Electrical and Electronic Equipment in France - Ré · PDF file"Waste electrical and...

20

2011 Data COLLECTION REPÈRES Electrical and Electronic Equipment in France Legislation Organisation Market Collection Outlook Treatment

Transcript of Electrical and Electronic Equipment in France - Ré · PDF file"Waste electrical and...

2011Data

COLLECTION REPÈRES

Electrical and ElectronicEquipment in France

Legislation Organisation Market Collection OutlookTreatment

Electrical and Electronic Equipment in France - 2011 Data

"Waste electrical and electronic equipment" or "WEEE" refers to electrical orelectronic equipment which has been discarded by its end-user. “Electrical andelectronic equipment" or "EEE" means equipment which is dependent onelectric currents or electromagnetic fields to function properly, as well asequipment for the generation, transfer and measurement of such currents andfields, designed for use with a voltage rating not exceeding 1,000 Volt foralternating current and 1,500 Volt for direct current.

Following the transposition of the European Directive 2002/96/EC (the WEEEDirective) into French law in July 2005, the collection and treatment of WEEEofficially began in France on 13 August 2005 for professional waste, and on 15November 2006 for household waste. Collection and treatment of householdWEEE in French overseas departments began one year later, on 15 November2007.

The law requires all producers of EEE to submit a declaration to the nationalWEEE Register, administered by ADEME, stating the quantities put onto theFrench market and the quantities of waste subsequently collected and treated.

A report on WEEE is released by ADEME each year, based on data drawn mainlyfrom the Register. The present summary is based on the report for 2011.

Updated data are posted annually at www.ademe.fr/publications

2 / 3

LegislationFrench legislationEuropean legislation

Decree 2005-829 of 20 July 2005(codified in articles R543-172 to R543-206

of the Environment Code)

Supplemented by:

Supplemented or modified by:

Decisions of 18/08/05, 13/10/05, 21/10/05, 21/04/06 and 12/10/06 on substances

Directive 2011/65/EU: RoHS/LdSD1 January 2013 (revision)

Completed or supplemented by:

Modified by:

Directive 2002/96/EC: WEEE13 August 2005

Decree 2012-617 of 2 May 2012

Directive 2002/95/EC: RoHS/LdSD1 July 2006

Directive 2003/108/EC: WEEE(modification)

Decision of 11/03/04:Questionnaire for national implementation reports

Decision of 03/05/05:Rules applicable to national monitoring procedures

Directive 2008/34/EC: WEEE(modification)

Directive 2012/19/EU: WEEE13 August 2012 (revision)

Order of 23/11/05: treatment procedures

Art-L541-10-2 of the Environment Code (art. 87 LRF 2005)

Notice of 26/10/05: annexe IB, scope

Order of 13/07/06: lamps

Order of 23/11/05: RoHS substances, modified by the Order of 18/03/11

Order of 30/06/09: Register of producers (abrogating the Order of 13/03/06)

5 Orders of 23/12/09: renewed approval of the 4 householdWEEE Producer Responsibility Organisations (PROs) and of the OCAD3E as coordinating organisation

Order of 18/03/11: RoHS substances

Order of the 05/06/12: approval procedure and specifications for PROs responsible for professional WEEE

(abrogating the Order of 23/11/2005)

4 Orders of 01/08/12: approval of the 4 professional WEEE PROs

RoHS Directives

WEEE Directives

European regulations

Directive 2002/96/EC, known as the“WEEE Directive”, and Directive 2002/95/EC,known as the “RoHS Directive”, set upthe European regulatory framework forthe separate collection and treatmentof electrical and electronic equipmentwaste in each Member State.

All EEE devices, whether household orprofessional, are classified into one ofthe following ten categories:

Electrical and Electronic Equipment in France - 2011 Data

The 10 Categories of Equipment

1 Large household appliances

2 Small household appliances

3 IT and telecommunications equipment

4 Consumer equipment

5 Lighting equipment

6 Electrical and electronic tools

7 Toys, leisure and sports equipment

8 Medical devices

9 Monitoring and control instruments

10 Automatic dispensers

The WEEE Directive specifically requires:

∎ EEE eco-design in order to facilitateWEEE reuse and treatment

∎ separate collection of WEEE, with acollection target of 4 kg/year/capitain 2006 for household waste and anobligation to take back old equipmentfree of charge when similar newhousehold equipment is purchased

∎ systematic treatment of specificcomponents (such as PCB condensers,printed circuit boards) and of substancesclassified as dangerous (such as mercury,CFCs) to prevent pollution

∎ reuse, recycling and recovery of col-lected WEEE with high recycling and re-covery targets, with the reuse of wholedevices being identified as the priority.

In addition, products put on the marketafter 13 August 2005 must bear the pro-

ducer’s name and the“crossed-out wheeled bin”symbol, as stipulated bythe EN 50419 standard.

The RoHS Directive lists substanceswhose use in the manufacturing of equip-ment is banned or strictly controlled.Most EEE devices are affected by thislist. Directive 2011/65/EU, published on1 July 2011, is a revision of the RoHS Di-rective and must be transposed by theMember States before 1 January 2013.

The regulatory framework will evolveagain in the coming years, following thepublication on 4 July 2012 of Directive2012/19/EU (recast WEEE Directive)amending Directive 2002/96/EC (WEEEDirective). The new Directive, which mustbe transposed into French law by 14February 2014 at the latest, reasserts

the principles laid down in the previouslegislation regarding the establishmentof a collection and treatment system andextends the scope of the WEEE Directive.

The key modifications will include:

∎ A broader scope for EEE and achange in definition of householdWEEE, now also covering WEEE thatcan be used both by professionalsor households

∎ A reduction of the number of EEEcategories from 10 to 6

∎ New collection targets:

∎ More ambitious reuse, recovery andrecycling objectives (5% increase)

∎ Reinforced controls on EEE exportedfor reuse

French regulations

• Distinction between Householdand Professional EEE

Equipment is considered to be professionalif its use is exclusively professional, or ifthe devices are distributed exclusivelyvia professional distribution channels. Equipment is regarded as household (or

domestic) if it is not considered as pro-fessional (equipment that is exclusivelyfor domestic or mixed use and is distrib-uted via household or mixed distributionchannels). If equipment is sold via a mixed distri-bution channel (open both to householdsand professionals) without any possibilityfor the producer to identify the end user,

the latter is considered, by decree, to behousehold equipment (for example: ITdevices for professional use).

• Producers The Decree defines an EEE producer asthe entity which puts the equipment onthe French market. According to that def-inition, there are five types of producers.

4 / 5

Les 5 statuts de producteur

Manufacturer Sells under its own brand products manufactured in France

Importer Imports from a country outside the EU

Introducer Imports from an EU Member State

Reseller under its own brand Resells products under its own brand

Distance seller Direct seller of household EEE from abroad by post of household equipment or Internet communication [status added after

publication of the Decree]

The 5 types of Producer Producers are responsible fororganising and financingthe collection and treat-ment of WEEE (see chapter‘Organisation’).

• DistributorsDecree 2005-829 imposes the followingobligations on distributors of householdEEE:

∎ Distributors must take back a usedproduct upon purchase of a new productof the same type (an obligation called“one for one” take-back).

∎ Distributors must inform buyers aboutthe legislation prohibiting the disposalof WEEE with regular household waste,the availability of collection systems,and the potential effects of hazardoussubstances contained in EEE on theenvironment and human health

• Visible Fee Producers and distributors of householdequipment are required to inform purchasersof the cost of WEEE disposal. They mustindicate, at the bottom of the invoice,the amount of the “eco-contribution”(or “eco-participation”) included therein,which varies depending on the type ofequipment in question and the ProducerResponsibility Organisation (PRO) towhich the producer belongs. This obligationof disclosure holds until 13 February 2013.

• The WEEE Register Producers of EEE or the collectiveschemes acting on their behalf mustdeclare annually the following infor-mation to the Register administeredby ADEME:

∎ quantities of EEE put on the Frenchmarket;

∎ quantities of WEEE collected in Franceand subsequently treated in Franceor abroad, as well as the amount ofspecific components and substancesextracted from WEEE during treatment.

The WEEE Register and the Batteries andAccumulators Register are accessible viaa single online platform at:

www.registres.ademe.fr

Electrical and Electronic Equipment in France - 2011 Data

OrganisationHousehold and professional WEEE streams are managed differently.

Household WEEE

The Decree offers two options to producersof household equipment:

∎ implementing an individual collectionand treatment scheme subject toapproval by public authorities (noindividual scheme has been approvedto date)

∎ joining an approved Producer Re-sponsibility Organisation (PRO)responsible for the collection andtreatment of household equipment.

Les éco-organismes agréés pour la collecte et le traitement des DEEE ménagers

www.ecologic-france.com

All WEEE except Category 5

Category 5 WEEE (Lighting equipment)

www.eco-systemes.com

www.erp-recycling.fr

www.recylum.com

In 2006, these four PROs foundedOCAD3E, the association responsible forcoordinating and managing relationshipsbetween Producer Responsibility Organ-isations and local authorities, who playa major role in household WEEE collection. The 5 Waste Streams

“ GEM F ”Large cooling appliances

“ GEM HF ” - Large household appliances (except for cooling appliances)

“ Ecrans ” - Screens

“ PAM ” - Other small appliances

“ Lampes ”- Lamps

CollectionHousehold WEEE is collected in fiveseparate waste streams.

• Household WEEE is collected byservice providers selected by thePROs from:

∎ local authorities having set up aselective collection scheme (drop-offcentres, collection districts) and signeda contract with the OCAD3E to receivecompensation for collection costs.By the end of 2011, 90% of Frenchcitizens had access to such a selectivecollection system for WEEE, notablythrough 4.000 drop-off centres

∎ distributors implementing ‘one-for-one’ take-back programmes. Bythe end of 2011, more than 20.000collection points were acceptingWEEE, with 16.000 accepting lamps

∎ not-for-profit and community organ-isations involved in reuse operations.

Treatment (household and professional WEEE)

Five types of WEEE treatment can be identified. They are ranked below according to the degree of priority given to them bythe legislation:

6 / 7

French designation Type of Treatment

Réemploi ou réutilisation Reuse of whole devices

Réutilisation en pièces Reuse of device components

Recyclage Material recycling

Valorisation énergétique Energy recovery

Destruction ou éliminationDisposal without material or energy recovery (landfill, incineration without energy recovery)

Professional WEEE

Owners of professional EEE are responsiblefor the end-of-life of products placed onthe market before 13 August 2005, exceptwhen such equipment is replaced by anew one (in this case the supplier musttake back the old equipment).

The end-of-life of professional EEE putinto circulation after 13 August 2005, orof older equipment having been theobject of a replacement, is the responsi-bility of the producer, who is given threeoptions:

∎ implementing an individual schemefor collection and treatment (no ap-proval is necessary, unlike for the house-hold sector). Since 2012, a certificateof conformity with the law, consistingin a formal commitment by the pro-ducer to fulfil his obligations, must be

provided when making the annual dec-laration to the WEEE Register.

∎ joining an approved Producer Re-sponsibility Organisation. Up until2011, this possibility was of a purelytheoretical nature since no PRO hadbeen established to specifically handleprofessional WEEE. However, the work carried out by theEnvironment Ministry since 2010 hasled to the accreditation, as of 15August 2012, of a number of PROsresponsible for the collection andtreatment of certain types of profes-sional WEEE:- ‘Ecologic’ for Category 3 and 4 equip-

ment (IT and telecommunicationsequipment, Consumer equipment)

- ‘Eco-systèmes’ for Category 10equipment (Automatic dispensers)

- ‘Recyclum’ for Category 5, 8 and 9

equipment (Lighting equipment,Medical devices and Monitoringand control instruments)

- ‘Récydent’ for Category 6 and 8equipment (Electrical and electronictools and Medical devices) fromthe dentistry sector

∎ delegating the disposal to the end-user. This option is available only whena direct contractual relationship existswith the end-user (i.e. no sales inter-mediary), and must be specified in theequipment’s terms of sale. It is the end-user’s right to negotiate the financialconditions of, or to simply refuse thisdelegation. Since 2012, producers re-sorting to this option must provide acertificate of conformity with the lawlaying down the conditions of the transferof responsibility when making their an-nual declaration to the WEEE Register.

Annual quantities of WEEE treated must be declared by product category as well as treatment type. This declaration also specifiesthe quantities of components or substances requiring special treatment and having been extracted during the treatment process.

English designation

Reuse

Component reuse

Recycling

Energy recovery

Disposal

Electrical and Electronic Equipment in France - 2011 Data

Market

0

20

40

60

80

100

120

140

160

1 2 3 4 5 6 7 8 9 10Categories

2008

2009

2010

2011

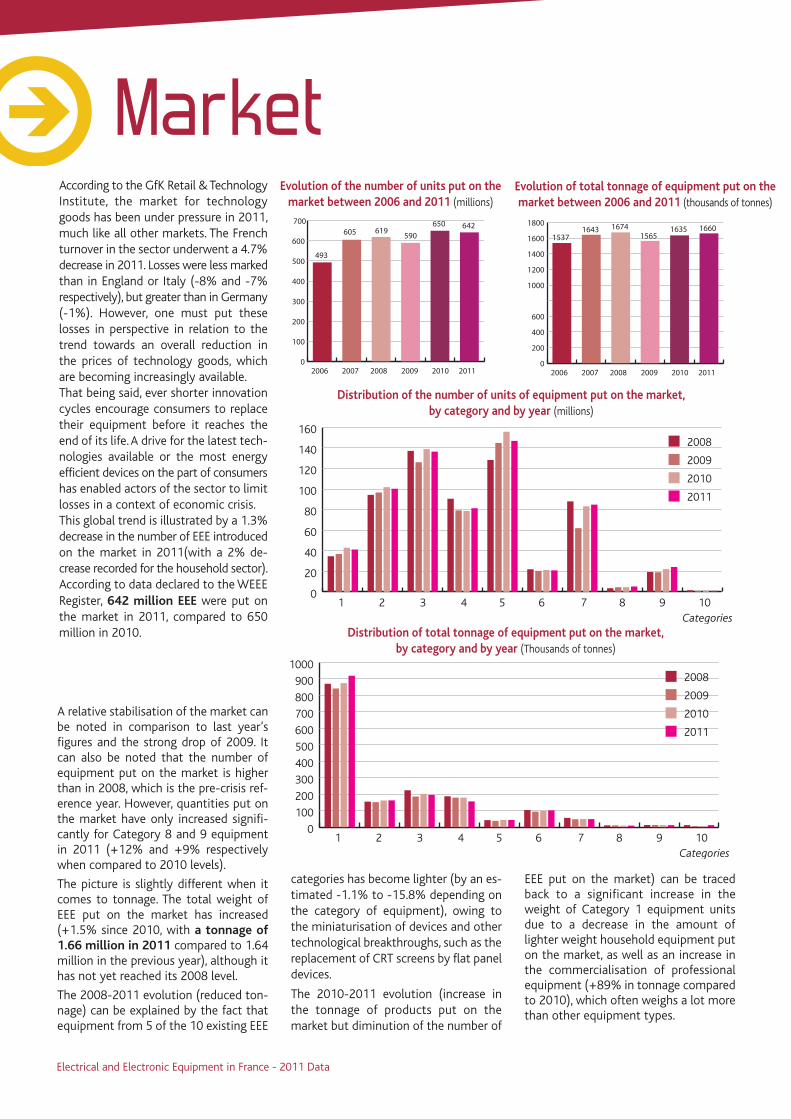

According to the GfK Retail & TechnologyInstitute, the market for technologygoods has been under pressure in 2011,much like all other markets. The Frenchturnover in the sector underwent a 4.7%decrease in 2011. Losses were less markedthan in England or Italy (-8% and -7%respectively), but greater than in Germany(-1%). However, one must put theselosses in perspective in relation to thetrend towards an overall reduction inthe prices of technology goods, whichare becoming increasingly available.That being said, ever shorter innovationcycles encourage consumers to replacetheir equipment before it reaches theend of its life. A drive for the latest tech-nologies available or the most energyefficient devices on the part of consumershas enabled actors of the sector to limitlosses in a context of economic crisis.This global trend is illustrated by a 1.3%decrease in the number of EEE introducedon the market in 2011(with a 2% de-crease recorded for the household sector).According to data declared to the WEEERegister, 642 million EEE were put onthe market in 2011, compared to 650million in 2010.

Evolution of total tonnage of equipment put on themarket between 2006 and 2011 (thousands of tonnes)

Distribution of total tonnage of equipment put on the market,by category and by year (Thousands of tonnes)

0

100

200

300

400

500

600

700

2006 2007 2008 2009 2010 2011

493

605 619590

650 642

0

200

400

600

1000

1200

1400

1600

1800

2006

15371643 1674

15651635 1660

2007 2008 2009 2010 2011

Evolution of the number of units put on themarket between 2006 and 2011 (millions)

Distribution of the number of units of equipment put on the market,by category and by year (millions)

A relative stabilisation of the market canbe noted in comparison to last year’sfigures and the strong drop of 2009. Itcan also be noted that the number ofequipment put on the market is higherthan in 2008, which is the pre-crisis ref-erence year. However, quantities put onthe market have only increased signifi-cantly for Category 8 and 9 equipmentin 2011 (+12% and +9% respectivelywhen compared to 2010 levels).

The picture is slightly different when itcomes to tonnage. The total weight ofEEE put on the market has increased(+1.5% since 2010, with a tonnage of1.66 million in 2011 compared to 1.64million in the previous year), although ithas not yet reached its 2008 level.

The 2008-2011 evolution (reduced ton-nage) can be explained by the fact thatequipment from 5 of the 10 existing EEE

categories has become lighter (by an es-timated -1.1% to -15.8% depending onthe category of equipment), owing tothe miniaturisation of devices and othertechnological breakthroughs, such as thereplacement of CRT screens by flat paneldevices.

The 2010-2011 evolution (increase inthe tonnage of products put on themarket but diminution of the number of

EEE put on the market) can be tracedback to a significant increase in theweight of Category 1 equipment unitsdue to a decrease in the amount oflighter weight household equipment puton the market, as well as an increase inthe commercialisation of professionalequipment (+89% in tonnage comparedto 2010), which often weighs a lot morethan other equipment types.

0

100

200

300

400

500

600

700

800

900

1000

1 2 3 4 5 6 7 8 9 10Categories

2008

2009

2010

2011

8 / 9

0

100

200

300

400

500

600

700

800

900

1000

1 2 3 4 5 6 7 8 9 10(Categories)

2008

2009

2010

2011

0

20

40

60

80

100

120

1 2 3 4 5 6 7 8 9 10(Categories)

2008

2009

2010

2011

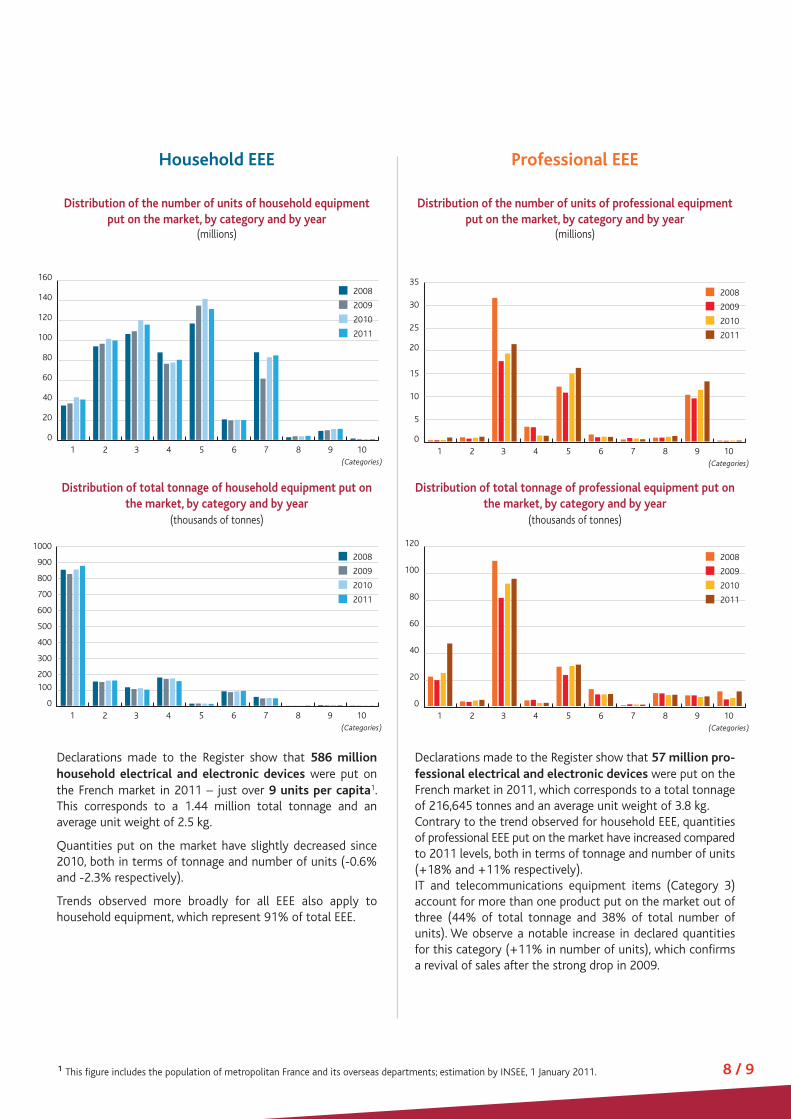

Declarations made to the Register show that 586 millionhousehold electrical and electronic devices were put onthe French market in 2011 – just over 9 units per capita1.This corresponds to a 1.44 million total tonnage and anaverage unit weight of 2.5 kg.

Quantities put on the market have slightly decreased since2010, both in terms of tonnage and number of units (-0.6%and -2.3% respectively).

Trends observed more broadly for all EEE also apply tohousehold equipment, which represent 91% of total EEE.

Declarations made to the Register show that 57 million pro-fessional electrical and electronic devices were put on theFrench market in 2011, which corresponds to a total tonnageof 216,645 tonnes and an average unit weight of 3.8 kg. Contrary to the trend observed for household EEE, quantitiesof professional EEE put on the market have increased comparedto 2011 levels, both in terms of tonnage and number of units(+18% and +11% respectively).IT and telecommunications equipment items (Category 3)account for more than one product put on the market out ofthree (44% of total tonnage and 38% of total number ofunits). We observe a notable increase in declared quantitiesfor this category (+11% in number of units), which confirmsa revival of sales after the strong drop in 2009.

1 This figure includes the population of metropolitan France and its overseas departments; estimation by INSEE, 1 January 2011.

Distribution of the number of units of household equipmentput on the market, by category and by year

(millions)

Distribution of the number of units of professional equipmentput on the market, by category and by year

(millions)

Household EEE Professional EEE

0

20

40

60

80

100

120

140

160

1 2 3 4 5 6 7 8 9 10(Categories)

2008

2009

2010

2011

0

5

10

15

20

25

30

35

1 2 3 4 5 6 7 8 9 10(Categories)

2008

2009

2010

2011

Distribution of total tonnage of household equipment put onthe market, by category and by year

(thousands of tonnes)

Distribution of total tonnage of professional equipment put onthe market, by category and by year

(thousands of tonnes)

Electrical and Electronic Equipment in France - 2011 Data

Household EEE Professional EEE

Tonnage of household devices put on the marketin 2011 by type of producer

Total tonnage put on the market: 1,443,614

Distribution of total tonnage of professional devicesput on the market, by type of producerTotal tonnage put on the market: 216,645

Introducer - 20 %

Manufacturer - 38 %

Importer - 35 %

Distance seller - <1 %

Reseller under own brand - 7 %

Manufacturer - 47 %

Reseller under own brand - 6 %

Importer - 17 %

Introducer - 31 %

Almost 40% (in tonnage) of household equipment put on theFrench market in 2011 was manufactured in France. Importsfrom countries outside the EU also constituted an importantproportion of products put on the market (35% in tonnage).

Almost half of the professional equipment (in tonnage) puton the market in 2011 was manufactured in France andaround 30% in other EU Member States.

Market share by PRO in 2011Total tonnage for all categories

Récylum - 0.8 %

ERP - 8.4 %

Ecologic - 16.6 %

Eco-systèmes - 74.2 %

Management by end-user - 16 %

Individual scheme - 84 %

PRO market shares correspond to the proportion of EEEtonnage put on the market by their members compared tothe overall tonnage of EEE put on the market. The estimationof these market shares has important financial consequencessince it is used as the basis for calculating the collection obli-gations of PROs.In 2011, contributions received by PROs for household EEEput on the market amounted to €193 million, a figure whichis less than contributions in 2010 (€197 million), owing to adecrease in the number of units sold.

Distribution by type of collection and treatment organisationremains relatively stable compared to 2010, with a small de-crease in the proportion of equipment items for which disposalis delegated to end-users (16% in 2011 compared to 17% in2010). Most EEE are still being treated through individualschemes.

DISTRIBUTION BY TYPE OF COLLECTION AND TREATMENT ORGANISATION

DISTRIBUTION BY TYPE OF PRODUCER

Distribution of total tonnage of professional equipment put onthe market in 2011, by type of organisationTotal tonnage put on the market: 216,645

10 / 11

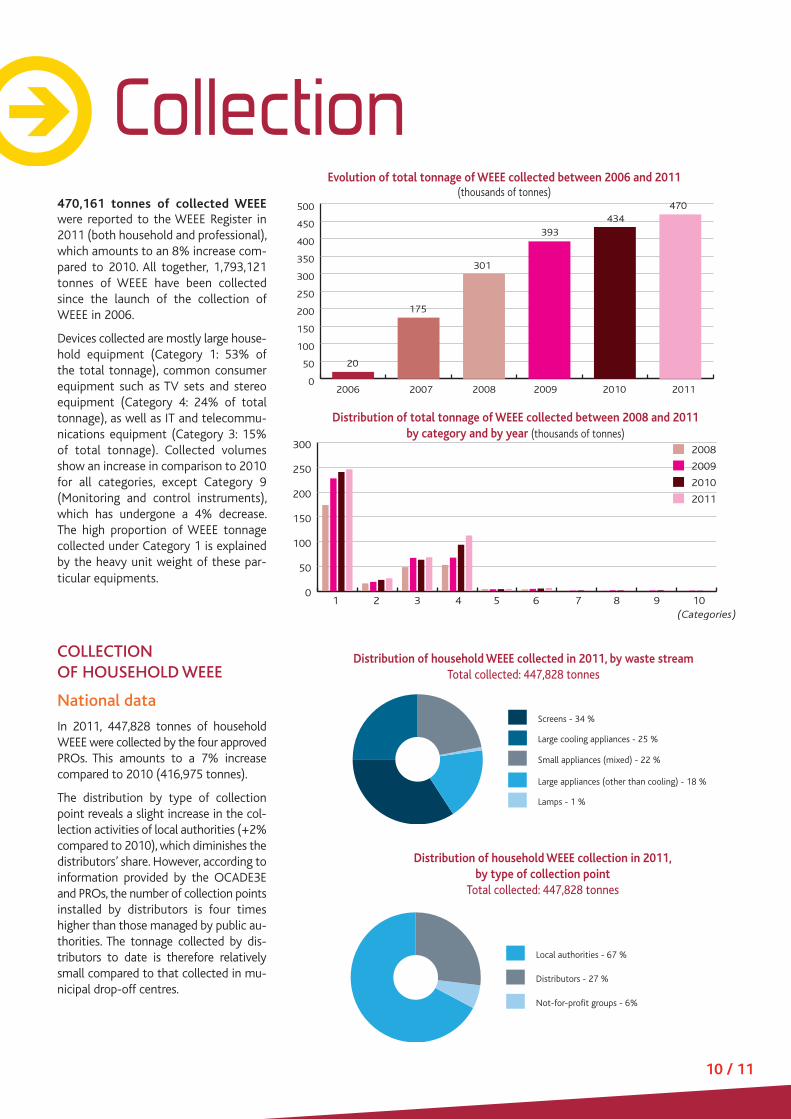

Collection470,161 tonnes of collected WEEEwere reported to the WEEE Register in2011 (both household and professional),which amounts to an 8% increase com-pared to 2010. All together, 1,793,121tonnes of WEEE have been collectedsince the launch of the collection ofWEEE in 2006.

Devices collected are mostly large house-hold equipment (Category 1: 53% ofthe total tonnage), common consumerequipment such as TV sets and stereoequipment (Category 4: 24% of totaltonnage), as well as IT and telecommu-nications equipment (Category 3: 15%of total tonnage). Collected volumesshow an increase in comparison to 2010for all categories, except Category 9(Monitoring and control instruments),which has undergone a 4% decrease.The high proportion of WEEE tonnagecollected under Category 1 is explainedby the heavy unit weight of these par-ticular equipments.

0

50

100

150

200

250

300

350

400

450

500

2006 2007 2008 2009 2010 2011

20

175

301

393434

470

Evolution of total tonnage of WEEE collected between 2006 and 2011(thousands of tonnes)

0

50

100

150

200

250

300

1 2 3 4 5 6 7 8 9 10(Categories)

2008

2009

2010

2011

Distribution of total tonnage of WEEE collected between 2008 and 2011by category and by year (thousands of tonnes)

COLLECTIONOF HOUSEHOLD WEEE

National data

In 2011, 447,828 tonnes of householdWEEE were collected by the four approvedPROs. This amounts to a 7% increasecompared to 2010 (416,975 tonnes).

The distribution by type of collectionpoint reveals a slight increase in the col-lection activities of local authorities (+2%compared to 2010), which diminishes thedistributors’ share. However, according toinformation provided by the OCADE3Eand PROs, the number of collection pointsinstalled by distributors is four timeshigher than those managed by public au-thorities. The tonnage collected by dis-tributors to date is therefore relativelysmall compared to that collected in mu-nicipal drop-off centres.

Large cooling appliances - 25 %

Screens - 34 %

Large appliances (other than cooling) - 18 %

Lamps - 1 %

Small appliances (mixed) - 22 %

Distribution of household WEEE collected in 2011, by waste streamTotal collected: 447,828 tonnes

Local authorities - 67 %

Not-for-profit groups - 6%

Distributors - 27 %

Distribution of household WEEE collection in 2011,by type of collection point

Total collected: 447,828 tonnes

Electrical and Electronic Equipment in France - 2011 Data

The collection streams of all householdequipment categories have increased since2010, except for large appliances (oven,dish-washer or washing machine type:-0.2%). A limited increase can also be ob-served for large cooling appliances (+5%).Collection of large household appliancesand large cooling appliances is still beingnegatively impacted by the pickup ofdiscarded items on the streets and thelooting of drop-off centres by individualswishing to sell their metallic components.Public authorities have taken several meas-ures to combat those illegal activities.

Collection of lamps has increased morein 2011 than during the previous year(+11% in 2011; +5% in 2010), thanksnotably to communication campaigns. Ithas reached its highest level since 2006.Thus, the return ratio for lamps (collectedquantities compared to volumes put onthe market under Category 5) amountsto more than 33% in 2011.

In addition, collection of small appliancesis still intensifying to a considerable extent(+13% compared to 2010 and +36%compared to 2009), owing to the multi-plication of available collection pointsfor this stream (collection by some localauthorities through sorting containers,by distributors or via drop-off centres).

Finally, the tonnage of collected TV screenshas increased sharply, but not as muchas in 2010 (+16% compared to 2010;+26% between 2009 and 2010). Thistrend can be explained by the replacementof CRT screens by flat panel ones withthe introduction of digital television.

In 2011, thanks to a denser network of collection points, theshare of the French population covered by WEEE collectionschemes amounts to more than 60 million people (all WEEEstreams except lamps) and to 48 million for lamps.

S2 2007S2 2008

S2 2009S2 2010

S2 2011

S : semester

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

General stream

Lamp stream

Share of the French population covered by collection schemes (Number of inhabitants - thousands)

For 2011, the collection shares of the four approved PROs arethe following:

Récylum - 1 %

ERP - 10 %

Ecologic - 16 %

Eco-systèmes - 73 %

Distribution of Household WEEE collected in 2011, by PROTotal collected: 447,828 tonnes

As Récylum is the only approved PRO for Category 5 waste, itmust handle the collection and treatment of the entire stream.

The three other PROs must collect a volume of WEEE that isproportional to their respective market shares. Potential dis-crepancies have to be taken into account during the followingyear.

0

50

100

150

200

250

300

350

400

450

500

Large appliances (other than cooling)

Large cooling appliances

Screens

Small appliances (mixed)

Lamps

2006 2007 2008 2009 2010 2011

Evolution of household WEEE collected, by waste stream between 2006 and 2011(thousands of tonnes)

12 / 13

At the local level

Réunion Guadeloupe MayotteMartinique Guyane

Less than 4

Household WEEE collectedin 2011, by department(kg per capita)

4 – 7

7 – 10

Above 10

29 22

56

44

85

49

5335

50 14

61

72

37

8679

1716

33

40

64

65

31

0911

66

34 13

30 84

83

0604

05

73

74

38

260748

12

8182

32

4746

2315 43

63

19

36

18

41

45

28

78

9177

89

58

03

42 69

01

71

21

5210

51

0260

95

8076

6259

08

55

54

57

67

8868

9070

25

39

94

93

92

75

24

87

27

2b

2a

Household WEEE collected in 2011, by department (kg per capita)

With an average of 6.9 kg WEEE collectedper capita in 20112, the target of 4 kg by31 December 2006 set by the EuropeanDirective has been surpassed at the na-tional level. However, the objective ofcollecting 7 kg per capita by 2011 assignedto PROs has not been reached. 28 French“Départements” (regional administrativeunits) have collected less than 7 kg,among which 8 have collected less than4 kg.

It should be noted that the WEEE collec-tion is done by collection point (fromdistributors, drop-off centers or not-for-profit groups) but the estimation of col-lected quantities is done at transfer sta-tions where PROs pick up WEEE. As WEEEregrouped from collection points to trans-fer stations can be in the neighbouring“département”, this may distort localcollection figures, notably in the case ofParis area.

Besides, in addition to disparities among“Départements”, collection rates are verydissimilar when one compares rural withsemi-urban areas on the one hand, andwith urban areas on the other. Of WEEEcollected, 49.2% (in tonnage) originatesfrom semi-urban areas, 33.7% from ruralareas and only 17.1% from cities3.

2 This figure includes the population of metropolitan France and its overseas departments; estimation by INSEE, 1 January 20103 OCAD3E data

Electrical and Electronic Equipment in France - 2011 Data

COLLECTION OFPROFESSIONAL WEEE

In 2011, 22,332 tonnes of professionalelectrical and electronic equipment wastehave been declared as collected by 385producers implementing individualschemes. This figure corresponds to a31% increase in tonnage compared to2010 (16,983 tonnes). This evolution isdue partly to a rise in the quantities de-clared as collected by producers of Cat-egory 3 equipment, and partly to thecollected quantities declared by a singlenewly registered producer, who had notreported any collected WEEE in 2010(collected quantities have reached their2009 level again).

Thus, as is also true for quantities puton the market, data from the Registeron the collection and treatment of pro-fessional WEEE can vary largely fromone year to another given that it dependsto a great extent on declarations madeby a small number of producers recordinghigh tonnages.

Collection of Category 3 professionalequipment has increased sharply (+30%compared to 2010). The 2009 peak hasbeen surpassed (18,557 tonnes collectedin 2011; 18,331 in 2009).

0

5

10

15

20

25

2006 2007 2008 2009 2010 2011

10

1617

22

17

22

Evolution in total tonnage of professional WEEE collected between 2006 and 2011(thousands of tonnes)

0

2

4

6

8

10

12

14

16

18

20

1 2 3 4 5 6 7 8 9 10(Categories)

2008

2009

2010

2011

Distribution of tonnage of professional WEEE collected,by category of equipment and by year (thousands of tonnes) / (Categories)

1 - Large household appliances - 3 %

2 - Small household appliances - <1 %

3 - IT and telecommunications equipment - 83 %

4 - Consumer equipment - <1 %

5 - Lighting equipment - 2 %

6 - Electrical and electronic tools - <1 %

8 - Medical devices - 6 %

9 - Monitoring and control instruments - <1 %

10 - Automatic dispensers - 5 %

Distribution of professional WEEE collected tonnage in 2011,by category of equipment4

Total collected: 22,332 tonnes

The distribution of collected professional WEEE tonnageby equipment category gives a better picture of therelative significance of different WEEE collection rates.

63 producers declared 18,557 tonnes of Category 3waste collected, representing 83% of the total tonnagecollected in 2011. Among those producers, 4 declaredmore than 75% of the volumes recorded under Category3 (i.e. 65% of the overall tonnage declared, all equipmentcategories included).

This distribution can be explained by the fact that thelifespan of some categories of equipment is longerthan that of others. For example, certain tools (Category6) or large household appliances (Category 1) introducedon the market in 2006 have not reached the end oftheir life yet, while Category 3 equipment items (ITand telecommunications equipment), which have ashorter lifespan, are for the most part being collected.

Recent agreements made with PROs for the collectionand treatment of Category 3, 4, 5, 6 (dentistry sectoronly), 8, 9 and 10 professional WEEE should have animpact on the collected volumes declared to theRegister in coming years.

4 No collection of professional equipment was declared for Category 7; this category is thus absent from the chart.

14 / 15

Treatment

The distribution of tonnage treated is logically very close to thedistribution of tonnage collected: large household appliances(Category 1 amounts to 53% of total tonnage treated), IT andtelecommunications equipment and consumer equipment (Cat-egories 4 and 3 respectively cover 24% and 14% of total tonnagetreated) account for the largest shares.

There are 220 treatment centres in France, which carry out oneor several of the following operations: reuse, depollution,dismantling, grinding, sorting, recycling, and physico-chemicaltreatment.

Recycling is the most common type of treatment (78% of totaltonnage), which highlights the added environmental value of WEEEcollection and treatment.

881 tonnes of WEEE have been declared as being reused ascomponent in 2011, compared to 390 tonnes in 2010. This 126%increase is due exclusively to a sharp rise in declared quantities ofreused WEEE as component in the professional sector (+162%compared to 2010).

Certain products (components or substances) mentioned in theWEEE Directive must be extracted during the treatment processowing to their pollution potential or high recyclability. These com-ponents and substances are the object of a specific declaration.

119,832 tonnes of such components and substances (from boththe household and the professional WEEE streams) have beendeclared to the Register in 2011, compared to 100,723 tonnes in2010. This represents a 19% increase. This evolution, more markedthan the increase in treated tonnage, can be explained by improve-ments in the separation of these sub-parts and, above all, by abetter monitoring of corresponding quantities.

Evolution in total tonnage of WEEE treated between 2006 and 2011

(thousands of tonnes)

0

100

200

300

400

500

600

700

2006 2007 2008 2009 2010 2011

9

153

286

386424

469

0

50

100

150

200

250

300

1 2 3 4 5 6 7 8 9 10(Categories)

2008

2009

2010

2011

Distribution of WEEE treated, by category and by year(thousands of tonnes)

469 401 tonnes of treated WEEE were reported to the Register in 2011 (both household and professional).

The tonnage treated in 2011 was slightly lower than the collected tonnage for the same period (470.1 kt) owing to stocking trendson the part of professional producers. This discrepancy hides the fact that the tonnage of treated household WEEE was superior tothe tonnage collected in 2011.

Energy recovery - 6 %

Disposal - 13 %

Recycling - 78 %

Component reuse - < 1 %

Reuse (whole appliances) - 3 %

Distribution of WEEE treated in 2011,by treatment type

Electrical and Electronic Equipment in France - 2011 Data

Energy recovery - 6 %

Disposal - 13 %

Recycling - 80 %

Component reuse - < 1 %

Reuse (whole appliances) - 1 %

HOUSEHOLD WEEE

451,679 tonnes of household WEEE weretreated by the four approved PROs in 2011- an 11% increase compared to 2010. Thetreated tonnage is superior to the collectedtonnage in 2011, owing to the destockingby PROs of WEEE collected in 2010.

Tonnage treated by waste stream

The evolution of treated quantities by waste stream logically follows that ofcorresponding collected quantities: 52% of the total tonnage consists of largehousehold appliances.

Large cooling appliances - 18 %

Screens - 25 %

Large appliances (other than cooling) - 34 %

Lamps - 1 %

Small appliances (mixed) - 22 %

Distribution of household WEEE treated in 2011, by waste streamTotal treated : 451,679 tonnes

Tonnage treated by country in which treatment occurred and treatment type

Belgium (less than 1%)

France - 99.9 %

Distribution of household WEEE treated in 2011, by country in which treatment occurred

Total treated : 451,679 tonnes

Over 99% of household equipment was treated inFrance (99,75%). Only 1,120 tonnes were treated inBelgium (lamps).

Recycling is the most common treatment mode usedfor household WEEE (80% of total tonnage).

Concerning reuse, quantities reused aswhole devices and declared as such to theRegister correspond to the tonnage ofequipment which goes back onto themarket for a second life after having beenrepaired. Those volumes are almost eighttimes smaller than the tonnage originallydestined for reuse. All equipment itemssent to reuse organisations do not findtheir way back to the market, eitherbecause they cannot be repaired, orbecause they are no longer marketable(obsolete technology, high energy con-sumption, etc.).

Evolution in the quantities sent to reuse organisations and actually reused, between 2007 and 2011 (tonnes)

Distribution of household WEEE treated in 2011, by type of treatment

Total treated : 451,679 tonnes

0

10000

20000

30000

40000

50000

60000

2007 2008 2009 2010 2011

40 900

4 415 4 715 5 676 5 704

43 446 44 666 45 50147 977

6 800

Quantities actually reusedQuantities sent to reuse organisations

PROFESSIONAL WEEE

17,722 tonnes of professional WEEE weredeclared as treated by 260 producersresorting to individual treatment schemes.This represents an 11% increase comparedto 2010, when 16,012 tonnes of treatedWEEE was declared. An additional 99producers made declarations in 2011,compared to 2010 (+61%). However,this tonnage is still small in relation tothe volume recorded in 2009 (21, 599tonnes); some producers having declaredimportant volumes that year did notmake declarations in 2010 and 2011 ordeclared smaller quantities.

According to a study by ADEME on WEEEtreatment centres, at least 140,000tonnes of professional WEEE were treatedin 20105. Most WEEE treated in 2010were historical WEEE (introduced on themarket before 13 August 2005), or WEEEthe disposal of which had been delegatedto the end-user and therefore was notdeclared.

Distribution of professional WEEE treated by equipment category

35 producers registered 14,428 tonnes of Category 3 WEEE, representing 81% of thetotal treated. Less than 275 tonnes were registered for Categories 2, 4, 5, 6 and 9.

1 - Large household appliances - 4 %

3 - IT and telecommunications equipment - 81 %

5 - Lighting equipment - 2 %

6 - Electrical and electronic tools - <1 %

8 - Medical devices - 8 %

9 - Monitoring and control instruments - <1 %

10 - Automatic dispensers - 4 %

Distribution of professional WEEE treated in 2011, by equipment category6

Total treated: 17,722 tonnes

Energy recovery - 4 %

Disposal - 5 %

Recycling - 49 %

Component reuse - 4 %

Reuse (whole appliances) - 38

Distribution of professional WEEE treated in 2011, by treatment typeTotal treated: 17,722 tonnes

Tonnage treated by countryin which treatment occurredand treatment type

Recycling is the most common treatmentmode for professional WEEE (49%).However, contrary to what holds forhousehold WEEE, reuse represents animportant share of the tonnage treated(38%). Indeed, the renewal of IT instal-lations offers interesting reuse opportu-nities, both qualitatively and quantitatively.

When we observe treatment modes bydestination countries, we note that 59%of whole devices reuse takes place outsidethe EU and 38% in France, while thereuse of components, recycling, energeticrecovery and disposal occur almost ex-clusively in the EU..

5 ADEME, Inventory 2010 of WEEE treatment centres, July 20126 Categories for which professional WEEE tonnage shares are inferior to 0.2 % are not represented on this chart (Categories 2 and 4 represent respectively

0.05 % and 0.13 % of total professional WEEE tonnage). No declaration was made for Category 7. Percentages have been rounded off, which explains that

the total does not equal 100 %

France - 53 %

Outside the EU - 23 %

Within the EU - 24 %

Distribution of professional WEEE treated in 2011, by country in which treatment occurred

Total treated: 17,722 tonnes

16 / 17

Synthèse Equipements électriques et électroniques - Données 2011

REGULATORY TARGETS FOR RECYCLING AND RECOVERY

In 2011, European regulatory targets for recycling and recovery were achieved in France for all equipment categories (householdand professional WEEE)7.

0 %

20 %

40 %

60 %

80 %

100 %

1 2 3 4 5 5a 6 7 8 9 10(Categories)

Regulatory targets

Reuse and recycling rates of WEEE

Reuse and recycling rates compared to regulatory targets, by equipment category

Recovery rates compared to regulatory targets, by equipment category

7 Reuse of whole devices is not considered as treatment here. Moreover, Category 5 has been divided into 2 sub-categories: discharge lamps

(neon tubes, energy efficient light bulbs, etc. : Category 5a) and professional lighting equipment (Category 5)

0 %

20 %

40 %

60 %

80 %

100 %

1 2 3 4 5 5a 6 7 8 9 10(Categories)

Regulatory targets

Rates of recovery of WEEE

18 / 19

Outlook for 2012On average, 6.9 kg of household WEEE per capita were collected in 2011. This outcome is slightly inferior to the objectiveassigned to PROs by public institutions (7kg). However, 46 “Départements” out of 101 had already reached the 2012 per capitatarget (8 kg) as of 2011. What is truly at stake in 2012 is the generalisation of that performance to the whole territory, while making sure that citizens bringtheir used equipment to a collection point and limiting the traffic of items containing valuable metals.

Comparison of distribution by department of household WEEE collected between 2009 and 2011 (kg per capita)

In the professional sector, approval of PROs for certain categories of equipment as of August 2012 will meet the expectations ofproducers wishing to assume their responsibilities but for whom the implementation of individual schemes is difficult and whotherefore tended up to now to delegate the management of products’ end-of-life to consumers.

Thus, the sector can be expected to structure itself in a way similar to that of household WEEE, with PROs organising the collectionand treatment of their members’ used equipment.

Réunion GuadeloupeMartinique Guyane

29 22

56

44

85

49

5335

50 14

61

72

37

8679

1716

33

40

64

65

31

0911

66

34 13

30 84

83

2b

2a

0604

05

73

74

38

260748

12

8182

32

4746

2315 43

63

19

36

18

41

45

28

78

9177

89

58

03

42 69

01

71

21

5210

51

0260

95

8076

6259

08

55

54

57

67

8868

9070

25

39

94

93

92

75

24

87

27

Réunion GuadeloupeMartinique Guyane Mayotte

29 22

56

44

85

49

5335

50 14

61

72

37

8679

1716

33

40

64

65

31

0911

66

34 13

30 84

83

2b

2a

0604

05

73

74

38

260748

12

8182

32

4746

2315 43

63

19

36

18

41

45

28

78

9177

89

58

03

42 69

01

71

21

5210

51

0260

95

8076

6259

08

55

54

57

67

8868

9070

25

39

94

93

92

75

24

87

27

2009 2011

Less than 4 Between 4 and 7 Between 7 and 10 Above 10

ADEMECorporate headquarters: 20, avenue du GrésilléF - BP 90406 49004 Angers Cedex 01

The French Environment and Energy Manage-

ment Agency (ADEME) is a public agency

under the joint authority of the Ministry of

Ecology, Sustainable Development and Energy,

and the Ministry for Higher Education and

Research. The agency is active in the imple-

mentation of public policy in the areas of the

environment, energy and sustainable develop-

ment. ADEME provides expertise and advisory

services to businesses, local authorities and

communities, government bodies and the

public at large, to enable them to establish and

consolidate their environmental action. As

part of this work the agency helps finance

projects, from research to implementation, in

the areas of waste management, soil conserva-

tion, energy efficiency and renewable energy,

air quality and noise abatement.

AAbout ADEMEbout ADEME

For more information:www.ademe.frWithin the section “Domaine d’intervention Déchets” (Waste intervention area)

“À chaque déchet des solutions”:The most recent data can be downloaded in the section “A solution for each type of waste” (À chaque déchet des solutions)- WEEE information sheet(Déchets d’équipements électriques et électroniques)

- EEE summary document updated annually (in French and in English)

- Full annual report compilated by the Observatory (in French)

For current recycling news check out our newsletter“L’Écho des filières”To subscribe (free): [email protected]

“

”7613

Décem

bre 20

12 - A4 éd

itions 02 41

720

700

- Crédit photos : ADEME, R.Bourget pour l’ADEME, Photodisc