Dublin Office Market - WordPress.com...betting company at unit 4, The Oval, Ballsbridge, Dublin 4....

12

Autumn Review 2012 Dublin Office Market

Transcript of Dublin Office Market - WordPress.com...betting company at unit 4, The Oval, Ballsbridge, Dublin 4....

Autumn Review 2012

Dublin Office Market

.

2

Following mixed performance during the first half of the year, activity in the Dublin office market was disappointing in the third quarter. Furthermore, the CBD also experienced a slowdown in activity during the quarter. That said, demand remains robust for well-located Grade A1 accommodation in the CBD with a 13% reduction in the supply of this space over the past twelve months. Availability of this grade of accommodation has now fallen to only 87,300 sq m.

Marian Finnegan, Director of Research, Chief Economist, DTZ Sherry FitzGerald

Transaction activity in the Dublin office weakened more than expected in

recent months amid persistent uncertainty in the international environment.

This tension continues to weigh heavily on the office market recovery.

Performance in the office market during the first nine months of the year

has been volatile. The level of take up recorded during the third quarter

fell sharply and remains significantly lower than the quarterly average. On

a positive note, the volume of space reserved rose during the quarter, this

was particularly evident in the CBD where the quantum of space reserved

increased by 31%.

Supply levels in the office market remain elevated but continue to

show increasing signs of stabilisation. However, the supply of Grade A

accommodation remains significantly lower than Grade B. The office market

and in particular the Central Business District continues to suffer from a

deficient supply of large floor plate Grade A stock. The stock of Grade A

space and in particular newer A1 continues to diminish and has not been

replenished. Furthermore, there are only three buildings that can provide

over 10,000 sq m of Grade A1 office accommodation in the CBD.

Prime rents in the capital have stabilised at €313 per sq m. As supply

levels in the CBD recede, prime rents are unlikely to increase. However, the

incentives available on existing new Grade A space will start to tighten and

lease flexibility will begin to diminish.

..

Dublin Office Market

3Source: DTZ Sherry FitzGerald Research

Dublin Office Market

4

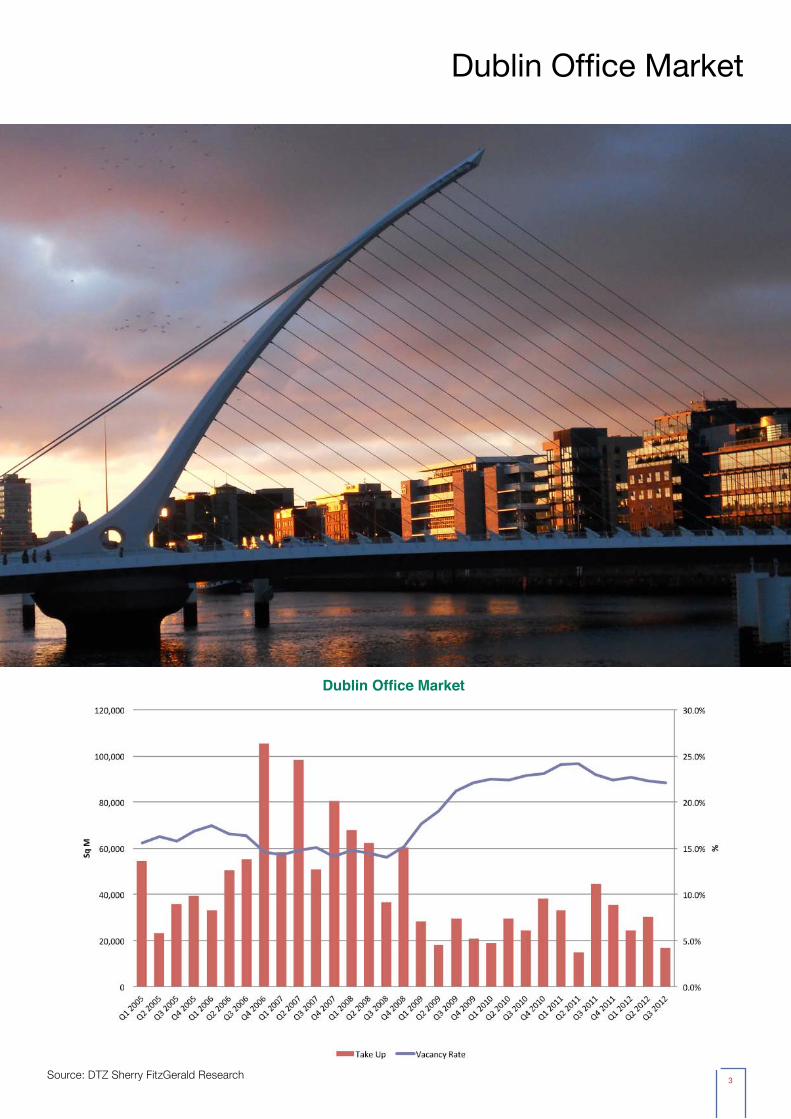

Take Up

Despite optimism last year that a sustained recover was in sight for 2012, the reality is that 2012 is unfolding to be yet another challenging year for the office market. International events, in particular those in Europe and the forthcoming US presidential election, continue to weigh heavily on performance in the Dublin office market. Performance during the year to September has been volatile with activity fluctuating considerably between quarters. After suffering a setback during the opening quarter of 2012, transaction activity in the Dublin office market strengthened during the second quarter. However, the momentum failed to build during the third quarter as activity weakened notably. The total quantity of space taken up in the three months to September fell to 16,800 sq m, reflecting a considerable reduction on the previous quarter.

The third quarter of 2012 witnessed a significant deterioration in activity during the three month period. The total quantity of space occupied fell to 16,800 sq m; this compares to approximately 30,200 sq m transacted in the previous quarter. The level of activity recorded during quarter three marked one of its weakest performing quarters since the onset of the downturn. An analysis of the space transacted in the year to date reveals a 23% reduction in activity levels when compared to the same period in 2011.

The level of net take up, which measures the change in occupied space, stood at 6,650 sq m at the end of September; representing a

53% reduction on the previous quarter. The CBD, on the other hand, witnessed a strong uplift in the level of net take up; rising by 21% when compared to the same period in 2011. This reflects the continued strength in demand for this area.

The largest deal transacted during quarter three was the occupation of approximately 1,550 sq m by MarketSpreads, a financial spread betting company at unit 4, The Oval, Ballsbridge, Dublin 4. However, an analysis of activity during the quarter reveals that demand remains prevalent for smaller sized deals measuring 1,000 sq m or less.

The Dublin office market remains divided. While demand remains strongest in the Central Business District (CBD), the third quarter also witnessed a deterioration in activity in this region. During the first nine months of the year, demand for space in the CBD fell by 8% when compared to the corresponding period in 2011. Active demand during the year remains strong for third generation space, in particular Grade A accommodation. Conversely, demand is more subdued for second generation space. That said if the location is right, there is demand for space that is refurbished to a high standard.

Source: DTZ Sherry FitzGerald Research

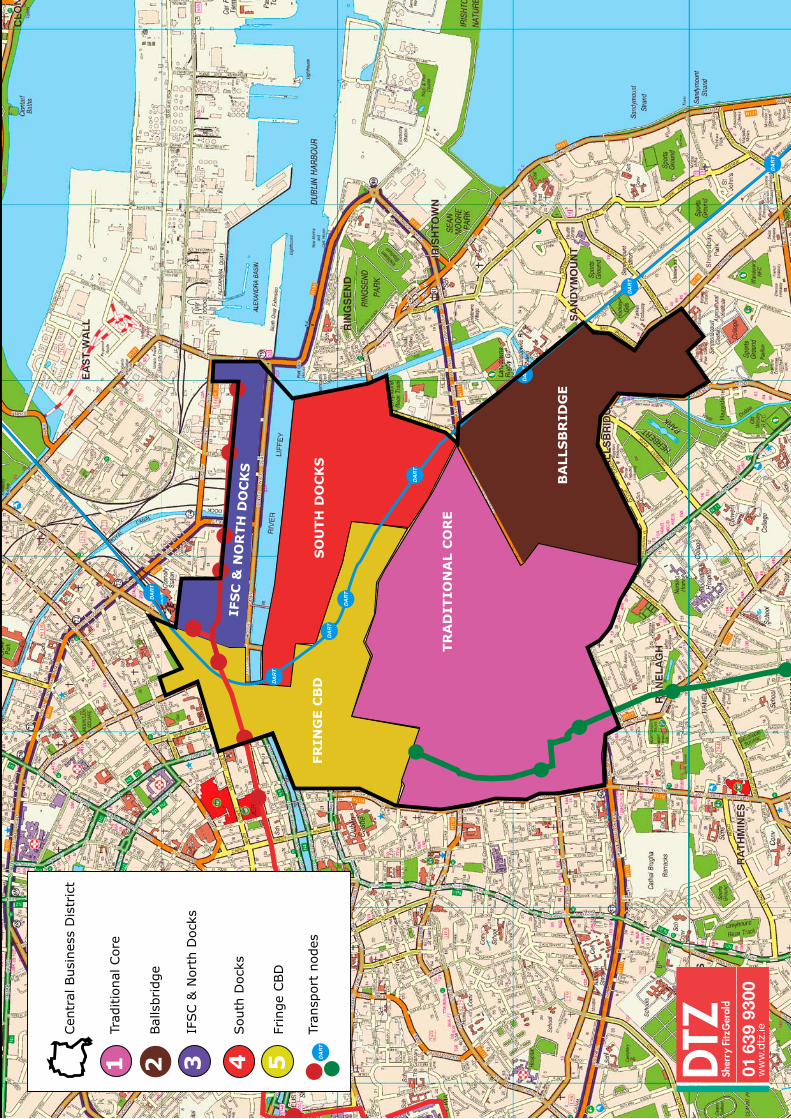

CBD Take Up by Area - Year to Q3 2012

Demand remains strongest for Grade A Accommodation

Dublin Office Market

The attractiveness of the Central Business District (CBD) as a location preference continued to dominate take up during the third quarter of 2012. An analysis of the space transacted in the year to date reveals that 64% of offices

taken up are located in the CBD. Furthermore, higher quality Grade A accommodation continues to be the most sought after, evidenced by the fact that 74% of space transacted in the CBD during the first nine months of the year comprised of Grade A space. Moreover, 48% comprised of newer Grade A1 space.

Within the CBD boundaries, the traditional core area remains the most sought after location, accounting for 46% of the CBD space taken up in the year to date. This was followed by the south docks area accounting for 18%. A combination of significantly reduced rents coupled with attractive lease lengths has seen the CBD continue to gain further ground over the suburban region as a location preference. The suburban region accounted for 33% of space occupied during the three month period.

With regard to future demand, while there are a number of active requirements in the market at present, the unresolved euro crisis is acting as a barrier and thus weighing on investor confidence. This is evident in the case of new entrants to the market and in particular multinational companies. A number of high profile companies with requirements for space include software giant Microsoft, Arthur Cox, Paypal, Salesforce.com, CITI Group and BNY Mellon. However, cautiousness and uncertainty on behalf of potential occupiers and in particular multi-national occupier’s, results in deals taking time to close. At the end of quarter two, there was a further 15,500 sq m of office space signed and awaiting occupation in the capital with a further 41,500 sq m reserved. Furthermore, the CBD witnessed a 31% increase in the proportion of space both reserved and signed during the quarter. This should positively impact take up in the coming quarters.

The opening half of 2012 saw demand driven by the finance sector. This trend continued to build momentum during the third quarter, with the finance cohort occupying a quarter of the space occupied during the first nine months of the year. The IT/telecommunications and the Pharmaceutical/Health sectors remain very active absorbing 20% and 15% respectively during the nine month period. The State, which remains constrained by policy, was inactive in the year to date.

5

Source: DTZ Sherry FitzGerald Research

Dublin Office Market

Supply levels fall by 4%

CBD Availability by Area, Q3 2012

Availability

Supply levels in the Dublin office market have shown signs of stabilisation. Having peaked at approximately 811,400 sq m during the second quarter of 2011, the level has fluctuated somewhat in the interim to stand at 739,700 sq m at the end of September. The rate of decline in availability in the CBD continued during the quarter, however at a more accelerated pace. In particular, grade A space receded by 13% during the twelve month period. Thus the CBD is potentially facing a looming shortage of top quality accommodation.

The opening quarter of 2012 witnessed a surge in the quantum of second hand space released to the market resulting in upward pressure on supply. However, the highly volatile nature of supply at present

returned in the second quarter; with availability declining by 2%. This trend continued during the third quarter; however the reduction in supply narrowed to 1% during the three month period. The total quantity of available space in the Dublin office market stood at 739,700 sq m at the end of September. A comparison with the corresponding period in 2011 reveals a 4% reduction in supply.

The modest reduction in supply evident during quarter three resulted largely from a further moderation in the rate of release of second hand space to the market as opposed to stronger demand during the quarter. A comparison with the previous quarter reveals that the quantum of second hand space entering the market halved during the three month period. While the rate of increase in the supply of second hand space has lessened considerably compared with rates witnessed at the onset of the downturn, upside risks remain both from potential future consolidations and also relocation activity.

The level of supply remains stubbornly high by historical standards. This is further highlighted by an analysis of the vacancy rate. The vacancy rate stood at 22.1% at the end of September. Furthermore, a comparison

6

Source: DTZ Sherry FitzGerald Research

with the corresponding period in 2011 reveals a very modest reduction from 23%. It is important to note that this rate is significantly greater than the equilibrium rate of 7%.

A significant proportion of the vacant space is older stock which is effectively obsolete. This stock has been on the market for a considerable number of years and therefore arguably masking the true vacancy rate in the market.

An analysis of the spread of available space in the office market at the end of quarter three reveals that the suburbs continues to account for the majority of accommodation, 41%. This would suggest that the vacancy rate in this region is significantly greater than the overall market rate of 22.1%. A further 24% of accommodation is located in the secondary region.

In the CBD, the total quantity of space fell to approximately 251,400 sq m or 34% of the total available space at the end of September. This represents a reduction of 5% when compared to the previous quarter and a reduction of 11% compared with twelve months previously. The corresponding vacancy rate in the CBD fell to 14.7%, down from 16.4% recorded in the previous year. Active demand for floorspace in the CBD rose sharply during the third quarter, the quantity of space under active negotiation stood at 41,700 sq m; representing an increase of 31% on the previous quarter. If this space is taken up, it could potentially reduce the vacancy rate for the area to 12.2%.

Furthermore, Grade A space continues to be the most sought after. In the CBD, the quantity of Grade A space stands at 164,100 sq m, down 13% on the level recorded twelve months previously. An occupier with a requirement for 10,000+ sq m of new space has limited choice with just three buildings which satisfy this requirement. Grade B space located in the CBD also contracted by 6% over the same period.

Under Construction Development activity in the Dublin office market has ceased with no space currently under construction. This marks the sixth quarter in which the market recorded no active construction. At the height of the market, the quantity of space under construction totalled 350,000 sq m; this has declined radically to a situation where there is now no development in the capital.

The volume of space under construction fell to zero during 2011. Since then, no new space has commenced construction and with no new developments starts scheduled at present, development activity is expected to be limited during 2012. Furthermore, it is highly unlikely there will be any speculative development given the large overhang of available space that exists in the market coupled with the lack of development finance and low rents. Strong demand for Grade A space, particularly in the CBD may see some occupiers forced to consider better Grade B space which may give an impetus to self financed landlords to refurbish Grade B space as the stock of Grade A space continues to diminish.

The total stock of office accommodation remained unchanged at approximately 3,350,100 sq m at the end of quarter three 2012.

As there is no space under construction, supply in the market stands at 739,700 sq m. Any increases in availability going forward will stem from the release of second hand space to the market. Comparing this to the average annual take up over the past decade suggests ample supply going forward.

Dublin Office Market

7

“While the take-up figures for the quarter may be disappointing, this has to be looked at in the context of the very uncertain economic climate; specifically in regard to the Euro at the beginning of 2012. The Euro crises has now calmed somewhat which has led to confidence returning and a notable increase in the amount of space reserved for the quarter”

Ronan Corbett, Director of Business Space, DTZ Sherry FitzGerald

Rental Levels Prime rents in the capital remain stable at €313 per sq m, unchanged from the previous quarter. In addition, incentives have also remained broadly stable across the Dublin office market. In the CBD, headline rents for third generation prime accommodation stood at approximately €313 per sq m, having remained static since the second quarter of 2011. However, there have been some deals recorded marginally above this rate, such as reported for No 2 Hume Street. While there have been some deals reported above this, rents may be subject to downward pressure over the coming year due to ongoing supply demand imbalances coupled with ongoing uncertainty in the world economy.

The level of incentives on offer such as rent free periods and other tenant inducements continue to be a fundamental part of tenant incentive packages. However, they have become intrinsically linked to the condition of the property. An example of this is that inducements are limited for turn key properties. Tenants acquiring new space can expect on average two months rent free per year term certain.

In the suburbs, rents can vary significantly depending on location and building specification, but have remained broadly unchanged during quarter two. The south suburbs continue to see the strongest suburban headline rental levels, particularly in Sandyford where rents range between €161 and €194 per sq m per annum. In the western suburbs rents typically range between €86 and €150 per sq m per annum. In the northern suburbs, headline rents generally range between €129 and €150 per sq m per annum. Similar to the prime region of Dublin, landlords in the suburbs are also tailoring incentive packages to secure those tenants active in the market.

8

Dublin Office Market

Outlook for the FutureThe course of office market recovery has dimmed somewhat as on-going uncertainty surrounding euro debt crisis and more recently the US presidential elections triggers more cautiousness on the part of occupiers; particularly multinational companies. The total volume and number of transactions in the Dublin office market weakened during the third quarter of the year; this follows largely mixed performance during the first half of the year. Activity for the first nine months of 2012 is down on last year and unless there is a significant uplift in activity during the final quarter; the current trajectory would suggest that transaction volumes for 2012 will be lower than those recorded in 2011. However, recent measures introduced by the European Central Bank to preserve collateral availability have proved more convincing and this marks a positive step towards stemming the debt crisis and reducing uncertainty among potential office occupiers.

The total volume of available office space stood at 739,700 sq m at the end of September, reflecting a marginal reduction on the level recorded in the previous quarter. Leading supply indicators would suggest that the market continues to show signs of stabilisation, albeit tentative. It is anticipated that overall availability will ease in the coming quarters as the delivery of new stock is static and the rate of release of second hand space shows signs of stabilising. In the CBD, The rate of decline in availability accelerated during the third quarter. In particular, grade A space receded by 13% during the twelve month period.

Prime rents in the capital have stabilised at €313 per sq m. Despite the fact that supply levels in the CBD continue to decline, prime rents are unlikely to increase. However, the incentives available on existing new Grade A space will start to tighten and lease flexibility will begin to diminish.

9

.

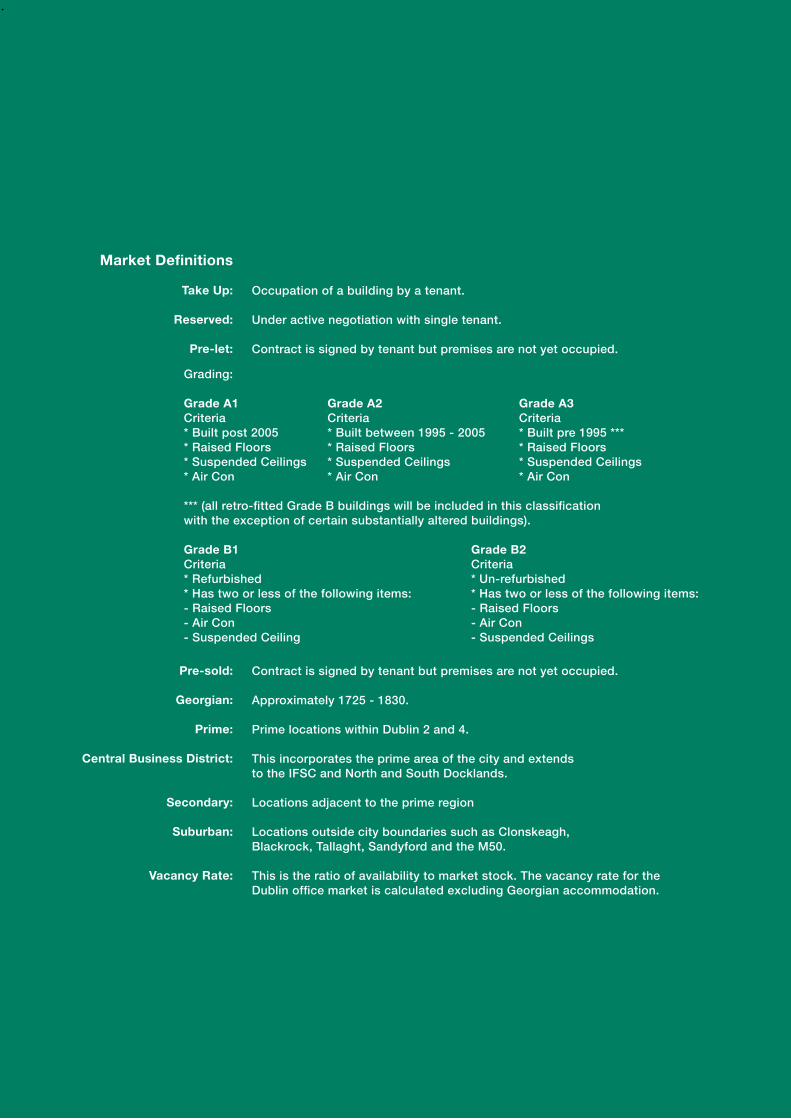

Market Definitions

Take Up:

Reserved:

Pre-let:

Pre-sold:

Georgian:

Prime:

Central Business District:

Secondary:

Suburban:

Vacancy Rate:

Occupation of a building by a tenant.

Under active negotiation with single tenant.

Contract is signed by tenant but premises are not yet occupied.

Contract is signed by tenant but premises are not yet occupied.

Approximately 1725 - 1830.

Prime locations within Dublin 2 and 4.

This incorporates the prime area of the city and extends to the IFSC and North and South Docklands.

Locations adjacent to the prime region Locations outside city boundaries such as Clonskeagh, Blackrock, Tallaght, Sandyford and the M50.

This is the ratio of availability to market stock. The vacancy rate for the Dublin office market is calculated excluding Georgian accommodation.

Grading: Grade A1 Grade A2 Grade A3Criteria Criteria Criteria* Built post 2005 * Built between 1995 - 2005 * Built pre 1995 **** Raised Floors * Raised Floors * Raised Floors* Suspended Ceilings * Suspended Ceilings * Suspended Ceilings* Air Con * Air Con * Air Con *** (all retro-fitted Grade B buildings will be included in this classification with the exception of certain substantially altered buildings). Grade B1 Grade B2Criteria Criteria* Refurbished * Un-refurbished* Has two or less of the following items: * Has two or less of the following items: - Raised Floors - Raised Floors- Air Con - Air Con- Suspended Ceiling - Suspended Ceilings

.

01 6

39 9

300

ww

w.d

tz.ie

DA

RT

DA

RT

DA

RT

DA

RT

DA

RT

DA

RT

DA

RT

DA

RT

4South

Dock

s

SO

UTH

DO

CK

S

Cen

tral

Busi

nes

s D

istr

ict

3IF

SC &

Nort

h D

ock

s

IFS

C &

NO

RTH

DO

CK

S

2Bal

lsbridge

BA

LLS

BR

IDG

E

1Tr

aditio

nal

Core

TR

AD

ITIO

NA

L C

OR

E

5Fr

inge

CBD

FR

ING

E C

BD

Tran

sport

nodes

DA

RT

.

This report should not be relied upon as a basis for entering transactions without seeking specific, qualified, professional advice. It is intended as a general guide only. This report has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. While reasonable care has been taken in the preparation of the report, neither Sherry FitzGerald nor any of directors, employees or affiliates guarantees the accuracy or completeness of the information contained in the report. Any opinion expressed (including estimates and forecasts) may be subject to change without notice. No warranty or representation, express or implied, is or will be provided by Sherry FitzGerald, its directors, employees or affiliates, all of whom expressly disclaim any and all liability for the contents of, or omissions from, this document, the information or opinions on which it is based. Information contained in this report should not, in whole or part, be published, reproduced or referred to without prior approval. Any such reproduction should be credited to Sherry FitzGerald.

© 2012

[email protected] | www.dtz.ie

BELFAST

DUBLINGALWAY

LIMERICK

CORK

DTZ is now part of UGL Services, a division of UGL Limited. The combined business creates one of the largest property services companies in the world, providing corporate/occupier clients with a global, integrated end-to-end service offering and best-in-class investor services capabilities in investment

agency, leasing agency, property and facilities management, project and building consultancy, valuation, and investment and asset management. The organization has 27,000 permanent employees and 43,000 contractors, operating across 225 offices in 45 countries.

CONTACTMarian FinneganDirector of Research, Chief Economist Siobhán MoloneyEconomist

Ronan CorbettDirector of Business Space

DUBLIN164 Shelbourne RoadBallsbridge, Dublin 4T: +353 1 237 6300F: +353 1 237 6347