Emerging Issues in the Life Science Industry

32

0 Emerging Issues in the Life Science Industry Marsh 2005 Life Science Conference „Effective Risk Management Solutions for the Life Science Industry“ 20 & 21 October 2005, Berlin

Transcript of Emerging Issues in the Life Science Industry

0

Emerging Issues in the Life Science Industry

Marsh 2005 Life Science Conference

„Effective Risk Management Solutionsfor the Life Science Industry“

20 & 21 October 2005, Berlin

1

Agenda

• Life Science Industry – a global overview• Markets and Gographies• Industry Issues

• Emerging Health Markets• Market Drivers and Industry Positioning• Therapeutic Areas

• Convergence of Life Science industry segments• Innovation Driver• Impact of Biotechnology• Deals

• Regulation and Risk• Transparency• Integrity• Value

• Ernst & Young – Advisor in the Life Science industry• Pharma-, Biotech-, Health Care Reports• Ernst & Young Risk Advisory Service

2

Life Science Industry – a global overview

Pharma – the global market

Source: IMS Health MIDAS MAT Dec 2004

0

50

100

150

200

250

300

350

400

450

500

550

1995 1996 1997 1998 1999 2000 2001 2002 2003 20040

2

4

6

8

10

12

14Market SizeGrowth Rate

% Growth

US$

North America

US$ (bn)

3

Life Science Industry – a global overview

Pharma – the global players

Top 10 Pharmaceutical Companies, LocationsPfizer

Bristol -Meyers Squibb

Johnson & JohnsonMerck

GlaxoSmithKline

AstraZeneca

Sanofi -Aventis

NovartisRoche

Abbott

4

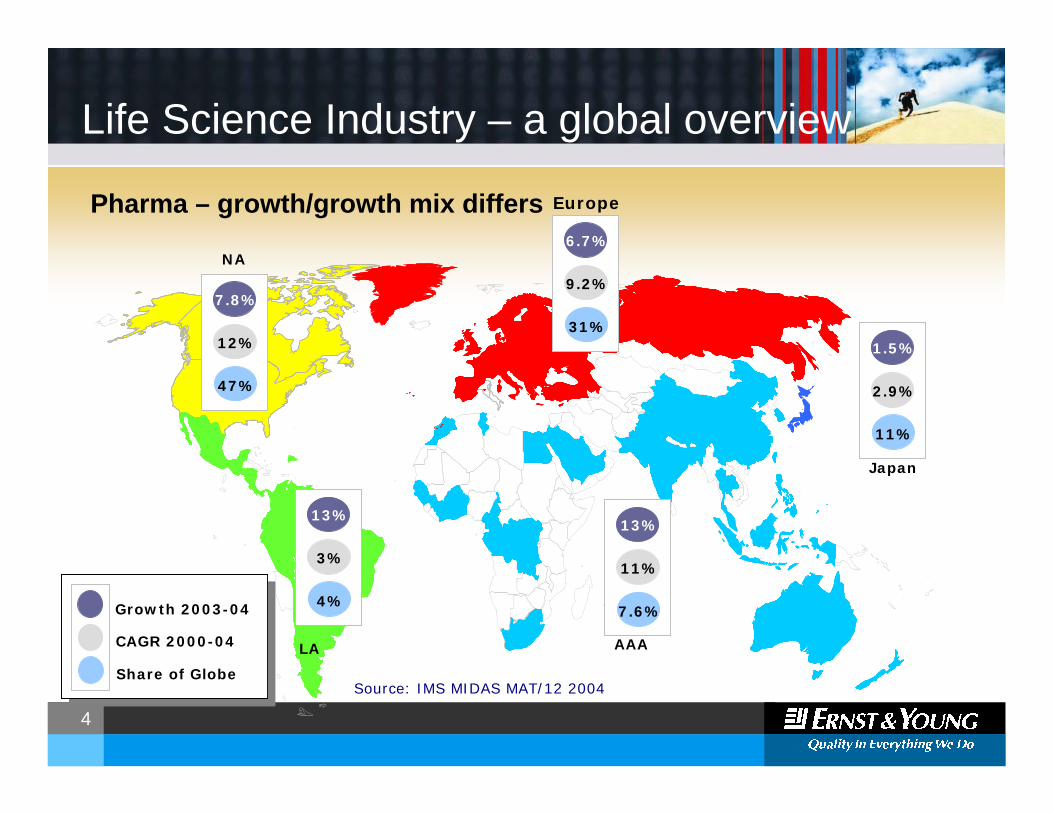

Life Science Industry – a global overview

Pharma – growth/growth mix differs

Source: IMS MIDAS MAT/12 2004

47%

12%

7.8%

47%

12%

7.8%

4%

3%

13%

4%

3%

13%

7.6%

11%

13%

7.6%

11%

13%

11%

2.9%

1.5%

11%

2.9%

1.5%

Japan

LA

NA

AAA

Europe

31%

9.2%

6.7%

31%

9.2%

6.7%

Growth 2003-04

CAGR 2000-04

Share of Globe

Growth 2003-04

CAGR 2000-04

Share of Globe

5

Life Science Industry – a global overview

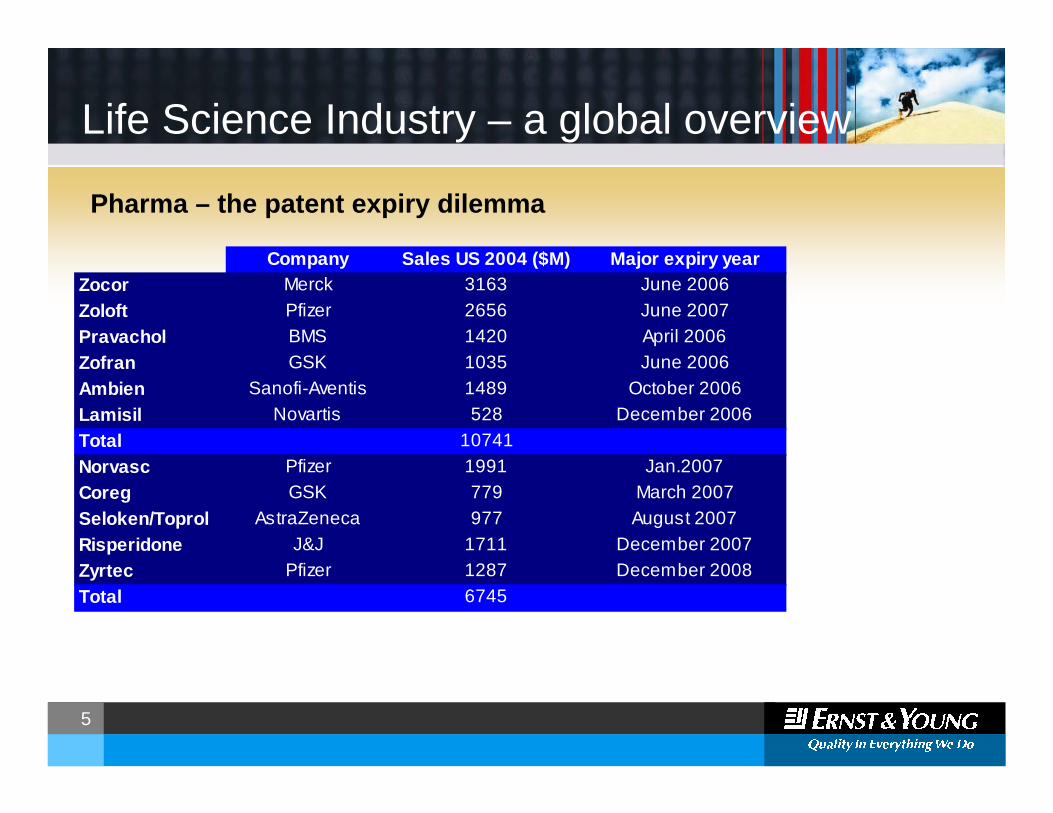

Pharma – the patent expiry dilemma

Company Sales US 2004 ($M) Major expiry yearZocor Merck 3163 June 2006Zoloft Pfizer 2656 June 2007Pravachol BMS 1420 April 2006Zofran GSK 1035 June 2006Ambien Sanofi-Aventis 1489 October 2006Lamisil Novartis 528 December 2006Total 10741Norvasc Pfizer 1991 Jan.2007Coreg GSK 779 March 2007Seloken/Toprol AstraZeneca 977 August 2007Risperidone J&J 1711 December 2007Zyrtec Pfizer 1287 December 2008Total 6745

6

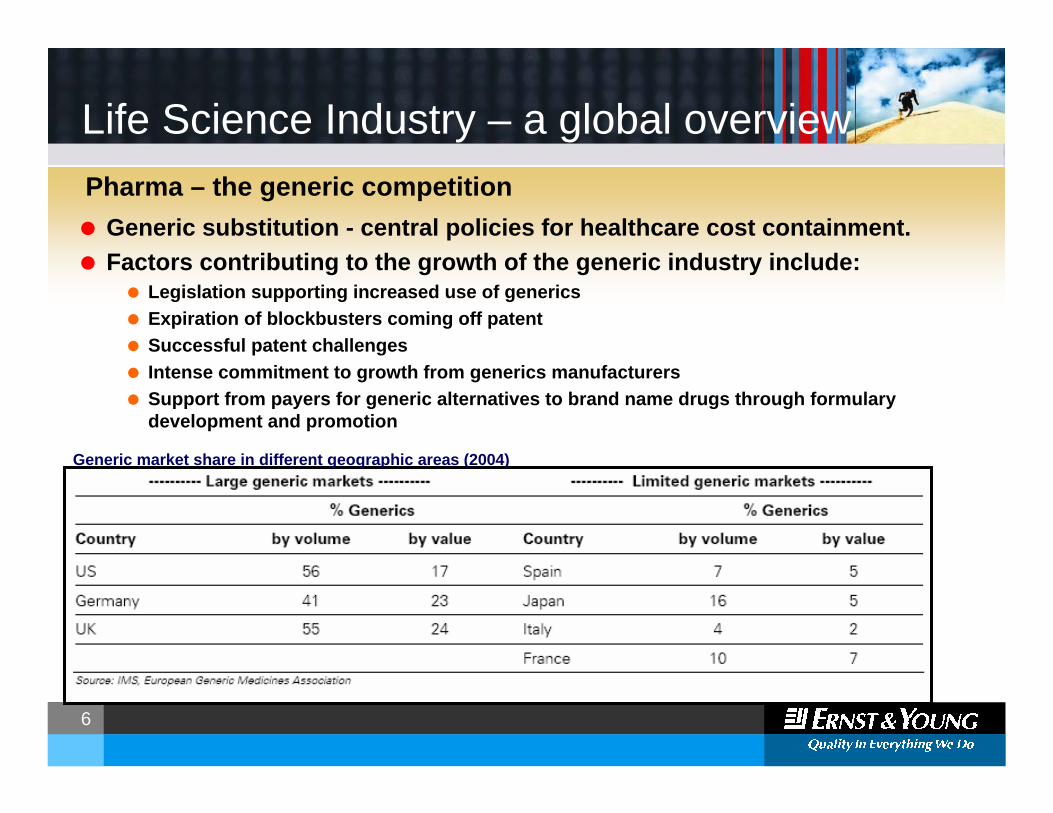

Life Science Industry – a global overviewPharma – the generic competition

Generic market share in different geographic areas (2004)

Generic substitution - central policies for healthcare cost containment. Factors contributing to the growth of the generic industry include:

Legislation supporting increased use of genericsExpiration of blockbusters coming off patentSuccessful patent challengesIntense commitment to growth from generics manufacturersSupport from payers for generic alternatives to brand name drugs through formulary development and promotion

7

Life Science Industry – a global overviewPharma – the innovation deficit dilemma

Year

Cost / benefit ratioTime to approval

8

Life Science Industry – a global overviewPharma – the innovation deficit dilemma and the biotech promise

$0

$10

$20

$30

$40

$50

$60

1998 1999 2000 2001 2002 2003 20040

5

10

15

20

25

30

Biotech R&D Big pharma R&D Biotech NME approvals Big pharma NME approvals

Source: Ernst & Young

Approvals inlcude only new molecular entities, and exclude label approvals, new formulations and combinations. Certain drugs partnered between biotech and big pharma companies are counted in both groups. Big pharma is defined as the 20 largest global pharmaceuitcal companies by market cap. Companies that do not meet the definition of big pharma and do not meet Ernst & Young's definition of biotechnology are excluded from the analysis. Biotech R&D expenditures include large acquired in-process R&D charges resulting from mergers in some years.

Biotech and big pharma R&D expenditures and FDA new molecular entity (NME) approvals

R&D expenditures New molecular entities

9

Market Cap($ billions)

Company

Source: Ernst & Young

$ 73.5$ 29.0$ 5.7Genentech$ 72.7$ 63.2$ 5.7Amgen

$ 358.0$ 330.8$ 41.0Biotech Industry

$ 204.5$ 252.8$ 19.3Pfizer$ 75.0$ 146.5$ 37.4Merck

2005 (May 10th)20001995

Historical pharma vs biotech

Life Science Industry – a global overviewBiotech is catching up

10

Source: Ernst & Young; Yahoo Finance

Biotech

$73.58Genentech$72.69Amgen

$75.17Merck & Co., Inc.

$204.51Johnson & Johnson$204.52Pfizer Inc.$143.03GlaxoSmithKline plc (ADR)$114.24Novartis AG (ADR)$103.85Roche Holding Ltd. (ADR)$77.06Abbott Laboratories

$72.410AstraZeneca PLC (ADR)$66.711Eli Lilly & Co.$59.812Wyeth

Market CapRankPharma

Bristol Myers Squibb Co. $51.013

Top therapeutic companies by market cap (in $ billions)

Biotech

$73.58Genentech$72.69Amgen

$75.17Merck & Co., Inc.

$204.51Johnson & Johnson$204.52Pfizer Inc.$143.03GlaxoSmithKline plc (ADR)$114.24Novartis AG (ADR)$103.85Roche Holding Ltd. (ADR)$77.06Abbott Laboratories

$72.410AstraZeneca PLC (ADR)$66.711Eli Lilly & Co.$59.812Wyeth

Market CapRankPharma

Bristol Myers Squibb Co. $51.013

Top therapeutic companies by market cap (in $ billions)

Biotech

$19.78Abbott Laboratories$21.7 7AstraZeneca PLC

$52.51Pfizer Inc.$47.42Johnson & Johnson$39.23GlaxoSmithKline PLC$28.9 4Roche Holding AG$28.2 5Novartis AG$23.46Merck & Co. Inc.

$19.49Bristol-Myers Squibb Co.$17.4 10Wyeth Pharmaceuticals$13.9 11Eli Lilly & Co.$11.0 12Amgen

RevenuesRank

Pharma

Genentech Source: Ernst & Young; Yahoo (represents total revenues for most recent 12 month period reported)

$ 5.815

Top therapeutic companies by revenues (in $ billions)

Biotech

$19.78Abbott Laboratories$21.7 7AstraZeneca PLC

$52.51Pfizer Inc.$47.42Johnson & Johnson$39.23GlaxoSmithKline PLC$28.9 4Roche Holding AG$28.2 5Novartis AG$23.46Merck & Co. Inc.

$19.49Bristol-Myers Squibb Co.$17.4 10Wyeth Pharmaceuticals$13.9 11Eli Lilly & Co.$11.0 12Amgen

RevenuesRank

Pharma

Genentech Source: Ernst & Young; Yahoo (represents total revenues for most recent 12 month period reported)

$ 5.815

Top therapeutic companies by revenues (in $ billions)

Life Science Industry – a global overviewBiotech is catching up

11

Life Science Industry – a global overviewBiotech is catching up with the US dominating

USA EU Asia-PacificNo.Comp.

2000

1500

1000

500

US

40

30

20

10

Mrd. US$ No.Comp. Mrd. US$2000

1500

1000

500

40

30

20

10

2000

1500

1000

500

40

30

20

10

No.Comp. Mrd. US$

2000

1500

1000

500

EU

40

30

20

10

No.Comp. Mrd. US$

400

300

200

100

D UK F CH

4

3

2

1(public companies)

12

Life Science Industry – a global overview

Asian governments: strategic investments, ambitious goals

New Zealand: $660M industry in next decade,

with 18,000 employees

India(Draft

policy): $5B

industry by 2010

Japan: $200B

market by 2010Korea: Global

ranking of 7th by 2012

Taiwan: Invest $4.5 B; 18

companies by 2010Malaysia: One of

five core technologies

Biotech is catching up in Asia-Pacific

13

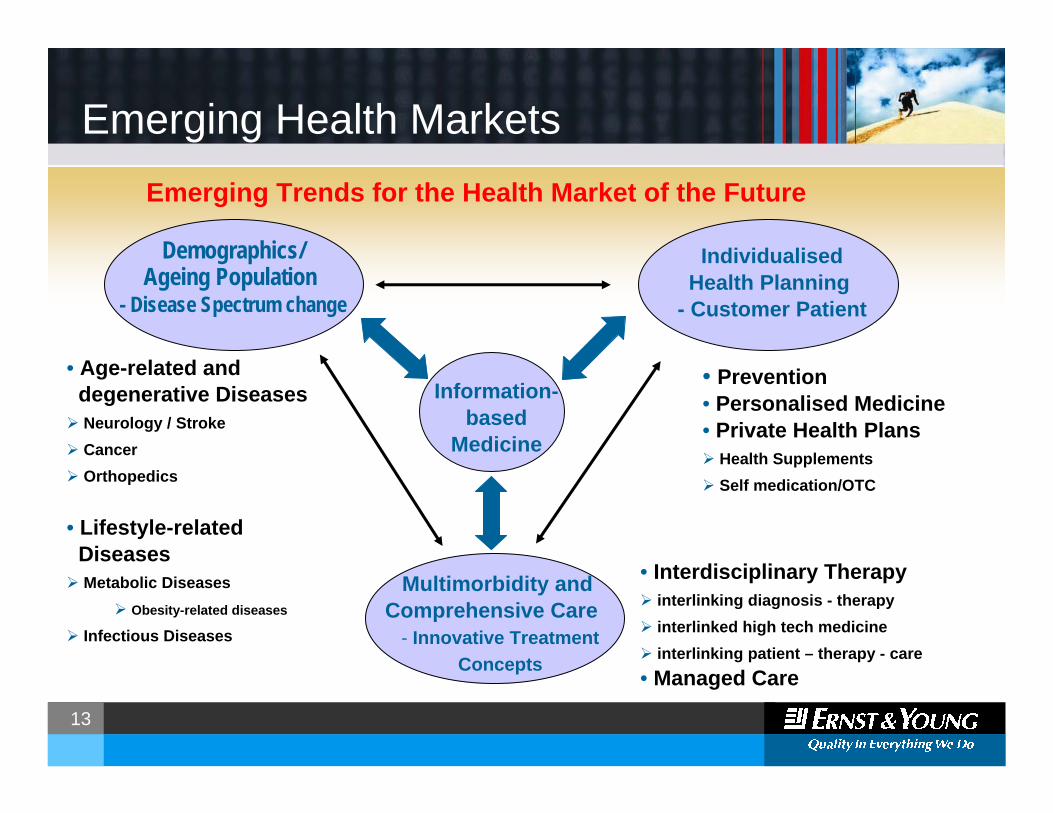

Emerging Health MarketsEmerging Trends for the Health Market of the Future

Information-based

Medicine

Demographics/Ageing Population

- Disease Spectrum change

IndividualisedHealth Planning

- Customer Patient

Multimorbidity and Comprehensive Care

- Innovative TreatmentConcepts

• Age-related and degenerative DiseasesNeurology / StrokeCancerOrthopedics

• Lifestyle-relatedDiseasesMetabolic Diseases

Obesity-related diseases

Infectious Diseases

• Prevention• Personalised Medicine• Private Health Plans

Health SupplementsSelf medication/OTC

• Interdisciplinary Therapyinterlinking diagnosis - therapyinterlinked high tech medicineinterlinking patient – therapy - care

• Managed Care

14

Emerging Markets – Health CareHealth Market as a significant economic factor in the future

HealthIT

Life ScienceIndustry

„Preventing, detecting, treating diseases“

Food and Health Supplement

Industry„Supporting health“

Health Care„Services within the

Health Market“

• Evidence-based and„Personalized“ Medicine

• Innovative Therapies• Innovative Diagnostics• Innovative Medical Devices

• Prevention Medicine• Convergence of Disciplines

• Theranostics• Molecular Imaging• Drug –coated Devices

• Nutrition /Neutraceuticals• Life Style-Products• Fitness-/Wellness-Products

• Physician Care (amb. u. stat.)• Care / Rehabilitation• Fitness / Wellness

15

Emerging Markets – Health Care

Leading Therapy Classes in 2004 ($bn)…$billion 1995 2005Statines 4 25Anti-cancer 4,5 26EPO 2 10Anti-psychotics 0,5 7Biphosphonates 0 4,5Total 11 72,5

16

Emerging Markets – Health Care

365 Phase III clinical products

Infectious Diseases 16%

Central Nervous System 12%

Cardiovascular 12%

Autoimmune 5%

Diabetes 2%

Cancer 28%Miscellaneous 25%

…and biotech pipelines address medical needs with preference

17

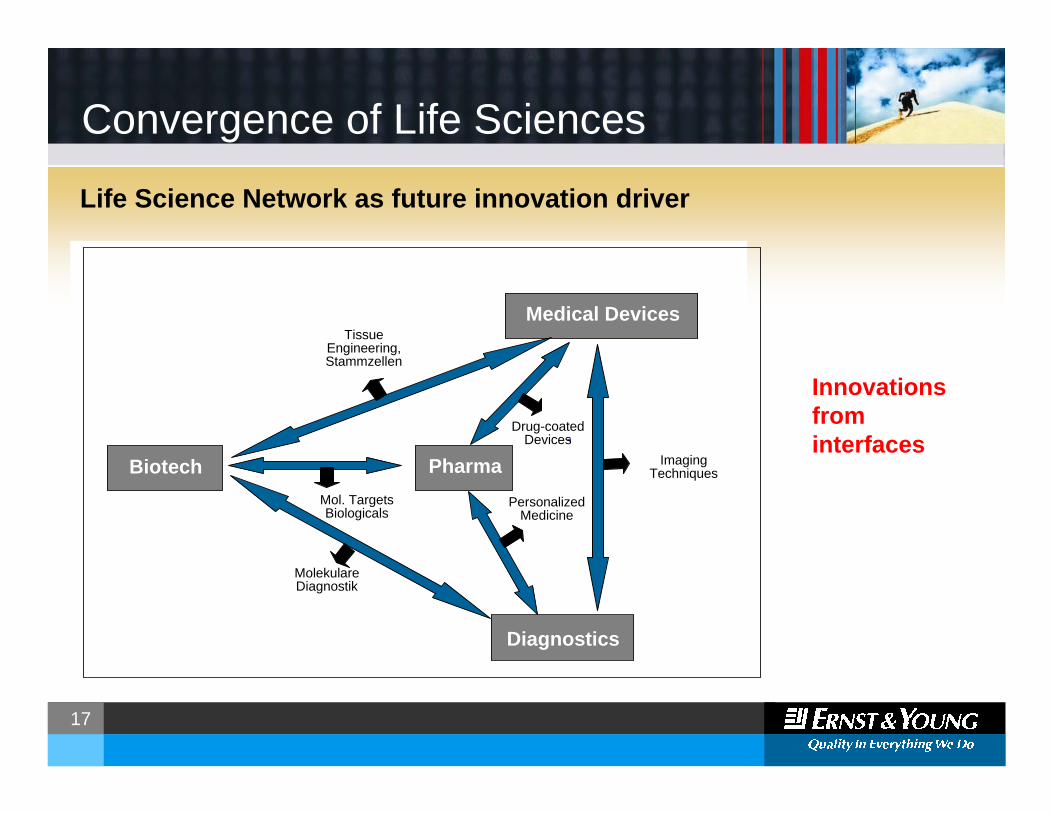

Convergence of Life Sciences

Life Science Network as future innovation driver

Pharma

Medical Devices

Biotech

Diagnostics

-

Molekulare Diagnostik

Mol. TargetsBiologicals

TissueEngineering,Stammzellen

Drug-coatedDevices

PersonalizedMedicine

ImagingTechniques

Innovationsfrominterfaces

18

Convergence of Life Sciences

Impact of Biotechnology

• Biologicals• therapeutic proteins• antibodies• peptides• biogenerics

• Molecular Diagnostics• gene testing• disease markers• theranostics• personalized medicine

• Cell Biology• Stem cells• vaccines• tissue engineering

• Nanobiotech• biotech/devices

$1,370Recombinant interferon alfa-2a modified with PEG (monotherapy; also in combination with Copegus [ribavirin])

10. Pegasys/Copegus

$1,417Recombinant interferon beta-1a9. Avonex$1,700PEGylated version of Neupogen8. Neulasta$1,826

Recombinant erythropoietin7. Epogin/NeoRecormon

$2,500Novel erythropoiesis-stimulating protein (2nd generation EPO)6. Aranesp$2,580Recombinant fusion protein; soluble TNF receptor linked to IgG15. Enbrel$2,600Recombinant erythropoietin4. Epogen$2,891Chimeric monoclonal antibody; anti-TNF-alpha3. Remicade$2,963Chimeric monoclonal antibody; anti-CD202. Rituxan$3,589Recombinant erythropoietin1. Procrit

2004 Sales, $MTypeProduct

$1,370Recombinant interferon alfa-2a modified with PEG (monotherapy; also in combination with Copegus [ribavirin])

10. Pegasys/Copegus

$1,417Recombinant interferon beta-1a9. Avonex$1,700PEGylated version of Neupogen8. Neulasta$1,826

Recombinant erythropoietin7. Epogin/NeoRecormon

$2,500Novel erythropoiesis-stimulating protein (2nd generation EPO)6. Aranesp$2,580Recombinant fusion protein; soluble TNF receptor linked to IgG15. Enbrel$2,600Recombinant erythropoietin4. Epogen$2,891Chimeric monoclonal antibody; anti-TNF-alpha3. Remicade$2,963Chimeric monoclonal antibody; anti-CD202. Rituxan$3,589Recombinant erythropoietin1. Procrit

2004 Sales, $MTypeProduct

Top biological therapeutics

Med

Dev

ices

Dia

gnos

tics

Pha

rma

19

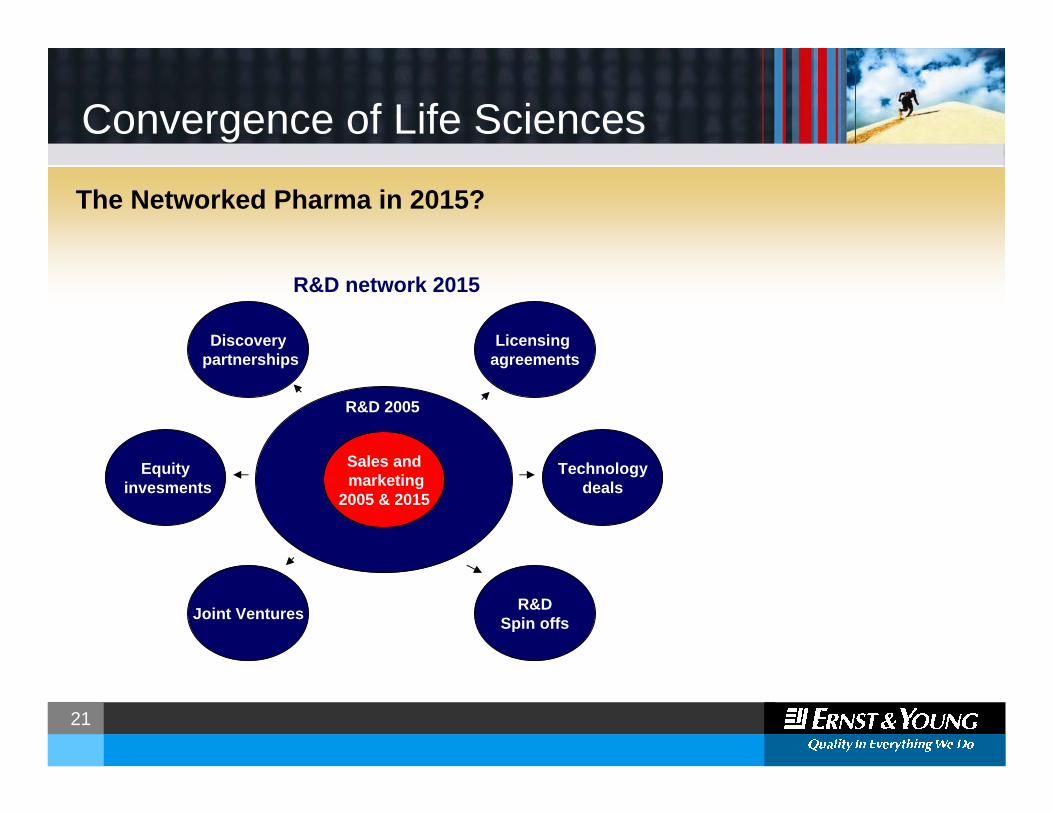

Convergence of Life Sciences

Consolidation through alliances and M&APharma M&As in 2004

20

Convergence of Life Sciences

Consolidation through alliances and M&A

21

Convergence of Life Sciences

Sales andmarketing

2005 & 2015

Technologydeals

Licensingagreements

R&DSpin offsJoint Ventures

Equityinvesments

Discoverypartnerships

R&D 2005

R&D network 2015

The Networked Pharma in 2015?

22

Regulation and Risk

Drivers of Change

Demands for greater transparency

Disclosing clinical resultsPricing strategiesFinancial controls

Questions about Pharma’svalue proposition

Economic value to society

Concern over regulatory compliance and integrity

Complex regulation & authority scrutinySecurity of Supply Chain, Products, IT-systems

Actions to be taken• Continuing to ask the right questions in

order to mitigate risks and take advantage of new opportunities

• Demonstrating and communicating the value that pharma companies add to society and shareholders

• Examining their relationships with third parties – from R&D collaborators to retail pharmacies – in addition to their internal controls and standard operating procedures

• Working collaborative with stakeholders in other sectors worldwide to enhance the security and integrity of the pharma supply chain

Risk

Life Science – the most heavily regulated industry

23

Regulation and Risk

Global Supply Chain Management

Product integrity, brand reputation, and patient safety rely on a series of third parties along the supply chain.

Upstream, risks and opportunities are associated with R&D collaboration, raw materials transactions

Downstream, risks and opportunities include diversion, counterfeiting, public safety, and evolving trade laws and regulations.

24

Regulation and Risk

Global Supply Chain Management

From factory to customer: a long road…

H

Enduser

Short liner

wholesalerwholesaler

wholesaler

25

Regulation and Risk

Assisted by the Economist Intelligence Unit225 respondents:

North America (33 percent), Europe (35 percent), Asia-Pacific (21 percent) representedPharmaceutical Manufacturers (33 percent), Wholesaler-distributors (31 percent), Pharmacies (24 percent) surveyed45 percent generate over $100 million in annual sales37 percent C-Level executives

Ernst & Young Global Supply Chain Survey

Distribution –a major risk carrier• diversion• conterfeit

26

Regulation and Risk

Argue for non dominanceQuotas/Cease Supply (non dominance)Pricing CorridorsAccessing data (IMS, Customs, Wholesalers)

Political LobbyingCreating ‘best case’

Supply Chain optimisationOrganisational alignmentProduct Launch StrategiesMinimising counterfeitsDeveloping Product Pricing StrategiesCreating Day Trading Capability Systems & Information Integration and enhancementProcess and IT Controls integritySales Force Compliance

Argue for non dominanceQuotas Lease Supply (non dominance)Pricing Corridors

Redesign incentive plans Global & Import data aspectsAutomation of performance measurement and assessment

Understanding volumeflows and associated pricingAccessing customer/wholesaler dataSystems integration and controlData warehousing

Industry Regulatory

Action

Supply Chain

Internal Action

PerformanceMeasurement& Motivation

Knowledge/Information

Management

‘Day Trading’Capabilities

Legal

Taking Effective Action to mitigate Margin Erosion

27

Ernst & Young and Health Sciences

Ernst & Young dedicated Health Science Competence Center

Dr. Manuel Bauer Dr. Susanne WoschMünchen KölnIndustry Specialist Industry Specialist

Dr. Siegfried BialojanMannheimIndustry Leader

Dr. Julia Schüler,MannheimSenior Industry Specialist

Dr. Ira Betz MannheimKnowledge Manager

Nina DunzweilerMannheimTeam Assistent

Account/Service Line/Client Support• Business Assessment/Development• Link to Service Lines• HS Solutions Development• Project Support

Thought Leadership/Marketing• Industry Analysis & Knowledge• Knowledge Management• Industry Reports• Public Relations• Marketing / Business Relations

Ernst & Young Health Sciences Competence CenterTel.: +49 621 4208 13 454 - [email protected] - www.de.ey.com

28

Ernst & Young and Health Sciences

Ernst & Young Health Sciences Thought Leadership

"Our Biotech Reports generate deep understanding of the industry and knowledge to be exploited in client projects."

"Our Pharmaceutical Reports take up major issues in Pharma and are the basis for the development of specific solutions for clients."

29

Ernst & Young and Pharma Risk Management

Ernst & Young Risk associated Advisory Services

Value proposition

Solution Sets

Core Competencies

Corporate SourcingCorporate SourcingCorporate ManagementCorporate ManagementCorporate Assuranceand Compliance

Corporate Assuranceand Compliance

Internal AuditFinancial Reporting ControlsIT Assurance & ControlsProgram & Project AssuranceEnterprise Security Mgmt.Forensic Advisory

Internal AuditFinancial Reporting ControlsIT Assurance & ControlsProgram & Project AssuranceEnterprise Security Mgmt.Forensic Advisory

Corporate Performance Mgmt.Corporate Risk Mgmt.Corporate Accountingand ReportingTreasury Management

Corporate Performance Mgmt.Corporate Risk Mgmt.Corporate Accountingand ReportingTreasury Management

Business Process OutsourcingIT OutsourcingIT Service ManagementPost Merger Integration

Business Process OutsourcingIT OutsourcingIT Service ManagementPost Merger Integration

Compliance – Cost – Quality - Performance

IT Management, Processes & Controls

Program & Project Management

Finance Processes, System & Controls

Advisory ServicesValue proposition

Solution Sets

Core Competencies

Corporate SourcingCorporate SourcingCorporate ManagementCorporate ManagementCorporate Assuranceand Compliance

Corporate Assuranceand Compliance

Internal AuditFinancial Reporting ControlsIT Assurance & ControlsProgram & Project AssuranceEnterprise Security Mgmt.Forensic Advisory

Internal AuditFinancial Reporting ControlsIT Assurance & ControlsProgram & Project AssuranceEnterprise Security Mgmt.Forensic Advisory

Corporate Performance Mgmt.Corporate Risk Mgmt.Corporate Accountingand ReportingTreasury Management

Corporate Performance Mgmt.Corporate Risk Mgmt.Corporate Accountingand ReportingTreasury Management

Business Process OutsourcingIT OutsourcingIT Service ManagementPost Merger Integration

Business Process OutsourcingIT OutsourcingIT Service ManagementPost Merger Integration

Compliance – Cost – Quality - Performance

IT Management, Processes & Controls

Program & Project Management

Finance Processes, System & Controls

Advisory Services

30

Ernst & Young and Pharma Risk Management

Ernst & Young Risk associated Advisory Services

Value proposition

Solution Sets

Core Competencies

Corporate SourcingCorporate SourcingCorporate ManagementCorporate ManagementCorporate Assuranceand Compliance

Corporate Assuranceand Compliance

Internal AuditFinancial Reporting ControlsIT Assurance & ControlsProgram & Project AssuranceEnterprise Security Mgmt.Forensic Advisory

Internal AuditFinancial Reporting ControlsIT Assurance & ControlsProgram & Project AssuranceEnterprise Security Mgmt.Forensic Advisory

Corporate Performance Mgmt.Corporate Risk Mgmt.Corporate Accountingand ReportingTreasury Management

Corporate Performance Mgmt.Corporate Risk Mgmt.Corporate Accountingand ReportingTreasury Management

Business Process OutsourcingIT OutsourcingIT Service ManagementPost Merger Integration

Business Process OutsourcingIT OutsourcingIT Service ManagementPost Merger Integration

Compliance – Cost – Quality - Performance

IT Management, Processes & Controls

Program & Project Management

Finance Processes, System & Controls

Advisory ServicesValue proposition

Solution Sets

Core Competencies

Corporate SourcingCorporate SourcingCorporate ManagementCorporate ManagementCorporate Assuranceand Compliance

Corporate Assuranceand Compliance

Internal AuditFinancial Reporting ControlsIT Assurance & ControlsProgram & Project AssuranceEnterprise Security Mgmt.Forensic Advisory

Internal AuditFinancial Reporting ControlsIT Assurance & ControlsProgram & Project AssuranceEnterprise Security Mgmt.Forensic Advisory

Corporate Performance Mgmt.Corporate Risk Mgmt.Corporate Accountingand ReportingTreasury Management

Corporate Performance Mgmt.Corporate Risk Mgmt.Corporate Accountingand ReportingTreasury Management

Business Process OutsourcingIT OutsourcingIT Service ManagementPost Merger Integration

Business Process OutsourcingIT OutsourcingIT Service ManagementPost Merger Integration

Compliance – Cost – Quality - Performance

IT Management, Processes & Controls

Program & Project Management

Finance Processes, System & Controls

Advisory Services

Risk:Advanced Security CentersAverage Sales Price (ASP) ComplianceBrand ProtectionContract AssuranceCorporate Social Responsibility (CSR) Data PrivacyEnterprise Risk ManagementGlobal Legislative and Regulatory RiskIdentity and Access Management Intellectual Property and Royalty Recovery ReviewsInternal Audit Outsourcing – TeamingMarketing & Advertising Risk ServicesMarketing Mix OptimizationMedicaid Drug Rebate Program Contract Services MMA Brand Impact AnalysisSales and Marketing Compliance AssessmentSecurity Information Management Supply Chain Risk MitigationRisk and Control Anchor SolutionWholesaler Audits

HealthSciencesSolutions

31

Ernst & Young and Pharma Risk Management

ContactHealth Sciences Competence [email protected]

Phone (0621) 4208-13454Fax (0621) 4208-42102

Theodor-Heuss-Anlage 268165 Mannheim

Thank you for your attention!