Discovering the Concealed Benefits of Auditor-Provided Tax ... · PDF fileDiscovering the...

46

2017-14 4/28/17 Discovering the Concealed Benefits of Auditor-Provided Tax Services Working Paper - April 2017 - Stephan Burggraef * [email protected] Christoph Watrin * [email protected] Falko Weiß * [email protected] Abstract: The paper investigates the effect of APTS on tax planning and earnings quality using a German sample. Our findings differ from previous US studies which we attribute to the tighter re- strictions on APTS in Germany. We find a negative association between APTS and tax planning suggesting that knowledge spillover to the tax department might not result in aggressive tax strategies and therefore might not drive the results in this case. Also, we find a positive relation between the level of APTS and the sustainability of tax strategies in client firms. Turning to the accounting perspective we find that APTS are positively related to accrual quality. This is con- sistent with the presence of beneficial knowledge spillover to the audit department while a loss of professional skepticism does not prevail. However, it appears that earnings persistence de- creases with APTS. Altogether, our study suggests the effectiveness and the advantages of the former German legislation. Therefore, the purpose of the recent reform is questionable. We conclude that the 2016 reform which restricted APTS even further might not be necessary ac- cording to our findings. JEL Classification: H26, H73, K23, L84, K23, L84, M41, M42, M48 Keywords: Auditor-Provided Tax Services, Regulation, Tax Planning, Tax Sustainability, Ac- crual Quality, Earnings Persistence We thank the participants of the Workshop on Empirical Tax Research at the Centre for Euro- pean Economic Research (ZEW) 2016, of the 3 rd Doctoral Research Seminar at Vienna Uni- versity of Economics and Business, and of the AAA International Accounting Section Midyear Meeting 2017 for their helpful comments. We especially appreciate the useful suggestions by Gopal Krishnan. * University of Münster, Institute of Accounting and Taxation, Universitätsstrasse 14-16, 48143 Münster, Germany

Transcript of Discovering the Concealed Benefits of Auditor-Provided Tax ... · PDF fileDiscovering the...

2017-14 4/28/17

Discovering the Concealed Benefits of Auditor-Provided Tax Services

Working Paper

- April 2017 -

Stephan Burggraef* [email protected]

Christoph Watrin*

Falko Weiß* [email protected]

Abstract:

The paper investigates the effect of APTS on tax planning and earnings quality using a German sample. Our findings differ from previous US studies which we attribute to the tighter re-strictions on APTS in Germany. We find a negative association between APTS and tax planning suggesting that knowledge spillover to the tax department might not result in aggressive tax strategies and therefore might not drive the results in this case. Also, we find a positive relation between the level of APTS and the sustainability of tax strategies in client firms. Turning to the accounting perspective we find that APTS are positively related to accrual quality. This is con-sistent with the presence of beneficial knowledge spillover to the audit department while a loss of professional skepticism does not prevail. However, it appears that earnings persistence de-creases with APTS. Altogether, our study suggests the effectiveness and the advantages of the former German legislation. Therefore, the purpose of the recent reform is questionable. We conclude that the 2016 reform which restricted APTS even further might not be necessary ac-cording to our findings.

JEL Classification: H26, H73, K23, L84, K23, L84, M41, M42, M48

Keywords: Auditor-Provided Tax Services, Regulation, Tax Planning, Tax Sustainability, Ac-crual Quality, Earnings Persistence

We thank the participants of the Workshop on Empirical Tax Research at the Centre for Euro-pean Economic Research (ZEW) 2016, of the 3rd Doctoral Research Seminar at Vienna Uni-versity of Economics and Business, and of the AAA International Accounting Section Midyear Meeting 2017 for their helpful comments. We especially appreciate the useful suggestions by Gopal Krishnan.

*University of Münster, Institute of Accounting and Taxation, Universitätsstrasse 14-16, 48143 Münster, Germany

2017-14 4/28/17

2

1 Introduction

The association between auditor provided tax services (APTS) and both tax avoidance and

earnings quality has been discussed for some time. However, most evidence is based on an US-

American background which is different from the European one. Even though the results in

prior literature were not unambiguous they point towards a deteriorating effect of APTS on tax

payments and earnings quality. Supposedly having those findings in mind, regulators in the EU

and Germany recently tightened the regulations on the provision of APTS. The goal of this

paper is to investigate whether APTS has a positive or negative effect in an EU setting and

whether the regulations prior to the recent reform were sufficient to maintain auditor independ-

ence and avoid negative outcomes. In our German sample 95% of the companies buy non-audit

services, and 60% obtain APTS. These numbers indicate the high relevance of these services

also in Germany.

By auditing the financial statement the auditor1 gains a tremendous insight into the firm. The

auditor can use this knowledge to give advice on tax planning2 and potentially can help to in-

troduce aggressive tax strategies (e.g. Hogan and Noga [2012]). The knowledge spillover to the

tax department makes the auditor especially suited to consult on tax planning (e.g. Gleason and

Mills [2011]). However, aggressive tax planning increases the risk of tax disputes. More tax

risks can result in financial statement restatements and auditor liability.3 Therefore, auditors

that provide tax services might also prefer less tax planning. In contrast, Kinney et al. [2004]

even find a negative association between APTS and restatements. It is thus an empirical ques-

tion whether APTS increase or decrease tax planning. Our finding is consistent with a negative

association between APTS and tax planning. There is also evidence that the tax planning level

of a firm influences the amount of APTS obtained. The reason for the negative association

might be that tax aggressive firms buy tax services from third parties.

Another facet of tax strategies is tax sustainability. As pointed out by McGuire et al. [2013] the

tax sustainability must not be mistaken for the level of tax planning. Instead it shows whether

1 If not pronounced otherwise the audit firm is meant by “auditor”. 2 There are different perceptions of the terms ‘tax avoidance’, ‘tax planning’ or ‘tax aggressiveness’. Hanlon and

Heitzman (2010) see tax avoidance as a continuum of tax planning strategies ranging from perfectly legal and relatively harmless measures to more dubious efforts such as tax sheltering. Although it appears that the legis-lator in this case aims at the more aggressive end of the continuum, in this paper we follow the broader defini-tion by Hanlon and Heitzman (2010), because our focus is generally on firms’ actions to influence their tax payments and not on the specific type of action taken. Therefore, we employ the term ‘tax planning’ because we believe it better represents the broader and more neutral approach.

3 See for example Laux and Newman [2012] for an analysis of the relation between auditor liability regulations and the decision of the auditor to take on clients depending on their riskiness.

2017-14 4/28/17

3

a company is able to maintain its level of tax planning over time. In contrast to a previous

finding by Francis et al. [2015], we find that the volatility of the effective tax rates decreases

with more APTS, i.e. the tax strategies are more sustainable. Our finding is in line with anec-

dotal evidence suggesting that advisory and audit companies actively promote sustainable tax

strategies (e.g. Deloitte [2013]).

If the auditor provides non-audit services to a client, his dependence on the client increases.

Economic bonding could potentially endanger auditor independence in fact or in appearance.

Despite of several studies highlighting the negative aspects of economic bonding (e.g. Srinidhi

and Gul [2007]) other studies such as Cook and Omer [2013] or Choudhary et al. [2016] have

already cleared economic bonding of concerns regarding the quality of the financial statement

(earnings quality or audit quality in particular). However, Choudhary et al. [2016] find evidence

for reduced professional skepticism in the presence of APTS. Though, this effect is said to be

due to the cognitive bias “in-group identification” instead. In contrast to these considerations,

knowledge spillover to the audit department from APTS might also strengthen audit quality

because of synergy effects. (Chung and Kullapur [2007] or Robinson [2008]). Our results are

mainly consistent with the view of knowledge spillovers to the audit department.

Earnings persistence is often viewed as an indicator of earnings quality (Dechow et al. [2010]).

However, if earnings persistence is the result of earnings smoothing it might be less desirable

in order to give a true and fair view of the real performance. Although an investor is interested

in less volatile earnings, it is important to face unsmoothed results to accurately evaluate the

company’s performance. Following this idea, persistent earnings due to earnings management

may not be desirable. Depending on the different interpretations of earnings persistence, a pos-

sible relation between APTS and earnings persistent may have another interpretation of earn-

ings quality. Accordingly, we also investigate the influence of APTS on earnings persistence

and find evidence for a negative relation following a positive association with audit quality.

In all aspects the legal background is important because it determines to what extent an auditor

can provide non-audit services at all. On the one hand, very strict restrictions may ensure a high

degree of auditor independence and could constrain economic bonding between the auditor and

his clients thereby avoiding negative effects such as high tax aggressiveness or low earnings

quality. However, a side-effect could be an inhibition of a reasonable amount of knowledge

spillovers resulting in inefficiencies and possibly even lower earnings quality. On the other

hand, a weak regulation of APTS may enable a potentially positive high degree of knowledge

spillover. Nevertheless, auditor independence and tax planning activities could be impaired.

2017-14 4/28/17

4

We contribute to prior literature in at least two aspects. First, we present evidence from Ger-

many which is one of the important EU member states. The German setting varies widely from

the US-American background. Due to this setting our results also mostly differ from previous

studies. Our data on auditor fees are hand-collected giving our sample a unique character. Sec-

ond, we are able to show that APTS can have positive influences with respect to reduced tax

planning and an increasing earnings quality. Since this finding occurs in the German legal back-

ground we infer that moderate restrictions on APTS are helpful in avoiding the negative aspects

without preventing the positive aspects. This could be a role model for the United States where

very loose restrictions appear to be accompanied with mostly negative outcomes. However, our

results are also not in favor of further tightening the law as it recently happened in Europe. It

remains an area for further research to actually evaluate the reform in a few years.

The paper proceeds as follows: Chapter 2 gives an overview of the legal situation in Europe

and Germany in particular. Chapter 3 presents prior research while chapter 4 builds on this and

develops our hypotheses. In chapter 5, we present the research design and the empirical results

for the tax perspective of APTS. We proceed analogously in chapter 6 for the accounting per-

spective of APTS. Chapter 7 concludes and gives perspectives for future developments and

fields of research.

2 EU and German Regulations of APTS

This paper is motivated by the reform of the German regulations on the provision of tax services

by the auditor. The Abschlussprüfungsreformgesetz (AReG) [Law on the reform of the audit

process]4 is an implementation of EU Directive No. 2014/56/EU and gives guidelines for the

application of EU Regulation No. 537/2014. It changed Sec. 319a I No. 2 of the German Com-

mercial Code effective June 17th, 2016. Before the reform, an audit firm was precluded from

offering audit services to a client if it also provides tax services or legal services in the same

year, which have a substantial influence on the financial statement and go beyond a presentation

of different tax planning alternatives.

In the amended version after the reform, the critical tax services are specified referring to EU

Regulation No. 537/2014. These services include the preparation of tax forms, the identification

of public subsidies and tax incentives, support regarding tax inspections, calculation of taxes

and deferred taxes, and the provision of tax advice in general. They remain possible but in a

more restricted way. First, the “substantial influence” is defined. According to the new law,

4 See BT-Drs. 18/7902 [German Bundestag Printed Paper No. 18/7902].

2017-14 4/28/17

5

substantial influence is assumed where aggressive tax planning strategies are pursued, i.e. there

is an extensive decrease in the domestic tax base or a significant shift of taxable income to

foreign countries. Second, the new Sec. 319a Ia Commercial Code directly refers to the ruling

in EU Regulation No. 537/2014, which restricts non-audit services to 70% of the average audit

fees in the last three years. In addition, the EU Regulation introduces a “black list” of services

which are prohibited in any case. This list includes services with regard to payroll taxes and

custom duties.

Under the new legislation APTS are highly limited or even forbidden. The intuition of the new

law appears to be that APTS have a detrimental influence on tax planning, because knowledge

spillover to the tax department and economic bonding might lead to more tax avoidance. The

new restriction on APTS is in line with past regulations of audit services. Sec. 319a Commercial

Code was first introduced in 2004 by the Bilanzrechtsreformgesetz (BilReG) and there were

further changes in this area by the Bilanzrechtsmodernisierungsgesetz (BilMoG) in 2009. These

reforms were mainly intended to improve financial statement quality and to strengthen auditor

independence.

In the US, APTS are far less restricted even when looking at the German situation before the

recent reform. If the audit committee agrees on APTS in advance, there are little further re-

strictions on the provision of these services in the US.5 Since the experience with largely un-

regulated APTS in the US setting is mostly negative or at least mixed, it is interesting to see

what effects the previously moderate German legislation had. Therefore, we investigate

whether APTS are as destructive as the European legislator suspects it to be. Since we employ

data before 2016, only the former legislation is subject of our analyses. Our results give insights

into whether the current further tightening of APTS is really necessary.

3 Prior Research

When the auditor provides both tax planning and auditing services, knowledge spillover effects

are likely, to the tax department as well as to the audit department. Several studies find a posi-

tive effect of APTS on tax avoidance. Cook and Omer [2013] observe a decrease in tax avoid-

ance after the termination or substantial decrease of APTS. According to Hogan and Noga

5 SEC Release No. 34-53677, File No. PCAOB-2006-01 (April 19th, 2006); SEC Release No. 34-72087, File

No. PCAOB-2013-03 (May 2nd, 2014)]; Rule 3524 of the PCAOB, available at: http://pcao-bus.org/Rules/PCAOBRules/pages/section_3.aspx. Also see SEC Release No. 33-8183 (January 28th, 2003); Sarbanes-Oxley Act, Section 201. Contingent-fee arrangements, confidential or overly aggressive tax market-ing, planning, or advice, and tax services to certain corporate managers and their family are prohibited (Krish-nan et al. [2013], Laffie [2006]).

2017-14 4/28/17

6

[2012] a reduction in APTS leads to higher tax payments in the long run and vice versa.

McGuire et al. [2012] add that APTS increases tax avoidance if the audit firm is a tax expert.

Dhaliwal et al. [2013] provide evidence that the positive effect of APTS is driven by tax plan-

ning fees in contrast to tax compliance fees. However, the effect is more pronounced if the

auditor provides both tax planning and tax compliance. All these findings suggest knowledge

spillover effects. Besides, Donohoe and Knechel [2014] find that due to knowledge spillover a

potential fee premium can be offset, which the auditor may demand for tax aggressive behavior

of the client.

Our second research question is related to tax sustainability. Francis et al. [2015] find that the

volatility of the ETR increases with an increase in APTS. McGuire et al. [2013] take a closer

look at tax sustainability. They discover that firms exhibit more persistent earnings if they pur-

sue sustainable tax strategies. Guenther et al. [2013] find that firms with a higher volatility in

Cash ETR, i.e. higher tax risk, are subject to a higher total firm risk. Therefore, it appears that

sustainable tax strategies are also value relevant.

Prior literature documents some negative effects of APTS on accounting and audit quality as

well as analyst’s forecasts. The study by Frankel et al. [2002] finds that the amount of discre-

tionary accruals is positively associated with non-audit fees, i.e. this points to a lower audit

quality due to a loss of auditor independence. On the other hand, Ashbaugh et al. [2003] find

no statistically significant relation between non-audit fees and the quality of financial state-

ments. This finding is reinforced for example by Chung and Kallapur [2003] and Huang et al.

[2007] with regard to non-audit fees in general. However, more closely related to our study, the

latter ones find a very weak hint that biased financial reporting is less likely when there are

higher values of APTS. In this line is the finding of Robinson [2008] that audit quality improves

through knowledge spillover if the auditor provides higher levels of tax services. Krishnan et

al. [2013] conclude that investors perceive the improved financial reporting quality through

knowledge spillover to be more important than a potentially lower auditor independence. The

study by Larcker and Richardson [2004] provides mixed evidence. They find that the absolute

value of accruals is positively related to the ratio of non-audit fees to total fees but it is nega-

tively related to the level of all (non-audit and audit) fees. In a study more closely related to

ours in terms of research design Srinidhi and Gul [2007] show that the level of non-audit fees

negatively affects the quality of accruals. In a German setting but with a smaller sample Sattler

[2011] gives evidence that the amount of APTS is generally not relevant for the level of earn-

ings management.

2017-14 4/28/17

7

Francis et al. [2015] identify a positive relation between the level of APTS and analysts’ fore-

cast error for both pre-tax earnings and tax expense. Their result is in line with Sattler [2011]

who identifies an independence violation assumption by external analysts. The main finding of

Choudhary et al. [2016] is a positive relation between the estimation error in the tax accounts

and APTS. If firms purchase a significant amount of APTS, the estimation error is nearly 10 %

higher compared to firms not buying APTS. In contrast, Ashbaugh et al. [2003] do not find

systematic evidence for decreasing independence of the auditor in the presence of APTS and

challenge the findings of Frankel et al. [2002].

Despite the potentially positive effect of knowledge spillover the mixed evidence regarding the

effect of APTS on accounting and audit quality hints at possible economic bonding effects

which impair auditor independence. However, reputation effects might restrain auditors to al-

low clients to engage in unusual accrual choices.

With regard to earnings persistence and APTS Francis et al. [2015] find a negative association.

Furthermore, some studies investigate the association between APTS and the earnings response

coefficient (ERC). For example, in a rather different setting Teoh and Wong [1993] find that

the audit quality (proxied by the size of the audit company) has an effect on the ERC. Gul et al.

[2006] discover that non-audit services have a negative influence on the value relevance of

earnings, also proxied by ERC. In terms of our measure of earnings persistence, we refer to the

common idea that future earnings are to a certain extent related to current earnings. This has

been often used in prior literature such as Sloan [1996], Richardson et al. [2005], Hanlon [2005]

or McGuire et al. [2013].

4 Hypotheses Development

An audit firm that provides non-audit services as well as audit services to a client, makes more

revenue with the client. This could result in economic bonding and impair auditor independ-

ence. Knowledge spillover to the tax department puts the audit firm in a good position to consult

on aggressive tax planning techniques if it has tax expertise (Dhaliwal et al. [2013]). The client

might demand advice on tax planning in order to reduce cash outflows to the tax authorities.

The increased importance of the client because of APTS makes it more difficult for the auditor

to resist any demands of the client. Economic bonding might thus lead to a positive effect of

APTS on tax avoidance.

However, the auditor must weight economic bonding against the reputational costs that might

result from a tax dispute. Further, the audit firm has to consider the risk of a restatement and a

2017-14 4/28/17

8

resulting liability to third parties. Recently, restatements related to tax positions have increased

in the US (Audit Analytics [2016]). This might induce an audit firm to advice on less risky tax

strategies and APTS could have a negative association with tax avoidance.

Most studies that find a positive association between APTS and tax avoidance are related to the

US market. Even before the recent reform, EU/German regulations on APTS were tighter than

the US standards. This is another argument for a negative relation between APTS and tax plan-

ning. We conclude that both the association of APTS with tax planning as well as its direction

are an empirical question in the EU setting and state:

Hypothesis 1: The level of APTS is associated with the level of tax planning.

Tax sustainability generally means that a company maintains certain tax outcomes over time.

McGuire et al. [2013] gather some evidence that tax sustainability is a primary goal for many

tax departments and that analysts may view unexpected changes in tax rates as a signal of poor

management. They also highlight a fact, which is especially relevant in our context, namely

that advisory and audit firms such as Deloitte actively promote sustainable tax strategies as

being relevant for firm value (Deloitte [2013]). Since the vast majority of firms in our sample

is audited by big-4 companies, which additionally provide tax services in many cases, this could

be a hint to a possible positive relation between APTS and tax sustainability. Moreover, it seems

to be intuitively logical, that an advisory firm, which is very familiar with its client’s business

model and accounting procedures due to the audit, is quite easily able to propose sustainable

tax strategies. However, any other tax adviser and the client’s own tax department might be as

able to consult on a sustainable tax strategy as the auditor. A third party firm might even have

an unbiased view and could be more motivated to introduce a new and sustainable tax strategy

while for the auditor the tax affairs of its client could only be a side business. If the audit firm

provides the tax services, it might prefer to concentrate on tax compliance and not tax planning

in order to reduce the risk from auditing the tax positions. The previous considerations have

shown that the direction of the relation between APTS and tax sustainability is not quite clear.

It even seems imaginable that there is no effect at all. Therefore, we state our next hypothesis

as follows:

Hypothesis 2: The level of APTS is associated with the level of tax sustainability.

Due to the insights into the client’s tax strategy provided by the audit firm’s tax department the

auditor gets a better understanding of the client’s business and the tax strategies in place. De

Simone et al. [2015] find that APTS enhance the overall quality of the financial reporting by

2017-14 4/28/17

9

improving the internal control quality in the sense that auditors are aware of material transac-

tions at an earlier stage. According to the principle of congruency of tax accounts and financial

statements, the understanding of the tax accounts yields an increase of audit quality. Providing

APTS, the audit quality rises due to knowledge spillover to the audit department. The rise in

audit quality due to the increased understanding of the underlying business would reduce ac-

crual management. The auditor is able to better identify window dressing in the accrual ac-

counts by the management to smooth earnings and meet analysts’ forecasts. Following this

argumentation, APTS is associated with a rise in accrual quality. The quality of accruals is often

regarded as a proxy for earnings quality (see for example Dechow et al. [2010]) which is in turn

a characteristic of audit quality (e.g. Ghosh and Moon [2005]).

The theory of reduced professional skepticism explains why a negative relation may be ob-

served, i.e. audit quality decreases in the presence of APTS. An auditor might rely on the work

done by his colleague in the tax department and might check the financial statements with less

skepticism. This phenomenon is known as in-group identification. Because of reduced profes-

sional skepticism due to in-group identification, the auditor may not identify earnings manage-

ment conducted by company executives. Therefore, a reduction of professional skepticism is in

line with a reduction of accrual quality. Another argument connected to reduced professional

skepticism is economic bonding. This means that due to the strong links between the auditor

and its client the auditor could be under pressure not to report a discovered issue in the financial

statement. Since an explanation for both a positive and a negative relation between APTS and

accrual quality exists, we formulate hypothesis 3 as follows:

Hypothesis 3: The level of APTS is associated with the level of accrual quality.

If a positive relation between APTS and accrual quality can be identified, the earnings manage-

ment in favor of earnings smoothing may decline. As a result, earnings persistence may decline,

too.6 However, if APTS decrease accrual quality, earnings persistence might also rise. We

therefore conclude:

Hypothesis 4: The level of APTS is associated with the level of earnings persistence.

6 Please note that we are aware of earnings persistence being evaluated as positive by the capital market. How-

ever, it is difficult to differentiate between the operative component due to the underlying business and the smoothed part due to earnings management. In contrast to prior literature, we interpret earnings persistence not exclusively positive but also want to give an alternative explanation for a negative association with audit qual-ity. While the firm value may be positively associated with earnings persistence, we want to give an explanation for a negative association with audit quality.

2017-14 4/28/17

10

5 The Tax Perspective

5.1 Research Design

To analyze hypothesis 1 empirically, this paper employs an OLS regression to investigate the

relation between APTS and tax planning. Equation (1) shows the regression model with

LRCASHETR being the dependent variable and ATR being the variable of interest.

LRCASHETRi,t = β0 + β1 ATRi,t + β2 SIZEi,t+ β3 LEVi,t + β4 PPEi,t + β5 ROAi,t

+ β6 INTANi,t+β7 INTLTYi,t + β8 Deloittei,t + β9 EYi,t + β10 KPMGi,t

+ β11 PwCi,t + Industry Fixed Effects + Year Fixed Effects + εi,t

(1)

The dependent variable is a long-run version of the cash ETR and proxies for tax planning. As

Dyreng et al. [2008] point out, long-run measures are helpful for eliminating one-year effects

from the ETR measures. LRCASHETR is calculated as the sum of income taxes paid from t-4

through t divided by the sum of pretax income from t-4 through t.7 Since all firms in the sample

are listed in the German prime standard and report their earnings to the German tax authority,

the underlying tax code is the same for all firms. Therefore, we are not dependent on the ad-

vantage of GAAP ETR measures’8 advantage of comparability due to a common IFRS code.

Additionally, as Hanlon and Heitzman [2010] point out, the advantage of cash ETR is that it

also captures tax planning strategies which induce the shifting of taxes over time.9 Therefore,

we believe LRCASHETR is the more appropriate proxy. For reasons of completeness, we also

run our tests using LRGAAPETR and we also use annual calculations of both versions, i.e.

CASHETR (GAAPETR) is computed by dividing income taxes paid (income tax expense) in a

period by the pretax income in the same period. In contrast to the potentially higher informative

value of LRCASHETR a potential advantage of the annual CASHETR is that we do not lose so

many observations due to data restrictions. When using long-run measures we exclude those

observations with negative ETR values and those being greater than one. For annual ETRs,

observations with negative values for pretax income and for income taxes paid and income tax

expense respectively are omitted due to issues of interpretation. A firm is defined to be engaged

in tax planning if it pays less taxes to the tax authorities and therefore has a low effective tax

7 Please note that measures of long-run ETRs must not be confused with the coefficient of variation of ETRs as

used in the analysis of H2. Although both concepts use data over several years, the intuition is different. Long-run ETRs still look at the level of ETR and thereby proxy for tax avoidance/planning. The coefficient of vari-ation does not specifically look at the level of ETR but captures to what extent a certain level is sustainable over time.

8 GAAP ETR measures use income tax expense instead of income taxes paid in the numerator. 9 This goal cannot be achieved using GAAPETR because it also comprises deferred taxes.

2017-14 4/28/17

11

rate. ATR is our measure of APTS. Specifically, it is the fee ratio of APTS to auditor-provided

audit services. According to Sec. 314 I No. 9 of the German Commercial Code firms have to

disclose the fees they paid to the auditor of the consolidated financial statement for audit ser-

vices, other audit related services, tax services (APTS), and other services. The auditor of the

consolidated financial statement is usually the local branch of the audit company, e.g. in case

of PricewaterhouseCoopers in Germany this would be PwC AG Wirtschaftsprüfungsgesell-

schaft. The fees represent all services provided by this local entity worldwide. However, we are

unable to obtain reliable information about the fees the entire network of an audit company

receives because only a few firms report this information. This could be a potential limitation

of our inferences.10 We use the fee ratio described above because we are interested in the impact

of additional tax services provided by auditors. We scale this measure with the fee for audit

services to make the values more comparable across firms.11 A previous study by Sattler [2011]

analyzing a German sample shows that the quality of the fee disclosure is sufficiently good and

reliable. Besides our variable of interest, we employ several control variables. SIZE is the nat-

ural logarithm of total assets, LEV indicates the companies leverage as long-term liabilities

scaled by total assets, PPE shows the company’s property, plant and equipment scaled by total

assets, ROA shows the return on assets, i.e. pretax income scaled by total assets, and INTAN the

intangible assets scaled by total assets. INTLTY is a variable indicating the degree of a firm’s

internationality and is calculated as the number of foreign subsidiaries divided by the total num-

ber of subsidiaries for each company in our sample.12 All continuous variables except for

CASHETR and INTLY are winsorized at a level of 0.01. Values of ETR measures are limited

between zero and one. Due to the construction, this also applies to INTLTY. Looking at account-

ing data and the impact of auditors, most researchers apply an indicator variable equal to one if

the firm is audited by a big-4 audit firm and zero otherwise. Since we are focusing on the Ger-

man prime standard, the portion of big-4 audits is quite high (ca. 85%). Nevertheless, there

might be a significant influence of the audit firm. We do not differentiate between big-4 audit

firm and others but each single big-4 firm. We employ indicator variables as shown in equation

10 We also run our tests with the limited data on network fees. The results are generally consistent. However, the

statistical relevance of such tests is much lower, because the sample is less than a sixth of the original size. 11 This ratio has been used in prior literature, e.g. Maydew and Shackelford [2005]. We also conduct our tests

with ATR defined as fees for tax-services divided by fees for audit services plus fees for tax services. This leads to similar results in terms of significance. The coefficients are slightly larger.

12 We are aware that internationalization of companies is usually proxied by control variables such as foreign income or foreign sales. Unfortunately, we cannot get reliable data for this approach from the relevant data-bases. Therefore, we construct an own indicator for internationalization by the given ratio. Data are obtained from the Amadeus database by Bureau van Dijk.

2017-14 4/28/17

12

(1) to identify the audit firm. Industry-fixed effects and year-fixed effects are included in the

model. The coefficient of interest is β1.

When including the proxy for internationality in the basic regressions as an additional control

variable, the number of observations decreases a lot due to data limitations compared to other

control variables. We show the effect of including this variable for hypothesis 1 while not in-

cluding the proxy in hypotheses two to four. However, untabulated results show that including

the proxy in the other hypotheses does not change the inferences of this paper.

In hypothesis 2, we analyze the relation between APTS and the sustainability of tax strategies

a company executes. Following the emerging literature on tax sustainability, e.g. Neuman et al.

[2013] or McGuire et al. [2013], we assume that a tax strategy is sustainable if there is a low

variation in the effective tax rates over the years. Specifically, the coefficient of variation of the

ETR is used as a proxy:

CV_ETRi,t = �∑ �ETRi,t – AvgETRi�

2Nt=1

abs�1N �∑ ETRi,t

Nt=1 ��

, (2)

where ETR is either CASHETR or GAAPETR. The coefficient of variation is determined by

scaling the standard deviation of the respective ETR over three years13 (N=3) by the absolute

value of the mean of the respective ETR over the same three-year period. As pointed out in

Neuman et al. [2013], the coefficient of variation reveals how consistently a company maintains

a certain tax outcome over the chosen period. In this respect, it is a measure of volatility without

unit. Lower values of CV_CASHETR and CV_GAAPETR indicate higher sustainability.

In order to investigate the hypothesis we run the OLS regression in equation (3) where the

coefficient of variation of both versions of ETR is the dependent variable. Our focus lies on the

coefficient on ATR, which is the same fee ratio as above. To control for the volatility of earnings

we also use the coefficient of variation of pretax book income (CV_PTBI) which is calculated

analogously to equation (2) (Newman et al. [2013]).

13 Neuman et al. [2013] and McGuire et al. [2013] use a window of five years to calculate the coefficient of

variation. However, we use only three years instead because our sample would be diminished too much other-wise. The three year period ranges from t-2 to t.

2017-14 4/28/17

13

CV_CASHETRi ,t or CV_GAAPETRi,t = β0 + β1 ATRi,t + β2 CV_PTBIi,t

+ β3 SIZEi,t + β4 LEVi,t + β5 PPEi,t + β6 ROAi,t + β7 INTANGi,t

+ Industry Fixed Effects + Year Fixed Effects + εi,t (3)

Again, we use indicator variables for the big-4 companies to control for a possible influence.

All continuous variables are winsorized to the 1 and 99 percentiles.

5.2 Descriptive Statistics and Empirical Results

Descriptive Statistics

Our sample comprises the four major indices of the DAX-family (number of companies in

brackets): DAX (30), MDAX (50), SDAX (50), and TecDAX (30), see Panel A of Table 1.

This makes 160 firms which are all listed in the Prime Standard of the Frankfurt Stock Ex-

change. Data on auditor fees are hand collected from the respective financial statements for

years 2009 through 2014. We use the indices’ composition as of January 2016. Companies are

excluded from the sample if they do not provide information about fees and if their headquarter

is not located in Germany because these firms do not necessarily disclose auditor fee infor-

mation according to German law.14 Panel B of Table 1 shows the distribution of audit firms.15

We obtain financial statement data from Compustat Global. All data are publicly available.

<Insert Table 1 here>

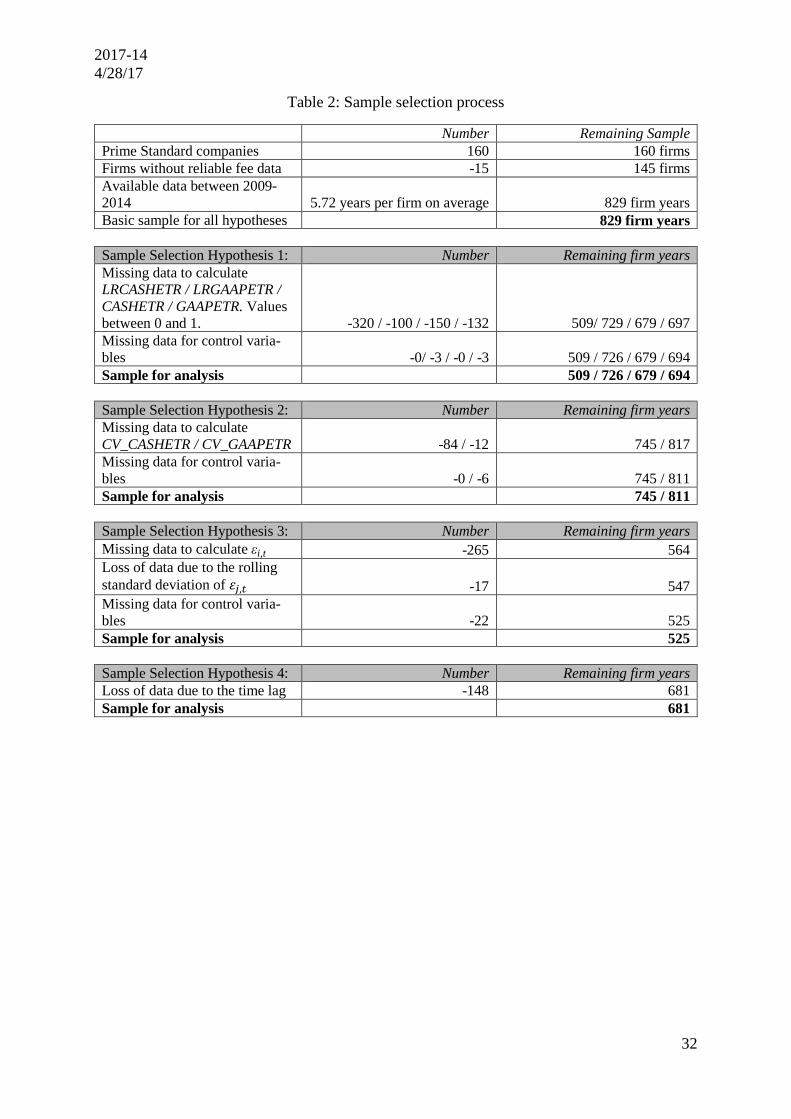

The sample selection is shown in Table 2. We collect fee data for 829 firms. In 495 firm-years

(60% of the sample) clients buy APTS.

<Insert Table 2 here>

Descriptive statistics are provided in Table 3.

<Insert Table 3 here>

Fees paid to the auditor for tax services make on average about 15% of the fees paid for audit

services. However, compared to the median firm’s ratio of 3 to 4%, it seems that there are some

companies with very high ratios in ATR. Within the subsample of those firms with non-zero

values for APTS the mean of ATR is 26% while the median amounts to 14.5% (not reported).

14 The number of firms varies between 131 and 142 per year (instead of 160). 15 It is interesting to see that the trend in our sample is towards concentration at the big-4 audit firms. There is a

drastic decline at the smaller companies in the item “Other”, while PwC and EY experience strong increases in their audit contracts and KPMG and Deloitte remain relatively steady.

2017-14 4/28/17

14

Looking at the different tax planning measures, we observe that the one-year measures CASH-

ETR and GAAPETR are slightly below the statutory tax rate, while both long-run measures

appear to be quite close to the statutory tax rate. This is a sign that the average firm in our

sample does not tend to engage in aggressive tax planning.

With regard to hypothesis 2, for the sake of brevity we include descriptive statistics for control

variables only for the regression using CV_CASHETR and on CV_GAAPETR. The variation in

the coefficients of variation is quite large even though the data are winsorized.

Panels A and B of Table 4 present the relevant correlation coefficients.

<Insert Table 4 here>

Empirical Results for Tax Planning

Table 5 shows the regression results of equation (1). The first and second (third and fourth)

columns of Panel A are designed to explain LRCASHETR (LRGAAPETR) as the dependent

variable. Since using INTLTY limits the number of firm-year observations more than any other

control variable, we show the regression results in column one (three) without INTLTY but

include it in column two (four). Anyway, the measure is not statistically significant in both

cases.

The coefficient of interest is β1 explaining the effect of ATR on the ETRs. The coefficients for

estimating LRCASHETR are statistically significant on a level of 1%. Column one and two

report a coefficient of about 0.09. The coefficient can be interpreted as the influence of ATR on

ETR. If the audit-tax ratio rises by 0.1 the LRCASHETR rises by 0.9 percentage points. Since

ATR is a ratio, it is difficult to interpret a change by 0.1 units. For reasons of simplicity, we

assume a mean company characterized by a mean APTS fee (€ 0.2099 million), a mean audit

fee (€ 1.8823 million), a mean LRCASHETR (30.38%) and a mean pretax income (€ 829.158

million). This firm would have an ATR of 0.1115. A rise in ATR by 0.1 units leads to a new

ATR of 0.2115. Assuming the audit fee not to change, the new ATR equals a tax service fee to

the audit firm of € 0.3981 million (a rise of about 90%).16 Given the above coefficient the mean

firm’s LRCASHETR therefore rises to 31.28%. If the long-run cash effective tax rate rises by

0.9 percentage points we assume this increase to be due to a rise in income taxes paid in time t

16 Assuming the audit fee not to change is a restrictive assumption but we apply the audit fee as a scaling variable

to generate the tax fee-to-audit fee ratio. The assumption is weak and limits the interpretation of the coefficient derived in the regression but is the only possibility to deal with a variable containing information about tax fees and audit fees. The ceteris paribus assumption is crucial for our interpretation.

2017-14 4/28/17

15

only. If the rise of a three-year cash ETR is due to a single-year rise of income taxes paid, the

effect on an theoretical single year ETR (which is easier to interpret) is three times as big.

Assuming the mean pretax income in all three years and the mean amount of taxes paid in years

t-2 and t-1 not to change the calculated amount of income taxes paid in t rises from € 251.898

million to € 274.286 million, an increase of € 22.388 in taxes. We are aware that this interpre-

tation only holds true for the mean firm while having constant values for pretax income. Nev-

ertheless, it gives an impression of the economic significance.

Most control variables are not statistically significant. Firms’ SIZE and ROA show significant

results meaning that bigger and less profitable firms tend to have higher CASHETRs. In the first

column it appears that being audited by KPMG leads to a lower ETR, but the significance is

weak. Running the regression without control variables gives consistent results.

In the LRGAAPETR case we do not find a significant association between ATR and tax plan-

ning. However, in Panel B using annual GAAPETR and not including the internationality meas-

ure shows significant results for the coefficient of interest on a 5%-level, including the interna-

tionality measure yields no statistical significance anymore. However, one might wonder if this

effect is due to INTLTY or due to the change in the sample size. Even in the absence of INTLTY,

the economic significance of the ATR coefficient is half compared to the results in column one

and two. SIZE is negatively associated with GAAPETR (on a significance level of 10%) indi-

cating that bigger firms tend to be characterized by lower GAAPETRs, while in the CASHETR

case we have an opposite finding. Regarding the association to ATR using annual CASHETR

yields similar inferences to the long-run case.

<Insert Table 5 here>

Taken together, these findings indicate that knowledge spillover from the audit to the tax de-

partment in favor of more tax planning are not an important issue in the German setting. More-

over, economic bonding does not appear to drive the association between APTS and tax plan-

ning. Instead reputational and liability concerns may be the key factors.

Empirical Results for Tax Sustainability

As Table 6 shows, we obtain negative and significant coefficients on ATR regardless of using

CV_CASHETR or CV_GAAPETR. The coefficient is slightly more significant in the first case.

This finding indicates that the volatility of the respective effective tax rates decreases with in-

creasing fees for APTS relative to audit fees. In our research setting, this means that there is a

2017-14 4/28/17

16

positive relation between APTS and the sustainability of tax strategies. This finding contradicts

the one by Francis et al. [2015] in an US-American setting. Nevertheless, our result is in line

with the view that audit/advisory firms market sustainable tax strategies as part of their services

and effectively implement these strategies in their clients’ firms. Furthermore, because of their

increased knowledge of the companies due to the audit cycles the audit firms may find it easier

to suggest suitable strategies, which lead to sustainable tax outcomes.

<Insert Table 6 here>

The control variables have various significance levels. It is worth mentioning that in contrast to

e.g. Francis et al. [2015] and Neuman et al. [2013] the volatility of earnings or pretax income

respectively appears to have no significant effect on the volatility of the tax outcomes (although

it is close in the case of CV_CASHETR). Moreover, in both cases we find a highly significant

negative coefficient on ROA indicating that more profitable firms have more sustainable tax

strategies, which seems to be plausible. Running the regressions without control variables pro-

duces consistent results.

5.3 Additional Tests

Controlling for Potential Endogeneity between Tax Planning and APTS

Several studies, e.g. Omer et al. [2006], Lassila et al. [2010], McGuire et al. [2012], or Krishnan

et al. [2013], argue that companies do not randomly decide on whether to buy tax services from

their auditor. Instead several factors which may be both observable and unobservable appear to

influence this decision. McGuire et al. [2012] explicitly point out that the level of tax avoidance

which is achieved by buying tax services from outside the audit firm may have an influence.

Since our German setting implies quite a regulated environment this reasoning is especially

important. Due to the regulations the auditor may not be in a good position to advise very ag-

gressive strategies. Therefore, it may be more useful for the firm to rely on the work of third

party tax advisory. Hence, the degree of tax planning a firm wants to achieve may also affect

the decision on how much APTS are to be bought. This would induce a serious endogeneity

problem in our model of hypothesis 1. To control for this issue we employ a Heckman [1979]

two-stage model and a simultaneous equations approach.

In the first stage of the Heckman procedure we estimate a probit model that predicts whether a

company will resort to its auditor for tax services. The model is similar to the ones used by

McGuire et al. [2012] and Krishnan et al. [2013], although some variables of these models

2017-14 4/28/17

17

cannot be used due to data restrictions. APTS is an indicator variable set to 1 if the firm obtains

any tax services from its auditor and 0 otherwise. For the definitions of the other variables we

refer to the appendix. A peculiarity of our model is that we explicitly control for tax planning

activity by including LRCASHETR.

APTSi ,t = β0 + β1 AUDINDi,t + β2 LAFi,t + β3 SIZEi,t + β4 LEVi,t + β5 PPEi,t

+ β6 ROAi,t + β7 CASHi,t + β8 DEPi,t+β9 LRCASHETRi,t + β10 Deloittei,t + β11 EYi,t

+ β12 KPMGi,t

+ β13 PwCi,t + Industry Fixed Effects + Year Fixed Effects + εi,t (4)

Results from this regression are reported in column 1 of Table 7. It is worth noticing that the

long-run cash ETR has a slightly significant positive impact on the probability to buy APTS.

The estimates from equation (4) are used to construct an inverse Mills Ratio which will be

included as an additional control variable in the second step. Apart from that, the second step

is basically identical to equation (1). Results are shown in columns 2 and 3 of Table 7. Column 2

follows Krishnan et al. [2013] and includes all remaining observations while column 3 omits

those observations with no APTS according to McGuire et al. [2012]. In both columns we still

find a highly significant positive association between ATR and LRCASHETR which is con-

sistent with our previous finding of less tax planning in the presence of APTS. Furthermore, the

inverse Mills Ratio being significant in both column 2 and 3 indicates that there may be poten-

tial endogeneity associated with the decision to buy APTS (Krishnan et al. [2013]). However,

this does not change our inferences. Additionally, it is striking that in column 3 the explanatory

value more than doubles compared to column 2 while all big-4 companies are now significantly

positive associated with tax planning.

<Insert Table 7 here>

In a second approach to deal with the endogeneity problem we use a simultaneous equations

estimation, specifically a three-stage least squares model. The detailed system of equations is

shown in Table 8. The first equation is identical to equation (1) and the second equation which

is estimated simultaneously has ATR as the dependent variable and the same independent vari-

ables as equation (4), because these are supposed to influence the decision on whether and to

what extent APTS are obtained. The results in column 1 of Table 8 are consistent with APTS

negatively influencing tax planning even after controlling for endogeneity by estimating the

2017-14 4/28/17

18

opposite direction, i.e. the amount of APTS depending on the level of tax planning, simultane-

ously. Moreover, the opposite direction in column 2 does not show a significant coefficient on

LRCASHETR suggesting that this direction may not be very important.17

<Insert Table 8 here>

Taken together, the above additional tests corroborate the findings in the main analysis that

APTS do not have an increasing influence on tax planning due to knowledge spillover to the

tax department of the audit firm. Although the decision on how much tax services are purchased

from the auditor and the pursued level of tax planning may be endogenous, our finding still

holds.

Splitting the Sample Depending on SIZE

In Panel B of Table 5, the statistically significant coefficients of SIZE for both GAAPETR and

CASHETR show different signs. This finding indicates that the firm size is somehow relevant

and the effect on the respective ETR measure is not quite obvious. To further analyze the effect

of ATR on the ETR while taking into account the special role of firm size, we split up the sample

into three groups based on the natural logarithm of total assets. Within the terciles we repeat

the baseline regression in equation (1). Untabulated results show that the effect found for the

whole sample using CASHETR seems to be driven by bigger firms since the coefficient for ATR

does not have statistical significance for the lowest tercile. Firms within the second and highest

tercile seem to provide evidence for an economically more significant influence of ATR on

CASHETR although being less statistically significant. We explain the lower statistical signifi-

cance by the small sample of less than 230 firm-year observations per group. However, the

adjusted R2 rises to over 33% in the second and third tercile. In contrast, the effect of ATR on

GAAPETR appears to be driven by those firm-year observations ranked in the lowest tercile.

The economic as well as the statistical significance increase for the first tercile while not yield-

ing any statistical significance for the second and third tercile. This finding is interesting be-

cause we interpret the altering statistical significance of ATR coefficients as evidence for the

different influence of APTS on ETR measures. It seems that for smaller18 firms rising levels of

APTS are associated with higher levels of GAAPETR while not affecting the CASHETR. For

17 However, the explanatory power in column 2 of Table 8 is poor. 18 Although labeling this group of firms “smaller firms” it is worth noting that all firms are listed in the German

prime standard and that these firms are not necessarily small firms but the smallest within the biggest listed firms in Germany.

2017-14 4/28/17

19

bigger and medium firms we provide evidence that rising levels of APTS are associated with

higher levels of CASHETR while not affecting the GAAPETR.

6 The Accounting Perspective

6.1 Research Design

We evaluate accrual quality (our proxy for audit quality and earnings quality in general) ac-

cording to the Francis et al. [2005] accrual quality model. In a first step, the following linear

time series regression is conducted in order to estimate total current accruals, while the focus is

on the remaining residuals.

TCAi,t = α0 + α1CFOi,t-1 + α2CFOi,t + α3CFOi,t+1 + α4∆Revi,t + α5PPEi,t + εi,t (5)

TCAi,t is a measure of total current accruals of firm i in year t calculated as TCAi,t= ∆CAi,t -

∆CLi,t - ∆CASHi,t - ∆DCLi,t where ∆CAi,t is the change in current assets between year t-1 and

t, ∆CLj,t denotes the change in current liabilities between year t-1 and t, ∆CASHi,t is the change

in cash between year t-1 and t and ∆DCLi,t denotes the change in debt in current liabilities

between year t-1 and t. The total current accruals are regressed on CFOi,t which is firm i’s cash

flow from operations in year t, its lag and lead values, on ∆Revi,t indicating the change in sales

revenue between year t-1 and t and on PPEi,t denoting the value of property, plant and equip-

ment in year t. As established by Francis et al. [2005] we use current accruals because there are

no long time lags between current accruals and cash flow realizations, which could be the case

if total accruals were used. We conduct a cross-sectional regression where we pool all firms in

the sample, which is different compared to Francis et al. [2005] where firms are pooled on an

industry level with each industry group having at least 20 observations. Due to the relatively

small size of our sample, this approach is not possible. We expect the same signs to appear as

in previous studies, which should be in line with the reasoning of Dechow and Dichev [2002].

The standard deviation of the residuals of equation (5) is the accrual quality proxy. However,

instead of a rolling window of five years we take a three-year window from t-2 through t. The

shorter window is due to the fact that we do not have time series in our sample that are suffi-

ciently long. To sum up, our measure of accruals quality is as follows:

AQi,t= σ(εi)t , calculated over t-2 through t.

Higher values of AQi,t indicate a lower accrual quality because the standard deviation is higher.

Following Francis et. al [2005] in our further analysis next to the raw data we also employ

2017-14 4/28/17

20

decile ranks of AQi,t (Dec_AQi,t) as a dependent variable in order to control for outliers and

non-linearities.

The association between audit quality and APTS is evaluated using the following OLS regres-

sion. The test variable ATR is the same as before.

Dec_AQi,t or AQi,t = γ0 + γ1 ATRi,t + γ2 SIZEi,t + γ3 SD_Revi,t + γ4 SD_CFOi,t

+ γ5 LOSSi,t + γ6 OPCYCi,t + γ7 Deloittei,t + γ8 EYi,t+ γ9 KPMGi,t

+ γ10 PwCi,t

+ Industry Fixed Effects + Year Fixed Effects + ϑi,t (6)

To control for other factors, which could influence the applied measure of accrual quality, we

include several control variables. These variables are extracted from Dechow and Dichev

[2002] who analyze various firm characteristics regarding their impact on accrual quality. Fran-

cis et al. [2005] also refer to these variables as being “innate” factors. To begin with, there is

SIZE, calculated as the natural logarithm of total assets. Dechow and Dichev [2002] expect

larger firms to have better accrual quality, because their operations are more stable and diver-

sified. A high standard deviation of sales revenue (SD_Rev, calculated over three years and

scaled by average total assets) is likely due to a volatile operating environment leading to larger

estimation errors and thereby reducing accrual quality. The same reasoning applies to the stand-

ard deviation of cash flow from operations (SD_CFO, calculated over three years and scaled

by average total assets). The variable LOSS is an indicator variable, which takes a value of 1 if

the pretax income is smaller than zero and a value of 0 otherwise. This approach proposed by

Srinidhi and Gul [2007] is easier to conduct for samples with a limited size compared to the

one employed by Francis et al. [2005] who take the number of negative income realizations in

the past ten years. Dechow and Dichev [2002] argue that accruals generated because of losses

are in general subject to greater estimation errors, because losses represent severe shocks. Fi-

nally, OPCYC is the natural logarithm of a firm’s operating cycle. Referring to Dechow [1994]

we calculate the operating cycle as [360/(Sales/Average Total Receivables) + 360/(Costs of

goods sold/Average Inventory)]. According to Dechow and Dichev [2002] longer operating

cycles lead to a lower accrual quality because they are usually indicative of a higher uncertainty

in the firm’s accounting. We also include indicator variables for the big-4-companies. All con-

tinuous variables are winsorized at a level of 0.01 to exclude extreme outliers. Furthermore, we

include industry and firm fixed effects.

2017-14 4/28/17

21

Finally, in hypothesis 4, we investigate the relation between APTS and the persistence of com-

pany earnings in Germany. To obtain the effects on earnings persistence we employ a rather

common model used for example by Hanlon [2005] or McGuire et al. [2013]. This model is

adapted to our research problem and gives us the following equation (7) which is estimated

using an OLS regression.

PTBIi,t+1 = β0 + β1 ATRi,t + β2 PTBIi,t + β3 PTBIi,t* ATRi,t

+ β4 Deloittei,t + β5 EYi,t+ β6 KPMGi,t

+ β7 PwCi,t

+ Industry Fixed Effects + Year Fixed Effects + 𝜀𝜀i,t

(7)

PTBIi,t+1 is the pretax book income of firm i in year t+1 and PTBIi,t is the pretax book income

of firm i in year t. Both variables are scaled by total assets at the end of the respective year.

ATRi,t is the fee ratio as specified above. In these terms, we investigate to what extent future

earnings are related to current earnings. According to Hanlon [2005], the interaction between

PTBI and ATR allows variation of the coefficient on current earnings depending on the level of

ATR. Therefore, we are interested in the significance of the coefficient β3. If hypothesis 4 were

true, we would expect β3 to be significantly different from zero. The sign could allow for further

implications. Again, we control for the effect of each big-4 audit company and industry and

year fixed effects. All continuous variables are winsorized to the 1 and 99 percentiles.

6.2 Descriptive Statistics and Empirical Results

Descriptive Statistics

Concerning the sample selection we refer to Table 2. Furthermore, Table 3 presents descriptive

statistics and Panels C and D of Table 4 present correlation coefficients.

With regard to hypothesis 3 the accrual quality measure with a mean of 0.0435 and a median

of 0.0304 has a very similar distribution to the one in Francis et al. (2005), where the measure

is developed, even though we have a much smaller and different sample and use standard devi-

ations over three years instead of five. Besides, firms in this sample are quite large (median

total assets of € 2,010 million), have experienced a loss in the previous year in 10% of the years,

and have a median operating cycle of nearly 130 days.

The variable PTBI used in the model of hypothesis 4 is identical with the variable ROA used

before, i.e. their definition is the same due to scaling pretax book income by total assets and

2017-14 4/28/17

22

their distribution only varies slightly because of different sample sizes. However, we use dis-

tinct names due to conventional issues. In most tax planning literature, the variable ROA is used

as a proxy for profitability and in papers concerning earnings persistence the variable PTBI is

a proxy for earnings which is scaled by total assets.

Empirical Results for Accrual Quality

The basic Francis et al. [2005] model shown in equation (5) which is used to obtain the residuals

shows the expected signs for the coefficients (untabulated). All three values of cash flow from

operations and the change in revenue are significantly related to the measure of total current

accruals. The value of PPE appears not to be a significant driver of current accruals in this case.

Turning to the effect of APTS on accrual quality we present the results in Table 9.

<Insert Table 9 here>

In both columns, we find a highly significant negative coefficient of ATR indicating an decrease

of accruals’ standard deviation and therefore an increase in accrual quality if the auditor pro-

vides more tax services relative to its audit services. This finding occurs after controlling for

several innate firm characteristics that are known to influence accrual quality. The coefficient

is slightly more significant if decile ranks of AQ are used. This is intuitive since the values are

less affected by outliers. Moreover, the explanatory power is considerably higher reaching a

value of 32.8%. Larger firms appear to have a better accrual quality. On the other hand, the

quality decreases with higher volatilities in revenues and cash flows from operations as well as

within loss years. The length of the operating cycle does not have a significant effect. None of

the big-4 indicator variables shows a significant effect. We use robust standard errors to control

for heteroscedasticity. Again, we also obtain consistent results when running the regressions

without control variables and fixed effects.

Our findings are in contrast to the related study by Srinidhi and Gul [2007] who find that accrual

quality decreases with increasing non-audit fees in US-American companies. However, despite

a different approach concerning the research design, our results are in line with the view of De

Simone et al. [2015] stating that the overall financial reporting quality increases due to APTS.

All in all, this finding supports the view of knowledge spillover to the audit department due to

insights from the tax service. On the other hand, it also suggests that a loss of professional

skepticism is not a major problem connected with APTS in Germany. Compared to the study

by Sattler [2011] we provide further insight into the role of APTS in Germany because in a

2017-14 4/28/17

23

smaller sample he does not find evidence of an effect of APTS on earnings management. Only

partially and with weak significance his results point to income-decreasing earnings manage-

ment accompanied by APTS.

Empirical Results for Earnings Persistence

The results of our investigation of the relation between APTS and earnings persistence are

shown in Column 1 of Table 10. Using robust standard errors, we find a significant and negative

coefficient on the interaction between ATR and PTBI (estimation of equation (7)). This result

indicates that APTS in fact influences the earnings persistence, i.e. earnings persistence declines

if the auditor provides more tax services. It is in line with the finding by Francis et al. [2015].

<Insert Table 10 here>

At first glance, this result may appear surprising since for hypothesis 3 we found that accrual

quality increases with ATR. As Dechow et al. [2010] point out both accrual quality and earnings

persistence are regularly used as proxies for earnings quality. However, in our case we infer

contradicting results from hypotheses 3 and 4. Though, we provide another possible explanation

for these findings. If the variation in accruals decreases, the accrual quality increases. This

means that managers do not change accruals from year to year largely, so the degree of earnings

management is limited. Due to lower earnings management, it can appear that earnings are less

persistent, because they are not subject to extreme smoothing.

6.3 Additional Tests

Innate and Discretionary Accrual Quality

While the quality of innate accruals depends on the general firm characteristics, which we used

as control variables in the above analysis, the discretionary accruals are subject to managerial

accounting choices, implementation decisions, and managerial error (Francis et al. [2005]).

Since the regression results for ATR in equation (6) emerge after controlling for innate factors,

they represent to some extent the effect of APTS on the quality of discretionary accruals. How-

ever, there is another possibility to disentangle the effects. Francis et al. [2005] suggest a

method of splitting their measure of accrual quality into innate and discretionary components.

To this end, they regress AQ on the five innate factors. Afterwards, the predicted estimate is

regarded as the innate component while residuals equal the discretionary component. To cor-

roborate our previous findings, we proceed accordingly, i.e. we first regress equation (8).

2017-14 4/28/17

24

AQi,t= 𝜃𝜃0 + 𝜃𝜃1SIZEi,t + 𝜃𝜃2SD_Revi,t + 𝜃𝜃3SD_CFOi,t + 𝜃𝜃4LOSSi,t + 𝜃𝜃5OPCYCi,t + 𝜇𝜇i,t (8)

The innate component is the linear prediction of the regression results and the discretionary

component is given by the error term.

In the next step, we regress the discretionary component and the innate component on ATR and

the remaining control variables from equation (6). Additionally, we employ decile ranks of both

components again. As Srinidhi and Gul [2007] point out, auditors’ fees are generally not ex-

pected to have a large impact on innate accruals since they could only be affected by firm char-

acteristics itself. Therefore, our focus is on discretionary accruals in the following analysis. We

expect significant negative coefficients on ATR in the case of discretionary accrual quality and

no significant impact of ATR on innate accrual quality.

As shown in Table 11, we find that there is a significant negative relation between ATR and the

quality of discretionary accruals. This applies to raw data and deciles of AQ. On the other hand,

there seems to be no relation between the ratio of auditor’s fees and the quality of innate accru-

als. This finding is consistent with our main analysis where we obtain a significant negative

relation between ATR and the overall accrual quality after controlling for innate factors. These

results suggest that APTS affect the way managers exercise their discretion concerning account-

ing practices. Specifically, with an increasing portion of APTS, the managers’ discretion seems

to improve the quality of the accruals and thereby the quality of the financial statement in its

entirety is enhanced.

Different Measures of Accrual Quality

In our main analysis, we employ a measure of accruals quality presented by Francis et al.

[2005]. This approach relies partly on the Jones [1991] model. Since the Jones model is also

very common in the research field of accruals, we also estimate our proxy of accrual quality

using this model in the first step. This means that we process the residuals of the Jones model

in a three-year standard deviation and take the resulting values as the accrual quality. With the

rest of the analysis remaining the same, we find (unreported) results being similar in quantity

and quality to our estimates using the Francis [2005] model. The same applies if we use the

modified Jones model proposed by Dechow et al. [1995].

2017-14 4/28/17

25

Influence of Extreme Values of APTS on Earnings Persistence

As an additional test, we attempt to show whether especially low or high values of ATR influ-

ence earnings persistence. To this end, we substitute ATR from equation (7) by dummy varia-

bles for the upper and lower ends of the distribution. Low_ ATRi,t is an indicator variable equal

to 1 if ATR is zero in the respective firm year. The number of firms concerned equals almost

exactly the lowest two quintiles in the distribution of ATR. On the other hand High_ ATRi,t is

an indicator variable equal to one if ATR is in the top two quintiles of the observations.19 Cor-

responding to the above reasoning our focus is on the coefficients β3 in each case.

In columns 2 and 3 of Table 10 we provide the results. In column 2, we see a positive and

significant coefficient on the interaction, showing that earnings persistence increases if the au-

ditor provides no tax services at all. On the contrary, in column 3 the interaction for high values

of ATR has a negative coefficient that is slightly significant, indicating that the persistence of

earnings decreases for companies, which buy a higher amount of APTS. These results seem to

corroborate the results of column 1. It becomes obvious that in the whole sample the decreasing

effect of ATR on earnings persistence prevails. Besides, unreported results show that for com-

panies in the middle quintile of ATR the interaction coefficient is also negative but statistically

insignificant.

7 Conclusion and Perspectives

The paper gives an overview of the role auditor-provided tax services play in Germany. It com-

prehensively and empirically analyzes several aspects in which APTS influence the clients’

firms. Therefore, this paper provides new insights, which are especially interesting considering

the legal background being significantly different to the US where most previous studies in this

area originated.

In contrast to an US setting, we find that tax planning does not increase if the auditor provides

more tax services. On the contrary, it even appears that an increasing amount of APTS is asso-

ciated with smaller tax planning activities proxied by different ETR measures. Regarding the

legal restrictions on APTS in Germany this finding is plausible. Due to these restrictions, audit

firms can only provide tax services to a limited extent, which may be of no use to a company

wishing to engage in tax planning. Third party tax advisors are not bound by these limitations

19 This approach is meant to approximately yield the two highest and lowest quintiles in ATR. It is not possible

to split ATR into regular quintiles because there are more observations with ATR=0 than would be in the lowest regular quintile.

2017-14 4/28/17

26

and their potential reputational damage may be smaller because they are not subject to a sus-

pected loss of professional skepticism with regard to an audit. Therefore, knowledge spillover

to the tax department followed by more aggressive strategies is not a relevant driver in the tax

planning perspective. In addition, we have some evidence of an endogenous relationship be-

tween APTS and tax planning policies, but our results are robust to controlling for this endoge-

neity.

In a further analysis of tax outcomes, we also find that companies with higher levels of APTS

appear to pursue more sustainable tax strategies in the sense of smaller variation in their effec-

tive tax rates. Although we cannot be certain about the reasons for this observation, we suggest

two possibilities. On the one hand, audit firms may market sustainable tax strategies as part of

their portfolio, and on the other hand, they may be in a better position to implement these strat-

egies than other potential tax advisors. In general, sustainable tax outcomes are regarded as

positive to the respective firm, so one might even conclude that audit firms have a positive

influence when providing tax services. The increased sustainability in the presence of APTS

strengthens the positive influence on decreasing tax planning activities. Higher levels of APTS

are not only associated with lower levels of tax planning but also with sustainably lower tax

planning activities.

Our finding that audit quality proxied by accrual quality increases if auditors provide more tax

services is interesting in at least two aspects. First, it provides evidence that the widespread

opinion of auditors’ conflict of interests resulting in lower quality financial statements appears

not to hold true at least in this respect. Rather, the double role of auditors appears to give rise

to an even better audit quality. Compared to the tax perspective where we cannot observe a

potential bad effect of knowledge spillover to the tax department, our results are consistent with

a positive influence of knowledge spillover to the audit department from the accounting per-

spective. Second, this finding can only be interpreted in the light of the legal background since

US studies came to opposite conclusions. It may be that the improved audit quality can only be

achieved if the APTS are subject to severe limitations. Going beyond these restrictions may

well increase auditors’ economic bonding and result in a loss of professional skepticism.

In our last hypothesis, we investigate the effect of APTS on earnings persistence. We find that

there is a negative relationship. Although this result may be astonishing it may be linked to our

findings on accrual quality. A greater consistency in the annual accruals (especially the discre-

tionary accruals) is possibly connected to smaller management-induced earnings smoothing.

2017-14 4/28/17

27

This, on the other hand, leads to a lower persistence of earnings because in the absence of

earnings smoothing the reported earnings are largely subject to the annual conditions.

Having our results in mind, the new restrictions of APTS seem at least questionable. Obviously,

the legislator’s underlying notion is that APTS have a detrimental influence on companies and

the economy in its entirety. This study suggests that there is no need to further limit APTS and

directly connect them to tax planning. Our findings indicate that with the former legislation in

place the effects of APTS should not be generally interpreted as a bad influence. Instead, we

can even show some positive effects. It appears that both the firms and the stakeholders benefit

from APTS by an increased audit quality. This enhances the reliability of the financial state-

ments which is positive for all stakeholders. The increasing sustainability of tax strategies may

also be beneficial to the firm and their shareholders including the government if it is value

relevant. With regard to the relation between tax planning and APTS there may also be benefi-

cial effects. Since the level of APTS appears to influence the level of tax planning negatively,

the positive effect of a higher level of APTS for the government is obvious. Arguing from the

companies’ perspective less tax planning may result in a higher outflow of funds to the govern-

ment, but the decision on the amount of APTS is up to the company itself. These arguments