Download 1.21 MB

74

Technical Assistance Consultant’s Report This consultant’s report does not necessarily reflect the views of ADB or the Government concerned, and ADB and the Government cannot be held liable for its contents. (For project preparatory technical assistance: All the views expressed herein may not be incorporated into the proposed project’s design. Project Number: 44447 August 2014 India: Preparing the Bond Guarantee Fund for India (Financed by the Japan Fund for Poverty Reduction) Prepared by CRISIL Risk and Infrastructure Solutions Limited Mumbai, India For Department of Financial Services, Ministry of Finance

Transcript of Download 1.21 MB

Technical Assistance Consultant’s Report

This consultant’s report does not necessarily reflect the views of ADB or the Government concerned, and ADB and the Government cannot be held liable for its contents. (For project preparatory technical assistance: All the views expressed herein may not be incorporated into the proposed project’s design.

Project Number: 44447 August 2014

India: Preparing the Bond Guarantee Fund for India (Financed by the Japan Fund for Poverty Reduction)

Prepared by CRISIL Risk and Infrastructure Solutions Limited

Mumbai, India

For Department of Financial Services, Ministry of Finance

Asian Development Bank

TA-8279 IND: Preparing the Bond Guarantee Fund for India

– 1 Consulting Firm (44447-012)

Market Assessment Report

August 2014

CRISIL Risk and Infrastructure Solutions Limited

Asian Development Bank

[iii] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

Abbreviations

ADB Asian Development Bank

AUM Assets Under Management

BGFI Bond Guarantee Fund for India

CAGR Compounded Annual Growth Rate

CDR Corporate Debt Restructuring

COD Commercial Operations Date

CRIS CRISIL Risk and Infrastructure Solutions

CRISIL Credit Rating and Information Services India Ltd.

CRR Cash Reserve Ratio

CSO Central Statistics Office

ECB External Commercial Borrowings

EPF Employee Provident Fund

EPFO Employees’ Provident Fund Organisation

GCF Gross Capital Formation

GDP Gross Domestic Product

GFCF Gross Fixed Capital Formation

GIC General Insurance Corporation of India

GNPA Gross Non-Performing Asset

HDFC Housing Development and Finance Corporation

HNI High Net-Worth Individual

HPCL Hindustan Petroleum Corporation Limited

IDBI Industrial Development Bank of India

IDF Infrastructure Debt Fund

IDFC Infrastructure Development & Finance Corporation

IFC International Finance Corporation

IFCI Industrial Finance Corporation of India

IIFCL India Infrastructure Finance Company Ltd.

IL&FS Infrastructure Leasing & Financial Services Ltd.

IRDA Insurance Regulatory and Development Authority

LIC Life Insurance Corporation of India

MOSPI Ministry of Statistics & Programme Implementation

MSME Micro, Small & Medium Enterprises

NBFC Non-Banking Finance Company

NCD Non-Convertible Debenture

NHAI National Highways Authority of India

NHB National Housing Bank

Asian Development Bank

[iv] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

NHDP National Highways Development Project

NPS National Pension System

NTPC National Thermal Power Corporation

ONGC Oil and Natural Gas Corporation

PCG Partial Credit Guarantee

PFC Power Finance Corporation

PFRDA Pension Fund Regulatory and Development Authority

PMI Purchasing Managers’ Index

PMS Portfolio Management Services

PPP Public-Private Partnership

PSU Public Sector Undertaking/Utility

RBI Reserve Bank of India

REC Rural Electrification Corporation

SARFAESI The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002

SBI State Bank of India

SEB State Electricity Board

SEBI Securities and Exchange Board of India

SIDBI Small Industries Development Bank of India

SLR Statutory Liquidity Ratio

SPV Special Purpose Vehicle

USA United States of America

USAID United States Agency for International Development

USD United States Dollar

UTI Unit Trust of India

WPI Wholesale Price Index

Asian Development Bank

[v] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

Executive Summary

The Bond Guarantee Fund for India (BGFI seeks to catalyze the nascent bond market…

BGFI is proposed to be a credit enhancement mechanism, giving guarantees to long-term bond

issuances (by entities (private and public) in the infrastructure and non-infrastructure sectors) of

issuers with credit rating less than AA (category); through this credit enhancement these bond issues

would achieve a structured rating of AA or above and would therefore be able to attract bond market

investors.

CRISIL Infrastructure Advisory (CRIS) has been appointed by ADB to design such a fund – ascertain

the business case through market assessment, analyze the financial viability, develop the structure

and frameworks and conduct road shows and seminars. A kick-off meeting with the Steering

Committee was conducted on June 2, 2014 and subsequently the inception report was submitted on

June 23, 2014. This report details out the first stage of the engagement i.e market assessment.

Based on the analysis conducted – investments required over a period of 10 years, supply of

traditional sources of funds and their constraints – it can be concluded that bond markets need to play

a significant part to fund these investments. There is a huge pool of lower rated entities, rated lower

than AA (and especially in the A and BBB categories) which are practically serviced only by banks

today and which would benefit from the bond market and therefore a mechanism such as BGFI.

Moreover all market participants, interacted with during the course of this stage, were positively

disposed towards the overall concept of BGFI.

A comprehensive market assessment exercise was undertaken to ascertain the business case

for BGFI over a period of 10 years…

The exercise undertaken was two-fold:

First, an analytical projection of investments and debt requirement (long term and for entities

rated less than AA) for both infrastructure and non-infrastructure sectors for 10 years was

done – against which supply of debt from the existing sources of finance such as banks,

NBFCs, ECBs, and bond investors was measured. The objective of this exercise was to arrive

at the potential gap in debt financing.

Second, extensive interactions were held with a cross-section of stakeholders

(government/ministry departments, regulators, investors, bond issuers, investment banks and

lenders) to gain perspectives on the overall concept and attractiveness of the same to them.

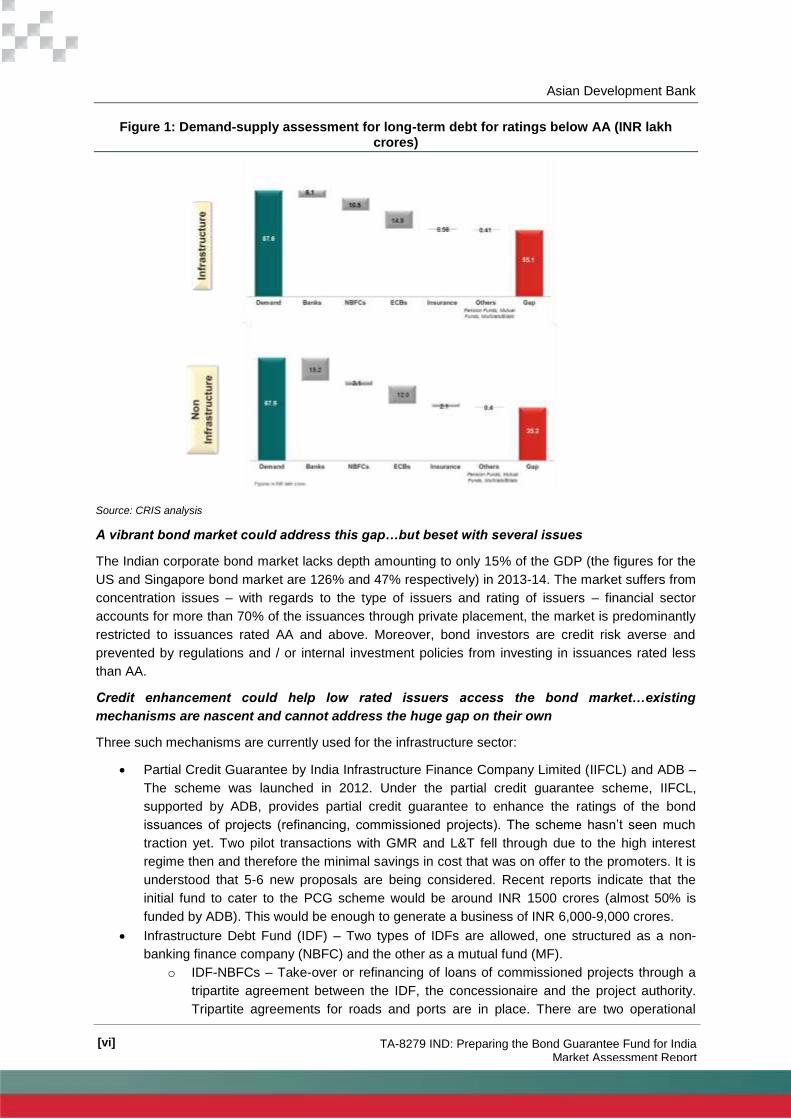

Projected gap of ~INR 551 lakh crores in infrastructure and ~INR 35 lakh crores in non-

infrastructure…

1 10 million = 1 crores, 1 trillion = 1 lakh crores

Asian Development Bank

[vi] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

Figure 1: Demand-supply assessment for long-term debt for ratings below AA (INR lakh crores)

Source: CRIS analysis

A vibrant bond market could address this gap…but beset with several issues

The Indian corporate bond market lacks depth amounting to only 15% of the GDP (the figures for the

US and Singapore bond market are 126% and 47% respectively) in 2013-14. The market suffers from

concentration issues – with regards to the type of issuers and rating of issuers – financial sector

accounts for more than 70% of the issuances through private placement, the market is predominantly

restricted to issuances rated AA and above. Moreover, bond investors are credit risk averse and

prevented by regulations and / or internal investment policies from investing in issuances rated less

than AA.

Credit enhancement could help low rated issuers access the bond market…existing

mechanisms are nascent and cannot address the huge gap on their own

Three such mechanisms are currently used for the infrastructure sector:

Partial Credit Guarantee by India Infrastructure Finance Company Limited (IIFCL) and ADB –

The scheme was launched in 2012. Under the partial credit guarantee scheme, IIFCL,

supported by ADB, provides partial credit guarantee to enhance the ratings of the bond

issuances of projects (refinancing, commissioned projects). The scheme hasn’t seen much

traction yet. Two pilot transactions with GMR and L&T fell through due to the high interest

regime then and therefore the minimal savings in cost that was on offer to the promoters. It is

understood that 5-6 new proposals are being considered. Recent reports indicate that the

initial fund to cater to the PCG scheme would be around INR 1500 crores (almost 50% is

funded by ADB). This would be enough to generate a business of INR 6,000-9,000 crores.

Infrastructure Debt Fund (IDF) – Two types of IDFs are allowed, one structured as a non-

banking finance company (NBFC) and the other as a mutual fund (MF).

o IDF-NBFCs – Take-over or refinancing of loans of commissioned projects through a

tripartite agreement between the IDF, the concessionaire and the project authority.

Tripartite agreements for roads and ports are in place. There are two operational

Asian Development Bank

[vii] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

IDFs, one promoted by ICICI and other by L&T. Interactions reveal that these funds

are finding it tough to find adequate assets in the market; primary reason is that

banks are not willing to sell off their assets after project commissioning as they

believe that risks come down substantially after commissioning of projects.

Discussions are also underway to do away with the tripartite agreement which could

result in lower credit rating for the respective IDFs, impacting their ability to attract

long term funds, as well as impacting their investments.

o IDF-MFs – Three IDFs set up by IL&FS, IIFCL and SREI. Investment guidelines

mandate them to invest at least 90% of AUM in infrastructure companies or

infrastructure projects/SPVs or bank loans in terms of completed and revenue

generating projects or public finance institutions or infrastructure finance companies.

Today while they are technically allowed to invest upto BBB, there are hardly any

investments in less than AA credits. The appetite of these funds for investment

directly in projects in the infrastructure sector is therefore questionable.

Credit enhancement by banks – The recent draft circular by RBI, which is open to public

comments allows restricted credit enhancement (by 20%/2 notches whichever is lower)

through provision of subordinate debt or a line of credit. Considering the fact that

infrastructure sector projects in general are rated not above BBB/BB, would need a higher

level of credit enhancement to take them to AA. Moreover, the current capital requirements as

mandated by the circular are prohibitive. Therefore, in the present form this mechanism is not

expected to be successful.

Clearly the viability of most of these mechanisms is in question. Moreover, the large market gap

cannot be addressed without new mechanisms being introduced. The RBI has recently issued a

circular, following the announcement in the Union Budget 2014-15, allowing banks to issue long-term

infrastructure bonds which are exempted from Cash Reserve Ratio (CRR), Statutory Liquidity Ratio

(SLR) and Priority Sector Lending limits. This initiative would help the banks two-fold, i) manage their

assets/liabilities better and ii) help the higher rated banks access cheaper sources of funds (due to

the exemptions) and thereby become aggressive in pricing of loans (interactions reveal that AAA

rated banks would probably enjoy pricing advantages to the tune of 50-120 bps). However the

initiative would do little to catalyze the bond market in terms of helping low rated entities access it.

Tremendous opportunity for BGFI…overall unanimous approval for such a mechanism, from

all stakeholders

A diverse set of stakeholders – government/ministry departments, regulators, investors, issuers,

lenders, and investment bankers – were consulted with during this stage. All of them were well

disposed towards such a concept and believed that such a mechanism could help kick-start the bond

market in the country.

Key issues were discussed and inputs were garnered from a wide cross-section of stakeholders on

the following issues:

Who will own this entity? – Strong ownership is required to attain AAA rating. Majority

government holding might create a moral hazard, while majority private sector holding might

not promote acceptability in the market. A widely held structure, professionally run, with

representation from both government and private sector could be explored along the lines of

IDFC – IDFC when set up had 35% government holding, 5% by IDBI, 40% by foreign

investors and 20% by domestic institutions. Government holding ensured easy access to

various stakeholders and forums within the government which helped in development of

IDFC.

Asian Development Bank

[viii] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

How will the entity be capitalized? – In addition to ownership, the entity should be sufficiently

capitalized to attain AAA rating. The capital could be upfront through direct infusion or by

means of callable capital. The government could also participate through a long-term

subordinate debt – case in point; the government has provided a 50-year subordinate debt

to IDFC.

What will be the legal structure of this entity? – The entity is meant to be a pure guarantee

company. Thus the operations of the entity do not strictly fall under the ambit of any of the

current regulated structures in India. A potential option is as a bond insurance company

(akin to a monoline insurer) under IRDA. Structuring the entity as a NBFC under RBI may

also be explored but it may lead to issues pertaining to exposure limits which NBFCs are

subjected to unless specific exemptions are obtained for the same.

What will be the business model of this entity?

o Products – Partial credit guarantee as an instrument is still nascent in India. It might

be prudent to employ a mix of full guarantees and partial guarantees to begin with to

establish credibility and acceptability.

o Rating enhancement – To begin with BGFI could target entities rated A and BBB

category, and enhance them to AA+/AAA. This would promote acceptability in the

market.

o Pricing – Pricing might be critical to wean away borrowers from the bank loan

market. Prominent bigger firms enjoy a long relationship with banks and therefore

favourable interest rates. The prospective cost savings in the bond market might not

be attractive enough to pull these firms away from their relationships. It would

therefore be advisable to target smaller promoters, with good credit quality, but who

do not enjoy favourable interest rates with the banks currently.

This report establishes the need for a facility such as BGFI. The next stage of the engagement,

which will be part of the interim report, will be to ascertain the financial viability of this facility

as a standalone business.

[ix]

Contents

1. Introduction ..................................................................................................................................... 1

1.1 Market estimation .................................................................................................................... 1

1.1.1 Classification of infrastructure and non-infrastructure sectors .................................. 2

1.2 Structure of the report ............................................................................................................. 3

2. Overview of the Indian Economy .................................................................................................... 4

2.1 Macroeconomic overview ........................................................................................................ 4

2.1.1 Sectoral trends ........................................................................................................... 4

2.2 Key indicators and outlook ...................................................................................................... 5

2.2.1 Infrastructure sector indicators .................................................................................. 5

2.2.2 Macroeconomic outlook ............................................................................................. 6

3. Investments in India and Debt Requirement ................................................................................... 8

3.1 Methodology to forecast investments and estimate debt requirement ................................... 8

3.2 Recent trends in investments .................................................................................................. 8

3.2.1 Investment in infrastructure sector............................................................................. 9

3.2.2 Investment in non-infrastructure sector ................................................................... 13

4. Financial Sector in India and Debt Supply .................................................................................... 16

4.1 Overview of the Indian financial sector ................................................................................. 16

4.2 Sources of debt financing and estimation of debt supply ..................................................... 17

4.2.1 Banks ....................................................................................................................... 17

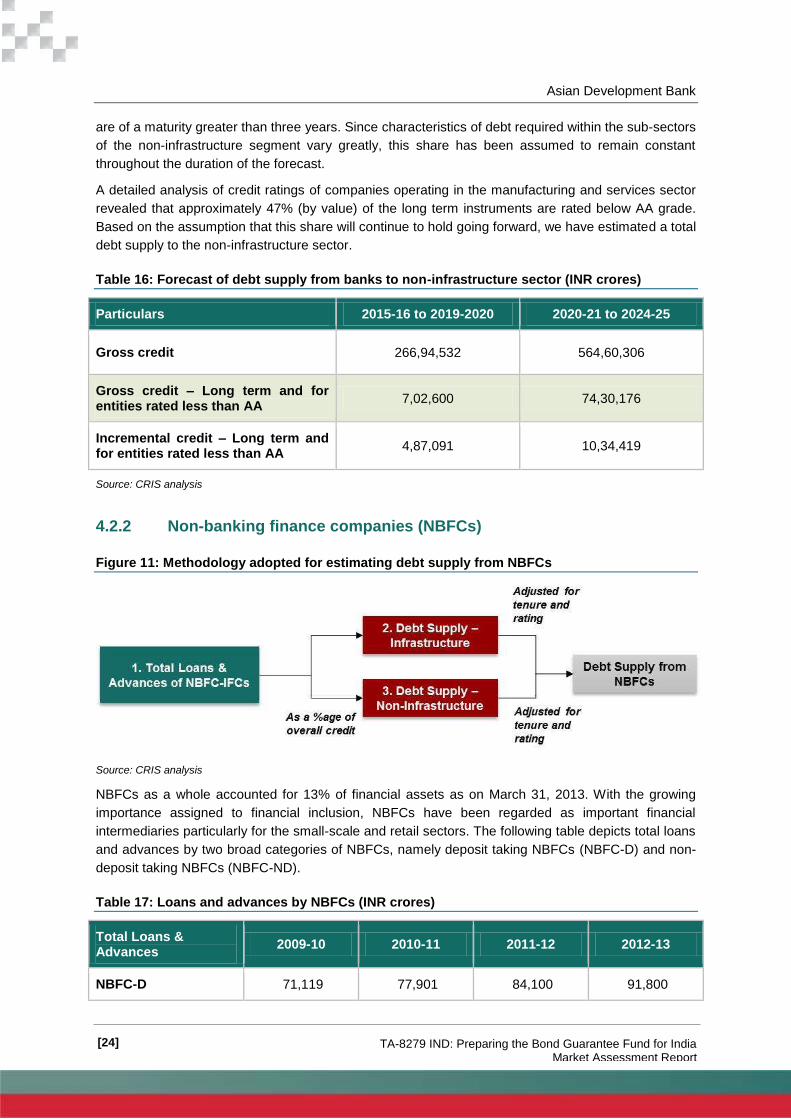

4.2.2 Non-banking finance companies (NBFCs) .............................................................. 24

4.2.3 External commercial borrowings (ECBs) ................................................................. 27

4.2.4 Insurance sector ...................................................................................................... 30

4.2.5 Other suppliers of debt ............................................................................................ 33

4.3 Gap assessment ................................................................................................................... 37

4.3.1 Infrastructure sector ................................................................................................. 37

4.3.2 Non-infrastructure sector ......................................................................................... 38

4.4 Sensitivity analysis ................................................................................................................ 38

4.4.1 Adjustment for credit ratings bracket ....................................................................... 38

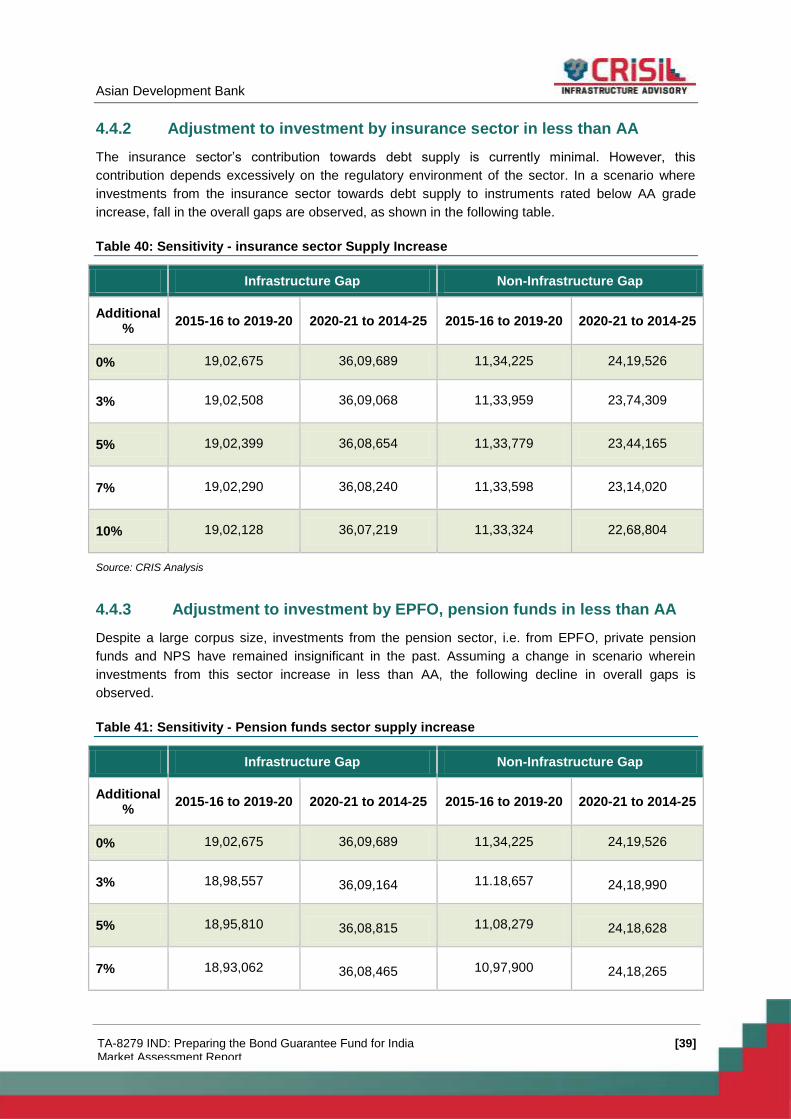

4.4.2 Adjustment to investment by insurance sector in less than AA ............................... 39

4.4.3 Adjustment to investment by EPFO, pension funds in less than AA ....................... 39

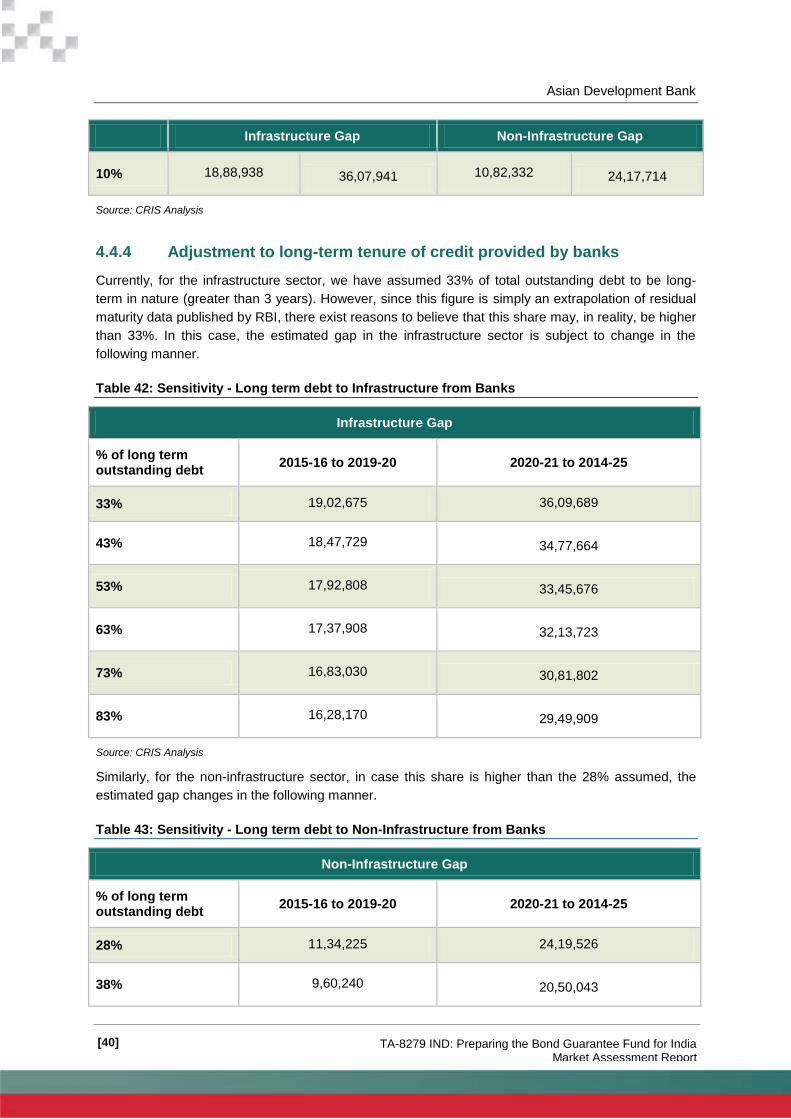

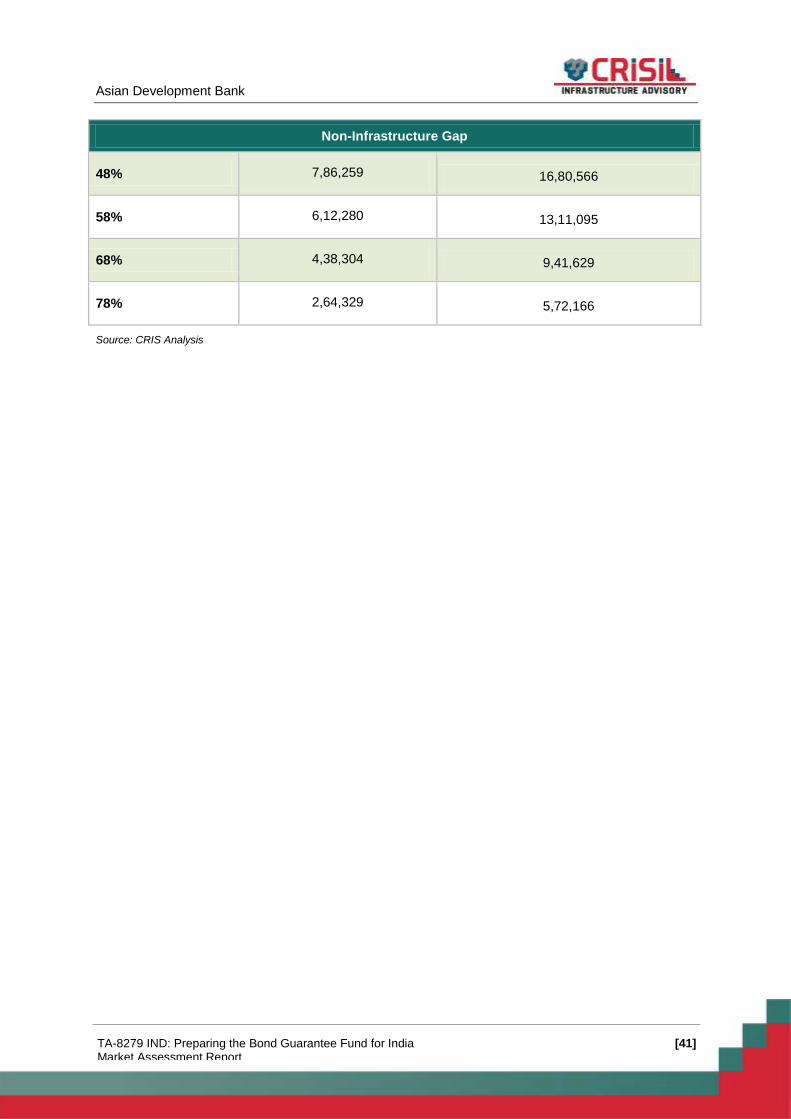

4.4.4 Adjustment to long-term tenure of credit provided by banks ................................... 40

5. Requirement of Bond Market in India ........................................................................................... 42

[x]

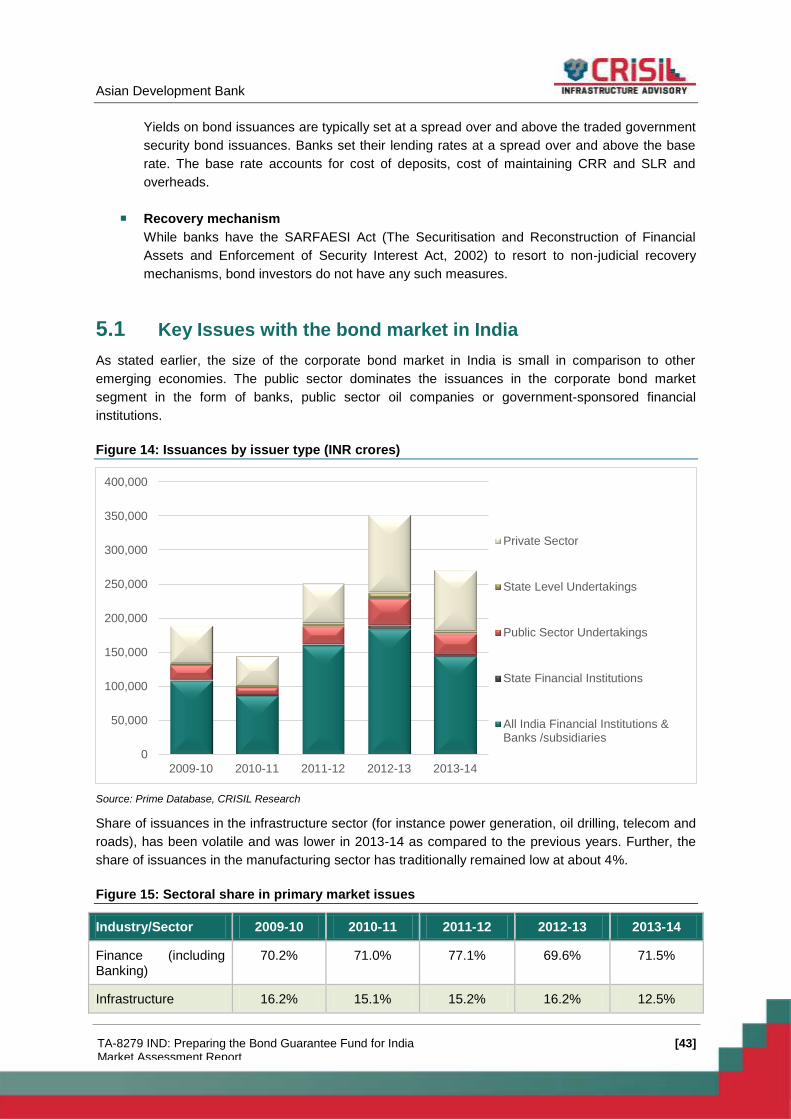

5.1 Key Issues with the bond market in India ............................................................................. 43

5.1.1 Lack of depth in corporate bond market in India ..................................................... 44

5.1.2 Low credit rating for infrastructure projects ............................................................. 44

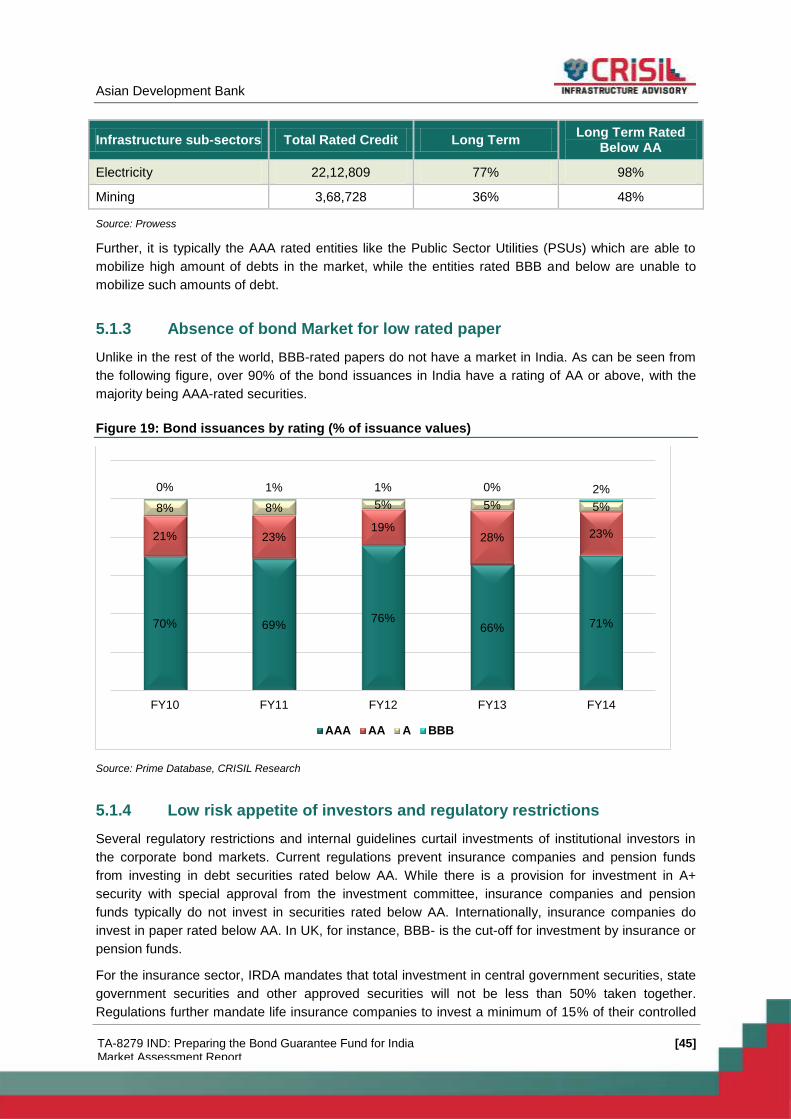

5.1.3 Absence of bond Market for low rated paper ........................................................... 45

5.1.4 Low risk appetite of investors and regulatory restrictions ........................................ 45

5.1.5 Limited secondary market activity............................................................................ 46

5.1.6 Lack of awareness and information ......................................................................... 46

5.2 Credit enhancement can help bridge the gap ....................................................................... 46

5.3 Sectors that can potentially tap the bond market through credit enhancement .................... 47

5.3.1 Infrastructure ............................................................................................................ 47

5.3.2 Non-infrastructure .................................................................................................... 47

5.4 Existing credit enhancement mechanisms in India ............................................................... 47

5.4.1 Partial Credit Guarantee Scheme (PCG) ................................................................ 47

5.4.2 Infrastructure Debt Fund (IDF) ................................................................................. 48

5.4.3 Credit enhancement by banks ................................................................................. 49

6. Initial Thoughts on Bond Guarantee Fund for India and Next Steps ............................................ 51

6.1 Stakeholder’s initial inputs on BGFI ...................................................................................... 51

6.2 Next steps ............................................................................................................................. 54

7. Annexure 1 – Stakeholder meetings ............................................................................................. 55

[xi]

List of Tables

Table 1: Classification of infrastructure and non-infrastructure sectors .................................................. 3

Table 2: Growth in GDP of India at constant prices (2004-05 prices (percent)) ..................................... 4

Table 3: Sectoral share in GDP (%) ........................................................................................................ 5

Table 4: Global Competitiveness Report - Ranking for Infrastructure .................................................... 6

Table 5: Contribution of investment to GDP in percentage terms (at current market prices) ................. 8

Table 6: Comparison of infrastructure investments across Five Year Plans – Planning Commission

(INR crores) ............................................................................................................................................. 9

Table 7: Planning Commission estimates for private corporate sector debt requirement in the

infrastructure sector during 12th Five Year Plan (INR crores) ............................................................... 11

Table 8: Forecast for investment and debt requirement in infrastructure sector (INR crores) ............. 13

Table 9: Investments in non-infrastructure sectors ............................................................................... 13

Table 10: Estimated Private Debt Requirement in non-infrastructure sector ....................................... 15

Table 11: Outstanding credit by scheduled commercial banks in India (INR crores) ........................... 18

Table 12: Incremental flow of bank credit to infrastructure (INR crores) .............................................. 18

Table 13: Outstanding bank credit to non-infrastructure sector (INR crores) ....................................... 19

Table 14: Overall and incremental credit by scheduled commercial banks .......................................... 21

Table 15: Forecast of debt supply from banks to infrastructure sector (INR crores) ............................ 23

Table 16: Forecast of debt supply from banks to non-infrastructure sector (INR crores) ..................... 24

Table 17: Loans and advances by NBFCs (INR crores) ....................................................................... 24

Table 18: Loans and advances by NBFC-IFCs (INR crores) ................................................................ 25

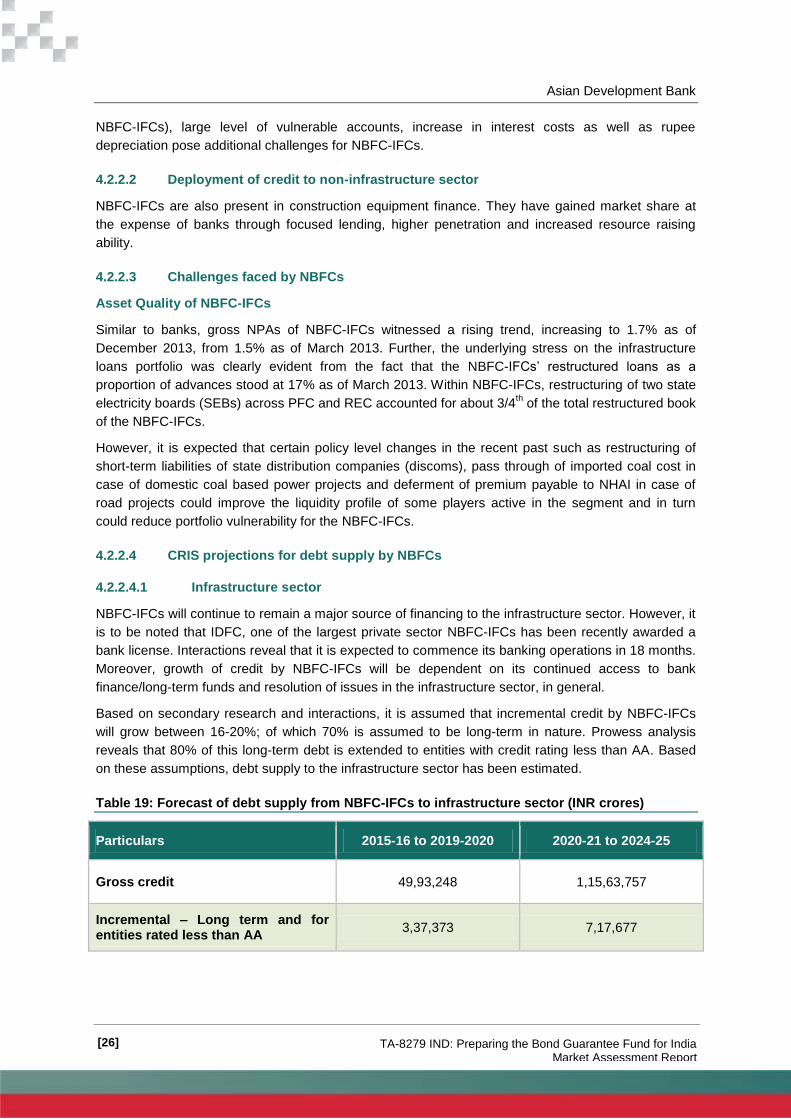

Table 19: Forecast of debt supply from NBFC-IFCs to infrastructure sector (INR crores) ................... 26

Table 20: Total ECB Inflow (INR crores) ............................................................................................... 28

Table 21: Flow of ECBs to infrastructure sector (INR crores) ............................................................... 28

Table 22: Data for ECBs to non-infrastructure sector for the period January-April 2014 ..................... 28

Table 23: Forecast of debt supply through ECBs to infrastructure sector (INR crores) ....................... 29

Table 24: Forecast of debt supply through ECBs to non-infrastructure sector (INR crores) ................ 30

Table 25: Incremental flow of credit from insurance companies into infrastructure sector (INR crores)

.............................................................................................................................................................. 31

Table 26: Investments in infrastructure sector by life insurance companies (INR crores) ................... 31

Table 27: Forecast of debt supply from insurance companies to infrastructure sector (INR crores) ... 32

Table 28: Forecast of debt supply from insurance companies to non-infrastructure sector (INR crores)

.............................................................................................................................................................. 32

[xii]

Table 29: EPFO corpus (INR crores) .................................................................................................... 33

Table 30: EPFO portfolio managers ..................................................................................................... 33

Table 31: Corporate Bonds Investment Pattern – EPFO (INR crores as of September 2013) ............ 34

Table 32: Corpus size and investment pattern – NPS (INR crores) ..................................................... 34

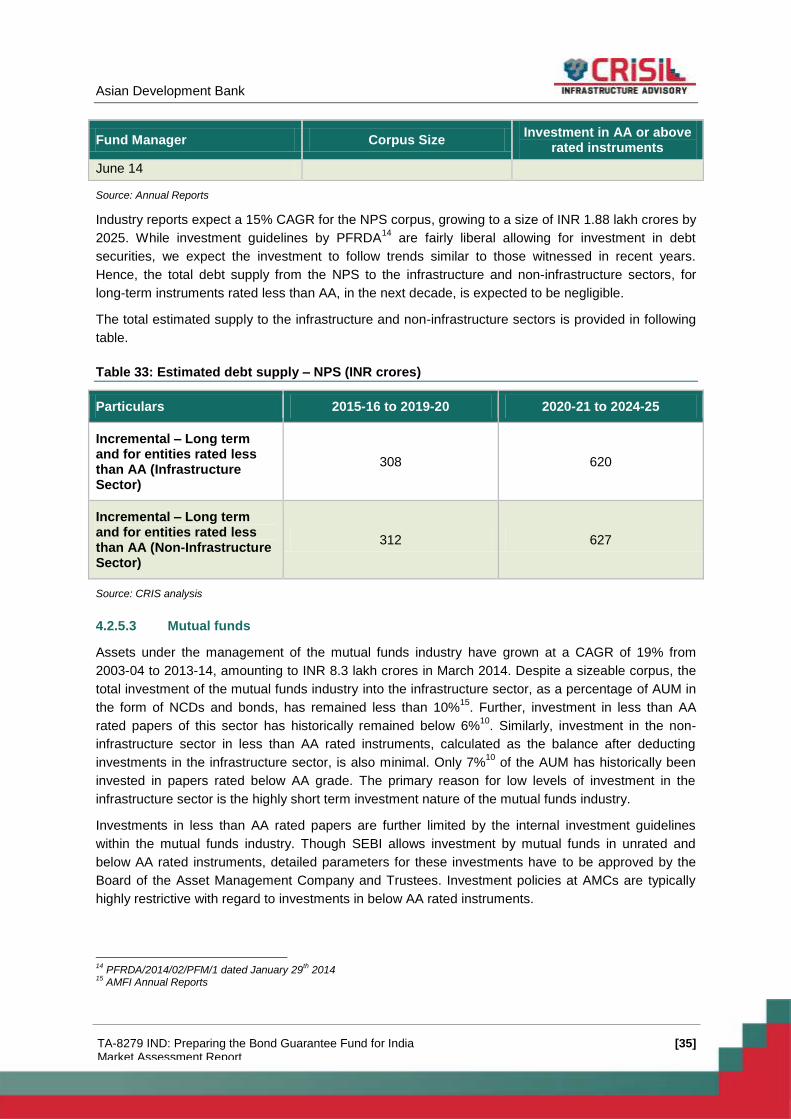

Table 33: Estimated debt supply – NPS (INR crores) .......................................................................... 35

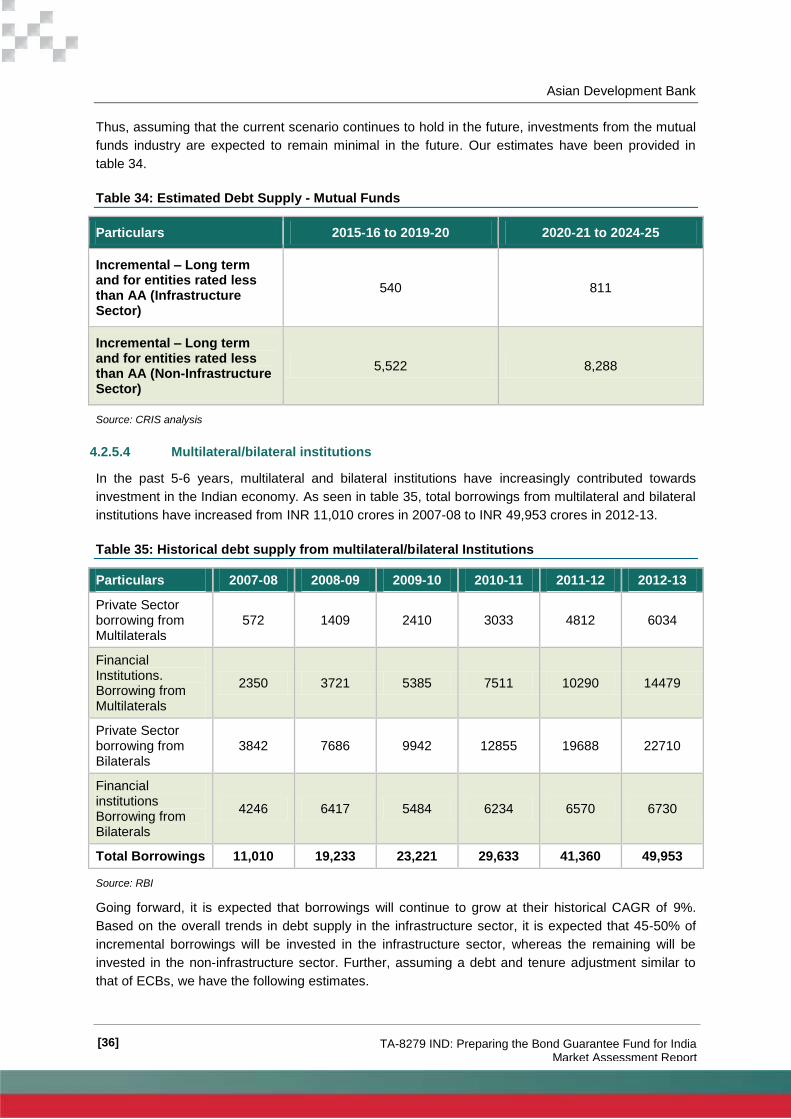

Table 34: Estimated Debt Supply - Mutual Funds ................................................................................ 36

Table 35: Historical debt supply from multilateral/bilateral Institutions ................................................. 36

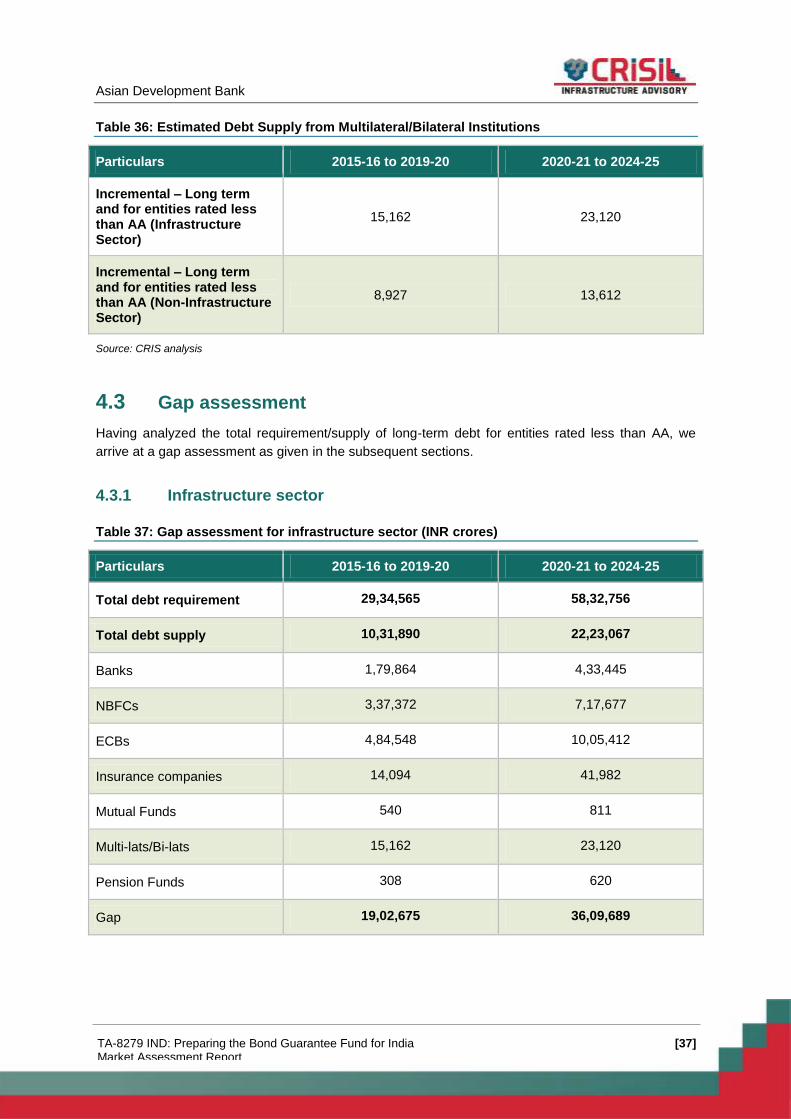

Table 36: Estimated Debt Supply from Multilateral/Bilateral Institutions .............................................. 37

Table 37: Gap assessment for infrastructure sector (INR crores) ........................................................ 37

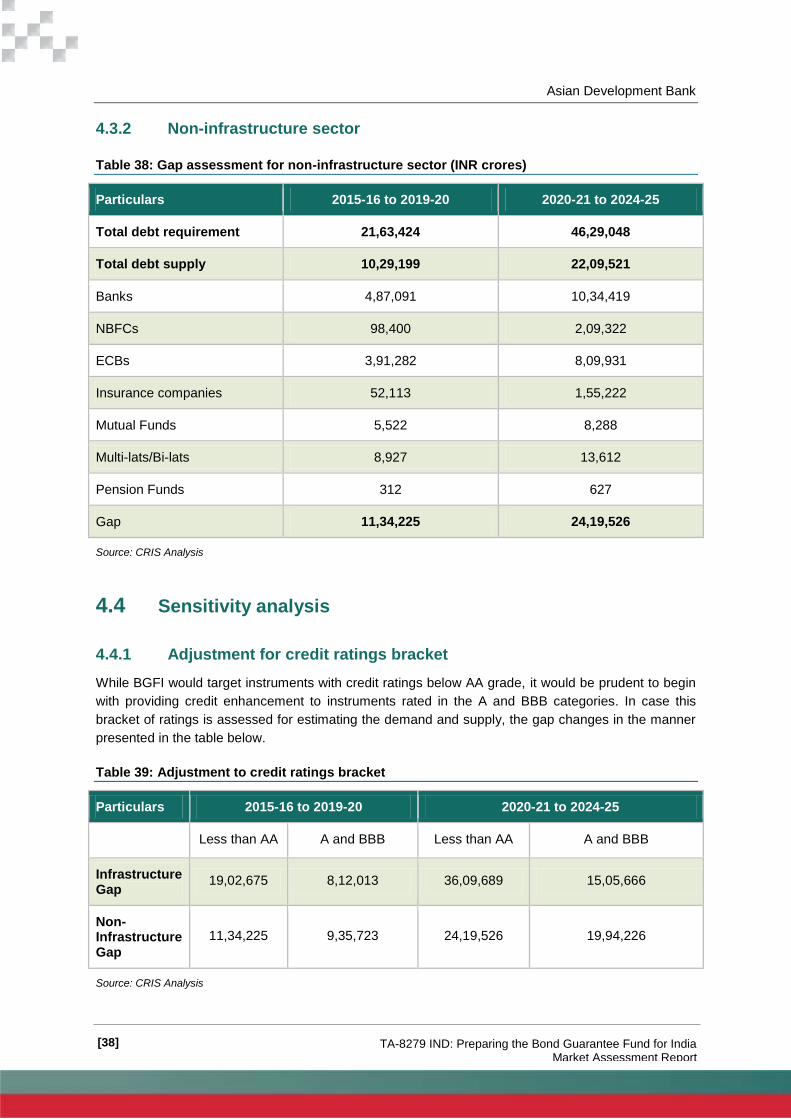

Table 38: Gap assessment for non-infrastructure sector (INR crores) ................................................. 38

Table 39: Adjustment to credit ratings bracket...................................................................................... 38

Table 40: Sensitivity - insurance sector Supply Increase ..................................................................... 39

Table 41: Sensitivity - Pension funds sector supply increase ............................................................... 39

Table 42: Sensitivity - Long term debt to Infrastructure from Banks ..................................................... 40

Table 43: Sensitivity - Long term debt to Non-Infrastructure from Banks ............................................. 40

Table 44: Past PCG transactions in India ............................................................................................. 48

Table 45: List of stakeholders met ........................................................................................................ 55

[xiii]

List of Figures

Figure 1: Demand-supply assessment for long-term debt for ratings below AA (INR lakh crores) ....... vi

Figure 2: Approach and methodology for market assessment ............................................................... 2

Figure 3: Sector-wise growth rate of GDP .............................................................................................. 5

Figure 4: Methodology to estimate debt requirement ............................................................................. 8

Figure 5: Investment in Infrastructure (% of GDP) for other emerging economies ............................... 12

Figure 6: Mode of financing of infrastructure investments .................................................................... 16

Figure 7: Corporate bonds outstanding as a percentage of GDP, 2013 – Replaced China with

Thailand................................................................................................................................................. 17

Figure 8: Methodology adopted for estimating debt supply from banks ............................................... 17

Figure 9: Banking sector GNPA and RA (%) ........................................................................................ 20

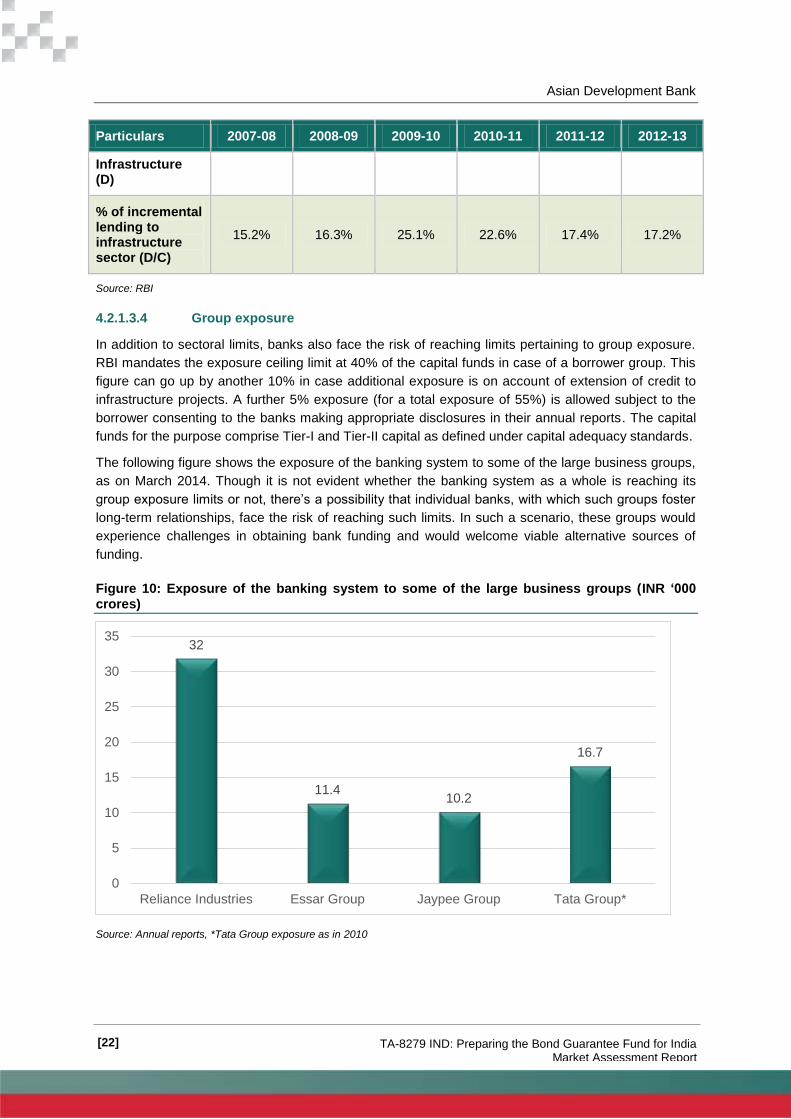

Figure 10: Exposure of the banking system to some of the large business groups (INR ‘000 crores) . 22

Figure 11: Methodology adopted for estimating debt supply from NBFCs ........................................... 24

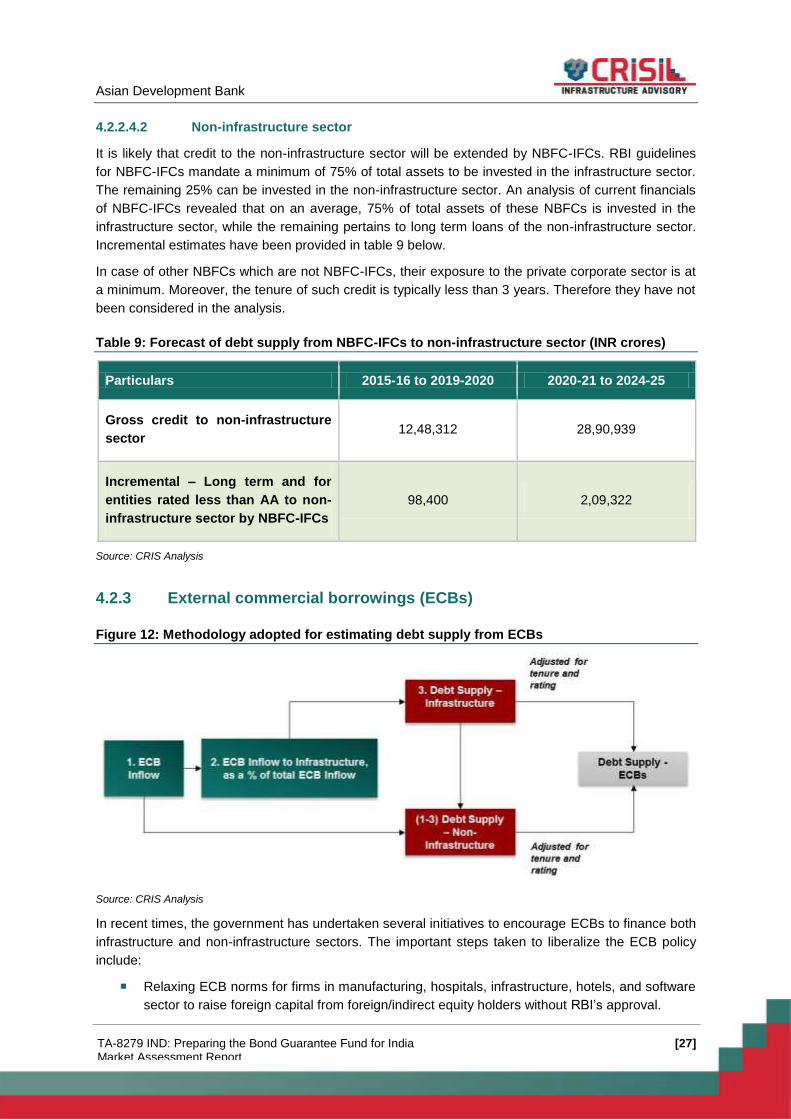

Figure 12: Methodology adopted for estimating debt supply from ECBs ............................................. 27

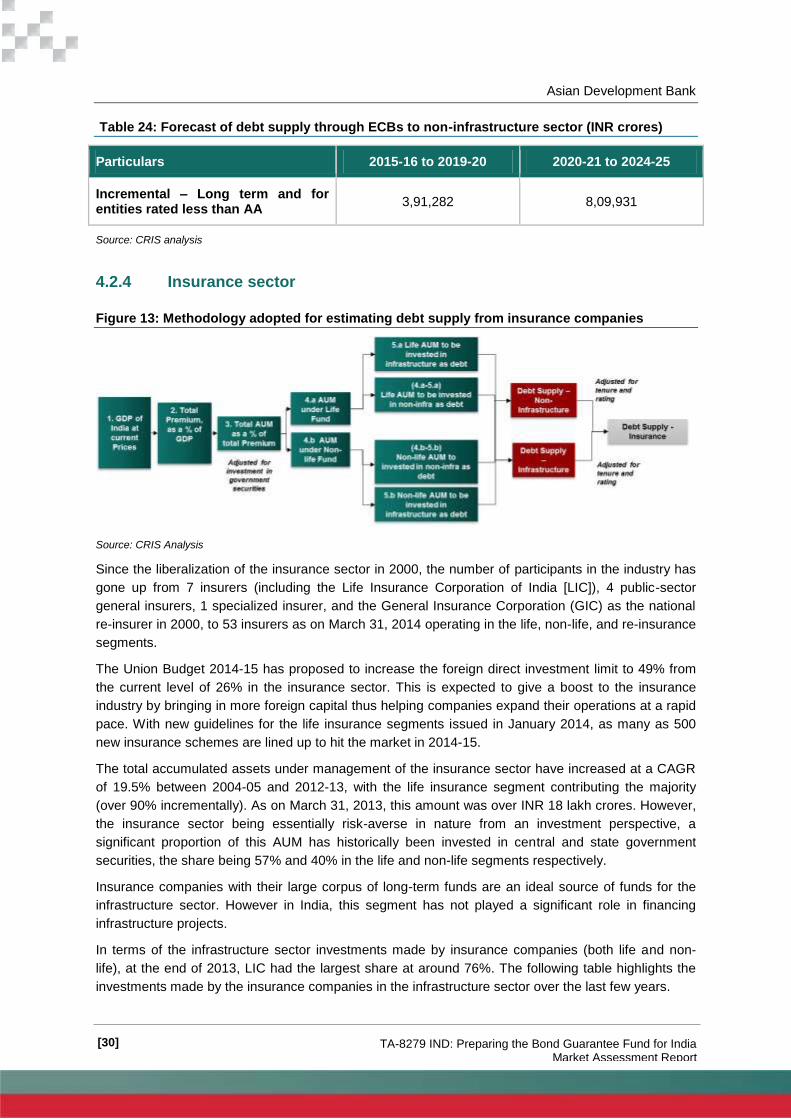

Figure 13: Methodology adopted for estimating debt supply from insurance companies .................... 30

Figure 14: Issuances by issuer type (INR crores) ................................................................................. 43

Figure 15: Sectoral share in primary market issues ............................................................................. 43

Figure 16: Amount raised through private debt placement (INR crores) .............................................. 44

Figure 17: Issuances by issuer type (INR crores) ................................................................................. 44

Figure 18: Long-term instruments rated below AA in infrastructure sectors (INR crores) .................... 44

Figure 19: Bond issuances by rating (% of issuance values) ............................................................... 45

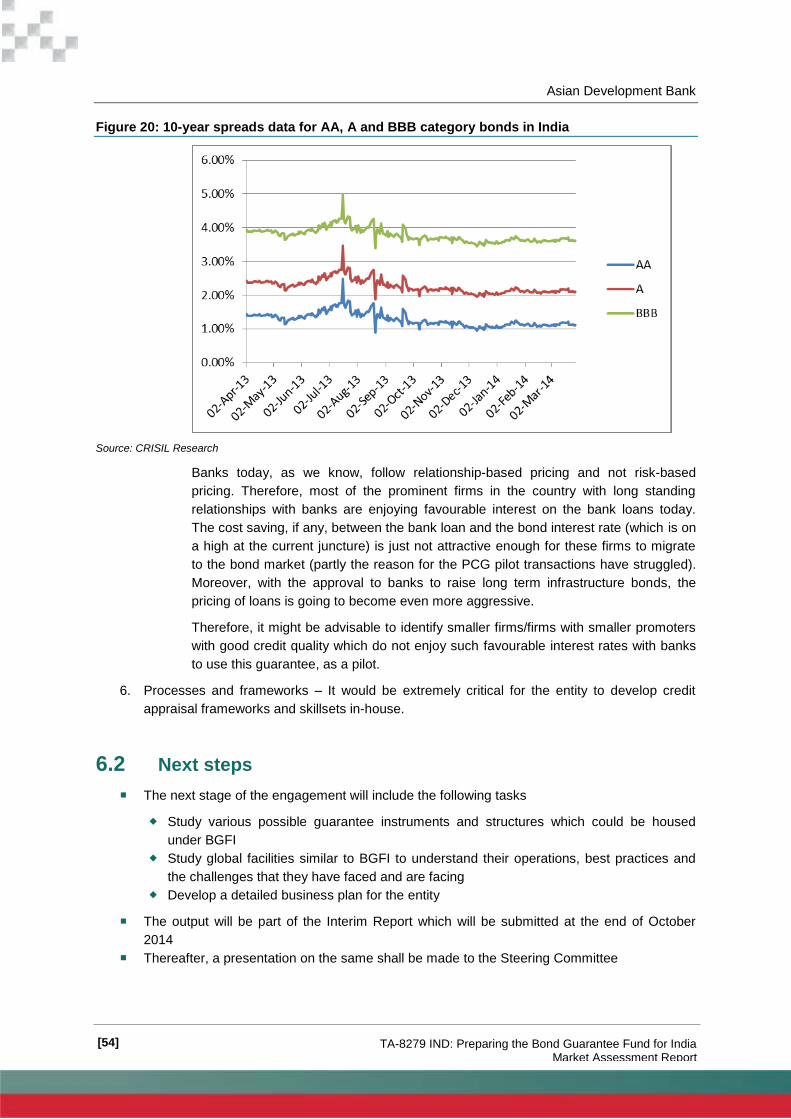

Figure 20: 10-year spreads data for AA, A and BBB category bonds in India ...................................... 54

Asian Development Bank

[1] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

1. Introduction

The Ministry of Finance (MOF) has requested the Asian Development Bank (ADB) to examine the

modalities, scope and potential for the establishment of the Bond Guarantee Fund for India (BGFI)

that supports the development of the local currency bond market to meet India’s infrastructure and

non-infrastructure financing requirements.

CRISIL Infrastructure Advisory (CRIS) has been appointed for designing such a fund. The assignment

is being undertaken under a technical assistance grant from ADB and under the aegis of the MOF.

The MOF has constituted a Steering Committee – to oversee the progress of this assignment –

comprising representatives from Department of Financial Services (DFS) – Chairperson, Department

of Economic Affairs (DEA) – Observer, Insurance Regulatory and Development Authority (IRDA),

Pension Fund Regulatory and Development Authority (PFRDA), Reserve Bank of India (RBI), and

Securities and Exchange Board of India (SEBI).

The first meeting with the Steering Committee was held on June 2, 2014 wherein CRIS presented the

objectives of the study and detailed work programme – approach and methodology, work plan and

deliverables’ schedule. Thereafter, a detailed Inception Report was submitted by CRIS on June 23,

2014 presenting the afore-mentioned details.

This document – market assessment report – forms the second deliverable of this study. It is advised

that this report is read post reading of the inception report.

1.1 Market estimation

BGFI is proposed to be a credit enhancement mechanism, giving guarantees to long-term bond

issuances (by entities (private and public) in the infrastructure and non-infrastructure sectors) with

credit rating less than AA (category); through this credit enhancement these bond issues would

achieve a structured rating of AA or above and would therefore be able to attract bond market

investors. With this background, this report strives to estimate a market/ a business case for BGFI.

The estimation is structured in the following broad manner for both the infrastructure and non-

infrastructure sectors.

Asian Development Bank

[2] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

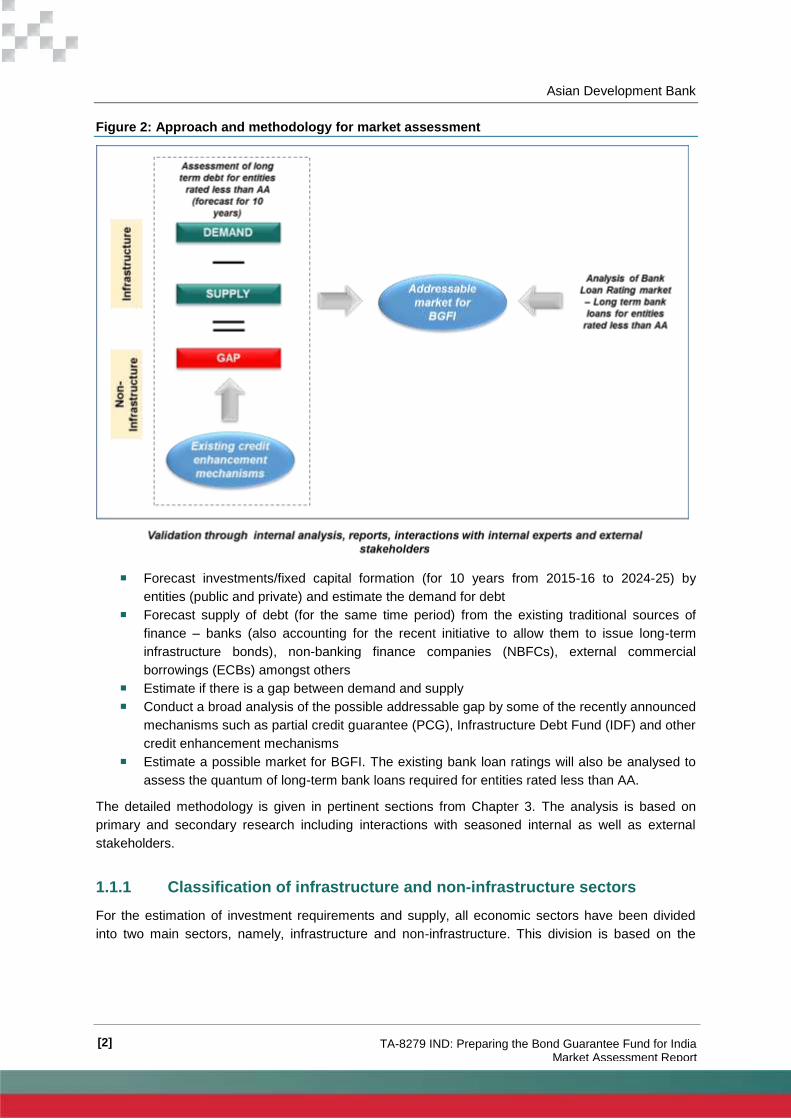

Figure 2: Approach and methodology for market assessment

Forecast investments/fixed capital formation (for 10 years from 2015-16 to 2024-25) by

entities (public and private) and estimate the demand for debt

Forecast supply of debt (for the same time period) from the existing traditional sources of

finance – banks (also accounting for the recent initiative to allow them to issue long-term

infrastructure bonds), non-banking finance companies (NBFCs), external commercial

borrowings (ECBs) amongst others

Estimate if there is a gap between demand and supply

Conduct a broad analysis of the possible addressable gap by some of the recently announced

mechanisms such as partial credit guarantee (PCG), Infrastructure Debt Fund (IDF) and other

credit enhancement mechanisms

Estimate a possible market for BGFI. The existing bank loan ratings will also be analysed to

assess the quantum of long-term bank loans required for entities rated less than AA.

The detailed methodology is given in pertinent sections from Chapter 3. The analysis is based on

primary and secondary research including interactions with seasoned internal as well as external

stakeholders.

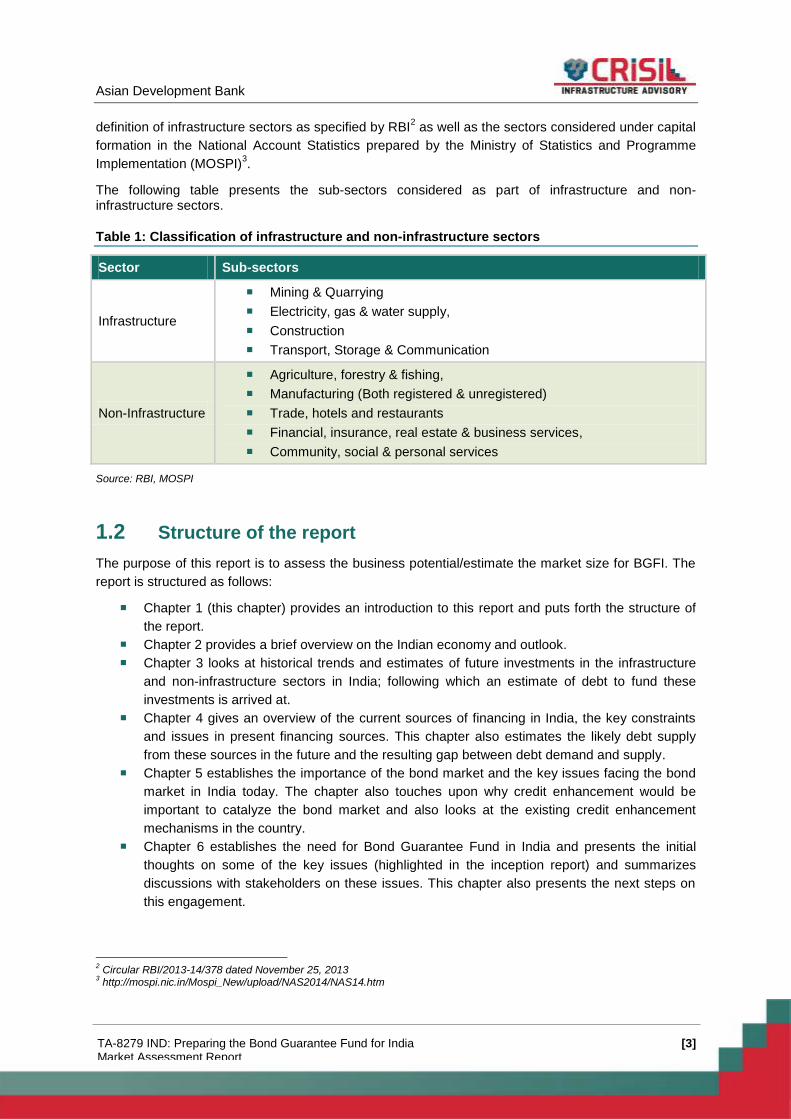

1.1.1 Classification of infrastructure and non-infrastructure sectors

For the estimation of investment requirements and supply, all economic sectors have been divided

into two main sectors, namely, infrastructure and non-infrastructure. This division is based on the

Asian Development Bank

[3] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

definition of infrastructure sectors as specified by RBI2 as well as the sectors considered under capital

formation in the National Account Statistics prepared by the Ministry of Statistics and Programme

Implementation (MOSPI)3.

The following table presents the sub-sectors considered as part of infrastructure and non-infrastructure sectors.

Table 1: Classification of infrastructure and non-infrastructure sectors

Sector Sub-sectors

Infrastructure

Mining & Quarrying

Electricity, gas & water supply,

Construction

Transport, Storage & Communication

Non-Infrastructure

Agriculture, forestry & fishing,

Manufacturing (Both registered & unregistered)

Trade, hotels and restaurants

Financial, insurance, real estate & business services,

Community, social & personal services

Source: RBI, MOSPI

1.2 Structure of the report

The purpose of this report is to assess the business potential/estimate the market size for BGFI. The

report is structured as follows:

Chapter 1 (this chapter) provides an introduction to this report and puts forth the structure of

the report.

Chapter 2 provides a brief overview on the Indian economy and outlook.

Chapter 3 looks at historical trends and estimates of future investments in the infrastructure

and non-infrastructure sectors in India; following which an estimate of debt to fund these

investments is arrived at.

Chapter 4 gives an overview of the current sources of financing in India, the key constraints

and issues in present financing sources. This chapter also estimates the likely debt supply

from these sources in the future and the resulting gap between debt demand and supply.

Chapter 5 establishes the importance of the bond market and the key issues facing the bond

market in India today. The chapter also touches upon why credit enhancement would be

important to catalyze the bond market and also looks at the existing credit enhancement

mechanisms in the country.

Chapter 6 establishes the need for Bond Guarantee Fund in India and presents the initial

thoughts on some of the key issues (highlighted in the inception report) and summarizes

discussions with stakeholders on these issues. This chapter also presents the next steps on

this engagement.

2 Circular RBI/2013-14/378 dated November 25, 2013

3 http://mospi.nic.in/Mospi_New/upload/NAS2014/NAS14.htm

Asian Development Bank

[4] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

2. Overview of the Indian Economy

2.1 Macroeconomic overview

The Indian economy grew at a fast clip of over 9% for three successive years before it slowed down

due to the global financial crisis in 2008-09. It however recovered strongly and posted almost

equivalent pre-crisis growth figures in the two subsequent years. In recent times, the economy has

suffered a slowdown, witnessing its lowest growth rate in 2012-13.

A combination of domestic factors, borne out of weak policy decisions, such as high inflation, weak

currency, and drop in foreign investment coupled with global stress factors such as the sovereign debt

crisis in the Euro-zone that unfolded in 2010-11 (and the subsequent recession in the Euro-area)

were primary reasons for the slow growth.

Table 2: Growth in GDP of India at constant prices (2004-05 prices (percent))

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

9.57 9.32 6.72 8.59 8.91 6.69 4.47 4.74

Source: CSO Release May 30, 2014, RBI, EAC to PM, Ministry of Finance; May 31, 2014

The economy began to show signs of recovery in 2013-14, with the second quarter of 2013-14

recording a growth of 4.8%. This follows a growth rate of 4.4% in the first quarter which was the

lowest growth recorded in 16 quarters. The external sector witnessed a turnaround after the first

quarter of 2013-14, the year ending with a current account deficit of 1.7% of GDP as against 4.7 per

cent in 2012-13. Improvement has also been observed on the fiscal front, with the fiscal deficit

declining from 5.7% of GDP in 2011-12 to 4.9% in 2012-13 and 4.5% in 2013-14. Other indications of

recovery are the moderation on year-on-year WPI inflation to 6.0% in 2013-14 vis-à-vis 8.9% in 2011-

12 and 7.4% in 2012-13, accelerated growth in agriculture and a mild recovery in manufacturing.

2.1.1 Sectoral trends

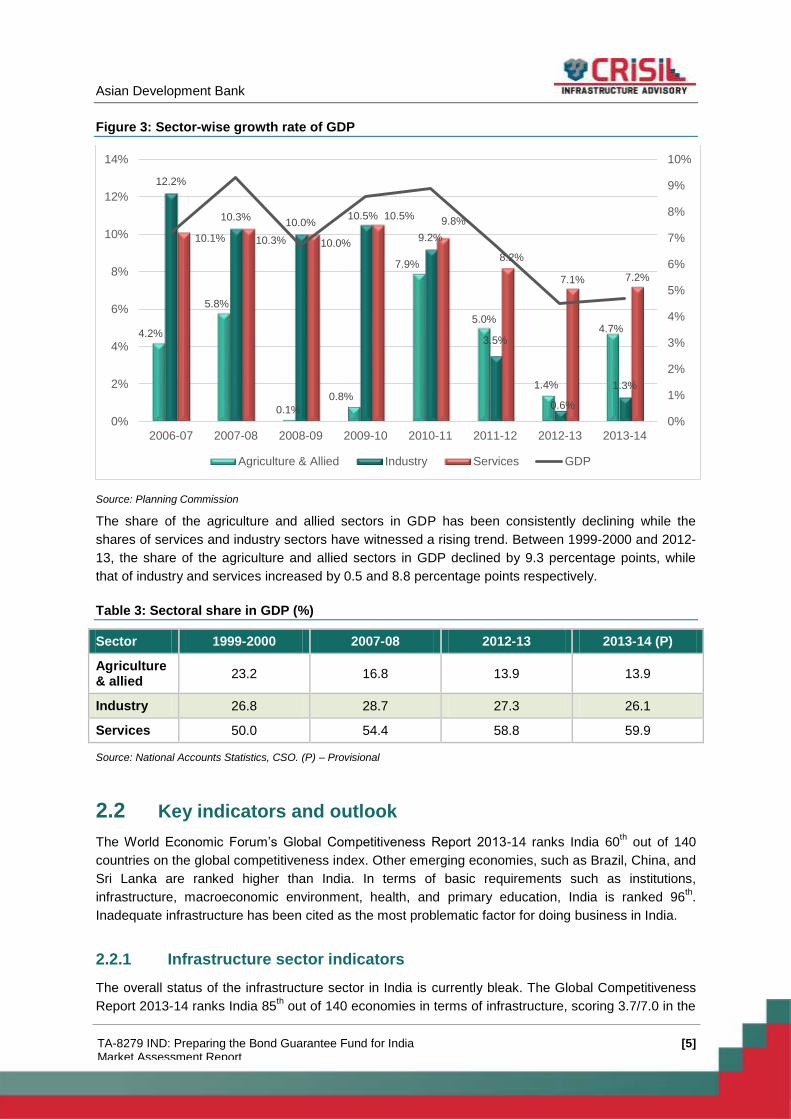

In the last decade, the biggest contributors to the economy growth were the services and industry

sectors. As seen in the subsequent graph, between 2006-07 and 2007-08 when the annual growth

rate of GDP was over 9 per cent, the performance of these two sectors was particularly strong.

The slowdown witnessed in the following years, however, was broad-based across all sectors. The

agriculture sector witnessed a steady decline in growth rate from 7.9 per cent in 2010-11 to 3.6% in

2011-12 and further to 1.9 per cent in 2012-13. Within the industry sector, mining and manufacturing

sectors have decelerated significantly over the period 2010-11 and 2012-13. Growth in services which

had averaged 10 per cent for six years, reduced to 8.2 per cent and 7.1% in 2011-12 and 2012-13

respectively. Within the services sector, transport (particularly railways) and communications, as well

as banking and insurance, slowed in 2012-13 vis-à-vis 2011-12.

In 2013-14, the agriculture and allied sectors achieved a growth of 4.7% due to favourable monsoons,

while business services also witnessed recovery due to moderate revival in the global economy.

Asian Development Bank

[5] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

Figure 3: Sector-wise growth rate of GDP

Source: Planning Commission

The share of the agriculture and allied sectors in GDP has been consistently declining while the

shares of services and industry sectors have witnessed a rising trend. Between 1999-2000 and 2012-

13, the share of the agriculture and allied sectors in GDP declined by 9.3 percentage points, while

that of industry and services increased by 0.5 and 8.8 percentage points respectively.

Table 3: Sectoral share in GDP (%)

Sector 1999-2000 2007-08 2012-13 2013-14 (P)

Agriculture & allied

23.2 16.8 13.9 13.9

Industry 26.8 28.7 27.3 26.1

Services 50.0 54.4 58.8 59.9

Source: National Accounts Statistics, CSO. (P) – Provisional

2.2 Key indicators and outlook

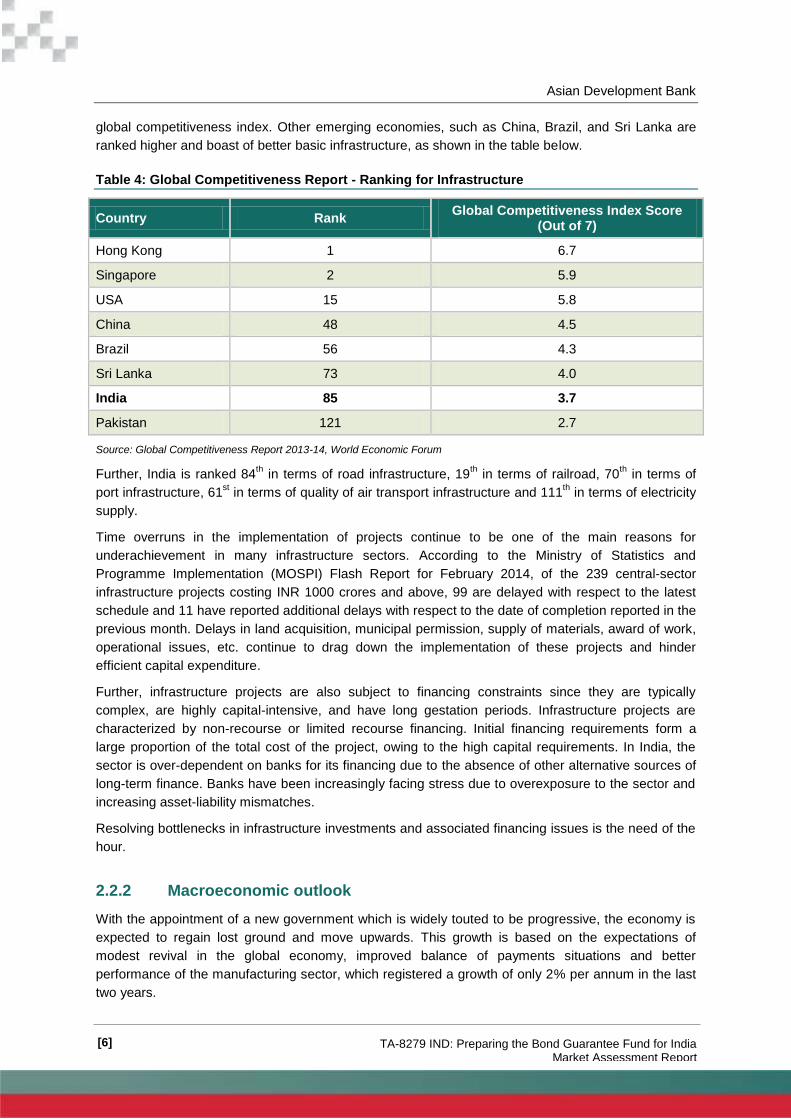

The World Economic Forum’s Global Competitiveness Report 2013-14 ranks India 60th out of 140

countries on the global competitiveness index. Other emerging economies, such as Brazil, China, and

Sri Lanka are ranked higher than India. In terms of basic requirements such as institutions,

infrastructure, macroeconomic environment, health, and primary education, India is ranked 96th.

Inadequate infrastructure has been cited as the most problematic factor for doing business in India.

2.2.1 Infrastructure sector indicators

The overall status of the infrastructure sector in India is currently bleak. The Global Competitiveness

Report 2013-14 ranks India 85th out of 140 economies in terms of infrastructure, scoring 3.7/7.0 in the

4.2%

5.8%

0.1%

0.8%

7.9%

5.0%

1.4%

4.7%

12.2%

10.3% 10.0%

10.5%

9.2%

3.5%

0.6%

1.3%

10.1% 10.3% 10.0%

10.5% 9.8%

8.2%

7.1% 7.2%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0%

2%

4%

6%

8%

10%

12%

14%

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Agriculture & Allied Industry Services GDP

Asian Development Bank

[6] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

global competitiveness index. Other emerging economies, such as China, Brazil, and Sri Lanka are

ranked higher and boast of better basic infrastructure, as shown in the table below.

Table 4: Global Competitiveness Report - Ranking for Infrastructure

Country Rank Global Competitiveness Index Score

(Out of 7)

Hong Kong 1 6.7

Singapore 2 5.9

USA 15 5.8

China 48 4.5

Brazil 56 4.3

Sri Lanka 73 4.0

India 85 3.7

Pakistan 121 2.7

Source: Global Competitiveness Report 2013-14, World Economic Forum

Further, India is ranked 84th in terms of road infrastructure, 19

th in terms of railroad, 70

th in terms of

port infrastructure, 61st in terms of quality of air transport infrastructure and 111

th in terms of electricity

supply.

Time overruns in the implementation of projects continue to be one of the main reasons for

underachievement in many infrastructure sectors. According to the Ministry of Statistics and

Programme Implementation (MOSPI) Flash Report for February 2014, of the 239 central-sector

infrastructure projects costing INR 1000 crores and above, 99 are delayed with respect to the latest

schedule and 11 have reported additional delays with respect to the date of completion reported in the

previous month. Delays in land acquisition, municipal permission, supply of materials, award of work,

operational issues, etc. continue to drag down the implementation of these projects and hinder

efficient capital expenditure.

Further, infrastructure projects are also subject to financing constraints since they are typically

complex, are highly capital-intensive, and have long gestation periods. Infrastructure projects are

characterized by non-recourse or limited recourse financing. Initial financing requirements form a

large proportion of the total cost of the project, owing to the high capital requirements. In India, the

sector is over-dependent on banks for its financing due to the absence of other alternative sources of

long-term finance. Banks have been increasingly facing stress due to overexposure to the sector and

increasing asset-liability mismatches.

Resolving bottlenecks in infrastructure investments and associated financing issues is the need of the

hour.

2.2.2 Macroeconomic outlook

With the appointment of a new government which is widely touted to be progressive, the economy is

expected to regain lost ground and move upwards. This growth is based on the expectations of

modest revival in the global economy, improved balance of payments situations and better

performance of the manufacturing sector, which registered a growth of only 2% per annum in the last

two years.

Asian Development Bank

[7] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

Global economic activity is expected to strengthen in the current year on the back of some recovery in

advanced economies. The World Bank has predicted a growth rate of above 1% for the Euro area as

against the contraction witnessed in 2012 and 2013. The growth outlook for emerging Asian

economies is generally benign with some grappling with inflation, structural bottlenecks, and external

imbalances.

The Union Budget 2014-15 has announced steps to raise private consumption growth as well as push

growth in the manufacturing and construction/infrastructure sectors. While these steps would help in

industrial recovery, weaker monsoons are likely to adversely impact growth in the short term.

The Economic Survey of India 2013-14 (July, 2014) has predicted a growth rate of GDP at constant

prices in the range of 5.4 – 5.9% in 2014-15 for the economy. This assumes the revival of growth in

the industrial sector witnessed in April 2014 to continue for the rest of the year, the generally benign

outlook on oil prices and the absence of pronounced destabilizing shocks. However, as per our

estimates, it is expected that GDP will grow at a lower growth rate of 5.5% in the short term, given the

likely deficit in monsoons in 2014-15 that could affect agriculture production.

Asian Development Bank

[8] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

3. Investments in India and Debt Requirement

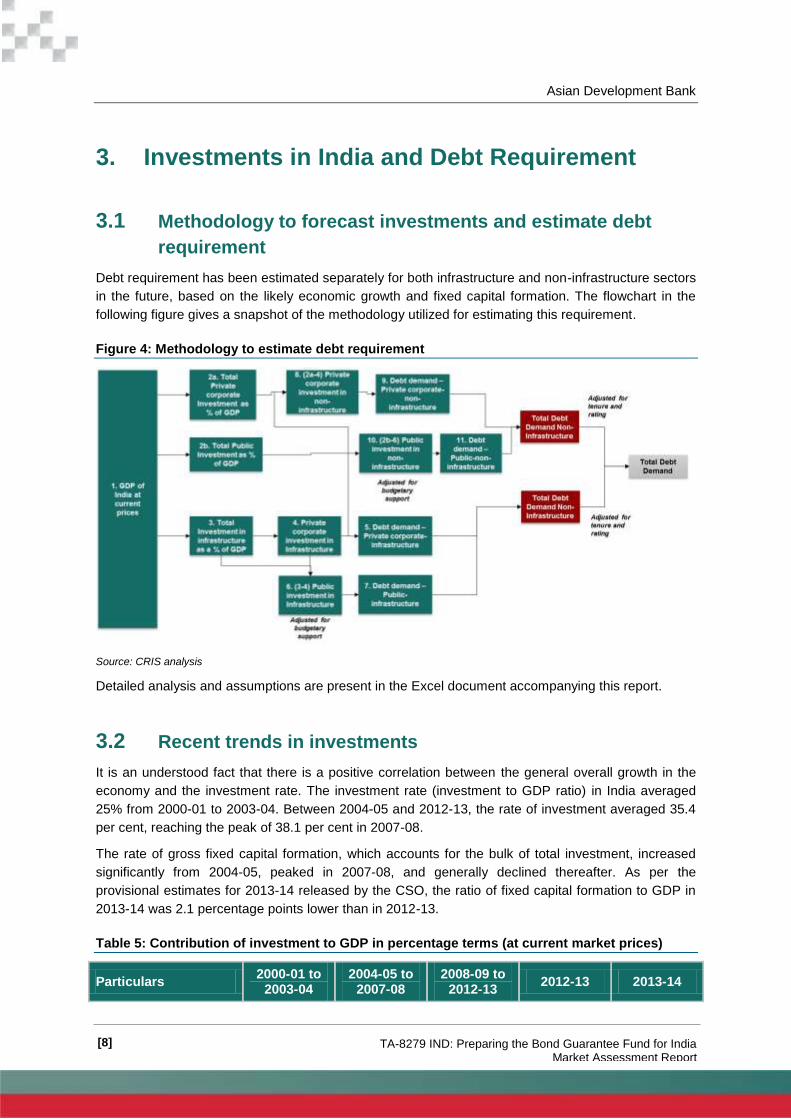

3.1 Methodology to forecast investments and estimate debt

requirement

Debt requirement has been estimated separately for both infrastructure and non-infrastructure sectors

in the future, based on the likely economic growth and fixed capital formation. The flowchart in the

following figure gives a snapshot of the methodology utilized for estimating this requirement.

Figure 4: Methodology to estimate debt requirement

Source: CRIS analysis

Detailed analysis and assumptions are present in the Excel document accompanying this report.

3.2 Recent trends in investments

It is an understood fact that there is a positive correlation between the general overall growth in the

economy and the investment rate. The investment rate (investment to GDP ratio) in India averaged

25% from 2000-01 to 2003-04. Between 2004-05 and 2012-13, the rate of investment averaged 35.4

per cent, reaching the peak of 38.1 per cent in 2007-08.

The rate of gross fixed capital formation, which accounts for the bulk of total investment, increased

significantly from 2004-05, peaked in 2007-08, and generally declined thereafter. As per the

provisional estimates for 2013-14 released by the CSO, the ratio of fixed capital formation to GDP in

2013-14 was 2.1 percentage points lower than in 2012-13.

Table 5: Contribution of investment to GDP in percentage terms (at current market prices)

Particulars 2000-01 to

2003-04 2004-05 to

2007-08 2008-09 to

2012-13 2012-13 2013-14

Asian Development Bank

[9] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

Particulars 2000-01 to

2003-04 2004-05 to

2007-08 2008-09 to

2012-13 2012-13 2013-14

Total Investment 25.0 35.3 35.5 34.8 35

Gross Fixed Capital Formation

24.0 30.8 31.4 30.4 28.3

Public Sector 6.7 7.6 7.9 7.8 NA

Private Corporate Sector 5.5 11.9 9.8 8.5

NA

Household Sector 11.8 11.3 13.7 14.1 NA

Source: CSO Release May 30, 2014, RBI, EAC to PM, Ministry of Finance; May 31, 2014, NA-Not Available

As can be seen from the previous table, the private sector (comprising private corporate sector and

household sector) is the major source of investment in the country. Increase in investment by the

private corporate sector explained the bulk of the increase in overall investment during the upswing

phase between 2004-05 and 2007-08.

3.2.1 Investment in infrastructure sector

3.2.1.1 Investment in infrastructure sector – Planning Commission estimates

Investments in the infrastructure sector in India over the period 2002-12 (10th & 11

th Five Year Plans)

were to the tune of INR 32.6 lakh crores. A comparison between the actual investments in

infrastructure during the 10th and 11

th Five Year Plans and the projected investments during the 12

th

Five Year Plan – as given by the Planning Commission – are given in the table below.

Table 6: Comparison of infrastructure investments across Five Year Plans – Planning Commission (INR crores)

Particulars 10th Five Year Plan (2002-07) - Actual

11th Five Year Plan (2007-12) - Actual

12th Five Year Plan (2012- 2017) Projected

GDP at market prices 1,65,98,847 3,36,04,450 6,81,63,208

Total investment 8,37,159 24,24,277 55,74,663

Total investment as percentage of GDP 5.04% 7.21% 8.18%

Public investment 6,51,136 15,36,773 28,90,823

Private corporate sector investment

1,86,023 8,87,504 26,83,840

Percentage share of private corporate sector investment in total investment

22% 37% 48%

Source: Planning Commission

The total investment in infrastructure, as a percentage of GDP, is projected to increase from around

5.08% during the 10th Five Year Plan to 8.18% by the end of 12

th Five Year Plan. Percentage share of

Asian Development Bank

[10] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

private investment in the total investment is projected to increase from 25% during the 10th Plan to

48% by the end of the 12th Plan.

The Union Budget 2014-15 has announced a slew of measures to boost infrastructure investments –

mainstreaming Public-Private Partnerships (PPPs) through the creation of 3P India, focusing on

increasing investments in infrastructure through various projects and increasing funding to the sector

amongst others; these measures are expected to boost the pace of growth in the infrastructure sector.

Overall spending on infrastructure is budgeted to rise 24% over last fiscal to INR 2.1 lakh crores.

While the budget provisions are positive, addressing on-the-ground issues like land acquisition,

environmental clearances, inflation, and uncertainties in regulations etc. is key to reinvigorate the

sector.

Keeping these teething issues in mind it is believed that the total investment in infrastructure as a

percentage of GDP might just fall short of the Planning Commission estimates for the 12th Plan period,

falling to an average of 7.3% of GDP for the same period. Contribution by private corporate sector in

the overall investment has been growing year on year. While a slowdown in investment was seen in

recent years, with the focus of the new government on increasing private sector participation it is

expected that their contribution to investments would increase further.

3.2.1.2 Outlook on investments in key infrastructure segments

In the following sub-section, details on investments in some of the key infrastructure segments are

provided.

3.2.1.2.1 Power/Electricity

The capacity-addition target for the 12th Plan period is estimated at 88,537 MW, comprising 26,182

MW in the central sector, 15,530 MW in the state sector, and 46,825 MW in the private sector. In

2012-13, a record capacity addition of 20,622.8 MW (20,121.8 MW in thermal and 501 MW in hydro)

was achieved, as against the set target of 17,956.3 MW. The capacity addition target for the year

2013-14 was 18,432.3 MW.

The government has also recently undertaken initiatives for augmenting power generation in India –

changes in the mega power policy for provisional mega power certified projects (February 2014),

allocation of new coal blocks to NTPC, Independent Coal Regulatory Bill, automatic approval for

foreign direct investment etc.

It is expected that another 37,000 MW of capacity will be added by 2017-18, out of which around 82%

will be based on coal. Private sector is expected account for around 54% of the capacity additions.

3.2.1.2.2 Roads

It is expected that roads and highways would see an investment of about INR 6.3 lakh crores between

2013-14 and 2017-18. Of this amount, the share of national highways would be 43%, followed by

state roads and rural roads at 30% and 27%, respectively.

Going forward, it is expected that the highway projects under the National Highways Development

Programme (NHDP) would pick up, with the main focus on Phase III, Phase IV and Phase V projects.

A total length of 21,787 km has been completed till March 2014 under various phases of the NHDP.

The Union Budget 2014-15 has announced the provision of INR 14,400 crores towards Pradhan

Mantri Gram Sadak Yojana Scheme and INR 37.900 crores for national highways and state roads.

Further, it has set aside INR 500 crores to initiate work on expressways.

Asian Development Bank

[11] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

3.2.1.2.3 Railways

The Indian Railways is currently working at close to 100% capacity utilization, highlighting the need to

augment its freight-carrying capacity in the near future. Keeping these constraints in mind, policies

have been developed to focus on the creation of additional capacity, modernization of the existing

network, improvement in asset utilization and productivity, and modernization of rolling stock and

maintenance practices to bring about overall improvement in the quality of railway services, while

augmenting profitability and internal resource generation. The 12th Five Year Plan envisages an

investment of over INR 5 lakh crores in Railways. It also envisages a larger role for PPP in projects

like high-speed rail corridors and direct freight corridors for effective project execution.

The Union Budget 2014-15 plans to introduce a bullet train on the Mumbai-Ahmedabad route and

create a diamond quadrilateral for high-speed trains. It further provides for permitting foreign direct

investment in railway projects.

3.2.1.2.4 Ports

Over INR 55,000 crores has been invested in the ports sector, in the last five years. More than 80% of

these investments are estimated to have been made by the private sector, majority towards non-major

ports, whereas public sector contribution in the investments has remained limited to maintenance of

draft and building of allied infrastructure like roads at major ports.

Going forward, it is expected that close to INR 60,000 crores will be invested in the ports sector in the

coming years. Based on the present status of ongoing/announced projects, it is likely that a higher

proportion of these investments would flow towards projects at major ports.

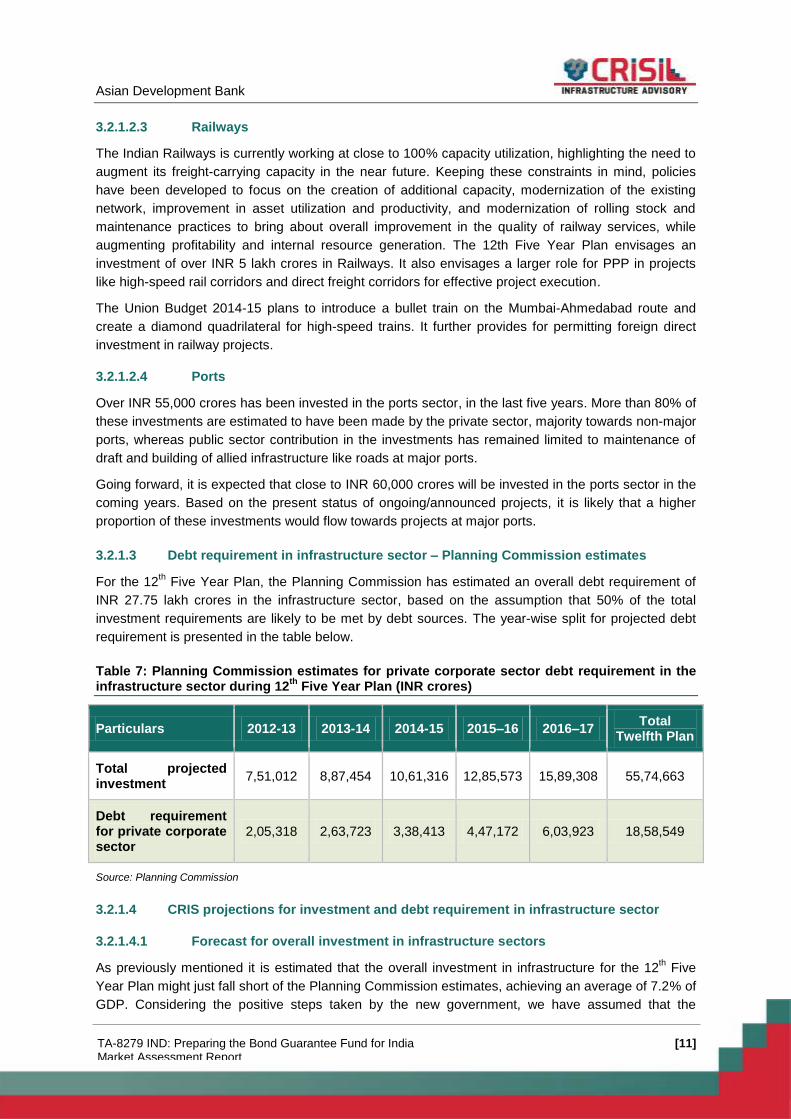

3.2.1.3 Debt requirement in infrastructure sector – Planning Commission estimates

For the 12th Five Year Plan, the Planning Commission has estimated an overall debt requirement of

INR 27.75 lakh crores in the infrastructure sector, based on the assumption that 50% of the total

investment requirements are likely to be met by debt sources. The year-wise split for projected debt

requirement is presented in the table below.

Table 7: Planning Commission estimates for private corporate sector debt requirement in the infrastructure sector during 12

th Five Year Plan (INR crores)

Particulars 2012-13 2013-14 2014-15 2015–16 2016–17 Total

Twelfth Plan

Total projected investment

7,51,012 8,87,454 10,61,316 12,85,573 15,89,308 55,74,663

Debt requirement for private corporate sector

2,05,318 2,63,723 3,38,413 4,47,172 6,03,923 18,58,549

Source: Planning Commission

3.2.1.4 CRIS projections for investment and debt requirement in infrastructure sector

3.2.1.4.1 Forecast for overall investment in infrastructure sectors

As previously mentioned it is estimated that the overall investment in infrastructure for the 12th Five

Year Plan might just fall short of the Planning Commission estimates, achieving an average of 7.2% of

GDP. Considering the positive steps taken by the new government, we have assumed that the

Asian Development Bank

[12] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

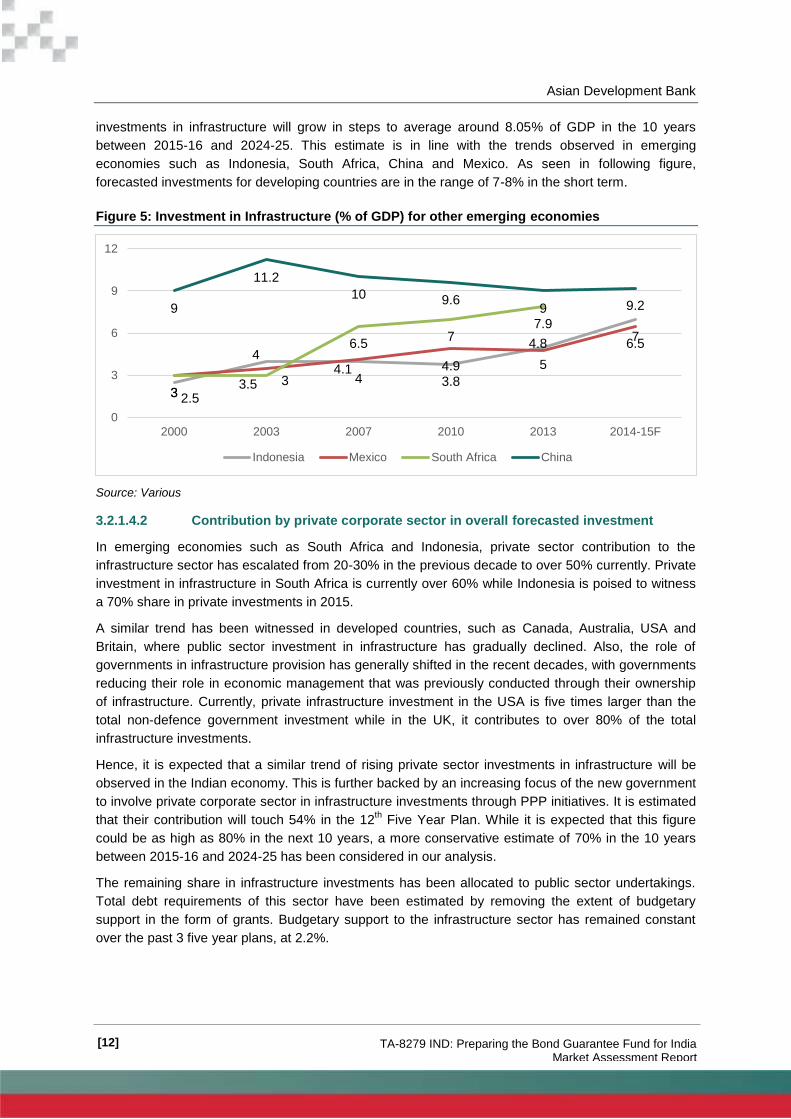

investments in infrastructure will grow in steps to average around 8.05% of GDP in the 10 years

between 2015-16 and 2024-25. This estimate is in line with the trends observed in emerging

economies such as Indonesia, South Africa, China and Mexico. As seen in following figure,

forecasted investments for developing countries are in the range of 7-8% in the short term.

Figure 5: Investment in Infrastructure (% of GDP) for other emerging economies

Source: Various

3.2.1.4.2 Contribution by private corporate sector in overall forecasted investment

In emerging economies such as South Africa and Indonesia, private sector contribution to the

infrastructure sector has escalated from 20-30% in the previous decade to over 50% currently. Private

investment in infrastructure in South Africa is currently over 60% while Indonesia is poised to witness

a 70% share in private investments in 2015.

A similar trend has been witnessed in developed countries, such as Canada, Australia, USA and

Britain, where public sector investment in infrastructure has gradually declined. Also, the role of

governments in infrastructure provision has generally shifted in the recent decades, with governments

reducing their role in economic management that was previously conducted through their ownership

of infrastructure. Currently, private infrastructure investment in the USA is five times larger than the

total non-defence government investment while in the UK, it contributes to over 80% of the total

infrastructure investments.

Hence, it is expected that a similar trend of rising private sector investments in infrastructure will be

observed in the Indian economy. This is further backed by an increasing focus of the new government

to involve private corporate sector in infrastructure investments through PPP initiatives. It is estimated

that their contribution will touch 54% in the 12th Five Year Plan. While it is expected that this figure

could be as high as 80% in the next 10 years, a more conservative estimate of 70% in the 10 years

between 2015-16 and 2024-25 has been considered in our analysis.

The remaining share in infrastructure investments has been allocated to public sector undertakings.

Total debt requirements of this sector have been estimated by removing the extent of budgetary

support in the form of grants. Budgetary support to the infrastructure sector has remained constant

over the past 3 five year plans, at 2.2%.

2.5

4

4 3.8

5

7

3 3.5

4.1 4.9

4.8 6.5

3 3

6.5 7

7.9 9

11.2

10 9.6 9 9.2

0

3

6

9

12

2000 2003 2007 2010 2013 2014-15F

Indonesia Mexico South Africa China

Asian Development Bank

[13] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

3.2.1.4.3 Forecast for debt requirement in infrastructure sector – adjusted for tenure and

rating

Considering the long-term nature of these investments it is estimated that they will be funded by long-

term debt – this is assumed at current levels of 70%4 of overall investments. Moreover, it is assumed

that 85%5 of this total debt requirement would pertain to entities rated less than AA category for the

private sector and 30%6 for the public sector.

Table 8: Forecast for investment and debt requirement in infrastructure sector (INR crores)

Particulars 2015-16 to 2019-2020 2020-21 to 2024-25

Total projected investment 71,45,297 137,50,732

(% of GDP) 7.70% 8.40%

Contribution by private corporate sector

48,35,005 96,25,512

(% of projected investment) 67% 70%

Contribution by PSUs 2,74,939 5,02,744

Debt requirement – Long term and by entities rated less than AA

29,34,565 58,32,756

Source: CRIS analysis

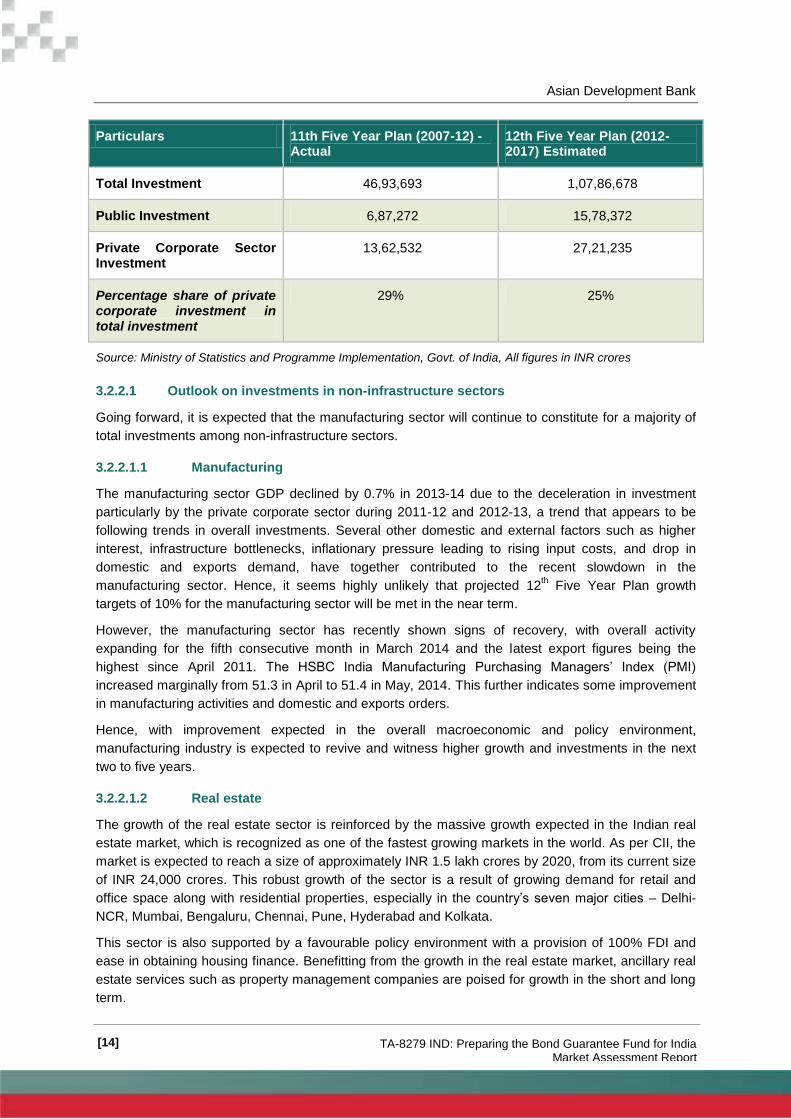

3.2.2 Investment in non-infrastructure sector

Investments in the non-infrastructure sectors have grown at a CAGR of 18% in the last decade. The

manufacturing and business services segments (real estate) constitute dominate investments in the

non-infrastructure sector, constituting approximately 70% of the total investments.

Estimated investment in the non-infrastructure sectors over the 11th & 12

th Five Year Plans and its

split between the public and private sectors has been highlighted in the table below. The private

corporate sector has contributed 29% of investments during the 11th Five Year Plan. Following the

decline in overall investments due to the economic slowdown, this share is expected to fall to an

average of 25% in the 12th Five Year Plan.

Table 9: Investments in non-infrastructure sectors

Particulars 11th Five Year Plan (2007-12) - Actual

12th Five Year Plan (2012- 2017) Estimated

4 Arrived at after Prowess analysis of outstanding liabilities of entities in the infrastructure sector

5 Arrived at after Prowess analysis of outstanding credit rating data

6 Arrived at after Prowess analysis of outstanding credit rating data

Asian Development Bank

[14] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

Particulars 11th Five Year Plan (2007-12) - Actual

12th Five Year Plan (2012- 2017) Estimated

Total Investment 46,93,693 1,07,86,678

Public Investment 6,87,272 15,78,372

Private Corporate Sector Investment

13,62,532 27,21,235

Percentage share of private corporate investment in total investment

29% 25%

Source: Ministry of Statistics and Programme Implementation, Govt. of India, All figures in INR crores

3.2.2.1 Outlook on investments in non-infrastructure sectors

Going forward, it is expected that the manufacturing sector will continue to constitute for a majority of

total investments among non-infrastructure sectors.

3.2.2.1.1 Manufacturing

The manufacturing sector GDP declined by 0.7% in 2013-14 due to the deceleration in investment

particularly by the private corporate sector during 2011-12 and 2012-13, a trend that appears to be

following trends in overall investments. Several other domestic and external factors such as higher

interest, infrastructure bottlenecks, inflationary pressure leading to rising input costs, and drop in

domestic and exports demand, have together contributed to the recent slowdown in the

manufacturing sector. Hence, it seems highly unlikely that projected 12th Five Year Plan growth

targets of 10% for the manufacturing sector will be met in the near term.

However, the manufacturing sector has recently shown signs of recovery, with overall activity

expanding for the fifth consecutive month in March 2014 and the latest export figures being the

highest since April 2011. The HSBC India Manufacturing Purchasing Managers’ Index (PMI)

increased marginally from 51.3 in April to 51.4 in May, 2014. This further indicates some improvement

in manufacturing activities and domestic and exports orders.

Hence, with improvement expected in the overall macroeconomic and policy environment,

manufacturing industry is expected to revive and witness higher growth and investments in the next

two to five years.

3.2.2.1.2 Real estate

The growth of the real estate sector is reinforced by the massive growth expected in the Indian real

estate market, which is recognized as one of the fastest growing markets in the world. As per CII, the

market is expected to reach a size of approximately INR 1.5 lakh crores by 2020, from its current size

of INR 24,000 crores. This robust growth of the sector is a result of growing demand for retail and

office space along with residential properties, especially in the country’s seven major cities – Delhi-

NCR, Mumbai, Bengaluru, Chennai, Pune, Hyderabad and Kolkata.

This sector is also supported by a favourable policy environment with a provision of 100% FDI and

ease in obtaining housing finance. Benefitting from the growth in the real estate market, ancillary real

estate services such as property management companies are poised for growth in the short and long

term.

Asian Development Bank

[15] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

3.2.2.2 CRIS projections for investment and debt requirement in non-infrastructure sectors

3.2.2.2.1 Forecast for total private corporate investment

As per our estimates, private corporate investment in both infrastructure and non-infrastructure

sectors has historically grown from 5.3% in 2002-03 to 10% currently. Following these trends, private

corporate investment is expected to increase in the future, given the limited investment ability of the

public sector due to the fiscal deficit target and an overall impetus to privatization in the economy.

Hence, private corporate gross fixed capital formation as a percentage of GDP is expected to rise by

another five percentage points over the next year, rising to 15% in 2025.

3.2.2.2.2 Forecast for total private corporate investment in the non-infrastructure sector

The estimates for private corporate investment in the non-infrastructure sector have been arrived at

by calculating the balancing figure for overall private corporate investment. It has been assumed that

the balance of private corporate investments to infrastructure sector will be invested in the non-

infrastructure sector.

3.2.2.2.3 Forecast for debt requirement in infrastructure sector – adjusted for tenure and

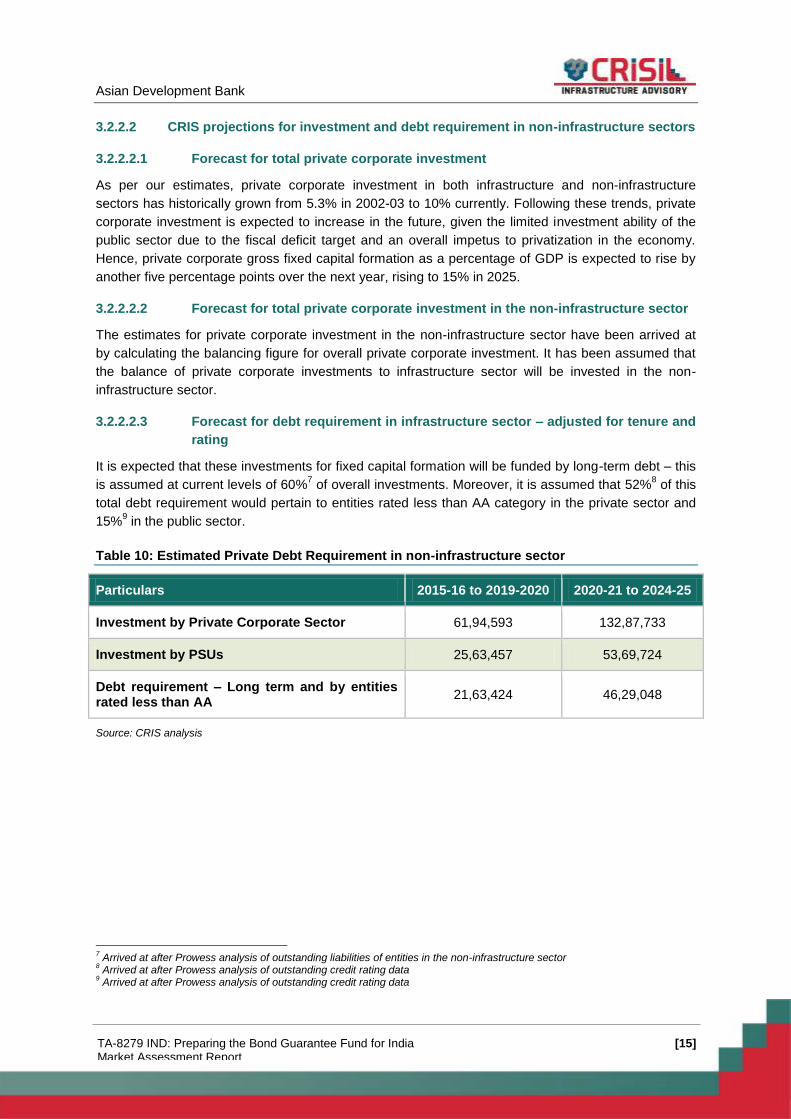

rating

It is expected that these investments for fixed capital formation will be funded by long-term debt – this

is assumed at current levels of 60%7 of overall investments. Moreover, it is assumed that 52%

8 of this

total debt requirement would pertain to entities rated less than AA category in the private sector and

15%9 in the public sector.

Table 10: Estimated Private Debt Requirement in non-infrastructure sector

Particulars 2015-16 to 2019-2020 2020-21 to 2024-25

Investment by Private Corporate Sector 61,94,593 132,87,733

Investment by PSUs 25,63,457 53,69,724

Debt requirement – Long term and by entities rated less than AA

21,63,424 46,29,048

Source: CRIS analysis

7 Arrived at after Prowess analysis of outstanding liabilities of entities in the non-infrastructure sector

8 Arrived at after Prowess analysis of outstanding credit rating data

9 Arrived at after Prowess analysis of outstanding credit rating data

Asian Development Bank

[16] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

4. Financial Sector in India and Debt Supply

4.1 Overview of the Indian financial sector

India has one of the better financial market systems in the world. The World Economic Forum’s Global

Competitiveness Report 2013-14 ranks India 45th out of 128 countries in availability of financial

services and 38th in both ease of access to loans and affordability of financial services, outperforming

most of its peers in the BRICS quintet such as Brazil, China, and Russia.

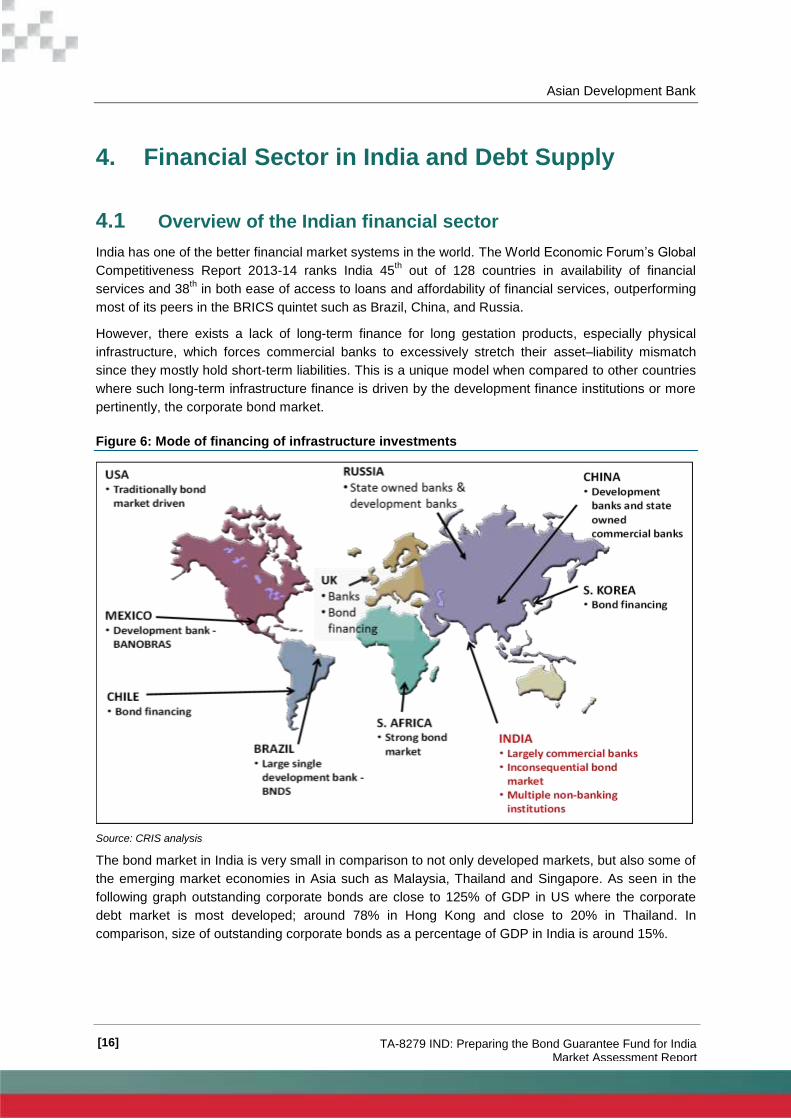

However, there exists a lack of long-term finance for long gestation products, especially physical

infrastructure, which forces commercial banks to excessively stretch their asset–liability mismatch

since they mostly hold short-term liabilities. This is a unique model when compared to other countries

where such long-term infrastructure finance is driven by the development finance institutions or more

pertinently, the corporate bond market.

Figure 6: Mode of financing of infrastructure investments

Source: CRIS analysis

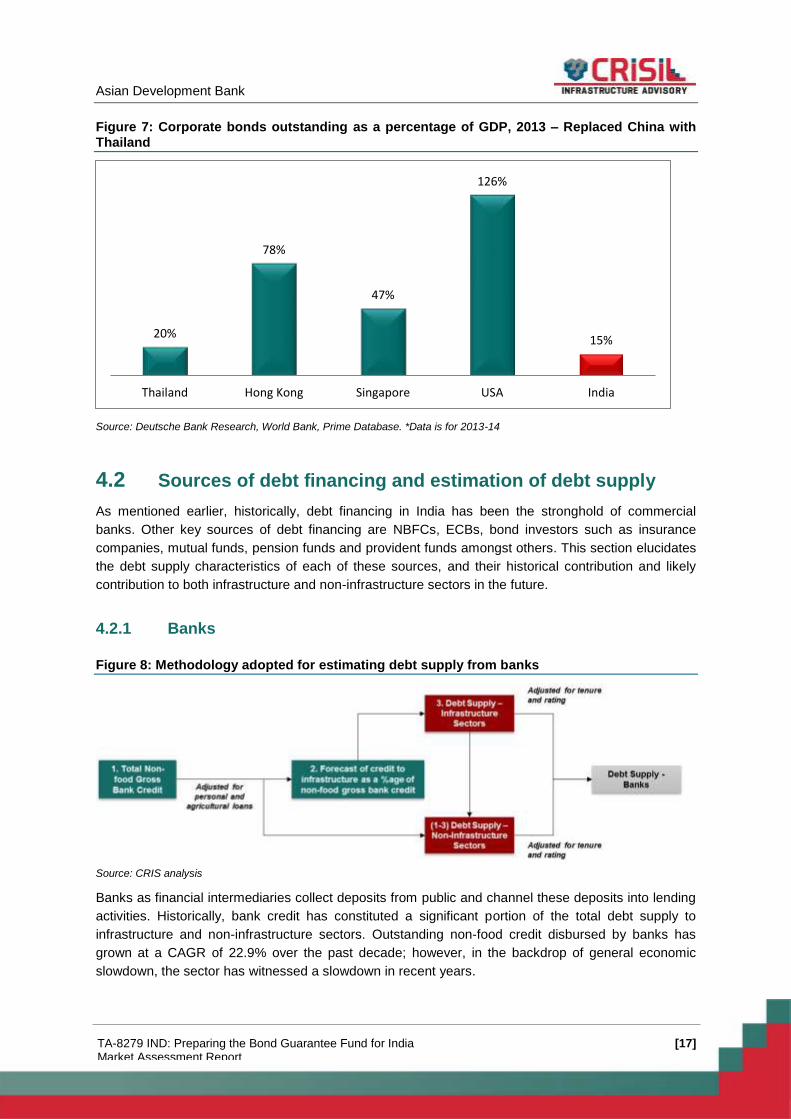

The bond market in India is very small in comparison to not only developed markets, but also some of

the emerging market economies in Asia such as Malaysia, Thailand and Singapore. As seen in the

following graph outstanding corporate bonds are close to 125% of GDP in US where the corporate

debt market is most developed; around 78% in Hong Kong and close to 20% in Thailand. In

comparison, size of outstanding corporate bonds as a percentage of GDP in India is around 15%.

Asian Development Bank

[17] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

Figure 7: Corporate bonds outstanding as a percentage of GDP, 2013 – Replaced China with Thailand

Source: Deutsche Bank Research, World Bank, Prime Database. *Data is for 2013-14

4.2 Sources of debt financing and estimation of debt supply

As mentioned earlier, historically, debt financing in India has been the stronghold of commercial

banks. Other key sources of debt financing are NBFCs, ECBs, bond investors such as insurance

companies, mutual funds, pension funds and provident funds amongst others. This section elucidates

the debt supply characteristics of each of these sources, and their historical contribution and likely

contribution to both infrastructure and non-infrastructure sectors in the future.

4.2.1 Banks

Figure 8: Methodology adopted for estimating debt supply from banks

Source: CRIS analysis

Banks as financial intermediaries collect deposits from public and channel these deposits into lending

activities. Historically, bank credit has constituted a significant portion of the total debt supply to

infrastructure and non-infrastructure sectors. Outstanding non-food credit disbursed by banks has

grown at a CAGR of 22.9% over the past decade; however, in the backdrop of general economic

slowdown, the sector has witnessed a slowdown in recent years.

20%

78%

47%

126%

15%

Thailand Hong Kong Singapore USA India

Asian Development Bank

[18] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

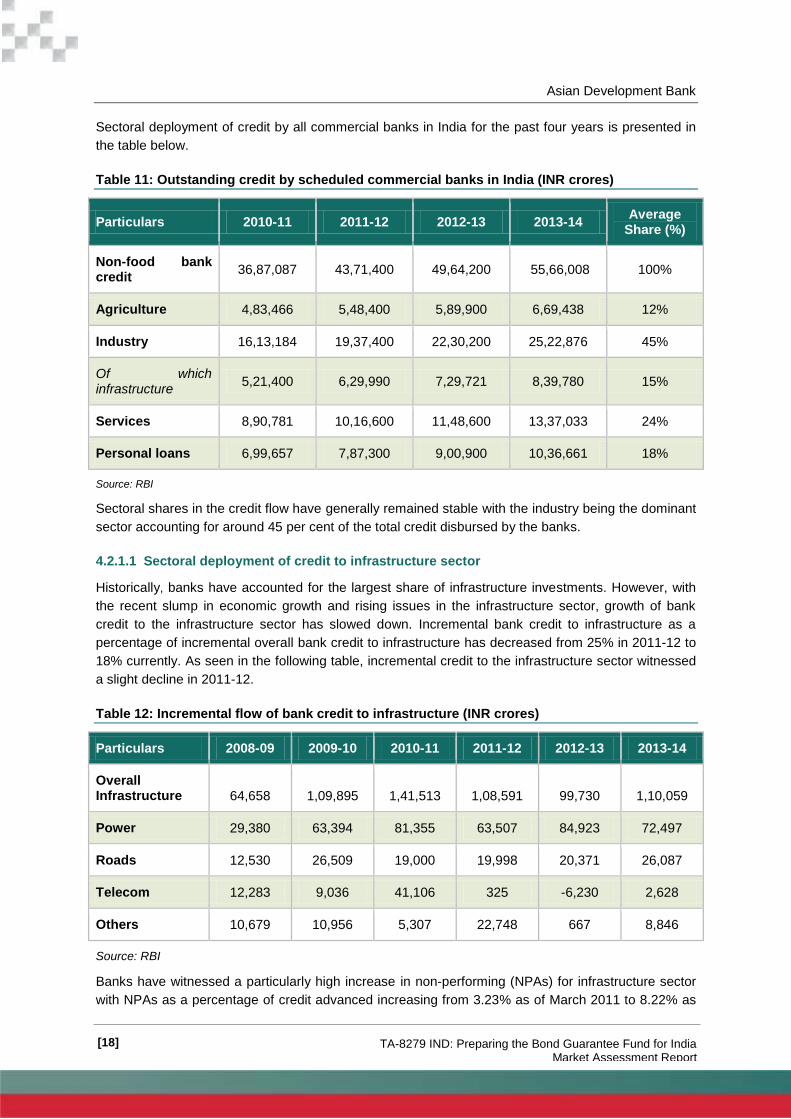

Sectoral deployment of credit by all commercial banks in India for the past four years is presented in

the table below.

Table 11: Outstanding credit by scheduled commercial banks in India (INR crores)

Particulars 2010-11 2011-12 2012-13 2013-14 Average

Share (%)

Non-food bank credit

36,87,087 43,71,400 49,64,200 55,66,008 100%

Agriculture 4,83,466 5,48,400 5,89,900 6,69,438 12%

Industry 16,13,184 19,37,400 22,30,200 25,22,876 45%

Of which infrastructure

5,21,400 6,29,990 7,29,721 8,39,780 15%

Services 8,90,781 10,16,600 11,48,600 13,37,033 24%

Personal loans 6,99,657 7,87,300 9,00,900 10,36,661 18%

Source: RBI

Sectoral shares in the credit flow have generally remained stable with the industry being the dominant

sector accounting for around 45 per cent of the total credit disbursed by the banks.

4.2.1.1 Sectoral deployment of credit to infrastructure sector

Historically, banks have accounted for the largest share of infrastructure investments. However, with

the recent slump in economic growth and rising issues in the infrastructure sector, growth of bank

credit to the infrastructure sector has slowed down. Incremental bank credit to infrastructure as a

percentage of incremental overall bank credit to infrastructure has decreased from 25% in 2011-12 to

18% currently. As seen in the following table, incremental credit to the infrastructure sector witnessed

a slight decline in 2011-12.

Table 12: Incremental flow of bank credit to infrastructure (INR crores)

Particulars 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Overall Infrastructure 64,658 1,09,895 1,41,513 1,08,591 99,730 1,10,059

Power 29,380 63,394 81,355 63,507 84,923 72,497

Roads 12,530 26,509 19,000 19,998 20,371 26,087

Telecom 12,283 9,036 41,106 325 -6,230 2,628

Others 10,679 10,956 5,307 22,748 667 8,846

Source: RBI

Banks have witnessed a particularly high increase in non-performing (NPAs) for infrastructure sector

with NPAs as a percentage of credit advanced increasing from 3.23% as of March 2011 to 8.22% as

Asian Development Bank

[19] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

of March 2014. As of March 31, 2014, banks had restructured INR 50,239 crores of infrastructure

loans – 21% of the total loans recast in the last fiscal year under the corporate debt restructuring

(CDR) mechanism.

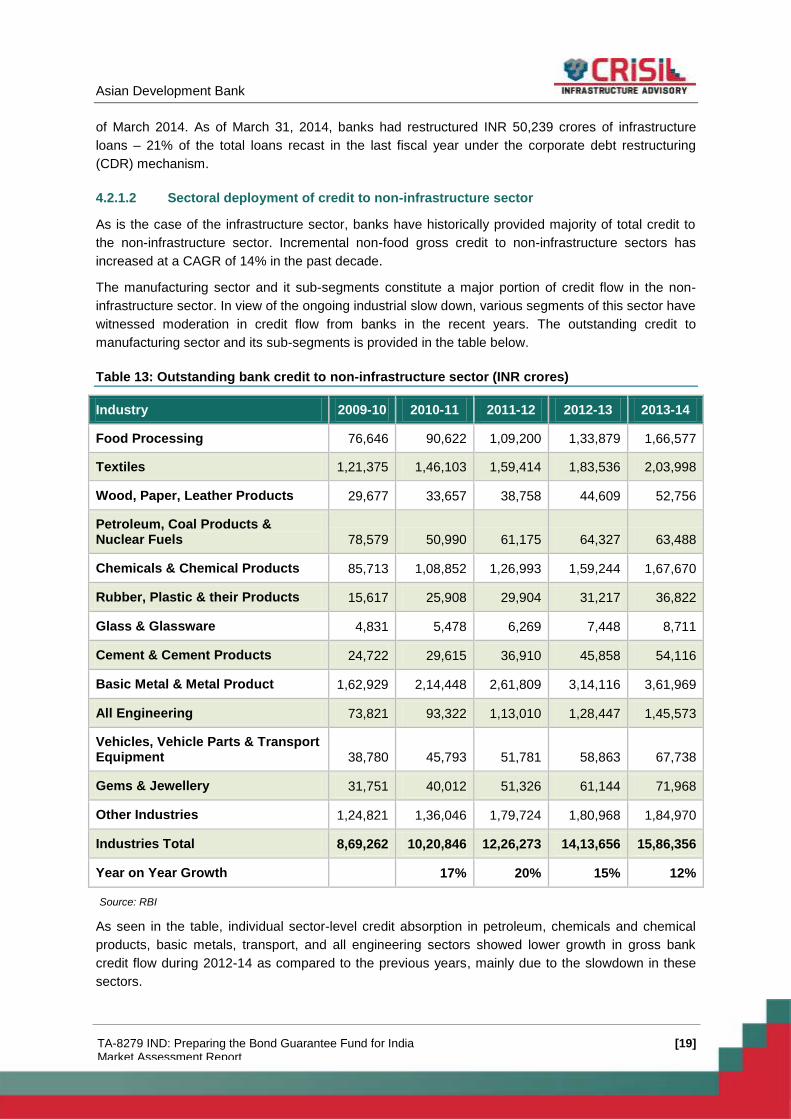

4.2.1.2 Sectoral deployment of credit to non-infrastructure sector

As is the case of the infrastructure sector, banks have historically provided majority of total credit to

the non-infrastructure sector. Incremental non-food gross credit to non-infrastructure sectors has

increased at a CAGR of 14% in the past decade.

The manufacturing sector and it sub-segments constitute a major portion of credit flow in the non-

infrastructure sector. In view of the ongoing industrial slow down, various segments of this sector have

witnessed moderation in credit flow from banks in the recent years. The outstanding credit to

manufacturing sector and its sub-segments is provided in the table below.

Table 13: Outstanding bank credit to non-infrastructure sector (INR crores)

Industry 2009-10 2010-11 2011-12 2012-13 2013-14

Food Processing 76,646 90,622 1,09,200 1,33,879 1,66,577

Textiles 1,21,375 1,46,103 1,59,414 1,83,536 2,03,998

Wood, Paper, Leather Products 29,677 33,657 38,758 44,609 52,756

Petroleum, Coal Products & Nuclear Fuels 78,579 50,990 61,175 64,327 63,488

Chemicals & Chemical Products 85,713 1,08,852 1,26,993 1,59,244 1,67,670

Rubber, Plastic & their Products 15,617 25,908 29,904 31,217 36,822

Glass & Glassware 4,831 5,478 6,269 7,448 8,711

Cement & Cement Products 24,722 29,615 36,910 45,858 54,116

Basic Metal & Metal Product 1,62,929 2,14,448 2,61,809 3,14,116 3,61,969

All Engineering 73,821 93,322 1,13,010 1,28,447 1,45,573

Vehicles, Vehicle Parts & Transport Equipment 38,780 45,793 51,781 58,863 67,738

Gems & Jewellery 31,751 40,012 51,326 61,144 71,968

Other Industries 1,24,821 1,36,046 1,79,724 1,80,968 1,84,970

Industries Total 8,69,262 10,20,846 12,26,273 14,13,656 15,86,356

Year on Year Growth 17% 20% 15% 12%

Source: RBI

As seen in the table, individual sector-level credit absorption in petroleum, chemicals and chemical

products, basic metals, transport, and all engineering sectors showed lower growth in gross bank

credit flow during 2012-14 as compared to the previous years, mainly due to the slowdown in these

sectors.

Asian Development Bank

[20] TA-8279 IND: Preparing the Bond Guarantee Fund for India Market Assessment Report

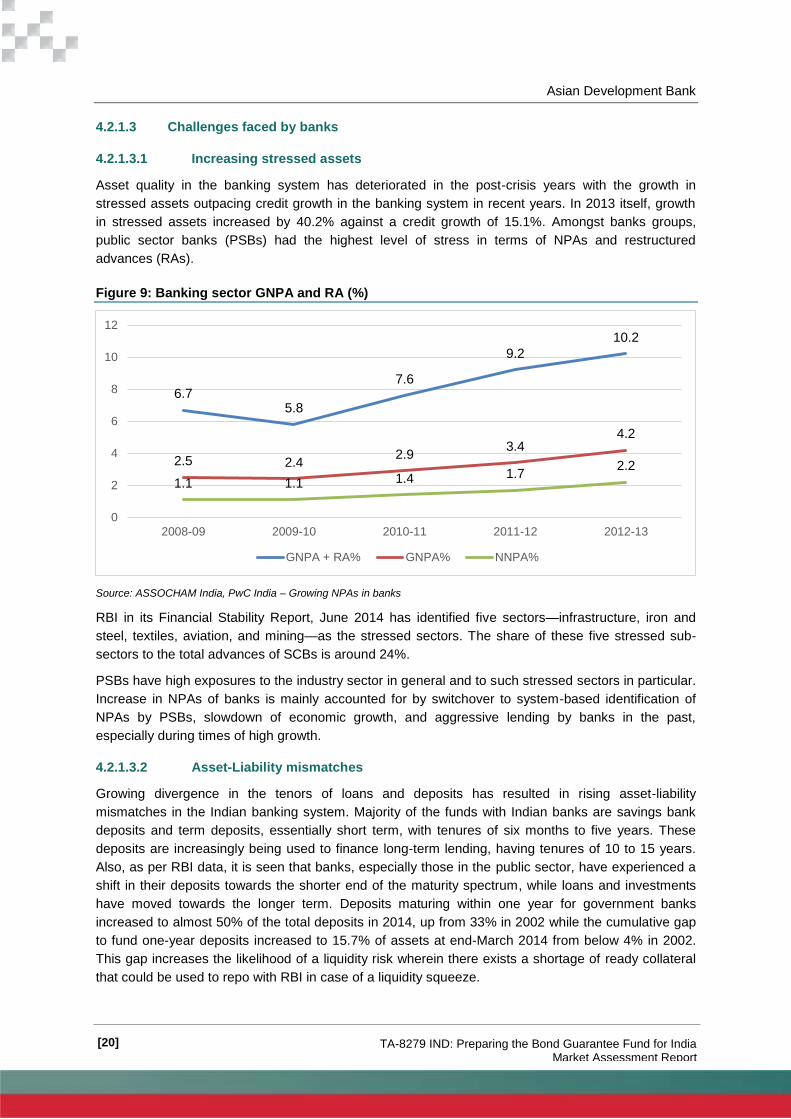

4.2.1.3 Challenges faced by banks

4.2.1.3.1 Increasing stressed assets

Asset quality in the banking system has deteriorated in the post-crisis years with the growth in

stressed assets outpacing credit growth in the banking system in recent years. In 2013 itself, growth

in stressed assets increased by 40.2% against a credit growth of 15.1%. Amongst banks groups,

public sector banks (PSBs) had the highest level of stress in terms of NPAs and restructured

advances (RAs).

Figure 9: Banking sector GNPA and RA (%)