Diversification and value additions of production and exports · Recapitulating constraints •...

16

Diversification and value additions of production and exports

Transcript of Diversification and value additions of production and exports · Recapitulating constraints •...

Diversification and value additions ofproduction and exports

What is diversification?• Horizontal, vertical, geographical

– Upgrading processes, products, functional, intersectoral

• It is not producing and exporting a varied basket at anycost

• Continuous process of seeking higher value addedretained in the country

• Dichotomy between diversification and specialization• Adding up problem (for significant producers)• Food security not strictly speaking “diversification”

Why diversify?

• Spread risks, especially from commodities– Reduce price, volume (supply and demand) volatility

and aggregate earnings volatility– Diversification itself is risky – entrepreneurial gamble

cost of discovery• More important

– Increase income, employment (especially women),promote linkages

– Towards structural change– Demonstration effect – diversifiers as change agents

Diversification in Brussels Programme of Action

Mentioned mostly in terms of agriculture, commodities,“Diversifying production and exports from low value added

to high value added products” agric paragraph 58“Intensifying horizontal and vertical diversification, including

local processing of primary commodities; paragraph 67“Encouraging diversification in economic activities that are

less prone to adverse external economic shocks,paragraph 72

Principal success stories not from LDCs (ExceptBangladesh jute to textiles) Possible backsliding, Niger

LDCs dependence on single commodities2006-2008

More than 50 per cent of total merchandise exports:

Petroleum - 5 countries (all of the petroleum exporters,lowest 61% Chad)

Aluminium, fruits, gold, tobacco, iron ore, uranium, spices,fish, wood

Change through years depends also on relative prices

Prerequisites for diversification• Identification of opportunities

– Prices, volumes (SS trade and SN trade, new uses)– Markets: China factor

• Supply capacity/competitiveness/management– Cost, quality, relationship with clients– Technology, finance– Inputs, including support services

• Demand (internal/regional market useful)• Market access (advantage for LDCs, especially for processed:

tariff escalation), but subsidies for temperate products)• Market entry• Raw materials – not critically important• Low income countries into new products – inverted U

Development of agro-food trade

Higher growth• Beer• Fruit juices• Fish (LDC increase)• Vegetables• Fruits• Processed products

in general

Slower growth• Vegetable oils• Rice• Sugar and confect.• Wheat and flour• Meat• Maize• Spices (LDC

increase)

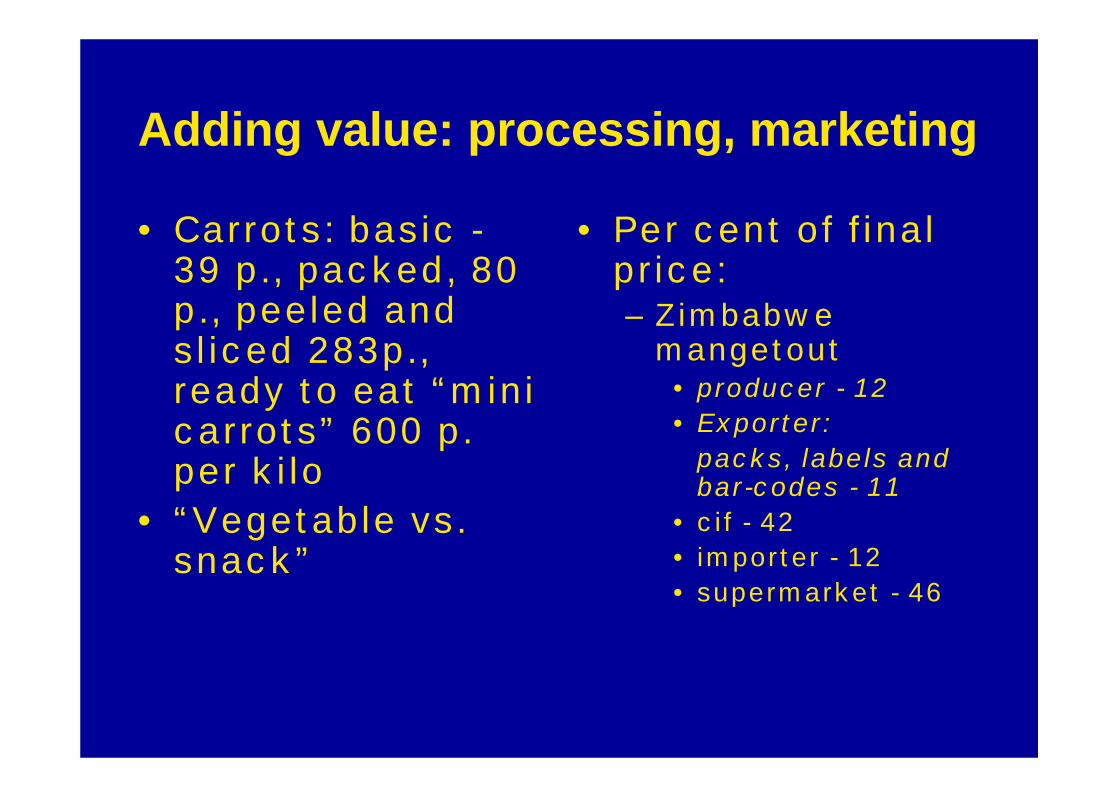

Adding value: processing, marketing

• Carrots: basic -39 p., packed, 80p., peeled andsliced 283p.,ready to eat “minicarrots” 600 p.per kilo

• “Vegetable vs.snack”

• Per cent of finalprice:– Zimbabwe

mangetout• producer - 12• Exporter:

packs, labels andbar-codes - 11

• cif - 42• importer - 12• supermarket - 46

Some crucial avenues

• Positioning in the value chain– Contract farming (Nestlé, >600000 in >80 countries)– Links with buyers

• Labeling, fair trade environmentallly preferable– About 600 labels worldwide– Fair trade supplies not prevalent in LDCs

• Differentiation, e.g. specialty coffees, but costly(coffee tasting)

• Supermarkets (cannot do without)

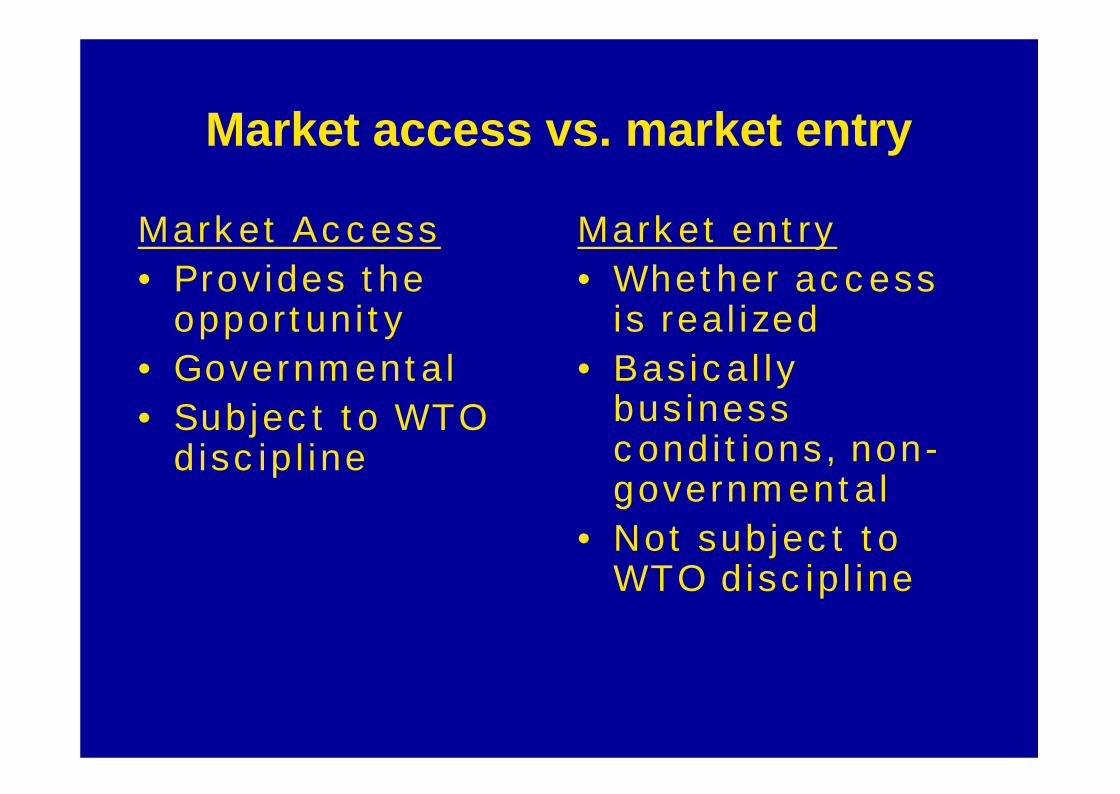

Market access vs. market entry

Market Access• Provides the

opportunity• Governmental• Subject to WTO

discipline

Market entry• Whether access

is realized• Basically

businessconditions, non-governmental

• Not subject toWTO discipline

Market structures concentrated

• Few buyers• Few processors• Few retailers• Technology often propriety• Simple food processing, e.g. of vegetables

escapes some of these constraints

Concentration in retailing:Dominance of supermarkets

The gold mine:http//:www.fas.usda.gov/scriptsw/attacherep/default.asp

• Austria: 5 largest - 90%• France: 75% mass distributors• Germany: top ten - 84%• Hungary: International chains - 43%• Netherlands: top four – 55%• UK: “Big five” – 80%• Italy and Spain low• Egypt, Slovakia, Turkey – relatively low but

rising

Meeting the standards of the international market placeMeeting the standards of the international market place

If farmers are to supply a newIf farmers are to supply a newmarket, they need to meet thatmarket, they need to meet thatmarket’s quality conditions andmarket’s quality conditions andcontract obligations.contract obligations.

This requires not just skills,This requires not just skills,but also an infrastructure thatbut also an infrastructure thatallows farmers to bring goodallows farmers to bring goodquality products to the buyers.quality products to the buyers.

Understanding the exigencies

In distant markets – difficult tofollow from home:

• Governmental standards andregulations under WTOagreements (SPS, TBT, TRIPS)

• Tastes• Private standards – more complex

and important

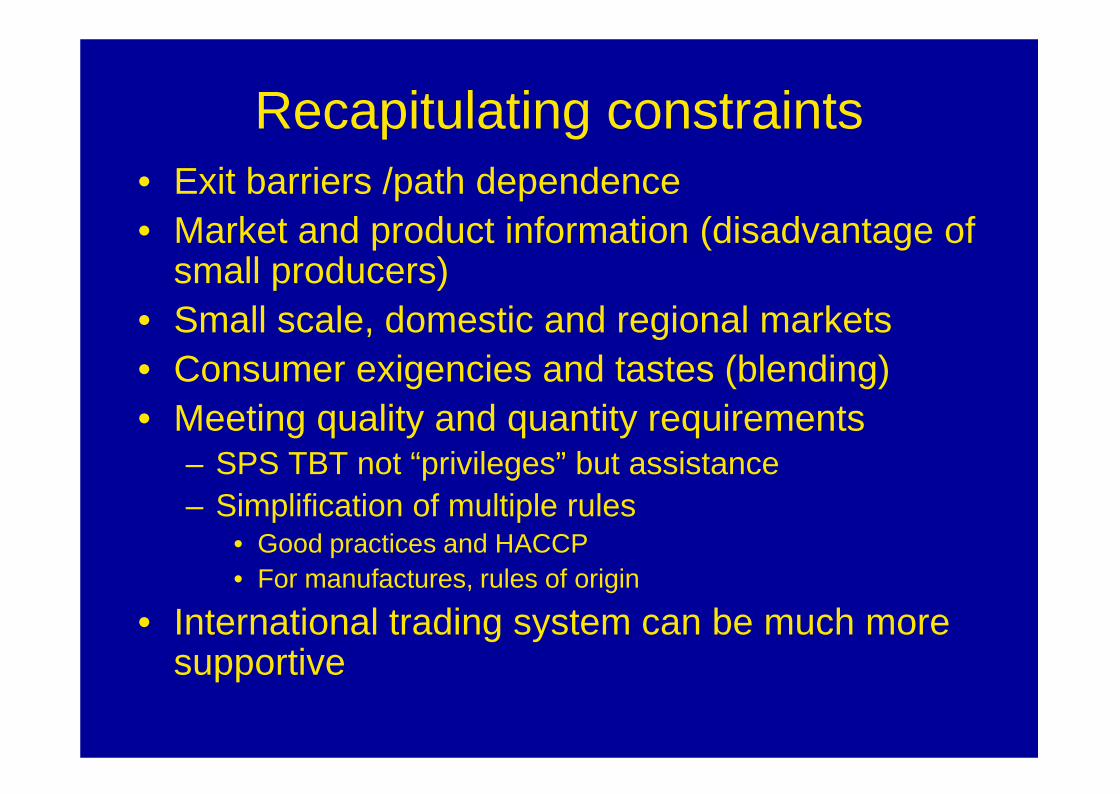

Recapitulating constraints• Exit barriers /path dependence• Market and product information (disadvantage of

small producers)• Small scale, domestic and regional markets• Consumer exigencies and tastes (blending)• Meeting quality and quantity requirements

– SPS TBT not “privileges” but assistance– Simplification of multiple rules

• Good practices and HACCP• For manufactures, rules of origin

• International trading system can be much moresupportive

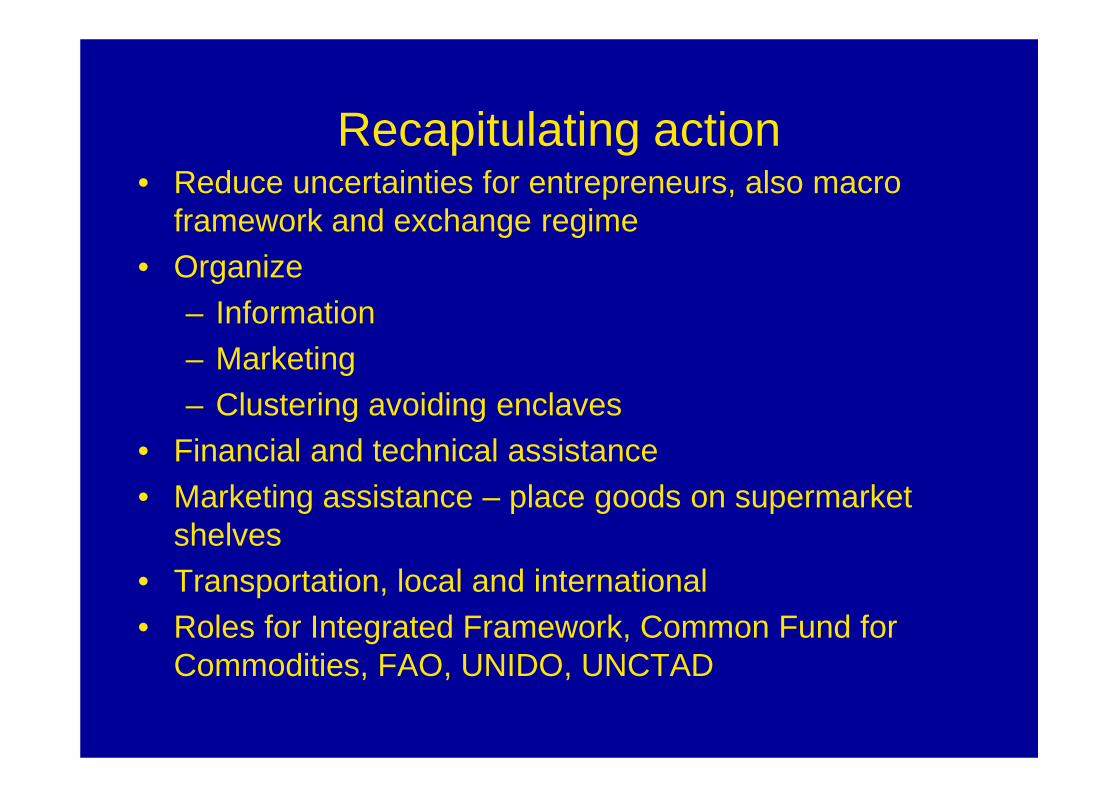

Recapitulating action• Reduce uncertainties for entrepreneurs, also macro

framework and exchange regime• Organize

– Information– Marketing– Clustering avoiding enclaves

• Financial and technical assistance• Marketing assistance – place goods on supermarket

shelves• Transportation, local and international• Roles for Integrated Framework, Common Fund for

Commodities, FAO, UNIDO, UNCTAD