Drivers of Future Energy Demand - U.S. Energy … · Drivers of Future Energy Demand in China ......

22

Drivers of Future Energy Demand in China Asian Energy Demand Outlook 2014 EIA Energy Conference July 14, 2014 Valerie J. Karplus MIT Sloan School of Management

Transcript of Drivers of Future Energy Demand - U.S. Energy … · Drivers of Future Energy Demand in China ......

Drivers of Future Energy Demand in China

Asian Energy Demand Outlook 2014 EIA Energy Conference

July 14, 2014

Valerie J. Karplus

MIT Sloan School of Management

2

www.china.org.cn

www.flickr.com www.wikimedia.org

globalchange.mit.edu

Global Climate Change

Human Development

Local Pollution

Industrial Development & Resource Needs

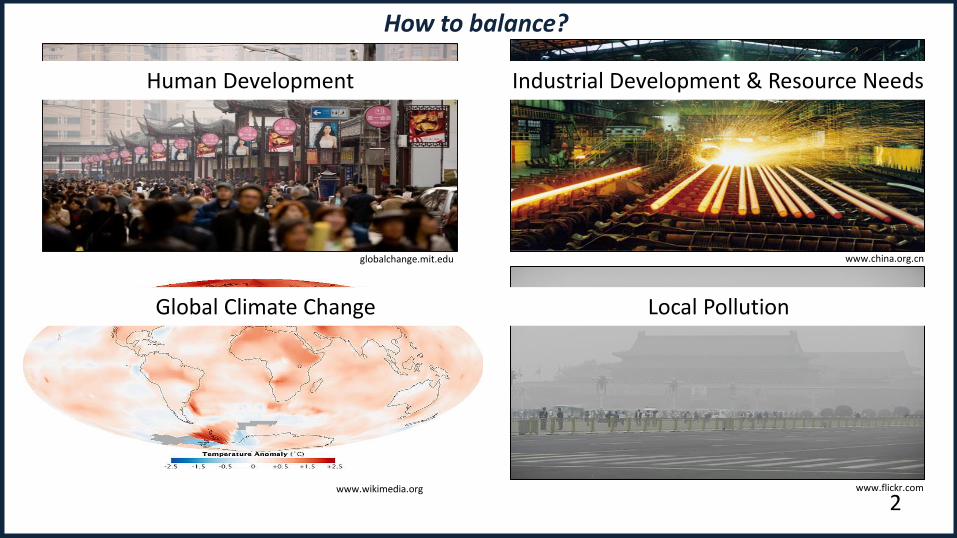

How to balance?

0

500

1000

1500

2000

2500

3000

3500

4000

1981 1991 2001 2011Non-material Sectors/Other ConstructionCommercial consumption Residential consumptionTransportation Agriculture

mtce/year

0

2000

4000

6000

8000

10000

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

20

13

Mainland China Asia Not Including China

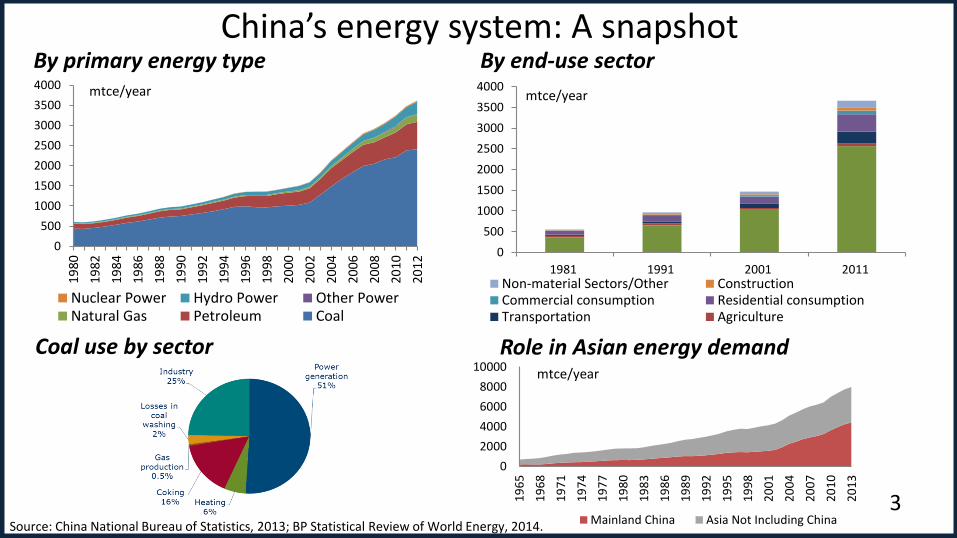

China’s energy system: A snapshot By primary energy type By end-use sector

Coal use by sector

3

0

500

1000

1500

2000

2500

3000

3500

40001

98

0

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

Nuclear Power Hydro Power Other PowerNatural Gas Petroleum Coal

mtce/year

Source: China National Bureau of Statistics, 2013; BP Statistical Review of World Energy, 2014.

mtce/year

Role in Asian energy demand

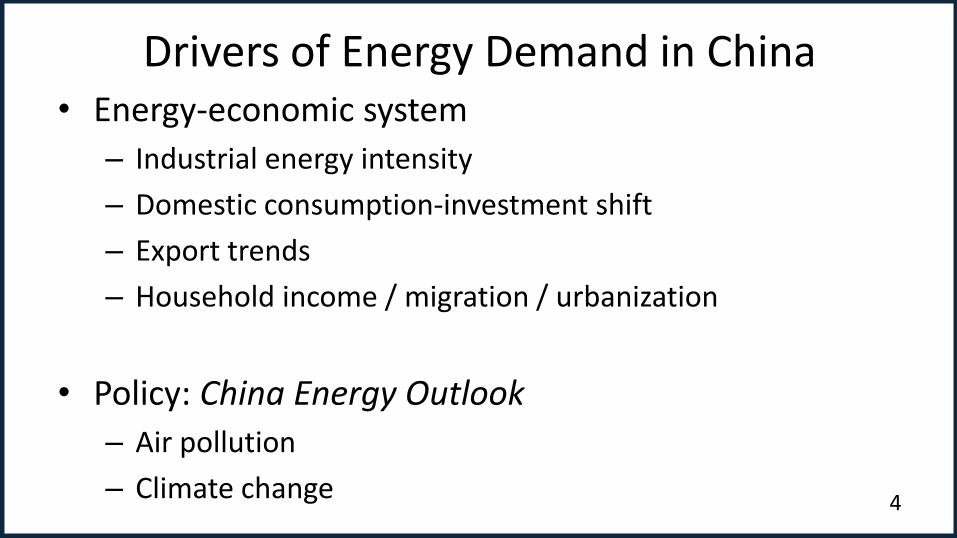

Drivers of Energy Demand in China • Energy-economic system

– Industrial energy intensity

– Domestic consumption-investment shift

– Export trends

– Household income / migration / urbanization

• Policy: China Energy Outlook

– Air pollution

– Climate change

4

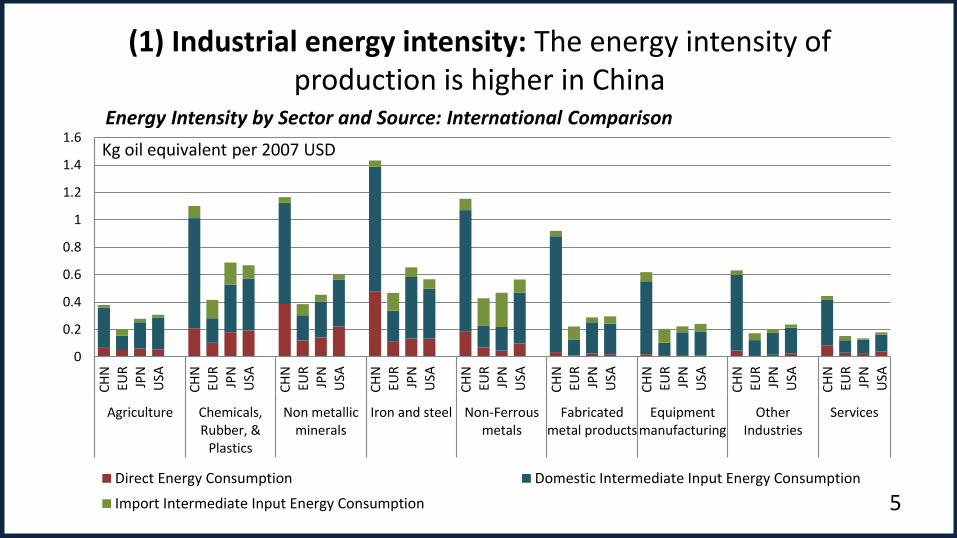

(1) Industrial energy intensity: The energy intensity of production is higher in China

5

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

CH

NEU

RJP

NU

SA

CH

NEU

RJP

NU

SA

CH

NEU

RJP

NU

SA

CH

NEU

RJP

NU

SA

CH

NEU

RJP

NU

SA

CH

NEU

RJP

NU

SA

CH

NEU

RJP

NU

SA

CH

NEU

RJP

NU

SA

CH

NEU

RJP

NU

SA

Agriculture Chemicals,Rubber, &

Plastics

Non metallicminerals

Iron and steel Non-Ferrousmetals

Fabricatedmetal products

Equipmentmanufacturing

OtherIndustries

Services

Direct Energy Consumption Domestic Intermediate Input Energy Consumption

Import Intermediate Input Energy Consumption

Kg oil equivalent per 2007 USD

Energy Intensity by Sector and Source: International Comparison

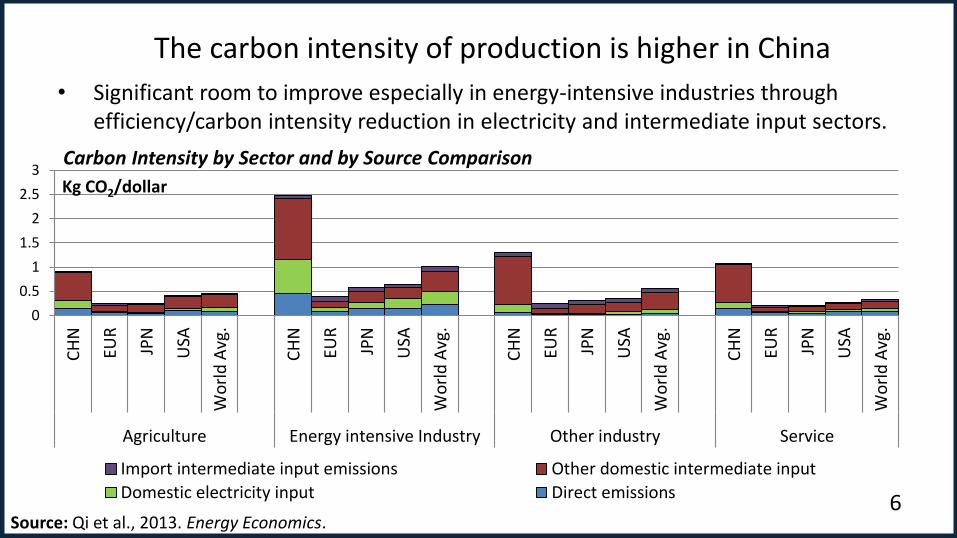

The carbon intensity of production is higher in China

6

• Significant room to improve especially in energy-intensive industries through efficiency/carbon intensity reduction in electricity and intermediate input sectors.

0

0.5

1

1.5

2

2.5

3

CH

N

EUR

JPN

USA

Wo

rld

Avg

.

CH

N

EUR

JPN

USA

Wo

rld

Avg

.

CH

N

EUR

JPN

USA

Wo

rld

Avg

.

CH

N

EUR

JPN

USA

Wo

rld

Avg

.

Agriculture Energy intensive Industry Other industry Service

Kg CO2/dollar

Import intermediate input emissions Other domestic intermediate input

Domestic electricity input Direct emissions

Carbon Intensity by Sector and by Source Comparison

Source: Qi et al., 2013. Energy Economics.

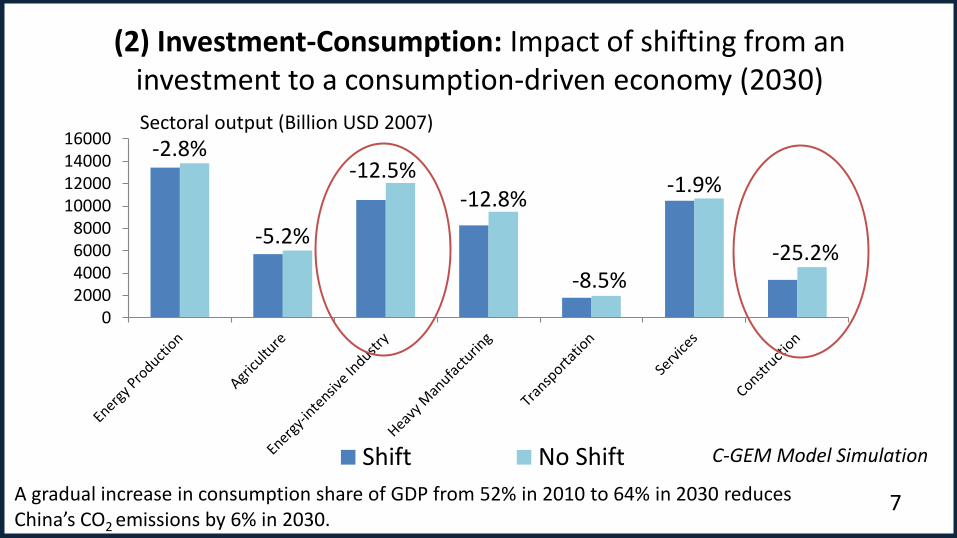

(2) Investment-Consumption: Impact of shifting from an investment to a consumption-driven economy (2030)

7

02000400060008000

10000120001400016000

Shift No Shift

A gradual increase in consumption share of GDP from 52% in 2010 to 64% in 2030 reduces China’s CO2 emissions by 6% in 2030.

-2.8%

-5.2%

-12.5% -12.8%

-8.5%

-1.9%

-25.2%

Sectoral output (Billion USD 2007)

C-GEM Model Simulation

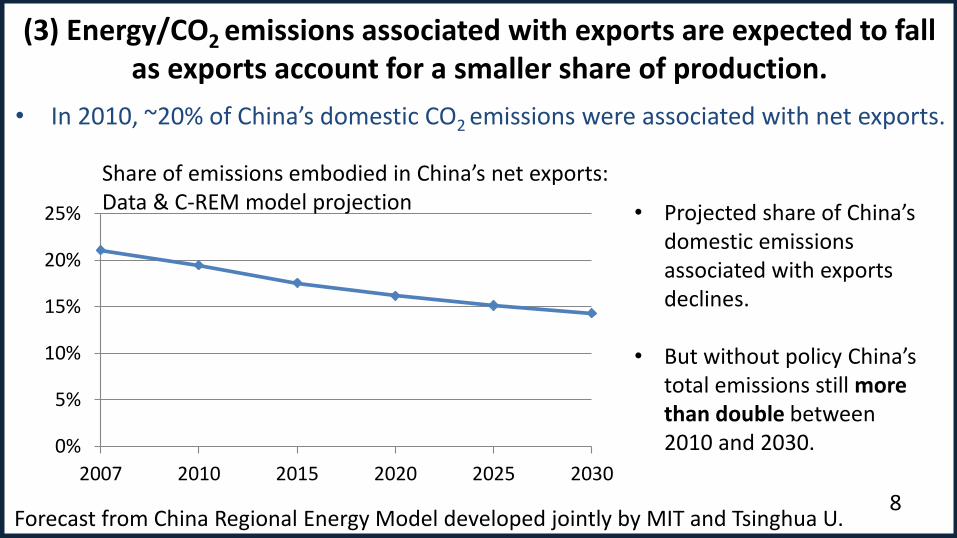

• In 2010, ~20% of China’s domestic CO2 emissions were associated with net exports.

8

0%

5%

10%

15%

20%

25%

2007 2010 2015 2020 2025 2030

• Projected share of China’s domestic emissions associated with exports declines.

• But without policy China’s total emissions still more than double between 2010 and 2030.

(3) Energy/CO2 emissions associated with exports are expected to fall as exports account for a smaller share of production.

Forecast from China Regional Energy Model developed jointly by MIT and Tsinghua U.

Share of emissions embodied in China’s net exports: Data & C-REM model projection

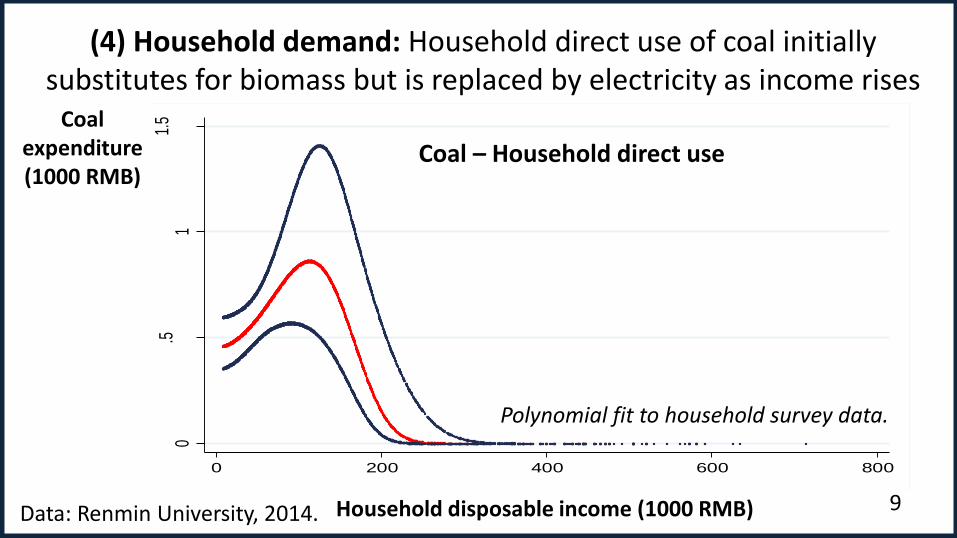

(4) Household demand: Household direct use of coal initially substitutes for biomass but is replaced by electricity as income rises

9

0.5

11.

5

0 200 400 600 800

Coal – Household direct use

Household disposable income (1000 RMB)

Coal expenditure (1000 RMB)

Data: Renmin University, 2014.

Polynomial fit to household survey data.

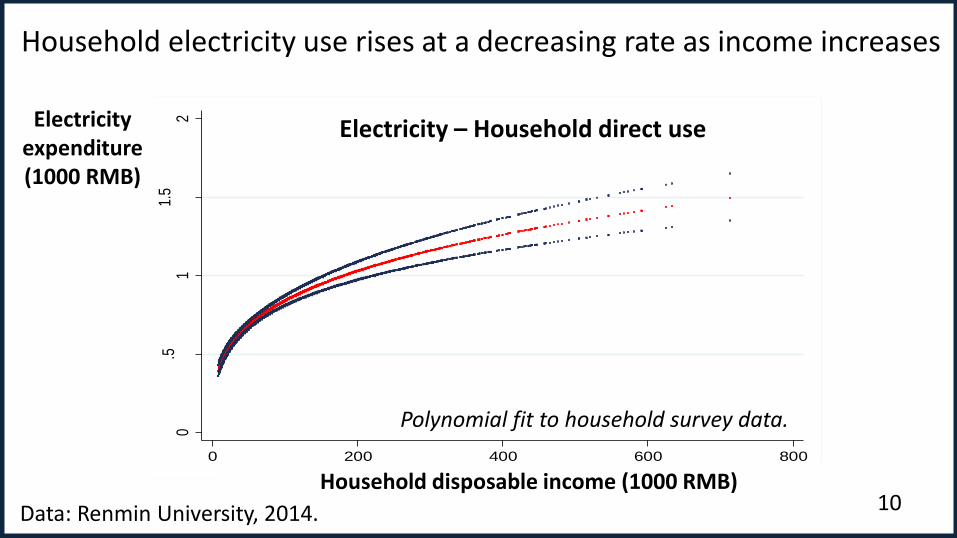

Household electricity use rises at a decreasing rate as income increases

10

0.5

11.

52

0 200 400 600 800

Electricity – Household direct use

Household disposable income (1000 RMB)

Electricity expenditure (1000 RMB)

Data: Renmin University, 2014.

Polynomial fit to household survey data.

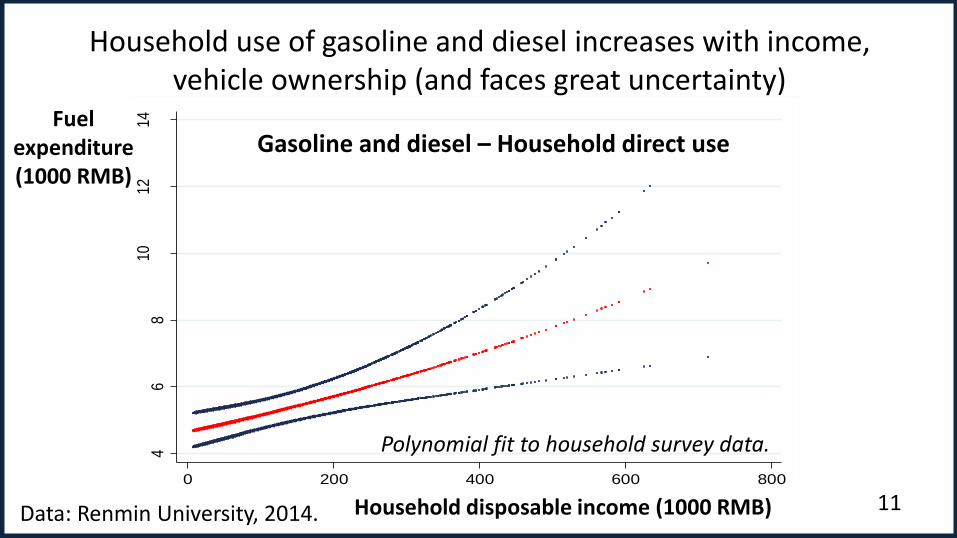

Household use of gasoline and diesel increases with income, vehicle ownership (and faces great uncertainty)

11

46

810

1214

0 200 400 600 800

Gasoline and diesel – Household direct use

Household disposable income (1000 RMB) Data: Renmin University, 2014.

Polynomial fit to household survey data.

Fuel expenditure (1000 RMB)

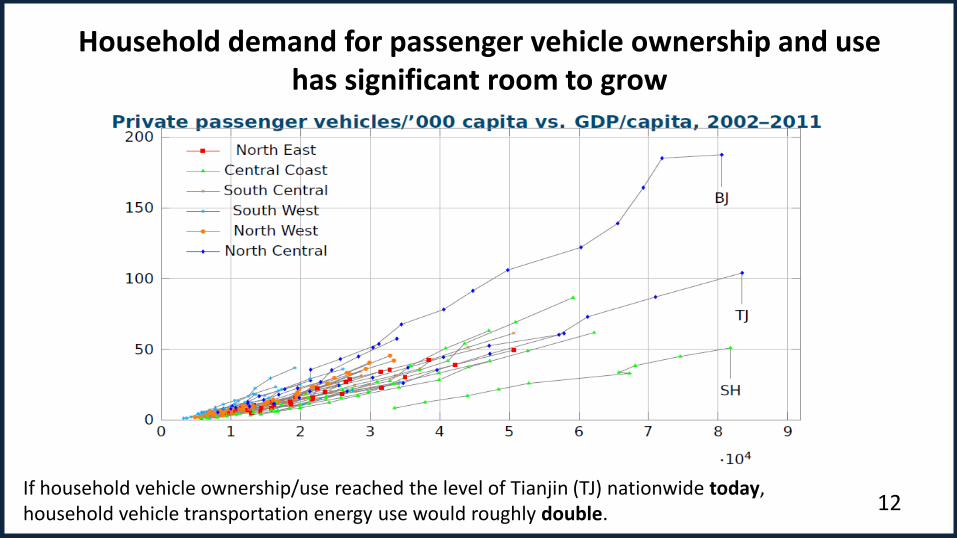

Household demand for passenger vehicle ownership and use has significant room to grow

12 If household vehicle ownership/use reached the level of Tianjin (TJ) nationwide today, household vehicle transportation energy use would roughly double.

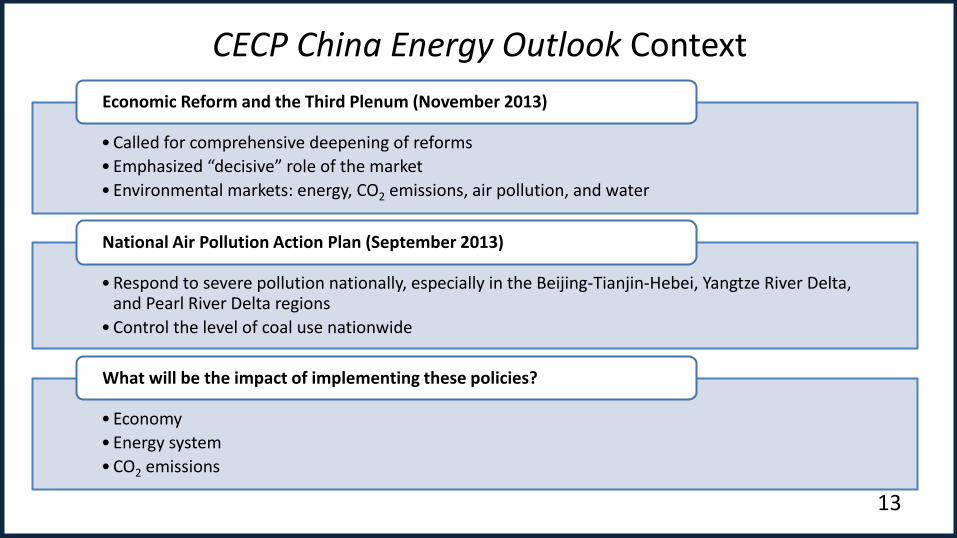

CECP China Energy Outlook Context

13

• Called for comprehensive deepening of reforms

• Emphasized “decisive” role of the market

• Environmental markets: energy, CO2 emissions, air pollution, and water

Economic Reform and the Third Plenum (November 2013)

• Respond to severe pollution nationally, especially in the Beijing-Tianjin-Hebei, Yangtze River Delta, and Pearl River Delta regions

• Control the level of coal use nationwide

National Air Pollution Action Plan (September 2013)

• Economy

• Energy system

• CO2 emissions

What will be the impact of implementing these policies?

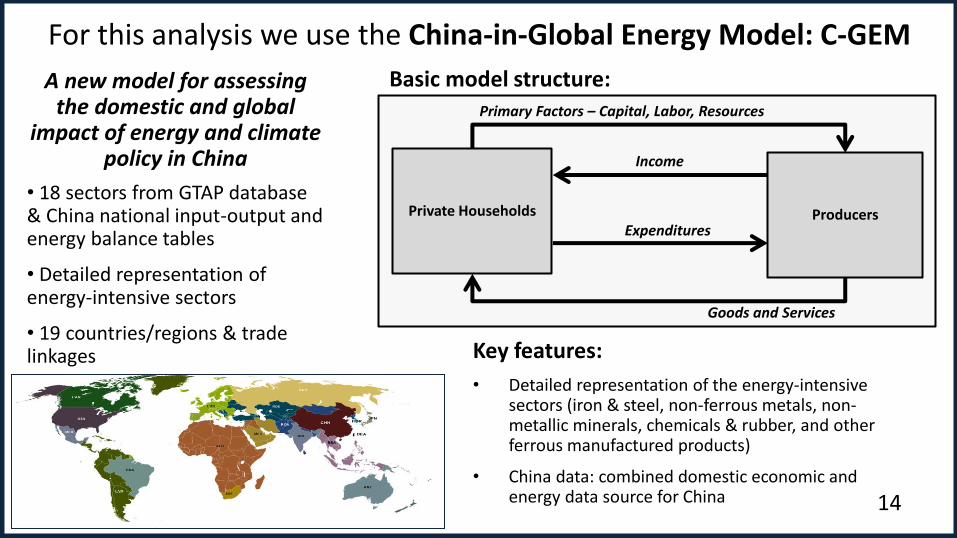

For this analysis we use the China-in-Global Energy Model: C-GEM

14

Private Households

Income

Expenditures

Goods and Services

Primary Factors – Capital, Labor, Resources

Producers

Basic model structure: A new model for assessing the domestic and global

impact of energy and climate policy in China

• 18 sectors from GTAP database & China national input-output and energy balance tables

• Detailed representation of energy-intensive sectors

• 19 countries/regions & trade linkages Key features:

• Detailed representation of the energy-intensive sectors (iron & steel, non-ferrous metals, non-metallic minerals, chemicals & rubber, and other ferrous manufactured products)

• China data: combined domestic economic and energy data source for China

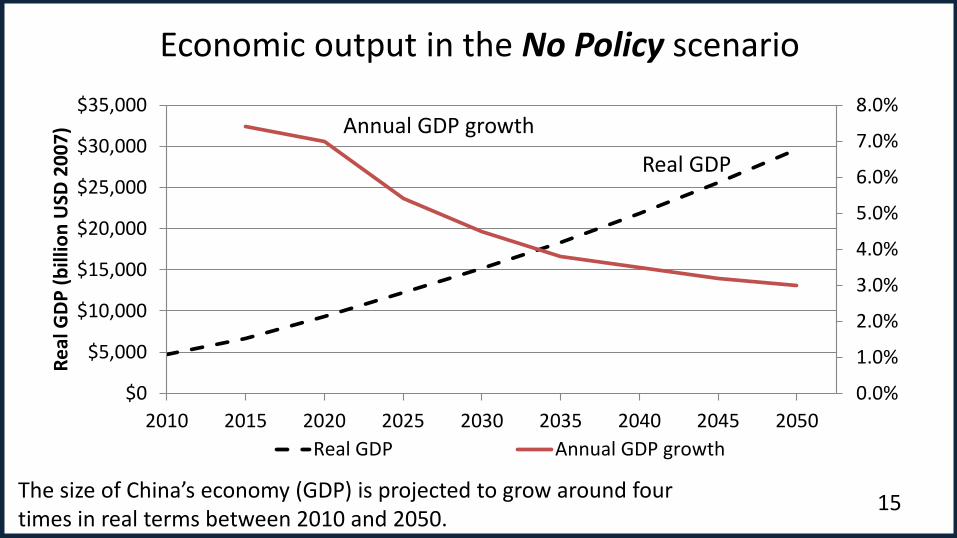

Economic output in the No Policy scenario

15 The size of China’s economy (GDP) is projected to grow around four times in real terms between 2010 and 2050.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

2010 2015 2020 2025 2030 2035 2040 2045 2050

Re

al G

DP

(b

illio

n U

SD 2

00

7)

Real GDP Annual GDP growth

Real GDP

Annual GDP growth

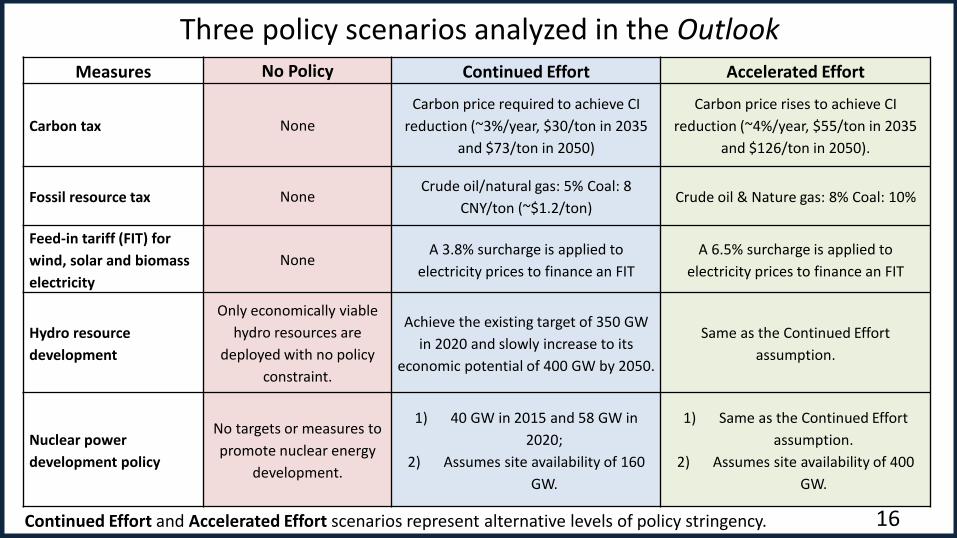

Three policy scenarios analyzed in the Outlook Measures No Policy Continued Effort Accelerated Effort

Carbon tax None

Carbon price required to achieve CI

reduction (~3%/year, $30/ton in 2035

and $73/ton in 2050)

Carbon price rises to achieve CI

reduction (~4%/year, $55/ton in 2035

and $126/ton in 2050).

Fossil resource tax None Crude oil/natural gas: 5% Coal: 8

CNY/ton (~$1.2/ton) Crude oil & Nature gas: 8% Coal: 10%

Feed-in tariff (FIT) for

wind, solar and biomass

electricity

None A 3.8% surcharge is applied to

electricity prices to finance an FIT

A 6.5% surcharge is applied to

electricity prices to finance an FIT

Hydro resource

development

Only economically viable

hydro resources are

deployed with no policy

constraint.

Achieve the existing target of 350 GW

in 2020 and slowly increase to its

economic potential of 400 GW by 2050.

Same as the Continued Effort

assumption.

Nuclear power

development policy

No targets or measures to

promote nuclear energy

development.

1) 40 GW in 2015 and 58 GW in

2020;

2) Assumes site availability of 160

GW.

1) Same as the Continued Effort

assumption.

2) Assumes site availability of 400

GW.

16 Continued Effort and Accelerated Effort scenarios represent alternative levels of policy stringency.

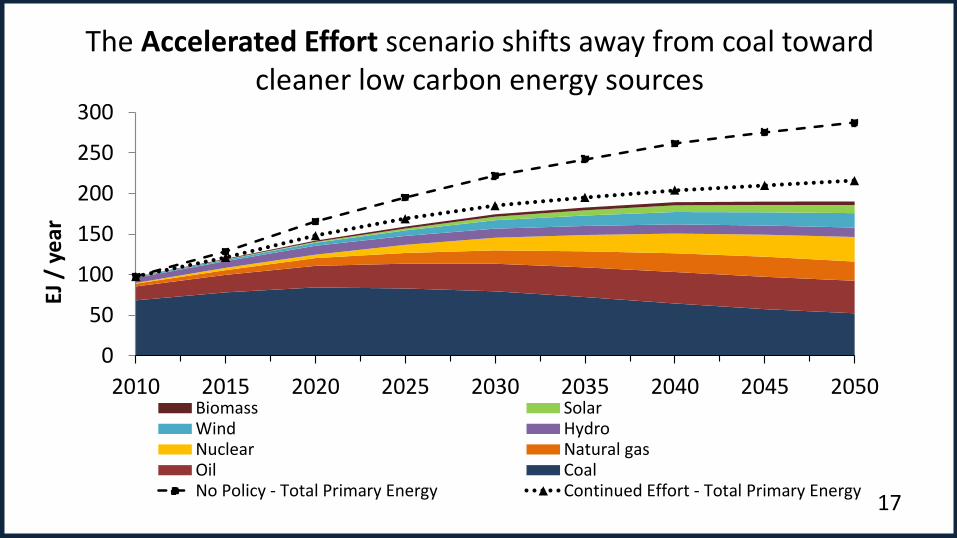

The Accelerated Effort scenario shifts away from coal toward cleaner low carbon energy sources

17

0

50

100

150

200

250

300

2010 2015 2020 2025 2030 2035 2040 2045 2050

EJ /

ye

ar

Biomass SolarWind HydroNuclear Natural gasOil CoalNo Policy - Total Primary Energy Continued Effort - Total Primary Energy

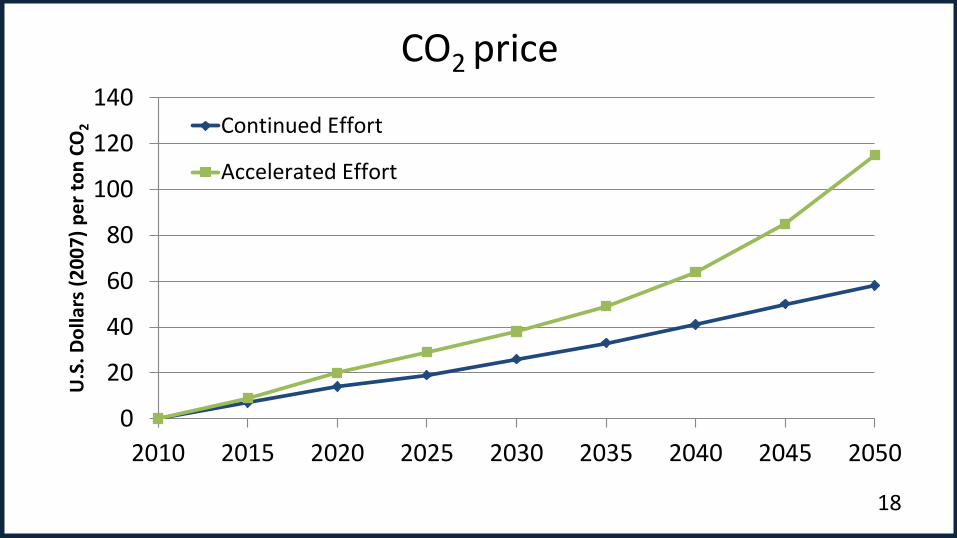

CO2 price

18

0

20

40

60

80

100

120

140

2010 2015 2020 2025 2030 2035 2040 2045 2050

U.S

. Do

llars

(2

00

7)

pe

r to

n C

O2

Continued Effort

Accelerated Effort

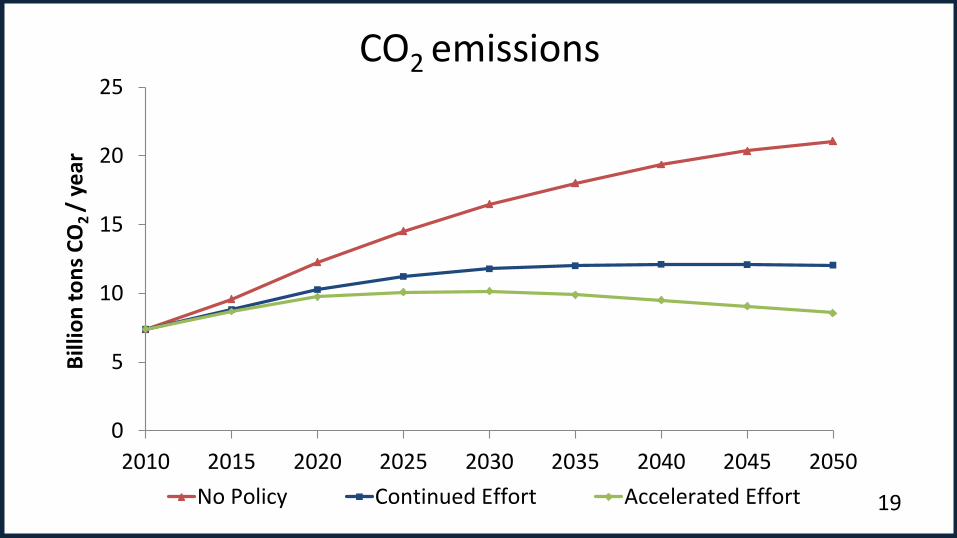

CO2 emissions

19

0

5

10

15

20

25

2010 2015 2020 2025 2030 2035 2040 2045 2050

Bill

ion

to

ns

CO

2 /

ye

ar

No Policy Continued Effort Accelerated Effort

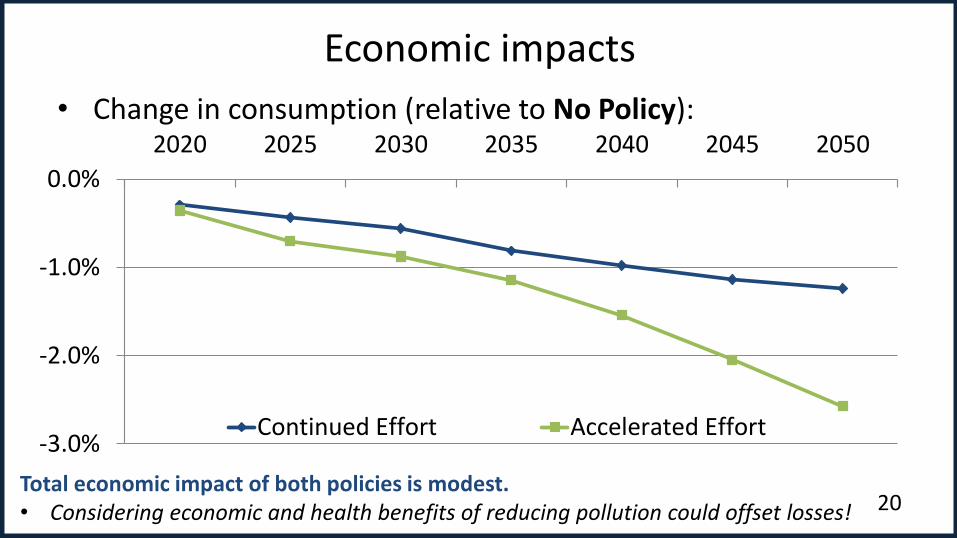

Economic impacts

20

• Change in consumption (relative to No Policy):

-3.0%

-2.0%

-1.0%

0.0%

2020 2025 2030 2035 2040 2045 2050

Continued Effort Accelerated Effort

Total economic impact of both policies is modest. • Considering economic and health benefits of reducing pollution could offset losses!

Insights

21

Significant CO2 reductions can be achieved at modest cost—with the right incentives.

Domestic action on air pollution that reduces coal will also cost-effectively reduce CO2.

Oil demand is the least sensitive to a CO2 price given limited substitutes and rising household demand.

Even substantial nuclear deployment will only be a partial solution.

Solar, wind, and biomass will expand, raising grid connection and integration challenges.

globalchange.mit.edu/cecp 22

Thank you 谢谢!

![Drivers of Demand for Travel in London[1]](https://static.fdocuments.net/doc/165x107/577cc47a1a28aba711997090/drivers-of-demand-for-travel-in-london1.jpg)