DOF Subsea Group Sub/IR/2013/DOF Subsea Group... · 2014-02-26 · DOF Subsea Group –In brief DOF...

36

Q4 2013 Presentation DOF Subsea Group

Transcript of DOF Subsea Group Sub/IR/2013/DOF Subsea Group... · 2014-02-26 · DOF Subsea Group –In brief DOF...

Q4 2013 Presentation

DOF Subsea Group

DOF Subsea

Agenda

In brief

Recent events

Group overview

Contract status

Financials

Outlook

Appendix

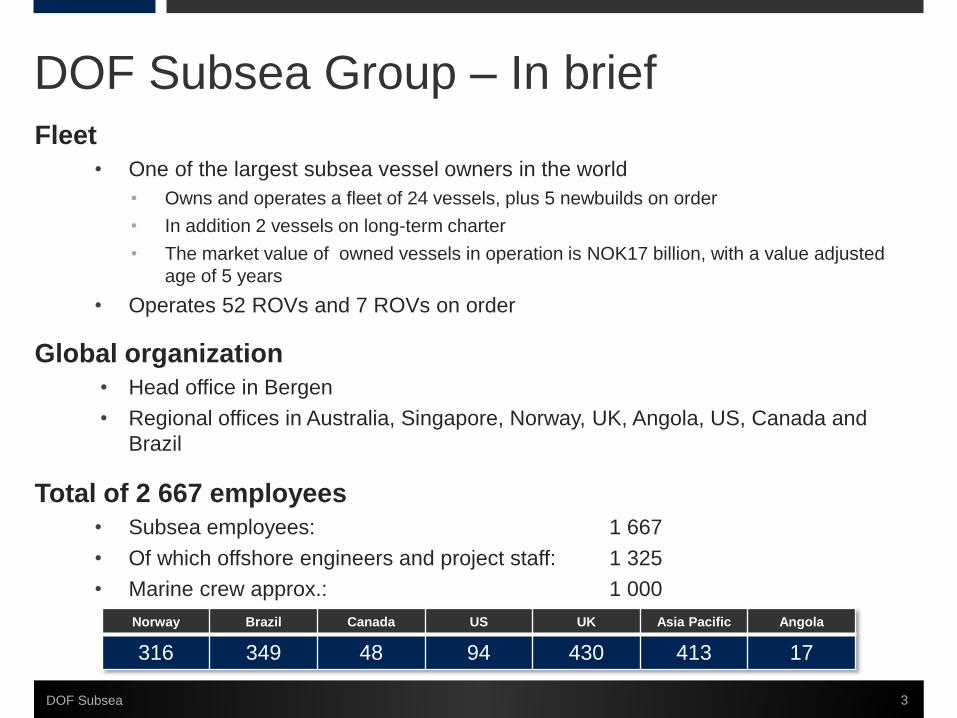

DOF Subsea Group – In brief

DOF Subsea 3

Fleet

• One of the largest subsea vessel owners in the world

• Owns and operates a fleet of 24 vessels, plus 5 newbuilds on order

• In addition 2 vessels on long-term charter

• The market value of owned vessels in operation is NOK17 billion, with a value adjusted

age of 5 years

• Operates 52 ROVs and 7 ROVs on order

Global organization

• Head office in Bergen

• Regional offices in Australia, Singapore, Norway, UK, Angola, US, Canada and

Brazil

Total of 2 667 employees

• Subsea employees: 1 667

• Of which offshore engineers and project staff: 1 325

• Marine crew approx.: 1 000

Norway Brazil Canada US UK Asia Pacific Angola

316 349 48 94 430 413 17

DOF Subsea Group – In brief

DOF Subsea 4

Key figures

Back-log incl. options NOK 34 billion

Market value of fleet NOK 17 billion

Number of shares 119 733 714

Total Per share

Book equity NOK 5.2 billion NOK 43.56

Value adj. equity NOK 8.5 billion NOK 71.05

Book equity ratio 26.8 %

Value adj. equity ratio 37.4 %

19.7 %

CAGR

20.1 %

CAGR

Quarterly figures

27%

28%

29%

30%

31%

32%

33%

-

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

Q4 2010 Q4 2011 Q4 2012 Q4 2013

NO

K m

illio

n

Operating revenue EBITDA EBITDA margin

Recent events

DOF Subsea 5

Fleet

• Chartered the Normand Reach for a 2 + 2 year period

• Skandi Bergen was delivered to new owners in beginning of January

• Skandi Aker purchase options was exercised by AKOFS 2 AS, transaction in February 2015

Contracts

• Statoil call-off under existing frame agreement, utilizing Geosund for minimum 4 months in

2014 and 8 months in 2015

• Several subsea contracts in the North America region, increasing the utilization of the vessel

Harvey Deep-Sea, including a two-year frame agreement

• Awarded mooring installation contract in Asia Pacific, utilizing Skandi Hercules for approx. 2

months

• Australian Customs and Border control extended the charter on Ocean Protector with 6 months

• Awarded 5 ROV contracts by Petrobras for a 4 + 4 years period

• Awarded an RSV contract with Petrobras for a period of 18 months

• Technip awarded DOF Subsea a 5 + 5 year charter agreement on the newbuild VARD800

Finance

• Sale of own holding in bonds DOFSUB05 and DOFSUB06 and bought back bonds in

DOFSUB04, with a total net cash effect of NOK 236 million

State-of-the-art PLSVs

DOF Subsea 6

PLSV 1+2 PLSV 3+4

• To be built in Brazil

• Delivered Q4 2016 and Q2 2017

• Design 316

• Type Pipe Lay support

• LOA 140 m

• Breadth 28 m

• VLS 340 t

• 2 ROVs

• DWT 10 800 t

• To be built in Norway, Søviknes

• Delivered Q2 2016 and Q4 2016

• Design 305

• Type Pipe Lay support

• LOA 150 m

• Breadth 30 m

• VLS 650 t

• 2 ROVs

• DWT 13 200 t

• Contract 8+8 years

• Norskan will provide Marine

Services

• Approx. USD 110 million in

annual EBITDA contribution for

DOF Subsea when all vessels

are in operations

• DOF Subsea part of CAPEX

approx. USD 625 million

DOF Subsea

Group overview

Ownership structure

DOF Subsea 8

Modern high-end fleet and equipment

A workforce of 2 667 highly skilled employees

24 owned subsea vessels in operation

5 vessels on order

2 vessels on charter

50 ROVs, 1 ROTV and 1 AUV in operation

7 ROVs on order

Leading subsea contractor

51% 49%

100%

DOF ASAFIRST RESERVE

CORPORATION

DOF SUBSEA

HOLDING AS

DOF SUBSEA AS

DOF Subsea AS

DOF Subsea Asia Pacific

Singapore

Australia

Indonesia

Malaysia

Mashhor DOF Subsea (50%)

Brunei

DOF Subsea Atlantic

UK

Angola

Norway

Arctic

Russia

DOF Subsea North America

US

Canada

DOF Subsea Brazil

Survey & Positioning

UK

US

Management companies

DOF Management

(34 %)

Marin IT

(35 %)

Engineering companies

CSL

Semar (50%)

Ship/asset owning

companies

DOF Subsea Rederi

DOF Subsea Rederi II

DOF Installer (83.66 %)

DOFTECH

(50 %)

TECHDOF

(50 %)

DOF Subsea ROV

DOF Subsea 9

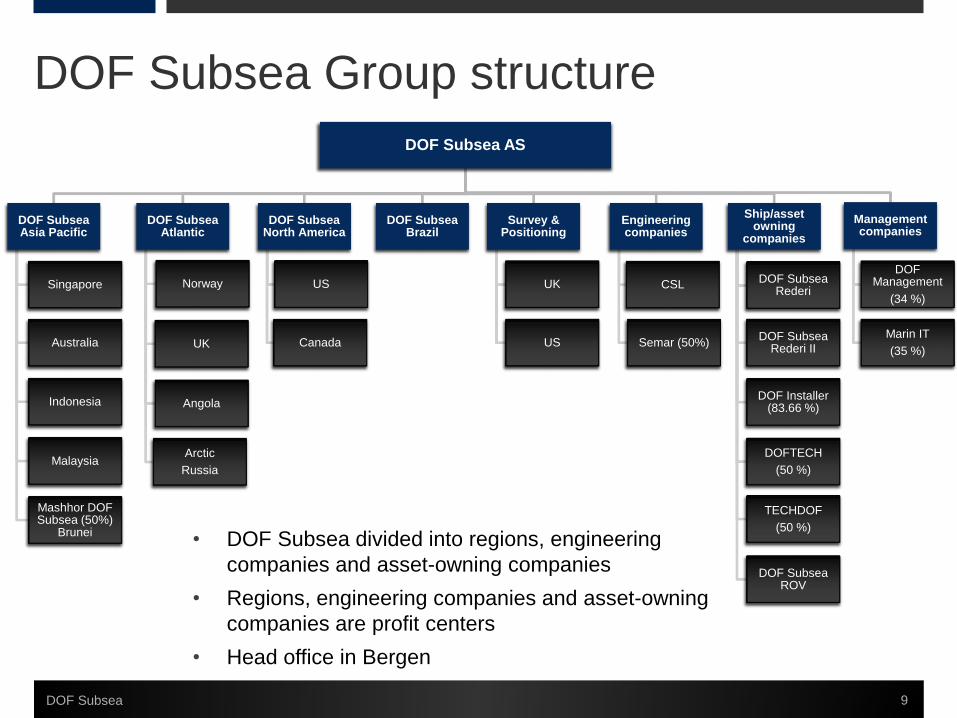

DOF Subsea Group structure

• DOF Subsea divided into regions, engineering

companies and asset-owning companies

• Regions, engineering companies and asset-owning

companies are profit centers

• Head office in Bergen

GEOGRAPHICAL FOCUS AREAS

PerthRio de Janeiro

Buenos Aires

Singapore

Houston

St. Johns

Aberdeen

Cairo

Brunei

Macaé

Jakarta

Manila

Angola

Moscow

Bergen

(142)

(349)

(17)

(413)

(746)

DOF Subsea - A global subsea player

10DOF Subsea

Malaysia

• Incorporated on 24th of May 2005 after DOF ASA acquired

GEO Group AS and its subsidiary Geoconsult AS

• DOF Subsea was established by DOF ASA in order to create a

more effective organization with the aim of establishing a

leading subsea services company

• DOF ASA transferred its multipurpose/ROV vessels to

DOF Subsea, constituting four vessels and one

newbuild

• DOF Subsea is headquartered in Bergen, Norway

DOF Subsea fleet evolution

-

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

0

4

8

12

16

20

24

28

2005 2006 2007 2008 2009 2010 2011 2012 2013

NO

K m

illio

n

Nu

mb

er

of o

pe

rate

d v

essels

Owned vessels Chartered vessels MV of owned fleet (r.a.)

MV of fleet

DOF Subsea – Company history

DOF Subsea 11

2005 2006 2007

Fleet: 11 vessels

May: DOF acquired Geoconsult and established GEO (now DOF Subsea)

May: Private placement of shares of NOK 715 mill

Nov: Listed on Oslo Stock Exchange

Nov: Acquisition of Century Subsea

Fleet: 11 vessels

Feb: Acquisition of Covus Corp

May: Set up of Geo do Brazil

Aug: Established 50/50 JV in Brunei

Fleet: 13 vessels

Jan: Acquired 50% of SEMAR

Jan: Acquired 100% of DOFCON

Mar: Establishment of Aker Oilfield Services

Mar: Name change to DOF Subsea

Apr: Acquisition of CSL

Aug: Merger of Mgmt company with DOF Management AS

2008

Fleet: 16 vessels

Feb: Delivery of Geograph

Jul: Delivery of Skandi Acergy

Nov: Delivery of Skandi Seven and sale of Geofjord

Dec: DOF Subsea acquired by DOF ASA and First Reserve

JV with Technip

2009 2010

Fleet: 18 vessels

Feb: Delivery of Skandi Salvador

Mar: Delivery of Skandi Arctic

Dec: Delivery of Skandi Santos

Fleet: 21 vessels

Jan: Delivery of Skandi Aker

Feb: Sale of GeoChallenger

Jun: Acquisition of SWG

Jul: Delivery of Skandi Vitoria and Skandi Skolten

Dec: Delivery of Skandi Hercules

JV with Technip

2011

Fleet: 24 vessels

Feb: Delivery of Skandi Niteroi

May: Sale of Geosounder

Jun: Acquisition Skandi Constructor

Jul: Delivery of Skandi Skansen

Sep: Delivery of Skandi Singapore

2012

Fleet: 25 vessels

Mar: Sale of OSCV newbuild.

Mar: Signed OSCV newbuildcontract

2013

Fleet: 26 vessels

Feb: Signed OSCV newbuildcontract

Feb: Chartered Harvey Deep-Sea

Mar: Sale ofGeobay

Jun: Delivery of Skandi Bergen

Aug: Signed newbuild contracts for 4 x PLSVs

Nov: Chartered Normand Reach

• DOF Subsea’s main presence is in segments with medium to high

barriers to entry and high complexity of operations

• Higher margins and earnings beyond the time charter rates

• DOF Subsea is gradually building engineering capabilities

12DOF Subsea

Le

ve

l o

f b

arr

iers

to

en

try

Incre

ase

d e

ng

ine

ering

re

qu

ire

me

nt

Complex

subsea operations

Marine transport/

services

Co

mp

lexity a

nd

siz

e o

f o

pe

ratio

ns

Incre

ase

d s

yste

m r

eq

uire

me

nt

Level of industry barriers to entry

New high-end fleet

DOF Subsea 13

• Majority of the fleet delivered after 2007

• Industry leading value adjusted average fleet age of 5 years

• High-end vessels capable of a wide scope of operations, world wide

Newbuild17 %

2007 - 201359 %

2000 - 200621 %

Before 20003 %

Building year DOF Subsea fleet

-

1,00

2,00

3,00

4,00

5,00

6,00

7,00

8,00

Average fleet age

Value adjusted

2009

Business management

Global business management system accredited by DNV to:

• Business Management System ISO 9001: 2008

• Health and Safety System OHSAS 18001:2007

• Environmental Management System ISO 14001:2004

• Global recertification by DNV December 2013

DOF Subsea 14

• DOF Subsea Lost Time Injury (LTI) frequencies compared with IMCA industry average

• High number of safety observations reported shows commitment to HSEQ

HSEQ key statistcs

DOF Subsea 15

Safety Observations 2013

0,00

2,00

4,00

6,00

8,00

10,00

12,00

2005 2006 2007 2008 2009 2010 2011 2012 2013

DOF Subsea LTI frequency

IMCA - LTI frequency

DOF Subsea - recordable incidentfrequency

IMCA - recordable incident frequency

0

200

400

600

800

1000

1200

1400

1600

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

* Figures frequency per million man hours

* Figures represent number of safety observations

DOF Subsea

Projects

DOF Subsea – Life-of-field services

DOF Subsea 17

• DOF Subsea offers integrated subsea solutions across life-of-field

• Field development

• Production phase

• Field abandonment / decommissioning

DOF Subsea – Projects

• DOF Subsea has built a global project

organization over the last 8 years

• DOF Subsea has developed the project

business gradually

• Increased project activity driving growth

• Project business going forward

• Hire more engineers

• Gradually increase the complexity

of work done (Step by Step)

• Build a larger project back-log

• Mix between owned and chartered

in vessels

DOF Subsea 18

2012 2013

Operating Revenue 5 248 6 579

EBITDA 1 788 1 945

-

1 000

2 000

3 000

4 000

5 000

6 000

7 000

NO

K m

illio

n

Operating Revenue EBITDA

* Excluding gain on sale of assets

DOF Subsea – Projects

DOF Subsea 19

OMV Emergency FPSO

Mooring System Repair

• Skandi Singapore Q1 ‘12 &’13,

Skandi Hercules, Skandi Skansen,

Skandi Atlantic, Skandi Emerald

Q3 & Q4 ‘13

• Initially routine IRM scope including

saturation diving in NZ. Emergency

FPSO Mooring System Repair,

stabilising vessel, Engineering,

Project Management and

replacement vessel for Galoc EPIC

project.

• Innovation for diverless solution to

handle significant loads involved.

Developed and built the equipment

in time Hercules arrived in New

Zealand.

DOF Subsea – Projects

DOF Subsea 20

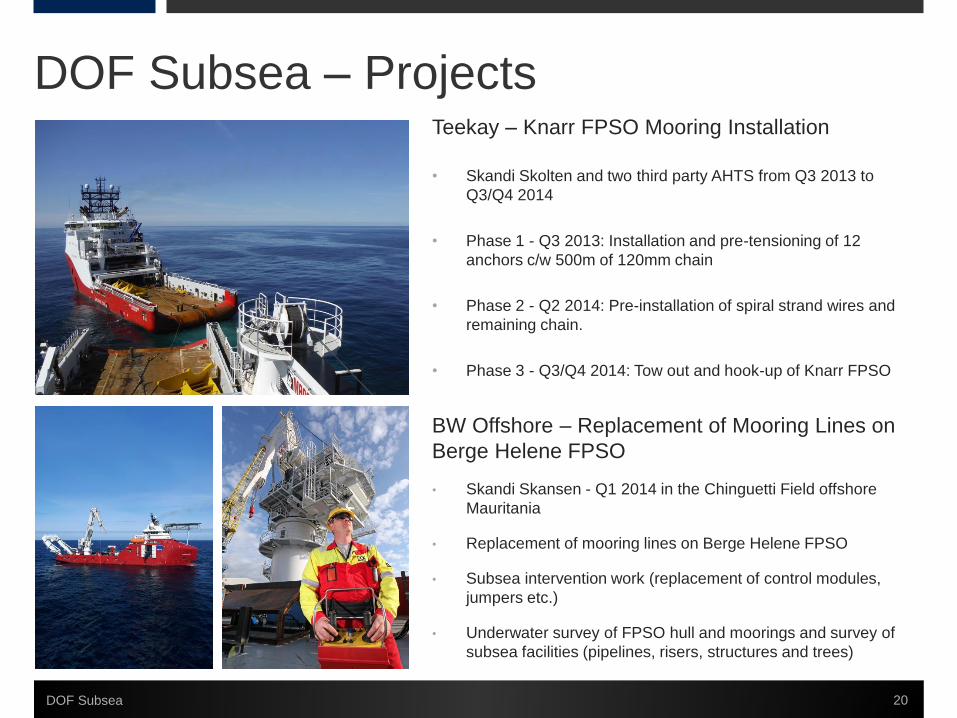

Teekay – Knarr FPSO Mooring Installation

• Skandi Skolten and two third party AHTS from Q3 2013 to

Q3/Q4 2014

• Phase 1 - Q3 2013: Installation and pre-tensioning of 12

anchors c/w 500m of 120mm chain

• Phase 2 - Q2 2014: Pre-installation of spiral strand wires and

remaining chain.

• Phase 3 - Q3/Q4 2014: Tow out and hook-up of Knarr FPSO

BW Offshore – Replacement of Mooring Lines on

Berge Helene FPSO

• Skandi Skansen - Q1 2014 in the Chinguetti Field offshore

Mauritania

• Replacement of mooring lines on Berge Helene FPSO

• Subsea intervention work (replacement of control modules,

jumpers etc.)

• Underwater survey of FPSO hull and moorings and survey of

subsea facilities (pipelines, risers, structures and trees)

DOF Subsea

Contract status

Contract coverage vessels

DOF Subsea 22

FIRM CONTRACTS

OPTIONAL PERIOD

CONSTRUCTION PERIOD

Chartered in vessels

Contract coverage vessels

DOF Subsea 23

• DOF Subsea Group has solid cash flow visibility over the next 3-5 years

• By December 2013 the total back-log (incl. options) was approx. NOK 34 billion

• Firm contracts counts for approx. NOK 17 billion

• Options counts for approx. NOK 17 billion

Note: includes options on long-term contracts

34

29

27

24

22

19

17

14

-

5

10

15

20

25

30

35

40

2014 2015 2016 2017 2018 2019 2020 2021

NO

K b

illio

n

DOF Subsea

Financials

Condensed profit & loss

• Operating income increased from NOK 1 288 million in Q4 2012 to NOK 1 871 million in Q4 2013.

• EBITDA (excl. gain on sale of assets) increased from NOK 417 million in Q4 2012 to NOK 550 million in Q4 2013.

• EBIT (excl. gain on sale of assets) increased from NOK 227 million in Q4 2012 to NOK 360 million in Q4 2013.

DOF Subsea 25

Condensed balance sheet

• From year end 2012 total fixed assets has increased from NOK 16 012 million to NOK 16 340 million

• From year end 2012 cash and cash equivalents has increased from NOK 1 478 million to NOK 1 833 million

• Total liabilities as per 31st December 2013 was NOK 14 594 million

• Net interest bearing debt of NOK 10 923 million as per 31st December 2013

• Book equity of NOK 5 216 million giving a ratio of 26.8 % to total assets as per 31st December 2013

• Value adjusted equity of NOK 8 507 million giving a ratio of 37.4 % as per 31st December 2013

DOF Subsea 26

Quarterly performance (excl. asset sales)

DOF Subsea 27

25.5 %

CAGR

34.0 %

CAGR

0%

5%

10%

15%

20%

25%

30%

35%

40%

-

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

Q4 2009Q1 2010Q2 2010Q3 2010Q4 2010Q1 2011Q2 2011Q3 2011Q4 2011Q1 2012Q2 2012Q3 2012Q4 2012Q1 2013Q2 2013Q3 2013Q4 2013

NO

K m

illio

n

Operating income EBITDA EBITDA margin

NOK million Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013

Operating income 754 730 944 851 1 080 900 1 028 1 152 1 246 1 223 1 384 1 354 1 288 1 225 1 679 1 804 1 871

EBITDA 171 186 306 282 320 241 325 370 406 411 470 489 417 329 471 595 550

EBITDA margin 22.6% 25.4% 32.4% 33.2% 29.7% 26.8% 31.6% 32.1% 32.6% 33.6% 34.0% 36.1% 32.4% 26.9% 28.1% 33.0% 29.4%

Current assets 2 670 2 467 2 919 3 192 3 366 2 829 3 003 2 938 2 923 2 782 2 962 2 704 2 612 3 077 3 319 3 119 3 470

Fixed assets 10 933 11 738 12 499 13 325 14 179 14 520 15 089 16 178 16 305 16 455 16 230 16 056 16 012 16 043 16 344 16 330 16 340

Total assets 13 603 14 205 15 418 16 517 17 545 17 349 18 092 19 117 19 228 19 238 19 192 18 760 18 624 19 120 19 663 19 450 19 810

Current liabilities 1 489 2 035 2 496 2 942 2 167 2 311 2 458 2 640 2 637 2 543 2 495 2 260 1 989 2 000 2 805 2 808 3 167

Non-current liabilities 8 279 8 350 8 867 9 109 10 154 9 946 10 542 11 694 11 759 11 723 11 735 11 439 11 534 12 051 11 862 11 474 11 427

Equity 3 833 3 819 4 054 4 466 5 224 5 091 5 092 4 782 4 832 4 970 4 963 5 061 5 102 5 069 4 996 5 167 5 216

Debt maturity profile

DOF Subsea 28

DOFSUB04

- NOK 750 million

- Maturity April 2014

- Net NOK 453.5 million

DOFSUB05

- NOK 750 million

- Maturity April 2016

- Net NOK 750 million

DOFSUB06

- NOK 700 million

- Maturity Oct 2015

- Net NOK 700 million

DOFSUB07

- NOK 1 300 million

- Maturity May 2018

• The figures reflects amortization and balloon payments on debt drawn as per 31st December 2013.

• Debt maturity profile excludes approx. NOK 0.6 billion in payments to Eksportfinans which is serviced by corresponding

amount of restricted cash.

* As per 31st December 2013

Debt maturity profile DOF Subsea AS level, 2014E – 2018E

-

500

1 000

1 500

2 000

2 500

3 000

2014E 2015E 2016E 2017E 2018E After

NO

K m

illio

n

Bond Loan Bank Debt Balloons

Stable asset values over the last years

DOF Subsea 29

200

300

400

500

600

700

800

900

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

NO

K m

illio

n

Skandi Seven Ocean Protector Geoholm Skandi Patagonia

• Fair market values of the DOF Subsea fleet have been stable over time.

* As per 31st December 2013

Market value development

Asset coverage

DOF Subsea 30

• The figures reflects amortization and balloon payments on debt drawn as per 31st December 2013, including newbuilds

to be delivered assuming standard DOF Subsea leverage. Bonds not included.

Gearing forecast – summary Total assets (NOK billion) Market value

Vessels 17.1

Other equipment (a) 1.3

Total assets 18.4

• Note: vessel values as per 31st December 2013

(a) Includes ROVs, AUV, diving systems and other equipment

• Combined market value of DOF Subsea’s fleet is NOK 17 billion

• Vessel level gearing on the existing fleet is estimated to 44 % at year end 2014, decreasing to 36 % at year end 2015

• Provides a significant equity cushion on top of the existing vessel level financing

• Significant gearing reduction on the existing fleet in the years to come

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

100 %

2014E 2015E 2016E 2017E 2018E

44 %36 % 34 % 32 % 28 %

56 %64 % 66 % 68 % 72 %

Loan to value Market Value Cushion

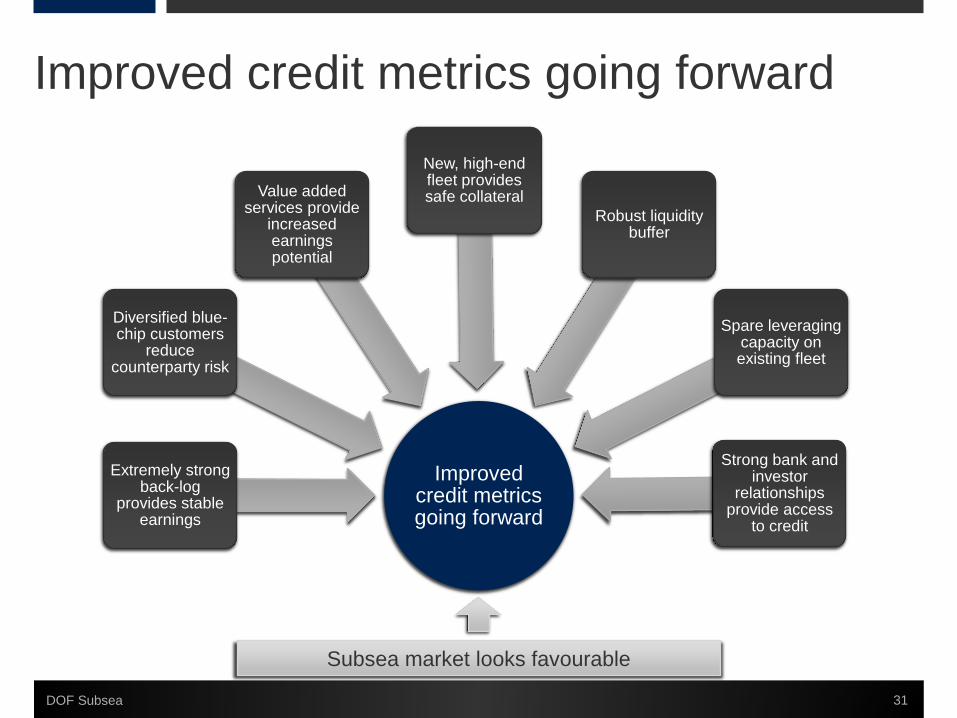

Improved credit metrics going forward

DOF Subsea 31

Improved credit metrics going forward

Extremely strong back-log

provides stable earnings

Diversified blue-chip customers

reduce counterparty risk

Value added services provide

increased earnings potential

New, high-end fleet provides safe collateral

Strong bank and investor

relationships provide access

to credit

Spare leveraging capacity on existing fleet

Robust liquidity buffer

Subsea market looks favourable

DOF Subsea

Outlook

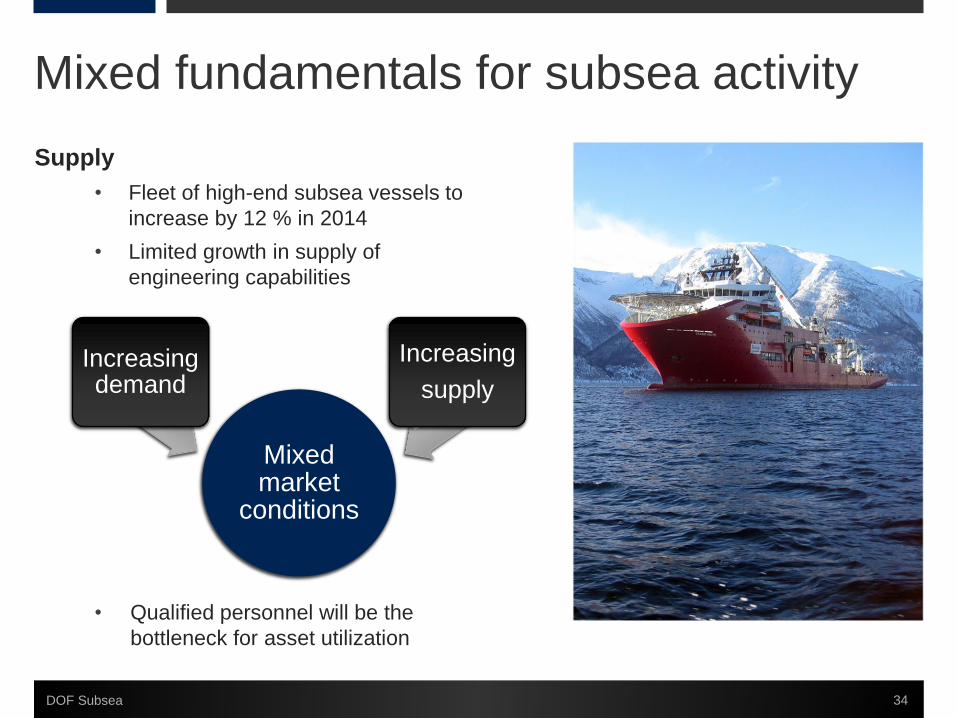

Mixed fundamentals for subsea activity

DOF Subsea 33

Demand

• Stable oil price

• Expected growth in E&P spending

in 2014

• Increased deep water spending

• Increased infrastructure spending

• Growth expected in Brazil, North

Sea and Gulf of Mexico

• Increased focus on newer, larger

and more technologically

advanced vessels and

engineering capabilities

• DOF Subsea owns the world’s

most sophisticated fleet and has a

global project organization

Mixed fundamentals for subsea activity

DOF Subsea 34

Supply

• Fleet of high-end subsea vessels to

increase by 12 % in 2014

• Limited growth in supply of

engineering capabilities

• Qualified personnel will be the

bottleneck for asset utilization

Mixed market

conditions

Increasing demand

Increasing

supply

Thank you

Disclaimer

DOF Subsea 36

This presentation by DOF Subsea AS (“DOF Subsea” or the “Company”) is designed to provide a high level overview of aspects of the

operations of DOF Subsea and the DOF Subsea group.

The material set out in the presentation is current as at 31st December 2013.

This presentation contains forward looking statements relating to operations of DOF Subsea and the DOF Subsea Group that are

based on management’s own current expectations, estimates and projections about matters relevant to DOF Subsea‘s future financial

performance. Words such as “likely”, “aims”, “looking forward”, “potential”, “anticipates”, “expects”, “predicts”, “plans”, “targets”,

“believes” and “estimates” and similar expressions are intended to identify forward looking statements.

References in the presentation to assumptions, estimates and outcomes and forward looking statements about assumptions, estimates

and outcomes, which are based on internal business data and external sources, are uncertain given the nature of the industry,

business risks, and other factors. Also, they may be affected by internal and external factors that may have a material effect on future

business performance and results.

No assurance or guarantee is, or should be taken to be, given in relation to the future business performance or results of DOF Subsea

or the DOF Subsea Group or the likelihood that the assumptions, estimates or outcomes will be achieved.

While management has taken every effort to ensure the accuracy of the material in the presentation, the presentation is provided for

information only. DOF Subsea, its officers and management exclude and disclaim any liability in respect of anything done in reliance on

the presentation.

All forward looking statements made in this presentation are based on information presently available to management and DOF

Subsea assumes no obligation to update any forward looking statements. Nothing in this presentation constitutes investment advice

and this presentation shall not constitute an offer to sell or the solicitation of any offer to buy any securities or otherwise engage in any

investment activity.