Jumpstart Our Business Startups (“JOBS”) Act · PDF fileJumpstart Our Business Startups (“JOBS”) Act

Disclosure and the JOBS Act: Information

Asymmetry, SEC Letters, and Post-IPO Liquidity∗

Sudip Gupta and Ryan D. Israelsen†

First draft: March 15, 2014

This draft: November 29, 2014

Abstract

This paper evaluates the impact of the recently passed JOBS Act on IPO outcomes. A significantnumber of IPO firms use provisions of this act. For firms taking advantage of the JOBS Act,we find that, relative to a matched set of peer firms, (1) IPO underpricing increases, (2) postIPO liquidity decreases and (3) disclosure affects the probability of informed trading (PIN).These three results suggest that there is an increased degree of asymmetry of information amonginvestors in JOBS Act firms. The easing of disclosure requirements in the JOBS Act thereforeadversely impacts these firms by increasing the asymmetric information induced cost. Using anovel textual analysis technique to extract a set of disclosed risk factors from the prospectus,we examine which disclosures are associated with these costs. The Securities and ExchangeCommission (SEC) provides a complementary information production role via its commentsduring the filing process. A one standard deviation increase in a proxy for the winner’s cursefrom the SEC’s public signal increases underpricing by about 5.3%. The SEC’s comments alsoact as valuable inputs for post IPO information production as measured by PIN.

Keywords: Disclosure, Information Asymmetry, IPO, JOBS Act, Liquidity, Probability ofInformed Trading, Underpricing, Textual Analysis, Topic Models

∗We thank Viral Acharya, Reena Agarwal, Azi Ben-Rephael, Matt Billett, Sudheer Chava, Gerard Hoberg, CraigHolden, NR Prabhala, Rangarajan Sundaram, and Suresh Sundaresan for detailed comments and suggestions andparticipants at the Indiana University finance brown bag for helpful comments. We thank Jun Wu for excellentresearch assistance.†The authors are at Kelley School of Business, Indiana University. Gupta: [email protected], Israelsen:

1 Introduction

The Jumpstart Our Business Startups (JOBS) Act became law in April 2012 with the goal of

reducing the costs and delays of the IPO filing process. The JOBS Act coined a new term for small

firms with revenues of less than $1 billion: emerging growth companies (EGCs).1 The act aimed

to reduce the cost of raising new equity by easing regulatory restrictions for EGCs and to thus

“jumpstart” growth. The IPO process – “going public” – is particularly costly for small firms. In

this paper, we test whether there are indirect costs associated with the JOBS Act in terms of IPO

underpricing, informed trading, and post-IPO, secondary market illiquidity.

Over time, the disclosure and filing requirements of IPOs had become increasingly stringent for

firms wanting to access equity markets. In addition to the standard fees charged by underwriters,

going public also involves paying various auditor and legal fees in order to certify and maintain the

standard, stringent disclosure requirements. The IPO process also involves significant uncertainty

about the amount of money to be raised and the fair offer price for the equity. The impact of these

costs and uncertainties is larger and has a significantly more discouraging effect on small firms

who want to raise equity to enhance their future prospects than on large firms. Small firms have

relatively weak bargaining positions with respect to alternative private funding sources such as

bank loans and venture capital financing. This, in turn, increases the cost of capital and makes new

projects unattractive which impacts the growth of the economy.

With the backdrop of the great recession and the associated “drying up” of the IPO market, the

JOBS Act was enacted to reduce the regulatory burden and make it less costly for small firms to go

public. The main provisions of the JOBS act were designed to reduce the costs mentioned above.

For example, with a “testing the waters” clause, EGC firms may solicit interest from qualified

institutional buyers (QIB) about a contemplated offering. These firms may also “confidentially”

file the registration with the Securities and Exchange Commission (SEC). These provisions were

intended to reduce the uncertainty of the potential offer price and issue size and to receive feedback

from the market, thus enhancing EGC firms’ IPO prospects. EGC firms may also take advantage of

certain “scaled financial disclosure provisions” and are exempt from “internal controls audits”, both

1Throughout this paper, we will refer to EGC firms using JOBS Act provisions to go public as JOBS Act IPOs orEGC IPOs.

1

of which should reduce the cost of auditor fees and the time taken to go public. EGC firms are also

exempted from various other costly disclosures which should further ease the process of going public.

However, reducing disclosure requirements has a negative side effect: it may increase other

indirect costs of going public. There may be significant information asymmetry among investors

about the future prospect of an IPO firm. Uninformed investors may require compensation to bear

the adverse selection risk which may lead to underpricing of the issue. IPO underpricing – defined as

the first day return relative to the offer price – is like an indirect cost to the firm as it leaves money

on the table to satisfy enough investors in order to attract enough investors. Some of the provisions

of the JOBS Act may indirectly increase the degree of information asymmetry. For example retail

and uninformed investors may worry about the true quality of the firm if lower disclosure norms or

lower accounting standards are used. This aggravates the adverse selection problem and investors

may demand even more compensation to bear the adverse selection risk. This in turn should further

increase the underpricing of EGCs.

In addition to the the direct impact on underpricing, the higher degree of asymmetric information

may impact trading and liquidity in the secondary market. This should be most pronounced in the

days and weeks immediately following the IPO. This asymmetric information induced liquidity risk

may force all investors to demand more compensation in anticipation of bearing the risk and hence

the IPO may be further underpriced.

In this paper, we examine the performance of firms that went public as EGCs relative to a

matched sample of their peer firms before the JOBS Act. To the best of our knowledge this is

the first paper which analyzes the IPO firms which went public via the JOBS Act and examines

how changes in disclosures of both soft and hard information affect the associated indirect costs.2

Specifically, we find evidence that the JOBS Act affects underpricing, asymmetric information, and

post-IPO, secondary market liquidity. EGC firms leave substantially more money on the table

in terms of the first day return, relative to their peers. On average, EGC firms, post JOBS Act,

have about 7% more underpricing relative to the similar sized (less than $1 billion in revenues)

firms which went public just before the JOBS Act. Interestingly, small firms which went public

2In a recent paper, Dambra, Field and Gustafson (2014) provide evidence that the JOBS Act led to an increase inIPO Volume. In contrast, Chaplinsky, Hanley and Moon (2014) find no reduction in the direct costs of IPOs underthe JOBS act and no impact on IPO Volume.

2

after the JOBS Act, but did not use the provisions of the JOBS Act, have significantly less (about

13%) underpricing relative to other small firms (less than $1 billion in revenues) who use JOBS Act

provisions and list themselves as EGC firms. Among the set of EGCs, we find that underpricing is

about 8% higher for firms that choose to confidentially submit their draft registration statement

to the SEC. These firms are more likely to be uncertain about their valuation and prospects. The

underpricing may be compensation for this uncertainty.

Motivated by the result that the disclosure provisions of the JOBS Act affect underpricing, we

examine whether general risk disclosures can explain underpricing. We use a novel textual analysis

technique – topic modeling – to analyze the variation in IPO firms’ disclosed risk factors and to

link them to underpricing and asymmetric information. Topic models are used to uncover a set of

“topics” in a body of documents by finding latent relationships between groups of words that tend

to appear together. Using a topic model, we categorize IPO firms’ risk disclosures from the risk

factors section of their prospectus into a set of “Disclosed Risk Factors.”3 We then test whether

variations in the frequency of disclosed risk can explain the differences in underpricing between EGC

firms and a matched sample of their counterparts. We find that firms disclosing relatively more

risks associated with litigation, with uncertainty surrounding the development of new products,

with corporate control/ownership, with systems failure, with fluctuations in demand for products

and services, and with disclosure tend to have more first-day IPO underpricing. These last two

risk factors are especially relevant for EGC IPOs given both the impact of the great recession on

demand, and the reduced disclosure environment of the JOBS Act.

It is the context of the words that matters, not just the words themselves. For example, the

words “product” “drug”, “market”, and “candidate” are very commonly used words in risk factor

disclosures associated with the research and development of new pharmaceutical products. However,

when the words “clinical”, trial”, “approval”, and “FDA” also appear with these words, they tend

to be associated with risks of the product approval process. The word “product” is commonly

found in a few other risk factors. Thus, simply counting the number of times the word “product”

appears will not capture this distinction. Topic models are designed to capture these differences in

an objective way that is not captured by word counts, or even manual classifications.

3For a list of extracted topics and the words that make up each topic, please refer to the appendix and Section 4.B

3

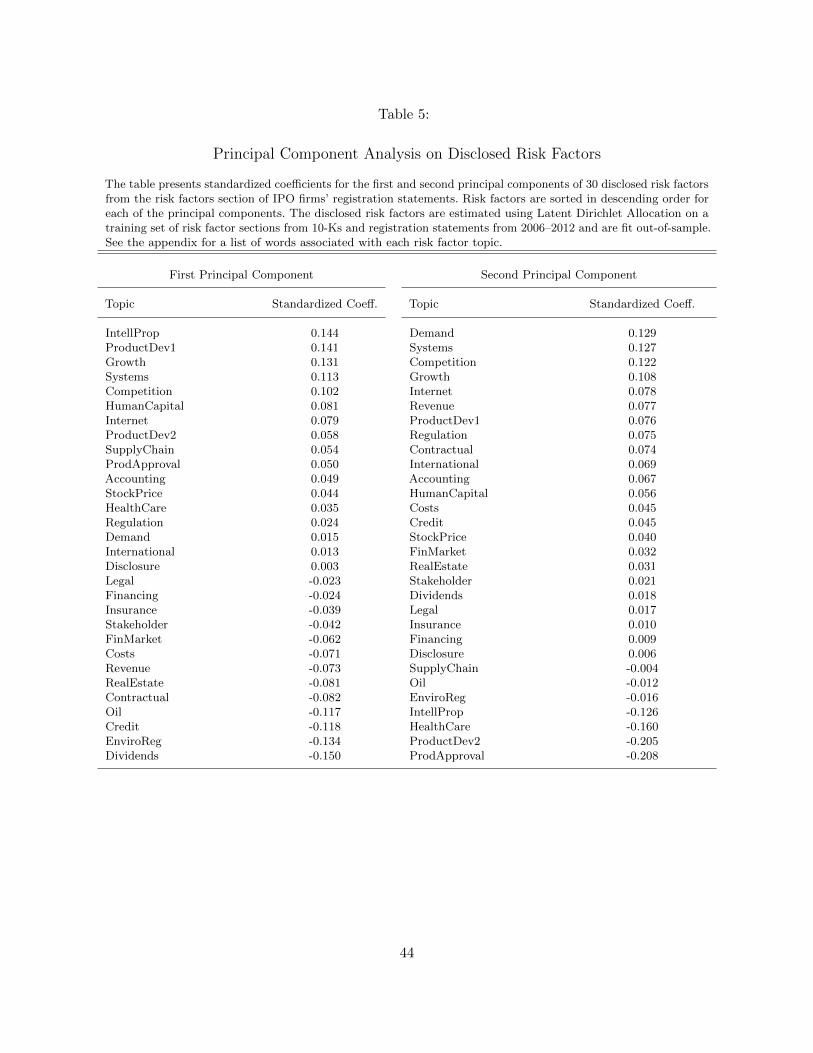

We summarize the variation in disclosed risks using the first and second principal components

and find that both significantly affect underpricing. A one-standard-deviation increase in the first

principal component is associated with 8% more underpricing. Differences in risk factor disclosures

can explain much (but not all) of the differences in underpricing between EGC firms and their coun-

terparts. The fit of the model doubles with the inclusion of the principal components. Importantly,

the impact of risk disclosures holds after controlling for the use of JOBS Act accommodations.

Several other papers examine the impact of the text of the prospectus on underpricing and

uncertainty.4 For example, Beatty and Welch (1996) provide evidence that the number of risk

factors disclosed in a firm’s prospectus is positively related to IPO underpricing. In terms of the

informational role of the prospectus, our paper is perhaps closest to Hanley and Hoberg (2010).

While they do not identify specific risk categories, they examine four sections of the prospectus

(including the “Risk Factors” section) and find that offers with more informative content (i.e., words

that deviate from those used in other IPOs in the same industry and from recent IPOs) have more

accurate initial offer prices and less underpricing. In a related paper, Hanley and Hoberg (2012)

examine the impact of revisions to the prospectus on price revisions during the issue process itself.

The tone of the language in the prospectus is also related to underpricing. Using a six sentiment

word lists created for financial documents, Loughran and McDonald (2013) find that the frequency

of uncertain, weak modal, and negative words in the prospectus are significantly related to IPO

underpricing. In contrast to the techniques used in the above papers which examine the number

of risks factors or the novelty or tone of the language, we examine the types of risks disclosed by

IPO firms and their individual impacts on underpricing and asymmetric information. Hence, our

approach is more consistent with the proposal by Ljungqvist (2007), in his review article, that a

“promising approach might be to identify specific . . . risk factors that, if present, indicate higher

uncertainty.”

Next, we examine the impact of the JOBS Act and its disclosure provisions on asymmetric

information and liquidity in the secondary market immediately following the IPO. Within the subset

of EGCs, we find evidence that informed trading increases with firms that take advantage of the

4A sample of papers examining the textual content of disclosures to the SEC after the IPO include Li (2008), Youand Zhang (2009), Hoberg and Phillips (2010), Loughran and McDonald (2011), Jegadeesh and Wu (2013), Lawrence(2013), and Loughran and McDonald (2014).

4

reduced disclosure provisions of the JOBS Act. In particular, there tends to be higher probabilities

of informed trading (PIN, Easley, Kiefer, O’Hara & Paperman (1996)) for firms disclosing fewer

years of selected financial data (about 1.7% higher per year of data) and omitting a discussion of

executive compensation (about 2% to 4% higher). When examining risk disclosures of EGCs and

a matched sample of their counterparts before the JOBS Act, we find that disclosed risk factors

explain a significant portion of the variation in informed trading after an IPO. A one-standard

deviation increase in the second principal component is associated with a reduction in PIN of more

than 3%. Moreover, the impact of risk disclosures on PIN changes after the JOBS Act. Additionally,

the number of words in the risk factor section is positively related to the probability of informed

trading after the IPO. Increased informed trading activity suggests that the secondary market plays

an important role in producing information in the environment of reduced disclosure following an

EGC’s IPO.

Next, we examine whether post-IPO liquidity changes as a result of the JOBS Act. We match a

sample of EGC firms with similar, pre-JOBS Act counterparts, and examine several measures of

spread for the first and second day following the IPO. Both unconditionally and controlling for firm

characteristics, we find that spreads are indeed generally larger after the JOBS Act. This, together

with the PIN and underpricing results described above, highlights the indirect costs of the JOBS

Act.

Finally, we examine the complementary role played by the Securities and Exchange Commission

following the enactment of the JOBS Act. Given the reduction in the amount of information

disclosed by most JOBS Act firms, public signals by the SEC about the IPO may affect investor

behavior. In particular, we examine the language used in the SEC’s comment letters to EGCs

following the submission of their draft registration statement. We find that when the SEC expresses

more uncertainty in their comments and uses more weak modal words relative to strong modal

words, underpricing tends to increase. This is consistent with “winner’s curse” from the standpoint

of an uninformed IPO investor. When there is more uncertainty, investors require a discount in the

IPO price. Thus, the SEC plays a complementary role to IPO firms in providing public information

to the market.

5

In addition to being the first paper to document the impact of changes in disclosure of hard and

soft information on the indirect costs of the JOBS Act, our paper relates to three broad strands

of literature: IPO underpricing, asymmetric information, and liquidity. Asymmetric information

is shown to affect both liquidity and IPO underpricing. If the JOBS Act increases information

asymmetry, it should impact both IPO underpricing, PIN, and post-IPO liquidity.

The impact of asymmetric information in the IPO process has been a topic of research for

decades (see Ljungqvist, 2007, for a survey). The issuing firm elicits information from informed

investors during the book-building process via the investment bank (Benveniste and Spindt,1989)

and IPO underpricing is a fair rent for producing information. The information asymmetry problem

among potential investors – both informed and uninformed – generates the winner’s curse problem

(Rock, 1986). The type of IPO mechanism use is shown to have a strong impact on information

revelation. Busaba and Chang (2002) showed that the use of a bookbuilding process elicits more

information during the IPO process than does a fixed price offering. Our paper examines the

impact of the JOBS Act and the role of information production during the IPO process on post-IPO

outcomes for EGCs.

Easley and O’Hara (2004) show that the differences in the composition of public and private

information can create asymmetric information induced systematic risk. In their model, uninformed

investors perceive different risk and return due to their information disadvantage and as a result

hold too many bad stocks in their portfolios. Anticipating this, these investors require compensation

for holding stocks with more asymmetric information. This risk is the greatest in stocks with less

public information. Thus, if the JOBS Act increased information asymmetry by reducing publicly

available information, this should lead to greater IPO underpricing. Consistent with this theory, we

find that compared to a matched sample, EGC IPO underpricing is almost 7% higher.

Easley and O’Hara also show that if more information about an asset is private, the difference

between the average holdings of informed versus uninformed investors will increase. Therefore, if

the JOBS Act increases private information, more informed investors should acquire shares during

the IPO process which will increase the dispersion of shareholdings.

6

Amihud and Mendelson (1986) model and test the relationship between liquidity and required

return for seasoned securities. Numerous follow-up papers (Acharya and Pedersen, 2002, among

others) show that investors demand compensation for bearing the systematic liquidity risk. A greater

degree of asymmetric information should reduce a stock’s liquidity as investors stop supplying

liquidity in order to avoid the asymmetric information induced winner’s curse. This should in turn

increase the expected return for stocks with more asymmetric information. In Vayanos and Wang

(2012), asymmetric information increases the expected return of a risky asset. They show that the

empirical relationship between illiquidity, as measured by lambda, and expected returns is positive

under asymmetric information.

Ellul and Pagano (2006) show that IPO underpricing may be related to the expected after-market

liquidity and that underpricing of the issue is required as compensation for investors bearing the

post-IPO liquidity risk. In their model, there are two types of private information about an IPO

firm. One is revealed during the IPO process and the other is revealed via trading in the post-IPO,

secondary market. If the second type of asymmetric information is higher that should lead to an

increase in the bid-ask spread, post-IPO, and a reduction in liquidity. The “flippers” who buy

during the IPO and sell immediately afterwards require compensation for the increased trading

costs induced by asymmetric information. The amount of information that remains undisclosed

after the IPO therefore depends on how much private information is revealed during the IPO stage.

We find evidence that JOBS Act IPO firms with more underpricing tend to have a lower probability

of informed trading after the IPO. This suggests that in an environment with lower disclosure

standards, these two types of information act as substitutes.

If the JOBS Act increases the degree of asymmetric information, there should be an increase in

the winner’s curse and hence a reduction the post-IPO liquidity. Expecting the increased illiquidity

induced by the increase in asymmetric information, investors will demand a larger return to bear

this secondary market illiquidity risk. Thus, IPO underpricing should increase. The above discussion

provides us the following formal hypotheses to be tested with respect to the JOBS Act:

H1: The IPO underpricing (as measured by the first day return relative to IPO offer price)

should be higher for a set of firms post-JOBS Act relative to a similar set of pre-JOBS Act firms.

7

H2: Probability of informed trading in the post-IPO period should be higher for small (EGC)

firms, post JOBS Act, relative to their similar sized peer group, pre-JOBS Act.

H3: Post-IPO, secondary market liquidity should be lower for small (EGC) firms, post JOBS

Act, relative to their similar sized peer group, pre-JOBS Act.

We find strong evidence in support of our hypotheses. Our paper makes several contributions to

the literature. First, we are the first to document the effect of the JOBS Act on IPO underpricing,

informed trading, and post-IPO liquidity. Second, we document the extent to which EGCs take

advantage of scaled disclosure requirements and other provisions of the JOBS Act in the IPO

process and examine their effects on underpricing, informed trading, and liquidity. Finally, using a

novel textual analysis technique we examine the effects of disclosed risk factors on underpricing and

informed trading.

To date, there has been little research on the impact of the JOBS Act. Dambra, Field, and

Gustafson (2014) also analyze the impact of the JOBS Act on the IPO decision and provide evidence

that the increase in the number of JOBS Act IPO relates to a reduction in the direct costs of

disclosures. On the other hand, Chaplinsky, Hanley and Moon (2014) find no reduction in the direct

costs of IPOs under the JOBS act and no impact on IPO Volume. By contrast, our paper focuses

on the indirect costs of the JOBS Act for EGC IPOs in terms of on underpricing, and post-IPO

PIN and liquidity. As described above we also use a novel textual analysis technique to link these

costs to various disclosed risk factors.

While this paper highlights negative impacts of the JOBS Act, these results do not imply that

the JOBS Act failed to help EGCs. As mentioned, there are undoubtedly significant benefits of the

JOBS Act on small firms. Whether the benefits outweigh the costs is an empirical question left for

future research.

The remainder of the paper is laid out as follows. In the following section, we describe the

provisions of the JOBS Act. In section 3, we describe our data. In section 4, we describe our

empirical methodology and our results. We conclude in section 5.

8

2 JOBS Act

The Jumpstart Our Business Startups (JOBS) Act became law on April 5, 2012 with the stated goal

“to increase American job creation and economic growth by improving access to the public capital

markets for emerging growth companies” (EGCs).5 Title I of the JOBS Act defines an EGC as a

company with revenues of no more than $1 billion in its most recent fiscal year. It also delineates

certain criteria by which such a company may lose its EGC status.6 Title I also lists a menu of

special provisions for the EGCs to chose from. The EGCs may choose all, some, or none of the

special provisions when going public. The main provisions are:

• Confidential SEC review: EGCs may make a confidential submission provided that the initial

confidential submission and all amendments are publicly filed with SEC no later than 21 days

before the commencement of the road show.

• Testing the waters: The EGC (or its underwriter) can engage in oral or written communications

with institutional investors, either before or after filing the first registration statement.

• Reduced financial disclosure: EGCs may disclose only two years of audited financial statements

instead of the three years norm. They may also disclose two years instead of five years of

selected financial data.

• Exemption from internal controls audit: The EGCs are exempt from an internal control audit

as stipulated by the Sarbanes-Oxley Act (2002).

• Reduced disclosure of executive compensation: EGCs are exempt from shareholders advisory

votes on executive compensation required by the Dodd-Frank act of 2010. Moreover, EGCs

5See H.R. 3606 “Jumpstart Our Business Startups Act” http://www.gpo.gov/fdsys/pkg/BILLS-112hr3606enr/

pdf/BILLS-112hr3606enr.pdf6Sections 101 (a) and (b) of the JOBS Act state that after the initial determination of EGC status, a company will

remain an EGC until the earliest of:

• the last day of any fiscal year in which company earns $1billion revenue or more

• the last date of the fiscal year following the fifth anniversary of IPO date

• the date of issuance, in a three year period of $1 billion or more of non-convertible debt

• the date on which the issuer is a ”large accelerated filer” with at least $ 700 million in public equity float

9

may omit a written discussion of executive compensation from its prospectus and may disclose

the compensation of as few as 3 executives instead of the 5 previously required.

• Extended phase-in for new GAAP: EGCs may continue to use private accounting phase-in

periods for new GAAP standards for a period after the IPO.

• Exemption from Public Company Accounting Oversight Board (PCAOB) rules

These provisions are intended to provide the EGC distinct advantages when going public. First,

they improve the ability of firms and underwriters to gather information about the costs/benefits of

going public without committing to an IPO or sending negative signals to the market. For example,

confidentially submitting a draft registration statement to the SEC for comments allows a company

to decide on the optimal timing of an IPO while significantly reducing the glare of publicity and

hiding its intentions from competitors. Similarly, the testing the waters clause enables the issuer

and its underwriter to gauge market sentiment – especially in industries where valuations are highly

uncertain.

Second, many of these provisions reduce the costs of the IPO process. For example, because a

confidential draft registration statement is not considered a filing, no filing fee needs to be paid.

Similarly, providing two years instead of three of audited financial statements may also save the EGC

auditor fees especially if they have recently changed auditors. Moreover, confidential submission

shields the issuer from the Sarbanes-Oxley Act until the registration is publicly filed. The EGCs

may also use private company phase-in period for accounting standards after the IPO.

In addition to the above provisions, the JOBS Act also relaxes standard norms for analyst

research reports of an EGC. Specifically, the JOBS Act suspended the existing FINRA rule of 40 day

of research quiet period immediately following the EGC IPO. It also includes provisions regarding

with pre-deal research communications.

There are minimal additional disclosure requirements for EGCs. For example, if the EGC does

not opt out of the private accounting standard then SEC requires them to mention that as an

additional risk factor in the prospectus to differentiate it from other public companies. EGC are

also required to disclose their EGC status in the prospectus as well as a summary of the exemptions

10

available to the EGC. Finally, if the EGC decides to opt out of the transitional accounting standards,

it must also mention that it is irrevocable.

In the following section, we examine the frequency with which EGCs take advantage of each of

the provisions of the JOBS Act and describe the data used in the analysis.

3 Data

We have three major sources of data in this paper. The IPO prospectus filed with the SEC provided

the stock price and other filling details of the firm as well as the pre-IPO accounting data and which

(if any) of the JOBS Act provisions are used by the firm. We hand collect information from the

EDGAR website about whether firm filed confidentially before the IPO. Additionally, we gather

SEC comment letters from EDGAR. Post-IPO share prices and trading information are collected

from Compustat, CRSP, and TAQ. Finally the IPO prospectuses are the sources of the textual risk

factor analysis.

A EGC Usage of JOBS Act Provisions

Before proceeding to the main analysis, we examine the frequency with which EGCs choose to

take advantage of the each of the JOBS Act provisions. To gather this information, we read the

prospectus of the EGCs in our sample to determine whether or not they took advantage of the

provisions of private accounting standards, omitted a discussion of executive compensation, provided

two years instead of three of audited financial statements, provided fewer than five years of selected

financial data, and provided compensation data on fewer than five executives. Panel A of Table 1

presents the frequency with which 220 IPO firms from 2012 and 2013 claiming EGC status take

advantage of each of these provisions and correlations between use of these provisions.

The use of various provisions of the JOBS Act is quite variable. The least used provision – the

choice to continue to use private accounting standards for a period after the IPO – is only used

by 20% of firms. The vast majority choose to opt out, perhaps as a signal of willingness to adopt

11

better corporate governance practice. 59% choose to file a confidential draft registration statement

with the SEC. Note that we can only observe those who chose to go public after a confidential filing,

so the true number is certainly higher.

Almost half of the firms omit a written discussion of their executive compensation from the

prospectus, and 80% report the amount of compensation for less than 5 executives. Surprisingly,

there is no correlation between the use of these two accommodations.

A significant majority (151 out of 220) chose to report fewer than five years of selected financial

data although almost half of the firms in our sample chose to provide at least three years of audited

financial statements. Interestingly, firms who disclose fewer than three years of audited statements

are more likely to provide fewer than five years of selected financial data as can be seen from the

correlations in Panel A. Panel B shows that about 86% of firms (68 of 79) providing fewer than five

years of selected financial data also provide fewer than three years of audited financial statements.

We find that 77% (34 out of 44) of those who chose to continue to use private accounting standards

also chose to disclose fewer than five years of selected financial data. Therefore, although there is a

considerable variation in the choice of the JOBS Act provisions, there are significant correlations

and disclosure patterns among EGCs.

B Summary Statistics

Table 2 presents summary statistics for the variables used in this study for four types of IPO firms.

The main group of interest is the 234 firms claiming EGC status under the JOBS Act between

April 2012 and December 2013. To qualify, a firm must have had revenues of less than $1 billion

in its most recent fiscal year. We use three types of IPO firms as controls. First, we match firms

on size, revenues and industry to create a matched sample of 186 firms with revenues less than $1

billion that had IPOs from the beginning of 2010 until just before the JOBS Act became law.7 For

the sake of simplicity we denote these firms as SMALL, though they are classified by revenues, not

assets. The next group we use as a control is firms that qualified as EGCs under the JOBS Act,

but chose not to claim EGC status in their filing. There are only 17 such firms. Finally, we use all

7In untabulated results, we also match on the additional variables number of employees, offer and offer amount,and results look very similar.

12

other IPO firms in the JOBS Act era as a control. We call these firms with more than $1 billion in

revenues LARGE. There are 45 such firms in out sample.

Panel A presents means, standard deviations, and standard errors for IPO-level variables for all

four groups of IPO firms. Variables include the IPO offer price, the size of the offering, the fees,

and the 1- and 3-day IPO returns for the four types of IPO firms. The first variable of interest is

the IPO offer price. The mean IPO offer price for EGC firms is statistically smaller than those of

the three other groups (as indicated by the asterisks in the table). The average size of the offerings

are $154 million for both the EGC companies and those from before the JOBS Act that would have

qualified as EGC. Not surprisingly, the set of firms ineligible for the JOBS Act due to high revenues

tend to have larger offerings and lower fees than EGC firms.

The next two variables are the 1-day IPO return - defined as the return based on the IPO offer

price and the closing price on the first day trading on the exchange - and the 3-day IPO return -

defines using the closing price on the third day. The average 1-day and 3-day IPO returns for the

EGCs are 18 and 21 percent, respectively. Strikingly, EGC companies, on average, have larger 1-day

and 3-day IPO returns than the three control groups, suggesting that their IPOs are underpriced

relatively more. Underpricing is 5% to 15% higher, on average. Additionally, Panel A presents 22-,

44-, and 66-day PIN for EGCs and their matched peers from before the JOBS Act as well as the

total number of words in the risk factors section of the prospectus. 66-day PIN is higher, on average,

for EGCs. In the next section, we test whether these differences can be explained by differences in

firm characteristics and risks.

Panel B provides the same metrics as Panel A for a set of accounting variables gathered from

each IPO firm’s prospectus including assets, liabilities, revenues, research & development expense,

and investment in property, plant & equipment. These variables will be used as controls when

examining underpricing and liquidity. As before, asterisks indicate that the mean is statistically

different from the mean of the EGC group.

EGCs have an average of $454 million in assets, and $319 million in liabilities. These averages

are not statistically different from the other post-JOBS Act firms with revenues less than $1 million,

but are slightly larger than their pre-JOBS Act peers. They do tend to have less debt than the

13

“LARGE” firms, and by definition, lower revenues – $244 million compared to $4.3 billion. The 17

firms that opted not to claim EGC status tend to have larger revenues – $244 million on average.

There are no statistically significant differences in R&D expense between the EGC firms and the

three other groups. However, they do invest less in PP&E than the larger firms and those opting

out of the JOBS Act.

4 Empirical Methodology and Results

To examine the indirect costs of the JOBS Act, we perform several tests. First, we explore the

determinants of the relatively larger underpricing for EGCs identified in the previous section. Next,

we examine the impact of the JOBS Act on the probability of informed trading. Finally, we test

whether liquidity in the secondary market is higher for EGCs than their counterparts. For part of

the analysis, we use a set of disclosed risk factors extracted from IPO firms’ filings.

A JOBS Act Provisions and IPO Underpricing

We begin by examining which – if any – of the disclosure accommodations under the JOBS Act are

associated with more underpricing by examining the subset of EGC firms. Given that unconditional

average underpricing is 5% lower for these firms than their matched counterparts before the JOBS

Act, it is of interest to know whether variation in the use of provisions plays a role. For 215

firms qualifying as EGCs under the JOBS Act, we regress the first-day underpricing on each of

six accommodations, individually and jointly, along with age, lagged revenues, and lagged assets.

Additionally, we include a dummy variable indicating that the IPO firm had venture capital backing

(from SDC Platinum), a dummy variable indicating that the IPO had a star lead underwriter (defined

as a lead underwriter with the highest rating on Jay Ritter’s website, using the methodology in

Ritter and Loughran, 2004), a dummy variable indicating the firm is in a technology industry (Tech:

defined as the Fama French industries Computers, Software, Electronic Equipment, Healthcare,

Medical Equipment, and Drugs).8 Table 3 presents the results.

8Results (available upon request) are very similar using the 12 Fama French industries. However, there are veryfew IPOs in some of the 12 industries.

14

Generally, smaller firms with a star lead underwriter and venture capital backing tend to

have more underpricing. Interestingly, when the accommodations are tested individually, the only

accommodation that is associated with underpricing is the number of years of selected financial data.

Moreover, the impact seems to be in the wrong direction. However, once the other 5 accommodations

are accounted for, the coefficient is no longer significant. As seen in column (7), firms who submit

a confidential registration statement tend to have more underpricing – 8% more than those who

don’t. These EGCs are more likely to be more uncertain about their potential valuation and higher

underpricing may reflect higher degree of asymmetric information. These may be firms that would

otherwise not have gone public, or it might be interepreted by the market as a sign of uncertainty.

By the time of the IPO, it is known whether firms took advantage of this provision.

B Topic Models and Risk Factors

Motivated by the result that the disclosure provisions of the JOBS Act affect underpricing, we

next examine whether the specific types of risk that firms disclose can explain underpricing and

asymmetric information. In order to classify risk disclosures into a set of categories, we use a novel

textual analysis technique which avoids subjectivity problems associated with manual classification.

Topic Models are probabilistic generative models used to describe a set of latent “topics” that

occur in a given collection of documents. Documents are modeled as mixtures of a smaller number

of topics and topics as probability distributions over words. In generating a document, words are

assumed to have been randomly chosen from the topics given the specific document’s distribution

over topics, θ(d), and the word distribution for the drawn topics, φ. Based on these models, Bayesian

statistics can be used to “uncover” the latent document-topic and topic-word distributions. These

models are particularly useful when corpora are large and when there are many topics. One benefit

of using a topic model is the classification technique is standardized and objective. The results of a

manual classifications may depend on the individual performing the classification and also may not

be internally consistent. Topic models allow the data to determine the classifications, which may

include latent connections that a researcher might otherwise miss.

15

One of the most commonly used topic models in machine learning and computational linguistics

is Latent Dirichlet Allocation (LDA) (Blei, 2003).9 LDA is a hierarchical model which chooses the

latent topics as well as probability distributions in order to maximize the likelihood of observing a

given set of D documents. In particular, if we have K topics, we can write the probability of the ith

word in the dth document as

P (wdi) =K∑k=1

P (wdi|zd = k)P (zd = k). (1)

Here zd is a latent variable indicating the topic from which the ith word in document d was

potentially drawn and P (wdi|zd = k) is the probability of the word wi under the kth topic. P (zi = k)

gives the probability of drawing a word from topic j in the current document, which will vary across

documents.

The K topics are defined as categorical distributions10 over W words with parameter vector

φ, such that P (w|z = k) = φ(k)w , and the the dth document is defined as multinomial distributions

over the K topics with parameter vector θd, such that P (z) = θd. LDA augments the model with

the addition of Dirichlet priors on both θ and φ Specifically, θ ∼ Dirichlet(α) and φ ∼ Dirichlet(β)

where α and β are hyperparameters. Dirichlet priors are assumed. These priors are conjugate to the

categorical distributions which means posterior distributions are Dirichlet. The inferential problem

that needs to be solved is to analyze the posterior distribution

P (z, θ, φ|w,α, η). (2)

With the introduction of the Dirichlet priors, estimation is a matter of maximizing the total

probability of the model

P (W,Z, θ, φ;α, β) =K∏i=1

P (φi;β)M∏j=1

P (θj ;α)

Nj∏t=1

P (Zj,t|θj)P (Wj,t|φZj,t) (3)

9See Chang, et al. (2009) who provide evidence from experiments that both humans and topic models arrive atsimilar topics.

10The categorical distribution is equivalent to the multinomial distribution with one trial.

16

by choosing the set of parameter vectors θ and φ. These two sets of estimates provide the

document’s probability distribution across topics, and the topic’s probability distribution across

words, respectively.

The Securities and Exchange Commission Regulation S-K instructs filers to provide “provide

under the caption ‘Risk Factors’ a discussion of the most significant factors that make the offering

speculative or risky.” Regulation S-K initially applies to a firm when it files Form S-1 - the

“Registration Statement Under the Securities Act of 1933”, but since 2005 it has also applied to

the 10-K. Using the “Risk Factors” section from 10-Ks and S-1s from 1995–2012, Israelsen (2014)

extracts 30 risk factor “topics” using LDA and examines how they relate to firm-level risk and

systematic risk. We use the same model trained on the data to fit, out of sample, the set of risk

factors disclosed in the IPO filings of our set of firms. The Appendix contains a discussion of all 30

risk factors.

Panel C of Table 2 provides the average fraction of the “Risk Factor” section of firms’ prospectuses

dedicated to each of the 30 risk factors for all four groups of IPO firms. As before, asterisks indicate

statistically significant differences with respect to the EGC group of firms. Compared to their

counterparts from before the JOBS Act was in effect, EGC firms make more disclosures of risk

associated with accounting, with financial markets, with health care, with insurance, with the

regulatory approval of products, and with regulation. On the other hand, they spend less time

discussing risks associated with product market competition, demand, human capital, international

markets, the development of new (non pharmaceutical/biotech) products, and the supply chain.

They differ much more from other Post-JOBS Act, non EGC companies in terms of disclosed risk

factors.

C Disclosed Risk Factors and Underpricing

To examine whether differences in disclosure of these risks may explain some of difference in

underpricing shown in Panel A of Table 2, we examine both the EGC firms and their matched

counterparts from before the enactment of the JOBS Act. In particular, we regress the first-day

17

IPO return, ret1 on the set of disclosed risk factor frequencies as well as lagged revenues, assets, and

a dummy variable indicating that the firm is an EGC. Table 4 presents the results of this regression.

Most of the coefficients on the risk factor variables are not statistically significant. However, firms

disclosing relatively more risks associated with changes in demand, with the problems associated

with disclosure, with litigation, with the development of new products or technologies (especially

pharmaceutical or biotech), with ownership/governance, and with systems failure are more likely to

have larger first-day IPO underpricing. The dummy variable EGC, which indicates that the firm

has claimed EGC status under the JOBS Act is now only marginally significant. Thus, differences

in disclosed risk factors can explain much of the statistical difference in underpricing between EGC

and non-EGC firms.

In addition to examining the effect of individual risk factors on underpricing, we also examine

the impact of their first and second principal components, which together explain almost one-third

of the variation in disclosed risk. Table 5 presents the standardized coefficients of both. The first

principal component – which explains 16% of the variation in the disclosed risk factors – has positive

coefficients on risk factors associated with intellectual property, the development of new products,

the need to grow, systems failure, competition, human capital, and the internet, and negative

coefficients on risks associated with the ability to pay dividends, environmental regulation, access to

credit, and the price of oil. These may be considered to be new economy (or high tech) versus old

economy (or low tech) risks. The second principal component – which explains 14% of the variation

– has positive coefficients on risks asociated with variable demand, systems failure, competition, and

growth and negative coefficients on risks associated with R&D, product approval, health care and

intellectual property. These latter risks tend to be disclosed by technology firms, particularly biotech

or pharmaceutical firms. We regress the first first-day IPO underpricing on these two principal

components, “riskfactor1” and “riskfactor2” as well as the EGC dummy, lagged revenues and assets.

Additionally, we include interaction terms between EGC and the two principal components and the

number of words in the risk factor section, and dummy variables indicating that the firm is in a

technology industry, has a star lead underwriter, and had venture capital backing. Table 6 presents

the results.

18

As was the case when examining JOBS Act accommodations and underpricing in the subset

of EGC firms in Table 3, small firms with star lead underwriters and VC backing tend to have

more underpricing in the larger sample of IPO firms. As shown in column 2, EGC firms have

underpricing of about 6% before controlling for their risk disclosures. In the column 3, we see that

both riskfactor1 and riskfactor2 are associated with more IPO underpricing, but the length of the

risk factor section is not, suggesting that the the type of risk disclosed – not the quantity – is what

matters. Controlling for the type of industry, a one-percent-increase in the first (second) principal

component is associated with an increase in underpricing of about 8% (5%). Though the types of

disclosed risks can explain a significant amount of underpricing, EGCs still an average first-day IPO

return of about 7%, controlling for the other variables.

Given that the type of risk disclosed in the prospectus is related to underpricing, we return

to the subset of EGC firms and examine whether there is an interaction between the JOBS Act

accommodations and disclosed risk factors. The first two columns in Table 9 provide results of

regressing 1st day underpricing on the JOBS Act Accommodations and the various control variables

both with and without the first two principal components of the disclosed risk factors and the

number of words in the risk factors section. There is very little change from Table 3. Moreover, the

adjusted R squared increases from 0.14 to 0.18.

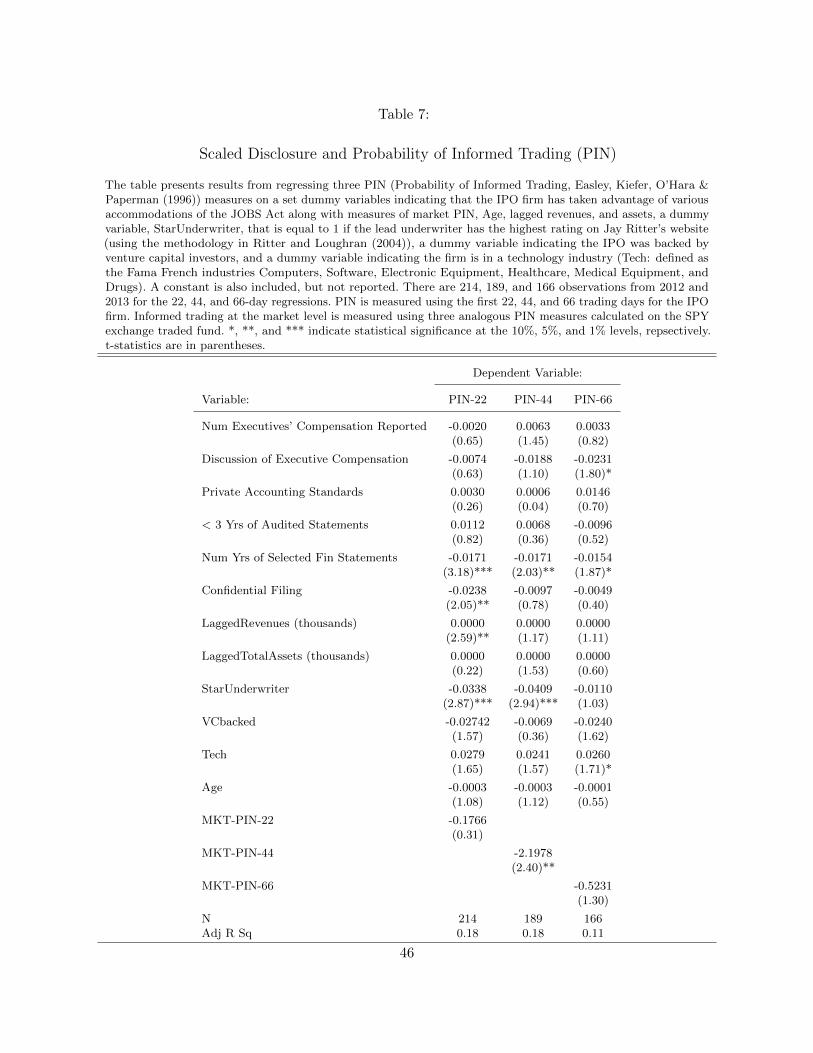

D Probability of Informed Trading

Now, we turn our attention to the impact of the JOBS Act, its disclosure provisions, and disclosed

risk factors on asymmetric information and liquidity in the secondary market immediately following

the IPO. While we focus on 66-day PIN, because it is likely to be more precisely estimated, we also

examine the impact on 22- and 44-day PIN.

Reducing the amount of information disclosed in the prospectus limits the information available

to the market and potentially increases opacity. As a result, following the IPO, there may be

more informed trading while new information production takes place. In Table 7, we find results

consistent with this story. For the subsample of EGCs, we regress each of our three our three PIN

measures (22-, 44-, and 66-day) on each of the disclosure provisions as well as age of the firm, lagged

19

revenues, lagged total assets, the star underwriter dummy, the venture capital dummy and the tech

industry dummy. Additionally, to control for changes in the general level of informed trading in the

market, we also include a measure of market pin (MKT-PIN-22, MKT-PIN-44, and MKT-PIN-66)

using data from the SPY ETF during the same window as the dependent variable is measured.

Firms who choose to disclose more years of selected financial data tend to have lower probabilities

of informed trading during the three months following the IPO. For each additional year, PIN

drops by between -0.015 and -0.017. This is statistically significant at the 1% level over the first

month, at the 5% level using over two months, and at the 10% level over a three-month window.

This is consistent with an asymmetric information story in which the reduction in information

initially allows informed investors to take advantage. Similarly, EGCs that choose to include a

detailed discussion of executive compensation in their prospectus tend to have less informed trading.

However, this result is only statistically significant over a three-month window.

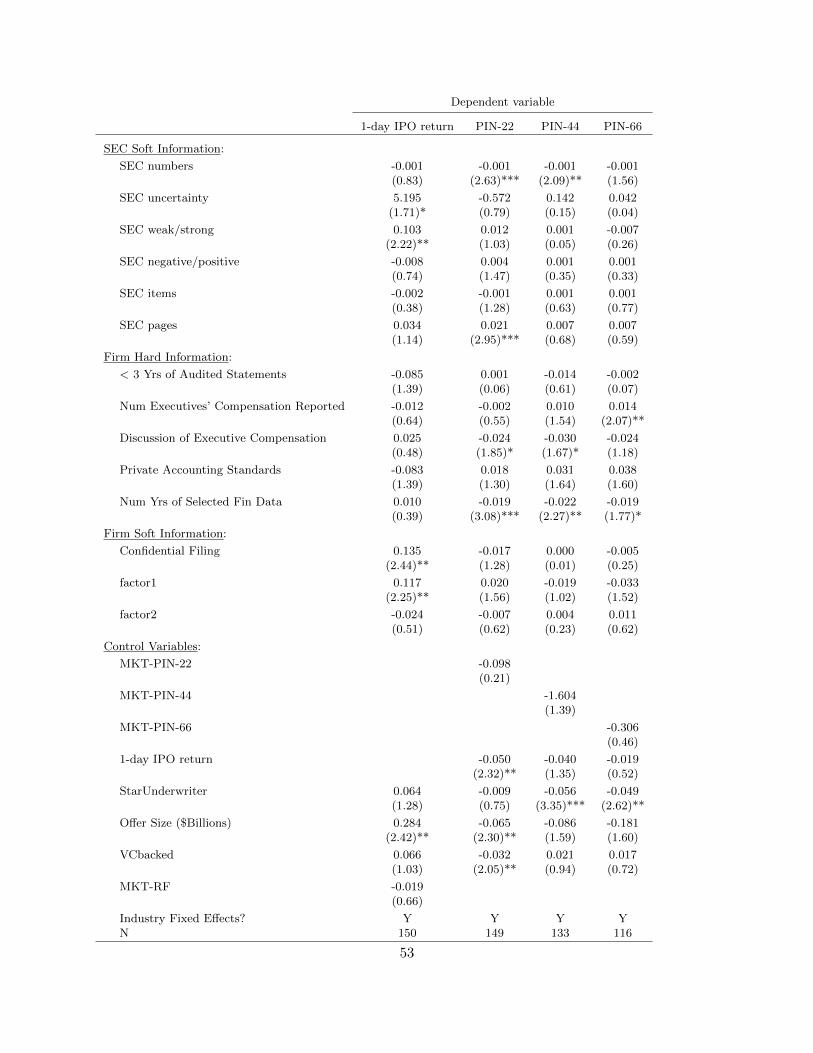

Motivated by the underpricing results, we examine the effect of disclosed risk factors on the

probability of informed trading for both EGC firms and their matched counterparts from before the

enactment of the JOBS Act. Table 8 provides the results of these regressions for the 22-, 44-, and

66-day PIN for 353 firms. Additionally, to examine whether information revealed in by the amount

of underpricing affects PIN after the JOBS Act, we interact EGC with first day underpricing. This

test is motivated by Ellul and Pagano who examine two types of private information about IPO

firms – one revealed during the IPO process and the other revealed via trading in the post-IPO,

secondary market. The independent variables are the same as those in Table 6 with the addition of

a 22-, 44-, or 66-day market PIN.

The first three columns present results for the 66-day PIN. There tends to be less informed

trading for firms with a star lead underwriter. This is consistent with the story that the underwriter

is skilled at providing information to the market. As seen in the third column, this remains even

after controlling for variation in risk factors. There is no impact of the first principal component of

the disclosed risk factors on the 66-day PIN. However, the second principal component (riskfactor2)

is negatively related. Firms disclosing more risks associated with product development and approval

and intellectual property tend to have more informed trading. Recall that firms with a higher

riskfactor2 measure had more underpricing – consistent with more uncertainty. Here, a negative

20

coefficient means a lower probability of informed trading, and thus, less informational asymmetry.

However, the interaction term shows that this effect is actually reduced after the JOBS Act. Thus,

the market interprets the disclosures differently under the new disclosure environment. In contrast

with the underpricing regressions, controlling for the other variables and interaction terms, there

is no direct treatment effect. Finally, the number of words in the disclosed risk factor section is

positively related to the probability of informed trading.

Interestingly, as shown by the interaction term between Underpricing and EGC, the information

revealed by the level of underpricing actually reduces the probability of informed trading, suggesting

that information revealed during the IPO process may substitute for information revealed via trading

in the post-IPO, secondary market. However, accounting for the interactions, and evaluating at

their means, PIN is significantly higher for EGCs than their peers, suggesting a higher degree of

information, post JOBS Act.

The final two columns provide results for 44- and 22-day pin. Results are generally similar,

though PIN is likely to be estimated with less precision. Interestingly, in the month following the

IPO, firms that had VC backing have less informed trading, though this difference disappears by

the second month. Similarly, firms with smaller revenues have more informed trading in the first

month or two of trading.

Next, we return to the subset of EGCs and examine the interaction between JOBS Act accom-

modations, disclosed risk factors, and PIN. The final two columns of Table 9 provide regressions

with and without the principal components of the risk factors. When the two principal components

and the number of words in the risk factor section are added, the adjusted R squared doubles, from

0.11 to 0.22. Moreover, the results are similar to what was found using the larger sample of IPO

firms. Namely, the second principal component has a negative coefficient, and the number of words

in the risk factor section is positively related to PIN-66. As was the case in Table 7, firms omitting a

discussion of executive compensation in their prospectus, and firms disclosing fewer years of selected

financial data tend to have more informed trading. Thus, both the JOBS Act accommodations and

the content of the risk factors section – both the type of risk factors, and the quantity of disclosure –

have an impact on the probability of informed trading immediately following the IPO.

21

E Liquidity

We have established that IPOs of EGCs are underpriced relative to their peers – some of which

is driven by differences in disclosed risk factors. Moreover, the probability of informed trading

is affected by risk disclosures and this relation changes after the JOBS Act. To the extent that

these differences are associated with an increased degree of asymmetry of information among IPO

investors, these results may show up in the secondary market in the form of larger spreads and

other information costs. To test this, we estimate measures of liquidity using TAQ data for the first

several days of trading following the IPO. We test whether there are differences in these measures

for EGC and non-EGC firms and examine the determinants.

We use TAQ data to estimate a large set of liquidity measures including effective spreads and

realized spreads. We use two weighting methods: dollar weighted (denoted with a subscript DW),

and share weighted (denoted with a subscript SW). To calculate spreads, we use three different

methods of classifying the midpoint: Lee and Ready (1991), which we denote with a subscript LR,

Ellis, Michaely and O’Hara (2000), which we denote with the subscript EMO, and Chakrabarty,

Li, Nguyen and Van Ness (2006), which we denote with the subscript CLNV.11 Table 10 presents

differences in summary statistics between EGC and non-EGC IPO firms for the first day of trading

(Panel A) and the second day (Panel B).

From Panel A, we see that on the first day of trading, spreads are generally larger for EGCs than

for their peers. By the second day, these differences are all statistically significant. Thus, on average,

there tends to be less liquidity for EGC firms, suggesting that the JOBS Act accommodations may

unintentionally play a role.

To test whether these differences in liquidity are driven by the lower disclosure standards from

the JOBS Act or other differences in EGC and non-EGC firms, we form a matched sample of firms

based on size, age, and industry and regress a subset of the liquidity measures from the first day

post-IPO on on lagged revenues, lagged R&D Expense, lagged total assets, and a dummy variable

indicating that the firm is claiming EGC status. Table 11 presents the regression results. Controlling

for these variables, there is still a significant difference in spreads in newly traded IPO firms. In

11See the appendix for a detailed description of the methodology.

22

particular, the spread is higher for EGC firms, consistent with the idea that lower IPO standards

mean higher asymmetry of information.

F Impact of SEC Comment Letters on JOBS Act IPOs

In this section, we analyze the information production role of the Securities and Exchange Commission

(SEC) during the IPO process. Specifically, we examine the impact of the information from the

SEC’s comment letters during the IPO process on firms’ underpricing and probability of informed

trading, given the interaction of the disclosure levels of hard and soft information of the IPO firm.

Draft registration statements are subject to review by the SEC in order to monitor compliance with

applicable disclosure requirements. The SEC reviews and suggests revisions of the prospectus with

the objective of increasing the overall quality of disclosure in the market. SEC comment letters and

the revised prospectus are available to investors via EDGAR before the IPO date. These comment

letters can therefore be thought of as “soft” information production by a regulator from the investors’

perspective. The role of SEC comment letters is particularly important for post JOBS Act IPOs

given the relaxed disclosure requirements of certain types of “hard” information in the prospectus.

The regulator (SEC) with its vast experience and informational advantage should therefore amend

its behavior in its review comments consistent with its objective of improving disclosure.

Thus, the soft information contained in the SEC’s comment letters should affect the firm’s

underpricing and the post-IPO probability of informed trading (PIN). We use a textual analysis

techniques in order to quantify this soft information and analyze its impact on IPO underpricing

and PIN, post JOBS Act. In particular, focusing on the first comment letter from the SEC to each

JOBS Act IPO firm in our sample, we count the number of pages, the number of numbers, the

number of words, and the number of itemized suggestions/comments from the SEC to the firm.

Additionally, using the Loughran and McDonald (2011) wordlists from Bill McDonald’s website, we

count the number of words in the comment letter that are classified as positive, negative, uncertainty,

weak modal and strong modal words. Using these categories, we form three textual measures: the

number of uncertainty words divided by total words, the number of weak modal words divided by

strong modal words, and the number of negative words divided by the number of positive words.

We hypothesize that if the SEC letters contain relatively more uncertainty words then it signifies

23

the uncertainty on the part of the regulator and hence increases the potential winner’s curse with

respect to the quality of the issue. As a result, investors should demand a premium to hold such

issue and hence higher underpricing. Similarly, more weak words relative to strong words and

negative words relative to positive words should signal an inferior quality and hence demand higher

underpricing. Post IPO information production should also depend on the nature of this public

information production.

In Table B we regress our measures of underpricing and PIN on the SEC soft information

variables as well as the firm-level measures of hard and soft information and control variables. We

find strong support for our hypotheses. The negative public signal about the quality of the issue

as proxied by weak over strong modal words has a strong positive impact on underpricing. The

coefficient is also economically meaningful: a one standard deviation increase of weak to strong

modal words increases underpricing by about 5.3%. Similarly, the frequency of uncertainty words

– our proxy for winner’s curse – also has a significant, positive impact. A one standard deviation

increase in uncertainty words over total words increases the required underpricing by about 4.7%.

The post IPO information production is also significantly increased by the amount of public

information produced by SEC letters as proxied by number of pages in the SEC comment letters.

During the first month after the IPO, the market assimilates the amount of public information

produced by SEC letters and produces additional information as measured by PIN. A one standard

deviation increase in number of pages in the SEC letter leads to a 7% increase in the probability of

informed trading (PIN) during the first month post IPO. This suggests the complementary nature of

the public information as an input to private information production by various market participants

immediately following the IPO.

5 Conclusion

The Jumpstart Our Business Startups Act was enacted to reduce the cost of going public for small

firms and encourage job creation. In this paper we evaluate the performance of the firms going

public via the JOBS Act and document their use of the act’s provisions. We find that underpricing

and post-IPO illiquidity are significantly higher for claiming firms claiming EGC status under the

24

JOBS Act relative to a set of matched peers going public before the act. Additionally, we identify

the disclosure provisions and risk factors associated with the underpricing, illiquidity, and probability

of informed trading in IPO firms. The SEC’s public signals about JOBS Act firms tend to affect

underpricing and PIN. The results point to higher degree of asymmetric information for JOBS Act

firms.

While this paper highlights negative impacts of the JOBS Act, these results do not imply that

the JOBS Act failed to help EGCs. As mentioned, there are undoubtedly significant benefits of the

JOBS Act on small firms. Whether the benefits outweigh the costs is an empirical question left for

future research.

25

References

[1] Acharya V. and L. Pedersen 2004. Asset Pricing with Liquidity Risk. Journal of Financial

Economics 77 (2005) 375–410.

[2] Amihud, Y., and H. Mendelson, 1986, ‘‘Asset Pricing and the Bid-Ask Spread,’’ Journal of

Financial Economics, 17(2), 223–249.

[3] Arosio, R., G. Giudici, and S. Paleari, 2001, “Why Do (or Did?) Internet-stock IPOs Leave So

Much Money on the Table?” Politecnico di Milano (Italy) Working Paper

[4] Balakrishnan, K., M.B. Billings, B. Kelly, and A. Ljungqvist, 2013, Shaping liquidity: On the

causal effects of voluntary disclosure. Journal of Finance, forthcoming.

[5] Baron, D., 1982, “A Model of the Demand of Investment Banking Advising and Distribution

Services for New Issues,” Journal of Finance 37, 955-976.

[6] Benveniste, L. M., and P. Spindt, 1989, ‘‘How Investment Bankers Determine the Offer Price

and Allocation of New Issues,’’ Journal of Financial Economics, 24(2), 343–361.

[7] Beatty, R.P., and I. Welch, 1996, “Issuer Expenses and Legal Liability in Initial Public Offerings,”

Journal of Law and Economics 39, 545-602.

[8] Blei, D., Ng, A., Jordan, M., 2003. Latent dirichlet allocation. the Journal of Machine Learning

Research 3, 9931022.

[9] Bradley, D.J. and B. Jordan, 2002, “Partial Adjustment to Public Information and IPO

Underpricing,” Journal of Financial and Quantitative Analysis 37, 595-616

[10] Busaba, W. Y., and C. Chang, 2002, ‘‘Bookbuilding vs. Fixed Price Revisited: The Effect of

Aftermarket Trading,’’ Working Paper, University of Minnesota, Moorhead.

[11] Carter, R.B., F.H. Dark, and A.K. Singh, 1998, “Underwriter Reputation, Initial Returns, and

the Long-run Performance of IPO Stocks,” Journal of Finance 53, 285-311.

[12] Chakrabarty, B., Li, B., Nguyen, V., Van Ness, R. A. (2007). Trade classification algorithms for

electronic communications network trades. Journal of Banking & Finance, 31(12), 3806-3821.

26

[13] Chang, J., Gerrish, S., Wang, C., Boyd-Graber, J. L., Blei, D. M., 2009. Reading tea leaves:

How humans interpret topic models. In: Advances in neural information processing systems.

pp. 288296.

[14] Chaplinsky, Susan, Kathleen Weiss Hanley, and S. Katie Moon. The JOBS Act and the Costs

of Going Public. Working paper.

[15] Dambra, M., Field, L. C., Gustafson, M. (2014). The Jobs Act and IPO Volume: Evidence

that Disclosure Costs Affect the IPO Decision. Journal of Financial Economics, forthcoming.

[16] Easley, D., O’Hara, M., 2004. Information and the cost of capital. Journal of Finance 59,

1553–1583

[17] Easley, D., Kiefer, N.M., O’Hara, M., Paperman, J.B., 1996. Liquidity, information, and

infrequently traded stocks. Journal of Finance 51, 1405–1436.

[18] Easley, D., Kiefer, N.M., O’Hara, M., 1997. One day in the life of a very common stock. Review

of Financial Studies 10, 805–835.

[19] Easley, D., O’Hara, M., Paperman, J.B., 1998. Financial analysts and information based trade.

Journal of Financial Markets 1, 175–201.

[20] Easley, D., Hvidkjaer, S., O’Hara, M., 2002. Is information risk a determinant of asset returns?

Journal of Finance 57, 2185–2221.

[21] Eleswarapu, V.R., Thompson, R., Venkataraman, K., 2004. The impact of Regulation Fair

Disclosure: trading costs and information asymmetry. Journal of Financial and Quantitative

Analysis 39, 209–225.

[22] Ellis, K., Michaely, R., O’Hara, M. (2000). The accuracy of trade classification rules: evidence

from Nasdaq. Journal of Financial and Quantitative Analysis, 35(04), 529-551.

[23] Ellul,A and M Pagano 2006. IPO Underpricing and After-Market Liquidity, Review of Financial

Studies

[24] Fama, E.F., French, K.R., 1993. Common risk factors in the returns on stocks and bonds.

Journal of Financial Economics 33, 3–56.

27

[25] Fama, E.F., MacBeth, J.D., 1973. Risk, return and equilibrium: empirical tests. Journal of

Political Economy 81, 607–636.

[26] Gintschel, A., Markov, S., 2004. The effectiveness of Regulation FD. Journal of Accounting

and Economics 37, 293–314.

[27] Gomes, A., Gorton, G., Madureira, L., 2008. SEC Regulation Fair Disclosure, information, and

the cost of capital. Journal of Corporate Finance

[28] Habib, M. and A. Ljungqvist, 2001, “Underpricing and Entrepreneurial Wealth Losses: Theory

and Evidence,” Review of Financial Studies 14, 433-458.

[29] Hanley, K. W., Hoberg, G. (2010). The information content of IPO prospectuses. Review of

Financial Studies, 23(7), 2821-2864.

[30] Hanley, K. W., Hoberg, G. (2012). Litigation risk, strategic disclosure and the underpricing of

initial public offerings. Journal of Financial Economics, 103(2), 235-254.

[31] Heflin, F., Subramanyam, K.R., Zhang, Y., 2003. Regulation FD and the financial information

environment: early evidence. Accounting Review 78, 1–37.

[32] Hoberg, G., Phillips, G. (2010). Product market synergies and competition in mergers and

acquisitions: A text-based analysis. Review of Financial Studies, 23(10), 3773-3811.

[33] Holden, C. W., Jacobsen, S. (2014). Liquidity measurement problems in fast, competitive

markets: expensive and cheap solutions. The Journal of Finance

[34] Israelsen, R., 2014. Tell it like it is: Disclosed risks and factor portfolios. Working Paper,

Indiana University.

[35] Jegadeesh, N., Wu, D. (2013). Word power: A new approach for content analysis. Journal of

Financial Economics, 110(3), 712-729.

[36] Jorion, P., Liu, Z., Shi, C., 2005. Informational effects of Regulation FD: evidence from rating

agencies. Journal of Financial Economics 76, 309–330.

[37] Lawrence, A. (2013). Individual investors and financial disclosure. Journal of Accounting and

Economics, 56(1), 130-147.

28

[38] Lee, C.M.C., Ready, M.J., 1991. Inferring trade direction from intraday data. Journal of Finance

46, 733–746.

[39] Li, F. (2008). Annual report readability, current earnings, and earnings persistence. Journal of

Accounting and economics, 45(2), 221-247.

[40] Litzenberger, R.H., Ramaswamy, K., 1979. The effect of personal taxes on dividends and capital

asset prices. Journal of Financial Economics 7, 163–195.

[41] Ljungqvist Alexander 2007. IPO Underpricing: A Survey. Handbook in Corporate Finance:

Empirical Corporate Finance. B. Espen Eckbo, ed.

[42] Loughran, T., McDonald, B. (2011). When is a liability not a liability? Textual analysis,

dictionaries, and 10-Ks. The Journal of Finance, 66(1), 35-65.

[43] Loughran, T., McDonald, B. (2013). IPO first-day returns, offer price revisions, volatility, and

form S-1 language. Journal of Financial Economics, 109(2), 307-326.

[44] Loughran, T., McDonald, B. (2014). Measuring readability in financial disclosures. The Journal

of Finance.

[45] Loughran, T., Ritter, J. R. (2004). Why has IPO underpricing changed over time?. Financial

management, 33(3).

[46] Merton, R., 1987. Presidential address: a simple model of capital market equilibrium with

incomplete information. Journal of Finance 42, 483–510.

[47] Ritter, J.R., 1984, “The ‘Hot Issue’ Market of 1980,” Journal of Business 57, 215-240.

[48] Ritter, J.R. and I. Welch, 2002, “A Review of IPO Activity, Pricing, and Allocations,” Journal

of Finance 57, 1795-1828.

[49] Sidhu, B., Smith, T., Whaley, R.E., 2006. Regulation fair disclosure and the cost of adverse

selection. Unpublished working paper. Vanderbilt University, Nashville, TN.

[50] Straser, V., 2002. Regulation Fair Disclosure and information asymmetry. Unpublished working

paper. University of Notre Dame, Notre Dame, IN.

29

[51] US Securities and Exchange Commission, 2012 Jumpstart Our Business ACT :

http://www.sec.gov/spotlight/jobs-act.shtml

[52] Vega, C., 2006. Stock price reaction to public and private information. Journal of Financial

Economics 82, 103–133.

[53] Vayanos D. and Wang 2012 Liquidity and Asset Returns under Asymmetric Information and

Imperfect Competition.Review of Financial Studies.

[54] You, Haifeng, and Xiao-jun Zhang, 2009, Financial reporting complexity and investor underre-

action to 10-K information, Review of Accounting Studies 14, 559586.

30

A Appendix

In this section, we include a slightly modified discussion of the 30 disclosed risk factorsextracted by Israelsen (2014) using Latent Dirichlet Allocation (Blei et al., 2003) on the riskfactor section of firms’ 10-K filings from 2006-2012. These are the same factors that are extracted(out-of-sample) from each firm’s prospectus and used in this paper.

A Disclosed Risk Factors (adapted from Israelsen, 2014)

Table A lists the 20 most common words for each of the 30 extracted risk factor topics. Foreach of the 30 extracted risk factors, a name is chosen based on the words and industries mostclosely associated with these factors and based on reading through a sample of disclosuresassigned to each topic. However, it is the words that define the topics, not the title. In thissubsection, we briefly examine each of the 30 disclosed risk factors. The discussion is based onthe word distributions from Table A, on the distribution of disclosures (in the 10-Ks) acrossindustries. The extracted risk factors are listed in alphabetical order.

Accounting contains words like reporting, accounting, result, statement, material andrequire and deals generally with the risk that statements may be incorrect. It is most likely tobe disclosed in the 10-K in industries such as “measuring and control equipment” (LabEq),“Recreation” (Toys), and “Business Services” (BusSv) as well as firms that are not easilyclassified into an industry (Other). Industries that are unlikely to disclose this risk in their10-K are “Agriculture” (Agric), “Coal” (Coal), and “Utilities” (Util).

Competition contains words associated with competition or product market competitionlike company, competition, compete, market, product and services. It is most commonly disclosedin industries where product market competition is most likely, such as “Textiles” (Txtls),“Candy & Soda” (Soda), “Beer & Liquor” (Beer), and “Food Products” (Food). Industriesthat are least likely to disclose competition risk in their 10-Ks are industries in which thereare larger barriers to entry such as “Petroleum and Natural Gas” (Oil), “Utilities” (Util),“Non-Metallic and Industrial Metal Mining” (Mines), “Precious Metals” (Gold), Coal, and“Pharmaceutical Products” (Drugs).

Contractual contains words associated with contract risk such as agreement, contract,terminate, terminate, obligation, and renew. This risk is commonly disclosed in firms 10-Ksin industries that rely on government contracts such as “Defense” (Guns), “Restaurants,Hotels, Motels” (Meals), Coal, and the “Aircraft” (Aero). At the other extreme are industrieslike “Banking” (Bank), “Medical Equipment” (MedEq), “Measuring and Control Equipment”(LabEq) and Gold.

Costs contains words associated with the risk that input prices may change such as costs,increase, labor, equipment, adversely, and affect. This risk is commonly disclosed in 10-Ks inindustries such as “Transportation” (Trans), “Shipbuilding, Railroad Equipment” (Ships),Aero, “Construction” (Cnstr), and Guns . At the other extreme are industries like “Banking”(Bank), “Medical Equipment” (MedEq), “Measuring and Control Equipment” (LabEq) andGold.

Credit contains words associated with credit or the ability to raise capital such as credit,debt, ability, capital, additional, and require. This risk is the most prevalent in industries like

31

Fun, FabPr, Txtls, and Coal. The industries least likely to disclose Credit risk are Comps,MedEq, Insur, Banks, and Drugs.

Demand contains words associated with changes in demand or the economic environmentsuch as economic, conditions, affect, result, customer, and demand. This is most commonlydisclosed in the 10-K in industries with seasonal or fluctuating demand such as Smoke. Meals,Clths, Rtail, Beer. Industries with inelastic demand such as Oil, MedEq, Hlth, and Drugsare less likely to disclose this risk. Gold is the industry least likely to disclose Demand risk.

Disclosure contains words such as risk, statement, forward, looking, uncertainty. Thisrisk is most commonly included in the 10-K as a disclaimer about relying on forward-lookingstatements. Industries most likely to emphasize this risk are Smoke, Soda, FabPr, Rubbr, andBooks. At the other extreme lie Telcm, Trans, MedEq, Drugs, and Coal.

Dividends contains words such as dividend, pay, distribution, capital, subsidiary. Theindustries Insur, Smoke, Banks, RlEst, and Fin are the industries most likely to discloseDividend risk in the 10-K while MedEq, Soda, Clths, LabEq, Guns are the industries leastlikely to disclose this risk.

EnviroReg contains words associated with environmental regulation or impact such asenvironmental, regulation, state, federal, permit, emission. The firms most likely to emphasizethis risk in the 10-K are those operating in industries subject to environmental regulationsuch as Coal, Gold, Util, and Mines. At the other extreme lie Clths, Smoke, Comps, Banks,Insur.

Financing contains words dealing with the need to acquire additional capital such asacquisition, acquire, additional, capital, operations, and need. Firms in RlEst, Boxes, Aero,and Mines are especially likely to disclose this risk in the 10-K, while firms in Rtail, Meals,Clths, Insur, Smoke are less likely.