Doing Business in Ireland - Matheson€¦ · Doing Business in Ireland. 3 Contents 1 Introduction 4...

48

driven by excellence DUBLIN LONDON NEW YORK PALO ALTO Doing Business in Ireland

Transcript of Doing Business in Ireland - Matheson€¦ · Doing Business in Ireland. 3 Contents 1 Introduction 4...

driven by excellence

DUBLIN LONDON NEWYORK PALOALTO

Doing Business in Ireland

3

Contents

1 Introduction 4

2 Why Invest in Ireland? 6

3 Ireland: An overview 8

4 Grants and other Fiscal Incentives 12

5 establishing in Ireland 14

6 taxation 18

7 employment and Labour Law 27

8 Real estate, Property, Construction, Planning and environmental Law 31

9 Intellectual Property and technology 35

10 Life sciences Regulatory 39

11 How can Matheson ormsby Prentice help you? 42

PageNo

4

1 Introduction

5

Over1,000internationalcompanieshaveoperationsinIreland.Thesecompaniesareinvolvedinawiderangeofactivitiesandsectorsincludingtechnology,pharmaceuticals,biosciences,financialservicesandmanufacturing.TheattractionofIrelandasaninvestmentlocationcanbeattributedtothepositiveapproachofsuccessiveIrishGovernmentstothepromotionofinwardinvestment,itsmembershipoftheEuropeanUnion(EU),averyfavourablecorporatetaxrateandaskilledandflexiblelabourpool.

ThepurposeofthisGuideistoprovideanintroductiontothemajorcommercialandlegalissuestobeconsideredby

internationalcompaniesestablishingbusinessoperationsinIrelandanditprovidesgeneralobservationsandguidancetothemanyquestionswehaveencounteredfromclients.Particularbusinessesorindustriesmayalsobesubjecttospecificlegalrequirementsandspecificadvicemayberequiredinthesecircumstances.

IfyouareconsideringIrelandasalocationforyourbusinesswelookforwardtohearingfromyou.

6

2 Why Invest in Ireland?

7

In2010,ForbesrankedIreland1stintheeurozoneas1ofthebestcountriesforbusiness.Irelandhassucceededinattractingsomeoftheworld’slargestcompaniestoestablishoperationshere.Thisincludessomeofthelargestcompaniesintheglobaltechnology,pharmaceutical,biosciences,manufacturingandfinancialservicesindustries.

TheyareinIrelandbecauseIrelanddelivers:

n lowcorporatetaxrate–corporationtaxontradingprofitsis12.5%andtheregimedoesnotbreachEUorOECDharmfultaxcompetitioncriteria;

n regulatory,economicandpeopleinfrastructureofahighly-developedOECDjurisdiction;

n benefitsofEUmembershipandofbeinganEnglish-speakingjurisdictionintheeurozone;

n commonlawjurisdiction,withalegalsystemthatisbroadlysimilartotheUSandtheUKsystems;

n refundabletaxcreditforresearchanddevelopmentactivityandotherincentives;and

n extensiveandexpandingdoubletaxtreatynetwork,withalmost60countries,includingtheUS,UK,ChinaandJapan.

Ourexperienceandresearchcarriedoutin2011bytheEconomistIntelligenceUnitonbehalfofourfirm,indicatesthatitistheuniquecombinationofthesefactors,andnot1specificelement,whichattractsinvestmenttoIreland.Forexample,whileothercountriesmaybecompetitiveinsomeoftheareashighlightedabove,Ireland’sabilitytocreatethemostcompellingsuiteofbothtangiblefactors(suchastaxationandtheregulatoryframework)andmoreintangibleelements(suchasa“cando”attitudetobusiness)isgenerallycitedascentraltoitsabilitytoattractinvestmentoverotherEUcountries.

8

3 Ireland: An overview

9

17 out oF tHe toP 25 GLoBAL MeDICAL DevICe CoMPAnIes

soMe oF tHe LARGest CoMPAnIes In tHe WoRLD HAve LoCAteD In IReLAnD, InCLuDInG:

8 out oF tHe toP 10 GLoBAL ICt CoRPoRAtIons

MoRe tHAn 50% oF tHe WoRLD’s LeADInG FInAnCIAL seRvICes oRGAnIsAtIons

10 toP “BoRn on tHe InteRnet” CoMPAnIes

9 out oF tHe toP 10 GLoBAL PHARMACeutICAL CoMPAnIes

3 out oF tHe toP 5 toP GAMInG CoMPAnIes

0

10

20

30

40

50

60

Non-Financial ServicesFinancial ServicesAll

Acc

ess

to E

Um

arke

ts

Lega

l & fi

scal

stab

ility

Cor

pora

te ta

xra

te r

egim

e

Acc

ess

tosk

ills

loca

lly

Ease

of d

oing

busi

ness

Acc

ess

toEU

ski

lls

Dou

ble-

taxa

tion

agre

emen

ts

Acc

ess

togo

vern

men

t

Sec

tor-s

peci

fic

ince

ntiv

es

Engl

ish-

spea

king

mem

ber

of e

uro

zone

Exis

ting

clus

ters

IT &

tel

ecom

sin

fras

truc

ture

8

12 12 13 14 15 15 15 16

22

10

23 23 23 24 25 24

2826

30 2927

31 3033

26

4649

43

12

16

9 10 911

6

%competitive advantages tHat ireland Has to offer

the economist Intelligence unit report on “Investing in Ireland: a survey of foreign direct investors”, commissioned by Matheson ormsby Prentice, examines the key factors that bring foreign investment to Ireland. the report identified 4 key cornerstones to Ireland’s FDI offering:

n access to the eu internal market

n the overall taxation infrastructure

n the ability to supply a skilled pool of labour

n a stable legal and fiscal framework

10

0

10

20

30

40

50

60

70

80

90

100

Finl

and

Aust

ria

Swed

en

New

mem

bers

Irel

and

Ger

man

y

Den

mar

k

Fran

ceUK

ther

land

s

Belg

ium

EU27

Gre

ece

Ital

y

Spai

n

Port

ugal

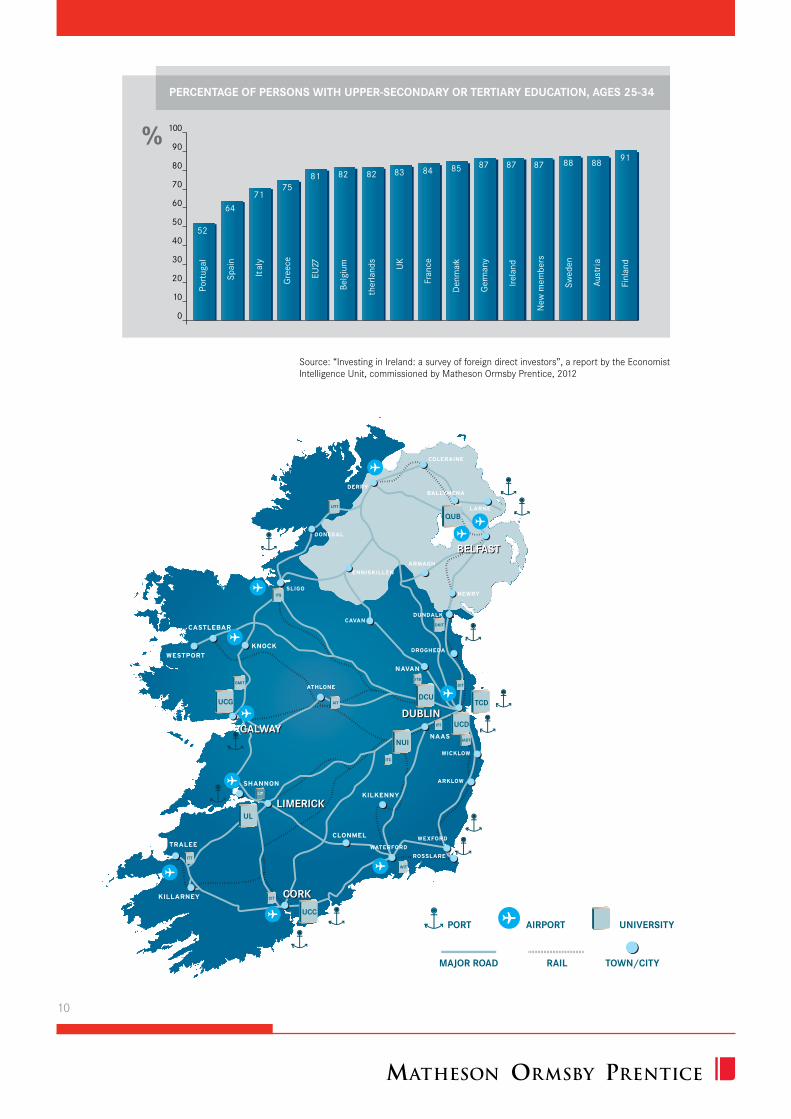

52

64

7175

81 82 82 83 84 85 87 87 87 88 88 91

%

percentage of persons witH upper-secondary or tertiary education, ages 25-34

Source:“InvestinginIreland:asurveyofforeigndirectinvestors”,areportbytheEconomistIntelligenceUnit,commissionedbyMathesonOrmsbyPrentice,2012

LIMERICK

GALWAYDUBLIN

CORK

BELFAST

LIMERICK

GALWAYDUBLIN

CORK

BELFAST

UCD

UCGDCU

ITB

AIT

LIT

ITT

WIT

ITT

CIT

ITC

ITS

GMIT

LYIT

DIT

IADT

DKIT

TCD

QUB

NUI

PORT

MAJOR ROAD RAIL TOWN/CITY

AIRPORT UNIVERSITY

UL

UCC

11

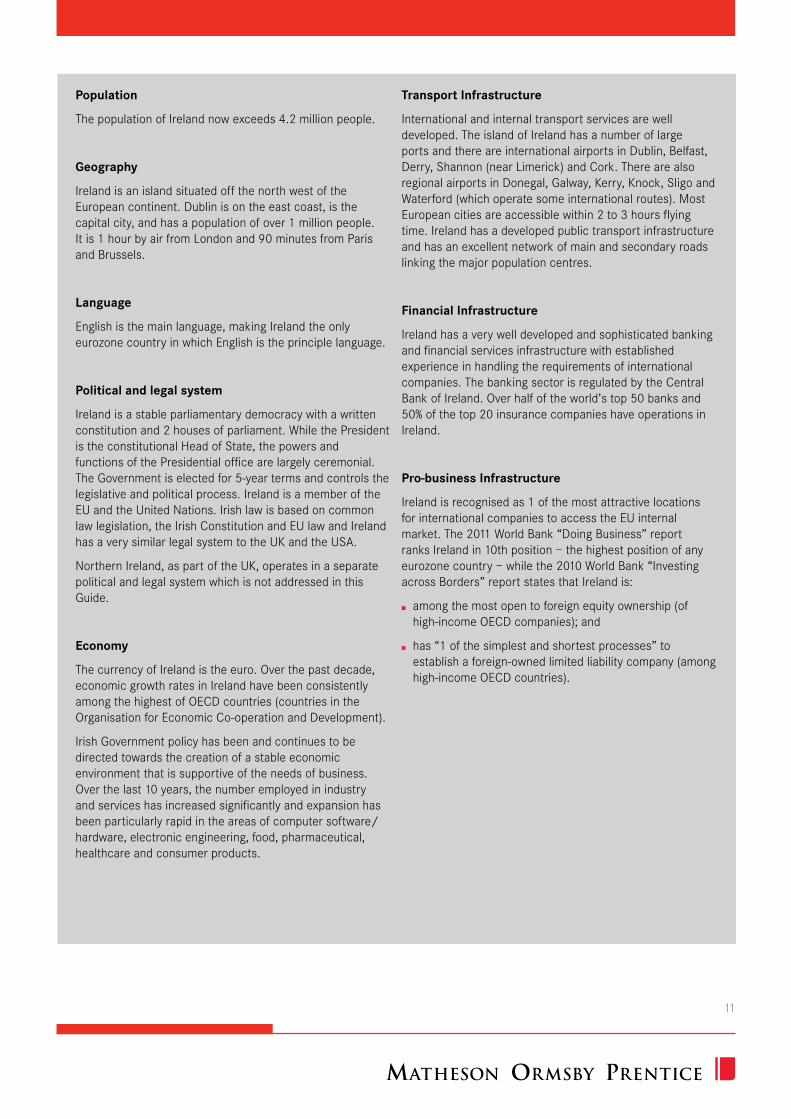

population

ThepopulationofIrelandnowexceeds4.2millionpeople.

geography

IrelandisanislandsituatedoffthenorthwestoftheEuropeancontinent.Dublinisontheeastcoast,isthecapitalcity,andhasapopulationofover1millionpeople.Itis1hourbyairfromLondonand90minutesfromParisandBrussels.

language

Englishisthemainlanguage,makingIrelandtheonlyeurozonecountryinwhichEnglishistheprinciplelanguage.

political and legal system

Irelandisastableparliamentarydemocracywithawrittenconstitutionand2housesofparliament.WhilethePresidentistheconstitutionalHeadofState,thepowersandfunctionsofthePresidentialofficearelargelyceremonial.TheGovernmentiselectedfor5-yeartermsandcontrolsthelegislativeandpoliticalprocess.IrelandisamemberoftheEUandtheUnitedNations.Irishlawisbasedoncommonlawlegislation,theIrishConstitutionandEUlawandIrelandhasaverysimilarlegalsystemtotheUKandtheUSA.

NorthernIreland,aspartoftheUK,operatesinaseparatepoliticalandlegalsystemwhichisnotaddressedinthisGuide.

economy

ThecurrencyofIrelandistheeuro.Overthepastdecade,economicgrowthratesinIrelandhavebeenconsistentlyamongthehighestofOECDcountries(countriesintheOrganisationforEconomicCo-operationandDevelopment).

IrishGovernmentpolicyhasbeenandcontinuestobedirectedtowardsthecreationofastableeconomicenvironmentthatissupportiveoftheneedsofbusiness.Overthelast10years,thenumberemployedinindustryandserviceshasincreasedsignificantlyandexpansionhasbeenparticularlyrapidintheareasofcomputersoftware/hardware,electronicengineering,food,pharmaceutical,healthcareandconsumerproducts.

transport infrastructure

Internationalandinternaltransportservicesarewelldeveloped.TheislandofIrelandhasanumberoflargeportsandthereareinternationalairportsinDublin,Belfast,Derry,Shannon(nearLimerick)andCork.TherearealsoregionalairportsinDonegal,Galway,Kerry,Knock,SligoandWaterford(whichoperatesomeinternationalroutes).MostEuropeancitiesareaccessiblewithin2to3hoursflyingtime.Irelandhasadevelopedpublictransportinfrastructureandhasanexcellentnetworkofmainandsecondaryroadslinkingthemajorpopulationcentres.

financial infrastructure

Irelandhasaverywelldevelopedandsophisticatedbankingandfinancialservicesinfrastructurewithestablishedexperienceinhandlingtherequirementsofinternationalcompanies.ThebankingsectorisregulatedbytheCentralBankofIreland.Overhalfoftheworld’stop50banksand50%ofthetop20insurancecompanieshaveoperationsinIreland.

pro-business infrastructure

Irelandisrecognisedas1ofthemostattractivelocationsforinternationalcompaniestoaccesstheEUinternalmarket.The2011WorldBank“DoingBusiness”reportranksIrelandin10thposition–thehighestpositionofanyeurozonecountry–whilethe2010WorldBank“InvestingacrossBorders”reportstatesthatIrelandis:

n amongthemostopentoforeignequityownership(ofhigh-incomeOECDcompanies);and

n has“1ofthesimplestandshortestprocesses”toestablishaforeign-ownedlimitedliabilitycompany(amonghigh-incomeOECDcountries).

12

4 Grants and other Fiscal Incentives

13

TheIrishGovernmentactivelyencouragesinternationalcompaniestochooseIrelandasaEuropeanbase.Partoftheincentivepackageofferedcanbetheavailabilityofstatefinancialassistance,intheformofgrants,todefraystart-uporothercosts.TheIndustrialDevelopmentAgency(IDA)andShannonDevelopmentaretheprimarygrant-awardingbodies.TheIDAistheprimarystate-sponsoredagencywithresponsibilityforthepromotionanddevelopmentofforeigninvestmentintoIreland.ShannonDevelopmentgrantsareconfinedtoprojectsintheShannonregion.Athirdbody,ÚdarásnaGaeltachta,isresponsibleforencouraginginvestmentintheIrish(Gaelic)speakingareasofIreland.Eachproposedinvestmentisassessedbytherelevantgrantauthorityagainstanumberofcriteria.Thelevelofgrantpayableisgenerallydeterminedthroughnegotiation.FurtherinformationcanbeobtainedbyvisitingthewebsitesoftheIDA(www.idaireland.com)andShannonDevelopment(www.shannondevelopment.ie)

what type of grants are available from the ida?

Avarietyofgrantsareavailableandcanbespecificallytailoredtomeettheneedsofeachcompany.Cashgrantsdonothavetoberepaidsaveincertainagreedcircumstances.Incertain“regions”approvedbytheEUforRegionalInvestmentAid(aidbasedonthegeographiclocationofaninvestment),aidmaybegivenintheformofcapitalgrantsfortheacquisitionoffixedassets(thatis,sitepurchaseanddevelopment,buildingsandnewplantandequipment).Incertaincases,aidmayalsobeavailablefortheacquisitionofintangibleassetssuchaspatentrights,licencesandknow-how.Thesubsequentdisposalofgrant-aidedassetsisinvariablyrestrictedbyagreement.Alternatively,regionalaidmayalsobegrantedintheformofemploymentgrantswhicharelinkedtotheamountofeachfull-timeandpermanentjobcreatedandwillvarydependingonthelocationoftheprojectandtheactivitiestobeundertaken.

what is the application procedure for ida grants?

TheprocesscantakeanumberofweeksandinvolvesthepreparationandsubmissionofaformalbusinessplantotheIDA,togetherwithsubsequentmeetingsandnegotiationsbetweentheapplicantandtheIDA.Inordertobeconsideredforgrantincentives,anapplicantmustsatisfytheIDAthatthefinancialassistanceisnecessarytoensuretheestablishmentordevelopmentoftheoperationandthattheinvestmentproposediscommerciallyviableandwillprovidenewemployment.

Iftheapplicationisapprovedandanincentivepackageisagreed,agrantagreementisthenenteredintobetweentheIDA,theIrishentityand/oritspromoter/parentcompany.Thiscontractsetsoutthetermsonwhichthegrantaidisgivenandwillvaryfromcasetocase.

How and when is the grant aid paid?

Grantsarepaidoncetherelevantexpenditureisincurred.WhenaclaimforagrantpaymentisreceivedbytheIDA,itisassignedtoadesignatedexecutiveintheirgrantsadministrationdepartmentwholiaiseswiththeclientcompanytomakesurethatthegrantispaidasquicklyandefficientlyaspossible.Inordertoclaimgrants,thecompanyisusuallyobligedtoprovidecertainspecifiedinformationtotheIDAincluding,forexample,copiesofsignedemploymentcontractsconfirmingtheappointmentoffull-timepermanentstaffforthepaymentofemploymentgrants.Anauditors’certificateisalsousuallyrequiredtosupportallclaimsforthepaymentofgrants.Itisimportantforthecompanytomaintainadequaterecordstofacilitatethisprocess.

14

5 establishing in Ireland

15

setting up a companywhat type of companies are available under irish law?

The2maintypesofcompanyinIrelandareprivatecompaniesandpubliccompanies.ThevastmajorityofcompaniesregisteredinIrelandareprivatecompanieslimitedbyshares.Theyarebyfarthemostpopularformofbusinessentityforinwardinvestmentprojects.Theshareholdersofaprivatelimitedcompanyhavelimitedliability.Publiclimitedcompaniesaretypicallyusedwheresecuritiesarelistedorofferedtothepublic.

what is the procedure for incorporation and how long does it take?

Toincorporateaprivatecompanylimitedbyshares,certaindocumentsmustbepubliclyfiledwiththeIrishCompaniesRegistrationOffice(CRO).Theseincludedetailsoftheproposednameoftheentity,theshareholders,directorsandcompanysecretary.Thecompleteddocumentationtogetherwiththememorandumandarticlesofassociation(theconstitutionandbye-laws)arefiledwiththeCRO.

Underanexpressincorporationscheme,itispossibletoincorporateacompanywithin5workingdays.Outsideoftheexpressscheme,itcantakeapproximately2to3weeksforacompanytobeincorporated.

can we choose any name we want for an irish company?

Notnecessarily,astherearerestrictionsonthechoiceofcompanyname.TheCROmayrefuseanameifitisidenticalto,ortoosimilartothenameofanexistingcompany,ifitisoffensiveorifitwouldsuggestStatesponsorship.Nameswhicharephoneticallyand/orvisuallysimilartoexistingcompanynameswillalsoberefusedbytheCRO.Thisincludesnameswherethereisaslightvariationinthespelling.Itisgenerallyrecommendedthatcompanynamesincludeextrawordssoastocreateasufficientdistinctionfromexistingnames.

Registrationdoesnotgivethecompanyanyproprietaryrightsinthecompanyname.AswellassearchingtheRegisterofCompanies,itcanalsobeimportanttocheckanyproposednameagainstthenamesontheIrishBusinessNamesRegisterandIrishandEUTradeMarksRegistries(andanyotherregisters,dependingonwhereitisproposedtocarryonbusiness).Thisistoensurethattheproposedcompanynamedoesnotconflictwithanexistingbusinessnameortrademark,sincethepersonclaimingtohavearighttothatnameormarkcouldtakelegalactiontoprotectitsinterest.

Itshouldalsobenotedthatcertainnamescannotbeusedunlessapprovedbyrelevantregulatorybodies.Bywayof

example,thewords“bank”,“insurance”,“society”and“university”cannotbeincludedinacompanynameunlesspriorpermissionisobtainedfromtherelevantregulatoryauthority.

can we reserve a company name in advance?

Companynamesmaybereservedforaperiodofupto28daysinadvanceofincorporation.

is the company obliged to carry on an activity in ireland?

AcompanywillnotbeincorporatedinIrelandunlessthecompanywill,whenregistered,carryonanactivityinIreland.AdeclarationconfirmingthismustbecompletedandfiledwiththeincorporationdocumentsattheCRO.

corporate governancewhat is the management and governance structure of an irish company?

Themanagementofacompanyisnearlyalwaysdelegatedtotheboardofdirectors.Allcompaniesmusthaveatleast1secretaryandaminimumof2directors,1ofwhomisrequiredtobearesidentoftheEuropeanEconomicArea(“EEA”).Thesecretarymayalsobe1ofthedirectorsofthecompany.Abodycorporatemayactassecretarytoanothercompany,butnottoitself.Abodycorporatemaynotactasadirector.ThedirectorsofacompanyhavewideresponsibilitiesunderIrishlaw.TheyareobligedtoactinthebestinterestsofthecompanyandtoensurethatthecompanyactsincompliancewithIrishcompanylaw.DirectorsshouldfamiliarisethemselveswiththeirdutiesunderIrishlaw.TheOfficeoftheDirectorofCorporateEnforcementhaspublishedaninformationbookletonthesubjectentitled‘ThePrincipalDutiesandPowersofCompanyDirectors’,andacopyisavailabletodownloadfromtheirwebsiteatwww.odce.ie.

are there residency requirements for directors?

Atleast1ofthedirectorsofanIrishcompanymustbearesidentofaMemberStateoftheEEA.Insofarasitistheperson’sresidenceinIrelandthatfallstobedetermined,apersonmusthavebeenpresentintheStateforaperiodamountinginaggregateto183daysormoreduringthe12monthsor280daysoverthe24months(excluding30daysorlessinany1year)precedingthedateofincorporationofthecompanyinordertoqualifyas“resident”.

AnEEAresidentdirectorisnotrequiredwherethecompanypostsabondintheprescribedform,tothevalueof€25,395.Thebondprovidesthat,intheeventofafailurebythecompany

16

topayafineimposedinrespectofanoffenceundercompanylaworapenaltyundertaxlegislation,anamountofmoneyuptothevalueofthebondwillbepaidbythesuretyindischargeofthecompany’sliability.ThebondfacilityisavailablefromanumberofinsurancecompaniesinIrelandandthe(non-refundable)premiumpayablefora2yearbondisapproximately€1,600.

Inaddition,acompanyisnotrequiredtohaveanEEAresidentdirector(orabondinlieu)wherethecompanyholdsacertificatefromtheCROconfirmingthatthecompanyhasarealandcontinuouslinkwith1ormoreeconomicactivitiesthatarebeingcarriedoninIreland.Thisoptionisonlyopentocompaniespost-incorporation.

what are the post-incorporation obligations?

Setoutbelowisabriefsummaryoftheprincipalobligations.Furtherdetailscanbeprovidedonincorporation.Finesandothersanctionscanbeimposedonacompanyandanyofficerofacompanywheretherelevantobligationsarenotmet.

maintenance of statutory registers

VariousstatutoryregistersandbooksofaccountmustbemaintainedbyacompanyunderIrishcompanylaw.Theregistersrequiredinclude:registerofmembers,registerofdirectorsandsecretaries,registerofdirectors’andsecretaries’interestsinsharesanddebentures,andaregisterofdebentureholders.Acompanyisalsoobligedtokeepminutesofitsgeneralmeetingsandthedirectorsarealsounderanobligationtokeepminutesofdirectors’meetings.Certainregistersareopentoinspectionbymembersofthegeneralpublic.

Inaddition,Irishcompanylawrequiresthedirectorstopreparefinancialstatementsforeachfinancialyearwhichgiveatrueandfairviewofthestateofaffairsofthecompanyandoftheprofitorlossofthecompanyforthatperiod.Inpreparingthosefinancialstatements,thedirectorsarerequiredto:

(a) selectsuitableinternationallyrecognisedaccounting policiesandthenapplythemconsistently;

(b) makejudgementsandestimatesthatarereasonable andprudent;and

(c) preparethefinancialstatementsonagoingconcern basis,unlessitisinappropriatetopresumethatthe companywillcontinueinbusiness.

Thedirectorsareresponsibleforkeepingproperaccountingrecordswhichdisclosewithreasonableaccuracyatanytimethefinancialpositionofthecompany.ThedirectorsmustensurethatthefinancialstatementsarepreparedinaccordancewitheitherInternationalFinancialReportingStandards(IFRS)or

withaccountingstandardsgenerallyacceptedinIreland.TheconsolidatedfinancialstatementsofEUlistedcompaniesthatareincorporatedinIrelandorelsewhereintheEUmustbepreparedinaccordancewithIFRS.

auditing financial statements

TheannualfinancialstatementsofIrishcompaniesarerequiredtobeauditedbyaregisteredauditor,subjecttolimitedexceptions.Theauditincludesanexamination,onatestbasis,ofevidencerelevanttotheamountsanddisclosuresinthefinancialstatements.Italsoincludesanassessmentofthesignificantestimatesandjudgementsmadebythedirectorsinthepreparationofthefinancialstatements,andofwhethertheaccountingpoliciesareappropriatetothecompany’scircumstances,consistentlyappliedandadequatelydisclosed.

Thereareexemptionsfromauditforcertainsmallercompaniesthatarenotpartofagroupofrelatedcompanies.

Irishlegislationrequiresauditorstoreporttotherelevantauthoritycertaininstancesoftheirclients,orofficers,committingindictableoffencesunderIrishcompanylawandtoreportanysuspicionsoftheft,fraudormoneylaunderingintheirclientcompanies.

annual return filing

CompaniesmustdeliveranannualreturntotheCROatleastonceayear.Theannualreturncontainsdetailsofthecompany’sdirectorsandsecretary,itsregisteredoffice,detailsofshareholders,sharecapitalandtheauditorregistrationnumber.Theannualreturnisrequiredtobemadeuptothecompany’sannualreturndate(ARD)andfiledwiththeCROwithin28daysofthatdate.Acompany’sfirstARDisthedatewhichis6monthsafteritsincorporation.Itispossibletochange,andinsomecasesextend,acompany’sARD.

Acompany’sauditedfinancialstatementsmustalsobeannexedtoacompany’sannualreturnexceptthefirstannualreturn.Smallercompaniesmayfileabridgedfinancialstatementsthatprovidelessinformationthantheannualfinancialstatementspreparedfortheshareholders.Inaddition,anIrishcompanythatisasubsidiaryofanEUparentmayfiletheconsolidatedfinancialstatementsoftheparentinsteadofitsownfinancialstatements,providedthattheEUparentcompanyguaranteestheliabilitiesoftheIrishsubsidiary.AfurtheroptionalexemptiontotheconsolidationobligationapplieswheretheIrishcompanyisitselfasubsidiaryofanotherundertakingestablishedoutsidetheEEA(so,forexample,anIrishholdingcompanywhoseparentinturnisalistedUScompany).Wherecertainconditionsaresatisfied,thenon-EEAparentcompany’sgroupaccounts(togetherwiththeIrishcompany’sstand-aloneaccounts)canbefiledasanalternativetotheIrishcompany

17

filingconsolidatedaccounts.Thefilingofauditedfinancialstatementsdoesnotapplytocertaincategoriesofprivateunlimitedcompanies.

obligations to publish company name and directors details

Acompanymustensurethatitsname,registeredaddressandregisterednumberarementionedonallbusinesslettersofthecompanyandonallcheques,invoicesandreceiptsofthecompany.Forprivatelimitedcompaniesandpubliclimitedcompaniesthisinformationmustalsobedisplayedonthecompany’swebsiteandcertainelectroniccommunications(forexample,email,lettersandelectronicorderforms).Thenamesofdirectorsandtheirnationality(ifnotIrish)mustbeincludedonallbusinesslettersonorinwhichthecompany’snamealsoappears.Acompanyisalsorequiredtopaintoraffixitsnameinaconspicuousplace,inlegibleletters,ontheoutsideofeveryofficeorplaceinwhichitsbusinessiscarriedon.

Business name

Whereacompanyusesabusinessnamethatisdifferentfromitscompanyname,thebusinessnamemustberegisteredbythatcompanywiththeIrishRegistrarofBusinessNamesattheCRO.

setting up a Branch

AnyforeigncompanytradinginIrelandthathastheappearanceofpermanency,anindependentIrishmanagementstructure,theabilitytonegotiatecontractswiththirdpartiesandareasonabledegreeoffinancialindependenceisconsideredabranchunderIrishcompanylaw.TherearecertainproceduressetdownfortheregistrationofbranchesinIrelandinvolvingthesubmissionandauthenticationofthememorandumandarticlesofassociationofthatcompanyand,incertainsituations,thefilingofannualaccountsforthatentity.

Insomecases,itmaymakesensefromataxperspectivetoestablishaforeignbranchinIreland,ratherthanincorporateaseparatelegalentity.IftradinglossesarelikelytoarisefollowingtheinitialestablishmentinIreland,suchlossesmaybecapableofbeingoffsetagainsttheprofitsoftheparentcompanyintheparentcompany’shomestate.IfitisenvisagedthattheoperationsinIrelandwouldcontinuetobeloss-making,thenabranchmaybepreferableuntilsuchtimeastheoperationbecomesprofitable.Themostadvantageousstructurewillonlybeidentifiedaftercarefulconsiderationoftheproposedbusiness,itsrelationshipwiththebusinessoftheforeignparentcompanyandtheprojectionsfortheprofitabilityofthebusinessinthefuture.

place of business in ireland

AforeigncompanycarryingonbusinessinIrelandfromafixedaddress,notbeingabranch,mustfileacopyofitsconstitutionaldocuments,togetherwithalistofdirectorsofthecompanyandtheaddressofitsestablishedplaceofbusinessinIreland,withtheCRO.

new irish company law regime

NewIrishcompanylawlegislationisinadvanceddraftform.ThismarksasignificantdevelopmentinthestrategicreformofIrishcompanylawandrepresentsastrongdesireonIreland’sparttoensurethatwehaveamoderncompanylawregimeinplacethatwillfurtherenhanceIreland’sattractivenessasaplacetodobusiness.

Wehavebeenactivelyinvolvedintheprogressionofthisnewlegislation.Wehaveplacedaparticularemphasisonthoseissueswehavediscussedwithmanyofourclientsandwhichoftenhaveacriticalbearingonthefeasibilityofvariousstrategiesorrestructuringsthathavebeenundertakeninthepast.

18

6 taxation

19

Formorethan50years,corporatetaxincentiveshavebeenthecornerstoneofthestrategypursuedbysuccessiveIrishGovernmentstoencourageinwardinvestmentintoIreland.Thisfocusedandunwaveringcommitmenttoimplementfiscal

policiesaimedatencouraginginwardinvestmentmakesIreland1ofthepre-eminentcountriesinandthroughwhichtodobusinessinEurope.

tax benefits of doing business in ireland

Theprimarybenefit,fromataxperspective,ofdoingbusinessinIrelandisIreland’sstandardcorporationtaxrateof12.5%.Ina2010surveypublishedintheIMDWorldCompetitivenessYearbookofkeymeasuresinfluencingFDI,Irelandranked1stforcorporatetaxes.The12.5%ratehasbeenapprovedbytheEUandappliestoactiveprofitsandisnotdependentonnegotiatingorsecuringincentives,rulingsorothertaxholidays.

Inrecentyearstheintroductionofanattractiveholdingcompanyregime,theavailabilityofimprovedcreditsforresearchanddevelopmentexpenditureandmostrecentlytheintroductionoftaxrelieffortheacquisitioncostsofIPandotherintangibles,hasgreatlyenhancedIreland’sattractivenessfromataxperspective.TheIrishGovernmenthasalsorepeatedlyreaffirmeditscommitmenttothe12.5%rateofcorporationtaxandanunrelentingwillingnesstofurtherenhancetheIrishtaxsystemtoattractfurtherinwardinvestment.ThefollowingrecentchangestotheIrishtaxsystememphasisethisongoingcommitment:

n DividendsreceivedbyanIrishholdingcompanyfromEUresidentcompanies,companiesresidentinjurisdictionswhichhaveataxtreatywithIreland(TreatyCountries)andcompaniesresidentincountrieswhichhaveenteredintocertainformsofexchangeofinformationtreatywithIrelandaretaxableattherateof12.5%(ratherthan25%).Since2010,the12.5%ratenowalsoappliestodividendsreceivedfromsubsidiarieslocatedinnon-TreatyCountries,wherethesharesofthesubsidiary(oritsultimate75%parent)aretradedonarecognisedstockexchange.Inbothcasesthelowerratewillonlyapplywheredividendsarepaidoutoftradingprofitsofthesubsidiary.

n Theintroductionofarelieffortheacquisitionofintellectualpropertyandotherintangiblesin2009allowscapitalexpenditureonintangiblestobeamortisedordepreciatedagainsttaxableincomederivedfromsuchintangibles.

n TheR&Dtaxcreditregime(seebelow)wasfurtherenhancedin2008byintroducingincreasedflexibilityfortheuseofR&Dtaxcredits.Suchcreditscannowbeusedtooffsetagainstprofitsfromtheprecedingaccountingperiod,andifanexcessstillremains2yearsafterthecreditarose,canberepaidtothetaxpayer.From2012creditscannowalsobesurrenderedtokeyemployeesengagedinR&Dactivitiesincertaincircumstances.

n Anumberofdomesticexemptions(includingdividendwithholdingtaxandinterestwithholdingtax)wereextendedin2008andnowconferthebenefitofexemptionsnotonlytopersonsresidentinTreatyCountries,butalsotopersonsresidentinjurisdictionswhichhavesignedadoubletaxationtreatywithIrelandandthattreatyhasnotyetbeenfullyratified.

n Irelandimposesawithholdingtaxonpatentroyalties.Adomesticexemptionfrompatentroyaltywithholdingtaxwasintroducedin2010inrespectofroyaltypaymentsmadetocompaniesresidentintheEUandTreatyCountries.Also,pursuanttoanadministrativepracticeintroducedin2010,incertaincircumstances,thepaymentofpatentroyaltiesbyanIrishcompanyinrespectofa“foreignpatent”toanynon-residentcompany(irrespectiveofitslocation)cannowbemadefreeofwithholdingtax,subjecttopriorapprovaloftheIrishRevenueCommissioners(Revenue).

n MeasurestofacilitatethedevelopmentofIslamicfinanceinIrelandwereintroducedin2010.Undertheseprovisions,thetaxtreatmentapplicabletoconventionalfinancetransactionswillapplyinthesamemannertoShari’acompliantdeposits,loansandbonds.

n TherecentlyintroducedSpecialAssigneeReliefProgramme(“SARP”)allowscertainexecutiveswhoareassignedtoworkinIrelandbyacompanyincorporatedandtaxresidentinanEUorTreatyCountry(assetoutonpage22)areductiononthetaxableincome,profitsorgainsliabletoIrishtaxwhichtheyreceivefromthatcompanyorarelatedcompany.

20

activities that qualify for the 12.5% rate

TheIrishcorporationtaxregimecharacterisesincomeinto2streams,withalltradingincome(broadlyequivalenttoactiveincome)taxableat12.5%andallnon-tradingincome(equivalenttopassiveincome)taxableat25%.

Practicallyallactivebusinesspursuitswillqualifyforthe12.5%rate.The12.5%rateisavailabletoallindustriesandsectors,makingIrelandattractivethroughoutallbusinesssectors.TheonlyissueinmostcaseswillbewhethertheactivityconductedinIrelandcomprisesthe“carryingonofatrade”inIrelandfortaxpurposes.Sincetheintroductionofthe12.5%rate,itisclearthatthelatestgenerationofinwardinvestorsinIrelandincludeinvestorsfromindustrysectorswhichmaynothavetraditionallyconsideredIrelandasapotentiallowtaxplatform.TheobjectiveunderpinningmostinvestmentsistoavailofthepossibilitiespresentedtounbundlethetraditionalvaluechainandlocateappropriateprofitgeneratingfunctionsinIreland.

ExamplesofactivitiesinthetraditionalvaluechainwhicharecapableofbeingunbundledandcarriedoninIrelandinclude:

n managementactivities(forexample,legal,accounting,humanresources,financeandreportingetc.);

n financialactivities(forexample,cashmanagement,banking,insuranceandriskmanagement);

n e-business(forexample,CRM,procurementanddistribution,supplychainmanagement,marketingandselling);

n technicalactivities(forexample,technicalsupport,datamanagement,security);

n researchand/ordevelopmentactivities;

n ownershipandexploitationofintellectualproperty;and

n distributionactivities.

Irelandoperatesaself-assessmentsystemforvarioustaxes,includingcorporationtax.However,incertaincircumstances,ataxpayercanrequestanopinionfromRevenueonthetaxconsequencesofaparticulartransactioninadvanceofthetransactiontakingplace.Revenuehaveanestablishedprocesswheretheywillgiveanopinionastoataxpayer’sentitlementtothe12.5%rate.OpinionsgivenbyRevenuearenotlegallybindingandarebasedsolelyonthefactspresentedtothem.ItisopentoRevenueofficialstoreviewthepositiontakeninanopinionwhenatransactioniscompleteandallthefactsarethenknown.

21

why choose ireland?

Taxlegislationthroughouttheglobeapplicabletointernationalbusinessisbecomingmorecomplexandsophisticatedeachyear.Inparticular,itisbecomingincreasinglydifficultformultinationalcompaniestopreservethetaxadvantagesoflocatinginalow-taxcountry.Inordertobeattractivetotheinternationalbusinesscommunity,therefore,alow-taxjurisdictionmustbeabletooffermorethanjustalowrateoftax.ItisforthisreasonthatIrelandisaparticularlyattractivelocationformultinationals.Forexample,thedecisionconcerningthechoiceoflocationsforcarryingontechnologyenabledactivitiesoftenturnsontheperceivedadvantagesanddisadvantagesbetweentaxhavensandonshorelow-taxlocationssuchasIreland.Theobviousadvantageofataxhavenistheabsenceofanylocalcorporationtaxonprofits.Theobviousdisadvantageofataxhavenistheabsenceofataxtreatynetwork.Thelessobviousdisadvantagesofestablishinginataxhaveninclude:

n constraintsoncreatingthenecessaryeconomicinfrastructuretowhichvalueandultimatelyprofitscanjustifiablybeattributed;and

n thegeneraldriveatEUandOECDlevelagainstharmfultaxcompetitionandtaxhavensinparticular.

Incontrast,Irelandcombinesthebenefitsof:

n anextensivetaxtreatynetwork;

n alowcorporationtaxenvironmentwhichdoesnotbreachEUorOECDharmfultaxcompetitioncriteria;

n theregulatoryandeconomicinfrastructureofahighly-developedOECDjurisdiction;

n thebenefitsofEUmembership(forexample,IrishregulatoryapprovalgenerallysufficesasaEuropeanpassportforregulatedgoodsandservicesthroughouttheEU);

n thephysicalandpeopleinfrastructuretoenabletheestablishmentofprofitgeneratingcentresdefensiblebyreferencetofunctions,risksandtangibleassetsoftheIrishoperation;and

n thephysicalproximitytoEurope,offeringarealgatewaytotheEUmarket.

Apartfromthelowrateofcorporationtax,otherkeytaxbenefitsoflocatinginIrelandinclude:

n nowithholdingtaxoninterestpaymentstoEU/TreatyCountries;

n wideexemptionsfromwithholdingtaxondividendpayments;

n nowithholdingtaxonroyaltiestoEU/TreatyCountries,andincertaincasestonon-EU/non-TreatyCountries;

n anextensiveandexpandingdoubletaxtreatynetwork;

n acomprehensiveunilateralforeigntaxcreditsystem;

n nocontrolledforeigncorporationrules;

n nospecificcodeofthincapitalisationrules;

n nocapitalgainstaxexitchargetoEU/TreatyCountries;

n anexemptionfromcapitalgainstaxinrespectofthedisposalofshareholdingsinqualifyingcompanies;

n nocompaniesregistrationtaxes(capitalduty);

n arefundabletaxcreditof25%forincrementalresearchanddevelopmentexpenditure;

n acorporatetaxrelieffortheacquisitioncostofIPandotherintangibles;and

n nocustomdutiesonIrishgoodsontheirimportationintootherpartsoftheEU.

22

Albania

Armenia*

Australia

Austria

Bahrain

Belarus

Belgium

Bosnia&Herzegovina*

Bulgaria

Canada

Chile

China

Croatia

Cyprus

CzechRepublic

Denmark

Egypt*

Estonia

Finland

France

Georgia

Germany

Greece

HongKong

Hungary

Iceland

India

Israel

Italy

Japan

Korea(Republicof)

Kuwait*

Latvia

Lithuania

Luxembourg

Macedonia

Malaysia

Malta

Mexico

Moldova

Montenegro

Morocco*

Netherlands

NewZealand

Norway

Pakistan

Panama*

Poland

Portugal

Romania

Russia

SaudiArabia*

Serbia

Singapore

SlovacRepublic

Slovenia

SouthAfrica

Spain

Sweden

Switzerland

Turkey

UnitedArabEmirates

UnitedKingdom

UnitedStates

Vietnam

Zambia

NegotiationsfornewagreementswithQatar,Thailand,UkraineandUzbekistanareexpectedtobesigned.TheIrishRevenueCommissionersintendtoinitiatenegotiationsforfurthernewagreementswithothercountriesinthenearfuture.

general scope of irish corporation taxcharge to tax and residence

CompanieswhichareresidentinIrelandfortaxpurposesaresubjecttocorporationtaxonworldwideincomeandgains.Anon-residentcompanyischargeabletocorporationtaxonprofitsarisingfromabusinessconductedthroughabranchoragencyinIreland.

AcompanywhichisincorporatedinIrelandwillberegardedastaxresidentinIreland,unless:

(a) thecompanyorarelatedcompanyiscarryingona tradeinIreland,andeither:

(i)thecompanyisultimatelycontrolledbytax residentsofanEUMemberStateoraTreatyCountry or

(ii)thecompanyorarelatedcompanyisquotedona recognisedstockexchangeofanEUMemberStateor aTreatyCountry;or

(b) thecompanyistreatedasresidentinacountryby virtueofadoubletaxtreatyenteredintobetweena TreatyCountryandIreland.

ireland’s network of double taxation treaties

IrelandhasaDoubleTaxationTreatywiththefollowingTreatyCountries.

* TreatieswithArmenia,Bosnia&Herzegovina,Egypt,Kuwait,Morocco,PanamaandSaudiArabiahavebeensigned,buthavenotyetbeenfullyratified.

ALBANIA

BULGARIA

BAHRAIN

CROATIA

FINLAND

AUSTRALIA

CHILE

EGYPT

BELGIUM

CZECH REPUBLIC

GEORGIA

ARMENIA

CANADA

BELARUS

CYPRUS

FRANCE

AUSTRIA

CHINA

ESTONIA

BOSNIA & HERZEGOVINA

DENMARK

GERMANY

GREECE

SOUTH KOREA

INDIA

LUXEMBOURG

MONTENEGRO

HUNGARY

LATVIA

MEXICO

ITALY

MALAYSIA

NETHERLANDS

KUWAIT

ISRAEL

MACEDONIA

MOROCCO

ICELAND

LITHUANIA

MOLDOVA

JAPAN

MALTA

NEW ZEALAND

NORWAY

SERBIA

PORTUGAL

SOUTH AFRICA

UNITED KINGDOM

PANAMA

SLOVAKIA

TURKEY

RUSSIANFEDERATION

SWEDEN

VIETNAM

PAKISTAN

SINGAPORE

ROMANIA

SPAIN

UNITED STATES OF AMERICA

POLAND

SLOVENIA

UNITED ARABEMIRATES

SAUDI ARABIA

SWITZERLAND

ZAMBIA

23

ForthosecompanieswhichfallwithintheaboveexceptionsandforcompanieswhicharenotincorporatedinIreland,taxresidenceisdeterminedbyreferencetotheplacewherethecentralmanagementandcontrolofthecompanyabides.

Inpracticeandintheabsenceofevidencetothecontrary,thecourtsgenerallyplaceconsiderableemphasisonmeetingsoftheboardofdirectorsindeterminingwhoexercisesthecentralmanagementandcontrolofacompany.Thereasonforthisisthat,ingeneral,thebusinessofcompaniesismanagedbytheirdirectorsandsuchmanagementisnormallyconductedatmeetingsoftheboardofdirectors.Ifmeetingsofthedirectorswhoactuallymanagethecompany’sbusinessinthismannerareheldinIreland,thecompanywouldgenerallyberegardedascentrallymanagedandcontrolledinIreland.

InordertobenefitfromIreland’staxtreaties,companiesmust,ingeneral,beresidentsofIrelandwithinthemeaningoftherelevanttreaty.

computation of taxable income

Aspreviouslymentioned,Irelandoperatesaself-assessmentsystemfortaxpurposes.Ingeneral,thetradingprofitsofacompanyarecomputedinaccordancewithgeneralaccountingprinciples.Itisimportant,however,totakeaccountofspecificstatutoryprovisionswhichmaydepartfromthegeneralaccountingtreatment.Forexample,onlyexpenseswhichareincurredwhollyandexclusivelyforthepurposesoftradingactivitiesareallowableasadeductionincalculatingtheprofitsofacompanyfortaxpurposes.Also,therearespecificprovisionsrelatingtothedeductibilityofentertainmentexpenses,motorvehicleexpenses,pre-tradingexpenses,provisions,interestandroyaltypayments.

DividendspaidbyanIrishresidentcompanyarenotdeductible.Suchdividendsareregardedas“frankedinvestmentincome”andthereforenottaxableinthehandsofanotherIrishresidentcompany.Therearedetailedrulesrelatingtothedeductibilityofinterestpaymentsinplace.Subjecttocertainlimitations,whereinterestispaidwhollyandexclusivelyforthepurposesofatradebyanIrishcompany,suchinterestwillbedeductible.Interestmayalsobedeductibleinotherlimitedcircumstanceswheretheloanisusedforinvestmentinothercompanies.

tax depreciation and loss relief

Taxlossesandtaxdepreciationaredeductibleinaccordancewithspecialrules.Ingeneral,thetaxlossesofacompanywhichformspartofataxgroupcanbeoffsetagainsttaxableprofitsofanothergroupcompany.ForthesepurposesagroupcanincludeEUresidentcompanies.LossesmayalsobesurrenderedfromEUsubsidiariesandbetweenbranchesofEUcompaniesandIrishsubsidiariesinlimitedcircumstances.It

shouldbenotedthattheconceptofagroupconsolidatedtaxreturnortaxunitydoesnotexistinIreland.

refundable research and development tax credit

Arefundablecorporationtaxcreditof25%forincrementalqualifyingR&DexpenditureisavailableinIreland.ThistaxcreditisavailableinrespectofqualifyingR&DexpenditureundertakenwithintheEEA.ThisR&DtaxcreditisinadditiontotheexistingdeductionandcapitalallowancesthatmaybeavailableforR&Dexpenditure.TheR&Dtaxcreditisallowedagainstacompany’scorporationtaxliabilityfortheyearinwhichitisincurred.ExcessR&Dtaxcreditscanbecarriedbackagainstacompany’scorporationtaxliabilityintheaccountingperiodprecedingtheaccountingperiodinwhichthequalifyingR&Dexpenditureisincurred.AnyexcessR&Dtaxcreditcanalsobecarriedforwardagainstfuturecorporationtaxprofitsand,importantlycannowbeclaimedbackasarefundfromRevenuewhereitisnotpossibletoutilisethecreditinthe2yearsfollowingtheaccountingperiodinwhichtheR&Dtaxcreditarises.From2012,itisalsopossibletosurrenderR&DtaxcreditstokeyemployeeswhoareengagedsubstantiallyinR&Dactivitiesforthecompanysubjecttocertainrestrictions.

tax relief for acquisition costs of ip and other intangibles

Capitalexpenditureincurredafter7May2009on“intangibleassets”whichareacquiredforthepurposesofatradecanbeoffsetagainsttaxableincomeforcorporatetaxpurposes.

Thetaxreliefavailablereflectsthestandardaccountingtreatmentoftheintangibleassetsandisbasedontheamountchargedtotheprofitandlossaccountinrespectoftheamortisationordepreciationoftherelevantintangibleasset.Alternatively,thetaxpayercanopttoclaimreliefover15yearsatarateof7%forthefirst14yearswiththeremaining2%ofthereliefclaimedinthefinalyear.Theaggregateamountofrelief,togetherwithrelatedinterestexpense,islimitedinany1yearto80%ofthetradingincomederivedfromtherelevantintangibleassets.Anyunutilisedreliefmaybecarriedforwardindefinitelyforoffsetagainstfuturetradingincomefromtheseparatetrade.Thedefinitionofintangiblesforthepurposesofthereliefhasbeenverywidelydraftedandincludesgoodwilldirectlyattributabletointangibles.

TheregimespecificallyprovidesthatwhereintangibleassetsareacquiredfromagroupcompanyincircumstanceswheresuchtransferorwouldbeentitledtoIrishcapitalgainstaxgrouprelief,theacquiringcompanywillbeabletoclaimthereliefontheassetsacquiredonlyifbothitandthetransferringcompanyelecttooptoutofthegroupreliefprovisions.

Reliefisnotavailableforcapitalexpenditureinrespectofwhichtaxreliefisotherwiseavailableorwheretheexpenditure

24

incurredexceedstheamountthatwouldbepayablebetweenindependentparties.Reliefisalsonotavailableinrespectofanyexpenditureincurredaspartofataxavoidancearrangement.Theintangibleassetmustcontinuetobeusedinatradefor10yearstoavoidtriggeringaclawbackofthereliefobtained.

incoming dividends

DividendsreceivedbyanIrishcompanyaretaxedateither12.5%or25%dependingontheprofileoftheunderlyingsubsidiary.However,Irelandoperatesacomprehensiveforeigntaxcreditsysteminrespectofdividendsreceived.Companiescanmixorpoolthecreditsforforeigntaxondifferentdividendstreamsforthepurposeofcalculatingtheoverallcredit(called“onshorepooling”).Creditisavailableforwithholdingtaxandunderlyingtax,includingcreditformanystate,localandmunicipaltaxessufferedincountrieswithwhichIrelandhasataxtreatybutwhichtaxesarenotcoveredbythetreaty(forexample,USStatetaxes).Thisunilateralcreditreliefrequiresashareholdingofatleast5%oftheordinarysharecapitalintheforeigncompany.Excesscreditsarisingfromdividendincometaxedat12.5%canonlybeusedtooffsetdividendincometaxedat12.5%.Excesscreditscanbecarriedforwardforoffsetinsubsequentaccountingperiods.

attractive Holding company and Headquarter regime

IrelandoffersanattractivetaxregimeforholdingcompaniesandthisisreflectedinthenumberofcompanieschoosingtorelocatetheirheadquarterstoIreland.The2mainfeaturesofthisregimeare(a)a‘substantialshareholders’exemptionfromIrishtaxonthesaleofsubsidiaries,and(b)anadvantageoustreatmentofforeigndividendincome.

exemption from irish tax on sale of subsidiaries

Ireland’s‘substantialshareholders’exemptionrelievesholdingcompaniesfromIrishcapitalgainstaxationondisposalsofsubsidiaries.2mainconditionsapply:(a)thesubsidiarymustberesidentintheEUoraTreatyCountry;and(b)aminimum5%shareholdingmusthavebeenheldforacontinuousperiodofatleast12monthswithintheprevious24months.

advantageous treatment of foreign dividend income

Generally,Irishholdingcompaniescanreceivedividendsfromtheirforeignsubsidiariesonaneffectivetax-freebasisinIreland(orwithaveryloweffectiverateofIrishtax).ThisisduetoacombinationofIreland’slowcorporationtaxrateformostdividendsandtheavailabilityofIrishcreditreliefforforeigntaxes.The12.5%corporationtaxrateappliesto

dividendincomereceivedbyanIrishcompanyfromitsforeignsubsidiariesinmanycases,includingwhere:(a)thesubsidiariesaretaxresidentineithertheEU,aTreatyCountryoracountrywhichhasratifiedtheConventiononMutualAssistanceinTaxMatterswithIreland,orthesubsidiary(oritsultimate75%parent)isquotedonarecognisedstockexchangeinanothermemberstateorTreatyCountry;and(b)thosedividendsarepaidoutof‘trading’profitsoftheforeignsubsidiaries.Ifthedividendsarepartiallypaidoutofnon-tradingprofits,thenthe12.5%stillappliesonce(broadlyspeaking)atleast75%oftheprofitsaretradingprofits.Ahigherrateof25%appliestootherdividendincome.

However,foreignwithholdingtaxesand(oncea5%shareholdingisheld)foreignunderlyingtaxesmaybecredited(orsetoff)againstthisIrishtaxliability.Onshoredividendmixingisalsopermittedsothatexcesstaxcreditscanbepooledagainstotherdividendincomesources.Typically,sufficientforeigntaxesarepayabletofullyoffsetthe12.5%(or,asthecasemaybe,the25%)Irishtaxdue.Wherethisisthecase,noIrishtaxispayableonsuchdividendincome.

Foreigndividendsreceivedonportfolioshareholdings(thatisaholdingthatrepresentslessthan5%ofthesharecapitalandvotingrights)byIrishdealersinsecuritiesarenowcompletelyexemptfromIrishcorporationtax.

other taxes capital gains tax

CompaniesresidentinIrelandfortaxpurposesaresubjecttocorporationtaxontheirgains.Non-residentcompaniesarechargeabletocapitalgainstaxondisposalsofcertainspecifiedassets(forexample,realestatesituatedinIreland).Thecurrentrateofcapitalgainstaxis30%.Taxablegainsarecalculatedbydeductingfromthesaleproceedsthecostsincurredonacquiringtheassets.Therearesignificantreliefsfromcapitalgainstaxonthetransferofassetsintragroupandinmerger/reconstructionsituations.

Asoutlinedabove,thedisposalofsharesinasubsidiarycompanybyanIrishholdingcompanyis,incertaincircumstances,exemptfromIrishcapitalgainstax.

value added tax (vat)

VAToperatesasaturnovertaxonallrelevantsuppliesuptoapointoffinalconsumptionordeemedconsumption.ThismeansthatataxablebusinessmustaccountforrelevantVATliabilitiesinrespectofitsIrishbasedtaxableturnoverbuthastherighttoclaimadeductionforVATincurredonitsownpurchases,acquisitionsandimportationsinrespectofwhichIrishVATisborne.

25

Ireland’sVATregimeisdictatedbyEUlegislationwiththeresultthatIreland’sVATsystemisbroadlyinlinewiththepan-Europeanharmonisedsystem.ThecurrentratesofVATare0%,4.8%,5.2%,9%,13.5%and23%.Thestandardrateof23%isapplicableunless1oftheotherratesisspecified.

Ingeneral,VATappliesonallimportsofgoodsfromoutsideoftheEU,thesupplyofgoodsandserviceswithinIrelandandtoservicesreceivedinIrelandfromsuppliersoutsideIreland.GoodsexportedtobusinessessituatedelsewhereintheEuropeanCommunityandtobusinessesorindividualssituatedoutsidetheEuropeanCommunitygenerallyattractthe0%rateofVAT.MostcategoriesofservicessuppliedtocustomerslocatedoutsideofIrelandmaynotbechargeabletoIrishVATastheplaceofsupplyisdeemedtobeoutsideofIreland.

IrelandoperatesaspecialVATincentiveforexportersofgoods.EntitieslocatedinIrelandthatsupplyinexcessof75%oftheirproductstootherEUlocationsorexporttonon-EUjurisdictionsmayqualifyforauthorisationtopurchasemostgoodsandservicesatthe0%rateofVAT.ThiscanprovideasubstantialcashflowadvantageforcompaniesestablishingtheirEuropeMiddleEastandAfrica(EMEA)regionoperationsinIreland.

stamp duty/capital duty

StampdutymayariseonwritteninstrumentsthatareexecutedinIrelandorwritteninstrumentsrelatingtoIrishproperty.Therateofstampdutyvariesdependingonthenatureoftheunderlyingassets.Generally,thetransferofsharesattractsa1%rateofstampduty,whilsttransfersofcommerciallandandbuildingsattractsstampdutyofupto2%.Transfersofintellectualpropertyrightsareexemptfromstampduty.Therearesignificantreliefsfromstampdutyonthetransferofassetsintragroupandinmergerandgroupreorganisationsituations.

NocapitaldutyarisesontheissueofsharesbyanIrishcompany.

custom duties

CustomsdutiesareessentiallyEUtaxeschargedontheimportationofgoodsfromnon-EUcountries.TheEUoperatesacommonsystemofcustomsduty.Applicableratesvarygreatlydependingontheclassofgoodsinquestion.Anumberofclassesofgoods,includinggoodswithinthecomputerandITsector,areliabletothe0%rateofduty.AnumberofreliefsexistincludingtheabilitytoimportgoodsforprocessingandonwardexportationbeyondtheEUfreeofcustomsduties.

payroll taxes

EmploymentincomeinIrelandissubjecttoawithholdingtax

knownasthePayAsYouEarn(PAYE)system.ThisPAYEsystemmustbeoperatedbyemployersandiseffectivelydesignedtoequatethetaxwithheldbytheemployerwiththefinalliabilityoftheemployeeinrespectofhis/heremploymentincomefortherelevanttaxyear.

PayRelatedSocialInsurance(PRSI)isanotherpayrolltaxoperatedbyemployers.UnlikePAYE,however,PRSIispaidpartlybytheemployerandpartlybytheemployee.Theemployer’scontributionisgenerally10.75%oftherelevantemployee’ssalary,whilstemployeesgenerallypay4%oftheirsalarysubjecttoaceilingof€75,036.Employeeswillalsopayauniversalsocialchargeof2,4or7%dependingontheamountofincomeearned.

transfer pricing

Transferpricing(TP)legislationwasintroducedinMay2010,witheffectforaccountingperiodsbeginningonorafter1January2011.Arrangementsenteredintopriorto1July2010areexcludedfromthescopeofthelegislationunderthegrandfatheringprovision.TheTPlegislationformallyadoptstheOECDarm’slengthprinciple.Whereanarrangementbetweenassociatedpersonsisotherwisethanatarm’slength,anadjustmentmustbemadewherethepricingresultsinthetradingprofitsoftheIrishresidentcompanybeingunderstated.

taxation of employees and special assignee relief programme

ThetaxtreatmentofanindividualforIrishtaxpurposeswilldependonwhethertheyareIrishresident,ordinarilyresidentand/orIrishdomiciled.

Apersonis“resident”forthedayiftheyarepresentinIrelandatanytimeduringaday.Inanongoingsituation,itispossibleforanindividualtospendupto139daysinIrelandinataxyearwithoutbecomingIrishresident.

Thelegalconceptof“domicile”andadefinitiveexplanationofitsmeaningisbeyondthescopeofthisGuide.Howeverdomicilecouldbebroadlydefinedasaperson’snaturalhome.Everyindividualisbornwithadomicileoforigin.Itispossibleforapersontolosetheirdomicileoforiginandacquireadomicileofchoice.Likewise,itispossibleforanindividualtolosetheirdomicileofchoiceandrevivetheirdomicileoforigin.DomicileisanimportantconceptunderIrishlawasitisrelevantnotonlyfortaxpurposesbutalsofordeterminingtherulesofsuccession,discussedfurtheroverleaf.

Whereanindividualisresident,ordinarilyresidentanddomiciledinIreland,theywillbetaxableontheirworldwideincomeandgains,regardlessoftheirsource.

26

IfapersonisresidentbutnotdomiciledinIreland,thenliabilitytoincometaxislimitedtoIrishsourceincome,incomefromanemploymentcontractinrespectofwhichthedutiesofsuchemploymentareexercisedinIrelandandworldwideincometotheextentremittedtoIreland.TheliabilityofapersontocapitalgainstaxwherethepersoniseitherresidentorordinarilyresidentbutnotdomiciledinIrelandislimitedtoIrishsourcegainsandworldwidegainstotheextentremittedtoIreland.Thisisknownasthe“remittancebasisoftaxation”.Fromanadministrativeperspective,itissufficienttorelyonnon-remittanceandthereisnoformalrequirementtoelect.

From2012,anemployeeassignedtoworkinIrelandbyacompanyincorporatedandtaxresidentinaTreatyCountryoracountrywithwhichIrelandhasaTaxInformationExchangeAgreementmayclaimadeductionfromtheirincometax.Therelief,referredtoastheSpecialAssigneeReliefProgramme(“SARP”),allowsassigneestoobtainataxdeductionofupto30%onemploymentincome,profitsorgains(includingstockoptions)liabletoIrishtaxinexcessof €75,000,uptoamaximumincomeof €500,000,thattheyreceivefromtheforeigncompany(orarelatedcompany).Inaddition,assigneesmayreceivecertainpersonalbenefits(anannualflighttotheassignee’scountryofresidence,schoolfeesofupto€5,000foreachchild)fromtheemployerwithoutincurringaliabilitytotax.

InordertobeeligibleforSARP,assigneesmustbeemployedbytheforeigncompanyforatleast12monthspriortoarrivinginIreland,theymusttakeupemploymentinIrelandwiththatcompanyand/oranassociatedcompanyforaminimumof12monthsandtheymusthavebeennon-Irishresidentforthe5taxyearsprecedingtheyearofarrival.

Thereliefmustbeclaimedbytheemployee,andtheemployermustcertifythatcertainrequirementsforthereliefhavebeensatisfied.

OtherreliefsareavailablefortemporaryassigneesandsecondeeswhoarenotresidentinIreland,underpublishedRevenuestatementsofpractice.

capital acquisitions tax (cat)

Itisimportantforanynon-domiciledpersonconsideringmovingtoIrelandtonotethepotentialexposuretoCAT.

CATisthegenericnameforthetaximposedongiftsandinheritancesinIreland,whichischargedat30%.CATisabeneficiarybasedtaxandisimposedonanyIrishsituateassetscomprisedinagiftorinheritanceandwhere,atthetimeofthegiftorinheritance,eitherthedonororbeneficiaryisresidentinIreland.Theleveloftaximposedwilldependonthedegreeofrelationshipbetweenthebeneficiaryandthedisponer.

Thereisastatutoryrelieffornon-domiciledindividuals.TheywillnotbedeemedtoberesidentforCATpurposesunlesstheyhavebeenresidentfor5consecutivetaxyearsattherelevanttime.Whereanon-domiciledIrishresidenthasbeenresidentinIrelandfor5consecutiveyearsthatpersonwillbewithintheIrishCATchargeontheirworldwideestates,aswillanytrustsofwhichtheyarethesettlor.

27

7 employment and Labour Law

28

IrishemploymentlawhasbeenconsiderablyinfluencedbyIreland’smembershipoftheEU,withmostIrishemploymentlegislationnowbasedonEUDirectives.

employee rights arising at commencement and during the course of employmentwhat information must be provided?

Eachemployeeisentitledtoawrittenstatementoftheirtermsandconditionsofemployment.Anemployeemustalsoreceivewrittendetailsoftheprocedurewhichwillbefollowediftheemployeeisgoingtobedismissed.Employeesarealsoentitledtowrittenstatementsshowingthegrosswagespayableandthenatureandamountofdeductionsapplied.

is there a minimum wage?

Allemployeesovertheageof18areentitledtothenationalminimumhourlyrateofpayunlesstheyfallintoacategorytowhichasub-minimumhourlyrateofpayapplies.Sub-minimumratesapplytoemployeesundertheageof18,jobentrantswhoenteremploymentforthefirsttimeaftertheageof18andtrainees.

what about restrictions on working time?

Themaximumaveragehoursthatanemployeemayworkis48hoursperweek,notincludingrestorlunchbreaks.Employeesareentitledtorestperiodsofatleast11consecutivehoursinevery24-hourperiodandmusthaveatleast1weeklyrestperiodof24consecutivehours.ThisrestperiodmustincludeaSundayunlesstheemployerspecificallyprovidesotherwiseinthecontractofemployment.Therearesignificantexceptionstotherulesonworkingtimeforvariouscategoriesofworkers.

is there employment equality legislation?

Discriminationonthefollowinggroundsisprohibitedregardingbothtermsandconditionsof,andaccessto,employment:gender,civilstatus,familystatus,sexualorientation,religiousbelief,age,disability,membershipoftheTravellercommunityandracewhichincludesnationality,ethnicoriginorcolour.

what about part-time workers?

Discriminationagainstpart-timeemployeesisprohibited.Part-timeworkersmustnotbetreatedinalessfavourablemannerthancomparablefull-timeworkerssolelybecausetheyworkpart-time,unlessdifferenttreatmentcanbeobjectivelyjustified.

what about fixed term workers?

Discriminationagainstemployeesonfixedtermorspecifiedpurposecontractsisprohibited.Fixedtermworkersmustnotbetreatedinalessfavourablemannerthancomparablepermanentemployeesunlesssuchdifferenceintreatmentcanbeobjectivelyjustified.

what about agency workers?

Agencyworkerswhoaretemporarilyassignedbyanemploymentagencytoworkforandunderthedirectionandsupervisionofahirer,areentitledduringtheirassignmenttothesamebasicemploymentconditions,includingbasicpay,overtimeetc,asiftheyweredirectlyemployedbythehirer.However,thisdoesnotincludesickpayoranyentitlementtopensionbenefits.

what are the statutory leave entitlements?

Everyfulltimeemployeeisentitledto4weeks(20days)paidannualleaveeachyear.Inadditiontopaidholidayleave,employeesarealsoentitledtomaternity,parental,forcemajeure,carers,adoptiveandhealthandsafetyleave.Thereisusuallynoobligationtopayanemployeewhileheorsheisonsuchtypesofleave,althoughyoumaychoosetodosodependingonthecircumstances.Employeesarealsoentitledto9furtherpaidleavedaysannuallyforpublicholidays(orpaymentinlieuofsame,dependingonthecircumstances).

what is the position with health and safety?

Thereisadutyonemployerstoprovideforthesafety,healthandwelfareofemployees.Thisincludesobligationstoprovideaworkplacethatissafesofarasreasonablypracticable,safeplantandmachineryandsuitableprotectiveclothingorequipment.Employersarealsoobligedtopreparea‘safetystatement’.Thisisareportsettingouthowemployersintendtosecurethehealth,safetyandwelfareofitsemployeesintheworkplaceandtoprovideforsafetyrepresentativeschosenfromemployees.

must employers pay sick pay?

Employersarenotobligedtoprovidesickpaybut,ifasickpayschemeisinplace,allemployeesmustgenerallybeentitledtoitequally.

29

employee rights arising on terminationHow much notice must be given to terminate an employee?

Whereeitheranemployeeoranemployerwishestoendacontractofemployment,minimumtermsofnoticeapplywheretherehasbeencontinuousserviceforatleast13weeks.Thenoticeperiodtobegivenbyanemployerdependsontheemployee’slengthofservice.Itvariesfrom1week,applicablewhereanemployeehasbeenemployedforupto2years,to8weeks’notice,applicablewhereanemployeehasbeenemployedfor15yearsandupwards.Employees,ontheotherhand,areonlyobligedtogivenoticeof1week,irrespectiveoftheirlengthofservice.Theseare,ofcourse,onlytheminimumprescribedtermsandthepartiesmayagreealongerperiodofnoticebycontract.

are all employees entitled to redundancy?

Anemployeeisentitledtoaredundancypaymentwhereheorshehasworkedcontinuouslyfor2yearsormoreandiseitherdismissedbyreasonofredundancyorislaidofforkeptonshorttimeforagivenperiodoftime.Statutoryentitlementis2weeksperyearofserviceplus1bonusweek.Employersof10makeanexgratiapaymentalongwiththestatutorypaymentbutarenotobligedbylawtodoso.Certainformalproceduresmustbeobserved.Employeesmustbegivenatleast2weeksnoticeofredundancy.Certainadditionalrulesandconsultationrequirementsapplywhereanemployerisconsideringanumberofredundanciesatthesametime.

is there unfair dismissal legislation?

Whereanemployeeisunfairlydismissed,heorshehasarighttocompensation,reinstatementorre-engagementundertheUnfairDismissalsActs.Unfairdismissallegislationappliestothoseemployeeswhohaveatleast1yearscontinuousservice.Thelegislationalsocoversinstanceswhereanemployeeisconstructivelydismissed.Thismayarisewheretheemployer’sbehaviourwassuchthattheemployeewasforcedtoleaveortheemployerunilaterallyimplementedamaterialvariationofanemployee’scontractofemploymentwithouthisorherconsent.

Employersmustapplyfairprocedureswhendismissinganemployee(forexample,warningsmustbegivenexceptincircumstancesamountingtogrossmisconduct).Theemployeemustbeheardandafairandproperinvestigationintothecircumstancesleadingtothedismissalmustbecarriedout.

do rules apply on the transfer of employees?

Detailedrulesapplyregardingthetreatmentofemployees

whereabusiness(orassetspertainingtothebusiness)isbeingtransferredfrom1employertoanother.Therulesdonotapplytoasharetransfer.Inessence,theobligationstheoriginalemployerhadtowardshisemployeeswillbetakenoverbythenewemployer.Thisincludesrightsarisingfromthecontractofemployment,collectiveagreementsandlegislation.Boththepreviousandnewemployerareobligedtoinformtheirrespectiveemployeesofthereasonsforthetransfer,theimplicationsofthetransfer,andthemeasuresenvisagedtobetakeninrelationtotheaffectedemployees,ingoodtimebeforethetransferiscarriedout.Theemployerisalsoobligedtoconsultwithemployeerepresentatives.

other employment matterswhat about industrial relations?

WhilstemployeesinIrelandhavearighttojoinatradeunion,employersarenotobligedtorecognisetradeunionsforcollectivebargainingpurposes(althoughwherecollectivebargainingdoesnottakeplace,employersmaybeobligedincertaincircumstancestodealindirectlywithunionsundertheauspicesoftheLabourRelationsCommissionortheLabourCourt).DependingonthenumberofemployeesanemployerhasinEUMemberStates,anemployermayberequiredtoestablishaEuropeanWorksCouncilfacilitatingemployeeaccesstomanagementinformationrelatingtotransnationalquestionswhichsignificantlyaffectemployeesinterests,thoughmanagementmaywithholdinformationthatitclaimsiscommerciallysensitive,andtoconsultwithmanagementonsuchquestions.EUlawrequirestheestablishmentofworkers’councilsbylargeremployers,whoemployatleast1,000employeesintheEUandwhichhaveundertakingsin2ormoreMemberStatesoftheEUwhichemployatleast150employeeseach.Againdependingonnumbers,anemployermayalsoberequiredtoestablishalocalworkscouncilwhichwillalsofacilitateaccesstoinformationandconsultation.However,suchlocalworkscouncilsarerelativelypowerlessincomparisontoworkscouncilsinsomeEuropeancivillawjurisdictions.Irishemployeesdonothaveanyrighttovetoanydecisionsoftheemployer.

employment permits for non-eea nationals?

Mostnon-EEAnationalsrequireanemploymentpermittoworkinIreland.Asaresult,employersshouldalwaysconfirmaprospectiveemployee’sentitlementtoworkinIrelandpriortocommencementofemployment.Therearevarioustypesofemploymentpermitswhichareavailablenamely:workpermits,greencardpermits,intra-companytransferpermitsandspousal/dependantpermits.Thepreferredpermitineachcasewilldependontheparticularcircumstances.Thereisusuallyafeeforpermitapplications(inmostcases

30

€1,000fora2yearpermit)andapplicationscantakeseveralmonthstoprocess.Insomecases,forexampleworkpermits,advertisingofthevacancyisrequiredpriortosubmittingtheapplication.Therefore,applicationsshouldbepreparedwellinadvanceoftheanticipatedstartdate.EmployeeswhoworkunderanemploymentpermitareentitledtotheprotectionofemploymentlegislationinIrelandinthesamewayasIrishorEUnationals.

Thereareseverepenaltiesforemployinganon-EEAnationalwithouttheappropriateemploymentpermit.Iffoundguiltyofsuchanoffence,finesuptoamaximumof€250,000canbeimposedontheemployerand/orimprisonmentuptoamaximumof10years.

employee benefits and pensions

Anemployermaywishtoprovideitsemployeeswithemployeebenefitssuchaslifeinsurance,pensions,privatehealthinsurance,sickpayandshareincentiveschemes.ThereisnolegalobligationinIrelandtoprovideanyofthesebenefits,saveforpensions,whereitisobligatoryforallemployerstoofferaccesstoaPersonalRetirementSavingsAccount(PRSA)toallemployees,unlesseachemployeehasaccesstoanOccupationalPensionSchemewithin6monthsofbeingemployed.ThereisnoobligationonanemployertocontributetoaPRSAonbehalfofanemployee.

PRSAproductsareavailablefromlifeassurancecompanies,banksandotherinvestmentfirms.EachproducthastobeapprovedbyboththeIrishPensionsBoardandtheIrishRevenueCommissionersbeforetheycanbesold.

AnOccupationalPensionSchemecaneitherbeonadefinedbenefitoradefinedcontributionbasis.MostlargerIrishemployersprovide1orothersuchscheme,withvaryingcontributionlevelsandeligibilitycriteria.

cross-border pension schemes

Undercurrentcross-borderpensionschemeslegislation,Irishemployersareabletoestablisharrangements(oradaptexistingarrangements)topermitinclusionofemployeesofsubsidiarycompaniesorbusinessesestablishedinotherEUMemberStateswhichhavealsoimplementedtheEUPensionsDirectiveandwhichwillallowIrishemployers(andemployees)tomakecontributionsonataxexemptbasistoapensionschemeestablishedinanotherEUMemberState.ForeignemployersestablishedinotherEUMemberStatesarealsoabletomakecontributionstopensionschemesestablishedinIreland.

Irish-basedpensionschemesthatwishtooperateacrossEUborders(thatis,toacceptcontributionsinrespectofmemberslocatedinotherEUMemberStates)mustobtainpriorauthorisationfromtheIrishPensionsBoard.TrusteesofIrish-basedschemesarerequiredtofurnishinformationtotheIrishPensionsBoardinrelationtocross-borderemployers.Detailednotificationrequirementsarenowprescribedinregulations.Theregulationsalsoprovidedetailsoftheregulatoryrequirementsforapprovalofcross-borderarrangements.

Thelegislationallowsmulti-nationalemployerswithoperationsinEuropetoestablishacompanyorbranchinIrelandwhichinturnwouldsponsoranoccupationalpensionarrangement.ThatarrangementcouldthenseekauthorisationfromtheIrishPensionsBoardtoacceptcontributionsfromoverseasemployerslocatedinotherEUMemberStates.

31

8 Real estate, Property, Construction, Planning and environmental Law

32

property

MostinwardinvestmentprojectswillinvolvetheacquisitionofsomeinterestinIrishrealestate,withassociatedregulatoryissuesincludingapplicationsforplanningpermission,buildingcontrolapprovalandenvironmentallicencesorpermitsalsolikelytoarise.Therearegenerallynorestrictionsonforeignindividualsorcorporationspurchasingorleasingland.

Dependingonthenatureoftheproject,itmaybenecessarytoretaintheservicesofapropertyconsultant(whocanassistwiththeidentificationandvaluationofanyproposedsiteorproperty),anarchitect/engineertocarryoutstructuralsurveysortodesignafacilityandenvironmentalconsultantswhomaybeneededtocarryoutenvironmentalassessments.Itisalsoimportantforpurchaserstoliaisewithlocalauthoritiesandutilitycompaniestoensurethatthereisadequateinfrastructureandthattherewillbeadequateutilitiesfortheintendedproject.

what is the process for the purchase of commercial property?

ThepurchaseofpropertyinIrelandisdealtwithbyrealestatelawyerswhoinvestigatethevendor’stitleandabilitytoselltheproperty,carryoutsearchesofthelocalauthorityregistersandadviseastothenecessarystructuralsurveysandenvironmentalassessmentsrequired.

Havingagreedthepurchasepricewiththevendororhisagentand,ifrequired,paidabookingdeposit,thepurchaseofcommercialpropertyinvolvesagreeingthetermsofacontractforsaleoftheproperty,thepaymentofadeposit(typically10%oftheoverallpurchaseprice)uponsigningofthecontract,followedsomeweekslaterbytheexecutionofthedeedsoftransferandpaymentofthebalancepurchasemonies.Thepurchaseofpropertycantakeanumberofmonthsfromthedateofaninitialoffertoformalcompletion.

what is the process for the leasing of commercial property?

Asanalternativetopurchasingpremises,businessesoftenopttoleasecommercialproperty,withtheflexibilityofnegotiatingatermwhichalignstotheirbusinessplans.While5yearleasesarecommonplaceforsmallofficespace,tenantsoflargerspacestendtotakeleasesfortermsrangingfrom10to20years.

Thereisnoautomaticrightto“break”thelease.However,itmaybepossibletonegotiateanentitlementtoterminatethelease,knownasa“breakclause”,normallymidwaythroughtheterm.Landlordsmayseekpaymentofacompensatorypenaltyforgrantingthebreakclause.Otherinducementswhichmaybeofferedtoprospectivetenantsincluderentfreeperiods,capitalcontributionsandfitoutallowances.

Rentreviewsnormallyoccurat5yearlyintervals.InIreland,upuntil28February2010,rentreviewswere“upwardsonly”,resultingintherenteitherincreasingifthemarketratewashigherorremainingthesamewhenthemarketratewaslower.Suchprovisionsareamatterfornegotiationbetweenthelandlordandthetenant.However,since28February2010therentreviewprovisioninanynewleaseisconstruedasprovidingthatonreviewtherentmayberevisedeitherupwardsordownwards,meaningtherentpayablecandecreaseonreview.Thisappliesonlyinrespectofleasescreatedsincethatdateandnotpre-existingleases.

LeasesinIrelandareusuallyona“fullrepairingandinsuring”basis,whichmeansthetenantisliableforthefullcostofrepairingandinsuringtheproperty.

AnewpublicdatabaseknownasTheCommercialLeasesDatabasewillrecorddetailsofeverycommercialleaseinIrelandenteredintoonorafter3April2012andrentreviewsunderthoseleases.Tenantsarerequiredbylawtosubmitinformationaboutthecommercialtermsofsuchleases,anyrentreviewsandanyassignmentorterminationoftheirinterestintheleases.TheCommercialLeasesDatabasewillprovidetransparencyinthemarket.

what are the property taxation issues?stamp duty

Stampdutyispayablebythepurchaserofcommercialpropertyonthepurchasepriceattherateof2%.Onthegrantofaleasethe2%rateappliestoanypremiumpaidbythetenantforthegrantoftheleaseandthetenantmustalsopaystampdutyatarateof1%ontheannualrentforanoccupationalleasenotexceeding35yearsandhigherratesforlongerleases.

value added tax (vat)

TheamountofVATrecoveryavailableisamaterialfactorinconsideringtheVATimplicationsofleasingorpurchasingpropertyinIreland.AnewVATregimeinrespectofpropertycommencedon1July2008,includingtheintroductionofaCapitalGoodsSchemeintoIreland.SpecialistVATadviceisgenerallyrecommendedforacquisitionofaninterestinpropertyinIreland.

Ifacquiringafreeholdinterestinproperty,theageofthebuilding,itshistoryintermsofoccupationanddevelopmentandtheVATstatusofanylettingsareallfactorswhichmaygotodeterminingwhetherVATispayableonacquisitionofafreeholdinterest.EvenifVATexempt,bothpartiesmayjointlyopttochargeVATonthetransaction,currentlyattherateof13.5%.

Allleasesgrantedafter1July2008mayattractVATontherentalpayments,currentlyattherateof23%.TheLandlordhastheoptionwhetherornottochargeVATontherent.

33

rates and water charges

Ratesareaformoflocaltaxationwhichappliestocommercialpropertyonly.LocalauthoritiesinIrelandraiseratesonthebasisofpropertyvaluations(rateablevaluations)providedtothemonrequestbytheValuationOfficewhichistheStatepropertyvaluationoffice.Theamountpayable(whichcanbesubstantial)ispaidtothelocalauthority.Ratesarenormallyincreasedannuallyinlinewiththeannualrateofinflation.

Inaddition,waterchargesarepayableifwaterisbeingsuppliedforusebybusiness,tradeormanufacture.Atpresentbusinessescaneitherpayaflatrateorhavetheirwaterusagemonitoredusingameter,butinthefutureallcommercialpremiseswillberequiredtohaveameter.

Building energy rating certificate

ABuildingEnergyRating(BER)Certificate,whichshowstheenergyperformance,C02emissionandapproximaterunningcostofabuilding,mustbeprovidedtoanypersonexpressinganinterestinpurchasingorleasingabuildingbeforetheyenterintoacontractforpurchaseorlease.EachBERmustbeaccompaniedbyanAdvisoryReportwhichwillconsistofrecommendationstoimprovetheenergyperformanceofthebuilding.

when is planning permission required?

Planningpermissionisrequiredbeforelandorbuildingscanbedevelopedortheexistinguseorappearanceoflandorbuildingscanbechanged.Initialconsultationwiththelocalplanningauthorityisrecommended.Publicnoticemustbegiven,afterwhichanapplicationforplanningpermissionissubmittedbytheengineer/architecttothelocalplanningauthority.Itmayalsobenecessarytoprepareanenvironmentalimpactstatement.

Thelocalplanningauthoritymaygrantorrefuseplanningpermissionorgrantpermissionsubjecttocertainconditions(whichisquitecommon).Rightsofappealexistandmembersofthepublicmayobjectinwritingbeforeanydecisionismade.Generallyspeaking,planningpermissioncantakeupto8weekstoobtainfromthedateofcompletedsubmissionsbeingmadeand,oncegranted,isstillsubjecttoappealwithin1monthofthedecision.IfanIntegratedPollutionPreventionControl(IPPC)Licenceisrequired,thiswillalsohaveanimpactonthetimingforanyotherplanningapplications.Theappealsprocessgenerallytakesupwardsof4months,withcomplexappealsonmajorprojects(whichofteninvolveoralhearings)lastingconsiderablylonger.Planningpermissiongenerallyhasalifespanof5years,butthisperiodcanbeextendedincertaincircumstancesuponapplicationtotheplanningauthority.

Oncompletionofdevelopmentthearchitectsand(where

appropriate)engineersarerequiredtoprovideOpinionsoncompliancewithplanningpermissionandbuildingregulations.Thesedocumentsarerequiredasevidenceofcomplianceonanysubsequentsaleorleaseoftheproperty.

environmental consents/permits

TheEnvironmentalProtectionAgencyofIreland(EPA)operatestheinstitutionalframeworkforthecontrolofenvironmentalpollution.Dependingonthenatureoftheproject,anIPPClicencemayberequired.TheIPPClicensingregimecoversair,water,solidwasteandnoisepollution.IfanIPPClicenceisnotrequired,itmaystillbenecessarytoapplytothelocalauthorityforawaterdischargepermitoranairemissionlicence.Itisalsoobligatorytoprovideforthedisposalofanywasteproducedbytheproject.Differentregimesapplytothedisposalofhazardousandnon-hazardouswaste.

construction

Manylargescaleinwardinvestmentprojectsinvolvetheconstructionofpurposebuiltfacilitiesongreenfieldsites.Typically,thiswillinvolvetheengagementofadesignteamtocarryouteitherfrontenddesign/preliminarydesignonlyoroveralldesign.Inaddition,aconstructioncontractorwillneedtobeselectedandengagedpursuanttoaconstructioncontract.Theconstructioncontractcaneitherbeabuildonlycontract(iewithnodesigninputbythecontractor)oradesignandbuildcontractwherebythecontractordesignstheentireprojectordevelopsthefrontend/preliminarydesignalreadyundertakenbyadesignteam.Formorecomplicatedbuilds,managementcontracting,mechanicalandelectricalandturnkey/engineer,procure,construction(EPC)formsofconstructioncontractscanbeused.ThekeyfeatureofanEPC/turnkeycontractisthatthereisarelativelyonerousrisktransfertothecontractorofprice,timeandquality.

engagement of consultants

Generally,amanufacturer/inwardinvestorwillappointitsowndesignteam/consultants,includinganarchitect,quantitysurveyor,structuralengineer,mechanicalandelectricalengineerandaprojectmanager(frequentlythequantitysurveyor).Insomecases,amanufacturer/inwardinvestorwillhavetheirownbespokesophisticatedsuiteofconsultantcontractsforuseandtheywillprefertocontractdirectlywitheachmemberofthedesignteam.Itisalsopossibletocontractdirectlywithsomeoftheconsultantsonly,forexample,themechanicalandelectricalengineerandtheprojectmanagerinthecaseoftheconstructionofamanufacturingplant.Theprojectmanagerwillthenenterintosub-consultancycontractswiththerestoftheconsultantsandtakesfullresponsibilityfor

34

theirco-ordinationanddeliveryofagreedoutput.Thereisnorecent“market”templateconsultantcontractforuseintheprivatesectorinIreland,butthereareanumberofstandardtermsandconditionswhichareconsidered“market”inthisjurisdiction.

Theprojectmanagerwillusuallyhaveresponsibilityforconductingthetendering/procurementprocesswithprospectivecontractors.

engagement of the contractor

Moststraightforward“buildonly”constructionandcivilengineeringprojectsinIrelandaretypicallygovernedbythegeneralconditionsproducedbyeithertheRoyalInstituteofArchitectsofIreland(RIAI)orEngineersIreland.Thesegeneralconditionsareusuallyheavilyamendedbythepartiestoreflectwhatiscurrentlyacceptableinthemarket.Thesecontractscanalsobeamendedtobecomedesignandbuildcontracts.

Inthecaseofmorecomplicatedprojectsormechanicalandelectricalcontracts,forexample,inthepharmaceutical,informationtechnologyandenergymarkets,therearenumber

ofothertypesofcontractswhicharecommonlyused,forexample:

(a) theFIDICsuiteofcontractswhichincludesabuildonly formofcontract,adesignandbuildmechanical andelectricalcontractandaturnkey/EPCcontract (asamended);

(b) managementcontracts;and

(c) EPC/turnkeycontracts.

Internationalcompaniesfrequentlyusetheirownbespokesubcontractsforkeyspecialistelements.

energy procurement

Priorityshouldbegiventoensuringthatyourbusinesshasthemostcosteffectiveandflexiblesupplyarrangementsinplace.Itwillbenecessarytoliaisewiththeelectricityandgasnetworkoperatorsandputinplacecontractstoconnectyourbusinesspremisestotheelectricityandgasgrids.Inaddition,itisnecessarytoliaisewithlocalauthoritiesinrelationtowaterandwastewaterconnectionandwatersupply.

35

9 Intellectual Property and technology

36

SubstantialeffortshavebeenmadeatapoliticalleveltoestablishIrelandasthepreferredlocationfore-commerceandothertechnologyindustriesandtherehasbeenheavyGovernmentinvestmentinthearea.

the patent protection regime

PatentprotectioninIrelandwill(a)inthecaseofafull-termpatent,lastforaperiodof20yearsfromthedateoffiling,and(b)inthecaseofashort-termpatent,lastforaperiodof10yearsfromthedateoffiling,subjecttothepaymentofrenewalfees.

AlthoughIrishpatentlegislationspecificallyexcludes“computerprograms”frompatentability,thisexclusionhadbeeninterpretedverynarrowly.AswiththeEuropeanPatentConvention(seebelow),theIrishPatentOfficehaspermittedcomputersoftwaretobepatentedprovideditmeetsthegeneralcriteriaforpatentabilityunderthePatentAct1992.

IrelandhasratifiedtheEuropeanPatentConvention(EPC)andthePatentCo-OperationTreaty(PCT).PatentscanthereforebeappliedforthroughthePCTsystem,theEPCsystem,orthroughtheIrishPatentsOffice.TheEPCsystemenablesapplicantstosecurepatentrightsinanumberofEuropeancountriesbywayoffilingasingleapplicationtotheEuropeanPatentOffice.Whengranted,thisapplicationresultsinabundleofnationalpatentsineachofthecountrieswhichtheapplicanthasdesignated.ThePCTsystemoperatesinasimilarmannertotheEPCsystem,allowingforasingleapplicationdesignatingasmanymemberstatesasdesiredandresultinginthegrantofabundleofnationalpatents.

Inaddition,IrelandhasbeenasignatorytoTheInternationalConventionfortheProtectionofIndustrialProperty(“theParisConvention”)since1925,pursuanttowhicheachConventioncountrymustgrant,asregardsintellectualpropertyrights,thesameprotectiontonationalsofallotherConventioncountriesasitgrantstoitsownnationals.

copyright in ireland

IrishcopyrightlawisinlinewiththecopyrightlawsofmanyotherEUcountrieswithprovisionformoralrights,performersrights,rentalandlendingrightsanddatabaserights(seebelow).Irishlawalsospecificallyprotectscopyrightincomputersoftware,asaliterarywork.

TherearenoregistrationformalitiesinIrelandinordertoobtaincopyrightprotection.Thestatutoryperiodofprotectionformostcopyrightworkslasts,inthemain,untiltheexpirationof70yearsafterthedateofdeathoftheauthor.

InadditiontobeingasignatorytotheParisConvention(seeabove),IrelandisalsoasignatorytotheBerneConventionfor

theProtectionofLiteraryandArtisticWorks,pursuanttowhichworksoriginatingin1ConventioncountryaregiventhesameprotectioninallotherConventioncountriesastheygranttoworksoftheirownnationals.

are databases protected in ireland?

TheEUDirectiveonthelegalprotectionofdatabaseshasbeenimplementedinIreland.Irishlawprovidesthatcopyrightsubsistsinoriginaldatabases,theperiodofprotectionlastinguntil70yearsafterthedeathoftheauthor,irrespectiveofthedateonwhichtheworkisfirstlawfullymadeavailabletothepublic.Databases(irrespectiveofwhetherthedatabaseisacopyrightwork)arealsoprotectedwheretherehasbeenasubstantialinvestmentinobtaining,verifyingorpresentingthecontentsofthedatabase.Thedatabaserightexpires15yearsfromtheendofthecalendaryearinwhichthemakingofthedatabasewascompleted.

is there legislation on industrial designs?

IrishlawgiveseffecttoDirective98/71/EContheLegalProtectionofDesignsandtotheGenevaActofTheHagueAgreementconcerningtheInternationalRegistrationofIndustrialDesigns.Protectionforregistereddesignslastsforamaximumperiodof25years,renewableat5-yearintervals.

Inaddition,IrelandbenefitsfromtheintroductionoftheRegisteredCommunityDesignRightandtheUnregisteredCommunityDesignRight,whichwereintroducedintoIrelandin2002.

TheRegisteredCommunityDesignsystemoffersasingleunitaryrightcoveringallMemberStatesoftheEU.Thesubstantiverequirementsforvalidregistrationarethatthedesignmustbenewandmusthaveindividualcharacter.Thetotaltermofprotectionis25years,renewableat5-yearintervals.

ThesubstantiverequirementsforprotectionaregenerallythesameasfortheRegisteredCommunityDesign,exceptthatinthiscasenoregistrationisrequired.AnunregisteredCommunityDesignRightexistsforaperiodof3yearsfromthedatethedesignisfirstmadeavailabletothepublicwithintheEUinsuchawaythat,inthenormalcourseofbusiness,thedisclosurecouldreasonablyhavebecomeknowntothecirclesspecialisedinthesectorconcerned,operatingwithintheEU.

Inaddition,IrelandhasimplementedtheDirectiveontheLegalProtectionofTopographiesofSemiconductorProducts(87/54/EEC),whichaffordsprotectiontothedesignandthelayoutoftheelementscomposingasemi-conductorproduct.Therighttoprotectiongenerallycommenceswhenthetopographyisfirstfixedorencodedandlastsfor10years.

37

can we fully protect our trade marks in ireland?

Anownerofatrademark,servicemarkorlogomayseekprotectionunderIrishstatutebyregisteringthemark/logoontheIrishTradeMarksRegistry.Aregistrationlastsforaperiodof10yearsandcanberenewedforfurther10-yearperiodsprovidedtherenewalfeeispaid.

WhilststatutoryprotectionextendsonlytothejurisdictionofIreland,Irelandis1oftheEUMemberStatesinwhichaCommunityTradeMark(registeredintheOfficeforHarmonisationoftheInternalMarketinAlicante,Spain),ifregistered,willbeeffective.

Also,IrelandhasratifiedtheMadridProtocol.ThisProtocolallowsforasingleapplicationforatrademarkregistrationtobefiledattheTradeMarkRegistryofanycountrywhichisapartytotheProtocolandtorequestthattheapplicationbeextendedtosuchothercountrieswhichareapartytotheProtocolastheapplicantmaydesignate.

Aninternationalregistrationproducesthesameeffectsasanapplicationforregistrationofthemarkmadeineachofthecountriesdesignatedbytheapplicant.