Elringklinger - Conference Call Q2 2014

22

Conference Call Results Q2 2014 August 7, 2014

-

Upload

company-spotlight -

Category

Investor Relations

-

view

449 -

download

2

description

Second Quarter 2014 Conference Call

Transcript of Elringklinger - Conference Call Q2 2014

Conference Call

Results Q2 2014

August 7, 2014

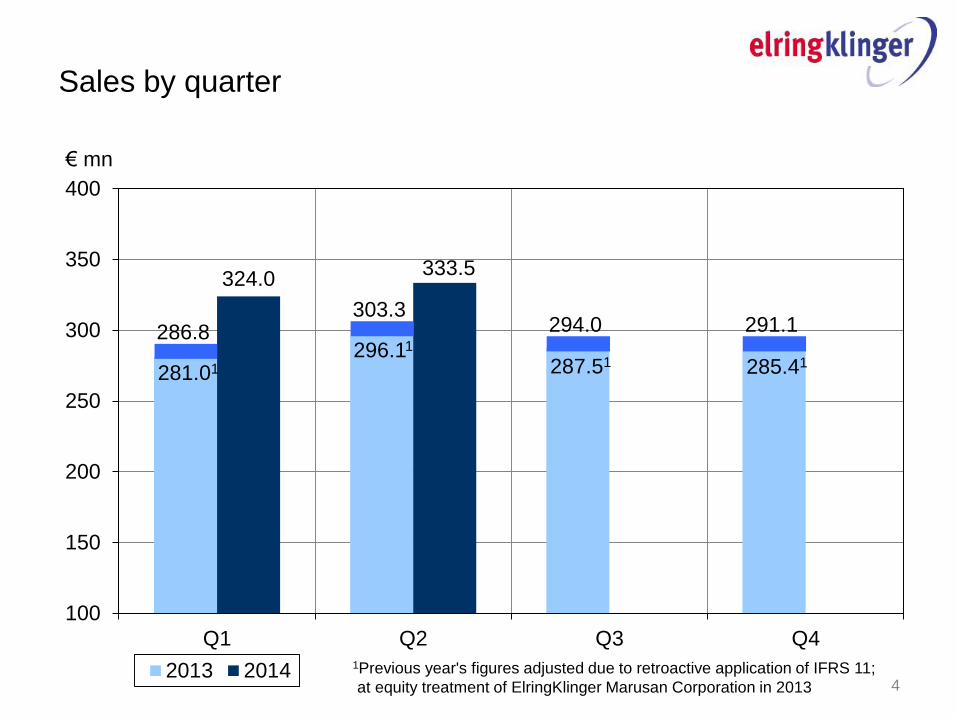

Group sales increased 12.6 % yoy to EUR 333.5 (296.1) mn; organic growth at

10.2 % again clearly outperforming world car production;

Higher share of tooling sales in preparation for ramp-ups

Sales up 2.9 % sequentially despite 4 days less of production (calendar effect)

Consolidation of EKMA in 2013 retroactively changed to equity method (IFRS 11)

resulting in slightly lower comparable sales and EBIT basis;

EKMA contributes an additional EUR 5.7 mn in sales in Q2 2014

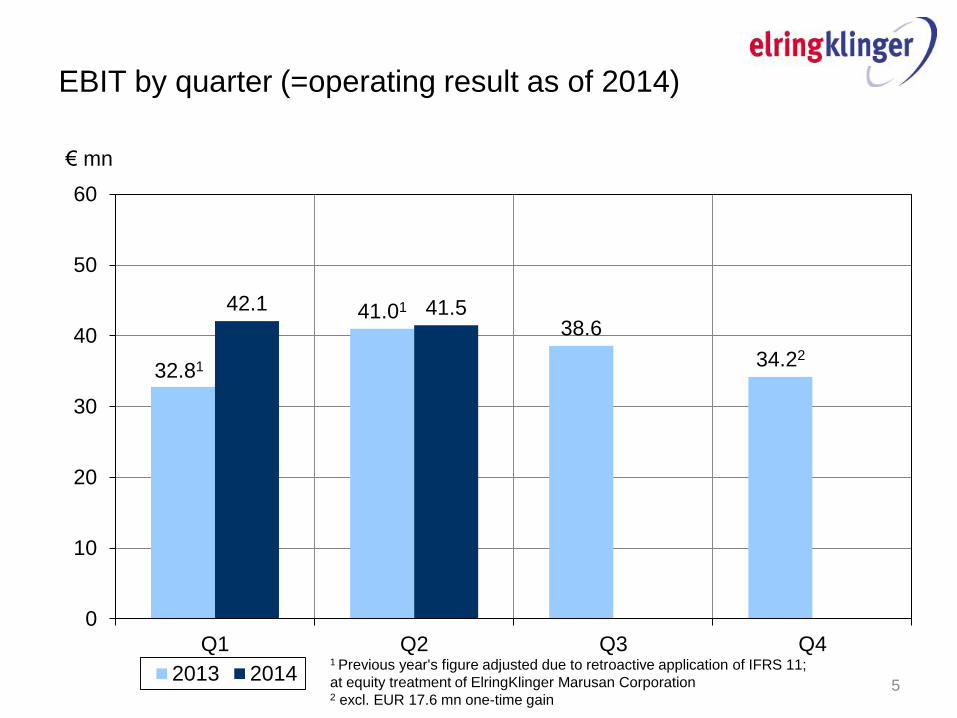

Continued high pre-expenses and start-up losses in battery technology (EBIT

EUR -1.9 mn), slightly better than in Q1 (EBIT EUR -2.2 mn)

Hug delivered solid earnings up y-o-y (EBIT margin 20%+); however at a more

normalized level compared to Q1 (EUR 4.0 mn as compared to EUR 7.7 mn)

EBIT(=operating result) up by 1.2 % to EUR 41.5 (41.0) mn incl. EUR 0.9 mn

ppa on high previous year’s basis

Q2 2014: Key developments

2

H1 2014: China and USA drive global car markets –

BRI markets drop sharply, production in Brazil -17%

3

New car registrations H1 2014 (yoy change)

14.5%

11.0%

5.5%

4.3%

-3.2%

-7.3%

-7.6%

-10% -5% 0% 5% 10% 15% 20%

Russia

Brazil

India

USA

Western Europe

Japan

China

281.01 296.11

287.51 285.41

324.0 333.5

100

150

200

250

300

350

400

Q1 Q2 Q3 Q4

2013 2014

286.8 303.3

294.0 291.1

Sales by quarter

1Previous year's figures adjusted due to retroactive application of IFRS 11;

at equity treatment of ElringKlinger Marusan Corporation in 2013

€ mn

4

EBIT by quarter (=operating result as of 2014)

32.81

41.01 38.6

34.22

42.1 41.5

0

10

20

30

40

50

60

Q1 Q2 Q3 Q4

2013 2014

€ mn

5

1 Previous year's figure adjusted due to retroactive application of IFRS 11;

at equity treatment of ElringKlinger Marusan Corporation 2 excl. EUR 17.6 mn one-time gain

Q2 2014: OEM sales up 13.7 % driven by core

business, higher tooling sales, EKMA

241.21

274.2

0

100

200

300

400

2013 20141Previous year's figures adjusted due to retroactive application of IFRS 11;

at equity treatment of ElringKlinger Marusan Corporation (- EUR 7.2 mn) in Q2 2013

EBIT

30.5 (30.6)

€ mn

6

Q2 2014: Aftermarket sales up 14.8%

29.0

33.3

0

10

20

30

40

50

2013 2014

EBIT +15.3%

6.8 (5.9)

€ mn

7

Q2 2014: Sales Engineered Plastics down 0.9%

22.9 22.7

0

10

20

30

40

2013 2014

EBIT -12.2%

3.6 (4.1)

€ mn

8

Group Sales by segment Q2 2014 (py): OE share up

driven by structural growth and new product ramp-ups

Industrial Parks

0.3% (0.4%) Services

0.7% (0.7%)

OEM

82.2% (81.4%)

Engineered Plastics

6.8% (7.7%)

Aftermarket

10.0% (9.8%)

9

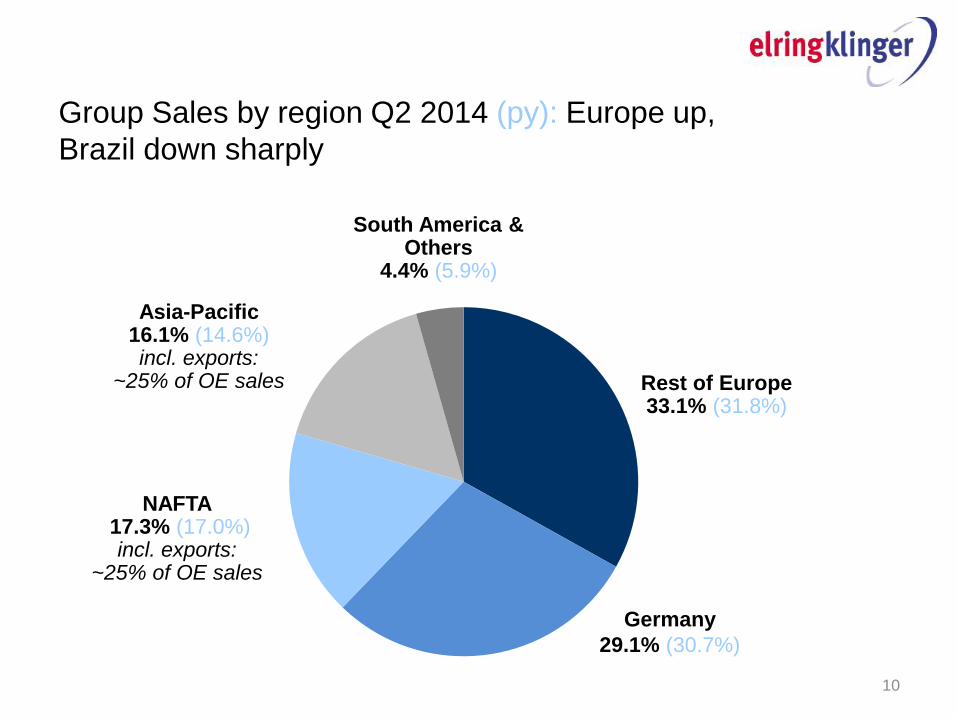

Group Sales by region Q2 2014 (py): Europe up,

Brazil down sharply

South America & Others

4.4% (5.9%)

Rest of Europe 33.1% (31.8%)

Germany

29.1% (30.7%)

Asia-Pacific 16.1% (14.6%) incl. exports:

~25% of OE sales

NAFTA 17.3% (17.0%)

incl. exports: ~25% of OE sales

10

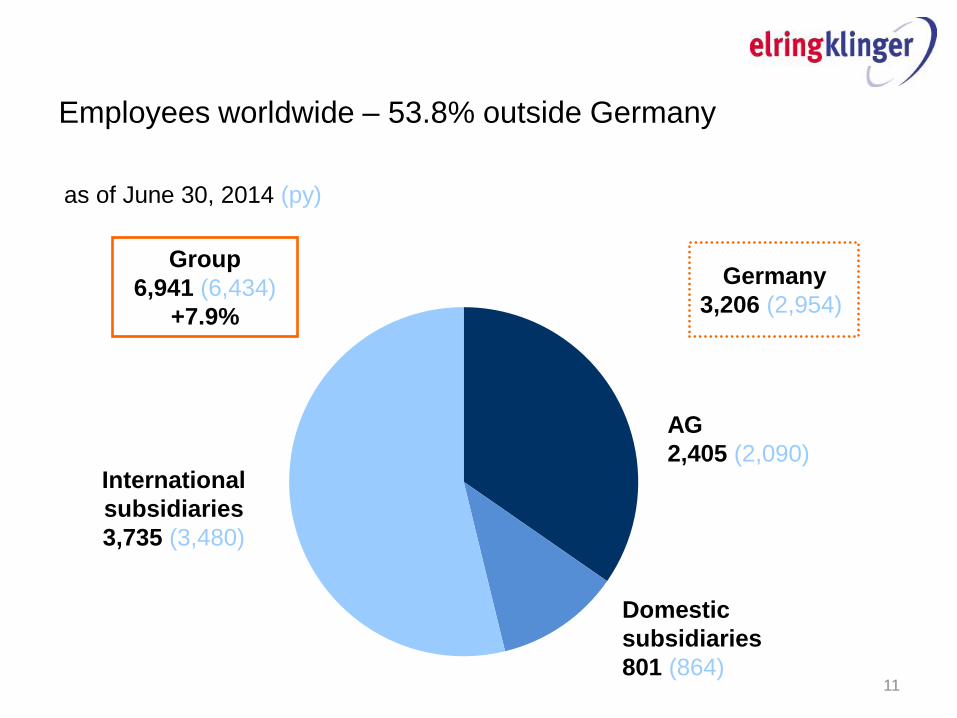

Employees worldwide – 53.8% outside Germany

AG

2,405 (2,090)

Domestic

subsidiaries

801 (864)

International

subsidiaries

3,735 (3,480)

Group

6,941 (6,434)

+7.9%

Germany

3,206 (2,954)

as of June 30, 2014 (py)

11

12

Q2 2014: Sequential improvement in net cash from

operating activities

€ mn

17.8 18.8

36.2 36.3

0

10

20

30

40

50

Q1 2013 Q1 2014 Q2 2013 Q2 2014

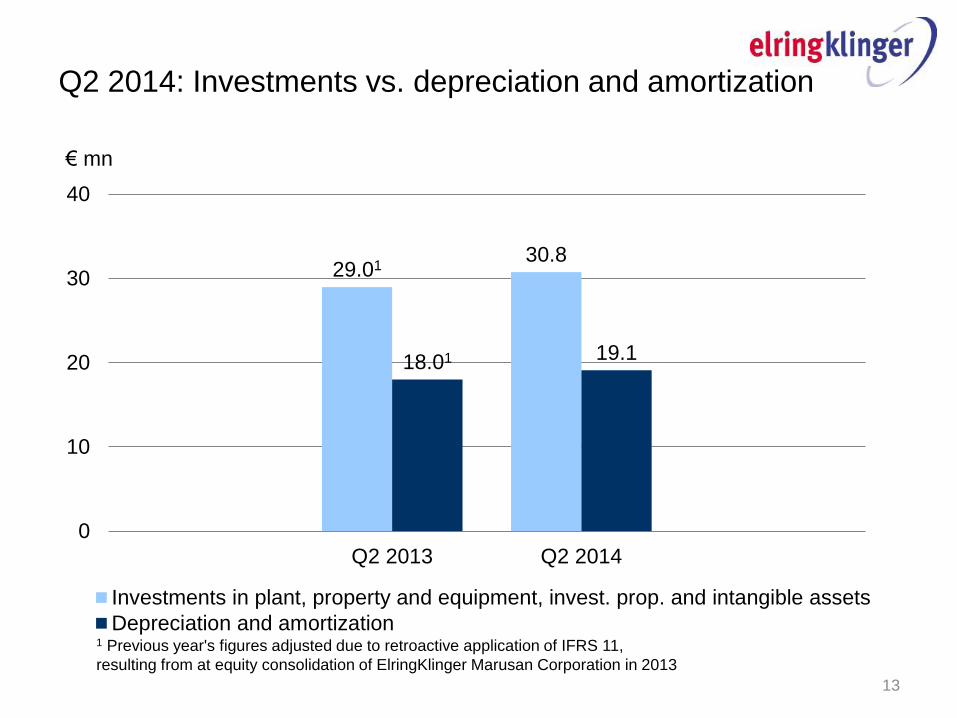

Q2 2014: Investments vs. depreciation and amortization

29.01 30.8

18.01 19.1

0

10

20

30

40

Q2 2013 Q2 2014

Investments in plant, property and equipment, invest. prop. and intangible assets

Depreciation and amortization1 Previous year's figures adjusted due to retroactive application of IFRS 11,

resulting from at equity consolidation of ElringKlinger Marusan Corporation in 2013

€ mn

13

14

Cash flow bridge first half 2014

62.9

+55.0

+33.6

-59.9

-32.8 60.1

0

40

80

120

160

200

Cash atDec 31,

2013

Net cashfrom

operatingactivities

Investments Dividendspaid

Change infinancialliabilities

Others Cash atJune 30,

2014

€ mn

1.3

41.5 42.5

26.7 24.1

58.5 57.5

24.6 26.1

48.7 49.8

June 30, 2013 June 30, 2014 June 30, 2013 June 30, 2014

Balance sheet structure as at June 30, 2014

Equity ratio slightly higher

Non-current liabilities

Current liabilities

Shareholder‘s equity Non-current assets

Current assets

Assets

in %

Liabilities and

shareholder’s equity in %

15

16

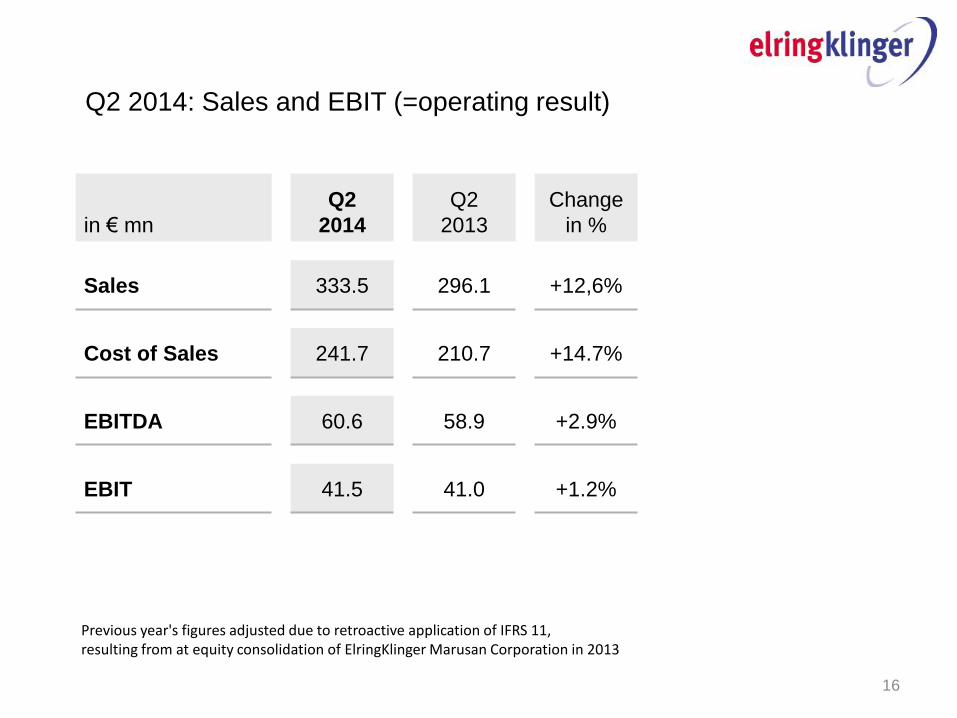

Q2 2014: Sales and EBIT (=operating result)

in € mn

Q2

2014

Q2

2013

Change

in %

Sales 333.5 296.1 +12,6%

Cost of Sales 241.7 210.7 +14.7%

EBITDA 60.6 58.9 +2.9%

EBIT 41.5 41.0 +1.2%

Previous year's figures adjusted due to retroactive application of IFRS 11, resulting from at equity consolidation of ElringKlinger Marusan Corporation in 2013

17

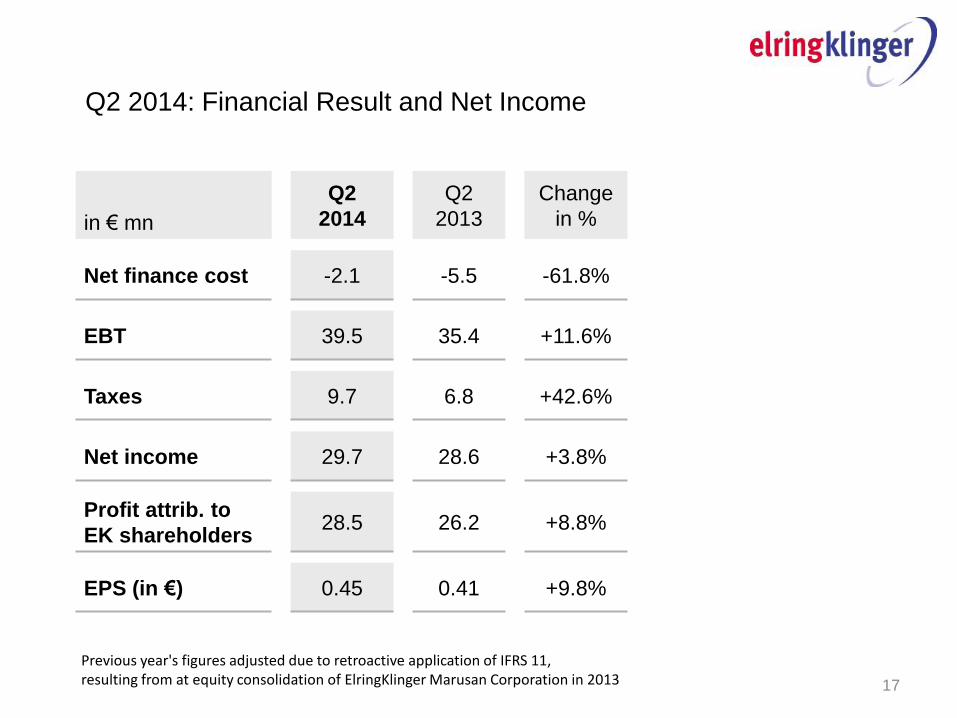

Q2 2014: Financial Result and Net Income

in € mn

Q2

2014

Q2

2013

Change

in %

Net finance cost -2.1 -5.5 -61.8%

EBT 39.5 35.4 +11.6%

Taxes 9.7 6.8 +42.6%

Net income 29.7 28.6 +3.8%

Profit attrib. to

EK shareholders 28.5 26.2 +8.8%

EPS (in €) 0.45 0.41 +9.8%

Previous year's figures adjusted due to retroactive application of IFRS 11, resulting from at equity consolidation of ElringKlinger Marusan Corporation in 2013

18

Q2 2014: Solid performance of Exhaust Gas Purification

division, following extraordinary Q1 2014

in € mn Hug Group

Q2

2014

Q2

2013

Q1

2014

∆ Q2

Sales 19.5 18.2 20.7 +1.3

EBIT 4.0 3.9 7.7 +0.1

PPA -0.3 -0.2 -0.3 -0.1

As expected, project-related and product-mix related business leads to

higher sales/earnings volatility over the quarters

Original sales target (high single digit %-growth) might be slightly exceeded

EBIT margin above Group average

Geopolitical risk factors have clearly increased (Russia, Mid East, Northern

Africa, South America)

EK still expects overall worldwide car production to grow by 2-3%; several

market researchers have been lowering their forecasts

Regional divergence is increasing: Demand primarily driven by China, NA

Modest Western European recovery from still historically low levels to

continue

Mixed picture in BRI markets: Sharp drop in vehicle sales in Brazil and

Russia (June 2014: -17 % each); India showing first signs of recovery

Truck sales in Europe following Euro VI pre-buying better than feared; for

the full year nevertheless moderate decline; EK increases value sold-in

Outlook 2014: Markets show a mixed picure

19

Outlook 2014: Financial performance

in € mn FY 2013

Guidance

FY 2014

Sales 1,175.2

5-7% organic growth

(+ close to EUR 25 mn

scope change) 2

Adj. EBIT1 149.2 160 - 165

Investments 127.2

100 - 110

(+ up to EUR 20 mn

for HFHT)

20

Full consolidation of ElringKlinger Marusan Corporation to add

close to EUR 25 mn in sales but 0.3 PP dilution to Group margin

Order intake Q2 up by 3.5% at EUR 380.0 (367.0) mn, up 14.7%

sequentially

Backlog exceeds prior year by 13.9 % (EUR 649.1 mn)

1 EBIT=operating result as is standard as from Dec. 31, 2013

Disclaimer – Forward-looking Statements and Predictions

This presentation contains statements about the future. These statements are based

on current expectations, market evaluations and predictions by the Management Board,

and on information that is currently available to them. The statements about the future

should not be interpreted as guarantees of the future developments and results that they

refer to. Whilst the Management Board are convinced that the statements that have

been made, and the convictions and expectations on which they are based, are realistic,

they rely on suppositions that may conceivably prove to be incorrect; future results and

developments are dependant on a multitude of factors, they involve various risks and

imponderabilities that can affect whether the ongoing development deviates from the

expectations that have been expressed. These factors include, for example, changes to

the general economic and business situation, variations of exchange rates and interest

rates, poor acceptance of new products and services, and changes to business strategy.

22