Edmonton Real Forum - · PDF fileProvince of Alberta projects $4.7 billion deficit for 2009...

47

Ron Gilbertson President and CEO Edmonton Economic Development Corporation Edmonton Real Estate Forum

Transcript of Edmonton Real Forum - · PDF fileProvince of Alberta projects $4.7 billion deficit for 2009...

Ron GilbertsonPresident and CEO

Edmonton Economic Development Corporation

Edmonton Real Estate Forum

DepressionEconomic Downturn

The Latest Economic News

• The Economy – What’s Going On?

• Edmonton and Alberta Today

• Opportunities and Threats

• The Challenge

Depression• In December, North American auto production

down over 40% from last 10 year average• Taiwan exports down 45% in DecemberCrisis• Virtual meltdown of global financial system• Bank bailouts over past 12 months in excess of

one trillion dollars, more required

It’s Everything ‐ Depending Where You Are

The Economy – What’s Going On

The Economy – What’s Going On

Recession• Latest IMF forecast is that world’s advanced

economies will decline by 2.0% in 2009, followed by modest growth in 2010

Downturn• IMF growth forecasts for developing nations

• China: 6.7% in 2009 (down from 13.0% in 2007)• India: 5.1% in 2009 (down from 9.3% in 2007)• Brazil: 1.8% in 2009 (down from 5.7% in 2007)

The Economy – What’s Going On

Economic Cycle• In good times, real temptation to believe the

party will never end • In bad times, real fear that things will never get

better• Most experts believe that this is a part of an

economic cycle• Periodic downturns are part of economic history• Usually the bigger the boom, the bigger the bust• Most forecasts projecting a return to growth by 2010

The Economy – What’s Going On

Correction• Recognition that accelerated and sustained

economic growth can create serious problems• Globally

• Over-leveraging, • Poor lending practises

• Alberta• Labour shortages• Dangerous price inflation• Infrastructure and service deficits

The Economy – What’s Going On

Economic Cycle• In good times, real temptation to believe the

party will never end • In bad times, real fear that things will never get

better• Most experts believe that this is a part of an

economic cycle• Periodic downturns are part of economic history• Usually the bigger the boom, the bigger the bust• Most forecasts projecting a return to growth by 2010

EEDC 2009 Economic Outlook LuncheonNovember 24, 2008

Where We Are Today

1. We are entering into a recession – it’s a normal part of the business cycle

2. The downturn will likely be longer and more severe than most originally believed

3. Canada, Alberta and Edmonton will fare better than most

EEDC 2009 Economic Outlook LuncheonUpdate

Where We Are Today

4. Alberta and Edmonton are now being impacted by the downturn• Impact is not evenly distributed

• Important to keep things in perspective

5. It’s not over yet• Expect more surprises

• Optimists seeing a “slowdown in bad news”

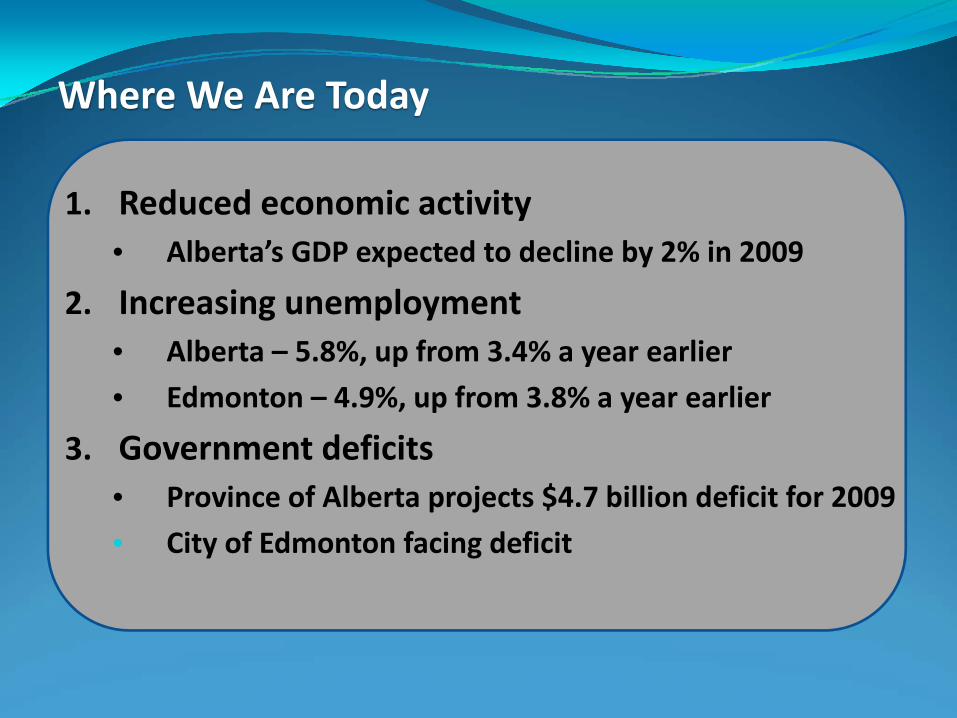

1. Reduced economic activity• Alberta’s GDP expected to decline by 2% in 2009

2. Increasing unemployment• Alberta – 5.8%, up from 3.4% a year earlier

• Edmonton – 4.9%, up from 3.8% a year earlier

3. Government deficits• Province of Alberta projects $4.7 billion deficit for 2009

• City of Edmonton facing deficit

Where We Are Today

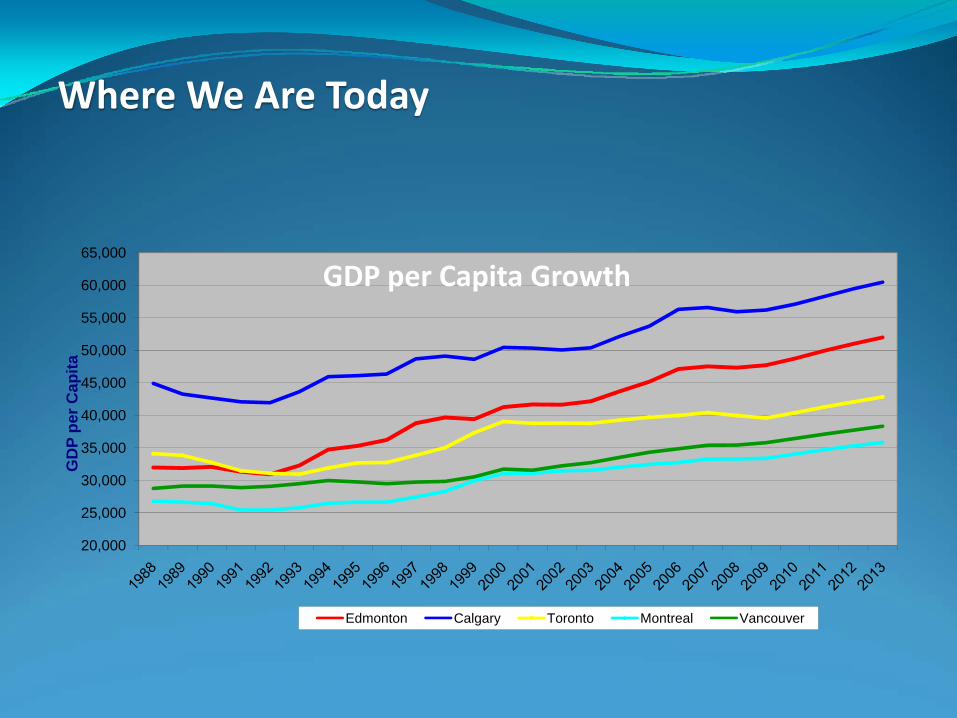

Overall Economic Performance• Edmonton’s overall economic activity ranking

• 2007 - #1 in Canada• 2008 - # 5 in Canada

• What changed?• Slowdown in population and employment growth• Drop in house prices, but increase in MLS sales

(year over year)• Fall off in housing starts, but significant increase in

non-residential construction

Overall Economic Performance

Where We Are Today

• Edmonton continues to have important economic strengths

• Key indexes• Unemployment rate - #2 – second lowest in Canada• Full time employment - #5 – fifth highest in Canada• Consumer bankruptcies - # 5 – fifth lowest in

Canada• Business bankruptcies - #1 – lowest in Canada

Overall Economic Performance

Where We Are Today

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

GD

P pe

r Cap

ita

Edmonton Calgary Toronto Montreal Vancouver

GDP per Capita Growth

Where We Are Today

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

B.C. Alberta Sask Man Ont Que N.B. N.S. P.E.I. N. & L.

GDP per Capita ‐ 2008/2009

20082009

Alberta• Down 2.3% in 2009• 35% above the Canadian average

Where We Are Today

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

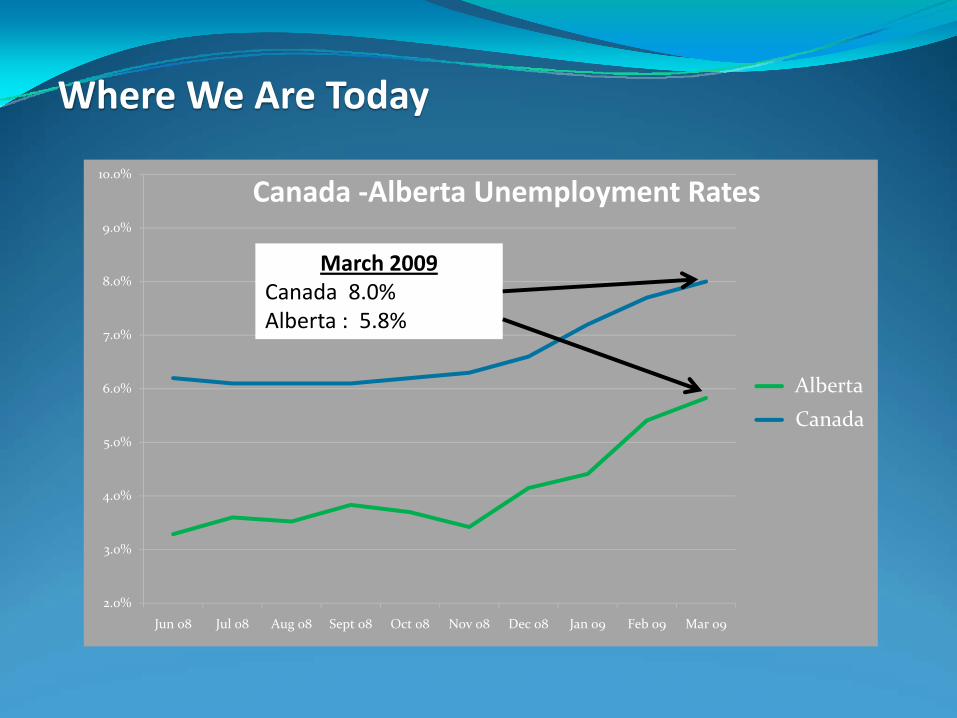

Jun 08 Jul 08 Aug 08 Sept 08 Oct 08 Nov 08 Dec 08 Jan 09 Feb 09 Mar 09

Canada ‐Alberta Unemployment Rates

AlbertaCanada

March 2009Canada 8.0%Alberta : 5.8%

Where We Are Today

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

Jun 08 Jul 08 Aug 08 Sept 08 Oct 08 Nov 08 Dec 08 Jan 09 Feb 09 Mar 09

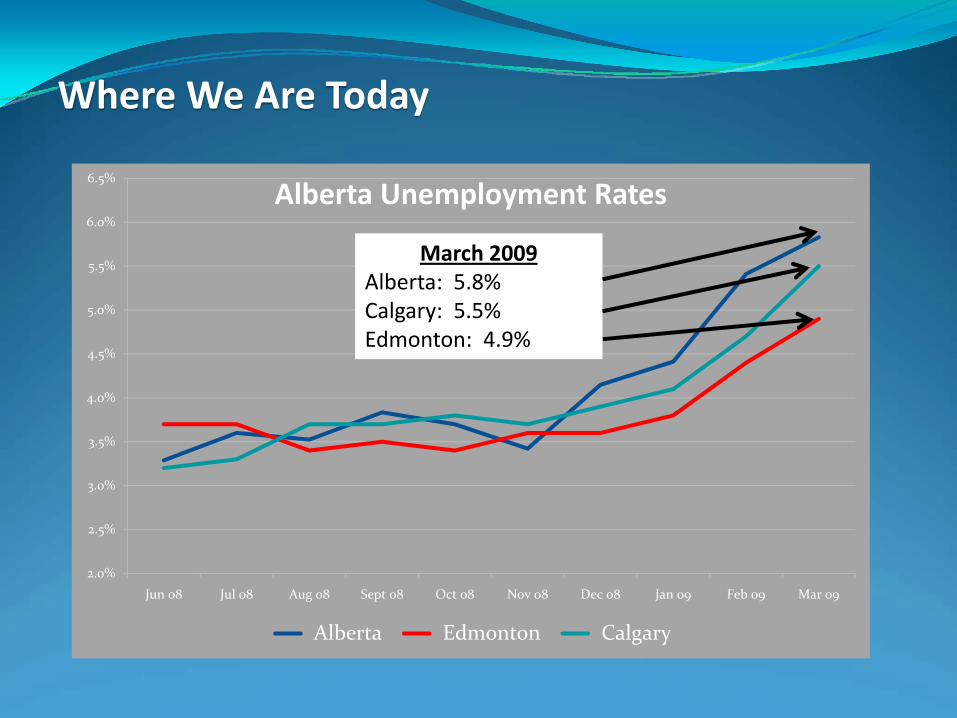

Alberta Unemployment Rates

Alberta Edmonton Calgary

March 2009Alberta: 5.8%Calgary: 5.5%Edmonton: 4.9%

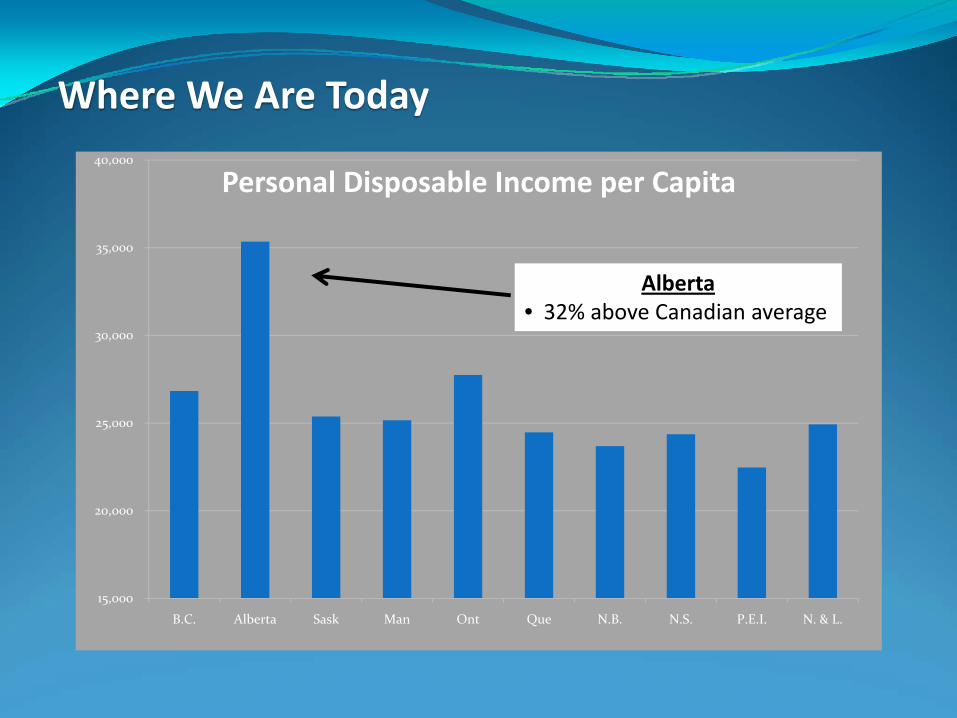

Where We Are Today

15,000

20,000

25,000

30,000

35,000

40,000

B.C. Alberta Sask Man Ont Que N.B. N.S. P.E.I. N. & L.

Personal Disposable Income per Capita

Alberta• 32% above Canadian average

Where We Are Today

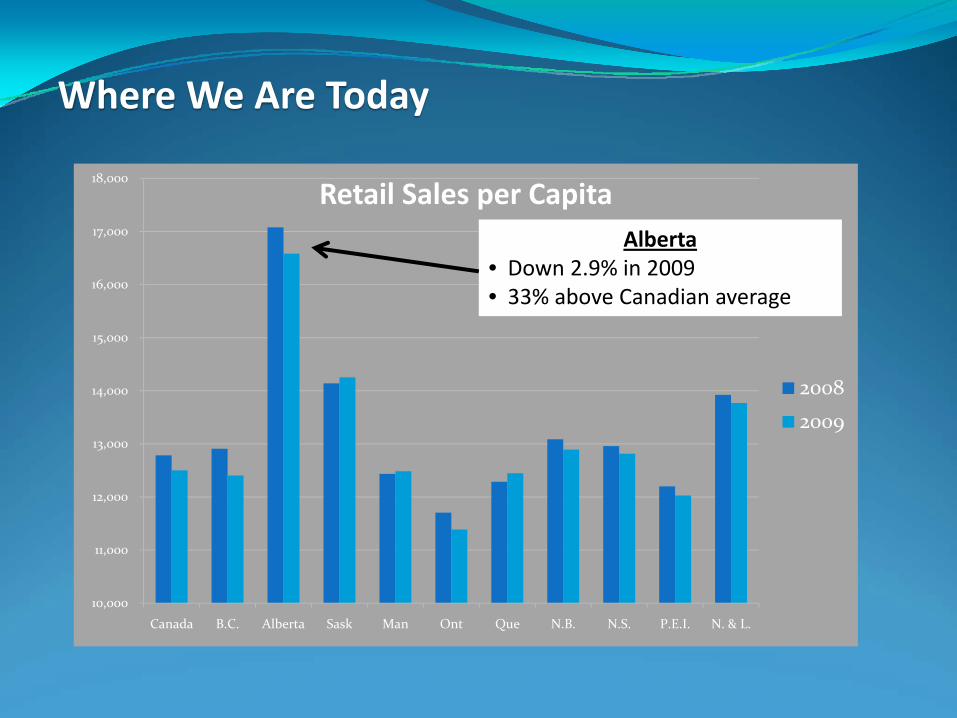

10,000

11,000

12,000

13,000

14,000

15,000

16,000

17,000

18,000

Canada B.C. Alberta Sask Man Ont Que N.B. N.S. P.E.I. N. & L.

Retail Sales per Capita

20082009

Alberta• Down 2.9% in 2009• 33% above Canadian average

Where We Are Today

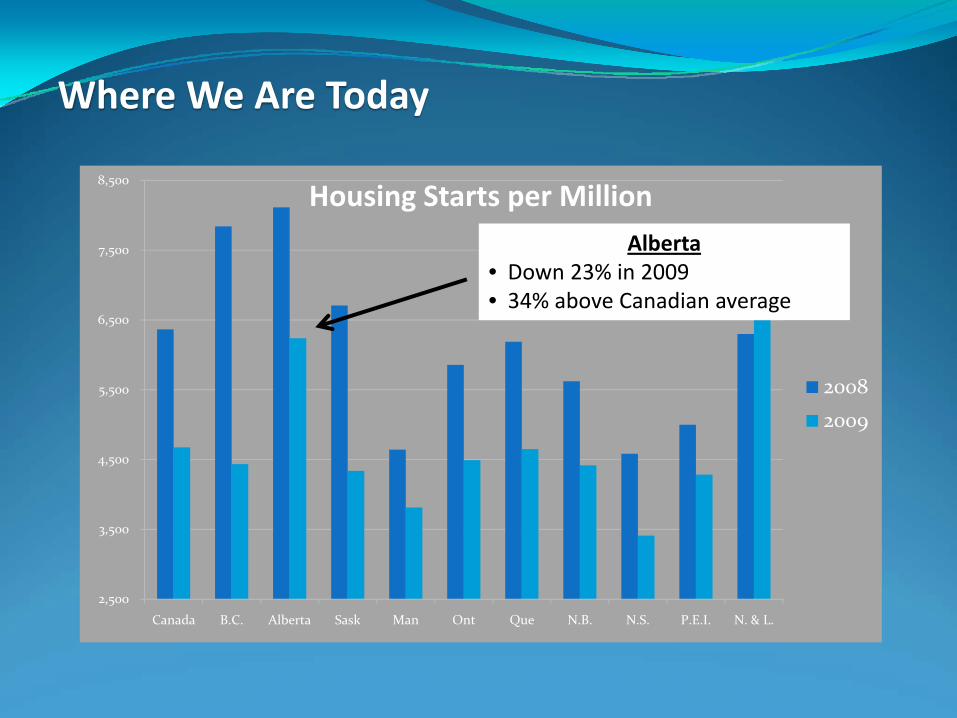

2,500

3,500

4,500

5,500

6,500

7,500

8,500

Canada B.C. Alberta Sask Man Ont Que N.B. N.S. P.E.I. N. & L.

Housing Starts per Million

20082009

Alberta• Down 23% in 2009• 34% above Canadian average

Opportunities and Threats

What The Future Looks Like

1. Changing global economy

2. World energy markets

3. Populations and labour forces

4. Critical success factors

5. Edmonton’s and Alberta’s economy of the future

What the Future Looks Like

• Dramatic shifts in the global economy can be expected over the next 3 to 4 decades

• These shifts being driven by, or reflected in, changes in:• Balance of power• Population• GDP• Globalization

A Changing World

What the Future Looks Like

Balance of Power

Cold WarA Bi‐Polar World

U.S.S.R.

U.S.A.

RecentA Uni‐Polar World

FutureA Multi‐Polar

World

U.S.A.

U.S.A.Russia

Japan

China

Europe

Gulf States

What the Future Looks Like

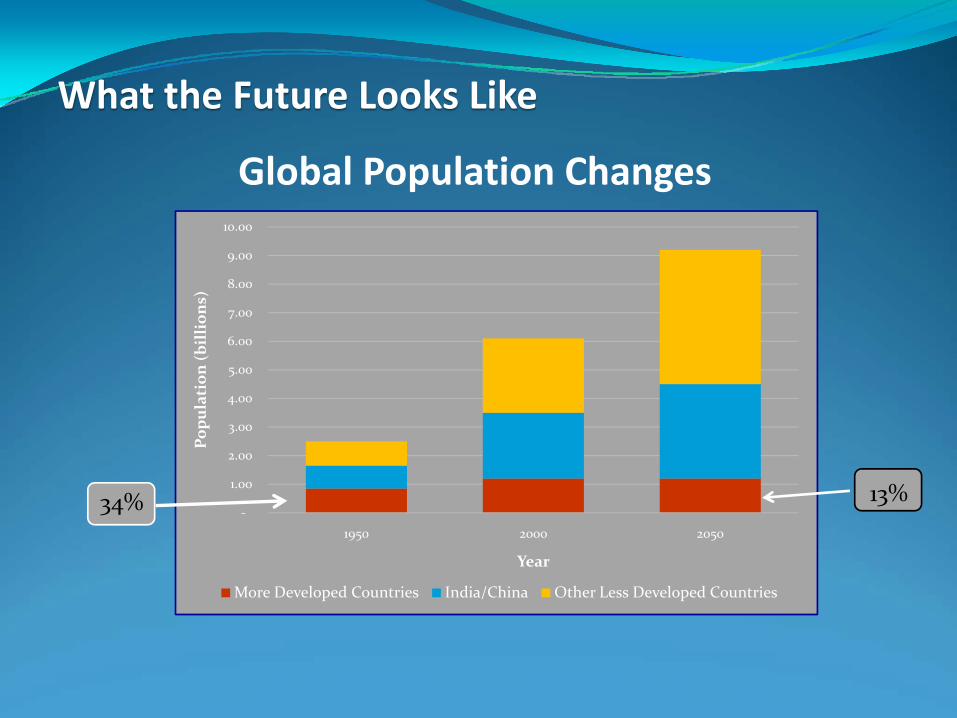

Global Population Changes

‐

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

1950 2000 2050

Popu

lation (b

illion

s)

Year

More Developed Countries India/China Other Less Developed Countries

34% 13%

What the Future Looks Like

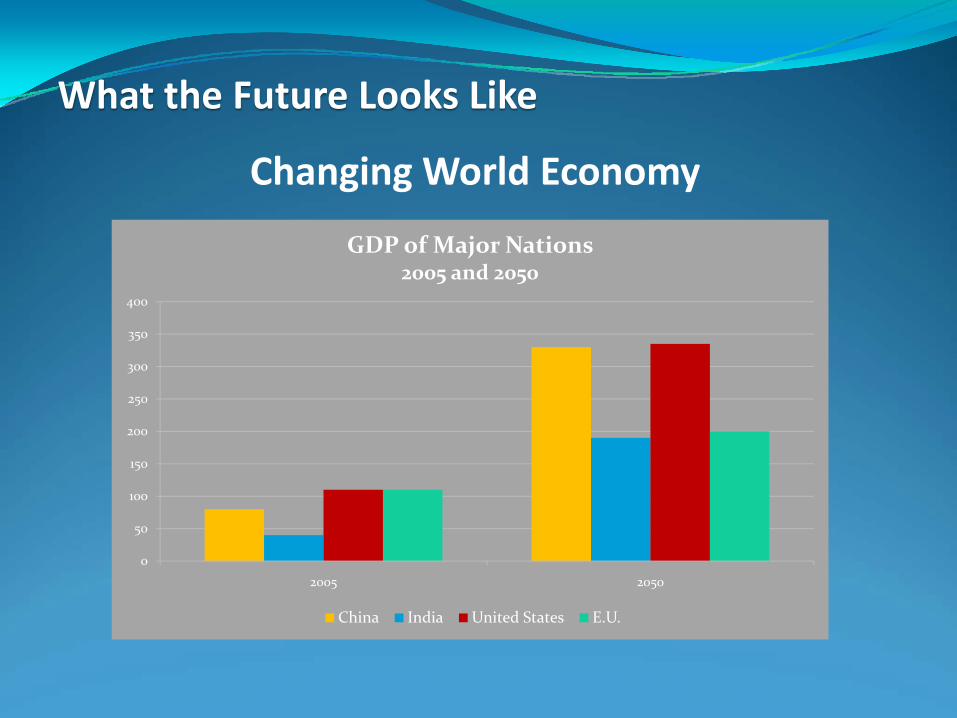

Changing World Economy

0

50

100

150

200

250

300

350

400

2005 2050

GDP of Major Nations2005 and 2050

China India United States E.U.

What the Future Looks Like

• Trend is to increased international trade and inter-dependence amongst nations

• Developing nations not standing still• Large populations and increasingly educated labour

forces• Equal access to advanced technologies• Improved access to investment capital

• Important complexities• Business environment• Distribution of value-add

Globalization

What the Future Looks Like

$224 Wholesale Price Where are revenues are captured

1% Taiwan / Korea / Other

8% USA

32% Japan

Manufacturers Headquartered In:

59%

Source: Personal Computing Industry Center: 2006

Apple:

The iPod Value Chain

Globalization

What the Future Looks Like

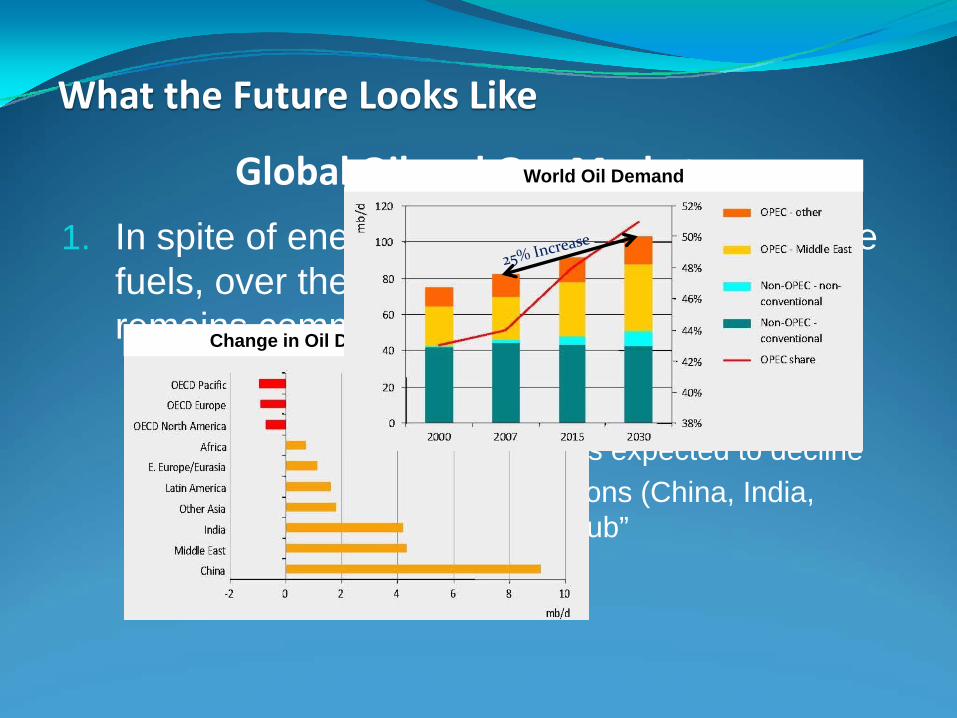

1. In spite of energy conservation and alternative fuels, over the foreseeable future the world remains committed to oil and gas

• World oil demand expected to rise an additional 25% by 2030 (from 85 to 106 million barrels daily)

• Demand in industrialized nations expected to decline• Major growth in developing nations (China, India,

Middle East) as they “join the club”

Global Oil and Gas Markets

Change in Oil Demand by Region

World Oil Demand

What the Future Looks Like

2. Globally, roughly 3 decades left to the conventional oil economy

• While global reserves increasing, the cost of exploration and production rising rapidly (95% increase since 2000)

• Production from existing sources expected to decline by over 50% by 2030

• To offset declines and meet new demands, world needs “6 new Saudi Arabia's” by 2030

• Long term pricing expected to be in the $100 - $120 a barrel range

Global Oil and Gas MarketsWorld Oil Production

6 Saudi Arabia’s

What the Future Looks Like

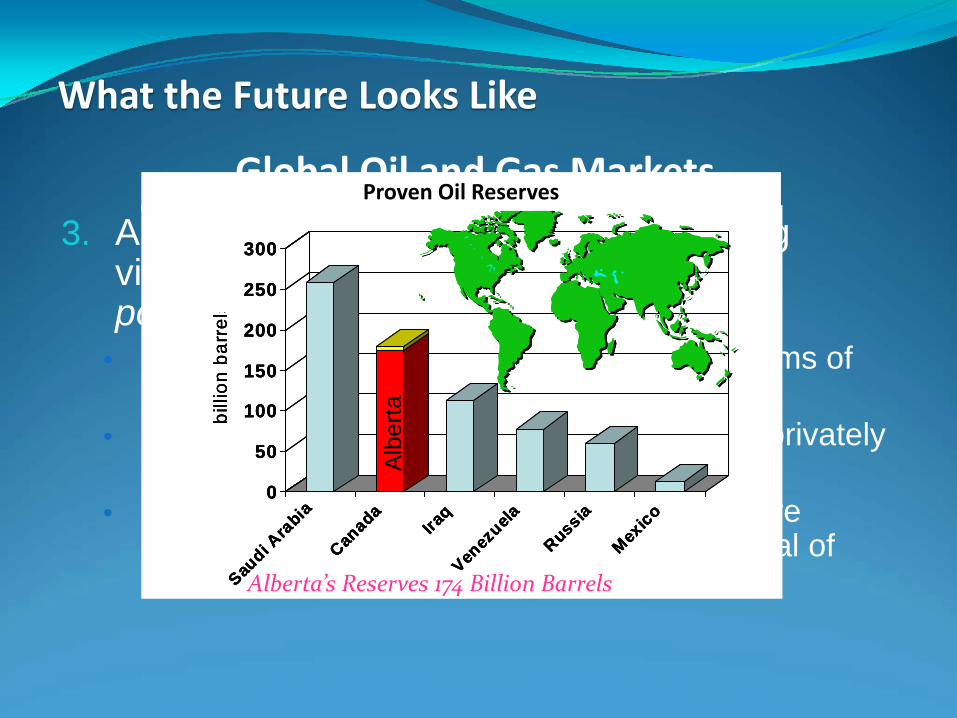

3. Alberta’s oil sands are increasingly being viewed as the world’s largest and most politically stable source of oil

• Alberta is second only to Saudi Arabia in terms of total proven reserves

• Alberta represents over 50% of the world’s privately developable oil reserves

• Cost escalation and environmental issues are critical to the long term development potential of heavy oil

Global Oil and Gas Markets

0

50

100

150

200

250

300bi

llion

bar

rels

Saudi A

rabia

Canada

Iraq

Venez

uela

Russia

Mexico

Alb

erta

0

50

100

150

200

250

300bi

llion

bar

rels

Saudi A

rabia

Canada

Iraq

Venez

uela

Russia

Mexico

Alb

erta

0

50

100

150

200

250

300bi

llion

bar

rels

Saudi A

rabia

Canada

Iraq

Venez

uela

Russia

Mexico

Alb

erta

Proven Oil Reserves

Alberta’s Reserves 174 Billion Barrels

What the Future Looks Like

• In virtually all industrialized nations, labour forces being impacted by 2 macro trends:• Declining populations• Aging populations

• As a result, in these nations’ unemployment levels are approaching all time lows

• Over the coming 50 years, labour shortages will be one of the most important challenges to be faced by industrialized nations

Populations and Labour Forces

What the Future Looks Like

• Education• Western world no longer has a monopoly on

advanced education• Innovation, productivity, global reach – all are directly

impacted by education levels• Innovation

• The primary driver of new market opportunities, and productivity and efficiency gains, will be innovation

• Innovation is as much a “culture” as anything else

Critical Success Factors

What the Future Looks Like

• Global View• Need to recognize that both competition and markets

will be increasingly global• Success will be dependent on identifying both

opportunities and threats within a global context• Entrepreneurial

• Having the drive or incentive to create new market and business opportunities, and to be competitive, essential to future success

• Developing an entrepreneurial culture is essential

Critical Success Factors

What the Future Looks Like

• We are becoming more productive• We are benefiting from higher incomes• We are becoming better educated• We are growing as a centre of economic activity

• Health care• Education• Advanced Technology• Oil and Gas, and in particular Oil Sands• Financial Services and Investment Management

Edmonton’s Economy of the Future

What the Future Looks Like

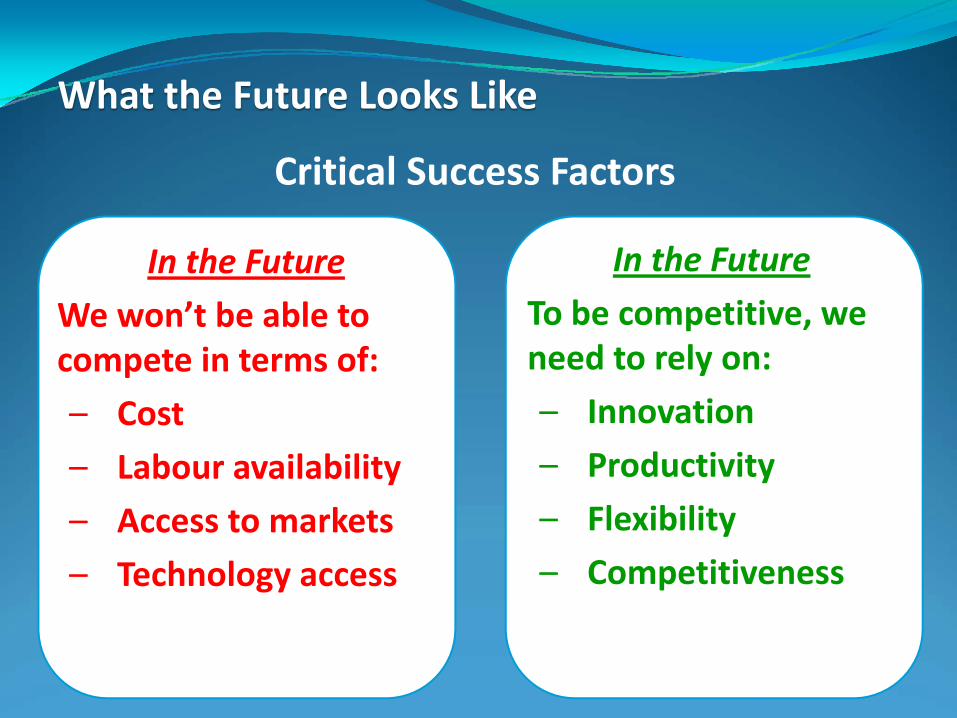

Critical Success Factors

In the Future

We won’t be able to compete in terms of:

– Cost

– Labour availability

– Access to markets

– Technology access2028 2038

In the Future

To be competitive, we need to rely on:

– Innovation

– Productivity

– Flexibility

– Competitiveness

What the Future Looks Like

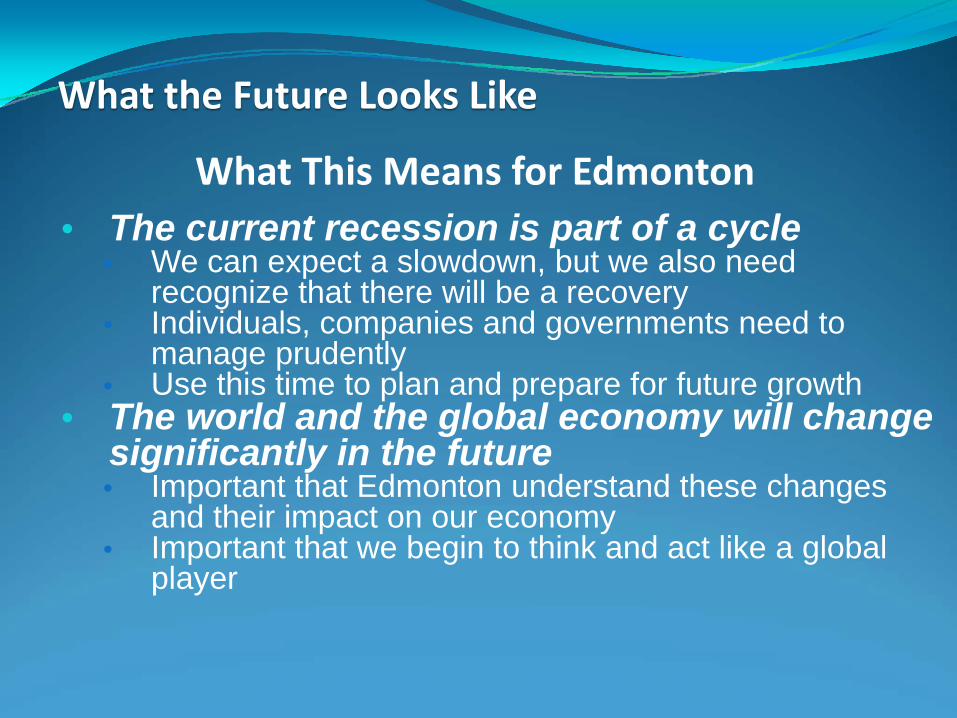

• The current recession is part of a cycle• We can expect a slowdown, but we also need

recognize that there will be a recovery• Individuals, companies and governments need to

manage prudently• Use this time to plan and prepare for future growth

• The world and the global economy will change significantly in the future• Important that Edmonton understand these changes

and their impact on our economy• Important that we begin to think and act like a global

player

What This Means for Edmonton

What the Future Looks Like

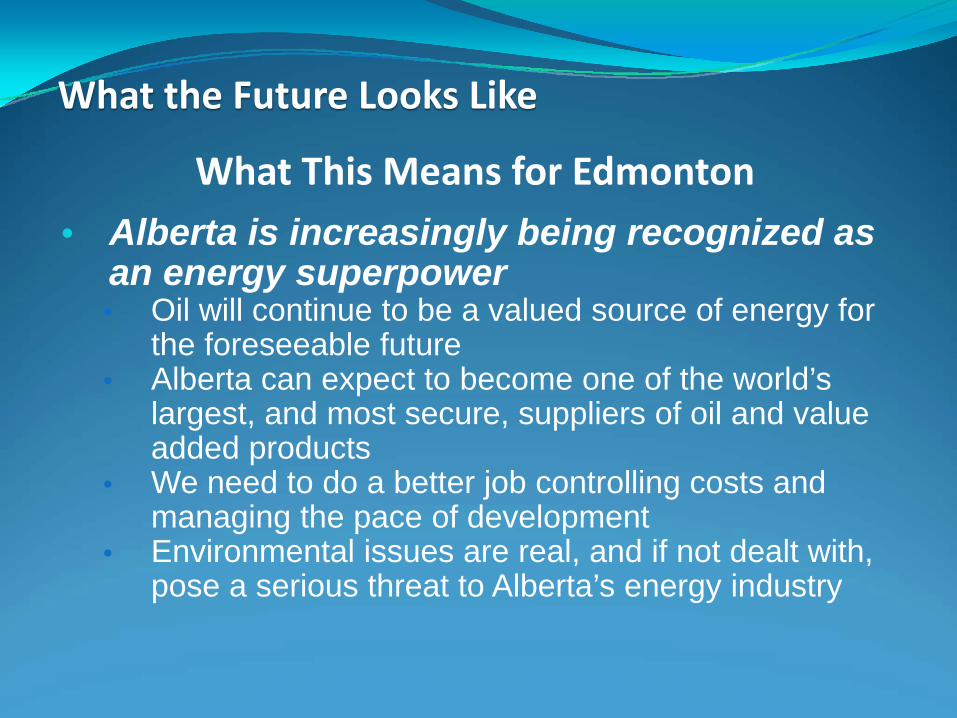

• Alberta is increasingly being recognized as an energy superpower• Oil will continue to be a valued source of energy for

the foreseeable future• Alberta can expect to become one of the world’s

largest, and most secure, suppliers of oil and value added products

• We need to do a better job controlling costs and managing the pace of development

• Environmental issues are real, and if not dealt with, pose a serious threat to Alberta’s energy industry

What This Means for Edmonton

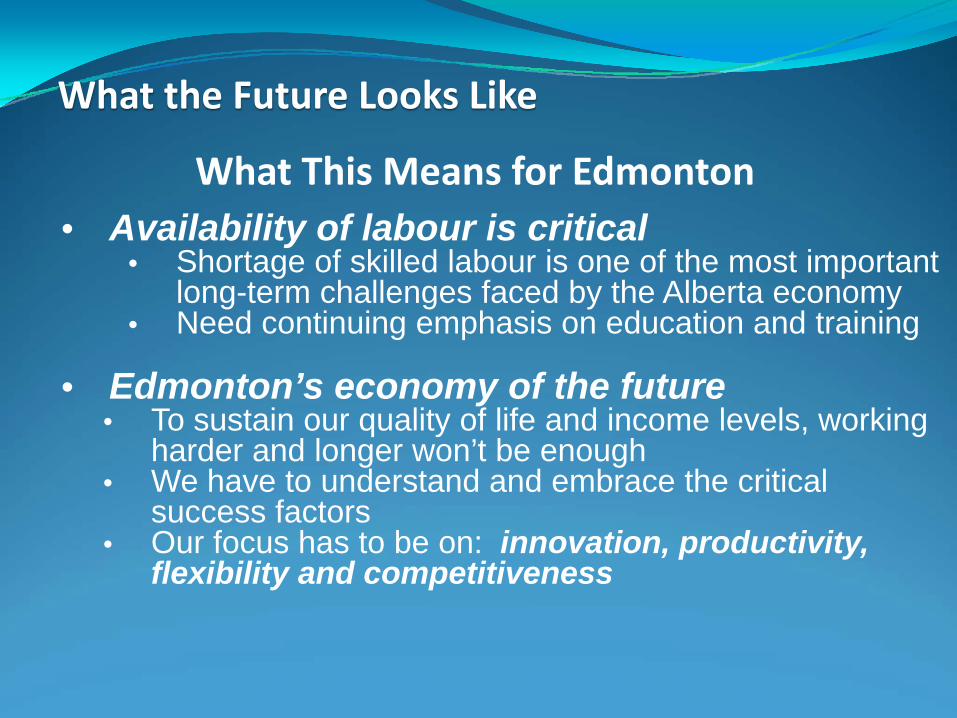

What the Future Looks Like

• Availability of labour is critical• Shortage of skilled labour is one of the most important

long-term challenges faced by the Alberta economy• Need continuing emphasis on education and training

• Edmonton’s economy of the future• To sustain our quality of life and income levels, working

harder and longer won’t be enough• We have to understand and embrace the critical

success factors• Our focus has to be on: innovation, productivity,

flexibility and competitiveness

What This Means for Edmonton

Core Sectors in the Future

Transportation& Logistics

Retail

Real Estate

Manufacturing

Real Estate

ProfessionalServices

Entertainment

Construction

Agriculture

Engineering

Hospitality

Utilities

Education

Tourism

Oil Sands

F.I.R.E.

HealthCare

Advanced Technology

F.I.R.E.

Health Care

Education

Advanced Technology

Oil Sands

Tourism

What the Future Looks Like

Where Do We Want to be 20 Years?

1. Establish a sustainable and internationally competitive economy

2. Offer high quality employment opportunities and good incomes

3. Provide citizens with a world‐class quality of life

4. Be globally recognized as a leading city

What the Future Looks Like

Setting a Goal

To have Edmonton become recognized as one of the world’s top 5 mid‐sized cities

The Challenge

City Type and Size Number of CitiesType Population North

AmericaRest of World

Total

Mega 20.0 M Plus 2 5 7Very Large 10.0 – 20.0 M 1 17 18Large 5.0 – 10.0 M 11 28 39Intermediate 2.5 – 5.0 M 11 86 97Mid-Size 1.0 – 2.5 M 43 264 307Total 68 400 468

The World’s Largest Cities

The Challenge

MunichLyonOrlandoSan AntonioAbu DhabiPretoriaStockholmVancouver

New OrleansCologneCalgaryAmsterdamXiamenGlasgowDubaiCopenhagen

Who are the Benchmarks?Who is our Competition?

• The Hague• Auckland• Memphis• Oslo• Ottawa• Fukuoka• Columbus• Brisbane

Conclusion

• Thank you for attending today

• Enjoy the rest of the Luncheon