Draft Report of the Committee to examine the Reserve Bank ...dcmsme.gov.in/reports/RBI.pdf · Draft...

57

Draft Report of the Committee to examine the Reserve Bank Of India (RBI)’s Proposal regarding Modifications in existing definition of sick micro and small enterprises (MSEs) and Procedure for assessing the viability of sick MSEs Ministry of Micro, Small & Medium Enterprises Office of the Development Commissioner (MSME) June 2012

Transcript of Draft Report of the Committee to examine the Reserve Bank ...dcmsme.gov.in/reports/RBI.pdf · Draft...

Draft Report of the Committee

to examine the Reserve Bank Of India (RBI)rsquos

Proposal regarding

Modifications in existing definition of sick micro and small enterprises (MSEs)

and

Procedure for assessing the viability of sick MSEs

Ministry of Micro Small amp Medium Enterprises

Office of the Development Commissioner

(MSME)

June 2012

1

DRAFT REPORT OF THE COMMITTEE TO EXAMINE THE RESERVE BANK OF INDIA (RBI)rsquoS PROPOSAL REGARDING MODIFICATIONS IN EXISTING DEFINITION OF SICK MICRO AND SMALL ENTERPRISES (MSEs) AND PROCEDURE FOR ASSESSING THE VIABILITY OF SICK MSEs

1 Introduction

Present status of sickness 11 The data on sick MSEs is compiled by the Reserve Bank of India (RBI) from

the scheduled commercial banks As at the end of March 2010 there were 77723

sick micro and small enterprises (MSEs) in the country There has been an increase

in the number of sick MSEs to 90141 as at the end of March 2011 The number of

sick MSEs potentially viable enterprises and the enterprises under nursing with the

amounts outstanding against them from March 2005 to 2011 are as under

(Amount in Rs Crore)

Source RBI 12 The above table shows that as at end of March 2010 banks found only 118

per cent of sick MSEs as viable Further the banks put only 258 per cent of the

viable units under nursing which constituted 3 of the total sick units Thus the

number of sick MSEs found viable and those put under nursing remained

insignificant The number of units found viable as a percentage of total sick MSEs

was still lower at 79 as at the end of March 2011 However units put under

nursing as a percentage of viable units has increased to 66 as at the end of March

2011 The number of sick units had decreased in 2010 by 25 but has increased by

16 in 2011 Number of viable enterprises put under nursing as percentage of total

sick MSEs at 52 at the end of March 2011 is very low

As at end of March

Total sick MSEs Potentially viable Viable enterprises under nursing

Number Amount Os

Number Amount Os

Number Amount Os

2005 138041 538013 3922 43467 2080 25993 2006 126824 498113 4594 49816 915 23377 2007 114132 526665 4287 42746 588 26893 2008 85187 308272 4210 24688 1262 12692 2009 103996 361990 8168 73168 2330 42426 2010 77723 523315 9160 96475 2360 47884 2011 90141 521125 7118 111298 4698 51830

2

2 Background 21 The RBI had constituted a Working Group on rehabilitation of sick SMEs (Chairman Dr KC Chakrabarty) The Working Group submitted its report in April 2008 The Committee inter alia made various recommendations on rehabilitation of sick SMEs The major recommendations of the Working Group relating to rehabilitation of sick MSEs are as under

i) Definition of sick small enterprises

A Micro or Small Enterprise (as defined in the MSMED Act 2006) may be said to have become sick if any of the borrowal account of the enterprise remains NPA for three months or more Or

There is erosion in the networth due to accumulated losses to the extent of 50 of its networth

The existing stipulation that the unit should have been in commercial production for at least two years may be removed so as to enable the banks to rehabilitate units where there is delay in commencement of commercial production and there is a need for handholding due to timecost overruns etc

However the accounts where willful default is identified (strictly in accordance with RBI guidelines) or the borrower is absconding shall not be classified as Sick units and accordingly shall not be eligible for any relief and concessions

ii) Definition of incipient sickness

An account may be treated to have reached the stage of incipient sickness potential sickness if any of the following events are triggered

a There is delay in commencement of commercial production by more than six months for reasons beyond the control of promoters and entailing cost overrun

b The company incurs losses for two years or cash loss for one year beyond the accepted timeframe on account of change in economic and fiscal policies affecting the working of MSEs or otherwise

c The capacity utilization is less than 50 of the projected level in terms of quantity or the sales are less than 50 of the projected level in terms of value during a year The rehabilitation process should start at the point of incipient sickness (and not

sickness) as defined above

iii) The existing criteria for viability are reasonable However decision on viability of a unit may be taken at the earliest but not later than 3 months of becoming sick under any circumstances

Procedure to declare sick units as unviable

In order to arrest the tendency of the banks to declare the sick micro small and medium enterprises as unviable and go for recovery it has been suggested that the following procedure should be adopted by the banks before declaring a micro small and medium enterprise unit as unviable However the banks may take decision in case of malfeasance or fraud without following the procedure

3

a A sick unit should be declared unviable only if the viability status is evidenced by a viability study

b The said viability study and the declaration of the unit as unviable should have the approval of the next higher authority (for micro small and medium enterprises) present sanctioning authority (for tiny micro enterprises)

c The next higher authority should take such decision only after giving an opportunity to the promoters of the unit to present their case They should be informed in writing about the reasons for declaring the unit as sick and unviable before giving this opportunity so that the promoters can present their case properly within 7 days from the date of such decision

d Decision of the above higher authority should be informed to the promoters in writing The above process should be completed in a time bound manner

iv) Rehabilitation measures

The existing guidelines on rehabilitation whether as regards the relief and concessions viability parameters or coordination between the banks FIs and Government agencies are adequate to manage the sickness in MSME sector It appears that the implementation of the guidelines has not been done properly More stringent monitoring at the level of HO of the banksFIs as also at the level of RBI may help in timely identification and treatment of sickness in MSME sector However minor modificationschanges have been suggested as under

Particulars Existing guidelines Suggested changes

Waiver of penal interest

Waiver of penal Interest from the beginning of the accounting year of the unit in which it started incurring cash losses continuously

The following words may be added ldquothe date of the account becoming NPA whichever is earlierrdquo

Rate of interest

NIL for FITL and different concessions for other facilities

The existing concessions on rate of interest may continue Interest may be made ballooning or staggered also

Repayment period

The repayment period permitted under DRM for SMEs is 10 years with concessions for 7 years and therefore no change is suggested in the same

Staggered or ballooning repayment may also be permitted so that the installments are aligned to the cash flows

Margin on funding of

While funding past and future losses margin of 40 may be prescribed in case

4

losses of small and medium enterprises

Some new suggestions

Banks may consider recovery of principal on the basis of tagging of sales starting from the quarter of commencement of repayment However tagging should not be more than the cash margins of the unit

In order to make the process of settlement of debt through OTS speedier and to provide resources to such intending borrowers RBI may consider allowing scaling down of debt burden to sustainable levels Further in order to incentivise lenders to fund the OTS and additional requirement of funds the new lenders may be allowed to convert a part of the debt into equity

As an incentive for proper restructuring package at the time of rehabilitation necessary support for business restructuring modernisation expansion diversification and technological upgradation as may be felt necessary by the lenders may also be encouraged Support of schemes like Credit Linked Capital Subsidy Scheme in case of units in other (than rural) areas KVIC Margin Money Scheme (for units in rural areas) may be extended for rehabilitation packages also

In terms of extant RBI guidelines an account gets downgraded if initial moratorium on interest payment is extended as a part of restructuring These guidelines need to be waived especially for MSMEs

22 The RBIrsquos circular dated 16th January 2002 to the banks regarding revised guidelines for Rehabilitation of Sick MSEs is at Annex I Based on the recommendations of the Working Group the RBI has issued circular RPCDSMEampNFS BC No 1020604012008-09 dated 4th May 2009 to all Scheduled Commercial Banks (Annex II)

23 RBIrsquos proposal to modify the existing definition of sick MSEs as recommended by the Working Group on Rehabilitation of Sick SMEs and procedure for assessing the viability of sick units

231 In the 13th meeting of Standing Advisory Committee to Review the Flow of

Institutional Credit to the MSME Sector held under the Chairmanship of Dr KC

Chakrabarty Dy Governor RBI at RBI Central Office Mumbai on 9th February 2012

the issue of Rehabilitation of Sick Micro and Small Enterprises was deliberated upon

Apart from reviewing the progress in rehabilitation of sick MSEs the Committee

deliberated on a proposal for modifying the existing definition of sick units as

recommended by the Working Group on Rehabilitation of Sick SMEs and procedure

for assessing the viability of sick units The detailed proposal of RBI in this regard

which was brought up in above meeting of Standing Advisory Committee is enclosed

(Annex III) On the agenda item of changing the definition of sick micro and small

5

units Secretary Ministry of MSME observed that the issue can be examined in more

detail and he proposed to set up a working group in the Ministry to look into the

issue

232 Accordingly a Committee was constituted under the chairpersonship of

Additional Development Commissioner amp Economic Adviser in the Office of the

DC(MSME) with representatives of Do Financial Services Mo Finance RBI RPCD

Mumbai and select banks viz State Bank of India Punjab National Bank and Bank

of Baroda as members to examine the RBIrsquos proposal and give viewssuggestions in

the matter A copy of Ministry of MSME Office of DC (MSME) OM no

E15(12)2011 dated 16th March 2012 regarding constitution of the Committee is at

Annex IV The names of Senior Officials included nominated as Members from

various Departments Organisations Banks are at Annex V

3 Meetings of the Committee

31 The Committee constituted under the chairpersonship of Additional

Development Commissioner amp Economic Adviser (ADCampEA) Office of the

Development Commissioner (MSME) to examine the Reserve Bank Of India (RBI)rsquos

proposal regarding modifications in existing definition of sick micro and small

enterprises (MSEs) and procedure for assessing the viability of sick MSEs met twice

on 2nd May 2012 and ------- in the Committee Room Nirman Bhawan New Delhi

The minutes of the meeting held on 2nd May 2012 is at Annex VI to the Report

32 The Committee deliberated on the various issues related to the proposed

modifications in existing definition of sick MSEs procedure for assessing the viability

of sick MSEs and other related issues like delayed payment to MSEs leading to

sickness stringent NPA norms and problems arising after the accounts turning

NPAs considering relaxation in NPA norms for MSEs need-based enhancement of

credit limits need for restructuringrehabilitation by banks at an early stage etc

Based on the suggestions of the members of the Committee participants the

Committee made the following observations and recommendations

6

4 Recommendations of the Committee

A Review of the existing definition of sick MSEs and changesmodifications therein

The Committee reviewed the existing definition of sick MSEs and observed

that there was there was considerable delay in rehabilitation of the potentially viable

units The Committee agreed on the proposed change in the definition of sick MSEs

as contained in the RBIrsquos proposal with some modificationschanges In case of

micro enterprises the borrowal accounts remaining NPA for three months or more to

declare a unit as sick may be too long and such enterprises immediately on being

declared NPA should be treated as sick and rehabilitation process initiated This

would enable banks to take timely corrective action for rehabilitation However in

case of small enterprises the overdue period could be 6 months as proposed

Recommendations

The proposed definition of sick MSEs may be adopted with some

modificationschanges are as under

(a) The first condition for identifying MSE as sick should stipulate ldquoif any of the

borrowal accounts becomes NPA in case of micro enterprises and remains

NPA for three months or more in case of small enterprisesrdquo

(b) The erosion in net worth due to accumulated losses to the extent of 50

has to be with reference to peak net worth to provide for a benchmarking

(c) The Committee recommends that it would be more appropriate to take

into consideration lsquoaccumulated lossesrsquo which is a larger concept and

finds better acceptability with banks instead of lsquoaccumulated cash lossesrsquo

for erosion in net-worth as it has been proposed

B Incipient sickness

The members of the Committeeparticipants suggested that the definition

recommended by the Working Group on Rehabilitation of Sick SME (Chairman Dr

7

KC Chakrabarty the then CMD of PNB) for incipient sickness may be adopted with

minor changes and restructuring rehabilitation measures started at that stage itself

The Working Group on Rehabilitation of Sick SMEs recommended the

definition of incipient sickness as under

An account may be treated to have reached the stage of incipient sickness

potential sickness if any of the following events are triggered

d There is delay in commencement of commercial production by more

than six months for reasons beyond the control of promoters and entailing

cost overrun

e The company incurs losses for two years or cash loss for one year

beyond the accepted timeframe on account of change in economic and fiscal

policies affecting the working of MSEs or otherwise

f The capacity utilization is less than 50 of the projected level in terms

of quantity or the sales are less than 50 of the projected level in terms of

value during a year

Recommendations

(i) The Committee recommends that the above definition may be adopted

However the Committee is of the view that the words ldquoentailing cost

overrunrdquo in (a) and ldquoon account of change in economic and fiscal policiesrdquo

in (b) are somewhat restrictive as there could be other implications of

delay in commercial production or reasons attributing to incurring losses

These aspects therefore need to be looked into

(ii) The restructuringrehabilitation process should start at the point of incipient

sickness in a timely manner so that sickness can be checked arrested at

an early stage The banks should consider providing financial assistance

depending on actual needs to such units to help sorting out the difficulties

(iii) The Committee further recommends that branch officials should keep a

close watch on the operations and identify the units reaching the stage of

incipient sickness within a period not exceeding one month and provide

assistance by way of restructuring additional finance if required etc to

bring back the units to healthy track It is also necessary to lay down

8

timelines for the Banks for taking remedial actionmeasures to ensure that

sickness is arrested at the incipient stage itself The restructuring of

accounts of such units should be undertaken and completed with a

maximum period of one month of detection of incipient sickness

C Procedure for assessing the viability of sick MSEs

It has been proposed by RBI that along with changing the definition of sick

units it is also necessary to prescribe a new set of guidelines to make viability study

an effective tool for rehabilitation of sick micro and small units Thus the suggestions

of the Working Group on procedure to be followed by the banks before declaring any

sick micro and small enterprise as unviable as follows may be accepted for

implementation

The proposed procedure to be followed by banks is as under

bull A unit should be declared unviable only if the viability status is

evidenced by a viability study However it may not be feasible to conduct

viability study in very small units and will only increase paperwork For tiny

micro enterprises Branch Manager may take a decision on viability and

record the same along with the justification

bull The said viability study and the declaration of the unit as unviable

should have the approval of the next higher authority present sanctioning

authority except in tiny micro enterprises However in tiny micro enterprises

an opportunity may be given to the borrower to present his case to the Branch

Manager before declaring a unit as unviable

bull The next higher authority should take such decision only after giving an

opportunity to the promoters of the unit to present their case

bull Decision of the above higher authority should be informed to the

promoters in writing The above process should be completed in a time bound

manner not later than 3 months However banks may take decision in cases

of malfeasance or fraud without following the above procedure

While deliberating on the procedure proposed for deciding on the viability of

sick MSEs it was suggested that a Committee with the representatives of DIC

9

Banks etc may decide on the viability of sick units The Committee is of the view

that assessing the viability of a sick MSE in a timely manner and faster relief and

concessionsrelief to the units identified as lsquoviablersquo is of critical importance in

addressing the problem of sickness among the MSEs The Committee while broadly

agreeing with the proposed procedure recommends certain changes in the

procedure to be followed by the banks before declaring a unit lsquounviablersquo The

Committee recommends that for lsquotiny micro enterprisesrsquo an opportunity should be

given to present the case before the sanctioning authority before such units are

declared lsquounviablersquo

Recommendations

(a) lsquoTiny micro enterprisesrsquo for which decision on viability is to be taken at the

Branch Manager level has not been clearly defined There is no such separate

category within micro enterprises provided in the definition as per the MSMED

Act 2006 However the Committee is of the view that micro (manufacturing)

enterprises having investment in plant and machinery up to Rs 5 lakh and

micro (service) enterprises having investment in equipment up to Rs 2 lakh for

which there is already earmarking of 40 within total advances to MSEs could

be considered as lsquoTiny micro enterprisesrsquo

(b) While the procedure proposed provides for an opportunity to tiny micro

enterprises to present case before Branch Manager it may be appropriate that

before such units are declared as unviable an opportunity be given for

presenting the case before sanctioning authority

(c) Timelines need to be clearly specified for the action to be taken at various

levels for deciding on the viability of sick MSEs The final decision on viability

of a sick MSEs may be taken within a maximum period of 3 months However

in case of lsquoTiny micro enterprisesrsquo for which decision on viability is to be taken

at the Branch Manager level the process to declare a unit as sick should be

taken within a shorter time period

(d) With regard to the suggestion to adopt a Committee approach for deciding on

the viability the Committee was of the view that it would lead to unnecessary

delays and may not be practically feasible However the RBI could issue

10

instructions to banks for ensuring that in all the cases where sick MSEs are

declared as lsquounviablersquo may be examined by a Committee The Committee may

be formed in each State under the chairmanship of the SecretaryDirector of

Industries with representatives from Lead Bank National and State Apex Level

MSE Associations MSME-DI DICs etc

(e) The extant guidelines of RBI provide that the rehabilitation package should be

fully implemented within six months from the date the unit is declared as

lsquopotentially viablersquo or lsquoviablersquo The Committee is of the view that the

implementation period should be reduced to 2-3 months as sick units need to

be provided reliefconcessions quickly and within a reasonable time period

D Relief and concessions extended to sick MSEs

The Committee observed that the relief and concessions extended to sick

MSEs as per the extant guidelines of RBI and recommendations of the lsquoWorking

Group on Rehabilitation of Sick SMEsrsquo in this regard also need to be looked into

though the proposal of RBI does not cover the same On the issue of relief and

concessions extended to sick MSEs the Committee agreed with the

recommendations of the Working Group that the extant guidelines though adequate

may require minor modifications to further strengthen the same

The changes suggested are as under

Particulars Existing guidelines Suggested changes

Waiver of

penal interest

Waiver of penal Interest from

the beginning of the

accounting year of the unit in

which it started incurring cash

losses continuously

The following words may be

added ldquothe date of the account

becoming NPA whichever is

earlierrdquo

Rate of

interest

NIL for FITL and different

concessions for other

facilities

The existing concessions on rate

of interest may continue Interest

may be made ballooning or

staggered also

11

Repayment

period

The repayment period

permitted under DRM for

SMEs is 10 years with

concessions for 7 years and

therefore no change is

suggested in the same

Staggered or ballooning

repayment may also be permitted

so that the instalments are

aligned to the cash flows

Margin on

funding of

losses

While funding past and future

losses margin of 25 may be

prescribed in case of MSEs

E Other related Issues (a) Relaxation in prudential guidelines to help MSE sector

As per the extant guidelines of RBI if any asset is restructured then the

asset classification of that asset is to be downgraded ie if it is standard

then after restructuring to sub-standard One of the exceptions to the

above rule is that if the restructured amount gets covered by 100

tangible security then the bank can retain the same classification ie if

the bank restructures any asset and if the restructured amount gets

covered by 100 by tangible security then bank can retain the asset

classification

There is exemption to the above provisions for SSI borrowers with

outstanding of Rs25 lakh

Recommendation

The Committee recommends that RBI may relax this norm and permit

restructuring of Micro and Small Enterprises without the tangible security cover

(b) Second restructuring

At present second restructuring is not permitted and it will downgrade the

asset classification of the account However if re-work is done by protecting

Net Present Value (NPV) then it will not be taken as a second restructuring

But again this provision is available ONLY UNDER CDR ROUTE

12

Recommendation

RBI may allow lenders to do rework of the earlier package without protecting

the NPV at their own level for MSME sector and lenders may be permitted to retain

the same asset classification

(c) Relaxation in NPA norms

The Committee deliberated at length on the issue of providing relaxations in

the NPA norms for MSMEs as the working capital cycle is stretched in the

present scenario and MSMEs facing the problems of delayed payments In

this context it was opined that the extant NPA norms are based on the

international standards and any sector-specific relaxations may not be

possible With the passage of the Factoring Regulation Bill 2011 and the

same becoming an Act the problems of liquidity faced by MSMEs would be

addressed to a large extent

As regards the relaxation in NPA norms the Committee was of the view that it

is suggesting pro-active measures at the incipient sickness stage itself in a

timely manner to checkarrest sickness and therefore the difficulties being

faced by MSEs would be taken care of

(Dr Sunita Chhibba)

Chairperson

(Dr Tarsem Chand) (Lily Vadera) (Subhranshu Mahapatra) Member Member Member

(G Rajkumar) (S G Chore) Member Member

Dated June 2012

Guidelines for Rehabilitation of Sick Small Scale Industrial Units

RPCD NO PLNFSBC570604012001-200216 January 2002

26 Pausha 1923 (S)All Scheduled Commercial Banks

Dear Sir

Guidelines for Rehabilitation of Sick Small Scale Industrial Units

Small Scale Industries (SSI) constitute an important and crucial segment of the

industrial sector This has been acknowledged by the Government of India by the

high priority it has accorded to the SSI sector The Reserve Bank of India have also

bestowed the status of Priority Sector to SSI lending by banks and various circulars

guidelines have been issued in this regard from time to time

2 Several internal and external factors have put considerable pressure on the

performance of the SSIs resulting in a number of them becoming sick Of late the

incidence of sickness in SSI Sector is showing an increasing trend and a large number

of SSI units identified as sick were not found potentially viable

3 To address this and other allied issues the Group of Ministers on SSI in their

meeting held on 16th August 2000 had desired that RBI should draw up a revised

detailed transparent and non-discretionary guidelines for rehabilitation of current sick

and potentially viable SSI units Accordingly a Working Group on Rehabilitation of

Sick SSI was constituted by RBI in November 2000 with the Chairman Indian

Banksrsquo Association Shri SSKohli as its Chairman The Group has since submitted

its report and all the major recommendations made therein including a change in the

criteria for identification and classification of sick units in the SSI Sector have been

accepted by the Reserve Bank of India The draft revised guidelines were put on RBI

website and also circulated among banks SSI Association etc for eliciting their

views The suggestions received have been considered while finalizing the revised

guidelines drawn up on the basis of the recommendations of the Working Group

4 Enclosed is a complete set of revised guidelines with regard to rehabilitation

of sick units in the SSI sector with specific reference to definition of sick SSI units its

monitoring viability norms incipient sickness as also relief and concessions from

banksfinancial institutions in the case of potentially viable units Although sickness

in the large medium and small industrial units exhibit many common features any

approach to sickness in SSI sector has to reckon with the relative weakness of such

units to withstand internal as well as external pressures The distinction between the

small scale and tiny sector units and between tiny sector and decentralized sector units

comprising artisans village and cottage industries units have also been taken into

consideration The emphasis of the rehabilitation effort in the case of SSI units is

therefore on early detection of signs of incipient sickness adequate and intensive

relief measures and their speedy application rather than giving a long span of time to

the units for rehabilitation Accordingly the revised guidelines are issued for

rehabilitation of sick units in the SSI sector as given in the Annexure-I This set of

guidelines will supercede all our earlier circulars and guidelines laid down in (i)

RPCD NO PLNFS BC 48 SIU20-87 dated 6 February 1987 (ii) RPCD NO

PLNFS BC 122 SIU-20 88-89 dated 8 June 1989 (iii) RPCD NO PLNFS BC

69 SIU20 90-91 dated 8 January 1991 (iv) RPCD NO PLNFS BC 1 SIU20

92-93 dated 1 July 1992 and (v) RPCD NO PLNFS BC 90 060401 95-96 dated

13 February 1996

5 The important changes brought out in guidelines based on the recommendations of

the Working Group vis-agrave-vis the existing guidelines on rehabilitation of sick SSI units

are furnished in Annexure II for ready reference

6 We need hardly emphasise that timely and adequate assistance to potentially

viable SSI units which have already become sick or are likely to become sick is of the

utmost importance not only from the point of view of the financing banks but also for

the improvement of the national economy in view of the sectorrsquos contribution to the

overall industrial production exports and employment generation The banks

should therefore take a sympathetic attitude and strive for rehabilitation in respect of

units in the SSI sector particularly wherever the sickness is on account of

circumstances beyond the control of the entrepreneurs However in cases of units

which are not capable of revival banks should try for a settlement and or resort to

other recovery measures expeditiously

7 Please acknowledge receipt and advise us of the action taken by your bank in

implementing the above guidelines

Yours faithfully

(Vani J Sharma )Chief General Manager

ANNEXURE - I

GENERAL GUIDELINES FORREHABILITATION OF SICK SSI UNITS

Incipient Sickness

1 It is of utmost importance to take measures to ensure that sickness is arrested

at the incipient stage itself The branch officials should keep a close watch on the

operations in the account and take adequate measures to achieve this objective The

managements of the units financed should be advised about their primary

responsibility to inform the banks if they face problems which could lead to sickness

and to restore the units to normal health The organizational arrangements at branch

level should also be fully geared for early detection of sickness and prompt remedial

action BanksFinancial Institutions will have to identify the units showing symptoms

of sickness by effective monitoring and provide additional finance if warranted so as

to bring back the units to a healthy track An illustrative list of warning signals of

incipient sickness that are thrown up during the scrutiny of borrowal accounts and

other related records eg periodical financial data stock statements reports on

inspection of factory premises and godowns etc is given in Appendix-I which will

serve as a useful guide to the operating personnel Further the system of asset

classification introduced in banks will be useful for detecting advances which are

deteriorating in quality well in time When an advance slips into the sub-standard

category as per norms the branch should make full enquiry into the financial health

of the unit its operations etc and take remedial action The branch officials who are

familiar with the day-to-day operations in the borrowal accounts should be under

obligation to identify the early warning signals and initiate corrective steps promptly

Such steps may include providing timely financial assistance depending on

established need if it is within the powers of the branch manager and an early

reference to the controlling office where the relief required are beyond his delegated

powers The branch manager may also help the unit in sorting out difficulties

which are non-financial in nature and require assistance from outside agencies like

Government departments undertakings Electricity Boards etc He should also keep

the term lending institutions informed about the position of the units wherever they

are also involved

2 The instructions issued to banks by RBI to set up cells at all regional centers

besides at Head Office to deal with sick industrial units and also provide expert staff

including technical personnel to such cells are reiterated

3 Definition of Sick SSI Unit

An SSI unit should be considered Sick if

a) any of the borrowal accounts of the unit remains substandard for more

than six months ie principal or interest in respect of any of its borrowal

accounts has remained overdue for a period exceeding one year The requirement

of overdue period exceeding one year will remain unchanged even if the present

period for classification of an account as sub-standard is reduced in due course

or

b) there is erosion in the net worth due to accumulated cash losses to the

extent of 50 per cent of its net worth during the previous accounting year

and

c) the unit has been in commercial production for at least two years

This would enable banks to take action at an early stage for revival of the units The

above definition may be adopted for the purpose of reporting the data for the half-year

ending 31 March 2002 while for the purpose of formulating nursing programme

banks should go by the above definition with immediate effect

4 Viability of Sick SSI Units

A unit may be regarded as potentially viable if it would be in a position after

implementing a relief package spread over a period not exceeding five years from the

commencement of the package from banks financial institutions Government (

Central State ) and other concerned agencies as may be necessary to continue to

service its repayment obligations as agreed upon including those forming part of the

package without the help of the concessions after the aforesaid period The

repayment period for restructured (past) debts should not exceed seven years from the

date of implementation of the package In the case of tinydecentralised sector units

the period of reliefsconcessions and repayment period of restructured debts which

were hitherto two years and three years respectively have been revised so as not to

exceed five and seven years respectively as in the case of other SSI units Based on

the norms specified above it will be for the banksfinancial institutions to decide

whether a sick SSI unit is potentially viable or not Viability of a unit identified as

sick should be decided quickly and made known to the unit and others concerned at

the earliest The rehabilitation package should be fully implemented within six

months from the date the unit is declared as potentially viable viable While

identifying and implementing the rehabilitation package banksFIs are advised to do

lsquoholding operation for a period of six months This will allow small-scale units to

draw funds from the cash credit account at least to the extent of their deposit of sale

proceeds during the period of such lsquoholding operation

5 Reliefs and Concessions for Rehabilitation of Potentially Viable Units

It is emphasised that only those units which are considered to be potentially viable

should be taken up for rehabilitation The reliefs and concessions specified are not to

be given in a routine manner and have to be decided by concerned bankfinancial

institution based on the commercial judgment and merits of each case Banks have

also the freedom to extend reliefs and concessions beyond the parameters in deserving

cases Only in exceptional cases concessions reliefs beyond the parameters should

be considered In fact the viability study itself should contain a sensitivity analysis in

respect of the risks involved that in turn will enable firming up of the corrective action

matrix Norms for grant of reliefs and concessions by banksfinancial institutions to

potentially viable sick SSI units for rehabilitation are furnished in Appendix-II

6 Units becoming sick on account of wilful mismanagement wilful default

unauthorized diversion of funds disputes among partners promoters etc should not

be considered for rehabilitation and steps should be taken for recovery of bankrsquos dues

The definition of wilful default as given by RBI vide its Circular DBOD

NoBCDL(W)1220016002(1)98-99 dated 20 February 1999 will broadly cover

the following

a) Deliberate non-payment of the dues despite adequate cash flow and

good networth

b) Siphoning off of funds to the detriment of the defaulting unit

c) Assets financed have either not been purchased or have been sold and

proceeds have been misutilised

d) Misrepresentationfalsification of records

e) Disposalremoval of securities without banks knowledge

f) Fraudulent transactions by the borrower

The views of the lending FIbanks in regard to wilful mismanagement of

fundsdefaults will be treated as final

7 Delegation of Powers

The delay in the implementation of agreed rehabilitation packages should be reduced

One of the factors contributing to such delay was found to be the time taken for

obtaining clearance from the Controlling Office for the relief and concessions As it

is essential to accelerate the process of clearance the banks and the financial

institutions may delegate sufficient powers to senior officers at various levels such as

district divisional regional zonal and also at head office to sanction the banks or the

financial institutions commitment to its share in the rehabilitation package drawn up

in conformity with the prescribed guidelines

APPENDIX-I

Illustrative list of warning signals of incipientsickness that are thrown up during the Scrutiny

of Borrowal Accounts and other Related Records(eg Periodical Financial Data Statements Report

on Inspection of Factory Premises and Godowns etc)

a) Continuous irregularities in cash creditoverdraft accounts such as inability tomaintain stipulated margin on continuous basis or drawings frequentlyexceeding sanctioned limits periodical interest debited remaining unrealised

b) Outstanding balance in cash credit account remaining continuously at themaximum

c) Failure to make timely payment of instalments of principal and interest onterm loans

d) Complaints from suppliers of raw materials water power etc about non-payment of bills

e) Non-submission or undue delay in submission or submission of incorrect stockstatements and other control statements

f) Attempts to divert sale proceeds through accounts with other banks

g) Downward trend in credit summations

h) Frequent return of cheques or bills

i) Steep decline in production figures

j) Downward trends in sales and fall in profits

k) Rising level of inventories which may include large proportion of slow ornon-moving items

l) Larger and longer outstandings in bill accounts

m) Longer period of credit allowed on sale documents negotiated through thebank and frequent return by the customers of the same as also allowing largediscount on sales

n) Failure to pay statutory liabilities

o) Utilization of funds for purposes other than running the units

p) Not furnishing the required informationdata on operations in time

q) Unreasonablewide variations in salesreceivables levels vis-agrave-vis level ofoperation of the unit

r) Non co-operation for stock inspections etc

s) Delay in meeting commitments towards payments of installments duecrystallized liabilities under LCBGs etc

t) Divertingrouting of receivables through non-lending banks

APPENDIX ndashII

Relief and concessions which can be extended bybanksfinancial institutions to potentially viable

sick SSI units under rehabilitation

The viability and the rehabilitation of a sick SSI unit would depend primarily on the

unitrsquos ability to continue to service its repayment obligations including the past

restructured debts It is therefore essential to ensure that ordinarily there is no write-

off or scaling down of debt such as by reduction in rate of interest with retrospective

effect except to the extent indicated in the guidelines The guidelines on various

parameters on reliefs and concessions are given below

i) Interest Dues on Cash Credit and Term Loan

If penal rates of interest or damages have been charged such charges should be

waived from the accounting year of the unit in which it started incurring cash losses

continuously After this is done the unpaid interest on term loans and cash credit

during this period should be segregated from the total liability and funded No interest

may be charged on funded interest and repayment of such funded interest should be

made within a period not exceeding three years from the date of commencement of

implementation of the rehabilitation programme

ii) Unadjusted Interest Dues

Unadjusted interest dues such as interest charged between the date up to which

rehabilitation package was prepared and the date from which actually implemented

may also be funded on the same terms as at (i) above

iii) Term Loans

The rate of interest on term loans may be reduced where considered necessary by not

more than three per cent in the case of tinydecentralised sector units and by not more

than two per cent for other SSI units below the document rate

iv) Working Capital Term Loan (WCTL)

After the unadjusted interest portion of the cash credit account is segregated as

indicated at (i) and (ii) above the balance representing principal dues may be treated

as irregular to the extent it exceeds drawing power This amount may be funded as

Working Capital Term Loan (WCTL) with a repayment schedule not exceeding 5

years The rate of interest applicable may be 15 to 3 points below the prevailing

fixed rate prime lending rate wherever applicable to all sick SSI units including tiny

and decentralized units

v) Cash Losses

Cash losses are likely to be incurred in the initial stages of the rehabilitation

programme till the unit reaches the break-even level Such cash losses excluding

interest as may be incurred during the nursing programme may also be financed by

the bank or the financial institution if only one of them is the financier But if both

are involved in the rehabilitation package the financial institution concerned should

finance such cash losses Interest may be charged on the funded amount at the rates

prescribed by SIDBI under its scheme for rehabilitation assistance

Future cash losses in this context will refer to losses from the time of implementation

of the package up to the point of cash break-even as projected Future cash losses as

above should be worked out before interest (ie after excluding interest) on working

capital etc due to the banks and should be financed by the financial institutions if it is

one of the financiers of the unit In other words the financial institutions should not

be asked to provide for interest due to the banks in the computation of future cash

losses and this should be taken care of by future cash accruals

The interest due to the bank should be funded by it separately Where however a

commercial bank alone is the financier the future cash losses including interest will

be financed by it

The interest on the funded amounts of cash lossesinterest will be at the rates

prescribed by Small Industries Development Bank of India under its scheme for

rehabilitation assistance

vi) Working Capital

Interest on working capital may be charged at 15 below the prevailing fixed prime

lending rate wherever applicable Additional working capital limits may be extended

at a rate not exceeding the PLR

vii) Contingency Loan Assistance

For meeting escalations in capital expenditure to be incurred under the rehabilitation

programme banksfinancial institutions may provide where considered necessary

appropriate additional financial assistance upto 15 per cent of the estimated cost of

rehabilitation by way of contingency loan assistance Interest on this contingency

assistance may be charged at the concessional rate allowed for working capital

assistance

viii) Funds for Start-up Expenses and Margin for Working Capital

There will be need to provide the unit under rehabilitation with funds for start-up

expenses (including payment of pressing creditors) or margin money for working

capital in the form of long-term loans Where a financial institution is not involved

banks may provide the loan for start-up expenses while margin money assistance

may either come from SIDBI under its Refinance Scheme for Rehabilitation or should

be provided by State Government where it is operating a Margin Money Scheme

Interest on fresh rehabilitation term loan may be charged at a rate 15 below the

prevailing fixed prime lending rate wherever applicable or as prescribed by SIDBI

NABARD where refinance is obtained from it for the purpose

All interest rate concessions would be subject to annual review depending on the

performance of the units

ix) Promoters Contribution

As per the extant RBI guidelines promoters contribution towards the rehabilitation

package is fixed at a minimum of 10 per cent of the additional long-term requirements

under the rehabilitation package in the case of tiny sector units and at 20 per cent of

such requirements for other units In the case of units in the decentralized sector

promoterrsquos contribution may not be insisted upon A need is felt for increasing the

promoters contribution towards rehabilitation from the present limits It is therefore

open to banks and financial institutions to stipulate a higher promoters contribution

where warranted At least 50 per cent of the above promoters contribution should be

brought in immediately and the balance within six months For arriving at promoters

contribution the monetary value of the sacrifices from banks financial institutions

and Government may be taken into account in addition to the long - term

requirement of funds under the rehabilitation package

While evolving packages it should be made a precondition that the promoters should

bring in their contribution within the stipulated time frame Further in regard to

concessions and relief made available to sick units banks should incorporate a lsquoRight

of Recompense clause in the sanction letter and other documents to the effect that

when such units turn the corner and rehabilitation is successfully completed the

sacrifices undertaken by the Fls and banks should be recouped from the units out of

their future profits cash accruals

ANNEXURE - II

Important changes brought out in the revised guidelines based on therecommendations of the Working Group on Rehabilitation of sick SSI units vis-

agrave-vis Existing Guidelines

New Guidelines Existing Guidelines

1 The definition of a sick SSI unit may be changed

as

a) If any of the borrowal accounts of the unit

remains substandard for more than six months ie

principal or interest in respect of any of its

borrowal accounts has remained overdue for a

period exceeding 1 year The requirement of

overdue period exceeding one year will remain

unchanged even if the present period for

classification of an account as sub-standard is

reduced in due course

OR

b) There is erosion in the net worth due to

An SSI is considered lsquosickrsquo when ndash

(i) any of its borrowal accounts has

become doubtful advance ie principal or

interest in respect of its borrowal accounts

has remained overdue for a period

exceeding 2frac12 years and

(ii) there is erosion in the net worth due

to accumulated cash losses to the extent of

50 per cent or more of its peak net worth

during the preceding two accounting years

accumulated cash losses to the extent of 50 per cent

of its net worth during the previous accounting year

and

AND

c) The unit has been in commercial production for

at least 2 years

2 In the case of tiny decentralized sector units the

period of reliefsconcessions and repayment period of

restructured debts have been revised so as not to

exceed five and seven years respectively as in the case

of other SSI units

(i) While the other existing norms for grant of relief

and concessions which can be extended by banks to

potentially viable sick SSI units may continue

additional working capital limits may be extended at a

rate not exceeding the PLR

(ii) Viability of a unit should be decided quickly

and made known to the unit and others concerned at

the earliest The rehabilitation package should be fully

implemented within six months from the date the unit

is declared as lsquopotentially viablersquo lsquoviablersquo While

identifying and implementing the rehabilitation

package banksFls may be asked to do lsquoholding

operationrsquo for period of six months This will allow

small-scale units to draw funds from the cash credit

account at least to the extent of the deposit of sale

proceeds during the period of such lsquoholding operationrsquo

(iii) There is a need for increasing the promotersrsquo

In the case of tiny decentralized sector

units the period of reliefs concessions

and repayment period of restructured debts

will be two years and three years

respectively

In the existing guidelines there was no

mention about providing additional

working capital

As per the extant guidelines the banks are

expected to take as far as possible a

decision on the viability or otherwise of a

unit identified as sick within a period of

three months from the date of receipt of

complete information on the relevant

aspects from the management of the unit

Further the finalization of the nursing

programme should be completed within a

period of three months from the date of

such decisions

As regards holding operation it is a new

conceptfacility which was not there in the

existing guidelines

contribution towards rehabilitation package from the

present limits It is open to the banksfinancial

Institutions to stipulate a higher promotersrsquo

contribution where warranted

Further in regard to concessions and reliefs made

available to sick units banks should incorporate ldquo

Right of Re-compenserdquo clause in the sanction letter

and other documents to the effect that when such units

turn the corner and rehabilitation is successfully

completed the sacrifices undertaken by the FIs and

banks should be recouped from the units out of their

future profitscash accruals

Promotersrsquo contribution towards

rehabilitation may be fixed at a minimum

of 10 of the additional long term

requirements under the rehabilitation

package in the case of tiny sector units and

20 of such requirements for other units

Banks have been advised to incorporate the

Right of Re- compenserdquo clause in cases

where the concessionsreliefs were beyond

the parameters laid down by RBI

भारतीय रज़व बक

_________________________RESERVE BANK OF INDIA________________________ wwwrbiorgin

RBI2008-09467

RPCD SMEampNFS BCNo1020604012008-09 May 4 2009

All Scheduled Commercial Banks

Dear Sir Madam

Credit delivery to the Micro and Small Enterprises Sector

In recognition of the problems being faced by the Micro and Small Enterprises (MSE)

sector particularly with respect to rehabilitation of potentially viable sick units the Reserve

Bank had constituted a Working Group under the Chairmanship of Dr K C Chakrabarty

Chairman amp Managing Director Punjab National Bank

2 The aforesaid Group submitted its report to Reserve Bank of India in April 2008

covering comprehensively the entire gamut of issues and problems (credit and non-credit

related) confronting the sector The Reserve Bank placed the report on its website and

invited comments from all stake holders The responses and comments on the report have

been carefully examined

3 The recommendations made by the Group need to be considered by Government of

India State Governments and commercial banks (Annexes I to III respectively) The

recommendations relating to Government of India have been forwarded to them for

consideration and necessary action The recommendations relating to the State Governments

have been forwarded to the SLBC Convenor banks for taking up the issue in the SLBC

meetings Other recommendations pertaining to SIDBI have been sent to them

__________________________________________________________________________________________________________________________________

aumleacuteecerCe Deesup3eespeocircee Deewj degeYacuteCe fJeYeeaumle kesAgraveecircrsup3e keAgraveesup3eeotildeuesup3e 13Jer cebfpeue kesAgraveecircrsup3e keAgraveesup3eeotildeuesup3e YeJeocirce cegbyeFotilde 400 001

igravesfueHeAgraveesocirce Tel No 91-22-22661602 HewAgravekeIgravemeFax No 91-22-226210112265827322658276 Fotilde-cesue Email IDcgmicrpcdrbiorgin Rural Planning amp Credit Department Central Office 13th Floor Central Office Building Post Box No 10014 Mumbai -400

001 Enor Deemeeocirce nw FmekeAgravee heacutesup3eesaumle yeŸeFsup3es

-2-

4 Several recommendations have been made regarding the Credit Guarantee Fund Trust for

Micro and Small Enterprises (CGTMSE) Scheme These recommendations will be considered by

the Standing Advisory Committee on Flow of Institutional Credit to MSEs in terms of

paragraph 114 of the Annual Policy for 2009-10

5 The Group has addressed problems being faced by the sector in getting adequate and

timely credit It has also made recommendations not only for timely detection and remedial

action with respect to incipient sickness but also rehabilitation of sick units which can be

revived

6 You are advised to consider for speedy implementation the recommendations made

by the Working Group set out in Annex III with regard to timely and adequate flow of credit

to the MSE sector

7 The Reserve Bank has carefully considered the Grouprsquos recommendations regarding

rehabilitation of potentially viable sick MSE unitsenterprises which essentially aim at timely

detection of sickness and adoption of remedial measures to rehabilitate the potentially viable

ones While fully appreciating the sense of the Grouprsquos recommendations attention of banks

is invited to the guidelines issued by the Reserve Bank on MSE debt restructuring in respect of

borrowal accounts that show symptoms of stickiness vide its circulars

i DBODBPBC No3421041322005-06 dated September 8 2005

ii DBODBPBCNo3721041322008-09 dated August 27 2008

These guidelines in fact subsume the incipient sickness stage and if implemented as

intended could significantly prevent or arrest sickness at the initial stages Such MSE

unitsenterprises which turn sick in spite of debt re-structuring are expected to be few and

would fall within the ambit of the extant guidelines on rehabilitation of potentially viable sick

unitsenterprises (vide circular RPCDNoPLNFSBC570604012001-2002 dated January 16

2002) Banks are therefore advised to apply the Reserve Bankrsquos guidelines on debt

restructuring optimally and in letter and spirit This would be to their advantage as well as

their MSE clients

-3-

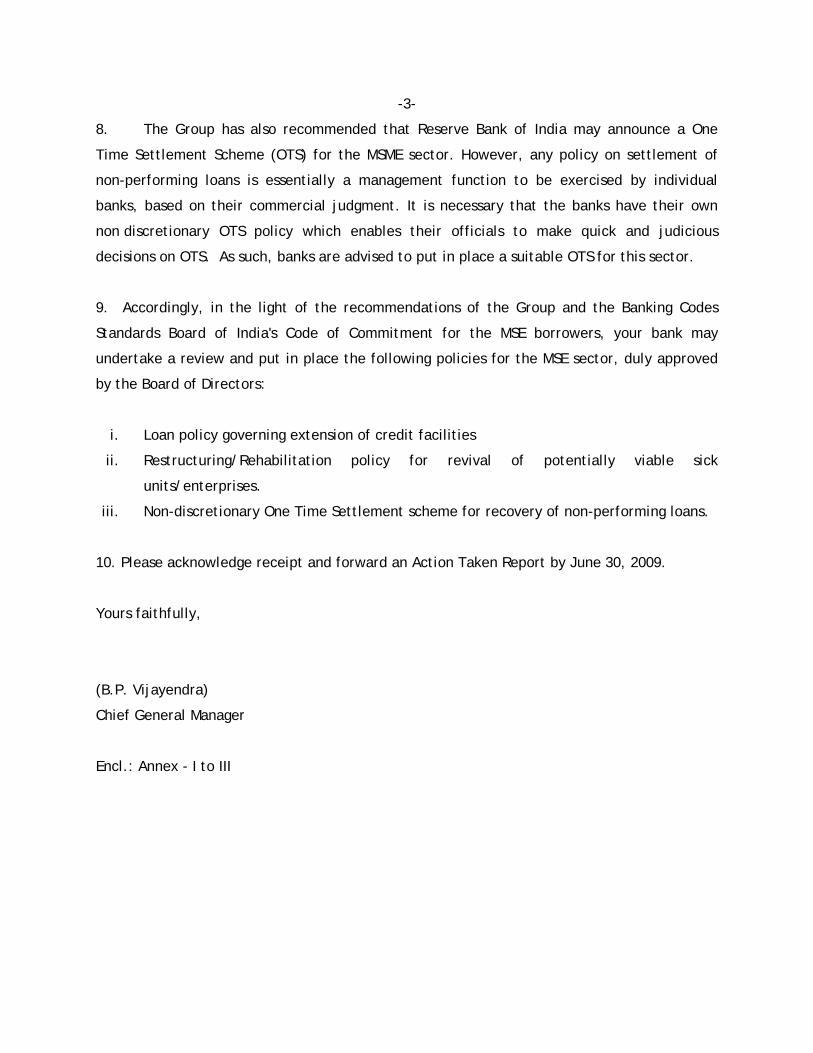

8 The Group has also recommended that Reserve Bank of India may announce a One

Time Settlement Scheme (OTS) for the MSME sector However any policy on settlement of

non-performing loans is essentially a management function to be exercised by individual

banks based on their commercial judgment It is necessary that the banks have their own

non discretionary OTS policy which enables their officials to make quick and judicious

decisions on OTS As such banks are advised to put in place a suitable OTS for this sector

9 Accordingly in the light of the recommendations of the Group and the Banking Codes

Standards Board of Indias Code of Commitment for the MSE borrowers your bank may

undertake a review and put in place the following policies for the MSE sector duly approved

by the Board of Directors

i Loan policy governing extension of credit facilities

ii RestructuringRehabilitation policy for revival of potentially viable sick

unitsenterprises

iii Non-discretionary One Time Settlement scheme for recovery of non-performing loans

10 Please acknowledge receipt and forward an Action Taken Report by June 30 2009

Yours faithfully

(BP Vijayendra)

Chief General Manager

Encl Annex - I to III

ANNEX-I

Sr No

Actions pertaining to GOI

1

As it has been observed that rehabilitation of sick SMEs could not be taken up due to non availability of promotersrsquo contribution in a large number of cases the Group recommends that the Government may create the following Funds to facilitate this sector i An independent Rehabilitation Fund may be created for rehabilitation of sick micro small and medium enterprises The fund may have a corpus of Rs 1000 crores While 75 of the corpus could be earmarked for assisting the micro and small enterprises balance could be utilized for assisting medium enterprises The fund could go a long way in rehabilitation of sick micro and small enterprises This fund may be utilized for providing soft loan at a concessional rate of interest say 5-6 quasi equity upto 50 of the required promotersrsquo contribution subject to a maximum of Rs 75 lacs (Para 321 e (i)) ii another fund may be created for contributing to the margin required to be brought in by the promoters of units taking up technological upgradation This assistance may be provided in the form of a soft loan quasi equity equity (Para 321 e (ii)) iii In order to encourage MSME units to market their products it will be desirable to set up a Marketing Development Fund which could interalia be used for providing financial assistance in setting up distribution and marketing infrastructure outlets This can also contribute resources to institutions organising exhibitions etc at various level (Para 321 e (iii) iv National Equity Fund Scheme should be restarted This fund could be utilized for green field or expansion projects (Para 321 e (iv) v In order to encourage the entrepreneurs to innovate new ideas it is necessary that venture capital mezzanine finance should be encouraged There should be a separate fund with the umbrella organisation (suggested in the report) SIDBI which should help venture capital funds in meeting the finance requirements of small enterprises by way of equity mezzanine finance soft loan etc (Para 321 e (v)) vi Support of schemes like Credit Linked Capital Subsidy Scheme (for units in other than rural areas) and KVIC Margin Money Scheme (for units in rural areas) may be extended for rehabilitation packages also (Para 321 e (vi))

2 Recognising their contribution of State Financial Corporations to industrialization of the respective regions and having regard to the potential of these

Sr No

Actions pertaining to GOI

Corporations GOI may direct the respective State Governments to provide a one time financial support for recapitalization of viable SFCs Those SFCs which are found unviable may be allowed to wind up their operations and the State Governments should settle the creditorslenders (Para 322)

3

There is little availability of funds with the promoters for technological upgradation Department of Science and Technology which is actively working for development of new technologies for the small and large industry may also consider adaptation of technology developed in other countries to the needs of Indian MSME sector for making the sector more cost effective and dovetailed to the requirements of the customer (Para 542)

4 It is necessary that all stakeholders extend financial support to Engineering CollegesIITs for undertaking research for technological upgradation in micro small and medium enterprises In order to encourage RampD towards upgradation of technology for micro small and medium enterprise units the Group propose that section 10 (21) of Income Tax Act may be amended to allow 150 deduction for contribution made towards funding of RampD work in Engineering Institutes (Para 543)

5 Government should introduce industry specific interest subsidy scheme for SMEs on the pattern of TUFS for technology upgradation and for setting up new units with latest technology However latest technology which may be covered in each industry has to be specified by the Ministry (Para 544)

6 The Government may set up more ITIs Tool room training centres etc for training of the workforce on the latest technology especially in the command areas of the user industry (Para 545)

ANNEX-II

SrNo

Action pertaining to State Government SLBC Convener banks

1 Creation of a Central Registry by the State Governments for registration of charges of all banks and other lending institutions in respect of all moveable and immovable properties of borrowers incorporated as proprietorship partnership cooperative society trust company or in any other form (Para 320d)

2 Stamp duty is payable on assignment of actionable claims Modification in these provisions for factors by way of exemption or prescribing a ceiling on the stamp duty would give impetus to the activity (Para 321 b)

3 A scheme for utilising specified NGOs to provide training services to tiny micro enterprises may be considered ( Para 410)

4 Each State Government may also have a separate Ministry for MSME In addition the State Governments may also have long term and short term policy for development promotion of MSME sector (Para 59)

5 State Government should provide preferential treatment to MSMEs in providing uninterrupted power supply In case the same is not possible the State Government may provide back ended subsidy on loans taken for purchase of DG sets (Para 511)

6 The State Governments may be encouraged to provide land at 50 of the normal rate for setting up Industrial Estates exclusively for MSMEs Further 50 subsidy may be provided on the capital cost of common facilities like effluent treatment plant power plant etc (Para 79)

7 The need for obtaining any clearance except registration with DIC for individual SME units set up in Industrial Estates developed by the State Industrial Development Corporations or DICs or approved Industrial Estates developed by private entrepreneurs for SMEs may not be considered necessary as they are developed as per the approved layouts Further the defunct Industrial Estates may be made active once again by putting in place the complete infrastructure putting national resources to good use(Para 710)

8 The niche industry or the activities having good concentration in the area may be identified by the banks and DIC The model cost of project for different sizes of commonly prevailing industry and overall viability of the activity may be assessed by a Committee comprising of 2-3 major banks of the District under the aegis of Lead Bank so as to obviate the need of any expertprofessional to prepare TEV study in individual cases The exercise may be carried out periodically after considering the price of machinery and other fixed assets required sources of raw material technical expertise and skilled labour availability access to market etc DIC may also be associated with the process Small entrepreneurs may use these project profiles and not take help from professionals in preparation of time consuming and costly TEV studyviability report While financing banks may not go for TEV study in individual cases To begin with this practice may be started for projects requiring terms loan upto 1 crore which may be raised after review (para 361)

Annex III

Action pertaining to banks 1 The model cost of project for different sizes of commonly prevailing industry

and overall viability of the activity may be assessed by a Committee comprising of 2-3 major banks of the District under the aegis of Lead Bank so as to obviate the need of any expertprofessional to prepare TEV study in individual cases The exercise may be carried out periodically after considering the price of machinery and other fixed assets required sources of raw material technical expertise and skilled labour availability access to market etc DIC may also be associated with the process Small entrepreneurs may use these project profiles and not take help from professionals in preparation of time consuming and costly TEV studyviability report Sufficient delegation of powers for sanctionrehabilitation of SMEs should be made at the field level (Para 361) Lead Banks may take necessary action

2 Lending in case of all advances upto Rs 2 crores may be done on the basis of scoring model Information required for scoring model should be incorporated in the application form itself No individual risk rating is required in such cases (Para 363 a)

3 Banks may start Central Registration of loan applications The same technology may be used for online submission of loan applications as also for online tracking of loan applications (Para 363 b)

4 The application forms may be so designed that all documents required to be executed by the borrower on sanction of the loan form its part The forms should invariably have a Checklist of the documents required to be submitted by the applicant along with the application and the formalities required to be completed post sanction (Para 363 c)

5 In case of all micro enterprises simplified application cum sanction form (which should also be printed in regional language) be introduced for loans upto Rs 1 crore and working capital under Nayak Committee norms (Para 363 d)

6 Banks who have sanctioned term loan singly or jointly must also sanction WC limit singly (or jointly in the ratio of term loan) to avoid delay in commencement of commercial production It may be ensured that there are no cases where term loan has been sanctioned and working capital facilities are yet to be sanctioned (Para 38)

7 Centralised Credit Processing Cells may be introduced These Cells may be utilized for single point appraisal sanction documentation renewal and enhancement The working of Centralised Processing Cell should be

Action pertaining to banks reviewed by the controlling office of the bank CPC should act as the back office of the bank (Para 39)

8 Committee Approach may be introduced for sanction of new loans as also rehabilitation cases This will not only improve the quality of decision as collective wisdom of the members shall be utilised especially while taking decision on loan applications for green-field projects in the micro small and medium enterprise sector or the rehabilitation proposals (Para 310)

9 The banks may consider a combined level of stock and receivables and no separate sub limit for debtors may be fixed Banks may allow CCOD against stock and receivables under one facility (Para 314)

10 In terms of the Nayak Committee norms the banks are required to provide minimum 20 of the turnover to the business enterprises as bank finance and 5 is to be obtained as margin This translates into a current ratio of 125 (Para 315)

11 Banks may develop appropriate Credit Appraisal and Rating Tool (CART) on the pattern of software developed by SIDBI or can take the help of such tools for processing the loanworking capital proposals of small and medium enterprises (Para 319)

12 The banks may focus on opening more specialised micro small and medium enterprise branches The expansion of specialised branch network in all identified clusters and Industrial Estates may be completed in a time bound manner say within next 3-5 years (Para 320 b)

13 The banks may use the platform provided by the technical institutions and send their staff to such institutions on a regular basis Training is also required to be imparted to the branch managers and their loan officers for change in their mindset away from the perceived risk in financing MSMEs A system of incentives for good performance in financing to MSMEs may be implemented which could be by way of special mention in the Performance Appraisal special training etc (Para 320 a)

14 Banks may consider introduction of Factoring Services particularly for MSMEs (Para 321 b)

15 Intervention of technology may be adopted for correct identification and reporting of sick micro small and medium enterprises (Para 919)

Modifying the existing definition of sick units as recommended by the Working Group

on Rehabilitation of Sick SMEs and procedure for assessing the viability of sick units

1 Definition of Sick Micro and Small Units

The increasing trend of sick MSME units was discussed in detail in the 8th meeting of

the Standing Advisory Committee on Flow of Institutional Credit to SME Sector held on

1612007 at RBI Mumbai The Committee observed that there was considerable delay

in rehabilitation nursing of the potentially viable units GOI suggested constitution of a

small Working Group under the Chairmanship of Dr K C Chakrabarty CMD of PNB

(then CMD of Indian Bank) with SBI and SIDBI as members to look into these issues and

suggest remedial measures so that potentially viable sick units can be rehabilitated at

the earliest

The Working Group in its Report observed that the identification of a unit is so late that

the possibilities of its revival recede To hasten the process of identification of a unit as

sick the WG had recommended a definition of sickness in order to remove the delay

factor The present definition of Sick Units in terms of our circular dated 16 January

2002 (Kohli Committee Recommendations) and the proposed definition of Sick Units is

given below in a Tabular form

Present Definition of Sick Units Proposed Definition of Sick Units

An SSI is considered lsquosickrsquo when ndash

a) If any of the borrowal accounts remains sub standard for more than six months ie principal or interest has remained overdue for a period exceeding 1 year The requirement of overdue period exceeding one year will remain unchanged even if the present period for classification

The definition of a sick MSE unit may be changed as

a) If any of the borrowal accounts remains NPA for three months or more

of an account as sub-standard is reduced in due course Or

b) There is erosion in the net worth due to accumulated cash losses to the extent of 50 per cent of its net worth during the previous accounting year And

The unit has been in commercial production for at least 2 years

Or

b) There is erosion in the net worth due to accumulated losses to the extent of 50

The existing stipulation that the unit should have been in commercial production for at least two years needs to be removed

The impact of the proposed definition vis-agrave-vis the present definition would be as under

A microsmall enterprise would be classified as sick if it has been classified as NPA for a

period of three months or more whereas earlier it was classified as substandard for

more than six months However as the period of delinquency for classification as NPA

had been reduced to 3 months from 6 months as prevailing on the date of last definition

of sickness a unit could be classified as sick only after 3 months after its classification as

NPA

For example If the date of default is 01012012

Under the current guidelines it becomes NPA on 30062012 and sick on 31122012

Under the proposed definition it becomes NPA on 31032012 and sick on 3062012

Justification for the Recommendations

bull Prior to 2002 the norms stipulated for identification of sick units were very

tough A unit had to wait for minimum two and half years before it is declared sick The

Kohli Committee submitted its report when 180 days norms were there for NPA

classification The committee reduced the time span from two and half years to one year

but suggested that the unit has to wait for one year to become sick even if NPA

classification norms are reduced from 180 days to 90 days Thus at present the unit is

declared sick after one year or Nine months after it became NPA Delay in identifying a

unit as sick considerably affects its rehabilitation By the time it is identified as a sick

unit its net worth is eroded to almost zero To keep pace with NPA classification norms

and in order to quicken the process of identification of sick units it is imperative that the

time span for declaring a unit be reduced from 160 days to 180 days In other words if

an MSE account remains NPA for more than 3 months it should be declared sick

bull The second condition for identifying a unit as sick is that there is erosion in the

net worth due to accumulated cash losses to the extent of 50 per cent during the

previous accounting year Cash loss refers to losses incurred on account of cash

transactions and they are computed without providing depreciation Such losses

normally reflect negative cash flows Accumulated loss on the other hand is a much

wider terminology and has a direct impact on capital In banking terminology

accumulated losses are used for calculation of net worth and not cash losses Hence

there is a strong case to migrate to accumulated losses from cash losses

bull The present stipulation of the unit in commercial production for at least 2 years

needs to be removed so as to enable the banks to rehabilitate units where there is delay

in commencement of commercial production and there is a need for handholding due to

timecost overruns etc

Feedback on the proposal Received

bull Department of Banking Operations And Development (DBOD)

The proposal had been referred to DBOD for clearance DBOD has since conveyed its

approval and advised that quickening the speed of identification of sick units will act as

an indicator to the bank that the unit could be restructured if considered viable DBOD

however has stated that if the bank has already taken up the account for restructuring

even before it is classified as sick then the sick classification would not have any

implication

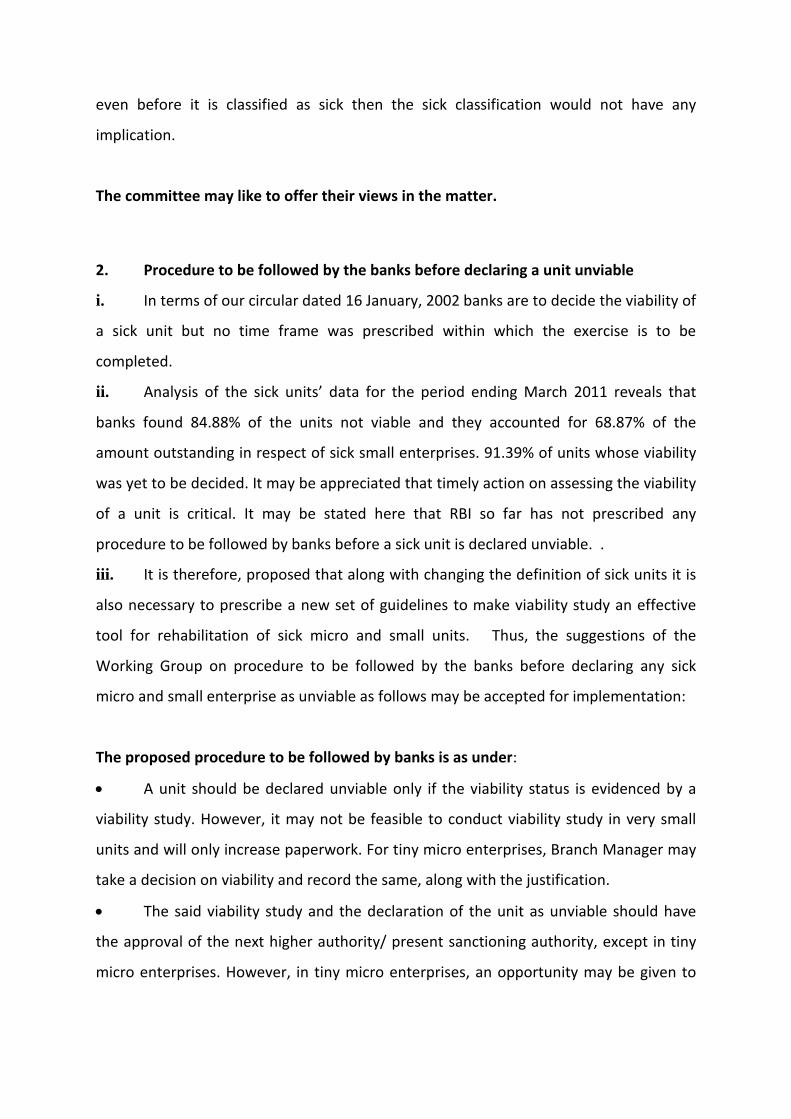

The committee may like to offer their views in the matter

2 Procedure to be followed by the banks before declaring a unit unviable

i In terms of our circular dated 16 January 2002 banks are to decide the viability of

a sick unit but no time frame was prescribed within which the exercise is to be

completed

ii Analysis of the sick unitsrsquo data for the period ending March 2011 reveals that

banks found 8488 of the units not viable and they accounted for 6887 of the

amount outstanding in respect of sick small enterprises 9139 of units whose viability

was yet to be decided It may be appreciated that timely action on assessing the viability

of a unit is critical It may be stated here that RBI so far has not prescribed any

procedure to be followed by banks before a sick unit is declared unviable

iii It is therefore proposed that along with changing the definition of sick units it is

also necessary to prescribe a new set of guidelines to make viability study an effective

tool for rehabilitation of sick micro and small units Thus the suggestions of the

Working Group on procedure to be followed by the banks before declaring any sick

micro and small enterprise as unviable as follows may be accepted for implementation

The proposed procedure to be followed by banks is as under

bull A unit should be declared unviable only if the viability status is evidenced by a