Economic and Commodity Outlook ASFMRA Denver, Colorado October 30, 2009

140

2009 Economic and Commodity Outlook ASFMRA Denver, Colorado October 30, 2009

-

Upload

harding-vinson -

Category

Documents

-

view

45 -

download

2

description

Economic and Commodity Outlook ASFMRA Denver, Colorado October 30, 2009. THREE BIGGEST EVENTS of LAST TWO WEEKS. October 17,2009 Purdue 26 THE Ohio State 18. October 24,2009 Purdue 24 Illinois 14. October 24,2009 Iowa State 9 Nebraska 7. General Economy. Where are we headed…. - PowerPoint PPT Presentation

Transcript of Economic and Commodity Outlook ASFMRA Denver, Colorado October 30, 2009

2009

Economic and Commodity Outlook

ASFMRA

Denver, Colorado

October 30, 2009

2009

THREE BIGGEST

EVENTS of

LAST TWO WEEKS

2009

October 17,2009

Purdue 26

THE Ohio State 18

2009

October 24,2009

Purdue 24

Illinois 14

2009

October 24,2009

Iowa State 9

Nebraska 7

2009

General Economy

Where are we headed…

2009

CASH for CLUNKERS

was

A GOOD DEAL

2009

GOT a LOT of

OBAMA BUMPER STICKERS

OFF THE ROAD

2009

Economic Overview While some economic indicators are

hinting the recession is ending – it isn’t. Unemployment remains high with little sign

of improvement. Deflation continues. This will be the decade of Three Bubbles:

1. The High Tech Bubble of 2000.2. The Housing Bubble of 2005-06.3. The Commodity Price Bubble of 2008.

2009

Name this country…

2009

Richest in the world Largest military Center of world business and finance Strongest education system World center of innovation and invention Currency the world standard of value Highest standard of living

2009

ENGLAND

2009

In 1900

2009

1 of every 8 couples married in the U.S. last year met online

2009

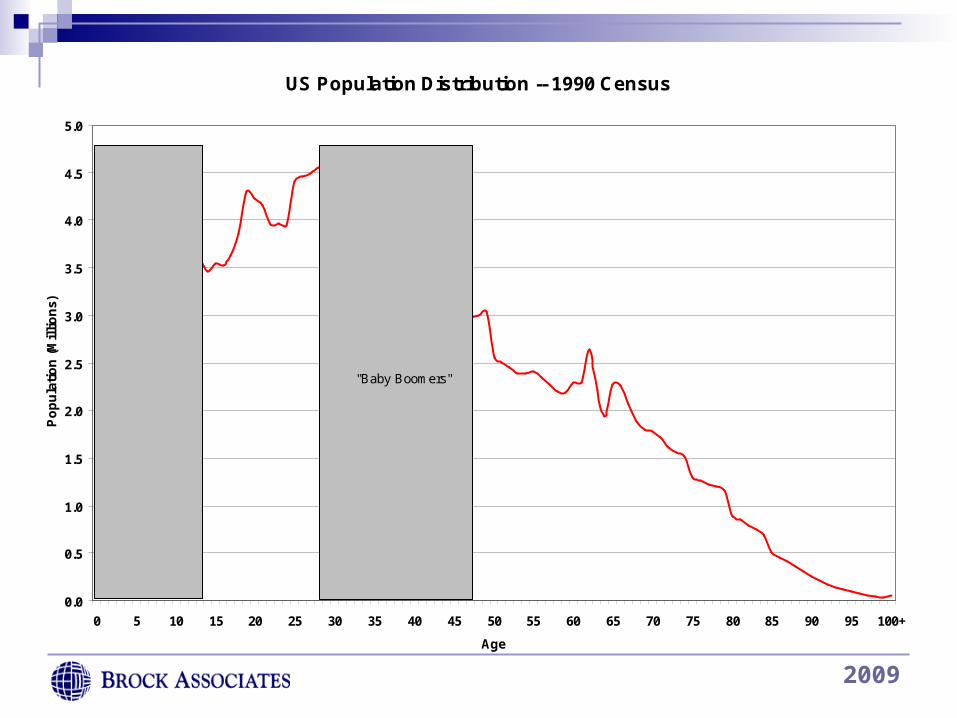

US Population Distribution -- 1990 Census

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100+

Age

Po

pu

lati

on

(M

illi

on

s)

"Baby Boomers""Boomlet"

2009

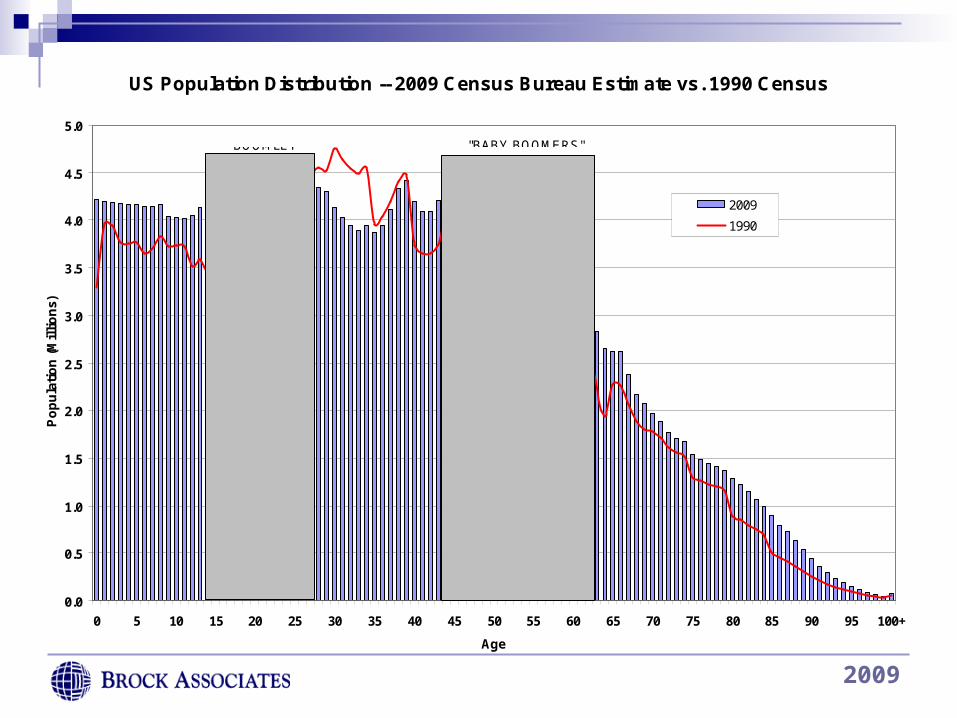

US Population Distribution -- 2009 Census Bureau Estimate vs. 1990 Census

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100+

Age

Po

pu

lati

on

(M

illi

on

s)

2009

1990

"BABY BOOMERS""BOOMLET"

2009

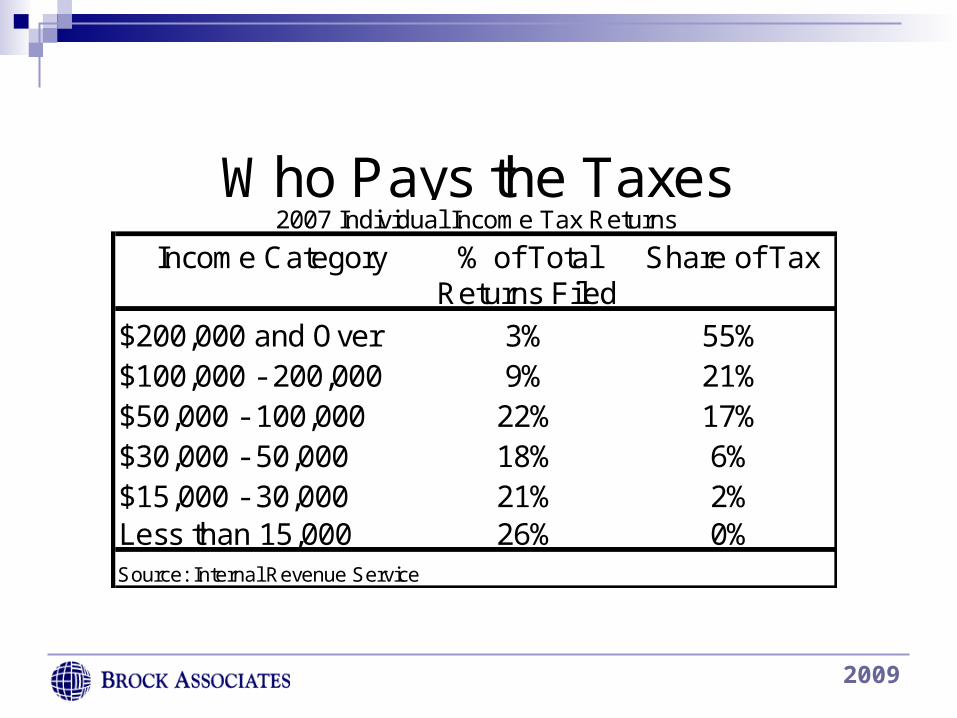

Income Category % of Total Share of TaxReturns Filed

$200,000 and Over 3% 55%$100,000 - 200,000 9% 21%$50,000 - 100,000 22% 17%$30,000 - 50,000 18% 6%$15,000 - 30,000 21% 2%Less than 15,000 26% 0%Source: Internal Revenue Service

Who Pays the Taxes2007 Individual Income Tax Returns

2009

2009

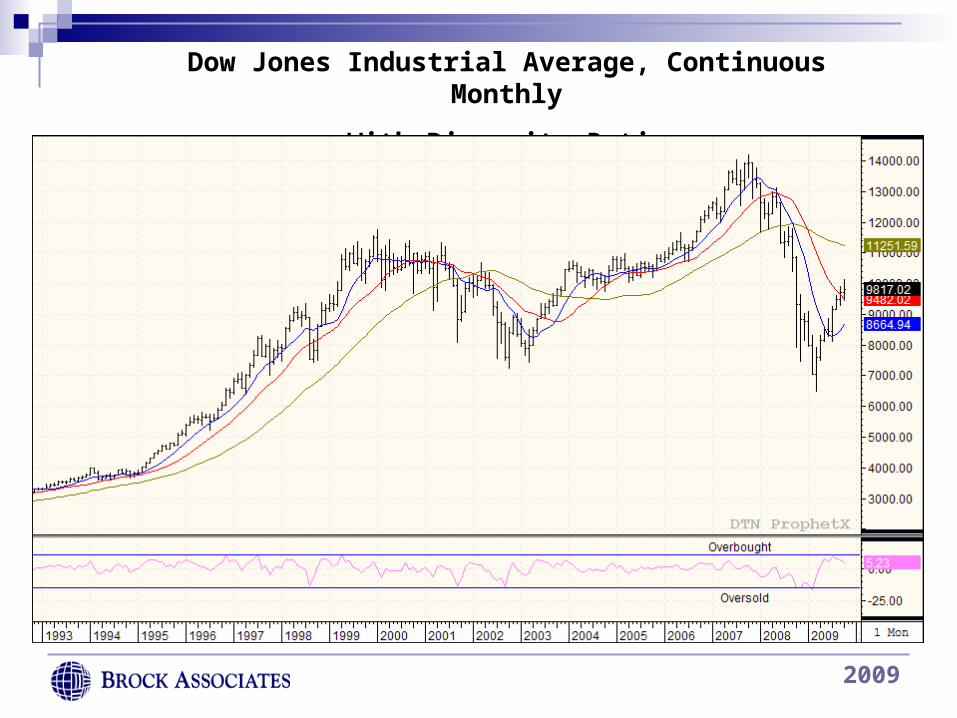

Dow Jones Industrial Average, Continuous Monthly

With Disparity Ratio

2009

Dow Jones Industrial Average, Daily

2009

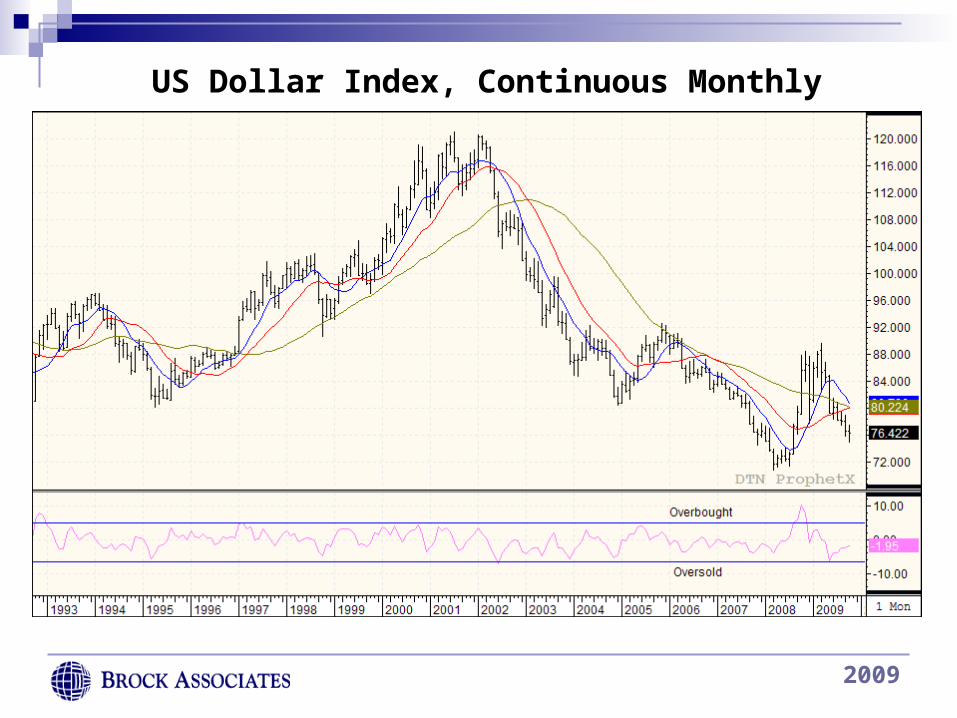

US Dollar Index, Continuous Monthly

2009

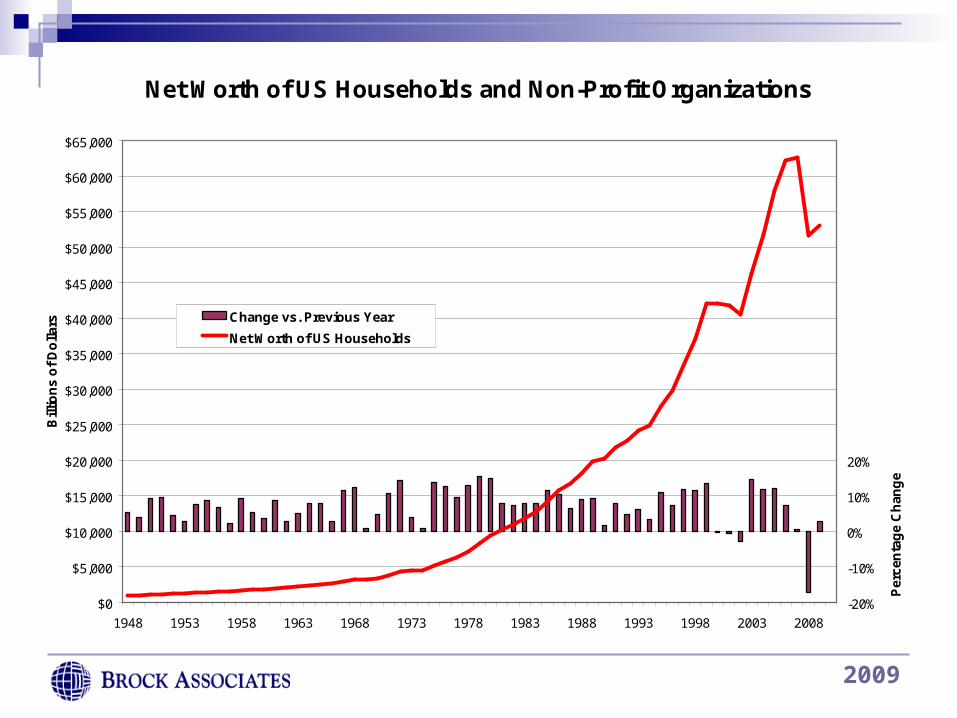

Net Worth of US Households and Non-Profit Organizations

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

$50,000

$55,000

$60,000

$65,000

1948 1953 1958 1963 1968 1973 1978 1983 1988 1993 1998 2003 2008

Bill

ion

s o

f D

olla

rs

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

Per

cen

tag

e C

han

ge

Change vs. Previous Year

Net Worth of US Households

Source: US Federal Reserve, Annual Data except 2009 through Second Quarter

2009

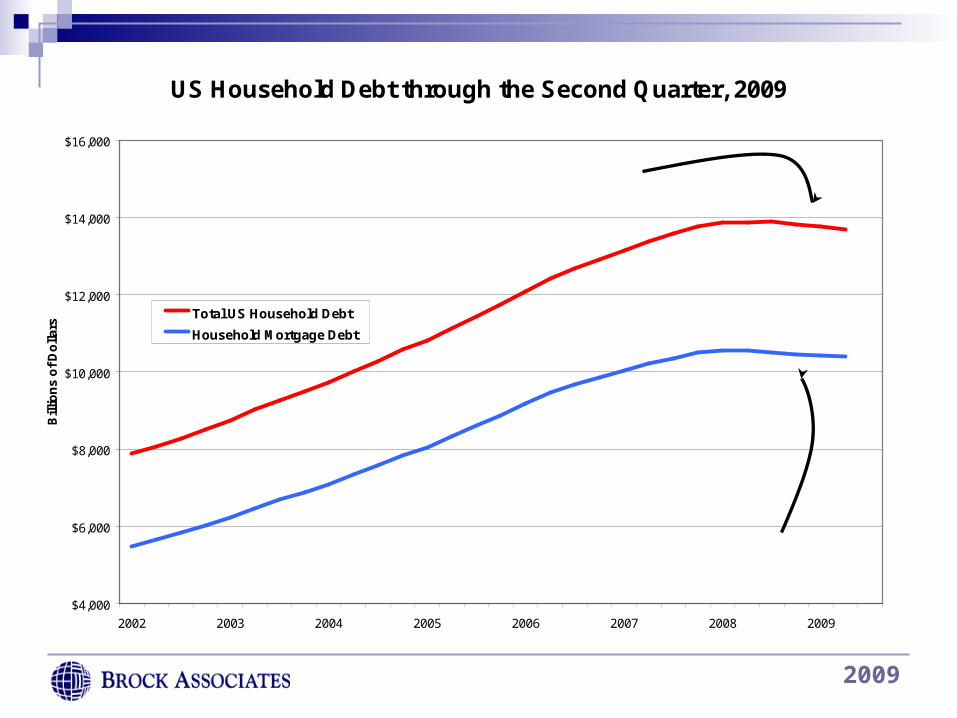

US Household Debt through the Second Quarter, 2009

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

2002 2003 2004 2005 2006 2007 2008 2009

Bill

ion

s o

f D

olla

rs

Total US Household Debt

Household Mortgage Debt

Source: US Federal Reserve

The third quarter 2008 drop from $13.943 trillion to $13.914 trillion was the first quarterly decline in Total US Household Debt since the data began being recorded (1952). Total Household debt has now declined for four consecutive quarters, dropping by $181 billion dollars.

Total Household debt has declined for five consecutive quarters, dropping by $157.4 billion dollars.

2009

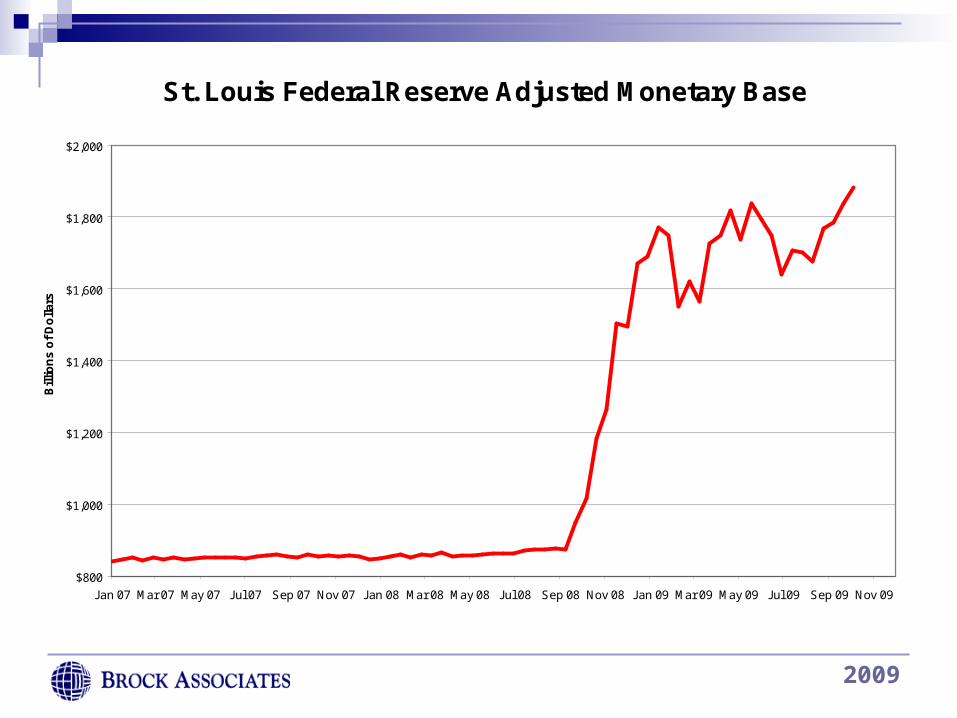

St. Louis Federal Reserve Adjusted Monetary Base

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

Jan 07 Mar 07 May 07 Jul 07 Sep 07 Nov 07 Jan 08 Mar 08 May 08 Jul 08 Sep 08 Nov 08 Jan 09 Mar 09 May 09 Jul 09 Sep 09 Nov 09

Bil

lio

ns

of

Do

llar

s

2009

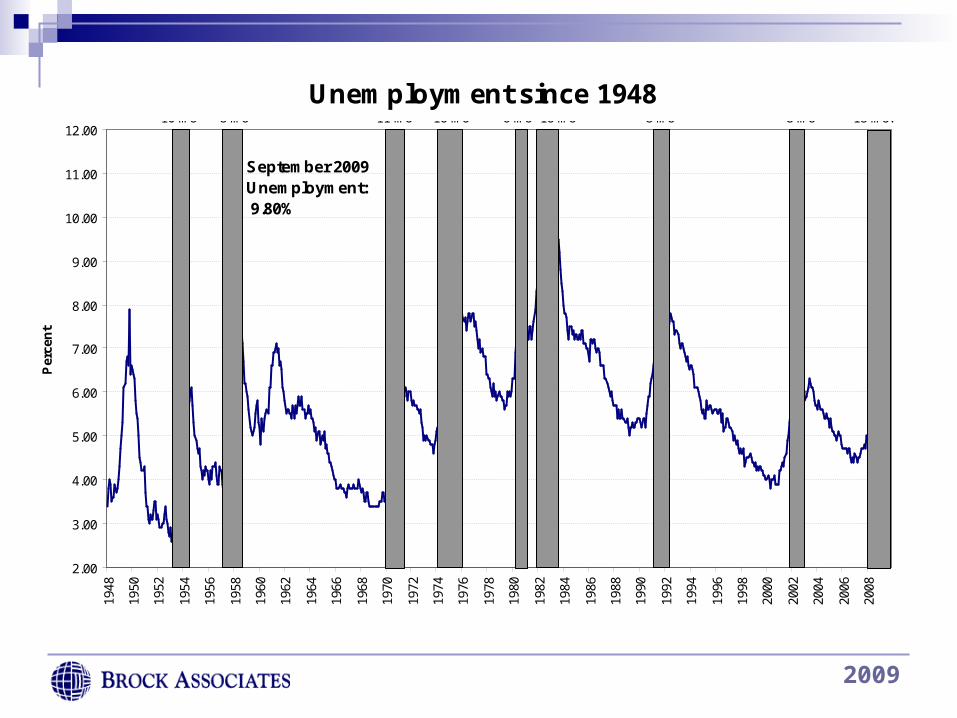

Unemployment since 1948

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

11.00

12.00

1948

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

Per

cen

t

September 2009 Unemployment: 9.80%

Source: Bureau of Labor Statistics Gray shaded area indicate recessions

8 mo8 mo6 mo 16 mo16 mo11 mo8 mo10 mo 18 mo?

2009

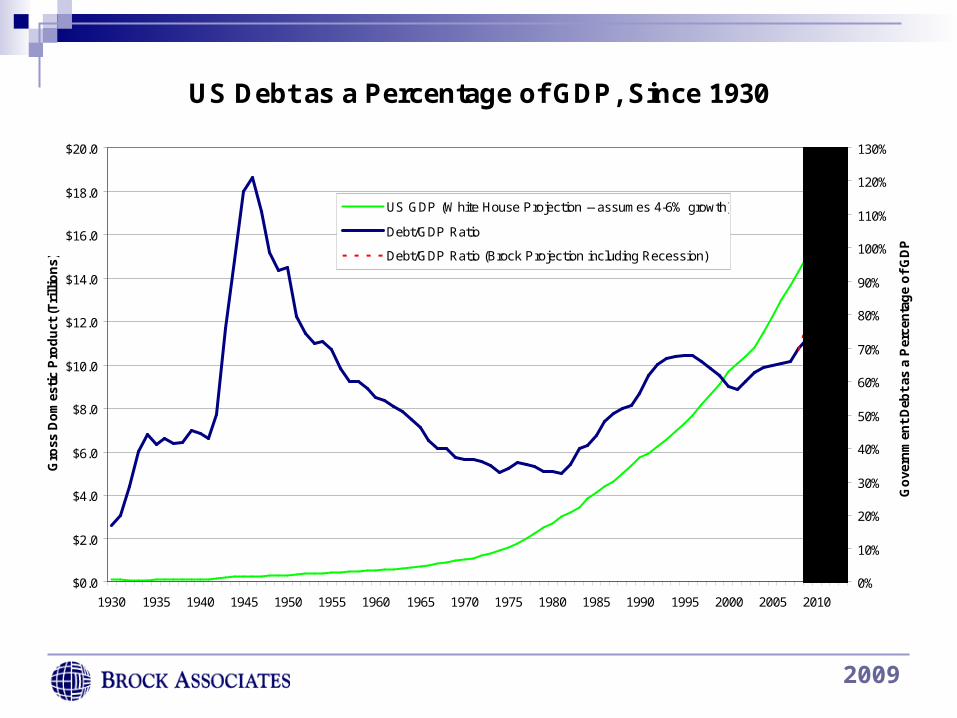

US Debt as a Percentage of GDP, Since 1930

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

$16.0

$18.0

$20.0

1930 1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Gro

ss D

om

esti

c P

rod

uct

(T

rill

ion

s)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

Go

vern

men

t D

ebt

as a

Per

cen

tag

e o

f G

DP

US GDP (White House Projection -- assumes 4-6% growth)

Debt/GDP Ratio

Debt/GDP Ratio (Brock Projection including Recession)

Source: White House, US Treasury, Brock Associates estimates Brock Associates Projections

2009

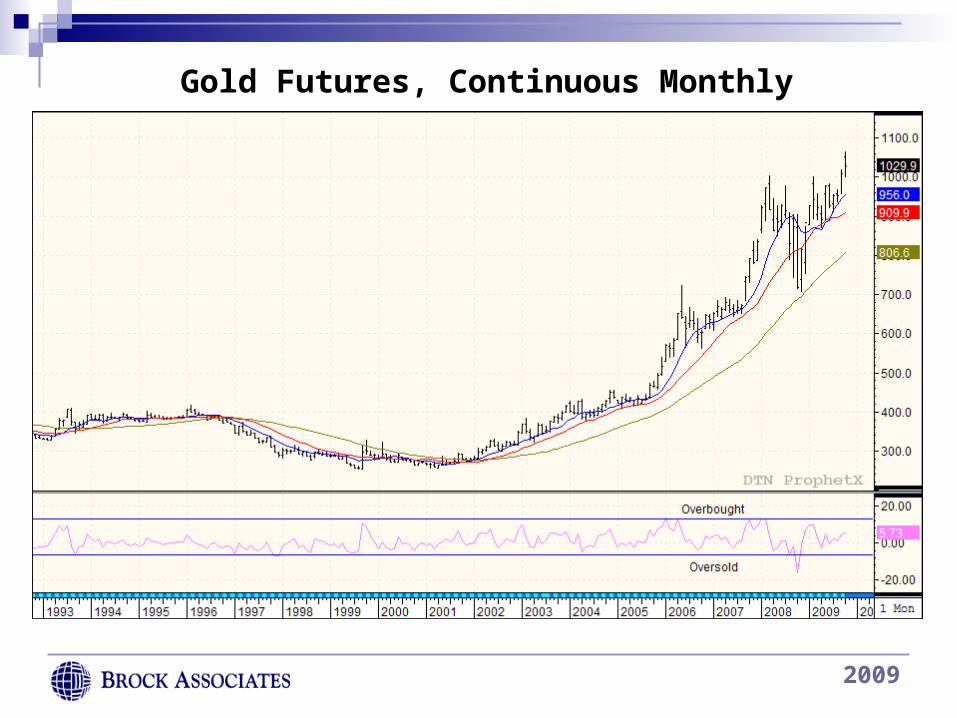

Gold Futures, Continuous Monthly

2009

GCZ9

2009

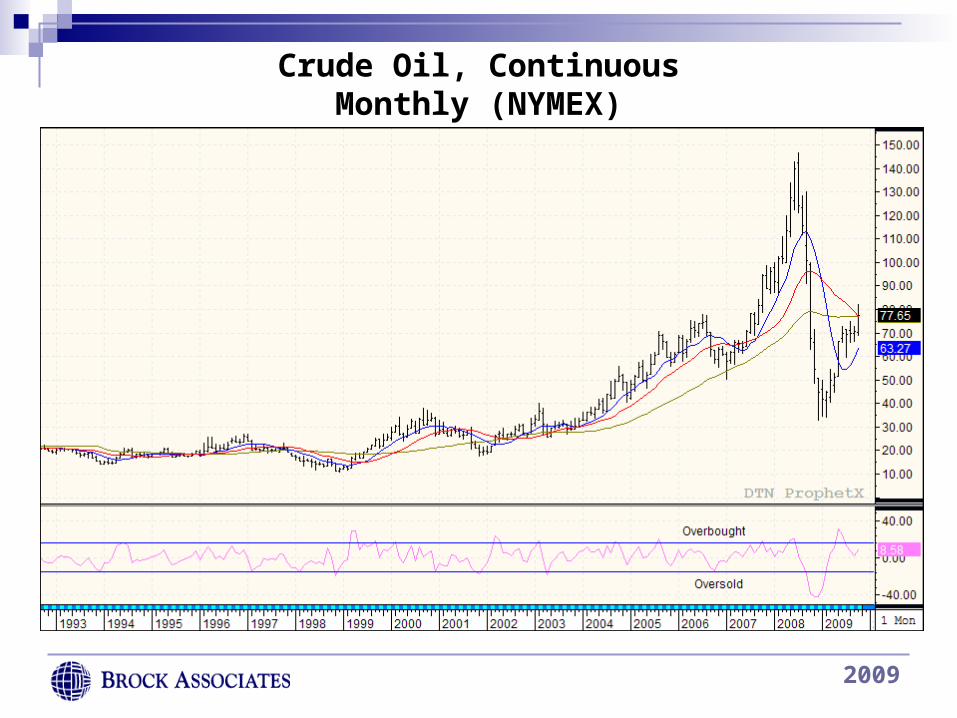

Crude Oil, Continuous Monthly (NYMEX)

2009

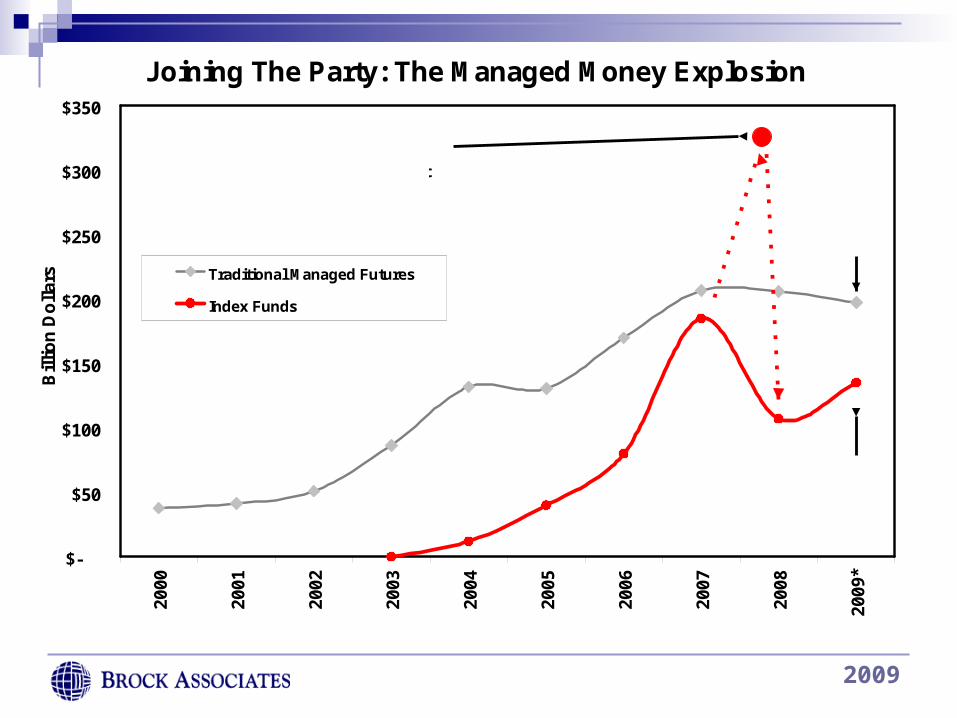

Joining The Party: The Managed Money Explosion

$-

$50

$100

$150

$200

$250

$300

$350

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

*

Bil

lio

n D

oll

ars Traditional Managed Futures

Index Funds

Source: The Barclay Group, Brock estimates

As of June 24, 2008$338 Billion wasunder management by index funds

$135.1 Billion as of October 20, 2009(Brock Estimate)

$197.3 Billionas of

October 20 2009

(Brock Estimate)

2009

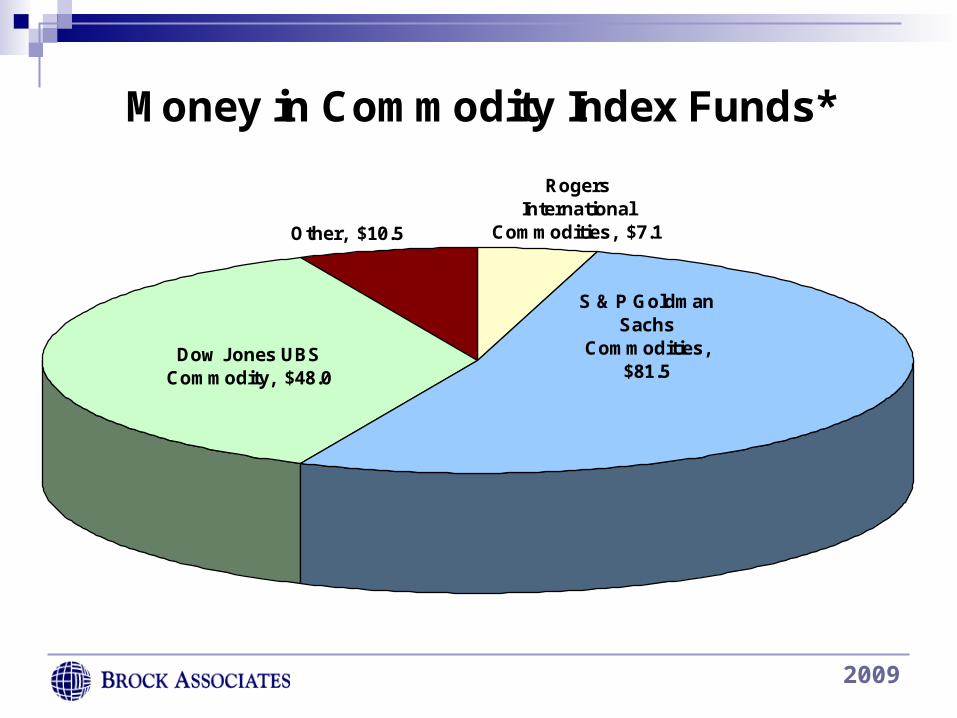

Money in Commodity Index Funds*

Rogers International

Commodities, $7.1 Other, $10.5

S & P Goldman Sachs

Commodities, $81.5

Dow Jones UBS Commodity, $48.0

*Figures are the industry's best estimate, as of October 20, 2009

2009

Commodity Index Funds

44.0%

66.9%

55.0%

39.0%

19.7%

13.8%

21.0%

22.5%

13.0%

3.0%

5.6%

6.7% 7.0%

12.2%

3.9%

21.0%

21.1%

9.8%

31.1%22.5% 20.0%

33.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Rogers InternationalCommodities

S & P Goldman SachsCommodities

Dow Jones UBSCommodity

Deutsche Bank LiquidCommodity

Reuters/Jefferies CRB

Energy Grain Livestock Softs Metals

8.2%

2009

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

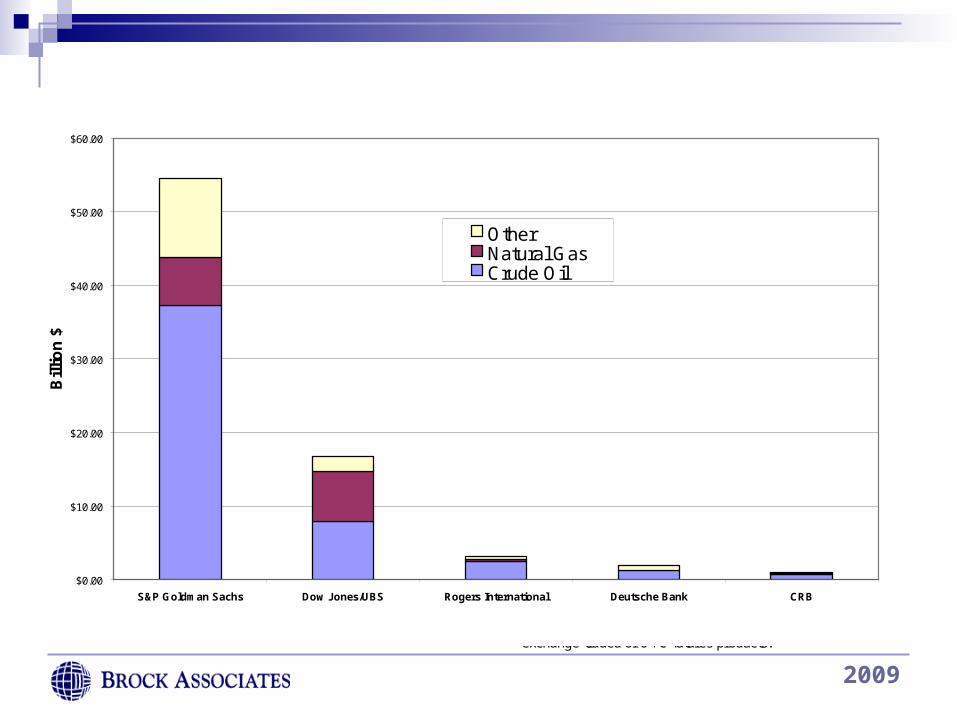

S&P Goldman Sachs Dow Jones/UBS Rogers International Deutsche Bank CRB

Bil

lio

n $

OtherNatural GasCrude Oil

Index Fund Buying Power:Estimated Energy Market Holdings by Investments Tracking Major Indexes

Source: Brock Associates Estimates Estimate includes holdings of all energy index components and may include exchange-traded or OTC futures products.

2009

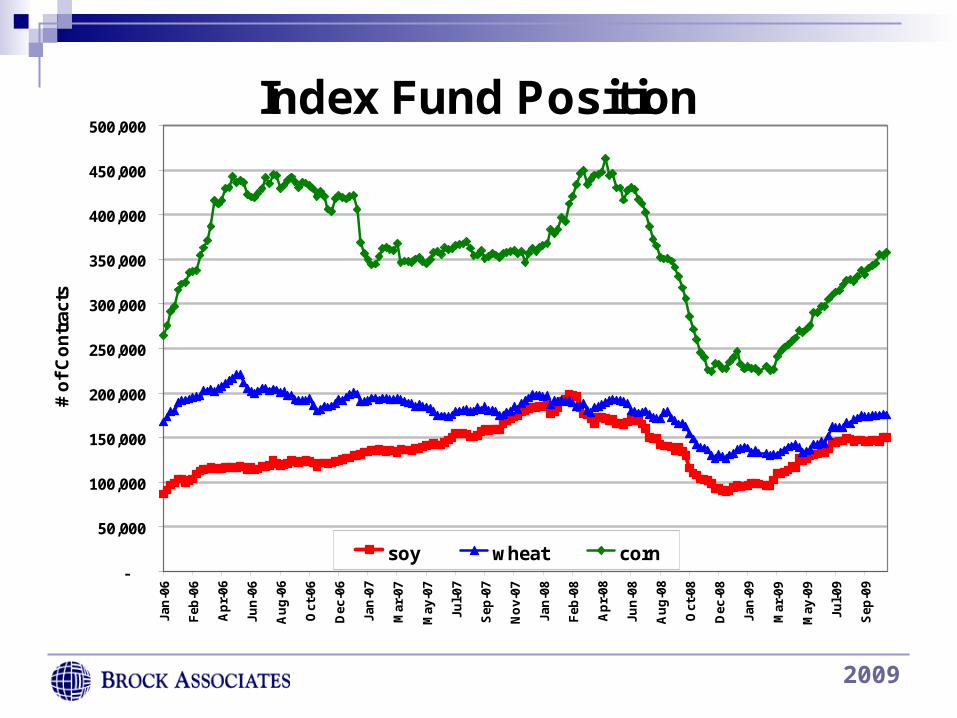

Index Fund Position

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

Jan

-06

Feb

-06

Ap

r-06

Jun

-06

Au

g-0

6

Oct

-06

Dec

-06

Jan

-07

Mar

-07

May

-07

Jul-

07

Sep

-07

No

v-07

Jan

-08

Feb

-08

Ap

r-08

Jun

-08

Au

g-0

8

Oct

-08

Dec

-08

Jan

-09

Mar

-09

May

-09

Jul-

09

Sep

-09

# o

f C

on

trac

ts

soy wheat corn

2009

Index Fund Net Position as % of Open Interest

0%

10%

20%

30%

40%

50%

Corn Ch. Wheat Soybeans Soy Oil Cattle Cotton Hogs KC Wheat

2009

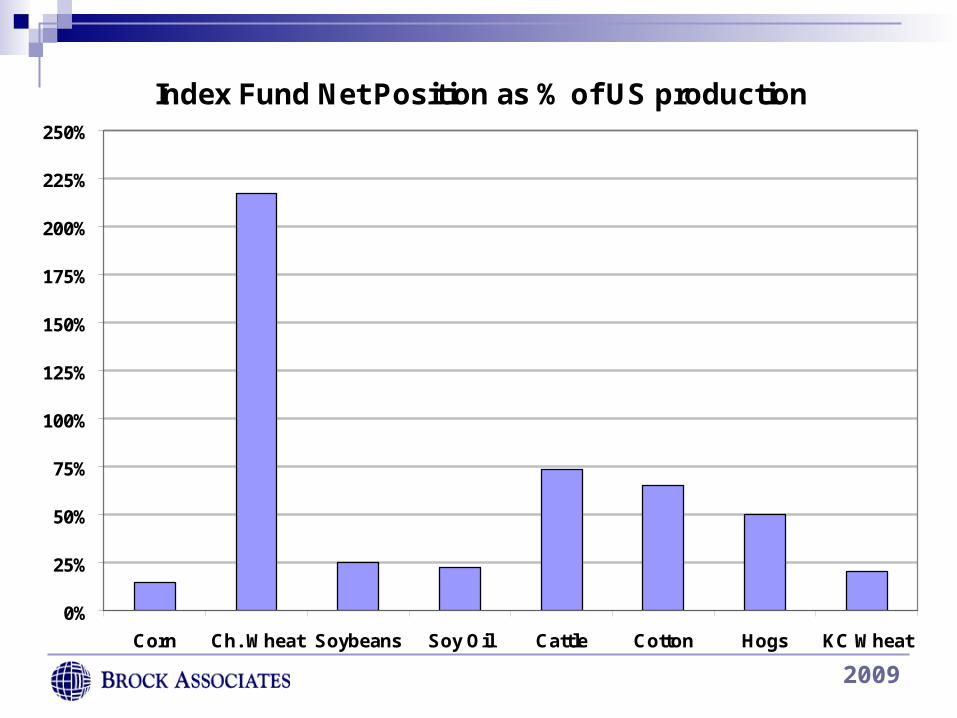

Index Fund Net Position as % of US production

0%

25%

50%

75%

100%

125%

150%

175%

200%

225%

250%

Corn Ch. Wheat Soybeans Soy Oil Cattle Cotton Hogs KC Wheat

2009

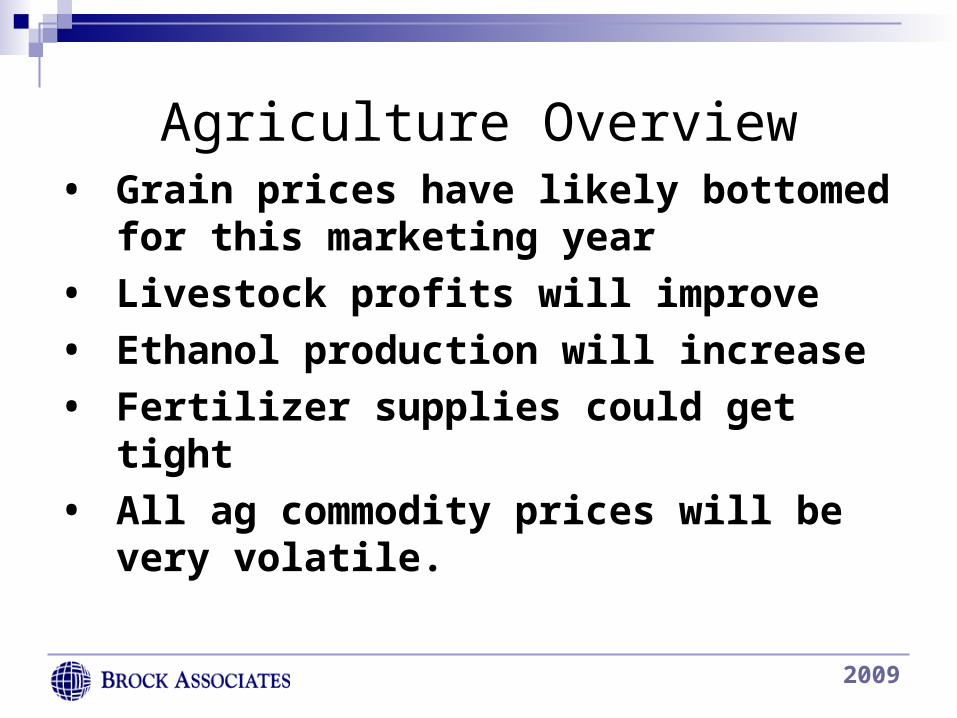

Agriculture Overview• Grain prices have likely bottomed for

this marketing year

• Livestock profits will improve

• Ethanol production will increase

• Fertilizer supplies could get tight

• All ag commodity prices will be very volatile.

2009

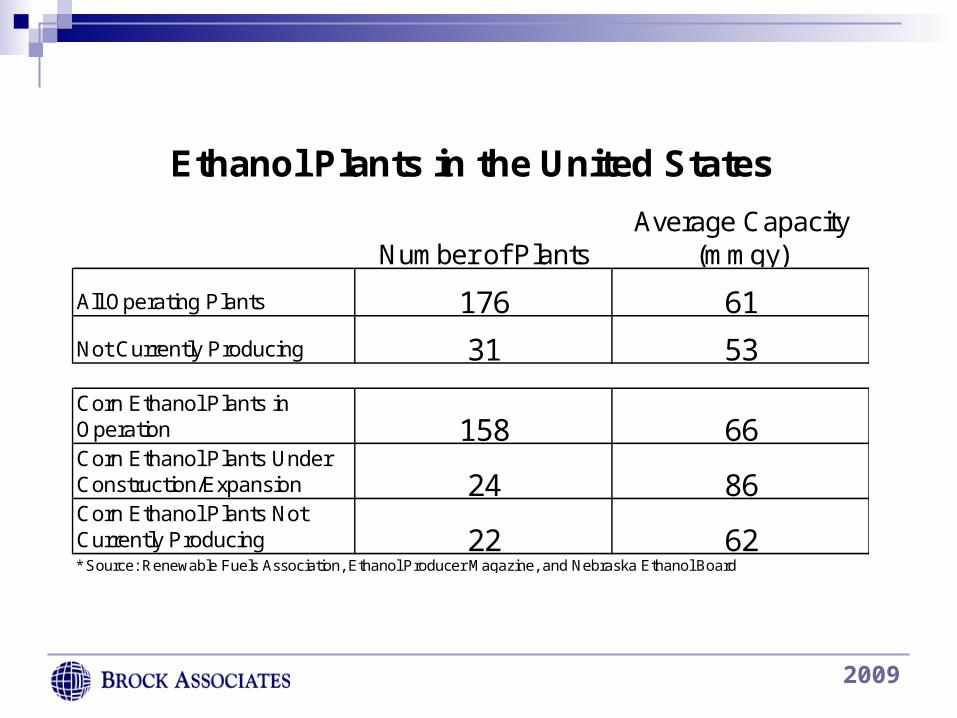

Number of PlantsAverage Capacity

(mmgy)

All Operating Plants 176 61

Not Currently Producing 31 53

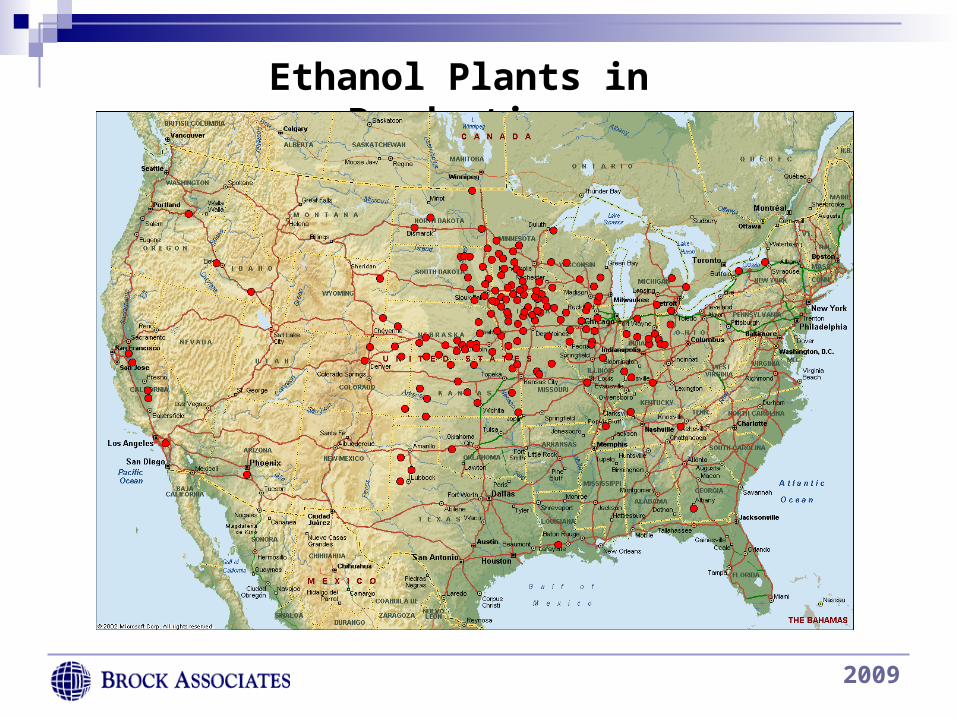

Corn Ethanol Plants in Operation 158 66Corn Ethanol Plants Under Construction/Expansion 24 86Corn Ethanol Plants Not Currently Producing 22 62* Source: Renewable Fuels Association, Ethanol Producer Magazine, and Nebraska Ethanol Board

Ethanol Plants in the United States

2009

Ethanol Plants in Production

2009

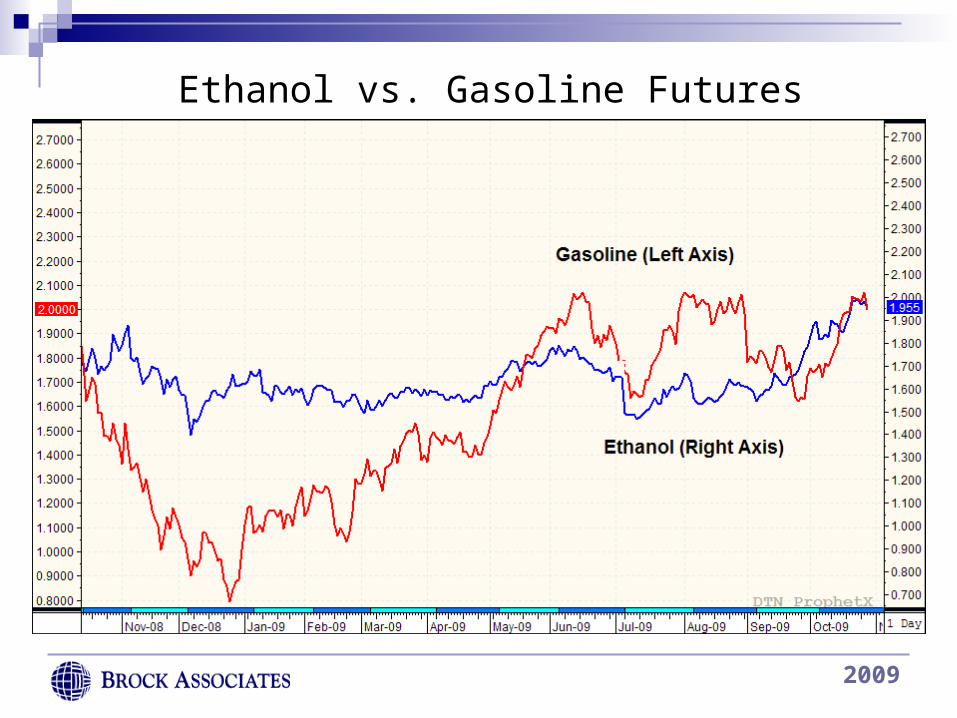

Ethanol vs. Gasoline Futures

2009

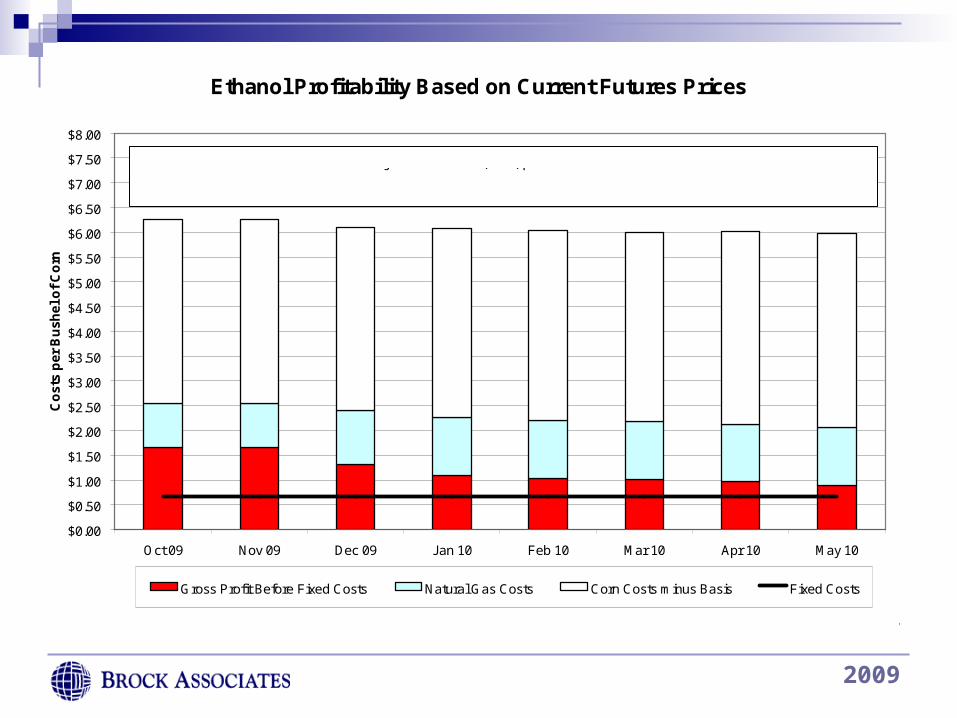

Ethanol Profitability Based on Current Futures Prices

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

$6.50

$7.00

$7.50

$8.00

Oct 09 Nov 09 Dec 09 Jan 10 Feb 10 Mar 10 Apr 10 May 10

Co

sts

per

Bu

shel

of

Co

rn

Gross Profit Before Fixed Costs Natural Gas Costs Corn Costs minus Basis Fixed Costs

Gross profit must exceed Fixed Costs line to realize a net profit

Per Bushel of Corn

Basis calculated as current average of 30 Midwest delivery points,Fixed costs assumed to be 67 cents/bushel

Projected Net Profit (Loss) per bushel of corn

$0.976 $0.976 $0.634 $0.428 $0.363 $0.342 $0.288 $0.221

2009

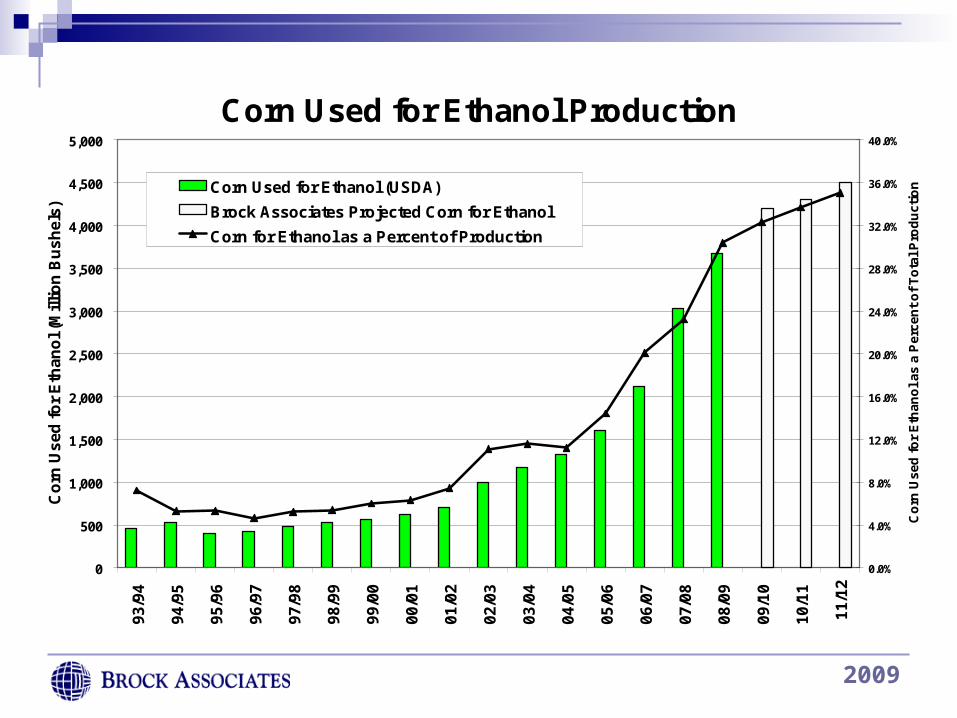

Corn Used for Ethanol Production

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,0009

3/9

4

94

/95

95

/96

96

/97

97

/98

98

/99

99

/00

00

/01

01

/02

02

/03

03

/04

04

/05

05

/06

06

/07

07

/08

08

/09

09

/10

10

/11

11

/12

Co

rn U

se

d f

or

Eth

ano

l (M

illi

on

Bu

sh

els

)

0.0%

4.0%

8.0%

12.0%

16.0%

20.0%

24.0%

28.0%

32.0%

36.0%

40.0%

Co

rn U

sed

fo

r E

than

ol

as

a P

erc

ent

of

To

tal

Pro

du

ctio

nCorn Used for Ethanol (USDA)

Brock Associates Projected Corn for Ethanol

Corn for Ethanol as a Percent of Production

Brock 2009/10 Projection: 4,200 Million Bushels

2009

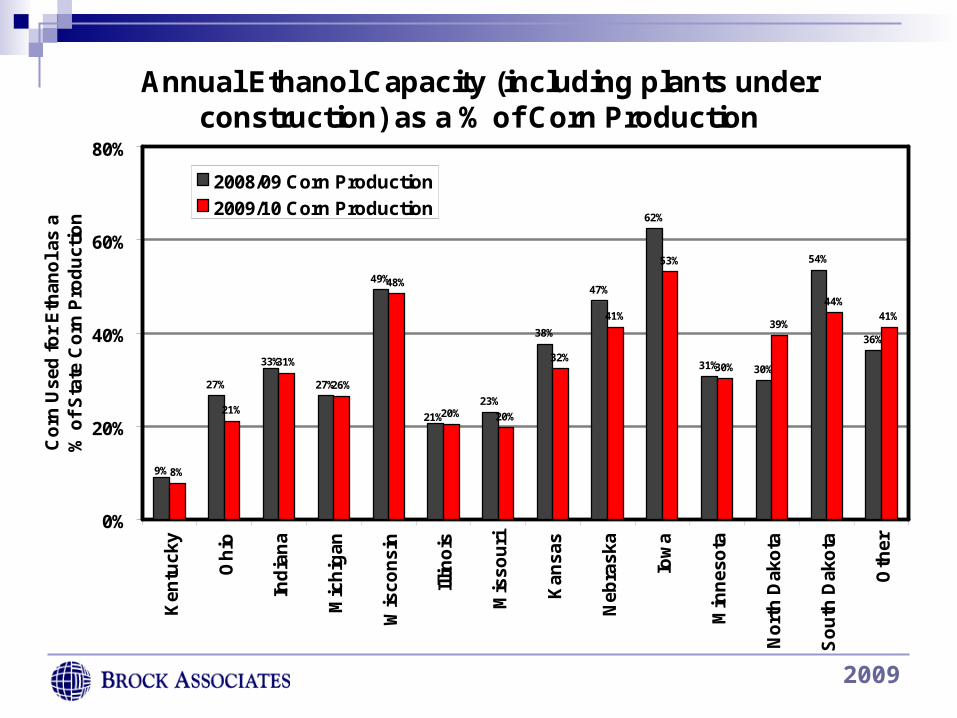

Annual Ethanol Capacity (including plants under construction) as a % of Corn Production

27% 27%

49%

23%

38%

47%

62%

31% 30%

54%

36%

8%

21%

31%

26%

48%

20% 20%

32%

41%

53%

30%

39%

44%41%

9%

33%

21%

0%

20%

40%

60%

80%K

entu

cky

Oh

io

Ind

ian

a

Mic

hig

an

Wis

con

sin

Illin

ois

Mis

sou

ri

Kan

sas

Neb

rask

a

Iow

a

Min

nes

ota

No

rth

Dak

ota

So

uth

Dak

ota

Oth

er

Co

rn U

sed

fo

r E

than

ol a

s a

% o

f S

tate

Co

rn P

rod

uct

ion

2008/09 Corn Production

2009/10 Corn Production

2009

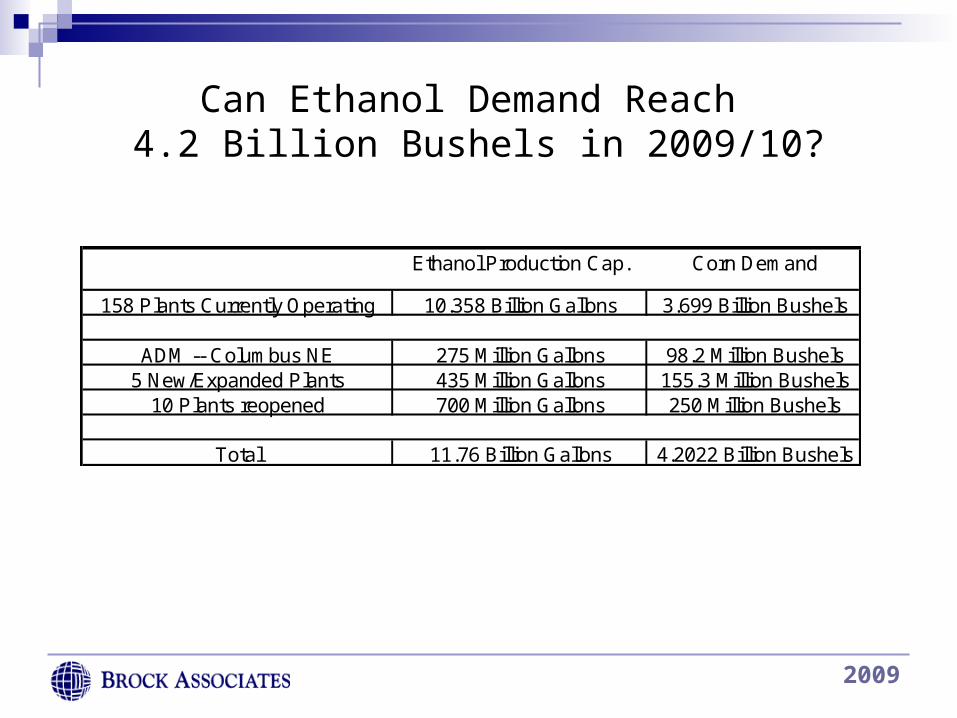

Can Ethanol Demand Reach 4.2 Billion Bushels in 2009/10?

Ethanol Production Cap. Corn Demand

158 Plants Currently Operating 10.358 Billion Gallons 3.699 Billion Bushels

ADM -- Columbus NE 275 Million Gallons 98.2 Million Bushels5 New/Expanded Plants 435 Million Gallons 155.3 Million Bushels

10 Plants reopened 700 Million Gallons 250 Million Bushels

Total 11.76 Billion Gallons 4.2022 Billion Bushels

2009

2009

Natural Gas Futures, Continuous Monthly

2009

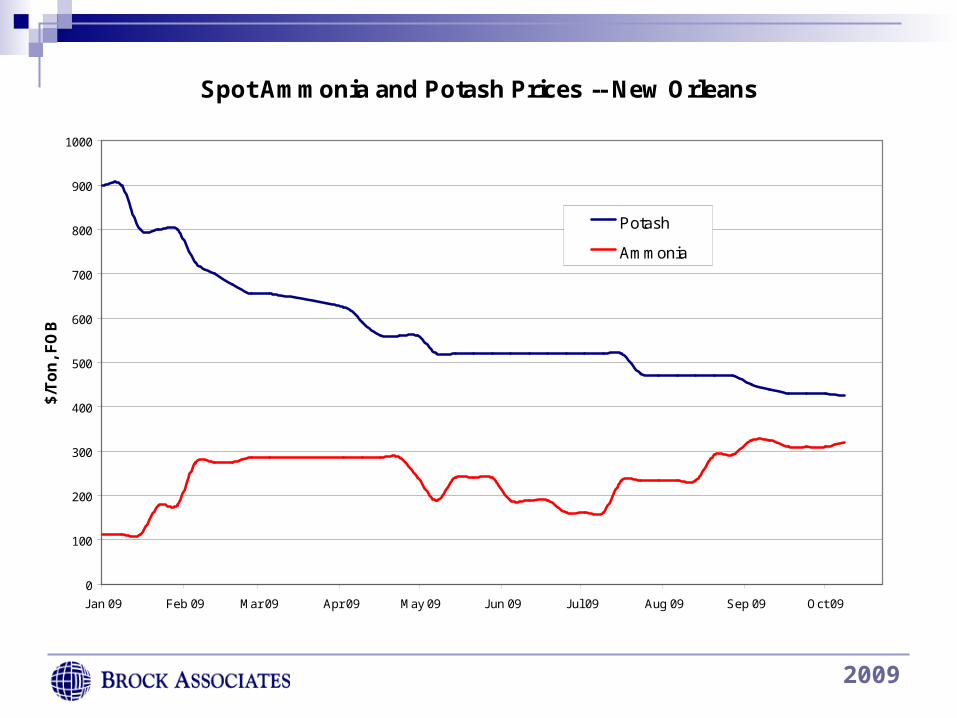

Spot Ammonia and Potash Prices -- New Orleans

0

100

200

300

400

500

600

700

800

900

1000

Jan 09 Feb 09 Mar 09 Apr 09 May 09 Jun 09 Jul 09 Aug 09 Sep 09 Oct 09

$/T

on

, F

OB

Potash

Ammonia

Source: Midwest Fertilizer Insight

2009

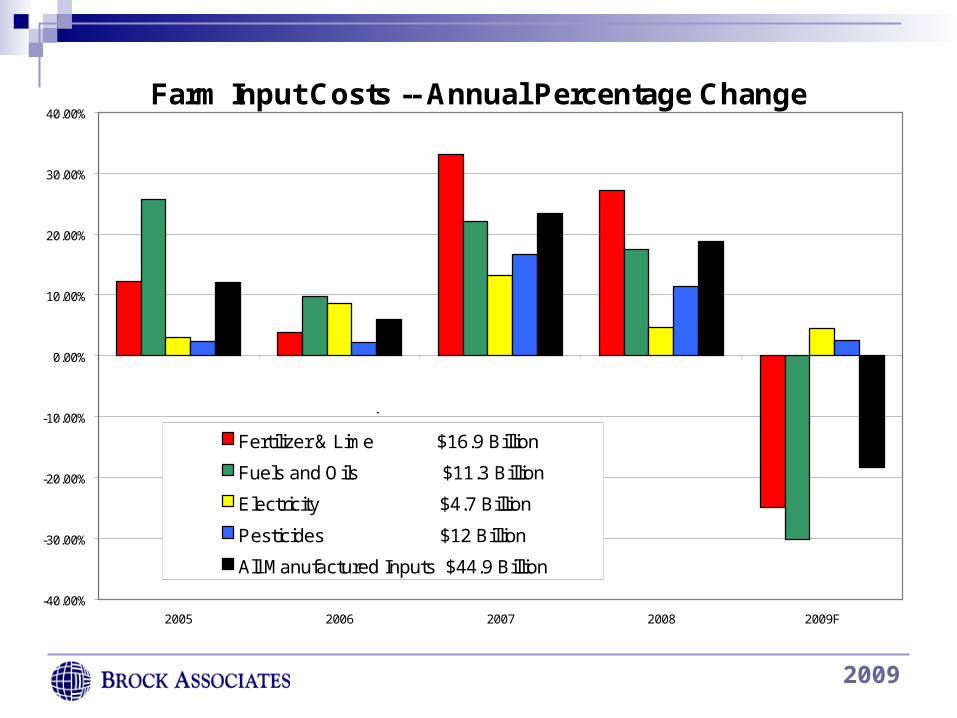

Farm Input Costs -- Annual Percentage Change

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

2005 2006 2007 2008 2009F

Fertilizer & Lime $16.9 Billion

Fuels and Oils $11.3 Billion

Electricity $4.7 Billion

Pesticides $12 Billion

All Manufactured Inputs $44.9 Billion

2009 Total Expenditures

Source: USDA

2009

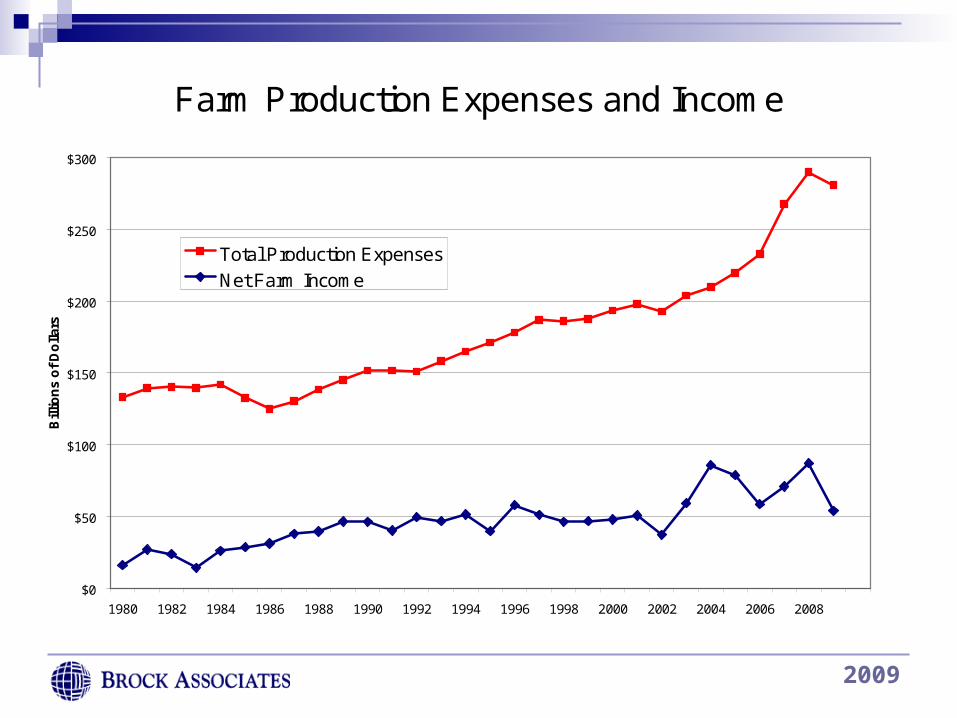

Farm Production Expenses and Income

$0

$50

$100

$150

$200

$250

$300

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Bill

ion

s o

f D

olla

rs

Total Production Expenses

Net Farm Income

Source: USDA

2009

2009

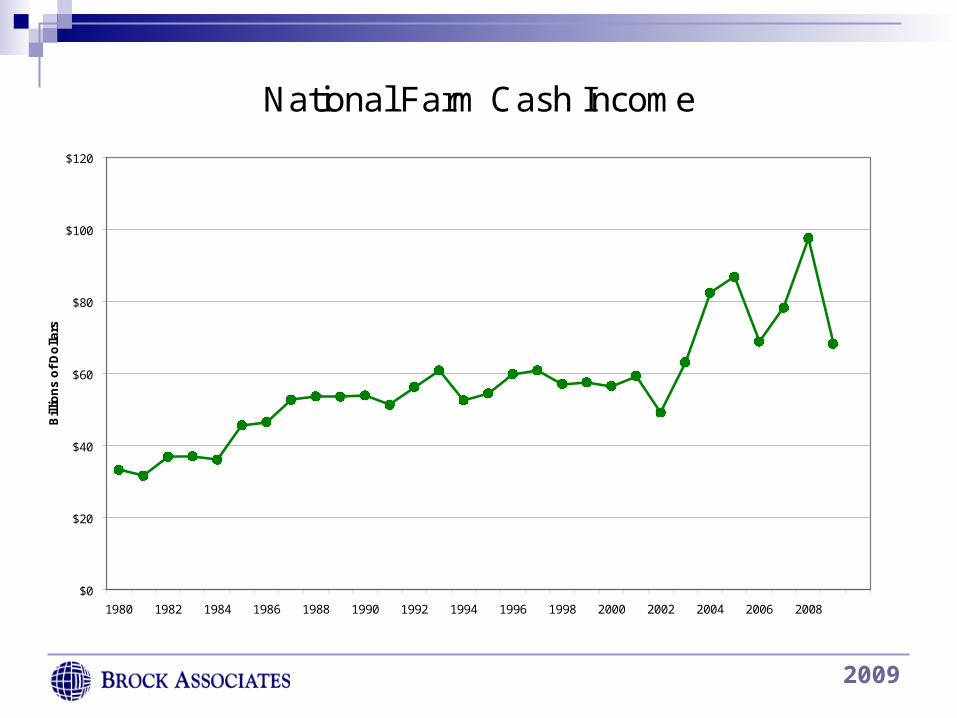

National Farm Cash Income

$0

$20

$40

$60

$80

$100

$120

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Bill

ion

s o

f D

olla

rs

Source: USDA

2009Proj

2009

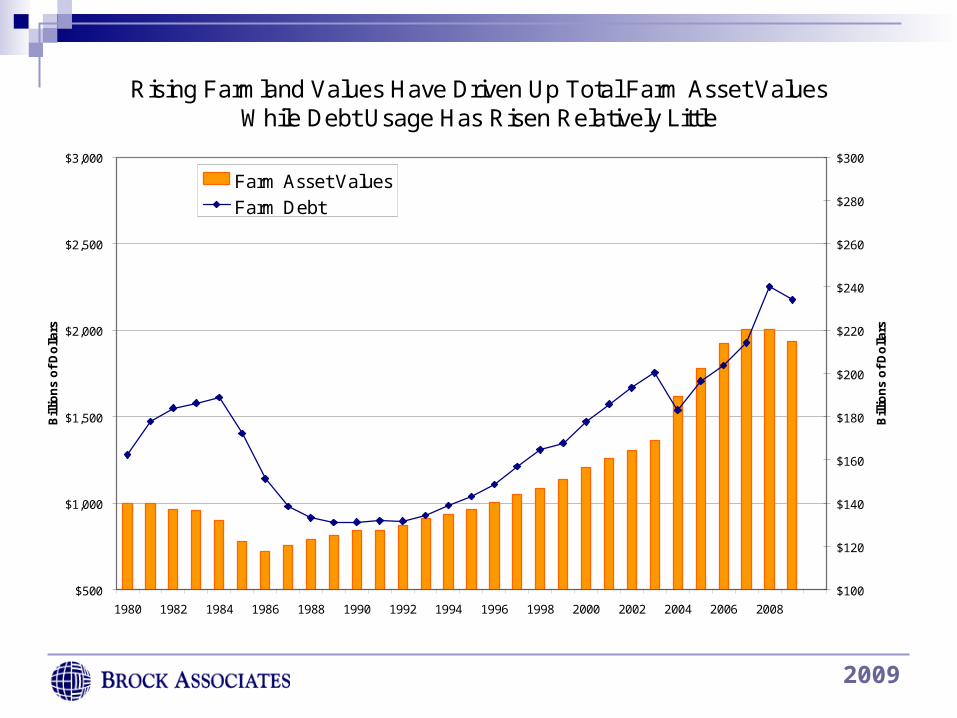

Rising Farmland Values Have Driven Up Total Farm Asset Values While Debt Usage Has Risen Relatively Little

$500

$1,000

$1,500

$2,000

$2,500

$3,000

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Bill

ion

s o

f D

olla

rs

$100

$120

$140

$160

$180

$200

$220

$240

$260

$280

$300

Bill

ion

s o

f D

olla

rs

Farm Asset Values

Farm Debt

Source: USDA

2009

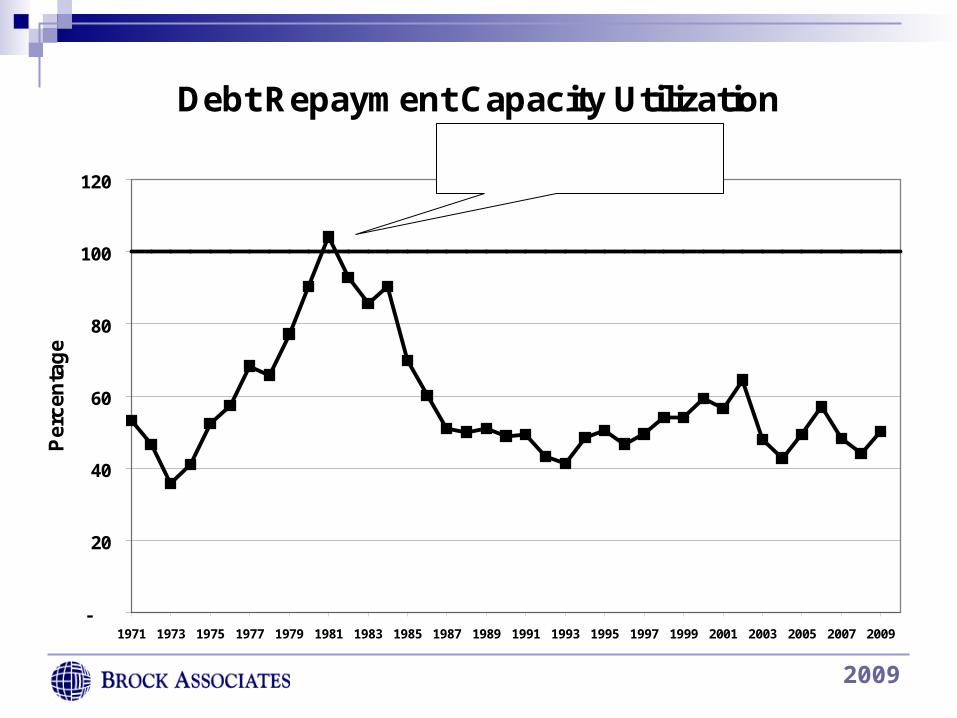

Debt Repayment Capacity Utilization

-

20

40

60

80

100

120

1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

Per

cen

tag

e

Debt use exceeded repayment capacity during 1980-82

Source: Agriculture Income and Finance Outlook

2009

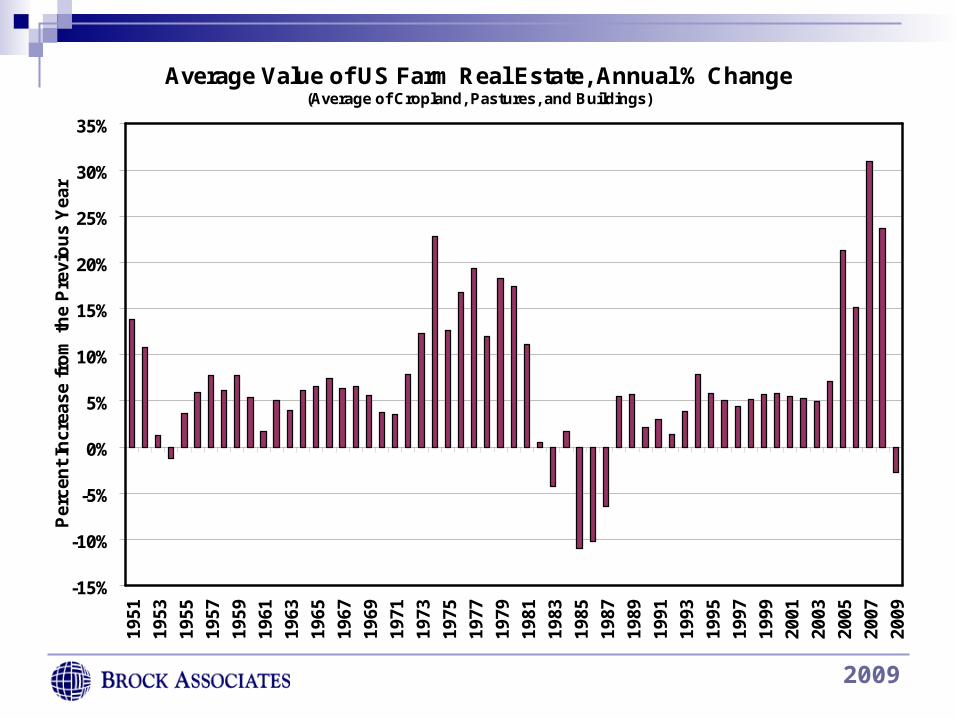

Average Value of US Farm Real Estate, Annual % Change(Average of Cropland, Pastures, and Buildings)

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%19

51

1953

1955

1957

1959

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

Per

cen

t In

crea

se f

rom

th

e P

revi

ou

s Y

ear

Source: USDA

2009

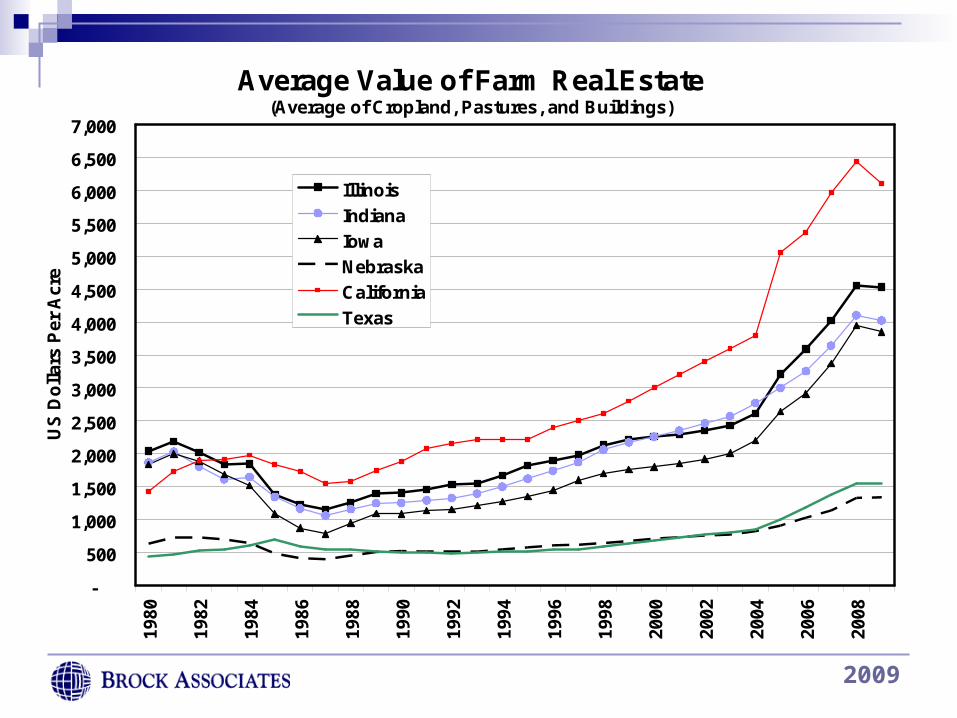

Average Value of Farm Real Estate(Average of Cropland, Pastures, and Buildings)

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

7,00019

80

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

US

Do

llar

s P

er A

cre

Illinois

Indiana

Iowa

Nebraska

California

Texas

Source: USDA, Brock Associates Estimates

2009

2009

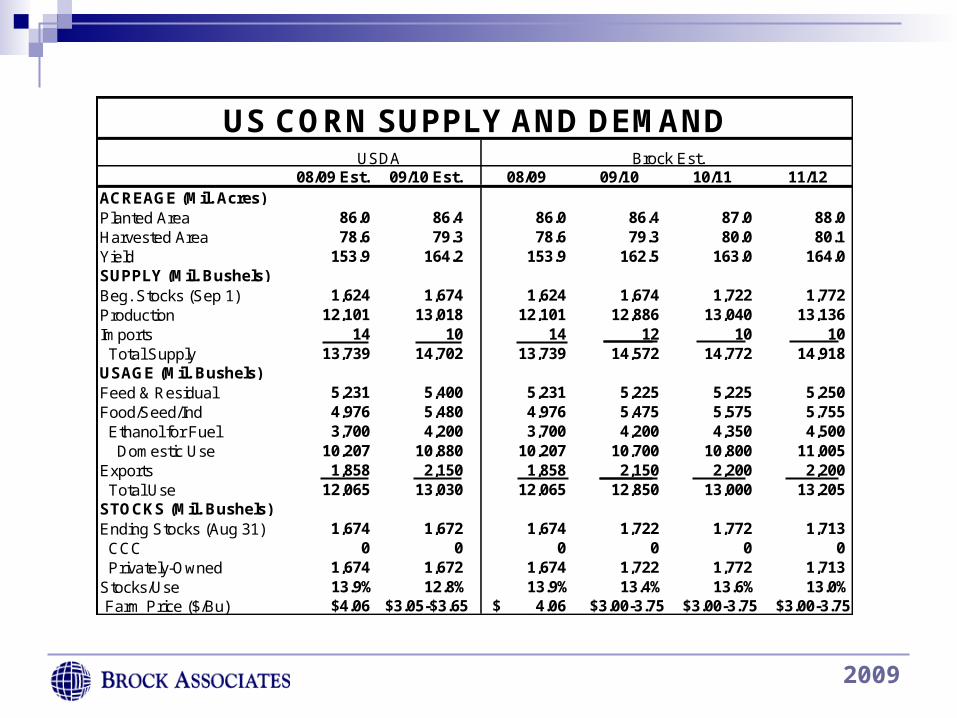

08/09 Est. 09/10 Est. 08/09 09/10 10/11 11/12ACREAGE (Mil. Acres)Planted Area 86.0 86.4 86.0 86.4 87.0 88.0Harvested Area 78.6 79.3 78.6 79.3 80.0 80.1Yield 153.9 164.2 153.9 162.5 163.0 164.0SUPPLY (Mil. Bushels)Beg. Stocks (Sep 1) 1,624 1,674 1,624 1,674 1,722 1,772Production 12,101 13,018 12,101 12,886 13,040 13,136Imports 14 10 14 12 10 10 Total Supply 13,739 14,702 13,739 14,572 14,772 14,918USAGE (Mil. Bushels)Feed & Residual 5,231 5,400 5,231 5,225 5,225 5,250Food/Seed/Ind 4,976 5,480 4,976 5,475 5,575 5,755 Ethanol for Fuel 3,700 4,200 3,700 4,200 4,350 4,500 Domestic Use 10,207 10,880 10,207 10,700 10,800 11,005Exports 1,858 2,150 1,858 2,150 2,200 2,200 Total Use 12,065 13,030 12,065 12,850 13,000 13,205STOCKS (Mil. Bushels)Ending Stocks (Aug 31) 1,674 1,672 1,674 1,722 1,772 1,713 CCC 0 0 0 0 0 0 Privately-Owned 1,674 1,672 1,674 1,722 1,772 1,713Stocks/Use 13.9% 12.8% 13.9% 13.4% 13.6% 13.0%Farm Price ($/Bu) $4.06 $3.05-$3.65 4.06$ $3.00-3.75 $3.00-3.75 $3.00-3.75

Brock Est.

US CORN SUPPLY AND DEMANDUSDA

2009

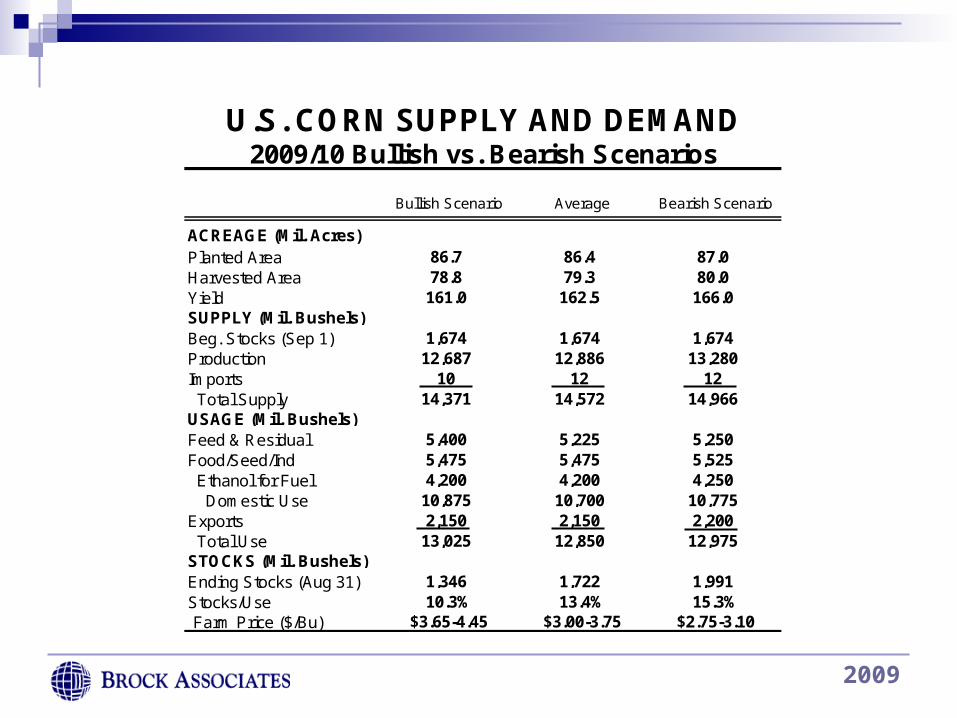

ACREAGE (Mil. Acres)Planted Area 86.7 86.4 87.0Harvested Area 78.8 79.3 80.0Yield 161.0 162.5 166.0SUPPLY (Mil. Bushels)Beg. Stocks (Sep 1) 1,674 1,674 1,674Production 12,687 12,886 13,280Imports 10 12 12 Total Supply 14,371 14,572 14,966USAGE (Mil. Bushels)Feed & Residual 5,400 5,225 5,250Food/Seed/Ind 5,475 5,475 5,525 Ethanol for Fuel 4,200 4,200 4,250 Domestic Use 10,875 10,700 10,775Exports 2,150 2,150 2,200 Total Use 13,025 12,850 12,975STOCKS (Mil. Bushels)Ending Stocks (Aug 31) 1,346 1,722 1,991Stocks/Use 10.3% 13.4% 15.3%Farm Price ($/Bu) $3.65-4.45 $3.00-3.75 $2.75-3.10

Average Bearish ScenarioBullish Scenario

U.S. CORN SUPPLY AND DEMAND2009/10 Bullish vs. Bearish Scenarios

2009

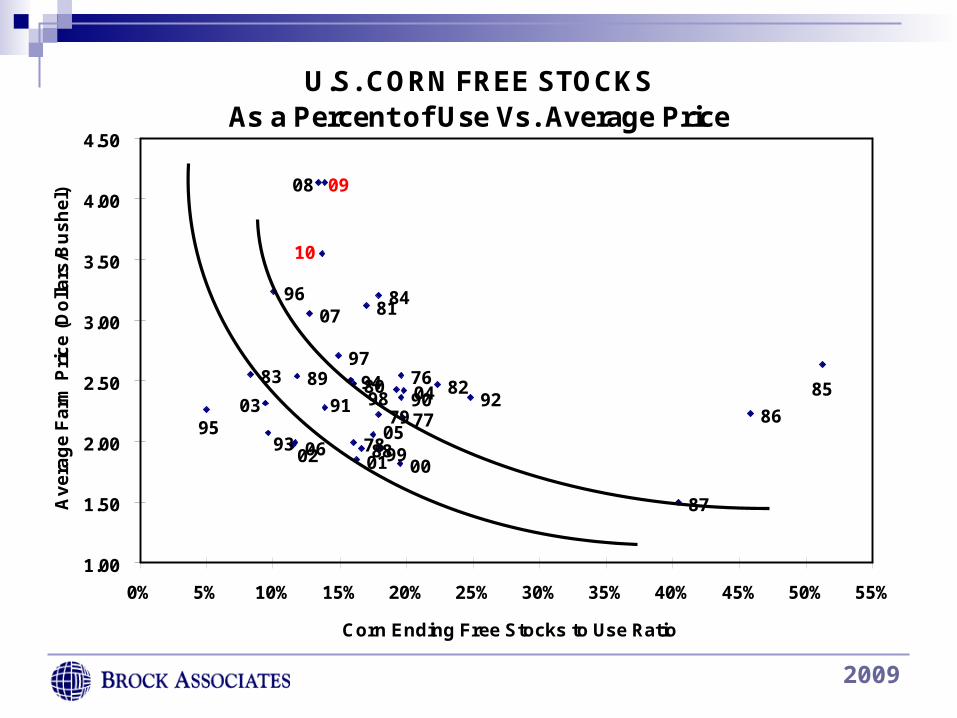

U.S. CORN FREE STOCKS As a Percent of Use Vs. Average Price

10

0908

07

0605

0403

02 01 0099

98

97

96

95

94

93

9291 9089

88

87

86

85

84

8382

81

80

79

7877

76

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55%

Corn Ending Free Stocks to Use Ratio

Av

era

ge

Fa

rm P

ric

e (

Do

llars

/Bu

sh

el)

2009

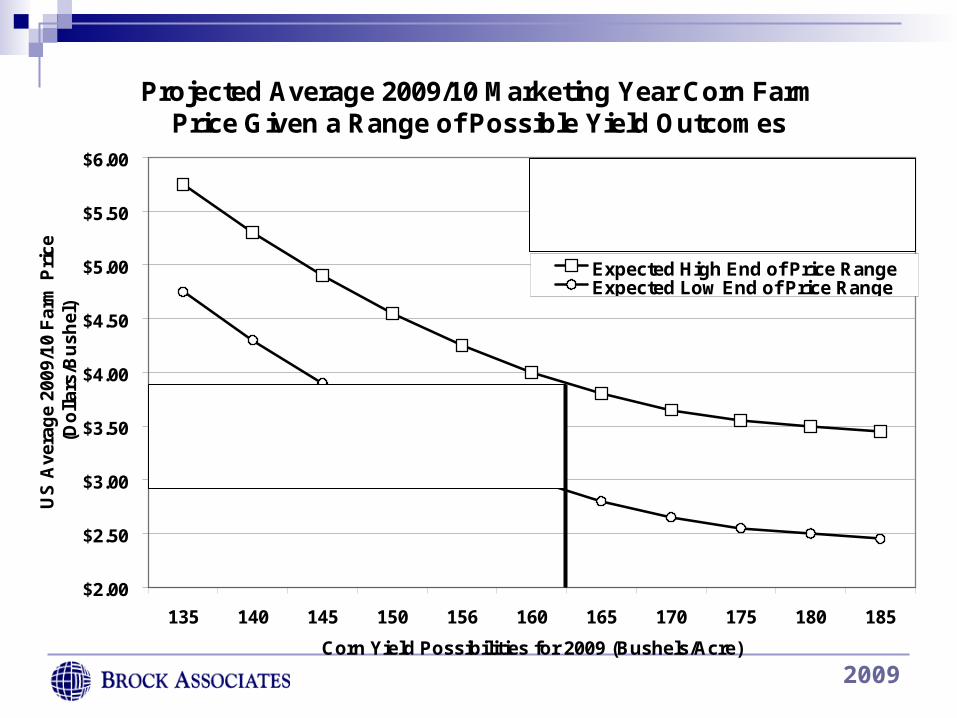

Projected Average 2009/10 Marketing Year Corn Farm Price Given a Range of Possible Yield Outcomes

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

135 140 145 150 156 160 165 170 175 180 185

Corn Yield Possibilities for 2009 (Bushels/Acre)

US

Ave

rag

e 20

09/1

0 F

arm

Pri

ce

(Do

llar

s/B

ush

el)

Expected High End of Price RangeExpected Low End of Price Range

The average marketing year farm price is projected between $3.00 and $3.75 given the current Brock Associates acreage estimate of 86.4 million acres, yield estimate of 162.5 bushels/acre and 12,850 million bushel demand expectation.

2009

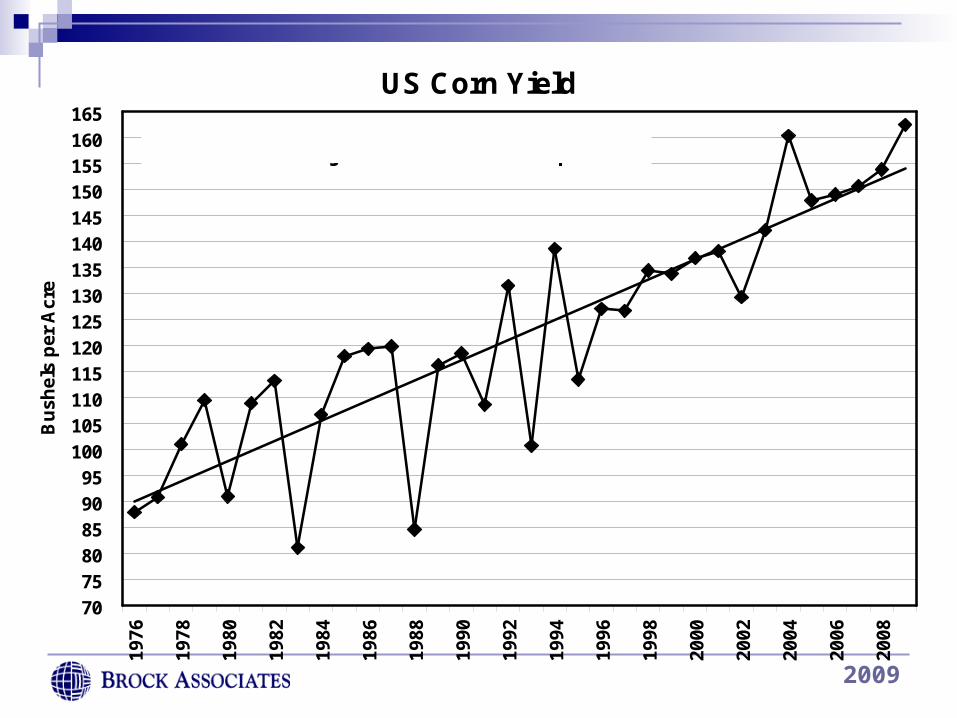

US Corn Yield

70

75

8085

90

95

100

105110

115

120

125130

135

140

145

150155

160

16519

76

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

Bu

shel

s p

er A

cre

Brock 2009/10 Projection: 162.5 Bushels per Acre

2009

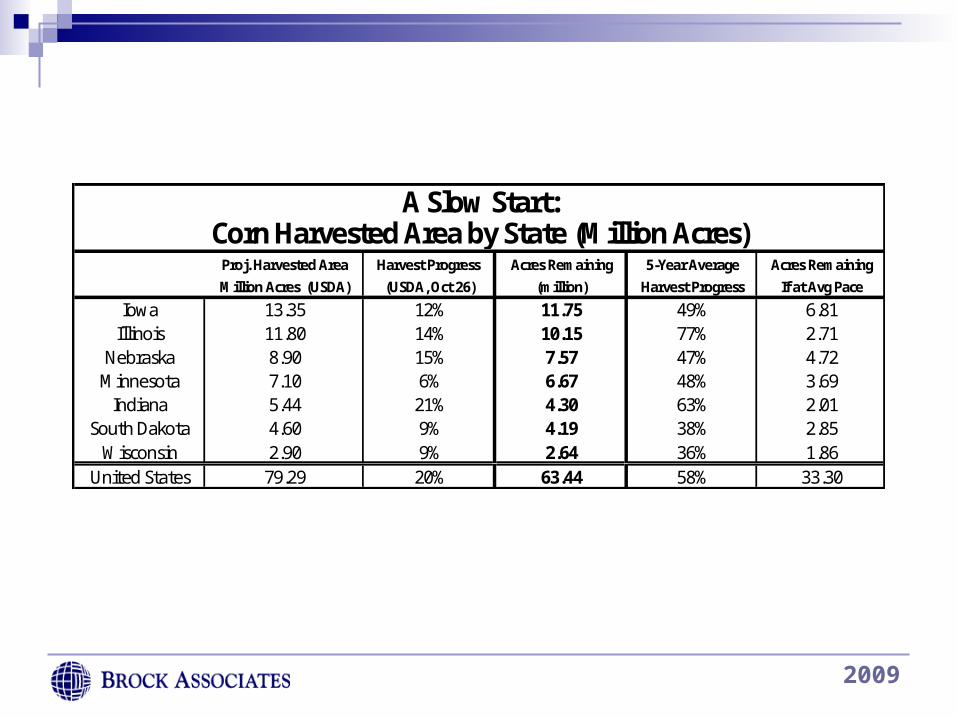

Proj. Harvested Area Harvest Progress Acres Remaining 5-Year Average Acres RemainingMillion Acres (USDA) (USDA, Oct 26) (million) Harvest Progress If at Avg Pace

Iowa 13.35 12% 11.75 49% 6.81Illinois 11.80 14% 10.15 77% 2.71

Nebraska 8.90 15% 7.57 47% 4.72Minnesota 7.10 6% 6.67 48% 3.69

Indiana 5.44 21% 4.30 63% 2.01South Dakota 4.60 9% 4.19 38% 2.85

Wisconsin 2.90 9% 2.64 36% 1.860.00United States 79.29 20% 63.44 58% 33.30

A Slow Start:Corn Harvested Area by State (Million Acres)

2009

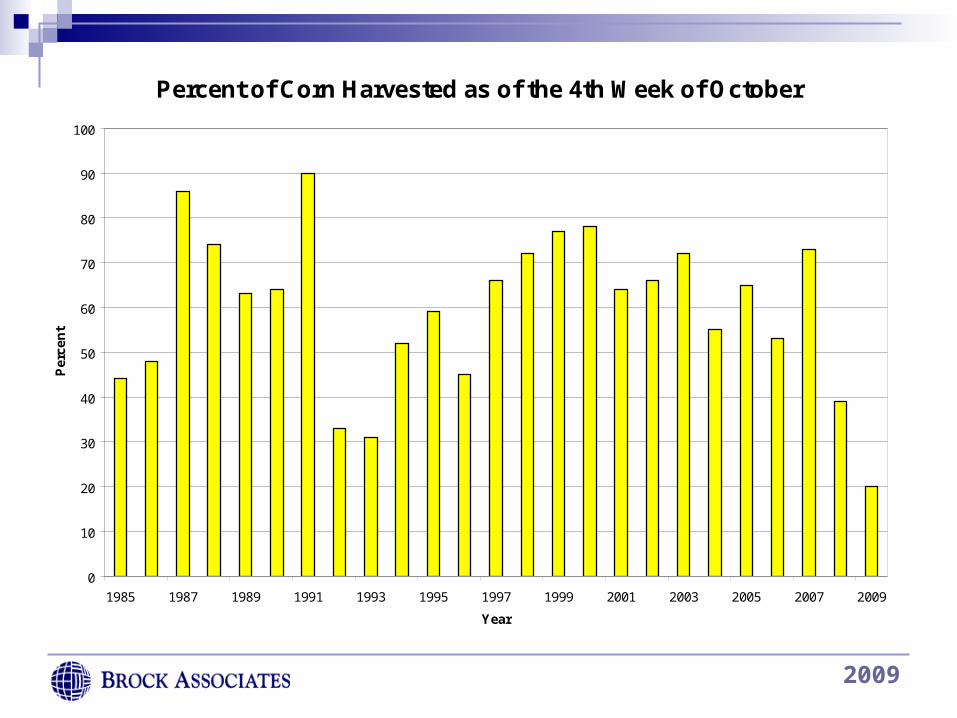

Percent of Corn Harvested as of the 4th Week of October

0

10

20

30

40

50

60

70

80

90

100

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

Year

Per

cen

t

Source: USDA

2009

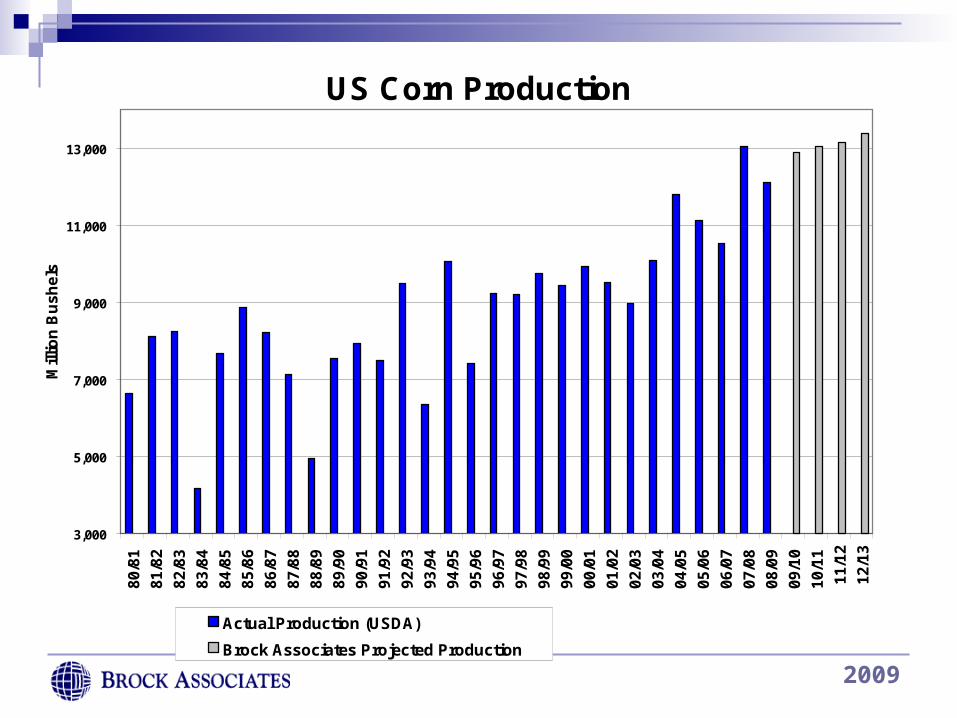

US Corn Production

3,000

5,000

7,000

9,000

11,000

13,0008

0/8

1

81/

82

82/

83

83/

84

84/

85

85/

86

86/

87

87/

88

88/

89

89/

90

90/

91

91/

92

92/

93

93/

94

94/

95

95/

96

96/

97

97/

98

98/

99

99/

00

00/

01

01/

02

02/

03

03/

04

04/

05

05/

06

06/

07

07/

08

08/

09

09/

10

10/

11

11/

12

12/

13

Mill

ion

Bu

sh

els

Actual Production (USDA)

Brock Associates Projected Production

Brock 2009/10 Projection: 12,886 Million Bushels

2009

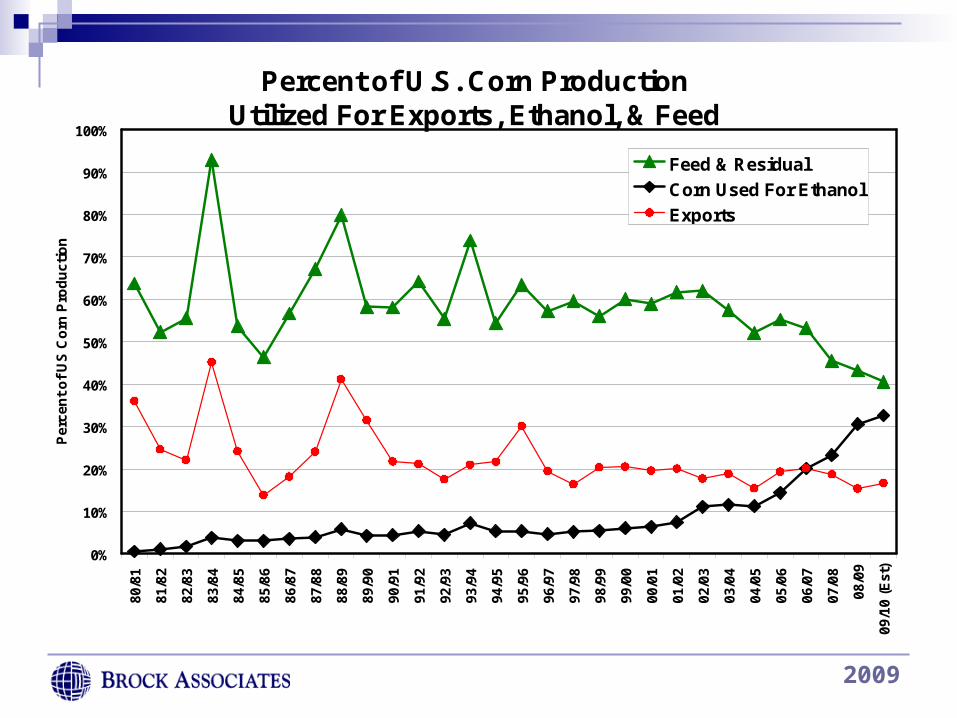

Percent of U.S. Corn Production Utilized For Exports, Ethanol, & Feed

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%80

/81

81/8

2

82/8

3

83/8

4

84/8

5

85/8

6

86/8

7

87/8

8

88/8

9

89/9

0

90/9

1

91/9

2

92/9

3

93/9

4

94/9

5

95/9

6

96/9

7

97/9

8

98/9

9

99/0

0

00/0

1

01/0

2

02/0

3

03/0

4

04/0

5

05/0

6

06/0

7

07/0

8

08/0

9

09/1

0 (E

st)

Per

cen

t o

f U

S C

orn

Pro

du

ctio

n

Feed & Residual

Corn Used For Ethanol

Exports

2009

Corn Ending Stocks

0

1,000

2,000

3,000

4,000

5,000

6,0008

0/8

1

81

/82

82

/83

83

/84

84

/85

85

/86

86

/87

87

/88

88

/89

89

/90

90

/91

91

/92

92

/93

93

/94

94

/95

95

/96

96

/97

97

/98

98

/99

99

/00

00

/01

01

/02

02

/03

03

/04

04

/05

05

/06

06

/07

07

/08

08

/09

09

/10

10

/11

11

/12

12

/13

Mil

lio

n B

us

he

ls

Actual Ending Stocks (USDA)

Brock Associates Projected Ending Stocks

Brock 2009/10 Projection: 1,722 Million Bushels

2009

YearBeginning

Stocks Production ConsumptionEnding Stocks

Stocks/Use Ratio

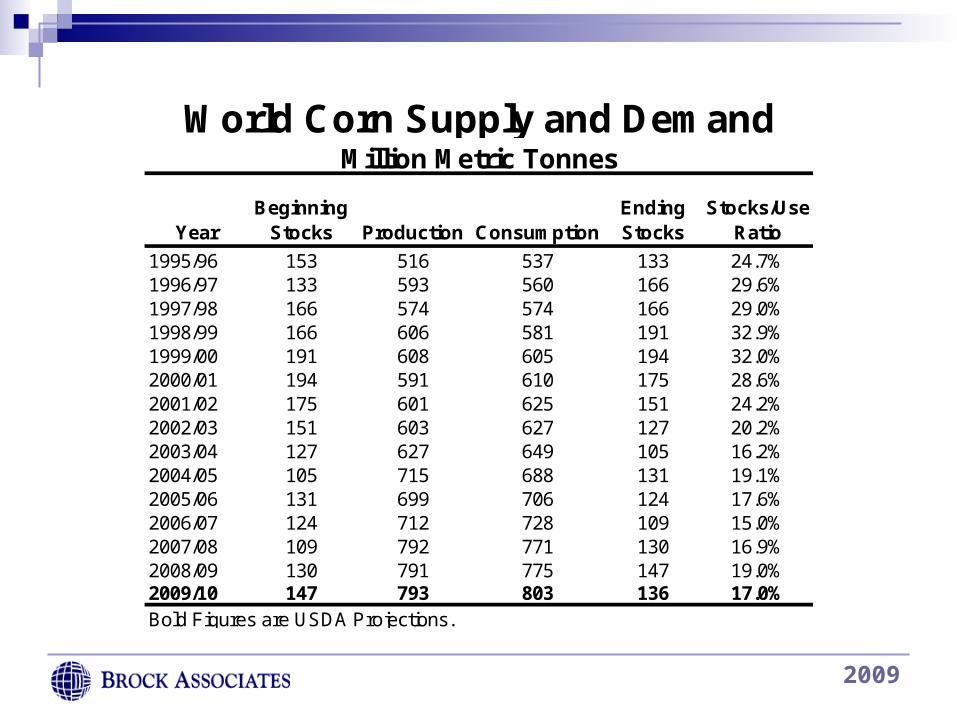

1995/96 153 516 537 133 24.7%1996/97 133 593 560 166 29.6%1997/98 166 574 574 166 29.0%1998/99 166 606 581 191 32.9%1999/00 191 608 605 194 32.0%2000/01 194 591 610 175 28.6%2001/02 175 601 625 151 24.2%2002/03 151 603 627 127 20.2%2003/04 127 627 649 105 16.2%2004/05 105 715 688 131 19.1%2005/06 131 699 706 124 17.6%2006/07 124 712 728 109 15.0%2007/08 109 792 771 130 16.9%2008/09 130 791 775 147 19.0%2009/10 147 793 803 136 17.0%

World Corn Supply and DemandMillion Metric Tonnes

Bold Figures are USDA Projections.

2009

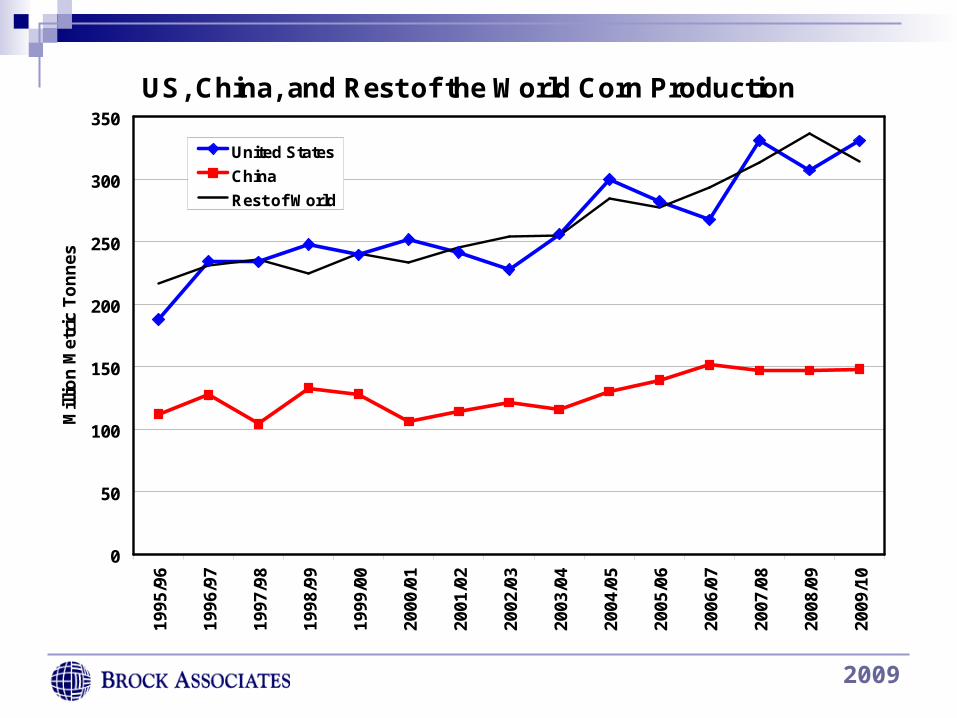

US, China, and Rest of the World Corn Production

0

50

100

150

200

250

300

350

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

Mil

lio

n M

etri

c T

on

nes

United States

China

Rest of World

2009

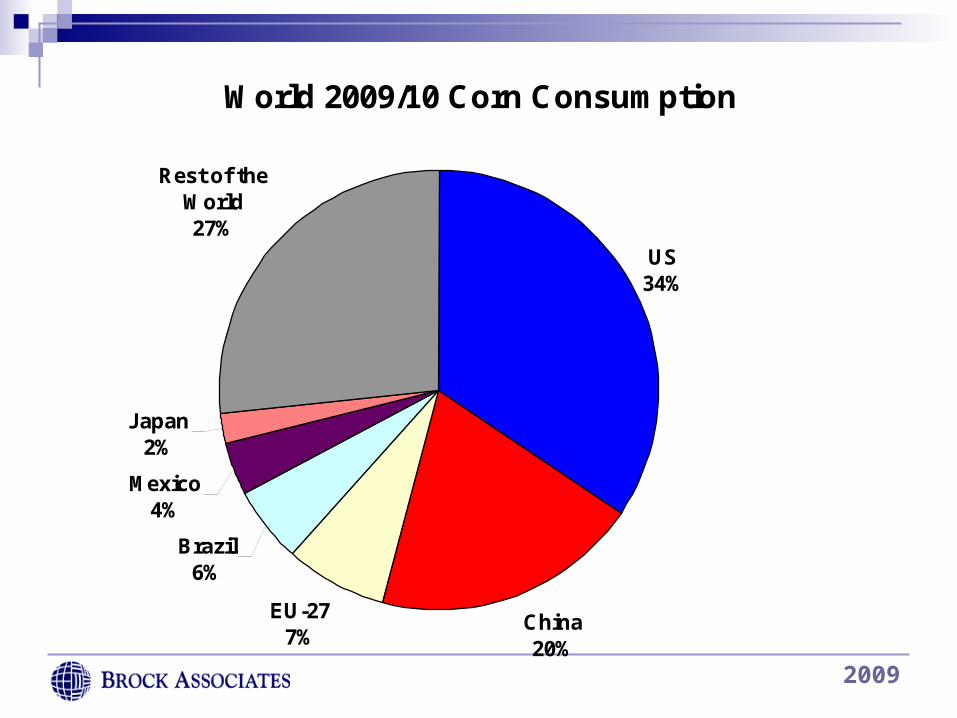

World 2009/10 Corn Consumption

US34%

China20%

EU-277%

Brazil6%

Mexico4%

Japan2%

Rest of the World27%

2009

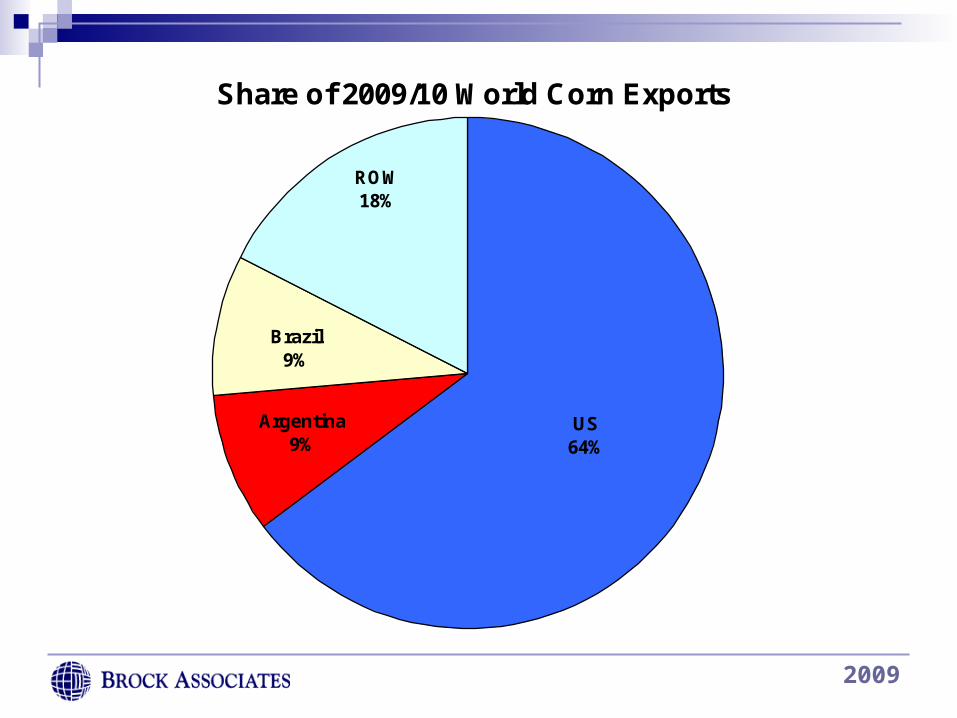

Share of 2009/10 World Corn Exports

US64%

Argentina9%

Brazil9%

ROW18%

2009

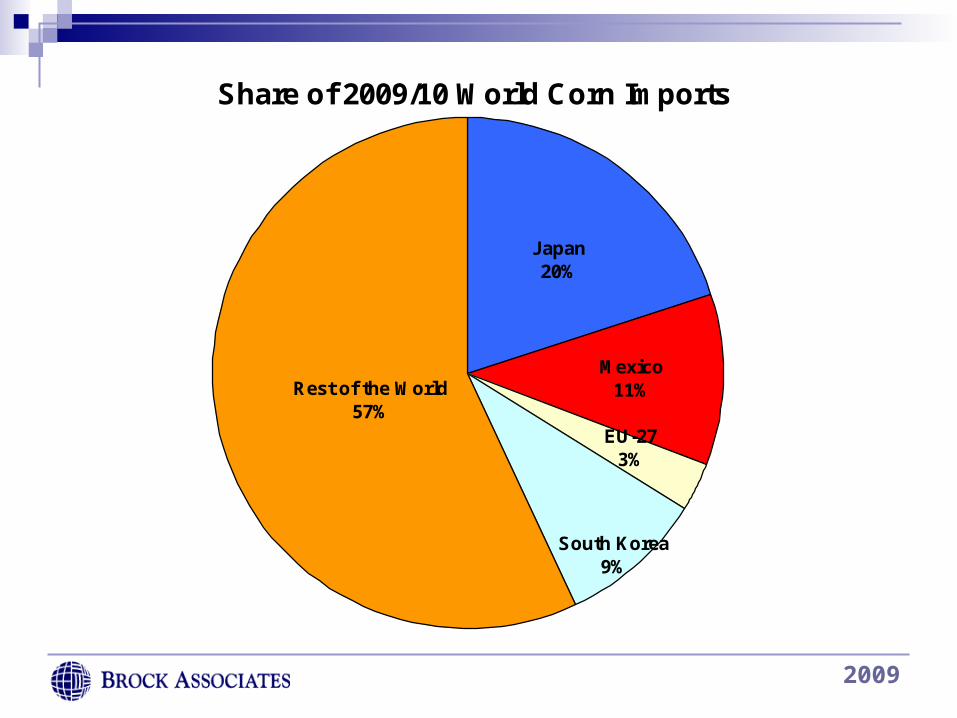

Share of 2009/10 World Corn Imports

Japan20%

Mexico11%

EU-273%

South Korea9%

Rest of the World57%

2009

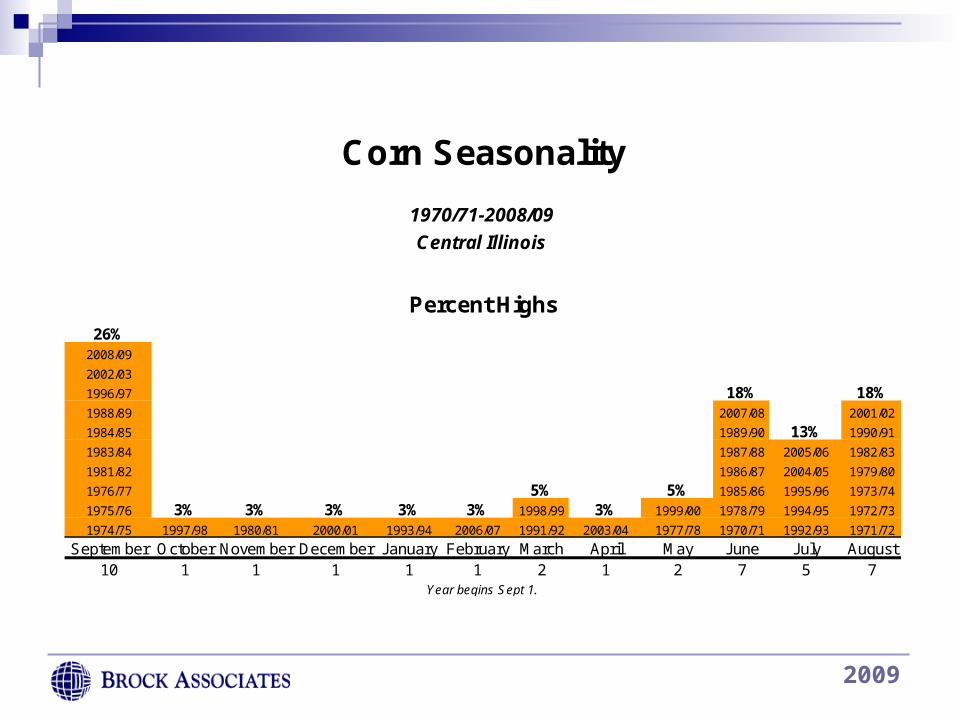

26%2008/09

2002/03

1996/97 18% 18%1988/89 2007/08 2001/02

1984/85 1989/90 13% 1990/91

1983/84 1987/88 2005/06 1982/83

1981/82 1986/87 2004/05 1979/80

1976/77 5% 5% 1985/86 1995/96 1973/74

1975/76 3% 3% 3% 3% 3% 1998/99 3% 1999/00 1978/79 1994/95 1972/73

1974/75 1997/98 1980/81 2000/01 1993/94 2006/07 1991/92 2003/04 1977/78 1970/71 1992/93 1971/72

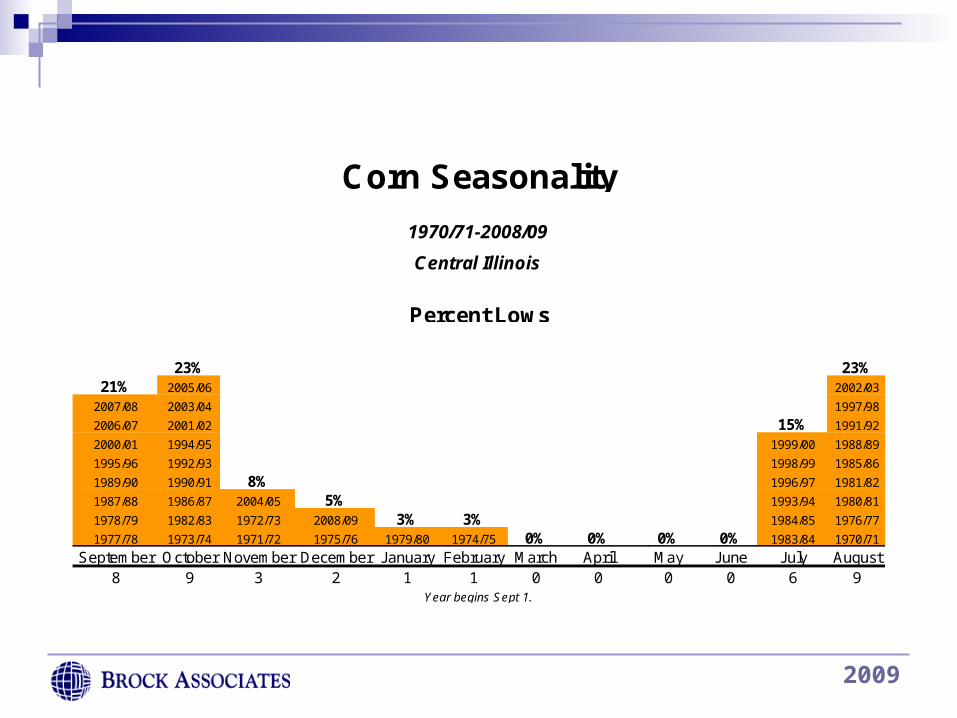

September October November December January February March April May June July August10 1 1 1 1 1 2 1 2 7 5 7

Corn Seasonality

Percent Highs

1970/71-2008/09

Central Illinois

Year begins Sept 1.

2009

23% 23%21% 2005/06 2002/03

2007/08 2003/04 1997/98

2006/07 2001/02 15% 1991/92

2000/01 1994/95 1999/00 1988/89

1995/96 1992/93 1998/99 1985/86

1989/90 1990/91 8% 1996/97 1981/82

1987/88 1986/87 2004/05 5% 1993/94 1980/81

1978/79 1982/83 1972/73 2008/09 3% 3% 1984/85 1976/77

1977/78 1973/74 1971/72 1975/76 1979/80 1974/75 0% 0% 0% 0% 1983/84 1970/71

September October November December January February March April May June July August8 9 3 2 1 1 0 0 0 0 6 9

1970/71-2008/09

Year begins Sept 1.

Central Illinois

Percent Lows

Corn Seasonality

2009

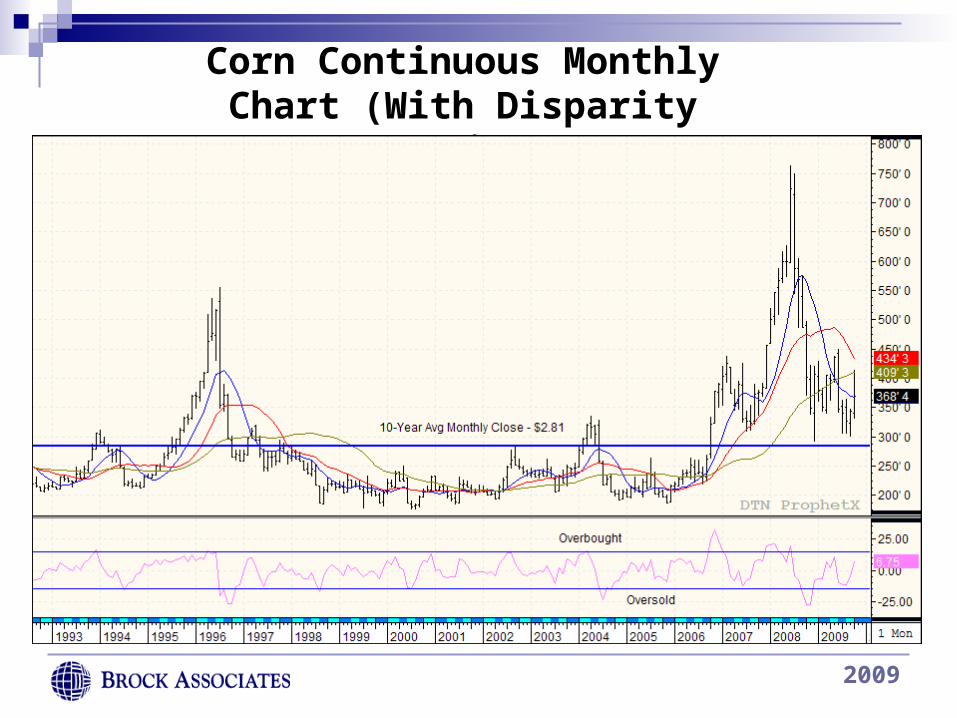

Corn Continuous Monthly Chart (With Disparity Ratio)

2009

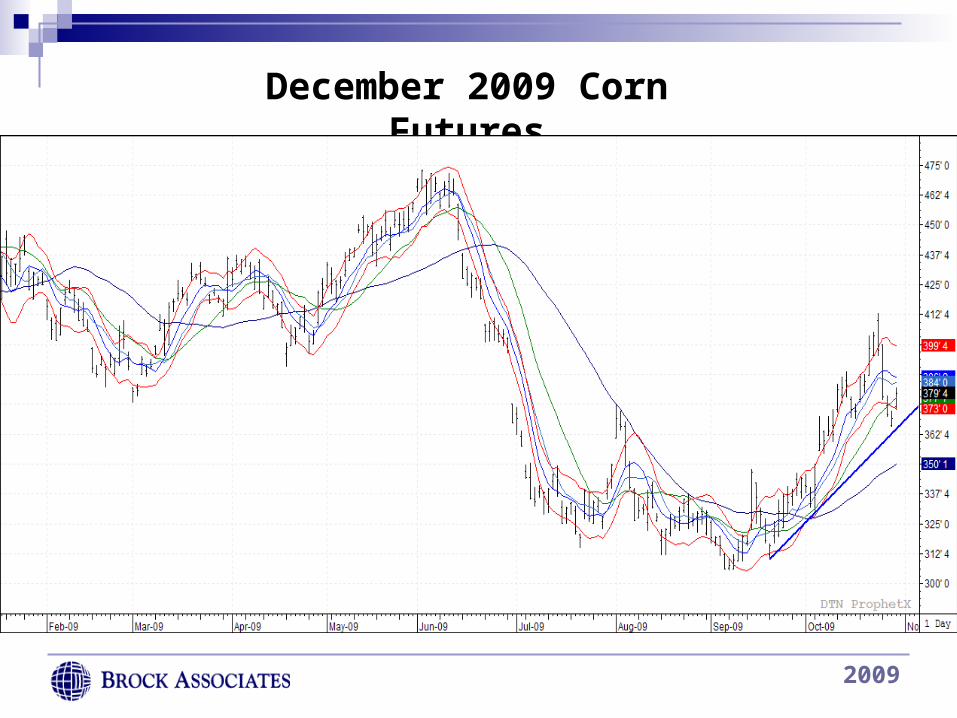

December 2009 Corn Futures

2009

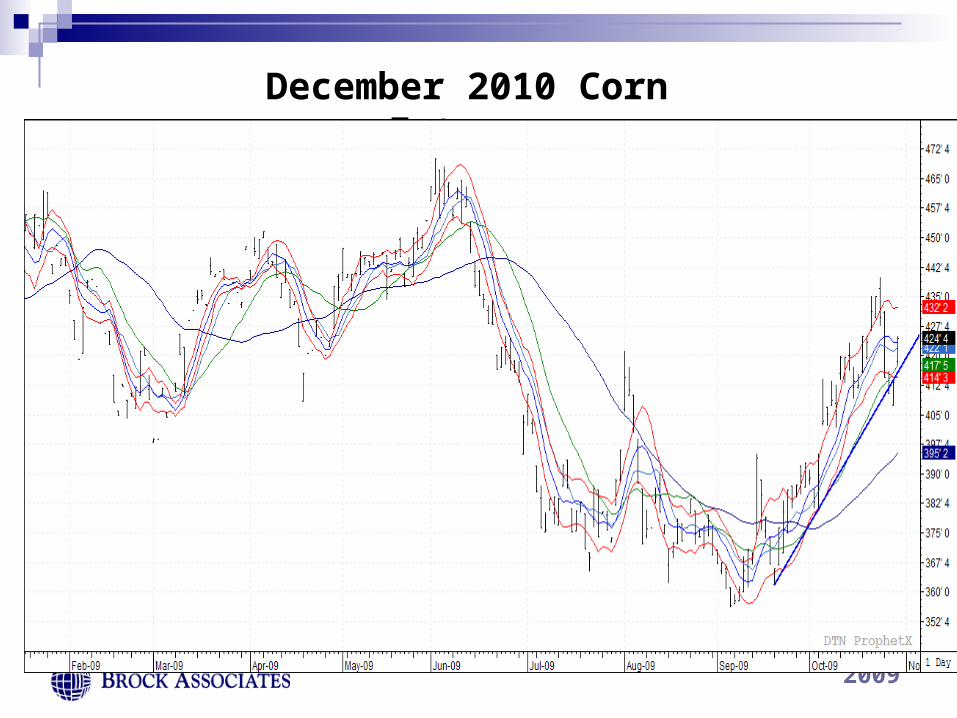

December 2010 Corn Futures

2009

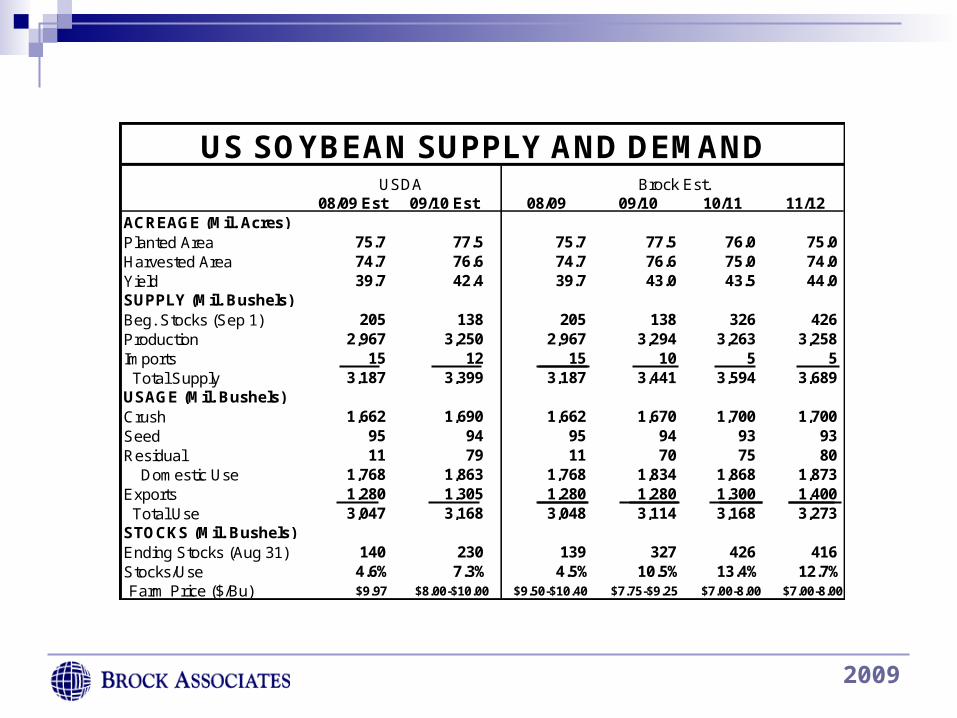

08/09 Est 09/10 Est 08/09 09/10 10/11 11/12ACREAGE (Mil. Acres)Planted Area 75.7 77.5 75.7 77.5 76.0 75.0Harvested Area 74.7 76.6 74.7 76.6 75.0 74.0Yield 39.7 42.4 39.7 43.0 43.5 44.0SUPPLY (Mil. Bushels)Beg. Stocks (Sep 1) 205 138 205 138 326 426Production 2,967 3,250 2,967 3,294 3,263 3,258Imports 15 12 15 10 5 5 Total Supply 3,187 3,399 3,187 3,441 3,594 3,689USAGE (Mil. Bushels)Crush 1,662 1,690 1,662 1,670 1,700 1,700Seed 95 94 95 94 93 93Residual 11 79 11 70 75 80 Domestic Use 1,768 1,863 1,768 1,834 1,868 1,873Exports 1,280 1,305 1,280 1,280 1,300 1,400 Total Use 3,047 3,168 3,048 3,114 3,168 3,273STOCKS (Mil. Bushels)Ending Stocks (Aug 31) 140 230 139 327 426 416Stocks/Use 4.6% 7.3% 4.5% 10.5% 13.4% 12.7%Farm Price ($/Bu) $9.97 $8.00-$10.00 $9.50-$10.40 $7.75-$9.25 $7.00-8.00 $7.00-8.00

US SOYBEAN SUPPLY AND DEMANDBrock Est.USDA

2009

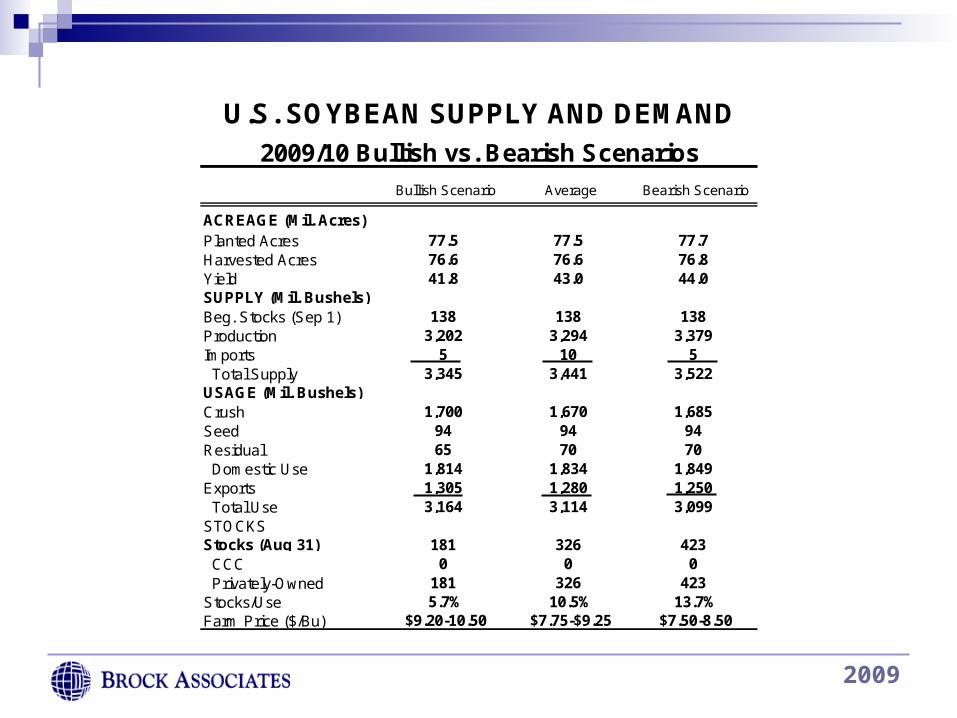

ACREAGE (Mil. Acres)Planted Acres 77.5 77.5 77.7Harvested Acres 76.6 76.6 76.8Yield 41.8 43.0 44.0SUPPLY (Mil. Bushels)Beg. Stocks (Sep 1) 138 138 138Production 3,202 3,294 3,379Imports 5 10 5 Total Supply 3,345 3,441 3,522USAGE (Mil. Bushels)Crush 1,700 1,670 1,685Seed 94 94 94Residual 65 70 70 Domestic Use 1,814 1,834 1,849Exports 1,305 1,280 1,250 Total Use 3,164 3,114 3,099STOCKSStocks (Aug 31) 181 326 423 CCC 0 0 0 Privately-Owned 181 326 423Stocks/Use 5.7% 10.5% 13.7%Farm Price ($/Bu) $9.20-10.50 $7.75-$9.25 $7.50-8.50

Bullish Scenario Average Bearish Scenario

U.S. SOYBEAN SUPPLY AND DEMAND

2009/10 Bullish vs. Bearish Scenarios

2009

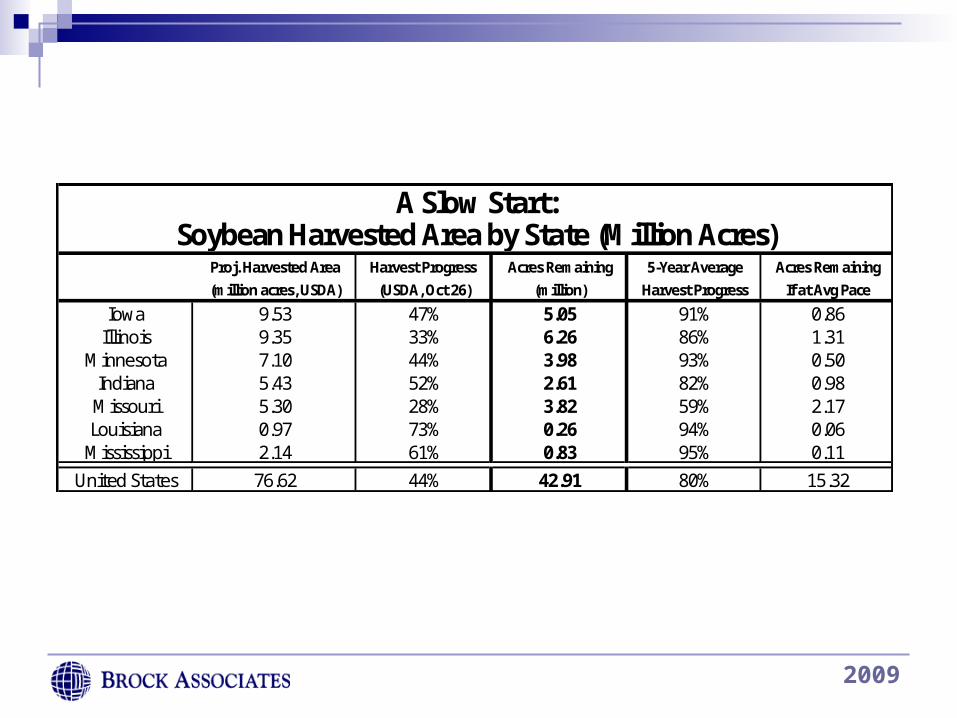

Proj. Harvested Area Harvest Progress Acres Remaining 5-Year Average Acres Remaining(million acres, USDA) (USDA, Oct 26) (million) Harvest Progress If at Avg Pace

Iowa 9.53 47% 5.05 91% 0.86Illinois 9.35 33% 6.26 86% 1.31

Minnesota 7.10 44% 3.98 93% 0.50Indiana 5.43 52% 2.61 82% 0.98

Missouri 5.30 28% 3.82 59% 2.17Louisiana 0.97 73% 0.26 94% 0.06

Mississippi 2.14 61% 0.83 95% 0.11United States 76.62 44% 42.91 80% 15.32

A Slow Start:Soybean Harvested Area by State (Million Acres)

2009

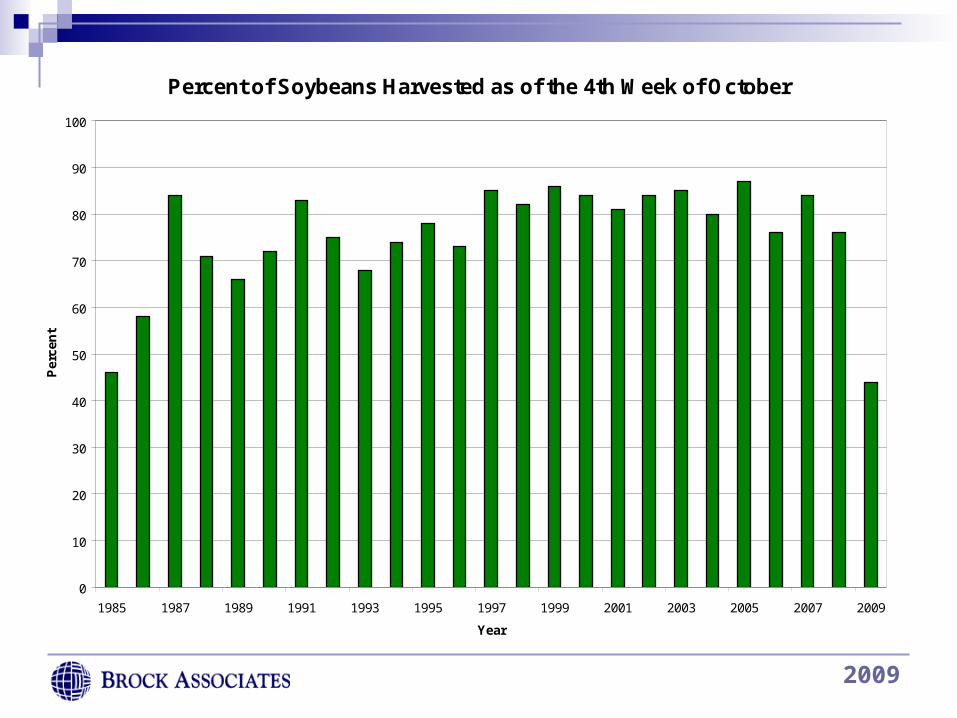

Percent of Soybeans Harvested as of the 4th Week of October

0

10

20

30

40

50

60

70

80

90

100

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

Year

Per

cen

t

Source: USDA

2009

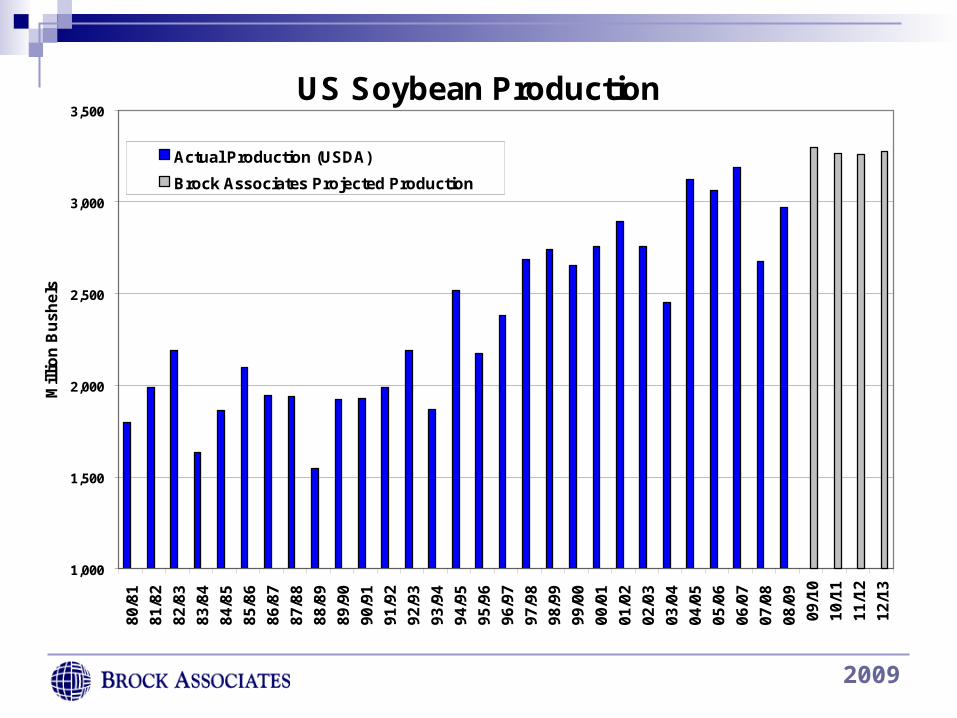

US Soybean Production

1,000

1,500

2,000

2,500

3,000

3,500

80

/81

81

/82

82

/83

83

/84

84

/85

85

/86

86

/87

87

/88

88

/89

89

/90

90

/91

91

/92

92

/93

93

/94

94

/95

95

/96

96

/97

97

/98

98

/99

99

/00

00

/01

01

/02

02

/03

03

/04

04

/05

05

/06

06

/07

07

/08

08

/09

09

/10

10

/11

11

/12

12

/13

Mil

lio

n B

us

he

ls

Actual Production (USDA)

Brock Associates Projected Production

Brock 2009/10 Projection: 3,294 Million Bushels

2009

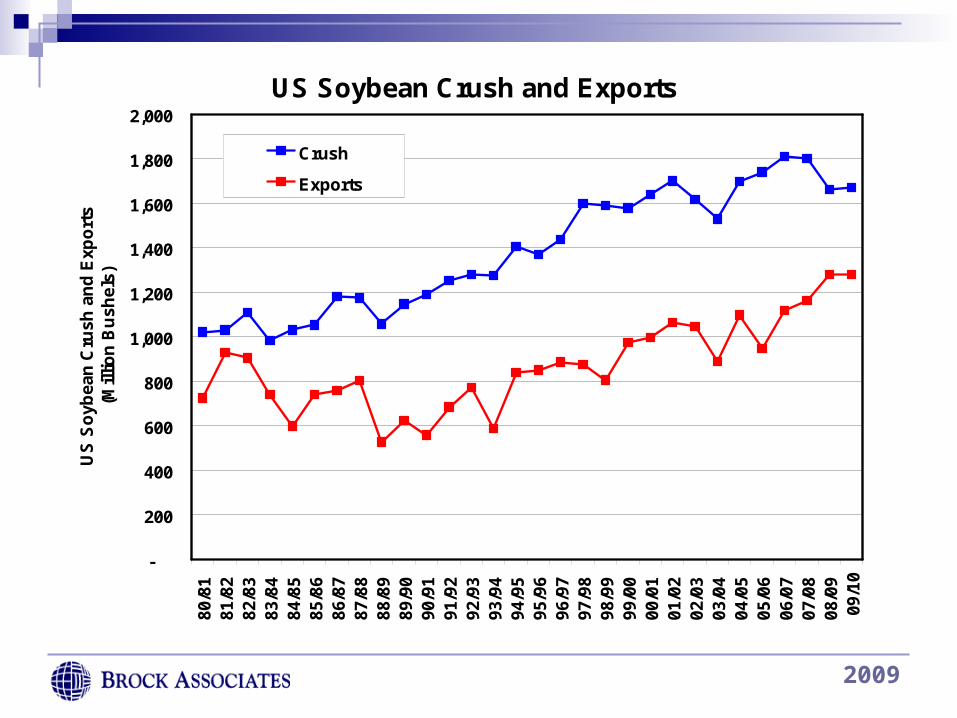

US Soybean Crush and Exports

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

80/8

1 81

/82

82/8

3 83

/84

84/8

5 85

/86

86/8

7 87

/88

88/8

9 89

/90

90/9

1 91

/92

92/9

3 93

/94

94/9

5 95

/96

96/9

7 97

/98

98/9

9 99

/00

00/0

1 01

/02

02/0

3 03

/04

04/0

5 05

/06

06/0

7 07

/08

08/0

9 09

/10

US

So

ybea

n C

rush

an

d E

xpo

rts

(Mil

lio

n B

ush

els)

Crush

Exports

2009

Soybean Export Commitments

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Wk 1

Wk 3

Wk 5

Wk 7

Wk 9

Wk 1

1

Wk 1

3

Wk 1

5

Wk 1

7

Wk 1

9

Wk 2

1

Wk 2

3

Wk 2

5

Wk 2

7

Wk 2

9

Wk 3

1

Wk 3

3

Wk 3

5

Wk 3

7

Wk 3

9

Wk 4

1

Wk 4

3

Wk 4

5

Wk 4

7

Wk 4

9

Wk 5

1

Week of Crop Year

Th

ou

san

d M

etri

c T

on

s

2005/06

2006/07

2007/08

2008/09

2009/10

2009

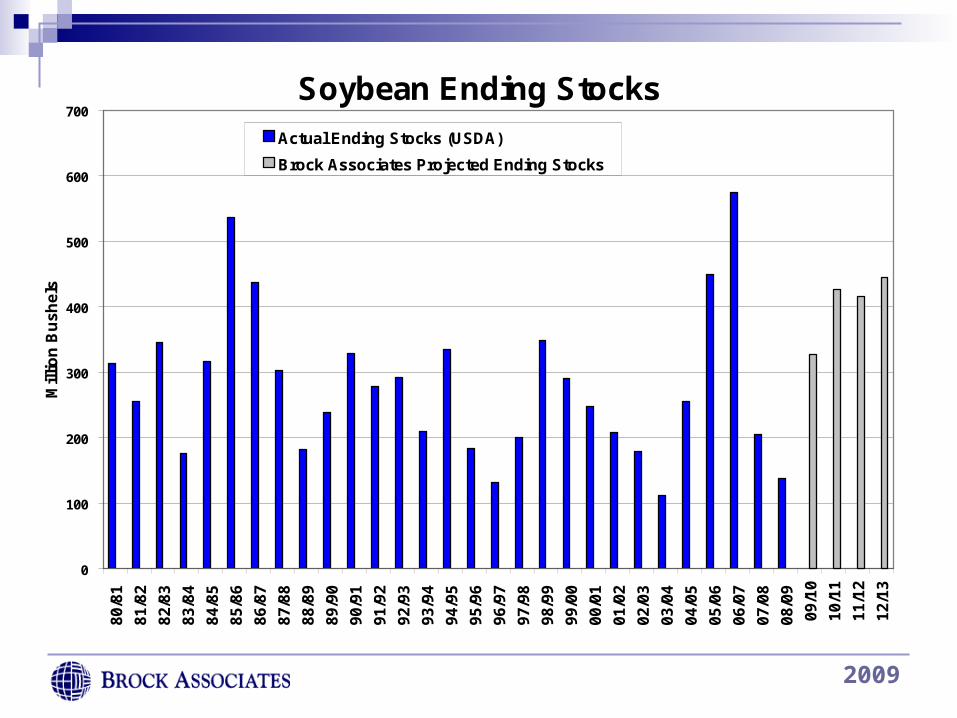

Soybean Ending Stocks

0

100

200

300

400

500

600

7008

0/8

1

81

/82

82

/83

83

/84

84

/85

85

/86

86

/87

87

/88

88

/89

89

/90

90

/91

91

/92

92

/93

93

/94

94

/95

95

/96

96

/97

97

/98

98

/99

99

/00

00

/01

01

/02

02

/03

03

/04

04

/05

05

/06

06

/07

07

/08

08

/09

09

/10

10

/11

11

/12

12

/13

Mil

lio

n B

us

he

ls

Actual Ending Stocks (USDA)

Brock Associates Projected Ending Stocks

Brock 2009/10 Projection: 326 Million Bushels

2009

YearBeginning

Stocks Production ConsumptionEnding Stocks

Stocks/Use Ratio

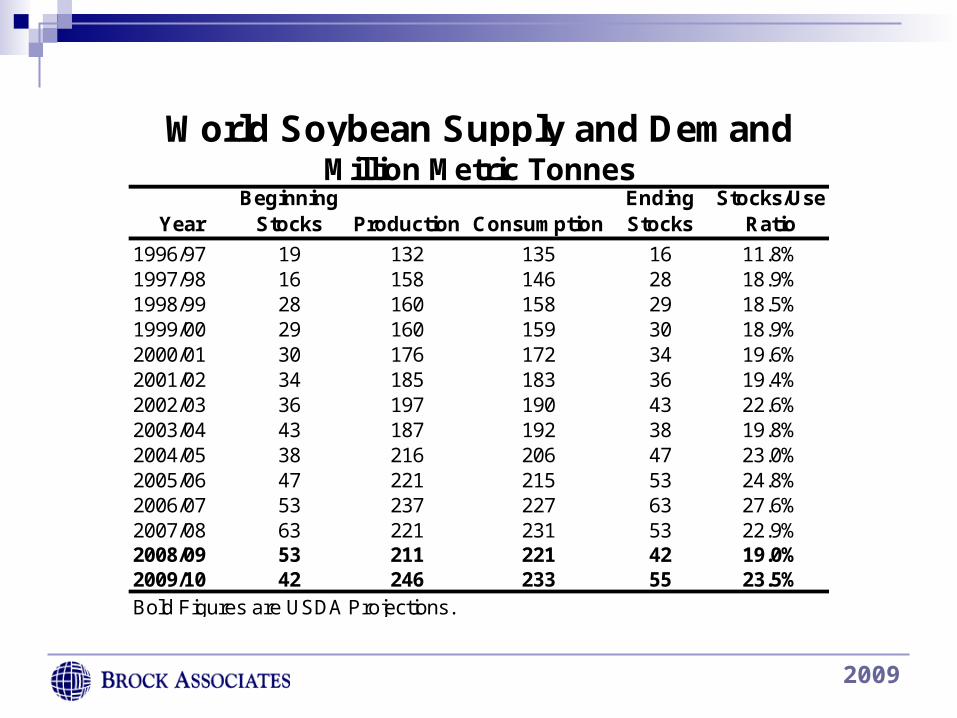

1996/97 19 132 135 16 11.8%1997/98 16 158 146 28 18.9%1998/99 28 160 158 29 18.5%1999/00 29 160 159 30 18.9%2000/01 30 176 172 34 19.6%2001/02 34 185 183 36 19.4%2002/03 36 197 190 43 22.6%2003/04 43 187 192 38 19.8%2004/05 38 216 206 47 23.0%2005/06 47 221 215 53 24.8%2006/07 53 237 227 63 27.6%2007/08 63 221 231 53 22.9%2008/09 53 211 221 42 19.0%2009/10 42 246 233 55 23.5%Bold Figures are USDA Projections.

World Soybean Supply and DemandMillion Metric Tonnes

2009

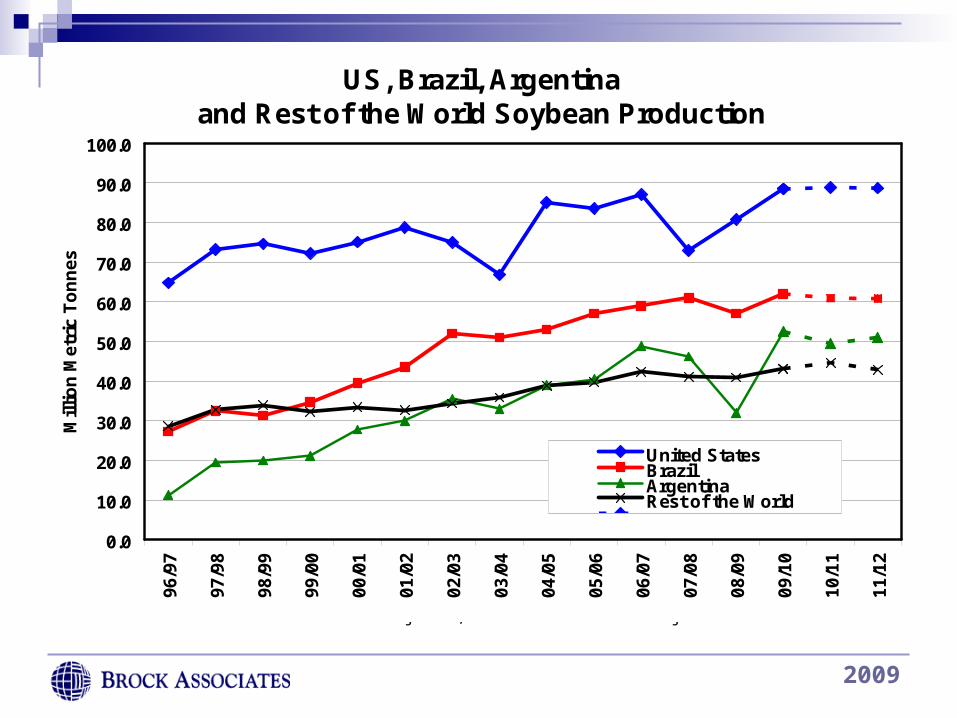

US, Brazil, Argentina and Rest of the World Soybean Production

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.096

/97

97/9

8

98/9

9

99/0

0

00/0

1

01/0

2

02/0

3

03/0

4

04/0

5

05/0

6

06/0

7

07/0

8

08/0

9

09/1

0

10/1

1

11/1

2

Mil

lio

n M

etri

c T

on

nes

United StatesBrazilArgentinaRest of the World

Series7Series8

Source: 1996-2009 USDA Data/Projections, 2010-11 Brock Associates Projections

2009

China Grain and Oilseed Imports

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

55.0

60.0

65.019

70/7

1

1972

/73

1974

/75

1976

/77

1978

/79

1980

/81

1982

/83

1984

/85

1986

/87

1988

/89

1990

/91

1992

/93

1994

/95

1996

/97

1998

/99

2000

/01

2002

/03

2004

/05

2006

/07

2008

/09

Mil

lio

n M

etri

c T

on

nes

Total Oilseed

Total Grain

2009

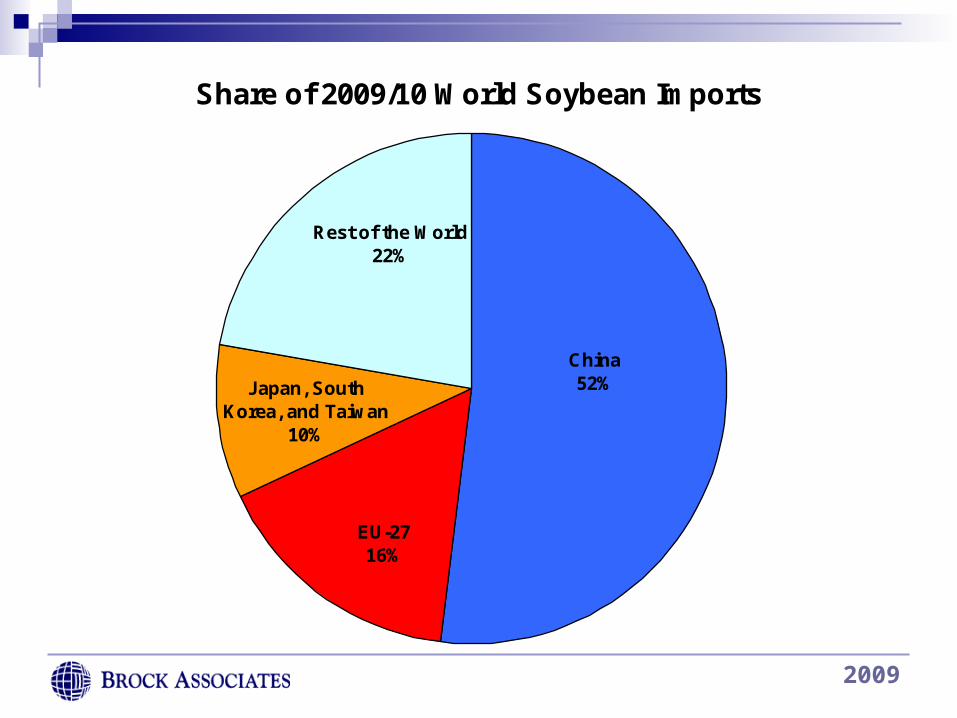

Share of 2009/10 World Soybean Imports

Rest of the World22%

EU-2716%

China52%Japan, South

Korea, and Taiwan10%

2009

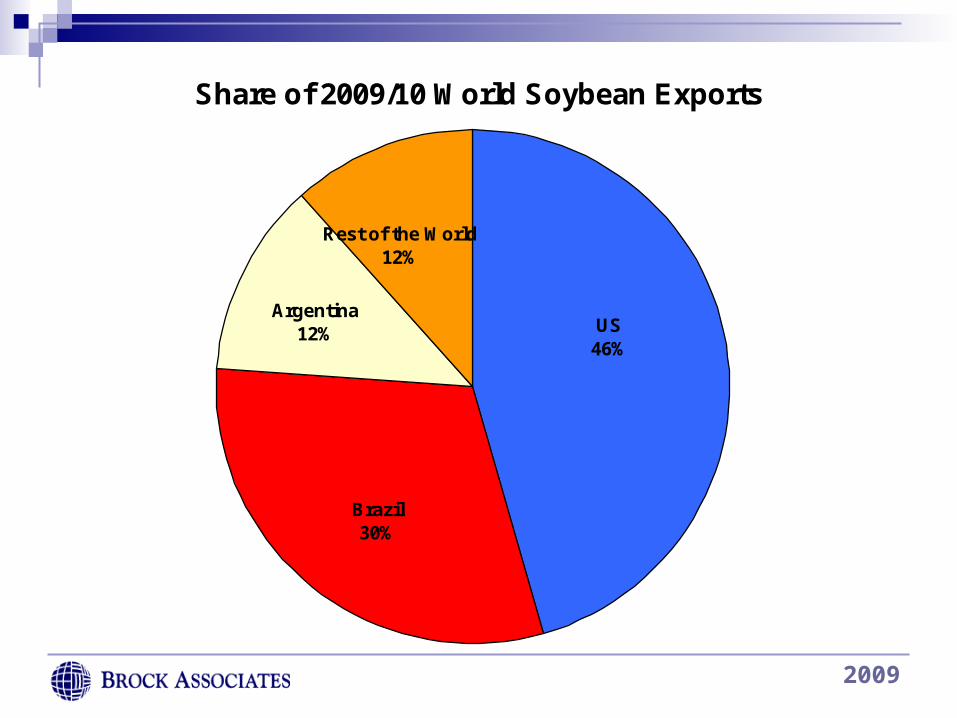

Share of 2009/10 World Soybean Exports

US46%

Brazil30%

Argentina12%

Rest of the World12%

2009

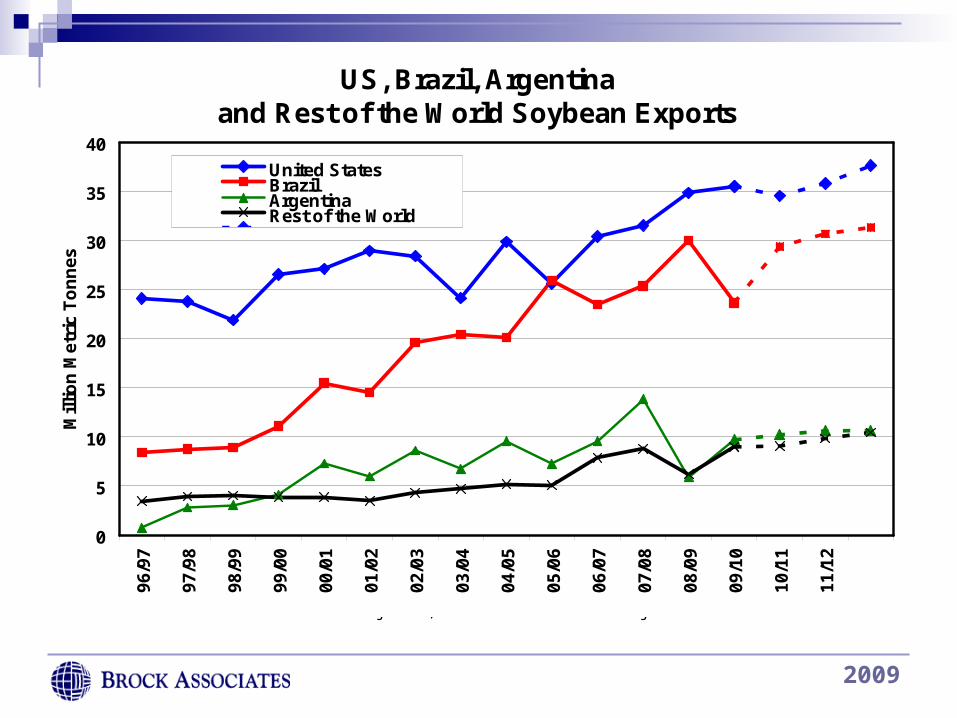

US, Brazil, Argentina and Rest of the World Soybean Exports

0

5

10

15

20

25

30

35

4096

/97

97/9

8

98/9

9

99/0

0

00/0

1

01/0

2

02/0

3

03/0

4

04/0

5

05/0

6

06/0

7

07/0

8

08/0

9

09/1

0

10/1

1

11/1

2

Mil

lio

n M

etri

c T

on

nes

United StatesBrazilArgentinaRest of the World

Series7Series8

Source: 1996-2009 USDA Data/Projections, 2010-11 Brock Associates Projections

2009

28%2007/082006/072000/01

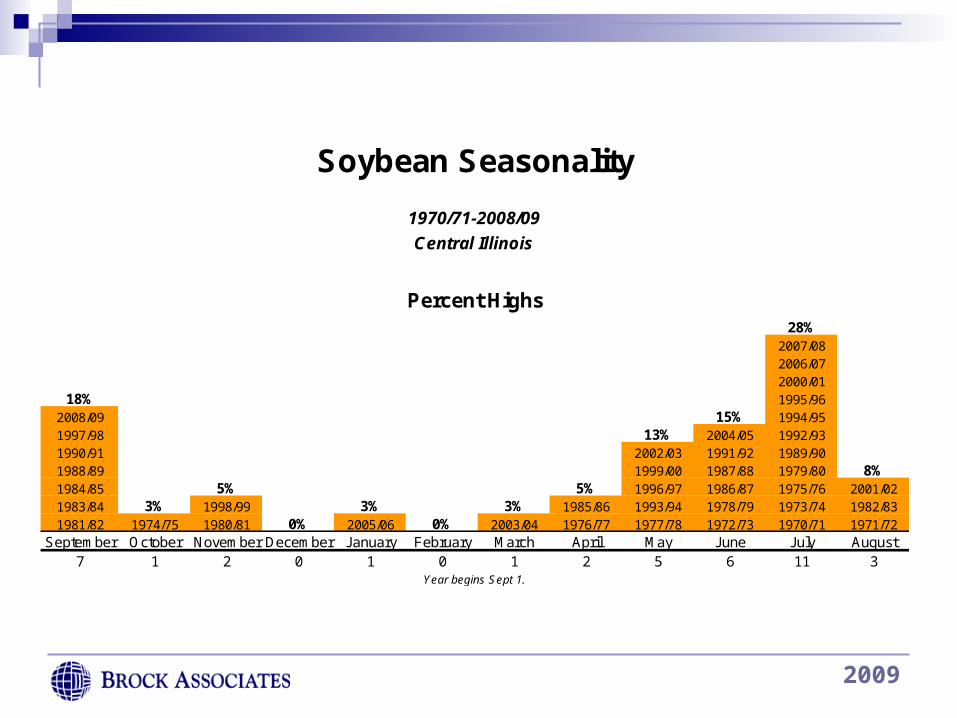

18% 1995/962008/09 15% 1994/951997/98 13% 2004/05 1992/931990/91 2002/03 1991/92 1989/901988/89 1999/00 1987/88 1979/80 8%1984/85 5% 5% 1996/97 1986/87 1975/76 2001/021983/84 3% 1998/99 3% 3% 1985/86 1993/94 1978/79 1973/74 1982/831981/82 1974/75 1980/81 0% 2005/06 0% 2003/04 1976/77 1977/78 1972/73 1970/71 1971/72

September October November December January February March April May June July August7 1 2 0 1 0 1 2 5 6 11 3

Soybean Seasonality

1970/71-2008/09

Central Illinois

Percent Highs

Year begins Sept 1.

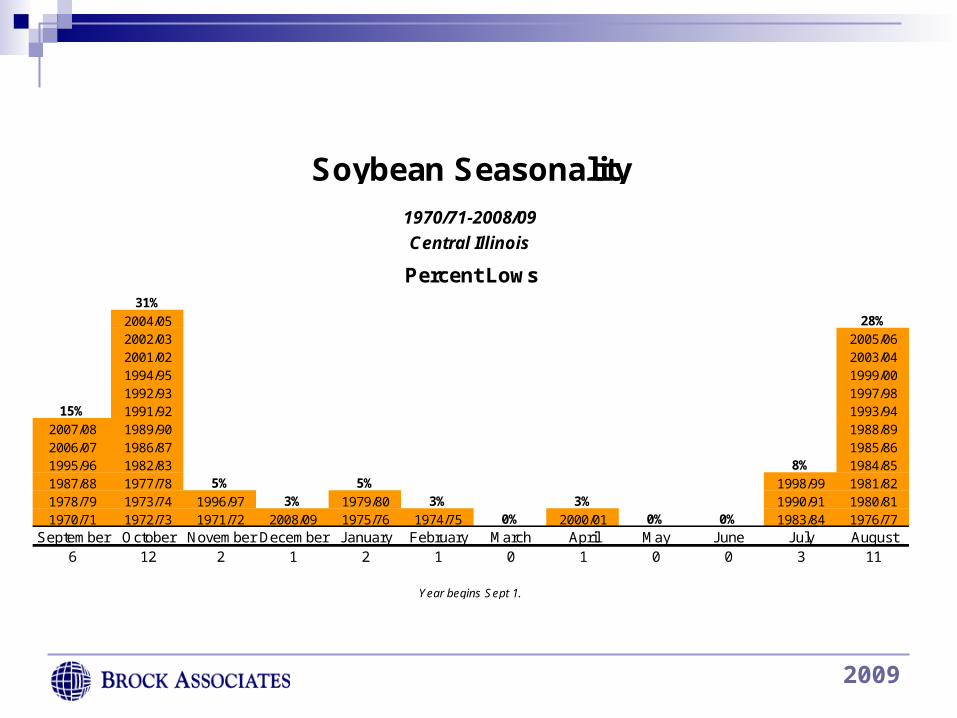

2009

31%

2004/05 28%

2002/03 2005/062001/02 2003/041994/95 1999/001992/93 1997/98

15% 1991/92 1993/942007/08 1989/90 1988/892006/07 1986/87 1985/861995/96 1982/83 8% 1984/851987/88 1977/78 5% 5% 1998/99 1981/821978/79 1973/74 1996/97 3% 1979/80 3% 3% 1990/91 1980/811970/71 1972/73 1971/72 2008/09 1975/76 1974/75 0% 2000/01 0% 0% 1983/84 1976/77

September October November December January February March April May June July August6 12 2 1 2 1 0 1 0 0 3 11

Percent Lows

Year begins Sept 1.

Soybean Seasonality

1970/71-2008/09

Central Illinois

2009

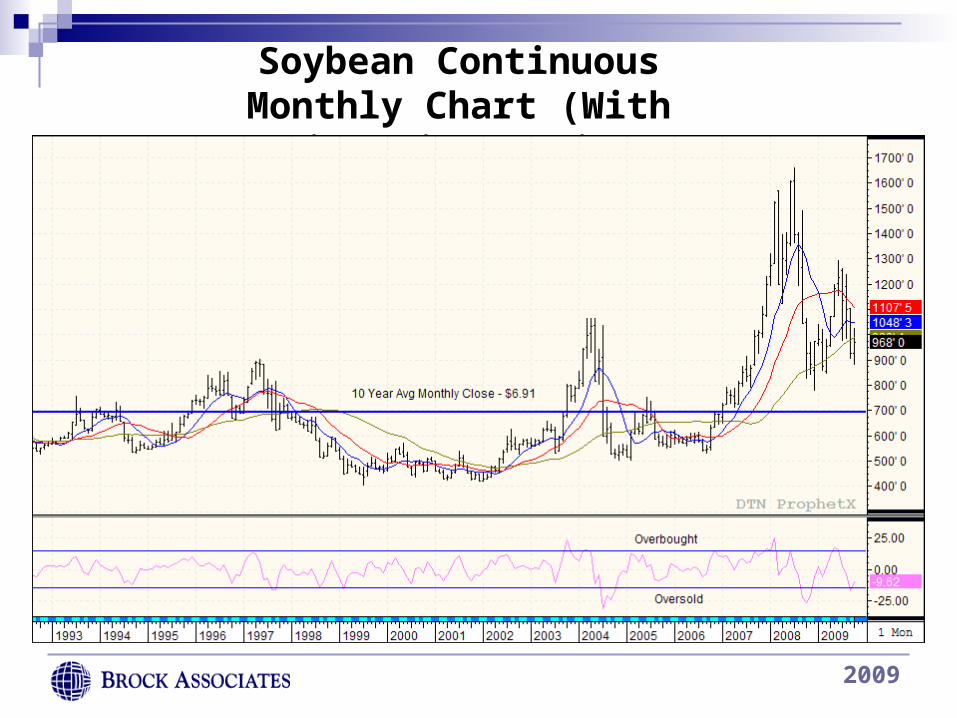

Soybean Continuous Monthly Chart (With Disparity Ratio)

2009

November 2009 Soybean Futures

2009

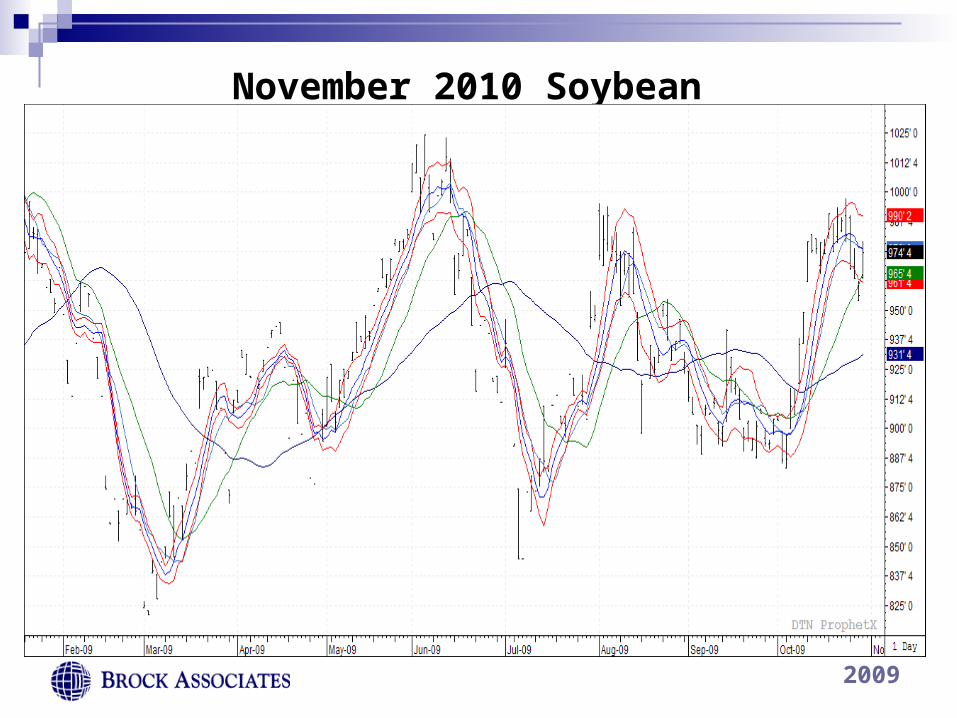

November 2010 Soybean Futures

2009

08/09 Est 09/10 Est 09/10 10/11 11/12 12/13ACREAGE (Mil. Acres)Planted Area 63.2 59.1 59.1 58.5 57.5 56.5Harvested Area 55.7 50.1 50.1 49.7 48.9 48.0Yield 44.9 44.4 44.4 43.1 43.4 44.0SUPPLY (Mil. Bushels)Beg. Stocks (Sep 1) 306 657 657 839 900 905Production 2,499 2,220 2,220 2,142 2,122 2,112Imports 127 110 110 100 100 75

Total Supply 2,932 2,987 2,987 3,081 3,123 3,092USAGE (Mil. Bushels)Food 925 955 955 968 977 977Seed 75 78 78 78 76 76Feed & Residual 260 190 200 210 215 215

Domestic Use 1,260 1,223 1,233 1,256 1,268 1,268Exports 1,015 900 915 925 950 950

Total Use 2,275 2,123 2,148 2,181 2,218 2,218STOCKS (Mil. Bushels)Ending Stocks (Aug 31) 657 864 839 900 905 874

CCC 0 0 0 0 0 0Privately Owned 657 864 839 900 905 874

Stocks/Use 28.9% 40.7% 39.1% 41.3% 40.8% 39.4%Farm Price ($/Bu) $6.78 $4.55-$5.15 $4.60-5.20 $4.75-5.50 $4.75-5.25 $5.00-5.75

US WHEAT SUPPLY AND DEMANDBrock Est.USDA

2009

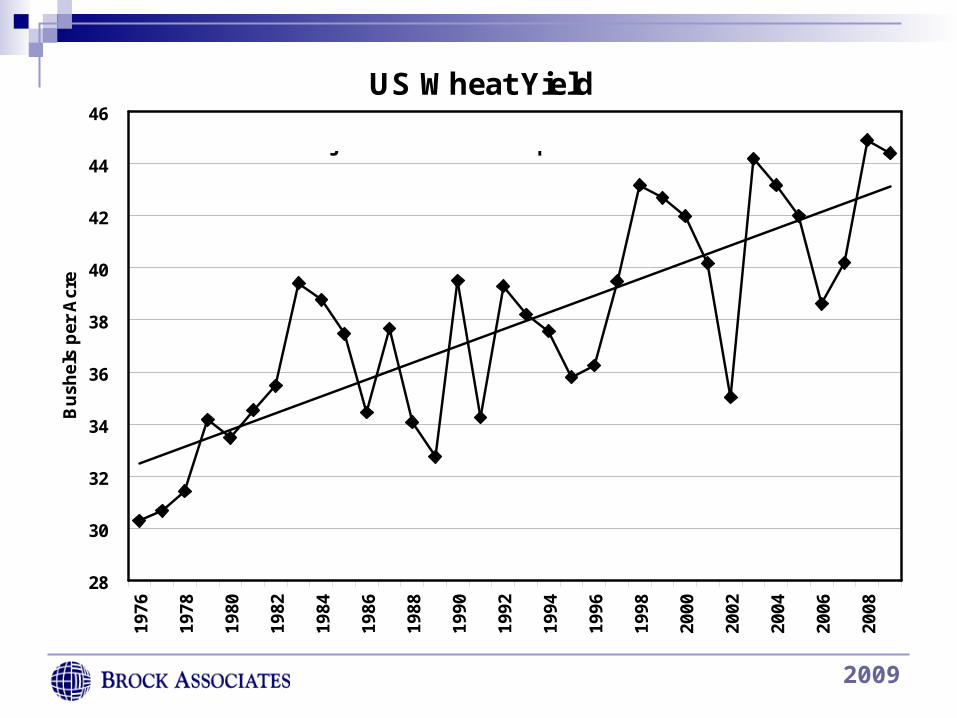

US Wheat Yield

28

30

32

34

36

38

40

42

44

46

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

Bu

shel

s p

er A

cre

Brock 2009/10 Projection: 44.4 Bushels per Acre

2009

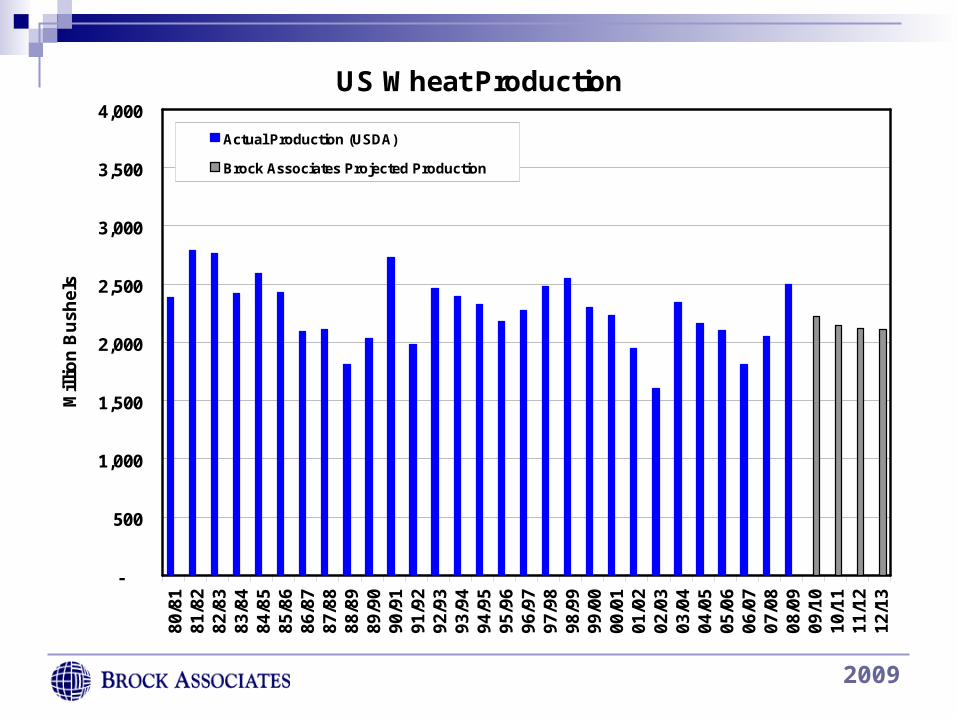

US Wheat Production

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

80/8

181

/82

82/8

383

/84

84/8

585

/86

86/8

787

/88

88/8

989

/90

90/9

191

/92

92/9

393

/94

94/9

595

/96

96/9

797

/98

98/9

999

/00

00/0

101

/02

02/0

303

/04

04/0

505

/06

06/0

707

/08

08/0

909

/10

10/1

111

/12

12/1

3

Mil

lio

n B

ush

els

Actual Production (USDA)

Brock Associates Projected Production

Brock 2009/10 Projection: 2,220 Million Bushels

2009

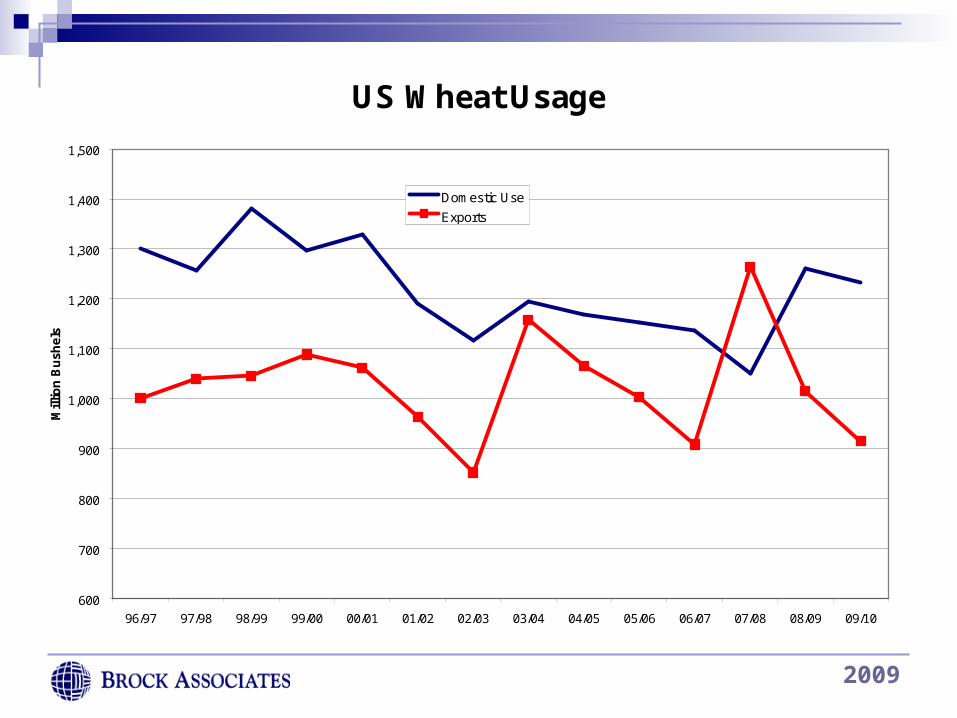

US Wheat Usage

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

96/97 97/98 98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10

Mill

ion

Bu

shel

s

Domestic Use

Exports

Source: USDA, Brock Estimates

2009

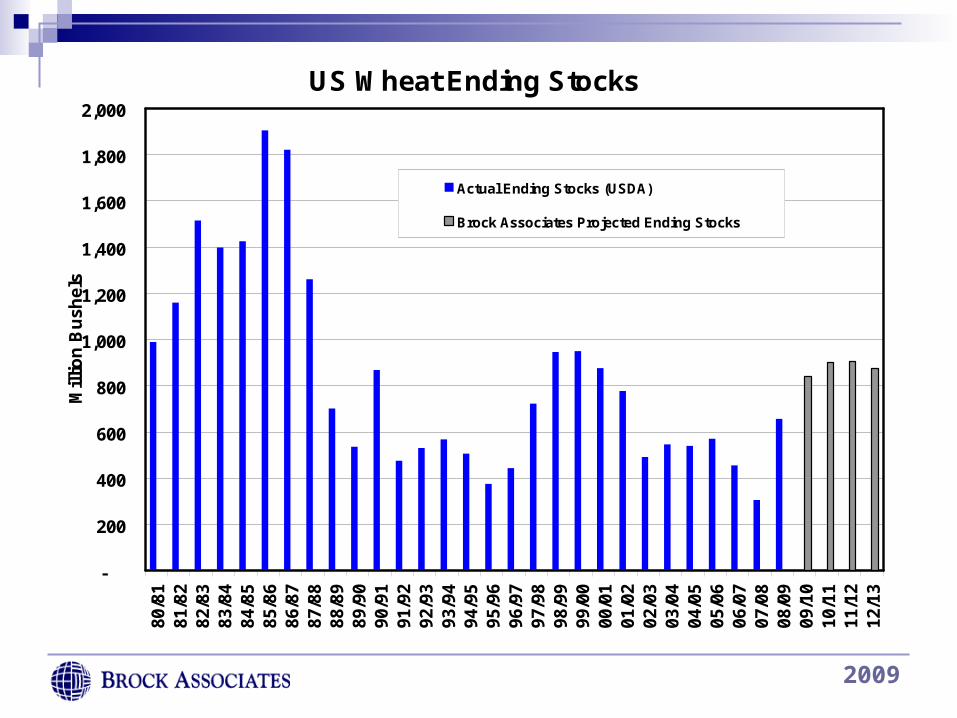

US Wheat Ending Stocks

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

80/8

181

/82

82/8

383

/84

84/8

585

/86

86/8

787

/88

88/8

989

/90

90/9

191

/92

92/9

393

/94

94/9

595

/96

96/9

797

/98

98/9

999

/00

00/0

101

/02

02/0

303

/04

04/0

505

/06

06/0

707

/08

08/0

909

/10

10/1

111

/12

12/1

3

Mil

lio

n B

ush

els

Actual Ending Stocks (USDA)

Brock Associates Projected Ending Stocks

Brock 2009/10 Projection: 839 Million Bushels

2009

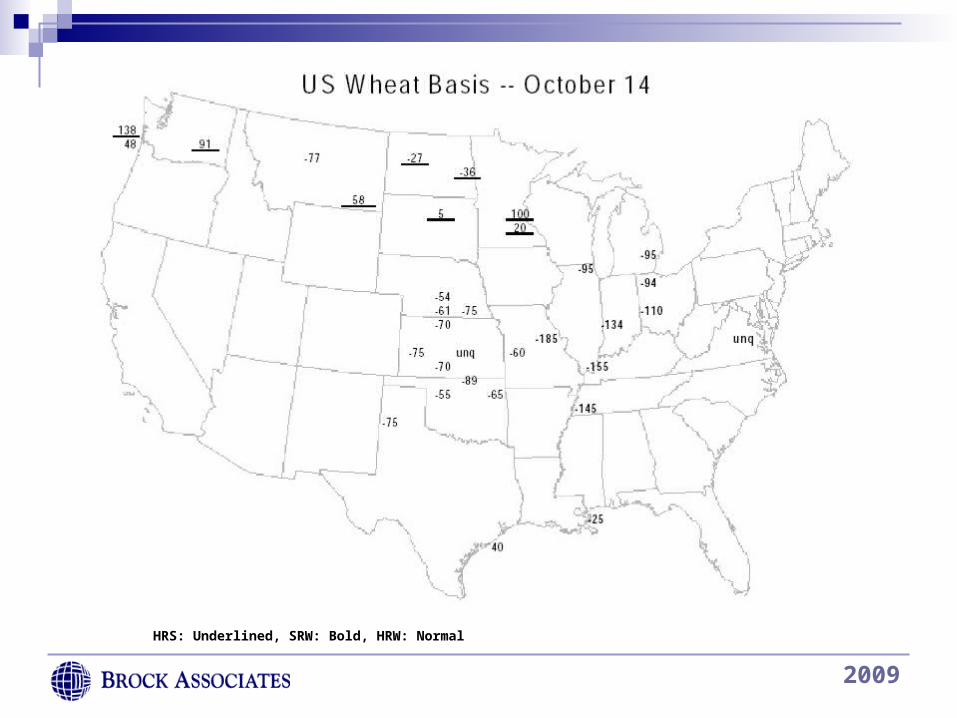

HRS: Underlined, SRW: Bold, HRW: Normal

2009

YearBeginning

Stocks Production ConsumptionEnding Stocks

Stocks/Use Ratio

1995/96 163 537 545 156 28.6%1996/97 156 581 573 163 28.5%1997/98 163 610 577 196 34.0%1998/99 196 590 579 208 35.9%1999/00 208 587 585 210 35.8%2000/01 210 583 585 207 35.4%2001/02 207 583 587 203 34.6%2002/03 203 568 604 167 27.6%2003/04 167 554 589 132 22.4%2004/05 132 626 607 150 24.7%2005/06 150 620 623 147 23.7%2006/07 147 596 615 128 20.7%2007/08 128 611 616 122 19.8%2008/09 122 682 638 167 26.2%2009/10 167 668 648 187 28.8%Bold Figures are USDA Projections.

World Wheat Supply and DemandMillion Metric Tonnes

2009

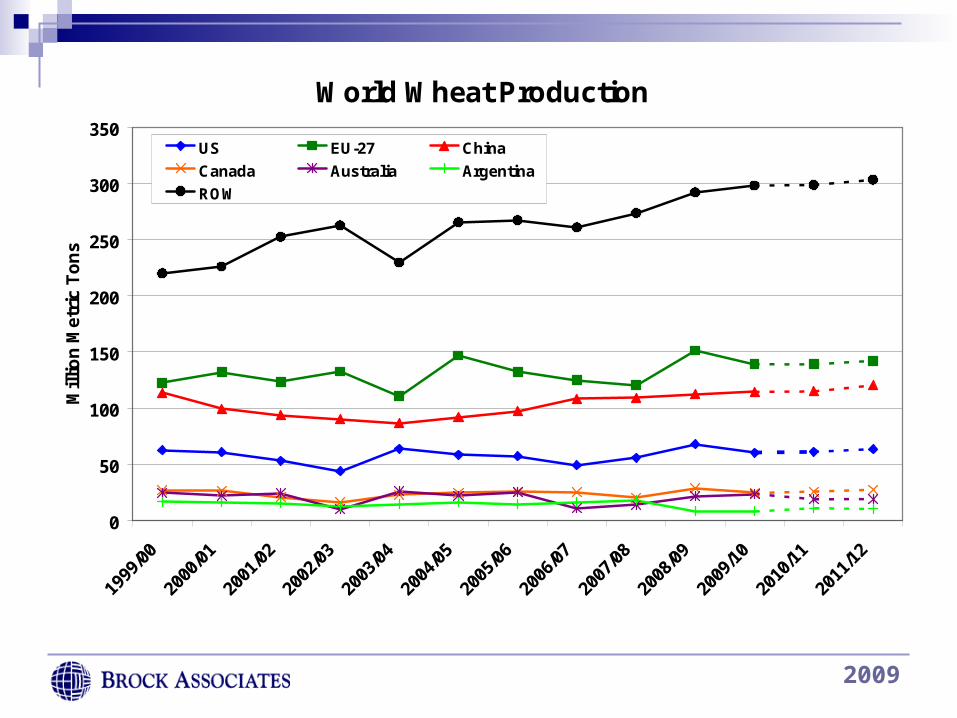

World Wheat Production

0

50

100

150

200

250

300

350

Mill

ion

Met

ric

To

ns

US EU-27 China

Canada Australia Argentina

ROW

Source: USDA, Dotted Lines are Brock Projections

2009

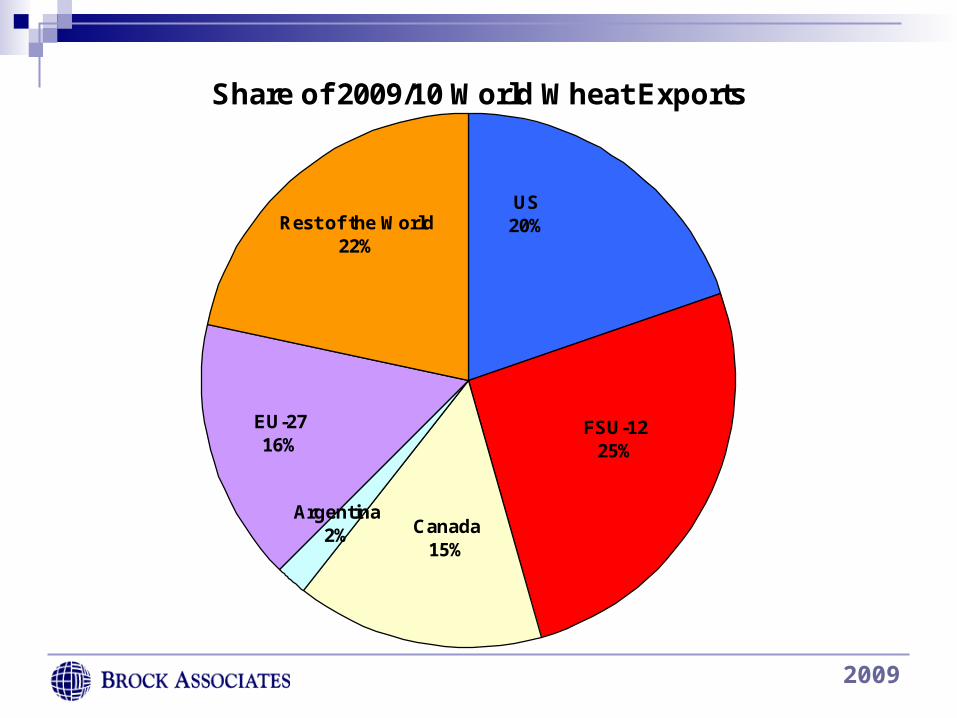

Share of 2009/10 World Wheat Exports

Rest of the World22%

US20%

FSU-1225%

Canada15%

Argentina2%

EU-2716%

2009

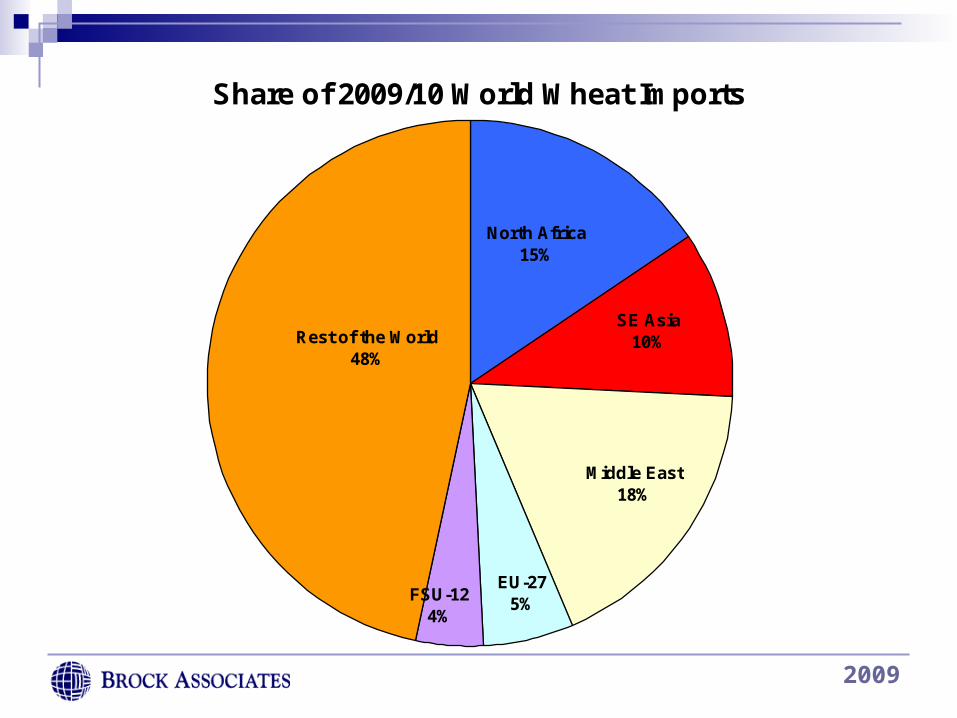

Share of 2009/10 World Wheat Imports

FSU-124%

EU-275%

Middle East18%

SE Asia10%

North Africa15%

Rest of the World48%

2009

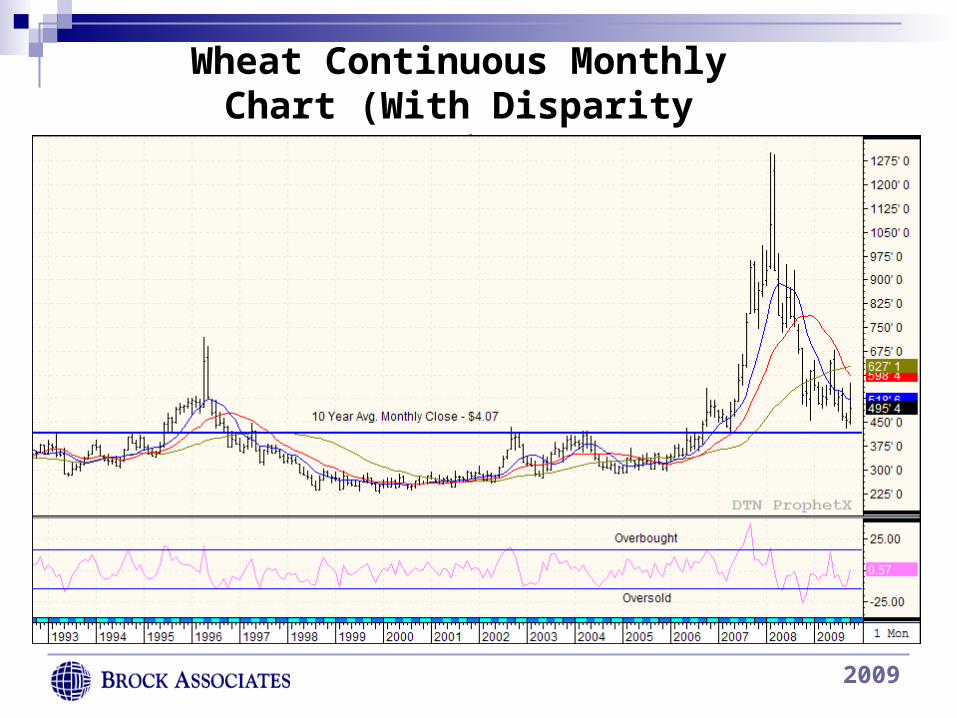

Wheat Continuous Monthly Chart (With Disparity Ratio)

2009

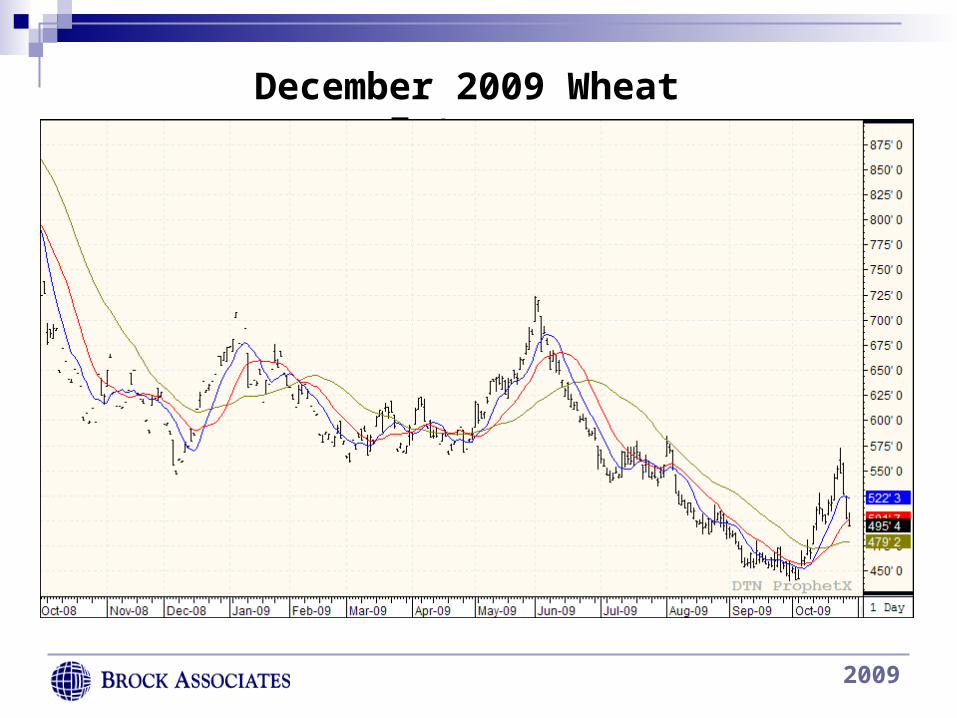

December 2009 Wheat Futures

2009

2009

US Meat Production

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Mill

ion

Po

un

ds

Beef

Pork

Broilers

Turkeys

2009

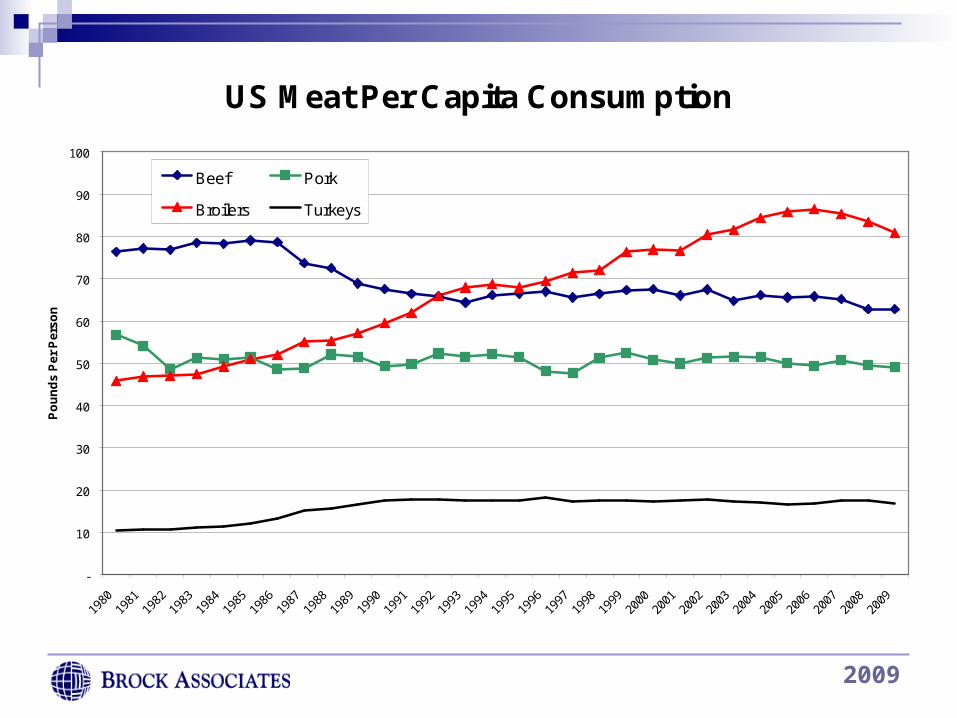

US Meat Per Capita Consumption

-

10

20

30

40

50

60

70

80

90

100

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Po

un

ds

Pe

r P

ers

on

Beef Pork

Broilers Turkeys

Source: USDA

2009

Year & Qtr Beef Pork Red Meat Broiler Turkey

Total Poultry

Red Meat & Poultry Egg Milk

Mil Doz Bil lbs

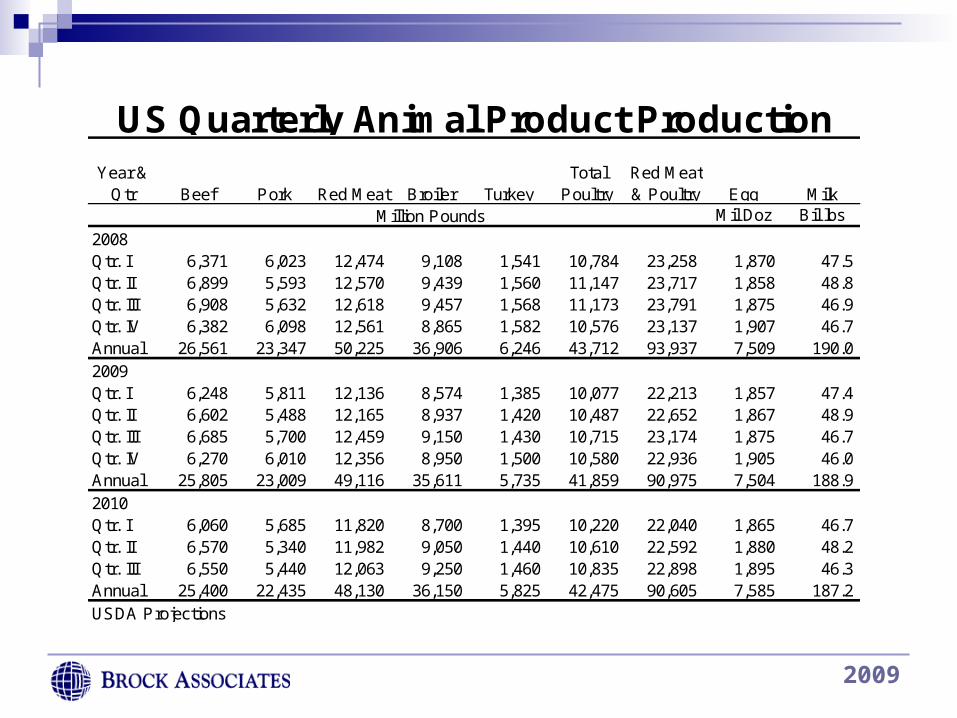

2008Qtr. I 6,371 6,023 12,474 9,108 1,541 10,784 23,258 1,870 47.5 Qtr. II 6,899 5,593 12,570 9,439 1,560 11,147 23,717 1,858 48.8 Qtr. III 6,908 5,632 12,618 9,457 1,568 11,173 23,791 1,875 46.9 Qtr. IV 6,382 6,098 12,561 8,865 1,582 10,576 23,137 1,907 46.7 Annual 26,561 23,347 50,225 36,906 6,246 43,712 93,937 7,509 190.0 2009Qtr. I 6,248 5,811 12,136 8,574 1,385 10,077 22,213 1,857 47.4 Qtr. II 6,602 5,488 12,165 8,937 1,420 10,487 22,652 1,867 48.9 Qtr. III 6,685 5,700 12,459 9,150 1,430 10,715 23,174 1,875 46.7 Qtr. IV 6,270 6,010 12,356 8,950 1,500 10,580 22,936 1,905 46.0 Annual 25,805 23,009 49,116 35,611 5,735 41,859 90,975 7,504 188.9 2010Qtr. I 6,060 5,685 11,820 8,700 1,395 10,220 22,040 1,865 46.7 Qtr. II 6,570 5,340 11,982 9,050 1,440 10,610 22,592 1,880 48.2 Qtr. III 6,550 5,440 12,063 9,250 1,460 10,835 22,898 1,895 46.3 Annual 25,400 22,435 48,130 36,150 5,825 42,475 90,605 7,585 187.2 USDA Projections

US Quarterly Animal Product Production

Million Pounds

2009

Year & Qtr

Choice Steers (Neb. Direct,

1100-1300 lb)

Barrows and Gilts (National Base, Live Eq. 51-52% Lean)

Broilers (Wholesale, 12-

City Avg.)Turkeys (8-16 lbs, hens East)

Eggs (Large, Grade A, New

York)

Milk (Prices Received by

Farmers)

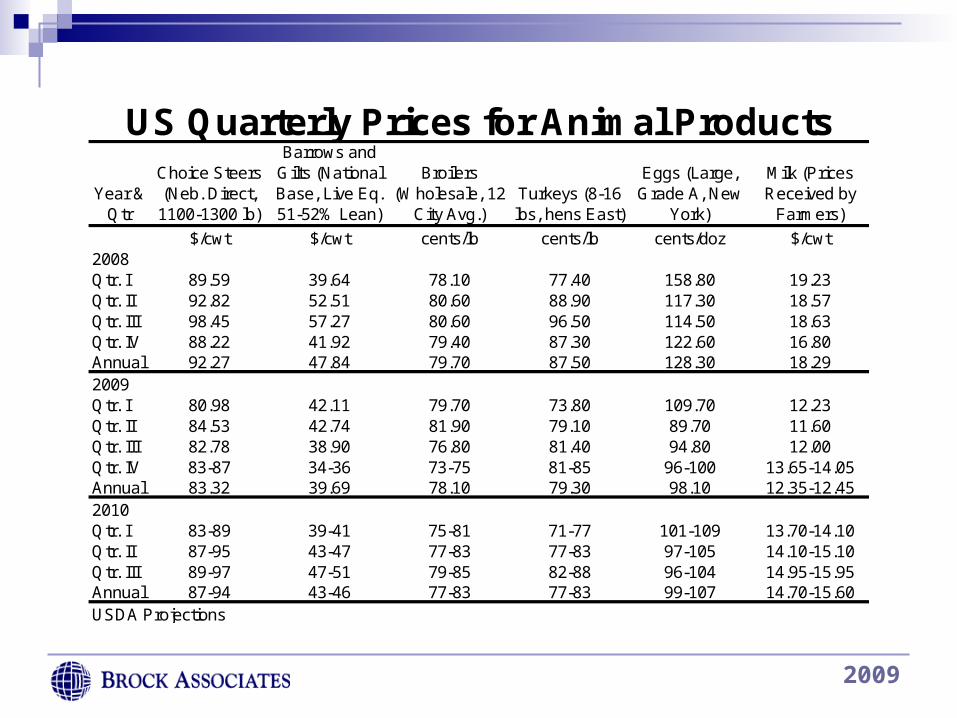

$/cwt $/cwt cents/lb cents/lb cents/doz $/cwt2008Qtr. I 89.59 39.64 78.10 77.40 158.80 19.23Qtr. II 92.82 52.51 80.60 88.90 117.30 18.57Qtr. III 98.45 57.27 80.60 96.50 114.50 18.63Qtr. IV 88.22 41.92 79.40 87.30 122.60 16.80Annual 92.27 47.84 79.70 87.50 128.30 18.292009Qtr. I 80.98 42.11 79.70 73.80 109.70 12.23Qtr. II 84.53 42.74 81.90 79.10 89.70 11.60Qtr. III 82.78 38.90 76.80 81.40 94.80 12.00Qtr. IV 83-87 34-36 73-75 81-85 96-100 13.65-14.05Annual 83.32 39.69 78.10 79.30 98.10 12.35-12.452010Qtr. I 83-89 39-41 75-81 71-77 101-109 13.70-14.10Qtr. II 87-95 43-47 77-83 77-83 97-105 14.10-15.10Qtr. III 89-97 47-51 79-85 82-88 96-104 14.95-15.95Annual 87-94 43-46 77-83 77-83 99-107 14.70-15.60USDA Projections

US Quarterly Prices for Animal Products

2009

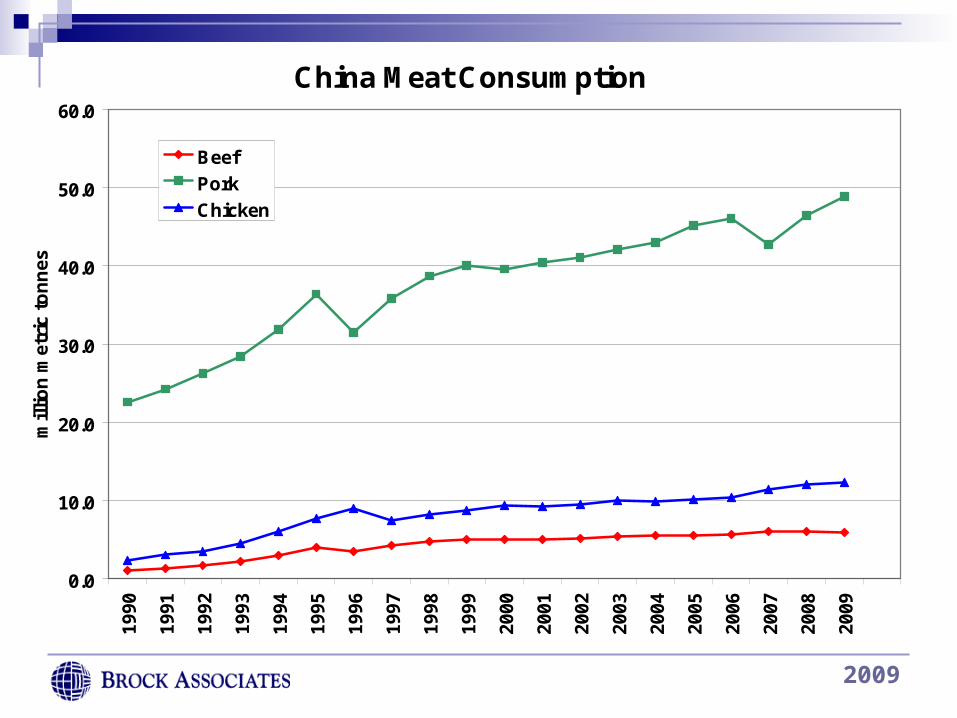

China Meat Consumption

0.0

10.0

20.0

30.0

40.0

50.0

60.019

90

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

mil

lio

n m

etri

c to

nn

es

Beef

Pork

Chicken

2009

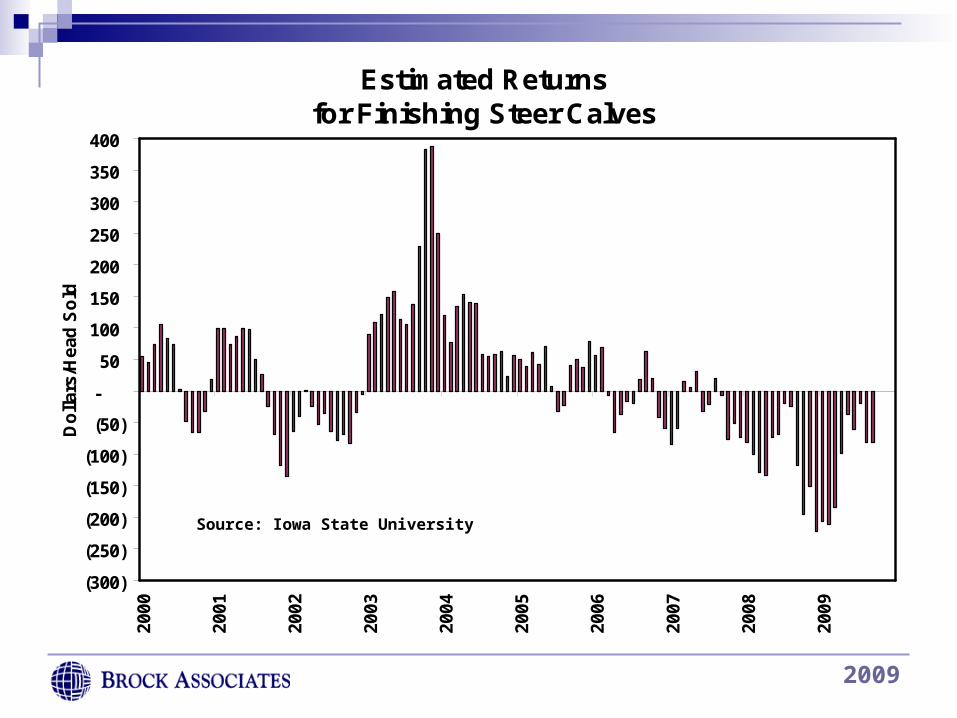

Estimated Returnsfor Finishing Steer Calves

(300)

(250)

(200)

(150)

(100)

(50)

-

50

100

150

200

250

300

350

40020

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

Do

llar

s/H

ead

So

ld

Source: Iowa State University

2009

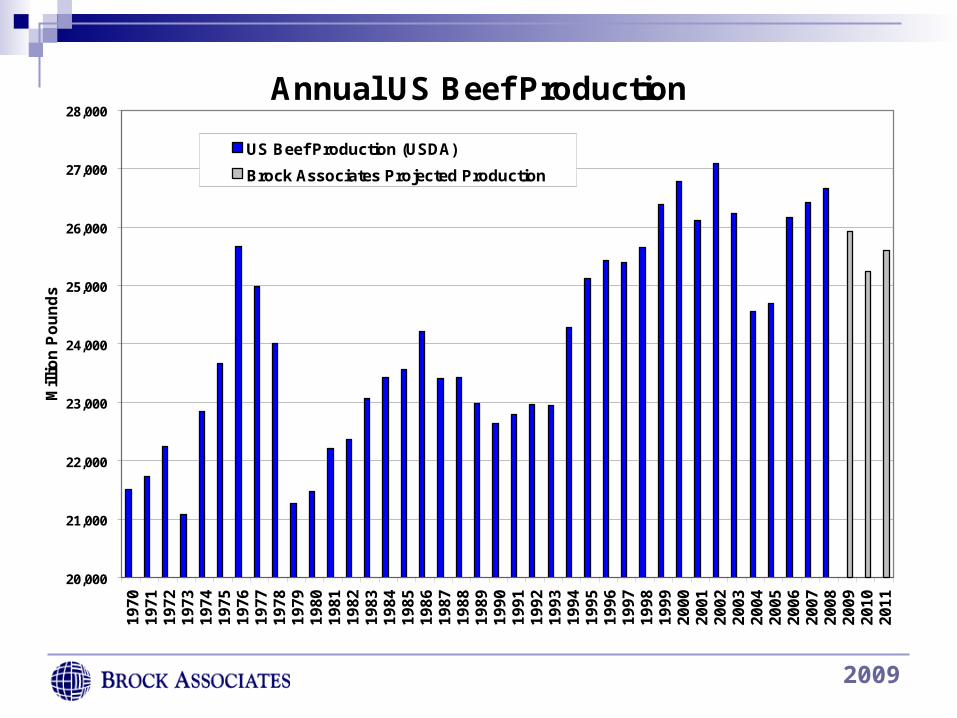

Annual US Beef Production

20,000

21,000

22,000

23,000

24,000

25,000

26,000

27,000

28,000

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Mil

lio

n P

ou

nd

s

US Beef Production (USDA)

Brock Associates Projected Production

2009

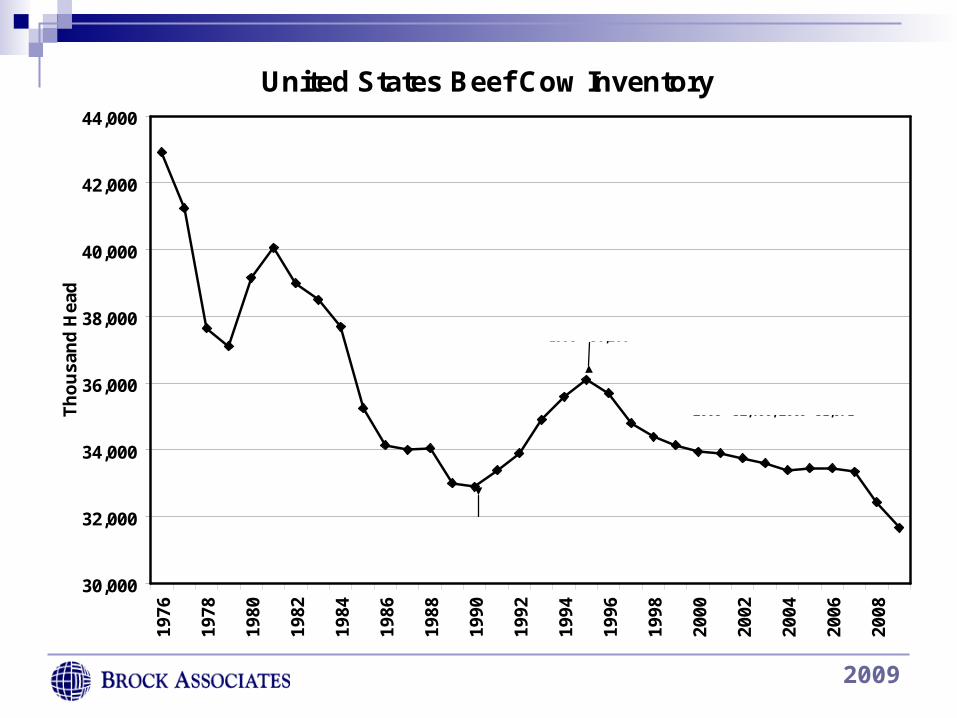

United States Beef Cow Inventory

30,000

32,000

34,000

36,000

38,000

40,000

42,000

44,000

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

Th

ou

san

d H

ead

Key Statistics:

2004 - 33,400, 2005 - 33,450

2006 - 33,450, 2007 - 33,3502008 - 32,400, 2009- 31,671

1990 - 32,900

1995 - 36,100

2009

Annual US Beef and Veal Exports

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500

2,750

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

Bee

f an

d V

eal

Exp

ort

s (M

illi

on

Po

un

ds)

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

Exp

ort

s as

a %

of

Pro

du

ctio

n

Beef and Veal Exports

Beef and Veal Exports as a % of Production

2009

Projected Finished Steer Profitability Based on Current Futures Prices

$0.00

$200.00

$400.00

$600.00

$800.00

$1,000.00

$1,200.00

$1,400.00

Oct 09 Nov 09 Dec 09 Jan 10 Feb 10 Mar 10 Apr 10 May 10

Co

st p

er S

teer

Gross Profit Before Fixed Costs Hay Costs Corn Costs w/Basis DDGS Cost Calf Purchase Fixed Costs

Net Profit is Gross Profit minus Fixed Cost -- Gross profit must exceed Fixed Cost line to realize a net profit

($30.58) ($43.05) ($45.42) ($47.04)($48.45) ($28.96) ($22.49) ($43.92)

Projected Net Profit (Loss) per head

2009

Live Cattle Continuous Monthly Chart (With Disparity Ratio)

2009

December 2009 Live Cattle Futures

2009

Estimated ReturnsIowa Farrow-to-Finish Hog Operations

(70)

(60)

(50)

(40)

(30)

(20)

(10)

-

10

20

30

40

50

6019

91

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Do

llar

s/H

ead

So

ld

Source: Iowa State University

2009

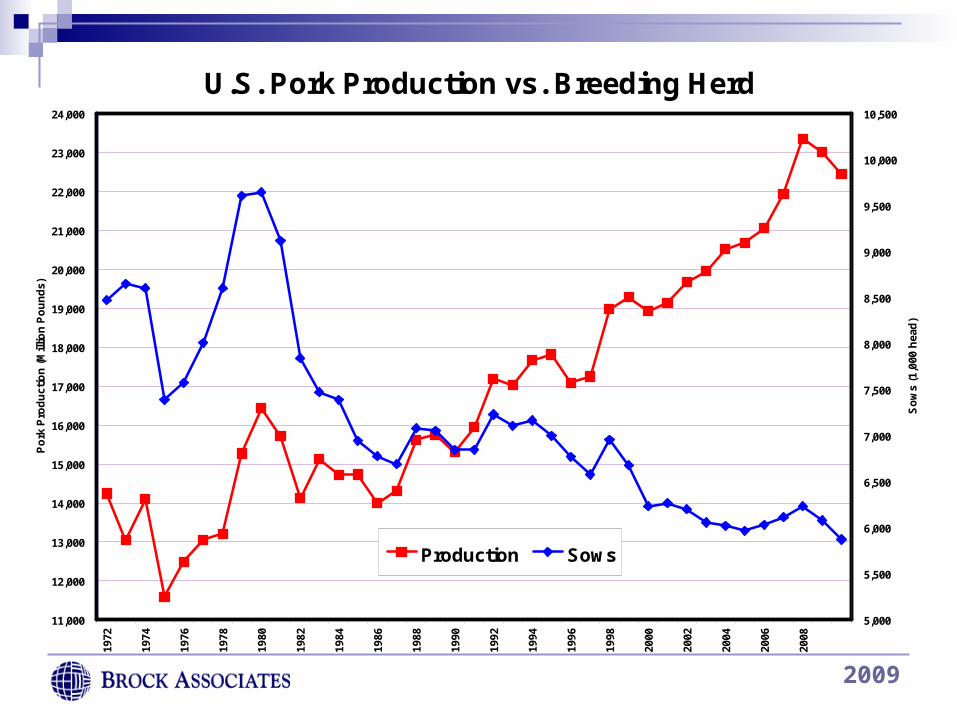

U.S. Pork Production vs. Breeding Herd

11,000

12,000

13,000

14,000

15,000

16,000

17,000

18,000

19,000

20,000

21,000

22,000

23,000

24,00019

72

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

Po

rk P

rod

uct

ion

(M

illio

n P

ou

nd

s)

5,000

5,500

6,000

6,500

7,000

7,500

8,000

8,500

9,000

9,500

10,000

10,500

So

ws

(1,0

00 h

ead

)

Production Sows

2009

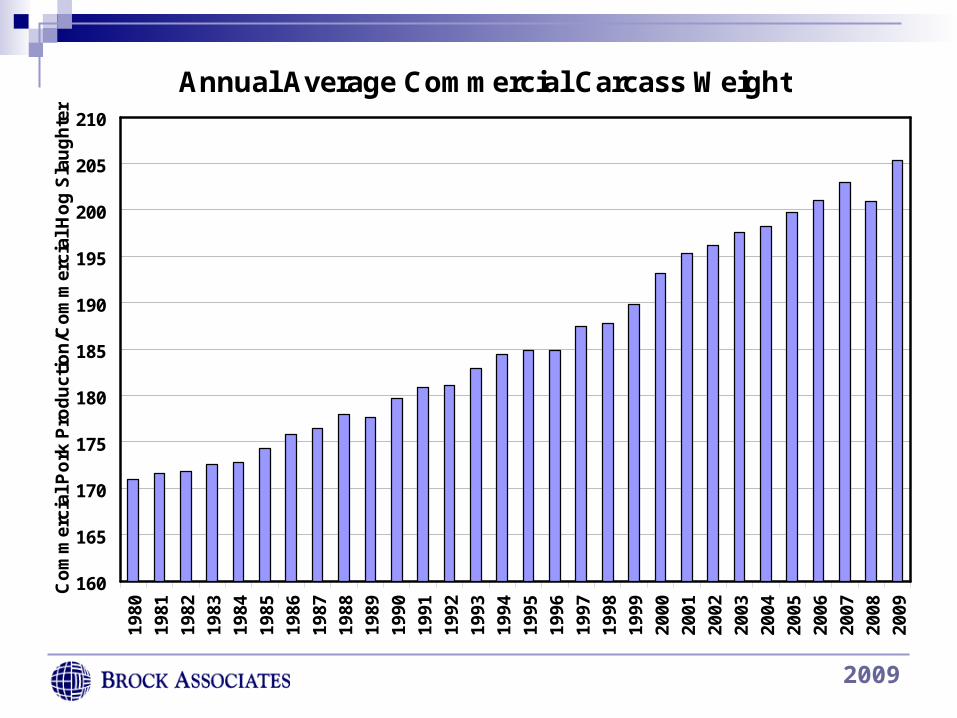

Annual Average Commercial Carcass Weight

160

165

170

175

180

185

190

195

200

205

21019

80

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Co

mm

erci

al P

ork

Pro

du

ctio

n/C

om

mer

cial

Ho

g S

lau

gh

ter

2009

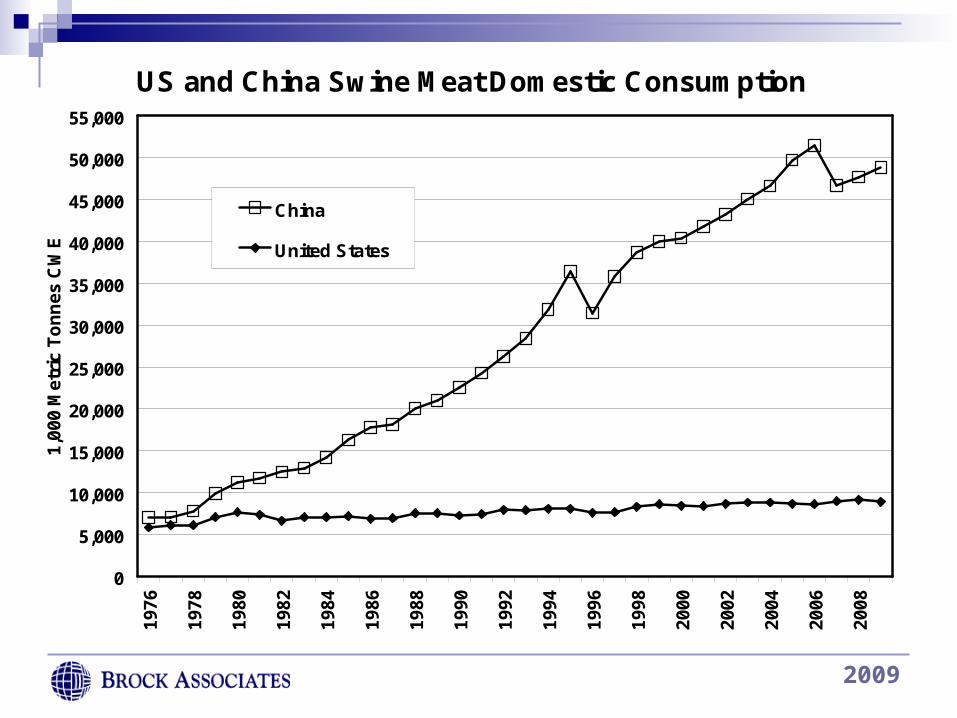

US and China Swine Meat Domestic Consumption

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

1,00

0 M

etri

c T

on

nes

CW

E

China

United States

2009

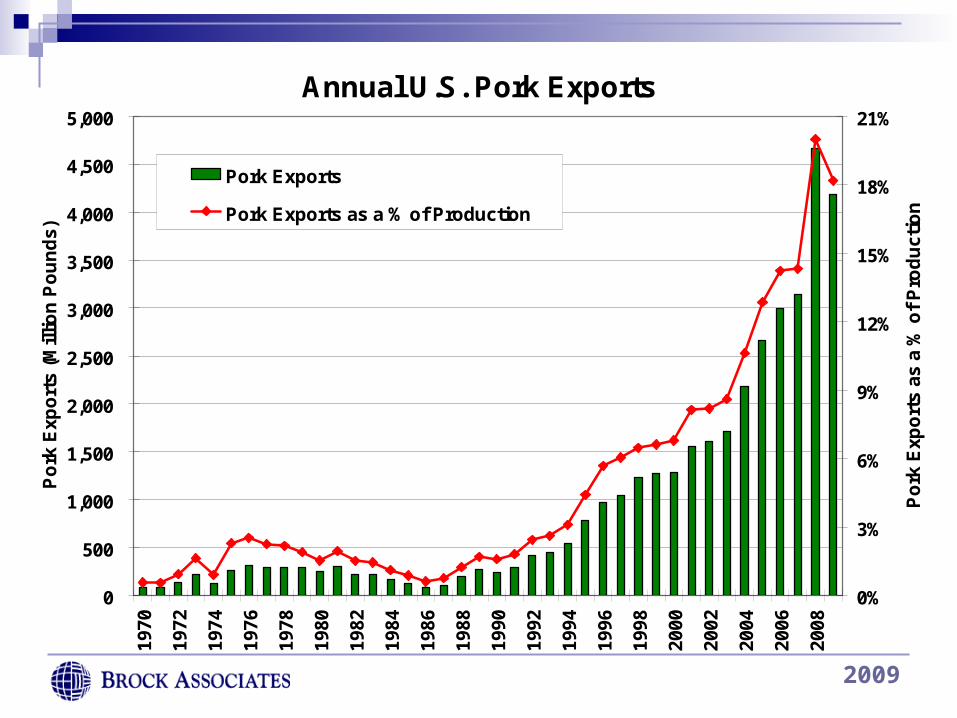

Annual U.S. Pork Exports

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,00019

70

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

Po

rk E

xpo

rts

(Mil

lio

n P

ou

nd

s)

0%

3%

6%

9%

12%

15%

18%

21%

Po

rk E

xpo

rts

as a

% o

f P

rod

uct

ion

Pork Exports

Pork Exports as a % of Production

2009

Projected Hog Profitability Based on Current Futures Prices

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

$180.00

Nov 09 Dec 09 Jan 10 Feb 10 Mar 10 Apr 10 May 10 Jun 10

Co

st p

er H

og

Gross Profit Before Fixed Costs Soybean Meal Costs w/Basis Corn Costs w/Basis DDGS Cost Fixed Costs

Net Profit is Gross Profit minus Fixed Cost -- Gross profit must exceed Fixed Cost line to realize a net profit

(270 pound live weight)

($26.13) ($26.13) ($13.66) ($4.05)($13.54) ($4.92) $12.71 $11.73

Projected Net Profit (Loss) per head

2009

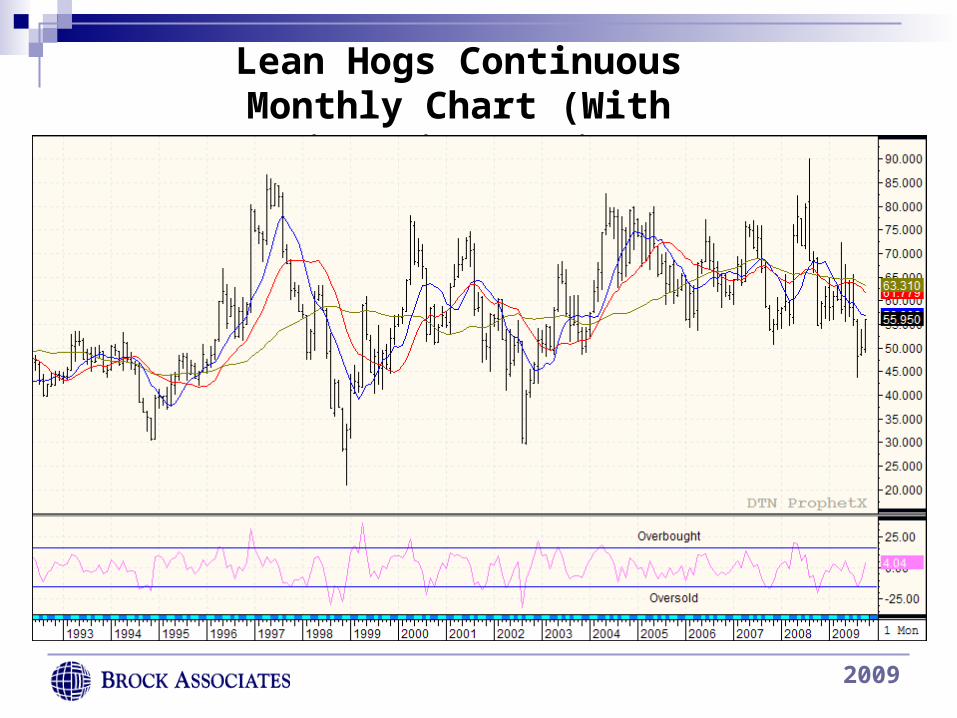

Lean Hogs Continuous Monthly Chart (With Disparity Ratio)

2009

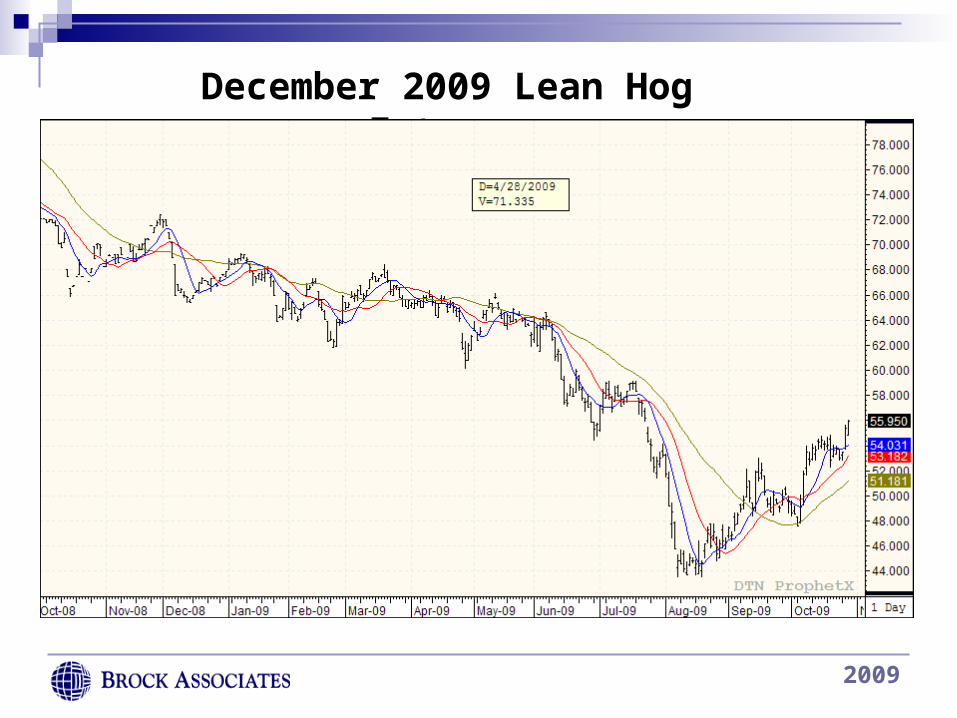

December 2009 Lean Hog Futures

2009

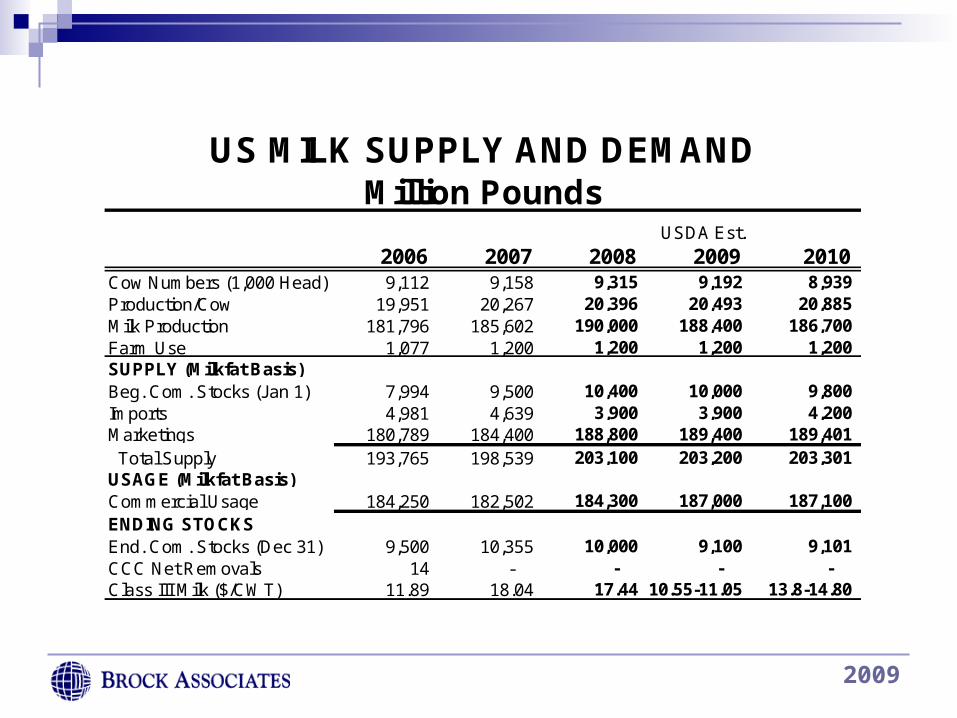

2006 2007 2008 2009 2010Cow Numbers (1,000 Head) 9,112 9,158 9,315 9,192 8,939 Production/Cow 19,951 20,267 20,396 20,493 20,885 Milk Production 181,796 185,602 190,000 188,400 186,700 Farm Use 1,077 1,200 1,200 1,200 1,200SUPPLY (Milkfat Basis)Beg. Com. Stocks (Jan 1) 7,994 9,500 10,400 10,000 9,800 Imports 4,981 4,639 3,900 3,900 4,200 Marketings 180,789 184,400 188,800 189,400 189,401 Total Supply 193,765 198,539 203,100 203,200 203,301 USAGE (Milkfat Basis)Commercial Usage 184,250 182,502 184,300 187,000 187,100 ENDING STOCKSEnd. Com. Stocks (Dec 31) 9,500 10,355 10,000 9,100 9,101 CCC Net Removals 14 - - - - Class III Milk ($/CWT) 11.89 18.04 17.44 10.55-11.05 13.8-14.80

USDA Est.

US MILK SUPPLY AND DEMANDMillion Pounds

2009

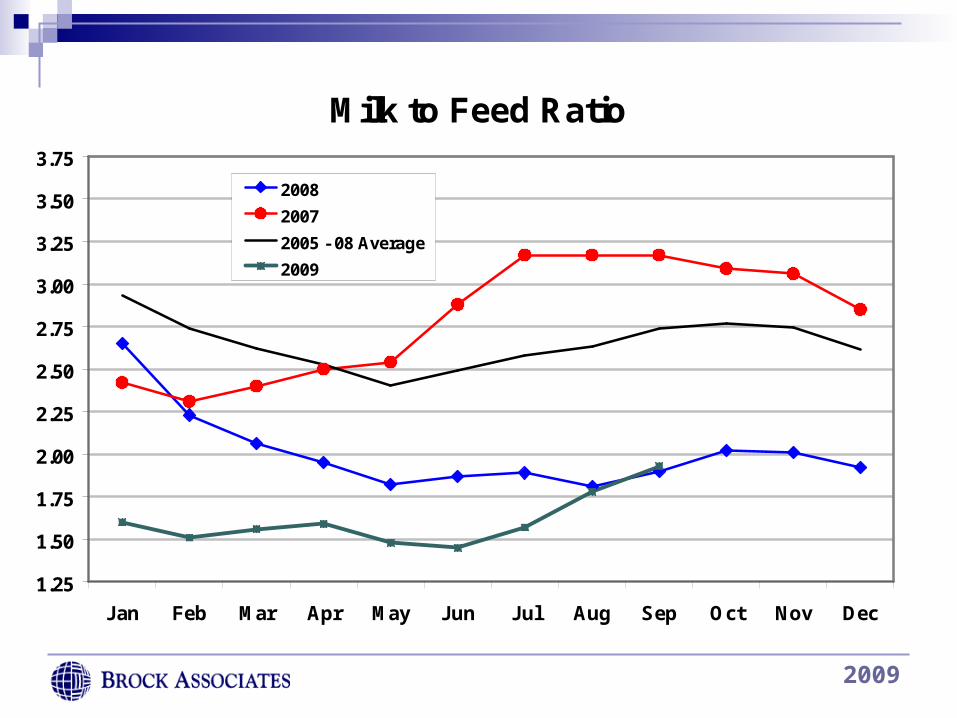

Milk to Feed Ratio

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

3.50

3.75

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2008

2007

2005 - 08 Average

2009

2009

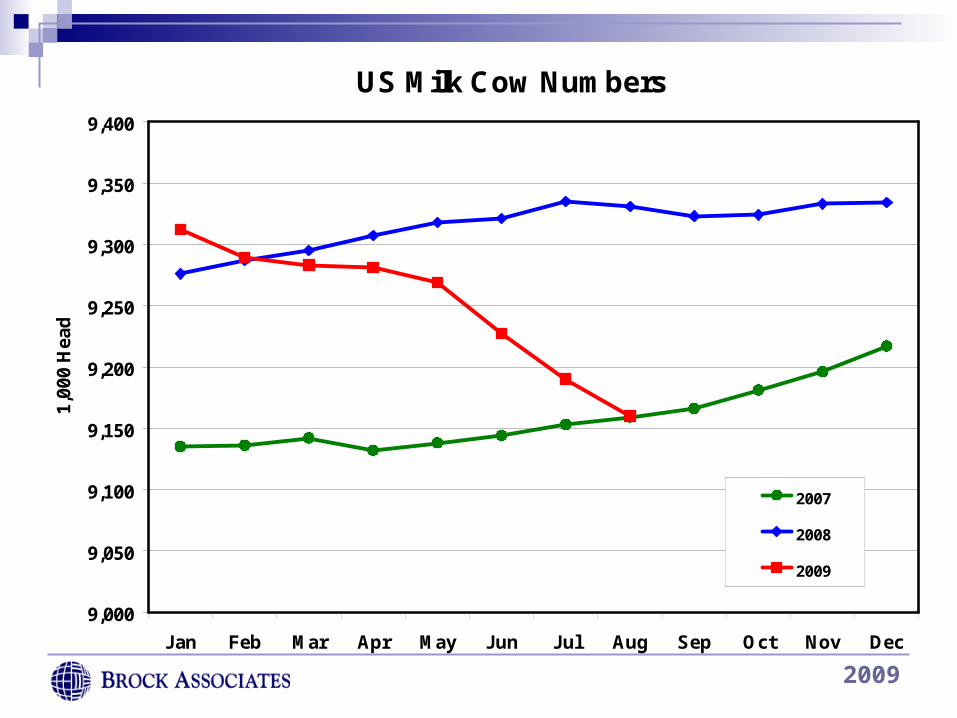

US Milk Cow Numbers

9,000

9,050

9,100

9,150

9,200

9,250

9,300

9,350

9,400

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1,00

0 H

ead

2007

2008

2009

2009

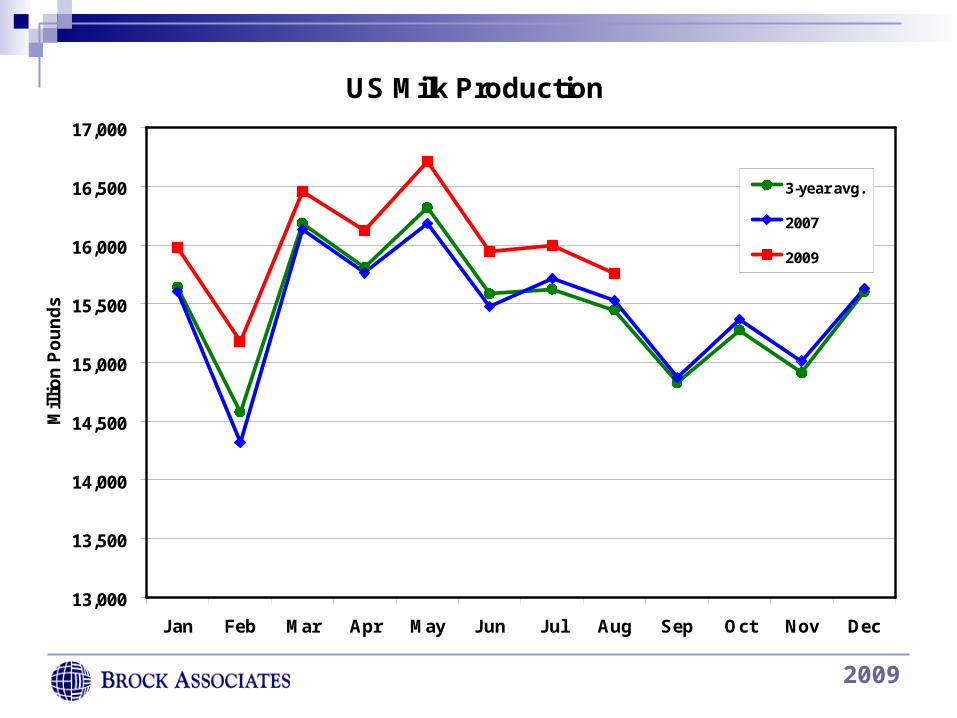

US Milk Production

13,000

13,500

14,000

14,500

15,000

15,500

16,000

16,500

17,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mil

lio

n P

ou

nd

s

3-year avg.

2007

2009

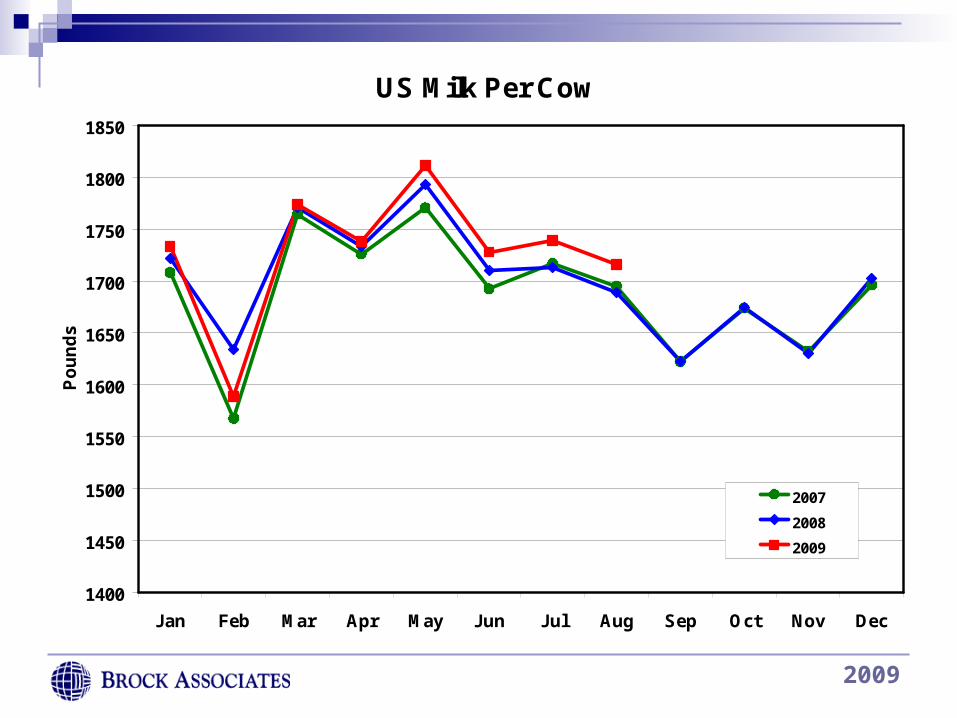

2009

US Milk Per Cow

1400

1450

1500

1550

1600

1650

1700

1750

1800

1850

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Po

un

ds

2007

2008

2009

2009

Annual US Milk Production and Commercial Use

100,000

110,000

120,000

130,000

140,000

150,000

160,000

170,000

180,000

190,000

200,000

197

0

197

2

197

4

197

6

197

8

198

0

198

2

198

4

198

6

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

Mil

lio

n P

ou

nd

s

Milk Production

Milk Commercial Use

Data, Projections: USDA

2009

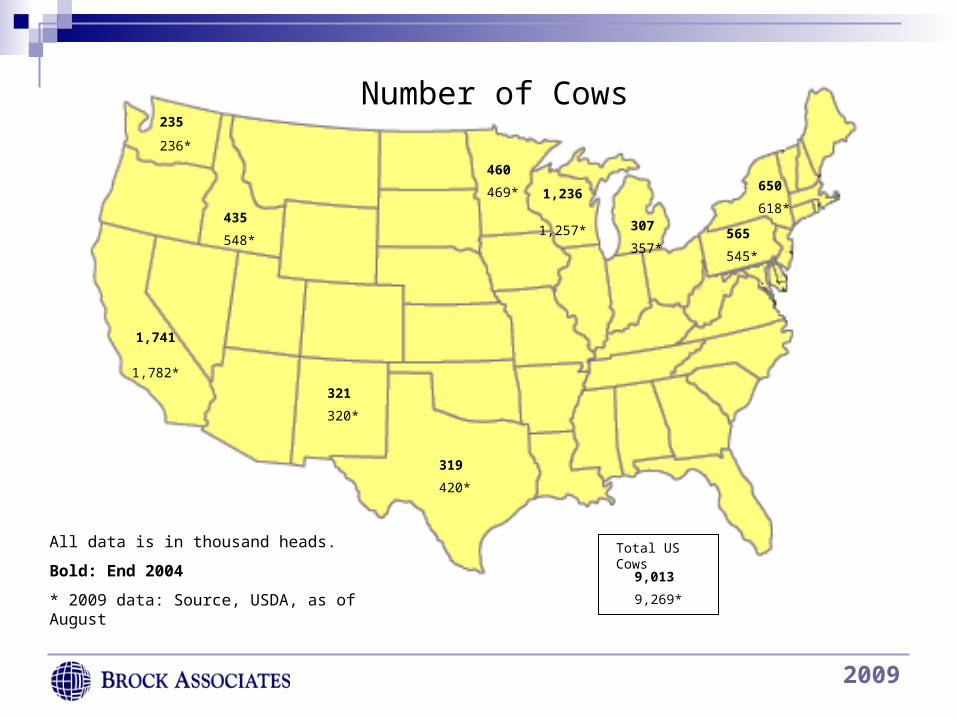

235

236*

All data is in thousand heads.

Bold: End 2004

* 2009 data: Source, USDA, as of August

435

548*

650

618*

565

545*

307

357*

1,236

1,257*

460

469*

319

420*

321

320*

1,741

1,782*

Number of Cows

9,013

9,269*

Total US Cows

2009

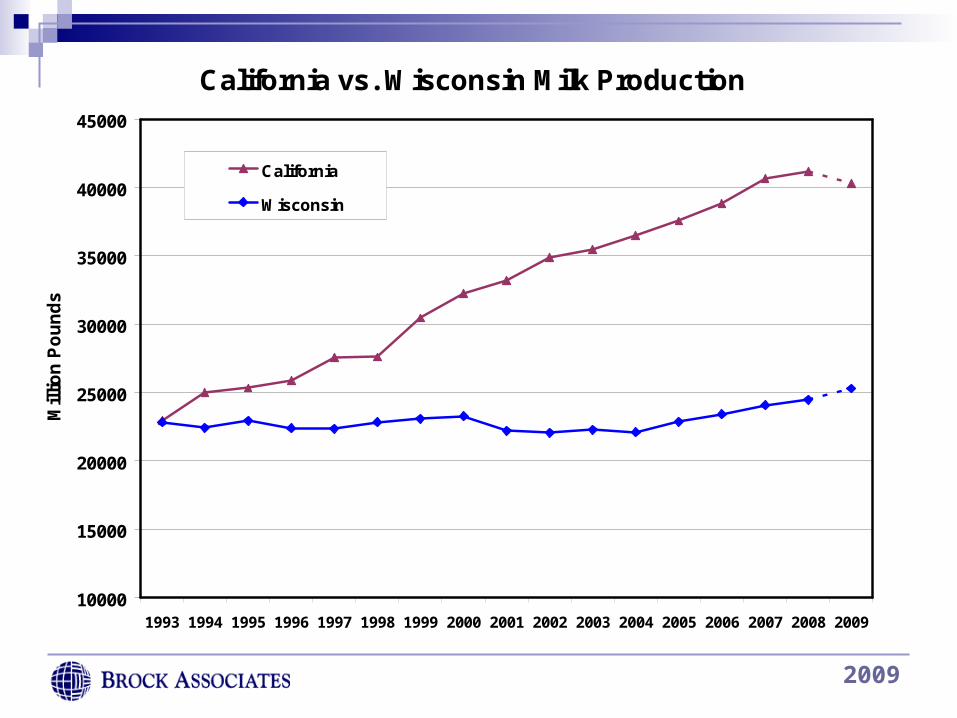

California vs. Wisconsin Milk Production

10000

15000

20000

25000

30000

35000

40000

45000

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Mil

lio

n P

ou

nd

s

California

Wisconsin

Source: USDA, 2009 Projection Brock Estimate

2009

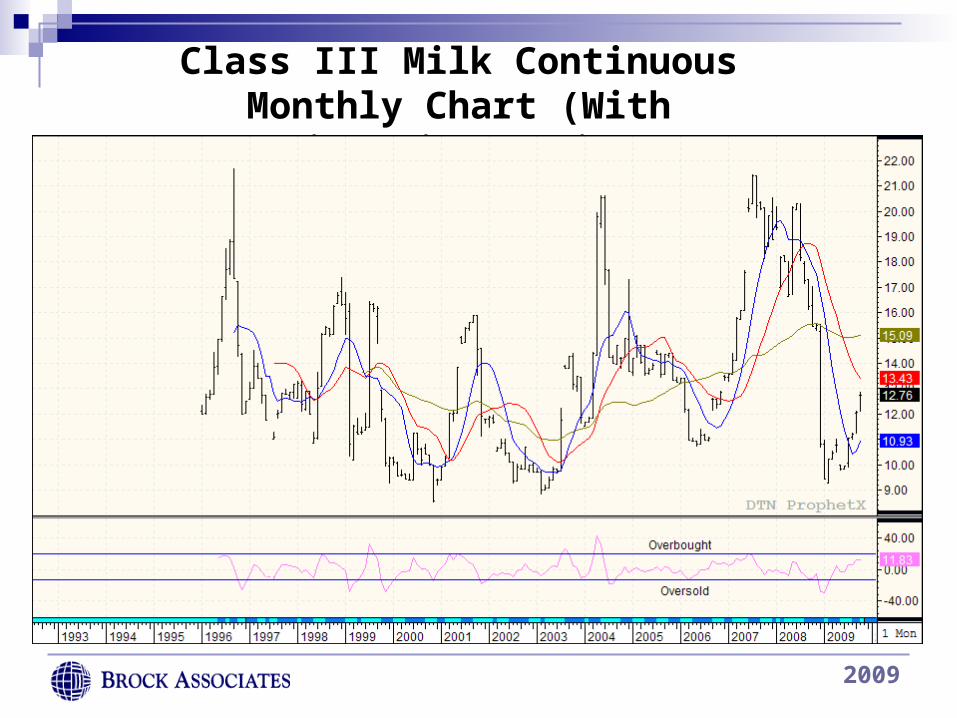

Class III Milk Continuous Monthly Chart (With Disparity Ratio)

2009

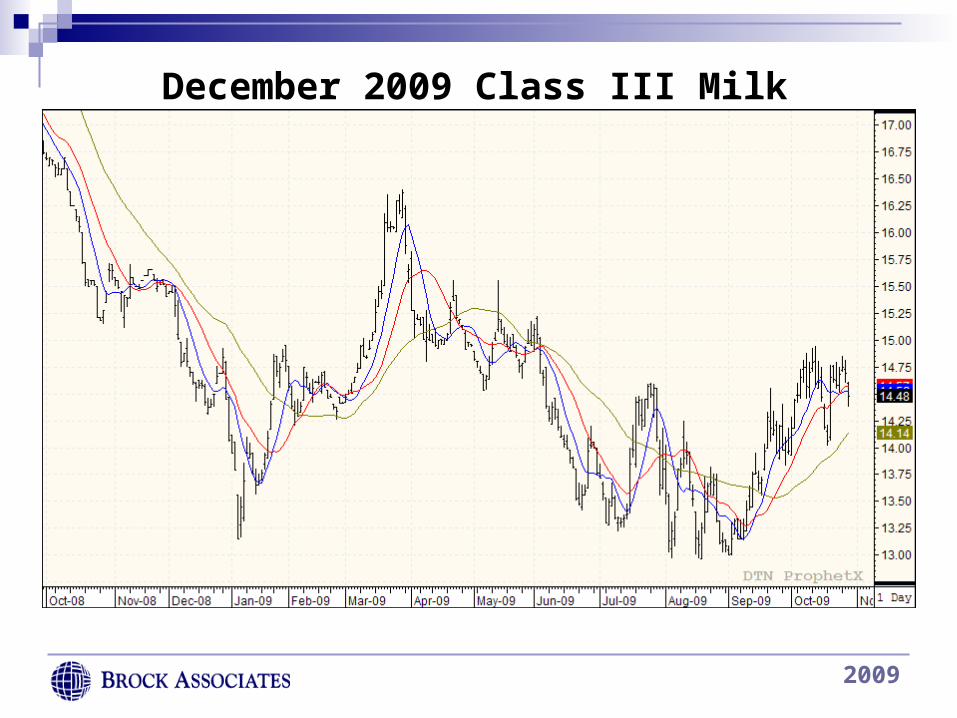

December 2009 Class III Milk Futures

2009

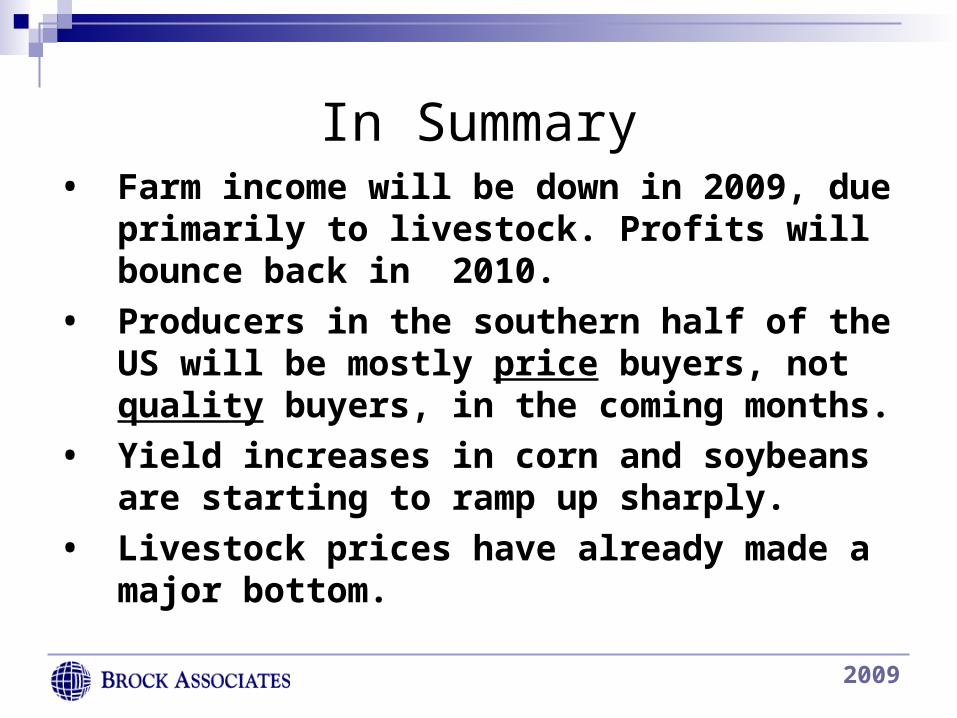

In Summary• Farm income will be down in 2009, due

primarily to livestock. Profits will bounce back in 2010.

• Producers in the southern half of the US will be mostly price buyers, not quality buyers, in the coming months.

• Yield increases in corn and soybeans are starting to ramp up sharply.

• Livestock prices have already made a major bottom.

2009

•Land prices and cash rents will stay strong in the Midwest. California and other states impacted by dairy losses, water availability and environmental issues will soften•Consolidation of farms will continue increasing the demand for farm management services and appraisals

2009

For More Information on the Brock Report, write, email or call

BROCK ASSOCIATES2050 W. Good Hope Rd.

Milwaukee, WI 53209(800) 558-3431

www.brockreport.com [email protected]

![[Commodity Name] Commodity Strategy](https://static.fdocuments.net/doc/165x107/568135d2550346895d9d3881/commodity-name-commodity-strategy.jpg)