E marketer indonesia_online-a_digital_economy_emerges_fueled_by_cheap_mobile_handsets

Digital Intelligence Copyright ©2012 eMarketer, Inc. All rights reserved.

Integrated Video Advertising: What’s Possible? 2

Forces for Fusion 3

Forces Against Fusion 5

Mixed Messages (Forces that Help and Hinder) 8

Conclusions 15

eMarketer Interviews 16

Related Links 16

About eMarketer 17

June 2012

Executive Summary: Someday, online video will almost certainly become so disruptive that TV advertising will have to integrate with it. Several forces are in play that will likely fuel that eventual fusion, most notably the availability of high-quality video content and associated advertising across five increasingly used digital screens—desktop computers, notebook computers, smartphones, tablets and connected TVs.140195

But this report focuses on a shorter timeline—about two years. And in the short term, the fusion of online video ads and TV commercials into singular campaigns will remain incomplete.

What’s standing in the way? The core factor is a fear of financial loss within the TV industry—broadcast and cable networks, and cable providers (which are often also ISPs). Those fears are leading to tactics such as broadband and mobile data caps, which can reduce video usage, and the use of authentication protocols to block cord-cutters from accessing TV content online.

Integration, then, is a question of extent. How far will advertisers go to blend their TV and digital advertising? This report looks at the factors that are speeding the process, as well as those that could impede it. In fact, many of the forces at play could go either way, helping or hindering the connection of digital video and TV advertising.

In the meantime, online video’s ad spending growth will far outstrip TV’s growth through 2016, fueled more by the desires of brand advertisers than by the actions of media companies and other established content owners. Brands need to engage their progressively more fragmented audiences, while media companies feel they have more to lose in the digital space.

Key Questions

■ What forces are making the fusion of TV and online video advertising inevitable?

■ How powerful are the forces that could block cross-media video advertising’s growth?

■ Will strategic factors entice large brand marketers to add more digital to their TV-focused ad budgets?

% change

US TV Ad Spending Growth vs. Online Video AdSpending Growth, 2010-2016

2010

39.6%

9.7%

2011

42.1%

2.8%

2012

54.7%

6.8%

2013

46.0%

1.3%

2014

40.2%

3.3%

2015

22.4%

1.7%

2016

18.9%

4.5%

Online video* TV**

Note: eMarketer benchmarks its US online ad spending projections againstthe IAB/PwC data, for which the last full year measured was 2010;*includes in-banner, in-stream (such as pre-roll and overlays) and in-text(ads delivered when users mouse-over relevant words); mobile included;**includes broadcast TV (network, syndication & spot) & cable TVSource: eMarketer, Jan 2012140195 www.eMarketer.com

David Hallerman [email protected]

Contributors Lauren Fisher, Tracy Tang, Mitch Winkels

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 2

Integrated Video Advertising: What’s Possible?

Over the next couple of years, online video advertising and TV commercials will become increasingly integrated. But it will be an incomplete blend.

Various players and observers, including this analyst, have long anticipated digital video becoming a central platform for brand advertising, but it still hasn’t happened.

This report looks at the different factors that could speed or slow integration over the next two years. Before considering those factors, let’s define the kinds of integration involved in blending digital video and TV:

■ Blend of content availability

■ Blend of media buys

■ Blend of measurement and metrics

■ Blend of campaign messaging

■ Blend of audiences

It’s also important to define the screens we are talking about. There are really six different screens all together, because along with television, digital or online refers to five possible delivery platforms, each with pros and cons for marketers:

■ Desktop computer

■ Notebook computer

■ Smartphone

■ Tablet

■ Connected TV (CTV)

That TV and video advertising are coming together is clear; the process less so. “There’s a spectrum,” said Toby Gabriner, president of Adap.tv, in an April 2012 interview. “There are those who treat online video as an extension or another form of display ad units. But there’s also a growing movement that is starting to look at video and TV paired together.”

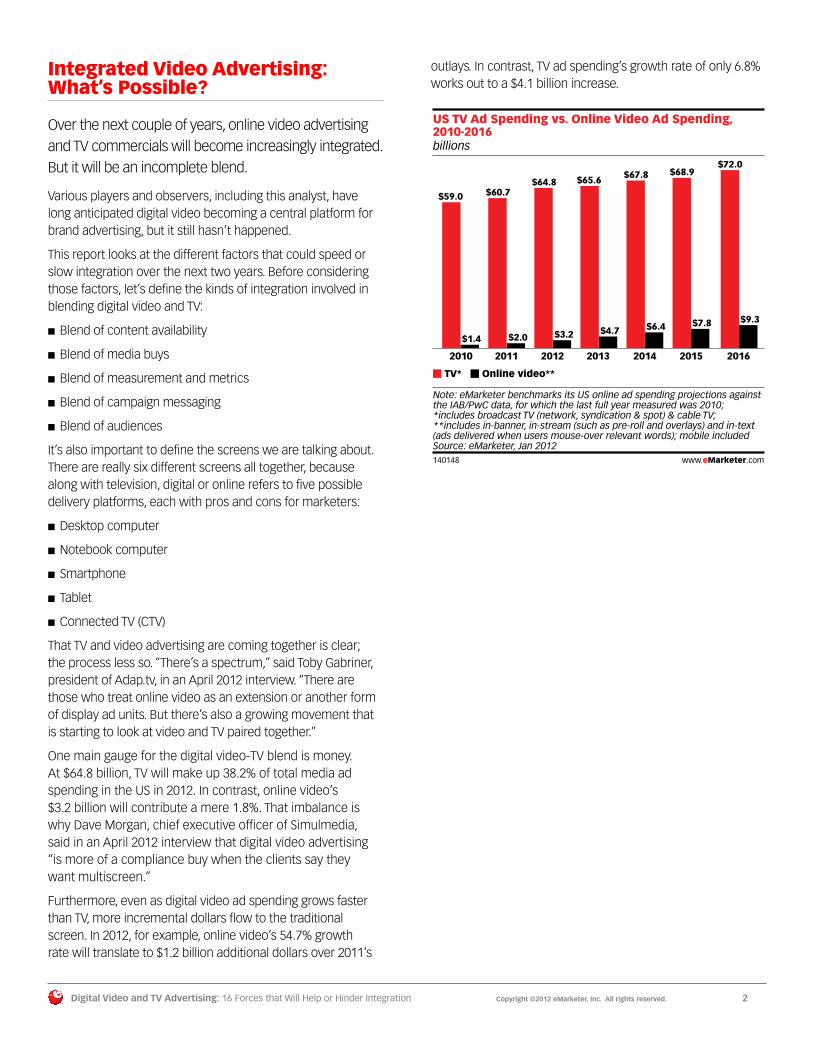

One main gauge for the digital video-TV blend is money. At $64.8 billion, TV will make up 38.2% of total media ad spending in the US in 2012. In contrast, online video’s $3.2 billion will contribute a mere 1.8%. That imbalance is why Dave Morgan, chief executive officer of Simulmedia, said in an April 2012 interview that digital video advertising “is more of a compliance buy when the clients say they want multiscreen.”

Furthermore, even as digital video ad spending grows faster than TV, more incremental dollars flow to the traditional screen. In 2012, for example, online video’s 54.7% growth rate will translate to $1.2 billion additional dollars over 2011’s

outlays. In contrast, TV ad spending’s growth rate of only 6.8% works out to a $4.1 billion increase.

billions

US TV Ad Spending vs. Online Video Ad Spending,2010-2016

2010

$59.0

$1.4

2011

$60.7

$2.0

2012

$64.8

$3.2

2013

$65.6

$4.7

2014

$67.8

$6.4

2015

$68.9

$7.8

2016

$72.0

$9.3

TV* Online video**

Note: eMarketer benchmarks its US online ad spending projections againstthe IAB/PwC data, for which the last full year measured was 2010;*includes broadcast TV (network, syndication & spot) & cable TV;**includes in-banner, in-stream (such as pre-roll and overlays) and in-text(ads delivered when users mouse-over relevant words); mobile includedSource: eMarketer, Jan 2012140148 www.eMarketer.com

140148

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 3

Forces for Fusion

Several factors make the blend between online and TV advertising seem inevitable. A shift in how people use digital devices, combined with a shift in how brands look to engage that changing audience, are creating several strong forces in favor of fusion between the two video advertising channels.

(1) Connected TVs Combine Strengths

Connected TVs offer two crucial elements that will help blend advertising across the two media—the big screen of a television and the digital delivery of the internet. Increasing numbers of US homes have connected TVs, which makes connected TV a prime digital channel for video ad growth. More than one-third of US connected-TV owners now use their TV sets to watch internet-sourced content at least once a week, according to March 2012 research from Strategy Analytics.

Another study, from the Leichtman Research Group, found that 38% of US households had at least one TV set connected to the internet as of February 2012, up from only 24% in 2010.

Increasingly known by its acronym, CTV, connected TV is also called over-the-top TV, smart TV, internet TV and IPTV. Too many names can create confusion, but the concept is simple: A TV set becomes a connected TV when whatever is being watched is sourced through internet protocol (IP), rather than through cable or broadcast.

The types of devices that are used to create a CTV environment include:

■ Standalone boxes, such as Roku or Apple TV

■ Game consoles (i.e., Sony PlayStation 3, Microsoft Xbox 360, Nintendo Wii)

■ Internet-enabled TVs

■ Internet-enabled DVD or Blu-ray players

■ Digital video recorders (DVRs)

■ Computers attached to TVs

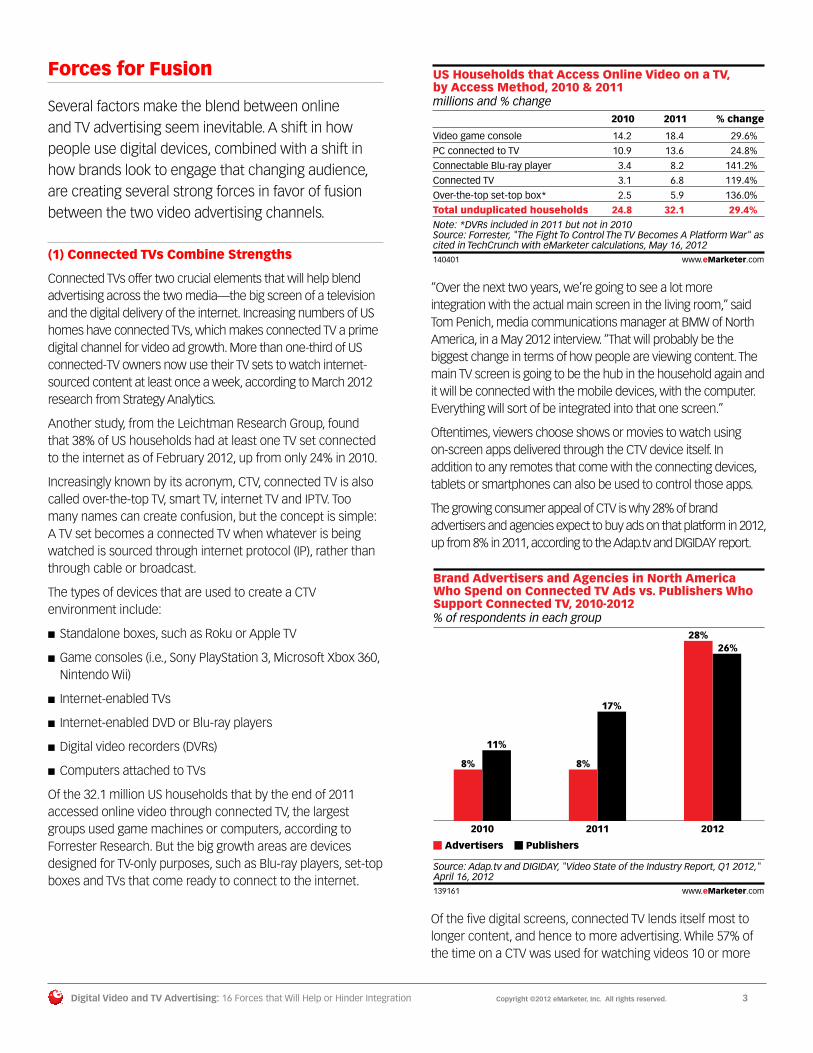

Of the 32.1 million US households that by the end of 2011 accessed online video through connected TV, the largest groups used game machines or computers, according to Forrester Research. But the big growth areas are devices designed for TV-only purposes, such as Blu-ray players, set-top boxes and TVs that come ready to connect to the internet.

millions and % change

US Households that Access Online Video on a TV, by Access Method, 2010 & 2011

2010 % change

Video game console 14.2 29.6%

PC connected to TV 10.9 24.8%

Connectable Blu-ray player 3.4 141.2%

Connected TV 3.1 119.4%

Over-the-top set-top box* 2.5 136.0%

Total unduplicated households 24.8

2011

18.4

13.6

8.2

6.8

5.9

32.1 29.4%Note: *DVRs included in 2011 but not in 2010Source: Forrester, "The Fight To Control The TV Becomes A Platform War" ascited in TechCrunch with eMarketer calculations, May 16, 2012140401 www.eMarketer.com

140401

“Over the next two years, we’re going to see a lot more integration with the actual main screen in the living room,” said Tom Penich, media communications manager at BMW of North America, in a May 2012 interview. “That will probably be the biggest change in terms of how people are viewing content. The main TV screen is going to be the hub in the household again and it will be connected with the mobile devices, with the computer. Everything will sort of be integrated into that one screen.”

Oftentimes, viewers choose shows or movies to watch using on-screen apps delivered through the CTV device itself. In addition to any remotes that come with the connecting devices, tablets or smartphones can also be used to control those apps.

The growing consumer appeal of CTV is why 28% of brand advertisers and agencies expect to buy ads on that platform in 2012, up from 8% in 2011, according to the Adap.tv and DIGIDAY report.

% of respondents in each group

Brand Advertisers and Agencies in North AmericaWho Spend on Connected TV Ads vs. Publishers WhoSupport Connected TV, 2010-2012

2010

8%

11%

2011

8%

17%

2012

28%26%

Advertisers Publishers

Source: Adap.tv and DIGIDAY, "Video State of the Industry Report, Q1 2012,"April 16, 2012139161 www.eMarketer.com

139161

Of the five digital screens, connected TV lends itself most to longer content, and hence to more advertising. While 57% of the time on a CTV was used for watching videos 10 or more

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 4

minutes long, according to an Ooyala study, the shares of time on the other screens for such content were smaller.

% of total

Share of Time Spent Watching Online VideosWorldwide, by Video Length and Device, Q4 2011

Desktop10% 29% 26% 10% 25%

Mobile6% 30% 23% 12% 29%

Tablet6% 26% 22% 11% 36%

<1 minute1-3 minutes

3-6 minutes6-10 minutes

10+ minutes

Source: Ooyala, "Video Index Report Q4 2011," Feb 15, 2012137882 www.eMarketer.com

Connected TV devices and game consoles15% 15% 9% 57%4%

137882

“The big TV is going to continue to dominate the overall video consumption, certainly in home. But what content is getting to it?” asked Brian Fuhrer, senior vice president for product leadership at Nielsen, in an April 2012 interview. “Connected TV is going to continue to accelerate, because if we have learned anything from our data, it’s that people really want to use the big screen.”

Rumors suggest that Apple—the dominant company in the tablet and smartphone space—will be coming out with “some type of a connected TV,” said Will Richmond, editor and publisher of the VideoNuze site, in an April 2012 interview. “As we’ve seen with the iPad, that could be a major game changer. . . . We do know that Apple brings a ton of momentum and innovation and brand loyalty to the party, and done right that could really roil the market.”

(2) Tablets Are Game Changers

More than 90% of US tablet owners in 2012 have watched a TV program or movie on their device, according to QuickPlay Media. But only 9% of US consumers in 2012 said they watched video on their tablet weekly, according to Leichtman Research Group.

The first datapoint shows how popular video is among those who have tablets. The second, though, shows that among a much larger group—US consumers in general—the share watching video on tablets is, at this point, still small.

“There’s a lot more hype around the actual penetration levels of tablets,” said Nielsen’s Fuhrer. “When you look at the number of computers, laptops and tablets out there, tablets are still, despite what you might hear, fairly nascent.”

Tablet penetration will need to be higher than it is currently to push it out of its niche base. But that can shift quickly, especially when you remember that the iPad was introduced only two years ago, in April 2010. “It is going to complement a lot of TV,” said Simulmedia’s Morgan.

eMarketer expects tablet usage to soar from substantially less than one-third of internet users in 2012 to more than one-half in 2015.

US Tablet Users and Penetration, 2010-2015

Tablet users (millions)—% change

—% of total population

—% of internet users

2010

13.0-

4.2%

5.8%

2011

33.7158.6%

10.8%

14.5%

2012

69.6106.5%

22.0%

29.1%

2013

99.042.3%

31.0%

40.4%

2014

119.320.5%

37.0%

47.5%

2015

133.511.9%

41.0%

51.9%

Note: individuals of any age who use a tablet at least once per monthSource: eMarketer, June 2012140848 www.eMarketer.com

140848

“Tablets strike a happy medium. They are more of an entertainment and leisure screen than your typical computer. Other mobile devices tend to be a mix of entertainment and utility,” said Colleen Soriano, senior vice president and managing partner for US integrated investment and digital innovation at Universal McCann, in an April 2012 interview.

No wonder, then, that 41% of US digital media professionals in a November 2011 DigiCareers survey said that tablets provided the best advertising experience. In contrast, only 8% cited smartphones.

% of respondents

Effect of Select Devices on Advertising* According toUS Digital Media Professionals, Nov 2011

Will not be a major factor in advertising6% 10% 10% 10% 65%

Tablet PC Smartphone TV Game console

Note: numbers may not add up to 100% due to rounding; *in 5 yearsSource: DigiCareers, March 27, 2012138522 www.eMarketer.com

Provides the best user experience61% 19% 13% 4%

2%

Provides the best advertising experience41% 21% 8% 27% 4%

Generates the majority of advertising dollars8% 17% 25% 48% 3%

138522

Fascinating data from Forrester shows that as of Q3 2011, more respondents decreased usage of 11 devices or media due to tablet ownership—including computers, print, MP3 players, mobile phones, TV and ereaders—than increased their usage. However, for online video, more tablet owners increased their usage than decreased it.

Perhaps more than any other datapoint, this makes the potential connection between TV and tablets clear and present.

“Tablets are where the money is actually going to flow,” said Rick Landsman, senior vice president for engineering at [x+1], in a May 2012 interview. “On the phone you’re really snacking, using specific apps to do specific things, and you’re often out and about. With the tablet, you’re sitting at home and there is an awful lot going on in integrating video.”

Forces for Fusion

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 5

Forces Against Fusion

Inertia is a powerful force against change. Advertisers and agencies often have separate digital and television departments, a silo approach that slows integration.

In addition, stakeholders with deep pockets—notably cable companies and TV broadcast and cable networks—are actively impeding a deeper integration of traditional and digital advertising for fear of a reduced bottom line.

(3) Fear of Cannibalization

TV executives saw what happened to the music industry in the digital era and don’t want to follow that same downward spiral. Many TV companies have a vested interest in keeping digital video from undercutting their current revenue streams. Cable TV providers make more money from television than the internet, and TV networks—broadcast and cable alike—gather more ad dollars from the tube than from all five digital screens put together.

The TV business is looking at several methods that might reduce the growth of digital video content, even if the consequence is a reduction in associated advertising. Two main tactics are bandwidth metering, also called a data cap, and authentication.

The elephant in the room that could stomp on digital video is greater bandwidth metering—in more areas of the country and to a greater extent than ISPs do now. If consumers need to think twice before watching another online video, because that viewing would cost them extra or result in their ISP slowing down (aka “throttling”) their internet connection, digital video viewing would likely tumble—and therefore so would accompanying advertising. In fact, why should ISPs that are also cable providers want online video to get too big unless they can get a little extra share out of the pot?

Bandwidth metering is already a fact of life for many mobile users, especially when their devices are connected via 3G or 4G wireless technologies.

“One of the things that is problematic today in delivery of video into the mobile space is that in most cases you’re going over the carrier networks. And in nearly all cases, you have tiered, high-priced data plans with low caps,” said [x+1]’s Landsman. “From an advertising perspective, video over the cellular net to mobile devices is actually being paid out of the data plan of the user. The advertisers are going to have to figure out a way of working with carriers to address the bandwidth issues in the mobile environment.”

Networks and cable operators are also considering requiring users to prove that they are paying subscribers before allowing them to access certain content online. As reported by the New York Post in late April 2012, Hulu is “taking its first steps to change

to a model where viewers will have to prove they are a pay-TV customer to watch their favorite shows” on its site.

However, since Hulu is the top property on the web for online video advertising, as reported monthly by comScore, cutting off a potentially large portion of its audience would most likely reduce the video ad spending it receives.

In addition to Hulu’s progression toward authentication, Comcast—the owner of NBC (which owns part of Hulu) and also a major ISP—is “expected to switch to an authentication model for this summer’s Olympic Games,” as the Post also reported.

The act of walling off content from certain digital channels means the larger TV companies are ceding much of the lower-end video market to more innovative competitors. This strategy could work in the short- and mid-term, maintaining profit levels for the major players, although it may fail over the longer term.

(4) Digital Pennies vs. Analog Dollars

Many content owners think that digital viewers are getting a “free ride” just because they cannot sell enough advertising to support the content. Therefore, they will limit the ad-supported video content available online because, in the now-famous warning from Jeff Zucker, former head of NBC Universal, they would be “trading analog dollars for digital pennies.”

Comparing current revenue between TV and digital video ads can be done only indirectly, but it’s still revealing. Using the typical 22-minute-long primetime TV comedy as an example, say ABC’s “Modern Family,” here’s how the numbers work out:

Data from Nielsen shows that in Q1 2011, the price of single 30-second primetime TV ad was nearly $97,000.

In contrast, the CPM for an online video ad associated with premium content, such as on Hulu or a TV network site, ranged from about $25 to $30 in late 2011, according to research from DIGIDAY and Adap.tv.

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 6

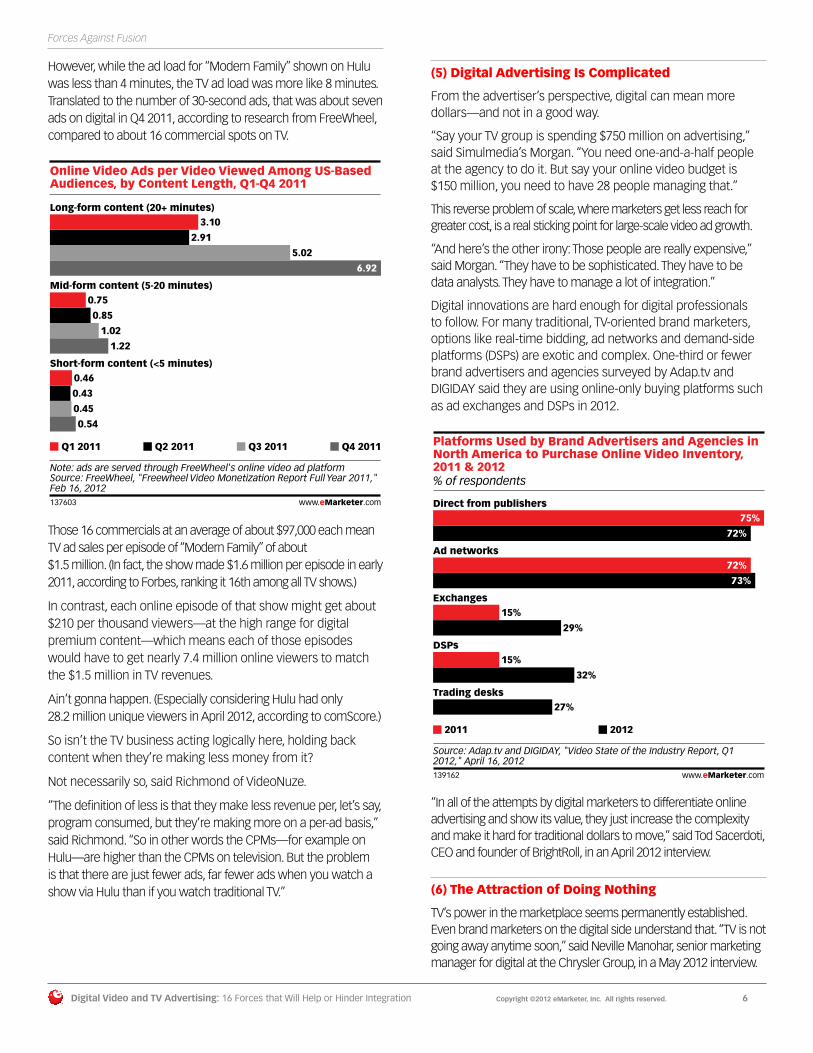

However, while the ad load for “Modern Family” shown on Hulu was less than 4 minutes, the TV ad load was more like 8 minutes. Translated to the number of 30-second ads, that was about seven ads on digital in Q4 2011, according to research from FreeWheel, compared to about 16 commercial spots on TV.

Online Video Ads per Video Viewed Among US-BasedAudiences, by Content Length, Q1-Q4 2011

Long-form content (20+ minutes)3.10

2.91

5.02

6.92

Mid-form content (5-20 minutes)0.75

0.85

1.02

1.22

Short-form content (<5 minutes)0.46

0.43

0.45

0.54

Q1 2011 Q2 2011 Q3 2011 Q4 2011

Note: ads are served through FreeWheel's online video ad platformSource: FreeWheel, "Freewheel Video Monetization Report Full Year 2011,"Feb 16, 2012137603 www.eMarketer.com

137603

Those 16 commercials at an average of about $97,000 each mean TV ad sales per episode of “Modern Family” of about $1.5 million. (In fact, the show made $1.6 million per episode in early 2011, according to Forbes, ranking it 16th among all TV shows.)

In contrast, each online episode of that show might get about $210 per thousand viewers—at the high range for digital premium content—which means each of those episodes would have to get nearly 7.4 million online viewers to match the $1.5 million in TV revenues.

Ain’t gonna happen. (Especially considering Hulu had only 28.2 million unique viewers in April 2012, according to comScore.)

So isn’t the TV business acting logically here, holding back content when they’re making less money from it?

Not necessarily so, said Richmond of VideoNuze.

“The definition of less is that they make less revenue per, let’s say, program consumed, but they’re making more on a per-ad basis,” said Richmond. “So in other words the CPMs—for example on Hulu—are higher than the CPMs on television. But the problem is that there are just fewer ads, far fewer ads when you watch a show via Hulu than if you watch traditional TV.”

(5) Digital Advertising Is Complicated

From the advertiser’s perspective, digital can mean more dollars—and not in a good way.

“Say your TV group is spending $750 million on advertising,” said Simulmedia’s Morgan. “You need one-and-a-half people at the agency to do it. But say your online video budget is $150 million, you need to have 28 people managing that.”

This reverse problem of scale, where marketers get less reach for greater cost, is a real sticking point for large-scale video ad growth.

“And here’s the other irony: Those people are really expensive,” said Morgan. “They have to be sophisticated. They have to be data analysts. They have to manage a lot of integration.”

Digital innovations are hard enough for digital professionals to follow. For many traditional, TV-oriented brand marketers, options like real-time bidding, ad networks and demand-side platforms (DSPs) are exotic and complex. One-third or fewer brand advertisers and agencies surveyed by Adap.tv and DIGIDAY said they are using online-only buying platforms such as ad exchanges and DSPs in 2012.

% of respondents

Platforms Used by Brand Advertisers and Agencies inNorth America to Purchase Online Video Inventory,2011 & 2012

Direct from publishers75%

72%

Ad networks72%

73%

Exchanges15%

29%

DSPs15%

32%

Trading desks27%

2011 2012

Source: Adap.tv and DIGIDAY, "Video State of the Industry Report, Q12012," April 16, 2012139162 www.eMarketer.com

139162

“In all of the attempts by digital marketers to differentiate online advertising and show its value, they just increase the complexity and make it hard for traditional dollars to move,” said Tod Sacerdoti, CEO and founder of BrightRoll, in an April 2012 interview.

(6) The Attraction of Doing Nothing

TV’s power in the marketplace seems permanently established. Even brand marketers on the digital side understand that. “TV is not going away anytime soon,” said Neville Manohar, senior marketing manager for digital at the Chrysler Group, in a May 2012 interview.

Forces Against Fusion

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 7

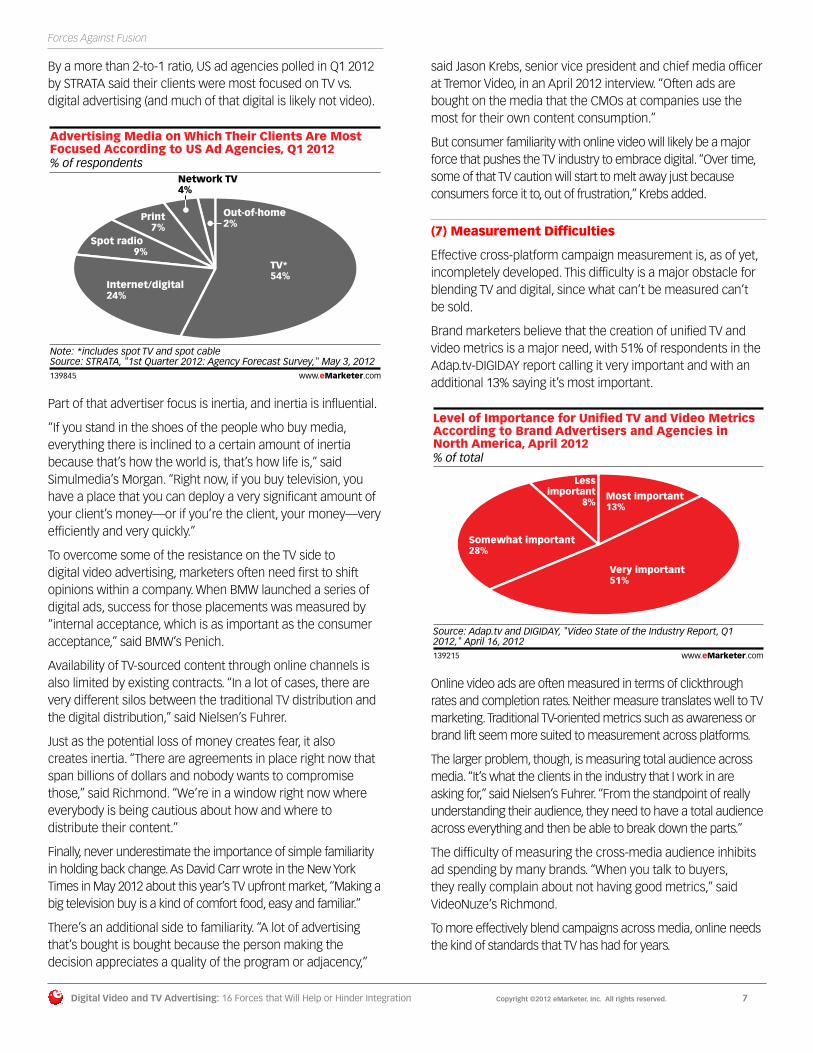

By a more than 2-to-1 ratio, US ad agencies polled in Q1 2012 by STRATA said their clients were most focused on TV vs. digital advertising (and much of that digital is likely not video).

% of respondents

Advertising Media on Which Their Clients Are MostFocused According to US Ad Agencies, Q1 2012

TV*54%

Internet/digital24%

Spot radio 9%

Print7%

Network TV4%

Out-of-home2%

Note: *includes spot TV and spot cableSource: STRATA, "1st Quarter 2012: Agency Forecast Survey," May 3, 2012139845 www.eMarketer.com

139845

Part of that advertiser focus is inertia, and inertia is influential.

“If you stand in the shoes of the people who buy media, everything there is inclined to a certain amount of inertia because that’s how the world is, that’s how life is,” said Simulmedia’s Morgan. “Right now, if you buy television, you have a place that you can deploy a very significant amount of your client’s money—or if you’re the client, your money—very efficiently and very quickly.”

To overcome some of the resistance on the TV side to digital video advertising, marketers often need first to shift opinions within a company. When BMW launched a series of digital ads, success for those placements was measured by “internal acceptance, which is as important as the consumer acceptance,” said BMW’s Penich.

Availability of TV-sourced content through online channels is also limited by existing contracts. “In a lot of cases, there are very different silos between the traditional TV distribution and the digital distribution,” said Nielsen’s Fuhrer.

Just as the potential loss of money creates fear, it also creates inertia. “There are agreements in place right now that span billions of dollars and nobody wants to compromise those,” said Richmond. “We’re in a window right now where everybody is being cautious about how and where to distribute their content.”

Finally, never underestimate the importance of simple familiarity in holding back change. As David Carr wrote in the New York Times in May 2012 about this year’s TV upfront market, “Making a big television buy is a kind of comfort food, easy and familiar.”

There’s an additional side to familiarity. “A lot of advertising that’s bought is bought because the person making the decision appreciates a quality of the program or adjacency,”

said Jason Krebs, senior vice president and chief media officer at Tremor Video, in an April 2012 interview. “Often ads are bought on the media that the CMOs at companies use the most for their own content consumption.”

But consumer familiarity with online video will likely be a major force that pushes the TV industry to embrace digital. “Over time, some of that TV caution will start to melt away just because consumers force it to, out of frustration,” Krebs added.

(7) Measurement Difficulties

Effective cross-platform campaign measurement is, as of yet, incompletely developed. This difficulty is a major obstacle for blending TV and digital, since what can’t be measured can’t be sold.

Brand marketers believe that the creation of unified TV and video metrics is a major need, with 51% of respondents in the Adap.tv-DIGIDAY report calling it very important and with an additional 13% saying it’s most important.

% of total

Level of Importance for Unified TV and Video MetricsAccording to Brand Advertisers and Agencies in North America, April 2012

Most important13%

Very important51%

Somewhat important28%

Lessimportant

8%

Source: Adap.tv and DIGIDAY, "Video State of the Industry Report, Q12012," April 16, 2012139215 www.eMarketer.com

139215

Online video ads are often measured in terms of clickthrough rates and completion rates. Neither measure translates well to TV marketing. Traditional TV-oriented metrics such as awareness or brand lift seem more suited to measurement across platforms.

The larger problem, though, is measuring total audience across media. “It’s what the clients in the industry that I work in are asking for,” said Nielsen’s Fuhrer. “From the standpoint of really understanding their audience, they need to have a total audience across everything and then be able to break down the parts.”

The difficulty of measuring the cross-media audience inhibits ad spending by many brands. “When you talk to buyers, they really complain about not having good metrics,” said VideoNuze’s Richmond.

To more effectively blend campaigns across media, online needs the kind of standards that TV has had for years.

Forces Against Fusion

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 8

“I would standardize on a single measurement company,” said BrightRoll’s Sacerdoti. “It almost doesn’t matter who it is, because there are flaws with everybody. It’s either Quantcast, comScore, Nielsen, one of the data vendors. It’s somebody who is the source of truth for measurement and, therefore, currency value.”

Among those looking for a fusion of TV and digital advertising, several say Nielsen would likely be best, since they’re so entrenched in the television industry.

“We definitely promote Nielsen more because of its TV credibility,” said Sacerdoti.

Mixed Messages (Forces that Help and Hinder)

Many of the factors that could influence the potential integration of digital video and TV advertising are not clear-cut for or against. Instead, these two-sided trends might help, hinder or, most likely, do a bit of both.

The three main areas that deliver a mixed message about helping or hindering are audience, measurement and content.

(8) The Video Audience: Real or Deceptive?

It isn’t clear that the audience for digital video is large enough, either in number of people or in time spent viewing content, to lead TV advertisers to spend more on digital screens. What is clear, though, is:

■ While there’s little question that the digital video audience is growing steadily in numbers, not all those people necessarily represent opportunities for advertisers.

■ While the online audience watches more and more video, often that content is still either unsafe for brands or too short to support substantial advertising.

■ While the amount of time the audience spends watching video online is increasing, it is a mere blip compared to how much time it spends watching TV.

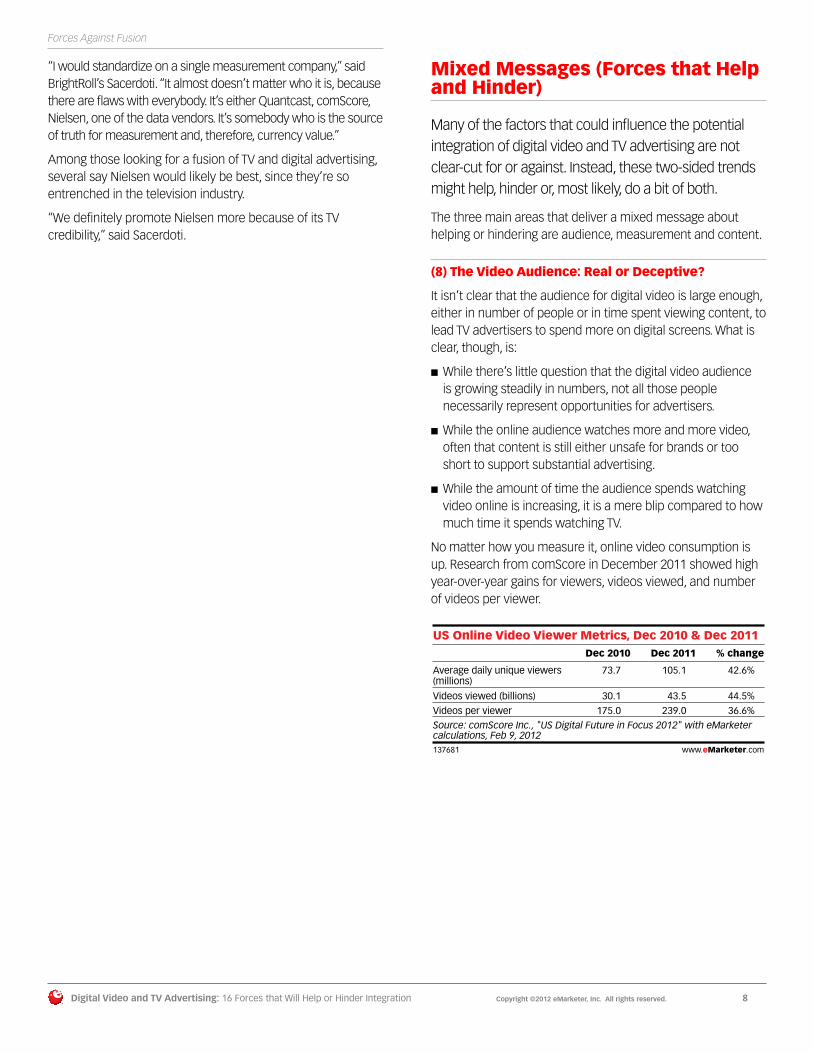

No matter how you measure it, online video consumption is up. Research from comScore in December 2011 showed high year-over-year gains for viewers, videos viewed, and number of videos per viewer.

US Online Video Viewer Metrics, Dec 2010 & Dec 2011

Average daily unique viewers(millions)

Videos viewed (billions)

Videos per viewer

Dec 2010

73.7

30.1

175.0

Dec 2011

105.1

43.5

239.0

% change

42.6%

44.5%

36.6%

Source: comScore Inc., "US Digital Future in Focus 2012" with eMarketercalculations, Feb 9, 2012137681 www.eMarketer.com

137681

Forces Against Fusion

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 9

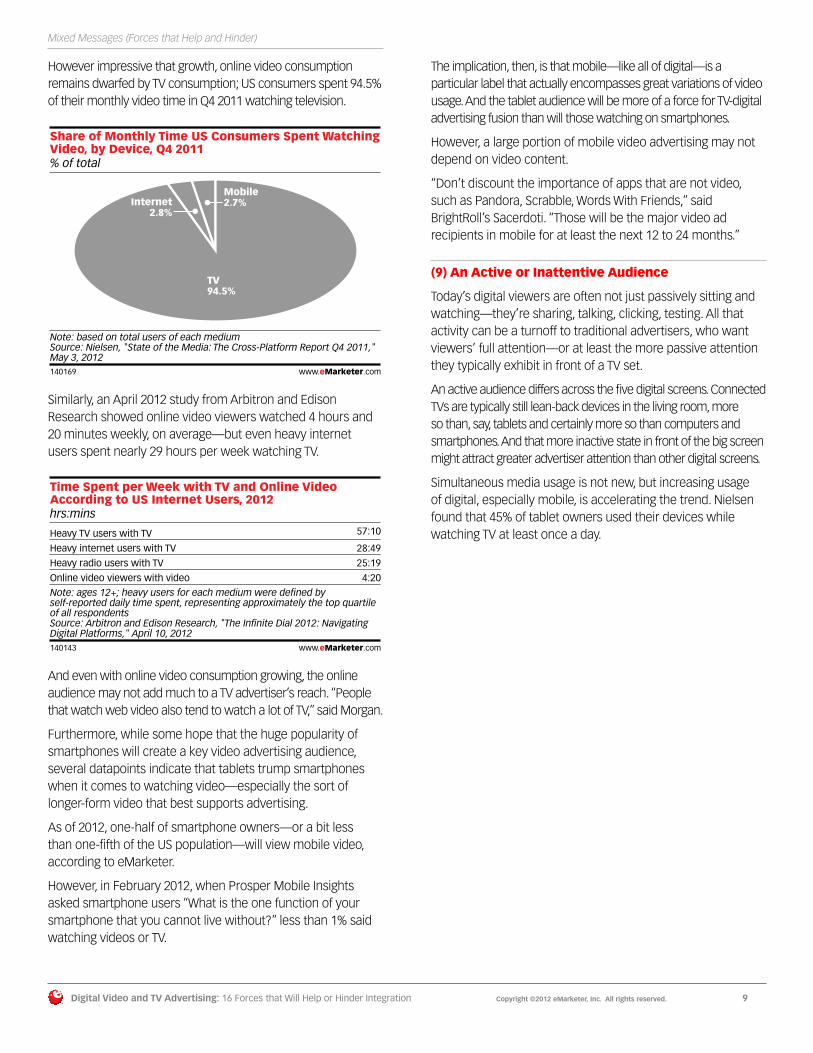

However impressive that growth, online video consumption remains dwarfed by TV consumption; US consumers spent 94.5% of their monthly video time in Q4 2011 watching television.

% of total

Share of Monthly Time US Consumers Spent WatchingVideo, by Device, Q4 2011

TV94.5%

Internet2.8%

Mobile2.7%

Note: based on total users of each mediumSource: Nielsen, "State of the Media: The Cross-Platform Report Q4 2011,"May 3, 2012140169 www.eMarketer.com

140169

Similarly, an April 2012 study from Arbitron and Edison Research showed online video viewers watched 4 hours and 20 minutes weekly, on average—but even heavy internet users spent nearly 29 hours per week watching TV.

hrs:mins

Time Spent per Week with TV and Online VideoAccording to US Internet Users, 2012

Heavy TV users with TV 57:10

Heavy internet users with TV 28:49

Heavy radio users with TV 25:19

Online video viewers with video 4:20

Note: ages 12+; heavy users for each medium were defined byself-reported daily time spent, representing approximately the top quartileof all respondentsSource: Arbitron and Edison Research, "The Infinite Dial 2012: NavigatingDigital Platforms," April 10, 2012140143 www.eMarketer.com

140143

And even with online video consumption growing, the online audience may not add much to a TV advertiser’s reach. “People that watch web video also tend to watch a lot of TV,” said Morgan.

Furthermore, while some hope that the huge popularity of smartphones will create a key video advertising audience, several datapoints indicate that tablets trump smartphones when it comes to watching video—especially the sort of longer-form video that best supports advertising.

As of 2012, one-half of smartphone owners—or a bit less than one-fifth of the US population—will view mobile video, according to eMarketer.

However, in February 2012, when Prosper Mobile Insights asked smartphone users “What is the one function of your smartphone that you cannot live without?” less than 1% said watching videos or TV.

The implication, then, is that mobile—like all of digital—is a particular label that actually encompasses great variations of video usage. And the tablet audience will be more of a force for TV-digital advertising fusion than will those watching on smartphones.

However, a large portion of mobile video advertising may not depend on video content.

“Don’t discount the importance of apps that are not video, such as Pandora, Scrabble, Words With Friends,” said BrightRoll’s Sacerdoti. “Those will be the major video ad recipients in mobile for at least the next 12 to 24 months.”

(9) An Active or Inattentive Audience

Today’s digital viewers are often not just passively sitting and watching—they’re sharing, talking, clicking, testing. All that activity can be a turnoff to traditional advertisers, who want viewers’ full attention—or at least the more passive attention they typically exhibit in front of a TV set.

An active audience differs across the five digital screens. Connected TVs are typically still lean-back devices in the living room, more so than, say, tablets and certainly more so than computers and smartphones. And that more inactive state in front of the big screen might attract greater advertiser attention than other digital screens.

Simultaneous media usage is not new, but increasing usage of digital, especially mobile, is accelerating the trend. Nielsen found that 45% of tablet owners used their devices while watching TV at least once a day.

Mixed Messages (Forces that Help and Hinder)

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 10

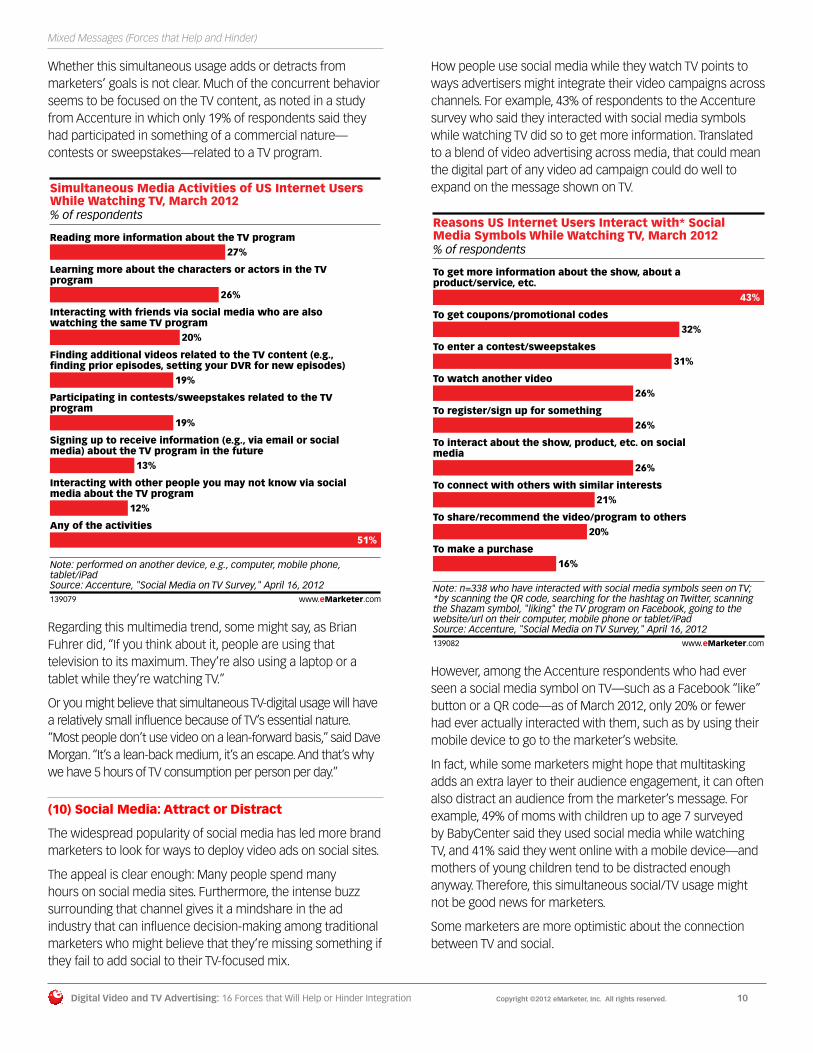

Whether this simultaneous usage adds or detracts from marketers’ goals is not clear. Much of the concurrent behavior seems to be focused on the TV content, as noted in a study from Accenture in which only 19% of respondents said they had participated in something of a commercial nature—contests or sweepstakes—related to a TV program.

% of respondents

Simultaneous Media Activities of US Internet UsersWhile Watching TV, March 2012

Reading more information about the TV program27%

Learning more about the characters or actors in the TVprogram

26%

Interacting with friends via social media who are alsowatching the same TV program

20%

Finding additional videos related to the TV content (e.g.,finding prior episodes, setting your DVR for new episodes)

19%

Participating in contests/sweepstakes related to the TVprogram

19%

Signing up to receive information (e.g., via email or socialmedia) about the TV program in the future

13%

Interacting with other people you may not know via socialmedia about the TV program

12%

Any of the activities51%

Note: performed on another device, e.g., computer, mobile phone,tablet/iPadSource: Accenture, "Social Media on TV Survey," April 16, 2012139079 www.eMarketer.com

139079

Regarding this multimedia trend, some might say, as Brian Fuhrer did, “If you think about it, people are using that television to its maximum. They’re also using a laptop or a tablet while they’re watching TV.”

Or you might believe that simultaneous TV-digital usage will have a relatively small influence because of TV’s essential nature. “Most people don’t use video on a lean-forward basis,” said Dave Morgan. “It’s a lean-back medium, it’s an escape. And that’s why we have 5 hours of TV consumption per person per day.”

(10) Social Media: Attract or Distract

The widespread popularity of social media has led more brand marketers to look for ways to deploy video ads on social sites.

The appeal is clear enough: Many people spend many hours on social media sites. Furthermore, the intense buzz surrounding that channel gives it a mindshare in the ad industry that can influence decision-making among traditional marketers who might believe that they’re missing something if they fail to add social to their TV-focused mix.

How people use social media while they watch TV points to ways advertisers might integrate their video campaigns across channels. For example, 43% of respondents to the Accenture survey who said they interacted with social media symbols while watching TV did so to get more information. Translated to a blend of video advertising across media, that could mean the digital part of any video ad campaign could do well to expand on the message shown on TV.

% of respondents

Reasons US Internet Users Interact with* SocialMedia Symbols While Watching TV, March 2012

To get more information about the show, about aproduct/service, etc.

43%

To get coupons/promotional codes32%

To enter a contest/sweepstakes31%

To watch another video26%

To register/sign up for something26%

To interact about the show, product, etc. on socialmedia

26%

To connect with others with similar interests21%

To share/recommend the video/program to others20%

To make a purchase16%

Note: n=338 who have interacted with social media symbols seen on TV;*by scanning the QR code, searching for the hashtag on Twitter, scanningthe Shazam symbol, "liking" the TV program on Facebook, going to thewebsite/url on their computer, mobile phone or tablet/iPadSource: Accenture, "Social Media on TV Survey," April 16, 2012139082 www.eMarketer.com

139082

However, among the Accenture respondents who had ever seen a social media symbol on TV—such as a Facebook “like” button or a QR code—as of March 2012, only 20% or fewer had ever actually interacted with them, such as by using their mobile device to go to the marketer’s website.

In fact, while some marketers might hope that multitasking adds an extra layer to their audience engagement, it can often also distract an audience from the marketer’s message. For example, 49% of moms with children up to age 7 surveyed by BabyCenter said they used social media while watching TV, and 41% said they went online with a mobile device—and mothers of young children tend to be distracted enough anyway. Therefore, this simultaneous social/TV usage might not be good news for marketers.

Some marketers are more optimistic about the connection between TV and social.

Mixed Messages (Forces that Help and Hinder)

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 11

“As TV ratings continue to decline, the volume and sentiment of social discussion around programming gives us an indicator of how engaged that viewership is,” said Colleen Soriano, “which starts to define value more by impact and behavior than reach alone. The implication there is that social media can help us start to evaluate TV more like we evaluate digital video.”

(11) GRPs—Or Not

Many ad industry executives say that because gross rating points (GRPs) are a central currency for buying TV ad inventory, they need an online equivalent. Having a common language in the form of GRPs can help brands and agencies better compare digital apples to TV apples.

“If you don’t have measurement that ties back to the way advertising has always been bought, you’ve introduced friction,” said VideoNuze’s Richmond, “because the buyers don’t know what something’s worth on its own and they don’t know what something’s worth relative to what they’ve been buying.”

But the detractors say GRPs dumb down digital, failing to measure engagement and interaction. “The downside of the online GRP is that it gets you back into valuing the medium on TV’s standards—reach and frequency—whereas this digital medium has so much more to offer,” said Richmond.

GRPs are a tool for combining reach and frequency, calculated by taking the percentage of the target audience that views an ad and multiplying that figure by how often it sees the ad in a given campaign. Therefore, if a TV commercial reaches 25% of the target audience and is shown 10 times, it has a GRP of 250. However, if the same commercial reaches 50% of the target audience and is shown only 5 times, it also has a GRP of 250.

You can see the problem there: the same GRPs. Yet with twice the number of ads, the first example could cost more than the second—all other pricing matters being equal.

Despite the general shortcomings and the digital naysayers, more and more online companies are grafting GRPs onto the online video advertising process.

“The objective is to utilize some of the strengths of the digital side and combine it with the existing television approach (GRPs), without having to make major changes in that side of it,” said Nielsen’s Fuhrer.

Recent digital GRP endeavors include:

■ September 2011. Nielsen announced that its Nielsen Online Campaign Ratings (NOCR) measurement system, which provides the equivalent of GRPs for online video ads, was accredited by the Media Rating Council (MRC).

■ December 2011. Nielsen announced a deal with Tremor Video’s VideoHub unit that lets the latter company’s clients access the measurement firm’s GRPs to give further insight into the audience’s demographics.

■ January 2012. comScore announced the launch of its vGRPs (validated gross rating points), which look to layer behavior onto reach and frequency.

■ March 2012. TubeMogul announced that it was bringing Nielsen’s GRP system to its real-time bidding (RTB) buying platform for digital video ads.

■ April 2012. Google announced its Active GRP metric that integrates into DoubleClick’s ad serving tools.

■ April 2012. AOL announced it would sell video ads using GRPs provided by Nielsen.

All those efforts to establish an online GRP sound hopeful, but there’s a problem built into the multiplicity—a lack of standards. If the purpose of GRPs is to make buying digital video ads both easier and comparable to TV, competing versions of the same metric could complicate matters.

That sticking point is one reason why several industry executives interviewed for this report look most to Nielsen for establishing online GRPs.

“You can criticize Nielsen all day long, but the reality is that they’re bringing an important service, which is sellers and buyers are agreeing that this is the metric that we’re going to use and here is a currency,” said Adap.tv’s Gabriner.

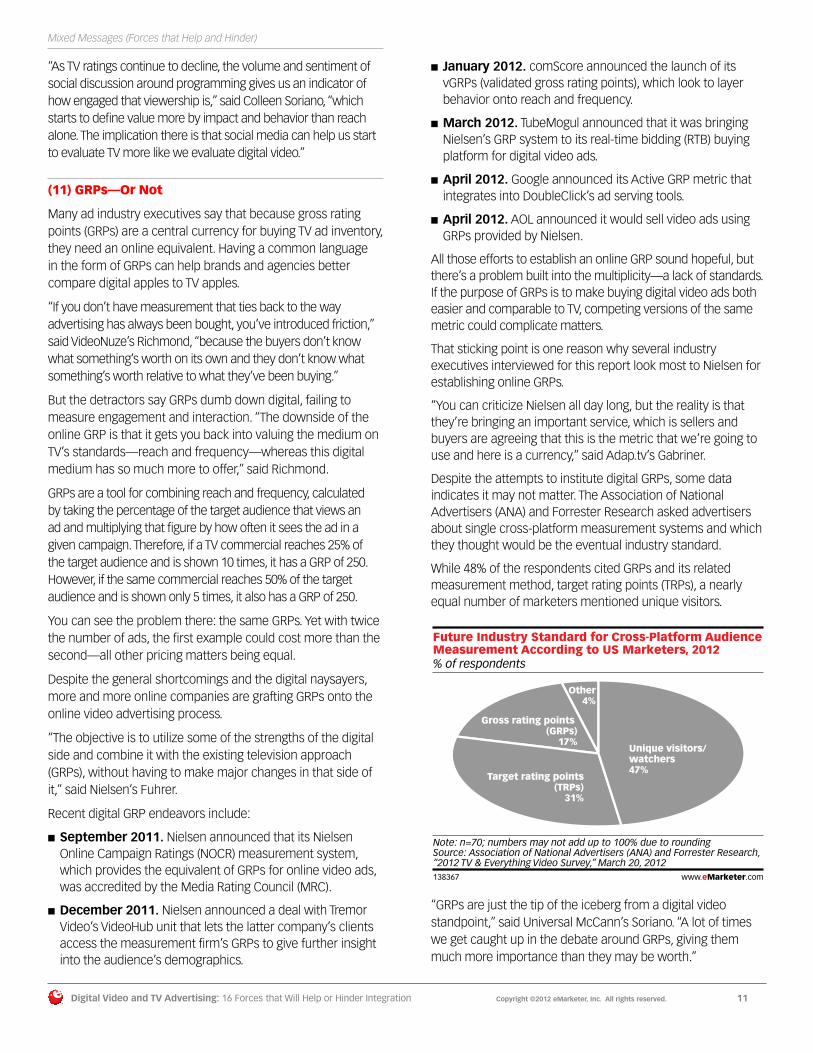

Despite the attempts to institute digital GRPs, some data indicates it may not matter. The Association of National Advertisers (ANA) and Forrester Research asked advertisers about single cross-platform measurement systems and which they thought would be the eventual industry standard.

While 48% of the respondents cited GRPs and its related measurement method, target rating points (TRPs), a nearly equal number of marketers mentioned unique visitors.

% of respondents

Future Industry Standard for Cross-Platform AudienceMeasurement According to US Marketers, 2012

Unique visitors/watchers47%

Target rating points(TRPs)

31%

Gross rating points (GRPs)

17%

Other4%

Note: n=70; numbers may not add up to 100% due to roundingSource: Association of National Advertisers (ANA) and Forrester Research, “2012 TV & Everything Video Survey,” March 20, 2012138367 www.eMarketer.com

138367

“GRPs are just the tip of the iceberg from a digital video standpoint,” said Universal McCann’s Soriano. “A lot of times we get caught up in the debate around GRPs, giving them much more importance than they may be worth.”

Mixed Messages (Forces that Help and Hinder)

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 12

But GRPs might be essential to draw more TV brand advertisers to include more digital video in their campaigns. “GRPs are a necessary evil,” said Tremor Video’s Krebs. “Table stakes, in order to get someone to pay attention to you. You can’t prove that you have something better until you have someone already trying you. And that’s where the digital industry is right now when it comes to video and GRPs.”

(12) Targeting vs. Reach

Online video offers a degree of targeting not generally available with TV advertising. But targeting reduces reach. Most brand advertisers look to video—that is, TV—for greater reach.

“Part of the friction point right now is that when you’re buying on targeting and reach, you can get below certain thresholds and there isn’t enough scale there to keep a brand interested,” said Richmond. “We’re still in that early phase of the market where it’s hard to accomplish both objectives, reach and targeting.”

However, some think that when you look at the amount of time people spend watching TV vs. how little they spend watching digital video, online video advertising won’t do much to increase reach.

“There isn’t incremental reach available in web video that’s not already being bought on TV,” said Simulmedia’s Morgan. “That is, if you buy TV, you’re already a significant TV advertiser. You can’t extend your reach more than about two [points], because there aren’t that many people who have really cut the cord.”

The resolution of the targeting/reach equation may not be solved over the next couple of years. However, the continued growth of audience viewing across the five digital screens, combined with a rising amount of content to support brand advertising, could resolve the paradox over time.

“Thinking about how the iPad universe is expanding and how connected TV is expanding, what happens is that the high-quality inventory that’s available just gets bigger and bigger and bigger and both targeting and reach objectives end up getting addressed,” said Richmond.

(13) Extra Costs vs. Unique Creative

Making ad creative just for online video is often too costly. Hence, most digital video ads are simply repurposed TV commercials. That isn’t necessarily a bad thing. Extended reach with engaging video ads can help boost brand performance at relatively low cost. But repurposed TV ads can’t take advantage of digital’s interactive capabilities.

“With the holistic buy, you want a single message across mobile, online and TV. It makes the most sense to shoot one portfolio of commercials for those three media,” said Sacerdoti. “What I see is 90%-plus repurposed television ads. Given the percentage of spend that digital video receives relative to television, that seems rational.”

The paucity of unique creative for digital may not be only about extra costs.

“Economics is one thing, and speed is another,” said agency executive Soriano. “It takes time to concept these out, to produce them and get them in the can. We’re not equipped right now as an industry to iterate as efficiently as we would like.”

Perhaps the use of TV commercials for online placements is shifting. A study from VINDICO found that of the 30 billion video ad impressions the company delivered in 2011, TV creative was used for 90% of them—down from 98% in 2010.

% of total

Types of Digital Video Ads Served to US-BasedAudiences, 2010 & 2011

TV creative98%

90%

Custom video environment*1%

6%

Interactive video1%

2%

Mobile2%

2010 2011

Note: digital video ad impressions served over the ad server VINDICO;mobile video ads are also repurposed TV creative ads; *include overlays,billboards and tiles but are not digital video adsSource: VINDICO, "Year in Review," April 11, 2012138956 www.eMarketer.com

138956

Brands at the leading edge of video advertising are seeing cross-media advantages in making ad creative specifically for the digital space.

For example, when BMW of North America launched its revamped 3 Series, the campaign began with a traditional TV buy and then the company “extended that into Hulu, ABC.com, NBC.com and YouTube,” said Penich at BMW.

And while “there was overlap in some of the creative,” he said, “we took the opportunity to create something that we call digital shorts. So these were 15 seconds, really quick concepts highlighting different features of the 3 Series.”

What made these digital-only ads effective for BMW was that they built recognition for the 15-second concept ads by connecting the creative to the main TV portion of the campaign. In this instance, the creative went two ways. “There was so much excitement around these pieces that were created for digital content that they actually made their way into traditional TV,” said Penich.

When you consider that about one-third of all TV commercials in 2011 were 15-second spots, according to Nielsen, that

Mixed Messages (Forces that Help and Hinder)

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 13

length might be prime for creating greater connections between digital and TV.

“The key thing the research shows is that the message needs to be the same across the different platforms, not necessarily that the creative is the same,” said Justin Evans, senior vice president for emerging media at Collective, in a May 2012 interview.

(14) Digital Content New Fronts

Over a two-week period in April 2012, several of the largest video sites banded together to offer ad buyers the kind of upfront market long-established in television. The event—called Digital Content New Fronts (New Fronts, for short) and organized by Digitas—should help ease the siloed process of buying media space for video advertising.

The video ad sellers involved in the New Fronts included Google/YouTube, Yahoo!, AOL, Microsoft and Hulu. Each company took a day or so to present advertisers and agencies with marketing opportunities and information about future video programming.

By looking to emulate TV’s upfront sales model with a combined effort, these large online media companies hope to persuade marketers to buy digital video advertising early and, overall, to increase spending in this space.

“The New Fronts are a great strategy for the video companies in adopting the upfront model,” said BMW’s Penich, “in the sense that Hulu and YouTube, for example, are trying to change the perception of how they are viewed. Right now they are very much viewed as a website that’s part of a digital buy and they want to change that perception. This is a step in the right direction.”

However, there’s some question whether the TV model of upfronts can work in the digital space to overcome other ongoing concerns. “For monies to transfer, you need a consistent measurement. And we don’t have that,” said Rino Scanzoni, GroupM’s chief investment officer, in an April 2012 article in AdWeek.

The piece noted that Scanzoni didn’t see the need for an online video upfront. “It’s kind of absurd,” he said. “With TV, there’s scarcity, and you can wrap your arms around the market.” But on the web, there’s a seemingly infinite supply of video advertising inventory.

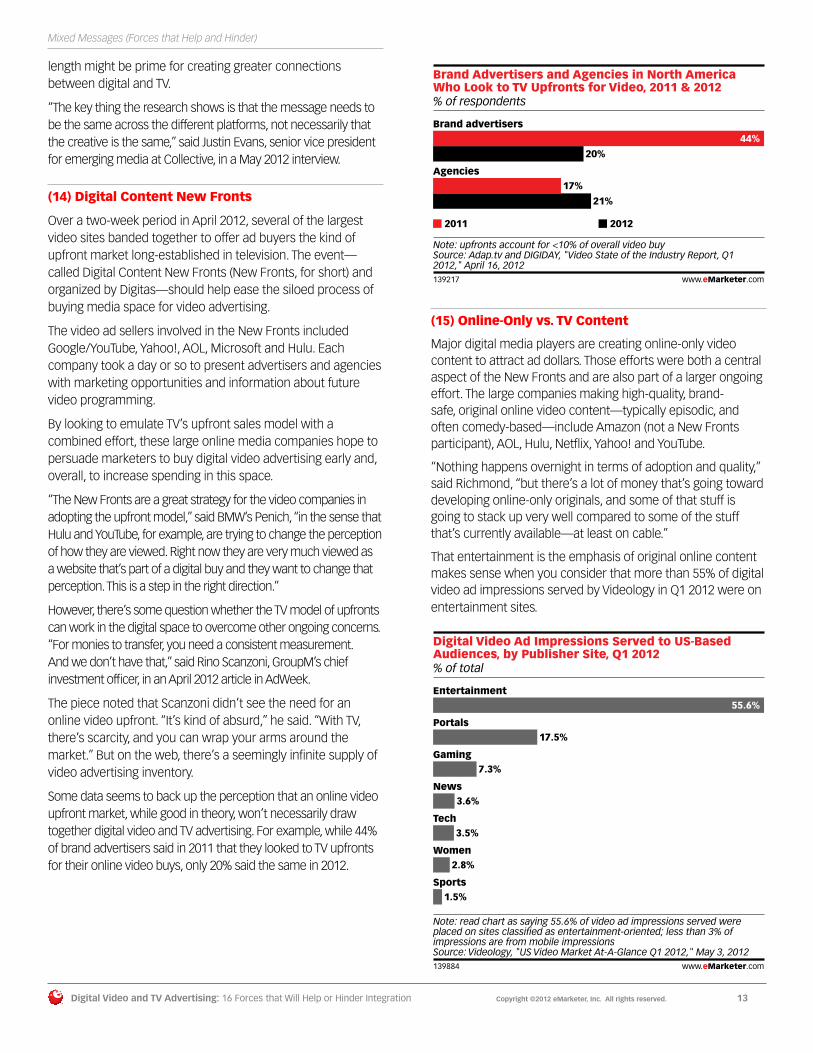

Some data seems to back up the perception that an online video upfront market, while good in theory, won’t necessarily draw together digital video and TV advertising. For example, while 44% of brand advertisers said in 2011 that they looked to TV upfronts for their online video buys, only 20% said the same in 2012.

% of respondents

Brand Advertisers and Agencies in North AmericaWho Look to TV Upfronts for Video, 2011 & 2012

Brand advertisers44%

20%

Agencies17%

21%

2011 2012

Note: upfronts account for <10% of overall video buySource: Adap.tv and DIGIDAY, "Video State of the Industry Report, Q12012," April 16, 2012139217 www.eMarketer.com

139217

(15) Online-Only vs. TV Content

Major digital media players are creating online-only video content to attract ad dollars. Those efforts were both a central aspect of the New Fronts and are also part of a larger ongoing effort. The large companies making high-quality, brand-safe, original online video content—typically episodic, and often comedy-based—include Amazon (not a New Fronts participant), AOL, Hulu, Netflix, Yahoo! and YouTube.

“Nothing happens overnight in terms of adoption and quality,” said Richmond, “but there’s a lot of money that’s going toward developing online-only originals, and some of that stuff is going to stack up very well compared to some of the stuff that’s currently available—at least on cable.”

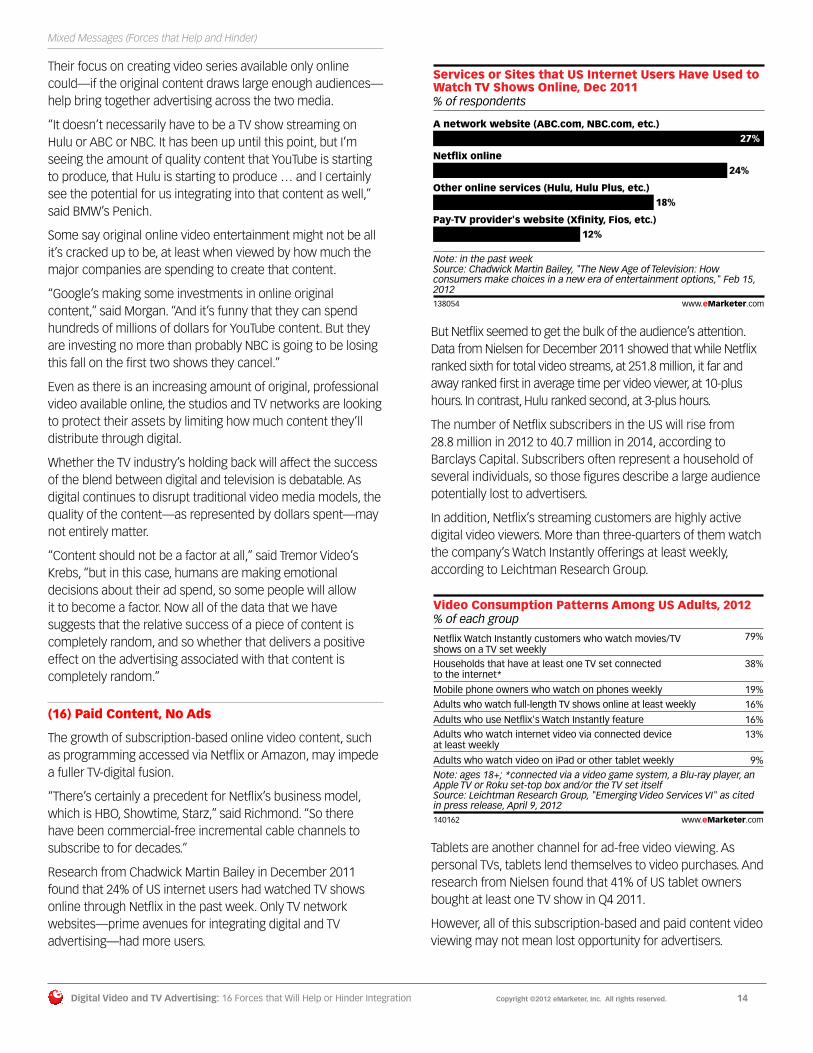

That entertainment is the emphasis of original online content makes sense when you consider that more than 55% of digital video ad impressions served by Videology in Q1 2012 were on entertainment sites.

% of total

Digital Video Ad Impressions Served to US-BasedAudiences, by Publisher Site, Q1 2012

Entertainment55.6%

Portals17.5%

Gaming7.3%

News3.6%

Tech3.5%

Women2.8%

Sports1.5%

Note: read chart as saying 55.6% of video ad impressions served wereplaced on sites classified as entertainment-oriented; less than 3% ofimpressions are from mobile impressionsSource: Videology, "US Video Market At-A-Glance Q1 2012," May 3, 2012139884 www.eMarketer.com

139884

Mixed Messages (Forces that Help and Hinder)

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 14

Their focus on creating video series available only online could—if the original content draws large enough audiences—help bring together advertising across the two media.

“It doesn’t necessarily have to be a TV show streaming on Hulu or ABC or NBC. It has been up until this point, but I’m seeing the amount of quality content that YouTube is starting to produce, that Hulu is starting to produce … and I certainly see the potential for us integrating into that content as well,” said BMW’s Penich.

Some say original online video entertainment might not be all it’s cracked up to be, at least when viewed by how much the major companies are spending to create that content.

“Google’s making some investments in online original content,” said Morgan. “And it’s funny that they can spend hundreds of millions of dollars for YouTube content. But they are investing no more than probably NBC is going to be losing this fall on the first two shows they cancel.”

Even as there is an increasing amount of original, professional video available online, the studios and TV networks are looking to protect their assets by limiting how much content they’ll distribute through digital.

Whether the TV industry’s holding back will affect the success of the blend between digital and television is debatable. As digital continues to disrupt traditional video media models, the quality of the content—as represented by dollars spent—may not entirely matter.

“Content should not be a factor at all,” said Tremor Video’s Krebs, “but in this case, humans are making emotional decisions about their ad spend, so some people will allow it to become a factor. Now all of the data that we have suggests that the relative success of a piece of content is completely random, and so whether that delivers a positive effect on the advertising associated with that content is completely random.”

(16) Paid Content, No Ads

The growth of subscription-based online video content, such as programming accessed via Netflix or Amazon, may impede a fuller TV-digital fusion.

“There’s certainly a precedent for Netflix’s business model, which is HBO, Showtime, Starz,” said Richmond. “So there have been commercial-free incremental cable channels to subscribe to for decades.”

Research from Chadwick Martin Bailey in December 2011 found that 24% of US internet users had watched TV shows online through Netflix in the past week. Only TV network websites—prime avenues for integrating digital and TV advertising—had more users.

% of respondents

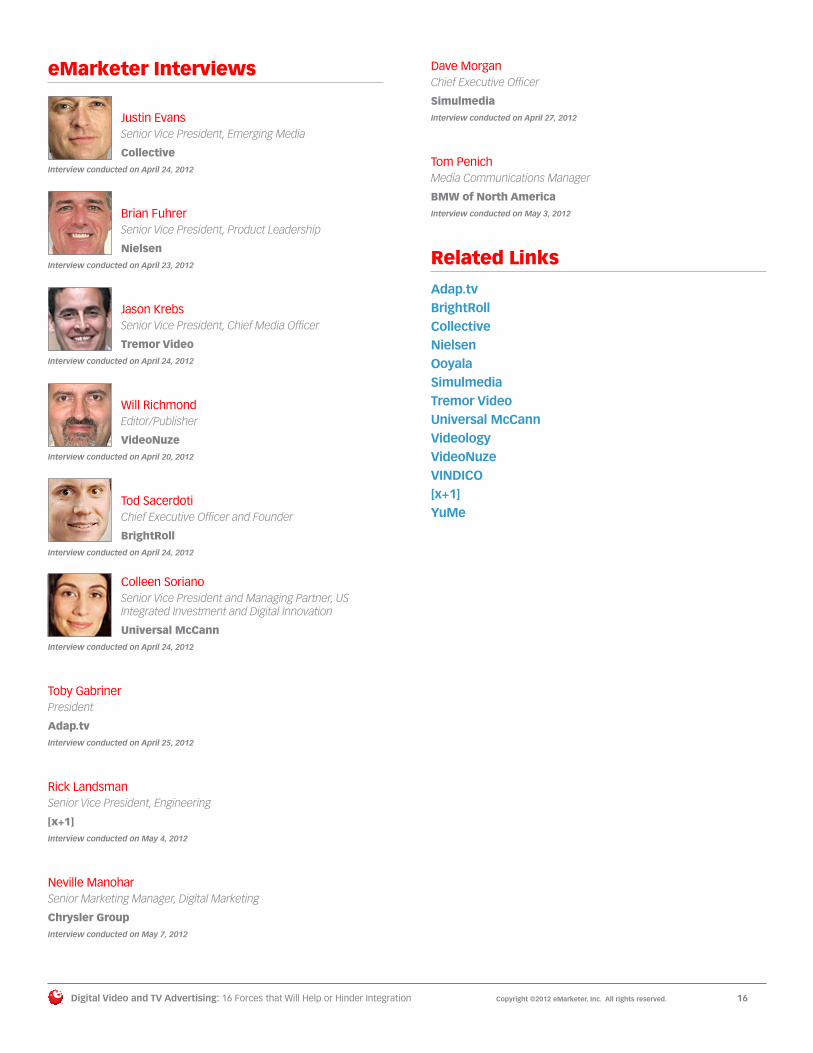

Services or Sites that US Internet Users Have Used toWatch TV Shows Online, Dec 2011

A network website (ABC.com, NBC.com, etc.)27%

Netflix online24%

Other online services (Hulu, Hulu Plus, etc.)18%

Pay-TV provider's website (Xfinity, Fios, etc.)12%

Note: in the past weekSource: Chadwick Martin Bailey, "The New Age of Television: Howconsumers make choices in a new era of entertainment options," Feb 15,2012138054 www.eMarketer.com

138054

But Netflix seemed to get the bulk of the audience’s attention. Data from Nielsen for December 2011 showed that while Netflix ranked sixth for total video streams, at 251.8 million, it far and away ranked first in average time per video viewer, at 10-plus hours. In contrast, Hulu ranked second, at 3-plus hours.

The number of Netflix subscribers in the US will rise from 28.8 million in 2012 to 40.7 million in 2014, according to Barclays Capital. Subscribers often represent a household of several individuals, so those figures describe a large audience potentially lost to advertisers.

In addition, Netflix’s streaming customers are highly active digital video viewers. More than three-quarters of them watch the company’s Watch Instantly offerings at least weekly, according to Leichtman Research Group.

% of each groupVideo Consumption Patterns Among US Adults, 2012

Netflix Watch Instantly customers who watch movies/TVshows on a TV set weekly

79%

Households that have at least one TV set connectedto the internet*

38%

Mobile phone owners who watch on phones weekly 19%

Adults who watch full-length TV shows online at least weekly 16%

Adults who use Netflix's Watch Instantly feature 16%

Adults who watch internet video via connected deviceat least weekly

13%

Adults who watch video on iPad or other tablet weekly 9%

Note: ages 18+; *connected via a video game system, a Blu-ray player, anApple TV or Roku set-top box and/or the TV set itselfSource: Leichtman Research Group, "Emerging Video Services VI" as citedin press release, April 9, 2012140162 www.eMarketer.com

140162

Tablets are another channel for ad-free video viewing. As personal TVs, tablets lend themselves to video purchases. And research from Nielsen found that 41% of US tablet owners bought at least one TV show in Q4 2011.

However, all of this subscription-based and paid content video viewing may not mean lost opportunity for advertisers.

Mixed Messages (Forces that Help and Hinder)

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 15

The large volume of video watching shows a growing audience for digital video. And it is quite possible that Netflix could move to a hybrid fee/advertising mix, much as cable TV did. That would help create a further integration between the two media.

And some indicate that paid content may not even matter for the ultimate blend of TV and online video advertising. “Some say if these subscription services choose not to serve ads, it will hurt the highly valued premium supply in the digital video category,” said Sacerdoti. “But my premise is that most analysts overestimate the importance of television content being online in order for TV and digital video buying to be in sync.”

Conclusions

Clearly, there is no straightforward path to integrating TV and digital video advertising.

Fear of the unknown—new audience measures, unfamiliar programming choices, and complex buying systems—has held back many advertisers. But an entirely different fear could actually drive increased digital advertising. That’s the fear of ad skipping.

A 2012 study from Arbitron and Edison Research found that 81% of DVR owners skipped commercials almost every time they came on. And consumers are being given more tools for ad skipping. For example, in May 2012, Dish Network, the satellite-TV company, unveiled a feature called “Auto Hop” that lets viewers automatically skip past commercials on shows recorded on the company’s DVRs.

Ad skipping doesn’t exist with online video content—at least not yet.

But many advertisers may be reluctant to shift to digital simply because they are still quite happy with TV.

It’s going to take years for digital video advertising to blend more fully with TV advertising, but time is on digital’s side. The five digital screens are where audiences increasingly watch TV and other video content, and brands need to reach them anytime and everywhere.

In general, TV marketers see balance as the most effective way to blend digital video into their messaging—a way to reach audiences they might not have touched otherwise, a way to engage their target customers in ways that TV doesn’t allow, a way to make their spending more cost-effective.

“We work with Fortune 100 brands and TV, for the foreseeable future, is going to be the centerpiece of those brands’ marketing campaigns,” said Collective’s Evans. “But they can make that very sizeable spend more effective by strategically complementing it with digital.”

Mixed Messages (Forces that Help and Hinder)

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 16

eMarketer Interviews

Justin Evans Senior Vice President, Emerging Media

Collective Interview conducted on April 24, 2012

Brian Fuhrer Senior Vice President, Product Leadership

Nielsen Interview conducted on April 23, 2012

Jason Krebs Senior Vice President, Chief Media Officer

Tremor Video Interview conducted on April 24, 2012

Will Richmond Editor/Publisher

VideoNuze Interview conducted on April 20, 2012

Tod Sacerdoti Chief Executive Officer and Founder

BrightRoll Interview conducted on April 24, 2012

Colleen Soriano Senior Vice President and Managing Partner, US Integrated Investment and Digital Innovation

Universal McCann Interview conducted on April 24, 2012

Toby Gabriner President

Adap.tv Interview conducted on April 25, 2012

Rick Landsman Senior Vice President, Engineering

[x+1] Interview conducted on May 4, 2012

Neville Manohar Senior Marketing Manager, Digital Marketing

Chrysler Group Interview conducted on May 7, 2012

Dave Morgan Chief Executive Officer

Simulmedia Interview conducted on April 27, 2012

Tom Penich Media Communications Manager

BMW of North America Interview conducted on May 3, 2012

Related Links

Adap.tv BrightRoll Collective Nielsen Ooyala Simulmedia Tremor Video Universal McCann VideologyVideoNuze VINDICO [x+1] YuMe

Digital Video and TV Advertising: 16 Forces that Will Help or Hinder Integration Copyright ©2012 eMarketer, Inc. All rights reserved. 17

About eMarketer

eMarketer publishes data, analysis and insights on digital marketing, media and commerce. We do this by gathering information from many sources, filtering it, and putting it into perspective. For more than a decade, leading companies have trusted this approach, and have relied on eMarketer to help them make better business decisions.

Benefits

Companies rely on eMarketer to:

■ Save time and resources by getting the right information, quickly.

■ Validate media decisions with reliable data to ensure productive investments.

■ Educate teams and senior executives on the latest digital marketing topics.

■ Evaluate emerging trends instantly and maintain competitive advantage.

■ Deliver impactful presentations with facts, figures and charts in a variety of downloadable formats.

Editorial and Production Contributors

Nicole Perrin Associate Editorial DirectorCliff Annicelli Senior Copy EditorEmily Adler Copy EditorDana Hill Director of ProductionJoanne DiCamillo Senior Production ArtistStephanie Gehrsitz Production ArtistAllie Smith Director of Charts