Eecfa forecast report_romania_2015_winter

46

FORECAST REPORT ROMANIA UNTIL 2017

-

Upload

andreas-laspadakis -

Category

Presentations & Public Speaking

-

view

23 -

download

0

Transcript of Eecfa forecast report_romania_2015_winter

FORECAST REPORT ROMANIAUNTIL 2017

ROMANIA © 2015 EECFA 02

This Forecast Report was written by

EBUILD srl, Romanian member institute of EECFA

Mr Sebastian Sipos-GugT: + 40 359 466 [email protected]

Editor: EECFAAnalytical approach and methodological background:Dr Aron Horvath – EECFA Research – ELTINGAJanos Gaspar – EECFA Research

www.eltinga.huwww.eecfa.com

Copyright shall be held by EECFA, Winter 2015

ROMANIA © 2015 EECFA 03

CONTENT

04 _ Summary

05 _ Summary: Forecast revision

06 _ Forecast table 1 | macro figures

07 _ Forecast table 2 | construction summary figures

08 _ Residential construction | graph

09 _ Residential model | graph

10 _ Residential construction | graph, text

13 _ Forecast table 3 | residential figures

14 _ Office construction | graph

15 _ Office construction | graph, text

17 _ Retail and wholesale construction | graph

18 _ Retail and wholesale construction | graph, text

21 _ Industrial and warehousing | graph

22 _ Industrial and warehousing | graph, text

24 _ Hotel construction | graph

25 _ Hotel construction | graph, text

26 _ Education- and Health-related construction | graph

27 _ Education- and Health-related construction | graph, text

29 _ Other non-residential | graph, text

30 _ Forecast table 4 | non-residential figures

31 _ Road construction | graph, text

34 _ Railway construction | graph, text

36 _ Other transport infrastructure | graph, text

37 _ Energy, pipeline, cable construction | graph, text

38 _ Public utility | graph, text

39 _ Forecast table 5 | civil engineering figures

40 _ Project data | table

ROMANIA SUMMARY © 2015 EECFA 04

2001 2017

35% of total constructionRenovation ratio* 11%

(2014)

*Renovation / Total

Residential (at constant price)2001 2017

25% of total constructionRenovation ratio 16%

(2014)

Non-Residential (at constant price)2001 2017

40% of total constructionRenovation ratio 27%

(2014)

Civil engineering (at constant price)

SUMMARY The economic growth continues its positive trend into 2015 and the Romanian economy is predicted

to grow with 3% per year in 2016 and 2017 as well. Industrial production and retail turnover are expected to rise as well, and this growth is set to be accompa-nied by increases in employment and real wages. The cumulative impact of these factors on the construction market overall is awaited to be quite benefic.

Residential construction has increased in 2015, and is foreseen to continue this trend in the future as well. Larger income, lower mortgage rates and state guar-anteed loans have helped the recovery of the market for new homes. While development is still relatively timid, the share of multi-unit buildings is increasing and so is the average size of new houses. With prices stable and rents on a declining trend, speculative investment into residential projects will likely increase.

Non-residential construction has contributed to the sta-bilization of the construction market, and is forecasted

to be on a positive trend in 2016 and 2017. The main drivers of this sector are office construction, expected to remain on a small positive trend, and industrial and transport construction, also hoped to grow over the forecasted period. Retail construction is to remain rel-atively stable; however, beyond 2017 a decline is likely in large-scale commercial construction.

Civil engineering was plagued by funding issues and delayed projects, thus it declined in 2014. 2015 has performed better, due to fears of losing EU funding on ongoing projects and political pressure. However, we expect 2016 to mark a new decline period, as transi-tion between EU financial exercises will mean delays and halted construction works. Political instability due to the elections will divert funding away from infra-structure investments. The situation should recover in 2017, when stability will be achieved, phased projects will continue and new investments will start.

Macro outlook until 2017 Population (20-29 age group) GDP Private consumption Industrial production Employment Income Financial conditionsGREEN: POSITIVE GREY: NEUTRAL RED: NEGATIVE

Summar y

ROMANIA SUMMARY: FORECA ST RE vISION © 2015 EECFA 05

All data for 2013 have been changed due to the revision of official data for the year. In general, this has led to

lower figures than previously reported; however, long term trends have remained largely unaffected by this update.

Residential forecast has been revised in the light of new data for 2014 and the change of several factors, the most important being the number of permits issued for new construction. While final information regarding construction output in 2014 is not final yet, preliminary data influenced our decision to move our estimate upwards. At the same time, increases in issued permits and expected income levels have made us adjust our forecast for 2016 and 2017 upwards.

In case of non-residential construction, we have also made several adjustments. Office growth rates for 2016 and 2017 have been raised because of increased activity on the market and the evolution of the employment indicators in the field. Small changes have also occurred

in case of the rest of the non-residential segments, which are attributable to the dynamics of ongoing and planned projects rather than to the long-term trend change.

For civil engineering, our forecast has generally been adjusted slightly downwards, due to a combination of factors. Firstly, EU funding absorption from the 2007-2013 exercise has been lower than hoped. Secondly, the entire year has been marked by political instability, culminating with the change of government in November. This will influence national budgets for 2016, the finalization of ongoing projects, and will cause delay in the start of new projects from the 2014-2020 exercise. Moreover, 2016 will be negatively impacted by the election year effects. And last, but not least, calls for proposals for infrastructure projects in the 2014-2020 exercise are set to start earliest in 2016, which means that, with the exception of phased projects, construction will greatly be reduced.

SUMMARY: FORECAST REVISION

2011 20172014Residential (index 2011 = 100)

2011 2017Non-Residential (index 2011 = 100)

Current forecast Previous forecast

2014 2011 2017Civil engineering (index 2011 = 100)

2014

Summar y: Forecast rev ision

ROMANIA FORECA ST TABLE 1 © 2015 EECFA 06

FORECAST TABLE 1

ROMANIA

MACRO CONDITIONS AND DEVELOPMENTS 2007 2008 2009 2010 2011 2012 2013 2014 2015(F) 2016(F) 2017(F)

POPULATION (´000) 21 131 20 635 20 440 20 295 20 199 20 096 20 020 19 947 19 898 19 858 19 813

POPULATION AGE GROUP 20-29 YEAR (´000) 3 160 2 921 2 726 2 701 2 677 2 659 2 618 2 585 2 548 2 500 2 431

GDP GROWTH (%) 6.9 8.5 -7.1 -0.8 1.1 0.6 3.4 2.9 2.8 3.0 3.3

PRIVATE CONSUMPTION GROWTH (%) 14.2 7.1 -10.5 1.0 1.0 0.8 1.1 5.0 3.0 2.7 2.5

RETAIL TURNOVER (%) 20.4 18.5 -9.4 -7.3 -1.1 4.3 0.6 6.5 5.8 2.3 1.8

INDUSTRIAL PRODUCTION (%) 10.2 2.1 -4.9 4.9 8.1 2.5 7.5 6.4 3.3 5.9 6.2

EMPLOYMENT (´000) 8 820 8 835 8 717 8 713 8 528 8 605 8 549 8 614 8 640 8 674 8 718

REAL WAGE GROWTH (%) 14.7 16.5 -1.5 -3.7 -1.9 1.0 0.8 6.4 7.6 6.2 2.6

CONSUMER PRICE INDEX (%) 4.8 7.9 5.6 6.1 5.8 3.3 4.0 1.1 -0.5 0.5 2.7

INTEREST RATE ON NEW HOUSING LOANS (% P.A.) 8.2 8.5 8.6 6.2 6.3 5.5 5.5 5.4 4.3 3.9 3.5

1 EUR IN RON 3.3 3.7 4.2 4.2 4.2 4.5 4.4 4.4 4.5 4.4 4.4

Forecast t able 1 | macro f igu res

ROMANIA FORECA ST TABLE 2 © 2015 EECFA 07

FORECAST TABLE 2

ROMANIA VALUE (RON MLN)

VALUE (EUR MLN) GROWTH RATES AT CONSTANT PRICE (%)

CONSTRUCTION MARKET SIZE AND DEVELOPMENT

2014 2014 2007 2008 2009 2010 2011 2012 2013 2014 2015(F) 2016(F) 2017(F)

RESIDENTIAL

NEW 18 878 4 247 -26.2 -14.3 -21.3 11.0 -17.0 12.5 9.0 15.9 10.3

RENOVATION 2 310 520 -4.7 -16.2 5.4 -1.2 27.8 -24.4 4.7 7.1 3.7

TOTAL 21 188 4 767 50.9 11.2 -24.6 -14.4 -18.9 9.6 -12.3 6.8 8.5 15.0 9.6

NON-RESIDENTIAL

NEW 12 686 2 854 -17.9 -13.6 14.0 -22.4 -13.6 6.0 7.9 6.0 5.5

RENOVATION 2 352 529 -11.9 -31.2 16.9 -11.0 -10.6 -0.5 7.9 6.0 5.5

TOTAL 15 038 3 383 18.1 33.0 -17.0 -16.6 14.4 -20.7 -13.1 4.9 7.9 6.0 5.5

BUILDING CONSTRUCTION

NEW 31 564 7 102 -23.1 -14.0 -7.1 -5.5 -15.6 9.8 8.5 12.0 8.5

RENOVATION 4 662 1 049 -8.9 -24.8 11.5 -6.6 7.6 -14.0 6.3 6.6 4.6

TOTAL 36 225 8 150 37.2 19.0 -21.6 -15.4 -5.0 -5.6 -12.6 6.0 8.2 11.3 8.0

CIVIL ENGINEERING

NEW 17 474 3 932 -5.5 -2.1 -1.1 -9.6 -7.8 -15.1 11.5 -3.8 6.0

RENOVATION 6 557 1 475 -11.1 -11.5 2.6 4.2 -15.8 -15.3 11.2 -4.0 5.7

TOTAL 24 031 5 407 26.8 27.0 -7.1 -4.7 -0.2 -6.0 -10.2 -15.2 11.4 -3.8 5.9

TOTAL CONSTRUCTION OUTPUT 60 256 13 557 33.4 21.8 -16.3 -11.0 -2.9 -5.8 -11.5 -3.6 9.5 5.1 7.2

Forecast t able 2 | const r uct ion summar y f igu res

RON 0bln

RON 5bln

RON 10bln

RON 15bln

RON 20bln

RON 25bln

RON 30bln

RON 35bln

RON 0bln

RON 5bln

RON 10bln

RON 15bln

RON 20bln

RON 25bln

RON 30bln

RON 35bln

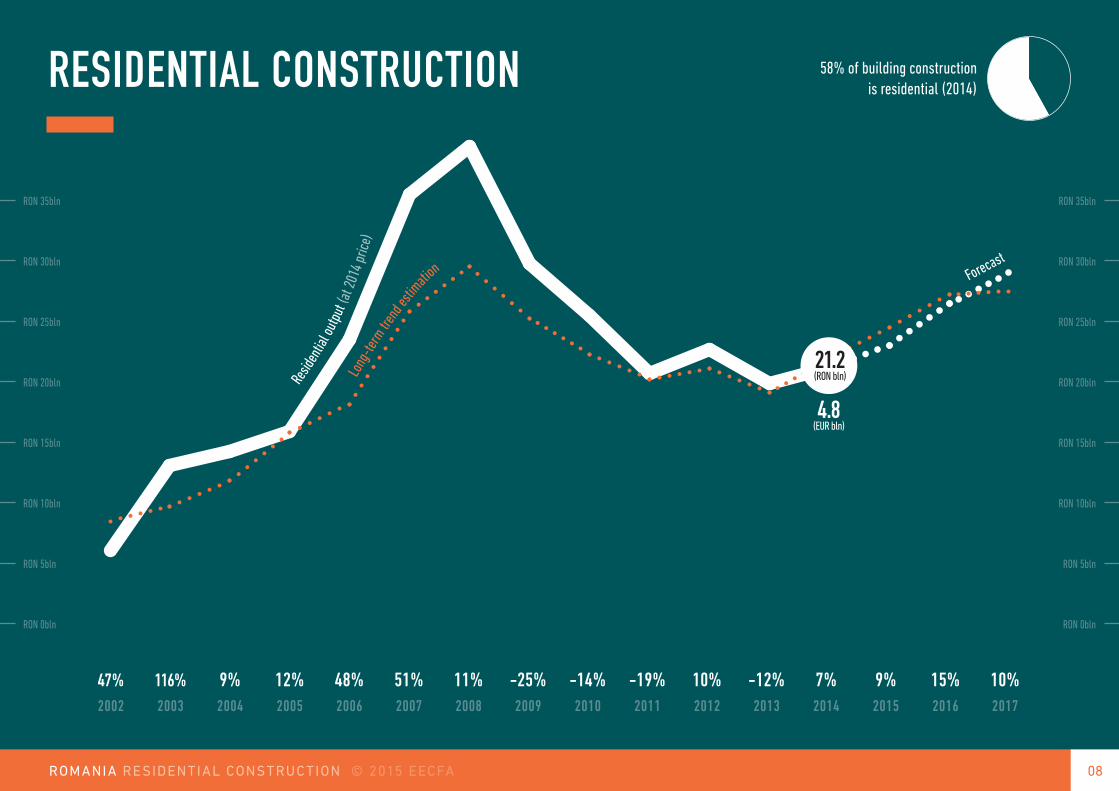

21.2(RON bln)

4.8(EUR bln)

58% of building constructionis residential (2014)

Forecast

Resid

entia

l out

put (

at 20

14 pr

ice)

Long

-term

tren

d esti

mation

RESIDENTIAL CONSTRUCTION

47% 116% 9% 12% 48% 51% 11% -25% -14% -19% 10% -12% 7% 9% 15% 10%2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

08ROMANIA RESIdENTIAL CONSTRUC TION © 2015 EECFA

Resident ial const r uct ion | g raph

RON 0bln

RON 10bln

RON 20bln

RON 30bln

RON 40bln

RON 50bln

RON 0bln

RON 10bln

RON 20bln

RON 30bln

RON 40bln

RON 50bln

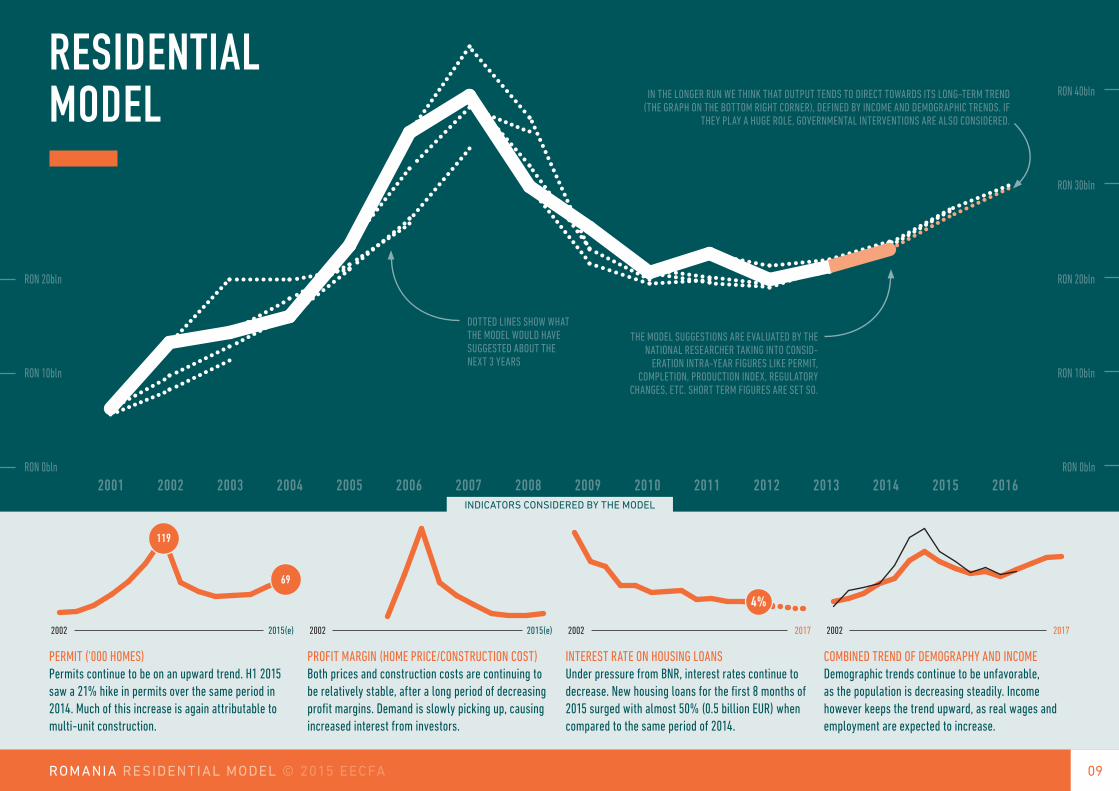

RESIDENTIAL MODEL

COMBINED TREND OF DEMOGRAPHY AND INCOMEDemographic trends continue to be unfavorable, as the population is decreasing steadily. Income however keeps the trend upward, as real wages and employment are expected to increase.

INTEREST RATE ON HOUSING LOANSUnder pressure from BNR, interest rates continue to decrease. New housing loans for the first 8 months of 2015 surged with almost 50% (0.5 billion EUR) when compared to the same period of 2014.

PROFIT MARGIN (HOME PRICE/CONSTRUCTION COST)Both prices and construction costs are continuing to be relatively stable, after a long period of decreasing profit margins. Demand is slowly picking up, causing increased interest from investors.

PERMIT ('000 HOMES)Permits continue to be on an upward trend. H1 2015 saw a 21% hike in permits over the same period in 2014. Much of this increase is again attributable to multi-unit construction.

2015(e)2002

69

119

2015(e)2002 2017200220172002

4%

INdICATORS CONSIdEREd BY THE MOdEL

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

IN THE LONGER RUN WE THINK THAT OUTPUT TENDS TO DIRECT TOWARDS ITS LONG-TERM TREND (THE GRAPH ON THE BOTTOM RIGHT CORNER), DEFINED BY INCOME AND DEMOGRAPHIC TRENDS. IF

THEY PLAY A HUGE ROLE, GOVERNMENTAL INTERVENTIONS ARE ALSO CONSIDERED.

THE MODEL SUGGESTIONS ARE EVALUATED BY THE NATIONAL RESEARCHER TAKING INTO CONSID-

ERATION INTRA-YEAR FIGURES LIKE PERMIT, COMPLETION, PRODUCTION INDEX, REGULATORY

CHANGES, ETC. SHORT TERM FIGURES ARE SET SO.

DOTTED LINES SHOW WHAT THE MODEL WOULD HAVE SUGGESTED ABOUT THE NEXT 3 YEARS

09ROMANIA RESIdENTIAL MOdEL © 2015 EECFA

Resident ial model | g raph

ROMANIA RESIdENTIAL CONSTRUC TION © 2015 EECFA 10

Residential construction has returned to an upward trend, with most indicators predicting strong growth

in 2016 and 2017. While fear of another "bubble" is still restraining some developers, increases in real wages and advantageous loaning rates lead to hiked demand and construction activity.

Permits for residential construction have continued to increase in number in 2015, with the first eight months of the year outperforming the equivalent period in 2014 by 8% in raw numbers and 20% in useful area. This confirms our prediction that the market will return to higher surfaces/building because of increases in income and relaxed loan rates. When looking at the type of permitted building, we see a rise in the share of multi-unit buildings, while the number of permits for one-family houses is actually lower in 2015 than in 2014.

After a slight drop in 2014, we expect home comple-tion to pick up in 2015 and continue an upward trend

into 2016 and 2017. The share of multi-unit building is predicted to increase; after bottoming at around 25% in 2013, we estimate it will reach around 35% in the fore-casted period. The average useful area per dwelling is also forecasted to grow as developments in govern-ment subsidy programs encourage owners to relocate to larger homes. At the same time, income increase will open more opportunities to do so.

Investors are regaining confidence in the residen-tial development market and several projects having been on hold for several years are now undergoing or have been completed. An example in this case is Cor-tina Residence project with 270 flats, which has been completed in 2015, though started in 2007 and stopped due to bankruptcy of the developer. At the same time, an increasing number of projects are underway or planned to start in the next two years.

The proportion of renovation works in total residential construction is on a downwards trend. Albeit a large

RESIDENTIAL CONSTRUCTION

2001 2017

48

31

Completion ('000 dwellings)

Total number of

dweli

ngs

1 dwelling buildings

Resident ial const r uct ion | g raph, text

ROMANIA RESIdENTIAL CONSTRUC TION © 2015 EECFA 11

number of the dwelling stock is old (65% of them con-structed before 1978), a small number of buildings has been rehabilitated and made energy efficient. Accord-ing to the current goals of the Romanian government, around 120000 buildings are planned to undergo investments into energy efficiency by 2023, with the help of FEdR funding.

Real estate prices have begun to increase after bot-toming out in 2014. In Q3 2015, the hike was 5%, when compared to the same period of 2014 (according to the IMO index by imobiliare.ro), and in the future we expect prices to be on a modest upward trend. As detailed in the previous report, many of the repossessed homes and speculative developments from 2008-2014 have not been sold, due to low market prices, and have instead been leased. However, with rents on a downward trend, and dwelling prices going upward, an increasing num-ber of these buildings will be sold instead; therefore, offer will continue to exceed demand in the next two

years. Thus, a sudden and significant surge in prices is unlikely.

Romania's population continues to decline, especially in the 20 to 29 segment. While birth rates remain rel-atively stable, the younger population has a tendency to migrate to another EU state after graduating high school or college. This has a mixed impact on demand for new homes. On the one hand, the population’s migration reduces the need for new homes, though a portion of young emigrants returns to Romania and invests their savings into real estate. Income trends however continue to favor a positive outlook for the construction market. Increases in net income coupled with raised employment should lead to more demand for new and larger homes.

Interest rates for mortgages remain on a downward trend, due to the pressure from the National Bank, and will likely remain so for the forecast period. The

RESIDENTIAL CONSTRUCTION

2015 2016 2017 2018

Ongoing and planned Residential construction projects

Neo Laguna Residence | Ovidiu, South-East region | 191,000 sqm

Basarabia Residence | Bucharest, sector 3 | 89,000 sqm

Cartierul Solar phase 2 | Bucharest, sector 4 | 50,000 sqm

Residential park | Bucharest, sector 5 | 1,800 flats

AFI City Bucureştii Noi phase 2 | Bucharest, sector 1 | 1,688 flats

Pacii Residence Phase 2 | Bucharest, sector 6 | 1,164 flats

Residential park | Bucharest, sector 1 | 100,000 sqm | 600 flats

Neo Peninsula Residences | Bucharest, sector 2 | 120,000 sqm | 3,400 flats

Frumusani Residential Park | Frumusani, South region | 2,850 flats

Brown Residence Metalurgiei Phase 2 | Bucharest, sector 4 | 50,000 sqm | 500 flats

Straulesti Lake Residence | Bucharest, sector 1 | 139,000 sqm

Nordic Residence Park | Dumbravita, West region | 50,000 sqm

One Herăstrău Park Residence | Bucharest, sector 1 | 27,000 sqm

Cosmopolis Phase 4 | Stefanesti de Jos, Bucharest-Ilfov region | 800 flats

Cartier Orizont phase 3 | Buzau, South-East region | 130,000 sqm

Condominiums | Craiova, South-West region | 182,000 sqm

Metalurgiei Park Residence Phase 1 | Bucharest, sector 4 | 185,000 sqm

Bujorului Residence | Craiova, South-West region | 28,000 sqm | 230 flats

Avantgarden 3 phase 2 | Brasov, Center region | 55,000 sqm

SOURCE: IBUILD.INFO

ROMANIA RESIdENTIAL CONSTRUC TION © 2015 EECFA 12

National Bank controls much of the mortgage marked by means of the ROBOR index. Loans through the gov-ernment program "Prima Casa" (accounting for more than 60% of total mortgage loans granted in 2014, and around 50% of outstanding mortgages in 2015) provide banks with state guarantees in exchange for obeying a fixed interest rate, tied to ROBOR.

Several public policy changes will also have an impact on the residential construction market:

• The "Prima Casa" program might not continue into 2016. Financial risk indicators for the program are higher than average and political support for it has been low in 2015. The suspension or the cancella-tion of the program will have a negative impact on the market, yet, currently there is a relative degree of stability that would prevent any major long-term consequences.

• Real estate taxes are set to increase in 2016 with around 25% for homes, reaching between 0.1% and 0.2% of the value of the building. The impact of this measure on residential construction will relatively be low (average yearly tax would reach around 1%-2% of average yearly income). However, coupled with new surface area calculation (built versus use-ful) and taxation of the land under the building, it might lead to more built multi-unit and multi-level buildings.

RESIDENTIAL CONSTRUCTION

ROMANIA FORECA ST TABLE 3 © 2015 EECFA 13

FORECAST TABLE 3

ROMANIA

RESIDENTIAL CONSTRUCTION 2007 2008 2009 2010 2011 2012 2013 2014 2015(F) 2016(F) 2017(F)

COMPLETED DWELLINGS (´000 UNIT)

1 DWELLING BUILDINGS 33.8 33.3 37.0 35.5 33.5 32.1 32.2 28.4 30.6 32.7 36.1

2+ DWELLING BUILDINGS 13.5 33.9 25.5 13.3 11.9 11.9 11.4 14.1 17.2 18.3 20.1

TOTAL 47.3 67.3 62.5 48.8 45.4 44.0 43.6 42.6 47.8 51.0 56.2

COMPLETED DWELLINGS (´000 UNIT)

1 ROOM 3.9 5.3 5.3 3.3 2.8 3.2 2.5 2.6 2.9 3.1 3.4

2 ROOM 8.7 16.7 14.7 9.2 8.4 8.6 8.9 8.9 10.2 11.2 12.7

3+ ROOM 34.7 45.2 42.5 36.4 34.1 32.3 32.2 31.2 34.7 36.7 40.1

TOTAL 47.3 67.3 62.5 48.9 45.4 44.0 43.6 42.6 47.8 51.0 56.2

CONSTRUCTION PERMITS (´000 DWELLINGS) 87.6 118.6 65.9 55.3 49.2 49.8 51.2 60.3 69.0 75.9 82.0

RESIDENTIAL STOCK (MILLION DWELLINGS) 8.23 8.27 8.33 8.38 8.43 8.47 8.51 8.51 8.55 8.58 8.61

HOME OWNERSHIP RATE (%) 97.7

Forecast t able 3 | resident ial f igu res

21% 45% 104% 5% 10% 48% 49% 12% -24% -14% -19% -3% 3% 8% 15%2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

RON 0bln

RON 5bln

RON 10bln

RON 0bln

RON 5bln

RON 10bln

O�ce

outp

ut (

at 20

14 pr

ice)

Forecast

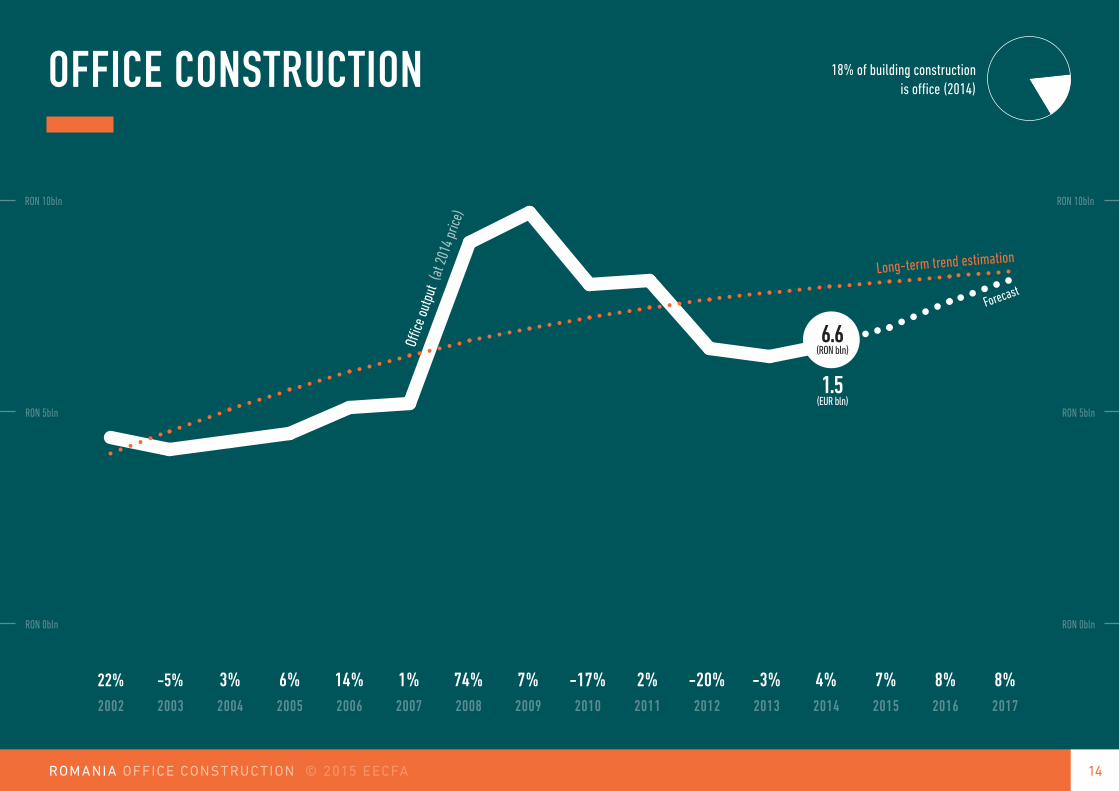

18% of building constructionis o�ce (2014)

Long-term trend estimation

6.6(RON bln)

1.5(EUR bln)

OFFICE CONSTRUCTION

22% -5% 3% 6% 14% 1% 74% 7% -17% 2% -20% -3% 4% 7% 8% 8%2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

14ROMANIA OFFICE CONSTRUC TION © 2015 EECFA

Off ice const r uct ion | g raph

ROMANIA OFFICE CONSTRUC TION © 2015 EECFA 15

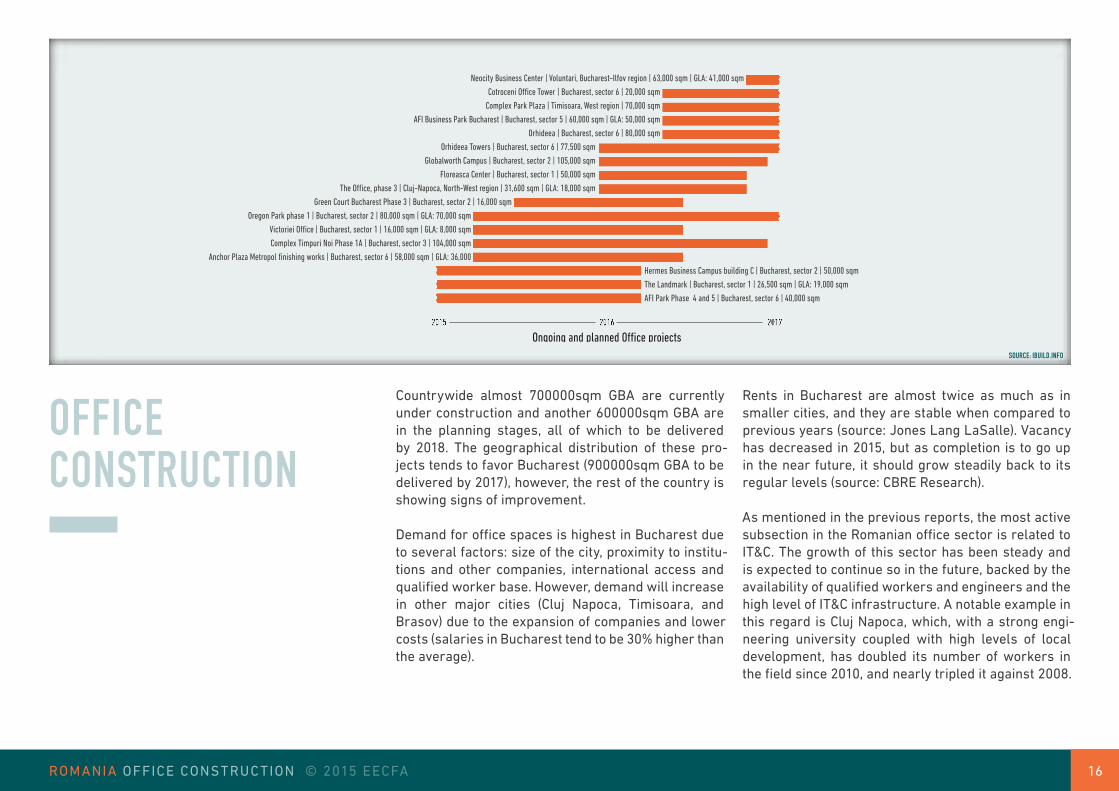

OFFICE CONSTRUCTION

The trend for office construction continues to be pos-itive into 2015 and growth is expected to continue in

2016 and 2017. As almost one-half of the population is employed in the services sector, demand for adminis-trative spaces continues to be high.

Permits for office buildings continued their recovery into H2 2015, with the first three quarters marking and increase of 9% in the number of permits and 24% in the useful permitted area over the same period of 2014. We predict this evolution to consolidate into an upward trend into 2016 and 2017 as well. Of note is the increasing average area per permit, indicating that more large-scale projects are being considered.

As previously mentioned, the most active location for office construction is the capital city, Bucharest. Completion here for H1 2015 has been of around 45-60 thousand sqm GLA, and by the end of the year we estimate around 120-140 thousand sqm GLA to

be delivered (sources: Jones Lang LaSalle, CBRE Research), marking a slight improvement over 2014.

Currently there are an additional 300000sqm GBA of office spaces under construction in Bucharest, to be delivered in 2016, and a further 77500sqm GBA to be delivered into 2017. Another 300000sqm GBA are planned to start construction in 2016, with delivery dates in 2017. We therefore expect 2016 and 2017 to outperform 2015 in Bucharest.

In the rest of the country, Cluj Napoca continues to be the most active location with 77000sqm GBA com-pleted in four projects in 2015. The largest of these projects, phase 2 of ”The Office” covers nearly half the completion (31600sqm GBA), and will be followed by phase 3 with the same scale, to be delivered in 2016. The project is representative for most of the ongoing and planned projects in Romania, featuring a focus on energy efficiency and sustainability (BREEAM certified).

2002 2015(e)

148

Permit ('000 m2)

Off ice const r uct ion | g raph, text

ROMANIA OFFICE CONSTRUC TION © 2015 EECFA 16

OFFICE CONSTRUCTION

Rents in Bucharest are almost twice as much as in smaller cities, and they are stable when compared to previous years (source: Jones Lang LaSalle). vacancy has decreased in 2015, but as completion is to go up in the near future, it should grow steadily back to its regular levels (source: CBRE Research).

As mentioned in the previous reports, the most active subsection in the Romanian office sector is related to IT&C. The growth of this sector has been steady and is expected to continue so in the future, backed by the availability of qualified workers and engineers and the high level of IT&C infrastructure. A notable example in this regard is Cluj Napoca, which, with a strong engi-neering university coupled with high levels of local development, has doubled its number of workers in the field since 2010, and nearly tripled it against 2008.

2015 2016 2017

Ongoing and planned O�ce projects

Neocity Business Center | Voluntari, Bucharest-Ilfov region | 63,000 sqm | GLA: 41,000 sqm

Cotroceni O�ce Tower | Bucharest, sector 6 | 20,000 sqm

Complex Park Plaza | Timisoara, West region | 70,000 sqm

AFI Business Park Bucharest | Bucharest, sector 5 | 60,000 sqm | GLA: 50,000 sqm

Orhideea | Bucharest, sector 6 | 80,000 sqm

Orhideea Towers | Bucharest, sector 6 | 77,500 sqm

Globalworth Campus | Bucharest, sector 2 | 105,000 sqm

Floreasca Center | Bucharest, sector 1 | 50,000 sqm

The O�ce, phase 3 | Cluj-Napoca, North-West region | 31,600 sqm | GLA: 18,000 sqm

Green Court Bucharest Phase 3 | Bucharest, sector 2 | 16,000 sqm

Oregon Park phase 1 | Bucharest, sector 2 | 80,000 sqm | GLA: 70,000 sqm

Victoriei O�ce | Bucharest, sector 1 | 16,000 sqm | GLA: 8,000 sqm

Complex Timpuri Noi Phase 1A | Bucharest, sector 3 | 104,000 sqm

Anchor Plaza Metropol finishing works | Bucharest, sector 6 | 58,000 sqm | GLA: 36,000

Hermes Business Campus building C | Bucharest, sector 2 | 50,000 sqm

The Landmark | Bucharest, sector 1 | 26,500 sqm | GLA: 19,000 sqm

AFI Park Phase 4 and 5 | Bucharest, sector 6 | 40,000 sqm

Countrywide almost 700000sqm GBA are currently under construction and another 600000sqm GBA are in the planning stages, all of which to be delivered by 2018. The geographical distribution of these pro-jects tends to favor Bucharest (900000sqm GBA to be delivered by 2017), however, the rest of the country is showing signs of improvement.

demand for office spaces is highest in Bucharest due to several factors: size of the city, proximity to institu-tions and other companies, international access and qualified worker base. However, demand will increase in other major cities (Cluj Napoca, Timisoara, and Brasov) due to the expansion of companies and lower costs (salaries in Bucharest tend to be 30% higher than the average).

SOURCE: IBUILD.INFO

21% 45% 104% 5% 10% 48% 49% 12% -24% -14% -19% -3% 3% 8% 15%2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

RON 0bln

RON 1bln

RON 2bln

RON 3bln

RON 4bln

RON 0bln

RON 1bln

RON 2bln

RON 3bln

RON 4bln

Forecast

3% of building constructionis commercial (2014)

Long-term trend estimation

Comm

ercial output (at 2014 price)

0.3(EUR bln)

1.2(RON bln)

RETAIL AND WHOLESALE CONSTRUCTION

15% 47% 32% 8% 47% 16% 55% -46% -10% 9% -44% -10% -2% 2% 1% 1%2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

17ROMANIA RE TAIL ANd WHOLESALE CONSTRUC TION © 2015 EECFA

Retai l and wholesale const r uct ion | g raph

ROMANIA RE TAIL ANd WHOLESALE CONSTRUC TION © 2015 EECFA 18

RETAIL AND WHOLESALE CONSTRUCTION

After a period of decline since 2008, we foresee retail and wholesale construction to return to an

upward trend starting with 2015 and into 2017. Eco-nomic growth, increasing real income as well as a more relaxed tax rate for some goods will encourage investments in this area.

Permits for commercial buildings have gone down in H1 2015, accounting only for around 60% of the figures registered in 2014 over the same period, however, this figure is actually very similar to the one in 2013. Since 2014 experienced a large hike in the number of issued permits, output growth should continue in 2016 and 2017.

Completion in 2015 has exceeded the one registered in 2014 in the shopping mall segment. One of the larg-est malls in the country, Mega Mall (70000sqm GLA) was completed in the first half of the year in Bucha-rest. In addition, the third quarter saw the opening of the first phase of the Coresi Shopping Center in Brasov

(55000sqm GBA), Targu Mures Plaza (143000sqm GBA) and the second phase of deva Shopping Center (an extension of the existing mall, adding more enter-tainment options). By the end of the year, the national shopping center stock is set to grow with another 70000sqm GBA, as Timisoara Shopping City is to be completed.

Main ongoing projects are:

• Afi Palace Bucuresti Noi phase 1 (35000sqm GBA, estimated completion in H2 2016) that, in its final form, is planned to include in addition to the shop-ping mall a retail park, hypermarket and office buildings.

• Parklake Plaza, Bucharest (180000sqm GBA), delayed in the past by several issues is now expected to open in 2016

2009 2015(e)

271

Permit ('000 m2)

Retai l and wholesale const r uct ion | g raph, text

ROMANIA RE TAIL ANd WHOLESALE CONSTRUC TION © 2015 EECFA 19

RETAIL AND WHOLESALE CONSTRUCTION

• veranda Shop & Stay Obor, Bucharest (66700sqm GBA), to open in late 2016.

• Extension of City Park Mall, in Constanta (46000sqm GBA) will be completed in 2016, almost doubling the existing leasable area, and adding more entertain-ment and food options

In addition to these ongoing projects, several other large-scale investments are currently planned, raising the estimated completion in 2016 to 400000sqm GBA in Bucharest and around 100000sqm GBA in the rest of the country.

When it comes to shopping malls, many large cities are now saturated. Nevertheless, the development contin-ues in a few large cities (Timisoara, Constanta, Brasov) as well as in Bucharest, but it is predicted to transition to smaller cities over the next decade.

The hypermarket segment construction is also an important segment, Kaufland, Carrefour and Auchan continuing their expansion into the Romanian market with more than 10 units opened in 2015. Supermarkets and proximity stores are contributing significantly to the new construction market, with Mega Image being one of the most active ones in 2015, having expanded its network with more than 100 units.

After a rough period, the dIY segment is being revital-ized, with dedeman expanding its network in 2015 and having several ongoing projects planned to be opened in 2016 and 2017.

Growth in the whole retail and wholesale construction segment is backed by several factors: increases in real income and consumption, rises in retail turnover and tax changes.

2015 2016 2017

Ongoing and planned Retail projects

IKEA store | Bucharest, sector 3

Marina Park Shopping Center | Constanta, South-East region | 51,000 sqm

Dedeman store | Hunedoara, West region

Victoria City Lifestyle Retail Center phase 2 | Bucharest, sector 1 | 15,000 sqm

Dedeman store | Oradea, North-West region | 14,000 sqm

AFI Palace Braşov | Brasov, Center region | | GLA: 56,000 sqm

Timisoara Centrum | Timisoara, West region | GLA: 80,000 sqm

Victoria City Lifestyle Retail Center | Bucharest, sector 1 | 68,000 sqm | GLA: 36,000 sqm

Kaufland Hypermarket | Bucharest, sector 5 | 16,000 sqm

Neamţ Shopping City | Piatra Neamt, North-East region | 29,000 sqm

Palatul Stirbei shopping centre | Bucharest, sector 1 | 31,000 sqm

Dedeman store | Bucharest, sector 1 | 51,000 sqm

Timişoara Plaza | Timisoara, West region | 60,000 sqm

Veranda Shop & Stay Obor | Bucharest, sector 2 | 66,700 sqm

City Park Mall & Hypermarket Cora | Constanta, South-East region | 46,000 sqm | extension

Timişoara Shopping City | Timisoara, West region | 70,000 sqm | GLA: 55,000 sqm

Parklake Plaza | Bucharest, sector 3 | 180,000 sqm | 67,000 GLA

Bucharest Mall | Bucharest, sector 3 | 37,000 sqm | renovation

Plaza Romania | Bucharest, sector 6 | 40,000 sqm | renovation

AFI Palace Bucuresti Noi | Bucharest, sector 1 | 35,000 sqm

SOURCE: IBUILD.INFO

ROMANIA RE TAIL ANd WHOLESALE CONSTRUC TION © 2015 EECFA 20

RETAIL AND WHOLESALE CONSTRUCTION

Retail turnover continues to be on an upward trend, giving more confidence to investors and fueling fur-ther growth. Internet shopping share is increasing steadily, however, as mentioned in the previous report, this is having a relatively low impact on the rest of the retail market, as electronic payment methods continue to be used only by a small portion of the Romanian population and most citizens have low confidence in e-commerce.

Romania is an attractive target for many interna-tional brands, especially those in fashion and food. Many known fashion brands have entered the Roma-nian market in the last years, especially in shopping centers. Unlike many other European countries' res-idents, Romanians prefer to shop inside malls, and so major brands usually focus on this segment, as opposed to high street.

Policy changes have had a positive impact on the retail market, especially in the food segment, as vAT has been reduced from 24% to 9% in their case. For 2016, vAT is planned to be reduced for all goods to 20%, and in 2017 to 19%. While this might not greatly influence retail companies directly, price reduction will likely lead to a hike in consumption and will boost sales.

21% 45% 104% 5% 10% 48% 49% 12% -24% -14% -19% -3% 3% 8% 15%2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

RON 0bln

RON 2bln

RON 4bln

RON 6bln

RON 8bln

RON 0bln

RON 2bln

RON 4bln

RON 6bln

RON 8bln

11% of building construction is industrialand warehouse (2014)

Forecast

Long-term trend estimation

0.9(EUR bln)

3.9(RON bln)

Indus

trial

and w

areho

use ou

tput (at 2014 price)

INDUSTRIAL AND WAREHOUSING

36% -13% 1% -13% 9% 37% 8% -30% -27% 59% -22% -25% 13% 9% 5% 5%2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

21ROMANIA INdUSTRIAL ANd WAREHOUSING © 2015 EECFA

Indust r ia l and warehousing | g raph

ROMANIA INdUSTRIAL ANd WAREHOUSING © 2015 EECFA 22

INDUSTRIAL AND WAREHOUSING Industrial construction is expected to be on a growth

path until 2017, due to a stronger economy and increased attractiveness for investors. A similar trend is forecasted for warehousing as Romanian transpor-tation infrastructure continues to develop slowly.

Completion in 2015 has been high, compared to pre-vious years, reaching 170000sqm GBA in units across the country. It includes, in addition the projects men-tioned in the previous report:

• Holzindustrie Schweighofer wood processing plant in Covasna (72000sqm),

• Star Transmission (daimler) assembly hall in Sebes (20000sqm),

• Olympian Park Timişoara TT Electronics Factory in Timis (20000sqm)

• Siniat Factory, in Turceni (25000sqm)

• Bistrita South Industrial Park (180000sqm)

Another 100000sqm GBA are expected to be com-pleted by the end of the year, marking a significant increase over the previous 2 years. For 2016 approxi-mately 100000sqm GBA are expected to be delivered in several projects currently under construction, in addition to over 2.3 million sqm in industrial parks in Craiova and Alexandria. Growth is also forecasted for 2017, with around 100000sqm GBA already planned to be delivered in several projects across the country.

2015 2016 2017

Ongoing and planned Industrial projects

KLG Logistic Center | Turda, North-West region

Logistic center | Popesti-Leordeni, Bucharest-Ilfov region | 72,000 sqm

Emerson factory, phase 2 | Oradea, North-West region | 7,000 sqm

Craiova Industrial Park 3 | Isalnita, South-West region | 2,100,000 sqm

SW Umwelttechnik factory | Cristesti, North-East region | 35,000 sqm

Karl Heinz Dietrich Logistic | Blaj, Center region | 20,000 sqm

Alexandria industrial park | Alexandria, South region | 186,000 sqm

Continental factory | Timisoara, West region | 19,000 sqm | extension

P3 Logistic Park | Chiajna, Bucharest-Ilfov region | 75,000 sqm

Lidl logistic centre | Lugoj, West region | 45,000 sqm

Martur Automotive Factory phase 2 | Cateasca, South region | 17,000 sqm

Prysmian cable factory | Slatina, South-West region | 20,000 sqm

Olympian Park Brasov | Brasov, Center region | 5,000 sqm

Mega Image Logistic Center | Ilfov, Bucharest-Ilfov region | 30,000 sqm

Karcher factory | Curtea de Arges, South region | 22,000 sqm

Leoni factory | Bistrita, North-West region | 22,000 sqm

Log Center Bucharest | Mogosoaia, Bucharest-Ilfov region | 148,000 sqm

Star Transmission (Daimler) assembly hall | Sebes, Center region | 67,000 sqm

SOURCE: IBUILD.INFO

Indust r ia l and warehousing | g raph, text

ROMANIA INdUSTRIAL ANd WAREHOUSING © 2015 EECFA 23

INDUSTRIAL AND WAREHOUSING

The trend for build-to-order construction in the indus-trial field continues, with only a few speculative developments planned in the future. This is quite typ-ical for the Romanian industrial market; however, the trend might change in the future as demand increases. A first indicator of this could be that vacancy rates are dropping and rents are being pushed upwards (source: CBRE Research).

In the case of logistics construction, completion in 2015 has exceeded 120000sqm across the country, with most projects taking place in the North-West and West regions. These continue to be the most attrac-tive for warehousing projects due to their proximity to the western border and easier access to the European market.

For 2016, expected completion will exceed 300000sqm, with two major projects near Bucharest: Log Center Bucharest phase I (148000sqm) under construction and P3 Logistic Park (75000sqm) planned.

Employment in the industry, especially manufacturing, and warehousing continues to be on an upward trend. Lower than EU average wages and development costs are competitive advantages for Romania and attract industry investors. Its geographical position and low

storage costs also make it attractive for logistic spaces developments. Therefore, we estimate employment to continue to rise in these fields at least until 2017. Universities in Romania continue to provide a steady supply of graduates for employment in industry; yet, there continue to be regions lacking in local qualified workforce, and many industrial-developed cities resort to attracting personnel from underdeveloped regions (with an impact also on residential construction).

The Romanian economy performed well over the last years and a GdP growth of over 3% per year is forecasted in 2016 and 2017 as well. At least for the forecast horizon, we predict the economy to continue to be stable, and industry and manufacturing production to increase. While 2015 inflation is currently estimated to be negative, its impact on the sector should be min-imal, as it is mainly due to the relaxation of tax policies.

The main hindering factor for warehouse investments in Romania continues to be the low level of transport infrastructure development. With the completion of several projects in the near future (such as highways, intermodal and harbors - detailed in the correspond-ing sections) we expect construction in warehousing and industry to pick up significantly.

21% 45% 104% 5% 10% 48% 49% 12% -24% -14% -19% -3% 3% 8% 15%2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

RON 0,3bln

RON 0,6bln

RON 0,9bln

RON 1,2bln

RON 0,3bln

RON 0,6bln

RON 0,9bln

RON 1,2bln

3% of building constructionis hotel (2014)

Long-term trend estimationHo

tel o

utpu

t (at

2014

price

)

Forecast

0.2(EUR bln)

0.9(RON bln)

HOTEL CONSTRUCTION

21% 78% -48% -5% 58% 12% 32% -41% -10% 49% -13% 4% 3% 2% 3% 3%2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

24ROMANIA HOTEL CONSTRUC TION © 2015 EECFA

Hotel const r uct ion | g raph

ROMANIA HOTEL CONSTRUC TION © 2015 EECFA 25

the average useful area per permit. Traditionally most investments (in number) were done in the bed-and-breakfast and rural tourism, with the market share of hotels dropping, a tendency likely to continue for the forecast period as well.

The completion of major projects for 2015 has raised the current stock with more than 60000sqm GBA. The largest of these is the Blaxy Premium Resort & Hotel (35000sqm) with 560 rooms opened in the first phase of the project in 2015, and another 400 to be delivered in 2016.

In 2016, most large-scale projects will take place on the shores of the Black Sea, with the construction of Hotel Cocorul in venus (8000sqm), Hilton Garden Inn in Constanta (10000sqm) and of Hotel Mamaia in Con-stanta (8000sqm).

Tourism trends in Romania are improving, with over-night stays on an upward trend in 2015, compared to

Tourism is showing signs of improvement, backing our forecast for increased hotel construction activity

up to and including 2017.

The useful surface area permitted for hotel construc-tion has grown in the first 8 months of 2015, over the same period in 2014, and we predict permits to con-tinue to go up in the near future. The trend for smaller investments seems to have stabilized, as evidenced by

2014 (17% improvement Jan-Sept). At the same time, the number of foreign visitors went up by almost 19%. vacancy rates have also improved, being on aver-age with 2 points lower in 2015 than in the equivalent months of 2014. We expect the situation to continue to improve in the future as well, as current investments in infrastructure will improve travel time and cost, once they are completed. At the same time, growth in income might open more travel options for Romanian tourists, which might actually have a negative impact on local hotels' turnover.

Another factor influencing tourism demand is tied to government and local administration. They are cur-rently trying to actively promote and stimulate tourism in many areas, and they are to receive EUR 120 mil-lion from EU funding in the 2014-2020 exercise to help them do this.

HOTEL CONSTRUCTION

2015 2016 2017

Ongoing and planned Hotel projects

Iride City Phase 2 | Bucharest, sector 2 | 60,000 sqm | 140 rooms

Hilton Garden Inn | Craiova, South-West region | 5,890 sqm, 108 rooms

Airport City Park | Otopeni, Ilfov | 25,000 sqm

Hotel Gemi Center | Arad, West region | 5,000 sqm

Hilton Garden Inn | Constanta, South-East region | 10,000 sqm, 145 rooms

Blaxy Premium Resort & Hotel Phase 2 | 23 August, South-East region | 35,000 sqm | 400 rooms

Hotel Cocorul | Venus, South-East region | 8,000 sqm | 204 rooms, renovation

Hotel Hampton by Hilton | Iasi, North-East region | 7,000 sqm, 123 rooms | renovation

Hotel Mamaia | Constanta, South-East region | 8,000 sqm

SOURCE: IBUILD.INFO

Hotel const r uct ion | g raph, text

21% 45% 104% 5% 10% 48% 49% 12% -24% -14% -19% -3% 3% 8% 15%2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

RON 0,5bln

RON 1,0bln

RON 1,5bln

RON 2,0bln

RON 2,5bln

RON 0,5bln

RON 1,0bln

RON 1,5bln

RON 2,0bln

RON 2,5bln

Forecast

4% of building construction is education-and health-related (2014)

Long-term trend estimation

0.3(EUR bln)

1.3(RON bln)

Educ

ation

-and

Hea

lth-re

lated

outpu

t (at 2

014 price

)

Regim

e Swi

tch

HEALTH- AND EDUCATION- RELATED CONSTRUCTION

-16% 56% 1% -46% 94% 38% 13% 4% -36% 20% -29% -14% 4% 16% 8% 4%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

26ROMANIA HE ALTH- ANd EdUCATION- REL ATEd CONSTRUC TION © 2015 EECFA

Educat ion- and Health-related const r uct ion | g raph

ROMANIA HE ALTH- ANd EdUCATION- REL ATEd CONSTRUC TION © 2015 EECFA 27

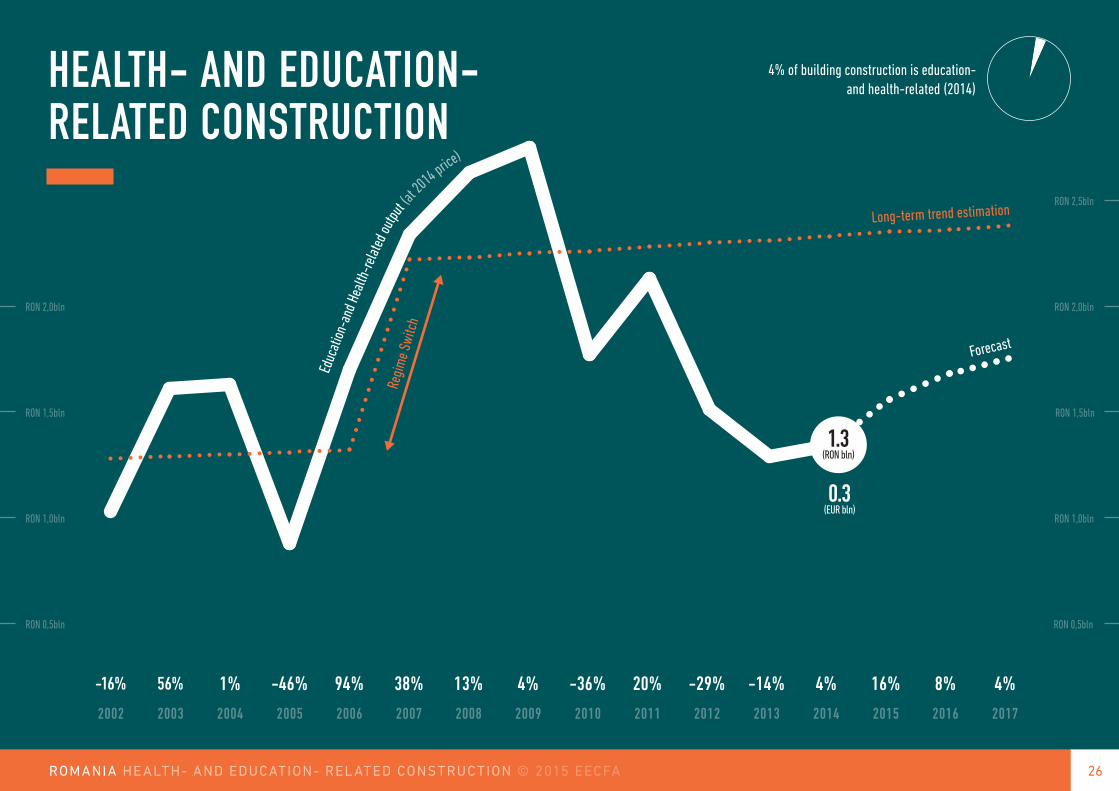

Due to increased demand, we predict health related construction to grow significantly in the near future.

At the same time, educational building construction is set to pick up, partly due to increased renovation activ-ity, but also due to investments in research facilities. We forecast this segment to go up rapidly in 2015 and 2016 and to be on an upward trend into 2017.

The aging infrastructure and lack of modern facilities in many medical units have been the consequence of low funding levels for the past two decades. With the help of private, government and local funding, several projects were completed in 2015, aimed especially at emergency hospitals in Craiova (2000sqm, extension), valcea (10000sqm, renovation), Brasov (4000sqm, renovation), Alexandria (9300sqm, renovation) and Bucharest (21000sqm, renovation).

New construction is more limited, with only few projects completed in 2015, the most notable of which being the Falticeni Municipal Hospital (16000sqm). For 2016, most

of the completion should again be due to renovation and extension works on existing hospitals, which will cover more than 51000sqm countrywide. The largest under-going projects expected to be finished in 2016 are the emergency hospitals in Timisoara (10000sqm, exten-sion) and Petrosani (15800sqm, renovation), as well as the dr.Fogolyan Kristof County Hospital in Covasna (147000sqm, renovation).

In 2016-2020, health-related construction might see an improvement, due to the EU funding directed towards the construction of regional hospitals and moderniza-tion/extension of emergency hospitals. Currently the estimated budget for the 2014-2020 period is of EUR 763 million, but as of date no concrete measures (calls for projects, contracts, works) have been taken to use these funds.

Education-related construction has taken mainly the form of research buildings, with around 46500sqm being constructed. The most important project in this

HEALTH- AND EDUCATION- RELATED CONSTRUCTION

2015 2016 2017

Ongoing and planned Health-related projects

Precista hospital | Roman, North-East region | 16,000 sqm | extension, renovation

Regional Oncology Center | Timisoara, West region | 22,000 sqm

Medgidia Hospital | Medgidia, South-East region | 3,700 sqm | renovation

County hospital Bacau | Bacau, North-East region | | EUR 5 million, extension, renovation

City Hospital | Mioveni, South region | 15,000 sqm |

Doctor Ioan Aurel Sbarcea Hospital | Brasov, Center region | 4,000 sqm | renovation

City Hospital | Sinaia, South region | 8,000 sqm | extension, renovation

Craiova County Hospital emergency unit | Craiova, South-West region | 2,800 sqm | EUR 4 million extension, renovation

Emergency Hospital Petrosani | Petrosani, West region | 15,800 sqm | renovation

Ilfov county hospital | Bucharest, sector 2 | 4,500 sqm | renovation

Dr. Fogolyan Kristof County Hospital | Covasna, Center region | 14,700 sqm | renovation

Louis Turcanu Hospital | Timisoara, West region | 10,000 sqm | extension

Foisor Hospital | Bucharest, sector 2 | 13,000 sqm | extension

Medical Clinic | Bucharest, sector 1 | 10,000 sqm

SOURCE: IBUILD.INFO

Educat ion- and Health-related const r uct ion | g raph, text

ROMANIA HE ALTH- ANd EdUCATION- REL ATEd CONSTRUC TION © 2015 EECFA 28

HEALTH- AND EDUCATION-RELATED CONSTRUCTION

field is the Extreme Light Infrastructure – Nuclear Physics Facility in Magurele (34000sqm) that will be completed by end 2015, including a high power laser and a gamma ray generator.

For 2016, four more research facilities are expected to reach completion, including the Research and devel-opment centre PRECIS (78000sqm) that will include 28 labs designed for "smart" technology research.

Renovation works are also ongoing in a number of edu-cational buildings across Romania, a process that we expect to increase in the near future, as for the 2014-2020 EU exercise EUR 352 million have been budgeted for this purpose, and so far, none of these funds have been contracted.

demographic trends in Romania are the same as in the previous years: decreased young population (espe-cially on the 20-30 years old segment) coupled with

an increase in the share of old persons. These trends favor health-related construction, as the aging popu-lation will require more assistance. At the same time, the decrease in the number of children and teenagers is reducing the need for education construction. The impact of these trends on actual output however is, for the time being, low. The condition of the stock and low investments in the past has led to high demand for renovation and extensions that will fuel construction at least until 2020.

2015 2016 2017

Ongoing and planned Education-related projects

Scientific and technology park | Bucharest, sector 3 | 13 ha

Tetapolis research and development centre | Cluj-Napoca, North-West region |

Advanced Research Institute | Timisoara, West region | 14,000 sqm

Tulcea educational centre | Babadag, South-East region | 80,000 sqm | renovation of 52 buildings

Renovation of schools, kindergartens | Bucharest, sector 1 | 334,000 sqm | EUR 69 million, renovation of 106 buildings

Radio-molecular imaging research centre | Magurele, Bucharest-Ilfov region | 9 million EUR

Emanuil Ungureanu Technical College | Timisoara, West region | 1,700 sqm | renovation

Transilvania Motorland research & development centre | Brasov, Center region | 11,000 sqm

Continental Powertrain testing laboratory | Ghimbav, Center region | 1,700 sqm

Medical research and development centre | Targu Mures, Center region | 4,000 sqm

Research and development centre | Bucharest, sector 6 | 78,000 sqm

Partenie Cosma National College & Vasile Voiculescu School | Oradea, North-West region | 16,000 sqm

M. Kogalniceanu High School | Snagov, Bucharest-Ilfov region | 8,100 sqm | extension, renovation

Cumpana School Campus | Constanta, South-East region | 3,900 sqm

Tertiary School | Bucharest, sector 5 | 7,300 sqm | extension

Research Center Campus | Bucharest, sector 6 | 8,500 sqm

Craiova University - Mechanics Faculty | Craiova, South-West region | 6,300 sqm | extension

Extreme Light Infrastructure - Nuclear Physics Facility | Magurele, Bucharest-Ilfov region | 34,000 sqm | EUR 224 million

SOURCE: IBUILD.INFO

ROMANIA OTHER NON-RESIdENTIAL © 2015 EECFA 29

For 2015, completion has been modest, however by the end of the year the renovations of the Palace of Justice in Oradea (15351sqm) and the Palace of the Patriarchate in Bucharest (16000sqm) are predicted to be finished.

In 2016, works on the Metropolitan Cathedral (18000sqm) and the Cultural Palace (34000sqm) in Iasi are expected to reach completion.

due to overcrowding and poor living conditions in Romanian prisons, there are plans to build several new facilities. The first of these, the P46 Caracal high secu-rity prison (27000sqm) is set to start construction in 2016, and should be completed in 2017.

EUR 2.4 billion are allocated from the 2014-2020 EU programs to renovation works for public buildings, aim-ing at increasing their energy efficiency. As previously stated, due to their age, most of these buildings were constructed before environmental protection or energy were an issue.

Romanian public institutions are generally housed into state-owned buildings that have been con-

structed during the communist era. Many of these buildings are either in poor condition due to lack of maintenance and renovation works, or have since became inadequate for their purpose, as institutions grew in size. Therefore, renovation and expansion works on civic buildings is taking up a large portion of the non-residential construction market.

Efforts are also being undertaken to preserve cultural buildings, with several projects currently ongoing at Capidava and Sucidava Fortresses, two of the very few remaining dacian and Roman sites. With almost EUR 0.5 billion allocated for the protection of cultural sites in the 2014-2020 EU funding exercise, we expect similar works to grow in number after 2016, once projects are elected.

Entertainment and sports buildings are also major contributors to growth in non-residential construction. Several projects for tourist attractions have been devel-oped in and near Oradea: Lotus Felixarium waterpark (20000sqm), completed in 2015 and Complex Wellness Termal Nymphaea, to be finished in 2016 (18000sqm).

Sports facilities are under construction in Craiova (41000sqm Stadium) and planned to be constructed in Bucharest (37000sqm Rugby sport centre) and Con-stanta (7 ha, sports arena); all of these are expected to be delivered in 2016.

OTHER NON-RESIDENTIAL

2015 2016 2017

Ongoing and planned Other non-residential projects

Underground parking Avram Iancu | Arad, West region | 18,083 sqm |

P46 Caracal prison | Caracal, South-West region | 27,000 sqm |

Mihai Flamaropol ice arena | Bucharest, sector 2 | 22,600 sqm |

Rugby sport centre | Bucharest, sector 1 | 37,000 sqm | extension, renovation

Craoiva Stadium | Craiova, South-West region | 41,000 sqm |

Capidava Fortress | Constanta, South-East region | | EUR 12 million, renovation

Complex Wellness Termal Nymphaea | Oradea, North-West region | 18,000 sqm | new construction, extension

Sport centre | Sfantu Gheorghe, Center region | 8,700 sqm |

Cultural Palace Iasi | Iasi, North-East region | 34,000 sqm | renovation

Sucidava fortress | Olt, South-West region | | EUR 184 million, renovation

Palace of the Patriarchate | Bucharest, sector 4 | 16,000 sqm | renovation

Metropolitan Cathedral Iasi | Iasi, North-East region | 18,000 sqm | renovation

Orthodox Cathedral - Catedrala Mantuirii Neamului | Bucaharest, sector 5 | 42,000 sqm |

SOURCE: IBUILD.INFO

Other non-resident ial | g raph, text

ROMANIA FORECA ST TABLE 4 © 2015 EECFA 30

FORECAST TABLE 4

ROMANIA VALUE (RON MLN)

VALUE (EUR MLN) GROWTH RATES AT CONSTANT PRICE (%)

NON-RESIDENTIAL MARKET SIZE AND DEVELOPMENT

2014 2014 2007 2008 2009 2010 2011 2012 2013 2014 2015(F) 2016(F) 2017(F)

HOTEL, ACCOMODATION BUILDINGS 907 204 12.4 32.2 -41.1 -9.7 49.2 -13.0 4.3 3.1 1.5 2.9 2.8

OFFICE BUILDINGS 6 568 1 478 1.2 74.2 7.1 -17.2 1.6 -19.5 -3.1 3.5 7.1 7.5 7.7

RETAIL AND WHOLESALE BUILDINGS 1 187 267 16.3 54.6 -46.1 -9.9 8.9 -43.7 -10.1 -1.5 2.3 1.0 1.4

TRANSPORT BUILDINGS 264 59 8.7 6.3 -32.3 137.7 -38.3 0.3 -41.6 -14.1 8.0 7.5 -6.2

INDUSTRIAL BUILDINGS AND WAREHOUSES 3 927 884 37.1 8.3 -29.6 -27.1 59.2 -22.5 -25.5 13.2 9.4 5.4 5.3

EDUCATION-RELATED BUILDINGS* 1 344 302 37.8 12.5 4.5 -35.6 20.3 -29.0 -14.3 3.8 15.7 8.3 4.2

HEALTH-RELATED BUILDINGS

AGRICULTURAL BUILDINGS

OTHER NON-RESIDENTIAL BUILDINGS 841 189 -5.6 -9.4 -28.2 33.3 -30.5 61.8 -22.3 1.4 9.1 2.8 3.3

TOTAL NON-RESIDENTIAL CONSTRUCTION 15 038 3 383 18.1 33.0 -17.0 -16.6 14.4 -20.7 -13.1 4.9 7.9 6.0 5.5

*EDUCATION AND HEALTH TOGETHER

Forecast t able 4 | non-resident ial f igu res

ROMANIA ROAd CONSTRUC TION © 2015 EECFA 31

ROAD CONSTRUCTION

After the low performance of the sector in 2014, 2015 has seen an increase in road construction activity.

Under the pressure of deadlines for EU funding, more projects have been initiated and restarted; yet, the effect is still far from enough to counterbalance the more negative effects of institutional instability. As such, we continue to expect 2015 to mark a hike compared to 2014. We predict a drop in output in 2016, as calls for the new EU programs will only start in Q1 2016 earliest and activity will consist only of phased and nationally funded projects. 2017, on the other hand, should see a return to an upward trend, as projects will be underway and the election year effects will wear off.

The Romanian road network is in a dire need of renova-tion and modernization works. Half of the total network has actual speeds under 70% of the target speeds (according the Romanian General Transport Master-plan). At the same time, only 35% of the road network is

registered as "modern", while 26% of the total network is made of stone covered roads and 36% of dirt roads. In 2014 around 600 km of roads were modernized, and we estimate this number to remain relatively stable, but on an upward trend in 2015 and 2016.

Highway construction in 2015 has continued at the usual slow pace, despite the threat of losing EU funding. So far, only 10.7 km have been constructed, and, at best, 68 km are to be completed by the end of the year. In addition, around 170 km are currently under construc-tion and expected to be completed in 2016. Around 180 are planned to be completed in 2017.

The main ongoing projects are:

• In case of A1 Highway, accounting for all of 2015 highway completion to date, work has been delayed repeatedly due to legal and technical issues, so deadlines have been moved into 2016 for all sections.

Road construction, RON bln (at 2014 prices)

2.1(EUR bln)

2002 2017

Road const r uct ion | g raph, text

ROMANIA ROAd CONSTRUC TION © 2015 EECFA 32

• A10 Highway Sebes-Turda is also under construc-tion. While initially scheduled for late 2015, it has also been delayed by administrative issues and is more likely to be pushed into H1 2016.

• Work continues on 79.2 km in several sections of A3 "Transilvania" Highway, expected to be completed in 2016. For the remainder currently the earliest start date would be 2016 and completion could be as late as 2021.

A number of projects are also under various stages of planning and predicted to begin by 2017, the most important being:

2015 2016 2017 2018

Ongoing and planned Road projects

Transfagarasan highway | Sibiu, Center region | 91,000 m | renovation

Mihailesti bypass | Mihailesti, South region | 13,800 m | 10 million EUR

Stei bypass road | Bihor, North-West region | 28 km | EUR 94 million

Satu Mare bypass road | Satu-Mare, North-West region | 13,5 km |

Sibiu-Fagaras highway | Brasov, Center region | 72,5 km |

A3 highway Gilau - Mihaiesti | Cluj, North-West region | 24 km |

A3 Highway Comarnic-Brasov | Center and South regions | 58 km |

Galati-Bratianu tunnel | Galati-Bratianu, South-East region | 2,000 m |

A3 highway Targu Mures-Ungheni section | Mures, Center region | 9,2 km |

A3 highway Ungheni-Ogra section | Mures, Center region | 10 km |

A3 Highway section 5 | Bihor, North-West region | 60 km | EUR 266 million

Targoviste bypass road | Targoviste, South region | 13,8 km | renovation

Bacau bypass road | Bacau, North-East region | 30,7 km |

Târgu Jiu bypass road | Gorj, South-West region | 20 km |

A 10 highway, segment 2 | Alba, Center region | 24,3 km |

A 10 highway, segment 1 | Alba, Center region | 17 km |

A 10 highway, segment 4 | Cluj, North-West region | 16,3 km |

A1 highway Lugoj - Deva segment 3 | Cosevita - Ilia, West region | 21,1 km |

A1 Highway, Timisorara-Lugoj segment 2 | Timis, West region | 25 km |

A1 highway Lugoj - Deva segment 4 | Ilia - Soimus, West region | 22,1 km |

A1 highway Lugoj - Deva segment 2 | Traian Vuia - Cosevita, West region | 28,6 km |

SOURCE: IBUILD.INFO

• Sibiu - Făgăraș (72,5 km) and Sibiu - Pitești (116 km) motorways are planned and likely to start construc-tion in 2016 and 2017, respectively

• Renovation of the ”Transfăgărășan” road, one of the most famous roads in Romania to undergo a road surface reconstruction over around 91 km, esti-mated to start in 2016 and to be finished in 2017

Large-scale projects are commonly funded with the aid of EU programs. At the start of October 2015, for the POST program (that helps fund all transport infra-structures) only 73% of the total budged was contracted and only 60% was absorbed. We had hoped the situa-tion to improve by the end of the year, as traditionally

ROAD CONSTRUCTION

ROMANIA ROAd CONSTRUC TION © 2015 EECFA 33

ROAD CONSTRUCTION

most works are paid in the last quarter of the year. But due to the low efficiency of use, we do not foresee total absorption rate to exceed 80%, and thus that would leave at least EUR 0.85 million to be spent from the 2014-2020 budget through phased projects. The total budget for road construction from the 2014-2020 EU programs is of EUR 2.6 billion, with an additional EUR 1 billion for local and regional roads.

due to delays in program calls, which are scheduled for January 2016 earliest in case of infrastructure, we expect investments to stop until projects are approved for refinancing, a process that can take up to a year in Romania. Thus, 2016 will mark a drop in road construc-tion; though we expect it to pick up in 2017.

A major impact factor in 2016 and 2017 in road con-struction is the influence of the political context. As of November 2015, due to internal struggles, the Romanian Government resigned. Until the situation is finalized,

all positions in the cabinet are temporary, and thus no major decisions are expected. This will most likely lead to lower than expected performance on EU funding absorption in 2015, as well as delays in the launch of new projects in 2016. Furthermore, as 2016 is an election year, we predict money to be diverted to social impact programs, in order to attract voters. This will cause a slight increase in road renovation activity, as local budg-ets are boosted for this purpose. However, as in the past, we forecast long-term investments (such as highways) to be underfunded, and overall the impact to be negative.

ROMANIA R AILWAY CONSTRUC TION © 2015 EECFA 34

Despite the poor condition of the railroad network in Romania, renovation and modernization works con-

tinue to be much lower than needed. We predict some improvement in 2015, but 2016 should see a reduction in activity, as the lack of funds and elections will cause interruptions and delays in projects. In 2017, we might see a return to normal activity, as projects phased from 2015 and planned investments will be implemented.

Previous analyses of traffic trends remain valid, with road transportation steadily increasing its share in both freight and passengers. According to NSI, railroad passenger transportation is down to 18% of market, and freight down to 15% of market, as of Q2 2015. This decrease in railroad network demand is coupled with the bad condition of the current infrastructure and leads to a vicious circle hindering both renovation and new investments.

More than 60% of the railroad infrastructure has exceeded its designated life expectancy, and needs capital repairs; the average age of a locomotive or carriage is 30 years (according to the Ministry of Transportation reports). Speed restrictions are in place, which causes delays. In 2014, total delays were 2.5 million minutes for passengers, and 16.1 million minutes for freight.

However, in the near future, the budget of the national railroad company (CFR SA) for maintenance is to remain relatively at the same level (around EUR 300 million/year) and even to drop in the near future. Since at best one-half of the needed maintenance and repair works are accomplished each year, we do not expect the situation to improve dramatically in the near future.

Funding for investments is assured from a combina-tion of national and EU funds. Out of the EUR 1.6 billion

RAILWAY CONSTRUCTION

2015 2017 2019

Ongoing and planned Railway projects

Subway - M4 Line | Bucharest | 15 km | EUR 159 million, extension

Bucharest-Giurgiu railway | Bucharest-Ilfov and South regions | 95 km | renovation

Rosiori de Nord station | Rosiori de Vede, South region | 400 sqm | renovation

Subway -M6 Line | Bucharest, sector 6 | 16 km |

Railway Corridor IV, section 3 | Simeria – Vintu de Jos, Center region | 42,7 km | EUR 320 million, renovation

Subway - M4 Line | Bucharest, sector 1 | | EUR 161 million

Railway Corridor IV, section 5 | Coslariu – Sighisoara, Center region | 91,6 km | EUR 528 million

Railway Corridor IV, section 4 | Vintu de Jos – Coslariu, Center region | 33,1 km | EUR 173 million

Railway Corridor IV, section 1 | border - Curtici - Arad, West region | 41,1 km | EUR 244 million, renovation

Subway - M5 Line | Bucharest, sector 6 | 10 km | EUR 256 million

SOURCE: IBUILD.INFO

Railway const r uct ion | g raph, text

ROMANIA R AILWAY CONSTRUC TION © 2015 EECFA 35

allocated to this sector in the 2007-2013 exercise, only around 75% had been contracted by end 2014. The absorption rate is most likely to be around 80% by end 2015, which has led to several projects being phased into the 2014-2020 budget (of approximately 1.5 billion EUR aimed at railroad construction and repair).

The main ongoing projects are related to the Iv Pan - European Corridor renovation works. Started in 2012, works on this section have been ongoing at a relatively low pace, partly due to the harsh terrain and partly due to bureaucratic reasons. The project is programmed to be phased into the 2014-2020 exercise, and is to be completed in 2018, with some sections to be delivered at the end of 2015.

Improvements of the network are also planned in sev-eral key areas, such as development of touristic lines with the goal of preserving historical features of train

transportation, and the electrification of railways that are currently still running on diesel, such as the Cluj-Napoca – Oradea line, planned to start in 2017 and to be completed by 2021.

Political instability will have an even greater effect on the railroad network construction than on road con-struction. As 2016 will be an election year and funding will switch from the 2007-2013 to the 2014-2020 exer-cise, we expect a drop in completion. However, due to the poor condition of the network, we forecast interest to pick up in the near future and investments to increase in 2017 and beyond.

RAILWAY CONSTRUCTION

ROMANIA OTHER TR ANSPORT REL ATEd CONSTRUC TION © 2015 EECFA 36

Most large-scale transport related construction in Romania is accompanied by additional bridges and

tunnel construction. Coupled with the aging infrastruc-ture, this has led to a lot of activity in this field, albeit usually on small projects.

Airport construction continues to be the most active subsector of this type of construction. As mentioned in the previous report, passenger air traffic in Romania is underperforming over the EU average, and the majority of flights take place from and between 3 major air-ports (Cluj Napoca, Timisoara and Bucharest). This has resulted in investments in the field, with the help of EU funding. Around EUR 72 million were contracted from the 2007-2013 exercise and EUR 42 million planned out of the 2014-2020 exercise to be used for renovation, extension and new construction in the field.

So far, in 2015, several projects have been completed, including the renovation of the ”Mihail Kogalniceanu” Airport terminal (EUR 28 million) and the construc-tion and extension of terminals in Iași and Suceava, totaling at EUR 57 million of completion for the whole year. Extensions of the runway are also undergoing in Oradea and are to be completed by the end of 2015, turning the local airport into an international one.

OTHER TRANSPORT RELATED CONSTRUCTION

2015 2016 2017 2018

Ongoing and planned Other transport projects

Bridge over Tisa river | Sighetu Marmatiei, North-West region | 2,000 m

Danube bridges | Calarasi-Turnu Magurele, South region and Bulgaria | EUR 209 million

Harghita Airport | Ciceu, Center region | 2,000 sqm | 1,200 m runway

Airport Transylvania - runway | Targu Mures, Center region | 3,600 m | extension

Bucharest-Domnesti overpass | Bucharest-Domnesti, Bucharest-Ilfov region | 260 m

Sport aircraft airport Phase 2 | Borcea, South region | 6,500 sqm | new construction, renovation

Railway tunnel renovation | Suceava, North-East region | 255 m | EUR 500,000

Baia Mare Airport | Tautii-Magheraus, North-West region | 2,150 m | extension

Sport aircraft airport Phase 1 | Borcea, South region | 1,500 sqm | new construction, renovation

Brasov-Ghimbav airport - runway and parking | Ghimbav | 17,700 sqm

Tulcea Danube Delta Airport | Tulcea, South-East region | 52,150 sqm | modernisation

Nicolina Tunnel | Iasi, North-East region | 15,560 sqm | renovation

Hangar, runway | Borcea, South region | 3,500 m | extension, renovation

Military airport | Otopeni, Ilfov | 1321 m | EUR 11 million

Vehicular overpass | Ploiesti, South region | 500 m

SOURCE: IBUILD.INFO

For 2016, ongoing projects would lead to at least six more renovation and extension projects being com-pleted, totaling in the value of around EUR 65 million. With the planned projects, total completion in 2016 might exceed EUR 100 million in the field, and thus be one of the best years in recent history for the airport construction segment in Romania. Yet, since this is largely dependent on EU co-funding, we expect delays to take place, similarly to road and railroad construc-tions (however at a smaller scale) and thus, some of these projects might get pushed into 2017.

The extension of the Bucharest's subway network is continuing, with M5 line (10km) expected to reach com-pletion in 2016 (after 5 years of delays) together with the extension of M4 line (1km). Planning for the two new lines (M6 and M7) continues, however construc-tion will likely only be completed in 2020 earliest.

Other t ranspor t in f rast r uct u re | g raph, text

ROMANIA ENERGY, PIPELINE, CABLE CONSTRUC TION © 2015 EECFA 37

ENERGY, PIPELINE, CABLE CONSTRUCTION

Energy production in Romania continues to be reliant on oil and gas, which account for more than 50% of

all energy produced in Romania. However, renewable energy sources continue to be on the rise, and in 2016 and onwards, we estimate the share of wind, solar and geothermal power to increase steadily.

Most of the current energy production network is rather old, and as such, renovation and modernization works are underway. Examples in this direction are the Paroseni and deva thermal-power plants and Ste-jaru hydro plant currently under construction, the total budget for these projects exceeding EUR 370 million.

New construction is mostly focused on renewable energy:

• Solar power - expected to increase in 2016 with about 700 MW across the country (according to Transelectrica forecast), with several projects underway and then remain relatively steady

• Wind power - expected to increase with 300 MW per year in the 2015 - 2017 period

• Biomass - expected to increase with 25 MW per year in the 2015 - 2017 period

• Geothermal power plant to be constructed in Oradea in 2016 - 2017

2015 2016 2017 2018

Ongoing and planned Energy-related projects

Nuclear power plant unit 3 and 4 | Cernavoda, South-East region | 1440 MW | new construction, renovation

ALFRED nuclear reactor | Mioveni, South region | 130 MW | EUR 1 billion

District heating | Oradea, North-West region | 20,300 m | EUR 26 million, renovation

Thermal power plant | Rovinari, South-West region | 600 MW

Pumped-storage hydroelectric power station | Tarnita-Lapustesti, Center region | 1,000 MW | EUR 1,1 billion

Thermal power plant | Mures, Center region | 250 MW | new construction, renovation

Thermal power plant | Arad, West region | 270 MW

Mintia thermal power plant | Mintia, West region | 5,000 sqm | renovation

Dumitra hydro power plant | Bumbesti-Jiu, South-West region | 24,5 MW |

Bumbesti-Jiu Hydro power plant | Bumbesti-Jiu, South-West region | 40,5 MW

Hidroelectrica Stejarul Bicaz hydro power plant | Neamt county, North-East region | 210 MW | EUR 136,9 million, renovation

Thermal power plant | Oradea, North-West region | 43 MW

Biomass power station | Prahova, South region | 6.8 Mw

Paroseni thermal power plant | Hunedoara, West region | 150 MW | EUR 65 million, renovation

Petrobrazi refinary | Prahova, South region | renovation

SOURCE: IBUILD.INFO

Funding for these projects is partially covered from EU programs, with around 200 EUR million budgeted from the 2014-2020 exercise for renewable and more efficient energy.

However, several projects also aim to increase the nuclear power output, with the doubling of the Cer-navodă power plant capacity, by adding reactors 3 and 4 expected to enter construction in early 2017. In the same year, construction is set to start at ALFREd, an experimental lead-cooled fast reactor in Mioveni, budgeted for EUR 1 billion.

The energy transportation network is also set for expansion, with 1000 km of new lines planned for con-struction between 2014 and 2023. Over this period, around EUR 1 billion from national funds will be invested in energy lines and around 1/2 of the amount will be directed to modernization works, coupled with EUR 66 million from EU 2014-2020 programs for energy transportation.

Energy, pipel ine, cable const r uct ion | g raph, text

ROMANIA PUBLIC UTIL IT Y © 2015 EECFA 38

PUBLIC UTILITY We predict public utility to pursue to be an important factor of civil engineering construction output as

the problems we evidenced in the last reports continue to plague the system. Water shortages in most major cities go on to be a relatively frequent occurrence due to the age of the system.

despite significant progress in the last few years, access to public utilities remains relatively low with only slightly more than one half of Romanians having their homes connected to a sewage system, as of the beginning of 2015 (source: NSI). There is also a high level of geographical disparity, with public utilities lacking especially in the rural areas.

Several public utility construction works have been completed so far in 2015, with more than EUR 400 mil-lion invested in water supply, wastewater treatment plants and sewer systems across the country.

2015 2016 2017

Ongoing and planned Utility and Other civil engineering projects

Glina Waste Water Treatment Plant phase 2 | Glina, Bucharest-Ilfov region | EUR 152 million, extension

Protection and Rehab. of the Southern Black See Coast, ph. 2 | South-East region | 20 km | extension, renovation

Waste management facility | Constanta, South-East region | 21,000 tons/year | EUR 13 million

Waste management facility | Vadeni, South-East region | 30,000 tons/year

Waste management plant | Alba, Central region | 1,900,000 m3

Waste management plant | Dolj, South-West region | 44,000 tons/year

Waste management facility | Remetea, Center region | 23,000 tons/year

Sanitary sewer | Salaj, North-West region | EUR 18 million, new construction, extension

Sanitary sewer | Prahova, South region | 37 km | extension

Waste water and water management | Sibiu, Center region | EUR 132 million

Waste water and water management | Maramures, North-West region | EUR 148 million

Waste water and water management | Timis, West region | EUR 119 million

In addition to new construction and improving access to water and sewer systems, many renovation works are also ongoing or planned. Public utility networks in most cities are a relic of the communist regime and at least 20 years old and their efficiency is diminishing, as evidenced by the frequent interruptions in service.

Currently, funding for the new projects is assured by a mixture of national, local and European sources. The absorption rate of EU funding from the 2007-2013 exercise continues to be low, and thus many projects are expected to be transferred or phased into the 2014-2020 exercise, where around EUR 300 million are budgeted for waste management investments and around EUR 2.6 billion for water and wastewater net-work development.

SOURCE: IBUILD.INFO

Publ ic ut i l it y | g raph, text

ROMANIA FORECA ST TABLE 5 © 2015 EECFA 39

FORECAST TABLE 5

ROMANIA VALUE (RON MLN)

VALUE (EUR MLN) GROWTH RATES AT CONSTANT PRICE (%)

CIVIL ENGINEERING MARKET SIZEAND DEVELOPMENT

2014 2014 2007 2008 2009 2010 2011 2012 2013 2014 2015(F) 2016(F) 2017(F)

TRANSPORT INFRASTRUCTURE 13 930 3 134 34.8 44.6 -7.1 -12.0 1.7 -7.3 -8.9 -17.4 12.7 -7.4 7.4

ROADS 9 297 2 092 24.9 31.1 -10.9 -11.3 6.4 -6.9 -12.8 -19.2 14.5 -9.4 8.7

RAILWAYS 764 172 165.3 -3.8 -37.4 -8.0 -11.7 -27.9 77.1 -14.1 13.3 -4.4 3.1

AIRFIELDS 102 23 140.4 -79.4 -24.9 -86.2 123.2 880.7 -5.9 21.2 3.4 0.0 0.0

BRIDGES AND TUNNELS 2 849 641 70.4 641.6 4.6 -6.9 -19.3 24.8 -6.8 -14.1 11.9 -4.4 6.2

HARBOURS 919 207 46.3 29.1 22.2 -23.7 13.2 -48.2 -7.8 -14.1 -2.8 1.0 2.9

ENERGY, COMPLEX INDUSTRIAL AND LONG TERM PIPELINES 3 563 802 83.8 -5.9 -15.5 19.4 -10.8 17.3 -12.6 -14.1 8.5 7.8 2.9

PUBLIC UTILITY 1 105 249 24.4 9.6 13.1 -28.8 11.3 -2.5 6.4 -14.1 17.5 -4.4 6.2

OTHER CIVIL ENGINEERING 5 432 1 222 -5.2 11.3 -5.8 9.6 -0.4 -14.6 -14.7 -9.8 8.7 -1.8 4.2

TOTAL CIVIL ENGINEERING CONSTRUCTION 24 031 5 407 26.8 27.0 -7.1 -4.7 -0.2 -6.0 -10.2 -15.2 11.4 -3.8 5.9

Forecast t able 5 | civ i l engineer ing f igu res

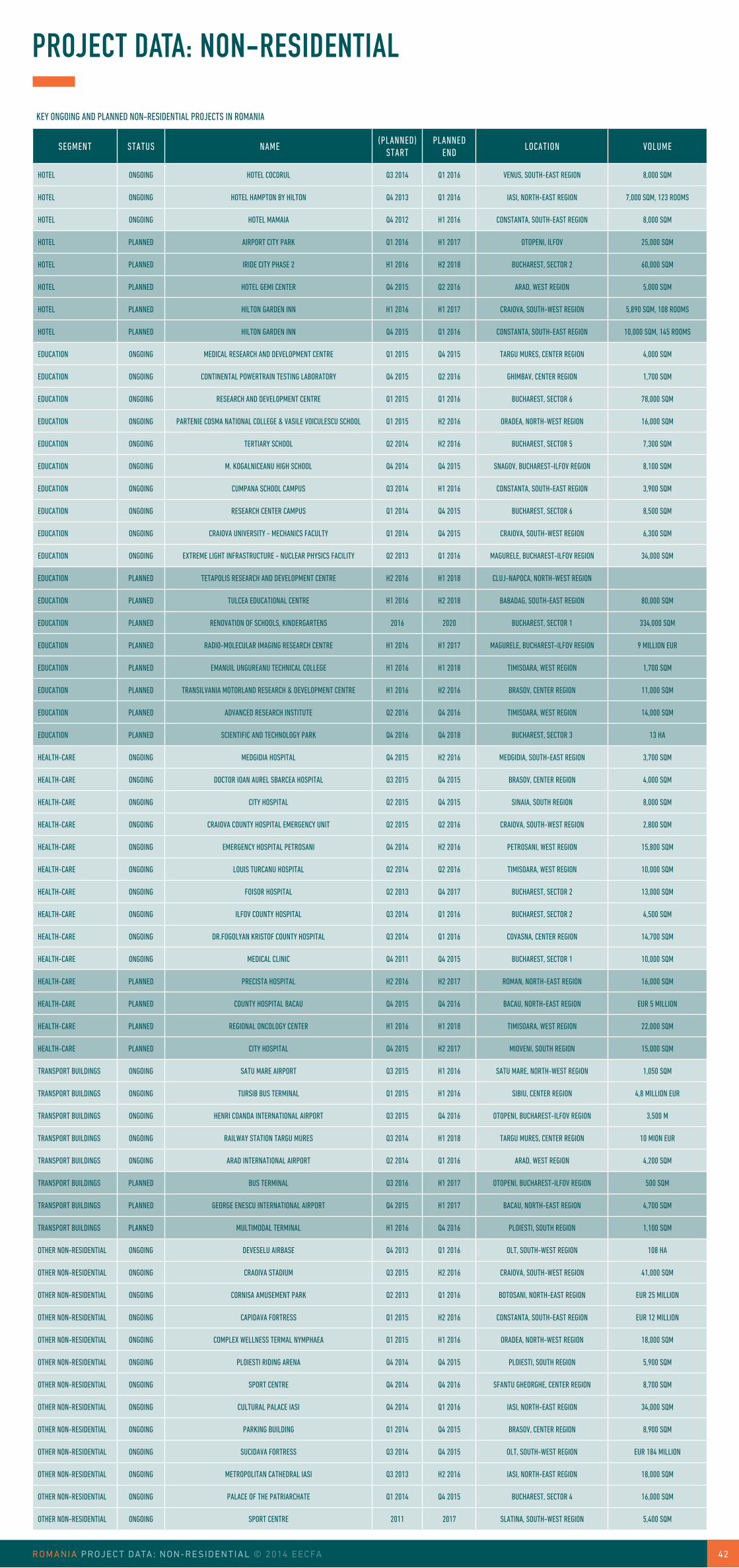

ROMANIA PROJEC T dATA: NON-RESIdENTIAL © 2014 EECFA 40

KEY ONGOING AND PLANNED NON-RESIDENTIAL PROJECTS IN ROMANIA

SEGMENT STATUS NAME (PLANNED)

START PLANNED

END LOCATION VOLUME

RESIDENTIAL ONGOING BEACHSIDE RESIDENCE Q3 2014 H1 2016 CONSTANTA, SOUTH-EAST REGION 16,000 SQM

RESIDENTIAL ONGOING CITY OF MARA PHASE 1 Q3 2015 H1 2016 TIMISOARA, WEST REGION 12,000 SQM

RESIDENTIAL ONGOING NORDIC RESIDENCE PARK Q4 2015 H1 2017 DUMBRAVITA, WEST REGION 50,000 SQM

RESIDENTIAL ONGOING ARENA RESIDENTIAL PARK PHASE 2 Q3 2015 H2 2016 IASI, NORTH-EAST REGION 22,000 SQM

RESIDENTIAL ONGOING CARTIER ORIZONT PHASE 3 Q2 2015 Q4 2018 BUZAU, SOUTH-EAST REGION 130,000 SQM

RESIDENTIAL ONGOING BUJORULUI RESIDENCE Q4 2014 Q4 2018 CRAIOVA, SOUTH-WEST REGION 28,000 SQM

RESIDENTIAL ONGOING ONE HERĂSTRĂU PARK RESIDENCE Q3 2015 H2 2016 BUCHAREST, SECTOR 1 27,000 SQM

RESIDENTIAL ONGOING EXIGENT ONE Q2 2015 Q2 2016 BUCHAREST, SECTOR 6 25,000 SQM

RESIDENTIAL ONGOING BLOCK OF FLATS - THERMAL INSULATION Q2 2015 H2 2017 BUCHAREST, SECTOR 2 EUR 22 MILLION, 597 FLATS

RESIDENTIAL ONGOING METALURGIEI PARK RESIDENCE PHASE 1 Q1 2015 H1 2016 BUCHAREST, SECTOR 4 185,000 SQM

RESIDENTIAL ONGOING CONDOMINIUMS Q2 2015 H2 2016 CRAIOVA, SOUTH-WEST REGION 182,000 SQM

RESIDENTIAL ONGOING DREAM TOWN RESIDENCE Q2 2014 H2 2016 POPESTI-LEORDENI, BUCHAREST-ILFOV REGION 30,000 SQM

RESIDENTIAL ONGOING MC METROCITY ACADEMIEI Q4 2014 Q4 2016 BUCHAREST, SECTOR 5 30,000 SQM

RESIDENTIAL ONGOING AVANTGARDEN 3 PHASE 2 Q3 2014 2018 BRASOV, CENTER REGION 55,000 SQM

RESIDENTIAL ONGOING THE PARK Q3 2014 H2 2017 BUCHAREST, SECTOR 4 20,000 SQM

RESIDENTIAL ONGOING COSMOPOLIS PHASE 4 Q3 2015 H2 2016 STEFANESTI DE JOS, BUCHAREST-ILFOV REGION 800 FLATS