Dufry AG · Dufry AG Domicile Switzerland ... international passenger traffic, ... will limit forex...

8

CORPORATES CREDIT OPINION 17 June 2016 Update RATINGS Dufry AG Domicile Switzerland Long Term Rating Ba3 Type LT Corporate Family Ratings - Dom Curr Outlook Stable Please see the ratings section at the end of this report for more information.The ratings and outlook shown reflect information as of the publication date. Contacts Ernesto Bisagno 4420-7772-5403 VP-Senior Analyst [email protected] Marina Albo 44-20-7772-5365 MD-Corporate Finance [email protected] Dufry AG Update Following Year End and Interim Results Summary Rating Rationale Dufry's Ba3 rating reflects Dufry's (1) leading market position with around 24% market share of the airport travel retail spending according to the company (2) strong geographical footprint; (3) track record and know-how in operating a travel retail business; (4) expectation of long term positive organic sales growth in line with growth of passenger air traffic. The rating is however constrained by the (1) high leverage reflecting Dufry's aggressive acquisition strategy; (2) the execution risk associated with the integration of World Duty Free (“WDF”) (3) the cyclical nature of the company's travel retail business, which is tied to international passenger traffic, with an exposure to certain discretionary items (e.g., perfumes and cosmetics, confectionary and luxury goods); (4) risks associated with the renewal of concession contracts as well as to certain event risks that would have implications on global travel behaviour. Positively, we expect Dufry's metrics to strengthen with adjusted leverage to decline towards 4.7x in 2016 down reflecting the full contribution from WDF and additional combined synergies from Nuance and WDF coming on stream, as well as return to positive organic growth , as guided by management. Exhibit 1 Dufry's Leverage To Decline From Fiscal 2015 High Adjusted (gross) debt/EBITDA Source: Moody's Investors Service estimates

Transcript of Dufry AG · Dufry AG Domicile Switzerland ... international passenger traffic, ... will limit forex...

CORPORATES

CREDIT OPINION17 June 2016

Update

RATINGSDufry AG

Domicile Switzerland

Long Term Rating Ba3

Type LT Corporate FamilyRatings - Dom Curr

Outlook Stable

Please see the ratings section at the end of this reportfor more information.The ratings and outlook shownreflect information as of the publication date.

Contacts

Ernesto Bisagno 4420-7772-5403VP-Senior [email protected]

Marina Albo 44-20-7772-5365MD-Corporate [email protected]

Dufry AGUpdate Following Year End and Interim Results

Summary Rating RationaleDufry's Ba3 rating reflects Dufry's (1) leading market position with around 24% marketshare of the airport travel retail spending according to the company (2) strong geographicalfootprint; (3) track record and know-how in operating a travel retail business; (4) expectationof long term positive organic sales growth in line with growth of passenger air traffic.

The rating is however constrained by the (1) high leverage reflecting Dufry's aggressiveacquisition strategy; (2) the execution risk associated with the integration of World DutyFree (“WDF”) (3) the cyclical nature of the company's travel retail business, which is tied tointernational passenger traffic, with an exposure to certain discretionary items (e.g., perfumesand cosmetics, confectionary and luxury goods); (4) risks associated with the renewal ofconcession contracts as well as to certain event risks that would have implications on globaltravel behaviour.

Positively, we expect Dufry's metrics to strengthen with adjusted leverage to decline towards4.7x in 2016 down reflecting the full contribution from WDF and additional combinedsynergies from Nuance and WDF coming on stream, as well as return to positive organicgrowth , as guided by management.

Exhibit 1

Dufry's Leverage To Decline From Fiscal 2015 HighAdjusted (gross) debt/EBITDA

Source: Moody's Investors Service estimates

MOODY'S INVESTORS SERVICE CORPORATES

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 17 June 2016 Dufry AG: Update Following Year End and Interim Results

Credit Strengths

» Leading travel retail operator

» Diversified revenue base by product and by geography

» Positive free cash flow generation

» Solid profitability compared to Moody's-rated specialty retailers

Credit Challenges

» Sales development correlated to international passenger flows

» Exposure to event risk

» High leverage driven by the company's aggressive acquisition strategy

» Execution risk from the integration of WDF

Rating OutlookThe stable outlook reflects our expectations that Dufry's credit metrics will improve as a result of the full contribution from WDFcombined with positive organic growth. With leverage to decline towards 4.7x in 2016, we expect the company to start buildingheadroom within the rating category. Whilst there is still some execution risk from the acquisition of WDF, management indicated thatthe initial phase of integration started well.

Factors that Could Lead to an UpgradeUpgrade pressure on the ratings would reflect Dufry's ability to restore positive organic growth and successfully integrate WDF withEBITDA (on a reported basis) margin strengthening above 12.5% and debt/EBITDA (fully adjusted for the concessions) trending towards4.5x, on a sustainable basis.

Factors that Could Lead to a DowngradeConversely, downward pressure on the rating would reflects operational weakness or difficulties in integrating the acquired assets.Quantitatively, downward pressure could be exerted on the ratings if Dufry's financial leverage does not return below 5.25x and RCF /net debt does not improve to 14% by the end of 2016.

MOODY'S INVESTORS SERVICE CORPORATES

3 17 June 2016 Dufry AG: Update Following Year End and Interim Results

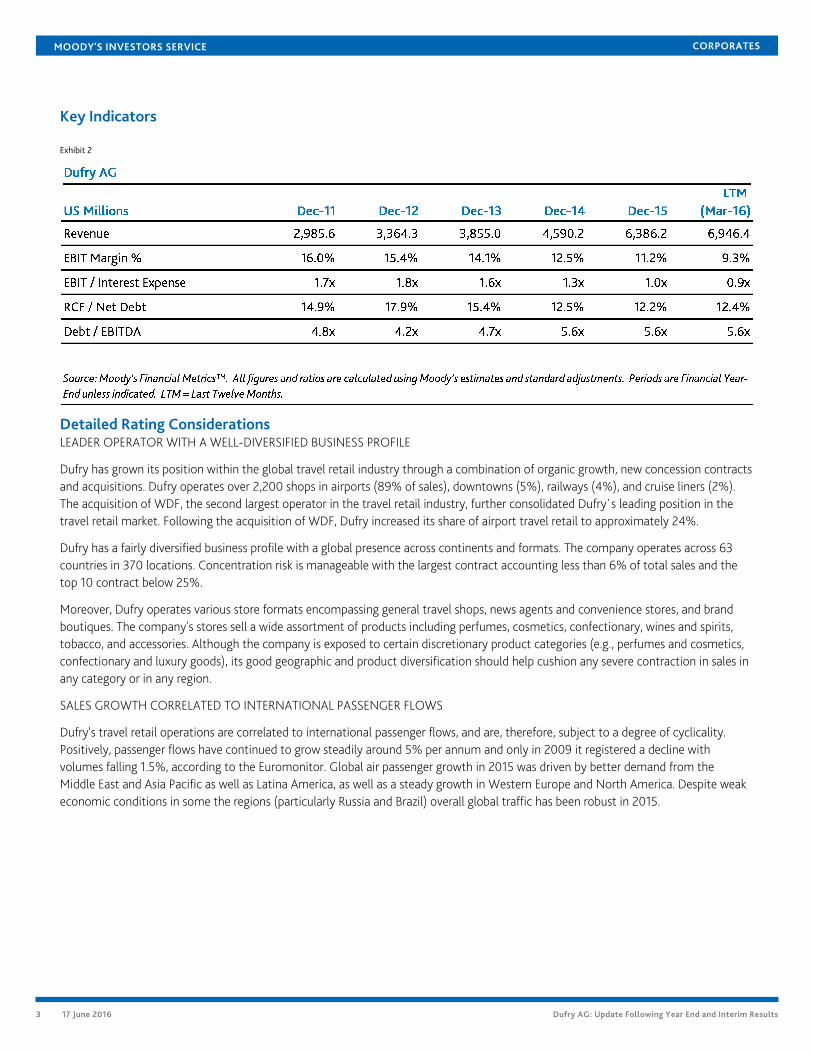

Key Indicators

Exhibit 2

Detailed Rating ConsiderationsLEADER OPERATOR WITH A WELL-DIVERSIFIED BUSINESS PROFILE

Dufry has grown its position within the global travel retail industry through a combination of organic growth, new concession contractsand acquisitions. Dufry operates over 2,200 shops in airports (89% of sales), downtowns (5%), railways (4%), and cruise liners (2%).The acquisition of WDF, the second largest operator in the travel retail industry, further consolidated Dufry`s leading position in thetravel retail market. Following the acquisition of WDF, Dufry increased its share of airport travel retail to approximately 24%.

Dufry has a fairly diversified business profile with a global presence across continents and formats. The company operates across 63countries in 370 locations. Concentration risk is manageable with the largest contract accounting less than 6% of total sales and thetop 10 contract below 25%.

Moreover, Dufry operates various store formats encompassing general travel shops, news agents and convenience stores, and brandboutiques. The company's stores sell a wide assortment of products including perfumes, cosmetics, confectionary, wines and spirits,tobacco, and accessories. Although the company is exposed to certain discretionary product categories (e.g., perfumes and cosmetics,confectionary and luxury goods), its good geographic and product diversification should help cushion any severe contraction in sales inany category or in any region.

SALES GROWTH CORRELATED TO INTERNATIONAL PASSENGER FLOWS

Dufry's travel retail operations are correlated to international passenger flows, and are, therefore, subject to a degree of cyclicality.Positively, passenger flows have continued to grow steadily around 5% per annum and only in 2009 it registered a decline withvolumes falling 1.5%, according to the Euromonitor. Global air passenger growth in 2015 was driven by better demand from theMiddle East and Asia Pacific as well as Latina America, as well as a steady growth in Western Europe and North America. Despite weakeconomic conditions in some the regions (particularly Russia and Brazil) overall global traffic has been robust in 2015.

MOODY'S INVESTORS SERVICE CORPORATES

4 17 June 2016 Dufry AG: Update Following Year End and Interim Results

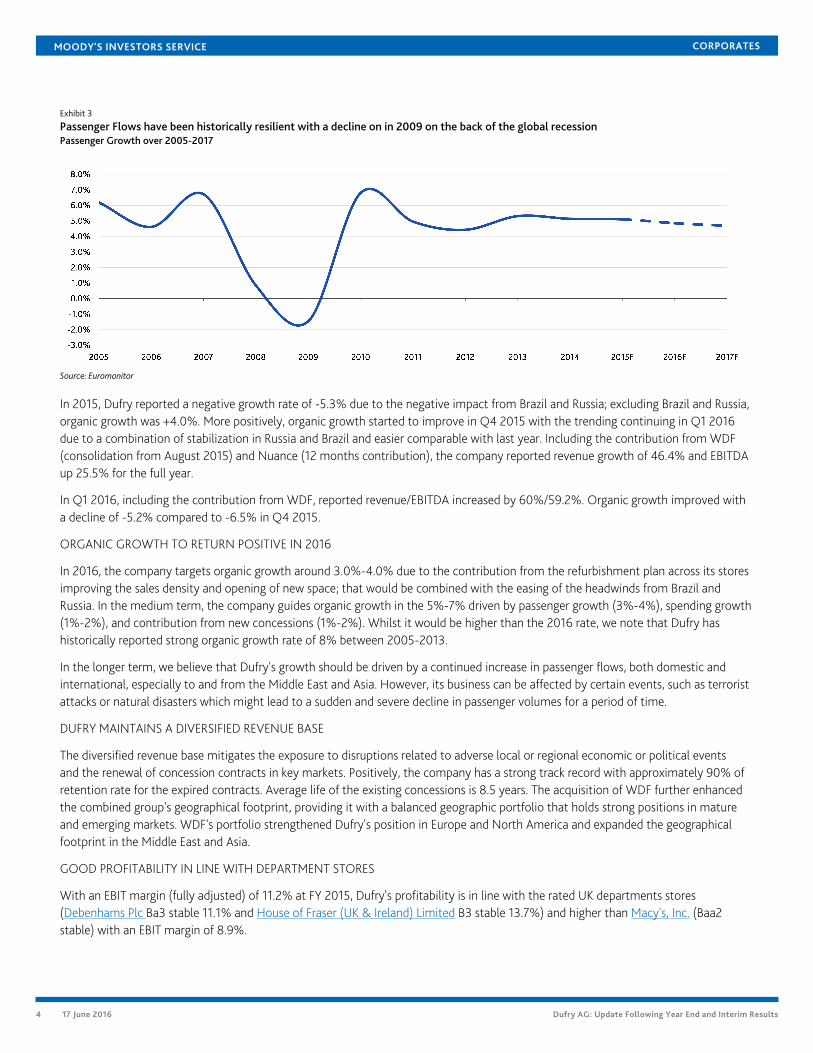

Exhibit 3

Passenger Flows have been historically resilient with a decline on in 2009 on the back of the global recessionPassenger Growth over 2005-2017

Source: Euromonitor

In 2015, Dufry reported a negative growth rate of -5.3% due to the negative impact from Brazil and Russia; excluding Brazil and Russia,organic growth was +4.0%. More positively, organic growth started to improve in Q4 2015 with the trending continuing in Q1 2016due to a combination of stabilization in Russia and Brazil and easier comparable with last year. Including the contribution from WDF(consolidation from August 2015) and Nuance (12 months contribution), the company reported revenue growth of 46.4% and EBITDAup 25.5% for the full year.

In Q1 2016, including the contribution from WDF, reported revenue/EBITDA increased by 60%/59.2%. Organic growth improved witha decline of -5.2% compared to -6.5% in Q4 2015.

ORGANIC GROWTH TO RETURN POSITIVE IN 2016

In 2016, the company targets organic growth around 3.0%-4.0% due to the contribution from the refurbishment plan across its storesimproving the sales density and opening of new space; that would be combined with the easing of the headwinds from Brazil andRussia. In the medium term, the company guides organic growth in the 5%-7% driven by passenger growth (3%-4%), spending growth(1%-2%), and contribution from new concessions (1%-2%). Whilst it would be higher than the 2016 rate, we note that Dufry hashistorically reported strong organic growth rate of 8% between 2005-2013.

In the longer term, we believe that Dufry's growth should be driven by a continued increase in passenger flows, both domestic andinternational, especially to and from the Middle East and Asia. However, its business can be affected by certain events, such as terroristattacks or natural disasters which might lead to a sudden and severe decline in passenger volumes for a period of time.

DUFRY MAINTAINS A DIVERSIFIED REVENUE BASE

The diversified revenue base mitigates the exposure to disruptions related to adverse local or regional economic or political eventsand the renewal of concession contracts in key markets. Positively, the company has a strong track record with approximately 90% ofretention rate for the expired contracts. Average life of the existing concessions is 8.5 years. The acquisition of WDF further enhancedthe combined group's geographical footprint, providing it with a balanced geographic portfolio that holds strong positions in matureand emerging markets. WDF's portfolio strengthened Dufry's position in Europe and North America and expanded the geographicalfootprint in the Middle East and Asia.

GOOD PROFITABILITY IN LINE WITH DEPARTMENT STORES

With an EBIT margin (fully adjusted) of 11.2% at FY 2015, Dufry's profitability is in line with the rated UK departments stores(Debenhams Plc Ba3 stable 11.1% and House of Fraser (UK & Ireland) Limited B3 stable 13.7%) and higher than Macy's, Inc. (Baa2stable) with an EBIT margin of 8.9%.

MOODY'S INVESTORS SERVICE CORPORATES

5 17 June 2016 Dufry AG: Update Following Year End and Interim Results

Although Dufry's profitability continue to benefit from higher-return emerging markets, the acquisitions of WDF had a negative impacton margins given the higher exposure to developed markets (64% of EBITDA generated from the developed markets at FY 2015compared to 47% in FY 2013). However, the lower exposure to emerging market, will limit forex headwinds and exposure to politicalrisk as well as to less stable economic environments.

In addition, the company's concession-based business model is considered to be more flexible than that of a traditional retailer becauseconcession fees are mostly variable, whereas rents tend to be mostly a fixed charge. Therefore, operating margins are less likely to beeroded as sharply when footfall and sales slow-down.

CREDIT METRICS TO STRENGTHEN OVER 2016-17

We expect margins to improve over 2016-17 driven by the synergies from acquired assets and a positive organic growth. Managementindicated that the integration of Nuance is completed with a total achieved synergies of CHF70 million of which CHF36 million will bereflected in 2016. Management also confirmed the original guidance of EUR100 million synergies from the integration of WDF by 2017with first synergies expected in the second half of 2016. Around EUR50-60 million include cost synergies and EUR40-50 million relatedto gross margin improvement reflecting the optimization of commercial policies and enhanced purchasing power. Whilst there is stillsome execution risk, management indicated the initial phase of the integration of WDF is progressing on track.

Leverage peaked at 2015 at 5.6x due to the acquisition of WDF which only contributed 5-months during the year. We expect Dufry todeleverage in 2016 down to 4.7x reflecting stronger earnings with full contribution from WDF and additional combined synergies fromthe acquired assets coming on stream and our assumption of a debt prepayment of CHF400 million. We model further improvementin leverage towards 4.1x over 2017-18 driven by positive organic growth in line with management long term guidance.

With small shareholder distributions and a modest level of capex at 3% of total sales, we expect the free cash flow generation tostrengthen. Whilst historically the company has been very acquisitive, we expect management will focus on organic growth anddeleverage and we expect a positive free cash flow of CHF400-500 million per annum over 2016-17 which we assume to be largelyutilized to pay down debt.

Despite the positive free cash flow, we expect gross adjusted debt to increase as a result of higher concession costs going forwardwhich we assumed to increase in line with sales growth. The adjustment for concession fees (CHF1,597 million in 2015), which weview as a proxy for rental expenses, accounts for the large majority of gross debt. Capitalized concession fees adjustment, addsapproximately CHF8 billion to Dufry's gross debt in 2015 and will increase to around CHF11 billion (using a 5x multiple) in 2015reflecting additional rental expenses from the full contribution from WDF.

Positively, we note that Dufry mostly operates under concessions with variable payments based upon the revenues of each shop whichprovides Dufry a more flexible debt structure when compared to the typical retailer. However, some concessions also include a fixedfee component called "MAG" which would be payable to the airport operator regardless of the amount of sales generated from theshop.

Liquidity AnalysisDufry's liquidity is good, underpinned by cash balances of CHF483.5 million (31 March 2016) and a CHF900 million RCF maturingin June 2019 (CHF718 million undrawn at 31 December 2015); and our expectation of ongoing positive free cash flow generationsupported by the absence of dividends and a moderate level of capital expenditure.

We note that the first quarter is seasonally the weakest for the company with Dufry having its strongest season of turnover and EBITDAbetween July and September corresponding to the summer time in the northern hemisphere.

During 2015, the company fully refinanced the bridge loans funding the acquisition of WDF through a combination of rights issuesof EUR2.1 billion, a new term loan of CHF800 million and a bond issuance of EUR700 million. Dufry will not have any material debtmaturities until June 2019 when around CHF1.8 billion bank facilities would mature.

Existing financial covenants as amended in January 2016, include a max net debt/ Adj. EBITDA threshold of 4.50x (to be reduced to4.25x in June 2016, to 4.00x in December 2016 and to 3.75x in March 2017) and Adj. EBITDA / Adj. interest expenses interest covenant

MOODY'S INVESTORS SERVICE CORPORATES

6 17 June 2016 Dufry AG: Update Following Year End and Interim Results

threshold to 3.5x. As of 31 March 2016, Dufry maintained ample headroom under its financial covenants (more than 50% for theinterest cover and around 15% for the leverage).

Structural ConsiderationsDufry's Ba3 senior unsecured instrument ratings are in line with the corporate family rating (CFR). This reflects the lack of significantsubordination with all the obligations benefiting from a guarantee from Dufry AG, Dufry Financial Services B.V. and the subsidiariesthat collectively represent 100% of the consolidated net assets and EBITDA of the company. However, these instruments rank behind asmall amount of secured debt and trade payables located at the operating subsidiaries' level.

ProfileHeadquartered in Basel, Switzerland, Dufry AG is a leading global travel retailer with operations in 63 countries. Dufry operates over2,200 shops in airports (89% of sales), downtown (5%), railways (4%), and cruise liners (2%). The acquisition of WDF, the secondlargest operator in the travel retail industry, further consolidated Dufry`s leading position in the travel retail market. Following theacquisition of WDF, Dufry increased its share of airport travel retail to approximately 24%.

Dufry's network includes general travel retail shops, `walk-through' shops, brand boutiques, news agents and convenience stores with aproduct offer spanning perfumes & cosmetics, wines & spirits, tobacco, watches & jewellery, and accessories.

Dufry is listed on SWX Swiss Exchange with a market capitalization of CHF6.4 billion and a free float of 77.6%. At 31 December 2015,there is a syndicate led by the long-term shareholder Travel Retail Investments, an holding company owned by Mr Andrés HolzerNeumann (vice-chairman of Dufry), amounting to 22.4%

Rating Methodology and Scorecard FactorsWe expect the company to start building headroom in the Ba3 rating reflecting full contribution from WDF and return to positiveorganic growth combined with the synergies coming on stream. With the integration of WDF at the initial phase, there is still someexecution risk constraining the rating.

MOODY'S INVESTORS SERVICE CORPORATES

7 17 June 2016 Dufry AG: Update Following Year End and Interim Results

Exhibit 4

Credit Metrics to strengthen over the next 12-18 months

Source: Moody’s Financial Metrics™

Ratings

Exhibit 5Category Moody's RatingDUFRY AG

Outlook StableCorporate Family Rating -Dom Curr Ba3

DUFRY FINANCE S.C.A.

Outlook StableBkd Senior Unsecured Ba3/LGD4

Source: Moody's Investors Service

MOODY'S INVESTORS SERVICE CORPORATES

8 17 June 2016 Dufry AG: Update Following Year End and Interim Results

© 2016 Moody's Corporation, Moody's Investors Service, Inc., Moody's Analytics, Inc. and/or their licensors and affiliates (collectively, "MOODY'S"). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES ("MIS") ARE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY'S ("MOODY'SPUBLICATIONS") MAY INCLUDE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKESECURITIES. MOODY'S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANYESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKETVALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY'S OPINIONS INCLUDED IN MOODY'S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICALFACT. MOODY'S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHEDBY MOODY'S ANALYTICS, INC. CREDIT RATINGS AND MOODY'S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDITRATINGS AND MOODY'S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDITRATINGS NOR MOODY'S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY'S ISSUES ITS CREDIT RATINGSAND PUBLISHES MOODY'S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY ANDEVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY'S CREDIT RATINGS AND MOODY'S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY'S CREDIT RATINGS OR MOODY'S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY'S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY'S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided "AS IS" without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY'S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody's Publications.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY'S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY'S.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY'S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY'S IN ANY FORM OR MANNER WHATSOEVER.

Moody's Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody's Corporation ("MCO"), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody's Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody's Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS's ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading "Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy."

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY'S affiliate, Moody's InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody's Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to "wholesale clients" within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY'S that you are, or are accessing the document as a representative of, a "wholesale client" and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to "retail clients" within the meaning of section 761G of the Corporations Act 2001. MOODY'S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY'S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. ("MJKK") is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody'sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody's SF Japan K.K. ("MSFJ") is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization ("NRSRO"). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1029982