Ecuador - iuj.ac.jp

57

COUNTRY PROFILE Ecuador Our quarterly Country Report on Ecuador analyses current trends. This annual Country Profile provides background political and economic information. 1998-99 The Economist Intelligence Unit 15 Regent Street, London SW1Y 4LR United Kingdom

Transcript of Ecuador - iuj.ac.jp

COUNTRY PROFILE

EcuadorOur quarterly Country Report on Ecuador analyses currenttrends. This annual Country Profile provides backgroundpolitical and economic information.

1998-99The Economist Intelligence Unit15 Regent Street, London SW1Y 4LRUnited Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through subscription products ranging from newslettersto annual reference works; through specific research reports, whether for general release or for particularclients; through electronic publishing; and by organising conferences and roundtables. The firm is amember of The Economist Group.

London New York Hong KongThe Economist Intelligence Unit The Economist Intelligence Unit The Economist Intelligence Unit15 Regent Street The Economist Building 25/F, Dah Sing Financial CentreLondon 111 West 57th Street 108 Gloucester RoadSW1Y 4LR New York Wanchai United Kingdom NY 10019, US Hong KongTel: (44.171) 830 1000 Tel: (1.212) 554 0600 Tel: (852) 2802 7288Fax: (44.171) 499 9767 Fax: (1.212) 586 1181/2 Fax: (852) 2802 7638E-mail: [email protected] E-mail: [email protected] E-mail: [email protected]

Website: http://www.eiu.com

Electronic deliveryEIU ElectronicNew York: Lou Celi or Lisa Hennessey Tel: (1.212) 554 0600 Fax: (1.212) 586 0248London: Jeremy Eagle Tel: (44.171) 830 1183 Fax: (44.171) 830 1023

This publication is available on the following electronic and other media:

Online databases Microfilm

FT Profile (UK) NewsEdge Corporation (US) World Microfilms Publications (UK)Tel: (44.171) 825 8000 Tel: (1.781) 229 3000 Tel: (44.171) 266 2202

DIALOG (US) University Microfilms Inc (US)Tel: (1.415) 254 7000 CD-ROM Tel: (1.800) 521 0600

LEXIS-NEXIS (US) The Dialog Corporation (US)Tel: (1.800) 227 4908 SilverPlatter (US)

M.A.I.D/Profound (UK)Tel: (44.171) 930 6900

Copyright© 1998 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author’s and the publisher’s ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

ISSN 0269-7971

Comparative economic indicators, 1997

0 100 200 300 400

Brazil

Mexico

Argentina

Colombia

Venezuela

Chile

Peru

Ecuador

Uruguay

Paraguay

Bolivia

Gross domestic product$ bn

Sources: EIU estimates; national sources.

798.8798.8798.8798.8798.8798.8798.8798.8

0 2,000 4,000 6,000 8,000 10,000

Argentina

Uruguay

Chile

Brazil

Mexico

Venezuela

Peru

Colombia

Paraguay

Ecuador

Bolivia

Gross domestic product per head$

Sources: EIU estimates; national sources.

0 2 4 6 8 10

Argentina

Peru

Chile

Mexico

Venezuela

Uruguay

Bolivia

Ecuador

Brazil

Colombia

Paraguay

Gross domestic product% change, year on year

Sources: EIU estimates; national sources.

0 10 20 30 40 50 60

Venezuela

Ecuador

Mexico

Uruguay

Colombia

Peru

Paraguay

Brazil

Chile

Bolivia

Argentina

Consumer prices% change, year on year

Sources: EIU estimates; national sources.

EIU Country Profile 1998-99 © The Economist Intelligence Unit Limited 1998

November 13th 1998 Contents

3 Basic data

4 Political background4 Historical background8 Constitution and institutions

10 Political forces11 International relations and defence

12 The economy12 Economic structure13 Economic policy16 Economic performance19 Regional trends

19 Resources19 Population20 Education21 Health22 Natural resources and the environment

23 Economic infrastructure23 Transport and communications24 Energy provision26 Financial services27 Tourism

28 Production28 Industry29 Mining30 Agriculture31 Construction

32 The external sector32 Merchandise trade35 Invisibles and the current account35 Capital flows and foreign debt36 Foreign reserves and the exchange rate

38 Appendices38 Sources of information39 Reference tables39 Government finances39 Money supply40 Interest rates40 Gross domestic product41 Gross domestic product by expenditure42 Gross domestic product by sector

1

© The Economist Intelligence Unit Limited 1998 EIU Country Profile 1998-99

42 Manufacturing gross domestic product43 Prices43 Earnings43 Population43 Labour force44 Transport statistics44 National energy statistics45 Banking statistics45 Stockmarket indicators46 Tourism46 Foreign direct investment in manufacturing46 Gold production46 Agricultural production47 Livestock numbers47 Fishing exports47 Construction statistics48 Exports48 Imports49 Key exports and imports49 Main trading partners50 Balance of payments, IMF estimates51 Balance of payments, national estimates51 Net foreign investment by sector51 Net foreign investment by source country52 External debt, World Bank estimates53 External debt, national estimates53 Exchange rates

2

EIU Country Profile 1998-99 © The Economist Intelligence Unit Limited 1998

Ecuador

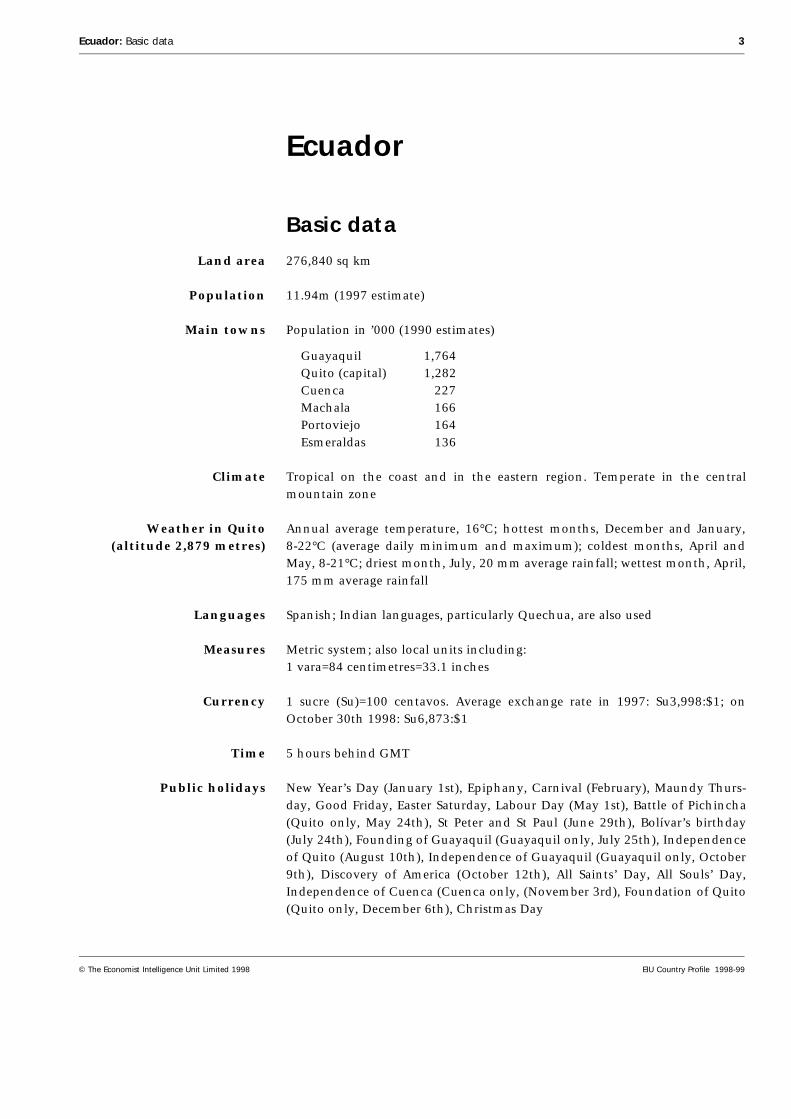

Basic data

Land area 276,840 sq km

Population 11.94m (1997 estimate)

Main towns Population in ’000 (1990 estimates)

Guayaquil 1,764Quito (capital) 1,282Cuenca 227Machala 166Portoviejo 164Esmeraldas 136

Climate Tropical on the coast and in the eastern region. Temperate in the centralmountain zone

Weather in Quito(altitude 2,879 metres)

Annual average temperature, 16°C; hottest months, December and January,8-22°C (average daily minimum and maximum); coldest months, April andMay, 8-21°C; driest month, July, 20 mm average rainfall; wettest month, April,175 mm average rainfall

Languages Spanish; Indian languages, particularly Quechua, are also used

Measures Metric system; also local units including:1 vara=84 centimetres=33.1 inches

Currency 1 sucre (Su)=100 centavos. Average exchange rate in 1997: Su3,998:$1; onOctober 30th 1998: Su6,873:$1

Time 5 hours behind GMT

Public holidays New Year’s Day (January 1st), Epiphany, Carnival (February), Maundy Thurs-day, Good Friday, Easter Saturday, Labour Day (May 1st), Battle of Pichincha(Quito only, May 24th), St Peter and St Paul (June 29th), Bolívar’s birthday(July 24th), Founding of Guayaquil (Guayaquil only, July 25th), Independenceof Quito (August 10th), Independence of Guayaquil (Guayaquil only, October9th), Discovery of America (October 12th), All Saints’ Day, All Souls’ Day,Independence of Cuenca (Cuenca only, (November 3rd), Foundation of Quito(Quito only, December 6th), Christmas Day

Ecuador: Basic data 3

© The Economist Intelligence Unit Limited 1998 EIU Country Profile 1998-99

Political background

Jamil Mahuad assumed the presidency on August 10th 1998 after defeating hismain opponent in a second-round election. His party, the centrist DemocraciaPopular (DP), is the largest in the country’s unicameral Congress, but does nothave an overall majority. Mr Mahuad will hold office until August 2002.

Historical background

Independence— Prior to the arrival of the Spanish in 1531, the territory which is now Ecuadorwas dominated by regional trading confederacies. For 80 years it was the north-ern outpost of the Inca empire, which introduced the Quechua language. Thecountry gained independence from Spain in 1822 and temporarily joined Vene-zuela, Colombia and Panama in Simón Bolívar’s Grancolombian Federation. In1830 it left to become an independent nation.

—leads to politicalinstability

The period after independence was characterised by government instabilityand economic and political rivalry between the coastal and highland regions.Political power was concentrated in the hands of a highland landowning classallied with the Catholic Church, yet growth of the banking sector and rapidexpansion in cocoa production created a wealthy coastal banking and agricul-tural middle class seeking greater political power. State power remained decen-tralised at a regional level until Gabriel García Moreno came to power in 1860and attempted to centralise public administration and tax collection. Externalshocks, in the shape of a collapse in the cocoa market in the 1920s and theGreat Depression of the 1930s, were at the root of severe instability from 1931to 1948. Of 21 governments, none survived to complete a term in office. JoséMaría Velasco Ibarra was a particularly important figure in the period. A popu-list who was first elected in 1933, he was to hold office a total of five times (thelast time in 1968), and was overthrown four times. From 1948 to 1960, how-ever, Ecuador enjoyed 12 years of stable civilian rule. Increasing banana ex-ports helped to finance development policies, and also stimulated theemergence of growers as a powerful economic group.

Modernisation and themilitary

A move towards industrial development took place in the 1960s. The influenceof the Cuban revolution coincided with growing social unrest, leading themilitary government of 1963-66 to take a strongly anti-communist stance.Great emphasis was placed upon economic modernisation, and the role of thestate in the economy was expanded. Another military dictatorship from 1972began the exploitation of extensive oil reserves under state control. The in-come from oil exports was used for modernisation, but also led to high levelsof indebtedness to foreign banks. In 1978 a referendum approved a new con-stitution which was to form the basis for a return to civilian rule and demo-cratic elections in 1979.

Democratic governmentsface economic crisis—

Jaime Roldós of the populist Concentración de Fuerzas Populares (CFP) led thenew government. Mr Roldós was killed in a plane crash in 1981, giving him thestatus of political martyr even though his reformist intentions had been under-

4 Ecuador: Historical background

EIU Country Profile 1998-99 © The Economist Intelligence Unit Limited 1998

mined by conflict within his government. Mr Roldós was succeeded by hismore moderate vice-president, Osvaldo Hurtado of Democracia Popular (DP).Mr Hurtado was able to provide more organised government but faced eco-nomic difficulties. Falling oil prices meant that the government was unable tomeet rising current spending commitments. An increasing debt burden con-tributed to a debt crisis in 1982 and the subsequent need for fiscal austerityprovoked social and labour protest.

—and initiate structuralreforms

A shift to the right followed in 1984 with the government of the centre-rightFrente de Reconstrucción Nacional, led by León Febres Cordero of the PartidoSocial Cristiano (PSC). Often authoritarian and corrupt in its methods, withsome notorious cases of human rights abuses, the administration moved awayfrom the state intervention of the military regimes of the 1970s, liberalising andopening the economy. Although the government was unpopular, an attemptedmilitary coup in March 1986 proved unsuccessful. A left-wing alliance won amajority in the mid-term congressional election of 1986, amid worsening rel-ations between Congress and the executive. The situation deteriorated furtherwhen oil prices collapsed and oil exports were suspended for six months after anearthquake damaged the cross-country oil pipeline in March 1987.

Although the left regained the presidency in the 1988 elections, under RodrigoBorja of Izquierda Democrática (ID), the administration implemented tightfiscal and monetary policies which weakened growth. The government’s popu-larity suffered because of shortages of basic commodities, high inflation andrising unemployment. Once again, a mid-term election resulted in the loss ofthe regime’s congressional majority and relations between the executive andthe legislature deteriorated further. At the same time there was an upsurge insocial unrest. Indigenous groups began to have a greater impact on the politicalscene, seeking land titles and recognition of Ecuador as a plurinational state.Disillusionment was reflected in the 1992 elections, where both presidentialfinalists were from the centre right.

Political stalemate underMr Durán Ballén—

The priorities of the new government of Sixto Durán Ballén were to reduceinflation, curb the public-sector deficit, modernise the state sector and normal-ise relations with foreign creditors. It faced several political problems, however.The government was unable to create a consensus in favour of its reformsamong key interest groups. Trade unions were unhappy about the govern-ment’s privatisation plans, which implied huge redundancies and publicspending cuts. This led to strikes and demonstrations, which disrupted publicservices. The government also lacked a majority in Congress, which led to theblocking of legislation on key issues such as privatisation, and the frequentimpeachment of government ministers. Government weakness and internaldivisions worsened when the vice-president, Alberto Dahik, an important fig-ure in the administration, fled to Costa Rica in October 1995 to avoid arrest oncorruption charges. This further discredited a government already widely un-popular because of its reform plans and the impact of austerity measures.

—and chaos underMr Bucaram

Abdalá Bucaram of the populist Partido Roldosista Ecuatoriano (PRE) managedto tap popular feeling to win the second round of the presidential election inJuly 1996. Although painfully crude, his platform of poverty reduction and the

Ecuador: Historical background 5

© The Economist Intelligence Unit Limited 1998 EIU Country Profile 1998-99

elimination of economic and political oligarchies from power led to victory in20 out of 21 provinces, with his strongest vote in both rural and urban mar-ginal areas. Mr Bucaram beat the PSC candidate, Jaime Nebot, who promisedpolicy continuity with the outgoing government. But with only 19 seats inCongress out of 82, the PRE was forced into a broad centre-left coalition whichincluded members of three of the four largest parties in Congress.

However, it was not long before Mr Bucaram’s flamboyant, heavy-handed, andunrefined style of government began to antagonise both coalition membersand his supporters in the electorate. His inability to present a coherent eco-nomic package added to growing political uncertainty. In February 1997 anationwide general strike took place in protest against Mr Bucaram’s cronyism,authoritarian tendencies, and contradictory economic policies. Protesters inQuito forced Mr Bucaram to barricade himself in the presidential palace underheavy military protection. Almost immediately, Congress voted by 44 votes to34 to dismiss Mr Bucaram from office on the grounds of mental incapacity.Although the constitutional basis for taking this step was unclear, the militarywithdrew its support for the Bucaram administration, forcing the president toflee the country. After a brief power struggle between Congress and the vice-president, Rosalía Arteaga, the legislature appointed its leader, Fabián Alarcón,to serve as interim president until August 1998.

Constitutional reformbegins under Mr Alarcón

Although Mr Alarcón had long been regarded as a skilful politician, the circum-stances under which his appointment was made did not provide him with astrong mandate for effective government at the outset of his term. To remedythis situation, Mr Alarcón held a referendum in May 1997 asking the electorateto support his appointment as interim president. Although this gamble paidoff, it soon became obvious that the interim president was both unable andunwilling to provide focused government. Instead of using his brief term topush through important economic measures which past incumbents hadfound too politically difficult to implement, Mr Alarcón used his tenure tostrengthen his personal support base and that of his small party, the populistFrente Radical Alfarista (FRA), with a view to regaining the presidency for a fullterm in 2002 (the constitution barred him from seeking the presidency in the1998 elections). This preoccupation made Mr Alarcón reluctant to address thecountry’s serious fiscal imbalance. In fact he worsened it by making substantialconcessions to powerful public-sector unions and regional lobbies. Towards theend of his term Mr Alarcón became embroiled in accusations that he andmembers of his administration had misappropriated state funds while inpower. These allegations are still being investigated.

The highlight of Mr Alarcón’s term in office was undoubtedly constitutionalreform. This reform was the direct result of the popular approval of variousproposals which were also put to the vote in the May 1997 referendum, andwas carried out by a popularly elected National Assembly between December1997 and April 1998. Although the deliberations of the National Assemblywere marred by inter-party squabbles and consequently failed to achieve asmuch as its supporters had hoped (particularly the reform of the social securitysystem), some important constitutional changes were approved (see box).

6 Ecuador: Historical background

EIU Country Profile 1998-99 © The Economist Intelligence Unit Limited 1998

Mr Mahuad assumes thepresidency promising

reforms

Ecuadorean political life returned to some degree of normality with the elec-tion to the presidency of the reform-minded Jamil Mahuad of the centristDemocracia Popular (DP). Mr Mahuad, who had two consecutive terms as apopular mayor of Quito, took office on August 10th 1998 after narrowly beat-ing the PRE’s populist candidate, Álvaro Noboa. Mr Mahuad gained 51% of thevote in a second-round run-off. Despite this narrow margin, the election ofMr Mahuad—who campaigned on a moderate platform emphasising free-market policies and reform coupled with a social element—gives three reasonsto believe that Ecuador is entering a period of greater political stability whichwill make long-awaited economic reform possible. First, Mr Mahuad is an expe-rienced public administrator who appears reform-minded. Second, the constit-utional reforms approved shortly before his accession to office should improvethe country’s governability by strengthening the presidency, especially in itsrelations with Congress, and open up the way for substantial structural reform.Third, in October 1998 Mr Mahuad signed a permanent peace agreement withPeru over the long-running border dispute, bringing to a close a peace processwhich began after the brief war between the two countries in 1995.

But before Mr Mahuad can contemplate reactivating growth he must stabilisethe economy, primarily by rectifying the fiscal imbalance. This will dependgreatly on the goodwill of Congress, where the DP is the largest party but doesnot enjoy a working majority. As always, relations with Congress will deter-mine the success of the president’s term in office. In particular, Mr Mahuad will

Key points of the 1998 constitutional reform

Political

• The abolition of mid-term congressional elections.

• The abolition of the legislature’s ability to impeach cabinet ministers.

• The institutionalisation of the corruption commission set up temporarily in1997 to investigate allegations of corruption made against Abdalá Bucaram.

• The expansion of Congress from 82 to 121 members. The expansion of thechamber will increase the number of deputies from densely populated areas,redressing imbalances which led to the disproportionately higher representationfrom marginal and sparsely populated provinces.

Economic

• Repeal of the state’s monopoly in the so-called strategic sectors of theeconomy, opening the way for greater private-sector participation in oil,electricity and telecommunications.

• The abolition of the Monetary Board, granting the Central Bank full autonomyover monetary policy.

• The budget will now require the approval of the whole Congress rather than ofa select committee. Once the budget has been approved, Congress will beunable to introduce extra expenditure items without specifying their source offunding.

Ecuador: Historical background 7

© The Economist Intelligence Unit Limited 1998 EIU Country Profile 1998-99

have to woo the PSC, which is the second largest party in Congress and has itsstronghold in the Pacific lowlands. The PSC, which was left without a pres-idential candidate in the 1998 elections after Jaime Nebot turned down theparty nomination, is the DP’s obvious ideological ally. Collaboration with thePSC would allow Mr Mahuad to compensate voters in the coastal region(Mr Mahuad is from the highlands) for shunning Mr Noboa (who is a bananamagnate from Guayaquil) in the 1998 elections.

Constitution and institutions

The executive The 1979 constitution established a unicameral parliament and presidentialgovernment. The president is elected for four years and may not be re-electedimmediately. The 1998 constitutional reforms will prevent legislators fromimpeaching ministers as they did in the past, although the president can stillbe impeached by a two-thirds majority. Constitutional reform also increasedthe number of congressmen (also elected for four years) from 82 to 121. Ofthese, 20 are national congressmen elected through proportional repre-sentation and the rest are provincial legislators elected by simple majority. Thereforms also scrapped mid-term congressional elections which had tradition-ally wiped out any support gained in the legislature by the president in the firsttwo years of his term. A strengthening of the power of the executive vis-à-visthe legislature may reduce the pressures which have pushed past presidentsinto underhand deals with congressmen in order to get measures passed.

Important recent events

November 1992: Ecuador enters the Andean Pact free-trade area.

November 1993: The government declares a state of emergency in response towidespread civil unrest.

January 1995: Fighting breaks out on the disputed border with Peru.

February 1997: Congress votes to oust the populist Abdalá Bucaram from officeafter widespread civic protests against his administration. The leader of Congress,Fabián Alarcón, is appointed interim president until August 1998 by thelegislature.

May 1997: Mr Alarcón’s interim presidency is endorsed in a plebiscite togetherwith plans to set up a National Assembly to reform the constitution.

May 1998: The constitutional reforms drawn up by the National Assembly areratified.

August 1998: The centrist Jamil Mahuad assumes the presidency after defeatingthe populist Álvaro Noboa in the second round of the presidential election.

October 1998: A permanent peace agreement is signed with Peru, ending thelong-running border dispute.

8 Ecuador: Constitution and institutions

EIU Country Profile 1998-99 © The Economist Intelligence Unit Limited 1998

Congress The congressional year begins on August 10th, when coalitions are establishedand a congressional chairman is elected. The latter has considerable power overlegislation as he can convoke extraordinary congressional sessions and deter-mine the agenda for discussion. He is a key negotiator between the executiveand the legislature. The formal parliamentary session is short, lasting only toearly October. However, extraordinary sessions are then called to continuecongressional business. Legislative commissions continue to sit even whenCongress is in recess.

Despite the fact that Ecuadorean voters tend to back the traditional parties, aproliferation of small parties forming shifting coalitions has contributed to thefragmentation of Congress in recent years. The 1998 constitutional reformsseek to reverse this by striking from the party register any political party thatfails to win less than 5% of the national vote in two consecutive elections.Independents have been allowed to run for Congress and other official posi-tions since 1996.

A new Supreme Court Judicial and regulatory bodies in Ecuador have traditionally been highly poli-ticised. Congress appoints officials to the Electoral Supreme Tribunal and Tri-bunal of Constitutional Guarantees, as well as the superintendents of banksand companies, the state attorney-general, procurator-general and comptroller-general. Until recently, Congress was also responsible for appointing judges tothe Supreme Court for fixed terms. This practice changed in July 1997, how-ever, when Congress voted to dismiss the 31 members of the Supreme Court,including its president. This unprecedented move followed the popular sup-port voiced in the May 1997 referendum for the modernisation of the judiciary.In removing the judges, Congress argued that the Supreme Court had becometoo politicised. In early October 1997 a new Supreme Court was appointed. Thejudges, who will serve for life, were selected by Congress from a shortlist pre-sented by a commission, which in turn received nominations from 12 electoralcolleges representing different civic groups as well as individuals. The extent ofdepoliticisation will only become clear once the new court begins taking dec-isions. Of particular significance will be the court rulings with respect to cor-ruption charges brought against the former president, Mr Alarcón (although heremains exiled in Panama, Mr Bucaram has already been found guilty for themisappropriation of funds by the new court). Mr Alarcón is currently underinvestigation over allegations that he approved the appointment of over 1,000pipones (individuals on the state’s payroll but doing little or no work) as con-gressional advisers during his time as leader of the legislature. As before, theSupreme Court is responsible for appointing the judges of provincial superiorcourts.

Political forces

A diverse party system Ecuador’s largest political parties in terms of congressional representation arethe centrist Democracia Popular (DP), the right-of-centre Partido Social Cris-tiano (PSC), the populist Partido Roldosista Ecuatoriano (PRE) and the left-of-centre Izquierda Democrática (ID). All have held power at some time since thetransition to democracy in 1979. The PSC was founded in the 1950s by a group

Ecuador: Political forces 9

© The Economist Intelligence Unit Limited 1998 EIU Country Profile 1998-99

of upper-middle-class Roman Catholics in Quito, but soon established a strongnational party organisation under Camilo Ponce, especially on the coast. TheDP developed in the 1970s out of the Partido Demócrata Cristiano, founded byuniversity students and Christian trade unionists in the 1960s. Although it hasclear left-wing roots, the party has evolved to espouse free-market policieswhile emphasising a concern for social issues. It derives its greatest supportfrom the highland middle classes. The populist PRE was founded in memory ofMr Roldós. It is strongest on the coast and in marginal urban and rural areas,but was discredited by Mr Bucaram’s brief tenure. The ID, founded in 1970,combined an offshoot of the Liberal Party and independent socialists. It has amoderate reformist wing and a more radical element. The MovimientoPachacutik is an umbrella group of indigenous organisations, social move-ments and trade unions which was formed in 1996 and achieved immediateelectoral success that year. Although it continues to be the main formal polit-ical vehicle for indigenous groups, organised in the Confederación de Nacion-alidades Indígenas del Ecuador (Conaie), its support diminished somewhat inthe 1998 elections.

Congressional election results(no. of seats)

1994 1996 1998

Partido Conservador 7 2 2

Partido Social Cristiano 26 24 26

Partido Roldosista Ecuatoriano 11 19 23

Izquierda Democrática 7 4 16

Democracia Popular 6 6 33

Movimiento Pachacutik-Nuevo País n/a 7 6

Movimiento Popular Democrático 8 3 2

Frente Radical Alfarista 4 4 4

Independents n/a 12 8

Other 1 1 1

Total 82 82 121Sources: Local press; Análisis Semanal.

The military Since leaving power in 1978, the Ecuadorean military has continued to play animportant political role. It exerts pressure behind the scenes, especially at timesof political instability. This was evident in February 1997 when the militaryplayed a key role in negotiating the agreement which brought a swift end tothe constitutional crisis after Mr Bucaram’s ousting. The silent threat of directintervention acts to some extent as a brake on civilian politicians. The armedforces occupy a type of moral high ground from which military leaders, such asa former general, Paco Moncayo, have criticised the corruption and ineffi-ciency of civilian political institutions. This contrasts with the relative effi-ciency and lack of corruption of the military, as proven in the economicsuccess of their extensive commercial interests. Their reputation was enhancedby their success on the battlefield against Peru in 1995. Deep respect for themilitary among the Ecuadorean population is also due to a role in providingeducation, infrastructure and health facilities in many marginal rural commu-nities, especially in the Amazon region. The military faces a period of adjust-ment now that a permanent peace agreement with Peru has been signed.

10 Ecuador: Political forces

EIU Country Profile 1998-99 © The Economist Intelligence Unit Limited 1998

International relations and defence

The conflict with Peru A border conflict with Peru, which lasted for more than five decades and led towar in 1941 and brief clashes as recently as 1995, finally came to an end whenMr Mahuad signed a permanent peace agreement with the Peruvian president,Alberto Fujimori, in October 1998. This agreement was the result of a five-stagepeace process agreed in the Itamaraty Declaration in February 1995. Observersfrom the four guarantor countries of the 1942 Rio Protocol (the US, Brazil, Chileand Argentina), the border treaty signed by Peru and Ecuador after the 1941 war,monitored demilitarisation of the conflict zone, which was in dense Amazonjungle. Tensions rose at various points, and when the two sides were unable toagree on a common border, Mr Mahuad and Mr Fujimori agreed to accept theruling of the guarantor countries.

The final agreement defines a permanent border, and awards Ecuador unlimited(not sovereign) perpetual navigation rights on the Amazon River. It will alsoallow the two countries to lower defence expenditure, which has risen consider-ably over the last decade. (Between 1985 and 1994 there was a 57% real increasein defence spending in Ecuador, while the armed forces increased in sizeby 35%.)

Internationalorganisations

Ecuador is a member of many international organisations, including the UN,the World Trade Organisation (WTO), the Organisation of American States

Main political figures

Jamil Mahuad: Prior to his election, Mr Mahuad was mayorof Quito, where he established a reputation as an able publicadministrator, a consensus-oriented politician and a skilfulnegotiator. Nonetheless, all of his skills will be stretched as heattempts to restore order to the public finances, restructure aweak economy, reduce the size of the state, restore investorconfidence and combat corruption. Mr Mahuad hasappointed able technocrats to his economic cabinet, and willbenefit from the permanent peace agreement with Peru.

Juan José Pons: The new leader of Congress is a close allyof the president. A polished consensus-builder and asuccessful businessman, Mr Pons will be critical to theadministration’s efforts to consolidate a working majority inCongress. Mr Pons has so far focused on forging a deal withthe Partido Social Cristiano (PSC), to which significantpolitical concessions may have to be made in order to securecontinued co-operation.

Jaime Nebot: A lawyer from Guayaquil and head of thePSC. Mr Nebot came second in his second attempt to winthe presidency in 1996, and disappointed his party byrefusing to run in 1998. As the leader of the powerful PSCbloc in Congress, Mr Nebot will wield considerable influence

in the party’s negotiations with the government. He has areputation for being single-minded and stubborn, and isregarded as having little patience for consensus building.

León Febres Cordero: Although aged, ill, and somewhatovershadowed by his protégé, Mr Nebot, the formerpresident is the current mayor of Guayaquil, Ecuador’s largestand richest city, where he enjoys overwhelming support.Mr Febres Cordero continues to wield considerable politicalclout and is still in a position to exert decisive influence overhis party, the PSC, and over many national-level politicalissues.

Paco Moncayo: The retired former chairman of the jointchiefs-of-staff was elected to Congress in May 1998 as anIzquierda Democrática (ID) legislator, quickly becoming theID’s leader in the legislature. As army chief, Mr Moncayoplayed a crucial role in the 1995 war against Peru. He is astaunch nationalist and moderate leftist. He and his party areopposed to most free-market reforms and neo-liberalpolicies. But Mr Moncayo has presidential ambitions, and thismay push him to adopt a more centrist stance on many keyissues. Mr Moncayo may become the informal leader of theleftist opposition.

Ecuador: International relations and defence 11

© The Economist Intelligence Unit Limited 1998 EIU Country Profile 1998-99

(OAS), the Inter-American Development Bank (IDB), the IMF, the InternationalBank for Reconstruction and Development (IBRD) and affiliates, the Inter-national Finance Corporation, the International Development Association(IDA), the World Health Organisation (WHO) and the Rio Group. Other inter-national bodies of which Ecuador is a member include the International SugarOrganisation (ISO), the International Cocoa Organisation (ICCO) and theLatin American Economic System (SELA). It is also a member of the AsociaciónLatinoamericana de Integración (ALADI), the Andean Community and theNon-Aligned Movement. Ecuador was a member of OPEC until November1992, when it downgraded its participation to observer status. Ecuador left theInternational Coffee Organisation (ICO) in October 1998 after the body votedto make increasing export cuts to counter falling world coffee prices.

The economy

Economic structure

Main economic indicators, 1997

Real GDP growth (%) 3.4

Consumer price inflation (av; %) 30.7

Current-account balance ($ m) –743

Total external debt ($ bn) 15.5

Exchange rate (av; Su:$) 3,998

Population (m) 11.9Sources: Banco Central del Ecuador, Información Estadística Mensual; EIU.

Comparative economic indicators, 1997

Ecuador Colombia Peru US

GDP ($ bn) 19.8 96.4 65.1 8,111

GDP per head ($) 1,656 2,293 2,674 30,263

Consumer price inflation (year-end; %) 30.5 18.4 6.5 2.4

Current-account balance ($ bn) –0.7 –5.5 –3.4 –166.8

Merchandise exports fob ($ bn) 5.3 11.7 6.8 680.3

Merchandise imports fob ($ bn) 4.7 14.4 8.6 877.3

Total merchandise foreign trade (% of GDP) 59.7 35.9 29.4 19.2Sources: IMF, International Financial Statistics; EIU.

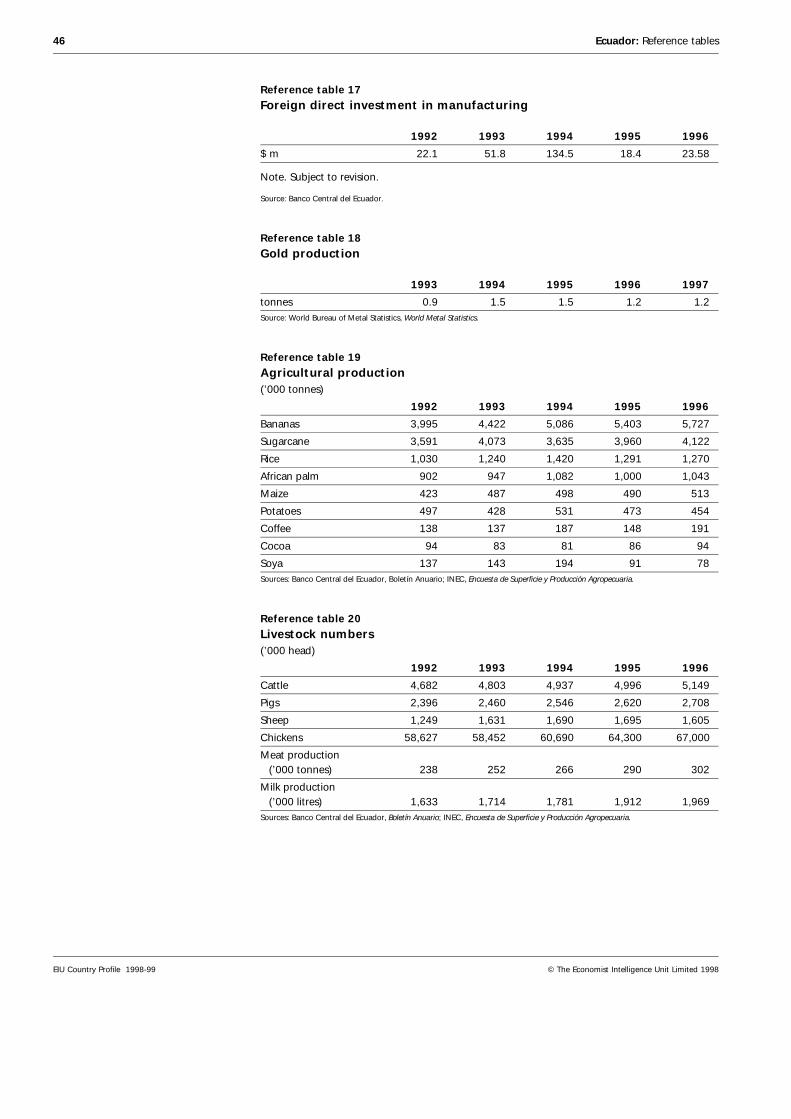

The agricultural, forestry and fishing sector is the most important in Ecuador’seconomy, having contributed an average of 17.5% of GDP over the last tenyears. The principal agricultural crops for export—bananas, coffee and cocoa—are grown on the coastal plain, with the banana industry centred in the south-western province of El Oro. The coast is also the basis for the fishing industry,with prawn farms concentrated around the Gulf of Guayaquil. Since seriouscommercial exploitation began in 1972, the oil sector has become extremelyimportant and is the area to which most longer-term foreign investment isattracted. The contribution of the oil and mining sector to GDP has grown

12 Ecuador: Economic structure

EIU Country Profile 1998-99 © The Economist Intelligence Unit Limited 1998

steadily during the 1990s from 11.7% in 1990 to 14% in 1997, although thecollapse of world oil prices in 1998 is likely to reverse this trend. Most oilexploration and production activity is found in the east of the country, in therain forests of the Amazon basin. Principal refining facilities are located atEsmeraldas on the northern coast and at La Libertad in the south.

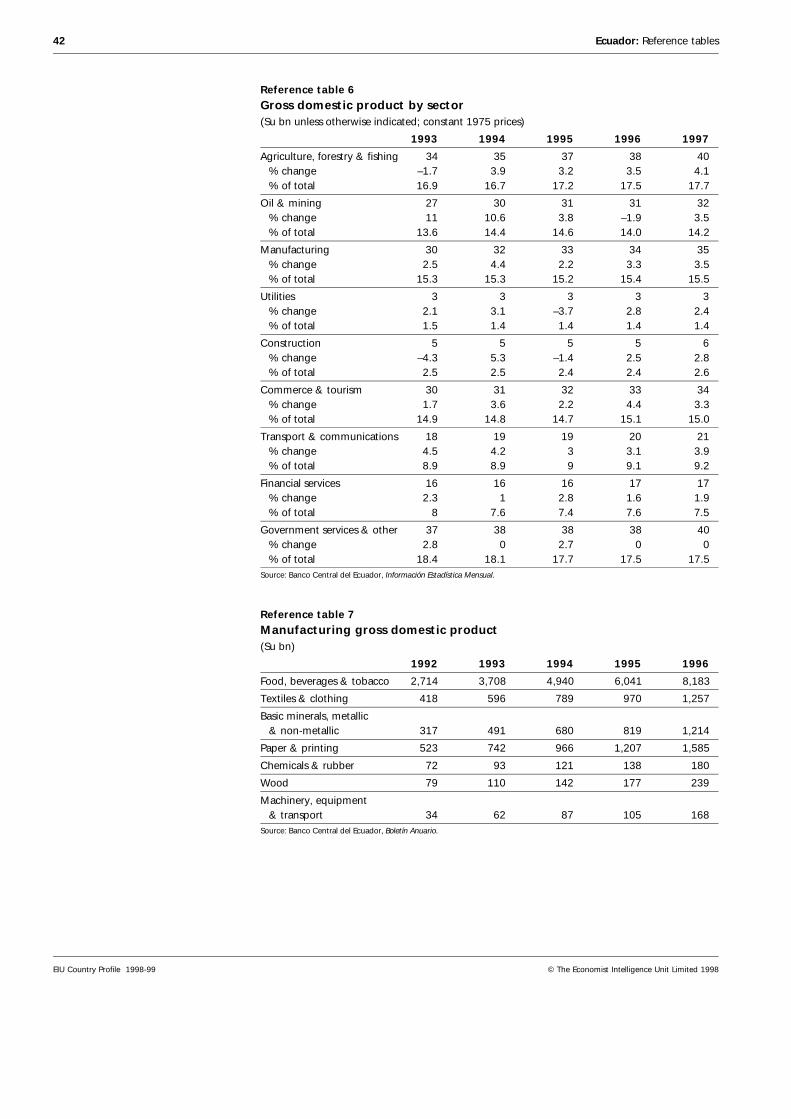

Manufacturing industry is located mainly around Ecuador’s two largest cities,Guayaquil and Quito. Trade liberalisation has stripped away the protectionpreviously enjoyed by industry which has been facing difficult trading condi-tions owing to high interest rates and scarce credit. Its contribution to GDPdropped from 18.1% in 1987 to 15.5% in 1990 and has since stood at around15.4%. Trade and tourism have represented an average of 15% of GDP over thelast ten years. The international tourism industry focuses on the GalapagosIslands, with the mainland a secondary attraction. The coast is the focus forlocal tourism but facilities for international visitors are as yet underdeveloped(see Reference table 6).

Economic policy

Central government finances(% of GDP)

1997

Revenue 17.1

Expenditure 18.6

Balance –1.5Source: Banco Central del Ecuador, Boletín Anuario.

Political considerationsprevent major reform—

Since the presidency of León Febres Cordero (1984-88), successive governmentshave attempted to liberalise the economy. This has involved dismantling tradebarriers and reducing state intervention in the face of political opposition fromprotected national producers and powerful public-sector unions. Such actions,along with attempts to slow inflation with tight fiscal and monetary policy,facilitated several foreign-debt renegotiations and stand-by agreements withthe IMF. Political pressures, however, led repeatedly to the loosening of policy,especially in the run-up to elections. A vicious cycle was established of deval-uations, austerity packages and debt agreements, followed by a slackening offiscal policy and accelerating inflation. (See Reference table 1 for historical dataon government finances.)

—but President DuránBallén makes some

headway

The Durán Ballén government, which came to power in August 1992, an-nounced major reforms, including financial sector liberalisation and a broadprivatisation programme. The country’s long-delayed entry into the AndeanPact free-trade area (now the Andean Community) was implemented, and inJanuary 1993 a new foreign investment code was announced. Political oppos-ition and divisions within the government itself stalled the privatisation pro-cess, although progress was made with preparations for the sale of the EmpresaEcuatoriana de Telecomunicaciones (EMETEL, the state telecommunicationscompany).

Ecuador: Economic policy 13

© The Economist Intelligence Unit Limited 1998 EIU Country Profile 1998-99

A precarious adjustmentstrategy

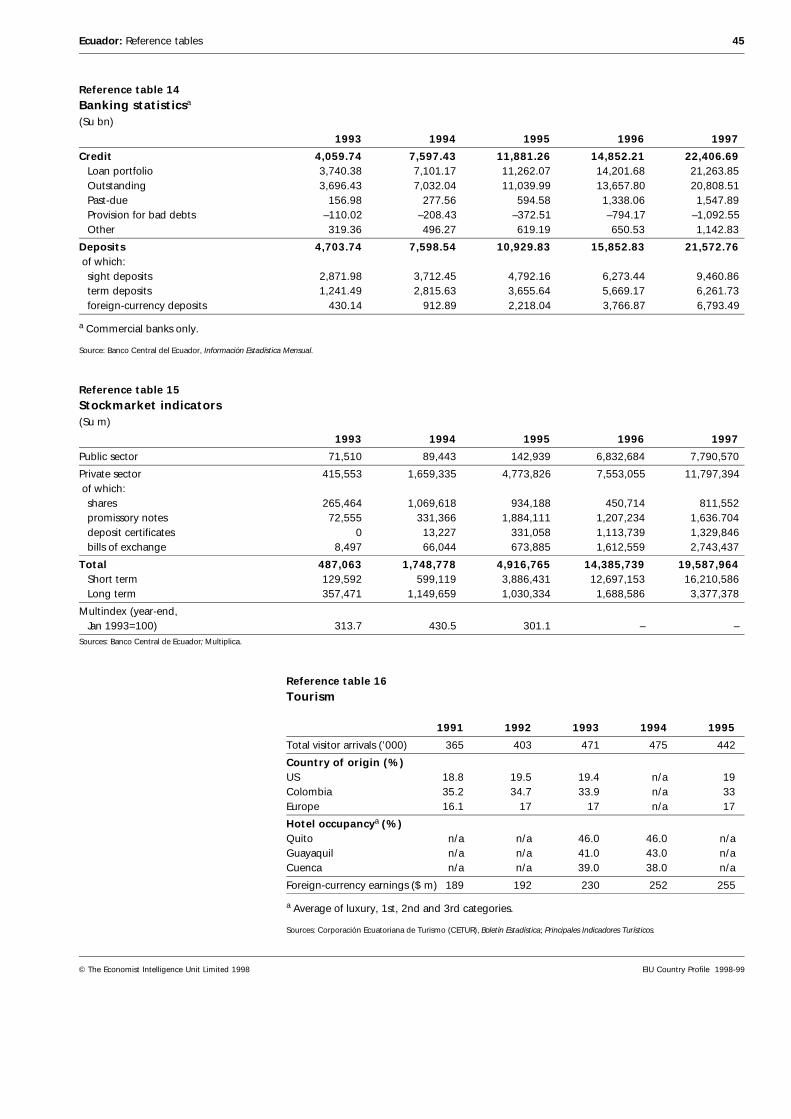

A key aim of the government’s economic policy was to slow down inflation bymeans of a nominal exchange-rate anchor and fiscal austerity. Growth in themoney supply, however, initially accelerated as financial liberalisation andshort-term capital inflows created aggressive competition for lending. This inturn led to inflationary pressures and a credit boom. However, towards the endof 1994 political crisis and the conflict with Peru reduced short-term capitalinflows. The Banco Central del Ecuador (the Central Bank) responded by rais-ing interest rates, causing a severe tightening of liquidity. Public spending wascut further and emergency war taxes imposed, and two minor devaluationstook place. Thus, large-scale capital flight was stemmed and a major deval-uation of the sucre averted, but the measures also caused recession and uncer-tainty surrounding the sustainability of the system of exchange-rate bands.Credit restrictions severely affected production and investment, while publicspending cuts and structural reforms harmed poorer sectors. In 1996 thegovernment was forced to bail out several banks hit by reduced liquidity and ahigh ratio of bad debts (see Reference tables 2, 3, 14 and 33).

Structural problemspersist

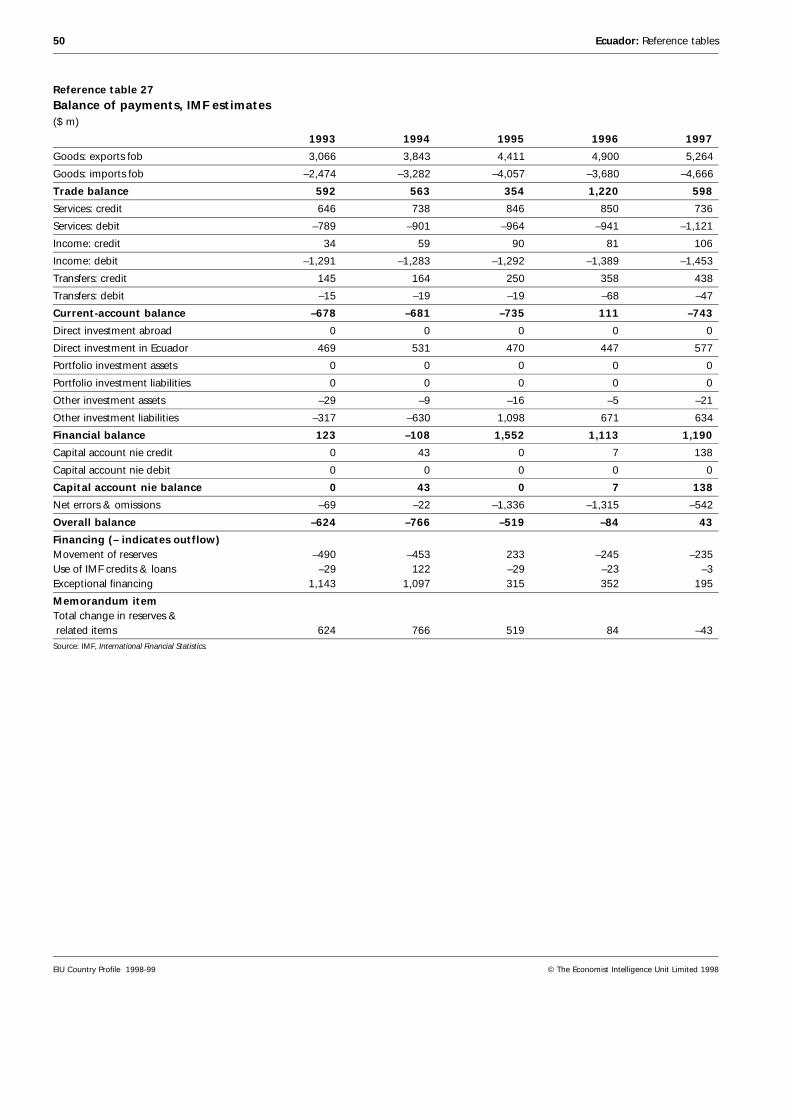

Several underlying problems remain, including: a weak financial sector; a de-pendence on short-term capital inflows to finance the current-account deficit;an overdependence on oil export receipts for fiscal revenue (oil-related revenueamounted to 34.6% of total central government revenue in 1997); tax evasion;and, finally, wage-indexation which obstructs progress on price stabilisation.Although trade liberalisation has stimulated the growth of non-traditional ex-ports, Ecuador remains overdependent on oil and bananas, which togetherrepresented 52% of exports in 1997. The other principal exports are agriculturalprimary products, exposing the economy to the external shocks of price anddemand movements in international markets (see Reference table 23 for his-torical data on exports). Finally, Ecuador’s low domestic savings rate has leftthe country dependent on external finance. As it has not developed the polit-ical or economic stability necessary to attract medium- and longer-term capitalinflows, it has had to rely on short-term speculative capital to finance itscurrent-account deficit.

Mr Alarcón missesopportunities owing to

political expediency

Repeated delays in the presentation of his promised economic plan meant thatAbdalá Bucaram implemented little in terms of economic policy during his sixmonths as president. His tentative plans to introduce a currency board put himin direct conflict with those who had elected him on a clearly populist plat-form, and it was the preparatory increases in utility tariffs that triggered theprotests that ultimately led to the president’s ousting.

Mr Bucaram’s drastic plans were scrapped by Fabián Alarcón as soon as heassumed office as interim president. Despite promises to lay the foundations fora recovery in production by stabilising the macroeconomic environment, itsoon became apparent that political expediency would keep Mr Alarcón frommaking progress on this front. A sound stance by the Central Bank did permitthe stabilisation of key macroeconomic variables (the devaluation rate of theexchange-rate band was increased in order to minimise the real appreciation ofthe currency in the face of rising inflation, and the introduction of daily foreign-exchange auctions curtailed currency volatility, leading to lower interest rates).But the government’s failure to tackle the fiscal deficit ensured this was

14 Ecuador: Economic policy

EIU Country Profile 1998-99 © The Economist Intelligence Unit Limited 1998

shortlived. Soon after partially reversing the utility tariff increases introduced byMr Bucaram, a set of emergency measures—import tariff surcharges and a$400m cut in public expenditure—were announced by the Alarcón governmentto curb the deterioration of public finances. These, however, were more thanoffset by Mr Alarcón’s willingness to give in to the demands made in late 1997for higher public-sector wages in the hope that this would strengthen his sup-port base. This, together with the collapse in world oil prices in late 1997 andearly 1998, put increasing pressure on public finances, fuelling inflation andultimately leading to a moderate devaluation of the sucre in March 1998. Thedegree of perceived policy uncertainty and regulatory inadequacy was behindthe government’s failure to sell a 35% stake of EMETEL on two separate occa-sions, the first in November 1997 and the second in April 1998.

Mr Mahuad promiseswide-ranging reforms

Jamil Mahuad has assumed the presidency at a time of deep economic crisis,and he has spared no effort in highlighting this to explain the need for far-reaching reform. Soon after he took office, the government eliminated utilitysubsidies on electricity and domestic gas, replacing these with “poverty cou-pons” to compensate the poorest families. Although this is a key step towardsrestoring balance to public finances (and one which his predecessors repeatedlyshied away from), the government must still address the problems posed byinefficient tax collection (income tax receipts are estimated at 1% of GDP),which lead to an overreliance on oil export receipts and a heavy debt-servicingburden. As regards tax collection, the government is considering a number ofproposals, including reducing value-added tax (VAT) exemptions and replacingincome tax with a flat tax on financial transactions.

Important economic policy initiatives of recent years

1992: Ecuador leaves OPEC in November, gaining completefreedom to produce and export oil.

1994: A stand-by agreement is signed with the IMF in May,running until end-1995. All targets are met.

1994: The Financial Institutions Law deregulates the financialsector, leading to a proliferation of institutions and intensecompetition for deposits. Interest rates are pushed up andaggressive marketing of credit leads to accelerating growth inmoney supply.

1994: A crawling-peg exchange-rate system from Decemberhas a Su50 band either side of the central parity rate.

1995: A Brady Plan debt-restructuring agreement iscompleted in February, re-establishing Ecuador’s sovereigncreditworthiness and opening the door to fresh credit. InAugust Congress approves the sale of 35% of the statetelecommunications institute to private operators and 10%to the workforce. Proceeds go to a Solidarity Fund for socialspending.

1995: Faced with a liquidity crisis in the financial sector, theCentral Bank provides emergency 60-day credits to 29institutions in December. Capital requirements are raised tostrengthen the sector and encourage mergers, a moratoriumis imposed on new institutions and limits placed onforeign-currency holdings.

1996: Ecuador joins the World Trade Organisation in Januaryand removes all remaining non-tariff barriers, while amaximum tariff 10 percentage points above the Andean Pactcommon external tariff is allowed.

1997: A daily auction system for foreign-exchange tradingbetween the Central Bank and commercial banks isintroduced in March in order to reduce exchange-rate andinterest-rate volatility.

1998: State subsidies on electricity and domestic gas areabolished in September.

Ecuador: Economic policy 15

© The Economist Intelligence Unit Limited 1998 EIU Country Profile 1998-99

But progress towards stabilisation will be slow, and will be complicated by aweakness in the financial system (the loan portfolios of many banks are dete-riorating, and this has prompted the authorities to reduce reserve requirementsfor all financial institutions) and an unfavourable international economic en-vironment. The collapse of investor confidence in emerging markets forcedanother devaluation in September 1998, raising further doubts about the feasi-bility of the exchange-rate regime, and caused interest rates to surge. Thepresident has also promised to speed up much-awaited structural reform, usingthe remit of the new constitution to encourage greater private-sector partici-pation in oil, telecommunications (the privatisation of the state telecoms com-panies will be a priority), electricity and other infrastructure projects with aclearer regulatory and legal environment. Mr Mahuad’s government will alsoprioritise rebuilding on the coast, which was battered by the El Niño weatherphenomenon in late 1997 and early 1998, and labour-market reform.

Further tradeliberalisation

Competitive pressures and trading opportunities are arising from the con-tinued process of regional integration. The Andean Community is enteringnegotiations on a possible trade agreement with Mercosur (the southern conecustoms union comprising Brazil, Argentina, Uruguay and Paraguay), whilethere are also plans to create a Free-Trade Area of the Americas (FTAA) by 2005,as proposed in 1994 by the US at the Summit of the Americas in Miami.

Economic performance

Oil-sector fortunesshape growth

Between 1970 and 1979 GDP grew at an annual average rate of 7.5%, thankslargely to the growth of the oil sector. During the 1980s growth was muchslower and even declined. The worst year was 1987, when a sharp drop in oiloutput following an earthquake caused a 6% contraction in GDP.

Growth picked up in 1990 and 1991. The recovery in 1990 mainly reflected theboost to government revenue and exports provided by higher world oil prices,while in 1991 the acceleration in growth was due to a recovery in the agricul-tural sector—particularly export-oriented activities such as bananas andprawns—and in mining. Private consumption also grew in 1991, followingsubstantial public-sector wage rises.

Growth slowed in 1992 and 1993 as a result of high interest rates, a tighterfiscal stance, a real appreciation in the sucre and slow growth in the worldeconomy. Particularly badly hit were construction and agriculture. The fastestgrowing sector in 1993 was oil and mining, with Ecuador’s departure fromOPEC allowing significant production increases. Economic stabilisation andderegulation, as well as debt renegotiation, made Ecuador a more attractivetarget for foreign investment but trade liberalisation meant tough competitionfor local manufacturers (see Reference tables 4, 5 and 6).

The 1994 credit boom— By the last quarter of 1994 GDP growth had accelerated to an annualised rate of6.3%. Expanding credit, rising consumer demand and expectations of con-tinued consumer confidence boosted manufacturing growth, which almostdoubled compared with 1993. The construction sector recovered and services,especially financial services, boomed. The downside to this was a deterioration

16 Ecuador: Economic performance

EIU Country Profile 1998-99 © The Economist Intelligence Unit Limited 1998

in the current-account balance, as an overvalued exchange rate sucked incheap imports.

—leads to bust in 1995 A series of external shocks, internal energy supply difficulties and increasedpolitical instability brought an abrupt end to this nascent boom in 1995.The sectors which had grown fastest in 1994 were among the worst affected—financial services and construction. The costs of the conflict with Peru strainedthe public-sector budget, and armaments imports contributed to a widening ofthe current-account deficit. Electricity rationing due to drought at the principalhydroelectric plant disrupted production and imposed alternative generationcosts. Political uncertainty increased following the flight of the vice-president,Alberto Dahik, and interest rates were raised to prevent capital leaving thecountry. Producers and the financial sector struggled against lower liquidity,rising interest rates and bad debts. The export sector was unable to compensatefully for these difficulties, with major products such as bananas, oil, coffee andprawns facing poor international trading conditions or domestic productionproblems.

The difficulties faced by producers and the financial sector continued into 1996with high interest rates, low liquidity and investor uncertainty as to the out-come of elections and the future of economic policy. Even after Mr Bucaramhad taken office, uncertainty continued to be fuelled by repeated delays in theannouncement of an economic package and, subsequently, by doubts over theviability of the planned currency board. As a result of this uncertainty, con-sumption and investment stagnated, prompting a fall in borrowing and adownward trend in interest rates. The problems facing production were com-pounded once again by power shortages towards the end of the year. Lowdomestic demand caused a sharp contraction in import levels, swinging thecurrent account into surplus for the first time in ten years. The contraction inimports meant that GDP was able to expand by 2% in that year despitethe problems.

Real growth in gross domestic product(% change)

Annual average1997 1993-97

Private consumption 2.4 2.4

Public consumption –0.3 –0.1

Gross fixed investment 4.0 3.3

Change in stocks –1.7 –0.1

Exports 4.3 5.2

Imports 8.8 3.9

GDP 3.4 2.8Source: Banco Central del Ecuador, Información Estadística Mensual.

The following year was another lost year for Ecuador. Although Mr Alarcón wassuccessful in restoring some degree of calm following the ousting of his prede-cessor in February 1997, consumption remained stagnant and investment dis-played only a modest improvement. The lack of demand for credit createdexcess liquidity in the banking system, making it increasingly difficult forcommercial banks to invest assets profitably at a time when interest rates had

Ecuador: Economic performance 17

© The Economist Intelligence Unit Limited 1998 EIU Country Profile 1998-99

already turned negative in real terms. On the supply side, oil production begana slow decline owing to a transport bottleneck, and towards the end of the yearmanufacturing was hit once again by electricity shortages, despite prior assur-ances by the government that the problem had been resolved. Agricultureperformed well throughout most of the year, with strong output rises partic-ularly visible in bananas and prawns. However, excess rainfall and floodingcaused by the arrival of the El Niño climatic pattern in late 1997 devastated keyexport crops on the coast, destroyed infrastructure and left thousands homelessuntil the early months of 1998. Despite ongoing political uncertainty in 1997,a moderate rate of recovery in domestic demand revived import growth andallowed the economy to expand by 3.4%, returning the current-account bal-ance to its customary deficit.

Fiscal imbalance drivesinflation—

Since the early 1980s inflation has been fuelled by large public-sector deficits,currency devaluations, production problems in the agricultural sector and thegradual reduction of fuel and utilities subsidies. The Durán Ballén governmentsucceeded in lowering the annual average rate from 54.6% in 1992 to 22.9% in1995, through a combination of fiscal austerity and a nominal exchange-rateanchor (see Reference table 8). However, price pressures were stirred once againin early 1997 by the rises in utility prices, causing year-end inflation to reach30.5%. Mr Alarcón’s refusal to exercise fiscal rectitude fuelled price pressuresfurther in early 1998. Currency weakness and President Mahuad’s abolitionof state subsidies on utilities put inflation at just under 44% in the year toOctober 1998.

—affecting real wages— The official monthly minimum wage and associated benefits are revised inter-mittently by a committee consisting of representatives of the government,unions and employers—usually twice a year. In the second half of the 1980sand early 1990s nominal increases failed to keep pace with inflation. The realaverage wage index (1990=100) fell from 162.2 in January 1986 to a low of 65.1in mid-1992. Although it rose to 130.8 in August 1997 as inflation eased, itplummeted back to 113.5 in September as price pressures gained once more(see Reference table 9).

—making poverty aproblem

The country’s failure to embark on a sustainable growth path has caused em-ployment to fall, forcing a growing proportion of the economically active pop-ulation into the informal sector (for historical data on the labour force, seeReference table 11). This trend has been made more acute because of barriers tolabour market entry placed by powerful trade unions—particularly in the exten-sive public-sector workforce—and a pro-labour legal framework. Rural-urbanmigration has increased the supply of unskilled labour in urban areas. Privatestudies indicate that the share in income of the poorest 20% of the urbanpopulation dropped from 2.55% to 1.68% between 1988 and 1993. The share ofthe richest 5% increased from 33% to 41%. In 1994, 25% of the urban popul-ation and 47% of the rural were considered poor, while 10% of the urbanpopulation and 22% of the rural were living in conditions of extreme poverty.

18 Ecuador: Economic performance

EIU Country Profile 1998-99 © The Economist Intelligence Unit Limited 1998

Inflation and wages

Annual average1997 1993-97

Consumer prices (% change) 30.7 30.0

Real minimum wage index (Jan 1990=100) 126.1 102.3Source: Banco Central del Ecuador, Información Estadística Mensual.

Regional trends

A move to devolution Opinion has been tilting in recent years towards the devolution of greaterfinancial and administrative control to the provinces. A constitutional reformto this effect was defeated in the November 1995 referendum only because themajority of the population used the referendum to express rejection of thegovernment, although the measure itself had majority support. There are alsogrowing pressures for central government allocation of funds to be distributedmore evenly on the basis of the size and needs of the local population. Cur-rently, distribution is determined by political pressures at the centre and byhistorical distribution.

Resources

Population

Ecuador’s population was 10.3m at the 1990 census, and is expected to reach12.6m by 2000. It grew by an average rate of 2.5% per year between 1982 (theprevious census) and 1990, and by an estimated 2.3% per year in the 1990s (seeReference table 10). The infant mortality rate fell from 60.4 per 1,000 childrenborn alive in 1982 to 52.7 in 1990, while the birth rate rose from 2.5% of thepopulation to 3.2%, and the death rate from 0.6% to 0.8% of the population.

Urbanisation Between 1982 and 1990 the urban population increased from 49.2% to 55.4%of the total population, and is forecast to reach 64% by 2000. The three prin-cipal cities, Quito, Guayaquil and Cuenca, accounted for a roughly constant30% of total population between 1982 and 1993, with the relative increase inthe urban population due to migration towards major secondary cities such asLoja, Santo Domingo and Machala—a trend expected to continue. The coastremains slightly more densely populated than the highlands.

Population indicators, Nov 1990 census(%)

By age0-14 38.815-24 20.325-59 34.560+ 6.4

continued

Ecuador: Regional trends 19

© The Economist Intelligence Unit Limited 1998 EIU Country Profile 1998-99

By regionHighlands 45.6Coast 49.7Amazon 3.9Galapagos & others 0.8Sources: Instituto Nacional de Estadística y Censos (INEC); Banco Central del Ecuador, Boletín Anuario.

A growing workforce The age trend of the 1980s is forecast to continue in the 1990s. The proportionof the population under 15 years of age is projected to fall from 38.8% in 1990to 33.8% by 2000. The proportion of those between 15 and 64 rose from 54.1%to 56.9% between 1982 and 1990. This trend implies less demand for educationbut an increase in those seeking employment.

Access to basic services, 1994(% of income category, unless otherwise indicated)

Poor Non-poor

Years spent in education by head of household 4.0 7.5

Informal health treatment 29.4 18.0

Sewage systems 29.6 63.8

Electricity 75.8 91.1

Drinking water 34.8 59.3Source: Gestión.

Race Indigenous people account for an estimated 43% of the population. The mes-tizo population includes descendants of foreign immigrants who have inter-married with indigenous people. These immigrants have included Spanishcolonialists and other European settlers; Arabs, especially Lebanese, who ar-rived at the beginning of this century and form an economically and politicallypowerful community, particularly on the coast; Chinese; and other LatinAmericans, especially from neighbouring Colombia. Two areas of northernEcuador, around the port of Esmeraldas and in the Chota valley near theColombian border, have a mainly black population, descendants of slaves ofAfrican origin.

Education

Universal education isunderfunded

Since the 1970s successive Ecuadorean governments have sought to reduceilliteracy and increase the output of trained professionals through the provi-sion of free education. Since the early 1980s, however, state resources availablefor education have been squeezed. Although the constitution requires 30% ofthe budget to be spent on education, parents have increasingly been requiredto contribute towards fees, materials and uniforms. The number of institutions,teachers and pupils has continued to rise at the expense of educational quality.Only a small proportion of the population can afford private education, whichis concentrated in urban areas at secondary and university levels.

According to the latest census in 1990, 10.2% of the population aged ten andover were illiterate (compared with 14.8% in 1982) and 87% of children aged6-11 years were in education although there are high rates of absenteeism,repetition and irregular attendance, especially in rural and the poorest urban

20 Ecuador: Education

EIU Country Profile 1998-99 © The Economist Intelligence Unit Limited 1998

areas. Poor health and nutrition, and a lack of transport, materials and teacherscompound these problems, which are further aggravated by uncreative, trad-itional teacher-training methods. Teachers are also underpaid and strikes causerepeated disruption.

Secondary education Only the first three years of secondary school are compulsory, but even theseprovide many with inadequate preparation for work. The subsequent threeyears are intended to prepare pupils for further study or provide technicaltraining. Most students graduate in science, social science or business studies.In technical colleges pupils favour business administration over industrial andagricultural studies. Although the proportion of children aged 12 to 14 years insecondary education totalled 63.9% in 1990, the value of this education islimited by a shortage of institutions, inadequate teacher training, the pupils’wide range of academic backgrounds and an excess of theoretical material overtechnical fieldwork.

Higher education The tertiary education sector has also seen a rapid rise in the number of institu-tions, pupils and teachers since the 1970s. The proportion of the populationover 24 years with higher education rose from 6.8% in 1982 to 12.7% in 1990.A policy of free entry to state universities combined with budget cuts, however,has inevitably led to a decline in quality. Most university courses are directedtowards training professionals for the services sector and bureaucracy ratherthan for industry.

Health

Treatment rather thanprevention

Financial constraints mean that public healthcare has tended to concentrateon treatment rather than prevention, although vaccination programmes sincethe 1970s have considerably reduced the incidence of illnesses such as measles,polio, diphtheria, tetanus and whooping cough. The diseases which most affectthe Ecuadorean population are those related to inadequate nutrition and poorsanitation and housing, especially in marginal urban and rural areas. Between1987 and 1990 the principal causes of death were intestinal infections andrespiratory diseases. There has been a resurgence of diseases such as cholera,dengue fever, malaria and rabies in recent years. Urbanisation and the shift ofemployment towards more sedentary, office-based activities have also led to anincrease in the diseases more prevalent in developed countries, such as heartdisease and stress-related illnesses.

Spending cuts Healthcare has been one of the public-service areas affected by governmentdrives to cut fiscal spending since the early 1980s. According to the WorldBank, Ecuador had one of the lowest levels of expenditure on health in LatinAmerica in 1990, at 3.7% of GDP (compared with 10% in Argentina). Com-pounding this is the fact that limited funds are not targeted effectively. TheMinistry of Health allocates funds on the basis of historical spending levels andpolitical pressures rather than population or need. Most of the budget is spenton salaries, yet services are frequently disrupted by strikes over low wages andpoor working conditions, leading to shortages of equipment and medicines.Public-health benefits are provided by the Instituto Ecuatoriano de Seguridad

Ecuador: Health 21

© The Economist Intelligence Unit Limited 1998 EIU Country Profile 1998-99

Social (IESS, the social security department). However, only 17% of the popul-ation—mostly employees—are affiliated. Private health-insurance schemeshave marketed their services aggressively in recent years.

Natural resources and the environment

Ecuador is situated on the Pacific coast of South America, and influences on itsclimate include the Andean mountain range and the warm El Niño and coldHumboldt currents. Its total area of 276,840 sq km includes the Galapagosarchipelago, 1,552 km off the coast. Owing to the country’s location on theequator, there are no extreme variations in climate during the year and thereare approximately 12 hours of daylight all year round. There are essentiallythree regions—the western coastal plain, the central highland corridor of vol-canoes and the eastern rainforest in the Amazon basin.

Biodiversity On the coast the rainy season lasts from January to May and the rest of the yearis dry. In the highlands the rainy season is from October to June. Rainfall isheavier throughout the year in the Amazon region. Around 78% of the countryhas a tropical or subtropical climate, 20% is temperate and there are 23 differ-ent microclimates, resulting in a high level of biodiversity. The alluvial soils ofthe coast and the Oriente are the most fertile and can be used to cultivate awide range of crops.

Agricultural resources Around 8.29m ha of land have potential for agricultural use, of which 74% liesin tropical and subtropical zones. Large oil and gas reserves are located in theOriente, although there is also gas in the Gulf of Guayaquil. Water is animportant potential source of hydroelectric energy.

Fishing resources Inland rivers and lakes, as well as the coastline, provide a wide variety of fishand sea products. Fresh-water prawn production for export has expanded rap-idly in recent years, especially in the Gulf of Guayaquil, and in Esmeraldas andManabí provinces.

Environmental conditions

Principal problems: Oil spillages; urban fumes and lack of waste-disposalfacilities; destruction of coastal mangrove swamps for prawn farming;deforestation and soil erosion; indiscriminate use of pesticides; mercurycontamination in unauthorised mining areas; and overfishing.

Legal framework: 1976 Law for Environmental Control and Protection andmany sector-specific regulations. The technical capacity, personnel and politicalwill necessary to fulfil regulations is lacking, however. Control is dissipated amonga number of organisations.

22 Ecuador: Natural resources and the environment

EIU Country Profile 1998-99 © The Economist Intelligence Unit Limited 1998

Economic infrastructure

Transport and communications

Investment in highwaysreceives a boost

Most transport in Ecuador is by road. The number of vehicles registered rose by25% to 463,000 between 1990 and 1994, although this figure understates thetrue quantity owing to evasion of the vehicle tax. Most of the road network isin poor condition for lack of public funds. The Durán Ballén government’sNational Highway Plan improved 35 major provincial motorways with anoverall investment of around $500m, partially financed by multilateral andbilateral credits. Work also began in 1996 on the Ecuadorean section of theInteroceanic Way, which will eventually join the Pacific and Atlantic oceansvia Ecuadorean roadways and Brazilian waterways.

In 1995 the Ministry of Public Works called for bids from private-sector con-tractors to repair, maintain and administer 1,315 km of roads under two-yearconcessions. Investment would be recovered through tolls. Progress hasonly been made with the first stage of bids for the Rumichaca-Guayllabambaroute in the north and Aloag-Riobamba route in the central highlands. Thesecond stage will include the Santo Domingo bypass and Santo Domingo-Jujánroutes. Floods caused by El Niño have destroyed much of the road network incoastal areas, and it must be rebuilt in 1999.

The rail system is indecline

The railway system, built at the turn of the century, is now of relatively littleimportance. Service is irregular and the track and rolling stock are in urgentneed of modernisation. The state modernisation body, Corporación Nacionalpor la Modernación del Estado (Conam), plans to wind up the state railway

Telecommunications privatisation

August 1995: Congress passes the Telecommunications Law, allowing theprivatisation of the state telecommunications company, Empresa Ecuatoriana deTelecomunicaciones (EMETEL).

January-June 1996: Tariff structure agreed by the regulatory Comisión deTelecomunicaciones (Conatel), EMETEL, government and private bidders.

September 1997: EMETEL converted into two regional companies—Andinateland Pacifictel. 100% of EMETEL valued at $1.82bn; qualified operators invited tobid.

November 1997: Auction to sell 35% of Andinatel and Pacifictel fails becauseonly one operator presented a bid (the law requires at least two bidders).

April 1998: Second attempt fails after all bidders withdraw from process, citingan uncertain legal and regulatory environment.

Ecuador: Transport and communications 23

© The Economist Intelligence Unit Limited 1998 EIU Country Profile 1998-99

company, which requires an annual state subsidy of around $8m, and is seek-ing private purchasers or subcontractors.

Air traffic is on theincrease

Ecuador’s two main airports are in Quito and Guayaquil. International passen-ger traffic is projected to increase over the next 30 years by 7% in Quito and 6%in Guayaquil, while freight volumes are expected to rise by 16.5%. The need foran expansion of capacity and improved safety means that the two airports areto be moved out of the city centres, and Conam recently called for private bids.There are three national airlines: TAME, SAETA and Ecuatoriana. TAME(military-owned) is the principal domestic airline, but it also began flying toChile, Panama and Cuba in 1996. SAETA, a private airline, operates inter-nationally, mainly to the US, and has a domestic wing, SAN SAETA. However,the former state airline, Ecuatoriana, was grounded in 1993, benefiting variousUS airlines. Ecuatoriana’s privatisation in 1995 and return to internationaloperations in June 1996 have since meant tough competition. A serious acci-dent in September 1998 involving a Cuban aircraft taking off from Quitoairport has increased pressure to finalise plans to build new airports forEcuador’s two main cities.

Telecommunications:privatisation has been

difficult

Ecuador has an average of eight telephone lines per 100 inhabitants (just overone-third of the Latin American average of 20), but the service is concentratedin urban areas. Years of underinvestment have led to a poorly maintained andinadequate infrastructure. The Durán Ballén government introduced the legalframework for the privatisation of the state-owned telecommunications sector.However, opposition from interest groups and a lack of political will has meantrepeated delays in the privatisation process. The auction to sell off a 35% stakein each of the two regional companies into which the state telecoms enterprisewas divided had to be abandoned at the last minute when only one operatorpresented a bid. An uncertain regulatory environment was probably the mainfactor prompting other registered bidders to withdraw from the process. Muchto the government’s embarrassment, a second attempt to sell the stake in theentities in April 1998 had to be cancelled, also at the last minute, when the twoprincipal bidders told the government that their previous concerns had notbeen addressed.

Port modernisation isunder way

Ecuador’s four main ports are Guayaquil, Esmeraldas, Manta and PuertoBolívar. Two additional ports, at Balao and La Libertad, are equipped to accom-modate oil tankers. Port trade has been rising rapidly and the number of shipsdeparting rose by 165% between 1990 and 1994, to 16,340. A modernisationprogramme is under way, which in the short term involves the subcontractingof port services to the private sector and in the longer term an internationalbidding round. Customs control, which was tightened as inspection washanded over to the private sector under the Durán Ballén government, deterio-rated following its renationalisation under Abdalá Bucaram. Customs control islikely to be handed back to the private sector in 1998 under new arrangements.(For historical data on transport see Reference table 12)

24 Ecuador: Transport and communications

EIU Country Profile 1998-99 © The Economist Intelligence Unit Limited 1998

Energy provision

The growth in oilproduction—

Oil production in Ecuador took off in the 1970s and has since risen steadilyfrom an average of 78,000 barrels/day (b/d) in 1972 to 389,000 b/d in 1997.Export volumes have also increased, from 25m barrles to 91m, although at aslower rate than overall production owing to growing domestic consumptionand internal transport bottlenecks. At the end of 1993 proven reservesamounted to 3.7bn barrels. Crude exports, which come mainly from Oriente,are of medium heaviness, 27°API, although the most recent discoveries havebeen of heavy crude (see Reference table 13).

Since the foundation of the state oil company, CEPE (now Petroecuador), in1972, the state has dominated production. In 1989, however, 13 risk-servicecontracts were signed with private operators, seven of which are still in force(with Occidental, Arco, Oryx, Tripetrol, Elf, Braspetro and Maxus). Most ofthese have started producing since 1990, reducing Petroecuador’s share ofproduction in 1994 to 88%. In 1993 a further reform to the Hydrocarbons Lawintroduced production-sharing contracts (PSCs), six of which were signed withthe private sector in 1994, followed by a further two in 1996.

—is limited by poorrefining and transport

facilities

The increasing production of derivatives has meant the need for expandedtransport and refining facilities. Refining capacity has increased from some31,500 b/d in 1972 to 157,000 b/d in 1995 but is still insufficient to meetdomestic demand, leading Ecuador to import fuel. Recent programmes havebeen aimed at further increasing capacity, producing lead-free and high-octanefuel and diesel, and processing heavier crude.

Lack of transport capacity has been the principal obstacle to increased oilproduction in recent years. Plans to expand pipeline capacity have been repeat-edly disrupted by political opposition to handing this “strategic” national assetover to private-sector management. A programme to expand transport capacityto 410,000 b/d by the end of 1999 has now been scrapped by President JamilMahuad, and is expected to be replaced with a project to build a second pipe-line dedicated to transporting heavy crude. The government is likely to look forgreater private-sector participation in this sector.

Gas production Ecuador has the refining capacity to process only around 20% of the natural gasproduced in the Oriente oilfields, and imports are necessary to meet about 50%of national demand. The existing national network of poliducts transportinggas and other derivatives is 1,300 km long, but there are plans to increase thisto 2,000 km. Mr Mahuad’s government plans to restructure the sector with thehelp of private investors. It has already abolished the state subsidy on domesticgas consumption.

Investment is sought inelectricity generation

Hydroelectric resources are estimated to represent 70% of Ecuador’s commer-cial energy resources, but only 3% is actually tapped for generation. Thecountry is dependent for around 65% of its electricity on the Paute hydro-electric plant, but low rainfall, inadequate water storage and the accumulationof silt due to deforestation have reduced generating capacity. At the same timethe contribution of thermal stations has declined markedly owing to poor

Ecuador: Energy provision 25

© The Economist Intelligence Unit Limited 1998 EIU Country Profile 1998-99

maintenance and a lack of investment in new technology. Until recently heav-ily subsidised tariffs discouraged international aid, as donors judge that theyare unlikely to recoup their investments.

A series of hydroelectric plants have been built by the private sector underconcession and build-operate-transfer (BOT) schemes. It was hoped that theserecently completed projects would provide the necessary capacity to meet theshortfall from the Paute plant in the dry season, but electricity rationing had tobe reimposed in late 1997 regardless, and more rationing is expected in late1998. The ratification of the Electricity Law in 1997 paves the way for thedivision of Inecel, the state electricity company, into regional entities whichwill be privatised in 1999.

Financial services

Deregulation leads to acredit boom—

The financial sector was deregulated by the 1994 Financial Institutions Law,which led to a large increase in the number of institutions and the expansionof banks into new activities such as leasing, credit cards and investment bank-ing. Ecuador now has over 300 financial institutions, including 31 banks,although 90% of assets are held by only ten institutions.