E DBS16 - Contactlabcontactlab.com/.../2016/10/EDBS_2016_Contactlab_Report_Excerpt.pdf · Global...

49

E + DBS16 This document and the global cross tabs are subject to copyright. Milan, October 2016 Global report - Focus on Italy EUROPEAN (+) DIGITAL BEHAVIOUR STUDY 2016 Research report presenting the results of the study conducted in April 2016, with a comparative analysis on the UK, Germany, France, Spain, Switzerland, New York, Korea, Shanghai, Tokyo, Moscow and St. Petersburg. EXCERPT

Transcript of E DBS16 - Contactlabcontactlab.com/.../2016/10/EDBS_2016_Contactlab_Report_Excerpt.pdf · Global...

E+DBS16

This document and the global cross tabs are subject to copyright.

Milan, October 2016

Global report - Focus on Italy

EUROPEAN (+) DIGITAL BEHAVIOUR STUDY 2016

Research report presenting the results of the study

conducted in April 2016, with a comparative

analysis on the UK, Germany, France, Spain,

Switzerland, New York, Korea, Shanghai, Tokyo,

Moscow and St. Petersburg.

EXCERPT

2© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

No materials, data or information internally published for the purposes of research within the ‘European+ Digital Behaviour Study 2016’ may be reproduced, distributed, transmitted, republished or otherwise used in any way, in part or in whole, without express written permission from Contactlab.

The materials, data and information contained within the statistics tables drawn up for each participant enterprise in the study may be employed for internal usage; the publication and communication of these results outside of the enterprise in question must be agreed by Contactlab.

For more information about the Report or to request permission to reproduce results or materials, please email [email protected]

COPYRIGHT

3© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

EDBS: A SINGLE SOURCE STUDY ON OPERATIVE DIGITAL TOPICS

AB

C

D

EF

G

H

I

E+dbs 2016:

30.500 cases

representative of 200M

+ of users |

11 markets |

90 questions |

F. E-CROSSBORDER AND EXPORT POTENTIAL

H. PROFILE & ATTITUDE

G. FASHION PURCHASES AND HIGH-END FASHION ATTITUDE

E. ECOMMERCE AND CLICK & COLLECT

B. INTERACTIVITY ONLINE AND DIGITAL ACTIVITIES

A. DEVICES AND MOBILE EVOLUTION

C. SOCIAL NETWORK AND BRAND INFLUENCE

D. DIGITAL DIRECT MARKETING AND ITS EFFECTIVENESS

Devices used in the past 4 weeks to connect to the internet (PC at home, sm.phone, tablet, sm.Tv, videogame console, etc.)

Time spent online Smartphone usage in-store to compare prices/ get prod.

information Intention to use a SmartTV/Smartphone/Tablet

General online activities (email, social media, ecommerce, home banking, multimedia, gaming, etc.)

Specific online activities (streaming, dating, job searching, e-government, QR code, etc.)

DII: Digital Interactivity index

Social accounting (FB, LinkedIn, Instagram, TW, G+, Tinder, etc.)

Brand engagement attitude via social networking (follow a brand, like/unlike, etc.)

Social login users SOI: Social Opportunity Index

Newsletter subscriptions Newsletter topics Channels for subscribing to newsletters (on brands’

websites, through self-service kiosks, etc.) Reasons for subscribing (stay up-to-date, get

exclusive benefits/ discounts, etc.) Effectiveness of newsletters vs. other channels DOI: Direct Opportunity Index

Ecommerce users and intention to shop online Products/ services bought online (27 prod/services cat.) Online shopping expenditure Information sources for online shopping Online sales channels (e-tailers, private sales, etc.) Preferred payment methods (standard c.card, PayPal, digital wallet, etc.) Click&collect use and propensity EXI: Ecommerce Expenditure Index (27 cat)

Products/ services bought online abroad Reasons for buying abroad (better prices, more choice,

etc.) Expenditure abroad Country shopped Recommendability of countries for ecommerce Country image

Sociodemographic profile (gender, age, geographical area, occupation, education, hh composition, age of children)

Offline buyer of: clothing/ footwear, cosmetics, tech products, holidays

I. CONSUMER SEGMENTATIONAND INDEXES

DII: Digital Interactivity Index DOI: Direct Opportunity Index SOI: Social Opportunity Index EXI: Ecommerce Expenditure Index FSI: Fashion Spending Index LAI: Luxury Attitude Index LCI: Luxury Consumption Index

Online/ offline fashion behaviour Target affluent behaviour Fashion concept evolution Luxury brand awareness/ attractiveness (27) LAI: Luxury Attitude Index LCI: Luxury Consumption Index

4© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

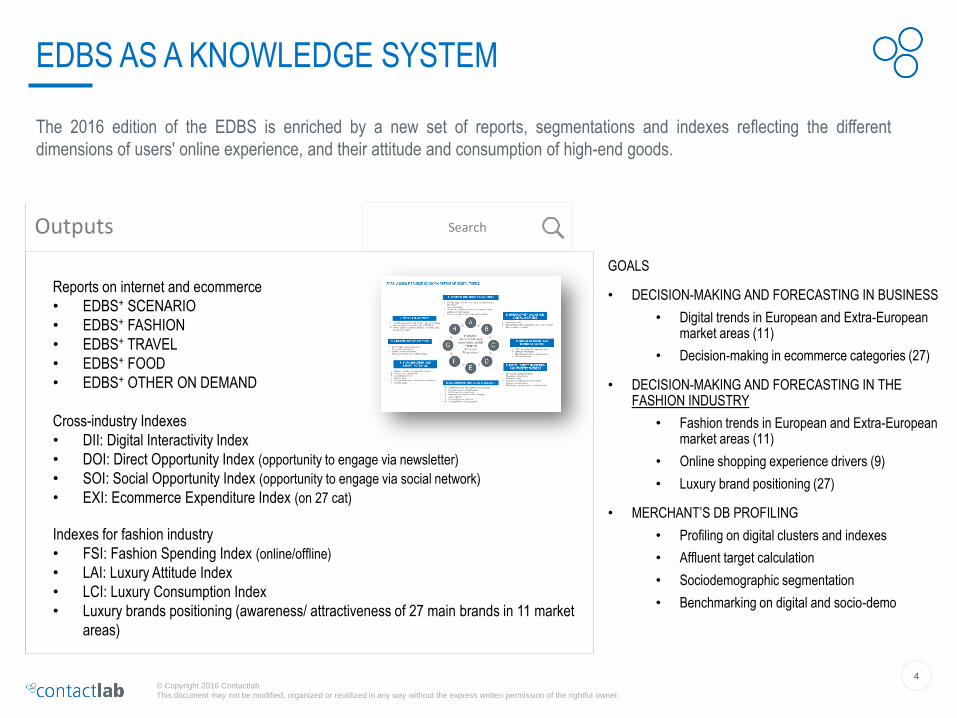

EDBS AS A KNOWLEDGE SYSTEM

The 2016 edition of the EDBS is enriched by a new set of reports, segmentations and indexes reflecting the different

dimensions of users' online experience, and their attitude and consumption of high-end goods.

GOALS

• DECISION-MAKING AND FORECASTING IN BUSINESS

• Digital trends in European and Extra-European market areas (11)

• Decision-making in ecommerce categories (27)

• DECISION-MAKING AND FORECASTING IN THE FASHION INDUSTRY

• Fashion trends in European and Extra-European market areas (11)

• Online shopping experience drivers (9)

• Luxury brand positioning (27)

• MERCHANT’S DB PROFILING

• Profiling on digital clusters and indexes

• Affluent target calculation

• Sociodemographic segmentation

• Benchmarking on digital and socio-demo

SearchOutputs

Reports on internet and ecommerce

• EDBS+ SCENARIO

• EDBS+ FASHION

• EDBS+ TRAVEL

• EDBS+ FOOD

• EDBS+ OTHER ON DEMAND

Cross-industry Indexes

• DII: Digital Interactivity Index

• DOI: Direct Opportunity Index (opportunity to engage via newsletter)

• SOI: Social Opportunity Index (opportunity to engage via social network)

• EXI: Ecommerce Expenditure Index (on 27 cat)

Indexes for fashion industry

• FSI: Fashion Spending Index (online/offline)

• LAI: Luxury Attitude Index

• LCI: Luxury Consumption Index

• Luxury brands positioning (awareness/ attractiveness of 27 main brands in 11 market

areas)

5© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

EDBS KNOWLEDGE SYSTEM: CROSS-INDUSTRY INDEXES

Dimension Cluster Index Goal

Online activities

1. Hyper-actives ++

2. Hyper-actives +

3. Actives

4. Passives -

5. Passives - -

► DII - Digital Interactivity

Index

• Find out how interactive your customers are online

• Identify the most effective means to communicate

and interact with them

• Understand the trade-off between advanced

solutions and digital education

Digital direct communication impact (opportunity to engage via newsletter)

1. Committed

2. Open

3. Passive

4. Opportunistic

5. Not disturb

6. Unaware

► DOI - Direct Opportunity

Index• Gain a detailed understanding of the relationship

between the direct channel (newsletter) and the

social media channel

• Calculate engagement opportunities through

owned media

• Help define the digital media plan Brand relationship via social network (opportunity to engage via social network)

1. Committed

2. Open

3. Passive

4. Not disturb

5. Non user

► SOI - Social Opportunity

Index

Online expenditure on different

products/ services (27 categories)

1. High

2. Medium

3. Low

► EXI - Ecommerce

Expenditure Index

• Quantify your industry’s online expenditure

• Identify trends with regards online spending

capacity

6© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

EDBS KNOWLEDGE SYSTEM: LUXURY INDUSTRY INDEXES

Dimension Cluster Index Goal

Fashion spending(online and/or offline purchase of fashion products)

1. High

2. Medium

3. Low

► FSI – Fashion

Spending Index

• Quantify (online/ offline) spending on fashion

products

High-end brands relationship(category attitude)

1. High-end lover

2. High-end assayer

3. High-end selector

4. High-end skeptic

5. High-end resistant

► LAI - Luxury

Attitude Index

• Identify targets respecting the affinity to/

distance from brand high-end products

• Drive segmentation for direct communication

Fashion luxury consumption(category attitude AND product buying)

1. Luxury staunch

2. Luxury committed

3. Luxury selector

4. Luxury detached

► LCI – Luxury

Consumption

Index

• Calculate an affluent target

• Identify trends

7© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

GLOBAL REPORT INDEX

EXECUTIVE SUMMARY FOR ITALY

ANALYSIS:

DIGITAL CLUSTERS AND INDEXES

INTERNET AND ECOMMERCE SCENARIO

DEVICE AND MOBILE EVOLUTION

LEVEL OF INTERACTIVITY ON THE INTERNET: ONLINE ACTIVITIES

SOCIAL NETWORKING AND BRAND INFLUENCE

DIGITAL DIRECT MARKETING

ECOMMERCE

(Available in the full report: "e-crossborder and the attractiveness of Italian ecommerce" , "fashion purchases and high-end fashion attitude"

METHODOLOGICAL NOTES

EXECUTIVE SUMMARY

Italy

9© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

EUROPEAN (+) DIGITAL BEHAVIOUR STUDY

Report 2016The rate of smartphone adoption by Italians is growing at almost double the rate of internet use, itself growing at 6%

In Italy in 2016, the number of individuals regularly using the internet (almost one time per week) reached 30,5 million, with

penetration among 16-65 y.o. of 78%.

Despite a +6% increase in the past 12 months, Italy remains significantly behind other European+ countries, with the UK and

Germany in first place.

The increase of internet users in Italy has resulted primarily from smartphone use (+13%), which has led to users connecting to

the internet increasingly frequently, confirming the default position of ‘always on’ already recognised in 2015.

69% of internet users are in fact mobile users; ‘triple players’ (users who connected to the internet with their smartphone/

tablet/ pc), reached 19%, confirming the strong trend for growth noted in recent years (2015: 15%; 2014: 10%; 2013: 6%).

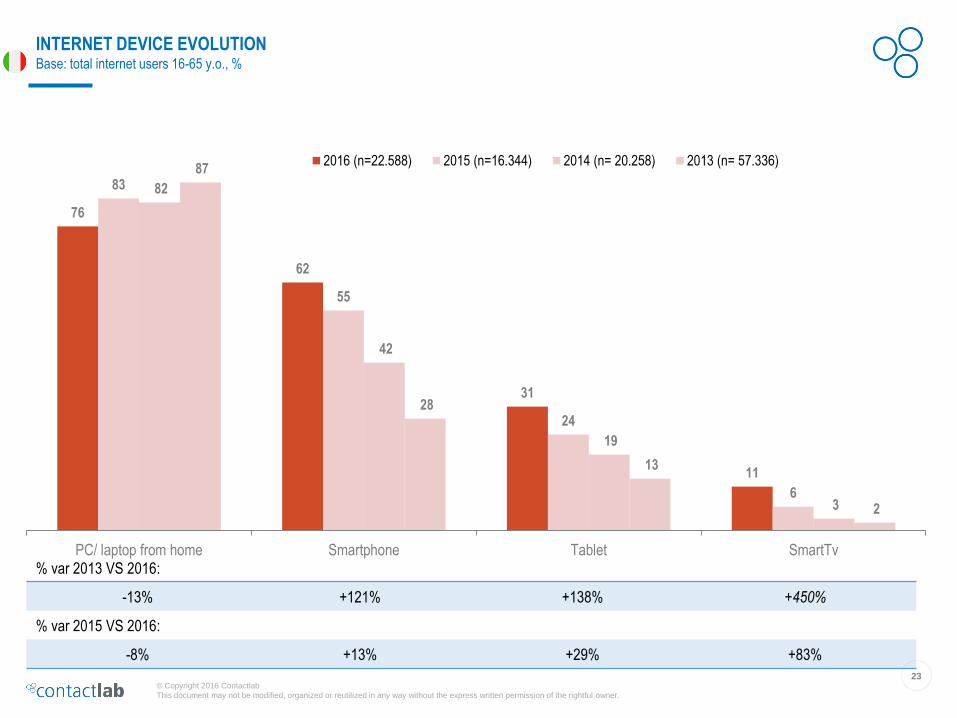

Despite a slight fall in use, desktop/laptop pc remains the standard primary device, used in the last month by 83% of users.

In 2016, SmartTv passed the 10% threshold, almost doubling with respect to 2015. There is significant interest in SmartTv –

12% of users intend to adopt it in the next 12 months (47% in an unspecified timeframe) – but the market offer is ineffective in

converting users.

Internet use is still “basic”, though online shopping and home banking saw a significant increase

The use of smartphones to connect to the internet is still growing. Likewise, the number of activities carried out regularly

(weekly) on this device is rising.

With regards online activities, there was a considerable rise in online shopping (+38% on 2013) and home banking (+18% on

2013).

Italian internet users remain ‘basic’, with an interactivity index (0-100) of 39, a score significantly lower than the other EU+

countries (UK 51, ES 49).

INTERNET USE IN ITALY: RISE PRIMARILY DUE TO EXPONENTIAL INCREASE IN THE USE OF

MOBILE DEVICES

10© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

EUROPEAN (+) DIGITAL BEHAVIOUR STUDY

Report 2016

THE OPPORTUNITY TO ENGAGE DIGITALLY THROUGH OWNED MEDIA

Report 2016Social media as an engagement opportunity has now spread to different platforms

The use of social networks remains pretty much stable over the last 12 months with about 80% penetration.

The opportunity to engage Italian users through social networks is slightly lower than in the rest of Europe; nonetheless almost

1 in 5 Italian internet users has a relationship that can be defined as “committed" with brands on social networks while overall,

37% are “open" towards communication from and “with” brands on s.n.

As regards the most popular social networks, Facebook confirms its number 1 position (82%), followed by Google+ (49%) and

YouTube (46%). Google+ and Instagram registered the highest growth over the last 36 months.

There has been a significant rise over the last 12 months for products/brands pages on Facebook as drivers of online

purchases.

The “social network login” (using an existing social account to register to another site) maintains its relevance both in Italy (with

a 29% of users) and in the other EU+ countries (used, on average, by 1 in 5 users).

Direct marketing is recognized as the most effective communication channel

Newsletter services confirm their role as the main channel by which users can stay up-to-date with brands.

This communication channel represents even more a starting point for purchases (online or offline): 65% of newsletter users

often or sometimes buy the products featured in the messages in physical stores (+3% on 2015), while half of users purchase

online from links within newsletters (+19% on 2015).

The opportunity to engage Italian users through direct marketing is also slightly lower than in the rest of EU+; nonetheless one

third of users have a neutral attitude toward this channel, an attitude that can with little effort be turned in an open one,

characterized by more active and engaged behaviours.

11© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

EUROPEAN (+) DIGITAL BEHAVIOUR STUDY

Report 2016

ONLINE SHOPPING: PENETRATION AND EXPENDITURE INCREASING WITH FURTHER POTENTIAL FOR

GROWTH

Report 201647% of internet users are online shoppers, and they spend 1,600€ online each year

Penetration of online shopping among internet users in Italy continues to grow, landing at 47%. Even though 14,3 million

people shop online, the full potential has not yet been reached.

Average online spending grew by more than 30%, reaching 1.600 € per year: the almost 2 million "ecommerce newbies"

contributed to this growth.

PayPal and prepaid credit cards remain the preferred payment methods for online purchases, preferred by 57% and 52% of

users respectively.

As regards the drivers of online purchases, the starting point for collecting information on the desired product/service remains

the brand website; more detailed information is then acquired from ecommerce portals with products specifications or from

reviews on specialized websites.

For their purchases, Italian online shoppers mainly use ecommerce portals with various product categories. This type of online

channel has a lower usage in the other EU areas, where the first place is held by sites of retailers that also have physical

shops.

The fashion sector maintains its first position among goods/services categories bought online

7,3 million individuals (+1,6 million on 2015), equal to 51% online shoppers, chose to buy online products belonging to this

category.

Second and the third position also remain unchanged over the last 12 months: 2nd place is held by transport tickets (6,3 million

individuals), and 3rd place is tech products/ home electronics (5,4 million buyers).

12© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

EUROPEAN (+) DIGITAL BEHAVIOUR STUDY

Report 2016

TRENDS IN THE DIGITAL ARENA

Report 2016 In the main European countries (UK, Germany, France, Spain), internet penetration reached 94%. With a linear trend based

on data from previous years, we expect this threshold to be reached in Italy over the next 4 years.

According to this forecast, there will be 37 million 16-65 y.o. Italian internet users, meaning 6.7 million new regular users.

As regards ecommerce, the average penetration of online shoppers in Europe is 78% (84% among internet users). Taking

into consideration the current distribution of online shoppers and past trends, a longer period is needed to reach this threshold.

The use of click&collect grew slightly for all the categories analysed. Nevertheless, this growth does not mirror the high level

of interest in purchasing with this method, recorded both in 2015 and 2016. There is huge potential in this interest.

The use of smartphone among Italian internet users is slightly below the European average. If trends recorded over the past

36 months continue and the behaviours of people who are not already mobile users are further consolidated, in 3 years

smartphones will be used by more than three-quarters of Italian internet users.

13© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

THE DIGITAL INTERACTIVITY INDEX – INTERNATIONAL VIEW

IT UK DE FR ES CH NY* KR* Shanghai* Tokyo*Moscow/

St. Pet.*

►DII

Digital Interactivity Index39 51 46 45 49 45 55 53 61 40 53

hyper-actives + + 13 36 26 27 39 21 44 40 59 18 39

hyper-actives + 17 21 22 17 16 22 17 22 19 15 27

actives 23 18 19 21 17 24 18 18 9 17 21

passives - 22 12 16 14 11 17 12 11 8 20 10

passives -- 25 13 17 21 17 16 9 9 5 30 3

*for these countries the total sample always refers to online shoppers

39 51 46 45 49 45 55 53 61 40 53

13 36 26 27 39 21 44 40 59 18 39

17 21 22 17 16 22 17 22 19 15 27

23 18 19 21 17 24 18 18 9 17 21

22 12 16 14 11 17 12 11 8 20 10

25 13 17 21 17 16 9 9 5 30 3

14© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

OPPORTUNITY TO ENGAGE VIA NEWSLETTERS/ SOCIAL NETWORKS – INTERNATIONAL VIEW

IT UK DE FR ES CH NY* KR* Shanghai* Tokyo*Moscow/

St. Pet.*

►DOI - Direct

Opportunity Index42 47 43 43 42 43 53 44 58 41 52

Committed 4 9 6 5 7 4 19 7 35 7 9

Open 19 33 22 27 28 22 35 37 32 23 39

Passive 33 23 26 25 20 32 14 12 2 21 23

Opportunistic 1 3 1 1 1 3 2 1

Not disturb 21 8 27 22 10 27 5 8 3 18 15

Unaware 22 27 16 20 35 14 26 33 28 29 13

►SOI - Social

Opportunity Index21 24 20 23 27 22 27 22 34 16 26

Committed 19 27 16 22 29 20 31 18 36 11 28

Open 18 23 21 22 26 22 23 29 42 17 26

Passive 33 24 32 27 31 33 26 38 20 31 34

Opportunistic 8 12 16 12 9 12 12 7 1 9 7

Non users 22 14 15 17 5 13 8 8 1 32 5

*for these countries the total sample always refers to online shoppers

21 24 20 23 27 22 27 22 34 16 26

19 27 16 22 29 20 31 18 36 11 28

18 23 21 22 26 22 23 29 42 17 26

33 24 32 27 31 33 26 38 20 31 34

8 12 16 12 9 12 12 7 1 9 7

22 14 15 17 5 13 8 8 1 32 5

42 47 43 43 42 43 53 44 58 41 52

4 9 6 5 7 4 19 7 35 7 9

19 33 22 27 28 22 35 37 32 23 39

33 23 26 25 20 32 14 12 2 21 23

1 3 1 1 1 3 2 1

21 8 27 22 10 27 5 8 3 18 15

22 27 16 20 35 14 26 33 28 29 13

15© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

FASHION AND AFFLUENT SEGMENTATION – INTERNATIONAL VIEW

IT UK DE FR ES CH NY* KR* Shanghai* Tokyo*Moscow/

St. Pet.*

►Fashion spending

Online/offline

High

Medium

Low

►LAI -

Luxury Attitude Index43 47 47 46 46 43 55 52 64 47 49

High-end experience lover 13 22 18 21 21 12 39 21 56 17 24

High-end assayer 12 15 16 13 15 12 17 23 20 14 14

High-end selector 43 37 41 37 38 43 30 45 20 49 39

High-end skeptic 14 9 11 11 10 13 7 5 3 8 12

High-end resistant 18 17 14 18 16 20 7 6 1 12 11

*for these countries the total sample always refers to online shoppers

43 47 47 46 46 43 55 52 64 47 49

13 22 18 21 21 12 39 21 56 17 24

12 15 16 13 15 12 17 23 20 14 14

43 37 41 37 38 43 30 45 20 49 39

14 9 11 11 10 13 7 5 3 8 12

18 17 14 18 16 20 7 6 1 12 11

18 29 27 26 32 31 49 39 65 30 28

30 37 45 37 36 38 32 33 26 29 36

52 34 28 37 31 31 19 28 10 41 35

16© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

LUXURY CONSUMPTION INDEX – INTERNATIONAL VIEW

IT UK DE FR ES CH NY* KR* Shanghai* Tokyo*Moscow/

St. Pet.*

►LCI

Luxury Consumption

Index

49 59 59 58 63 55 74 66 86 58 60

Staunch 14 29 24 26 30 17 47 31 67 25 26

Committed 15 15 18 15 20 20 19 24 16 18 18

Selector 23 22 30 24 22 29 18 22 12 22 24

Detached 48 35 28 35 27 35 17 22 5 35 31

*for these countries the total sample always refers to online shoppers

16

13

41

13

17

H-Experience lover

H-Assayer

H-Selector

H-Skeptic

H-Resistant

LCIluxury consumptionindex and clusters

EXPENDITURE ON FASHION

HIGH MEDIUM LOW

49 59 59 58 63 55 74 66 86 58 60

14 29 24 26 30 17 47 31 67 25 26

15 15 18 15 20 20 19 24 16 18 18

23 22 30 24 22 29 18 22 12 22 24

48 35 28 35 27 35 17 22 5 35 31

INTERNET AND E-COMMERCE SCENARIO

• The spread of the Internet in Europe – Last 5 years*

• Online shoppers last 12 months in Europe – Last 5 years

• E+DBS16 universes – Regular Internet users and online shoppers in Italy

• E+DBS16 represented universes: Europe and extra-EU areas

• E+DBS16 represented universes in Europe: trends

*The sections denoted in light grey are part of the full report only

*Definition by “Eurostat – Information Society”: frequency of internet access: once a week (including every day). Users 16-74 y.o.

Only for Switzerland , the value for 2015 is an estimate by Contactlab based on the official BFS/ Eurostat data

THE SPREAD OF INTERNET IN EUROPE – LAST 5 YEARSSource: EUROSTAT* data processed by Contactlab

81

84

8789 90

82 8385 86 86

77 7880

8284

74

78

8081

61

65 66

71

75

5153

56

59

63

30

40

50

60

70

80

90

100

2011 2012 2013 2014 2015

UK

CH

DE

FR

ES

IT

+2,9%

is the average growth of

internet pop in Europe +

from 2014 to 2015

19© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

* Source: “Eurostat – Information Society”: Last online purchase in the 12 months, % of individuals 14-74 y.o.

ONLINE SHOPPERS LAST 12 MONTHS IN EUROPE – LAST 5 YEARSSource: EUROSTAT* data processed by Contactlab

7173

7779

81

5659

6467

69

64 65

69 70

73

53

5759

6265

2730

32

37

42

1517

2022

26

0

10

20

30

40

50

60

70

80

90

100

2011 2012 2013 2014 2015

UK

CH

DE

FR

ES

IT

+7,7%

The average amount

ecommerce rose in

Europe+ between 2014

and 2015

20© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

E+DBS16 REPRESENTED UNIVERSE - REGULAR INTERNET USERS AND ONLINE SHOPPERS IN ITALYSource: EUROSTAT ICT/ ContactLab

100%

78%

36%

Total

national

population

Regular

internet users

(weekly)

Online

shoppers

(at least one

product in the last

12 months)

Individuals

16-65 years old (.000)39.400 30.500 14.300

100% 78% 36%

21© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

E+DBS16 UNIVERSES: EUROPE AND EXTRA-EU AREASSource: EUROSTAT/ National bureaus of statistics for each country, data processed by Contactlab

ITALY(.000)

UK(.000)

GERMANY(.000)

FRANCE(.000)

SPAIN(.000)

SWITZERLAND(.000)

Nr of interviews n=22.,588 n=1,000 n=1,001 n=1,002 n=1,004 n=1,001

Total population 16-65 39,400 41,900 53,600 41,800 30,900 5,500

Internet population (16-65) 30,500 41,000 51,700 37,600 28,000 5,300

Online shoppers (16-65) 14,300 38,100 47,500 33,000 18,000 4,700

New York(.000)

Korea(.000)

Shanghai(.000)

Tokyo (.000)

Moscow/ St. Pet(.000)

Nr of interviews n=473 n=475 n=437 n=462 n=1.049

Total population 16-65 8,400 37,600 19,600 8,900 12,600

Online shoppers (16-65) 6,600 25,700 11,300 6,500 5,800

Tot. USA Tot. China Tot. Japan Tot. Russia

Online shoppers (16-65) 252,000 370,400 79,000 26,000

DEVICE AND MOBILE EVOLUTION

• Internet devices (connecting for personal reasons) – last 4 weeks (eu)*

• Internet device evolution (it)

• Access to the internet: always online vs connection when needed

• Time spent online during a regular day

• Italy: device overlapping & mobile segments - last 4 weeks

• Device and mobile evolution – worldwide overview

• Non-smart tv users: intention to adopt in the near future

• Non-smartphone users: intention to adopt in the near future | forecast to 2018

• Non-tablet users: intention to adopt in the near future | forecast to 2018

*The sections denoted in light grey are part of the full report only

23© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

% var 2013 VS 2016:

-13% +121% +138% +450%

% var 2015 VS 2016:

-8% +13% +29% +83%

INTERNET DEVICE EVOLUTIONBase: total internet users 16-65 y.o., %

76

62

31

11

83

55

24

6

82

42

19

3

87

28

13

2

PC/ laptop from home Smartphone Tablet SmartTv

2016 (n=22.588) 2015 (n=16.344) 2014 (n= 20.258) 2013 (n= 57.336)

24© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

5

3

4

35

53

I think I will start to use onewithin the next 3 months

I think I will start to use one in3 - 6 months

I think I will start to use one in6 - 12 months

I think I will start to use one,but I do not know when

No, I do not think that I willconnect to the Internet in this

way

47

total

prospect

12

Next 12

months

(non users/ owners smartTv, n=16.343)

11

17 72

SmartTv last 4 weeks users

SmartTv occasional users

Non users

NON-SMART TV USERS: INTENTION TO ADOPT IN THE NEAR FUTUREBase: total internet users 16-65 y.o., n=22.588; %

Thinking about the use of a smart Tv, which of the following statements is true for you?

LEVEL OF INTERACTIVITY ON THE INTERNET: ONLINE ACTIVITIES

• Interactivity level – last 36 months trend (it)*

• Interactivity level

• Main online activities carried out yearly (total users - eu)

• Main online activities carried out yearly - last 36 months trend (it)

• Other online activities - last 4 weeks (eu)

• Smartphone: main activities carried out online weekly (eu)

• Smartphone: main activities carried out online weekly - last 24 months trend (it)

• Use of the smartphone in stores to compare prices (often+sometimes) (trend it)

• Main online activities weekly - worldwide overview

*The sections denoted in light grey are part of the full report only

INTERACTIVITY LEVEL – LAST 36 MONTHS TRENDBase: total internet users 16-65 y.o., %

DII - Digital Interactivity

Index (0-100)39 37 36 35

25

22

23

17

13

2016 (n=22.588)

hyper-actives + +

hyper-actives +

actives

passives -

passives -- 27

21

22

17

13

2015 (n=16.334)

28,7 M individuals

28

24

23

14

11

2014 (n=20.258)

29

25

21

15

10

2013 (n=57.336)

30,5 M individuals

26,5 M individuals

25,0 M individuals

14,3 M

9,2 M

7,0 M

13,8 M 13,5 M

6,3 M6,6 M

6,1 M 5,2 M

13,8 M

8,6 M

6,3 M

27© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

INTERACTIVITY LEVELBase: total internet users 16-65 y.o., %

DII - Digital Interact.

Index (0-100)39 51 46 45 49

25

1317

2117

22

12

1614

11

23

18

1921

17

17

21

22 17

16

13

36

26 27

39

ITALY (n=22.588) UK (n=1.000) GERMANY (n=1.001) FRANCE (n=1.002) SPAIN (n=1.004)

hyper-actives + +

hyper-actives +

actives

passives -

passives --

28© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

ecommerce

SMARTPHONE: MAIN ACTIVITIES CARRIED OUT ONLINE WEEKLYBase: smartphone users 16-65 y.o. (It 62%, Uk 69%; De 65%; Fr 61%, Es 66%) %

82

75

68

54

47

36

30

24

18 17

83

76

68

42

46

42

52

34

19

35

79

72

64

49 48

37

3235

12

27

80

73

57

42

49

3336 37

15

20

85 84

63

5552

41

49

37

19

27

Email Socialnetworking

News Information onproducts/services

Multimediaentertainment

Sports &hobbies

Home-banking efinance online

Online gaming E-learning/onlineeducation

Online shopping

ITALY (n=13.990) UK (n=691) GERMANY (n=652) FRANCE (n=612) SPAIN (n=667)

29© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

MAIN ONLINE ACTIVITIES WEEKLY – WORLDWIDE OVERVIEWBase: total internet users 16-65 y.o., %

U M/stPt.: 5,8 M*

U SH: 11,3 M*

U NY: 6,6M*U: 5,3 M

U: 51,7 MU: 41,0 M

U: 30,5 MU: 28,0 M

U: 37,6 M

*In

NY

, KR

, Sha

ngha

i, T

okyo

, Mos

cow

/St.

Pet

the

tota

lsam

ple

alw

ays

refe

rsto

onl

ine

shop

pers

U : 25,7 M*

IT UK DE FR ES CH NY KR Shanghai TokyoMoscow/

St. Pet.

% % % % % % % % % % %

Email 84 90 89 90 90 91 90 86 74 87 96

Reading news 64 68 60 54 64 61 67 76 73 59 85

Social networking 63 70 63 68 82 64 70 66 73 49 85

Info. on prod./services 45 43 40 38 53 31 41 47 53 54 69

Multimedia entertainment 41 47 39 43 47 38 52 52 61 35 63

Sports & hobbies 32 43 28 25 41 23 40 37 47 42 38

Home banking 29 60 42 40 52 28 46 50 38 18 19

Online gaming 22 31 28 33 33 24 37 41 44 25 40

E-Learning 16 17 8 11 19 11 22 21 30 8 13

Online shopping 12 39 22 16 32 14 41 48 47 29 21

DII - Digital Interactivity Index (0-100) 39 51 46 45 49 45 55 53 61 40 53

U Tokyo: 6,5 M*

SOCIAL NETWORKING AND BRAND INFLUENCE

• Main online activities carried out yearly: focus on social networking*

• Social networking: distribution of accounts by all users (it)

• Social networking: distribution of main accounts by all users - last 36 months trend (it)

• Brand engagement via social network - ways of interacting (it)

• SOI: the social opportunity index (the opportunity to engage via social media)

• Spread of the "social login" - last 36 months trend

• Social networking - worldwide overview

*The sections denoted in light grey are part of the full report only

31© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

SOCIAL NETWORKING: DISTRIBUTION OF ACCOUNTS BY ALL USERS Base: social network users 16-65 y.o., (78%); %

82

49

46

38

34

33

32

23

22

14

13

11

7

4

3

2

2

1

Google+

Youtube

Amazon

Paypal

Microsoft/ Windows Live ID

Yahoo

Telegram

Snapchat

Flickr

MySpace

Foursquare

Tinder

Happn

ITALY (n=17.546)

On which of the following sites do you have an account?

32© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

Social Opportunity Index

(SOI)21 24 20 23 27

SOI: THE SOCIAL OPPORTUNITY INDEX (OPPORTUNITY TO ENGAGE VIA SOCIAL MEDIA)Base: total internet users 16-65 y.o., %

2214 15 17

5

8

1216 12

9

33

24

32

27

31

18

23

21

22

26

1927

1622

29

ITALY (n=22.588) UK (n=1.000) GERMANY (n=1.001) FRANCE (n=1.002) SPAIN (n=1.004)

Committed

Open

Passive

Not disturb

Non user

33© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

SPREAD OF THE "SOCIAL LOGIN" – LAST 36 MONTHS TRENDBase: social network users 16-65 y.o., %

2016 2015 2014 2013 2016 2015 2014 2013 2016 2015 2014 2013 2016 2015 2014 2013 2016 2015 2014 2013

(n=17.546) (n=12.552) (n=15.759) (n=41.638) (n=856) (n=894) (n= 950) (n= 1.004) (n=846) (n=833) (n= 850) (n= 869) (n=835) (n=821) (n= 827) (n= 825) (n=951) (n=946) (n= 927) (n= 941)

…To use my social network account to subscribe automatically to another website

(e.g. using Facebook Connect, Twitter Login or Google+ sign-In, etc.)

29

25 2526

2523

13

24

2018

16

12

20

13

19

1211

14

1113

ITALY UK GERMANY FRANCE SPAIN

DIGITAL DIRECT MARKETING

• Number of active email addresses*

• Email providers

• Newsletter subscriptions

• Main newsletter topics (it)

• Newsletter topics (eu)

• The newsletter attitude

• Online vs offline channel for subscribing to newsletters

• Benefits sought for subscribing to newsletters

• Responses to communication from newsletters

• DOI: the direct opportunity index (the opportunity to engage via newsletter)

• Digital direct marketing - worldwide overview

• Effectiveness of different communication methods used by brands/ companies

*The sections denoted in light grey are part of the full report only

35© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

18

5

8

22

16

13

10

8

I am not subscribed to any newsletters

1 newsletter

2 different newsletters

3/4 different newsletters

5/6 different newsletters

7/10 different newsletters

10/20 different newsletters

more than 20 different newsletters

ITALY (n=21.647)

NEWSLETTER SUBSCRIPTIONSBase: email users 16-65 y.o. (96%); %

• Newsletter users on

internet users:

– 78

– 73

– 84

– 80

– 65

• Avg. nr. =

– 5,6

– 4,8

– 6,7

– 6,4 – 4,1

82%

newsletter users(on email users)

Now we’ll refer to emails that are sent periodically from brands, business, organizations after a user has subscribed.

These types of emails will all be defined as newsletters.

Thinking about all of the email you receive, how many different newsletters are you subscribed to?

36© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

RESPONSES TO COMMUNICATION FROM NEWSLETTERSBase: newsletter users 16-65 y.o., (78%), %

11

13

8

7

54

37

35

21

when I receive an offer in a newsletter, Igo to the store and buy the products /

services reported in the message

I buy online (…) from a link within the newsletter

I forward a newsletter to a friend if Ithink he/she might be interested

I share a newsletter on social networks,when it contains interesting promotions

Yes, often Yes, sometimes

TOP2

(often+sometimes)

2016 2015

65 63

50 42

43 n.a.

28 28

Thinking about newsletters, in which of the following situations do you recognize yourself?

37© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

DOI: THE DIRECT OPPORTUNITY INDEX (THE OPPORTUNITY TO ENGAGE VIA NEWSLETTER)Base: total internet users 16-65 y.o., %

Direct Opportunity Index

(DOI)42 47 43 43 42

2227

1620

35

21 8 27 22

101 3

1

33

23

2625 20

19

33

22 2728

49 6 5 7

ITALY (n=22.588) UK (n=1.000) GERMANY (n=1.001) FRANCE (n=1.002) SPAIN (n=1.004)

Committed

Open

Passive

Opportunistic

Not disturb

Unaware

38© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

DIGITAL DIRECT MARKETING – WORLDWIDE OVERVIEWBase: total internet users 16-65 y.o., %

U M/stPt.: 5,8 M*

U SH: 11,3 M*

U NY: 6,6M*U: 5,3 M

U: 51,7 MU: 41,0 M

U: 30,5 MU: 28,0 M

U: 37,6 M

U : 25,7 M*

IT UK DE FR ES CH NY* KR* Shanghai* Tokyo*Moscow/

St. Pet.

* % % % % % % % % % % %

Newsletter subscribers 78 73 84 80 65 87 74 67 72 71 87

=100 =100 =100 =100 =100 =100 =100 =100 =100 =100 =100

On FASHION 47 35 52 46 47 44 33 31 40 35 35… … … … … … … … … … … …

Avg nr of subscriptions 5,6 4,8 6,7 6,4 4,1 6,1 4,3 3 2,7 6,4 6,5

SUBSCRIPTIONS:

Via online 77 92 95 90 92 91 88 87 85 88 92

Via offline 50 32 22 43 30 29 46 41 72 44 55

ENGAGEMENT (often+sometimes):

Go to shop and buy the prod. 65 78 68 74 79 70 84 84 97 70 79

Go to website and buy the prod. 50 85 82 77 74 73 92 90 94 77 86

Direct Opportunity Index (DOI) 42 47 43 43 42 43 53 44 58 41 52

*In

NY

, KR

, Sha

ngha

i, T

okyo

, Mos

cow

/St.

Pet

the

tota

lsam

ple

alw

ays

refe

rsto

onl

ine

shop

pers

U Tokyo: 6,5 M*

39© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

EFFECTIVENESS OF DIFFERENT COMMUNICATION METHODS USED BY BRANDS/ COMPANIESBase: total internet users 16-65 y.o., n=22.588; %

«TOP2»AVG

(5-1)

66 3,9

49 3,5

38 3,1

32 3,1

Thinking about brands, companies or organisations that you like to follow closely, how useful do you personally find these

communication methods?

26

19

16

10

40

30

22

22

12

14

15

18

6

10

13

13

4

8

14

13

12

19

20

24

communication via email/ newsletter

communication via social media

communication via chat (whatsapp, Skype…)

communication via app notifications/pushmessages

Very useful Fairly useful Neither much nor little useful Not much useful Not at all useful I do not know

ECOMMERCE

• E-commerce trend - online shoppers «at least once in the past 12 months» (it)

• Non online shoppers: intention to purchase online in the near future*

• Product categories purchased online in the last 12 months

• EXI - ecommerce expenditure index 2016 (main categories)

• Average online shopping expenditure for each category (last 12 months)

• Information channels for online shopping

• Favourite methods of payment for online purchases

• Ecommerce channels used

• Recommendability of ecommerce channels

• Use/ recommendability of ecommerce channels

• Main barriers to ecommerce - last 24 months trend

• Categories purchased/ interest to purchase with "click&collect“

• Ecommerce - worldwide overview

*The sections denoted in light grey are part of the full report only

41© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

34

4043

47

2013 (n=57.336) 2014 (n=20.258) 2015 (n=16.344) 2016 (n=22.588)

E-COMMERCE TREND – "SHOPPED ONLINE AT LEAST ONCE IN THE PAST 12 MONTHS" Base: total internet users 16-65 y.o., %

last 12m + 18%

last 12m + 9%

2013 vs 2016

+38%

10.6 M online sh.

8.5 M online sh.

12.4 M online sh.14.3 M online sh.

last 12m + 8%

2013 vs 2015

+26%

42© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

EXI* - ECOMMERCE EXPENDITURE INDEX 2016 (MAIN CATEGORIES)Base: online shoppers 16-65 y.o.for each category

184

136

164

184 186

135 140127

117

73

120

97

50

100

150

200

250

300

350

400

450

UK

CH

DE

FR

ES

IT

*EXI. = expenditure over previous 12 months by category/ avg exp across 27 categ in 6 EU countries *100

43© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

USE/ RECOMMENDABILITY OF ECOMMERCE CHANNELSBase: online shoppers 16-65 y.o., n=10.575, (47%), %

...ecommerce portals with various product categories

… sites of retailers that also have shops

… online shop of the brand

...specialized websites by type of product/ e-tailer

… comparison sites of offers and prices

… private sales sites

...purchasing groups online with coupon

... from online private ads

0

10

20

30

40

50

60

0 10 20 30 40 50 60

PROMOTERS (10+9) (%) (avg.24.5)

US

ER

S(%

) (a

vg. 2

9,5)

44© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

ECOMMERCE – WORLDWIDE OVERVIEW (1/2)Base: online shoppers 16-65 y.o., %

U M/stPt.: 5,8 M

U SH: 11,3 M

U NY: 6,6MU: 4,7 M

U: 47,5 MU: 38,1 M

U: 14,3 M

IT UK DE FR ES CH NY* KR* Shanghai* Tokyo*Moscow/ St.

Pet.*% % % % % % % % % % %

Most used ecommerce channels:

1°Ecomm.

portals

53

Sites with

shops

58

Sites with

shops

53

Sites with

shops

46

E-tailers

49

Sites with

shops

48

Sites with

shops

47

Compar. e-

sites

55

Ecomm. portals

55

Ecomm.

portals

44

E-tailers

54

2°Sites with

shops

45

Brand’s

e-shops

43

E-tailers

50

E-tailers

38

Brand’s

e-shops

44

Brand’s

e-shops

47

Brand’s

e-shops

39

Ecomm.

Portals

42

E-tailers

53

Sites with

shops

40

Ecomm.

portals/ e-

tailers 41

U: 18,0 M

U: 33,0 M

U : 25,7 M

U Tokyo: 6,5 M

45© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

ECOMMERCE – WORLDWIDE OVERVIEW (2/2)Base: total internet users 16-65 y.o., %

U M/stPt.: 5,8 M*

U SH: 11,3 M*

U NY: 6,6M*U: 5,3 M

U: 51,7 MU: 41,0 M

U: 30,5 M

IT UK DE FR ES CH NY* KR* Shanghai* Tokyo*Moscow/

St. Pet.*% % % % % % % % % % %

Main barriers for ecommerce:

1°can't check

in person

39

high costs

of shipping

33

can't check

in person

30

can't

check in

person

33

can't

check in

person

28

can't

check in

person

35

high

costs of

shipping

43

can't

check in

person

40

can't check

in person

39

high

costs of

shipping

40

can't

check in

person

33

2°

afraid of

not

receiving

29

can't check

in person

32

high costs

of shipping

25

high costs

of

shipping

31

afraid of

not

receiving

22

high

costs of

shipping

30

can't

check in

person

35

afraid of

not

receiving

34

can't find

online what

I want 23

can't

check in

person

28

afraid of

not

receiving

31

Users of Click&Collect 12 17 10 10 15 9 7 6 3 7 15

Users + prospect of C&C 53 64 45 54 61 47 63 60 81 37 63

U: 28,0 M

U: 37,6 M

*In

NY

, KR

, Sha

ngha

i, T

okyo

, Mos

cow

/St.

Pet

the

tota

lsam

ple

alw

ays

refe

rsto

onl

ine

shop

pers

U : 25,7 M*

U Tokyo: 6,5 M*

METHODOLOGICAL NOTES

47© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

EUROPEAN (+) DIGITAL BEHAVIOUR STUDY

Report 2016

EUROPEAN (+) DIGITAL BEHAVIOUR STUDY

2016The European Digital Behaviour Study is a study analysing the digital behaviour of internet users with

reference to all types of internet use in Europe+ (6 countries). Since the 2015 edition, the study has also looked

at users outside Europe (including, in 2016, 4 metropolitan areas – Tokyo, Shanghai, Moscow, St. Petersburg –

and the Republic of Korea).

By providing a complete and detailed overview of digital behaviour, the objective of the report is to provide

useful information to enterprises seeking new opportunities in electronic communication and relations, and new

commercial openings.

The study was conducted using a total sample of over 30,000 cases. This includes users interviewed during the

sampling process, as well as those who accessed the study through participating merchants who sent the

invitation to their database of Italian users asking them to take part in the research.*

The country samples represent individuals between 16 and 65 years of age who connect to the internet at least

once a week, irrespective of device and purpose of use (c.f. interview methods in methodology notes).

*Each merchant that took part in the study in Italy was sent, as a reward for participating, the complete set of

statistic tables referring to their own customer base, on a confidential basis.

This report and the related statistics tables demonstrate the aggregate results and do not contain any data that

can be attributed to the specific customer base of a participating merchant.

48© Copyright 2016 Contactlab

This document may not be modified, organized or reutilized in any way without the express written permission of the rightful owner.

ecommerce

Interview method

Europe+ (Italy, UK, Germany, France, Spain, Switzerland):

CAWI survey on ‘regular’ internet users aged 16 – 65, who connect at least once a week, regardless of the device and reason.

Extra-EU markets (New York, Shanghai, Tokyo, Moscow/St Petersburg, Korea):

CAWI survey on ‘online shoppers’ aged 16-65, who purchased/ordered online goods/services in the last year.

Sample design

In the European countries, a representative sample was formed based on the latest data provided by the Eurostat – Information Society and by national

bureaus of statistics. As regards the other extra-EU markets, have been used data from OECD and national bureaus of statistics.

Boost from merchants

In Italy, the representative sample was combined with the sample taken from the lists of merchants. Profiles were then re-balanced to maximize their

representativeness.

The numbers

30.492 cases, composed of 22.588 Italian internet users.

Average duration of online interview: 25 minutes.

EUROPEAN (+) DIGITAL BEHAVIOUR STUDY: INTERVIEW METHOD AND SAMPLING

Need a deep dive on those data?

Ask for more information:

www.contactlab.com

![CONFIRMING CEDENTES · CONFIRMING CEDENTES Para acceder a CONFIRMING: [Imagen1] Ir a Financiación Desplegar Confirming (emisores de pagos) Imagen1 · Podrá obtener la información](https://static.fdocuments.net/doc/165x107/5f07bf467e708231d41e89f0/confirming-cedentes-confirming-cedentes-para-acceder-a-confirming-imagen1-ir.jpg)