Disclaimer: Forward Looking Statements - Kerry Group · other things, the ompany’s strategy,...

50

Transcript of Disclaimer: Forward Looking Statements - Kerry Group · other things, the ompany’s strategy,...

Disclaimer: Forward Looking Statements

This presentation/announcement may contain forward looking statements with projections regarding, among other things, the Company’s strategy, revenues, earnings, trading profit, trading margin, finance costs, tax rate, capital expenditure, dividends, cash flow, net debt or other financial measures, the impact of foreign exchange fluctuations, the impact of raw material fluctuations and other competitive pressures. These and other forward looking statements reflect management expectations based on currently available data.

However actual results will be influenced by, among other things, macro-economic conditions, food industry supply and demand issues, foreign exchange fluctuations, raw material and commodity fluctuations, the successful acquisition and integration of new businesses, the successful execution of business transformation programmes and other, as of today, unknown factors and therefore actual results may differ materially from these projections.

These forward looking statements speak only as of the date they were made and the Company undertakes no obligation to publicly update any forward looking statement, whether as a result of new information, future events or otherwise.

2

2015 Preliminary Statement of Results

Stan McCarthyCEO Kerry Group

Review of Business

Brian MehiganCFO Kerry Group

Financial Review

1

2

Outlook & Future Prospects

3

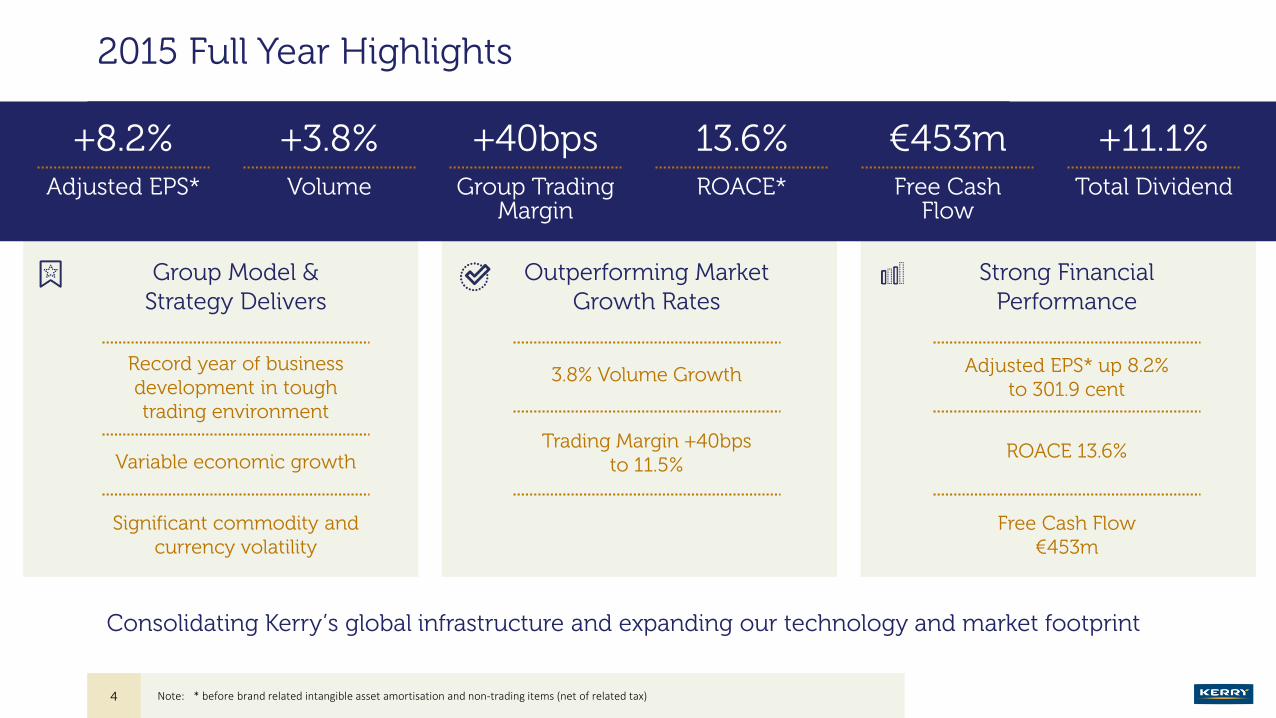

2015 Full Year Highlights

Adjusted EPS*

+8.2%Volume

+3.8%Group Trading

Margin

+40bpsROACE*

13.6%Free Cash

Flow

€453mTotal Dividend

+11.1%

Consolidating Kerry’s global infrastructure and expanding our technology and market footprint

Group Model & Strategy Delivers

3.8% Volume Growth

Trading Margin +40bps to 11.5%

Outperforming Market Growth Rates

ROACE 13.6%

Free Cash Flow €453m

Strong Financial Performance

Adjusted EPS* up 8.2% to 301.9 cent

Variable economic growth

Significant commodity and currency volatility

Record year of business development in tough trading environment

4 Note: * before brand related intangible asset amortisation and non-trading items (net of related tax)

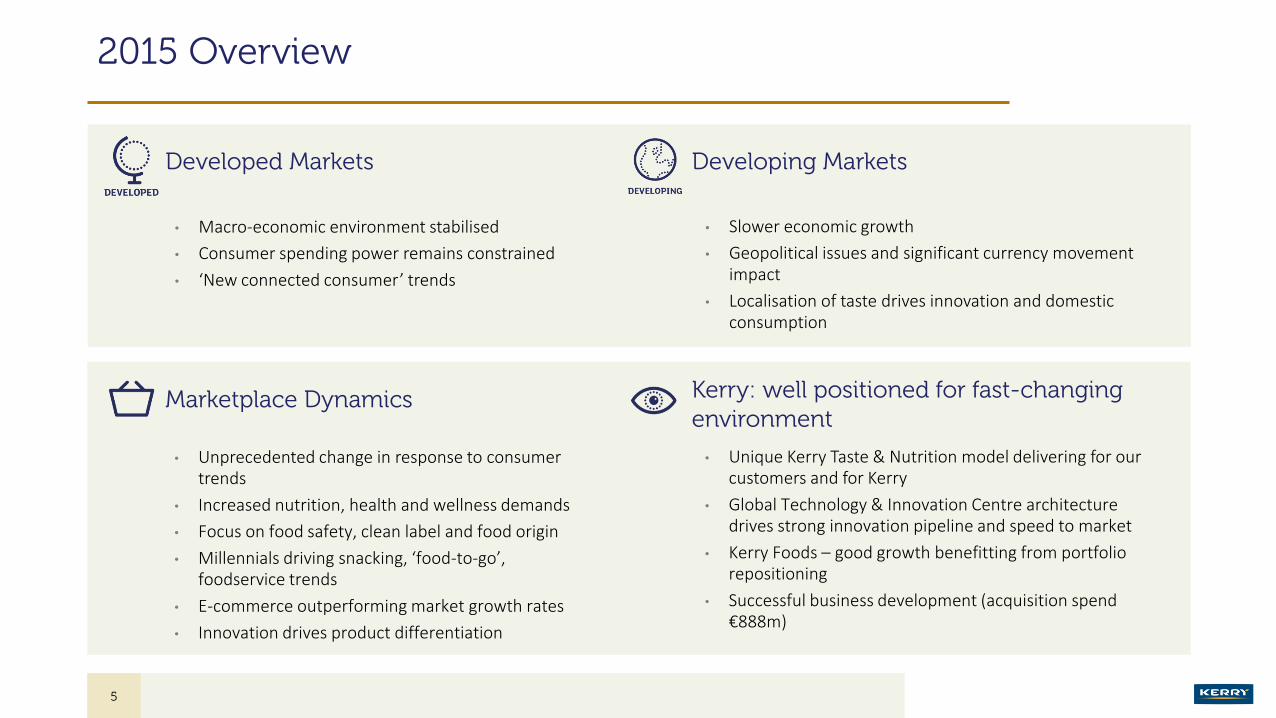

2015 Overview

Developed Markets

Marketplace Dynamics

Developing Markets

Kerry: well positioned for fast-changing environment

• Macro-economic environment stabilised

• Consumer spending power remains constrained

• ‘New connected consumer’ trends

• Unprecedented change in response to consumer trends

• Increased nutrition, health and wellness demands

• Focus on food safety, clean label and food origin

• Millennials driving snacking, ‘food-to-go’, foodservice trends

• E-commerce outperforming market growth rates

• Innovation drives product differentiation

• Slower economic growth

• Geopolitical issues and significant currency movement impact

• Localisation of taste drives innovation and domestic consumption

• Unique Kerry Taste & Nutrition model delivering for our customers and for Kerry

• Global Technology & Innovation Centre architecture drives strong innovation pipeline and speed to market

• Kerry Foods – good growth benefitting from portfolio repositioning

• Successful business development (acquisition spend €888m)

5

Revenue and Margin Overview

€6,105mVolume +3.8%

Margin +40bps

Group

€4,716mVolume +4.0%

Margin +40bps

Taste & Nutrition

€1,476mVolume +3.0%

Margin +20bps

Consumer Foods

6

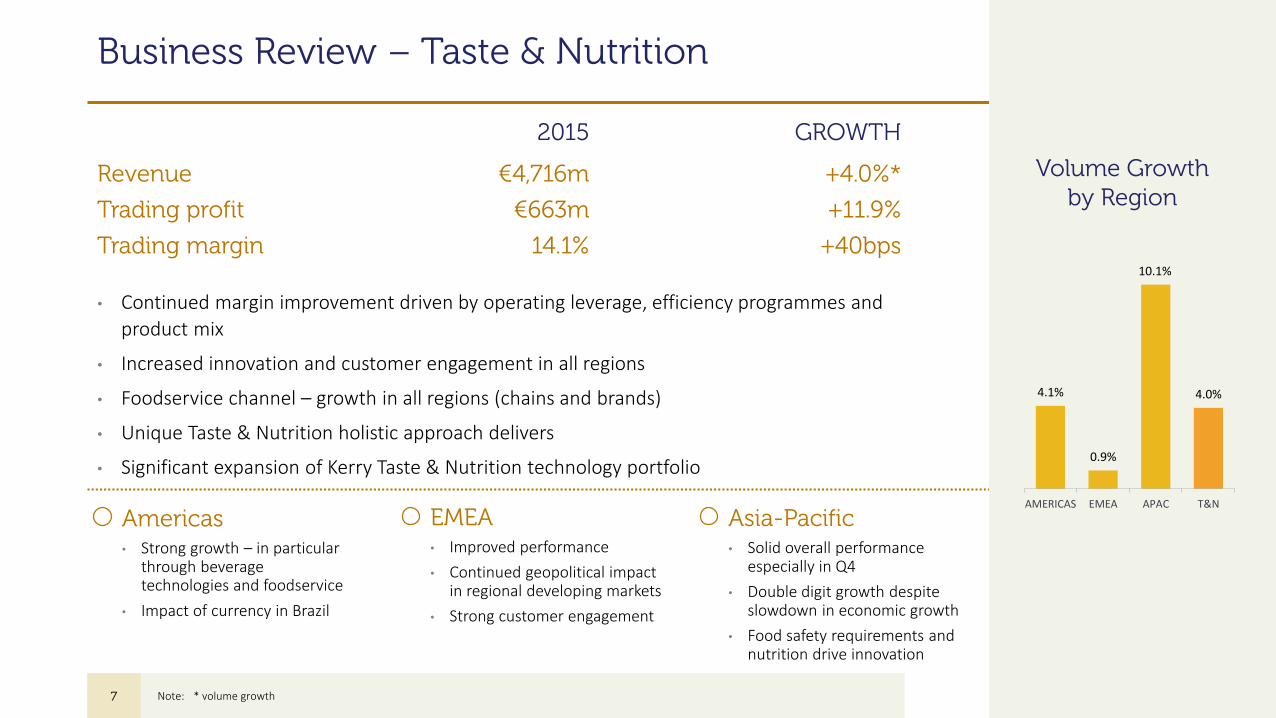

Business Review – Taste & Nutrition

• Continued margin improvement driven by operating leverage, efficiency programmes and

product mix

• Increased innovation and customer engagement in all regions

• Foodservice channel – growth in all regions (chains and brands)

• Unique Taste & Nutrition holistic approach delivers

• Significant expansion of Kerry Taste & Nutrition technology portfolio

2015 GROWTH

Revenue €4,716m +4.0%*

Trading profit €663m +11.9%

Trading margin 14.1% +40bps

Americas EMEA Asia-Pacific

4.1%

0.9%

10.1%

4.0%

AMERICAS EMEA APAC T&N

Volume Growth by Region

7

• Strong growth – in particular through beverage technologies and foodservice

• Impact of currency in Brazil

• Improved performance

• Continued geopolitical impact in regional developing markets

• Strong customer engagement

• Solid overall performance especially in Q4

• Double digit growth despite slowdown in economic growth

• Food safety requirements and nutrition drive innovation

Note: * volume growth

Our Taste & Nutrition Business Today

8

+3.4%Savoury & Dairy

Systems & Flavours

+8.6%Beverage Systems

& Flavours

(1.4%)Cereal & Sweet

Systems & Flavours

+8.5%Pharma/Functional

Ingredients

Regional Ingredients

24% Beverage

18% Meats

9% Dairy

9% Bakery

6% Cereal & Bars

6% Soups, Sauces & Dressings

5% Ice-cream & Desserts

5% Prepared Meals & Side

Dishes

5% Savoury Snacks

5% Pharma

4% Confectionery

2% Appetisers

2% Others

End Use MarketTechnology

Year On Year Volume Growth Revenue By End Use Market

Developed 74%

Developing 26%

50% 33% 17%

Americas EMEA Asia-Pacific

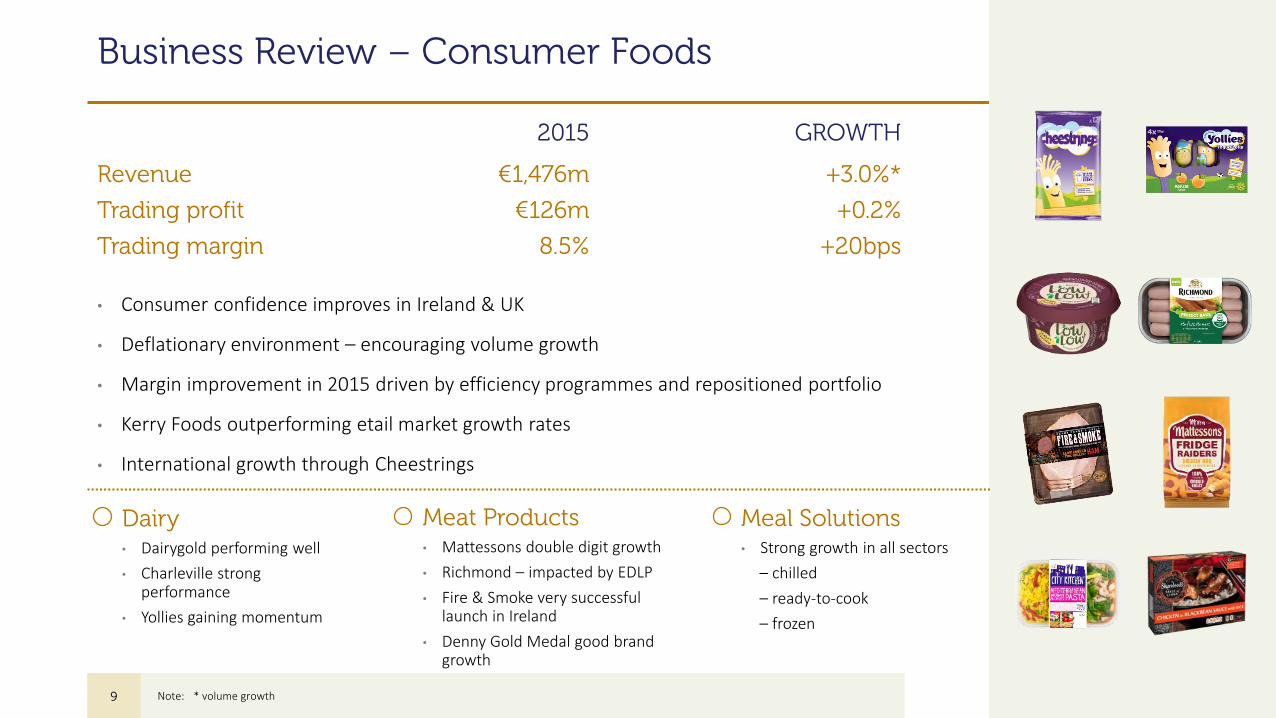

Business Review – Consumer Foods

• Consumer confidence improves in Ireland & UK

• Deflationary environment – encouraging volume growth

• Margin improvement in 2015 driven by efficiency programmes and repositioned portfolio

• Kerry Foods outperforming etail market growth rates

• International growth through Cheestrings

2015 GROWTH

Revenue €1,476m +3.0%*

Trading profit €126m +0.2%

Trading margin 8.5% +20bps

9

Dairy• Dairygold performing well

• Charleville strong performance

• Yollies gaining momentum

Meat Products• Mattessons double digit growth

• Richmond – impacted by EDLP

• Fire & Smoke very successful launch in Ireland

• Denny Gold Medal good brand growth

Meal Solutions• Strong growth in all sectors

– chilled

– ready-to-cook

– frozen

Note: * volume growth

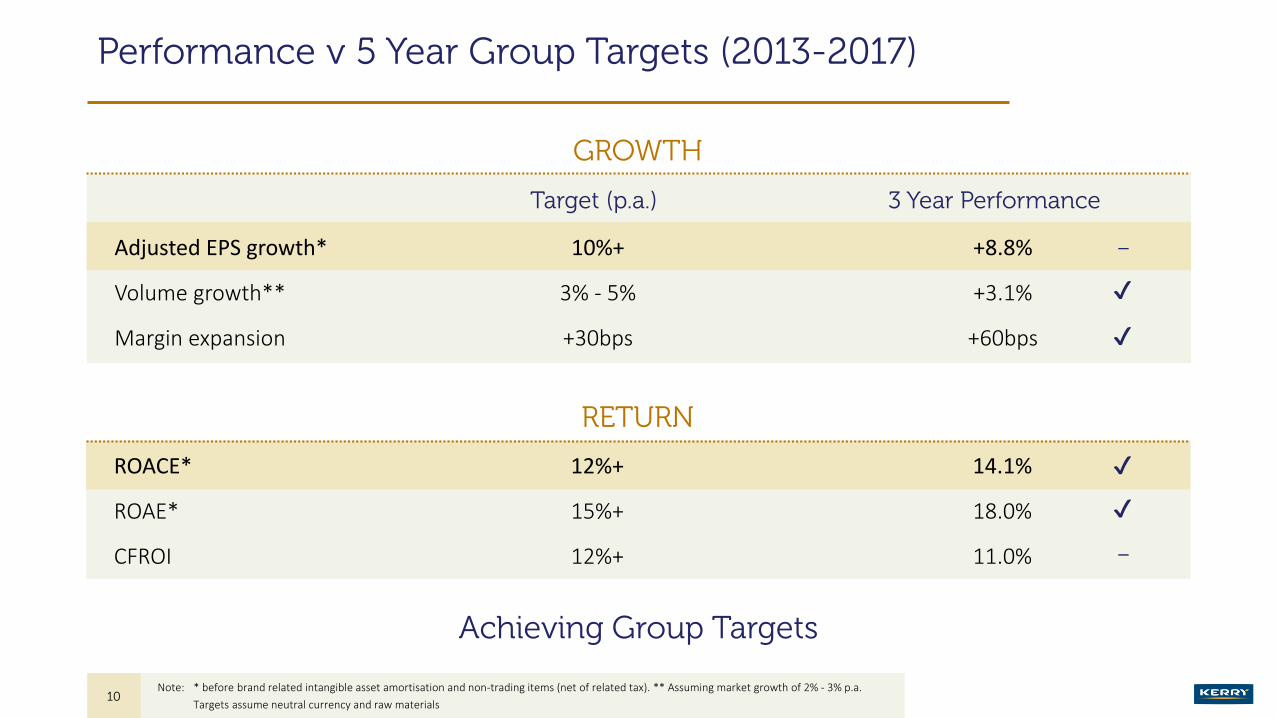

Performance v 5 Year Group Targets (2013-2017)

Target (p.a.) 3 Year Performance

Adjusted EPS growth* 10%+ +8.8%

Volume growth** 3% - 5% +3.1%

Margin expansion +30bps +60bps

RETURN

ROACE* 12%+ 14.1%

ROAE* 15%+ 18.0%

CFROI 12%+ 11.0%

Achieving Group Targets

✔

✔

✔

–

✔

10

GROWTH

Note: * before brand related intangible asset amortisation and non-trading items (net of related tax). ** Assuming market growth of 2% - 3% p.a.

Targets assume neutral currency and raw materials

–

Financial Highlights

Revenue

€6,105m

Trading Profit

€700m

Adjusted EPS

301.9

Brian MehiganCFO Kerry Group

11

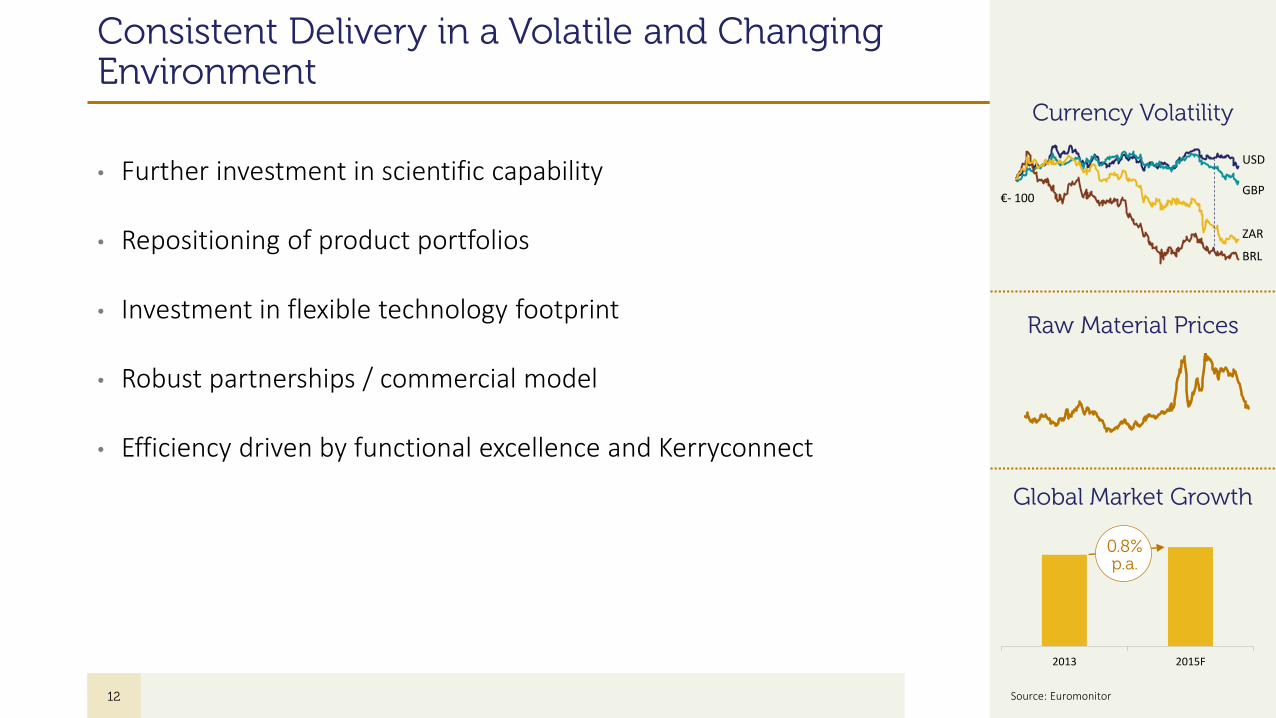

Consistent Delivery in a Volatile and Changing Environment

• Further investment in scientific capability

• Repositioning of product portfolios

• Investment in flexible technology footprint

• Robust partnerships / commercial model

• Efficiency driven by functional excellence and Kerryconnect

12

Currency Volatility

Raw Material Prices

Global Market Growth

€- 100

USD

GBP

ZAR

BRL

2013 2015F

0.8%p.a.

Source: Euromonitor

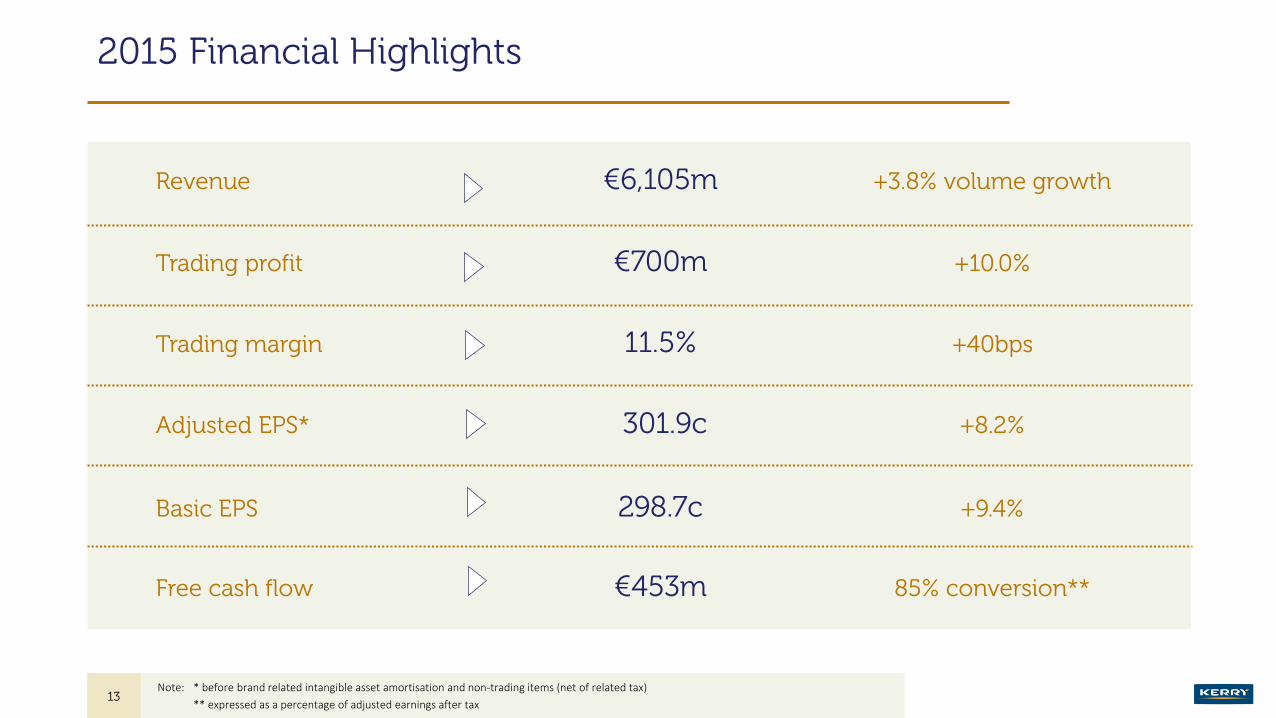

2015 Financial Highlights

+3.8% volume growth €6,105mRevenue

+10.0%€700mTrading profit

+40bps11.5%Trading margin

+8.2%301.9cAdjusted EPS*

+9.4%298.7cBasic EPS

85% conversion**€453mFree cash flow

13Note: * before brand related intangible asset amortisation and non-trading items (net of related tax)

** expressed as a percentage of adjusted earnings after tax

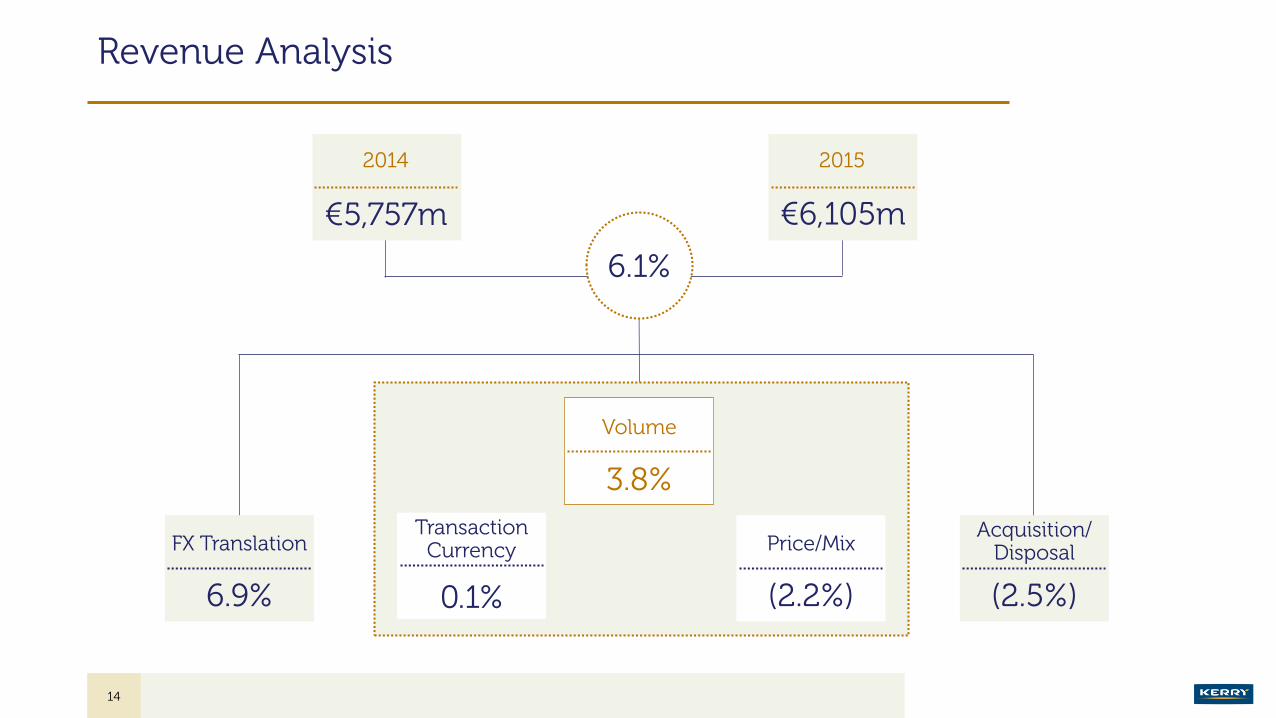

Revenue Analysis

€5,757m

2014

€6,105m

2015

6.1%

6.9%

FX Translation

0.1%

Transaction Currency

3.8%

Volume

(2.2%)

Price/Mix

(2.5%)

Acquisition/Disposal

14

Revenue – Volume Growth Ahead of Markets

€6,105

€4,716

€1,476

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Group Taste & Nutrition Consumer Foods

€m

+3.8%

+4.0%

+3.0%

Volume Growth

15

Group Volume Growth by Quarter

2.5%

2.9%

4.1%

5.7%

Q1 Q2 Q3 Q4

2014 2015

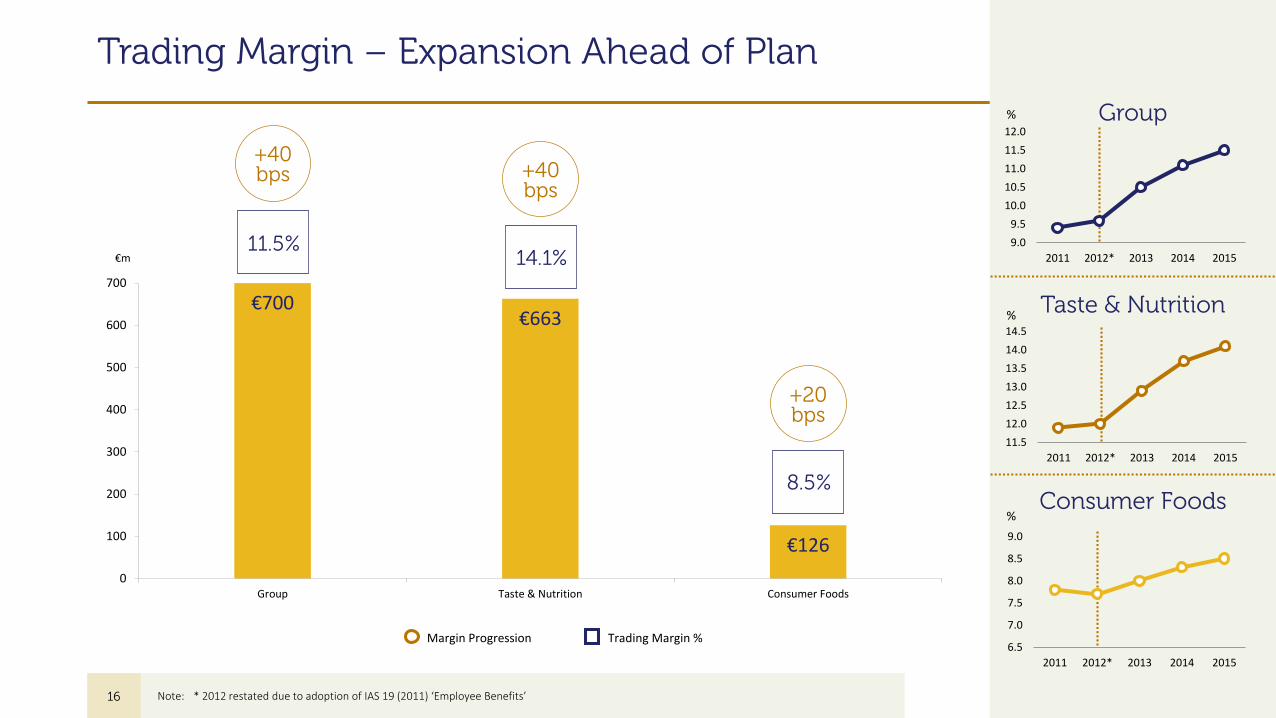

Trading Margin – Expansion Ahead of Plan

€700€663

€126

0

100

200

300

400

500

600

700

Group Taste & Nutrition Consumer Foods

€m11.5%

+40bps

14.1%

+40bps

Margin Progression Trading Margin %

16

Group

Taste & Nutrition

Consumer Foods8.5%

+20bps

9.0

9.5

10.0

10.5

11.0

11.5

12.0

2011 2012* 2013 2014 2015

6.5

7.0

7.5

8.0

8.5

9.0

2011 2012* 2013 2014 2015

11.5

12.0

12.5

13.0

13.5

14.0

14.5

2011 2012* 2013 2014 2015

%

%

%

Note: * 2012 restated due to adoption of IAS 19 (2011) ‘Employee Benefits’

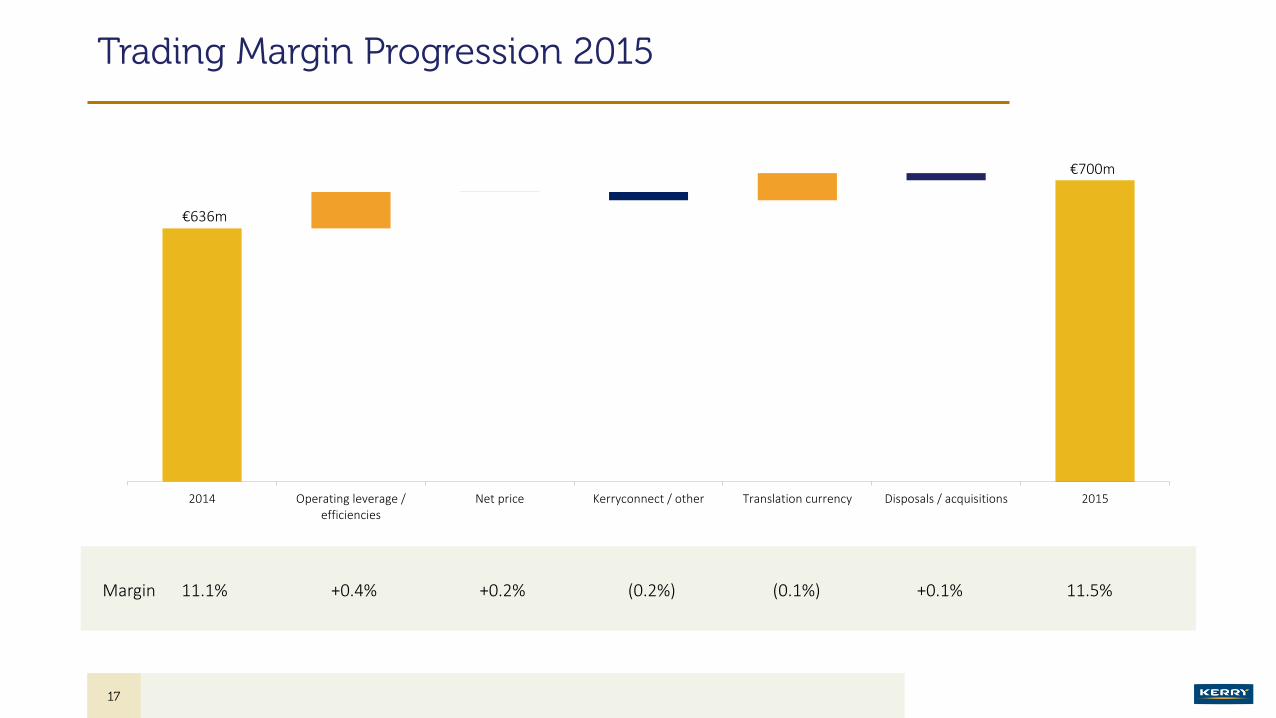

Trading Margin Progression 2015

Margin 11.1% +0.4% +0.2% (0.2%) (0.1%) +0.1% 11.5%

17

2014 Operating leverage /efficiencies

Net price Kerryconnect / other Translation currency Disposals / acquisitions 2015

€636m

€700m

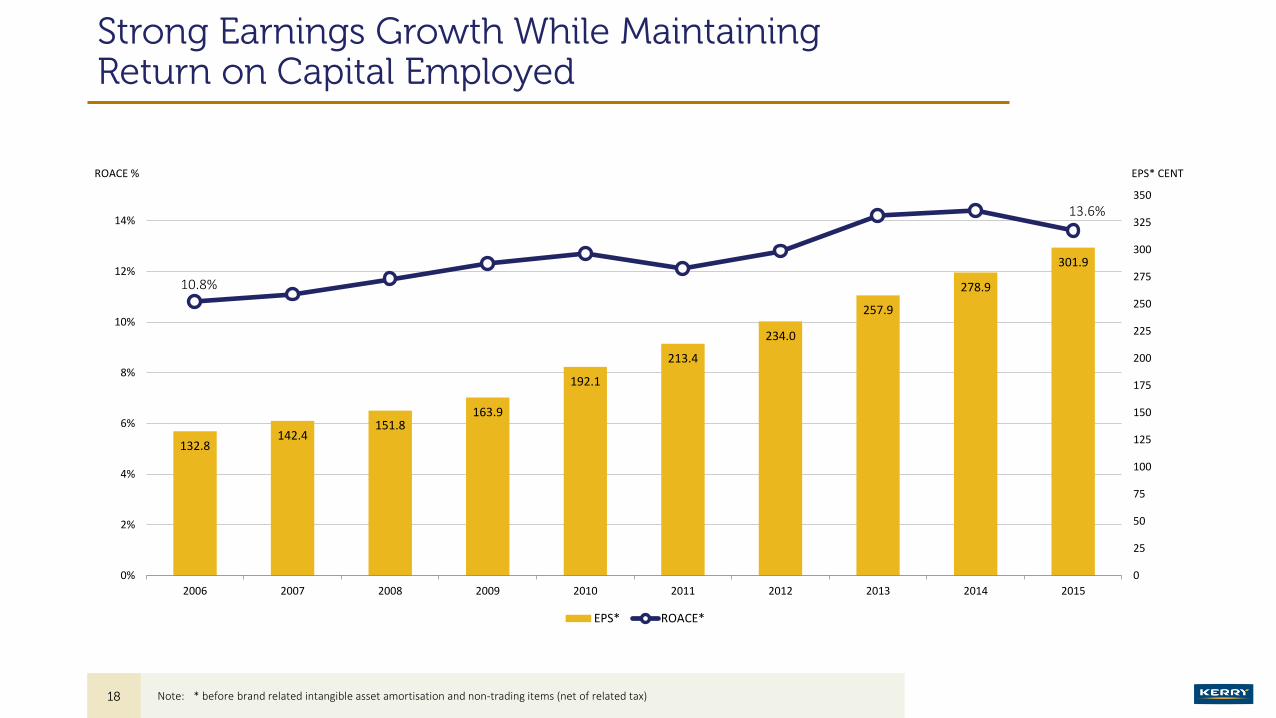

Strong Earnings Growth While Maintaining Return on Capital Employed

132.8142.4

151.8163.9

192.1

213.4

234.0

257.9

278.9

301.9

0

25

50

75

100

125

150

175

200

225

250

275

300

325

350

0%

2%

4%

6%

8%

10%

12%

14%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

EPS* ROACE*

ROACE % EPS* CENT

18 Note: * before brand related intangible asset amortisation and non-trading items (net of related tax)

13.6%

10.8%

Free Cash Flow

2015 2014

€m €m

Trading profit 700 636

Depreciation (net) 126 104

Movement in average working capital (2) (59)

Pension contributions paid less pension expense (57) (48)

Cash inflow from operations 767 633

Finance costs (47) (42)

Taxation (38) (31)

Capital expenditure (net) (229) (257)

Free cash flow 453 303

19

Financial Ratios

Banking Ratios 2015 2014

Net debt: EBITDA* 1.9x 1.6x

EBITDA: net interest* 17.3x 17.2x

Return Ratios

ROACE** 13.6% 14.4%

ROAE** 17.5% 18.6%

CFROI 11.3% 9.1%

20Note: * calculated in accordance with lender covenants

** before brand related intangible asset amortisation and non-trading items (net of related tax)

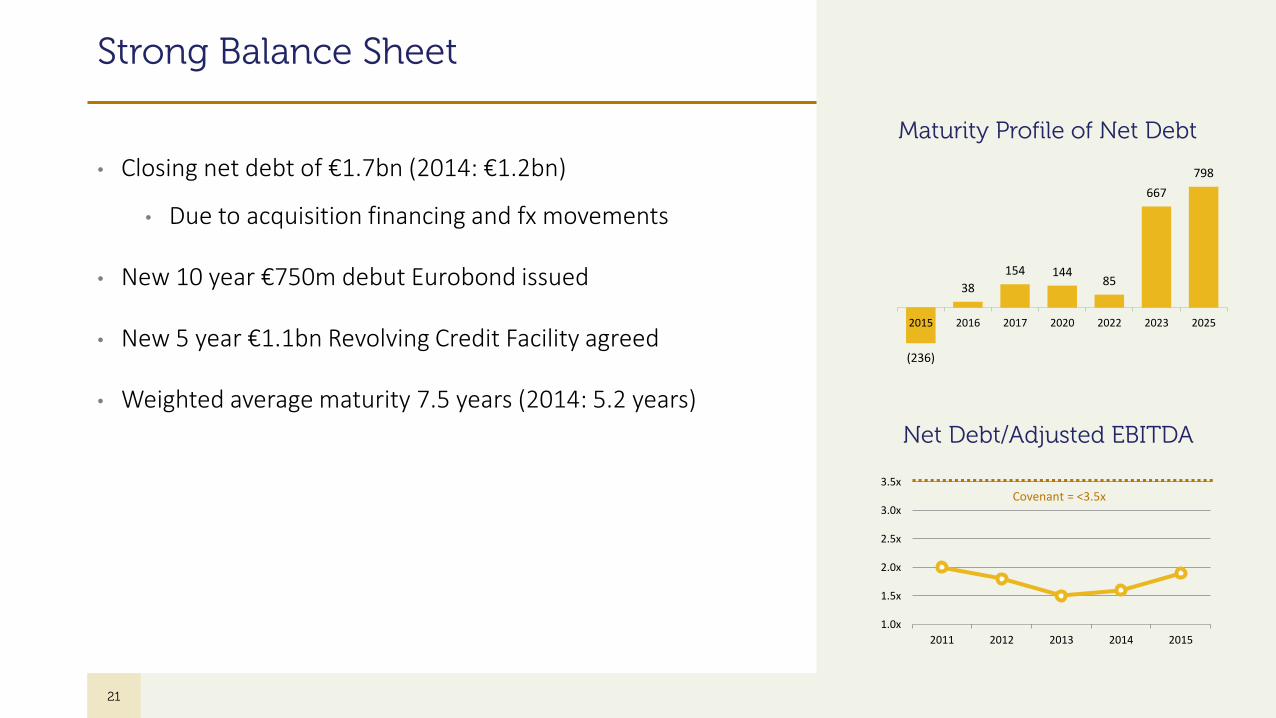

Strong Balance Sheet

• Closing net debt of €1.7bn (2014: €1.2bn)

• Due to acquisition financing and fx movements

• New 10 year €750m debut Eurobond issued

• New 5 year €1.1bn Revolving Credit Facility agreed

• Weighted average maturity 7.5 years (2014: 5.2 years)

21

Maturity Profile of Net Debt

Net Debt/Adjusted EBITDA

(236)

38

154 14485

667

798

2015 2016 2017 2020 2022 2023 2025

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

2011 2012 2013 2014 2015

Covenant = <3.5x

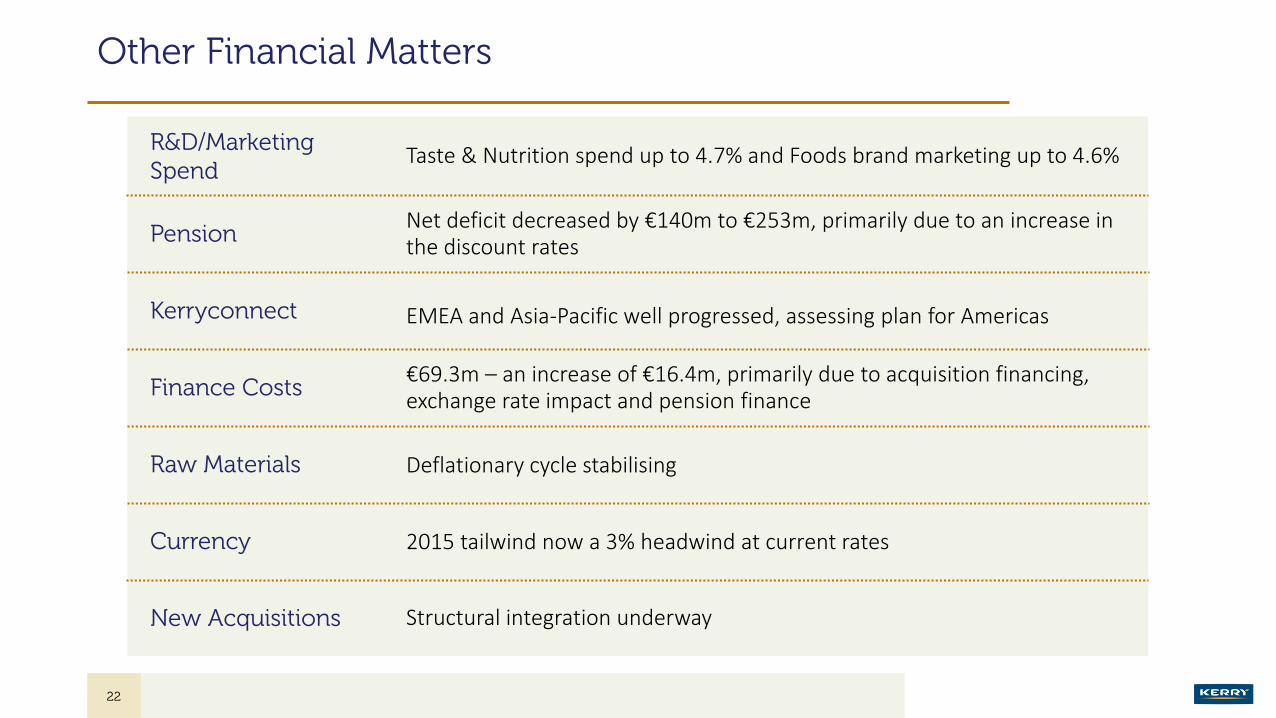

Other Financial Matters

22

R&D/Marketing Spend

Taste & Nutrition spend up to 4.7% and Foods brand marketing up to 4.6%

2015 tailwind now a 3% headwind at current rates

Net deficit decreased by €140m to €253m, primarily due to an increase in the discount rates

EMEA and Asia-Pacific well progressed, assessing plan for Americas

Deflationary cycle stabilising

Structural integration underway

€69.3m – an increase of €16.4m, primarily due to acquisition financing, exchange rate impact and pension finance

Pension

Kerryconnect

Finance Costs

Raw Materials

Currency

New Acquisitions

Outlook & Future Prospects

Stan McCarthyCEO Kerry Group

23

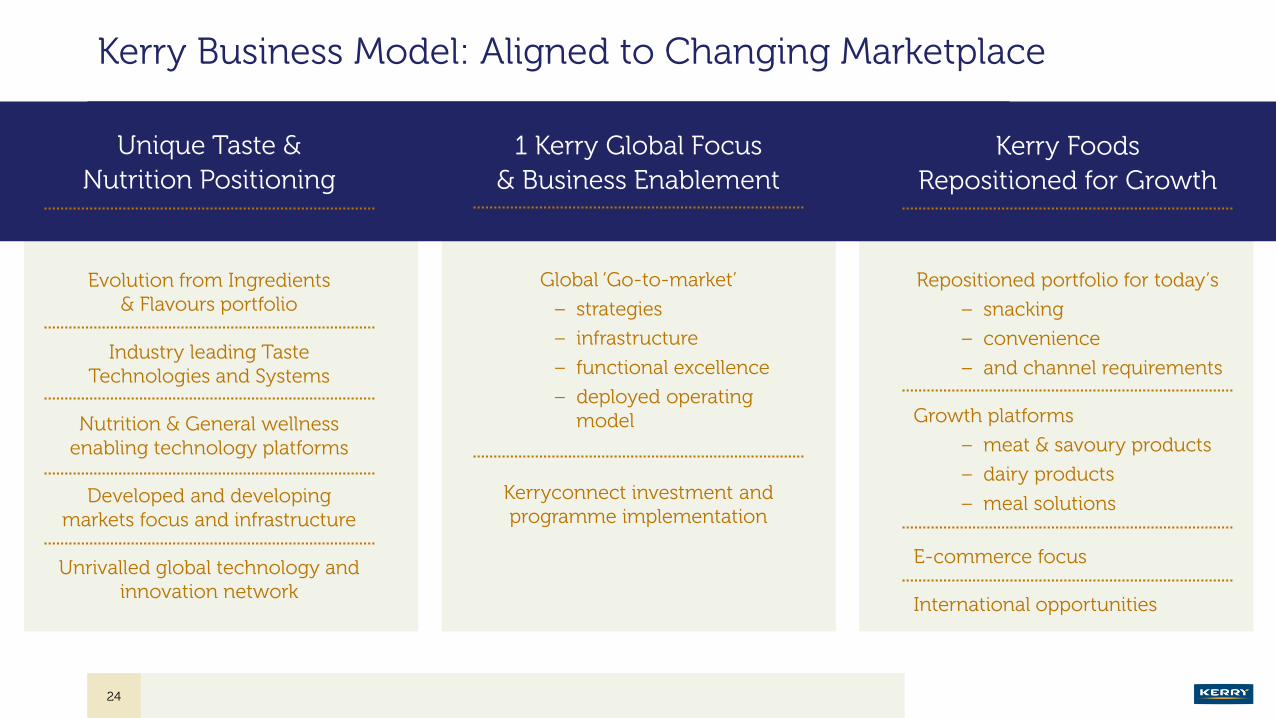

Kerry Business Model: Aligned to Changing Marketplace

Unique Taste &

Nutrition Positioning

Evolution from Ingredients & Flavours portfolio

Industry leading Taste Technologies and Systems

Nutrition & General wellness enabling technology platforms

Developed and developing markets focus and infrastructure

Unrivalled global technology and innovation network

24

1 Kerry Global Focus

& Business Enablement

Kerry Foods

Repositioned for Growth

Global ‘Go-to-market’

– strategies

– infrastructure

– functional excellence

– deployed operating model

Kerryconnect investment and programme implementation

Repositioned portfolio for today’s

– snacking

– convenience

– and channel requirements

Growth platforms

– meat & savoury products

– dairy products

– meal solutions

E-commerce focus

International opportunities

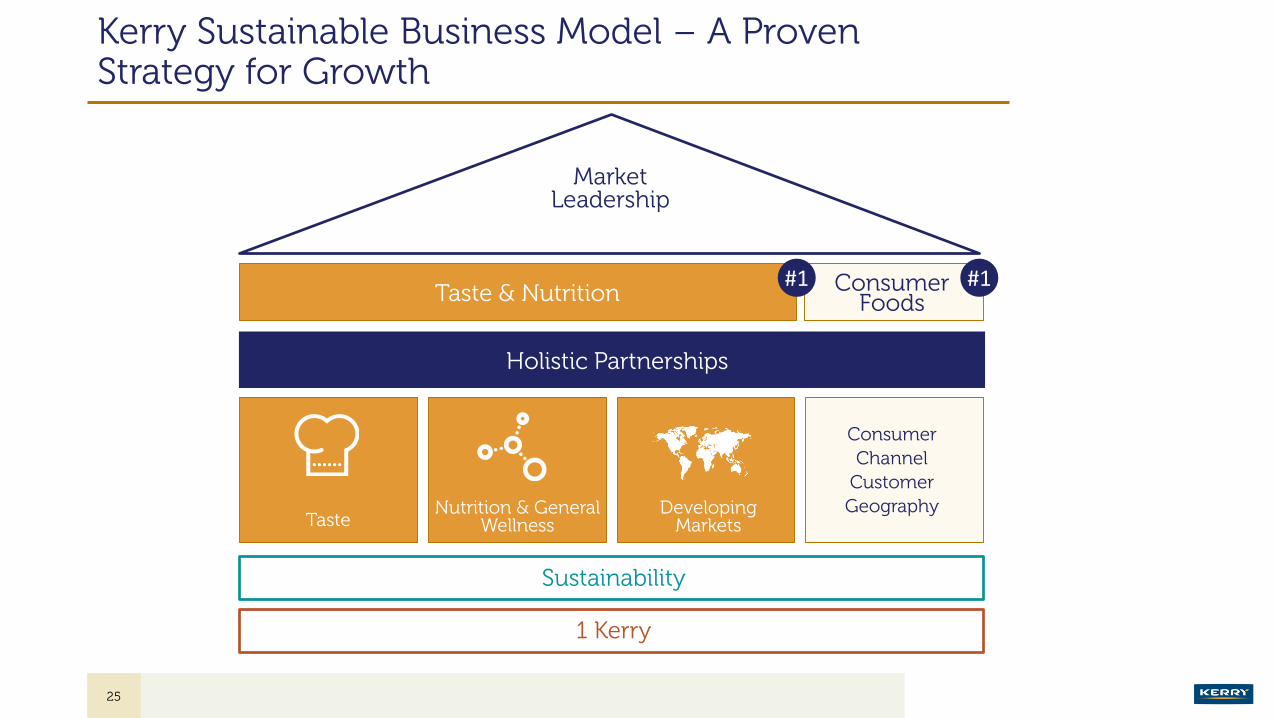

Kerry Sustainable Business Model – A Proven Strategy for Growth

25

Market Leadership

Taste & Nutrition Consumer Foods

Holistic Partnerships

Sustainability

1 Kerry

TasteNutrition & General

WellnessDeveloping

Markets

Consumer

Channel

Customer

Geography

#1 #1

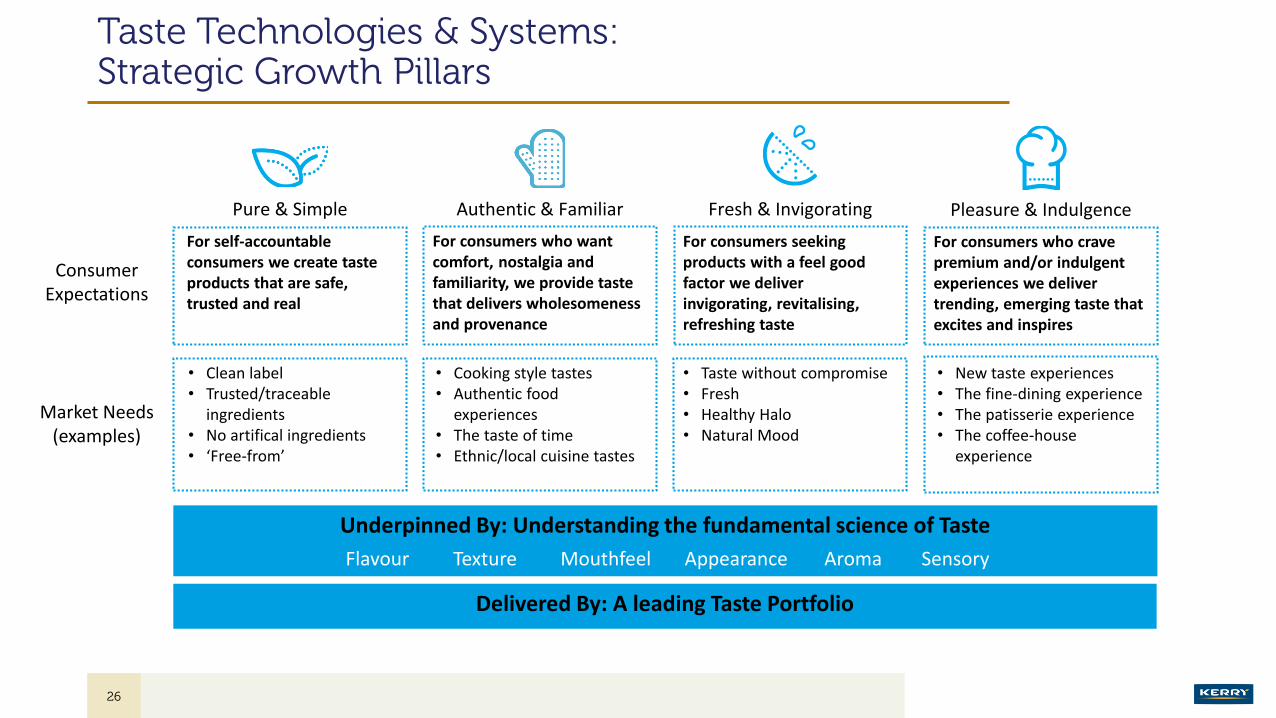

Taste Technologies & Systems: Strategic Growth Pillars

26

Underpinned By: Understanding the fundamental science of Taste

Flavour Texture Mouthfeel Appearance Aroma Sensory

Delivered By: A leading Taste Portfolio

Consumer Expectations

Market Needs(examples)

For self-accountable consumers we create taste products that are safe, trusted and real

• Clean label • Trusted/traceable

ingredients• No artifical ingredients • ‘Free-from’

Pure & Simple

For consumers who want comfort, nostalgia and familiarity, we provide taste that delivers wholesomeness and provenance

• Cooking style tastes • Authentic food

experiences• The taste of time• Ethnic/local cuisine tastes

Authentic & Familiar

• Taste without compromise• Fresh• Healthy Halo• Natural Mood

Fresh & Invigorating

For consumers seeking products with a feel good factor we deliver invigorating, revitalising, refreshing taste

• New taste experiences• The fine-dining experience• The patisserie experience• The coffee-house

experience

Pleasure & Indulgence

For consumers who crave premium and/or indulgent experiences we deliver trending, emerging taste that excites and inspires

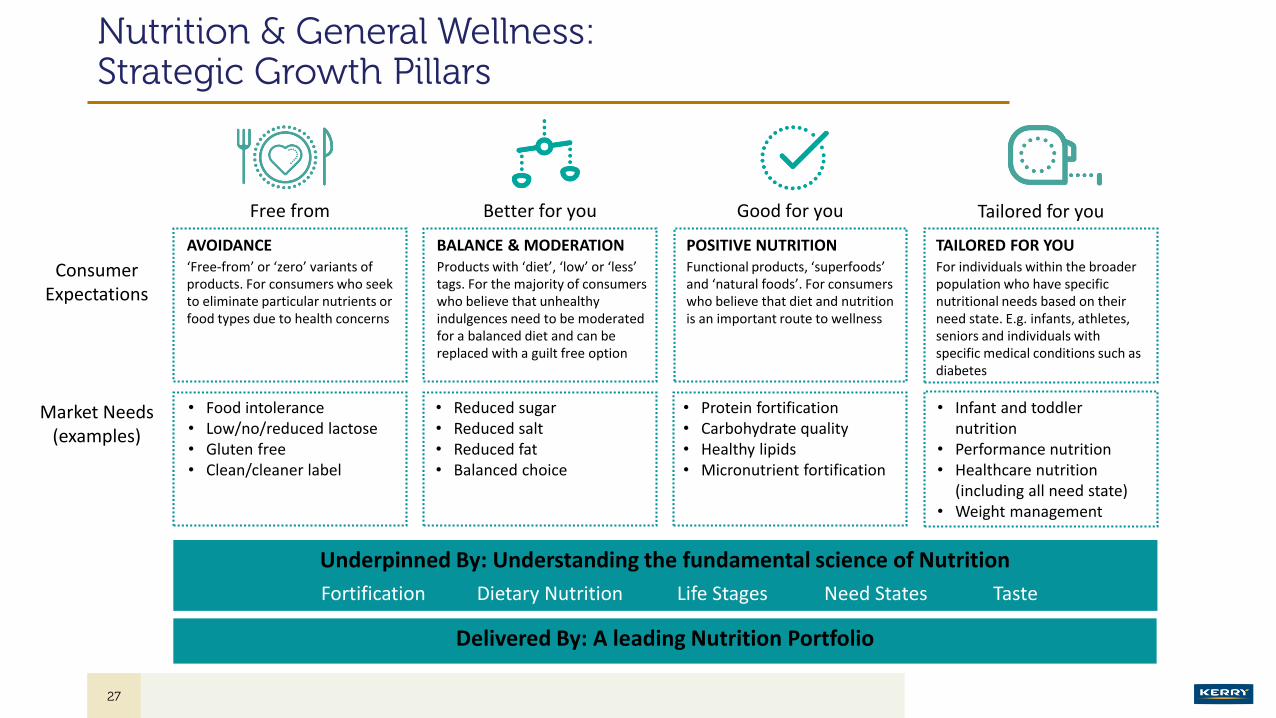

Nutrition & General Wellness: Strategic Growth Pillars

27

Underpinned By: Understanding the fundamental science of Nutrition

Fortification Dietary Nutrition Life Stages Need States Taste

Delivered By: A leading Nutrition Portfolio

AVOIDANCE‘Free-from’ or ‘zero’ variants of products. For consumers who seek to eliminate particular nutrients or food types due to health concerns

• Food intolerance• Low/no/reduced lactose• Gluten free• Clean/cleaner label

Free from

BALANCE & MODERATIONProducts with ‘diet’, ‘low’ or ‘less’ tags. For the majority of consumers who believe that unhealthy indulgences need to be moderated for a balanced diet and can be replaced with a guilt free option

• Reduced sugar• Reduced salt• Reduced fat• Balanced choice

Better for you

• Protein fortification• Carbohydrate quality• Healthy lipids• Micronutrient fortification

Good for you

• Infant and toddler nutrition

• Performance nutrition• Healthcare nutrition

(including all need state)• Weight management

Tailored for you

POSITIVE NUTRITIONFunctional products, ‘superfoods’ and ‘natural foods’. For consumers who believe that diet and nutrition is an important route to wellness

TAILORED FOR YOUFor individuals within the broader population who have specific nutritional needs based on their need state. E.g. infants, athletes, seniors and individuals with specific medical conditions such as diabetes

Consumer Expectations

Market Needs(examples)

Taste & Nutrition: Foodservice Growth Strategies

28

Trends Driving Foodservice Traffic

• Foodservice has grown at three times the pace of retail (+3.0% v +1.0% 2013-2015)

• Foodservice has overtaken retail as the No.1 channel for food and beverage sales in the U.S.

• Growth across all markets – in particular developing markets

• Kerry expertise across all channels, menus and ‘day-parts’

• Brand and Channel strategies

• Leveraging Kerry’s:

Beverage | Dairy | Meat |Nutritional

Chains

Restaurants

C-Stores

Fast Casual

Bars

HospitalityTaste Technologies & Delivery Systems

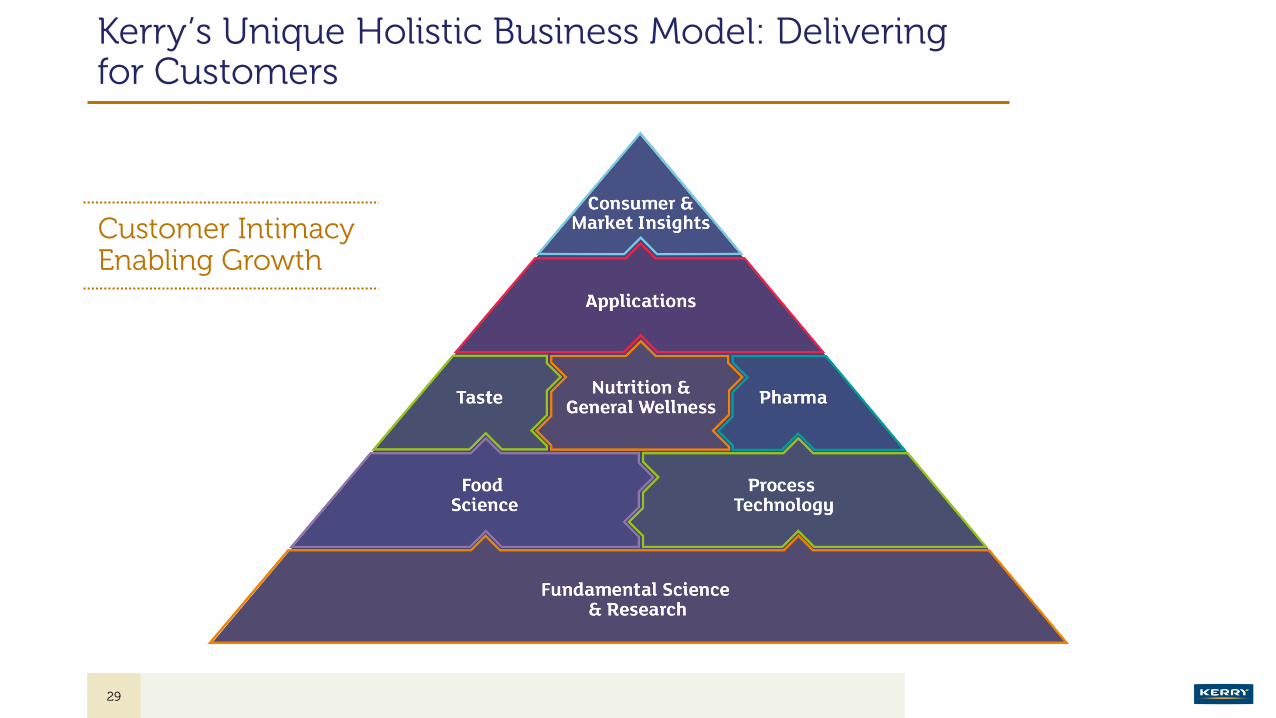

Kerry’s Unique Holistic Business Model: Delivering for Customers

29

Customer Intimacy Enabling Growth

Kerry Case Study:The Industry’s Broadest Portfolio of Beverage Solutions

30

Taste

Natural Flavours

Natural Extracts

– Citrus

– Vanilla

– Cocoa

– Coffee

– Botanicals

Taste Enhancers

Functional & Nutritional Ingredients

Enzymes

Foaming Systems

Proteins

Fibre

Emulsifiers & texturants

Wellmune

Brewing Ingredients

Beverage Systems

Nutritional Beverage Systems

Foodservice Beverage Systems

Dry Beverage Systems

Foodservice Automation

Aseptic Packaging

Complete Canned

Nutritional Systems

Syrups & Sauces

Smoothies & Juices

Juice Units/ Concentrates

Tea & Coffee Concentrates

Creaming & Whipping Systems

Agglomeration & Encapsulation

Complete Packaged Customised

Solutions

Kerry Foods: Growth Platforms

31

Consumer

We will use consumer-led insight & innovative

technology to develop compelling propositions that delight shoppers in our core

categories – meat, dairy and meals.

Channel

We will ensure our products are readily available to all our consumers, across all channels, when ever and

where ever they shop.

Customer

We will work collaboratively with our customers to

ensure we create products that they, and their

consumers, love to buy.

Geography

We’re committed to expanding our footprint

beyond the UK and Ireland into new markets, to

reach new consumers.

Underpinned by high performing teams

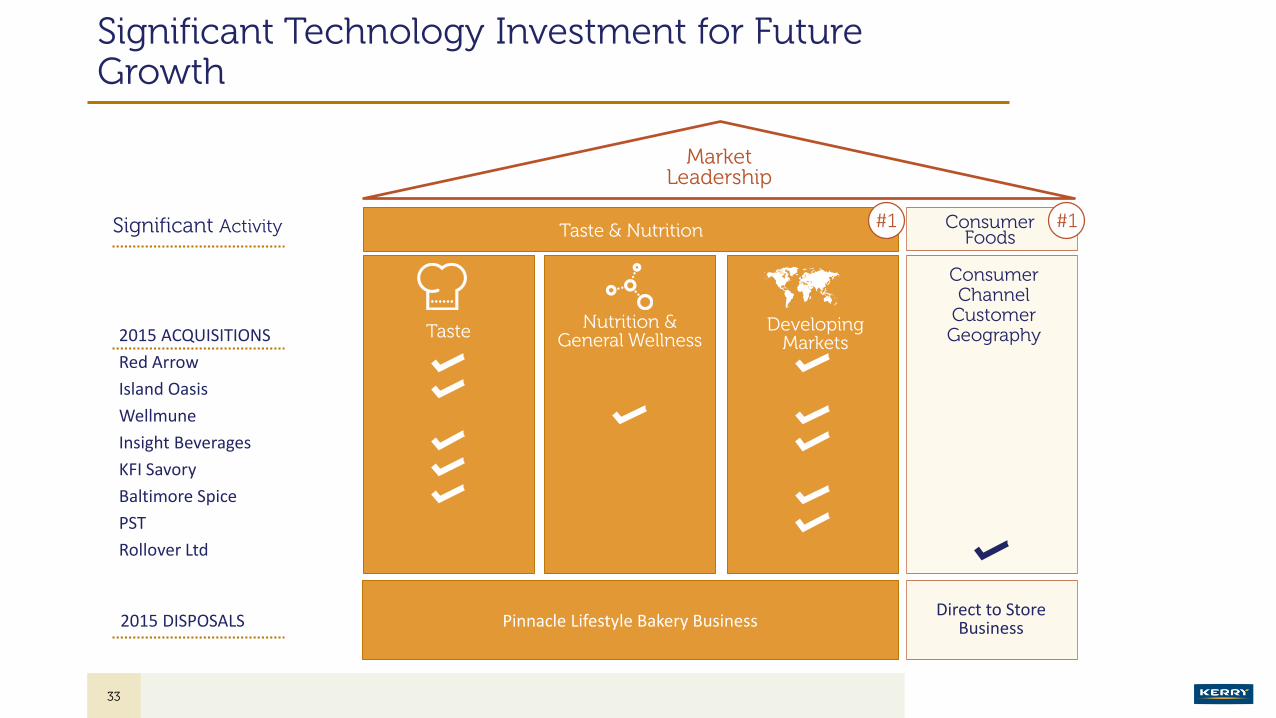

Kerry Foods’ Offerings: Differentiation Through Technology and Brand Investment

32

Kerry Foods’ Offerings

Significant Technology Investment for Future Growth

2015 ACQUISITIONS

Red Arrow

Island Oasis

Wellmune

Insight Beverages

KFI Savory

Baltimore Spice

PST

Rollover Ltd

Market Leadership

Taste & Nutrition Consumer Foods

TasteNutrition &

General WellnessDeveloping

Markets

ConsumerChannel

CustomerGeography

Significant Activity

Pinnacle Lifestyle Bakery Business2015 DISPOSALSDirect to Store

Business

#1 #1

33

Future Prospects

• Strong underlying business development momentum – benefiting from changing marketplace

• solid innovation pipeline driven by our Taste & Nutrition and General Wellness technology platforms

• Kerry Foods performing well and delivering for today’s consumer requirements

• Group will continue to invest in extending and broadening newly acquired technologies into wider Taste &

Nutrition markets

• and in organic development of Kerry’s technology and manufacturing facilities in developing markets

• supporting customer initiatives in advancing continued food safety improvements

• Group will continue to pursue strategic acquisition opportunities

We expect to achieve 6% to 10% growth in adjusted EPS* to a range of 320 to 332 cent per share in

2016 (2015: 301.9 cent) taking into account a 3% currency headwind at current exchange rates

34 Note: * before brand related intangible asset amortisation and non-trading items (net of related tax)

Appendix

Business Review: Taste & Nutrition – Americas

• Volume +4.1%, pricing (1.9%)

• Increased innovation in wellness, nutrition and snacking categories

• Taste technologies drive innovation as customers focus on evolving consumer requirements

• Good growth in foodservice channel

• Continued progress through ‘clean label’ technologies in meat and bakery sectors

• Beverage sector continued to provide good growth opportunities for Kerry solutions and brands

• LATAM impacted by significant currency devaluation – but Kerry records good growth in Mexico and Central America

• Acquisition of KFI Savory, Red Arrow, Baltimore Spice, Insight Beverages and Island Oasis – performing in line with expectations

• Solid growth through cell nutrition and excipient pharma solutions

• Acquisition of Biothera Inc’s ‘Wellmune’ business – global opportunity

2015 GROWTH

Revenue €2,308m +4.1%*

37 Note: * volume growth

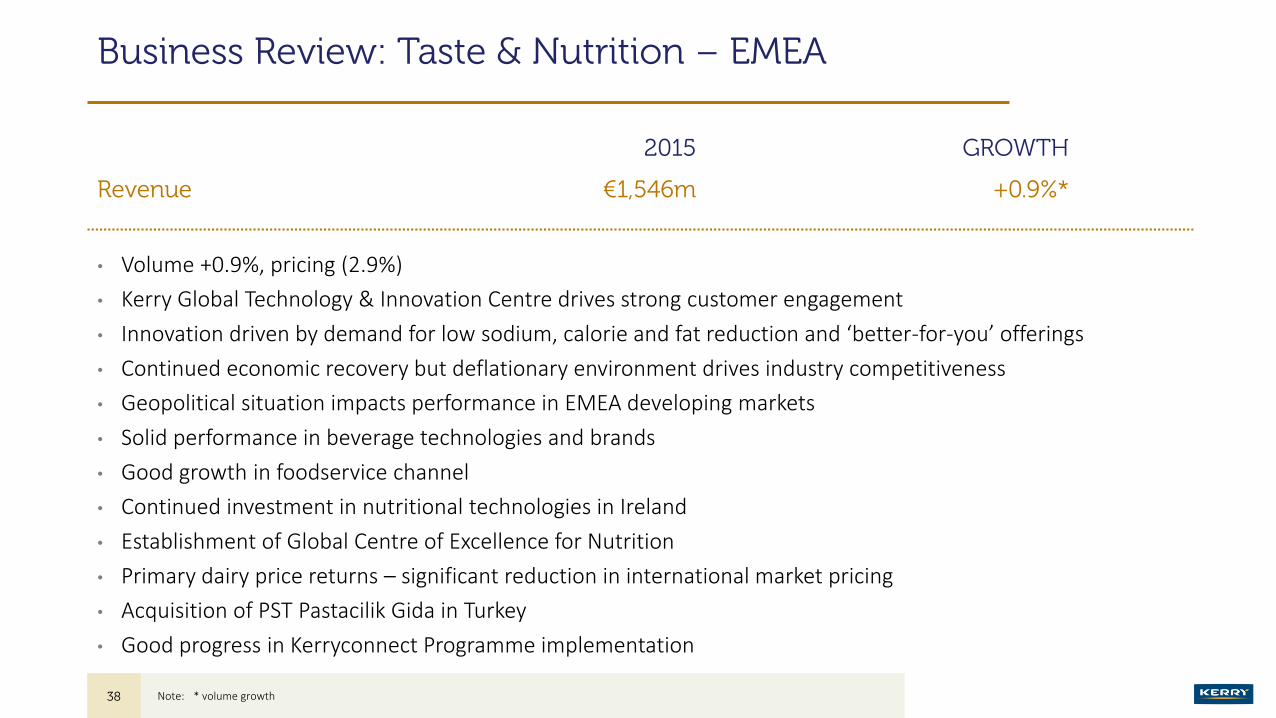

Business Review: Taste & Nutrition – EMEA

• Volume +0.9%, pricing (2.9%)

• Kerry Global Technology & Innovation Centre drives strong customer engagement

• Innovation driven by demand for low sodium, calorie and fat reduction and ‘better-for-you’ offerings

• Continued economic recovery but deflationary environment drives industry competitiveness

• Geopolitical situation impacts performance in EMEA developing markets

• Solid performance in beverage technologies and brands

• Good growth in foodservice channel

• Continued investment in nutritional technologies in Ireland

• Establishment of Global Centre of Excellence for Nutrition

• Primary dairy price returns – significant reduction in international market pricing

• Acquisition of PST Pastacilik Gida in Turkey

• Good progress in Kerryconnect Programme implementation

2015 GROWTH

Revenue €1,546m +0.9%*

38 Note: * volume growth

Business Review: Taste & Nutrition – Asia-Pacific

• Volume +10.1%, pricing (2.1%)

• Strong Kerry performance – realising benefits of Group investment

• Regional economic growth slower but urbanisation and consumer trends increase demand for innovation and speed of launch

• Dairy Taste – good growth in Indonesia, Vietnam, China and the Philippines

• Solid growth in beverage sector, in particular in foodservice channel

• Excellent growth through ‘life-stage’ nutritional solutions

• Growth of e-commerce in Chinese infant nutrition sector

• Phase 1 of major expansion of Nantong, China production facility complete

• India market development progressing well

• Sale of Pinnacle Lifestyle bakery business in Australia completed in May

2015 GROWTH

Revenue €784m +10.1%*

39 Note: * volume growth

Revenue Growth Components FY 2015

Trading Reporting Disposals/ TotalVolumes Price Currency Currency Acquisitions

Taste & Nutrition 4.0% (2.3%) 0.0% 6.9% 0.1% 8.7%

Consumer Foods 3.0% (1.9%) 0.4% 6.6% (10.3%) (2.2%)

Group 3.8% (2.2%) 0.1% 6.9% (2.5%) 6.1%

40

Trading Margin by Business

2015 2014Revenue Trading Profit Revenue Trading Profit

€m €m % €m €m %

Taste & Nutrition 4,716 663 14.1% 4,337 593 13.7%

Consumer Foods 1,476 126 8.5% 1,509 125 8.3%

Eliminations/unallocated (87) (89) – (89) (82) –

Group 6,105 700 11.5% 5,757 636 11.1%

41

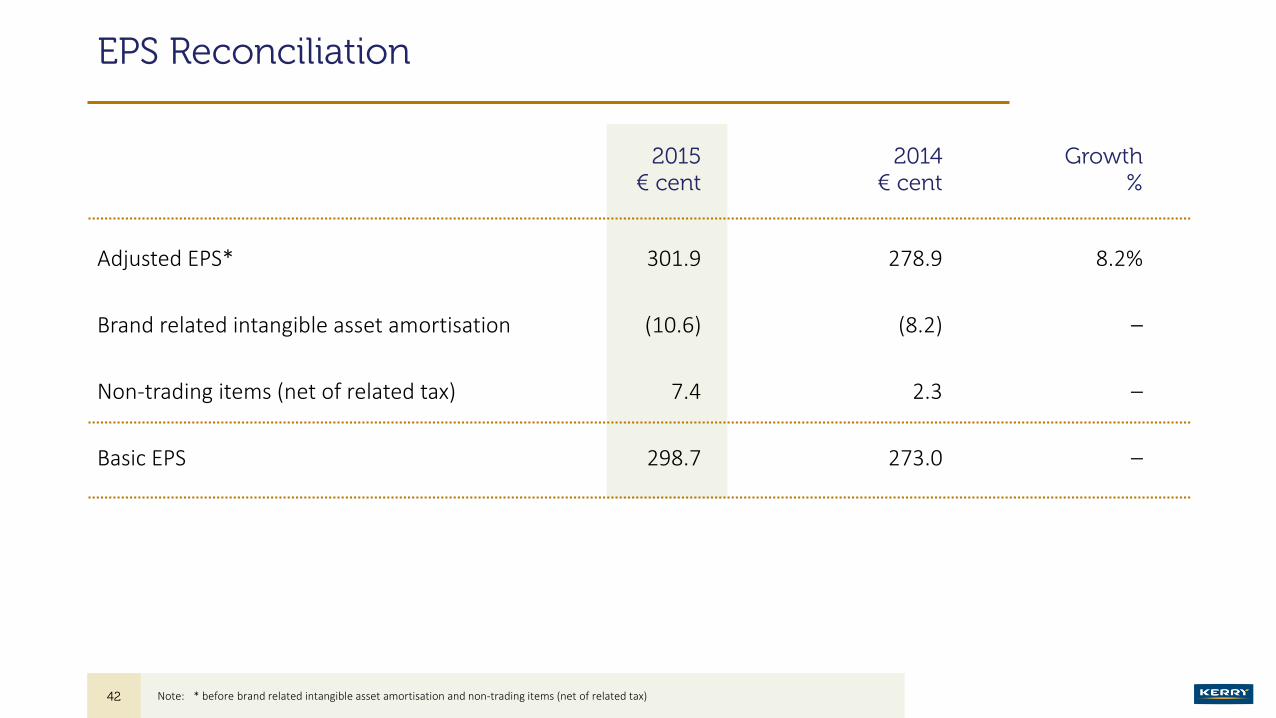

EPS Reconciliation

2015 2014 Growth€ cent € cent %

Adjusted EPS* 301.9 278.9 8.2%

Brand related intangible asset amortisation (10.6) (8.2) –

Non-trading items (net of related tax) 7.4 2.3 –

Basic EPS 298.7 273.0 –

42 Note: * before brand related intangible asset amortisation and non-trading items (net of related tax)

Free Cash Flow (€m)

Earnings conversion 74% 84% 91% 62% 85%

43

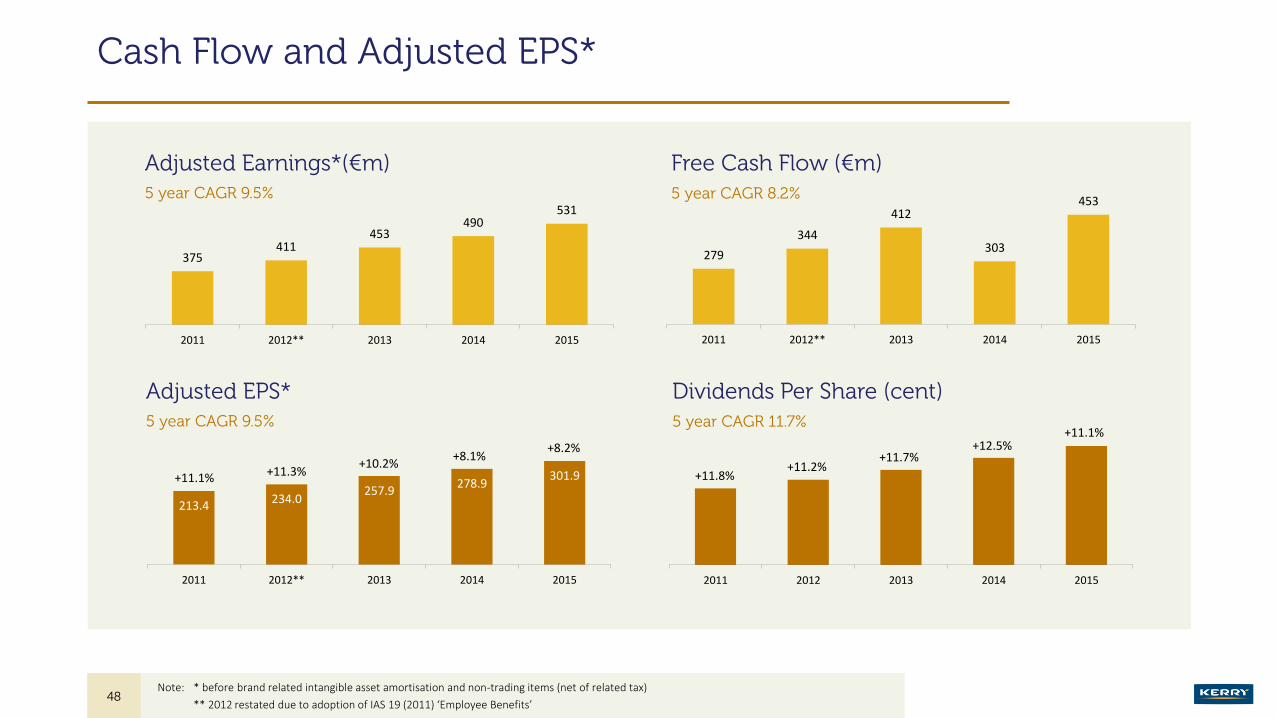

5 year free cash flow of €1.8bn

€279m

€344m

€412m

€303m

€453m

0

50

100

150

200

250

300

350

400

450

500

2011 2012 2013 2014 2015

Note: * free cash flow as a % of adjusted earnings after tax

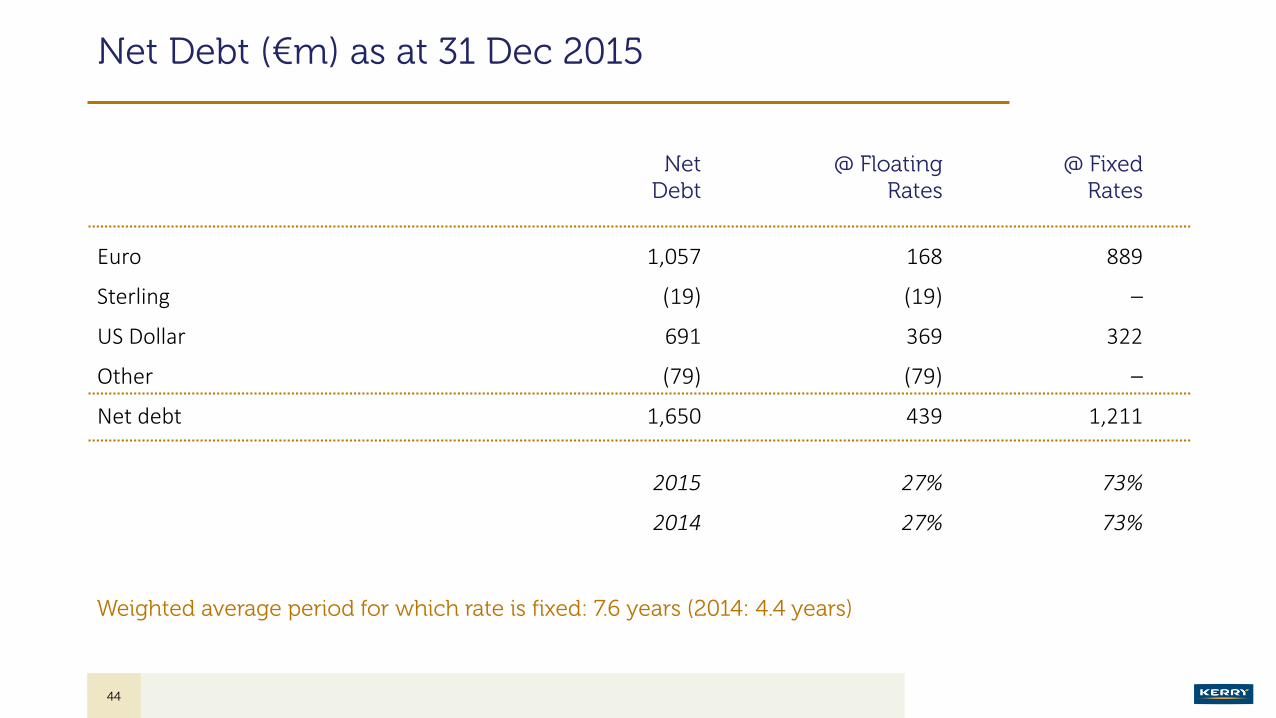

Net Debt (€m) as at 31 Dec 2015

Net @ Floating @ FixedDebt Rates Rates

Euro 1,057 168 889

Sterling (19) (19) –

US Dollar 691 369 322

Other (79) (79) –

Net debt 1,650 439 1,211

2015 27% 73%

2014 27% 73%

44

Weighted average period for which rate is fixed: 7.6 years (2014: 4.4 years)

16%

10%

0%

-18%

1% 0%4% 3%

-34%

USD GBP MXN BRL MYR AUD CAD ZAR RUB

1%

-6%

-16%

-21%

-9%-7% -8%

-23%-25%

USD GBP MXN BRL MYR AUD CAD ZAR RUB

Exchange Rate Movements

Latest Exchange Rates – 2016* v Average 2015

Average 2015 v 2014

45 Note: * source – ECB foreign exchange rates as of 19 February 2016

Group Long Term Targets (5 Years 2013-2017)

46Note: * before brand related intangible asset amortisation and non-trading items (net of related tax)

Targets assume neutral currency and raw materials

Growth

VOLUME GROWTH

Taste & Nutrition 4% to 6% p.a.

Consumer Foods 2% to 3% p.a.

Group 3% to 5% p.a.**

(** assumes market growth rate of 2% to 3% p.a.)

MARGIN EXPANSION

Taste & Nutrition 50bps p.a.

Consumer Foods 20bps p.a.

Group 30bps p.a.

(plus an additional 100bps from Kerryconnect project)

Adjusted EPS* 10%+ p.a. by:

CFROI 12%+ ROAE* 15%+

ROACE* 12%+

Return

Revenues and Profitability

Taste & Nutrition Trading Profit

Group Trading Profit (€m)

Consumer Foods Trading Profit

Group Revenues (€m)

47 Note: * 2012 restated due to adoption of IAS 19 (2011) ‘Employee Benefits’

5,302

5,848 5,837 5,757

6,105

2011 2012 2013 2014 2015

5 year CAGR 4.2% 5 year CAGR 8.3%

501559

611636

700

2011 2012* 2013 2014 2015

7.8% 7.7%8.0%

8.3% 8.5%

3.5%

5.5%

7.5%

0

20

40

60

80

100

120

140

160

180

2011 2012* 2013 2014 2015Trading profit Trading profit margin

11.9% 12.0%

12.9%

13.7% 14.1%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

100

200

300

400

500

600

700

800

2011 2012* 2013 2014 2015

Trading profit Trading profit margin

2011 2012 2013 2014 2015

279

344

412

303

453

2011 2012** 2013 2014 2015

375411

453490

531

2011 2012** 2013 2014 2015

Dividends Per Share (cent)Adjusted EPS*5 year CAGR 9.5% 5 year CAGR 11.7%

Cash Flow and Adjusted EPS*

48Note: * before brand related intangible asset amortisation and non-trading items (net of related tax)

** 2012 restated due to adoption of IAS 19 (2011) ‘Employee Benefits’

Free Cash Flow (€m)Adjusted Earnings*(€m)5 year CAGR 9.5% 5 year CAGR 8.2%

213.4234.0

257.9278.9

301.9

2011 2012** 2013 2014 2015

+11.1% +11.3%+10.2%

+8.1%+8.2%

+11.8%+11.2%

+11.7%+12.5%

+11.1%

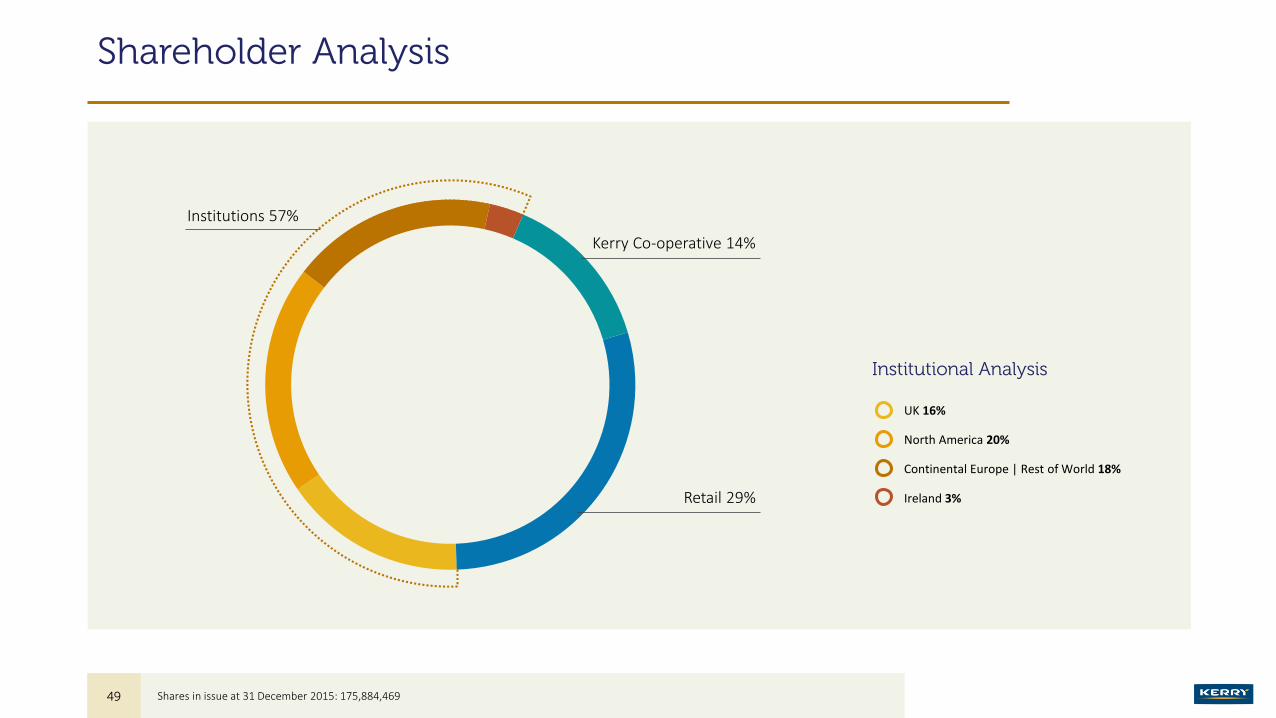

Shareholder Analysis

49 Shares in issue at 31 December 2015: 175,884,469

UK 16%

North America 20%

Continental Europe | Rest of World 18%

Ireland 3%Retail 29%

Kerry Co-operative 14%

Institutions 57%

Institutional Analysis