(e-bulletin for Executive & Professional Students) · Diwali- the festival of lights- is one of the...

66

Dear Students Goodness is the only investment which never fails. Henry David Thoreau Diwali- the festival of lights- is one of the biggest festivals celebrated in India. The festival is not only about crackers, lighting lamps, shopping and sweets but behind the festival is a great history of struggle between the forces of Good and Evil and the victory of good over evil. In true sense it is about overcoming the darkness of ignorance and propagating the light of knowledge. The story behind Diwali signifies that good and evil are not something outside the human body rather every human being faces the struggle between the inner good and evil every day. The inner strength lies in empowering good to always win over evil. This Diwali, I wish we defeat our inner evil and let our inner truth to win. CS Mamta Binani President [email protected] Inside This Issue Academic Guidance Practice Manual Hindi Books relevant for CS Course Curriculum Legal World Student – ICSI Academic Connect Student Services Precious ‘You’ Training Corporate Compliance Executive Certificate for Students Licentiate – ICSI News from Region Student Company Secretary (e-bulletin for Executive & Professional Students)

Transcript of (e-bulletin for Executive & Professional Students) · Diwali- the festival of lights- is one of the...

Dear Students

Goodness is the only investment which never fails.

Henry David Thoreau

Diwali- the festival of lights- is one of the biggest festivals celebrated in India. The festival is not only about crackers, lighting lamps, shopping and sweets but behind the festival is a great history of struggle between the forces of Good and Evil and the victory of good over evil. In true sense it is about overcoming the darkness of ignorance and propagating the light of knowledge. The story behind Diwali signifies that good and evil are not something outside the human body rather every human being faces the struggle between the inner good and evil every day. The inner strength lies in empowering good to always win over evil. This Diwali, I wish we defeat our inner evil and let our inner truth to win.

CS Mamta Binani President [email protected]

Inside This Issue

Academic Guidance Practice Manual Hindi Books relevant for

CS Course Curriculum Legal World Student – ICSI Academic

Connect Student Services Precious ‘You’ Training Corporate Compliance

Executive Certificate for Students

Licentiate – ICSI News from Region

Student Company Secretary (e-bulletin for Executive & Professional Students)

e- bulletin 2 November 2016

Academic Guidance

Child Labour (Prohibition and Regulation) Amendment Act, 2016*

The Child Labour (Prohibition and Regulation) Act, 1986 provides for prohibition of the engagement of children in certain employments and for regulating the conditions of work of children in certain other employments.

To prohibit employment of children in all occupations and processes to facilitate their enrolment in schools in view of the Right of Children to Free and Compulsory Education Act, 2009 and to prohibit employment of adolescents (persons who have completed fourteenth year of age but have not completed eighteenth year) in hazardous occupations and processes and to regulate the conditions of service of adolescents in line with the ILO Convention 138 and Convention 182, respectively, the Child Labour (Prohibition and Regulation) Amendment Act, 2016 is passed by the Parliament.

The salient features of the Child Labour (Prohibition and Regulation) Amendment Act, 2016, are as under:

Child and Adolescent Labour (Prohibition and Regulation) Act, 1986

The title i.e. the Child Labour (Prohibition and Regulation) Act, 1986 has been amended and renamed as the Child and Adolescent Labour (Prohibition and Regulation) Act, 1986 to prohibit employment of children below fourteen years in all occupations and processes and to prohibit employment of adolescents (persons who have completed fourteenth year of age but have not completed eighteenth year) in hazardous occupations and processes set forth in the Schedule.

“Adolescent”

Inserted a new definition of “Adolescent” that means a person who has completed his fourteenth year of age but not completed his eighteenth year in section 2 of the said Act;

“Child”

Amended the definition of “Child” to provide that child means a person who has not completed his fourteenth year of age or such age as may be specified in the Right of Children to Free and Compulsory Education Act, 2009, whichever is more.

Prohibition of employment of children in any occupation and process

Amended Section 3 of the Child Labour (Prohibition and Regulation) Act, 1986 to prohibit employment of children in all occupations and processes except where the child helps his family after his school hours or during vacations or works as an artist in an audio-visual entertainment industry, including advertisement, films, television serials or any such other entertainment or sports activities except the circus, subject to such conditions and safety measures, as may be prescribed:

However, no such work under this clause shall affect the school education of the child.

* Chittaranjan Pal, Assistant Director, ICSI.

The views expressed are personal views of the author and do not necessarily reflect those of the Institute.

e- bulletin 3 November 2016

Prohibition of employment of adolescents in certain hazardous occupations and processes

Inserted a new Section 3A to prohibit employment of adolescents in any hazardous occupations and processes specified in the Schedule.

Central Government may, by notification, specify the nature of the non-hazardous work to which an adolescent may be permitted to work under the Act.

Power to amend the Schedule

Amended Section 4 of the Act to empower the Central Government to add or omit any hazardous occupations and processes from the Schedule to the Act.

Penalties

Amended Section 14(1) to enhance the punishment from imprisonment for a term which shall not be less than three months but which may extend to one year or with fine which shall not be less than ten thousand rupees but which may extend to twenty thousand rupees, to imprisonment for a term which shall not be less than six months but which may extend to two years, or with fine which shall not be less than twenty thousand rupees but which may extend to fifty thousand rupees, or with both, for employment or permitting any children to work in any occupations or processes in contravention of section 3. However, the parents or guardians of such children shall not be liable for such punishment unless they permit such children for commercial purposes;

Inserted new sub-section (1A) in section 14 to provide punishment of imprisonment for a term which shall not be less than six months but which may extend to two years, or with fine which shall not be less than twenty thousand rupees but which may extend to fifty thousand rupees, or with both for employment or permitting to work any adolescent in any hazardous occupations or processes. However, the parents or guardians of such adolescents shall not be liable for punishment unless they permit such adolescents to work in contravention of the provisions of section 3A.

Amended Section 14(2), which provides punishment for the convicted offender who commits a like offence afterwards, to enhance the minimum punishment existing therein from six months to one year and maximum punishment from two years to three years.

Inserted new sub-section (2A) in section 14, which provides that if the parents or guardians having been convicted of an offence under section 3 or section 3A, commits a like offence afterwards, he shall be punishable with a fine which may extend to ten thousand rupees.

Offences to be Cognizable

Inserted a new Section 14A to provide that the offences under the proposed legislation shall be cognizable notwithstanding anything contained in the Code of Criminal Procedure, 1973 .

Child and Adolescent Labour Rehabilitation Fund

Inserted a new Section 14B. It states that:

(1) The appropriate Government shall constitute a Fund in every district or for two or more districts to be called the Child and Adolescent Labour Rehabilitation Fund to which the amount of the fine realized from the employer of the child and adolescent, within the jurisdiction of such district or districts shall be credited.

(2) The appropriate Government shall credit an amount of fifteen thousand rupees to the Fund for each child or adolescent for whom the fine amount has been credited under sub-section (1).

e- bulletin 4 November 2016

(3) The amount credited to the Fund under sub-section (1) and (2) shall be deposited in such banks or invested in such manner, as the appropriate Government may decide.

(4) The amount deposited or invested, as the case may be under sub-section (3), and the interest accrued on it, shall be paid on the child or adolescent in whose favour such amount is credited, in such manner as may be prescribed.

Explanation:— For the purposes of appropriate Government the Central Government shall include the Administrator or the Lieutenant Governor of a Union territory under article 239A of the Constitution.

Compounding of offences

Inserted a new Section 14D. It provides that

(1) Notwithstanding anything contained in the Code of Criminal Procedure, 1973, the District Magistrate may, on the application of the accused person, compound any offence committed for the first time by him, under sub-section (3) of section 14 or any offence committed by an accused person being parent or a guardian, in such manner and on payment of such amount to the appropriate Government, as may be prescribed.

(2) If the accused fails to pay such amount for composition of the offence, then, the proceedings shall be continued against such person in accordance with the provisions of this Act.

(3) Where any offence is compounded before the institution of any prosecution, no prosecution shall be instituted in relation to such offence, against the offender in relation to whom the offence is so compounded.

(4) Where the composition of any offence is made after the institution of any prosecution, such composition 'shall be brought in writing, to the notice of the Court in which the prosecution is pending and on the approval of the composition of the offence being given, the person against whom the offence is so compounded, shall be discharged."

District Magistrate to implement the provisions

Inserted a new Section 17A to empower the appropriate Government to confer such powers and impose such duties on a District Magistrate as may be necessary to ensure that the provisions of the proposed legislation are properly carried out and to empower the District Magistrate to specify the officer subordinate to him who shall exercise all or any of the powers and perform all or any of the duties so conferred or imposed and the local limits within which such powers or duties shall be carried out by the officer in accordance with the rules made by the appropriate Government;

Inspection and monitoring

Inserted a new Section 17B which empowers the appropriate Government to make periodic inspection or cause such inspection to be made, of the places at which the employment of the children is prohibited and the hazardous occupation or process are carried out, at such intervals as it thinks fit and monitor the issues relating to the provisions of the Act; and

Schedule

Substitution of the existing Schedule(Part A & Part B) to the Child Labour (Prohibition and Regulation) Act, 1986 by new Schedule in view of the prohibition of children in all occupations and processes and regulation of employment of adolescents in hazardous occupations and processes.

***

e- bulletin 5 November 2016

Mutual Funds*

Put not your trust in money, but put your money in trust. - Oliver Wendell Holmes

A Mutual Fund is a trust that pools the savings of a number of investors who share a common financial goal and investments may be in shares, debt securities, money-market securities or a combination of these. These securities are professionally managed on behalf of the unit holders and each investor holds a pro-rata share of the portfolio, that is, entitled to profits as well as losses. Income earned through these investments and the capital appreciation realized is shared by its unit holders in proportion to the number of units owned by them.

A mutual fund is the most suitable investment scope for common people as it offers an opportunity to invest in a diversified, professionally managed basket of securities at a relatively lower cost.

History of Mutual Funds

The mutual fund industry in India began in 1963 with the formation of the Unit Trust of India (UTI) as an initiative of the Government of India and Reserve Bank of India. Much later, in 1987, SBI Mutual Fund became the first non-UTI mutual fund in India.

Subsequently, the year 1993 indicated a new era in the mutual fund industry. This was marked by the entry of private companies in the sector. After that the Securities and Exchange Board of India (SEBI) Act was passed in 1992 and SEBI also formulate the new regulation on Mutual Fund in 1996 i.e., SEBI (Mutual Fund) Regulations, 1996, which for the first time, established a comprehensive regulatory framework for the mutual fund industry. Since then, several mutual funds have been set up by the private and joint sectors.

Currently there are around 44 mutual fund organizations in India together handling assets. Today, the Indian mutual fund industry has opened up many exciting investment opportunities for investors. As a result, we have started witnessing the phenomenon of savings now being entrusted to the funds rather than in banks alone. Mutual Funds are now perhaps one of the most sought-after investment options for most investors. We can also use mutual funds for a better post-retirement life.

As financial markets become more sophisticated and complex, investors need a financial intermediary who can provide the required knowledge and professional expertise on taking informed decisions. Mutual funds act as this intermediary.

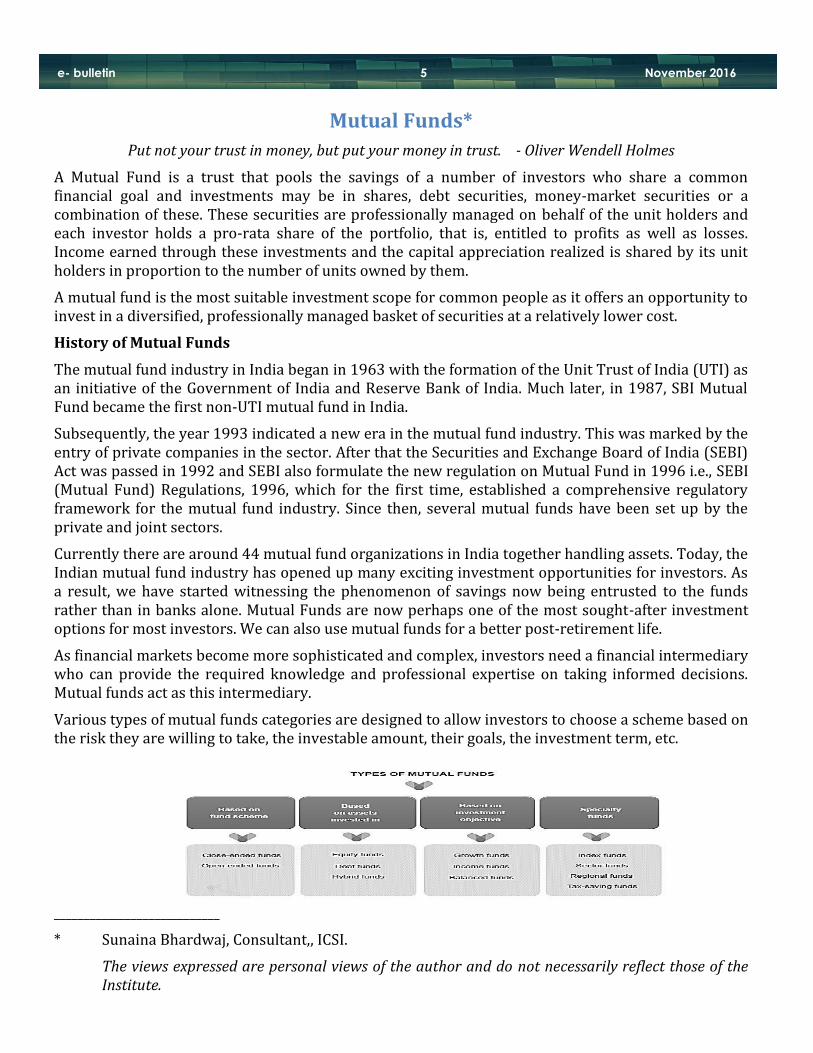

Various types of mutual funds categories are designed to allow investors to choose a scheme based on the risk they are willing to take, the investable amount, their goals, the investment term, etc.

____________________________

* Sunaina Bhardwaj, Consultant,, ICSI.

The views expressed are personal views of the author and do not necessarily reflect those of the Institute.

e- bulletin 6 November 2016

There are also other types of funds that one can invest in i.e., Closed-end investment funds, Exchange-traded funds (ETFs), Segregated funds etc. The level of risk and return depends on what the fund invests in.

Mutual funds are extended beyond the limits of equity i.e., Investor can also invest in Debt Instruments. The same principle is applicable i.e., higher the risk, the higher the returns.

Markets regulator, SEBI will soon issue norms which will allow e-commerce platforms for sale of mutual fund products, among other measures, to boost the Mutual Fund industry. The Securities and Exchange Board of India (SEBI) is also planning to implement know-your-client (KYC) procedure online, to simplify the process for mutual fund investors and attract wider number of customers.

Mutual Funds: How to Buy and Sell

Mutual funds have been around in India for nearly three decades now, but the number of people who actively buy and sell mutual funds in the country remains terribly low as a percentage of the population.

The fundamental reason for poor participation in the mutual fund market is the lack of awareness; not just about the benefits of mutual funds, but also the knowledge of how to buy and sell them.

The following is the process of buying and selling mutual funds:-

1. How to Buy Mutual Funds

Mutual funds are useful instruments that can be bought and sold in a variety of ways. Once all your paperwork is in order, here are some of the various ways one can acquire mutual funds in India:

Once one has decided which way to go and which mutual fund scheme(s) to invest in, he will have to place the order. Here’s the step-by-step procedure of buying a mutual fund:

Get a demat account

Go to the Mutual Funds section. Login and then click on ‘Place order’ or, you can call your broker.

Select the name of the mutual fund or the AMC’s name that you wish to invest in.

Then select the correct scheme as many fund houses offer multiple schemes.

e- bulletin 7 November 2016

Specify the amount you wish to invest in the scheme.

In case of a dividend scheme, select one of the two dividend options - payout or reinvestment. If he select the payout option, the mutual fund’s dividends will be credited to his bank account. The reinvestment option allows the amount to be used to buy additional units of the scheme. He thus won’t get the dividends credited to his bank account. Select the former if one want a secondary source of income. The reinvestment option, however, helps increase the size of holdings and increase returns.

2. How to Sell Mutual Funds:

There are two ways to sell your mutual funds –

sell to another investor or

back to the mutual fund.

The latter i.e., back to mutual fund is called redemption of mutual fund. Mutual funds are best redeemed the same route through which they are purchased. This means could choose to redeem them online or offline, through an agent or broker or directly by himself.

Redemption of Mutual Funds

A redemption is the return of an investor's principal in a fixed-income security, such as a preferred stock or bond, or the sale of units in a mutual fund. Redemption involves careful research about the performance of the fund and clarity about the reasons for redemption.

Some of instances for when mutual funds have to be redeemed:

Most people sell their mutual funds to finance some immediate or upcoming financial requirement, like buying a house or car, paying for children’s education, a health crisis or even an upcoming foreign holiday.

Another good time to sell off your mutual funds is when your investment requirements undergo a change – this could be due to inherent growth or changes in your existing portfolio or due to a life event that reorganizes your priorities.

If the performance of a mutual fund dips consistently below expectations and other comparable funds for a sustained period of time. Here, ‘sustained’ refers to a time period of 1 to 5 years at least.

Changes on the part of the mutual fund – a reset of its investment objectives or strategy, a rejig of its favoured stock picks or sectors in which it invests or even the departure of a trusted fund manager often leads to the sale of such mutual funds by investors.

Mutual funds are managed by professional fund managers who take proactive decisions and try to factor-in the perceived market movements. However, if a mutual fund scheme is consistently underperforming for a very long period (vis-a-vis its benchmark) one may choose exit.

Once the reason for redemption is clear, here are a few points to make the process straight forward.

1. Redemption if Purchased through the AMC or Distributors

The most common route for investing in mutual funds is through the AMC (direct) or through a distributor. In order to redeem funds through offline modes, one need to send a duly signed redemption request to the AMC's or the distributor's office. A standard redemption form asks for details like your name, folio number, plan and scheme details, and number of units one wish to

e- bulletin 8 November 2016

redeem. In addition, all the holders have to sign the slip. The proceeds from the redemption will be credited to the registered bank account.

2. Redemption if bought online

Mutual funds can also be purchased online. Such units can be redeemed online through a trading account or the AMCs website. One simply has to log in, select the fund and the number of units one wish to redeem and confirm your order. In addition, Central Service Providers like CAMS (Computer Age Management Services Pvt. Ltd.), Karvy, etc. offer the option of redeeming mutual fund bought from several AMCs. One can download the form online or visit the nearest office.

Points to be Remember:

Applicable Net Asset Value (NAV)

Turnaround Time i.e., Once the redemption request is successfully received and verified, it takes up to 3 working days for the proceeds to be credited to the registered bank account.

Funds with Lock-In Period i.e., unlike the units of a close-ended scheme, open-ended schemes can be redeemed anytime. Schemes like Equity Linked Savings Scheme (ELSS) cannot be redeemed up to 3 years from the date of investment.

Exit Loads and Applicable Taxes i.e., Based on the duration after which one is redeeming the funds, transaction might attract certain amount of taxes and exit loads. Like every investment decision, it is advisable to consult financial advisor beforehand. Remember, redeeming from one scheme and investing into another scheme of the similar kind is called 'churning' and is not advisable unless backed by sound logic.

Rights of Mutual Fund Investors

Every mutual fund investor enjoys certain rights, guaranteed by market regulator SEBI and other legal provisions. The following are the rights of Mutual fund investors:-

The documents, called Scheme Information Document (SID) and Statement of Additional Information (SAI), and Key Information Document (KIM), which gives some important information about the scheme and the fund house. If there is any change in these documents, the fund house have to inform the investor about those changes.

Annual Reports, Statements of accounts, Periodic updates etc., through newspapers advertisements, shall be inform to the investor.

Right of investor to receive redemption proceeds within 10 working days. In case a fund house sends the proceeds after 10 days, the investor has the right to receive interest at the rate of 15% per annum for the period of delay after the expiry of the 10th day.

In case the fund house in which one has invested makes any fundamental change to a scheme, the investors in that scheme can exit his investments without paying any exit load.

Every investor has the right to know the amount of money, or the commission, that his mutual fund distributor gets by selling the scheme. The distributor should also tell the investor the commissions or remunerations that he gets by selling other competing schemes.

Every fund house has an appointed officer to attend the investor grievances. In case an investor has any complaints against the fund house, scheme or anything, he can approach the designated officer at the fund house. If the complaint grievance is not resolved by the fund house as to the investor's satisfaction, he can escalate this to the compliance officer of the fund

e- bulletin 9 November 2016

house. If the same is not resolved by these officers too, the investor can move AMFI, the fund industry trade body or even SEBI, the industry regulator.

Conclusion:

Mutual funds are funds that pool the money of several investors to invest in equity or debt markets. The main disadvantages of Mutual Funds is it gives fluctuating returns, very costly due to professional management fees and misleading advertisements of different funds which can guide investors in wrong path. Even though the disadvantages, the mutual fund industry in India has prospered due to transparency and disclosures. Most fund houses come out with a fund fact sheet for each scheme every month. They provide information about the investment particulars of the corpus (company and sector-wise), credit ratings, market value of investments, NAVs, returns, repurchase and sale price of the schemes.

Sources: -

1. https://www.amfiindia.com/

2. http://www.sebi.gov.in/

*****

e- bulletin 10 November 2016

PRACTICE MANUAL

To build competency in practical oriented subjects by providing the students with a pool of solved practical problems, Practice Manual for the following papers have been released by the Institute.

Cost and Management Accounting (Executive Programme) Company Accounts and Auditing Practices (Executive Programme) Advanced Tax Laws and Practice (Professional Programme) Financial Treasury and Forex Management (Professional Programme)

Soft copies of the Practice Manuals are available on ICSI website under the head Academic corner at the link : https://www.icsi.edu/AcademicCorner.aspx. The students, who wish to procure printed copies, may purchase from sale counters at ICSI Regional offices/ Chapter offices or order it online through e-cart on ICSI website.

For any feedback / queries, students may please write at [email protected].

e- bulletin 11 November 2016

Hindi Books relevant for CS Course Curriculum

From Shree Mahavir Publications:

Vyavsayik Arthshasttra, Part – I, by M D Aggarwal

Vyavsayik Vatavaran Avem Udhiamitta by Gupta & Chaturvedi

Vyavasayik Prabandh, Neeti shastra Avem Sanchar, by Sharma & Chaturvedi,

Vyavasayik Arthashasttra Part – II, by S C Sharma,

Lekhankan Ke Mool tatv Avem Ankenshan, by P C Gupta & C L Chaturvedi

Aarthik Avem Samanaye Vidhi, by Jain & Gupta

Prabhandh Lekhanken by M D Aggarwal & N P Aggarwal

Lagat Lekhanken by S N Maheshwari & S N Mittal

Cost Accounting – Theory & Problems by Maheshwari SN & Mittal SN

Cost Accounting & Financial Management, by S N Maheshwari & S N Mittal

Audhyogik, Shram Avem Samanye Vidhi by Jain & Gupta

Pratibhouti Sanniyam Avem Anupalan, by Jain & Gupta

Adhunik Bhartiya Company Adhiniyam by M C Kuchhal

Adhunik Bhartiya Company Law by M C Kuchhal

From Taxmann Publications:

Vyaparik Evam Samanya Vidhi by Shubham Aggarwal

Bharat Law House:

Systematic Approach to Taxation Containing Income Tax & Indirect Taxes by Dr. Girish Ahuja & Dr Ravi Gupta

Eastern Book Company:

Adminstrative Law (Prashasanik Vidhi) by C K Tekwani

Consumer Protection Law (Upbhokta Sanrakshan Vidhi) by S P Gupta

Company Law (Company Vidhi) by Avtar Singh

Constitution of India (Bharat KaSamvidhan) by EBC

Art of Conveyancing and Pleading (Abhivachonon ke Prarooparn aur Abhihastaantarn - lekhan ki kala) by Murli Manohar

Systematic Approach to Income Tax, Service Tax & VAT (Hindi Edn.) by Dr. Girish Ahuja

***

e- bulletin 12 November 2016

Attention Students

Applicability of the Finance Act for December 2016 Examinations

Students appearing in the following Papers in December 2016 Examinations

Executive Programme

(i) Tax Laws and Practice (Module-1, Paper-4)

Professional Programme

(ii) Advanced Tax Laws and Practice (Module-3, Paper-7)

May note as follows:

1. For Direct taxes, Finance Act, 2015 is applicable.

2. Applicable Assessment Year is 2016-17 (Previous Year 2015-16).

3. Since, Wealth Tax Act, 1957 has been abolished w.e.f. 1st April, 2016. The questions from the same will not be asked in examination from December, 2015 session onwards.

4. For Indirect Taxes, all changes made by the Finance Act, 2016 are also applicable.

5. Students are also required to update themselves on all the relevant Notifications, Circulars, Clarifications, etc. issued by the CBDT, CBEC & Central Government, on or before six months prior to the date of December, 2016 Examination.

Supplements covering major Amendments, Notifications, Circulars etc. relevant for December, 2016 Examination has been uploaded under the ‘Academic Corner’ of the Institute’s website : https://www.icsi.edu/GuidanceforDec2016Exam.aspx

Director PD, PP & Studies

e-bulletin 13 November 2016

Legal World

CORPORATE LAWS

Landmark Judgement

SINGER INDIA LTD v. CHANDER MOHAN CHADHA & ORS [SC]

Civil Appeals No. 387 & 388 of 2004

R.C. Lahoti, G. P. Mathur & C. K. Thakker, JJ. [Decided on 13/08.2004]

Equivalent citations: (2004) 122 Comp Cas 468(SC); (2004) 62 CLA 213 (SC); AIR 2004 SC 4368.

Companies Act, 1956 read with Delhi Rent Control Act- shop let out to American company- the company merged with Indian company- landlord initiated eviction proceedings on the ground of sub-letting- contested that the transfer was due to merger which is by operation of law- whether tenable-Held, No.

Brief facts: Respondent landlord let out one Shop to M/s. Singer Sewing Machine Company, incorporated under the laws of the State of New Jersey, USA, (hereinafter referred to as 'American Company'), vide a registered lease deed dated 11.7.1966. In the year 1982, the landlord filed an eviction petition on the ground, inter alia, that the American Company, without obtaining any written consent from the landlord, had parted with the possession of the premises in dispute in favour of Indian Sewing Machine Company Limited, and it was the said company which was in exclusive possession of the premises and thereby it was liable for eviction in view of Section 14(1)(b) of the Delhi Rent Control Act (hereinafter referred to as the 'Act').

The eviction petition was contested by the appellant on the ground, inter alia, that a direction was issued to the American Company to reduce its share capital to 40 per cent in order to carry on business in India in view of Section 29 of Foreign Exchange Regulation Act, 1973 (hereinafter referred to as 'FERA'). Accordingly, Company Petition was filed by the Indian Company before the Bombay High Court under which a scheme of amalgamation was sanctioned whereby the undertaking in India of the American Company was amalgamated with the Indian Company. It was submitted that the Indian Company is no other entity except the legal substitute of the American Company and in substance there is no case of sub-tenancy.

The Additional Rent Controller, Delhi dismissed the eviction petition, but this was reversed by the Rent Control Tribunal in the appeal preferred by the landlord and eviction petition was allowed. The Second Appeal preferred by the appellant was dismissed by the High Court. During the pendency of the appeal before the Rent Control Tribunal, the name of M/s. Indian Sewing Machine Company was changed as Singer India Limited which is the appellant herein.

Decision: Appeal dismissed.

Reason:The effect of parting of possession of the tenanted premises as a result of sanction of scheme of amalgamation of companies under Section 394 of the Companies Act by the High Court has also been considered in two decisions of this Court. In M/s. General Radio and Appliances Co. Ltd and others v. M.A. Khader 1986 (2) SCC 656, which is a decision by a bench of three learned Judges, the premises had been let out to M/s. General Radio and Appliances Co. Ltd. On account of a scheme of amalgamation sanctioned by the High Court, all property, rights and powers of every description

e-bulletin 14 November 2016

including tenancy right, held by M/s. General Radio and Appliances Co. Ltd. had been blended with M/s. National Ekco Radio & Engineering Co. Ltd. Thereafter the landlord instituted proceedings for eviction on the ground of unauthorized sub-letting. It was held that the order of amalgamation was made by the High Court on the basis of the petition filed by the Transferor Company in the Company Petition and, therefore, it cannot be said that this is an involuntary transfer effected by the order of the Court. It was further held that appellant No. 1 Company was no longer in existence in the eyes of law and it had effaced itself for all practical purposes. The appellant No. 2 Company i.e., the Transferee Company, was not a tenant in respect of the suit premises and it was appellant No. 1 Company which had transferred possession of the suit premises in favour of the appellant No. 2 Company. The Court further took the view that under the relevant Act, there was no express provision that in case of any involuntary transfer or transfer of the tenancy right by virtue of a scheme of amalgamation sanctioned by the High Court, such a transfer will not come within the purview of Section 10(ii) (a) of Andhra Pradesh Building (Lease, Rent and Eviction) Control Act. On this finding, it was held that the appellant was liable for eviction.

Cox & Kings Ltd. & Anr v. Chander Malhotra 1997 (2) SCC 687 is also a decision by a bench of three learned Judges and arose out of proceedings for eviction under Section 14(1)(b) of Delhi Rent Control Act. Here, the premises were given on lease to Cox & Kings (AGENTS) Limited, a company incorporated under the United Kingdom Companies Act (for short, "Foreign Company"). A petition for eviction was filed on several grounds and one of the grounds was of sub-letting to Cox & Kings Limited, a company registered under the Indian Companies Act (for short an "Indian Company"). It was urged that the transfer of leasehold interest from the Foreign Company to the Indian Company was by compulsion, it was an involuntary one and, therefore, it was not a case of sub-letting within the meaning of Section 14(1) (b) of the Act. It was held that under FERA, there was no compulsion that the premises demised to the Foreign Company should be continued or given to the Indian Company. On the other hand, under the agreement executed between the Foreign Company and the Indian Company, incidental to the assignment of the business as a growing concern, the Foreign Company also assigned the monthly and other tenancies and all rented premises of the assignor in India to the Indian Company. The Court, accordingly, concluded that though by operation of FERA the Foreign Company had wound up its business, but under the agreement it had assigned the leasehold interest in the demised premises to the Indian Company which was carrying on the same business in the tenanted premises without obtaining the written consent of the landlord and, therefore, it was a clear case of sub-letting.

These cases clearly hold that even if there is an order of a Court sanctioning the scheme of amalgamation under the Companies Act where under the leases, rights of tenancy or occupancy of the Transferor Company get vested in and become the property of the Transferee Company, it would make no difference in so far as the applicability of Section 14(1)(b) is concerned, as the Act does not make any exception in favour of a lessee who may have adopted such a course of action in order to secure compliance of law.

It was next contended that on amalgamation Singer Sewing Machine Company (American Company) merged into Indian Sewing Machine Company (Indian Company) shedding its corporate shell, but for all practical purposes remained alive and thriving as part of the larger whole. He has submitted that this Court should lift the corporate veil and see who are the directors and shareholders of the Transferee Company and who are in real control of the affairs of the said company and if it is done it will be evident there has been no sub-letting or parting with possession by the American Company.

e-bulletin 15 November 2016

It is not open to the Company to ask for unveiling its own cloak and examine as to who are the directors and shareholders and who are in reality controlling the affairs of the Company. This is not the case of the appellant nor could it possibly be that the corporate character is employed for the purpose of committing illegality or defrauding others. It is not open to the appellant to contend that for the purpose of FERA, the American Company has effaced itself and has ceased to exist but for the purpose of Delhi Rent Control Act, it is still in existence. Therefore, it is not possible to hold that it is the American Company which is still in existence and is in possession of the premises in question. On the contrary, the inescapable conclusion is that it is the Indian Company which is in occupation and is carrying on business in the premises in question rendering the appellant liable for eviction.

TAX LAWS

LARSEN & TOUBRO LIMITED v. ADDITIONAL DY.COMMISSIONER OF COMMERCIAL TAXES & ANR [SC]

Civil Appeal No. 2956 of 2007 with Civil Appeal No. 2318 of 2013 and Civil Appeal No. 7241 OF 2016

A.K. Sikri & Rohinton Fali Nariman, JJ. [Decided on 05/09/2016]

Karnataka Sales Tax Act, 1957 – works contract- turnover tax- assesse sub-contracted works to subcontractor- value of sub-contracted works included in the total turnover of the assesse for turnover tax purposes- whether tenable- Held, No.

Brief facts: Same parties are entangled in these three appeals which arise out of the provisions of the Karnataka Sales Tax Act, 1957 (hereinafter referred to as the 'Karnataka Act'). Two appeals are preferred by the assessee, viz. Larsen & Toubro Ltd., and one appeal is filed by the Revenue, i.e. the Sales Tax Department of Karnataka.

The assessee sub-contracted works contract and the tax on the same was paid by the sub-contractor. The Department imposed turnover tax on the assesse including the value of the works contract sub-contracted. The contention of the assesse was that value of the contract given to sub-contractors should not be taxed again by including the same in the total turnover for the purpose of turnover tax.

Decision: Assessee’s appeal allowed; Revenue’s appeal dismissed.

Reason: The appellant/assessee, made a fervent plea for not including such payments made to the sub-contractor, as component of total turnover, because of the reason that the sales tax is payable on the transfer of property and the 'turnover' also meant aggregate amount for which goods are bought or sold, etc. Therefore, transfer of property in goods was the necessary concomitant in ascertaining the sale and, thus, in the process calculating the turnover/total turnover. It was submitted that there was no sale of goods involved in the execution of a works contract as in such contracts the property does not pass as movables. Tracing the history of works contract, the learned senior counsel submitted that in the case of The State of Madras v. Gannon Dunkerley & Co. (Madras) Limited AIR 1958 SC 560, while speaking of a building contract, this Court held that the property in goods involved in the execution of a works contract does not pass as movables but on the theory of accretion on the principle quicquid plantatur solo, solo cedit, i.e. whatever is attached to the soil, becomes part of it. He argued that this Court, in Builders' Association of India & Ors. v. Union of India & Ors (1989) 2 SCC 645, reiterated that in a works contract property in goods passes out as movable but on the theory of accretion. It was further submitted that the property passes by accession just once which, by a fiction, is taxed as a sale. The Article also identifies the transferor and transferee effecting the deemed sale and deemed purchase. The taxable person is the contractor executing the works contract so that the

e-bulletin 16 November 2016

main contractor, who assigns the work to another person to execute the work, cannot be a transferor, nor any property in goods vest in the main contractor, when the contract is executed by a sub-contractor.

Proceeding further, by taking the aforesaid line of argument, the learned senior counsel submitted that if the point of view of the Revenue is accepted, it would amount to double taxation inasmuch as sub-contractors were also registered dealers who had paid sales tax under the Karnataka Act and by including the payments made to them in the total turnover of the assessee, tax was sought to be levied on the same amount all over again. On the aforesaid premise, the learned senior counsel for the assessee submitted that precisely this argument in law has been accepted by this Court in the Andhra Pradesh judgment. He referred to the discussion contained in the said judgment in extenso.

The Revenue, per contra, heavily relied upon the reasoning given by the High Court in the judgment which has taken the view in favour of the Revenue. He submitted that one had to keep in mind the distinction between Section 5-B and Section 6-B of the Karnataka Act by pointing out that when it comes to levy of turnover tax, it speaks of 'total turnover', whereas tax payable under Section 5-B is on the 'taxable turnover'. He submitted that since we are concerned with the levy of tax under Section 6-B of the Karnataka Act, total turnover becomes relevant and, therefore, the value of the work entrusted to the sub-contractors is includible at the hands of the assessee. He further submitted that the High Court was right in pointing out that sales tax is leviable at a single point, whereas turnover tax is leviable at a multi-point, both at the hands of the main contractor and sub- contractor and, therefore, the question of double taxation does not arise.

After bestowing our due consideration to the respective submissions, we find that the position taken by the assessee has to prevail, which appears to be meritorious. This result follows even from the bare perusal of the Karnataka Act and Rules.

The question which is raised before us is whether the turnover of the sub-contractors (whose names are also given in the original writ petition) is to be added to the turnover of L&T. In other words, the question which we are required to answer is whether the goods employed by the sub- contractors occur in the form of a single deemed sale or multiple deemed sales. In our view, the principle of law in this regard is clarified by this Court in Builders' Assn. of India as under: (SCC p. 673, para 36)

“36 … Ordinarily unless there is a contract to the contrary in the case of a works contract, the property in the goods used in the construction of a building passes to the owner of the land on which the building is constructed, when the goods or materials used are incorporated in the building.” (emphasis supplied by us)

As stated above, according to the Department, there are two deemed sales, one from the main contractor to the contractee and the other from sub-contractor(s) to the main contractor, in the event of the contractee not having any privity of contract with the sub-contractor(s).

If one keeps in mind the above quoted observation of this Court in Builders' Assn. of India the position becomes clear, namely, that even if there is no privity of contract between the contractee and the sub- contractor, that would not do away with the principle of transfer of property by the sub-contractor by employing the same on the property belonging to the contractee. This reasoning is based on the principle of accretion of property in goods. It is subject to the contract to the contrary. Thus, in our view, in such a case, the work executed by a sub-contractor, results in a single transaction and not as multiple transactions. This reasoning is also borne out by Section 4(7) which refers to the value of goods at the time of incorporation in the works executed.

e-bulletin 17 November 2016

In our view, if the argument of the Department is to be accepted, it would result in plurality of deemed sales which would be contrary to Article 366(29-A) (b) of the Constitution as held by the impugned judgment of the High Court. Moreover, it may result in double taxation which may make the said 2005 Act vulnerable to challenge as violative of Articles 14, 19(1) (g) and 265 of the Constitution of India as held by the High Court in its impugned judgment.”

This raison d'etre shall apply, in full force, while answering the question even in the context of the Karnataka Act.

We, therefore, hold that the value of the work entrusted to the sub- contractors or payments made to them shall not be taken into consideration while computing total turnover for the purposes of Section 6-B of the Karnataka Act. As a consequence, the two appeals which are filed by the assessee are allowed and the appeal preferred by the Revenue is dismissed.

NIMESH N. KAMPANI v. ASST. CIT, CIRCLE-4(2) MUMBAI [ITAT-MUM]

I.T.A. No. 3316/Mum/2013

R. C. Sharma & Pawan Singh. [Decided on 16/06/2016]

Income tax Act- allowable expenditure- professional independent director- incurred legal expenditure in defending cases- whether allowable as business expenditure- Held, Yes.

Brief facts: The assessee debited an amount of Rs.55,65,938/- under the head "legal fees and related expenses". In respect of this expenditure, the assessee explained to the Assessing Officer that the assessee was Director on Board of many companies including on the Board of M/s. Nagarjuna Finance Ltd. This company M/s. Nagarjuna Finance Ltd. received fixed deposit from the public. This company was charged with default in repayment of fixed deposits and interest thereon. The assessee had been mentioned as one of the accused among several others for non-payment of these fixed deposits by M/s. Nagarjuna Finance Ltd. The Andra Pradesh Government had filed suit against directors of M/s. Nagarjuna Finance Ltd. including against the assessee. To defend himself, the assessee had appointed various advocates to represent his case before various courts viz., District Court, High Court, Supreme Court. The appellant paid fees to the advocates and other expenses incurred. The details of such expenses were furnished by the assessee to the Assessing Officer. The assessee argued before the Assessing Officer that the expenditure was incurred to protect his business interest and, therefore, the same should be fully allowable u/s.37 (1) of the Act. As per A.O. the expenditure were personal in nature, he therefore disallowed the same. By the impugned order, the ld. CIT (A) confirmed the action of the A.O. against which the assessee is in further appeal before us.

Decision: Appeal allowed.

Reason: We have considered the rival contentions and found from the record that the assessee is merchant broker. During the year net profit of Rs.15.50 crores was offered to tax. Against of the income so offered the assessee has claimed legal fees and related expenditure of Rs.55,65,938/-, which was disallowed by the A.O. on the plea of personal expenses. From the record we found that that the expenditure is incurred by the assessee in his character as a professional and is not an expenditure which is personal in nature. The assessee has in his professional capacity been a director of various limited companies has earned professional fees for the services rendered to these companies. He was a director of Nagarjuna Finance Limited (NFL) from 14-12-1982 to 28-04-1999. The assessee has earned professional income during all the years, he was, a director of NFL.

The assessee serves as an Independent Director on the Board of several leading Indian Companies such as Apollo Tyres Limited, Britannia Industries Limited, Deepak Nitrite Limited and KSB Pumps

e-bulletin 18 November 2016

Limited and also a member of various Governing Boards of Centre for Policy Research, Indian Institute of Capital Markets, CII, SEBI etc. He regularly gets sitting fees and commission from many of these Companies. The assessee was also an independent Director on the board of Nagarjuna Finance Limited. Nagarjuna Finance Limited had collected Fixed Deposits from the public. Nagarjuna Finance Limited was charged with default in repayment of fixed deposits and interest thereon. Mr. Nimesh Kampani has been mentioned as one of the accused among several others, for non-payment of these fixed deposits by Nagarjuna Finance Limited. The Andhra Pradesh Government had since filed suit against directors of Nagarjuna Finance Limited including Mr. Kampani. To defend himself, Mr. Kampani has appointed various advocates to represent his case before various courts viz, District Court, High Court of Andhra Pradesh, Supreme Court of India. As the expenditure is incurred to protect his business interest the same is required to be allowed u/s. 37(1) of the Act. Accordingly we direct the A.O. to allow legal expenses of Rs.40,72,750/-.

In the result, the assessee’s appeal is allowed in part.

GENERAL LAW

THE CHANCELLOR, MASTERS & SCHOLARS OF THE UNIVERSITY OF OXFORD & ORS v. RAMESHWARI PHOTOCOPY SERVICES & ANR [DEL]

CS (OS) 2439/2012

Rajiv Sahai Endlaw, J. [Decided on 16/09/2016]

Copyrights Act, - infringement of copy right- photocopying of portions of book for preparation of its course material by university- allowing photocopying the same in mass scale to distribute the same to students through contractor- whether results in infringement of copyright- Held, No.

Brief facts: The five plaintiffs, namely i) Oxford University Press, ii) Cambridge University Press, United Kingdom (UK), iii) Cambridge University Press India Pvt. Ltd., iv) Taylor & Francis Group, U.K. and, v) Taylor & Francis Books India Pvt. Ltd., being the publishers, including of textbooks, instituted this suit for the relief of permanent injunction restraining the two defendants namely Rameshwari Photocopy Service (carrying on business from Delhi School of Economic (DSE), University of Delhi) and the University of Delhi from infringing the copyright of the plaintiffs in their publications by photocopying, reproduction and distribution of copies of plaintiffs' publications on a large scale and circulating the same and by sale of unauthorised compilations of substantial extracts from the plaintiffs' publications by compiling them into course packs / anthologies for sale.

The plaintiffs, in the plaint, have given particulars of at least four course packs being so sold containing photocopies of portions of plaintiffs' publication varying from 6 to 65 pages. It is further the case of the plaintiffs that the said course packs sold by the defendant No.1 are based on syllabi issued by the defendant No.2 University for its students and that the faculty teaching at the defendant No.2 University is directly encouraging and recommending the students to purchase these course packs instead of legitimate copies of plaintiffs' publications. It is yet further the case of the plaintiffs that the libraries of the defendant No.2 University are issuing books published by the plaintiffs stocked in the said libraries to the defendant No.1 for photocopying to prepare the said course packs.

Decision: Suit dismissed.

Reason: Applying the tests as aforesaid laid down by the Courts of (i) integral part of continuous flow; (ii) connected relation; (iii) incidental; (iv) causal relationship; (v) during (in the course of time, as time goes by); (vi) while doing; (vii) continuous progress from one point to the next in time and

e-bulletin 19 November 2016

space; and, (viii) in the path in which anything moves, it has to be held that the words “in the course of instruction” within the meaning of Section 52(1)(i) supra would include reproduction of any work while the process of imparting instruction by the teacher and receiving instruction by the pupil continues i.e. during the entire academic session for which the pupil is under the tutelage of the teacher and that imparting and receiving of instruction is not limited to personal interface between teacher and pupil but is a process commencing from the teacher readying herself/himself for imparting instruction, setting syllabus, prescribing text books, readings and ensuring, whether by interface in classroom/tutorials or otherwise by holding tests from time to time or clarifying doubts of students, that the pupil stands instructed in what he/she has approached the teacher to learn. Similarly the words “in the course of instruction”, even if the word “instruction” have to be given the same meaning as “lecture”, have to include within their ambit the prescription of syllabus the preparation of which both the teacher and the pupil are required to do before the lecture and the studies which the pupils are to do post lecture and so that the teachers can reproduce the work as part of the question and the pupils can answer the questions by reproducing the work, in an examination. Resultantly, reproduction of any copyrighted work by the teacher for the purpose of imparting instruction to the pupil as prescribed in the syllabus during the academic year would be within the meaning of Section 52 (1)(i) of the Act.

The matter can be looked at from another angle as well. Though I have held Section 52(1)(a)to be not applicable to the action of the defendant no.2 University of making photocopies of copyrighted works but the issuance by the defendant no.2 University of the books purchased by it and kept in its library to the students and reproduction thereof by the students for the purposes of their private or personal use, whether by way of photocopying or by way of copying the same by way of hand would indeed make the action of the student a fair dealing therewith and not constitute infringement of copyright. The counsel for the plaintiffs also on enquiry did not argue so. I have wondered that if the action of each of the students of having the book issued from the library of defendant No.2 University and copying pages thereof, whether by hand or by photocopy, is not infringement, whether the action of the defendant no.2 University impugned in this suit, guided by the reason of limited number of each book available in its library, the limited number of days of the academic session, large number of students requiring the said book, the fear of the costly precious books being damaged on being subjected to repeated photocopying, can be said to be infringement; particularly when the result/effect of both actions is the same. The answer, according to me, has to be in the negative.

Copyright, especially in literary works, is thus not an inevitable, divine, or natural right that confers on authors the absolute ownership of their creations. It is designed rather to stimulate activity and progress in the arts for the intellectual enrichment of the public. Copyright is intended to increase and not to impede the harvest of knowledge. It is intended to motivate the creative activity of authors and inventors in order to benefit the public. For this reason only, Section 14(a)(ii) as aforesaid, applies the principle of “exhaustion” to literary works and which, this court in Warner Bros. Entertainment Inc. Vs. Mr. Santosh V.G. MANU/DE/0406/2009 has held, to be not applicable to copyright in an artistic work or in a sound recording or in a cinematographic film. Once it is found that the doctrine of exhaustion applies to literary work as the works with which we are concerned are, it has but to be held that it is permissible for the defendant No.2 University to on purchasing book(s) and stocking the same in its library, issue the same to different students each day or even several times in a day. It is not the case of the plaintiffs that the said students once have so got the books issued would not be entitled to, instead of laboriously copying the contents of the book or taking notes therefrom, photocopy the relevant pages thereof, so that they do not need the book again.

e-bulletin 20 November 2016

I thus conclude that the action of the defendant no.2 University of making a master photocopy of the relevant portions (prescribed in syllabus) of the books of the plaintiffs purchased by the defendant no.2 University and kept in its library and making further photocopies out of the said master copy and distributing the same to the students does not constitute infringement of copyright in the said books under the Copyright Act.

The next question is, whether the action of the defendant no.2 University of supplying the master copy to the defendant no.1, granting licence to the defendant no.1 to install photocopiers in the premises of the defendant no.2 University, allowing the defendant no.1 to supply photocopies made of the said master copy to the students, permitting the defendant no.1 to charge therefor and also requiring the defendant no.1 to photocopy up to 3000 pages per month free of cost for the defendant no.2 University and whether the action of the defendant no.1 of preparation of such course packs and supplying the same to the students for charge, constitutes ‗publication' within the meaning of Section 52(1)(h) or would tantamount to infringement by the defendant no.1 or the defendant no.2 University of the copyright of in the said books. In my opinion, it would not.

***

e-bulletin 21 November 2016

Student-ICSI Academic CONNECT Students may clarify their subject specific academic queries related to study material between 2.00 p.m. to 3.00 p.m. on all working days (Monday- Friday) at 011-45341074.

Students may also write their academic queries on [email protected]

Dear Students,

We are pleased to share that with a view to update the students on important developments

on daily basis, the Institute has initiated ‘News Headlines‘ on the Academic corner of the

Institute’s website www.icsi.edu.

Students are requested to take advantage of this new initiative.

Our best wishes for all your endeavors.

Team ICSI

, ह ह

( ह २.०० ३.०० ) . 011-45341074 ह ई-

e-bulletin 22 November 2016

Student Services

The details of National Level Competitions for the students for the year 2016 are as follows:

S.No Activities Scheduled Date Host Winners

1 All India Elocution

Competition 8th July 2016 NIRO

Ms. Mega Balyan (440205129/08/2014)- AHMEDABAD (WIRC)

2 All India Company

Law Quiz 15th July 2016 EIRO

Mr. Chirag Kular (440128509/02/2014 )-RAJKOT (WIRC)

Mr. Kamil Lakhani (440170151/05/2014 )-RAJKOT (WIRC)

3 All India Moot

Court Competition 30th July 2016 PUNE Chapter

Ms. Nikita Nagori (140081380/02/2014)-BANGALORE (SIRC)

Ms. Ramya C (340141893/02/2015)-BANGALORE (SIRC)

4 All India Essay

Writing Competition

26th July 2016 EIRO Mr. Anish Shankar Menon (320557992/01/2010)- BANGALORE (SIRC)

e-bulletin 23 November 2016

e-bulletin 24 November 2016

The Institute has initiated various steps to provide instantaneous services to its stakeholders by the use of technology. More and more services are being added in this march for automation. The study material is now fully available to one and all through the online portal. Some of services and their uses which are important for awareness are listed:

CALL CENTRE

The Institute has established a dedicated call centre with Phone Nos. 011-33132333, 011-66204999. The Call Centre provides for Interactive Voice Response as well as a Ticketing Mechanism.

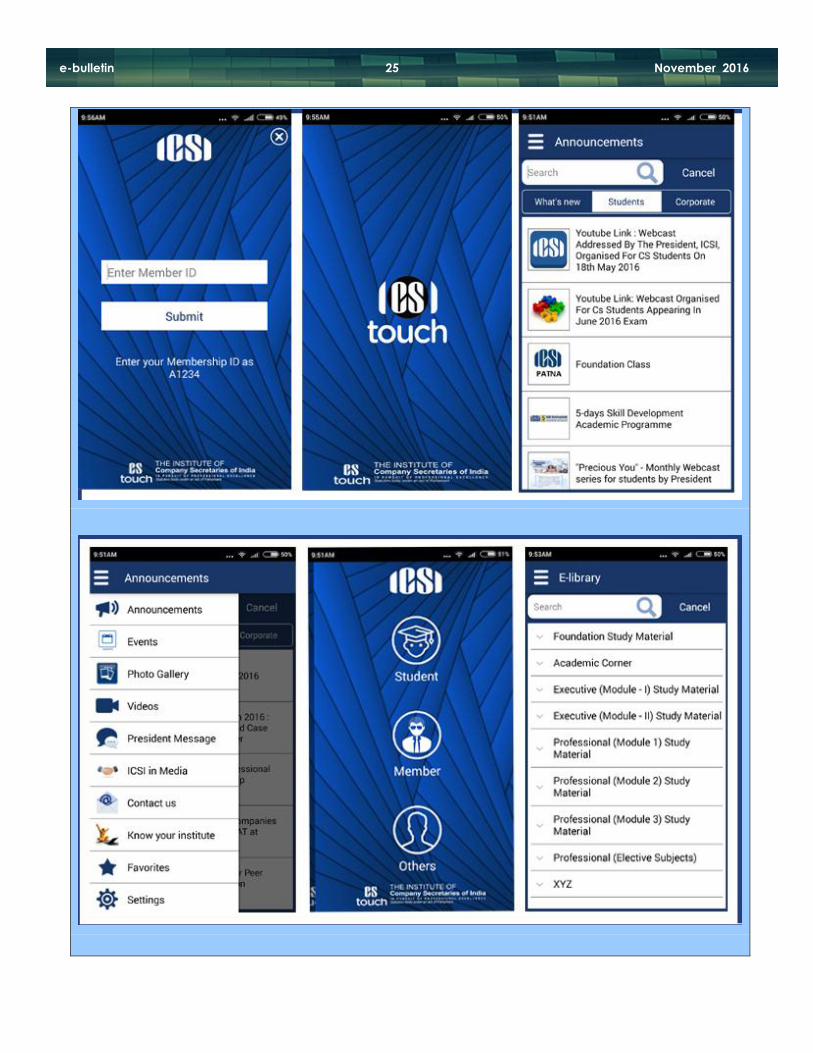

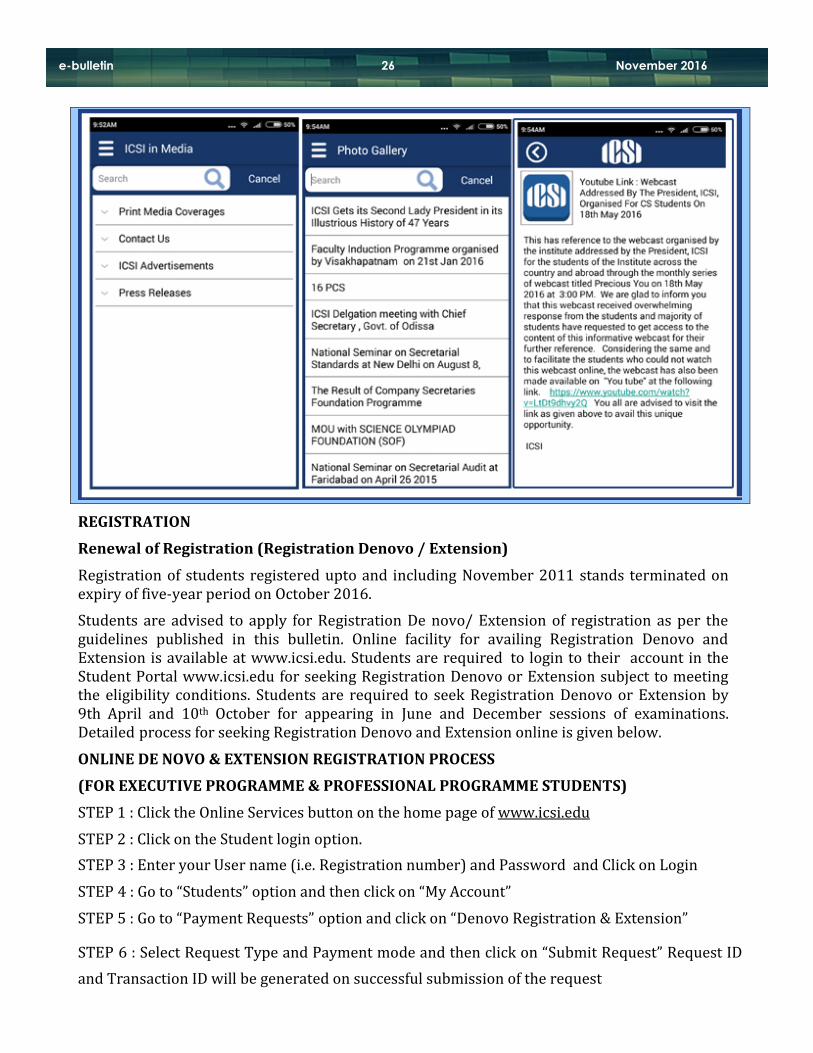

CS TOUCH - ANDROID BASED MOBILE APPLICATION

The Institute of Company Secretaries of India has launched ‘CS touch’ an android a n d I O S based mobile application for students and members recently. CS touch is an android and I O S based mobile application for web based content Management system. The application features are Splash screen, home screen, top menu screen. Following categories will be available to end users in times to come like Announcements, Events, Photo Gallery, Videos, President message, ICSI in media, Contact us, Know your Institute, Favourite, Setting and Info among others. CS touch is available in Google play store. You can download the same from Google play store.

e-bulletin 25 November 2016

e-bulletin 26 November 2016

REGISTRATION

Renewal of Registration (Registration Denovo / Extension)

Registration of students registered upto and including November 2011 stands terminated on expiry of five-year period on October 2016.

Students are advised to apply for Registration De novo/ Extension of registration as per the guidelines published in this bulletin. Online facility for availing Registration Denovo and Extension is available at www.icsi.edu. Students are required to login to their account in the Student Portal www.icsi.edu for seeking Registration Denovo or Extension subject to meeting the eligibility conditions. Students are required to seek Registration Denovo or Extension by 9th April and 10th October for appearing in June and December sessions of examinations. Detailed process for seeking Registration Denovo and Extension online is given below.

ONLINE DE NOVO & EXTENSION REGISTRATION PROCESS

(FOR EXECUTIVE PROGRAMME & PROFESSIONAL PROGRAMME STUDENTS)

STEP 1 : Click the Online Services button on the home page of www.icsi.edu

STEP 2 : Click on the Student login option.

STEP 3 : Enter your User name (i.e. Registration number) and Password and Click on Login

STEP 4 : Go to “Students” option and then click on “My Account”

STEP 5 : Go to “Payment Requests” option and click on “Denovo Registration & Extension”

STEP 6 : Select Request Type and Payment mode and then click on “Submit Request” Request ID

and Transaction ID will be generated on successful submission of the request

e-bulletin 27 November 2016

STEP 7 : Proceed for payment through Credit Card / Debit Card / Net Banking/Challan.

For all successful payments an acknowledgement receipt is generated and an intimation will be sent on the respective email ID. In case acknowledgement is not generated due to any reason, follow the procedure as given below:

Click Student-> select My Account

Click payment request->Generate payment Receipt

Write Request id and Transaction id and click on check status.

STEP 8 : Please download the de novo registration Letter from Section “Letter for student” in “other” option

STEP 9 : In case of unsuccessful payment please resubmit your request

REGULARISATION OF EXECUTIVE PROGRAMME ADMISSION

Students provisionally admitted to the Executive Programme are advised to upload the scanned copies of their graduation Pass Certificates or marksheets for regularizing their admission at their online account at www.icsi.edu. They are required to login at their account to upload the desired marks sheets/certificates at manage account option. Subsequently they are required to go to qualification tab option to upload their graduation pass marksheet/certificate. Students, who have already uploaded / submitted their graduation pass certificate/Marksheet and have not received any confirmation with regard to approval of their admission, must contact the Institute immediately either through online grievance Redressal module or ticketing Mechanism of the Institute quoting the following particulars through online grievance redressal module:

Name

Details of Fee paid

Admission No.

Email Address

Complete Postal Address with Pin code

CANCELLATION OF PROVISIONAL ADMISSION

Provisional admission of the students, who fail to submit/upload the requisite proof of having passed the graduation examinations within the stipulated time period of six months shall stand cancelled and no refund of fee will be made. It is informed further that the students registered provisionally in Executive stage and have not submitted their graduation pass certificate or marksheet, will not be allowed to appear in December 2016 examination.

Change of Address/Resetting Password

Students are advised to update their addresses instantly through online services option at www.icsi.edu. Their Registration Number shall be their user Id itself. Students can also reset their password anytime (The new password will be displayed on the screen). The process is given

e-bulletin 28 November 2016

below:

Your registration number in Username

1) Visit Institute’s website www.icsi.edu

2) Click on ON-LINE SERVICES (top right side of your screen)

3) Click on Student Login

4) Type your registration number in Username

5) Click on Reset password (students only)

6) Enter your all details (i.e. Your Programme, Registration Number, Gender, DOB, Pin Code etc.)

7) Click on Proceed.

8) Enter your correct e-mail id & mobile number

9) Click on Reset Password and Get the password on screen.

Note: Students who have registered from 15th June 2016 onwards in Foundation stage and 23rd September 2016 onwards in CS Executive stage may kindly follow the process given at the link for change of communication.

https://www.icsi.in/Student/Portals/0/Sitemap/UserManuals/SMASH_Registration_Edit_Change_AddressCommunication_Detail_Manual.pdf

Updation of E-Mail Address/ Mobile

Students are advised to update their E-Mail Id and Mobile Numbers timely so that important communications are not missed as the same are sent through bulk mail/SMS nowadays. Students may update their E-mail Id/ Mobile Number instantly after logging into their account at www.icsi.edu at request option.

Student Identity Card Identity Card can be downloaded after logging into the Student Portal at www.icsi.edu. After downloading the Identity card, students are compulsorily required to get it attested by any of the following authorities with his/her seal carrying name, professional membership No., designation and complete official address:

1. Member of the Institute, with ACS/FCS No.

2. Gazetted Officer of the Central or State Government.

3. Manager of a Nationalised Bank.

4. Principal of a recognized School/College.

5. Officer of ICSI

Unattested Identity Cards are not valid and the students are advised to carry duly attested

e-bulletin 29 November 2016

Identity Card for various services during their visits to the offices of the Institute, Examination Centres, etc.

Registration to Professional Programme

Students who have passed/completed both modules of Executive examination are advised to seek registration to Professional Programme through online mode. The prescribed fee is Rs.12,000/-.Eligibility of students registered to professional programme for appearing in the Examinations shall be as under: -

Students Registered During Will be eligible for appearing in

1st December, 2015 to 29th February, 2016 All Modules in December 2016 Session

1st March, 2016 to 31st May, 2016 Any One Module in December 2016 Session

1st June, 2016 to 31st August, 2016 All Modules in June 2017 Session

1st September, 2016 to 30th November, 2016 Any One Module in June 2017 Session

While registering for Professional Programme, students are required to submit their option for the Elective Subject under Module 3 as per details given below:-

Electives subject 1 out of below 5 subjects

1. Banking Law and Practice

2. Capital, Commodity and Money Market

3. Insurance Law and Practice

4. Intellectual Property Rights - Law and Practice

5. International Business-Laws and Practices

Notwithstanding the original option of Elective Subject, students may change their option of Elective Subject at the time of seeking enrolment to the Examinations. There will be no fee for changing their option for elective subject, but the study material if needed will have to be purchased by them against requisite payment. Soft copies of the study materials are available on the website of the Institute.

Clarification Regarding Paper wise Exemption

(a) Paperwise exemption is granted only on the basis of specific request received online through website www.icsi.edu from a registered student and complying all the requirements. There is one time payment of Rs. 1000/- (per subject).

(b) Students are required to apply for paper wise exemption on-line by logging into their

account on www.icsi.edu before 9th April for June session of examinations and before

10th October for December session of examinations. (c) The paperwise exemption once granted holds good during the validity period of

registration or passing/completing the examination, whichever is earlier. (d) Paper-wise exemptions based on scoring 60% marks in the examinations are being

granted to the students automatically and in case the students are not interested in availing the exemption they may seek cancellation of the same by sending a formal request at [email protected]. If any student appears in the examinations disregarding the exemption granted on the basis of 60% marks and shown in the Admit Card, the appearance will be treated as valid and the exemption will be cancelled.

e-bulletin 30 November 2016

(e) It may be noted that candidates who apply for grant of paper wise exemption or seek cancellation of paper wise exemption already granted, must see and ensure that the exemption has been granted/cancelled accordingly. Candidates who would presume automatic grant or cancellation of paper wise exemption without obtaining written confirmation on time and absent themselves in any paper(s) of examination and/or appear in the exempted paper(s) would do so at their own risk and responsibility and the matter will be dealt with as per the above guidelines.

(f) Exemption once cancelled on request in writing shall not be granted again under any circumstances.

(g) Candidates who have passed either module of the Executive/Professional examination under the old syllabus shall be granted the paper wise exemption in the corresponding subject(s) on switchover to the new/latest syllabus.

(h) No exemption fee is payable for availing paper wise exemption on the basis of switchover or on the basis of securing 60% or more marks in previous sessions of examinations.

(i) Please check at https://www.icsi.edu/Docs/Website/Paperwise%20ExemptionforHigh Qual.pdf for exemptions granted on the basis of higher qualification of the student.

(j) Please check at http://www.icsi.edu/docs/website/faq_exemption.pdf for exemptions granted on the basis on 60% or aggregate of 60%

Important

Paper-wise Exemptions are available only on the basis of passing (i) ICAI (The Institute of Cost Accountants of India) Final Examinations (ii) LL.B. Examinations (with 50% marks) or (iii) Members of ICSA-UK in selected subjects of Executive Programme & Professional Programme and no other exemptions are admissible on the basis of any other higher qualifications.

Attention Students !!!

There is no provision for submitting the exemption at the time of submitting the examination form.

If you have already been granted the exemption,it is reflected in your online account under “Programme Info”, Examination Enrollment Status and Admit Card issued for examination through online mode.

It may be noted that in some cases, the exemptions granted in accordance with the various provisions contained under the regulations are inter-related with other exemptions granted and cancellation (or appearance) in any one of the papers may result in cancellation of exemptions in all the inter-related papers. For example, if a candidate has been granted paper-wise exemptions in three papers on the basis of scoring 60, 62, 58 & 10 Marks respectively in the four papers contained under Module-I of Executive Programme in previous session and in case he/she appears or cancels the exemption in any one out of the three exempted papers, all the three exemptions shall be cancelled since the exemption criteria in this case is applicable only if all the three papers are taken together. Candidates are, therefore, advised to be extremely careful while seeking cancellation or while appearing in the exempted papers, as the final result will be computed considering the actual marks scored on reappearance and/ or the deemed absence in the papers as the case may be. In other words, candidates appearing in the exempted papers

e-bulletin 31 November 2016

despite an endorsement to the effect in the Admit Card shall be doing so at their own risk and responsibility and the Institute may not be held responsible for any eventuality which may arise at a later date. In case of any doubt regarding the applicability of rules regarding the exemptions, it would be better if the candidates seek prior clarifications from the Institute by writing at [email protected] before appearing in the examination of exempted subjects or seeking cancellation of exemptions granted.

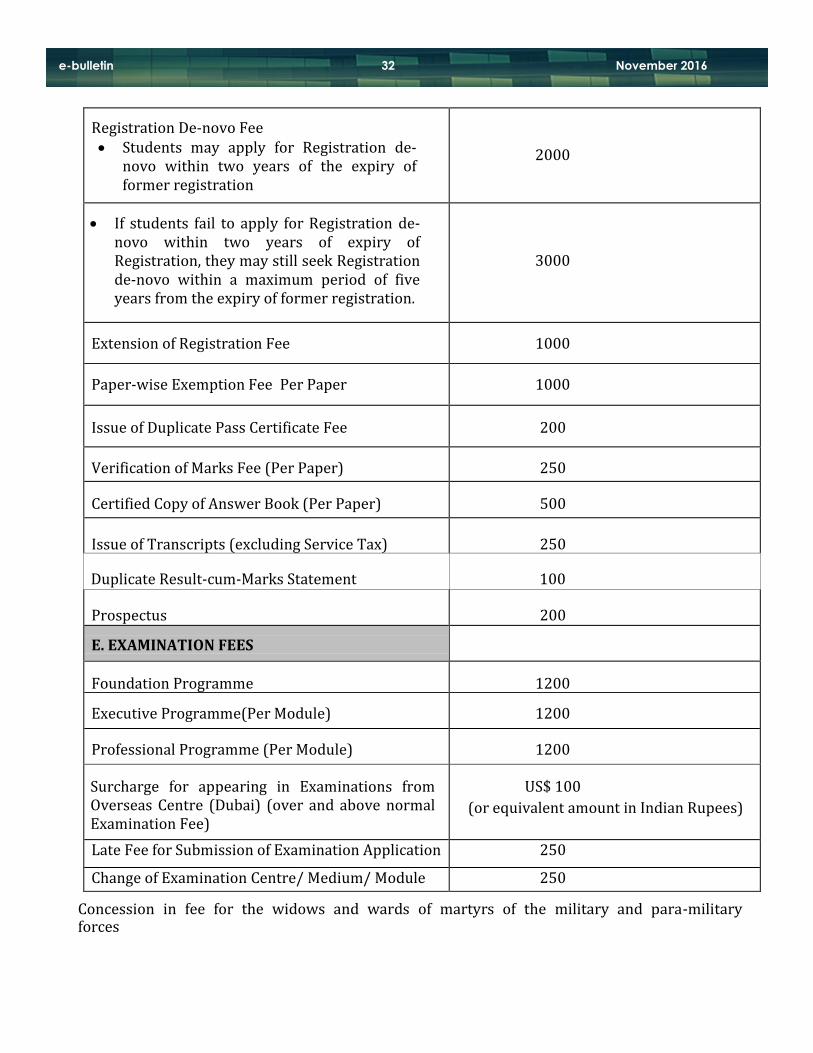

Schedule of Fees

A.) The details of fee applicable for availing various services are as under:-

PARTICULARS FEE (Rs.) A. FOUNDATION PROGRAMME

(i) Admission Fee 1500

(ii) Education Fee 3000

Total 4500

B. *EXECUTIVE PROGRAMME

(i) Foundation Examination Exemption Fee

500 (Commerce and non-commerce graduates) 4000 (ICAI-CPT/ICAI (Cost) Foundation Pass Students)

(ii) Registration Fee 2000

(iii) Education Fee for Executive Programme 6500

(iv) Education fee for Foundation Programme payable by non-commerce graduates who are seeking exemption from passing the Foundation Programme examination under clause (iii) of Regulation 38

1000

Total

8500 (CS Foundation Pass Students) 9000 (Commerce Graduates) 12500 ICAI-CPT/ICAI(Cost) Foundation Pass Students) 10000 (Other Graduates)

C. *PROFESSIONAL PROGRAMME

Education Fee

12000

D. OTHER FEES

e-bulletin 32 November 2016

Registration De-novo Fee Students may apply for Registration de-

novo within two years of the expiry of former registration

2000

If students fail to apply for Registration de-

novo within two years of expiry of Registration, they may still seek Registration de-novo within a maximum period of five years from the expiry of former registration.

3000

Extension of Registration Fee

1000

Paper-wise Exemption Fee Per Paper

1000

Issue of Duplicate Pass Certificate Fee

200

Verification of Marks Fee (Per Paper)

250

Certified Copy of Answer Book (Per Paper)

500

Issue of Transcripts (excluding Service Tax)

250

Duplicate Result-cum-Marks Statement

100

Prospectus

200

E. EXAMINATION FEES

Foundation Programme

1200

Executive Programme(Per Module)

1200

Professional Programme (Per Module)

1200

Surcharge for appearing in Examinations from Overseas Centre (Dubai) (over and above normal Examination Fee)

US$ 100

(or equivalent amount in Indian Rupees)

Late Fee for Submission of Examination Application 250

Change of Examination Centre/ Medium/ Module 250

Concession in fee for the widows and wards of martyrs of the military and para-military forces

e-bulletin 33 November 2016

Registration to Foundation Programme, Executive Programme & Professional Programme Stages

50% of the fee applicable to general category students

Examination Fee

50% of the fee applicable to general category students

Discontinuation of Public Private Partnership Scheme for Class Room Teaching

The Public Private Partnership Scheme for conducting Class Room Teaching has been discontinued and presently no Centres are authorized to conduct the classes under the Scheme. Students registering at these centres will be doing so at their own risk and responsibility. Students are advised to the approach the nearest Regional and Chapter Offices of the Institute for availing the Class Room Teaching facility.

Discontinuation of Requirement of Coaching Completion Certificate

The requirement of coaching completion certificate has been discontinued. This would make students eligible for enrolment to Executive / Professional Programme examinations after expiry of six months or nine months as the case may be, from the date of registration to the respective stage.

Henceforth, students of Executive Programme and Professional Programme are not required to:

a) submit response sheets to test papers on various subjects to the Institute under Postal Tuition Scheme, or

b) obtain coaching completion certificate from the Institute or from Class Room Teaching Centres of the Institute, or

c) submit coaching completion certificate for enrollment to examinations of Executive and Professional Programmes.

Simplified process for seeking Registration Denovo / Extension of registration

The process for seeking Registration Denovo and Extension of Registration has been simplified. For details, please follow the path given below :

ONLINE DE NOVO & EXTENSION REGISTRATION PROCESS

(FOR EXECUTIVE PROGRAMME & PROFESSIONAL PROGRAMME STUDENTS)

STEP 1 : Click the Online Services button on the home page of www.icsi.edu

STEP 2 : Click on the Student login option.

STEP 3 : Enter your User name (i.e. Registration number) and Password and Click on Login

STEP 4 : Go to “Students” option and then click on “My Account”

STEP 5 : Go to “Payment Requests” option and click on “Denovo Registration & Extension”

STEP 6 : Select Request Type and Payment mode and then click on “Submit Request” Request ID and Transaction ID will be generated on successful submission of the request

e-bulletin 34 November 2016

STEP 7 : Proceed for payment through Credit Card / Debit Card / Net Banking/Challan.

For all successful payments an acknowledgement receipt is generated and an intimation will be sent on the respective email ID. In case acknowledgement is not generated due to any reason, follow the procedure as given below:

Click Student-> select My Account

Click payment request->Generate payment Receipt

Write Request id and Transaction id and click on check status.

STEP 8 : Please download the de novo registration Letter from Section “Letter for student” in “other” option

STEP 9 : In case of unsuccessful payment please resubmit your request

Re-Registration to Professional Programme

The Institute has introduced a Re-registration Scheme, whereby students who have passed Intermediate Course/ Executive Programme under any old syllabus but not eligible for seeking Registration Denovo may resume CS Course from Professional Programme Stage. It is an opportunity to come back to the profession for those students who had to discontinue the CS Course due to compelling reasons. Detailed FAQ, Prescribed Application Form, etc. may be seen at “for students” option at home page of Institute”s website www.icsi.edu.

Please check FAQ & Application Form for Re-Registration at http://www.icsi.edu/docs/Webmodules/REREGISTRATION.pdf

e-bulletin 35 November 2016

ATTENTION STUDENTS !

EXPECTATIONS FROM THE STUDENTS DURING THE EXAMINATION ENROLLMENT FOR DECEMBER, 2016 CS EXAMINATIONS