DRIVES US TOWARD FURTHER SUCCESS · Financial Highlight: 3Q18 & 9M18 performance Hyvahl & RDCC...

36

GDP DRIVES US TOWARD FURTHER SUCCESS

Transcript of DRIVES US TOWARD FURTHER SUCCESS · Financial Highlight: 3Q18 & 9M18 performance Hyvahl & RDCC...

GDP

DRIVES US TOWARD FURTHER SUCCESS

Performance by Business

Financial Performance

Strategic Direction

3Q18 Highlight

2

Projects Update

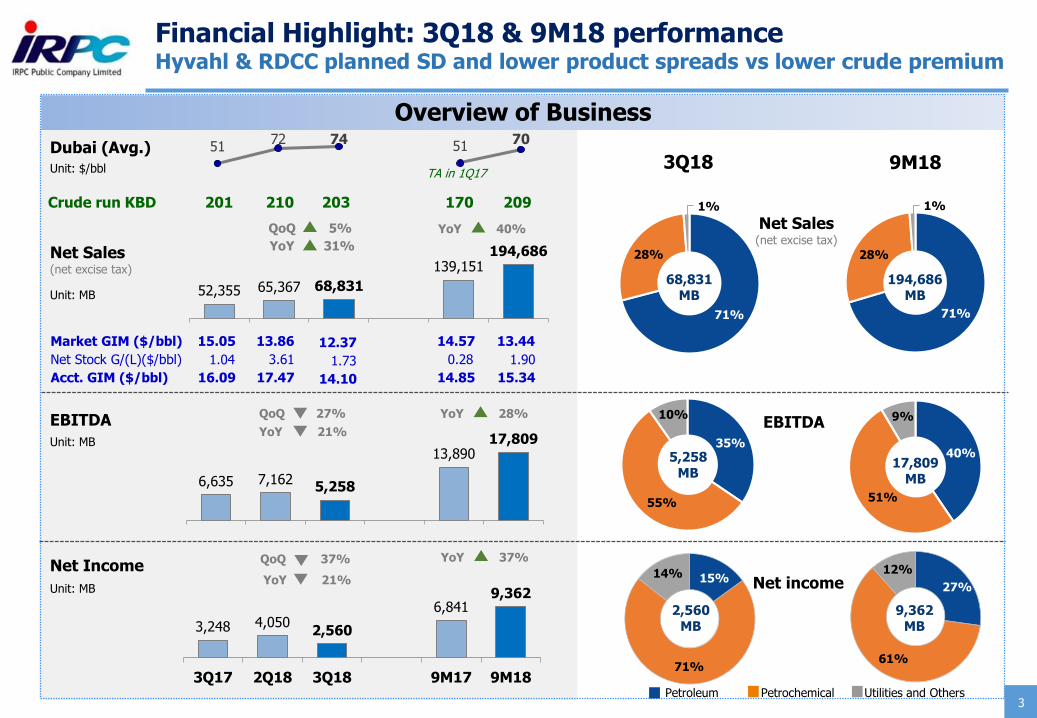

Financial Highlight: 3Q18 & 9M18 performanceHyvahl & RDCC planned SD and lower product spreads vs lower crude premium

27%

61%

12%

52,355 65,367 68,831

139,151 194,686

QoQ 5%

YoY 31%

Overview of Business

Net Sales(net excise tax)

Dubai (Avg.)

Unit: $/bbl

Net Income

Unit: MB

Unit: MB

YoY 21%

QoQ 37%

EBITDA

Unit: MB

6,635 7,162 5,258

13,890 17,809

QoQ 27%

YoY 21%

Petroleum Petrochemical Utilities and Others

Net Sales(net excise tax)

EBITDA

Net income

9M18

40%

51%

9%

71%

28%

1%

194,686MB

17,809MB

3,248 4,050 2,560

6,841 9,362

3Q17 2Q18 3Q18 9M17 9M18

9,362MB

Market GIM ($/bbl) 15.05 13.86 12.37

5172 74

5170

Crude run KBD 201 210 203

Acct. GIM ($/bbl) 16.09 17.47 14.10

3

3Q18

35%

55%

10%

71%

28%

1%

68,831MB

5,258MB

15%

71%

14%

2,560MB

Net Stock G/(L)($/bbl) 1.04 3.61 1.73

YoY 37%

YoY 28%

YoY 40%

170 209

TA in 1Q17

14.57

15.34

1.90

13.44

14.85

0.28

Awards & Achievement in 3Q18

received outstanding plant management

“Best SET Sustainability Awards 2018

And Thailand Sustainability

Investment”

4

IRPC’s Achievement

Social Contribution Marketing

By The Stock Exchange of Thailand (SET)

“Thailand Energy Awards 2018”

For Plant Management

By Department of Alternative Energy Development and Efficiency,

Ministry of Energy

“Excellent CG Scoring Company”

Corporate Governance Report : CGR

By Thai Institute of Directors (IOD)and The Stock Exchange

of Thailand (SET)

“Dow Jones Sustainability Indices (DJSI) Member”

In Oil and Gas Refining & Marketing Industry

The 5th consecutive year, with the highest score

By RobecoSAM

“IRPC Join Guangzhao SaijuPerformance Polymer Ltd.”

Investment in plastic product E-Commerce business in

The PRC and incorporation a subsidiary under the

laws of Thailand

“Top Community Care Companies in Asia 2018”

By Asia Corporate Excellence & Sustainability Awards

5

IRPC’s DJSI Achievements DJSI member for the 5th consecutive year

2018

2014

2015

2016

2017

Listed in “The Sustainability Year Book 2014”

1st yearDJSI Member Listed

2nd yearDJSI Member Listed

3rd yearDJSI Member Listed

4th yearDJSI Member Listed

2013

5th yearDJSI Member ListedAnd ranked as Industry Leader

IRPC received the highest scores from Dow Jones Sustainability Indices (DJSI):Oil and Gas Refining and Marketing Industry Leader and being DJSI member for the 5th consecutive year

Expecting RobecoSAMSustainability Award Gold Class 2019

2019

Performance by Business

Financial Performance

Strategic Direction

3Q18 Highlight

6

Projects Update

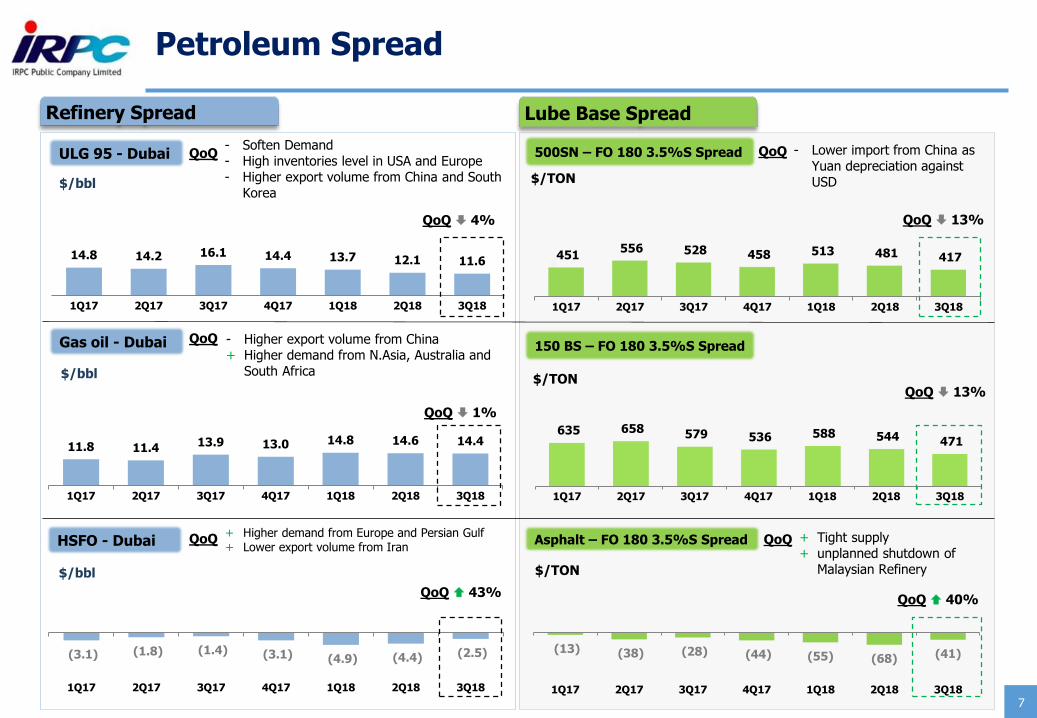

Petroleum Spread

7

+ Higher demand from Europe and Persian Gulf+ Lower export volume from Iran

11.8 11.4 13.9 13.0 14.8 14.6 14.4

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

- Soften Demand- High inventories level in USA and Europe- Higher export volume from China and South

Korea

14.8 14.2 16.1 14.4 13.7 12.1 11.6

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

(3.1) (1.8) (1.4) (3.1) (4.9) (4.4) (2.5)

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

500SN – FO 180 3.5%S Spread

150 BS – FO 180 3.5%S Spread

Asphalt – FO 180 3.5%S Spread

$/bbl

$/bbl

$/bbl

Lube Base SpreadRefinery Spread

Gas oil - Dubai

ULG 95 - Dubai

HSFO - Dubai

(13) (38) (28) (44) (55) (68) (41)

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

635 658 579 536 588 544 471

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

451 556 528 458 513 481 417

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

QoQ 13%

QoQ 43%

QoQ 13%

QoQ 1%

QoQ 40%

- Higher export volume from China + Higher demand from N.Asia, Australia and

South Africa

QoQ 4%

+ Tight supply + unplanned shutdown of

Malaysian Refinery

QoQ

QoQ

QoQ

QoQ

QoQ

$/TON

$/TON

$/TON

- Lower import from China as Yuan depreciation against USD

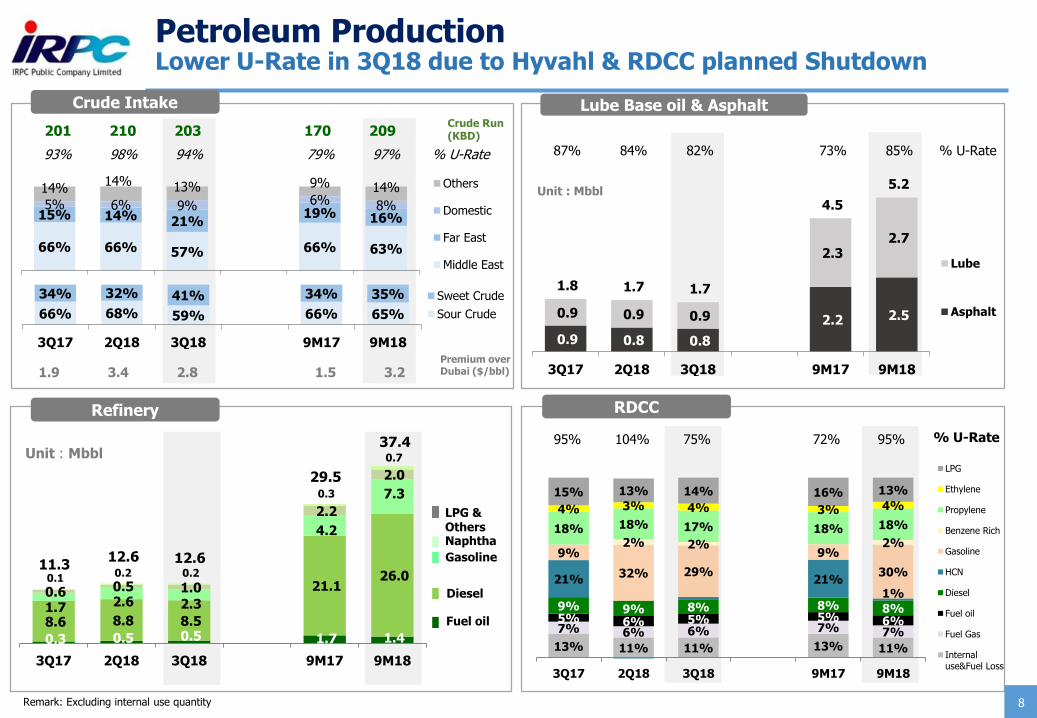

13% 11% 11% 13% 11%

7% 6% 6% 7% 7%5% 6% 5% 5% 6%

9% 9% 8% 8% 8%

21% 21%1%

9%

32% 29%

9%

30%

2% 2% 2%18% 18% 17% 18% 18%

4% 3% 4% 3% 4%15% 13% 14% 16% 13%

3Q17 2Q18 3Q18 . 9M17 9M18

LPG

Ethylene

Propylene

Benzene Rich

Gasoline

HCN

Diesel

Fuel oil

Fuel Gas

Internaluse&Fuel Loss

0.9 0.8 0.8

2.2 2.5 0.9 0.9 0.9

2.3 2.7

1.8 1.7 1.7

4.5

5.2

3Q17 2Q18 3Q18 9M17 9M18

Lube

Asphalt66% 68% 59% 66% 65%

34% 32% 41% 34% 35%

3Q17 2Q18 3Q18 9M17 9M18

Sweet Crude

Sour Crude

201 210 203 170 209

Petroleum ProductionLower U-Rate in 3Q18 due to Hyvahl & RDCC planned Shutdown

1.9 3.4 2.8 1.5 3.2

93% 98% 94% 79% 97% % U-Rate

Unit : Mbbl

Unit : Mbbl

LPG & OthersNaphtha

Gasoline

Diesel

Fuel oil

Remark: Excluding internal use quantity

Premium over Dubai ($/bbl)

95% 104% 75% 72% 95% % U-Rate

Crude Intake

RDCC Refinery

Lube Base oil & Asphalt

87% 84% 82% 73% 85% % U-Rate

0.3 0.5 0.5 1.7 1.4 8.6 8.8 8.5

21.1 26.0

1.7 2.6 2.3

4.2

7.3

0.6 0.5 1.0

2.2

2.0

0.1 0.2 0.2

0.3

0.7

11.3 12.6 12.6

29.5

37.4

3Q17 2Q18 3Q18 9M17 9M18

8

66% 66% 57% 66% 63%

15% 14% 21%19% 16%

5% 6% 9% 6% 8%

14%14% 13% 9% 14% Others

Domestic

Far East

Middle East

Crude Run (KBD)

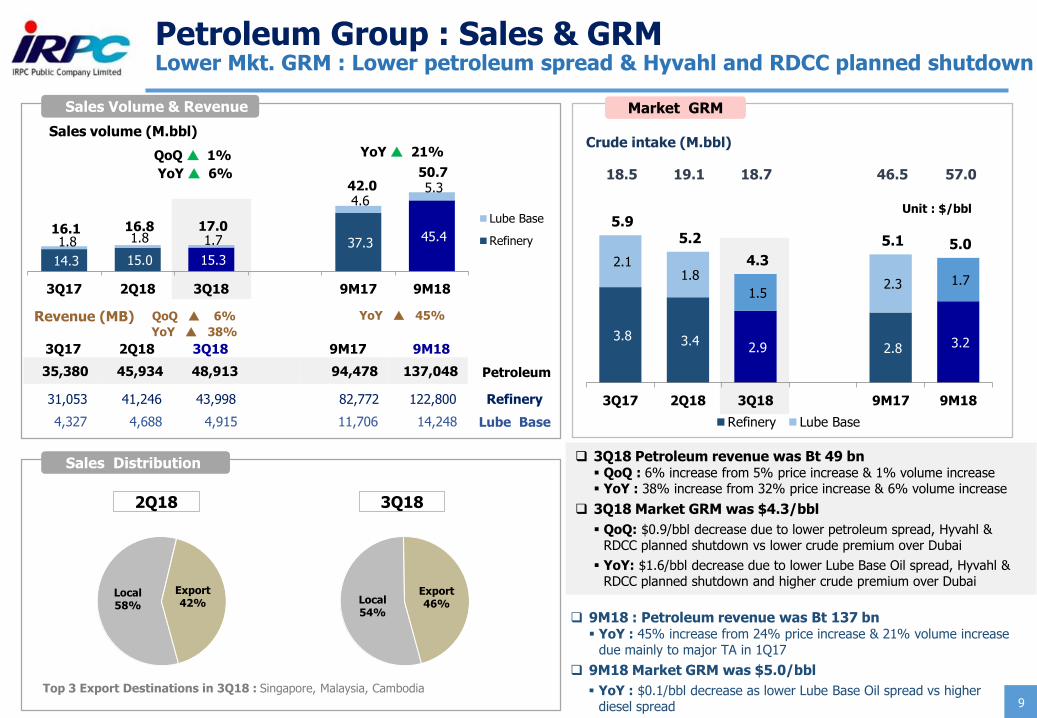

Petroleum Group : Sales & GRMLower Mkt. GRM : Lower petroleum spread & Hyvahl and RDCC planned shutdown

3.8 3.4 2.9 2.8 3.2

2.1 1.8

1.5 2.3 1.7

5.9 5.2

4.3

5.1 5.0

3Q17 2Q18 3Q18 9M17 9M18

Refinery Lube Base4,327 4,688 4,915 11,706 14,248

14.3 15.0 15.3

37.3 45.4 1.8 1.8 1.7

4.6 5.3

16.1 16.8 17.0

42.0 50.7

3Q17 2Q18 3Q18 9M17 9M18

Lube Base

Refinery

31,053 41,246 43,998 82,772 122,800 Refinery

35,380 45,934 48,913 94,478 137,048

Sales Volume & Revenue

18.5 19.1 18.7 46.5 57.0

Crude intake (M.bbl)

Unit : $/bbl

Sales Distribution

Top 3 Export Destinations in 3Q18 : Singapore, Malaysia, Cambodia

YoY 6%

QoQ 1%

YoY 38%

QoQ 6%

Sales volume (M.bbl)

Revenue (MB)

❑ 9M18 : Petroleum revenue was Bt 137 bn▪ YoY : 45% increase from 24% price increase & 21% volume increase

due mainly to major TA in 1Q17

❑ 9M18 Market GRM was $5.0/bbl

▪ YoY : $0.1/bbl decrease as lower Lube Base Oil spread vs higher diesel spread

3Q17 2Q18 3Q18 9M17 9M18

Market GRM

❑ 3Q18 Petroleum revenue was Bt 49 bn▪ QoQ : 6% increase from 5% price increase & 1% volume increase▪ YoY : 38% increase from 32% price increase & 6% volume increase

❑ 3Q18 Market GRM was $4.3/bbl

▪ QoQ: $0.9/bbl decrease due to lower petroleum spread, Hyvahl & RDCC planned shutdown vs lower crude premium over Dubai

▪ YoY: $1.6/bbl decrease due to lower Lube Base Oil spread, Hyvahl & RDCC planned shutdown and higher crude premium over Dubai

9

YoY 21%

YoY 45%

Petroleum

Lube Base

Local58%

Export42%

2Q18

Local54%

Export46%

3Q18

10

Petrochemical Spread

200 170 159

109 137 115 121

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

591 544 622 626 659 581 550

171 286 201 284 367 427 267

762 830 823 910 1,026 1,008

817

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

Ethylene-NP HDPE-Ethylene

192 202 182 114

182 164 217

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

1,029 878 977 905 998 945 898

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

435 296 323 258 406 362 361

228 365 356 363 287 298 256

663 661 679 621 693 660 617

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

Propylene-NP PP-Propylene

HDPE-Ethylene –Naphtha Spread

PP-Propylene –Naphtha Spread

MX – Naphtha SpreadToluene – Naphtha Spread

PS –Naphtha SpreadABS –Naphtha Spread

Ole

fin

sS

tyre

nic

sA

rom

ati

cs

1,382 1,226 1,377 1,353 1,428 1,379 1,248

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

- Lower demand from Monsoon

QoQ 19% QoQ 7%

QoQ 5%

QoQ 5% QoQ 9%

QoQ 32%

- Higher utilization rate - Soften demand from China

- Lower Chinese demand due to weaken Yuan

+ Tight supply from turnaround

QoQ

QoQ

QoQ

QoQ

QoQ

QoQ

+ Increasing demand

$/TON

$/TON

$/TON$/TON

$/TON

$/TON

+ Higher PX demand+ Tight supply from turnaround in

N.E.A.

- High production volume in China- Weaken demand

109 106 87

253 297

4 4 6

9

14

81 87 86

229

250

194 197 179

490

561

100 75 61 192 209

162 196 202

401

592

261 271 263

592

801

Polyolefins

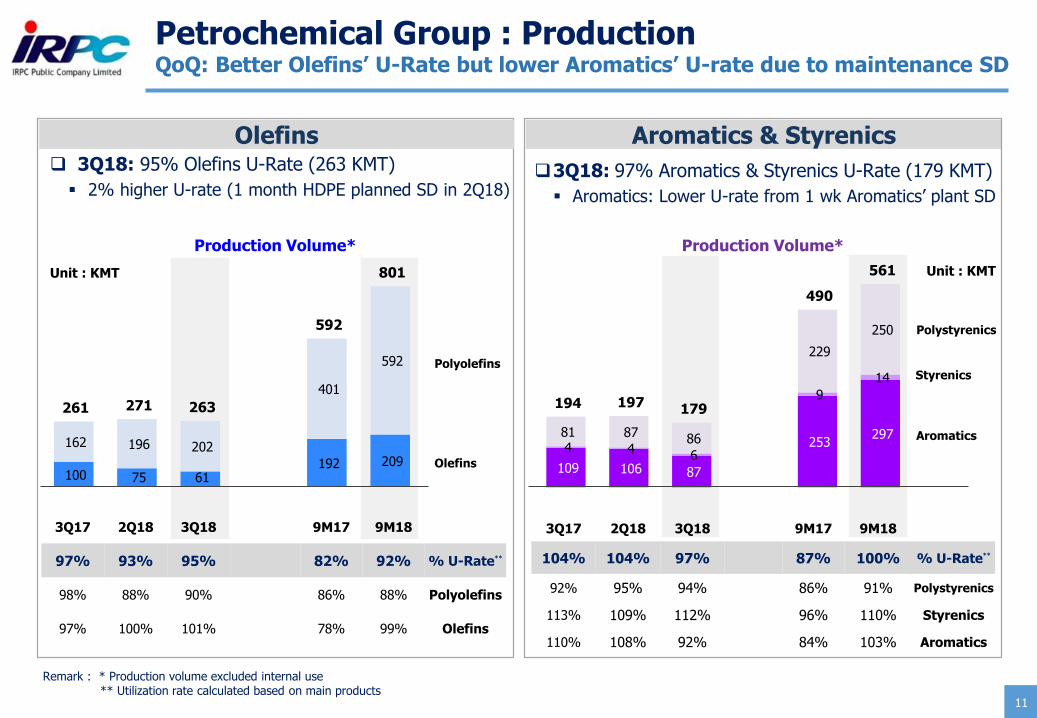

Petrochemical Group : ProductionQoQ: Better Olefins’ U-Rate but lower Aromatics’ U-rate due to maintenance SD

3Q17 2Q18 3Q18 9M17 9M18

97% 93% 95% 82% 92% % U-Rate**

98% 88% 90% 86% 88% Polyolefins

97% 100% 101% 78% 99% Olefins

Aromatics & StyrenicsOlefins

3Q17 2Q18 3Q18 9M17 9M18

104% 104% 97% 87% 100% % U-Rate**

92% 95% 94% 86% 91% Polystyrenics

113% 109% 112% 96% 110% Styrenics

110% 108% 92% 84% 103% Aromatics

Olefins

Unit : KMT

Remark : * Production volume excluded internal use** Utilization rate calculated based on main products

❑ 3Q18: 95% Olefins U-Rate (263 KMT)

▪ 2% higher U-rate (1 month HDPE planned SD in 2Q18)

Polystyrenics

Styrenics

Aromatics

❑3Q18: 97% Aromatics & Styrenics U-Rate (179 KMT)

▪ Aromatics: Lower U-rate from 1 wk Aromatics’ plant SD

Unit : KMT

11

Production Volume* Production Volume*

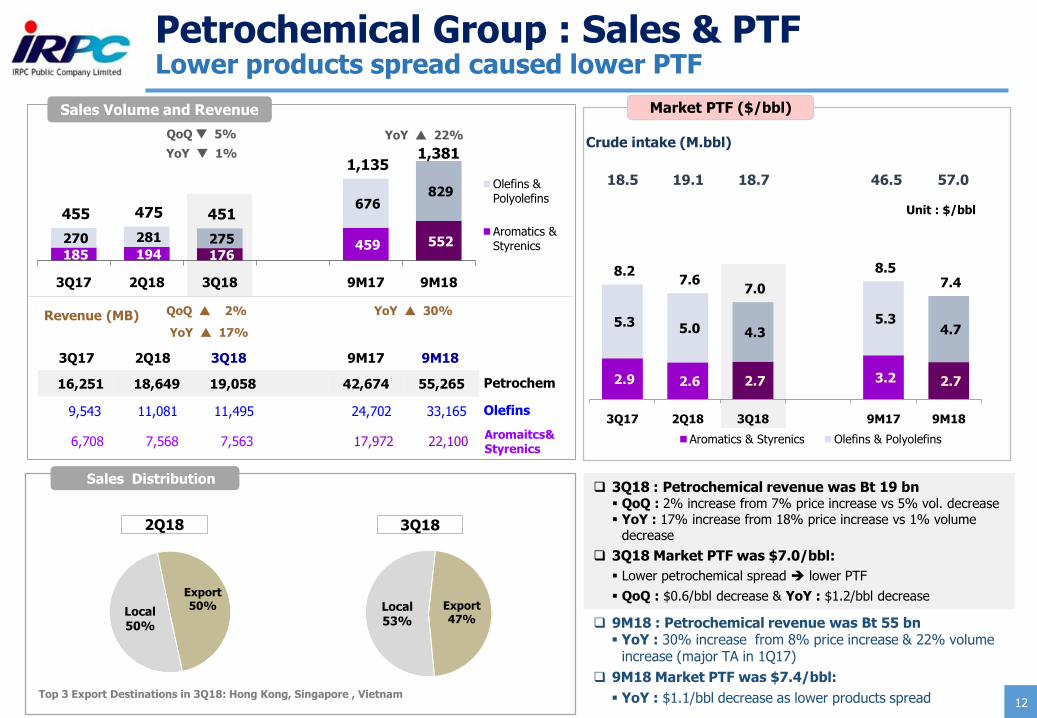

Petrochemical Group : Sales & PTFLower products spread caused lower PTF

185 194 176 459 552 270 281 275

676 829

455 475 451

1,135 1,381

3Q17 2Q18 3Q18 9M17 9M18

Olefins &Polyolefins

Aromatics &Styrenics

2.9 2.6 2.7 3.2 2.7

5.3 5.0 4.3 5.3

4.7

8.2 7.6

7.0

8.5 7.4

3Q17 2Q18 3Q18 9M17 9M18

Unit : $/bbl

Aromatics & Styrenics Olefins & Polyolefins

Sales Volume and Revenue

Sales Distribution

Top 3 Export Destinations in 3Q18: Hong Kong, Singapore , Vietnam

QoQ 5%

QoQ 2% Revenue (MB)

3Q17 2Q18 3Q18 9M17 9M18

YoY 1%

YoY 17%

Market PTF ($/bbl)

16,251 18,649 19,058 42,674 55,265

9,543 11,081 11,495 24,702 33,165

6,708 7,568 7,563 17,972 22,100

12

YoY 22%

YoY 30%

Petrochem

Olefins

Aromaitcs&Styrenics

❑ 9M18 : Petrochemical revenue was Bt 55 bn▪ YoY : 30% increase from 8% price increase & 22% volume

increase (major TA in 1Q17)

❑ 9M18 Market PTF was $7.4/bbl:

▪ YoY : $1.1/bbl decrease as lower products spread

❑ 3Q18 : Petrochemical revenue was Bt 19 bn▪ QoQ : 2% increase from 7% price increase vs 5% vol. decrease▪ YoY : 17% increase from 18% price increase vs 1% volume

decrease

❑ 3Q18 Market PTF was $7.0/bbl:

▪ Lower petrochemical spread ➔ lower PTF

▪ QoQ : $0.6/bbl decrease & YoY : $1.2/bbl decrease Local53%

Export47%

3Q18

Local50%

Export50%

2Q18

18.5 19.1 18.7 46.5 57.0

Crude intake (M.bbl)

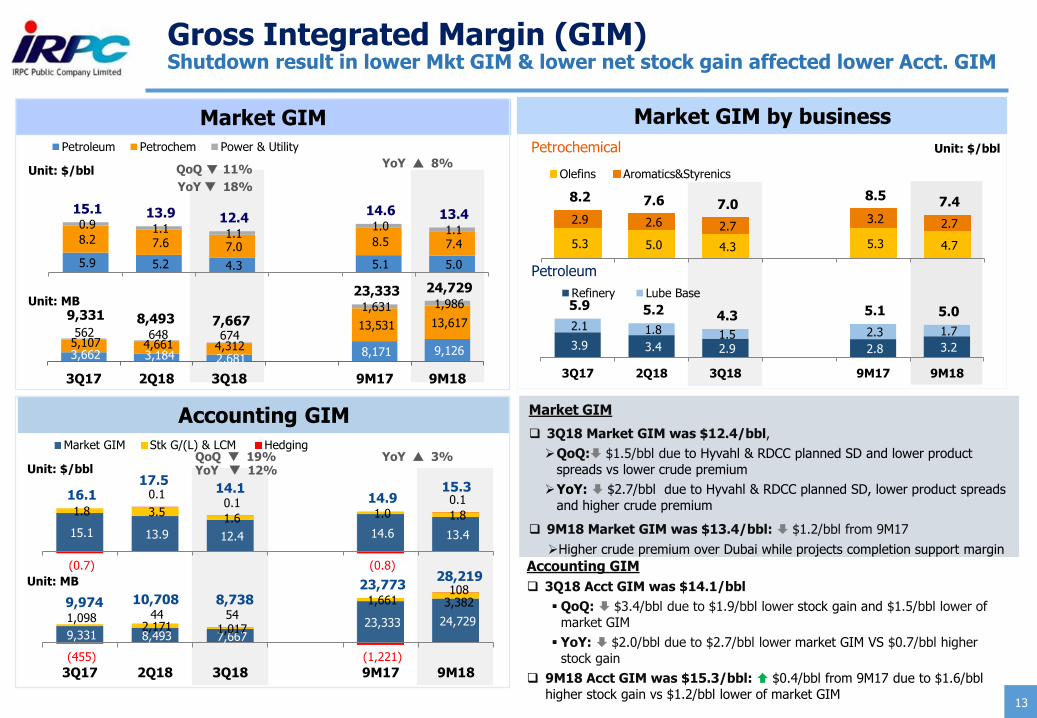

Market GIM

❑ 3Q18 Market GIM was $12.4/bbl,

➢QoQ: $1.5/bbl due to Hyvahl & RDCC planned SD and lower product

spreads vs lower crude premium

➢YoY: $2.7/bbl due to Hyvahl & RDCC planned SD, lower product spreads

and higher crude premium

❑ 9M18 Market GIM was $13.4/bbl: $1.2/bbl from 9M17

➢Higher crude premium over Dubai while projects completion support margin

3.9 3.4 2.9 2.8 3.2

2.1 1.8 1.5 2.3 1.7

5.9 5.2 4.3 5.1 5.0

3Q17 2Q18 3Q18 9M17 9M18

Refinery Lube Base

5.3 5.0 4.3 5.3 4.7

2.9 2.6 2.7 3.2 2.7

8.2 7.6 7.0 8.5 7.4

Olefins Aromatics&Styrenics

5.9 5.2 4.3 5.1 5.0

8.2 7.6 7.0 8.5 7.4

0.9 1.1 1.1 1.0 1.1

15.1 13.9 12.4 14.6 13.4

Petroleum Petrochem Power & Utility

3,662 3,184 2,681 8,171 9,126

5,107 4,661 4,312

13,531 13,617 562 648 674

1,631 1,986 9,331 8,493 7,667

23,333 24,729

3Q17 2Q18 3Q18 9M17 9M18

9,331 8,493 7,667 23,333 24,729 1,098

2,171 1,017

1,661 3,382

(455)

44 54

(1,221)

108 9,974 10,708 8,738

23,773 28,219

3Q17 2Q18 3Q18 9M17 9M18

15.1 13.9 12.4 14.6 13.4

1.8 3.5 1.6 1.0 1.8

(0.7)

0.1 0.1

(0.8)

0.1 16.1 17.5

14.114.9

15.3

Market GIM Stk G/(L) & LCM Hedging

Market GIM

Unit: $/bbl

Accounting GIM

Unit: $/bbl

Unit: MB

Market GIM by business

Unit: $/bblPetrochemical

Petroleum

Unit: MB

13

Gross Integrated Margin (GIM)Shutdown result in lower Mkt GIM & lower net stock gain affected lower Acct. GIM

YoY 18%

QoQ 11%

YoY 8%

YoY 12% YoY 3% QoQ 19%

Accounting GIM

❑ 3Q18 Acct GIM was $14.1/bbl

▪ QoQ: $3.4/bbl due to $1.9/bbl lower stock gain and $1.5/bbl lower of

market GIM

▪ YoY: $2.0/bbl due to $2.7/bbl lower market GIM VS $0.7/bbl higher

stock gain

❑ 9M18 Acct GIM was $15.3/bbl: $0.4/bbl from 9M17 due to $1.6/bbl

higher stock gain vs $1.2/bbl lower of market GIM

Performance by Business

Financial Performance

Strategic Direction

3Q18 Highlight

14

Projects Update

QoQ YoY 3Q17 2Q18 3Q18

Net Sales 52,355 65,367 68,831 5% 31% 84.44 106.65 111.15

Market GIM 9,331 8,493 7,667 (10)% (18)% 15.05 13.86 12.37

Stock Gain/(Loss) 1,098 2,177 1,017 (53)% (7)% 1.77 3.55 1.64

LCM (0) (6) - 100% 100% (0.00) (0.01) -

Oil Hedging Gain/(Loss) (455) 44 54 22% 112% (0.73) 0.07 0.09

Net Stock Gain/(Loss) 643 2,215 1,070 (52)% 67% 1.04 3.61 1.73

Accounting GIM 9,974 10,708 8,738 (18)% (12)% 16.09 17.47 14.10

OPEX + Selling Exp. (3,715) (3,942) (3,851) 2% (4)% (5.99) (6.43) (6.22)

Other Incomes 376 396 371 (6)% (1)% 0.61 0.65 0.60

EBITDA 6,635 7,162 5,258 (27)% (21)% 10.71 11.69 8.48

Depreciation (2,029) (2,047) (2,046) 0% (1)% (3.27) (3.34) (3.30)

Cost of Finance (710) (437) (500) (14)% 30% (1.15) (0.71) (0.81)

FX Gain/(Loss) 90 (73) 57 179% (36)% 0.15 (0.12) 0.09

Impairment Gain/(Loss) - 51 (5) - - - 0.08 (0.01)

Investment Gain/(Loss) 109 202 203 1% 87% 0.17 0.33 0.33

Other Expenses - (0) (2) - - - - (0.00)

Income Tax (846) (795) (395) 50% 53% (1.36) (1.30) (0.64)

Net Profit 3,248 4,050 2,560 (37)% (21)% 5.25 6.62 4.12

Unit: $/bbl3Q17 2Q18 3Q18

% Change

15

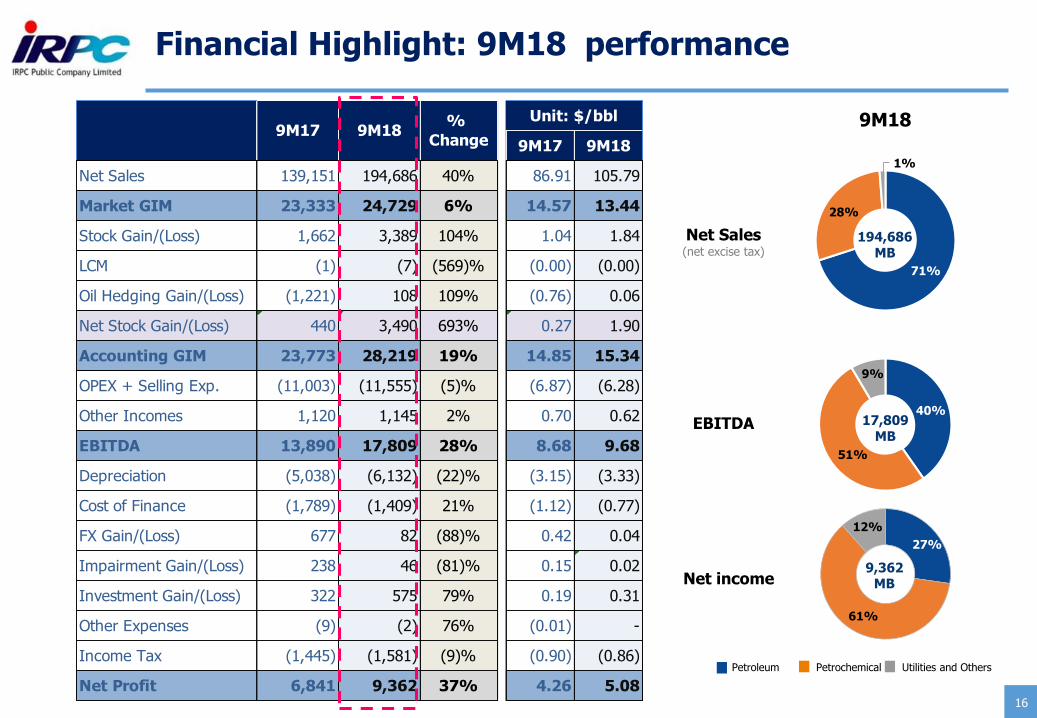

Financial Highlight: 3Q18 performance

Net Sales(net excise tax)

EBITDA

Net income

3Q18

35%

55%

10%

71%

28%

1%

68,831MB

5,258MB

15%

71%

14%

2,560MB

Petroleum Petrochemical Utilities and Others

9M17 9M18

Net Sales 139,151 194,686 40% 86.91 105.79

Market GIM 23,333 24,729 6% 14.57 13.44

Stock Gain/(Loss) 1,662 3,389 104% 1.04 1.84

LCM (1) (7) (569)% (0.00) (0.00)

Oil Hedging Gain/(Loss) (1,221) 108 109% (0.76) 0.06

Net Stock Gain/(Loss) 440 3,490 693% 0.27 1.90

Accounting GIM 23,773 28,219 19% 14.85 15.34

OPEX + Selling Exp. (11,003) (11,555) (5)% (6.87) (6.28)

Other Incomes 1,120 1,145 2% 0.70 0.62

EBITDA 13,890 17,809 28% 8.68 9.68

Depreciation (5,038) (6,132) (22)% (3.15) (3.33)

Cost of Finance (1,789) (1,409) 21% (1.12) (0.77)

FX Gain/(Loss) 677 82 (88)% 0.42 0.04

Impairment Gain/(Loss) 238 46 (81)% 0.15 0.02

Investment Gain/(Loss) 322 575 79% 0.19 0.31

Other Expenses (9) (2) 76% (0.01) -

Income Tax (1,445) (1,581) (9)% (0.90) (0.86)

Net Profit 6,841 9,362 37% 4.26 5.08

Unit: $/bbl%

Change9M17 9M18

16

Financial Highlight: 9M18 performance

27%

61%

12%

9M18

40%

51%

9%

71%

28%

1%

194,686MB

17,809MB

9,362MB

Net Sales(net excise tax)

EBITDA

Net income

Petroleum Petrochemical Utilities and Others

699 3,734 6,358 6,438

17,416 1,936

4,516

3,363

6,887

699

7,098 8,294

13,325

21,932

2018 2019 2020 2021 >2021

THB Bond

USD Loan

THB Loan

128,324 126,970

8,637 9,220

45,438 52,753

2,145 2,336

87,650 88,996

2,378 2,537

55,812 51,347

38,704 48,399

Financial PositionIncrease ST loans to support crude payment due to high crude oil price

Maturity of Long-term Debt

Debt ProfileStatements of Financial Position

Cash Flow

Unit : MB

Remark: Long-term debt as at 30 Sep 2018

Unit: MB

PP&E

Other Non-C/A

Cash

184,544

Other CurrentLiabilities

LT Liabilities incl. current port.

Shareholders’Equity

Sep. 2018

191,279

Dec. 2017

Other CA

Other Non-CurrentLiabilities

Beginning Cash

1 Jan 2018

Ending Cash30 Sep 2018

Cash Flow from

Operating

Unit: MB

Cash Flow from

Investing

Cash Flow from

Financing

Net Debt = 61,412 MB

Ex. Rate = 32.58 Baht/$

Financial Ratios

< 1.0x

Net D/E CA/CL

17

0.74 0.61 0.69

3Q17 2Q18 3Q18

0.85 0.90 1.00

3Q17 2Q18 3Q18

ST Loan20%

LT Loan (USD)10%

LT Loan (THB)54%

Bond (THB)16%

Float 84 THB 66

Fixed 16 USD 34

Currency (%) Interest Rate (%)

Performance by Business

Financial Performance

Strategic Direction

3Q18 Highlight

18

Projects Update

19

UHV project : Major CAPEXImprove product yield and earnings

IRPC’s refined Production Yield

Upstream project for Hygiene & Value-added Products

Objective : Upgrade low value to high valued-added products

Investment : $ 1.1 bn

COD : Jul. 2016

Benefit : GIM 1.5-2.0 $/ bblAssumption : Spread propylene to FO ~ 500-600 $/ton

RDCC unit➢ Feed Cut-in

@ Jun 16➢ COD @ Jul 16

HYVAHL unit➢ Feed Cut-in

HS-ATB @ Jul 16➢ COD @ Jul 16

Performance Guarantee Test➢ RDCC run 100%

@ Oct 2016

Plant Acceptance

(PAC)

Jan 2017

43%

78%

95%

2016A 2017A 2018F

Upgrade to High Valued-Added products

131

123

163

367

220

326

74

HS-ATB

LPG

Ethylene

HYVAHL

Propylene

Naphtha

FO/FG

Middle Distillates

RDCC

C4 Raffinate III

Internal use & Loss

Unit : KTA

16%

5%

23%

9%

9%

26%

12%

Flow Diagram

LS-ATB

UHV

Designed Yield

23%8% 11%

4% 4%

14%

10%

15%

12% 10%

40%

38%

45%

47% 48%

5%

10%

8%

9% 12%

16%

21%

16%18% 16%

2%

5%3% 5% 5%

6%1% 4% 4%

2% 1% 1%

IRPC IRPC+UHV IRPC2015A

IRPC2017A

IRPC2018F

Ethylene

Propylene

LPG

Naphtha

Gasoline

Diesel/JetFuelLube Oil

Fuel Oil

Designed Yield

20

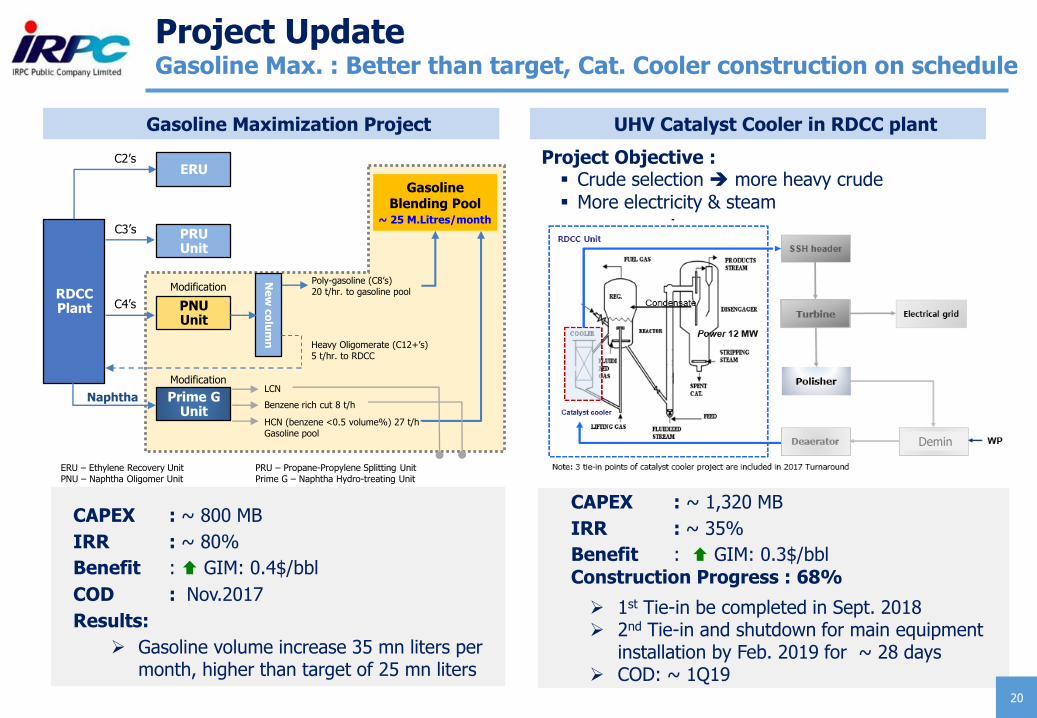

Project UpdateGasoline Max. : Better than target, Cat. Cooler construction on schedule

Gasoline Maximization Project UHV Catalyst Cooler in RDCC plant

CAPEX : ~ 800 MB

IRR : ~ 80%

Benefit : GIM: 0.4$/bbl

COD : Nov.2017

Results:

➢ Gasoline volume increase 35 mn liters per month, higher than target of 25 mn liters

Demin

RDCC Plant

ERU

PRU Unit

PNU Unit

Prime G Unit

Ne

w c

olu

mn

GasolineBlending Pool

~ 25 M.Litres/month

C2’s

C3’s

C4’s

Naphtha

Modification

Modification

Poly-gasoline (C8’s)20 t/hr. to gasoline pool

Heavy Oligomerate (C12+’s)5 t/hr. to RDCC

HCN (benzene <0.5 volume%) 27 t/h Gasoline pool

Benzene rich cut 8 t/h

LCN

ERU – Ethylene Recovery Unit PRU – Propane-Propylene Splitting Unit PNU – Naphtha Oligomer Unit Prime G – Naphtha Hydro-treating Unit

CAPEX : ~ 1,320 MB

IRR : ~ 35%

Benefit : GIM: 0.3$/bblConstruction Progress : 68%

➢ 1st Tie-in be completed in Sept. 2018➢ 2nd Tie-in and shutdown for main equipment

installation by Feb. 2019 for ~ 28 days➢ COD: ~ 1Q19

Project Objective :▪ Crude selection ➔ more heavy crude▪ More electricity & steam

21

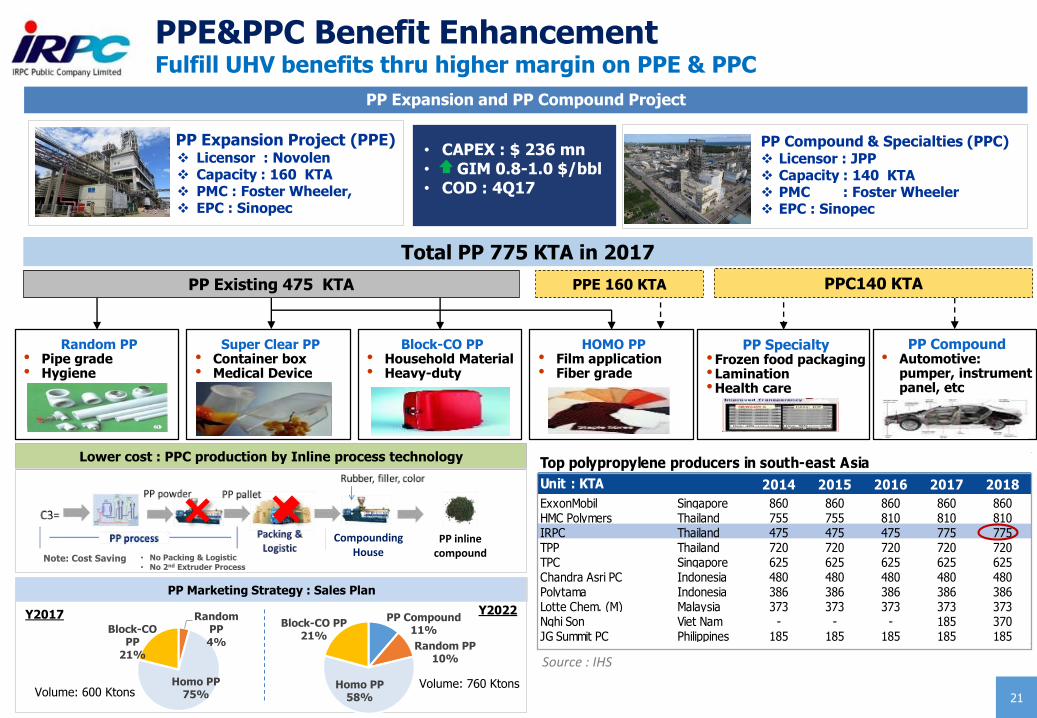

PPE&PPC Benefit EnhancementFulfill UHV benefits thru higher margin on PPE & PPC

Random PP• Pipe grade• Hygiene

Super Clear PP• Container box• Medical Device

Block-CO PP• Household Material• Heavy-duty

HOMO PP• Film application• Fiber grade

PP Specialty•Frozen food packaging•Lamination•Health care

PP Compound• Automotive:

pumper, instrument panel, etc

PPE 160 KTA PPC140 KTA

Total PP 775 KTA in 2017

PP Existing 475 KTA

PP Expansion and PP Compound Project

CompoundingHouse

PP inline compound

Lower cost : PPC production by Inline process technology

Note: Cost Saving • No Packing & Logistic• No 2nd Extruder Process

PP Marketing Strategy : Sales Plan

Y2017

Volume: 600 Ktons

Y2022

Volume: 760 Ktons

PP Expansion Project (PPE)❖ Licensor : Novolen ❖ Capacity : 160 KTA ❖ PMC : Foster Wheeler, ❖ EPC : Sinopec

• CAPEX : $ 236 mn• GIM 0.8-1.0 $/bbl• COD : 4Q17

Top polypropylene producers in south-east Asia

2014 2015 2016 2017 2018

ExxonMobil Singapore 860 860 860 860 860HMC Polymers Thailand 755 755 810 810 810IRPC Thailand 475 475 475 775 775TPP Thailand 720 720 720 720 720TPC Singapore 625 625 625 625 625Chandra Asri PC Indonesia 480 480 480 480 480Polytama Indonesia 386 386 386 386 386Lotte Chem. (M) Malaysia 373 373 373 373 373Nghi Son Viet Nam - - - 185 370JG Summit PC Philippines 185 185 185 185 185

Unit : KTA

Source : IHS

Random PP4%

Homo PP75%

Block-CO PP

21%

PP Compound11%

Random PP10%

Homo PP58%

Block-CO PP21%

PP Compound & Specialties (PPC) ❖ Licensor : JPP❖ Capacity : 140 KTA❖ PMC : Foster Wheeler ❖ EPC : Sinopec

22

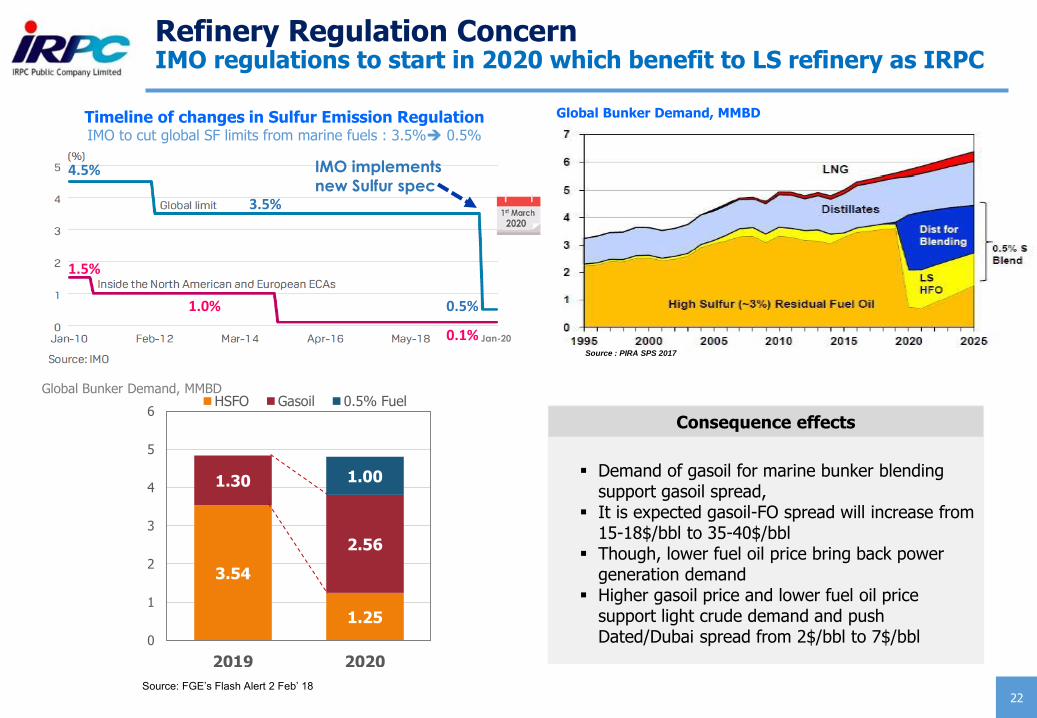

Refinery Regulation ConcernIMO regulations to start in 2020 which benefit to LS refinery as IRPC

Source : PIRA SPS 2017

1.5%

1.0%

4.5%

3.5%

0.5%

Jan-200.1%

IMO implements

new Sulfur spec

Timeline of changes in Sulfur Emission RegulationIMO to cut global SF limits from marine fuels : 3.5%➔ 0.5%

Global Bunker Demand, MMBD

Source: FGE’s Flash Alert 2 Feb’ 18

Consequence effects

▪ Demand of gasoil for marine bunker blending support gasoil spread,

▪ It is expected gasoil-FO spread will increase from 15-18$/bbl to 35-40$/bbl

▪ Though, lower fuel oil price bring back power generation demand

▪ Higher gasoil price and lower fuel oil price support light crude demand and push Dated/Dubai spread from 2$/bbl to 7$/bbl

3.54

1.25

1.30

2.56

1.00

0

1

2

3

4

5

6

2019 2020

HSFO Gasoil 0.5% FuelGlobal Bunker Demand, MMBD

23

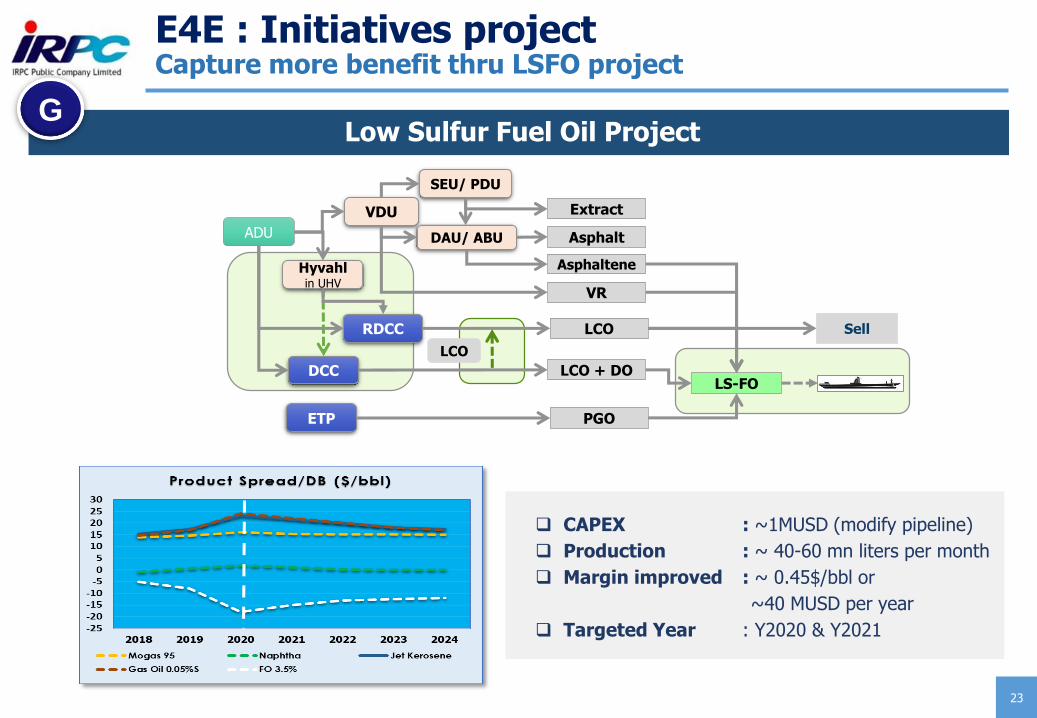

E4E : Initiatives projectCapture more benefit thru LSFO project

❑ CAPEX : ~1MUSD (modify pipeline)

❑ Production : ~ 40-60 mn liters per month

❑ Margin improved : ~ 0.45$/bbl or

~40 MUSD per year

❑ Targeted Year : Y2020 & Y2021

Price Assumption to Study IMO effect.Low Sulfur Fuel Oil Project

ADU

VDU

RDCC

Hyvahlin UHV

DCC

SEU/ PDU

DAU/ ABU Asphalt

Extract

VR

Asphaltene

LCO + DO

LCO

ETP PGO

LS-FO

LCO

Sell

G

24

Petroleum and Petrochemical Value Chain Optimized Configuration & Product Diversification

Olefins Plant PropyleneEthyleneAcetylene Butadiene

180 KTA360 KTA6 KTA56 KTA

Vacuum Gas Oil (VGO)

PP

PS

ABS/SAN

EPS

CCM

Acetylene Black

HDPEEthylene

Acetylene

Propylene

Benzene

TolueneMixed Xylene

Butadiene

CD1

Ethylene

EBSM

Long Residue

4 KTA

140 KTA

775 KTA

Ethylene Rich Gas

DCC

Propylene 132 KTA

ADU (1,2)

215 KBD

Naphtha

Reformate

UHV

Ethylene Propylene 320 KTA

73 KTA

Lube BaseLube Base Oil Asphalt

320 KTA600 KTA

BTX Benzene TolueneMixed Xylene

114 KTA132 KTA121 KTA 31 KTA

57 KTA

179 KTA

125 KTA

48 KTA

260 KTAStyrene Monomer

Acrylonitrile

Feed (Crude Oil / Condensate)Transportation FuelGasoline,

Jet

Diesel

PRP

HS ATB

Propylene 100 KTA

Pyrolysis Gasoline Raffinate

Styrene Monomer

LS ATB

65% 18% 7% 10%

Crude/Condensate Portfolio

Middle east Far east Domestic Others

For sale

16%

22%

31%34% 35%

39%43%

45%

50%

55%

60%

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

25

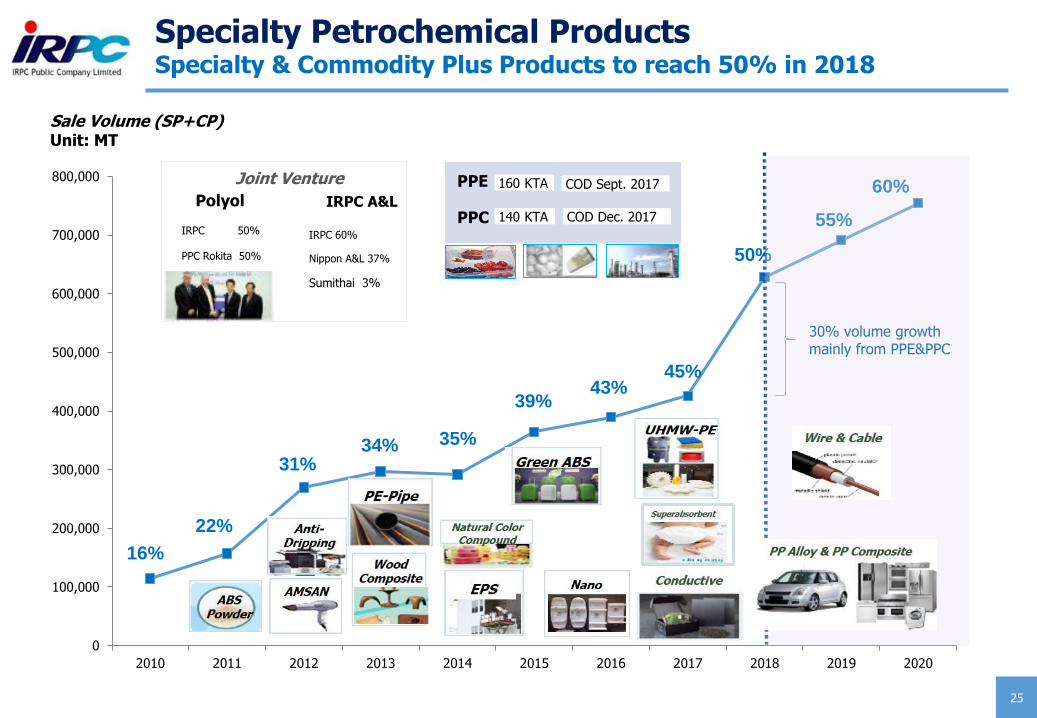

Specialty Petrochemical ProductsSpecialty & Commodity Plus Products to reach 50% in 2018

IRPC 50%

PPC Rokita 50%

IRPC A&L

IRPC 60%

Nippon A&L 37%

Sumithai 3%

Joint Venture

Polyol

Sale Volume (SP+CP) Unit: MT

PPE

PPC

160 KTA

140 KTA COD Dec. 2017

COD Sept. 2017

30% volume growth mainly from PPE&PPC

Performance by Business

Financial Performance

Strategic Direction

3Q18 Highlight

26

Projects Update

27

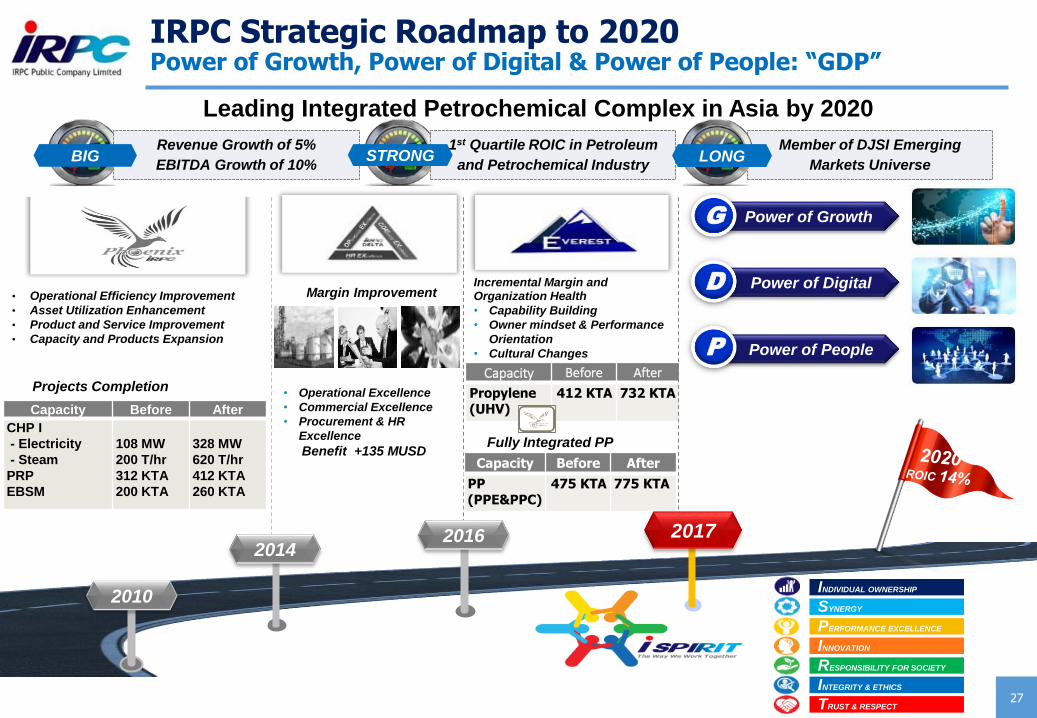

IRPC Strategic Roadmap to 2020Power of Growth, Power of Digital & Power of People: “GDP”

Capacity Before After

Propylene (UHV)

412 KTA 732 KTA

2010

2014

Margin Improvement

• Operational Excellence

• Commercial Excellence

• Procurement & HR

Excellence

Benefit +135 MUSD

INDIVIDUAL OWNERSHIP

SYNERGY

PERFORMANCE EXCELLENCE

INNOVATION

RESPONSIBILITY FOR SOCIETY

INTEGRITY & ETHICS

TRUST & RESPECT

Projects Completion

• Operational Efficiency Improvement

• Asset Utilization Enhancement

• Product and Service Improvement

• Capacity and Products Expansion

Incremental Margin and Organization Health

• Capability Building

• Owner mindset & Performance

Orientation

• Cultural Changes

Fully Integrated PP

Revenue Growth of 5%

EBITDA Growth of 10%

1st Quartile ROIC in Petroleum

and Petrochemical Industry STRONG

Member of DJSI Emerging

Markets Universe

Capacity Before After

PP (PPE&PPC)

475 KTA 775 KTA

20172016

Capacity Before After

CHP I

- Electricity

- Steam

PRP

EBSM

108 MW

200 T/hr

312 KTA

200 KTA

328 MW

620 T/hr

412 KTA

260 KTA

BIG LONG

Leading Integrated Petrochemical Complex in Asia by 2020

Power of GrowthG

Power of DigitalD

Power of PeopleP

28

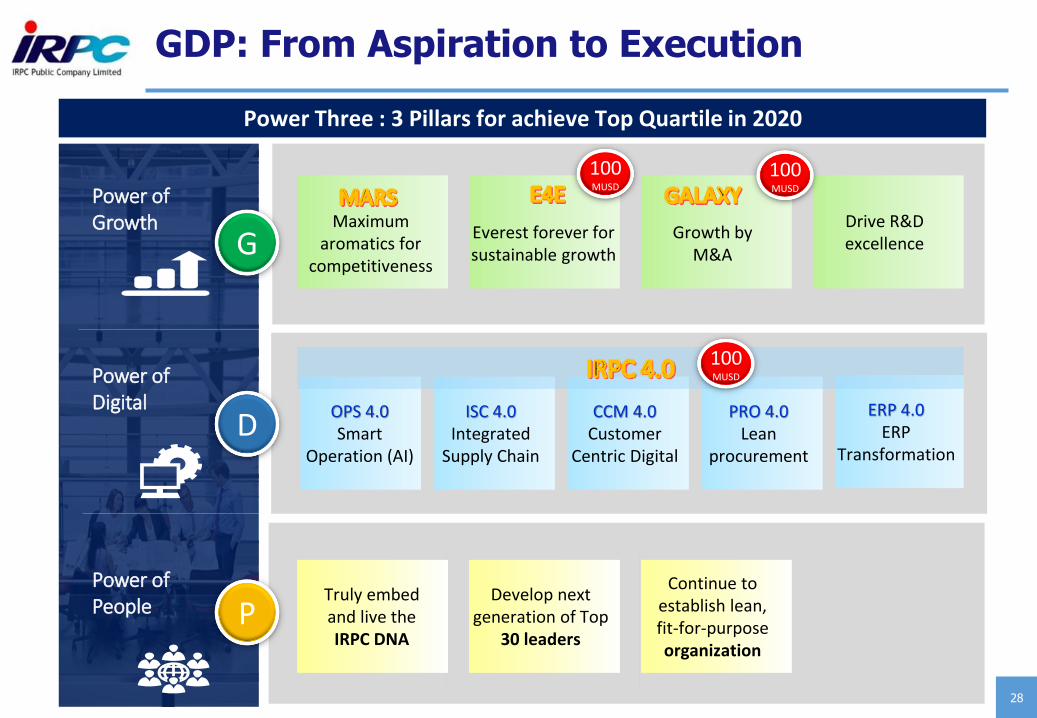

GDP: From Aspiration to Execution

Power Three : 3 Pillars for achieve Top Quartile in 2020

Power of Digital

Power of People

Truly embedand live the IRPC DNA

Develop next generation of Top

30 leaders

Continue to establish lean, fit-for-purpose organization

P

Power of Growth Maximum

aromatics for competitiveness

Growth byM&A

Everest forever for sustainable growth

Drive R&D excellenceG

100MUSD

100MUSD

OPS 4.0Smart

Operation (AI)

ISC 4.0Integrated

Supply Chain

CCM 4.0Customer

Centric Digital

ERP 4.0ERP

Transformation

PRO 4.0Lean

procurement

100MUSD

D

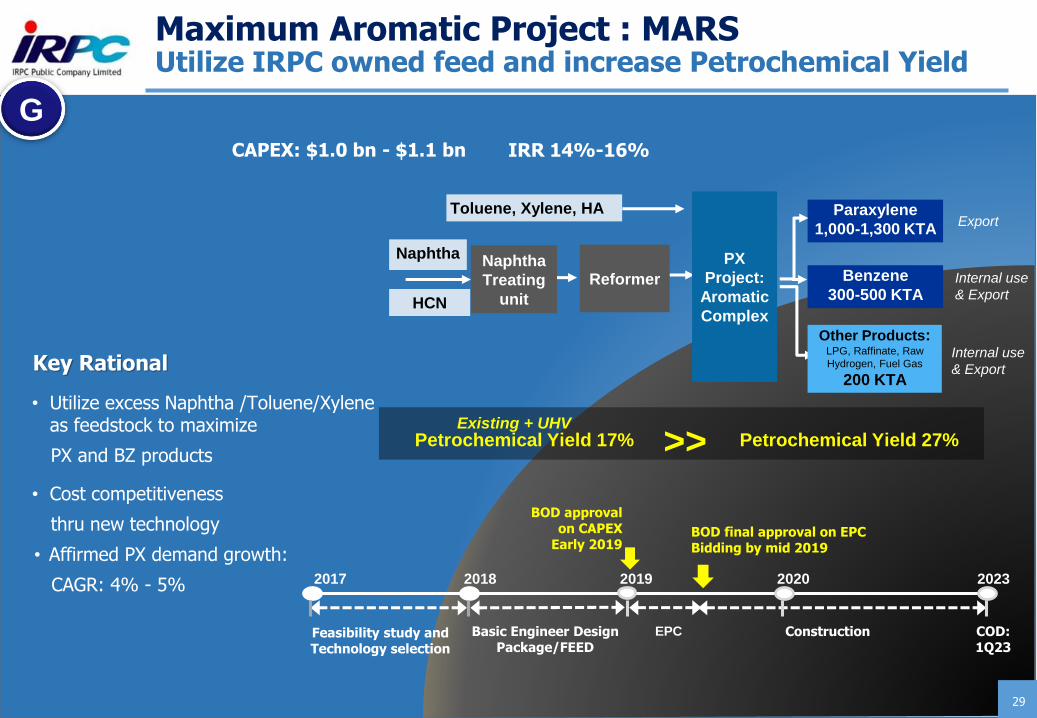

MARS - Maximum Aromatics

Reformer Benzene

300-500 KTA

Paraxylene

1,000-1,300 KTA

Naphtha PX

Project:

Aromatic

Complex

Internal use

& Export

Export

Naphtha

Treating

unitHCN

Toluene, Xylene, HA

Internal use

& Export

Other Products: LPG, Raffinate, Raw

Hydrogen, Fuel Gas

200 KTA

CAPEX: $1.0 bn - $1.1 bn IRR 14%-16%

Petrochemical Yield 17% Existing + UHV

Petrochemical Yield 27% >>

Key Rational

• Utilize excess Naphtha /Toluene/Xylene as feedstock to maximize

PX and BZ products

• Cost competitiveness

thru new technology

• Affirmed PX demand growth:

CAGR: 4% - 5%

G

Maximum Aromatic Project : MARSUtilize IRPC owned feed and increase Petrochemical Yield

COD:1Q23

Feasibility study and Technology selection

Basic Engineer Design Package/FEED

Construction

202320192017 20202018

EPC

BOD approval on CAPEX

Early 2019BOD final approval on EPC Bidding by mid 2019

29

30

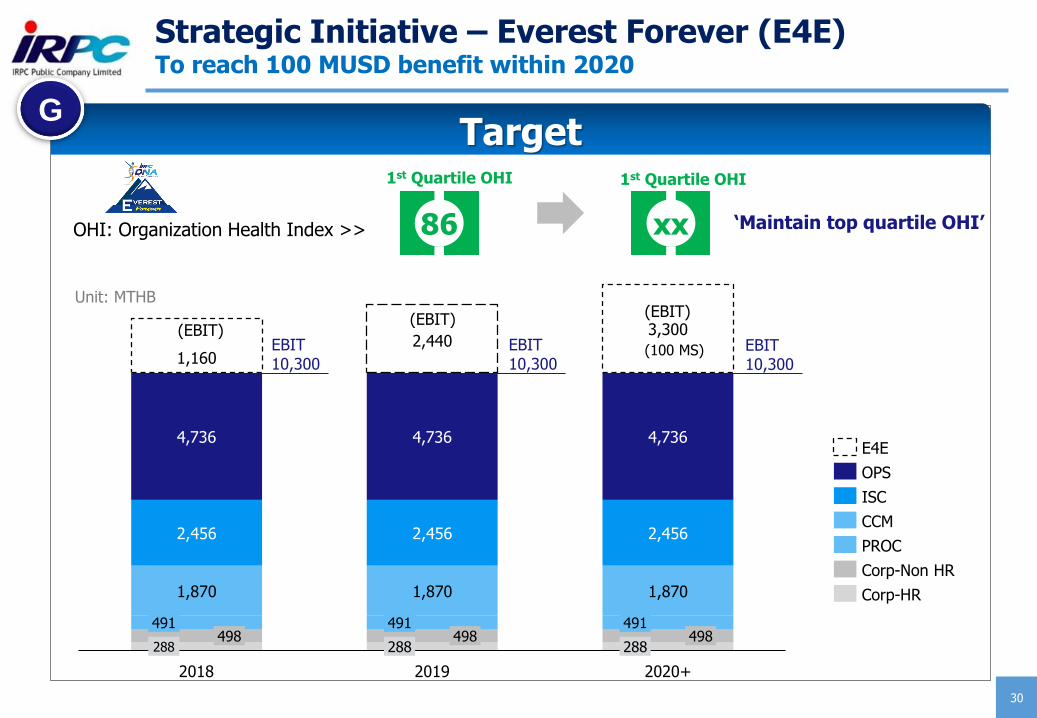

Strategic Initiative – Everest Forever (E4E)To reach 100 MUSD benefit within 2020

1,870 1,870 1,870

2,456 2,456 2,456

4,736 4,736 4,736

1,1602,440

3,300

491498

491

288

2018

498491

2019

288498

288

2020+

E4E

ISC

OPS

CCM

Corp-Non HR

PROC

Corp-HR

OHI: Organization Health Index >> 86

1st Quartile OHI

xx

1st Quartile OHI

(EBIT)(EBIT)

(EBIT)

‘Maintain top quartile OHI’

Unit: MTHB

EBIT10,300

EBIT10,300

EBIT10,300

Target

(100 MS)

G

31

M&A under “Galaxy” projectFocus in Petrochemical Industry

▪ Petrochemical and/ or related petrochemical business with synergy value

▪ Why Galaxy :• Align with aspiration: “Leading Integrated Petrochemical Complex in Asia by 2020”

• Growth Ambition: Invest to deliver targeted EBITDA of $100-200 Million

• Expeditious success

G

32

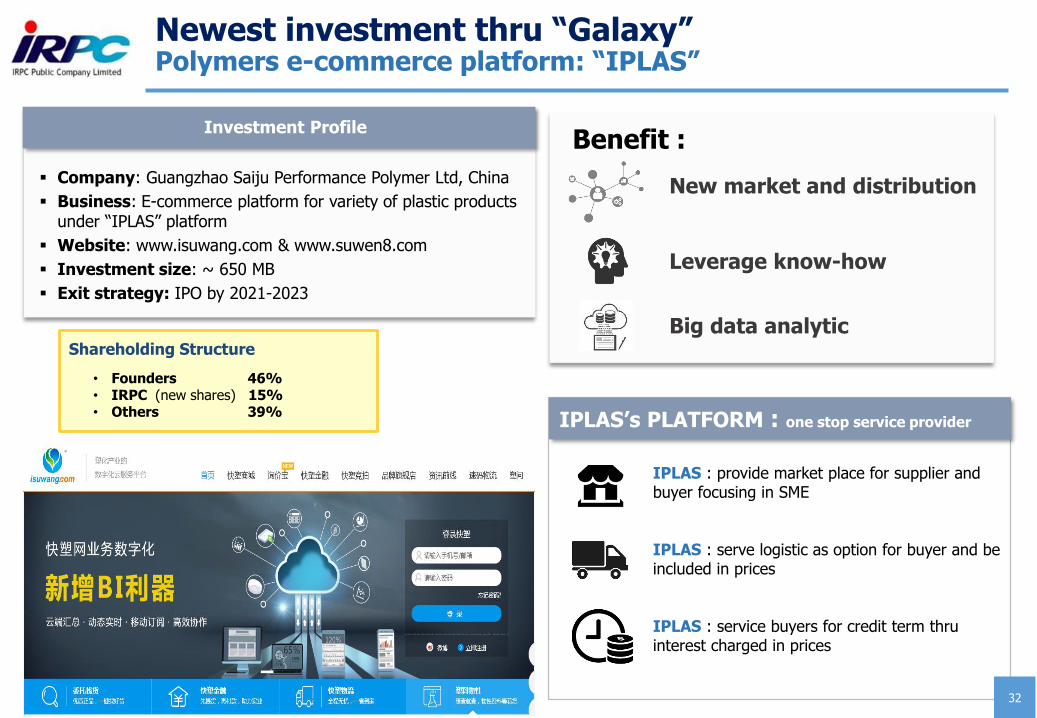

Newest investment thru “Galaxy”Polymers e-commerce platform: “IPLAS”

Investment Profile

▪ Company: Guangzhao Saiju Performance Polymer Ltd, China

▪ Business: E-commerce platform for variety of plastic products under “IPLAS” platform

▪ Website: www.isuwang.com & www.suwen8.com

▪ Investment size: ~ 650 MB

▪ Exit strategy: IPO by 2021-2023

Shareholding Structure

• Founders 46%• IRPC (new shares) 15%• Others 39%

Investment Profile

New market and distribution

Benefit :

Big data analytic

Leverage know-how

IPLAS : provide market place for supplier and buyer focusing in SME

IPLAS : serve logistic as option for buyer and be included in prices

IPLAS : service buyers for credit term thru interest charged in prices

IPLAS’s PLATFORM : one stop service provider

33

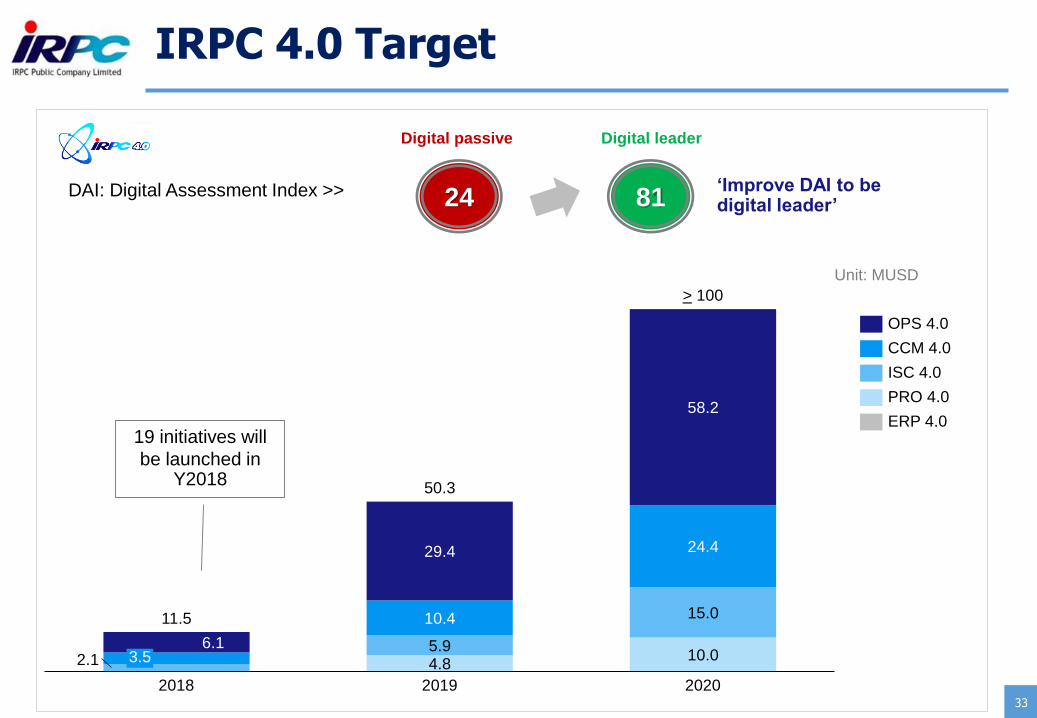

IRPC 4.0 Target

2.1 4.810.0

5.9

15.0

6.1

10.4

24.429.4

58.2

2020

3.5

> 100

2018 2019

11.5

50.3

OPS 4.0

CCM 4.0

PRO 4.0

ISC 4.0

ERP 4.0

24

Digital passive

81

Digital leader

DAI: Digital Assessment Index >> ‘Improve DAI to be digital leader’

Unit: MUSD

19 initiatives will

be launched in Y2018

34

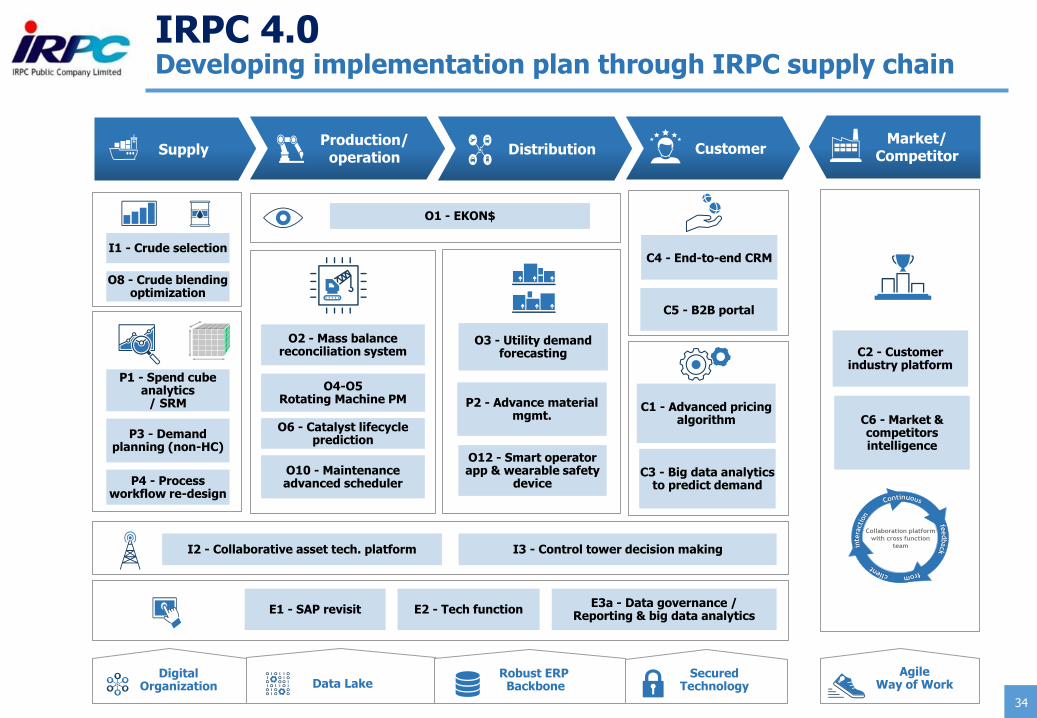

IRPC 4.0 Developing implementation plan through IRPC supply chain

O3 - Utility demand forecasting

O2 - Mass balance reconciliation system

E1 - SAP revisit

I3 - Control tower decision making

O4-O5Rotating Machine PM

O1 - EKON$

P1 - Spend cube analytics

/ SRM

I1 - Crude selection

SupplyProduction/

operationDistribution Customer

Market/Competitor

Digital Organization Data Lake

Robust ERPBackbone

Secured Technology

Agile Way of Work

Collaboration platform

with cross function

team

P2 - Advance material mgmt.

C4 - End-to-end CRM

C1 - Advanced pricing algorithm C6 - Market &

competitors intelligence

C3 - Big data analytics to predict demand

E2 - Tech functionE3a - Data governance /

Reporting & big data analytics

I2 - Collaborative asset tech. platform

P3 - Demand planning (non-HC)

C5 - B2B portal

P4 - Process workflow re-design

C2 - Customer industry platform

O6 - Catalyst lifecycle prediction

O10 - Maintenance advanced scheduler

O8 - Crude blending optimization

O12 - Smart operator app & wearable safety

device

35

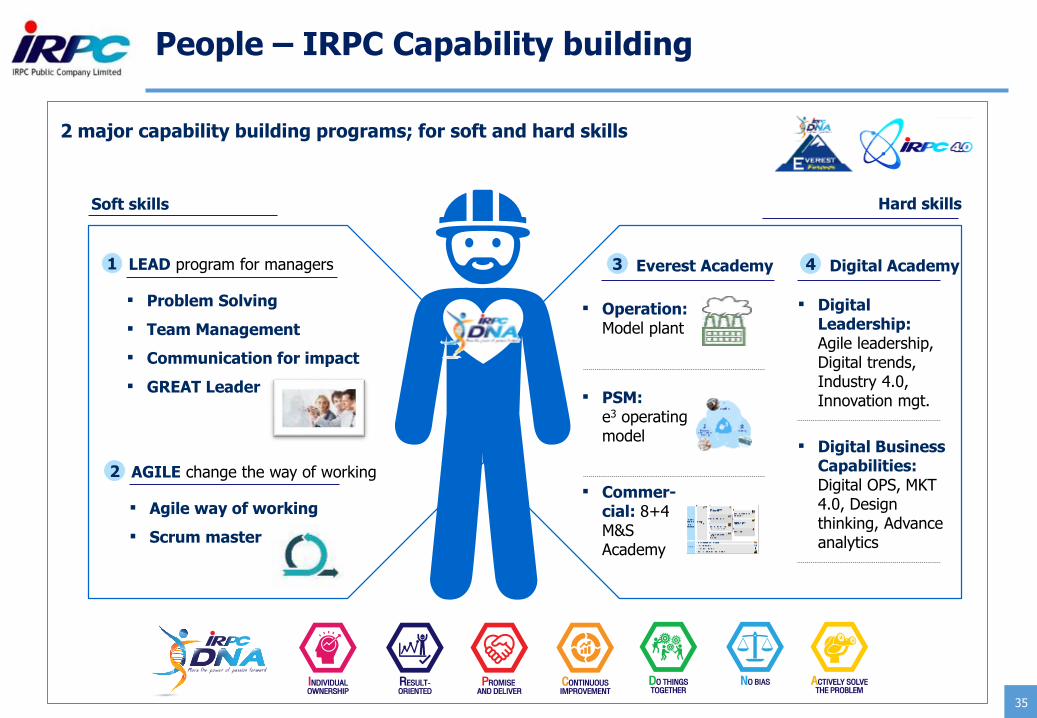

People – IRPC Capability building

2 major capability building programs; for soft and hard skills

1 3

Soft skills Hard skills

Everest AcademyLEAD program for managers

▪ Problem Solving

▪ Team Management

▪ Communication for impact

▪ GREAT Leader

▪ Operation: Model plant

▪ PSM: e3 operating model

▪ Commer-cial: 8+4 M&SAcademy

4 Digital Academy

▪ Digital Leadership: Agile leadership, Digital trends, Industry 4.0, Innovation mgt.

▪ Digital Business Capabilities: Digital OPS, MKT 4.0, Design thinking, Advance analytics

2 AGILE change the way of working

▪ Agile way of working

▪ Scrum master

Thank You

This presentation material has been prepared solely for informational purposes only. IRPC is furnishing it solely for use by prospective investors / analysts in

the proposed event. IRPC makes no representations or warranties as to the accuracy or completeness of such information. By accepting this material each

recipient agrees that IRPC shall not have any liability for any representations (express or implied) contained in, or for any omissions from this presentation.

The information contained herein does not purport to be all-inclusive or to contain all of the Information that may be material to the recipient’s decision. Each

recipient of the information and data contained herein should perform its own independent investigation and analysis of the transaction and the creditworthiness of IRPC . Reference in this Disclaimer to this shall include references to the Appendices (if any) hereto.

Investor Relations Contact: [email protected]

Tel. +662-765-7380, Fax. +662-765-7379