Editor in Chief Editorial Board Associate Editor in Chief ...

EDITORIAL BOARD

CHIEF EDITOR MANAGING EDITOR

DR. PAVAN MISHRA DR.SONIYA RAJPOOT Professor ,Department of Commerce

Barkatullah University,Bhopal INDIA

Ph.D(Management) , M.Phil (Management) Ex. MBA

(HRM), MBA(Finance),B.Com.(Computer), F.I.C.E.R..

EDITORIAL BOARD

DR.SAMEER SHARMA DR.KAMRAN SULTAN

Director Former Director

People's Institute of Management & Research,

Bhopal, INDIA

Pt. Jawaharlal Institute of Management

Vikram University, Ujjain, INDIA

DR. MANORAMA SAINI ADRIAN FARLEY

Reader& Head, Humanities Department Managing Director

Smart Ashok Technological Institute, Vidisha,

INDIA

Farley & Associates Ltd (UK Immigration Specialists)

LONDON

SAMEER ELWIN BHAGIRATHI MAHIMA AGOCHIYA

735 Queen Street East Toronto, Ontario

CANADA

Business Development, Advisor at McMaster University

Toronto, Ontario, CANADA

PUBLICITY AND PUBLICATION BOARD

DR. RAJESH KUMAR SHARMA, Faculty of Management, VNS Group of Institutions, Bhopal (MP)

Dr. Bhagwan Singh, LNCT-MBA, Bhopal(M.P.)

ADVISORY BOARD

DR. ARUN K.TRIVEDI DR. P.K. MISHRA

Managing Director Professor

Global Business Development Consultant C.R.I.M., Barkatullah University, Bhopal

At Vorse Solutions (UK) Limited, LONDON Ex-Vice Chancellor (DAVV. Indore)INDIA

DR. NAGESHWAR RAO DR. JAVAID AKHTAR

Pro Vice Chancellors Professor

Indira Gandhi National Open University (IGNOU) Ex- Former Chairmen & Dean

Ex-Vice Chancellor(Open University Allahabad)

INDIA

Department Business Administration, Aligarh Muslim

University, Aligarh , INDIA

DR. RAJ KUMAR DR. Y.S.THAKUR

Professor Head & Professor

Faculty of Management Studies Faculty of Management Studies

Banaras Hindu University, Varanasi INDIA Dr. Harisingh Gour University, Sagar, INDIA

DR. VIVEK SHARMA DR. P.K. CHOPRA

Director Director

CRIM Barkatullah University, Bhopal, INDIA Oriental College of Management, Bhopal INDIA

DR. K.K. SAXENA DR. L.P. PATERIYA

Head & Professor Head & Professor

Deptt. of Humanities &Social Science Deptt. of Management Studies

IIT Kanpur INDIA Guru Ghasidas University, Bilaspur, INDIA

ONLINE SHOPPING BEHAVIOUR OF CONSUMERS IN BHOPAL CITY-

A STUDY

By

Dr. Bhagwan Singh

Asst. Prof., LNCT-MBA, Bhopal

E-mail: [email protected]

ABSTRACT

This paper studies the behaviour of consumers in Bhopal city with respect to online shopping.

The variables included are familiarty with online shopping, familiarty with specific websites

engaged in e-retailing, purchased products from these websites etc. Data is collected directly

by interviewing the respondents according to a self-constructed schedule. Random sampling

technique is applied for gathering the data. Data analysis and statistical testing is performed

with the help of SPSS 16.0 and MS-Excel 2007 softwares. Results answer the questions like,

how consumers are aware of online shopping method?, how they use to purchase?, what

online shopping websites are chosen?, what kind of products are purchased? etc.

Keywords: Online shopping, consumer behaviour, online shopping websites, Bhopal city.

INTRODUCTION:

Online shopping is pioneered by Micheal Aldrich in 1980s. In India, it has been

successfully started by Indian Railway Catering and Tourism Corporation (IRCTC) by

opening online ticketing for public around 2002. Now-a-days, it is very popular for

purchasing various assortments, bill payments, ticket booking, mobile recharging etc. Most of

the companies maintain their well-developed websites to entertain online purchasing and

services. Various websites exclusively dealing with online-retailing are also prevalent in

common parlance these days. In present scenario many products and services are available on

virtual world i.e., internet. There are so many words that are synonymously used such as,

online shopping, electronic shopping, e-commerce etc. for the same concept and retailing is

the another aspect of the same environment. Whether brick & mortar or online retailing;

customer is the king everywhere. That is why most of the studies and researches at market

place are customer centric, so the current study too. Here in this research, consumer behavior

which is the study of groups, individuals or organizations relating to their purchase and

selection of products or services is studied with regard to online shopping. The study of

available literature on the topic is essential for full understanding, so the same is mentioned

further:

LITERATURE REVIEW:

Various literatures are studied for this purpose and important ones are mentioned

below with their conclusions:

Sonwalkar, Jayant and Nema, Geeta (2008) concluded that brand persona is the

most effective factor that affects the brand preference. The same deals with the personality

aspects or the external attributes of a brand. Thus, it can be said that the customer prefer any

brand by looking at the external attributes of a brand. . Gupta and Hiremath (2011) found

that there was a significant difference between the selected retail formats with respect to

merchandise, and services offered. Malls and discount store attracted many customers but

there was no difference found in quality, variety, style, brand, service and prices offered

among the outlets. Even the service factors like ambience, parking space, personal

assistance, sitting lounge, loyalty program and home delivery were not differed within the

outlets. It is also expressed that there was a need for better pricing, availability of more

brands and enhanced apparel service like the appointment of trained personnel. Sharma,

Himani (2008) concluded in her study that the technology helps in improving sophistication

that can develop ways to differentiate themselves and cultivate distinctive capabilities that

help achieve high performance. Dawn, Suman Kumar and Kar, Uttiya (2011) suggested

that the convenience in using internet websites and technologies should be emphasized by

the retailers. Online customers are more aware, more sensitive and therefore more difficult

to retain. The industry should ensure that customers must feel safe and secure while

transacting online. Goswami, Shubham and Mathur, Meera (2011) expected in their

studies that India would have an exponential growth in online retail industry due some

favorable driving forces like- demographics, economy, changing lifestyle, exposure to new

ideas etc. Shukre, Anagha (2011) concluded that the websites must be accessible and

operate efficiently. The retailers are suggested to join up the two retailing methods i.e.,

traditional and online. Vasanth, Kiran et. al. (2013) concluded that the internet savvy

generation is using social networking sites that can easily be used as promotional and selling

purposes. Technologies like- “Google Wallets” and other virtual wallets, customers need not

to carry cash and physical wallets. Hence it is expected that online sales in India is a

promising sector in coming future. Ghosh, Debasis (2014) suggested in this research study

that online vendors should design e-commerce portals with more interactivity options,

feelings, emotions and sense of enjoyments along with the detailed information about their

offerings, transparent business terms and conditions with special focus on privacy and

security aspects of customers’ information with the help of advanced technologies will

definitely help in growing the online consumers trust on those portals. Some issues of

concern are durability, delivery quickness, special offers, discounts, after sales service etc.

Poonia, Rashmi Siag ( 2015) studied on emerging online-retail market in India and found

that online retailing gives growth opportunities to many industries such as air cargo services,

warehousing industries, transportation industries, packaging, IT sector, telecom sector etc. It

is also helpful in generating employment opportunities.

OBJECTIVES OF THE STUDY:

To analyze the research problem, smaller objectives are defined that are given below:

i) To find out the behavior of consumers of Bhopal city, with regard to online shopping.

ii) To identify the popular shopping websites among the consumers of Bhopal city.

iii) To identify the kind of assortments being purchased from these websites by the

consumers of Bhopal city.

HYPOTHESES FORMULATED:

H01: There is no significant difference between age of the customers and naming the online

shopping websites.

H02: Familiarity with online shopping is independent of age of the customers.

H03: There is no significant difference between the sex of the consumers and the overall

satisfaction with regard to online shopping websites.

RESEARCH METHODOLOGY:

The research is conducted in Bhopal city. It is a survey based description type of

research study based on primary data. The data is gathered using random sampling technique

with the help of a schedule. The data is collected by conducting face to face interviews with

respondents. A total number of 200 samples were collected but only 196 samples were found

suitable for analysis as rest of them were not complete. Data so collected were tabled in MS-

Excel 2007 worksheet containing all the questions and variables. Later this datasheet was

exported to SPSS 16.0 and proper coding and labeling were done to get the output with

proper headings. The result outputs are drawn with the help of SPSS 16.0 software. For

validation of hypotheses constructed, Chi-Square and ANOVA are applied.

HYPOTHESES TESTING:

The hypotheses testing is performed as here under:

H01: There is no significant difference between age of the customers and identifying the

online shopping websites.

There are two variables in this hypothesis; age of the customers is the independent

one while identifying the online shopping websites is the dependent one. To validate the

hypothesis, one-way ANOVA is conducted. The output of ANOVA analysis is given in the

table 1. In this table, f-Value is 1.422 with degrees of freedom of 4 and 191. The p-Value is

0.228 which is greater than 0.05 hence the null hypothesis is statistically failed to reject at 5%

of significance level. It means that there is no statistically significant difference between the

age of the consumers and the identifying the online shopping websites.

Table 1: ANOVA test for identifying the online shopping websites

Sum of

Squares df

Mean

Square F Sig.

Between

Groups 52.362 4 13.091 1.422 0.228

Within Groups 1757.775 191 9.203

Total 1810.138 195

H02: Familiarity with online shopping is independent of age of the consumers.

Here, the independence of consumers’ familiarity with online shopping and their age

is tested. For this purpose, Chi- Square test of independence is conducted to find the

relationship between the two variances. The output of Chi- Square test is displayed in the

table 2 given further:

Table 2: Chi-Square tests

Value df

Asymp. Sig. (2-

sided)

Pearson Chi-Square 0.964 1 0.326

Likelihood Ratio 0.936 1 0.333

Linear-by-Linear

Association 0.959 1 0.327

N of Valid Cases 196

a. 0 cells (.0%) have expected count less than 5. The minimum

expected count is 11.48.

The Chi-Square table shows that the Pearson Chi-Square value is 0.964 with a degree

of freedom of 1 and p-Value is 0.326. The p-Value is greater than 0.05 hence the null

hypothesis is statistically failed to reject at a significance level of 5%. It means that the

familiarity with online shopping is independent of age of the consumers. In other words it can

be said that there is no significant relationship between the familiarity with online shopping

and age of the consumers.

H03: There is no significant difference between sex of the consumers and the

overall satisfaction with regard to online shopping websites.

There are two variables in this hypothesis; sex of the customers is the independent one

while identifying the online shopping websites is the dependent one. To validate the

hypothesis, one-way ANOVA is conducted. The output of ANOVA analysis is given in the

table 3.

Table 3: ANOVA test for overall satisfaction of the consumers with

online shopping websites

Overall satisfaction with

the online websites

Sum of

Squares df

Mean

Square F Sig.

Between Groups 5.621 1 5.621 5.920 0.016

Within Groups 184.195 194 0.949

Total= 189.816 195

It can be observed in the table 4 that the f-Value is 5.920 with degrees of freedom of 1

and 194. The p-Value is 0.016 which is less than than 0.05 hence the null hypothesis is

statistically rejected at 5% of significance level. It means that there is statistically a

significant difference between the sex of the consumers and the overall satisfaction with

online shopping websites.

RESULTS AND DISCUSSIONS:

1. Data gathered with regard to the variable termed as familiarity with online shopping is

undergone for frequency distribution. It is found in the analysis that the consumer

respondents of Bhopal city are aware of online shopping in majority, responded with the

option as yes.

2. It is found in the study that majority of consumers are familiar with the online

shopping website amazon.com. The next website which is popularly known is flipkart.com

followed by snapdeal.com. These websites are very popular and active in the online retail

industry in India which is supported with various studies. These websites also use strong

promotional strategies and supply chain system in cities like Bhopal.

3. It is also found that majority of consumers used to purchase electrical & electronics

items from online shopping websites. Next product category that is used to be purchased is

footwear followed by cloths & apparels. The electronics & electrical items include mobiles,

laptops, tablets, gadgets, electronic savers, computer accessories, and cameras etc. which are

favorite of young population. These products are offered on lesser prices as compared to

brick & mortar retail outlets. So due to lucrative discounts on branded products, customers

are attracted to shop from online stores.

4. It is found in testing the satisfaction level of the consumers with regard to online

shopping websites on Likert Scale that majority of the respondents were satisfied. Second

majority was identified for the response named as highly satisfied and the third for the

response neither satisfied nor dissatisfied that shows the neutrality of the consumers.

5. By performing one way ANOVA, it is validated that there is no statistically

significant difference between the age of the consumers and the identifying the online

shopping websites. In other words, it can be said that consumers’ knowledge about online

shopping websites is same irrespective of their age.

6. Chi-Square test has verified that the familiarity with online shopping is independent

of age of the consumers. It means that there is no significant relationship between the

familiarity with online shopping and age of the consumers. In simpler words, it can be said

that the knowledge of online shopping is not age specific of the consumers in Bhopal city.

7. One way ANOVA verifies that there is statistically a significant difference between

the sex of the consumers and the overall satisfaction with online shopping websites. So in

simpler words it can be said that the overall satisfaction with online shopping websites

differs with respect to the sex of the customer in Bhopal city.

CONCLUSION:

Finally, it can be concluded that the consumers of Bhopal city are familiar with online

shopping. The consumers are popularly known to online shopping websites such as,

amozone.com, flipkart.com, snapdeal.com etc. The satisfaction of the consumers is found

satisfied with regard to online shopping websites on five point Likert scale. One way

ANOVA testify that age is not a diterminant in respect of consumers’ knowledge about

online shopping websites. ANOVA also verifies that overall satisfaction of the consumers

with regard to online shopping websites differs with sex of the consumers. Chi-Square

validated that the knowledge of online shopping is not age specific of the consumers in

Bhopal city.

REFERENCES:

1. Dawn, Suman Kumar and Kar, Uttiya (2011) E-Tailing in India: Its Issues, Opportunities

and Effective Strategies for Growth and Development, International Journal of

Multidisciplinary Research, Vol.1 Issue 3. (Accessed on 08/01/2014 from

http://zenithresearch.org.in/images/stories/pdf/2011/July/9%20SUMAN%20E-

tailing_Paper.pdf)

2. Ghosh, Debasis (2014)/ Why Indian E-Retailing Market is Still a Partly Success and a

Partly Failure Story?, Journal of Accounting and Marketing, Volume 1, Issue 3.

(Accessed on 20/12/2014 from http://omicsgroup.org/journals/why-indian-eretailing-

market-is-still-a-partly-success-and-a-partly-failure-story-2168-9601.1000113.pdf)

3. Goswami, Shubham and Mathur, Meera (2011).Retail goes online- An Indian

Perspective, International Journal of Management and Tourism, Volume 19, Issue 2, pp

1-11. Accessed on 5/06/2014 from

http://ijmtpublication.com/files/IJMT_volume%2019_2_1.pdf

4. Gupta, Mathala Juliet and Hiremath, Chetan V. (2011). Apparel Retail Outlet Selection:

Influence Of Service Levels In Goa. Indian Journal of Marketing, Vol. 41, Issue 11: pp.

4-14.

5. Sharma, Himani (2008). Leveraging Technology: Retail Industry Gaining Competitive

Advantage. Journal of IMS Group, Vol. 5 No 2: pp 7-11.

6. Shukre, Anagha (2011) Youths’ Perception Towards Online Shopping: An Empirical

Study in Delhi/ NCR, Vishwakarma Business Review, Volume I, Issue 2, pp 9-19.

(Accessed on 15/08/2014 from

http://vbrjournal.net/index.php/vbr/article/view/52575/42204)

7. Sonwalkar, Jayant and Nema, Geeta (2008). A Study of the Factors Responsible for

Brand Preference in FMCG Products among College Students. Journal of IMS Group,

Volume 5, No. 1, pp 44-49.

8. Vasanth, Kiran and others (2013)/ Online Sales in India- Opportunities and challenges,

Global Journal of Commerce & Management Perspective, Vol. 2(2), pp 73-80. (Accessed

on 06/08/2014 from http://www.gifre.org/admin/papers/gjcmp/Online%20Sales.pdf).

9. http://shodhganga.inflibnet.ac.in/bitstream/10603/8374/4/04 accessed on 12-7-14

10. http://ripublication.com/ijmibs-spl/ijbmisv4n1spl_10.pdf (Fatima/ Flipkart-Myntra)

11. http://www.technopak.com/files/E-tailing_in_India.pdf (E-tailing in India: Unlocking the

Potential)

12. Kothari, C.R. (2002). Research Methodology: Methods & techniques, New Age

International, 2e.

13. Kotler, Phillip (2003). Marketing Management, Pearson Education, 11th ed., pg. 535.

Author:

Dr. Bhagwan Singh: The author is presently associated with Lakshmi Narain College of

Technology, Bhopal. He has multidisciplinary expertise with qualifications of Certificate in

French language, B.Ed., PGDCA, MLIS, MPhil. (LIS), MBA, and PhD (Mgmt). He has got

six research papers published in reviewed journals, books, and conference proceedings. He

has attanded one international and various national conferences. He has been participating

periodically in capacity building programmes. He is a life member of ISTE and ILA and

member of AIMA. His fields of interest are research methodology, retail management,

marketing management, computer applications etc.

ROLE OF EFFECTIVE COMMUNICATION IN ORGANIZATION

By

Dr. Dharmesh Jain

Head and Reader

Department of Management of Studies

S.A.T.I. Vidisha (M.P.)

ABSTRACT

Communication is one of the most important aspects of management. Without strong

communication, employees won't even understand what the manager wants them to

accomplish. Effective communication also helps employees to value their jobs more by

minimizing conflicts and letting each employee communication feel heard.

Key Words: Communication, Management, Employees, Effective

1. One way Communication Process

Communication may be defined as a process concerning exchange of facts or ideas between

persons holding different positions in an organisation to achieve mutual harmony. The

communication process is dynamic in nature rather than a static phenomenon.

Sender Encoding Message Channel Decoding Receiver

2. Two way Communication Process

Perceived Message &

Internal Response

A communication cycle and two-way communication cycle are in point of fact two majorly

different things. If we scrutinize closely the composition of communication – the actual

formation and parts – we will realize that a cycle of communication is not a two-way

communication in its whole. Meaning, two way communications is not as simple as one may

conclude. One can improve two-way or interpersonal communication by focusing on the eyes

of the person speaking, making eye contact, watching body language, responding

appropriately with comments, questions, and paraphrasing, and summarizing to authenticate

main points and an precise perceptive.

Two-way communication involves feedback from the receiver to the sender. This allows the

sender to know the message was received exactly by the receiver. Communication is also

negotiated which means that the sender and receiver listen to each other, the messages then

gathers information to respond. One person is the sender, which means they send a message

to another person via face to face, email, telephone, etc. The other person is the receiver,

which means they are the one getting the senders message. Once receiving the message, the

receiver sends a response back. For example, Person A sends an email to Person B --> Person

B responds with their own email back to Person A. The cycle then continues. This chart

demonstrates two-way communication and feedback

Encoder/ Sender

Encoding Ideas

(Verbal/Non Verbal)

Decoding of feedback

Decoder / Receiver

Decoding

Encoding of Response

Feedback

Message

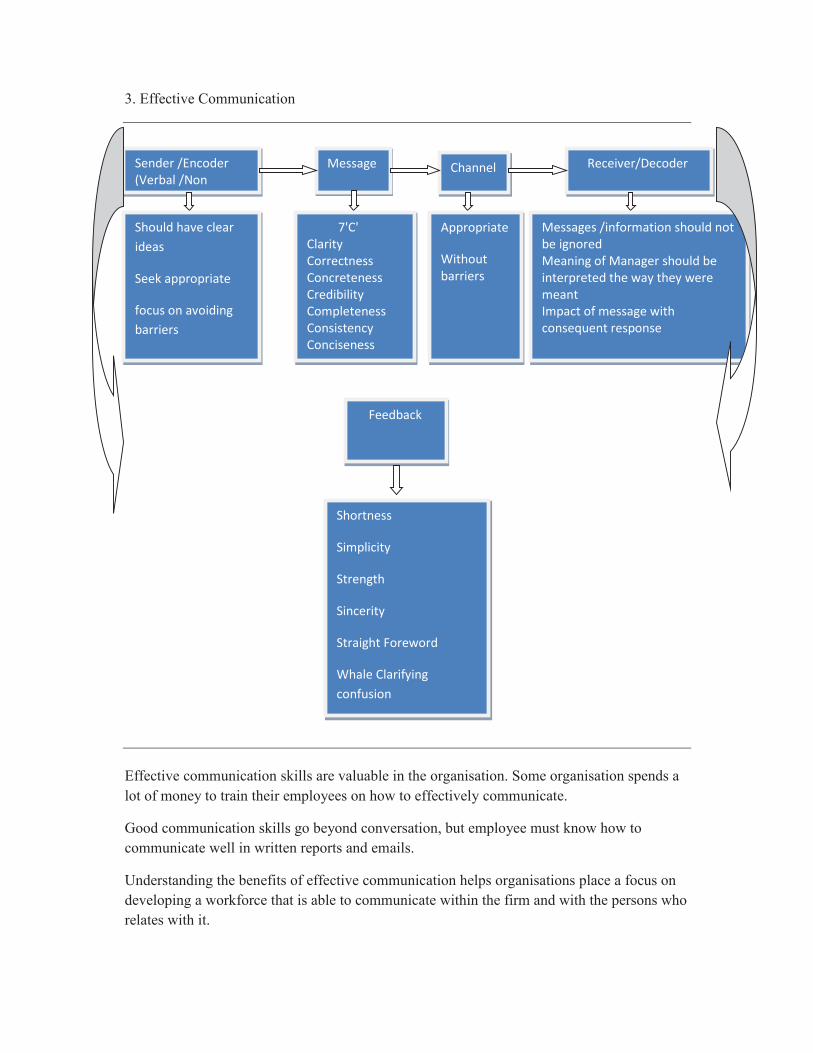

3. Effective Communication

Effective communication skills are valuable in the organisation. Some organisation spends a

lot of money to train their employees on how to effectively communicate.

Good communication skills go beyond conversation, but employee must know how to

communicate well in written reports and emails.

Understanding the benefits of effective communication helps organisations place a focus on

developing a workforce that is able to communicate within the firm and with the persons who

relates with it.

Sender /Encoder

(Verbal /Non

Message Receiver/Decoder Channel

Should have clear

ideas

Seek appropriate

focus on avoiding

barriers

7'C'

Clarity

Correctness

Concreteness

Credibility

Completeness

Consistency

Conciseness

Appropriate

Without

barriers

Messages /information should not

be ignored

Meaning of Manager should be

interpreted the way they were

meant

Impact of message with

consequent response

Feedback

Shortness

Simplicity

Strength

Sincerity

Straight Foreword

Whale Clarifying

confusion

Effective workplace communication is important in companies with workplace diversity.

Good communication skills help to reduce the barriers erected because of language and

cultural differences.

Message

1. Courtesy; Be polite and respectful for others, focus on 'YOU' attitude instead of 'I' attitude.

2. Clarity; Arrange appropriate words to have main ideas in the given sentence.

3. Correctness; Maintain proper grammar, punctuation and spelling with acceptable writing

mechanism.

4. Concreteness; Use specific facts, figure with image-building words.

5. Credibility; The sender should establish his credibility by building trust, sp the receiver

feel no problem in accepting the sender's statement.

6. Completeness & consistency; provide all necessary information with answering all

questions asked in desirable way.

7. Conciseness; Using the fewest possible words i.e., by keeping the message short and sweet

by avoiding unnecessary repetition to save the time of both sender and receiver.

Feedback

1. Sincerity; The geniuses & sincerity shown up in the tone communication and the language

that the sender writes.

2. Shortness; Brevity is the soul of wit i.e. the ability of sender to draft message in a crisp

simple style.

3. Simplicity; The ability to understand & explain even the most complex issue in a simple

way by using simple language and ideas.

4. Strength; The strength of any message comes from the fact that it convey the meaning

intended i.e. the message emanates from the credibility of the sender.

Conclusion

1. Communication is the process of transmitting information and common understanding

from one person to another by using elements of communication. the effective

communication can be retarded by number of barriers.

2. While giving feedback one should focus on avoiding criticism of particular person directly

by not highlighting the negative area too much and also look at area that can be improved

upon.

3. Effective communication is a two way process that requires efforts and skills by both

sender and receiver.

The success of business depends not only on what you communicate but also on how well

you communicate.

The individual employee and the organization together make success and failure by

communication with their internal & external customers.

The advantages of effective communication have better interpersonal relationship, better

information availability, better decision making, improved productivity, high employee

satisfaction.

Bibliography

Agee, W.K., R.H. Ault and E. Emery, eds, 1979, Introduction to Mass Communication, New

York: Harper and Row, Publishers.

Ahuja, B.N. and S.S. Chopra, 1989, Communication, New Delhi: Surjeet Publications.

Albrecht, T.L. and M.B. Adelman, eds, 1987a, Communicating social support, Newbury

Park, CA: Sage.

———, 1987, ‘Dilemmas of Supportive Communication’ in T.L. Albrecht, and M.B.

Adelman, eds, Communicating Social Support, Newbury Park, CA: Sage, pp. 240–254.

Allport, G.W., 1937, Personality: A Psychological Interpretation, New York: Holt.

Baxter, Leslie A., and Dawn O. Braithwaite, eds. 2008. Engaging theories in interpersonal

communication: Multiple perspectives. Thousand Oaks, CA: SAGE.

Canary, Daniel J., Michael J. Cody, and Valerie L. Manusov. 2008. Interpersonal

communication: A goals-based approach. 4th ed. Boston: Bedford/St. Martin’s.

DeVito, John A. 2009. The interpersonal communication book. 12th ed. Boston: Allyn &

Bacon.

“CORPORATE GOVERNANCE AND SEBI”

By

Dr. Anil Kothari

Professor and Coordinator (MBA Integrated)

RGPV Bhopal (M.P)

E-mail – [email protected]

ABSTRACT

Aims and Objectives:

The aim of this paper is to highlight the role of SEBI in Corporate Governance in

India and the impact caused by it. Corporate governance is the management of the rights of

shareholders as the true owners of the corporation on behalf of the shareholders. SEBI’s

regulatory framework will strengthen existing governance practices and also provide a strong

incentive to avoid corporate failures. Companies that do not employ meaningful governance

procedures will have to pay a significant risk premium when competing for scarce capital in

today’s public markets.

Materials and Methods:

This retrospective study was done using data collected from various sources like

books, newspapers, magazines and websites. Gathered data was further sorted, analysed and

converted into useful information through evaluation.

Conclusion:

With the recent increase in corporate scandals a plethora of corporate governance norms and

standards have sprouted around the country. Development of norms and guidelines should be

first step in a serious effort to improve corporate governance. The bigger challenge in India is

proper implementation of the rules at the ground level. It appears that outside agencies like

analysts and stock markets have the most influence on the actions of managers in the leading

companies of the country. Nevertheless, with industry organizations and SEBI themselves

pushing for an improved corporate governance system, the future of corporate governance in

India promises to be distinctly better than the past.

Key Words: Corporate Governance, SEBI, Scandals, Committees

INTRODUCTION

Investment is done by keeping faith in the ability of a corporation’s management.

Investor expects the board and the management for the safety of the capital and also earns a

rate of return that is higher than the cost of capital. Corporate governance is the management

of the rights of shareholders as the true owners of the corporation on behalf of the

shareholders. “The corporate governance systems should be in place to avoid corporate

misconduct and ensure discipline”1The Securities and Exchange Board of India (“SEBI”)

believes that corporate governance standards in India must improve. This is because these

standards themselves were evolving in keeping with market dynamics. Accordingly, the

Committee on Corporate Governance was constituted by SEBI, to evaluate the adequacy of

existing corporate governance practices and further improve these practices. The Committee

comprised members from various fields of public and professional life. This includes captains

of industry, academicians, public accountants and people from financial press and from

industry forums. The issues discussed by the Committee primarily related to audit

committees, audit reports, independent directors, related parties, risk management,

directorships and director compensation, codes of conduct and financial disclosures. The

Committee’s recommendations in the final report were selected based on parameters

including their relative importance, fairness, and accountability, and transparency, ease of

implementation, verifiability and enforceability. Some recommendations focus on

strengthening the responsibilities of audit committees; improving the quality of financial

disclosures, including those related to related party transactions and proceeds from initial

public offerings; requiring corporate executive boards to assess and disclose business risks in

the annual reports of companies; introducing responsibilities on boards to adopt formal codes

of conduct; the position of nominee directors; and stock holder approval and improved

disclosures relating to compensation paid to non-executive directors. Non-mandatory

recommendations include moving to a regime where corporate financial statements are not

qualified; instituting a system of training of board members; and the evaluation of

performance of board members. The Committee believes that these recommendations will

result in governance into specific requirements. SEBI’s regulatory framework will strengthen

existing governance practices and also provide a strong incentive to avoid corporate failures.

Companies that do not employ meaningful governance procedures will have to pay a

significant risk premium when competing for scarce capital in today’s public markets.

Table: Recommendations of various committees on Corporate Governance in India

CII Code recommendations

(1997)

Birla Committee (SEBI)

recommendations (2000)

Narayana Murthy

committee (SEBI)

recommendations (2003)

a) No need for German

style two-tiered board

b) For a listed company

with turnover exceeding

Rs.100 crores, if the

Chairman is also the MD,

at least half of the board

should be Independent

directors, else at least 30%

c) No single person should

hold directorships in more

than 10 listed companies.

d) Non-executive directors

should be competent and

active and have clearly

defined responsibilities like

in the Audit Committee.

e) Directors should be paid

a commission not exceeding

1% (3%) of net profits for

a company with (out) an

MD over and above sitting

fees. Stock options may be

considered too.

f) Attendance record of

directors should be made

explicit at the time of re-

appointment. Those with

less than 50% attendance

should not be reappointed.

g) Key information that

must be presented to the

board is listed in the code.

h) Audit Committee: Listed

companies’ with turnover

over Rs. 100 crores or paid-

up capital of Rs. 20 crores

should have an audit

committee of at least three

members, all non-executive,

competent and willing to

work more than other non-

executive directors, with

clear terms of reference

and access to all financial

a) At least 50% non-

executive members

b) For a company with an

executive Chairman, at least

half of the board should be

independent directors¨, else

at least one-third.

c) Non-executive Chairman

should have an office and be

paid for job related expenses.

d) Maximum of 10

directorships and 5

chairmanships per person.

e) Audit Committee: A

board must have a qualified

and independent audit

committee, of minimum 3

members, all non-executive,

majority and chair

independent with at least one

having financial and

accounting knowledge. Its

chairman should attend AGM

to answer shareholder

queries. The committee

should confer with key

executives as necessary and

the company secretary should

be he secretary of the

committee. The committee

should meet at least thrice a

year -- one before

finalization of annual

accounts and one necessarily

every six months with the

quorum being the higher of

two members or one-third of

members with at least two

independent directors. It

should have access to

information from any

employee and can investigate

matter within its TOR, can

seek outside

legal/professional service as

a) Training of board

members suggested.

b) There shall be no nominee

directors. All directors to be

elected by shareholders with

same responsibilities and

accountabilities.

c) Non-executive director

compensation to be fixed by

board and ratified by

shareholders and reported.

Stock options should be

vested at least a year after

their retirement. Independent

directors should be treated

the same way as non-

executive directors.

d) The board should be

informed every quarter of

business risk and risk

management strategies.

e) Audit Committee: Should

comprise entirely of

“financially literate” non-

executive members with at

least one member having

accounting or related

financial management

expertise. It should review a

mandatory list of documents

including information

relating to subsidiary

companies. “Whistle blowers” should have direct access to it and all employees

be informed of such policy

(and this should be affirmed

annually by management).

All “related party” transactions must be

approved by audit

committee. The committee

should be responsible for the

appointment, removal and

remuneration of chief

information in the company

and should periodically

interact with statutory

auditors and internal

auditors and assist the

board in corporate

accounting and reporting.

i) Reduction in number of

nominee directors. FIs

should withdraw nominee

directors from companies

with individual FI

shareholding below 5% or

total FI holding below 10%.

well as secure attendance of

outside experts in meetings.

It should act as the bridge

between the board, statutory

auditors and internal auditors

with far ranging powers and

responsibilities.

f) Remuneration

Committee: The

Remuneration committee

should decide remuneration

packages for executive

directors. It should have at

least 3 directors, all non

executive and be chaired by

an independent director.

g) The board should decide

on the remuneration of non-

executive directors and all

remuneration information

should be disclosed in annual

report

h) At least 4 board meetings

a year with a maximum gap

of 4 months between any 2

meetings. Minimum

information available to

boards stipulated.

internal auditor.

f) Boards of subsidiaries

should follow similar

composition rules as that of

parent and should have at

least one independent

director s of the parent

company.

g) The Board report of a

parent company should have

access to minutes of board

meeting in subsidiaries and

should affirm reviewing its

affairs.

h) Performance evaluation of

non-executive directors by all

his fellow Board members

should inform a re-

appointment decision.

i) While independent and

non-executive directors

should enjoy some protection

from civil and criminal

litigation, they may be held

responsible of the legal

compliance in the company’s affairs.

j) Code of conduct for Board

members and senior

management and annual

affirmation of compliance to

it.

Source: http://unpan1.un.org/intradoc/groups/public/documents/APCITY/UNPAN023826.pdf

A comparison of the three sets of recommendations in above Table reveals the progress in the

corporate governance in India over the years. An outline provided by the CII supported the

Birla Committee report of SEBI. SEBI implemented the recommendations of the Birla

Committee through the enactment of Clause 49 of the Listing Agreements. “They were

applied to companies in the BSE 200 and S&P C&X Nifty indices, and all newly listed

companies, on March 31, 2001; to companies with a paid up capital of Rs. 10 crore or with a

net worth of Rs. 25 crore at any time in the past five years, as of March 31, 2002; to other

listed companies with a paid up capital of over Rs. 3 crore on March 31, 2003.”2 The

Narayana Murthy committee worked on further refining the rules. The recommendations also

show that much of the thrust in Indian corporate governance reform has been on the role and

composition of the board of directors and the disclosure laws. The Birla Committee paid

much-needed attention to the subject of share transfers. In the area of corporate governance,

the spirit of the laws and principles is much more important. Developing a positive culture

and atmosphere of corporate governance is essential. Corporate governance norms should not

become just another legal item to be checked off by managers at the time of filing regulatory

papers.

CHANGES SINCE LIBERALIZATION

Liberalization has witnessed wide-ranging changes in both laws and regulations driving

corporate governance as well as general consciousness about it. “In the aftermath of

economic liberalisation corporate heavyweights have started mulling over the buzz phase of

corporate governance.”3

1. Most important development in the field of corporate governance and investor

protection in India has been the establishment of the Securities and Exchange Board

of India (SEBI) in 1992 and its gradual empowerment since then. It has played a

crucial role in establishing the basic minimum ground rules of corporate conduct in

the country. Concerns about corporate governance in India were started in the early

90’s – the Harshad Mehta stock market scam of 1992 followed by incidents of

companies allotting preferential shares to their promoters at deeply discounted prices

as well as those of companies simply disappearing with investors’ money.

2. These concerns about corporate governance stemming from the corporate scandals as

well as opening up to the forces of competition and globalization gave rise to several

investigations into the ways to fix the corporate governance situation in India. One of

the first among such endeavours was the CII Code for Desirable Corporate

Governance developed by a committee chaired by Rahul Bajaj. The committee was

formed in 1996 and submitted its code in April 1998.

3. SEBI constituted two committees to look into the issue of corporate governance. The

first chaired by Kumar Mangalam Birla that submitted its report in early 2000 and the

second by Narayana Murthy three years later.

4. The SEBI committee recommendations have had the maximum impact on changing

the corporate governance situation in India. The Advisory Group on Corporate

Governance of RBI’s Standing Committee on International Financial Standards and

Codes also submitted its own recommendations in 2001.

CORPORATE GOVERNANCE SCAMS

1. Vyapam scam

It is an admission & recruitment scam involving politicians, senior officials and businessmen

in the Indian state of Madhya Pradesh. Vyapam is a self-financed and autonomous body

incorporated by the State government responsible for conducting several entrance tests in the

state. These entrance exams are held for recruitment in government jobs and admissions in

educational institutes of the state. The scam involved a admission of undeserving candidates,

who bribed politicians and MPPEB officials through middlemen, to get high ranks in these

entrance tests. The scam also led to between 23 and 40 'unnatural' deaths of involved

individuals.

The scam involved 13 different exams conducted by Vyapam, for selection of medical

students and state government employees (including food inspectors, transport constables,

police personnel, school teachers, dairy supply officers and forest guards). The exams were

taken by around 3.2 million students.

2. Satyam Scam

The biggest corporate scam in India has come from one of the most respected businessmen.

Satyam founder Ramalinga Raju had to resign as chairman after admitting to manipulating

the account books. He filled the fictitious assets with real ones through Maytas acquisition

which failed, after that he decided to confess the crime. “Notwithstanding his constant

exhortations that his employees adopt a global mindset in the shrinking world, Ramalinga

Raju never followed this advice. In the end it was his lust for land that felled the IT czar and

took him to jail.”4 It was a fraud that involve about Rs 8,000 crore, Satyam is heading for

more trouble in the days ahead.

3. Harshad mehta scam

Harshad Mehta triggered a rise in the Bombay Stock Exchange in the year 1992 by trading in

shares at a premium across many segments. Taking advantages of the flaws in the banking

system, Harshad Mehta diverted Rs 4000 crore from the banks to stockbrokers between April

1991 to May 1992. Harshad Mehta moved money from one bank account to another,

especially illegally or dishonestly from several banks and millions of investors were conned

in the process. He was exposed, the markets crashed and he was arrested and banned for life

from trading in the stock markets. “Once the scam was exposed, though, a lot of banks were

left holding BRs which did not have any value - the banking system had been swindled of a

whopping Rs 4,000 crore.”5 He died in 2002 with many litigations still pending against him.

4. Ketan Parekh

Ketan Parekh targeted smaller exchanges like the Allahabad Stock Exchange and the Calcutta

Stock Exchange, and bought shares in fictitious names. His dealings revolved around shares

of ten companies like Himachal Futuristic, Global Tele-Systems, SSI Ltd, DSQ Software,

Zee Telefilms, Silverline, Pentamedia Graphics and Satyam Computer (K-10 scrips). “In

2001, a payment crisis triggered by Kolkata-based beers brought Parekh, who was known as

KP, down. A probe by market regulator SEBI along with other investigating agencies

unearthed the skeletons and KP was proclaimed a rogue trader. He was banned in the stock

market since 2001.”6 He borrowed Rs 250 crore from Global Trust Bank to fuel his

ambitions. Ketan alongwith his associates also managed to get Rs 1,000 crore from the

Madhavpura Mercantile Co-operative Bank. According to RBI regulations, a broker is

allowed a loan of only Rs 15 crore.

5. C.R.Bhansali Scam

He launched the finance company such as CRB Capital Markets, CRB Mutual Fund and CRB

Share Custodial Services. He collected money from the public through fixed deposits, bonds

and debentures during 1992-96. The money was transferred to companies that never existed.

The Bhansali scam resulted in a loss of over Rs 1,200 crore. Bhansali also succeeded to rise

about Rs 900 crore from the markets. “Bhansali was arrested as soon as he landed in Delhi.

Bhansali's advocate however maintained that his client had surrendered himself to CBI

officials 'as soon as he came to know that he was embroiled in an alleged case of fraud by the

company, which was being investigated by the CBI.”7 Bhansali tried borrowing more money

from the market. This led to a financial crisis. It became difficult for Bhansali to sustain

himself. The Reserve Bank of India (RBI) refused banking status to CRB and he was in the

dock. SBI was one of the banks to be hit by his huge defaults

6. Sohin daya scam

The main accused in the multi-crore shoes scam was Sohin Daya, son of a former Sheriff of

Mumbai. Others were Rafique Tejani of Metro Shoes, and Kishore Signapurkar of Milano

Shoes arrested for creating several leather co-operative societies which did not exist. They

raised loans of crores of rupees on behalf of fictitious societies. “The scam had cost the

government around Rs 1200 crore, while the poor Cobblers of Mumbai were severely

affected.”8 The scam was exposed in 1995. The accused created a fictitious cooperative

society of cobblers to take advantage of government loans through various schemes.

7. DINESH DALMIA’S” STOCK SCAM

Dinesh Dalmia was the managing director of DSQ Software Limited. He was involved in a

stocks scam of Rs 595 crore. His group included DSQ Holdings Ltd, Hulda Properties and

Trades Ltd, and Power flow Holding and Trading Pvt Ltd. “Mr. Dalmia, accused of criminal

breach of trust, cheating and fraud, is alleged to have induced National Securities Depository

Limited (NSDL) to dematerialise and credit 130 lakh equity shares of the software company

as fully paid shares.”9 He fled to US in 2003 and arrested by CBI in 2006.

8. Abdul KarimTelgi

He uses to sell fruits and vegetables on trains. He was the man behind one of the big scam

that rocked India. The fake stamp racket involving Abdul Karim Telgi was exposed in 2000.

The loss is estimated to be Rs 171.33 crore. In 1994, Abdul Karim Telgi acquired a stamp

paper license from the Indian government and began printing fake stamp papers. Telgi bribed

to get into the government security press in Nashikand bought special machines to print fake

stamp papers. “Several cases were against him in the '90s. Denied bail but not arrested. He

was arrested in August 2001, after he's made crores in a business spanning 72 centres in 12

states over 10 years.”10

9. The money market fraud

Virendra Rastogi chief executive of RBG Resources was deceiving banks worldwide of an

estimated $1 billion. “After fooling the world of finance with a sophisticated fraud spanning

three continents and six years from 1996 to 2002, Rastogi's RBG Resources fell under the

suspicion of Britain's Serious Fraud Office (SFO) because of a simple unintended human

error. In 2002 a PricewaterhouseCoopers auditor in Romania became suspicious when six

documents - purporting to be sent from six different companies all over the world - were all

sent from the same fax machine in Hong Kong.”11 According to CBI five companies, whose

directors were the four Rastogi brothers named Subash, Virender, Ravinde and Narinder

exported bicycle parts during 1995-96 to Russia and Hong Kong by heavily over invoicing

the value of goods for claiming excess duty draw back from customs.

CONCLUSION

With the recent increase in corporate scandals corporate governance norms and

standards have grew around the country. Different rules have been identified in recent

surveys and their number is increasing. India has been no exception to the rule. Several issues

deserve the attention. The problems for private companies, that form a vast majority of Indian

corporate entities, are not given any attention. It must be understood that ownership and

control are separate. Minority shareholders are exploited. Serious efforts should be done to

develop guidelines for corporate governance. The implementation of the rules at the ground

level is necessary. The influence of top companies dominates the role of analysts and stock

market. Adequate corporate governance is needed in the Indian company. Even the strictest

norms can be flawed in a system with widespread corruption. The industry organizations and

SEBI themselves pushing for an improved corporate governance system, the future of

corporate governance in India promises to be distinctly better than the past.

References:

1. Bhole, L.M. (2009): “Financial Markets & SEBI”, Tata Mcgraw Hill Private Ltd., New Delhi, p. 235

2. Vashisht, A.K., Tandon, B.B., and Arya, P.P. (2006): “Corporate Governance”, Deep and Deep Publications, New Delhi, Page 196

3. Fernando A.C. (2009): “Business Ethics and Corporate Governance”, Dorling Kindersley (India) Pvt Ltd., New Delhi, Page 12

4. Kingshuk Nag: “Satyam case: Ramalinga Raju's lust for land tripped him”, Apr 10, 2015

5. http://indianeconomyataglance.blogspot.in/2009/03/harshad-mehtas-scam.html

6.http://indiatoday.intoday.in/story/ketan-parekh-stock-market-share-prices-sebi-k-10-

stocks/1/208342.html

7. http://www.icmrindia.org/free%20resources/casestudies/Finance%20freecasep2.htm

8. http://www.dnaindia.com/mumbai/report-7-high-profile-scams-that-rocked-maharashtra-

and-their-net-worth-2003438

9. “Stock scam: Dinesh Dalmia arrested”: The Hindu, February 14, 2006

10. “Abdul Karim Telgi Ki Ajeeb Dastan”: The Times of India, Nov 16, 2003

11. Sarkar, Dipankar De: “Rastogi's multi-million dollar scam was right out of Bollywood”, Hindustan Times, June 06, 2008

WOMEN EMPOWERMENT AND RURAL PROGRAMMES

By

Dr. Jitendra Kumar Yadav

Principal , Laxmi Bai Sahuji Institute of Management

Jabalpur (MP)

ABSTRACT

----------------------------------------------------------------------------------------------------------------

Women empowerment and Rural Programmes is a debatable subject. After independence of

India, the constitutional makers and national leaders strongly demand equal social position of

women with men. The past three decades have witnessed a steadily increasing awareness of

the need to empower women through measures to increase social economic and political

equity, the border access to fundamental human rights, improvement in nutrition, basic health

and education. Along with awareness of the subordinate status of women has come the

concept of gender as an overarching socio-cultural variable, seem in relation to other factors,

such as race, class, age and ethnicity. Gender equality refers to that stage of human social

development at which “the rights, responsibilities and opportunities of individuals will not be

determined by the fact of being born male or female”, in other words, a stage when both men

and women realize their full potential. Today we have seen the women occupied the

respectable positions in all walks of the fields. Yet, they have not absolutely freed some

discrimination and harassment of the society. Therefore, each and every one should be

careful to promote the women status.

In the changing scenario of the Indian society efforts has been made to empower

women so that they can not only joins hand in making important decisions in the family or

society but also hold the public office for development.

Keywords: Women Empowerment , Rural Programmes, Opportunity.

INTRODUCTION:

The very issue of women empowerment arises because of the stark reality that women are

still marginalized and sidelined from the mainstream as a use-and-throw commodity. The

patriarchal canopy had always denied women the warm rays of autonomy and freedom.

Empowerment of women involves many things, economic opportunity, property rights,

political representation, social equality, personal rights

Women comprise nearly half of the national population of a country. Of Course, the

Globalization provided opportunities of education and employment to urbanwomen and

helped them to develop and possess all the rights equally with men. Butthe problem is that

the women in rural areas are still backward in education, socialstatus, economic background,

political matters, etc. Hence, the development of thecountry is inescapably linked with the

status of development of rural women. Economic empowerment is one approach to enable

women to realize their inherent knowledge, skills and competences for creation of small

business enterprises. There are shining examples from the developing countries to illustrate

women entrepreneurs who started small and grew to large enterprises. Women are considered

as a focal point and the unifying force in the family. While their contribution to the family

and society is considerable, they are subjected to numerous constraints undermining their

potentials. They receive only small share indevelopment opportunities and are often excluded

from education, better jobs, participation in political system and better health care, decision

making, etc. Besides, they suffer from physiological, physiological, social and cultural

barriers, which hinder their empowerment. In rural areas, women are preoccupied with

mostly household work including the bearing and rearing of children. Accordingly, the

opportunities for improving their conditions are limited. The Government of India and state

governments have already been formulated social welfare, women empowerment and rural

development Programmes for the betterment of women, backward classes and vulnerable

groups. These Programmes are discussed as under.

WELFARE PROGRAMMES OF GOVERNMENT:

Following are a few Government Programmes, which aimed at empowerment of women,

social welfare and rural development in different aspects:

1.Integrated development programme (IRDP)

2. Training of Rural Youth for self-Employment (TRYSEM)

3. Jawahar Rozgar Yojana (JRY)

4. Professional women’s Development Network (PWDN)

5. The National Employment Guarantee Act(NREGA)

6. Pradhan Mantri Gram Sadak Yojana (PMGSY)

7. Indiara Awas Yojana (IAY)

8. Swarnajayanti Gram Swarozgar Yojana (SGSY)

9. Sampoorna Grameen Rozgar Yojana (SGRY)

10. Swarna Jayanti Shahari Rozgar Yojana (SJSRY)

These Programmes are helping Empowering Women and Rural development.

1.Integrated development programme (IRDP): Various kinds of agencies are carrying on

the task of providing ruralemployment. They include, Employment Guarantee Scheme, Food

for Work Programme, small Farmers Development Agency, Marginal Farmers and

Agricultural Laborers, Drought prone Areas Development Proramme, Desert Development

Programme, Command Area Development Programme, etc. TheSixth plan (1980-85)

proposed that such multiplicity of programmes for the ruralpoor operated through a

multiplicity of agencies should be ended and replaced byone single integrated programme

operative throughout the country. This programme was named the Integrated Rural

Development Programme (IRDP), which was initiated on 2nd October 1980 in all the 5011

blocks in India. The IRDP aims at providing self-employment opportunities to the rural poor

through assistance in the form of subsidy and bank credit to enable them acquire productive

assets and appropriate skills to cross the poverty line.

2. Training of Rural Youth for self-Employment (TRYSEM): TRYSEM is centrally

sponsored scheme. It started functioning since15th August 1979. It aimed at providing basis

technical and entrepreneurial skills to the rural youth from families below the poverty line to

enable them to take up self-employment in the broad fields of agriculture and allied sectors,

industries,services and business activities.

3. Jawahar Rozgar Yojana (JRY): On 28th April 1989, Prime Minister Rajiv Gandhi

launched the Jawahar RozgarYojana and the primary objective which is general of gainful

employment for the unemployed and underemployed, men and women in the rural areas.

4. Professional women’s Development Network (PWDN): PWDN was established in 1992

in order to offer a comprehensive service of women’s development and training to both

employers and individuals in areas of consultancy, research training, development,

monitoring and such other training programme

5. The National Employment Guarantee Act (NREGA): The National Employment

Guarantee Act was notified on 7th September,2005, aims at enhancing live hood security of

households in rural areas of the country by providing at least 100 days of guaranteed wage

employment in afinancial year to every household whose adult member’s volunteers to do

unskilled manual work. The NREGA Act which came into existence on Feb 2, 2006 was

initially

Implemented into 200 districts of the country in the I Phase. In the II Phase beginning 2007-

08, it was further extended to 130 more districts for implementation. From April 2008, it

extended across the country. Over the three years since it became operational, NREGA

(2005) has had a positive impact on the lives of millions of people across the poorest district

in the country. In particular, it holds the powerful prospect of bringing major changes in the

lives of women. It is rechristened as MAHATHMA GANDHI NATIOAL RURAL

EMPLOYMENT GUARANTEE SCHEME (MGNREGS) on the occasion of 140th Birth of

Mahatma Gandhi.

6. Pradhan Mantri Gram Sadak Yojana (PMGSY): Launched in December 2000 as a 100

percent CSS, PMGSY aims to provide allwearer connectivity to all the eligible unconnected

rural habitations. Bharat Nirman emerges connectivity by 2009 to all the habitations with a

population of 1000 or more in the lains of 500 or more in the hilly, desert and tribal areas.

7. Indiara Awas Yojana (IAY): Indira Awas Yoyana was implemented since 1985-86 under

the Rural Landless Employment Gurantee Scheme (RLEGP).Indira Awas Yojana aims to

provide dwelling units free of cost – sharing basis in the rates of 75:25 between the Center

and the States.

8. Swarnajayanti Gram Swarozgar Yojana (SGSY):SGSY, launched in April 1999 after

restructuring the integrated Rural DevelopmentProgramme and allied schemes, is the only

self-employment programme for therural poor. The objective is to bring the self-employed

above the poverty line by providing them income-generating assets through bank credit and

Government subsidy.

9. Sampoorna Grameen Rozgar Yojana (SGRY): SGRY launched on September 25, 2001

to provide additional wage employment inthe rural areas, has cash and food grains

component and the Centre bears 75 percent and 100 percent of the cost of the two with the

balance borne by the

States/Union Territories.

10. Swarna Jayanti Shahari Rozgar Yojana (SJSRY): In December 1997, the Urban Self-

Employment Programme (USEP) and theUrban Wage Employment Programme (UWEP),

which are the two specialcomponents of SJSRY, substitute for various programmes operated

earlier forurban poverty alleviation. The SJSRY is founded on a 75:25 basis between

theCenter and States.

While the benefits of the above mentioned programmes flowing to the women can be

measured in quantitative terms, for other programmes such as Pradhan Mantri Gram Sadak

Yojana (PMGSY), it isnot always possible to collect the segregated data reflecting the direct

benefits flowing to the rural women. But this programme does have a significant impact on

the living conditions of the rural women in terms of providing connectivity through the rural

roads, which may enhance the opportunities for the girl child to have an access to the

educational facilities.

Similarly, due to better rural roads women may have easier access to the health facilities and

local market which may not only increase their productivity but may also increase their

awareness which goes a long way in changing the traditional social structure and resulting in

improvement of the rural women.

We will see percentage of benefiters from someof these Govt. Programmes:

Name of Programmes Percentages of Benefiters

Swarna Jayanti Gram Swarazgar Yojana

(SGSY)

78.33

Indira Awas Yojana (IAY) 39.17

Ashraya Yojana 55.00

Prime Minister’s Rozgar Yojana(PMRY) 28.33

Navagram Yojana 23.33

Stree Shakti Yojana 95.00

National Rural Employee Guarantee

Scheme (NGEGS)

17.50

Now-a-days economic development is one of the factors that have changed the entire

scenario of social and cultural environment within the country especially for the women. The

rural women are engaged in small-scale entrepreneurship programme with the help of Self

Help Groups. Through that they were economically empowered and attaining status in family

and community.

Rural women play a vital role in farm and home system. She contributes substantially inthe

physical aspect of farming, livestock management, post-harvest and allied activities. Her

direct and indirect contribution at the farm and home level along with livestock management

operation has not only help to save their assets but also led to increase the family income. She

performs various farm, livestock, post-harvest and allied activities and possesses skills and

indigenous knowledge in these areas. The women were empowering themselves technically

to cope with the changing times and productively using their free time and existing skills for

setting and sustaining enterprises. They were engaged in starting individual or collective

income generation programme with the help of self-help group. This will not only generate

income for them but also improve the decision-making capabilities that led to overall

empowerment.

Empowering women particularly rural women is a challenge. Following are some of the

personal and social capabilities, which were developed as result of taking up enterprise

among rural women.

• Economic empowerment

• Improved standard of living

• Self confidence

• Enhance awareness

• Sense of achievement

• Increased social interaction

• Engaged in political activities

• Increased participation level in gram-sabha meeting

• Improvement in leadership qualities

• Involvement in solving problems related to women and community

• Decision making capacity in family and community

Economic empowerment of women by micro entrepreneurship led to the empowermentof

women in many things such as socio-economic opportunity, property rights, political

representation, social equality, personal right, family development, market development,

community development and at last the nation development.

Standing on the threshold of the twenty-first century as one looks back a question that

confronts us is where indeed are the women in India in terms of empowerment and socio-

economic emancipation? In the changing scenario of the Indian society efforts has been made

to empower women so that they can not only joins hand in making important decisions in the

family or society but also hold the public office for development.

Rural development is an integral process of economic growth and social progress. It implies

the development of rural sector which has many dimensions. The role of microfinance and

women empowerment in this context is important because it provides an environment of

sustainable improvement in the quality of life of rural womenfolk enabling them to form

S.H.Gs, and providing them equal opportunities in decisionmaking process and participation

in community life.

CONCLUSION

Still the rural areas is underdeveloped. As suchthere was employment –gap among the rural

people, as many of the small scaleindustries, cottage industries and handicrafts are ended.

Further, even thoughwomen constitute half of the population, they have no adequate

representation, uneducated and employment, especially in rural areas. The rural

development,women empowerment and employment generation policies discussed above are

very helpful for the rural women so as to start income generating activitiesindependently or

give at least 100 days of employment for the rural women. But it is emphasized that still there

is no or less awareness about the government Programmes among the rural people and

particularly among rural women. Hence, the voluntaryorganization and Non-Governmental

Organizations have to act to increase theawareness among the rural women on the

government Programmes.

Rural development symbolizes rural industrialization. Rural industrialization provides the

best solution to tackle with the twin problems of unemployment and poverty in the rural areas

of the country particularly women employees. However, the development of rural

industrialization is plagued by some major problems like inadequate flow of credit; use of

obsolete technology, machinery and equipment, and inadequate infrastructural facilities.

Solving these problems is necessary for developing rural industries in the country. The

NGOs have proved as an effective agent in developing industries in rural areas with effective

empowerment of women in our country.

The Govt. of India planning to facilitate Road, House, Electricity, Drinking Water and

minimum needs to Rural area such that Rural Development has to be taken place and get a

chance to employability in Rural youth, and give maximum protection to women,in that

context Govt. of Madhya Pradesh implemented a programme called Ladli Laxmi

Yojana,Sukanya Yojana , Beti bachao it speaks about give an importance to girl child.

There is no cast for poverty and there is no cast for hungry .So that empowering rural women.

1. http:/indiabudget.nic.in

2. http://www.indiatogether.org

3. http://gcra.in

4. http://mgnrage.in

5. http://google.com

6. http://govt.ap.in

“IMPACT OF FINANCIAL REPORTING QUALITY ON EPS: AN EMPIRICAL

STUDY OF INDIAN FINANCING COMPANIES”

By

Ms. Saumya Singh

UGC Net & ICSSR Fellow,

Faculty of Management Studies, Banaras Hindu University, Varanasi (U.P.)

Dr. Raj Kumar

Professor, Faculty of Management Studies,

Banaras Hindu University, Varanasi (U.P.)

ABSTRACT

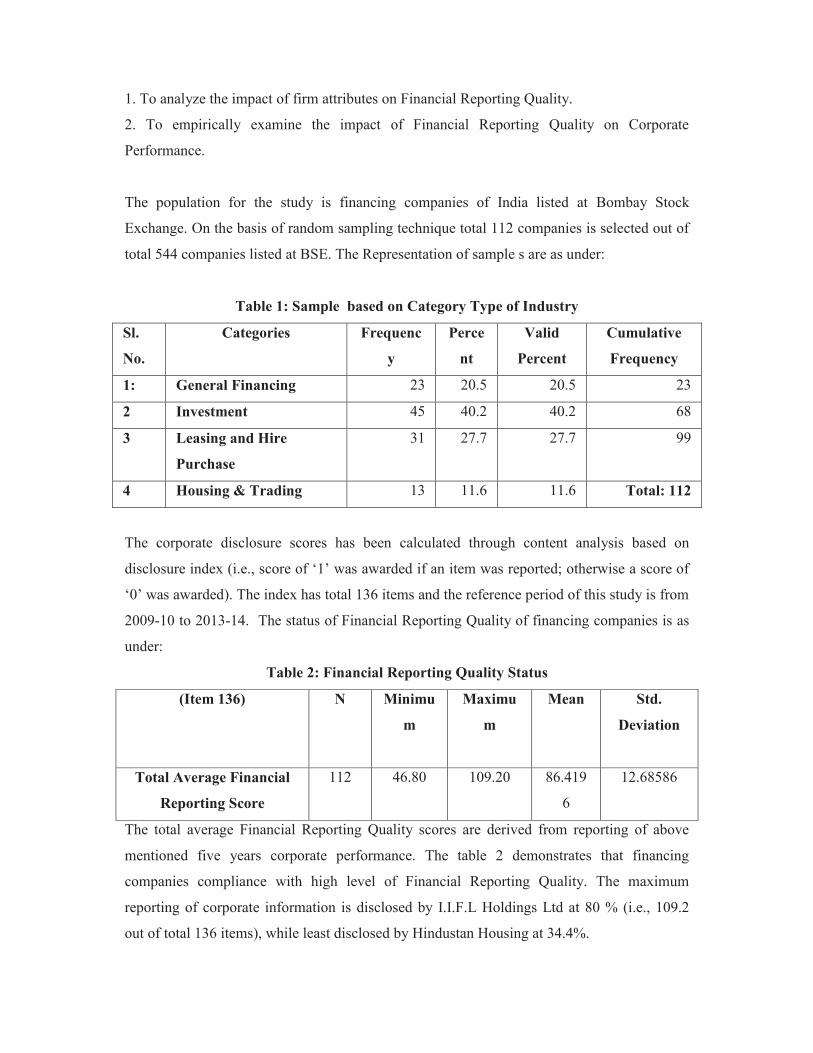

The paper examines the effect of Financial Reporting Quality on Company Performance of

Indian financing companies. The data are extracted from 112 sample firms representing the

quoted financing companies in India as the population of the study. Multiple step-wise

regressions are conducted for the analysis of data. The results from regression analysis

suggest that there is positive impact of firm attributes on financial reporting quality of quoted

financing firms in India. In addition, the Fishers statistics of significant change in step-wise

analysis indicates model II is a good fit. Therefore, the model reveals that the Financial

Reporting Quality of quoted financing firms in India has positive influence in performance of

the company. It is therefore, recommended that the company should report reliable and error

free information based on prevailing standards to ensure higher quality of financial reporting.

Keywords: Financial Reporting Quality (FRQ), Earning Per Share (EPS), Firm attributes,

Financing Companies.

1. INTRODUCTION

The word corporate disclosure and Financial Reporting is used interchangeably in the

accounting research. Financial Reporting is a process through which an undertaking

communicates with especially external parties. It is the Communication of various details

regarding the activities of the business, which are to be disclosed either statutorily or

otherwise, to convey a true and fair view of the operating results and performance for the

particular years. Information about corporate activities is essential for investors and other

users in order to reach appropriate decisions. The aim of financial reporting to promote

transparency is accomplished through comprehensive reporting of corporate actual performed

activities which was a global concern since long time.

In order to have to good predictive value or better feedback, the reporting must be timely and

pertinent. Moreover, annual reports are most crucial avenues for corresponding companies’

performance to different stakeholders. As annual reports helps on decision making, therefore

it, should always present reliable and error free information. It was also viewed that, it can

never be completely free from bias, as various estimates, assumptions and economic

phenomena are integrated in the annual report under situations of uncertainty (Jonas and

Blanchet, 2000). Although it is not possible to achieve complete lack of bias, a definite level

of exactitude in reporting is always required for decision to be purposeful. Therefore, it is

important that the information presentation in the annual report should not be misleading or

ambiguous and should present financial/ non-financial performance of corporate clearly.

Users should be able to understand the information presented by the companies according to

prevailing standards and practices of reporting. To achieve this, the annual reports should

contain full disclosure and higher level of transparency. The study, therefore, centered on

evaluating the effect of firms’ attributes and Financial Reporting Quality on EPS of Indian

financing companies.

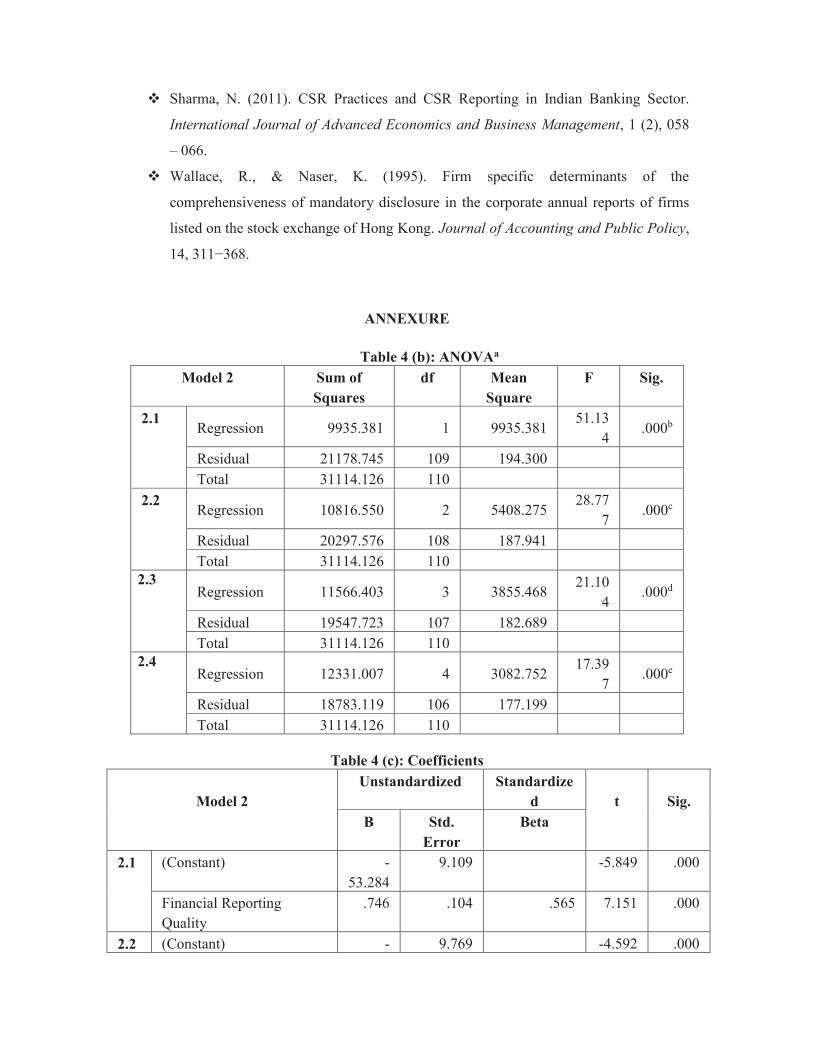

2. THEORETICAL BACKGROUND

Corporate disclosure of financial reports helps the investors, lenders and several other users

to analyze the past performance of the company and to compare its performance with other

peer companies’ performance for the particular years. The disclosure can be done through

various ways similarly the disclosure through annual report plays an important role. Previous

study on this area was initiated by Cerf (1964) and afterwards, several researches have

conducted on the reporting of quality of information in various contexts. The glimpses of

such studies are: Owusu- Ansah (1998); Ho and Wong (2001), Chau and Gray (2002); Naser

et al. (2006); Akhtaruddin (2005) and Ofoegbu and Okoye (2006). Each of these studies has

been differentiated by research objectives, differences in nature of independent variables,

differences in corporate reporting index calculation and differences in statistical tools for the

analysis. These studies identified the corporate attributes which are used as analyst in

explaining the quality of financial reporting. The most popular characteristics that were

studied in prior researches are selected and incorporated in the present research to know the

influence of financial reporting quality on corporate performance. The variables include

profitability i.e. EPS, Age of Company, Board Composition, Firm Structural Complexity,

Firm Multiple Listing and Number of Shares which are explained as:

2. 1. Profitability

Earnings Per Share (EPS) is the portion of distributable company’s revenue which is

allocated among outstanding equity share holders. EPS is considered as indicator of the

profitability of any corporate performance, and it is also widely used as measures for

calculating profitability. Previous studies by Cerf, 1964; Singhvi and Desai, 1971; Wallace

and Naser, 1995; Inchausti, 1997; Owusu-Ansah, 1998, examined EPS are capable of

persuading the extent of corporate financial reporting. Such studies generated that EPS is a

good measure of corporate performance, and also depicted from the above studies that

profitable firm is likely to disclose more information. More of previous studies i.e, Singhvi

and Desai (1971); Wallace and Naser (1995); Meek et al.(1995); Inchausti (1997); Glaum and

Street (2003) and Akhtaruddin (2005) have empirically tested the relationship between EPS

as profitability and extent corporate reporting, in which they found the mixed results.

For instance, Singhvi and Desai (1971) & Owusu-Ansah (1998) found positive and

significant connection between profitability and corporate reporting, whereas Meek et al.

(1995) found that profitability has no impact on reporting of corporate information. Wallace

and Naser (1995) described a negative relationship between EPS and corporate reporting.

Lang and Lundholm (1993) pointed that the influence of profitability on corporate reporting

can be positive, neutral or negative, depending on its level of performance.

2.2 Age of Company

Age of company is a crucial indicator of firm attribute as older company tends to produce

more information when compared to newly constructed company. It is believed that old

companies might have improved its financial reporting practices over time, and therefore,

they are expected to provide more disclosure than newly established companies

(Akhtaruddin, 2005; Al-Shammari, 2005; Patelli, L.& Prencipe, A., 2007; Barako, et. al. ,

2006). In 1988, Owusu-Ansah in his study proved that company age has a statistically

significant & positive influence on corporate disclosure and reporting practices in Hong

Kong. In New Zealand, Owusu-Ansah and Yeho (2005) also found company age as the vital

factor in explaining the extent of mandatory disclosure practices. Al Shammari et al (2007)

examined the association between the age and reporting practices; he found the significant

association between them.

Moreover, Kakani et al. (2001) have a slight different opinion that newer and smaller firm

must have lack of capital, not established brand name and reputation unlike older firms;

However, it is not possible to reach a conclusion that long-established firms can disclose

more information or be more compliant than newly-established firms.

2.3 Size of Board Members

The board of directors is another important component of corporate reporting and governance

system. Board size is considered as an interesting variable as it will indirectly replicate the

existence of executive and non executive directors on the board (Haniffa and Cook, 2002).

According to agency theory, the board should be more effective when composed of a

majority of unrelated directors (Jensen and Meckling, 1976 & Berle and Means, 1991).

Mangel and Singh (1993) expressed that outside directors have more opportunity for their

control and greater flexibility in decision making as it was amplified by their equity position