Emerging Consumer Survey Databook 2014 - Credit Suisse€¦ · Brazil: Brand penetration...

240

Emerging Consumer Survey Databook 2014 Research Institute Thought leadership from Credit Suisse Research and the world’s foremost experts February 2014

Transcript of Emerging Consumer Survey Databook 2014 - Credit Suisse€¦ · Brazil: Brand penetration...

Emerging ConsumerSurvey Databook 2014

Research InstituteThought leadership from Credit Suisse Research

and the world’s foremost experts

February 2014

Contents

For more information, please contact:

Mujtaba Rana, Vice President

Thematic Equity Research

Credit Suisse Investment Banking

+44 20 7883 3773

3 Introduction

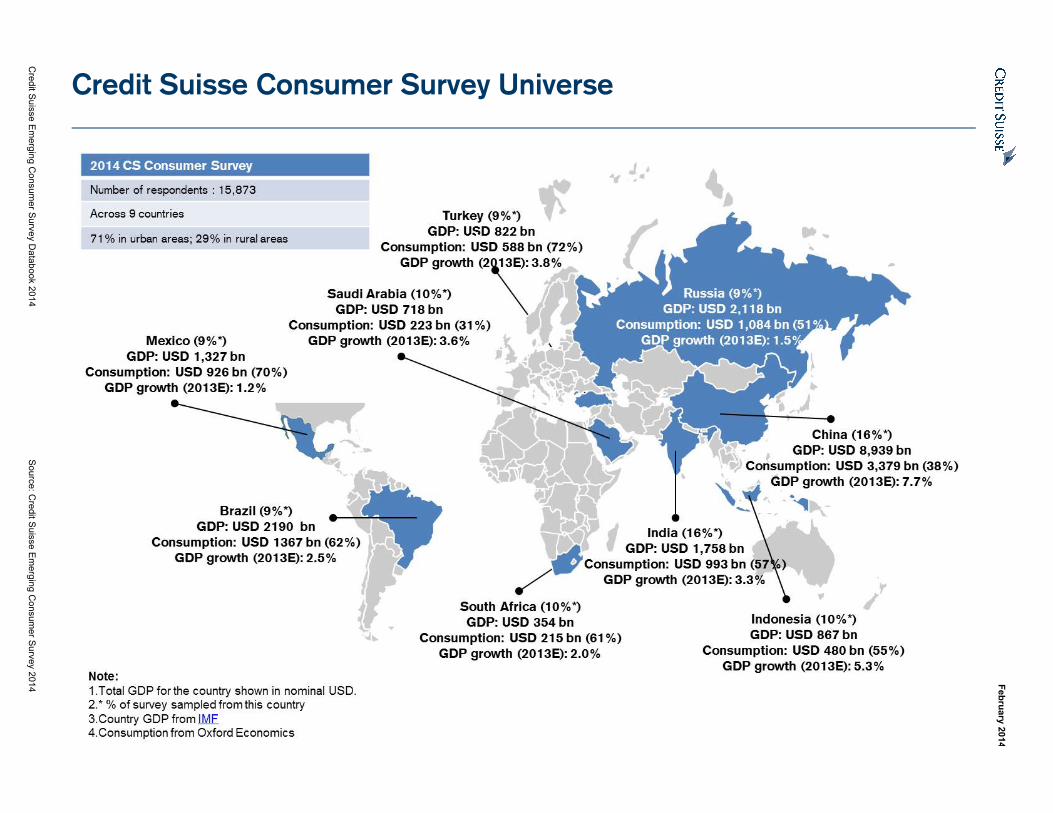

4 Credit Suisse Consumer Survey Universe

5 Brazil

30 China

58 India

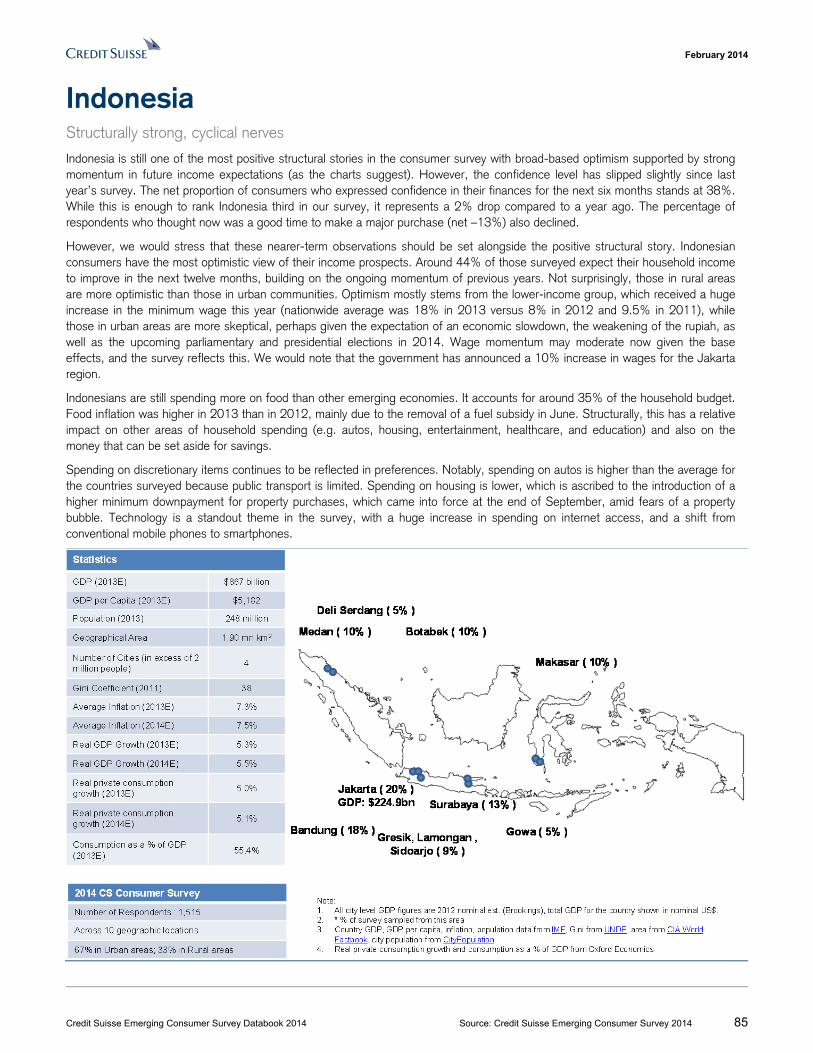

85 Indonesia

110 Mexico

136 Russia

162 Saudi Arabia

185 South Africa

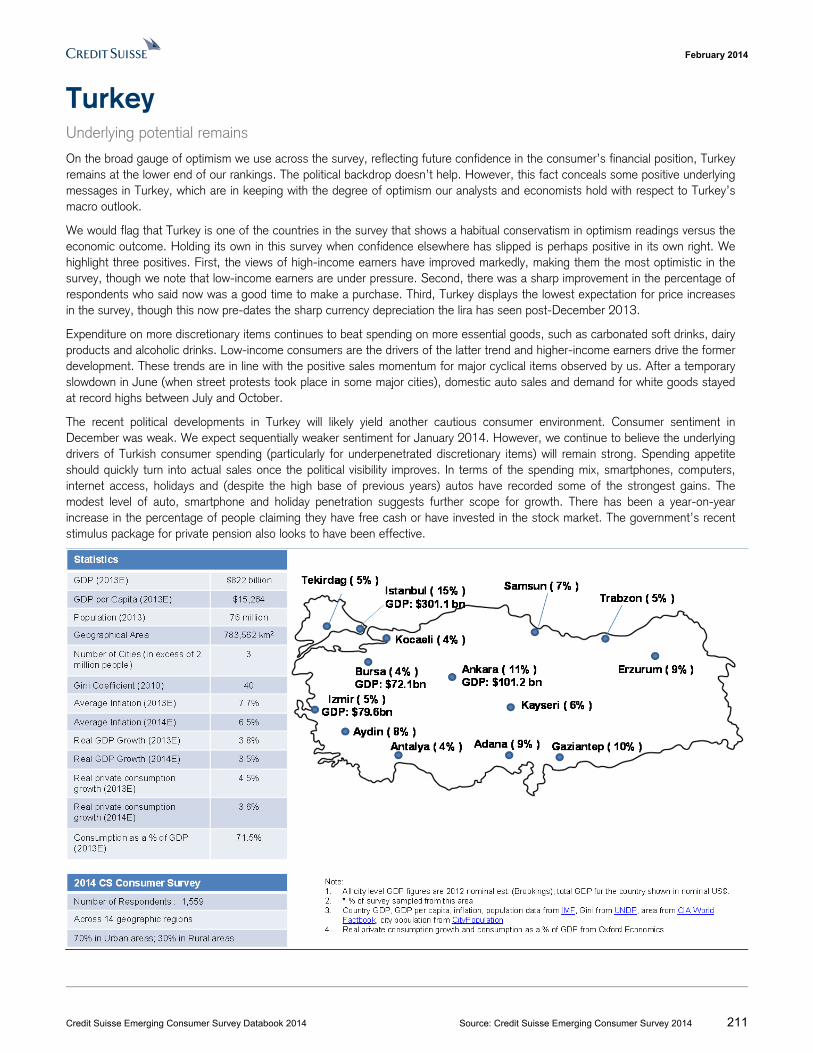

211 Turkey

237 Appendix: Methodology

238 About the survey

239 Imprint

240 General disclaimer/Important information

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014

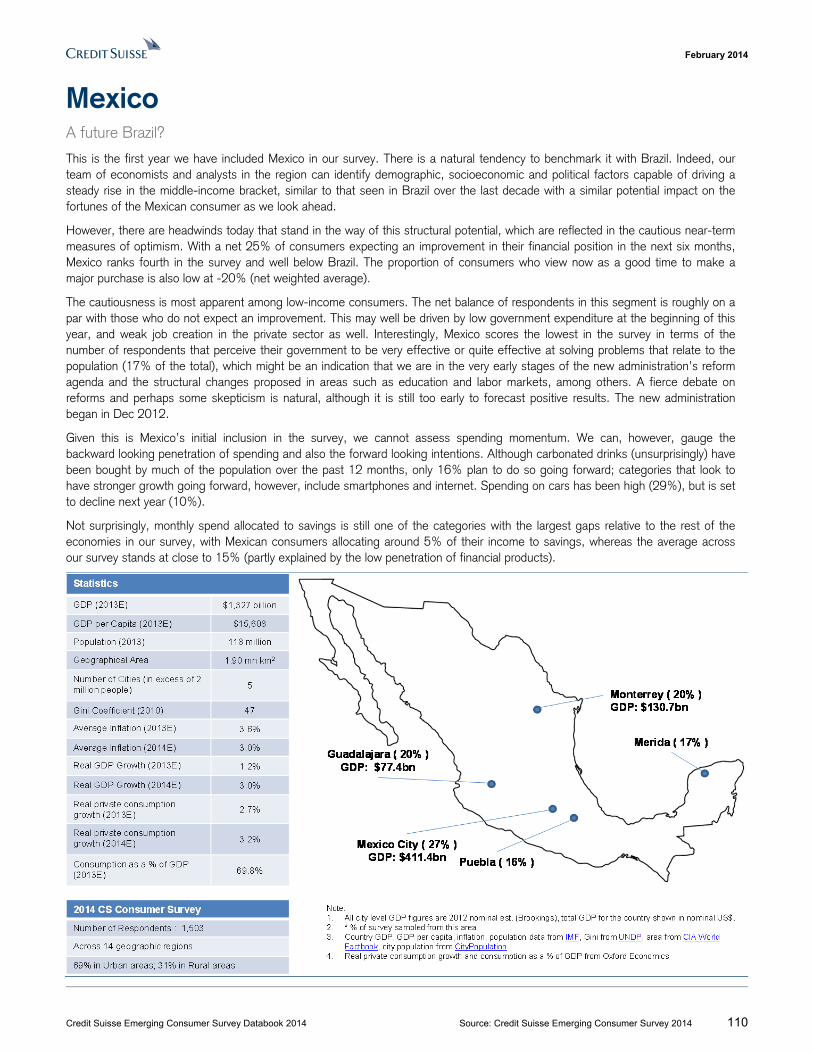

Introduction This Credit Suisse Emerging Consumer Survey Databook provides granular detail of the market research that underpins the conclusions and themes highlighted in the Credit Suisse Emerging Consumer Survey 2014, a comprehensive and exclusive study of the consumption patterns and plans of individuals residing in nine key economies across the emerging world. Specifically, the markets we have incorporated in this survey are China, India, Brazil, Russia, Mexico, Saudi Arabia, South Africa, Indonesia and Turkey. In total, these markets account for almost 3.5 billion people.

As comprehensive as this Databook is, we have not provided every aspect of the detail which can be derived from the survey along the lines of gender, age, city and rural/urban locations. This is available on request. The pages that follow have focused on income bands as a source of disaggregation of the responses which was a principal feature of the themes we have explored.

This report builds on work Credit Suisse published on consumption trends in emerging markets over the past 36 months. The Emerging Consumer Surveys in 2013, 2012 and 2011 were in themselves an extension to the China Consumer Survey, a publication released annually since 2005. The survey structure and questionnaire used in this previous work has been used as a template for this project, ensuring both a degree of consistency with previous work and a comparable dataset across the different countries.

To conduct the primary research for this project, the Credit Suisse Research Institute engaged the global market research firm Nielsen to advise on the questionnaire construction and to undertake the interview process on our behalf. Using a global firm with local offices has provided a consistent approach to this multi-region survey, as well as allowing sufficient flexibility to incorporate questions specific to the countries concerned.

This survey is designed to capture information regarding the spending patterns (past, present and future) and general lifestyles and aspirations of the consumers across these markets. The data is proprietary to Credit Suisse and is based on face-to-face interviews carried out in 91 distinct regional areas, spread over the nine different countries. Data from such a sample will vary in quality due to the sampling and non-sampling problems inherent in all surveys. Approximately 1,500 respondents were surveyed for each region, with the largest two markets (India and China) having a larger sample size of 2,500 each. The male-to-female split between respondents was roughly 50:50 in all cases, with rural-to-urban split varying by country.

A total of 16,000 respondents were screened and surveyed on questions within 12 categories: 1) general income and wealth, 2) autos, 3) food and beverages, 4) household and personal care, 5) luxury goods, 6) technology, 7) telecoms, 8) internet, 9) travelling, 10) property, 11) education and 12) healthcare. Detailed results from each of the eight markets are shown in the "Country Specific Data" section from page 5 onwards. The survey methodology is described in the appendix.

Although each respondent was asked up to 120 questions during the course of the survey, the Databook aims to present detailed information on those areas which investors may find most compelling and those which garnered the most thought-provoking ideas during the course of our study. Certain topics are more pertinent in some markets than others: questions on holiday plans yielded far more interesting results in Russia and Saudi Arabia than they did in Indonesia, for instance. Similarly, questions on stock market investments are more pertinent in China than they are in India. Nevertheless, for the sake of consistency, we have included a standard set of results for each market in this Databook. Numbered references within the tables, such as A7 and D5, allude to specific questions surveyed. More detail is available on request.

Mujtaba Rana Equity Research, Credit Suisse Investment Banking

Feb

ruary 2014

Credit S

uisse Em

erging Consum

er Survey D

atabook 2014 Source: C

redit Suisse E

merging C

onsumer S

urvey 2014

Credit Suisse Consumer Survey Universe

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 5

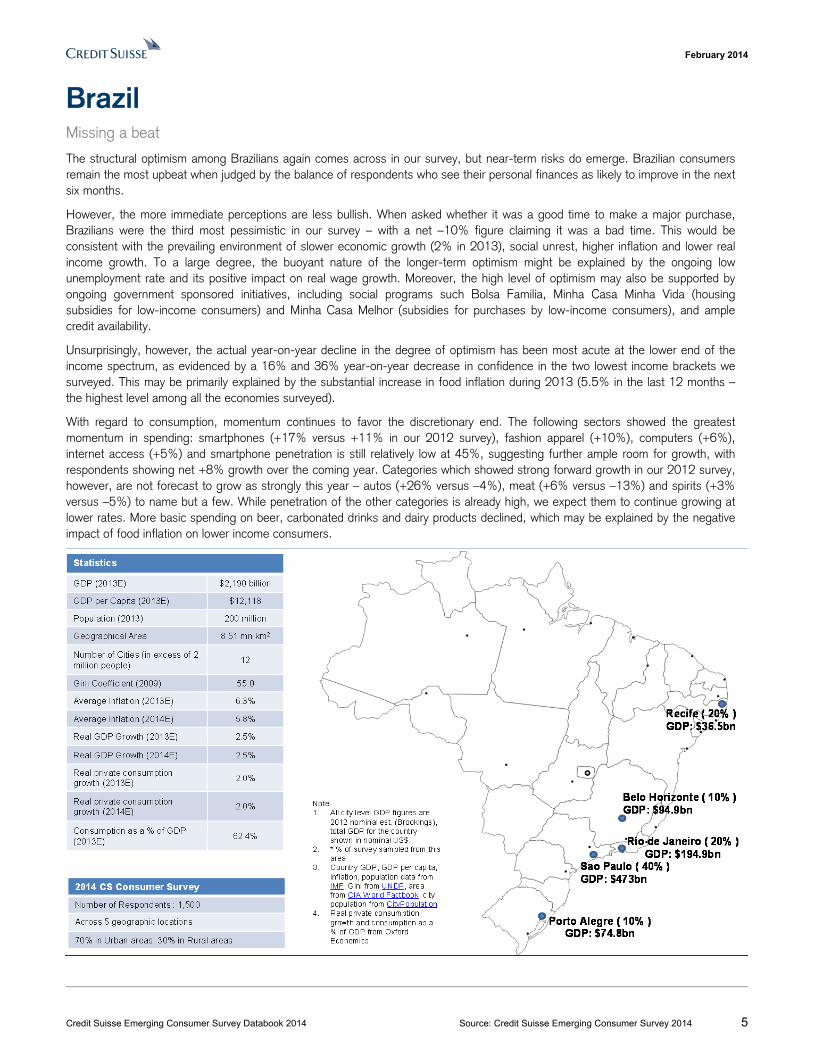

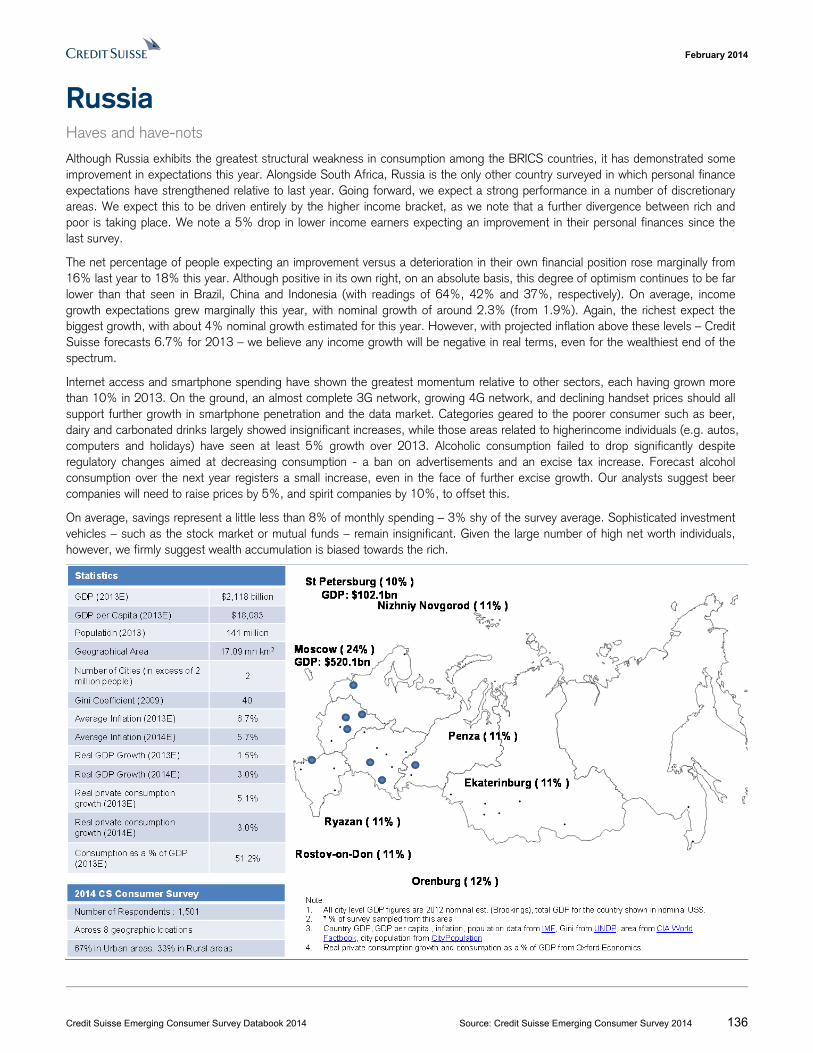

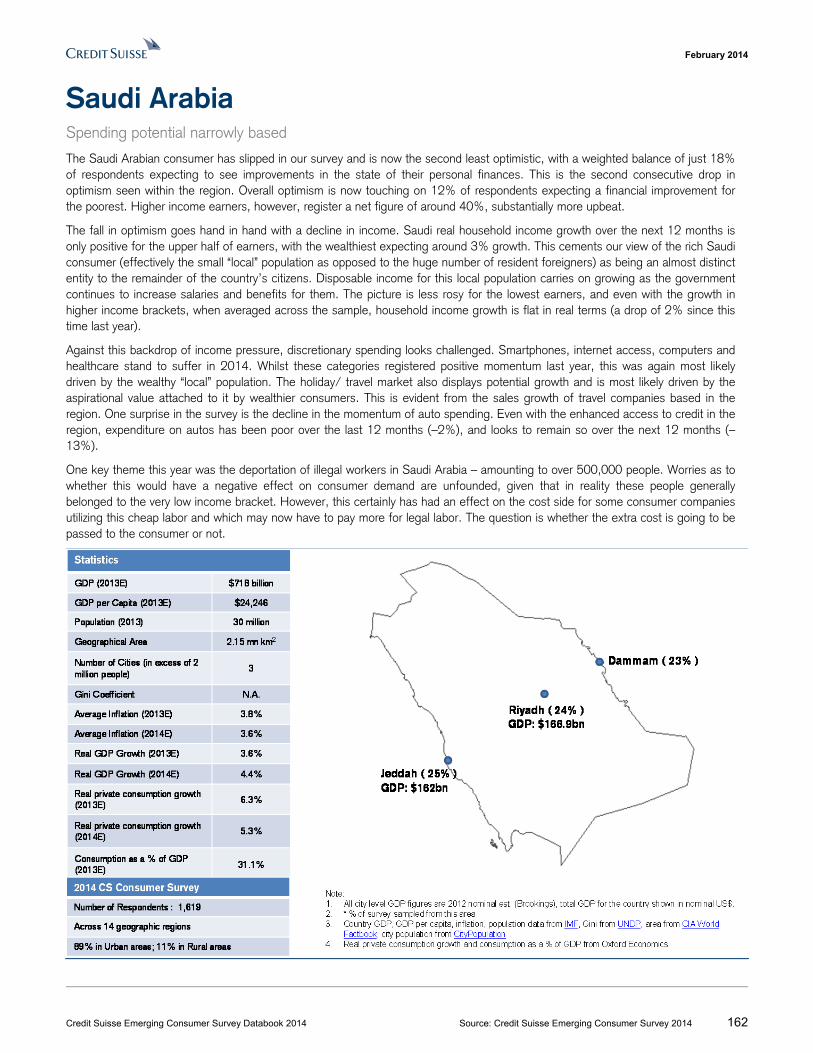

Brazil Missing a beat

The structural optimism among Brazilians again comes across in our survey, but near-term risks do emerge. Brazilian consumers remain the most upbeat when judged by the balance of respondents who see their personal finances as likely to improve in the next six months.

However, the more immediate perceptions are less bullish. When asked whether it was a good time to make a major purchase, Brazilians were the third most pessimistic in our survey – with a net –10% figure claiming it was a bad time. This would be consistent with the prevailing environment of slower economic growth (2% in 2013), social unrest, higher inflation and lower real income growth. To a large degree, the buoyant nature of the longer-term optimism might be explained by the ongoing low unemployment rate and its positive impact on real wage growth. Moreover, the high level of optimism may also be supported by ongoing government sponsored initiatives, including social programs such Bolsa Familia, Minha Casa Minha Vida (housing subsidies for low-income consumers) and Minha Casa Melhor (subsidies for purchases by low-income consumers), and ample credit availability.

Unsurprisingly, however, the actual year-on-year decline in the degree of optimism has been most acute at the lower end of the income spectrum, as evidenced by a 16% and 36% year-on-year decrease in confidence in the two lowest income brackets we surveyed. This may be primarily explained by the substantial increase in food inflation during 2013 (5.5% in the last 12 months – the highest level among all the economies surveyed).

With regard to consumption, momentum continues to favor the discretionary end. The following sectors showed the greatest momentum in spending: smartphones (+17% versus +11% in our 2012 survey), fashion apparel (+10%), computers (+6%), internet access (+5%) and smartphone penetration is still relatively low at 45%, suggesting further ample room for growth, with respondents showing net +8% growth over the coming year. Categories which showed strong forward growth in our 2012 survey, however, are not forecast to grow as strongly this year – autos (+26% versus –4%), meat (+6% versus –13%) and spirits (+3% versus –5%) to name but a few. While penetration of the other categories is already high, we expect them to continue growing at lower rates. More basic spending on beer, carbonated drinks and dairy products declined, which may be explained by the negative impact of food inflation on lower income consumers.

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 6

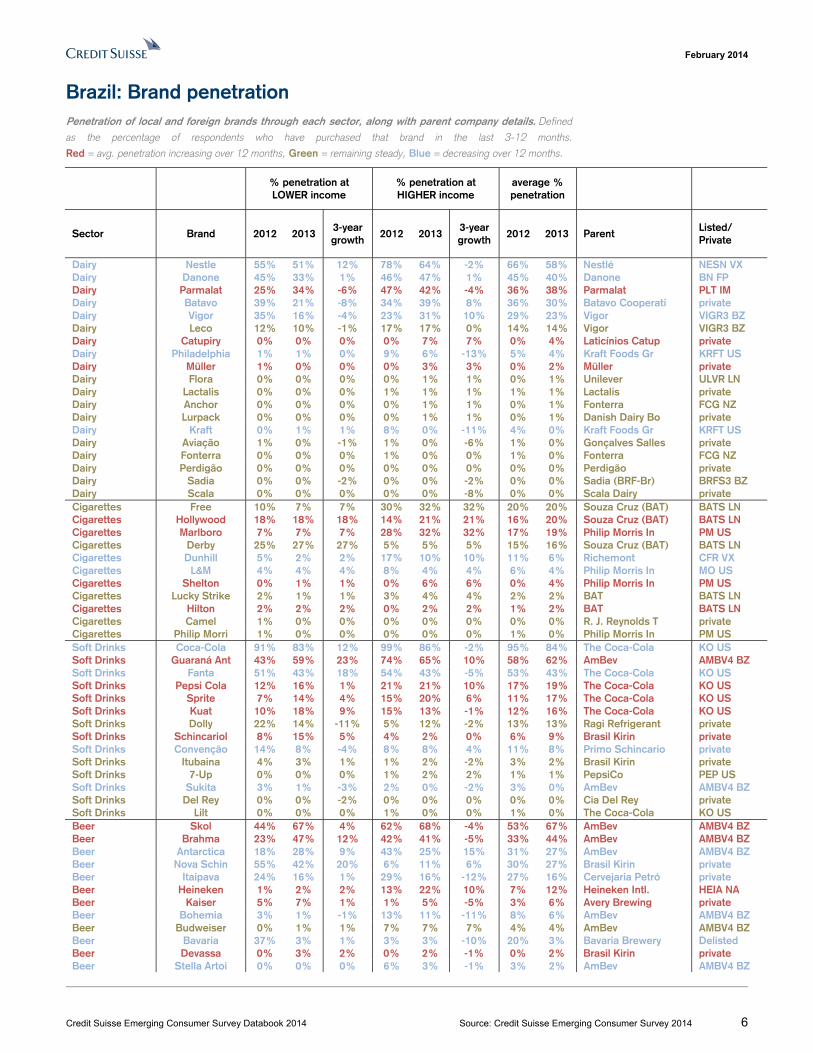

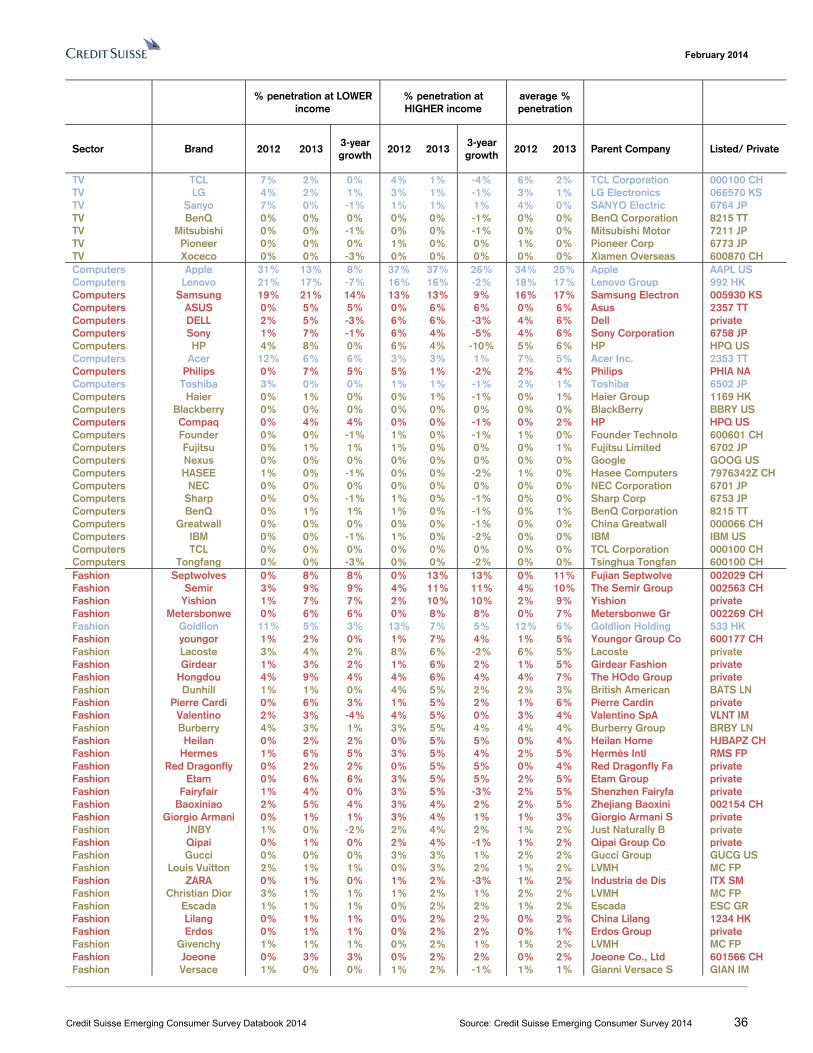

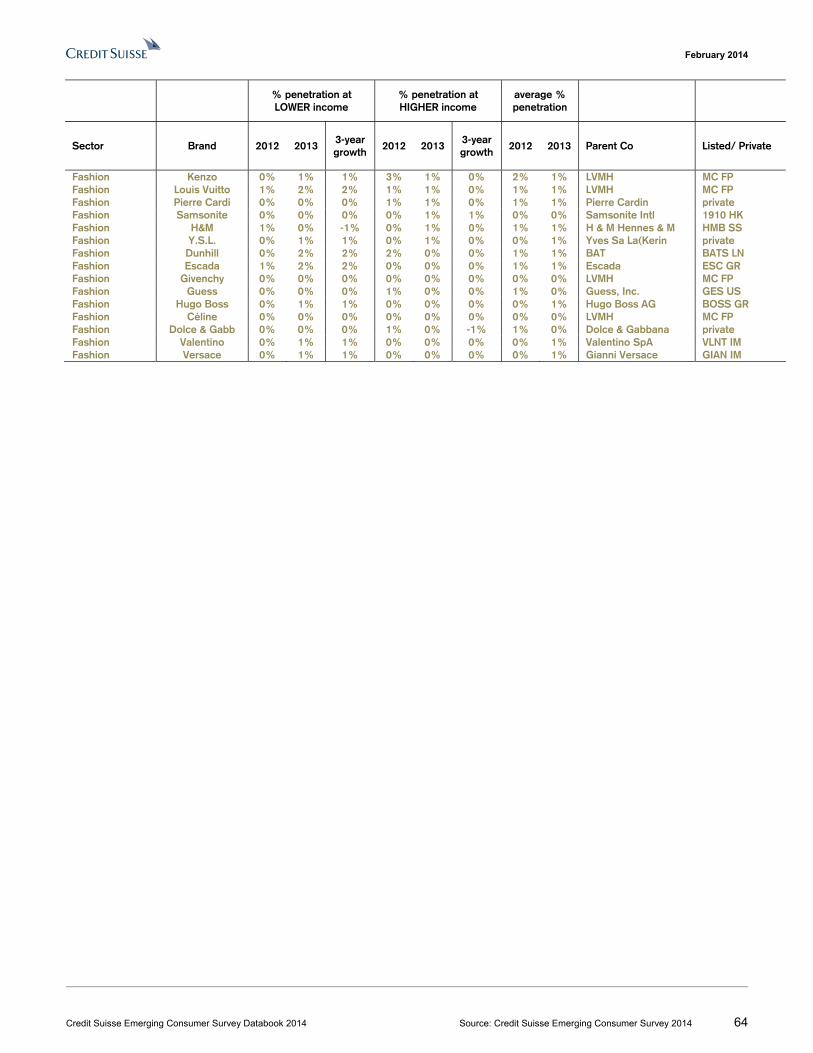

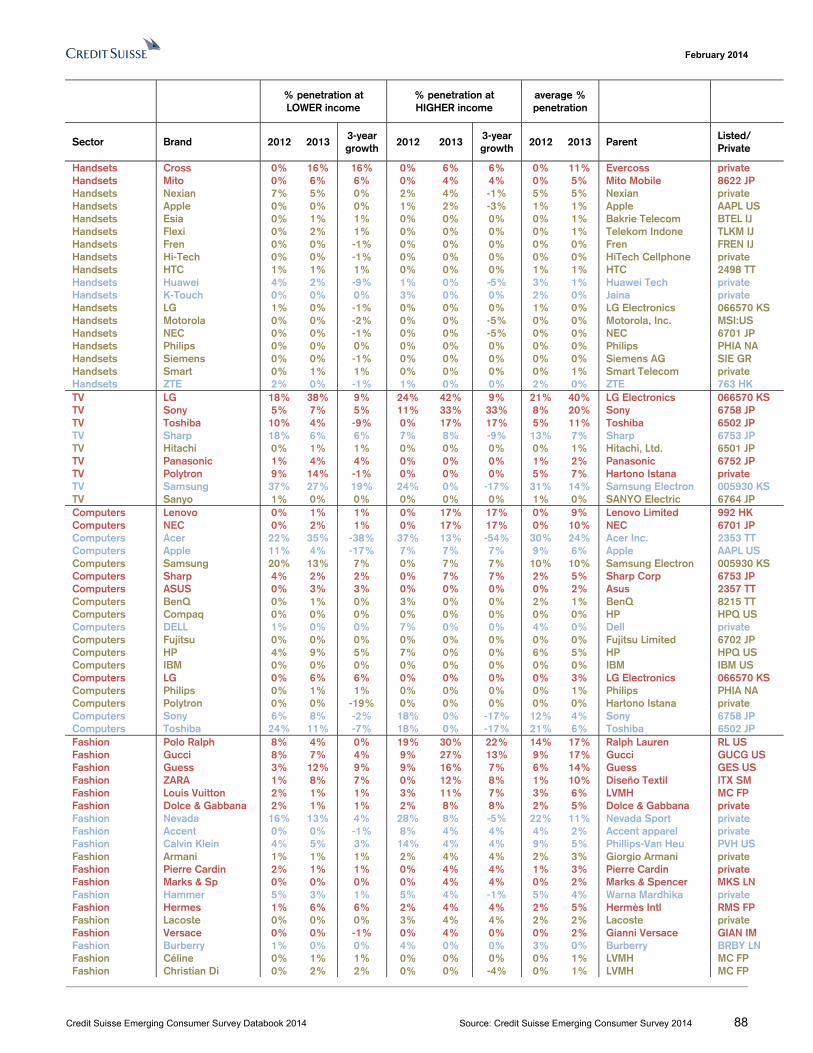

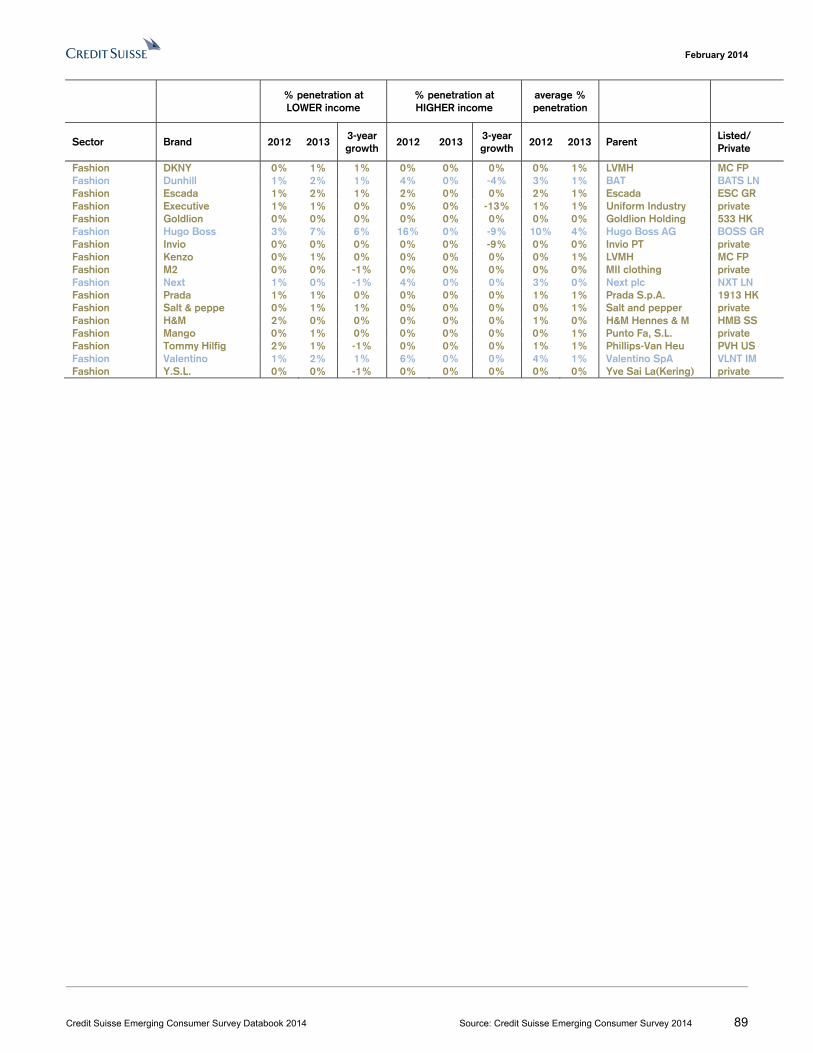

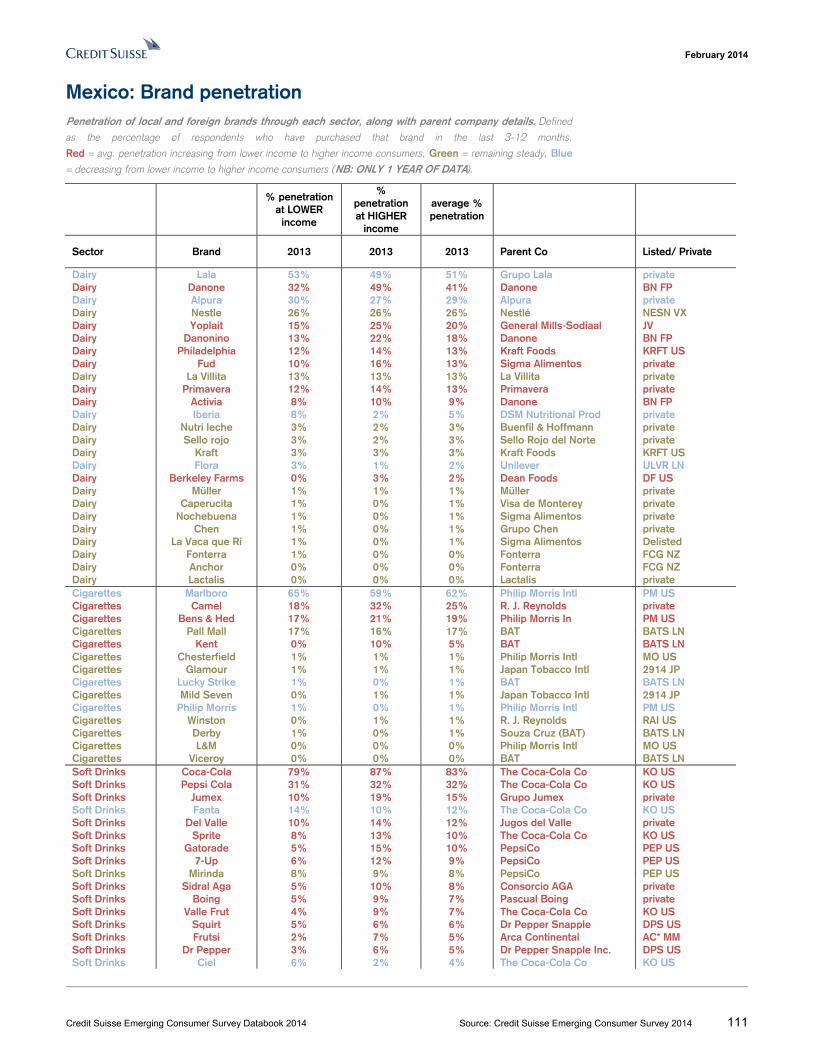

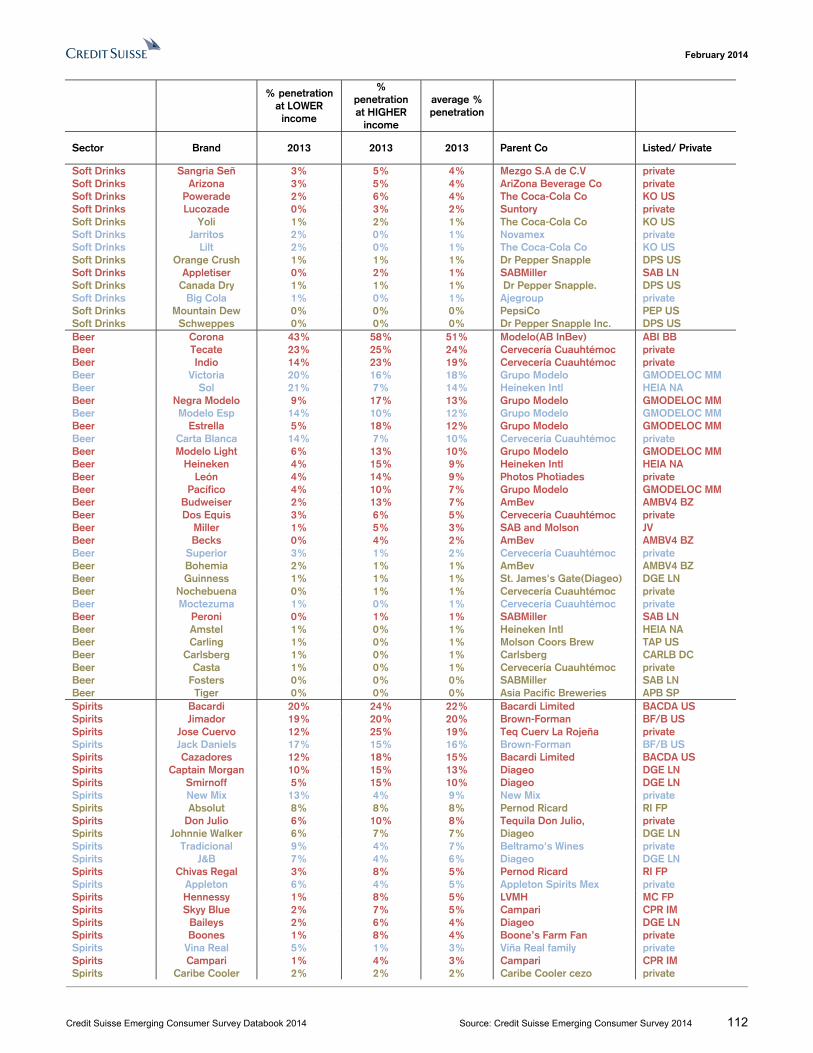

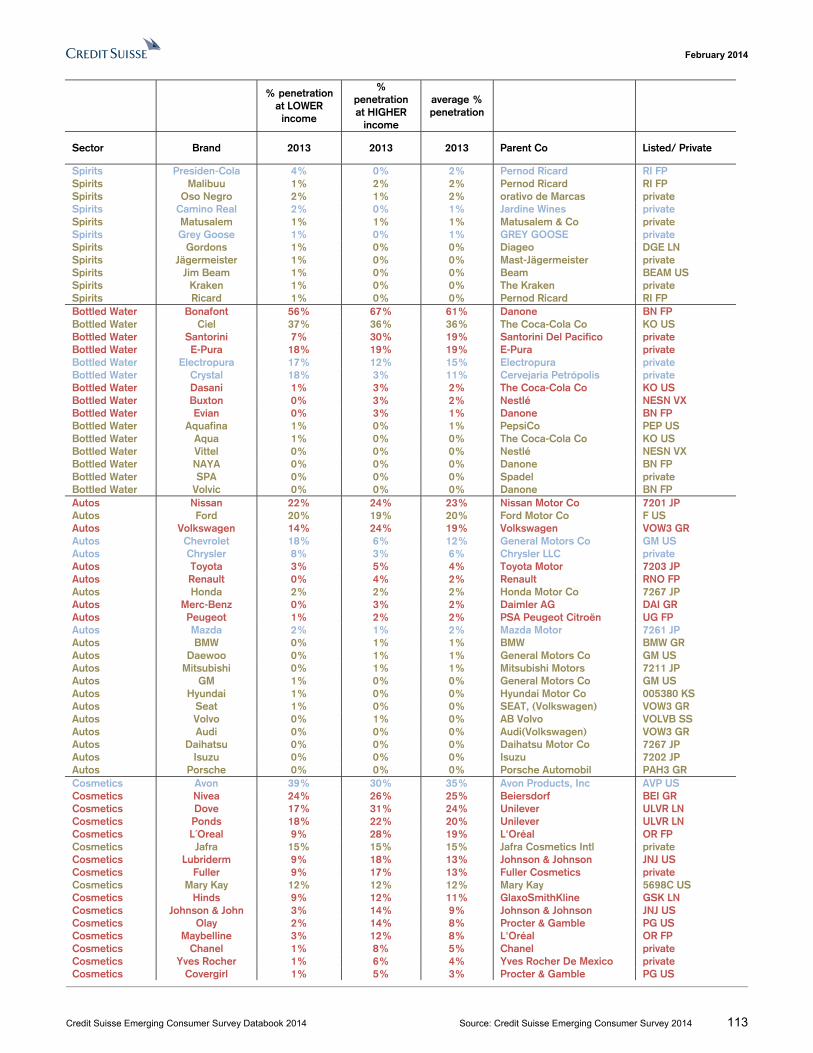

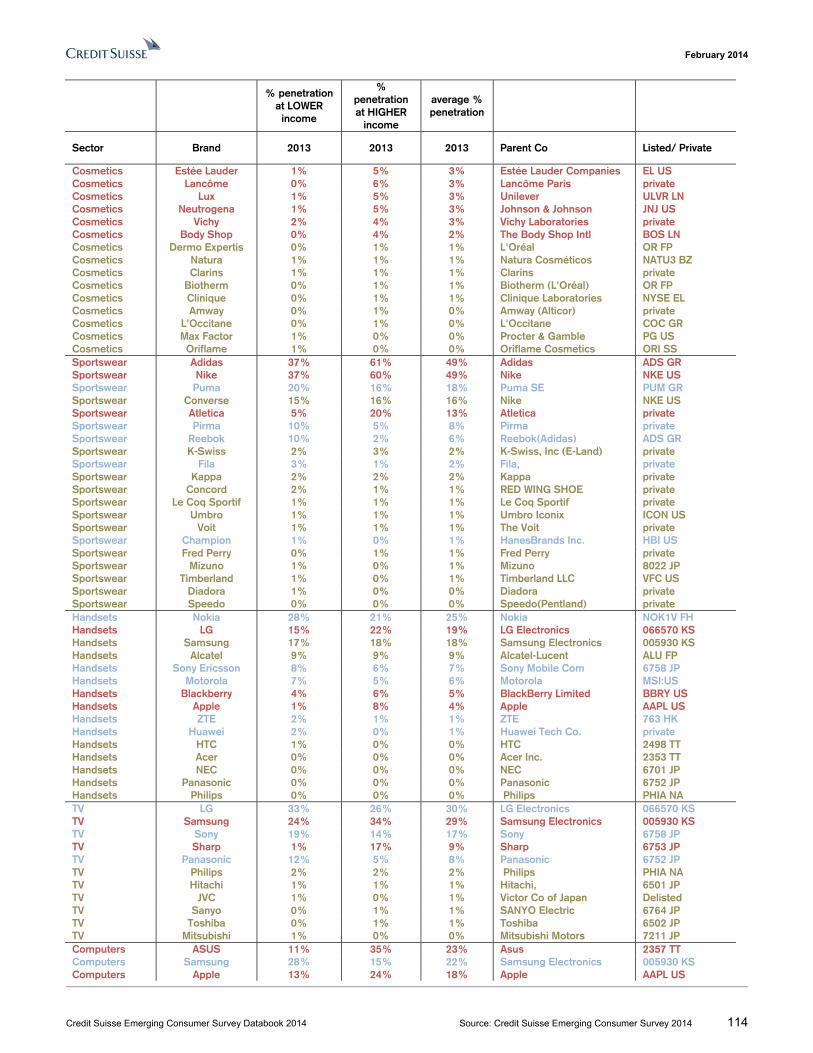

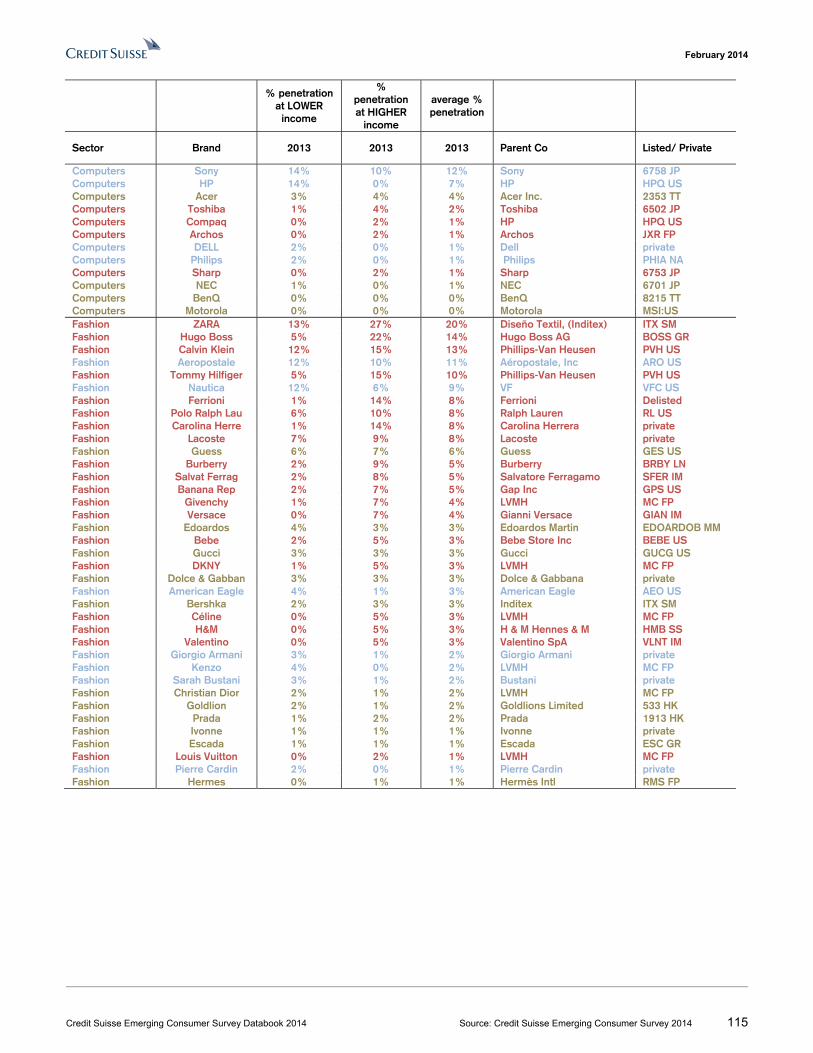

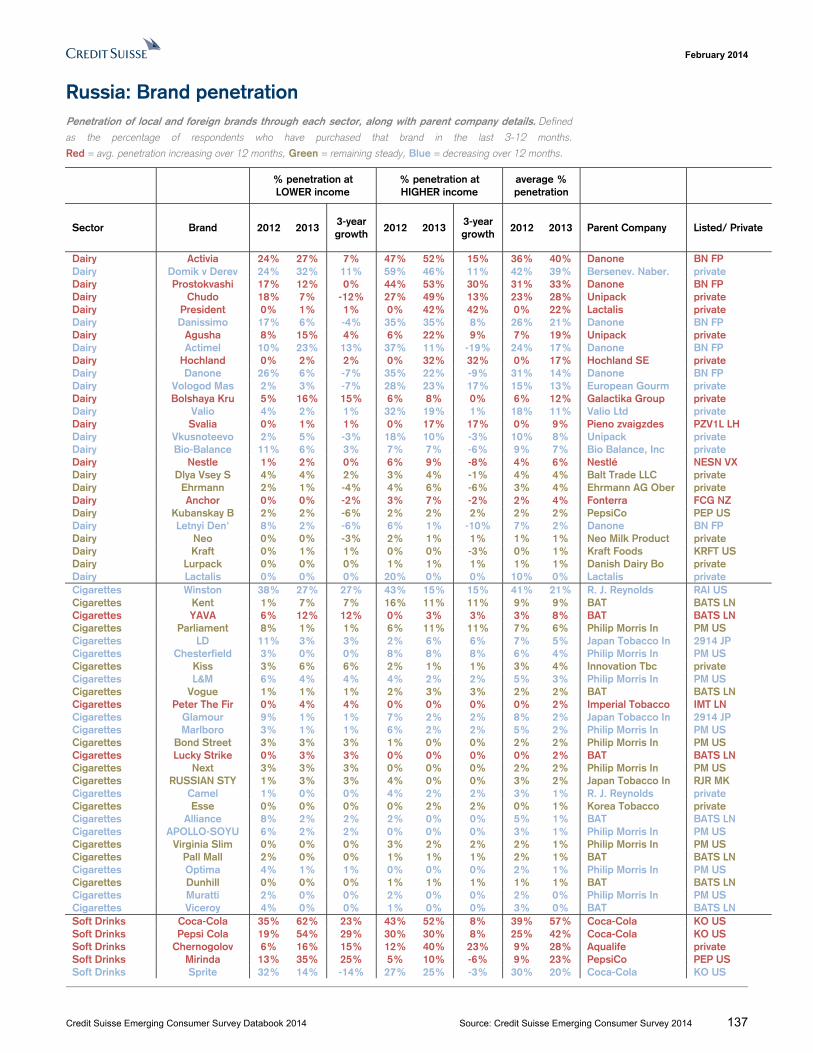

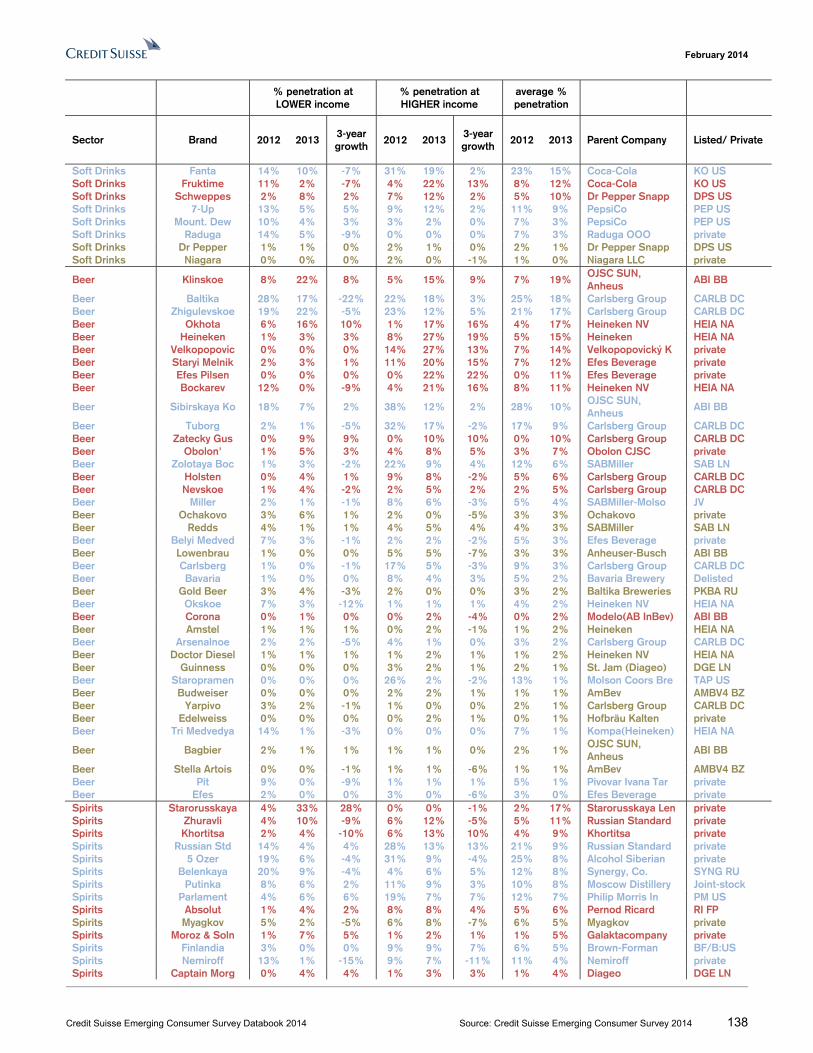

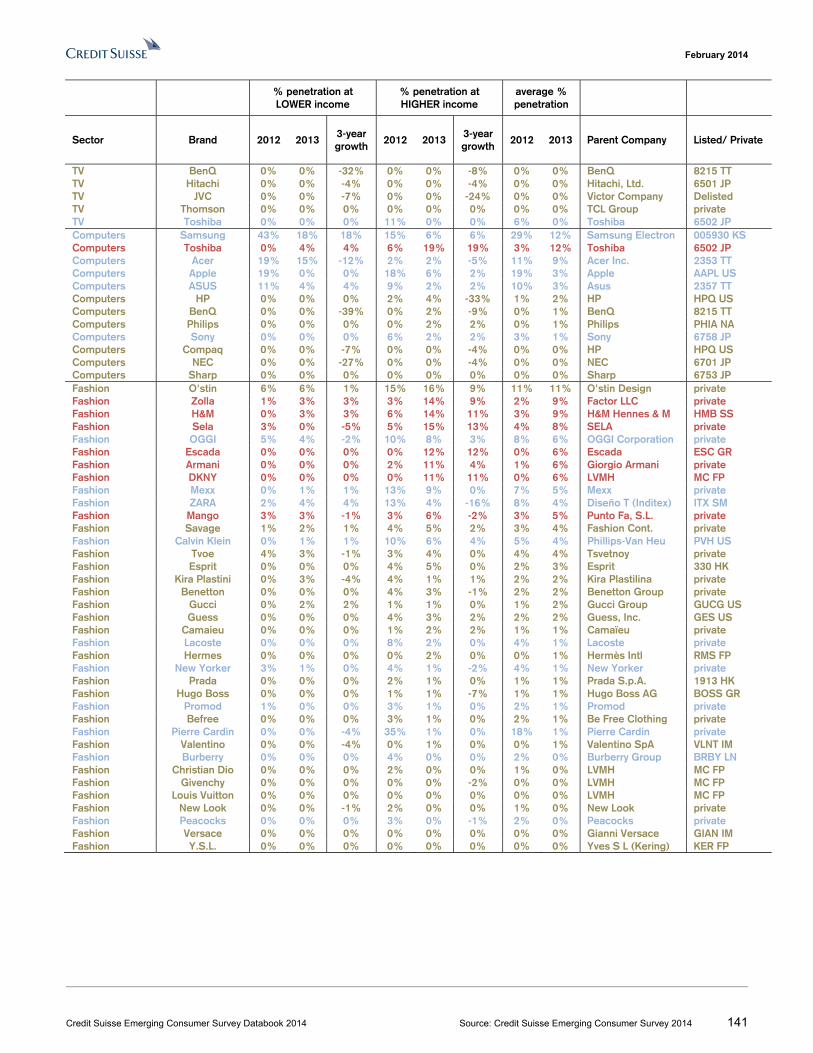

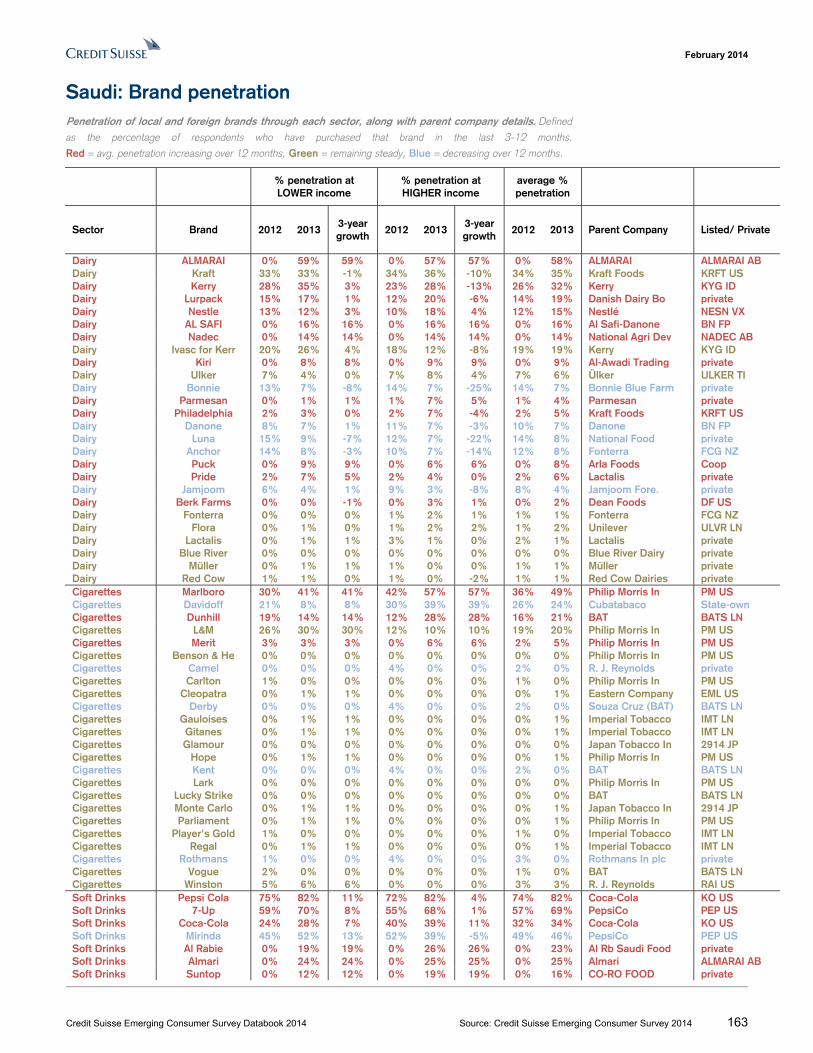

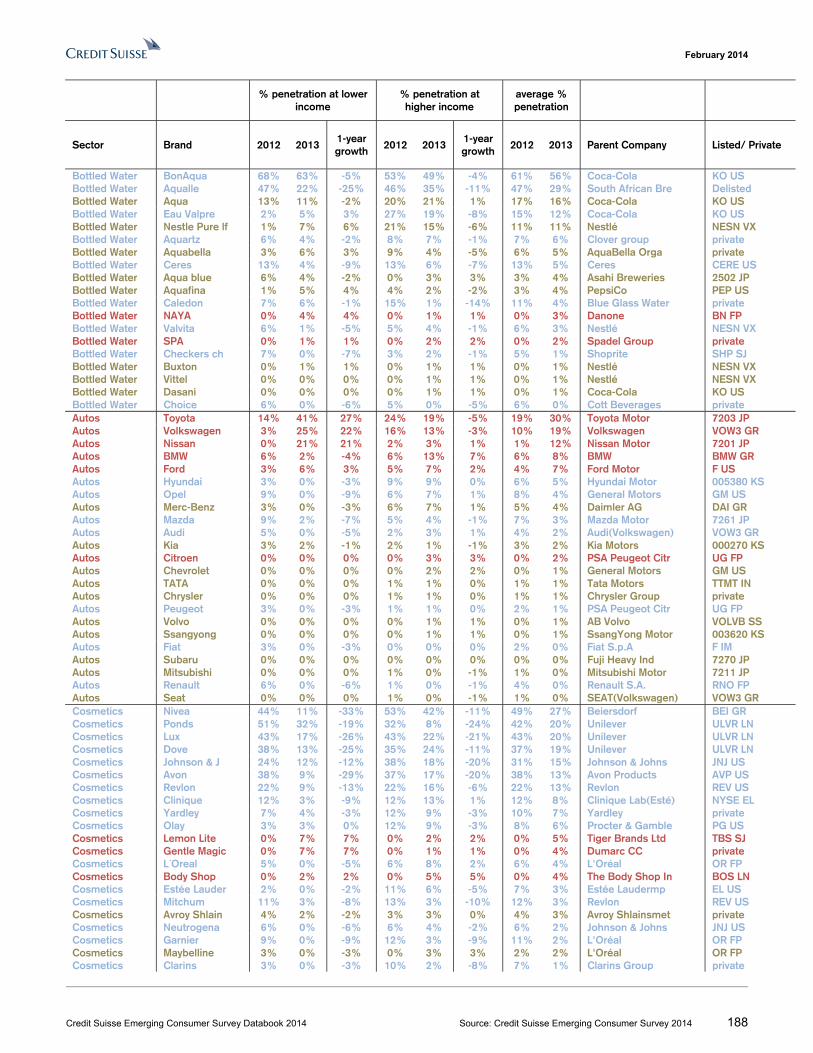

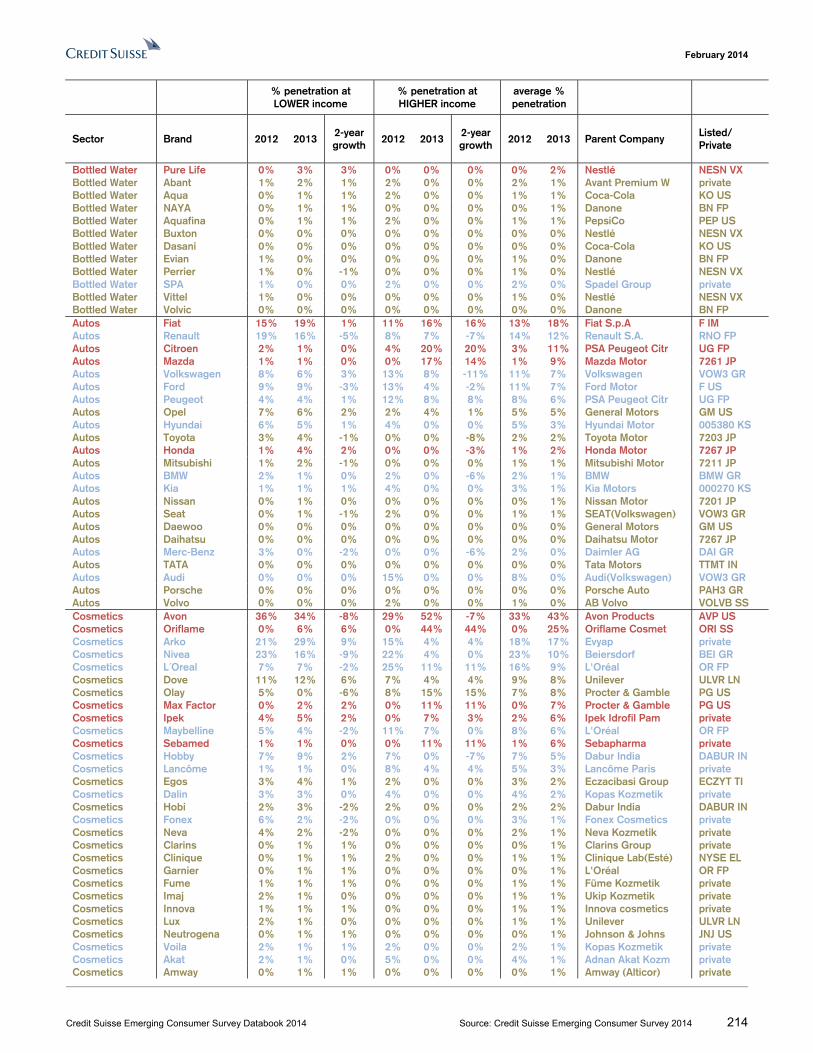

Brazil: Brand penetration Penetration of local and foreign brands through each sector, along with parent company details. Defined

as the percentage of respondents who have purchased that brand in the last 3-12 months.

Red = avg. penetration increasing over 12 months, Green = remaining steady, Blue = decreasing over 12 months.

% penetration at LOWER income

% penetration at HIGHER income

average % penetration

Sector Brand 2012 2013 3-year growth

2012 2013 3-year growth

2012 2013 Parent Listed/ Private

Dairy Nestle 55% 51% 12% 78% 64% -2% 66% 58% Nestlé NESN VX Dairy Danone 45% 33% 1% 46% 47% 1% 45% 40% Danone BN FP Dairy Parmalat 25% 34% -6% 47% 42% -4% 36% 38% Parmalat PLT IM Dairy Batavo 39% 21% -8% 34% 39% 8% 36% 30% Batavo Cooperati private Dairy Vigor 35% 16% -4% 23% 31% 10% 29% 23% Vigor VIGR3 BZ Dairy Leco 12% 10% -1% 17% 17% 0% 14% 14% Vigor VIGR3 BZ Dairy Catupiry 0% 0% 0% 0% 7% 7% 0% 4% Laticínios Catup private Dairy Philadelphia 1% 1% 0% 9% 6% -13% 5% 4% Kraft Foods Gr KRFT US Dairy Müller 1% 0% 0% 0% 3% 3% 0% 2% Müller private Dairy Flora 0% 0% 0% 0% 1% 1% 0% 1% Unilever ULVR LN Dairy Lactalis 0% 0% 0% 1% 1% 1% 1% 1% Lactalis private Dairy Anchor 0% 0% 0% 0% 1% 1% 0% 1% Fonterra FCG NZ Dairy Lurpack 0% 0% 0% 0% 1% 1% 0% 1% Danish Dairy Bo private Dairy Kraft 0% 1% 1% 8% 0% -11% 4% 0% Kraft Foods Gr KRFT US Dairy Aviação 1% 0% -1% 1% 0% -6% 1% 0% Gonçalves Salles private Dairy Fonterra 0% 0% 0% 1% 0% 0% 1% 0% Fonterra FCG NZ Dairy Perdigão 0% 0% 0% 0% 0% 0% 0% 0% Perdigão private Dairy Sadia 0% 0% -2% 0% 0% -2% 0% 0% Sadia (BRF-Br) BRFS3 BZ Dairy Scala 0% 0% 0% 0% 0% -8% 0% 0% Scala Dairy private Cigarettes Free 10% 7% 7% 30% 32% 32% 20% 20% Souza Cruz (BAT) BATS LN Cigarettes Hollywood 18% 18% 18% 14% 21% 21% 16% 20% Souza Cruz (BAT) BATS LN Cigarettes Marlboro 7% 7% 7% 28% 32% 32% 17% 19% Philip Morris In PM US Cigarettes Derby 25% 27% 27% 5% 5% 5% 15% 16% Souza Cruz (BAT) BATS LN Cigarettes Dunhill 5% 2% 2% 17% 10% 10% 11% 6% Richemont CFR VX Cigarettes L&M 4% 4% 4% 8% 4% 4% 6% 4% Philip Morris In MO US Cigarettes Shelton 0% 1% 1% 0% 6% 6% 0% 4% Philip Morris In PM US Cigarettes Lucky Strike 2% 1% 1% 3% 4% 4% 2% 2% BAT BATS LN Cigarettes Hilton 2% 2% 2% 0% 2% 2% 1% 2% BAT BATS LN Cigarettes Camel 1% 0% 0% 0% 0% 0% 0% 0% R. J. Reynolds T private Cigarettes Philip Morri 1% 0% 0% 0% 0% 0% 1% 0% Philip Morris In PM US Soft Drinks Coca-Cola 91% 83% 12% 99% 86% -2% 95% 84% The Coca-Cola KO US Soft Drinks Guaraná Ant 43% 59% 23% 74% 65% 10% 58% 62% AmBev AMBV4 BZ Soft Drinks Fanta 51% 43% 18% 54% 43% -5% 53% 43% The Coca-Cola KO US Soft Drinks Pepsi Cola 12% 16% 1% 21% 21% 10% 17% 19% The Coca-Cola KO US Soft Drinks Sprite 7% 14% 4% 15% 20% 6% 11% 17% The Coca-Cola KO US Soft Drinks Kuat 10% 18% 9% 15% 13% -1% 12% 16% The Coca-Cola KO US Soft Drinks Dolly 22% 14% -11% 5% 12% -2% 13% 13% Ragi Refrigerant private Soft Drinks Schincariol 8% 15% 5% 4% 2% 0% 6% 9% Brasil Kirin private Soft Drinks Convenção 14% 8% -4% 8% 8% 4% 11% 8% Primo Schincario private Soft Drinks Itubaina 4% 3% 1% 1% 2% -2% 3% 2% Brasil Kirin private Soft Drinks 7-Up 0% 0% 0% 1% 2% 2% 1% 1% PepsiCo PEP US Soft Drinks Sukita 3% 1% -3% 2% 0% -2% 3% 0% AmBev AMBV4 BZ Soft Drinks Del Rey 0% 0% -2% 0% 0% 0% 0% 0% Cia Del Rey private Soft Drinks Lilt 0% 0% 0% 1% 0% 0% 1% 0% The Coca-Cola KO US Beer Skol 44% 67% 4% 62% 68% -4% 53% 67% AmBev AMBV4 BZ Beer Brahma 23% 47% 12% 42% 41% -5% 33% 44% AmBev AMBV4 BZ Beer Antarctica 18% 28% 9% 43% 25% 15% 31% 27% AmBev AMBV4 BZ Beer Nova Schin 55% 42% 20% 6% 11% 6% 30% 27% Brasil Kirin private Beer Itaipava 24% 16% 1% 29% 16% -12% 27% 16% Cervejaria Petró private Beer Heineken 1% 2% 2% 13% 22% 10% 7% 12% Heineken Intl. HEIA NA Beer Kaiser 5% 7% 1% 1% 5% -5% 3% 6% Avery Brewing private Beer Bohemia 3% 1% -1% 13% 11% -11% 8% 6% AmBev AMBV4 BZ Beer Budweiser 0% 1% 1% 7% 7% 7% 4% 4% AmBev AMBV4 BZ Beer Bavaria 37% 3% 1% 3% 3% -10% 20% 3% Bavaria Brewery Delisted Beer Devassa 0% 3% 2% 0% 2% -1% 0% 2% Brasil Kirin private Beer Stella Artoi 0% 0% 0% 6% 3% -1% 3% 2% AmBev AMBV4 BZ

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 7

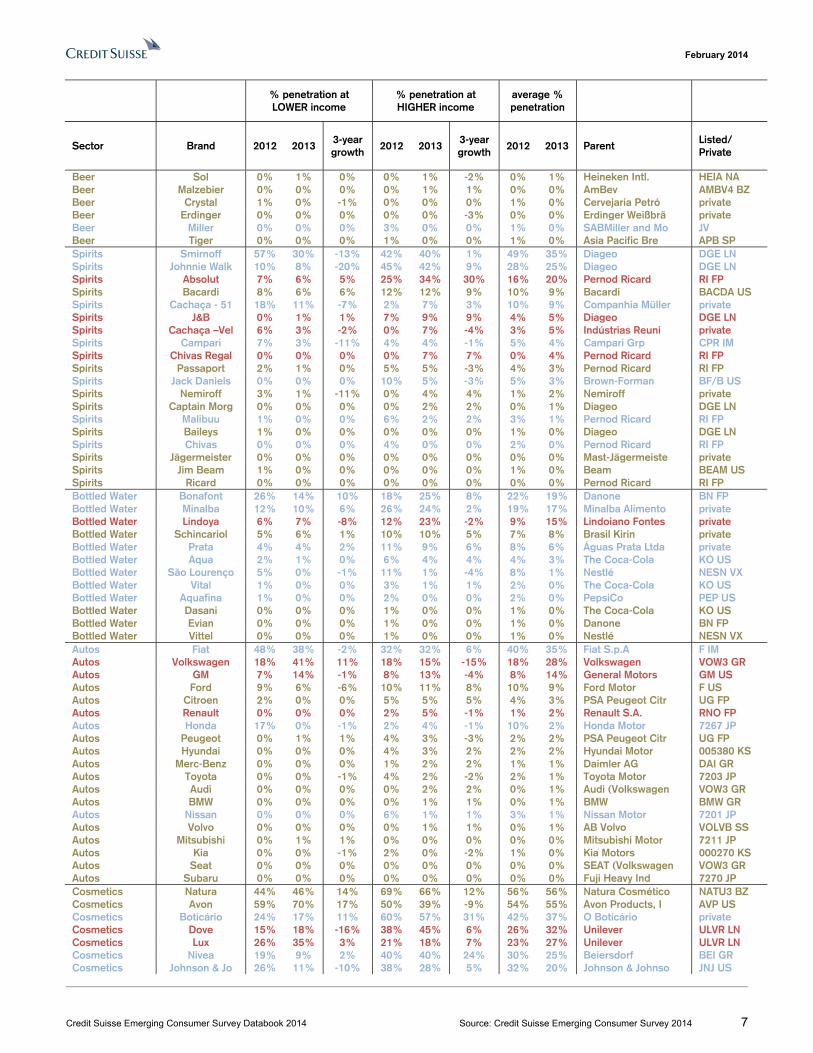

% penetration at LOWER income

% penetration at HIGHER income

average % penetration

Sector Brand 2012 2013 3-year growth

2012 2013 3-year growth

2012 2013 Parent Listed/ Private

Beer Sol 0% 1% 0% 0% 1% -2% 0% 1% Heineken Intl. HEIA NA Beer Malzebier 0% 0% 0% 0% 1% 1% 0% 0% AmBev AMBV4 BZ Beer Crystal 1% 0% -1% 0% 0% 0% 1% 0% Cervejaria Petró private Beer Erdinger 0% 0% 0% 0% 0% -3% 0% 0% Erdinger Weißbrä private Beer Miller 0% 0% 0% 3% 0% 0% 1% 0% SABMiller and Mo JV Beer Tiger 0% 0% 0% 1% 0% 0% 1% 0% Asia Pacific Bre APB SP Spirits Smirnoff 57% 30% -13% 42% 40% 1% 49% 35% Diageo DGE LN Spirits Johnnie Walk 10% 8% -20% 45% 42% 9% 28% 25% Diageo DGE LN Spirits Absolut 7% 6% 5% 25% 34% 30% 16% 20% Pernod Ricard RI FP Spirits Bacardi 8% 6% 6% 12% 12% 9% 10% 9% Bacardi BACDA US Spirits Cachaça - 51 18% 11% -7% 2% 7% 3% 10% 9% Companhia Müller private Spirits J&B 0% 1% 1% 7% 9% 9% 4% 5% Diageo DGE LN Spirits Cachaça –Vel 6% 3% -2% 0% 7% -4% 3% 5% Indústrias Reuni private Spirits Campari 7% 3% -11% 4% 4% -1% 5% 4% Campari Grp CPR IM Spirits Chivas Regal 0% 0% 0% 0% 7% 7% 0% 4% Pernod Ricard RI FP Spirits Passaport 2% 1% 0% 5% 5% -3% 4% 3% Pernod Ricard RI FP Spirits Jack Daniels 0% 0% 0% 10% 5% -3% 5% 3% Brown-Forman BF/B US Spirits Nemiroff 3% 1% -11% 0% 4% 4% 1% 2% Nemiroff private Spirits Captain Morg 0% 0% 0% 0% 2% 2% 0% 1% Diageo DGE LN Spirits Malibuu 1% 0% 0% 6% 2% 2% 3% 1% Pernod Ricard RI FP Spirits Baileys 1% 0% 0% 0% 0% 0% 1% 0% Diageo DGE LN Spirits Chivas 0% 0% 0% 4% 0% 0% 2% 0% Pernod Ricard RI FP Spirits Jägermeister 0% 0% 0% 0% 0% 0% 0% 0% Mast-Jägermeiste private Spirits Jim Beam 1% 0% 0% 0% 0% 0% 1% 0% Beam BEAM US Spirits Ricard 0% 0% 0% 0% 0% 0% 0% 0% Pernod Ricard RI FP Bottled Water Bonafont 26% 14% 10% 18% 25% 8% 22% 19% Danone BN FP Bottled Water Minalba 12% 10% 6% 26% 24% 2% 19% 17% Minalba Alimento private Bottled Water Lindoya 6% 7% -8% 12% 23% -2% 9% 15% Lindoiano Fontes private Bottled Water Schincariol 5% 6% 1% 10% 10% 5% 7% 8% Brasil Kirin private Bottled Water Prata 4% 4% 2% 11% 9% 6% 8% 6% Águas Prata Ltda private Bottled Water Aqua 2% 1% 0% 6% 4% 4% 4% 3% The Coca-Cola KO US Bottled Water São Lourenço 5% 0% -1% 11% 1% -4% 8% 1% Nestlé NESN VX Bottled Water Vital 1% 0% 0% 3% 1% 1% 2% 0% The Coca-Cola KO US Bottled Water Aquafina 1% 0% 0% 2% 0% 0% 2% 0% PepsiCo PEP US Bottled Water Dasani 0% 0% 0% 1% 0% 0% 1% 0% The Coca-Cola KO US Bottled Water Evian 0% 0% 0% 1% 0% 0% 1% 0% Danone BN FP Bottled Water Vittel 0% 0% 0% 1% 0% 0% 1% 0% Nestlé NESN VX Autos Fiat 48% 38% -2% 32% 32% 6% 40% 35% Fiat S.p.A F IM Autos Volkswagen 18% 41% 11% 18% 15% -15% 18% 28% Volkswagen VOW3 GR Autos GM 7% 14% -1% 8% 13% -4% 8% 14% General Motors GM US Autos Ford 9% 6% -6% 10% 11% 8% 10% 9% Ford Motor F US Autos Citroen 2% 0% 0% 5% 5% 5% 4% 3% PSA Peugeot Citr UG FP Autos Renault 0% 0% 0% 2% 5% -1% 1% 2% Renault S.A. RNO FP Autos Honda 17% 0% -1% 2% 4% -1% 10% 2% Honda Motor 7267 JP Autos Peugeot 0% 1% 1% 4% 3% -3% 2% 2% PSA Peugeot Citr UG FP Autos Hyundai 0% 0% 0% 4% 3% 2% 2% 2% Hyundai Motor 005380 KS Autos Merc-Benz 0% 0% 0% 1% 2% 2% 1% 1% Daimler AG DAI GR Autos Toyota 0% 0% -1% 4% 2% -2% 2% 1% Toyota Motor 7203 JP Autos Audi 0% 0% 0% 0% 2% 2% 0% 1% Audi (Volkswagen VOW3 GR Autos BMW 0% 0% 0% 0% 1% 1% 0% 1% BMW BMW GR Autos Nissan 0% 0% 0% 6% 1% 1% 3% 1% Nissan Motor 7201 JP Autos Volvo 0% 0% 0% 0% 1% 1% 0% 1% AB Volvo VOLVB SS Autos Mitsubishi 0% 1% 1% 0% 0% 0% 0% 0% Mitsubishi Motor 7211 JP Autos Kia 0% 0% -1% 2% 0% -2% 1% 0% Kia Motors 000270 KS Autos Seat 0% 0% 0% 0% 0% 0% 0% 0% SEAT (Volkswagen VOW3 GR Autos Subaru 0% 0% 0% 0% 0% 0% 0% 0% Fuji Heavy Ind 7270 JP Cosmetics Natura 44% 46% 14% 69% 66% 12% 56% 56% Natura Cosmético NATU3 BZ Cosmetics Avon 59% 70% 17% 50% 39% -9% 54% 55% Avon Products, I AVP US Cosmetics Boticário 24% 17% 11% 60% 57% 31% 42% 37% O Boticário private Cosmetics Dove 15% 18% -16% 38% 45% 6% 26% 32% Unilever ULVR LN Cosmetics Lux 26% 35% 3% 21% 18% 7% 23% 27% Unilever ULVR LN Cosmetics Nivea 19% 9% 2% 40% 40% 24% 30% 25% Beiersdorf BEI GR Cosmetics Johnson & Jo 26% 11% -10% 38% 28% 5% 32% 20% Johnson & Johnso JNJ US

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 8

% penetration at LOWER income

% penetration at HIGHER income

average % penetration

Sector Brand 2012 2013 3-year growth

2012 2013 3-year growth

2012 2013 Parent Listed/ Private

Cosmetics L´Oreal 4% 3% -1% 27% 19% -1% 15% 11% L'Oréal OR FP Cosmetics Chanel 0% 0% 0% 4% 10% 10% 2% 5% Chanel S.A. private Cosmetics Mary Kay 0% 0% 0% 0% 10% 10% 0% 5% Mary Kay, 5698C US Cosmetics Vult 0% 1% 0% 9% 6% 4% 5% 3% Vult Cosmetics private Cosmetics Vita Derm 1% 0% 0% 3% 5% 3% 2% 3% Vita Derm private Cosmetics Biotherm 0% 0% 0% 1% 4% 4% 1% 2% Biotherm (L'Oréa OR FP Cosmetics Lancôme 0% 0% 0% 8% 4% 0% 4% 2% Lancôme Paris private Cosmetics Neutrogena 0% 0% 0% 0% 4% 4% 0% 2% Johnson & Johnso JNJ US Cosmetics Olay 0% 0% 0% 2% 3% 3% 1% 2% Procter & Gamble PG US Cosmetics Ponds 0% 0% 0% 0% 3% 3% 0% 2% Unilever ULVR LN Cosmetics Maybelline 0% 0% 0% 1% 3% 3% 1% 1% L'Oréal OR FP Cosmetics Estée Lauder 0% 0% 0% 1% 2% 2% 1% 1% Estée Lauder Com EL US Cosmetics Marcelo Beau 0% 0% 0% 2% 2% 2% 1% 1% Marcelo Beauty C private Cosmetics Amway 0% 1% 1% 0% 1% 1% 0% 1% Amway (Alticor) private Cosmetics Artistry 0% 0% 0% 0% 1% 1% 0% 0% Access Business private Cosmetics Clinique 0% 0% 0% 5% 1% 1% 2% 0% Clinique Laborat NYSE EL Cosmetics Max Factor 0% 0% 0% 0% 0% 0% 0% 0% Procter & Gamble PG US Cosmetics Clarins 0% 0% 0% 1% 0% 0% 1% 0% Clarins Grp private Cosmetics Covergirl 0% 0% 0% 2% 0% 0% 1% 0% Procter & Gamble PG US Sportswear Adidas 24% 67% 52% 22% 44% 19% 23% 56% Adidas ADS GR Sportswear Nike 28% 32% 22% 38% 56% 21% 33% 44% Nike, NKE US Sportswear Puma 3% 6% 3% 7% 29% 25% 5% 17% Puma SE PUM GR Sportswear Reebok 3% 10% -4% 10% 21% 3% 6% 15% Reebok (Adidas) ADS GR Sportswear Olympikus 13% 12% 3% 23% 18% 5% 18% 15% Vulcabrasǀazalei VULC3 BZ Sportswear Mizuno 2% 6% -4% 2% 24% 13% 2% 15% Mizuno 8022 JP Sportswear Penalty 3% 5% 4% 2% 9% 9% 2% 7% Penalty private Sportswear Fila 4% 5% 4% 3% 8% -11% 3% 6% Fila. private Sportswear Topper 3% 5% 3% 8% 6% 6% 5% 6% Topper (Alpargat private Sportswear Diadora 1% 2% 2% 0% 7% 7% 1% 4% Diadora private Sportswear Umbro 0% 3% 2% 0% 6% 6% 0% 4% Umbro (Iconix) ICON US Sportswear Wilson 0% 1% 1% 0% 6% 6% 0% 3% Wilson Sporting AMEAS FH Sportswear Speedo 0% 1% 1% 0% 5% 5% 0% 3% Speedo Intl. (Pe private Sportswear Le Coq Sport 0% 0% 0% 0% 4% 4% 0% 2% Le Coq Sportif private Sportswear Asics 0% 1% 1% 0% 3% 3% 0% 2% ASICS 7936 JP Sportswear Champion 0% 0% -9% 3% 3% 3% 1% 1% HanesBrands HBI US Sportswear Kappa 0% 0% 0% 3% 1% 1% 1% 1% Kappa private Sportswear K-Swiss 0% 0% 0% 3% 1% 1% 1% 1% K-Swiss, Inc (E- private Sportswear Converse 1% 0% -1% 0% 1% 1% 1% 0% Nike, NKE US Sportswear Fred Perry 0% 0% 0% 2% 0% 0% 1% 0% Fred Perry private Sportswear Timberland 0% 0% -1% 6% 0% -7% 3% 0% Timberland LLC VFC US Handsets Samsung 16% 31% 19% 32% 34% 14% 24% 32% Samsung Electron 005930 KS Handsets Nokia 55% 38% 2% 28% 22% -3% 42% 30% Nokia NOK1V FH Handsets Motorola 10% 16% 0% 11% 10% -27% 11% 13% Motorola, MSI:US Handsets LG 11% 9% -9% 12% 13% 4% 12% 11% LG Electronics 066570 KS Handsets Apple 0% 0% 0% 8% 8% 6% 4% 4% Apple AAPL US Handsets Blackberry 0% 0% 0% 6% 4% 4% 3% 2% BlackBerry BBRY US Handsets Sony Ericsso 2% 1% -9% 1% 3% -1% 2% 2% Sony Mobile Com 6758 JP Handsets Alcatel 0% 2% 2% 1% 1% 1% 1% 1% Alcatel-Lucent ALU FP Handsets Huawei 0% 0% 0% 0% 2% 2% 0% 1% Huawei Tech private Handsets Google 0% 0% 0% 0% 1% 1% 0% 1% Google GOOG US Handsets Philips 0% 0% 0% 0% 0% 0% 0% 0% Koninklijke Phil PHIA NA Handsets Sharp 0% 0% 0% 1% 0% 0% 1% 0% Sharp 6753 JP Handsets Siemens 1% 0% 0% 0% 0% 0% 0% 0% Siemens AG SIE GR Handsets NEC 0% 0% 0% 0% 0% 0% 0% 0% NEC 6701 JP Handsets Panasonic 0% 0% 0% 0% 0% 0% 0% 0% Panasonic 6752 JP TV Samsung 63% 28% -10% 35% 51% -13% 49% 39% Samsung Electron 005930 KS TV Panasonic 2% 35% 34% 0% 5% 5% 1% 20% Panasonic 6752 JP TV LG 11% 11% 0% 18% 11% 0% 14% 11% LG Electronics 066570 KS TV Sony 8% 2% -14% 23% 17% 6% 16% 10% Sony 6758 JP TV Philips 2% 7% -4% 0% 0% 0% 1% 4% Koninklijke Phil PHIA NA TV Toshiba 4% 6% 0% 0% 0% 0% 2% 3% Toshiba 6502 JP TV Sanyo 1% 1% -1% 0% 0% 0% 1% 1% SANYO Electric 6764 JP TV Sharp 1% 1% -1% 6% 0% 0% 3% 1% Sharp 6753 JP

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 9

% penetration at LOWER income

% penetration at HIGHER income

average % penetration

Sector Brand 2012 2013 3-year growth

2012 2013 3-year growth

2012 2013 Parent Listed/ Private

TV Mitsubishi 1% 0% -2% 0% 0% 0% 1% 0% Mitsubishi Elect 6503 JP Computers Samsung 45% 20% -33% 50% 30% 30% 47% 25% Samsung Electron 005930 KS Computers Apple 2% 6% 5% 6% 22% -5% 4% 14% Apple AAPL US Computers Positivo 11% 15% 15% 0% 4% 4% 5% 10% Positivo Informá POSI3 BZ Computers HP 2% 3% 1% 11% 10% 10% 7% 6% HP HPQ US Computers Sony 0% 2% -1% 0% 6% 6% 0% 4% Sony 6758 JP Computers LG 0% 1% 1% 0% 7% 7% 0% 4% LG Electronics 066570 KS Computers Acer 13% 5% 4% 0% 0% 0% 7% 3% Acer 2353 TT Computers ASUS 0% 3% 3% 0% 2% 2% 0% 2% Asus 2357 TT Computers Philips 2% 1% -5% 0% 3% -8% 1% 2% Koninklijke Phil PHIA NA Computers DELL 5% 1% -1% 0% 2% -9% 2% 2% Dell private Computers Toshiba 1% 1% -2% 0% 2% 2% 1% 2% Toshiba 6502 JP Computers Motorola 0% 0% 0% 0% 2% 2% 0% 1% Motorola, MSI:US Computers Sharp 0% 1% 0% 0% 0% 0% 0% 0% Sharp 6753 JP Computers Compaq 1% 0% 0% 0% 0% 0% 1% 0% HP HPQ US Computers Itautec 1% 0% 0% 6% 0% 0% 3% 0% Itautec ITEC3 BZ Computers Semp Toshiba 1% 0% 0% 0% 0% 0% 1% 0% Toshiba 6502 JP Fashion C & A Marisa 48% 54% 17% 36% 30% 8% 42% 42% C&A private Fashion Renner 12% 27% 7% 29% 34% 13% 20% 31% Lojas Renner S.A LREN3 BZ Fashion Lacoste 2% 13% 13% 6% 25% 20% 4% 19% Lacoste private Fashion Calvin Klein 1% 3% 3% 10% 18% 10% 5% 11% Phillips-Van Heu PVH US Fashion Hering 7% 5% 4% 24% 13% 2% 16% 9% CIA HERING HGTX3 BZ Fashion Levi's 0% 2% 2% 0% 16% 16% 0% 9% Levi Strauss & private Fashion Forum 1% 1% 0% 10% 17% 3% 5% 9% Colcci private Fashion TNG 4% 3% 3% 16% 15% -3% 10% 9% TNG Comércio de private Fashion ZARA 0% 1% 0% 5% 15% 12% 3% 8% Industria de Dis ITX SM Fashion Louis Vuitto 0% 0% 0% 5% 15% 15% 3% 8% LVMH MC FP Fashion Dolce & Gabb 1% 2% -1% 10% 12% 7% 6% 7% Dolce & Gabbana private Fashion Hugo Boss 1% 3% 3% 8% 10% 6% 4% 7% Hugo Boss AG BOSS GR Fashion Armani 0% 0% 0% 2% 13% 11% 1% 7% Giorgio Armani S private Fashion Gucci 0% 1% 1% 9% 12% 12% 5% 7% Gucci Grp GUCG US Fashion Polo Ralph L 0% 1% -6% 10% 11% 7% 5% 6% Ralph Lauren RL US Fashion Guess 0% 1% 0% 2% 11% 11% 1% 6% Guess GES US Fashion Tommy Hilfig 0% 0% 0% 3% 11% 11% 2% 6% Phillips-Van Heu PVH US Fashion Pierre Cardi 0% 2% -2% 8% 8% 4% 4% 5% Société de Gesti private Fashion Christian Di 1% 0% 0% 2% 7% 2% 2% 4% LVMH MC FP Fashion Carmim 0% 0% 0% 2% 7% 2% 1% 4% Carmim private Fashion Dunhill 0% 1% 1% 0% 6% 6% 0% 3% BAT BATS LN Fashion Kenzo 0% 2% 2% 5% 4% 4% 3% 3% LVMH MC FP Fashion Prada 0% 0% -3% 7% 4% 4% 3% 2% Prada S.p.A. 1913 HK Fashion Hermes 8% 1% 0% 2% 2% 2% 5% 2% Hermès Intl. S.A RMS FP Fashion Givenchy 0% 0% 0% 2% 3% 3% 1% 1% LVMH MC FP Fashion Goldlion 0% 0% 0% 0% 2% 2% 0% 1% Goldlion Holding 533 HK Fashion H&M 0% 1% 0% 0% 1% 1% 0% 1% H & M Hennes & M HMB SS Fashion Mango 0% 0% 0% 3% 1% 1% 2% 1% Punto Fa, S.L. private Fashion Escada 0% 0% 0% 0% 1% 1% 0% 1% Escada ESC GR Fashion Iódice 0% 0% 0% 4% 1% 1% 2% 1% Valdermar Iodice private Fashion Osmoze 1% 0% 0% 0% 1% -2% 0% 1% Osmoze Grp private Fashion Y.S.L. 0% 0% 0% 0% 1% 1% 0% 0% Yves Saint Laure private Fashion Burberry 0% 0% 0% 0% 0% 0% 0% 0% Burberry Grp BRBY LN Fashion Levi’s 1% 0% 0% 15% 0% 0% 8% 0% Levi Strauss & private Fashion Valentino 1% 0% 0% 4% 0% 0% 2% 0% Valentino SpA VLNT IM Fashion Versace 0% 0% 0% 6% 0% 0% 3% 0% Gianni Versace S GIAN IM

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 10

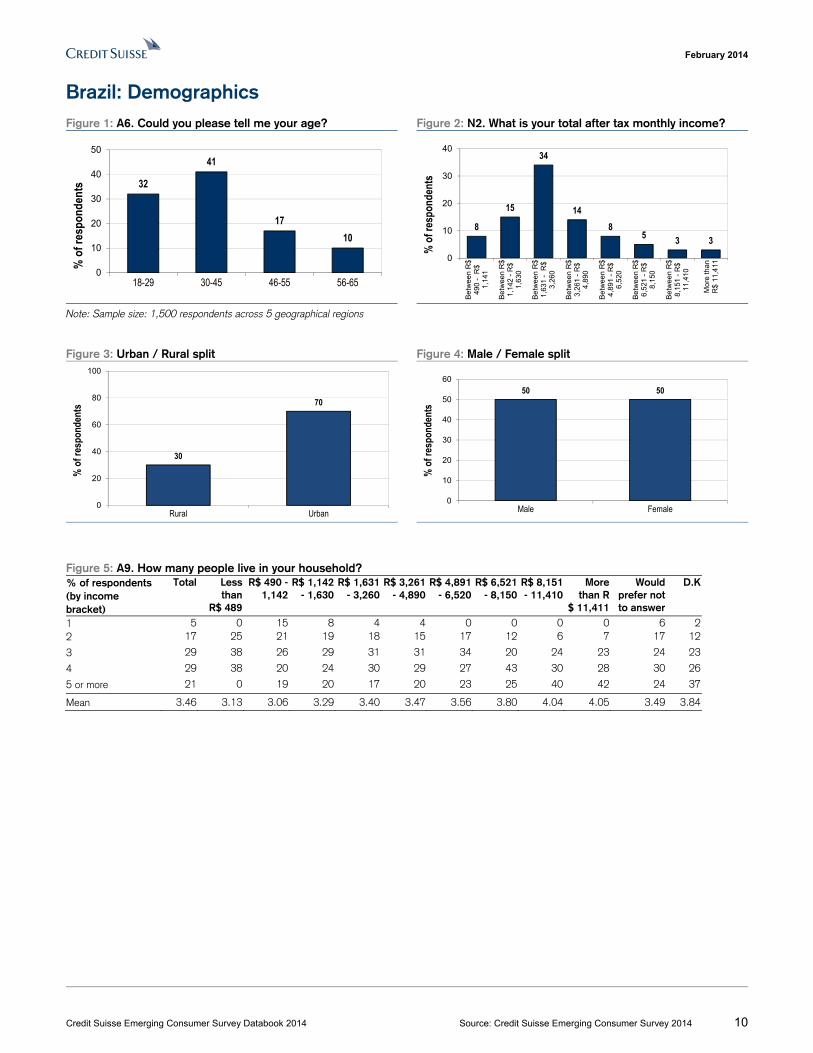

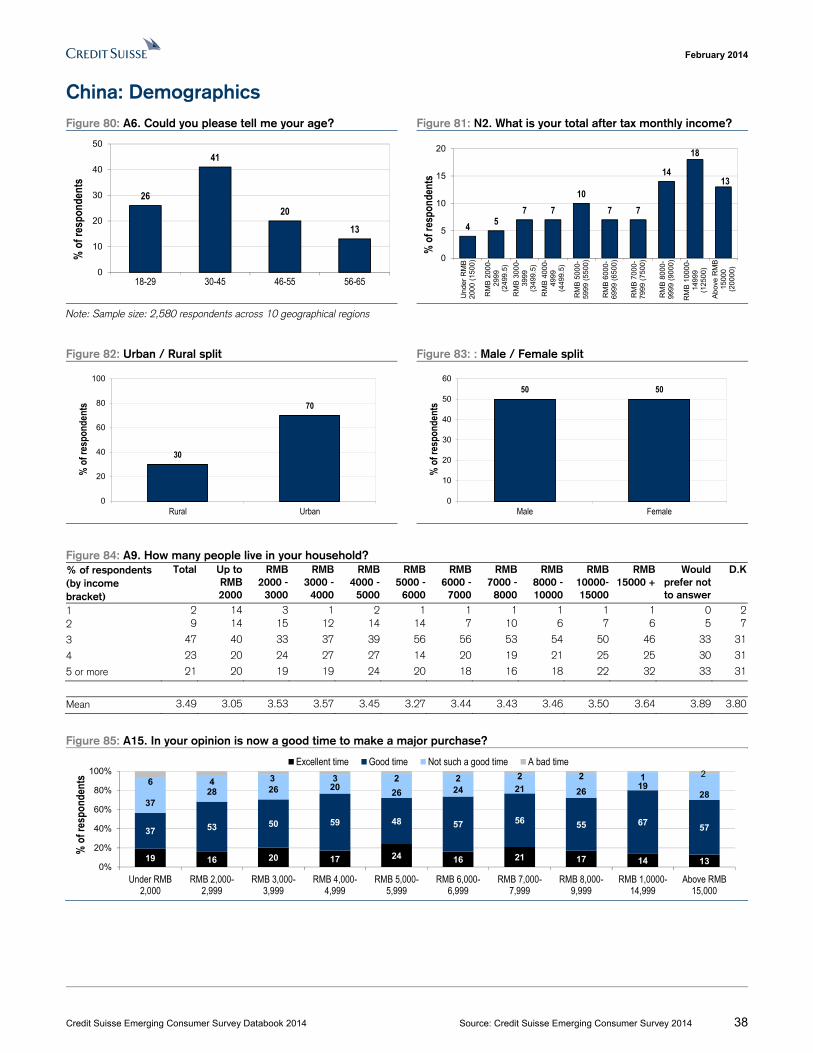

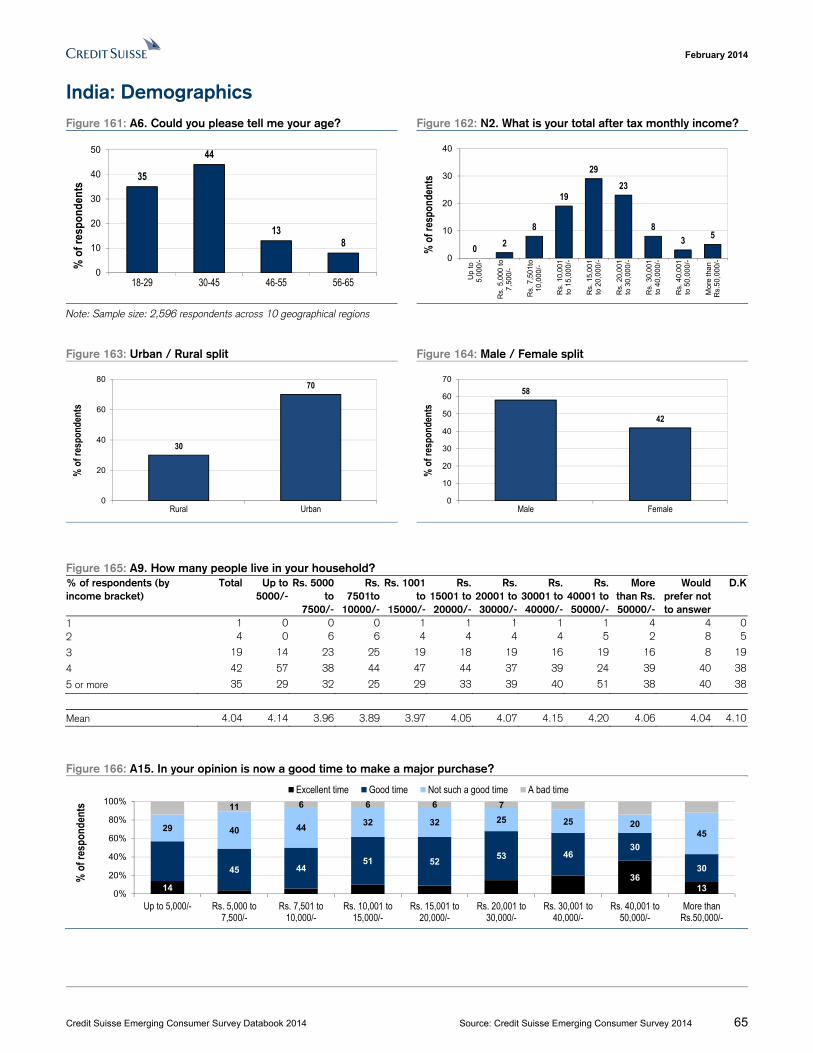

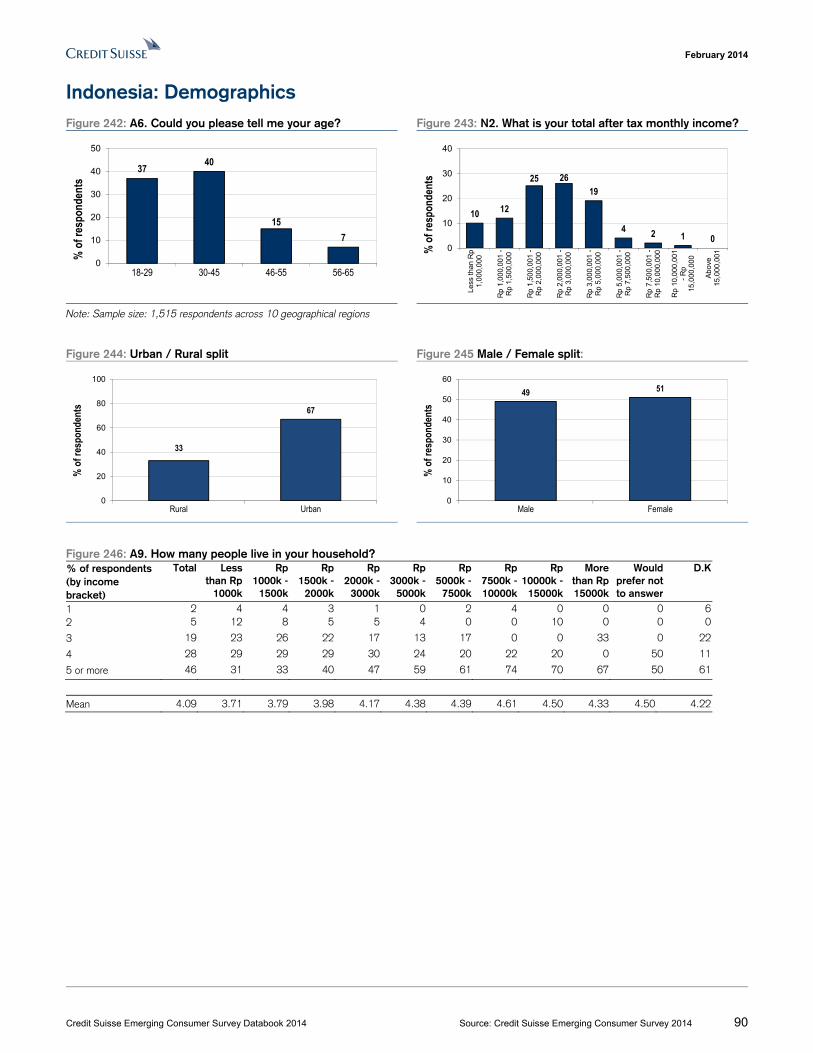

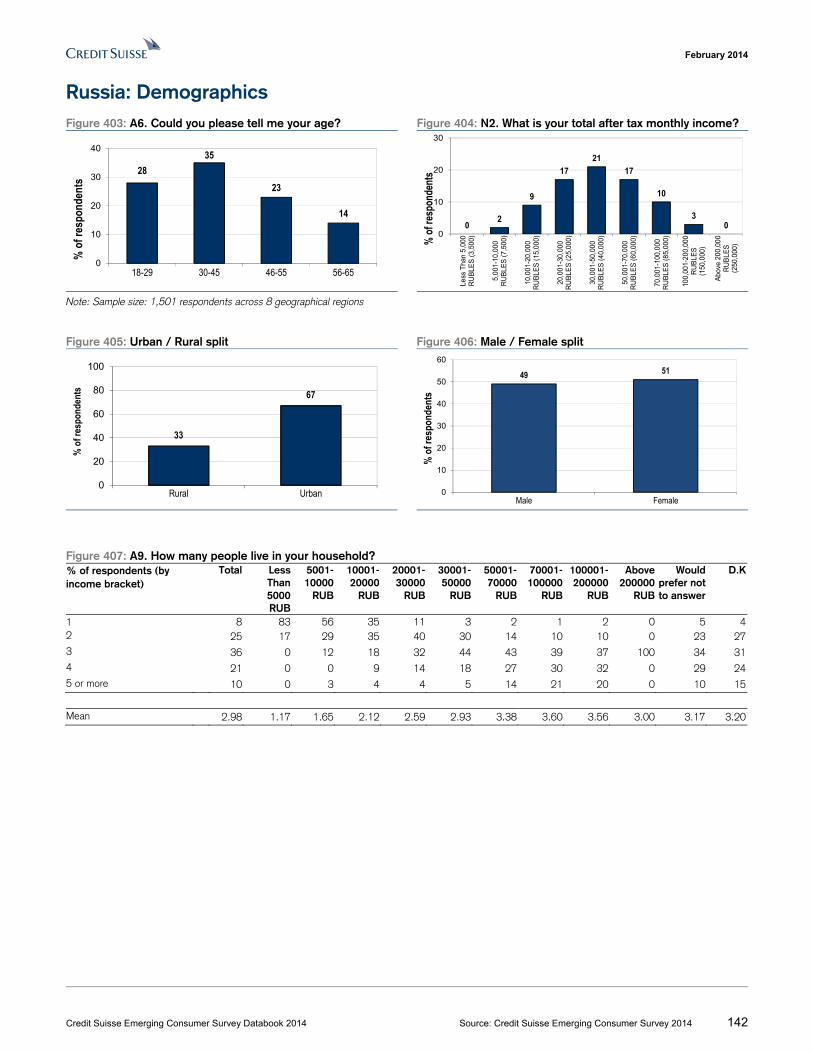

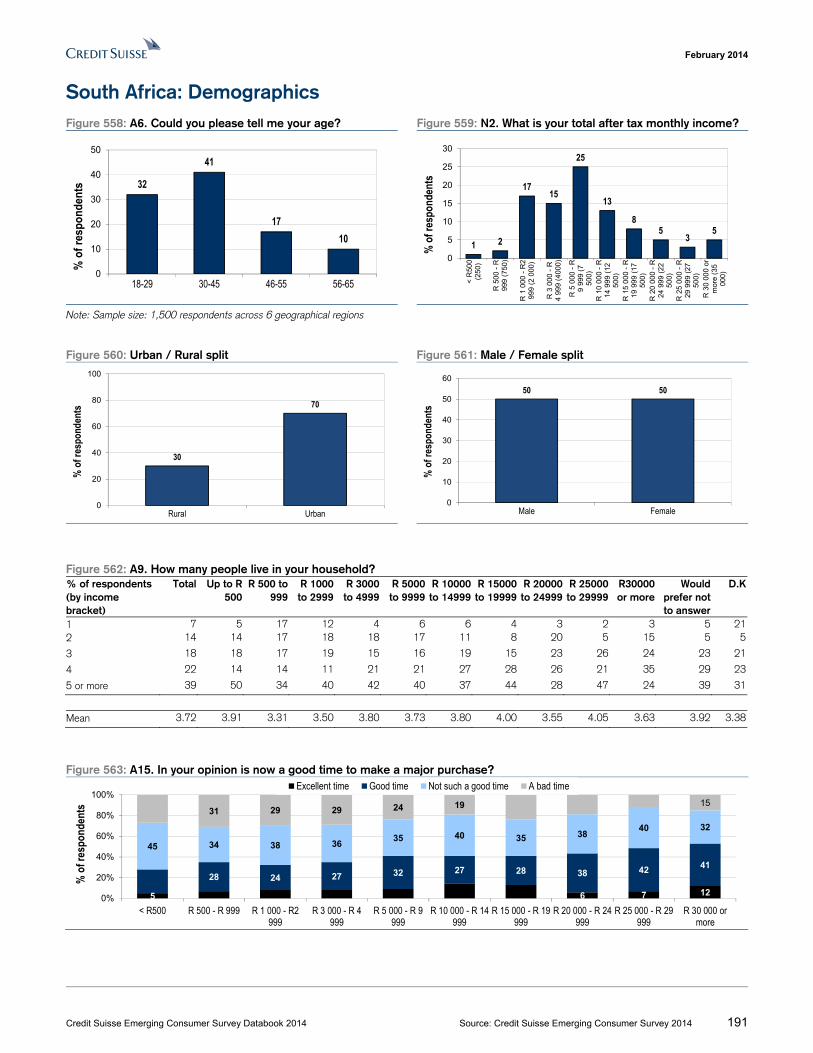

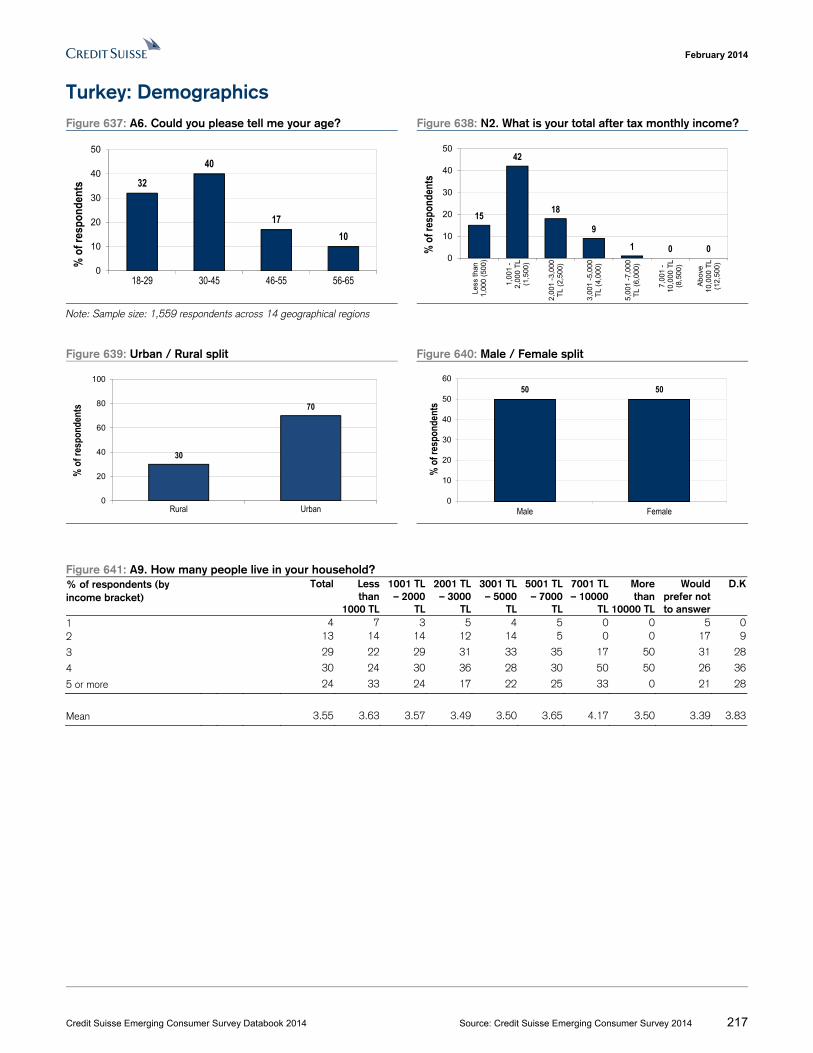

Brazil: Demographics Figure 1: A6. Could you please tell me your age? Figure 2: N2. What is your total after tax monthly income?

Note: Sample size: 1,500 respondents across 5 geographical regions

Figure 3: Urban / Rural split Figure 4: Male / Female split

Figure 5: A9. How many people live in your household? % of respondents (by income bracket)

Total Less than

R$ 489

R$ 490 - 1,142

R$ 1,142 - 1,630

R$ 1,631 - 3,260

R$ 3,261 - 4,890

R$ 4,891 - 6,520

R$ 6,521 - 8,150

R$ 8,151 - 11,410

More than R

$ 11,411

Would prefer not to answer

D.K

1 5 0 15 8 4 4 0 0 0 0 6 22 17 25 21 19 18 15 17 12 6 7 17 12

3 29 38 26 29 31 31 34 20 24 23 24 23

4 29 38 20 24 30 29 27 43 30 28 30 26

5 or more 21 0 19 20 17 20 23 25 40 42 24 37

Mean 3.46 3.13 3.06 3.29 3.40 3.47 3.56 3.80 4.04 4.05 3.49 3.84

32

41

1710

0

10

20

30

40

50

18-29 30-45 46-55 56-65

% o

f res

pond

ents

8

15

34

148

5 3 3

0

10

20

30

40

Be

twee

n R

$49

0 -

R$

1,14

1

Be

twee

n R

$1,

142

- R

$1,

630

Be

twee

n R

$1,

631

- R

$3,

260

Be

twee

n R

$3,

261

- R

$4,

890

Be

twee

n R

$4,

891

- R

$6,

520

Be

twee

n R

$6,

521

- R

$8,

150

Be

twee

n R

$8,

151

- R

$11

,410

Mor

e th

anR

$ 11

,411

% o

f res

pond

ents

30

70

0

20

40

60

80

100

Rural Urban

% o

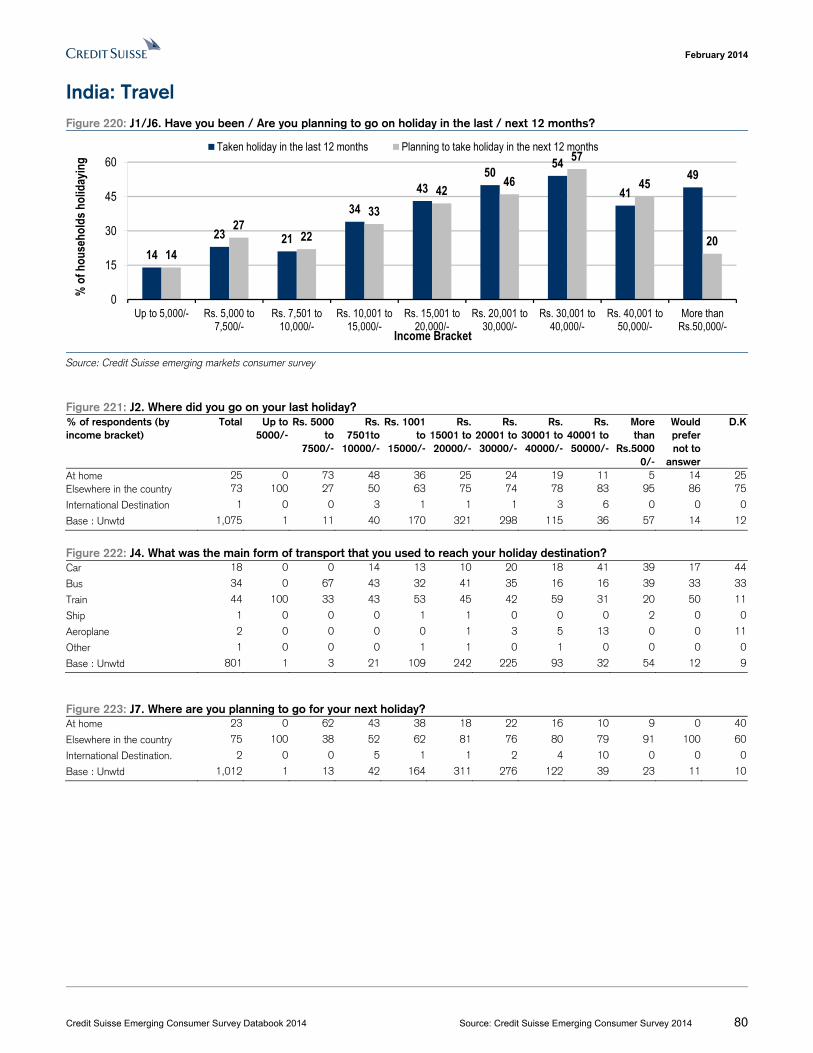

f res

pond

ents

50 50

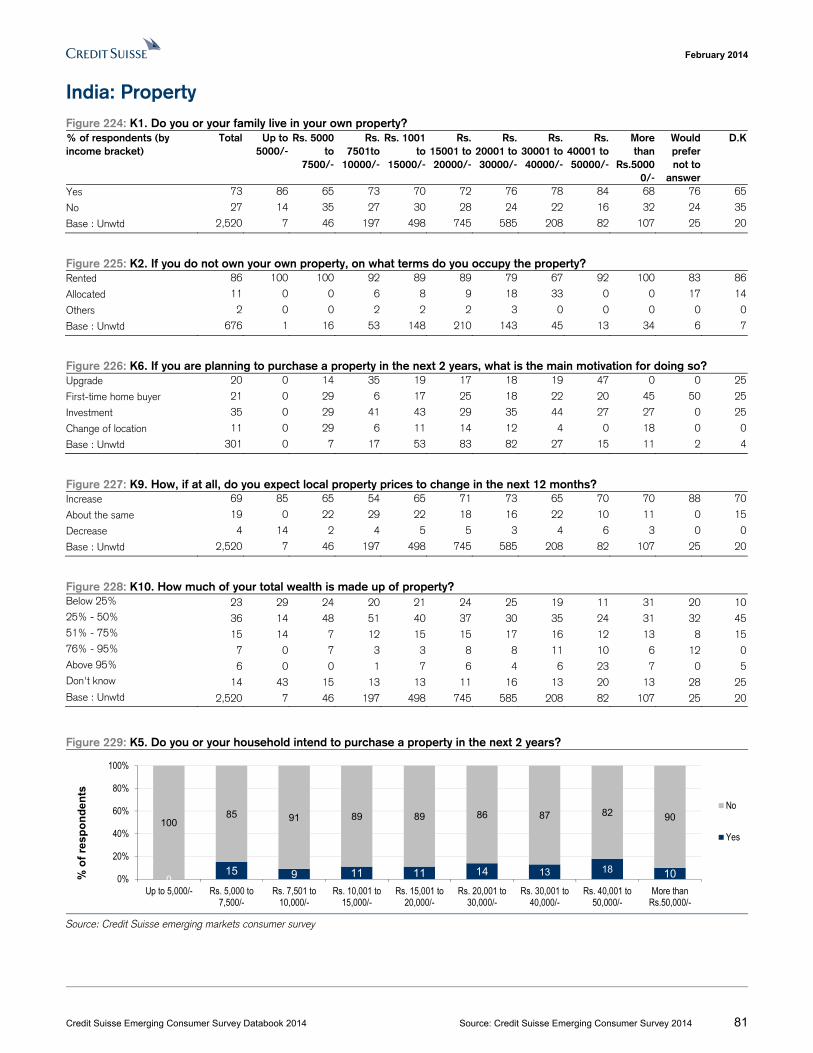

0

10

20

30

40

50

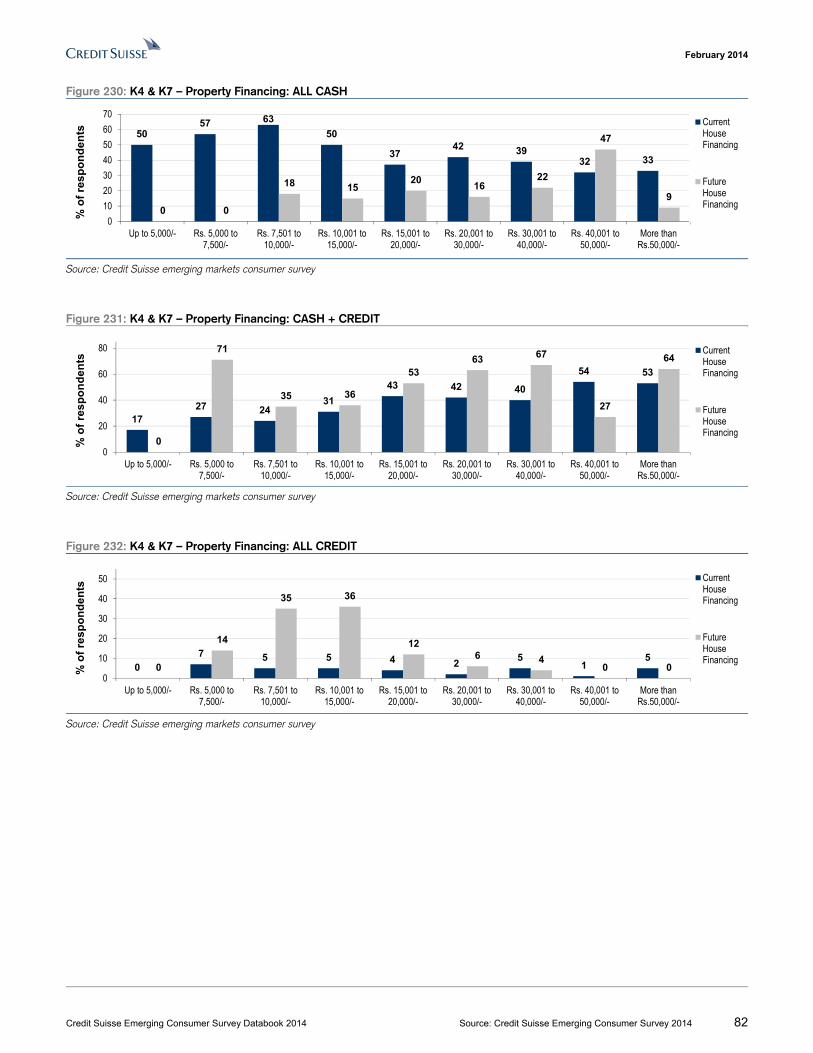

60

Male Female

% o

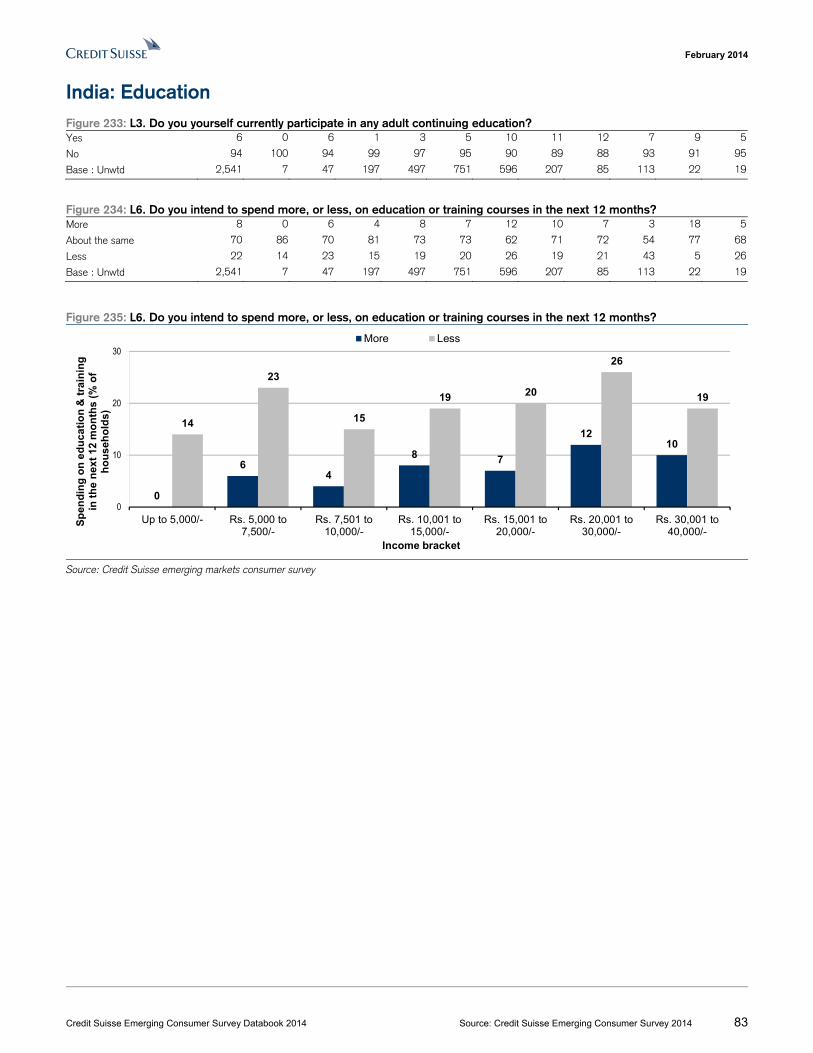

f res

pond

ents

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 11

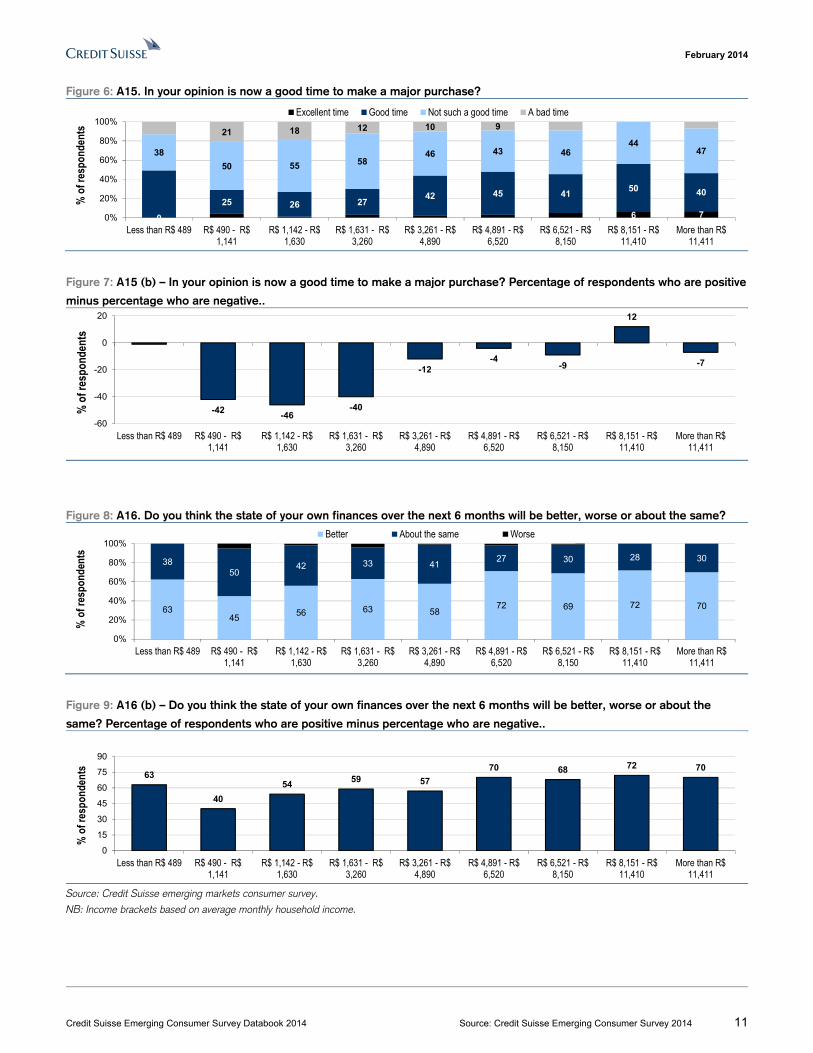

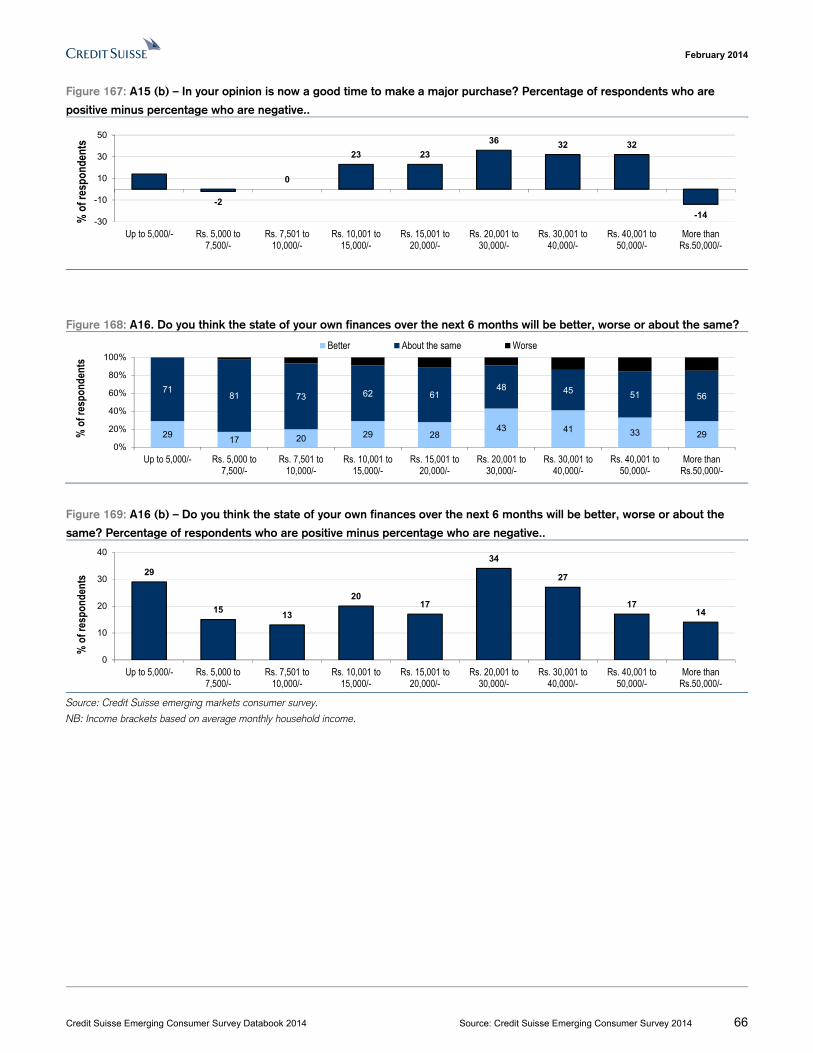

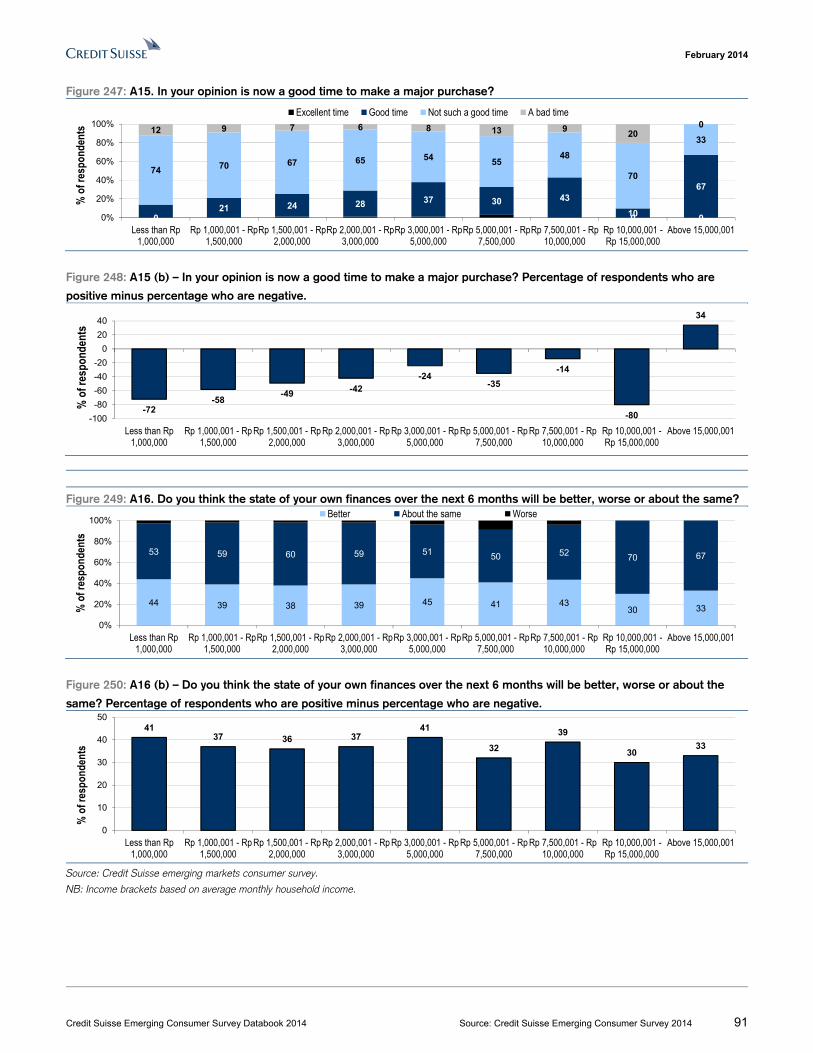

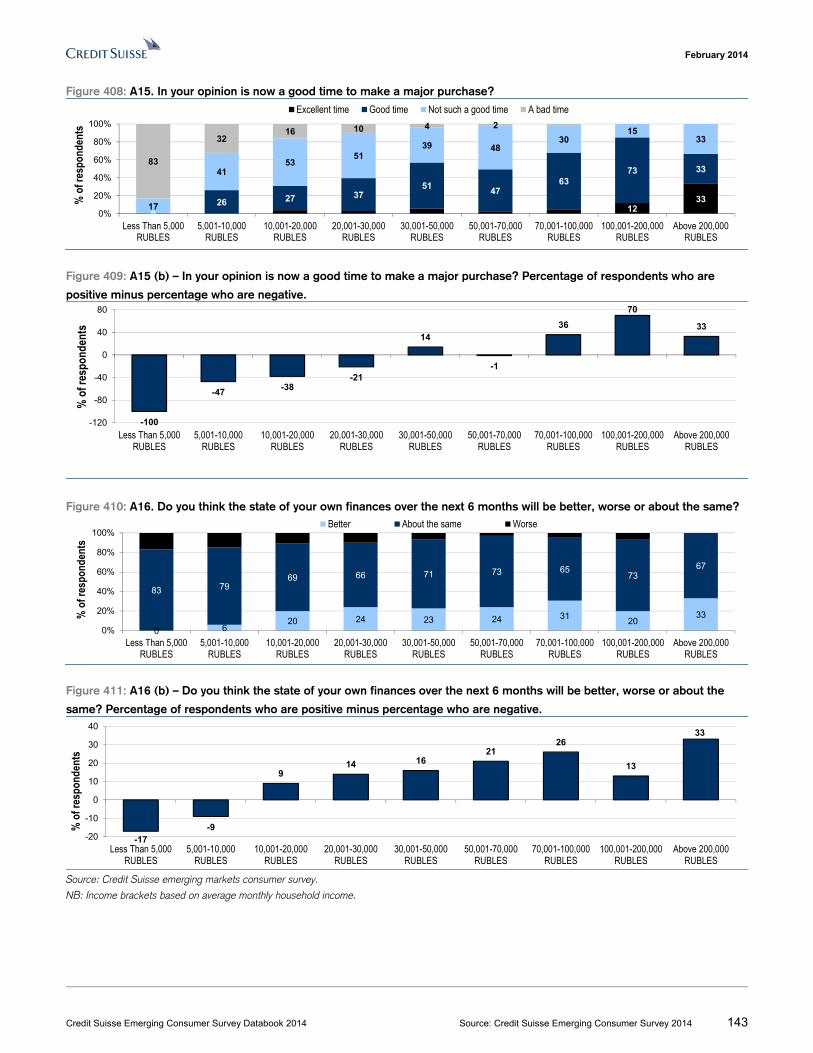

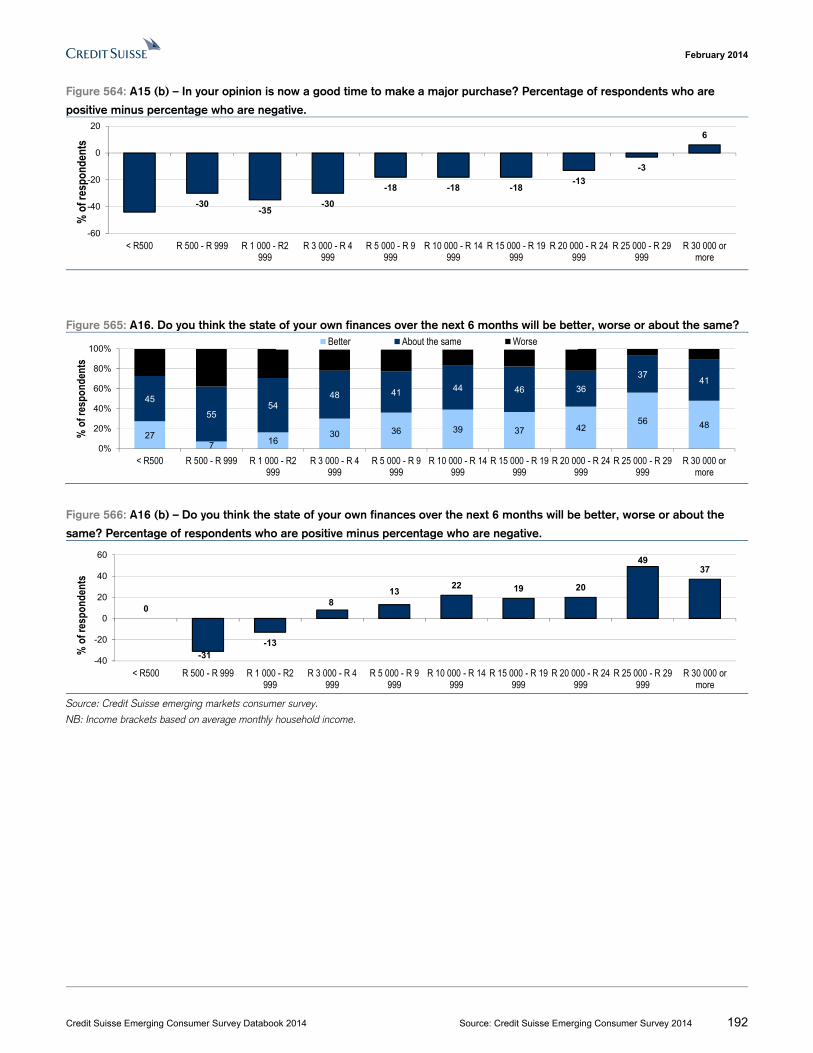

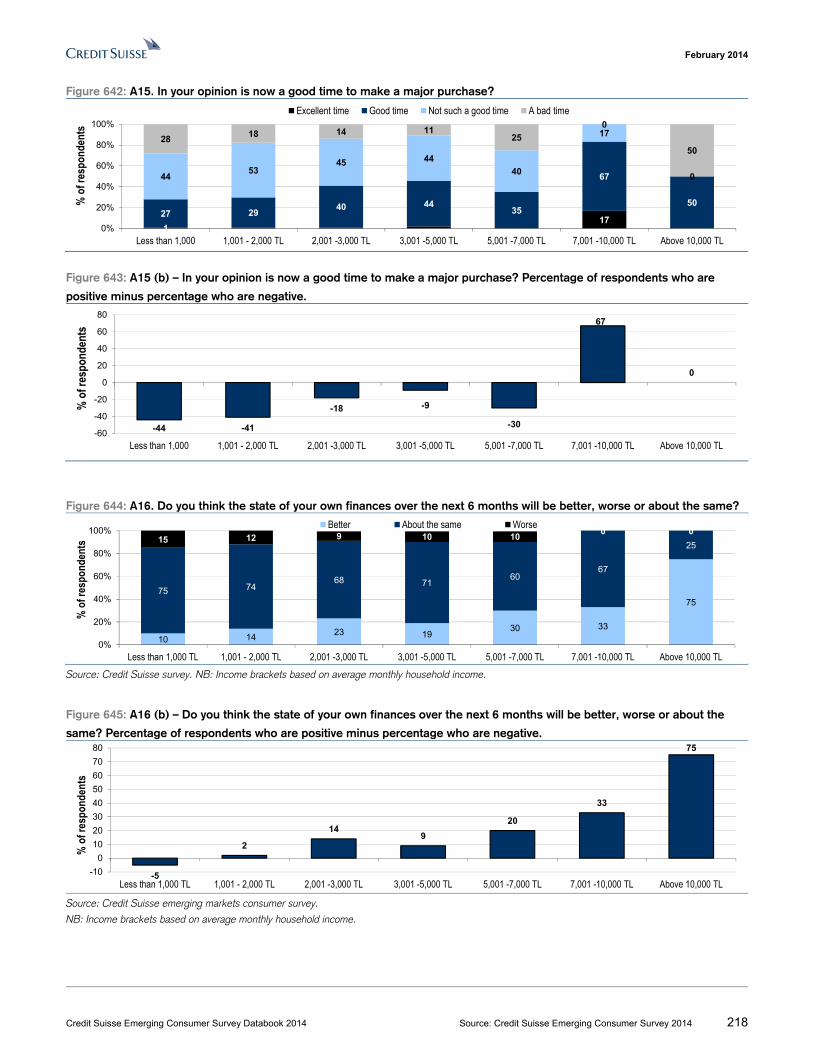

Figure 6: A15. In your opinion is now a good time to make a major purchase?

Figure 7: A15 (b) – In your opinion is now a good time to make a major purchase? Percentage of respondents who are positive

minus percentage who are negative..

Figure 8: A16. Do you think the state of your own finances over the next 6 months will be better, worse or about the same?

Figure 9: A16 (b) – Do you think the state of your own finances over the next 6 months will be better, worse or about the

same? Percentage of respondents who are positive minus percentage who are negative..

Source: Credit Suisse emerging markets consumer survey.

NB: Income brackets based on average monthly household income.

0 6 725 26 27

42 45 4150 40

38

50 55 5846 43 46

4447

21 18 12 10 9

0%

20%

40%

60%

80%

100%

Less than R$ 489 R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

R$ 8,151 - R$11,410

More than R$11,411

% o

f res

pond

ents

Excellent time Good time Not such a good time A bad time

-42-46

-40

-12-4

-9

12

-7

-60

-40

-20

0

20

Less than R$ 489 R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

R$ 8,151 - R$11,410

More than R$11,411

% o

f res

pond

ents

6345

56 63 5872 69 72 70

3850

42 33 4127 30 28 30

0%

20%

40%

60%

80%

100%

Less than R$ 489 R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

R$ 8,151 - R$11,410

More than R$11,411

% o

f res

pond

ents

Better About the same Worse

63

40

5459 57

70 68 72 70

0

15

30

45

60

75

90

Less than R$ 489 R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

R$ 8,151 - R$11,410

More than R$11,411

% o

f res

pond

ents

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 12

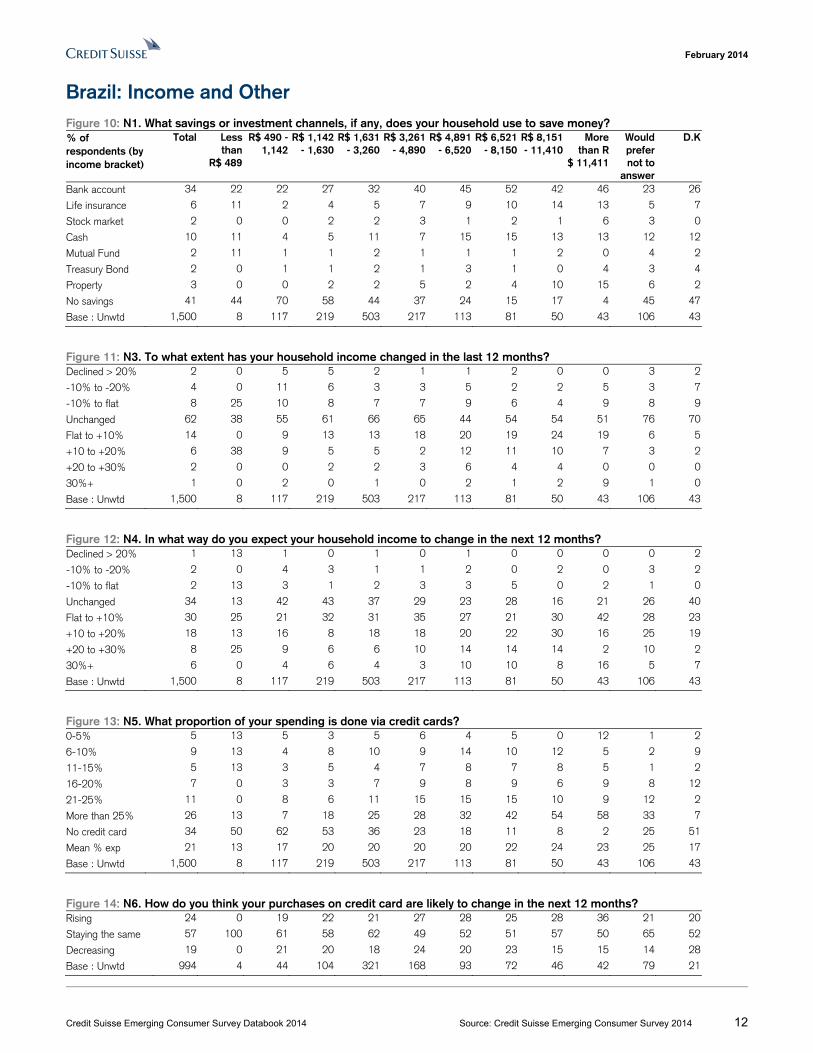

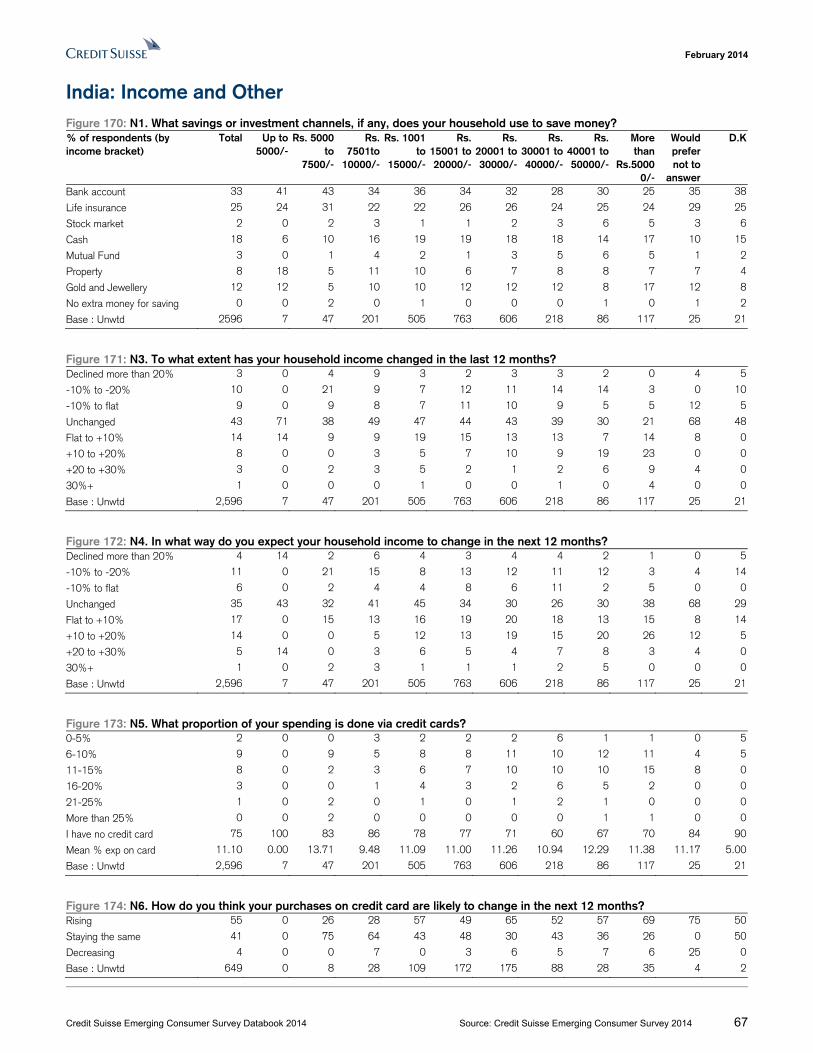

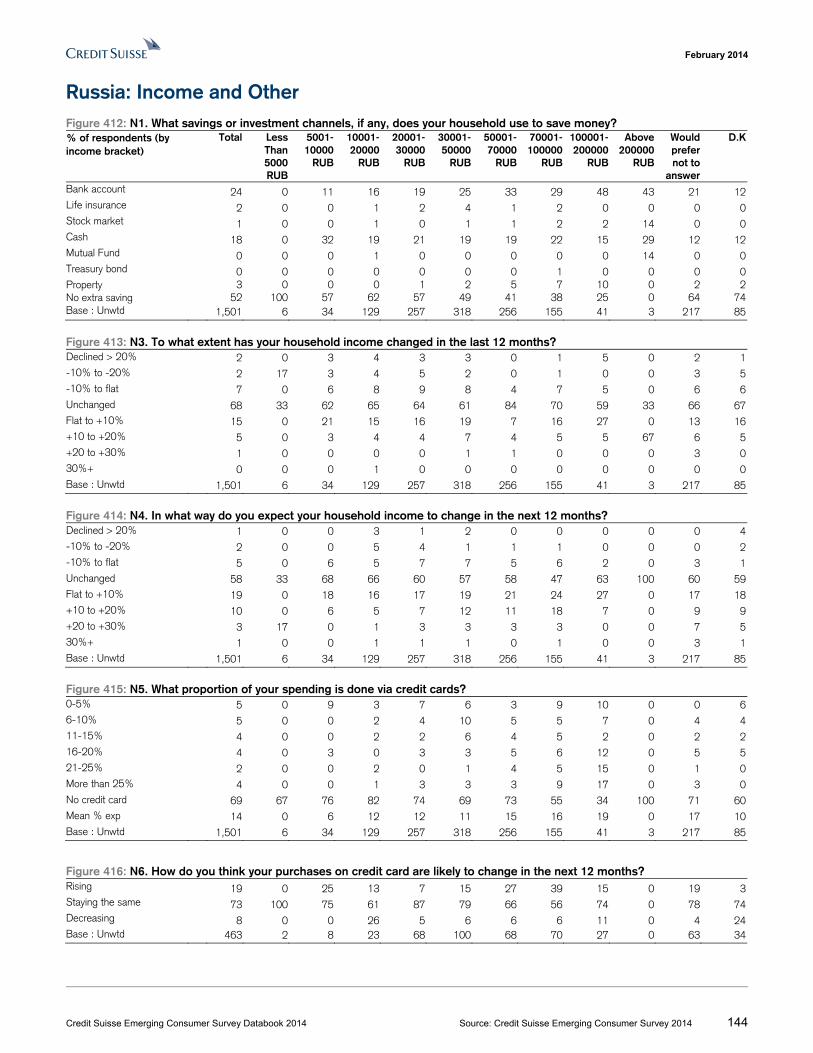

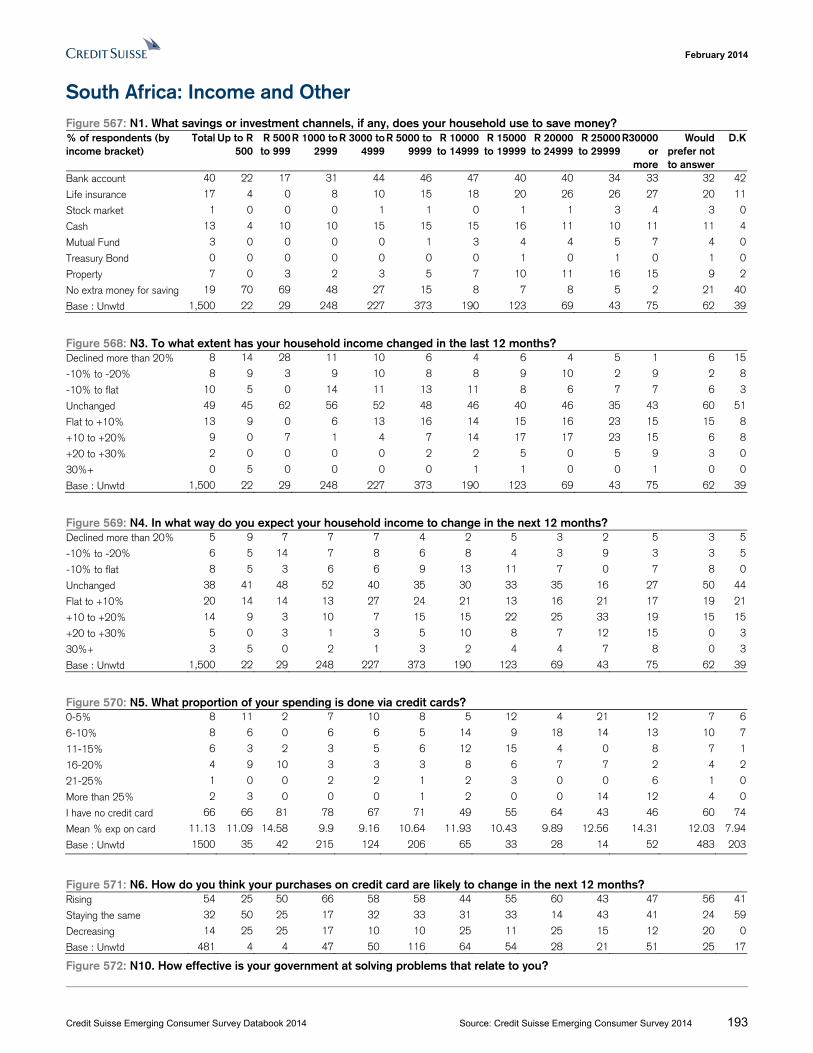

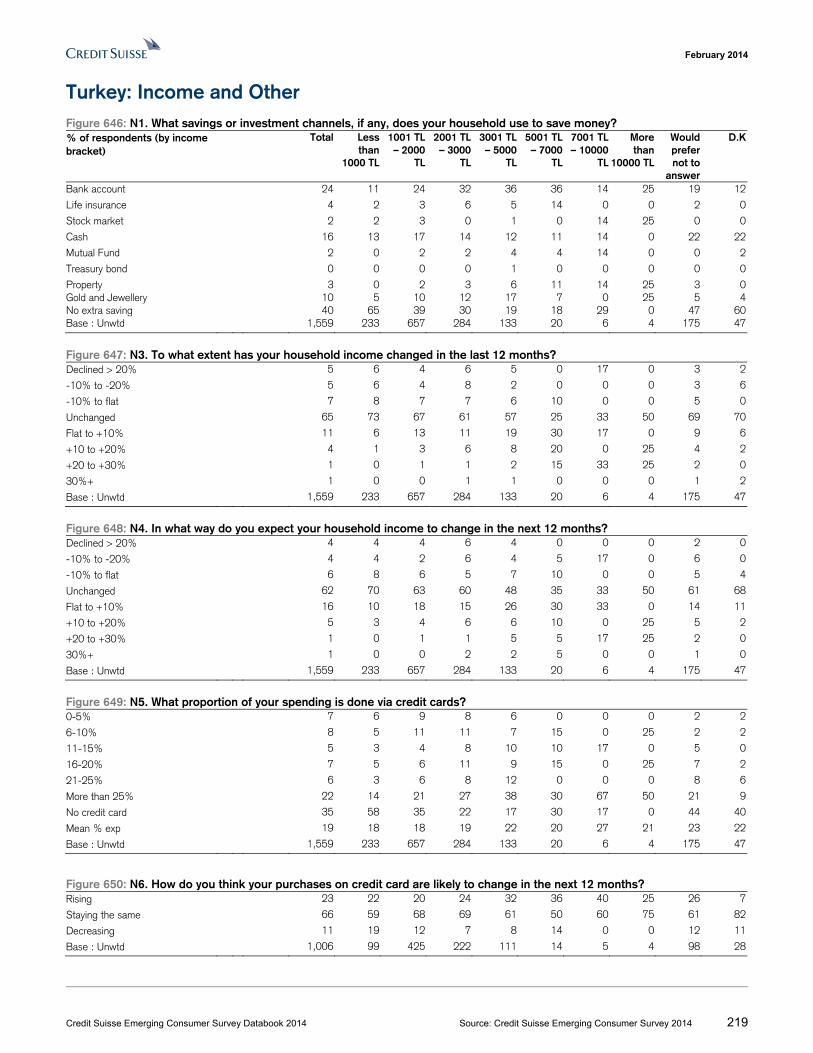

Brazil: Income and Other Figure 10: N1. What savings or investment channels, if any, does your household use to save money? % of respondents (by income bracket)

Total Less than

R$ 489

R$ 490 - 1,142

R$ 1,142 - 1,630

R$ 1,631 - 3,260

R$ 3,261 - 4,890

R$ 4,891 - 6,520

R$ 6,521 - 8,150

R$ 8,151 - 11,410

More than R

$ 11,411

Would prefer not to

answer

D.K

Bank account 34 22 22 27 32 40 45 52 42 46 23 26

Life insurance 6 11 2 4 5 7 9 10 14 13 5 7

Stock market 2 0 0 2 2 3 1 2 1 6 3 0

Cash 10 11 4 5 11 7 15 15 13 13 12 12

Mutual Fund 2 11 1 1 2 1 1 1 2 0 4 2

Treasury Bond 2 0 1 1 2 1 3 1 0 4 3 4

Property 3 0 0 2 2 5 2 4 10 15 6 2

No savings 41 44 70 58 44 37 24 15 17 4 45 47

Base : Unwtd 1,500 8 117 219 503 217 113 81 50 43 106 43

Figure 11: N3. To what extent has your household income changed in the last 12 months? Declined > 20% 2 0 5 5 2 1 1 2 0 0 3 2

-10% to -20% 4 0 11 6 3 3 5 2 2 5 3 7

-10% to flat 8 25 10 8 7 7 9 6 4 9 8 9

Unchanged 62 38 55 61 66 65 44 54 54 51 76 70

Flat to +10% 14 0 9 13 13 18 20 19 24 19 6 5

+10 to +20% 6 38 9 5 5 2 12 11 10 7 3 2

+20 to +30% 2 0 0 2 2 3 6 4 4 0 0 0

30%+ 1 0 2 0 1 0 2 1 2 9 1 0

Base : Unwtd 1,500 8 117 219 503 217 113 81 50 43 106 43

Figure 12: N4. In what way do you expect your household income to change in the next 12 months? Declined > 20% 1 13 1 0 1 0 1 0 0 0 0 2

-10% to -20% 2 0 4 3 1 1 2 0 2 0 3 2

-10% to flat 2 13 3 1 2 3 3 5 0 2 1 0

Unchanged 34 13 42 43 37 29 23 28 16 21 26 40

Flat to +10% 30 25 21 32 31 35 27 21 30 42 28 23

+10 to +20% 18 13 16 8 18 18 20 22 30 16 25 19

+20 to +30% 8 25 9 6 6 10 14 14 14 2 10 2

30%+ 6 0 4 6 4 3 10 10 8 16 5 7

Base : Unwtd 1,500 8 117 219 503 217 113 81 50 43 106 43

Figure 13: N5. What proportion of your spending is done via credit cards? 0-5% 5 13 5 3 5 6 4 5 0 12 1 2

6-10% 9 13 4 8 10 9 14 10 12 5 2 9

11-15% 5 13 3 5 4 7 8 7 8 5 1 2

16-20% 7 0 3 3 7 9 8 9 6 9 8 12

21-25% 11 0 8 6 11 15 15 15 10 9 12 2

More than 25% 26 13 7 18 25 28 32 42 54 58 33 7

No credit card 34 50 62 53 36 23 18 11 8 2 25 51

Mean % exp 21 13 17 20 20 20 20 22 24 23 25 17

Base : Unwtd 1,500 8 117 219 503 217 113 81 50 43 106 43

Figure 14: N6. How do you think your purchases on credit card are likely to change in the next 12 months? Rising 24 0 19 22 21 27 28 25 28 36 21 20

Staying the same 57 100 61 58 62 49 52 51 57 50 65 52

Decreasing 19 0 21 20 18 24 20 23 15 15 14 28

Base : Unwtd 994 4 44 104 321 168 93 72 46 42 79 21

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 13

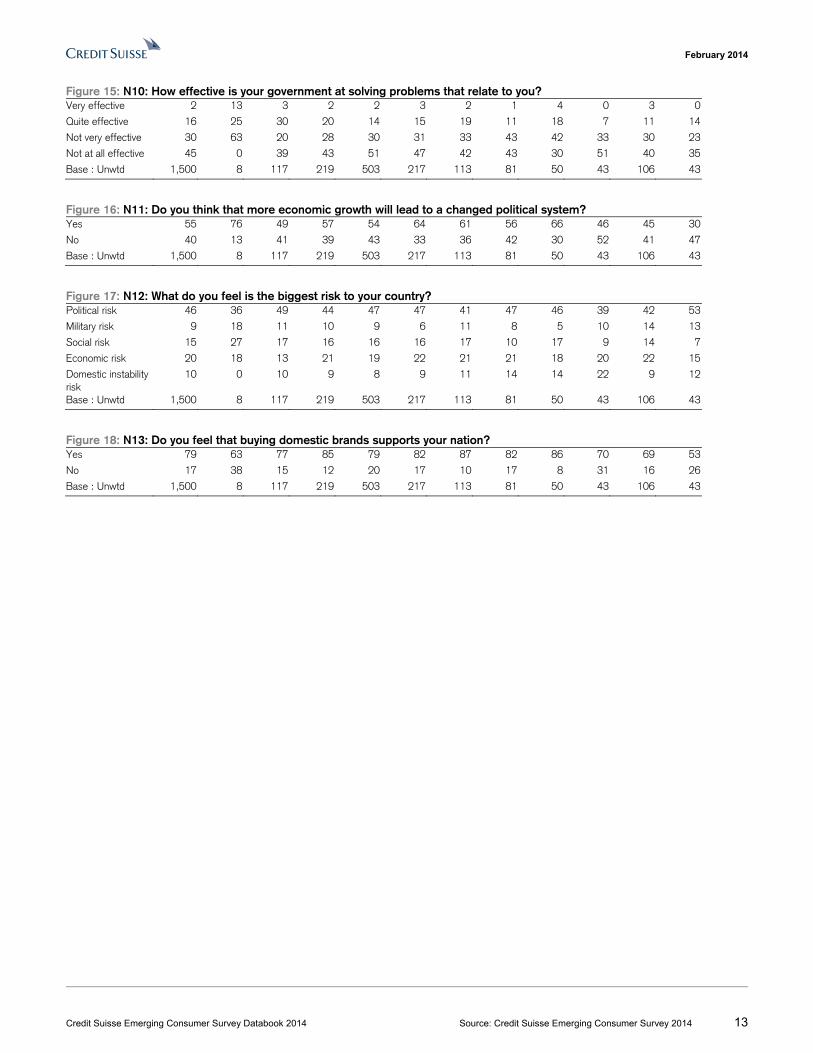

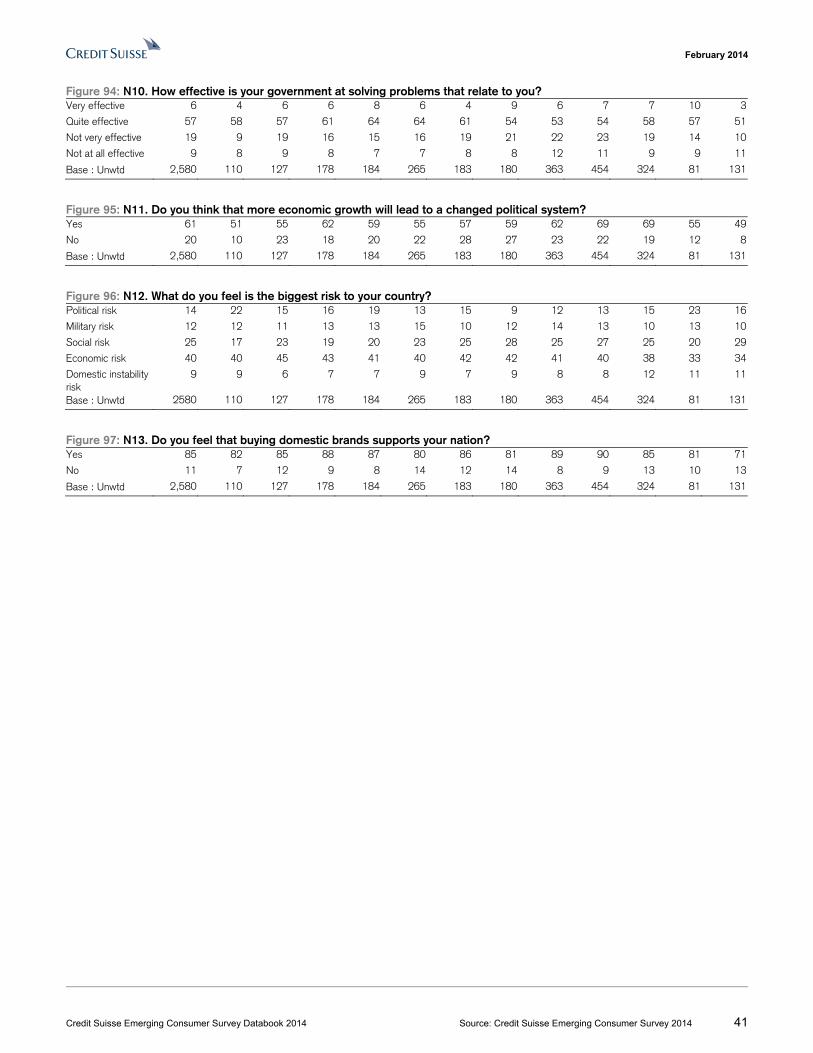

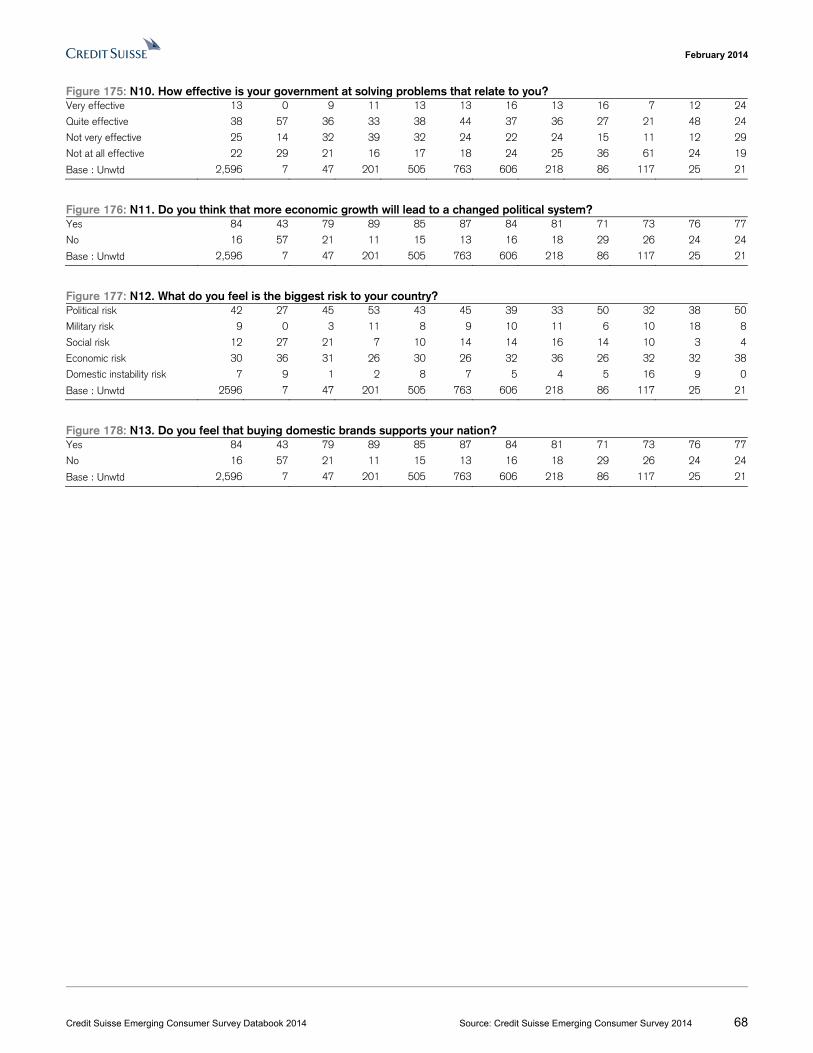

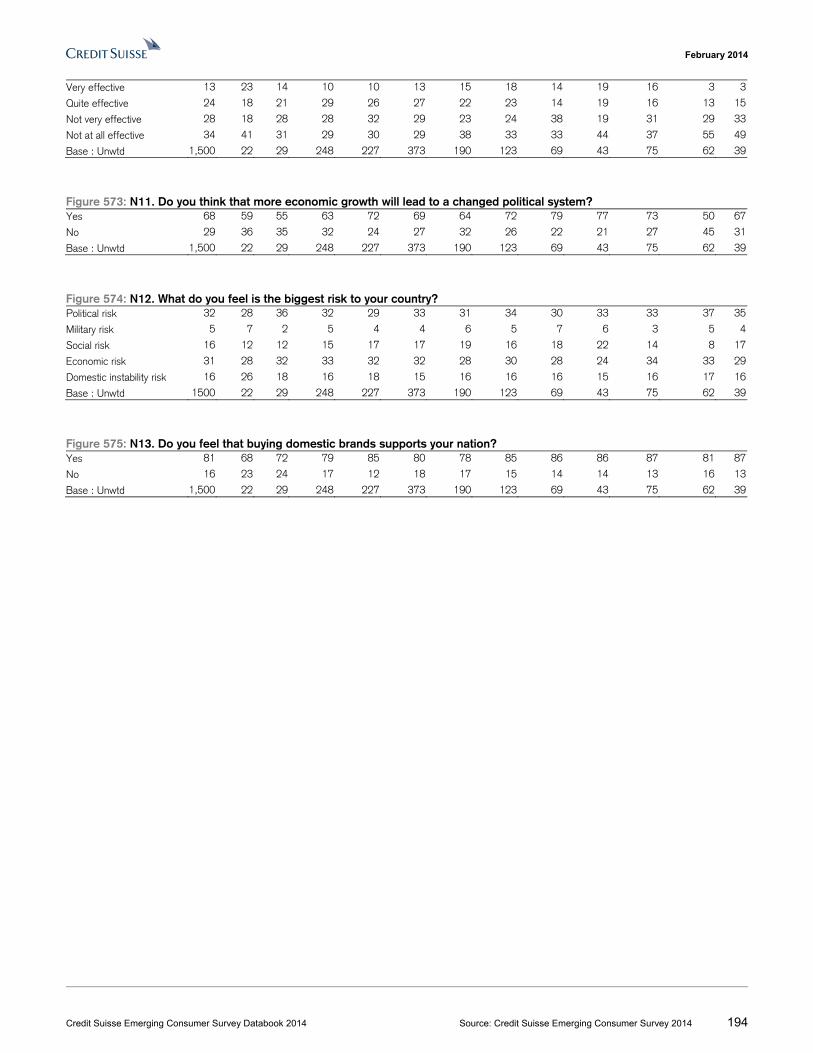

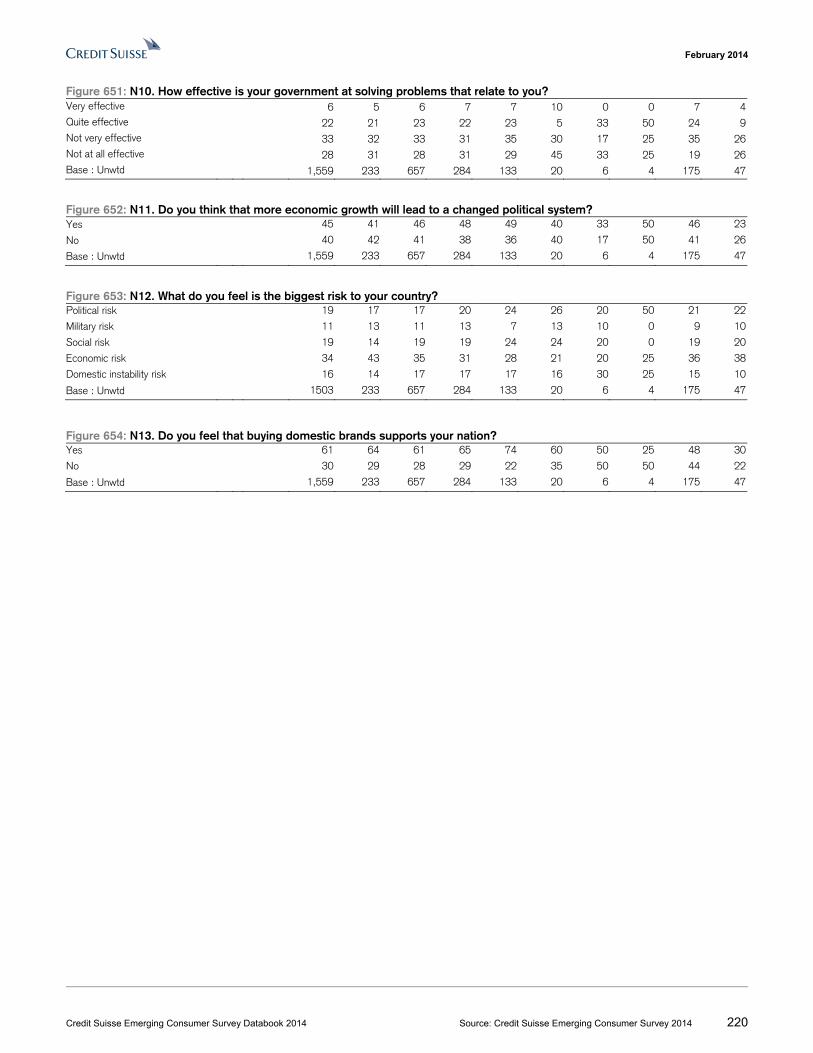

Figure 15: N10: How effective is your government at solving problems that relate to you? Very effective 2 13 3 2 2 3 2 1 4 0 3 0

Quite effective 16 25 30 20 14 15 19 11 18 7 11 14

Not very effective 30 63 20 28 30 31 33 43 42 33 30 23

Not at all effective 45 0 39 43 51 47 42 43 30 51 40 35

Base : Unwtd 1,500 8 117 219 503 217 113 81 50 43 106 43

Figure 16: N11: Do you think that more economic growth will lead to a changed political system? Yes 55 76 49 57 54 64 61 56 66 46 45 30

No 40 13 41 39 43 33 36 42 30 52 41 47

Base : Unwtd 1,500 8 117 219 503 217 113 81 50 43 106 43

Figure 17: N12: What do you feel is the biggest risk to your country? Political risk 46 36 49 44 47 47 41 47 46 39 42 53

Military risk 9 18 11 10 9 6 11 8 5 10 14 13

Social risk 15 27 17 16 16 16 17 10 17 9 14 7

Economic risk 20 18 13 21 19 22 21 21 18 20 22 15

Domestic instability risk

10 0 10 9 8 9 11 14 14 22 9 12

Base : Unwtd 1,500 8 117 219 503 217 113 81 50 43 106 43

Figure 18: N13: Do you feel that buying domestic brands supports your nation? Yes 79 63 77 85 79 82 87 82 86 70 69 53

No 17 38 15 12 20 17 10 17 8 31 16 26

Base : Unwtd 1,500 8 117 219 503 217 113 81 50 43 106 43

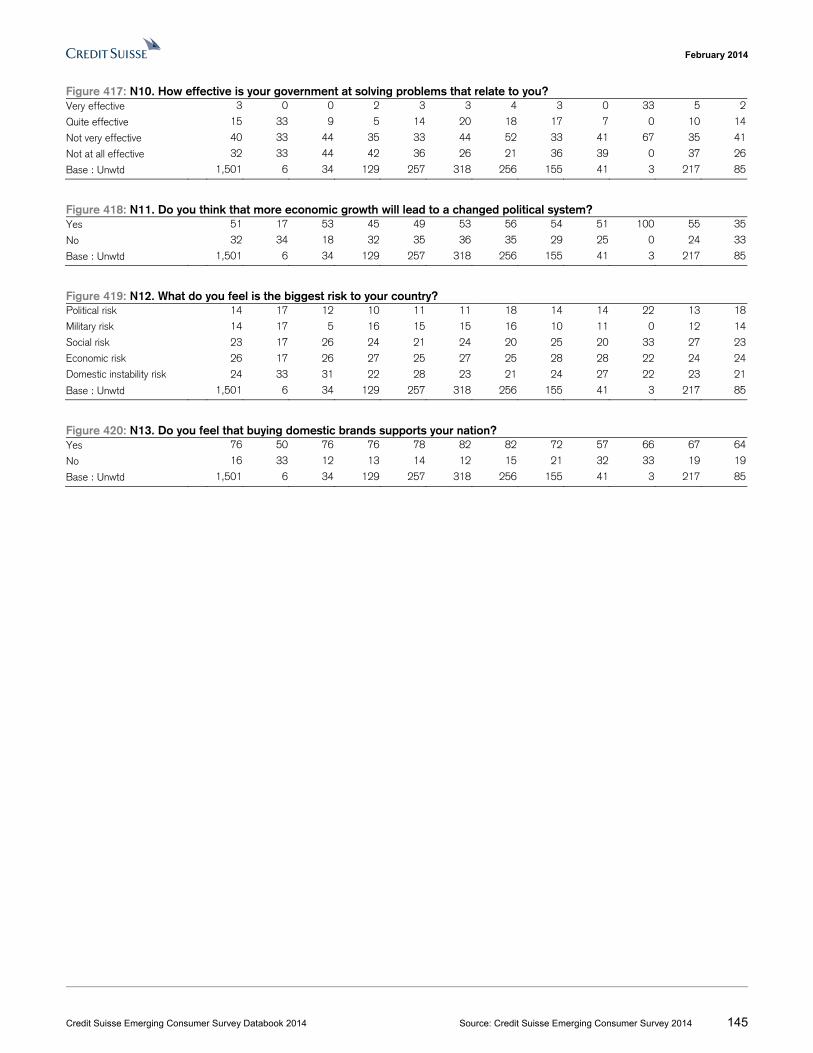

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 14

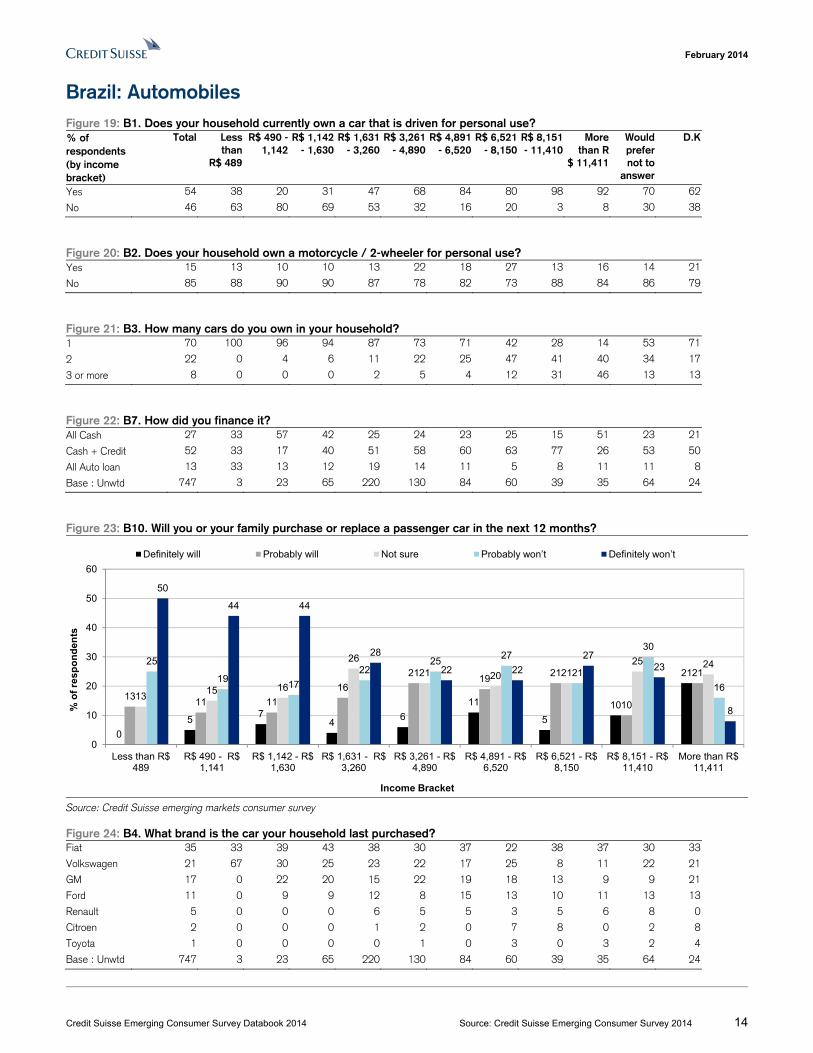

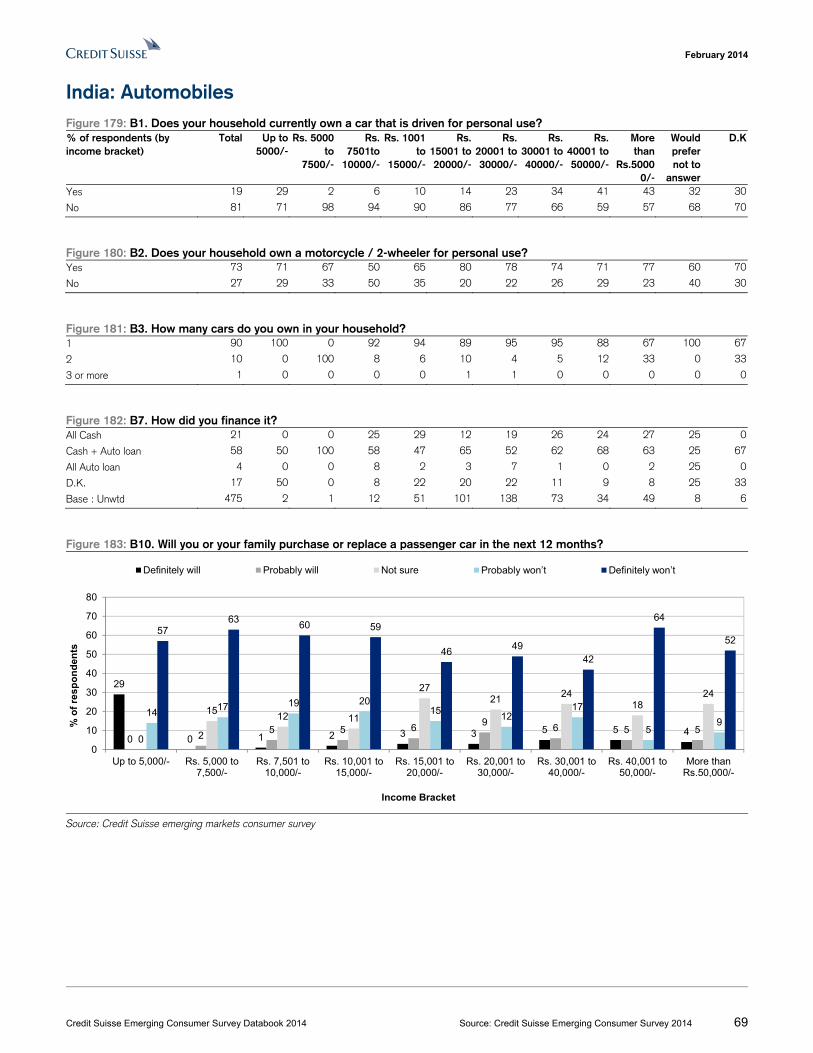

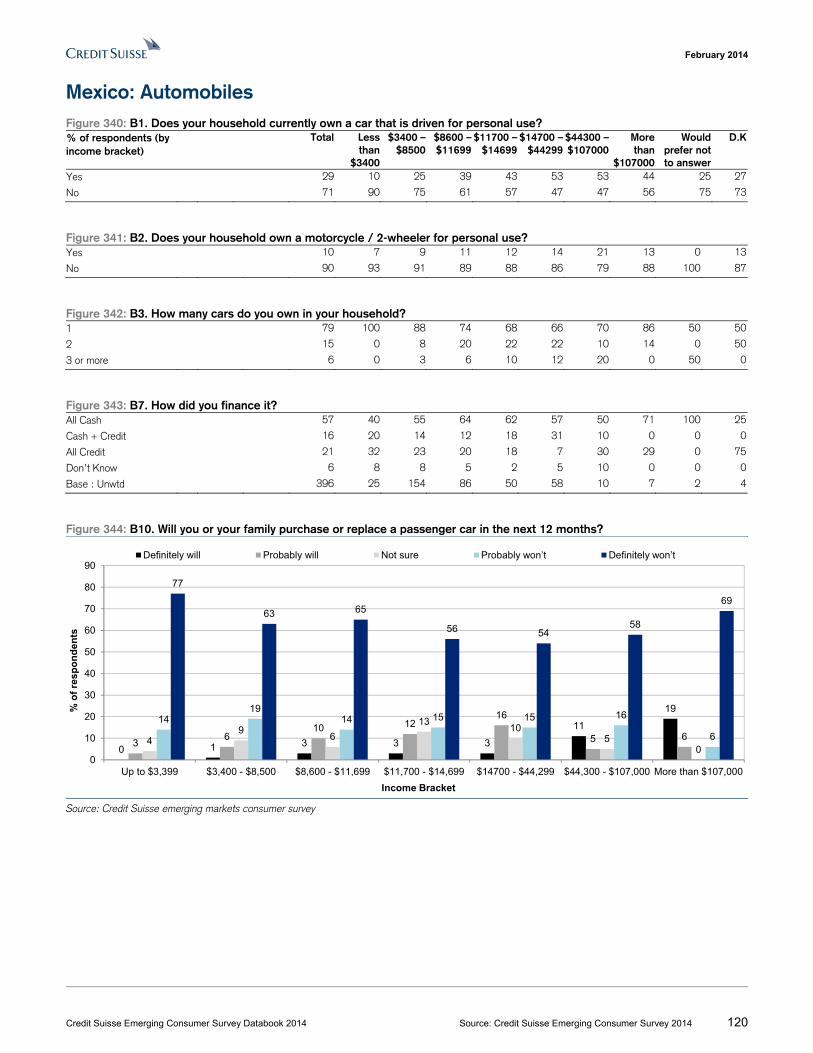

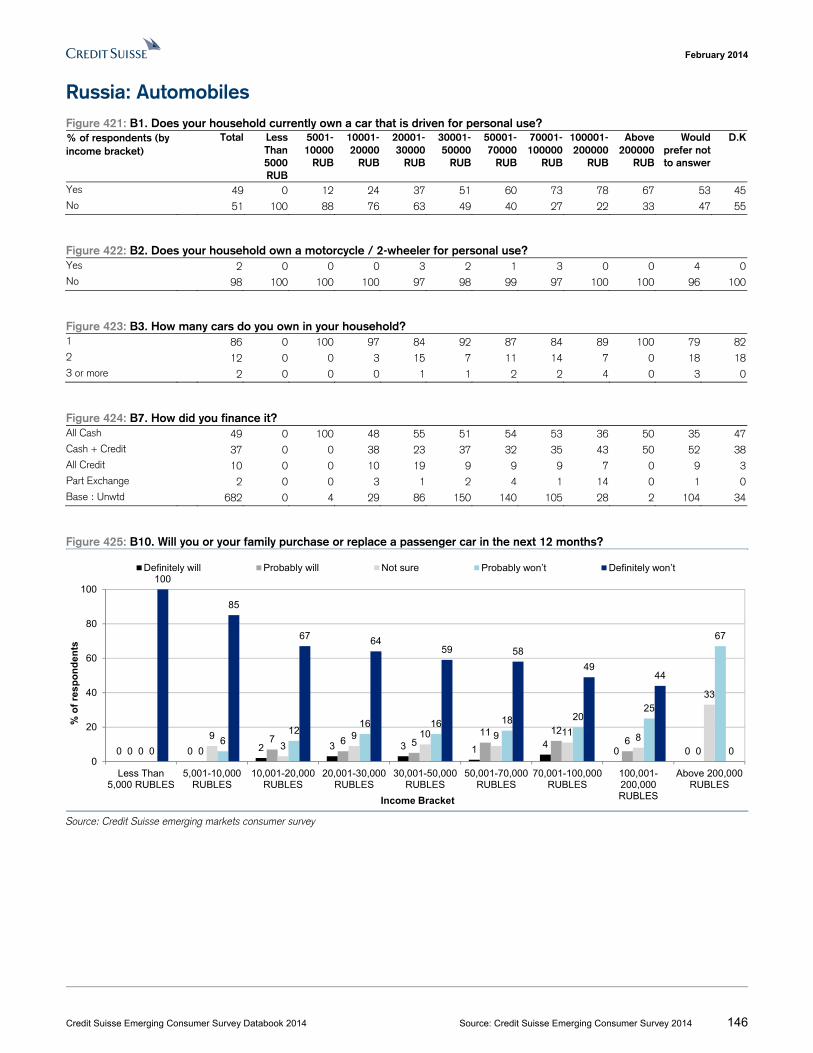

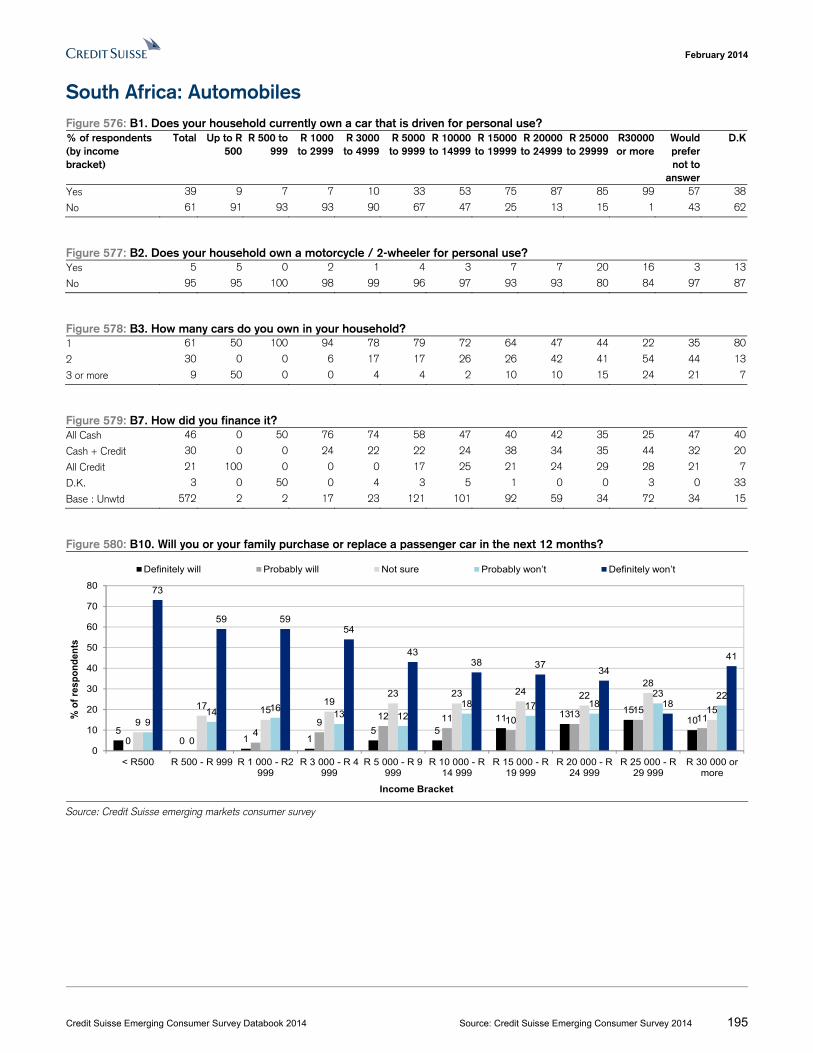

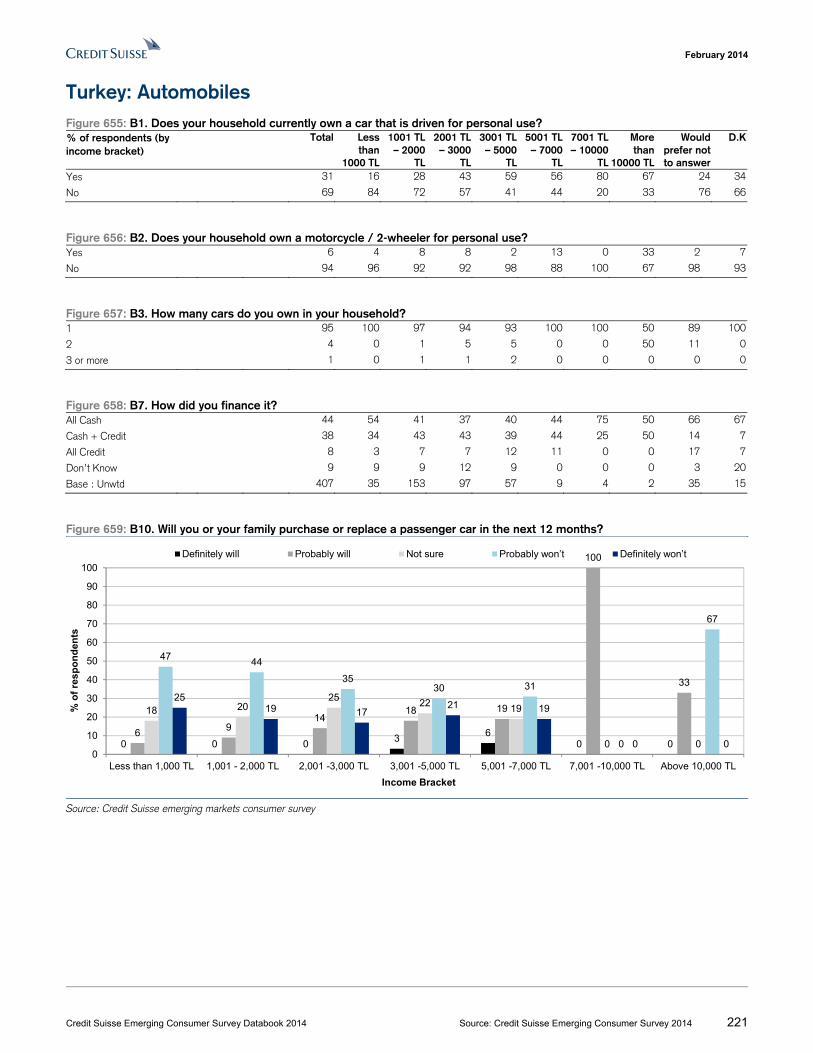

Brazil: Automobiles Figure 19: B1. Does your household currently own a car that is driven for personal use? % of respondents (by income bracket)

Total Less than

R$ 489

R$ 490 - 1,142

R$ 1,142 - 1,630

R$ 1,631 - 3,260

R$ 3,261 - 4,890

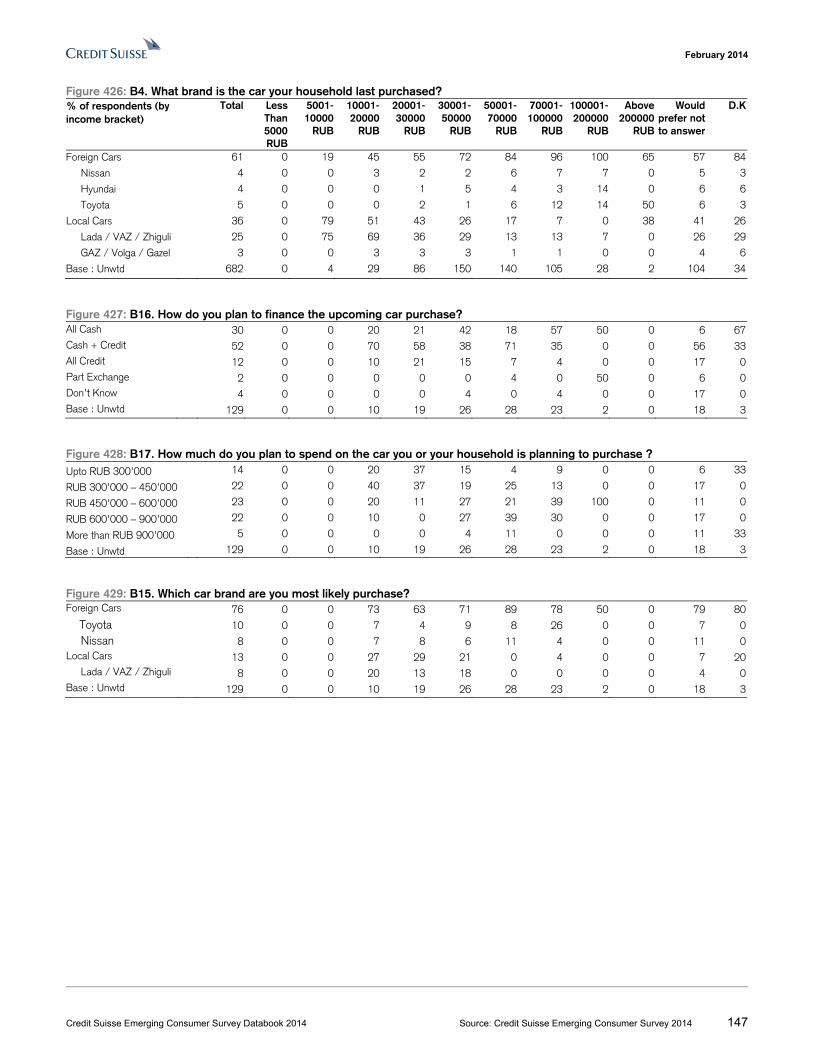

R$ 4,891 - 6,520

R$ 6,521 - 8,150

R$ 8,151 - 11,410

More than R

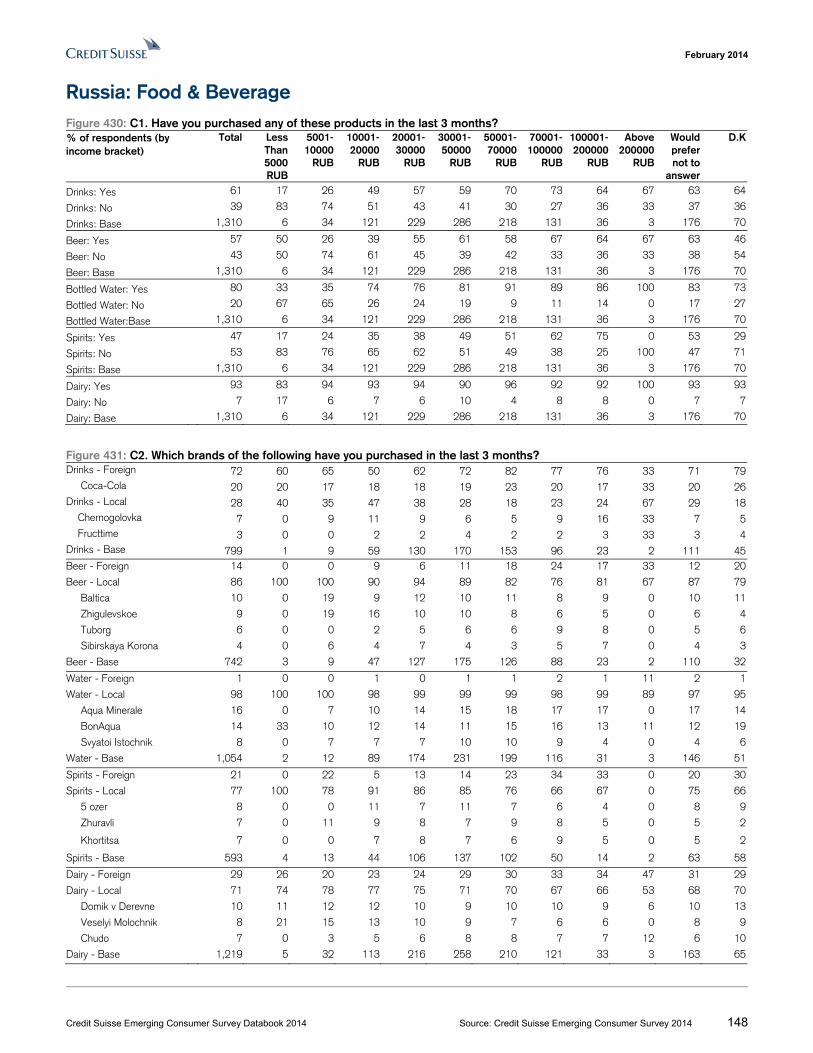

$ 11,411

Would prefer not to

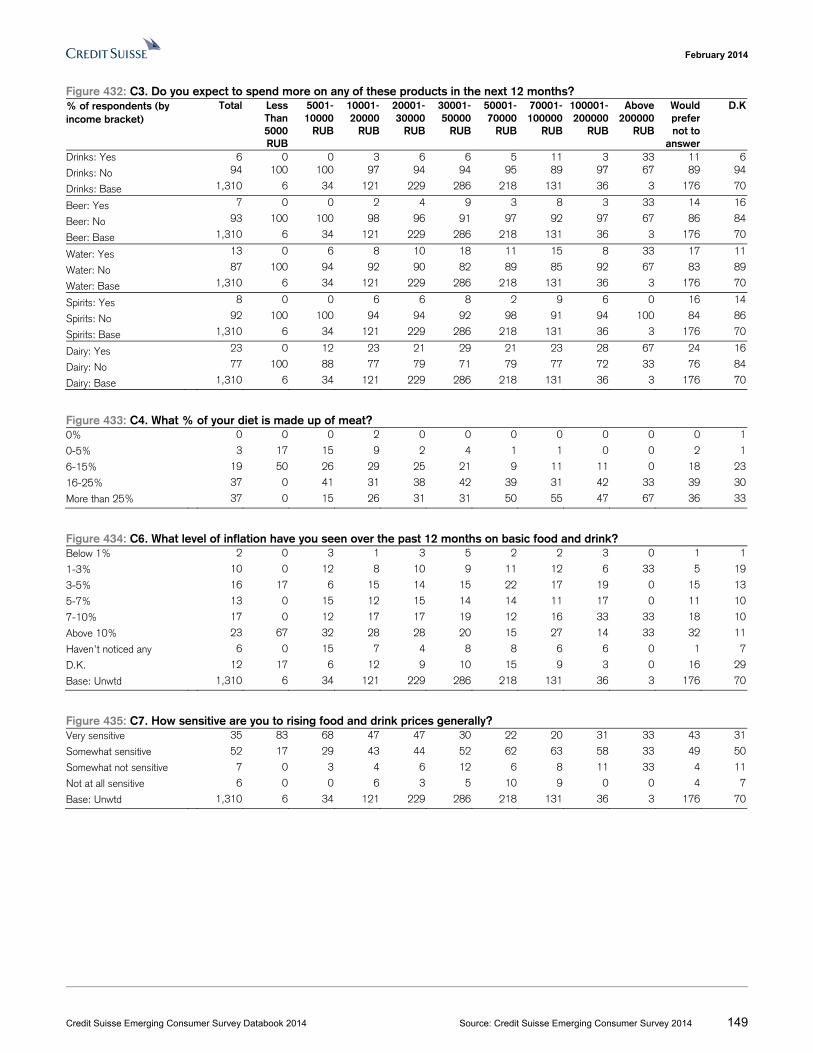

answer

D.K

Yes 54 38 20 31 47 68 84 80 98 92 70 62

No 46 63 80 69 53 32 16 20 3 8 30 38

Figure 20: B2. Does your household own a motorcycle / 2-wheeler for personal use? Yes 15 13 10 10 13 22 18 27 13 16 14 21

No 85 88 90 90 87 78 82 73 88 84 86 79

Figure 21: B3. How many cars do you own in your household? 1 70 100 96 94 87 73 71 42 28 14 53 71

2 22 0 4 6 11 22 25 47 41 40 34 17

3 or more 8 0 0 0 2 5 4 12 31 46 13 13

Figure 22: B7. How did you finance it? All Cash 27 33 57 42 25 24 23 25 15 51 23 21

Cash + Credit 52 33 17 40 51 58 60 63 77 26 53 50

All Auto loan 13 33 13 12 19 14 11 5 8 11 11 8

Base : Unwtd 747 3 23 65 220 130 84 60 39 35 64 24

Figure 23: B10. Will you or your family purchase or replace a passenger car in the next 12 months?

Source: Credit Suisse emerging markets consumer survey

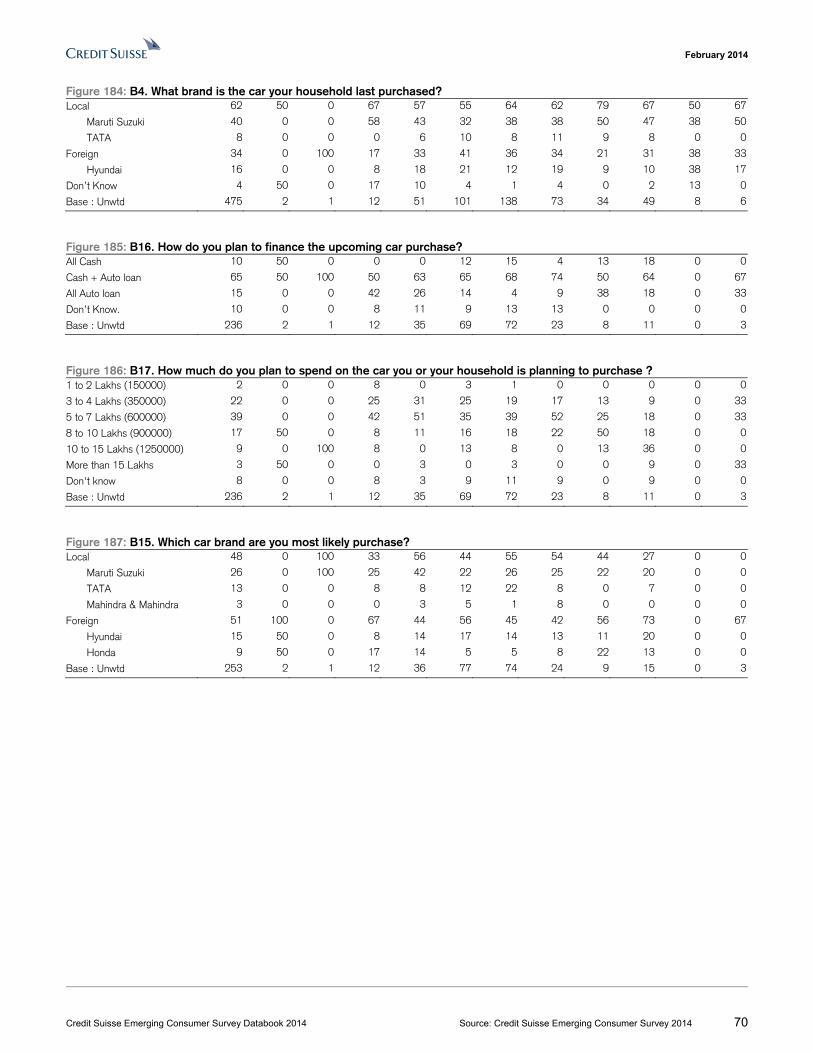

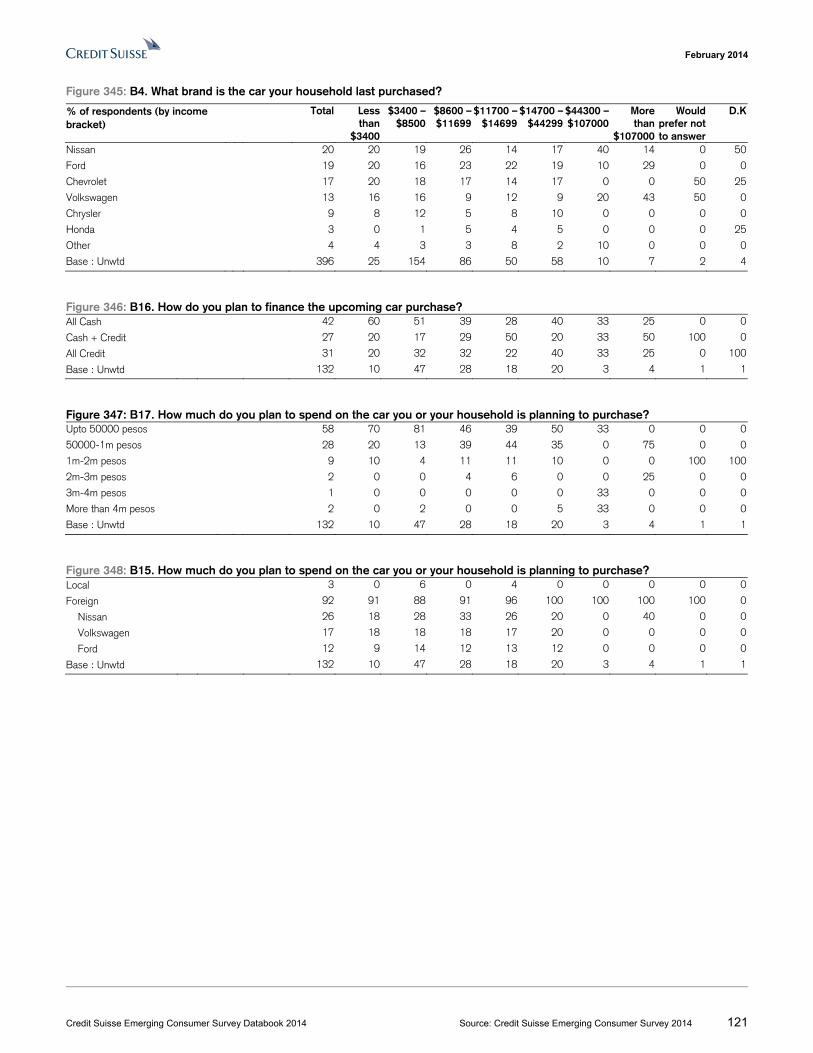

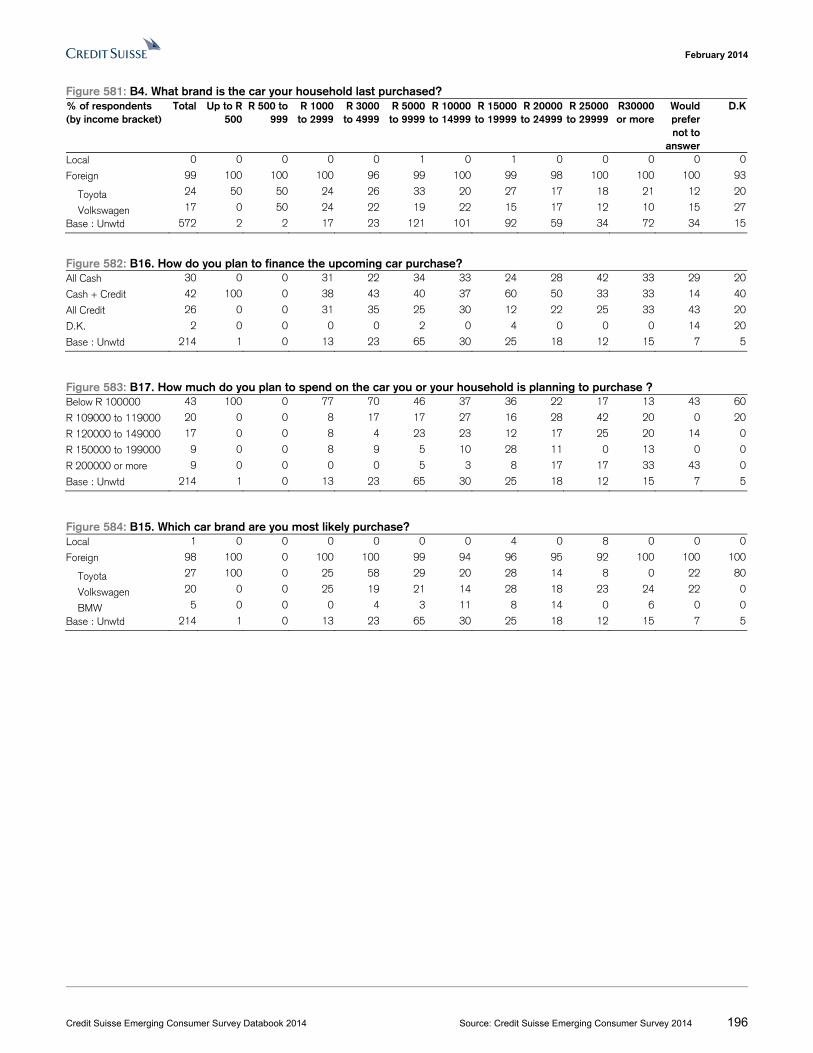

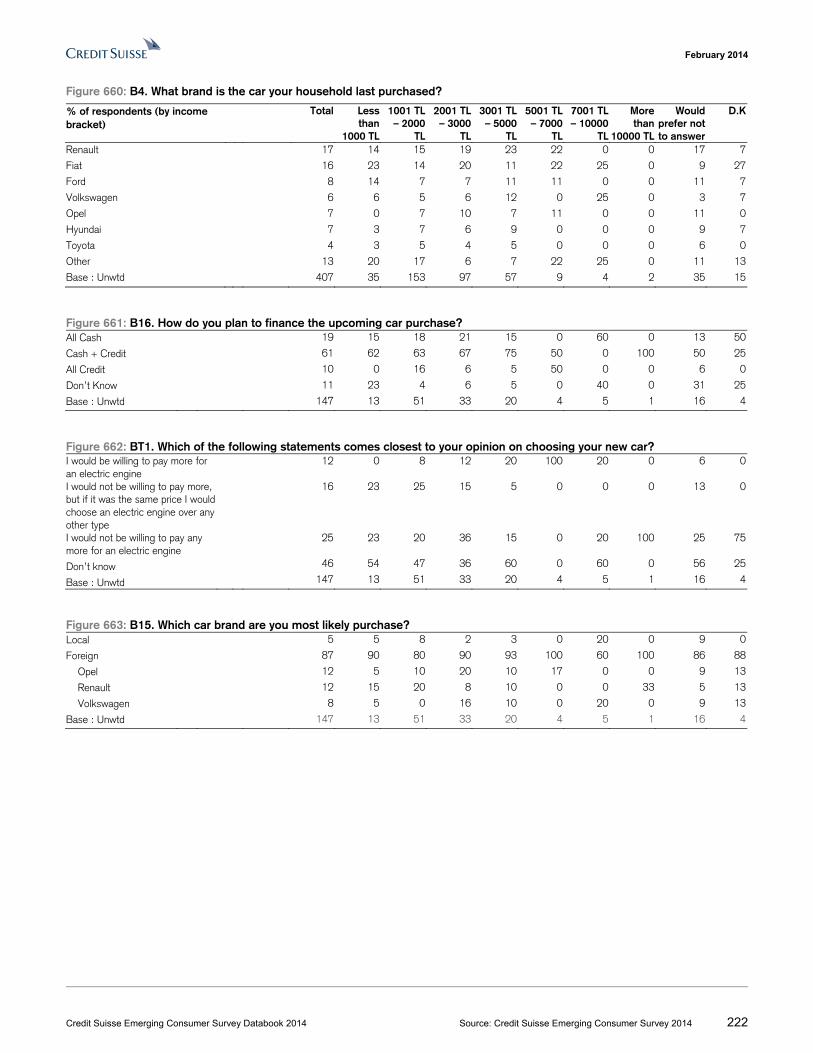

Figure 24: B4. What brand is the car your household last purchased? Fiat 35 33 39 43 38 30 37 22 38 37 30 33

Volkswagen 21 67 30 25 23 22 17 25 8 11 22 21

GM 17 0 22 20 15 22 19 18 13 9 9 21

Ford 11 0 9 9 12 8 15 13 10 11 13 13

Renault 5 0 0 0 6 5 5 3 5 6 8 0

Citroen 2 0 0 0 1 2 0 7 8 0 2 8

Toyota 1 0 0 0 0 1 0 3 0 3 2 4

Base : Unwtd 747 3 23 65 220 130 84 60 39 35 64 24

0

57

46

11

5

10

21

1311 11

16

2119

21

10

21

1315 16

26

21 20 2125 2425

1917

2225

27

21

30

16

50

44 44

28

22 22

2723

8

0

10

20

30

40

50

60

Less than R$489

R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

R$ 8,151 - R$11,410

More than R$11,411

% o

f re

spo

nd

ents

Income Bracket

Definitely will Probably will Not sure Probably won’t Definitely won’t

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 15

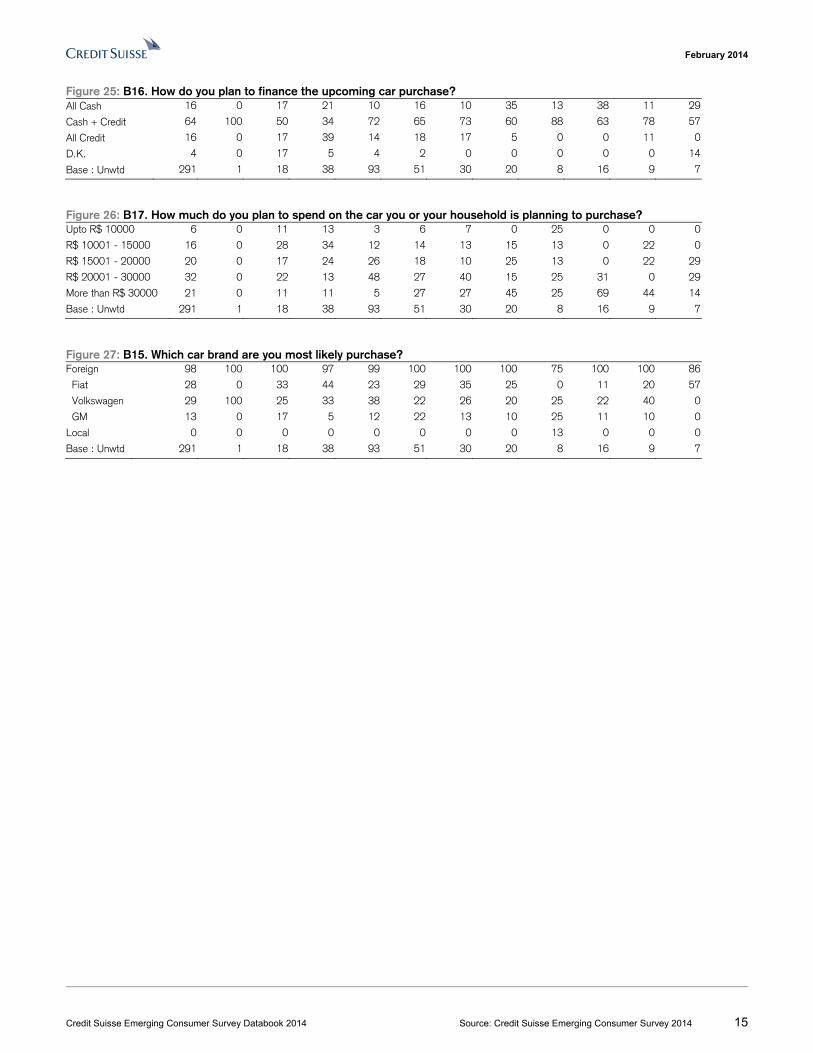

Figure 25: B16. How do you plan to finance the upcoming car purchase? All Cash 16 0 17 21 10 16 10 35 13 38 11 29

Cash + Credit 64 100 50 34 72 65 73 60 88 63 78 57

All Credit 16 0 17 39 14 18 17 5 0 0 11 0

D.K. 4 0 17 5 4 2 0 0 0 0 0 14

Base : Unwtd 291 1 18 38 93 51 30 20 8 16 9 7

Figure 26: B17. How much do you plan to spend on the car you or your household is planning to purchase? Upto R$ 10000 6 0 11 13 3 6 7 0 25 0 0 0

R$ 10001 - 15000 16 0 28 34 12 14 13 15 13 0 22 0

R$ 15001 - 20000 20 0 17 24 26 18 10 25 13 0 22 29

R$ 20001 - 30000 32 0 22 13 48 27 40 15 25 31 0 29

More than R$ 30000 21 0 11 11 5 27 27 45 25 69 44 14

Base : Unwtd 291 1 18 38 93 51 30 20 8 16 9 7

Figure 27: B15. Which car brand are you most likely purchase? Foreign 98 100 100 97 99 100 100 100 75 100 100 86

Fiat 28 0 33 44 23 29 35 25 0 11 20 57

Volkswagen 29 100 25 33 38 22 26 20 25 22 40 0

GM 13 0 17 5 12 22 13 10 25 11 10 0

Local 0 0 0 0 0 0 0 0 13 0 0 0

Base : Unwtd 291 1 18 38 93 51 30 20 8 16 9 7

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 16

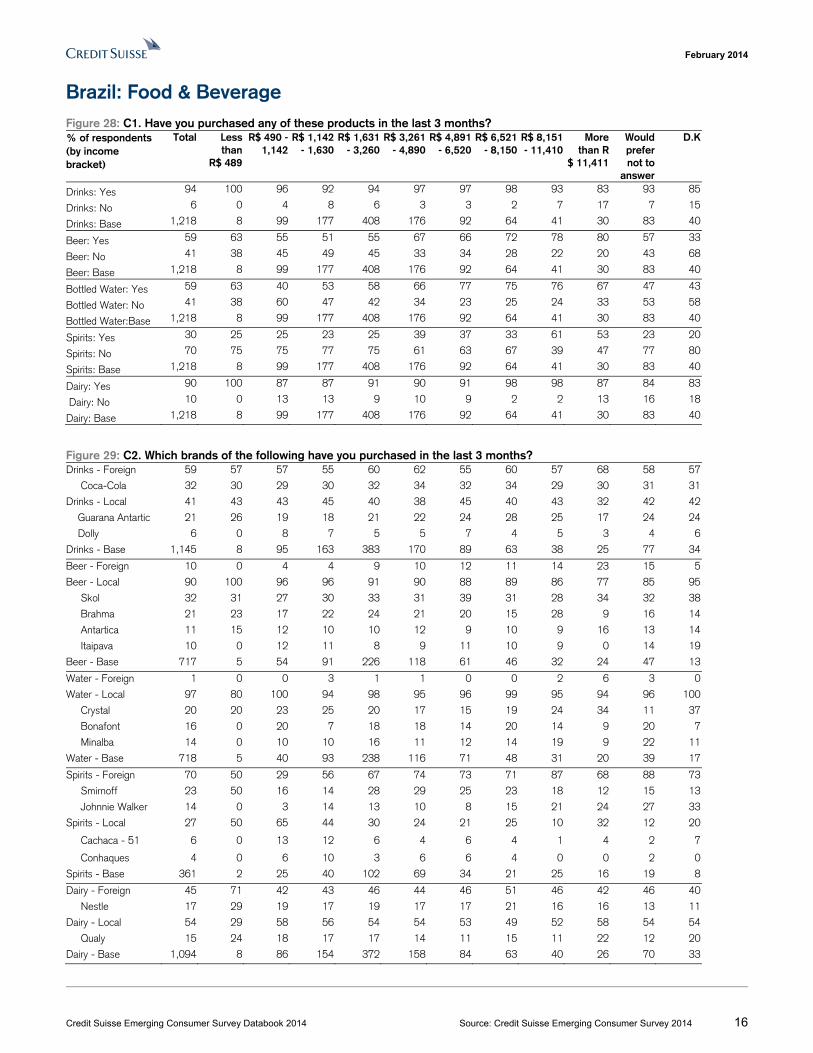

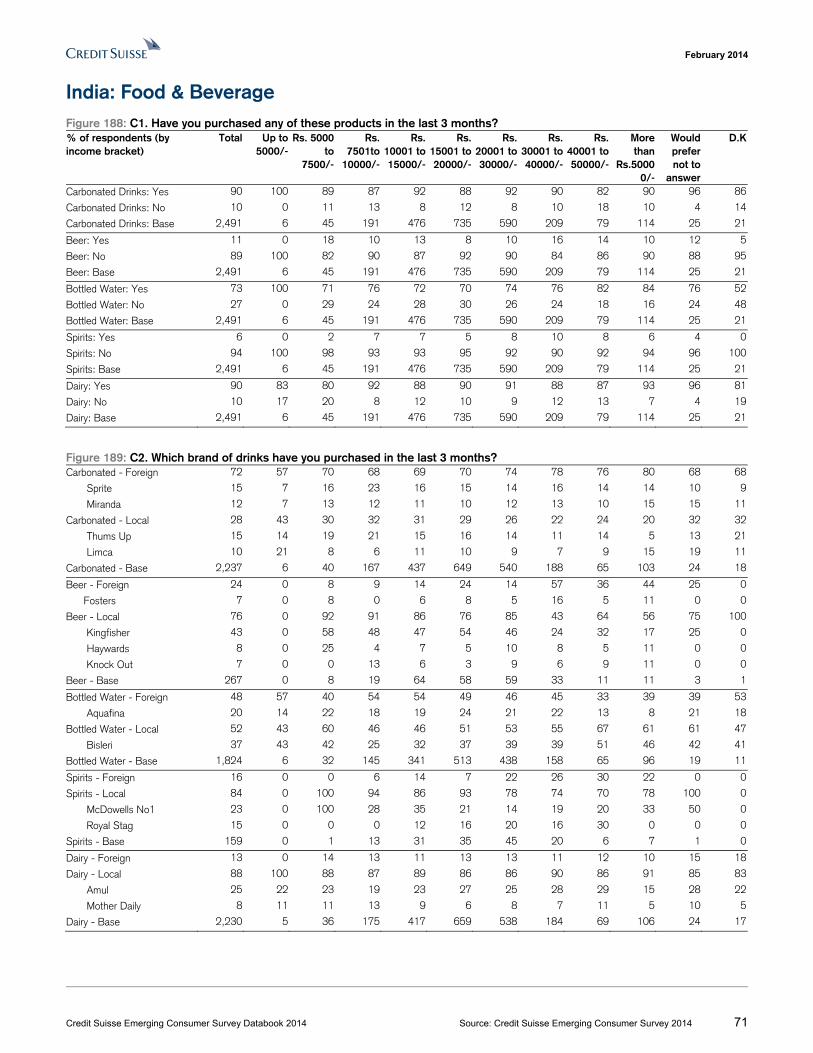

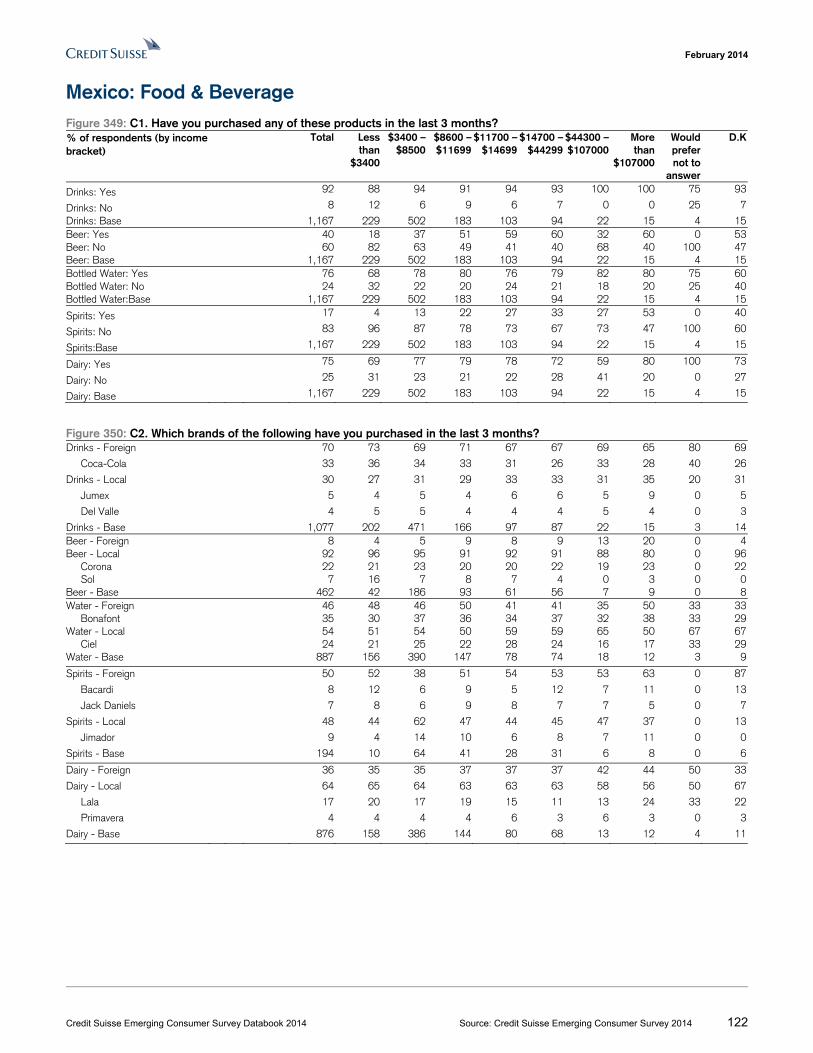

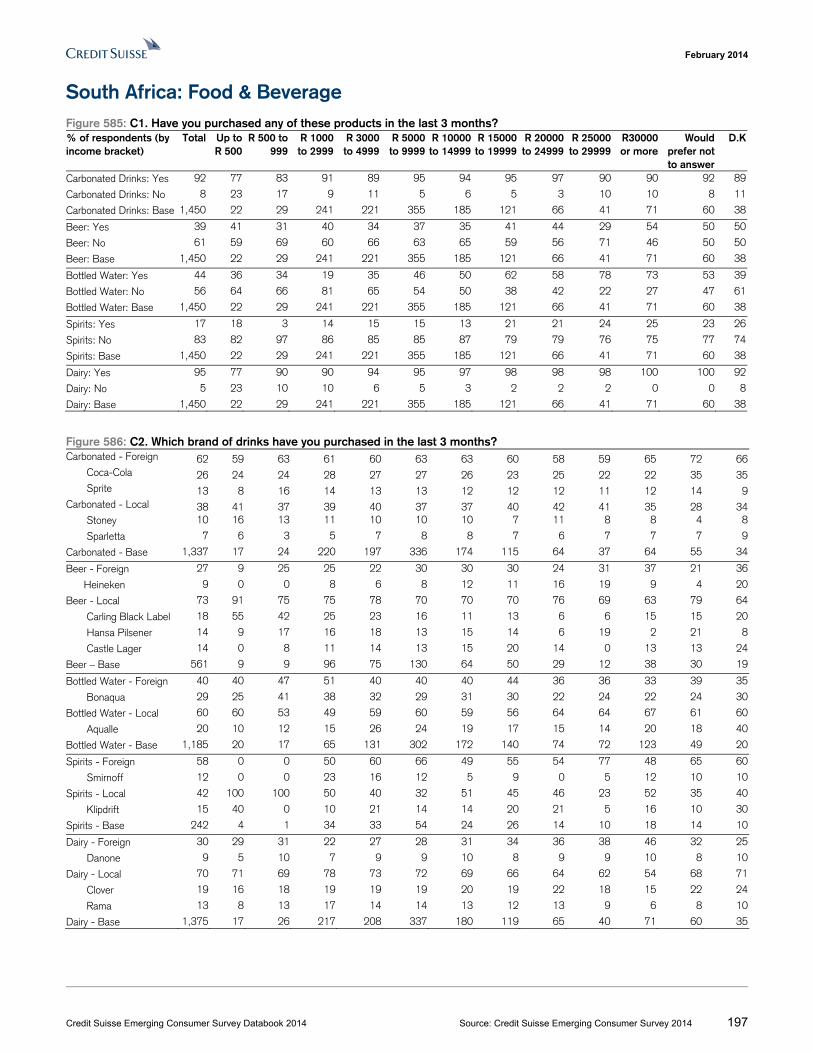

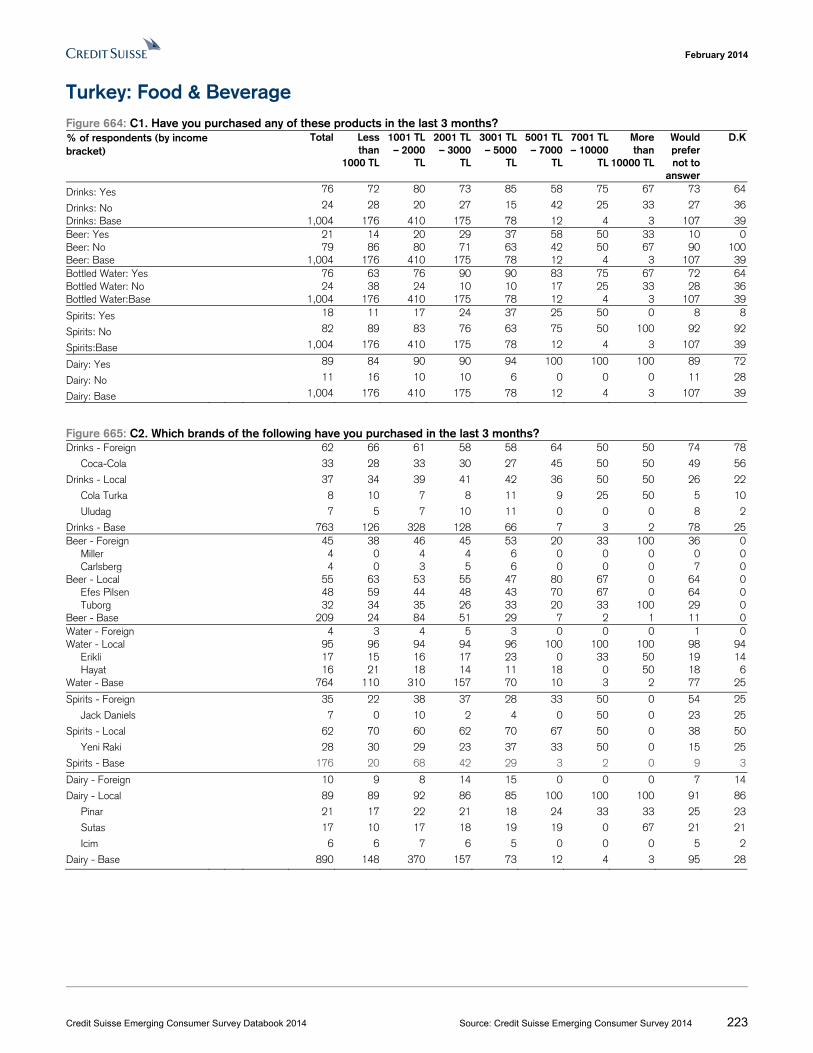

Brazil: Food & Beverage Figure 28: C1. Have you purchased any of these products in the last 3 months? % of respondents (by income bracket)

Total Less than

R$ 489

R$ 490 - 1,142

R$ 1,142 - 1,630

R$ 1,631 - 3,260

R$ 3,261 - 4,890

R$ 4,891 - 6,520

R$ 6,521 - 8,150

R$ 8,151 - 11,410

More than R

$ 11,411

Would prefer not to

answer

D.K

Drinks: Yes 94 100 96 92 94 97 97 98 93 83 93 85

Drinks: No 6 0 4 8 6 3 3 2 7 17 7 15

Drinks: Base 1,218 8 99 177 408 176 92 64 41 30 83 40

Beer: Yes 59 63 55 51 55 67 66 72 78 80 57 33

Beer: No 41 38 45 49 45 33 34 28 22 20 43 68

Beer: Base 1,218 8 99 177 408 176 92 64 41 30 83 40

Bottled Water: Yes 59 63 40 53 58 66 77 75 76 67 47 43

Bottled Water: No 41 38 60 47 42 34 23 25 24 33 53 58

Bottled Water:Base 1,218 8 99 177 408 176 92 64 41 30 83 40

Spirits: Yes 30 25 25 23 25 39 37 33 61 53 23 20

Spirits: No 70 75 75 77 75 61 63 67 39 47 77 80

Spirits: Base 1,218 8 99 177 408 176 92 64 41 30 83 40

Dairy: Yes 90 100 87 87 91 90 91 98 98 87 84 83

Dairy: No 10 0 13 13 9 10 9 2 2 13 16 18

Dairy: Base 1,218 8 99 177 408 176 92 64 41 30 83 40

Figure 29: C2. Which brands of the following have you purchased in the last 3 months? Drinks - Foreign 59 57 57 55 60 62 55 60 57 68 58 57

Coca-Cola 32 30 29 30 32 34 32 34 29 30 31 31

Drinks - Local 41 43 43 45 40 38 45 40 43 32 42 42

Guarana Antartic 21 26 19 18 21 22 24 28 25 17 24 24

Dolly 6 0 8 7 5 5 7 4 5 3 4 6

Drinks - Base 1,145 8 95 163 383 170 89 63 38 25 77 34

Beer - Foreign 10 0 4 4 9 10 12 11 14 23 15 5

Beer - Local 90 100 96 96 91 90 88 89 86 77 85 95

Skol 32 31 27 30 33 31 39 31 28 34 32 38

Brahma 21 23 17 22 24 21 20 15 28 9 16 14

Antartica 11 15 12 10 10 12 9 10 9 16 13 14

Itaipava 10 0 12 11 8 9 11 10 9 0 14 19

Beer - Base 717 5 54 91 226 118 61 46 32 24 47 13

Water - Foreign 1 0 0 3 1 1 0 0 2 6 3 0

Water - Local 97 80 100 94 98 95 96 99 95 94 96 100

Crystal 20 20 23 25 20 17 15 19 24 34 11 37

Bonafont 16 0 20 7 18 18 14 20 14 9 20 7

Minalba 14 0 10 10 16 11 12 14 19 9 22 11

Water - Base 718 5 40 93 238 116 71 48 31 20 39 17

Spirits - Foreign 70 50 29 56 67 74 73 71 87 68 88 73

Smirnoff 23 50 16 14 28 29 25 23 18 12 15 13

Johnnie Walker 14 0 3 14 13 10 8 15 21 24 27 33

Spirits - Local 27 50 65 44 30 24 21 25 10 32 12 20

Cachaca - 51 6 0 13 12 6 4 6 4 1 4 2 7

Conhaques 4 0 6 10 3 6 6 4 0 0 2 0

Spirits - Base 361 2 25 40 102 69 34 21 25 16 19 8

Dairy - Foreign 45 71 42 43 46 44 46 51 46 42 46 40

Nestle 17 29 19 17 19 17 17 21 16 16 13 11

Dairy - Local 54 29 58 56 54 54 53 49 52 58 54 54

Qualy 15 24 18 17 17 14 11 15 11 22 12 20

Dairy - Base 1,094 8 86 154 372 158 84 63 40 26 70 33

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 17

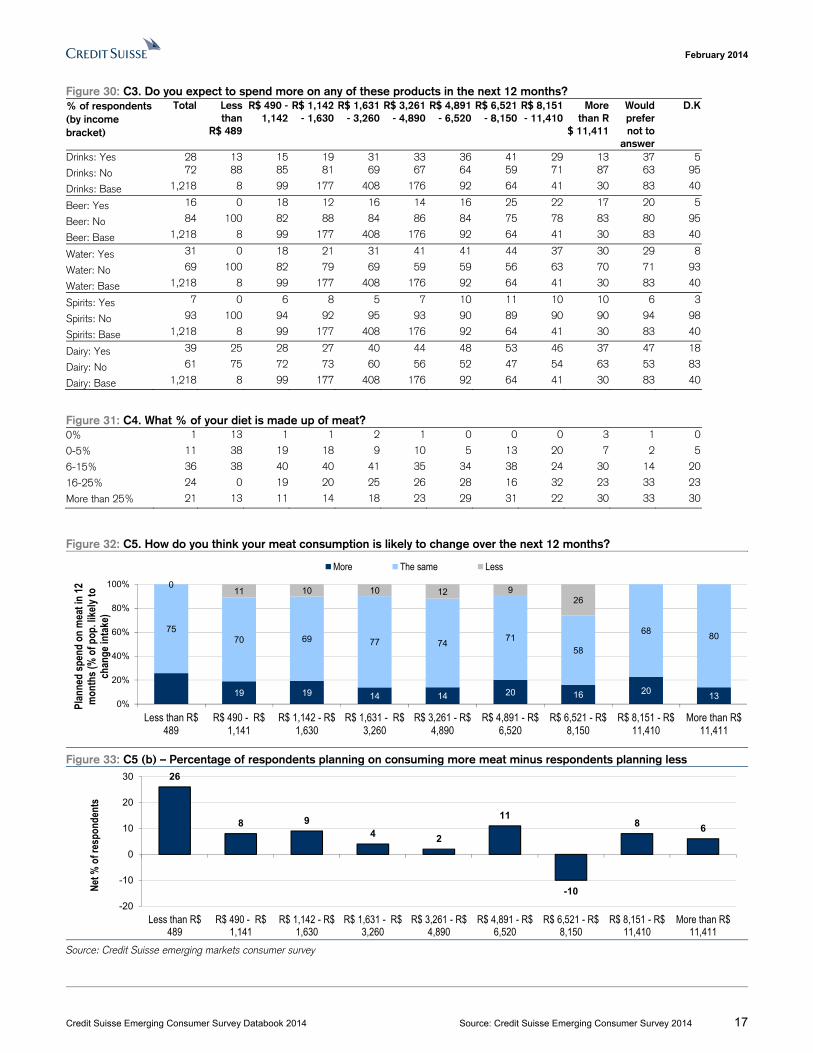

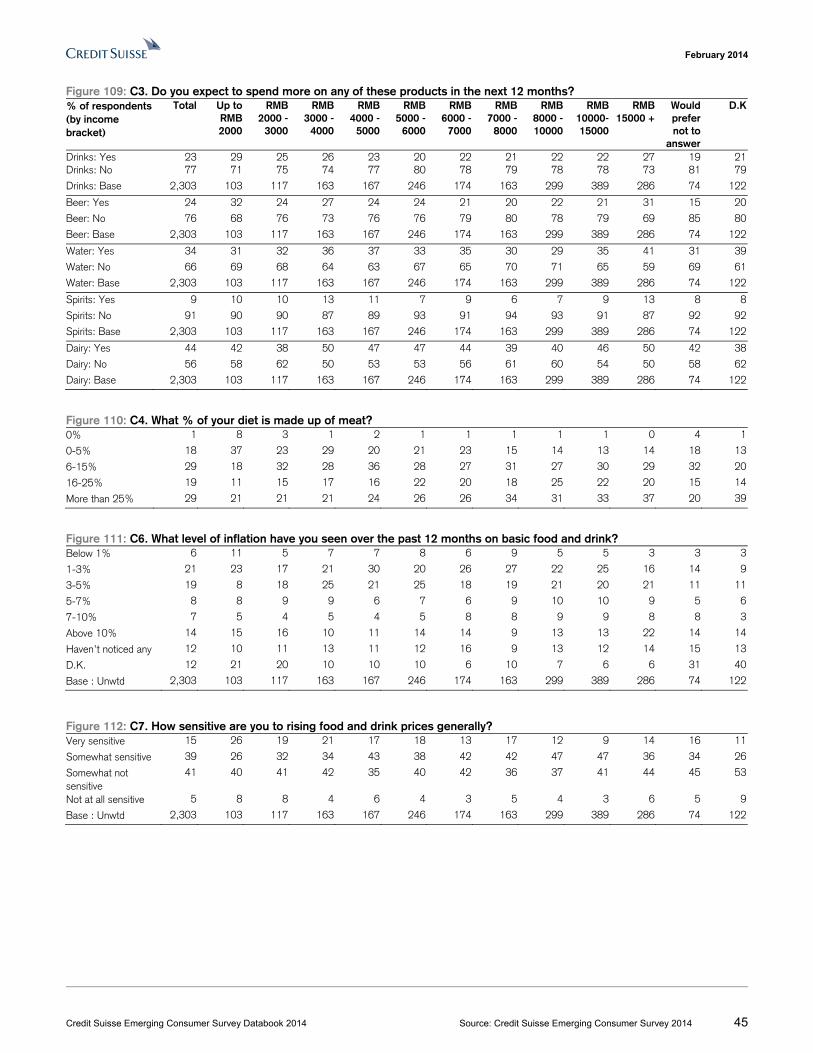

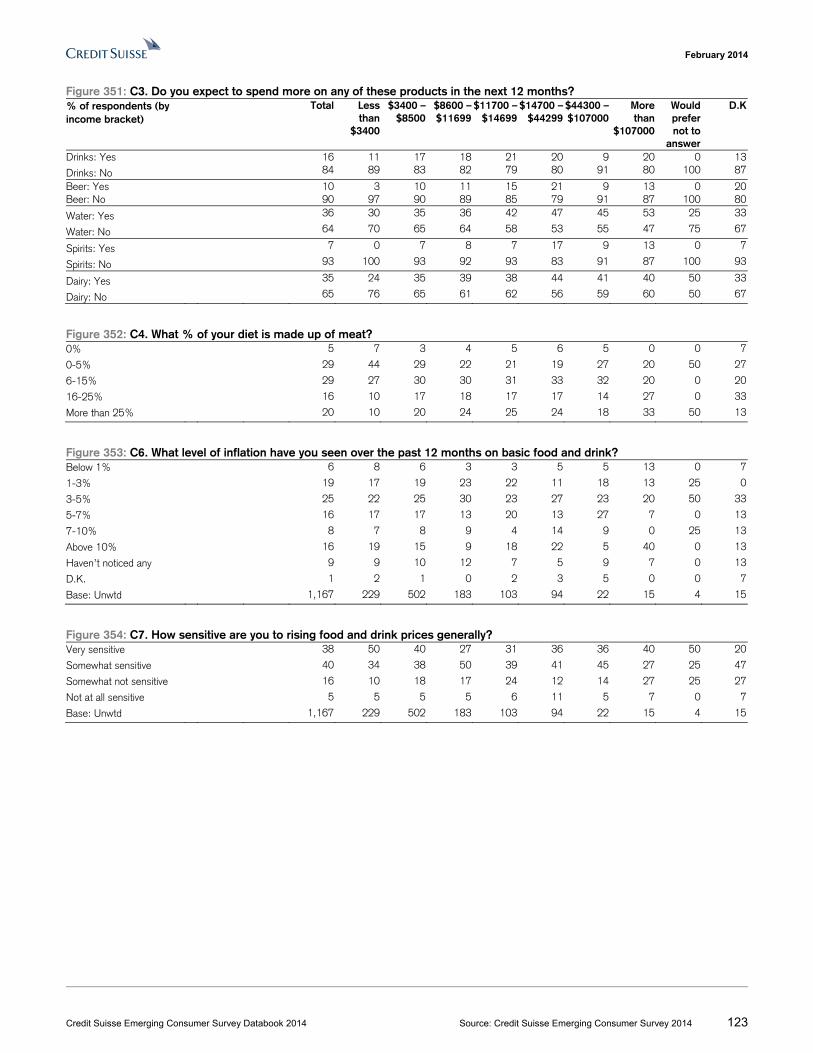

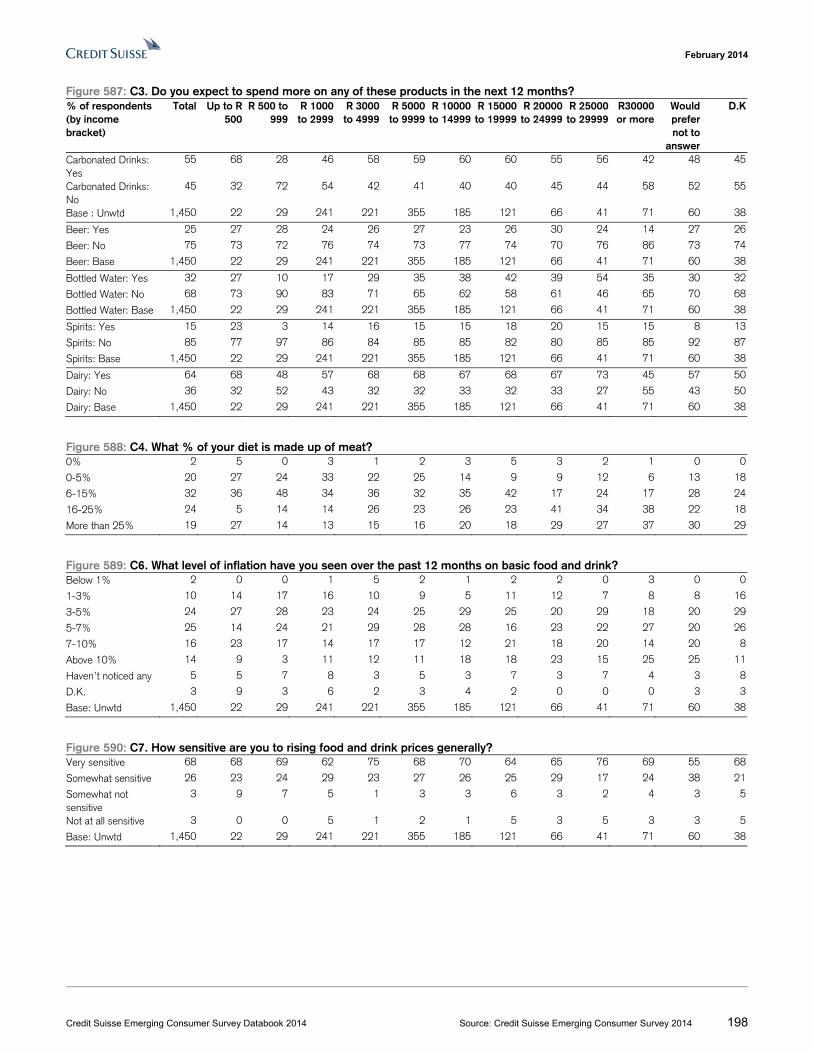

Figure 30: C3. Do you expect to spend more on any of these products in the next 12 months? % of respondents (by income bracket)

Total Less than

R$ 489

R$ 490 - 1,142

R$ 1,142 - 1,630

R$ 1,631 - 3,260

R$ 3,261 - 4,890

R$ 4,891 - 6,520

R$ 6,521 - 8,150

R$ 8,151 - 11,410

More than R

$ 11,411

Would prefer not to

answer

D.K

Drinks: Yes 28 13 15 19 31 33 36 41 29 13 37 5

Drinks: No 72 88 85 81 69 67 64 59 71 87 63 95

Drinks: Base 1,218 8 99 177 408 176 92 64 41 30 83 40

Beer: Yes 16 0 18 12 16 14 16 25 22 17 20 5

Beer: No 84 100 82 88 84 86 84 75 78 83 80 95

Beer: Base 1,218 8 99 177 408 176 92 64 41 30 83 40

Water: Yes 31 0 18 21 31 41 41 44 37 30 29 8

Water: No 69 100 82 79 69 59 59 56 63 70 71 93

Water: Base 1,218 8 99 177 408 176 92 64 41 30 83 40

Spirits: Yes 7 0 6 8 5 7 10 11 10 10 6 3

Spirits: No 93 100 94 92 95 93 90 89 90 90 94 98

Spirits: Base 1,218 8 99 177 408 176 92 64 41 30 83 40

Dairy: Yes 39 25 28 27 40 44 48 53 46 37 47 18

Dairy: No 61 75 72 73 60 56 52 47 54 63 53 83

Dairy: Base 1,218 8 99 177 408 176 92 64 41 30 83 40

Figure 31: C4. What % of your diet is made up of meat? 0% 1 13 1 1 2 1 0 0 0 3 1 0

0-5% 11 38 19 18 9 10 5 13 20 7 2 5

6-15% 36 38 40 40 41 35 34 38 24 30 14 20

16-25% 24 0 19 20 25 26 28 16 32 23 33 23

More than 25% 21 13 11 14 18 23 29 31 22 30 33 30

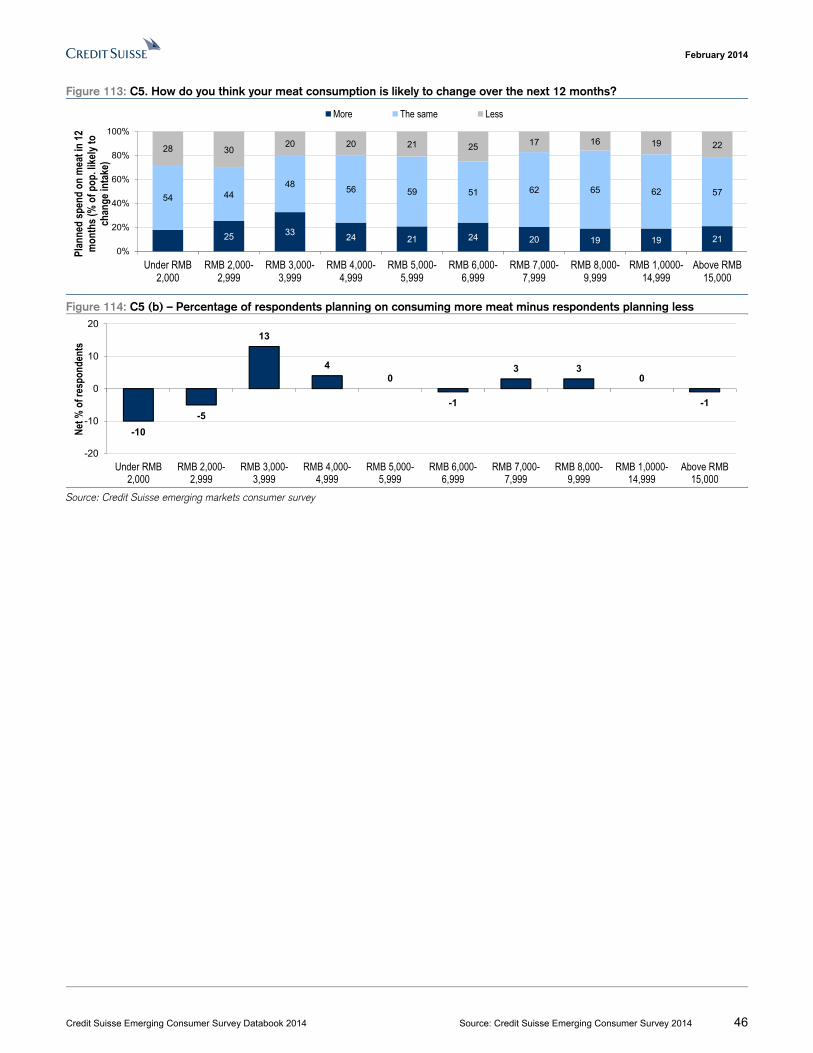

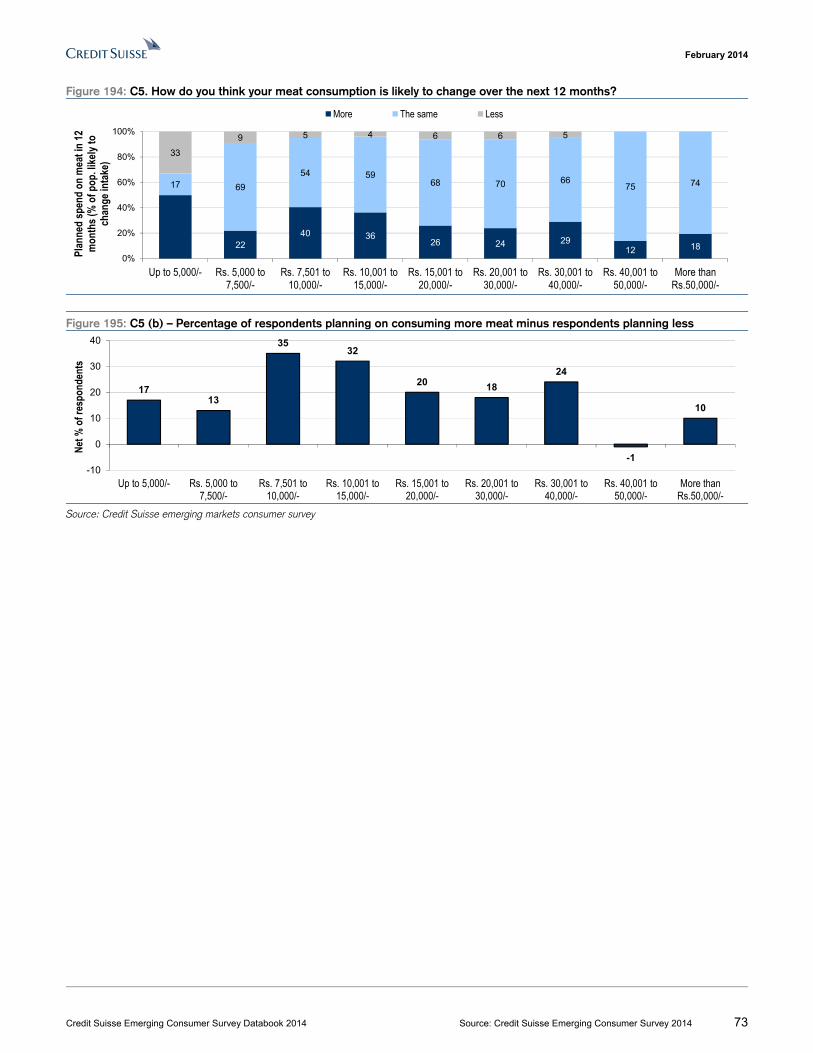

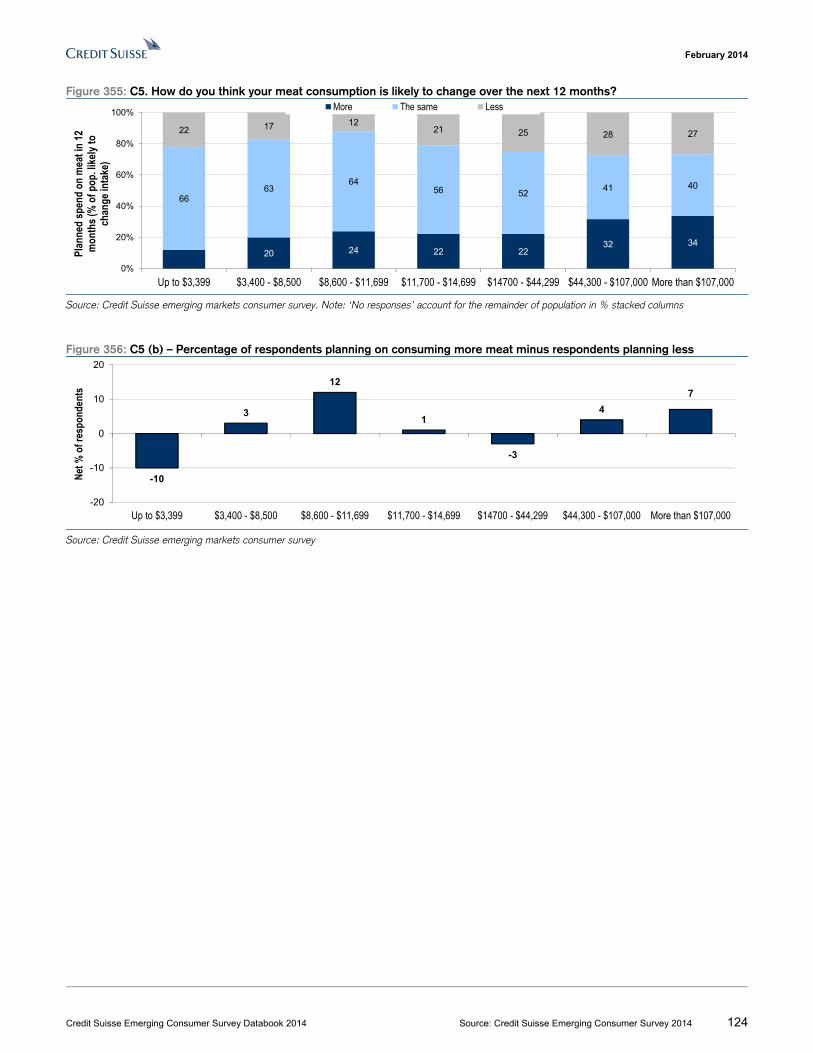

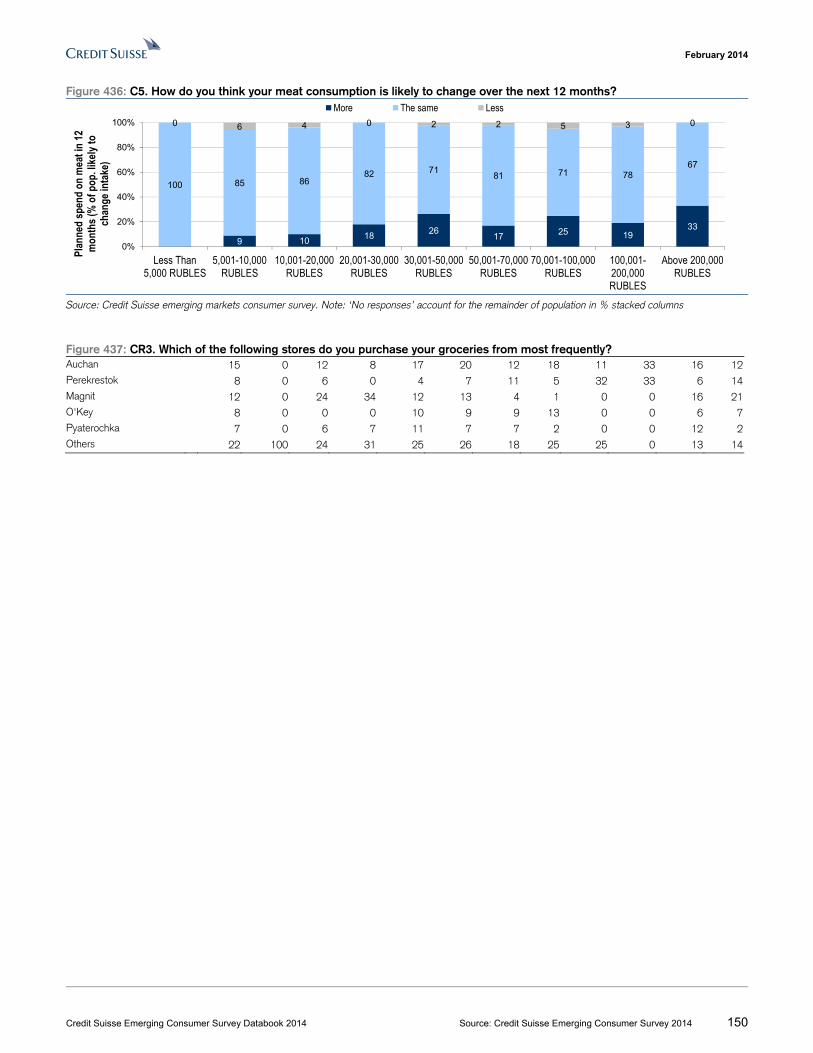

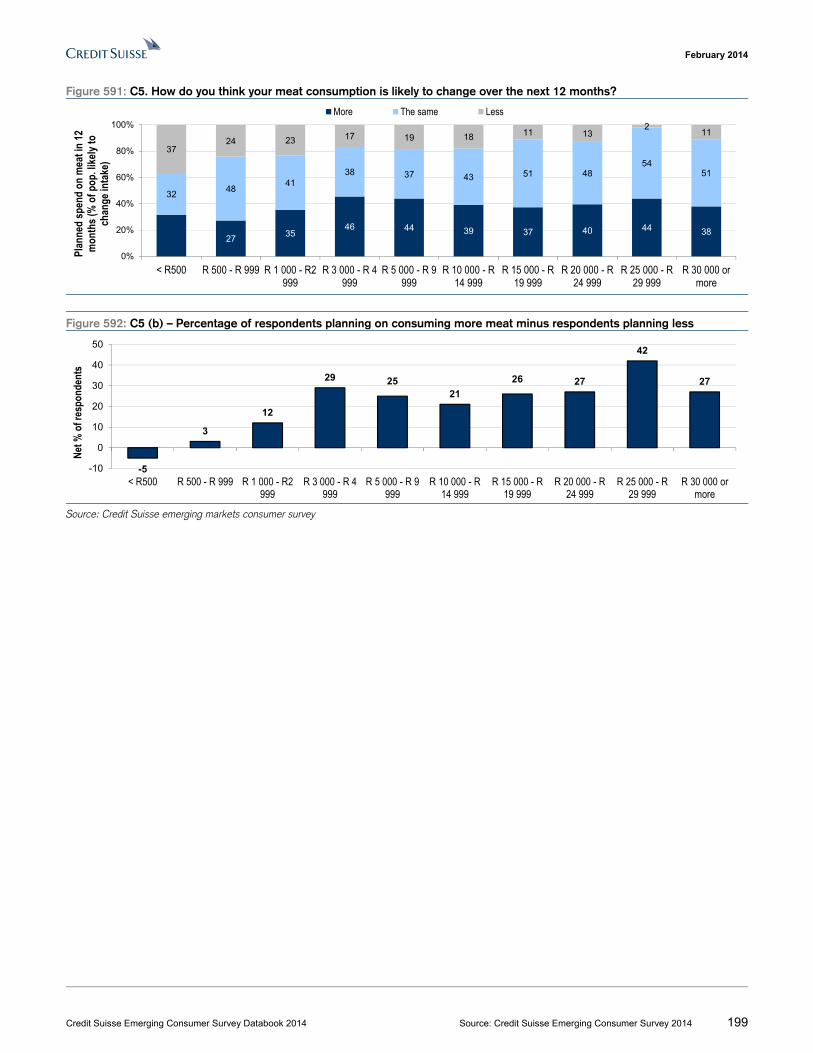

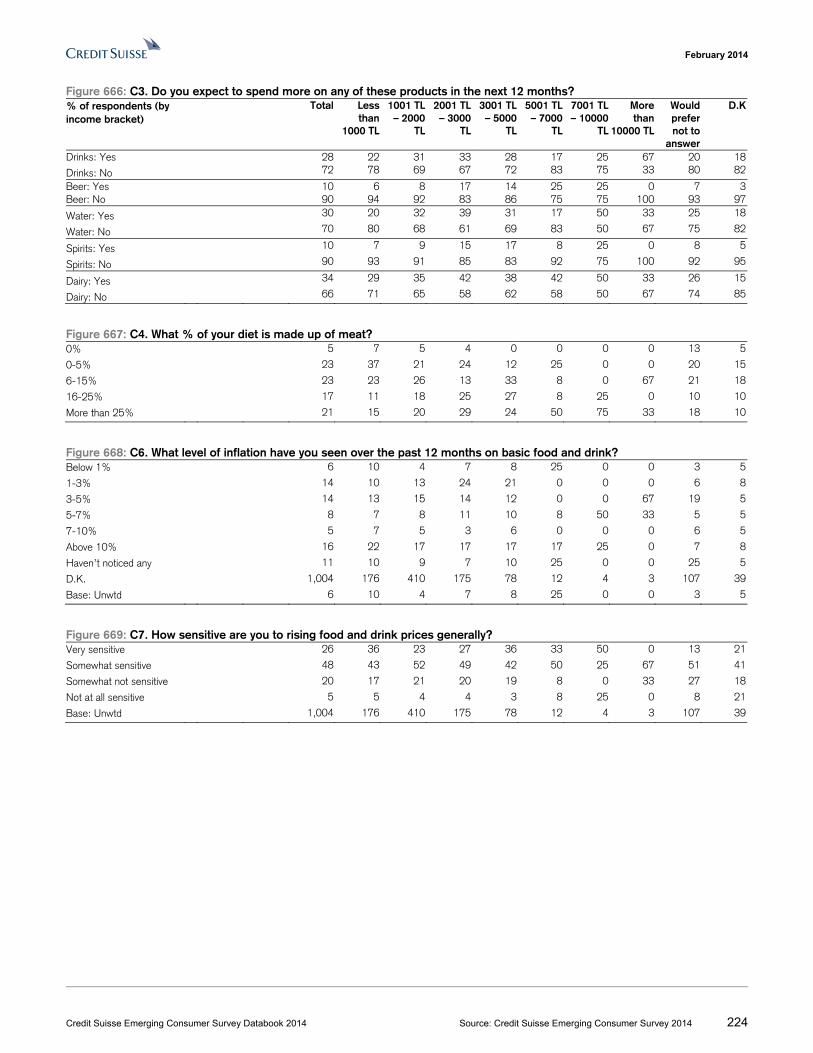

Figure 32: C5. How do you think your meat consumption is likely to change over the next 12 months?

Figure 33: C5 (b) – Percentage of respondents planning on consuming more meat minus respondents planning less

Source: Credit Suisse emerging markets consumer survey

19 19 14 14 20 16 2013

7570 69 77 74

71

58

6880

011 10 10 12 9

26

0%

20%

40%

60%

80%

100%

Less than R$489

R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

R$ 8,151 - R$11,410

More than R$11,411

Plan

ned

spen

d on

mea

t in

12

mon

ths (

% o

f pop

. like

ly to

ch

ange

inta

ke)

More The same Less

26

8 94 2

11

-10

8 6

-20

-10

0

10

20

30

Less than R$489

R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

R$ 8,151 - R$11,410

More than R$11,411

Net %

of r

espo

nden

ts

February 2014

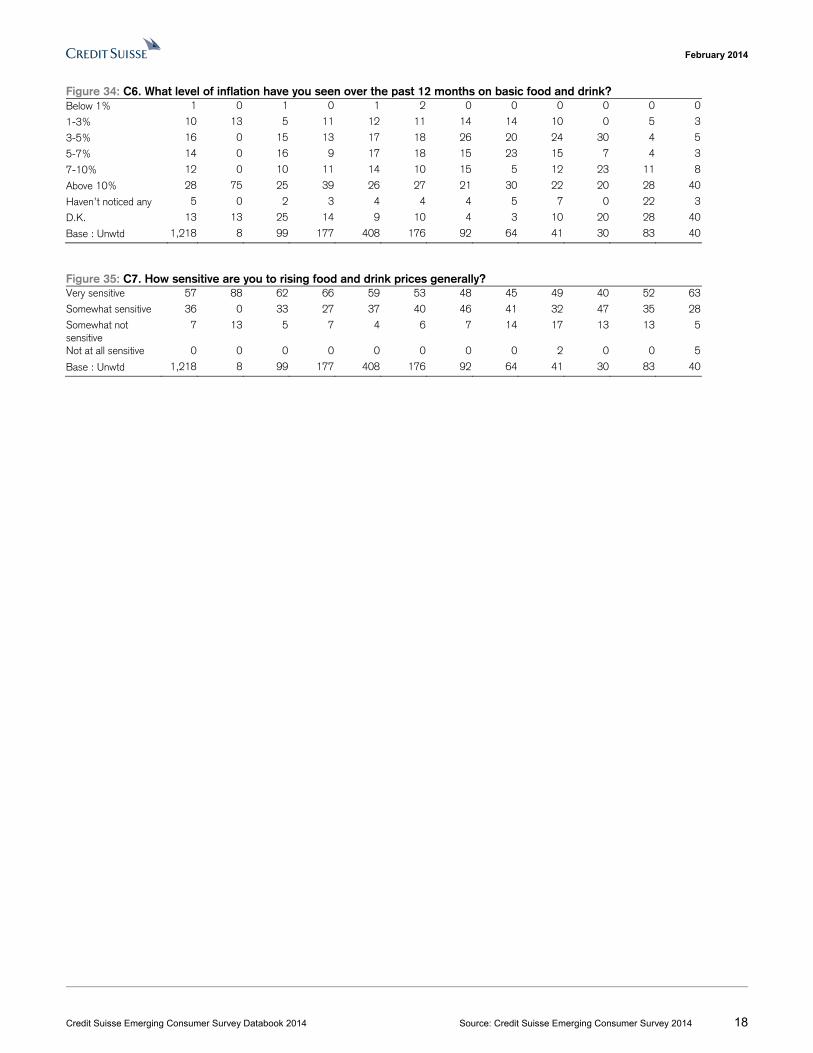

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 18

Figure 34: C6. What level of inflation have you seen over the past 12 months on basic food and drink? Below 1% 1 0 1 0 1 2 0 0 0 0 0 0

1-3% 10 13 5 11 12 11 14 14 10 0 5 3

3-5% 16 0 15 13 17 18 26 20 24 30 4 5

5-7% 14 0 16 9 17 18 15 23 15 7 4 3

7-10% 12 0 10 11 14 10 15 5 12 23 11 8

Above 10% 28 75 25 39 26 27 21 30 22 20 28 40

Haven’t noticed any 5 0 2 3 4 4 4 5 7 0 22 3

D.K. 13 13 25 14 9 10 4 3 10 20 28 40

Base : Unwtd 1,218 8 99 177 408 176 92 64 41 30 83 40

Figure 35: C7. How sensitive are you to rising food and drink prices generally? Very sensitive 57 88 62 66 59 53 48 45 49 40 52 63

Somewhat sensitive 36 0 33 27 37 40 46 41 32 47 35 28

Somewhat not sensitive

7 13 5 7 4 6 7 14 17 13 13 5

Not at all sensitive 0 0 0 0 0 0 0 0 2 0 0 5

Base : Unwtd 1,218 8 99 177 408 176 92 64 41 30 83 40

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 19

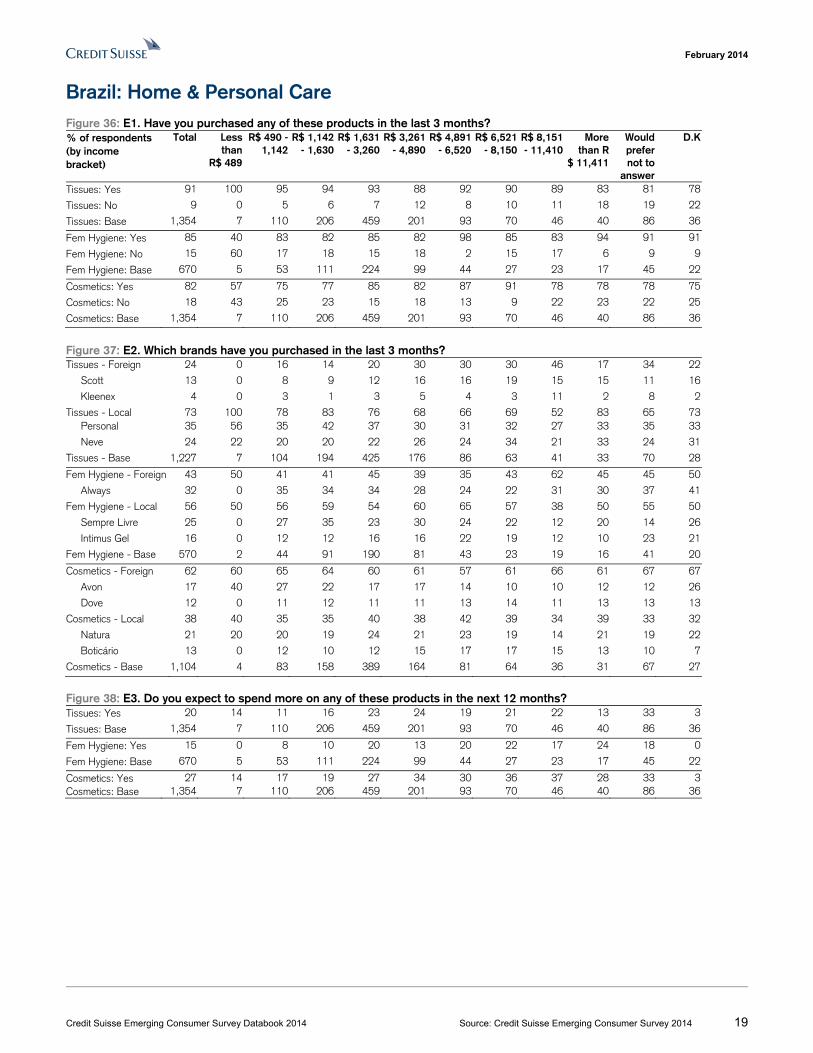

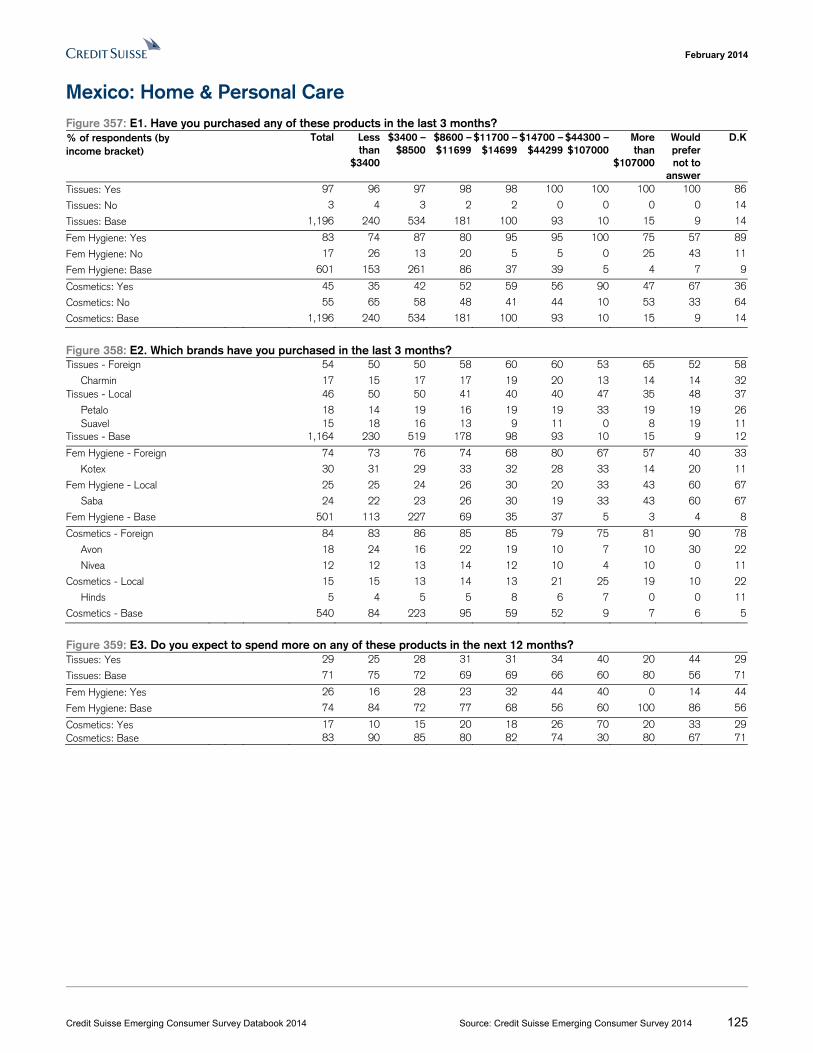

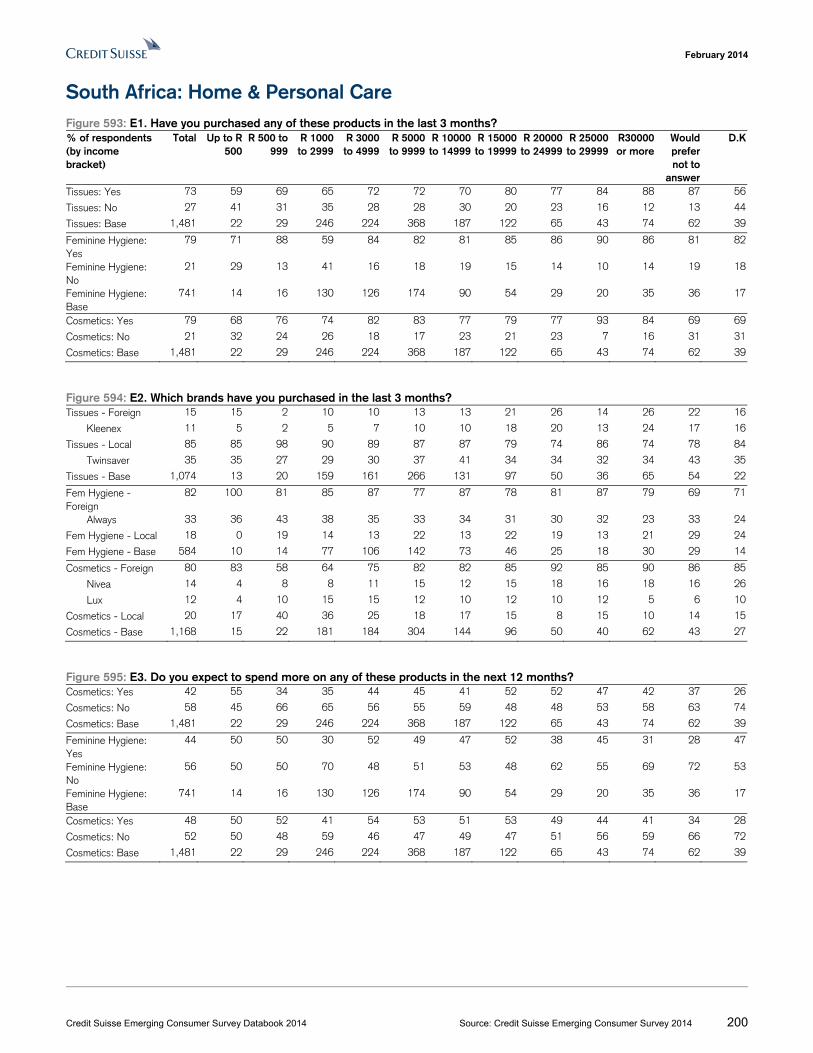

Brazil: Home & Personal Care Figure 36: E1. Have you purchased any of these products in the last 3 months? % of respondents (by income bracket)

Total Less than

R$ 489

R$ 490 - 1,142

R$ 1,142 - 1,630

R$ 1,631 - 3,260

R$ 3,261 - 4,890

R$ 4,891 - 6,520

R$ 6,521 - 8,150

R$ 8,151 - 11,410

More than R

$ 11,411

Would prefer not to

answer

D.K

Tissues: Yes 91 100 95 94 93 88 92 90 89 83 81 78

Tissues: No 9 0 5 6 7 12 8 10 11 18 19 22

Tissues: Base 1,354 7 110 206 459 201 93 70 46 40 86 36

Fem Hygiene: Yes 85 40 83 82 85 82 98 85 83 94 91 91

Fem Hygiene: No 15 60 17 18 15 18 2 15 17 6 9 9

Fem Hygiene: Base 670 5 53 111 224 99 44 27 23 17 45 22

Cosmetics: Yes 82 57 75 77 85 82 87 91 78 78 78 75

Cosmetics: No 18 43 25 23 15 18 13 9 22 23 22 25

Cosmetics: Base 1,354 7 110 206 459 201 93 70 46 40 86 36

Figure 37: E2. Which brands have you purchased in the last 3 months? Tissues - Foreign 24 0 16 14 20 30 30 30 46 17 34 22

Scott 13 0 8 9 12 16 16 19 15 15 11 16

Kleenex 4 0 3 1 3 5 4 3 11 2 8 2

Tissues - Local 73 100 78 83 76 68 66 69 52 83 65 73 Personal 35 56 35 42 37 30 31 32 27 33 35 33

Neve 24 22 20 20 22 26 24 34 21 33 24 31

Tissues - Base 1,227 7 104 194 425 176 86 63 41 33 70 28

Fem Hygiene - Foreign 43 50 41 41 45 39 35 43 62 45 45 50

Always 32 0 35 34 34 28 24 22 31 30 37 41

Fem Hygiene - Local 56 50 56 59 54 60 65 57 38 50 55 50

Sempre Livre 25 0 27 35 23 30 24 22 12 20 14 26

Intimus Gel 16 0 12 12 16 16 22 19 12 10 23 21

Fem Hygiene - Base 570 2 44 91 190 81 43 23 19 16 41 20

Cosmetics - Foreign 62 60 65 64 60 61 57 61 66 61 67 67

Avon 17 40 27 22 17 17 14 10 10 12 12 26

Dove 12 0 11 12 11 11 13 14 11 13 13 13

Cosmetics - Local 38 40 35 35 40 38 42 39 34 39 33 32

Natura 21 20 20 19 24 21 23 19 14 21 19 22

Boticário 13 0 12 10 12 15 17 17 15 13 10 7

Cosmetics - Base 1,104 4 83 158 389 164 81 64 36 31 67 27

Figure 38: E3. Do you expect to spend more on any of these products in the next 12 months? Tissues: Yes 20 14 11 16 23 24 19 21 22 13 33 3

Tissues: Base 1,354 7 110 206 459 201 93 70 46 40 86 36

Fem Hygiene: Yes 15 0 8 10 20 13 20 22 17 24 18 0

Fem Hygiene: Base 670 5 53 111 224 99 44 27 23 17 45 22

Cosmetics: Yes 27 14 17 19 27 34 30 36 37 28 33 3Cosmetics: Base 1,354 7 110 206 459 201 93 70 46 40 86 36

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 20

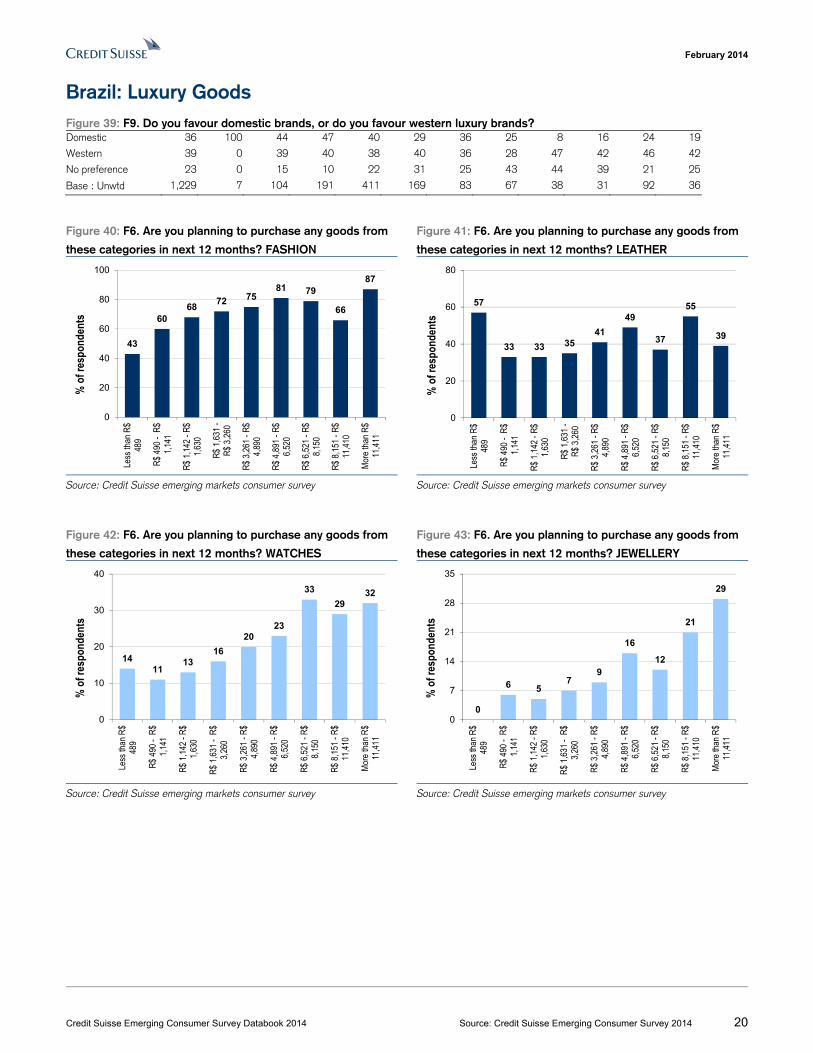

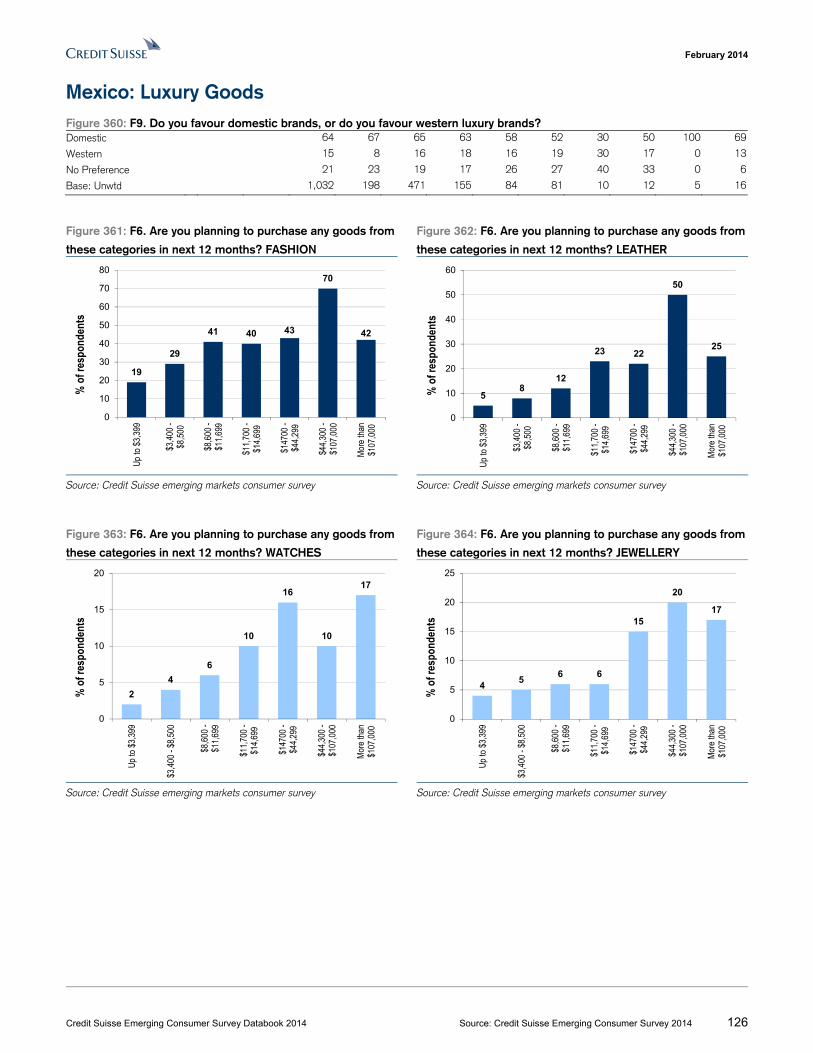

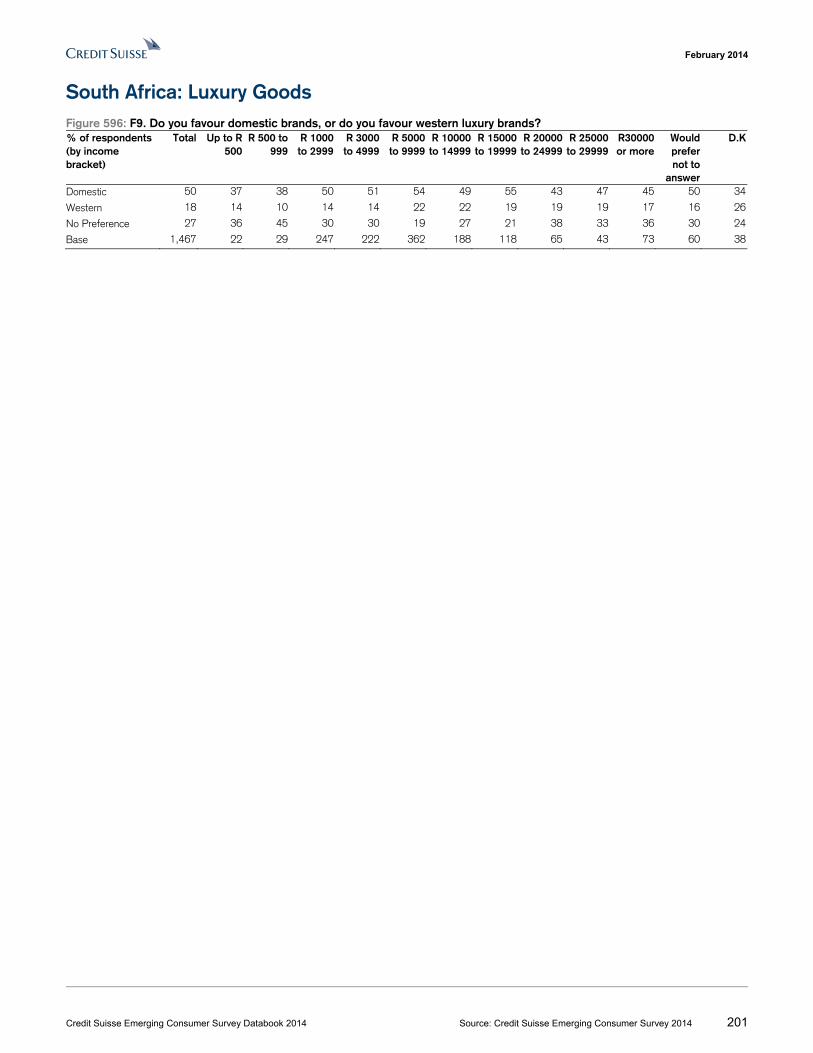

Brazil: Luxury Goods Figure 39: F9. Do you favour domestic brands, or do you favour western luxury brands? Domestic 36 100 44 47 40 29 36 25 8 16 24 19

Western 39 0 39 40 38 40 36 28 47 42 46 42

No preference 23 0 15 10 22 31 25 43 44 39 21 25

Base : Unwtd 1,229 7 104 191 411 169 83 67 38 31 92 36

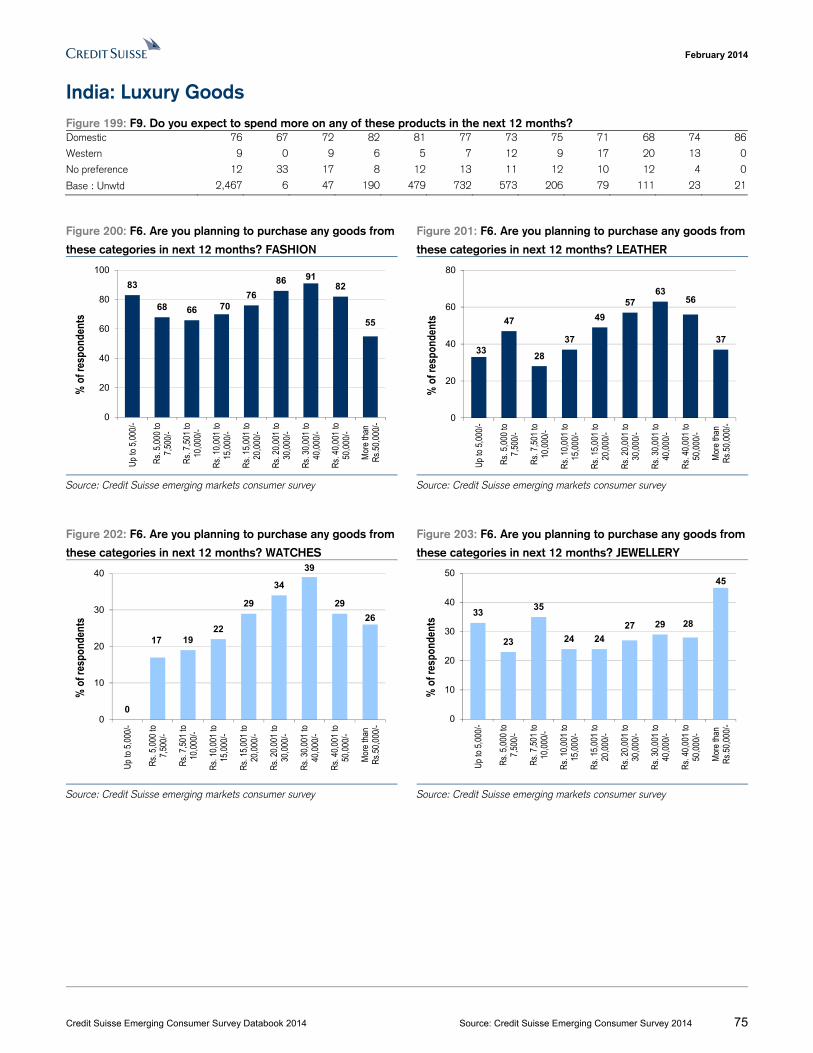

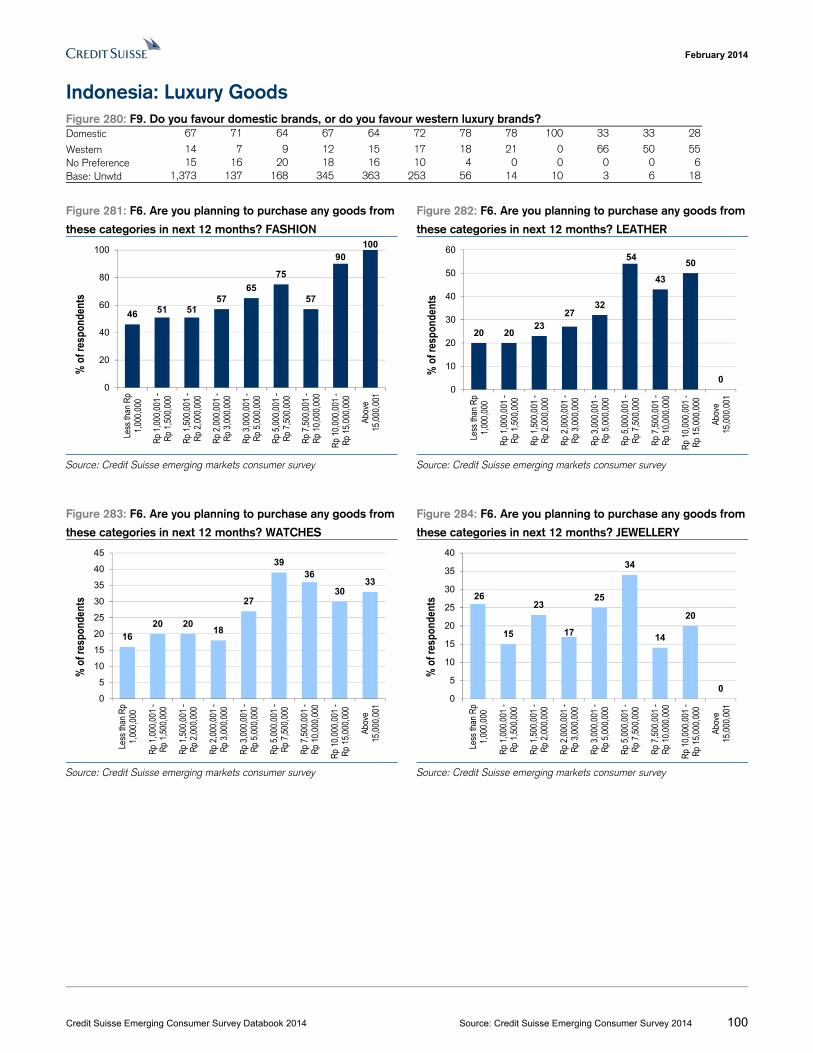

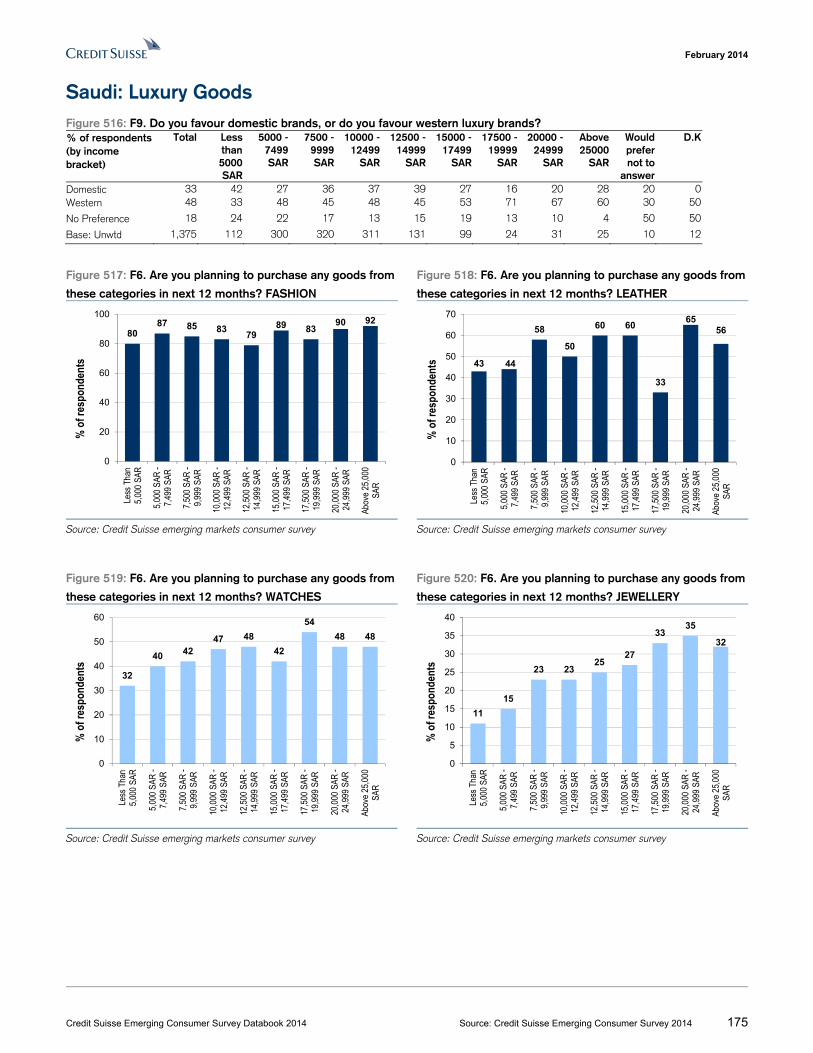

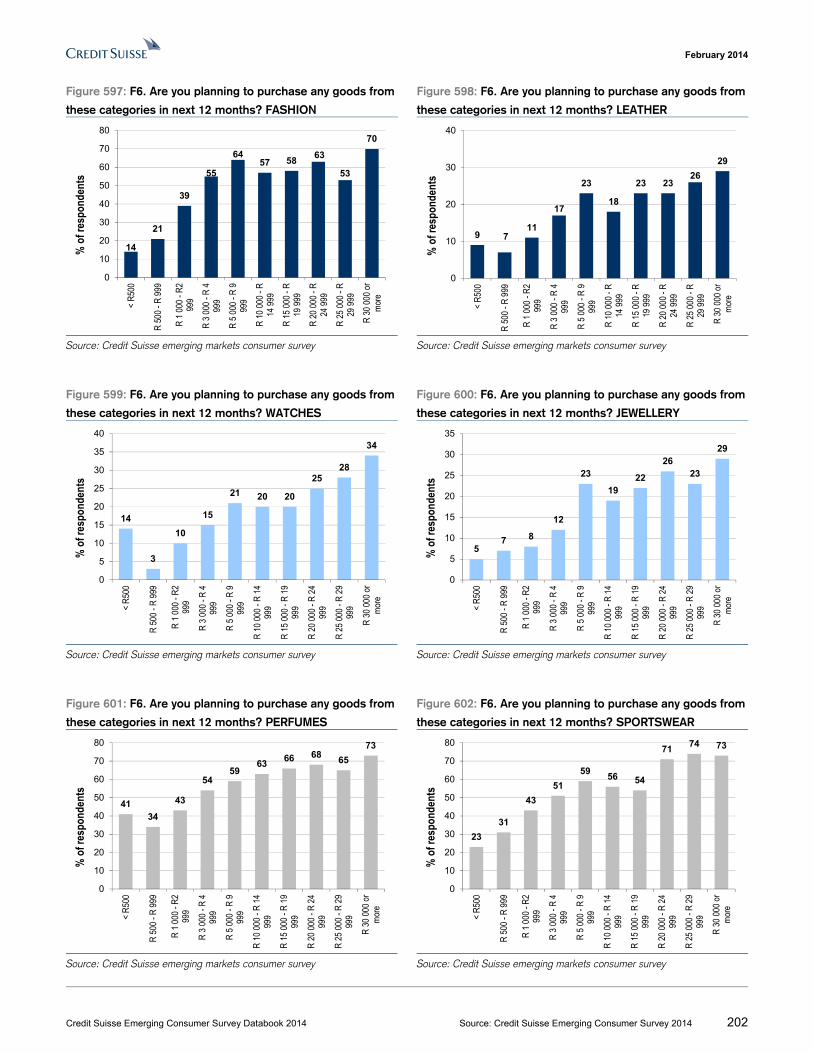

Figure 40: F6. Are you planning to purchase any goods from

these categories in next 12 months? FASHION

Figure 41: F6. Are you planning to purchase any goods from

these categories in next 12 months? LEATHER

Source: Credit Suisse emerging markets consumer survey Source: Credit Suisse emerging markets consumer survey

Figure 42: F6. Are you planning to purchase any goods from

these categories in next 12 months? WATCHES

Figure 43: F6. Are you planning to purchase any goods from

these categories in next 12 months? JEWELLERY

Source: Credit Suisse emerging markets consumer survey Source: Credit Suisse emerging markets consumer survey

43

6068

72 7581 79

66

87

0

20

40

60

80

100

Less

than

R$

489

R$

490

- R

$1,

141

R$

1,14

2 - R

$1,

630

R$

1,63

1 -

R$

3,26

0

R$

3,26

1 - R

$4,

890

R$

4,89

1 - R

$6,

520

R$

6,52

1 - R

$8,

150

R$

8,15

1 - R

$11

,410

Mor

e th

an R

$11

,411

% o

f res

pond

ents

57

33 33 3541

49

37

55

39

0

20

40

60

80

Less

than

R$

489

R$

490

- R

$1,

141

R$

1,14

2 - R

$1,

630

R$

1,63

1 -

R$

3,26

0

R$

3,26

1 - R

$4,

890

R$

4,89

1 - R

$6,

520

R$

6,52

1 - R

$8,

150

R$

8,15

1 - R

$11

,410

Mor

e th

an R

$11

,411

% o

f res

pond

ents

1411

1316

2023

33

2932

0

10

20

30

40

Less

than

R$

489

R$

490

- R

$1,

141

R$

1,14

2 - R

$1,

630

R$

1,63

1 -

R$

3,26

0

R$

3,26

1 - R

$4,

890

R$

4,89

1 - R

$6,

520

R$

6,52

1 - R

$8,

150

R$

8,15

1 - R

$11

,410

Mor

e th

an R

$11

,411

% o

f res

pond

ents

0

6 57

9

16

12

21

29

0

7

14

21

28

35

Less

than

R$

489

R$

490

- R

$1,

141

R$

1,14

2 - R

$1,

630

R$

1,63

1 -

R$

3,26

0

R$

3,26

1 - R

$4,

890

R$

4,89

1 - R

$6,

520

R$

6,52

1 - R

$8,

150

R$

8,15

1 - R

$11

,410

Mor

e th

an R

$11

,411

% o

f res

pond

ents

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 21

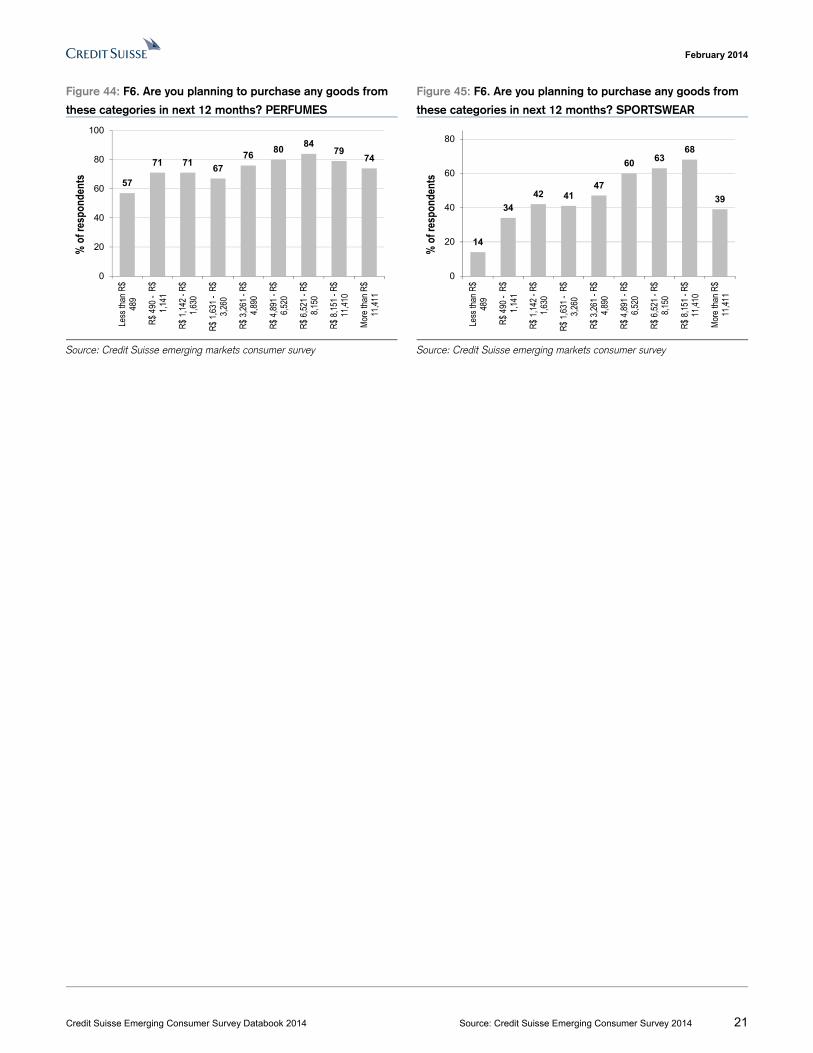

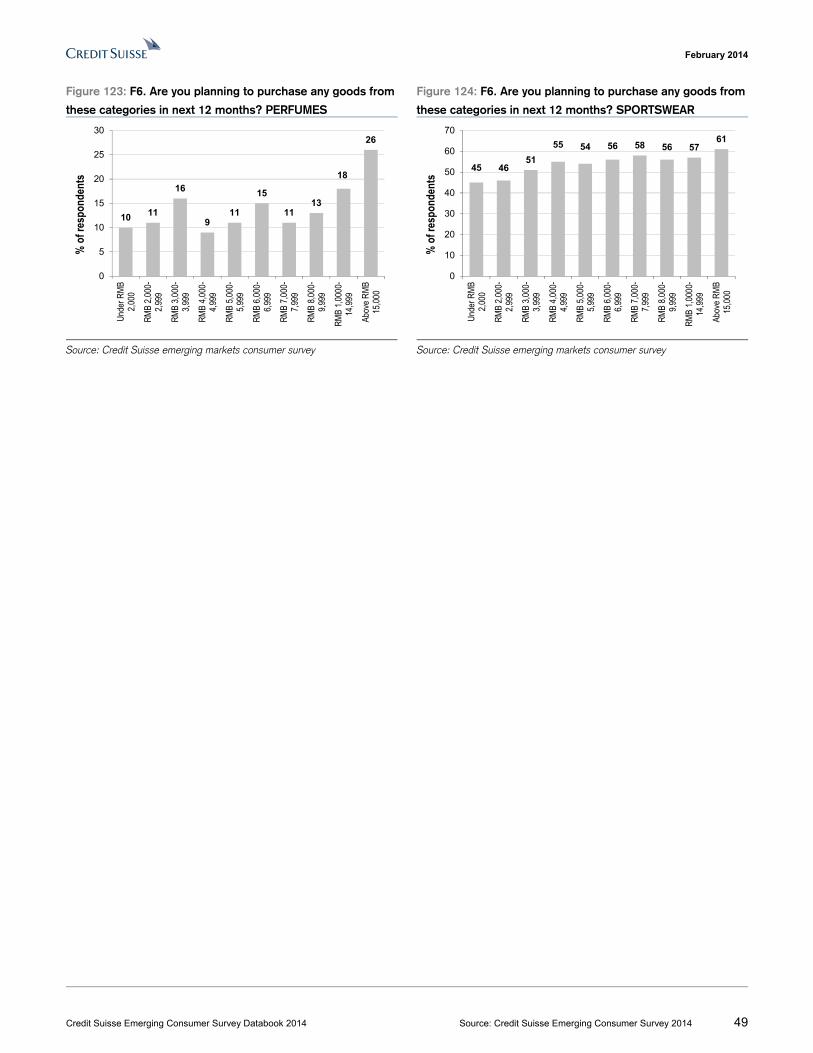

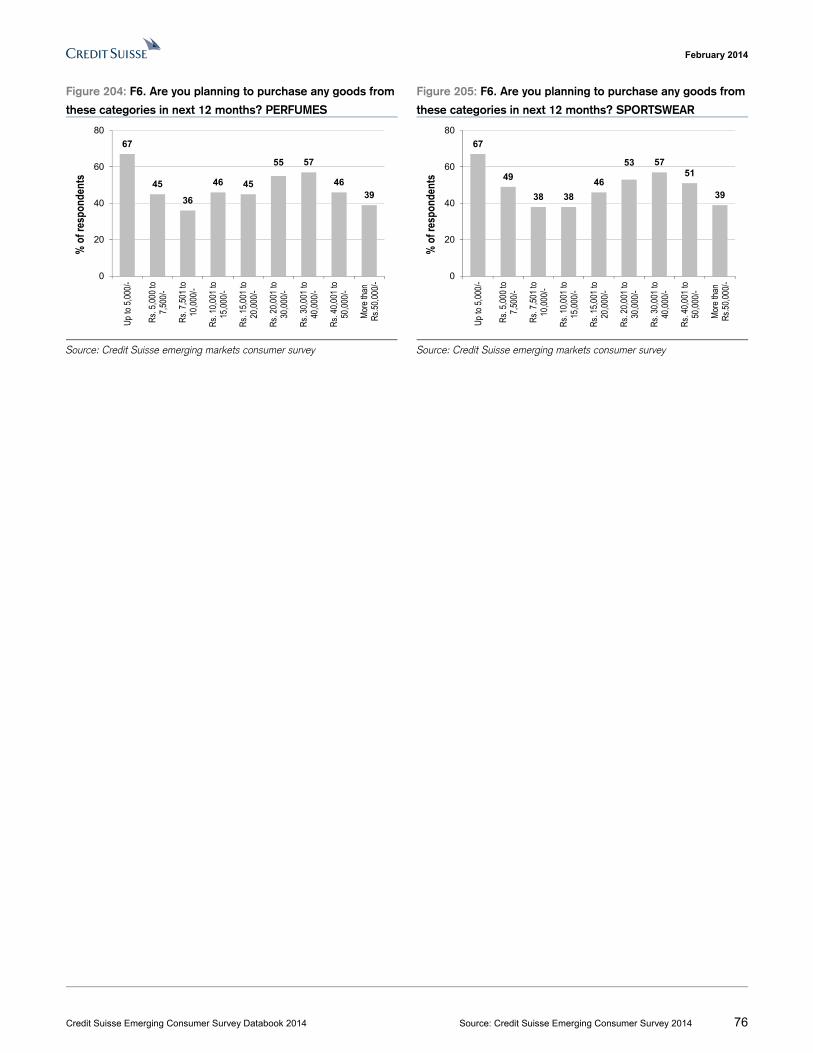

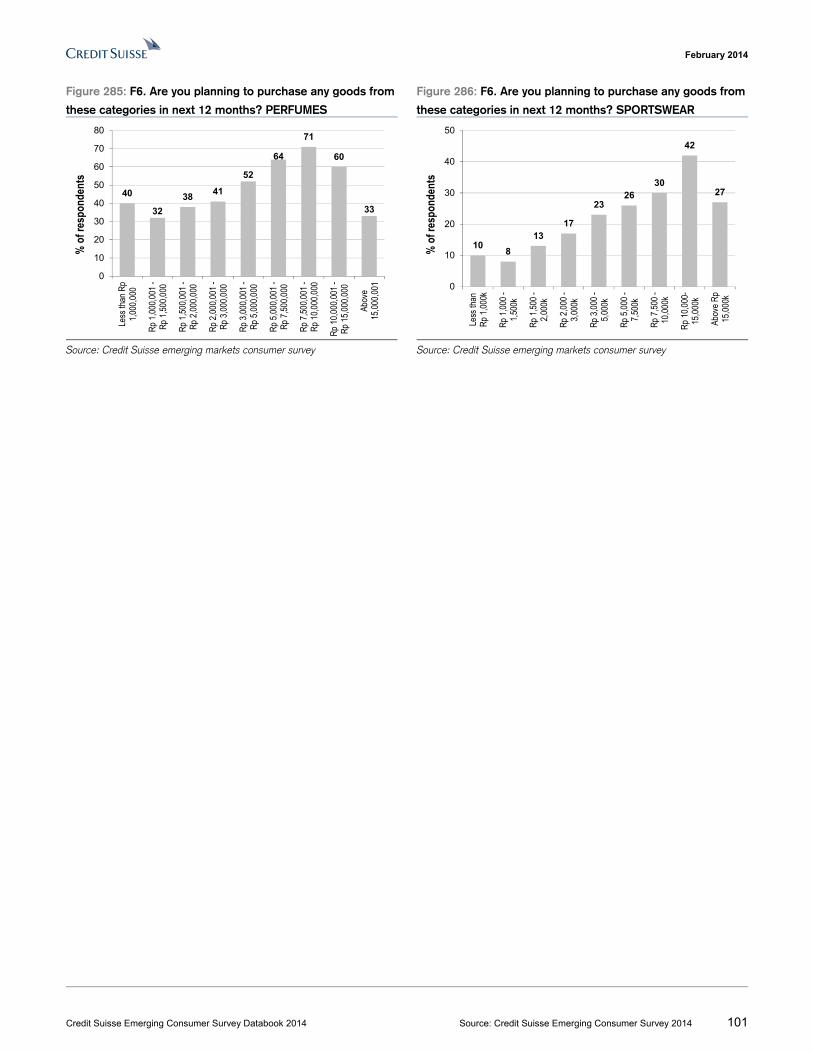

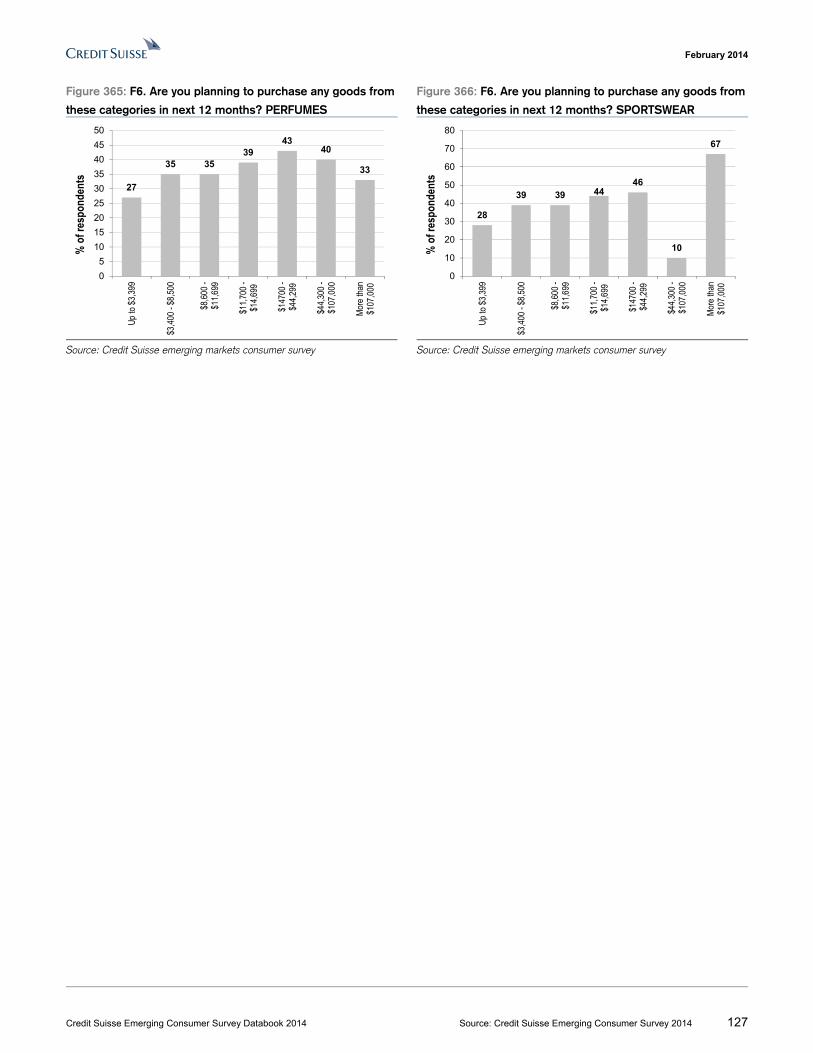

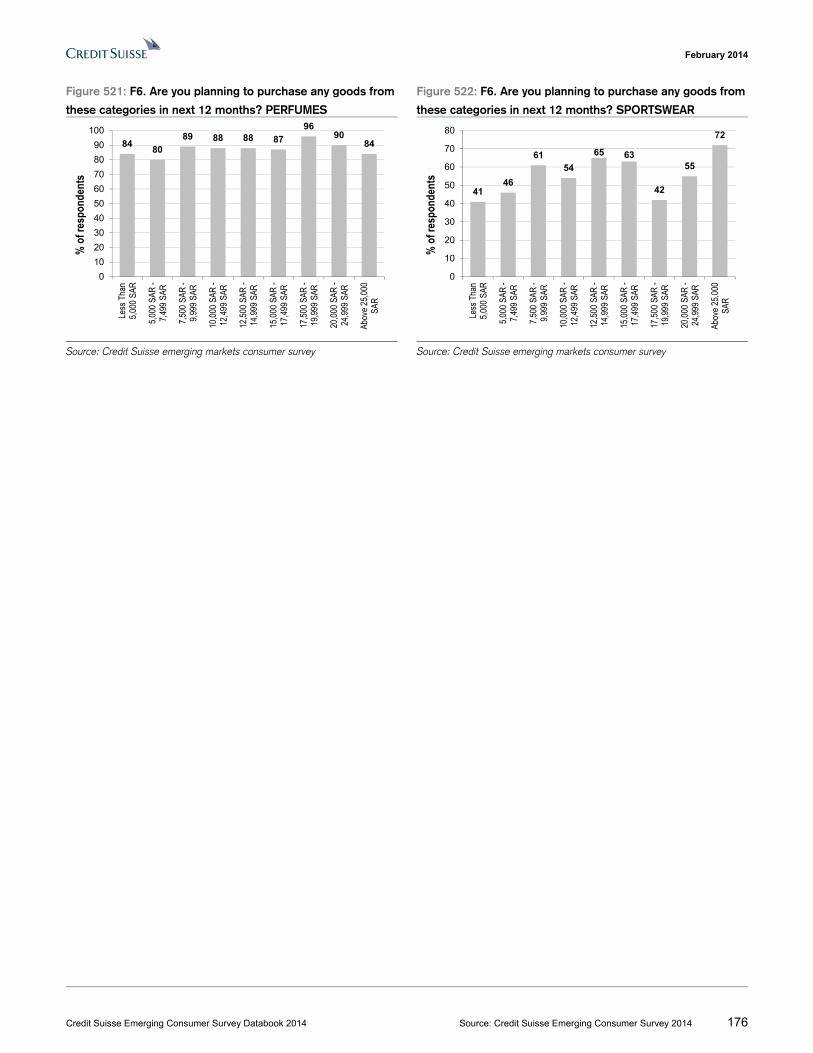

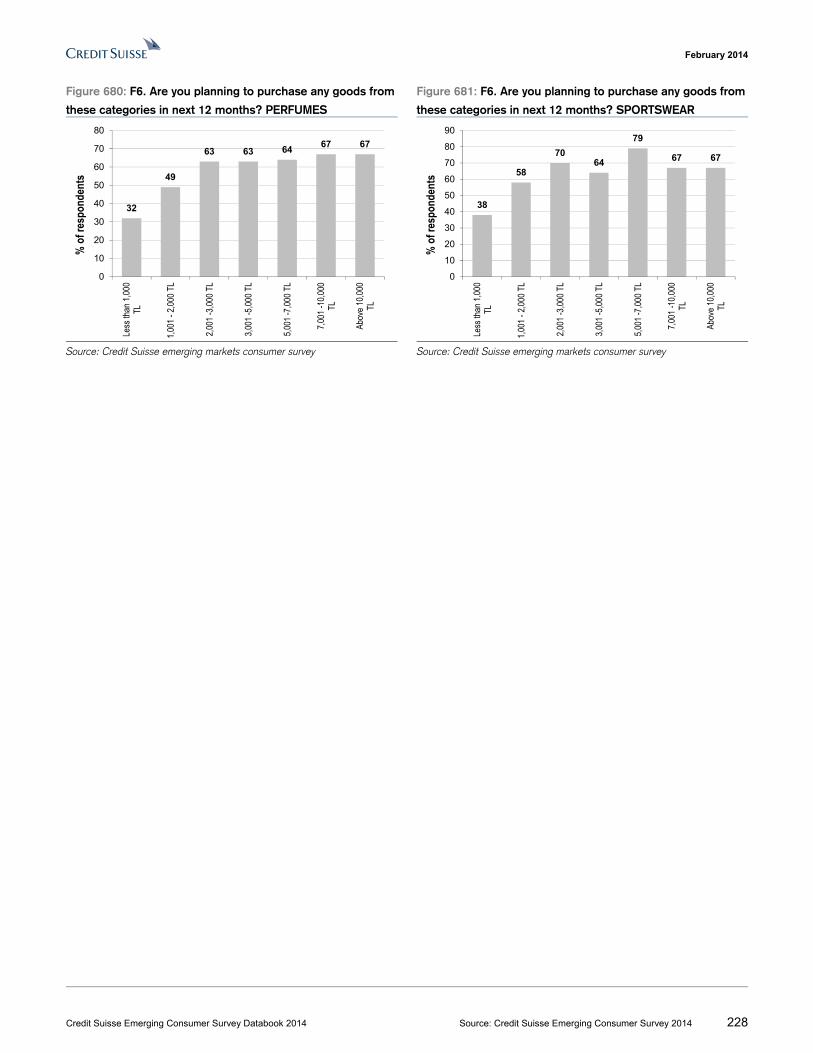

Figure 44: F6. Are you planning to purchase any goods from

these categories in next 12 months? PERFUMES

Figure 45: F6. Are you planning to purchase any goods from

these categories in next 12 months? SPORTSWEAR

Source: Credit Suisse emerging markets consumer survey Source: Credit Suisse emerging markets consumer survey

57

71 7167

7680

8479

74

0

20

40

60

80

100Le

ss th

an R

$48

9

R$

490

- R

$1,

141

R$

1,14

2 - R

$1,

630

R$

1,63

1 -

R$

3,26

0

R$

3,26

1 - R

$4,

890

R$

4,89

1 - R

$6,

520

R$

6,52

1 - R

$8,

150

R$

8,15

1 - R

$11

,410

Mor

e th

an R

$11

,411

% o

f res

pond

ents

14

34

42 4147

60 6368

39

0

20

40

60

80

Less

than

R$

489

R$

490

- R

$1,

141

R$

1,14

2 - R

$1,

630

R$

1,63

1 -

R$

3,26

0

R$

3,26

1 - R

$4,

890

R$

4,89

1 - R

$6,

520

R$

6,52

1 - R

$8,

150

R$

8,15

1 - R

$11

,410

Mor

e th

an R

$11

,411

% o

f res

pond

ents

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 22

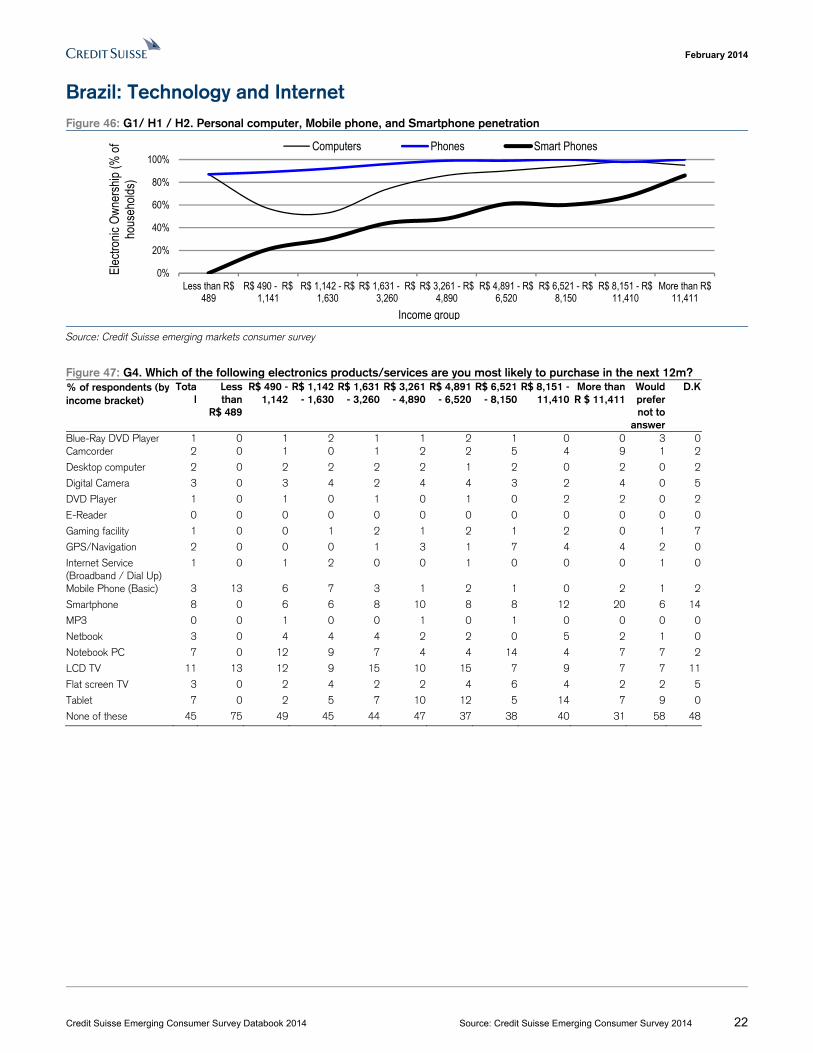

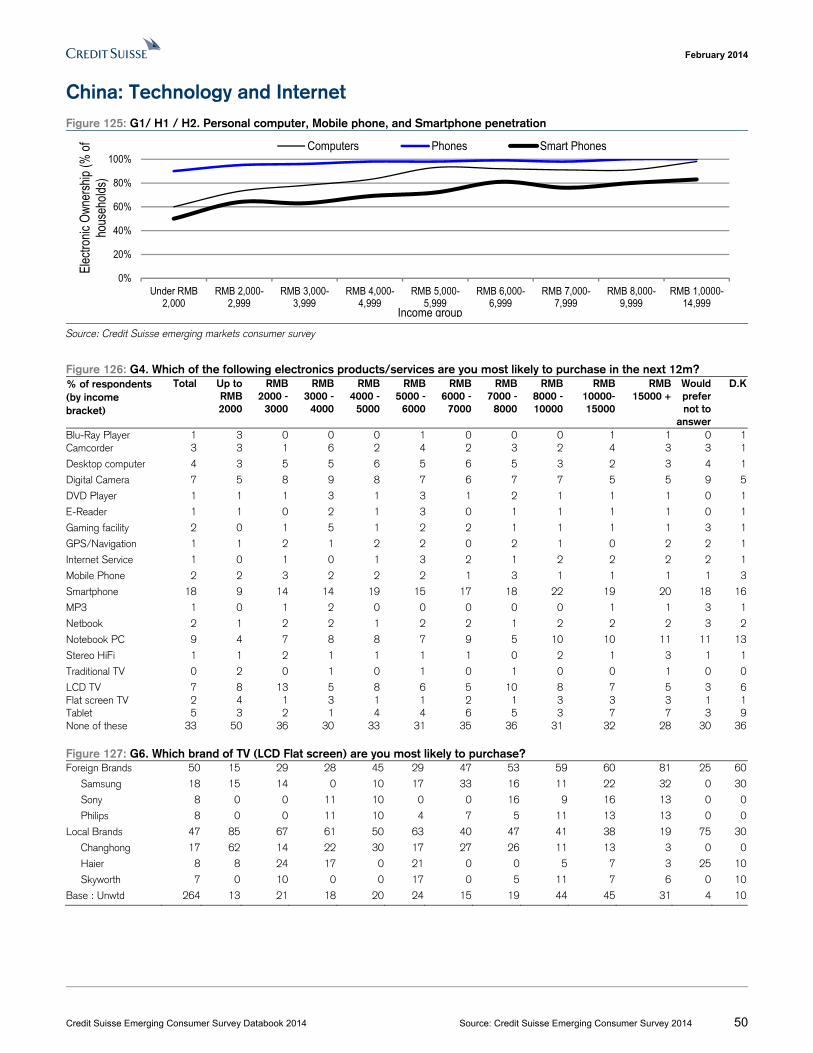

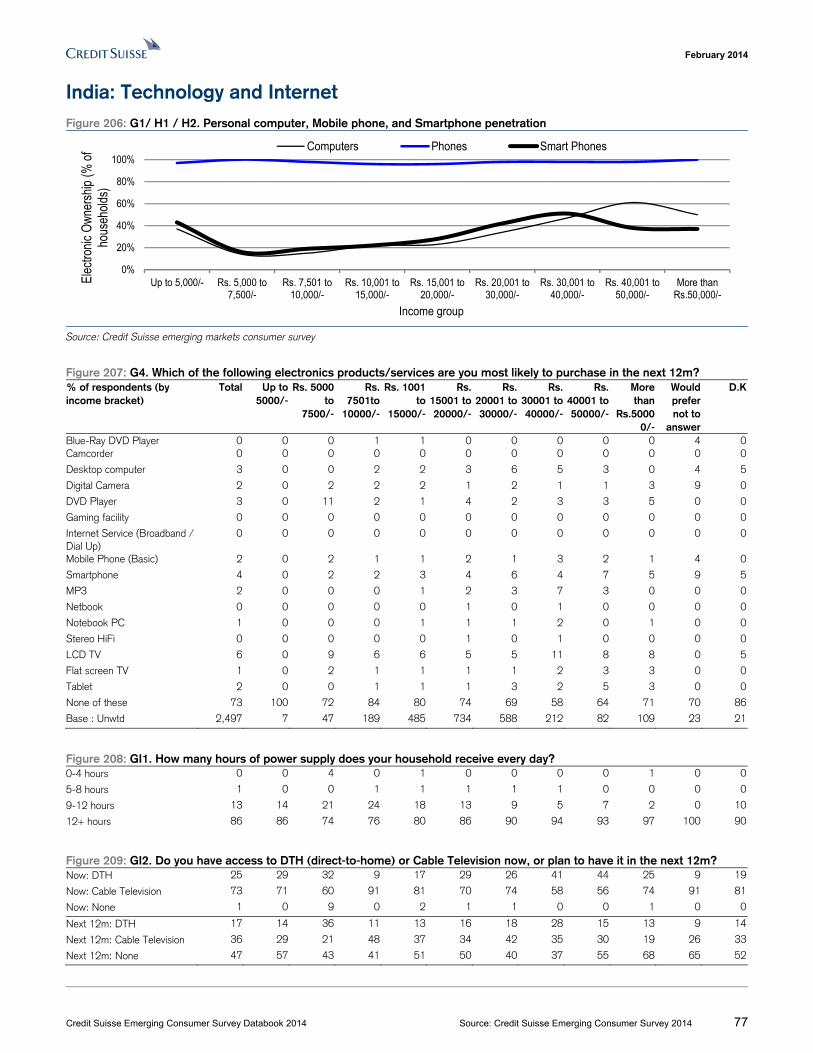

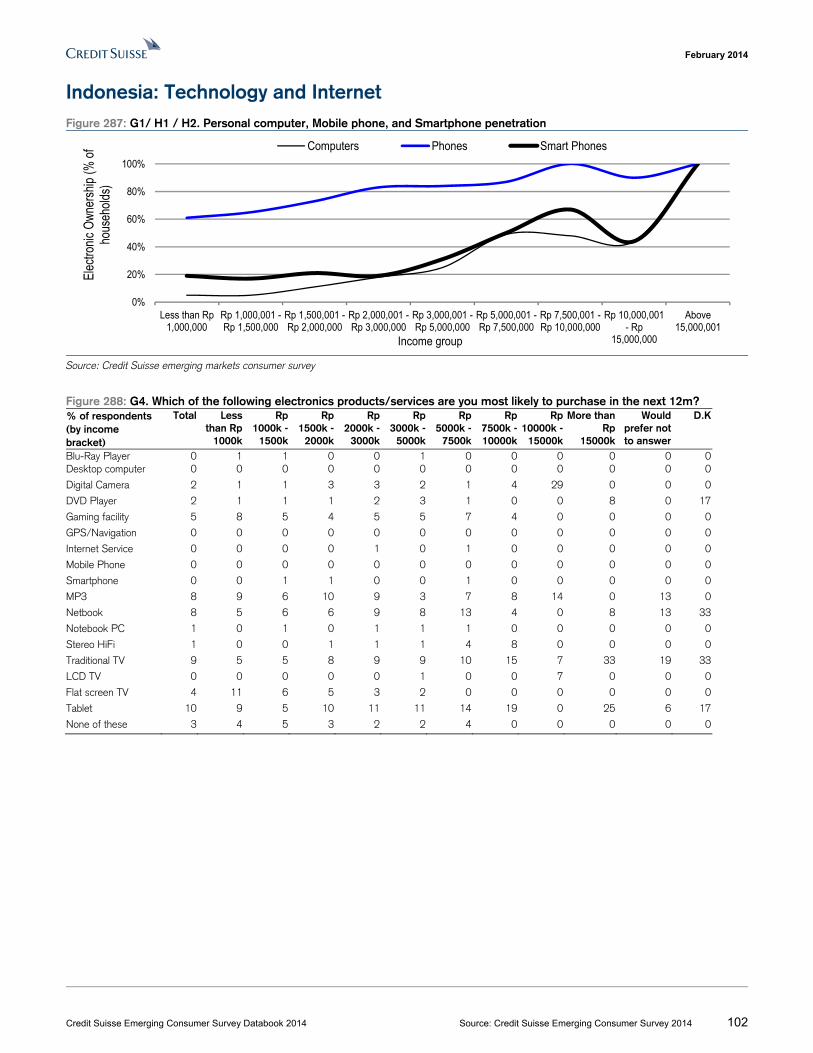

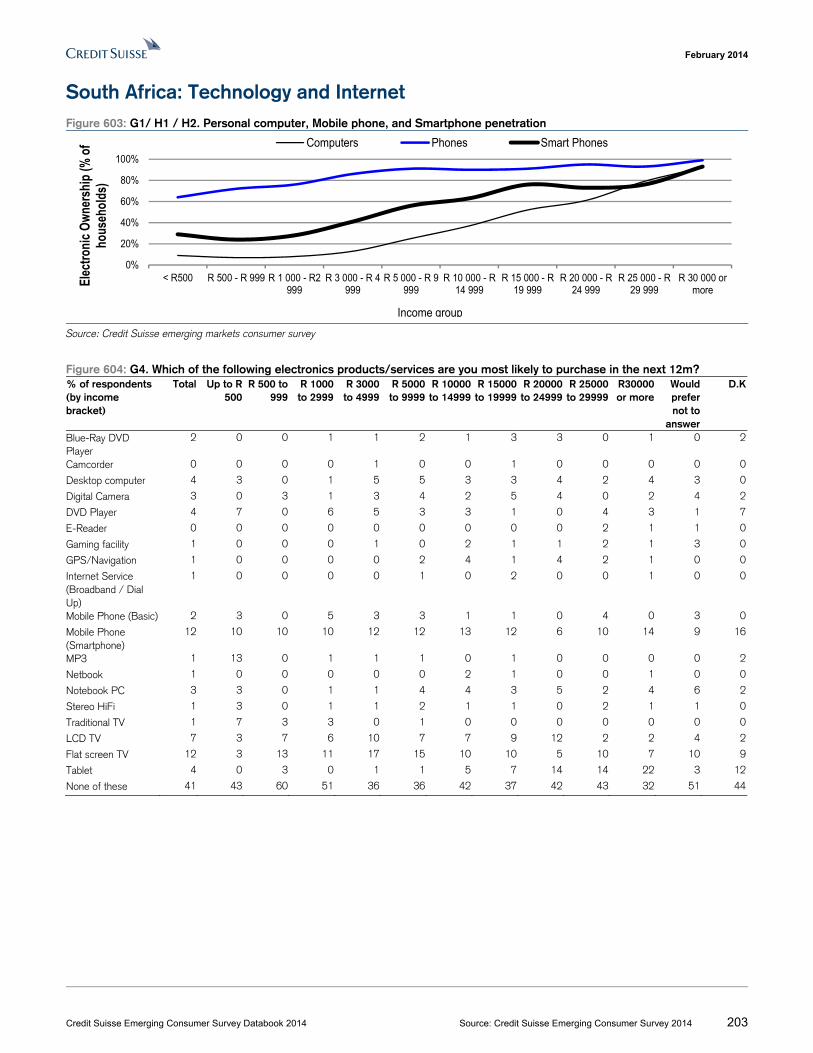

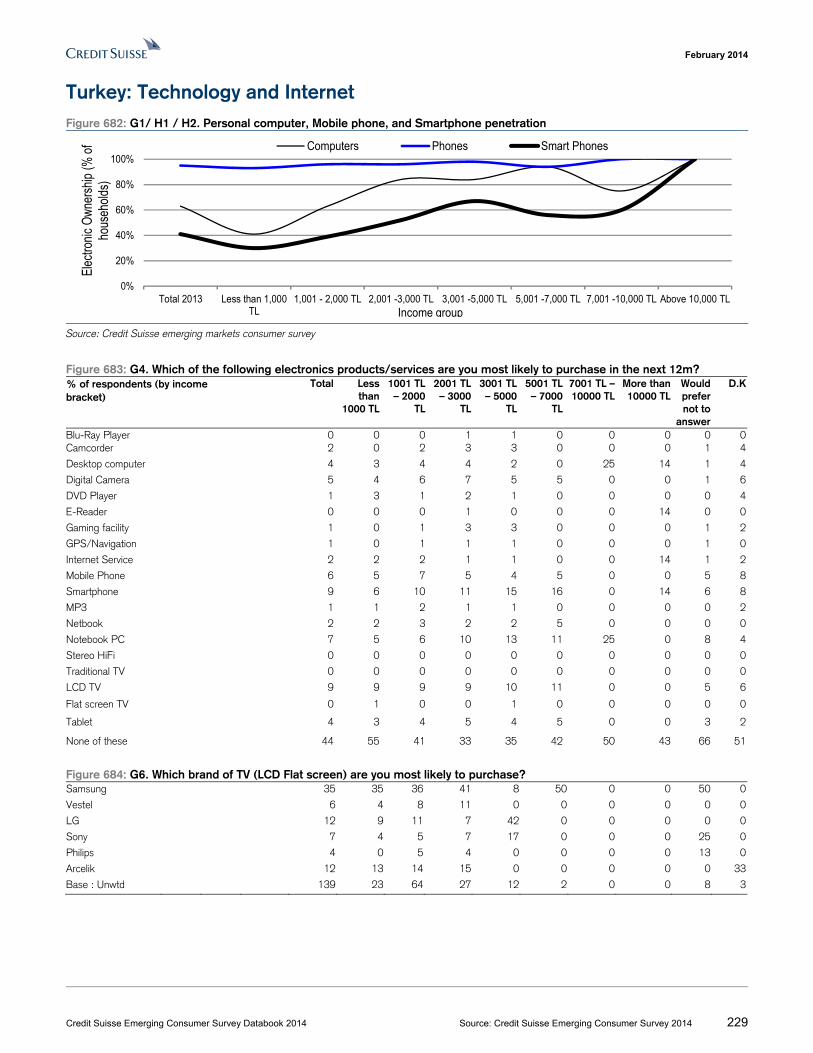

Brazil: Technology and Internet Figure 46: G1/ H1 / H2. Personal computer, Mobile phone, and Smartphone penetration

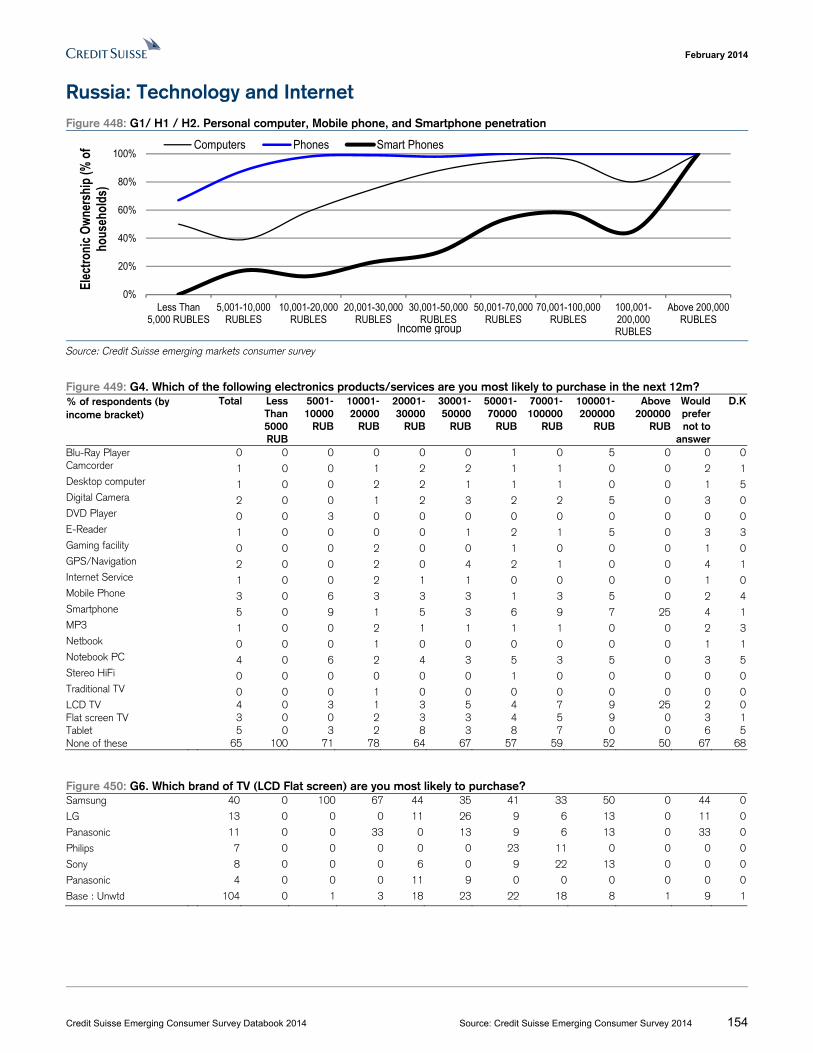

Source: Credit Suisse emerging markets consumer survey

Figure 47: G4. Which of the following electronics products/services are you most likely to purchase in the next 12m? % of respondents (by income bracket)

Total

Less than

R$ 489

R$ 490 - 1,142

R$ 1,142 - 1,630

R$ 1,631 - 3,260

R$ 3,261 - 4,890

R$ 4,891 - 6,520

R$ 6,521 - 8,150

R$ 8,151 -11,410

More than R $ 11,411

Would prefer not to

answer

D.K

Blue-Ray DVD Player 1 0 1 2 1 1 2 1 0 0 3 0Camcorder 2 0 1 0 1 2 2 5 4 9 1 2

Desktop computer 2 0 2 2 2 2 1 2 0 2 0 2

Digital Camera 3 0 3 4 2 4 4 3 2 4 0 5

DVD Player 1 0 1 0 1 0 1 0 2 2 0 2

E-Reader 0 0 0 0 0 0 0 0 0 0 0 0

Gaming facility 1 0 0 1 2 1 2 1 2 0 1 7

GPS/Navigation 2 0 0 0 1 3 1 7 4 4 2 0

Internet Service (Broadband / Dial Up)

1 0 1 2 0 0 1 0 0 0 1 0

Mobile Phone (Basic) 3 13 6 7 3 1 2 1 0 2 1 2

Smartphone 8 0 6 6 8 10 8 8 12 20 6 14

MP3 0 0 1 0 0 1 0 1 0 0 0 0

Netbook 3 0 4 4 4 2 2 0 5 2 1 0

Notebook PC 7 0 12 9 7 4 4 14 4 7 7 2

LCD TV 11 13 12 9 15 10 15 7 9 7 7 11

Flat screen TV 3 0 2 4 2 2 4 6 4 2 2 5

Tablet 7 0 2 5 7 10 12 5 14 7 9 0

None of these 45 75 49 45 44 47 37 38 40 31 58 48

0%

20%

40%

60%

80%

100%

Less than R$489

R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

R$ 8,151 - R$11,410

More than R$11,411

Elec

troni

c O

wne

rshi

p (%

of

hous

ehol

ds)

Computers Phones Smart Phones

Income group

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 23

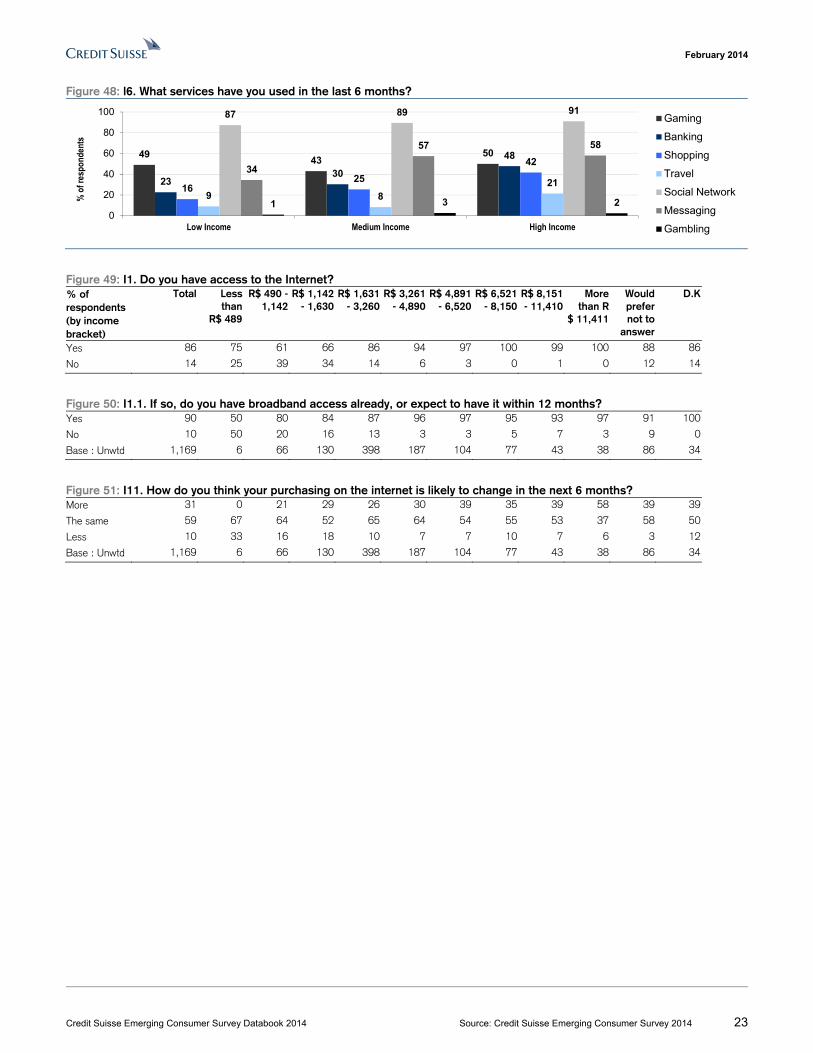

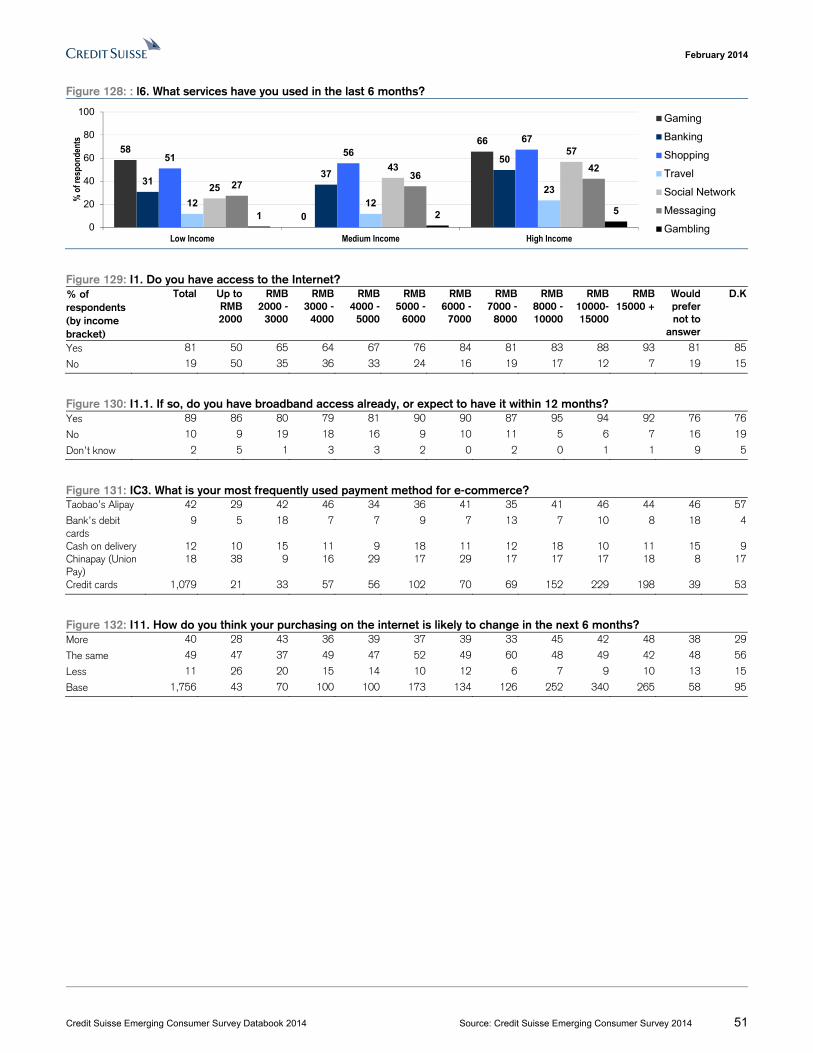

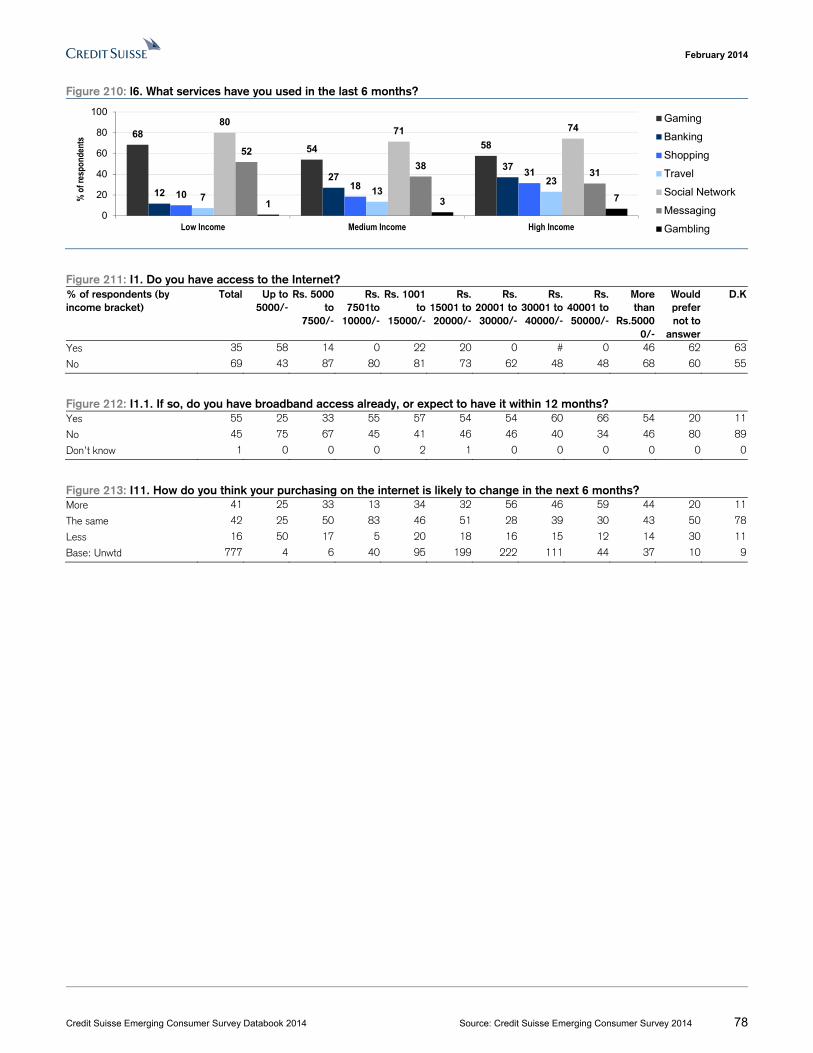

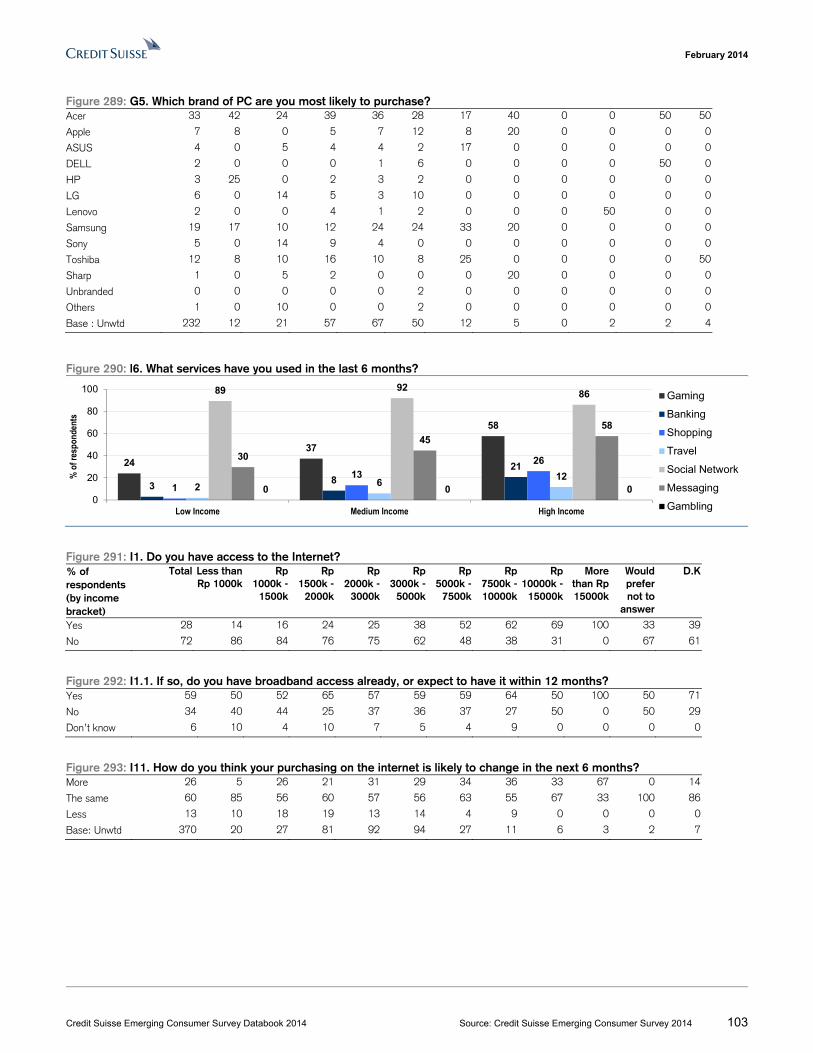

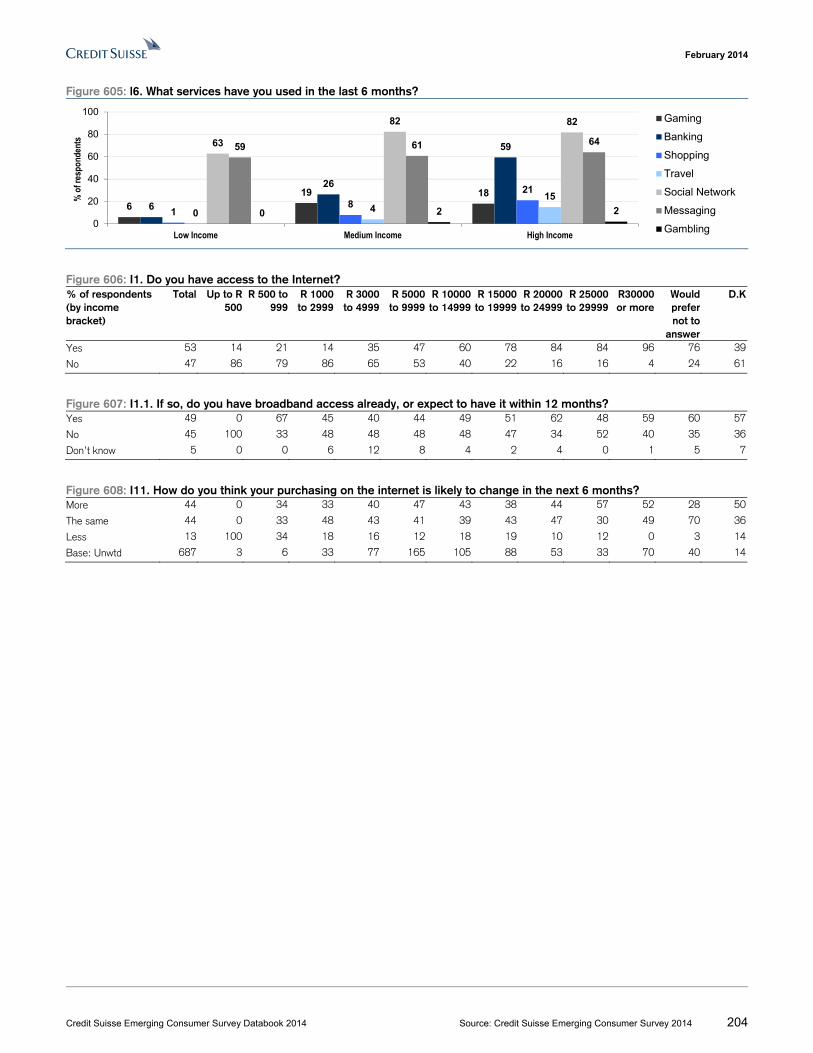

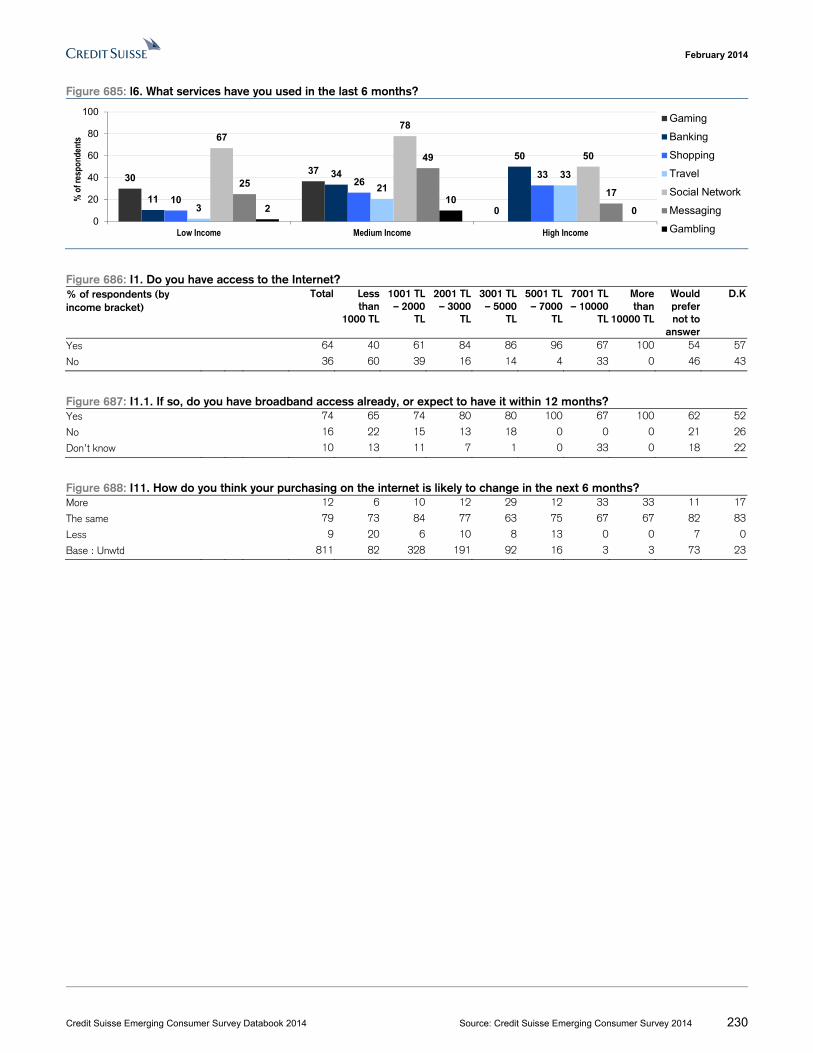

Figure 48: l6. What services have you used in the last 6 months?

Figure 49: I1. Do you have access to the Internet? % of respondents (by income bracket)

Total Less than

R$ 489

R$ 490 - 1,142

R$ 1,142 - 1,630

R$ 1,631 - 3,260

R$ 3,261 - 4,890

R$ 4,891 - 6,520

R$ 6,521 - 8,150

R$ 8,151 - 11,410

More than R

$ 11,411

Would prefer not to

answer

D.K

Yes 86 75 61 66 86 94 97 100 99 100 88 86

No 14 25 39 34 14 6 3 0 1 0 12 14

Figure 50: I1.1. If so, do you have broadband access already, or expect to have it within 12 months? Yes 90 50 80 84 87 96 97 95 93 97 91 100

No 10 50 20 16 13 3 3 5 7 3 9 0

Base : Unwtd 1,169 6 66 130 398 187 104 77 43 38 86 34

Figure 51: I11. How do you think your purchasing on the internet is likely to change in the next 6 months? More 31 0 21 29 26 30 39 35 39 58 39 39

The same 59 67 64 52 65 64 54 55 53 37 58 50

Less 10 33 16 18 10 7 7 10 7 6 3 12

Base : Unwtd 1,169 6 66 130 398 187 104 77 43 38 86 34

4943

50

2330

48

1625

42

9 821

87 89 91

34

57 58

1 3 20

20

40

60

80

100

Low Income Medium Income High Income

% o

f res

pond

ents

Gaming

Banking

Shopping

Travel

Social Network

Messaging

Gambling

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 24

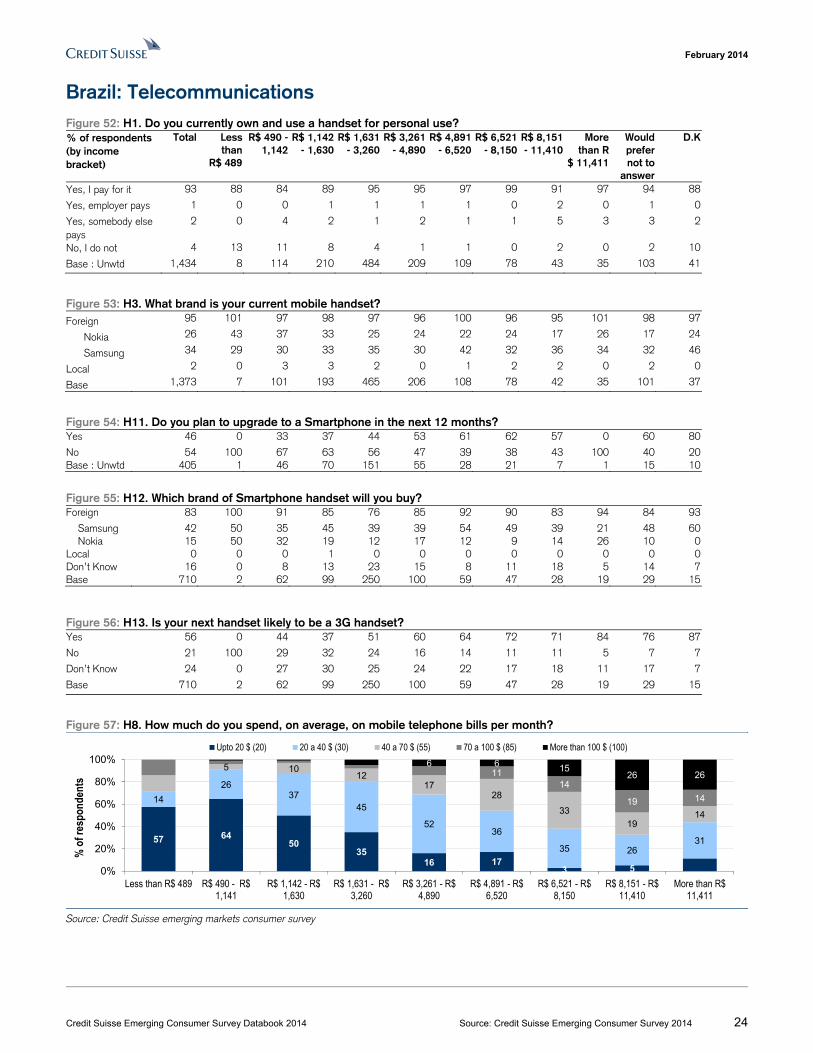

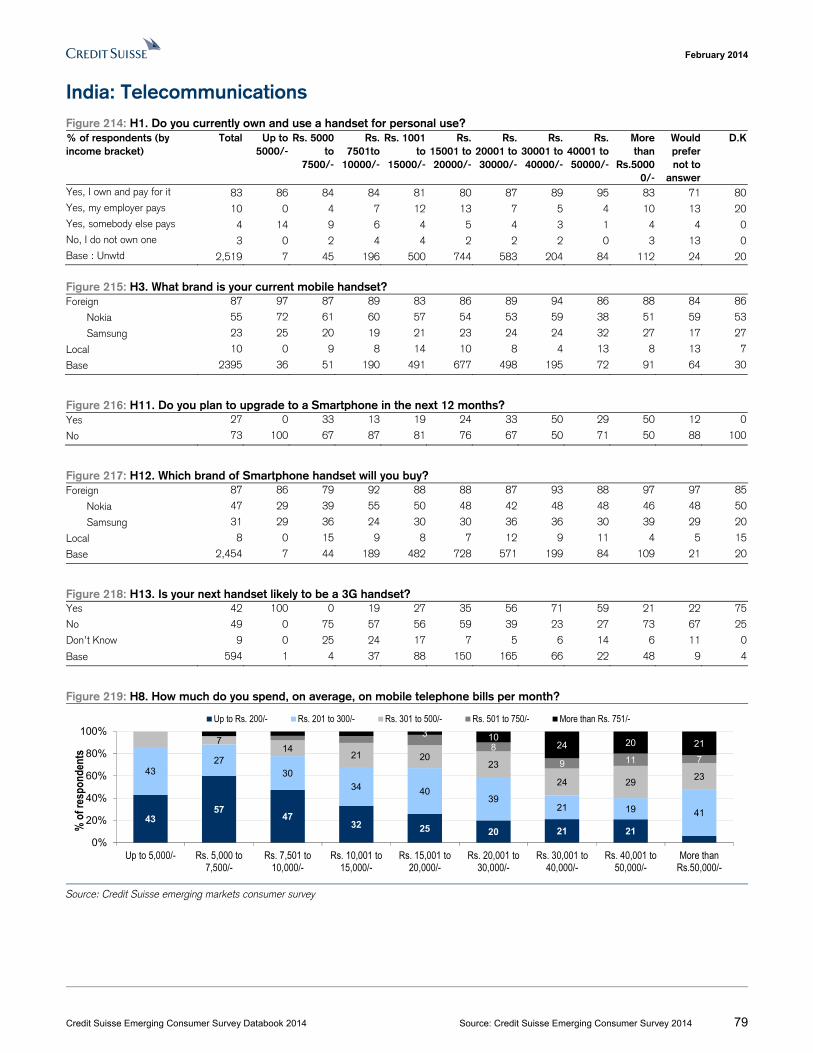

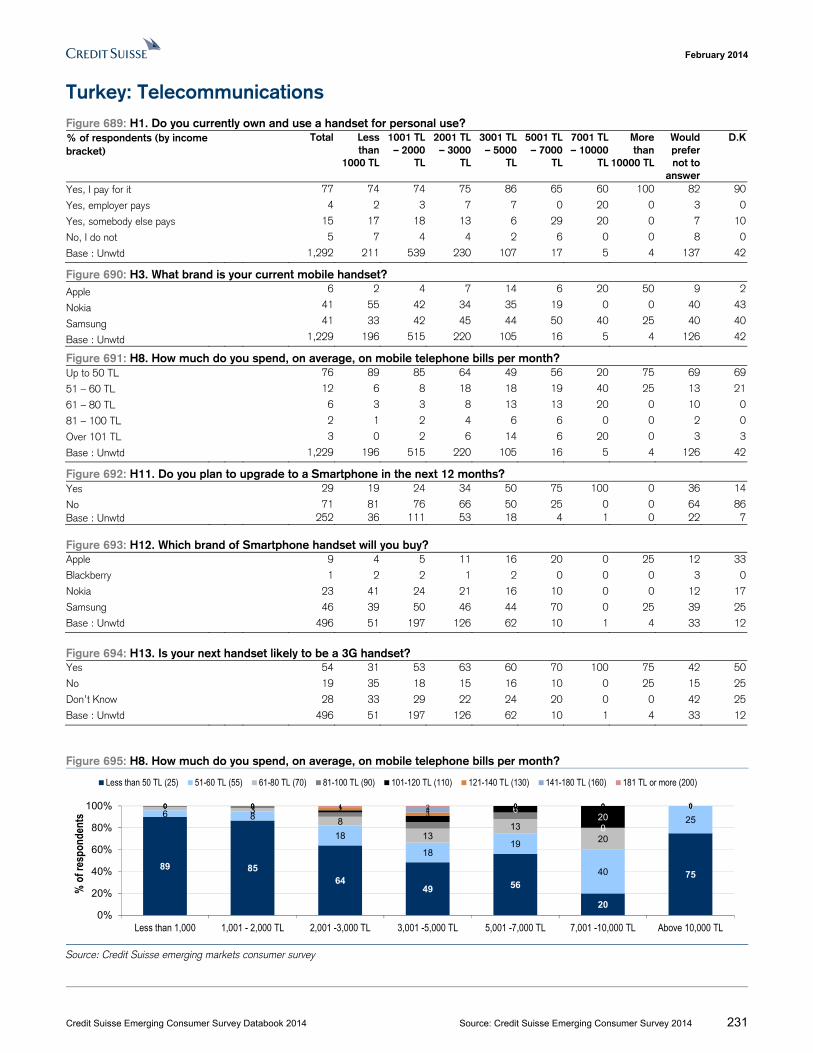

Brazil: Telecommunications Figure 52: H1. Do you currently own and use a handset for personal use? % of respondents (by income bracket)

Total Less than

R$ 489

R$ 490 - 1,142

R$ 1,142 - 1,630

R$ 1,631 - 3,260

R$ 3,261 - 4,890

R$ 4,891 - 6,520

R$ 6,521 - 8,150

R$ 8,151 - 11,410

More than R

$ 11,411

Would prefer not to

answer

D.K

Yes, I pay for it 93 88 84 89 95 95 97 99 91 97 94 88

Yes, employer pays 1 0 0 1 1 1 1 0 2 0 1 0

Yes, somebody else pays

2 0 4 2 1 2 1 1 5 3 3 2

No, I do not 4 13 11 8 4 1 1 0 2 0 2 10

Base : Unwtd 1,434 8 114 210 484 209 109 78 43 35 103 41

Figure 53: H3. What brand is your current mobile handset? Foreign 95 101 97 98 97 96 100 96 95 101 98 97

Nokia 26 43 37 33 25 24 22 24 17 26 17 24

Samsung 34 29 30 33 35 30 42 32 36 34 32 46

Local 2 0 3 3 2 0 1 2 2 0 2 0

Base 1,373 7 101 193 465 206 108 78 42 35 101 37

Figure 54: H11. Do you plan to upgrade to a Smartphone in the next 12 months? Yes 46 0 33 37 44 53 61 62 57 0 60 80

No 54 100 67 63 56 47 39 38 43 100 40 20Base : Unwtd 405 1 46 70 151 55 28 21 7 1 15 10

Figure 55: H12. Which brand of Smartphone handset will you buy? Foreign 83 100 91 85 76 85 92 90 83 94 84 93

Samsung 42 50 35 45 39 39 54 49 39 21 48 60 Nokia 15 50 32 19 12 17 12 9 14 26 10 0Local 0 0 0 1 0 0 0 0 0 0 0 0Don’t Know 16 0 8 13 23 15 8 11 18 5 14 7Base 710 2 62 99 250 100 59 47 28 19 29 15 Figure 56: H13. Is your next handset likely to be a 3G handset? Yes 56 0 44 37 51 60 64 72 71 84 76 87

No 21 100 29 32 24 16 14 11 11 5 7 7

Don’t Know 24 0 27 30 25 24 22 17 18 11 17 7

Base 710 2 62 99 250 100 59 47 28 19 29 15

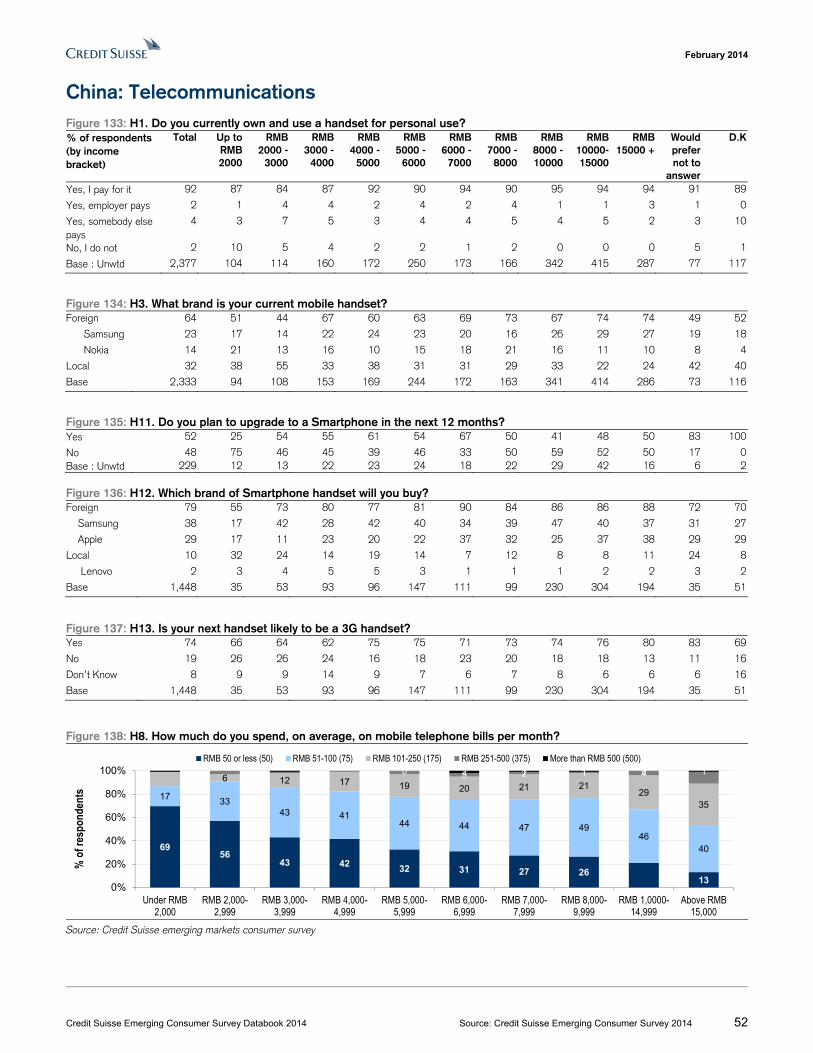

Figure 57: H8. How much do you spend, on average, on mobile telephone bills per month?

Source: Credit Suisse emerging markets consumer survey

57 6450

3516 17

3 5

14

2637

45

5236

35 2631

5 1012

1728

33

1914

1114

19 14

6 6 1526 26

0%

20%

40%

60%

80%

100%

Less than R$ 489 R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

R$ 8,151 - R$11,410

More than R$11,411

% o

f res

pond

ents

Upto 20 $ (20) 20 a 40 $ (30) 40 a 70 $ (55) 70 a 100 $ (85) More than 100 $ (100)

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 25

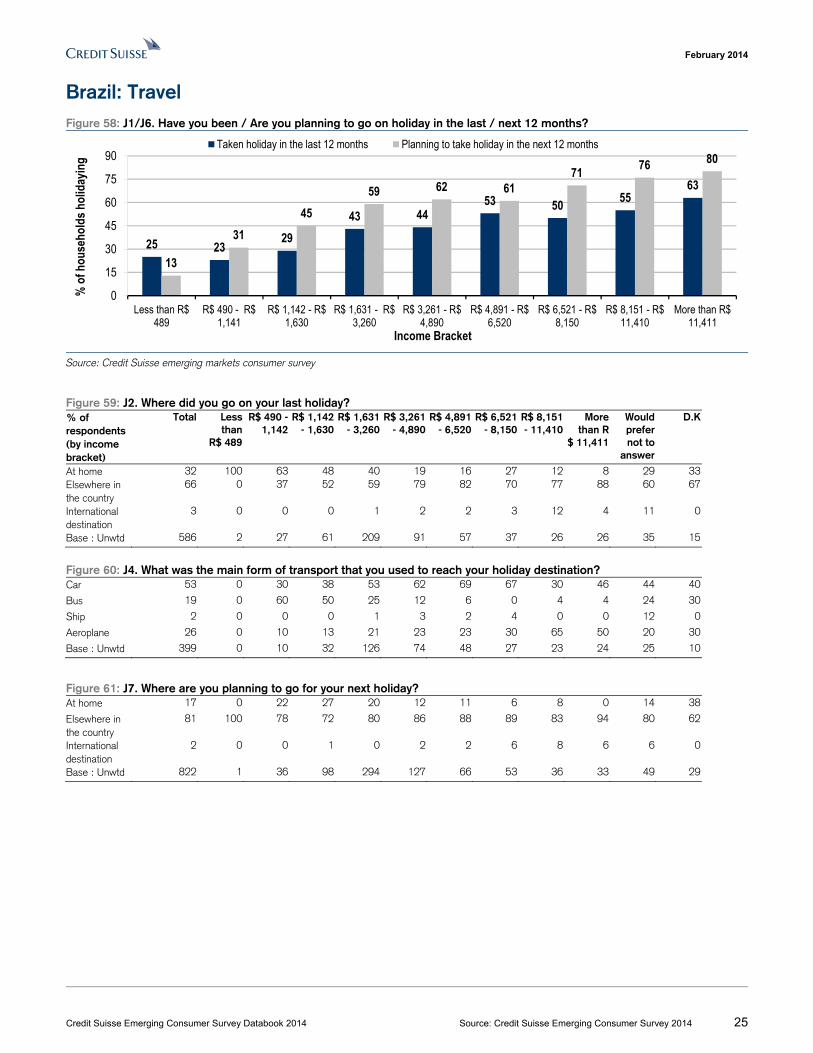

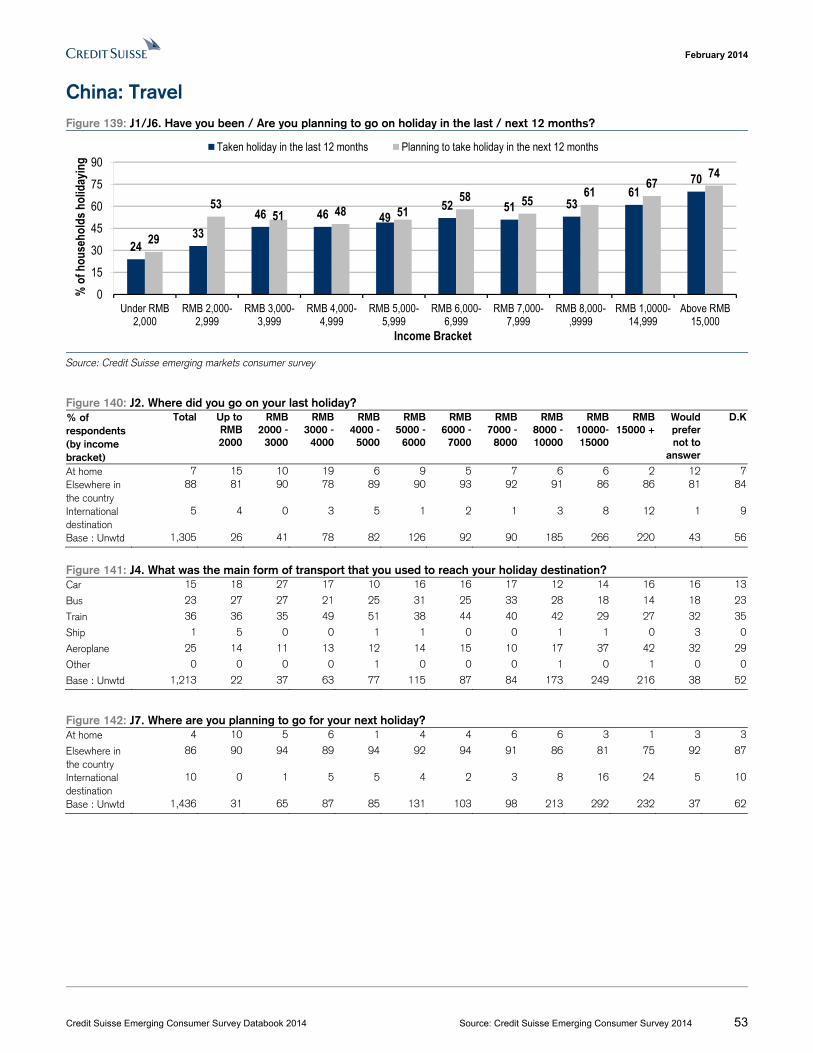

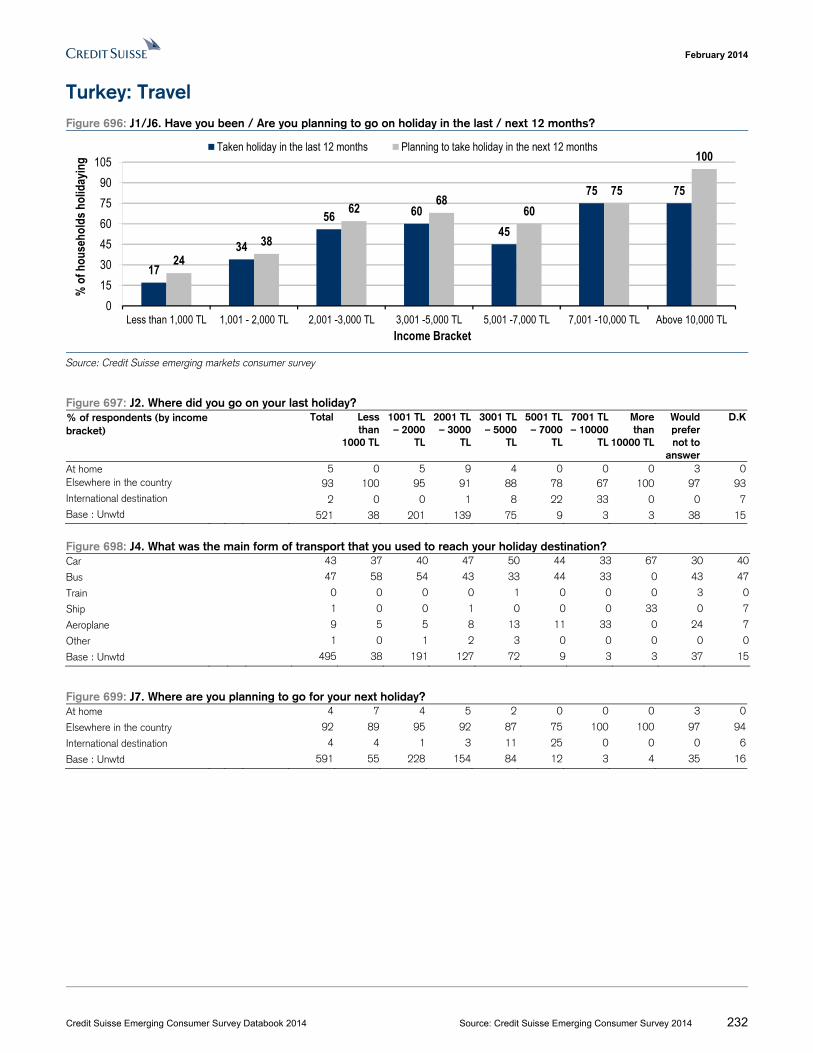

Brazil: Travel Figure 58: J1/J6. Have you been / Are you planning to go on holiday in the last / next 12 months?

Source: Credit Suisse emerging markets consumer survey

Figure 59: J2. Where did you go on your last holiday? % of respondents (by income bracket)

Total Less than

R$ 489

R$ 490 - 1,142

R$ 1,142 - 1,630

R$ 1,631 - 3,260

R$ 3,261 - 4,890

R$ 4,891 - 6,520

R$ 6,521 - 8,150

R$ 8,151 - 11,410

More than R

$ 11,411

Would prefer not to

answer

D.K

At home 32 100 63 48 40 19 16 27 12 8 29 33Elsewhere in the country

66 0 37 52 59 79 82 70 77 88 60 67

International destination

3 0 0 0 1 2 2 3 12 4 11 0

Base : Unwtd 586 2 27 61 209 91 57 37 26 26 35 15

Figure 60: J4. What was the main form of transport that you used to reach your holiday destination? Car 53 0 30 38 53 62 69 67 30 46 44 40

Bus 19 0 60 50 25 12 6 0 4 4 24 30

Ship 2 0 0 0 1 3 2 4 0 0 12 0

Aeroplane 26 0 10 13 21 23 23 30 65 50 20 30

Base : Unwtd 399 0 10 32 126 74 48 27 23 24 25 10

Figure 61: J7. Where are you planning to go for your next holiday? At home 17 0 22 27 20 12 11 6 8 0 14 38

Elsewhere in the country

81 100 78 72 80 86 88 89 83 94 80 62

International destination

2 0 0 1 0 2 2 6 8 6 6 0

Base : Unwtd 822 1 36 98 294 127 66 53 36 33 49 29

25 2329

43 4453 50 55

63

13

3145

59 62 6171 76 80

0

15

30

45

60

75

90

Less than R$489

R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

R$ 8,151 - R$11,410

More than R$11,411

% o

f hou

seho

lds h

olid

ayin

g

Income Bracket

Taken holiday in the last 12 months Planning to take holiday in the next 12 months

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 26

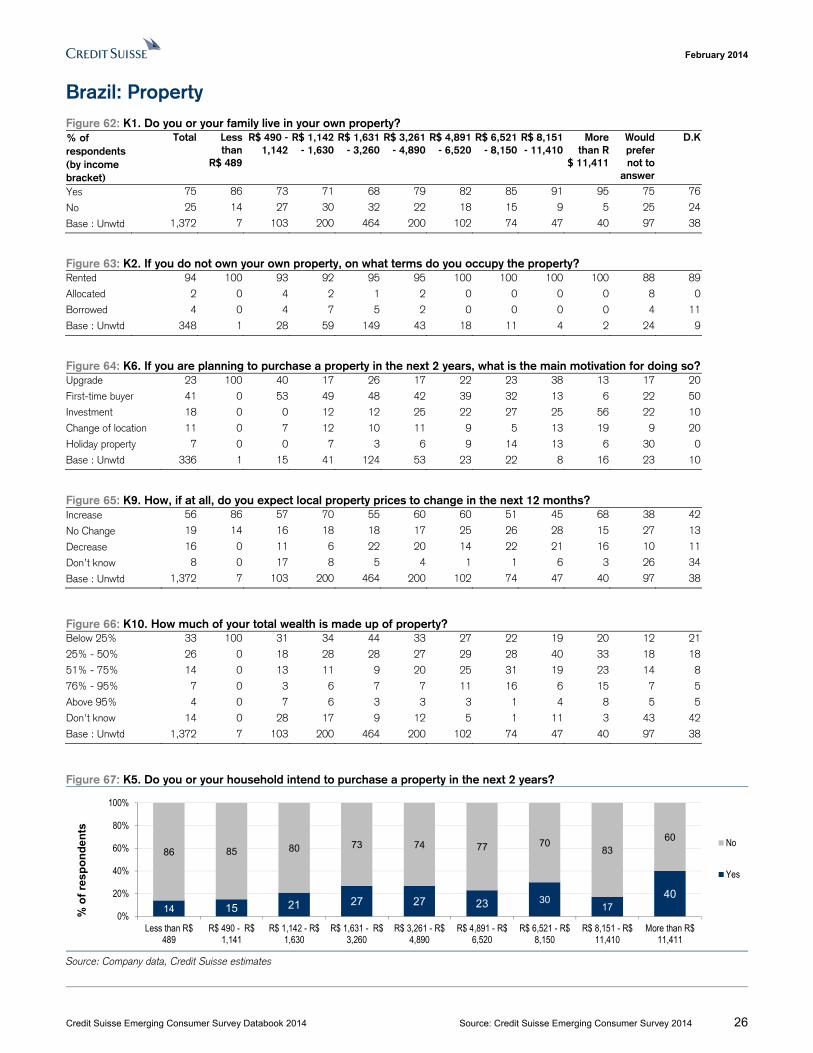

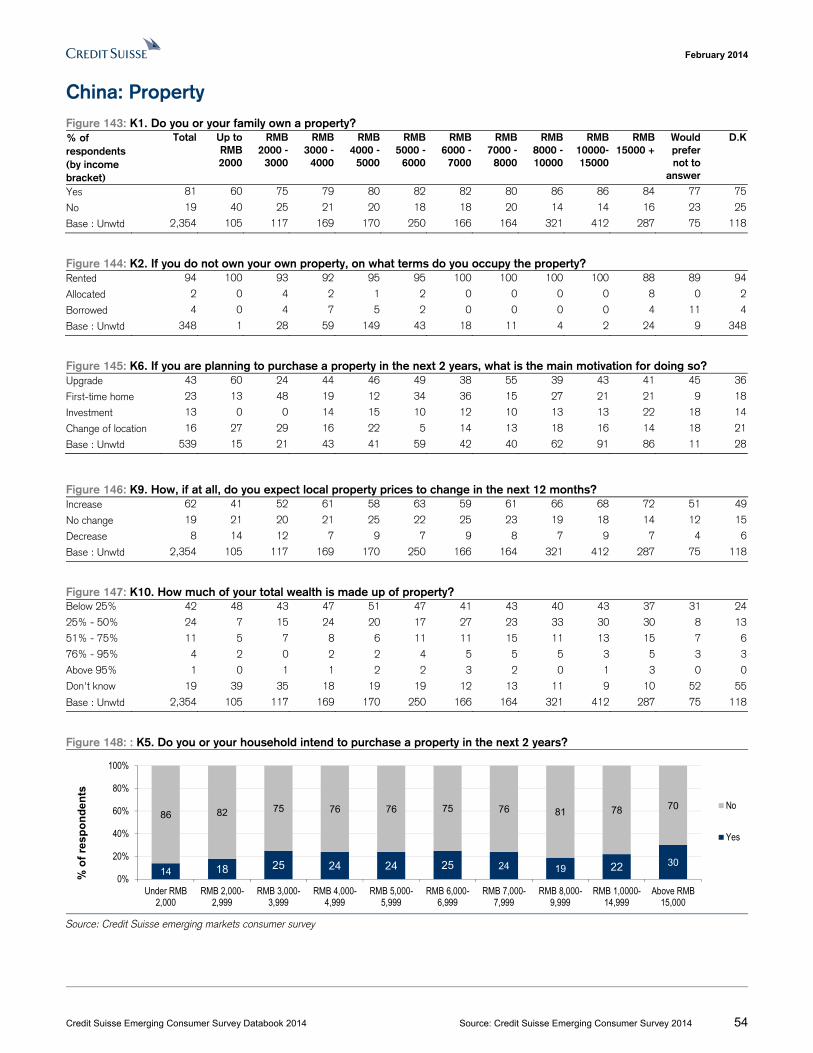

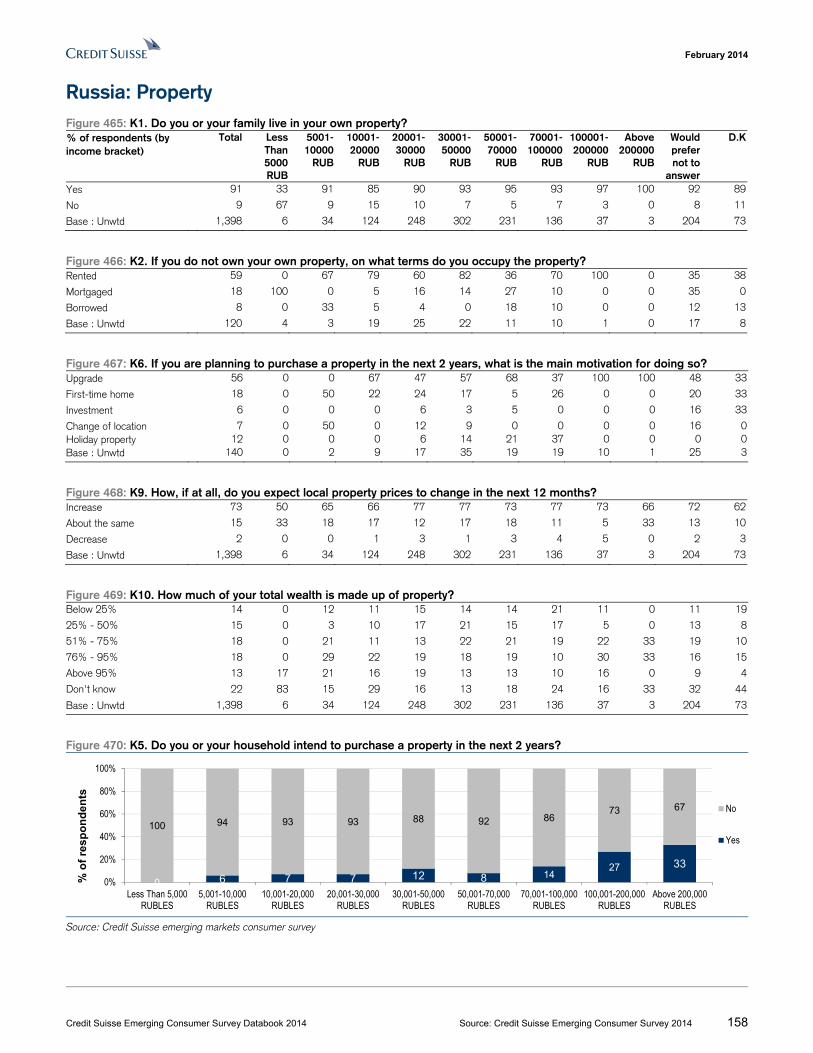

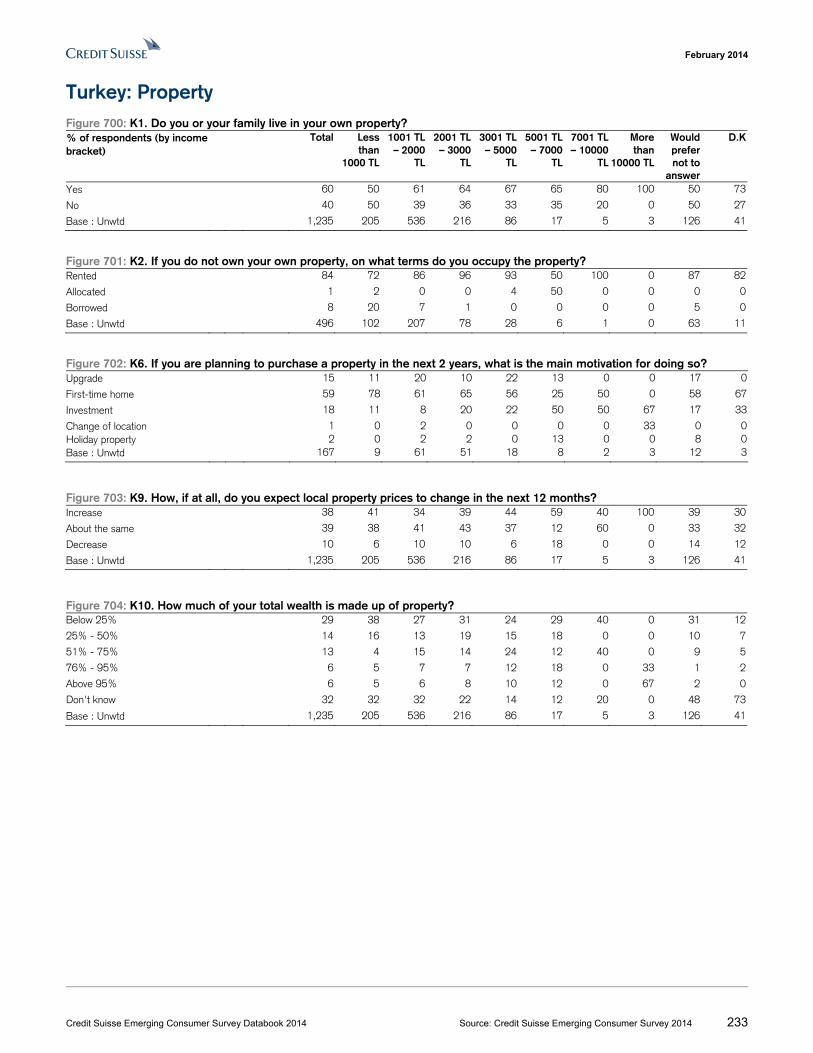

Brazil: Property Figure 62: K1. Do you or your family live in your own property? % of respondents (by income bracket)

Total Less than

R$ 489

R$ 490 - 1,142

R$ 1,142 - 1,630

R$ 1,631 - 3,260

R$ 3,261 - 4,890

R$ 4,891 - 6,520

R$ 6,521 - 8,150

R$ 8,151 - 11,410

More than R

$ 11,411

Would prefer not to

answer

D.K

Yes 75 86 73 71 68 79 82 85 91 95 75 76

No 25 14 27 30 32 22 18 15 9 5 25 24

Base : Unwtd 1,372 7 103 200 464 200 102 74 47 40 97 38

Figure 63: K2. If you do not own your own property, on what terms do you occupy the property? Rented 94 100 93 92 95 95 100 100 100 100 88 89

Allocated 2 0 4 2 1 2 0 0 0 0 8 0

Borrowed 4 0 4 7 5 2 0 0 0 0 4 11

Base : Unwtd 348 1 28 59 149 43 18 11 4 2 24 9

Figure 64: K6. If you are planning to purchase a property in the next 2 years, what is the main motivation for doing so? Upgrade 23 100 40 17 26 17 22 23 38 13 17 20

First-time buyer 41 0 53 49 48 42 39 32 13 6 22 50

Investment 18 0 0 12 12 25 22 27 25 56 22 10

Change of location 11 0 7 12 10 11 9 5 13 19 9 20

Holiday property 7 0 0 7 3 6 9 14 13 6 30 0

Base : Unwtd 336 1 15 41 124 53 23 22 8 16 23 10

Figure 65: K9. How, if at all, do you expect local property prices to change in the next 12 months? Increase 56 86 57 70 55 60 60 51 45 68 38 42

No Change 19 14 16 18 18 17 25 26 28 15 27 13

Decrease 16 0 11 6 22 20 14 22 21 16 10 11

Don’t know 8 0 17 8 5 4 1 1 6 3 26 34

Base : Unwtd 1,372 7 103 200 464 200 102 74 47 40 97 38

Figure 66: K10. How much of your total wealth is made up of property? Below 25% 33 100 31 34 44 33 27 22 19 20 12 21

25% - 50% 26 0 18 28 28 27 29 28 40 33 18 18

51% - 75% 14 0 13 11 9 20 25 31 19 23 14 8

76% - 95% 7 0 3 6 7 7 11 16 6 15 7 5

Above 95% 4 0 7 6 3 3 3 1 4 8 5 5

Don't know 14 0 28 17 9 12 5 1 11 3 43 42

Base : Unwtd 1,372 7 103 200 464 200 102 74 47 40 97 38

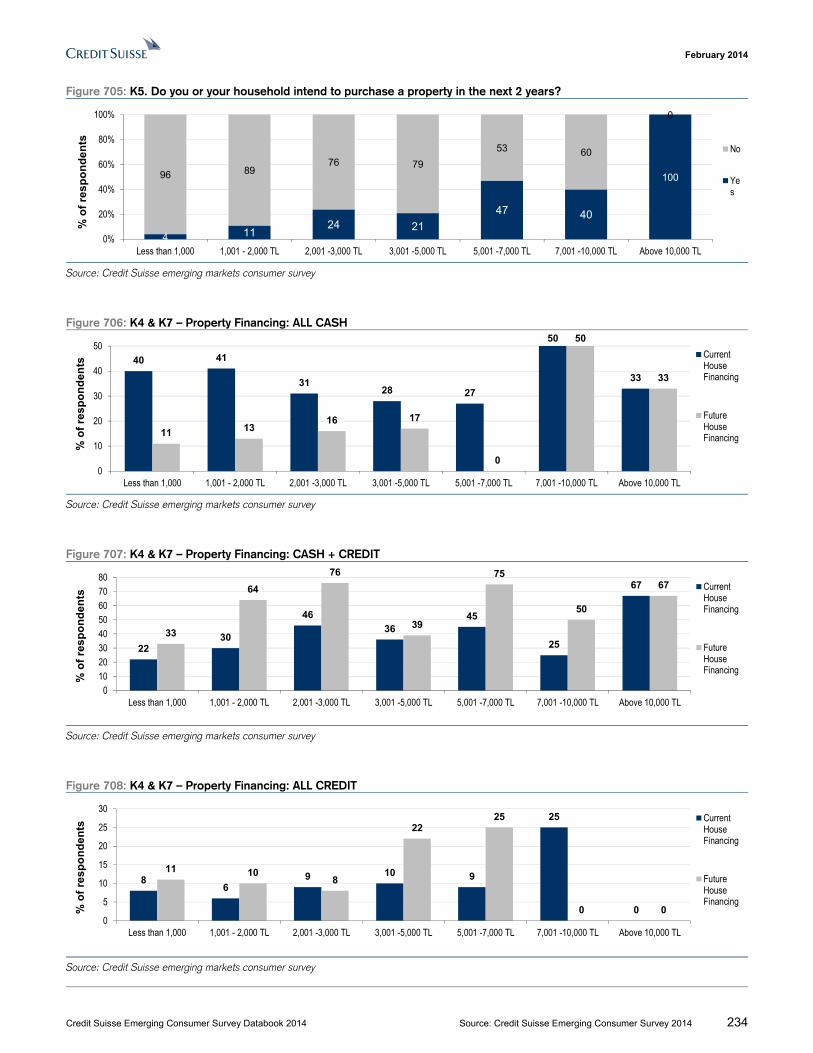

Figure 67: K5. Do you or your household intend to purchase a property in the next 2 years?

Source: Company data, Credit Suisse estimates

14 15 21 27 27 23 3017

40

86 85 80 73 74 77 7083

60

0%

20%

40%

60%

80%

100%

Less than R$489

R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

R$ 8,151 - R$11,410

More than R$11,411

% o

f re

sp

on

de

nts

No

Yes

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 27

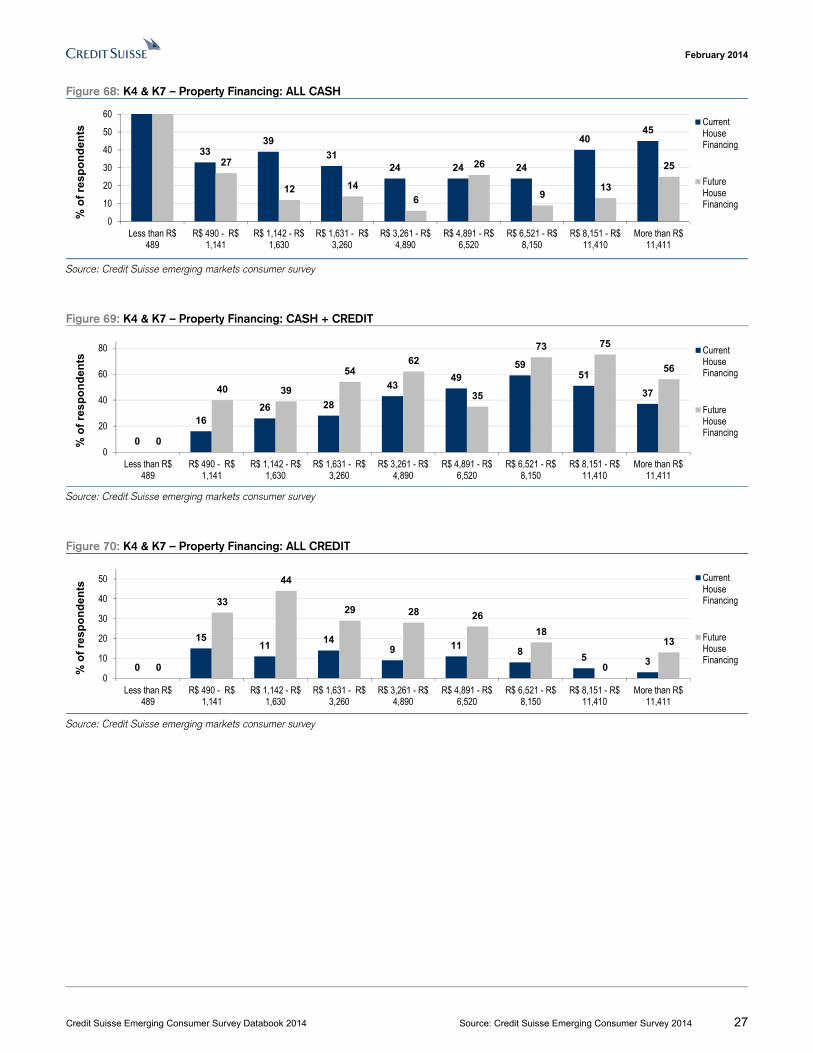

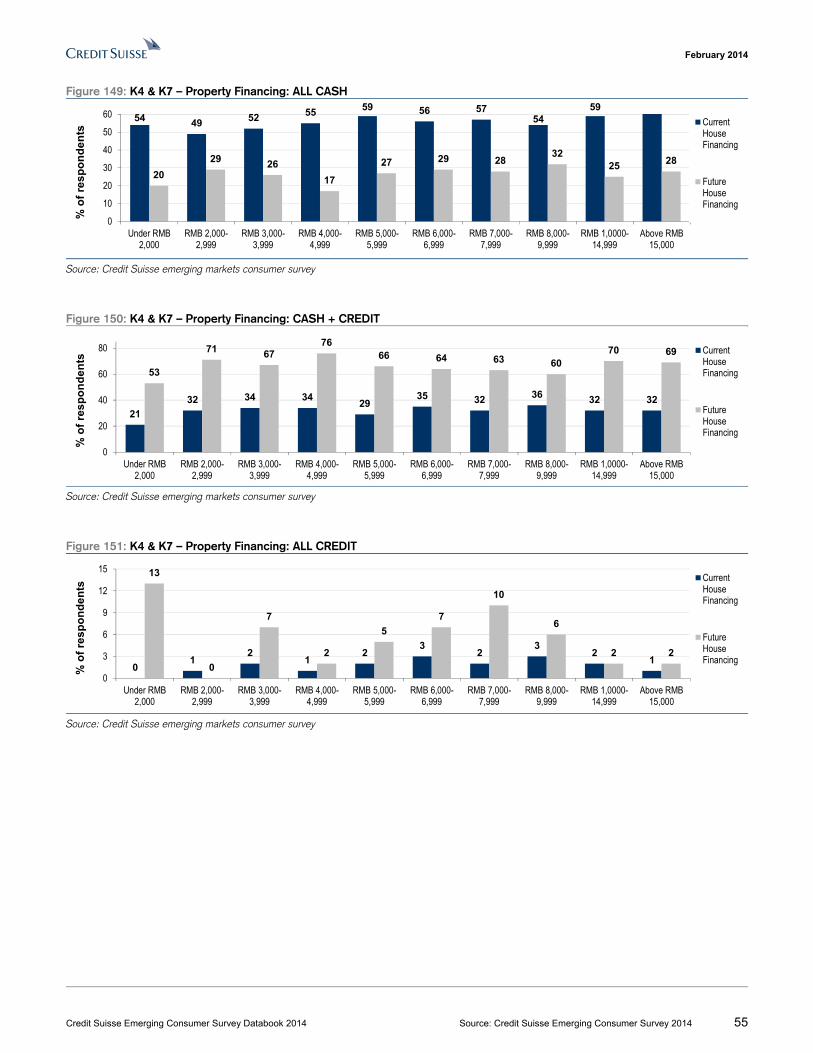

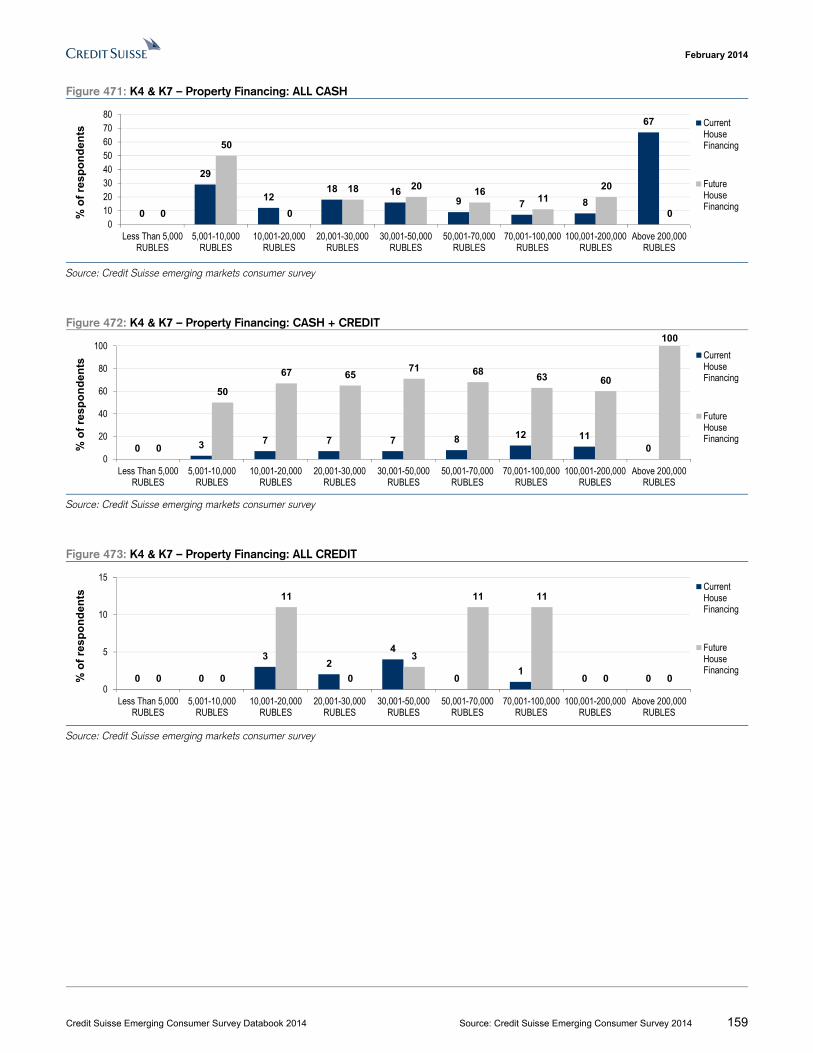

Figure 68: K4 & K7 – Property Financing: ALL CASH

Source: Credit Suisse emerging markets consumer survey

Figure 69: K4 & K7 – Property Financing: CASH + CREDIT

Source: Credit Suisse emerging markets consumer survey

Figure 70: K4 & K7 – Property Financing: ALL CREDIT

Source: Credit Suisse emerging markets consumer survey

3339

3124 24 24

4045

27

12 14

6

26

913

25

0

10

20

30

40

50

60

Less than R$489

R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

R$ 8,151 - R$11,410

More than R$11,411

% o

f re

sp

on

de

nts

CurrentHouseFinancing

FutureHouseFinancing

0

1626 28

4349

5951

37

0

40 39

5462

35

73 75

56

0

20

40

60

80

Less than R$489

R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

R$ 8,151 - R$11,410

More than R$11,411

% o

f re

sp

on

de

nts

CurrentHouseFinancing

FutureHouseFinancing

0

1511

149 11

85 3

0

33

44

29 28 26

18

0

13

0

10

20

30

40

50

Less than R$489

R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

R$ 8,151 - R$11,410

More than R$11,411

% o

f re

sp

on

de

nts

CurrentHouseFinancing

FutureHouseFinancing

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 28

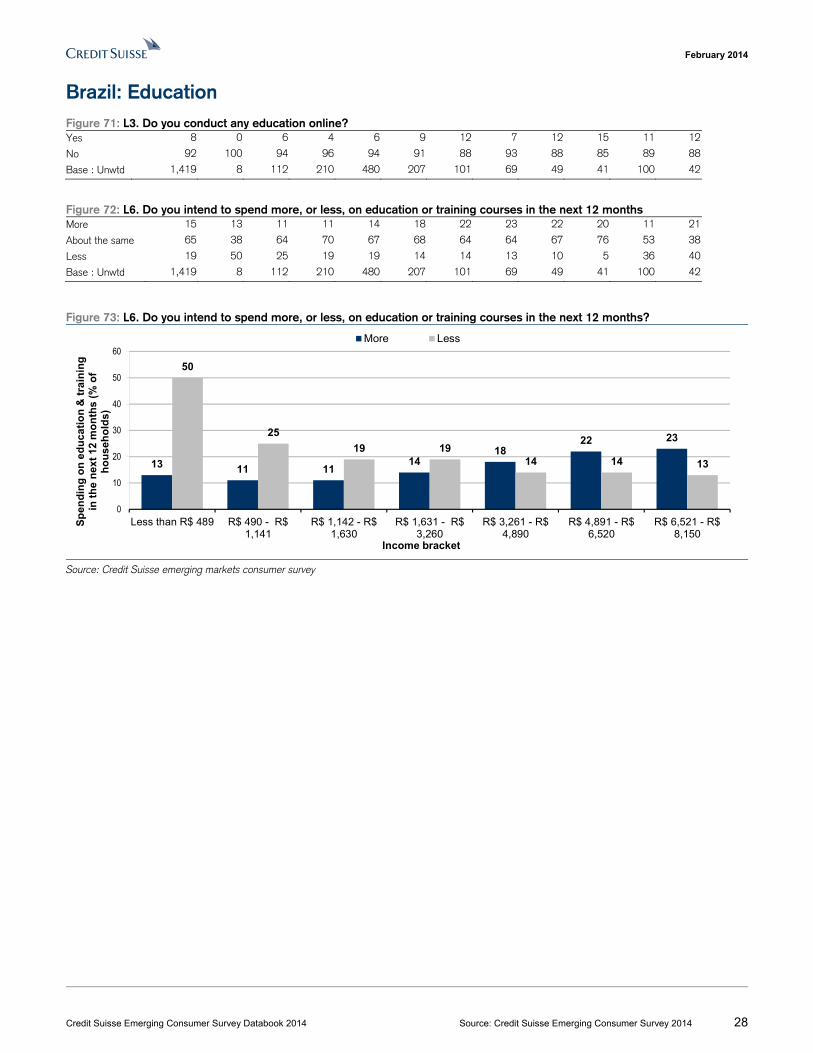

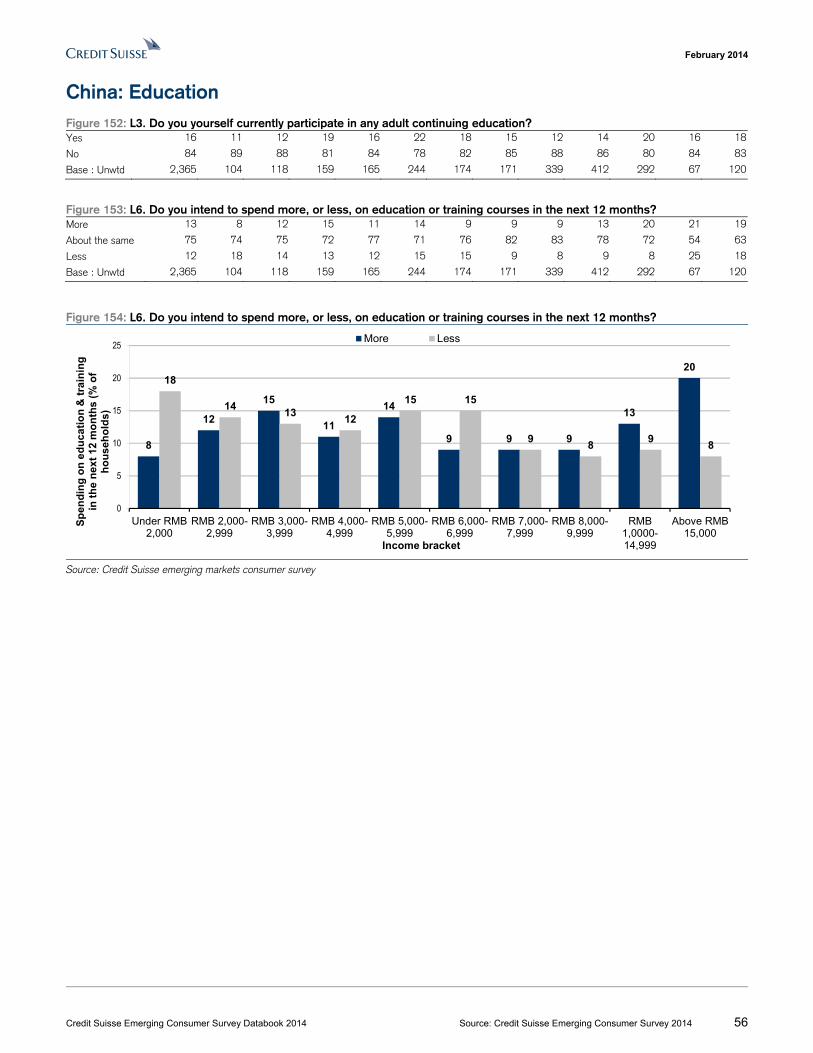

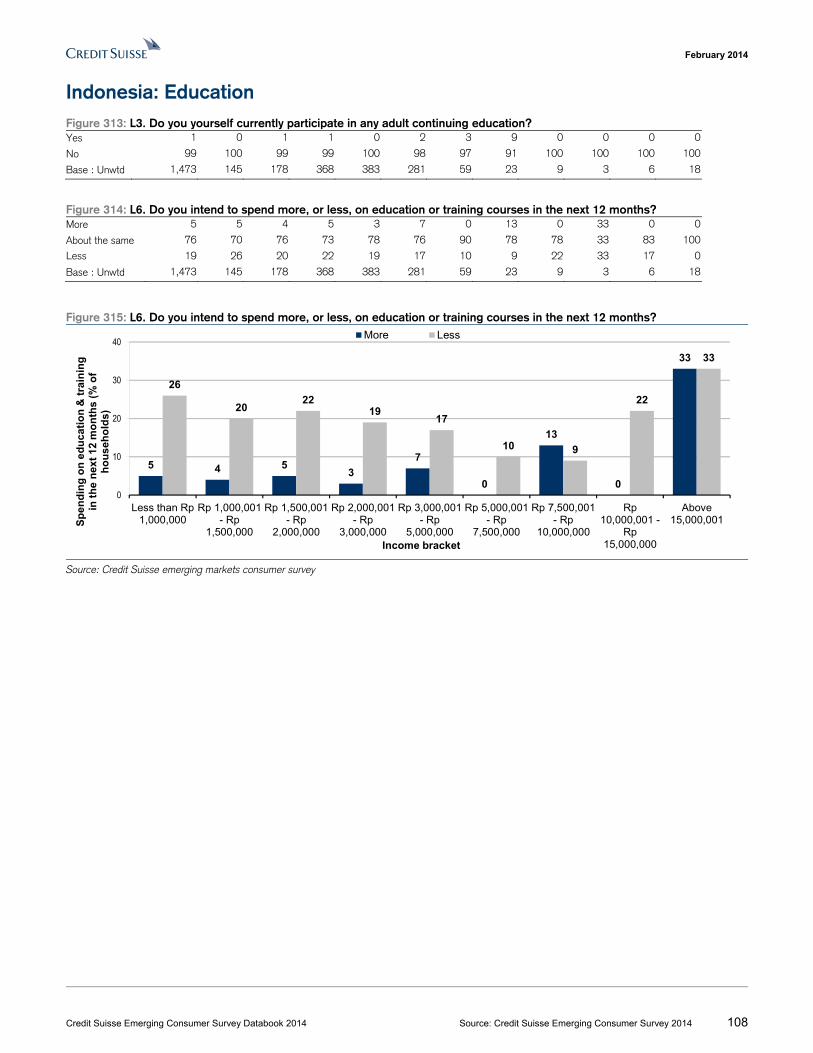

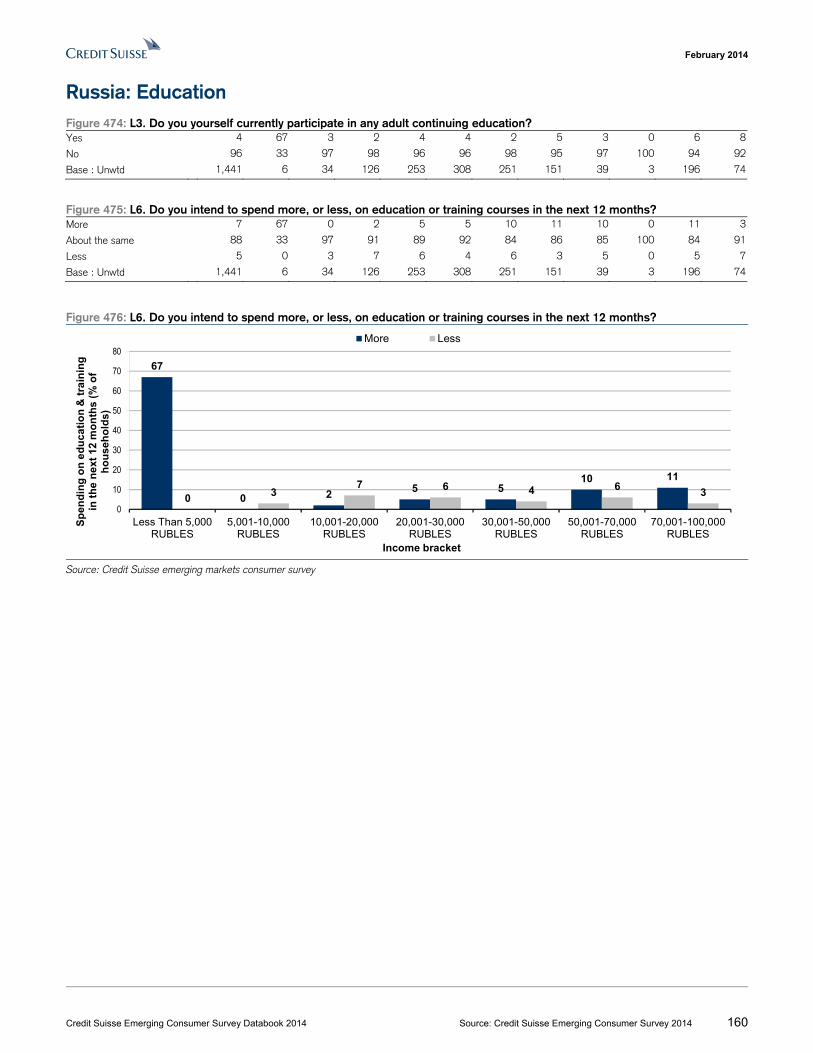

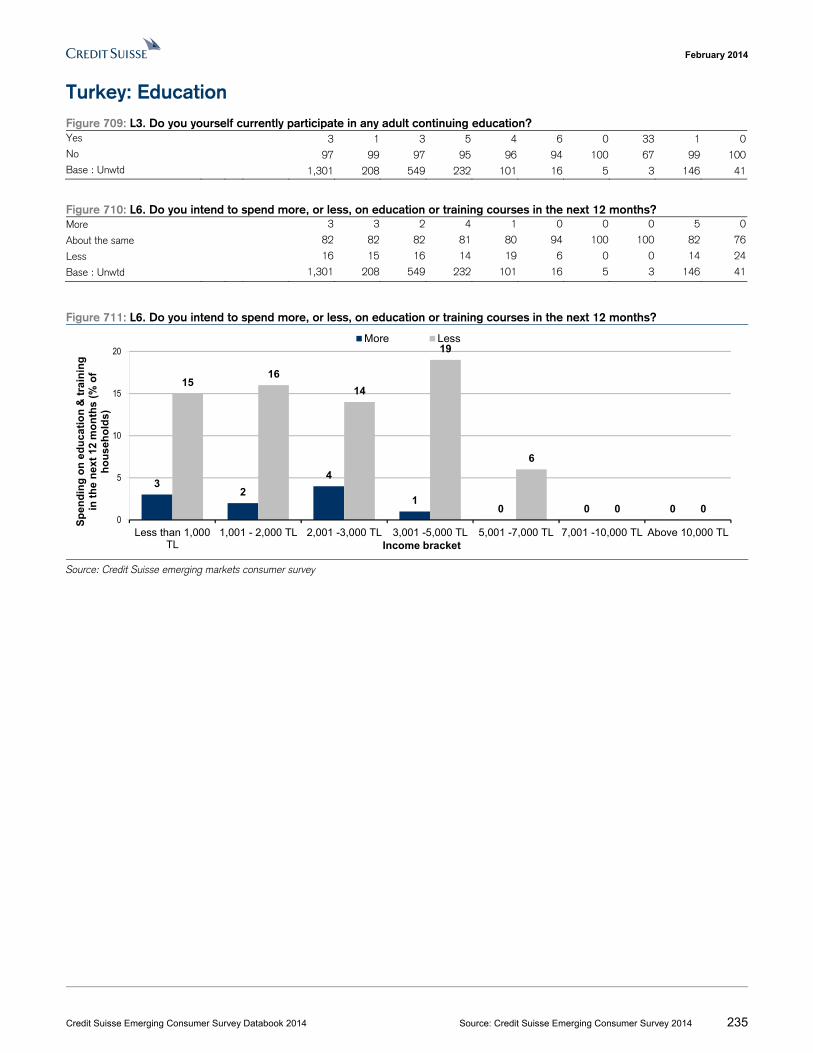

Brazil: Education Figure 71: L3. Do you conduct any education online? Yes 8 0 6 4 6 9 12 7 12 15 11 12

No 92 100 94 96 94 91 88 93 88 85 89 88

Base : Unwtd 1,419 8 112 210 480 207 101 69 49 41 100 42

Figure 72: L6. Do you intend to spend more, or less, on education or training courses in the next 12 months More 15 13 11 11 14 18 22 23 22 20 11 21

About the same 65 38 64 70 67 68 64 64 67 76 53 38

Less 19 50 25 19 19 14 14 13 10 5 36 40

Base : Unwtd 1,419 8 112 210 480 207 101 69 49 41 100 42

Figure 73: L6. Do you intend to spend more, or less, on education or training courses in the next 12 months?

Source: Credit Suisse emerging markets consumer survey

13 11 1114

1822 23

50

25

19 1914 14 13

0

10

20

30

40

50

60

Less than R$ 489 R$ 490 - R$1,141

R$ 1,142 - R$1,630

R$ 1,631 - R$3,260

R$ 3,261 - R$4,890

R$ 4,891 - R$6,520

R$ 6,521 - R$8,150

Sp

end

ing

on

ed

uca

tio

n &

tra

inin

g

in t

he

nex

t 12

mo

nth

s (

% o

f h

ou

seh

old

s)

Income bracket

More Less

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 29

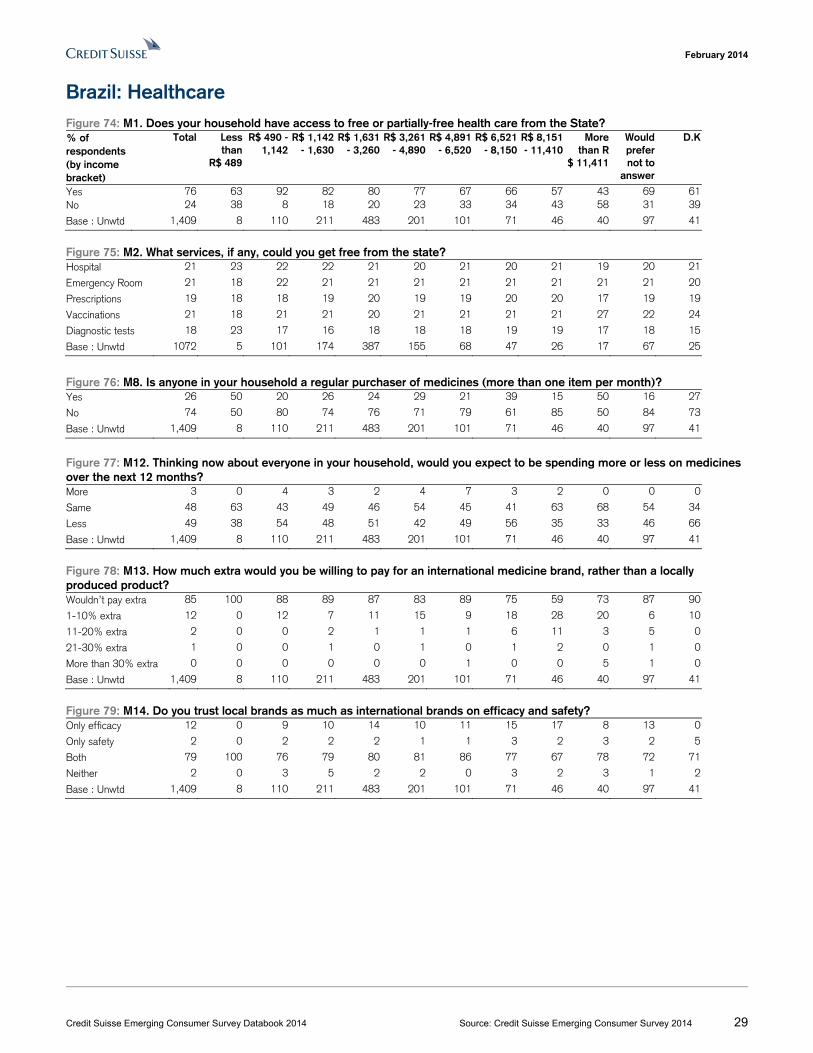

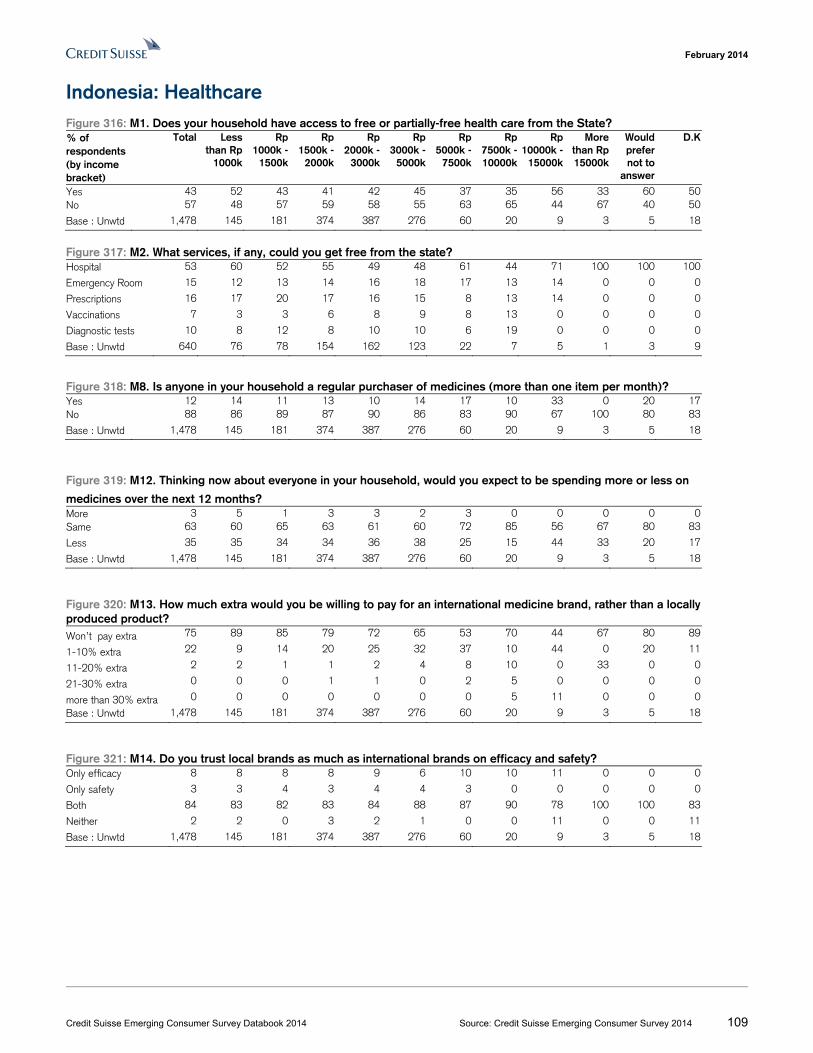

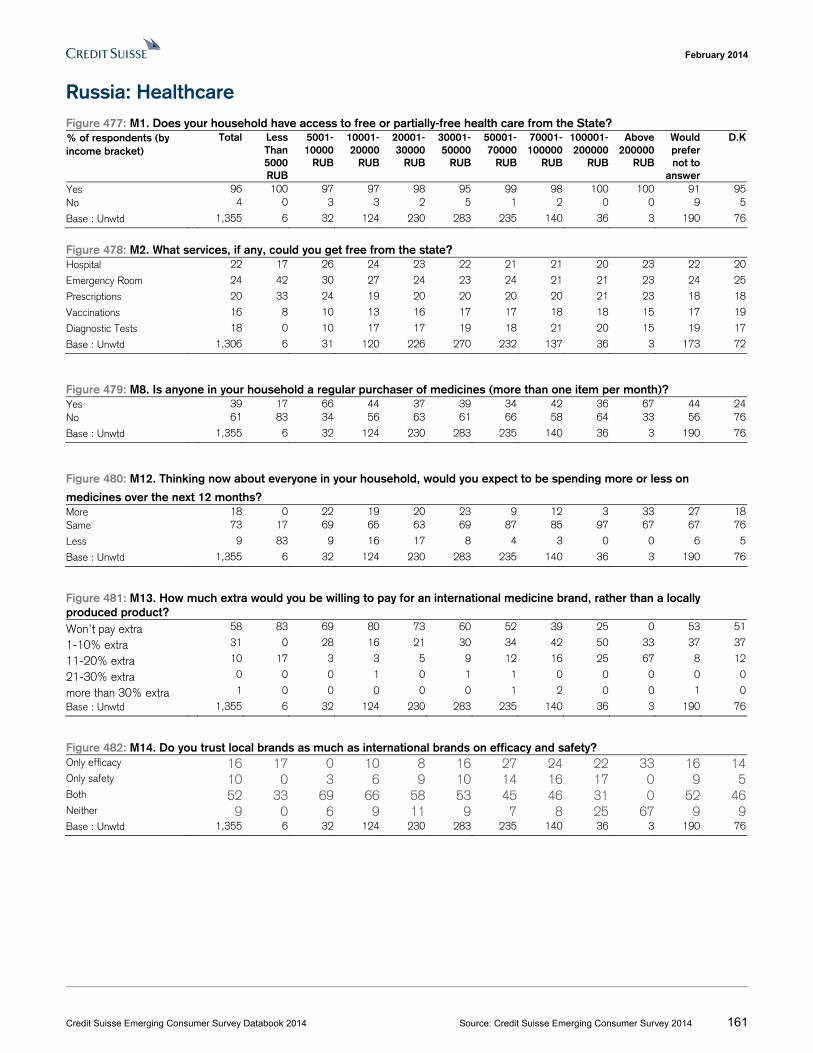

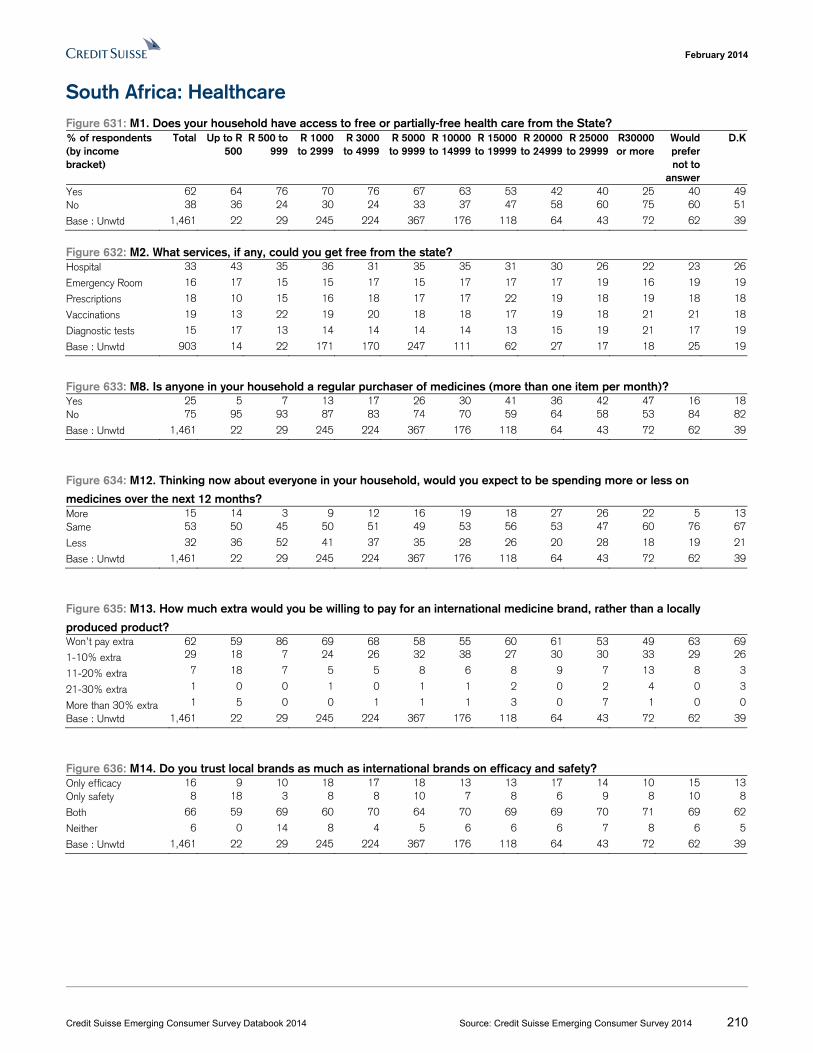

Brazil: Healthcare Figure 74: M1. Does your household have access to free or partially-free health care from the State? % of respondents (by income bracket)

Total Less than

R$ 489

R$ 490 - 1,142

R$ 1,142 - 1,630

R$ 1,631 - 3,260

R$ 3,261 - 4,890

R$ 4,891 - 6,520

R$ 6,521 - 8,150

R$ 8,151 - 11,410

More than R

$ 11,411

Would prefer not to

answer

D.K

Yes 76 63 92 82 80 77 67 66 57 43 69 61No 24 38 8 18 20 23 33 34 43 58 31 39

Base : Unwtd 1,409 8 110 211 483 201 101 71 46 40 97 41

Figure 75: M2. What services, if any, could you get free from the state? Hospital 21 23 22 22 21 20 21 20 21 19 20 21

Emergency Room 21 18 22 21 21 21 21 21 21 21 21 20

Prescriptions 19 18 18 19 20 19 19 20 20 17 19 19

Vaccinations 21 18 21 21 20 21 21 21 21 27 22 24

Diagnostic tests 18 23 17 16 18 18 18 19 19 17 18 15

Base : Unwtd 1072 5 101 174 387 155 68 47 26 17 67 25

Figure 76: M8. Is anyone in your household a regular purchaser of medicines (more than one item per month)? Yes 26 50 20 26 24 29 21 39 15 50 16 27

No 74 50 80 74 76 71 79 61 85 50 84 73

Base : Unwtd 1,409 8 110 211 483 201 101 71 46 40 97 41

Figure 77: M12. Thinking now about everyone in your household, would you expect to be spending more or less on medicines over the next 12 months? More 3 0 4 3 2 4 7 3 2 0 0 0

Same 48 63 43 49 46 54 45 41 63 68 54 34

Less 49 38 54 48 51 42 49 56 35 33 46 66

Base : Unwtd 1,409 8 110 211 483 201 101 71 46 40 97 41

Figure 78: M13. How much extra would you be willing to pay for an international medicine brand, rather than a locally produced product? Wouldn’t pay extra 85 100 88 89 87 83 89 75 59 73 87 90

1-10% extra 12 0 12 7 11 15 9 18 28 20 6 10

11-20% extra 2 0 0 2 1 1 1 6 11 3 5 0

21-30% extra 1 0 0 1 0 1 0 1 2 0 1 0

More than 30% extra 0 0 0 0 0 0 1 0 0 5 1 0

Base : Unwtd 1,409 8 110 211 483 201 101 71 46 40 97 41

Figure 79: M14. Do you trust local brands as much as international brands on efficacy and safety? Only efficacy 12 0 9 10 14 10 11 15 17 8 13 0

Only safety 2 0 2 2 2 1 1 3 2 3 2 5

Both 79 100 76 79 80 81 86 77 67 78 72 71

Neither 2 0 3 5 2 2 0 3 2 3 1 2

Base : Unwtd 1,409 8 110 211 483 201 101 71 46 40 97 41

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 30

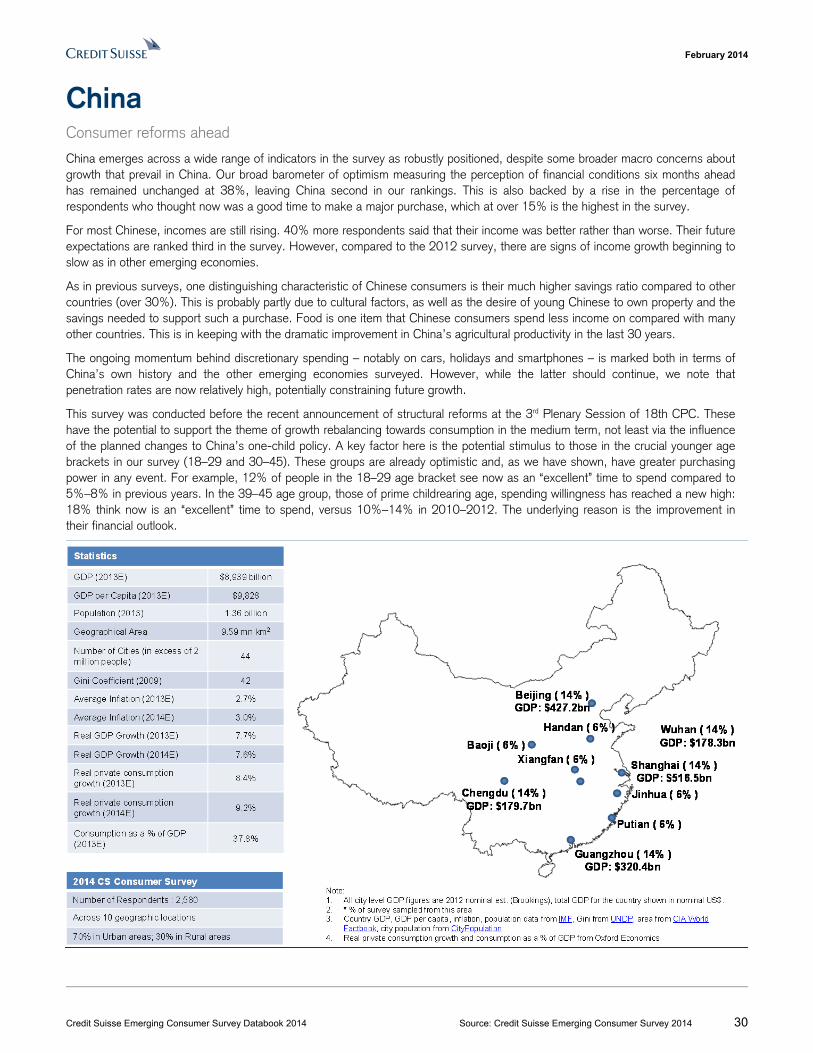

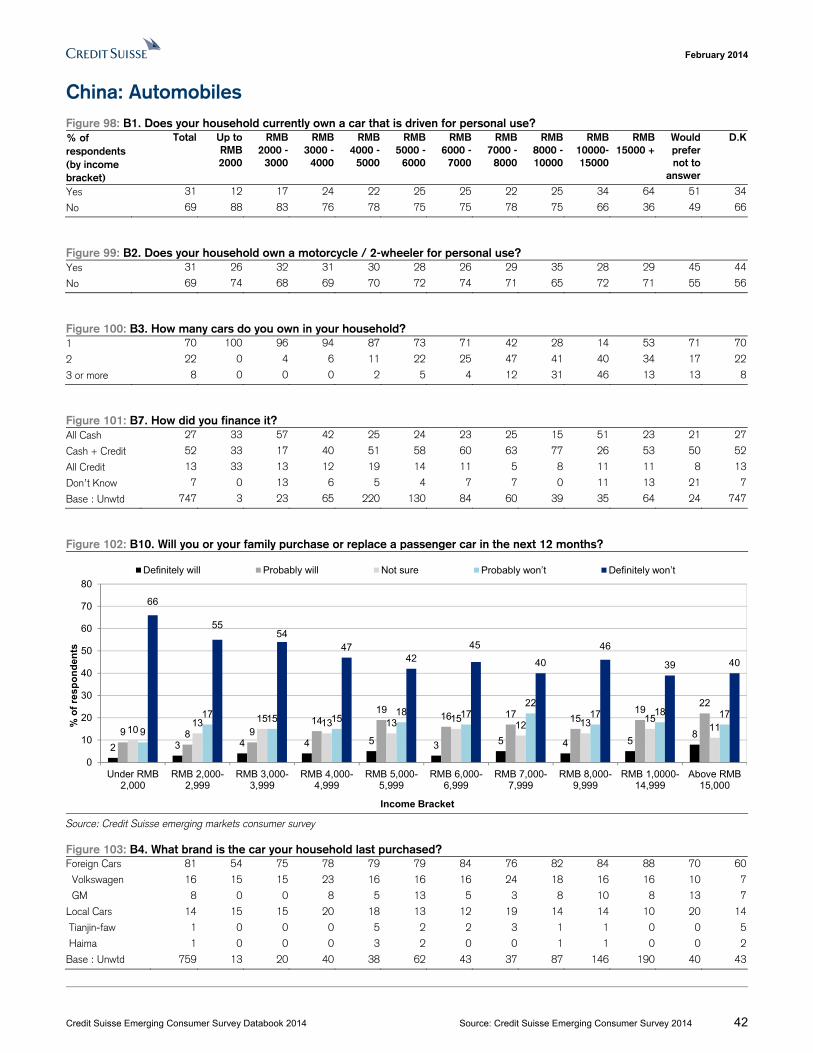

China Consumer reforms ahead

China emerges across a wide range of indicators in the survey as robustly positioned, despite some broader macro concerns about growth that prevail in China. Our broad barometer of optimism measuring the perception of financial conditions six months ahead has remained unchanged at 38%, leaving China second in our rankings. This is also backed by a rise in the percentage of respondents who thought now was a good time to make a major purchase, which at over 15% is the highest in the survey.

For most Chinese, incomes are still rising. 40% more respondents said that their income was better rather than worse. Their future expectations are ranked third in the survey. However, compared to the 2012 survey, there are signs of income growth beginning to slow as in other emerging economies.

As in previous surveys, one distinguishing characteristic of Chinese consumers is their much higher savings ratio compared to other countries (over 30%). This is probably partly due to cultural factors, as well as the desire of young Chinese to own property and the savings needed to support such a purchase. Food is one item that Chinese consumers spend less income on compared with many other countries. This is in keeping with the dramatic improvement in China’s agricultural productivity in the last 30 years.

The ongoing momentum behind discretionary spending – notably on cars, holidays and smartphones – is marked both in terms of China’s own history and the other emerging economies surveyed. However, while the latter should continue, we note that penetration rates are now relatively high, potentially constraining future growth.

This survey was conducted before the recent announcement of structural reforms at the 3rd Plenary Session of 18th CPC. These have the potential to support the theme of growth rebalancing towards consumption in the medium term, not least via the influence of the planned changes to China’s one-child policy. A key factor here is the potential stimulus to those in the crucial younger age brackets in our survey (18–29 and 30–45). These groups are already optimistic and, as we have shown, have greater purchasing power in any event. For example, 12% of people in the 18–29 age bracket see now as an “excellent” time to spend compared to 5%–8% in previous years. In the 39–45 age group, those of prime childrearing age, spending willingness has reached a new high: 18% think now is an “excellent” time to spend, versus 10%–14% in 2010–2012. The underlying reason is the improvement in their financial outlook.

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 31

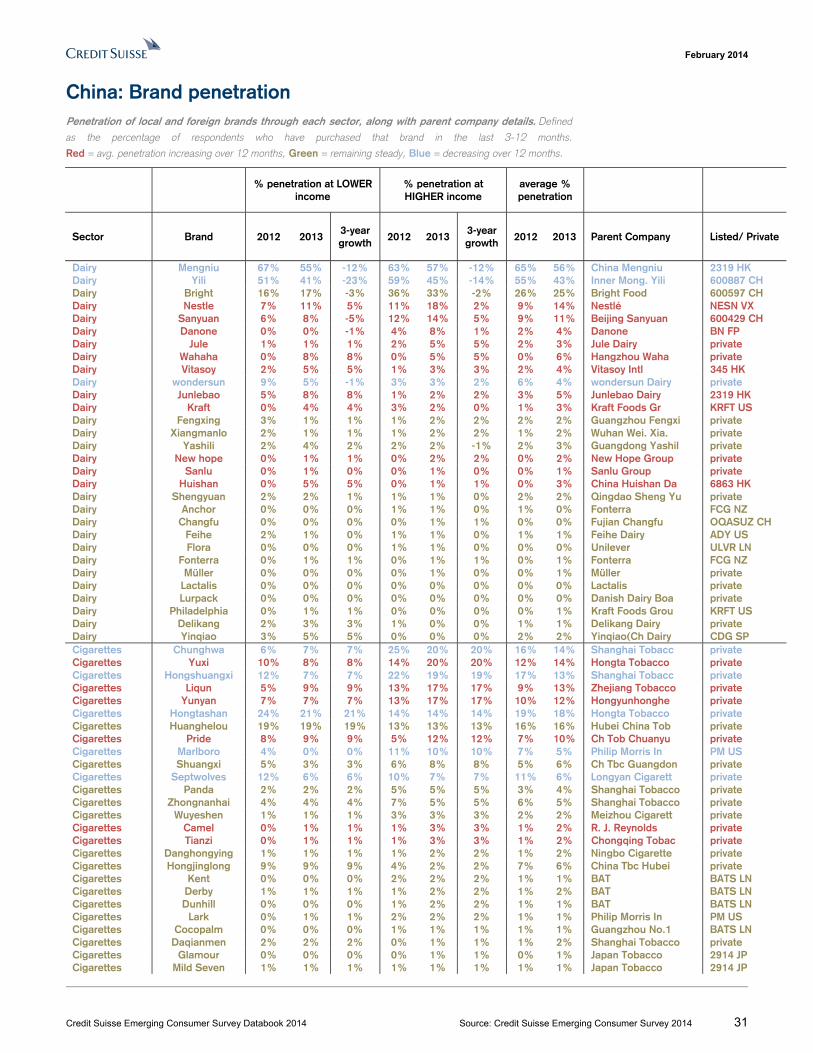

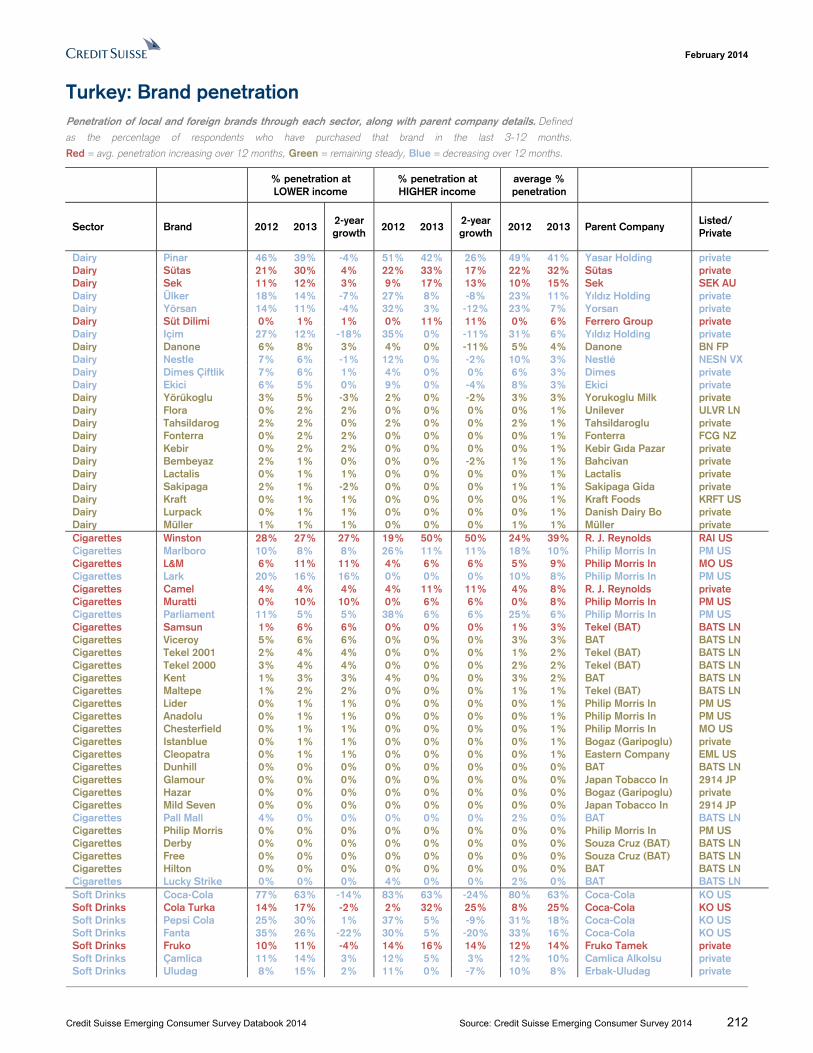

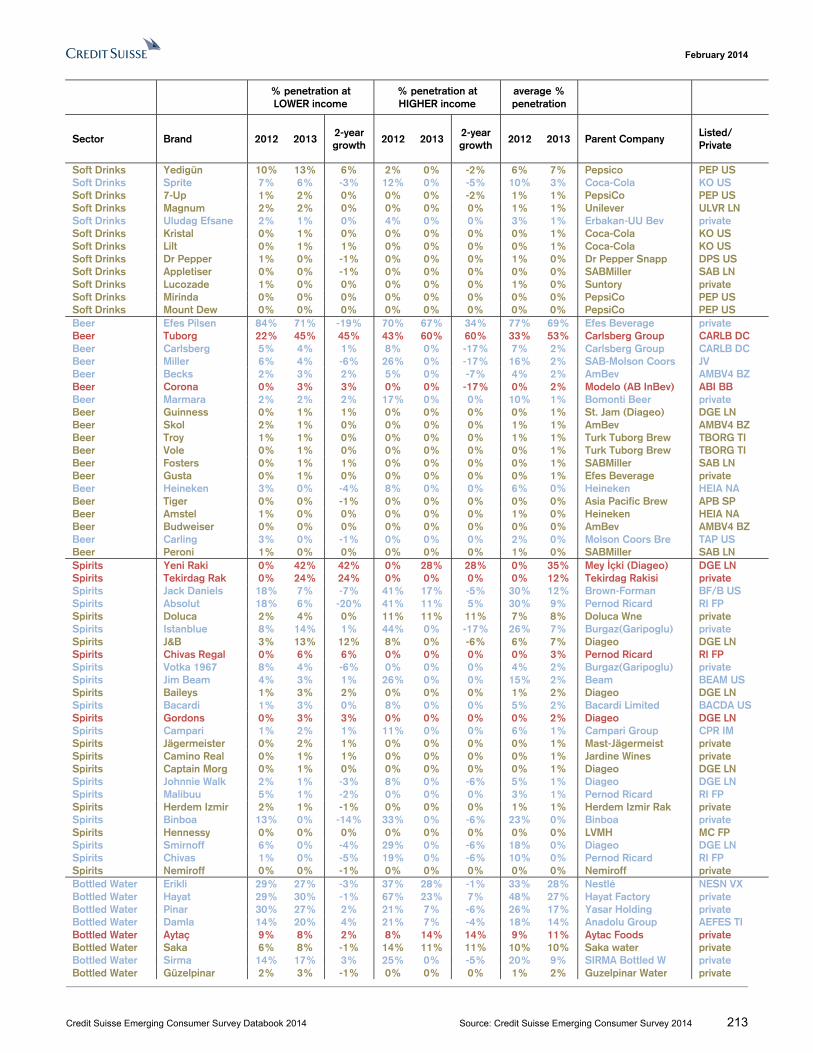

China: Brand penetration Penetration of local and foreign brands through each sector, along with parent company details. Defined

as the percentage of respondents who have purchased that brand in the last 3-12 months.

Red = avg. penetration increasing over 12 months, Green = remaining steady, Blue = decreasing over 12 months.

% penetration at LOWER income

% penetration at HIGHER income

average % penetration

Sector Brand 2012 2013 3-year growth

2012 2013 3-year growth

2012 2013 Parent Company Listed/ Private

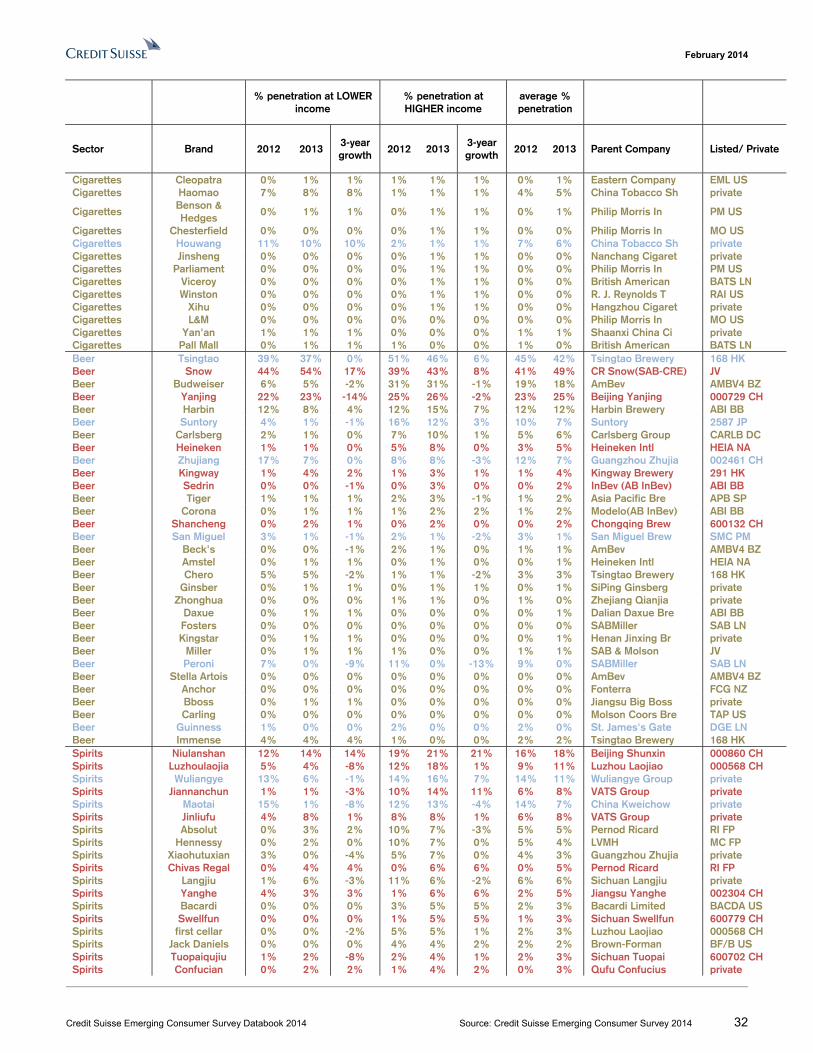

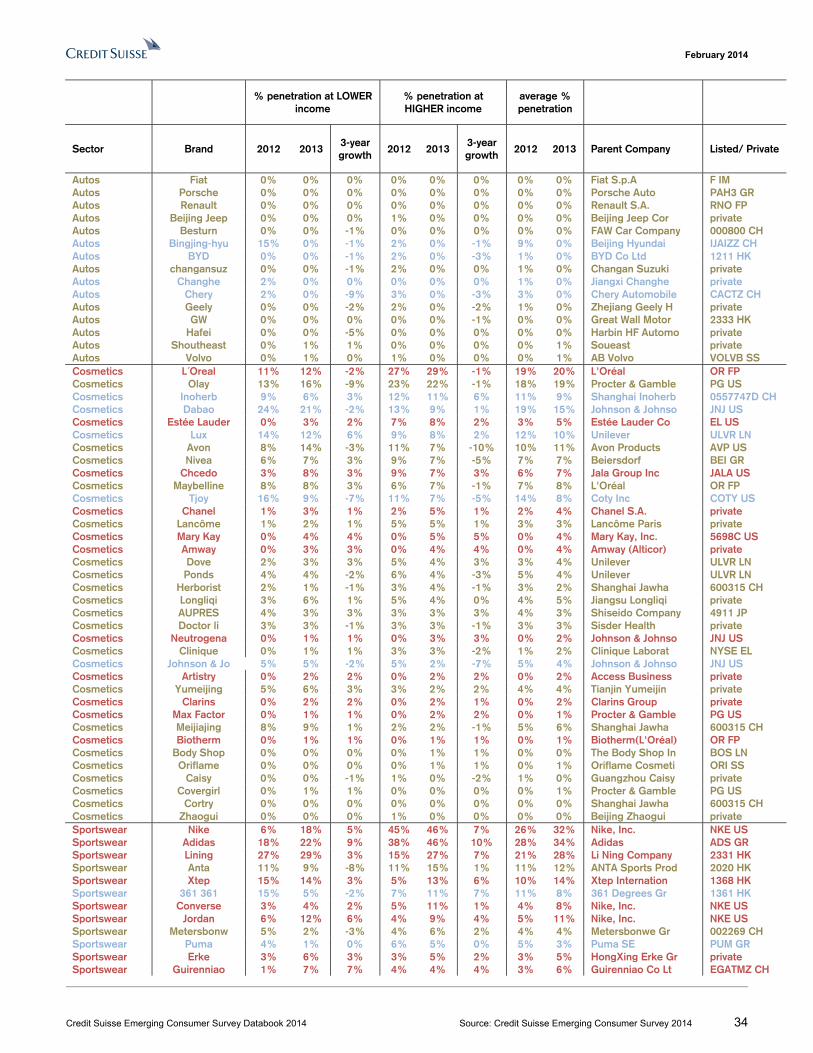

Dairy Mengniu 67% 55% -12% 63% 57% -12% 65% 56% China Mengniu 2319 HK Dairy Yili 51% 41% -23% 59% 45% -14% 55% 43% Inner Mong. Yili 600887 CH Dairy Bright 16% 17% -3% 36% 33% -2% 26% 25% Bright Food 600597 CH Dairy Nestle 7% 11% 5% 11% 18% 2% 9% 14% Nestlé NESN VX Dairy Sanyuan 6% 8% -5% 12% 14% 5% 9% 11% Beijing Sanyuan 600429 CH Dairy Danone 0% 0% -1% 4% 8% 1% 2% 4% Danone BN FP Dairy Jule 1% 1% 1% 2% 5% 5% 2% 3% Jule Dairy private Dairy Wahaha 0% 8% 8% 0% 5% 5% 0% 6% Hangzhou Waha private Dairy Vitasoy 2% 5% 5% 1% 3% 3% 2% 4% Vitasoy Intl 345 HK Dairy wondersun 9% 5% -1% 3% 3% 2% 6% 4% wondersun Dairy private Dairy Junlebao 5% 8% 8% 1% 2% 2% 3% 5% Junlebao Dairy 2319 HK Dairy Kraft 0% 4% 4% 3% 2% 0% 1% 3% Kraft Foods Gr KRFT US Dairy Fengxing 3% 1% 1% 1% 2% 2% 2% 2% Guangzhou Fengxi private Dairy Xiangmanlo 2% 1% 1% 1% 2% 2% 1% 2% Wuhan Wei. Xia. private Dairy Yashili 2% 4% 2% 2% 2% -1% 2% 3% Guangdong Yashil private Dairy New hope 0% 1% 1% 0% 2% 2% 0% 2% New Hope Group private Dairy Sanlu 0% 1% 0% 0% 1% 0% 0% 1% Sanlu Group private Dairy Huishan 0% 5% 5% 0% 1% 1% 0% 3% China Huishan Da 6863 HK Dairy Shengyuan 2% 2% 1% 1% 1% 0% 2% 2% Qingdao Sheng Yu private Dairy Anchor 0% 0% 0% 1% 1% 0% 1% 0% Fonterra FCG NZ Dairy Changfu 0% 0% 0% 0% 1% 1% 0% 0% Fujian Changfu OQASUZ CH Dairy Feihe 2% 1% 0% 1% 1% 0% 1% 1% Feihe Dairy ADY US Dairy Flora 0% 0% 0% 1% 1% 0% 0% 0% Unilever ULVR LN Dairy Fonterra 0% 1% 1% 0% 1% 1% 0% 1% Fonterra FCG NZ Dairy Müller 0% 0% 0% 0% 1% 0% 0% 1% Müller private Dairy Lactalis 0% 0% 0% 0% 0% 0% 0% 0% Lactalis private Dairy Lurpack 0% 0% 0% 0% 0% 0% 0% 0% Danish Dairy Boa private Dairy Philadelphia 0% 1% 1% 0% 0% 0% 0% 1% Kraft Foods Grou KRFT US Dairy Delikang 2% 3% 3% 1% 0% 0% 1% 1% Delikang Dairy private Dairy Yinqiao 3% 5% 5% 0% 0% 0% 2% 2% Yinqiao(Ch Dairy CDG SP Cigarettes Chunghwa 6% 7% 7% 25% 20% 20% 16% 14% Shanghai Tobacc private Cigarettes Yuxi 10% 8% 8% 14% 20% 20% 12% 14% Hongta Tobacco private Cigarettes Hongshuangxi 12% 7% 7% 22% 19% 19% 17% 13% Shanghai Tobacc private Cigarettes Liqun 5% 9% 9% 13% 17% 17% 9% 13% Zhejiang Tobacco private Cigarettes Yunyan 7% 7% 7% 13% 17% 17% 10% 12% Hongyunhonghe private Cigarettes Hongtashan 24% 21% 21% 14% 14% 14% 19% 18% Hongta Tobacco private Cigarettes Huanghelou 19% 19% 19% 13% 13% 13% 16% 16% Hubei China Tob private Cigarettes Pride 8% 9% 9% 5% 12% 12% 7% 10% Ch Tob Chuanyu private Cigarettes Marlboro 4% 0% 0% 11% 10% 10% 7% 5% Philip Morris In PM US Cigarettes Shuangxi 5% 3% 3% 6% 8% 8% 5% 6% Ch Tbc Guangdon private Cigarettes Septwolves 12% 6% 6% 10% 7% 7% 11% 6% Longyan Cigarett private Cigarettes Panda 2% 2% 2% 5% 5% 5% 3% 4% Shanghai Tobacco private Cigarettes Zhongnanhai 4% 4% 4% 7% 5% 5% 6% 5% Shanghai Tobacco private Cigarettes Wuyeshen 1% 1% 1% 3% 3% 3% 2% 2% Meizhou Cigarett private Cigarettes Camel 0% 1% 1% 1% 3% 3% 1% 2% R. J. Reynolds private Cigarettes Tianzi 0% 1% 1% 1% 3% 3% 1% 2% Chongqing Tobac private Cigarettes Danghongying 1% 1% 1% 1% 2% 2% 1% 2% Ningbo Cigarette private Cigarettes Hongjinglong 9% 9% 9% 4% 2% 2% 7% 6% China Tbc Hubei private Cigarettes Kent 0% 0% 0% 2% 2% 2% 1% 1% BAT BATS LN Cigarettes Derby 1% 1% 1% 1% 2% 2% 1% 2% BAT BATS LN Cigarettes Dunhill 0% 0% 0% 1% 2% 2% 1% 1% BAT BATS LN Cigarettes Lark 0% 1% 1% 2% 2% 2% 1% 1% Philip Morris In PM US Cigarettes Cocopalm 0% 0% 0% 1% 1% 1% 1% 1% Guangzhou No.1 BATS LN Cigarettes Daqianmen 2% 2% 2% 0% 1% 1% 1% 2% Shanghai Tobacco private Cigarettes Glamour 0% 0% 0% 0% 1% 1% 0% 1% Japan Tobacco 2914 JP Cigarettes Mild Seven 1% 1% 1% 1% 1% 1% 1% 1% Japan Tobacco 2914 JP

February 2014

Credit Suisse Emerging Consumer Survey Databook 2014 Source: Credit Suisse Emerging Consumer Survey 2014 32

% penetration at LOWER income

% penetration at HIGHER income

average % penetration

Sector Brand 2012 2013 3-year growth

2012 2013 3-year growth

2012 2013 Parent Company Listed/ Private

Cigarettes Cleopatra 0% 1% 1% 1% 1% 1% 0% 1% Eastern Company EML US Cigarettes Haomao 7% 8% 8% 1% 1% 1% 4% 5% China Tobacco Sh private

Cigarettes Benson & Hedges

0% 1% 1% 0% 1% 1% 0% 1% Philip Morris In PM US