EMERGING DIGITAL MARKETING TRENDS · 6 Summary of key themes Digital marketing is now considered...

48

1 EMERGING DIGITAL MARKETING TRENDS AUSTRALIA & NEW ZEALAND 2013

Transcript of EMERGING DIGITAL MARKETING TRENDS · 6 Summary of key themes Digital marketing is now considered...

1

EMERGING DIGITAL MARKETING TRENDS AUSTRALIA & NEW ZEALAND 2013

I love it. . . and the possibilities seem ENDLESS!!! (Just give me a budget) ;)

Contents

Executive Summary 4Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

Summary of key themes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

A snapshot of the Australian & NZ sectors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7

What’s in the digital toolkit? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8

How do marketers feel about working in the digital environment? . . . . . . . . . . . . . . . .8

Managing the digital marketing strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

What constitutes digital success and how is it measured? . . . . . . . . . . . . . . . . . . . . . . .9

Barriers to the acceleration of digital marketing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10

Research Methodology and Profile of Participants 11Sample profile . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12

Findings in Detail 13Part 1.

A Context for Digital Marketing in Australia & New Zealand…

Findings in Detail 25Part 2.

Current patterns of behaviour in digital marketing

About Sitecore 48

4

EXECUTIVE SUMMARY

1

5

Introduction

Thank you for your interest in the attitudes and behaviour of marketers across Australia and New Zealand .Sitecore together with First Point Research and Consulting are pleased to present a uniquely Australian and New Zealand study into the marketer’s relationship with and understanding of digital marketing.

Digital marketing is a rapidly evolving industry. Marketers are faced with a diverse and growing range of channels, a consumer journey with multi-channel touch points, different technologies to deliver to each channel and no consistent approach to the measurement of marketing effectiveness. With these challenges comes greater scrutiny of marketing budgets and demands for increased linkages to sales. With this survey we analyse the current state of digital marketing and attitudes to the challenges and opportunities within the Australian and New Zealand markets.

It’s not uncommon to see reports discussing the trends within this space, however many only

focus on the United States or United Kingdom and presume these countries reflect the stance in Australia and New Zealand. Other reports simply confirm what is already known – that it’s happening now and will continue long into the future. With that in mind, we wanted to get to the truth of digital marketing in Australia and New Zealand, even if that meant some potentially disruptive insights.

Read on and find out how your organisation and role compares to others in your industry, seniority and organisation size.

Robert Holliday

Managing DirectorSitecore Australia & New Zealand

This research study conducted with 330 marketing managers examines:

• Current patterns of behaviours in digital marketing

• The current digital toolkit and how it is expected to change

• Attitudes of marketers working in a digital world

• Managing the digital marketing strategy

• What constitutes digital success and how it is measured

• The barriers to the acceleration of digital marketing

6

Summary of key themes

Digital marketing is now considered mainstream within the marketing repertoire. Marketers have seen the opportunities presented and are now embracing them. (page 35)

Large companies are now leading the investment in digital marketing activities.While smaller companies were the early adopters of digital marketing, the big spenders are now catching up and are the most likely to be investing more in digital over the next 12 months. (page 21)

Experienced marketers (15yrs+ in the industry) are more likely to have undertaken specific training in digital marketing (relative to those with 10yrs or less in the industry) and this is reflected in their knowledge of the digital tools available to them, application of more sophisticated digital tools and higher rates of measurement of ROI.Less experienced marketers are less knowledgeable about digital, are less likely to measure ROI and are generally less confident about the digital marketing strategies they implement. (page 32)

Web analytics are used primarily for periodic reporting and most marketers are frustrated in their knowledge that they could be used far more effectively. Web analytics is the number one area marketers would like to see their organisations improve. (page 31)

Predictive analytics is largely viewed as the next ‘golden ticket’ but most feel ill equipped to move in that direction. (page 31)

ROI of digital activity is still evolving and most are still focused on visits to the website as a primary measure of success. 20% are not measuring ROI at all. (page 40)

Digital marketing is no longer niche.

Big companies are waking up to the advantages.

Web analytics is not being used effectively.

Big appetite for predictive analytics.

Digital ROI is a work in progress.

Senior marketers are building their own skills in digital marketing but greater emphasis is now needed at the junior-mid levels.

7

A snapshot of the Australian & NZ sectors

The majority of the marketing budget is still being spent offline but within the next 12 months the spend on digital marketing activities is likely to outstrip offline.

• 73% intend to spend more on digital in the next 12 months (only 2% will spend less on digital); and

• Only 11% intend to increase spend on traditional marketing (while 33% will spend less).

The top 5 ‘areas of growth’ all fall within the scope of digital marketing.

• Social media (22% perceive it as the greatest opportunity for future growth); emailing to their own database (14%); personalisation (12%); mobile (10%) and paid search (8%) are perceived as the key growth areas.

Two of the top three most common marketing activities in late 2013 are digital activities.

• Social media & email marketing to existing customer databases (both used by more than 80% of the organisations surveyed) are currently the most widely used marketing activities.

The top 5 ‘over-rated marketing channels’ are all traditional marketing channels.

• Print (38% perceive it as over-rated); TV (24%); trade shows (16%); direct mail (15%) & radio (13%).

The most significant differences in the application of digital marketing activities is observed across the scale of organisations.

• Organisations with turnover of $20million+ are still more traditional in their marketing activities while smaller companies (turnover of $2million or less) are using digital marketing more extensively.

• The indication however is that larger companies have now realised they need to ‘get on board’. Large companies are the most likely to be spending more on digital in the next 12 months (75% of high turnover companies indicate they will invest more money in digital in the next 12 months, compared with 50% of companies with a turnover of $2million or less).

8

What’s in the digital toolkit?

What’s hot right now?

• Web analytics (currently used by 88% of companies).• Email marketing (currently used by 85% of companies).

What are the priorities for the next 12 months?

• Predictive analytics (44% planning to use within 12 months).• Content profiling (40% planning to use within 12 months).• Integration to CRM (40% planning to use within 12 months).• Personalisation (40% planning to use within 12 months).• Mobile adapted version of the website (37%

planning to use within 12 months).

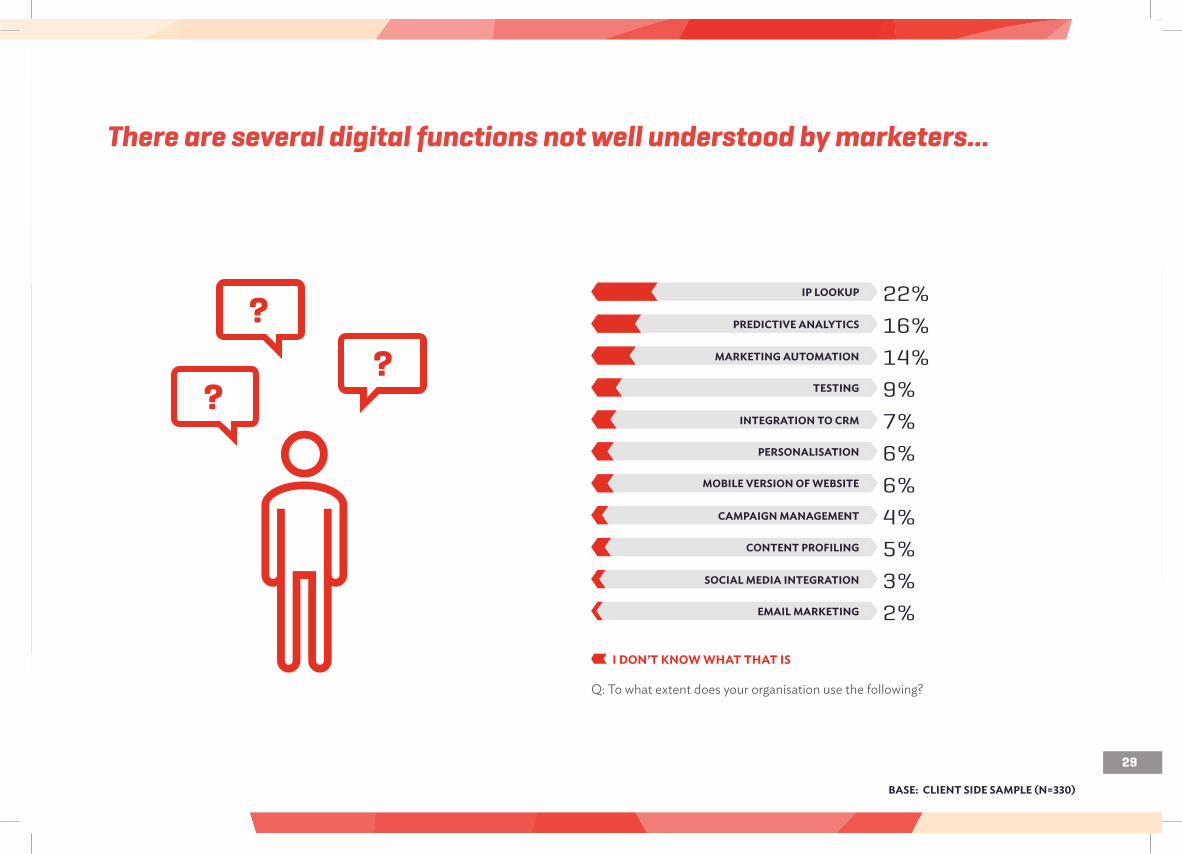

What are the knowledge roadblocks?

• IP Lookup for sales (22% don’t know what this is).• Predictive analytics (16% don’t know what this is).• Marketing automation (14% don’t know what this is).

Analytics & personalisation are the areas marketers want to see their organisations improve.

• Web analytics (51% want to see their organisation get better at this).

• Predictive analytics (50% want to see their organisation get better at this).

• Personalisation (50% want to see their organisation get better at this).

How do marketers feel about working in the digital environment?

There is a clear need to deliver enhanced training to junior and mid-level marketers.

• Formal training in digital marketing is heavily skewed to marketers with 15 years or more experience (53% vs 38%). It appears as an industry there is an assumption that young marketers are obtaining the necessary skills in their undergraduate courses… and this doesn’t appear to be the case.

While most feel relatively confident with their digital marketing skills, younger marketers are much less confident in their skills, which is not surprising given they are far less likely to be completing specific training courses in digital marketing.

• While 27% of marketers with 15yrs or more experience in marketing rate their digital skills as ‘excellent’, only 13% of marketers with less than 5 years experience view their digital skills as ‘excellent’.

The enhanced training received by senior marketers is reflected not only in their higher level of digital competency, but also in a competitive edge.

• While 33% of senior marketers think their organisation is ‘ahead of most competitors’, only 22% of junior to mid level marketers believe that.

Digital marketing is no longer considered niche. Marketers feel more confident about it and are embracing the opportunities presented by the sector.

• 95% now view digital marketing as mainstream;• 83% find digital marketing stimulating and exciting.

Mid-Larger companies have been slower to invest in digital but are now seeing success and are feeling more confident in the process.

9

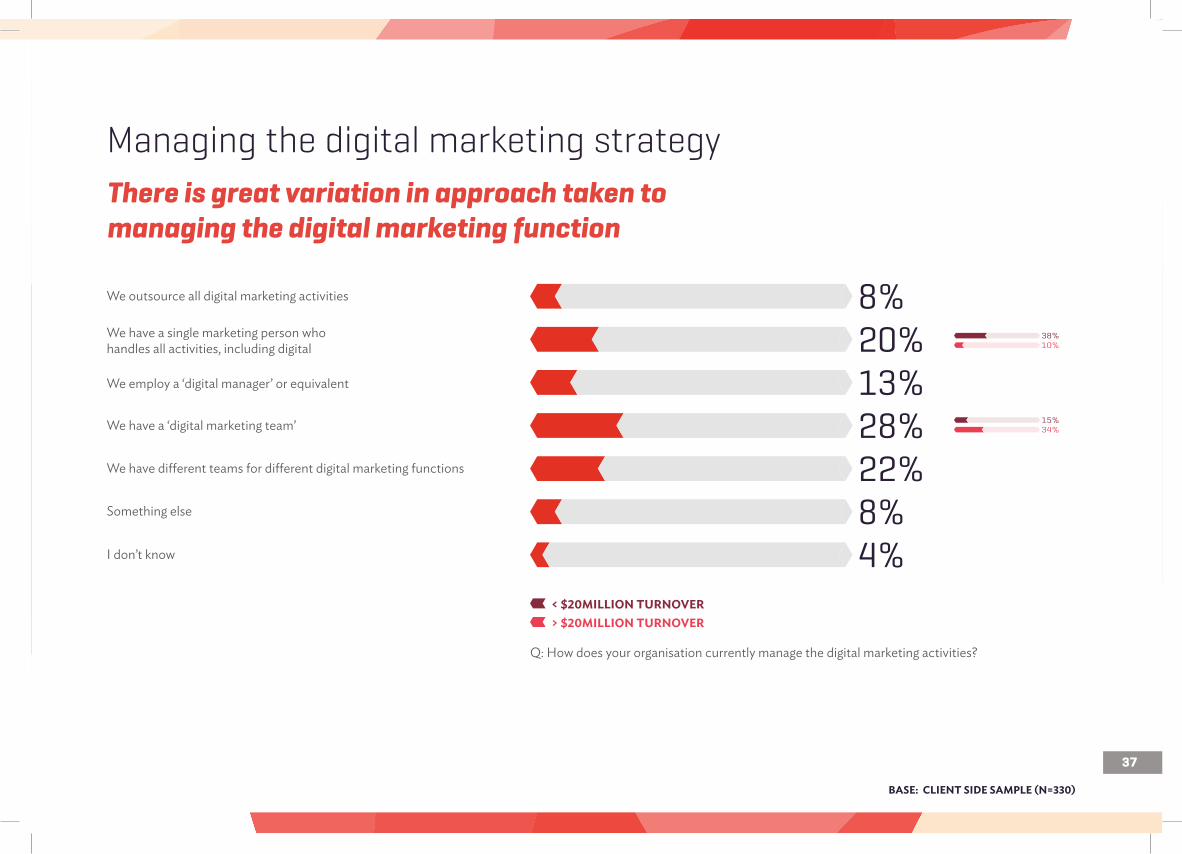

Managing the digital marketing strategy

There is great variation in the way the digital marketing function is managed across organisations.

• As might be expected, there are significant differences between small-medium size companies compared with larger firms.

• While the most common scenario is now to have a ‘digital marketing team’ (28% overall), this increases to 34% amongst large companies and only 15% amongst smaller companies.

• A large proportion still rely on a single marketing person to handle all marketing activities (20% overall) but this is more prevalent in smaller companies (38%) and far less so in larger companies (10%).

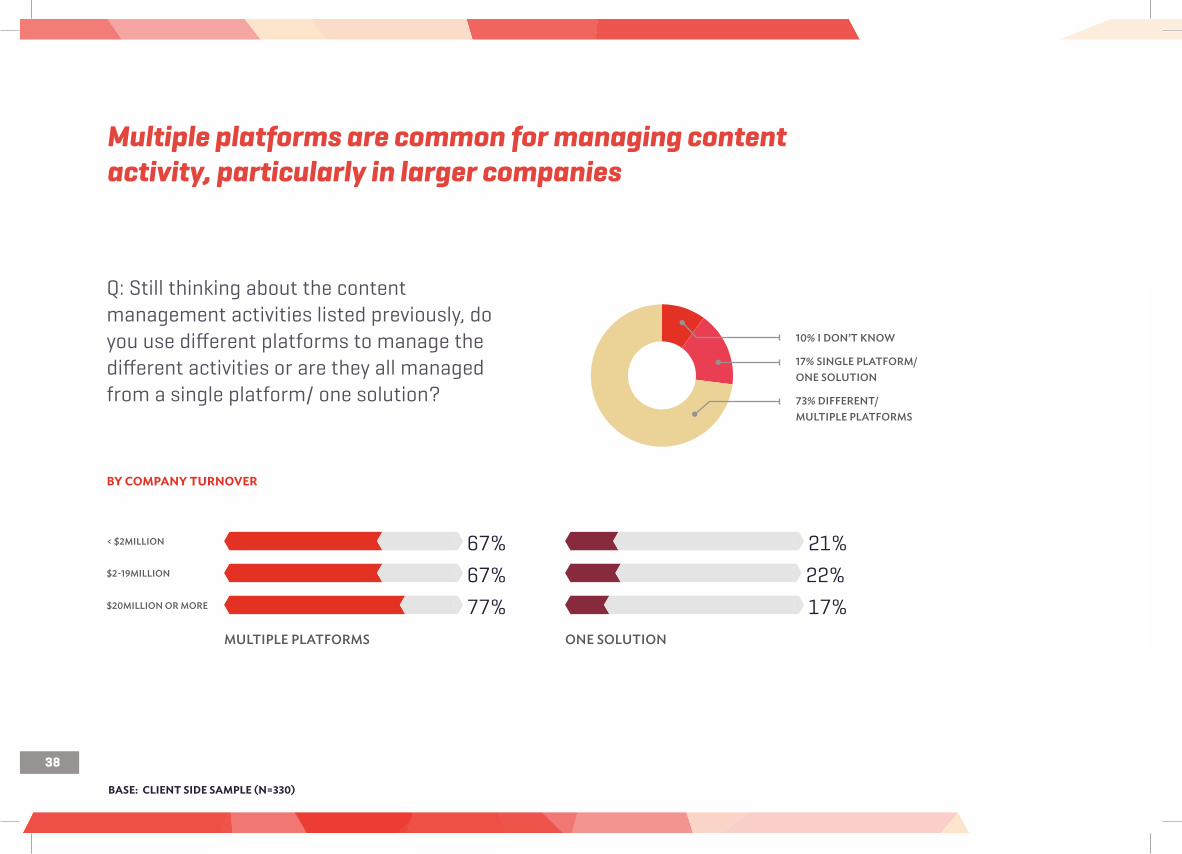

Multiple platforms are common for managing content activity, particularly in larger companies.

• 73% on average are using multiple platforms and only 17% are using a single platform.

Social media is the area that marketers are most vigilant about the activities of their competitors.

• 47% think their competitors have an edge over them in social media.

What constitutes digital success and how is it measured?

While the vast majority (80%) of organisations track ROI on their digital marketing activities, the big surprise is that 20% are not tracking ROI on digital activities at all.

• The largest proportion (46%) use ROI to report back to management.• A small but significant segment (14%) are tracking the ROI but are unsure of how to use it.

The most common measure of digital success is the use of website traffic. The three most common measures of success are:

• Visits to the website (73%);• Conversions/ sales/ new customer acquisitions (57%); and• Leads generated (44%)

Most marketers are in no doubt though about how ‘the boss’ measures success:

• Conversions/ sales/ new customer acquisitions (43%) is cited by the largest proportion as the key indicator sought by the management team, followed by having KPIs aligned with the business objectives (14%).

Web analytics could be used far more effectively in most organisations.

• They are generally used in periodic marketing meetings (in 48% of organisations) and few are using them in real time (only 8%).

• The most common use of web analytics is in reporting (38% using them extensively for reporting) and to a lesser extent for insights (22%).

• Few are using web analytics for recommendations for content for market automation, or site or content optimisation (only around 10% are using them regularly for these functions).

10

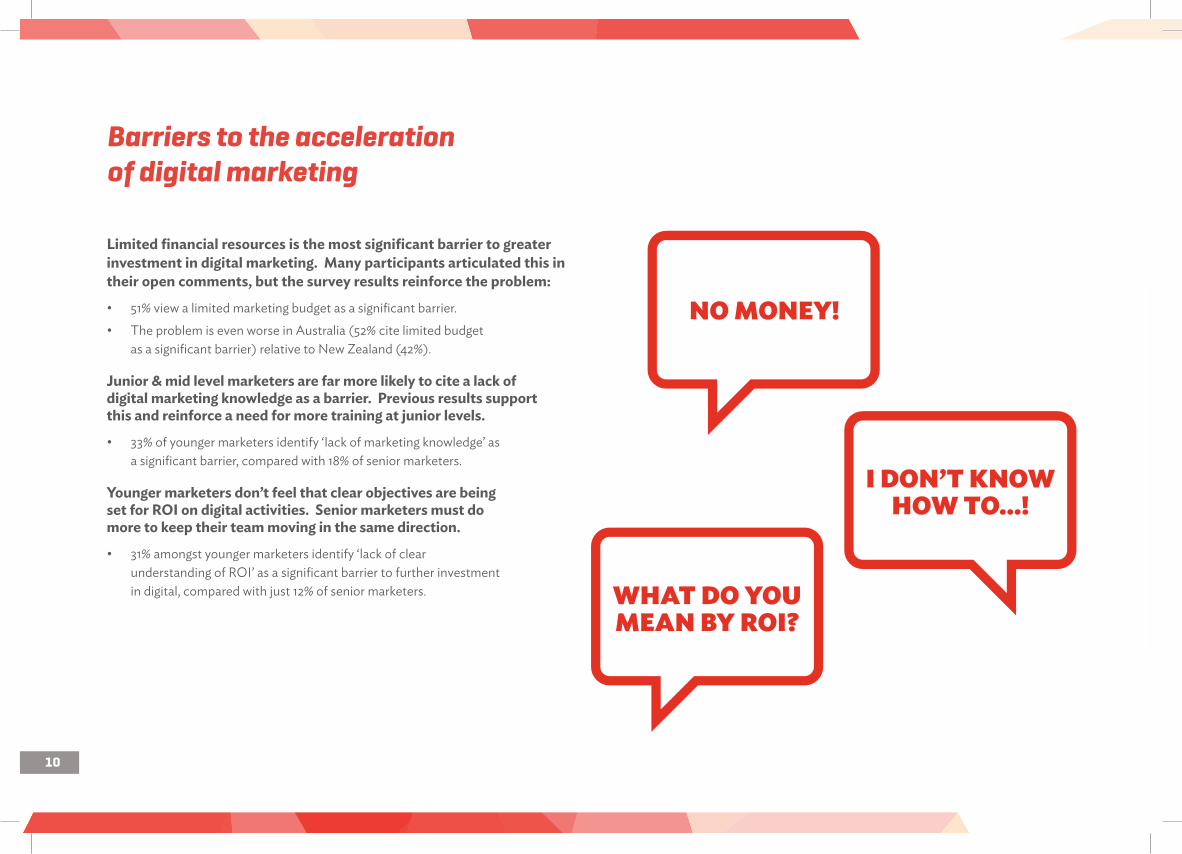

Barriers to the acceleration of digital marketing

Limited financial resources is the most significant barrier to greater investment in digital marketing. Many participants articulated this in their open comments, but the survey results reinforce the problem:

• 51% view a limited marketing budget as a significant barrier.• The problem is even worse in Australia (52% cite limited budget

as a significant barrier) relative to New Zealand (42%).

Junior & mid level marketers are far more likely to cite a lack of digital marketing knowledge as a barrier. Previous results support this and reinforce a need for more training at junior levels.

• 33% of younger marketers identify ‘lack of marketing knowledge’ as a significant barrier, compared with 18% of senior marketers.

Younger marketers don’t feel that clear objectives are being set for ROI on digital activities. Senior marketers must do more to keep their team moving in the same direction.

• 31% amongst younger marketers identify ‘lack of clear understanding of ROI’ as a significant barrier to further investment in digital, compared with just 12% of senior marketers.

NO MONEY!

I DON’T KNOW HOW TO...!

WHAT DO YOU MEAN BY ROI?

11

RESEARCH METHODOLOGY AND PROFILE OF PARTICIPANTS

2

12

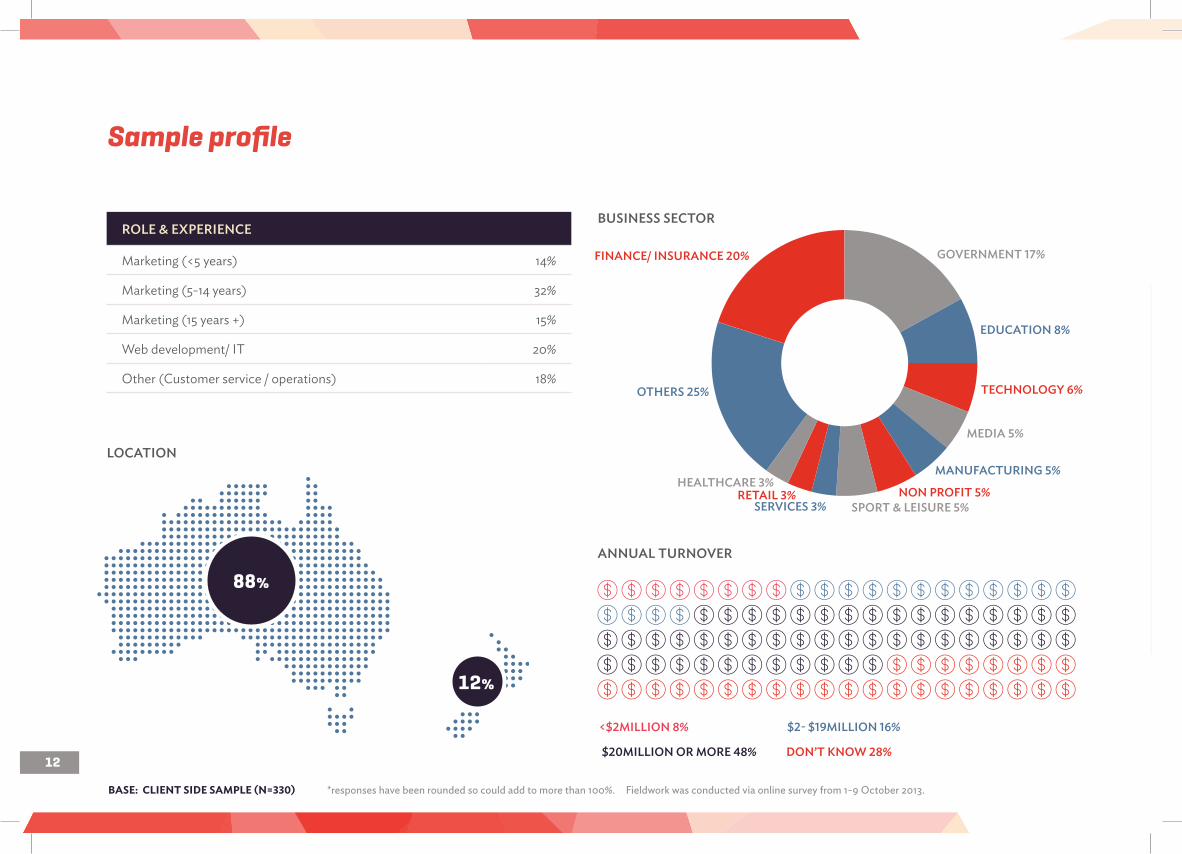

BASE: CLIENT SIDE SAMPLE (N=330)

$20MILLION OR MORE 48%

Sample profile

ROLE & EXPERIENCE

Marketing (<5 years) 14%

Marketing (5-14 years) 32%

Marketing (15 years +) 15%

Web development/ IT 20%

Other (Customer service / operations) 18% 17+8+6+5+5+5+5+3+3+3+20+20+xFINANCE/ INSURANCE 20% GOVERNMENT 17%

EDUCATION 8%

TECHNOLOGY 6%

MEDIA 5%

MANUFACTURING 5%

NON PROFIT 5%SPORT & LEISURE 5%SERVICES 3%

RETAIL 3%HEALTHCARE 3%

OTHERS 25%

BUSINESS SECTOR

ANNUAL TURNOVER

LOCATION

88%

12%

<$2MILLION 8% $2- $19MILLION 16%

DON’T KNOW 28%

*responses have been rounded so could add to more than 100%. Fieldwork was conducted via online survey from 1-9 October 2013.

13

EDUCATION 8%

TECHNOLOGY 6%

FINDINGS IN DETAIL

Part 1 .

A Context for Dig ita l Market ing in Austral ia & New Zealand…

3

14

The sentiment amongst marketers is largely positive…

It is the place to be! It is growing, evolving and in the next 12-18

months we will see a lot of dinosaurs leaving traditional methods

and jumping into the “”new”” digital marketing space. Mobile is the tip of

the iceberg, and where a lot of money & efforts will be concentrated on.

I’m excited about new platforms

and possibilities for reaching our

target audience which has grown up with

technology and are first embracers.

Digital marketing is fast moving and it takes time and effort to keep up

with the technology. If you can keep up there are exciting times ahead.

I’m excited, with Google Glass about to disrupt social media,

and Pebble leading the charge into smartwatch technology,

wearable digital devices will become integrated, more so, into

every aspect of life. And marketers need to be able to harness these

technologies and provide customers with better brand experiences.

Australian marketing is about 10

years behind the UK in strategy

and channel optimisation, however, the

need to satisfy and focus on the customer

is always at the forefront of strategic

conversations. If companies don’t

have a plan in place to implement an

effective digital marketing plan, including

reporting through to optimisation and

trigger based CRM, then they are already

5 years behind their competitors.

15

But there are still plenty of cynics…

Digital is simply another advertising/marketing

medium, we use it alongside traditional media

at different weights depending on the campaign

objectives. It’s not a silver bullet, it may work in some

cases and not in others... like any other medium!

Stop making out it’s something

it isn’t. Digital is just another set

of channels - some work, some don’t.

I wish the BS and noise would die.

It’s still full of digi-spruikers

conning money out of marketers

by pretending there is something

special about digital. With all these digi-

experts we have not seen any market

share shifts, nor any reduction in

budgets from testing and analytics.

Digital marketing is just another tool in the tool

kit. It’s not always the answer, sometimes it is the

best/sole solution and sometimes it is part of an integrated

strategy. It’s probably going to grow in importance

as many more people spend more time online.

16

A number of challenges have been identified…

I think digital marketing is evolving as we

speak. There’s little differentiation between

editorial content and sponsored content and I think

that this is going to be a problem. Many people want

to buy native advertising, but if there is too much

vendor content, then it will significantly reduce

the value of such content and their proposition.

Digital marketing has much

potential but the rapidly

evolving nature of it makes long term

usage strategies difficult to plan for.

There is always something new, lots

of static about social media, frauds

purporting to be experts, people who

don’t understand specific industries,

a disconnect between reality and fact

which will continue into the future.

As a marketing manager I feel overwhelmed at the enormity

of creating and implementing a digital marketing plan

with very little budget. I feel like our organisation has left it all up

to my department and there is no support for us. My working

week is now 80% digital and I am not sure when that turning point

occurred. Over the next 12-18 months I can see that the digital task

will continue to be my team’s focus as we strive to harness its many

facets. It will be unlikely that we employ digital specialists, so we are

all trying to get up to speed with digital marketing as best we can.

It will become a very crowded space so we

need to develop effective new ways to cut

through the clutter and connect with potential clients.

Positive as far as ROI and insight goes, apprehensive as to how long it will last,

fear consumers will say enough is enough with the stalking style tactics.

17

Lack of resources is a common theme…

There is a lot for our organisation to learn from how digital

marketing can benefit our business. We currently need more

resources to even look at digital within the next 12 - 18 months.

Lots of potential for creating great campaigns,

however resources are often understated

and great tools end up being under-utilised.

Exciting opportunities exist. However, as a Government body that sets industry standards and ensures

industry compliance we are greatly restricted in terms of budget in the current economic environment.

I feel agnostic and

yet resigned to not

doing anything about it,

knowing there is absolutely

no budget for such activities.

I love it... and the possibilities seem

ENDLESS!!! (Just give me a budget) ;)

18

Many are concerned about isolating digital activity from the broader marketing mix

Growing, critical, but part of the greater marketing mix, integrated

campaigns still provide best return. digital alone won’t succeed.

Awash with opportunity but must be part of overall business strategy. Requires a huge corporate

cultural shift but those that embrace it and move forward with it will reap the rewards.

Digital marketing will grow

however it should not be looked

at in isolation in the total marketing mix.

I feel that people have very high exceptions of

digital marketing and that they need to understand

it is one platform of a good multi-channel campaign.

19

But the overwhelming tone is of EXCITEMENT & OPTIMISM

I am very excited about the

outlook for the digital marketing

industry. I am only a newbie and not

formally trained, but the last two years

working in this space have convinced

me that this is the career I want.

I feel very passionately about digital marketing and would like to partake in more

training courses to keep up to date with new technologies and improvements.

Bring it on...!

Excited! So much opportunity and if we don’t

lose the NBN plans in Australia then we’ll have

exponential growth in digital marketing. Marketers will need

to be creative to stay one step ahead of the media savvy

public. But the challenges and opportunities excite me!

20

BASE: CLIENT SIDE SAMPLE (N=330)

Spend on offline activities still outstrips online spend by more than 60%

390+610= 39%

610+390= 61%100 AVERAGE PROPORTION OF THE MARKETING BUDGET SPENT ONLINE VS OFFLINE

Q: Approximately what proportion of your marketing budget would currently be spent online (ie. on digital marketing activities) compared with offline marketing activities?

ONLINE/DIGITAL MARKETING ACTIVITIES

OFFLINE MARKETING ACTIVITIES

Smaller firms are leading the way in their investment in digital

39+61+x 39%BY COMPANY TURNOVER

550+450= 55%

460+540= 46%

330+670= 33%

< $2MILLION

$2-19MILLION

$20MILLION OR MORE

The average proportion of the marketing budget, on average, spent on DIGITAL marketing activities

21

BASE: CLIENT SIDE SAMPLE (N=330)

The momentum however is clearly towards an increased spend on digital marketing

73+20+2+5+0+1+48+33+8100 INCREASE SPEND100 MAINTAIN SPEND100 DECREASE SPEND100 DON’T KNOW

Q: Looking ahead to the next 12-18 months, what is planned for your digital marketing budget and your offline marketing budgets?

ONLINE/DIGITAL MARKETING OFFLINE MARKETING

73% 11%20% 48%2% 33%5% 8%

And it is larger firms now driving the increased spend in digital and ‘catching up’

73+27+x 73%BY COMPANY TURNOVER

500+500= 50%

760+240= 76%

750+250= 75%

$2-19MILLION

$20MILLION OR MORE

Indicates they will increase their spend on DIGITAL marketing activities

< $2MILLION

22

BASE: CLIENT SIDE SAMPLE (N=330)

The use of social media & customer databases feature heavily in current marketing activities

ONLINE

840+160= 84%

810+190= 81%

600+400= 60%

550+450= 55%

320+680= 32%

310+690= 31%

270+730= 27%

210+790= 21%

170+830= 17%

150+850= 15%

120+880= 12%

90+910= 9%

OFFLINE

820+180= 82%

650+350= 65%

590+410= 59%

470+530= 47%

460+540= 46%

360+640= 36%

180+820= 18%

180+820= 18%

Q: Looking at the extensive list below of offline and online marketing channels, please indicate which channels currently feature within your marketing mix (or the marketing mix of the organisation you deal with most often). (Multiple answers possible)

EMAIL TO OWN DATABASE PRINT

SOCIAL MEDIA TRADE SHOWS

DISPLAY ADS DIRECT MAIL

PAID SEARCH RADIO

MOBILE TV

BUSINESS/ WEB ANALYTICS OTHER EVENTS

EMAIL TO EXTERNAL DATABASE TELEMARKETING

VIDEO ADS OUT OF HOME

WEBINARS

AFFILIATE MARKETING

PERSONALISATION

PRICE COMPARISON SITES

23

BASE: CLIENT SIDE SAMPLE (N=330)

The top 5 over-rated marketing channels are all OFFLINE

380+620= 38%

240+760= 24%

160+840= 16%

150+850= 15%

130+870= 13%

110+890= 11%

60+940= 6%

60+940= 6%

60+940= 6%

50+950= 5%

40+960= 4%

40+960= 4%

30+970= 3%

20+980= 2%

50+950= 5%

Q: Of those channels that currently feature in your marketing mix, which, if any, do you think are over-rated and would prefer to see less of your marketing budget spent on?

TV

TRADE SHOWS

DIRECT MAIL

RADIO

DISPLAY ADS

SOCIAL MEDIA

TELEMARKETING

PAID SEARCH

EMAIL MARKETING

OUT OF HOME

PRICE COMPARISON SITES

AFFILIATE MARKETING

WEBINARS

OTHERS

24

BASE: CLIENT SIDE SAMPLE (N=330)

Q: Looking again at the comprehensive list of marketing channels, which ONE channel, do you perceive offers the greatest opportunity for growth of your organisation (or the organisation you deal with most often) over the next 12-18 months?

The top 5 growth opportunities are all ONLINE

220+780= 22%

140+860= 14%

120+880= 12%

100+900= 10%

80+920= 8%

60+940= 6%

30+970= 3%

SOCIAL MEDIA

EMAIL TO OWN DATABASE

PERSONALISATION

MOBILE

PAID SEARCH

TV

ALL OTHERS

25

FINDINGS IN DETAIL

Part 2 .

Current patterns of behaviour in d ig ita l market ing

3

26

BASE: CLIENT SIDE SAMPLE (N=330)

What is in the digital toolkit and how is that expected to change?What’s hot right now?

88+85+63+57+55+53+40+40+38+26+24+18+11W

EB A

NA

LYTI

CS

EMA

IL M

ARK

ETIN

G

CAM

PAIG

N M

AN

AG

EMEN

T

SOCI

AL

MED

IA IN

TEG

RATI

ON

TEST

ING

MO

BILE

AD

APT

ED

VER

SIO

N O

F W

EBSI

TE

PERS

ON

ALI

SATI

ON

ECO

MM

ERCE

SER

VIC

ES

INTE

GRA

TIO

N T

O C

RM/

CUST

OM

ER R

EPO

SITO

RIES

CON

TEN

T PR

OFI

LIN

G

MA

RKET

ING

AU

TOM

ATIO

N

PRED

ICTI

VE

AN

ALY

TICS

IP L

OO

KUP

88% 85% 63% 57% 55% 53% 40% 40% 38% 26% 24% 18% 11%

WEB ANALYTICS AND EMAIL

MARKETING ARE ON FIRE!

Q: To what extent does your organisation use the following?

27

BASE: CLIENT SIDE SAMPLE (N=330)

Some interesting observations about the different digital activities being implemented

<5 YEARS MARKETING EXPERIENCE 5-14 YEARS MARKETING EXPERIENCE 15YEARS + MARKETING EXPERIENCE

Web analytics 81% 91% 88%

Email marketing 85% 88% 90%

Campaign management 71% 58% 78%

Social media integration 67% 59% 47%

Testing 52% 46% 57%

Mobile adapted version of the website 48% 41% 55%

Personalisation 54% 37% 55%

Ecommerce services 27% 40% 61%

Integration to CRM 46% 33% 31%

Content profiling 35% 19% 29%

Marketing automation 27% 23% 33%

Predictive analytics 23% 12% 24%

IP Lookup 17% 10% 12%

Q: To what extent does your organisation use the following?

28

BASE: CLIENT SIDE SAMPLE (N=330)

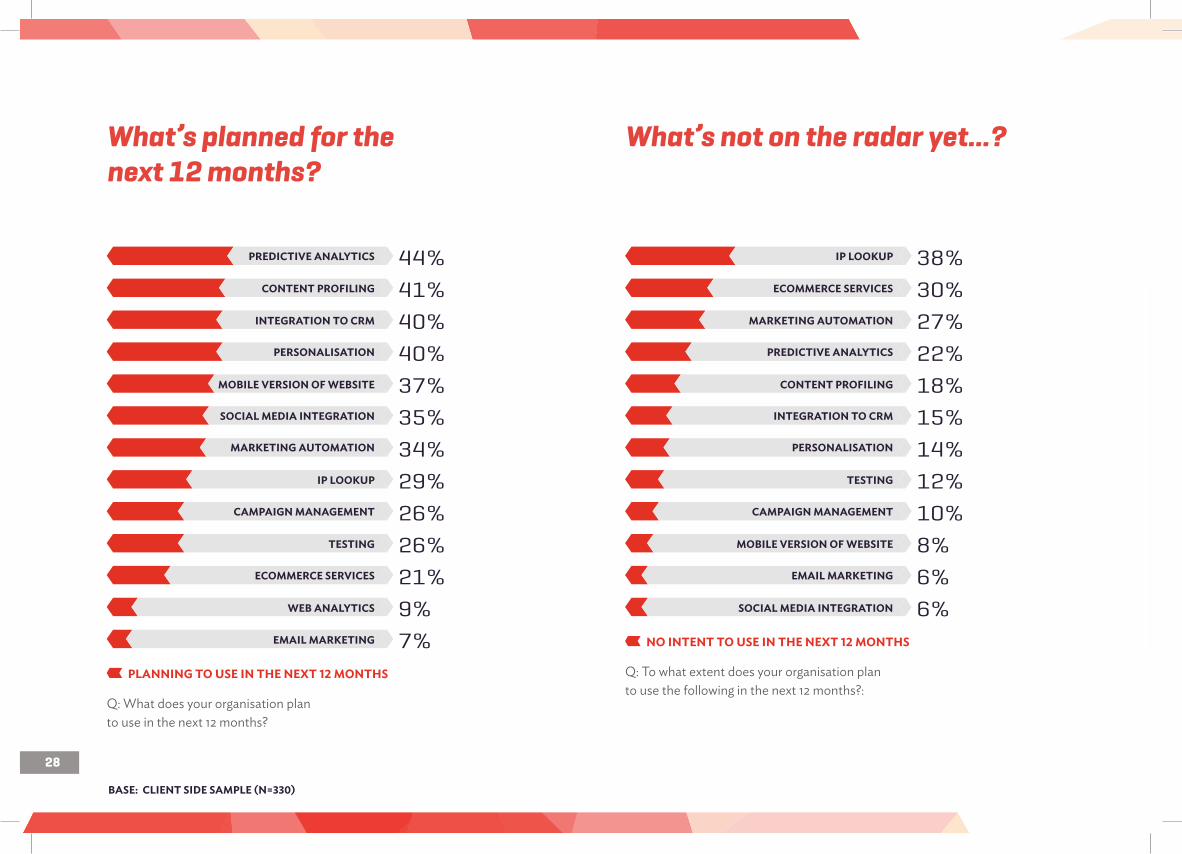

What’s planned for the next 12 months?

440+560= 44%

410+590= 41%

400+600= 40%

400+600= 40%

370+630= 37%

350+650= 35%

340+660= 34%

290+710= 29%

260+740= 26%

260+740= 26%

210+790= 21%

90+910= 9%

70+930= 7%100 PLANNING TO USE IN THE NEXT 12 MONTHS

Q: What does your organisation plan to use in the next 12 months?

PREDICTIVE ANALYTICS

CONTENT PROFILING

INTEGRATION TO CRM

PERSONALISATION

MOBILE VERSION OF WEBSITE

SOCIAL MEDIA INTEGRATION

MARKETING AUTOMATION

IP LOOKUP

CAMPAIGN MANAGEMENT

TESTING

ECOMMERCE SERVICES

WEB ANALYTICS

EMAIL MARKETING

What’s not on the radar yet…?

380+620= 38%

300+700= 30%

270+730= 27%

220+780= 22%

180+820= 18%

150+850= 15%

140+860= 14%

120+880= 12%

100+900= 10%

80+920= 8%

60+940= 6%

60+940= 6%100 NO INTENT TO USE IN THE NEXT 12 MONTHS

Q: To what extent does your organisation plan to use the following in the next 12 months?:

IP LOOKUP

ECOMMERCE SERVICES

MARKETING AUTOMATION

PREDICTIVE ANALYTICS

CONTENT PROFILING

INTEGRATION TO CRM

PERSONALISATION

TESTING

CAMPAIGN MANAGEMENT

MOBILE VERSION OF WEBSITE

EMAIL MARKETING

SOCIAL MEDIA INTEGRATION

29

BASE: CLIENT SIDE SAMPLE (N=330)

There are several digital functions not well understood by marketers…

220+780= 22%

160+840= 16%

140+860= 14%

90+910= 9%

70+930= 7%

60+940= 6%

60+940= 6%

40+960= 4%

50+950= 5%

30+970= 3%

20+980= 2%

100 I DON’T KNOW WHAT THAT IS

Q: To what extent does your organisation use the following?

IP LOOKUP

PREDICTIVE ANALYTICS

MARKETING AUTOMATION

TESTING

INTEGRATION TO CRM

PERSONALISATION

MOBILE VERSION OF WEBSITE

CAMPAIGN MANAGEMENT

CONTENT PROFILING

SOCIAL MEDIA INTEGRATION

EMAIL MARKETING

??

?

30

BASE: CLIENT SIDE SAMPLE (N=330)

The knowledge gaps lie most significantly with junior-mid level marketers

<5 YEARS MARKETING EXPERIENCE 5-14 YEARS MARKETING EXPERIENCE 15 YEARS + MARKETING EXPERIENCE

IP Lookup 27% 22% 14%

Predictive analytics 13% 22% 4%

Marketing automation 17% 13% 6%

Testing 10% 12% 2%

Content profiling 10% 18% 10%

Integration to CRM 2% 7% 4%

Personalisation 4% 5% 0%

Mobile adapted version of the website 8% 6% 0%

Campaign management 4% 3% 2%

Social media integration 4% 1% 0%

Q: To what extent does your organisation use the following: (I DON’T KNOW WHAT THAT IS)

31

BASE: CLIENT SIDE SAMPLE (N=330)

Analytics & personalisation are the areas most want to be doing better…

51+50+50+42+38+35+34+33+32+32+32+19+17Q: Which of the following, if any, do you think your organisation should be doing better? Please select all that apply . (Multiple responses possible)

100 WHAT COULD YOUR ORGANISATION BE DOING BETTER?

WEB

AN

ALY

TICS

51%

PRED

ICTI

VE

AN

ALY

TICS

50%

PERS

ON

ALI

SATI

ON

50%

SOCI

AL

MED

IA IN

TEG

RATI

ON

42%

CON

TEN

T PR

OFI

LIN

G 3

8%

MO

BILE

VER

SIO

N O

F W

EBSI

TE 3

5%

EMA

IL M

ARK

ETIN

G 3

4%

CAM

PAIG

N M

AN

AG

EMEN

T 33

%

INTE

GRA

TIO

N T

O C

RM 3

2%

TEST

ING

32%

MA

RKET

ING

AU

TOM

ATIO

N 3

2%

ECO

MM

ERCE

SER

VIC

ES 19

%

IP L

OO

KUP

17%

32

BASE: CLIENT SIDE SAMPLE (N=330)

40+60+x‘YES’, THEY HAVE UNDERTAKEN A TRAINING COURSE

380+620= 38%

530+470= 53%

540+460= 54%

5-14 YEARS IN MARKETING

< 5 YEARS IN MARKETING

15 YEARS+ IN MARKETING

Q: Have you undertaken any training courses in digital marketing?

40% YES

60% NO

Attitudes & behaviour of marketers working in a digital world There is a clear need to deliver enhanced training to those new to the industry

SOME OF THE TRAINING UNDERTAKEN INCLUDED..

• Undergraduate degrees (units within)• Post-graduate degrees• Industry Association courses• Sitecore training courses• ADMA courses• Google Adwords• Google Analytics• SEO/SEM• Short courses (1-2 days)• Seminars• Webinars• In-house training

33

BASE: CLIENT SIDE SAMPLE (N=330)

While most feel quietly confident about their own skills in digital marketing…

Q: How would you rate your own knowledge of digital marketing?

170+830= 17%

430+570= 43%

280+720= 28%

110+890= 11%

10+990= 1%

EXCELLENT

GOOD

ADEQUATE

LIMITED

POOR

The more concentrated training directed at senior marketers is reflected in their own confidence… and also lack of confidence amongst younger marketers

17+83+x 17%MARKETING EXPERIENCE

130+870= 13%

230+770= 23%

270+730= 27%

Marketers that rate their own digital marketing skills as ‘excellent’

5-14 YEARS IN MARKETING

< 5 YEARS IN MARKETING

15 YEARS+ IN MARKETING

34

BASE: CLIENT SIDE SAMPLE (N=330)

Almost one in four think their organisation is more digitally competent than their competitors…

240+760= 24%

300+700= 30%

180+820= 18%

120+880= 12%

120+880= 12%

40+960= 4%100 DIGITAL COMPETENCY WITHIN THE ORGANISATION

Q: Which of the following best describes your impression of the digital competence within your organisation?

AHEAD OF MOST OF OUR COMPETITORS

ABOUT THE SAME AS OUR COMPETITORS

ABOUT 6 MONTHS BEHIND OUR COMPETITORS

ABOUT 12 MONTHS BEHIND OUR COMPETITORS

MORE THAN 12 MONTHS BEHIND OUR COMPETITORS

I DON’T KNOW/ COULDN’T SAY

EDUCATION SECTOR: 19%GOVERNMENT SECTOR : 30%

Senior marketers feel particularly confident about their competitive position. The enhanced training received by senior marketers is reflected not only in their higher level of digital competency… but also in a competitive edge

24+76+x 24%MARKETING EXPERIENCE

220+780= 22%

230+770= 23%

330+670= 33%

Marketers believe they are ahead of most of their competitors in terms of digital competency

5-14 YEARS IN MARKETING

< 5 YEARS IN MARKETING

15 YEARS+ IN MARKETING

35

BASE: CLIENT SIDE SAMPLE (N=330)

Digital marketing is now mainstream. Marketers feel more confident about it and are embracing the opportunities.

950+50= 95%830+170= 83%720+280= 72%650+350= 65%600+400= 60%80+600+320= 8%70+830+100= 7%70+830+100= 7%100 STRONGLY AGREE/ AGREE100 DISAGREE

I now see digital marketing as part of mainstream marketing

I find working on digital marketing activities both stimulating and exciting

I feel more confident executing digital marketing activities than I did 12 months ago

Measurement of the impact of digital marketing activities continues to be a major challenge for the industry

I continue to be impressed by the outcomes achieved by our digital marketing activities

I prefer traditional, offline marketing methods as they have a proven ROI

I avoid getting involved in digital marketing activities when I can

I don’t really ‘get’ the fuss about digital marketing

Q: Listed below are a number of statements other people have shared with us about how they are feeling about digital marketing . Using a scale from 1 to 5 please indicate the extent to which you agree or disagree with each statement .

60% DISAGREE

83% DISAGREE

83% DISAGREE

36

BASE: CLIENT SIDE SAMPLE (N=330)

Mid-size companies are the most likely to be seeing rewards from their digital activities

60+40+x 60%BY COMPANY TURNOVER

550+450= 55%

690+310= 69%

590+410= 59%

Continue to be impressed by the outcomes achieved by their digital marketing activities

$2-19MILLION

$20MILLION OR MORE

< $2MILLION

Digital success amongst mid-size companies is now translating to increased confidence

72+28+x 72%BY COMPANY TURNOVER

630+370= 63%

750+250= 75%

700+300= 70%

Feel more confident executing digital marketing activities than they did 12 months ago

$2-19MILLION

$20MILLION OR MORE

< $2MILLION

37

BASE: CLIENT SIDE SAMPLE (N=330)

Managing the digital marketing strategyThere is great variation in approach taken to managing the digital marketing function

80+920= 8%200+800= 20%130+870= 13%280+720= 28%220+780= 22%80+920= 8%40+960= 4%100 < $20MILLION TURNOVER100 > $20MILLION TURNOVER

Q: How does your organisation currently manage the digital marketing activities?

We outsource all digital marketing activities

We have a single marketing person who handles all activities, including digital

We employ a ‘digital manager’ or equivalent

We have a ‘digital marketing team’

We have different teams for different digital marketing functions

Something else

I don’t know

150+850= 15%340+660= 34%

380+620= 38%100+900= 10%

38

BASE: CLIENT SIDE SAMPLE (N=330)

Multiple platforms are common for managing content activity, particularly in larger companies

10+17+73+xBY COMPANY TURNOVER

Q: Still thinking about the content management activities listed previously, do you use different platforms to manage the different activities or are they all managed from a single platform/ one solution?

10% I DON’T KNOW

17% SINGLE PLATFORM/ ONE SOLUTION

73% DIFFERENT/ MULTIPLE PLATFORMS

670+330= 67%

670+330= 67%

770+230= 77%MULTIPLE PLATFORMS

210+790= 21%

220+770= 22%

170+830= 17%ONE SOLUTION

$2-19MILLION

$20MILLION OR MORE

< $2MILLION

39

BASE: CLIENT SIDE SAMPLE (N=330)

Most marketers feel vulnerable about their social media strategy & keep a close eye on competitor activity

470+530= 47%

410+590= 41%

390+610= 39%

370+630= 37%

270+730= 27%

150+850= 15%100 WHERE DO YOUR COMPETITORS HAVE AN EDGE

Q: In which of the following areas, if any, do you feel that your competitors have an edge over what your organisation is doing (or the organisation you are dealing with most often)?

SOCIAL MEDIA TECHNOLOGY

APPS

MOBILE

BUSINESS/ WEB ANALYTICS

EMAIL PLATFORMS

OTHERS RESPONSES

NZ marketers are feeling left behind in the area of business and web analytics

37+63+x 37%

350+650= 35%

500+500= 50%

Overall feel that competitors have an edge in business/ web analytics

NEW ZEALAND

AUSTRALIA

40

BASE: CLIENT SIDE SAMPLE (N=330)

What constitutes digital success and how is it measured?

Most track ROI to report back to the executive team… But 20% are NOT TRACKING ROI on digital activities at all!

500+500= 50%380+620= 38%160+840= 16%140+860= 14%200+800= 20%Q: Does your organisation track the ROI on digital marketing activities?

YES, TO REPORT BACK TO THE EXECUTIVE TEAM

YES, TO DETERMINE WHERE TO SPEND MORE FUNDS OR WHERE TO CUT BACK

YES, FOR ADDITIONAL FUNDING

YES, BUT I’M NOT SURE HOW TO USE THE INFORMATION YET

NO, WE DON’T TRACK THE ROI ON DIGITAL ACTIVITIES

Smaller companies tend to be the ones not tracking ROI

20+80+x 20%BY COMPANY TURNOVER

250+750= 25%

150+850= 15%

160+840= 16%

$2-19MILLION

$20MILLION OR MORE

< $2MILLION

Don’t track the ROI on their digital marketing activities

41

BASE: CLIENT SIDE SAMPLE (N=330)

Marketers with weak digital marketing skills are also far less likely to be measuring digital ROI

20+80+x 20%BY DIGITAL MARKETING COMPETENCY

50+950= 5%

120+880= 12%

250+750= 25%

540+460= 54%

On average, do NOT track the ROI on their digital marketing activities

EXCELLENT

GOOD

ADEQUATE

LIMITED

Most marketers are still anchored to website traffic as an indicator of digital success

730+270= 73%570+430= 57%440+560= 44%380+620= 38%380+620= 38%290+710= 29%230+770= 23%70+930= 7%40+960= 4%30+970= 3% 100 MEASURES OF DIGITAL SUCCESS CURRENTLY USED?

Q: How does your organisation measure the success of digital marketing activities? Please select all that apply (multiple answers possible).

VISITS TO THE WEBSITE

CONVERSIONS/ SALES/ NEW CUSTOMER ACQUISITIONS

LEADS GENERATED

KPIS ALIGNED WITH BUSINESS OBJECTIVES

MARKETING OBJECTIVES ACHIEVED

INCREASED SITE PERFORMANCE

HIGHER CUSTOMER SATISFACTION

KPIS ALIGNED WITH CUSTOMER LIFECYCLE ACROSS MULTIPLE CHANNELS

SHORTENED TIME FROM CONTENT CREATION TO PUBLISHING

WE DON’T MEASURE THE IMPACT OF OUR DIGITAL ACTIVITIES

42

BASE: CLIENT SIDE SAMPLE (N=330)

Marketers are in no doubt about what the boss is looking for!

430+570= 43%140+860= 14%100+900= 10%90+910= 9%60+940= 6%60+940= 6%100+900= 10%100 MEASURE MOST VALUED BY MANAGEMENT

Q: Which measurement do you believe is valued most highly by the management team? Please just choose one of the options below

CONVERSIONS/ SALES/ NEW CUSTOMER ACQUISITIONS

KPIS ALIGNED WITH BUSINESS OBJECTIVES

LEADS GENERATED

VISITS TO THE WEBSITE

MARKETING OBJECTIVES ACHIEVED

HIGHER CUSTOMER SATISFACTION

OTHER RESPONSES

Web analytics could be used more effectively in most organisations

480+520= 48%80+920= 8%280+720= 28%160+840= 16%Q: Are the analytics that are gathered used primarily in ‘real time’ or for discussion and reviews during periodic marketing meetings?

PERIODIC MARKETING MEETINGS

REAL TIME

BOTH OF THESE

I DON’T KNOW/ COULDN’T SAY

43

BASE: CLIENT SIDE SAMPLE (N=330)

Use of web analytics

FUNCTIONS USED EXTENSIVELY USED MODERATELY LIMITED/ NO USE

For reporting 38% 41% 16%

For insights 22% 43% 28%

For recommendations about SEO/SEM 17% 35% 38%

For recommendations about content optimisation 12% 34% 40%

For recommendations about conversion optimisation 10% 30% 51%

For recommendations about Site optimisation 10% 37% 45%

For recommendations about which content should be used for market automation

5% 19% 62%

Q: To what extent does your organisation currently use web analytics for each of the following functions?

44

BASE: CLIENT SIDE SAMPLE (N=330)

Barriers to the acceleration of digital marketing

Limited financial resources is the most significant barrier to greater investment in digital marketing

510+490= 51%340+660= 34%330+670= 33%300+700= 30%290+710= 29%270+730= 27%160+840= 16%150+850= 15%110+890= 11%

Limited marketing budget

Lack of understanding/ education about digital marketing

Lack of capabilities in digital software

Lack of executive support and buy-in

Lack of clear understanding of ROI

Reliance on traditional marketing

A fear of failure

Difficulty recruiting digital staff

Difficulty retaining digital staff

260+740= 26%330+670= 33%

300+700= 30%530+470= 53%

520+480= 52%420+580= 42%

100 AUSTRALIA100 NZ

100 SIGNIFICANT BARRIER

Q: Listed below are a number of factors that have been identified as barriers to increasing the investment in digital marketing at different organisations. How significant do you perceive each of these issues as a barrier in your organisation?

45

BASE: CLIENT SIDE SAMPLE (N=330)

51+49+x 51%BY COMPANY TURNOVER

710+290= 71%

650+350= 65%

430+570= 43%

Limited budgets are a more significant problem for smaller companies who would like to invest more in digital

Overall identify a ‘limited marketing budget’ as a significant barrier to further investment in digital marketing

$2-19MILLION

$20MILLION OR MORE

< $2MILLION

34+66+x 34%BY MARKETING EXPERIENCE

330+670= 33%

350+650= 35%

180+820= 18%

Junior & mid level marketers are far more likely to cite a lack of digital marketing knowledge as a barrier. Previous results support this and reinforce a need for more training at junior levels

Overall identify ‘lack of understanding/ education about digital marketing’ as a significant barrier to further investment in the area

5-14 YEARS IN MARKETING

< 5 YEARS IN MARKETING

15 YEARS+ IN MARKETING

46

BASE: CLIENT SIDE SAMPLE (N=330)

29+71+x 29%BY MARKETING EXPERIENCE

310+690= 31%

290+710= 29%

120+880= 12%

Younger marketers do not feel that clear objectives are being set for ROI on digital activities. Senior marketers must do more to keep their team moving in the same direction

Overall, identify ‘lack of clear understanding of ROI’ as a significant barrier to further investment in digital marketing .

5-14 YEARS IN MARKETING

< 5 YEARS IN MARKETING

15 YEARS+ IN MARKETING

ROI?

47

Summary of key themes

Digital marketing is now considered mainstream within the marketing repertoire. Marketers have seen the opportunities presented and are now embracing them.

Large companies are now leading the investment in digital marketing activities.While smaller companies were the early adopters of digital marketing, the big spenders are now catching up and are the most likely to be investing more in digital over the next 12 months.

Experienced marketers (15yrs+ in the industry) are more likely to have undertaken specific training in digital marketing (relative to those with 10yrs or less in the industry) and this is reflected in their knowledge of the digital tools available to them, application of more sophisticated digital tools and higher rates of measurement of ROI.Less experienced marketers are less knowledgeable about digital, are less likely to measure ROI and are generally less confident about the Digital Marketing strategies they implement.

Web analytics are used primarily for periodic reporting and most marketers are frustrated in their knowledge that they could be used far more effectively. Web analytics is the number one area marketers would like to see their organisations improve.

Predictive analytics is largely viewed as the next ‘golden ticket’ but most feel ill equipped to move in that direction.

ROI of digital activity is still evolving and most are still focused on visits to the website as a primary measure of success. 20% are not measuring ROI at all.

Digital marketing is no longer niche.

Big companies are waking up to the advantages.

Web analytics is not being used effectively.

Big appetite for predictive analytics.

Digital ROI is a work in progress.

Senior marketers are building their own skills in digital marketing but greater emphasis is now needed at the junior-mid levels.

48

About Sitecore

Sitecore is the global leader in customer experience management software for delivering the marketing that matters most – highly relevant content and personalised digital experiences that delight customers, increase loyalty and

drive revenue. With Sitecore’s fully unified, powerful, and easy-to-use software suite, marketers can focus on engaging customers instead of managing data – to deliver experiences that are relevant, immediate, and integrated

across channels. More than 3000 of the world’s leading brands – including Nissan Australia, Network 10, AustralianSuper, Canon, Blackmores, Jenny Craig,

Sydney Airport, AGL, Water Corporation, and TAL.

e. [email protected]. +61 2 8014 8857

Level 4, 50 Pitt StreetSYDNEY NSW 2000

Level 1, 27-31 King StMELBOURNE VIC 3000

www.sitecore.net