Employee Benefit Plan Audits: Asking the Right...

50

Employee Benefit Plan Audits: Asking the Right Questions and Avoiding Critical Errors WEDNESDAY, DECEMBER 17, 2014, 1:00-2:50 pm Eastern WHOM TO CONTACT For Additional Registrations: -Call Strafford Customer Service 1-800-926-7926 x10 (or 404-881-1141 x10) For Assistance During the Program: -On the web, use the chat box at the bottom left of the screen If you get disconnected during the program, you can simply log in using your original instructions and PIN. IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit you must: • Participate in the program on your own computer connection (no sharing) – if you need to register additional people, please call customer service at 1-800-926-7926 x10 (or 404-881-1141 x10). Strafford accepts American Express, Visa, MasterCard, Discover. • Listen on-line via your computer speakers. • Record verification codes presented throughout the seminar. If you have not printed out the “Official Record of Attendance”, please print it now. (see “Handouts” tab in “Conference Materials” box on left-hand side of your computer screen). To earn Continuing Education credits, you must write down the verification codes in the corresponding spaces found on the Official Record of Attendance form. • Complete and submit the “Official Record of Attendance for Continuing Education Credits,” which is available on the program page along with the presentation materials. Instructions on how to return it are included on the form. • To earn full credit, you must remain connected for the entire program.

Transcript of Employee Benefit Plan Audits: Asking the Right...

Employee Benefit Plan Audits:

Asking the Right Questions and Avoiding Critical Errors

WEDNESDAY, DECEMBER 17, 2014, 1:00-2:50 pm Eastern

WHOM TO CONTACT

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x10 (or 404-881-1141 x10)

For Assistance During the Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register additional people,

please call customer service at 1-800-926-7926 x10 (or 404-881-1141 x10). Strafford accepts American Express, Visa,

MasterCard, Discover.

• Listen on-line via your computer speakers.

• Record verification codes presented throughout the seminar. If you have not printed out the “Official Record of

Attendance”, please print it now. (see “Handouts” tab in “Conference Materials” box on left-hand side of your computer

screen). To earn Continuing Education credits, you must write down the verification codes in the corresponding spaces found

on the Official Record of Attendance form.

• Complete and submit the “Official Record of Attendance for Continuing Education Credits,” which is available on the

program page along with the presentation materials. Instructions on how to return it are included on the form.

• To earn full credit, you must remain connected for the entire program.

Tips for Optimal Quality

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides and the Official Record of Attendance for today's program.

• Double-click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Employee Benefit Plan Audits

Dec. 17, 2014

Danielle J. Kimmell

Bober Markey Fedorovich

Cindy H. Mitchell

Bober Markey Fedorovich

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

Employee Benefit Plan Audits: Asking the Right Questions and

Avoiding Critical Errors

By: Danielle Kimmell, CPA

Cindy Mitchell, CPA

What we will cover

• Form 5500 from an audit perspective

• Form 5500 errors and corrections

• Plan errors

• Types of plan failures

• Correction programs available

• Seven most common plan failures

• How to avoid plan failures

• Best practices for audit preparation

7

Form 5500

8

Form 5500 – Plan Audit Requirements

• General requirements

– > 100 audit is required

– Except… The 80/120 Rule; Plan Audit Waiver

– Measurement period – first day of the plan year

– Measurement criteria

• Active participants

• Eligible to participate

• Participant accounts

– Other criteria: Qualifying plan assets / bonding and Summary Annual Report (SAR) and document & other administrative communications to participants/beneficiaries

9

Form 5500 – Plan Audit Requirements

• Other audit requirement considerations

– 403(b) plans – “governmental” and “church” are exempt; otherwise, apply audit requirements

– Welfare plans – Voluntary Employee Beneficiary Association (VEBA) Trust, apply audit requirements

– Short period – 7 months or less, election to defer the audit requirements to the following year does exist

– Controlled group provisions

• Members of a controlled group don’t have to participate in a plan

• However, the controlled group impacts plan testing rules (nondiscrimination, ADP/ACP, top heavy, etc…)

10

Form 5500 – Plan Audit Requirements

• Full scope audit

• Limited scope audit - Disclaimer of opinion; no testing of investments IF…

– Financial institution properly qualified – bank or similar institution or by an insurance carrier that is regulated, supervised and subject to periodic exam

– Certification must cover the “accuracy and completeness” of information submitted

• Cautionary note: loans and hard to value assets are sometimes not covered or are erroneously not excluded from the certification

11

Form 5500

• Audit requirement to review Form 5500

• Auditors are required to review anything on the Form 5500 that have a direct impact to the financials.

• Most of the time this is Sch H and Sch SB if it is a defined benefit plan

• Should also scan all other schedules for reasonableness

12

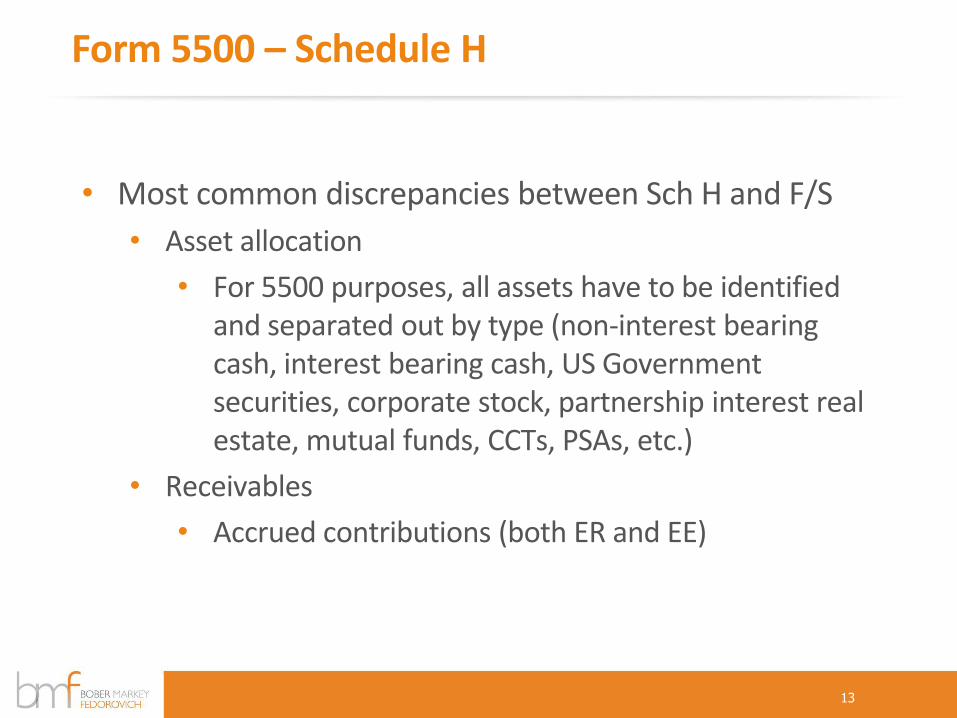

Form 5500 – Schedule H

• Most common discrepancies between Sch H and F/S

• Asset allocation

• For 5500 purposes, all assets have to be identified and separated out by type (non-interest bearing cash, interest bearing cash, US Government securities, corporate stock, partnership interest real estate, mutual funds, CCTs, PSAs, etc.)

• Receivables

• Accrued contributions (both ER and EE)

13

Form 5500 – Schedule H

• Most common discrepancies between Sch H and F/S

• Adjustment for fully benefit responsive contracts

• For F/S purposes, reported at contract value

• For 5500 purposes, reported at FMV

• Typically requires a footnote to explain the discrepancy between the 5500 and the F/S

• Income allocation

• Dividends for Mutual funds on line 2b(2)(C)

• All other income from mutual funds (realized and unrealized capital gains) reported on line 2b(10)

14

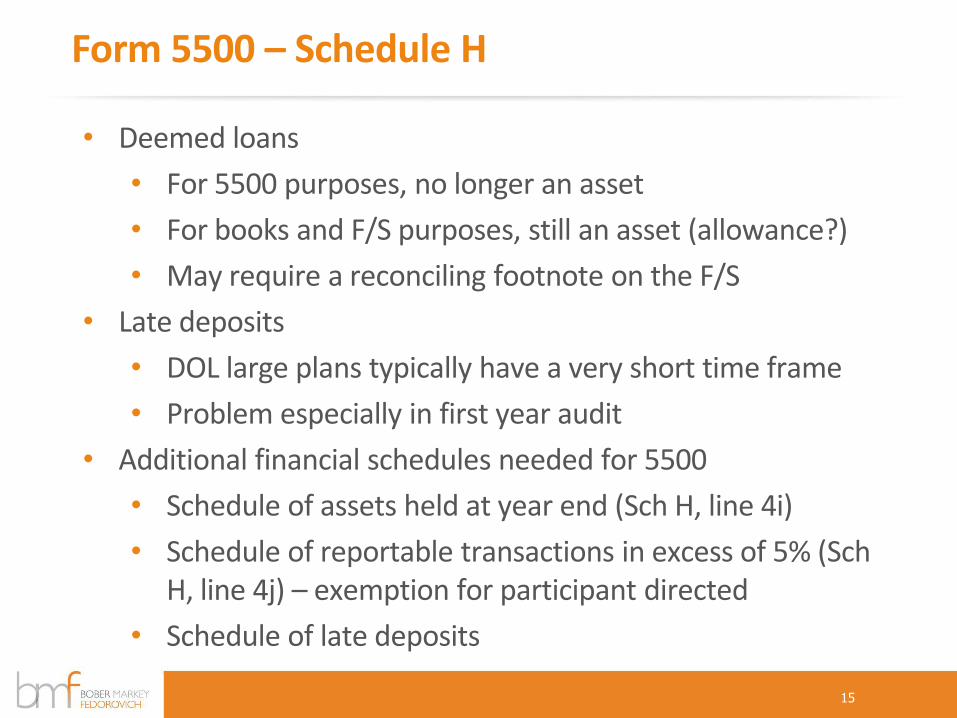

Form 5500 – Schedule H

• Deemed loans

• For 5500 purposes, no longer an asset

• For books and F/S purposes, still an asset (allowance?)

• May require a reconciling footnote on the F/S

• Late deposits

• DOL large plans typically have a very short time frame

• Problem especially in first year audit

• Additional financial schedules needed for 5500

• Schedule of assets held at year end (Sch H, line 4i)

• Schedule of reportable transactions in excess of 5% (Sch H, line 4j) – exemption for participant directed

• Schedule of late deposits

15

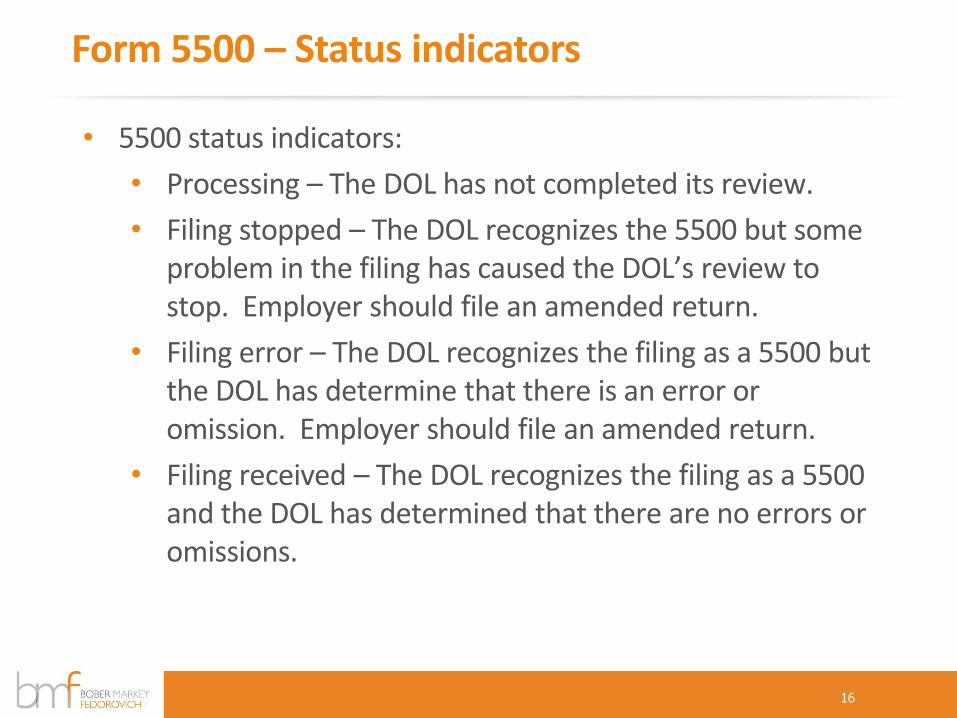

Form 5500 – Status indicators

• 5500 status indicators:

• Processing – The DOL has not completed its review.

• Filing stopped – The DOL recognizes the 5500 but some problem in the filing has caused the DOL’s review to stop. Employer should file an amended return.

• Filing error – The DOL recognizes the filing as a 5500 but the DOL has determine that there is an error or omission. Employer should file an amended return.

• Filing received – The DOL recognizes the filing as a 5500 and the DOL has determined that there are no errors or omissions.

16

Slide Intentionally Left Blank

Plan errors

18

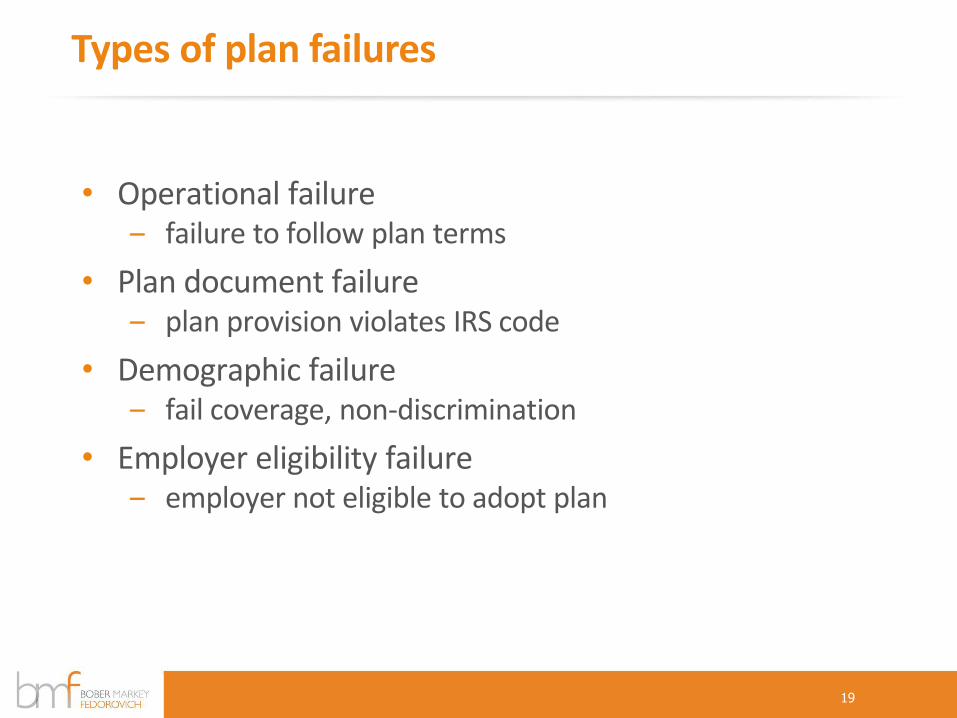

Types of plan failures

• Operational failure ‒ failure to follow plan terms

• Plan document failure ‒ plan provision violates IRS code

• Demographic failure ‒ fail coverage, non-discrimination

• Employer eligibility failure ‒ employer not eligible to adopt plan

19

Correction Programs Available

• IRS Programs – SCP: Self Correction Program

– VCP: Voluntary Correction Program

– Audit Cap: Audit Closing Agreement program

• DOL Programs – VFCP: Voluntary Fiduciary

Corrections Program

– DFVCP: Delinquent Filer Voluntary Corrections Program

20

Features: • Easy

• Free

• No IRS involvement

• Few guarantees

• Limited to operational failures only

• Must have practices and procedures in place to avoid future failures

IRS - Self Corrections Program

Types of failures: • Operational failures only - not

following the plan document provisions

Timing of correction: • If insignificant error: correct any time

• If significant error: correct within two years after the end of the plan year of failure

21

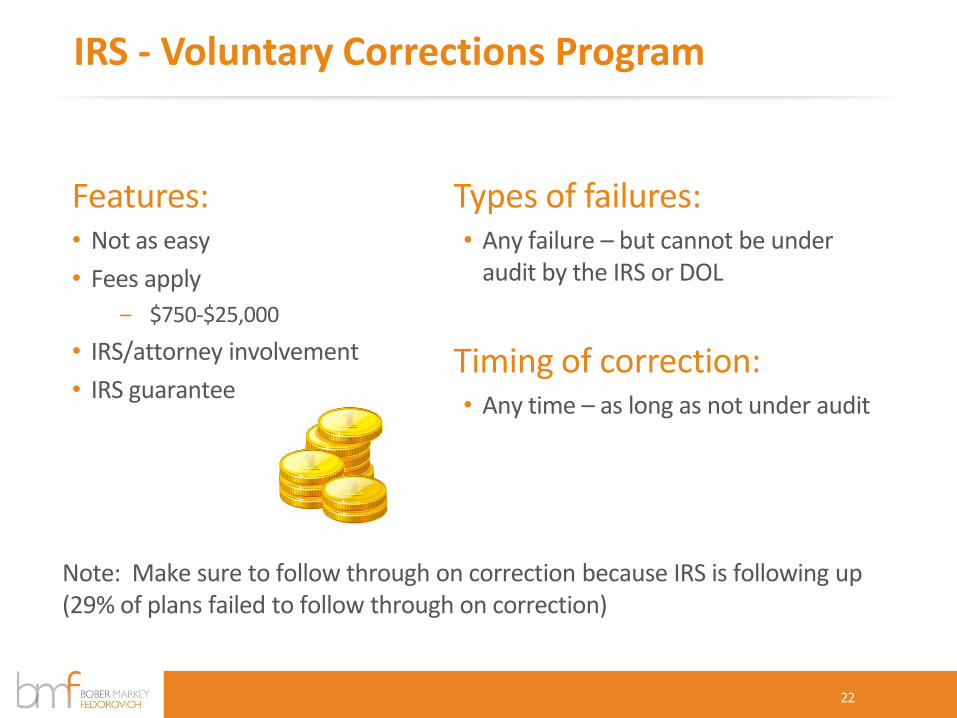

Features: • Not as easy

• Fees apply

‒ $750-$25,000

• IRS/attorney involvement

• IRS guarantee

IRS - Voluntary Corrections Program

Types of failures: • Any failure – but cannot be under

audit by the IRS or DOL

Timing of correction: • Any time – as long as not under audit

Note: Make sure to follow through on correction because IRS is following up (29% of plans failed to follow through on correction)

22

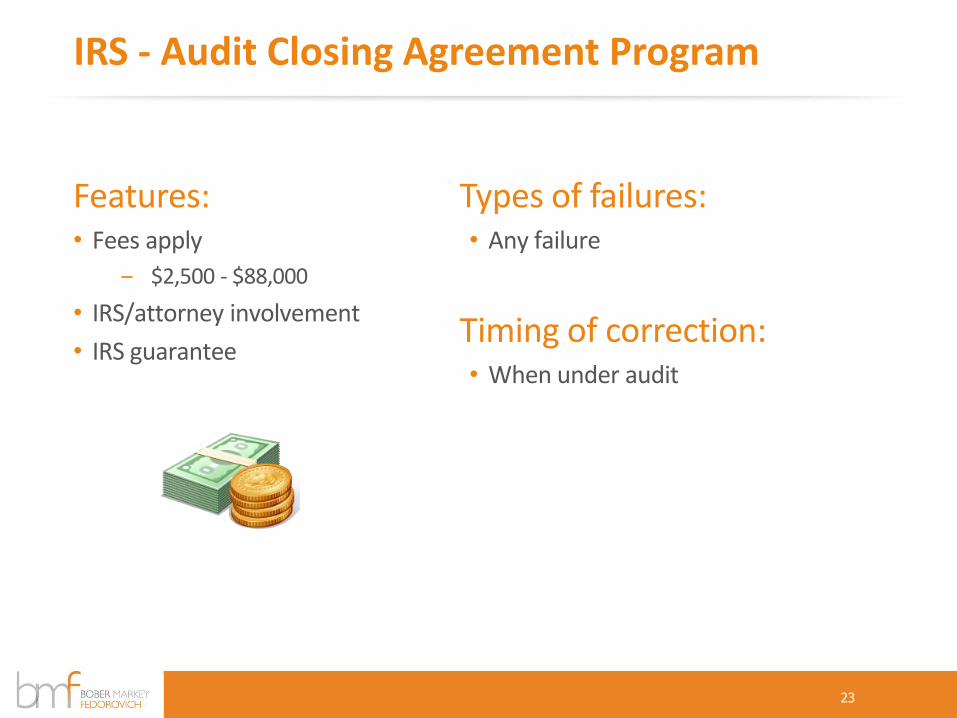

Features: • Fees apply

‒ $2,500 - $88,000

• IRS/attorney involvement

• IRS guarantee

IRS - Audit Closing Agreement Program

Types of failures: • Any failure

Timing of correction: • When under audit

23

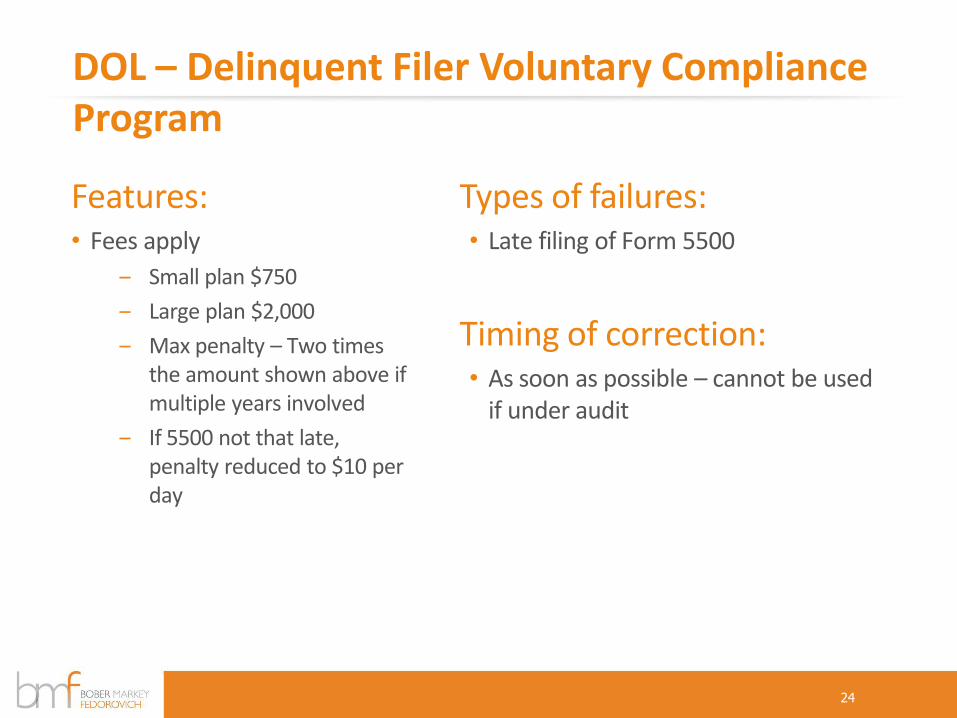

Features: • Fees apply

‒ Small plan $750

‒ Large plan $2,000

‒ Max penalty – Two times the amount shown above if multiple years involved

‒ If 5500 not that late, penalty reduced to $10 per day

DOL – Delinquent Filer Voluntary Compliance Program

Types of failures: • Late filing of Form 5500

Timing of correction: • As soon as possible – cannot be used

if under audit

24

Features: • May avoid paying IRS excise

tax

• Time consuming

• DOL “no action letter”

• Must notify interested parties of the filing and correction

DOL – Voluntary Fiduciary Corrections Program

Types of failures: • Delinquent participant contributions

• Loan failures

• Party-in-interest transactions

• Plan expenses

Timing of correction: • As soon as possible – cannot be used

if under audit

25

Slide Intentionally Left Blank

Most common plan failures

• Failure to deposit employee deferrals timely

• Failure to file Form 5500 timely

• Plan loan failure

• Failure to use correct definition of compensation

• Eligibility failure

• Vesting failure

• Failure to provide RMD (required minimum distribution)

27

Late deposit of participant contributions

• Employee contributions become plan assets on “the earliest date on which such contributions can reasonably be segregated from the employer’s general assets” but no later than the 15th business day of the following month. Employee contributions include deferrals and loan payments ‒ Must deposit money into the trust with lost earnings

‒ Must report late deposits on Form 5500

• Correction programs available: ‒ SCP

‒ VCP (if significant and past the two year period)

‒ VFCP

28

Failure to file Form 5500 timely

• Form 5500 due seven months after the plan year end ‒ Can file for a 2 ½ month extension using Form 5558

‒ Can rely on automatic extension using corporate extension

‒ Watch welfare plans (possibly more than one plan)

o Funded welfare plans (large or small) – filing required

o Small unfunded/fully insured welfare plans – no filing

o Large unfunded/fully insured welfare plans – filing required

• Correction programs available: ‒ SCP

‒ VCP (if significant and past the two year period)

‒ VFCP

29

Plan loan failure

• Plan document does not allow for loans but loans are permitted

‒ Retroactively amend the plan to permit loans and file under VCP

• Loan terms exceed five years with no evidence that it was used to purchase primary residence

‒ Re-amortize the loan over the maximum remaining period from the date of the original loan

• Loan amount exceeds dollar limit

‒ Participant repays the excess amount and remaining principal balance is re-amortized over original loan’s remaining period

• Loan payments are not made timely

‒ Participant to make a lump sum payment for missed installments or deemed distribution of loan balance – employer must issue 1099-R to participant

30

Failure to use correct definition of compensation

• Several different definitions of compensation – know which definition is used by your plan ‒ Section 3401(a) – (FIT withholding)

‒ W-2 Box 5 wages

‒ Include or exclude bonuses

‒ Include or exclude fringe benefits

‒ Include or exclude overtime, commissions, etc.

• When compensation used to practice is larger than the definition of compensation in the plan ‒ Improper employee contribution and earnings returned to

participant

‒ Improper matching contribution and earnings to be forfeited

31

Failure to use correct definition of compensation

• When compensation used in practice is less than the definition in the plan: ‒ Contribute 50% of the employees missed elective deferral

‒ Contribute 100% of the missed match

‒ Contribute earnings on all of the above

• Correction programs available: ‒ SCP

‒ VCP (if significant and past the two year period)

32

Eligibility failures

• Types of eligibility failures: ‒ Missed entry date – employer required to provide participant

o 50% of missed deferral

o 100% of missed match

o 100% of lost earnings

‒ Entry allowed too early

o Excess deferral and earnings should be returned to participant

o Excess match and earnings should be forfeited and used in

accordance with plan terms

• Correction programs available: ‒ SCP

‒ VCP (if significant and past the two year period)

33

Vesting failures

• Improper application of years of service ‒ Too few years of vesting service credited

o Forfeitures and earnings must be restored to participant

‒ Too many years of vesting service credited

o Employer match and excess earnings should be forfeited and used in accordance with plan terms

• Correction programs available: ‒ SCP

‒ VCP (if significant and past the two year period)

34

Failure to distribute required minimum distribution

• Two problems for failing to distribute RMD ‒ Operational failure for the plan

‒ 50% penalty for the participant

• Correction procedures ‒ Distribute RMD

• Correction programs available: ‒ SCP

‒ VCP

o If filed under VCP, IRS can forgive 50% penalty

o Reduced filing fee of $500 if less than 50 participants

35

How to avoid failures in the future

• Make sure to read the plan documents and know the definitions provided

• Have practices and procedures in place to be compliant with plan documents (good internal controls)

• Monitor new legislation and impact on plan

• Follow through on corrections as the DOL is following through

36

Slide Intentionally Left Blank

Audit Best Practices / Common Issues

• Overarching comments

– Audit personnel should be well versed in:

• Plan industry, operations, rules, regulations

• The plan’s document and related provisions

– If they don’t know the above:

• They can’t tailor the audit for proper risks and plan provision

• They won’t be able to identify issues, risks or errors when they find them

– 32% audit deficiencies rates – DOL findings; they call this unacceptable

38

Audit Best Practices / Common Issues

• Internal Controls

– Yes, plan’s have internal controls; IRS and DOL have various tools and guidance on their websites related to what they expect to see

– Appropriate identification and audit procedures are required

– Internal controls play into your assessment of risk and, if tested, could help you reduce your testing

– Can’t assessment control risk below maximum if they are not tested

– Consider dual purpose testing to leverage work

– Consider ability to leverage SOC reporting

39

Audit Best Practices / Common Issues

• Service Organizations

– Documentation • The appropriate report for the appropriate service provider

• Watch for carve-outs; you may need to get additional reports

• User controls – documenting them; identify key controls; perform relevant procedures on those controls

• Utilize and leverage AICPA EBPAQC checklist to meet minimum documentation requirements related to SOC reports

– Overreliance • Auditors often rely to heavily on the receipt of a SOC report from a TPA

• Read the report - Don’t presume no errors and don’t presume no qualifications in the report

• Cannot eliminate required testing because a SOC report exists

40

Audit Best Practices / Common Issues

• Actuaries

– Overreliance is a common issue; failure to test of validate census data

– Documentation requirements related to use of an expert

– Must gain comfort with key assumptions underlying calculations; clients should take ownership in this process

– Make sure you have the right report for the plan financials

• TPA reporting

– Watch for overreliance of TPA reports

– They frequently have inaccurate data

– Make sure you are obtaining the best source documents; original sources

41

Audit Best Practices / Common Issues

• Participant Data

– Common issue… failure to test

– Lost participants

42

Audit Best Practices / Common Issues

• Contribution testing - Audit procedures tend to not be properly modified for special provisions and / or errors are often found when these areas are audited:

– Catch-up contributions

– 402(g) limits

– Auto-enrollment & opt-out provisions

• Timeliness of remittance testing

• Payroll / compensation testing - Common failure related lack of auditor testing on the basis for which contributions are made

43

Audit Best Practices / Common Issues

• Plan loans

– Timely repayment

– Cessation of payments after loan is fully repaid

– Proper administration within rules and limits of the plan document and IRS limits

– Loans in default not properly accounted or allowed for

– Loans not tested by auditor

• Values not tested when certification doesn’t cover loans

• Administration of loans not tested even though required regarding of whether or not loan value are tested

44

Audit Best Practices / Common Issues

• Distributions testing

– Minimum distribution requirements

– Corrective distributions – timeliness; booking the liability

– Un-cashed benefit payment checks

– Vesting errors

• Transfers between plans

• Hire / re-hire / layoff

• Partial plan termination

– Pension plans

• Calculation errors due to complex nature

• Amounts not appropriately adjusted at different points in time (surviving spouse or term certain elections)

45

Audit Best Practices / Common Issues

• Hardship distributions

– Plan documents – Are they actually allowed?

– Generally, contributions to the plan should cease for a period of time after the hardship distribution. Common for this to not be treated timely or properly.

– Potential for risk of fraudulent applications for hardship

• Internal controls and proper administration is important

• Overreliance on TPAs often occurs

• Possible safe harbor depending on administrative and plan set up

46

Audit Best Practices / Common Issues

• Plan expenses

– Auditors often skip testing considerations related to plan expenses

– 408(b) fee disclosures now required – Has the plan sponsor complied? Has the auditor asked or obtained copies?

– Sch C on Form 5500

47

Noteworthy Websites

• http://www.irs.gov/retirement-plans/

• http://www.dol.gov/ebsa/

• http://www.aicpa.org/InterestAreas/EmployeeBenefitPlanAuditQuality/Pages/EBPAQhomepage.aspx

• http://www.401khelpcenter.com/

48

Bober Markey Fedorovich

• Danielle J. Kimmell

– 330-255-2459

• Cindy Mitchell

– 330-255-2454

49

Questions

50