Empresas CMPC S.A Company Overview 09

23

Empresas CMPC S.A. Company Overview Presentation prepared for Santander’s Materials Conference, New York 09.10 2010 1920

Transcript of Empresas CMPC S.A Company Overview 09

Empresas CMPC S.A.Company OverviewPresentation prepared for Santander’s Materials Conference, New York 09.10

2010

1920

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

Agenda

Overview 3

Business Divisions 7

Social Responsibility and Sustainability 14

Financial Review 16

21

2

Concluding Remarks

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

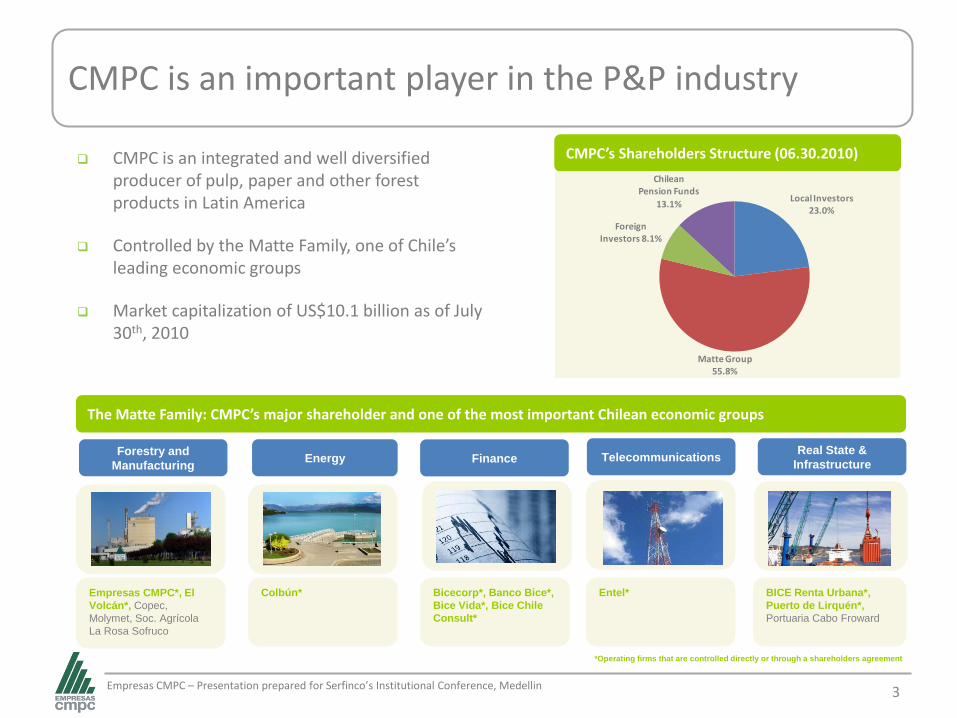

CMPC is an important player in the P&P industry

CMPC is an integrated and well diversified producer of pulp, paper and other forest products in Latin America

Controlled by the Matte Family, one of Chile’s leading economic groups

Market capitalization of US$10.1 billion as of July 30th, 2010

3

The Matte Family: CMPC’s major shareholder and one of the most important Chilean economic groups

Forestry and

Manufacturing Energy Finance Telecommunications

Real State &

Infrastructure

BICE Renta Urbana*,

Puerto de Lirquén*,

Portuaria Cabo Froward

*Operating firms that are controlled directly or through a shareholders agreement

Empresas CMPC*, El

Volcán*, Copec,

Molymet, Soc. Agrícola

La Rosa Sofruco

Colbún* Bicecorp*, Banco Bice*,

Bice Vida*, Bice Chile

Consult*

Entel*

CMPC’s Shareholders Structure (06.30.2010)

Local Investors 23.0%

Matte Group 55.8%

Foreign Investors 8.1%

Chilean Pension Funds

13.1%

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

Balanced growth in all business segments provides CMPC a diversified revenue mix

Fore

stry

Pu

lpP

aper

Tiss

ue

Pap

er

Pro

du

cts

Total Capacity% of Total Sales* % of Total EBITDA*

1,025 Th. Ha(659 Th. Plant)8.4 MM m3/y

11% 6%

29% 54%

18% 15%

34% 19%

9% 5%

* Figures in US$ million for the LTM as of June 2010 Main Figures

Sales: 787

Sales 3rd parties: 648

EBITDA: 139

EBITDA margin: 17%

Sales: 1,251

Sales 3rd parties: 1,248

EBITDA: 173

EBITDA margin: 14%

Sales: 335

Sales 3rd parties: 317

EBITDA: 46

EBITDA margin: 14%

2.5 MM tons/y

1.1 MM tons/y

470,000 tons/y

340,000 tons/y

Sales: 584

Sales 3rd parties: 389

EBITDA: 51

EBITDA margin: 9%

Sales: 1,224

Sales 3rd parties: 1,077

EBITDA: 481

EBITDA margin: 39%

4

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

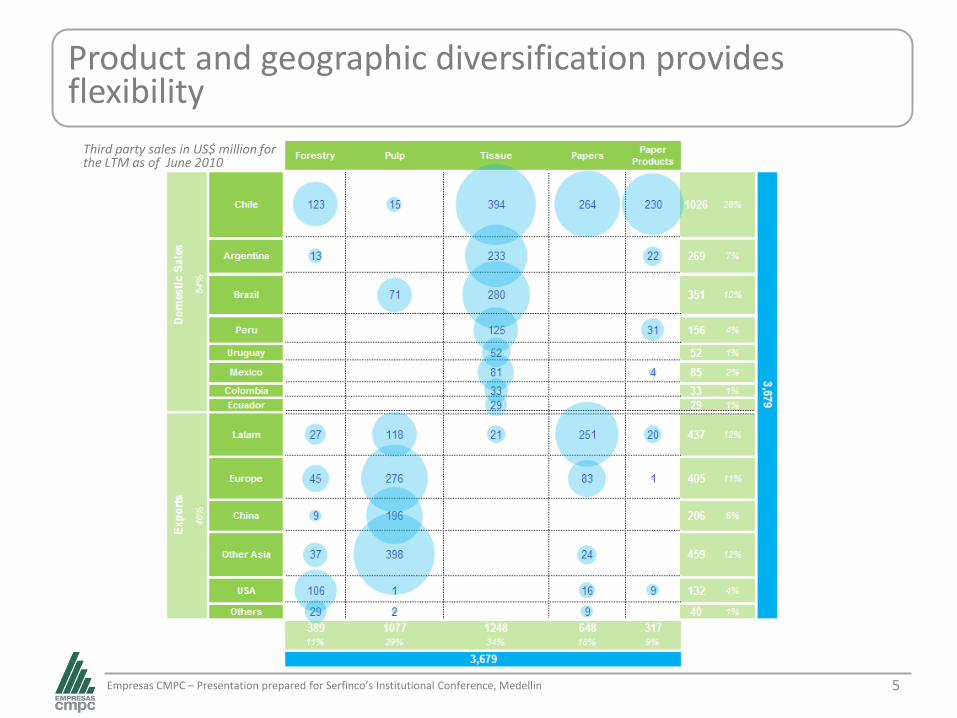

Product and geographic diversification provides flexibility

5

Third party sales in US$ million for the LTM as of June 2010

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

Agenda

Overview 3

Business Divisions 7

Social Responsibility and Sustainability 14

Financial Review 16

21

6

Concluding Remarks

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

Chile:

717,462 Hectares

498,872 Planted Hectares

Brazil:

213,592 Hectares

94,806 Planted Hectares

Argentina:

94,283 Hectares

65,164 Planted Hectares

Forestry Division: the root of CMPC’s competitive advantage

Forestry Sawnwood

Chile - 4 Sawmills:

• Bucalemu, Las Cañas,

Mulchén and Nacimiento

Total capacity: 1.4 MM m3/yr

Remanufactured Wood

Chile - 2 Remanufacturing plants:

• Coronel and Los Ángeles

Total capacity: 180,000 m3/yr

Plywood

Chile - 1 Plywood mill:

• Mininco

Total capacity: 240,000 m3/yr

7

• 100% planted and certified forests

• Genetic and silvicultural practices / forest management to

continuously improve yields

• Faster growth cycle than northern hemisphere forests

• Young and growing forestry base.

• Average age of CMPC’s Pine Forests: 11.8 years

• Average age of CMPC’s Eucalyptus Forests: 9.2 years

• Proximity of forests to industrial facilities and ports

Overview

1.82 X

Harvesting (million m3)

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

Pulp Division: CMPC has one of the lowest cash costs of the pulp industry Key drivers

• First class assets for the production of:

Softwood (pine) 760 Th. Tons annually

Hardwood (eucalyptus) 1.8 MM Tons annually

• Strategic locations (mills near to forests and ports)

• World’s lowest cost producer of softwood

• Sales diversification

• ISO, OHSAS Certified

What’s ahead…

• Consolidation of Guaíba’s assets in Brazil, which increased

CMPC’s hardwood capacity in 450 Th. tons per year

• Chile: rebuilding of Laja mill

• Environmental upgrades at the Pacífico and Santa Fe mills

• Debottlenecking of Santa Fe II mill

• New turbo generator in the Santa Fe II mill

8

0

100

200

300

400

500

600

700

0 5,000 10,000 15,000 20,000 25,000

(US$

/To

n d

el N

. Eu

rop

e)

(Thousand metric tonnes)

Source: CMPC and Hawkins Wright as of April, 2010

Source: CMPC and Hawkins Wright as of April, 2010

0

100

200

300

400

500

600

700

800

0 5,000 10,000 15,000 20,000 25,000

(US$

/To

n in

N.

Euro

pe)

(Thousand metric tonnes)

BSKP Supply Curve (US$/ton)

BHKP Supply Curve (US$/ton)

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

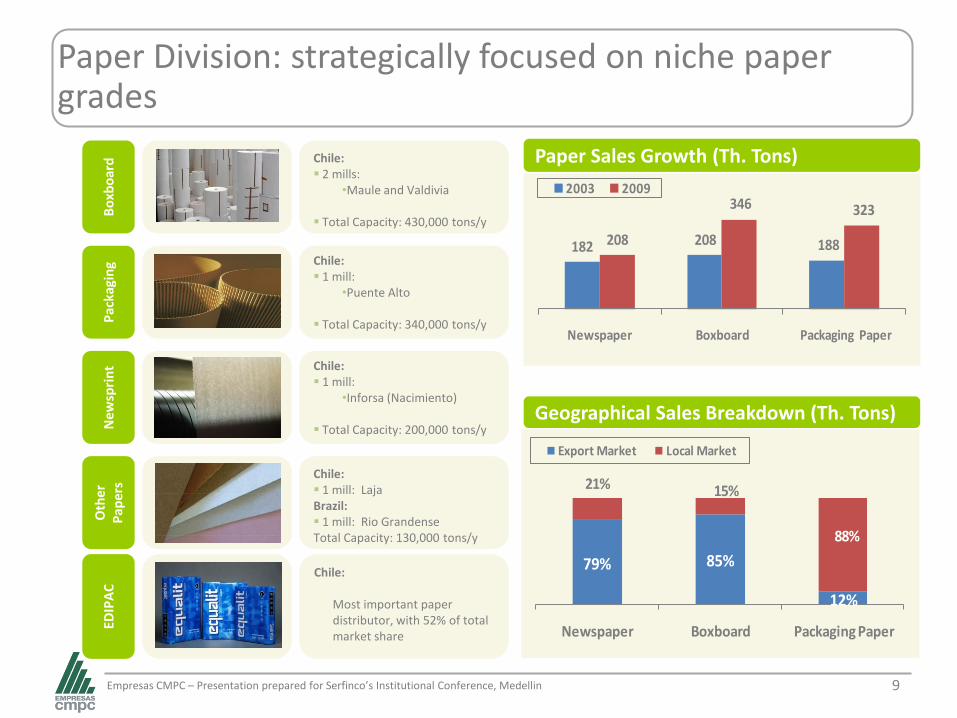

Paper Division: strategically focused on niche paper grades

Bo

xbo

ard Chile:

2 mills: •Maule and Valdivia

Total Capacity: 430,000 tons/y

Pac

kagi

ng Chile:

1 mill: •Puente Alto

Total Capacity: 340,000 tons/y

New

spri

nt Chile:

1 mill: •Inforsa (Nacimiento)

Total Capacity: 200,000 tons/y

Oth

er

Pap

ers

Chile: 1 mill: LajaBrazil: 1 mill: Rio GrandenseTotal Capacity: 130,000 tons/y

EDIP

AC

Chile:

Most important paper distributor, with 52% of total market share

Geographical Sales Breakdown (Th. Tons)

9

182 208 188208

346 323

Newspaper Boxboard Packaging Paper

2003 2009

79% 85%

12%

21% 15%

88%

Newspaper Boxboard Packaging Paper

Export Market Local Market

Paper Sales Growth (Th. Tons)

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

Tissue Division: CMPC is a leading Latin American player

Key drivers

• One of the largest tissue company in Latin America

• Strong branding

• Broad market segmentation

• Extensive distribution network

• High growth opportunities

• Flexible product mix

What’s ahead…

• Colombia: New Tissue Paper mill (27,000 tons/y), starting in

3Q10

• Mexico: New Tissue Paper Machine (double width, 50,000

tons/y), starting in 3Q10

• Brazil: New Tissue Paper Machine (double width, 50,000

tons/y), starting in 2011

• Peru: New Tissue Paper Machine (12,000 tons/y), starting in

2011

10

Market Share:Capacity: 87,000 tons/yr

5%

Mexico (Since 2006)

Market Share: 6%

Colombia (Since 2007)

Market Share:Capacity: 75,000 tons/yr

10%

Brazil (Since 2009)

Uruguay (since 1994)

Market Share:Capacity: 37,000 tons/yr

84%

Market Share: Only Conversion Process

15%

Ecuador (Since 2009)

Market Share:Capacity: 57,000 tons/yr

51%

Peru (Since 1996)

Market Share:Capacity: 118,000 tons/yr

75%

Chile (Since 1980)

Market Share:Capacity: 96,000 tons/yr

50%

Argentina (Since 1991)

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

State of the art projects has been developed in Colombia, Mexico and Brazil

• Latin-American countries have a low tissue per capita

consumption according to its per capita GNI.

• CMPC entered Mexico (2006), Colombia (2007) and Brazil

(2009), through the acquisition of Absormex, Drypers Andina

and Melhoramentos respectively.

• The new projects developed in the countries mentioned

above will add 130 Th. tons of tissue paper capacity per year.

11

Some of our tissue brands…

India

PeruChina Brazil

Colombia

MexicoChile

ArgentinaUruguay

Ecuador

SpainGermany

Portugal Japan

USA

0.0

5.0

10.0

15.0

20.0

25.0

30.0

0 10 20 30 40 50

Ap

pa

ren

t C

on

sum

tio

n p

/c (k

/ha

b.)

GNI p/c ppp (Thousand US$/hab.)

Tissue per Capita Consumption

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

Paper Products Division: Local sales mainly oriented to export industries

Co

rru

gate

d

Bo

xes

Chile: 3 mills:

•Buin, Quilicura and Til Til

Total Capacity: 252,000 tons/y

Pap

er

Bag

s

Chile: 1 mill: ChillánArgentina 1 mill: HinojoPeru: 1 mill: LimaMexico: 1 mill: Guadalajara

Total Capacity: 70,000 tons/y

Mo

lde

d P

ulp

Tr

ays

Chile: 1 mill:

•Puente Alto

Total Capacity: 18,000 tons/y

12

Key drivers

• Market leader in corrugated boxes and multiwall bags

markets in Chile

• Well diversified sales among different segments of

the market in corrugated boxes

• Manufacturing process benefits from backward

integration

• Although the lions share of all sales are local, CMPC is

also expanding its exports

What’s ahead…

• New 35,000 tons corrugating mill in the south of

Chile

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

Agenda

Overview 3

Business Divisions 7

Social Responsibility and Sustainability 14

Financial Review 16

21

13

Concluding Remarks

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

Social Responsibility and Sustainability

Social responsibility is an integral part of the CMPC business and organizational models allowing effective linking to all stake holders.

CMPC and the Environment

CMPC and the Community

CMPC and its Business Chain

CMPC and its Workers

CMPC’sCSR

• Producing and selling quality products

• Strong relationships with suppliers and customers

• Sound and transparent financial reporting

• Safe working environment

• Strict compliance with labor regulations and union agreements

• Comprehensive employee benefit policy

• Jorge Alessandri Educational Park

• Good Neighborhood Plan

• Fundación CMPC: improve language and math education in the primary schools where CMPC has facilities

• Plantations

• Clean processes

• Replacement of fossil fuels with biomass

• Recollection and recycling of waste paper

14

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

Agenda

Overview 3

Business Divisions 7

Social Responsibility and Sustainability 14

Financial Review 16

21

15

Concluding Remarks

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

Financial Summary

16

Financial Summary (US$ million)

2Q09 2009 1Q10 2Q10 QoQ% YoY%

Sales 691 3,124 938 1,007 7% 46%

Operating Costs (460) (2,066) (604) (596) -1% 29%

Other Operating Expenses (101) (414) (101) (130) 29% 29%

EBITDA 130 644 233 281 21% 116%

Depreciation & Stumpage (79) (327) (96) (96) 0% 22%

Change in Net Value if Biological Assets 4 52 32 21 -34% 429%

Operating Income 55 369 169 206 22% 272%

Financial Costs (22) (104) (33) (33) -1% 49%

Other Non Operational Items (5) 3 (55) (50) -9% 843%

Net Income 28 268 80 123 53% 338%

EBITDA Margin 19% 21% 25% 28% 3% 9%

Total Assets 10,116 12,291 12,207 12,322 1% 22%

Total Liabilities 3,549 5,033 4,896 4,941 1% 39%

Shareholder's Equity 6,567 7,258 7,312 7,382 1% 12%

2Q10

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

CMPC follows a conservative financial policy

*Figures as of 2006, 2007 and 2008 are under Chilean GAAPs. Figures for the LTM as of March 2010 are under the IFRS accounting standard.

17

Debt Evolution (US$ million) *

Net Debt / EBITDA *

1,397 1,362 1,3492,130 2,175

144 167 229

761 565

2006 2007 2008 2009 LTM

Net Debt Cash

7.4

11.910.1

6.37.2

2006 2007 2008 2009 LTM

2.7

1.5 1.7

3.3

2.5

2006 2007 2008 2009 LTM

0.36

0.280.33

0.42 0.40

2006 2007 2008 2009 LTM

Debt / Equity *

EBITDA / Interest Expenses *

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

A well structured debt profile delivers value to shareholders

Debt Description as of June 30th

• Average term of debt: 6.2 years

• Average cost of debt: 4.6%

• Composition of debt:

44% banks / 56% Bonds

• Debt breakdown by currencies:

19% UF / 71% US$ / 10% Other currencies

Last Financial Transactions

International Benchmark Bond: in November 2009,

CMPC issued an International Benchmark Bond under

the 144A-S regulation. The transaction conditions

were:

- 10 year bullet bond: for MUS$500 @ CT10 + 275 bps

18

Amortization Schedule

Debt Description as of June 30th (%)

90

194270

341 365

237153

266

500

2010 2011 2012 2013 2014 2015 2019 2027 2030

New Credit Note Amortizations

82% 86% 88%74% 80%

18% 14% 12%26% 20%

2006 2007 2008 2009 LTM

Floating Rate Fix Rate

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin 19

The Riograndense acquisition: the biggest project in the history of CMPC

On October 8th 2009, Empresas CMPC

S.A. and Aracruz Celulose S.A. signed a sale

contract for the transfer of ownership of a

group of assets known as the Guaíba Unit

for a total price of US$1,432 million

The Guaíba Unit includes:

• A pulp mill with annual production capacity of

approx. 450,000 tons

• A paper mill with annual production capacity

of approx. 60,000 tons

• Approximately 212,000 hectares of land of

which 102,000 are planted and 23,000 are

plantable

• Licenses and authorizations to execute an

expansion project for the pulp mill, to increase

its annual capacity to around 1.75 million

tons

What is CMPC buying?

Sizable entry to Brazil

Strategic location, complementary to

existing facilities, to serve customers

worldwide

Ability to reconfigure sales, delivery and

increase customers

Ability to easily increase production to

1.75 million tons of pulp in the near future

Potential to replicate CMPC Chile in one of

the largest and most dynamic economies

in the world

Substantial forestry base and sylvicultural

know-how

Opportunity to further improve CMPC’s

low cost producer status

What is CMPC getting?

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

Agenda

Overview 3

Business Divisions 7

Social Responsibility and Sustainability 14

Financial Review 16

21

20

Concluding Remarks

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

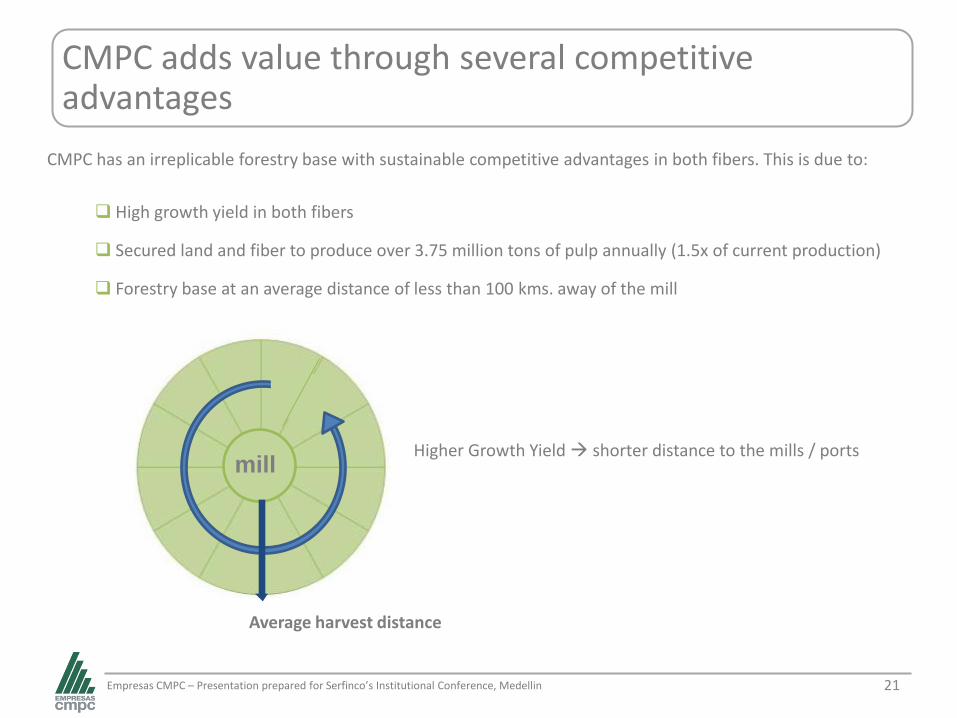

CMPC adds value through several competitive advantages

21

CMPC has an irreplicable forestry base with sustainable competitive advantages in both fibers. This is due to:

High growth yield in both fibers

Secured land and fiber to produce over 3.75 million tons of pulp annually (1.5x of current production)

Forestry base at an average distance of less than 100 kms. away of the mill

mill

Average harvest distance

Higher Growth Yield shorter distance to the mills / ports

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

CMPC adds value through several competitive advantages

22

CMPC’s tissue products have presence in :

10,592 stores

146 wholesalers

34 Drugstore Chains

In store service (over 2,800 people)

Countries with more than a 90% coverage :

ChileUruguay

ArgentinaColombia

Peru

Countries with more than a 70% and less than a 90% coverage:

MexicoEcuador

Brazil

High brand recognition Strong and efficient distribution network

Elevated market share and a recognized leadership in the tissue industry

Empresas CMPC – Presentation prepared for Serfinco’s Institutional Conference, Medellin

Q&A

This presentation will be available at CMPC’s Web Site www.cmpc.cl

Disclaimer:

This document provides information about Empresas CMPC SA. In any case this constitutes acomprehensive analysis of the financial, production and sales situation of the company, so to evaluatewhether to purchase or sell securities of the company, the investor must conduct its own independentanalysis.

In compliance with the applicable rules, Empresas CMPC SA. publishes this document in its web site(www.cmpc.cl) and sends to the Superintendencia de Valores y Seguros, the financial statements of thecompany and its corresponding notes, which are available for consultation and review.