DISTANCE EDUCATION B.B.A. DEGREE EXAMINATION, MAY … · 2019-05-15 · Ws19 DE–3529 DISTANCE...

64

Ws19 DE–3529 DISTANCE EDUCATION B.B.A. DEGREE EXAMINATION, MAY 2018. BUSINESS COMMUNICATION Time : Three hours Maximum : 100 marks SECTION A — (5 8 = 40 marks) Answer any FIVE questions. 1. Bring out the various qualities of a business letter. J¸ ÁoPU Piuzvß £À÷ÁÖ ußø©PøÍ Â›ÁõP GÊxP. 2. Write short notes on: (a) Execution of an order. (b) Cancellation of an order. ]Ö SÔ¨¦ ÁøμP. (A) Bønø¯ {øÓ÷ÁØÓ® (B) Bønø¯ μzx ö\´uÀ 3. What is a circular letter? What are the factors to be governed while drafting a circular letter? _ØÓÔUøP Piu® GßÓõÀ GßÚ? _ØÓÔUøPU Piu® GÊx®ö£õÊx PÁÚzvÀ öPõÒÍ ÷Ási¯ PõμoPÒ ¯õøÁ? 4. What are the objectives of collection letter? Á`À Piuzvß ÷|õUP[PÒ ¯õøÁ? Sub. Code 11

Transcript of DISTANCE EDUCATION B.B.A. DEGREE EXAMINATION, MAY … · 2019-05-15 · Ws19 DE–3529 DISTANCE...

Ws19

DE–3529

DISTANCE EDUCATION

B.B.A. DEGREE EXAMINATION, MAY 2018.

BUSINESS COMMUNICATION

Time : Three hours Maximum : 100 marks

SECTION A — (5 8 = 40 marks)

Answer any FIVE questions.

1. Bring out the various qualities of a business letter.

J¸ ÁoPU Piuzvß £À÷ÁÖ ußø©PøÍ Â›ÁõP GÊxP.

2. Write short notes on:

(a) Execution of an order.

(b) Cancellation of an order.

]Ö SÔ¨¦ ÁøμP.

(A) Bønø¯ {øÓ÷ÁØÓ®

(B) Bønø¯ μzx ö\´uÀ

3. What is a circular letter? What are the factors to be governed while drafting a circular letter?

_ØÓÔUøP Piu® GßÓõÀ GßÚ? _ØÓÔUøPU Piu®

GÊx®ö£õÊx PÁÚzvÀ öPõÒÍ ÷Ási¯ PõμoPÒ

¯õøÁ?

4. What are the objectives of collection letter?

Á`À Piuzvß ÷|õUP[PÒ ¯õøÁ?

Sub. Code 11

DE–3529

2

Ws19

5. What are the elements of a good banking correspondence?

Kº ]Ó¢u Á[Q°¯À Piuz öuõhº¤ß EmTÖPÒ ¯õøÁ?

6. What are the different types of Insurance? Explain.

Põ¨¥miß £À÷ÁÖ ÁøPPÒ ¯õøÁ? ÂÁ›.

7. What is an Agenda? Explain.

‘Tmh {PÌa] {μÀ’ GßÓõÀ GßÚ? ÂÍUSP.

8. Define: Report. What are the content of a reports? Explain.

Áøμ¯Ö : AÔUøP, AÔUøP°À Ch®ö£Ö® EmTÖPÒ

¯õøÁ? ÂÍUSP.

SECTION B — (4 15 = 60 marks)

Answer any FOUR questions.

9. What are the essential pieces of information required for composing an order? Give an examples.

J¸ BønU Piuzøu ÁiÁø©UPz ÷uøÁ¯õÚ uPÁÀPÒ

¯õøÁ? J¸ BønU PiuzvØS Euõμn® u¸P.

10. What are the reasons on which an order for goods may be refused?

\μUSPÐUPõÚ J¸ Bøn ©ÖUP¨£kÁuØS›¯ Põμn[PÒ

¯õøÁ?

11. Draft a reply to your customer who has complained about the poor quality of the goods sent by you.

}[PÒ Aݨ¤¯ ö£õ¸mPÒ uμ® SøÓ¢x C¸¨£uõP

öu›Âzx GÊu¨£mh E[PÒ ÁõiUøP¯õÍ›ß PiuzvØS

uS¢u £vÀ Piu® GÊxP.

DE–3529

3

Ws19

12. Write a letter to a banker asking extension of time for repayment of loan instalment

Phß uÁøn ö\¾zxÁuØPõÚ Põ» AÍøÁ }miUPU÷Põ›

Á[Q¯¸US Kº Piu® ÁøμP.

13. Explain the essential points you would consider in writing minutes.

Tmh |hÁiUøPU SÔ¨¦ GÊx®÷£õx PÁÛUP ÷Ási¯

•UQ¯ ÂÁμ[PøÍ ÂÍUSP.

14. Draft the minutes of the Annual General Meeting of a company.

J¸ {Ö©zvß Bsk¨ ö£õxUTmhzvß Tmh |hÁiUøP

SÔ¨¦ JßÖ ÁøμP.

15. Discuss the various classifications of reports in a company.

J¸ {ÖÁÚzv¾ÒÍ £À÷ÁÖ ÁøP¯õÚ AÔUøPPøÍ

ÂÁ›.

–––––––––––––

Ws 5

DE–3530

DISTANCE EDUCATION

B.B.A. DEGREE EXAMINATION, MAY 2018.

PRINCIPLES OF ECONOMICS

Time : Three hours Maximum : 100 marks

PART A — (5 × 8 = 40 marks)

Answer any FIVE questions.

1. Describe the features of perfect competition.

{øÓĨ ÷£õmi°ß C¯À¦PøÍ ÂÁ›.

2. State the bases of price discrimination.

Âø» ÷£u® PõmkÁuØPõÚ Ai¨£øh°øÚ TÖP.

3. Explain the causes for the emergency monopoly.

•ØÖ›ø© ÷uõßÖÁuØPõÚ Põμn[PøÍ ÂÍUSP.

4. Explain the standard of living theory of wages.

T¼°ß ÁõÌUøPz uμU ÷Põm£õmiøÚ ÂÍUSP.

5. What is real wage? Distinguish real wage from money wages.

Esø©U T¼ GßÓõÀ GßÚ? Esø©U T¼US® £n

T¼US® EÒÍ Âzv¯õ\zøu ÷ÁÖ£kzv TÖP.

6. Write a note on quasi-rent.

÷£õ¼ Áõμ® & J¸ SÔ¨¦ ÁøμP.

7. State and explain the risk theory of profit.

C»õ£zvß Chº uõ[S® ÷Põm£õmiøÚz TÔ ÂÁ›UPÄ®.

Sub. Code 12

DE–3530

2

Ws 5

8. State and illustrate the Cobb-Douglas production function.

Põ¨&hU»ì EØ£zv ö\¯À£õkPøÍ GkzxUPõmkhß

ÂÍUSP.

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. Explain the process of price determination under perfect competition.

{øÓĨ ÷£õmi°À Âø» GÆÁõÖ {ºn°UP¨£kQÓx

Gߣøu ÂÍUSP.

10. Discuss the welfare implications of monopoly.

•ØÖ›ø©°ÚõÀ ö£õ¸Íõuõμ |»ÛÀ HØ£k® uõUPzøu

ÂÁõv.

11. Examine the Ricardian theory of rent.

›UPõº÷hõÂß ÁõμU ÷Põm£õmøh B´P.

12. Critically analyse the modern theory of wages.

|ÃÚ T¼U ÷Põm£õmøhz vÓÚõ´P.

13. Explain Keynesian liquidity preference theory.

Rß]ß }ºø© ¸¨£U ÷Põm£õmiøÚ ÂÍUSP.

14. State and explain the neo-classical theory of interest.

Ámi öuõhº£õÚ ¦v¯ öuõßø©¨ ö£õ¸Î¯¼ß

÷Põm£õmøh TÖP.

15. Explain the criticism of indifference curve analysis.

\©÷|õUS ÁøÍ÷PõkPÒ Bμõ´uÀ £ØÔ Â©º\Ú® ö\´P.

————————

Sp 6

DE–3531

DISTANCE EDUCATION

B.B.A. DEGREE EXAMINATION, MAY 2018.

PRINCIPLES OF MANAGEMENT

Time : Three hours Maximum : 100 marks

PART A — (5 × 8 = 40 marks)

Answer any FIVE questions.

1. Describe the importance of management.

÷©»õsø©°ß •UQ¯zxÁzøu ÂÁ›UP.

2. Briefly explain the different types of decisions.

•iÄPÎß £À÷ÁÖ ÁøPPøÍa _¸UP©õP ÂÍUSP.

3. State the principles of delegation of authority.

AvPõμ J¨£øhÂß öPõÒøPPøÍU TÖP.

4. Describe strategic and tactical plans.

uÍzuøP ©ØÖ® u¢vμ vmh[PÒ £ØÔ ÂÁ›UP.

5. Write notes on line organization.

÷|ºQøh Aø©¨¦ £ØÔ SÔ¨¦PÒ GÊxP.

6. State the principles of direction.

ÁÈPõmh¼ß öPõÒøPPøÍU TÖP.

Sub. Code 13

DE–3531

2

Sp 6

7. Compare and contrast democratic and autocratic leadership.

áÚ|õ¯P ©ØÖ® \ºÁõvPõμ uø»ø©zxÁ[PøÍ J¨¤mk®

÷ÁÖ£kzv²® PõmkP.

8. What is coordination? Briefly explain the different types of coordination.

J¸[QønzuÀ GßÓõÀ GßÚ? J¸[Qønzu¼ß £À÷ÁÖ

ÁøPPøÍa _¸UP©õP ÂÍUSP.

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. Explain the different approaches to the study of modern management.

|ÃÚ ÷©»õsø©ø¯U PØ£uØPõÚ £À÷ÁÖ AqS

•øÓPøÍ ÂÍUSP.

10. Describe the various steps in the planning process.

vmhªhÀ ö\¯À•øÓ°ß £À÷ÁÖ £iPøÍ ÂÁ›UP.

11. What are the merits and limitations of decentralization?

AvPõμ¨ £μÁ»õUP¼ß |ßø©PÒ ©ØÖ® SøÓ£õkPÒ

¯õøÁ?

12. Explain Herzberg’s two factor theory of motivation.

öíºìö£ºQß C¸Põμo FUS¨¦U ÷Põm£õmøh

ÂÍUSP.

13. What is a matrix organization? Discuss its merits and limitations.

Ao Aø©¨¦ GßÓõÀ GßÚ? Auß |ßø©PÒ ©ØÖ®

SøÓ£õkPøÍ ÂÁõvUP.

DE–3531

3

Sp 6

14. Describe the process of communication? What are the main barriers in a communication system? Suggest measures to overcome the barriers.

uPÁÀ öuõhº¤ß ö\¯À•øÓø¯ ÂÁ›UP. uPÁÀ

öuõhº¤ß •UQ¯ uøhPÒ ¯õøÁ? AzuøhPøÍz

uPº¨£uØPõÚ B÷»õ\øÚ ÁÇ[SP.

15. Explain the various techniques of control.

Pmk¨£õmiß £À÷ÁÖ ²UvPøÍ ÂÍUSP.

–––––––––––––––

SP 5

DE–3532

DISTANCE EDUCATION

B.B.A. DEGREE EXAMINATION, MAY 2018.

BUSINESS ENVIRONMENT

Time : Three hours Maximum : 100 marks

SECTION A — (5 8 = 40 marks)

Answer any FIVE questions.

1. Define Business. Explain the basic aspects of business.

Áøμ¯Ö ÁoP®. ÁoPzvß Ai¨£øh A®\[PøÍ

ÂÍUSP.

2. What are the advantages and disadvantages of joint family system?

TmkU Sk®£zvß |ßø© ©ØÖ® wø©PÒ ¯õøÁ?

3. How does the political factors affect the environment of business?

ÁoPa `Çø» Aμ]¯À PõμoPÒ GÆÁõÖ £õvUQßÓÚ?

4. Explain the meaning and nature of directive principle of the state policy.

©õ{»U öPõÒøP°ß ÁÈPõmk® ÷Põm£õk Gߣuß

Aºzu® ©ØÖ® ußø©PøÍ ÂÍUSP.

Sub. Code 14

DE–3532

2

SP 5

5. “Sociological factors affect economic environment”. Do you agree?

“\‰PU PõμoPÒ ö£õ¸Íõuõμa `Çø» £õvUQÓx” CuøÚ

}º HØÖU öPõÒQÕºPÍõ?

6. What are the merits and demerits of Multi National Corporation?

£ßÚõmk {ÖÁÚ[PÎß |ßø© ©ØÖ® wø©PÒ ¯õøÁ?

7. Discuss the nature of technological environment.

öuõÈÀ~m£a `Ç¼ß ußø©ø¯ ÂÍUSP

8. Explain the advantages and disadvantages of a business being socially responsible.

J¸ ÁoP {ÖÁÚ® \‰P ö£õÖ¨¦nº÷Áõk

ö\¯À£kÁuõÀ HØ£k® |ßø©PÒ ©ØÖ® wø©PøÍ

ÂÍUSP.

SECTION B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. Explain various Environmental Factors affecting Business.

ÁoPzøu¨ £õvUS® £À÷ÁÖ _ØÖa`ÇÀ PõμoPøÍ

ÂÍUSP.

10. What is Social Environment? Explain its importance in developing a business.

\‰Pa`ÇÀ GßÓõÀ GßÚ? J¸ ÁoP Áͺa]°À \‰Pa

`Ç¼ß •UQ¯zxÁzøu ÂÁ›.

DE–3532

3

SP 5

11. Explain the several types of changes in political environment field.

Aμ]¯À `ǼÀ HØ£k® £À÷ÁÖ ©õØÓ[PÎß ÁøPPøÍU

SÔ¨¤mk ÂÍUSP.

12. Explain the importance of Centre — State relationships in the Indian Economic Development.

C¢v¯¨ ö£õ¸Íõuõμ Áͺa]°À ©zv¯, ©õ{» Aμ_PÎß

EÓÂß •UQ¯zxÁzøu ÂÍUSP.

13. Describe the economic role of Government in India.

C¢v¯õÂÀ Aμ]ß ö£õ¸Íõuõμ¨ £[PΨ¦ £ØÔ ÂÍUSP.

14. What are the problems faced by industries in selecting the appropriate technology? Explain.

\›¯õÚ öuõÈÀ ~m£zøu ÷uº¢öukUS®÷£õx J¸

öuõÈØ\õø»US HØ£k® ¤μa]øÚPÒ ¯õøÁ? ÂÁ›UPÄ®.

15. Explain the social responsibility of business concerns towards various groups.

£À÷ÁÖ SÊUPÒ «xÒÍ ÁoPzvß \‰P ö£õÖ¨¦ £ØÔ

ÂÍUSP.

–––––––––––––––

wk7

DE–3533

DISTANCE EDUCATION

B.B.A. DEGREE EXAMINATION, MAY 2018.

FINANCIAL ACCOUNTING

Time : Three hours Maximum : 100 marks

PART A — (5 8 = 40 marks)

Answer any FIVE questions.

1. State the Rule of Accountancy.

PnUQ¯¼ß ÂvPÒ ¯õøÁ?

2. What is the need for preparing Trial Balance?

C¸¨¦a ÷\õuøÚ¨ £mi¯À u¯õ›¨££vß AÁ]¯® ¯õx?

3. What are the differences between Consignment and Joint Venture?

Aݨ¥miØS® CønÂøÚUS® EÒÍ ÷ÁÖ£õkPÒ

¯õøÁ?

4. Distinguish between Receipts and payments account and Income and Expenditure account.

ö£ÖuÀ ö\¾zuÀ PnUQøÚ²®, ÁμÄ ö\»Ä PnUQøÚ²®

÷ÁÖ£kzv Põs¤.

5. X, Y and Z’s capital being Rs.90,000, Rs.60,000 and Rs.30,000 respectively. The value of goodwill Rs.6,000 and general Reserve Rs.4,500. The profit sharing Ratio is 3:2:1. Prepare capital of the three partners.

X, Y ©ØÖ® Zß •uÀ ¹.90,000, ¹.60,000 ©ØÖ® ¹.30,000.

|ß©v¨¦ ¹.6,000 GÚ ©v¨¤h¨£kQÓx. Põ¨¤ {v ¹.4,500

CÁºPÎß »õ£ ÂQu® 3:2:1 C®‰Á›ß •uÀ PnUøP u¸P.

Sub. Code 15

DE–3533

2

wk76. What is Garner Vs Murray? How does its Judgement

affect the accounts of partners?

PõºÚº Gvº •º÷μ GßÓõÀ GßÚ? Cx GÆÁõÖ

TmhõÎPÎß PnUøP £õvUQÓx?

7. How is interest recorded in instalment transactions?

uÁøn •øÓ°À Ámi GÆÁõÖ PnUQÀ £v¯¨£kQÓx?

8. Explain the methods of valuation of shares?

{Ö©® £[SPøÍ ©v¨¤k® •øÓPÒ £ØÔ ÂÍUSP.

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. From the following balances and additional information for the year ended 31.2.2004, prepare the final accounts in the books of a company.

Rs. Rs.

Purchases 9,25,000 Preliminary

Wages 4,24,325 expenses 25,000

Manufacturing Calls in arrear 37,500

Expenses 65,575 Machinery 15,00,000

Salaries 70,000 Building 16,50,000

Bad debts 10,550 Interim dividend 1,87,500

General Expenses 84,175 Furniture 35,000

Stock (1.4.2003) 3,75,000 Debtors 4,36,000

Goodwill 1,00,000 Capital 4,36,000

Cash in hand 2,28,250 P & L a/c (Cr) 72,500

Director’s fees 31,125 Creditors 1,67,500

Interest on debentures 45,000 Bills payable 2,90,000

6% Debentures 15,00,000 General Reserve 1,25,000

Sales 20,75,000

DE–3533

3

wk7 Additional Information:

(a) Closing Stock – Rs. 4,55,000

(b) Depreciation – Machinery 10%

(c) Write off Rs.2,500 from preliminary expenses

(d) Provision for doubtful debts Rs.4,250.

¤ßÁ¸® C¸¨¦UPÒ ©ØÖ® Cuμ £μ[Pμ¸¢x ©õºa 31,

2004À •iÁøh¢u BsiØPõÚ CÖvU PnUPPøÍ J¸

{Ö©zvÒ HkPÎÀ u¯õ›UPÄ®.

¹. ¹.

öPõÒ•uÀ 9,25,000 B쮣ö\»Ä 25,000

{¾øÁ°¾ÒÍ

T¼ 4,24,325 AøǨ¦ £n® 37,500

EØ£zva ö\»Ä 65,575 C¯¢vμ® 15,00,000

\®£Í® 70,000 Pmih® 16,50,000

ÁõμUPhß 10,550 Cøh{ø»

ö£õxa ö\»Ä 84,175 £[Põuõ¯® 1,87,500

\μUS (1.4.2003) 3,75,000 ©øÚxøn¨

|ß©v¨¦ 1,00,000 ö£õ¸mPÒ 35,000

öμõUP øP°¸¨¦ 2,28,250 PhÚõÎPÒ 4,36,000

C¯US|º Pmhn® 31,125 ‰»uÚ® 4,36,000

Phߣzvμ Ámi 45,000 C»õ£ |mhU

6% Phß £zvμ[PÒ 15,00,000 P/S (ÁμÄ) 72,500

ÂØ£øÚ 20,75,000 PhÜ¢÷uõº 1,67,500

ö\¾zuØS›¯

©õØÖa ^mk 2,90,000

ö£õxUPõ¨¦ 1,25,000

DE–3533

4

wk7 TkuÀ £μ[PÒ:

(A) CÖva \μUQ¸¨¦ ¹.4,55,000

(B) ÷u´©õÚ® – C¯¢vμ® 10%

(C) B쮣a ö\»ÂÀ 2,500 IU PÈUP

(D) I¯U Phß Põ¨¦ ¹.4,250.

10. Sundar and Rajan were independent contractors. They undertook a Joint Venture to construct building for a company. They opened a joint bank account and deposited Rs.50,000 by Sundar and Rs.30,000 by Rajan. The contract price was Rs.3,00,000 which was to be discharged Rs.2,50,000 in cash (in instalments) and Rs.50,000 in shares. Sundar paid Architect fees Rs.10,000. Rajan paid wages Rs.20,000. Sundar supplied a Truck for Rs.20,000 into the Venture. Rajan was entitled to a commission of Rs.10,000. Materials purchased totalled Rs.1,00,000 and other expenses totalled Rs.75,000. Materials costing Rs.5,000 were last in an accident.

The Venture was completed and the contract price was duly discharged. Sundar took shares at a value of Rs.55,000 and took back the truck at Rs.16,000.

Prepare necessary ledger accounts assuming that seperate books are maintained for the venture.

_¢uº, μõáß GßÝ® Cμsk Pmih PõsmμõUhºPÒ ÷\º¢x

J¸ {Ö©zvØPõP Pmih® Pmk® J¸ CønÂøÚø¯

÷©ØöPõshÚº. Cøn Á[Q PnUS JßÖ xÁ[Q AvÀ

_¢uº ¹.50,000, μõáß ¹.30,000, öh£õêm ö\´uÚº. J¨£¢u

Âø» ¹.3,00,000. Cøu {Ö©® ¹.2,50,000 öμõUP©õPÄ®

(]» uÁønPÎÀ) ¹.50,000 £[SPÍõPÄ® öPõkUS®.

Pmih Pø»b›ß Pmhn® ¹.10,000 _¢uμõÀ

öPõkUP¨£mhx. μõáß ¹.20,000 T¼ ö\¾zvÚõº. _¢uº

¹.20,000 ©v¨¦ÒÍ Fºv JßÖ CønÂønUS AÎzuõº.

J¨£¢u¨£i μõáÝUS ¹.10,000 Pªåß öPõkUP¨£h

DE–3533

5

wk7÷Ásk®. ö£õ¸mPÒ ¹.1,00,000 Cuμ ö\»ÄPÒ ¹.75,000

Cøn Á[Q°¼¸¢x ö\¾zu¨£mhx. ¹.5,000 ©v¨¦ÒÍ

ö£õ¸mPÒ J¸ £zvÀ AÈ¢x ÷£õ°Ú.

CønÂøn •i¢x J¨£¢u Âø» ö£Ó¨£mhx. _¢uº

£[SPøÍ ¹.55,000US GkzxUöPõshõº. Fºvø¯

¹.16,000US _¢uº v¸®£ GkzxU öPõshõº.

uÛ HkPÎÀ ÷uøÁ¯õÚ ÷£÷μmkU PnUSPøÍ

u¯õ›UPÄ®.

11. Given below are Receipts and payments Account and Income and Expenditure Account of a Club for the year ending 31st December 2001. Prepare Balance sheets both in beginning and at the end.

Receipts and Payments Account for the year ending 31.12.2001.

Receipts Payments

Rs. Rs.

To Bal b/d 4,000 By Electricity 500

To Endowment By Salaries 6,000

fund 2,000 By Advertisement 1,200

To Subscription 10,200 By Provision 6,800

To Entrance fee 800 By printing and

To Donation for stationery 700

Books 1,300 By Deposit in Bank 1,000

To Entertainment 4,000 By sports material 2,300

To sale of furniture By Creditors (2000) 1,300

(Cost price Rs.800 700 By Investment at 96

purchased on

1.7.2000 interest @ 4% 1,920

By Balance c/d 1,280

23,000 23,000

DE–3533

6

wk7 Income and Expenditure Account for the year ended 31st

December 2001. Expenditure Rs. Income Rs.

To sale of furniture By Subscription 10,000(loss) 100 By Entrance fee 400To salaries 6,700 By Interest on Investment atTo Advertisement 1,000 4% on Rs.2,000 80To Audit fee 300 By Entertainment 4,000To provisions 6,000 By Excess of Expenditure To printing and over Income 2,370stationery 750 To sports material 2,000

16,850 16,850

R÷Ç öPõkUP¨£mkÒÍx J¸ PÇPzvß i\®£º 31, 2001À

•iÁøh²® BsiØPõÚ ö£ÖuÀ ö\¾zxuÀ ©ØÖ® ö\»Ä

PnUSPÒ BS®. B쮣 C¸¨¦ {ø»U SÔ¨£¦ ©ØÖ®

CÖv C¸¨¦ {ø»U SÔ¨¦ BQ¯ÁØøÓz u¯õº ö\´P.

i\®£º 31, 2001À •iÁøh²® BsiØPõÚ ö£ÖuÀ ö\¾zuÀ

PnUS.

ö£ÓuÀ ö\¾zuÀ ¹. ¹.

öuõhUP C¸¨¦ 4,000 ªß\õμ® 500

{ø»¯õÚ {v 2,000 \®£Í® 6,000

\¢uõ 10,200 ÂÍ®£μ® 1,200

~øÇÄU Pmhn® 800 ö£õ¸mPÒ 6,800

¦zuP[PÐUPõÚ Aa_ GÊxö£õ¸Ò 700

|ßöPõøh 1,300 Á[Q°À øÁ¨¦ 1,000

÷PÎUøP 4,000 Âøͯõmk ©øÚz xøn¨ ö£õ¸mPÒ 2,300

ö£õ¸Ò TÜ¢÷uõº (2000) 1,300

ÂØ£øÚ 1.7.200À 96US

(AhUPÂø» Áõ[Q¯ •u½kPÒ

¹.800) 700 Ámi 4% 1,920

CÖv C¸¨¦ 1,280

23,000 23,000

DE–3533

7

wk7 i\®£º 31, 2001À kiÁøh²® BsiØPõÚ ÁμÄ ö\»Ä

PnUS ö\»Ä ¹. ÁμÄ ¹.

©øÚz \¢uõ 10,000xøn¨ö£õ¸Ò ~øÇÄU Pmhn® 400ÂØ£øÚ (|mh®) 100

\®£Í® 6,700 ¹.2000UPõÚ •u½kPÒ

ÂÍ®£μ® 1,000 «uõÚ 4% Ámi 80uoUøP Pmhn® 300 ÷PÎUøP 4,000ö£õ¸mPÒ 6,000 ÁμÂß ªS¢u ö\»Ä 2,370Aa_ GÊxö£õ¸Ò 750 Âøͯõmk¨ ö£õ¸Ò 2,000

16,850 16,850

12. The Balance sheet of A, B and C who were sharing profit in the ratio of 4: 3: 2 respectively stood as follows on 31st Dec 1996.

Rs. Rs.

Creditors 4,140 Cash at Bank 3,300

Capital Accounts: Debtors 3045

A 12,000 (-) provision 105 2940

B 9,000 Stock 4,800

C 6,000 Plant 5,100

Land 15,000

31,140 31,140

‘B’ having given notice to retire from the firm, the following adjustment in the books of the firm were agreed upon:

(a) The land be appreciated by 10%

(b) Provision for bad debts is no longer necessary

(c) Stock be appreciated by 20%

DE–3533

8

wk7 (d) The adjustment be made in the accounts to rectify a

mistake previously made whereby B was credited in excess by Rs.810 while A and C were debited in excess by Rs.420 and Rs.390 respectively.

(e) That the goodwill of the firm be valued at Rs.5,400 and B’s share of the same be adjusted in the ratio of 2: 1.

(f) That the entire capital of the firm as newly constituted will be readjusted by the ratio of 2: 1.

Pass Journal entries and prepare a Balance Sheet.

R÷Ç öPõkUP¨£mkÒÍ C¸¨¦ {ø»U SÔ¨£õÚx A, B ©ØÖ® C BQ¯ TmhõÎPÎß 31.12.1996® ÷uv°À

EÒÍuõS®. C»õ£zvøÚ 4: 3: 2 GßÓ ÂQuzvÀ ¤›zxU

öPõÒQßÓÚº.

¹. ¹.

PhÚõÎPÒ 4,140 öμõUP® 3,300

•uÀ PnUS PhÚõÎPÒ 3045

A 12,000 (&) Põ¨¦ 105 2940

B 9,000 \μUQ¸¨¦ 4,800

C 6,000 ö£õÔ 5,100

{»® 15,000

31,140 31,140

‘B’ Tmhõsø©°¼¸¢x »SÁuõP AÔUøP AÎzu¤ß

RÌUPsh ©õØÓ[PÒ ö\´¯¨£mhÚ.

(A) {»zvß ©v¨¦ 10% AvP›UP¨£mhx

(B) ÁõμUPhß Põ¨¦ CÛ ÷uøÁ°Àø»

(C) \μUQ¸¨¦ ©v¨¦ 20% AvP›¨¦

DE–3533

9

wk7 (D) ‘B; °ß PnUQÀ ¹.810 AvP©õP ÁμÄ®. A°ß

PnUQÀ ¹.420 AvP ©ØÖ® C°ß PnUQÀ AvP©õP

¹.390® £ØÖ øÁUP¨£mhx. C¢u uÁÖ \›ö\´¯¨£h

÷Ásk®.

(E) |Øö£¯º ¹.5,400US ©v¨¤h¨£mh, B °ß £[QøÚ A ©ØÖ® C 2: 1 GßÓ •øÓ°À ¤›zxU öPõÒͨ£k®.

÷uøÁ¯õÚ SÔ¨÷£mk¨ £vÄPÒ ©ØÖ® C¸¨¦{ø»

SÔ¨¤øÚ²® u¯õº ö\´P.

13. A company issued 2,000 shares of Rs.10 each at a premium of Rs.2 per share. The share amount is to be received as

Rs.

On application 2

On allotment 5 (including premium)

On I Call 3

On II Call 2

Applications were received for 3,000 shares. The total shares were allotted to the applicants of 2,400 shares prorata. Mohan to whom 60 shares were allotted did not pay the two calls and his shares were forfeited. Then 40 of such shares were received at Rs.9 per share. Show the journal entries in the books of the company.

J¸ P®ö£Û £[S JßÖ ¹.10 Ãu® 2,000 £[SPøͨ £[S

JßÖUS ¹.2 •øÚ©zvÀ öÁΰmhx. £[SzöuõøP

RÌUPshÁõÖ ö\¾zu¨£h ÷Ásk®.

¹.

Âsn¨£zvß ÷£õx 2

JxURmiß ÷£õx 5(•øÚ©® Em£h0

•uÀ AøǨ¦ 3

Cμshõ® AøǨ¦ 2

DE–3533

10

wk7 3,000 £[SPÐUPõÚ Âsn¨£[PÒ Á¢uÚ. 2,400

£[SPÐUPõÚ Âsn¨£[PÎøh÷¯ ö©õzu £[SPÒ

ÂQuõa\õμ Ai¨£øh°À JxUP¨£mhÚ. ÷©õPÝUS

JxUP¨£mh 60 £[SPÒ «x AÁº C¸ AøǨ¦UPõÚ

öuõøPPøÍa ö\¾zuõuõÀ AÁμx £[SPÒ JÖ¨¤Ç¨¦

ö\´¯¨£mhÚ. ¤ÓS A¨£[SPÎÀ 40 £[SPÒ ¹.9 Ãu®

ÂØP¨£mhÚ. P®ö£Û°ß HkPÎÀ SÔ¨÷£mk®

£vÄPøÍz u¯õ›UPÄ®.

14. Write the differences between provision and Reserve.

JxURmiØS®, Põ¨¦US® EÒÍ Âzv¯õ\[PøÍ GÊxP.

15. Discuss the methods and valuation of goodwill in partnership.

Tmhõsø©°À |ß©v¨¦ PnUQkPÒ •øÓPøÍ ÂÍUSP.

————————

sp4

DE–3534

DISTANCE EDUCATION

B.B.A./B.B.A. (Lateral) DEGREE EXAMINATION, MAY 2018.

BANKING THEORY, LAW AND PRACTICE

Time : Three hours Maximum : 100 marks

PART A — (5 8 = 40 marks)

Answer any FIVE questions.

1. What do you mean by commercial bank?

ÁoP Á[Q GßÓõÀ GßÚ?

2. “Central Bank is the Banker to the Government” Discuss.

“ø©¯ Á[Q Aμ\õ[PzvØS Á[Q” ÂÍUSP.

3. What is meant by selective credit control?

÷uº¢öukUP¨£mh Phß Pmk¨£õk GßÓõÀ GßÚ?

4. What are the advantages of Branch Banking?

QøÍ Á[QPÎß |ßø©PÒ GßÚ?

5. Define the terms “Banker” and “Customer”.

Á[Q¯º ÁõiUøP¯õͺ – Áøμ¯Ö.

6. What are the main features of fixed deposit?

{ø» øÁ¨¦ {v°ß •UQ¯ A®\[PÒ GßÚ?

Sub. Code 21

DE–3534

2

sp47. What is an organized money market?

JÊ[S£kzu¨£mh £na\¢øu GßÓõÀ GßÚ?

8. Discuss the position of a banker when an undated cheque is presented for payment.

÷uv SÔ¨¤mh¨£hõu Põ÷\õø» Á[Q°À ö\¾zu¨£k®

÷£õx Á[Q¯›ß {ø»¨£õk SÔzx ÂÁ›.

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. What are the functions of commercial banks?

ÁoP Á[Q°ß £oPÒ GßÚ?

10. Give a specimen of a cheque and discuss its features.

J¸ Põ÷\õø»°ß ©õv›ø¯z u¢x Auß ußø©PøÍ ÂÁ›.

11. Discuss the formalities which a banker has to observe before opening a new account.

Á[Q°À ¦v¯uõP PnUS öuõh[S® ÷£õx Á[Q¯º

PÁÛUP ÷Ási¯ |øh•øÓPÒ ¯õøÁ?

12. What are the different components of Indian money market?

C¢v¯ £na \¢øu°ß £À÷ÁÖ A[P[PÒ ¯õøÁ?

13. What do you mean by unit banking? What are its merits and demerits?

A»S Á[Q GßÓõÀ GßÚ? Auß |ßø©, wø©PÒ GßÚ?

DE–3534

3

sp414. Explain the different forms of advances.

•ß øÁ¨¦PÎß ÁiÁ[PøÍ ÂÍUSP.

15. What are the methods used by a Central Bank to control the credit?

G¢u •øÓPøͨ £¯ß£kzv ø©¯ Á[Q¯õÚx PhßPøÍU

Pmk¨£kzxQÓx?

————————

SER

DE-3535

DISTANCE EDUCATION

B.B.A./ B.B.A. (Lateral) DEGREE EXAMINATION, MAY 2018.

COMPANY LAW

Time : Three hours Maximum : 100 marks

SECTION A — (5 8 = 40 marks)

Answer any FIVE questions.

1. What are the privileges enjoyed by a private company?

uÛ {Ö©zvÝÒÍ \¾øPPÒ ¯õøÁ?

2. What is memorandum of association? Explain the procedure for alteration in any clause of the same.

Aø©¨¦ £zvμ® GßÓõÀ GßÚ? Auß \μzxUPøÍ ©õØÓ

ÁÈ•øÓPøÍ ÂÁ›.

3. Describe the different types of secretaries.

£À÷ÁÖ ÁøP¯õÚ ö\¯»õͺPøÍ ÂÁ›.

4. What is statutory report? What are its contents?

\mh•øÓ AÔUøP GßÓõÀ GßÚ? Auß EÒÍhUP®

¯õøÁ?

5. Who is an official liquidator? Explain its powers.

A¾Á»P Pø»¨£õͺ GߣÁº ¯õº? AÁ›ß AvPõμ[PøÍ

ÂÁ›.

6. Explain any five features of joint stock company.

Tmk¨ £[S {ÖÁÚzvß C¯À¦PøÍ H÷uÝ® I¢vøÚ

ÂÁ›.

Sub. Code 22

DE-3535

2

SER

7. State the rules relating to quorum for meeting under the Companies Act. 1956.

J¸ Tmhzøu |hzu SøÓ¢u£m\ |£ºPÒ GßÖ GÆÁÍÄ

÷uøÁ Gߣøu {¸© \mh® 1956 °ß Âv¨£i TÖP.

8. Distinguish between transfer and transmission of shares.

£[S E›ø© ©õØÓzøu²® ©ØÖ® ©μ¦ ÁÈ E›ø©

©õØÓzøu²® ÷ÁÖ£kzxP.

SECTION B — (4 15 = 60 marks)

Answer any FOUR questions.

9. Differentiate between a private and a public company when does a private company become a public company.

uÛ ©ØÖ® ö£õx {Ö©zøu ÷ÁÖ£kzxP. uÛ {ÖÁÚ®

G¨ö£õÊx ö£õx {Ö©©õP BQÓx?

10. Explain the different steps to be taken to float a public limited company from its inaction to the commencement of business.

J¸ ö£õx Áøμ¯Ö {Ö©zøu Auß ÷uõØÖ¨¦

{ø»°¼¸¢x öuõÈÀ öuõh[S® {ø»USU öPõsk

ö\ÀÁuØPõÚ £À÷ÁÖ £iPøÍ ÂÁ›.

11. Distinguish between managing director and whole time director.

÷©»õsø© C¯US|º ©ØÖ® •Ê÷|μ C¯US|º –

÷ÁÖ£kzxP.

12. What is special resolution? For what purposes are each resolutions necessary?

]Ó¨¦z wº©õÚ® GßÓõÀ GßÚ? AÆÁøPz wº©õÚ[PÒ

G¢u Põμn[PÐUSz ÷uøÁ£kQÓx?

DE-3535

3

SER

13. Discuss the duties and powers of directors.

C¯US|ºPÎß Phø©PÒ ©ØÖ® AvPõμ[PøÍ ÂÁ›.

14. Explain the different types of shares.

£[SPÎß £À÷ÁÖ ÁøPPøÍ ÂÁ›.

15. “A promoter is not a trustee or an agent of the company but he stands in a fiduciary position towards it” – comments.

÷uõØÖ¨£õͺ GߣÁº {Ö©zvß iμìi÷¯õ (A)

•PÁ÷μõ Qøh¯õx BÚõÀ Aøu ÷|õUQ¯ {ø»°À

EÒÍõº? ÂÁõv.

______________

Ws 5

DE–3536

DISTANCE EDUCATION

B.B.A./B.B.A. (Lateral) DEGREE EXAMINATION, MAY 2018.

BUSINESS STATISTICS

Time : Three hours Maximum : 100 marks

PART A — (5 × 8 = 40 marks)

Answer any FIVE questions.

1. State the functions of statistics.

¦Òΰ¯¼ß £oPÒ ¯õøÁ?

2. What are the qualities of a good average?

|À» \μõ\›°ß C¯À¦PÒ ¯õøÁ?

3. What is median? What are its merits and demerits?

Cøh{ø» GßÓõÀ GßÚ? Auß {øÓPøͲ®

SøÓPøͲ® TÖP.

4. Find the range and co-efficient of range from the

following :

27, 30, 35, 36, 38, 40, 43.

RÌUPsh ÂÁμ[PÎÀ C¸¢x Ãa_ ©ØÖ® Ãa_U öPÊ

PõsP :

27, 30, 35, 36, 38, 40, 43.

Sub. Code 23

DE–3536

2

Ws 5

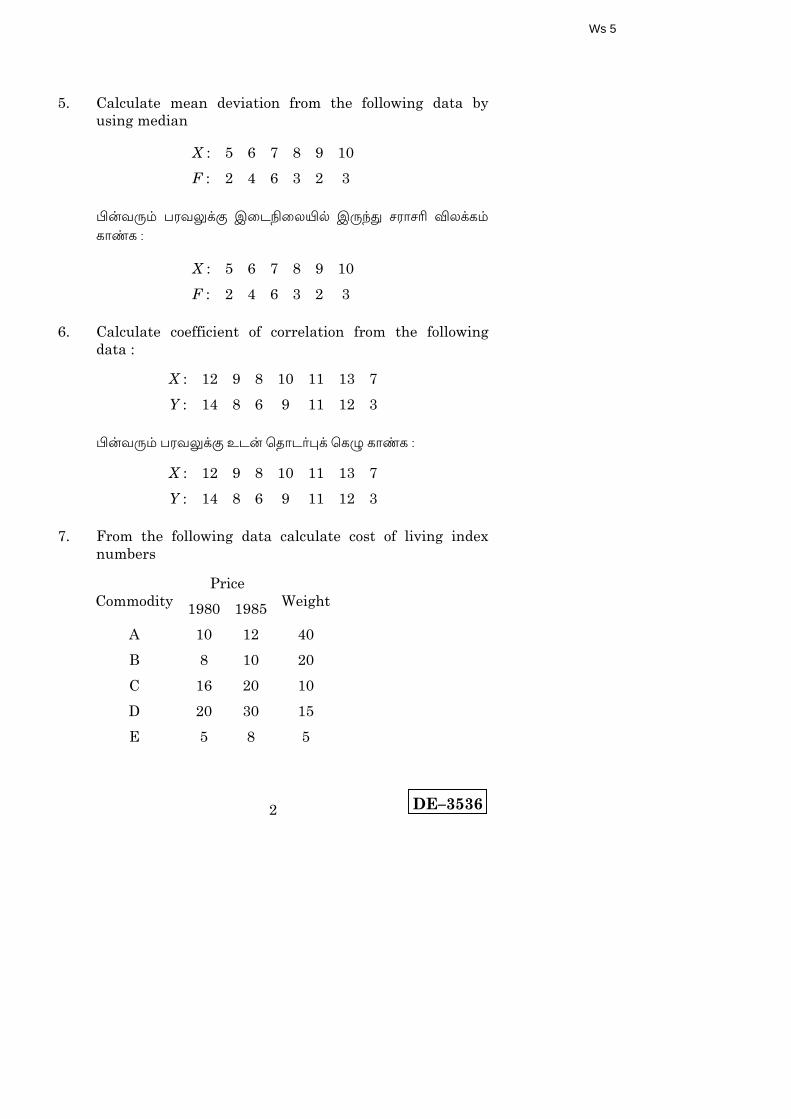

5. Calculate mean deviation from the following data by using median

X : 5 6 7 8 9 10

F : 2 4 6 3 2 3

¤ßÁ¸® £μÁ¾US Cøh{ø»°À C¸¢x \μõ\› »UP®

PõsP :

X : 5 6 7 8 9 10

F : 2 4 6 3 2 3

6. Calculate coefficient of correlation from the following data :

X : 12 9 8 10 11 13 7

Y : 14 8 6 9 11 12 3

¤ßÁ¸® £μÁ¾US Ehß öuõhº¦U öPÊ PõsP :

X : 12 9 8 10 11 13 7

Y : 14 8 6 9 11 12 3

7. From the following data calculate cost of living index numbers

Price Commodity 1980 1985

Weight

A 10 12 40

B 8 10 20

C 16 20 10

D 20 30 15

E 5 8 5

DE–3536

3

Ws 5

¤ßÁ¸® ÂÁμ[PÐUS ÁõÌUøPa ö\»ÄU SÔ±möhs

Aø©UP :

Âø»

ö£õ¸Ò 1980 1985

{øÓ

A 10 12 40

B 8 10 20

C 16 20 10

D 20 30 15

E 5 8 5

8. Calculate five yearly moving average of the following data :

Year : 1971 1972 1973 1974 1975

Students : 332 317 357 392 402

Year : 1976 1977 1978 1979 1980

Students : 405 410 427 405 438

¤ßÁ¸® Põ»z öuõhº Á›ø\US 5 Bsk |P¸® \μõ\›

Bsk : 1971 1972 1973 1974 1975

©õnÁºPÒ : 332 317 357 392 402

Bsk : 1976 1977 1978 1979 1980

©õnÁºPÒ : 405 410 427 405 438

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. Explain the scope of business statistics.

¦Òΰ¼ß Áøμ GÀø»ø¯ ÂÍUSP.

DE–3536

4

Ws 5

10. Draw a histogram for the following data :

Wages : 50–55 55–60 60–65 65–70 70–75 75–80

No. of workers : 16 20 25 10 8 3

RÌUPõq® ÂÁμ[PÐUS ö\ÆÁP¨ £h® ÁøμP :

ÁõμU T¼ : 50–55 55–60 60–65 65–70 70–75 75–80

öuõÈ»õͺPÎß GsoUøP : 16 20 25 10 8 3

11. For the following data, find mean, median and mode :

X : 0–200 200–400 400–600 600–800 800–1000 1000–1200

F : 80 165 230 80 32 13

RÌUPõq® ÂÁμ[PÐUS \μõ\›, Cøh{ø» ©ØÖ® •Pk

PõsP :

X : 0–200 200–400 400–600 600–800 800–1000 1000–1200

F : 80 165 230 80 32 13

12. Find standard deviation for the following data :

X : 5 15 25 35 45 55

F : 1 2 4 6 1 1

RÌUPõq® £μÁ¾US vmh»UPzøuU PõsP :

X : 5 15 25 35 45 55

F : 1 2 4 6 1 1

DE–3536

5

Ws 5

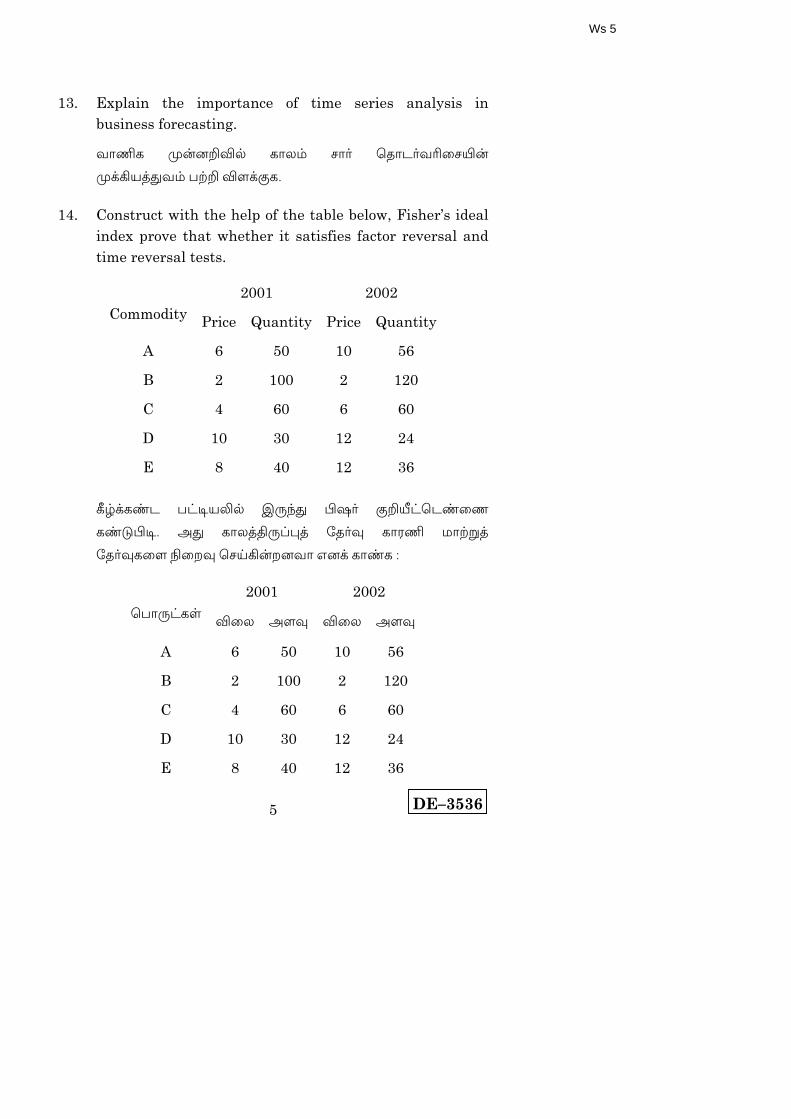

13. Explain the importance of time series analysis in business forecasting.

ÁõoP •ßÚÔÂÀ Põ»® \õº öuõhºÁ›ø\°ß

•UQ¯zxÁ® £ØÔ ÂÍUSP.

14. Construct with the help of the table below, Fisher’s ideal index prove that whether it satisfies factor reversal and time reversal tests.

2001 2002 Commodity Price Quantity Price Quantity

A 6 50 10 56

B 2 100 2 120

C 4 60 6 60

D 10 30 12 24

E 8 40 12 36

RÌUPsh £mi¯¼À C¸¢x ¤åº SÔ±möhsøn

Psk¤i. Ax Põ»zv¸¨¦z ÷uºÄ Põμo ©õØÖz

÷uºÄPøÍ {øÓÄ ö\´QßÓÚÁõ GÚU PõsP :

2001 2002 ö£õ¸mPÒ

Âø» AÍÄ Âø» AÍÄ

A 6 50 10 56

B 2 100 2 120

C 4 60 6 60

D 10 30 12 24

E 8 40 12 36

DE–3536

6

Ws 5

15. The annual sales of a concern are given below. Assuming the conditions of market to be the same, estimate the sales for 2002.

Year : 1997 1998 1999 2000 2001 2002

Sales : 125 163 204 238 282 ?

J¸ {ÖÁÚzvß Á¸hõ¢vμ ÂØ£øÚ R÷Ç u쨣mkÒÍx.

\¢øu°ß {»Áμ® ©õÓÂÀø» GÚU P¸zvÀ öPõsk 2002®

BsiØPõÚ ÂØ£øÚø¯U Psk¤i :

Á¸h® : 1997 1998 1999 2000 2001 2002

ÂØ£øÚ : 125 163 204 238 282 ?

————————

sp3

DE–3537

DISTANCE EDUCATION

B.B.A./B.B.A. (Lateral) DEGREE EXAMINATION, MAY 2018.

BUSINESS (COMMERCIAL) LAW

Time : Three hours Maximum : 100 marks

SECTION A — (5 8 = 40 marks)

Answer any FIVE questions.

1. Give a brief account on :

(a) Lapse of an offer. (4)

(b) Counter offer. (4)

(A) Põ»õÁv¯õÚ •øÚÄ

(B) SÖUS •øÚÄ ÷£õßÓÁØøÓ¨ £ØÔ ]Ö SÔ¨¦

ÁøμP.

2. State the rules regarding revocation of offer and acceptance.

Hئ ©ØÖ® •øÚÄ ÷£õßÓÁØøÓz v¸®£¨ ö£ÖÁvÀ

EÒÍ ÂvPÒ ¯õøÁ?

3. What are the implied conditions in a contract of sale of goods by sample?

©õv›¨ ö£õ¸mPÒ Ai¨£øh°À GÊ® ÂØ£øÚ

J¨£¢uzvß ©øÓ•P {£¢uøÚPÒ ¯õøÁ?

4. What is meant by termination of bailment?

J¨£øhÄ •iÄ GßÓõÀ GßÚ?

Sub. Code 24

DE–3537

2

sp3

5. What are the differences between liquidated damages and penalty?

•iÄ Pmh¨£mh CǨ¥kPÐUS® A£μõuzvØS® EÒÍ

÷ÁÖ£õkPÒ ¯õøÁ?

6. State how the surety is discharged from his liability by revocation.

GÆÁõÖ ¤øn¯õÒ uÚx ö£õÖ¨¤¼¸¢x ©ÖzuȨ¦ ‰»®

Âk¨¦ ö£ÖQÓõº GߣøuU SÔ¨¤kP.

7. "Nemo dat quod non habet" – Explain the maxim.

""ußÛh® CÀ»õu JßøÓ ©ØÓÁ¸USU öPõkUP •i¯õx'' –

C¢uU ÷Põm£õmøh ÂÍUSP.

8. 'A surety is a favoured debtor' – Explain.

"¤øn¯õͺ J¸ BuμÄ ö£ØÓ PhÚõÎ' – ÂÁ›.

SECTION B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. Describe the rules regarding fire insurance.

w Põ¨¥miß ÂvPøͨ £ØÔ ÂÁ›.

10. Explain the rules relating to contingent contract.

I¯¨£õkøh¯ J¨£¢u[PÒ \®£¢u©õÚ ÂvPøÍ ÂÍUSP.

11. Explain the term 'Delivery'. Discuss the rules relating to delivery in Sale of Goods Act.

"ÁÇ[SuÀ' GßÓ ö\õÀ¼ß ö£õ¸øÍ ÂÁ›. \μUS

ÂØ£øÚa \mh Ÿv¯õÚ Âv•øÓPøÍ Bμõ´P.

DE–3537

3

sp3

12. Explain the different types of damages.

CǨ¥miß ÁøPPøÍ ÂÍUSP.

13. Distinguish between an unpaid seller's is right of lein and right of stoppage in transit.

Âø» ö£Óõu ÂØ£øÚ¯õÍ›ß £ØÖ›ø© ©ØÖ®

ö\À¾øP°À {Özx® E›ø© – ÷ÁÖ£kzxP.

14. What is quantum merit? When quantum merit can be claimed? What are the limitations of the doctrine of quanture of merit?

£oUSP¢u öuõøP GßÓõÀ GßÚ? £oUSP¢u öuõøP

G¨÷£õx ÷Põ쨣h»õ®? £oUSP¢u öuõøP GßÓ

÷Põm£õmiÀ EÒÍ SøÓ£õkPÒ ¯õøÁ?

15. Explain the exceptions to the doctrine of privity of contract.

J¨£¢u EÓÄU ÷Põm£õmiØPõÚ Âv»USPøÍ ÂÁ›.

–––––––––––––––

WK 6

DE–3538

DISTANCE EDUCATION

B.B.A./B.B.A. (Lateral) DEGREE EXAMINATION, MAY 2018.

COST ACCOUNTING

Time : Three hours Maximum : 100 marks

PART A — (5 × 8 = 40 marks)

Answer any FIVE questions.

1. What are the merits of cost accounting?

AhUP Âø» PnUQ¯¼ß |ßø©PÒ GßÚ?

2. Show the model of a cost sheet.

AhUPÂø»U PnURmkz uõÎß ©õv›ø¯ PõmkP.

3. What is EOQ? How is it calculated?

]UPÚ Bøn AÍÄ GßÓõÀ GßÚ? Ax GÆÁõÖ

PnUQh¨£kQÓx?

4. Explain about variable overheads.

©õÖ® ÷©Øö\»ÄPÒ £ØÔ GÊxP.

5. A worker rates 9 hours to complete a job on daily wages and 6 hours on a scheme of payment of results. His day rate is 0.75 paise per hour, the material cost of the product is Rs. 4 and the overheads are recovered at 150% of the total direct wages. Calculate the factory cost of the product under (a) Piece work plant (b) Rowan plan and (c) Halsey plan.

Sub. Code 25

DE–3538

2

WK 6

J¸ ÷Áø»¯õÒ J¸ £oø¯ •i¨£uØS 9 ©o ÷|μ®

BQÓx. BÚõÀ A÷u ÷Áø»ø¯ ÷Áø» ÃuU T¼ •øÓ°À

6 ©o°À •izx ÂkQßÓÚº. A¨£o¯õÍ›ß vÚUTÔ

0.75 ø£\õ BS®. ‰»¨ö£õ¸ÒPÐUS ¹. 4 ö\»ÁõQÓx.

ö\»ÄPÒ T¼°À 150% GßÓ •øÓ°À «mP¨£kQÓx.

A¨ö£õ¸Îß öuõÈØ\õø» AhUP Âø»ø¯

(A) EØ£zvØ÷PØÓ T¼ •øÓ (B) ÷μõÁß vmh®

(C) íõÀ] vmh® BQ¯ÁØÔß ‰»® PnUQhÄ®.

6. From the following data segregate fixed cost and variable

cost.

Level of Activity

Capacity % 80% 100%

Labour hours 400 500

Maintenance expenses of plants (Rs.) 2600 2750

¤ßÁ¸ÁÚÁØÔ¼¸¢x ©õÖ® ©ØÖ® ©õÓõ ÷©Ø

ö\»ÄPøͨ ¤›zöukUPÄ®.

ö\¯À ÂQu®

vÓø© AÍÄ % 80% 100%

EøǨ¦ T¼ ©oPÒ 400 500

C¯¢vμz uÍÁõhzvØPõÚ £μõ©›¨¦a ö\»Ä (¹.) 2600 2750

DE–3538

3

WK 6

7. Prepare a cost sheet from the following details :

Rs.

Opening stock of raw materials 2,00,000

Opening stock of work in progress 60,000

Closing stock of raw materials 1,80,000

Closing stock of work in progress 50,000

Materials purchased 5,00,000

Direct wages 1,50,000

Manufacturing expenses 1,00,000

RÌUPõq® £μ[Pμ¸¢x AhUP Âø» AÔUøPz u¯õº

ö\´P.

¹.

‰»¨ö£õ¸mPÎß öuõhUP C¸¨¦ 2,00,000

Áͺ{ø»¨ ö£õ¸mPÎß öuõhUP C¸¨¦ 60,000

‰»¨ö£õ¸mPÎß CÖv C¸¨¦ 1,80,000

Áͺ{ø»¨ ö£õ¸mPÎß CÖv C¸¨¦ 50,000

‰»¨ö£õ¸mPÒ öPõÒ•uÀ 5,00,000

÷|μiU T¼ 1,50,000

EØ£zva ö\»ÄPÒ 1,00,000

8. What is standard costing? What are its advantages?

uμ AhUP Âø»°¯À GßÓõÀ GßÚ? Auß |ßø©PÒ

¯õøÁ?

DE–3538

4

WK 6

PART B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. A particular brand at oil paised through three important process. During the week ended 15th January, 600 bottles were produced. The cost book showed the following information :

Particulars Process A Process B Process C

Rs. Rs. Rs.

Materials 4,000 2,000 1,500

Labour 3,000 2,500 2,300

Direct expenses 6,000 200 500

Cost of bottles Nil 2,030 Nil

Cost of corks Nil Nil 325

The indirect expenses for the period were Rs. 1,600. The by products were sold for Rs. 240 from Process B. The residue was sold for Rs. 125.50 from process C. Indirect charges should be apportioned on the basis of labour charges.

Prepare the a/cs in respect of each process.

J¸ SÔ¨¤mh ÁøP Gsön´ 3 ö\´•øÓPøÍU Ph¢u

¤ß¦ QøhUQÓx. áÚÁ› 15 Ehß •i¢u ÁõμzvÀ 600

£õmiÀPÒ EØ£zv ö\´¯¨£mhÚ. AhUP Âø» HkPÎÀ

RÌUPõq® uPÁÀPÒ EÒÍÚ.

uPÁÀPÒ ö\´•øÓ A ö\´•øÓ B ö\´•øÓ C

¹. ¹. ¹.

ö£õ¸mPÒ 4,000 2,000 1,500

T¼ 3,000 2,500 2,300

÷|μia ö\»ÄPÒ 6,000 200 500

£õmiÀ Âø» - 2,030 -

PõºU Âø» - - 325

DE–3538

5

WK 6

÷©ØPsh ÁõμzvÀ ©øÓ•Pa ö\»ÄPÒ ¹. 1,600. ö\´•øÓ

B °¼¸¢x E£ö£õ¸mPÒ ¹. 240 US ÂØP¨£mhÚ.

ö\´•øÓ C °¼¸¢x P\kPÒ ¹. 125.50US ÂØP¨£mhÚ.

©øÓ•Pa ö\»ÄPÒ T¼a ö\»ÄPÒ Ai¨£øh°À £Q쨣h

÷Ásk®.

JÆöÁõ¸ ö\´•øÓUS® PnUS u¯õº ö\´P.

10. What are the common bases used for allocation of overheads? Explain.

÷©Ø ö\»ÄPøͨ £QºÁuØSU øP¯õͨ£k® ö£õxÁõÚ

Ai¨£øhPÒ ¯õøÁ? ÂÍUSP.

11. Explain the following : (a) Material price variance (b) Material cost variance (c) Material usage variance.

RÌUPshÁØøÓ ÂÍUSP.

(A) ‰»¨ö£õ¸Ò Âø» ÷ÁÖ£õk

(B) ‰»¨ö£õ¸Ò AhUP Âø» ÷ÁÖ£õk

(C) ‰»¨ö£õ¸Ò £¯ß ÷ÁÖ£õk.

12. From the following data, calculate total monthly remuneration of 3 workers X, Y and Z.

(a) Standard production per month per worker is 1000 units.

(b) Actual production during a month :

X - 800 units, Y - 700 units, Z - 900 units.

(c) Piece work rate per unit of actual production 15 paise.

(d) DA Rs. 40 per month.

(e) House rent allowance Rs. 20 per month.

(f) Additional production hours at the rate of Rs. 5 for each percentage of actual production exceeding 75% of standard.

DE–3538

6

WK 6

¤ßÁ¸® £μ[Pμ¸¢x X, Y ©ØÖ® Z GßÓ ‰ßÖ

öuõÈ»õͺPÐUS ö©õzu ©õua \®£Í® PnUQkP.

(A) {ºn°UP¨£mh uμ EØ£zv J¸ öuõÈ»õÎUS J¸

©õuzvØS 1000 A»SPÒ

(B) J¸ ©õuzvØPõÚ Esø©¯õÚ EØ£zv :

X - 800 A»SPÒ, Y - 700 A»SPÒ, Z - 900 A»SPÒ

(C) J¸ A»QØPõÚ E¸¨£i ÂQu® 15 ø£\õ

(D) Ãmk ÁõhøP¨i J¸ ©õuzvØS ¹. 20

(E) £g\¨£i J¸ ©õuzvØS ¹. 40

(F) TkuÀ EØ£zv ÷£õÚì : uμ EØ£zv°À 75% US ÷©À

C¸US®, JÆöÁõ¸ \uÃuzvØS® ¹. 5 GßÓ ÃuzvÀ.

13. The following receipts and issues were made of a new

item of stores.

Receipts Issues

Units Rs. Units

1st January 1000 1000 -

1st February 1000 800 -

28th February - - 1200

1st March 1000 1200 -

31st March - - 1200

Estimate weighted average prices for issued stores.

DE–3538

7

WK 6

J¸ ¦v¯ \μUS \®£¢u©õP ö£Ó¨£mh ©ØÖ® ÁÇ[P¨£mh

£μ[PÒ ¤ßÁ¸©õÖ.

ö£Ó¨£mhøÁ ÁÇ[P¨£mhøÁ A»SPÒ

A»SPÒ ¹. A»SPÒ

áÚÁ› 1 1000 1000 -

¤¨μÁ› 1 1000 800 -

¤¨μÁ› 28 - - 1200

©õºa 1 1000 1200 -

©õºa 31 - - 1200

‰»¨ö£õ¸Îß ÁÇ[PÀ Âø»ø¯ Gøh°mh \μõ\› Âø»

•øÓ°À PõsP.

14. ABC company Ltd. has prepared a budged for the production of 1,00,000 units. The cost details per unit is given below.

Per UnitRs.

Raw materials 2.52

Direct labour 0.75

Direct expenses 0.10

Works overhead (60% fixed) 2.50

Administrate on overhead (80% fixed) 0.40

Selling overhead (50% fixed) 0.20

The actual production during the period was only 60000 units. Calculate the revised budgeted cost per unit.

DE–3538

8

WK 6

ABC {Ö©® 1,00,000 A»SPÒ EØ£zv ö\´ÁuØS J¸

©v¨¥k ö\´v¸UQÓx.

J¸ A»SUS

¹. ø£

Pa\õ¨ ö£õ¸Ò 2.52

÷|º T¼ 0.75

÷|º ö\»ÄPÒ 0.10

£o ÷©Øö\»ÄPÒ (60% ©õÓõux) 2.50

{ºÁõPa ö\»ÄPÒ (80% ©õÓõx) 0.40

ÂØ£øÚa ö\»ÄPÒ (50% ©õÓõx) 0.20

60,000 A»SP÷Í |h¨¦U Põ»zvÀ EØ£zv ö\´¯¨£mhÚ.

J¸ A»Qß ¦v¯ AhUP Âø»ø¯U PnUQkP.

15. What are the bases of apportionment used for apportioning the service department costs? Explain.

÷\øÁzxøÓa ö\»ÄPøͨ £QºÄ ö\´ÁuØS

£¯ß£kzu¨£k® £À÷ÁÖ Ai¨£øhPÒ ¯õøÁ? ÂÍUSP.

————————

wk 3

DE–3539

DISTANCE EDUCATION

B.B.A./B.B.A. (Lateral) DEGREE EXAMINATION, MAY 2018.

PRODUCTION AND MATERIALS MANAGEMENT

Time : Three hours Maximum : 100 marks

PART A — (5 8 = 40 marks)

Answer any FIVE questions.

1. List the functions of a Store-keeper.

ö£õ¸mPÒ ÷\ªUS® Qh[Qß Eu¯õÍ›ß £oPøÍ

£mi¯¼kP.

2. Explain the integrated materials management concept.

J¸[Qøn¢u ö£õ¸mPÒ ÷©»õsø©°ß P¸zvøÚ

ÂÁ›UPÄ®.

3. Define production and operations management and list four of its objectives.

EØ£zv ©ØÖ® C¯UP ÷©»õsø© GßÓõÀ GßÚ? AÁØÔß

|õßS SÔU÷PõÒPøÍ £mi¯¼kP.

4. Explain the role of Government in location decision.

öuõÈØ\õø» Aø©²® Chzøu wº©õÛUS® •iÂÀ

Aμ]ß £[PΨø£ ÂÁ›UPÄ®.

5. List out the principles of good layout.

|À» ChÁiÁø©¨¤ß öPõÒøPPøÍ £mi¯¼kP.

Sub. Code 31

DE–3539

2

wk 3

6. Explain Make (or) Buy decisions.

ö£õ¸mPÒ EØ£zv ö\´¯ AÀ»x Áõ[S® •iÂøÚ

ÂÍUSP.

7. Explain Gnatt charts.

‘‘Põsm AmhÁøn’’ – ÂÍUSP.

8. Explain the layout of service facilities.

÷\øÁ Á\vPÐUPõÚ ChÁø©¨¤øÚ £ØÔ ÂÍUSP.

PART B — (4 15 = 60 marks)

Answer any FOUR questions.

9. Explain the inventory control techniques.

\μUøP Pmk£kzu¼À EÒÍ ÁÈ•øÓPøÍ ÂÍUSP.

10. Comment on EOQ, ABC analysis in store control.

ö£õ¸mPÒ ÷\ªUS® Qh[QøÚ Pmk£kzxu¼À EOQ, ABC B´øÁ P¸zxÖ ö\´P.

11. Explain the following :

(a) routing

(b) scheduling

(c) despatching.

¤ßTÔ¯ÁØøÓ ÂÁ›UPÄ® :

(A) ¹mi[

(B) ö\m²Î[

(C) öhì£õa][.

12. Explain the components of production system.

EØ£zv •øÓ°ß TÖPøÍ ÂÁ›UPÄ®.

DE–3539

3

wk 3

13. Differentiate product and process layout.

EØ£zv¨ ö£õ¸Îß uø쨣h® ©ØÖ® ÷Áø»UQμ©

uø쨣h® Âz¯õ\¨£kzxP.

14. Discuss the features of job production.

÷Áø» EØ£zv°ß ]Ó¨¦UPøÍ ÂÁõvUPÄ®.

15. Explain the advantages and disadvantages of Intermittent production system.

Âmk Âmk ö\´²® EØ£zv •øÓ°ß |ßø©PÒ,

wø©PøÍ ÂÁ›UPÄ®.

————————

wk14

DE–3540

DISTANCE EDUCATION

B.B.A./B.B.A. (Lateral) DEGREE EXAMINATION, MAY 2018.

ELEMENTS OF MARKETING

Time : Three hours Maximum : 100 marks

SECTION A — (5 8 = 40 marks)

Answer any FIVE questions.

1. Distinguish between Consumer marketing and Services marketing.

“~Pº÷Áõº \¢øu” ©ØÖ® “÷\øÁPÒ \¢øu” BQ¯ÁØÔØPõÚ

÷ÁÖ£õkPøÍ SÔ¨¤kP.

2. What are the components of marketing mix? Explain.

\¢øu°¯À P»øÁ°ß EmTÖPÒ ¯õøÁ? ÂÍUSP.

3. Explain the process of developing a new product.

J¸ ¦v¯ ö£õ¸øÍ E¸ÁõUSÁuØPõÚ £À÷ÁÖ ÁÈ•øÓPøÍ

ÂÍUSP.

4. Write a note on :

(a) Product Elimination

(b) Product Modification.

]ÖSÔ¨¦ ÁøμP :

(A) ö£õ¸Ò }USuÀ

(B) ö£õ¸Ò ©õØÓ® ö\´uÀ.

5. Discuss the various kinds of pricing.

Âø»°ku¼ß £À÷ÁÖ ÁøPPøÍ ÂÁ›UP.

Sub. Code 32

DE–3540

2

wk14

6. Define : Physical Distribution. Why it is needed in the modern marketing?

Áøμ¯Ö : ö£õ¸mPÒ Â{÷¯õP®. Cx Hß ¦v¯ \¢øu

C¯¼À ÷uøÁ¨£kQÓx?

7. Describe the various methods of Sales Promotion.

ÂØ£øÚ ö£¸UPzvß £À÷ÁÖ ÁøPPøÍ ÂÁ›UP.

8. What are the relevant steps in personal selling? Explain.

uÛ|£º ÂØ£øÚ÷¯õk öuõhº¦øh¯ {ø»PÒ ¯õøÁ?

ÂÍUSP.

SECTION B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. What is meant by marketing concept? What are the factors influencing marketing concept? Explain.

“\¢øu°¯À P¸zx¸” Gߣuß Aºzu® GßÚ? \¢øu°¯À

P¸zx¸øÁ £õvUS® PõμoPÒ ¯õøÁ? ÂÍUSP.

10. What do you mean by Market Segmentation? Explain its objectives and importance.

\¢øu £S¨¦ GßÓõÀ GßÚ? \¢øu¨ £S¨¤ß ÷|õUP[PÒ

©ØÖ® •UQ¯zxÁzøu ÂÍUSP.

11. Explain the various factors which affect the consumer buying behaviour.

~Pº÷Áõº ö£õ¸Ò Áõ[S® |hÁiUøPø¯¨ £õvUS®

£À÷ÁÖ PõμoPøÍ ÂÍUSP.

12. What do you mean by product life cycle? Analyse the various stages in the produce life cycle.

“ö£õ¸Ò ÁõÌUøP _ÇØ]” GßÓõÀ GßÚ? ö£õ¸Ò ÁõÌUøP

_ÇØ]°ß £À÷ÁÖ {ø»PøÍ B´Ä ö\´P.

DE–3540

3

wk14

13. List down the factors influencing pricing decisions.

Âø»°kuÀ •iÄPøͨ £õvUS® PõμoPøÍ £mi¯¼kP.

14. What is Channels of Distribution? Explain the factors determining the choice of a suitable channel of distribution.

“Â{÷¯õP ÁÈzuh[PÒ” GßÓõÀ GßÚ? Â{÷¯õP

ÁÈzuh[PøÍz ÷uº¢öukUP EuÄ® uS¢u PõμoPøÍ

ÂÍUSP.

15. Describe the types of advertising media. Discuss their merits and demerits.

ÂÍ®£μ FhPzvß ÁøPPøÍ ÂÁ›UP. AuØPõÚ |ßø©PÒ

©ØÖ® wø©PøÍ ÂÁ›UP.

–––––––––––––––

wk12

DE–3541

DISTANCE EDUCATION

B.B.A./B.B.A. (Lateral) DEGREE EXAMINATION, MAY 2018.

MANAGEMENT ACCOUNTING

Time : Three hours Maximum : 100 marks

PART A — (5 8 = 40 marks)

Answer any FIVE questions.

1. What are the functions of Management Accounting?

÷©»õsø© PnUQ¯¼ß £oPÒ ¯õøÁ?

2. From the following information, find out the amount of profit earned during the year using marginal costing technique :

Fixed cost Rs. 5,00,000

Variable cost Rs. 10 per unit

Selling price Rs. 15 per unit

Output level 1,50,000 units.

RÌUPsh £μ[Pμ¸¢x C»õ£® Dmi¯øu Áøμ{ø»

AhUPÂø» ‰»® PnUQkP :

{ø»¯õÚ ö\»Ä ¹. 5,00,000

©õÖ£k® ö\»Ä ¹. 10 J¸ A»SUS

ÂØ£øÚ Âø» ¹. 15 J¸ A»SUS

öÁαk {ø» 1,50,000 A»SPÒ.

Sub. Code 33

DE–3541

2

wk12

3. The following information was obtained from a company in a certain year :

Sales Rs. 1,00,000

Variable costs Rs. 60,000

Fixed costs Rs. 30,000

Find out the P/V ratio, Break even point and Margin of safety.

RÌUPsh £μ[PÒ J¸ {ÖÁÚzv¼¸¢x J¸ SÔ¨¤mh

BskUS ö£Ó¨£mhx :

ÂØ£øÚ ¹. 1,00,000

©õÖ£k® ö\»Ä ¹. 60,000

{ø»¯õÚ ö\»Ä ¹. 30,000

£[PΨ¦ ÂQu®, \©{ø»¨ ¦ÒÎ ©ØÖ® £õxPõ¨¦ AÍÄ

PnUQkP.

4. What are the advantages of Ratio Analysis?

ÂQu B´Âß |ßø©PÒ ¯õøÁ?

5. The expenses budgeted for an annual production of 10,000 units in a factory are given below :

Raw materials – Rs. 140 per unit

Labour – Rs. 25 per unit

Variable work expenses – Rs. 20 per unit

Fixed works overhead – Rs. 1,00,000 for the year

Selling and office expenses (20% fixed) – Rs. 25 per unit

Prepare a budget for production of 8,000 units.

DE–3541

3

wk12

J¸ öuõÈ»PzvÀ BsöhõßÖUS 10,000 A»SPÒ EØ£zv

ö\´vh BS® ö\»ÄPÒ R÷Ç u쨣mkÒÍÚ :

J¸ A»QØS ‰»¨ö£õ¸ÒPÒ – ¹. 140

J¸ A»QØS T¼ – ¹. 25

J¸ A»QØS ©õÖ® £oa ö\»ÄPÒ – ¹. 20

J¸ BsiØPõÚ {ø»¯õÚ £oa ö\»ÄPÒ – ¹. 1,00,000

ÂØ£øÚ ©ØÖ® A¾Á»Pa ö\»ÄPÒ (20% ©õÓõux) J¸

A»QØS – ¹. 25

8,000 A»SPÒ EØ£zv ö\´vh J¸ vmh® u¯õ›UP.

6. What is Break-even analysis? What are its assumptions?

\›\© B´Ä GßÓõÀ GßÚ? AÁØÔß FP[PÒ ¯õøÁ?

7. Distinguish between Funds flow statement and Cash flow statement.

{v |h©õmh AÔUøPUS®, öμõUP |h©õmh AÔUøPUS®

EÒÍ ÷ÁÖ£õkPÒ ¯õøÁ?

8. What do you mean by Capital Budgeting? What are its merits and demerits?

•uÀ vmh® GßÓõÀ GßÚ? Auß |ßø©, wø©PÒ GßÚ?

PART B — (4 15 = 60 marks)

Answer any FOUR questions.

9. From the following summarized balance sheets of a company prepare cash flow statement : Liabilities 1998 1999 Assets 1998 1999

Rs. Rs. Rs. Rs.

Share capital 2,00,000 2,50,000 Building 2,00,000 1,90,000

General reserve 50,000 60,000 Machinery 1,50,000 1,69,000

Profit and Loss a/c 30,500 30,600 Stock 1,00,000 79,000

DE–3541

4

wk12

Liabilities 1998 1999 Assets 1998 1999

Rs. Rs. Rs. Rs.

Long term bank loan 70,000 – Debtors 80,500 64,200

Creditors 1,50,000 1,35,200 Cash – 8,600

Taxation provision 30,000 35,000

5,30,500 5,10,800 5,30,500 5,10,800

Additional information :

(a) Dividend paid Rs. 23,000.

(b) Purchase of machinery Rs. 38,000.

(c) Depreciation written off on machinery Rs. 12,000.

(d) Income tax provided in the year Rs. 33,000.

(e) Loss on sale of machinery Rs. 1,200 written off to General Reserve.

RÌUPsh J¸ P®ö£Û°ß C¸¨¦{ø»U SÔ¨¦Pμ¸¢x

J¸ öμõUP |h©õmh AÔUøP°øÚz u¯õ›UP :

ö£õÖ¨¦PÒ 1998 1999 ö\õzxUPÒ 1998 1999

¹. ¹. ¹. ¹.

£[S •uÀ 2,00,000 2,50,000 Pmih® 2,00,000 1,90,000

ö£õxU Põ¨¦ 50,000 60,000 ö£õÔ 1,50,000 1,69,000

C»õ£ |mhU PnUS 30,500 30,600 \μUQ¸¨¦ 1,00,000 79,000

}shPõ» Á[QU Phß 70,000 – PhÚõÎPÒ 80,500 64,200

PhÜ¢÷uõºPÒ 1,50,000 1,35,200 öμõUP® – 8,600

Á›U Põ¨¦ 30,000 35,000

5,30,500 5,10,800 5,30,500 5,10,800

TkuÀ uPÁÀPÒ :

(A) C»õ£ DÄPÒ ö\¾zv¯x ¹. 23,000

(B) ö£õÔ Áõ[Q¯x ¹. 38,000

DE–3541

5

wk12

(C) ö£õÔ°ß «x ÷u´©õÚ® ¹. 12,000

(D) C¢u Bsk Á¸©õÚ Á› JxUQ¯x ¹. 33,000

(E) ö£õÔ ÂØ£øÚ «uõÚ |mh® ¹. 1,200 ö£õxUPõ¨¤ØS

GÊu¨ ö£ØÓx.

10. From the following particulars, prepare the balance sheet of A Ltd. :

Sales for the year – Rs. 6,00,000

Gross profit ratio – 25%

Current ratio – 1.75

Liquid ratio – 1.25

Stock turnover ratio – 15

Average collection period – 1 21 months

Turnover to fixed assets – 1.5

Ratio of reserves to capital – 1: 3

Fixed assets to network – 5 : 6

(Turnover refers to cost of sales, the stock refers to closing stock).

RÌUPsh ÂÁμ[Pμ¸¢x A ¼ªöhmiß C¸¨¦{ø»U

SÔ¨¤øÚz u¯õ›UP :

BsiØPõÚ ÂØ£øÚ – ¹. 6,00,000

ö©õzu »õ£ ÂQu® – 25%

|h¨¦ ÂQu® – 1.75

}ºø© ÂQu® – 1.25

\μUQ¸¨¦ ÂØ£øÚ ÂQu® – 15

\μõ\› Á`À Põ»® – 1 21 ©õu[PÒ

DE–3541

6

wk12

{ø»¯õÚ ö\õzxUPÐUS ÂØ£øÚ – 1.5

•u¾US Põ¨¦UPÎß ÂQu® – 1 : 3

{Pμ ö£Ö©õÚzvØS {ø»¯õÚ ö\õzxUPÒ – 5 : 6

(ÂØ£øÚ Gߣx ÂØ£øÚ AhUPzøu²®, ‘\μUQ¸¨¦’ Gߣx CÖva \μUQ¸¨¤øÚ²® SÔUQÓx).

11. Explain the scope of Management Accounting.

÷©»õsø© PnUQ¯¼ß £μ¨ö£Àø»ø¯ ÂÍUSP.

12. Enumerate the managerial uses of the marginal costing.

CÖv{ø»a ö\»ÄU PnUSPÎß, {ºÁõP £¯ß£õkPøÍ

ÂÁ›.

13. L & T Ltd wishes to arrange overdraft facility with their bankers during April to June 1998. Prepare a cash budget for the above period from the following data indicating the extent of bank facilities, the company will require at the end of each month :

(a) Month 1998

Credit sales

Purchases Wages

February 1,80,000 1,24,800 12,000

March 1,92,000 1,44,000 14,000

April 1,08,000 2,43,000 11,000

May 1,74,000 2,46,000 10,000

June 1,26,000 2,68,000 15,000

(b) 50% of the credit sales are realised in the month following sales and the remaining 50% in the second month following.

(c) Creditors and wages are paid in the month following the month of purchases.

(d) Cash at bank on 1.4.98 (estimated) Rs. 25,000.

DE–3541

7

wk12

GÀ ©ØÖ® i ¼ªöhm u[PÒ Á[Q°¼¸¢x 1998 H¨μÀ

•uÀ áüß Áøμ ÷©ÀÁø쨣ØÖUS ÁøP ö\´¯

¸®¦QÓx. RÌUPõq® ÂÁμ[Pμ¸¢x öμõUP ÁμÄ

ö\»Ä vmh® u¯õ›zx, JÆöÁõ¸ ©õu CÖv°¾®

÷uøÁ¨£k® Á[Qz öuõøP°øÚ²® SÔ¨¤kP.

(A) ©õu® 1998 Phß

ÂØ£øÚ

öPõÒ•uÀ T¼

¤¨μÁ› 1,80,000 1,24,800 12,000

©õºa 1,92,000 1,44,000 14,000

H¨μÀ 1,08,000 2,43,000 11,000

֩ 1,74,000 2,46,000 10,000

áüß 1,26,000 2,68,000 15,000

(B) Phß ÂØ£øÚ°À 50% ÂØ£øÚø¯z öuõhº¢x Á¸®

Akzu ©õuzv¾®, «u® 50% CμshõÁx ©õuzv¾®

Á`»õS®.

(C) T¼ ©ØÖ® PhÜ¢÷uõºUS® öPõÒ•uÀ ö\´¯¨£mh

©õuzvØS Akzu ©õu® ö\¾zu¨£k®.

(D) 1.4.98&À Á[Q C¸¨¦ (Gvº÷|õUP¨£mhx) ¹. 25,000.

14. For two years sales and profit were as under : I year II year

Rs. Rs.

Sales 4,00,000 5,00,000

Profit 1,00,000 1,40,000

Find :

(a) BEP

(b) Sales for a profit of Rs. 2,00,000

(c) Profit when sales are Rs. 6,00,000

(d) Margin of safety when profit is Rs. 50,000.

DE–3541

8

wk12

Cμsk Á¸h[PÐUPõÚ ÂØ£øÚ ©ØÖ® »õ£®

¤ßÁ¸©õÖ :

I Á¸h® II Á¸h®

¹. ¹.

ÂØ£øÚ 4,00,000 5,00,000

»õ£® 1,00,000 1,40,000

Psk¤i :

(A) »õ£ |mh©ØÓ ¦ÒÎ.

(B) ¹. 2,00,000 »õ£® DmhUTi¯ ÂØ£øÚ.

(C) ¹. 6,00,000 ÂØ£øÚ°À DmhUTi¯ »õ£®.

(D) ¹. 50,000 »õ£zvÀ £õxPõ¨¦ £Sv.

15. Explain the important steps in the capital budgeting process.

•uÀ vmh •øÓPÎß •UQ¯©õÚ £iPøÍ ÂÍUSP.

———————

Sp 1

DE–3542

DISTANCE EDUCATION

B.B.A./B.B.A. (Lateral) DEGREE EXAMINATION, MAY 2018.

FINANCIAL MANAGEMENT

Time : Three hours Maximum : 100 marks

SECTION A — (5 8 = 40 marks)

Answer any FIVE questions.

1. State the significance of finance function.

{v¨ £o°ß uÛa ]Ó¨ø£U TÖP.

2. Explain the traditional approach of financial management.

{v ÷©»õsø©°ß £õ쮣›¯ AqS•øÓø¯ ÂÍUSP.

3. Define financial planning. State its objectives.

{vz vmhzøu Áøμ¯Ö. Auß ÷|õUP[PøÍU TÖP.

4. What do you understand by capitalisation? How is it different from capital?

‰»uÚ©õUPÀ GßÓõÀ GßÚ? Ax •u½miÀ C¸¢x G¨£i

÷ÁÖ£kQÓx?

5. What do you mean by corporate debt? State its significance.

{Ö©U Phß GßÓõÀ GßÚ? Auß uÛa ]Ó¨¦PøÍU TÖP.

Sub. Code 34

DE–3542

2

Sp 1

6. What are the advantages of public deposit?

ö£õx øÁ¨¤ß |ßø©PÒ GßÚ?

7. State the importance of working capital.

|øh•øÓ ‰»uÚzvß •UQ¯zxÁzøuU TÖP.

8. Describe and explain the various types of securities.

£À÷ÁÖ ÁøP¯õÚ ¤øn¯¨ £zvμ[Pøͨ £ØÔ ÂÍUSP.

SECTION B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. Discuss in detail, the functions of financial management.

{v ÷©»õsø©°ß £oPøÍ Â›ÁõP ÂÍUSP.

10. Explain the characteristics of a sound financial plan.

Kº ]Ó¢u {vz vmhzvß £s¦PøÍ ÂÁ›UP.

11. Explain the significance of ploughing back of profits as a source of corporate finance.

{Ö© {v°ß ‰»©õP EÒÍ »õ£zøu ©Ö •u½k ö\´Ávß

•UQ¯zxÁzøu ÂÍUSP.

12. Explain the factors which determine the working capital needs of a firm.

J¸ {Ö©zvß |øh•øÓ ‰»uÚzøu wº©õÛUS®

PõμoPÒ ¯õøÁ?

13. Distinguish between preference shares and equity shares.

\© E›ø©¨ £[SPÐUS® \¾øP¨£[SPÐUS® EÒÍ

Âzv¯õ\zøuU TÖP.

DE–3542

3

Sp 1

14. Discuss the advantages and limitations of term loan as a source of finance.

{v vμmkÁuØS EÒÍ ÁÈPÎÀ JßÓõP Põ»U PhøÚU

P¸xÁuõÀ EÒÍ |ßø©, wø©PøÍU TÖP.

15. “The consequences of over capitalisation are for more serious and fatal than under capitalisation” – Discuss.

“ªøP ‰»uÚzvÚõÀ HØ£k® ÂøÍÄPÒ, SøÓ

‰»uÚzvßõÀ Á¸® ÂøÍÄPøÍ Âh B£zuõÚx ©ØÖ®

B£zxPøÍ ÂøÍÂUPUTi¯x” & ÂÁõvUP.

–––––––––––––––

wk7

DE–3543

DISTANCE EDUCATION

B.B.A./B.B.A. (Lateral) DEGREE EXAMINATION, MAY 2018.

PRINCIPLES OF PERSONNEL MANAGEMENT

Time : Three hours Maximum : 100 marks

SECTION A — (5 8 = 40 marks)

Answer any FIVE questions.

1. Explain the systems approach to Personnel Management.

£o¯õͺ ÷©»õsø©°ß AqS•øÓPøÍ ÂÍUSP.

2. Discuss the need and importance of Human Resource Planning.

©ÛuÁÍ vmhªh¼ß ÷uøÁPÒ ©ØÖ® •UQ¯zxÁ® £ØÔ

ÂÍUSP.

3. Explain the need for training in industries

öuõÈÀ {ÖÁÚ[PÎÀ £°Ø]°ß ÷uøÁø¯¨ £ØÔ

ÂÍUSP.

4. What are the different types of Promotion? Explain.

£u E¯ºÂß £À÷ÁÖ ÁøPPÒ ¯õøÁ? ÂÍUSP.

5. What is performance appraisal system? What are the merits and demerits?

‘£ozvÓß ©v¨¥k Aø©¨¦’ GßÓõÀ GßÚ? AÁØÔß

|ßø© ©ØÖ® wø©PÒ ¯õøÁ?

Sub. Code 35

DE–3543

2

wk76. What are the various techniques of performance

appraisal?

£ozvÓß ©v¨¥miß £À÷ÁÖ ~qUP[PÒ ¯õøÁ?

7. Explain the methods of Job Evaluation.

£o ©v¨¥miß ÁøPPøÍ ÂÁ›UP.

8. What are the causes of grievances in Industries?

öuõÈÀ {ÖÁÚ[PÎÀ SøÓPÒ HØ£kÁuØPõÚ Põμn[PÒ

¯õøÁ?

SECTION B — (4 × 15 = 60 marks)

Answer any FOUR questions.

9. Discuss the organizational structure of a personnel department with suitable example.

£o¯õͺ xøÓ°ß Aø©¨¦ Áøμ£h® £ØÔ \›¯õÚ

Euõμnzxhß ÂÍUSP.

10. What is meant by Job Analysis? Explain the need and importance of Job Analysis.

£o £S¨£õ´Ä GßÓõÀ GßÚ? £o £S¨£õ´Âß ÷uøÁ

©ØÖ® •UQ¯zxÁ® £ØÔ ÂÁ›.

11. What do you understand by selection of employees? Explain the steps involved in selection procedure

‘£o¯õͺ ÷uºÄ’ £ØÔ }º AÔ¢uøÁ GßÚ? £o¯õÍU

÷uºÄ •øÓ°ß {ø»PøÍ ÂÍUSP.

12. What do you mean by demotion? What are the causes of demotion?

£o CÓUP® GßÓõÀ GßÚ? AuØPõÚ Põμn[PÒ ¯õøÁ?

DE–3543

3

wk713. Explain various methods of performance appraisal.

£ozvÓß ©v¨¥miß £À÷ÁÖ ÁøPPøÍ ÂÍUSP.

14. Discuss the incentives offered to employees by the Indian organisations.

C¢v¯ öuõÈÀ Aø©¨¦PÎÀ £o¯õͺPÐUS

ÁÇ[P¨£k® FUPzöuõøP ¯õøÁ?

15. Explain the various welfares measures for workers in an Industry.

J¸ öuõÈÀ\õø»°¾ÒÍ £À÷ÁÖ £o¯õͺ |»

|hÁiUøPPøÍ ÂÍUSP.

————————

![No. [5516]-101 B.B.A. (I Semester) EXAMINATION, 2019 ...collegecirculars.unipune.ac.in/sites/examdocs/APRIL2019/B.B.A ( 20… · Journalise the following transactions in the books](https://static.fdocuments.net/doc/165x107/5f71938dd9eab820a163e5c0/no-5516-101-bba-i-semester-examination-2019-20-journalise-the-following.jpg)