Dr Katarzyna Sum Chair of International Finance Warsaw School of Economics

35

Finance Dr Katarzyna Sum Chair of International Finance Warsaw School of Economics THE PUBLIC DEBT AS A GLOBAL PROBLEM

-

Upload

timothy-terry -

Category

Documents

-

view

29 -

download

0

description

Dr Katarzyna Sum Chair of International Finance Warsaw School of Economics. THE PUBLIC DEBT AS A GLOBAL PROBLEM. Lecture outline. Increasing debt levels in the world Debt crisis - definition and mechanism The case of the euro area sovereign debt crisis. Government debt to GDP in the world. - PowerPoint PPT Presentation

Transcript of Dr Katarzyna Sum Chair of International Finance Warsaw School of Economics

Finance 110631-1165

Dr Katarzyna SumChair of International FinanceWarsaw School of Economics

THE PUBLIC DEBT AS A GLOBAL PROBLEM

Finance 110631-1165

Lecture outline

Increasing debt levels in the world

Debt crisis- definition and mechanism

The case of the euro area sovereign debt

crisis

Finance 110631-1165

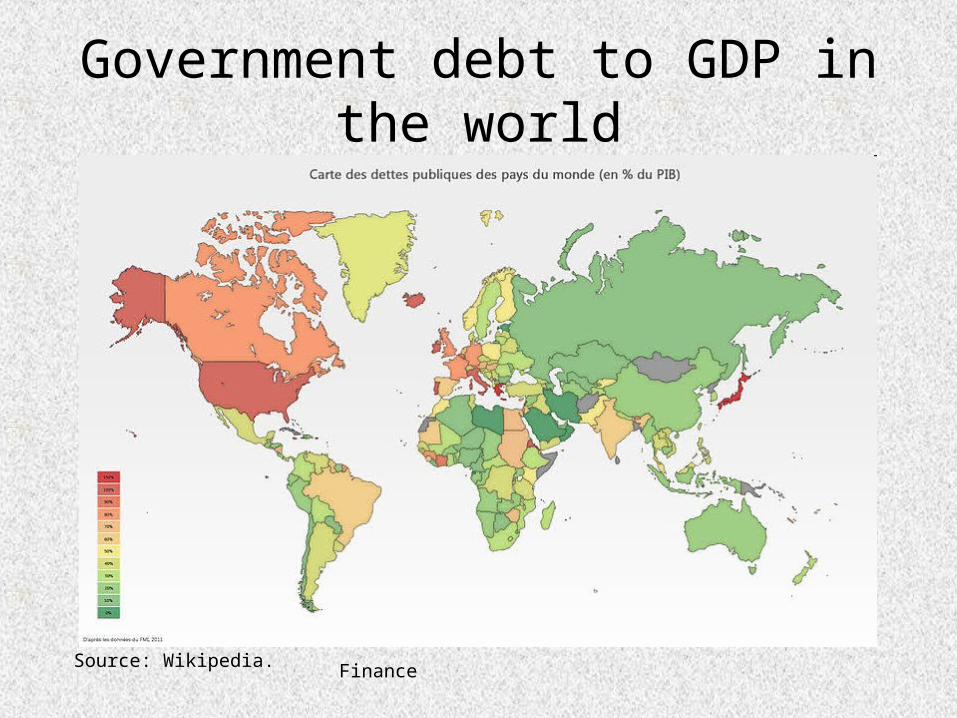

Government debt to GDP in the world

Source: Wikipedia.

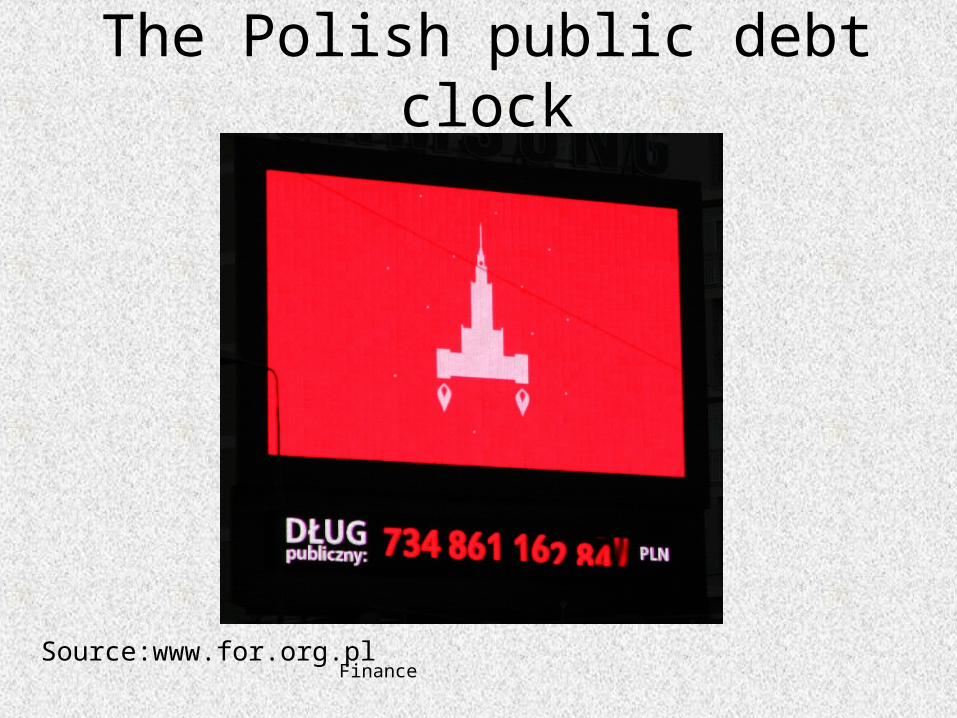

The Polish public debt clock

Source:www.for.org.plFinance 110631-1165

Finance 110631-1165

Government bonds

National government bonds- issued in domestic currency

Sovereign bonds- issued in foreign currency

Finance 110631-1165

Government bonds

Low risk premium of government bonds: Governments are able to undertake policy

measures to pay off their debt (taxes, expenses)

The risk premium depends on the credibility of the government

Sovereign bonds – additional risk related to exchange rate movements and availability of foreign currency

Finance 110631-1165

Problems related to public debt accummulation

Decreasing credibility Increasing risk premia

Investors start demanding a much higher compensation

for the risk of holding the increasingly large amounts of

public debt that authorities are going to issue

Finance 110631-1165

Accummulation of public debt globally

Individual country factors

Global factors-

the financial crisis from 2007-2009,

Global unequilibrium

Accummulation of public debt globally

The need to recapitalize banks after the crisisGovernments had to take over a large part of the debts of failing

financial institutionsThe introduction of large stimulus programmes to revive demand Prospects of further debt increase due to demographic tendencies

Finance 110631-1165

Finance 110631-1165

Accummulation of public debt globally

Total industrialised country public sector

debt is exceeded 100% of GDP in 2011!!!

(OECD)

Strong deterioration in countries which

had a balanced situation before the crisis

Finance 110631-1165

Further development will depend on:

The ultimate costs of the financial crisis

The rate of real growth

The level of interest rates,

Political decisions about spending and taxes

Finance 110631-1165

Short term and long term spending

Short term- to mitigate the effects of the

financial crisis

Long term- to deal with the ageing of societies

Finance 110631-1165

Unfunded liabilities arising from ageing

The pension system is based on the pay-as you

go method

This means that current pensions has to be

financed by current contributions

Ageing of the population creates the need of

additional borrowing

Finance 110631-1165

Age related government expenditure

Source: Stephen G Cecchetti, M S Mohanty and Fabrizio Zampolli, The future of public debt: prospects and implications, BIS Working Paper 2010.

Finance 110631-1165

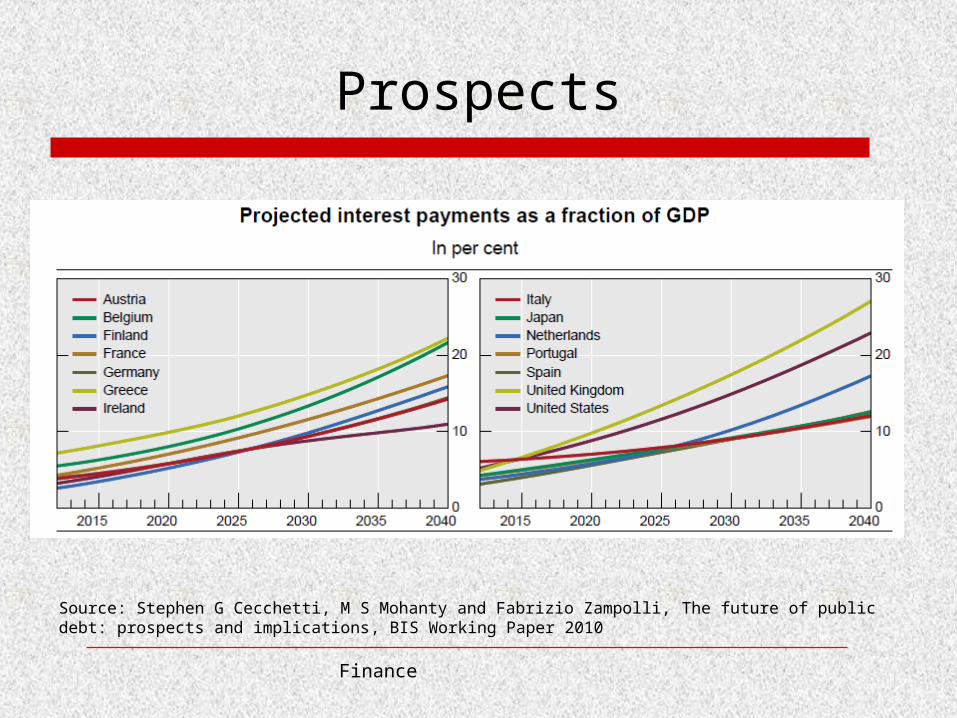

Prospects

Source: Stephen G Cecchetti, M S Mohanty and Fabrizio Zampolli, The future of public debt: prospects and implications, BIS Working Paper 2010

Finance 110631-1165

Finance 110631-1165

Debt crisis

A situation of excessive government debt

accummulation which renders an economy

incapable of paying off its debt without the help

of third parties

A type of financial crisis

Finance 110631-1165

Debt crisis

Initially high level of public debt creates the risk

of unstable debt dynamics

Increasing risk premia

Lower long term growth due the higher cost of

servicing the debt

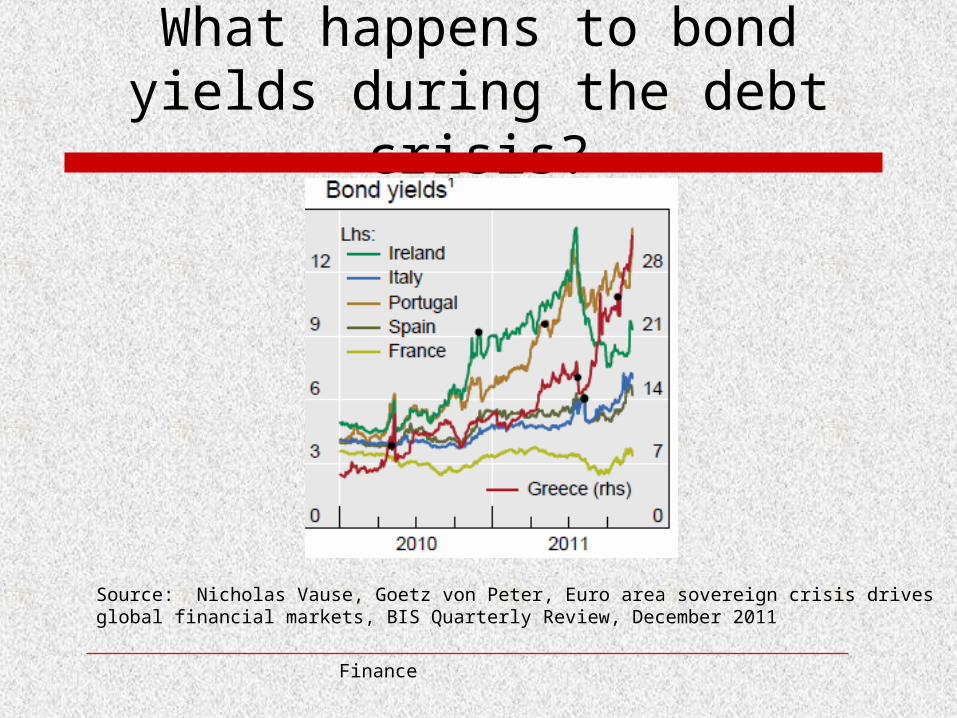

What happens to bond yields during the debt crisis?

Finance 110631-1165

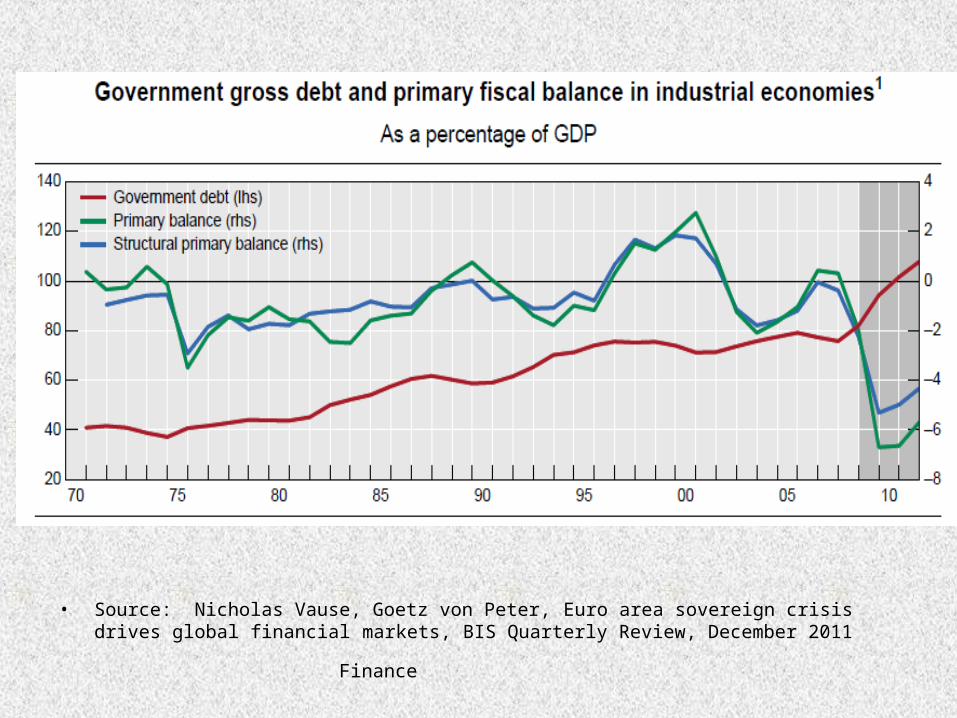

Source: Nicholas Vause, Goetz von Peter, Euro area sovereign crisis drives global financial markets, BIS Quarterly Review, December 2011

What triggered the sovereign debt crisis in the Eurozone?

The performance of respective Eurozone countries

Excessive lending, asset price bubbles

and a loss of competitiveness Overheating combined with structural

problems PIIGS

Finance 110631-1165

Finance 110631-1165

Did the euro zone try to prevnet the debt crisis?

The Stability and Growth Pact Aimed at

preventing excessive deficits and public debt

The no-bail out principle- the respective euro

area member states are not liable for the debt of

other member states

Finance 110631-1165

• Source: Nicholas Vause, Goetz von Peter, Euro area sovereign crisis drives global financial markets, BIS Quarterly Review, December 2011

Finance 110631-1165

The preventive measures

undertaken were not sufficient!

Even before the financial crisis countries did not

comply with the Pact reqirements

The situation worsened when the governments

had to fight the consequences of the crisis

Finance 110631-1165

The reaction of the financial markets

High volatility of equity and bond markets

Downgrades of country ratings exerted

additional upward pressure on government

bond yields

Finance 110631-1165

The reaction of the financial markets

The financial markets demanded higher

risk premia- financing contsraint

Additionaly- bank funding problems

This created the need of policy measures

to restore confidence

Finance 110631-1165

Political measures

Debt remission for Greece

Leveraging of the European Financial Stability

Facility

Recapitalisation of banks

Finance 110631-1165

Political measures

The political measures undertaken

contradict the no-bailout clause

The need of redefining the fiscal rules of

the eurozone

Finance 110631-1165

Securities Markets Programme

Interventions by the Eurosystem in public and

private debt securities markets in the euro area

to ensure depth and liquidity

Finance 110631-1165

Securities Markets Programme

Source: Nicholas Vause, Goetz von Peter, Euro area sovereign crisis drives global financial markets, BIS Quarterly Review, December 2011

Finance 110631-1165

Global spillovers

After the decrease of the euro area soveriegn

debt and bank debt the financial institutions

which held the securities were exposed to

increased costs

This affected institutions globally

Finance 110631-1165

Debt crisis resolution

In the past debt crises were resolved by:

Economic growth

Substantive fiscal adjustment/austerity plans;

Explicit default or restructuring of private and/or

public debt;

A sudden surprise burst in inflation

Financial repression

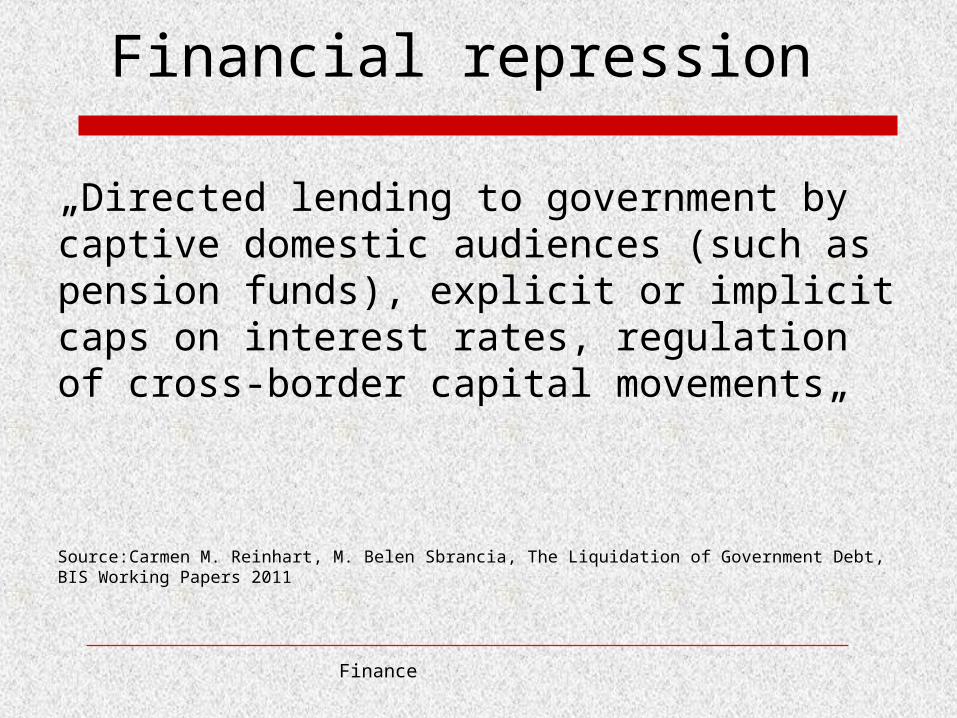

Financial repression

„Directed lending to government by captive domestic audiences (such as pension funds), explicit or implicit caps on interest rates, regulation of cross-border capital movements„

Source:Carmen M. Reinhart, M. Belen Sbrancia, The Liquidation of Government Debt, BIS Working Papers 2011

Finance 110631-1165

Debt crisis resolution

The resolution of the euro area sovereign debt crisis should consider:

Changing economic conditions Demographical tendencies

Finance 110631-1165

Finance 110631-1165

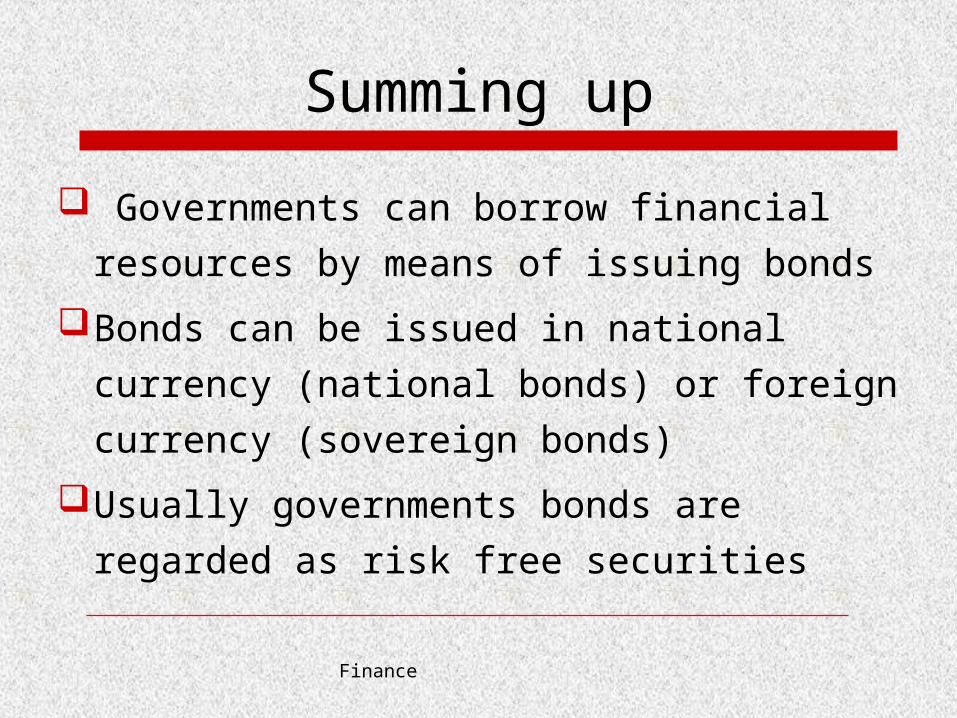

Summing up

Governments can borrow financial resources by

means of issuing bonds

Bonds can be issued in national currency

(national bonds) or foreign currency (sovereign

bonds)

Usually governments bonds are regarded as risk

free securities

Finance 110631-1165

Summing up

The excessive accummulation of debt

leads to an increase of risk premia and

increases to costs of debt servicing

A debt crisis occurs if a country can jot

repay its debt without the help of a third

party

Finance 110631-1165

Literature

Source: Stephen G Cecchetti, M S Mohanty and Fabrizio Zampolli, The future of public debt: prospects and implications, BIS Working Paper 2010

Nicholas Vause, Goetz von Peter, Euro area sovereign crisis drives global financial markets, BIS Quarterly Review, December 2011

Carmen M. Reinhart, M. Belen Sbrancia, The Liquidation of Government Debt, BIS Working Papers 2011