Economics Exercises - Bloomberg Professional … · Economics Exercises Rich Jakotowicz...

13

Transcript of Economics Exercises - Bloomberg Professional … · Economics Exercises Rich Jakotowicz...

Three ExamplesCentral Banking Policy

Software integrated lecture for students to understand the effects of central banking policy and to observe the impact on markets currently and historically

Yield Curves Goal is to deepen understanding of yield relative to ratings, over

time, and versus other countries Assignment to test Implied Forward Rates

Multi Factor Modeling Goal is to learn how to build a multi factor model, which factors and

how many to include, and test for significance and stability.

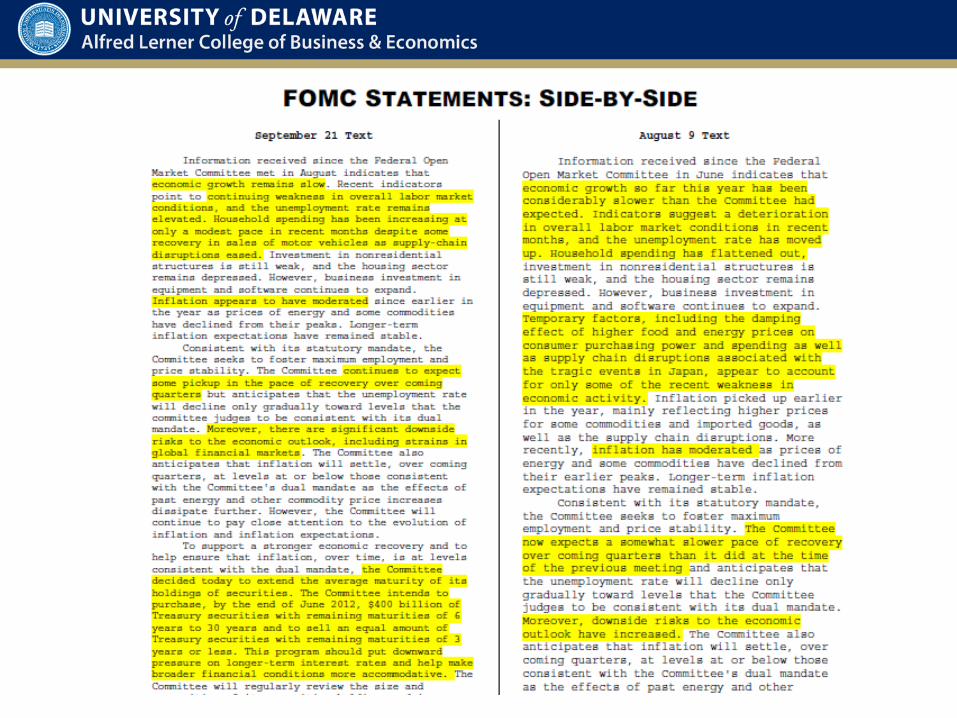

Central Banking PolicyFunctions used: • FOMC: View current policy and announcements.

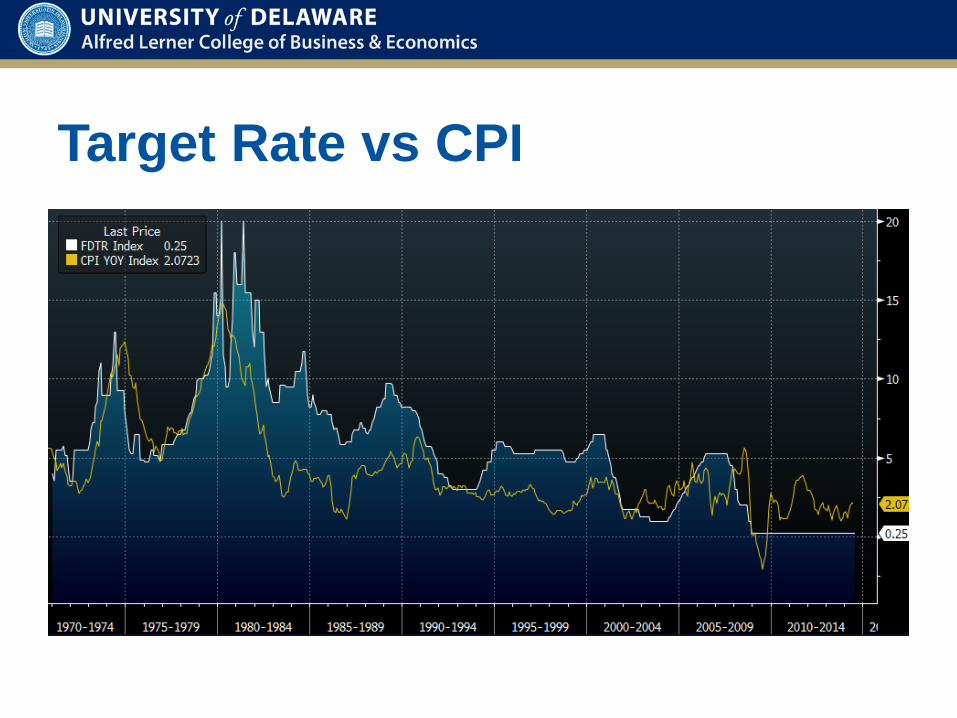

• OLR: View historic target rate.• Overlay CPI YOY

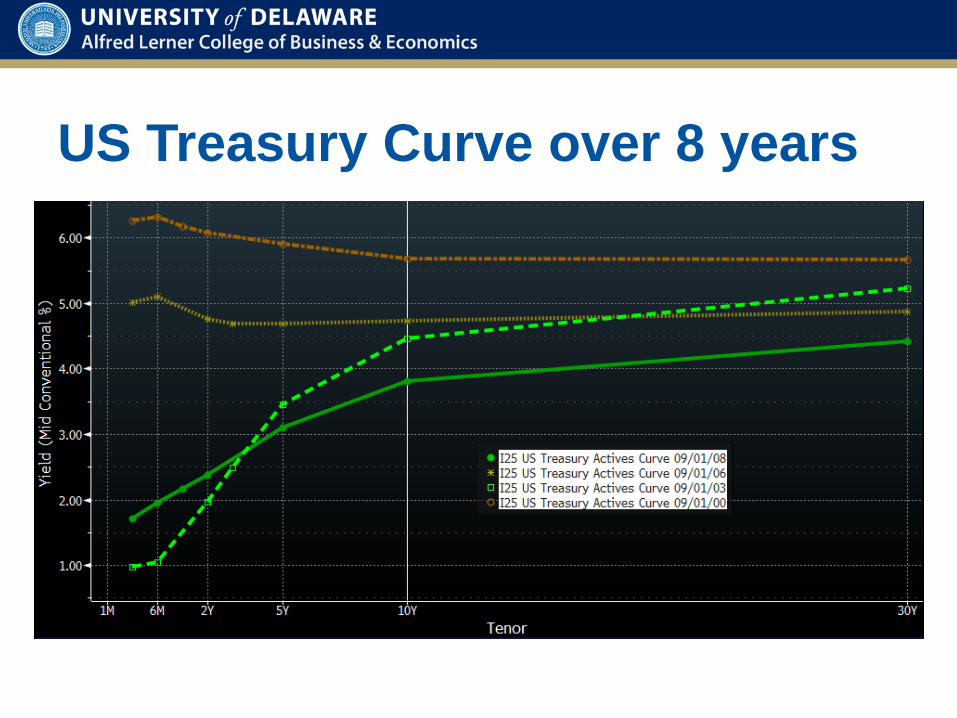

• Set historic target rate on one screen and Treasury Curve on the other. Use GC and start at 9/1/00. Then 9/1/03, 9/1/06, and 9/1/08. Discuss Term Structure Theory.

• GC & FOMS: Compare Treasury Curve before and after most recent FOMC Announcement• Discuss QE and Operation Twist (9/21/2011)

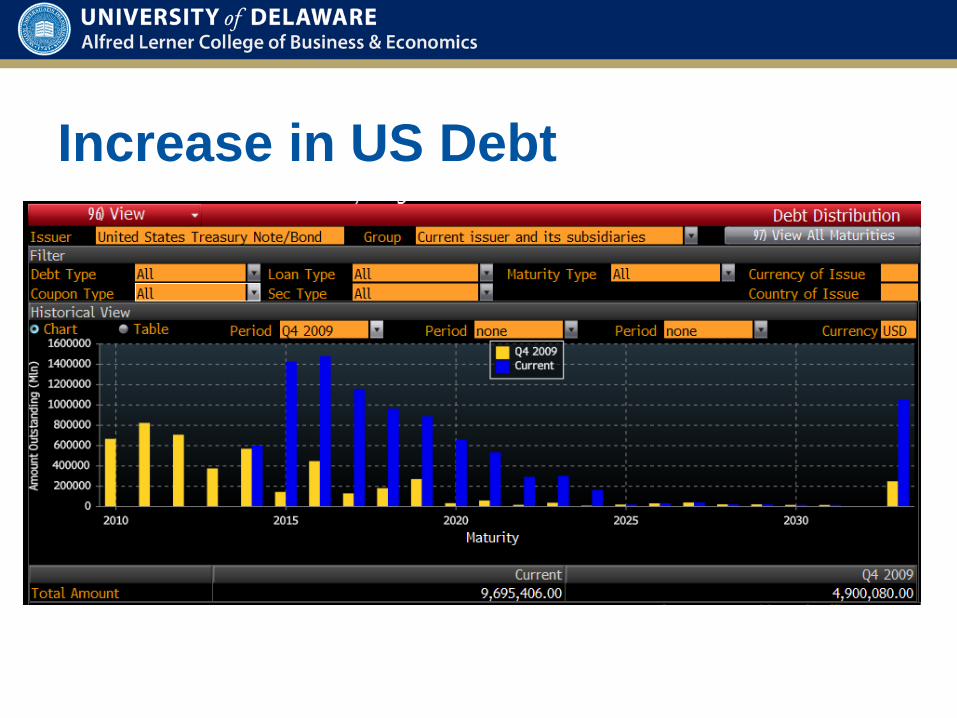

• DDIS to see debt expansion since the Financial Crisis

Target Rate vs CPI

US Treasury Curve over 8 years

Increase in US Debt

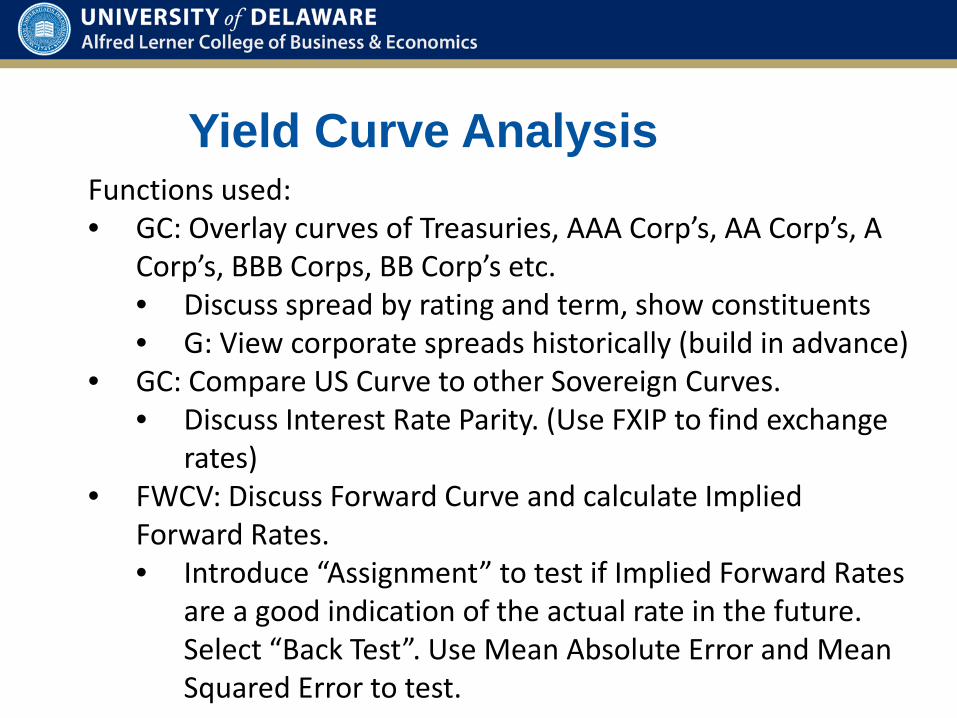

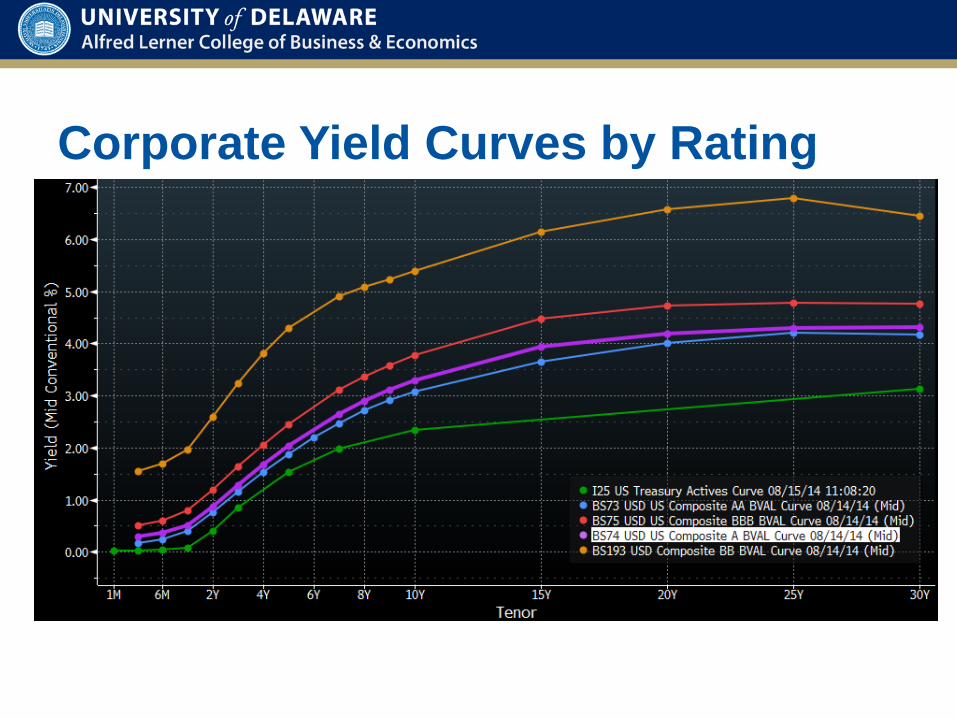

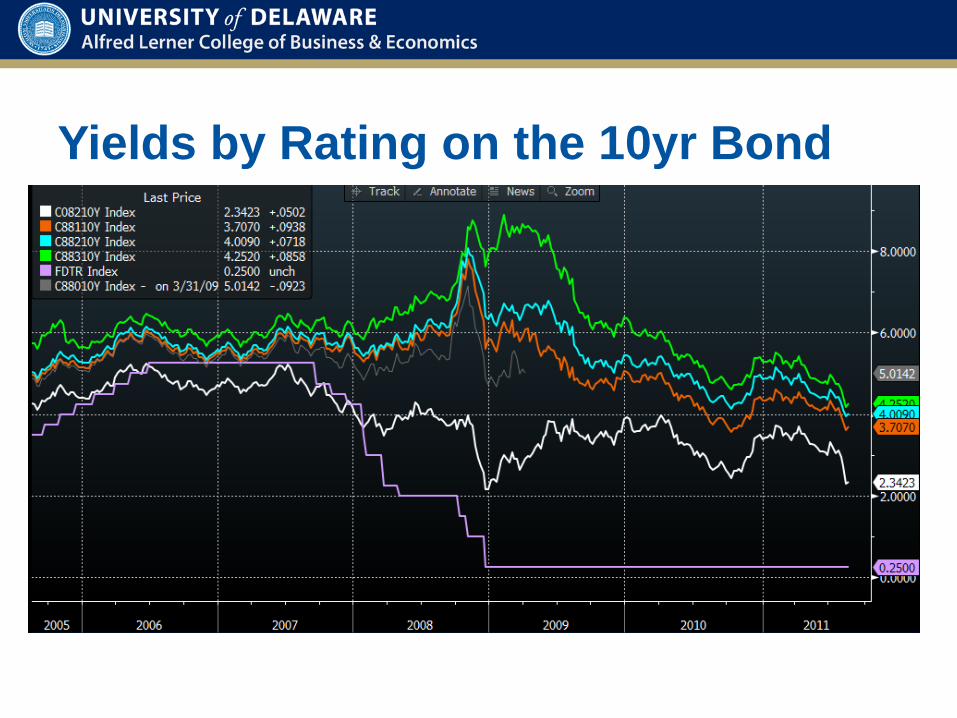

Yield Curve AnalysisFunctions used: • GC: Overlay curves of Treasuries, AAA Corp’s, AA Corp’s, A

Corp’s, BBB Corps, BB Corp’s etc. • Discuss spread by rating and term, show constituents• G: View corporate spreads historically (build in advance)

• GC: Compare US Curve to other Sovereign Curves.• Discuss Interest Rate Parity. (Use FXIP to find exchange

rates)• FWCV: Discuss Forward Curve and calculate Implied

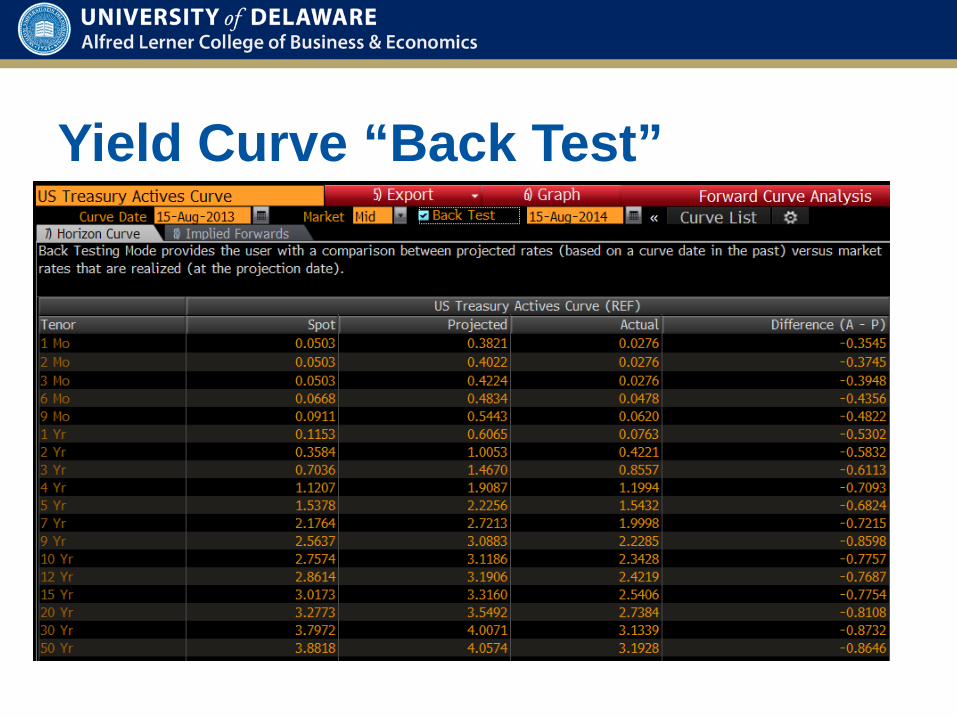

Forward Rates.• Introduce “Assignment” to test if Implied Forward Rates

are a good indication of the actual rate in the future. Select “Back Test”. Use Mean Absolute Error and Mean Squared Error to test.

Corporate Yield Curves by Rating

Yields by Rating on the 10yr Bond

Yield Curve “Back Test”

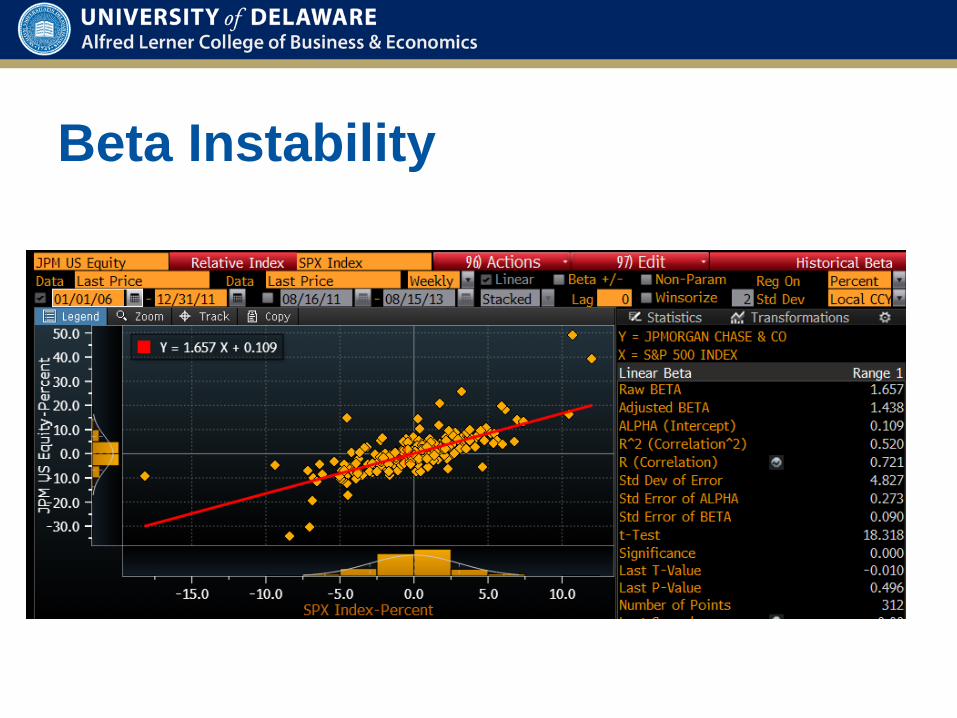

Multi Factor ModelingFunctions used:• BETA: Perform regressions over long period, then over 2

smaller inclusive periods. Discuss coefficient instability.• Ex: JPMorgan Beta from 1/1/06-12/31/11 versus from

1/1/06-12/31/08 and 1/1/9-12/31/11.• Could have this be an assignment.

• GP: Collect data to build a 5 factor model• Use Fama-French Data plus a factor for the spread

between ST and LT Treasuries and a factor for the spread between Treasuries and Corporates.

• At the graduate level, students must create their own multi factor model

• Introduce “Assignment” to test the model for significance and stability using Chow Tests.

Beta Instability