Drug Security in Nigeria: Technology for supply chain ... · Drug Security in Nigeria Technology...

36

Drug Security in Nigeria Technology for Supply Chain Integrity November 2017

Transcript of Drug Security in Nigeria: Technology for supply chain ... · Drug Security in Nigeria Technology...

Drug Security in NigeriaTechnology for Supply Chain Integrity

November 2017

PwC 2

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers does not accept or assume any liability, responsibility or duty of care for the consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

Caveat

PwC

Contents

3

State of the Nigerian Economy

Health Landscape in Nigeria

Technology for Drug Security

What else can be done

1

2

3

4

PwC

State of the Nigerian Economy

4

PwC

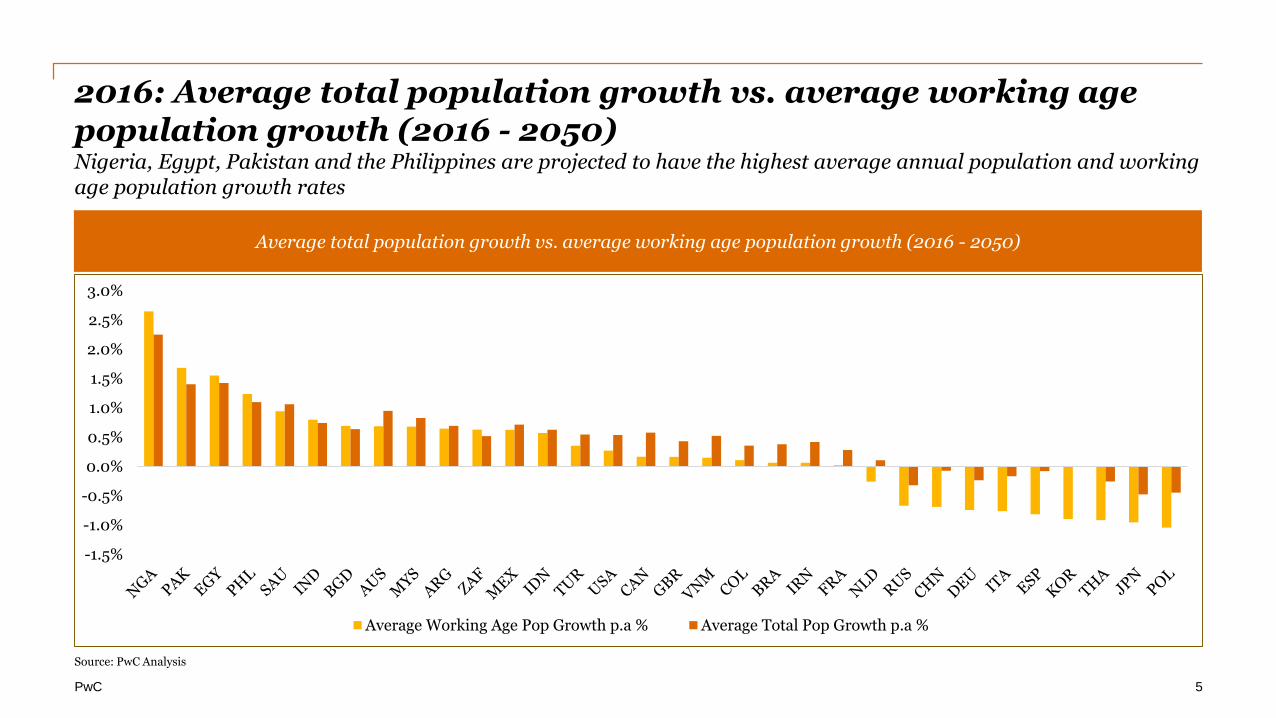

2016: Average total population growth vs. average working age population growth (2016 - 2050)Nigeria, Egypt, Pakistan and the Philippines are projected to have the highest average annual population and working age population growth rates

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Average Working Age Pop Growth p.a % Average Total Pop Growth p.a %

Source: PwC Analysis

Average total population growth vs. average working age population growth (2016 - 2050)

5

PwC

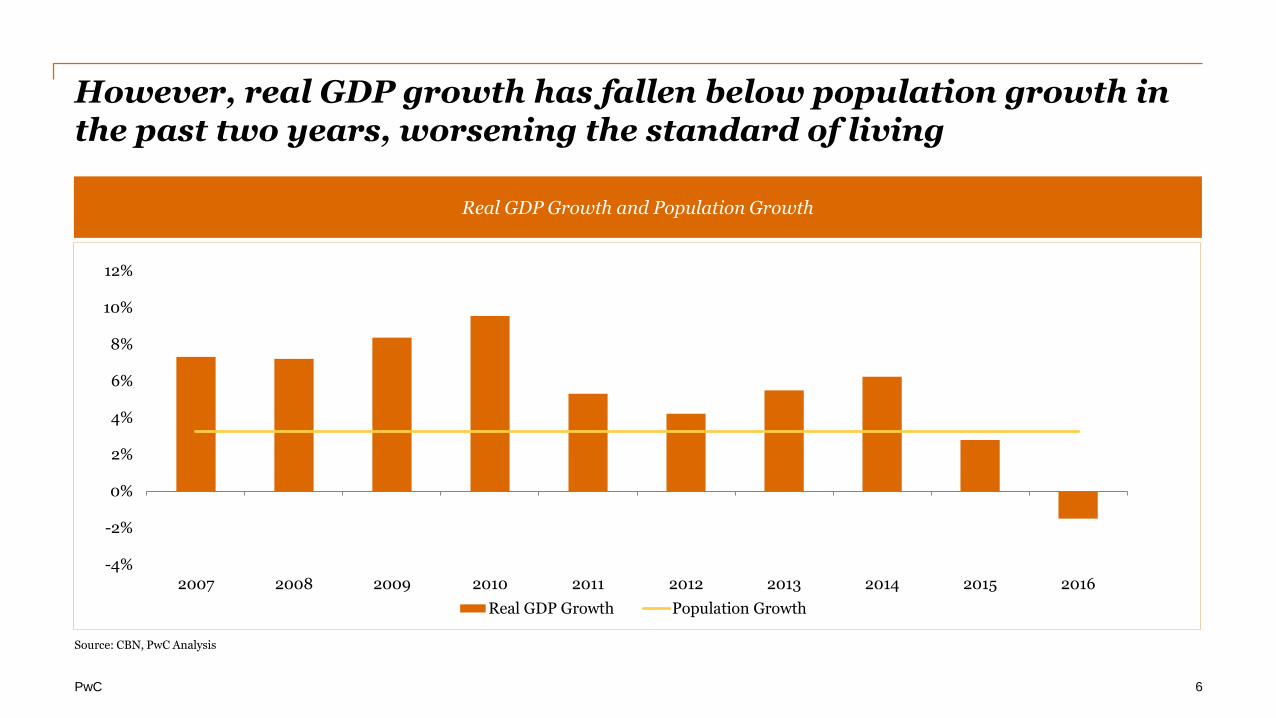

However, real GDP growth has fallen below population growth in the past two years, worsening the standard of living

Source: CBN, PwC Analysis

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Real GDP Growth Population Growth

Real GDP Growth and Population Growth

6

PwC

The Nigerian economy has turned a corner; recent macroeconomic trends strongly suggest a return to positive growth by YE2017

Q2’2017 Real GDP growth

0.55% y/y – best in six quarters

Inflation moderates to 15.9% y/y as at

September from a peak of 18.7% y/y in January 2017

Q3’2017 Purchasing Managers Index

average at54.3 points – best

since Q3’2014

NSEASI YtD35.3%* vs -6.2% in 2016

Reserves up by

40.6% in the past 12 months to USD33.3

billion

Source: CBN, NBS, NSE, PwC Analysis • NSEASI YtD is as at 23 October 2017• Reserves is as at 18 October 2017• YE – Year End 7

PwC

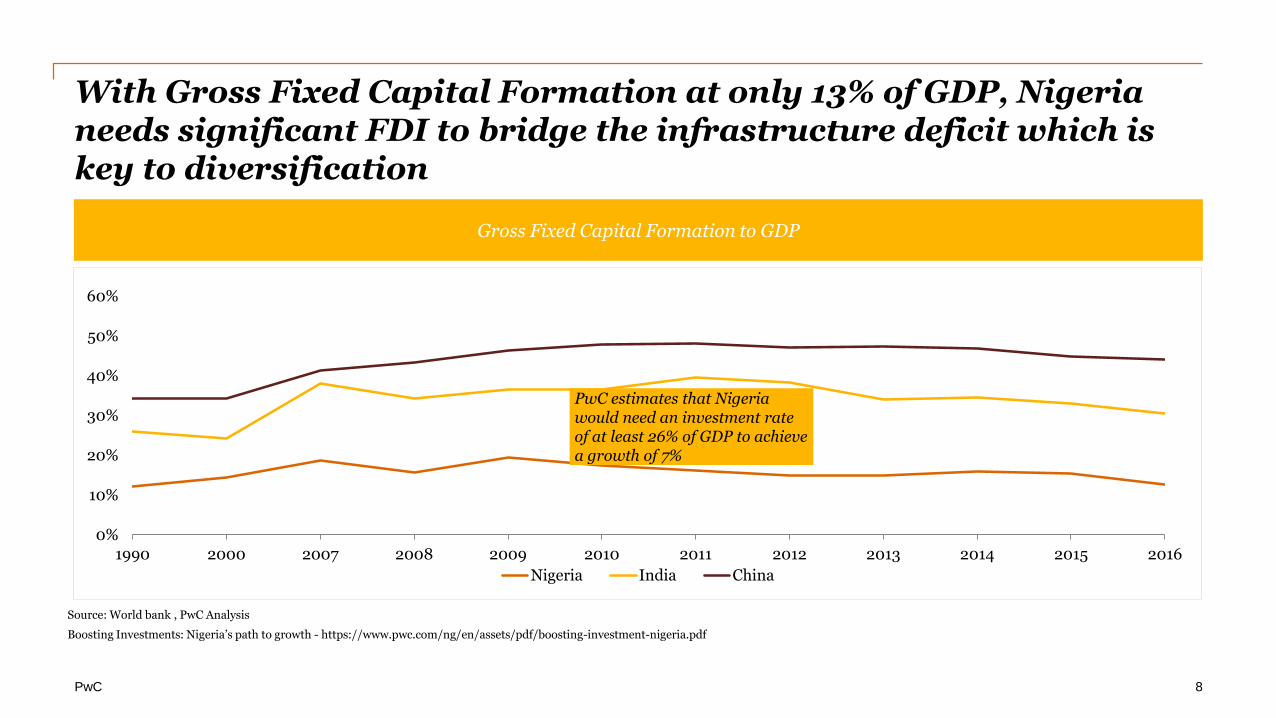

With Gross Fixed Capital Formation at only 13% of GDP, Nigeria needs significant FDI to bridge the infrastructure deficit which is key to diversification

Source: World bank , PwC Analysis

Boosting Investments: Nigeria’s path to growth - https://www.pwc.com/ng/en/assets/pdf/boosting-investment-nigeria.pdf

0%

10%

20%

30%

40%

50%

60%

1990 2000 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Nigeria India China

PwC estimates that Nigeria would need an investment rate of at least 26% of GDP to achieve a growth of 7%

Gross Fixed Capital Formation to GDP

8

PwC

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2013 Qrt. Avg. 2014 Qrt. Avg. 2015 Qrt. Avg. Q1'2016 Q2'2016 Q3'2016 Q4'2016 Q1'2017 Q2'2017

Foreign Portfolio Investment Foreign Direct Investment

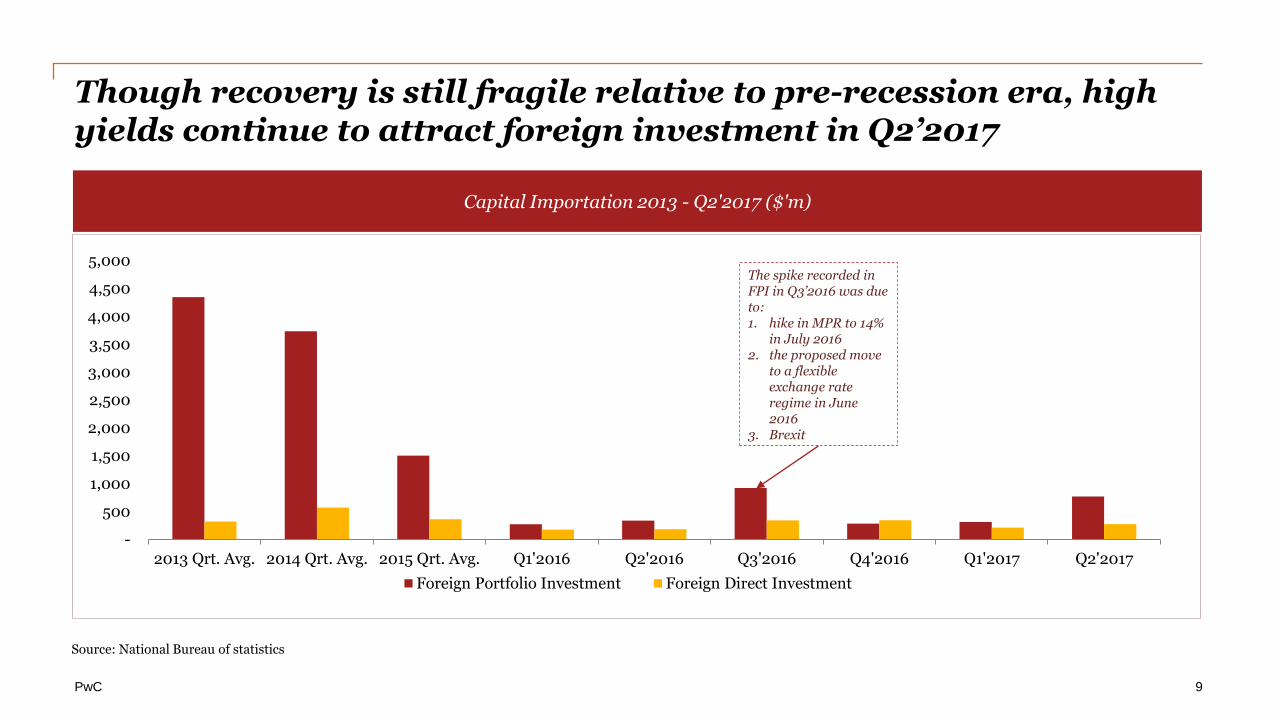

Though recovery is still fragile relative to pre-recession era, high yields continue to attract foreign investment in Q2’2017

Source: National Bureau of statistics

The spike recorded in FPI in Q3’2016 was due to: 1. hike in MPR to 14%

in July 2016 2. the proposed move

to a flexible exchange rate regime in June 2016

3. Brexit

Capital Importation 2013 - Q2'2017 ($'m)

9

PwC

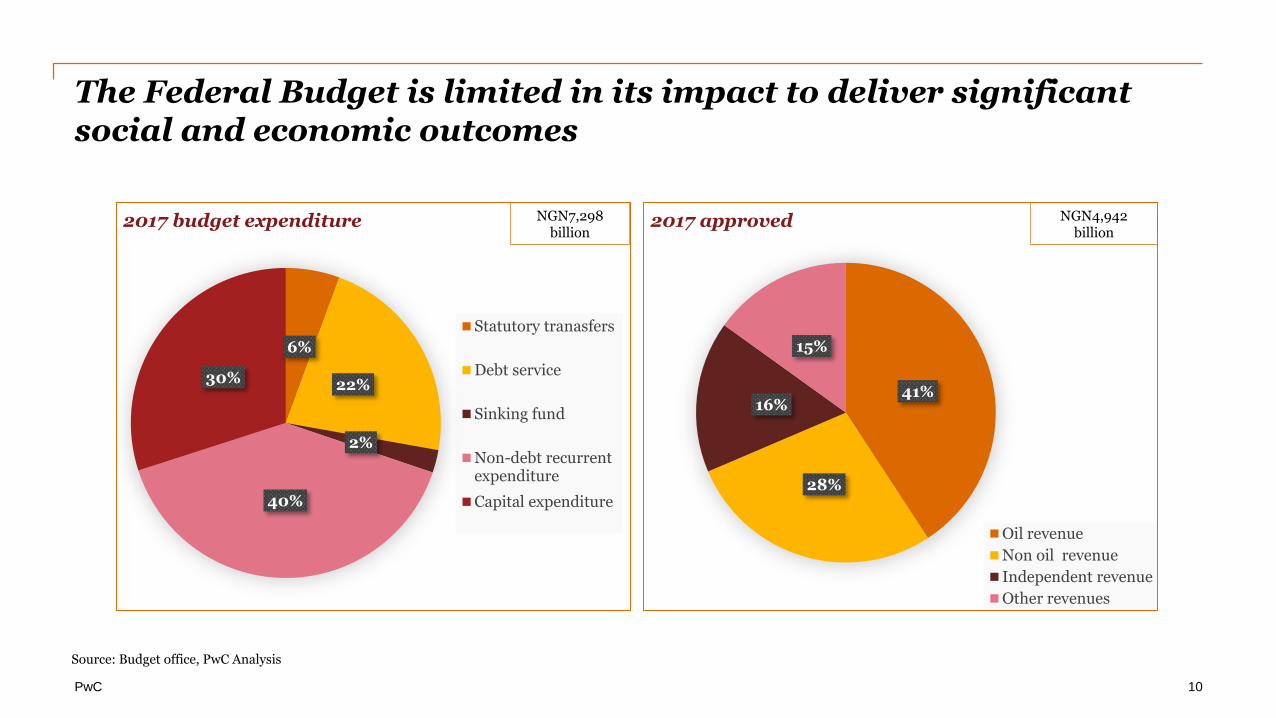

The Federal Budget is limited in its impact to deliver significant social and economic outcomes

41%

28%

16%

15%

2017 approved

Oil revenue

Non oil revenue

Independent revenue

Other revenues

NGN4,942 billion

6%

22%

2%

40%

30%

2017 budget expenditure

Statutory tranasfers

Debt service

Sinking fund

Non-debt recurrentexpenditure

Capital expenditure

NGN7,298 billion

Source: Budget office, PwC Analysis

10

PwC

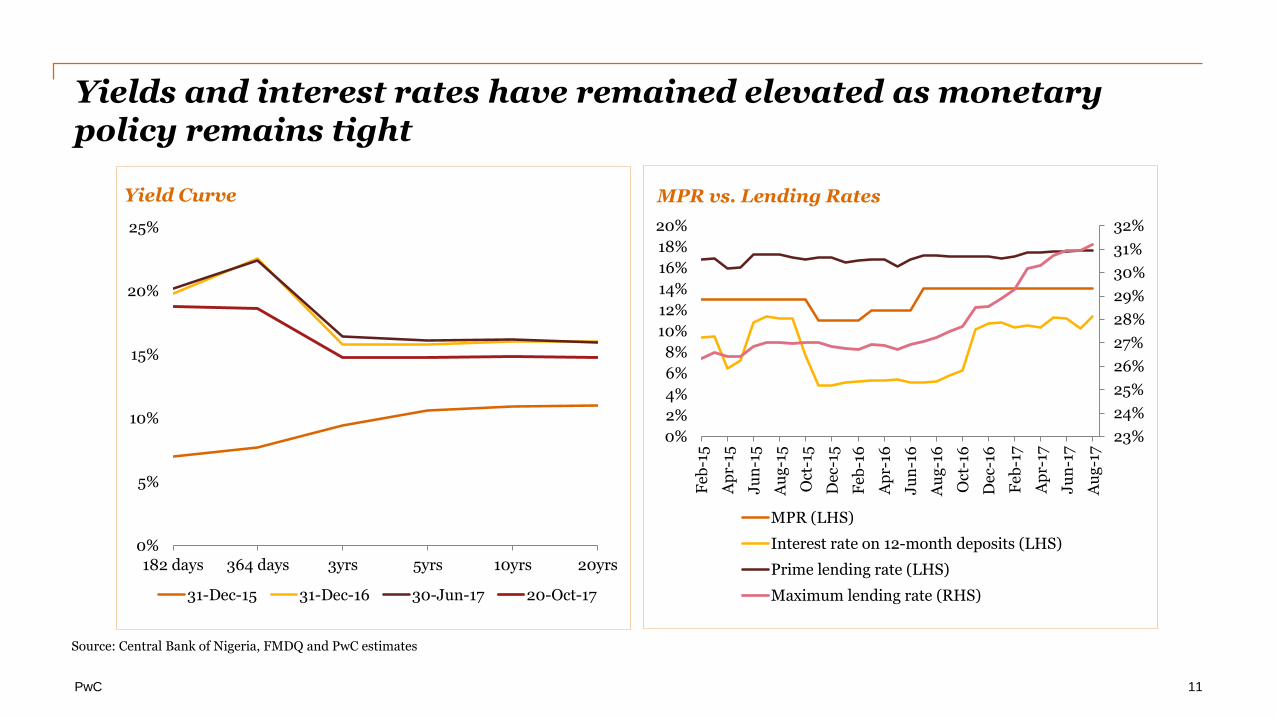

Yields and interest rates have remained elevated as monetary policy remains tight

Source: Central Bank of Nigeria, FMDQ and PwC estimates

23%

24%

25%

26%

27%

28%

29%

30%

31%

32%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Feb

-15

Ap

r-15

Ju

n-1

5

Au

g-1

5

Oct

-15

Dec

-15

Feb

-16

Ap

r-16

Ju

n-1

6

Au

g-1

6

Oct

-16

Dec

-16

Feb

-17

Ap

r-17

Ju

n-1

7

Au

g-1

7

MPR vs. Lending Rates

MPR (LHS)

Interest rate on 12-month deposits (LHS)

Prime lending rate (LHS)

Maximum lending rate (RHS)

0%

5%

10%

15%

20%

25%

182 days 364 days 3yrs 5yrs 10yrs 20yrs

Yield Curve

31-Dec-15 31-Dec-16 30-Jun-17 20-Oct-17

11

PwC

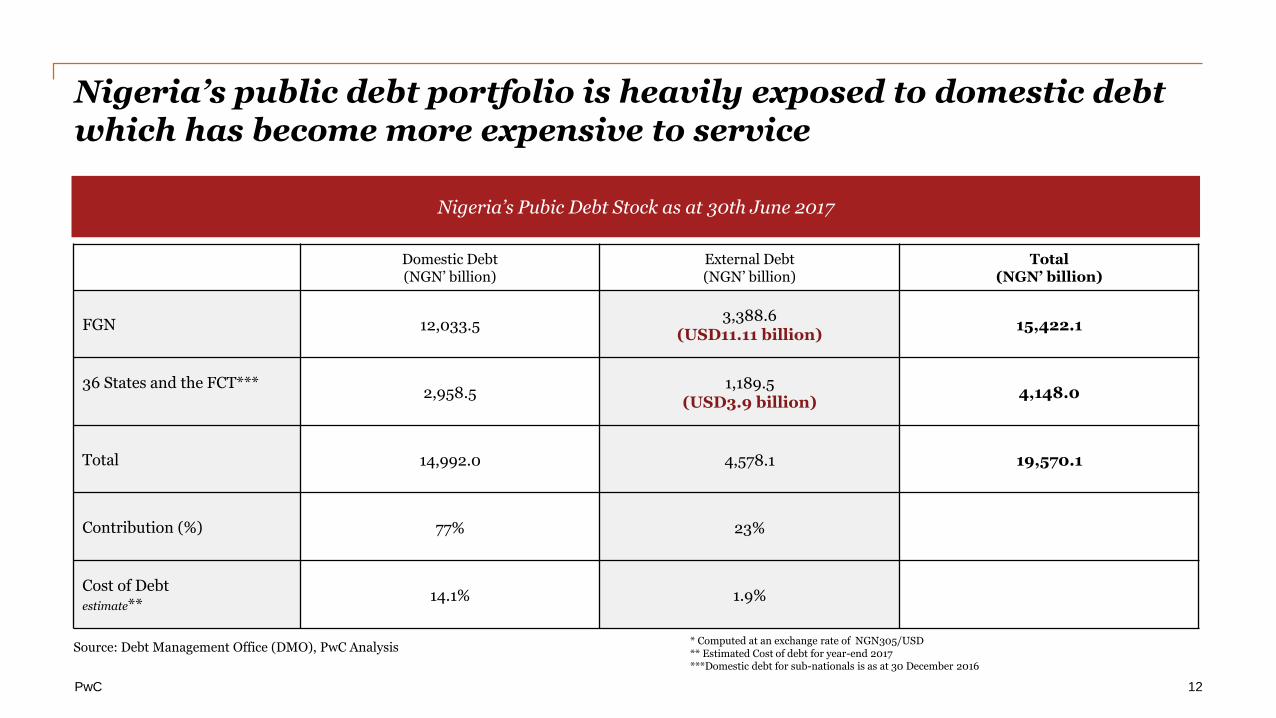

Nigeria’s public debt portfolio is heavily exposed to domestic debt which has become more expensive to service

Domestic Debt(NGN’ billion)

External Debt (NGN’ billion)

Total (NGN’ billion)

FGN 12,033.53,388.6

(USD11.11 billion)15,422.1

36 States and the FCT***2,958.5

1,189.5(USD3.9 billion)

4,148.0

Total 14,992.0 4,578.1 19,570.1

Contribution (%) 77% 23%

Cost of Debtestimate**

14.1% 1.9%

Source: Debt Management Office (DMO), PwC Analysis* Computed at an exchange rate of NGN305/USD** Estimated Cost of debt for year-end 2017***Domestic debt for sub-nationals is as at 30 December 2016

Nigeria’s Pubic Debt Stock as at 30th June 2017

12

PwC

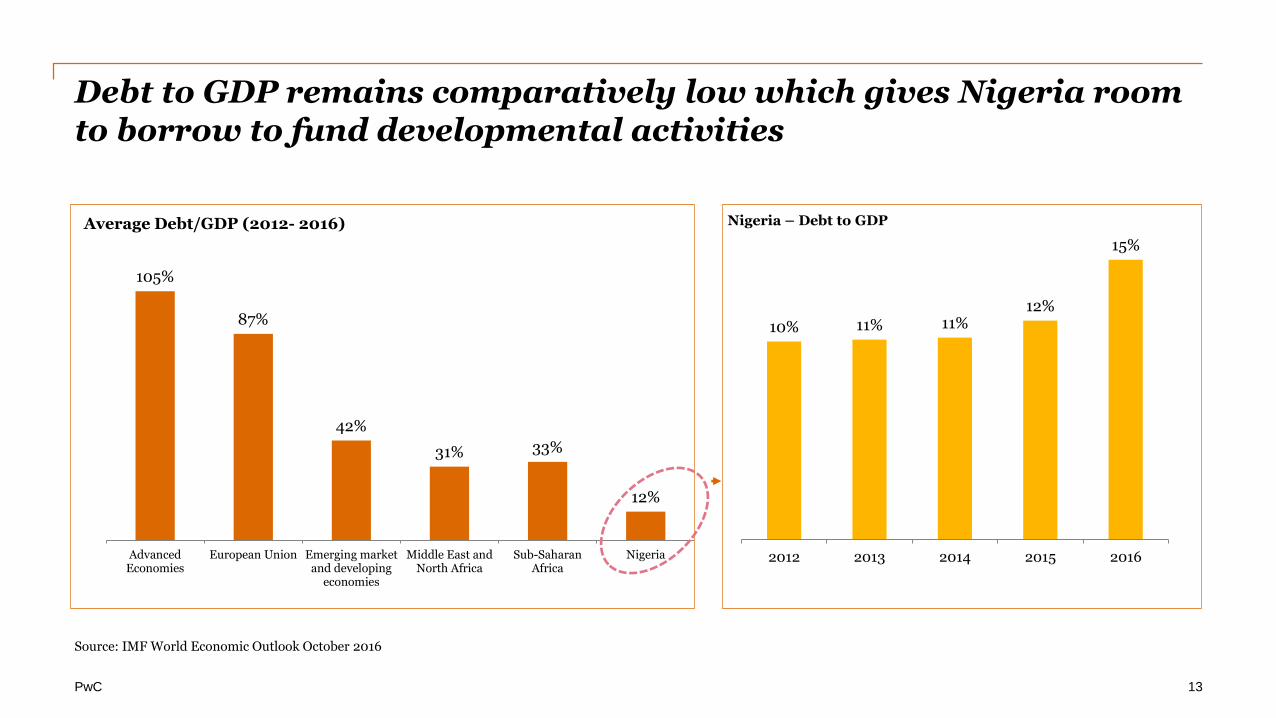

Debt to GDP remains comparatively low which gives Nigeria room to borrow to fund developmental activities

Source: IMF World Economic Outlook October 2016

105%

87%

42%

31% 33%

12%

AdvancedEconomies

European Union Emerging marketand developing

economies

Middle East andNorth Africa

Sub-SaharanAfrica

Nigeria

Average Debt/GDP (2012- 2016)

10% 11% 11%12%

15%

2012 2013 2014 2015 2016

Nigeria – Debt to GDP

13

PwC

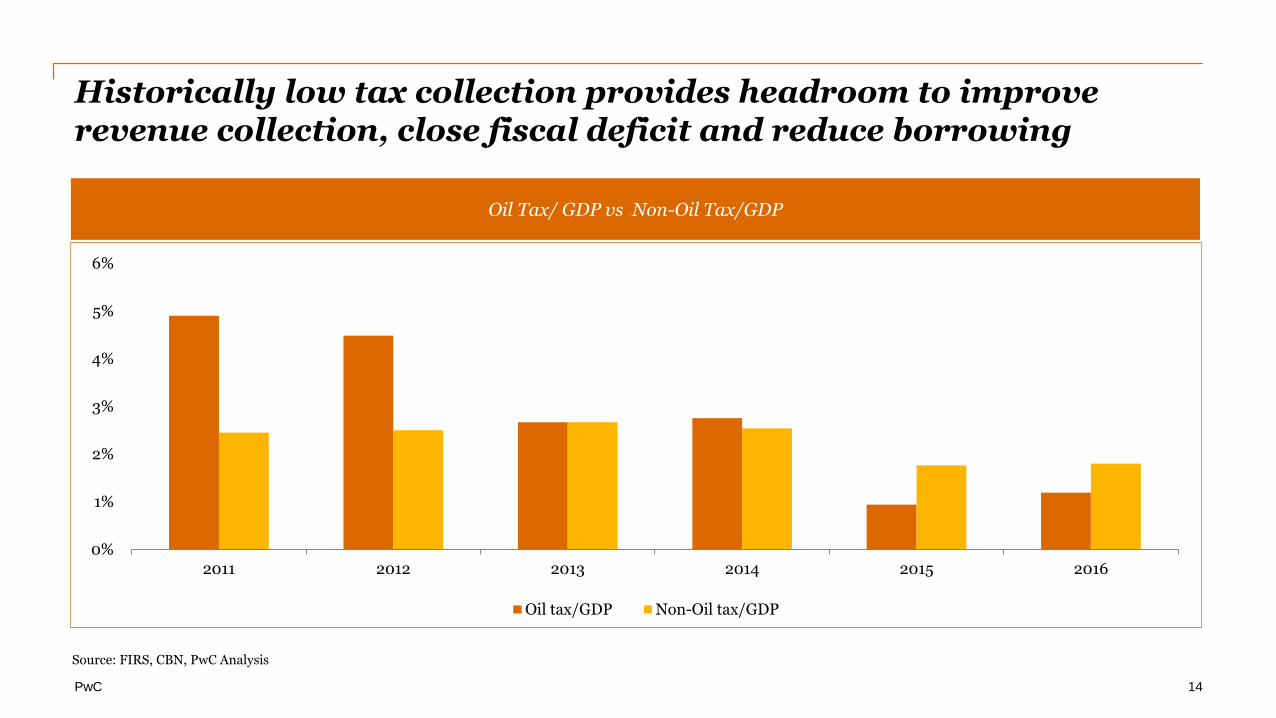

Historically low tax collection provides headroom to improve revenue collection, close fiscal deficit and reduce borrowing

Source: FIRS, CBN, PwC Analysis

0%

1%

2%

3%

4%

5%

6%

2011 2012 2013 2014 2015 2016

Oil tax/GDP Non-Oil tax/GDP

Oil Tax/ GDP vs Non-Oil Tax/GDP

14

PwC

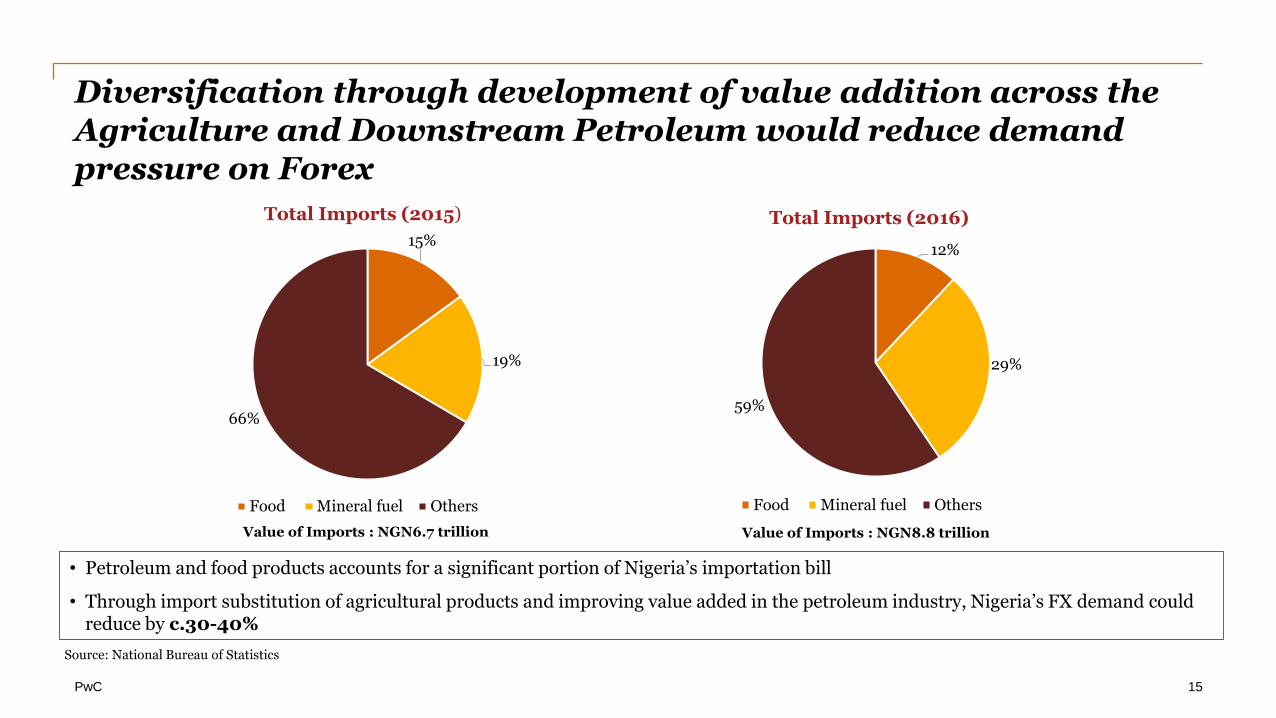

Diversification through development of value addition across the Agriculture and Downstream Petroleum would reduce demand pressure on Forex

• Petroleum and food products accounts for a significant portion of Nigeria’s importation bill

• Through import substitution of agricultural products and improving value added in the petroleum industry, Nigeria’s FX demand could reduce by c.30-40%

15%

19%

66%

Total Imports (2015)

Food Mineral fuel Others

12%

29%

59%

Total Imports (2016)

Food Mineral fuel Others

Value of Imports : NGN6.7 trillion Value of Imports : NGN8.8 trillion

Source: National Bureau of Statistics

15

PwC

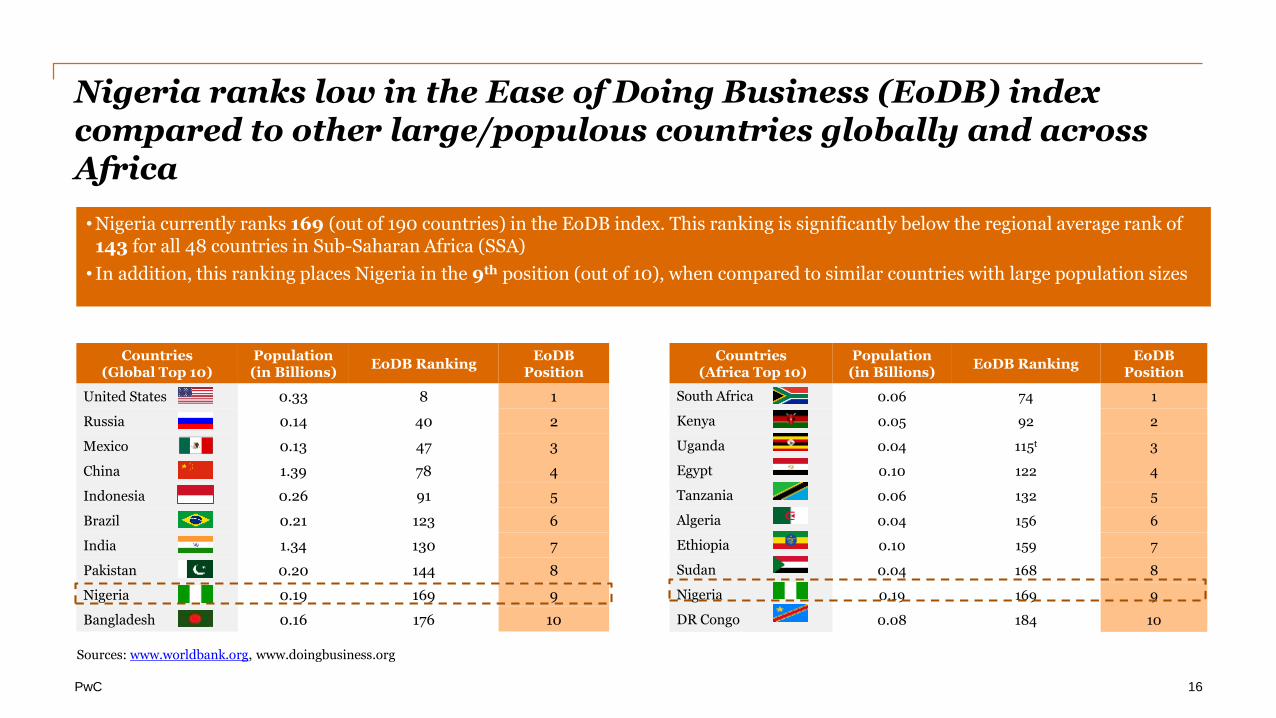

•Nigeria currently ranks 169 (out of 190 countries) in the EoDB index. This ranking is significantly below the regional average rank of 143 for all 48 countries in Sub-Saharan Africa (SSA)

• In addition, this ranking places Nigeria in the 9th position (out of 10), when compared to similar countries with large population sizes

Sources: www.worldbank.org, www.doingbusiness.org

Countries (Global Top 10)

Population (in Billions)

EoDB RankingEoDB

Position

United States 0.33 8 1

Russia 0.14 40 2

Mexico 0.13 47 3

China 1.39 78 4

Indonesia 0.26 91 5

Brazil 0.21 123 6

India 1.34 130 7

Pakistan 0.20 144 8

Nigeria 0.19 169 9

Bangladesh 0.16 176 10

Countries(Africa Top 10)

Population (in Billions)

EoDB RankingEoDB

Position

South Africa 0.06 74 1

Kenya 0.05 92 2

Uganda 0.04 115t 3

Egypt 0.10 122 4

Tanzania 0.06 132 5

Algeria 0.04 156 6

Ethiopia 0.10 159 7

Sudan 0.04 168 8

Nigeria 0.19 169 9

DR Congo 0.08 184 10

Nigeria ranks low in the Ease of Doing Business (EoDB) index compared to other large/populous countries globally and across Africa

16

PwC

Health Landscape in Nigeria

17

PwC

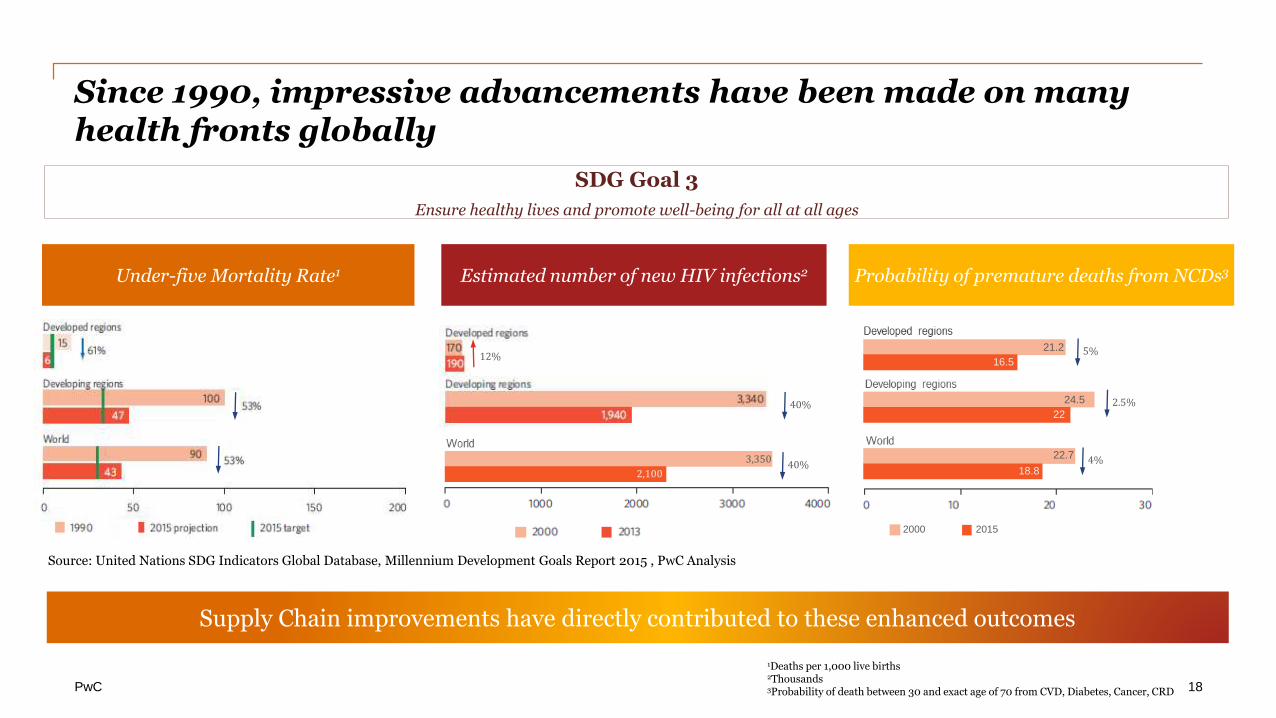

Since 1990, impressive advancements have been made on many health fronts globally

1Deaths per 1,000 live births2Thousands3Probability of death between 30 and exact age of 70 from CVD, Diabetes, Cancer, CRD

Source: United Nations SDG Indicators Global Database, Millennium Development Goals Report 2015 , PwC Analysis

SDG Goal 3

Ensure healthy lives and promote well-being for all at all ages

Supply Chain improvements have directly contributed to these enhanced outcomes

2015

Under-five Mortality Rate1 Estimated number of new HIV infections2

2,100

3,350

Probability of premature deaths from NCDs3

18.8

22.740%

40%22

24.5

16.5

21.2

2.5%

2000 2015

5%

4%

12%

18

PwC

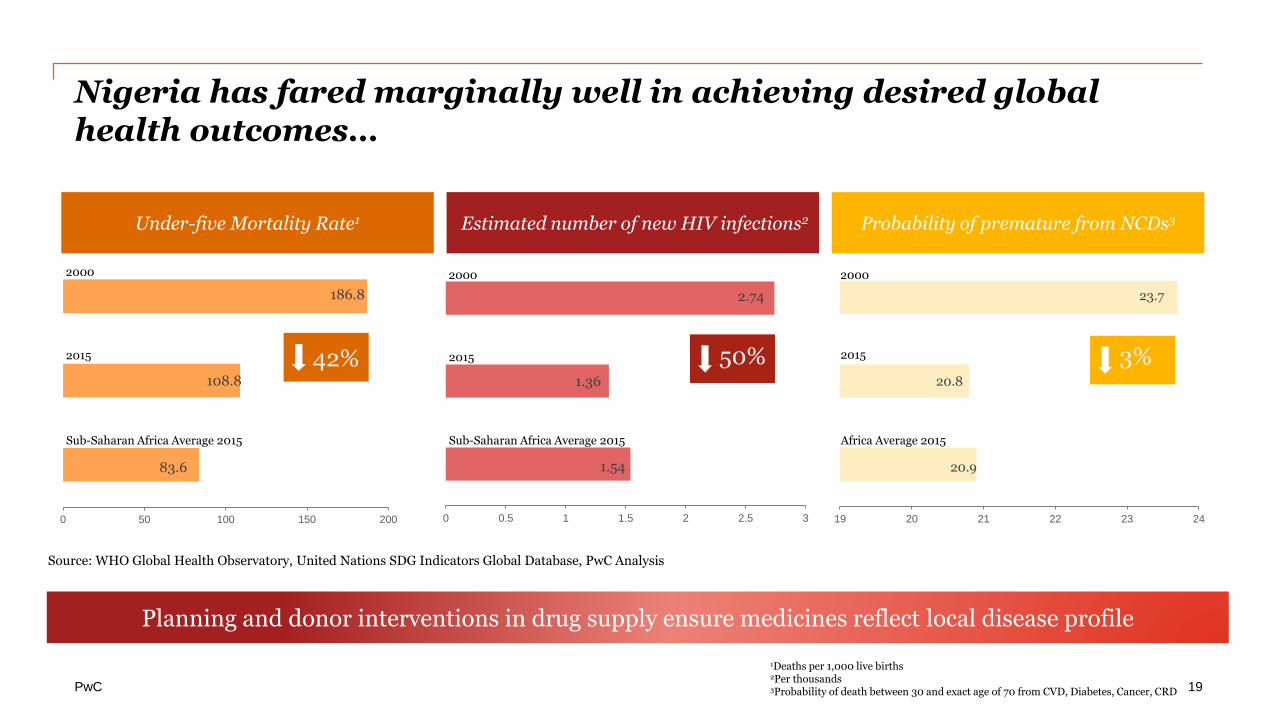

Nigeria has fared marginally well in achieving desired global health outcomes…

Under-five Mortality Rate1 Estimated number of new HIV infections2

83.6

108.8

186.8

0 50 100 150 200

Probability of premature from NCDs3

1.54

1.36

2.74

0 0.5 1 1.5 2 2.5 3

20.9

20.8

23.7

19 20 21 22 23 24

2000

2015

Sub-Saharan Africa Average 2015

2000

2015

Sub-Saharan Africa Average 2015

2000

2015

Africa Average 2015

42% 50% 3%

1Deaths per 1,000 live births2Per thousands3Probability of death between 30 and exact age of 70 from CVD, Diabetes, Cancer, CRD

Planning and donor interventions in drug supply ensure medicines reflect local disease profile

Source: WHO Global Health Observatory, United Nations SDG Indicators Global Database, PwC Analysis

19

PwC

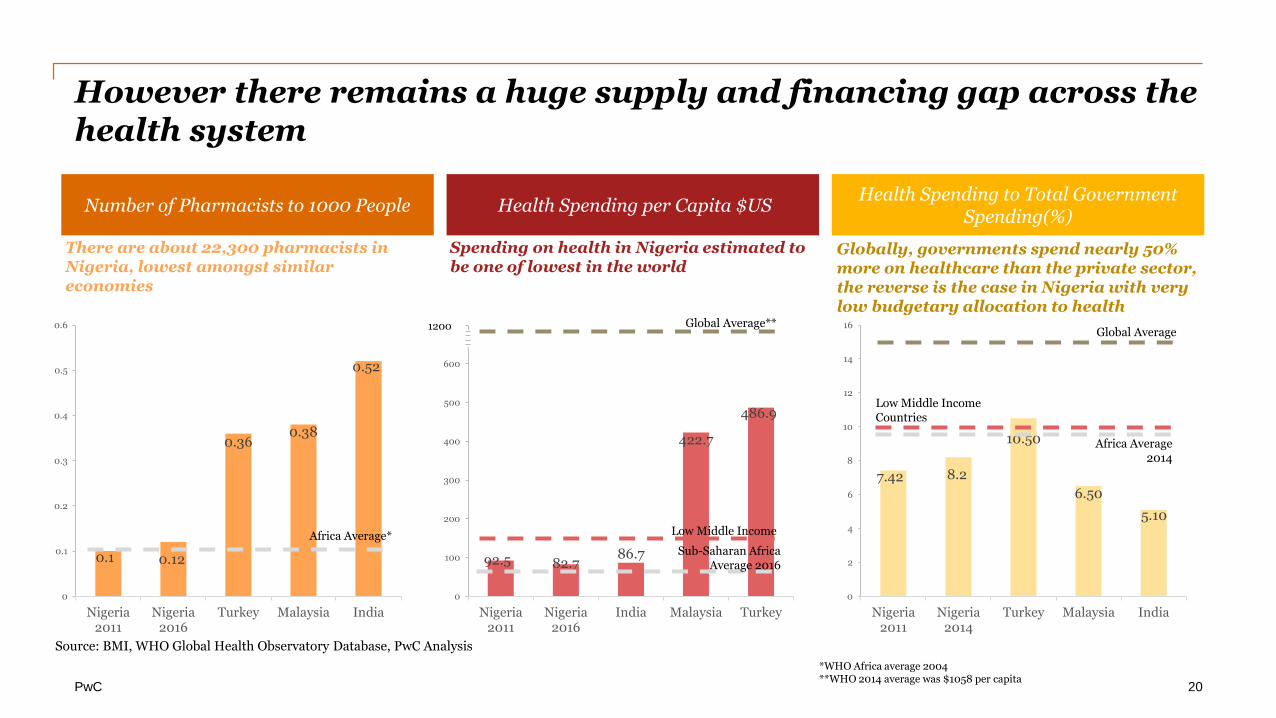

However there remains a huge supply and financing gap across the health system

Number of Pharmacists to 1000 People Health Spending per Capita $US

0.1 0.12

0.360.38

0.52

0

0.1

0.2

0.3

0.4

0.5

0.6

Nigeria2011

Nigeria2016

Turkey Malaysia India

Health Spending to Total Government Spending(%)

Africa Average*

There are about 22,300 pharmacists in Nigeria, lowest amongst similar economies

92.5 82.786.7

422.7

486.9

0

100

200

300

400

500

600

700

Nigeria2011

Nigeria2016

India Malaysia Turkey

Spending on health in Nigeria estimated to be one of lowest in the world

7.42 8.2

10.50

6.50

5.10

0

2

4

6

8

10

12

14

16

Nigeria2011

Nigeria2014

Turkey Malaysia India

Sub-Saharan Africa Average 2016

Global Average**

Low Middle Income

1200

*WHO Africa average 2004**WHO 2014 average was $1058 per capita

Source: BMI, WHO Global Health Observatory Database, PwC Analysis

Global Average

Africa Average 2014

Low Middle Income Countries

Globally, governments spend nearly 50% more on healthcare than the private sector, the reverse is the case in Nigeria with very low budgetary allocation to health

20

PwC

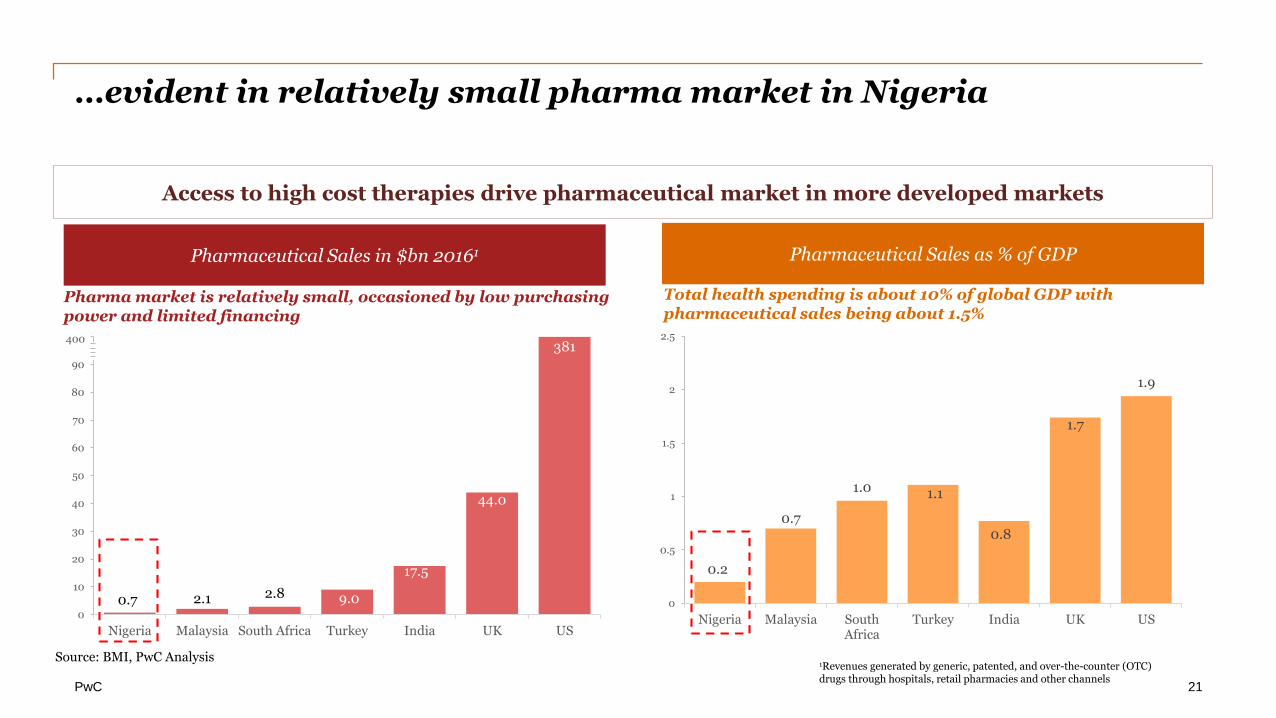

…evident in relatively small pharma market in Nigeria

Pharmaceutical Sales in $bn 20161

0.7 2.1 2.8 9.0

17.5

44.0

381

0

10

20

30

40

50

60

70

80

90

100

Nigeria Malaysia South Africa Turkey India UK US

400

Total health spending is about 10% of global GDP with pharmaceutical sales being about 1.5%

Access to high cost therapies drive pharmaceutical market in more developed markets

Pharma market is relatively small, occasioned by low purchasing power and limited financing

Pharmaceutical Sales as % of GDP

0.2

0.7

1.0 1.1

0.8

1.7

1.9

0

0.5

1

1.5

2

2.5

Nigeria Malaysia SouthAfrica

Turkey India UK US

1Revenues generated by generic, patented, and over-the-counter (OTC) drugs through hospitals, retail pharmacies and other channels

Source: BMI, PwC Analysis

21

PwC

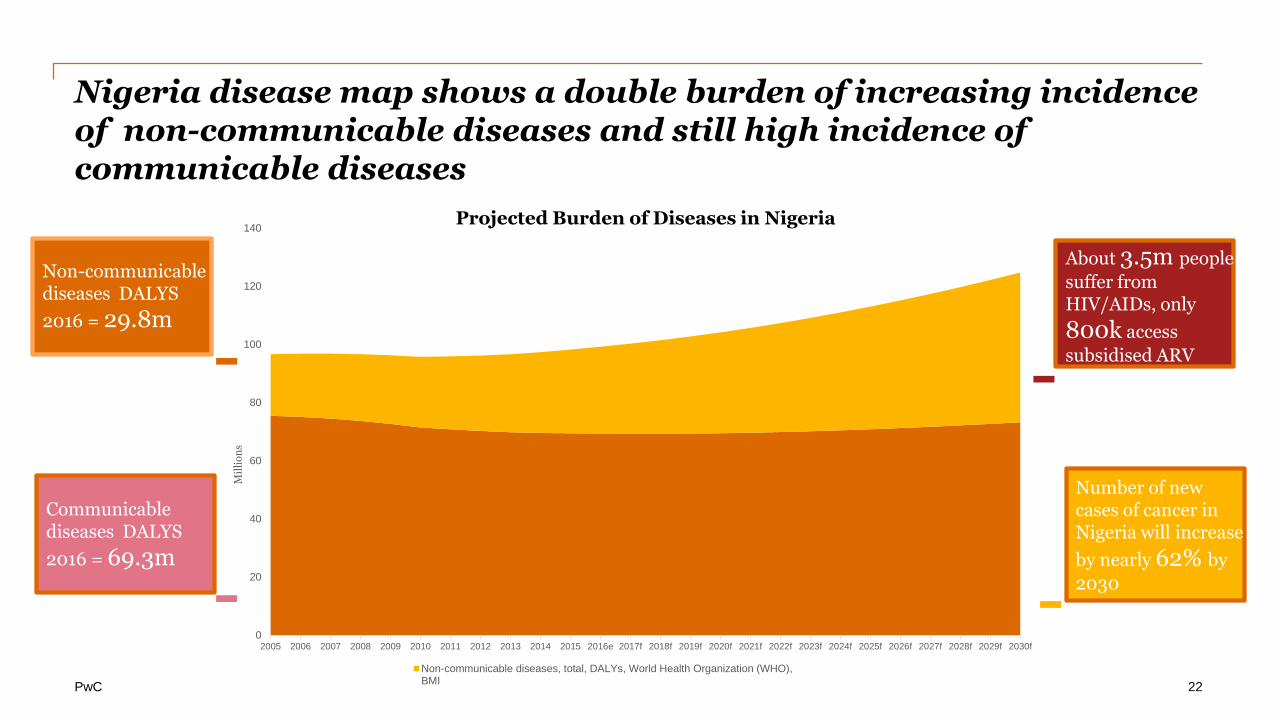

Nigeria disease map shows a double burden of increasing incidence of non-communicable diseases and still high incidence of communicable diseases

Projected Burden of Diseases in Nigeria

Number of new cases of cancer in Nigeria will increase

by nearly 62% by

2030

Non-communicable diseases DALYS

2016 = 29.8m

About 3.5m people

suffer from HIV/AIDs, only

800k access

subsidised ARV

Co

mm

un

ica

ble

Dis

ease

s

0

20

40

60

80

100

120

140

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016e 2017f 2018f 2019f 2020f 2021f 2022f 2023f 2024f 2025f 2026f 2027f 2028f 2029f 2030f

Mil

lio

ns

Non-communicable diseases, total, DALYs, World Health Organization (WHO),BMI

Communicable diseases DALYS

2016 = 69.3m

22

PwC

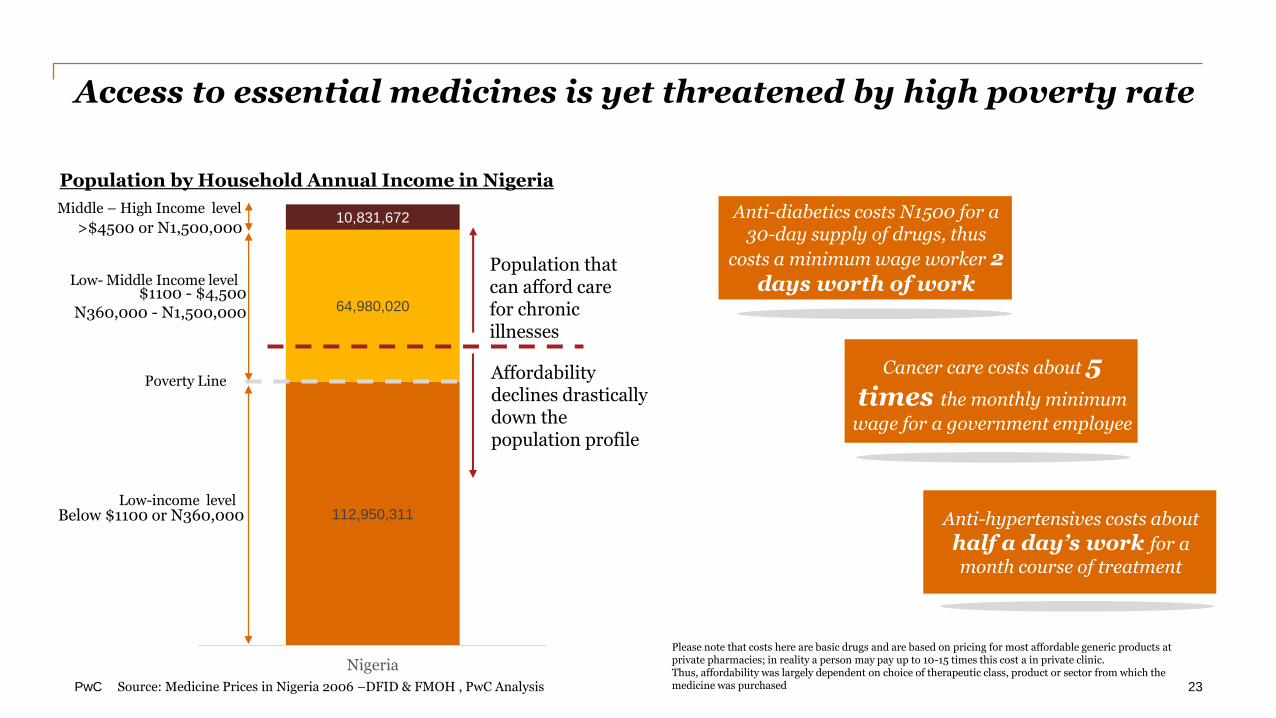

Access to essential medicines is yet threatened by high poverty rate

Population by Household Annual Income in Nigeria

112,950,311

64,980,020

10,831,672

Nigeria

Middle – High Income level

Low- Middle Income level

Low-income level

>$4500 or N1,500,000

$1100 - $4,500N360,000 - N1,500,000

Below $1100 or N360,000

Please note that costs here are basic drugs and are based on pricing for most affordable generic products at private pharmacies; in reality a person may pay up to 10-15 times this cost a in private clinic. Thus, affordability was largely dependent on choice of therapeutic class, product or sector from which the medicine was purchased

Cancer care costs about 5 times the monthly minimum

wage for a government employee

Anti-hypertensives costs about

half a day’s work for a

month course of treatment

Anti-diabetics costs N1500 for a 30-day supply of drugs, thus

costs a minimum wage worker 2 days worth of work

Population that can afford care for chronic illnesses

Affordability declines drastically down the population profile

Poverty Line

Source: Medicine Prices in Nigeria 2006 –DFID & FMOH , PwC Analysis 23

PwC

Technology for Drug Security

24

PwC

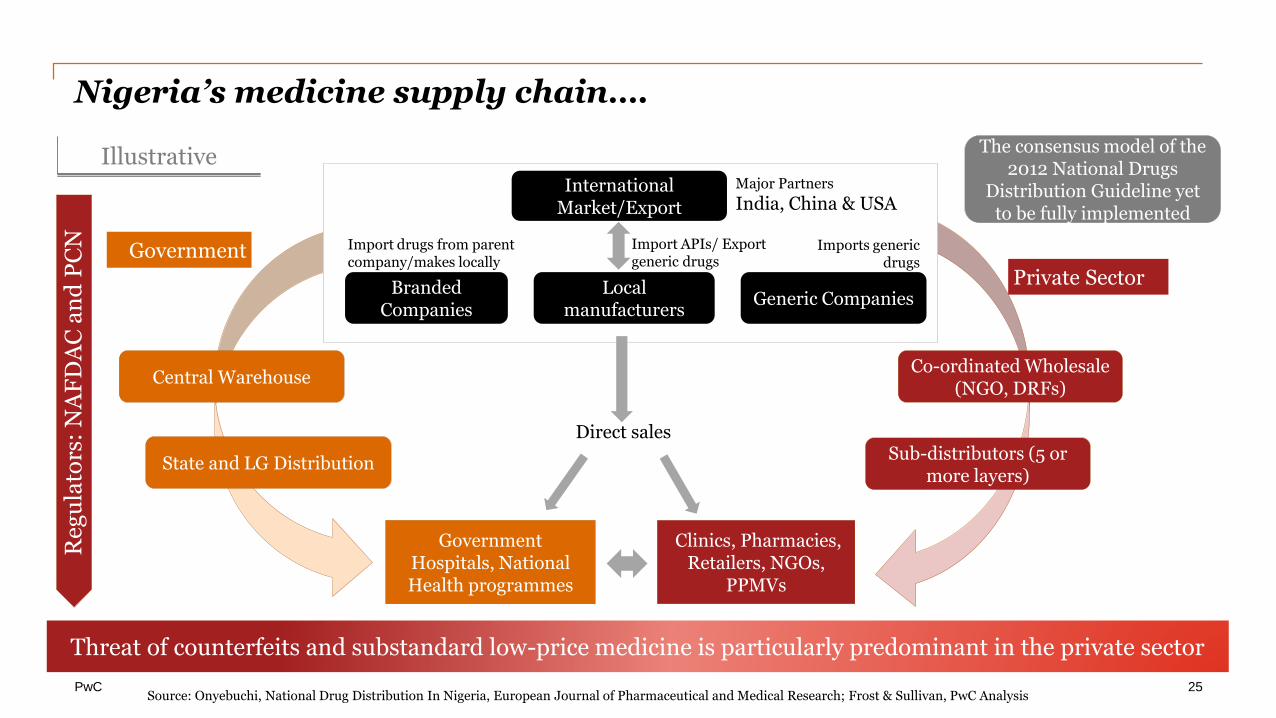

Nigeria’s medicine supply chain….

Local manufacturers

Branded Companies

Generic Companies

Government Hospitals, National Health programmes

Co-ordinated Wholesale (NGO, DRFs)

State and LG Distribution

Clinics, Pharmacies, Retailers, NGOs,

PPMVs

International Market/Export

Central Warehouse

Direct sales

Major Partners

India, China & USA

Government

Private Sector

Import APIs/ Export generic drugs

Imports generic drugs

Threat of counterfeits and substandard low-price medicine is particularly predominant in the private sector

Sub-distributors (5 or more layers)

Illustrative

Reg

ula

tors

: N

AF

DA

C a

nd

PC

N

Source: Onyebuchi, National Drug Distribution In Nigeria, European Journal of Pharmaceutical and Medical Research; Frost & Sullivan, PwC Analysis

The consensus model of the 2012 National Drugs

Distribution Guideline yet to be fully implemented

Import drugs from parent company/makes locally

25

PwC

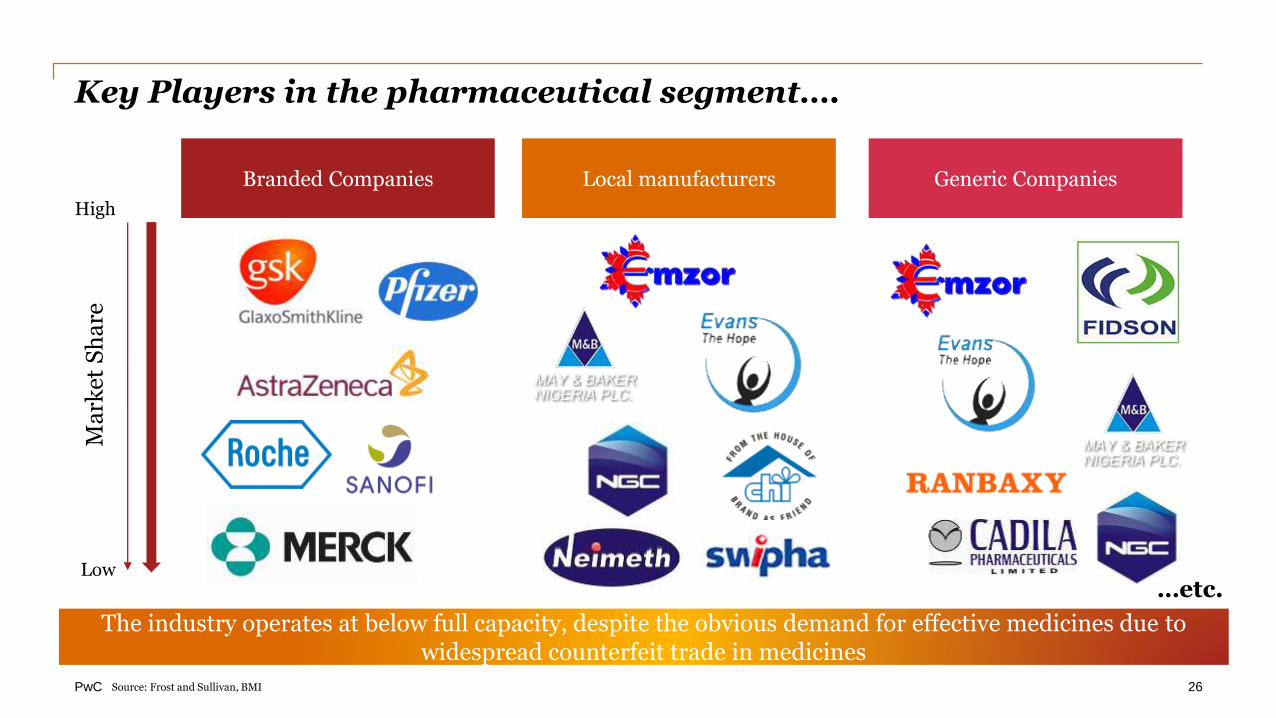

Key Players in the pharmaceutical segment….

Local manufacturersBranded Companies Generic Companies

Ma

rket

Sh

are

High

Low…etc.

The industry operates at below full capacity, despite the obvious demand for effective medicines due to widespread counterfeit trade in medicines

Source: Frost and Sullivan, BMI 26

PwC

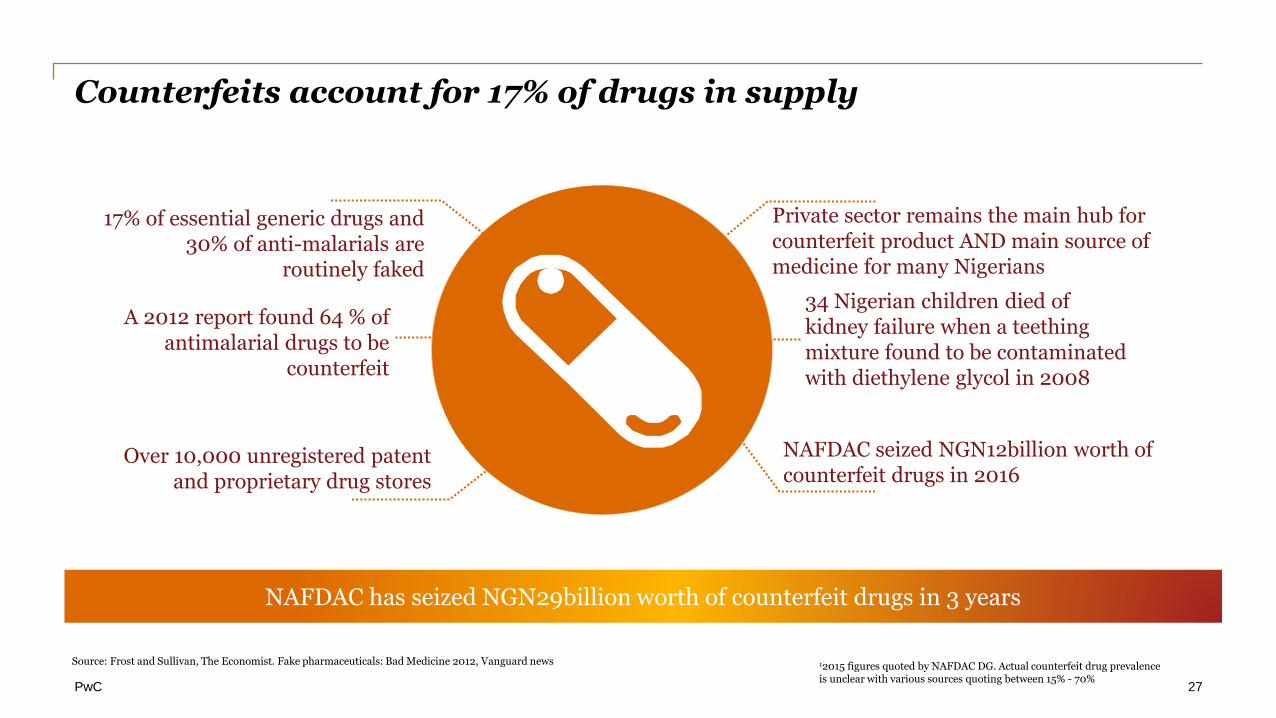

Counterfeits account for 17% of drugs in supply

17% of essential generic drugs and 30% of anti-malarials are

routinely faked

Private sector remains the main hub for counterfeit product AND main source of medicine for many Nigerians

NAFDAC seized NGN12billion worth of counterfeit drugs in 2016

NAFDAC has seized NGN29billion worth of counterfeit drugs in 3 years

Source: Frost and Sullivan, The Economist. Fake pharmaceuticals: Bad Medicine 2012, Vanguard news

A 2012 report found 64 % of antimalarial drugs to be

counterfeit

Over 10,000 unregistered patent and proprietary drug stores

34 Nigerian children died of kidney failure when a teething mixture found to be contaminated with diethylene glycol in 2008

27

12015 figures quoted by NAFDAC DG. Actual counterfeit drug prevalence is unclear with various sources quoting between 15% - 70%

PwC

NAFDAC has pioneered several authentication technologies targeted at fighting counterfeit drugs

NAFDAC is the first regulatory agency in the world to use the Truscan

Mobile Authentication service

Black eye Infra-red scanners to enhance packaging security

Radio Frequency Identification System to authenticate high-value

brands

More needs to be done in securing the supply chain end-to-end

On the back of technology adoption, circulation of counterfeit medicines dropped from 40% in 2001 to

16.7% in 20151

12015 figures quoted by NAFDAC DG. Actual counterfeit drug prevalence is unclear with various sources quoting between 15% - 70%

28

PwC

A new mandatory method called “mass serialization,” often combined with “track-and-trace” requirements, is becoming the worldwide standard for regulators in securing the supply chain

Experts say the backing technologies may still be inadequate

Serialization

Track-and-trace

29

PwC

The use case for blockchain technology

30

yolojo-kosoko

Typewritten text

https://youtu.be/9_Dvnz7aBRc

PwC

Advantages

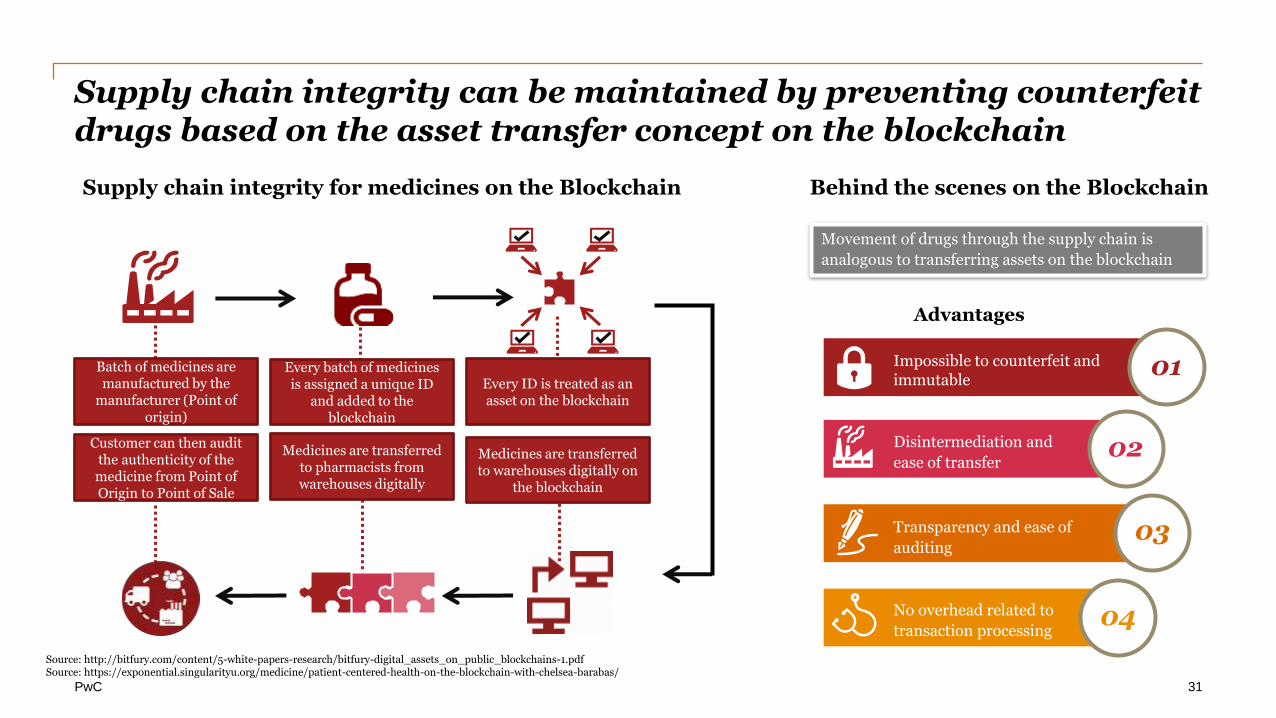

Supply chain integrity can be maintained by preventing counterfeit drugs based on the asset transfer concept on the blockchain

Batch of medicines are manufactured by the

manufacturer (Point of origin)

Every batch of medicines is assigned a unique ID

and added to the blockchain

Every ID is treated as an asset on the blockchain

Medicines are transferred to warehouses digitally on

the blockchain

Medicines are transferred to pharmacists from warehouses digitally

Customer can then audit the authenticity of the medicine from Point of Origin to Point of Sale

Supply chain integrity for medicines on the Blockchain Behind the scenes on the Blockchain

01

02

03

04

Impossible to counterfeit and immutable

Disintermediation and

ease of transfer

Transparency and ease of

auditing

No overhead related to

transaction processing

Movement of drugs through the supply chain is

analogous to transferring assets on the blockchain

Source: http://bitfury.com/content/5-white-papers-research/bitfury-digital_assets_on_public_blockchains-1.pdfSource: https://exponential.singularityu.org/medicine/patient-centered-health-on-the-blockchain-with-chelsea-barabas/

31

PwC

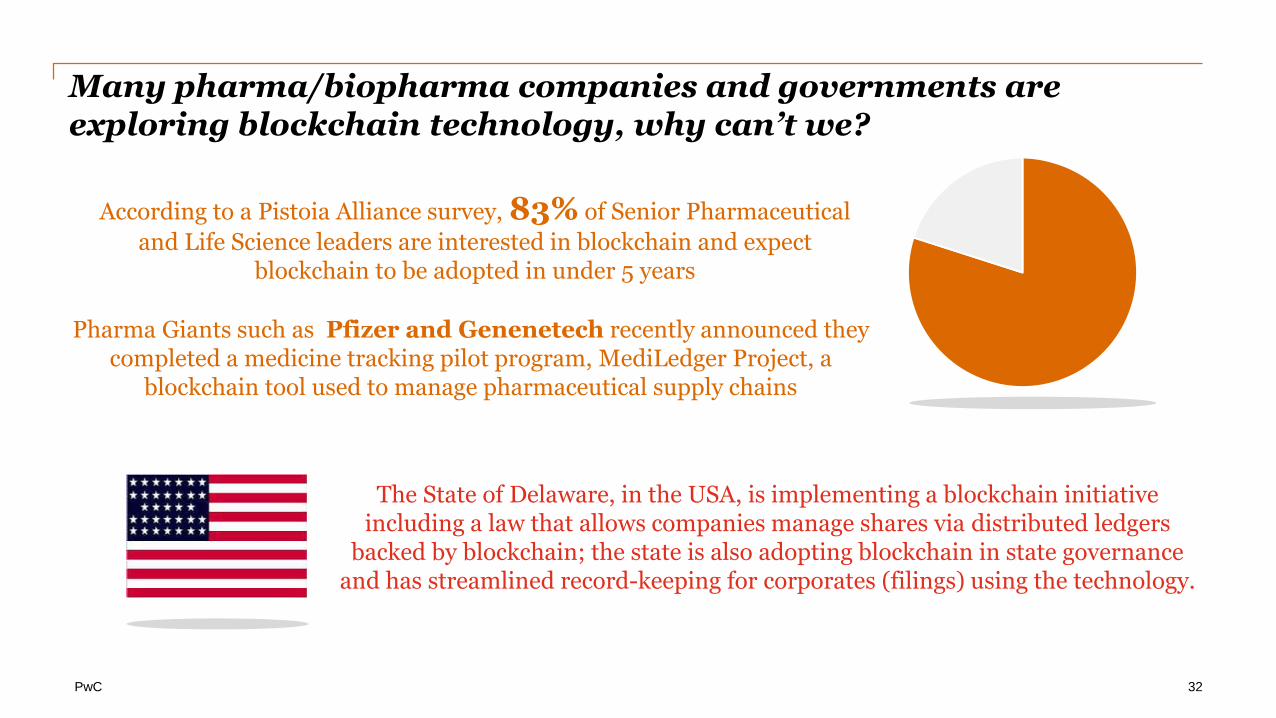

Many pharma/biopharma companies and governments are exploring blockchain technology, why can’t we?

According to a Pistoia Alliance survey, 83% of Senior Pharmaceutical

and Life Science leaders are interested in blockchain and expect blockchain to be adopted in under 5 years

Pharma Giants such as Pfizer and Genenetech recently announced they completed a medicine tracking pilot program, MediLedger Project, a

blockchain tool used to manage pharmaceutical supply chains

The State of Delaware, in the USA, is implementing a blockchain initiative including a law that allows companies manage shares via distributed ledgers

backed by blockchain; the state is also adopting blockchain in state governance and has streamlined record-keeping for corporates (filings) using the technology.

32

PwC

What else can be done?

33

PwC

Mandatory licensing of patented drugs to improve access to essential treatments for NCDs and infectious diseases

Advocacy for increased funding for health

Get behind a system

1

2

3

Industry including pharma companies and the government, consider the following…

34

PwC

Do NOT turn a blind eye to malpractices and counterfeits in the system. Remember about 100,000 people die annually in Africa from fake drugs

Provide pharmaceuticals in the best interest of patients

1

Every pharmacist must also remember their duty

35

PwC

Thank You

36