EDUCATIONAL LOANS AT SBH eddited.docx

126

A PROJECT REPORT ON EDUCATIONAL LOANS FROM PUBLIC SECTOR BANK Submitted in partial fulfillment for the award of Degree of MASTER OF BUSINESS ADMINISTRATION From OSMANIA UNIVERSITY Department of Business Management OSMANIA UNIVERSITY,

-

Upload

ravikumarreddyt -

Category

Documents

-

view

8 -

download

2

Transcript of EDUCATIONAL LOANS AT SBH eddited.docx

A PROJECT REPORTON

EDUCATIONAL LOANS FROMPUBLIC SECTOR BANK

Submitted in partial fulfillment for the award of Degree ofMASTER OF BUSINESS ADMINISTRATION

From OSMANIA UNIVERSITY

Department of Business Management OSMANIA UNIVERSITY,

HYDERABADTELANGANA.

2013-15

.

INTRODUCTION

Today's knowledge century has rendered the professional qualification as a must have. Good quality professional education is not cheap, thus putting tremendous strain on the ordinary middle-class parents' pocket. There are various funding avenues available to a student viz. Educational Loans from national/ co-operative/ a few private banks, scholarships from various trusts and scholarship/freeship schemes from the institute where the student is applying.

Why Educational Loans?

• No deprivation of opportunity to study due to lack of funds• Education loan schemes offer repayment holiday of Course period + 1 year or 6

months after getting a job, whichever is earlier• Tax benefit to the parents under section 80E of the Income Tax Act• Lower interest rates (subject to changes as advised by RBI/Bank)• Wide spectrum of courses covered

Who provides education loans?

Most scheduled nationalised and co-operative banks offer educational loans to students under the Educational Loan Scheme. Few private banks like, HSBC have also launched educational loan schemes in the recent past.

How to obtain an Educational Loan?

1. Shortlist the courses you want to pursue based on a Career Assessment by a Professional Career Advisor

2. Research the courses and institutes so as to obtain a rough estimate of costs Involved

3. Check with the institute about educational loan tie-ups and scholarship /free ship schemes

4. Research and shortlist lenders well before results are announced. Check if your course/institute is recognized by the bank. You may use lender search, EMI calculators and loan comparators available with websites like www.myiris.com.

5. Keep all the documents ready so that delays are avoided.6. Get a life insurance policy in your name. Many banks ask for at least an Amount

equivalent to the loan amount as a security.7. Opt for a loan only for the amount needed so that your repayment burden is

reduced.8. Once you obtain admission, procure a proof of admission along with a detail fee

structure and payment schedule from your institute9. Before submitting the documents to the bank, photocopy all the forms and show

them to the concerned bank officer. This will minimise any errors that may delay the disbursal process.

10. The loan disbursement process takes about a week and since the loan amount will be disbursed directly to the institute, it may be a good idea to check whether the disbursement is taking place on time.

Checklist of documents

• Proof of Admission• Loan agreement (with parents)• Residence Proof• Age Proof• Proof of parents' income (salary statements, IT returns etc.)• Student's resume showing past academic records

Indicative list.

You are eligible if you: Are an Indian National Have secured admission to professional/technical courses through Entrance test/Selection process Have secured admission to foreign university/institutions

Which courses will be funded by the Educational Loan Schemes?

A) Studies in India:

i) School education including +2 stageii) Graduation/Post Graduationiii) Professional courses by recognised/ reputed institutesiv) Evening courses of approved institutes

B) Studies Abroad:

i) Graduation: job oriented Professional / technical courses offered by reputed universities

ii) Post Graduation: MCA, MBA, MS etc.iii) Courses conducted by CIMA, London, CPA, USA etc

Usually, the courses financed should be for durations of more than a year i.e. 12months. The courses must be recognised by the University Grants Commission (UGC) or the All India Council for Technical Education (AICTE) or else the courses should be from institutes recognised as 'reputed' by the bank. A detailed list of courses is available in the RBI circular dated May 4, 2001 - URL

http://www.education.nic.in/htmlweb/circulars/eduloan.htm#banks. Many reputed institutes make loan facility and information easily accessible and available through Loan

helpdesks set up on the campus itself. Institutes are also striving to maintain a high academic standard so that they enter the bank's 'reputed institutes' list.

What costs are covered under the Educational Loan Scheme?• Fee payable to college/school/hostel• Examination/Library/Laboratory fee• Purchase of books/equipments/instruments/uniforms• Caution deposit/building fund/refundable deposit• Travel expenses/passage money for studies abroad• Purchase of computers• Other expenses required to complete the course e.g. study tours, projects, thesis etc.

Education Loans in India

Education is the essence of life. To ensure that no deserving student is denied education for want of funds government is promoting education loans in a big way.

Any student who has secured admission in any institute of repute, whose degree/diploma is recognized by University/Institute affiliated to any Central/State Statutory Body or recognized by AICTE (All India Council of Technical Education) and other institutes of repute, is eligible for educational loan.

Education loans cover cost of the school/college fee, hostel expenses, and cost of books and stationery. Apart from this, any other expense required to complete the course can also be considered. Maximum amount of education loan available is upto Rs. 7.50 lakhs in case of studies in India and Rs 15 lakhs for studying abroad.

The loan has to be repaid within 84 months in equated monthly instalments (EMIs) commencing 12 months after course completion or 6 months after getting the job, whichever is earlier. Following document are required to be submitted with the loan application:

• Mark sheet of last qualifying examination for school and graduate studies in India• Proof of admission to the course• Schedule of expenses for the course• Copies of letter confirming scholarship, etc.• Copies of foreign exchange permit, if applicable.• 2 passport size photographs• Statement of Bank account for the last six months of borrower• Income tax assessment order not more than 2 years old

THE STUDENT LOAN INDUSTRY

The student loan industry is complex, in part due to the detailed statutory and regulatory framework of federal loan programs. Richard George, the President and CEO of the Great Lakes Higher Education Corporation offer the following list of industry players. 81 Increasingly large providers like Sallie Mae provide a full range of activities. Fees and charges may be added at every point of service.

Lenders (banks, credit unions, savings and loan associations, private lenders) Secondary markets (buy student loans from lenders, freeing up funds for additional

lending) Bursars, registrars and financial aid officers (university/college employees who are key

intermediaries between schools and lenders) Originators (assist borrowers to obtain their loans including schools, banks, Private

lenders, credit unions, and savings and loan associations) Services (collect payments from borrowers and pass them on to the investors who

own the loans, and levy fees and other charges) Guaranty agencies (insure student loans against default and reimburse the lender for

the balance of a defaulted loan). Collection agencies (engage in receivables management, helping lenders and guaranty

agencies recover funds from borrowers who default on their loans) Securitization teams (issuer, bankers/underwriters, bond counsel, trustee, rating

agencies, underwriter's counsel, and accountants) U.S. Department of Education although it is beyond the scope of this report to fully

analyze the industry, the following discussion focuses on key players and the state's role.

SALLIE MAE

When the Higher Education Act was enacted in 1965, there was no private market for student loans. Students presented an unknown quantity to lenders because they did not have assets to secure a loan (like a house, for example), but rather an uncertain but likely

increase in long term earnings potential. For this reason the federal government created and financed the Student Loan Marketing Association (SLMA or Sallie Mae) in 1972, as a "government sponsored enterprise" or GSE. GSEs are a hybrid form of a corporation that uses privately-provided capital to increase investment in a specific sector of the economy.* Congress also authorized the creation of state-chartered guaranty agencies, which are discussed below, to manage the student loan guarantee program under the supervision of the U.S. Department of Education. Sallie Mae was created to encourage private banks to loan to students who were considered to be a credit risk; it did not make the loans itself. For many years, Sallie Mae Functioned as a "secondary lender," buying and managing loans from banks and other lenders, which used the proceeds to make new loans. This role, of freeing up more capital for private funding for student loans, was the reason that Congress created Sallie Mae.

Sallie Mae received valuable benefits as a GSE, including exemption from state and local taxes, and access to low-cost funds from the U.S. Department of the Treasury. Sallie Mae paid only a fraction of a percent in interest on the funds it borrowed from the U.S. Treasury...earnings—from interest payments made by students and subsidies paid by the federal government on student loans—were also tied to the Treasury bill rates. Therefore, if interest rates were up Sallie Mae paid more to the Treasury for its funds, but got even more back in subsidies….an easy path to profits.

In 1997, Sallie Mae began privatizing its operations. In 2004, Congress terminated its federal charter and it became a private company. In that time, its stock price increased by nearly 2,000 percent. The company is the country's largest originator of federally insured student loans and provides debt management services and technical and business products to colleges, universities and loan guarantors. Sallie Mae has the ability to control the entire loan process—making loans, guaranteeing them and collecting on them. Sallie Mae has an estimated 12,000 employees in 19 states and manages $142 billion in student loans. The company's loans comprised 27 percent of all federal student lending in 2006, four percent more than the Department of Education's direct lending program and 21 percent more than the next largest student lender, Citibank.84 According to the economist magazine, Sallie Mac's recent five year average return on equity was an "astonishing 52% a year."85 Its profits in 2006 were $1.3 billion. In April 2007, Sallie Mae announced that an investor group including J.C. Flowers & Co, Bank of America, JP Morgan Chase and the private equity firm Friedman Fleischer & Lowe had agreed to purchase the company for $25 billion. However the purchasers are attempting to withdraw, primarily because of"... changes in the legislative and economic environment," due to a reduction in federal subsidies to for-profit lenders by 0.55 percent in the newly-enacted College Cost Reduction and Access Act of 2007 (H.R. 2669). Sallie Mac's stock price has since fallen considerably and its operations have been affected by the tightening credit market.

FEDERAL SUBSIDIZES AND GUARANTEES

The federal government subsidizes federally-guaranteed student loans in several ways. It pays the interest on subsidized Stafford Loans while a student is in school, and assumes the lender's risk by guaranteeing repayment of the loan.

Once a student borrower goes into default, the government pays all the principal and compounded interest that have accrued. The loan then passes into a collection phase, in which the collector gets to keep up to 25 percent of whatever is recovered. The same financial entities that make loans can also gain revenues from collecting on defaulted loans. For example, Sallie Mae earns nearly a fifth of its revenues from its collection business.

The federal government also pays private lenders the difference between the interest rate that is actually charged to the student and a higher rate that is determined by Congress. This is the most profitable subsidy. The newly enacted College Cost Reduction and Access Act cut about $18-$ 19 billion in these lender subsidies over the next five years. Those savings were channeled into increased Pell Grants and capped loan repayments (as described above).

SECONDARY MARKETS

The original lender may sell its portfolio of student loans to a for-profit secondary-market organization such as Sallie Mae or Nelnet, or to a tax-exempt state-chartered institution such as the Pennsylvania Higher Education Assistance Authority. Much like home mortgages, student loans may be packaged into asset-based securities, a popular method for raising low cost capital. The loans are pooled, often by risk categories, into securities and sold. Some financial organizations specialize in securitization transactions, a profitable undertaking.

In general, securitizations of federal and private student loans have been marketed separately. When student loans are sold to a new lender, future benefits (prepayment incentives, for example) promised by the original lender may be lost. The New York Attorney General recommends that: It is important to make sure that if your loan is sold, the "back-end" benefits will travel with the loan. In some instances, the sale of the loan will terminate the very benefits that caused you to take out that particular loan in the first place! To preserve these benefits, have your lender commit to them in writing.

STATE GUARANTY AGENCIES

At the time the Higher Education Act was enacted, Congress authorized the creation of state-chartered guaranty agencies along with Sallie Mae to ensure sufficient capital for

student loans. There are currently 35 state and non-profit federally-designated guaranty agencies. The Student Aid Commission is California's guaranty agency. Guaranty agencies perform an intermediary fiscal role in the federal student loan system. Students first apply to a participating lender through their school. The school verifies the student's eligibility and determines the loan amount the student is eligible to receive, he student then receives the loan from the lender. The guaranty agency guarantees the loan against default, thereby reducing lender risk and resulting in lower borrower interest rates and the increased availability of capital for student loans. If a student defaults on a loan, the lender files a claim with the guaranty agency for reimbursement of most of its loss. The U.S. Department of Education, which is the final guarantor, reimburses the guaranty agency for most of those claims and for some administrative costs.

Guaranty agencies also counsel students to keep them out of default, rehabilitate loans, and collect on defaulted loans, keeping up to 16 percent of the collected payments (as of October 1, 2007). They have their own underwriting criteria and separate credit ratings.

They may guarantee private as well as federal student loans. Guaranty agencies receive the majority of their revenues from student post-default loan Rehabilitation and collection revenues. This reality creates an inherent conflict in their role as advocates for borrowers, since they receive less revenue for preventing defaults.

A 2001 agreement between California's Student Aid Commission and the U.S. Department of Education was designed to reduce this conflict by providing incentive payments to lower the default rate of student borrowers (however this program will cease at the end of this year).*

Federal reimbursement policies and rates greatly impact the financial health of state guaranty agencies. In 2005, the federal Higher Education Reconciliation Act required guaranty agencies to collect and deposit a default fee on loans issued after July 1, 2006. The California State Auditor opined that as a result of this requirement, the Student Aid Commission's ability to generate sufficient revenues to sustain its status as a guarantor was at risk.88 Recent changes in federal law further decrease payments to guaranty agencies by $4.5 billion nationally.

THE STUDENT AID COMMISSION AND EDFUND

The California Student Aid Commission was established in 1955 and is the federally designated guaranty agency for California. The Commission is governed by a 15-member board whose members serve four year terms. It guarantees the outstanding principal and interest due to lenders when student loan borrowers fail to repay as required, primarily by purchasing delinquent loans. In federal FY 2005-06, the Commission, through its auxiliary Ed Fund, guaranteed new federal student loans totaling more than $6.8 billion.90 It is the second largest student loan guaranty agency in the country.

Ed Fund was created pursuant to state legislation in January 1997, and is a 501(c)(3) public benefit corporation. It serves the Student Aid Commission as the state's official guarantor for student loans, while operating under "... private sector employment and procurement standards."91 Ed Fund's President is a former Executive Director of the Student Aid Commission. According to the governor's 2004 Performance Revision Commission, Ed Fund spent $89 million on operations.92 Ed Fund Board members are appointed by and accountable to the Commission, which has oversight responsibilities over the fund. A 2006 report by the State Auditor found ongoing tension between the Student Aid Commission and Ed Fund that resulted in a lack of cooperation and hampered business operations.93 Ed Fund administers an outstanding loan portfolio worth more than $27 billion and has more than 600 employees.94 Half of the loans it administers are made to students who live and go to school outside California. In federal FY 2006-07, 30 percent of all Ed Fund loan dollars were committed to students at nonprofit private institutions ($2.058 billion).

Four-year for-profit proprietary schools accounted for almost 28 percent of total loan dollars. The University of Phoenix is Ed Fund's largest school as measured by loan volume.95 Ed Fund student loan default claims totaled $703 million in FY 2006-07, a 35.5 percent increase from the previous year. Sixty-five percent of the defaults were from students at "high risk" segments, two-year public and private schools and all for-profit proprietary schools. The aggregate default rate for the year was 4.46 percent. Ed Fund is placing more emphasis on loan rehabilitations (regular payments on defaulted loans) and wage garnishments than direct loan consolidations, prompted in part by changes in federal reimbursement policies.96

State legislation that became operative in August 2007, (SB 89, Chapter 182, Statutes of 2007) authorizes the Director of the Department of Finance, in consultation with the State Treasurer, to act as the state's agent in the sale and transfer of Ed Fund's student loan guarantee portfolio. The transaction is to be completed by January 2009. The legislation also requires the Director of the Department of Finance to approve all Student Aid Commission activity relating to the federal student loan program.

In his May Budget Revision, Governor Schwarzenegger estimated that the sale of Ed Fund would realize one-time revenues of $980 million for the General Fund. The actual sale price would likely be less given recently-enacted decreased federal lender subsidies that also have resulted in the withdrawal of a $25 billion offer to buy Sallie Mae (as discussed above). The Legislative Analyst Office estimates a potential sale price of $500 million.97 Potential buyers of Ed Fund are to be assessed on a variety of criteria, as provided in SB 9, including:

• Borrower transparency or disclosure policies for products and/or services offered to students outside of the federal student loan program

• The quality of student services offered, including borrower training in budgeting and financial management, debt management and other financial literacy skills

The State of Missouri considered selling its state-chartered student loan guarantee agency, the Missouri Higher Education Loan Authority, but instead has directed the Authority to transfer $350 million in assets to a special fund. Money in the fund can be appropriated to finance capital projects at public colleges and universities, and to fund the Missouri Technology Corporation to commercialize technologies developed by academic researchers. In return, the Authority was granted the power to issue a specified amount of private activity bonds.

PRIVATE STUDENT LOANS

Rapid Growth

Fueled by higher demand for postsecondary education due to changes in the economy, and diminishing public financial aid relative to rising fees, the private student loan industry has been growing rapidly. Private student loans: "...make up a large and fast-growing asset class, with a demand fueled by student enrollment growth, college tuition costs that are rising faster than the rate of inflation, and aggressive marketing efforts by loan companies and financial aid offices."

Market forces similar to those in the subprime mortgage market have also contributed to the explosive growth of private student loans. Demand for bundled student loans sold to institutional investors worldwide has fueled lending to students. The market for private student loan-backed securities leapt 76 percent in 2006, to $16.6 billion, from $9.4 billion in 2005, according to Moody's Investors Service.

These loans may be certified by a. financial aid office at an institution of higher education, but increasingly many are direct-to-consumer loans. They usually require students to show a positive credit history or have a co-borrower (generally a parent).

Since private loans are not subsidized or guaranteed by the federal government, they have higher, variable market-based interest rates (that can reach 20 percent) and charge guarantee fees, making them more expensive. Applications are generally shorter, easier to understand, and require less personal information than for federal student loans.

Many private student loans, like home mortgages, carry adjustable rates and are resetting to higher levels, thereby increasing student repayment obligations and creating the potential for problems in the student loan credit market. Under provisions of the federal bankruptcy law enacted in 2005, private student loans may not be discharged in bankruptcy.

Federal oversight responsibility for private student lending activities falls under the jurisdiction of banking regulatory agencies including the Comptroller of the Currency, the Securities and Exchange Commission, the Federal Deposit Insurance Corporation and the Federal Trade Commission.

According to Sallie Mae, profit on private loans exceeds five percent, compared to less than two percent for federally subsidized loans. In its quarterly earnings report, the company projected growth in private loans in 2008 of up to 20 percent.

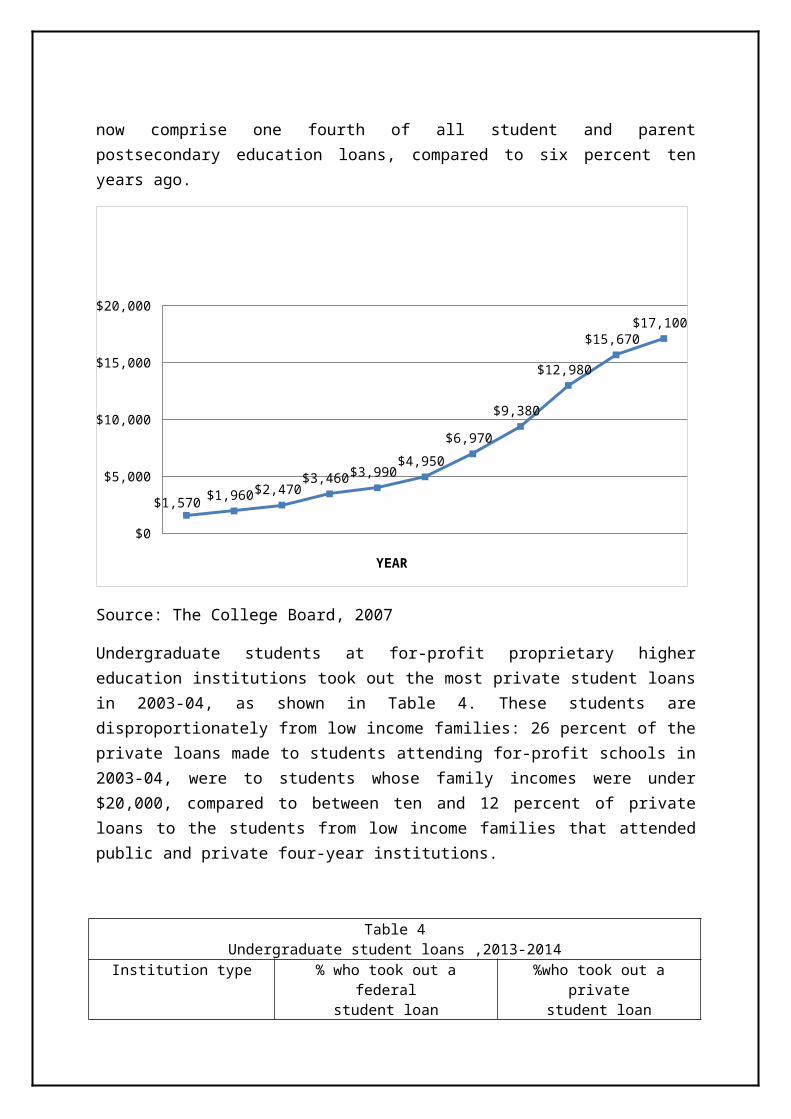

Private student loan volume grew from $1.57 billion in 1996-97 to $17.1 billion in 2013-14, including student and parent loans for undergraduate and graduate education. These loans now comprise one fourth of all student and parent postsecondary education loans, compared to six percent ten years ago.

$0

$5,000

$10,000

$15,000

$20,000

$1,570 $1,960 $2,470 $3,460 $3,990

$4,950

$6,970

$9,380

$12,980

$15,670 $17,100

YEAR

Source: The College Board, 2007

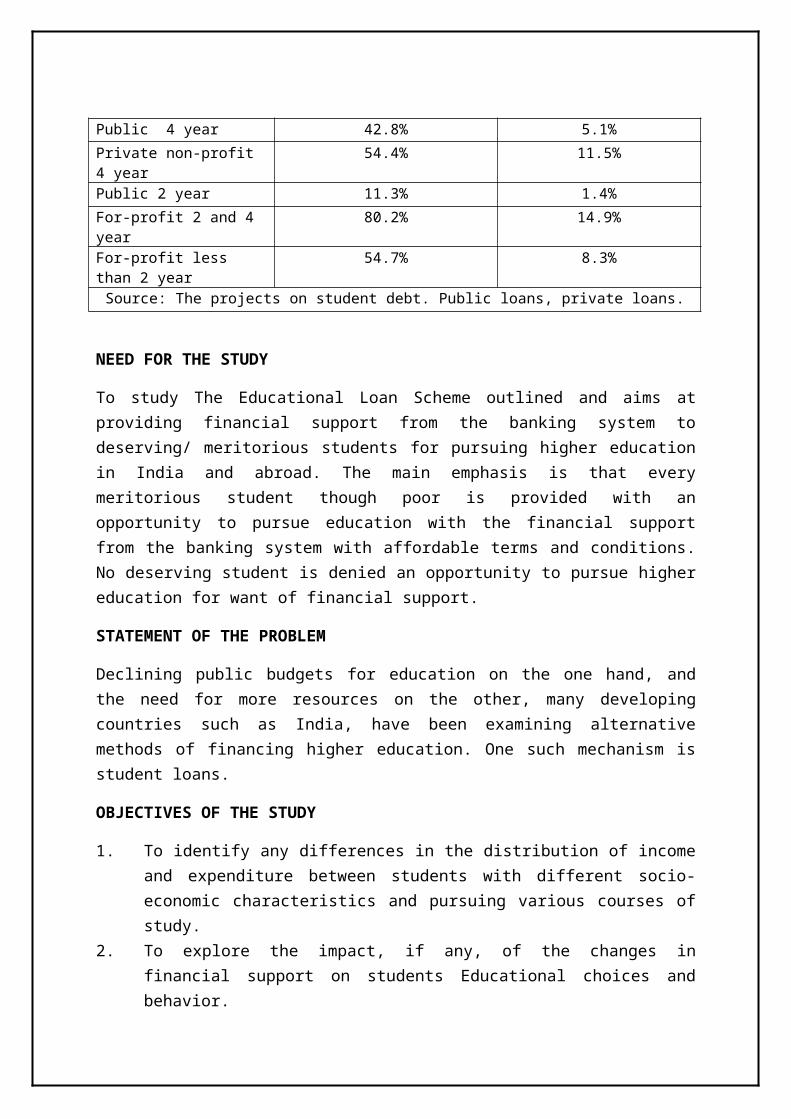

Undergraduate students at for-profit proprietary higher education institutions took out the most private student loans in 2003-04, as shown in Table 4. These students are disproportionately from low income families: 26 percent of the private loans made to students attending for-profit schools in 2003-04, were to students whose family incomes were under $20,000, compared to between ten and 12 percent of private loans to the students from low income families that attended public and private four-year institutions.

Table 4Undergraduate student loans ,2013-2014

Institution type % who took out a federalstudent loan

%who took out a privatestudent loan

Public 4 year 42.8% 5.1%

Private non-profit 4 year 54.4% 11.5%

Public 2 year 11.3% 1.4%

For-profit 2 and 4 year 80.2% 14.9%

For-profit less than 2 year 54.7% 8.3%

Source: The projects on student debt. Public loans, private loans.

NEED FOR THE STUDY

To study The Educational Loan Scheme outlined and aims at providing financial support from the banking system to deserving/ meritorious students for pursuing higher education in India and abroad. The main emphasis is that every meritorious student though poor is provided with an opportunity to pursue education with the financial support from the banking system with affordable terms and conditions. No deserving student is denied an opportunity to pursue higher education for want of financial support.

STATEMENT OF THE PROBLEM

Declining public budgets for education on the one hand, and the need for more resources on the other, many developing countries such as India, have been examining alternative methods of financing higher education. One such mechanism is student loans.

OBJECTIVES OF THE STUDY

1. To identify any differences in the distribution of income and expenditure between students with different socio-economic characteristics and pursuing various courses of study.

2. To explore the impact, if any, of the changes in financial support on students Educational choices and behavior.

3. To identify the characteristics of those students who might be experiencing Financial hardship.

4. to provide insights into the initial effects, if any, of the new funding policies on student finances.

SCOPE OF THE STUDY

Once upon a time the reason for not continuing the higher studies was the money problem. The financial position of the individual matters during that time. But now a days for that reason government had introduced the educational loan system. IT has a lot of benefits for

the individual. Their ambition, interest can be achieved through this. In some families the financial position consisting of retired father, mother and younger brother, made many of the people to work stopping their education. Because of the economical situation many of them have been opted the institutions costing less compared to the best one.

This complete study will help to understand the students with different socio-economic characteristics and pursuing various courses, of study, Nationalized banks financial support on students Educational choices and also it provides information about those students who might be experiencing Financial hardship, any new funding policies for students.

COMPANY PROFILE

A PROFILE OF STATE BANK OF HYDERABAD

The STATE BANK OF HYDERABAD became, through an Act of parliament with effect from October 1st 1959, a wholly owned subsidiary of State Bank of India under the SBI(Subsidiary Banks) Act, 1959.

Mission of the Bank :

To achieve Pre-eminence in banking and financial sectors with commitment to excellence in customer satisfaction, profit maximization and continued emphasis on developmental banking through a skilled and committed work force by providing training facilities and "Technological up gradations"

HISTORY OF THE BANK:

Based on a "Hyderabad Banking Enquiry Report" complied in 1932 a special committed under Mr. K. M. Baruch recommended the establishment of a Bank for the State. Accordingly, the "Hyderabad State Bank act" was enacted in August 8th 1941 for the establishment of the Hyderabad State Bank (herein after referred to as "Hyderabad Bank")

The Hyderabad Bank was formally inaugurated on the April 5th 1942, by Late Shirr Nawab Sir Aqeel Jung Bahadur, one of the Directors of the Bank and the then Member,Cinnerce and Industries. Nizam's Executive Council and the first branch of the Bank, viz., its main office (Present Gunfoundary Branch), Opened its doors to the Public.

Under the Hyderabad State Bank Act (XIX of!35 OF), the Bank was enjoined upon to regulate the circulation of currency (viz., the Osmania Sicca), to maintain in the fullest degree its stability and security, to facilitated the payment of money in the HEH. The Nizam's Dominions and aboard, to provide credit to encourage growth of agriculture, commerce and industry they carrying on the functions of a Central Bank and also that of a Commercial Bank in the Nizam's territories.

After the financial integration of the State of Hyderabad with the Union of India, the Hyderabad State Bank was taken over by the Reserve Bank of India on April 1st 1956, and subsequently, with GOI setting in a process of integrating the Banks of erstwhile Princely States the Bank became a subsidiary of the SBI (Subsidiary Banks) Act, 1959.

MAIN OBJECTS OF THE BANK:

State bank of India (subsidiary. Banks) Act, 1959 (Act No.38 of 1959) was enacted providing for formation of subsidiaries of the State bank of India (including state Bank of Hyderabad) and for the constitution, management and control of the Subsidiary Banks so formed, and for matters connected therewith, or incidental thereto.

Section 4(3) of Chapter II of the State Bank of India (Subsidiary Banks) Act, 1959 provides that the Bank shall carry on the business of Banking and other business in accordance with the provision of the SB Act., and shall have power to acquire and hold property, Whether moveable or immovable ,for the purpose of the business or to dispose of the same. Section7(3) of the SB Act provides that the state Bank shall, as soon as may be after determination, if any, by the Tribunal of the amount of compensation payable in respect of

an existing Bank, consider whether any increase in or reduction of, the issued capital of the corresponding new Bank as fixed under sub section(I), by way of adjustment or transfer from, or to, the reserves of such Bank, or in any other manner, is necessary or expedient and may, there after with approval of the Reserve Bank, direct that Bank to increase or reduce its issued capital.

The main object for constitution of State Bank of Hyderabad was for extension of banking facilities’ particularly in the rural and semi-urban areas and for other diverse public purpose and also to act as an agent to SBI/RBI at such centers where they do mat have their offices. However, over the years the Bank has spread its network all over the country and is now operating as a Banking institution of all India stature, It has branch network covering 14 states and 2 Union Territories at most of the important Banking Centers in the country.

BANK'S BUSINESSED AND ACTIVITIES - AN OVERVIEW:

The Bank's key activities are as follows: -

Accepting deposits for the purpose of lending and investment. Facilitating payments mechanism through local/outstation clearing of Cheques,

remittances etc., Offering services like safe custody, lockers, trusteeship etc., Acting as the Banker to the Central Government and State Governments of Andhra

pradesh, Karnataka and Maharashtra.

ORGANIZATION:

He bank's Board of Directors, comprises of Union Government, Reserve Bank of India and State bank of India, from the filed of commerce, industry and academics besides workmen/officers' nominee directors. The Chairman of State Bank of India is ex office Chairman of the Board of Directors.

The day-to -day affairs of the Bank are looked after by the Managing Director nominated by State Bank of India under clause (aa) of sub-section 25 of the SBI (Subsidiary Banks) Act, 1959 who is supported by experienced executive. There is also a Management Committee comprising the Managing Directors, Chief General Manager and General Managers which meets generally every week for collective decisions on operational matters.

The Bank has decentralized operational se up with 8 (Eight) Zonal Offices consisting of 32 Regional Offices at Hyderabad, Secunderabad, Warangal and Vizag zones in Andhra Pradesh state and Gulbarga in Karnataka State, Aurangabad , Mumbai in Maharastra and Delhi. A Deputy General Manager heads each Zonal Offices. The Bank is authorized dealer in Foreign Exchange and has full fledged Foreign Department at Chennai and correspondents at all major financial / commercial centers throughout the world. The Bank also extends diverse

merchant banking services and is registered with SEBI as Category-I Merchant Banker. The Bank has also become Depository Participant of National Securities Depository Ltd.(NSBL) and Central Depository Services Ltd.(CDSL).

NETWORK::

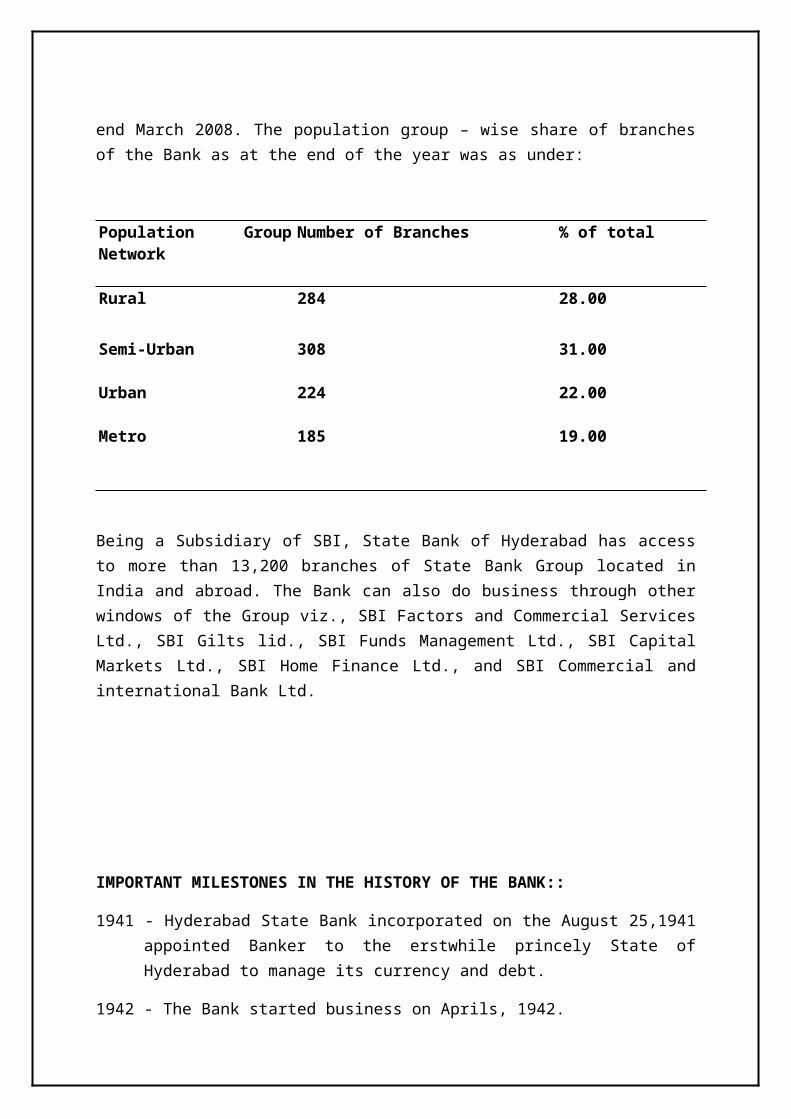

The network of branches grew to 1,001 as on 31st March 2008. The total number of extension counters stood at 45 as at the end March 2008. The population group – wise share of branches of the Bank as at the end of the year was as under:

Population Group Network Number of Branches % of total

Rural 284 28.00

Semi-Urban 308 31.00

Urban 224 22.00

Metro 185 19.00

Being a Subsidiary of SBI, State Bank of Hyderabad has access to more than 13,200 branches of State Bank Group located in India and abroad. The Bank can also do business through other windows of the Group viz., SBI Factors and Commercial Services Ltd., SBI Gilts lid., SBI Funds Management Ltd., SBI Capital Markets Ltd., SBI Home Finance Ltd., and SBI Commercial and international Bank Ltd.

IMPORTANT MILESTONES IN THE HISTORY OF THE BANK::

1941 - Hyderabad State Bank incorporated on the August 25,1941 appointed Banker to the erstwhile princely State of Hyderabad to manage its currency and debt.

1942 - The Bank started business on Aprils, 1942.

1953 -The Bank became the agent of the RBI for maintaining currency chest, handling Government transactions and remittance facilities. The bank took over the Mercantile bank of Hyderabad Ltd., on the April 1, 1953.

1954 - The Bank was authorized to deal in foreign exchange.

1956 - The Bank become a fully owned subsidiary of the RBI under the name of State Bank of Hyderabad on October 22,1956 (vide State Bank of Hyderabad Act, 1956).

1959 - The Bank became a fully owned subsidiary of SBI with effect from October 1,1959 under the State Bank of India ( Subsidiary Banks) Act, 1959.

1976 - Reorganization of the Bank's operations and introduction of performance. Budgeting System and evolution of the present organizational structure.

1995-96 -Bond issue (Subordinated Debt) concluded to strengthen capital funds and the Bank achieved a capital adequacy ration of 9.90%as on 31.03.1996.

1998-99- Deposits crossed the 10,000 crore mark.

INDUSTRIAL PROFILES

Allahabad Bank

Andhra Bank

Bank of Baroda

Bank of India

Bank of Indore

Bank of Karnataka

Bank of Maharashtra

Bank of Rajasthan

Canara Bank

Catholic Syrian Bank

Central Bank

Dena Bank

Development Credit Bank

Federal Bank

HDFC Bank

IDBI

Indian Bank

Mysore Bank

Oriental Bank

Overseas Bank

Punjab and Sind Bank

Punjab National Bank

State Bank of Hyderabad

State Bank of India

State Bank of Mysore

State Bank of Saurashtra

ALLAHABAD BANK

Allahabad Bank, the oldest joint stock bank of the nation was established in the year 1865. It is a nationalized bank and offers various kinds of financial services including Education loan

to its customers. The education loan scheme offered by the Allahabad Bank was launched to provide financial assistance to meritorious students on reasonable terms. Scroll down the page to know more about Allahabad Bank Education Loan.

Eligibility Criteria for Allahabad Bank Education Loan

a) Eligibility Criteria for Students

• Students seeking education loans should be an Indian National.

• An applicant will be considered eligible for the loan if he gets admission to professional or technical course in India or abroad through an entrance exam or a merit-based selection procedure.

b)Courses Eligible for Getting Loan

Education in India

• Bachelor Degree courses like B.COM, B.A, B.Sc and others

• Master Degree courses and Ph.D programs

• Professional courses like Management, Engineering, Law, Computer, Agriculture, Dental, Medical, Veterinary and others.

• Certificate courses in Computer offered by reputed institutes which are accredited to the Department of electronics or institutions certified by a university.

• Other courses like CA, ICWA and CFA.

• Programs which are conducted by the reputed institutions like IIT, XLRI, IIM, NIFT, IISc.

• Regular diploma and degree courses like pilot training, Aeronautical, shipping and others. The courses offered should be approved by the Director General of Civil Shipping or Aviation.

• Courses that are conducted by the renowned foreign universities.

• Evening courses which are conducted by the approved institutes.

• Various diploma and degree courses conducted by various colleges and universities approved by Govt., ICMR, UGC, AIBMS, AICTE and others.

Education Abroad

• Bachelor's Degree-Professional and technical courses which are offered by various reputed universities.

• Master's Degree-MS, MBA, MCA and others.

• Programs offered by CPA in USA and CIMA in London.

• Various regular diploma and degree courses in pilot training, aeronautics or shipping approved or recognized by the competent local shipping or aviation authority.

Quantum of Loan

The maximum amount given as loan for studies in India is Rs. 10 lacs. Rs. 20 lacs is the maximum amount for studies abroad.

Expenses to be considered for Loan

• The loan includes fees to be paid for colleges, hostel charges, examination fees, and laboratory and library fees.

• It also covers expenses for purchasing all the necessary articles required for completion of the courses.

• Travel expenses and money for purchasing computers are also provided to the students.

• Other payments like building fund, refundable deposit and caution money are also included.

website : http://www.allahabadbank.com/

ANDHRA BANK

Andhra Bank offers education loan to meritorious students, who wish to pursue higher education either in India or abroad. This bank was founded by Dr. Bhogaraju Pattabhi Sitaramayya. Registered on 20th November, 1923, it started operations from 28th November, 1923 with a capital of Rs.1 lacs and an authorized capital of Rs.10 lacs. Browse through this page to collect more information on Andhra Bank education loans, also known as Dr. Pattabhi Vidya Jyothi (education loan).

Eligibility of the Candidates

Candidates applying for education loans need to fulfill certain eligibility criteria as specified by the Andhra Bank.

Studies in India

Candidates should be within 12-30 years of age.

Studies Abroad-

Candidates applying for Dr. Pattabhi Vidya Jyothi education loan should be within 18-35 years of age

Quantum of Loan

For studies in India the maximum amount of Andhra Bank Student Loan offered is Rs.10 lacs. Candidates applying for education loan to study abroad can get a maximum amount of Rs.20 lacs.

Expenses Covered by the Andhra Bank Education Loan

The education loan covers tuition fee, examination fee, expense of study tours, hostel charges, cost of books and refundable deposits. The travel expenses and passage money are also included in the loan.

Margin

There is no margin for loans up to Rs.4 lacs. For loans above Rs.4 lacs the margin stated is 5% and 15% for India and abroad respectively.

Security

Parents need to act as guarantor for Andhra Bank education loan amount up to Rs. 4 lacs. For loans up to Rs.7.50 lacs, guarantee of the parents is essential. Both collateral security and guarantee by parent are required for education loans above Rs. 7.50. web site : http://andhrabank.in/

BANK OF BARODA

Bank of Baroda offers education loan to students willing to continue their higher education in India or abroad. The various loan options provided by Bank of Baroda are Baroda Vidya, Baroda Gyan and Baroda Scholar. Scroll down the page to learn more about Bank of Baroda education loan.

BARODA VIDYA

It is an education loan scheme offered to the parents of students undergoing school education. These loans are provided for studies between Nursery and 12th standard. Processing and documentation charges, margin and security are not required for taking loans under this scheme. However, the candidates are required to meet certain criteria for getting the loans. He or she has to be an India national who resides in India. Students are required to take admission in a recognized school, high school or junior school. The maximum loan amount offered is Rs. 4 lacs.

BARODA GYAN

It is a loan scheme specially meant for the students pursuing undergraduate, postgraduate, professional and other type of courses in India.

Eligible Courses

• All undergraduate and postgraduate courses. Loans are also provided for doctorate programs.

• Professional courses in areas like fashion technology, engineering, event management, agriculture, mass communication, medical, architecture, agriculture, hospital management, veterinary, hotel management, interior designing, management and others. Certificate courses in computer offered by reputed institutions certified under the Department of electronics or institutions which are affiliated to universities.

• Programs that are offered by XLRI, IIM, NIFT, IISC, IIT, diploma and degree courses and ICWA, CA, CS, CFA other courses.

• Diploma and degree courses offered by various colleges and universities which are approved by UGC, AICTE, ICMR, Govt., AIBMS and others.

• Courses, which are conducted by renowned foreign universities in India.

• Evening courses offered by institutes, which are approved by reputed associations or courses, which are conducted by reputed national and private institutions.

Eligibility Required for Students

Students should be Indian nationals residing in India. Applications will be considered eligible for the loan if they have received admission through entrance test for merit based selection procedure. The maximum loan offered is 10 lacs.

BARODA SCHOLAR:

It is offered to the students willing to go abroad for pursuing their technical and professional studies. The various courses eligible for this loan are graduate, doctorate, post graduate, technical courses and professional courses offered by renowned universities. Candidates seeking loans need to be Indian Nationals. The maximum amount of loan offered is Rs. 20 lacs.

Web : http://www.bankofbaroda.com

BANK OF INDIA

Bank of India has Star Educational Loan on offer for the students willing to pursue higher education. Meritorious students are offered Bank of India Education Loan so that they can study a graduate, computer certificate, diploma, postgraduate, specialized or professional course in India or abroad.

Courses:

Bank of India Education Loan is offered for studying several kinds of programs.

• You can apply for an educational loan from Bank of India if you want to pursue a graduate, postgraduate and doctoral program.

• A student can also obtain this loan if he plans to study a professional program including Engineering, Law and Medical programs.

• Even students willing to study computer certificate courses of recognized institutes or specialized programs like CFA, ICWA and CA can apply for the loan.

• An applicant, planning to pursue programs from institutes recognized by government, UGC, AICTE, a national body or a recognized foreign university in Indian, is also considered eligible for the loan.

Eligibility:

• For pursuing PG programs such as MS or MBA, employment-oriented programs from recognized universities or courses by CPA in the US and CIMA-London in abroad, you can also apply for the educational loan. Education Loans of Bank of India are offered to Indian nationals, who have no outstanding loan taken for education from any other body. The parent of the student should also act as a co-borrower. A student will be considered eligible for the loan if he has good academic record and gets admitted to a professional or technical course in India or abroad through a selection procedure based on merit or entrance test.

Expenses taken into account:

The educational loan covers college, school or hostel fee as well as that of exam, laboratory or library. Even the expenses of books, instruments and uniforms are also taken into account. The caution deposit, refundable deposit or building fund is also considered. The student's travel expenses as well as other necessary costs related with the program are covered by the loan.

Amount of Loan, Margin & Security:

For studying in India, you can apply for a maximum loan of Rs 10 lacs and Rs 20 lacs for studying abroad.

• There is also a margin of 5% and 15% for studying in India and abroad respectively and it is applicable for a loan amount above Rs 4 lacs.

• The borrower needs to keep a guarantee of a 3rd party if a loan amount is above Rs 4 lacs. If the amount exceeds Rs 7.5 lacs, then a collateral security or a third party (if allowed by the bank) should be kept as a guarantee.

• In addition, the student should assign his future income for paying the installments.

Repayment procedure:

The loan can be repaid in 5 to 7 years after the repayment is commenced. The moratorium period is considered till 6 months after employment or the period of study plus 1 year, whichever is earlier.

Web: http://www.bankofindia.com

BANK OF MAHARASTRA

Bank of Maharashtra offers several finance schemes and credit facilities to its customers. Students who want to pursue higher studies in India and abroad, can avail of the Education Loan Scheme of Bank of Maharashtra. As the history goes, this bank began its operation in 1936 and was nationalized in 1969. You can scroll through this page to gather information on Bank of Maharashtra Education Loan.

Courses:

Various courses are considered eligible for Student Loan of Bank of Maharashtra.

• You can apply for this loan for your school education in India.

• Even for graduate, postgraduate and doctoral programs in India, you can get the loan.

• An applicant planning to study professional courses in streams such as Engineering, Medicine or Agriculture in India can also apply for the loan.

• Certificate courses of recognized institutes or evening programs certified by government in India are eligible for the loan. Specialized programs like CA, ICWA or CFA, program of foreign universities or those of IIM, IISc NIFT and others in India are also considered for loan.

• You will also be considered eligible if you study diploma or degree program certified by UGC, AICTE, government or ICMR in India.

• For studying academic programs by CPA in the US or CIMA-London in abroad, your application can be considered.

• An applicant planning to study employment-oriented professional or technical course or even postgraduate program such as MS, MBA or MCA in abroad, will be eligible for the education loan of Bank of Maharashtra.

Eligibility:

Student Loan of Bank of Maharashtra is sanctioned to those candidates, who are Indian Nationals. You can also apply if you get admission to a professional or technical program through selection procedure or entrance test. An applicant will also be considered eligible if he gets admission to a foreign institute.

Amount of Loan, Margin & Security:

The maximum amount of loan sanctioned by Bank of Maharashtra for studying in India and abroad is Rs 10 lacs and 20 lacs respectively. There is a margin of 5% and 15% on a loan amount above Rs 4 lacs.

Security needs to be submitted by a borrower applying for a loan amount above Rs 4 lacs. The securities can be submitted in the form of one category or in combinations.

Repayment:

The repayment holiday covers 1 year after completing the course or 6 months after getting a job. Once you start repaying the student loan, you can complete repayment in 5 years.

Expenses taken into Consideration:

Education Loan Scheme of Bank of Maharashtra covers cost of books, instruments and other equipments, travel expenses, tuition fees and other costs related to completing the course.

Web: http:// bankofmaharashtra.in

CANARA BANK

Canara Bank offers a diverse range of personal banking services as well as priority credit schemes suiting the customized needs of an individual. It also has education loan known as Vidyasagar Loan, on offer for meritorious students willing to pursue higher studies in India or abroad. Canara Bank was established by Ammembal Subba Rao Pai, a renowned philanthropist at a port in Mangalore, Karnataka in 1906 and nationalized in 1969. You can gather information on Canara Bank Student Loans from this page.

Courses:

A graduate course or postgraduate program including employment-oriented technical or professional course in India is eligible for the student loan of Canara Bank. All these courses should be offered by colleges or universities approved by UGC, AICTE, IMC and government or other reputed institutes in India.

Employment-oriented, technical or professional program at graduate or post-graduate level in abroad, are also considered eligible for Vidya Sagar Loan.

Expenses taken into Account:

Educational Loan of Canara Bank covers expenses of equipment, uniform and instruments as well as that of travel and study. It also includes fees of courses, hostel and exam.

Amount of Loan, Margin & Security:

Educational Loan of Canara Bank is sanctioned on the basis of an individual's requirements. You can get a maximum loan of Rs 10 lacs and Rs 20 lacs for studying in India and abroad respectively.

• For loan amount upto Rs 4 lacs, no margin is charged.

• However, there is a margin of 5% and 15% for studying in India and abroad respectively. This is applicable for a loan amount above Rs 4 lacs.

• Canara Bank education loan is given to both the student and his guardian jointly and the future income of the student is pledged for paying the installments.

• If you take a loan above Rs 4 lacs, you need to pledge guarantee of a 3rd party.

• When the loan amount exceeds Rs 7.5 lacs, you can submit a collateral security equal to the full amount of the loan.

Repayment:

The borrower can begin repaying one year after completing the course or 6 months after getting the job, whichever happens earlier.

The loan amount as well as the interest is to be repaid in 5 to 7 years of time.

Web: http://www.canarabank.com

CENTRAL BANK

There are several banks which offer education loans in India. The education loan offered by Central Bank of India is also known as Cent Vidyarthi Loan. It is offered to meritorious students willing to pursue their higher education in India or abroad. Central Bank of India established in the year 1911 was regarded as the first commercial bank of India entirely managed and owned by Indians. Being the first Swadeshi Bank of India, it was nationalized in the year 1969. In order to know more about Central Bank student loans, scroll down the page.

Candidate's Eligibility

Candidates applying for the education loan need to satisfy certain eligibility criteria as specified by the bank.

• Applicants should be Indian Nationals and aged between 16-40 years.

• Students applying for the Central bank of India student loan are considered eligible if they get admission to various professional or technical courses through merit based selection process or entrance examination.

Courses Eligible for Central Bank Student Loans

There are plenty of professional and technical courses which are eligible for the Central Bank education loan in India.

Studies in India

• School education which includes +2 standard, graduation, post graduation and professional courses in the areas of Agriculture, Law, Engineering, Veterinary Science, Medicine, Management, Dental Science, Computer and others.

• The courses should be offered by reputed colleges or institutions approved by Department of Electronics or Institutions certified by the University.

• IIM, NIFT, XLRI, IIT offered courses, reputed regular diploma and degree courses, evening courses and courses that are conducted by foreign universities in India.

Studies Abroad

• Graduation, post graduation and courses conducted by reputed institutions like CIMA-London and CPA-USA.

Expenses Covered by Central Bank Student Loans

The loan amount covers hostel charges, examination fees, laboratory and library fee, building fund, caution deposit, refundable deposit and other expenses. The education loan also covers the travel expenses of the students traveling abroad for education.

Quantum of Finance

The maximum amount of loan offered is Rs.7.50 lacs and Rs.15 lacs for studies in India and abroad respectively.

Margin

There is no margin for education loans up to Rs.4 lacs. For loans above Rs. 4 lacs the margin is 5% and 15% respectively for India and abroad.

Security

Various types of securities are charged for the students willing to take education loan of Central Bank of India.

Education loan up to Rs.4 lacs- co-obligation security.

Education loan more than Rs.4 lacs and up to Rs.7.50 lacs-Collateral security

Education loan more than Rs.7.50 lacs-collateral security or co-obligation of any of the following-parents, guardians and third party.

Web: http://www.centralbankofindia.co.in

DENA BANK

Dena Bank offers educational loans to meritorious students who aspire for the best of higher education in India and abroad. The education loan offered by this bank is also known as the Dena Vidya Laxmi educational loan. Dena Bank was established by the family of Devkaran Nanjee on 26th May, 1938. The bank aims at providing premier financial services to its customers. It was nationalized in the year 1969 along with thirteen other banks in India. If you wish to know more about student loans from Dena Bank, then scroll down the page.

Candidate's Eligibility

Candidates who have applied for Dena Bank education loan need to meet certain eligibility criteria.

• Applicants who get admission to a professional or technical course in an Indian or foreign university are eligible to apply. They should also be Indian Nationals.

• Mark sheet of the qualifying examination and admission proof are the two documents required for application.

Courses Eligible for Dena Bank Student Loan

There are various courses, which are considered eligible for Dena Bank education loans in India.

Studies in India:

Student loans from Dena Bank are available for candidates willing to join various graduation, post graduation, masters, Ph.D and professional courses.

Studies Abroad:

Various job oriented graduation and post graduation courses are eligible for the education loan offered by Dena Bank.

Quantum of Loan

The maximum amount of education loan offered is Rs.10 lacs (Studies in India) and Rs. 20 lacs (Studies in Abroad) respectively.

Expenses Covered by Vidya Laxmi Educational Loan

Vidya Laxmi loan scheme covers the fees paid for school and hostel charges. It also includes the cost of purchasing books, uniforms, equipments, instruments, computer and other

necessary things. The passage fare for students traveling abroad is also covered by the Dena Bank education Loan.

Margin

For education loans above Rs. 4lacs, 5% and 15% are the margins stated for studies in India and abroad respectively.

Repayment of Dena Dank Loan for Education

Candidates are given a time period of five to seven years to repay the loan. The repayment starts either one year after the completion of the course or six month after the candidate gets employed.

Web: http://www.denabank.com

FEDERAL BANK LTD

Federal Bank education loans were launched to provide financial assistance to meritorious students willing to pursue their higher education. The bank offers two types of loans namely Federal Vidya Loan and Federal Special Vidya Loan.

Federal Bank Limited founded by Kulangara Paulo Hormis, started its operations with an authorized capital of Rs. 5000. If you want to know more about Federal Bank Ltd, educational loans, then scroll down the page.

Candidate's Eligibility

Candidates applying for Federal Bank student loan should be Indian nationals. Applicants will be considered eligible only if they get admission to various professional or technical courses through merit based selection process or entrance examination.

Courses Eligible for Federal Bank Ltd, Educational Loans

There are various undergraduate and postgraduate courses which are eligible for Federal Bank student loan. The courses should be offered by reputed institutions affiliated to universities and government statutory bodies.

Quantum of Loan

Federal Vidya Loan-The maximum education loan offered under this scheme is Rs.25 lacs. Federal Special Vidya Loan-The maximum education loan offered is Rs.7.5 lacs (Studies in India) and Rs.15 lacs (Studies abroad) respectively.

Repayment of Federal Bank Ltd, Educational Loan

Federal Vidya Loan-Eleven years is the maximum time period given for the repayment of loan. Federal Special Vidya Loan-Five to seven years of time is given to the candidates for paying back the loan.

Security

Federal Bank charges various kinds of securities for issuing education loans.

Federal Vidya Loan-Co-obligant or collateral security is required for the bank to issue the education loan.

Web: http://www.federalbank.co.in

HDFC BANK

Housing Development Finance Corporation Limited or HDFC Bank started its operations in the year 1995 as a scheduled commercial bank. It is one of the Indian banks, which offer education loans to students willing to pursue higher education in India or abroad. Scroll down the page to learn more about HDFC Bank education loans.

Candidates Eligibility Required for Education Loan

Candidates willing to apply for HDFC Bank education loan should be Indian Nationals. Applicants should be between 16-35 years of age. Collateral security is essential for loans above Rs. 7.5 lacs. A co-applicant is required if you are applying for full time courses.

Eligible Courses

The eligible courses for HDFC student loan are undergraduate and postgraduate courses in the fields of management, engineering, medicine, computer applications, fine arts and designing, hotel and hospitality, architecture and pure science.

The other courses eligible for loans are distance learning programs, air hostess training courses, SAP, GNIIT and ERP. The institutes should be recognized by competent government body or even by AICTE.

Features and Benefits offered by HDFC Bank

• The maximum amount of loan granted for education in India is Rs.10 lacs and Rs. 20 lacs for education in abroad. The rate of interest offered is attractive.

• Repayment of loan commences either one year after the course ends or six months after one gets a job. It depends on which one is earlier to the other.

• Tenure of seven years is available for the loans and the customers also get tax benefit.

• The entire procedure is hassle free and approvals are given at the earliest.

• Candidates may also fill and submit the online application form available. The representatives of the bank get in touch with the applicants as soon as possible.

Expenses Covered by the Loans

• The expenses covered by HDFC Bank education loan includes money to be paid as college and hostel charges, examination fees, library and laboratory fees, refundable deposit, caution deposit and other charges.

• The loan also covers travel expenses for studying abroad, essential articles required for completing the course and other educational costs.

Web: http://www.hdfcbank.com

IDBI BANK

It is great that you want to opt for education loan in order to pursue higher studies. There are several banks in India, which offer education loans to meritorious students willing to study higher education in India or abroad. Even IDBI Bank provides financial assistance to deserving candidates. If you to know more about education loans from IDBI, scroll down the page

Courses Eligible for IDBI Education Loans

There are plenty of courses considered eligible for IDBI Student Loan and the easy repayment options make the loan scheme attractive among the students.

Studies in India

• Various graduation, post graduation, professional and computer certificate courses.

• Other courses like CA, ICWA, CFA, courses conducted by reputed institutions like IIT, XLRI, IIT, NIFT, evening courses and those conducted by reputed foreign universities and institutions in India.

• Diploma and degree courses conducted by various universities and colleges which are approved by AICTE, ICMR, AIBMS, Government and UGC.

Studies Abroad

• Undergraduate, postgraduate and courses conducted by CPA in USA and CIMA-London.

Quantum of Loan

The maximum amount of education loan offered for studies in India is Rs.10 lacs and for studies abroad it is Rs. 20 lacs.

Expenses Covered by IDBI Student Loan

The expenses covered by IDBI education loan include fees to be paid for examination and hostel charges, library and laboratory fees, books, instruments, caution deposit, refundable deposit, instruments and building fund. The loan also covers the travel expenses of the students going abroad.

Repayment of IDBI Education Loan

The repayment commences either one year after the completion of the course or six months after one gets employed, whichever happens earlier.

The loan should be paid back within 5 to 7 years.

Web: http://www.idbi.com

INDIAN BANK

With the boom in banking sector in the recent past, several banks offer education loans in India these days. Indian Bank is no exception and offer education loans to students interested to pursue education in India or abroad. Gather information on learning loans: Indian Bank from this page and pursue your dream education.

Course:

Indian Bank learning loan is offered for a number of courses.

• You can apply for the education loan of Indian Bank if you want to pursue a graduate, diploma or post graduate program.

• The loan is also sanctioned for studying computer certificate courses of recognized bodies, which are accredited to the Department of Electronics.

• If you plan to study employment-oriented vocational or professional course, a program of CPA in the US or CIMA-London or specialized programs like MBA or MCA, you can apply for a loan in Indian Bank.

Eligibility:

Learning Loans are offered by Indian Bank to only Indian Nationals. The applicant should get admission to a professional or vocational course through a selection procedure based on merit or entrance test. The student will be considered eligible for studying in India if aged 15 to 30 years. A student should be aged between 18 to 35 years, if applying for studies abroad.

Expenses taken into account:

The educational loan covers insurance premium for the student as well as caution deposit, refundable deposit or building fund up to 10%. The educational cost of the course including travel expense, cost of essential purchases and fee of college, hostel, school and exam are taken into consideration.

Amount of Loan and Repayment:

You can borrow an education loan of maximum Rs 10 lacs for studying in India whereas a maximum amount of Rs 20 lacs can be borrowed for studying in abroad. The amount may increase in special cases.

• For loans above Rs 4 lacs taken for studying in India and abroad, there is a margin of 5% and 15% respectively. The loan can be repaid in 5 to 7 years.

• If you borrow a loan of above Rs 4 lacs, then you should provide the bank with a guarantee of a 3rd party.

• If the amount borrowed is more than Rs 7.5 lacs, then the co-obligation of parents or guardian of the student along with a collateral security need to be guaranteed.

The future income of the student also needs to be assigned for paying the installments.

Web: http://www.indian-bank.com

ORIENTAL BANK OF COMMERCE

The bank Oriental Bank of Commerce offers education loans for students who want to pursue higher education in India and abroad. This bank was set up on 19th February, 1943 in Lahore. It was founded by the first chairman of the bank Late Rai Bahadur Lala Sohan Lal. Within four years of its establishment, the Oriental Bank of Commerce shifted its base to Amritsar as problems aroused due to partition of India. If you want to know more about education loans from Oriental Bank of Commerce scroll down the page.

Candidate's Eligibility

Candidates applying for the Oriental Bank of Commerce education loan should be Indian Nationals and not more than forty five years of age.

An applicant will be considered eligible if he takes admission into the recognized courses, which are approved by recognized bodies.

Courses Eligible for Oriental Bank of Commerce Student Loan

The various courses eligible for the Oriental Bank of Commerce education loan are undergraduate, postgraduate, doctorate, professional and technical courses.

Amount of loan

The maximum amount of loan offered for education in India is Rs.10 lacs. Students taking admission in foreign institutes and universities may apply for a maximum loan amount of Rs.20 lacs.

Security

No collateral security is required for education loans up to Rs.4 lacs but co-obligation of guardian or parents is essential. For loans above Rs. 4lacs and up to Rs. 7.50 lacs no collateral security is required for approval. However, co-obligation of either parents or guardians and one third party guarantee is required for the loan. For loans more than Rs.7.50 lacs, mortgage of immovable property or other security (tangible) is required.

Margin

There is no margin for education loans up to Rs.4 lacs. For education loans above Rs.4 lacs, 5% and 15% are the margins stated for India and abroad respectively.

Repayment

The education loans from Oriental Bank of Commerce should be returned within 84 EMIs. The repayment commences either after six months of getting a job or after one year completion of the course, whichever, seems to be earlier.

Web: https://www.obcindia.co.in

INDIAN OVERSEAS BANK

The education loan offered by Indian Overseas Bank is also known as Vidya Jothi Scheme. Shri. M.Ct.M. Chidambaram Chettyar founded Indian Overseas Bank on 10th February, 1937 with the objective of specializing in overseas banking and business related to foreign exchange. It was nationalized in the year 1969. To know more about Indian Overseas Bank education loans, scroll down the page.

Eligibility of the Candidate

Candidates applying for the education loan from Indian Overseas Bank should be Indian nationals. Students who get admission to various professional and technical courses through merit based selection process or entrance examination are eligible to apply.

Courses Eligible for Indian Overseas Bank Educational Loans

There are various kinds of courses which are eligible for Indian Overseas Bank student loans.

• Loans are available for various graduation, post graduation, computer education and diploma courses offered by recognized universities or government statutory bodies in India.

• Indian Overseas Bank student loan is also provided for technical and professional courses, regular diploma and degree courses as well as courses conducted by reputed foreign universities in India.

• In case of studies abroad, the institutes offering the courses should be approved by the competent authority of the nation.

Quantum of Loan

A maximum of Rs.10 lacs is provided for studying in India and Rs.20 lacs for education abroad.

Margin

For Indian Overseas Bank Student Loan up to Rs.4 lacs there is no margin. However, the margin is 5% and 15% for loans more than Rs. 4 lacs in case of education in India and abroad respectively.

Security

Indian Overseas Bank charges various securities for issuing education loans under Vidya Jothi Scheme.

• For education loans up to Rs.4 lacs co-obligation of parents is required.

• For loans more than Rs.4 lacs and up to Rs.7.50 lacs- collateral security and Co-obligation of parents are needed.

• For loans more than Rs.7.50 lacs, you need to submit tangible collateral security and ensure co obligation of parents.

Repayment of Indian Overseas Bank Student Loan

A maximum time period of five to seven years is given to the students for the repayment of the education loan.

Web: http://www.iob.in

PUNJAB NATIONAL BANK

Students, who are willing to pursue higher education in India or abroad, can count on several kinds of education loans offered by the banks in India. They just need to gather comprehensive information on the scheme of all these loans before approaching a bank with their requirement. Even Punjab National Bank offers personalized educational loans for various kinds of academic programs. The scheme of Punjab National Bank (PNB) Educational Loan is also known as Vidyalakshyapurti. It also includes insurance coverage for the borrowers of educational loans in collaboration with Kotak Mahindra Insurance.

Courses:

Punjab National Bank offers educational loans for graduate and postgraduate programs. A student, who is pursuing a professional course or a vocational course from a recognized body, university or nationally known institute can apply for PNB educational loan as well.

Education Loans are also given for studying certificate or diploma programs.

Eligibility:

PNB has laid down a set of eligibility criteria for sanctioning the education loans.

• A student, who is an Indian national, can apply for the loan.

• An applicant is considered eligible for PNB educational loan, if he gets admitted to a professional or vocational course through a selection process or into a foreign institute.

• A student applying for a graduate program can also get the loan if he obtains at least pass marks in the qualifying exam.

Expenses, taken into account:

The education loan of Punjab National Bank covers the college, school or hostel fee and expenses for buying books, instruments or uniform. It also includes exam, laboratory or library fee apart from money for buying computer, if necessary for pursuing the program. Your travel and lodging expenses will also be covered by the loan. Even Caution Deposit, refundable deposit or building fund and any other cost essential for studying the program will be considered for loan.

Amount, Ceiling, Margin & Security of Loan

The amount of PNB Loan is sanctioned evaluating the need and the repaying capability of the parent or the student. Additionally, some ceilings and margins are also applied by PNB.

• You can borrow a maximum of Rs 7.5 lacs and Rs 15 lacs for studying in India or abroad respectively.

• Besides, there is a margin of 5% if you borrow above Rs 4 lacs for studying in India. The margin is 15% for studying abroad.

• An applicant needs to present a 3rd party as guarantee for borrowing above Rs 4 lacs.

• If the amount is above Rs 7.5 lacs, the bank asks for a collateral security or guarantee of a 3rd party.

Mode of repayment:

You can repay the principal sum and the interest in a time period of 5 to 7 years after you begin repaying. In case, a student fails to complete his study in the stipulated time period, he will be given an extended time of 2 years in maximum for completing the program.

Web: www.pnbindia.com

STATE BANK OF HYDERABAD

State Bank of Hyderabad Student Loans are sanctioned to meritorious students, who aspire to pursue their higher education in India or abroad. Apart from its education loan scheme, this bank offers diverse types of loans for personal advances. As the history goes, State Bank of Hyderabad was formed in the name of Hyderabad State Bank in 1941 under Hyderabad State Bank Act, 1941. Its first branch began operations at Gunfoundry in Hyderabad in 1942. This bank was given the existing name when it was taken over by RBI in 1956. Later in 1959, it started functioning as a subsidiary of State Bank of India.

Courses:

State Bank of Hyderabad Student Loans are offered for several kinds of academic programs in India and abroad.

• Education loan can be sanctioned for pursuing school education in India.

• A student can also apply for this loan if he plans to study graduate, postgraduate and doctoral programs in India.

• Professional Courses like Engineering and Medical programs, specialized courses like ICWA, CFA or CA, programs by nationally reputed institutes like IIM and IISc or computer certificate programs of recognized institutes in India can be considered for this loan.

• Even courses by recognized foreign universities, diploma programs sanctioned by the likes of UGC, AICTE and the government in India, can be taken into consideration for sanctioning this loan.

• If you plan to study employment-oriented graduate courses, postgraduate programs like MS or MBA, or courses by CPA in the US or CIMA-London in abroad, you can apply too.

Eligibility:

Only an Indian national can apply for an education loan from State Bank of Hyderabad. The student also should have been admitted to a vocational or professional course on the basis of a selection procedure or entrance test. You will also be considered eligible if you get admission to a foreign institute.

Amount of Loan, Margin & Security:

The amount of loan is decided on the basis of a person's requirement as well as the repaying capability of the student borrower or his parents.

A maximum amount of Rs 10 lacs is sanctioned for studying in India. The amount for studying in abroad is Rs 20 lacs. The bank also has guidelines in regard to the margin and security of its Educational Loan Scheme.

• No amount of margin and security is there for loan amount upto Rs 4 lacs.

• However, for a loan amount above Rs 4 lacs, there is a margin of 5% and 15% if you pursue studies in India and abroad respectively.

• A borrower needs to present guarantee of a 3rd party for a loan amount above Rs 4 lacs.

• When the loan amount exceeds Rs 7.5 lacs, a collateral security of considerable value should be submitted. Or there should a co-obligation of guardian, parents or a 3rd party. Even the future income of the student needs to be assigned for paying the installments.

Repayment:

The student loan obtained from State Bank of Hyderabad can be repaid in a time period of 5 to 7 years after repayment is begun.

Web: http://www.sbhyd.com

STATE BANK OF INDIA

State Bank of India provides its customers with a variety of personal banking services. SBI, which is actively engaged in Community Services Banking, also offers education loans to students aspiring to continue higher studies. SBI Study Loans are sanctioned only to Indian Nationals. A study loan is sanctioned for studies both in India and abroad.

Courses Eligible for Education Loans:

A candidate, who applies for a program with prospects of employment, can apply for the loan. Whether you apply for a graduate, professional or postgraduate program or any other course sanctioned by UGC, AICTE or the government, you will be considered eligible for the loan.

Expenses taken into account:

• The student loan covers school, college or hostel fees as well as cost for buying books and other necessary items.

• Apart from the library, exam or library fees, even caution deposit, refundable deposit and building fund are considered for the loan.

• Other expenses, which are mandatory for completing the course, travel expense as well as a maximum cost of Rd 50,000 for buying a 2 wheeler, are taken into account.

Quantum of Loan & Security:

An applicant is sanctioned a loan of maximum Rs 10 lacs for studying in India and Rs 20 lacs for studying in abroad. On a loan above Rs 4 lacs, there is a margin of 5% and 15% for studying in India and abroad respectively.

• No security is required for loan amount upto Rs 4 lacs.

• A borrower should present a 3rd party as guarantee for a loan amount above Rs 4 lacs. However, on SBI discretion, this clause of 3rd party guarantee may be waived off in certain cases.

• If you borrow a loan amount above Rs 7.5 lacs, you need to offer a material collateral security and assign the future income of the student for paying installments.

• The guardians or parents of a borrowing student should secure an education loan.

• If the borrower is married, his or her spouse, parents-in-law or parents can act as the co-obligator.

Repayment of Education Loan:

The borrower can begin repaying 6 months after getting job or one year after the course is completed, whichever happens earlier. The loan can be repaid in a period of 5 to 7 years.

Education Loan for ISM students:

Education loans are also offered to the students of ISB. An ISB student can borrow upto 95% of costs. There is also a margin of 5% on the loan amount, which needs to be repaid in 7 years. For detailed information on this loan scheme for ISB students, you can contact the branch at Hyderabad University Campus Branch.

Web: http://www.sbi.co.in

UCO BANK