Economic Summit Recent decline in oil prices March 6, 2015 Reza Varjavand Associate Professor of...

34

Economic Summit Recent decline in oil prices March 6, 2015 Reza Varjavand Associate Professor of Economics GSM, Saint Xavier University

-

Upload

juliet-matthews -

Category

Documents

-

view

214 -

download

1

Transcript of Economic Summit Recent decline in oil prices March 6, 2015 Reza Varjavand Associate Professor of...

Economic SummitRecent decline in oil

pricesMarch 6, 2015

Reza Varjavand

Associate Professor of Economics

GSM, Saint Xavier University

US crude oil market, facts and figures

The US is the biggest consumer, importer, and now the leading producer according to many analysts

Total spending on crude oil = 8.5% of GDP, $1.5 trillion

Daily consumption of 20 million barrel, almost 45% domestic production and 55% imported (74% from Canada, Mexico, Venezuela, and Saudi Arabia)

The US domestic production almost doubled since 2008 to about 9 million barrel/day

The booming shale oil industry accounts for 3.5 million barrel/day, nearly 40% of domestic production and 17.5% of total consumption

Crude oil is still the number one source of energy in the US, 36% of total

With surge in domestic production and import from non-OPEC sources, the US dependency on Middle Eastern oil is diminishing.

Top ten oil producing countries

Top ten oil consuming countries (millions of barrels per day)

Rank ConsumersTotal Oil Consumption

1. United States 20.5

2. China 6.5

3. Japan 5.4

4. Germany 2.6

5. Russia 2.6

6. India 2.3

7. Canada 2.3

8. Brazil 2.2

9. South Korea 2.1

10. France 2.0

http://www.nytimes.com/video/business/energy-environmen }

OPEC VS the US, Shares of world oil production, 10 to 50%

Fracking boom

Recent decline in price of crude oil

The contributing factors: Demand related Supply related Product related Strength of US dollar Changes in consumers priorities Popularity of services Environmental and fuel efficiency

concerns Geopolitical factors including conflict of

interests among OPEC nations

Latest crude oil price from NASDAQ

Effects of falling oil prices on the US economy

Dropping prices signify a mixed blessing for the economy, there are many gainers and a few losers.

US consumers are the biggest gainers, aggregate and per household

Manufacturing sectors: automobile, transportation, airline, and other businesses

Shale oil industry and its future economic viability Effects on different states and the US economy as

a whole

Oil consumption goes hand-in-hand with economic growth

Breakeven Prices for different kinds of crude oil

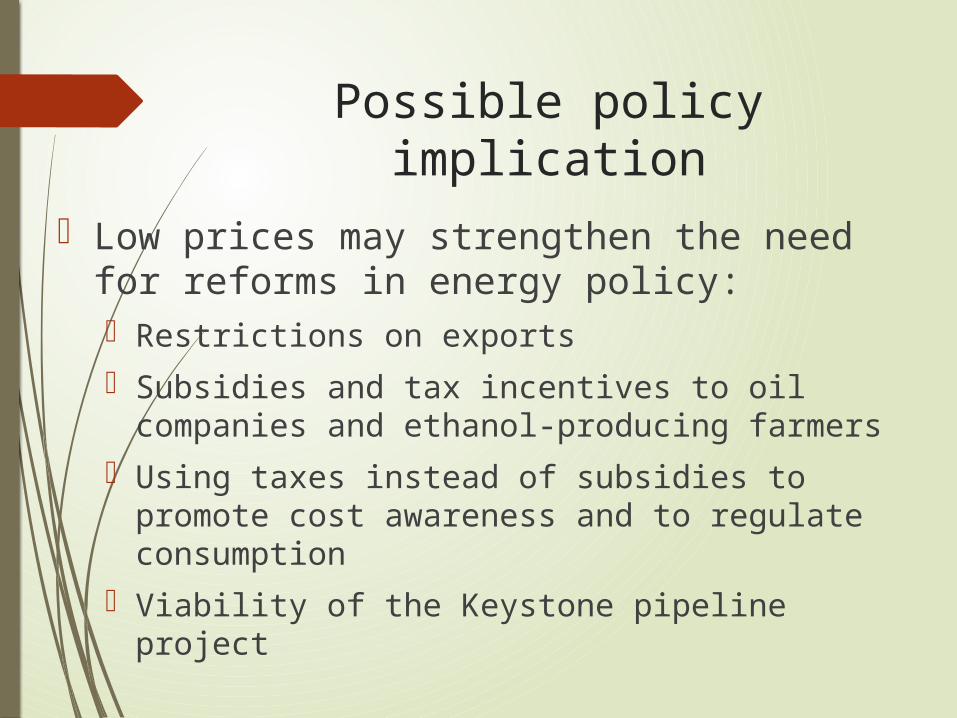

Possible policy implication

Low prices may strengthen the need for reforms in energy policy: Restrictions on exports Subsidies and tax incentives to oil companies

and ethanol-producing farmers Using taxes instead of subsidies to promote

cost awareness and to regulate consumption Viability of the Keystone pipeline project

Possibility of price rebound

Expectations of economic recovery worldwide

OPEC acting as an collaborative oligopoly (cartel) again, member nations may change their strategy and their attitudes toward one another

Law of demand and supply becomes relevant instead of geopolitical factors

Increasing world's stockpiles of crude oil

Effects of low prices on oil-exporting nations

Saudi Arabia

Russia

Iran

Venezuela

Nigeria

Structure of crude oil market Size, about 90 million barrel/day production (each barrel

contains 42 gallons)

Stages of operation: Exploration, Development, and Production

The types of benchmark crude Oil: WTI, West Texas Intermediate, for the US domestic producers and Brent for the global market.

Key producers in global market: USA, Saudi Arabia, Russia, China, and Canada, the share of top ten producers = 64% of total.

OPEC share is currently 40% of the world market. Non-OPEC producers 48% and t he US share is about 12%,

7 Companies dominating the global oil market: BP, Gulf, Standard of CA, Chevron, Shell, Standard of NJ, Exxon.

Major Players in global oil market

Share of world oil production

50

%

PROJ.

OPEC countries

40

30

20

United States

10

0

’96

’00

’04

’08

’12

’16

Source: Energy Information Administration