Impact of Air Services Liberalisation on Growth of Tourism in Asia

Ministry of Transport

Report 13 August 2013

Economic Effects of Air Services Liberalisation in New Zealand

Prepared for

Disclaimer

Although every effort has been made to ensure the accuracy of the material and the integrity

of the analysis presented herein, Covec Ltd accepts no liability for any actions taken on the

basis of its contents.

Authorship

Aaron Schiff and John Small

[email protected] | (09) 916 2012

© Covec Ltd, 2013. All rights reserved.

Contents

Executive Summary i

Effects of Liberalisation ii

Analysis of Foreign Airline Capacity iii

1 Introduction 1

2 Measuring Liberalisation 4

2.1 Background 4

2.2 Air Liberalisation Indexes 4

2.3 Case Studies 7

3 Estimating the Effects of Liberalisation 12

3.1 Theory 12

3.2 Empirical Methodology 14

3.3 Data 16

3.4 Determining which ALIs are Relevant 17

3.5 Regression Results 18

3.6 Interpretation of Results 21

3.7 Limitations of the Analysis 23

4 Analysis of Foreign Airline Capacity 24

4.1 General Trends 24

4.2 Volatility Analysis 26

4.3 Tenure Analysis 32

4.4 Discussion 34

5 Concluding Remarks 36

References 37

Appendix 1: Calculation of ALIs 38

Appendix 2: Regression Results 39

International visitor arrivals models 39

NZ Resident Departure Models 42

Trade Models 44

New Zealand Real GDP Models 46

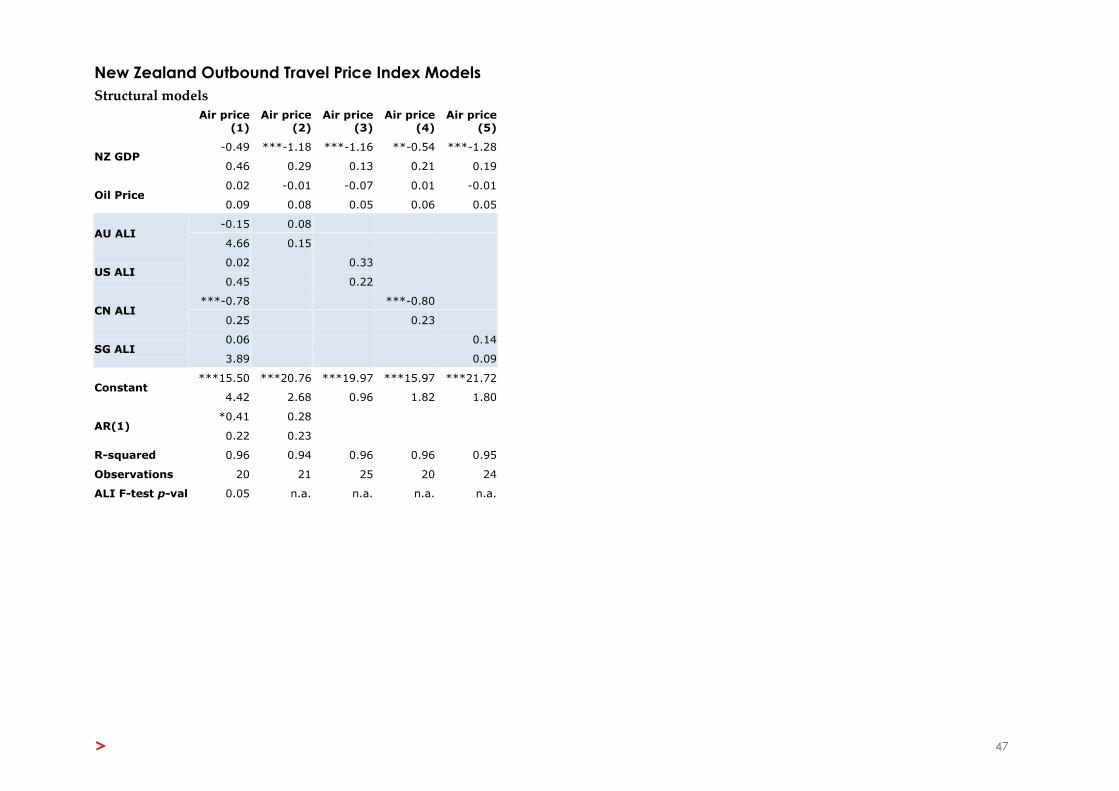

New Zealand Outbound Travel Price Index Models 47

i

Executive Summary

New Zealand has progressively deregulated markets for commercial air services since

the mid-1980s, and now has one of the most liberal international air transport policies in

the world. The New Zealand government has renegotiated existing air services

agreements (ASAs) with other countries and negotiated new ASAs, in order to reduce

regulatory barriers to competition on international air routes to and from New Zealand,

and in some cases on domestic routes within New Zealand.

Many of New Zealand’s ASAs are now “open skies” agreements, with no restrictions on

routes and capacity, and a liberal attitude towards foreign airline ownership. New

Zealand played a key role in the introduction of the Multilateral Agreement on the

Liberalisation of International Air Transportation (MALIAT). The MALIAT provides for

open skies between member states, and unlike standard bilateral ASAs it is open to

accession by other states, thus allowing open skies to propagate between members

without the need for bilateral negotiations.

Overall, liberalisation of New Zealand’s ASAs has been successful at attracting foreign

airlines to operate on international routes to and from New Zealand, although

competition on domestic routes remains limited. In 2013, 17 foreign airlines operated

services on New Zealand international routes, providing around 60% of total

international capacity, up from 50% in 2000 (Figure 1). The period of liberalisation has

coincided with strong growth in international travel volumes to and from New Zealand,

and falling real international airfares, in spite of increasing real fuel costs.

Figure 1 Total inbound capacity on flights arriving in New Zealand (seats per month).

Source: Covec calculations from Sabre-ADI data. Air New Zealand capacity includes Freedom Air.

0

100,000

200,000

300,000

400,000

500,000

600,000

20

00-1

20

00-7

20

01-1

20

01-7

20

02-1

20

02-7

20

03-1

20

03-7

20

04-1

20

04-7

20

05-1

20

05-7

20

06-1

20

06-7

20

07-1

20

07-7

20

08-1

20

08-7

20

09-1

20

09-7

20

10-1

20

10-7

20

11-1

20

11-7

20

12-1

20

12-7

20

13-1

20

13-7

Air NZ Foreign TotalAir NZ - Moving Average Foreign - Moving Average Total - Moving Average

ii

Effects of Liberalisation

We examined the effects of New Zealand’s air services liberalisation since the mid-1990s

on international visitor arrivals, outbound travel by New Zealand residents, exports and

imports by air, real GDP and real international outbound airfares. We tested for

relationships between these variables of interest and the liberalisation of New Zealand’s

ASAs with four countries: Australia, the United States, China and Singapore.

We calculated “air liberalisation indexes” (ALIs) using a methodology developed by the

World Trade Organisation, for each of the four case studies (Figure 2). We used time-

series econometric models to estimate relationships between the ALIs and the variables

of interest while controlling for other factors and trends that occurred at the same time.

Figure 2 Calculated ALIs for New Zealand’s ASAs with the case study countries. Higher values reflect

more liberal terms in the ASA; the maximum possible value is 50.

Source: Calculated from Ministry of Transport data.

The ALIs reflect policy settings that affect market outcomes indirectly via the

commercial decisions of airlines to take advantage of the opportunities created. It is

therefore difficult to empirically isolate the effects of liberalisation, particularly on

aggregate measures of economic activity. With this caveat in mind, the econometric

analysis leads us to the following conclusions for the four case studies:

International visitor arrivals: Liberalisation does not appear to be associated

with a significant increase in international visitors travelling point-to-point, ie

visitors from the case study countries. Rather, the effects appear to be on indirect

travel via the case study countries to New Zealand. This highlights the

importance of connectivity provided by ASAs, given New Zealand’s geographic

isolation from many inbound visitor markets.

0

5

10

15

20

25

30

35

40

45

50

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Air

lib

era

lisat

ion

in

de

x

Australia USA China Singapore

iii

Short-term departures by New Zealand residents: There is relatively strong

evidence of a relationship between the total number of short-term departures by

New Zealand residents and all of the ALIs except for the United States. This

suggests positive welfare benefits to New Zealanders from increased

competition in international air services and greater access to international

destinations. We analysed the total number of departures only; substitution by

outbound travellers between destinations may reflect additional welfare benefits

of liberalisation.

Real outbound travel prices: Real airfares have been falling in spite of

increasing fuel costs, likely due to increased competition and technological

improvements. There is evidence of a relationship between real outbound travel

prices and the ALI for China, suggesting that opening access to new markets

where there is substantial travel demand may reduce travel prices and generate

welfare benefits for travellers.

Imports and exports by air: There is no clear evidence of a relationship between

liberalisation and the real value of New Zealand’s international trade by air,

except for weak evidence of a link to the ALI for Australia. This likely reflects

the small amount of New Zealand trade by air, while Australia is New

Zealand’s largest trading partner and a relatively low cost destination for air

freight compared to elsewhere. Effects on trade appear to be secondary benefits

of liberalisation, relative to benefits from competition in passenger services.

Real GDP: There is no empirical evidence of a relationship between

liberalisation and total economic activity in New Zealand. This is likely due to

the fact that GDP is affected by a large number of factors, and it is difficult to

empirically isolate the effects of liberalisation from other trends.

Analysis of Foreign Airline Capacity

As noted above, foreign airlines now provide more than half of the international air

capacity to and from New Zealand. Between 2000 and 2013 foreign airlines increased

capacity by about 1.5 million seats per annum on flights arriving in New Zealand, while

Air New Zealand increased capacity by about 0.5 million seats per annum.

Foreign airlines have different incentives to operate routes to and from New Zealand

compared to domestic airlines, given the place of New Zealand in their route networks.

For most foreign airlines, New Zealand is at the end of a long ‘spoke’ in their network,

while New Zealand is a hub for domestic airlines.

Given these differences, we analysed the volatility of capacity on flights arriving in New

Zealand between 2000 and 2013, and the duration of time over which airlines

continuously operate routes to New Zealand (route tenure). The objective was to

determine whether foreign airlines behave differently to Air New Zealand in terms of

volatility and route tenure. The analysis was performed using capacity data published

by Sabre-ADI, which is based on flight schedules.

iv

Capacity Volatility

Volatility is measured by variance over time around an average or trend. Capacity on

air routes to New Zealand is affected by short-term seasonal factors as well as medium-

and long-term strategic behaviour by airlines.

Figure 3 shows variations of 12-month moving averages of capacity around a linear

trend. The moving averages remove seasonal effects, so this figure shows medium-term

volatility around the long-term trend. On this measure, total capacity provided by

foreign airlines on international routes to New Zealand is around twice as volatile as Air

New Zealand’s capacity. However, there are some individual foreign airlines that have

similar capacity volatility as Air New Zealand for this and other measures (Figure 4).

Figure 3 Analysis of deviations of 12-month moving average capacity from a linear trend.

Monthly normalised deviation Distribution of normalised deviations

Source: Calculated from Sabre-ADI data.

Figure 4 Normalised deviations of capacity for all airlines.

Source: Calculated from Sabre-ADI data.

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

20

00

-12

200

1-8

200

2-4

20

02

-12

200

3-8

200

4-4

20

04

-12

200

5-8

200

6-4

20

06

-12

200

7-8

200

8-4

20

08

-12

200

9-8

201

0-4

20

10

-12

201

1-8

201

2-4

20

12

-12

201

3-8

No

rmal

ise

d D

evi

atio

n

Air NZ Foreign

05

101520253035404550556065

-0.15to -0.11

-0.11to -0.07

-0.07to -0.03

-0.03to

0.01

0.01to

0.05

0.05to

0.09

0.09to

0.13

0.13to

0.17

0.17to

0.21

0.21to

0.25

Co

un

t

Normalised Deviation

Air NZ Foreign

0.00 0.05 0.10 0.15 0.20 0.25 0.30 0.35 0.40 0.45 0.50 0.55 0.60 0.65

Normalised Deviation

Foreign airlines Total foreign capacity Air NZ

Monthly capacity relative to

constant mean

Monthly capacity relative to 12-month

moving average

Monthly capacity relative to

linear trend

12-month moving average relative to

linear trend

v

Route Tenure

We calculated route tenure as the duration of time that an airline operated a route,

taking account of the fact that some routes are seasonal. Figure 5 shows the distribution

of route tenure (calculated over the period from 2000 to 2013) for Air New Zealand and

all foreign airlines combined. Overall we estimate average route tenure of 97 months for

Air New Zealand (median 87 months) and 70 months for foreign airlines (median 44

months). In aggregate, foreign airlines were more likely than Air New Zealand to

operate New Zealand routes for a short period only.

Figure 5 Number of international routes to New Zealand operated for various durations between 2000

and 2013.

Source: Calculated from Sabre-ADI data.

Figure 6 compares average route tenure for Air New Zealand with individual foreign

airlines. Several foreign airlines have route tenures similar to Air New Zealand.

However, Air New Zealand operates a significantly greater number of international

routes than any foreign airline. Those airlines that have the highest route tenure operate

only one or two unique routes.

Summary

There are some differences in volatility and route tenure between Air New Zealand and

foreign airlines as a group, although some large individual foreign airlines have similar

characteristics to Air New Zealand. Therefore, if stability is a desirable characteristic, it

is difficult to suggest favouring domestic over foreign airlines in air transport policy.

Furthermore, it is not clear that stability is desirable. There is uncertainty about the

profitability of routes, and profitability changes over time. Markets work to discover

new economically viable routes partly through a process of experimentation. Thus a

0

5

10

15

20

25

< 1

yea

r

1 -

2 y

ear

s

2 -

3 y

ear

s

3 -

4 y

ear

s

4 -

5 y

ear

s

5 -

6 y

ear

s

6 -

7 y

ear

s

7 -

8 y

ear

s

8 -

9 y

ear

s

9 -

10

ye

ars

10

- 1

1 ye

ars

11

- 1

2 ye

ars

12

- 1

3 ye

ars

13

- 1

4 ye

ars

14

ye

ars

Air NZ Foreign

vi

pattern of entry on routes followed by quick exit may be a sign of an efficiently

functioning market responding to changes in costs, demand and technology, and

working to discover new viable routes, rather than a problem that needs to be solved.

Figure 6 Average route tenure and number of unique international routes operated by airlines serving

New Zealand between 2000 and 2013.

Source: Calculated from Sabre-ADI data.

0

5

10

15

20

25

30

35

40

45

50

55

60

0

20

40

60

80

100

120

140

160

180

CX

NF

SB SQ LA

QF/

JQ AR

TN NZ

MH TG BR BI

GA EK

DJ/

VA FJ KE

PH CZ CI

UA

OZ

D7

WR

HA

CA YE

Nu

mb

er

of

Un

iqu

e R

ou

tes

Op

era

ted

Ave

rage

Te

nu

re (

mo

nth

s)

Average Tenure (left)

Number of Unique Routes (right)

1

1 Introduction

Markets for commercial air services in New Zealand have been progressively

deregulated since the mid-1980s, facilitating greater competition on international and

domestic routes. Liberalisation of New Zealand’s air services agreements (ASAs) with

other countries has been a key part of deregulation. This report examines the effects of

New Zealand’s international air services liberalisation since the mid-1990s across a

number of dimensions. The objectives are to estimate the observed effects of

liberalisation, and to give guidance for future air services negotiating priorities.

Liberalisation has involved the New Zealand government renegotiating ASAs with

existing partner countries, and negotiating new agreements with other countries, in

order to reduce regulatory barriers to competition on international routes to and from

New Zealand, and in some cases competition on domestic routes within New Zealand.

This has included New Zealand granting additional “freedoms of the air” to foreign

airlines,1 and reduction or removal of restrictions on capacity, price setting, ownership,

and cooperative arrangements such as code-sharing. Under the bilateral agreements,

New Zealand airlines also face lower barriers to operating services to and from other

countries.

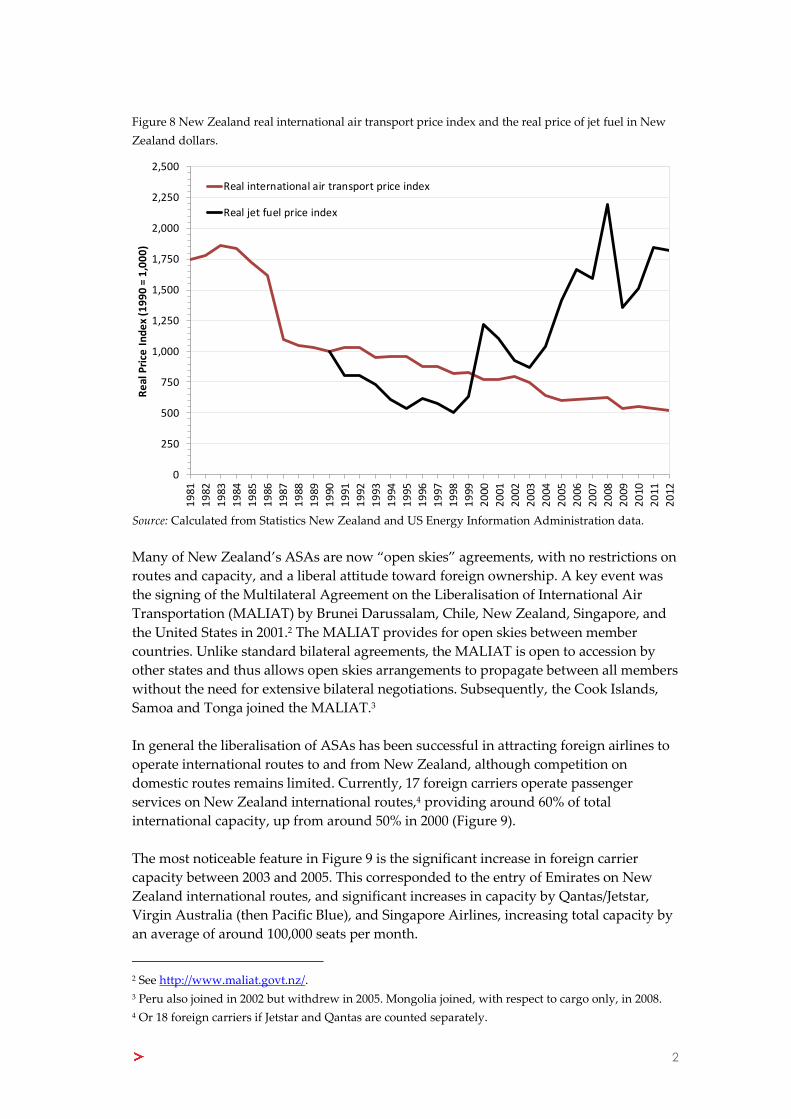

The period of liberalisation has coincided with strong growth in international travel to

and from New Zealand (Figure 7), and falling prices for international travel, in spite of

increasing fuel costs (Figure 8).

Figure 7 International travel to and from New Zealand.

Source: Statistics New Zealand.

1 See http://en.wikipedia.org/wiki/Freedoms_of_the_air for an overview of the standard air freedoms.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

Mill

ion

s

International Visitor Arrivals

NZ Resident Short-Term Departures

2

Figure 8 New Zealand real international air transport price index and the real price of jet fuel in New

Zealand dollars.

Source: Calculated from Statistics New Zealand and US Energy Information Administration data.

Many of New Zealand’s ASAs are now “open skies” agreements, with no restrictions on

routes and capacity, and a liberal attitude toward foreign ownership. A key event was

the signing of the Multilateral Agreement on the Liberalisation of International Air

Transportation (MALIAT) by Brunei Darussalam, Chile, New Zealand, Singapore, and

the United States in 2001.2 The MALIAT provides for open skies between member

countries. Unlike standard bilateral agreements, the MALIAT is open to accession by

other states and thus allows open skies arrangements to propagate between all members

without the need for extensive bilateral negotiations. Subsequently, the Cook Islands,

Samoa and Tonga joined the MALIAT.3

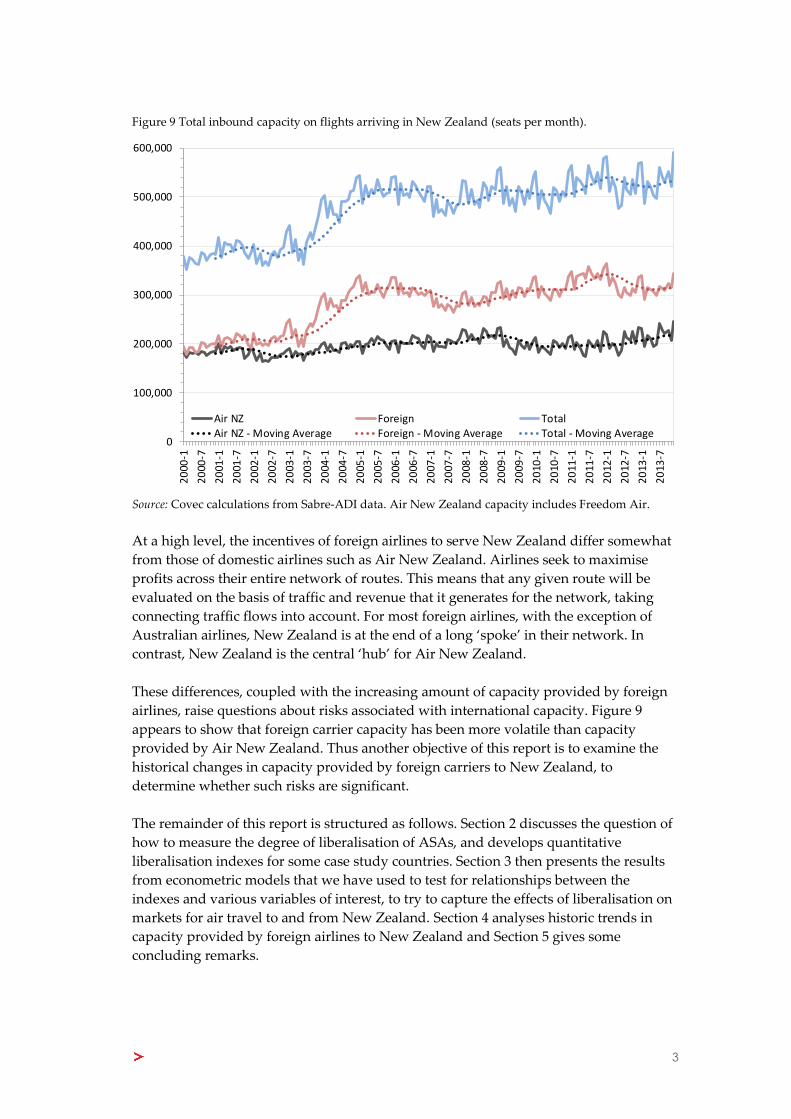

In general the liberalisation of ASAs has been successful in attracting foreign airlines to

operate international routes to and from New Zealand, although competition on

domestic routes remains limited. Currently, 17 foreign carriers operate passenger

services on New Zealand international routes,4 providing around 60% of total

international capacity, up from around 50% in 2000 (Figure 9).

The most noticeable feature in Figure 9 is the significant increase in foreign carrier

capacity between 2003 and 2005. This corresponded to the entry of Emirates on New

Zealand international routes, and significant increases in capacity by Qantas/Jetstar,

Virgin Australia (then Pacific Blue), and Singapore Airlines, increasing total capacity by

an average of around 100,000 seats per month.

2 See http://www.maliat.govt.nz/.

3 Peru also joined in 2002 but withdrew in 2005. Mongolia joined, with respect to cargo only, in 2008. 4 Or 18 foreign carriers if Jetstar and Qantas are counted separately.

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Re

al P

rice

In

de

x (1

99

0 =

1,0

00

)

Real international air transport price index

Real jet fuel price index

3

Figure 9 Total inbound capacity on flights arriving in New Zealand (seats per month).

Source: Covec calculations from Sabre-ADI data. Air New Zealand capacity includes Freedom Air.

At a high level, the incentives of foreign airlines to serve New Zealand differ somewhat

from those of domestic airlines such as Air New Zealand. Airlines seek to maximise

profits across their entire network of routes. This means that any given route will be

evaluated on the basis of traffic and revenue that it generates for the network, taking

connecting traffic flows into account. For most foreign airlines, with the exception of

Australian airlines, New Zealand is at the end of a long ‘spoke’ in their network. In

contrast, New Zealand is the central ‘hub’ for Air New Zealand.

These differences, coupled with the increasing amount of capacity provided by foreign

airlines, raise questions about risks associated with international capacity. Figure 9

appears to show that foreign carrier capacity has been more volatile than capacity

provided by Air New Zealand. Thus another objective of this report is to examine the

historical changes in capacity provided by foreign carriers to New Zealand, to

determine whether such risks are significant.

The remainder of this report is structured as follows. Section 2 discusses the question of

how to measure the degree of liberalisation of ASAs, and develops quantitative

liberalisation indexes for some case study countries. Section 3 then presents the results

from econometric models that we have used to test for relationships between the

indexes and various variables of interest, to try to capture the effects of liberalisation on

markets for air travel to and from New Zealand. Section 4 analyses historic trends in

capacity provided by foreign airlines to New Zealand and Section 5 gives some

concluding remarks.

0

100,000

200,000

300,000

400,000

500,000

600,000

20

00-1

20

00-7

20

01-1

20

01-7

20

02-1

20

02-7

20

03-1

20

03-7

20

04-1

20

04-7

20

05-1

20

05-7

20

06-1

20

06-7

20

07-1

20

07-7

20

08-1

20

08-7

20

09-1

20

09-7

20

10-1

20

10-7

20

11-1

20

11-7

20

12-1

20

12-7

20

13-1

20

13-7

Air NZ Foreign TotalAir NZ - Moving Average Foreign - Moving Average Total - Moving Average

4

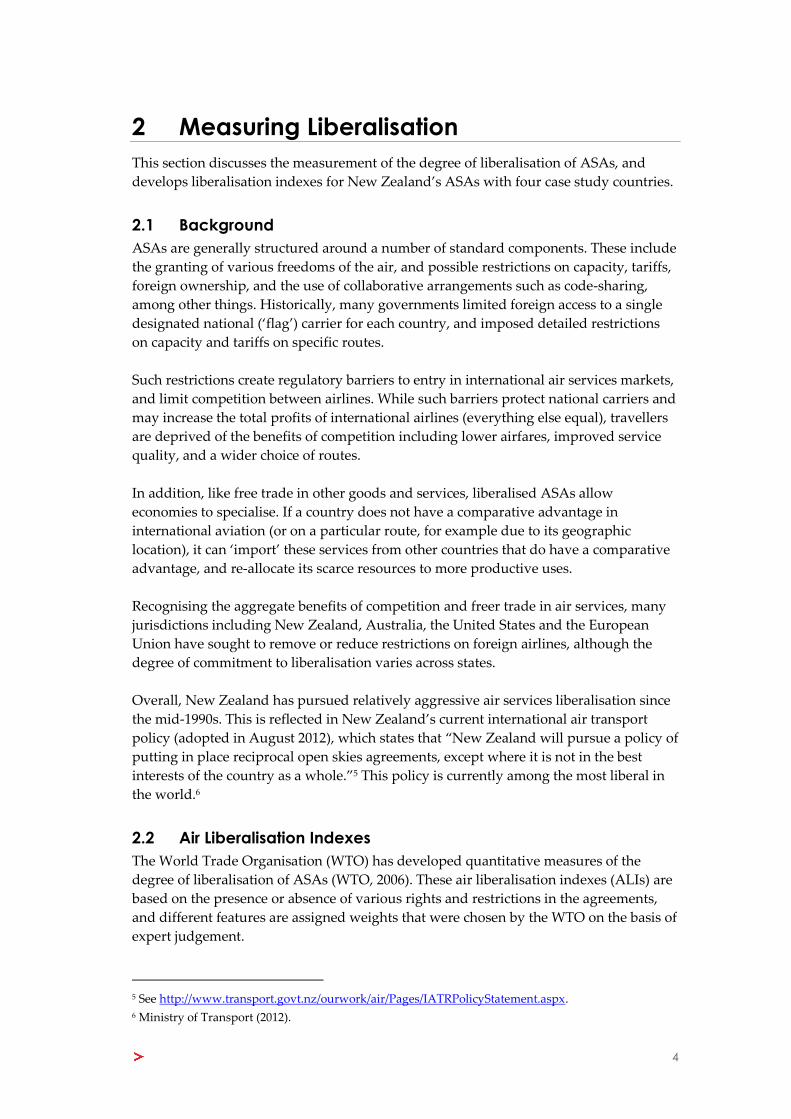

2 Measuring Liberalisation

This section discusses the measurement of the degree of liberalisation of ASAs, and

develops liberalisation indexes for New Zealand’s ASAs with four case study countries.

2.1 Background

ASAs are generally structured around a number of standard components. These include

the granting of various freedoms of the air, and possible restrictions on capacity, tariffs,

foreign ownership, and the use of collaborative arrangements such as code-sharing,

among other things. Historically, many governments limited foreign access to a single

designated national (‘flag’) carrier for each country, and imposed detailed restrictions

on capacity and tariffs on specific routes.

Such restrictions create regulatory barriers to entry in international air services markets,

and limit competition between airlines. While such barriers protect national carriers and

may increase the total profits of international airlines (everything else equal), travellers

are deprived of the benefits of competition including lower airfares, improved service

quality, and a wider choice of routes.

In addition, like free trade in other goods and services, liberalised ASAs allow

economies to specialise. If a country does not have a comparative advantage in

international aviation (or on a particular route, for example due to its geographic

location), it can ‘import’ these services from other countries that do have a comparative

advantage, and re-allocate its scarce resources to more productive uses.

Recognising the aggregate benefits of competition and freer trade in air services, many

jurisdictions including New Zealand, Australia, the United States and the European

Union have sought to remove or reduce restrictions on foreign airlines, although the

degree of commitment to liberalisation varies across states.

Overall, New Zealand has pursued relatively aggressive air services liberalisation since

the mid-1990s. This is reflected in New Zealand’s current international air transport

policy (adopted in August 2012), which states that “New Zealand will pursue a policy of

putting in place reciprocal open skies agreements, except where it is not in the best

interests of the country as a whole.”5 This policy is currently among the most liberal in

the world.6

2.2 Air Liberalisation Indexes

The World Trade Organisation (WTO) has developed quantitative measures of the

degree of liberalisation of ASAs (WTO, 2006). These air liberalisation indexes (ALIs) are

based on the presence or absence of various rights and restrictions in the agreements,

and different features are assigned weights that were chosen by the WTO on the basis of

expert judgement.

5 See http://www.transport.govt.nz/ourwork/air/Pages/IATRPolicyStatement.aspx. 6 Ministry of Transport (2012).

5

The result is an index that generally reflects the degree of liberalisation of an ASA, with

a higher index corresponding to a more liberal agreement, although the absolute level of

the index does not have a meaningful interpretation. Thus it is only possible to interpret

changes in the index for an ASA over time, or relative differences between ASAs.

Table 1 on the next page summarises the calculation of the WTO index for a given ASA.

The maximum value is 50, representing very minimal regulatory barriers to entry.

Piermartini and Rousová (2008) calculated average ALIs for a sample of 184 countries.

The data used to calculate the ALIs were from around 2005, and at the time New

Zealand was ranked the 145th most liberal country out of 184 countries overall, with an

average ALI of 15.7. This compared with 10.4 for Australia, 12.3 for Singapore, 18.9 for

the United Kingdom and 25.0 for the United States. Around 70% of ASAs were found to

have an ALI of below 15, while only 15% were found to be in excess of 40 (and none in

excess of 45). Most of the high ALIs were for ASAs within the European Union, for

which the ALI was calculated to be 43.

Piermartini and Rousová used the ALIs, together with a sample of air passenger

volumes between 2,299 country pairs, to test the effects of liberalisation on the volume

of passengers. Everything else equal, it is expected that greater liberalisation will

increase passenger volumes. In general the increase in passenger volumes as a result of

liberalisation is a proxy for the increase in wellbeing (or welfare) as it can be assumed

that a voluntary increase in consumption of a good or service corresponds to an increase

in wellbeing in proportion to the change in quantity.

Cross-country regression models were used by Piermartini and Rousová to explain

passenger volumes as a function of the ALIs, while controlling for the distance between

countries using a ‘gravity’ model,7 and controlling for whether or not the countries

shared a border, whether or not one country was a former colony of the other, whether

the countries shared a common language, income levels in the two countries, and the

age of each ASA.

The results from that study, using various regression methodologies, strongly

supported a positive relationship between greater liberalisation and increased passenger

volumes. Overall it was estimated that increasing the degree of liberalisation from the

25th to the 75th percentile of ASAs increases passenger traffic by around 30%, everything

else equal. The most beneficial liberalisation measures were found to be the removal of

restrictions on capacity and tariffs, granting cabotage (eighth and ninth freedom) rights,

and multiple designation, ie allowing airlines other than a nominated flag carrier of the

foreign country to operate services.

7 Gravity models assume that the ‘attraction’ of travel between two places decreases exponentially with

distance, similar to the effect of physical gravity.

6

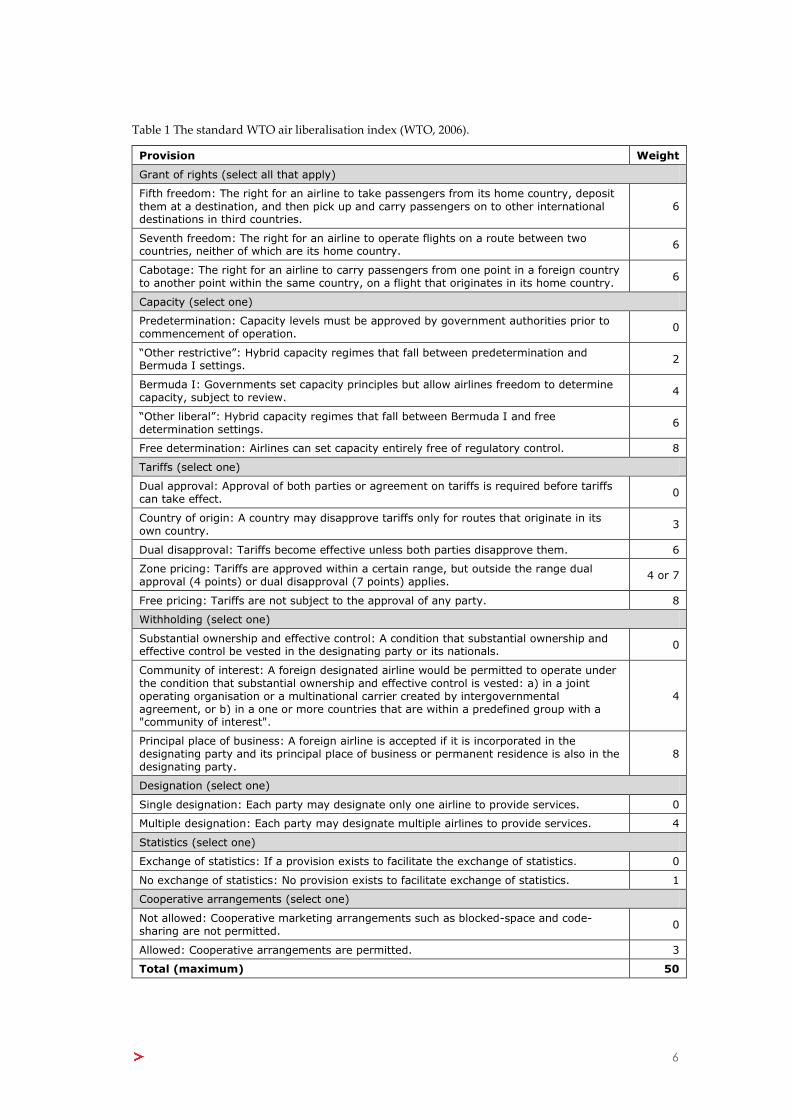

Table 1 The standard WTO air liberalisation index (WTO, 2006).

Provision Weight

Grant of rights (select all that apply)

Fifth freedom: The right for an airline to take passengers from its home country, deposit

them at a destination, and then pick up and carry passengers on to other international destinations in third countries.

6

Seventh freedom: The right for an airline to operate flights on a route between two countries, neither of which are its home country.

6

Cabotage: The right for an airline to carry passengers from one point in a foreign country to another point within the same country, on a flight that originates in its home country.

6

Capacity (select one)

Predetermination: Capacity levels must be approved by government authorities prior to commencement of operation.

0

“Other restrictive”: Hybrid capacity regimes that fall between predetermination and Bermuda I settings.

2

Bermuda I: Governments set capacity principles but allow airlines freedom to determine capacity, subject to review.

4

“Other liberal”: Hybrid capacity regimes that fall between Bermuda I and free determination settings.

6

Free determination: Airlines can set capacity entirely free of regulatory control. 8

Tariffs (select one)

Dual approval: Approval of both parties or agreement on tariffs is required before tariffs can take effect.

0

Country of origin: A country may disapprove tariffs only for routes that originate in its own country.

3

Dual disapproval: Tariffs become effective unless both parties disapprove them. 6

Zone pricing: Tariffs are approved within a certain range, but outside the range dual approval (4 points) or dual disapproval (7 points) applies.

4 or 7

Free pricing: Tariffs are not subject to the approval of any party. 8

Withholding (select one)

Substantial ownership and effective control: A condition that substantial ownership and effective control be vested in the designating party or its nationals.

0

Community of interest: A foreign designated airline would be permitted to operate under

the condition that substantial ownership and effective control is vested: a) in a joint operating organisation or a multinational carrier created by intergovernmental agreement, or b) in a one or more countries that are within a predefined group with a "community of interest".

4

Principal place of business: A foreign airline is accepted if it is incorporated in the designating party and its principal place of business or permanent residence is also in the designating party.

8

Designation (select one)

Single designation: Each party may designate only one airline to provide services. 0

Multiple designation: Each party may designate multiple airlines to provide services. 4

Statistics (select one)

Exchange of statistics: If a provision exists to facilitate the exchange of statistics. 0

No exchange of statistics: No provision exists to facilitate exchange of statistics. 1

Cooperative arrangements (select one)

Not allowed: Cooperative marketing arrangements such as blocked-space and code-sharing are not permitted.

0

Allowed: Cooperative arrangements are permitted. 3

Total (maximum) 50

7

2.3 Case Studies

For the purposes of the empirical analysis in section 3 below, case studies were selected

to test the effects of New Zealand’s air services liberalisation. The case studies were

chosen on the basis of significant liberalisation occurring over time since the mid-1990s:

between New Zealand and Australia, the United States, China and Singapore.

Appendix 1 gives details of the calculation of the four ALIs. The standard WTO (2006)

methodology was applied, with two minor modifications:

While all the relevant ASAs provide for the exchange of statistics, in practice this

is never enforced in New Zealand, hence the weight for “no exchange of

statistics” was used. In any case this condition has not changed in any of the

ASAs and so will not affect the value of the ALIs over time.

The allowance of cooperative arrangements was further divided into two sub-

categories to better reflect the detail of New Zealand’s ASAs:

o Regular codesharing allowed (2 points)

o Regular and third-country codesharing allowed (3 points)

The resulting ALIs for the four case studies are shown in Figure 10. All have increased

substantially over time. Following the 2001 MALIAT Protocol, the ASA with Singapore

achieves the maximum possible ALI of 50. The MALIAT itself achieves an ALI of 38.

Figure 10 Calculated ALIs for New Zealand’s ASAs with the case study countries.

Source: Calculated from Ministry of Transport data.

0

5

10

15

20

25

30

35

40

45

50

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Air

lib

era

lisat

ion

in

de

x

Australia USA China Singapore

8

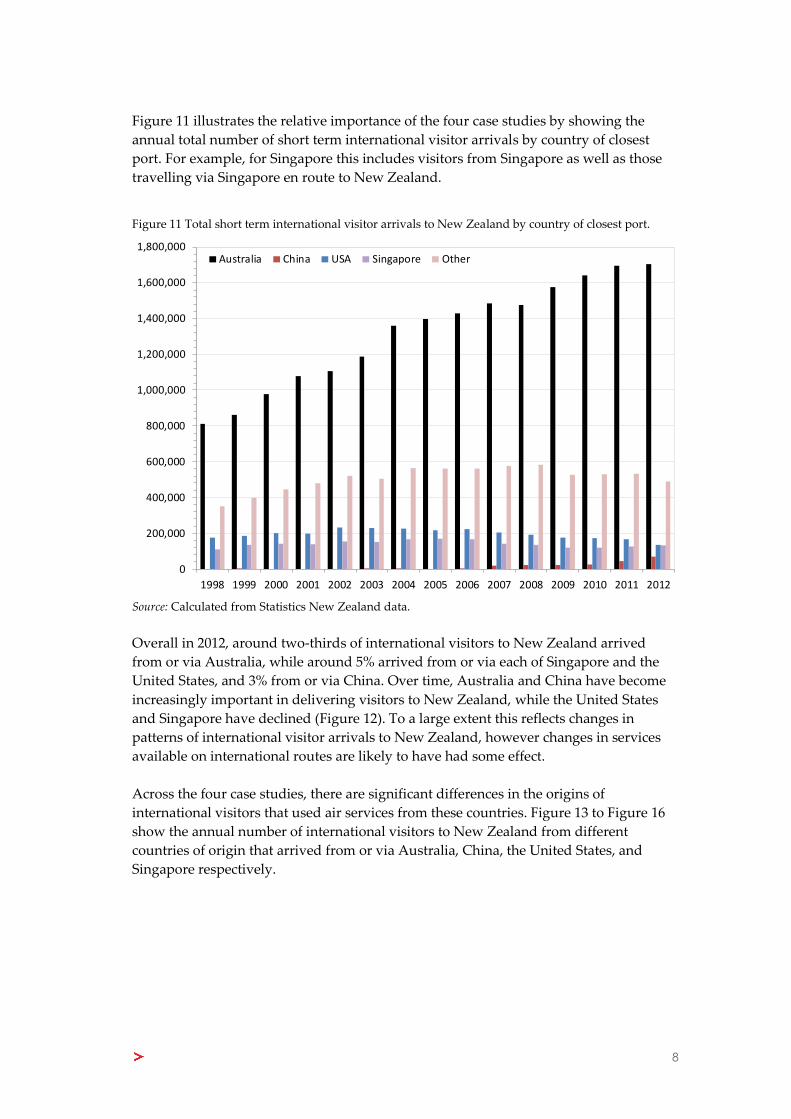

Figure 11 illustrates the relative importance of the four case studies by showing the

annual total number of short term international visitor arrivals by country of closest

port. For example, for Singapore this includes visitors from Singapore as well as those

travelling via Singapore en route to New Zealand.

Figure 11 Total short term international visitor arrivals to New Zealand by country of closest port.

Source: Calculated from Statistics New Zealand data.

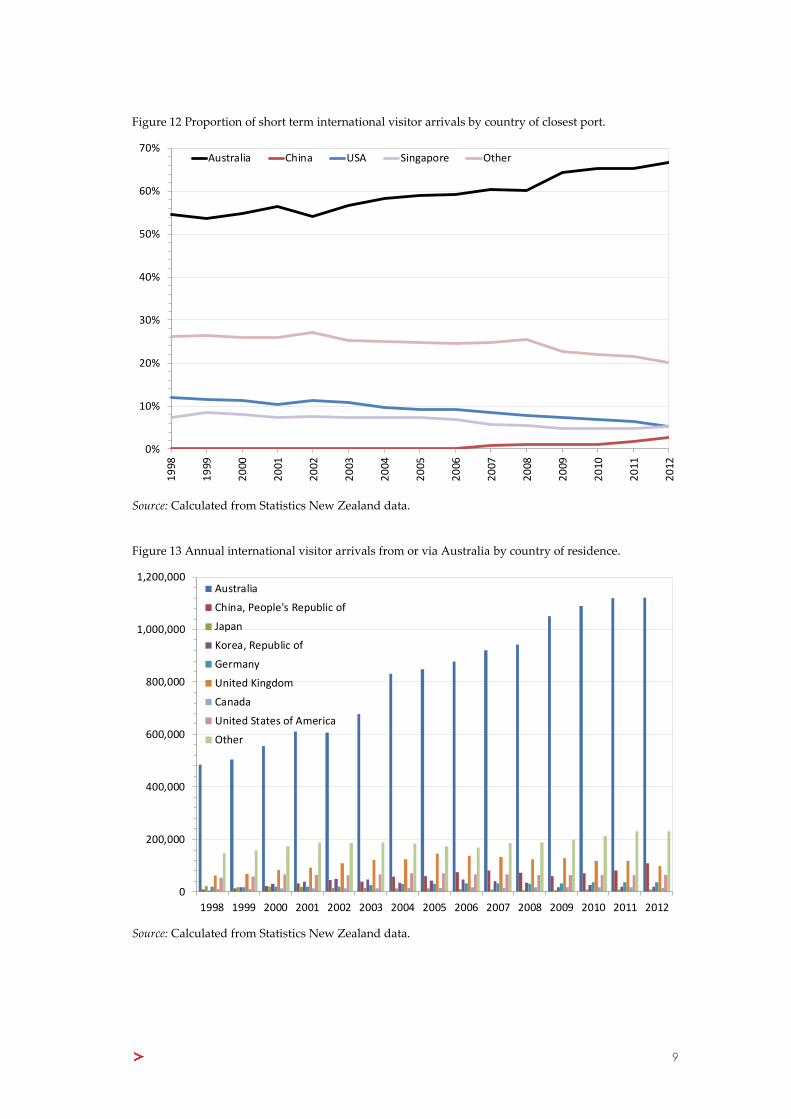

Overall in 2012, around two-thirds of international visitors to New Zealand arrived

from or via Australia, while around 5% arrived from or via each of Singapore and the

United States, and 3% from or via China. Over time, Australia and China have become

increasingly important in delivering visitors to New Zealand, while the United States

and Singapore have declined (Figure 12). To a large extent this reflects changes in

patterns of international visitor arrivals to New Zealand, however changes in services

available on international routes are likely to have had some effect.

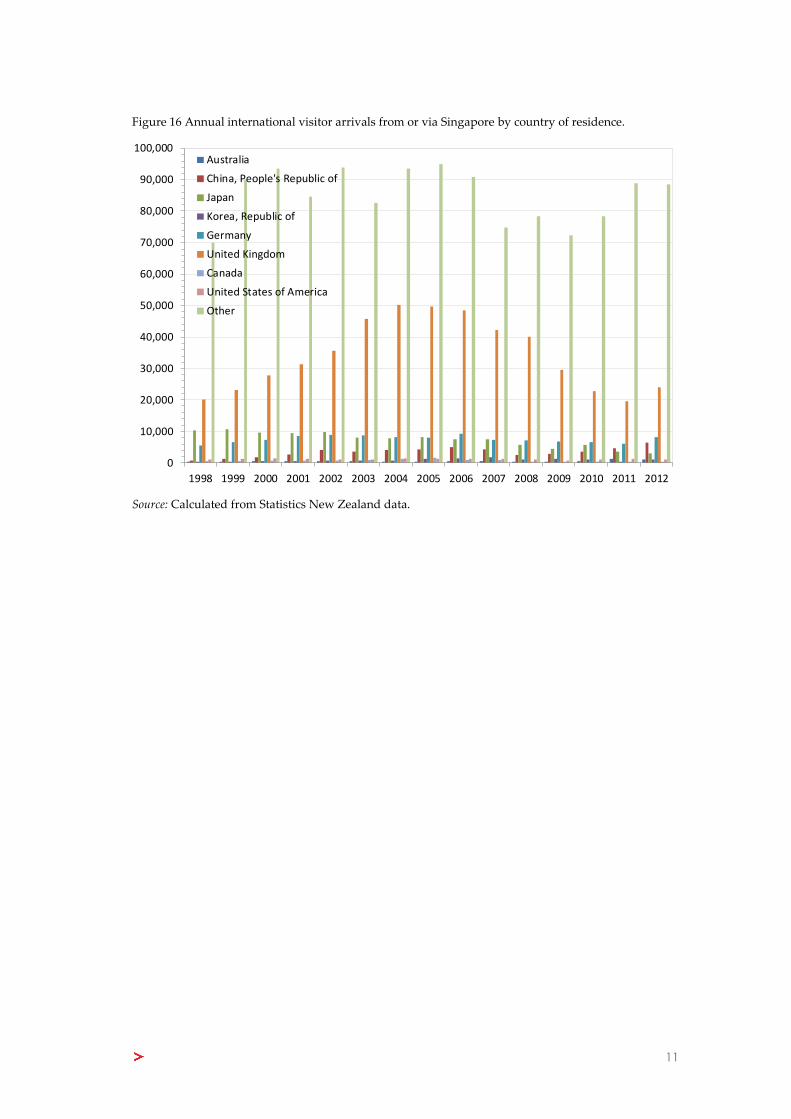

Across the four case studies, there are significant differences in the origins of

international visitors that used air services from these countries. Figure 13 to Figure 16

show the annual number of international visitors to New Zealand from different

countries of origin that arrived from or via Australia, China, the United States, and

Singapore respectively.

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Australia China USA Singapore Other

9

Figure 12 Proportion of short term international visitor arrivals by country of closest port.

Source: Calculated from Statistics New Zealand data.

Figure 13 Annual international visitor arrivals from or via Australia by country of residence.

Source: Calculated from Statistics New Zealand data.

0%

10%

20%

30%

40%

50%

60%

70%

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Australia China USA Singapore Other

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Australia

China, People's Republic of

Japan

Korea, Republic of

Germany

United Kingdom

Canada

United States of America

Other

10

Figure 14 Annual international visitor arrivals from or via China by country of residence.

Source: Calculated from Statistics New Zealand data.

Figure 15 Annual international visitor arrivals from or via the United States by country of residence.

Source: Calculated from Statistics New Zealand data.

0

10,000

20,000

30,000

40,000

50,000

60,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Australia

China, People's Republic of

Japan

Korea, Republic of

Germany

United Kingdom

Canada

United States of America

Other

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Australia

China, People's Republic of

Japan

Korea, Republic of

Germany

United Kingdom

Canada

United States of America

Other

11

Figure 16 Annual international visitor arrivals from or via Singapore by country of residence.

Source: Calculated from Statistics New Zealand data.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Australia

China, People's Republic of

Japan

Korea, Republic of

Germany

United Kingdom

Canada

United States of America

Other

12

3 Estimating the Effects of Liberalisation

In this section the effects on some interesting variables of the progressive liberalisation

of ASAs for each of the four case studies are investigated using econometric analysis.

We take a broad wellbeing (or total welfare) approach to the measurement of effects.

This includes effects on economic activity in New Zealand, for example due to changes

in inbound visitor numbers.

Our analysis also includes effects on New Zealand consumer welfare such as outbound

travel and changes in international airfares that are more aviation-specific than

aggregate economic activity measures such as GDP. Such outcomes reflect changes in

the wellbeing of New Zealanders and thus are relevant for development of international

air transport policy.

3.1 Theory

Before undertaking empirical analysis, it is important to establish a theoretical

connection between air services liberalisation and economic activity and welfare. In

general, liberalisation can be thought of as removing regulatory barriers to entry and

expansion on New Zealand international routes.

Historically, barriers to entry and expansion have been created by ASAs that limited the

ability of foreign carriers to operate New Zealand routes, for example by limiting access

to one nominated ‘flag’ carrier per country. Capacity restrictions and tariff approval

processes also limit the ability of airlines to compete on New Zealand routes. Similar

restrictions imposed by foreign countries have limited the ability of New Zealand

airlines to compete on routes to other countries. These barriers are quite apart from any

barriers created by the costs of operating any given route, or technological limitations.

Reduction of regulatory barriers to entry and expansion can be expected to stimulate

competition on New Zealand international air routes. Overall, we should observe entry

of new airlines and/or expansion of existing operators, and a move towards more equal

market shares of airlines serving New Zealand.

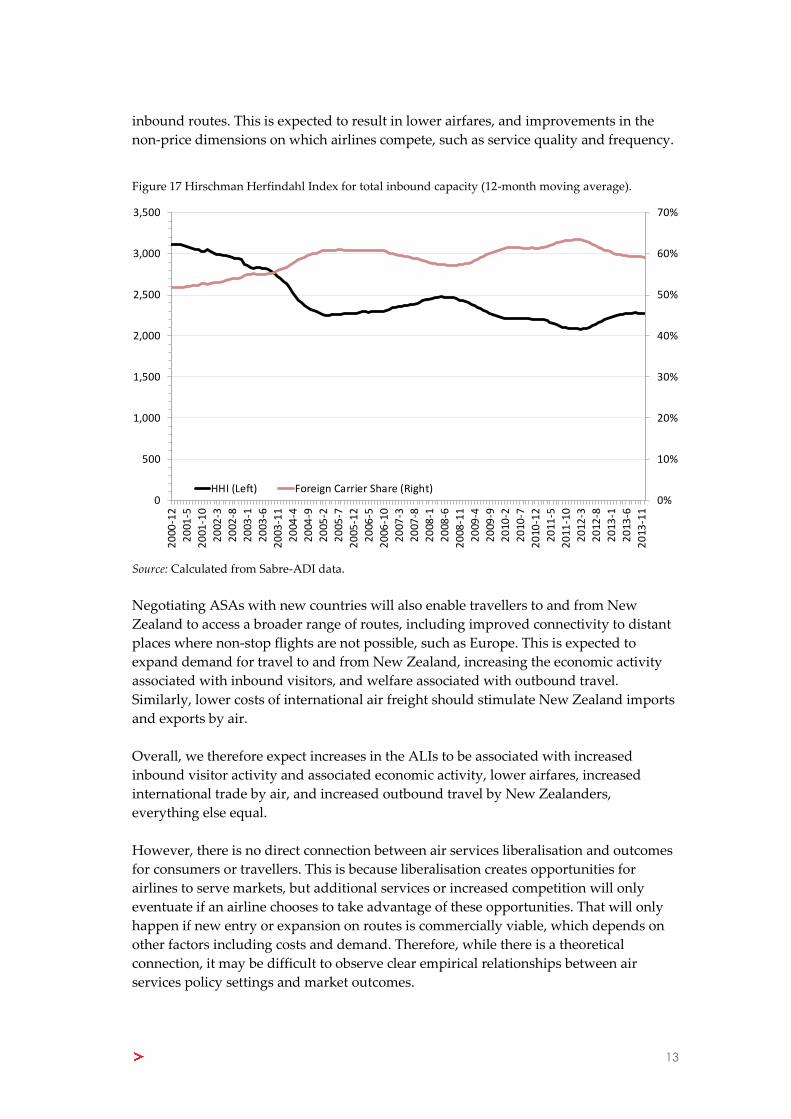

The Hirschman Herfindahl Index (HHI) is a commonly used measure of the diversity of

supply and intensity of competition in an industry. The HHI is calculated as the sum of

squared market shares, and reflects the number of suppliers as well as the distribution

of their market shares. Lower values of the HHI reflect a larger number of suppliers

and/or more evenly distributed market shares. For example, an industry with a single

supplier will have an HHI of 10,000. With two suppliers sharing the market equally, the

HHI will be 5,000. If one supplier had 90% market share and the other had 10%, the HHI

will be 8,200. If ten suppliers have equal market share, the HHI will be 1,000.

Figure 17 shows the HHI calculated on the basis of total inbound capacity to New

Zealand by airline. In general the HHI has been declining over time, while the share of

capacity supplied by foreign carriers has been increasing. This is consistent with the

entry of foreign carriers leading to an increase in overall competition on New Zealand

13

inbound routes. This is expected to result in lower airfares, and improvements in the

non-price dimensions on which airlines compete, such as service quality and frequency.

Figure 17 Hirschman Herfindahl Index for total inbound capacity (12-month moving average).

Source: Calculated from Sabre-ADI data.

Negotiating ASAs with new countries will also enable travellers to and from New

Zealand to access a broader range of routes, including improved connectivity to distant

places where non-stop flights are not possible, such as Europe. This is expected to

expand demand for travel to and from New Zealand, increasing the economic activity

associated with inbound visitors, and welfare associated with outbound travel.

Similarly, lower costs of international air freight should stimulate New Zealand imports

and exports by air.

Overall, we therefore expect increases in the ALIs to be associated with increased

inbound visitor activity and associated economic activity, lower airfares, increased

international trade by air, and increased outbound travel by New Zealanders,

everything else equal.

However, there is no direct connection between air services liberalisation and outcomes

for consumers or travellers. This is because liberalisation creates opportunities for

airlines to serve markets, but additional services or increased competition will only

eventuate if an airline chooses to take advantage of these opportunities. That will only

happen if new entry or expansion on routes is commercially viable, which depends on

other factors including costs and demand. Therefore, while there is a theoretical

connection, it may be difficult to observe clear empirical relationships between air

services policy settings and market outcomes.

0%

10%

20%

30%

40%

50%

60%

70%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

20

00-1

2

20

01-5

20

01-1

0

20

02-3

20

02-8

20

03-1

20

03-6

20

03-1

1

20

04-4

20

04-9

20

05-2

20

05-7

20

05-1

2

20

06-5

20

06-1

0

20

07-3

20

07-8

20

08-1

20

08-6

20

08-1

1

20

09-4

20

09-9

20

10-2

20

10-7

20

10-1

2

20

11-5

20

11-1

0

20

12-3

20

12-8

20

13-1

20

13-6

20

13-1

1

HHI (Left) Foreign Carrier Share (Right)

14

3.2 Empirical Methodology

Our empirical analysis is based on testing the relationships between ALIs and certain

variables of interest, for each of the four case studies. The following variables were

selected to measure the effects of liberalisation, based on the theoretical relationships

described above, and data availability:

The number of short-term international visitor arrivals to New Zealand, in total

and from various countries of origin expected to be affected by liberalisation in

each of the four case studies.

Total short-term departures by New Zealand residents.

The real value of New Zealand exports and imports by air.

Total New Zealand real GDP.

Real prices for international outbound travel from New Zealand.

For international visitor arrivals, we model arrivals from various countries and regions

of origin separately, in order to understand the effects of liberalisation on different types

of visitor to New Zealand. However, for New Zealand resident departures we model

only total departures, rather than departures to specific destinations. This is because

liberalisation may have caused some substitution between destinations by outbound

New Zealand travellers. If individual destinations were modelled, substitution between

destinations may appear to be as a net gain, when in fact it is offset by a reduction in

travel to another destination.8

In each case, we estimate time series models relating the variable of interest to the

relevant ALIs from the case studies.9 A key issue in this analysis is controlling for other

factors that have changed at the same time and that are also expected to affect the

variables of interest. We handle this by including other relevant variables in each

regression model, where possible and appropriate. Thus the results for the ALI variable

can be interpreted as the relationship between the ALI and the variable of interest,

holding constant the other variables included in the regression model.

Specifically, for each variable of interest, , we estimated a regression model of the form:

where is a vector of the relevant ALIs, is a vector of other controlling variables,

is a random error, and , and are parameters to be estimated.

8 Such substitution would also reflect a welfare gain if outbound travellers are choosing to travel to a

more favoured destination. However the extent of substitution and associated welfare benefits are

difficult to measure, and hence we focus on aggregate outbound travel.

9 Not all of the four ALIs were determined to be relevant for every variable of interest; we discuss this

further below.

15

In addition to the above ‘structural’ time series models, we also tested the effects of

liberalisation against simple linear time trends for each variable of interest.10 These

models have the basic form:

where is the slope of the time trend. In some cases where clear breaks in the trend of

the variable of interest were apparent, we used a piecewise trend model, with

potentially different intercept and/or slope before and after the break.

When working with time-series data it is important to test for the presence of

autocorrelation in the estimated model and correct for it if necessary. Autocorrelation

refers to a situation where the estimated residuals of the model ( ) are correlated over

time. This occurs if random shocks that disturb the estimated regression relationship

take time to dissipate, and is a common feature of time series models. We tested for

autocorrelation in each estimated model using statistical tests including the Durbin-

Watson statistic and the estimated autocorrelation function of the residuals.

If autocorrelation is found to be present, it is necessary to correct for this in order to

produce valid estimates from the regression model. We have done this by modifying the

error term of the model to model the autocorrelation if present. This is known as an

autoregressive (AR) model, where the error is modelled as a function of one or more

of its own past values. For example, an AR(1) model takes the form:

where is a parameter to be estimated along with the other parameters of the model

and is a random error. In some cases it was necessary to include a second lag of .

This is referred to as an AR(2) model but is conceptually similar to the AR(1) model.

Following the inclusion of autoregressive parameters as appropriate, we applied

diagnostic tests to the estimated models to check the validity of the results. These

included testing the stationarity of the regression residuals,11 testing the joint

significance of the estimated coefficients with F-tests, and measures of goodness of fit

with the data.

10 In a small number of cases, only trend variables were used, as suitable controlling variables for the

structural model are not available.

11 Regression residuals are ‘stationary’ if their mean and variance are constant over time. This is

necessary to generate valid estimates from time series regression models, and was checked by

conducting Augmented Dickey Fuller tests on the regression residuals.

16

3.3 Data

The following annual time series were obtained for use as dependent variables in the

regression analysis:

International visitor arrivals to New Zealand: In total, and from various

countries and regions of origin, published by Statistics New Zealand.

Total international short-term departures by New Zealand residents: To all

destinations, published by Statistics New Zealand.

Total real value of New Zealand imports and exports by air: Between New

Zealand and all countries. Imports are valued on a cost plus insurance plus

freight (CIF) basis, while exports are valued on a free-on-board (FOB) basis,

published by Statistics New Zealand. These were converted to real values using

Statistics New Zealand GDP deflators for exports and imports.

Total New Zealand real GDP: In constant prices, published by Statistics New

Zealand.

New Zealand real international outbound travel price index: Calculated from

Statistics New Zealand’s nominal outbound travel price index, deflated by the

Consumer Price Index to estimate the real price of travel.

The following annual time series were used as control variables in the structural models:

Foreign real GDP: In the international visitor arrivals models, GDP of the

relevant country of origin, obtained from the OECD and national statistics

agencies where OECD data was unavailable.

Exchange rates: Relative to the New Zealand dollar, published by the PACIFIC

Exchange Rate Service.

Oil prices: Real benchmark crude oil prices in US dollars, from the US Energy

Information Administration.

New Zealand real GDP: Used as a control variable in the outbound travel

model and imports models, obtained from Statistics New Zealand.

Terms of trade: The ratio of New Zealand export prices to import prices,

published by Statistics New Zealand.

Jet fuel prices: Real prices, converted to New Zealand dollars at prevailing

exchange rates, calculated from data from the US Energy Information

Administration.

Not all of these variables were used as control variables in all regression models. In

some cases, control variables that were found to be statistically insignificant were

omitted from the models. The details of each model are reported in the Appendix.

17

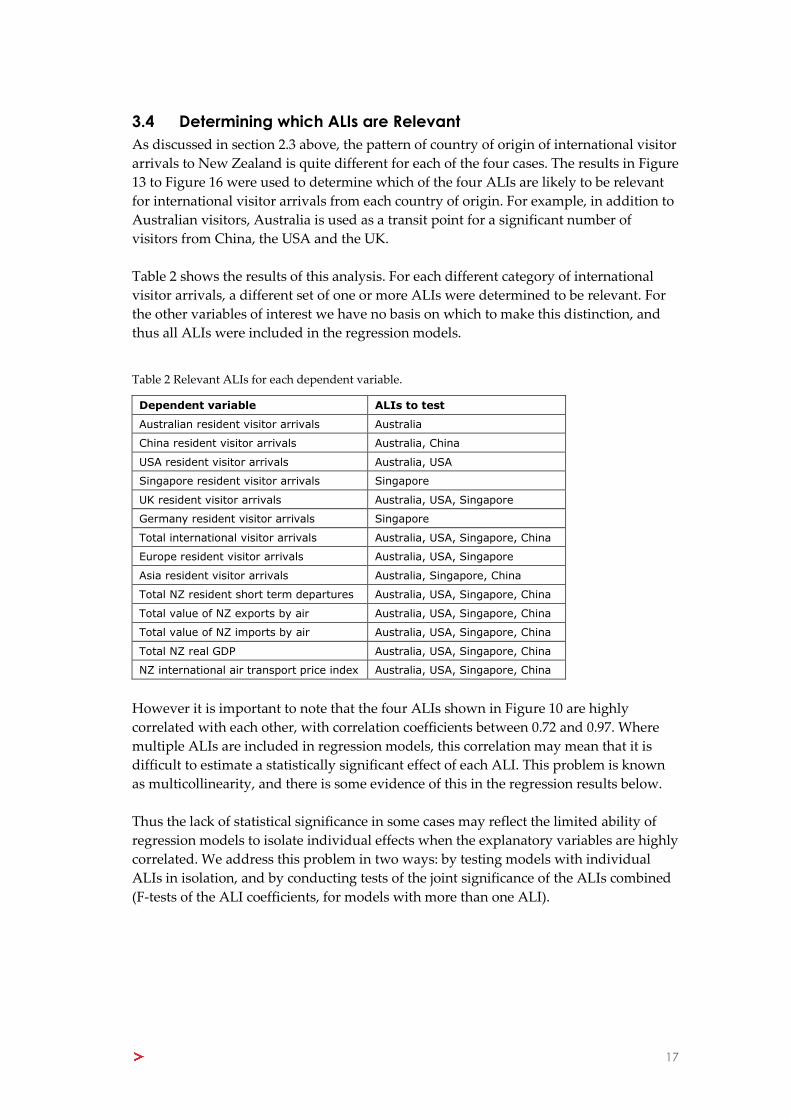

3.4 Determining which ALIs are Relevant

As discussed in section 2.3 above, the pattern of country of origin of international visitor

arrivals to New Zealand is quite different for each of the four cases. The results in Figure

13 to Figure 16 were used to determine which of the four ALIs are likely to be relevant

for international visitor arrivals from each country of origin. For example, in addition to

Australian visitors, Australia is used as a transit point for a significant number of

visitors from China, the USA and the UK.

Table 2 shows the results of this analysis. For each different category of international

visitor arrivals, a different set of one or more ALIs were determined to be relevant. For

the other variables of interest we have no basis on which to make this distinction, and

thus all ALIs were included in the regression models.

Table 2 Relevant ALIs for each dependent variable.

Dependent variable ALIs to test

Australian resident visitor arrivals Australia

China resident visitor arrivals Australia, China

USA resident visitor arrivals Australia, USA

Singapore resident visitor arrivals Singapore

UK resident visitor arrivals Australia, USA, Singapore

Germany resident visitor arrivals Singapore

Total international visitor arrivals Australia, USA, Singapore, China

Europe resident visitor arrivals Australia, USA, Singapore

Asia resident visitor arrivals Australia, Singapore, China

Total NZ resident short term departures Australia, USA, Singapore, China

Total value of NZ exports by air Australia, USA, Singapore, China

Total value of NZ imports by air Australia, USA, Singapore, China

Total NZ real GDP Australia, USA, Singapore, China

NZ international air transport price index Australia, USA, Singapore, China

However it is important to note that the four ALIs shown in Figure 10 are highly

correlated with each other, with correlation coefficients between 0.72 and 0.97. Where

multiple ALIs are included in regression models, this correlation may mean that it is

difficult to estimate a statistically significant effect of each ALI. This problem is known

as multicollinearity, and there is some evidence of this in the regression results below.

Thus the lack of statistical significance in some cases may reflect the limited ability of

regression models to isolate individual effects when the explanatory variables are highly

correlated. We address this problem in two ways: by testing models with individual

ALIs in isolation, and by conducting tests of the joint significance of the ALIs combined

(F-tests of the ALI coefficients, for models with more than one ALI).

18

3.5 Regression Results

Table 3 summarises the results from the regression models, in terms of the statistical

significance of each of the ALI variables for each variable of interest. The full regression

results are presented in the Appendix.

The results in Table 3 reflect the results of statistical hypothesis testing on the estimated

coefficients of the regression models. In each case the hypothesis tested is that the

estimated coefficient is equal to zero, ie there is no relationship between the ALI given

by the column of Table 3 and the variable of interest given by the row of the table. A

finding of “weak” or “strong” reflects the degree of confidence that this hypothesis of

no relationship is false, ie that there may be a relationship between the ALI and the

variable of interest. In particular, the results in Table 3 reflect the following:

No evidence: No statistically significant relationship was found between the ALI

and the variable of interest.

Weak evidence: Some evidence was found of a relationship between the ALI

and the variable of interest, but there is a 5 - 10% possibility that the observed

relationship is by chance rather than real.

Strong evidence: Evidence of a relationship between the ALI and the variable of

interest was found, and the possibility that the relationship is by chance is less

than 5%.

Wrong sign: A statistically significant relationship was found, but the estimated

direction is the opposite to what was expected, eg increased liberalisation was

associated with a reduction in visitor arrivals. This likely arises from the

estimated model not fitting the data well.

n.a.: Variable was not tested in the model.

19

Table 3 Summary of results from the regression models.

Australia ALI US ALI China ALI Singapore ALI Joint ALIs Control variables

International visitor arrivals

Structural models

Australia No evidence n.a. n.a. n.a. n.a. Foreign GDP, exchange rate

US No evidence No evidence n.a. n.a. No evidence Foreign GDP, exchange rate

UK No evidence No evidence n.a. No evidence No evidence Foreign GDP, exchange rate

China Weak evidence n.a. No evidence Strong evidence Strong evidence Foreign GDP, exchange rate

Singapore n.a. n.a. n.a. No evidence n.a. Foreign GDP, exchange rate

Germany n.a. n.a. n.a. No evidence n.a. Foreign GDP, exchange rate

Trend models

Australia No evidence n.a. n.a. n.a. n.a. Linear time trend

US No evidence No evidence n.a. n.a. No evidence Linear time trend

UK No evidence Strong evidence n.a. No evidence No evidence Linear time trend with break

China No evidence n.a. No evidence Weak evidence Strong evidence Linear time trend

Singapore n.a. n.a. n.a. No evidence n.a. Linear time trend

Germany n.a. n.a. n.a. Wrong sign n.a. Linear time trend with break

Asia No evidence n.a. No evidence No evidence No evidence Linear time trend with break

Europe No evidence Weak evidence n.a. Wrong sign Weak evidence Linear time trend with break

All origins No evidence Strong evidence No evidence Strong evidence Strong evidence Linear time trend

20

Australia ALI US ALI China ALI Singapore ALI Joint ALIs Control variables

NZ resident short term departures

Structural models Strong evidence Wrong sign Strong evidence No evidence Strong evidence NZ GDP, fuel price, exchange rate

Trend models Weak evidence No evidence Strong evidence Strong evidence Strong evidence Linear time trend

Value of international trade by air

Structural models

Exports No evidence No evidence No evidence No evidence No evidence Foreign GDP, oil price, terms of trade

Imports No evidence No evidence No evidence Wrong sign No evidence NZ GDP, oil price, terms of trade

Trend models

Exports Strong evidence No evidence No evidence No evidence No evidence Linear time trend

Imports Weak evidence No evidence Weak evidence No evidence No evidence Linear time trend

NZ real GDP

Trend models No evidence Strong evidence No evidence No evidence No evidence Linear time trend

NZ real international outbound travel price index

Structural models No evidence No evidence Strong evidence No evidence Strong evidence NZ GDP, oil price

Trend models No evidence No evidence Strong evidence No evidence Strong evidence Linear time trend

21

3.6 Interpretation of Results

The regression analysis described above tested the relationships between the ALIs and

the variables of interest in different ways using different models. In our view, for the

purposes of policy evaluation and development, it is most appropriate to interpret the

overall patterns and features of the results as a whole, rather than focussing on

individual numerical results from the regressions.

In the following we give our views on the estimated effects of New Zealand’s

liberalisation of air services that appear to be relatively robust.

International visitor arrivals

The estimated effects of liberalisation on international visitor arrivals are mixed. In each

of the four case studies, there is no significant relationship between the ALI and the

relevant point-to-point market. For example, visitor arrivals of Singapore residents do

not appear to depend on the Singapore ALI.

Rather, effects show up more frequently for indirect travel. Singapore in particular

appears to be important for travel from a variety of origins, and the Singapore ALI is

positively related to arrivals from China and all origins in total. Similarly there is some

evidence of a relationship between the US ALI and arrivals from the UK and Europe.

These observations may reflect the changes that have taken place during the period of

analysis used for this study. Prior to the mid-1990s, New Zealand did have ASAs and

air services with a number of countries, but competition was generally limited to

national carriers and capacity was constrained. Liberalisation since the mid-1990s has

permitted greater services by fifth-freedom carriers, stimulating indirect travel. Given

New Zealand’s relative geographic isolation from many of its inbound tourism markets

and outbound travel destinations, stimulating indirect travel via air services

liberalisation appears to have been relatively effective.

Short-term departures by New Zealand residents

The evidence for a link between liberalisation and short-term departures by New

Zealand residents is relatively strong. Significant positive relationships were observed

for all of the ALIs except the United States. This suggests that greater competition and

better access to international destinations has stimulated outbound travel by New

Zealanders.

Between 1998 and 2012, annual outbound trips by New Zealanders almost doubled,

from 1.2 million to 2.2 million. The majority of this increase has come from greater

holiday and visiting friends and relatives travel, although outbound travel for all

purposes has increased during this timeframe. Leisure travel is generally more price

sensitive than business travel, leading to a potentially larger response of leisure travel to

increased competition on international routes.

As noted above, additional outbound travel by New Zealanders may not stimulate

economic activity in New Zealand (particularly outbound leisure travel), but the fact

that people have chosen to travel more reflects the fact that it is something they value.

22

Thus greater outbound travel can be assumed to represent welfare benefits to New

Zealanders, and is a positive effect of liberalisation.

New Zealand outbound travel price index

Real prices for international outbound travel from New Zealand have been falling

almost continuously since the mid-1980s, in spite of generally increasing aviation fuel

prices (Figure 8 above). This is very likely due to increased competition among airlines,

as well as technological improvements that have reduced per-unit operating costs.

There is evidence of a relationship between liberalisation of air services between New

Zealand and China, and falling real outbound travel prices. Services between New

Zealand and China are relatively recent, facilitated by new ASAs, while China has

rapidly become increasingly important for both New Zealand inbound and outbound

travel. This suggests that opening access to new markets for which there is substantial

travel demand is associated with overall downwards pressure on travel prices.

Imports and Exports

There is no clear evidence of a relationship between the ALIs and New Zealand’s

international trade, except for the Australian ALI, which appears to be positively related

to the value of both imports and exports. This is consistent with Australia being New

Zealand’s largest trading partner, and the low cost of air freight between New Zealand

and Australia, compared to elsewhere.

Overall, air freight is a relatively small fraction of New Zealand’s total international

trade, and very few dedicated air freight services operate to New Zealand. Instead most

freight is carried on passenger aircraft, and to the extent that liberalisation stimulates

competition in passenger services, it should also stimulate competition in air freight,

leading to lower freight prices and increased volumes of international trade. However

this is more likely to be a secondary benefit of liberalisation, relative to benefits from

competition in passenger services.

New Zealand real GDP

The regression models indicate generally no evidence of a relationship between

liberalisation and New Zealand’s real GDP. This may be due to the fact that aggregate

economic activity is affected by a large number of trends, of which air services

liberalisation is comparatively minor. There is some evidence of a relationship between

the US ALI and real GDP, although this result should be interpreted cautiously as the

GDP models only control for the trend in GDP, due to the complexity of developing a

model containing exogenous drivers of GDP.

23

3.7 Limitations of the Analysis

The econometric analysis above has limitations that are primarily driven by the

availability of data and the difficulty of isolating effects of general policy settings such

as air services liberalisation. The following limitations should be borne in mind when

interpreting the results:

As mentioned above, high correlation between the individual ALIs means that

models with multiple ALIs may not find a statistically significant effect when

one exists.

In the trend models, the trend variable itself may capture some of the effects of

liberalisation if growth is partially created by the increased capacity facilitated

by air services liberalisation.

The effects of air services liberalisation may occur with a considerable time lag,

as effects will only be observed after airlines choose to offer new services. The

timeframe for this study limits the opportunity to estimate lag effects.

As noted above, analysis of outbound travel by New Zealanders is limited to the

total number of short-term departures and welfare-enhancing substitutions

between destinations have not been analysed. The welfare effects of air services

liberalisation on New Zealanders due to increased opportunities for outbound

travel are therefore probably underestimated.

As noted above, the analysis of effects on GDP is limited by the number of other

factors that will have affected GDP over time. It is difficult to isolate the effects

of air services policy from the great number of other factors that affect aggregate

economic activity.

At the same time as liberalising air transport markets, New Zealand has been

liberalising its trade agreements with other countries. Increased international

trade due to trade liberalisation may also stimulate demand for air travel. The

regression models do not directly estimate or control for this interaction.

24

4 Analysis of Foreign Airline Capacity

As noted in the introduction, foreign airlines have provided much of the increase in

capacity on international routes to and from New Zealand since 2000. This section

reviews features and trends of the capacity provided by foreign airlines between 2000

and 2013, with the objective of determining whether there is any evidence of risk

associated with reliance on foreign carriers.

Two features of foreign capacity are analysed – volatility and route tenure. Volatility

refers to fluctuations of capacity around its average or long-term trend. Route tenure

refers to the length of time that a route is operated by an airline. We compare foreign

airline capacity against capacity provided by Air New Zealand in terms of volatility and

route tenure.

The analysis in this section is based on monthly flight schedule data obtained from

Sabre-ADI for the period from January 2000 to December 2013.12 All figures refer to

capacity on inbound international routes only, however outbound capacity will be very

similar. For routes with more than one segment (eg Dubai-Sydney-Auckland), capacity

has been calculated for the segment arriving in New Zealand only (eg Sydney-

Auckland).13 The analysis in this section thus refers to the total number of seats arriving

in New Zealand each month.

The analysis also combines capacities for Qantas (QF) and Jetstar (JQ and 3K), Air New

Zealand (NZ) and Freedom Air (SJ), and Virgin Australia (VA) and Pacific Blue (DJ).14

4.1 General Trends

Figure 18 demonstrates the significance of the change in international capacity to New

Zealand by showing the cumulative change in total inbound capacity relative to the

level in 2000. Air New Zealand’s total annual capacity has increased by around 450,000

seats, while annual capacity provided by foreign carriers has increased by around

1,500,000 seats. Much of this growth occurred between 2003 and 2005.

Figure 9 and Figure 18 also show that there appear to be medium-term cycles of

capacity around the long-term trend. For example following the expansion between

2003-05, capacity declined during 2006 and 2007. A similar pattern is observed following

other periods of capacity expansion.

12 Sabre-ADI data is only available back to 2000, hence the time period for this analysis is shorter than

in the previous section.

13 It is not possible to know how many seats on other legs (eg Dubai-Sydney) were available for New

Zealand-bound passengers, and in any case all such passengers would eventually have to be on a flight

arriving in New Zealand.

14 This is because although some airlines have more than one brand (eg Qantas and Jetstar), common

ownership means there is a strong incentive for coordination of capacities across these brands. In

addition, combining capacities in this way is necessary for comparing with other airlines that operate a

single brand but strongly differentiate services within that brand (eg Air New Zealand’s current Seat,

Seat+Bag, Works products).

25

Figure 18 Cumulative change in total New Zealand inbound capacity relative to 2000.

Source: Calculated from Sabre-ADI data.

Figure 19 shows entry and exit of foreign airlines on New Zealand routes between 2000

and 2013. There is a stable set that have served the market for the entire period (and

significantly longer in some cases), while some other airlines entered only briefly.

Figure 19 Entry and exit of foreign carriers on any New Zealand inbound route.

Source: Calculated from Sabre-ADI data.

-250,000

0

250,000

500,000

750,000

1,000,000

1,250,000

1,500,000

1,750,000

2,000,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Seat

s p

er

ann

um

Air NZ Foreign

20

00-1

20

00-7

20

01-1

20

01-7

20

02-1

20

02-7

20

03-1

20

03-7

20

04-1

20

04-7

20

05-1

20

05-7

20

06-1

20

06-7

20

07-1

20

07-7

20

08-1

20

08-7

20

09-1

20

09-7

20

10-1

20

10-7

20

11-1

20

11-7

20

12-1

20

12-7

20

13-1

20

13-7

QF + JQSQTG

MHKECXFJSBNFTNARLAEK

DJ + VABI

GABRPHCI

UACZ

WROZYED7HACA

26

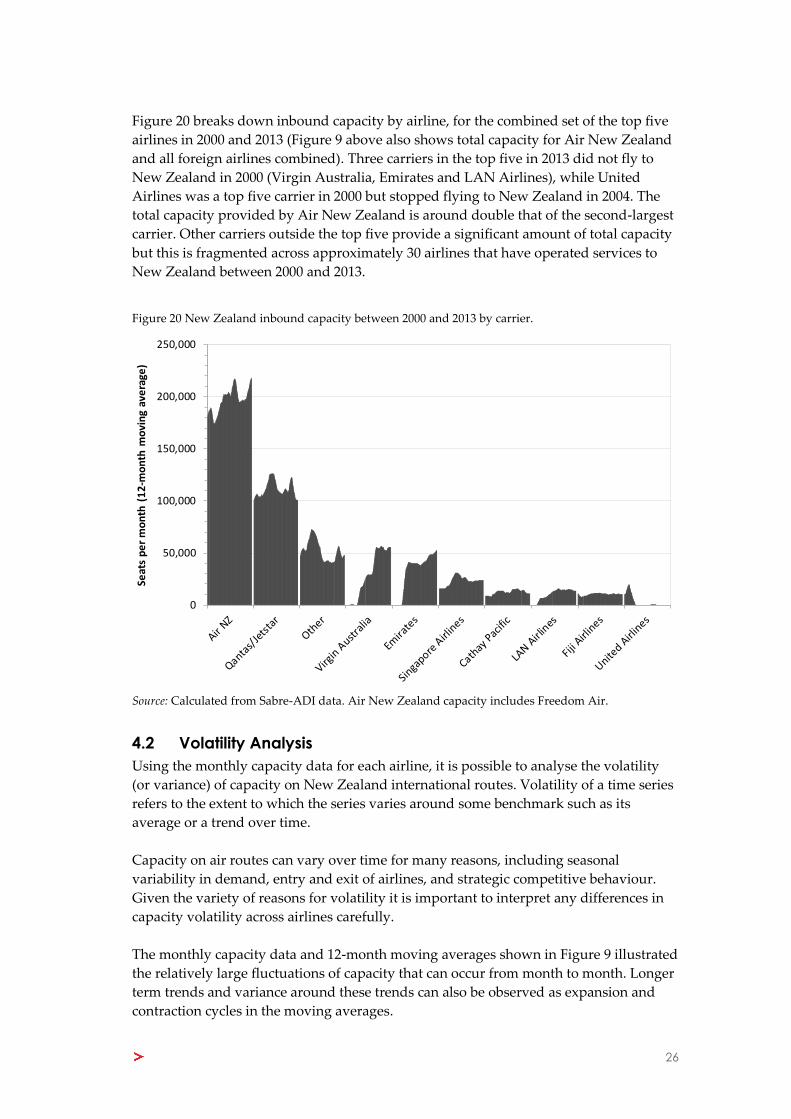

Figure 20 breaks down inbound capacity by airline, for the combined set of the top five

airlines in 2000 and 2013 (Figure 9 above also shows total capacity for Air New Zealand

and all foreign airlines combined). Three carriers in the top five in 2013 did not fly to

New Zealand in 2000 (Virgin Australia, Emirates and LAN Airlines), while United

Airlines was a top five carrier in 2000 but stopped flying to New Zealand in 2004. The

total capacity provided by Air New Zealand is around double that of the second-largest

carrier. Other carriers outside the top five provide a significant amount of total capacity

but this is fragmented across approximately 30 airlines that have operated services to

New Zealand between 2000 and 2013.

Figure 20 New Zealand inbound capacity between 2000 and 2013 by carrier.

Source: Calculated from Sabre-ADI data. Air New Zealand capacity includes Freedom Air.

4.2 Volatility Analysis

Using the monthly capacity data for each airline, it is possible to analyse the volatility

(or variance) of capacity on New Zealand international routes. Volatility of a time series

refers to the extent to which the series varies around some benchmark such as its

average or a trend over time.

Capacity on air routes can vary over time for many reasons, including seasonal

variability in demand, entry and exit of airlines, and strategic competitive behaviour.

Given the variety of reasons for volatility it is important to interpret any differences in

capacity volatility across airlines carefully.

The monthly capacity data and 12-month moving averages shown in Figure 9 illustrated

the relatively large fluctuations of capacity that can occur from month to month. Longer

term trends and variance around these trends can also be observed as expansion and

contraction cycles in the moving averages.

0

50,000

100,000

150,000

200,000

250,000

Seat

s p

er

mo

nth

(1

2-m

on

th m

ovi

ng

ave

rage

)

27

Much of the short-term fluctuations are due to seasonal changes in demand. Overall, we

estimate that 54% of the fluctuations in Air New Zealand’s monthly capacity around the

12-month moving average can be explained by seasonal factors. Similarly, 41% of the

fluctuations in total foreign carrier capacity around the 12-monthly moving average are

estimated to be seasonal.15

Figure 9 also showed that capacity provided by foreign airlines, and to a lesser extent

Air New Zealand, is trending upwards over time, while total capacity provided by

foreign airlines is greater than that provided by Air New Zealand. This presents two

problems for comparison of the variance of Air New Zealand’s capacity relative to the

total for foreign airlines:

1. A simple calculation of variance (or standard deviation) is based on an

assumption of variation around a constant mean level, but capacities are

generally trending upwards over time.

2. Time series with higher levels also naturally tend to have higher variance, and

this should be taken into account when comparing volatility across airlines.

To resolve these problems and facilitate meaningful comparisons, we have compared

capacity trends on the basis of normalised deviations from a given average or trend. In

particular our analysis is based on a sequence of normalised deviations calculated as:

Where is the normalised deviation at time , is the capacity observation and is

the benchmark against which deviations are being compared.

For example, if we were to benchmark against a constant average capacity then we

would calculate

Thus in this case reflects variations of capacity around its overall average level,

relative to the average.

Volatility of capacity can be analysed by looking at changes in over time and

calculation of the variance or standard deviation of . In the simple case where the

benchmark is the constant average capacity then the standard deviation of is the same

as the coefficient of variation of capacity, ie the standard deviation of capacity divided

by its average.

15 These percentages are the R-squared values obtained from regressing monthly deviations from the