Emerging Issues in Government Accounting & Auditing · 2019-04-22 · Emerging Issues in Government...

93

Emerging Issues in Government Accounting & Auditing 38 th Annual Tennessee Government Auditing Training Seminars 2

Transcript of Emerging Issues in Government Accounting & Auditing · 2019-04-22 · Emerging Issues in Government...

Emerging Issues in Government Accounting & Auditing38th Annual TennesseeGovernment Auditing Training Seminars

2

Today’s Agenda• State Fiscal Outlook• Legislative and Regulatory Issues• Uniform Guidance Implementation• Auditing and Accounting Issues• Other Emerging Issues

3

State Fiscal Outlook

4

NATIONAL OVERVIEW

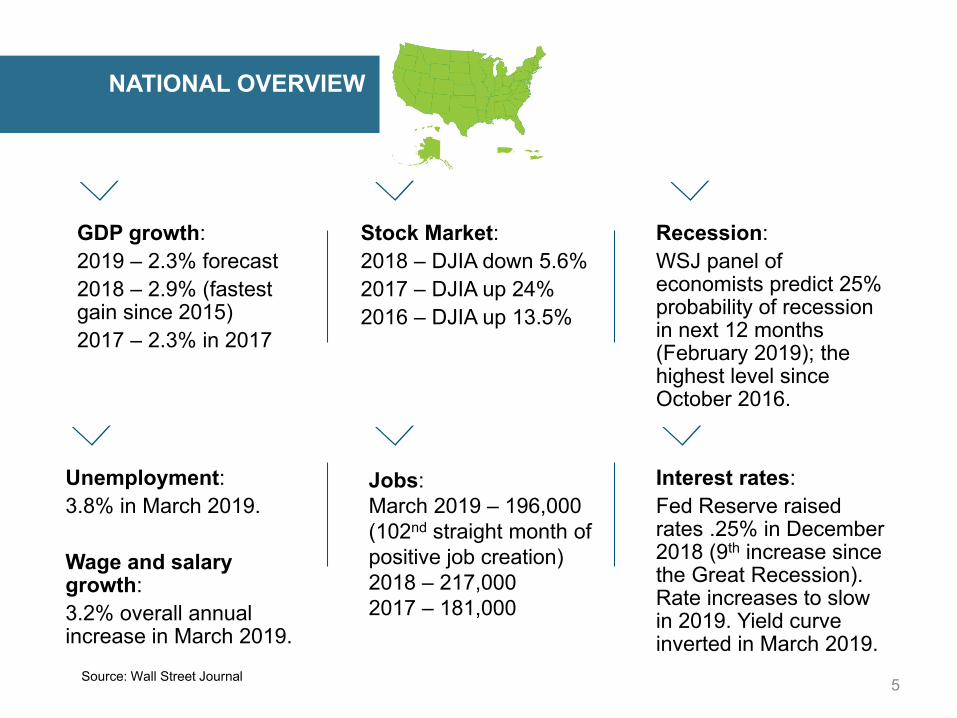

GDP growth: 2019 – 2.3% forecast2018 – 2.9% (fastest gain since 2015)2017 – 2.3% in 2017

Recession: WSJ panel of economists predict 25% probability of recession in next 12 months (February 2019); the highest level since October 2016.

Unemployment:3.8% in March 2019.

Wage and salary growth:3.2% overall annual increase in March 2019.

Jobs:March 2019 – 196,000 (102nd straight month of positive job creation)2018 – 217,0002017 – 181,000

Stock Market:2018 – DJIA down 5.6%2017 – DJIA up 24%2016 – DJIA up 13.5%

Source: Wall Street Journal 5

Interest rates:Fed Reserve raised rates .25% in December 2018 (9th increase since the Great Recession). Rate increases to slow in 2019. Yield curve inverted in March 2019.

Governors’ budgets for fiscal 2019 recommend a general fund spending increase of 3.2 percent, as fiscal conditions have improved compared to this time last year.

Only 9 states have had to make mid-year budget cuts, and 47 states reported meeting or exceeding budgeted revenue projections for fiscal 2018.

Governors proposed mostly modest tax changes for fiscal 2019, some in response to the new federal tax law, with a net revenue impact of +$2.8 billion.

Most states continue to strengthen their rainy day funds, with the forecasted median balance as a share of general fund spending rising to 6.2 percent in fiscal 2019, from a recent low of 1.9 percent in fiscal 2011.

Medicaid spending is projected to slow in fiscal 2019, with a median growth rate of 1.9 percent from all funds (1.5 percent state funds), but the program continues to pose spending pressures over the long term.

Revenue growth picked up in fiscal 2018 after 2 years of weakness, and is estimated at 4.9 percent, though growth varies by state and the median is lower at 2.7 percent.

STATE OVERVIEW

6Source: NASBO Spring 2018 Fiscal Survey

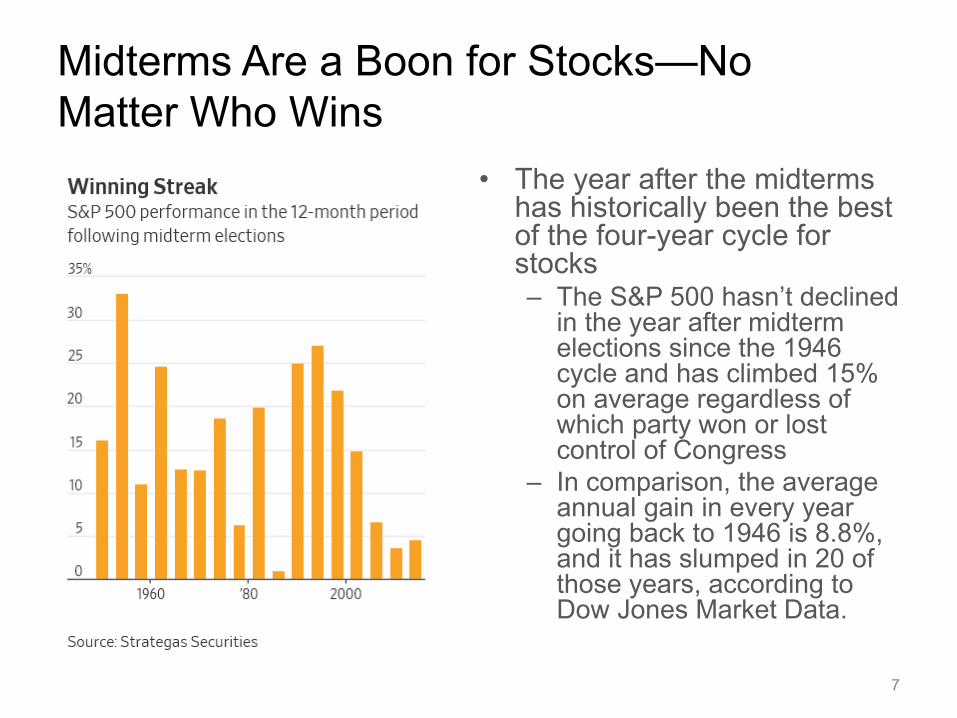

Midterms Are a Boon for Stocks—No Matter Who Wins

• The year after the midterms has historically been the best of the four-year cycle for stocks– The S&P 500 hasn’t declined

in the year after midterm elections since the 1946 cycle and has climbed 15% on average regardless of which party won or lost control of Congress

– In comparison, the average annual gain in every year going back to 1946 is 8.8%, and it has slumped in 20 of those years, according to Dow Jones Market Data.

7

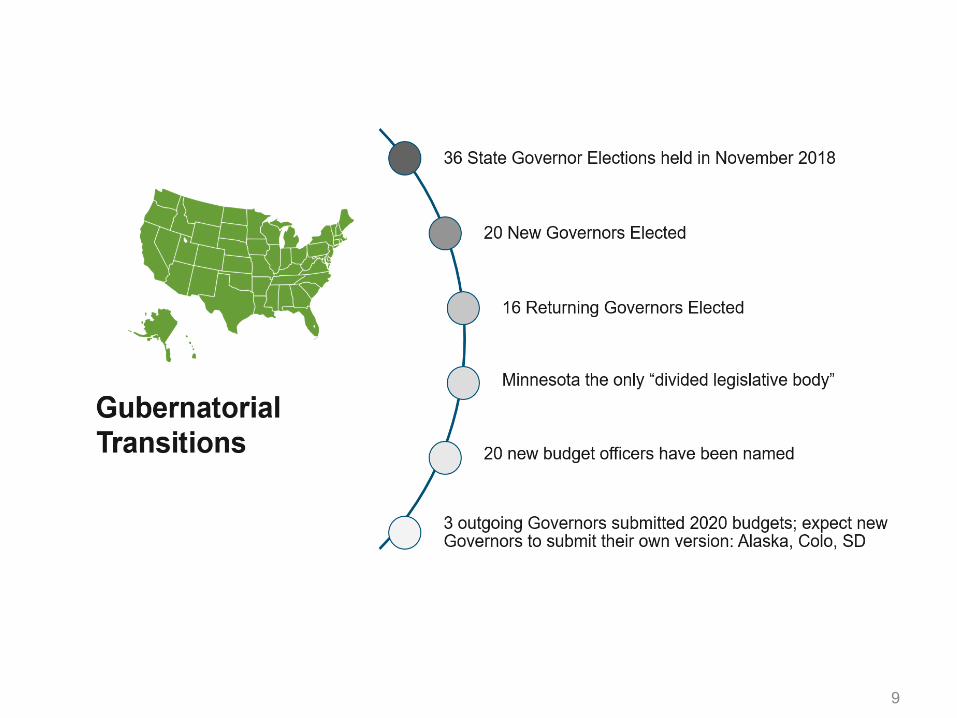

2019 Transitions

36 State Governor Elections

8

9

GENERAL FUND SPENDING

10

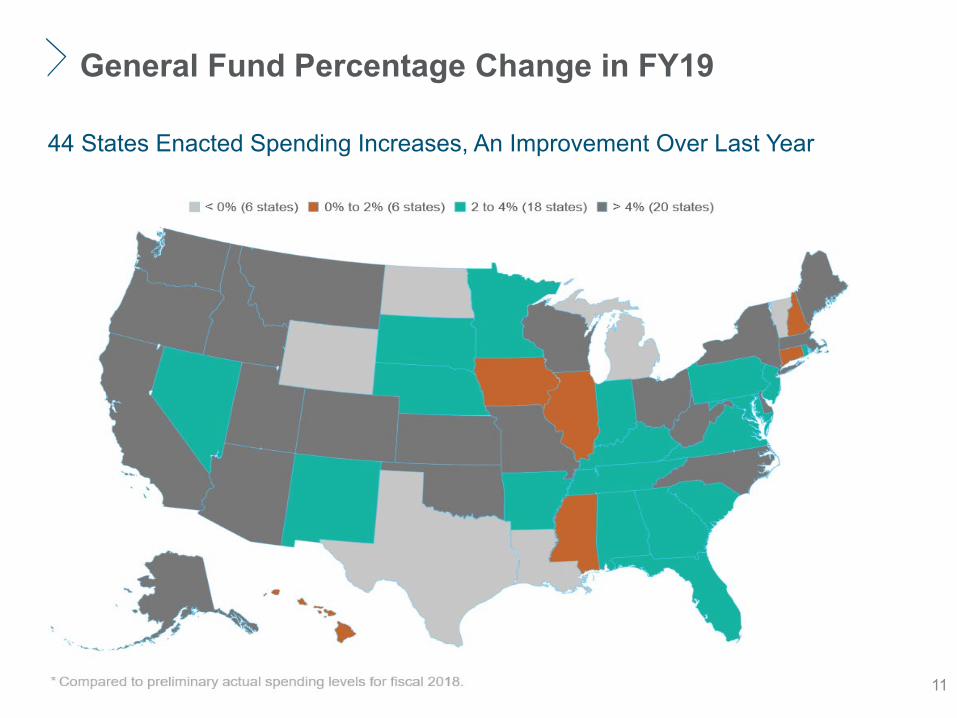

General Fund Percentage Change in FY19

44 States Enacted Spending Increases, An Improvement Over Last Year

11

General Fund Spending: FY 2008 – FY 2019

FY 2018 Falls Below Inflation Adjusted Pre-Recession Peak

12

STATE GENERAL FUND SPENDING EXPECTED TO SEE MODEST INCREASE IN FISCAL 2019

Source: NASBO Fiscal Survey of States

13

General Fund Expenditures

By Function

14

GENERAL FUND REVENUE

15

General Fund Revenue Collections Compared to Budget Projections

40 States Had FY 2018 Revenue Collections Exceed Budget Projections

16

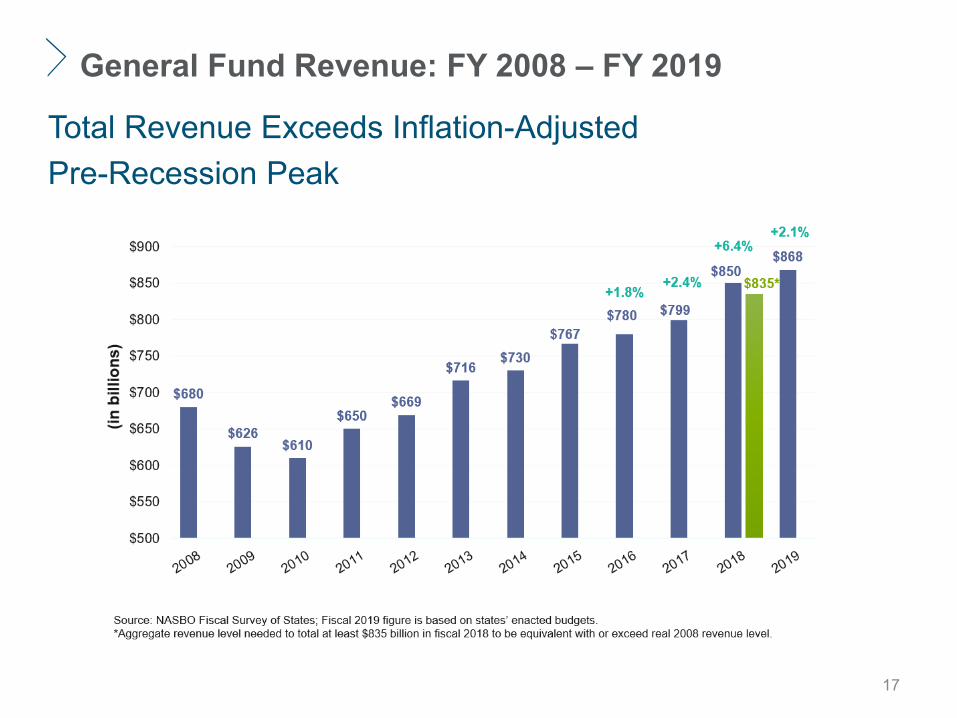

General Fund Revenue: FY 2008 – FY 2019

Total Revenue Exceeds Inflation-Adjusted Pre-Recession Peak

17

General Fund Revenue Sources – Est. FY 2018

18

Median General Fund Revenue Percentage Change

FY 2018 & 2019

19

RATINGS: IMPROVEMENTS FROM LAST YEAR

20

State G.O. Ratings as of December 2018, Citi

21

STATE SAVINGS ACCOUNTS(RAINY DAY FUNDS)

22

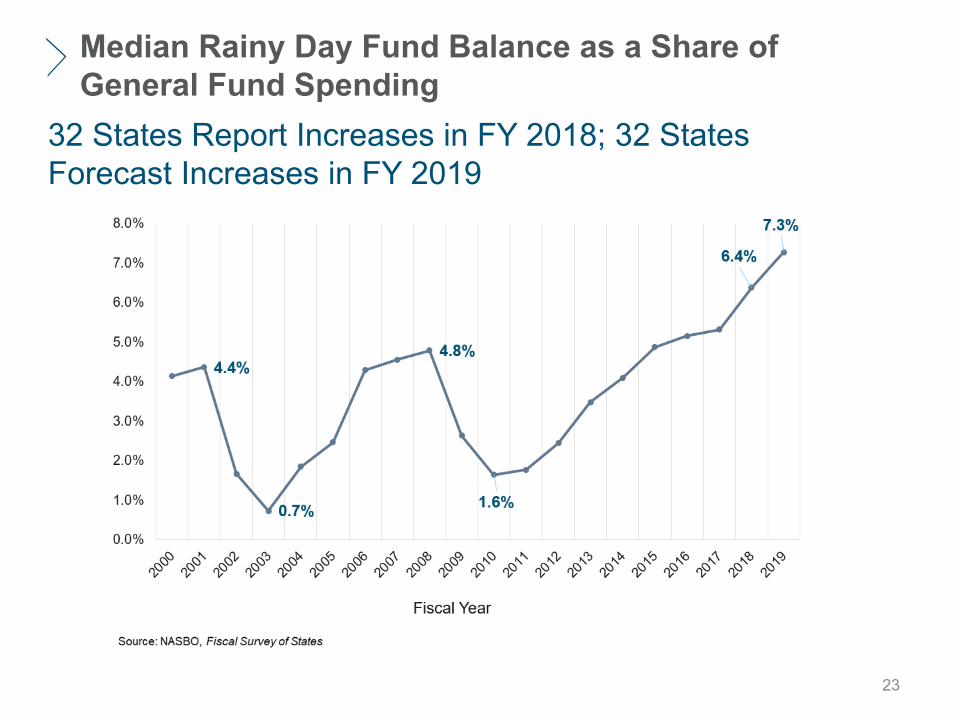

Median Rainy Day Fund Balance as a Share of General Fund Spending

32 States Report Increases in FY 2018; 32 States Forecast Increases in FY 2019

23

Two Recent Revenue Raisers:

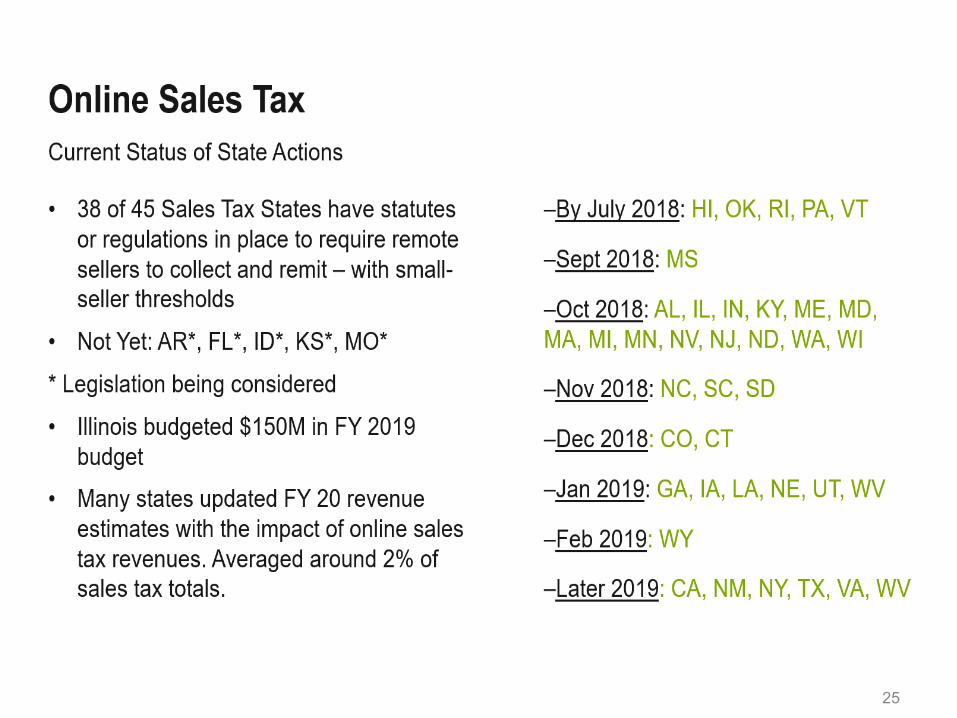

Online Sales Tax & Sports Betting

24

25

26

WHAT DOES THIS MEAN?

27

28

Legislative and Regulatory Issues

29

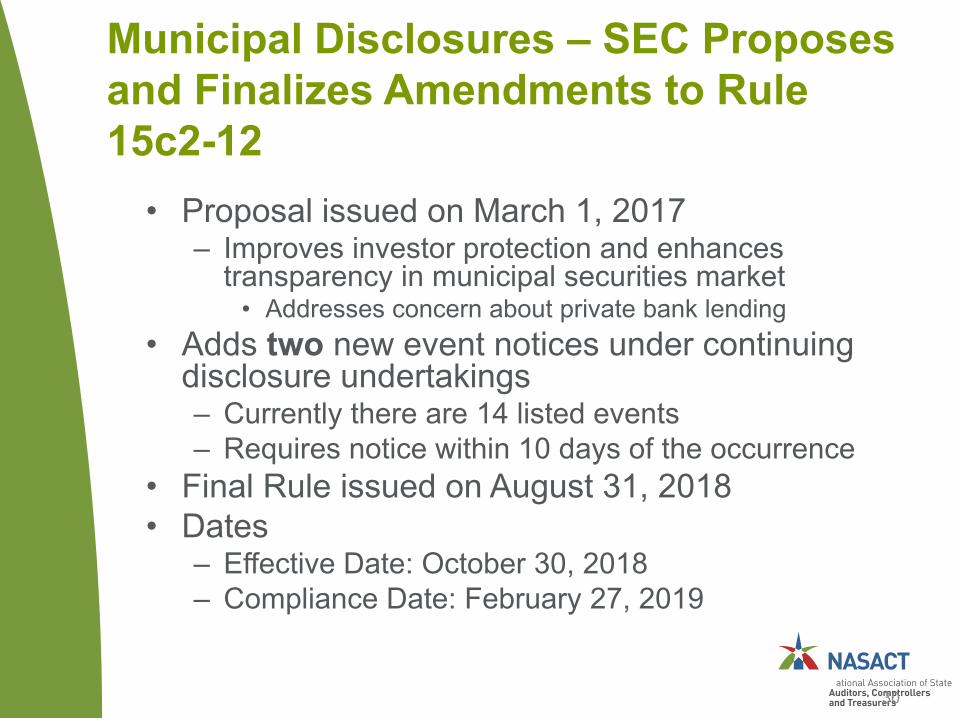

Municipal Disclosures – SEC Proposes and Finalizes Amendments to Rule 15c2-12

• Proposal issued on March 1, 2017– Improves investor protection and enhances

transparency in municipal securities market• Addresses concern about private bank lending

• Adds two new event notices under continuing disclosure undertakings– Currently there are 14 listed events– Requires notice within 10 days of the occurrence

• Final Rule issued on August 31, 2018• Dates

– Effective Date: October 30, 2018– Compliance Date: February 27, 2019

30

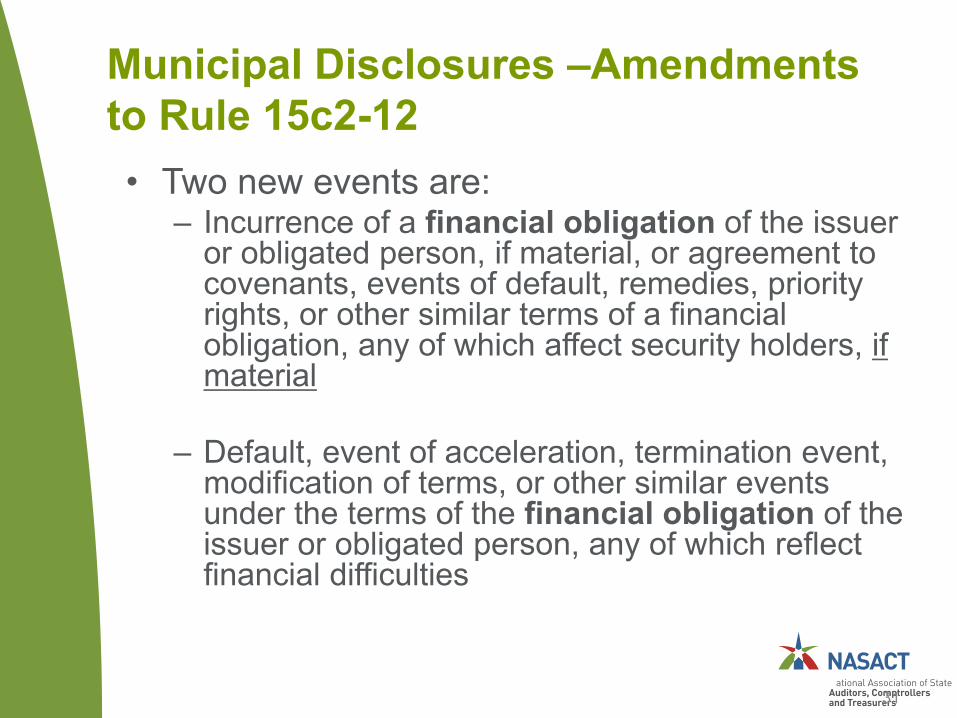

Municipal Disclosures –Amendments to Rule 15c2-12• Two new events are:

– Incurrence of a financial obligation of the issuer or obligated person, if material, or agreement to covenants, events of default, remedies, priority rights, or other similar terms of a financial obligation, any of which affect security holders, if material

– Default, event of acceleration, termination event, modification of terms, or other similar events under the terms of the financial obligation of the issuer or obligated person, any of which reflect financial difficulties

31

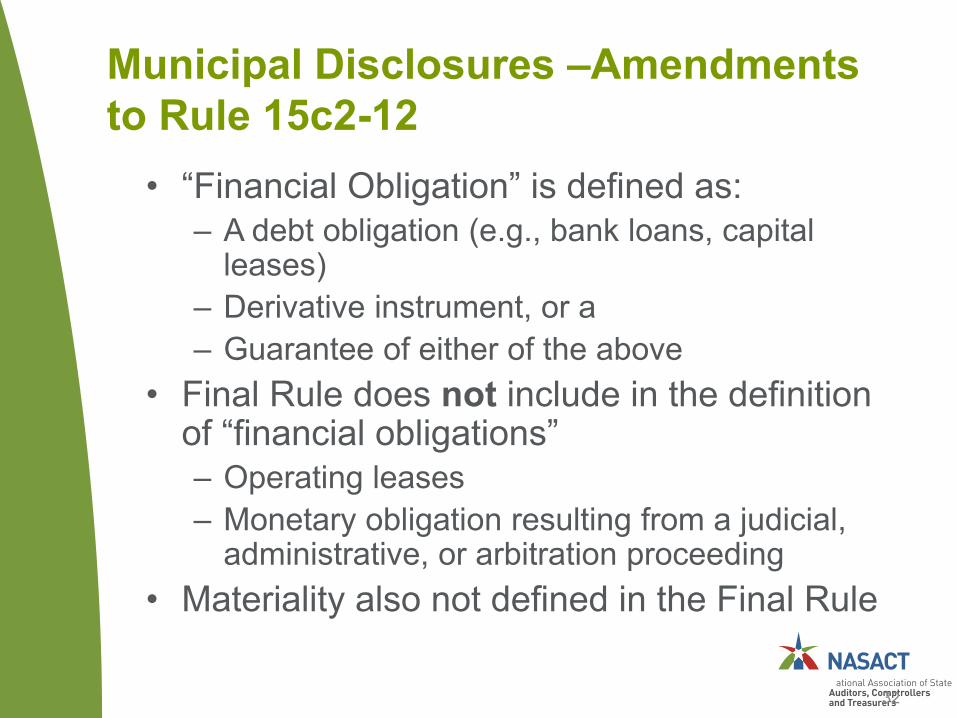

Municipal Disclosures –Amendments to Rule 15c2-12

• “Financial Obligation” is defined as:– A debt obligation (e.g., bank loans, capital

leases)– Derivative instrument, or a– Guarantee of either of the above

• Final Rule does not include in the definition of “financial obligations”– Operating leases– Monetary obligation resulting from a judicial,

administrative, or arbitration proceeding • Materiality also not defined in the Final Rule

32

Municipal Disclosures –Amendments to Rule 15c2-12

• What should be disclosed?– A description of the material terms of the

financial obligation, including:• Date of incurrence• Principal amount• Maturity and amortization• Interest rate (or method of computation of the

interest rate)• Default rates

33

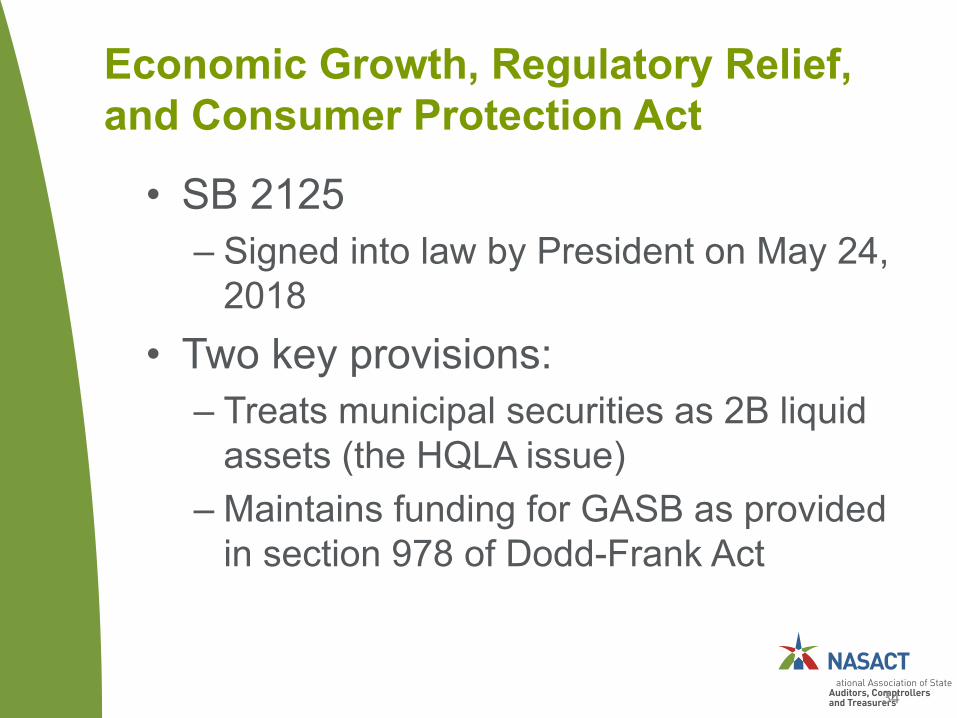

Economic Growth, Regulatory Relief, and Consumer Protection Act

• SB 2125– Signed into law by President on May 24,

2018• Two key provisions:

– Treats municipal securities as 2B liquid assets (the HQLA issue)

– Maintains funding for GASB as provided in section 978 of Dodd-Frank Act

34

Transparency IssuesFFATA, DATA, GREAT Act

35

Increasing Transparency: The Continuing Story

• FFATA (2006)– Ongoing monthly reporting of Federal

awards and contracts at prime/first-tier sub levels

• DATA (2014)– Amends FFATA– Now fully operational at Federal level

• GREAT (2018)– Proposed legislation to further DATA

36

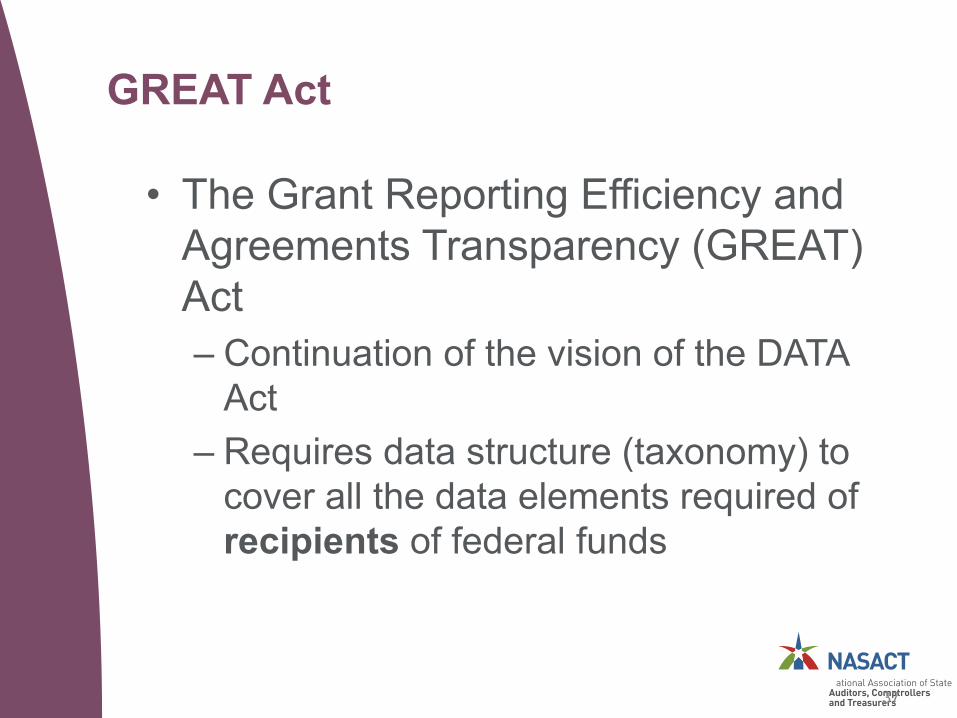

GREAT Act

• The Grant Reporting Efficiency and Agreements Transparency (GREAT) Act– Continuation of the vision of the DATA

Act– Requires data structure (taxonomy) to

cover all the data elements required of recipients of federal funds

37

GREAT Act

• House and Senate bills in 2018 had same requirements:– Establish government-wide data standards for

information related to federal awards reported by recipients of federal awards (within 1 year)

– Issue guidance to grantmaking agencies on how to utilize new technologies and implement new data standards into existing reporting practices with minimum disruption (within 2 years)

– Amends the Single Audit Act to provide for grantee audits to be reported in an electronic format consistent with the data standards (guidance to be issued within 2 years)

38

GREAT Act

• Legislative Update– 2018 (115th Congress)

• House (H.R. 4887)– Passed House on September 26, 2018

• Senate (S. 3484) – Homeland Security and Government Affairs

Committee passed on September 26, 2018– Did not move to full Senate vote

– 2019 (116th Congress)• House (H.R. 150)

– Passed unanimously on January 17, 2019• Senate

– Still waiting for companion bill

39

OMB Uniform Guidance

40

OMB Uniform Guidance

• Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (“Uniform Guidance”)– Final Rule issued on December 26, 2013

• Contained in 2 CFR Part 200 • Effective dates:

– Federal agencies on December 13, 2014– Subpart F audit requirements are applicable to fiscal

years beginning on or after December 26, 2014

– Interim Rule (for agencies) issued on December 19, 2014

– Resources:• http://www.whitehouse.gov/omb/grants_docs/

41

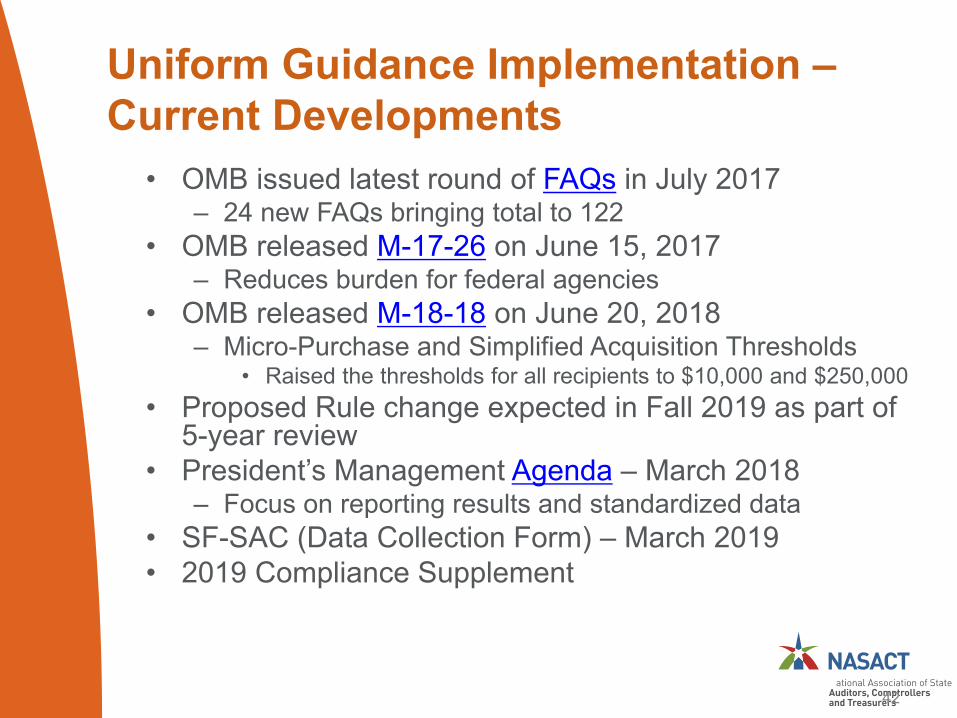

Uniform Guidance Implementation –Current Developments

• OMB issued latest round of FAQs in July 2017– 24 new FAQs bringing total to 122

• OMB released M-17-26 on June 15, 2017– Reduces burden for federal agencies

• OMB released M-18-18 on June 20, 2018– Micro-Purchase and Simplified Acquisition Thresholds

• Raised the thresholds for all recipients to $10,000 and $250,000 • Proposed Rule change expected in Fall 2019 as part of

5-year review• President’s Management Agenda – March 2018

– Focus on reporting results and standardized data• SF-SAC (Data Collection Form) – March 2019• 2019 Compliance Supplement

42

Implementation Issue: Pension and OPEB Costs Allowability

• Section 200.431(g)(3)– “For entities using accrual based accounting,

the cost assigned to each fiscal year is determined in accordance with GAAP”

• GASB 68 calculated pension costs differ from the amounts funded

– HHS DCA is currently allowing amounts funded in excess of GASB 68 amount (but awaiting OMB guidance)

– OMB hopes to release a proposed revision in summer 2018

• Similar issue for OPEB costs

43

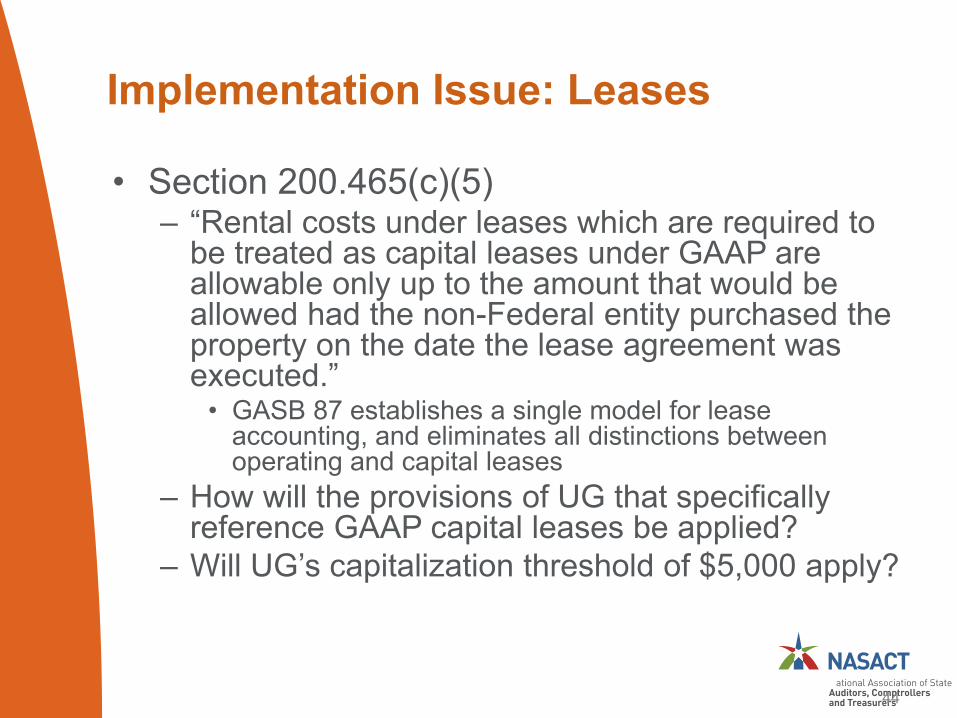

Implementation Issue: Leases

• Section 200.465(c)(5)– “Rental costs under leases which are required to

be treated as capital leases under GAAP are allowable only up to the amount that would be allowed had the non-Federal entity purchased the property on the date the lease agreement was executed.”

• GASB 87 establishes a single model for lease accounting, and eliminates all distinctions between operating and capital leases

– How will the provisions of UG that specifically reference GAAP capital leases be applied?

– Will UG’s capitalization threshold of $5,000 apply?

44

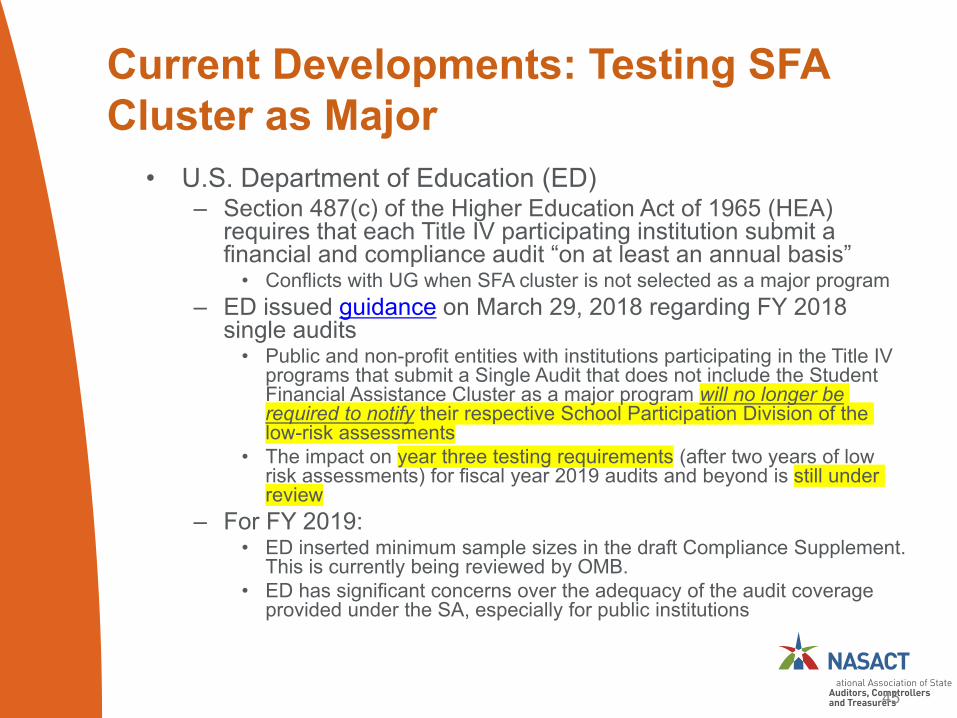

Current Developments: Testing SFA Cluster as Major

• U.S. Department of Education (ED)– Section 487(c) of the Higher Education Act of 1965 (HEA)

requires that each Title IV participating institution submit a financial and compliance audit “on at least an annual basis”

• Conflicts with UG when SFA cluster is not selected as a major program – ED issued guidance on March 29, 2018 regarding FY 2018

single audits• Public and non-profit entities with institutions participating in the Title IV

programs that submit a Single Audit that does not include the Student Financial Assistance Cluster as a major program will no longer be required to notify their respective School Participation Division of the low-risk assessments

• The impact on year three testing requirements (after two years of low risk assessments) for fiscal year 2019 audits and beyond is still under review

– For FY 2019:• ED inserted minimum sample sizes in the draft Compliance Supplement.

This is currently being reviewed by OMB.• ED has significant concerns over the adequacy of the audit coverage

provided under the SA, especially for public institutions

45

Current Developments: Securing Student Information

• Securing Student Information – Financial institutions under the Gramm-Leach-Bliley Act – New special test in draft 2019 Compliance Supplement

• Audit Objectives– Determine whether the IHE designated an individual to coordinate the

information security program, performed a risk assessment and documented safeguards for identified risks for:

» Employee training and management» Information systems, including network and software design, as well

as information processing, storage, transmission and disposal; and » Detecting, preventing and responding to attacks, intrusions, or other

systems failures • Suggested Audit Procedures

– Verify that the IHE has designated an individual to coordinate the program– Verify that the institution has performed a risk assessment that addresses

the three required areas noted above– Verify that the institution has documented safeguards for risk areas

46

2019 SF-SAC (Data Collection Form)

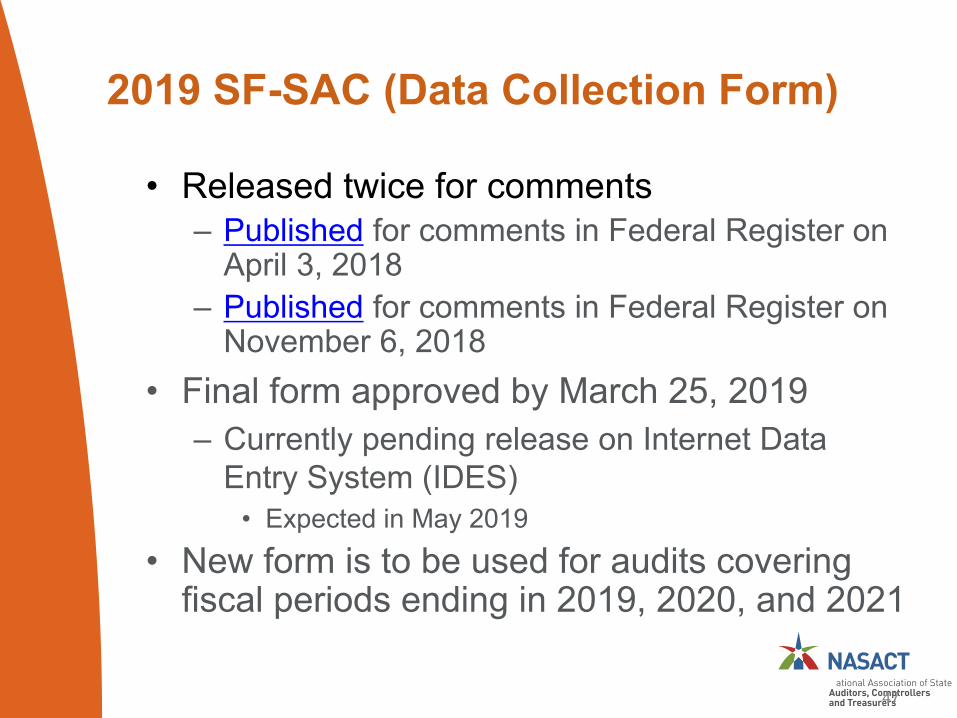

• Released twice for comments– Published for comments in Federal Register on

April 3, 2018– Published for comments in Federal Register on

November 6, 2018• Final form approved by March 25, 2019

– Currently pending release on Internet Data Entry System (IDES)

• Expected in May 2019• New form is to be used for audits covering

fiscal periods ending in 2019, 2020, and 2021

47

2019 SF-SAC (Data Collection Form)

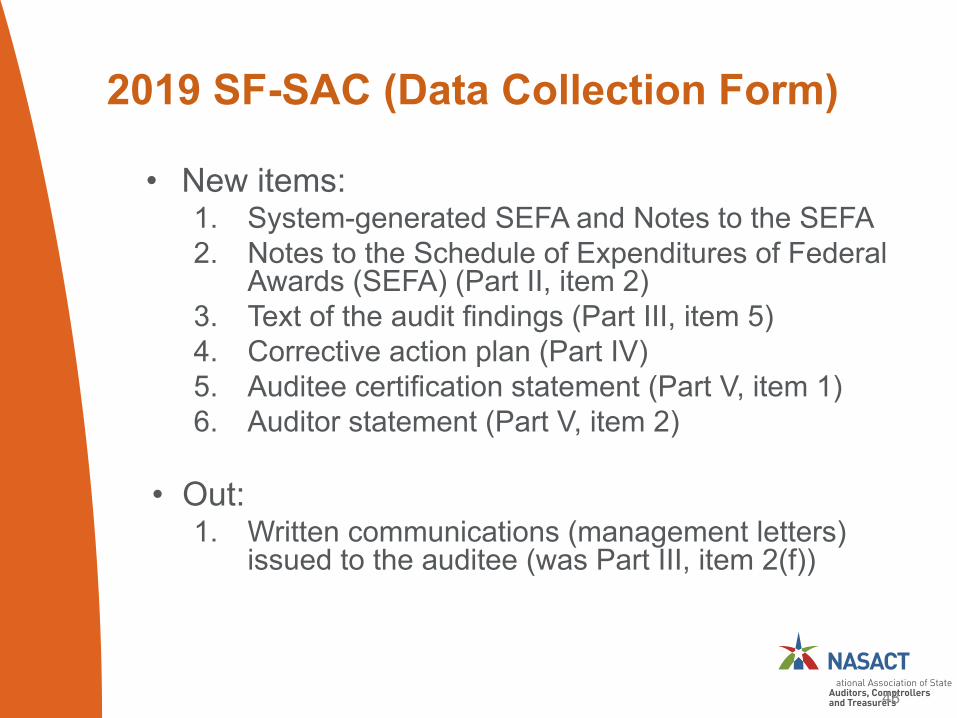

• New items:1. System-generated SEFA and Notes to the SEFA2. Notes to the Schedule of Expenditures of Federal

Awards (SEFA) (Part II, item 2)3. Text of the audit findings (Part III, item 5)4. Corrective action plan (Part IV)5. Auditee certification statement (Part V, item 1) 6. Auditor statement (Part V, item 2)

• Out:1. Written communications (management letters)

issued to the auditee (was Part III, item 2(f))

48

2019 SF-SAC (Data Collection Form)

• System-generated SEFA and Notes– Collections system now allows all respondents

to enter Federal awards and Notes to the SEFA• A customizable SEFA and Notes is generated for

inclusion in the reporting package• Part of 2016 Section 5 Pilot Program of DATA Act

– System-generated notes include:• Description of significant accounting policies used in

preparing the SEFA (2 CFR 200.510(b)(6))• Whether the auditee elected to use the de minimis

cost rate (2 CFR 200.414(f))• Any additional notes included in the reporting package

(excluding charts or tables)

49

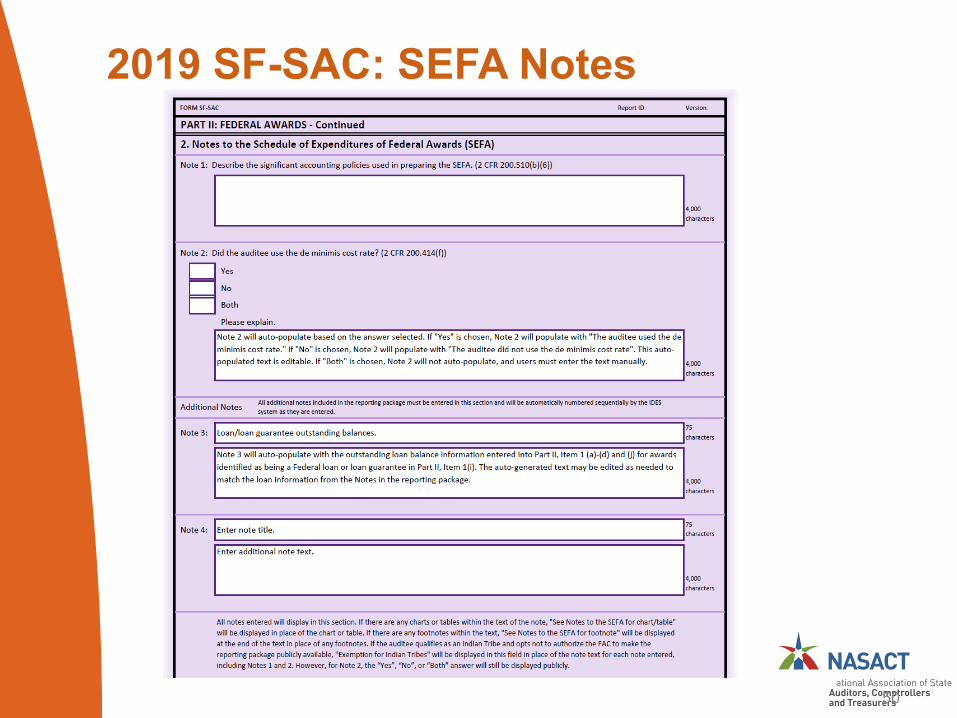

2019 SF-SAC: SEFA Notes

50

2019 SF-SAC (Data Collection Form)

• Text of Audit Findings (Part III, item 5)– Information is obtained from the Schedule of

Findings and Questioned Costs• Audit finding reference numbers from Part III, Item 4(e)

will be auto-generated in Part III, Item 5(a)• For findings related to more than one program, the text

must only be entered once by audit finding reference number

• Enter full, detailed text and the auditee’s response(s)excluding any charts or tables

– May copy and paste text from the reporting package• If there are any charts or tables, enter

– See “Schedule of Findings and Questioned Costs” for chart/table in the place of the chart or table within the text

• Do not enter “See reporting package” for all other text

51

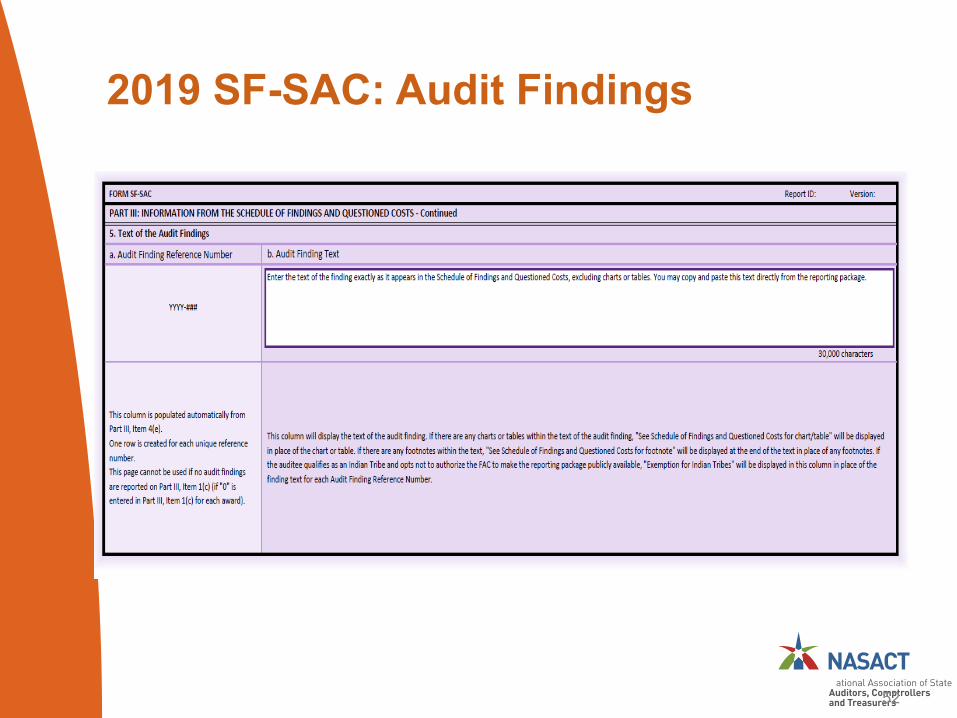

2019 SF-SAC: Audit Findings

52

2019 SF-SAC (Data Collection Form)• Corrective Action Plan (Part IV)

– Information obtained from the auditee’s CAP• Audit finding reference numbers from Part III, Item 4(e)

will be auto-generated in Part III, Item 5(a)• For findings related to more than one program, the text

must only be entered once by audit finding reference number

• Enter full, detailed text of the corrective action plan excluding any charts or tables

– May copy and paste text from the reporting package• If there are any charts or tables, enter

– “See Corrective Action Plan” for chart/table in place of the chart or table within the text

• Do not enter “See reporting package” for all other text

53

2019 SF-SAC: Corrective Action Plan

54

• Who to contact with questions– For technical audit questions:

• Contact the auditee’s Federal cognizant or oversight agency for audit

• “Federal Agency Single Audit Contacts” are listed in Appendix III of CS

– For questions related to specific Federal programs:• Contact Federal awarding agency• “Federal Agency Program Contacts” are listed in Appendix III of CS

– For questions concerning the Form SF-SAC or submission process:

• Contact FAC at (866) 306-8779 or [email protected]

55

2019 SF-SAC (Data Collection Form)

2019 Compliance Supplement• OMB is considering some interesting concepts:

– Compliance review areas limited to 6 compliance areas (“pick six”)

• All 12 compliance areas remain applicable• Program specific• Rotate on a year to year basis• Key practice issue

– What is the auditor’s responsibility for a compliance type marked with an “N,” but yet has a direct and material effect on the program?

– Will the auditor still have to test this type of compliance in order to issue an opinion on the program’s compliance?

– Timing:• Vett Draft started in December 2018; last round of programs

received April 2019• Final in June 2019 (?)

56

Auditing Issues

57

Update on the Developments in Government Auditing Standards

• 2018 Government Auditing Standards Revision (aka, Yellow Book or GAGAS)

• Exposure Draft was issued on April 5, 2017– 95 comment letters with

over 1,700 individual comments received

• Final version issued July 17, 2018– First revision since 2011

58

Summary of Key Changes from 2011 Revision

• New format and organization • Common terms and definitions• Independence threats related to preparing

financial statements• Updates to independence guidance• Competence of auditors• Guidance for CPE requirements• Competence of specialists• Peer review requirements

59

Summary of Key Changes from 2011 Revision

• Quality control and monitoring of quality• Internal control: financial audits and

examination engagements• Internal control: performance audits• New considerations for addressing waste• Standards for reviews of financial statements• Criteria for performance audits• Management assertions

60

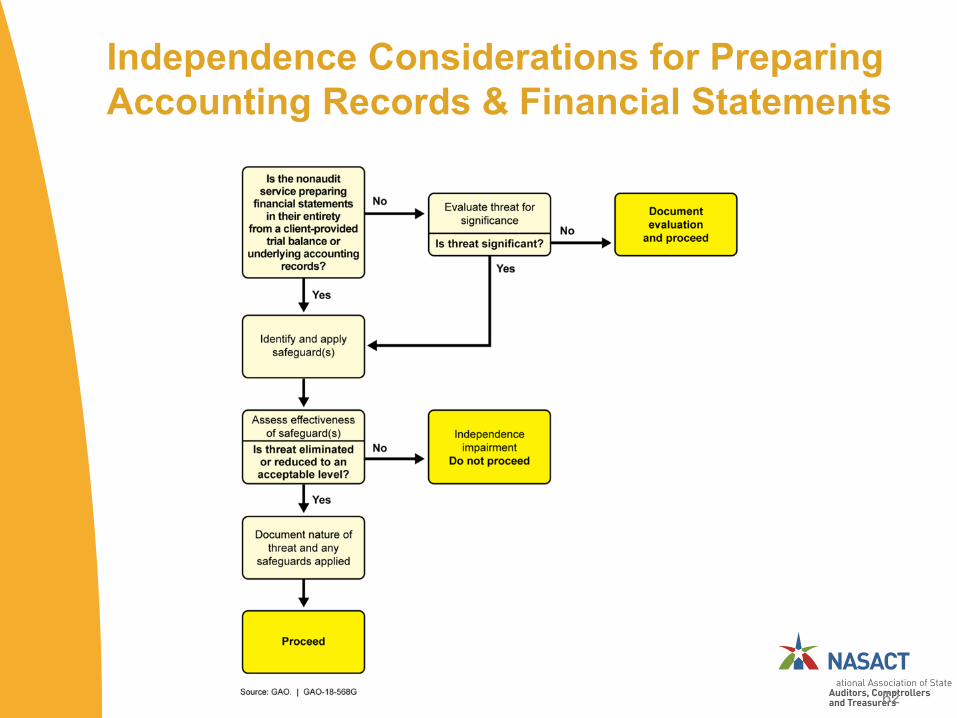

Independence Threats Related to Preparing Financial Statements & Accounting Records

Nonaudit services performed by auditors related to financial statements and accounting records either:

61

Impair Independence

Are Significant Threats

The auditor prepares financial statements in their entirety (para. 3.88).OR The auditor determines that a service related to preparing financial statements or accounting records is a significant threat (para. 3.93).

Are Threats • Evaluate threat and document evaluation (para. 3.90).• Typing, formatting, printing, binding: not likely significant (para.

3.95)

No change from 2011 Yellow Book (para. 3.87)

Document the threats and safeguards applied to eliminate and reduce threats to an acceptable level (para. 3.33).ORDecline to perform the service (para. 3.88).

Independence Considerations for Preparing Accounting Records & Financial Statements

62

Additional Updates to Independence Guidance

• Added application guidance to define management's “Skills, Knowledge and Experience” (SKE) an indicator is management’s ability to recognize a material error (para. 3.79).

• Updated application guidance to clarify that certain services provided by government audit organizations would generally not create threats to independence allowability of certain functions such as investigations (para. 3.72).

63

CPE Requirements and Guidance

• Removed the 4-hour GAGAS Qualification CPE requirement proposed in the exposure draft

• Added application guidance related to obtaining GAGAS specific CPE each time a new Yellow Book revision is issued (para. 4.19)

64

Competence of Specialists

• Engagement team should determine whether specialists are qualified and competent in their areas of specialization (para. 4.12)

• External specialists are not subject to Yellow Book CPE requirements (para. 4.30)

• Internal specialists who are not involved in planning, directing, performing engagement procedures, or reporting are not subject to Yellow Book CPE requirements (para. 4.30)

• IT auditors are considered auditors and thus are subject to the CPE requirements (para. 4.13)

65

Peer Review Requirements

Peer review section differentiates requirements for those audit organizations affiliated with a recognized organization.

66

Audit organization affiliated with a

recognized organization?

Yes

No

Peer Review Requirements

All audit organizations comply with GAGAS peer review requirements for:

• Assessment of peer review risk (paras. 5.66 & 5.67),

• Peer review report ratings (paras. 5.72 –5.74), and

• Availability of peer review report to the public (paras. 5.77 – 5.80).

67

Peer Review Requirements: Not Affiliated

Audit organizations not affiliated with a recognized organization also comply with additional GAGAS peer review requirements in areas including:• Peer review scope (para. 5.82) • Peer review intervals (para. 5.84) • Written agreement for peer review (para. 5.86)• Peer review team (para. 5.89) • Report content (para. 5.91) and• Audit organization’s response to the peer review

report (paras. 5.93 – 5.94)

68

Waste and Abuse

• Auditor considerations related to waste and abuse are intended to be consistent

• Auditors are not required to perform procedures to detect waste or abuse

• Evaluating internal control in a government environment may include consideration of internal control deficiencies that result in waste or abuse

(paras. 6.20, 7.22, & 8.119)

69

Effective Date

• 2018 Revision is effective for- Financial audits, attestation engagements, and reviews of financial statements for periods ending on or after June 30, 2020, and

- Performance audits beginning on or after July 1, 2019

• Early implementation is not permitted

70

Where to Find the Yellow Book

• The Yellow Book is available on GAO’s website at:www.gao.gov/yellowbook

• For technical assistance, contact us at:[email protected] call (202) 512-9535

71

AICPA Professional Ethics Division: State and Local Government Entities

• Exposure Draft issued July 7, 2017– Formerly Entities Included in State and

Local Government Financial Statements (ET sec. 1.224.020)

– Addresses a member’s (of the AICPA) independence with respect to entities that are required to be included in a state or local government’s financial reporting entity

• Exposure Draft issued January 11, 2019– Addresses questions about overall clarity

72

AICPA Professional Ethics Division: State and Local Government Entities (2017)

• Makes use of terms downstream, upstream and brother-sister entities– Downstream: refers to those entities that are “below” the

f/s attest client in its organization structure• e.g., financial statement attest client is the primary government, funds

and component units to be evaluated are those required to be included in the primary government’s financial reporting entity

– Upstream: refers to those entities that are “above” the f/s attest client

• e.g., financial statement attest client is a fund or component unit

– Brother-sister: refers to other funds and component units that the member does not provide attest services to but are included in the same upstream financial reporting entity as the financial statement attest client

73

AICPA Professional Ethics Division: SLG Client Affiliates (2019)

• Revisions/clarifications:– Replace terms upstream and downstream terminology

with affiliate• Revised ED uses the term affiliate and provides examples of

when to use the Conceptual Framework

– Replace the term primary government with affiliate and entity for consistency with the GASB definition

– Members do not need to evaluate investments of all downstream affiliates; rather, they need to evaluate only investments of:

• The financial attest client, and• Any entity included in the f/s attest client’s f/s when the member

does not make reference to another auditor’s report on the entity when determining whether the investment is an affiliate

74

• Revisions/clarifications:– When determining affiliate status, presume minimal

influence over funds and blended component units• For discretely presented CUs, members will need to evaluate on

a case-by-case basis

– Additional guidance on determining materiality• Should be applied at the financial statement attest client’s

financial reporting entity as a whole, rather than individual opinion units

– Replace the term de minimus to trivial and clearly inconsequential

• Confusion over whether an investment was de minimus• New terms are discussed in AU-C 450, Evaluations of

Misstatements Identified During the Audit, and should be easier to apply

75

AICPA Professional Ethics Division: SLG Client Affiliates (2019)

• There is an affiliate relationship between an SLG and an entity if any apply:– An entity is in the SLG’s f/s and the SLG’s

auditor’s report does not make reference to the report by the entity’s auditor

– An entity is included in the SLG’s financial statements and the SLG’s auditor’s report does make reference to the report by the entity’s auditor, and both of the following conditions exist:

• The entity is material to the SLG’s f/s as a whole, and • The SLG being audited has more than minimal

influence over the entity’s accounting or financial reporting process

76

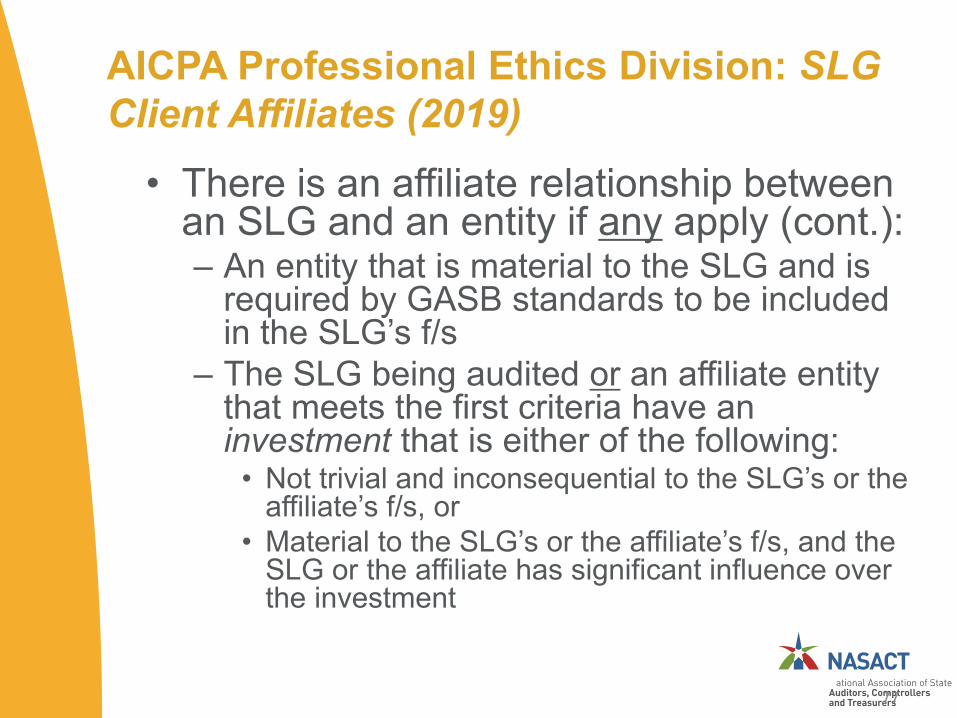

AICPA Professional Ethics Division: SLG Client Affiliates (2019)

• There is an affiliate relationship between an SLG and an entity if any apply (cont.):– An entity that is material to the SLG and is

required by GASB standards to be included in the SLG’s f/s

– The SLG being audited or an affiliate entity that meets the first criteria have an investment that is either of the following:

• Not trivial and inconsequential to the SLG’s or the affiliate’s f/s, or

• Material to the SLG’s or the affiliate’s f/s, and the SLG or the affiliate has significant influence over the investment

77

AICPA Professional Ethics Division: SLG Client Affiliates (2019)

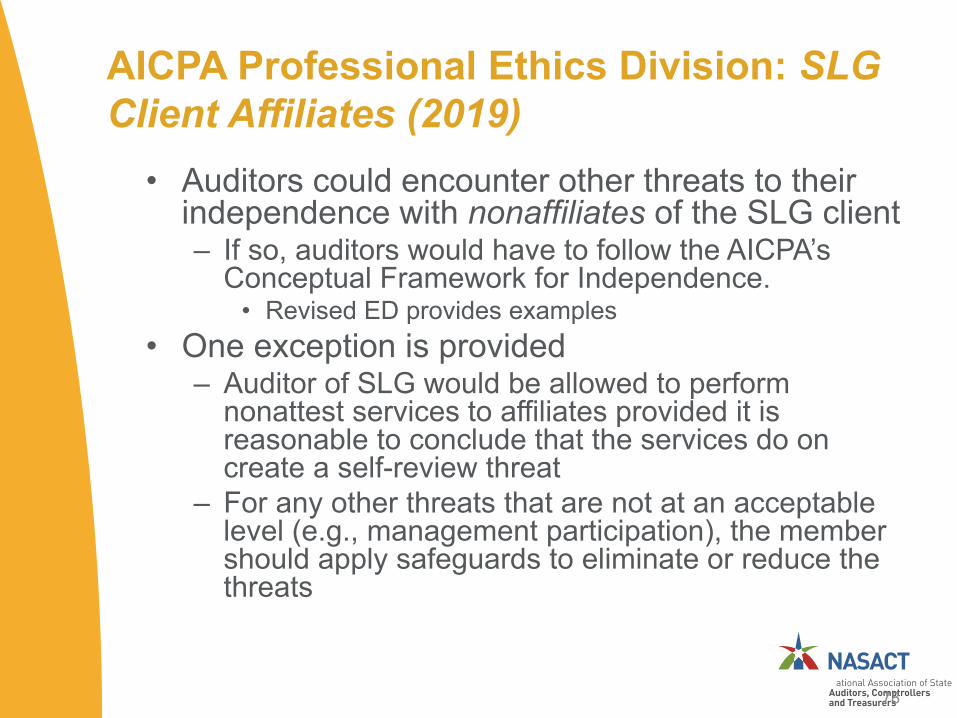

• Auditors could encounter other threats to their independence with nonaffiliates of the SLG client– If so, auditors would have to follow the AICPA’s

Conceptual Framework for Independence.• Revised ED provides examples

• One exception is provided– Auditor of SLG would be allowed to perform

nonattest services to affiliates provided it is reasonable to conclude that the services do on create a self-review threat

– For any other threats that are not at an acceptable level (e.g., management participation), the member should apply safeguards to eliminate or reduce the threats

78

AICPA Professional Ethics Division: SLG Client Affiliates (2019)

• Effective Date– PEEC believes members will need significant time to

implement the proposed revisions– PEEC recommends the interpretation be effective one

year after adoption• Early implementation allowed

• Current status– PEEC will review in May 2019– AICPA plans to issue a number of educational tools to

assist members with implementation, including:• Flowcharts - affiliate consideration for entities and investments• Practice aid including an electronic checklist (Excel)• FAQs and slides• Courses at conferences

79

AICPA Professional Ethics Division: SLG Client Affiliates (2019)

Accounting Issues

80

GASB’s Current Projects – The “Big Three”

• GASB is working on three related efforts that will help reshape state and local governmental accounting and financial reporting 1. The financial reporting model

reexamination2. Revenue and expense recognition, and3. Research reexamining most existing

note disclosures

81

GASB’s Reexamination of the Reporting Model

• Added to technical agenda on September 1, 2015– Targeted review (not “wholesale” changes)

• First phase of the project– Financial Reporting Model Improvements –

Governmental Funds– ITC released December 7, 2016

• ITC introduces three alternative recognition approaches for governmental fund financial statements:– Near-term financial resources– Short-term financial resources, and– Long-term financial resources

82

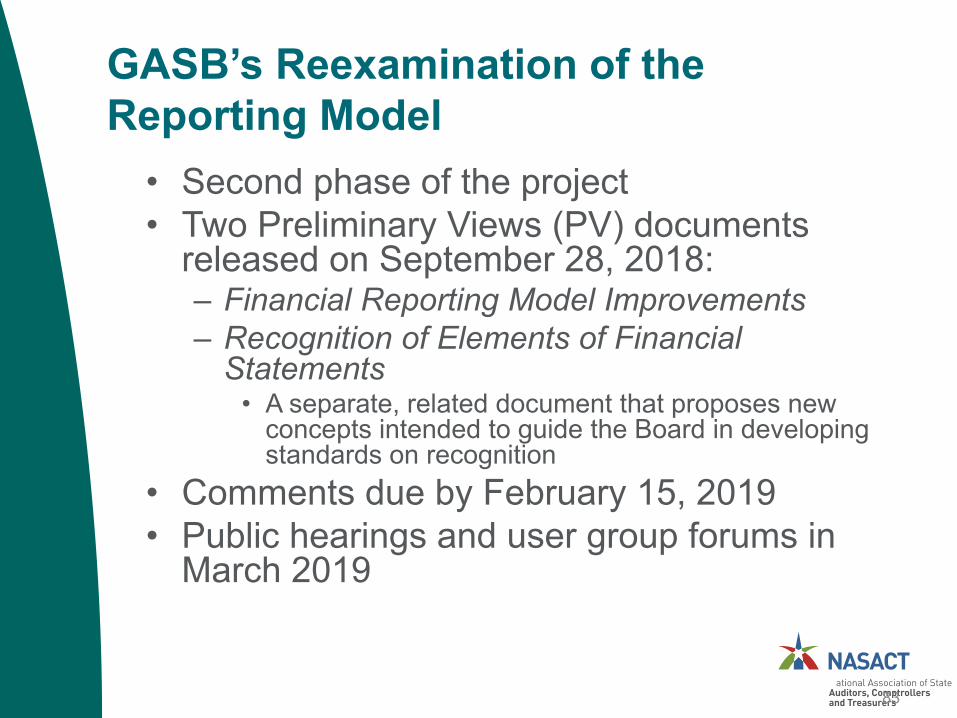

GASB’s Reexamination of the Reporting Model

• Second phase of the project• Two Preliminary Views (PV) documents

released on September 28, 2018:– Financial Reporting Model Improvements– Recognition of Elements of Financial

Statements• A separate, related document that proposes new

concepts intended to guide the Board in developing standards on recognition

• Comments due by February 15, 2019• Public hearings and user group forums in

March 2019

83

Financial Reporting Model Improvements PV

• Short-term financial resources measurement focus

• Elements from short-term transactions recognized as the underlying transaction occurs

• Elements from long-term transactions recognized when payments are due

84

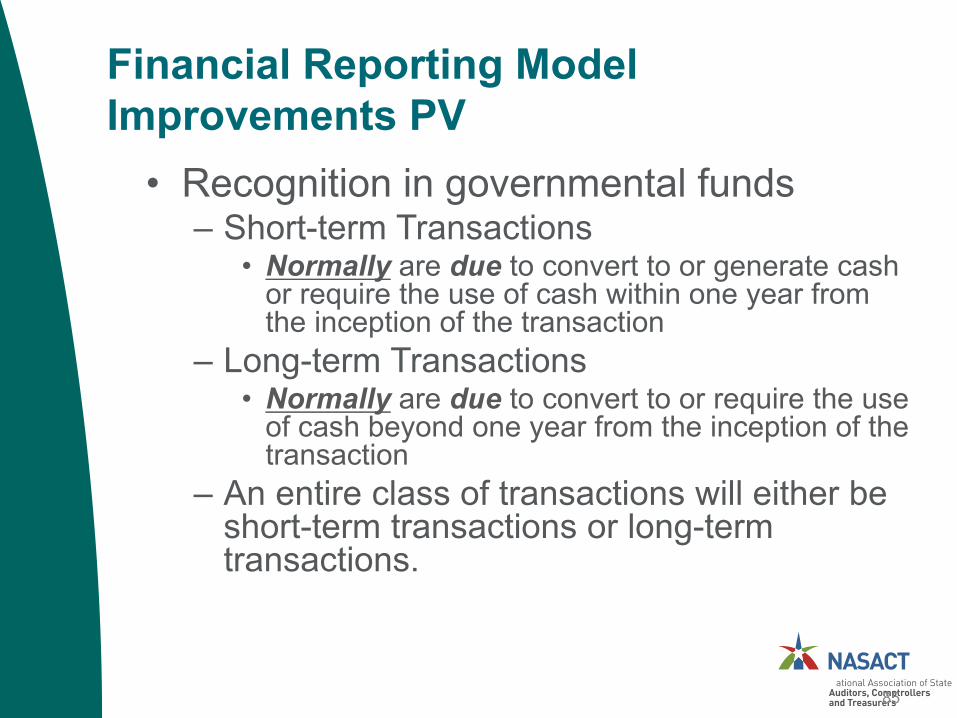

Financial Reporting Model Improvements PV

• Recognition in governmental funds– Short-term Transactions

• Normally are due to convert to or generate cash or require the use of cash within one year from the inception of the transaction

– Long-term Transactions• Normally are due to convert to or require the use

of cash beyond one year from the inception of the transaction

– An entire class of transactions will either be short-term transactions or long-term transactions.

85

Financial Reporting Model Improvements PV – Alternative View

• Modify short-term financial resources– Include all financial assets that represent cash or are

expected to be converted to cash (or other fund financial resources) with one year from date of f/s

– Include the portion of all financial liabilities that matures or is expected to be paid in cash (or other fund financial resources) within one year from date of f/s

• Replace concept of normally with contractual maturities (or amounts otherwise expected to be paid in cash or other fund financial resources)

• Proposes a government-wide statement of cash flows in the basic financial statements

86

GASB’s Reexamination of the Reporting Model – What’s Next?

• Items that will be included in the Exposure Draft:– Management’s Discussion and Analysis

• Consider alternatives for enhancing financial statement analysis, eliminating boilerplate components that are no longer necessary for understanding the financial reporting model, and

• Clarify guidance for presenting currently known facts, decisions, or conditions that are expected to have a significant effect.

– Debt Service Fund Presentation• Consider alternatives for providing additional information about

debt service funds (either individually or in aggregate).– Extraordinary and Special Items

• Consider alternatives to improve the consistency of application of the guidance for reporting extraordinary and special items.

– Other Issues• Consider alternatives that could permit more timely financial

reporting or that could reduce complexity overall.

87

GASB’s Reexamination of the Reporting Model – What’s Next?

• Timing– Deliberations began in October 2015– December 2016: Invitation to Comment– September 2018: Preliminary Views– April 2020: Exposure Draft– November 2021: Final Statement– Implementation dates: sometime in 2022,

2023

88

Other Emerging IssuesThings on the radar…

89

XBRL Developments: State and Local Governments

• XBRL US has formed a state and local government workgroup – Developing a taxonomy for a CAFR

• Florida HB 1073– Authorizes the creation of Florida Open Financial Statement

System• An interactive data repository for government financial statements• Requires the Florida CFO to determine whether a suitable XBRL

taxonomy has been developed• Effective for FY ending on or after September 1, 2022

• California SB 548– Introduced in February 2019; has not passed Senate yet– Requires the state, counties, cities, school districts, special

districts and pension funds submit financial statements in XBRL• Will other states follow?

90

Medicaid: An increased focus by state auditors

• Senate Homeland Security and Governmental Affairs Committee– At August 21, 2018, hearing, GAO encouraged greater use of

state auditors’ work • Group of state auditors have been meeting with GAO and

CMS– Trying to reduce improper payments in Medicaid– Draft 2019 Compliance Supplement will require testing of

eligibility by single auditor• However, more focus on managed care in the CS is needed• In Louisiana, almost 90% of the 1.7 million recipients are enrolled in

managed care• “Joint Audit”

– At March 26, 2019 meeting, group of state auditors decide to conduct “joint audit” of Medicaid eligibility

– 15 to 20 states are expected

91

Timeliness of Audited Financial Statements

• SEC chair Jay Clayton calls for improved municipal market disclosure including timelier financial reporting– December 6, 2018, speech indicates SEC may

be interested in taking additional regulatory action to improve municipal market disclosure

– SEC’s Office of Municipal Securities is working with MSRB to improve transparency and increase timeliness of issuer financial information.

• State and local government groups monitoring closely

92

These continue to be interesting times…

93