Dorado TrendWatch Q4 2016

19

TRENDWATCH 2.0 Q4 2016 PAYMENTS SYSTEM INDUSTRY SYNOPSIS Notice: Materials contained in this document are drawn from several media sources, and Dorado Industries is not responsible for their accuracy. Opinions expressed herein are presented without warranty. Brand names are the trademarks of their respective service offerors. The Next Fraud Nexus CNP Fraudsters TRENDWATCH 2.0 PERSPECTIVE Online SNAP (EBT) Attacks

-

Upload

city-of-rancho-palos-verdes -

Category

Business

-

view

44 -

download

1

Transcript of Dorado TrendWatch Q4 2016

TRENDWATCH 2.0 Q4 2016

PAYMENTS SYSTEM INDUSTRY SYNOPSIS

Notice: Materials contained in this document are drawn from several media sources, and Dorado Industries is not responsible for their accuracy. Opinions expressed herein are presented without warranty. Brand names are the trademarks of their respective service offerors.

The Next Fraud Nexus

CNP Fraudsters

TRENDWATCH 2.0 PERSPECTIVE

Online SNAP (EBT) Attacks

2

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

Contents Random Thoughts ............................................................ 3

2016 Predictions and Results ........................................... 4

2017 Predictions ............................................................... 7

TrendWatch Summary – Q4 2016 ..................................... 8

2016 Payments Industry YTD Yields ................................. 9

Interesting News This Quarter ........................................ 10

M&A and Alliance Activity ............................................... 15

Useful Links for More Information ................................... 18

Back in the Day! .............................................................. 19

3

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

Random Thoughts What if? Life is filled with bushel baskets full of coulda, shoulda, woulda opportunities; the electronic payments industry is no exception. For instance:

What if, when the card brands first set about formulating credit and debit interchange pricing, they had equally weighted the three pricing principles – cost, competition, and value – instead of focusing solely on value?

What if, when the EFT networks first set about formulating interchange pricing for PIN debit, they focused on competition and value as well as cost?

What if the five California banks that created Interlink, the first PIN debit network in America, had had the gumption to hold on to that asset rather than sell it to Visa?

What if Merchant Customer Exchange (MCX) had invested more (some?) resources developing an issuer value position?

What if Apple, Samsung, and Google had agreed on a plan for interoperability before launching their digital and wearable wallets?

What if Starbucks were to offer its closed loop order-and-pay application to other major (and smaller) retailers?

What if we all stopped whining about Dodd-Frank, Durbin, PCI, and EMV and began to focus on how to make the customer experience better through use of artificial intelligence, machine learning, and augmented reality?

What if The Democratic Party had put up a candidate for POTUS other than Senator Clinton? Oops. Sorry; wrong rant.

Here’s the point; the Fintech industry isn’t burdened with coulda, shoulda, woulda issues and wants to move full steam ahead with their plans for payments which might even include special banking charters. If the OCC caves, we’re in for a fistfight.

On the Other Hand . . . . The past ten years of Fintech-fed innovation in payments, customer experience, and retailing has kept us all engaged and scurrying to keep up. We’ve seen credit democratized, retailing commoditized and banking unbundled. We once relied on “twisted copper pairs” (Google it) to conduct credit and debit transactions; now, we leverage cell phone ether and DARPA’s Internet connectivity to buy, rent, borrow, and invest.

Yet, those who seriously watch VC and PE investments tell us that 2016 was major downer as privately-owned Fintech companies fail to deliver expected returns. Indeed, only the Asia marketplace will post YoY increases on hard cash investments in technology novelties while the rest of the world sees a slump. Why?

Well, for one thing, the massive rounds (say, $100 million or more) are becoming a thing of the past as investors opt for smaller bets and a broader investment field – more verticals and wider geography. Second, as noted elsewhere, Brexit and the US election results tossed cold water on more than the UK and US markets. Despite the very nature of their business, investors really do hate uncertainty. Third, perhaps its time for proof-of-concept technologies to get off the schneid and actually perform – blockchain being the poster child. It might also be helpful if the CNP authentication industry got its ducks in a row before the inevitable spike in e-commerce fraud hits US retailers like a freight train. So, more steak, less sizzle.

And then we have Alexa and her gaggle of chatterbox buddies. Just how much time will we give Amazon, Google, Apple and Microsoft to show us what these voice activated assistants can do to make our lives (and those of our banking and retailing cohorts) better before these “nice to have” gizmos become this decade’s Pet Rock?

Got a marathon to train for

Until next time..

4

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

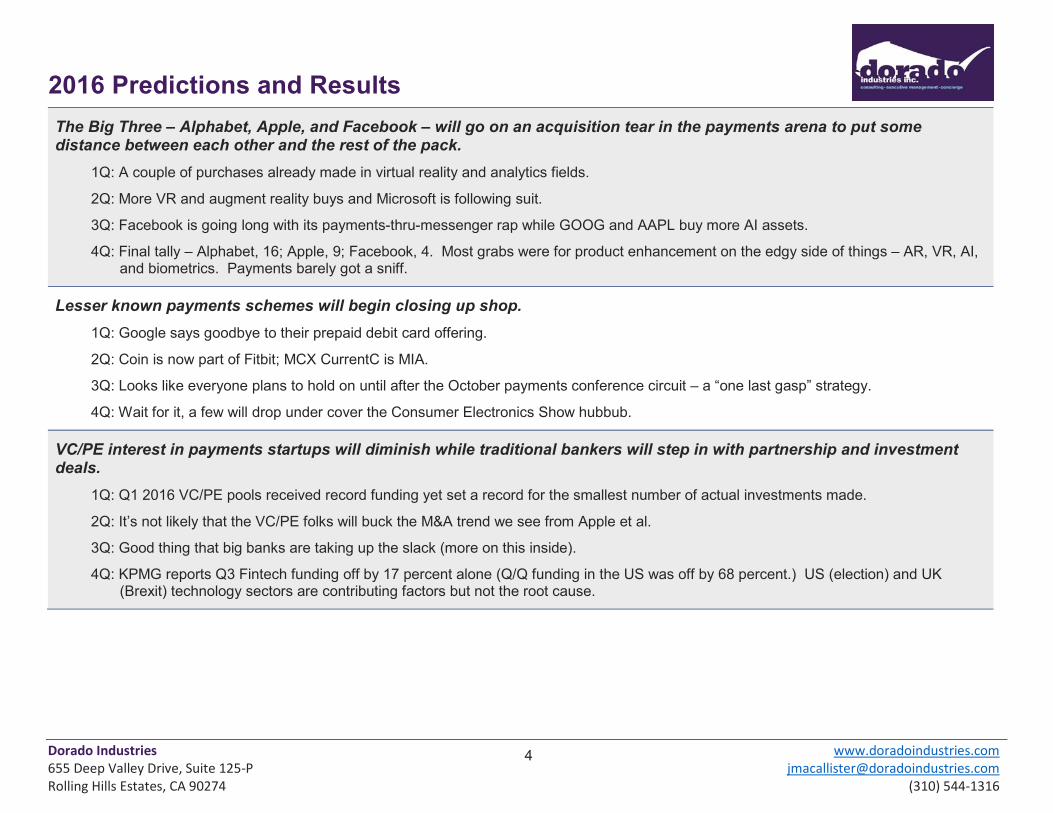

2016 Predictions and Results The Big Three – Alphabet, Apple, and Facebook – will go on an acquisition tear in the payments arena to put some distance between each other and the rest of the pack.

1Q: A couple of purchases already made in virtual reality and analytics fields.

2Q: More VR and augment reality buys and Microsoft is following suit.

3Q: Facebook is going long with its payments-thru-messenger rap while GOOG and AAPL buy more AI assets.

4Q: Final tally – Alphabet, 16; Apple, 9; Facebook, 4. Most grabs were for product enhancement on the edgy side of things – AR, VR, AI, and biometrics. Payments barely got a sniff.

Lesser known payments schemes will begin closing up shop. 1Q: Google says goodbye to their prepaid debit card offering.

2Q: Coin is now part of Fitbit; MCX CurrentC is MIA.

3Q: Looks like everyone plans to hold on until after the October payments conference circuit – a “one last gasp” strategy.

4Q: Wait for it, a few will drop under cover the Consumer Electronics Show hubbub.

VC/PE interest in payments startups will diminish while traditional bankers will step in with partnership and investment deals.

1Q: Q1 2016 VC/PE pools received record funding yet set a record for the smallest number of actual investments made.

2Q: It’s not likely that the VC/PE folks will buck the M&A trend we see from Apple et al.

3Q: Good thing that big banks are taking up the slack (more on this inside).

4Q: KPMG reports Q3 Fintech funding off by 17 percent alone (Q/Q funding in the US was off by 68 percent.) US (election) and UK (Brexit) technology sectors are contributing factors but not the root cause.

5

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

2016 Predictions and Results Despite intrigue created by CFPB’s interest in foreign transfers, the cross-border money movement sector will heat up – new players and some M&A.

1Q: Transferwise gains another $58 million in VC funds to expand globally. Meanwhile, WorldRemit raked in $45 million. More “follow the money” evidence.

2Q: Two new players have acquired their way into the U.S. market.

3Q: $180 million more for Payoneer suggests we’ve going to see more and more digital transfer options.

4Q: Check out what Western Union is doing with its strategic partnerships.

Banks and credit unions will throw caution to the wind and begin offering their depositors proprietary branded digital wallets to combat the zeal merchants have for steering customer loyalty.

1Q: No major announcements as yet.

2Q: Some minor movement but no marquee players following Chase Pay yet.

3Q: We may have blown this one; merchant apps are proliferating at a torrid rate. Perhaps consumers prefer their merchants’ brands to their banks’? Heavenly days!

4Q: Citibank and a few others joined the lemming rush. Not a game for the feint-hearted.

In another search for scale, two established merchant services processors will merge. 1Q: All quiet so far; waiting to see the Global Payments/Heartland deal close. The TransFirst/TSYS deal comes close but the buyer falls

short of the “established” qualifier.

2Q: Crickets. Might be an end-of-year event.

3Q: A couple of small deals – if one considers a $10 billion MSP small?

4Q: Guess we blew this one although the Vantiv/Moneris $425 million deal isn’t chump change. We were thinking a bit bigger.

6

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

2016 Predictions and Results Blockchain will remain the new “glowing object on the horizon” but efforts to institutionalize it will not move the needle much in 2016.

1Q: Lots of activity; BofA looking to patent apps and processing, over $1.0 billion has been invested in blockchain through new VC pools or direct plays.

2Q: Huge number of small investments being made in blockchain exchanges. Lots of folks following a Roulette Wheel investment strategy – small bets made across the full field of offerings.

3Q: Watch shows like Money2020 for new announcements. Credit unions are getting into “kicking the tires” mode.

4Q: Blockchain consortium R3 loses a handful of key investors and its new funding round struggles. Meanwhile, competing player, Hyperledger, gains new players and announces expansion plans. A BetaMax v. VHS redux? Pass the popcorn, please.

In-app payment options (e.g., “One Click” by Amazon) will go on autopilot and become less of an “end” and more of a “means to an end.”

1Q: It appears that the “steering wars” has begun with both Visa (Visa Checkout) and MasterCard (MasterPass) offering up new partnership deals with key mPOS and e-commerce retailers.

2Q: Lots of announcements with delayed go-live dates. We’ll see.

3Q: Hell, even Echo’s Alexa can make a payment for us while ordering concert tickets. What more proof do we need? And, PayPal and Visa Direct are playing nice together. Who would have thought?

4Q: Pretty soon Volkswagens will not only find their own parking places but pay for them too? Oy vey!

7

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

2017 Predictions Card brands and major retailers will announce new relationships in acceptance and consumer benefits.

Merchants will dazzle consumers with new value-added services tied to using their digital wallets.

At least one e-tailer will utilize virtual reality to enhance shopper’s e-commerce buying experiences.

Smaller retailers and those not yet EMV-compliant will experience a sharp rise is fraud losses.

There will be one significant acquisition in the payments processing marketplace and then we’re done.

The bloom will come off the blockchain rose; those in it, will stay. Others will adopt a wait-and-see attitude.

8

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

TrendWatch Summary – Q4 2016

Rec

ent

Act

ivity

Lev

el

Indu

stry

Im

pact

En

tren

ched

Pl

ayer

Impa

ct

Market and Industry Situation Focus Area Recent Movements

L New Payment Forums Some new Bitcoin and cybercurrency apps is about it.

M ATM Restructuring More card-less solutions and Diebold’s beacon play.

H POS Volume Trend Volume from Christmas way up; huge mobile uplift.

L Legal/Regulatory Issues Congress was on hiatus; won’t be after January 20.

L New Venture Growth Someone stole the spigot.

H Earnings Announcements Everyone except a few large brick-and-mortar retailers are way ahead.

L Industry Investments Augmented and Virtual Reality gaining all the investment interest.

L Payments Industry Security Other than government hacks, things have been suspiciously quiet.

Positive

Mixed

Negative

Industry Players to Watch AMEX: With most of its legal wranglings behind it, now’s the time to get serious again.

Card Brands: What, if anything, does the DoJ have to say about cross-tokenization and antitrust?

Fed Faster Payments: The final work product from nearly two years of effort is due out in June. Will we move into the 21st century by fiat or just wait for it to happen?

Chase Pay: Chase is stuffing its proprietary wallet with all the bells and whistles it can find. Wonder what’s next?

Amazon: The mega-retailer will soon lose patent/trade mark protection on its 1-Click checkout service. So, what’s next?

Echo and Google Home: Both started out as audio speakers and can now start your coffee and all but walk your dog. Is dog-walking the next skill?

9

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

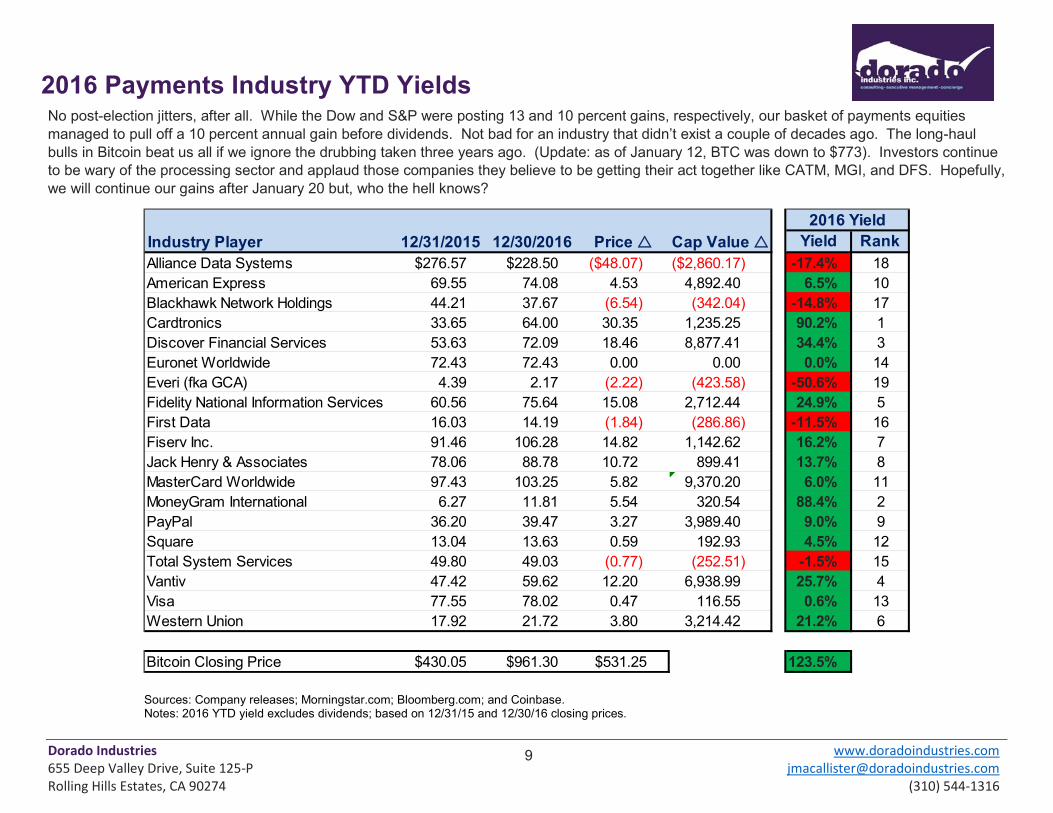

2016 Payments Industry YTD Yields No post-election jitters, after all. While the Dow and S&P were posting 13 and 10 percent gains, respectively, our basket of payments equities managed to pull off a 10 percent annual gain before dividends. Not bad for an industry that didn’t exist a couple of decades ago. The long-haul bulls in Bitcoin beat us all if we ignore the drubbing taken three years ago. (Update: as of January 12, BTC was down to $773). Investors continue to be wary of the processing sector and applaud those companies they believe to be getting their act together like CATM, MGI, and DFS. Hopefully, we will continue our gains after January 20 but, who the hell knows?

Yield RankAlliance Data Systems $276.57 $228.50 ($48.07) ($2,860.17) -17.4% 18American Express 69.55 74.08 4.53 4,892.40 6.5% 10Blackhawk Network Holdings 44.21 37.67 (6.54) (342.04) -14.8% 17Cardtronics 33.65 64.00 30.35 1,235.25 90.2% 1Discover Financial Services 53.63 72.09 18.46 8,877.41 34.4% 3Euronet Worldwide 72.43 72.43 0.00 0.00 0.0% 14Everi (fka GCA) 4.39 2.17 (2.22) (423.58) -50.6% 19Fidelity National Information Services 60.56 75.64 15.08 2,712.44 24.9% 5First Data 16.03 14.19 (1.84) (286.86) -11.5% 16Fiserv Inc. 91.46 106.28 14.82 1,142.62 16.2% 7Jack Henry & Associates 78.06 88.78 10.72 899.41 13.7% 8MasterCard Worldwide 97.43 103.25 5.82 9,370.20 6.0% 11MoneyGram International 6.27 11.81 5.54 320.54 88.4% 2PayPal 36.20 39.47 3.27 3,989.40 9.0% 9Square 13.04 13.63 0.59 192.93 4.5% 12Total System Services 49.80 49.03 (0.77) (252.51) -1.5% 15Vantiv 47.42 59.62 12.20 6,938.99 25.7% 4Visa 77.55 78.02 0.47 116.55 0.6% 13Western Union 17.92 21.72 3.80 3,214.42 21.2% 6

Bitcoin Closing Price $430.05 $961.30 $531.25 123.5%

2016 YieldIndustry Player 12/31/2015 12/30/2016 Price U Cap Value U

Sources: Company releases; Morningstar.com; Bloomberg.com; and Coinbase. Notes: 2016 YTD yield excludes dividends; based on 12/31/15 and 12/30/16 closing prices.

10

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

Interesting News This Quarter Subject Source / Date Summary Walmart Canada & Visa

Finextra January

We had hoped that the fracas between Walmart Canada and Visa would fuel at least a couple of quarters of TrendWatch issues but one of them blinked. In one of those “terms of the deal were not disclosed” announcements, the two combatants said they had kissed and made up so the three Canadians who use Visa instead of Interac may now shop at their local Manitoba and Thunder Bay Walmart stores. The original Walmart plan was to stop accepting Visa credit cards in its 370 Canadian stores with Manitoba and Thunder Bay, Ontario being the first sites to take action. Either Walmart felt the pain from lost sales at these sites (not likely) or Visa decided that “Everywhere you want to be” might include Canada. One wonders how much Visa shaved off its interchange rate to get the deal done. So it goes.

Visa & MasterCard

BI Intelligence December

MasterCard and Visa have taken a collaborative step in tokenization that is tantamount in importance to when they entered into duality agreements decades ago. The ability of each card company to provision tokens for the other’s cards brings a bit of comfort to the digital wallet industry and may spur faster consumer adoption of both stand-alone wallets like Apple Pay and Android Pay as well as wallets created by merchants – Walmart, Dunkin Donuts, etc. Duality led to an inquiry and litigation by the Department of Justice on antitrust grounds a decade ago and we may see the same outcome with this compact. In the meantime, it would be nice to see consumers react positively to the lack of brand clutter and start using those damn wallets.

Samsung Pay Payments Briefing November

Users of Samsung Pay may now earn reward points on a per-transaction basis. More active users can gain premium status levels because of usage frequency just like with airline rewards programs. Samsung Pay points can be redeemed for company products (naturally) as well as retailer gift cards or a prepaid Samsung Visa card. By providing a wallet-specific rewards scheme, Samsung is attempting to differentiate itself for other Android wallets and to jump-start the competition for transaction volume supremacy. We’ll see how that works out. We’d prefer an extra 2 percent off the price of the goods being bought or a free half-dozen donuts but time will tell if Samsung Pay leads to the sale of more Samsung crock pots. Follow-up: Samsung announced at the Consumer Electronics Show (CES) last week that Samsung Pay transaction volumes have doubled since launching the rewards program in November. Math lesson: a small number times two is still a small number.

Diebold Nixdorf

ATM Marketplace November

Let’s talk ATMs. Venerable ATM manufacturer, Diebold Nixdorf, is testing beacon technology with Cuscal, Ltd., an Australian payments processor owned by credit unions and savings banks. By installing Diebold programmed beacons near their ATMs, the company claims the ability to communicate with ATM users during the “approach” phase of the user/device relationship. In theory, the beacons will transmit custom-tailored marketing messages to consumers as they queue up to use the devices for cash withdrawals and other permitted functions. If consumer reaction is favorable, the devices will be tested in branch lobbies and other sites where consumers congregate.

11

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

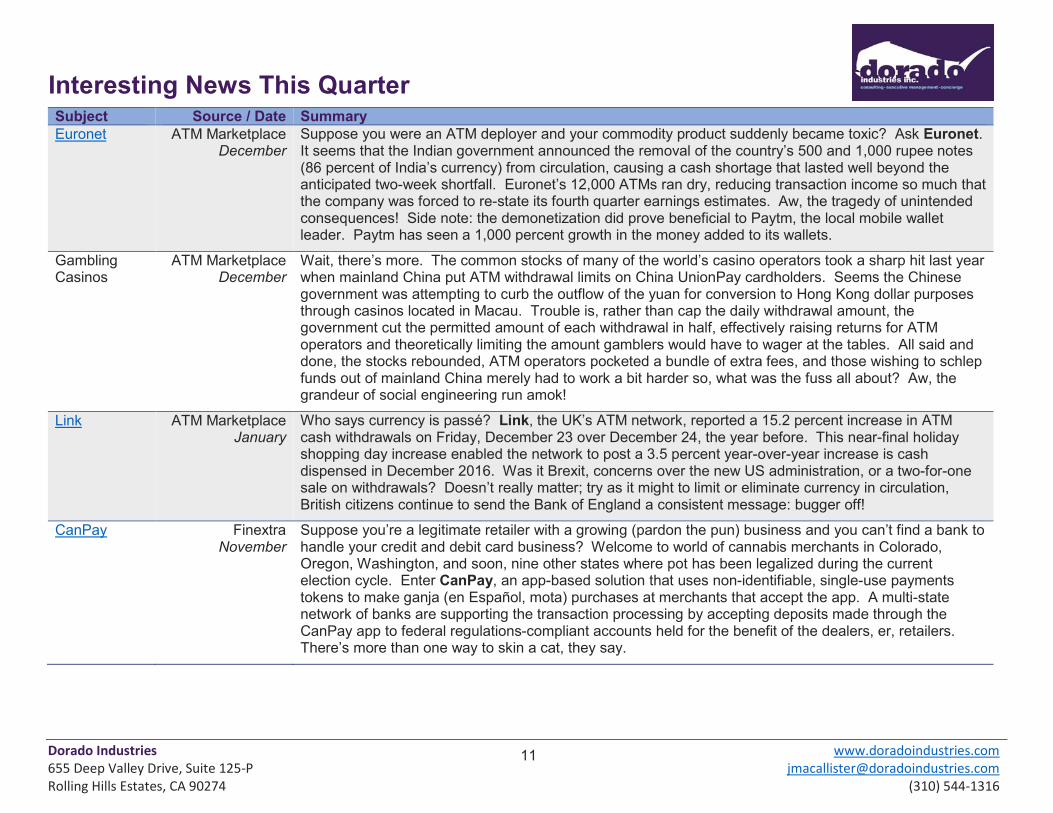

Interesting News This Quarter Subject Source / Date Summary Euronet ATM Marketplace

December Suppose you were an ATM deployer and your commodity product suddenly became toxic? Ask Euronet. It seems that the Indian government announced the removal of the country’s 500 and 1,000 rupee notes (86 percent of India’s currency) from circulation, causing a cash shortage that lasted well beyond the anticipated two-week shortfall. Euronet’s 12,000 ATMs ran dry, reducing transaction income so much that the company was forced to re-state its fourth quarter earnings estimates. Aw, the tragedy of unintended consequences! Side note: the demonetization did prove beneficial to Paytm, the local mobile wallet leader. Paytm has seen a 1,000 percent growth in the money added to its wallets.

Gambling Casinos

ATM Marketplace December

Wait, there’s more. The common stocks of many of the world’s casino operators took a sharp hit last year when mainland China put ATM withdrawal limits on China UnionPay cardholders. Seems the Chinese government was attempting to curb the outflow of the yuan for conversion to Hong Kong dollar purposes through casinos located in Macau. Trouble is, rather than cap the daily withdrawal amount, the government cut the permitted amount of each withdrawal in half, effectively raising returns for ATM operators and theoretically limiting the amount gamblers would have to wager at the tables. All said and done, the stocks rebounded, ATM operators pocketed a bundle of extra fees, and those wishing to schlep funds out of mainland China merely had to work a bit harder so, what was the fuss all about? Aw, the grandeur of social engineering run amok!

Link ATM Marketplace January

Who says currency is passé? Link, the UK’s ATM network, reported a 15.2 percent increase in ATM cash withdrawals on Friday, December 23 over December 24, the year before. This near-final holiday shopping day increase enabled the network to post a 3.5 percent year-over-year increase is cash dispensed in December 2016. Was it Brexit, concerns over the new US administration, or a two-for-one sale on withdrawals? Doesn’t really matter; try as it might to limit or eliminate currency in circulation, British citizens continue to send the Bank of England a consistent message: bugger off!

CanPay Finextra November

Suppose you’re a legitimate retailer with a growing (pardon the pun) business and you can’t find a bank to handle your credit and debit card business? Welcome to world of cannabis merchants in Colorado, Oregon, Washington, and soon, nine other states where pot has been legalized during the current election cycle. Enter CanPay, an app-based solution that uses non-identifiable, single-use payments tokens to make ganja (en Español, mota) purchases at merchants that accept the app. A multi-state network of banks are supporting the transaction processing by accepting deposits made through the CanPay app to federal regulations-compliant accounts held for the benefit of the dealers, er, retailers. There’s more than one way to skin a cat, they say.

12

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

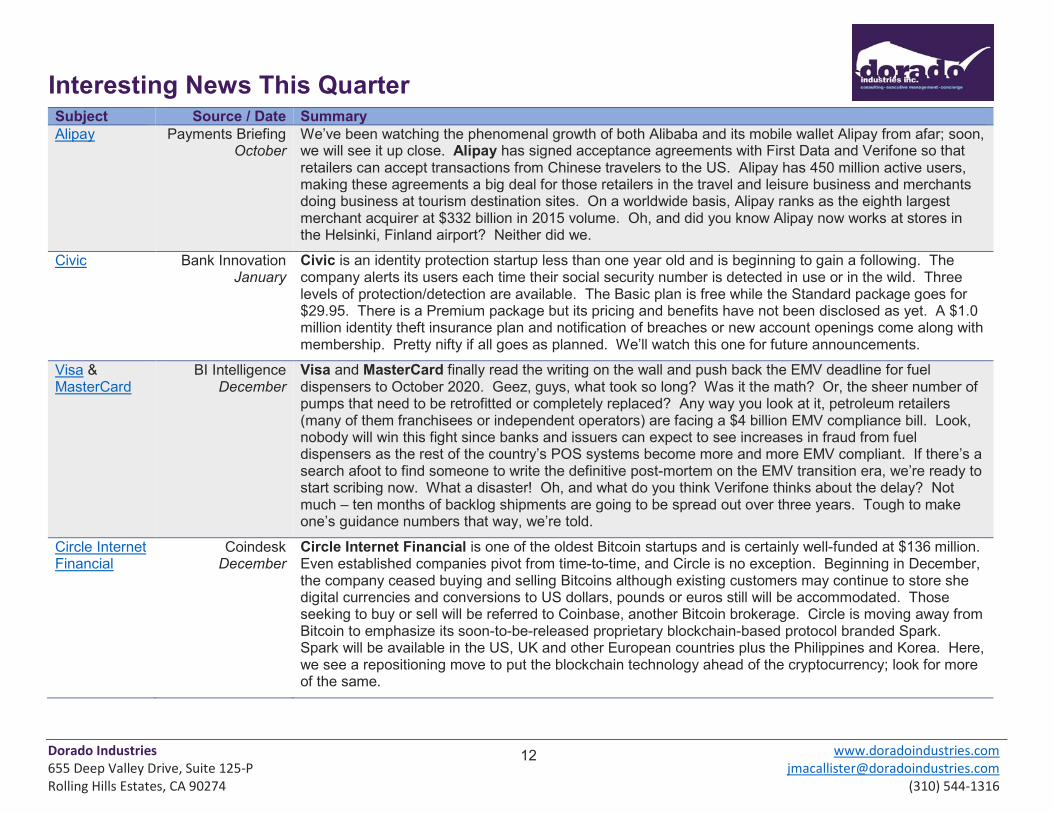

Interesting News This Quarter Subject Source / Date Summary Alipay Payments Briefing

October We’ve been watching the phenomenal growth of both Alibaba and its mobile wallet Alipay from afar; soon, we will see it up close. Alipay has signed acceptance agreements with First Data and Verifone so that retailers can accept transactions from Chinese travelers to the US. Alipay has 450 million active users, making these agreements a big deal for those retailers in the travel and leisure business and merchants doing business at tourism destination sites. On a worldwide basis, Alipay ranks as the eighth largest merchant acquirer at $332 billion in 2015 volume. Oh, and did you know Alipay now works at stores in the Helsinki, Finland airport? Neither did we.

Civic Bank Innovation January

Civic is an identity protection startup less than one year old and is beginning to gain a following. The company alerts its users each time their social security number is detected in use or in the wild. Three levels of protection/detection are available. The Basic plan is free while the Standard package goes for $29.95. There is a Premium package but its pricing and benefits have not been disclosed as yet. A $1.0 million identity theft insurance plan and notification of breaches or new account openings come along with membership. Pretty nifty if all goes as planned. We’ll watch this one for future announcements.

Visa & MasterCard

BI Intelligence December

Visa and MasterCard finally read the writing on the wall and push back the EMV deadline for fuel dispensers to October 2020. Geez, guys, what took so long? Was it the math? Or, the sheer number of pumps that need to be retrofitted or completely replaced? Any way you look at it, petroleum retailers (many of them franchisees or independent operators) are facing a $4 billion EMV compliance bill. Look, nobody will win this fight since banks and issuers can expect to see increases in fraud from fuel dispensers as the rest of the country’s POS systems become more and more EMV compliant. If there’s a search afoot to find someone to write the definitive post-mortem on the EMV transition era, we’re ready to start scribing now. What a disaster! Oh, and what do you think Verifone thinks about the delay? Not much – ten months of backlog shipments are going to be spread out over three years. Tough to make one’s guidance numbers that way, we’re told.

Circle Internet Financial

Coindesk December

Circle Internet Financial is one of the oldest Bitcoin startups and is certainly well-funded at $136 million. Even established companies pivot from time-to-time, and Circle is no exception. Beginning in December, the company ceased buying and selling Bitcoins although existing customers may continue to store she digital currencies and conversions to US dollars, pounds or euros still will be accommodated. Those seeking to buy or sell will be referred to Coinbase, another Bitcoin brokerage. Circle is moving away from Bitcoin to emphasize its soon-to-be-released proprietary blockchain-based protocol branded Spark. Spark will be available in the US, UK and other European countries plus the Philippines and Korea. Here, we see a repositioning move to put the blockchain technology ahead of the cryptocurrency; look for more of the same.

13

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

Interesting News This Quarter Subject Source / Date Summary iPayYou Paybefore

January So, you’re a hipster with a satchel of Bitcoins and a caffeine habit. What to do? Download the iPayYou app, link your Bitcoins and you’re on your way to that half-caff, soy latte. The iPayYou mobile app is now accepted at Starbucks for food and drink purchases. Well, sort of. You use the app to transfer your Bitcoin funds to your Starbucks account and then use your phone, Apple Watch, or the prepaid card to make your purchase. And why not? After all, you paid $250 for your Bitcoins and they’re worth $1,000 (again); so have a grande Americano courtesy of the market! By the way, did you know that under certain circumstances – a Starbucks store located in a grocery or other retailer location, cold drinks, not hot, etc. – you can use your EBT card at Starbucks? Go figure.

Chase Pay Businesswire December

Starting in early December, Chase Pay users gained an extra benefit through use of the mobile wallet at quick-service restaurants. Chase has partnered with LevelUp to provide order-ahead services at participating Boston locations. A full national roll-out is planned for 2017. As noted elsewhere, the mobile wallet competition is heating up fast and those offering plain vanilla payments through their applications are going to be quickly left behind. Nice job, Chase Pay.

Bluetooth 5 IoT Briefing December

Coming to a household near you soon – Bluetooth 5. The Bluetooth 5 standard has won approval and we should see it rolling out in products by mid-2017. Those most impacted with be drinkers of the Internet of Things Kool-Aid and those of us wanting to have the latest and greatest in automotive connectivity. The new specification allows for fatter data packets and longer range communication. Bluetooth 5 zealots believe that the new spec can compete effectively with WiFi for IoT connectivity. Imagine being able to hear your baby monitor in Boston while whizzing down the 405 freeway in Santa Monica. Oh, the joys of the electronic age (which should have ended with the demise of BetaMax.)

Apple Pay Mobile Payments Today

December

We had been waiting to see what Apple Pay will do to compete against the rewards scheme put up by Samsung Pay earlier in the year. Now we know. One of these early actions involves a new partnership with Blackhawk Network (yes, the J-hook folks). Through the new arrangement, Apple Pay users can make payments via provisioned prepaid, gift cards, e-gifts, and loyalty programs supported by Blackhawk. By adding a more expansive form of loyalty to its wallet, Apple Pay appears to have stepped up the wallet-wars leading a few pundits to wonder when a shakeup in the industry might start. Proprietary issuers and white label wallet providers might want to consider plans for a viable and face-saving exit. Or, give Blackhawk a call.

14

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

Interesting News This Quarter Subject Source / Date Summary SNAP PYMNTS.com

January Well, it was inevitable; particularly in light of how the 1964 Food Stamp Act was drafted – discrimination in just about any form against SNAP recipients is prohibited. There is going to be a two-year pilot to test the viability of using food stamps to purchase grocery items online. Participating pilot retailers include Amazon, FreshDirect, Safeway, ShopRite, Hy-Vee, Hart’s Local Grocers and Dash’s Market. SNAP cannot be used to cover service and delivery charges and purchases will be limited to a menu of eligible items in much the same way food stamps operate in the physical world. SNAP administrators acknowledge the need for additional security protections; hence, the pilot will not begin until this summer. Older readers, particularly those with bank management trainee experience, might recall what a pain in the tuckus physical food stamp reconciliation used to be.

Visa & Intel

BI Intelligence October

Now, this is both interesting and confusing. Visa and Intel have partnered to provide greater security for Visa transactions on PCs, mobile handsets, IoT devices, and wearables. Logical right? Almost. With the exception of PCs, very few of the other devices utilize Intel chips. Instead, smartphones, tablets and the like are powered by ARM (Advanced RISC Machine) chipsets, of which, Intel’s share of the 50 billion in use today hardly moves the needle. Could Intel be signaling a major pivot in its manufacturing emphasis? Definitely. Still think the Internet of Things is a passing fancy? Think again after a refreshing gulp of Kool-Aid.

Citi Pay Finextra November

Citibank is joining major rival JPMorgan Chase in the proprietary wallet wars as it announces plans to launch Citi Pay first in Singapore, Australia, and Mexico and then in the US in 2017. The user wallet will run on MasterCard’s MasterPass technology and will be available in online, in-app, and tap-and-pay flavors. With Chase Pay’s major head start in the wallet wars, Citi is going to have to stoke the boiler pretty hard to catch up and very likely will.

PayPal & Apple

Finextra November

PayPal continues to accelerate its run at mobile and online payments dominance. This time, the processor has partnered with Apple to enable device users to make P2P remittances by voice command with Siri, Apple’s personal agent system. PayPal’s arrangement with Apple dovetails with the inclusion of Siri support in the Venmo menu of services this past September. And, Siri is really getting around; Square Cash and Azimo both have integrated voice money transfer services in 2016. Might want to keep that in mind, Chase Pay and Citi Pay.

Apple Presser December

Finally, hipsters driving electric vehicles will have less to worry about if they also own iPhones running iOS 10. Apple Maps now denotes ChargePoint charging stations as electric vehicle owners cruise around the country. Apple Pay enables EV drivers to pay for their juice-ups while Apple Maps will help them navigate to the next recharge station. Nice integration, Apple. Now, if you could stretch out the distance between charges, you’d have the world by the tail, or cord.

15

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

M&A and Alliance Activity

Buyer/Investor Target Payments Emphasis Possible Strategy

Volkswagen Financial

PayByPhone Parking spot payments

Context is a wonderful thing. Three years ago, a gaggle of parking spot-seeking and payments-making apps hit the scene, evoking a TrendWatch chortle. After all, how many players could gain meaningful market share in the ten or so metro areas where parking is a problem? That was then; now, we have the emergence of connected mobility and the acquisition of PayByPhone by Volkswagen makes sense. VW gains new technology and existing parking site relationships while taking a big step forward in the IoT/connectivity race. PBP is VW’s second dive into the mobility connectivity pool; Sunhill Technologies was gobbled up in 2015.

Goldman Sachs

nanoPay MintChip digital currency

GS and others put $10 million on the table to energize nanoPay’s expansion of deployment of its MintChip digital currency beyond the confines of the City of Toronto. MintChip was developed by the Royal Canadian Mint and spun off prior to a commercial launch. Canadians in Toronto currently use their app wallets and MintChip for P2P payments and a few in-store site purchases. Funds are targeted for more geographic expansion and development of B2B and B2C markets. A Canadian faster payments gambit? Perhaps.

Samsung Harman Automobile audio While VW takes the direct route toward mobile connectivity, Samsung appears to be sneaking in the backdoor. Automotive audio pioneer, Harman, has agreements with General Motors and Fiat Chrysler to provide car audio systems. It’s $24 billion backlog might be attractive to any potential investor but we believe Samsung plans to do a bit more with the $8 billion acquisition. Just look at what the Korean technology giant did with its own refrigerator line. Could “smart radios” be next? We think so.

Vantiv Moneris USA Merchant services Number 2 merchant services processor, Vantiv (old-timers know the company better as Midwest Payments), pays $425 million for Moneris USA and gets 350,000 merchant locations in the deal. Vantiv offers its now 1.2 million merchant sites both online and brick-and-mortar acceptance services which ought to appeal to the Moneris merchants. Moneris USA never reached the market penetration that its Canadian parent (a joint venture of Bank of Montreal and RBC) expected, making the US operation expendable.

16

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

M&A and Alliance Activity

Buyer/Investor Target Payments Emphasis Possible Strategy

Bain Capital, Advent

Concardis Card payments group

Nothing succeeds like success, they say, and, speaking of Vantiv, its former PE owner Advent, and Bain Capital are reported to be close to a deal to acquire Concardis for 700 million euros. Sellers include a number of German banking firms that have decided that the business line is no longer core to their efforts. The company manufactures payments terminals and builds payments technology for e-commerce vendors. If the deal goes through, Bain and Advent will be paying almost 1.5 times revenues and 21 times earnings (just in case you’re interested in knowing what your Fintech company might be worth these days.)

CapitalG (Alphabet), General Catalyst Partners, others

Stripe Digital payments Alphabet’s late-stage investment arm, CapitalG, leads a $150 million round which pegs Stripe’s value at $9 billion. Amazing what being on 60 Minutes can do for you! JPMorgan Chase and other bankers added a $250 million credit line for additional comfort (and to stake a potential claim as one of the inevitable IPO bankers.) Stripe is one of only a few standout startups in 2016, due in large part to its ability to attract all-star clients including Target, Macy’s, and Facebook. Not bad for a couple of Irishmen.

Visa CardinalCommerce e-commerce payments authentication

Visa pays an undisclosed price (naturally) for CardinalCommerce in an effort to get ahead of the curve in mobile app, browser, wearable, and IoT e-commerce. The CardinalCommerce solution aims at bringing more transparency to transaction authentication, enabling both merchants and issuers to observe the process and adapt to the results of each transaction.

American Express

InAuth e-commerce payments authentication

Birds of a feather, we see. American Express acquires InAuth, a six-year-old mobile transaction authentication firm that it both uses and had invested in previously. InAuth had raised $30 million in funding since its founding; side note – Bain gets a nice payback as one of the investors despite the acquisition price being undisclosed. Aw, the rich get richer.

Western Union Walletron Billing wallet While it may be difficult for a zebra to change its stripes, venerable (and frequently overlooked) money movement company, Western Union, is methodically trying to apply new paint to its old veneer. Walletron enables its customers to communicate with wallet users with notifications, bill information and payment options. These features could be important to WU as year over year growth in mobile phone access to biller sites topped 42 percent in 2016. WU has taken an undisclosed amount of strategic investment in Walletron, among others.

17

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

M&A and Alliance Activity

Buyer/Investor Target Payments Emphasis Possible Strategy

Daimler Financial Services

PayCash Mobile payments Not to be outdone by VW, Daimler has acquired Luxembourg-based PayCash for an undisclosed amount. PayCash will empower “Mercedes pay” under the Daimler Mobility division which also includes the company’s Uber-like car2go ride sharing service and its mytaxi app. PayCash deals in cybercurrencies as well as euros and other market currencies. So there!

Dead Pool Pebble Smartwatch Well, there’s no chance that we will see “Pebble Pay” anytime soon since Fitbit swooped in to claim the carcass of what once was the best low-cost smartwatch on the market. Fitbit already owns the payments assets of the old Coin screen-on-card startup. There goes over $50 million in Fintech funding, a warranty that no longer warrants, and a sizeable backlog of Pebble 2 device orders which will go unfulfilled. Too bad, too, since $16 million of the funding came from crowdsourcing; not a good message for youthful investors.

Amphora Capital, Digital Currency Group, Draper Associates

Wyre Money transfer platform

Cross-border transfer startup, Wyre, attracts investors eager to fund Series A monies totaling $5.6 million. The blockchain-based platform currently operates in the US and China (Amphora is a Chinese VC house.) Wyre settles up in about six hours and charges between 1 and 4.5 percent for its services. At its current run-rate of $1.0 million in transaction volume per day and a posted month-over-month growth rate of 25 percent, Wyre might be something to watch for in the MTS options arena.

Lloyds Banking Group

BofA’s MBNA (UK portfolio)

Credit card issuer Older readers might recall that Bank of America acquired MBNA (which stands/stood for Maryland Bank, NA) in 2005 for $35 billion. Over time, pieces of the MBNA portfolio has been sold to players like TD Bank and Virgin Money. Now, BofA is selling the entire UK estate to Lloyds for £1.9 billion. Lloyds has announced plans to wipe out 30 percent of MBNA’s cost base to save £100 million. The transaction was announced on December 20th which may have soured the holiday season for just a few Brits.

Hillhouse Magneto Commerce

e-commerce processor

Magneto provides e-commerce technology for Burger King, Fraport Airport Group, Oliver Sweeney, Venroy and many others. Hillhouse, a Chinese VC firm, plows $250 million into the company to fund pan-Asia expansion and to improve sales and marketing efforts. Magneto retailers generate $50 billion in online and physical revenues. More pressure on the old merchant services establishment, we opine.

18

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

M&A and Alliance Activity

Buyer/Investor Target Payments Emphasis Possible Strategy

Edison Partners, others

MoneyLion Consumer credit and PFM

MoneyLion is both a consumer lender and provider of personal financial management software apps to enable consumers to borrow, spend, and save wisely. Edison Partners leads a group of investors to provide Series A fund totaling $22.5 million. The company also has $650 million in existing debt facilities and a consumer loan portfolio of 150,000 loans. Didn’t banks use to lend money, too?

BlueCross BlueShield Venture Partners, others

Payfone e-commerce payments authentication

Payfone completes the authentication investment trifecta by raising $23.5 million in Series E funding from BCBS and others. Payfone’s patented mobile service provides protection against identity theft and social engineering attacks. See the pattern yet? Big forecasts for transaction volumes via mobile channels garners interest from the investment community in avoiding or deferring security lapses. Side note: one of the Series E investors in this round is Early Warning Services, a bank-owned player in the account verification space and recent entrant in the faster payments footrace.

Useful Links for More Information Here are some companies referenced earlier should you care to learn more about them.

Company Role Link Circle Internet Financial Cybercurrency brokerage www.circle.com

iPayYou Bitcoin-to-Starbucks app www.iPayYou.io

Walletron Mobile wallet marketing www.walletron.com

Wyre Money transfer service www.sendwyre.com

Payfone Mobile authentication www.payfone.com

MoneyLion Consumer lending/PFM apps www.moneylion.com

19

Dorado Industries www.doradoindustries.com

655 Deep Valley Drive, Suite 125-P [email protected]

Rolling Hills Estates, CA 90274 (310) 544-1316

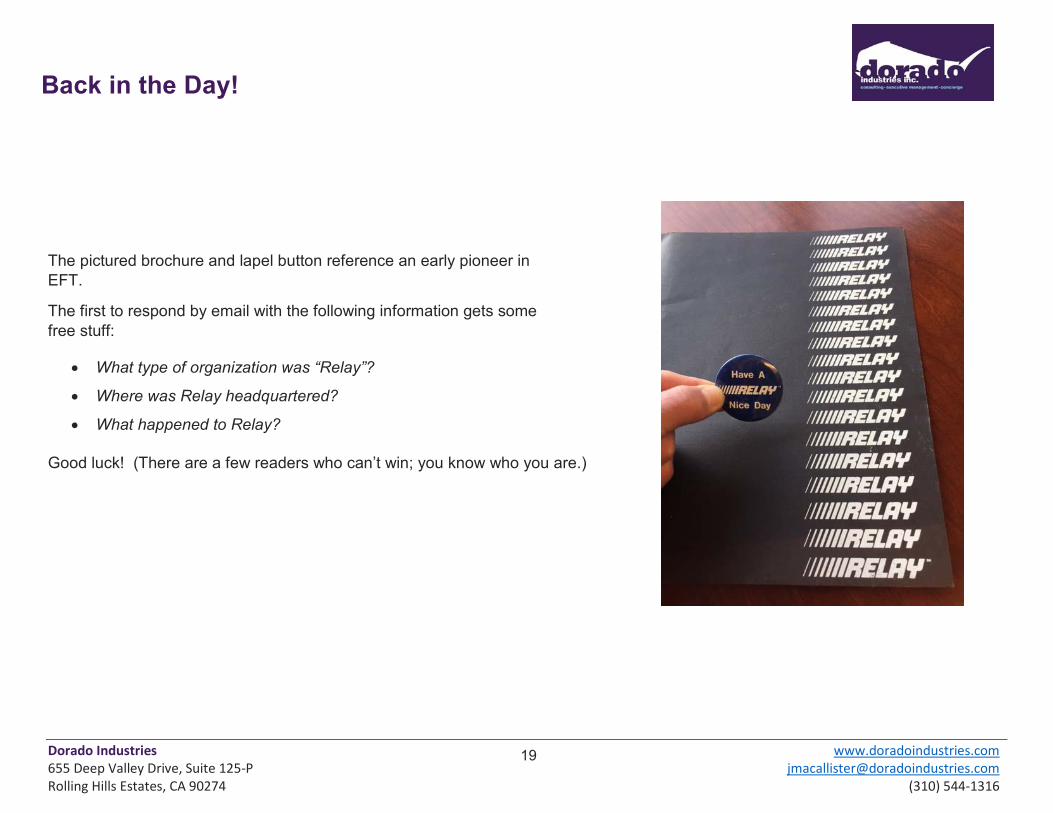

Back in the Day!

The pictured brochure and lapel button reference an early pioneer in EFT.

The first to respond by email with the following information gets some free stuff:

• What type of organization was “Relay”?

• Where was Relay headquartered?

• What happened to Relay?

Good luck! (There are a few readers who can’t win; you know who you are.)