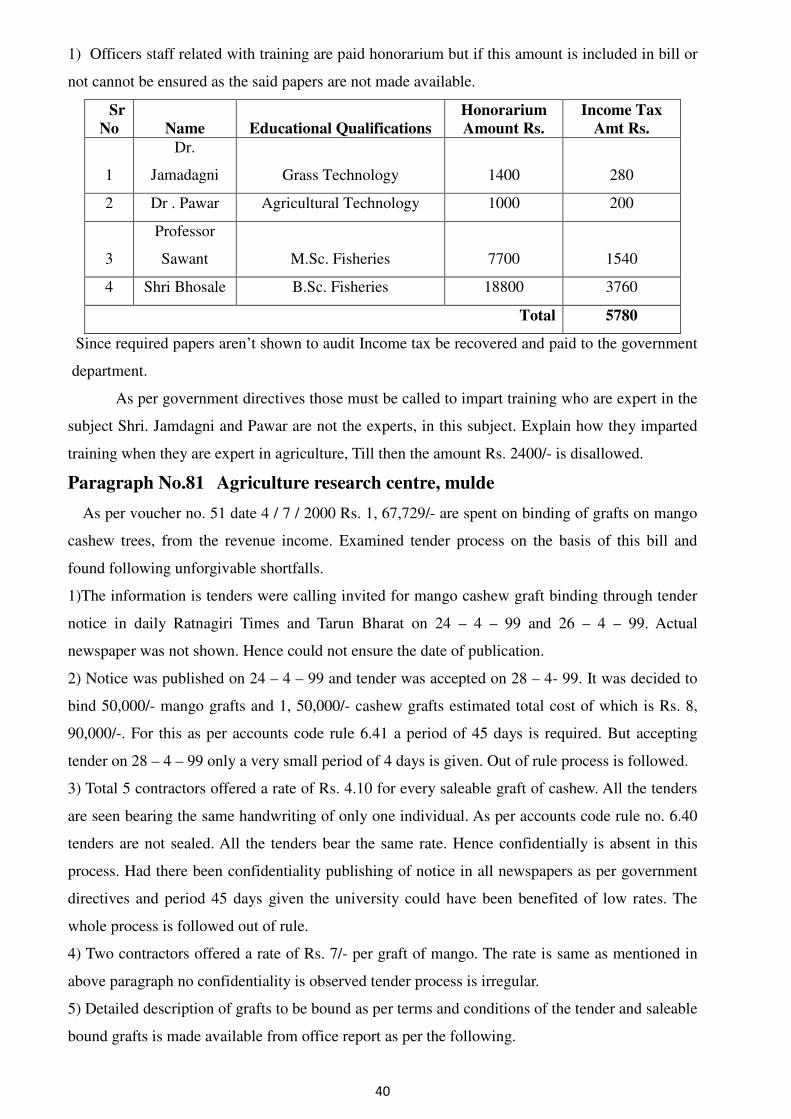

DR. BALASAHEB SAWANT KONKAN KRISHI …mls.org.in/pdf/MahaMandal/DBSKKV2000-01.pdfdr. balasaheb...

226

DR. BALASAHEB SAWANT KONKAN KRISHI VIDYAPEETH DAPOLI, DIST. RATNAGIRI AUDIT REPORT & ANNUAL ACCOUNTS FOR THE YEAR 2000 -2001

Transcript of DR. BALASAHEB SAWANT KONKAN KRISHI …mls.org.in/pdf/MahaMandal/DBSKKV2000-01.pdfdr. balasaheb...

DR. BALASAHEB SAWANT KONKAN KRISHI

VIDYAPEETH

DAPOLI, DIST. RATNAGIRI

AUDIT REPORT & ANNUAL

ACCOUNTS

FOR THE YEAR 2000 -2001

0

Publishers,

The Registrar,

Dr. Balasaheb Sawant Konkan Krishi Vidyapeeth,

Dapoli, Dist. Ratnagiri.

1

Dr. BALASAHEB SAWANT KONKAN KRISHI VIDYAPEETH

DAPOLI, Audit Report For the year 2000 – 2001

No. Local 18 / Dr.B.S.K.K.V. / MuVi /1547

Dy. Chief Auditor (Sr)

Local Fund Audits, Konkan Division Office

Konkan Bhavan, Sixth Floor,

Navi Mumbai 400 614

Date: 31.1.2007

From,

The Deputy Chief Auditor (Sr.)

Local Fund Accounts, Konkan Bhavan

Navi Mumbai 400 614

To,

The Registrar,

Dr. Balasaheb Sawant Konkan Krishi Vidyapeeth,

Dapoli, Dist. Ratnagiri.

There are 22 Institutions and offices working under Dr. Balasaheb Sawant Konkan

Krishi Vidyapeeth, Dapoli and considering the earnings and expenditures of various institutes

under the Vidyapeeth, the financial accounts of these 22 Institutions / centers for the period 2000 –

2001 were audited during the period between 21/11/2005 and 15/11/2006 by the following

officers.

Shri B. P. Chavhan between 21/11/2005 and 15/11/2006

The finalization of the audit report was done by Shri. Sudhakar Dange, The Deputy Chief

Auditor (Senior), Local Fund Audit, Konkan Bhavan, New Mumbai on 24/01/2007.

The following were the officers during the period between 01/04/2000 and 31/03/2001 for the

financial year 2000-20001

Hon. Vice-Chancellor

1. Dr. S.S.Magar Dates 01/04/2000 to 31/03/2001

Hon. Registrar

Shri. A. R. Kale Dates 01/04/2000 to 19/04/2000

Shri. Ghanashyam Bhise Dates 20/04/2000 to 16/01/2000

Shri. S. A. Chavhan Dates 16/01/2001 to 31/03/2001

Hon. Comptroller

Shri. Ghanashyam Bhise Dates 01/04/2000 to 16/01/2001

Shri. R. N. Madav Dates 17/01/2001 to 31/03/2001

2

PART 1: Previous Audit

a) The Audit objection under this scheme up to year 1982 -1983 are included in the audit report of

Vice-Chancellor’s office.

b) The Audit reports during the period form the year 1984-1985 to 99-2000 are issued separately

and the Audit reports on the accounts of Dr. Balasaheb Sawant Konkan Krishi Vidyapeeth, Dapoli

during the period of the year 2000-2001 were started at the same time separately and are issued

vide the letter No. Local/ B/K.K.V.D/MUVI/ 1547 Date: 10.08.2007 of this office of the year

2000-2001. Compliance of paragraphs as per provisions of Act should be done and procedure of

deletion of Paragraphs should be executed.

PART 2 : (CURRENT AUDIT REPORTS)

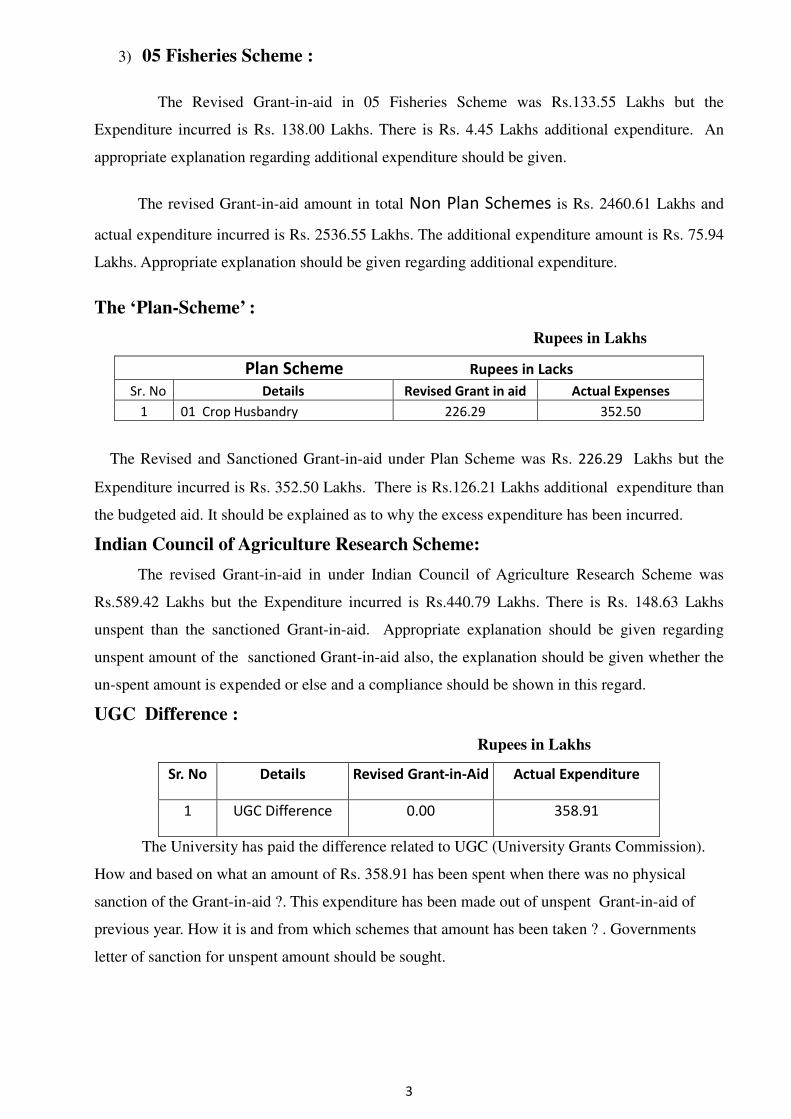

Paragraph No. 03 : BUDGET

Dr. Balasaheb Sawant Konkan Krishi Vidyapeeth, Dapoli, Dist. Ratnagiri receives Grant-in-aid

from the State Government and Indian Council of Agriculture Research. (I.C.A.R.)

Vidyapeeth receives itemized Grant-in-aid from Maharashtra Govt. Agriculture Animal

Husbandry Dairy development and Fisheries Department after presenting the Budget estimates

through Maharashtra Agriculture Education and Research Council to Government.

The details of sanctioned Grant in aid by Government and the actual expenditure are as

follows.

Non Plan Scheme Rupees in Lacs

Sr. No Details Revised Grant Actual Expenses

1 01 Crop Husbandry 1821.47 1828.92

2 03 Animal Husbandry 505.59 569.63

3 05 Fisheries 133.55 138.00

Total 2460.61 2536.55

1) 01 Crop Husbandry Scheme :

The total Re-vise Grant-in-aid in 01 Crop Husbandry Scheme was Rs.1821.47 Lakhs but the

actual Expenditure incurred is Rs. 1828.92 Lakhs. There is Rs. 7.45 Lakhs additional expenditure.

The explanation should be presented regarding additional expenditure than the sanctioned Grant-

in-aid. Government condition should be obtained regarding additional expenses .

2) 03 Animal Husbandry Scheme :

The Revised Grant-in-aid in 03 Animal Husbandry Scheme was Rs.505.59 Lakhs but the

Expenditure incurred is Rs. 569.63 Lakhs. There is Rs. 64.04 Lakhs additional expenses. An

appropriate explanation regarding additional expenditure should be given.

3

3) 05 Fisheries Scheme :

The Revised Grant-in-aid in 05 Fisheries Scheme was Rs.133.55 Lakhs but the

Expenditure incurred is Rs. 138.00 Lakhs. There is Rs. 4.45 Lakhs additional expenditure. An

appropriate explanation regarding additional expenditure should be given.

The revised Grant-in-aid amount in total Non Plan Schemes is Rs. 2460.61 Lakhs and

actual expenditure incurred is Rs. 2536.55 Lakhs. The additional expenditure amount is Rs. 75.94

Lakhs. Appropriate explanation should be given regarding additional expenditure.

The ‘Plan-Scheme’ :

Rupees in Lakhs

Plan Scheme Rupees in Lacks

Sr. No Details Revised Grant in aid Actual Expenses

1 01 Crop Husbandry 226.29 352.50

The Revised and Sanctioned Grant-in-aid under Plan Scheme was Rs. 226.29 Lakhs but the

Expenditure incurred is Rs. 352.50 Lakhs. There is Rs.126.21 Lakhs additional expenditure than

the budgeted aid. It should be explained as to why the excess expenditure has been incurred.

Indian Council of Agriculture Research Scheme:

The revised Grant-in-aid in under Indian Council of Agriculture Research Scheme was

Rs.589.42 Lakhs but the Expenditure incurred is Rs.440.79 Lakhs. There is Rs. 148.63 Lakhs

unspent than the sanctioned Grant-in-aid. Appropriate explanation should be given regarding

unspent amount of the sanctioned Grant-in-aid also, the explanation should be given whether the

un-spent amount is expended or else and a compliance should be shown in this regard.

UGC Difference :

Rupees in Lakhs

Sr. No Details Revised Grant-in-Aid Actual Expenditure

1 UGC Difference 0.00 358.91

The University has paid the difference related to UGC (University Grants Commission).

How and based on what an amount of Rs. 358.91 has been spent when there was no physical

sanction of the Grant-in-aid ?. This expenditure has been made out of unspent Grant-in-aid of

previous year. How it is and from which schemes that amount has been taken ? . Governments

letter of sanction for unspent amount should be sought.

4

Paragraph No.-4 : Regional Agricultural Research Station – Karjat.

A Farm Yard Manure (Cow dung fertilizer) of Rs. 62100/- is purchased vide Voucher No.

1152, Dated – 31.3.2001 and Voucher No. 1211, Dated – 1.3.2001. The expenditure has been

made out of Grant-in-aid from Central Government’s A.I.C.R.I.P. scheme.

1) Though the total purchase was above Rs. 50000 i.e. Rs. 62100 hence it was necessary to invite

tenders by advertising publicly. but farm yard manure was purchased by inviting quotations. Why

ignored inviting Tenders is to be explained. Because of this the university did not get any benefit

of appropriate low price.

2) According to Accounts Code Rule 6.40 & 7.7, quotation envelopes should be sealed at the time

of accepting; but have accepted even when these were not sealed. Confidentiality has not

remained since these were not sealed. Rules were not followed in this behalf.

3) According to Accounts Code Rule 7.7, rule number 6.40 is applicable to quotations. According

to this rule there is no reference of approximate cost, seal and related matters in the quotation.

There is no clarity if there is enough competition. It is clear that rules were avoided.

4) According to Accounts Code Rule 2.6, 2.7 schedule – 5 rule 20 (K) and Income tax Act clause

194 c recover Rs. 1242 by 2% and surcharge Rs. 186 ; Total Rs. 1428 and should submit to related

government office.

5) Buffalos are reared by university at Goregaon. There though farm yard manure was available it

has been purchased by inviting quotations explain be submitted.

Paragraph No. 5 – Regional Agricultural Research Station, Karjat

Under the scheme of Employment, Self employment training for mushroom production

has been taken from 18th

January 2000 to 17th

January 2000.

1) 25 kits were purchased for total of 25 beneficiaries as per Rs. 1500 each. Out of these

beneficiaries one was absent and hence the kit was not given to him. Kit was remained unused

from the year 2000 till the year 2006. memo was issued in this behalf. The object of purchased of

kit was not fulfilled was the objection to which it is replied that as per the objective of the scheme

the kit purchased for beneficiary was used in laboratory. The above reply is inappropriate as the

Grant was not used properly responsibility be fixed on person concerned and the amount be

recovered. It’s not wise to say that the Kit which was purchased as per the aim of scheme is used

in laboratory. Since there is no appropriate use of the donation and the amount spent; it should be

recovered from the concern persons by defining accountability.

2) There were four quotations invited for purchase of kits. As per Accounts Code Rule 7.7 and

6.40 not a single quotation was sealed and hence there is no confidentiality. Why the quotations

were accepted without seal is to be explained.

3) In one contractor’s quotation the name was Hastimal Kankariya but in the comparison chart

this was mentioned as Kantimal; why this is so is to be explained. There is a finding that the rates

by Hastimal & Manoj steel are same. A rate by Hastimal for cooker is Rs. 1100 each & for drum it

is Rs. 330 with rent. Rate by Manoj steel for cooker was Rs. 1100 and for drum it was Rs. 300; it

5

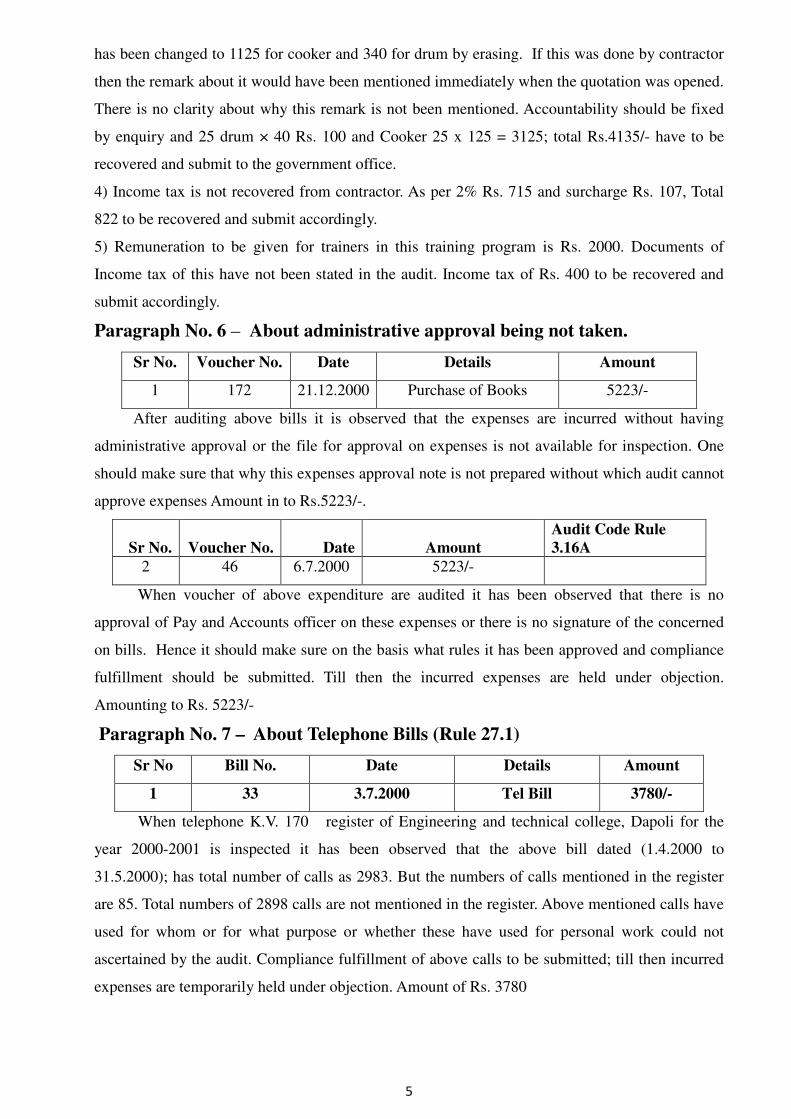

has been changed to 1125 for cooker and 340 for drum by erasing. If this was done by contractor

then the remark about it would have been mentioned immediately when the quotation was opened.

There is no clarity about why this remark is not been mentioned. Accountability should be fixed

by enquiry and 25 drum × 40 Rs. 100 and Cooker 25 x 125 = 3125; total Rs.4135/- have to be

recovered and submit to the government office.

4) Income tax is not recovered from contractor. As per 2% Rs. 715 and surcharge Rs. 107, Total

822 to be recovered and submit accordingly.

5) Remuneration to be given for trainers in this training program is Rs. 2000. Documents of

Income tax of this have not been stated in the audit. Income tax of Rs. 400 to be recovered and

submit accordingly.

Paragraph No. 6 – About administrative approval being not taken.

Sr No. Voucher No. Date Details Amount

1 172 21.12.2000 Purchase of Books 5223/-

After auditing above bills it is observed that the expenses are incurred without having

administrative approval or the file for approval on expenses is not available for inspection. One

should make sure that why this expenses approval note is not prepared without which audit cannot

approve expenses Amount in to Rs.5223/-.

Sr No. Voucher No. Date Amount

Audit Code Rule

3.16A

2 46 6.7.2000 5223/-

When voucher of above expenditure are audited it has been observed that there is no

approval of Pay and Accounts officer on these expenses or there is no signature of the concerned

on bills. Hence it should make sure on the basis what rules it has been approved and compliance

fulfillment should be submitted. Till then the incurred expenses are held under objection.

Amounting to Rs. 5223/-

Paragraph No. 7 – About Telephone Bills (Rule 27.1)

Sr No Bill No. Date Details Amount

1 33 3.7.2000 Tel Bill 3780/-

When telephone K.V. 170 register of Engineering and technical college, Dapoli for the

year 2000-2001 is inspected it has been observed that the above bill dated (1.4.2000 to

31.5.2000); has total number of calls as 2983. But the numbers of calls mentioned in the register

are 85. Total numbers of 2898 calls are not mentioned in the register. Above mentioned calls have

used for whom or for what purpose or whether these have used for personal work could not

ascertained by the audit. Compliance fulfillment of above calls to be submitted; till then incurred

expenses are temporarily held under objection. Amount of Rs. 3780

6

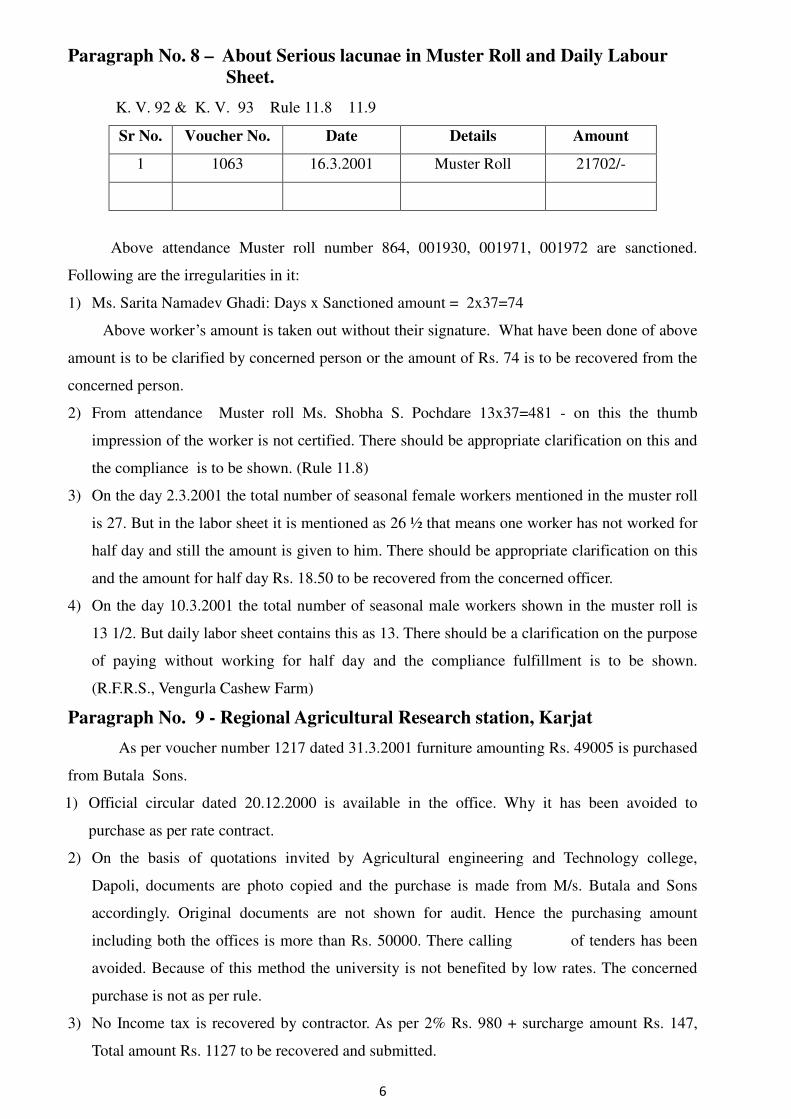

Paragraph No. 8 – About Serious lacunae in Muster Roll and Daily Labour

Sheet.

K. V. 92 & K. V. 93 Rule 11.8 11.9

Sr No. Voucher No. Date Details Amount

1 1063 16.3.2001 Muster Roll 21702/-

Above attendance Muster roll number 864, 001930, 001971, 001972 are sanctioned.

Following are the irregularities in it:

1) Ms. Sarita Namadev Ghadi: Days x Sanctioned amount = 2x37=74

Above worker’s amount is taken out without their signature. What have been done of above

amount is to be clarified by concerned person or the amount of Rs. 74 is to be recovered from the

concerned person.

2) From attendance Muster roll Ms. Shobha S. Pochdare 13x37=481 - on this the thumb

impression of the worker is not certified. There should be appropriate clarification on this and

the compliance is to be shown. (Rule 11.8)

3) On the day 2.3.2001 the total number of seasonal female workers mentioned in the muster roll

is 27. But in the labor sheet it is mentioned as 26 ½ that means one worker has not worked for

half day and still the amount is given to him. There should be appropriate clarification on this

and the amount for half day Rs. 18.50 to be recovered from the concerned officer.

4) On the day 10.3.2001 the total number of seasonal male workers shown in the muster roll is

13 1/2. But daily labor sheet contains this as 13. There should be a clarification on the purpose

of paying without working for half day and the compliance fulfillment is to be shown.

(R.F.R.S., Vengurla Cashew Farm)

Paragraph No. 9 - Regional Agricultural Research station, Karjat

As per voucher number 1217 dated 31.3.2001 furniture amounting Rs. 49005 is purchased

from Butala Sons.

1) Official circular dated 20.12.2000 is available in the office. Why it has been avoided to

purchase as per rate contract.

2) On the basis of quotations invited by Agricultural engineering and Technology college,

Dapoli, documents are photo copied and the purchase is made from M/s. Butala and Sons

accordingly. Original documents are not shown for audit. Hence the purchasing amount

including both the offices is more than Rs. 50000. There calling of tenders has been

avoided. Because of this method the university is not benefited by low rates. The concerned

purchase is not as per rule.

3) No Income tax is recovered by contractor. As per 2% Rs. 980 + surcharge amount Rs. 147,

Total amount Rs. 1127 to be recovered and submitted.

7

4) The original file of quotation was avoided and not shown to audit..

Hence it was not possible to carry out appropriate audit of this purchase. Till the time

concerned copy is shown in next audit; the concerned purchase is temporarily unacceptable.

Paragraph No. 10 - Regional Agricultural Research Station, Karjat

Voucher number 1216 dated 31.07.2001; as per N.A.P centre government donation

Rs. 24900 projector is purchased.

1) According to Accounts Code Rule 7.7 and 8.60; approximate amount is not mentioned in the

quotation. All quotations are not sealed and hence there is no confidentiality about it.

2) Quotations are invited for the purchase of 19 things. Out of these, purchase is made only for

two things. People having these two things did not participate in the purchase because of other

things. So university is not benefited of competitive low rates. Similarly there is no comment in

the quotation as to which company the material can be purchased from.

3) According to Accounts Code Rule 2.6, 2.7 schedule 5, rule 20 (K) and Income tax Act section

194 (C), as per 2% Rs. 498 + surcharge Rs. 75, total amount Rs. 573 to be recovered and be

deposited.

4) After accepting quotations there are confusing notes on page number 19 and 20 as to date

20.01.2001 and again 20.02.2001 in the outward register. These pages have been cancelled and

new entries have been made on next pages. It can be observed that the quotations are not raised

timely and have received post dates. Inward numbers are noted at two places on the envelope.

Concern act is out of rule. There is no signature of the concern officer on the cancelled pages.

Enquiry should be held and concerns should be penalized accordingly.

Paragraph No. 11 – Regarding the Irregularities in the Telephone Register

KV -170, Rule (271) Sr No. Voucher No. Date Details Amount

1 338 28.7.2000 Telephone Bill 11977/-

(1.5.2000 to 30.6.2000)

Sr. No. Bill No. Meter Reading Call Free Balance Numbers

1 1696983/9956 8035 150 7885/-

2 1696386/2011 1769 150 1619/-

After observing the telephone register of bill number 1 as mentioned above there is an entry

of 134 calls only. However there is no clarification on the above calls as to for what official

purpose these have been made. There is no appropriate clarification on the above calls which are

questioned in the half margin letter number 4 at 20/04/2006. There has to be appropriate certainty

on the above calls and it should be followed. Similarly there should be a clarification on the 7751

number of calls in bill number 1. Motive should be made cleared as to not making entries of the

above mentioned calls and compliance should be shown.

8

Appropriate precaution should be taken about telephone as the telephone bill amount is

high. As the register concern with bill number 2 is not presented audit. As such it was not possible

to ascertain the legitimacy of call. Telephone register to be made available and compliance should

be shown.

Paragraph No. 12 - Rule (6.38) About quotation R.F.R.S Vengurla

Voucher No. Date Details Amount

744 12.12.2000 Karsharil Sevin 15 Kgs 8275/-

744 18.12.2000 Neem Oil 6700/-

After auditing above vouchers it has been observed that the last day for submitting

quotations was 25.10.2000, but these have been raised lately. Letter from Konkan Agricultural

Services Centre was received on 27.10.2000 in the office. Similarly quotations by Shriram

Agricultural Service Goa are reached on 30.10.2000 in the office.

1032/9.3.2001 Board Painting 6260/- , 3484/-

Following are the irregularities in the above voucher:

1) There should be a clarification as to why the instruction sheets of quotations do not have

timings on the last day.

2) There is no clarification is given to audit report as to date on which the work order is given.

Appropriate clarification to be given explaining the motive behind not issuing the work order

and compliance should be shown.

Paragraph No. 13 – About Stamp register of 17.4.2006 not made available to

Audit. Audit of Regional fruits research station, Vengurla has started on 17.4.2006. But the stamp

stock register was not made available for inspection to the audit. Hence audit can not ascertain the

remaining stamp or used stamp vide half margin memo No.2 at 18/4/2006. it was asked produce

stamp register for verification of audit. However till it is not submitted to audit. Non submission

of stamp register to audit may be explained. Compliance be submitted with action taken on

persons concerned.

Paragraph No. 14 – about recovery of credit sale

Credit sale amount of Rs. 2750 is yet to be recovered from the financial year 2000 – 2001.

Till date there is no recovery of the above mentioned amount. There has to be a clarification about

what action has been taken by the office to recover above amount; and the amount should be

recovered from the concern person.

Paragraph No. 15 – About making Record unavailable

Audit for financial year 2000-2001 of Regional fruits research station, Vengurla was

completed. However some vouchers of July 2000 of Nursery area of this institute were not made

available for audit. Similarly expenses vouchers of December 2000 and March 2001 were not

9

made available for audit relevant record was not made available even after it was asked for vide

half margin memo No. 1 at 18/04/2006.

Hence appropriate official action should be taken by defining accountability and intention

behind record not made available to be clarified. Till then the expenditure incurred in this month

is not accepted in the audit report.

Paragraph No. 16 – Irregularity in attendance Muster.

There are two vouchers Rs. 8995 & Rs. 6438 shown by Nursery division in the financial

year 2000-2001 of voucher number 173 dated 31.7.2000 by attendance muster.

Irregularity in it is as below:

1) Why K.V. 97 daily work labor sheet is not kept in the prescribed format since Accounts Code

1991 was came into force to be clarified and appropriate clarification to be presented.

2) After inspecting daily work labor sheet it has been observed that on 16.3.2001 3 workers

worked in head office and laboratory etc. It should be clarified if peons were there in the office

that time then what type of work was given to labour in office this should be clarified.

3) On 19.6.2000 it has been shown in the daily labor sheet that the 4 workers were given with a

task of gramoczone medicine spraying on the grass of green house. In fact the concern work

could have been completed in half day using 3 workers. Intention to pay remuneration to 4

workers to be explained or the respective amount to be recovered by defining accountability.

Amount of Rs. 96 – 3 ×18.50=55.50, 37.50=95.50.

4) Thumb impression is taken by Mrs. L.N. Temkar at the time of paying. But it is not been

certified. According to Accounts Code number 11.8 it is necessary to certify above thumb

impression. But it has not been done and the amount is paid. Hence there is a doubt about

above amount to the audit; so it should be clarified accordingly.

Till the time above 1 to 4 is completed, the expenditure amounting to Rs. 15433/- is held

under objection.

Paragraph No. 17 – Irregularity in Vouchers

Voucher No. Date Details Amount

249 4.7.2000 Purchase of Water B 7040/-

Following are the irregularities in the vouchers:

1) After inspecting above voucher it has been observed that the log book shares water trips for 87

times. But the water trips are done for 88 times in the bill. That means one water trip is shown

extra. 1 trip is for Rs. 20. One trip is shown extra and the bill is paid to the concern person.

Extra paid amount to be recovered from the concern person.

2) There are alterations at Rs. 20 in the final date of quotation instruction sheet. Why is this

erasing in the final date mentioned to be clarified appropriately.

10

3) Audit Connect ascertain the date on which the work order is issued or not at all issued. To be

clarified if at all the work order is given and compliance to be followed. Till the time number

1 to 3 is complied, The amount of . Rs. 7040/- is held under objection.

Paragraph No. 18 – Irregularities in the log book

Following are the irregularities about vehicle number MH-08 A–9568 & MH-07-11 in the

log book of Regional fruits research station, Vengurla for the financial year 2000-2001.

1) According to Accounts Code Rule 10.10 and 10 it is necessary to fill all the columns of log

book however these are not updated fully. There is no signature of officer in charge at column

number 15 of log book. Intention of concern officials not signing to be cleared and appropriate

clarification to be presented.

2) It is necessary to enter details of work in column number 12 however it has not been done.

Reason behind so be explained and appropriate clarification to be presented.

3) Abstract of information of vehicle number MH-08 A-9568 & MH-07-11 at the month end is

not done in the log book which was necessary as per the rule. Since it has not been done

vehicle it is not clear How much amount of fuel was balance with how much fuel was used

and average of running of vehicle was not known why abstract of information was not drawn

to be clarified and appropriate official action to be taken by defining accountability.

Paragraph No. 19 - Regional Agricultural Research station, Karjat

Voucher number 1218 dated 31.3.2001, furniture of Rs. 49987 was purchased from M/S

Dipak Industrial Co-Operative Society, Kurla as per rate contract under government scheme

N.A.T.P.

1) Purchase is made as per Maharashtra Government Trade Directorate Central Deposit Purchase

Association circular number 2/2000-2001/B-67244 dated 20.12.2000.Circular is photocopied.

There is no signature as true copy. Similarly rate list is separately attached and there is no

signature of concern government officer. Also there is no signature on it as true copy hence there

is no surety as to these are the rates finalized by government. Documents to be presented in next

audit by taking appropriate actions.

2) According to Accounts Code Rule 2.6, 2.7 schedule 5 rule 20 (K) and Income Tax Act section

194, Rs. 1000 by charging 2% and surcharge Rs. 150; total amount of Rs. 1150 needs to be

recovered and submitted.

Paragraph No. 20 - Regional Agricultural Research station, Karjat

There is a purchase of Air conditioners from M/S. Vaidya furniture, Karjat as per voucher

number B dated 31.3.2001. Rs.40480/-

1) Sealed quotations are invited on 8.5.2000 however unsealed quotations were accepted hence

there was no confidentiality in the purchase. According to Accounts Code Rule 6.40 and 7.7

there is no approximate cost mentioned in the instructions of quotation similarly there is no

information as to how much pieces are going to be purchased. Quotation contains name of the

11

companies such as Voltas/Blue Star, Godrej. Capability characteristic size of these three is not

same so the quotation can’t be compared. There are many deficiencies in the quotation.

2) No formal letter of company is presented for audit whether the supplier is authorized seller.

3) At the time of 1st quote the rate presented by M/S Basu for Godrej was Rs. 13050/- each. This

rate was not accepted even if this was the lowest after that. On 30.11.2000 tax quotations were

raised and out of three contractors rate of Mr. Vaidya was accepted which was Rs. 20240/- and

purchases were made.

4) Even if specifications in both were same the low rate quoted for 1st time was denied and

purchase is made at high rate for 2nd

time. Official action needs to be taken against concern

persons and difference amounting Rs. 20240 – 13050 = 7190×2 = 14380 needs to be

recovered and refunded to government.

5) No tax was recovered from contractor. As per 2% Rs. 810 and surcharge Rs. 121, total

amount of Rs. 931 to be recovered and submitted.

6) According to Accounts Code schedule 5 rule 13 no financial propriety and transparency was

followed during this purchase. Purchase made is not as per rule. Hence Rs. 14380 are

permanently denied.

Paragraph No. 21 – About advance registers (KV 30, 31)

1) Register KV 30 is not kept as per prescribed format. Clarification to be given as regards this.

2) Register KV 31 is not kept as per prescribed format. Clarification to be given as regards this

and fulfillment to be presented.

3) When advance register of financial years 2000-2001 is audited it was observed that advance

taken according to rule 8.11 has to be deposited and returned in that particular financial year

only; however this is not done and the advance has been recouped in next financial year. Why

the recuipment has not made in that financial year is to be clarified.

Date Amount Details Returned Date

19/7/2000 2000/- 20.10.2000 V. G. Sodaye 19.4.2001-2000

4) It is necessary to adjust entries in three months when the advance is taken.(Rule 8.6 to 8.10)

Following employees and officers has neither returned the amount within 3 months nor there

are adjustments of expenses. Appropriate justification to be presented about this.

Sr No. Date Amount Details Recoup Date Amount

1 5.5.2000 3000/- A.G. Deshpande 22.10.2000 3580/-

2 5.5.2000 2500/- M.R. Nagarale 31.3.2001 2500/-

5) There is no abstract drawn of Advance register K.V. 30 every month and at year end.

Clarification to be given as regards why this has not done and fulfillment to be presented.

12

Paragraph No. 22 – About irregularities in Cash book (K.V.22)

Following are the observed deficiencies when main cashbook (K.V. Number 22) of

Regional Agricultural Research, Station Karjat is inspected. 2000-2001

1) There is an attempt of hiding all the entries in the month of March 2001 by scratching and

using whitener. According to Accounts Code Rule 3.9 actions against scratching are ignored.

Clarification to be given as regards this and fulfillment to be presented.

2) Abstract from 14.3.2001 to 31.3.2001 and further abstract are not signed by Pay and Accounts

officer for about 5 years until the audit for the month of November 2005. Clarification to be

given as regards this and compliance fulfillment to be followed.

3) From 29.3.2001 to 31.3.2001 there is no entry of daily balance cash in words.

Clarification to be given as regards this and fulfillment to be presented.

4) Amount of Rs. 1436000/- and Rs. 6,00,000/- total amount of Rs. 20,36,000/- is cleared by

cheque dated 31.3.2001 but has not deposited in account and the entry is shown in the cash

book. That means in fact the cheque is drawn even when the amount was not deposited in

account on 31.3.2001. This is a serious issue. Why the entry is shown in cash book even when

that entry is not there in the passbook is to be clarified appropriately and compliance

fulfillment to be followed.

Paragraph No. 23 – Irregularities in Voucher

In the year 2000-2001 following irregularities are observed while auditing scheme of Rice

cultivation centre, Karjat

1) Voucher number 172 in the muster dated 3.7.2000 Mr. G. T. Shinde has paid with a

remuneration of 1 day. However in the audit of daily labor sheet there is no note of above

worker or there is no note of type of work given to him. Hence there is no assurance if the

above worker has worked. Above worker has paid with an amount of Rs. 37/-. Above amount

of Rs. 37 needs to be assured or amount of Rs. 37 to be recovered from responsible person

quickly.

There are no thumb impressions of following workers in above muster:

1) Ms. N. Khandagale 259/-

2) Mr. L. K. Thakare 222/-

Assurance to be given in audit as to why these thumb impressions are not taken or

clarification to be presented.

3) Diesel engine of Rs. 37840/- has been purchased as per voucher number 1214 dated

31.3.2001

4) There is erasing in the date in quotation by V. R. Talwalkar brothers Ltd. justifiable

clarification to be presented about this erasing.

5) Diesel engine was purchased even when there was electric motor available for use.

13

Paragraph No. 24 – Irregularities in the log book

Following irregularities has been observed in the audit of log book of extention

department for the financial year 2000-2001.

1) There is no entry of petrol and oil in appropriate column number 2 & 3 at some places in the

log book which was necessary. Those entries needs to be taken and compliance fulfillment to

be followed.

2) Details description is necessary in column number 12; however it is not being written.

Justifiable clarification and compliance fulfillment to be presented.

3) Only remark for vehicle number M H-01 - 1886 in column number 12 is “Clinic”. Hence the

motive behind using this vehicle to be assured. According to Accounts Code 1991sub-section

2 of rule 10.10 details description is mandatory hence expenses incurred at that time is not

acceptable to the audit.

4) According to rule 10.10 it is necessary to take abstract every month end; however this has not

been done. Certainty to be given about this and fulfillment of compliance to be presented by

taking abstract.

Paragraph No. 25 – Regarding repair of vehicle

Voucher No. Date Details Amount

1673 31.3.2001 Repair of vehicle 26850/-

Expenses are incurred as per above voucher and objections regarding this is as below:

1) According to Accounts Code Rule 1991 chapter 10 rule 10.7 it is necessary to keep scrap

material register which is not kept. Similarly it is necessary to keep a note of old parts in the

scrap material register; certainty to be given as to why this has not maintained by concern

division’s office in-charge and compliance fulfillment to be followed.

Motive to be explained behind not signing the entries by office-in-charge made in the

history sheet. Appropriate clarification to be given and compliance fulfillment to be followed.

Paragraph No. 26 – Regarding Potassium permanganate

Voucher No. Date Details Amount

1422 15.3.2001 Purchase of Potassium Permanganate 10994/-

Potassium permanganate is purchased as per above voucher. Note of above drugs is

made in consumable register. However this register has a note of 500 gm and subsequent

application is shown. But the use of 1000 gm or respective Potassium permanganate is not noted.

Cost of 1000 gm is Rs. 452.36. Respective amount to be recovered by fixing responsibility and

fulfillment of compliance to be presented. Amount of Rs. 452.36

Paragraph No. 27 – Regarding purchase of Garlic grass and carrot

Voucher No. Date Details Amount

1387 12.3.2001 Purchase of Garlic Grass & Carrot 5049/-

14

Garlic grass and carrot is purchased as per above voucher. It was necessary to keep a note

of above in daily feed register K.V.104 but concern department has kept a general register. There

are no signatures of responsible worker and officer on daily expenses incurred hence expenses

incurred above can’t be accepted by the audit. Compliance fulfillment to be presented by keeping

K.V. 104

Paragraph No. 28 – Regional Agriculture Research Station, Karjat

Office of Regional Research Station, Karjat has not maintained very important registers

about audit. Following are the comments about it:

1) K.V. 85 land notebook is not maintained. It was not shown even if asked at the time of audit.

Later on the answer given in Half- Margin Letter was wrong. Even general notebook was not

shown. Either University engineer or Research centre has not maintained a register as per

Accounts Code Rule 6.67

2) Register number K.V.86 plot history register is not maintained. University has not provided

the same is the clarification in Half- Margin Letter about this. Similarly it is mentioned that

register K.V. 87, K.V. 88, K.V. 89, K.V. 90 is not maintained as these are not provided with by

the university.

3) Since K.V. 94 which is the extremely important register is not maintained agricultural produce

and its sale can’t be reconciled. Immovable assets register number K.V. 74 is not maintained

in the format.

All above mentioned registers should be kept as per Accounts Code format. Appropriate

inspection of assets in the audit could not be done as these registers were not maintained.

Paragraph No. 29 - Regional Agriculture Research Station, Karjat

When delivery memo and other things of K.V. 96 was inspected as per Accounts Code

Rule 11.12, following deficiencies are observed in it and action were not taken as per rule.

1) As per rule double sided carbon was not used while noting details of material. It was

necessary to give two copies to a storekeeper out of three and he is needed to give one original

copy to office-in-charge. How ever this is not followed.

2) According to Accounts Code Rule 3.5 seal of university was not taken on receipt book and all

registers.

3) Printed page numbers of receipt book and notebook are not verified serially and there are no

remarks about it on the back side of pages.

4) According to Accounts Code Rule3.39 Personal security bond has been taken from cashier

Mr. Sawant is Security bond. But certificate is not taken whether sureties are eligible and

alive. Certificate to be taken and presented.

5) According to Accounts Code Rule 3.40 Security bond Register was not presented to the audit

as per format number K.V. 18. It should be updated and kept ready for the audit.

15

6) This office has unusable material lying. Efforts should be taken for its auction or writing off of

material.

Paragraph No. 30 – Agricultural engineering and technical institute, Dapoli

During the audit of 2000-2001 vouchers of expenditure for purchase of goods were

scrutinized. In which advances were scrutinized, it is observed that vouchers of adjustment were

not submitted to audit .

1) Half- Margin Letter number 5 is given on 15.12.2005. 24 bills of adjustments of amount of

Rs. 1177591/- were not presented for the audit. It was told that the bills of adjustments were

not passed.

2) As per Half- Margin Letter number 6 dated 21.12.2005 24 bill of amount of Rs. 3672252/-

were not passed in last five years and it was told that hence these are not yet presented for

audit.

Both of the half margin memo were forwarded to comptroller office by Associate Dean, vide

letter No. ART/Audit/255 Dt. 25/1/2006. it is also communicated some of the bills were passed

and some are getting passed while replying half margin memo it is communicated that 11 bills are

not passed.

Bills of adjustments are not passed for last five years. This is extremely serious. All advance

bills are entered in annual account in ledger and are presented for annual audit.

It is necessary to mention all the adjustment bills at actual in annual account and to be

presented for annual audit. After 5 years bills were passed and presented to audit this is very

serious matter. Vidyapeeth should take review of all the offices including these bills that whether

bills passed now are correct. And enquit be as to why the delay and take appropriate

administrative action.

Paragraph No. 31 – College of Agriculture, Engineering and Technology,

Dapoli Following deficiencies are observed when amount collected by receipt books and receipts

are inspected.

1) As per Accounts Code Rule 3.8 there are no signatures by Drawing and Disbursing Officer by

inspecting receipts pages. Receipt books number 202, 199, 203, 204 are of such kind. Using

receipt books prior to registering a certificate and signing violates the rule. There is no

university seal on each page of receipt book.

2) According to Accounts Code Rule 3.8 (1) it is necessary to intimate Pay and Accounts Officer

and Comptroller if the receipt book in financial year is to be reused on account of not being

used completely. Such intimation is not given.

3) According to Accounts Code Rule 3.8 (G) there should a signature with date on back side of

last receipt of the used receipt book by year end. Similarly as per rule this signature should be

of Drawing and Disbursing officer but have signed on it.

4) According to Accounts Code Rule 3.10 there is no Rs. 1 stamp on the receipts amounting

above Rs. 500/- hence there is no reference of counterfoil of receipts. So amount remaining

after checking for whole year to be submitted in government office.

16

5) Number 199 is scratched and the new number is entered as 200 in the receipt book. There is a

whitener on number 199. There are no remarks by concern officer by inspecting pages.

Amount is accepted by three unnumbered receipts after receipt number 24.

Sr No. Date Amount Remarks

1 9.3.2001 645/- Receipt Number not available.

2 12.3.2001 1000/- Receipt Number not available.

3 12.3.2001 1000/- Receipt Number not available.

After accepting amount by three unnumbered receipts, number 25 is given to the next

receipt. This irregularity is because of the pages of receipts being not checked.

6) According to Accounts Code Rule 3.10 there is no use of double sided carbon. Similarly there

is a writing using carbon paper at specific places. And later on there is a writing on

counterfoil by removing carbon.

Sr No. Receipt No. Date

1 57 31.3.2001

2 61 30.3.2001

3 62 30.3.2001

4 63 30.3.2001

Paragraph No. 32 – about trinoclular microscope

Voucher No. Date Details Amount

1868 31.3.2001 Trinocular Microscope 32900/-

There is a purchase of tin ocular microscope by Anatomy department as per above

voucher. Objections in it are as below:

1) No timing is mentioned for last of accepting applications in the quotation calling instruction

sheet. Certainty is to be given as to why this time has not mentioned and compliance

fulfillment to be presented.

2) Certainty is to be given if the enquiry for purchase was done at Central Repository Purchase

organization. Appropriate clarification and compliance fulfillment to be presented.

3) Test certificate for audit to be made available by office of Director of D.G.S and D with

respect to the supplied material and compliance fulfillment to be presented.

Paragraph No. 33 – about servicing of Monocular and binocular microscope

Voucher No. Date Details Amount

1871 31.3.2001

Yasraj Consultee Mono Bio

Microscope Servicing 22800/-

Servicing of trinocular and binocular microscope is done by microbiology department as

per above voucher. Objections in it are as below:

17

1) Calling quotations are not sealed when they are necessary to be sealed. Certainty to be given

about this and appropriate clarification to be presented.

2) Terms of conditions are not mentioned in the instruction sheet. Appropriate clarification to be

given about this.

3) Repairing and servicing register is not kept in prescribed format. Fulfillment to be made by

keeping in prescribed format.

4) Appropriate clarification and compliance fulfillment to be presented as to why the enquiry

about servicing or quotation is not invited by organization called Central Repository Purchase.

Paragraph No. 34 – Irregularities of purchasing in voucher

Voucher No. Date Details Amount

1707 31.3.2001 Repairs of Vehicle No. MH01-8196 32600/-

Vehicle is repaired by concern department as per above voucher. Estimate of repaired

vehicle is not made available for audit. Reason behind so is to be clarified.

It is necessary to register old parts in scrap material register; however register is not kept.

Motive behind not keeping scrap material register is to be clarified and appropriate certainty is to

be given.

Clarification by concern department is to be given as to not deducting the income tax of

suppliers.

Voucher No. Date Details Amount

1710 31.3.2001 Purchase of Pet Food 39440/-

1) Concern department has not invited quotations for purchasing food. Hence there is no

certainty if the advantage in terms of comparative prices is taken at the time of purchasing.

Motive behind not calling quotations is to be clarified and compliance fulfillment is to be

presented.

2) As per Accounts Code Rule 11.12, 12.6 and 12.16 (4) K.V. 104 it is necessary to keep a daily

note of prescribed food. However no note or register is kept by concern department hence

certainty can’t be given if the accounts are used appropriately. Compliance fulfillment is to be

presented by keeping K.V. 104.

Paragraph No. 35 – Irregularities in vouchers

Following irregularities are observed when department of medical science is audited fot the year

2000-2001.

1) Lab material is purchased by voucher number 1407 dated 19.3.2001 of amount Rs. 9883. No

certainty in the audit can be given as to which registers has notes of above material.

Completion is to be presented by registering these.

2) Rat feed is purchased by voucher number 1809 dated 31.3.2001 of amount Rs. 2967/-

Documents for above purchase couldn’t be available for audit hence certainty is to be given

for above amount in audit. It is necessary to keep above material in store ledger Register

18

format as per Accounts Code Rule number 7.8 (3) K.V. 73. Certainty is to be given as to why

these have not kept in the prescribed format. Certainty can’t be given about feed distribution

in the audit. It is necessary to keep a register about feed distribution as per format of K.V. 104

however these registers are not yet maintained since 1991. Appropriate clarification is to be

given about this and compliance fulfillment is to be presented.

3) Following expenses amounting Rs. 4205 are incurred by voucher number 1811 dated

31.3.2001

1) 9.50 couriers are sent by Tej courier. (Jadhav Communication) certainty is to be given as to

why this has sent by Tej courier as institute has its own post division.

2) On 20.9.2000 color Xerox is taken from shop Shiridhar Consumer Repository Paral. Reason

behind taking Xerox from outside is to be clarified as institute has its own Xerox machine.

Amount spent is Rs. 1605. Forgiveness of honorable Vice-Chancellor is to be obtained for

above expenses.

3) Amount Rs. 120 is spent on phone bills as per above voucher. Certainty is to be given as to

why these calls are made from outside when there is a phone in the office. Certainty is to be

given in the audit whether these calls are made for personal or official work or recovery of

amount of Rs. 120 is to be done by fixing accountability and completion to be presented.

4) Grass, carrot of Rs. 1932/- is purchased as per voucher number 1865 dated 31.3.2001.

Certainty can’t be given about feed distribution in audit. As per rule it was necessary to keep

the information of above distribution in the format of K.V. 104 however it is not kept in the

prescribed format. Certainty is to be given about this and compliance fulfillment to be

presented. Similarly no documents in the audit are available which reflect whether permission

for above expenses was taken. Compliance fulfillment to be presented by making above

documents available.

5) Dead stock register as per rule 7.8 (4) was not available for audit. Completion to be presented

by making it available.

Paragraph No. 36 – About incompletion of Stamp stock register B

Audit of financial year 2000-2001 was started on 6.12.2005. when current stamp register

was inspected it was observed that details of tickets were not entered in the register from

16.7.2005 to 6.12.2005. Last balance tickets are of amount Rs. 8301 in register B on 15.7.2005.

But amount is Rs. 2929 when balanced stamp are inspected on 6.12.2005. Difference in

amount is of Rs. 5372. There is no entry of accounts of stamp of above amount in register B.

hence there is no certainty about above stamp if they are misappropriated. Clarification was

invited by Half- Margin Letter 2 at the time of audit however no clarification or completion was

presented. Hence appropriate clarification is to be made of above stamp amounting Rs. 5372 or

respective amount to be recovered by defining accountability.

19

Paragraph No. 37 – Irregularities in vouchers

Following irregularities one observed when department of Extension is audited for the

year 2000-01

Sr No. Voucher No. Date Amount Remarks

1 1609 31.3.2001 15000/-

2 867 6.12.2000 7200/-

3 1468 28.3.2001 10019/-

4 1498 28.3.2001 31600/-

5 1818 31.3.2001 6748/-

Clarification about above documents was invited by Half- Margin Letter 29 however it

was not fulfilled. Appropriate clarification is to be given about this. Till then expenses amounting

Rs. 70567 are kept in audit objection.

Paragraph No. 38 – Regarding purchasing of hay

Voucher No. Date Details Amount

1665 31.3.2001 Purchase of Fodder (7 Metric Tons) 368775/-

Hay is purchased by Animal Nutrition department as per above voucher. Objections in it

are as below:

1) Date for opening quotations was 20.2.2001 but work order to concern supplier is given on

8.3.2001. Certainty of motive behind giving work order lately is to be given and appropriate

clarification is to be presented.

2) Entry of hay cottage is maintained in general notebook but hay cottage is already used daily.

There is no entry of this in K.V. 104 which was necessary. Hence certainty can’t be given

about appropriate utilization of hay cottage and doubt is generated about its utilization.

Appropriate clarification and documents in prescribed format to be made available for audit

and fulfillment compliance to be presented.

Paragraph No. 39 – about use of electric material

Voucher No. Date Details Amount

1575 31.3.2001 Purchase of Electrical Material 990/-

Material is purchased by poultry farming department as per above voucher. Junior electric

engineer has given an approximate note about the material however there is no assessment by

senior electric engineer whether the material is used at appropriate place. K.V. 63 (Rule 6.57 (i) )

is not given which was necessary. Assessment by senior electric engineer is to be obtained or K.V.

63 to be obtained and compliance fulfillment to be presented. Till then expenses amounting Rs.

990 are kept in objection.

20

Paragraph No. 40 – About purchase of layer birds

102 layer birds have been purchased amounting Rs. 1560 as per voucher number 1618

dated 31.3.2001. It was necessary to invite quotations as per account code 6-38; but the poultry

farming department has not invited any quotations for purchasing above mentioned birds.

Certainty is to be given as to why these quotations are not been invited. Benefit could have been

availed of competitive rates if quotations were invited but this have not done hence forgiveness of

Vice chancellor is to be obtained and compliance fulfillment to be presented.

Paragraph No. 41 – About dead stock register (Rule 7.8)

When dead stock register is audited it was observed that physical verification certificate

for the financial year 2000-20001 is obtained on 28.8.2003. Above physical verification was

needed to obtained on 31.3.2001 however was obtained two years later. Certainty is to be given in

the audit about this. As per rule it was necessary to obtain physical verification certificate on

31.3.2001 as soon as the financial year ends and copy of it should have been given by comptroller

till 10th

April, which is not done. (As per rule 7.9) Motive about this is to be clarified.

Paragraph No. 42 – About not having quotations

Sr No Voucher No. Date Details Amount

1 1576 31.3.2001 Purchase of Buffalo Calf 10200/-

2 1630 31.3.2001 Purchase of Buffalo Calf 17520/-

Total 27520/-

Buffalo pan is purchased by surgery department as per above voucher. No quotations are

invited for purchasing above pan. Certainty is to be given as quotations were not invited even if it

was necessary to invite quotations as per rule 6.38. Benefit could have been availed of

competitive rates if quotations were invited; clarification to be given about why this has not done

so. Appropriate clarification is to be given as why this above pan is purchased from Devnar

slaughter house only and compliance fulfillment to be presented.

Paragraph No. 43 – About irregularity in medicine purchase

Sr No. Voucher No. Date Details Amount

1 1676 27.3.2001 Purchase of Medicines 8143/-

2 1490 27.3.2001 Purchase of Medicines 9330/-

Total 17473/-

Medicines are purchased by surgery department as per above voucher. Irregularities in it are as

follows:

1) Terms and conditions are not mentioned in the final quotation instruction sheet which

was necessary. Certainty is to be given about this and clarification to be presented.

21

2) It was necessary to mention time details about last day of accepting quotations which was not

mentioned. Completion to be presented by mentioning it. Motive behind not mentioning the

time detail is to be clarified.

3) There is no entry of Godrej lock 6 & 7 liver medicine. Certainty is to be given as to why this

entry has not made and compliance fulfillment is to be presented whether above medicine is

utilized.

4) 10 dettol soaps amounting Rs. 135 have been purchased. But there is no entry of above

purchased soaps in K.V. 172 daily issue medicine register so there is no certainty about this in

audit. Certainty is to be given if above purchased soaps are utilized; appropriate clarification is

to be given about this and compliance fulfillment to be presented.

No test certificate was available in audit to know whether the quality of above material was

good. Else test certificate of Director of Inspection D.G.S. and G income tax centre, Mumbai to be

made available for audit and completion to be presented or appropriate clarification to be

presented about the unavailability of this timely manner.

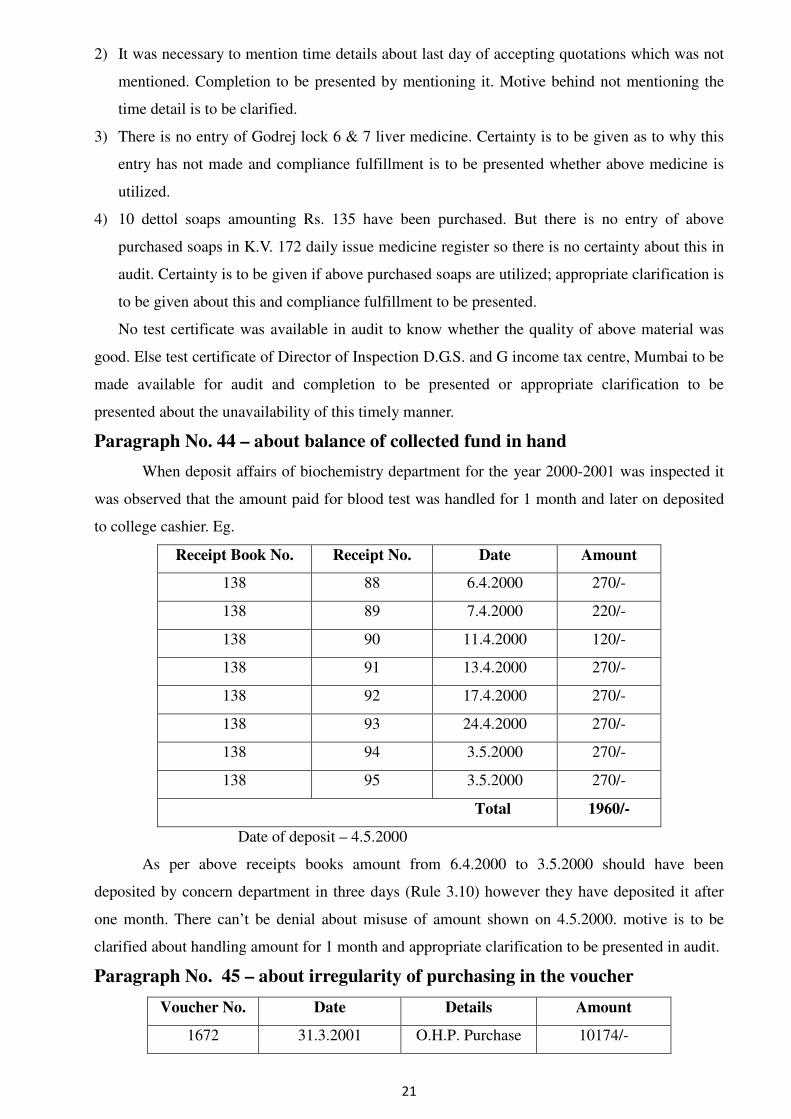

Paragraph No. 44 – about balance of collected fund in hand

When deposit affairs of biochemistry department for the year 2000-2001 was inspected it

was observed that the amount paid for blood test was handled for 1 month and later on deposited

to college cashier. Eg.

Receipt Book No. Receipt No. Date Amount

138 88 6.4.2000 270/-

138 89 7.4.2000 220/-

138 90 11.4.2000 120/-

138 91 13.4.2000 270/-

138 92 17.4.2000 270/-

138 93 24.4.2000 270/-

138 94 3.5.2000 270/-

138 95 3.5.2000 270/-

Total 1960/-

Date of deposit – 4.5.2000

As per above receipts books amount from 6.4.2000 to 3.5.2000 should have been

deposited by concern department in three days (Rule 3.10) however they have deposited it after

one month. There can’t be denial about misuse of amount shown on 4.5.2000. motive is to be

clarified about handling amount for 1 month and appropriate clarification to be presented in audit.

Paragraph No. 45 – about irregularity of purchasing in the voucher

Voucher No. Date Details Amount

1672 31.3.2001 O.H.P. Purchase 10174/-

22

1) O.H.P machine is purchased as per above voucher. However there is no signature of Head of

Department when note is kept for sanction. Appropriate clarification in the audit and

compliance fulfillment is to be presented reflecting the rule by which Honorable Associate

Dean and Assistant comptroller sanctioned the note.

2) Above machine is purchased from Decta standard Pvt. Ltd. Pune certainty is to be given about

non calling quotations from other authorized companies.

Voucher No. Date Details Amount

1615 31.3.2001 Poultry Feed Prabhat Poultry Abhibag 31500/-

1) Clarification is to be presented about rubbing out at several places in quotations.

2) Motive behind not mentioning the time for last day of accepting quotations in the notice is

to be clarified. Motive should also be explained about not mentioning the opening period of

quotations.

3) According to Accounts Code Rule 11.22, 12.6, 12.16 (4) it is necessary to maintain K.V.

104 daily poultry feeding register. However since the appropriate register is not maintained

there is no clarification in the audit about distribution of purchased poultry feed.

Compliance fulfillment to be presented by maintaining above registers. Till then incurred

expenses amount Rs. 31500 will be treated as objectionable in audit.

4) K.V. 116 Bird register is not available for audit. Completion to be presented by making it

available.

Paragraph No. 46 – purchase of A. C. - 2

Voucher No. Date Details Amount

1659 31.3.2001 Purchase of A. C. 42000/-

AC is purchased by poultry farming department as per above voucher. Irregularities in it

are as follows:

1) Above AC is purchased at Daman. Certainty in the audit to given as why these quotations are

not calling from any other authorized company. Clarity can be taken whether benefit of

comparative rates could be taken if quotations from other companies were invited.

Appropriate clarification is to be given as why this is not done so.

2) Company at Daman AC Price list not submitted curtaining is to be given about this.

3) As per Maharashtra Government, Industry, Energy and Labor division decision number

bks/1088/2512/ Industry-6 ministry, dated 2.11.92 it was necessary to purchase above AC

from Maharashtra Small Business Development Corporation but this purchase is made from a

private company. Certainty is to be given about this and forgiveness or no objection certificate

to be obtained from the concern corporation and compliance fulfillment to be presented.

23

Paragraph No. 47 – Regional Fruits Research Station, Vengurla

(Cashew Farm)s Some important deficiencies are observed when Cashew farm’s receipts and receipt books

are inspected. Following are the comments about it:

1) As per Accounts Code 3.8 pages of receipt book number 174, 253, 266, 75, 285 are not

inspected by Drawing and Disbursing Officer and there is no certificate on the back page.

There is no university seal on every receipt of the receipt book. Similarly no action is taken as

per Accounts Code Rule 3.8 (F) and (G).

2) There is no revenue stamp on receipts amounting more than Rs. 500 as per Accounts Code

3.10. There are no comments about stamp on counterfoil.

As stated above these conditions are there on all over the farm of Regional Fruits Research

Station, Vengurla. All formalities as per rule should be completed before using receipts however

there is out of order use.

Paragraph No. 48 – Agricultural Research Station, Phondaghat

Following are the comments about audit of accounts related documents:

1) There is no certificate on the back page of receipts after inspection as per Accounts Code Rule

3.8. No use of double sided carbon can be seen.

2) No comments about receipt are taken after giving receipts to the concerns.

3) Voucher file was presented for audit but no serial numbers were marked on it by Pay and

Accounts officer. Serial numbers should be given as per Accounts Code Rule 3.51 (IV)

4) Advance register format number K.V. 30 is not maintained. Since this was no maintained as

per the rule, advance adjustments couldn’t be verified.

5) Advance of Rs. 11700/- is given to Mr. B.P. Rajput for transfer. An adjustment of this advance

was not shown. Adjustment Bill certificate or amount of Rs. 11700/- with interest should be

recovered and deposited.

Paragraph No. 49 – About purchase of Chemicals – BVC Paral

Voucher No. Date Details Amount Rs.

1870 31.3.2001 Purchase of Chemicals 19178/-

Chemical is purchased as per above voucher by Parasite Science department in the year

2000-2001. Irregularities in it are as below:

1) No timing for last day of accepting quotations was mentioned in the notice. Clarification is to

be given about it. Similarly there is no comment about date on which quotations will be

opened. Also comments should be there as in in front of whom these quotations will be

opened. Motive behind not mentioning above details to be clarified and compliance

fulfillment to be presented.

2) No certainty can be given in the audit for source of delivery of quotation came from company

based in Bangalore. Certainty is to be given about this.

24

3) It was necessary to maintain a record of chemical purchased by company in K.V. 171 stock

register of medicine or Store ledger K.V. 73 however this record is maintained in simple

notebook. Certainty is to be given as to why these records are not maintained in the prescribed

format and compliance fulfillment to be presented.

4) Motive behind not maintaining Daily issue register is to be clarified when it is necessary to

maintain K.V. 172 describing utilization of chemicals; and compliance fulfillment to be

presented.

5) Receipt book stock register was not available for audit hence receipt book account or provided

by university is to be clarifies and compliance fulfillment is to be presented.

6) No test certificate of authorized institute was available in the audit prescribing standard of the

purchased chemical. (eg. National Chemical Laboratory, Pashan, Pune 411008). Compliance

fulfillment to be presented by making it available.

Paragraph No. 50 – about outdated insecticides. C.E.S. Wakavli.

Voucher No. Date Details

629 4.12.2000 Purchase of Pesticides-886 [validity expired]

Monokochafoy 1 Ltr 415 Exp-12/2000

Insecticide is purchased by Irrigation Research Scheme as per above voucher. Expiry date

of Monochrotophoy medicine was December 2000 but use of this insecticide is mentioned in the

store ledger K.V. 73 as 200 ml on 19.3.2001. Similarly stock of 800 ml is shown on 31.3.2001.

Above insecticides are sprinkled on crops like chilly, lady finger after their expiry. There

can’t be certainty about basis on which concern department has used these outdated medicines and

effect of these medicines.

Expired medicines may not have given effective results on the crop hence audit can’t

accept the expenses incurred on purchasing above insecticides.

Paragraph No. 51 – About irregularities in K.V. number 22 cash book and

vouchers – C.E.S. Wakawali Following irregularities are observed after auditing for the year 2000-2001:

1) After tracing vouchers it was observed that the voucher number is not registered on vouchers.

Appropriate clarification to be given about this as it was necessary to do so.

2) According to Accounts Code Rule 3.51 (IV) it is necessary to arrange vouchers serially but

some vouchers are not arranged serially. Clarification to be given about this and completion to

be presented by arranging these vouchers serially.

3) After auditing K.V. 22 cash book it is necessary to register agreement circular in the cash book

as per Accounts Code Rule 3.12. But such registration is not done for the month of July 2000.

Hence audit for back agreement of this month could not happen. Why this is not done by back

agreement Pay and Accounts Officer is to be clarified and compliance fulfillment to be

presented.

25

4) Back agreement entries are not done for the month of November 2000. Hence audit for back

agreement of December 2000 could not happen. Clarification to be given about not registering

back agreement circular for the month of November 2000 and compliance fulfillment to be

presented.

5) Prior audit team has not maintained submitted registers of K.V. 23, K.V. 26, and K.V. 28.

Hence related documents were not available for the audit. Compliance fulfillment to be

presented by making those available.

Paragraph No. 52 – About bill of Xerox

Sr No. Voucher No. & Date Details Paid Amount

1 1010/13.12.2000 Xerox Bill Prashant Xerox, Dapoli 634-75

2 1067/26.12.2000 Xerox Bill R R Enterprises, Dapoli 468/-

Total 1102-75

After auditing Irrigation Research Scheme as per above vouchers it was observed that the

concern department has made Xerox copies from private shopkeeper. Certainty in the audit is to

be given about not making these Xerox copies at Centrali Experimental Station, Wakavali since

they have a Xerox machine or if the concern head office is not allowing to make Xerox copies

over there. And appropriate clarification is to be presented.

If above bill could have Xerox copied in the office, university could have saved

Rs. 1102.75

Motive to be clarified for not doing so or respective amount needs to be recovered from

concerns by defining accountability.

Paragraph No. 53 - About not having Advance adjustments – B.V.C. Paral

Advance was taken by the name M/S Arambh Computers, Mumbai for purchasing laser

printer as per voucher number 1046 dated 11.1.2001 of amounting Rs. 44000/-. Following are the

deficiencies in it:

1) Advance amounting Rs. 44000/- was taken by the name of M/S Arambh Computers, Mumbai

as per Invoice from M/S Arambh Computers, Mumbai dated 8.12.2000. Clarification is to be

given as to rule by which the advance is sanctioned to suppliers.

2) As per Accounts Code Rule number 8.11 it is necessary to adjust advance in 1 month after

giving advance to the concerns. There are 5 years now for which this advance is not adjusted.

Clarification to be given about this.

3) Clarification is to be given for adjusted advance as Rs. 44000 given to supplier was a

responsibility of Associate Comptroller / Pay and Accounts officer.

4) Not having adjustments in advance bills is a serious matter and out of order. Action to be taken

by considering concerns responsible.

5) Annual accounts can’t be accepted unless clarification is given about how this advance bills

are included in the final expenses annual accounts and final advance adjustment is done.

26

Paragraph No. 54 – Agricultural Research Station, Phondaghat

Accounts related very important registers are not maintained in the format prescribed by

Accounts Code. Since these were extremely important registers it was not possible to inspect as

per assets rule.

Sr No.

Registers

Form No. Subject Remarks

1 K.V.85 Land Register Not kept.

2 K.V86 Plot History Register Not kept.

3 K.V.87 Nursery Plants Register Plain papers. Not in proper form.

4 K.V.88 Plants Register Plain papers. Not in proper form.

5 K.V.89 Plants Register Not kept.

6 K.V.90 Fruit Trees Register

Plain papers. Not in proper form. No

proper entries.

7 K.V.94

Record Book of Farm

Produce

Not kept. Due to this Audit of

physically sold goods and produced

goods not verified.

8 K.V.101 Credit Sales Register plain papers. Not in proper form.

9 K.V.102 Unsold Goods Register Not kept.

This situation can be seen all over the university by more or less difference. University

did not provide registers in the prescribed format.

Paragraph No. 55 - Agricultural Research Station, Mulade

Registers are not maintained as per rule and provisions of Agricultural University

Accounts Code. Registers are maintained as per format of K.V. 85, 86, 87, 88, 89, 90, 94, 101,

and 102 hence review of land registers, plot history, number and variety of produce crops and the

current situation in comparison with it, number of fruits giving trees, quantity of agricultural

income, sold quantity, registers at the time of extracting fruits, product sold on credit etc. was not

possible in the audit.

It was observed that extremely important registers are not provided since establishment of

the university. Immediate decision should be taken by the university and registers should be

supplied by printing. Similarly updated registers should be kept for inspection of matters like

assets at the time of establishment of the university and current assets, loss if any and reasons etc.

Paragraph No. 56 - About not having Advance adjustments – B.V.C. Paral

An advance amounting Rs. 62909/- was taken by medicine department as per voucher number

1105 dated 17.1.2001. Following are the serious deficiencies observed in it:

27

1) Advance of Rs. 62909/- for the purchase of computers was taken by the name of M/S. Zenith

computers Ltd., Mumbai as per voucher number 1105 dated 17.1.2001. clarification is necessary

as to by which rule the name of the supplier is payment.

2. As per provisions of Accounts Code Rule 8.11 advance should be sanctioned for rare cases;

clarification is to be given about how the advance is given in such a huge extent.

3. As per Accounts Code Rule 8.11 when advance is given to the concerns it is necessary to adjust

that in one month. Advance amount given to supplier was 62909/- however it is not adjusted even

after five years. Half margin letter number 16 dated 27.2.2006 is sent.

4. Clarification to be given as according to Accounts Code Rule number 3.6 it is a

responsibility of Assistant Comptroller and Pay and Accounts officer to do final adjustment of

concern bill which was not done; and without adjustment of advance the next advance is

sanctioned by the chief.

5.Amount can’t be considered as expenses until Pay and Accounts Officer pass for payment.

Clarification is to be given as how the advance given in the year 2000-2001 is considered as

expenses without final adjustments.

6.Unadjusted final bills is a serious matter and it is out of order. Compliance to be presented in

audit by taking actions on concern responsible persons.

Paragraph No. 57 – About purchase of chemicals by Gynecology department

– B.V.C. Paral

Chemical amounting Rs. 20460/- was purchased by Gynecology department as per

voucher number 1491 dated 28.3.2001. Following are the deficiencies observed in it. Half-

Margin Letter number 24 dated 1.3.2006 is sent.

1) Rate contract was done for chemical purchase by university for the year 2000-2001. However

rate contract file was not made available for inspection.

2) There are comments accepting rate contract on the back side of the bill but rate catalogue of

rate contract was not presented for inspection hence certainty can’t be given about rates.

3) Certainty is to be given in the audit for not sending rate catalogue to College as per rate

contract after the rate contract is accepted by the university; and how to be sure about the rates

of chemicals purchased by the department.

4) While inspecting bill of M/S. Amy Chemicals, Mumbai as per Accounts Code Rule appendix

5 section B sub-section 2 rule number 20 (K) it is observed that the income tax is not deducted

from the bill. Clarification is needed about this.

5) As per Income tax section 194 (C) 2% income tax and surcharge of 15%, total amount of Rs.

470/- needs to be recovered from the supplier and to be submitted to the income tax

department and compliance to be presented.

28

6) There are entries about chemicals as per bills in the ETT register maintained by the

department. However there are no signatures of office In-Charge indicating inspection of it.

Hence there is no certainty if the chemicals are received.

7) There is no record of chemical utilization in the register. Clarifications to be given if the

separate register is maintained for this and if yes the compliance to be presented for the audit.

Compliance to be presented for audit by fulfilling as per above.

Paragraph No. 58 – About serious irregularities in the rate contract –B.V.C.

Paral Purchase of Bench shield of Rs. 49920/- and 3200/- lead brick interlocking of Rs. 18720/-

as per voucher number 1702 Dt. 31.3.2001 is done by medicine department by calling quotations.

Following are the serious irregularities in respective quotation.

1) Quotations are calling from suppliers for the purchase of bench shield as per office letter

number bvc/med/30-32/2000 dated 10.3.2001. Similarly quotations are calling for the

purchase of lead brick interlocking as per office letter number bvc/med/33-35/2000 dated

10.3.2001. Accepted quotations from suppliers are not sealed as per Accounts Code Rule

number 6.40 (1).

2) Only three quotations are invited for the purchase of above which are as below:

i) Saxons biotech (P) Ltd. Mumbai

ii) S.A.S. sales corporation, Mumbai

iii) Trirstar international, Mumbai

No envelope is attached with above three quotations. It can be seen that the quotations are

not received in the envelope. Clarification is to be given about accepting quotations without

envelope from suppliers. This is a serious matter which is out of order. Clarification is to be given

by Office In-Charge as to why these quotations can’t be treated as invalid.

3) It is observed that the action as per Accounts Code Rule number 6.40 (2) is not taken at the

time of calling quotations. Last day of calling quotations is mentioned as 29.3.2001 and date

written on the quotation is 29.3.2001. Clarification is to be given about receiving all the three

quotations on the same day.

4) Invoice, quotation and delivery challan of M/S Saxons biotech (P) Ltd. Mumbai is

computerized. Why the printed bill is not accepted.

5) Clarification is to be given about non deducting income tax from the bill of M/S Saxons

biotech (P) Ltd. Mumbai as per Accounts Code Rule appendix 5 section B sub section B sub

section

2. 20K

6) According to Income tax department article number 194 C 2% income tax and 15% surcharge,

total amount of Rs. 1148/- to be recovered from suppliers and to be submitted to income tax

department. Compliance to be presented.

Respective expenses amounting Rs. 49920/- incurred on the purchase are objected.

29

Paragraph No. 59 – Agricultural Research Station, Mulade

Action as per order while using receipts is not taken by Agricultural Research Station, Mulade.

Deficiencies in it are as below:

1) No inspection of all the receipts and remarks at the end on the back page was given by

Drawing and Disbursing officer as per Accounts Code Rule 3.8

There is no seal of university on each receipt of the receipt book. Similarly there is no signature

with date by Drawing and Disbursing officer on last page at year end after the receipt book was

used.

2) Double sided carbon was not used as per Accounts Code Rule 3.10. Similarly no revenue

stamp is used for the receipts amounting more than Rs. 500. Amount of tickets should be

submitted by counting all the receipts.

3) Clarification is to be given about ignoring actions as per rule by concern Office In-Charge

and Drawing and Disbursing officer.

Paragraph No. 60 – About presenting rate contracts for the purchase of AC –

B.V.C. Paral 1) 3 air conditioners of Rs. 68340/- are purchased by medicine department as per voucher

number 1660 dated 31/3/2001. Air conditioners are purchased as per 22780/- each from 1.5

Trultra global services.

2) Air conditioners are purchased from M/S Carrier aircon Ltd., Mumbai by rate contract as per

bill dated 31st March 2001. But concern rate contract were not made available for inspection

till the time of audit. Clarification is to be given since the terms and conditions were not be

able to inspect in the audit as bill did not have any comments about the rate contract and rate

contract was not presented.

Clarification is to be given about not deducting income tax from supplier as per Accounts

Code Rule appendix 5 section B sub section 2 – Rule number 20 K. Income tax of 2% and

surcharge of 15% total amount of Rs. 1572/- to be recovered from the supplier and to be

submitted to Income tax department and compliance to be presented. Stamp receipt showing

amount paid to M/S Carrier aircon Ltd., Mumbai can’t be seen.

Fulfillment to be done as per above.

Paragraph No. 61 – About purchase of chemical glassware – B.V.C. Paral

Chemical glassware amounting Rs. 22470/- were purchased by Animal genetics and

breeding department as per voucher number 1384 dated 20.2.2001. This purchase by department

is made by calling quotations.

1) Clarification is to be given about calling quotations as university has sanctioned the purchase

of chemicals and glassware for the year 2000-2001.

2) Remarks can’t be seen if the rate contract sanctioned by the university did not have accepted

rates for the chemical glassware. Half- Margin Letter number 26 dated 1.3.2006 is sent.

30

3) Quotations are not accepted in the sealed envelope as per provisions of Accounts Code Rule

number 6.40.

4) No taxes are included while accepting the quotation from M/S. Modi and Modi, Mumbai.

5) Appropriate clarification is to be given about not deducting income tax from the bill of M/S.

Modi and Modi, Mumbai as per Accounts Code Rule appendix 5 section B sub section 2 – Rule

number 20(K.)

6) As per Income tax department article number 194 C, Income tax of 2% and surcharge of 15%