Effective planning for international employees - tax, social security, immigration 18 November 2013...

20

Effective planning for international employees - tax, social security, immigration www.pwcias.com 18 November 2013 Monica Xu Senior Manager PwC International Assignment Services - Hong Kong

-

Upload

florence-booker -

Category

Documents

-

view

216 -

download

1

Transcript of Effective planning for international employees - tax, social security, immigration 18 November 2013...

Effective planning for international employees - tax, social security, immigration

www.pwcias.com

18 November 2013

Monica XuSenior ManagerPwC International Assignment Services - Hong Kong

PwC

Agenda

1. An overview of key issues surrounding international assignees

2. Individual income tax

3. Social security & immigration

4. Possible planning tactics

5. Q&A

2

PwC

Key issues surrounding international assignees

3

International assignees

Individualtax

Corporate tax

Social securityImmigration

Labour requirement

PwC

Individual income tax

4

PwC

International assignees

• Business travellers – meetings, marketing, etc.

• Short- term assignees – projects, trainings, etc.

• Long-term assignees – executives, management

• Internal firm services – internal audits, IT Support, trainers, etc.

• Roles – regional functions

5

PwC

De minimis threshold under domestic laws

• Mainland China 90 days

• Hong Kong 60 days

• India 90 days

• Singapore 60 days

• Malaysia 60 days

• Australia 0 day

• Japan 0 day

• Thailand 0 day

• Indonesia 0 day

• Vietnam 0 day

6

PwC

Protection under income tax treaty

The following conditions must be satisfied for exemption of employment income in other contracting parties:

1. Presence ≤ 183 days in the other contracting party in a calendar year / any 12-month period; and

2. Remuneration is paid by, or on behalf of, an employer who is not a resident in the other contracting party; and

3. Remuneration is not borne by a permanent establishment (PE) [or a fixed base] which the employer has in the other contracting party; and

4. Remuneration is taxable in the contracting party according to the laws in that party.

7

PwC

TaxProject leader

Finance

Employees

HR

Common problems

8

PwC

Common questions

• Individuals:

- Who is tracking? “Who knows I am here?”

- What income is taxable?

- Double taxation?

- Tax filing requirements?

• Employers:

- Who is here?

- Cost charges?

- Withholding/ payroll taxes?

9

PwC

Risks and exposures

• Individuals:

- Non-compliance: tax and immigration

- Financial penalties

- Inconveniences

• Employers:

- Corporate income tax and immigration exposure

- Financial penalties

- Unexpected/ unbudgeted costs

- Reputational

10

PwC

Social security and immigration

11

PwC

Social security requirement

• Hong Kong: Mandatory provident fundExemption criteria

• China: social security Law enacted in July 2011

12

PwC 13

Social security - China

Who can be exempted?

How much is the monthly

contribution?

Are there any refund upon departure?

What are the types of

contributions ?Who need to participate?

Is it fully implemented?

What if the employer pays for my contributions?

PwC

Permanent establishment

creation

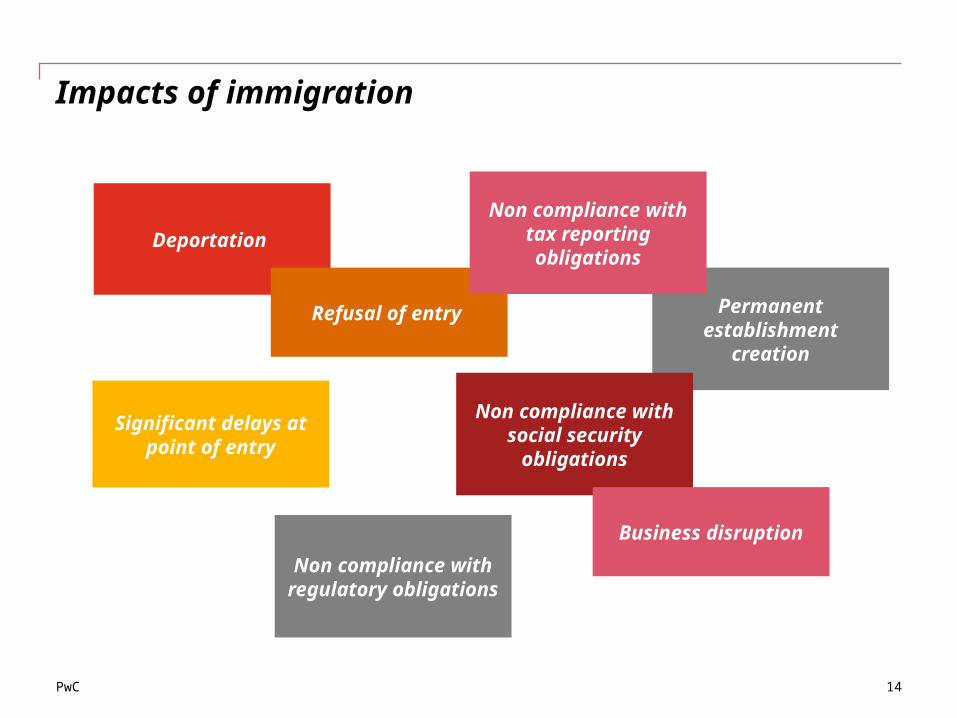

Impacts of immigration

14

Deportation

Refusal of entry

Significant delays at point of entry

Non compliance with tax reporting

obligations

Non compliance with social security

obligations

Business disruptionNon compliance

with regulatory obligations

PwC

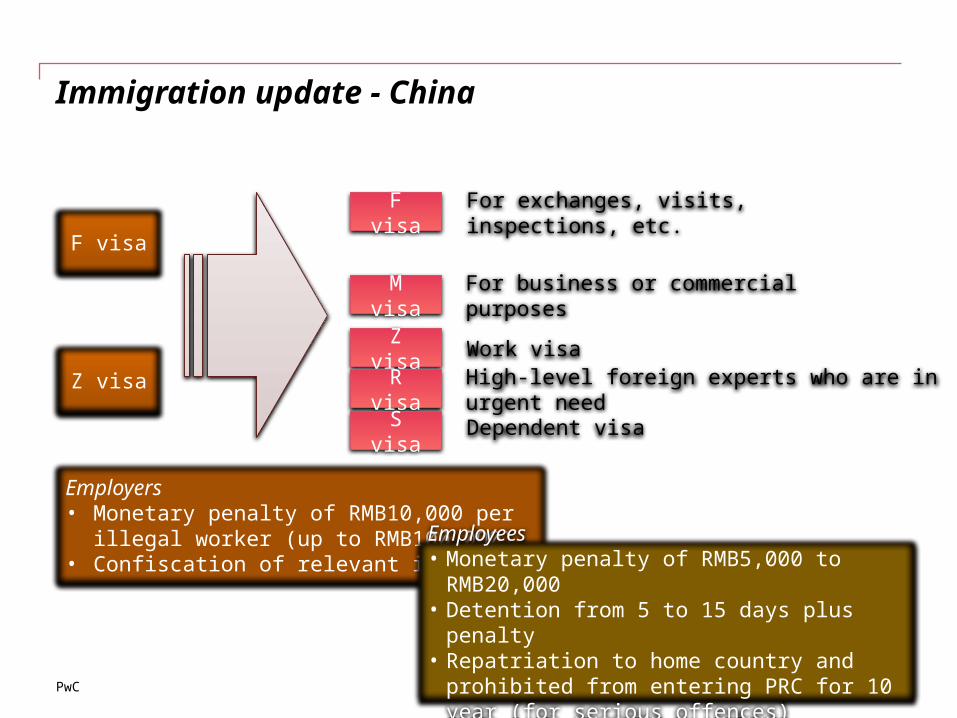

Immigration update - China

15

Z visa

F visaF visa

For exchanges, visits, inspections, etc.

M visa

Z visa

R visa

S visa

For business or commercial purposes

Dependent visa

Work visaHigh-level foreign experts who are in urgent need

Employers• Monetary penalty of RMB10,000 per

illegal worker (up to RMB100,000)• Confiscation of relevant income

Employees• Monetary penalty of RMB5,000 to

RMB20,000• Detention from 5 to 15 days plus penalty• Repatriation to home country and

prohibited from entering PRC for 10 year (for serious offences)

PwC

Best practices in immigration

• Centralised immigration policies

• Ensuring holistic stance

• Immigration governance structure with visible board level input

• Awareness to anticipate immigration changes

• Short term business visitor tracking

• Crisis management planning

16

Best Practic

e compliance

solutions

Sustainable business

growth

PwC

Possible planning ideas

17

PwC

Planning strategies and considerations

Bonus, equity compensation, deferred compensation

Onshore and offshore roles and responsibilities

• Potential challenges from the tax authorities

• Compliance registration fulfillment

Tax efficient remuneratio

n items (e.g.,

housing)

• Whether supporting policy and documentation are in place

• Whether companies are exercising proper control over the policy

• The eligibility for income exemption or time apportionment claim

• The way to mitigate double taxation

Possible planning tactics

Slide 18

PwC

Business commuter policy

Key messages

19

Proper planning

Effective tracking system

Individual and corporate tax cost estimatesCommunicate

internally and externally

Stay ahead of the changing regulatory requirements

Timely tax and other regulatory compliance

Thank you.

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PwC International Assignment Services Holdings Pte Ltd, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2013 PwC International Assignment Services Holdings Pte Ltd. All rights reserved. In this document, “PwC” refers to PwC International Assignment Services Holdings Pte Ltd which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.