Do Short Sellers Affect Corporate Decisions? · DoShortSellersAffectCorporateDecisions? Mahdi...

53

Do Short Sellers Affect Corporate Decisions? Mahdi Nezafat, Tao Shen, Qinghai Wang * January, 2015 Abstract We study the effects of short selling activities on corporate investment. In a model with short-term managerial incentives, we show that short sellers can cause firms to overinvestment. The overinvestment is more severe for managers with low productivity and/or with high short-term incentives. Empirically, we find that short interest is strongly and positively associated with subsequent corporate investment. The impact of short selling activities on investment is greater when a firm’s investment prospect is poor and/or when the sensitivity of a CEO’s compensation to stock price performance is strong. Additionally, both short interest and corporate investment are negatively associated with subsequent stock returns. JEL Codes: G30, G31 Keywords: Short Selling, Corporate Investment, Stock Returns * Mahdi Nezafat, Broad College of Business, Michigan State University, East Lansing, MI 48824. E-mail: [email protected]. Tao Shen, School of Economics and Management, Tsinghua University, China, Beijing 100084. Email: [email protected]. Qinghai Wang, Lubar School of Business, University of Wisconsin-Milwaukee, Milwaukee, WI 53201. E-mail: [email protected]. We thank Charles Hadlock and Xu Jiang for helpful comments. We thank Lalitha Naveen and Alex Edmans for making their data publicly available. We alone are responsible for any errors.

Transcript of Do Short Sellers Affect Corporate Decisions? · DoShortSellersAffectCorporateDecisions? Mahdi...

Do Short Sellers Affect Corporate Decisions?

Mahdi Nezafat, Tao Shen, Qinghai Wang∗

January, 2015

Abstract

We study the effects of short selling activities on corporate investment. In a modelwith short-term managerial incentives, we show that short sellers can cause firms tooverinvestment. The overinvestment is more severe for managers with low productivityand/or with high short-term incentives. Empirically, we find that short interest isstrongly and positively associated with subsequent corporate investment. The impactof short selling activities on investment is greater when a firm’s investment prospect ispoor and/or when the sensitivity of a CEO’s compensation to stock price performanceis strong. Additionally, both short interest and corporate investment are negativelyassociated with subsequent stock returns.

JEL Codes: G30, G31Keywords: Short Selling, Corporate Investment, Stock Returns

∗Mahdi Nezafat, Broad College of Business, Michigan State University, East Lansing, MI 48824. E-mail:[email protected]. Tao Shen, School of Economics and Management, Tsinghua University, China,Beijing 100084. Email: [email protected]. Qinghai Wang, Lubar School of Business, Universityof Wisconsin-Milwaukee, Milwaukee, WI 53201. E-mail: [email protected]. We thank Charles Hadlock andXu Jiang for helpful comments. We thank Lalitha Naveen and Alex Edmans for making their data publiclyavailable. We alone are responsible for any errors.

1 Introduction

Do short sellers affect corporate decisions? Lamont (2012) documents that the management

takes a variety of legal and regulatory actions in response to short selling pressure to impede

short selling and concludes that “firms are not just passively responding to market signals,

but are in fact actively trying to prop up their stock prices.”1 In this paper, we study the

effects of short selling on corporate investment. We show theoretically that short selling

activities, in combination with short-term managerial objectives, can cause managers to

overinvestment. The overinvestment is more severe for managers with low productivity

and/or with high short-term incentives. The empirical analysis provides strong support for

the model’s predictions.

We introduce short sellers in the model described in Bebchuk and Stole (1993) to highlight

how short sellers can play an important role in corporate decisions. In our two-period

model, there are a manager and two types of investors: long investors and short sellers.

The manager’s utility depends on both the first and the second period firm’s valuation.

The manager decides to allocate a limited capital to two projects: a short-term project,

and a long-term project. The payoff of the long-term project is a function the manager’s

unobservable productivity. The long and short investors have different priors about the

productivity of the manager.

We show that short-term managerial objectives cause the manager to overinvest in the

long-term project and the presence of short sellers exacerbates the overinvestment problem.

Why does a manager overinvest? In this model, the market can observe the level of invest-

ment, but it has incomplete information about the productivity of the manager. Since the

manager’s utility depends on firm’s valuations in both periods, a manager with high produc-

tivity wants to invest more in the long-term project (relative to the first-best) to signal to

the market that the long-term project is valuable and therefore boost the firm’s valuation1These actions mainly include legal maneuvers such as lawsuits or the threat of lawsuits, as well as

actions such as stock splits or appeals to shareholders to limit the supply of shares. Liu and Swanson (2011)document that the management also employs share repurchases to fight short sellers.

1

in the first period. The existence of the short sellers reduces the market assessment of the

productivity of the manager and therefore the firm’s valuation in the short-term. This re-

duction in firm’s valuation reduces the total utility of the manager and hence increases his

incentive to overinvest even more (relative to a manager that does not face short sellers) in

the long-term project.

We also show that the overinvestment problem is more severe for managers with low

productivity. A manager with high productivity is already overinvesting to signal his high

productivity and due to resource constraints cannot increase his investment in the long-term

project aggressively in response to the short sellers. Whereas, a manager with low productiv-

ity is investing closer to the efficient investment level in the absence of short selling activities

and thus responds more aggressively to the short sellers. In addition, the overinvestment

problem is more severe for managers with strong short-term incentives. This is because a

manager whose utility is more sensitive to short-term firm’s valuation has a stronger incentive

to overinvest in the long-term project in order to increase the short-term firm’s valuation.

We find strong empirical support for the model’s predictions. We show that short interest

strongly and positively predicts subsequent firm’s investment over time periods of one quarter

to one year. For corporate investment over the next quarter, if the short interest of a

firm increases to the top 20th percentile in the sample, the investment to assets ratio will

increase by approximately five percent. For investment over the next year, the increase is

approximately three percent. The main results are robust with respect to different measures

of short selling activities, different time horizons, and different estimation methodologies.

We explore two predictions of the model to understand the cross-sectional differences of

short sellers’ roles in corporate decisions. The model suggests that the lower the produc-

tivity of a manager, the stronger the effects of short selling on investment. The manager’s

productivity in the model determines the payoff of the long-term project, thus the manager’s

productivity can be interpreted as the quality of the investment opportunities that the firm

has. We use Tobin’s Q as a proxy for the quality of a firm’s investment opportunity. We find

2

that the effects of short interest on investment remain significant for firms with low Tobin’s

Q, whereas the effects are much weaker for firms with high Tobin’s Q. The model also sug-

gests that the higher the sensitivity of a manager’s utility to the short-term firm’s valuation,

the greater the effects of short selling on investment. We use a CEO’s pay-performance sen-

sitivity (PPS), i.e., dollar change in wealth associated with a 1% change in the firm’s stock

price, as a proxy for the sensitivity of a manager’s utility to the firm’s short-term valuation.

We find that the high PPS firms respond more strongly to short interest in their investment

decisions than the low PPS firms do.

We conduct several tests to address concerns that reverse causality and endogeneity

problems could drive the evidence we have documented. We first investigate the concern

that firms with high short interest are overpriced and a firm’s overvaluation rather than

short selling activities causes the firm to overinvestment (see, e.g., Polk and Sapienza 2009).

We follow Polk and Sapienza (2009) and use discretionary accruals as a measure of mispricing

and study the effects of short interest on investment while controlling for the overvaluation

effects. We find that the inclusion of discretionary accruals does not subsume the effects of

short interest on investment.

We next investigate the concern that (over)investment and the associated overvaluation

drive short selling activities, and because investment is persistent, we observe a spurious

relation between short interest and subsequent investment. We employ three different tests

to address this concern. In the first test, we directly include past investment in the baseline

regression model to control for the possible relation between past investment and short

interest. We find that the inclusion of past investment does not subsume the effects of

short interest on investment. In the second test, we employ a two-stage least-squares (2SLS)

regression to tease out the effects of short interest on investment. Again, the effects of short

interest on investment remains significant in most specifications.

We develop our third test based on a prediction of the reverse causality argument in the

presence of short-sale constraints. For the reverse causality argument, it is what drives the

3

possible short selling, i.e., overinvestment or overvaluation, and not the actual short interest

that relates to the subsequent investment. Because short-sale constraints affect short selling

activities, if reverse causality explains our empirical findings, the relation between short

interest and investment should be stronger in firms that are short-sale constrained. We find

that short-sale constraints have a negative rather than a positive impact on the documented

relation between short interest and investment which is opposite to the prediction of the

reverse causality argument. Taken together, these three separate tests provide support on

the robustness of our main empirical finding as they show that even after controlling for the

possible confounding effects on short selling activities, short interest still exhibits substantial

influence on corporate investment decisions.

Lastly, we examine the relation between corporate investment and stock returns in the

presence of short selling activities. We find that both short interest and corporate investment

are negatively associated with subsequent stock returns. The literature refers to the negative

relation between investment and future return as investment or asset growth anomaly, and

different theories have been proposed to explain this anomaly (see, e.g., Titman, Wei, and

Xie 2004, Zhang 2005, Xing 2008, Cooper, Gulen, and Schill 2008, and Lam and Wei 2011).

Our model and empirical findings suggest a new mechanism in which overinvestment driven

by short-term managerial incentives leads to an inefficient allocation of capital and hence

the abnormal negative future returns. This mechanism is consistent with empirical findings

in Titman, Wei, and Xie (2004) and Cooper, Gulen, and Schill (2008) in which they show

that asset growth effect is weaker in times of increased corporate oversight.

Our paper is related to models in Goldstein and Guembel (2008) and Brunnermeier and

Oehmke (2013). Goldstein and Guembel (2008) present a model in which short sellers can

cause under-investment due to price manipulation and the feedback effect from the stock price

to the real investment decisions. Brunnermeier and Oehmke (2013) present a model in which

predatory short selling forces financial firms to liquidate long-term investment at a discount.

In contrast to these models, our model implies that short sellers can cause overinvestment

4

and the presented empirical evidence supports the overinvestment prediction.

Our paper is also related to studies on the effects of short-sale constraints on corporate

decisions. Massa, Zhang, and Zhang (2013a) and Massa, Zhang, and Zhang (2013b) find

that stock lending supply, i.e., the amount of shares available to be lent for short selling,

has a negative relation with earnings manipulation and a positive relation with internal

governance. Chang, Lin, and Ma (2014) show a negative relation exists between stock

lending supply and investment spikes. The stock lending supply is an ex ante threat to

the firm, and this threat could discipline managers. Our paper focuses on impact of the

observed short selling activities which is an ex post action taken by investors. Grullon et al.

(forthcoming) study the effects of short-sale constraints on corporate decisions. They find

that the relaxation of short-sale constraints affects the investment and financing decisions

of only small firms. Our findings, along with the findings of Liu and Swanson (2011), differ

from Grullon et al. (forthcoming) as we investigate the impact of the observed short sellers’

decisions and not the constraints that can affect the short selling activities.

The rest of the paper is organized as follows. The model is presented in Section 2. Section

3 describes the data and Section 4 presents the empirical results. Section 5 offers concluding

remarks.

2 Model

In this section we develop a simple model to show how short sellers can affect corporate

investment decisions. Our model follows the theoretical framework described in Bebchuk

and Stole (1993) while introducing short sellers into the model. There are two periods, a

manager and a unit measure of two types of investors: a fraction of 1 − w investors are

equity holders who are holding one divisible outstanding share, and a fraction of w are short

sellers. We assume that w is exogenous and there are a sufficient number of long and short

investors for each type to take positions in the firm. The assumption that w is exogenous is

5

not a restrictive assumption in our model as we are investigating the effects of short sellers

on the investment choice of a manager. The manager has capital K and he allocates this

capital to two projects. The first project, the short-term project, will realize a return in the

first period and the second project, the long-term project, will realize a return in the second

period.

Let x represent the investment in the long-term project. The realization of the short-term

project’s return is S̃ = S(K−x)+ εs, where S ′(.) > 0, S ′′(.) < 0, and εs is a random variable

with mean zero and unbounded support. The realization of the long-term project’s return

is L̃ = θL(x) + εl, where θ represents the productivity of the manager, L′(.) > 0, L′′(.) < 0,

and εl is a random variable with mean zero and unbounded support that is independent of

εs. It is common knowledge by the investors and the manager that the long investors believe

that θ is distributed according to the continuous probability function f(θ) on [θl, θl]. The

short sellers are in disagreement with the long investors and it is also common knowledge

by the investors and the manager that short sellers believe that θ is distributed according

to the continuous probability function g(θ) on [θs, θs] such that θs < θl and θs ≤ θl. These

differences in priors can be interpreted as arising rationally due to difference in information

acquired by the investors, or as irrational overconfidence (see, e.g., Scheinkman and Xiong

2003).

Let x∗(θ) represent the value-maximizing level of investment in the long-term project. In

particular x∗(θ) is the solution to the following maximization problem:

x∗(θ) = arg maxx∈[0,K]

W (x) = S(K − x) + θL(x). (1)

This first-best solution can be achieved in a principal-agent setting in which θ is publicly

observable and contractible.

Let Vt represent the stock market’s valuation of the firm in period t over both periods.

The manager’s utility depends on both the first and the second period firm’s valuation. In

particular, the manager’s utility is:

6

U(V1, V2) = α0 + α1V1 + α2V2,

where α1 > 0 and α2 > 0 are respectively the sensitivity of the manager to the first and

second period firm’s valuation.

We assume that the manager knows his productivity, i.e., θ. The investors cannot observe

θ but they form rational expectations. The output of the short-term project will be known

by the manager and the investors in the first period, and the investors can observe the level

of investment in the long-term project. We consider separating equilibrium in which the

manager signals his productivity through the level of investment in the long-term project. A

pure strategy equilibrium will have that a manager of type θ who observe a short interest of

w chooses xw, and therefore we can represent the equilibrium by function xw(θ). Let Θw(xw)

be the set of all θ that choose xw for a given level of short interest w. The market will have

expectation of θ which will be a function of xw and w. In particular,

θwE(xw) = E[θ|xw, w] = (1− w)

´Θw(x)

θf(θ)dθ´Θw(x)

f(θ)dθ+ w

´Θw(x)

θg(θ)dθ´Θw(x)

g(θ)dθ.

The manager’s expected utility can be written as:

U(xw, w, θ) = α0 + α1[S(K − xw) + θwE(xw)L(xw)] + α2[S(K − xw) + θL(xw)].

In this framework, we can prove the following three propositions (see Appendix A for

detail).

Proposition 1. A manager that faces short sellers invests more than a manager that does

not.

Proposition 2. The lower the productivity of a manager, the more severe the overinvestment

problem caused by short sellers.

Proposition 3. The higher the sensitivity of a manager’s utility to the first period firm’s

7

valuation, the more severe the overinvestment problem.

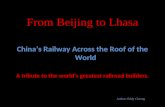

Figure 1 illustrates the solution of the model. We plot xw as a function of θ, for managers

that face short sellers, xo as a function of θ, for managers that do not face short sellers, and

x∗ as a function of θ. In all figures we set S(x) = log(x), L(x) = log(x), K = 10, θs = 1,

θs = 3, θl = 1.5, and θl = 3. In the top figure, we set α1 = 0.1 and α2 = 1. In the middle

figure, we set α1 = 1 and α2 = 1. In the bottom figure, we set α1 = 1 and α2 = 0.1. The

relative value of α1 and α2 highlights differences in the sensitivities of the manager’s utility

to the firm’s valuations in the two periods.

The figures and the comparison of the figures reveal the main results of the model: (1)

investment in the long-term project is higher in the presence of short sellers, (2) the effects

of short sellers on investment are stronger when the productivity of the manager is lower,

and (3) the larger the ratio of α1/α2, i.e., the greater the managerial utility’s sensitivity to

first period firm’s valuation, the higher the overinvestment in the long-term project,

Why does the manager overinvest in this model? The results here resemble those in

Bebchuk and Stole (1993). In this model, the market can observe the level of investment, but

it has incomplete information about the productivity of the manager. Since the manager’s

utility depends on firm’s valuations in both periods, a manager with high productivity wants

to invest more in the long-term project to signal to the market that the long-term project is

valuable (as it depends on the productivity of the manager) and therefore boost the firm’s

valuation in the first period. Whereas, a manager with low productivity prefers to invest

more efficiently and overinvest less than managers with high productivity. This is because

overinvestment is more costly for managers with low productivity. The comparison between

the first-best solution and the solution without short sellers in Figure 1 illustrates this point.

Why does the overinvestment problem become more severe when the manager faces short

sellers? The existence of the short sellers reduces the market assessment (the expected value)

of the productivity of the manager and therefore the firm’s valuation in the first period.

This reduction in firm’s value reduces the total utility of the manager and hence increases

8

his incentive to overinvest in the long-term project. As Figure 1 illustrates, investment in

the long-term project is always higher in the presence of short sellers.

Moreover, the overinvestment problem due to short selling activities is more severe for

managers with low productivity. A manager with high productivity is already overinvesting

to signal its high productivity and due to resource constraints cannot increase his investment

in the long-term project aggressively in response to short selling. Whereas, a manager with

low productivity is investing closer to the efficient investment level in the absence of short

selling activities and thus responds more aggressively to the short sellers. In addition, the

overinvestment problem is more severe for managers with strong short-term incentives. This

is because a manager whose utility is more sensitive to short-term firm’s valuation has a

stronger incentive to overinvest in the long-term project in order to increase short-term

firm’s valuation.

This simple model provides us a framework to understand the roles that short sellers may

play in corporate decisions. The model further highlights that the channel that transmits

the effects of short selling activities on corporate decisions is the agency problems between

the shareholders and the managers. We organize our empirical tests on the relation between

short selling activities and corporate investment based on the propositions presented here

and discuss the results in Section 4.

3 Data

We obtain quarterly and annual accounting data from CRSP/Compustat Merged database.

The sample period is from 1987 to 2011. We exclude foreign firms, and firms with SIC

codes between 4900-4999 (utilities) and 6000-6999 (financial services). To control errors in

quarterly data file, we exclude firm-quarter with negative or missing values in total assets,

net property plant & equipment, sales, or book equity. Short selling is sometimes driven by

mergers and acquisitions (see, e.g., Mitchell, Pulvino, and Stafford 2004). First, we follow

9

Whited and Wu (2006) and exclude any firm-quarter that experienced a merger accounting

for more than 15% of the book value of its assets. Second, we obtain the merger and

acquisition information from SDC and exclude any firm-year that has a match in SDC.

We use the capital expenditure as a proxy for the long-term project in our model. This

is due to the modeling assumption that the source of information asymmetry between the

investors and the manager is θ which only affects the long-term project and not the short-

term project. To investigate whether short selling activities affects capital expenditure over

different time horizons, we construct one-, two-, and four-quarter investment as Ii,t/Ki,t−1,

(∑1

m=0 Ii,t+m)/Ki,t−1, and (∑3

m=0 Ii,t+m)/Ki,t−1 respectively. Ii,t is firm’s i investment in

quarter t and Ki,t−1 is firm’s i total assets in quarter t. We construct one-, two-, and

four-quarter R&D in a similar way.

We obtain monthly short interest data from the New York Stock Exchange (NYSE),

the American Stock Exchange (AMEX), and NASDAQ for the period of January 1988 to

December 2011. The level of short interest in individual stocks is reported to the exchanges

by member firms. Exchanges report short interest twice per month since September 2007.

To be consistent with the short interest data from the earlier period we keep the data at the

monthly frequency. Nasdaq short interest data start from July of 1988.

Following the literature (see, e.g., Christophe, Ferri, and Angel 2004 and Henry, Kisgen,

and Wu 2014), we use abnormal change in short interest to measure short selling activities

in a stock. Let SIji be the short interest for firm i at the end of month j, where short

interest is defined as the number of shares that are shorted divided by the number of shares

outstanding. We define the relative short interest denoted by RSIji as:2

RSIji = SIji −1

3(SIj−3

i + SIj−2i + SIj−1

i ).

In other words, we subtract from a stock’s monthly short interest, its moving average2Here we omit the quarter subscript t which the month i belongs to, because the month j− 1, j− 2, and

j − 3 may be in quarter t or quarter t− 1.

10

over the past three months to represent the change of a firm’s short interest. The implicit

assumption in this approach is that the average short interest over the past three months is

a fair representation of the firm’s typical short interest. This approach also corrects for time

invariant omitted variables that might lead to high short interest. A large increase suggests

abnormally high short interest relative to its own recent shorting activity.

In our regression models we use the following three measures for abnormal short selling

activities to ensure that our results are not driven by the specific choice of the short selling

measure. Suppose quarter t has months j−2, j−1, and j, then RSIji,t represents the relative

short interest at the end of the quarter t for firm i.

The first abnormal short interest measure, denoted by ABSI(1), is a dummy variable

which equals to one if RSIji,t is above the top 20th percentile cutoff point, and zero otherwise.

The second abnormal short interest measure, denoted by ABSI(2), is the relative short

interest at the end of each quarter, i.e., ABSI(2)i,t = RSIji,t. The third abnormal short

interest measure, denoted by ABSI(3), is the maximum of relative short interest in the

three months within each quarter, i.e., ABSI(3)i,t = max{RSIji,tRSIj−1i,t , RSIj−2

i,t }. In the

remainder of the paper, we drop the term ‘abnormal’ and refer to the three measures of

abnormal short selling activities as ‘short interest’.3

Table 2 provides summary statistics for our variables of interest. To reduce the impact

of outliers, all variables are winsorized at 1st and 99th percentile in each year. The mean

of one-quarter investment is about 2%, while the median is about 1%. Not surprisingly, the

one-year investment is about 4 times the one-quarter investment. The firm’s book value of

total assets is about 1200 millions in 2004 dollars, while the median is about 103 millions.

The size variable is highly skewed, so we use its logarithm value in the regressions.

The variable SI in Table 2 is the raw short interest ratio at the end of a quarter. It has

an average of 2.3%, and a median of 0.54%. This high skewness is well documented in the3 In addition to the three main variables for measuring abnormal short interest, we further construct

several alternative measures of abnormal short interest. Details of the alternative short selling activitymeasures are presented in Section 4.

11

literature (see, e.g., Asquith, Pathak, and Ritter 2005). The three short interest measures

exhibit different characteristics. ABSI(1) is a dummy variable which by construction has

a mean of 0.2. ABSI(2) has a mean of 0.057% and ABSI(3) has a mean of 0.436%. The

standard deviations of these two measures are around 1%.

4 Empirical Results

4.1 Short Selling and Corporate Investment

We begin with a test of our first hypothesis which predicts that high short interest lead to

overinvestment. Following the literature (see, e.g., Kaplan and Zingales 1997, and Almeida

and Campello 2007), we augment the traditional investment equation with our measures of

short selling activities that we defined in Section 3. Given that we are interested in examining

the effects of short selling activities on investment over different horizons, we estimate the

following investment model.

∑nm=0 Ii,t+mKi,t−1

= fi + λt + β1Qi,t−1 + β2

∑nm=0CFi,t+mKi,t−1

+ β3Sizei,t+n + β4ABSIi,t−1 + εi,t. (2)

where i represents the firm, Ii,t+m is the one-quarter capital expenditure at the end of quarter

t+m, Ki,t−1 is total assets at the beginning of the quarter t, Qi,t−1 is the Tobin’s Q at the end

of quarter t− 1, CFi,t+m is the one-quarter cashflow at the end of quarter t+m, Sizei,t+n is

the logarithm of total assets (in 2004 constant dollar) at the end of quarter t+n, ABSIi,t−1 is

the short interest at the end of quarter t− 1. We set n = 0, n = 1, and n = 3 for investment

over one quarter, two quarters, and four quarters respectively. fi is the firm fixed effect, and

λt is year-quarter fixed effect. Our first hypothesis predicts that the coefficient β4 will be

positive.

Table 3 shows the quarterly results with different short interest measures and over dif-

12

ferent investment horizons.4 In all columns, both firm and year-quarter fixed effects are

included, and the standard errors are clustered at firm level. Table 3 shows that there is

indeed a strong positive relation between short interest and investment over one-quarter to

one-year horizons. The coefficients of all three short interest measures for all investment

horizons are significant at 1% level.

Table 3 shows that for investment over one quarter, if the short interest of a firm increases

to the top 20th percentile in the sample, the investment to asset ratio will increase by 0.001.

The average of one-quarter investment is 0.02 in the sample, so that represents a 5% increase.

The economic impact of short interest is not trivial even after we control for some well-known

first order determinants of corporate investment. For investment over two quarters and four

quarters, if the short interest of a firm is in the top 20th percentile in the sample, the

investment to asset ratio will increase approximately 4% over two quarters and 3% over

four quarters for the average firm. For investment over two and four quarters, the economic

impact of short interest declines, as the magnitude of their coefficients increases less than

two- and four-folds. This is expected because short interest is less persistent than other

determinants, and corporate investment is likely to respond to the most recent changes in

short selling activities.

We conduct several robustness checks to confirm our main results. These additional tests

include alternative measures of short interest, different control variables and their lagging

schemes in the regressions. For example, for alternative measures of short selling activities,

we use different lagged values for short interest, different cutoff points, and employ different

methodologies to measure short selling activities.5 These tests produce no qualitative change4In Table 2, the logarithm of the firm’s size is much larger than one-quarter investment. To properly

display the estimates in tables, we multiply all investment by 10. The short interest measures are in theiroriginal level, not in percentage.

5We use RSIj−1i,t , RSIj−2i,t , the average of relative short interest∑2

n=0 RSIj−ni,t

3 , and the zero instead ofthe top 20th percentile as the cutoff for dummy. In addition, we construct benchmark portfolios to adjustrelative short interest. Specifically, we construct 27 (3 × 3 × 3) portfolios at the beginning of each monthby independently sorting stocks on market capitalization, book-to-market, and momentum, all measured atthe end of the prior month. Prior literature shows that short interest is related to these firm characteristics.Momentum is defined as a stock’s cumulative returns over the past 12 months. We take the differencebetween a firm’s relative short interest and its benchmark portfolio, and use the differences as the proxy.

13

to our empirical findings and are omitted from the paper for space considerations. Next,

we report results from the tests that provide important information in addition to the main

findings.

Most corporate investment studies employ annual data in empirical analysis. Due to

the high frequency nature of the short interest data, it is more appropriate to use quarterly

investment in our setting though we show the results are consistent across time horizons from

one quarter to four quarters. In order to compare with other studies of corporate investment,

we also perform tests at annual frequency and report the panel regression results in Table

4.6 In columns (1) to (3), short interest all positively predicts next year’s investment and

the significance is at least at 5% level. The evidence from annual data is consistent with

our main results from quarterly data. The economic magnitude is also similar. If the short

interest of a firm is in the top 20th percentile in the sample, the annual investment to asset

ratio in next year will increase by 0.02.

The last question we address in our baseline tests is the concern that (over-)investment is

driven by investment opportunities for which Tobin’s Q fails to control for sufficiently (see,

e.g., Erickson and Whited 2000). Therefore, the positive relation between short interest

and investment could be spurious, and in fact may reveal a relation between short selling

and efficient investment. To address this concern, we study the effects of short interest

on research and development (R&D). Eberhart, Maxwell, and Siddique (2004) find that

high R&D firms have significantly positive long-term abnormal operating performance and

subsequent abnormal stock returns. Therefore, if short selling is positively related with

investment opportunities rather than overinvesting, then the short interest should also be

All measure give qualitatively similar results. To save space, we focus on the three short interest measuresthroughout the paper.

6At annual frequency, the relative short interest RSIji,t for firm i in month j and year t is defined asSji,t − Sj

i,t−1. We use three measures of annual short interest to predict next year investment. Assume in ayear the last month with RSIji,t available is December. The first is a dummy of the year-end relative shortinterest ABSI(1)i,t which equals to one if RSI12i,t is in top 20th percentile of the sample. The second is therelative short interest at the end of each year, ABSI(2)i,t = RSI12i,t . The third is the maximum in year t,ABSI(3)i,t = max{RSIji,t}j=1,..,12.

14

positively related with R&D.

To test this hypothesis, we construct R&D expenditures over one quarter, two quarters

and four quarters and replace the left-hand-side of the regression model (2) with R&D

expenditures. Table 5 shows the quarterly results with different short interest measures and

R&D horizons.7 We can see that there is a strong negative relation between short interest

and R&D over both short term and long-term horizons. Short interest negatively predicts

R&D expenditure, except for the second measure which is not significant.

The results in Tables 3 and 5 illustrate striking differences on the relation between short

interest and two corporate investment decisions. Short selling activities are associated with

increases in capital expenditures but decreases in R&D expenditures. Even though R&D

investment can increase the quality of a firm in the long-term (see, e.g., Eberhart, Maxwell,

and Siddique 2004), R&D is classified as an expense (while capital expenditure increases

long-term assets) and may depress the earnings and thus the current stock price (see, e.g.,

McConnell and Muscarella 1985). The result on R&D provides evidence against the argument

that firms with high short interest may have good investment opportunities for which Tobin’s

Q fails to fully control for in the regressions, and further highlights the differences between

the two corporate decisions (see also Kumar and Li 2014).

In sum, investment in tangible assets, i.e., capital expenditure, increases significantly

in response to short selling activities, whereas investment in intangible assets, i.e., R&D,

decreases significantly in response to short selling activities. These findings are consistent

with the signalling model that we presented in Section 2.7There is a missing value problem in the R&D data, and some early studies (see, e.g., Himmelberg,

Hubbard, and Palia 1999) set missing R&D values to zeros. We drop the missing values in R&D from thesample and perform the analysis. Because our sample covers a relative long time period, this choice doesnot affect our results in a significant way. Our results remain unchanged when we set the missing values tobe zeros and include a dummy for the observations with missing values.

15

4.2 Short Interest, Investment, and Firms’ Characteristics

We next turn to our hypotheses which relate the severity of the overinvestment problem to the

quality of investment opportunities and to the managerial incentives. The empirical analyses

in this subsection provide direct tests on the predictions of the model. These predictions

and the associated tests help us to disentangle the effects of short selling on investment from

other confounding effects.

The second prediction of the model relates to the unobserved productivity of the manager,

i.e., the variable θ in the model. In our simple model, θ is the single variable that determines

the payoff of the long-term project. We showed that the effects of short selling on investment

are stronger when θ is lower. One interpretation of θ is that it summarizes the quality of the

investment opportunities that a firm has. Therefore, one testable prediction of the model

is that managers in firms with lower quality investment opportunities react more strongly

when facing short sellers.

We use Tobin’s Q as a proxy for the quality of a firm’s investment opportunity. Because

Tobin’s Q is highly significantly related to investment decisions, an interaction of Tobin’s

Q with our short selling measures may only capture the marginal effects of Tobin’s Q on

investment. We use a different approach to examine the effects of short selling on high and

low Tobin’s Q firms. We first divide the full sample into two sub-samples based on Tobin’s

Q in the previous quarter, and then examine the effects of short interest on investment in

the two sub-samples of firms.

Table 6 reports the results. The first and second panels report the results for low and

high Tobin’s Q firms respectively. The short selling activity affects the firms with low

Tobin’s Q, though two proxies become insignificant in the four-quarter horizon. For high

Tobin’s Q firms, the impact of short selling on investment is much weaker. The evidence

appears consistent with our hypothesis that managers in firms with lower quality investment

opportunities react more strongly when facing short sellers.

The third prediction of the model relates to the incentives of a manager. In the model

16

that we present in Section 2, we assumed that the manager’s expected utility is:

U(V1, V2) = α0 + α1V1 + α2V2,

where Vt represents the stock market’s valuation of the firm in period t over both periods.

We showed that the effects of short selling on investment are stronger if the sensitivity of

a manager’s utility to the first period firm’s valuation is higher (i.e., the value of α1/α2

is greater). Thus, one direct prediction of the model is that managers who have stronger

short-term incentives react more aggressively when facing short sellers.

We follow the empirical literature and quantify the sensitivity of a manager’s wealth

from his stock and options holdings to the stock price as a proxy for the sensitivity of the

manager’s utility to the firm’s performance (see, e.g., Hall and Liebman 1998). To test the

hypothesis that the greater the sensitivity of a manager’s wealth to the firm’s short-term

performance, the stronger the effects of short selling activities on investment, we use the

CEO pay-performance sensitivity (PPS), i.e., dollar change in wealth associated with a 1%

change in the firm’s stock price, as a proxy for the short-term incentive. We obtain CEO’s

PPS, or the delta, from Coles, Daniel, and Naveen (2006) which use the method in Core and

Guay (2002) to calculate the delta for the period 1992-2010 for executives in the Compustat

Execucomp database.

In each year, we sort firms into quintiles based on the previous year CEO’s PPS. The

variable “High PPS” is a dummy which equals to one if the PPS is in the highest quintile,

and the variable “Low PPS” is a dummy which equals to one if PPS is in the lowest quintile.

We interact those two dummies with our short interest measures. Because the PPS is firm

specific, we use two-digit industry SIC fixed effects in the regressions. The model predicts

that the loading on the interaction term of the high PPS firms is higher than that of the low

PPS firms.

Table 7 reports results in three panels for one-, two-, and four-quarter investment respec-

17

tively. The sample of firms for which we have executive compensation data is a subset of

our full sample firms. The estimates in columns (1), (3), and (5) in all three panels show

that the coefficients on the three measures of short interest are positive and significant in

this sub-sample, consistent with our full sample results.

The interaction terms in all three panels have the expected sign, and are all significant

except for the second measure of short interest. The high PPS firms tend to invest more,

while the low PPS firms invest less than average. For one-quarter investment, if the short

interest increases to the top 20th percentile in the sample, the investment to assets ratio of

the firms with high PPS will be about 0.0039, higher than that of the low PPS firms. The

coefficient magnitude on the interaction term of low PPS firms (-0.019) is larger than that

of unconditional short interest (0.015). It suggests that investment of firms in the low PPS

quintile do not respond significantly to short selling activities. Similar results are also found

for two- and four-quarter investment in the second and the third panels. The significance of

the first measure (a dummy) and the third measure (quarterly maximum) of short interest is

also consistent with the intuition that only the high short interest would attract managers’

attention. The second measure does not capture this intuition as well as the other two.

As a robustness check, we also use the scaled wealth-performance sensitivity proposed

by Edmans, Gabaix, and Landier (2009) as an alternative proxy for the managerial incen-

tive. This is the dollar change in CEO’s wealth for a 100 percentage point change in firm’s

value, divided by the annual flow compensation. We find that the results are qualitatively

unchanged.8 Overall, the results

In sum, we find strong evidence that the effects of short selling activities on investment

are stronger for firms with poor investment prospects measured by Tobin’s Q. In addition,

firms whose CEOs’ compensation is more sensitive to the stock price respond more strongly

to short selling activities. These results are broadly consistent with the predictions of the8Edmans, Gabaix, and Landier (2009) argue that “The key advantage of this incentive measure is that,

empirically, it is independent of firm size, and thus comparable across firms and over time. Theoretically, itis generated by a model where effort has a multiplicative effort on both firm value and CEO utility.”

18

model and provide insight on the agency problem channel that transmits the effects of short

selling activities into corporate decisions.

4.3 Addressing Concerns on Endogeneity and Reverse Causality

We now address concerns that the documented relation between short interest and invest-

ment is driven by forces other than those emphasized in our model. Although one cannot

completely rule out all the forces that can drive our main result, but the analyses in this sub-

section provide evidence that is broadly consistent with the forces emphasized in the model.

We focus on two closely related questions that are essential for establishing the causal effects

of short selling on investment decisions: (1) the effects of overvaluation on short interest and

overinvestment, and (2) the possible reverse causality between overinvestment and shorting

interest.

Overvaluation can lead to corporate overinvestment. Polk and Sapienza (2009) argue

that managers may try to boost short-term share prices by catering to temporary market

overvaluation. They use discretionary accruals as a proxy for mispricing and find that it

is positively related to investment. The overinvestment channel in our model is different

from the catering channel described in Polk and Sapienza (2009). However, it is possible

that short sellers react to overvaluation, and the observed short interest can be driven by

overvaluation. In this case, the relation between short interest and corporate investment

could be driven by overvaluation.

We first examine how short interest is directly related to the overvaluation measure. We

follow Polk and Sapienza (2009) and use discretionary accruals as a measure of overvaluation.

In particular, the discretionary accruals is:

DACCRi,t = ACCRi,t −NORMALACCRi,t,

where ACCRi,t = 4NCCAi,t − 4CLi,t − DPi,t represents accrual for firm i in year t,

19

4NCCAi,t is the change in noncash assets, 4CLi,t is the change in current liabilities minus

change in debt included in current liabilities and minus the change in income taxes payable,

and DPi,t is depreciation and amortization. Appendix B provides more details on the vari-

able construction. In unreported results, we find that the correlation between discretionary

accruals and short interest measures ranges from -5% to 3%, and the correlation among the

three short interest measures ranges from 33% to 61%. Given the low correlations between

discretionary accruals and short interest measures, it is unlikely that the short selling mea-

sures we employ in the study that are based on changes in short selling activities are driven

by the levels of mispricing.

To further see whether the inclusion of the mispricing proxy will subsume our results, we

include the discretionary accruals variable in our baseline regression model in equation (2).

Columns (4) to (6) in Table 4 report the estimates from annual data. The short interest

measure is from the previous year, while as in Polk and Sapienza (2009) the measure of

accruals is contemporaneous. These columns show that when we control for investment

opportunities, firm size, cashflow, and discretionary accruals, we still find that firms with

higher short interest invest more. This relation is significant at least at 5% level. Therefore,

the inclusion of discretionary accruals does not subsume the effects of short interest. The

coefficients on short interest are smaller than those in columns (1) to (3), except for the third

measure.

We also include discretionary accruals in quarterly investment regressions, and present

the results in Table 8. The coefficients on short interest are positive and significant in all

specifications. Again, the inclusion of discretionary accruals does not subsume the effects

of short interest. Nonetheless, the discretionary accruals do explain part of the investment

as the coefficients on short interest are smaller and the discretionary accruals are significant

in the regressions. This suggests that corporate overinvestment could be driven by both

channels. On the other hand, the results in this table should be read with some caution.

The accruals here are at the end of each year, while one- and two-quarter investment are

20

during the year. To avoid this time alignment issue, we also experiment with lagged accruals.

Though not reported, accruals are not significant in any of the specifications, whereas the

results are stronger for short interest.

In sum, our evidence on discretionary accruals alleviates the concern that short interest

is a proxy for overvaluation and the relation between short interest and investment is driven

by the overvaluation effects. Short interest and the mispricing measure have low correlation

and including overvaluation in our baseline regression model does not subsume the effects of

short interest on investment.

We next examine the possibility that reverse causality, i.e., the effects of (over)investment

on short interest, drives the evidence we have documented. Short sellers may target firms

that overinvest and hence, the relation that we document between the short interest and the

firm’s investment is simply a manifestation of the reaction of short sellers to overinvestment.

Ruling out, or adequately controlling for the reverse causality effects in our empirical tests is

a challenging task. We provide three different tests to assess how much the possible reverse

causality affects our results.

In our first test, we directly include the past investment in the baseline regression model

in equation (2). To the extent that past investment predicts future investment and may

affect short selling activities, including the past investment in the regression can at least

partly control for the possible relation between past investment and short interest. Table 9

reports the results from the regression model that include the lagged value of investment.

We measure the past investment over the same length of the time periods as we measure

the subsequent investment. Compared with the baseline results, the results on short selling

measures are weaker, but remain significant for most specifications.

For our second test, we employ a two-stage least-squares (2SLS) regression to tease out

the effects of short interest on investment. The challenge for this approach is the selection of a

valid instrumental variable. The industry median of each ABSIi,t−1 measure in each quarter

is used as the excluded instrumental variable for ABSIi,t−1. The intuition is that an industry

21

level common shock may affect the short interest of all firms and this common shock could

affect a firm’s investment through the firm’s short interest. The model is exactly identified

with one excluded instrumental variable. Table 11 reports the two-stage least-squares (2SLS)

regression results. To save space, only the second stage results are reported. The LM test

statistics for under-identification indicate that the excluded instrumental variable is strongly

correlated with the endogenous regressor. The effects of short interest remains significant,

except the last proxy in the four-quarter horizon.

We develop our third test based on a prediction of the reverse causality argument in

the presence of short-sale constraints. For the reverse causality argument, it is what drives

the possible short selling, i.e., overinvestment or overvaluation, and not the actual short

interest that relates to subsequent investment. Because short-sale constraints affect short

selling activities, if reverse causality explains our empirical findings, the relation between

short interest and investment should be stronger in firms that are short-sale constrained.

The difference in short-sale constraints across firms allows us to explore this prediction.

We use idiosyncratic risk obtained from the Fama-French three-factor model over the past

three-year period as a proxy for short-sales constraints (see, e.g., Pontiff 2006). We include

the variable of idiosyncratic risk and an interaction variable of idiosyncratic risk and short

interest in our baseline regression model in equation (2). Table 12 reports the results and

show that the interaction variable has a negative relation with subsequent investment which

is the opposite to the prediction of the alternative argument. This result suggests that the

alternative argument does not drive our findings.

Overall, the three separate tests provide support on the robustness of our main empirical

findings. Although we cannot completely rule out all the forces that can drive our main

result, the presented results in this subsection show that after controlling for the possible

confounding effects on short interest, short selling activities still exhibit substantial influence

on corporate investment decisions which is broadly consistent with our model.

22

4.4 Short Interest, Investment, and Stock Returns

We have shown that high short interest leads to corporate overinvestment. The inefficient

allocation of capital by a manager could have important implications for firm’s subsequent

performance. If the market recognizes, possibly with some delay, the overinvestment by self-

interest driven managers, those firms that overinvest will have subsequent negative abnormal

returns. We next investigate this hypothesis that relates investment and short interest to

subsequent stock returns.

The relation between investment and subsequent stock returns has been studied exten-

sively in the literature. Titman, Wei, and Xie (2004) and Cooper, Gulen, and Schill (2008),

among others, show that firms that invest more or grow their total assets more have lower

subsequent risk-adjusted returns. The relation between short interest and subsequent stock

returns has also been studied in the literature. Asquith and Meulbroek (1995) and Desai,

Ramesh, Thiagarajan, and Balachandran (2002), among others, show that firms with high

short interest have significant negative abnormal returns.

Our test is different from the two strands of the literature. First and foremost, we

argue that short interest could cause low subsequent stock return through its real effects on

corporate decisions. Existing studies on the relation between short interest and stock returns

largely focus on the informational role of short interest and examine whether short interest

predicts subsequent stock returns. Second, on the relation between corporate investment

and stock returns, we highlight the causes of such a relation by including short interest as

one of the possible causes of overinvestment.

Our return regression model controls for the firm’s characteristics and is analogous to

investment regression model of equation (2) which incorporates different investment horizons.

In addition, we test subsequent returns using the Fama and MacBeth (1973) method. In

23

particular, our specification is,

CumReti,(t+n+1, t+2n+1) = β0 + β1 log

(∑nm=0 Ii,t+mKi,t−1

)+ β2ABSIi,t−1 + β3 log(Qi,t−1)

+ β4

∑nm=0 CFi,t+mKi,t−1

+ β5MEi,t−1 + β6MOMi,t−1 + εi,j, (3)

where CumReti,(t+n+1, t+2n+1) is the firm i’s cumulative quarterly stock returns from the

quarter t+n+1 to the quarter t+2n+1. The variableMOMi,t−1 is the momentum, defined

as a stock’s cumulative returns over the past 12 months. The variable MEi,t−1 is the market

value of equity. Other variables are the same as those in equation (2). We set n = 0, n = 1,

and n = 3 for investment over one quarter, two quarters, and four quarters respectively.

Table 13 presents the Fama and MacBeth (1973) cross sectional results for investment and

subsequent stock returns. Consistent with our hypothesis, in the first panel, the subsequent

returns are strongly and negatively related with investment, after controlling for the short

interest and other firm characteristics. The choice of short interest measures does not change

the coefficients of the logarithm of investment to assets ratio. One standard deviation increase

in one-quarter investment leads to about a cumulative -0.44% abnormal returns in the next

quarter, equivalent to annualized abnormal returns of -1.77%. The overinvestment effect

diminishes in long horizon. One standard deviation increase in four-quarter investment leads

to about a cumulative -1.24% abnormal returns in the next year. This finding is consistent

with our evidence in Table 3 that the impact of short interest on investment diminishes

in long horizon. Overall, the result suggests that although managers try to counteract the

effects of short selling activities by signalling firms’ quality through overinvestment, over

time the market realizes the increase in investment has been inefficient.

Controlling for the short interest is important. Table 13 shows that if the short interest

of a firm increases to the top 20th percentile in sample, the cumulative abnormal returns in

the next quarter is about -0.6%, equivalent to annualized abnormal returns of -2.4%. This

magnitude is larger than that of the investment. It suggests that both short selling activities

24

and overinvestment lead to abnormal negative future returns.

The evidence on investment and returns is consistent with previous studies. In addition,

we show that the negative relation between investment and future returns is robust after

controlling for short selling activities, and the magnitude diminishes in long horizon. These

new findings can be explained by our model and are consistent with our baseline regression

results in Table 3.

The literature refers to the negative relation between investment and future return as

investment or asset growth anomaly, and different theories have been proposed to explain this

anomaly.9 Our model and empirical findings suggest a new mechanism in which signalling

through investment leads to an inefficient allocation of capital and hence the abnormal

negative future returns. This mechanism is consistent with empirical findings in Titman,

Wei, and Xie (2004) and Cooper, Gulen, and Schill (2008) in which they show that asset

growth effect is weaker in times of increased corporate oversight.

5 Conclusions

Investors who short stocks may have real impacts on corporate decisions. In this paper we

focus on one central corporate decision, namely the investment. In a simple model we show

that short sellers can cause firms to overinvestment. The overinvestment is more severe for

managers with low productivity and/or with high short-term incentives. Empirically, we

find that investment in tangible assets, i.e., capital expenditures, increases significantly in

response to an increase in short selling activities, whereas investment in intangible assets,

i.e., R&D expenditures, decreases significantly in response to an increase in short selling

activities. In particular, for corporate investment over the subsequent quarter, if the short

interest of a firm increases to the top 20th percentile in the sample, the investment to assets

ratio will increase approximately by five percent. For investment over the next year, the9For example, Zhang (2005), and Xing (2008), among others, provide q-theory based rational explana-

tions. Titman, Wei, and Xie (2004), and Cooper, Gulen, and Schill (2008) among others, provide behavioralexplanations. Lam and Wei (2011) find supporting empirical evidence for both.

25

increase is approximately three percent. We also find that the impact of short selling on

investment is larger for firms with poor investment prospects and for firms whose CEO’s

compensation is more sensitive to its stock performance.

Investment policy is not the only corporate decision that could be affected by short selling

activities. Firms may increase payout to shareholders, either through dividend or share

repurchase, to boost stock price and increase the cost of short selling. Liu and Swanson

(2011) indeed find that firms employs share repurchases to fight short sellers. In view of the

increased payout, the evidence on increased investment is even more striking. These results,

along with the argument we presented in the theoretical model, further suggest that short

selling activities can also affect firm’s financing decisions and capital structure. Exploring

the real effects of short selling activities on aspects of firm’s policies other than investment

remain a topic of future research.

26

Appendix A: Proofs

To prove Proposition 1, 2 and 3, we need to prove the following two propositions.

Proposition 4. In any Nash equilibrium of the signaling game and given level of short-

interest w, xw(θ) will be a nondecreasing function of θ.

Proof: We prove this proposition by contradiction. Let (xw, θ) and (x′w, θ′) be two investment-

type pairs used in equilibrium by the managers who faces the same level of short-interest

and θ > θ′ but x′w > xw. By revealed preference

U(xw, w, θ) > U(x′w, w, θ)

U(x′w, w, θ′) > U(xw, w, θ′)

which leads to

(θ − θ′)(L(xw)− L(x′w)) > 0

which contradicts the initial assumption.

Proposition 5. A unique fully separating Perfect Bayesian equilibrium exists which involves

over-investment in the second project relative to the first-best with probability one and where

the equilibrium choice of investment, xw(θ), is such that xw(θs) = x∗(θs) and for all θ ∈

(θs, θl]

dxw

dθ=

α1

α1 + α2

L(xw)

S ′(K − xw)− θL′(xw).

Proof: For simplicity of notation we drop the superscript w in xw. Any Perfect Bayesian

equilibrium must have beliefs that are a nondecreasing function of investments. Since

limx→0∂U(x,w,θ)

∂x= +∞ and limx→K

∂U(x,w,θ)∂x

= −∞, necessary conditions for the manager’s

choice of investment are

∂U(x,w, θ)

∂x= 0, and

∂2U(x,w, θ)

∂x26 0 (4)

27

Differentiating the first order condition we get that

∂2U(x,w, θ)

∂θ∂x+∂2U(x,w, θ)

∂x2

∂x

∂θ= 0

Therefore, the necessary local second-order condition can be restated as ∂2U(x,w,θ)∂θ∂x

> 0,

which is true by the assumption that L′(x) > 0. Furthermore, if x(θ) is nondecreasing, the

local conditions for a maximum is sufficient. To see that the monotonicity of x(θ) and the

first-order condition are sufficient for a separating equilibrium, suppose x(θ) satisfies these

conditions but the manager prefers to choose otherwise. Suppose that x′ = x(θ′) rather than

x is the chosen investment by a manager with productivity θ. Then, revealed preference

implies U(x(θ′), w, θ)− U(x(θ), w, θ) > 0. Therefore

ˆ θ′

θ

Ux(x(s), w, θ)dx(s)

dsds > 0

But by hypothesis, Ux(x(θ), w, θ) = 0 for all θ. Therefore,

ˆ θ′

θ

(Ux(x(s), w, θ)− Ux(x(s), w, s))dx(s)

dsds > 0

which implies that ˆ θ′

θ

ˆ θ

s

Uxθ(s, w, t)dx(s)

dsdtds > 0

But by assumption, the above double integral is always non-positive, which contradicts

our hypothesis. Therefore, if our solution satisfies the local first-order condition and the

manager’s investment function is a nondecreasing in θ, we have characterized the equilibrium

path of a Perfect Bayesian Nash equilibrium.

The first order condition is

∂U(x,w, θ)

∂x= (α1 + α2)[θL′(x)− S ′(K − x)] + α1

dθ

dxL(x) = 0

28

Or equivalentlydθ

dx=α1 + α2

α1

S ′(K − x)− θL′(x)

L(x)(5)

Let x∗(θ) be the efficient level of investment for a given productivity θ. In a fully sepa-

rating equilibrium, the worst inference which the investors can place on a manager is that

the productivity of the second project is θs, and consequently the worst firm’s manager must

earn at least U(x∗(θs), w, θs). Thus, in a fully separating equilibrium, x(θs) = x∗(θs) which

is an initial condition of differential equitation (5).

We must specify beliefs off the equilibrium path. Let X = [x, x] be the set of all investment

levels which arise with positive probability in the proposed equilibrium of signaling game.

One set of arbitrary beliefs which holds together the equilibrium has the market believing

that for any x ∈ [0, x) the firm’s type is θs, and for any x > x the firm’s type is θl.

Differential equation (5) implies that ∂x∂θ

= ∞ at θs and at any other points where

x(θ) = x∗(θ). Since x(θ) is monotonic in θ and x∗(θ) has finite slope, x(θ) must remain

above x∗(θ) for all θ ∈ [θs, θl]. Therefore, we have a uniquely defined fully separating

equilibrium which exhibit over-investment with probability one.

Proof of Proposition 1: Let xw(θ) denote the investment of a manager with productivity

θ that faces short sellers and let xo(θ) denote the investment of a manager with productivity

θ that does not face short-sellers. The functions xw(.) and xo(.) are characterized by the

following differential equations:

dxw

dθ=

α1

α1 + α2

L(xw)

S ′(K − xw)− θL′(xw), xw(θs) = x∗(θs) (6)

dxo

dθ=

α1

α1 + α2

L(xo)

S ′(K − xo)− θL′(xo), xo(θl) = x∗(θl) (7)

We need to show that xw(θ) ≥ xo(θ) for ∀θ. Dropping w and o in the above differential

equations, they are of the following form:

dθ

dx= h1(x)− θh2(x) (8)

29

where

h1(x) =

(1 +

α2

α1

)S ′(K − x)

L(x), h2(x) =

(1 +

α2

α1

)L′(x)

L(x)

The solution to differential equation (8) is of the form:

θ =

´h1(t)e

´h2(t)dt + c

e´h2(t)dt

or equivalently

θ = z1(x) + cz2(x)

where

z1(x) =

´h1(t)e

´h2(t)dt

e´h2(t)dt

, z2(x) =1

e´h2(t)dt

Therefore, the solutions to the differential equations (6) and (7) are characterized by

θw = z1(xw) + cwz2(xw)

θo = z1(xo) + coz2(xo)

where, cw and co are constant that are determined based on initial conditions xw(θs) = x∗(θs)

and xo(θl) = x∗(θl). For a given level of investment x,

θw(x)− θo(x) = z2(x)(cw − co)

Given that z2(.) > 0, in order to show that xw(θ) > xo(θ) we can equivalently show that

co > cw. We prove this by contradiction. Suppose that cw > co. Consider the level of

investment x∗ such that θo(x∗) = θl = z1(x∗) + coz2(x∗). Given that cw > co we have that

θw(x∗) = z1(x∗) + cwz2(x∗) > θl. Given the monotonicity of θw and x, this implies that

xw(θ1) < xo(θ1) = x∗. However, this is not consistent with Proposition 1 as we showed that

xw(θ) > x∗(θ).

30

Proof of Proposition 2: Let xw(θ) denote the investment of a manager with productivity

θ that faces short sellers and let xo(θ) denote the investment of a manager with productivity

θ that does not face short-sellers. The functions xw(.) and xo(.) are characterized by the

following differential equations:

dxw

dθ=

α1

α1 + α2

L(xw)

S ′(K − xw)− θL′(xw), xw(θs) = x∗(θs)

dxo

dθ=

α1

α1 + α2

L(xo)

S ′(K − xo)− θL′(xo), xo(θl) = x∗(θl)

Define f(θ) as f(θ) = xw(θ)− xo(θ). We need to show that f ′(θ) 6 0 for θ ∈ (θs, θl).

We know that xw(θ) and xo(θ) are increasing functions. To show that xw(θ)− xo(θ) is a

decreasing function, we need to show that θo(x)− θw(x) is a decreasing function.10

From proof of Proposition 1 we know that

θw = z1(xw) + cwz2(xw)

θo = z1(xo) + coz2(xo)

where, cw and co are constant that are determined based on initial conditions xw(θs) = x∗(θs)

and xo(θl) = x∗(θl). Therefore,

θo(x)− θw(x) = z2(x)(co − cw)

Since co > cw and z2(.) is a decreasing function, we get that θo(x) − θw(x) is a decreasing

function.

Proof of Proposition 3: We need to show that dxw

dα1> 0. We know that

10It is straightforward to show that if f(x) and g(x) are increasing functions, h(x) = f(x) − g(x) isdecreasing iff g−1(.)− f−1(.) is a decreasing function.

31

dxw

dθ=

α1

α1 + α2

L(xw)

S ′(K − xw)− θL′(xw)

Therefored2xw

dα1dθ=

α2

α1(α1 + α2)

dxw

dθ

Thereforedxw

dα1

=α2

α1(α1 + α2)xw

Given that xw > 0 we get that dxw

dα1> 0.

Appendix B: Variable Definitions

We obtain quarterly and annual firm accounting data from CRSP/Compustat Merged

database. The sample period is from 1987 to 2011. We exclude foreign firms, and firms

with SIC codes between 4900-4999 (utilities) and 6000-6999 (financial services). We exclude

firm-quarter with negative or missing values in total assets, net property plant & equipment,

sales, or book equity, and firm-quarter that experienced a merger accounting for more than

15% of the book value of its assets. We obtain the merger and acquisition information from

SDC and exclude any firm-year that has a match in SDC. Item names refer to Compustat

quarterly data items.

Variable Definition

IK CAPXYQ / Item ATQ. Data Item ATQ is lagged. CAPXYQ

is the difference between the current and previous quarter of

Item CAPXY in each fiscal year.

Size The logarithm of the 2004-dollar deflated Item ATQ

Tobin’s Q (Item PRCCQ × Item CSHOQ - Item CEQQ - Item TXDBQ)

/ Item ATQ

32

Variable Definition

CF (Item IBQ + Item DPQ)/ Item ATQ. Data Item ATQ is

lagged.

RnD Item XRDQ / Item ATQ. Data Item ATQ is lagged.

ABSI See Section Data for details.

DACCR See Table 4 for details.

33

ReferencesAlmeida, H., and M. Campello. 2007. Financial constraints, asset tangibility, and corporateinvestment. Review of Financial Studies 20:1429–1460.

Asquith, P., and L. K. Meulbroek. 1995. An empirical investigation of short interest. WorkingPaper .

Asquith, P., P. A. Pathak, and J. R. Ritter. 2005. Short interest, institutional ownership,and stock returns. Journal of Financial Economics 78:243–276.

Bebchuk, L. A., and L. A. Stole. 1993. Do short-term objectives lead to under-or overinvest-ment in long-term projects? Journal of Finance 48:719–730.

Brunnermeier, M. K., and M. Oehmke. 2013. Predatory short selling. Review of Finance .

Chang, E. C., T.-C. Lin, and X. Ma. 2014. Does short selling discipline managerial empirebuilding? Working Paper .

Christophe, S. E., M. G. Ferri, and J. J. Angel. 2004. Short-selling prior to earnings an-nouncements. Journal of Finance 59:1845–1876.

Coles, J. L., N. D. Daniel, and L. Naveen. 2006. Managerial incentives and risk-taking.Journal of Financial Economics 79:431–468.

Cooper, M. J., H. Gulen, and M. J. Schill. 2008. Asset growth and the cross-section of stockreturns. Journal of Finance 63:1609–1651.

Core, J., and W. Guay. 2002. Estimating the value of employee stock option portfolios andtheir sensitivities to price and volatility. Journal of Accounting Research 40:613–630.

Desai, H., K. Ramesh, S. R. Thiagarajan, and B. V. Balachandran. 2002. An investigationof the informational role of short interest in the Nasdaq market. Journal of Finance57:2263–2287.

Eberhart, A. C., W. F. Maxwell, and A. R. Siddique. 2004. An examination of long-termabnormal stock returns and operating performance following R&D increases. Journal ofFinance 59:623–650.

Edmans, A., X. Gabaix, and A. Landier. 2009. A multiplicative model of optimal CEOincentives in market equilibrium. Review of Financial Studies 22:4881–4917.

Erickson, T., and T. M. Whited. 2000. Measurement error and the relationship betweeninvestment and q. Journal of Political Economy 108:1027–1057.

Fama, E. F., and J. D. MacBeth. 1973. Risk, return, and equilibrium: Empirical tests.Journal of Political Economy pp. 607–636.

Goldstein, I., and A. Guembel. 2008. Manipulation and the allocational role of prices. Reviewof Economic Studies 75:133–164.

34

Grullon, G., S. Michenaud, and J. P. Weston. forthcoming. The real effects of short-sellingconstraints. Review of Financial Studies .

Hall, B. J., and J. B. Liebman. 1998. Are CEOS really paid like bureaucrats? QuarterlyJournal of Economics pp. 653–691.

Henry, T. R., D. J. Kisgen, and J. J. Wu. 2014. Equity short selling and bond ratingdowngrades. Journal of Financial Intermediation .

Himmelberg, C. P., R. G. Hubbard, and D. Palia. 1999. Understanding the determinantsof managerial ownership and the link between ownership and performance. Journal ofFinancial Economics 53:353–384.

Kaplan, S. N., and L. Zingales. 1997. Do investment-cash flow sensitivities provide usefulmeasures of financing constraints? Quarterly Journal of Economics 112:169–215.

Kumar, P., and D. Li. 2014. Capital Investment, option generation, and stock return.Working paper .

Lam, F., and K.-C. Wei. 2011. Limits-to-arbitrage, investment frictions, and the asset growthanomaly. Journal of Financial Economics 102:127–149.

Lamont, O. A. 2012. Go down fighting: Short sellers vs. firms. Review of Asset PricingStudies 2:1–30.

Liu, H., and E. P. Swanson. 2011. Do corporate managers trade against short sellers?Working Paper .

Massa, M., B. Zhang, and H. Zhang. 2013a. Governance through threat: Does short sellingimprove internal governance? Working Paper .

Massa, M., B. Zhang, and H. Zhang. 2013b. The invisible hand of short selling: Does shortselling discipline earnings manipulation? Working Paper .

McConnell, J. J., and C. J. Muscarella. 1985. Corporate capital expenditure decisions andthe market value of the firm. Journal of Financial Economics 14:399–422.

Mitchell, M., T. Pulvino, and E. Stafford. 2004. Price pressure around mergers. Journal ofFinance 59:31–63.

Polk, C., and P. Sapienza. 2009. The stock market and corporate investment: A test ofcatering theory. Review of Financial Studies 22:187–217.

Pontiff, J. 2006. Costly arbitrage and the myth of idiosyncratic risk. Journal of Accountingand Economics 42:35–52.

Scheinkman, J. A., and W. Xiong. 2003. Overconfidence and speculative bubbles. Journalof Political Economy 111:1183–1220.

35

Titman, S., K.-C. Wei, and F. Xie. 2004. Capital investments and stock returns. Journal ofFinancial and Quantitative Analysis 39:677–700.

Whited, T. M., and G. Wu. 2006. Financial constraints risk. Review of Financial Studies19:531–559.

Xing, Y. 2008. Interpreting the value effect through the Q-theory: An empirical investigation.Review of Financial Studies 21:1767–1795.

Zhang, L. 2005. The value premium. Journal of Finance 60:67–103.

36

Figure 1: Solution to the Model

The figure plots the solution of the model for three set of parameters. In the top figureα1 = 0.1 and α2 = 1. In the middle figure α1 = 1 and α2 = 1. In the bottom figure α1 = 1and α2 = 0.1.

1.0 1.5 2.0 2.5 3.05

6

7

8

9

10

Productivity of the Manager HΘL

Inves

tmen

tin

the

Lon

g-

Ter

mP

roje

ctHxL

Without Short Sellers

1.0 1.5 2.0 2.5 3.05

6

7

8

9

10

Productivity of the Manager HΘL

Inves

tmen

tin

the

Lon

g-

Ter

mP

roje

ctHxL

With Short Sellers

First-Best

1.0 1.5 2.0 2.5 3.05

6

7

8

9

10

Productivity of the Manager HΘL

Inves

tmen

tin

the

Lon

g-

Ter

mP

roje

ctHxL

1.0 1.5 2.0 2.5 3.05

6

7

8

9

10

Productivity of the Manager HΘL

Inves

tmen

tin

the

Lon

g-

Ter

mP

roje

ctHxL

Without Short Sellers

1.0 1.5 2.0 2.5 3.05

6

7

8

9

10

Productivity of the Manager HΘL

Inves

tmen

tin

the

Lon

g-

Ter

mP

roje

ctHxL

With Short Sellers

First-Best

1.0 1.5 2.0 2.5 3.05

6

7

8

9

10