Down, but not out - The Tungsten Market in Europe · PDF filefrom the Euro zone financial...

13

Tungsten Market Europe www.hcstarck.com www.hcstarck.com Slide 1 Insert title here Technology Metals I Advanced Ceramics Down, but not out - The Tungsten Market in Europe ITIA – 26 th Annual General Meeting, Sydney Kurt Wandaller, Gunnar Kunz 24. Sep. 2013

Transcript of Down, but not out - The Tungsten Market in Europe · PDF filefrom the Euro zone financial...

Tungsten Market Europe

www.hcstarck.com www.hcstarck.com Slide 1

Insert title here

Technology Metals I Advanced Ceramics

Down, but not out - The Tungsten Market in Europe ITIA – 26th Annual General Meeting, Sydney Kurt Wandaller, Gunnar Kunz 24. Sep. 2013

Tungsten Market Europe

www.hcstarck.com www.hcstarck.com

Europe Economy Outlook

Slide 2

• The Euro zone remains in recession with GDP is forecast to shrink by -0.4% in 2013 (after -0.6% in 2012).

• Although leading indicators signal improvement, it will take time to feed through to the real economy.

• There is a severe disparity between northern & southern EU countries in terms of economic performance & unemployment rates

• In 2013 external demand is the main driver for economic stabilization. Domestic demand is held back by the impact of deleveraging in the private & public sector

• By 2014 domestic demand will be taking over as main demand driver.

• EU economic recovery may still take >5 years on back of an improving global economy.

EU economy bottoming out…

Source: European Union 2013 / The Economist / RBS market insight

Quarterly GDP Growth, EU and Euro Area ~ q-o-q% ~

Employment Growth and Unemployment Rate, EU ~ % of labour force ~

Euro Area EU

Unemployment rate Employment

Tungsten Market Europe

www.hcstarck.com www.hcstarck.com

Tungsten Consumption in Europe

Slide 3

~ 85% of European Tungsten Consumption

A fistful of countries consume about 85% of Europe‘s Tungsten consumption.

Euro area

Currency pegged to Euro

Floating currency

Sweden

UK

Austria

France

Germany

Luxembourg

Italy

Tungsten Market Europe

www.hcstarck.com www.hcstarck.com

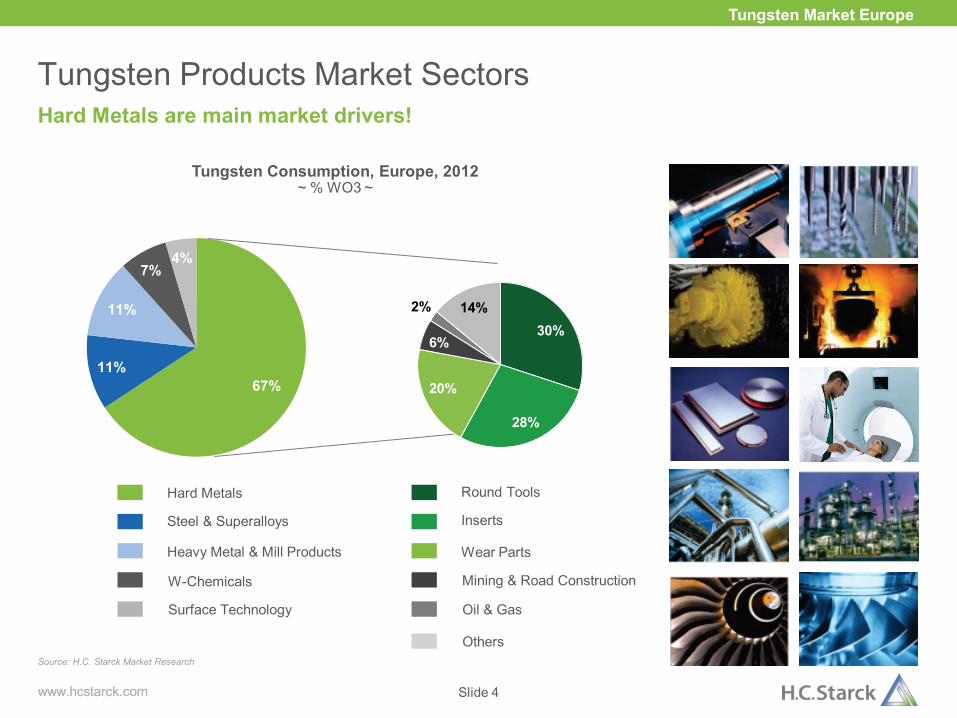

Tungsten Products Market Sectors

Slide 4

Tungsten Consumption, Europe, 2012 ~ % WO3 ~

Hard Metals

Steel & Superalloys

W-Chemicals

Heavy Metal & Mill Products

Hard Metals are main market drivers!

Source: H.C. Starck Market Research

Surface Technology

67%11%

11%

4%7%

30%

28%

20%

6%

2% 14%

Round Tools

Inserts

Mining & Road Construction

Wear Parts

Oil & Gas

Others

Tungsten Market Europe

www.hcstarck.com www.hcstarck.com Slide 5

Automotive Industry

Energy Industry

Industrial Engineering

Special Steel Industry

Mining & Road Construction

Tungsten End Market Drivers

0

20

40

60

80

10 0

12 0

14 0

0

20

40

60

80

10 0

12 0

14 0

20 06 20 07 20 08 20 09 20 10 20 11 20 12 20 13 20 14 20 15 20 16 20 17 20 18

31,400

17,300

26,900

31,300

29,000 29,300 29,800

30,800 31,800

32,900 34,000

21,700

10,900

19,300

21,700

19,200 19,200 19,400 20,100 20,800 21,500 22,300

3,800

2,100

2,500

3,200

3,300 3,300 3,400 3,500

3,600 3,700

3,700

2,600

2,000

2,500

3,100

3,200 3,300 3,500 3,600

3,700 3,800

3,900

2,000

1,400

1,600

2,000

2,100 2,100 2,200

2,300 2,400

2,400 2,500

1,200

900

1,000

1,200

1,200 1,300 1,300

1,400 1,400

1,500 1,500

0

5,0 00

10 ,000

15 ,000

20 ,000

25 ,000

30 ,000

35 ,000

40 ,000

0

5,0 00

10 ,000

15 ,000

20 ,000

25 ,000

30 ,000

35 ,000

40 ,000

20 08 20 09 20 10 20 11 20 12 20 13 20 14 20 15 20 16 20 17 20 18

19,950

17,348

15,784

16,614

18,096

19,722

22,679

24,430

16,861 16,625

19,842

0

22,725

20 01 20 02 20 03 20 04 20 05 20 06 20 07 20 08 20 09 20 10 20 11 20 12 20 13

196185

210204

163 164 167 174185

52 52 49 50 50 50 5135 40

17 16 15 13 14 1410 10

52 53 58 63 72 79 89100

110

23 23 23 2427

2829

2025

13 13 1314

1314

10

12

7 8 88

1013

15

10

13

16

14

2002 2003 2004 2005 2006 2007 2008 2009 2010

Presenter

Presentation Notes

Tungsten end market index, developed based on development and split of major underlying end markets.

Tungsten Market Europe

www.hcstarck.com www.hcstarck.com

End Markets – Automotive Global

Slide 6

Source: PwC Autofacts (2006-2013)

Global Light Vehicle Assembly, 2006 - 2018 ~ million units ~

European Union East Europe, incl. Russia China Japan, Korea, Taiwan

India ASEAN Middle East Africa NAFTA

Capacity Utilization Rate

South America Excess Capacity

0

20

40

60

80

100

120

140

0

20

40

60

80

100

120

140

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

71.5 74.7 79.2 80.9 86.7

93.2 98 101 105.1

65.2 69.0 66.0 57.6

81% 83%

76%

67%

79% 78% 77% 75% 76%

78% 80%

82% 82%

50%

55%

60%

65%

70%

75%

80%

85%

90%

• For 2013 global car assembly is forecasted as 81mio units, +2% YoY. Main growth markets are China & NAFTA, while EU & Japan are shrinking.

• In 2018 global car assembly is fore-casted as 105mio units, however, with downside risks of up to -15%

• The majority of growth contribution comes from emerging markets (China, India) with increasing urbanization & growing middle-class.

• China’s forecast was downgraded early 2013, but in recent months the GDP y-o-y again rose above 7%.

• The European union is stuck in a financial crisis.

• North America sees continuous growth on back of economic recovery.

• For Japan the long-term trend of assembly-localization to current end markets continues.

Tungsten Market Europe

www.hcstarck.com www.hcstarck.com

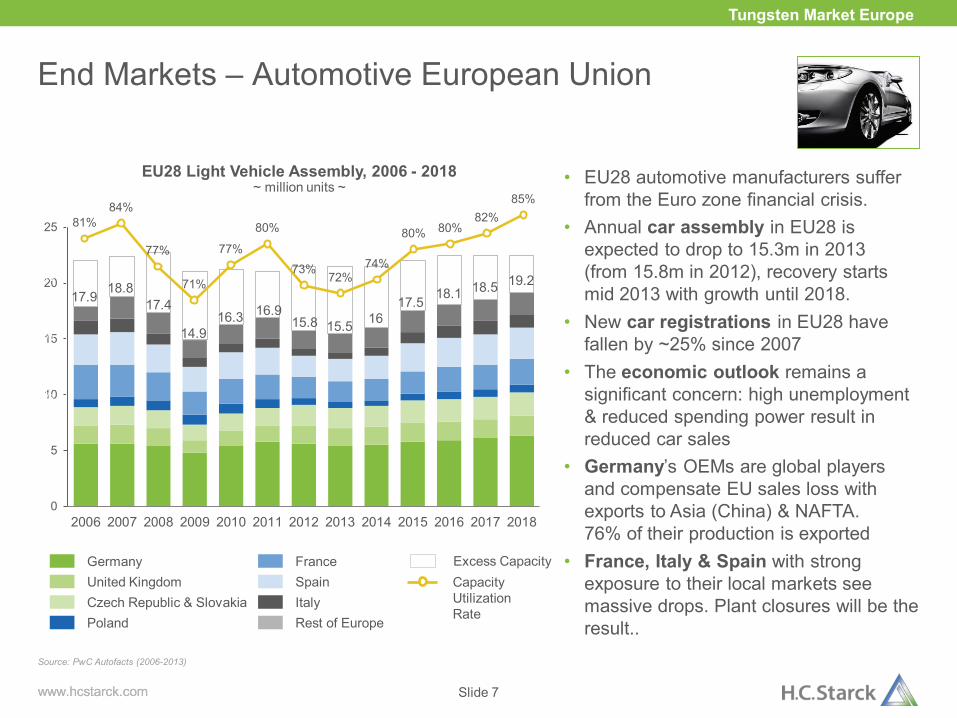

End Markets – Automotive European Union

Slide 7

• EU28 automotive manufacturers suffer from the Euro zone financial crisis.

• Annual car assembly in EU28 is expected to drop to 15.3m in 2013 (from 15.8m in 2012), recovery starts mid 2013 with growth until 2018.

• New car registrations in EU28 have fallen by ~25% since 2007

• The economic outlook remains a significant concern: high unemployment & reduced spending power result in reduced car sales

• Germany’s OEMs are global players and compensate EU sales loss with exports to Asia (China) & NAFTA. 76% of their production is exported

• France, Italy & Spain with strong exposure to their local markets see massive drops. Plant closures will be the result..

Source: PwC Autofacts (2006-2013)

Germany United Kingdom Czech Republic & Slovakia Poland

France Spain Italy Rest of Europe

Capacity Utilization Rate

EU28 Light Vehicle Assembly, 2006 - 2018 ~ million units ~

Excess Capacity

0

5

10

15

20

25

0

5

10

15

20

25

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

81% 84%

77%

71%

77%

80%

73% 72%

74%

80% 80% 82%

85%

50%

55%

60%

65%

70%

75%

80%

85%

90%

18.8 17.4

14.9

17.9 16

17.5 18.1 18.5 19.2

16.3 15.5

16.9 15.8

Tungsten Market Europe

www.hcstarck.com www.hcstarck.com

Demand for Construction and Mining Equipment by Region ~ units ~

End Markets – Mining & Road Construction

Slide 8

• Europe’s Mining Activity had already it’s peak in the 19th century.

• There’s a ongoing shift of mining locations & road construction works from developed to under-developed countries.

• However, there’s high global demand for mining equipment industry manufactured in Europe.

• Main demand growth happens in China, South East Asian (Indonesia), Latin America and Australia against the backdrop of booming resources development.

• In 2011 there was a strong rise in demand mainly to replace aging equipment.

• Growth prospects of 7-8% in the coming years.

Sources: ICMM (10/2012) / Komatsu Annual Report 2012

Location of World Mining Regions, 1850 to Present ~ % of world mining ~

Europe

North America

Japan

China

Others

Europe USA China USSR / CIS AU & CA

CL, BR, PR, SA, DRC

Tungsten Market Europe

www.hcstarck.com www.hcstarck.com

End Markets – Europe Machine Tools Industry

Slide 9

• European Machine Tools are highly competitive at the world market • The industry sees slowing growth: in 2012 EU demand contracted by 2%, while exports to non-EU grew by 9% • There is an increasing dependence on exports: > 60% of production is exported to Asia(China), USA & Russia • In H1 2013 exports to Asia (China) slowed by 10%, indicating that China’s industrial growth peak might be over • Restoring growth in the Europe domestic market will be vital for securing the future of the MT industry.

Global Machine Tools Production Share, 2012

Source: CECIMO European Machine Tools Industry

19,950

17,348 15,784 16,614

18,096 19,722

22,679 24,430

16,861 16,625

19,842

22,725

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Europe Machine Tools Production, 2001 – 2013 ~ million Euro ~

Germany Italy Switzerland

Spain Austria France

UK Czech Republic Turkey

TOTAL

EU 28, 31%

China, 30%

Japan, 20%

South Korea,

6%

Taiwan, 5%

USA, 4% Brazil, 1% Others, 2%

48%

19%

11%

22%

others

22.594

Tungsten Market Europe

www.hcstarck.com www.hcstarck.com

End Markets – Energy

Slide 10

• The EU produces just 48% of it’s energy needs, the rest is imported.

• The import dependency on fossil fuel is for oil 84%, gas 62% & coal 58%.

• The EU energy production declined by 13% over the last 20 years – less coal mined in Germany and North Sea oil&gas is depleting.

• The production of renewable energies rose by 110% in the same period.

• 2/3 of energy production comes from 5 EU states: - UK: Oil & Gas - France: Nuclear - Germany & Poland: Coal - Netherlands: Gas

• There is an expected shale gas boom in UK & Poland that will change the energy landscape and open new potentials for hard metal manufacturers. Source: Eurostat (08/2013) / European Commission Market Observation for Energy (2011)

213 211 209 208 200 195 191 185 177 165 163 166

173 161 166 156 145 133 121 120 112 105 97 85

208 208 204 200 203 189 179 167 168 153 156 140

244 253 256 257 260 258 255 241 242

231 237 234

96 100 97 104 112 116 123 134 142 149 167 162

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Energy Production in the EU28 ~ million tons of oil equivalent ~

Coal Oil Gas

Nuclear Renewables

Presenter

Presentation Notes

The Oil & Gas industry also suffered from declining economic and industrial growth. In 2009 major oil companies delayed or canceled planned investments in increasing or sustaining production.

Tungsten Market Europe

www.hcstarck.com www.hcstarck.com

End Markets – Special Steel Industry

• Europe remains an important location for special steel production.

• Germany + Sweden account for 94% of Europe’s demand and 40% of world production.

• Between 2002 - 2010 China showed the highest growth rates.

• Tungsten is added to steel in form of FeW. Different types of tool steel contain 1 – 20% W.

• China & Vietnam are the main suppliers of FeW to the European Tool Steel Industry.

Slide 11

Source: Roskill (2011)

Special Steel Industry – a profitable business in Europe!

High Speed Steel Production by Region ~ thousand tons ~

196185

210204

163 164 167 174185

52 52 49 50 50 50 5135 40

17 16 15 13 14 1410 10

52 53 58 63 72 79 89100

110

23 23 23 2427

2829

2025

13 13 1314

1314

10

12

7 8 88

1013

15

10

13

16

14

2002 2003 2004 2005 2006 2007 2008 2009 2010

China USA Europe

Others CIS Other Asia

Presenter

Presentation Notes

In 2009 global steel production dropped by 8%, making the decline by far the biggest in the industry since the end of the second world war.

Tungsten Market Europe

www.hcstarck.com www.hcstarck.com

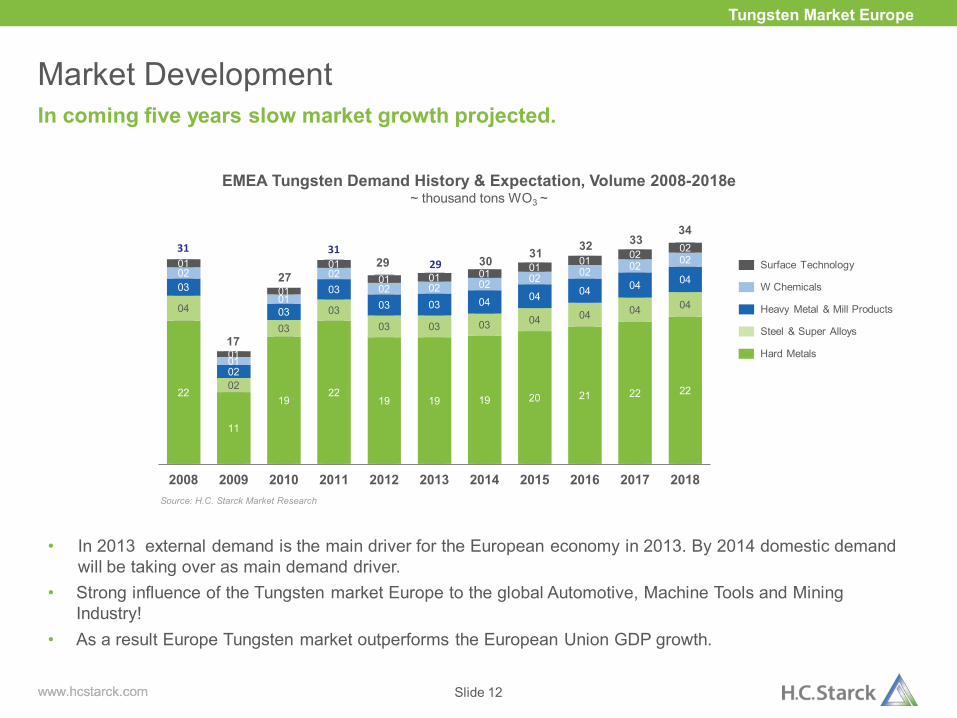

Market Development

Slide 12

In coming five years slow market growth projected.

• In 2013 external demand is the main driver for the European economy in 2013. By 2014 domestic demand will be taking over as main demand driver.

• Strong influence of the Tungsten market Europe to the global Automotive, Machine Tools and Mining Industry!

• As a result Europe Tungsten market outperforms the European Union GDP growth.

Source: H.C. Starck Market Research

EMEA Tungsten Demand History & Expectation, Volume 2008-2018e ~ thousand tons WO3 ~

Hard Metals

Surface Technology

W Chemicals

Steel & Super Alloys

Heavy Metal & Mill Products

31

17

27

31 29 29 30 31 32 33

34

22

11

19 22

19 19 19 20 21 22 22

04

02

03

03 03 03 03 04 04 04 04

03

02

03

03 03 03 04 04 04 04 04 02

01

01

02 02 02 02 02 02 02 02 01

01

01

01 01 01 01 01 01 02 02

0

5

10

15

20

25

30

35

40

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Tungsten Market Europe

www.hcstarck.com www.hcstarck.com Slide 13

Thank you for your attention!

Kurt Wandaller Senior Vice President

Business Line Tungsten Landberger Str. 94-98, 80339 Munich Germany / European Community T +49 89 5009 42 0 F +49 89 5009 42 499