Energy “Blueprints”for Pakistan - pip.org.pk 2010-11 to 2024-25.pdf · The current price &...

42

Energy “Blueprints” for Pakistan … 1 Blueprint # 1 – Normalization of Natural Gas Prices

Transcript of Energy “Blueprints”for Pakistan - pip.org.pk 2010-11 to 2024-25.pdf · The current price &...

Energy “Blueprints” for Pakistan …

1

Blueprint # 1 –

Normalization of Natural Gas Prices

Blueprint # 1 - Normalization of NaturalGas Prices – Recommendations

2

• It is recommended that natural gas pricing in Pakistan be

progressively normalized to its replacement /replenishment

value via a “gas normalization levy” for existing gas supplies

and de-regulation for new gas supplies, local or imports.

(Currently this means adjusting the natural gas price to the level

of the nearest replacement fuel in each economic sector - LPG

for residential , commercial & transport, and fuel oil for industrial

& power. In due course this will mean adjustment to the

replenishment pricing of natural gas imports).

• It is further recommended that gas pricing slabs be abolished

and a single gas price, similar to oil pricing, be applied for all

volumes. Direct subsidies may be given to life-line customers

using the additional revenues from the “gas normalization levy”.

Blueprint # 1 - Normalization of NaturalGas Prices - Benefits

3

1. Reduced Gas Demand via Energy Conservation - an immediate

benefit of normalized natural gas prices would be a 15 – 20%

reduced demand from the economic sectors through energy

conservation and use of efficient gas appliances.

2. Increased Gas Supplies – normalized market-based natural gas

prices will incentivize increased E&P activity in the country. The

revenue from the gas normalization levy (estimated $ 1

billion/year for each $ 1/mmbtu price increase) will also enable the

government to fund gas imports infrastructure.

3. Enhanced GDP Growth Rate – increased gas availability should

enhance Pakistan’s GDP growth rate through assured gas supply

for industry & power. These segments will also need to modernize

and improve their production efficiencies to remain competitive in

a market-based gas pricing environment.

Energy “Blueprints” for Pakistan …

4

Blueprint # 2 –

Re-structuring of the Natural Gas Sector

Blueprint # 2 – Restructuring of the Natural Gas Sector – Issues

5

1. Natural gas supply has become a political tool The state-controlled gas utilities SNGPL & SSGC remain under

consistent political pressure to supply gas to non-viable

consumers regardless of business merit or availability of natural

gas, which has resulted in over-commitment and growing gas

shortages for all consumer segments.

2. Increasing Natural Gas theft & non-paymentThe quantum of unaccounted for gas (UFG) is reaching alarming

proportions, with 8 – 10% of gas supply lost, and the state-

controlled gas utilities being unable to implement strong

administrative and legal measures to control the situation due to

political pressures.

Blueprint # 2 – Restructuring of the Natural Gas Sector – Recommendations

6

It is recommended that the natural gas sector be re-structured as

follows:

• A single state-controlled natural gas transmission company -

for transmitting natural gas on an open-access basis for all

suppliers / consumers at a regulator-controlled grid tariff. This

company would have no gas purchase or marketing role.

• Multiple natural gas distribution & marketing companies in the

private sector - each company managing the gas distribution

grid in a particular region or city, with the ability to purchase &

market gas at de-regulated prices to all consumer segments

within its zone, while at the same time providing open-access to

third-party gas suppliers against a regulator-controlled grid

tariff to create a competitive market.

• Gas theft to be declared a “non-bailable offence” with a high

penalty

Blueprint # 2 – Restructuring of the Natural Gas Sector – Benefits

7

1. Security of Gas Transmission infrastructureState control of the vital high-pressure gas transmission trunk-line

will ensure long-term viability of this crucial infrastructure in the

national interest.

2. Business Discipline & Reduced LossesPrivatization of natural gas distribution & marketing should lead to

reduced political pressures in this sector, allowing better business

& financial discipline and more stringent control of gas losses.

3. A Competitive Gas MarketOpen access to the gas market for all third-party gas suppliers,

together with de-regulated prices, will increase natural gas

supplies into the market and, in due course, lead to healthy

competition and reducing gas prices.

Energy “Blueprints” for Pakistan …

8

Blueprint # 3 –

Dynamic Exploration & Production (E&P)

Blueprint # 3 – A Dynamic E&P Sector - Issues

9

1. Unattractive Price IncentivesThe current price & fiscal regime for the E&P sector in Pakistan

is not attractive for major investments to be undertaken which

are critical for creating a dynamic E&P environment, particularly

for offshore drilling and unconventional gas resources such as

tight gas, shale gas, coal bed methane, gas hydrates etc.

2. Uncertain Security & Political Environment Innovative political solutions will be required to open-up access

to large E&P acreage in the country which is currently off-limits

for security reasons, and assured continuity of policies by

successive governments will be a pre-requisite for major E&P

investments in Pakistan.

Blueprint # 3 – A Dynamic E&P Sector- Recommendations

10

In a major bid to raise the level of E&P development in Pakistan it is

recommended that:

• The E&P sector be progressively de-regulated and, as the first

step, be allowed to sell new natural gas discoveries, both

conventional and unconventional, at market based de-regulated

pricing under standard government taxation & royalty

conditions (with exemption from any gas normalization levy).

• E&P sector have open access to the gas transmission &

distribution grids at regulator-controlled grid tariff and be able

to sell natural gas directly to the proposed private sector

natural gas distribution & marketing companies as well as to

bulk consumers in the industry and power segments.

Blueprint # 3 – A Dynamic E&P Sector- Benefits

11

1. Attracting Large-scale Investment in the E&P Sector An early benefit of normalization of natural gas prices and

opening up the gas market in Pakistan should be to attract large-

scale investment in the E&P sector, resulting in dynamic activity

in both onshore & offshore exploration areas and for

conventional & unconventional gas resources.

2. A Better Security & Policy environmentWith attractive market conditions, the E&P companies are likely to

work closely with the federal & provincial governments to develop

suitable security & policy arrangements for sustainable E&P

development.

Energy “Blueprints” for Pakistan …

12

Blueprint # 4 –

Fast-tracking Liquefied Natural Gas (LNG)

Imports

Blueprint # 4 – Fast-tracking Liquefied Natural Gas (LNG) Imports - Issues

13

1. Pakistan’s Ability to Pay for LNGUnlike oil imports which can be bought on short-term/spot

contracts due to a highly liquid market, LNG has been typically

sold against long-term, take-or pay contracts which require the

buyer to have a high credit rating for assurance of long-term

payments. Pakistan’s current credit rating of below investment

grade is not conducive for long-term LNG contracts.

2. Lack of Infrastructure & Inadequate Port ConditionsLNG import terminals will require significant investment (either

as capital expenditure for land-based facilities or as operating

cost for floating terminals), as well as port accessibility for large-

sized LNG vessels, which no investor can undertake without

government support.

Blueprint # 4 – Fast-tracking LNG Imports- Recommendations

14

With the global LNG market becoming more liquid on the back of

increasing global LNG production and reduced demand in the

USA due to its enormous shale-gas discoveries, it is

recommended that Pakistan take benefit of this evolving market

change and fast-track LNG imports as follows:

• Merchant (tolling) LNG import terminals be set-up by the

private-sector to enable early spot/short-term LNG imports.

These terminals to be provided capacity-utilization guarantees

by the government for an initial period, and to have open-

access for third-party LNG suppliers/consumers at a regulator-

controlled terminal tariff to create a competitive market.

• Development of ports be undertaken by the government on fast-

track basis, using revenues from the proposed “gas

normalization levy”, to provide accessibility for large-sized LNG

vessels, a key requirement for sustainable LNG imports.

Blueprint # 4 – Fast-tracking Liquefied Natural Gas (LNG) Imports – Benefits

15

1. Competitive LNG/Gas PricesBy fast-tracking LNG imports, Pakistan will benefit from

competitive LNG import prices through spot/short-term purchases,

which will also provide a check on local gas prices as the gas

market de-regulates.

2. Increased Gas Supplies & GDP GrowthLNG imports will be a key element in meeting the energy short-fall

in Pakistan and providing assured gas availability for the industry

& power sectors, leading to higher revenue generation and

accelerated GDP growth.

3. Improving Port AccessibilityProviding port access for large-sized shipping is a crucial step

towards reducing the cost of oil and gas imports, and making

Pakistan an attractive destination for energy supplies.

Energy “Blueprints” for Pakistan …

16

Blueprint # 5 –

Rationalization of the Power Tariff

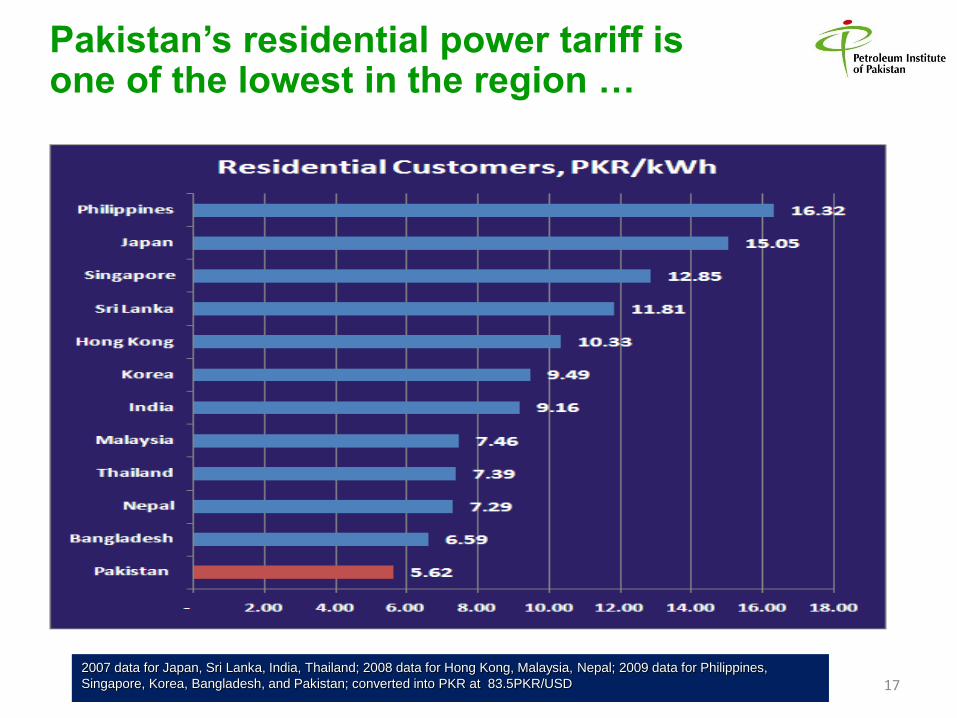

172007 data for Japan, Sri Lanka, India, Thailand; 2008 data for Hong Kong, Malaysia, Nepal; 2009 data for Philippines,

Singapore, Korea, Bangladesh, and Pakistan; converted into PKR at 83.5PKR/USD

Pakistan’s residential power tariff is one of the lowest in the region …

18

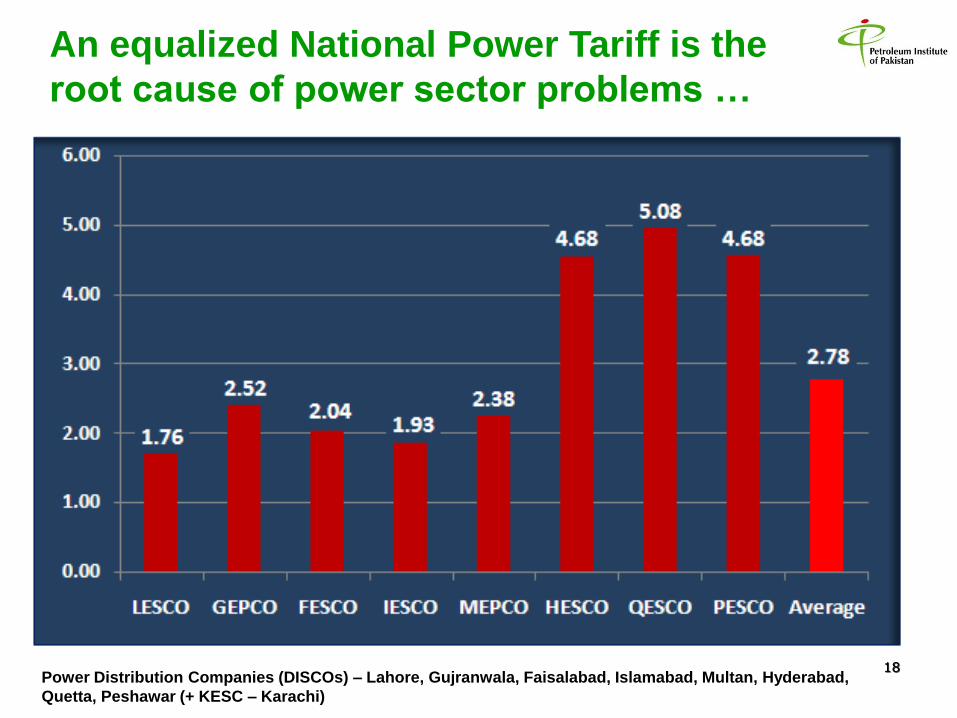

An equalized National Power Tariff is the

root cause of power sector problems …

Power Distribution Companies (DISCOs) – Lahore, Gujranwala, Faisalabad, Islamabad, Multan, Hyderabad,

Quetta, Peshawar (+ KESC – Karachi)

Blueprint # 5 – Rationalization of the Power Tariff - Issues

19

1. Low, Regulated Power Tariff & Circular DebtThe current power tariff in Pakistan does not reflect the change

in ground realities whereby there has been a significant shift

from hydel to thermal power generation over the past decade,

and successive governments have failed to recover true costs

from the consumer or provide sufficient subsidies, leading to a

crippling circular debt.

2. A Single, National Tariff & Pricing Slabs are not viableA single, nation-wide power tariff does not recognize the wide

disparities in power generation & distribution costs in different

regions of the country and provides no incentive for efficiency

or reduced costs, while pricing slabs force the consumer to

resort to unfair means (multi-metering etc) to remain in the

lowest pricing slab and contributes to under-recovery of costs.

Blueprint # 5 – Rationalization of thePower Tariff - Recommendations

20

With the power sector in Pakistan in a state of serious crisis and

becoming a significant barrier for national development with

growing power shortages, it is recommended as follows:

• The power tariff be de-centralized to distribution circles (initially

DISCOs & KESC) to reflect the true costs of power generation &

distribution that exist in different parts of the country.

• The power tariff for each distribution circle be de-regulated,

with no pricing slabs and no government subsidy (lifeline

consumers may be given a direct subsidy).

• Open access to the power transmission & distribution grids be

provided for all third-party power suppliers to create a

competitive market.

• Tariffs for hydel & nuclear power be gradually adjusted to

reflect replacement value, which includes the high cost of

building new dams & nuclear plants.

Blueprint # 5 – Rationalization of thePower Tariff – Benefits

21

The key benefits of de-centralization and de-regulation of the power

tariff will be:

• True reflection & recovery of power generation & distribution

costs in each distribution circle

• Elimination of government subsidies and burden on exchequer

• Providing a solid business grounding for the main-stream power

sector and reducing the rapid growth of small-scale “captive”

power generation in Pakistan which is the consumer response to

growing power shortages

• Cost impact of inefficiencies (line losses, non-payment) becoming

localized within each distribution circle

• De-regulation of the power tariff providing incentives for large-

scale investment in power generation capacity

• Power supply becoming a business issue instead of a political

entitlement

Energy “Blueprints” for Pakistan …

22

Blueprint # 6 –

Transforming the Power Sector

Blueprint # 6 – Transforming the Power Sector - Issues

23

1. Power Supply has become a political tool – the power

sector in Pakistan is centrally controlled and heavily regulated

by the government, with the state-owned power utilities being

under political pressure to supply power to consumers

regardless of business merit, which has resulted in growing

shortages for all consumer segments.

2. Non-payment Culture and High T&D Losses - a

dangerous sense of entitlement has crept into the power sector

whereby both government and private consumers feel they do

not need to pay for power consumed, and are able to resort to

power theft & non-payment without fear of repercussions.

3. No Incentives for Investment – multiple problems in the

power sector, particularly low tariff and high losses leading to

circular debt, have made it unattractive for new investment.

Blueprint # 6 – Transforming the Power Sector – Recommendations

24

It is recommended that the power sector in Pakistan be re-

structured to create a competitive & vibrant sector:

• NTDC/WPPO to continue functioning as the state-owned high-

voltage power transmission company, with open-access for all

power suppliers at a regulator-controlled grid tariff, but its role

as central power purchaser to be diluted and eventually

eliminated, as power purchase is progressively de-centralized

to the distribution circles.

• All power distribution & marketing companies (DISCOs) to be

privatized, with each company purchasing & marketing power

to consumer segments within its distribution circle while

providing open-access to third-party power suppliers against a

regulator-controlled grid tariff to create an open and

competitive market.

• Power theft to be declared a “non-bailable offence” with a high

penalty.

Blueprint # 6 – Transforming the Power Sector – Benefits

25

1. Security of High-Voltage Transmission infrastructureState control of the vital high-voltage power transmission &

distribution trunk-lines will ensure long-term viability of this crucial

infrastructure in the national interest.

2. Business DisciplinePrivatization of the power distribution & marketing companies

(DISCOs) and a de-regulated power tariff should lead to a

transparent and efficient power sector with improved consumer

interface allowing better business & financial discipline.

3. Competitive MarketOpen access to the power sector will create a multi-buyer market

with directly negotiated pricing, allowing power suppliers the

opportunity to create innovative “power packages” for the

consumer based on specific requirements and paying ability.

Energy “Blueprints” for Pakistan …

26

Blueprint # 7 –

Growing Power Generation Capacity

Blueprint # 7 – Growing the Power Generation Capacity - Issues

27

1. Insufficient Power GenerationPakistan’s current installed power generation capacity of 19,000

MW (effective 14,000 MW) is insufficient to meet the country’s

needs and will require to be at least doubled in the next 15 years.

2. Inefficient Public-sector Power PlantsThe state-owned thermal power plants (4,000 MW), with the older

steam-turbine technology, have low conversion efficiencies and

are expensive to maintain and operate.

3. Under-utilized Private-sector Power Plants (IPPs)The IPPs (currently 4,000 MW) based on newer and more

efficient oil & gas fired technologies, have multiple problems

including insufficient gas availability and the circular debt,

which are resulting in their under-utilization.

Blueprint # 7 – Growing the Power Generation Capacity - Recommendations

28

The following key steps are recommended for growing the power

generation capacity in Pakistan:

• Hydel and nuclear power generation remain a state

responsibility, and their tariffs be progressively adjusted to

provide funds for the government to install new hydel

generation and nuclear power plants.

• All thermal power generation based on oil, gas and coal to be in

the private sector, and the state-owned thermal power plants

privatized. With the power tariff de-centralized and de-regulated,

these power plants will operate in a competitive market with no

requirement of government support.

• Legislation to be passed by the government to allow

disconnection of power to government bodies on account of

non-payment of power bills.

• Limited period subsidies be provided for development of wind

and solar power generation.

Blueprint # 7 – Growing the Power Generation Capacity – Benefits

29

1. Increased Investment Open access to the power grid and the power market, deregulated

tariffs and reduced regulatory hurdles will be powerful incentives

for the private sector to invest in new power generation capacity in

Pakistan and, in due course, will lead to healthy competition and

reduced power tariffs.

2. Enhanced Conversion EfficienciesAll thermal power plants, being in the private sector, will need to

operate at high conversion efficiencies to be able to compete in a

de-regulated power market.

3. Accelerated GDP GrowthSustained and reliable power supply to all economic segments will

provide a strong push for accelerated GDP growth in Pakistan.

Energy “Blueprints” for Pakistan …

30

Blueprint # 8 –

Oil Sector: Introduction of Future Fuels

Blueprint # 8 – Oil Sector: Introduction of Future Fuels - Issues

31

1. Regulated Oil Pricing Regulated pricing & margins of the main fuels, petrol and diesel,

is a significant disincentive for the introduction of future fuels in

Pakistan as it does not allow differentiated pricing for higher

quality fuels.

2. Low Quality SpecificationsGovernment specifications for petrol and diesel are out-dated

and not in line with global innovations in fuels quality,

particularly to meet modern automotive requirements and

international emissions standards.

3. Need to Upgrade Local RefineriesMost of the local refineries do not have the capability to produce

future fuels and require fiscal support for upgrading their

refining assets & processes.

Blueprint # 8 – Oil Sector: Introduction of Future Fuels - Recommendations

32

• With significant competition existing in the oil marketing sector,

it is recommended that pricing & margins of the main fuels be

de-regulated and the regulatory authority be tasked with

ensuring fair competition for consumer protection.

• It is further recommended that minimum specifications for fuels

quality be progressively aligned with international

specifications and the capability of local refineries be enhanced

through time-bound fiscal support to enable them to produce

future fuels.

• Subsequent to de-regulation of oil pricing & margins, a road-

map be agreed between government and the oil sector for the

introduction of first generation bio-fuels to meet modern

emissions standards and to support the long-term development

of the agricultural sector in Pakistan.

Blueprint # 8 – Oil Sector: Introduction of Future Fuels – Benefits

33

1. Consumer Choice De-regulated oil prices will open the door for the introduction of

differentiated fuels in Pakistan, allowing consumers the choice to

select from different performance fuels as per vehicle requirement.

2. Clean Fuels De-regulated oil prices & margins will allow the government to set

a time-line for the oil sector to phase out high-sulfur diesel & high-

aromatics petrol and phase-in the introduction of clean fuels in line

with international & regional standards.

3. Bio-fuels DevelopmentDe-regulation of oil prices & margins is a pre-condition for the

introduction of bio-fuels in any market, and will enable the

government and oil sector to agree a mandate for marketing of first

generation bio-fuels.

Energy “Blueprints” for Pakistan …

34

Blueprint # 9 –

Thar Coal-fields as a Game-Changer for

Pakistan

Blueprint # 9 – Thar Coal-fields as a Game-changer – Challenges

35

1. Highly Complex Mining The Thar coal-fields present a significant mining challenge with

thin coal seams buried deep under-ground (high over-hang) and

being immersed in vast saline aquifers.

Coal mining at Thar will be highly capital intensive and will

require very special incentives to attract the necessary foreign

expertise and investment for this giant-scale project.

2. Low Transportability of Thar CoalWith a high ash content, Thar coal cannot be readily transported

and will require to be utilized at the “mine-mouth”. This will

entail significant infrastructure development (water supply,

effluent disposal, road network, power grid etc) for transforming

Thar into a major industrial zone for utilizing its giant coal

reserves.

Blueprint # 9 – Thar Coal-fields as a Game-changer - Recommendations

36

To position the Thar coal-fields as a game-changer in the economic

development of Pakistan, it is recommended that:

1. A “Thar Coal Development Master-plan” be formulated with

international support, setting out the road-map for the use of

Thar coal for large-scale power generation and for conversion

into high-value hydrocarbon products, both for domestic

consumption and as a major source of foreign exchange

earnings via exports.

2. The Thar coal-fields be designated as an “export processing

zone” with duty-free imports of equipment, machinery and raw

materials for industrial use, and stream-lined exports of its

products, including power, to within Pakistan (duty-paid) or

outside Pakistan (duty-free) at de-regulated prices directly

negotiated with buyers.

Blueprint # 9 – Thar Coal-fields as a Game-changer - Recommendations

37

3. The federal and provincial governments urgently approve and

allocate funds for key infrastructure development of the Thar

coal-fields, including provision of raw water, drainage & effluent

disposal, road network and power transmission line.

4. The Government of Pakistan initiate strategic discussions for

development of Thar Coal reserves with potential international

investors including World Bank, IFC, ADB, China, US, UK,

Japan, Middle East and major global energy companies.

5. Since the Pakistani banking system is not capable of financing

infrastructure projects of this scale, there is an urgent need for

creation of a Domestic Infrastructure Bank to finance large-scale

energy sector infrastructure projects such as Thar Coal.

Energy “Blueprints” for Pakistan …

38

Blueprint # 10 –

Effective Governance of the Energy Sector

Blueprint # 10 – Effective Governance of the Energy Sector – Issues

39

1. Excessive Regulation The heavily regulated energy sector in Pakistan has resulted in a

large bureaucratic structure which has not allowed the market

supply & demand forces to operate, leading to severe problems

in both the natural gas and the power sectors.

2. Conflicting Objectives of Major MinistriesThe often conflicting objectives of the two major energy sector

ministries, petroleum and power, and their affiliated bodies are

contributing to the on-going issues in the energy sector.

3. Unclear Role of the Regulatory AuthoritiesOGRA & NEPRA’s key purpose of ensuring transparency and

competitiveness in a de-regulated energy market has not been

achieved as the sector continues to remain heavily regulated,

and the role of the two regulatory authorities is unclear.

Blueprint # 10 – Effective Governance of the Energy Sector - Recommendations

40

It is recommended that the governance of the energy sector be re-

structured in line with its proposed de-regulation as follows:

1. All energy sector functions of the government be consolidated

under a single Ministry of Energy, with major responsibilities

including development of hydel & nuclear power, management

of the natural gas and power transmission grids, setting out the

de-regulation policies of the government and facilitating energy

sector investments.

2. The regulatory functions of the energy sector be consolidated

under a single Energy Regulatory Authority, with major

responsibilities including monitoring the de-regulated energy

markets for fair competition, ensuring open third-party access

to the gas and power sectors infrastructure and tariff-setting for

such access, and monitoring safety and customer service

standards in the energy sector.

Blueprint # 10 – Effective Governance of the Energy Sector – Benefits

41

1. A Vibrant Energy Sector Reduced bureaucratic role in the energy sector should enable the

market demand and supply forces to operate effectively to meet

the consumer needs, leading to a vibrant energy sector

contributing to healthy national development.

2. Clarity of Roles & ResponsibilitiesSimplifying the government role and empowering an independent

regulatory authority to oversee a de-regulated energy sector will

provide clarity of roles for growing this sector.

3. Facilitating Investment GrowthA de-regulated and competitive energy sector with reduced

bureaucratic hurdles is expected to create a positive investment

climate in this vital sector, contributing to accelerated GDP growth

in Pakistan.

“Blueprints” will bring accelerated GDP

growth through sustained Energy availability …

42

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

120.0

130.0

140.0

1994-9

5

1996-9

7

1998-9

9

2000-0

1

2002-0

3

2004-0

5

2006-0

7

2008-0

9

2010-1

1

2012-1

3

2014-1

5

2016-1

7

2018-1

9

2020-2

1

2022-2

3

2024-2

5

(Million

TO

Es)

Natural Gas Oil Products

Coal Hydel

Nuclear Renew ables

Electricity Import

“Blueprints” Scenario

Historical Consumption