DOING BUSINESS IN INDIA - eepcindia.com · Doing Business in India ... Today, the FDI policy in...

56

INDIA DOING BUSINESS IN EEPC INDIA ‘DOING BUSINESS’ SERIES

Transcript of DOING BUSINESS IN INDIA - eepcindia.com · Doing Business in India ... Today, the FDI policy in...

INDIADOING BUSINESS IN

EEPC INDIA ‘DOING BUSINESS’ SERIES

INDIADOING BUSINESS IN

EEPC INDIA ‘DOING BUSINESS’ SERIES

Disclaimer: Neither EEPC India nor any person acting on behalf of the Council is responsible for the use which might be made of the following information.

Doing Business in India© EEPC India November 2014

EEPC India Doing Business Series | 5

Doing Business in India

INDIA IS POISED TO BECOME A $2 TRILLION ECONOMY this year, while its GDP size would cross another milestone of $3 trillion after five years in 2019. Latest data from the International Monetary Fund (IMF) show that the Indian economy is set to be worth $2.05 trillion this year, increasing its size from $1.88 trillion in 2013.

After relaxing a number of foreign direct investment (FDI) norms earlier this year, India has emerged as the most attractive destination for investment, ac-cording to a new report by leading consultancy firm Ernst and Young (EY). In-dian markets have significant potential and offer prospects of high profitability and favourable regulatory regime for investors.

The infrastructure sector is a focus area with over $1 trillion envisaged to be in-vested on infrastructure in coming years. The government of India has facilitated 100 percent FDI under the automatic route for port development projects.

The report has highlighted details regarding India’s existing tax structure, FDI policy, trade, etc. It also includes details of Indian engineering industry.

I am certain that this report will be a valuable reference for global businesses and investors in doing business with India.

Anupam Shah Chairman, EEPC India

6 | EEPC India Doing Business Series

ForewordTHE GLOBAL ECONOMY seems to be on the mend. The IMF fore-casts global growth to rise from 3.3 percent in 2014 to 3.8 percent in 2015. The Indian economy also has shown an upward growth trajectory in recent months. The IMF has re-vised India’s 2014 GDP growth pro-jection marginally upwards to 5.6

percent from its July forecast of 5.4 percent. According to its flagship World Economic Outlook (WEO) Report, the growth in India is likely to increase in the remaining period of 2014 as well as entire 2015 because exports and investment will continue to pick up.

At present India is one of the fastest growing economies in the world and has emerged as a key destination for for-eign investors in recent years. It is now the world’s third-largest economy in terms of purchasing power parity, ahead of Japan and behind the US and China.

Since 1991, India has witnessed wide-ranging economic reforms in its policies governing international trade and foreign direct investment (FDI) flows which has conse-

quently led to a dramatic rise in both trade and FDI flows since then.

Today, the FDI policy in India is widely reckoned to be among the most liberal in the emerging economies and FDI up to 100 percent is allowed under the automatic route in most sectors and activities. A global survey by leading con-sultancy firm Ernst and Young (EY) has ranked India as the most attractive investment destination followed by Brazil and China at second and third positions, respectively.

This report highlights various aspects of India’s economy such as trade, investment, tax structure, visa regulations and so on. The report also identifies a list of attractive sectors for investment.

The report has been prepared for global businesses, in-vestors and international trade associations.

Bhaskar Sarkar Executive Director & Secretary, EEPC India

EEPC India Doing Business Series | 7

Doing Business in India

Contents

8 | EEPC India Doing Business Series

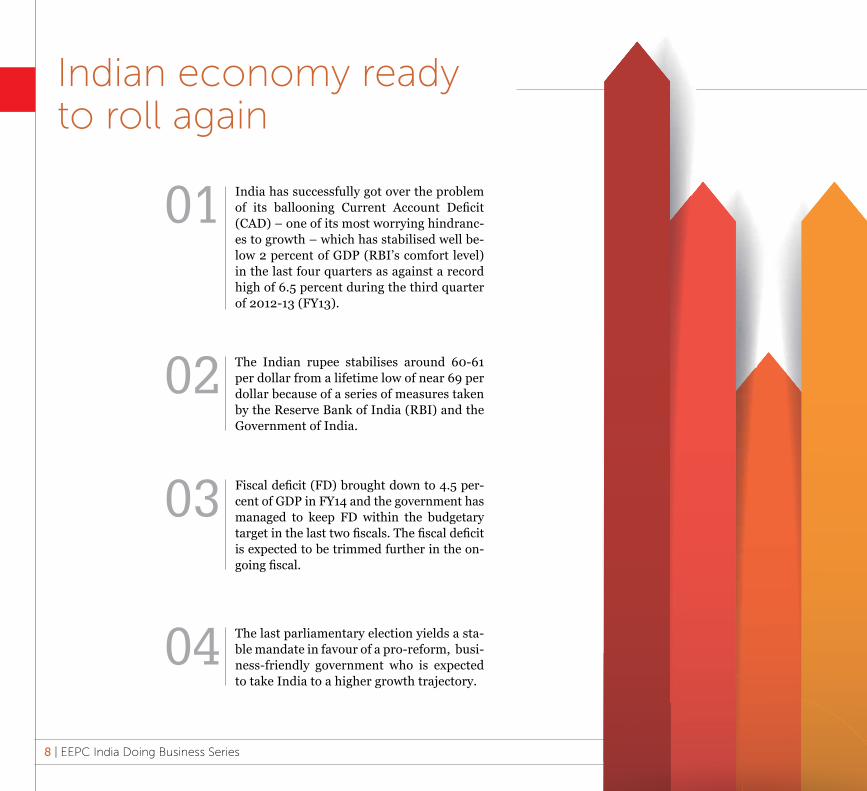

Indian economy ready to roll again

India has successfully got over the problem of its ballooning Current Account Deficit (CAD) – one of its most worrying hindranc-es to growth – which has stabilised well be-low 2 percent of GDP (RBI’s comfort level) in the last four quarters as against a record high of 6.5 percent during the third quarter of 2012-13 (FY13).

01

The Indian rupee stabilises around 60-61 per dollar from a lifetime low of near 69 per dollar because of a series of measures taken by the Reserve Bank of India (RBI) and the Government of India.

02

Fiscal deficit (FD) brought down to 4.5 per-cent of GDP in FY14 and the government has managed to keep FD within the budgetary target in the last two fiscals. The fiscal deficit is expected to be trimmed further in the on-going fiscal.

03

The last parliamentary election yields a sta-ble mandate in favour of a pro-reform, busi-ness-friendly government who is expected to take India to a higher growth trajectory.

04

EEPC India Doing Business Series | 9

Doing Business in India

The new government already shows its strong intent for aggressive economic re-form and elimination of unnecessary regula-tory laws through its ‘minimum government, maximum governance’ stand.

05

India shrugs off the threat of the downgrade of its sovereign credit rating to ‘junk’ status after the decline in CAD, stable rupee, low-er FD and expectations of reforms from the new government; rather, international rating agencies have upgraded India’s outlook to stable from negative.

06

Government focus on more disinvestments and lower subsidy will shift India’s focus solely to growth and help upgrade its credit rating.

07

Hope of an economic recovery strengthens with real GDP growth reaching a nine quarter high of 5.7 percent during April-June 2014 after remaining below 5 percent in seven of the previous eight quarters.

08

Consumer price inflation (CPI) or retail in-flation cools off in line with the projections of RBI. Core components of CPI has stabi-lised at lower levels bringing relief to poli-cymakers.

10

Interest rates likely to soften in early 2015 – CPI is RBI’s primary measure for framing monetary policy and once CPI comes within the target level of RBI (8 percent), India may see a downward movement of interest rate cycle from early-2015.

11

The manufacturing sector bounces back dur-ing the current fiscal after remaining vulner-able in the last fiscal. However, manufactur-ing output contracted in July 2014, driven by dismal consumer goods production, and it may take 2-3 more months for manufactur-ing to see stable growth.

09CAD shrinksIndia successfully got over the problem of its ballooning Current Account Deficit (CAD), one of the most worrying hindrances to growth which has stabilised well below 2 percent of GDP in the last four quarters against a record high of 6.5 percent during the third quarter of 2012-13

10 | EEPC India Doing Business Series

IntroductionINDIA IS THE SEVENTH-LARGEST COUNTRY by area, the second-most populous country with over 1.2 billion people, and the most populous democracy in the world. India’s economy is the third-largest in purchasing power parity (PPP) and it has the 10th-largest nominal gross domestic product (GDP) at $1.8 trillion.

India has seen a systematic transition from being a closed-door economy to an open economy since the start of economic reforms in the country in 1991. These reforms have had a far-reaching impact and have helped India unlock its enormous potential for growth.

Today, India is one of the fastest-growing economies in the world and has emerged as a key destination for foreign investors. UNC-TAD’s World Investment Prospects Survey 2012–2014 says India is the third-most attractive destination for FDI after China and the US.

India’s GDP has grown at about 7.9 percent between 2003 and 2012. This trend, according to the International Monetary Fund (IMF), is likely to continue for the next five years with an average GDP growth rate of 7.7 percent per annum till 2017. India’s GDP for 2013, valued at $1.8 trillion at current prices is the 10th-largest in the world.i

Mizoram

Odisha

Gangtok

Shimla

Bengaluru

Thiruvananthapuram

Aizawl

i http://www.investindia.gov.in

Doing Business in India

EEPC India Doing Business Series | 11

India – A snapshotCapitalNew Delhi

CoastlineIndia’s 7000-km coastline encircles the mainland and the Andaman and Nicobar and Lakshadweep islands

LocationIndia, located in South Asia, is bordered by Pakistan in the west, China and Nepal in the north to northeastern part, Bhutan in the northeast and Myanmar in the east

Languages English, Hindi (official)

Exports – partners (%) UAE (12.3), US (12.2), China (5), Singapore (4.9), Hong Kong (4.1) (2012)

Imports – commodities Crude oil, precious stones, machinery, fertiliser, iron and steel, chemicals

Imports – partners (%) China (10.7), UAE (7.8), Saudi Arabia (6.8), Switzerland (6.2), US (5.1) % (2012)

Exchange rate INR 61.6475: USD1 (as on 17 Nov 2014, RBI)

Source: CIA Factbook

GDP (official exchange rate) $1.758 trillion (2013 est.) (official)

Industries Textiles, chemicals, food processing, steel, transportation equipment, cement, mining, petroleum, machinery, software, pharmaceuticals

Exports $313.2 billion (2013 est.)

Exports – commodities Petroleum products, precious stones, machinery, iron and steel, chemicals, vehicles, apparel

Imports $467.5 billion (2013 est.)

GDP – per capita (PPP) $4000 (2013 est.)

States and Union TerritoriesIndia comprises 29 states and 7 union territories

Natural resourcesCoal (fourth-largest reserve in the world), manganese, bauxite, iron-ore, chromites, diamond, limestone, titanium ore, natural gas, petroleum and arable land

Mizoram

Odisha

Gangtok

Shimla

Bengaluru

Thiruvananthapuram

Aizawl

12 | EEPC India Doing Business Series

T HE sharp fall in imports and moderate export growth last year resulted in a sharp decline in In-dia’s trade deficit by 27.8 percent. India’s exports

grew by a little less than 4 percent in the year ending 31 March 2014, while imports dipped by over 8 percent dur-ing the period. Overall, exports grew to $312.35 billion, while imports declined to $450.94 billion.

India is the leading exporter of petroleum products, gems and jewellery, textiles, engineering goods, chemi-cals and services. The country’s main trading partners are European Union countries, United States, China and UAE. Table1 and Figure1 show India’s overall trade pattern in the past five years.

The share of the top ten countries in India’s trade basket was a little over 50 percent in 2013-14 (Figure2). Countries with a high share in India’s ex-port basket include the US, UAE, China, Hong Kong and Singapore.

Trade

Table1: India’s trade performance in the last five years ($ billion)

Trade flow 2009-10 2010-11 2011-12 2012-132013-

14

India’s total exports

178.8 251.1 306.0 300.4 313.5

India’s total imports

288.4 369.8 489.3 490.7 450.6

Balance of trade

-109.6 -118.6 -183.3 -190.3 -137.1

Total trade 467.1 620.9 795.3 791.1 764.1

Source: DGCI&S, Government of India

State-wise export performance in IndiaThe state-wise export data show the domination of two states – Gujarat at the top followed by Maharashtra – while Tamil Nadu and Karnataka are a distant third and fourth. Among the other states, Uttar Pradesh, West Ben-gal and Orissa had double-digit export growth. Table2 depicts India’s state-wise export performance.

1000

800

600

400

200

0

-200

-400

2009-10

India,s total exports

Balance of trade Total tradeIndia,s total exports

2010-11

$bill

ion

2011-12 2012-13 2013-14

Figure1: Trend of India’s trade

USA

UAEChina

SingaporeSaudi Arabia

Japan

Germany

Nether lands

UK

Hong Kong

12.5

9.74,7

4.1

4.0

3.9

3.1

2.5

2.4

2.0

0.0 2.0 4.0 6.0 8.0 12.0 14.0

Source: DGCI&S, Government of India

Figure2: India’s top 10 trade partners and their shares (%)

Source: DGCI&S, Government of India

Trade agreementsOver the years, India has signed numerous bilateral and regional trade agreements with key trading part-ners. Apart from offering preferential tariff rates on the trading of goods among member countries, these agree-ments also enable increased economic intellectual prop-erty rights, resulting in enhanced trade liberalisation.

The first free trade agreement (FTA) entered into by India was in 1975 when the Government of India signed the Bangkok Agreement. It started as a regional initiative between developing countries of the Asia-Pacific region but was very limited in its scope. It was only after it re-incarnated in 2005 as the Asia-Pacific Trade Agreement (APTA) that trade started in a meaningful way between its members – Bangladesh, China, India, Republic of Korea, Lao People’s Democratic Republic and Sri Lanka. Members of the South Asian Association for Regional Cooperation (SAARC)ii formed a PTA (SAPTA) in 1995, which was another regional initiative between the na-tions of South Asia under the ambit of SAARC. It was upgraded to an FTA (SAFTA) in 2006, though SAPTA will be in place till 2016 when tariff liberalisation under SAFTA is complete. India’s first bilateral FTA was with Sri Lanka – the India-Sri Lanka Free Trade Agreement (ISFTA). It took effect in March 2000. Subsequently, many other FTAs were signed.

Some of the existing key trade agreements entered into by India include:

| 13

Table2: State-wise export performance (US$ million)

State Exports in 2013-14

Gujarat 73,498

Maharashtra 71,661

Tamil Nadu 26,937

Karnataka 17,821

Andhra Pradesh 15,353

Uttar Pradesh 13,309

Haryana 10,657

West Bengal 10,496

Delhi 9329

Punjab 7063

Rajasthan 5915

Madhya Pradesh 4374

Kerala 4285

Orissa 4005

Source: DGCI&S, Government of India

SEZs in India

In about eight years since the SEZ Act and Rules were notified in February 2006, formal approvals have been granted to 566 SEZs, of which 388 have been notified. A total of 184 SEZs are exporting at present. Exports from the SEZs increased from Rs4,76,159 crore in 2012-13 to Rs4,94,077 crore in 2013-14, a growth of four percent in rupee terms. The total investment in SEZs till 31 March 2014 is approximately Rs2,96,663 crore includ-ing Rs2,73,379 crore in the newly-notified SEZs set up after the SEZ Act 2005. 100 percent FDI is allowed in SEZs through the automatic route.

ii Bangladesh, Bhutan, India, Maldives, Nepal, Pakistan and Sri Lanka established the South Asian Association for Regional Cooperation (SAARC) on 8 December 1985 to facilitate regional cooperation. In April 2007, at SAARC’s 14th summit, Afghanistan became its eighth member

14 | EEPC India Doing Business Series

• Comprehensive Economic Partnership Agreement (CEPA) with Japan

• Comprehensive Economic Cooperation Agreement (CECA) with Malaysia

• Comprehensive Economic Partnership Agreement (CEPA) with Korea

• India-ASEAN Trade in Goods Agreement• Comprehensive Economic Cooperation Agreement

(CECA) with Singapore• Free Trade Agreement with Sri Lanka (Trade in Goods) • Agreement on South Asia Free Trade Area executed by

India with Bangladesh, Bhutan, Maldives, Nepal, Paki-stan and Sri Lanka

• Framework Agreement with Thailand• Preferential Trade Agreement with MERCOSUR coun-

tries• Preferential Trade Agreement with Chile

• Asia-Pacific Trade Agreement with Bangladesh, Re-public of Korea, China and Sri Lanka

• Preferential Trade Agreement with Afghanistan• Global System of Trade Preference with 46 countries• India-Bhutan Trade Agreement• India-Nepal Trade Treaty• Economic Cooperation Agreement with Finland

Trade agreements under negotiationSome of India’s key prospective trade agreements that are currently under negotiation include:• India-European Union FTA• India-ASEAN (Services and Investment) CECA• India-Thailand Comprehensive Economic Cooperation

Agreement• India-New Zealand FTA• India-European Free Trade Association FTA• India Canada Comprehensive Economic Cooperation

Agreement• India-Mauritius Comprehensive Economic Coopera-

tion and Partnership Agreement• India-South African Customs Union PTA• India-Sri Lanka FTA (to be expanded to include ser-

vices and investment)• Bay of Bengal Initiative for Multi-sectoral Technical

and Economic Cooperation• India-Gulf Cooperation Council FTA• India-Australia Comprehensive Economic Coopera-

tion Agreement• India-Israel FTA• India-MERCOSUR PTA (scope to be expanded)• India-Chile PTA (scope to be expanded)

India’s first FTAThe first free trade agreement (FTA) entered into by India was in 1975 when the Government of India signed the Bangkok Agreement. It started as a regional initiative between developing countries of the Asia-Pacific region but was very limited in its scope. It was only after it reincarnated in 2005 as the Asia-Pacific Trade Agreement (APTA) that trade started in a meaningful way between its members

EEPC India Doing Business Series | 15

Doing Business in India

‘Make in India’ initiativeThe new Government has launched an ambitious campaign “Make in India” which aims to turn the country into a global manufacturing hub. It includes cutting red tape, developing infrastructure and making it easier for companies to do business. The following sectors have been included by the Government in this campaign.

Automobile, auto-components, automobile components, aviation, biotechnology, chem-icals, construction, defence manufacturing, electrical machinery, electronic systems, food processing, IT and BPM, leather, media and entertainment, mining, oil and gas, pharma-ceuticals, ports, railways, renewable energy, roads and highways, space, textiles and gar-ments, thermal power, tourism and hospitality and wellness.

16 | EEPC India Doing Business Series

INDIA’s infrastructure has been improving: • The domestic telecom sector is the second-largest in the world, after China. The country’s wireless and

wire line subscriber base stood at 867.8 million and 30.2 million, respectively.• The installed capacity of power increased by 12 percent

y-o-y to 223,343.6 MW• The capacity of refineries stood at 215 MT• Many infrastructure facilities in other sectors such as

railways, airways and ports are also being either con-structed or revamped to support higher capacity.In order to support infrastructure development in the

12th Five-Year Plan period, the Government of India has envisaged an investment of $1 trillion. The private sector is expected to play a major role in sectors such as power, airports, metro-rail and roads.

According to the World Economic Forum’s Global Competitiveness Report 2012-13, India’s ranking im-proved in many infrastructure subsectors (including ports and power supply). The country fares well in rail-road infrastructure with a ranking of 27/144, followed by airways with a ranking of 68/144. It is expected that continued government support will lead to expansion in infrastructure and improved ranks.

Infrastructure

EEPC India Doing Business Series | 17

Doing Business in India

Mizoram

Odisha

Gangtok

Shimla

Bengaluru

Surendranagar

Nandurbar

JN Port

Thiruvananthapuram

Aizawl

Nasik

Anand

Ahmedabad

Udaipur

Chittaurgarh

Bhilwara

Jodhpur

Dausa

DadriAligarh

Alwar

New Delhi

HisarBhiwani

KarnalMuza�arnagarMeerut

Godhra

Surat

AjmerAjmer

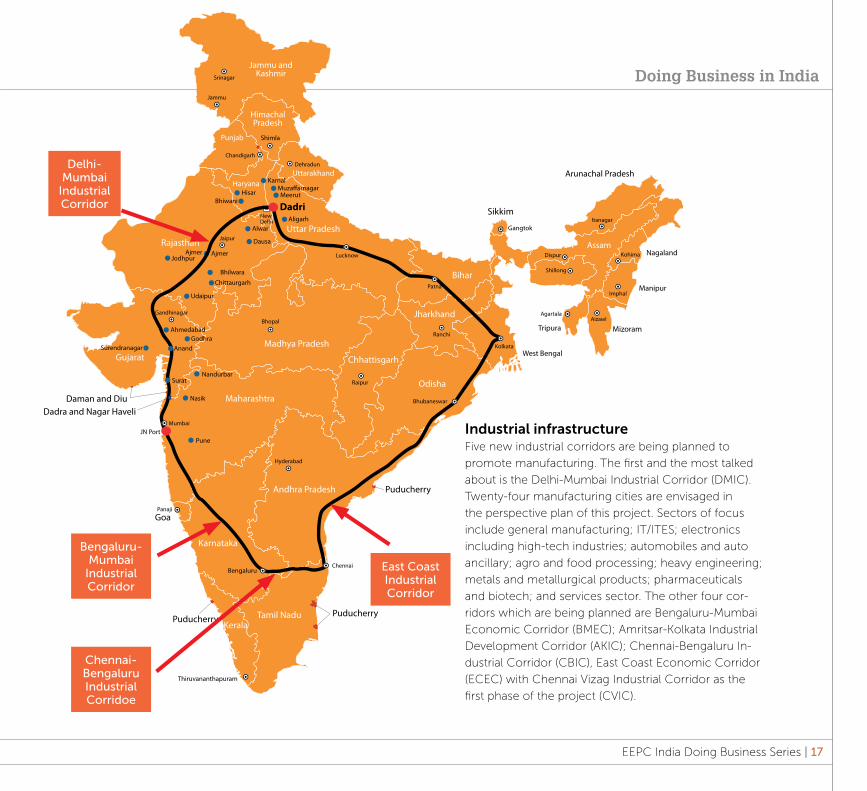

PuneIndustrial infrastructureFive new industrial corridors are being planned to

promote manufacturing. The first and the most talked

about is the Delhi-Mumbai Industrial Corridor (DMIC).

Twenty-four manufacturing cities are envisaged in

the perspective plan of this project. Sectors of focus

include general manufacturing; IT/ITES; electronics

including high-tech industries; automobiles and auto

ancillary; agro and food processing; heavy engineering;

metals and metallurgical products; pharmaceuticals

and biotech; and services sector. The other four cor-

ridors which are being planned are Bengaluru-Mumbai

Economic Corridor (BMEC); Amritsar-Kolkata Industrial

Development Corridor (AKIC); Chennai-Bengaluru In-

dustrial Corridor (CBIC), East Coast Economic Corridor

(ECEC) with Chennai Vizag Industrial Corridor as the

first phase of the project (CVIC).

East Coast Industrial Corridor

Chennai-Bengaluru Industrial Corridoe

Bengaluru-Mumbai

Industrial Corridor

Delhi-Mumbai

Industrial Corridor

18 | EEPC India Doing Business Series

Urban infrastructureTo develop India’s urban infrastructure, the new Govern-ment is focusing on following key areas:A. Smart CitiesB. Digital India C. Affordable housingD. Swachh Bharat project

A. Smart citiesIn an ambitious plan to upgrade urban India, the new Government in India announced to establish 100 smart cities across the nation. The five main elements of the proposed smart cities identified by the Urban Develop-ment Ministry, Government of India are:1. In terms of infrastructure, the smart cities should have 24x7 availability of high quality utility services like water and power;2. A robust transport system that emphasizes on public transport is also a key element;3. In social infrastructure, the cities should provide op-portunities for jobs and livelihoods for its inhabitants;4. The smart cities should also have proper facilities for entertainment and the safety and security of the people. State-of-the-art health and education facilities are also a must;5. The smart cities should minimize waste by increas-ing energy efficiency and reducing water conservation. Proper recycling of waste materials must be done in such cities.

B. Digital IndiaDigital India is another major initiative of Government of India to transform India into digital empowered so-ciety and knowledge economy. Three key areas of this

project are (also see graphic on opposite page): • Digital Infrastructure as a Utility to Every Citizen;• Governance & Services on Demand; and• Digital Empowerment of Citizens.

C. Affordable housing• The Government has announced to set up a Mission on

Low Cost Affordable Housing anchored in the National Housing Bank (NHB).

• A sum of Rs. 4,000 crore for NHB is provided with a view to increase the flow of cheaper credit for afford-able housing

• Projects which commit at least 30% of total project cost for low cost affordable housing to be exempted from the built-up and capitalization conditions

D. Swachh Bharat • The Government also intends to cover every household

by total sanitation by the year 2019, the 150th year of the Birth anniversary of Mahatma Gandhi through Swachh Bharat Abhiyan.

EEPC India Doing Business Series | 19

Doing Business in India

1. BROADBAND HIGHWAYS

2. UNIVERSAL ACCESS TO PHONES

3. PUBLIC INTERNET ACCESS PROGRAMME

4. E-GOVERNANCE – REFORMING GOVERNMENT THROUGH TECHNOLOGY

5. EKRANTI – ELECTRONIC DELIVERY OF SERVICES

6. INFORMATION FOR ALL

7. ELECTRONICS MANUFACTURING – TARGET NET ZERO IMPORTS

8. IT FOR JOBS

9. EARLY HARVEST PROGRAMMES

The plan for Digital India

Today, India is one of the fastest-growing economies in the world and has emerged as a key destination for foreign investors. UNCTAD’s World Investment Prospects Survey 2012–2014 says India is the third-most attractive destination for FDI, after China and the US

22 | EEPC India Doing Business Series

Investment

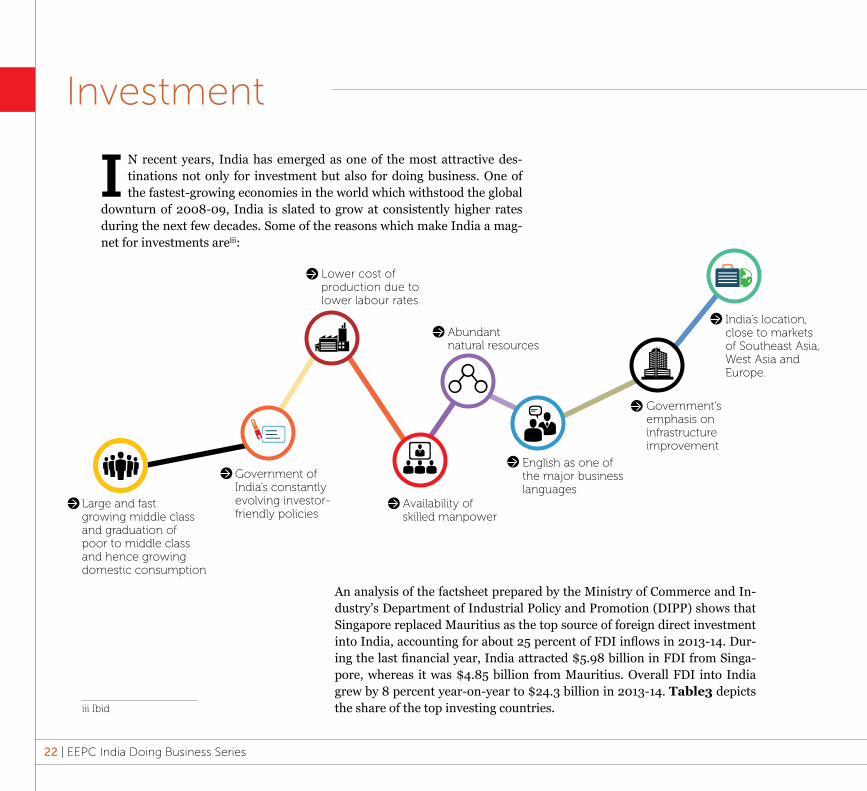

I N recent years, India has emerged as one of the most attractive des-tinations not only for investment but also for doing business. One of the fastest-growing economies in the world which withstood the global

downturn of 2008-09, India is slated to grow at consistently higher rates during the next few decades. Some of the reasons which make India a mag-net for investments areiii:

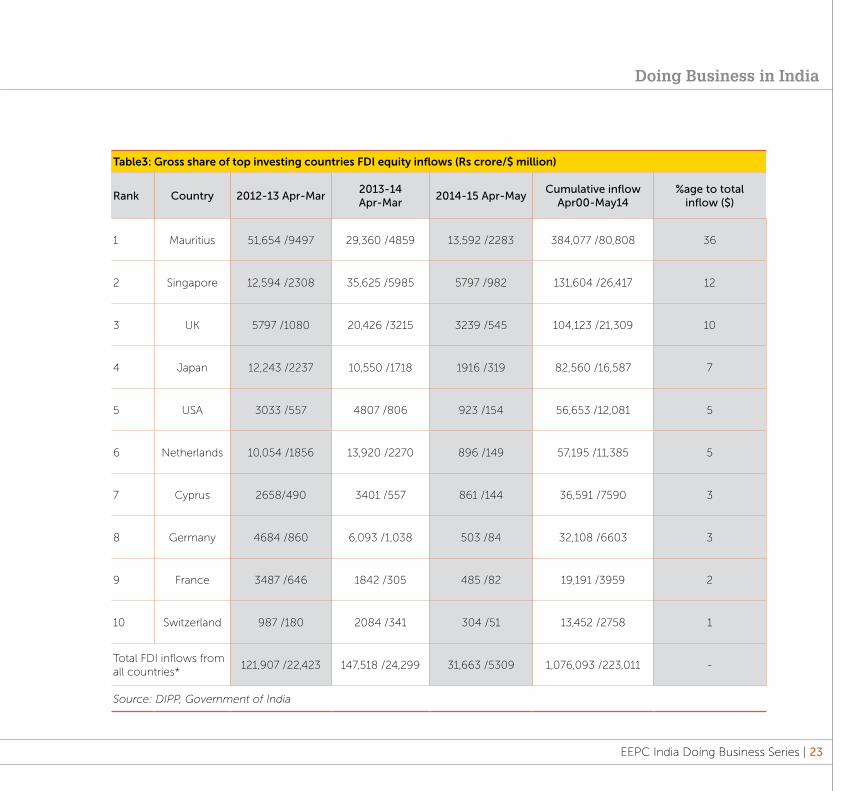

An analysis of the factsheet prepared by the Ministry of Commerce and In-dustry’s Department of Industrial Policy and Promotion (DIPP) shows that Singapore replaced Mauritius as the top source of foreign direct investment into India, accounting for about 25 percent of FDI inflows in 2013-14. Dur-ing the last financial year, India attracted $5.98 billion in FDI from Singa-pore, whereas it was $4.85 billion from Mauritius. Overall FDI into India grew by 8 percent year-on-year to $24.3 billion in 2013-14. Table3 depicts the share of the top investing countries.

Large and fast growing middle class and graduation of poor to middle class and hence growing domestic consumption

Government of India’s constantly evolving investor-friendly policies

Lower cost of production due to lower labour rates

Availability of skilled manpower

English as one of the major business languages

Government’s emphasis on infrastructure improvement

India’s location, close to markets of Southeast Asia, West Asia and Europe.

Abundant natural resources

iii Ibid

EEPC India Doing Business Series | 23

Doing Business in India

Table3: Gross share of top investing countries FDI equity inflows (Rs crore/$ million)

Rank Country 2012-13 Apr-Mar2013-14 Apr-Mar

2014-15 Apr-MayCumulative inflow

Apr00-May14%age to total

inflow ($)

1 Mauritius 51,654 /9497 29,360 /4859 13,592 /2283 384,077 /80,808 36

2 Singapore 12,594 /2308 35,625 /5985 5797 /982 131,604 /26,417 12

3 UK 5797 /1080 20,426 /3215 3239 /545 104,123 /21,309 10

4 Japan 12,243 /2237 10,550 /1718 1916 /319 82,560 /16,587 7

5 USA 3033 /557 4807 /806 923 /154 56,653 /12,081 5

6 Netherlands 10,054 /1856 13,920 /2270 896 /149 57,195 /11,385 5

7 Cyprus 2658/490 3401 /557 861 /144 36,591 /7590 3

8 Germany 4684 /860 6,093 /1,038 503 /84 32,108 /6603 3

9 France 3487 /646 1842 /305 485 /82 19,191 /3959 2

10 Switzerland 987 /180 2084 /341 304 /51 13,452 /2758 1

Total FDI inflows from all countries*

121,907 /22,423 147,518 /24,299 31,663 /5309 1,076,093 /223,011 -

Source: DIPP, Government of India

24 | EEPC India Doing Business Series

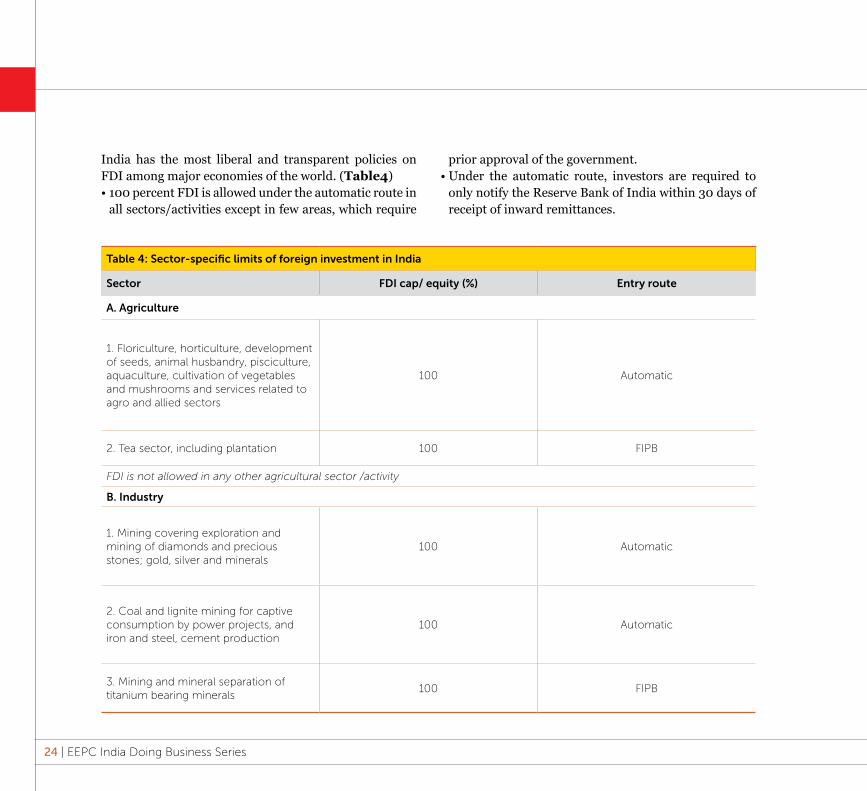

India has the most liberal and transparent policies on FDI among major economies of the world. (Table4)• 100 percent FDI is allowed under the automatic route in

all sectors/activities except in few areas, which require

prior approval of the government. • Under the automatic route, investors are required to

only notify the Reserve Bank of India within 30 days of receipt of inward remittances.

Table 4: Sector-specific limits of foreign investment in India

Sector FDI cap/ equity (%) Entry route

A. Agriculture

1. Floriculture, horticulture, development of seeds, animal husbandry, pisciculture, aquaculture, cultivation of vegetables and mushrooms and services related to agro and allied sectors

100 Automatic

2. Tea sector, including plantation 100 FIPB

FDI is not allowed in any other agricultural sector /activity

B. Industry

1. Mining covering exploration and mining of diamonds and precious stones; gold, silver and minerals

100 Automatic

2. Coal and lignite mining for captive consumption by power projects, and iron and steel, cement production

100 Automatic

3. Mining and mineral separation of titanium bearing minerals

100 FIPB

EEPC India Doing Business Series | 25

Doing Business in India

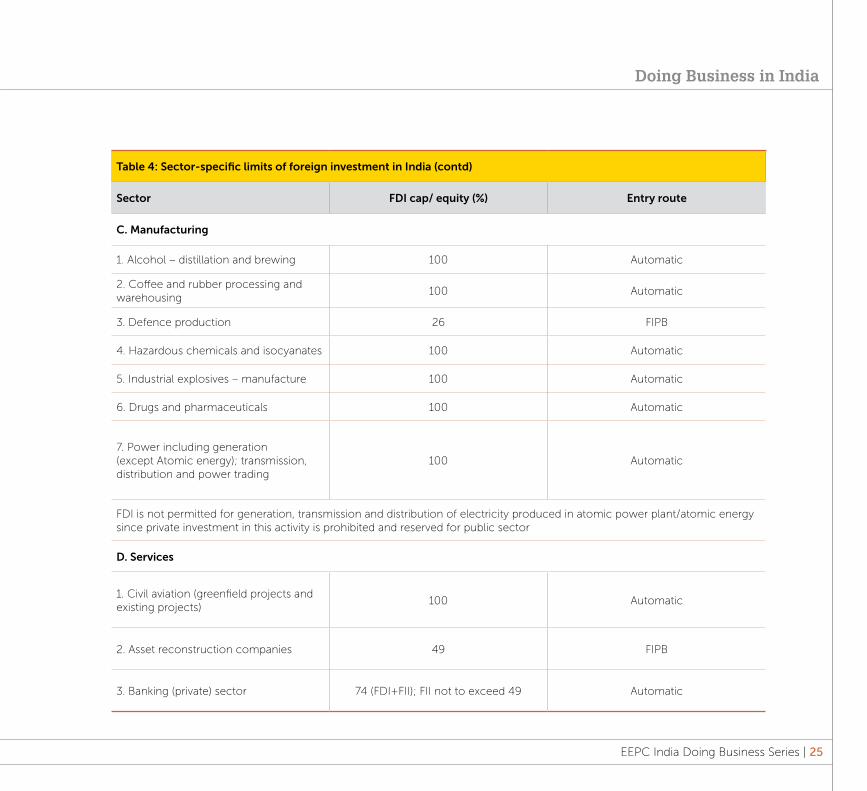

Table 4: Sector-specific limits of foreign investment in India (contd)

Sector FDI cap/ equity (%) Entry route

C. Manufacturing

1. Alcohol – distillation and brewing 100 Automatic

2. Coffee and rubber processing and warehousing

100 Automatic

3. Defence production 26 FIPB

4. Hazardous chemicals and isocyanates 100 Automatic

5. Industrial explosives – manufacture 100 Automatic

6. Drugs and pharmaceuticals 100 Automatic

7. Power including generation (except Atomic energy); transmission, distribution and power trading

100 Automatic

FDI is not permitted for generation, transmission and distribution of electricity produced in atomic power plant/atomic energy since private investment in this activity is prohibited and reserved for public sector

D. Services

1. Civil aviation (greenfield projects and existing projects)

100 Automatic

2. Asset reconstruction companies 49 FIPB

3. Banking (private) sector 74 (FDI+FII); FII not to exceed 49 Automatic

26 | EEPC India Doing Business Series

Table 4: Sector-specific limits of foreign investment in India (contd)

Sector FDI cap/ equity (%) Entry route Other conditions

4. NBFCs: Underwriting, portfolio management services, investment advisory services, financial consultancy, stock broking, asset management, venture capital, custodian, factoring, leasing and finance, housing finance, forex broking, etc

100 AutomaticST minimum capitalisation

norms

5. Broadcasting

a. FM Radio 20 FIPB

b. Cable network; c. Direct to home; d. Hardware facilities such as up-linking, HUB

49 (FDI+FII)

e. Up-linking a news and current affairs TV channel

100

6. Commodity exchanges 49 (FDI+FII); (FDI 26 FII 23) FIPB

7. Insurance 26 Automatic Clearance from IRDA

8. Petroleum and natural gas

49 (PSUs) FIPB (PSUs)

a. Refining 100 (pvt. companies) Automatic (pvt.)

EEPC India Doing Business Series | 27

Doing Business in India

Table 4: Sector-specific limits of foreign investment in India (contd)

Sector FDI cap/ equity (%) Entry route Other conditions

9. Print Media

FIPBST guidelines by the

Ministry of Information and Broadcasting

a. Publishing of newspaper and periodicals dealing with news and current affairs

26

b. Publishing of scientific magazines/speciality journals/periodicals

100

10. Telecommunications

74 (including FDI, FII, NRI, FCCBs, ADRs/GDRs, convertible preference

shares, etc

Automatic up to 49 and FIPB beyond 49

a. Basic and cellular, unified access services, national/international long-distance, V-SAT, public mobile radio trunked services (PMRTS), global mobile personal communication services (GMPCS) and others

Source: Reserve Bank of India

Sectors where FDI is bannedFDI is prohibited under the government route as well as the automatic route in the following sectors:• Atomic energy• Lottery business• Gambling and betting• Business of chit fund• Nidhi company• Agricultural (excluding floriculture, horticulture, de-

velopment of seeds, animal husbandry, pisciculture and cultivation of vegetables, mushrooms, etc. under controlled conditions and services related to agro and allied sectors) and plantations activities (other than tea plantations)

• Housing and real estate business (except development of townships, construction of residential/commercial

premises, roads or bridges• Trading in transferable development rights (TDRs)• Manufacture of cigars, cheroots, cigarillos and ciga-

rettes, of tobacco or of tobacco substitutes• Source: Reserve Bank of India

Modes of payment for FDI in Indian companyAn Indian company issuing shares/convertible deben-tures under FDI to a person resident outside India shall receive the amount of consideration required to be paid for such shares/convertible debentures by:• Inward remittance through normal banking channels• Debit to NRE/FCNR account of person concerned

maintained with an AD category I bank• Conversion of royalty/lump sum/technical knowhow

fee due for payment or conversion of ECB shall be

28 | EEPC India Doing Business Series

treated as consideration for issue of shares• Conversion of import payables/pre-incorporation ex-

penses/share swap can be treated as consideration for issue of shares with the approval of FIPB

• Debit to non-interest bearing Escrow account in Indi-an Rupees in India which is opened with the approval from AD Category – I bank and is maintained with the AD Category I bank on behalf of residents and non-residents towards payment of share purchase consid-eration.If the shares or convertible debentures are not issued

within 180 days from the date of receipt of the inward remittance or date of debit to NRE/FCNR(B)/Escrow ac-count, the amount shall be refunded. Further, Reserve Bank may on an application made to it and for sufficient reasons permit an Indian company to refund/allot shares for the amount of consideration received towards issue of security if such amount is outstanding beyond the period of 180 days from the date of receipt.Source: Reserve Bank of India

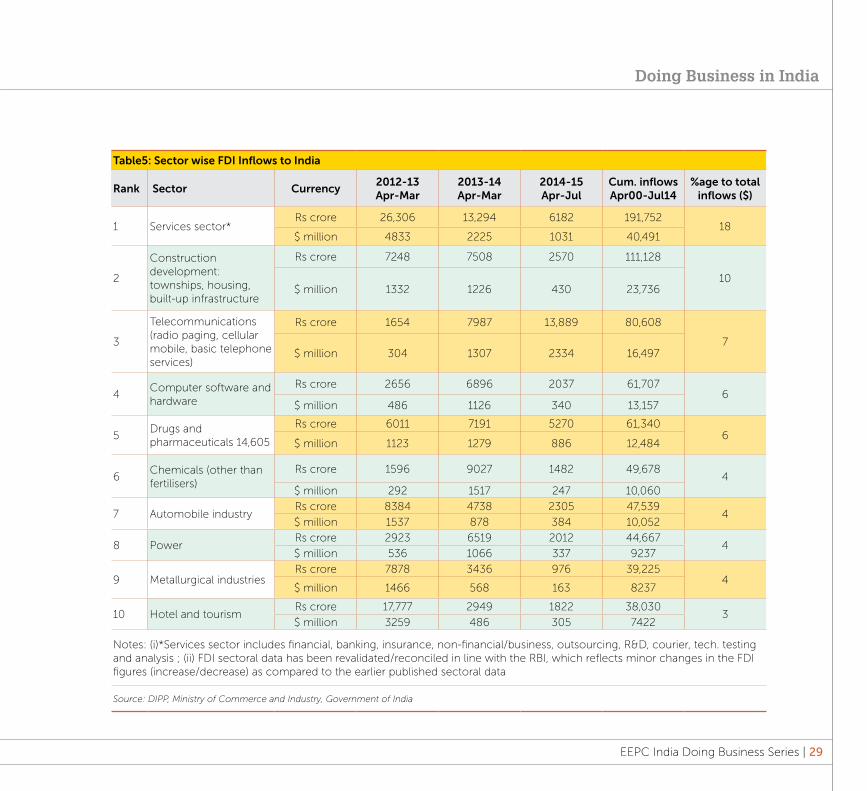

Sector-wise FDI inflowFrom a sectoral perspective, FDI in India mainly flowed into the services sector (with an average share of 40 percent) fol-lowed by the manufacturing sector. Table 5 depicts sectoral information on the recent trends in FDI flows to India.

FDI in the automobile industry has experienced huge growth in the past few years. The increase in the demand for cars and other vehicles is powered by the increase in the levels of disposable income in India. The options have increased with quality products from foreign car manufacturers. The introduction of tailor-made finance schemes and easy repayment schemes has also helped the growth of the automobile sector.

For the past few years the pharmaceutical industry is also performing very well. The varied functions such as contract research and manufacturing, clinical research, research and development pertaining to vaccines are the strengths of the pharma industry in India. Multinational pharmaceutical corporations outsource these activities and help the growth of the sector. The Indian pharmaceu-tical industry has been experiencing a vast inflow of FDI.

FDI inflow in the cement industry has increased with some of the Indian cement giants merging with major ce-ment manufacturers in the world such as Holcim, Hei-delberg, Italcementi, Lafarge, etc. FDI in the semicon-ductor sector was crucial for the development of the IT and the ITES sector in India. Electronic hardware is the major component of several industries such as informa-tion technology, telecommunication, automobiles, elec-tronic appliances and special medical equipment.

State-wise FDI inflowIndia aims to enter a new era of inclusive growth – though it might take longer to experience fully-inclusive growth, significant progress will be visible in terms of growth per-colating to a larger section of the society during the cur-rent decade. Some of the potential Indian states that can contribute significantly to India’s growth story during the current decade include Maharashtra, Gujarat, Andhra Pradesh and Tamil Nadu.

Maharashtra, Dadra and Nagar Haveli, Daman and Diu together received Rs3,20,281 crore FDI. Delhi, parts of UP and Haryana have together attracted Rs2,12,376 crore FDI. Tamil Nadu and Pondicherry have together at-tracted FDI of Rs67,964 crore. Karnataka has also shown considerable openness with FDI of Rs61,721 crore. Fol-lowing table depicts RBI regional office wise FDI data.

EEPC India Doing Business Series | 29

Doing Business in India

Table5: Sector wise FDI Inflows to India

Rank Sector Currency2012-13 Apr-Mar

2013-14 Apr-Mar

2014-15 Apr-Jul

Cum. inflows Apr00-Jul14

%age to total inflows ($)

1 Services sector* Rs crore 26,306 13,294 6182 191,752

18 $ million 4833 2225 1031 40,491

2

Construction development: townships, housing, built-up infrastructure

Rs crore 7248 7508 2570 111,128

10 $ million 1332 1226 430 23,736

3

Telecommunications (radio paging, cellular mobile, basic telephone services)

Rs crore 1654 7987 13,889 80,608

7 $ million 304 1307 2334 16,497

4Computer software and hardware

Rs crore 2656 6896 2037 61,7076

$ million 486 1126 340 13,157

5Drugs and pharmaceuticals 14,605

Rs crore 6011 7191 5270 61,3406

$ million 1123 1279 886 12,484

6Chemicals (other than fertilisers)

Rs crore 1596 9027 1482 49,6784

$ million 292 1517 247 10,060

7 Automobile industry Rs crore 8384 4738 2305 47,539

4 $ million 1537 878 384 10,052

8 Power Rs crore 2923 6519 2012 44,667

4 $ million 536 1066 337 9237

9 Metallurgical industries Rs crore 7878 3436 976 39,225

4 $ million 1466 568 163 8237

10 Hotel and tourism Rs crore 17,777 2949 1822 38,030

3 $ million 3259 486 305 7422

Notes: (i)*Services sector includes financial, banking, insurance, non-financial/business, outsourcing, R&D, courier, tech. testing and analysis ; (ii) FDI sectoral data has been revalidated/reconciled in line with the RBI, which reflects minor changes in the FDI figures (increase/decrease) as compared to the earlier published sectoral data

Source: DIPP, Ministry of Commerce and Industry, Government of India

30 | EEPC India Doing Business Series

Table6: FDI equity inflows to RBI’s regional offices – April 2000-May 2014 (Rscrore/$ million)

No.RBI regional

officeStates covered

2012-13 Apr-Mar

2013-14 Apr-Mar

2014-15 Apr-May

Cum. inflows Apr00-May14

%age to total inflows ($)

1 MumbaiMaharashtra, Dadra/

Nagar Haveli, Daman/Diu

47,359 /8716 20,595 /3420 6192 /1038 320,281 /67,795

30

2 New DelhiDelhi, parts of UP,

Haryana17,490 /3222 38,190 /6242 5605 /936

212,376 /43,472

20

3 ChennaiTamil Nadu, Pondicherry

15,252 /2807 12,595 /2116 2558 /429 67,964 /13,625 6

4 Bangalore Karnataka 5,553 /1023 11,422 /1892 854 /142 61,721 /12,819 6

5 Ahmedabad Gujarat 2676 /493 5282 /860 526 /88 44,908 /9599 4

6 Hyderabad Andhra Pradesh 6290 /1159 4,024 /678 992 /166 41,906 /8811 4

7 KolkataWest Bengal, Sikkim, Andaman/Nicobar

Islands2319 /424 2659 /436 143 /24 13,307 /2766 1

8 ChandigarhChandigarh, Punjab, Haryana, Himachal

Pradesh255 /47 562 /91 15 /3 6142 /1295 0.6

9 BhopalMadhya Pradesh,

Chattisgarh1208 /220 708 /119 0 /0 5495 /1115 0.5

EEPC India Doing Business Series | 31

Doing Business in India

Table6: FDI equity inflows to RBI’s regional offices – April 2000-May 2014 (Rscrore/$ million) (contd)

No.RBI regional

officeStates covered

2012-13 Apr-Mar

2013-14 Apr-Mar

2014-15 Apr-May

Cum. inflows Apr00-May14

%age to total inflows ($)

10 Kochi Kerala, Lakshadweep 390 /72 411 /70 41 /7 4773 /988 0.4

11 Panaji Goa 47 /9 103 /17 2 /0.3 3658 /789 0.4

12 Jaipur Rajasthan 714 /132 233 /38 53 /9 3611 /732 0.3

13 Bhubaneshwar Orissa 285 /52 288 /48 20 /3 1926 /392 0.2

14 KanpurUttar Pradesh,

Uttaranchal167 /31 150 /25 108 /18 1873 /390 0.2

15 Guwahati

Assam, Arunachal Pradesh, Manipur,

Meghalaya, Mizoram, Nagaland, Tripura

27 /5 4 /0.6 0 /0 352 /79 0

16 Patna Bihar, Jharkhand 41 /8 9 /1 29 /5 228 /44 0

17 Jammu Jammu and Kashmir 0 /0 1 /0.2 25 /4 26 /4 0

18 Region not indicated 21,833 /4004 50,283 /8245 14,500 /2437 285,016 /58,176

26.1

Subtotal121,907 /22,424

147,518 /24,299

31,663 /5309 1,075,560 /222,890

100

19 RBI’s NRI schemes 2000-02 0 0 0 533 /121 -

Grand total121,907 /22,424

147,518 24,299

31,663 /5309 1,076,093 /223,011

-

Source: The region-wise FDI inflows are classified as per RBI’s Regional Office received FDI inflows, furnished by RBI, Mumbai

Attractive sectors for investment

AEROSPACE AND DEFENCE India’s national budget for 2012-

13 pegged the defence outlay at $35.16 billion. Of this, capital

expenditure, which primarily caters to acquisition of defence hardware

and modernisation requirements of defence services, accounted for

$14.47 billion.

CAPITAL MARKETS The Indian capital market has made significant progress over the last decade, which spans several dimensions of development such as accessibility, regulatory framework, market infrastructure, transparency, liquidity and the types of instru-ments available. All these factors have culminated in the emergence of a much deeper and resilient primary as well as secondary capital markets in India.

AUTOMOTIVE The Indian automobile industry

was estimated to have a total turn-over of $74 billion for the 12-month

period ending 31 March 2012.

BANKING Financial markets in India have ac-

quired enhanced depth and liquidity over the years. However, in recent

times, weak global economic pros-pects and continuing uncertainties in

the financial market have impacted emerging market economies, leading to constraints in availability of funding

for banks and corporate entities.

LIFE SCIENCES (PHARMACEUTICAL, MEDICAL DEVICES AND EQUIPMENTS AND DRUGS) The Indian pharmaceutical market is highly frag-mented with the top 10 players accounting for nearly 38 percent of total sector revenues, which was estimated at $21.5 billion in 2011. India is the fourth-largest medical device industry in Asia after Japan, China and South Korea. The Indian industry was valued at $2.4 billion in 2010, growing at a CAGR of 12 percent for 2007-10.

32 | EEPC India Doing Business Series

INFORMATION TECHNOLOGY According to the IT Annual Report 2011-12, issued by the Department of Information Technology, it is estimated that the IT industry’s contribution to India’s GDP had increased to 7.5 percent in 2011-12, from about 7.1 percent in 2010-11. Although the IT sector is export driven, its revenues from the domestic market were also substantial – the domestic sector was esti-mated at $19 billion in 2011-12, as against $17.3 billion in 2010-11, an increase of around 9.8 percent.

INSURANCE The Indian insurance industry has undergone a major transformation over the past decade and has evolved into a considerable competitive market. The total penetration of insurance (premium as a percentage of GDP) had increased manifold from 1.90 percent in FY00 to 5.10 percent in FY11.

MEDIA AND ENTERTAINMENT India’s vibrant media and entertainment (M&E) industry provides attractive growth opportunities for global corporations. The industry was estimat-ed to have achieved a growth rate of 13 percent in 2012 to touch Rs825 billion and is projected to reach Rs1500 billion by 2016, at a CAGR of close to 15 percent.

MINING AND METALS The mineral wealth of a country is piv-otal to its industrial development. India

develops 87 minerals, which includes 4 fuels, 10 metallic, 47 non-metallic, 3 atomic and 23 minor minerals (includ-

ing building and other material).

OIL AND GAS India is the world’s fourth-largest consumer of primary energy, the

consumption of which has grown at a CAGR of 6.5 percent between 2001

and 2011 as compared to a global average of 2.7 percent.

PORTS India has 13 major ports and ap-

proximately 200 non-major ports, accounting for 95 percent of the

country’s total trade in terms of vol-ume and approximately 70 percent in

terms of value.

EEPC India Doing Business Series | 33

Doing Business in India

34 | EEPC India Doing Business Series

RETAIL AND CONSUMER PRODUCTS

With an estimated market size of US$440 billion in 2011, India’s retail sector is at attractive-best for inter-

national and Indian players.

POWER AND UTILITIES India’s power generation capacity, as on 30 June 2012, according to the Ministry of Power, Govern-ment of India, was estimated at around 205.3401 gigawatt (with captive power generating capac-ity of 31.51 gigawatt), wherein the private sector contribution just exceeds 27.75 percent of the installed capacity.

REAL ESTATE The real estate sector is a key contributor to the GDP of the country and most of the fac-tors underpinning economic growth have a direct impact on the growth of the sector. With the GDP for FY13 expected to grow approximately at the rate of 7.6 percent, the real estate sector is expected to show a measured growth in the next year.

TELECOMMUNICATIONS The contribution of the telecom

sector has had a multiplier effect on socioeconomic growth due to as-

sociated individuals and businesses.

ROADS AND HIGHWAYS India has one of the largest road

networks in the world, spread across approximately 4.1 million km. Roads are the preferred mode of transpor-

tation in the country and account for 87 percent of passenger traffic and

63 percent of freight traffic.

EEPC India Doing Business Series | 35

Doing Business in India

For certain transactions listed in Schedules II and III of the Foreign Exchange Management (Current Account Transactions) (Amendment) Rules, 2009, prior approv-al of the Government of India and Reserve Bank of India is not required if the payment is made out of funds held in resident foreign currency (RFC) accounts or exchange earners’ foreign currency (EEFC) accounts of the remit-ter. Remittances for all other current account transac-tions can generally be made directly through the AD bank without any specific approval. Some of the relevant current account payments are discussed here. • Dividends: Dividends declared by an Indian com-

pany can be freely remitted overseas to foreign share-holders (net after tax deduction at source or dividend distribution tax, if any, as the case may be) without any restrictions excepting remittance of dividend requires permission when investment was allowed subject to

dividend balancing condition.

• Foreign technology collaboration: The govern-ment’s liberalised policy permits payments for royal-ty, lump-sum payment under technical collaboration agreements and payments for use of trademark/brand name under the automatic route without any restric-tions/ceilings.

• Consultancy services: Remittances up to $10 mil-lion per project for any consultancy services in respect of infrastructure projects and $1 million per project, for other consultancy services procured from outside India can be made without any prior approval of the RBI. However, no such prior approval is necessary if the remittance exceeding this ceiling is made out of an EEFC account of the remitter.

Repatriation of foreign exchange

36 | EEPC India Doing Business Series

Direct taxesIndia follows a residence based taxation system. Broadly, taxpayers may be classified as residents or non-residents. Individual taxpayers may also be classified as ‘residents but not ordinary residents.’

Kinds of taxesCorporate income-tax – Indian companyFor a domestic company, tax is levied @30 percent on its global income. Moreover, surcharge is 5 percent if the net income is in the range of Rs1 crore to Rs10 crore. If net income exceeds Rs10 crore then surcharge is 10 percent. Education cess of 2 percent and secondary and higher secondary education cess @ 1 percent is calcu-lated on income-tax and surcharge.

Minimum alternate tax (MAT)• MAT is levied at 18.5 percent of the adjusted book prof-

it for companies where income-tax payable on the total income (according to the normal provisions of the Act) is less than 18.5 percent of the adjusted book profit.

• A 5 percent surcharge is applicable in case of domes-tic companies, if the adjusted book profit exceeds Rs1 crore but does not exceed Rs10 crore. Marginal relief is available.

• A 10 percent surcharge is applicable in case of domes-tic companies, if the adjusted book profit exceeds Rs10 crore. Marginal relief is available.

• A 3 percent education cess is applicable on income-tax (inclusive of surcharge, if any).

• MAT credit is available for ten years.

Tax and other regulatory measures

EEPC India Doing Business Series | 37

Dividends earned by an Indian company Dividends earned by an Indian company from a foreign company in which it holds 26 percent or more equity shares shall be taxable at the rate of 15 percent (plus ap-plicable surcharge and education cess) on gross amount of such dividends.

Dividend distribution tax (DDT)Dividends distributed by a domestic company are ex-empt from income-tax in the hands of all shareholders. The domestic company is liable to pay DDT at 16.995 per-cent (inclusive of surcharge and education cess) on such dividends.

Buyback of sharesAn unlisted domestic company is liable to additional in-come-tax at the rate of 20 percent to the extent of distrib-uted income paid to the shareholder in a buyback scheme for purchase of its own shares.

Tonnage tax scheme for Indian shipping firmsTax is levied on the notional income (determined on the basis of the tonnage of a ship) of an Indian shipping com-pany arising from the operation of ships at normal cor-porate tax rates.

Securities transaction taxSTT is levied on the value of taxable securities transactions. The taxable securities transactions are listed in Table7.

Commodity transaction taxCTT is levied on the sale of commodity derivative (other than agricultural commodities) entered in a recognised association @0.01 percent payable by the seller.

Wealth taxWealth tax is levied on specified assets at 1 percent on the value of the net wealth as held by a taxpayer (net of debts incurred in respect of such assets) in excess of the basic exemption of $48,387 [Taking $1 = Rs 62].

Doing Business in India

Table7: Taxable securities transactions

Total income Rates w.e.f. 01.10.14 Payable by

Purchase/sale of equity shares (delivery-based) 0.1 Purchaser/seller

Purchase of units of equity-oriented mutual fund (delivery-based) Nil Purchaser

Sale of units of equity-oriented mutual fund (delivery-based) 0.001 Seller

Sale of equity shares, units of equity-oriented mutual fund (non-delivery-based) 0.025 Seller

Sale of an option in securities 0.017 Seller

Sale of an option in securities, where option is exercised 0.125 Purchaser

Sale of a futures in securities 0.01 Seller

Sale of unit of equity oriented fund to mutual fund 0.001 Seller

Source: Direct Taxes Ready Reckoner: Assessment Year 2015-2016

38 | EEPC India Doing Business Series

Personal taxesResident individuals (excluding senior citizens), any non-resident individual, every HUF/AOP/BOI/artificial juridical person are liable to tax in India at progressive rates of tax as given in Table8.

Notes a. For a resident senior citizen (60 years or more), the

basic exemption limit is Rs3 lakh.b. For a resident super senior citizen (who is 80 years or

more), the basic exemption limit is Rs5 lakh.c. A resident individual with annual income less than

Rs5 lakh can avail rebate of Rs2000 or 100 percent on income-tax payable, whichever is less.

d. A 10 percent surcharge shall be levied if the net in-come exceeds Rs1 crore. It is subject to marginal re-lief (in case of a person having net income exceeding Rs1 crore, the amount payable as income-tax and sur-charge shall not exceed the total amount payable as income-tax on total income of Rs1 crore by more than the amount of income that exceeds Rs1 crore).

e. Education cess and secondary and higher education cess is applicable at the rate of 3 percent on income-tax and surcharge if any.

Capital gains tax• The profits arising from the transfer of capital assets

are liable to be taxed as capital gains. • Long-term capital gains arise from assets held for 36

months or more (12 months for shares, listed in a recog-nised stock exchange) are eligible for indexation benefit. For debt or mutual fund, the long-term capital gain tax arises if the assessee held assets for 36 months or more.

• Long-term capital gains arising on transfer of equity shares or units of equity oriented mutual funds liable to STT are exempt from tax. Long-term capital gains from transfer of other assets are taxed at a concessional rate of 20 percent plus surcharge, if any plus education cess.

• Short-term capital gains arising on transfer of securi-ties liable to STT are taxed at a rate of 15 percent (plus surcharge, if any plus education cess).

• Taxability of foreign nationals and/or non-residents• Indian tax law provides exemption of income earned

by a foreign national, employed by a foreign enterprise during his/her stay in India, subject to the following conditions: » The total period of the stay in India does not exceed 90 days in a tax year.

» The foreign national is not engaged in any trade or business in India.

» Remuneration is not charged to any entity subject to Indian income-tax.

Salary earned from working abroad• Compensation received outside India for work per-

formed by an employee abroad, which is not in connec-tion with the services being rendered in India, is not taxable in India, unless the same is received in India, where the employee is NR or NOR in India.

Table8: Progressive rates of tax

Total income Income-tax rate (%)

Up to Rs2,50,000 Nil

Rs2,50,000-5,00,000 10

Rs5,00,000-10,00,000 20

Rs10,00,000-1crore 30

Above 1 crore 30 + 10 IT surcharge

Source: Direct Taxes Ready Reckoner: Assessment Year 2015-2016

Tax Rates

EEPC India Doing Business Series | 39

Doing Business in India

• If the expatriate qualifies as an ordinary resident of In-dia, the salary earned for working abroad will be tax-able in India even if the same is received outside India.

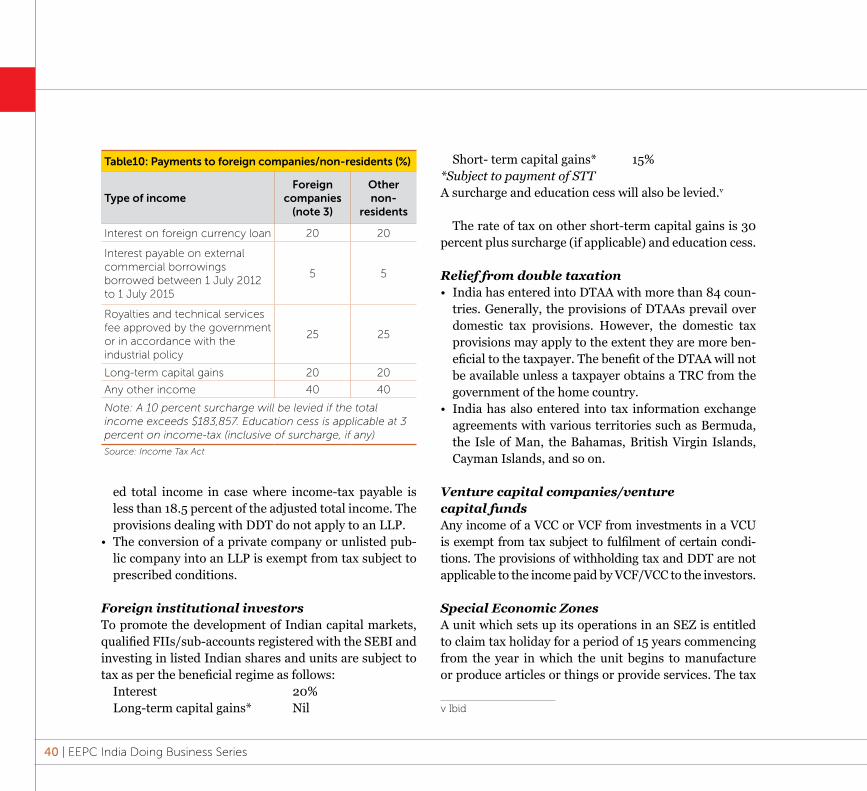

Taxability of foreign companiesA non-resident company is taxed at 40 percent on income which is received/accrued or deemed to accrue/arise in India, along with surcharge and education cessiv.

Modes of taxationGross basis of taxationInterest and royalties/FTS earned by non-residents are li-able to tax on a gross basis at 20 percent and 25 percent respectively along with surcharge and educational cess. However, DTAA protection may be available.

Presumptive basis of taxationForeign companies engaged in certain specified business

activities are subject to tax on a presumptive basis as shown in Table9.

Withholding of taxesGenerally, incomes payable to residents or non-resi-dents are liable to withholding tax by the payer. Howev-er, in most cases individuals are not obliged to withhold tax on payments made by them. Under the Act, pay-ments to foreign companies/non-residents are listed in Table10 (on the next page).

Carry forward of losses and unabsorbed depreciation Business loss (including that of speculation business), unabsorbed depreciation, and capital loss (long-term as well as short-term) can be carried forward and set off as per the prescribed provisions of the law. Business losses can currently be carried forward for a period of eight years whereas unabsorbed depreciation can be carried forward infinitely.

Limited liability partnerships• The LLP Act was introduced in 2008 in India. LLPs are

subject to AMT at the rate of 18.5 percent of the adjust-

Table9: Presumptive basis of taxation

Activity Basis of taxationEffective tax rate (inc surcharge (2%/5% and education cess 3%)

Oil and gas services Deemed profit of 10% of revenues 4.2024/4.326

Execution of certain turnkey contracts Deemed profit of 10% of revenues 4.2024/4.326

Air transport Deemed profit of 5% of revenues 2.1012/2.16

Shipping operations Deemed profit of 7.5% of freight revenues 3.1518/3.24

Source: Income Tax Act

iv Surcharge: If the total income exceeds $183,857 - 2 percent on income-tax. If total income exceeds $1,838,573 - 5 percent on income-tax. Education cess: Applicable at 3 percent on income-tax (inclusive of surcharge, if any)

40 | EEPC India Doing Business Series

ed total income in case where income-tax payable is less than 18.5 percent of the adjusted total income. The provisions dealing with DDT do not apply to an LLP.

• The conversion of a private company or unlisted pub-lic company into an LLP is exempt from tax subject to prescribed conditions.

Foreign institutional investorsTo promote the development of Indian capital markets, qualified FIIs/sub-accounts registered with the SEBI and investing in listed Indian shares and units are subject to tax as per the beneficial regime as follows:

Interest 20%Long-term capital gains* Nil

Short- term capital gains* 15%*Subject to payment of STTA surcharge and education cess will also be levied.v

The rate of tax on other short-term capital gains is 30 percent plus surcharge (if applicable) and education cess.

Relief from double taxation• India has entered into DTAA with more than 84 coun-

tries. Generally, the provisions of DTAAs prevail over domestic tax provisions. However, the domestic tax provisions may apply to the extent they are more ben-eficial to the taxpayer. The benefit of the DTAA will not be available unless a taxpayer obtains a TRC from the government of the home country.

• India has also entered into tax information exchange agreements with various territories such as Bermuda, the Isle of Man, the Bahamas, British Virgin Islands, Cayman Islands, and so on.

Venture capital companies/venture capital fundsAny income of a VCC or VCF from investments in a VCU is exempt from tax subject to fulfilment of certain condi-tions. The provisions of withholding tax and DDT are not applicable to the income paid by VCF/VCC to the investors.

Special Economic ZonesA unit which sets up its operations in an SEZ is entitled to claim tax holiday for a period of 15 years commencing from the year in which the unit begins to manufacture or produce articles or things or provide services. The tax

v Ibid

Table10: Payments to foreign companies/non-residents (%)

Type of incomeForeign

companies (note 3)

Other non-

residents

Interest on foreign currency loan 20 20

Interest payable on external commercial borrowings borrowed between 1 July 2012 to 1 July 2015

5 5

Royalties and technical services fee approved by the government or in accordance with the industrial policy

25 25

Long-term capital gains 20 20

Any other income 40 40

Note: A 10 percent surcharge will be levied if the total income exceeds $183,857. Education cess is applicable at 3 percent on income-tax (inclusive of surcharge, if any)

Source: Income Tax Act

EEPC India Doing Business Series | 41

Doing Business in India

holiday of 15 years is as follows:• 100 percent for the first five years. • 50 percent for the next five years. • 50 percent for the next five years (with restriction to

create reserves).

The benefits are available against export profits.However, MAT and DDT provisions are applicable to

SEZ units.

Special Economic Zone developerA 100 percent tax holiday (on profits and gains derived from any business of developing an SEZ) for any ten con-secutive years out of 15 years has been provided to under-takings involved in developing SEZs. However, MAT and DDT provisions are applicable to the SEZ developers.

Tax holiday for infrastructure projectsUndertakings engaged in prescribed infrastructure pro-jects are eligible for a tax holiday for a consecutive period of any ten years out of a block period of 20 years.

Tax holiday for power projectsA tax holiday of ten years in a block of 15 years is available to undertakings set up before 31 March 2014, with respect to generation/generation and distribution of power, lay-ing of a network of new lines for transmission or distri-bution, undertaking a substantial renovation (more than 50 percent) and modernisation of the existing network of transmission or distribution lines.

Investment allowanceAn investment allowance is available at 15 percent on in-vestments made by a manufacturing company in new plant

and machinery acquired and installed between 1 April 2013 and 31 March 2015 if the same exceeds $18.4 million.

Transfer pricing in IndiaDomestic transfer pricingThe transfer pricing regulations apply to certain domes-tic transactions defined as SDT covering the following:• Payments (i.e. only expenditure) to specific related

parties. • Transactions between tax holiday eligible units and

other business of the same taxpayer. • Computation of ordinary profits of a tax holiday unit of

the taxpayer where there are transactions with entities with close connection.

• Such other transactions as may be prescribed. These provisions shall be applicable in cases where the

aggregate amount of all such domestic transactions ex-ceeds $919,286 in a financial year.

Safe harbour rulesTo reduce increasing number of transfer pricing audits and prolonged disputes, the CBDT notified the Safe Har-bour Rules in September 2013, applicable for a period of five years starting with assessment year 2013-14 for vari-ous sectors. The Rules provide for a time-bound procedure for determination of the eligibility of the taxpayer and of the international transactions for Safe Harbour Rules.

Advance pricing agreementsRecently, APA provisions have been introduced in the Act and the salient legislative provisions of this are as fol-lows:• APA provisions have been introduced with effect from

1 July 2012.

42 | EEPC India Doing Business Series

• Option of unilateral/bilateral/multilateral APA possi-ble.

• The ALP will be determined on the basis of prescribed methods or any other method.

• Valid for a maximum of five consecutive years unless there is a change in provisions of the Act having a bear-ing on international transactions.

• Pre-filing consultation mandatory (option of anony-mous filing available).

• In case an APA covering a particular year is obtained af-ter filing the return of income, a modified return should be filed based on the APA and assessment or reassess-ment to be completed based on such modified return.

• APA to be declared void ab initio if obtained by fraud or misrepresentation of facts.

• No regular TP audits – only an annual compliance au-dit.

• Taxpayer can withdraw the APA application at any stage.

• Option of renewal of APA available. • New Direct Taxes Code Bill, 2010 – ProposedThe DTC Bill, 2010 aims to replace the Act and the Wealth-Tax Act, 1957. Several proposals of the DTC are path-breaking and aim to bring changes to the ways we have traditionally understood tax laws in India.

General provisionsThe concept of previous year is replaced with a new con-cept of financial year which means a period of 12 months commencing from the 1st day of April.

Corporate taxTax rates for domestic companies (See Table).

Taxation of non-residentsThe rates under the DTC for a foreign company is 30 per-cent, with additional branch profits tax of 15 percent (on post-tax income) for income attributable directly or indi-rectly to PE of foreign companies in India.

Indirect taxesCustoms dutyCustoms duty is applicable on import of goods into India. It is payable by the importer of the goods.

The applicable customs duty rate on the import of any goods into India is based on the universally accepted HSN code assigned to the said goods.

The generic basic customs duty (BCD) rate is 10 per-cent at present and the effective customs duty rate (i.e. the aggregate of the components – BCD, ACD, SAD and cesses) with BCD at 10 percent is 28.85 percent (with ACD at 12 percent, SAD at 4 percent and cesses at 3 per-cent).

CENVATCENVAT, also known as excise duty, is applicable on manufacture of goods in India. It is payable by the person

Category Rates under the DTC

Income-tax 30%

MAT

Levied at 20 percent of the adjusted book profits for companies whose income-tax payable on taxable income according to normal provisions of the DTC is lower than the tax at 20 percent on book profits

DDT 15%

Source: Direct Taxes Ready Reckoner: Assessment Year 2015-2016

undertaking the manufacturing activity. It is recoverable from the buyer of the goods.

The applicable CENVAT rate on the manufacture of any goods in India is based on the universally accepted HSN code assigned to the said goods.

The generic CENVAT rate is 12.36 percent (including 2 percent education cess and 1 percent secondary and higher education cess).

Service taxService tax is applicable on the provision of all services except 17 services specified in the Negative List and 39 exempted services specified in a Mega-exemption Noti-fication.

The generic service tax rate is 12.36 percent (includ-ing 2 percent education cess and 1 percent secondary and higher education cess).

Central sales taxIndia has both Central and State-level indirect tax levies on sale or purchase of goods. The rate of CST is equiva-lent to the VAT rate prevailing in the state from where the movement of goods has commenced. There is a conces-sional rate of 2 percent (1 percent in a few states), if the buyer can issue a declaration in Form C subject to fulfil-ment of specified conditions.

CST paid by the buyer while procuring the goods is not available as set-off for payment against any liability and hence is a cost to the business.

Research and development cessR&D Cess is leviable at the rate of 5 percent on import of technology directly or through deputation of foreign technical personnel under a foreign collaboration.

EEPC India Doing Business Series | 43

Foreign Trade PolicyThe FTP is outlined by the Ministry of Commerce and provides a broad policy framework for pro-moting exports and regulating imports into the country.

The FTP outlines various export promotion schemes for enterprises in designated areas such as software technology parks and EOUs which enable them to procure raw materials free from customs duty/CENVAT.

The FTP also outlines various export promotion schemes providing benefits such as import of goods at nil or concessional customs duty rates if the goods manufactured/services provided us-ing such imported goods are exported subject to fulfilment of prescribed export obligations. Such schemes among other things include:

Export promotion capital goods scheme Under the EPCG scheme, capital goods (includ-ing second-hand capital goods) can be imported at a concessional customs duty rate, i.e. nil rate with the export obligation of six times the amount of duty saved over a period of six years.

Served from India scheme Under the SFIS, service providers exporting their services are allowed to import goods without payment of customs duty against an SFIS issued to them. The value of SFIS issued is up to 10 percent of the realisations from service exports in the current/previous financial year.

Duty free import authorisation scheme Under the DFIA scheme, raw materials can be imported without payment of customs duty, if the goods manufactured using the imported raw materials are exported subject to fulfilment of specified conditions.

44 | EEPC India Doing Business Series

Value added taxVAT is applicable on sale of goods where the movement of goods takes place within the same state. The VAT rate ranges from nil to 30 percent across different states and is also dependent upon the nature of the goods.

Entry taxEntry tax is levied on the entry of specified goods into a state for use, consumption or sale therein. The entry tax rates vary from state to state and are applicable only on specified goods. Local body taxLBT (in lieu of Octroi) rates vary from 0 to 10 percent across municipal areas and are also dependent upon the nature of the goods.

Goods and service taxTo reduce the complexities and streamline various indi-rect taxes at the central and the state levels, an empow-ered committee was set up to look into various aspects of integrating multiple indirect taxes into a common GST.

The salient features of GST are as follows:• GST is a broad-based and single unified consumption

tax on supply of goods and services. • GST would be levied on the value addition at each stage

of the supply chain. • The taxable event for GST would be supply of goods

and services and therefore, will no longer be manufac-ture or sale of goods.

• Full input credit of the taxes paid in the supply chain would be available. However, there would be no cross credit available between central GST (CGST) and state GST (SGST);

• GST proposes to subsume the following taxes: • Central taxes: CENVAT, CST, CVD, SAD, service tax,

surcharges, cesses, etc. • State taxes: VAT, entertainment tax, luxury tax, state

cesses and surcharges, entry tax, etc. • Exports would be zero-rated under GST. • Basic customs duty on imports would not be subsumed

with GST and hence, the levy would continue. • Five specified petroleum products – crude petroleum,

diesel, petrol, aviation turbine fuel, and natural gas may be kept out of the ambit of GST. It is understood that the Government might peg the

revenue neutral rate of GST at a rate between 18% and 22%. This represents the aggregate of CGST and SGST payable on the transaction.

The GST implementation is actively under considera-tion and proposed to be introduced soon.

Other lawsCompanies Act 2013 – salient features• The Companies Act 2013 to replace the existing Com-

panies Act, 1956.• Mandatory for certain company to spend at least 2 per-

cent of the average net profits for social purposes.• Increase in the limit of members in a private limited

company to 200.• Financial year defined as April to March.• One director of a company has to be resident in India

(i.e. stay over 182 days or more).• A body, National Financial Reporting Authority (NFRA)

to constitute for monitoring the compliance and over-seeing the quality of service of professionals.

• Transfer to reserves is not mandatory before declaring the dividend.

EEPC India Doing Business Series | 45

Doing Business in India

• Consolidated financial statements of companies are re-quired to also include financial statements of associate companies and joint ventures.

• Merger of Indian companies with a foreign company (incorporated in notified countries) permitted.

Types of companiesThe Companies Act provides for incorporation of differ-ent types of companies, the most popular ones engaged in commercial activities being private limited and public limited companies (liability of members being limited to the extent of their shareholding).

Private companyA private company is required to be incorporated with a minimum paid-up capital of $1838 and two subscribers.

Broadly, the Companies Act 2013 removes the condi-tion relating to non-acceptance of deposits from the pub-lic and increases the limits of the company’s members

(shareholders) to 200.

Public companyA public company is a company which is not a private company. A public company is required to be incorporated with a minimum paid-up capital of $9191 and seven sub-scribers. The profit-and-loss account and balance sheet, along with the reports of the directors and auditors, of a public company are required to be filed with the RoC and are available for inspection by the public at large.

Usually, foreign corporations set up their subsidiary companies as private companies. A private company is a more popular form as it is less cumbersome to incorpo-rate and also has less stringent reporting requirements.

One-man companyThe Companies Act 2013 proposes insertion of a new concept of ‘One-man company,’ having one shareholder and requiring a minimum of one director.

46 | EEPC India Doing Business Series

Business visa• A business visa may be granted to a foreign national

who to establish an industrial/business venture or to explore possibilities to set up an industrial/business venture in India.

• The guidelines issued by the MHA provides various il-lustrative scenarios under which business visas may be granted to the foreign nationals.

• Business visas with multiple-entry facility can be grant-ed up to a maximum period of five years and for US na-tionals up to a maximum period of 10 years. Generally, a maximum stay stipulation of six months is prescribed for each business visit.

Employment visa• An employment visa may be granted to a highly

skilled and/or a qualified foreign national who de-sires to come to India for employment and if his/her salary is in excess of $25,000 per annum. A foreign national who desires to come to India for honorary work (without salary) with a non-govern-mental organisation may be granted an employ-ment visa.

Entry (X) visa• An entry (X) visa is granted to the spouse and depend-

ents of a foreign national who wants to visit India or is already in India on any other type of visa, i.e. business, employment, etc.

Project visa• The MHA, within the employment visa regime intro-

duced a new visa regime known as project visa which has initially been made applicable to the foreign na-

Visa regulations

EEPC India Doing Business Series | 47

Doing Business in India

tionals employed in the power and steel sector. The number of project visas that may be granted per power and steel project is subject to a ceiling.

Conference visa• A conference visa may be granted to a foreign national

who intends to visit India with the sole objective of attending a conference, seminar or workshop (event) and is of assured financial standing.

Tourist visa• A tourist visa is generally granted to a foreign national

whose primary objective of visiting India is sightsee-ing, recreation, casual visit, etc., and does not involve any economic or business activity.

• The visa-on-arrival has been extended to citizens of 11 countries – Cambodia, Finland, Indonesia, Japan, Laos, Luxembourg, Myanmar, New Zealand, the Phil-ippines, Singapore and Vietnam.

Investments in Indian engineering sectorThe FDI inflows in miscellaneous mechanical and engineering industries during April 2000 to March 2014 stood at $2,606.83 million, as per data released by the Department of Industrial Policy and Promotion (DIPP).

India’s engineering sector

E ngineering exports from India have been steadily growing and the performance has exceeded all ex-

pectations ever since the birth of EEPC India. Apart from being one of the largest stakeholders in the total exports out of India, engineering exporters are the foremost net foreign exchange earners in the country. Figure3 shows the upward trend in India’s engineering exports over the last five years.

The top five export destinations of Indian engineering products are the US, UAE, Sri Lanka, Singapore and UK.

49.9

2013-142009-10 2012-132011-122010-11

Figure3: India’s engineering exports in last five years ($ billion)

70.0

60.0

50.0

40.0

30.0

20.0

10.0

0.0

32.6

58.6 56.862.2

Source: DGCI&S, Government of India

48 | EEPC India Doing Business Series

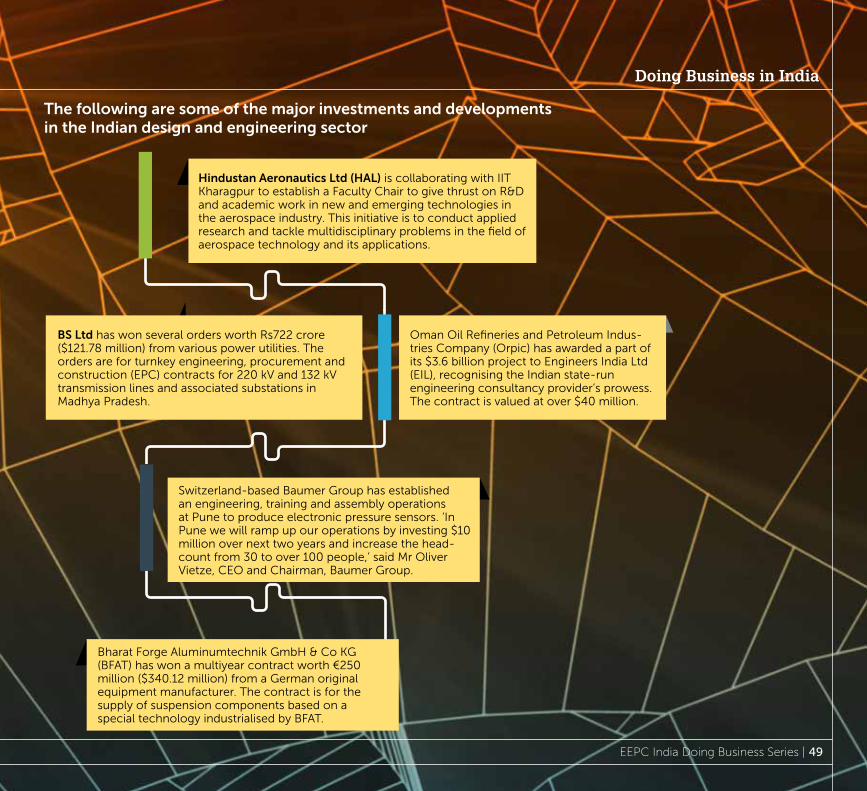

The following are some of the major investments and developments in the Indian design and engineering sector

Hindustan Aeronautics Ltd (HAL) is collaborating with IIT Kharagpur to establish a Faculty Chair to give thrust on R&D and academic work in new and emerging technologies in the aerospace industry. This initiative is to conduct applied research and tackle multidisciplinary problems in the field of aerospace technology and its applications.

Oman Oil Refineries and Petroleum Indus-tries Company (Orpic) has awarded a part of its $3.6 billion project to Engineers India Ltd (EIL), recognising the Indian state-run engineering consultancy provider’s prowess. The contract is valued at over $40 million.

Switzerland-based Baumer Group has established an engineering, training and assembly operations at Pune to produce electronic pressure sensors. ‘In Pune we will ramp up our operations by investing $10 million over next two years and increase the head-count from 30 to over 100 people,’ said Mr Oliver Vietze, CEO and Chairman, Baumer Group.

Bharat Forge Aluminumtechnik GmbH & Co KG (BFAT) has won a multiyear contract worth €250 million ($340.12 million) from a German original equipment manufacturer. The contract is for the supply of suspension components based on a special technology industrialised by BFAT.

BS Ltd has won several orders worth Rs722 crore ($121.78 million) from various power utilities. The orders are for turnkey engineering, procurement and construction (EPC) contracts for 220 kV and 132 kV transmission lines and associated substations in Madhya Pradesh.

Doing Business in India

EEPC India Doing Business Series | 49

50 | EEPC India Doing Business Series

Important information

Trade information sources

Ministry of External Affairs, Government of India

www.mea.gov.in

Ministry of Commerce and Industry, Government of India

www.commerce.nic.in

Directorate General of Commercial Intelligence and Statistics

http://www.dgciskol.nic.in

Director General of Foreign Trade, Government of India

http://dgft.gov.in

Reserve Bank of India – Foreign Trade Statistics

www.rbi.org.in, dbie.rbi.org.in

Ministry of Statistics and Programme Implementation

http://mospi.nic.in

Department of Industrial Policy http://dipp.nic.in

Department of Heavy Industry http://dhi.nic.in

Industry associations in India

EEPC India www.eepcindia.org

All Indian Cycle Manufacturers Association

www.aicma.org

Associated Chambers of Commerce and Industry (ASSOCHAM)

www.assocham.org

Association of Indian Forging Industry

www.indianforging.org

Automotive Component Manufacturers Association of India (ACMA)

www.acma.in

Chemical and Allied Products Export Promotion Council (CAPEXIL)

www.capexil.com

Confederation of Indian Industry (CII)

www.cii.in

Consulting Engineers Association of India

www.ceaindia.com

Federation of Indian Chambers of Commerce and Industry (FICCI)

www.ficci.com

Federation of Indian Export Organisations (FIEO)

www.fieo.org

Gem and Jewellery Export Promotion Council (GJEPC)

www.gjepc.org