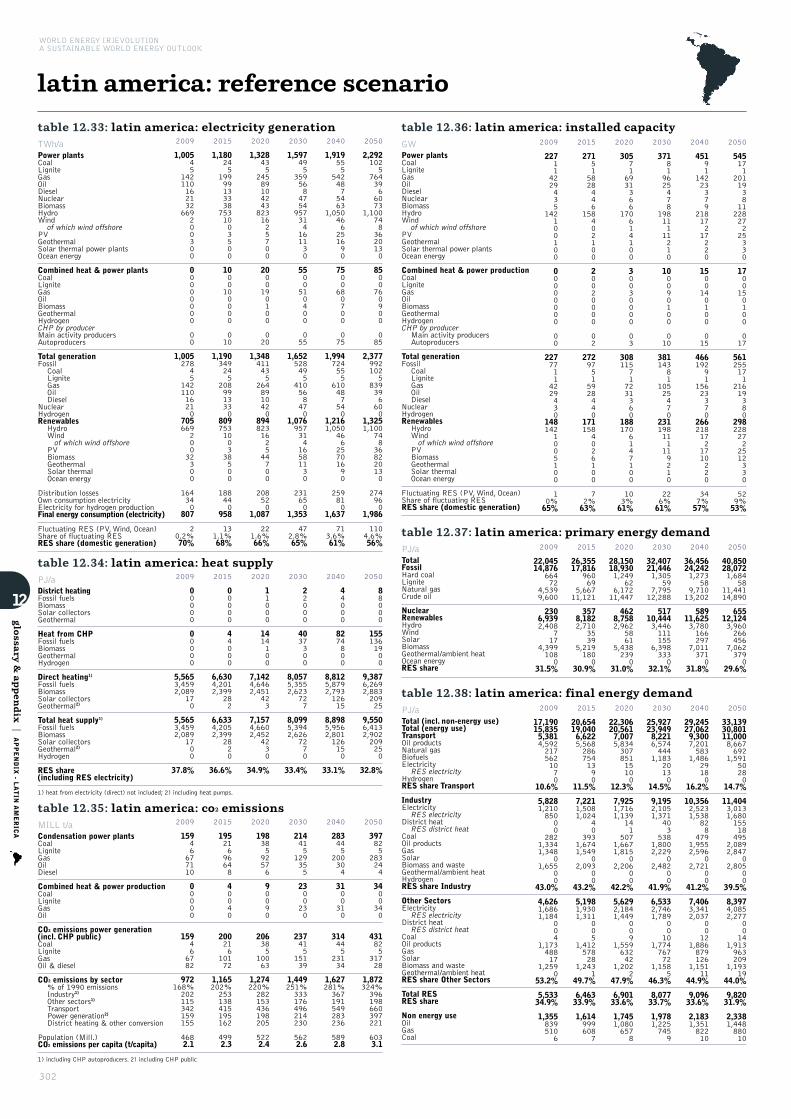

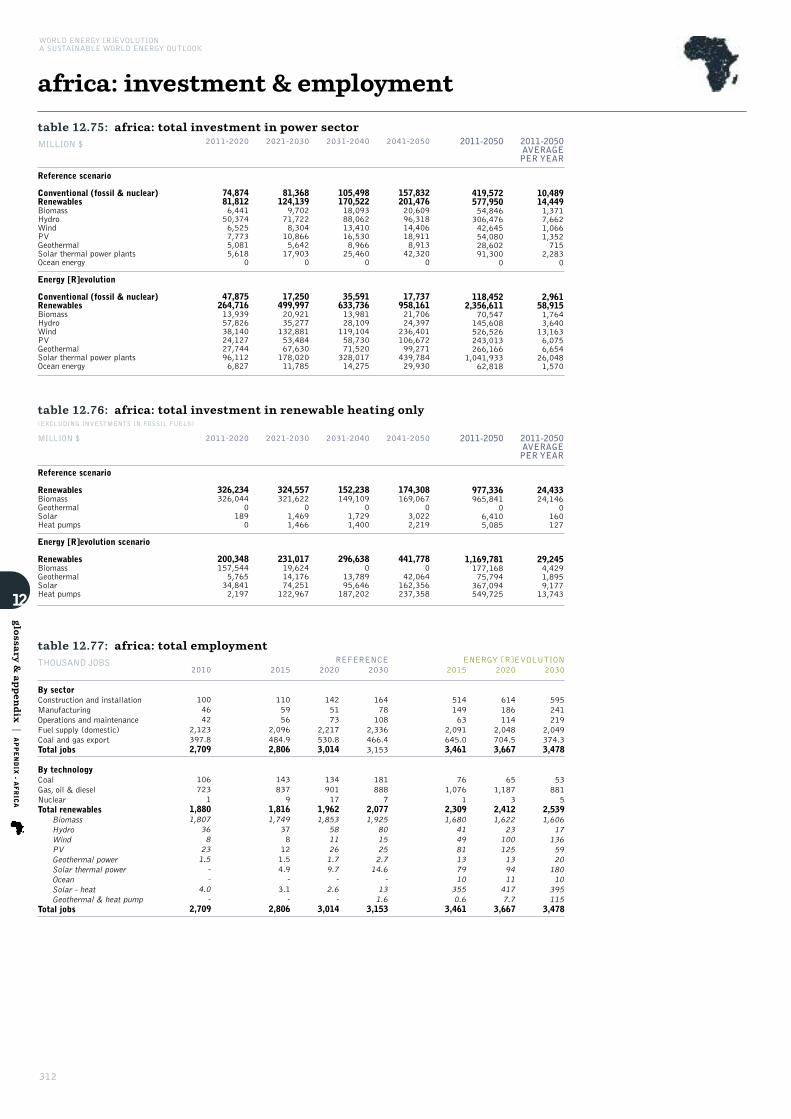

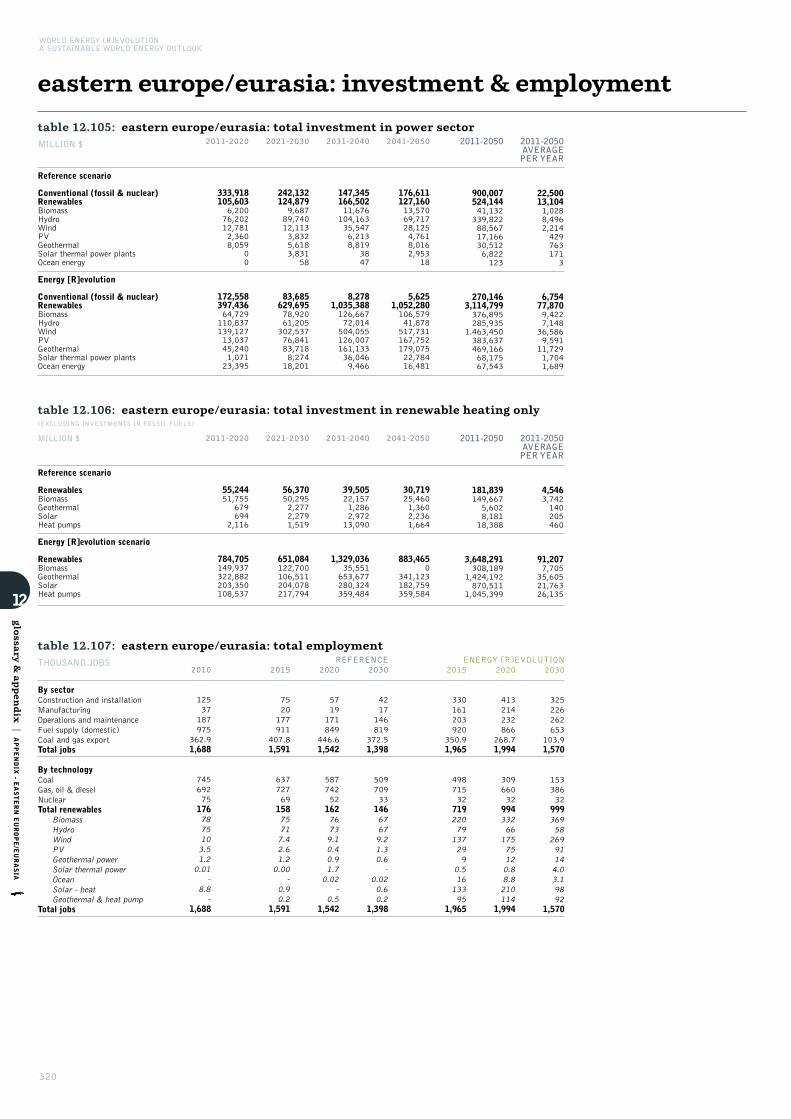

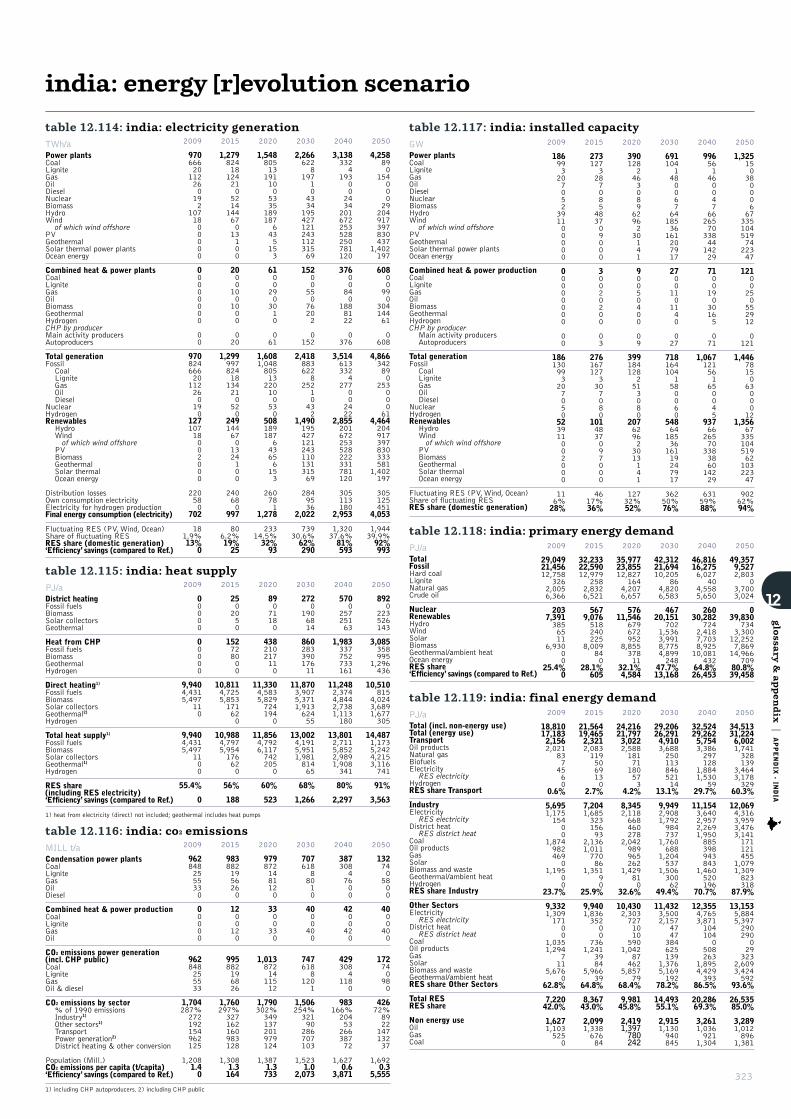

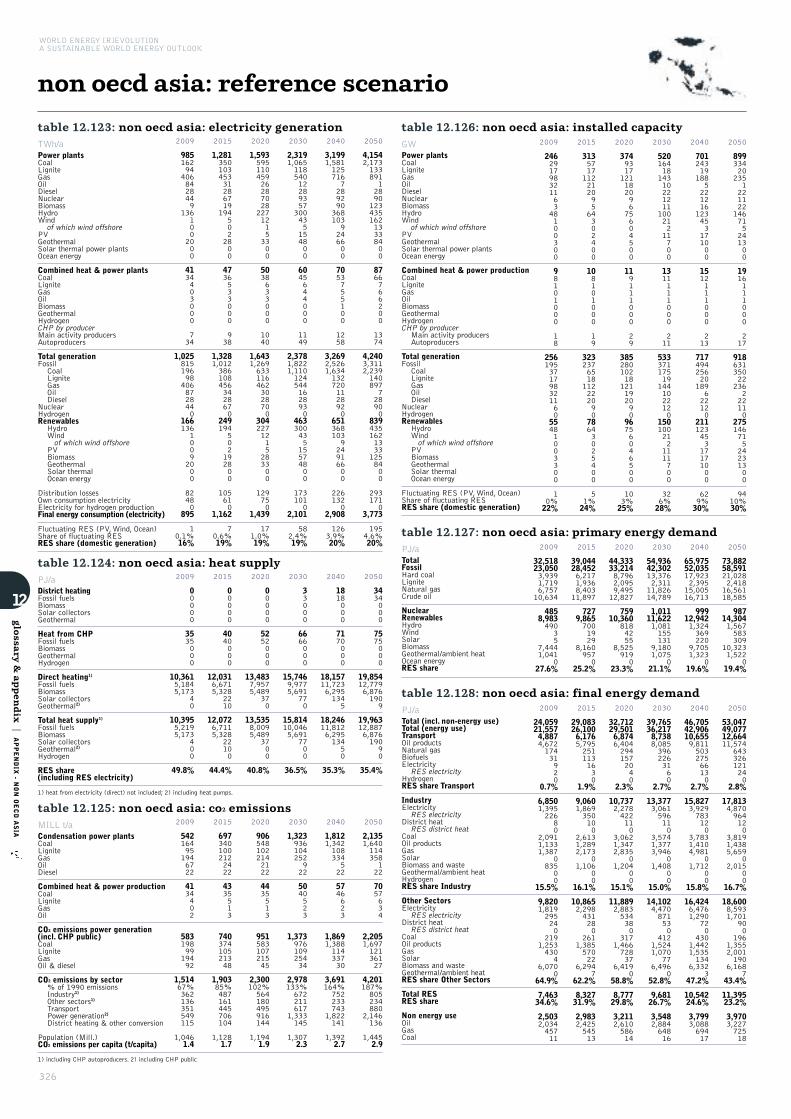

table 12.1 conversion factors – fossil fuels 292table 12.2 conversion factors – different energy units 292table 12.3-12.17 global scenario results 293table 12.18-12.32 latin america america scenario results 297table 12.33-12.47 oecd europe scenario results 301table 12.48-12.62 africa scenario results 305table 12.63-12.77 middle east scenario results 309table 12.78-12.92 eastern europe/eurasia scenario results 313table 12.93-12.107 india scenario results 317table 12.108-12.122 oecd north america scenario results 321table 12.123-12.137 non oecd asia scenario results 325table 12.138-12.152 china scenario results 329table 12.153-12.167 oecd asia oceania scenario results 333

map 8.1 oil reference scenario and the energy [r]evolution scenario 212

map 8.2 gas reference scenario and the energy [r]evolution scenario 214

map 8.3 coal reference scenario and the energy [r]evolution scenario 216

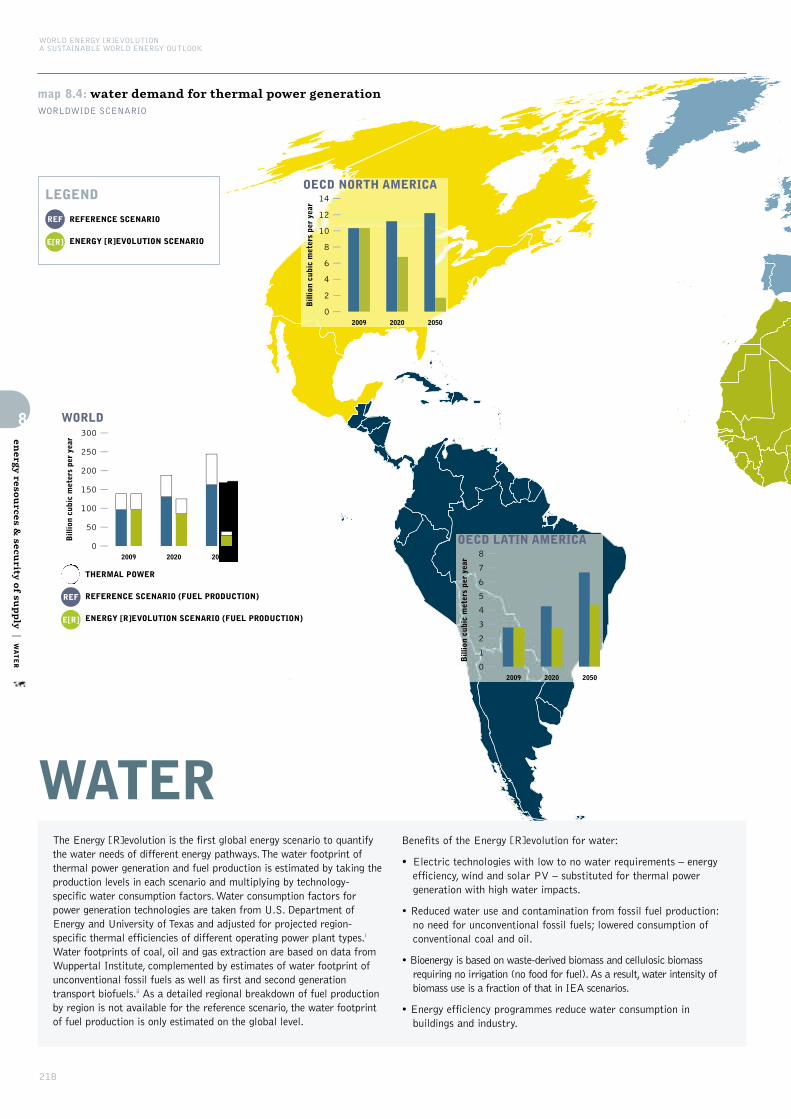

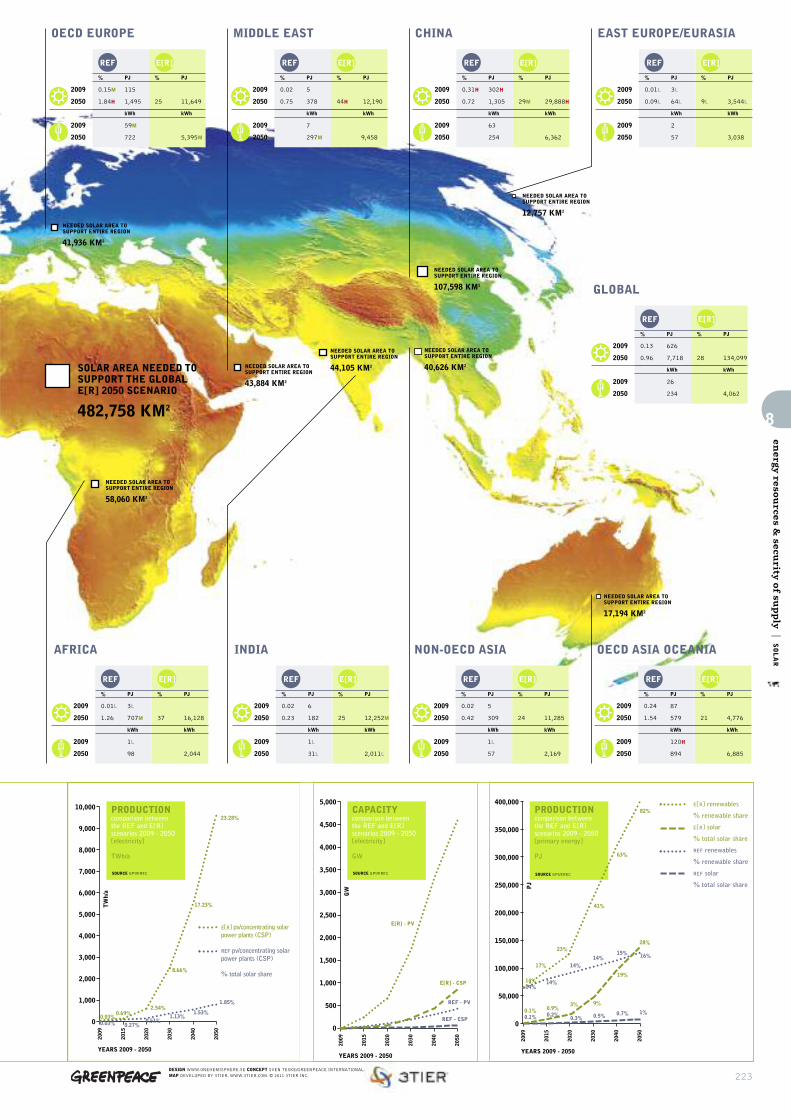

map 8.4 water demand for thermal power generation 218map 8.5 solar reference scenario and the

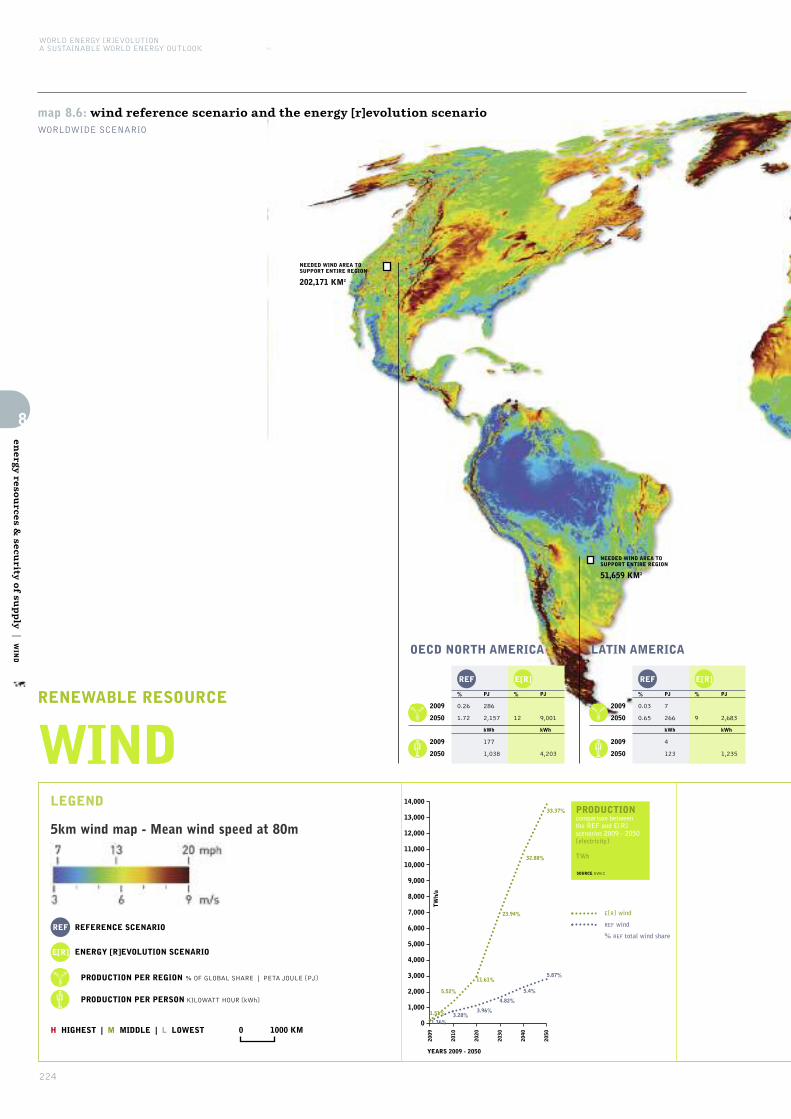

energy [r]evolution scenario 222map 8.6 wind reference scenario and the

energy [r]evolution scenario 224map 8.7 regional renewable energy potential 227

list of maps

89

10

11

12

image DUST IS SEEN BLOWING ACROSS THE WEST COAST OF SOUTHERN AFRICA FROM ANGOLA TO SOUTH AFRICA.

© SEAWIFS PROJECT, NASA/GODDARD SPACE FLIGHT CENTER, AND ORBIMAGE

“FOR THE SAKE OF A SOUND ENVIRONMENT, POLITICAL STABILITY AND THRIVING ECONOMIES, NOW IS THE TIME TO COMMIT

TO A TRULY SECURE AND SUSTAINABLE ENERGY FUTURE.”

introduction

greenhouse gas emissions. This is much faster than anythingexperienced in human history. As average temperature increasesapproach 2°C or more, damage to ecosystems and disruption to theclimate system increases dramatically, threatening millions of peoplewith increased risk of hunger, disease, flooding and water shortage.

A certain amount of climate change is now “locked in”, based onthe amount of carbon dioxide and other greenhouse gases alreadyemitted into the atmosphere since industrialisation began. No oneknows how much warming is “safe” for life on the planet.However, what we know is that the effects of climate change arealready being felt by populations and ecosystems. We can alreadysee melting glaciers, disintegrating polar ice, thawing permafrost,dying coral reefs, rising sea levels, changing ecosystems and fatalheat waves that are made more severe by a changed climate.

Japan’s major nuclear accident at Fukushima in March 2011following a tsunami came 25 years after the disastrous explosion inthe Chernobyl nuclear power plant in former Soviet Union, showingthat nuclear energy is an inherently unsafe source of power. TheFukushima disaster triggered a surge in global renewable energyand energy efficiency deals. At the same time, the poor state of theglobal economy has resulted in decreasing carbon prices, somegovernments reducing support for renewables, and a stagnation ofoverall investment, particularly in the OECD.

The world’s energy system has bestowed great benefits on society,but it has also come with high price tag: climate change, which isoccurring due to a build of carbon dioxide and other greenhousegases in the atmosphere caused by human activity; military andeconomic conflict due to uneven distribution of fossil resources;and millions of premature deaths and illness due to the air andwater pollution inherent in fossil fuel production and consumption.

The largest proportion of global fossil fuel use is to generate power, forheating and lighting, and for transport. Business-as-usual growth offossil-fuels is fundamentally unsustainable. Climate change threatensall continents, coastal cities, food production and ecosystems. It willmean more natural disasters such as fire and floods, disruption ofagriculture and damage to property as sea levels rise.

The pursuit of energy security, while remaining dependent on fossilfuel will lead to increasing greenhouse gas emissions and moreextreme climate impacts. Rising demand and rising prices drives thefossil fuel industry towards unconventional sources such as tar sands,shale gas and super-coal mines which destroy ecosystems and putwater supplies in danger. The inherent volatility of fossil fuel pricesputs more strain on an already stressed global economy.

According to the Intergovernmental Panel on Climate Change,global mean temperatures are expected to increase over the nexthundred years by up to 6.4° C if no action is taken to reduce

WORLD ENERGY [R]EVOLUTIONA SUSTAINABLE WORLD ENERGY OUTLOOK

12

Rapid cost reductions in the renewable energy sector have made itpossible to increase their share in power generation, heating andcooling and the transport sector faster than in previous editions. Forthe first time, this report takes a closer look at required investmentcosts for renewable heating technologies. The employment calculationhas been expanded to the heating sector as well and the overallmethodology of the employment calculation has been improved.

For the urgently needed access to energy for the almost 2 billionpeople who lack it at present, we have developed a new “bottomup” electrification concept in the North Indian state of Bihar (seechapter 2). New technology coupled with innovative finance mayresult in a new wave of rural electrification programs implementedby local people. A power plant market analysis of the past 40 yearshas been added to further develop the replacement strategy for oldpower plants. While the solar photovoltaic and wind installationhave been increased, the use of bio-energy has been reduced due toenvironmental concerns (see page 212). Concentrated solar powerstations and offshore wind remain cornerstones of the Energy[R]evolution, while we are aware that both technologies experienceincreasing difficulty raising finance than some other renewabletechnologies. Therefore we urge governments to introduce therequired policy frameworks to lower the risks for investors. Newstorage technologies need to move from R&D to marketimplementation; again this requires long term policy decisions.Without those new storage technologies, e.g. methane producedfrom renewables (see chapter 9), a transition towards more efficientelectric mobility will be more difficult.

Last but not least, the automobile industry needs to movetowards smaller and lighter vehicles to bring down the energydemand and introduce new technologies. We urge carmanufactures to finally move forward and repeat the hugesuccesses of the renewable energy industry.

This fourth edition of the Energy [R]evolution shows that with only1% of global GDP invested in renewable energy by 2050, 12 million jobs would be created in the renewable sector alone; andthe fuel costs savings would cover the additional investment twotimes over. To conclude, there are no real technical or economicbarriers to implementing the Energy [R]evolution. It is the lack ofpolitical will that is to blame for the slow progress to date.

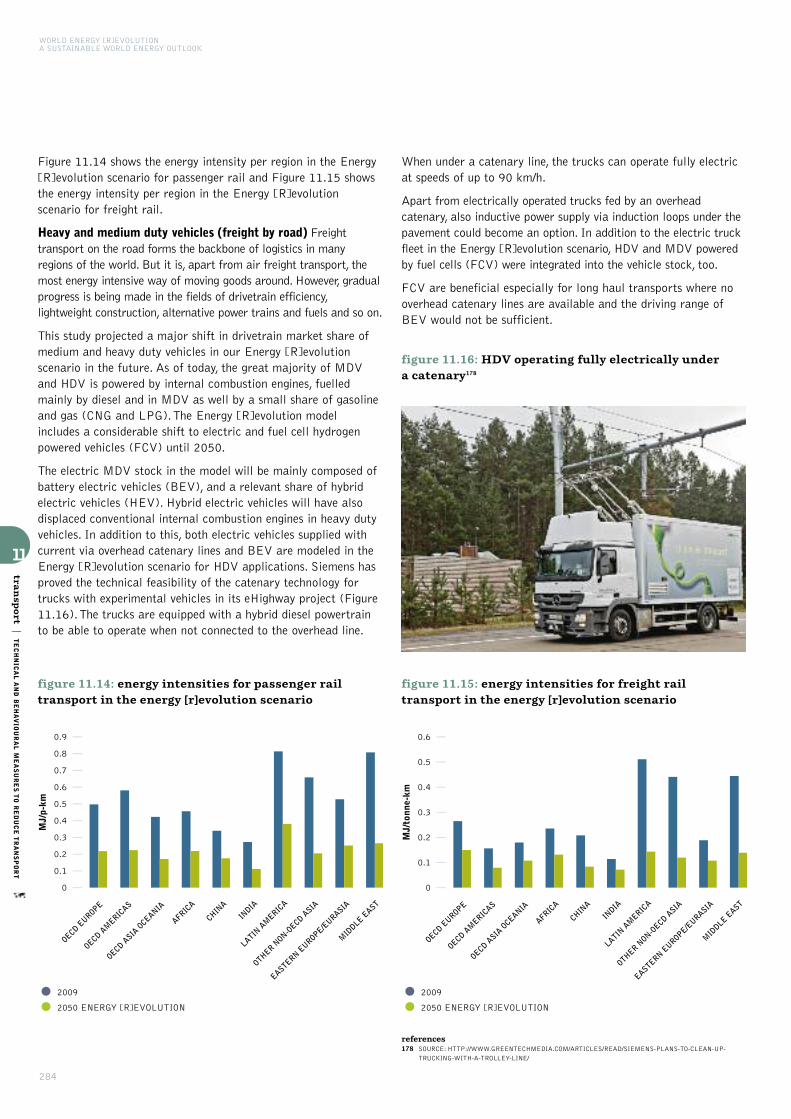

image WIND TURBINES AT THE NAN WIND FARM INNAN’AO. GUANGDONG PROVINCE HAS ONE OF THEBEST WIND RESOURCES IN CHINA AND IS ALREADYHOME TO SEVERAL INDUSTRIAL SCALE WIND FARMS.

© GP/XUAN CANXIONG

Rising oil demand is putting pressure on supply causing prices torise which make possible increased exploration for “marginal andunconventional” oil resources, such as regions of the Arctic newlyaccessible due to retreating polar ice, and the environmentallydestructive tar sands project in Canada.

For almost a decade it looked as if nothing could halt the growthof the renewable industries and their markets. The only way wasup. However the economic crisis in 2008/2009 and its continuingaftermath slowed growth and dampened demand. While therenewable industry is slowly recovering, increased competition,particularly in the solar PV and wind markets has driven downprices and shaved margins to the point where most manufacturersare struggling to survive. This is good news for the consumer,however, as the prices for solar PV fell more than 60% between2010 and 2012, and wind turbine prices have also decreasedsubstantially. This means that renewables are directly competitivewith heavily subsidized conventional generation in an increasingnumber of markets, but for the industry to meet its full potentialgovernments need to act to reduce the 600 billion USD/annum insubsidies to fossil fuels, and move ahead with pricing CO2 emissionsand other external costs of conventional generation.

As renewables play an increasing role in the energy system, one can nolonger speak of ‘integration’ of renewables’ but ‘transformation’, movingaway from the reliance on a few large power plants, or single fuels to aflexible system based on a wide variety of renewable sources of supply,some of which are variable. Investments in new infrastructure, smartergrids, better storage technologies and a new energy policy which takesall these new technologies into account are required.

the new energy [r]evolution

The IPCC’s Special Report on Renewable Energy and ClimateChange (SRREN) chose the last Energy [R]evolution edition(published in 2010) as one of the four benchmark scenarios forclimate mitigation energy scenarios. The Energy [R]evolution wasthe most ambitious, combining an uptake of renewable energy andrigorous energy efficiency measures to put forward the highestrenewable energy share by 2050, although some other scenariosactually had higher total quantities of renewables. Following thepublication of the SRREN in May 2011 in Abu Dhabi, the Energy[R]evolution has been widely quoted in the scientific literature.

The Energy [R]evolution 2012 takes into account the significantchanges in the global energy sector debate over the past two years. InJapan, the Fukushima Nuclear disaster following the devastatingtsunami triggered a faster phase-out of nuclear power in Germany, andraised the level of debate in many countries. The Deepwater Horizondisaster in the Gulf of Mexico in 2010 highlighted the damage that canbe done to eco-systems and livelihoods, while oil companies started newoil exploration in ever-more sensitive environments such as the ArcticCircle. The Energy [R]evolution oil pathway is based on a detailedanalysis of the global conventional oil resources, the currentinfrastructure of those industries, the estimated production capacitiesof existing oil wells in the light of projected production decline ratesand the investment plans known by end 2011. To end our addiction tooil, financial resources must flow from 2012 onwards to developingnew and larger markets for renewable energy technologies and energyefficiency to avoid “locking in” new fossil fuel infrastructure.

13

Sven TeskeCLIMATE & ENERGY UNIT

GREENPEACE INTERNATIONAL

JUNE 2012

Josche MuthPRESIDENT

EUROPEAN RENEWABLE

ENERGY COUNCIL (EREC)

Steve SawyerSECRETARY GENERAL

GLOBAL WIND ENERGY

COUNCIL (GWEC)

14

WORLD ENERGY [R]EVOLUTIONA SUSTAINABLE WORLD ENERGY OUTLOOK

The Energy [R]evolution Scenario has became a well known andwell respected energy analysis since it was first published forEurope in 2005. This is the fourth Global Energy [R]evolutionscenario; earlier editions were published in 2007, 2008 and 2010.

The Energy [R]evolution 2012 provides a consistent fundamentalpathway for how to protect our climate: getting the world fromwhere we are now to where we need to be by phasing out fossilfuels and cutting CO2 emissions while ensuring energy security.

The evolution of the scenarios has included a detailedemployment analysis in 2010, and now this edition expands theresearch further to incorporate new demand and transportprojections, new constraints for the oil and gas pathways andtechno-economic aspects of renewable heating systems. While the2010 edition had two scenarios – a basic and an advancedEnergy [R]evolution, this edition puts forward only one; based onthe previous ‘advanced’ case.

the fossil fuel dilemma

Raising energy demand is putting pressure on fossil fuel supplyand now pushing oil exploration towards “unconventional” oilresources. Remote and sensitive environments such as the Arcticare under threat from increased drilling, while theenvironmentally destructive tar sands projects in Canada arebeing pursued to extract more marginal sources. However,scarcity of conventional oil is not the most pressing reason tophase-out fossil fuels: cutting back dramatically is essential tosave the climate of our planet. Switching from fossil fuels torenewables also offers substantial benefits such as independencefrom world market fossil fuel prices and the creation of millionsof new green jobs. It can also provide energy to the two billionpeople currently without access to energy services. The Energy[R]evolution 2012 took a closer look at the measures required tophase-out oil faster in order to save the Arctic from oilexploration, avoid dangerous deep sea drilling projects and toleave oil shale in the ground.

executive summary

“AT THE CORE OF THE ENERGY [R]EVOLUTION WILL BE A CHANGE IN THE WAY THAT ENERGY IS PRODUCED, DISTRIBUTED AND CONSUMED.”

© MARKEL REDONDO/GREENPEACE

image GEMASOLAR, A 15 MWE SOLAR-ONLY POWER TOWER PLANT. IT’S 16-HOUR MOLTEN SALT STORAGE SYSTEM CAN DELIVER POWER AROUND THE CLOCK. IT RUNS THEEQUIVALENT OF 6,570 FULL HOURS OUT OF A 8,769 TOTAL. GEMASOLAR IS OWNED BY TORRESOL ENERGY AND HAS BEEN COMPLETED IN MAY 2011.

15

climate change threats

The threat of climate change, caused by rising globaltemperatures, is the most significant environmental challengefacing the world at the beginning of the 21st century. It hasmajor implications for the world’s social and economic stability,its natural resources and in particular, the way we produce our energy.

In order to avoid the most catastrophic impacts of climatechange, the global temperature increase must be kept as farbelow 2°C as possible. This is still possible, but time is runningout. To stay within this limit, global greenhouse gas emissions willneed to peak by 2015 and decline rapidly after that, reaching asclose to zero as possible by the middle of the 21st century. Themain greenhouse gas is carbon dioxide (CO2) produced by usingfossil fuels for energy and transport. Keeping the globaltemperature increase to 2°C is often referred to as a ‘safe level’of warming, but this does not reflect the reality of the latestscience. This shows that a warming of 2°C above pre-industriallevels would pose unacceptable risks to many of the world’s keynatural and human systems.1 Even with a 1.5°C warming,increases in drought, heat waves and floods, along with otheradverse impacts such as increased water stress for up to 1.7billion people, wildfire frequency and flood risks, are projected inmany regions. Neither does staying below 2°C rule out large-scale disasters such as melting ice sheets. Partial de-glaciation ofthe Greenland ice sheet, and possibly the West Antarctic icesheet, could even occur from additional warming within a rangeof 0.8 – 3.8°C above current levels.2 If rising temperatures are tobe kept within acceptable limits then we need to significantlyreduce our greenhouse gas emissions. This makes bothenvironmental and economic sense.

global negotiation

Recognising the global threats of climate change, the signatoriesto the 1992 UN Framework Convention on Climate Change(UNFCCC) agreed to the Kyoto Protocol in 1997. The Protocolentered into force in early 2005 and its 193 members meetcontinuously to negotiate further refinement and development ofthe agreement. Only one major industrialised nation, the UnitedStates, has not ratified the protocol. In 2011, Canada announcedits intention to withdraw from the protocol. In Copenhagen in2009, the members of the UNFCCC were not able to deliver anew climate change agreement towards ambitious and fairemission reductions. At the 2012 Conference of the Parties inDurban, there was agreement to reach a new agreement by 2015and to adopt a second commitment period at the end of 2012.However, the United Nations Environment Program’s examinationof the climate action pledges for 2020 shows a major gapbetween what the science demands to curb climate change andwhat the countries plan to do. The proposed mitigation pledgesput forward by governments are likely to allow global warming toat least 2.5 to 5 degrees temperature increase above pre-industrial levels.3

© GP/PETER CATON

image SOVARANI KOYAL LIVES IN SATJELLIA ISLAND AND IS ONE OF THE MANY PEOPLEAFFECTED BY SEA LEVEL RISE: “NOWADAYS, HEAVY FLOODS ARE GOING ON HERE. THE WATERLEVEL IS INCREASING AND THE TEMPERATURE TOO. WE CANNOT LIVE HERE, THE HEAT ISBECOMING UNBEARABLE. WE HAVE RECEIVED A PLASTIC SHEET AND HAVE COVERED OURHOME WITH IT. DURING THE COMING MONSOON WE SHALL WRAP OUR BODIES IN THE PLASTIC TOSTAY DRY. WE HAVE ONLY A FEW GOATS BUT WE DO NOT KNOW WHERE THEY ARE. WE ALSOHAVE TWO CHILDREN AND WE CANNOT MANAGE TO FEED THEM.”

the nuclear issue

The nuclear industry promises that nuclear energy can contributeto both climate protection and energy security, however theirclaims are not supported by data. The most recent EnergyTechnology Perspectives report published by the InternationalEnergy Agency includes a Blue Map scenario including aquadrupling of nuclear capacity between now and 2050. Toachieve this, the report says that on average 32 large reactors(1,000 MWe each) would have to be built every year from nowuntil 2050. According to the IEA’s own scenario, such massivenuclear expansion would cut carbon emissions by less than 5%.More realistic analysis shows the past development history ofnuclear power and the global production capacity make suchexpansion extremely unviable. Japan’s major nuclear accident atFukushima in March 2011 following a tsunami came 25 yearsafter the disastrous explosion in the Chernobyl nuclear powerplant in former Soviet Union, illustrating the inherent risks ofnuclear energy. Nuclear energy is simply unsafe, expensive, hascontinuing waste disposal problems and can not reduce emissionsby a large enough amount.

climate change and security of supply

Security of supply – both for access to supplies and financialstability – is now at the top of the energy policy agenda. Recentrapidly fluctuating oil prices are lined to a combination of manyevents, however one reason for these price fluctuations is thatsupplies of all proven resources of fossil fuels are becomingscarcer and more expensive to produce. Some ‘non-conventional’resources such as shale oil have become economic, withdevastating consequences for the local environment. The days of‘cheap oil and gas’ are coming to an end. Uranium, the fuel fornuclear power, is also a finite resource. By contrast, the reservesof renewable energy that are technically accessible globally arelarge enough to provide more than 40 times more energy thanthe world currently consumes, forever, according to the latestIPCC Special report Renewables (SRREN). Renewable energytechnologies are at different levels of technical and economicmaturity, but a variety of sources offer increasingly attractiveoptions. Cost reductions in just the past two years have changedthe economic of renewables fundamentally, especially wind andsolar photovoltaics. The common feature of all renewable energysources, the wind, sun, earth’s crust, and ocean is that theyproduce little or no greenhouse gases and are a virtuallyinexhaustible ‘fuel’. Some technologies are already competitive;the solar and the wind industry have maintained double digitgrowth rates over 10 years now, leading to faster technologydeployment world wide.

references1 W. L. HARE. A SAFE LANDING FOR THE CLIMATE. STATE OF THE WORLD. WORLDWATCH INSTITUTE. 2009.

2 JOEL B. SMITH, STEPHEN H. SCHNEIDER, MICHAEL OPPENHEIMER, GARY W. YOHE, WILLIAM HARE,

MICHAEL D. MASTRANDREA, ANAND PATWARDHAN, IAN BURTON, JAN CORFEE-MORLOT, CHRIS H. D.

MAGADZA, HANS-MARTIN FÜSSEL, A. BARRIE PITTOCK, ATIQ RAHMAN, AVELINO SUAREZ, AND JEAN-

PASCAL VAN YPERSELE: ASSESSING DANGEROUS CLIMATE CHANGE THROUGH AN UPDATE OF THE

INTERGOVERNMENTAL PANEL ON CLIMATE CHANGE (IPCC) “REASONS FOR CONCERN”. PROCEEDINGS

OF THE NATIONAL ACADEMY OF SCIENCES. PUBLISHED ONLINE BEFORE PRINT FEBRUARY 26, 2009, DOI:

10.1073/PNAS.0812355106. THE ARTICLE IS FREELY AVAILABLE

AT:HTTP://WWW.PNAS.ORG/CONTENT/EARLY/2009/02/25/0812355106.FULL.PDF. A COPY OF THE GRAPH

CAN BE FOUND ON APPENDIX 1.

3 UNITED NATIONS ENVIRONMENT PROGRAMME (UNEP): ‘BRIDGING THE EMISSIONS GAP’. A UNEP

SYNTHESIS REPORT, NOV. 2011.

16

WORLD ENERGY [R]EVOLUTIONA SUSTAINABLE WORLD ENERGY OUTLOOK

Energy efficiency is a sleeping giant – offering the most costcompetitive way to reform the energy sector. There is enormouspotential for reducing our consumption of energy, while providingthe same level of energy services. New business models toimplement energy efficiency must be developed and must getmore political support. This study details a series of energyefficiency measures which can substantially reduce demandacross industry, homes, business and services as well as transport.

the energy [r]evolution key principles

The expert consensus is that this fundamental shift in the way weconsume and generate energy must begin immediately and be wellunderway within the next ten years in order to avert the worstimpacts of climate change.4 The scale of the challenge requires acomplete transformation of the way we produce, consume anddistribute energy, while maintaining economic growth. The five keyprinciples behind this Energy [R]evolution will be to:

• Implement renewable solutions, especially throughdecentralised energy systems and grid expansions

• Respect the natural limits of the environment

• Phase out dirty, unsustainable energy sources

• Create greater equity in the use of resources

• Decouple economic growth from the consumption of fossil fuels

Decentralised energy systems, where power and heat areproduced close to the point of final use reduce grid loads andenergy losses in distribution. Investments in ‘climateinfrastructure’ such as smart interactive grids and transmissiongrids to transport large quantities of offshore wind andconcentrating solar power are essential. Building up clusters ofrenewable micro grids, especially for people living in remoteareas, will be a central tool in providing sustainable electricity tothe almost two billion people around who currently don’t haveaccess to electricity.

the energy [r]evolution – key results

Renewable energy sources account for 13.5% of the world’sprimary energy demand in 2009. The main source is biomass,which is mostly used in the heat sector.

For electricity generation renewables contribute about 19.3%and for heat supply, around 25%, much of this is from traditionaluses such as firewood. About 81% of the primary energy supplytoday still comes from fossil fuels and 5.5% from nuclear energy.

The Energy [R]evolution scenario describes developmentpathways to a sustainable energy supply, achieving the urgentlyneeded CO2 reduction target and a nuclear phase-out, withoutunconventional oil resources. The results of the Energy[R]evolution scenario which will be achieved through thefollowing measures:

• Curbing global energy demand: The world’s energy demand isprojected by combining population development, GDP growthand energy intensity. Under the Reference scenario, totalprimary energy demand increases by 61% from about 500 EJ(Exajoules) per year in 2009 to 806 EJ per year in 2050. Inthe Energy [R]evolution scenario, demand increases by only10% compared to current consumption until 2020 anddecreases slightly afterwards to 2009 levels.

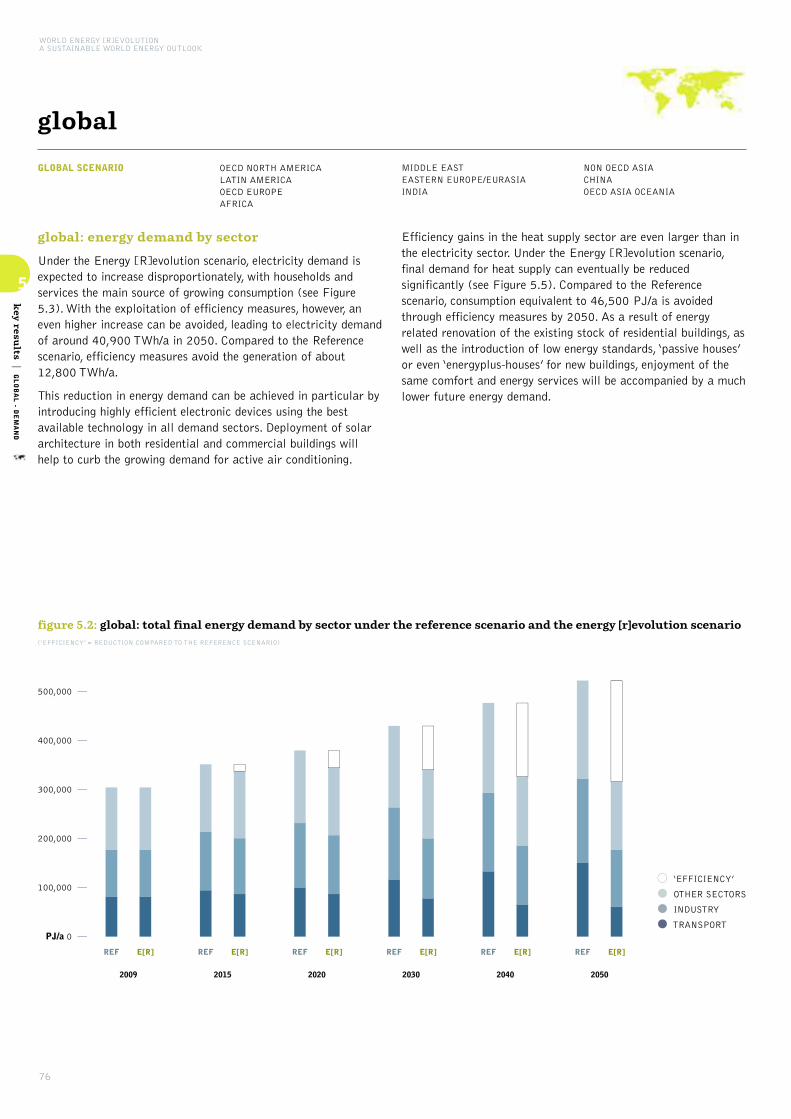

• Controlling global power demand: Under the Energy[R]evolution scenario, electricity demand is expected toincrease disproportionately, the main growth in households andservices. With adequate efficiency measures, however, a higherincrease can be avoided, leading to electricity demand ofaround 41,000 TWh/a in 2050. Compared to the Referencescenario, efficiency measures avoid the generation of 12,800 TWh/a.

• Reducing global heating demand: Efficiency gains in the heatsupply sector are even larger than in the electricity sector.Under the Energy [R]evolution scenario, final demand for heatsupply can eventually be reduced significantly. Compared to theReference scenario, consumption equivalent to 46,500 PJ/a isavoided through efficiency measures by 2050. The lowerdemand can be achieved by energy-related renovation of theexisting stock of residential buildings, introduction of lowenergy standards; even ‘energy-plus-houses’ for new buildings,so people can enjoy the same comfort and energy services.

references4 IPCC – SPECIAL REPORT RENEWABLES, CHAPTER 1, MAY 2011.

projections to reality

Projection of global installed wind power capacity at theend of 2010 in the first Global Energy [R]evolution,published in January 2007.

>> 156 GW

Actual global installed wind capacity at the end of 2010.

>> 197 GW

While at the end of 2011 already 237 GW have beeninstalled. More needs to be done.

17

© GP/ALBERTO CESAR ARAUJOimage THOUSANDS OF FISH DIE AT THE DRY RIVER

BED OF MANAQUIRI LAKE, 150 KILOMETERS FROMAMAZONAS STATE CAPITOL MANAUS, BRAZIL.

• Development of global industry energy demand: The energydemand in the industry sector will grow in both scenarios.While the economic growth rates in the Reference and theEnergy [R]evolution scenario are identical, the growth of theoverall energy demand is different due to a faster increase ofthe energy intensity in the alternative case. Decouplingeconomic growth with the energy demand is key to reach asustainable energy supply by 2050, the Energy [R]evolutionscenario saves 40% less energy per $ GDP than the Reference case.

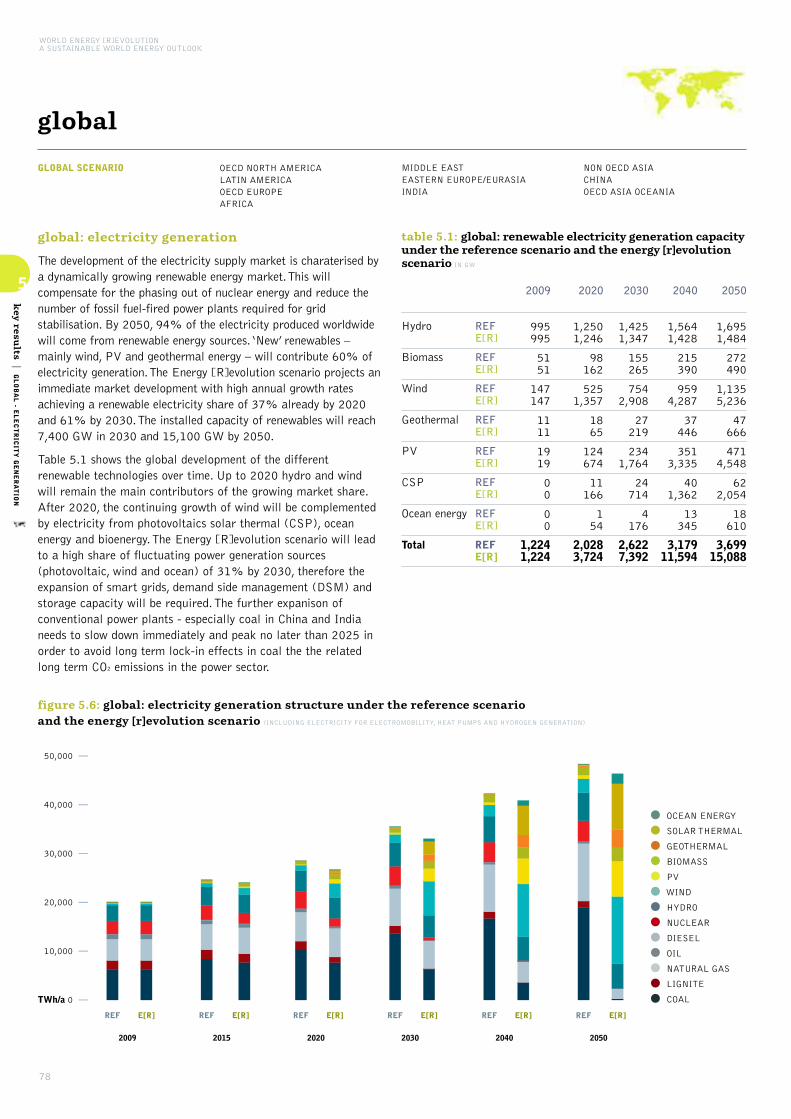

• Electricity generation: A dynamically growing renewableenergy market compensates for phasing out nuclear energy andfewer fossil fuel-fired power plants. By 2050, 94% of theelectricity produced worldwide will come from renewableenergy sources. ‘New’ renewables – mainly wind, PV andgeothermal energy – will contribute 60% of electricitygeneration. The Energy [R]evolution scenario projects animmediate market development with high annual growth ratesachieving a renewable electricity share of 37% already by2020 and 61% by 2030. The installed capacity of renewableswill reach almost 7,400 GW in 2030 and 15,100 GW by 2050.

• Future costs of electricity generation: Under the Energy[R]evolution scenario the costs of electricity generationincrease slightly compared to the Reference scenario. Thisdifference will be on average less than 0.6 $cent/kWh up to2020. However, if fossil fuel prices go any higher than themodel assumes, this gap will decrease. Electricity generationcosts will become economically favourable under the Energy[R]evolution scenario by 2025 and by 2050, costs will besignificantly lower: about 8 $cents/kWh – or 45% below thosein the Reference version

• The future electricity bill: Under the Reference scenario, theunchecked growth in demand, results in total electricity supplycosts rising from today’s $ 2,364 billion per year to more than$ 8,830 billion in 2050. The Energy [R]evolution scenariohelps to stabilise energy costs, increasing energy efficiency andshifting to renewable energy supply means long term costs forelectricity supply are 22% lower in 2050 than in the Referencescenario (including estimated costs for efficiency measures).

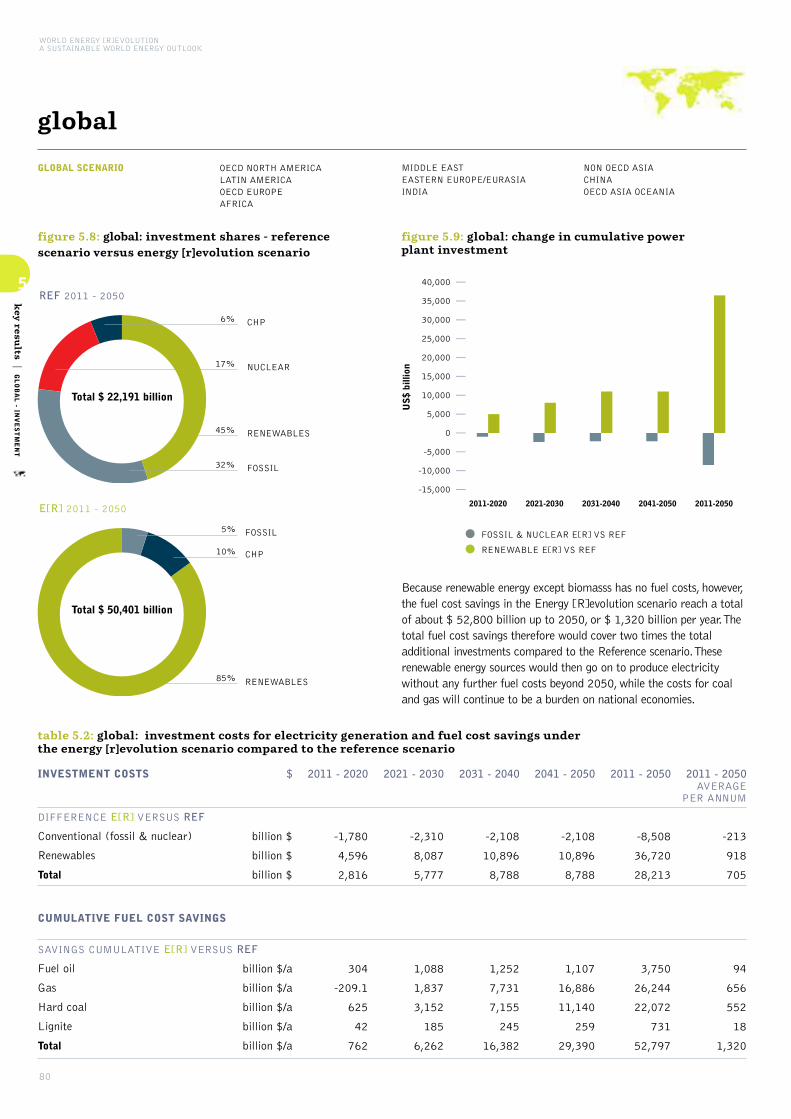

• Future investment in power generation: The overall global levelof investment required in new power plants up to 2020 will bein the region of $ 11.5 trillion in the Reference case and $ 20.1 trillion in the Energy [R]evolution. The need to replacethe ageing fleet of power plants in OECD countries and toinstall new power plants in developing countries will be themajor investment drivers. Depending on the local resources,renewable energy resources (for example wind in a high windarea) can produce electricity at the same cost levels as coal orgas power plants. Solar photovoltaic already reach ‘grid parity’in many industrialised countries. For the Energy [R]evolutionscenario until 2050 to become reality would require about $ 50,400 billion in investment in the power sector (includinginvestments for replacement after the economic lifetime of theplants). Under the Reference scenario, total investment would

be split 48% to 52% between conventional power plants andrenewable energy plus cogeneration (CHP) up to 2050. Underthe Energy [R]evolution scenario 95% of global investmentwould be in renewables and cogeneration. Up to 2030, thepower sector investment that does go to fossil fuels would befocused mainly on cogeneration plants. The average annualinvestment in the power sector under the Energy [R]evolutionscenario from today to 2050 would be $ 1,260 billion,compared to $ 555 billion in the Reference case.

• Fuel costs savings: Because renewable energy, except biomass,has no fuel costs, the fuel cost savings in the Energy[R]evolution scenario reach a total of $ 52,800 billion up to2050, or $ 1320 billion per year. The total fuel cost savingstherefore would cover more than two times the total additionalinvestments compared to the Reference scenario. Theserenewable energy sources would then go on to produceelectricity without any further fuel costs beyond 2050, whilethe costs for coal and gas will continue to be a burden onnational economies.

• Heating supply: Renewables currently provide 25% of theglobal energy demand for heat supply, the main contributioncoming from the use of biomass. In the Energy [R]evolutionscenario, renewables provide more than 50% of the world’stotal heat demand in 2030 and more than 90% in 2050.Energy efficiency measures can decrease the current demandfor heat supply by 10 %, and still support improving livingstandards of a growing population.

• Future investments in the heat sector: The heat sector in theEnergy [R]evolution scenario would require a major revision ofcurrent investment strategies in heating technologies. Inparticular enormous increases in installations are required torealise the potential of the not yet common solar andgeothermal technologies and heat pumps. Installed capacityneeds to increase by a factor of 60 for solar thermal and by afactor of over 3,000 for geothermal and heat pumps. Becausethe level of technological complexity in this sector is extremelyvariable, the Energy [R]evolution scenario can only be roughlycalculated, to require around $ 27 trillion investment inrenewable heating technologies up to 2050. This includesinvestments for replacement after the economic lifetime of theplant and is approximately $ 670 billion per year.

18

WORLD ENERGY [R]EVOLUTIONA SUSTAINABLE WORLD ENERGY OUTLOOK

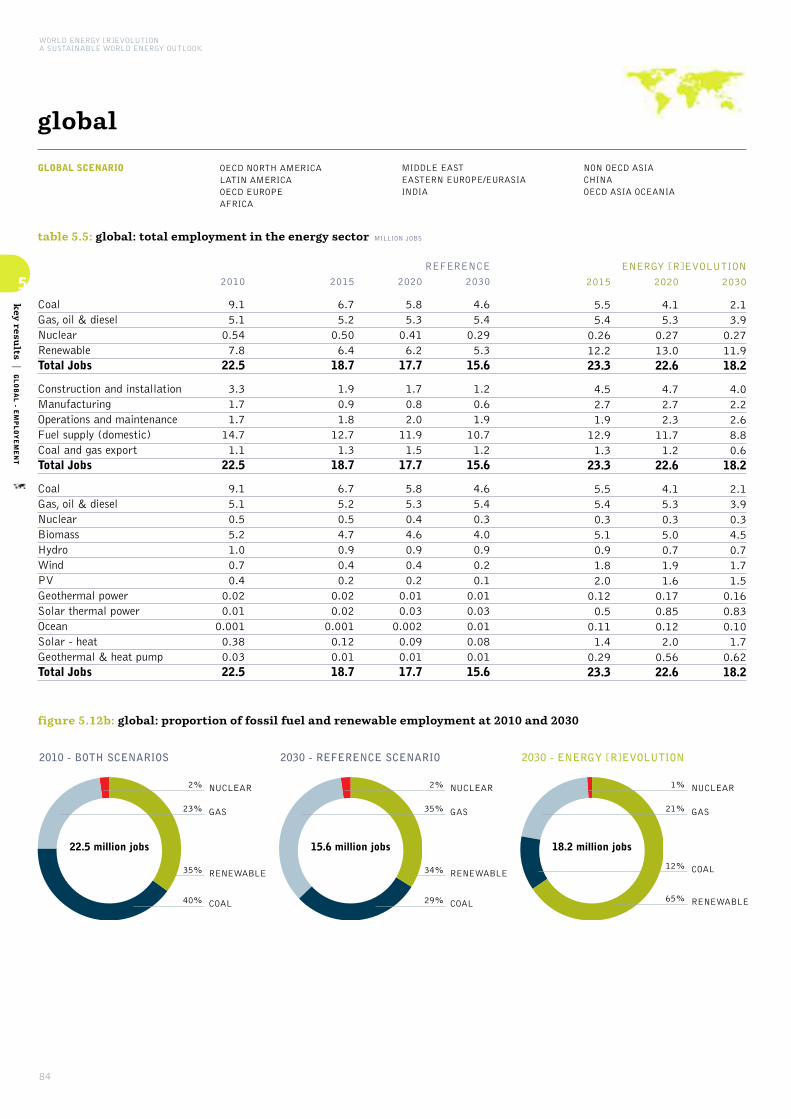

• Future employment in the energy sector: The Energy[R]evolution scenario results in more global energy sector jobsat every stage of the projection.

There are 23.3 million energy sector jobs in the Energy [R]evolution in 2015, and 18.7 million in theReference scenario.

In 2020, there are 22.6 million jobs in the Energy [R]evolution scenario, and 17.8 million in the Reference scenario.

In 2030, there are 18.3 million jobs in the Energy [R]evolution scenario and 15.7 million in the Reference scenario.

There is a decline in overall job numbers under both scenariosbetween 2010 and 2030. Jobs in the coal sector declinesignificantly in both scenarios, leading to a drop of 6.8 millionenergy jobs in the Reference scenario by 2030. Strong growth inthe renewable sector leads to an increase of 4% in total energysector jobs in the Energy [R]evolution scenario by 2015. Jobnumbers fall after 2020, so jobs in the Energy [R]evolution are19% below 2010 levels at 2030. However, this is 2.5 millionmore jobs than in the Reference scenario. Renewable energyaccounts for 65% of energy jobs by 2030, with the majorityspread over wind, solar PV, solar heating, and biomass.

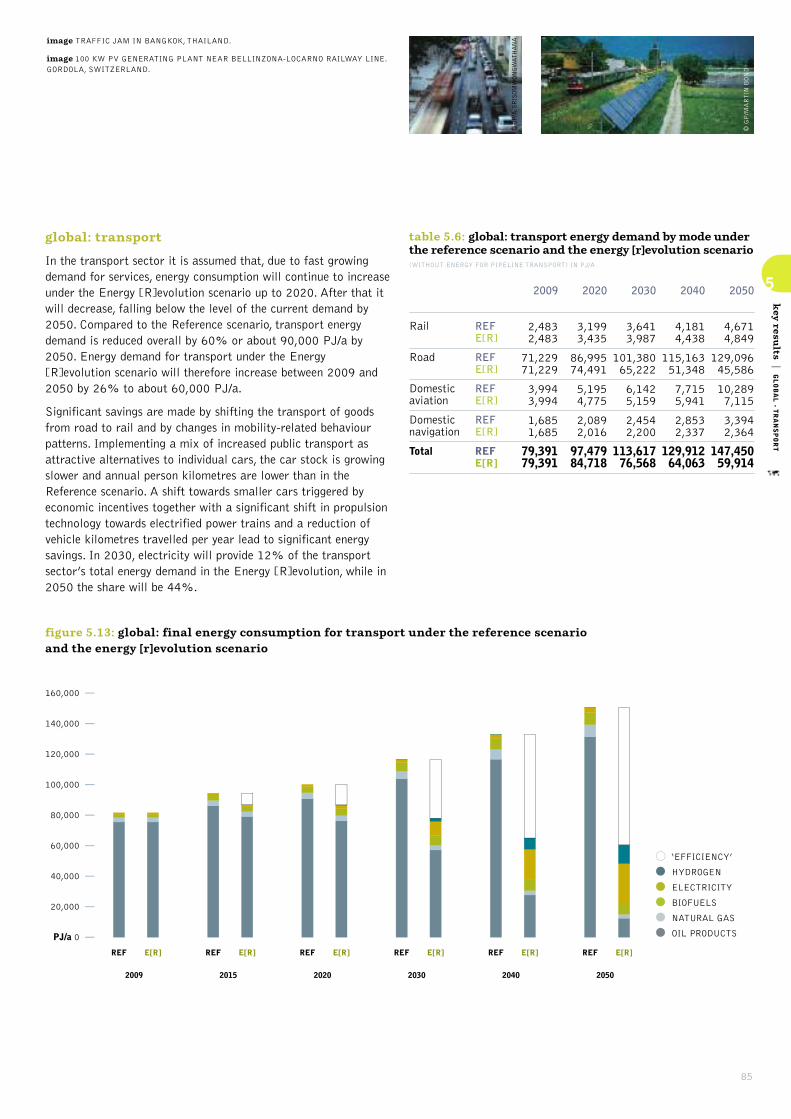

• Global transport: In the transport sector it is assumed that,energy consumption will continue to increase under the Energy[R]evolution scenario up to 2020 due to fast growing demandfor services. After that it falls back to the level of the currentdemand by 2050. Compared to the Reference scenario,transport energy demand is reduced overall by 60% or about90,000 PJ/a by 2050. Energy demand for transport under theEnergy [R]evolution scenario will therefore increase between2009 and 2050 by only 26% to about 60,500 PJ/a.Significant savings are made from a shift towards smaller carstriggered by economic incentives together with a significantshift in propulsion technology towards electrified power trains –together with reducing vehicle kilometres travelled per year. In2030, electricity will provide 12% of the transport sector’stotal energy demand in the Energy [R]evolution, while in 2050the share will be 44%.

• Primary energy consumption: Under the Energy [R]evolutionscenario the overall primary energy demand will be reduced by40% in 2050 compared to the Reference scenario. In thisprojection almost the entire global electricity supply, includingthe majority of the energy used in buildings and industry, wouldcome from renewable energy sources. The transport sector, inparticular aviation and shipping, would be the last sector tobecome fossil fuel free.

• Development of CO2 emissions: Worldwide CO2 emissions in theReference case will increase by 62% while under the Energy[R]evolution scenario they will decrease from 27,925 milliontons in 2009 to 3,076 million t in 2050. Annual per capitaemissions will drop from 4.1 tonne CO2 to 2.4 tonne CO2 in2030 and 0.3 tonne CO2 in 2050. Even with a phase out ofnuclear energy and increasing demand, CO2 emissions willdecrease in the electricity sector. In the long term, efficiencygains and greater use of renewable electricity for vehicles willalso reduce emissions in the transport sector. With a share of33% of CO2 emissions in 2050, the transport sector will be themain source of emissions ahead of the industry and powergeneration. By 2050 the Global Energy related CO2 emissionsare 85% under 1990 levels.

policy changes

To make the Energy [R]evolution real and to avoid dangerousclimate change, Greenpeace, GWEC and EREC demand that the following policies and actions are implemented in the energy sector:

1. Phase out all subsidies for fossil fuels and nuclear energy.

2. Internalise the external (social and environmental) costs ofenergy production through ‘cap and trade’ emissions trading.

3. Mandate strict efficiency standards for all energy consumingappliances, buildings and vehicles.

4. Establish legally binding targets for renewable energy andcombined heat and power generation.

5. Reform the electricity markets by guaranteeing priorityaccess to the grid for renewable power generators.

6. Provide defined and stable returns for investors, for exampleby feed-in tariff programmes.

7. Implement better labelling and disclosure mechanisms toprovide more environmental product information.

8. Increase research and development budgets for renewableenergy and energy efficiency.

19

1climate and energy policy

image HURRICANE BUD FORMING OVER THE EASTERN PACIFIC OCEAN, MAY 2012.

THE UNFCCC AND THE KYOTO PROTOCOL

INTERNATIONAL ENERGY POLICY

RENEWABLE ENERGY TARGETS

POLICY CHANGES IN THE ENERGY SECTOR

FTSM: A SPECIAL FEED-IN LAWPROPOSAL FOR DEVELOPINGCOUNTRIES

FINANCING THE ENERGY[R]EVOLUTION WITH FTSM

bridgingthe gap”“

© NASA/JEFF SCHMALTZ

1

If we do not take urgent and immediate action to protect theclimate, the threats from climate change could become irreversible.

The goal of climate policy should be to keep the global meantemperature rise to less than 2°C above pre-industrial levels. Wehave very little time within which we can change our energysystem to meet these targets. This means that global emissionswill have to peak and start to decline by the end of the nextdecade at the latest.

The only way forwards is a rapid reduction in the emission ofgreenhouse gases into the atmosphere.

1.1 the UNFCCC and the kyoto protocol

Recognising the global threats of climate change, the signatoriesto the 1992 UN Framework Convention on Climate Change(UNFCCC) agreed the Kyoto Protocol in 1997. The Protocolentered into force in early 2005 and its 193 members meetcontinuously to negotiate further refinement and development ofthe agreement. Only one major industrialised nation, the UnitedStates, has not ratified the protocol. In 2011, Canada announcedits intention to withdraw from the protocol.

In Copenhagen in 2009, the 195 members of the UNFCCC weresupposed to deliver a new climate change agreement towardsambitious and fair emission reductions. Unfortunately theambition to reach such an agreement failed at this conference.

At the 2012 Conference of the Parties in Durban, there wasagreement to reach a new agreement by 2015. There is alsoagreement to adopt a second commitment period at the end of2012. However, the United Nations Environment Program’sexamination of the climate action pledges for 2020 shows thatthere is still a major gap between what the science demands tocurb climate change and what the countries plan to do. Theproposed mitigation pledges put forward by governments arelikely to allow global warming to at least 2.5 to 5 degreestemperature increase above pre-industrial levels.5

This means that the new agreement in 2015, with the FifthAssessment Report of the IPCC on its heels, should strive forclimate action for 2020 that ensures that the world stay as farbelow an average temperature increase of 2°C as possible. Such anagreement will need to ensure:

• That industrialised countries reduce their emissions on averageby at least 40% by 2020 compared to their 1990 level.

• That industrialised countries provide funding of at least $140billion a year to developing countries under the newly establishedGreen Climate Fund to enable them to adapt to climate change,protect their forests and be part of the energy revolution.

• That developing countries reduce their greenhouse gas emissionsby 15 to 30% compared to their projected growth by 2020.

1.2 international energy policy

At present there is a distortion in many energy markets, whererenewable energy generators have to compete with old nuclearand fossil fuel power stations but not on a level playing field. Thisis because consumers and taxpayers have already paid theinterest and depreciation on the original investments so thegenerators are running at a marginal cost. Political action isneeded to overcome market distortions so renewable energytechnologies can compete on their own merits.

While governments around the world are liberalising theirelectricity markets, the increasing competitiveness of renewableenergy should lead to higher demand. Without political support,however, renewable energy remains at a disadvantage,marginalised because there has been decades of massivefinancial, political and structural support to conventionaltechnologies. Developing renewables will therefore require strongpolitical and economic efforts for example, through laws thatguarantee stable tariffs over a period of up to 20 years.Renewable energy will also contribute to sustainable economicgrowth, high quality jobs, technology development, globalcompetitiveness and industrial and research leadership.

1.3 renewable energy targets

A growing number of countries have established targets forrenewable energy in order to reduce greenhouse emissions andincrease energy security. Targets are usually expressed asinstalled capacity or as a percentage of energy consumption andthey are important catalysts for increasing the share ofrenewable energy worldwide.

However, in the electricity sector the investment horizon can beup to 40 years. Renewable energy targets therefore need to haveshort, medium and long term steps and must be legally binding inorder to be effective. They should also be supported by incentivemechanisms such as feed-in tariffs for renewable electricitygeneration. To get significant increases in the proportion ofrenewable energy, targets must be set in accordance with thelocal potential for each technology (wind, solar, biomass etc) andbe complemented by policies that develop the skills andmanufacturing bases to deliver the agreed quantity.

20

box 1.1: what does the kyoto protocol do?

The Kyoto Protocol commits 193 countries (signatories) toreduce their greenhouse gas emissions by 5.2% from their1990 level. The global target period to achieve cuts was2008-2012. Under the protocol, many countries andregions have adopted regional and national reductiontargets. The European Union commitment is for overallreduction of 8%, for example. In order to help reach thistarget, the EU also created a target to increase itsproportion of renewable energy from 6% to 12% by 2010.

reference5 UNEP EMISSIONS GAP REPORT.

1

climate &

energ

y policy

|THE UNFCCC & THE KYOTO PROTOCOL, IN

TERNATIONAL ENERGY POLICY, R

ENEWABLE ENERGY TARGETS

1

climate &

energ

y policy

|POLICY CHANGES IN

THE ENERGY SECTOR

21

© GP/NICK COBBING

image GREENPEACE AND AN INDEPENDENT NASA-FUNDED SCIENTIST COMPLETEDMEASUREMENTS OF MELT LAKES ON THEGREENLAND ICE SHEET THAT SHOW ITSVULNERABILITY TO WARMING TEMPERATURES.

Data from the wind and solar power industries show that it ispossible to maintain a growth rate of 30 to 35% in therenewable energy sector. In conjunction with the EuropeanPhotovoltaic Industry Association,6 the European Solar ThermalPower Industry Association7 and the Global Wind EnergyCouncil,8 the European Renewable Energy Council, Greenpeacehas documented the development of these clean energy industriesin a series of Global Outlook documents from 1990 onwards andpredicted growth up to 2020 and 2040.

1.4 policy changes in the energy sector

Greenpeace and the renewable energy industry share a clearagenda for the policy changes which need to be made toencourage a shift to renewable sources.

The main demands are:

1. Phase out all subsidies for fossil fuels and nuclear energy.

2. Internalise external (social and environmental) costs through‘cap and trade’ emissions trading.

3. Mandate strict efficiency standards for all energy consumingappliances, buildings and vehicles.

4. Establish legally binding targets for renewable energy andcombined heat and power generation.

5. Reform the electricity markets by guaranteeing priorityaccess to the grid for renewable power generators.

6. Provide defined and stable returns for investors, for examplethrough feed-in tariff payments.

7. Implement better labelling and disclosure mechanisms toprovide more environmental product information.

8. Increase research and development budgets for renewableenergy and energy efficiency.

Conventional energy sources receive an estimated $409 billion9 insubsidies in 2010, resulting in heavily distorted markets.Subsidies artificially reduce the price of power, keep renewableenergy out of the market place and prop up non-competitivetechnologies and fuels. Eliminating direct and indirect subsidiesto fossil fuels and nuclear power would help move us towards alevel playing field across the energy sector. Renewable energywould not need special provisions if markets factored in the costof climate damage from greenhouse gas pollution. Subsidies topolluting technologies are perverse in that they are economicallyas well as environmentally detrimental. Removing subsidies fromconventional electricity supply would not only save taxpayers’money, it would also dramatically reduce the need for renewableenergy support.

1.4.1 the most effective way to implement the energy[r]evolution: feed-in laws

To plan and invest in energy infrastructure whether forconventional or renewable energy requires secure policyframeworks over decades.

The key requirements are:

a. Long term security for the investment The investor needs to knowif the energy policy will remain stable over the entire investmentperiod (until the generator is paid off). Investors want a “good”return on investment and while there is no universal definition of agood return, it depends to a large extent on the inflation rate of thecountry. Germany, for example, has an average inflation rate of 2%per year and a minimum return of investment expected by thefinancial sector is 6% to 7%. Achieving 10 to 15% returns is seenas extremely good and everything above 20% is seen as suspicious.

b. Long-term security for market conditions The investor needs toknow, if the electricity or heat from the power plant can be soldto the market for a price which guarantees a “good” return oninvestment (ROI). If the ROI is high, the financial sector willinvest, it is low compared to other investments financialinstitutions will not invest.

c. Transparent Planning Process A transparent planning process iskey for project developers, so they can sell the planned project toinvestors or utilities. The entire licensing process must be clearand transparent.

d. Access to the grid A fair access to the grid is essential forrenewable power plants. If there is no grid connection availableor if the costs to access the grid are too high the project will notbe built. In order to operate a power plant it is essential forinvestors to know if the asset can reliably deliver and sellelectricity to the grid. If a specific power plant (e.g. a wind farm)does not have priority access to the grid , the operator might haveto switch the plant off when there is an over supply from otherpower plants or due to a bottleneck situation in the grid. Thisarrangement can add high risk to the project financing and itmay not be financed or it will attract a “risk-premium” whichwill lower the ROI.

references6 ‘SOLARGENERATION IV’, SEPTEMBER 2009.

7 ‘GLOBAL CONCENTRATED SOLAR POWER OUTLOOK – WHY RENEWABLES ARE HOT!’ MAY, 2009.

8 ‘GLOBAL WIND ENERGY OUTLOOK 2008’, OCTOBER 2008.

9 ‘IEA WORLD ENERGY OUTLOOK 2011’, PARIS NOVEMBER 2011, CHAPTER 14, PAGE 507.

WORLD ENERGY [R]EVOLUTIONA SUSTAINABLE WORLD ENERGY OUTLOOK

1

climate &

energ

y policy

|POLICY CHANGES IN

THE ENERGY SECTOR

22

box 1.2: example of a sustainable feed-in tariff

The German Feed-in Law (“Erneuerbare Energien Gesetz” =EEG) is among the most effective pieces of legislation tophase in renewable energy technologies. Greenpeace supportsthis law and encourages other countries to implement a similareffective renewable energy law.

Structure of the German renewable energy Act:

a. Definitions & Purpose Chapter 1 of the law provides ageneral overview about the purpose, the scope of theapplications, specific definitions for all used terms in the lawas well as the statutory obligation.

b. Regulation of all grid related issues Chapter 2 of the lawprovides the general provisions of grid connection, technical andoperational requirements, how to establish and use gridconnection and how the renewable electricity purchase, thetransmission and distribution of this electricity must be organised.