Economic and financial trends - Danske...

39

www.danskeresearch.com Investment Research 25 June 2015 Nordic Outlook Economic and financial trends Denmark: Denmark’s recovery on a firm footing - We are at the start of a new upswing Sweden: An ambivalent and reactive Riksbank set to miss its target - We expect solid growth but Riksbank will be forced to act again Norway: The end is in sight - Oil investment now looks set to flatten out next year Finland: Signs of a slow recovery - New government struggles with both cyclical and structural problems

Transcript of Economic and financial trends - Danske...

www.danskeresearch.com

Investment Research

25 June 2015

Nordic OutlookEconomic and financial trends

� Denmark: Denmark’s recovery on a firm footing - We are at the start of a new upswing

� Sweden: An ambivalent and reactive Riksbank set to miss its target - We expect solid growth but Riksbank will be forced to act again

� Norway: The end is in sight - Oil investment now looks set to flatten out next year

� Finland: Signs of a slow recovery - New government struggles with both cyclical and structural problems

2 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Analysts

Editorial deadline 24 June 2015 Investment Research

Editor-in-Chief:

Steen Bocian

Chief Economist

+ 45 45 12 85 31

Macro economics:

Las Olsen Denmark +45 45 12 85 36 [email protected]

Mikael Olai Milhøj Denmark +45 45 12 76 07 [email protected]

Mark Thybo Naur Denmark +45 45 12 85 26 [email protected]

Roger Josefsson Sweden +46 (0)8-568 805 58 [email protected]

Frank Jullum Norway +47 85 40 65 40 [email protected]

Pasi Petteri Kuoppamäki Finland +358 (0)10 546 7715 [email protected]

Henna Mikkonen Finland +358 (0) 10 546 6619 [email protected]

This publication can be viewed at www.danskebank.com/danskeresearch

Statistical sources: Datastream, Macrobond Financial, OECD, IMF, National Institute of Social and Economic Research,

Statistics Denmark and other national statistical institutes as well as proprietary calculations.

Important disclosures and certifications are contained from page 38 of this report.

3 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Contents

Nordic Outlook At a glance 4

Denmark Denmark�s recovery on a firm footing 7

Forecast at a glance 13

Sweden An ambivalent and reactive Riksbank set to miss its target 14

Forecast at a glance 19

Norway The end is in sight 20

Forecast at a glance 26

Finland Signs of a slow recovery 27

Forecast at a glance 33

Global overview Reflation theme building 34

Economic forecast 36

Financial forecast 37

The Nordic Outlook is a quarterly publication that presents Danske Bank�s view on the economic outlook for

the Nordic countries. The semi-annual publication The Big Picture sets out our global economic outlook.

4 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Nordic Outlook At a glance A strong region The Nordic region still looks to be one of the strongest and most stable economic regions globally when we look at the prospects for the forthcoming years. We expect GDP growth in Sweden, Norway and Denmark to be around the level of 1.5-2.0% in 2015 and even above 2% in 2016. Only Finland is still cyclically weak and even though growth looks set to pick up the economy still looks very fragile. Growth in the Nordic region is likely to come from an expected continued strengthening of the overall European economy, but domestic challenges also seem limited, leaving room for growth in domestic demand.

We have only made quite small revisions to our economic forecasts for the Nordic countries compared to our latest edition of Nordic Outlook from March. The most significant change is that GDP growth in Norway seems to be more negatively affected by the lower oil price than what we expected. We now forecast growth in Norway of 1.5% in 2015, but seen in the light of the very significant decline in oil prices the Norwegian economy still looks strong as it benefits from strong consumer spending and the weaker NOK.

Impact from a Grexit not devastating The economic and financial situation in Greece is attracting attention as the risk of Greece leaving the eurozone has increased in recent months. Our base case is that the politicians in Europe will in the end strike a deal ensuring that Greece stays in the eurozone, but as the game of chicken between Greece and the rest of Europe intensifies we cannot rule out the risk of something going wrong. The Nordic region will not be significantly affected by a Grexit if that were to happen, in our view. Its trade with Greece is limited and the financial exposure is close to zero. If Greece does leave the euro we would expect to see a strengthening of NOK and SEK but less than in 2011/2012. DKK is pegged to the euro, thus the appreciation pressure we saw in January and February this year will probably re-emerge, but the peg is indisputable and the central bank would likely react accordingly. We expect the first line of defence to be FX intervention and that interest rates would only be lowered in an extreme case, which we do not expect. We expect the financial and economic turmoil following a Grexit to be limited as we expect a strong political response and that the ECB would do whatever it takes to stabilise the markets through additional QE.

Even though we expect the financial and economic impact of a Grexit to be limited in the Nordic region, it is important to stress that there is not a lot of experience to draw upon when it comes to currency areas splitting up, thus there is a risk of a more substantial economic and financial effect in Europe than what we expect. If European growth is more significantly affected, then Denmark and Finland will be the most vulnerable as the two economies are in a more fragile economic situation than Sweden and Norway. Also Finland and Denmark’s business cycles are more in sync with the rest of Europe than Sweden and Norway. That being said, a more significant strengthening of SEK and NOK if the European crisis gets worse than expected could pose a significant macroeconomic challenge to the central banks in Norway and Sweden. The impact on inflation would argue for lower interest rates giving an increased risk of unbalanced growth led by overheating housing markets.

Nordic GDP growth still looking strong

Source: National statistics offices, Danske Bank Markets

Low inflation � except in Norway

Source: National statistics offices, Danske Bank Markets

Insignificant exports to Greece...

Source: National statistics offices

...as are imports

Source: National statistics offices

5 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Non-standard Swedish monetary policy increases the risk of bubbles

Monetary policy is extreme in all western countries. It is also extreme in the

Nordic region where central bank rates are negative in three out of four

countries. Only Norway has a positive interest rate, but it is as low as 1%

despite the fact that Norway is running very close to full capacity in the

economy.

We expect additional monetary easing in Sweden only. In Norway and

Finland we expect interest rates to be left unchanged, and we do not expect

additional QE in Europe or Sweden. In Denmark, monetary policy might be

tightened slightly as the appreciation pressure has fallen in recent months.

When the financial uncertainty linked to Greece levels off we expect the

Danish central bank to be able to start normalising Danish rates slowly by

increasing Danish CD rates by 25 bp before yearend, leaving the interest rate

at minus 0.5% instead of the current minus 0.75%.

We expect Sweden to ease monetary policy further by lowering the interest

rate an additional 10 bp to minus 0.35% by the end of the year. Our

expectation of a lower Swedish rate is a consequence of the low inflation, and

as we do not expect inflation to increase as quickly as the Riksbank foresees,

thus we expect the Riksbank to react to ensure that inflation expectations are

anchored.

The very low interest rates are leading to an increased risk of unbalanced

growth and bubbles building up. We have long been concerned about the

Swedish housing market, and the continued sharp price increases driven by

the low short-term interest rates is only adding to that concern. The

Norwegian market has also been increasing rapidly. The rapid price growth

has so far been justified by strong income growth, but as income growth is

decelerating due to the lower oil price, one has to be worried if the housing

market continues to rise – we see a clear risk of this given the historically low

interest rates.

Denmark has long struggled with a weak housing market although house and

apartment prices have actually been increasing in the larger cities since 2012.

Over the last year price increases of apartments in Copenhagen and Aarhus

have started to accelerate and if this continues there is a risk of regional

bubbles in our view. The acceleration in the price development in the

Copenhagen and Aarhus markets is closely linked to the historically low

Danish interest rates.

One way to address the risk of bubbles in the housing market is macro

prudential initiatives. But so far Sweden has not had success in implementing

tighter regulation to deal with the risks linked to the housing market and the

increasing household debt. Meanwhile Norway is yet to see the desired

results from the tightening measures that have been implemented. So far it

seems as though the effect on the household sector is quite limited. The

challenge to the authorities in Denmark is that the pressure is not nationwide

– there are no strong regional macro prudential tools.

Extremely low policy rates

Source: National central banks

Inflation expectations below target in Sweden

Source: Prospera

Houses prices to drop in Sweden

Source: National statistics offices

Hot housing markets in Sweden and Norway

Source: National statistics offices

6 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

New governments in Finland and Denmark

There has been a change in government in both Finland and Denmark. The

new Finnish government probably has a more challenging task ahead of it

than the Danish as it is being forced to tighten budgets quite substantially and

reform the retirement system. The Finnish government also aims at achieving

a “social contract” with the labour market unions in which annual working

hours would be extended, locally negotiated wage agreements encouraged

and income tax cut. The aim is to improve competitiveness by what could be

called an internal devaluation. The negotiations take place during the

summer, and could cause turmoil in the Finnish economy if a deal is not

struck.

On 18 June Danes also voted for a change in government. Although the

parliamentary situation may be challenging for the new Danish government

led by the liberal party, there is no reason to expect a major change in

economic policy as a consequence of the change in government. Denmark

has to run tight budgets to avoid large public deficits and this challenge does

not depend on the colour of the government.

It is not only in Finland that labour market negotiations will attract attention

in the forthcoming quarters. The next round of centralised wage negotiations

in Sweden starts at the beginning of 2016. As inflation expectations are

extremely low at the moment, the Riksbank is being forced to act to ensure

that inflation expectations are not too low compared to the Riksbank target

for inflation. This is the main reason for our forecast of a lower Riksbank rate

by the end of this year.

Government debt to exceed 60% limit in Finland

Source: Statistics Finland, Danske Bank

Limited room for more expansive fiscal policy in

Denmark

Source: Convergence Programme 2015

7 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

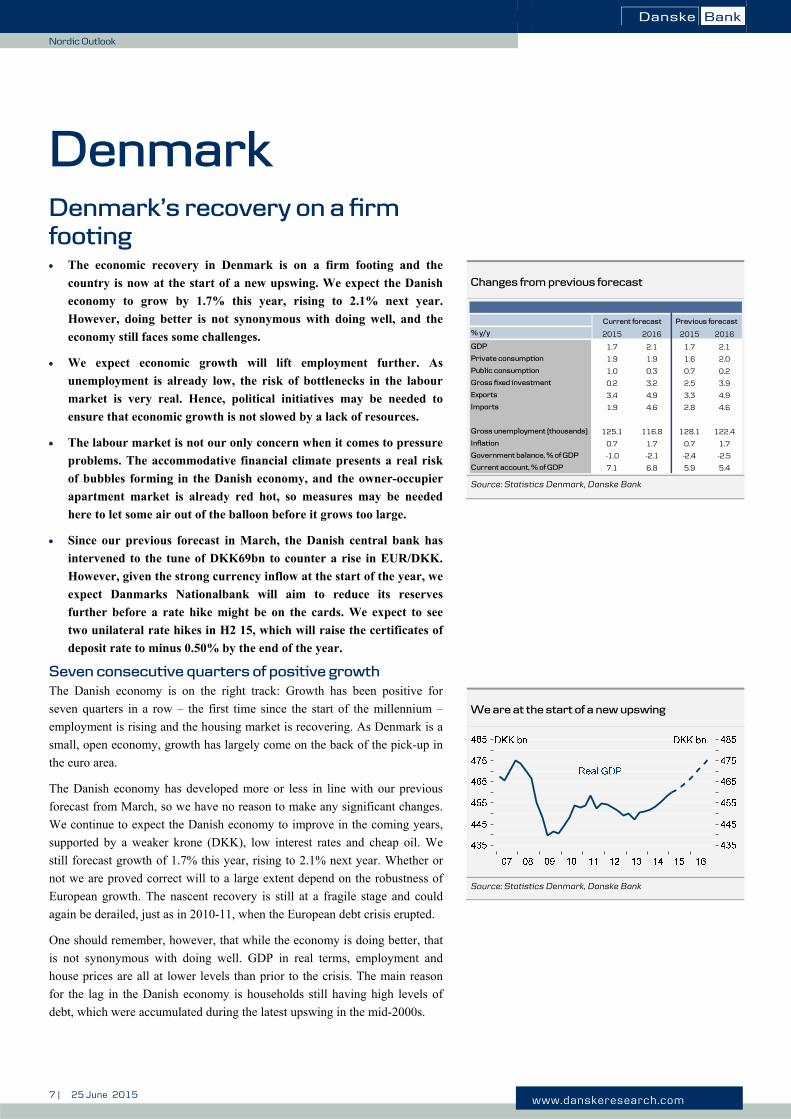

Denmark Denmark�s recovery on a firm footing The economic recovery in Denmark is on a firm footing and the

country is now at the start of a new upswing. We expect the Danish

economy to grow by 1.7% this year, rising to 2.1% next year.

However, doing better is not synonymous with doing well, and the

economy still faces some challenges.

We expect economic growth will lift employment further. As

unemployment is already low, the risk of bottlenecks in the labour

market is very real. Hence, political initiatives may be needed to

ensure that economic growth is not slowed by a lack of resources.

The labour market is not our only concern when it comes to pressure

problems. The accommodative financial climate presents a real risk

of bubbles forming in the Danish economy, and the owner-occupier

apartment market is already red hot, so measures may be needed

here to let some air out of the balloon before it grows too large.

Since our previous forecast in March, the Danish central bank has

intervened to the tune of DKK69bn to counter a rise in EUR/DKK.

However, given the strong currency inflow at the start of the year, we

expect Danmarks Nationalbank will aim to reduce its reserves

further before a rate hike might be on the cards. We expect to see

two unilateral rate hikes in H2 15, which will raise the certificates of

deposit rate to minus 0.50% by the end of the year.

Seven consecutive quarters of positive growth The Danish economy is on the right track: Growth has been positive for

seven quarters in a row – the first time since the start of the millennium –

employment is rising and the housing market is recovering. As Denmark is a

small, open economy, growth has largely come on the back of the pick-up in

the euro area.

The Danish economy has developed more or less in line with our previous

forecast from March, so we have no reason to make any significant changes.

We continue to expect the Danish economy to improve in the coming years,

supported by a weaker krone (DKK), low interest rates and cheap oil. We

still forecast growth of 1.7% this year, rising to 2.1% next year. Whether or

not we are proved correct will to a large extent depend on the robustness of

European growth. The nascent recovery is still at a fragile stage and could

again be derailed, just as in 2010-11, when the European debt crisis erupted.

One should remember, however, that while the economy is doing better, that

is not synonymous with doing well. GDP in real terms, employment and

house prices are all at lower levels than prior to the crisis. The main reason

for the lag in the Danish economy is households still having high levels of

debt, which were accumulated during the latest upswing in the mid-2000s.

Changes from previous forecast

Source: Statistics Denmark, Danske Bank

We are at the start of a new upswing

Source: Statistics Denmark, Danske Bank

% y/y 2015 2016 2015 2016

GDP 1.7 2.1 1.7 2.1

Private consumption 1.9 1.9 1.6 2.0

Public consumption 1.0 0.3 0.7 0.2

Gross fixed investment 0.2 3.2 2.5 3.9

Exports 3.4 4.9 3.3 4.9

Imports 1.9 4.6 2.8 4.6

Gross unemployment (thousands) 125.1 116.8 128.1 122.4

Inflation 0.7 1.7 0.7 1.7

Government balance, % of GDP -1.0 -2.1 -2.4 -2.5

Current account, % of GDP 7.1 6.8 5.9 5.4

Current forecast Previous forecast

8 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Pressure on DKK eases further in recent months

Denmark and its EUR/DKK peg attracted an unaccustomed degree of

attention at the start of the year due to strong appreciation pressures on the

currency. The upward pressure prompted four rate cuts and intervention in

the FX market by Danmarks Nationalbank (DN), which lowered the

certificates of deposit rate to -0.75% and increased Denmark’s currency

reserves to almost 38% of GDP in February compared to 23.2% at the end of

2014. Pressure began to ease in late February, causing DN to increase the

central bank current account limits twice and to buy krone for DKK68.9bn in

all in April and May. Ordinarily, intervention to buy krone for DKK10-20bn

would result in a unilateral Danish rate hike, but the current situation is by no

means ordinary, and we expect that DN will prefer to reduce its currency

reserves further before a rate cut might be on the cards. The unresolved

situation with Greece is another reason for DN’s hesitancy at the moment.

We expect that Greece and its creditors will eventually reach an agreement,

which would mean an outflow of DKK. Given this, we estimate that DN will

hike rates twice by the end of the year, taking the certificates of deposit rate

up to -0.50%. Thus even if we are correct, policy rates will continue to be

extremely low and still a long way from the norm.

While slightly longer rates have corrected to some extent, in part due to better

economic key figures in Europe and rising inflation expectations, rates

generally remain low – and extremely low rates have consequences. First,

they put pressure on the bank system, as the banks have to place their money

with DN at a negative rate once they have used up their current account limit.

This means the banks have an incentive to ‘put their money to work’, which

can increase the probability of them taking on too much risk. Hence, credit

growth should come under increasing scrutiny in the coming years. Second,

very low interest rates increase the risk of asset bubbles in, for example, the

equity or housing markets – and indeed there has been an increasing focus on

the housing market of late. It is less than 10 years since the Danish economy

last experienced a housing market collapse and record-low interest rates have

stoked fears of a new bubble forming, especially in the Copenhagen

apartment market.

Housing market steams ahead in H1

While the Danish housing market has been undergoing a slow recovery over

the past few years, the pace of improvement has picked up in the first half of

this year. Figures from Statistics Denmark show that house and apartment

prices rose by 2.6% and 3.8%, respectively, between Q4 14 and Q1 15. We

have to go all the way back to 2006 to find similarly steep price increases

over a single quarter. Figures from property sales website Boligsiden and

estate agents home indicate that price growth has continued in Q2. The

pronounced increases in property prices are primarily due to extremely low

interest rates, which despite rising in recent weeks remain incredibly low

from a historical perspective. Low interest rates have made home financing

cheap, which has helped increase demand and therefore prices – as has labour

market growth. We expect house prices will continue to rise in the coming

years, though increases in interest rates will probably put a damper on the

most extreme examples. Nevertheless, we still expect to see solid price

appreciation of 7.1% this year and 5.8% next year. Hence the outlook is for

house prices to increase by more than nominal income growth would

indicate.

Extremely low policy rates in Denmark

Source: Danmarks Nationalbank, Danske Bank

FX reserves still very substantial

Source: Danmarks Nationalbank, Statistics Denmark

Mortgage rates still low in spite of correction

Note: Including trading margins; excluding administration fees

Source: Danske Bank Markets

House prices set to rise further

Source: Statistics Denmark, Danske Bank

9 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

We do not currently see any reason to fear a bubble in the housing market though, as prices remain moderate. This is also supported by the continued absence of growth in household borrowing despite low interest rates. Housing bubbles usually go hand-in-hand with high lending growth, as was the case in the mid-2000s. However, the current appreciation trend in the housing market is not being driven by growing indebtedness among households. One important proviso, however, is that lending figures only cover the country as a whole, and so say nothing about regional differences.

Another item of good news for the Danish economy is that the housing market pick-up is no longer solely concentrated in and around the major urban conurbations. According to Housing Market Statistics (Boligmarkedsstatistikken), house prices in all regions except Bornholm were higher in Q1 15 compared to Q1 14. We expect that the nationwide improvement will continue in the coming years, though still with the Greater Copenhagen area as the main driving force. However, while things are generally going better in many parts of the country, we would underline that some areas remain very fragile, with house prices here still substantially below pre-crisis levels.

Furthermore, while price appreciation has spread, prices are clearly still rising fastest in Copenhagen and Aarhus. Given that apartment prices have now reached pre-crisis levels in these areas, it is worth considering the risk of localised bubbles. Prices beating their previous record do not define a bubble. Demand for housing in Copenhagen and Aarhus may also be driven by more fundamental factors – such as relocation and strong income growth. One way of putting apartment price growth into an economic perspective to assess the risk of bubble formation is to consider prices in terms of regional GDP growth. When doing this for Copenhagen, developments in H1 do give some grounds for concern – for while prices are still 14.5% from their peak in these terms, the gap has narrowed by around 10 percentage points since Q4 14. Hence the apartment market is running at full steam at the moment.

Moreover, whether or not a bubble exists in the economic sense can quickly become a theoretical discussion – what is important for an ordinary homebuyer is not to take on too much debt, believe in eternally rising prices or be blinded by incredibly low interest rates. We can certainly not rule out property prices starting to fall – especially in the major towns and cities – in a few years’ time when interest rates begin to normalise. If so, price falls could hit hard, regardless of whether or not there has been an actual bubble or not.

Weaker DKK a boon to Danish economy

Both the EUR and hence the DKK – due to the EUR/DKK peg – have

weakened very substantially since December 2014 and the effective DKK

exchange rate is now 3.6% below its level of last December. The pronounced

fall in the effective exchange rate has given Danish exporters a competitive

boost, as Danish goods have become relatively cheaper abroad. This has

already had a major impact, with Danish goods exports rising by 4.4% in the

course of Q1. Quarterly growth in goods exports has only exceeded this level

five times since the start of the 1990s. Service exports in constant prices fell

in Q1, though this was largely due to technicalities connected with a highly

fluctuating deflator. In current prices, service exports rose by 2.3% over the

quarter. Hence, exports have generally got off to a good start in 2015.

While the DKK has strengthened a little in May and June, we would have to

go back to the end of 2002 – apart from a brief period in 2012 – to find a

weaker krone. As we expect the DKK to remain weak for the immediate

Housing market pick-up spreading to more areas of

the country

Note: Bornholm not included in graph.

Source: DK Mortgage Banks� Fed., Danske Bank

Rising house prices not due to increased net

borrowing

Note: Data break September 2013

Source: Danmarks Nationalbank, Danske Bank

Apartment prices corrected for wages, inflation

and relocation approach peak

Note: Regional GDP figures for 14/15 extrapolated by correcting

nom. GDP growth nationwide with an excess growth of 0.8

percentage points. H1 apartment prices extrapolated using figures

from �Boligsiden�.

Source: Statistics Denmark, �Boligsiden�, Danske Bank

Marked weakening of effective DKK exchange rate

Source: Danmarks Nationalbank

10 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

future and we forecast faster growth in our export markets, the outlook for

Danish exports is bright. We expect exports to grow 3.4% overall this year,

rising to 4.9% next year.

Consumption rising

Private consumption growth hit a six-year high in the six months around the

turn of the year. A sharp rise in heating consumption caused overall

consumption to increase by 1.2% in the final quarter of 2014, while a more

broadly based increase pushed consumption up a further 0.7% in Q1 this

year. Consumption is now 2.4% up on last year. Hence, a consumption

recovery is clearly under way, supported by rising real income, more people

in work, low interest rates and extremely high consumer confidence.

However, the recovery still does not resemble the strong, loan-financed

consumption upswing that has previously got the Danish economy going

after a crisis. In fact, the first two months of Q2 have seen a rather sharp fall

in Dankort (Danish debit card) transactions. Moreover, the increase in

heating consumption in Statistics Denmark’s figures has been from an

extremely low level in the early part of 2014 and is unlikely to recur. That is

why we have not really changed our forecast for private consumption, though

developments so far mean that some growth has been shifted from 2016 to

2015 when calculating the figures for the year as a whole.

Essentially, our position remains that consumption is being stymied by the

unusually large amount of debt owed by households. For households overall,

debt currently amounts to roughly three years’ income, which is the same as

in 2007. However, the value of owner-occupier dwellings has fallen from 4.2

to 3 years’ income, in other words, basically the same as the debt. Hence,

households still need to adjust their debt levels to the new house prices. We

have estimated that private consumption will more or less follow income

growth in the coming years, which means debt will be largely unchanged in

kroner terms. It is also quite possible that households could react to the

upswing by increasing debt levels and thus pushing consumption growth

higher. The relatively strong increase in house prices so far this year has

clearly made that possibility more likely. However, there is also a real chance

that some households will use rising income to pay off their debt and thus

dampen consumption growth relative to our expectations.

Another aspect of this story is that during the crisis households increased

their pension savings to more or less match the fall in housing wealth.

However, pension savings are tied up and most of it will be taxed when paid

out – plus there is solid evidence to suggest households look much more

closely at the equity in their homes rather than their pension wealth when

planning consumption.

Exports set to contribute to growth in coming years

Source: Statistics Denmark, Danske Bank

Heating consumption dragged private consumption

down in 2014

Source: Statistics Denmark and Danske Bank

Consumption recovery likely to be modest

Source: Statistics Denmark and Danske Bank

House prices have fallen, but not debt

Note: Not corrected for conversion of lump sum (capital) pensions.

Pension savings are excl. bank account savings. Data break in

2012.

Sources: Danmarks Nationalbank, Statistics Denmark, Realkredit

Danmark, own calculations

0

50

100

150

200

250

300

350

400

450

2000 2002 2004 2006 2008 2010 2012 2014

Debt Pension assets

Housing assets Other financial assets

11 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Prices rising faster

As we expected, inflation rose quite sharply in the opening months of the

year; from 0.1% in January to 0.6% at present – and the outlook is for the

upward trend to continue. The impact of the decline in the oil price will

gradually fall out of the statistic, which will instead be pulled higher by the

increase in the oil price since it bottomed out in January. The effect of the cut

in energy duties, which has lowered inflation by 0.2 percentage points, will

also disappear from 2016. Furthermore, the DKK weakening by 5% relative

to our trading partners between December 2014 and March 2015 will

increase import prices in Denmark, though the effect will be gradual and will

contribute to pushing inflation higher for an extended period. Underlying

inflationary pressures remain modest in Denmark, however, and as yet show

no signs of increasing. Wage growth is still modest, even though we expect it

to pick up slightly as employment increases. Real income does not look set to

experience the same solid growth in 2016, though rising employment will

help pull total household income higher.

Beware bottlenecks in the labour market

Employment has remained a bright spot in recent years. According to the

national accounts figures, the number of employed people rose by a further

5,400 from Q4 14 to Q1 15. Since bottoming out in Q2 13, total employment

has risen by 38,200 – the result of 44,600 new jobs being created in the

private sector, while the public sector has shed 5,400 jobs. Private sector

employment performing so well despite just modest GDP growth is in part

due to GDP growth being held down by less labour-intensive industries.

Hence, gross value added (GVA) in private sector non-farm and non-oil

industries has actually been positive every year since 2010 and showed

growth of 1.9% last year compared to total GDP growth of 1.1%.

We have been surprised by the pace of employment growth and now expect

more than 50,000 new jobs will be created between Q4 14 and Q4 16, taking

total employment to 2,830,000. We assume that job growth will mainly stem

from the private sector, but also expect public sector employment to rise

modestly, as this is assumed in the government’s economic policy.

Average gross unemployment fell to 126,600 or 4.8% of the labour force in

April this year. However, while gross unemployment has fallen, it has done

so at a somewhat slower pace than the pickup in employment. This is no bad

thing though, as it signals that the workforce is expanding. We forecast gross

unemployment to continue falling as employment rises, but still at a slower

pace, as we expect more people to enter the labour market due to improving

job prospects and as a result of various labour market reforms, such as the

changes to early retirement schemes. We forecast gross unemployment to fall

by a further 13,700 by the end of 2016. If we are correct, gross

unemployment will stand at 113,000 or 4.3% of the labour force, which is a

very low level of unemployment in historical terms. That employment

growth should come from the labour force means an increased risk of labour

market bottlenecks, as it is not certain the labour force can be expanded

relatively significantly in such a short space of time without creating regional

or professional bottlenecks. Hence, labour market flexibility should be a key

focus area in the coming quarters and years. It is worth pointing out here that

the normal warning signals such as wage pressure and pressure on the current

account are less effective at a time when there is labour immigration from the

rest of Europe and a structural surplus on the current account.

Inflation heading higher

Source: Statistics Denmark, Danske Bank

Solid growth in private sector non-farm and non-oil

industries explains employment growth in recent

years

Source: Statistics Denmark, Danske Bank

Higher economic growth will help lift employment

Source: Statistics Denmark, Danske Bank

Government has consistently overestimated

number of public sector employees

Source: Statistics Denmark, Economic Survey, Danske Bank

12 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

No scope for fiscal easing

General elections held in Denmark on Thursday 18 June resulted in a win for

the ‘blue block’ – the centre-right parties. As we write, negotiations to form a

new government have only just begun, so we do not yet know what the

economic policy of the future government will be. A change of government

in Denmark often does not result in any great change to short-term economic

policy and we expect this will once again be the case. Naturally, economic

policy differs between the political parties, but the budget and EU rules limit

the scope of politicians to act in the short term. Hence, our forecast for the

coming years is not particularly affected by the shift in government, although

it naturally constitutes a source of uncertainty with respect to our estimates

for government finances next year.

Last year was the first year since the financial crisis kicked off that Denmark

had a budget surplus – of DKK34.6bn, or 1.8% of GDP. The surplus was in

particular due to the bringing forward of a tax on pension savings and

extraordinary income from the PAL (pension yield) tax. However, Denmark

looks set to have a budget deficit again this year and next. We do not expect

the deficit to exceed the EU limit of 3% of GDP, but significant deficits mean

there is little scope for fiscal easing in the coming years. We estimate

economic policy will be tightened slightly in the coming years, which fits

well with the state of the economy.

Labour shortages could soon be looming again

Source: Statistics Denmark, Danske Bank

Budget deficit close to � but below � EU limit

Source: Statistics Denmark, Danske Bank

13 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Denmark: Forecast at a glance

Sources: Danmarks Statistik, Nationalbanken, Macrobond Financial, Danske Bank

National account 2013 2013 2014 2015 2016

DKK bn (current prices)

Private consumption 890.2 0.0 0.6 1.9 1.9

Government consumption 504.0 -0.5 1.4 1.0 0.3

Gross fixed investment 345.7 1.0 3.7 0.2 3.2

- Business investment 205.6 3.4 1.1 2.0 5.3

- Housing investment 70.7 -5.0 6.5 -2.4 3.3

- Government investment 69.3 0.3 8.6 -1.9 -3.2

Growth contribution from inventories -0.2 -0.2 0.3 -0.4 0.1

Exports 1023.8 0.8 2.6 3.4 4.9

- Goods exports 626.9 1.8 -0.3 5.8 4.7

- Service exports 396.9 -0.8 7.1 -0.3 5.2

Imports 915.5 1.5 3.8 1.9 4.6

- Goods imports 574.9 3.6 2.3 3.2 4.3

- Service imports 340.6 -2.0 6.4 -0.3 5.1

Growth contribution from net exports -0.3 -0.3 -0.5 0.9 0.5

GDP 1886.4 -0.5 1.1 1.7 2.1

Economic indicators 2013 2014 2015 2016

Current account, DKK bn 136.0 120.9 140.0 140.0

- % of GDP 7.2 6.3 7.1 6.8

General government balance, DKK bn -20.0 34.6 -20.4 -44.1

- % of GDP -1.1 1.8 -1.0 -2.1

General government debt, DKK bn 849.8 867.9 762.5 776.9

- % of GDP 45.0 45.2 38.6 37.9

Employment (annual average, thousands) 2748.8 2768.3 2791.4 2818.9

Gross unemployment (annual average, thousands) 152.9 134.6 125.1 116.8

- % of total work force (DST definition) 5.8 5.1 4.7 4.4

Oil price - USD/barrel (annual average) 109 99 66 78

House prices, % y/y 2.7 3.4 7.1 5.8

Private sector wage level, % y/y 1.2 1.3 1.6 2.2

Consumer prices, % y/y 0.8 0.6 0.7 1.7

Financial figures 24/06/2015 +3 mths +6 mths +12 mths

Lending rate, % p.a. 0.05 0.05 0.05 0.05

Certificates of deposit rate, % p.a. -0.75 -0.60 -0.50 -0.50

2-yr swap yield, % p.a. 0.27 0.15 0.15 0.25

10-yr swap yield, % p.a. 1.50 1.45 1.55 1.85

EUR/DKK 7.460 7.455 7.455 7.455

USD/DKK 6.67 7.17 7.03 6.78

% y/y

Forecast

14 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Sweden An ambivalent and reactive Riksbank set to miss its target Thus far in 2015, most economic developments have been in line with

what we chiselled out in December last year. Growth is improving in the sense that it is becoming increasingly more balanced as stronger external demand and a weak SEK are pushing exports up, while domestic demand growth (id est, mainly consumption and housing investment) is coming back down from the unsustainably high growth rates of yesteryear.

Inflation seems to be bottoming out and is expected to rise during H2, mainly due to statistical base effects as previous year’s sharp fall in energy and interest rate related costs are dropped from the inflation calculations. However, albeit expecting a pronounced rise in inflation during autumn, our forecast pales compared to the Riksbank’s path forward where inflation is calculated to rise by 1.75 percentage point (p.p.) from August to December.

Albeit directionally in line with the Riksbank’s forecasts for the Swedish economy, the above developments will pose a near-term challenge to the Riksbank. After undershooting the inflation target for long and by far, confidence in the inflation target has clearly deteriorated which is why the Riksbank has set its aim on coming across as ‘inflation nutters’.

In Sweden, centralised wage negotiations are widespread, deciding the level of wage inflation for considerably more than three million workers out of a total of less than five million workers. (Of course, there is room for some wage drift but that has rarely been a major issue in Swedish wage formation, especially when controlling the local wage bargaining agreements common among engineers et alia.)

The next wage bargaining round is concluded in the beginning of 2016 and inflation and inflation expectations are at historically low levels. In addition, both unions and industry organisations have expressed previously unheard of doubts about using the inflation target as an anchor for negotiations. In other words, the Riksbank has only limited time to push up inflation (-expectations) and should be extremely responsive to indications of negative developments vis-à-vis its preferred path forward or continued low inflation expectations among labour market participants.

Taken together, we believe that the continued lowflation prevalent in

our forecast and an acute need to lift inflation expectations, will be

sufficient to make the Riksbank act again. In relation to earlier

expectations we have, nevertheless, chosen to postpone policy action

to December.

Risks are still tilted to the downside and to earlier rather than later

policy action. In particular, we fear a swift SEK appreciation could

bring the Riksbank to act, even in the very near term.

Changes from previous forecast

Source: Danske Bank

Swedish economy at a glance

Source: Statistics Sweden (SCB). Danske calculations

Same same but different

Source: SCB, Riksbank. Danske calculations

The Riksbank trigger?

Source: National Institute for Economic Research (KI), Macrobond

% y/y 2015 2016 2015 2016

GDP, calendar adjusted 2.1 2.1 2.1 2.1

Private consumption 2.0 2.0 2.0 1.8

Public consumption 1.6 1.1 1.2 1.5

Gross fixed investment 5.3 3.6 6.0 3.8

Exports 3.8 5.3 5.5 4.9

Imports 4.9 5.2 6.6 5.1

Unemployment rate 7.8 7.6 7.7 7.5

Inflation 0.2 1.5 0.3 1.2

Government balance, % of GDP -1.8 -0.9 -2.0 -1.0

Current account, % of GDP 5.4 5.4 5.6 5.7

Current forecast Previous forecast

Sweden

15 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

The binarities of external demand

The Swedish economy is continuing to perform well in relation to most other

developed countries. However, in order to make demand composition more

balanced and to make economic policy long term sustainable, external

demand will have to pick up the pace in coming quarters. Danske Bank’s

international forecasts do forebode strong(er) growth in many of Sweden’s

main export markets. Details in the forecast, however, paint a less exuberant

image of the export outlook. The Swedish export industry consists mainly of

investment and input goods, while international demand growth currently

seems to be a function mainly of consumption goods and services. Indeed, in

2014, preliminary GDP data showed that service exports grew an impressive

7.2% y/y, with R&D and tourism being among the main contributing

industries. In the goods exporting industries, so called merchanting (exempli

gratia, tri-party trading) was the main contributor.

That said, external demand is ameliorating and as the improvement in

international demand progresses, we expect growth to increasingly come

from investments (and input) goods, which should enhance the Swedish

export outlook. In addition, at current levels, the SEK is weak against most

major currencies, lending additional support to a more benign export outlook

– especially for the Swedish input goods industry. Export orders have been

on the rise, over the past few months, and we take note of several leading

export companies having announced production increases during spring.

Also, despite the expected recoil in Q1 15, services exports should continue

on a strong note throughout the forecast horizon.

World market growth, id est the weighted import growth on Swedish export

markets, is calculated to gradually approach, and even exceed, 5% y/y at the

end of the forecast horizon. This implies that 2015 should mark the last year

with falling market shares for Swedish export industries, as Swedish export

growth is finally calculated to surpass market growth. Needless to say, given

renewed worries about Greece and recurrent skirmishes between the fighting

parties in Ukraine, risks to this forecast are tilted to the downside.

In quantitative terms, Swedish export growth is expected to rise 3.5 % y/y

(vol., cal. adj.) in 2015 and 5.0% y/y (vol., cal. adj.) in 2016.

Financial conditions to remain supportive

In line with developments in international financial markets, Sweden has

experienced a very high volatility in (longer-dated) interest rates and FX

markets during the first half of 2015. However, short-term interest rates are

fixed at low – even negative – levels due to the Riksbank’s repo rate

currently standing at -0.25%. The far below target inflation has made us, and

financial markets, believe that current low rates are here to stay for a longer

period of time. To be certain, we have a hard time identifying any near-term

risks that could push underlying inflation and short rates upwards and the

renewed volatility in the longer interest rate spectra and in FX markets, while

noteworthy, is apparently stuck in a wide but constructive range from a

Swedish standpoint.

Stock markets have risen strongly for a longer period of time which is why

we need to acknowledge some downside risks to our outlook. Partly due to

these risks, we expect the pace of gains to moderate and gradually align to

nominal GDP-growth.

GDP and investments growth on Swedish export

markets

Source: National Institute of Economic and Social Research

(NIESR), Macrobond. Danske calculations

World markets and Swedish exports

Source: NIESR, SCB, KI. Danske calculations

Financial conditions remain supportive

Source: Macrobond. Danske calculations

16 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Housing markets are taking out new highs by the day it seems and we have

long highlighted the risk of a major correction of 20-30%, where we believe a

fundamentally warranted price level is located. Simultaneously taking into

account an institutional lack of affordable housing, we have opted for a more

gradual, smoother, adjustment process with incomes rising and prices only

slowly dropping, eventually reaching a sustainable equilibrium a few years

hence.

Turning, lastly, to the fiscal situation, we do expect fiscal policy to become

less supportive to growth over the coming years as the fiscal targets, in

particular the surplus target, have become increasingly strained. The cyclical

improvement has not sufficed to restore government tax incomes to pre-crisis

trends or levels and a large influx of immigrants weigh on public

expenditures, even though the net economic impact on Sweden’s economy

may be positive. Views on the amount of saving necessary to restore the

surplus target is diverging but calculations from the semi-independent

National Institute for Economic Research suggests a need for structural

savings of close to SEK100bn over the coming years.

To sum up, despite increased volatility and in the presence of downside risks,

we expect financial and economic conditions to remain strongly supportive to

growth way past the forecast horizon.

Not only housing investments

Disregarding a temporary boost to R&D investments during the latter part of

last year, investments growth has been very weak in private sectors in the

wake of the financial crisis. The main exception, in particular over the past

couple of years, has been housing investments that have even increased some

25% y/y certain quarters! Investments have not been bad in service sectors

but far from what could have been expected when studying, exempli gratia,

growth in service industries (and exports). Public investments in various

infrastructure projects and other large scale projects instigated in the wake of

the crisis are now on a downward trajectory and we do not expect this trend

to shift much over the forecast horizon.

However, as capacity utilisation is increasing and as the export outlook firms

on the back of more benign international developments, we expect business

investments to finally pick up pace as well. Housing investment growth,

though, is expected to decelerate over the coming quarters. All in all,

investment growth is expected to reach 4.9 % y/y (vol., cal. adj.) this year

and to come in a tad lower, at 3.2% y/y (vol., cal. adj.), in 2016.

Frugal Swedish households

Last year, private consumption increased 2.5% y/y (vol., cal. adj.) and strong

consumption growth has been a trait of the Swedish economy ever since the

international financial crisis struck in 2008. This has many explanations,

lower tax burden, lower interest rate costs, increased wage share of GDP,

strong immigration, wealth effects from housing and stock markets etc.

However, this has also gone hand in hand with a very high savings ratio,

currently above 15% of disposable incomes, which has more than doubled

from 2008 until now. Most forecasters assume and have assumed that this

situation would ‘normalise’, meaning the savings ratio would/will decrease

and consumption – hence – increase as the labour market situation improves.

Asset prices are soaring, risks are building

Source: Macrobond

Fiscal policy is overly expansionary

Source: SCB, KI Danske bANK calculations

Domestic demand has driven Swedish GDP-growth

Source: SCB, KI Danske Bank calculations

High savings ratio remains the main upside risk

Source: SCB, KI. Danske Bank calculations

17 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Since the employment continues to be benign, wages are expected to increase

further and most evidence points towards continued decent demand growth,

the consumption outlook is almost by default only a question of how

optimistic you feel. Alas, we continue to foresee a high degree of uncertainty,

low to negative wealth effects, further fiscal contraction, low wage increases

and have all sorts of sombre views on the future, which is why our forecasts

for private consumption, albeit still respectable from a historical perspective,

imply a diminishing contribution to growth from consumption.

In numbers, in both 2015 and 2016, private consumption growth is forecasted

to come in at 1.9% y/y (vol., cal. adj.), suggesting, inter alia, a virtually

constant savings ratio in coming years.

Imports and GDP

Due to strong domestic demand, imports have been growing steadily over the

past years. Imported content is high also in exports, which is why we see no

reason to expect a dramatic change in import growth over the forecast

horizon. In 2015 imports are expected to grow 4.5% y/y (vol., cal. adj.) and

in 2016 we estimate an even higher import growth, 4.9% y/y (vol., cal. adj.).

Net exports will thus start to contribute strongly from now on and over the

forecast period, but leave, as year average a -0.3 p.p. y/y (vol., cal. adj.)

contribution on growth this year and a 0.2 p.p. (y/y) positive contribution to

growth in 2016.

Summing up the various components discussed above, we reach a GDP-

estimate somewhat below market consensus and the Riksbank but it is still

decent when comparing to other economies and post-crisis developments. It

is particularly pleasing to see a more balanced demand, as current domestic

developments would be unsustainable from a longer-term perspective given

the substantial (unsustainable) economic policy stimuli to domestic demand.

All in all, GDP is expected to come in at 2.1% y/y (vol., cal. adj.) in both

2015 and 2016 but, again, with a gradually improved composition.

Resource utilisation, inflation and the Riksbank

If only we could call it a Freudian slip but we are honestly and genuinely

uncertain about the future for resource utilisation and inflation and thus also

about the ‘Risk’bank. The unemployment rate is elevated and current

inflation is unarguably low. However, the explanation for the high

unemployment rate is not only an increased number of unemployed in the

wake of the financial crisis, but also due to a very strong influx of immigrants

with an unknown skill set and thus, perhaps, questionable employability on

Swedish labour markets. In this respect we are quite optimistic as many of

the jobs added after the crisis are to be found in the low-skilled service

sectors and an unusual high percentage of the new entrants have post-

secondary education.

High import content in exports

Source: SCB, KI. Danske Bank calculations

GDP, hours worked and productivity

Source: SCB, KI. Danske Bank calculations

18 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Together with a seemingly low utilisation of capital (i.e., machinery etc), our

belief is that resource utilisation is still low, despite us sporting a low

potential GDP-growth (of 1.5-1.75% y/y). The low resource utilisation

explains the low current inflation but the low potential growth implies that

even our below consensus forecasts of actual GDP will suffice to narrow the

output cap throughout the forecast horizon. It is only, however, late 2017 –

beyond the forecast horizon that the output gap reaches balance and we

foresee an underlying inflation closer to the inflation target.

In the near term and due to statistical base effects from the dramatic fall in

energy prices last autumn, we foresee a pronounced rise in inflation over the

coming months. In our forecast, (CPIF) inflation rises from -0.3% (in June)

to above 1½% y/y in January 2016. Thenceforth, inflation will again ebb – at

least in the medium term – as true inflation, wage inflation, is set to come in

all too low to produce the underlying inflationary impetus necessary to reach

the inflation target. Together with still weak pricing power in large parts of

the business sector, we believe that the inflation target is a long way hence, at

least when looking at core inflation measures. Overall, inflation is set to

average 0.2% y/y in 2015 and 1.3% y/y in 2016.

The Riksbank should be able to see through the energy-driven near-term rise

in inflation which we, to be sure, expect will be less dramatic than what the

Riksbank is forecasting. And with the Riksbank concentrating on its inflation

nutter credentials, particularly in the run up to the conclusion of the wage

negotiations, we expect the Riksbank will not be satisfied at all. In short, we

still expect the Riksbank to increase the monetary policy accommodation (a

10bp cut at the December meeting). It is a pity it is too late.

Under any circumstances, we continue to hold a strong SEK as the main risk

for early policy actions and we would also like to underline that

developments of external demand are key to forming an opinion on the future

of Swedish economic policy. In terms of domestic demand, economic policy

is already a success.

Resource utilization remains low

Source: SCB, KI. Danske calculations

�Lowflation� becoming a permanent trait of the

Swedish economy?

Source: SCB, Riksbank. Danske calculations

Sub zero rates and no thaw in sight

Source: Riksbank. Danske calculations

19 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Sweden: Forecast at a glance

Note: The national account figures relates to actual growth rates (i.e. not calendar adjusted or wda)

Source: Danske Bank

National account 2013 2013 2014 2015 2016

SEK bn (current prices)

Private consumption 1718.2 1.9 2.4 2.0 2.0

Government consumption 955.7 0.7 1.9 1.6 1.1

Gross fixed investment 674.2 -0.4 7.4 5.3 3.6

Growth contribution from inventories -4.4 0.0 0.2 0.1 0.0

Domestic demand 3348.1 1.0 3.4 2.7 2.1

Exports 1722.4 -0.2 3.3 3.8 5.3

Aggregate demand 3343.7 1.1 3.6 2.7 2.1

Imports 1516.4 -0.7 6.6 4.9 5.2

Growth contribution from net exports 206.1 0.2 -1.1 -0.3 0.2

GDP 3549.7 1.3 2.3 2.3 2.3

GDP, calendar adjusted 1.3 2.4 2.1 2.1

Economic indicators 2013 2014 2015 2016

Trade balance, SEK bn 142.2 123.5 107.3 121.4

- % of GDP 3.8 3.2 2.6 2.9

Current Account, SEK bn 260.4 224.9 220.7 228.3

- % of GDP 6.9 5.7 5.4 5.4

Public sector savings, SEK bn -45.3 -82.2 -73.0 -37.9

- % of GDP -1.2 -2.1 -1.8 -0.9

Public debt ratio, % of GDP* 38.7 43.9 44.5 44.8

Unemployment, % of labour force 8.0 7.9 7.8 7.6

Hourly wages, % y/y 1.9 2.8 2.8 2.5

Consumer prices, % y/y 0.0 -0.2 0.2 1.5

House prices, % y/y 3.6 5.0 -3.0 -2.0

* Maastricht definition

Financial figures +3 mths +6 mths +12 mths

Repo rate, % p.a. -0.25 -0.25 -0.35 -0.35

2-yr swap yield, % p.a. -0.04 0.05 0.00 0.00

10-yr swap yield, % p.a. 1.61 1.60 1.70 1.95

EUR/SEK 9.2 9.3 9.2 9.0

USD/SEK 8.2 8.9 8.7 8.2

24/06/2015

% y/y

Forecast

20 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Norway The end is in sight The decline in oil investment is now having a very clear impact on the

economy and there are some signs of second-round effects. The worst

is probably still to come, with higher unemployment and more

bankruptcies.

Oil investment now looks set to flatten out next year, which should

mean that the bottom is reached in the autumn.

A much weaker Norwegian krone has also offset much of the impact

of lower oil investment.

The central bank’s rate cuts are working as intended, with both

private consumption and housing investment on the increase.

Unemployment is set to increase but we believe it will be limited by

economic adaptation and a flexible labour market.

One unknown is the amount of excess capacity in the supply sector.

Norges Bank lowered its key rate again in June and is signalling a

good chance of further reductions but we believe interest rates have

hit the bottom.

The NOK should gradually strengthen again as oil investment

flattens out.

The wage model also appears to be working, as wage growth is

slowing without unemployment rising.

Beginning of the end

Growth in the Norwegian economy was surprisingly strong in Q1 but the fall

in oil investment since late 2013 is now beginning to affect oil-related

industries seriously. Nevertheless, we expect the downturn to be both mild

and short-lived.

For one thing, the Norwegian economy is actually relatively robust, even

against large swings in the oil price. The decline in the Norwegian krone that

has accompanied the slide in oil prices has given the export industry a lift.

The central bank’s rate cuts have also increased households’ purchasing

power and contributed to higher private consumption and housing demand,

so boosting housing investment. Together with expansionary fiscal policy

and continued positive bank lending policies, this has helped limit the

second-round effects of the fall in oil prices. Although unemployment has

begun to rise, the increase has not been as bad as many feared and has been

confined largely to oil-related industries and oil-dominated regions.

For another, oil prices have moved off the bottom and the oil investment

survey suggests oil investment will flatten out next year. This may mean that

the deterioration in the economy in the spring proves to be the beginning of

the end for the oil-driven downturn in Norway. This also has implications for

financial markets, as we believe interest rates have hit the bottom and that the

krone is set for a prolonged uptrend.

Changes from previous forecasts

Source: Danske Bank Markets

Growth slowing

Source: Statistics Norway, Danske Bank Markets

% y/y 2015 2016 2015 2016

GDP (mainland) 1.5 2.3 1.7 2.2

Private consumption 1.9 2.0 1.8 2.0

Public consumption 2.3 2.2 2.4 2.2

Gross fixed investment -1.8 1.9 -6.5 1.0

Exports 1.6 1.5 2.5 1.0

Imports 3.4 3.0 1.0 3.0

Unemployment (LFS) 4.0 3.8 3.7 3.7

Inflation 2.1 2.0 2.8 2.0

Current forecast Previous forecast

Norway

21 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Looking ahead two to three years, we still believe oil prices will have to

return to levels that will make the upcoming development of new fields in the

North Sea profitable. This is not, therefore, the start of a long-term decline in

the Norwegian oil sector but a short, sharp correction that will soon be

history.

Oil-related industries hit hard

Oil investment has been in decline since late 2013 and will probably continue

to fall through to spring 2016. This has put a dampener on economic

expansion but the slowdown appears to have gone largely as we expected in

March despite a deterioration in oil-related industries. It is very encouraging

that the second-round effects still seem to be moderate. Indeed, we are seeing

signs of consumption growth accelerating and of housing demand holding up

and helping push up housing investment. The weaker krone and continued

gradual global economic recovery have also meant that mainland exports are

still growing. Mainland GDP grew 0.5% q/q in Q1, more or less in line with

last year, but Norges Bank’s regional network survey is suggesting somewhat

weaker growth over the summer. We now expect mainland GDP to grow

1.5% this year, slightly less than forecast in Nordic Outlook: March 2015, 25

March.

Unemployment is beginning to rise but the increase is still confined to oil-

related industries and oil-dominated regions. Although employment has

stopped climbing, slower growth in labour supply will restrict the increase in

unemployment. This last factor seems to be due largely to net immigration

having fallen in response to the slacker labour market, which illustrates how

flexible the Norwegian labour market has become since the enlargement of

the EU in 2005.

The most important change since Nordic Outlook: March 2015 comes from

the oil investment survey. The oil companies have revised up their estimate

for this year slightly but we are still looking at a decrease in oil investment of

13%. On the other hand, the survey now suggests that oil investment will be

more or less unchanged in 2016, whereas we previously forecast a decrease

of 5% y/y. Besides pushing up our GDP forecast for 2016, this also removes

some of the downside risk to the Norwegian economy.

As mentioned above, the decline in oil investment since late 2013 is now

plain to see in activity in oil-related industries. New orders have dried up,

profitability has fallen and the focus is on cost cutting and downsizing. This

is now resulting in lower industrial production and a decrease in overall

business investment. One positive, though, is that the first contracts for the

new Johan Sverdrup oilfield have been awarded mainly to the Norwegian

supply sector.

We also expect oil prices to begin to climb after the summer, with the result

that oil investment should also stabilise gradually elsewhere in the world.

With several relatively large projects due to start up from late 2015, we

expect the fall in oil investment to be short-lived rather than mark the start of

a long-term decline in the Norwegian oil sector. Internal cost-cutting and

lower costs for rig hire have also pulled down breakeven levels for all

projects. This means the need for economic reorganisation will be limited,

which will decrease the downside risk for now.

Weaker growth over the summer

Source: Norges Bank

Oil investments will be more or less unchanged

next year

Source: Statistics Norway, Danske Bank Markets

We expect oil prices to climb further

Source: Macrobond

22 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

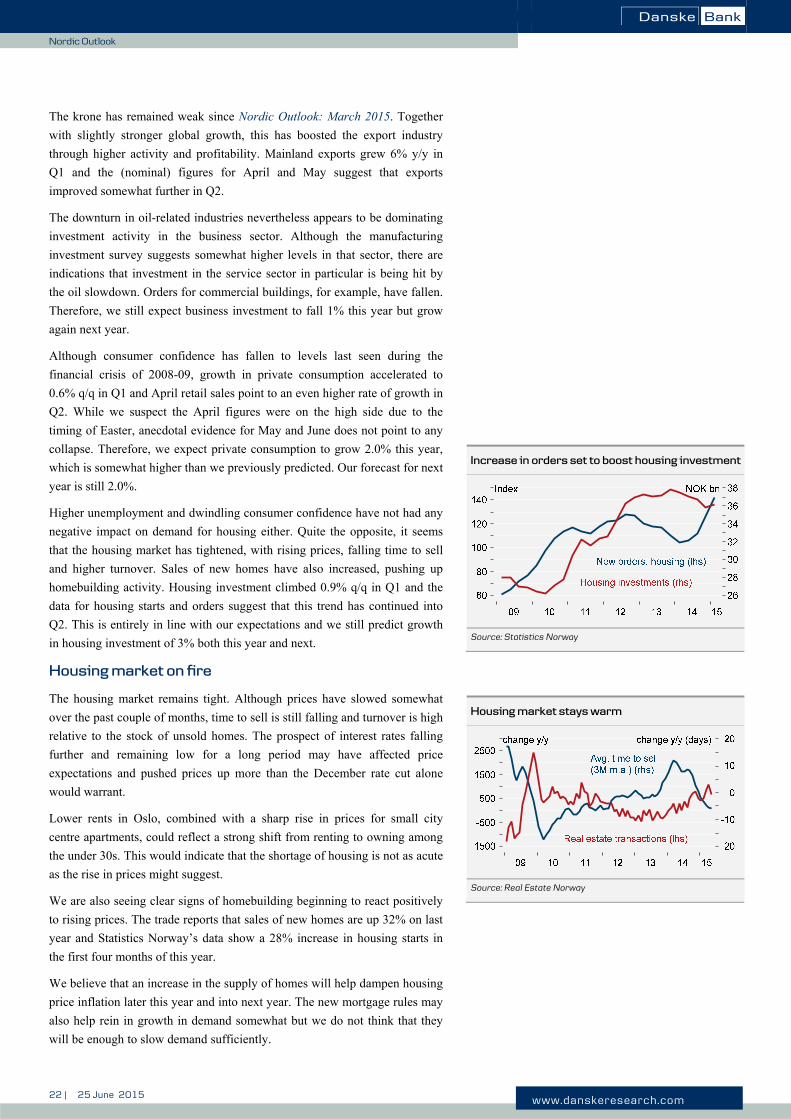

The krone has remained weak since Nordic Outlook: March 2015. Together

with slightly stronger global growth, this has boosted the export industry

through higher activity and profitability. Mainland exports grew 6% y/y in

Q1 and the (nominal) figures for April and May suggest that exports

improved somewhat further in Q2.

The downturn in oil-related industries nevertheless appears to be dominating

investment activity in the business sector. Although the manufacturing

investment survey suggests somewhat higher levels in that sector, there are

indications that investment in the service sector in particular is being hit by

the oil slowdown. Orders for commercial buildings, for example, have fallen.

Therefore, we still expect business investment to fall 1% this year but grow

again next year.

Although consumer confidence has fallen to levels last seen during the

financial crisis of 2008-09, growth in private consumption accelerated to

0.6% q/q in Q1 and April retail sales point to an even higher rate of growth in

Q2. While we suspect the April figures were on the high side due to the

timing of Easter, anecdotal evidence for May and June does not point to any

collapse. Therefore, we expect private consumption to grow 2.0% this year,

which is somewhat higher than we previously predicted. Our forecast for next

year is still 2.0%.

Higher unemployment and dwindling consumer confidence have not had any

negative impact on demand for housing either. Quite the opposite, it seems

that the housing market has tightened, with rising prices, falling time to sell

and higher turnover. Sales of new homes have also increased, pushing up

homebuilding activity. Housing investment climbed 0.9% q/q in Q1 and the

data for housing starts and orders suggest that this trend has continued into

Q2. This is entirely in line with our expectations and we still predict growth

in housing investment of 3% both this year and next.

Housing market on fire

The housing market remains tight. Although prices have slowed somewhat

over the past couple of months, time to sell is still falling and turnover is high

relative to the stock of unsold homes. The prospect of interest rates falling

further and remaining low for a long period may have affected price

expectations and pushed prices up more than the December rate cut alone

would warrant.

Lower rents in Oslo, combined with a sharp rise in prices for small city

centre apartments, could reflect a strong shift from renting to owning among

the under 30s. This would indicate that the shortage of housing is not as acute

as the rise in prices might suggest.

We are also seeing clear signs of homebuilding beginning to react positively

to rising prices. The trade reports that sales of new homes are up 32% on last

year and Statistics Norway’s data show a 28% increase in housing starts in

the first four months of this year.

We believe that an increase in the supply of homes will help dampen housing

price inflation later this year and into next year. The new mortgage rules may

also help rein in growth in demand somewhat but we do not think that they

will be enough to slow demand sufficiently.

Increase in orders set to boost housing investment

Source: Statistics Norway

Housing market stays warm

Source: Real Estate Norway

23 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

On balance, we consider the risk of a serious downturn in the housing market

is still relatively limited in the short term despite weaker economic growth

and slightly higher unemployment. Lower real wage growth will be more

than offset by lower interest rates, with the result that households’ debt-

servicing capacity will actually improve.

Unemployment set to peak early next year; wage growth set to slow

Unemployment has risen slightly further than we expected in Nordic

Outlook: March 2015, 25 March. It is mainly in oil-related industries and oil-

dominated regions that the number of jobless is rising and the increase in

other regions and sectors has been limited to date. According to the

Norwegian Labour and Welfare Administration (NAV), for example, the

entire increase in registered unemployment over the past year has been in

Rogaland, the heart of the offshore industry.

The two sources of jobless data also paint rather different pictures: while the

NAV figures show an increase of around 5,000 people, Statistics Norway’s

labour force survey suggests an increase of almost 25,000. We normally set

most store by the NAV’s figures, which show the number of people actually

registered as unemployed, whereas the LFS numbers are survey based and

therefore will always be associated with more uncertainty. Historically, the

NAV statistics have also presented a much more stable and accurate picture

of developments in the labour market than the LFS. On the other hand, the

use of severance packages in the oil sector means that the LFS may be better

at capturing the rise in unemployment there.

Either way, the rise in unemployment is being tempered by overall economic

growth holding up relatively well to date thanks to stronger growth in other

sectors. The Norwegian labour market has also become very flexible since

the enlargement of the EU in 2005. Net immigration has fallen by more than

10,000 since last year, curbing growth in the labour supply and keeping

unemployment down. On top of this, many of the jobs that have disappeared

in the oil sector were held by temporary foreign workers who are now

heading home without showing up in any of the jobless data.

We expect unemployment to rise somewhat in H2 as the slowdown in oil-

related sectors intensifies. However, we also expect the decline in oil

investment to flatten out early next year, which may mean the weakest period

in the labour market is through to next summer. In this case, we believe

unemployment will peak in H1 next year.

As expected, the Norwegian wage model appears to be working. The national

talks led to very moderate increases. The fall in oil prices will also erode

profitability in many industries, which will affect the wages they pay.

Together with rising unemployment, this will probably result in low local pay

increases too. Therefore, we expect wage growth to end up around 2.7% this

year and 3.0% next year.

Rise in unemployment still moderate

Source: Statistics Norway

24 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

Inflation holding up

Core inflation has held just below 2.5% over the past year but has fallen

somewhat lately despite higher imported inflation. This is probably because

the economic downturn has put a dampener on cost increases and squeezed

margins in the retail trade. The fall in inflation in March and April also

seemed to be linked to unusually weak movements in Norway’s ever-volatile

food prices and airfares. The May figures indicate a degree of normalisation,

with core inflation returning to 2.4% y/y.

We expect the underlying price drivers – lower wage growth and higher

productivity growth – to dampen domestic inflation further but the

deterioration in the krone in the spring will push up import prices over the

autumn and winter. Higher energy prices will also feed through gradually

into higher prices for both inputs and finished goods at importer level in

Norway. Therefore, we expect core inflation to hold around 2.25% y/y before

beginning to drift down towards 2.00% at the end of the year.

No more rate cuts; krone set to rally strongly

As expected, Norges Bank cut its key rate to 1.0% at the meeting on 18 June.

This was no surprise but the bank also signalled a significant chance of

further reductions, mainly because the growth outlook for the Norwegian

economy is weaker than previously thought. The latest regional network

survey results confirm that growth this year will probably be lower than

previously assumed and the bank also lowered its forecast for mainland GDP

next year despite an upward revision of the estimate for oil investment. The

change in the growth forecast for next year was due almost entirely to a

downward revision of private consumption despite unchanged projections of

real wage growth and unemployment.

It seems that the central bank is now much less worried about the risks to

financial stability from rapid growth in housing prices and credit. This is

probably a result of the government unveiling tougher new rules for banks’

mortgage lending. The Ministry of Finance has also announced that the

countercyclical capital buffer at banks is set to rise from 1.0% to 1.5%, partly

to ease the pressure in the housing market through tighter credit policies

and/or higher interest margins. However, when the buffer was first

introduced, it hit lending to businesses and had only a marginal impact on

lending to households, so this seems a very risky policy in the current

climate. Fortunately, it seems that banks are largely on course to meet higher

capital requirements, so with luck the effect will only be moderate.

Nevertheless, we believe that interest rates have now hit bottom and believe

that the growth outlook, even if it deteriorates, will not be as bad as Norges

Bank fears. We are also very doubtful whether the measures announced to

slow housing prices will work as intended. If they do not, growth in both

house prices and credit will be higher than the central bank is assuming.

Lower wage growth to ease upward pressure on

inflation

Source: Statistics Norway

Negative rates not on the cards

Source: Norges Bank, Danske Bank Markets

25 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

In the short term, we expect the krone to remain relatively weak, due to

expectations of further rate cuts and limited liquidity over the summer

months. On a six-month view, however, we expect the data to show gradual

stabilisation of the Norwegian economy and continued pressure on the

housing market. We also expect oil prices to climb during the period. This

would exert upward pressure on the krone towards the end of this year and

into 2016.

In the longer term, we are setting great store by the oil investment survey

now suggesting that oil investment in the Norwegian sector will flatten out as

early as next year. If so, the downturn in the Norwegian oil sector is drawing

to a close and we can see both the cycle bottoming out and unemployment

peaking next spring. We would then be looking at a relatively prolonged

uptrend in the krone once the worst of the dust has settled.

NOK expected to appreciate

Source: Norges Bank, Danske Bank Markets

26 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

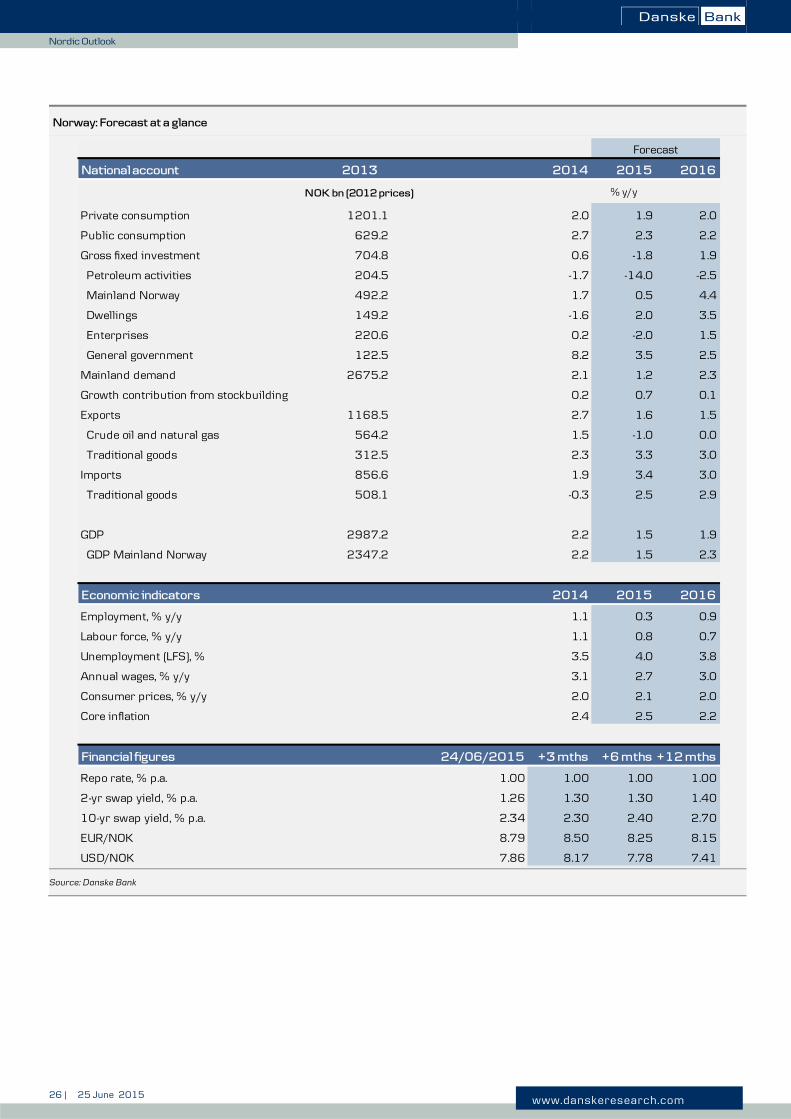

Norway: Forecast at a glance

Source: Danske Bank

National account 2013 2014 2015 2016

NOK bn (2012 prices)

Private consumption 1201.1 2.0 1.9 2.0

Public consumption 629.2 2.7 2.3 2.2

Gross fixed investment 704.8 0.6 -1.8 1.9

Petroleum activities 204.5 -1.7 -14.0 -2.5

Mainland Norway 492.2 1.7 0.5 4.4

Dwellings 149.2 -1.6 2.0 3.5

Enterprises 220.6 0.2 -2.0 1.5

General government 122.5 8.2 3.5 2.5

Mainland demand 2675.2 2.1 1.2 2.3

Growth contribution from stockbuilding 0.2 0.7 0.1

Exports 1168.5 2.7 1.6 1.5

Crude oil and natural gas 564.2 1.5 -1.0 0.0

Traditional goods 312.5 2.3 3.3 3.0

Imports 856.6 1.9 3.4 3.0

Traditional goods 508.1 -0.3 2.5 2.9

GDP 2987.2 2.2 1.5 1.9

GDP Mainland Norway 2347.2 2.2 1.5 2.3

Economic indicators 2014 2015 2016

Employment, % y/y 1.1 0.3 0.9

Labour force, % y/y 1.1 0.8 0.7

Unemployment (LFS), % 3.5 4.0 3.8

Annual wages, % y/y 3.1 2.7 3.0

Consumer prices, % y/y 2.0 2.1 2.0

Core inflation 2.4 2.5 2.2

Financial figures +3 mths +6 mths +12 mths

Repo rate, % p.a. 1.00 1.00 1.00 1.00

2-yr swap yield, % p.a. 1.26 1.30 1.30 1.40

10-yr swap yield, % p.a. 2.34 2.30 2.40 2.70

EUR/NOK 8.79 8.50 8.25 8.15

USD/NOK 7.86 8.17 7.78 7.41

24/06/2015

% y/y

Forecast

27 | 25 June 2015 www.danskeresearch.com

Nordic Outlook

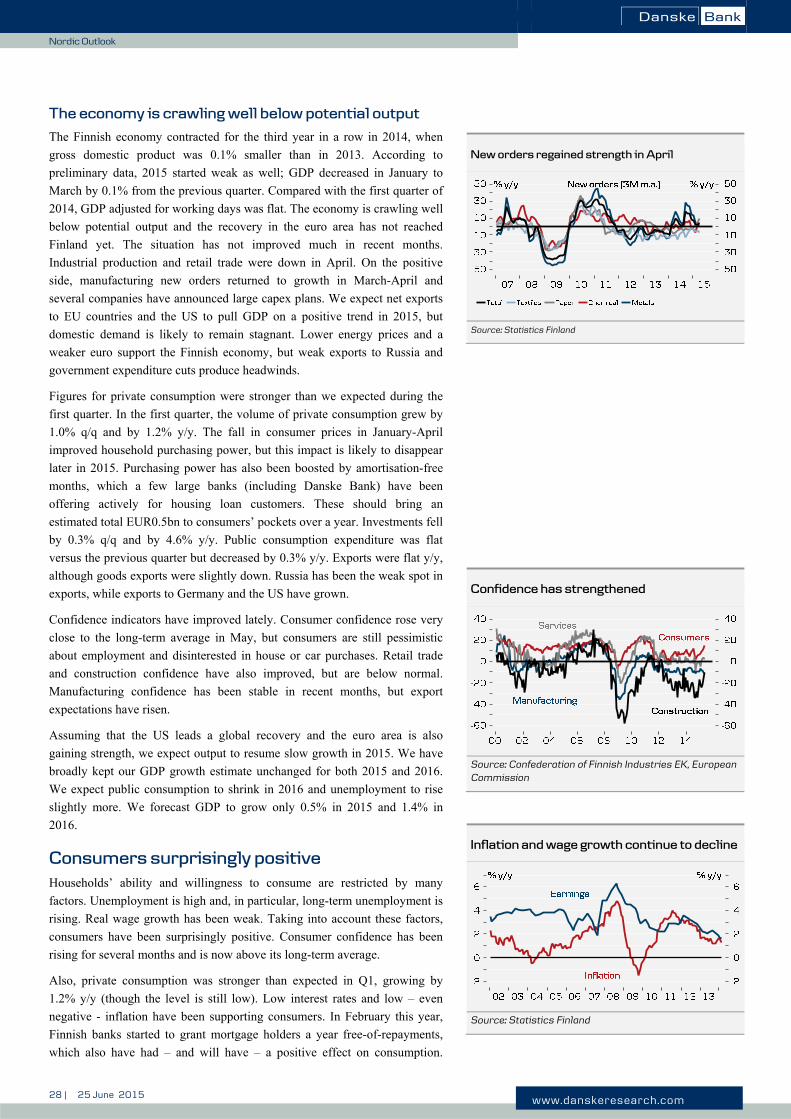

Finland Signs of a slow recovery We have largely kept our forecast unchanged and expect Finnish

GDP to grow by 0.5% in 2015. Exports have grown disappointingly

slowly, but private consumption surprised on the upside in Q1. We

continue to expect modest growth in exports on the back of growth in

western markets, despite weak Russian demand.

The outlook for domestic demand continues to be dull. Household

purchasing power remains weak, due to unemployment and a

moderate wage agreement. A fall in consumer prices boosted private

consumption in early 2015, but the impact is unlikely to last.

Investment activity is also weak, but manufacturing capex shows

early signs of a recovery.

The new conservative three-party government is reform oriented and

fiscal policy will be tightened significantly. The government aims to

adjust public finances by a total of EUR10bn with a combination of

short-term and long-term measures. An investment package worth

EUR1.6bn will soften the negative blow from frontloaded

expenditure cuts, but growth is set to slow down in 2016. Failure to

carry out major reforms could put Finland on a slow growth path

and lead to a downgrade of sovereign ratings.

The government aims to achieve a ‘social contract’ in which annual

working hours would be extended, locally negotiated wage

agreements encouraged and income tax rates cut. Unit labour costs

should fall by 5% at least. The aim is to improve cost competitiveness

by an internal devaluation. Negotiations with the labour unions are

set to be tough this summer.

The housing market outlook is dull, and prices have decreased, but

trade volumes stabilised during the spring. Cautious supply of new

housing and low interest rates are helping to keep housing prices

relatively stable.

Thanks to manageable debt levels and low interest rates, the weak

GDP figures have not translated into a full-scale depression with

mass unemployment, bankruptcies and credit losses. Loan