Economy at a glance: Calgary’s advantages · Economy at a glance: Calgary’s advantages ......

58

August 2013 Slide 1 Economy at a glance: Calgary’s advantages August 2013

Transcript of Economy at a glance: Calgary’s advantages · Economy at a glance: Calgary’s advantages ......

August 2013

Slide 1

Economy at a glance: Calgary’s advantages

August 2013

August 2013

Slide 2

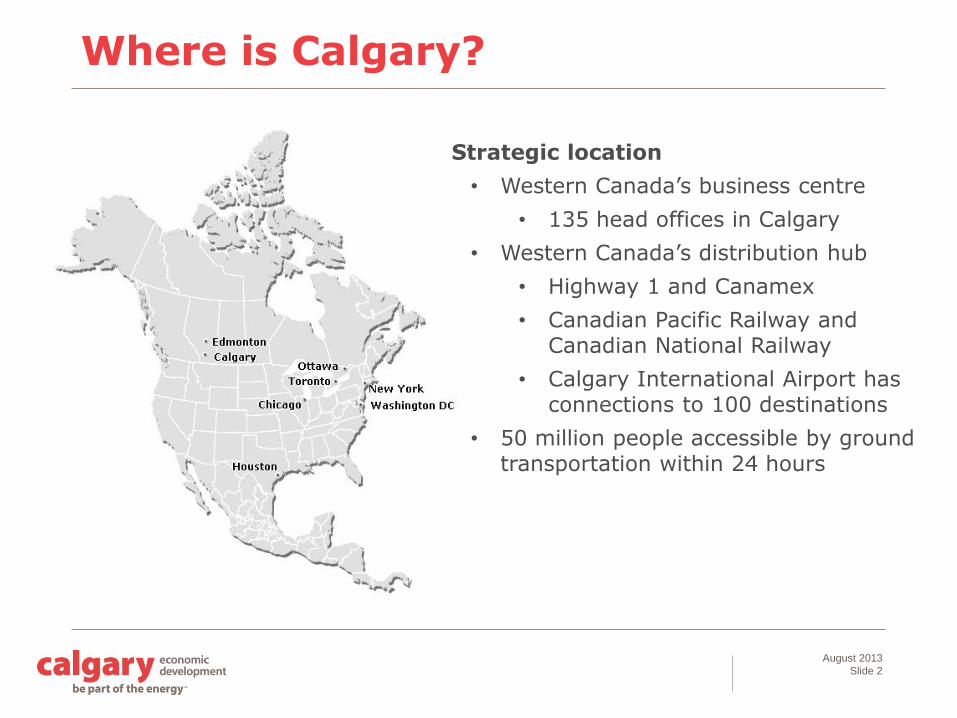

Where is Calgary?

Strategic location

• Western Canada’s business centre

• 135 head offices in Calgary

• Western Canada’s distribution hub

• Highway 1 and Canamex

• Canadian Pacific Railway and Canadian National Railway

• Calgary International Airport has connections to 100 destinations

• 50 million people accessible by ground transportation within 24 hours

August 2013

Slide 3

About Calgary Economic Development

• Promotional agency

• Lead economic development agency

• Non-profit organization

• Arms length to City of Calgary; Funded via grant from council

• Mandated to support / connect business

• Business expansion, investment and attraction

• Trade development

• Workforce development

• Research and information

August 2013

Slide 4

10-year Economic Development Strategy

A strategy to make a global city – competitive, successful and unique

Focus on People and Community

• Educate and exchange

• Remove barriers to meaningful employment

• Enhance the city’s sense of place and experience

Focus on Business and Enterprise

• Strategically develop Calgary’s economy

• Provide smart infrastructure

• Create an environment for smart ideas and innovation

Focus on International Reach

• Promote the Calgary brand and identity

• Diversify tourism and convention activity

• Enhance international business development and connections

August 2013

Slide 5

Sources: MoneySense, Conference Board of Canada

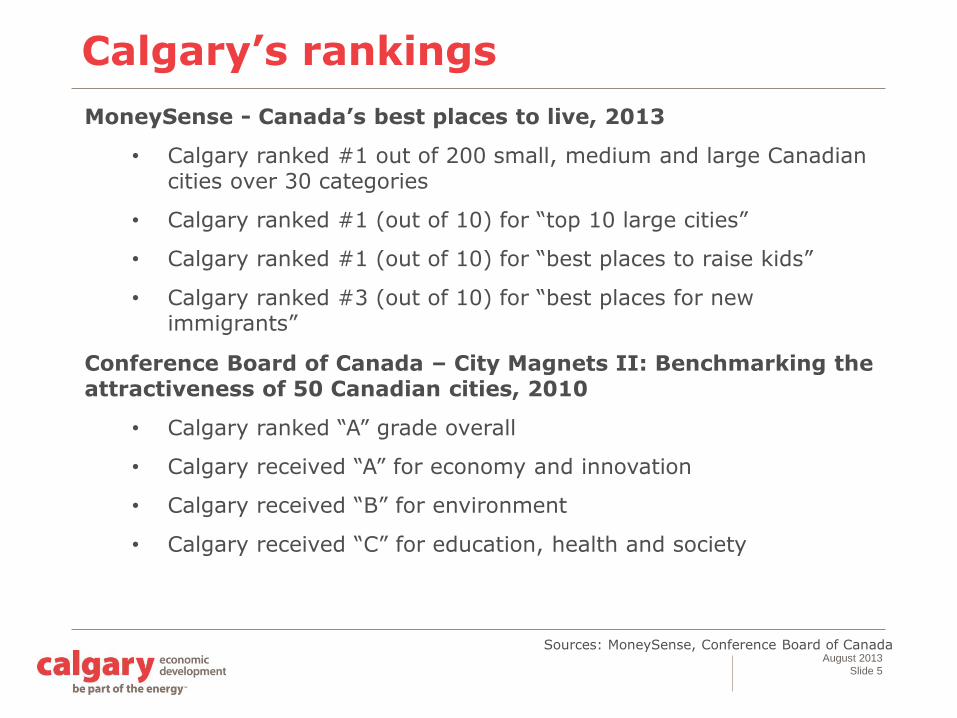

Calgary’s rankings

MoneySense - Canada’s best places to live, 2013

• Calgary ranked #1 out of 200 small, medium and large Canadian cities over 30 categories

• Calgary ranked #1 (out of 10) for “top 10 large cities”

• Calgary ranked #1 (out of 10) for “best places to raise kids”

• Calgary ranked #3 (out of 10) for “best places for new immigrants”

Conference Board of Canada – City Magnets II: Benchmarking the attractiveness of 50 Canadian cities, 2010

• Calgary ranked “A” grade overall

• Calgary received “A” for economy and innovation

• Calgary received “B” for environment

• Calgary received “C” for education, health and society

August 2013

Slide 6

Source: Economist Intelligence Unit, Mercer

Calgary’s rankings

Economist Intelligence Unit – Most livable city in the world

• Calgary #5 in 2012 (#5 for 2010 and 2011)

• Ranking of 140 global cities with 30 indicators

• Criteria: stability, healthcare, culture and environment, education, infrastructure

Mercer – Quality of living survey

• Calgary is #32 in the world in 2012 (up from #33 in 2011 ranking)

• Ranking of 221 global cities with 39 criteria ranked against New York as base city

• Criteria: political, social, economic and environmental factors

Mercer – Quality of living: eco-city ranking

• Calgary #1 in the world in 2010 – Mercer’s first eco-city ranking

• Criteria: water availability and potability, waste removal, sewage, air pollution and traffic congestion

August 2013

Slide 7

Source: Canadian Council on Learning; Maclean’s. May 20, 2010

Enviable lifestyle

Canada’s Smartest City

• Calgary ranked #3 in 2010 – based on Learning to Know (formal education), Learning to Do (applied skills), Learning to Live Together (social values of community) and Learning to Be (cultural opportunities and spending)

Canada’s Most Wired City

• Calgary ranked #1 in 2010 – based on spending for services, access to broadband

Canada’s Most Cultured City

• Calgary ranked #4 in 2010 – based on per cent of households who spend money on attending museums and live performing arts

Canada’s Most Active City

• Calgary ranked #6 in 2010 – based on per cent who spend on sports and recreation

August 2013

Slide 8

Enviable lifestyle

A focus on family and a sense of community

• Calgary schools consistently top performers in Alberta

• Boasts one of the most successful transit systems in the world (ridership of 94.4 million; 4,205 route kilometres)

• 55 per cent of Albertans volunteer -- higher than the national average of 47 per cent (2010)

• Calgary had second highest median charitable donation for 2011 among Canadian CMAs at $400

August 2013

Slide 9

Enviable lifestyle

Active and healthy lifestyle

• An hour’s drive to spectacular Banff and the Rocky Mountains

• The most extensive urban pathway and bikeway system in North America (700 km along rivers; 290 km on-street bikeways)

• World-class attractions and sporting amenities, including: Calgary Stampede, Calgary Zoo, WinSport Canada’s Canada Olympic Park, National Sports Hall of Fame, Telus Spark

• Abundant green space and parks (3,000 sites)

• A community rich in the arts, culture, entertainment and leisure activities and venues

August 2013

Slide 10

Source: “World Capitals of the Future”, Forbes, September 3, 2009

Rankings

World Capitals of the Future / World’s Fastest Growing Cities

• Forbes Magazine listed Calgary as one of the “world capitals of the future” – one of the “emerging global cities” (2009)

• Forbes Magazine ranked Calgary as one of North America’s fastest-growing cities (2010)

• Reasons:

• Calgary is center of Canada’s powerful energy industry

• Calgary has lower taxes and less stringent regulations

• Calgary has room to grow

• Calgary has better housing price-to-income ratio than many Canadian cities

August 2013

Slide 11

Global Scorecard on Prosperity

Fifth annual report benchmarking 24 global metropolitan areas with 33 indicators in two domains:

Economic performance - (18 indicators)

Labour attractiveness – (15 indicators)

• Overall ranking: Calgary ranks #2

• Economy overall ranking: Calgary ranks #8 - Grade B

• Economic update for North America: Calgary ranks #5 - Grade C

• Labour attractiveness: Calgary ranks #6 – Grade B

• Human capital lens (focus of report for 2013)

− Calgary ranks #1 – Grade A

Source: Toronto Region Board of Trade. Toronto as a Global City: Scorecard on Prosperity, 2013

August 2013

Slide 12

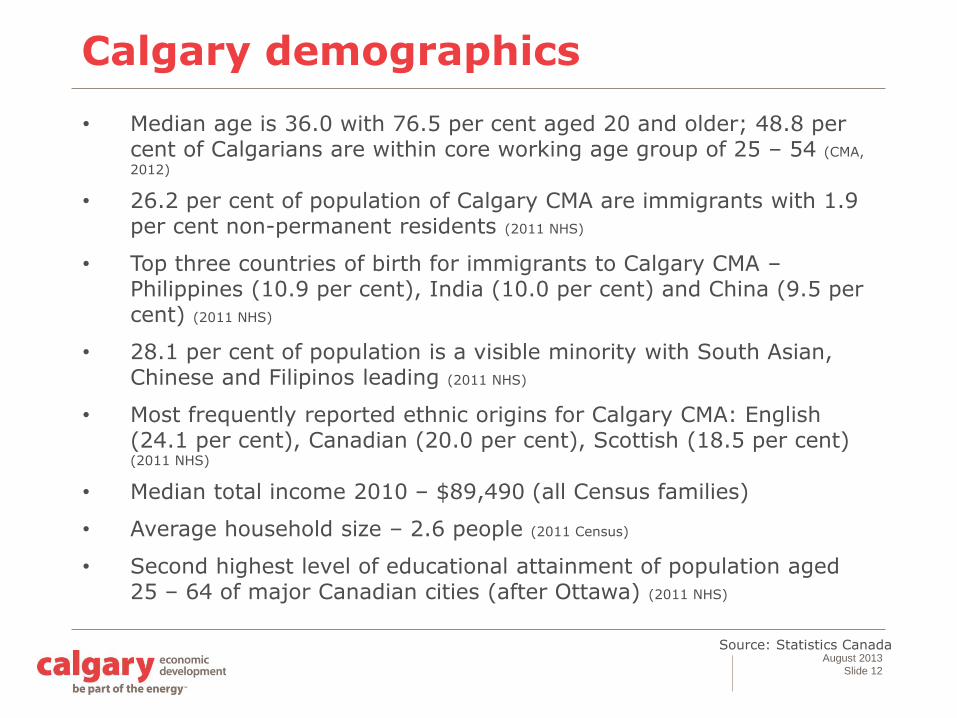

Calgary demographics

• Median age is 36.0 with 76.5 per cent aged 20 and older; 48.8 per cent of Calgarians are within core working age group of 25 – 54 (CMA,

2012)

• 26.2 per cent of population of Calgary CMA are immigrants with 1.9 per cent non-permanent residents (2011 NHS)

• Top three countries of birth for immigrants to Calgary CMA –Philippines (10.9 per cent), India (10.0 per cent) and China (9.5 per cent) (2011 NHS)

• 28.1 per cent of population is a visible minority with South Asian, Chinese and Filipinos leading (2011 NHS)

• Most frequently reported ethnic origins for Calgary CMA: English (24.1 per cent), Canadian (20.0 per cent), Scottish (18.5 per cent) (2011 NHS)

• Median total income 2010 – $89,490 (all Census families)

• Average household size – 2.6 people (2011 Census)

• Second highest level of educational attainment of population aged 25 – 64 of major Canadian cities (after Ottawa) (2011 NHS)

Source: Statistics Canada

August 2013

Slide 13

Source: Statistics Canada, Conference Board of Canada

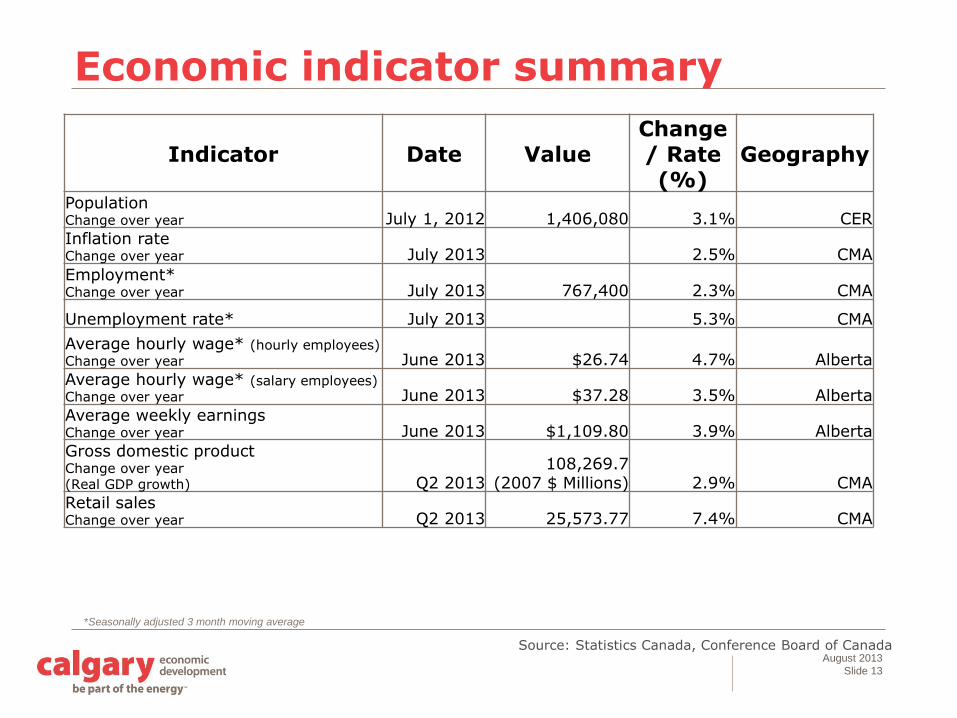

Economic indicator summary

*Seasonally adjusted 3 month moving average

Indicator Date ValueChange / Rate (%)

Geography

PopulationChange over year July 1, 2012 1,406,080 3.1% CER

Inflation rate Change over year July 2013 2.5% CMA

Employment*Change over year July 2013 767,400 2.3% CMA

Unemployment rate* July 2013 5.3% CMA

Average hourly wage* (hourly employees)

Change over year June 2013 $26.74 4.7% Alberta

Average hourly wage* (salary employees)

Change over year June 2013 $37.28 3.5% Alberta

Average weekly earningsChange over year June 2013 $1,109.80 3.9% Alberta

Gross domestic productChange over year (Real GDP growth) Q2 2013

108,269.7(2007 $ Millions) 2.9% CMA

Retail sales Change over year Q2 2013 25,573.77 7.4% CMA

August 2013

Slide 14

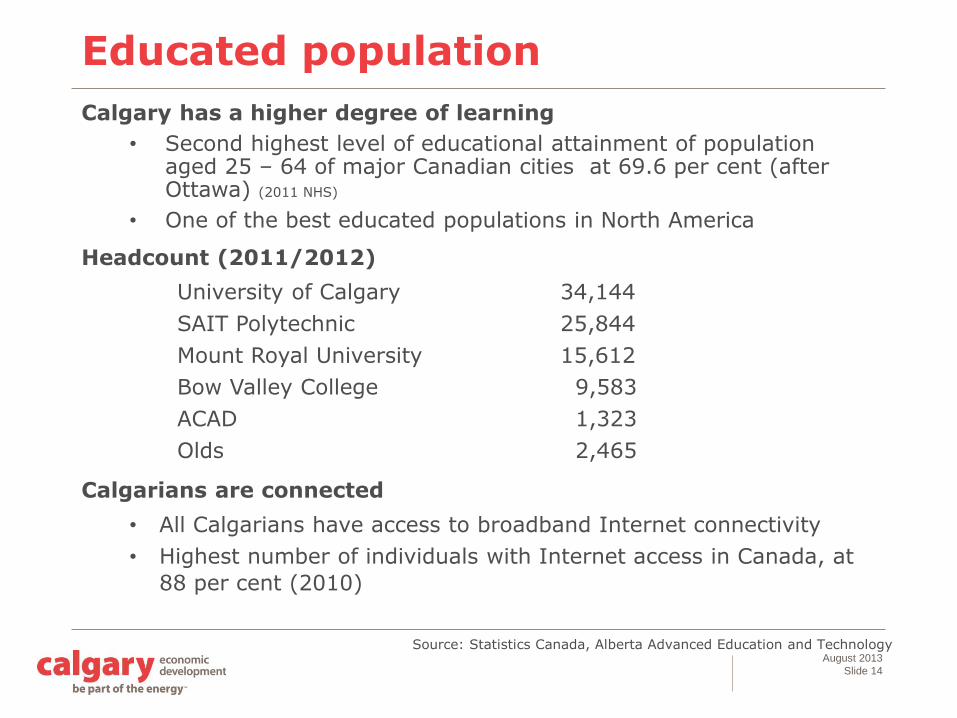

Source: Statistics Canada, Alberta Advanced Education and Technology

Educated population

Calgary has a higher degree of learning

• Second highest level of educational attainment of population aged 25 – 64 of major Canadian cities at 69.6 per cent (after Ottawa) (2011 NHS)

• One of the best educated populations in North America

Headcount (2011/2012)

University of Calgary 34,144

SAIT Polytechnic 25,844

Mount Royal University 15,612

Bow Valley College 9,583

ACAD 1,323

Olds 2,465

Calgarians are connected

• All Calgarians have access to broadband Internet connectivity

• Highest number of individuals with Internet access in Canada, at

88 per cent (2010)

August 2013

Slide 15

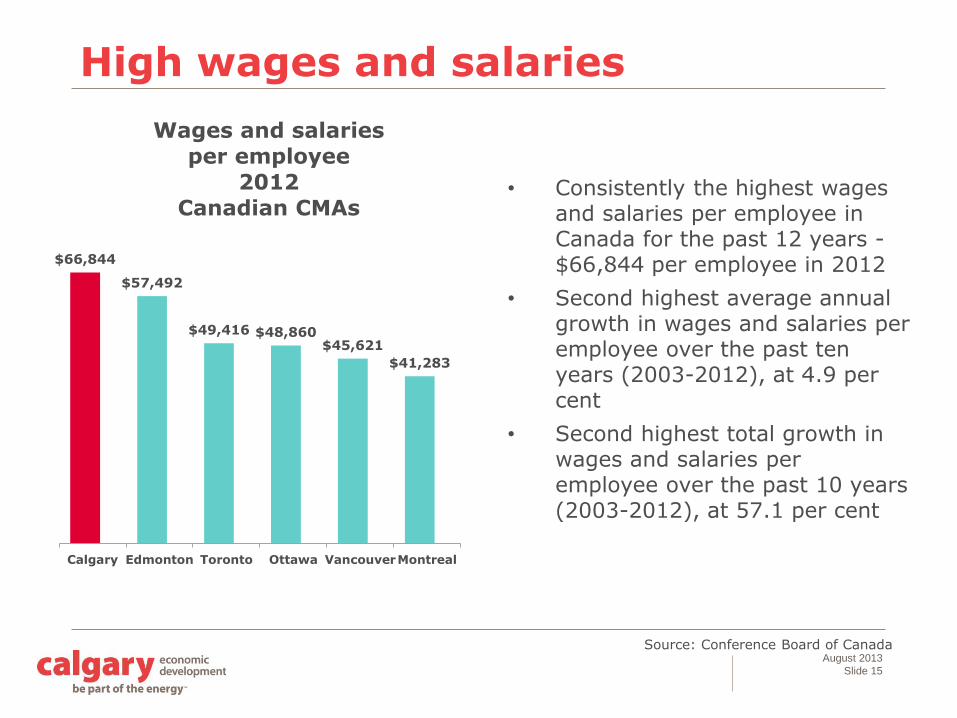

High wages and salaries

$66,844

$57,492

$49,416 $48,860$45,621

$41,283

Calgary Edmonton Toronto Ottawa VancouverMontreal

Wages and salaries

per employee

2012

Canadian CMAs• Consistently the highest wages

and salaries per employee in Canada for the past 12 years -$66,844 per employee in 2012

• Second highest average annual growth in wages and salaries per employee over the past ten years (2003-2012), at 4.9 per cent

• Second highest total growth in wages and salaries per employee over the past 10 years (2003-2012), at 57.1 per cent

Source: Conference Board of Canada

August 2013

Slide 16

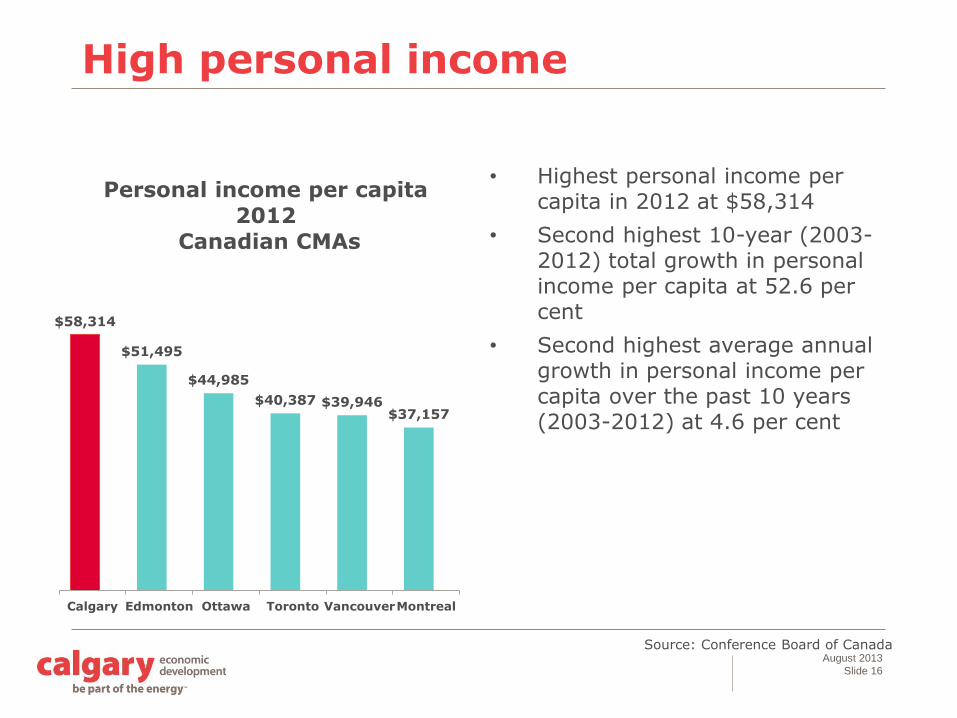

High personal income

$58,314

$51,495

$44,985

$40,387 $39,946$37,157

Calgary Edmonton Ottawa Toronto VancouverMontreal

Personal income per capita

2012

Canadian CMAs

• Highest personal income per capita in 2012 at $58,314

• Second highest 10-year (2003-2012) total growth in personal income per capita at 52.6 per cent

• Second highest average annual growth in personal income per capita over the past 10 years (2003-2012) at 4.6 per cent

Source: Conference Board of Canada

August 2013

Slide 17

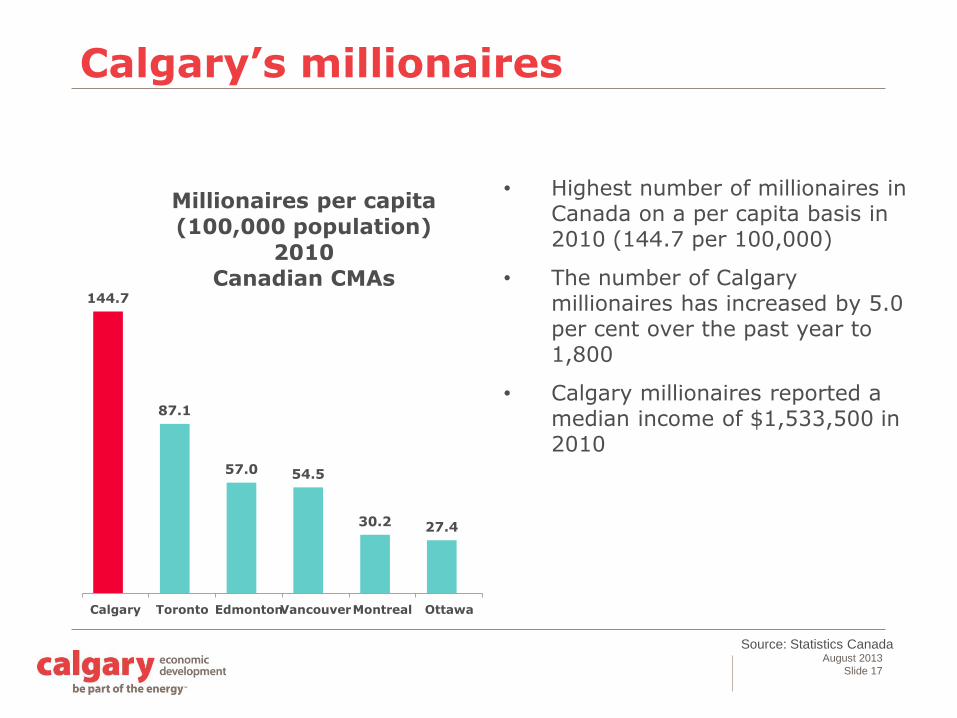

Calgary’s millionaires

144.7

87.1

57.0 54.5

30.2 27.4

Calgary Toronto EdmontonVancouverMontreal Ottawa

Millionaires per capita

(100,000 population)

2010

Canadian CMAs

• Highest number of millionaires in Canada on a per capita basis in 2010 (144.7 per 100,000)

• The number of Calgary millionaires has increased by 5.0 per cent over the past year to 1,800

• Calgary millionaires reported a median income of $1,533,500 in 2010

Source: Statistics Canada

August 2013

Slide 18

Calgary and region population

Source: City of Calgary Civic Census, Statistics Canada

1,042,8921,065,455

1,071,515

1,090,9361,120,225

1,149,5521,188,5951,222,491

1,244,2071,268,704

1,309,2211,278,273

1,314,711 1,338,859

1,364,172 1,406,080

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

2008 2009 2010 2011 2012 2013

Calgary’s population

City of

Calgary

Calgary

CMA

Calgary

EconomicRegion

• City of Calgary population is forecast to be 1.239 million in 2017 (City of Calgary Corporate Economics, Fall

2012)

• Calgary CMA is forecast to have a population of 1.443 million in 2017 (Conference Board of Canada)

• Calgary Economic Region is forecast to have a population of 1.544 million in 2017 (City of Calgary

Corporate Economics, Fall 2012)

August 2013

Slide 19

Population growth

12,920

-4,154

9,563

19,658 19,067

9,643

10,214

9,858

9,361 10,260

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2009 2010 2011 2012 2013

Population growth

2009-2013

City of Calgary

Natural Increase

Net Migration

1.9%

-73.1%

220.5%

50.8% 0.1% Annual growthrate (%)

Source: City of Calgary Civic Census

August 2013

Slide 20

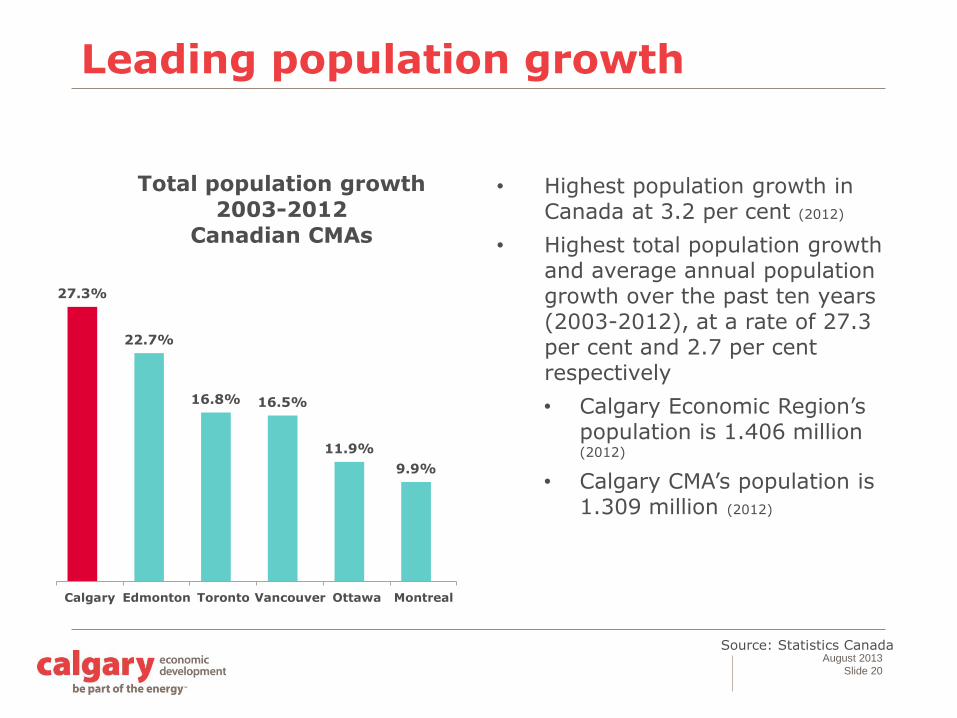

Leading population growth

27.3%

22.7%

16.8% 16.5%

11.9%

9.9%

Calgary Edmonton Toronto Vancouver Ottawa Montreal

Total population growth

2003-2012

Canadian CMAs

• Highest population growth in Canada at 3.2 per cent (2012)

• Highest total population growth and average annual population growth over the past ten years (2003-2012), at a rate of 27.3 per cent and 2.7 per cent respectively

• Calgary Economic Region’s population is 1.406 million (2012)

• Calgary CMA’s population is 1.309 million (2012)

Source: Statistics Canada

August 2013

Slide 21

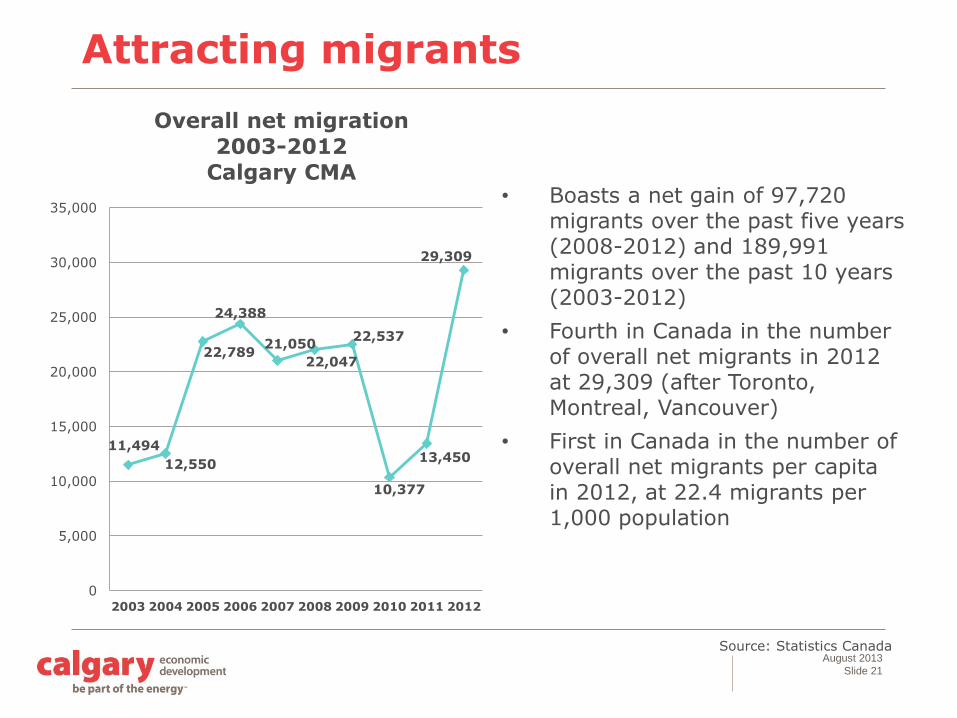

Attracting migrants

11,494

12,550

22,789

24,388

21,050

22,047

22,537

10,377

13,450

29,309

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Overall net migration

2003-2012

Calgary CMA• Boasts a net gain of 97,720

migrants over the past five years (2008-2012) and 189,991 migrants over the past 10 years (2003-2012)

• Fourth in Canada in the number of overall net migrants in 2012 at 29,309 (after Toronto, Montreal, Vancouver)

• First in Canada in the number of overall net migrants per capita in 2012, at 22.4 migrants per 1,000 population

Source: Statistics Canada

August 2013

Slide 22

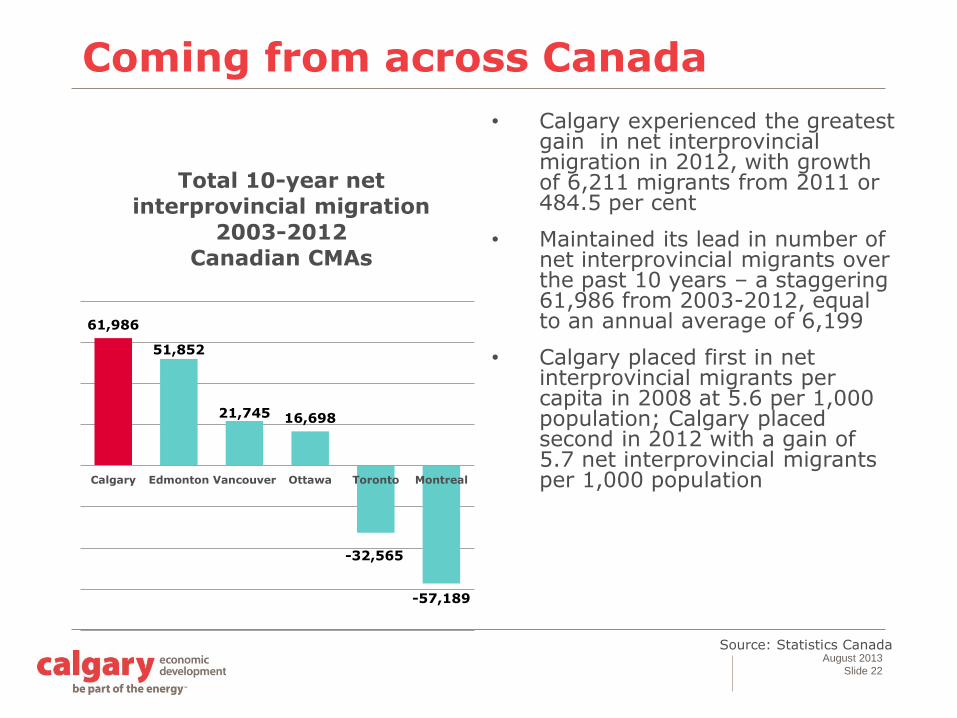

Coming from across Canada

61,986

51,852

21,745 16,698

-32,565

-57,189

Calgary Edmonton Vancouver Ottawa Toronto Montreal

Total 10-year net

interprovincial migration

2003-2012

Canadian CMAs

• Calgary experienced the greatest gain in net interprovincial migration in 2012, with growth of 6,211 migrants from 2011 or 484.5 per cent

• Maintained its lead in number of net interprovincial migrants over the past 10 years – a staggering 61,986 from 2003-2012, equal to an annual average of 6,199

• Calgary placed first in net interprovincial migrants per capita in 2008 at 5.6 per 1,000 population; Calgary placed second in 2012 with a gain of 5.7 net interprovincial migrants per 1,000 population

Source: Statistics Canada

August 2013

Slide 23

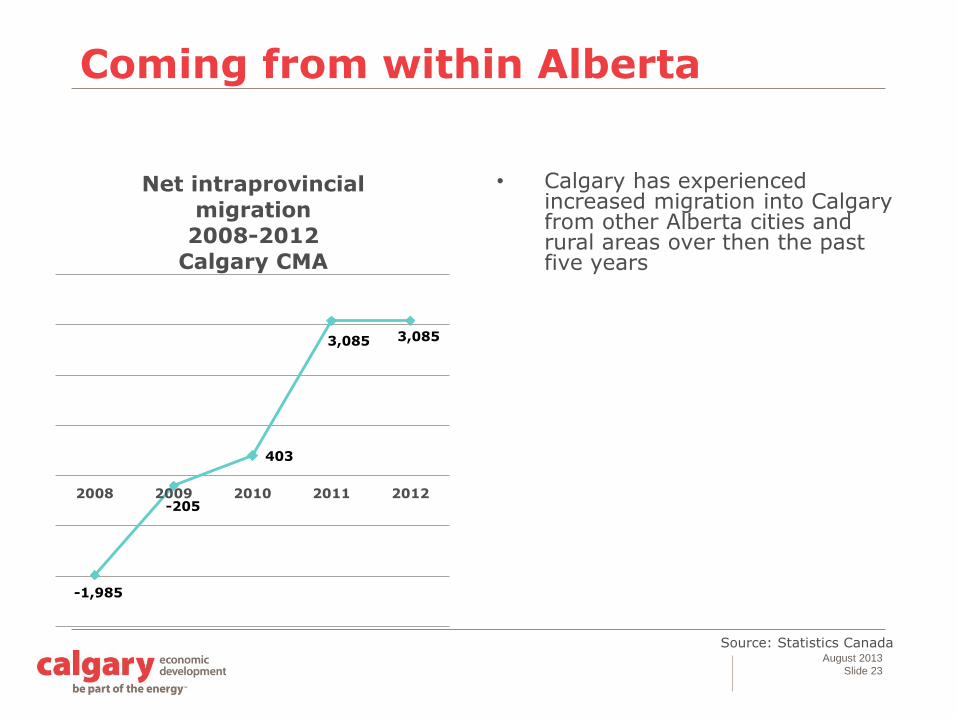

Coming from within Alberta

-1,985

-205

403

3,085 3,085

2008 2009 2010 2011 2012

Net intraprovincial

migration

2008-2012

Calgary CMA

• Calgary has experienced increased migration into Calgary from other Alberta cities and rural areas over then the past five years

Source: Statistics Canada

August 2013

Slide 24

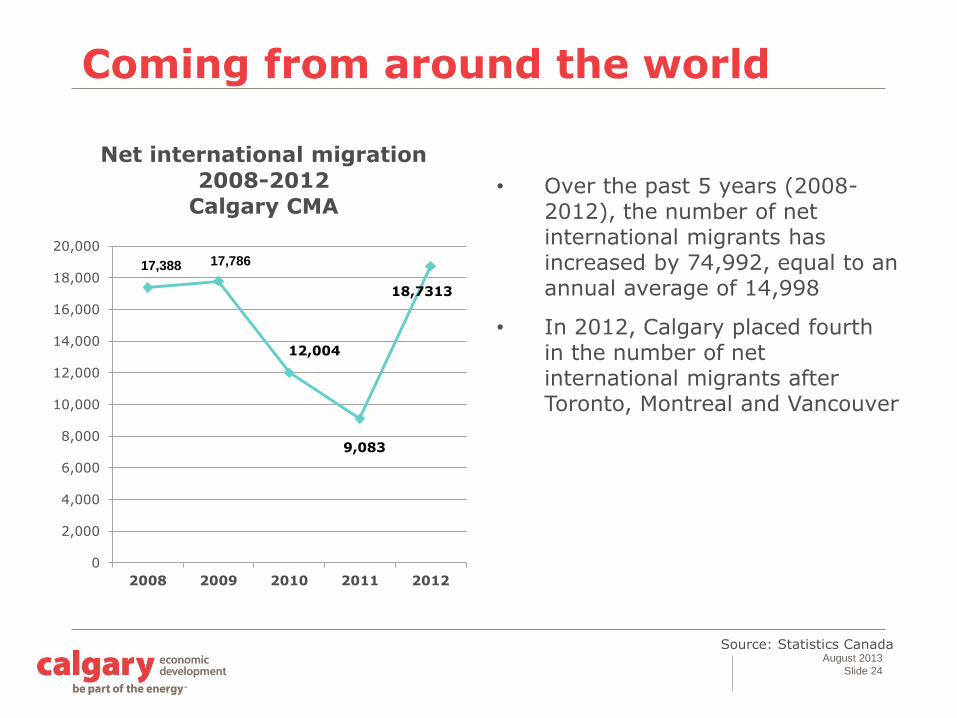

Source: Statistics Canada

Coming from around the world

17,388 17,786

12,004

9,083

18,7313

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2008 2009 2010 2011 2012

Net international migration

2008-2012

Calgary CMA• Over the past 5 years (2008-

2012), the number of net international migrants has increased by 74,992, equal to an annual average of 14,998

• In 2012, Calgary placed fourth in the number of net international migrants after Toronto, Montreal and Vancouver

August 2013

Slide 25

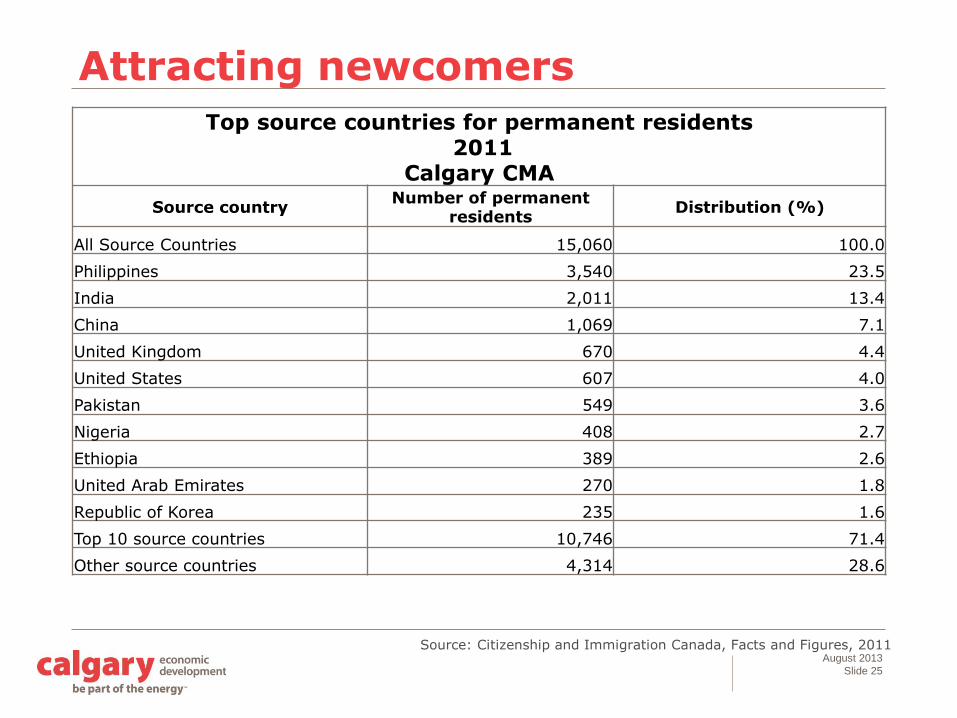

Attracting newcomers

Top source countries for permanent residents2011

Calgary CMA

Source countryNumber of permanent

residentsDistribution (%)

All Source Countries 15,060 100.0

Philippines 3,540 23.5

India 2,011 13.4

China 1,069 7.1

United Kingdom 670 4.4

United States 607 4.0

Pakistan 549 3.6

Nigeria 408 2.7

Ethiopia 389 2.6

United Arab Emirates 270 1.8

Republic of Korea 235 1.6

Top 10 source countries 10,746 71.4

Other source countries 4,314 28.6

Source: Citizenship and Immigration Canada, Facts and Figures, 2011

August 2013

Slide 26

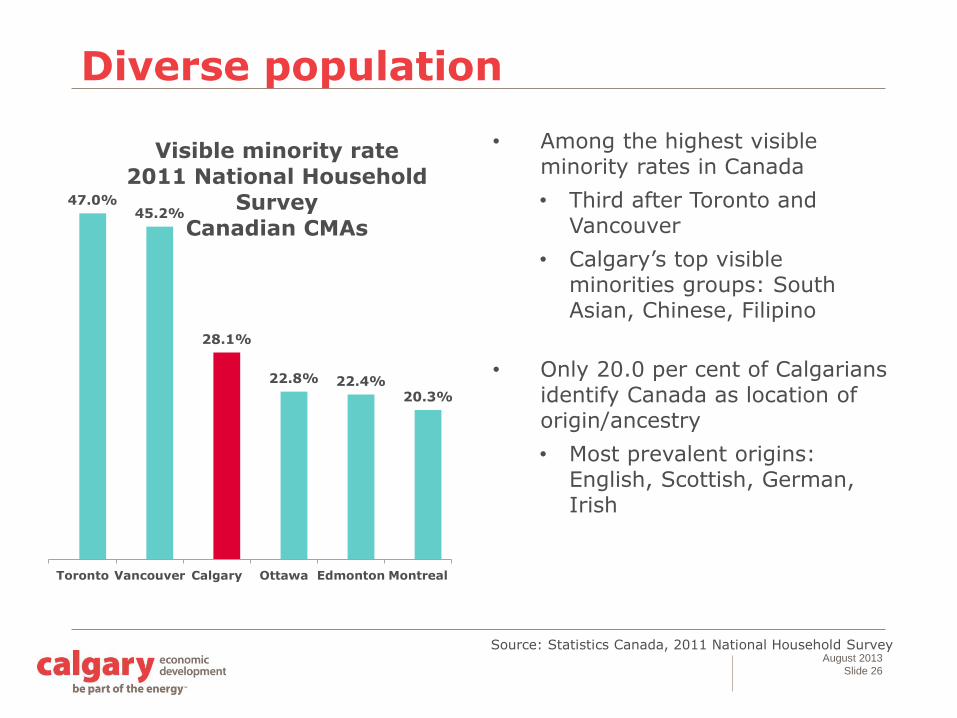

Diverse population

47.0%45.2%

28.1%

22.8% 22.4%20.3%

Toronto Vancouver Calgary Ottawa Edmonton Montreal

Visible minority rate

2011 National Household

Survey

Canadian CMAs

• Among the highest visible minority rates in Canada

• Third after Toronto and Vancouver

• Calgary’s top visible minorities groups: South Asian, Chinese, Filipino

• Only 20.0 per cent of Calgarians identify Canada as location of origin/ancestry

• Most prevalent origins: English, Scottish, German, Irish

Source: Statistics Canada, 2011 National Household Survey

August 2013

Slide 27

Labour force growth

27.0%26.5%

16.4% 16.1%15.0%

8.7%

Calgary Edmonton Ottawa Vancouver Toronto Montreal

Total labour force growth

2003-2012

Canadian CMAs

• Tied with Edmonton for second highest labour force growth in 2012 at 2.6 per cent (after Ottawa)

• Highest total labour force growth over the past 10 years (2003-2012) at 27.0 per cent

• Tied with Edmonton for highest average annual labour force growth over the past 10 years (2003-2012) at 2.7 per cent

Source: Statistics Canada

August 2013

Slide 28

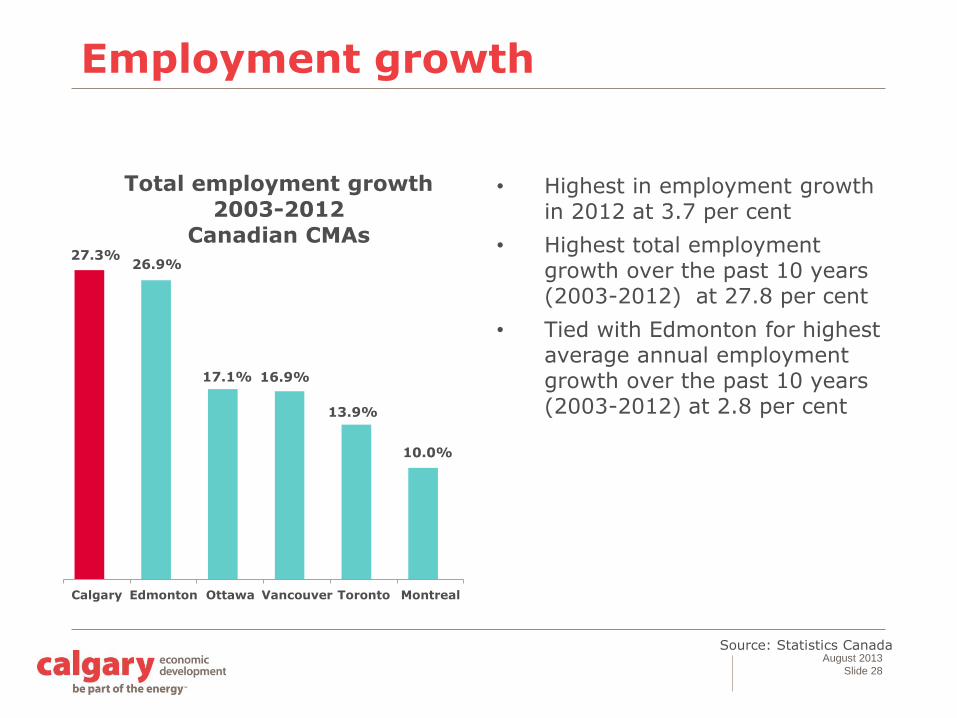

Employment growth

27.3%26.9%

17.1% 16.9%

13.9%

10.0%

Calgary Edmonton Ottawa Vancouver Toronto Montreal

Total employment growth

2003-2012

Canadian CMAs

• Highest in employment growth in 2012 at 3.7 per cent

• Highest total employment growth over the past 10 years (2003-2012) at 27.8 per cent

• Tied with Edmonton for highest average annual employment growth over the past 10 years (2003-2012) at 2.8 per cent

Source: Statistics Canada

August 2013

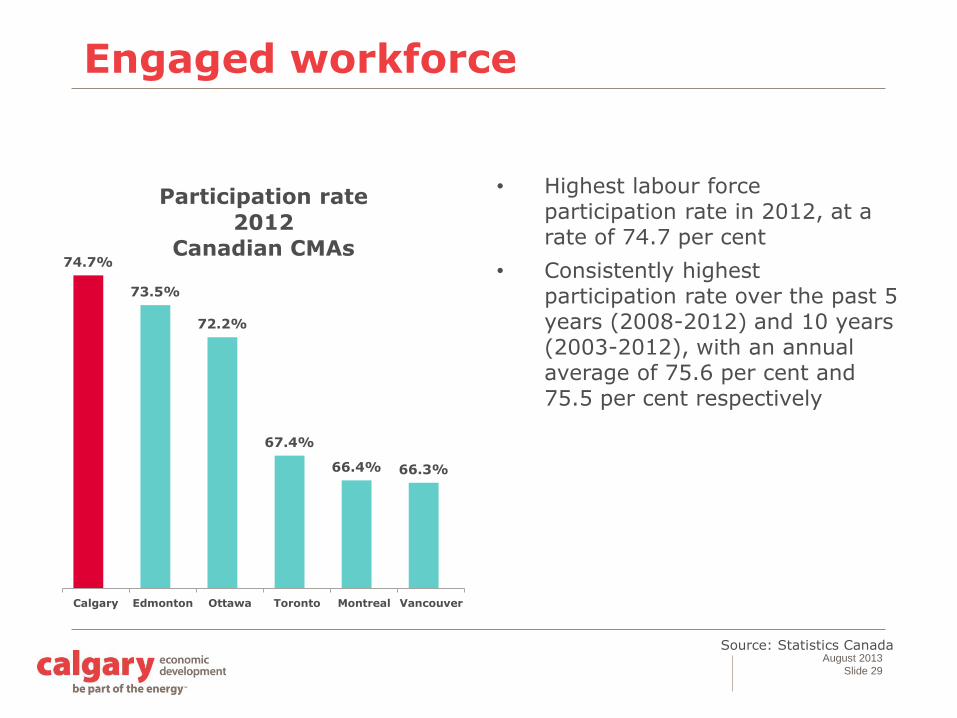

Slide 29

Engaged workforce

74.7%

73.5%

72.2%

67.4%

66.4% 66.3%

Calgary Edmonton Ottawa Toronto Montreal Vancouver

Participation rate

2012

Canadian CMAs

• Highest labour force participation rate in 2012, at a rate of 74.7 per cent

• Consistently highest participation rate over the past 5 years (2008-2012) and 10 years (2003-2012), with an annual average of 75.6 per cent and 75.5 per cent respectively

Source: Statistics Canada

August 2013

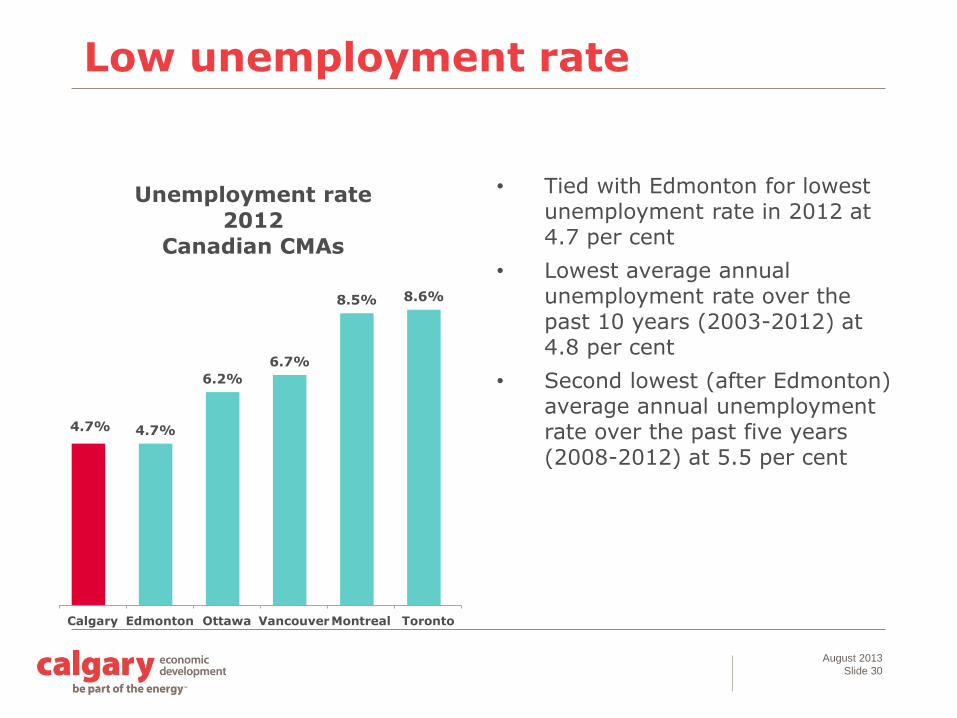

Slide 30

Low unemployment rate

4.7% 4.7%

6.2%

6.7%

8.5% 8.6%

Calgary Edmonton Ottawa VancouverMontreal Toronto

Unemployment rate

2012

Canadian CMAs

• Tied with Edmonton for lowest unemployment rate in 2012 at 4.7 per cent

• Lowest average annual unemployment rate over the past 10 years (2003-2012) at 4.8 per cent

• Second lowest (after Edmonton) average annual unemployment rate over the past five years (2008-2012) at 5.5 per cent

August 2013

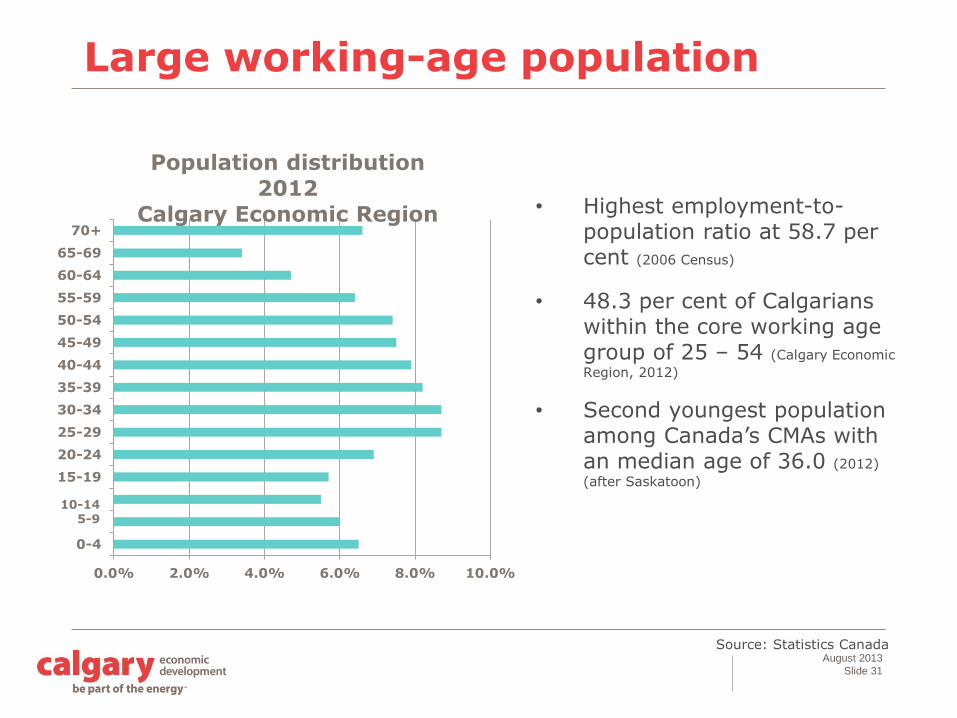

Slide 31

Large working-age population

• Highest employment-to-population ratio at 58.7 per cent (2006 Census)

• 48.3 per cent of Calgarians within the core working age group of 25 – 54 (Calgary Economic

Region, 2012)

• Second youngest population among Canada’s CMAs with an median age of 36.0 (2012)

(after Saskatoon)

Source: Statistics Canada

0.0% 2.0% 4.0% 6.0% 8.0% 10.0%

0-4

09-May

14-Oct

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70+

Population distribution

2012

Calgary Economic Region

10-145-9

August 2013

Slide 32

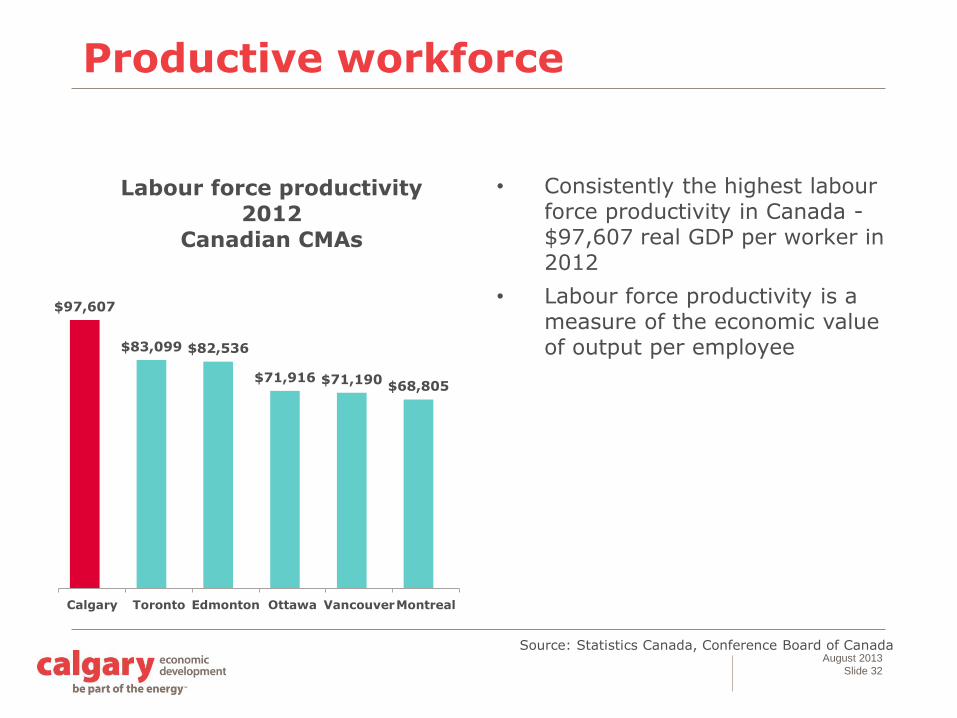

Productive workforce

$97,607

$83,099 $82,536

$71,916 $71,190$68,805

Calgary Toronto Edmonton Ottawa VancouverMontreal

Labour force productivity

2012

Canadian CMAs

• Consistently the highest labour force productivity in Canada -$97,607 real GDP per worker in 2012

• Labour force productivity is a measure of the economic value of output per employee

Source: Statistics Canada, Conference Board of Canada

August 2013

Slide 33

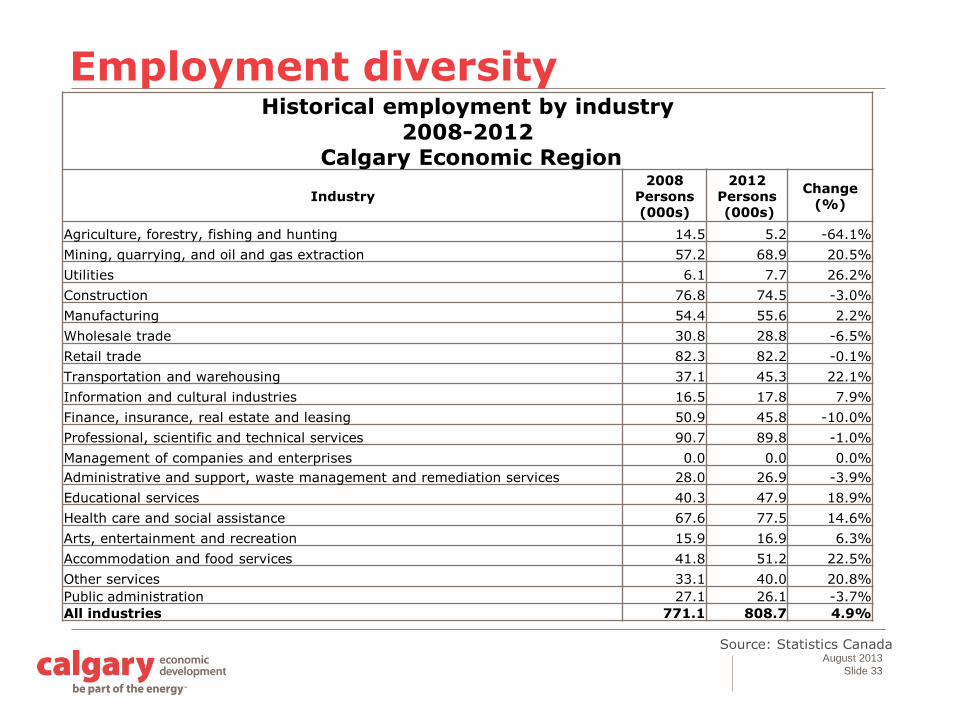

Source: Statistics Canada

Employment diversityHistorical employment by industry

2008-2012Calgary Economic Region

Industry2008

Persons (000s)

2012 Persons(000s)

Change (%)

Agriculture, forestry, fishing and hunting 14.5 5.2 -64.1%

Mining, quarrying, and oil and gas extraction 57.2 68.9 20.5%

Utilities 6.1 7.7 26.2%

Construction 76.8 74.5 -3.0%

Manufacturing 54.4 55.6 2.2%

Wholesale trade 30.8 28.8 -6.5%

Retail trade 82.3 82.2 -0.1%

Transportation and warehousing 37.1 45.3 22.1%

Information and cultural industries 16.5 17.8 7.9%

Finance, insurance, real estate and leasing 50.9 45.8 -10.0%

Professional, scientific and technical services 90.7 89.8 -1.0%

Management of companies and enterprises 0.0 0.0 0.0%

Administrative and support, waste management and remediation services 28.0 26.9 -3.9%

Educational services 40.3 47.9 18.9%

Health care and social assistance 67.6 77.5 14.6%

Arts, entertainment and recreation 15.9 16.9 6.3%

Accommodation and food services 41.8 51.2 22.5%

Other services 33.1 40.0 20.8%

Public administration 27.1 26.1 -3.7%

All industries 771.1 808.7 4.9%

August 2013

Slide 34

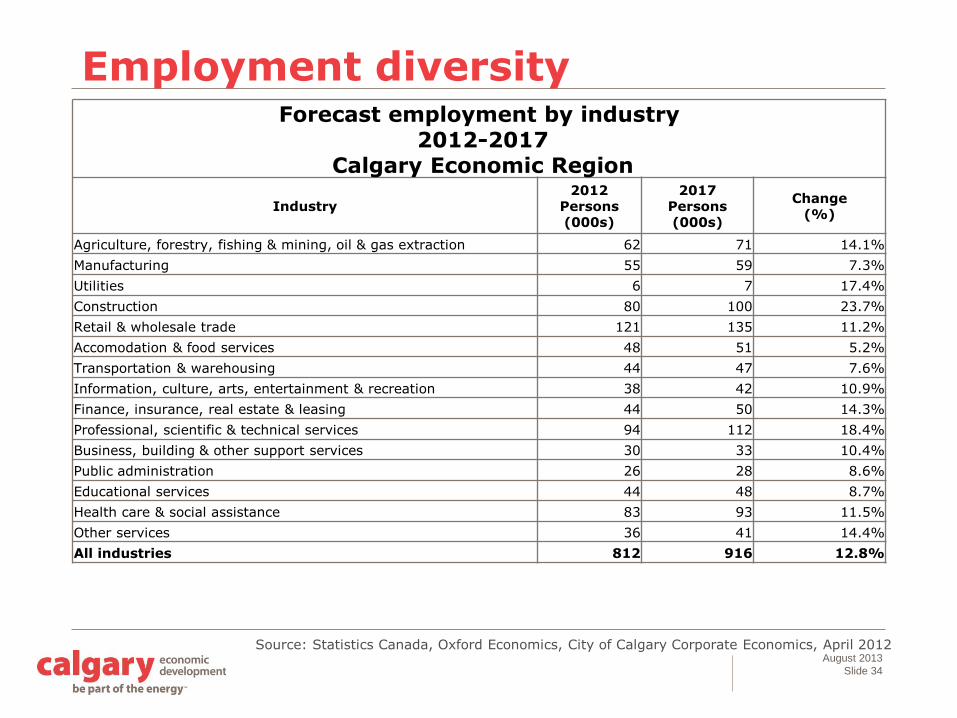

Source: Statistics Canada, Oxford Economics, City of Calgary Corporate Economics, April 2012

Employment diversityForecast employment by industry

2012-2017Calgary Economic Region

Industry2012

Persons (000s)

2017Persons (000s)

Change(%)

Agriculture, forestry, fishing & mining, oil & gas extraction 62 71 14.1%

Manufacturing 55 59 7.3%

Utilities 6 7 17.4%

Construction 80 100 23.7%

Retail & wholesale trade 121 135 11.2%

Accomodation & food services 48 51 5.2%

Transportation & warehousing 44 47 7.6%

Information, culture, arts, entertainment & recreation 38 42 10.9%

Finance, insurance, real estate & leasing 44 50 14.3%

Professional, scientific & technical services 94 112 18.4%

Business, building & other support services 30 33 10.4%

Public administration 26 28 8.6%

Educational services 44 48 8.7%

Health care & social assistance 83 93 11.5%

Other services 36 41 14.4%

All industries 812 916 12.8%

August 2013

Slide 35

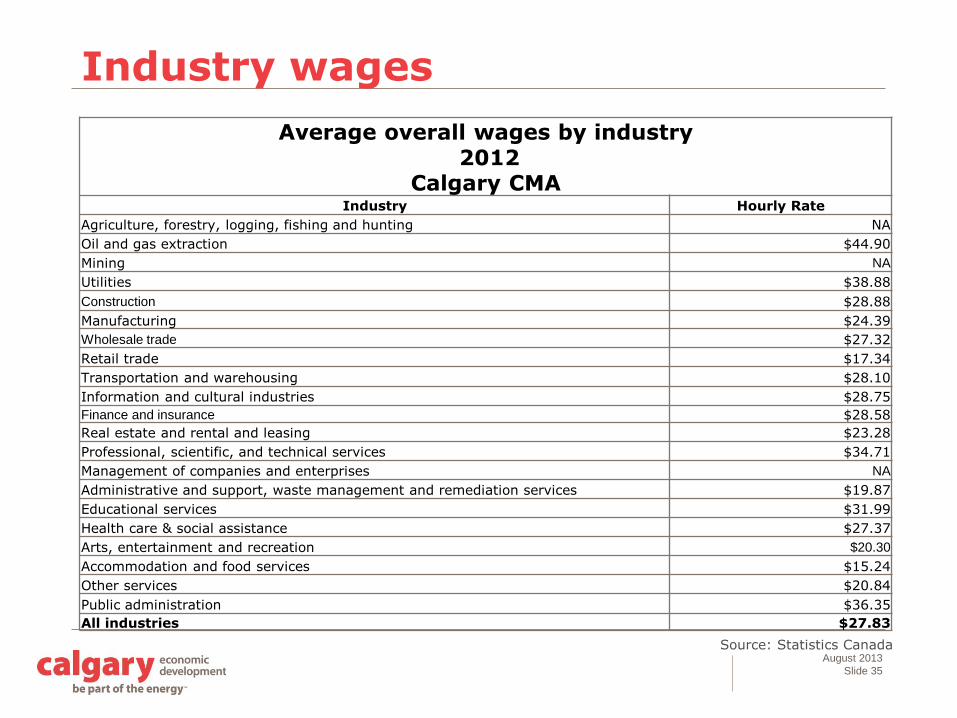

Source: Statistics Canada

Industry wages

Average overall wages by industry2012

Calgary CMAIndustry Hourly Rate

Agriculture, forestry, logging, fishing and hunting NA

Oil and gas extraction $44.90

Mining NA

Utilities $38.88

Construction $28.88

Manufacturing $24.39

Wholesale trade $27.32

Retail trade $17.34

Transportation and warehousing $28.10

Information and cultural industries $28.75

Finance and insurance $28.58

Real estate and rental and leasing $23.28

Professional, scientific, and technical services $34.71

Management of companies and enterprises NA

Administrative and support, waste management and remediation services $19.87

Educational services $31.99

Health care & social assistance $27.37

Arts, entertainment and recreation $20.30

Accommodation and food services $15.24

Other services $20.84

Public administration $36.35

All industries $27.83

August 2013

Slide 36

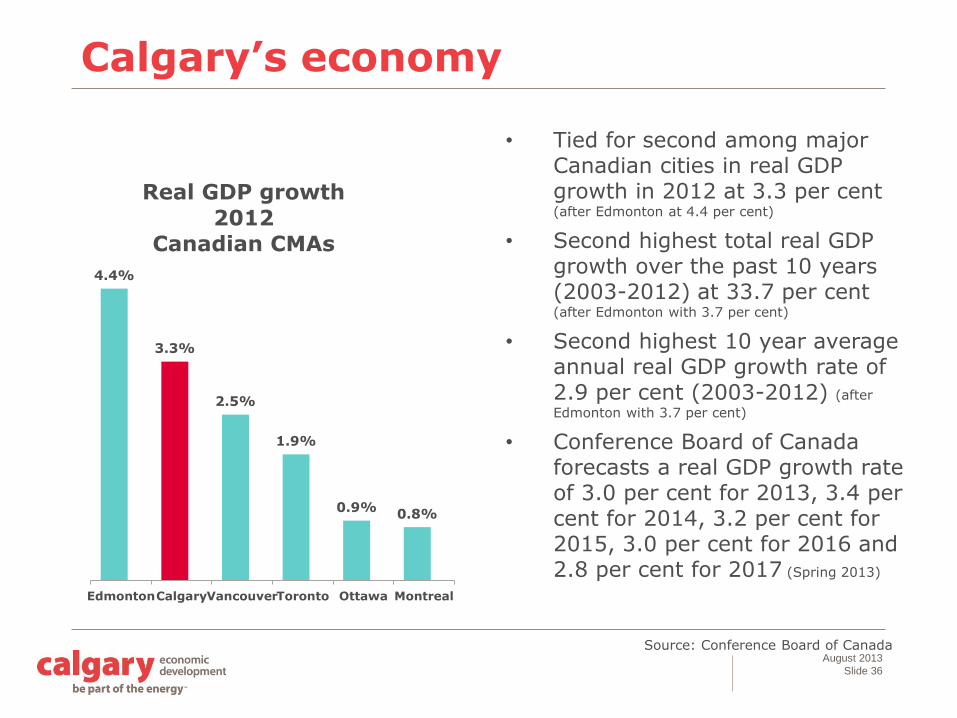

Calgary’s economy

4.4%

3.3%

2.5%

1.9%

0.9%0.8%

EdmontonCalgaryVancouverToronto Ottawa Montreal

Real GDP growth

2012

Canadian CMAs

• Tied for second among major Canadian cities in real GDP growth in 2012 at 3.3 per cent (after Edmonton at 4.4 per cent)

• Second highest total real GDP growth over the past 10 years (2003-2012) at 33.7 per cent (after Edmonton with 3.7 per cent)

• Second highest 10 year average annual real GDP growth rate of 2.9 per cent (2003-2012) (after

Edmonton with 3.7 per cent)

• Conference Board of Canada forecasts a real GDP growth rate of 3.0 per cent for 2013, 3.4 per cent for 2014, 3.2 per cent for 2015, 3.0 per cent for 2016 and 2.8 per cent for 2017 (Spring 2013)

Source: Conference Board of Canada

August 2013

Slide 37

Highest retail sales

77.2% 76.9%

39.9%

35.0% 33.5% 31.8%

Edmonton Calgary Ottawa Toronto Montreal Vancouver

Total retail sales growth

2003-2012

Canadian CMAs

• Second highest total growth in retail

sales over the past 10 years (2003-

2012) at 76.9 per cent (after Edmonton with

77.2 per cent)

• Tied with Edmonton for highest

average annual retail sales growth

over the past 10 years (2003-2012)

at 6.5 per cent

• Highest retail sales per capita in 2012

at $18,990

• Second highest total growth and

average annual growth in retail sales

per capita over the past 10 years

(2003-2012) at 38.9 per cent and 3.7

per cent respectively

Sources: Conference Board of Canada, Statistics Canada

August 2013

Slide 38

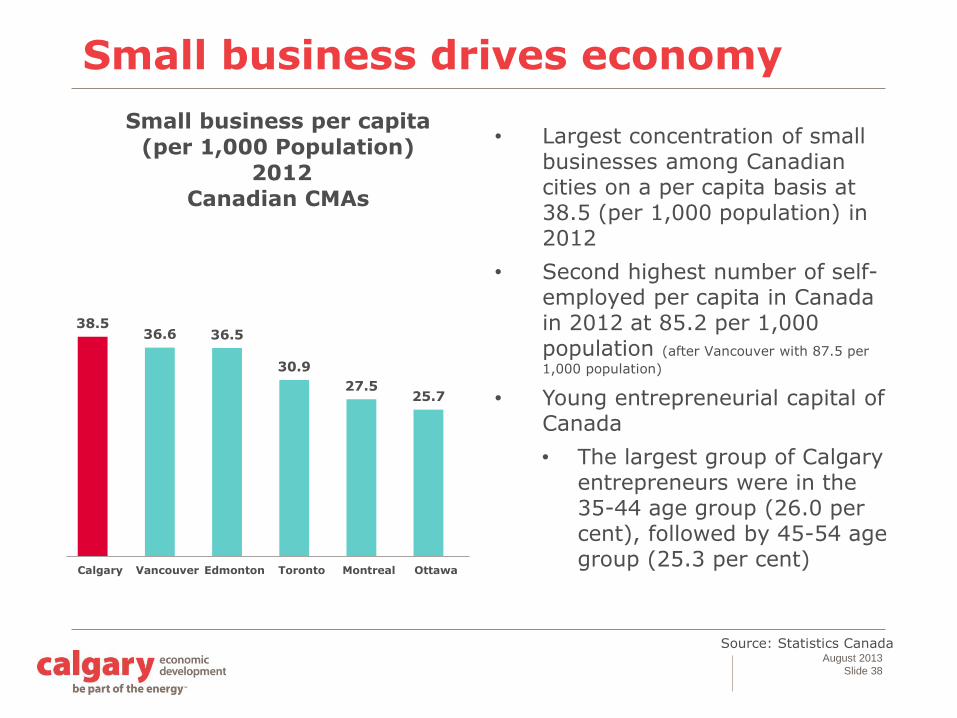

Small business drives economy

38.536.6 36.5

30.9

27.525.7

Calgary Vancouver Edmonton Toronto Montreal Ottawa

Small business per capita

(per 1,000 Population)

2012

Canadian CMAs

• Largest concentration of small businesses among Canadian cities on a per capita basis at 38.5 (per 1,000 population) in 2012

• Second highest number of self-employed per capita in Canada in 2012 at 85.2 per 1,000 population (after Vancouver with 87.5 per

1,000 population)

• Young entrepreneurial capital of Canada

• The largest group of Calgary entrepreneurs were in the 35-44 age group (26.0 per cent), followed by 45-54 age group (25.3 per cent)

Source: Statistics Canada

August 2013

Slide 39

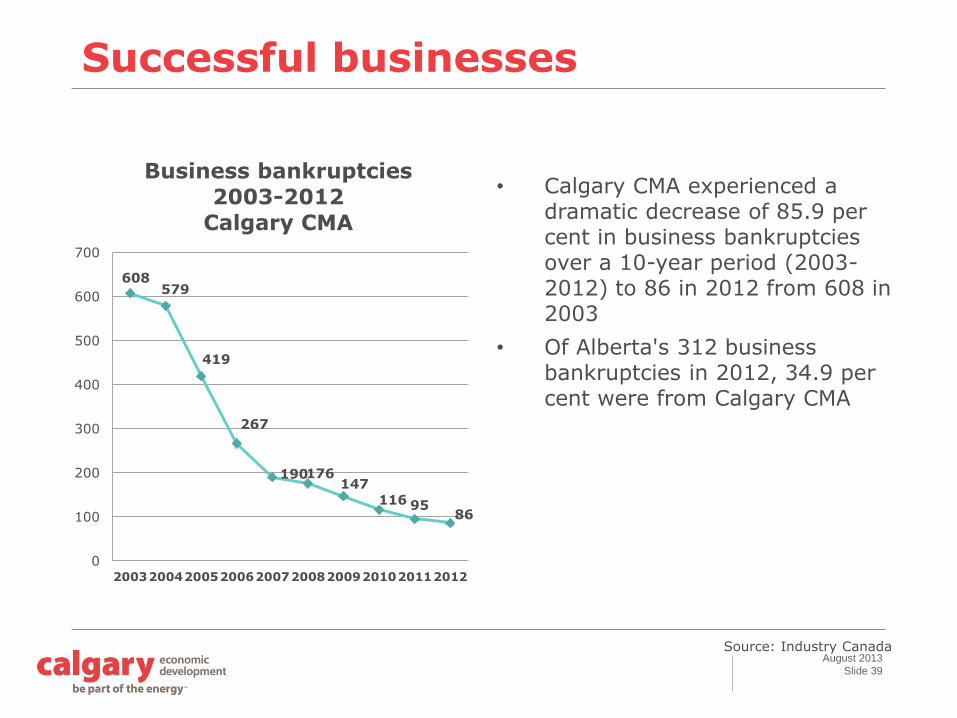

Successful businesses

• Calgary CMA experienced a dramatic decrease of 85.9 per cent in business bankruptcies over a 10-year period (2003-2012) to 86 in 2012 from 608 in 2003

• Of Alberta's 312 business bankruptcies in 2012, 34.9 per cent were from Calgary CMA

Source: Industry Canada

608579

419

267

190176147

116 9586

0

100

200

300

400

500

600

700

2003200420052006200720082009201020112012

Business bankruptcies

2003-2012

Calgary CMA

August 2013

Slide 40

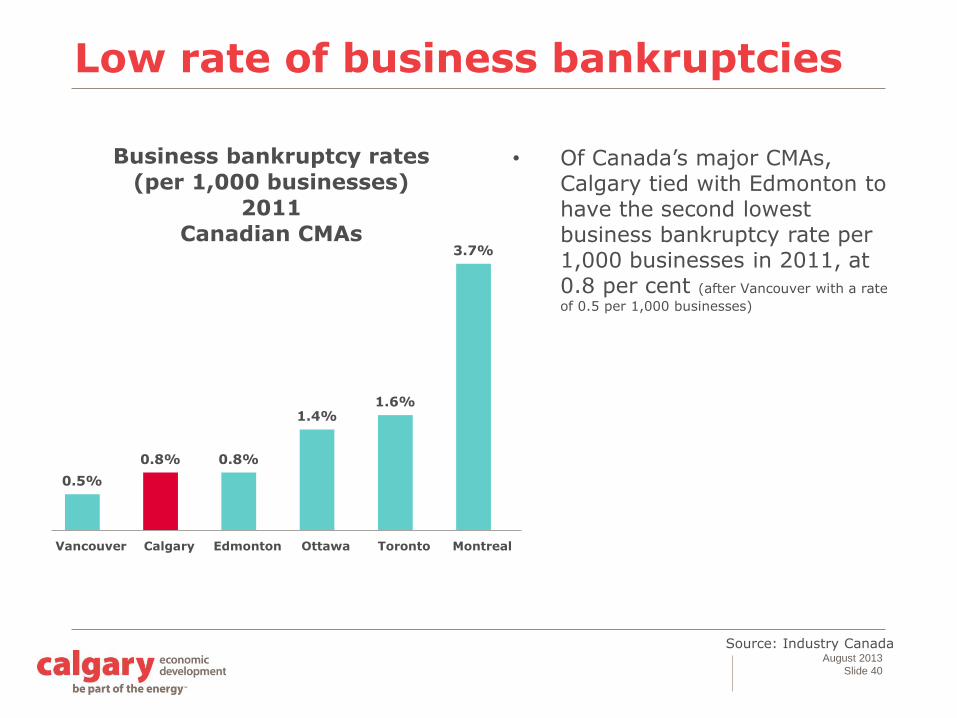

Low rate of business bankruptcies

• Of Canada’s major CMAs, Calgary tied with Edmonton to have the second lowest business bankruptcy rate per 1,000 businesses in 2011, at 0.8 per cent (after Vancouver with a rate

of 0.5 per 1,000 businesses)

Source: Industry Canada

0.5%

0.8% 0.8%

1.4%1.6%

3.7%

Vancouver Calgary Edmonton Ottawa Toronto Montreal

Business bankruptcy rates

(per 1,000 businesses)

2011

Canadian CMAs

August 2013

Slide 41

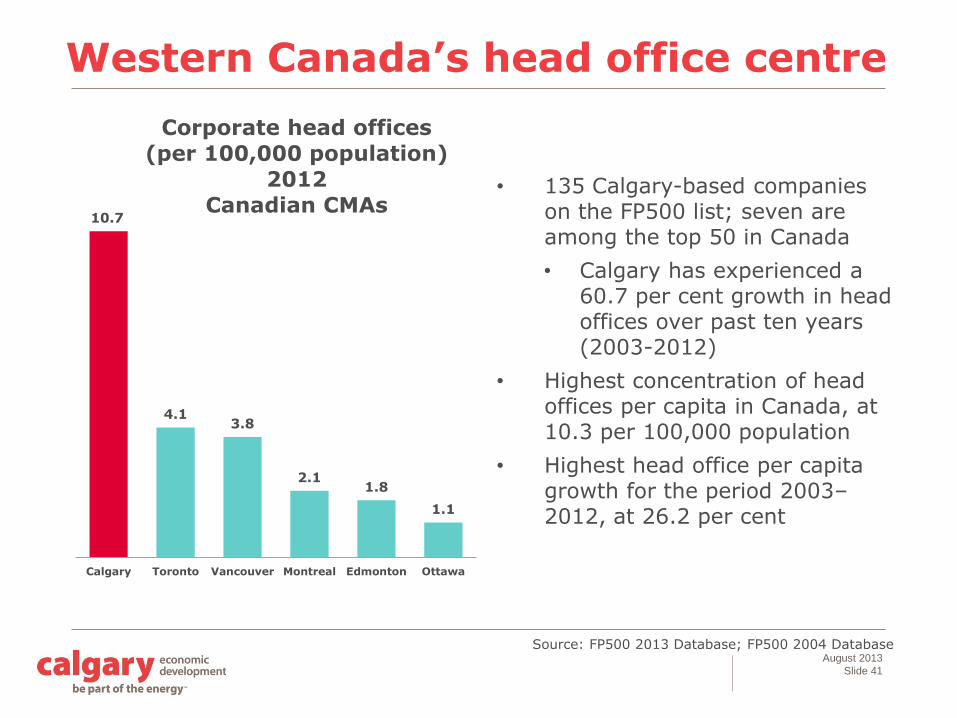

Western Canada’s head office centre

10.7

4.13.8

2.11.8

1.1

Calgary Toronto Vancouver Montreal Edmonton Ottawa

Corporate head offices

(per 100,000 population)

2012

Canadian CMAs• 135 Calgary-based companies

on the FP500 list; seven are among the top 50 in Canada

• Calgary has experienced a 60.7 per cent growth in head offices over past ten years (2003-2012)

• Highest concentration of head offices per capita in Canada, at 10.3 per 100,000 population

• Highest head office per capita growth for the period 2003–2012, at 26.2 per cent

Source: FP500 2013 Database; FP500 2004 Database

August 2013

Slide 42

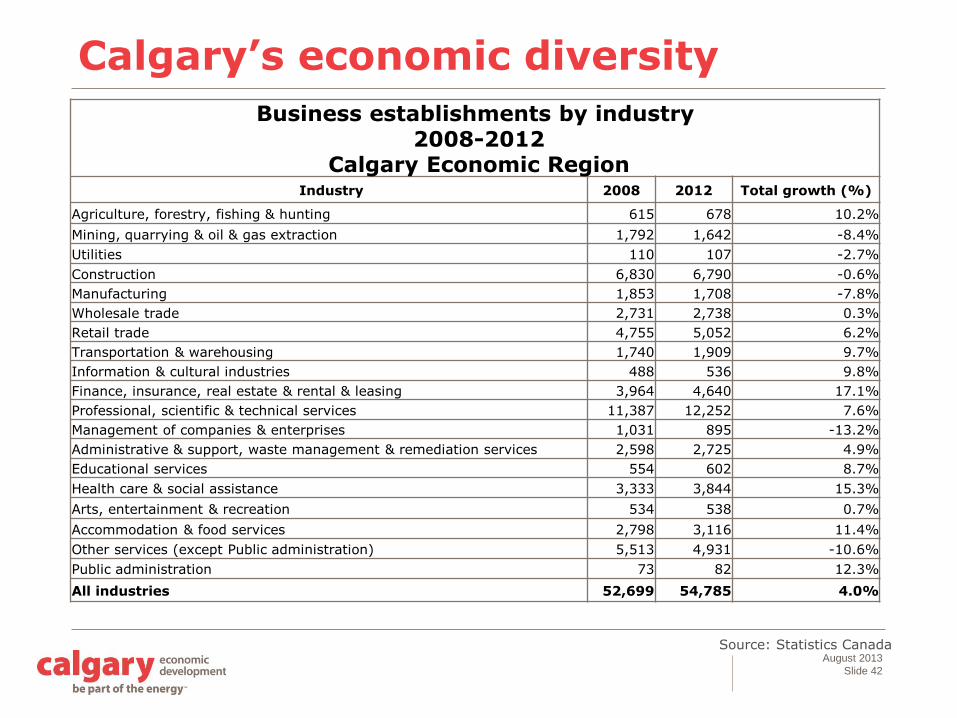

Source: Statistics Canada

Calgary’s economic diversity

Business establishments by industry2008-2012

Calgary Economic RegionIndustry 2008 2012 Total growth (%)

Agriculture, forestry, fishing & hunting 615 678 10.2%

Mining, quarrying & oil & gas extraction 1,792 1,642 -8.4%

Utilities 110 107 -2.7%

Construction 6,830 6,790 -0.6%

Manufacturing 1,853 1,708 -7.8%

Wholesale trade 2,731 2,738 0.3%

Retail trade 4,755 5,052 6.2%

Transportation & warehousing 1,740 1,909 9.7%

Information & cultural industries 488 536 9.8%

Finance, insurance, real estate & rental & leasing 3,964 4,640 17.1%

Professional, scientific & technical services 11,387 12,252 7.6%

Management of companies & enterprises 1,031 895 -13.2%

Administrative & support, waste management & remediation services 2,598 2,725 4.9%

Educational services 554 602 8.7%

Health care & social assistance 3,333 3,844 15.3%

Arts, entertainment & recreation 534 538 0.7%

Accommodation & food services 2,798 3,116 11.4%

Other services (except Public administration) 5,513 4,931 -10.6%

Public administration 73 82 12.3%

All industries 52,699 54,785 4.0%

August 2013

Slide 43

Source: Conference Board of Canada

Calgary’s economic diversityHistorical GDP by industry

2008-2012Calgary CMA

Industry2008

(2007 $ Millions)2012

(2007 $ Millions)

Total Change 2008-2012

(%)

Goods-producing industries 45,383 49,696 9.5%

Manufacturing 6,496 7,338 13.0%

Construction 8,348 8,608 3.1%

Primary and utilities 30,539 33,750 10.5%

Services-producing industries 51,726 55,834 7.9%

Transportation and warehousing 4,145 4,510 8.8%

Information and cultural industries 2,889 3,237 12.0%

Wholesale and retail trade 7,802 8,641 10.8%

Finance, insurance and real estate and leasing 13,772 14,864 7.9%

Business services 9,711 9,604 -1.1%

Personal services 3,803 4,265 12.1%

Non-commercial services 6,618 7,556 14.2%

Public administration and defence 2,985 3,157 5.8%

All industries 97,109 105,530 8.7%

August 2013

Slide 44

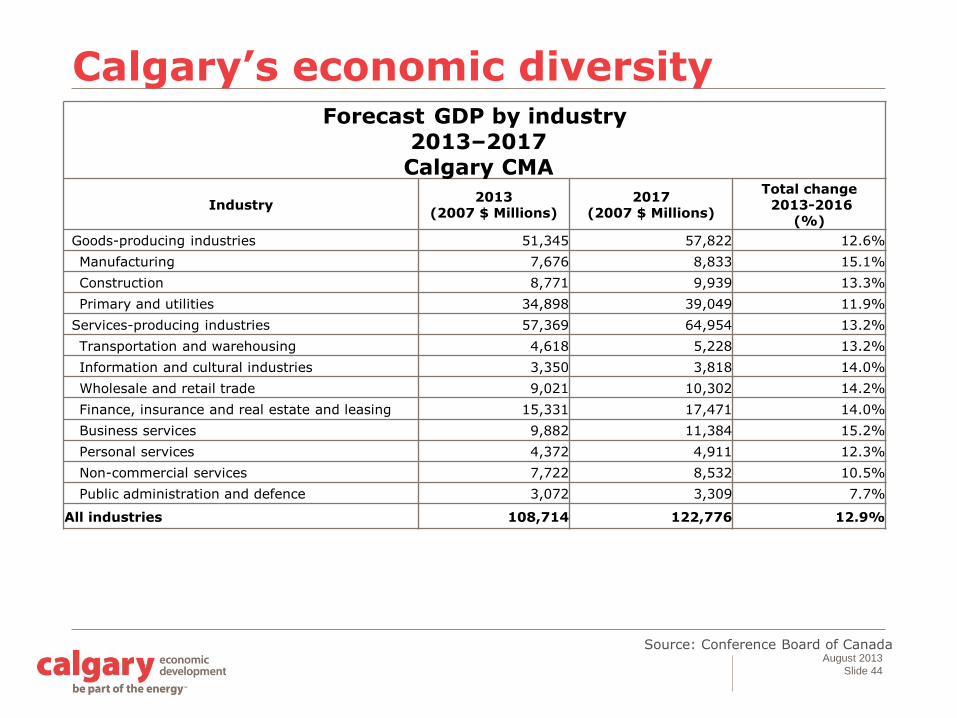

Source: Conference Board of Canada

Calgary’s economic diversityForecast GDP by industry

2013–2017Calgary CMA

Industry2013

(2007 $ Millions)2017

(2007 $ Millions)

Total change2013-2016

(%)

Goods-producing industries 51,345 57,822 12.6%

Manufacturing 7,676 8,833 15.1%

Construction 8,771 9,939 13.3%

Primary and utilities 34,898 39,049 11.9%

Services-producing industries 57,369 64,954 13.2%

Transportation and warehousing 4,618 5,228 13.2%

Information and cultural industries 3,350 3,818 14.0%

Wholesale and retail trade 9,021 10,302 14.2%

Finance, insurance and real estate and leasing 15,331 17,471 14.0%

Business services 9,882 11,384 15.2%

Personal services 4,372 4,911 12.3%

Non-commercial services 7,722 8,532 10.5%

Public administration and defence 3,072 3,309 7.7%

All industries 108,714 122,776 12.9%

August 2013

Slide 45

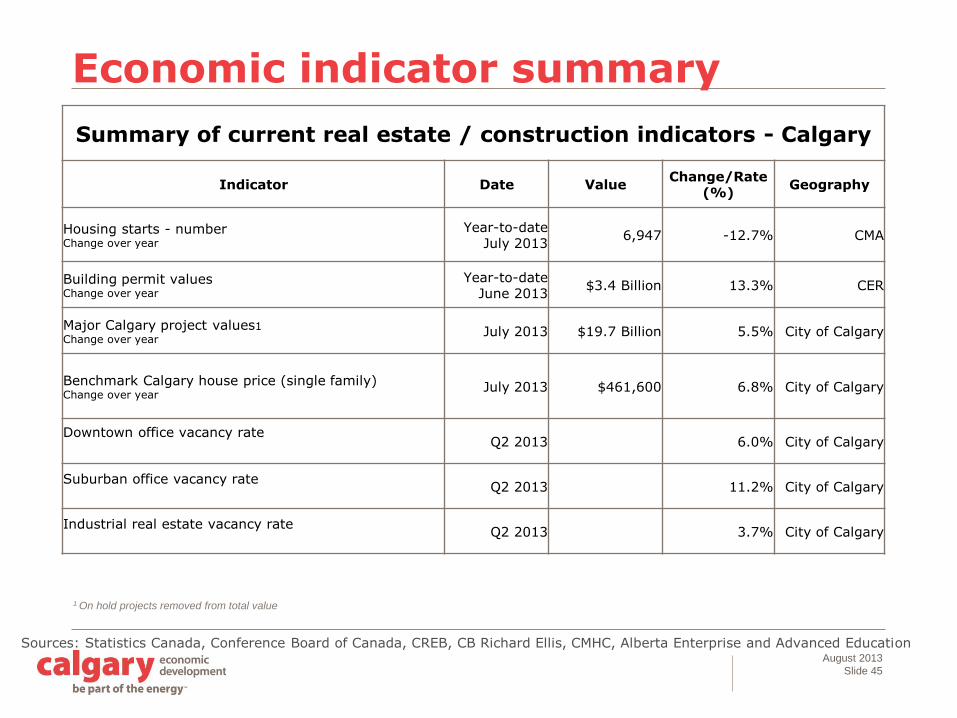

Economic indicator summary

Sources: Statistics Canada, Conference Board of Canada, CREB, CB Richard Ellis, CMHC, Alberta Enterprise and Advanced Education

Summary of current real estate / construction indicators - Calgary

Indicator Date ValueChange/Rate

(%)Geography

Housing starts - numberChange over year

Year-to-date July 2013

6,947 -12.7% CMA

Building permit values Change over year

Year-to-dateJune 2013

$3.4 Billion 13.3% CER

Major Calgary project values1

Change over year July 2013 $19.7 Billion 5.5% City of Calgary

Benchmark Calgary house price (single family)Change over year

July 2013 $461,600 6.8% City of Calgary

Downtown office vacancy rateQ2 2013 6.0% City of Calgary

Suburban office vacancy rateQ2 2013 11.2% City of Calgary

Industrial real estate vacancy rate Q2 2013 3.7% City of Calgary

1 On hold projects removed from total value

August 2013

Slide 46

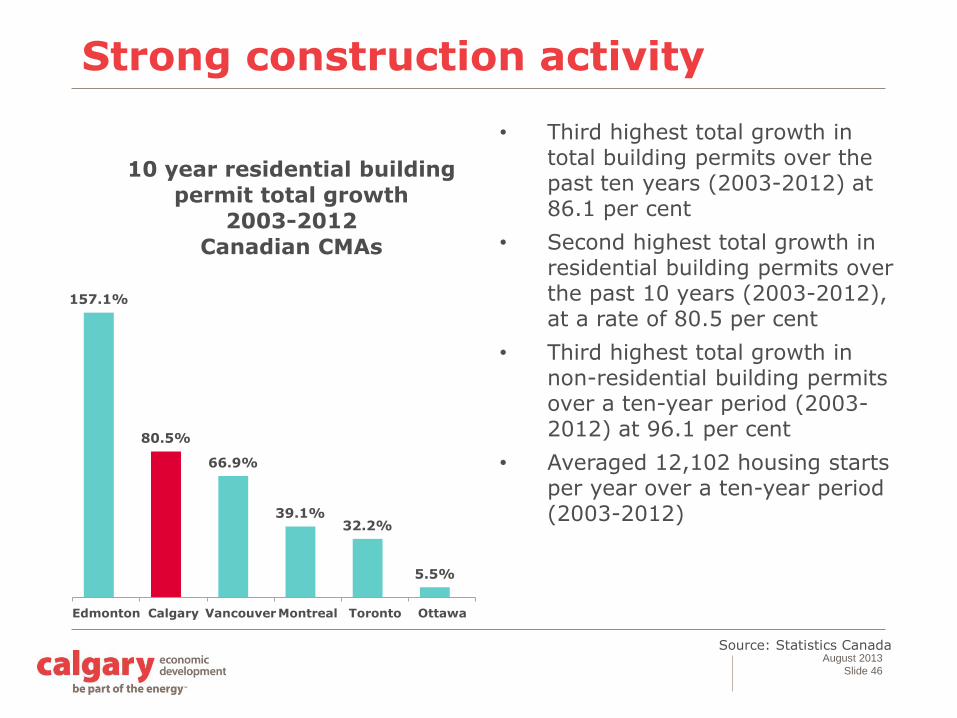

Strong construction activity

157.1%

80.5%

66.9%

39.1%32.2%

5.5%

Edmonton Calgary VancouverMontreal Toronto Ottawa

10 year residential building

permit total growth

2003-2012

Canadian CMAs

• Third highest total growth in total building permits over the past ten years (2003-2012) at 86.1 per cent

• Second highest total growth in residential building permits over the past 10 years (2003-2012), at a rate of 80.5 per cent

• Third highest total growth in non-residential building permits over a ten-year period (2003-2012) at 96.1 per cent

• Averaged 12,102 housing starts per year over a ten-year period (2003-2012)

Source: Statistics Canada

August 2013

Slide 47

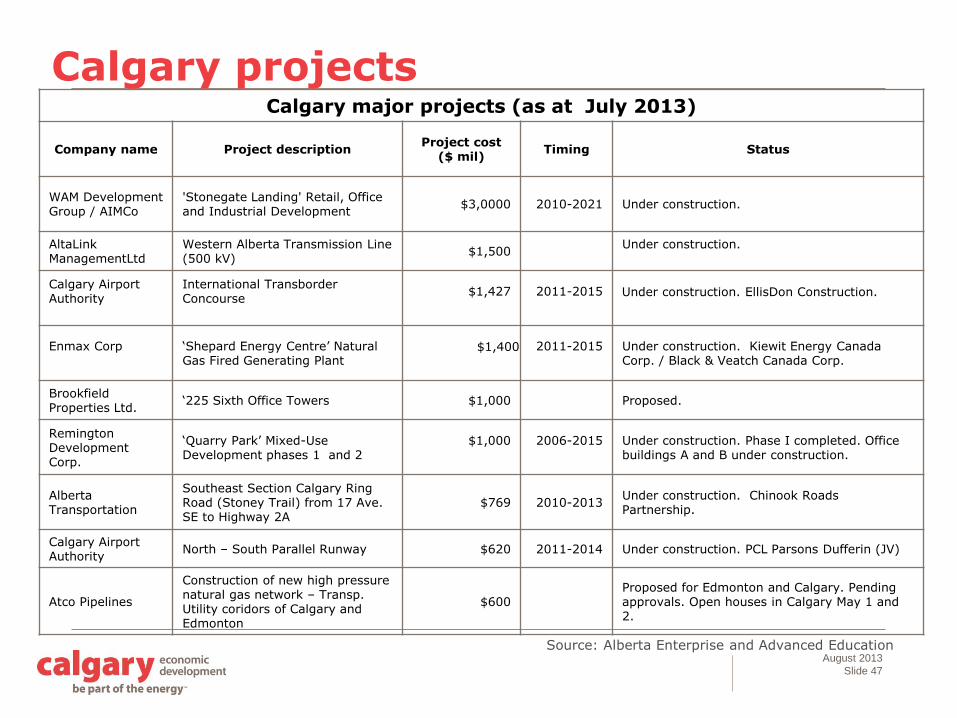

Source: Alberta Enterprise and Advanced Education

Calgary major projects (as at July 2013)

Company name Project descriptionProject cost

($ mil)Timing Status

WAM Development Group / AIMCo

'Stonegate Landing' Retail, Office and Industrial Development

$3,0000 2010-2021 Under construction.

AltaLinkManagementLtd

Western Alberta Transmission Line (500 kV)

$1,500Under construction.

Calgary Airport Authority

International TransborderConcourse

$1,427 2011-2015 Under construction. EllisDon Construction.

Enmax Corp ‘Shepard Energy Centre’ Natural Gas Fired Generating Plant

$1,400 2011-2015 Under construction. Kiewit Energy Canada Corp. / Black & Veatch Canada Corp.

Brookfield Properties Ltd.

‘225 Sixth Office Towers $1,000 Proposed.

Remington Development Corp.

‘Quarry Park’ Mixed-Use Development phases 1 and 2

$1,000 2006-2015 Under construction. Phase I completed. Office buildings A and B under construction.

Alberta Transportation

Southeast Section Calgary Ring Road (Stoney Trail) from 17 Ave. SE to Highway 2A

$769 2010-2013Under construction. Chinook Roads Partnership.

Calgary Airport Authority

North – South Parallel Runway $620 2011-2014 Under construction. PCL Parsons Dufferin (JV)

Atco Pipelines

Construction of new high pressure natural gas network – Transp. Utility coridors of Calgary and Edmonton

$600Proposed for Edmonton and Calgary. Pending approvals. Open houses in Calgary May 1 and 2.

Calgary projects

August 2013

Slide 48

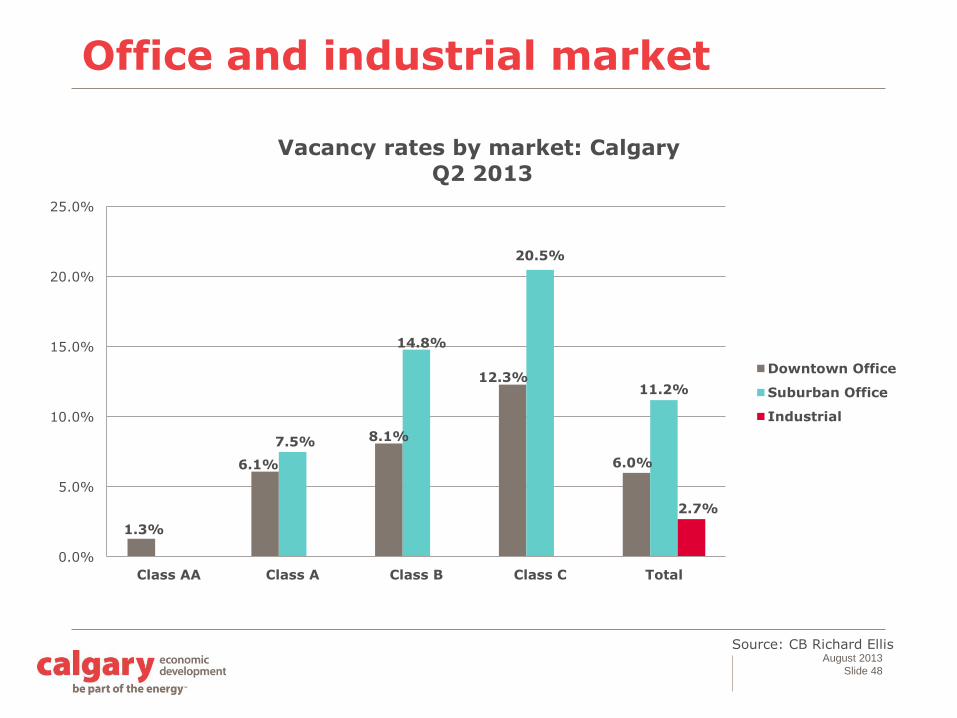

Source: CB Richard Ellis

Office and industrial market

1.3%

6.1%

8.1%

12.3%

6.0%

7.5%

14.8%

20.5%

11.2%

2.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Class AA Class A Class B Class C Total

Vacancy rates by market: Calgary

Q2 2013

Downtown Office

Suburban Office

Industrial

August 2013

Slide 49

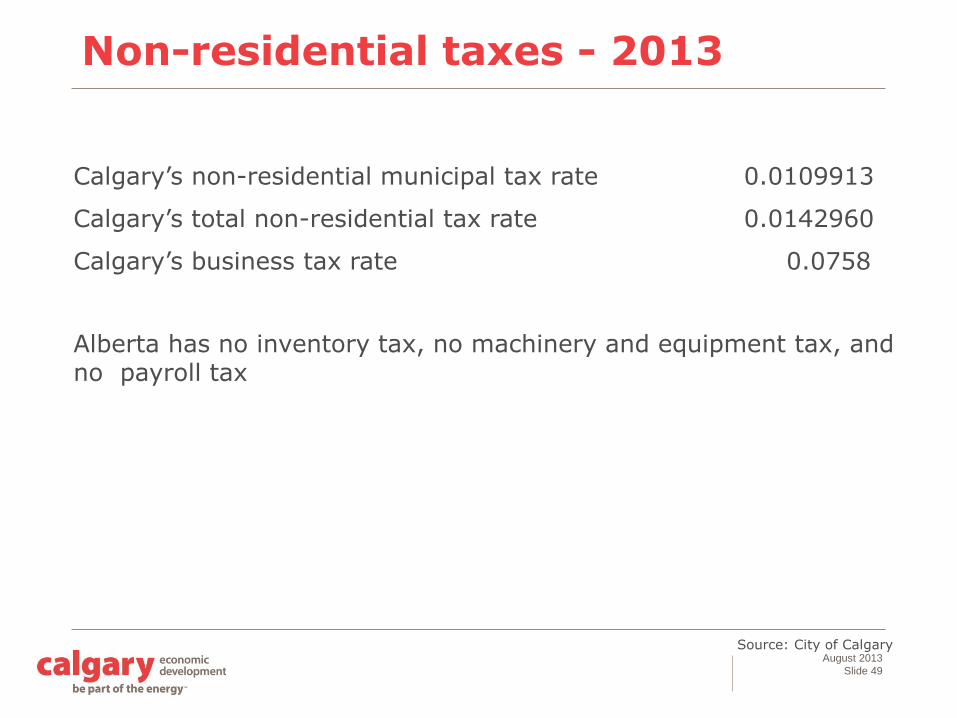

Source: City of Calgary

Non-residential taxes - 2013

Calgary’s non-residential municipal tax rate 0.0109913

Calgary’s total non-residential tax rate 0.0142960

Calgary’s business tax rate 0.0758

Alberta has no inventory tax, no machinery and equipment tax, and no payroll tax

August 2013

Slide 50

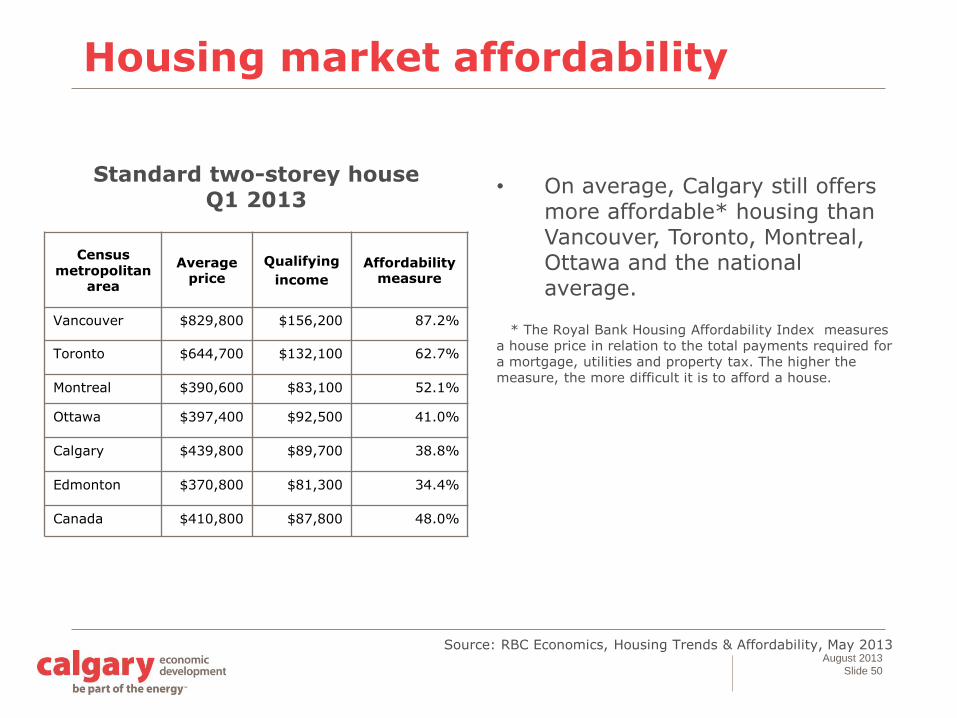

Housing market affordability

Census metropolitan

area

Average price

Qualifying

income

Affordability measure

Vancouver $829,800 $156,200 87.2%

Toronto $644,700 $132,100 62.7%

Montreal $390,600 $83,100 52.1%

Ottawa $397,400 $92,500 41.0%

Calgary $439,800 $89,700 38.8%

Edmonton $370,800 $81,300 34.4%

Canada $410,800 $87,800 48.0%

• On average, Calgary still offers more affordable* housing than Vancouver, Toronto, Montreal, Ottawa and the national average.

* The Royal Bank Housing Affordability Index measures a house price in relation to the total payments required for a mortgage, utilities and property tax. The higher the measure, the more difficult it is to afford a house.

Standard two-storey house Q1 2013

Source: RBC Economics, Housing Trends & Affordability, May 2013

August 2013

Slide 51

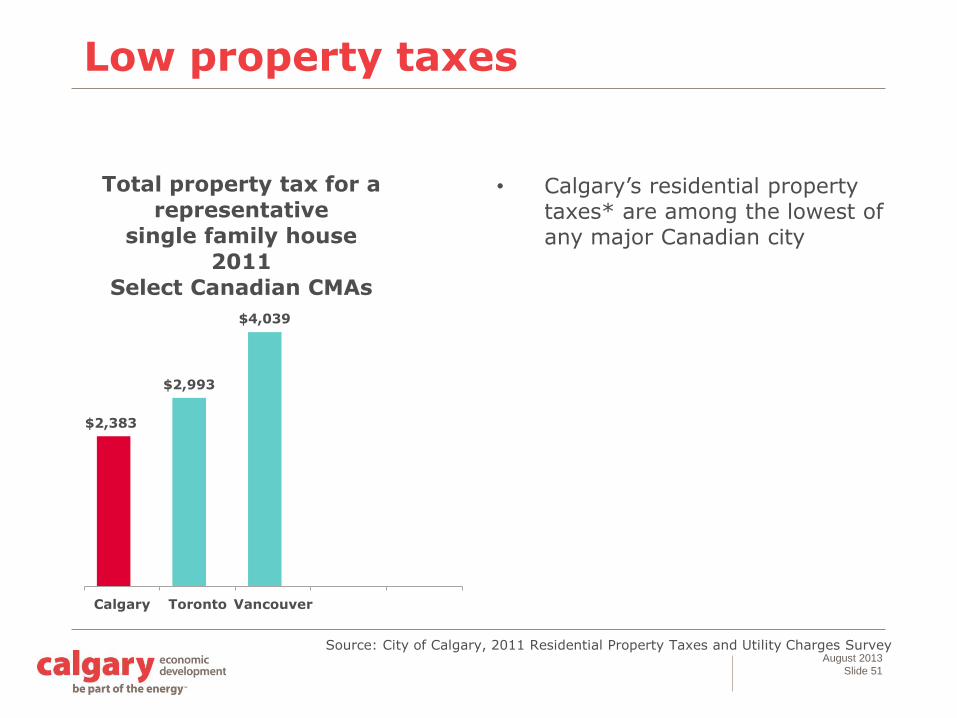

Low property taxes

$2,383

$2,993

$4,039

Calgary Toronto Vancouver

Total property tax for a

representative

single family house

2011

Select Canadian CMAs

• Calgary’s residential property taxes* are among the lowest of any major Canadian city

Source: City of Calgary, 2011 Residential Property Taxes and Utility Charges Survey

August 2013

Slide 52

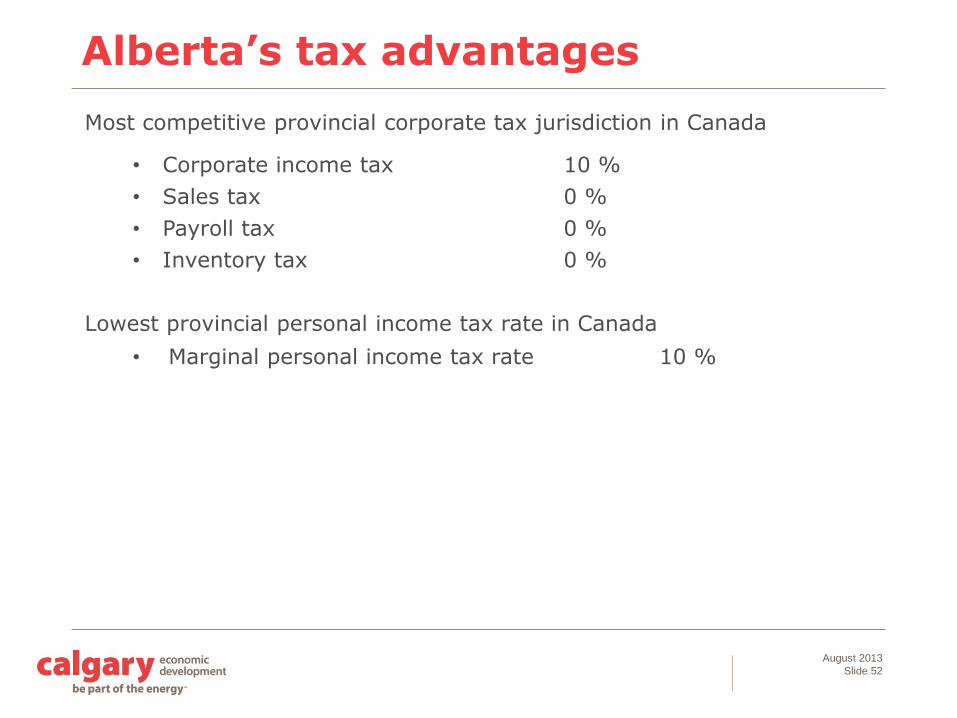

Alberta’s tax advantages

Most competitive provincial corporate tax jurisdiction in Canada

• Corporate income tax 10 %

• Sales tax 0 %

• Payroll tax 0 %

• Inventory tax 0 %

Lowest provincial personal income tax rate in Canada

• Marginal personal income tax rate 10 %

August 2013

Slide 53

Source: Alberta International and Intergovernmental Relations

Alberta’s trade strength

Alberta’s exports in 2011 ($93.2 billion)

• Oil (including oil sands) - $52.0 billion

• Gas & natural gas liquids - $12.9 billion

• Energy (including mining) - $67.2 billion (72.7 per cent of total Alberta exports)

• Chemicals - $7.2 billion

• Food, feed & beverage - $3.4 billion

United States - $15.7 billion

China - $2.6 billion

Mexico - $1.3 billion

August 2013

Slide 54

Source: Alberta International and Intergovernmental Relations

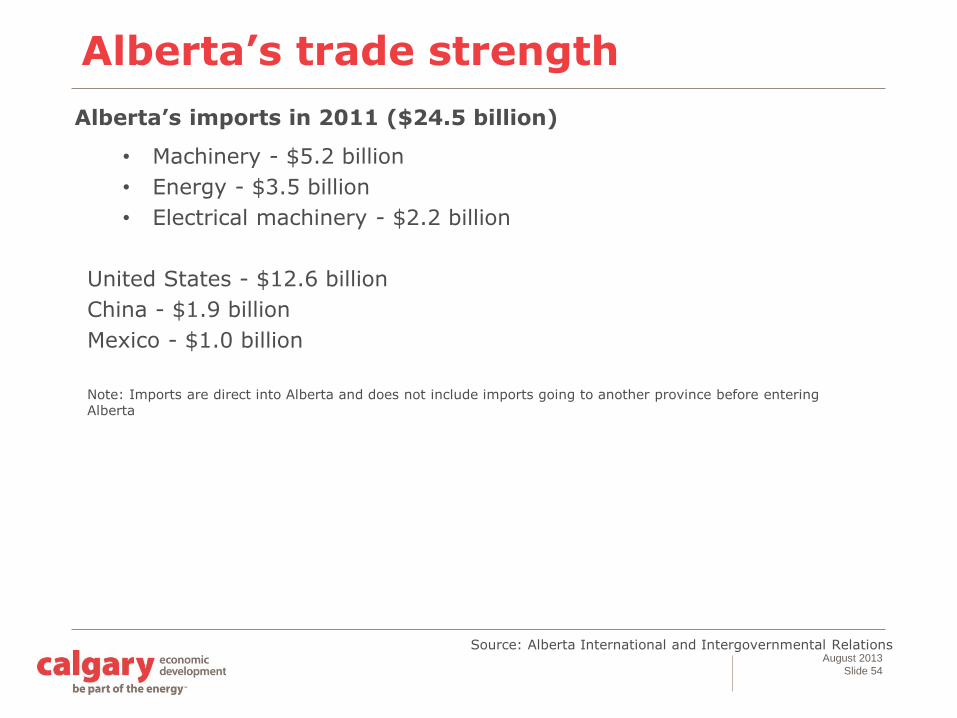

Alberta’s trade strength

Alberta’s imports in 2011 ($24.5 billion)

• Machinery - $5.2 billion

• Energy - $3.5 billion

• Electrical machinery - $2.2 billion

United States - $12.6 billion

China - $1.9 billion

Mexico - $1.0 billion

Note: Imports are direct into Alberta and does not include imports going to another province before entering Alberta

August 2013

Slide 55

Source: Alberta Enterprise and Advanced Education

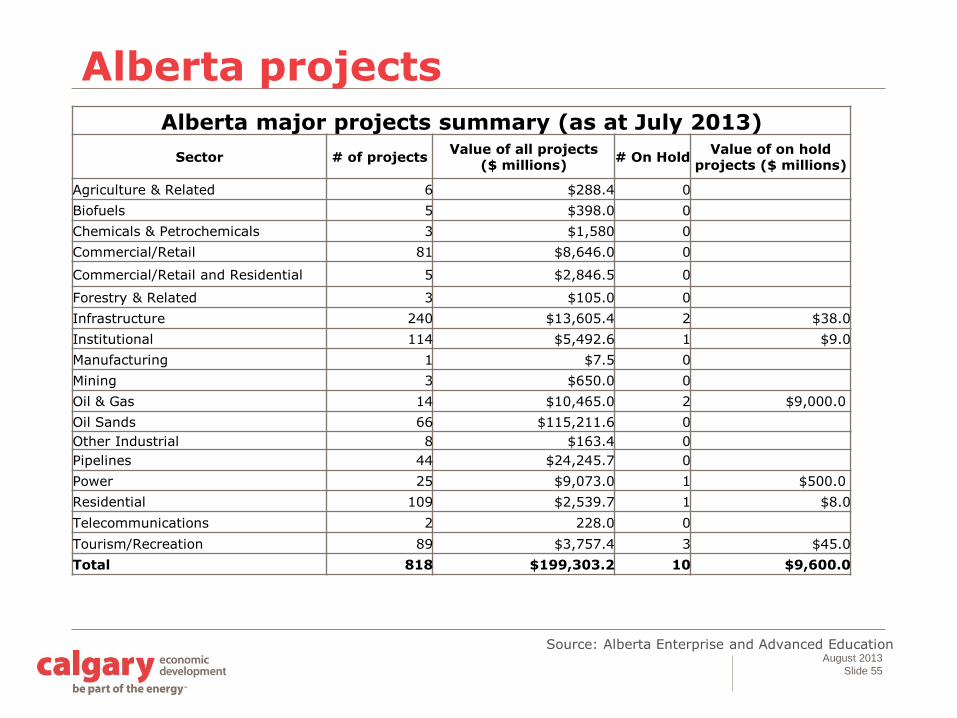

Alberta projects

Alberta major projects summary (as at July 2013)

Sector # of projectsValue of all projects

($ millions)# On Hold

Value of on hold projects ($ millions)

Agriculture & Related 6 $288.4 0

Biofuels 5 $398.0 0

Chemicals & Petrochemicals 3 $1,580 0

Commercial/Retail 81 $8,646.0 0

Commercial/Retail and Residential 5 $2,846.5 0

Forestry & Related 3 $105.0 0

Infrastructure 240 $13,605.4 2 $38.0

Institutional 114 $5,492.6 1 $9.0

Manufacturing 1 $7.5 0

Mining 3 $650.0 0

Oil & Gas 14 $10,465.0 2 $9,000.0

Oil Sands 66 $115,211.6 0

Other Industrial 8 $163.4 0

Pipelines 44 $24,245.7 0

Power 25 $9,073.0 1 $500.0

Residential 109 $2,539.7 1 $8.0

Telecommunications 2 228.0 0

Tourism/Recreation 89 $3,757.4 3 $45.0

Total 818 $199,303.2 10 $9,600.0

August 2013

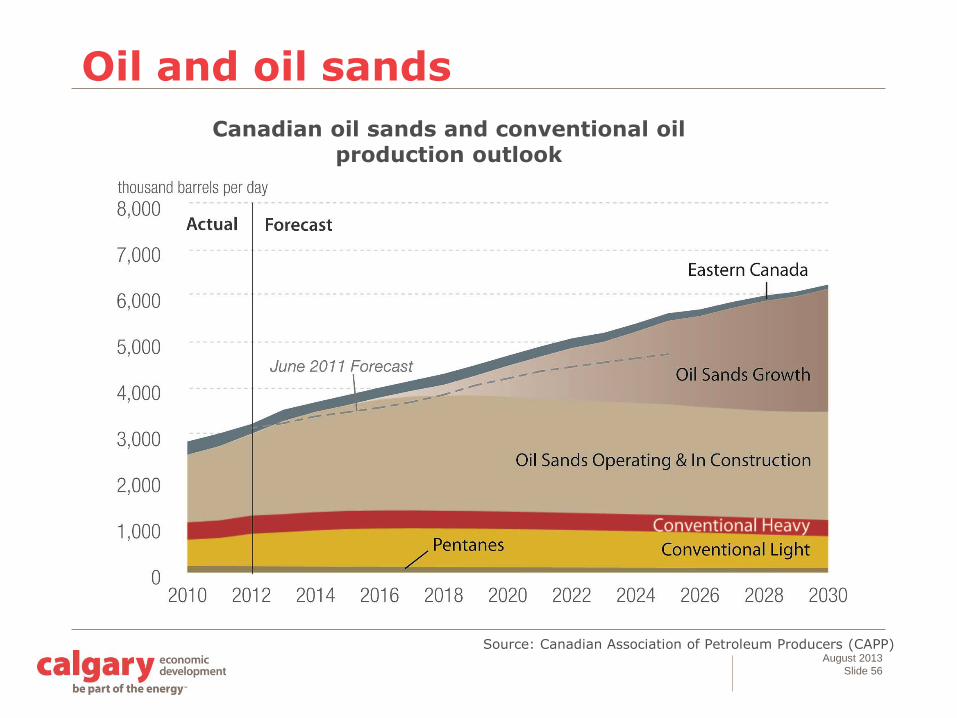

Slide 56

Source: Canadian Association of Petroleum Producers (CAPP)

Canadian oil sands and conventional oil production outlook

Oil and oil sands

August 2013

Slide 57

Source: Canadian Association of Petroleum Producers (CAPP)

Western Canadian oil sands and conventional oil production outlook

Oil sands in Western Canada

August 2013

Slide 58

Contact us

403-221-7831

www.calgaryeconomicdevelopment.com

Connect with us: @calgaryeconomic LinkedIn