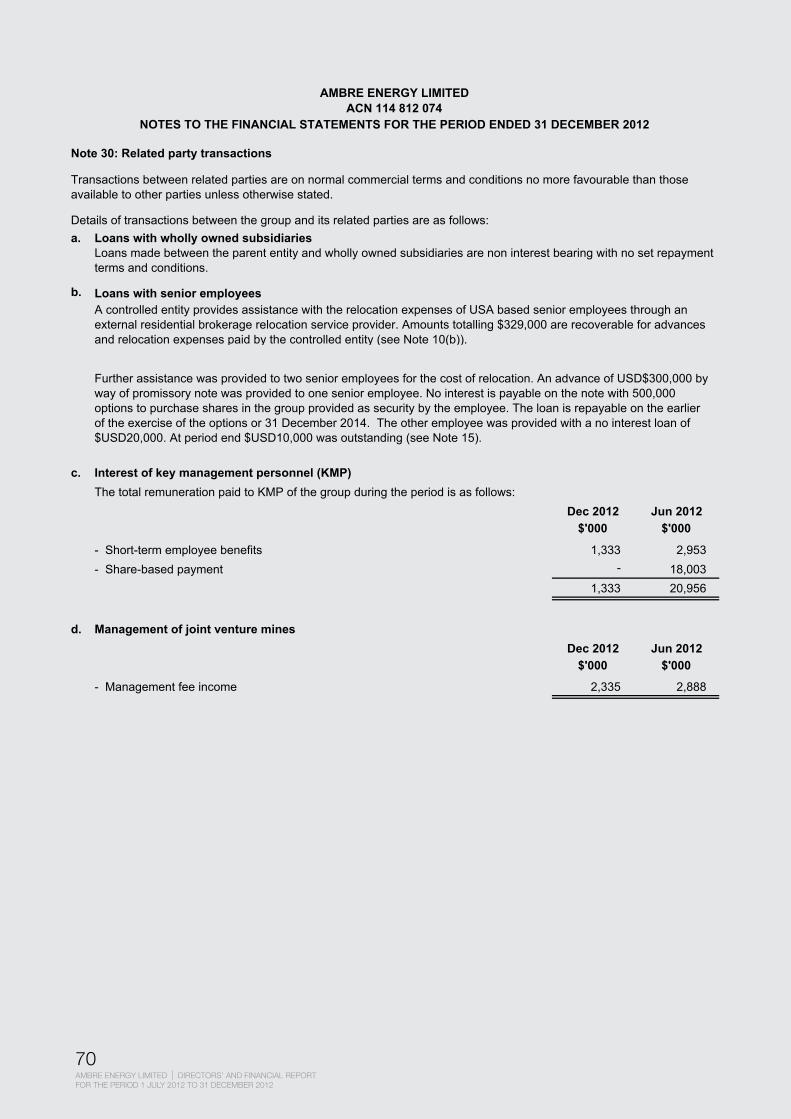

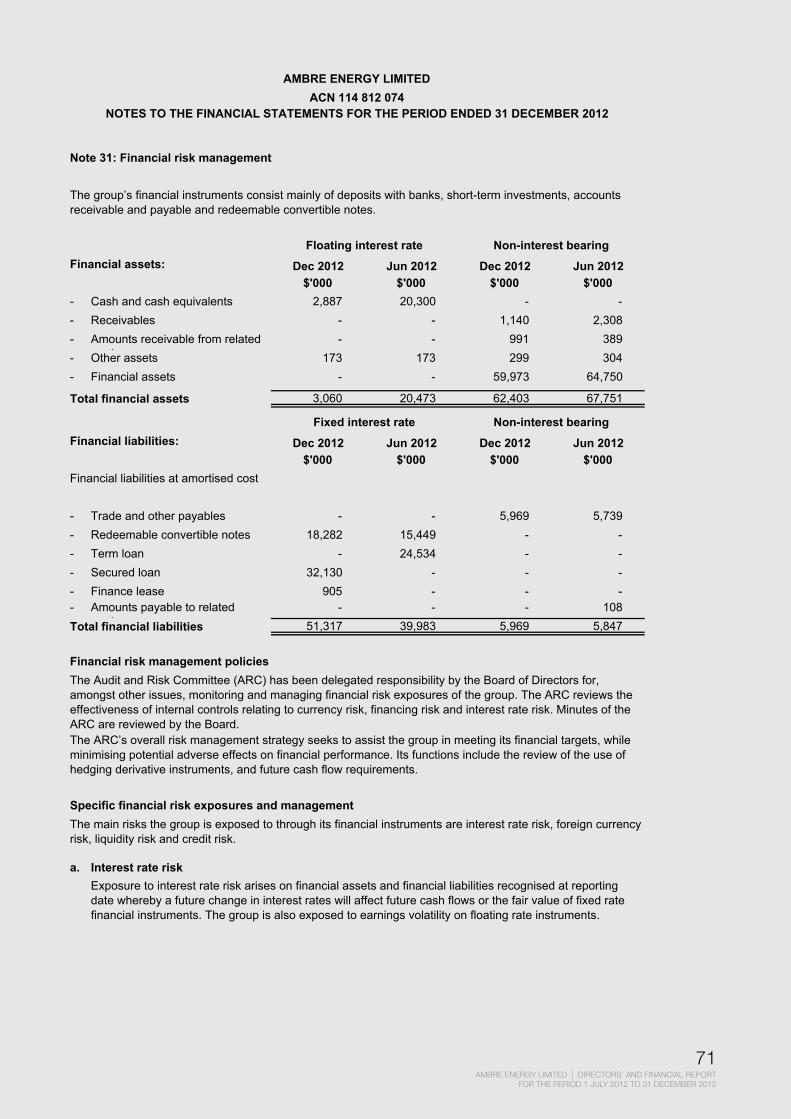

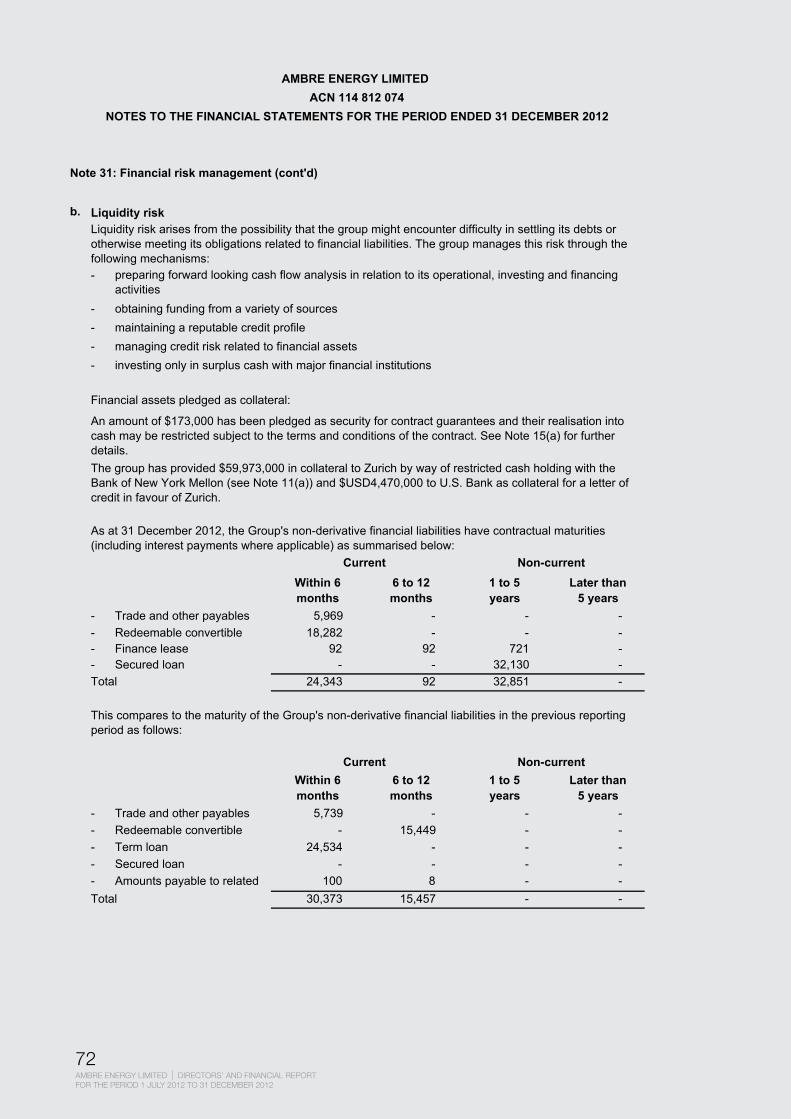

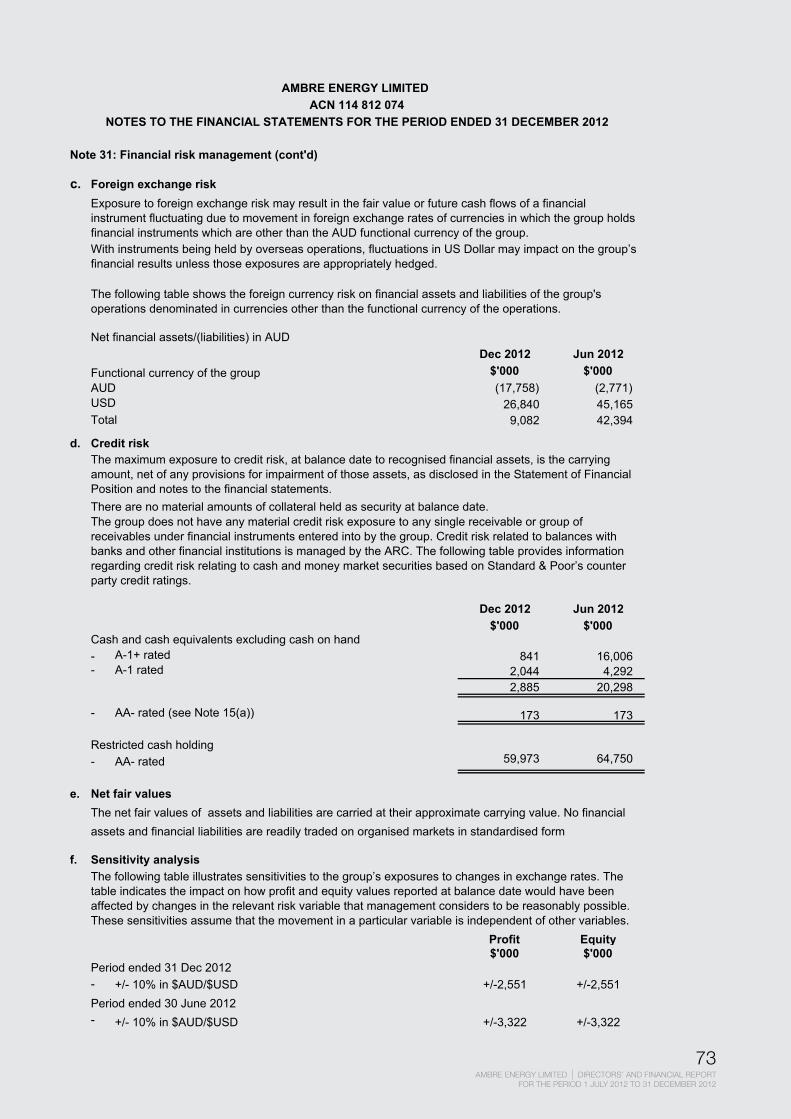

Uji toksisitas fraksi daun ambre (Geranium radula terhadap ...

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

1

directors’ and financial report for the period 1 July 2012 to 31 December 2012

Ambre Energy Limited

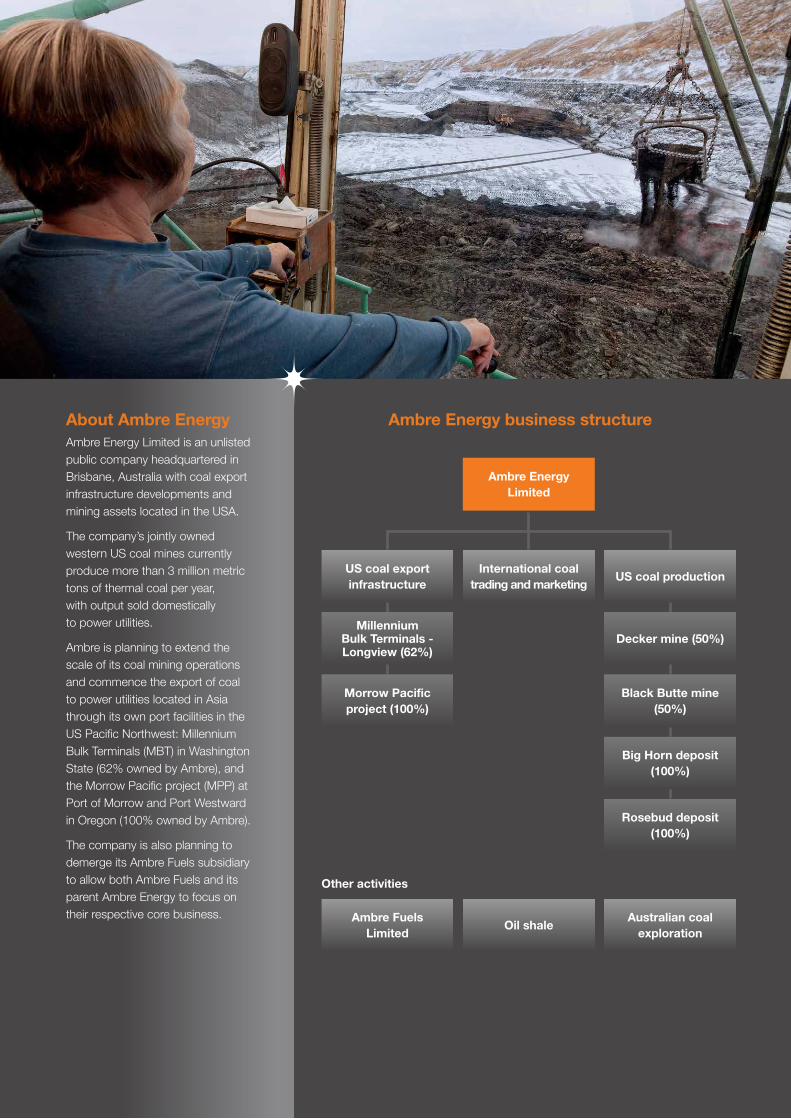

About Ambre EnergyAmbre Energy Limited is an unlisted public company headquartered in Brisbane, Australia with coal export infrastructure developments and mining assets located in the USA.

The company’s jointly owned western US coal mines currently produce more than 3 million metric tons of thermal coal per year, with output sold domestically to power utilities.

Ambre is planning to extend the scale of its coal mining operations and commence the export of coal to power utilities located in Asia through its own port facilities in the US Pacific Northwest: Millennium Bulk Terminals (MBT) in Washington State (62% owned by Ambre), and the Morrow Pacific project (MPP) at Port of Morrow and Port Westward in Oregon (100% owned by Ambre).

The company is also planning to demerge its Ambre Fuels subsidiary to allow both Ambre Fuels and its parent Ambre Energy to focus on their respective core business.

Ambre Energy business structure

Other activities

Oil shaleAmbre Fuels

LimitedAustralian coal

exploration

Ambre Energy Limited

International coal trading and marketing

US coal export infrastructure

Millennium Bulk Terminals - Longview (62%)

Morrow Pacific project (100%)

US coal production

Decker mine (50%)

Black Butte mine (50%)

Big Horn deposit (100%)

Rosebud deposit (100%)

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

3

CONTENTS

Directors’ report ................................................................................................. 4

Auditor’s independence declaration ............................................................... 19

Financial report ................................................................................................. 20

Consolidated statement of comprehensive income ...................................21

Consolidated statement of financial position .............................................22

Consolidated statement of cash flows .......................................................23

Consolidated statement of changes in equity ............................................24

Notes to the financial statements ...............................................................25

Directors’ declaration ...................................................................................... 78

Independent auditor’s report ........................................................................... 79

Corporate directory .......................................................................................... 84

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

4

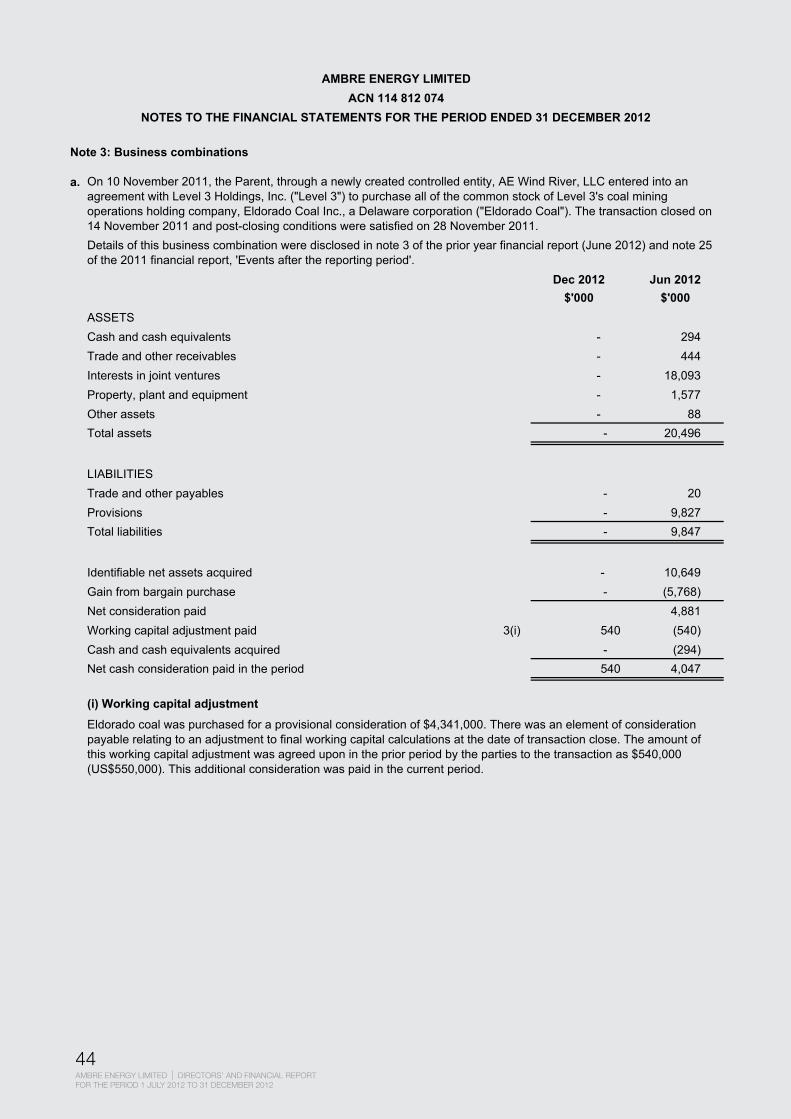

DIRECTORS’ REPORTAmbre Energy Limited, in December 2012, changed its financial year end from 30 June to 31 December. Due to the change of year end, Ambre Energy is required to report on the six month period 1 July 2012 to 31 December 2012 (the period). The annual report subsequent to this report will account for the year 1 January 2013 to 31 December 2013.

The annual report for the financial year ended 30 June 2012 was signed on behalf of directors on 12 December 2012. Consequently, certain information in this report overlaps with information in the annual report for the financial year ended 30 June 2012.

The directors of Ambre Energy Limited present their report together with the financial statements of the consolidated group, being Ambre Energy Limited (the parent) and its controlled entities (the group), for the period 1 July 2012 to 31 December 2012.

Directors The following persons were directors of the parent entity during the whole of the period and up to the date of this report, unless otherwise noted:

Terry O’Reilly BCom, MBA, MApplied Finance, CPA, FAICD, FAIMChairman

Appointed: 23 January 2012 Chairman of Nomination and Remuneration Committee Member of Audit and Risk Management Committee Terry O’Reilly has extensive board, chief executive and senior executive experience after working principally in the resources, energy and manufacturing sectors in Australia and internationally.

Terry has served as managing director of: Conzinc Asia, based in Singapore; Pacific Coal, based in Brisbane; and Coal and Allied Industries, based in Sydney. He has also served on the boards of the Port Waratah and Dalrymple Bay coal terminals.

With a commerce degree and MBA from Melbourne University, and a Masters in Applied Finance from Macquarie University, Terry is a Certified Practicing Accountant, a Fellow of the Australian Institute of Company Directors and a Fellow of the Australian Institute of Management.

Terry has served as Chairman of the Australian Coal Association, Queensland Coal Operators, the NSW Minerals Council and the World Coal Institute Promotions Committee, and was President of the Australia Philippines Business Council.

On the board of Macarthur Coal from October 2008 to October 2011, he served on the Audit and Special Projects committees and as Chairman of the Nomination and Remuneration Committee. Terry is a non-executive director with Thomas & Coffey Limited and Bandanna Energy Limited.

Edek Choros MSc (Geol), BE (Mining)Chief Executive Officer and Managing Director

Appointed: 17 June 2005

Edek Choros founded Ambre Energy in June 2005. With more than 25 years of geological and engineering experience, Edek has demonstrated an innate ability to identify and develop new project opportunities.

Before forming Ambre Energy, Edek established and sold the Millennium Coal Project in Queensland’s Bowen Basin. His experience developing innovative and profitable ventures ensures Ambre Energy continues to attract investment and international interest.

Edek gained his qualifications as a geologist and mining engineer in Krakow, Poland before moving to Australia in 1989. He worked for the Electricity Trust of South Australia and as a private consultant in the coal mining industry before establishing Millennium Coal.

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

5

Michael Mewing BEc

Executive Director, Coal Business Development and Marketing

Appointed: 14 April 2008 Michael Mewing joined the board of Ambre Energy in April 2008 as Non-Executive Chairman and assumed a full-time executive role in September 2008.

Michael was President of Ambre Energy’s US subsidiary, Ambre Energy North America, from December 2008 to December 2010 and is now an executive director based in Brisbane. His primary responsibilities include strategic development and coal trading and marketing.

Instrumental in progressing Ambre Energy’s US acquisition and development program, Michael joined Ambre Energy with 30 years of experience in the international energy field, working in New South Wales, Queensland, Japan, Indonesia and the USA. He has held commercial, marketing and business development roles with BP Oil, BP Coal, Rio Tinto, PT Berau Coal and Millennium Coal.

Michael van Baarle BCom, LLBExecutive Director, Corporate Development

Appointed: 10 April 2006 Michael van Baarle has been an executive director of Ambre Energy Limited since 2006, shortly after the company’s inception. In that time, he has assisted with business and corporate development, which has seen Ambre grow from a small coal exploration and technology business starting out in Brisbane to a global resources group that employs and manages over 300 personnel.

Michael’s role has included raising capital in Australia and internationally, attending to the legal and corporate requirements involved in various acquisitions, including US technology and mining companies and port assets, managing communication with shareholders and other stakeholders, and overseeing corporate development generally. Prior to this time, Michael was a solicitor for 20 years, mainly in private practice in Brisbane. He is a graduate of the University of Queensland with degrees in law and commerce.

David Usasz BCom, FCA

Non-Executive Director

Appointed: 1 February 2009 Chairman of Audit and Risk Management Committee Member of Nomination and Remuneration Committee David Usasz is an expert in financial and strategic affairs with 31 years of service at PricewaterhouseCoopers, including 20 years as a partner. Throughout his career, David has advised businesses in both government and the private sector on management issues around success and growth.

David gained extensive experience in corporate finance with a focus on tax and mergers and acquisitions. Three years working in Hong Kong, coupled with extensive travel to Japan, Taiwan, Jakarta and Singapore, gives David a strong understanding of Asian markets and investors.

David is currently a non-executive director of the publicly listed corporation Cromwell Group and of Queensland owned corporation Queensland Investment Corporation Limited. He was Chairman of Queensland Mining Corporation (2007-2013) and director of unlisted company URBIS Pty Ltd (2008–2013).

David’s diversified interests and networks are boosted by former directorship of the Australian Rugby Union Limited (2005–2007) and honorary positions held with the Princess Alexandra Hospital Research Foundation and the Australia Taiwan Business Council.

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

6

Jayson Newitt BSc, MBA

Non-Executive Director

Appointed: 1 December 2010 Member of Nomination and Remuneration Committee

Jayson Newitt holds a Bachelor of Science from Brigham Young University and received a Master of Business Administration degree from the Marriott School of Management (BYU).

Jayson is co-founder and managing director of Ritchie Opportunity Fund I, a private equity and investment fund with investment allocations in energy, manufacturing and healthcare, based in Salt Lake City, Utah. He is also a principal of The Ritchie Group, a private equity company with investments and projects across a diversified industry base, across two countries and across nine US states.

Jayson has substantial experience in project management, real estate, healthcare and private equity projects as a manager, limited partner, investor and board member.

Dr Ross Bhappu BSc, MSc, PhD (Mineral Econ.)

Non-Executive Director

Appointed: 16 November 2011 Member of Audit and Risk Management Committee Since 2005, Ross has been a partner with Resource Capital Funds, a series of private equity funds investing in the mining and minerals industry. From 2001 until 2005, he was vice-president/principal of Resource Capital Funds.

Since 2010, Ross has served as Chairman of the board of Molycorp Inc. and since 2008 has been on the board of directors of EMED Mining Public Ltd, a copper mining company. He has been a director of Traxys SA, a metal trading and distribution company, since 2007.

From July 2002 until November 2007, Ross served on the board of directors of copper mining company Constellation Copper Corporation, and from November 2005 until September 2006 on the board of gold mining company Anglo Asian Mining.

Ross has experience in constructing and operating complex mining and processing operations, as well as mining-related merger and acquisition activities. He has worked for Newmont Mining Corporation, GTN Copper Corporation and Cyprus Minerals Company.

Company SecretaryNeil McGregor BMus, MMus, MBA

Appointed: 15 March 2012 Neil McGregor joined Ambre Energy in August 2008. He has held the position of Company Secretary for Ambre Fuels Limited since September 2011 and was appointed as Company Secretary and GM Corporate Communications for Ambre Energy Limited in March 2012. Neil holds a Masters of Business Administration and is currently studying for a Graduate Diploma in Applied Corporate Governance. Prior to joining Ambre Energy, Neil was Director of Bands/Head of Woodwind at a Brisbane private school and enjoyed an active performance schedule as a professional clarinettist with symphony orchestras in Australia, New Zealand and the USA for 14 years.

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

7

PRINCIPAL ACTIVITIESAmbre Energy is engaged in the following principal activities:

Export infrastructurea) Jointly with partner Arch Coal, Inc., operating and rehabilitating a bulk commodities terminal, Millennium Bulk Terminals-

Longview, on the Columbia River in Washington State, USA, and developing an expansion of the terminal to handle up to 44 million metric tons of coal per year for delivery into the international seaborne market

b) Developing a proposed coal barging and transloading project known as the Morrow Pacific project on the Columbia River in Oregon, USA, with the capacity to handle up to 8 million metric tons of coal per year for delivery into the international seaborne market

International coal marketing and tradinga) Developing an international coal marketing business to sell US coal into the seaborne market, principally to service

North Asian power utilities in South Korea, Japan and Taiwan

Coal mininga) Operating the Decker coal mine in south-east Montana, USA, on behalf of itself and joint venture partner,

Cloud Peak Energy, and selling the coal to domestic US power utilities

b) Operating the Black Butte coal mine in south-west Wyoming, USA on behalf of itself and joint venture partner, Anadarko Petroleum, and selling the coal to domestic US power utilities

Alternative fuelsa) Developing processing facilities in the USA for the production of liquid fuels and chemicals from coal.

REVIEW OF OPERATIONS AND ASSETSThe following review of operations and assets provides further detail on the separate businesses in the Ambre Energy group.

Principal activities

US bulk commodities terminal operation and coal export infrastructure developmentAmbre Energy’s infrastructure business is responsible for operating and implementing expansion projects at the jointly-owned Millennium Bulk Terminals (Washington State, USA), and the wholly-owned Morrow Pacific project (Oregon, USA).

Millennium Bulk Terminals-Longview

Millennium Bulk Terminals-Longview (MBTL) is a bulk materials port on the Columbia River in Washington State, USA.

Ambre Energy owns 62 per cent of MBTL, with the remaining 38 per cent owned by Arch Coal, Inc. The site operated as an aluminum smelter from 1941 through 2000. Since 1968, the dock has been used to import alumina and materials for smelting.

A significant works program to maintain and upgrade the existing facilities is underway, including clean-up projects related to decades of aluminum smelting. The works have improved the safety and condition of the site for staff while addressing government requirements and community expectations. On 16 February 2012, Barlow Point Land Company, LLC, a State of Washington limited liability company wholly owned by MBTL, acquired the 20 acre Barlow Point property adjacent to the site for future environmental mitigation.

Since the company commenced operations in January 2011, MBTL has registered one loss time injury and no environmental citations. MBTL annually handles approximately 300,000 to 350,000 metric tons of alumina for Alcoa and 100,000 metric tons of coal for the neighbouring Weyerhaeuser paper mill. The company employed an average of 35 people on site during the reporting period, led by Chief Executive Officer, Ken Miller.

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

8

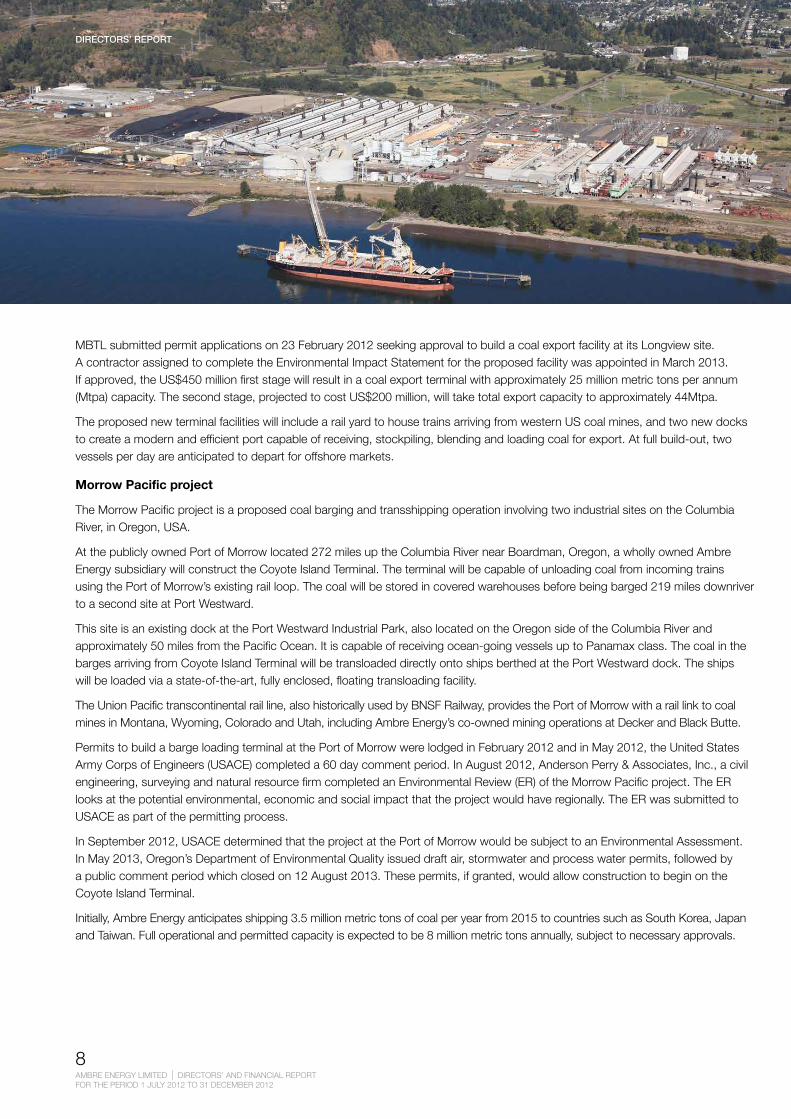

MBTL submitted permit applications on 23 February 2012 seeking approval to build a coal export facility at its Longview site. A contractor assigned to complete the Environmental Impact Statement for the proposed facility was appointed in March 2013. If approved, the US$450 million first stage will result in a coal export terminal with approximately 25 million metric tons per annum (Mtpa) capacity. The second stage, projected to cost US$200 million, will take total export capacity to approximately 44Mtpa.

The proposed new terminal facilities will include a rail yard to house trains arriving from western US coal mines, and two new docks to create a modern and efficient port capable of receiving, stockpiling, blending and loading coal for export. At full build-out, two vessels per day are anticipated to depart for offshore markets.

Morrow Pacific project

The Morrow Pacific project is a proposed coal barging and transshipping operation involving two industrial sites on the Columbia River, in Oregon, USA.

At the publicly owned Port of Morrow located 272 miles up the Columbia River near Boardman, Oregon, a wholly owned Ambre Energy subsidiary will construct the Coyote Island Terminal. The terminal will be capable of unloading coal from incoming trains using the Port of Morrow’s existing rail loop. The coal will be stored in covered warehouses before being barged 219 miles downriver to a second site at Port Westward.

This site is an existing dock at the Port Westward Industrial Park, also located on the Oregon side of the Columbia River and approximately 50 miles from the Pacific Ocean. It is capable of receiving ocean-going vessels up to Panamax class. The coal in the barges arriving from Coyote Island Terminal will be transloaded directly onto ships berthed at the Port Westward dock. The ships will be loaded via a state-of-the-art, fully enclosed, floating transloading facility.

The Union Pacific transcontinental rail line, also historically used by BNSF Railway, provides the Port of Morrow with a rail link to coal mines in Montana, Wyoming, Colorado and Utah, including Ambre Energy’s co-owned mining operations at Decker and Black Butte.

Permits to build a barge loading terminal at the Port of Morrow were lodged in February 2012 and in May 2012, the United States Army Corps of Engineers (USACE) completed a 60 day comment period. In August 2012, Anderson Perry & Associates, Inc., a civil engineering, surveying and natural resource firm completed an Environmental Review (ER) of the Morrow Pacific project. The ER looks at the potential environmental, economic and social impact that the project would have regionally. The ER was submitted to USACE as part of the permitting process.

In September 2012, USACE determined that the project at the Port of Morrow would be subject to an Environmental Assessment. In May 2013, Oregon’s Department of Environmental Quality issued draft air, stormwater and process water permits, followed by a public comment period which closed on 12 August 2013. These permits, if granted, would allow construction to begin on the Coyote Island Terminal.

Initially, Ambre Energy anticipates shipping 3.5 million metric tons of coal per year from 2015 to countries such as South Korea, Japan and Taiwan. Full operational and permitted capacity is expected to be 8 million metric tons annually, subject to necessary approvals.

DIRECTORS’ REPORT

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

9

International coal marketing and tradingAmbre Energy’s international coal marketing and trading business is aiming to source, market and sell high quality US thermal coal to customers predominantly in the Asia-Pacific market.

Total coal demand from Asia until 2030 is forecast to grow at 6.7 per cent per year – 1.3 billion additional metric tons of coal. The US is currently a minor supplier of thermal coal into the Pacific export market, accounting for only 8 million of Asia’s 650 million metric tons of thermal coal demand.

As export facilities are commissioned on the US north-west coast, western US coal producers will increase their share of the Asian market. Ambre Energy believes its port developments, the Morrow Pacific project and Millennium Bulk Terminals-Longview, will be among the first projects to be permitted and developed.

Ambre Energy’s international coal marketing and trading business will optimise sales from its current operations and underpin the potential development of the company’s new projects. The marketing business will also seek to buy coal from other western US producers and export through Ambre Energy’s wholly and jointly owned export infrastructure, once commissioned. The primary markets will be South Korea, Japan and Taiwan – the markets geographically closest to the US west coast.

New sales will build on Ambre Energy’s current 10-year coal supply agreements with two South Korean companies: Korea South East Power Co. Ltd (KOSEP) and Korea Southern Power Co. Ltd (KOSPO). In May 2012, KOSEP entered into an agreement to purchase up to three million metric tons of coal each year from Ambre Energy for 10 years and in June 2012, KOSPO agreed to purchase up to two million metric tons from Ambre Energy for 10 years. The agreements with KOSEP and KOSPO will commence from commissioning of Ambre Energy’s first US coal export terminal.

Within the US, Ambre Energy’s marketing focuses on expanding sales to current and new customers for its jointly held Decker and Black Butte mines.

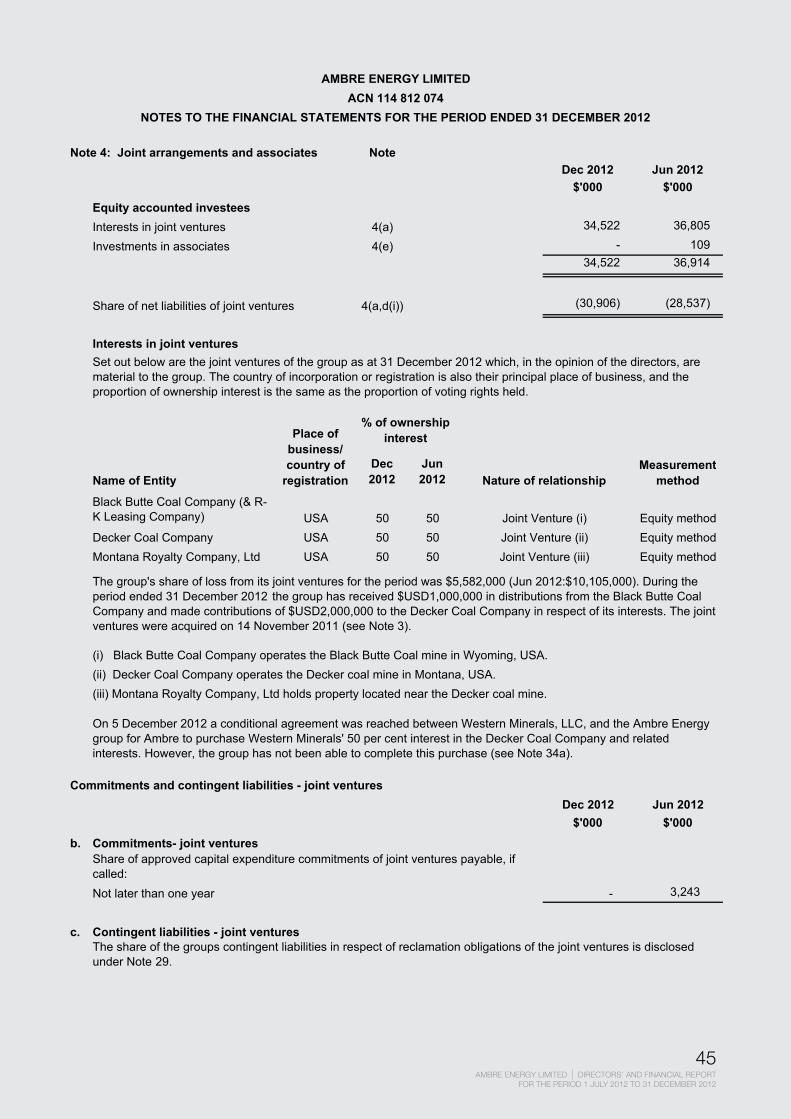

US thermal coal productionIn November 2011, through the purchase of a US company, KCP, Inc., Ambre Energy assumed the operation of, and acquired a 50 per cent ownership interest in, the Decker coal mine in Montana and the Black Butte coal mine in Wyoming, USA. The company also secured interests in two reclaimed Wyoming mines with significant remaining coal resources, Big Horn and Rosebud.

Ambre Energy’s thermal coal production business fulfills operating and marketing responsibilities for the Decker and Black Butte mines, and is also responsible for investigating the viability of redeveloping the Big Horn and Rosebud deposits.

Decker coal mine

The Decker coal mine is in the northern Powder River Basin. Located within Montana’s Big Horn County, the mine is divided into two areas – East Decker and West Decker – each with its own rail loadout facilities. The mine is serviced by BNSF Railway.

Since operations began in the 1970s, Decker has produced approximately 300 million metric tons of coal. Decker coal has the highest calorific value in the Powder River Basin (PRB) at 5000 Kcal/kg NAR, making it attractive for the export market as well as offering domestic users a quality premium to other PRB coals. Decker mine also has the shortest railing distance to Canadian and prospective US Pacific Northwest ports of all PRB mines.

Ambre Energy has operated the Decker mine since acquiring its 50% interest on 14 November 2011. In the period 1 July 2012 to 31 December 2012:

+ Decker had one lost time injury and zero significant environmental citations

+ Decker sold approximately 1.6 million metric tons of coal into the US domestic market, thereby achieving total sales for 2012 of 2.6 million metric tons

+ A new geological model for the Decker resource was completed, which has resulted in an improved mine plan and a better understanding of the extent of the resource

+ Ambre Energy was sued (on 9 July 2012) by its joint venture partner (a subsidiary of Cloud Peak Energy) in connection with, inter alia, the future plans for Decker mine, and Ambre Energy counterclaimed. As set out below, there was a subsequent agreement between the parties to resolve the dispute

+ Ambre Energy and Cloud Peak Energy (CPE) entered into a series of agreements on 5 December 2012 (through respective subsidiaries) whereby the parties would discontinue their lawsuits against each other, and Ambre Energy would purchase CPE’s indirect 50% joint venture share in the Decker Coal Company and related assets, including entitlement to certain royalties payable by Decker.

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

10

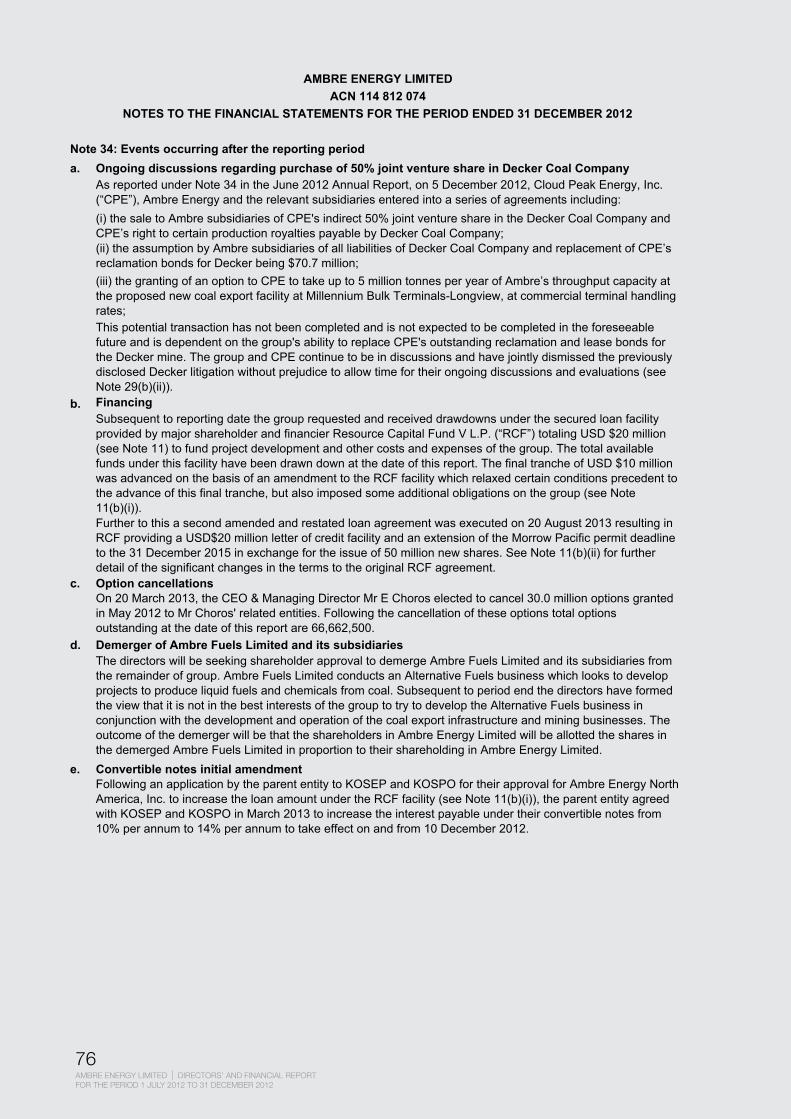

On 28 August 2013, Ambre Energy and CPE announced jointly that the potential transaction related to the agreements reached in December 2012 has not been completed and is not expected to be completed in the foreseeable future. The timing of any potential closing is uncertain and will depend on Ambre Energy’s ability to replace CPE’s outstanding reclamation and lease bonds for the Decker Mine. The companies continue to be in discussions and have jointly dismissed the previously disclosed Decker litigation without prejudice to allow time for their ongoing discussions and evaluations. For further information, see Note 34 (a) in the financial statements.

Black Butte coal mine

Black Butte coal mine is in the Green River Basin in Sweetwater County, south-west Wyoming, USA. The mine is a 50/50 joint venture between Ambre Energy and Anadarko Petroleum Corporation (APC). As with the Decker mine, Ambre Energy operates the mine and is responsible for marketing.

Ambre Energy has operated the Black Butte mine since acquiring its 50% interest on 14 November 2011. During the period, one loss time injury and one citation has occurred.

The mine, a combination of dragline and truck and shovel stripping, is serviced by Union Pacific Railroad and the existing rail loop can support throughput of 14.5 million metric tons per annum. The mine targets production of approximately 3.6 million metric tons of coal each year and in the period 1 July 2012 to 31 December 2012, the mine sold approximately 1.2 metric tons, thereby achieving total sales for 2012 of 2.6 million metric tons. An average of 186 people were employed during the period.

Along with supplying the existing domestic market, Ambre Energy is working towards exporting coal from Black Butte to the international market.

Rosebud deposit

Rosebud coal mine – located north of Hanna, in the Hanna Basin, Carbon County, Wyoming – opened in 1955 and operated until the early 1990s. The mine produced approximately 2.7 million metric tons per year at the height of its productivity in the 1970s. Today, the mine is nearly fully reclaimed and no coal production occurs.

As with the Big Horn deposit, there are significant remaining resources available at Rosebud. Developing these deposits is a potential future option for Ambre Energy.

Big Horn deposit

Located in the Northern Powder River Basin in Sheridan County, Wyoming, a mine operated at the Big Horn site from 1944 until 2000, producing up to 4.1 million metric tons of coal per year at its peak.

While the Big Horn deposit is not currently being mined, it has significant remaining resources.

DIRECTORS’ REPORT

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

11

Additional Ambre Energy group activities

Ambre Fuels Limited

Ambre Fuels Limited, a wholly-owned subsidiary of Ambre Energy, is developing projects and technologies in Australia and the USA to convert coal into transport fuels. An independent board directs Ambre Fuels Limited.

Ambre Fuels has investigated sites in Queensland, Wyoming, Montana, Colorado and Texas to identify the location of the company’s first coal-to-liquids project, while working with US research partners to investigate alternative methods for fuel production. At this stage, Wyoming is the most prospective location for the first project.

In Australia, while Ambre Fuels continues to maintain coal exploration permit EPC935 near Pittsworth, Queensland, there are no longer any immediate prospects for developing a project within the permit area. This will be reviewed periodically.

It is Ambre Energy’s intention to demerge Ambre Fuels Limited and its subsidiaries from the Ambre Energy group at the earliest opportunity, subject to approval from shareholders and secured creditors. The demerger will provide the necessary independence for Ambre Fuels Limited to pursue its strategy to develop coal-to-liquids projects in North America and will allow Ambre Energy to dedicate its resources to the company’s US coal export business.

Research and development

During the financial period, Ambre Fuels pursued the development and application of the following technologies:

+ Coal gasification to produce liquid fuels such as methanol, unleaded petrol, LPG and next-generation fuels such as DME

+ Catalyst for syngas conversion

+ Converting biomass and municipal waste to alternate fuels

+ Co-firing biomass and coal

+ Lignin-to-fuels conversion technologies

+ Coal liquefaction (dissolving coal).

Oil shale

Ambre Energy is the largest private owner of oil shale leases in Utah, USA, with 38,000 acres across 18 mineral leases and in-place resources of 8.7 billion metric tons containing 5.5 billion in-situ barrels of oil.

Approximately 1 billion in-situ barrels of this oil are contained in shale resources occurring at less than 500ft of cover, with the majority of near-surface resources well placed for surface mining techniques1.

Australian coal exploration

Ambre Energy holds coal exploration permits in Queensland, located roughly between Millmerran, Pittsworth and Warwick.

These exploration permits are located within the region currently under review as part of the Queensland Government’s statutory regional planning process.

Due to uncertainty and in accordance with Australian accounting standards, Ambre Energy’s coal exploration tenements were written down to zero value.

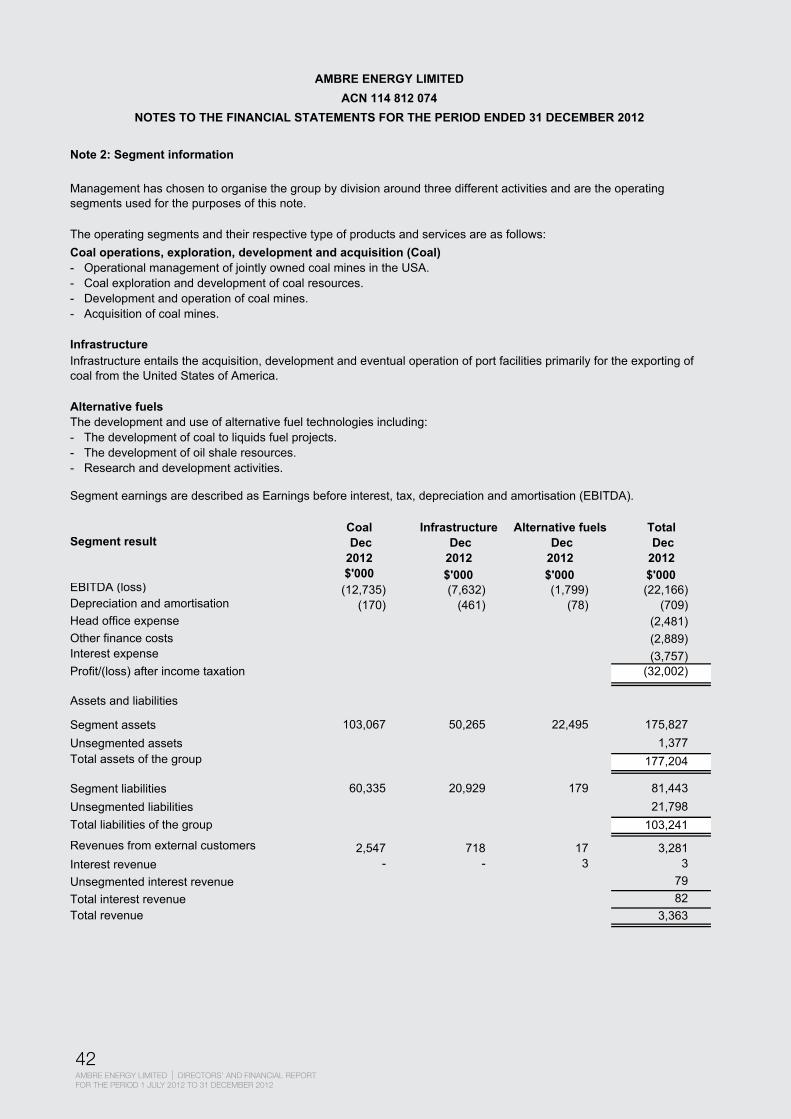

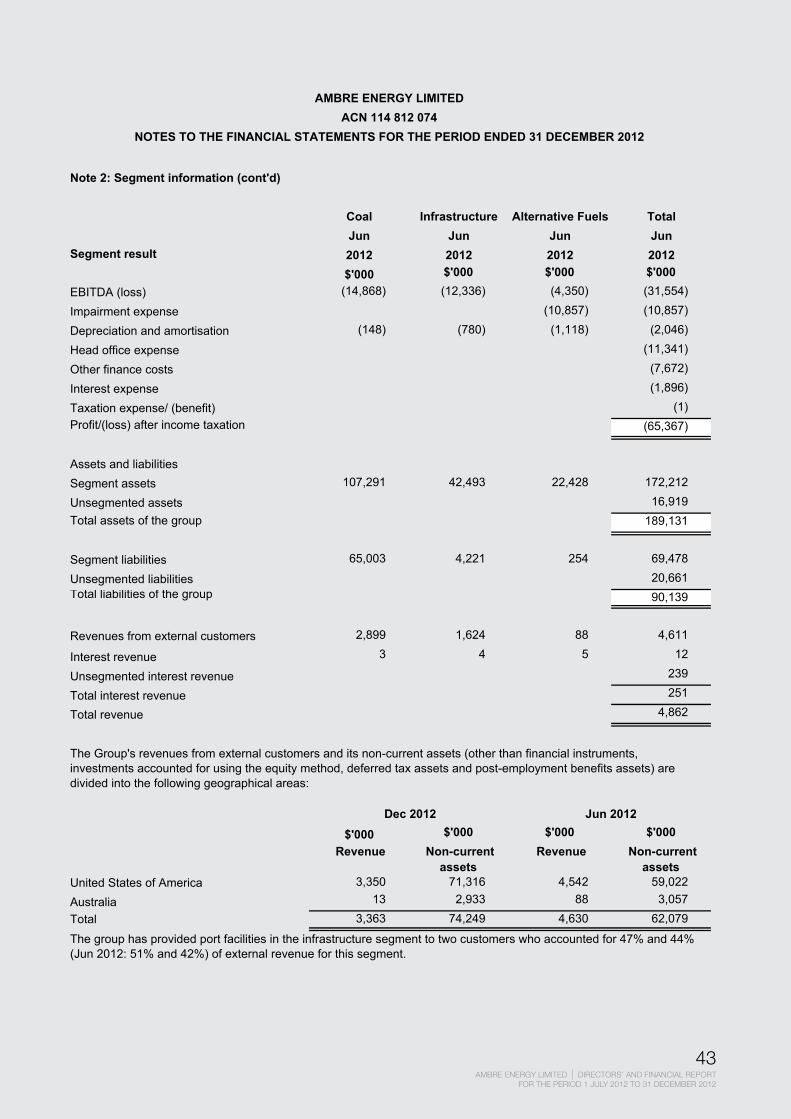

Operating results (Corporate and financial position)The net accounting loss for the group for the period was $30,741,000 (Jun 2012: $62,759,000). Cash flow (negative) from operations was $17,644,000 (Jun 2012: $26,366,000).

1 Ambre Energy Oil Shale Resource Determination Report, Norwest Corporation, August 2011

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

12

SIGNIFICANT CHANGES IN THE STATE OF AFFAIRS During the reporting period, the following significant changes in the state of affairs occurred:

+ Prior to the period, permit applications were lodged seeking approval to build a coal storage and barge loading terminal at the Port of Morrow, Oregon, as part of the Morrow Pacific project. In August 2012, Ambre Energy subsidiary Coyote Island Terminal, LLC (CIT) submitted an Environmental Review to USACE which investigates the potential environmental, economic and social impact that the coal barging terminal would have on the Port of Morrow region. In September 2012, CIT was informed that USACE will move forward with an Environmental Assessment of works proposed at the Port of Morrow.

+ Ambre Fuels Limited was informed by the Queensland Government in August 2012 that its Australian coal-to-liquids project, ambreCTL, would not be declared a significant project for which an environmental impact statement is required. The Queensland Government announced its intentions to undertake a regional planning process to resolve land use conflicts such as those arising between agricultural and mining activities.

+ On 9 July 2012, the 50% joint venture owner of the Decker Mine, Western Minerals LLC, filed a Complaint and Jury Demand with the US District Court in Billings, Montana. The defendants named in the Complaint were KCP, Inc., Ambre Energy North America, Inc. (AENA) and Ambre Energy Limited. KCP and AENA filed an Answer and Counterclaim on 30 July 2012, which Counterclaim also added Cloud Peak Energy, Inc. (CPE) as a defendant. Western Minerals and CPE filed a Response and Jury Demand to Counterclaims and Third Party Claims on 10 September 2012.

+ On 5 December 2012, a subsidiary of Ambre Energy Limited entered into an agreement with a CPE subsidiary to purchase CPE’s indirect 50% joint venture share in the Decker Coal Company and related assets, including entitlement to certain royalties payable by Decker. The terms of this agreement included a settlement of the previously disclosed Decker litigation.

+ On 5 December 2012, the board of directors resolved to change the financial year end for the Ambre Energy group to 31 December. Therefore, this financial period is for the six months ending 31 December 2012.

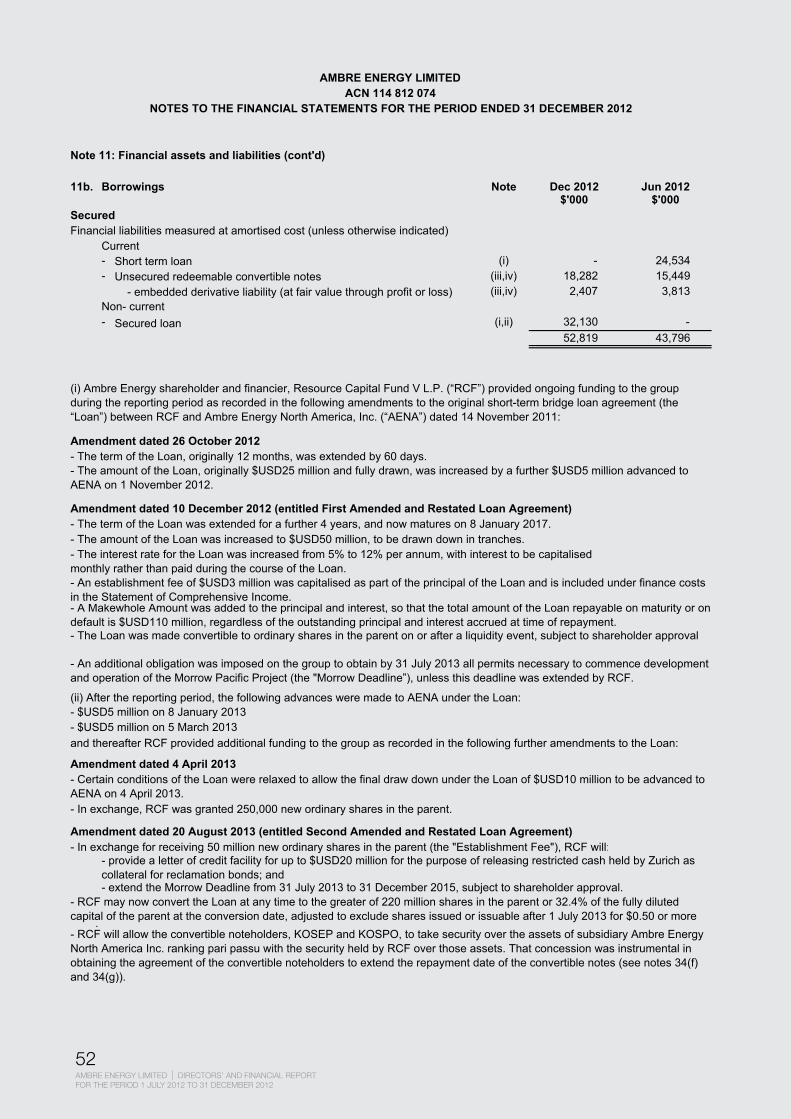

+ On 10 December 2012, Ambre and Resource Capital Fund V L.P. (RCF) agreed to amend, restate, modify, extend and continue their existing loan agreement. Under the amended agreement RCF made available to Ambre Energy North America, Inc. an additional $25 million senior, secured, non-revolving, convertible loan, of which $5 million was drawn down in the period and the remaining $20 million was drawn down between 1 January 2013 and 4 April 2013.

DIRECTORS’ REPORT

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

13

EVENTS ARISING AFTER BALANCE SHEET DATEThe following events occurred after the end of the financial period:

+ On 20 March 2013, the company’s Managing Director elected to cancel 30 million options over Ambre Energy Limited shares. Refer to note 34 (c) in the financial statements for further information.

+ Subsequent to the loan agreement executed by Ambre Energy and RCF on 10 December 2012, Ambre Energy and RCF entered into a second amended and restated loan agreement on 20 August 2013 to provide an additional financing facility to Ambre Energy. For further information on these agreements see note 11 (b) i. ii, and note 34 (b).

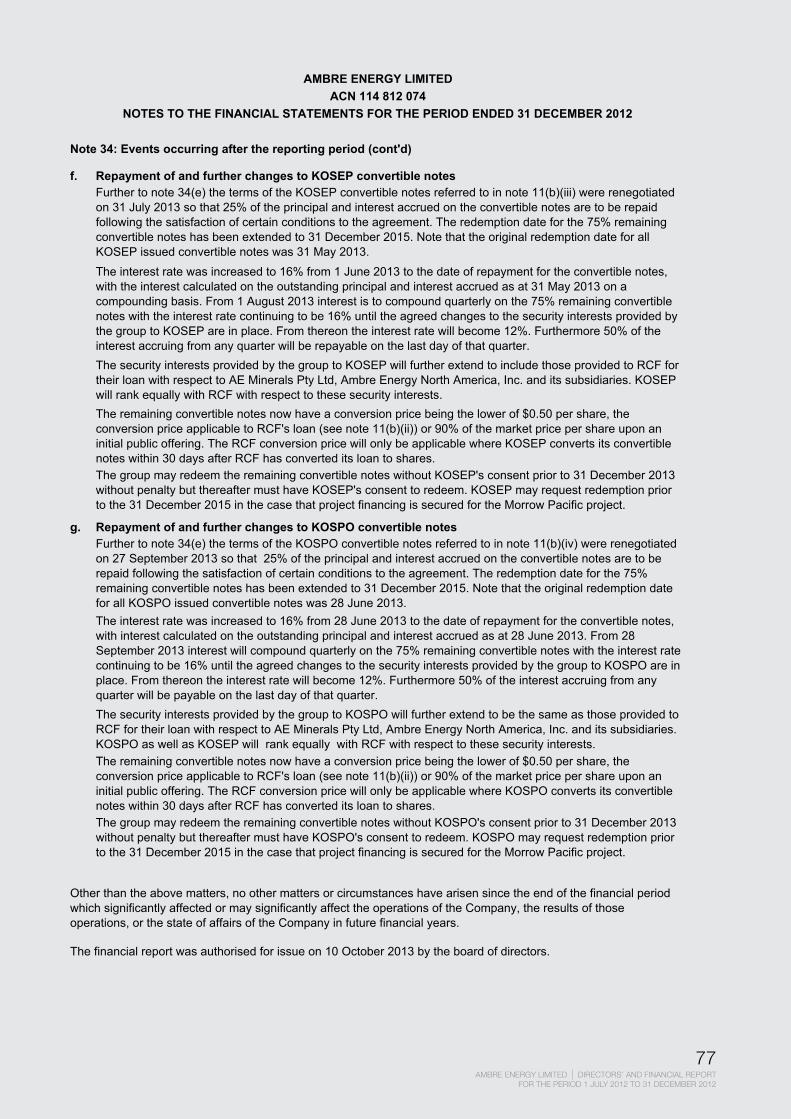

+ Ambre Energy entered into agreements with KOSEP and KOSPO to restructure the repayment terms of convertible notes held by the Korean power companies, which were originally due for repayment in May and June 2013 respectively. For further information see note 34 (f), (g).

+ On 28 August 2013, Ambre Energy and CPE announced jointly that the potential transaction related to agreements reached in December 2012 whereby Ambre Energy was to purchase CPE’s 50% interest in Decker mine has not been completed and is not expected to be completed in the foreseeable future. Nevertheless, the parties agreed to dismiss the Decker litigation without prejudice.

Otherwise, there has not been any matter or circumstance that has significantly affected, or may significantly affect, the operations of the group, the results of those operations, or the state of affairs of the group in future financial periods, other than those matters disclosed on pages 76 and 77 of the financial report.

LIKELY DEVELOPMENTSLikely developments include:

+ progress on permitting for the Morrow Pacific project and the Environmental Impact Statement for Millennium Bulk Terminals

+ a demerger of the alternative fuels division from the group, subject to approval from Ambre Energy shareholders and secured creditors

+ restructuring of the board of directors and changes to the company’s staffing requirements to reflect Ambre Energy’s increased focus on its North American export infrastructure and mining business.

DIRECTORS’ REPORT

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

14

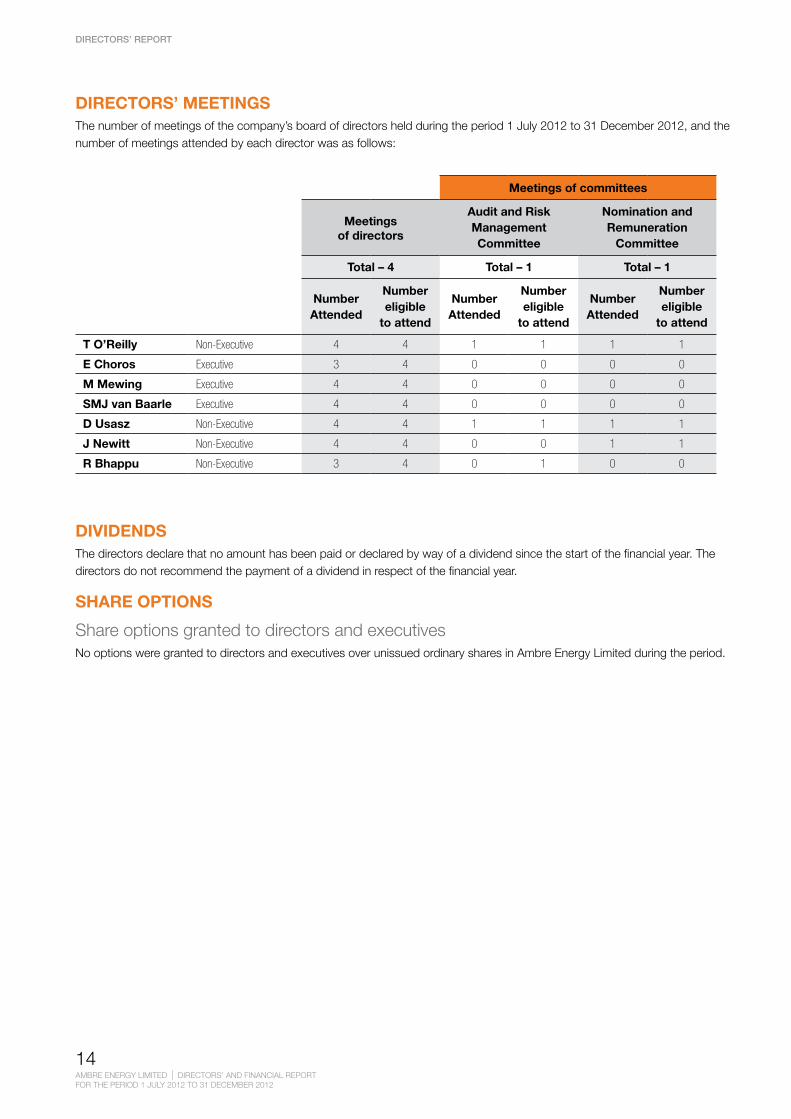

DIRECTORS’ MEETINGSThe number of meetings of the company’s board of directors held during the period 1 July 2012 to 31 December 2012, and the number of meetings attended by each director was as follows:

DIVIDENDSThe directors declare that no amount has been paid or declared by way of a dividend since the start of the financial year. The directors do not recommend the payment of a dividend in respect of the financial year.

SHARE OPTIONS

Share options granted to directors and executivesNo options were granted to directors and executives over unissued ordinary shares in Ambre Energy Limited during the period.

EvENTS ARISING AFTER BALANCE SHEET DATEDetails of events arising since the end of the financial period are disclosed in the significant changes in the state of affairs on page 14 of the annual report. otherwise, there has not been any matter or circumstance that has significantly affected, or may significantly affect, the operations of the group, the results of those operations, or the state of affairs of the group in future financial periods, other than those matters disclosed on pages xx of the financial report

LIkELy DEvELOPMENTSLikely developments include:

+ closing of the acquisition of Cloud Peak energy’s 50 % interest in the Decker mine

+ progress on permitting for the Morrow Pacific project and the environmental impact statement for Millennium Bulk terminals

+ expansion of Decker mine based on a revised geological model and mine plan

+ a demerger of the alternative fuels division from the group and restructuring resulting in a Us entity becoming the head entity of the fuels business. shareholder approval for the demerger will be sought at the next annual general meeting of the company. the restructure will allow the fuels business to focus on the development of projects to convert coal and oil shale to liquid fuels while the parent will concentrate on the development and operation of the coal mining, export and infrastructure businesses.

DIRECTORS’ MEETINGSthe number of meetings of the company’s board of directors held during the period 1 July 2012 to 31 December 2012, and the number of meetings attended by each director was as follows:

Meetings of committees

Full meetings of directors

Audit and Risk Management Committee

Nomination and Remuneration

Committee

Total – 4 Total – 1 Total – 1

Number Attended

Number eligible

to attend

Number Attended

Number eligible

to attend

Number Attended

Number eligible

to attend

T O’Reilly Non-Executive 4 4 1 1 1 1

E Choros Executive 3 4 0 0 0 0

M Mewing Executive 4 4 0 0 0 0

SMJ van Baarle Executive 4 4 0 0 0 0

D Usasz Non-Executive 4 4 1 1 1 1

J Newitt Non-Executive 4 4 0 0 1 1

R Bhappu Non-Executive 3 4 0 1 0 0

DIvIDENDSthe directors declare that no amount has been paid or declared by way of a dividend since the start of the financial year. the directors do not recommend the payment of a dividend in respect of the financial year.

SHARE OPTIONS

share options granted to directors and executivesno options were granted to directors and executives over unissued ordinary shares in Ambre energy Limited during the period.

AMBRE ENERGY LIMITEDDIRECTORS’ AND FINANCIAL REPORT FOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

16

Meetings of directors

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

15

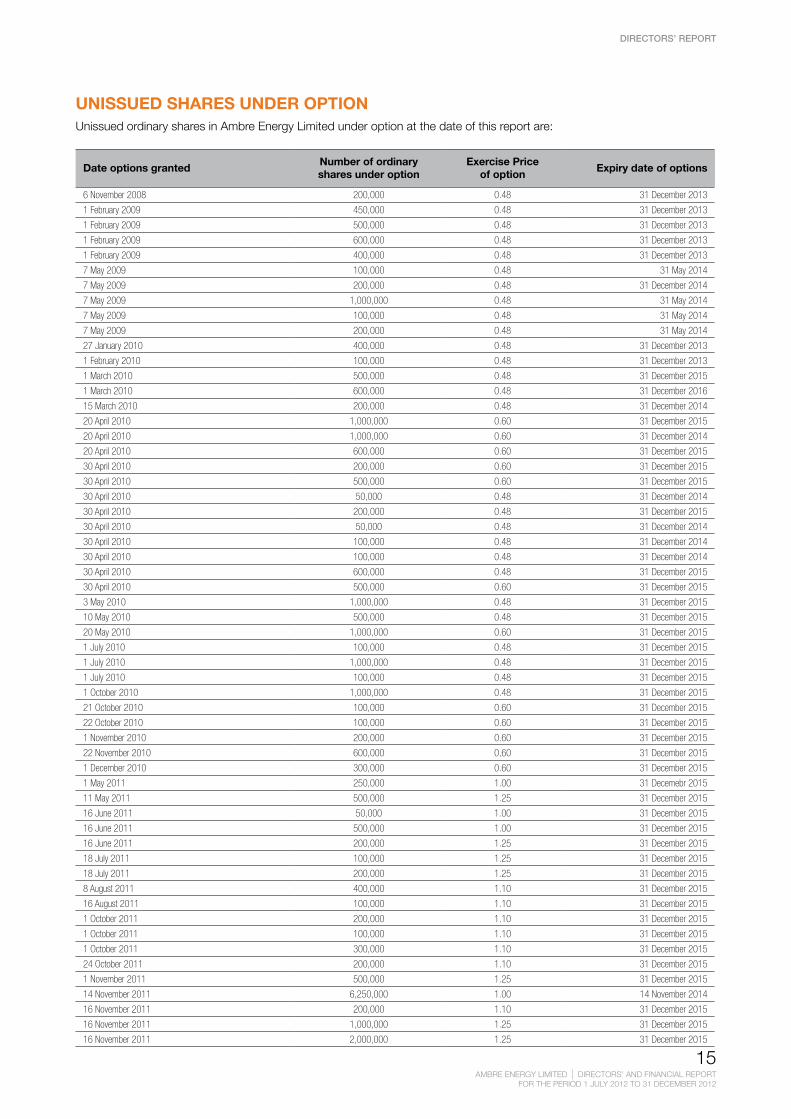

UNISSUED SHARES UNDER OPTIONUnissued ordinary shares in Ambre Energy Limited under option at the date of this report are:

Date options grantedNumber of ordinaryshares under option

Exercise Priceof option

Expiry date of options

6 November 2008 200,000 0.48 31 December 2013

1 February 2009 450,000 0.48 31 December 2013

1 February 2009 500,000 0.48 31 December 2013

1 February 2009 600,000 0.48 31 December 2013

1 February 2009 400,000 0.48 31 December 2013

7 May 2009 100,000 0.48 31 May 2014

7 May 2009 200,000 0.48 31 December 2014

7 May 2009 1,000,000 0.48 31 May 2014

7 May 2009 100,000 0.48 31 May 2014

7 May 2009 200,000 0.48 31 May 2014

27 January 2010 400,000 0.48 31 December 2013

1 February 2010 100,000 0.48 31 December 2013

1 March 2010 500,000 0.48 31 December 2015

1 March 2010 600,000 0.48 31 December 2016

15 March 2010 200,000 0.48 31 December 2014

20 April 2010 1,000,000 0.60 31 December 2015

20 April 2010 1,000,000 0.60 31 December 2014

20 April 2010 600,000 0.60 31 December 2015

30 April 2010 200,000 0.60 31 December 2015

30 April 2010 500,000 0.60 31 December 2015

30 April 2010 50,000 0.48 31 December 2014

30 April 2010 200,000 0.48 31 December 2015

30 April 2010 50,000 0.48 31 December 2014

30 April 2010 100,000 0.48 31 December 2014

30 April 2010 100,000 0.48 31 December 2014

30 April 2010 600,000 0.48 31 December 2015

30 April 2010 500,000 0.60 31 December 2015

3 May 2010 1,000,000 0.48 31 December 2015

10 May 2010 500,000 0.48 31 December 2015

20 May 2010 1,000,000 0.60 31 December 2015

1 July 2010 100,000 0.48 31 December 2015

1 July 2010 1,000,000 0.48 31 December 2015

1 July 2010 100,000 0.48 31 December 2015

1 October 2010 1,000,000 0.48 31 December 2015

21 October 2010 100,000 0.60 31 December 2015

22 October 2010 100,000 0.60 31 December 2015

1 November 2010 200,000 0.60 31 December 2015

22 November 2010 600,000 0,60 31 December 2015

1 December 2010 300,000 0.60 31 December 2015

1 May 2011 250,000 1.00 31 Decemebr 2015

11 May 2011 500,000 1.25 31 December 2015

16 June 2011 50,000 1.00 31 December 2015

16 June 2011 500,000 1.00 31 December 2015

16 June 2011 200,000 1.25 31 December 2015

18 July 2011 100,000 1.25 31 December 2015

18 July 2011 200,000 1.25 31 December 2015

8 August 2011 400,000 1.10 31 December 2015

16 August 2011 100,000 1.10 31 December 2015

1 October 2011 200,000 1.10 31 December 2015

1 October 2011 100,000 1.10 31 December 2015

1 October 2011 300,000 1.10 31 December 2015

24 October 2011 200,000 1.10 31 December 2015

1 November 2011 500,000 1.25 31 December 2015

14 November 2011 6,250,000 1.00 14 November 2014

16 November 2011 200,000 1.10 31 December 2015

16 November 2011 1,000,000 1.25 31 December 2015

16 November 2011 2,000,000 1.25 31 December 2015

EvENTS ARISING AFTER BALANCE SHEET DATEDetails of events arising since the end of the financial period are disclosed in the significant changes in the state of affairs on page 14 of the annual report. otherwise, there has not been any matter or circumstance that has significantly affected, or may significantly affect, the operations of the group, the results of those operations, or the state of affairs of the group in future financial periods, other than those matters disclosed on pages xx of the financial report

LIkELy DEvELOPMENTSLikely developments include:

+ closing of the acquisition of Cloud Peak energy’s 50 % interest in the Decker mine

+ progress on permitting for the Morrow Pacific project and the environmental impact statement for Millennium Bulk terminals

+ expansion of Decker mine based on a revised geological model and mine plan

+ a demerger of the alternative fuels division from the group and restructuring resulting in a Us entity becoming the head entity of the fuels business. shareholder approval for the demerger will be sought at the next annual general meeting of the company. the restructure will allow the fuels business to focus on the development of projects to convert coal and oil shale to liquid fuels while the parent will concentrate on the development and operation of the coal mining, export and infrastructure businesses.

DIRECTORS’ MEETINGSthe number of meetings of the company’s board of directors held during the period 1 July 2012 to 31 December 2012, and the number of meetings attended by each director was as follows:

Meetings of committees

Full meetings of directors

Audit and Risk Management Committee

Nomination and Remuneration

Committee

Total – 4 Total – 1 Total – 1

Number Attended

Number eligible

to attend

Number Attended

Number eligible

to attend

Number Attended

Number eligible

to attend

T O’Reilly Non-Executive 4 4 1 1 1 1

E Choros Executive 3 4 0 0 0 0

M Mewing Executive 4 4 0 0 0 0

SMJ van Baarle Executive 4 4 0 0 0 0

D Usasz Non-Executive 4 4 1 1 1 1

J Newitt Non-Executive 4 4 0 0 1 1

R Bhappu Non-Executive 3 4 0 1 0 0

DIvIDENDSthe directors declare that no amount has been paid or declared by way of a dividend since the start of the financial year. the directors do not recommend the payment of a dividend in respect of the financial year.

SHARE OPTIONS

share options granted to directors and executivesno options were granted to directors and executives over unissued ordinary shares in Ambre energy Limited during the period.

AMBRE ENERGY LIMITEDDIRECTORS’ AND FINANCIAL REPORT FOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

16

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

16

SHARES ISSUED DURING OR SINCE THE END OF THE PERIOD AS A RESULT OF EXERCISEDuring or since the end of the period, Ambre Energy Limited issued ordinary shares as a result of the exercise or net (cashless) exercise of options as follows:

Under the parent entity’s employee share option plan, option holders are entitled, as an alternative to exercising their options through payment of the exercise price, to exchange their options for a lesser number of shares based on the prevailing value of the company’s shares (commonly referred to as “cashless exercise”). During the period, 2,727,941 options were exchanged for 1,855,000 ordinary shares by way of cashless exercise. No consideration was paid to the company for these share issues.

Date options grantedNumber of ordinary shares under option

Price per shareNumber of ordinary shares

issued as a result of exercise

26 June 2008 100,000 0 68,000

26 June 2008 100,000 0 68,000

26 June 2008 100,000 0 68,000

26 June 2008 100,000 0 68,000

30 June 2008 136,765 0 93,000

1 September 2008 191,176 0 130,000

1 September 2008 225,000 0 153,000

4 September 2008 125,000 0 85,000

30 September 2008 800,000 0 544,000

1 October 2008 750,000 0 510,000

28 January 2009 100,000 0 68,000

26 June 2008 100,000 0.48 100,000

30 June 2008 100,000 0.48 100,000

30 June 2008 100,000 0.48 100,000

1 September 2008 275,000 0.48 275,000

Total 3,302,941 Total 2,430,000

Date options grantedNumber of ordinaryshares under option

Exercise Priceof option

Expiry date of options

16 November 2011 4,000,000 1.10 31 December 2015

16 November 2011 4,000,000 1.25 31 December 2015

16 November 2011 500,000 1.10 31 December 2015

16 November 2011 200,000 1.10 31 December 2015

16 November 2011 4,000,000 1.25 31 December 2015

25 November 2011 200,000 1.25 31 December 2015

5 December 2011 200,000 1.10 31 December 2015

31 December 2011 6,250,000 1.00 31 December 2014

23 January 2012 1,600,000 1.80 31 December 2016

7 March 2012 100,000 1.80 31 December 2015

1 April 2012 12,500,000 1.00 1 April 2015

27 April 2012 100,000 1.50 31 December 2016

27 April 2012 100,000 1.50 31 December 2016

27 April 2012 500,000 1.50 31 December 2016

27 April 2012 250,000 1.50 31 December 2016

30 April 2012 100,000 1.25 31 December 2015

14 May 2012 500,000 1.80 31 December 2016

28 May 2012 100,000 1.50 31 December 2016

28 May 2012 400,000 1.50 31 December 2016

28 May 2012 100,000 1.50 31 December 2016

28 May 2012 50,000 1.50 31 December 2016

28 May 2012 100,000 1.50 31 December 2016

28 May 2012 100,000 1.50 31 December 2016

5 June 2012 12,500 1.80 31 December 2016

6 June 2012 200,000 1.50 31 December 2016

1 November 2012 500,000 1.50 31 December 2016

23 January 2013 100,000 1.50 31 December 2016

25 January 2013 400,000 1.50 31 December 2016

Total 66,662,500

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

17

ENVIRONMENTAL LEGISLATIONThe group’s operations are subject to various environmental laws and regulations under the relevant government‘s legislation. Full compliance with these laws and regulations is regarded as a minimum standard for all operations to achieve.

Instances of environmental non–compliance by an operation are identified either by external compliance audits or inspections by relevant government authorities.

There have been no significant breaches by the group during the period.

INDEMNIFICATIONS OF OFFICERS AND AUDITORSDuring the period the company’s parent entity, Ambre Energy Limited, paid a premium in respect of a contract insuring the directors of the company (as named above), the company secretary, and all executive officers of the company and of any related body corporate against a liability incurred as a director, secretary or executive officer to the extent permitted by the Corporations Act 2001. The contract of insurance prohibits disclosure of the nature of the liability and the amount of the premium.

Directors’ DeedsAmbre Energy Limited entered into a Deed of Indemnity, Insurance and Access (Directors’ Deeds) with current directors of the parent. These Deeds formalise the arrangements between the company and the directors as to indemnities, insurance and access to board records. Under each Deed the company indemnifies the director to the extent permitted by law against any liability (including liability for legal defence costs) incurred by the director as an officer of the company or any operating company or while acting at the request of the company or any operating company as an officer of a non-controlled entity.

PROCEEDINGS ON BEHALF OF A COMPANYNo person has applied to the Court under section 237 of the Corporations Act 2001 for leave to bring proceedings on behalf of the Company, or to intervene in any proceedings to which the Company is a party, for the purpose of taking responsibility on behalf of the Company for all or part of those proceedings.

AUDITOR’S INDEPENDENCE DECLARATIONThe auditor’s independence declaration for the period 1 July 2012 to 31 December 2012 has been received and can be found on page 19 of the annual report.

The report is made in accordance with a resolution of the directors.

________________________________

Edward (Edek) Choros Director 10 October 2013

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

18

DIRECTORS’ REPORT

AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

DIRECTORS’ REPORT

19

AUDITOR’S INDEPENDENCE DECLARATION

20AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

FINANCIAL REPORT

Consolidated statement of comprehensive income ...................................21

Consolidated statement of financial position .............................................22

Consolidated statement of cash flows ......................................................23

Consolidated statement of changes in equity ............................................24

Notes to the financial statements ..............................................................25

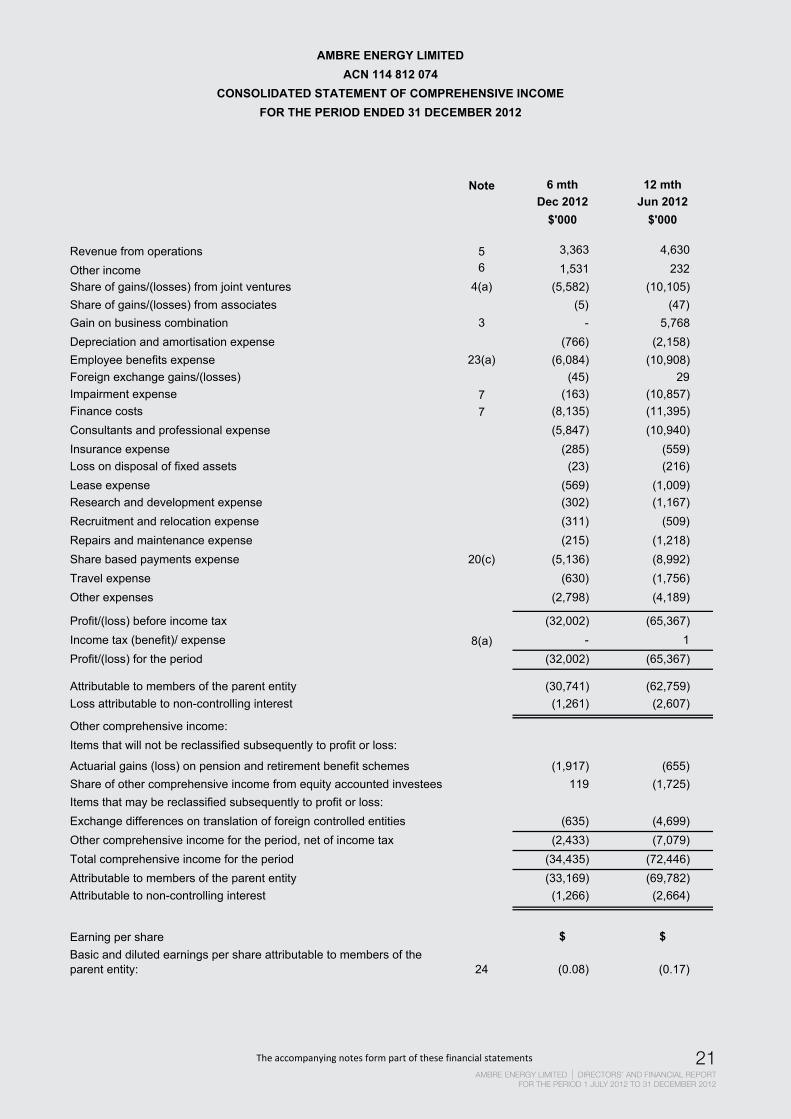

Note 6 mth 12 mthDec 2012 Jun 2012

$'000 $'000

Revenue from operations 5 3,363 4,630

Other income 6 1,531 232 Share of gains/(losses) from joint ventures 4(a) (5,582) (10,105)Share of gains/(losses) from associates (5) (47)Gain on business combination 3 - 5,768 Depreciation and amortisation expense (766) (2,158)Employee benefits expense 23(a) (6,084) (10,908)Foreign exchange gains/(losses) (45) 29 Impairment expense 7 (163) (10,857)Finance costs 7 (8,135) (11,395)Consultants and professional expense (5,847) (10,940)Insurance expense (285) (559)Loss on disposal of fixed assets (23) (216)Lease expense (569) (1,009)Research and development expense (302) (1,167)Recruitment and relocation expense (311) (509)Repairs and maintenance expense (215) (1,218)Share based payments expense 20(c) (5,136) (8,992)Travel expense (630) (1,756)Other expenses (2,798) (4,189)

Profit/(loss) before income tax (32,002) (65,367)Income tax (benefit)/ expense 8(a) - 1 Profit/(loss) for the period (32,002) (65,367)

Attributable to members of the parent entity (30,741) (62,759)Loss attributable to non-controlling interest (1,261) (2,607)

Other comprehensive income:Items that will not be reclassified subsequently to profit or loss:

Actuarial gains (loss) on pension and retirement benefit schemes (1,917) (655)Share of other comprehensive income from equity accounted investees 119 (1,725)Items that may be reclassified subsequently to profit or loss:Exchange differences on translation of foreign controlled entities (635) (4,699)Other comprehensive income for the period, net of income tax (2,433) (7,079)Total comprehensive income for the period (34,435) (72,446)Attributable to members of the parent entity (33,169) (69,782)Attributable to non-controlling interest (1,266) (2,664)

Earning per share $ $Basic and diluted earnings per share attributable to members of the parent entity: 24 (0.08) (0.17)

AMBRE ENERGY LIMITED ACN 114 812 074

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME FOR THE PERIOD ENDED 31 DECEMBER 2012

The accompanying notes form part of these financial statements 21AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORT

FOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

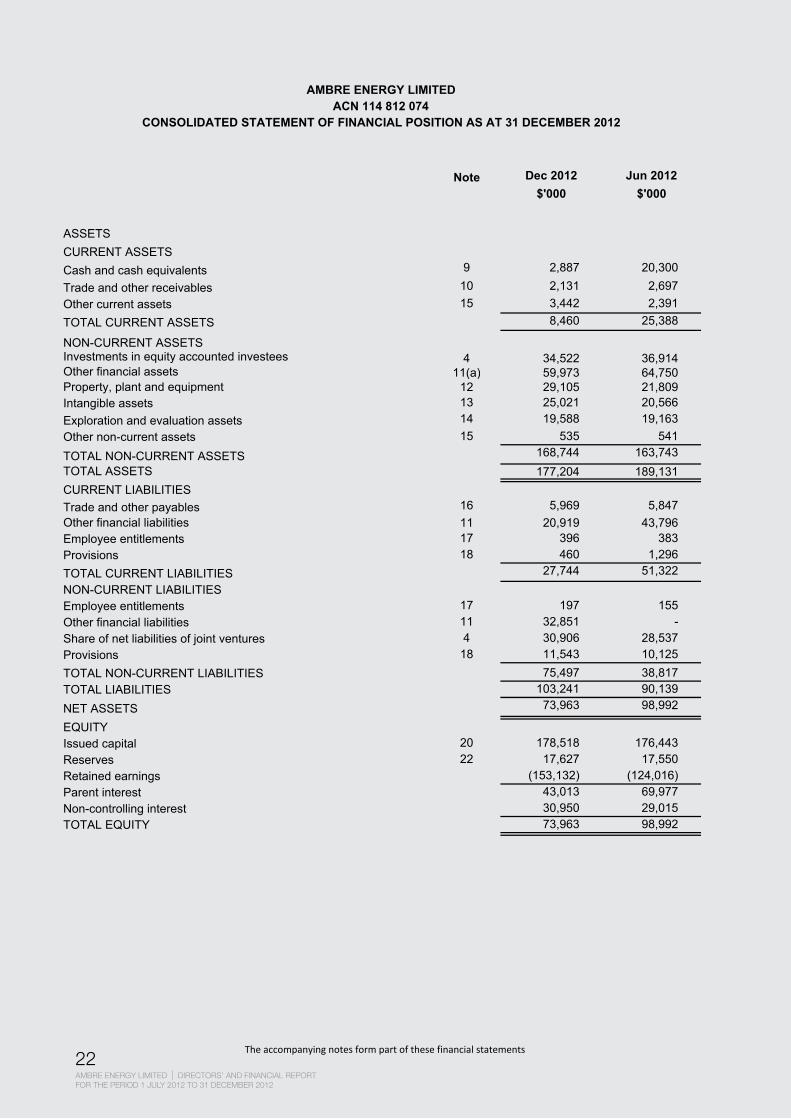

Note Dec 2012 Jun 2012$'000 $'000

ASSETSCURRENT ASSETSCash and cash equivalents 9 2,887 20,300

Trade and other receivables 10 2,131 2,697 Other current assets 15 3,442 2,391 TOTAL CURRENT ASSETS 8,460 25,388

NON-CURRENT ASSETSInvestments in equity accounted investees 4 34,522 36,914 Other financial assets 11(a) 59,973 64,750 Property, plant and equipment 12 29,105 21,809 Intangible assets 13 25,021 20,566 Exploration and evaluation assets 14 19,588 19,163 Other non-current assets 15 535 541

TOTAL NON-CURRENT ASSETS 168,744 163,743 TOTAL ASSETS 177,204 189,131 CURRENT LIABILITIESTrade and other payables 16 5,969 5,847 Other financial liabilities 11 20,919 43,796 Employee entitlements 17 396 383 Provisions 18 460 1,296 TOTAL CURRENT LIABILITIES 27,744 51,322 NON-CURRENT LIABILITIESEmployee entitlements 17 197 155 Other financial liabilities 11 32,851 - Share of net liabilities of joint ventures 4 30,906 28,537 Provisions 18 11,543 10,125 TOTAL NON-CURRENT LIABILITIES 75,497 38,817 TOTAL LIABILITIES 103,241 90,139 NET ASSETS 73,963 98,992

EQUITYIssued capital 20 178,518 176,443 Reserves 22 17,627 17,550 Retained earnings (153,132) (124,016)Parent interest 43,013 69,977 Non-controlling interest 30,950 29,015 TOTAL EQUITY 73,963 98,992

AMBRE ENERGY LIMITEDACN 114 812 074

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 2012

The accompanying notes form part of these financial statements22AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

Note 6 mth 12 mthDec 2012 Jun 2012

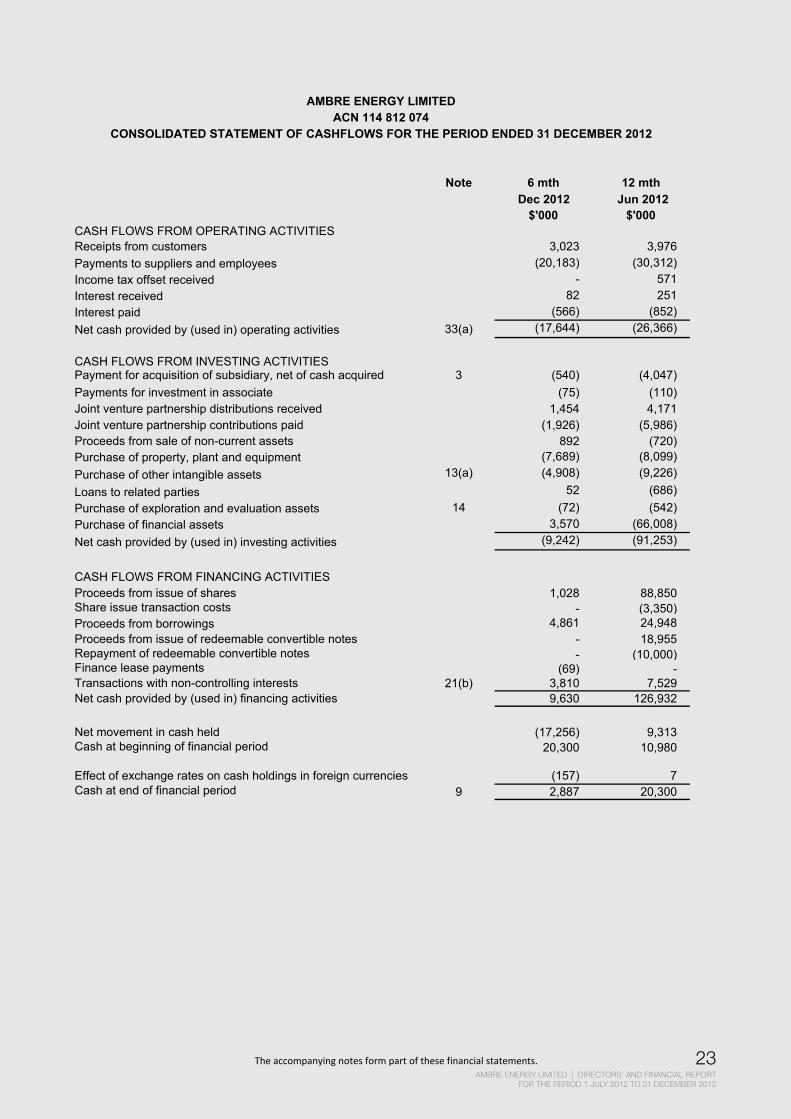

$'000 $'000CASH FLOWS FROM OPERATING ACTIVITIESReceipts from customers 3,023 3,976 Payments to suppliers and employees (20,183) (30,312)Income tax offset received - 571 Interest received 82 251 Interest paid (566) (852)Net cash provided by (used in) operating activities 33(a) (17,644) (26,366)

CASH FLOWS FROM INVESTING ACTIVITIESPayment for acquisition of subsidiary, net of cash acquired 3 (540) (4,047)Payments for investment in associate (75) (110)Joint venture partnership distributions received 1,454 4,171 Joint venture partnership contributions paid (1,926) (5,986)Proceeds from sale of non-current assets 892 (720)Purchase of property, plant and equipment (7,689) (8,099)Purchase of other intangible assets 13(a) (4,908) (9,226)Loans to related parties 52 (686)Purchase of exploration and evaluation assets 14 (72) (542)Purchase of financial assets 3,570 (66,008)Net cash provided by (used in) investing activities (9,242) (91,253)

CASH FLOWS FROM FINANCING ACTIVITIESProceeds from issue of shares 1,028 88,850 Share issue transaction costs - (3,350)Proceeds from borrowings 4,861 24,948 Proceeds from issue of redeemable convertible notes - 18,955 Repayment of redeemable convertible notes - (10,000)Finance lease payments (69) -Transactions with non-controlling interests 21(b) 3,810 7,529 Net cash provided by (used in) financing activities 9,630 126,932

Net movement in cash held (17,256) 9,313 Cash at beginning of financial period 20,300 10,980

Effect of exchange rates on cash holdings in foreign currencies (157) 7 Cash at end of financial period 9 2,887 20,300

AMBRE ENERGY LIMITEDACN 114 812 074

CONSOLIDATED STATEMENT OF CASHFLOWS FOR THE PERIOD ENDED 31 DECEMBER 2012

The accompanying notes form part of these financial statements. 23AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORT

FOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

Sharecapital

Retainedearnings

Foreigncurrency

translationreserve

Optionreserve

Otherreserves

Convertiblenotes

Non-controlling

interest Total$'000 $'000 $'000 $'000 $'000 $'000 $'000 $'000

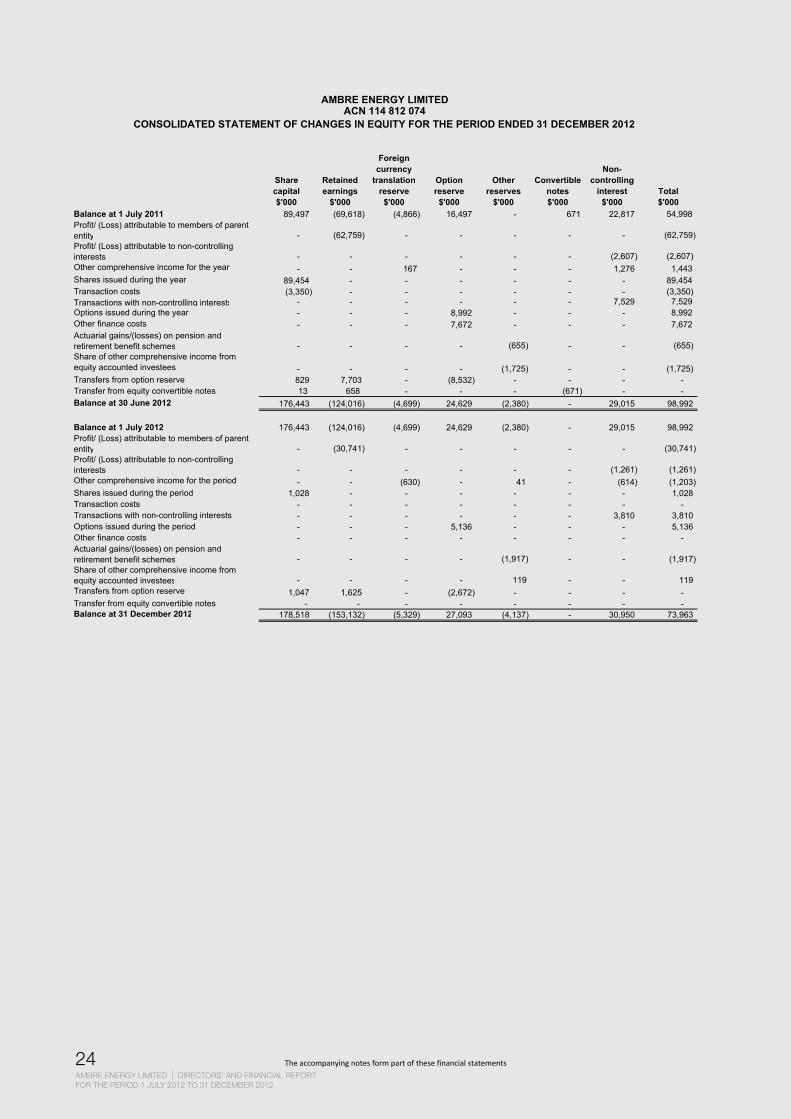

Balance at 1 July 2011 89,497 (69,618) (4,866) 16,497 - 671 22,817 54,998 Profit/ (Loss) attributable to members of parent entity - (62,759) - - - - - (62,759)Profit/ (Loss) attributable to non-controlling interests - - - - - - (2,607) (2,607)Other comprehensive income for the year - - 167 - - - 1,276 1,443 Shares issued during the year 89,454 - - - - - - 89,454 Transaction costs (3,350) - - - - - - (3,350)Transactions with non-controlling interests - - - - - - 7,529 7,529 Options issued during the year - - - 8,992 - - - 8,992 Other finance costs - - - 7,672 - - - 7,672 Actuarial gains/(losses) on pension and retirement benefit schemes - - - - (655) - - (655)Share of other comprehensive income from equity accounted investees - - - - (1,725) - - (1,725)Transfers from option reserve 829 7,703 - (8,532) - - - - Transfer from equity convertible notes 13 658 - - - (671) - - Balance at 30 June 2012 176,443 (124,016) (4,699) 24,629 (2,380) - 29,015 98,992

Balance at 1 July 2012 176,443 (124,016) (4,699) 24,629 (2,380) - 29,015 98,992 Profit/ (Loss) attributable to members of parent entity - (30,741) - - - - - (30,741) Profit/ (Loss) attributable to non-controlling interests - - - - - - (1,261) (1,261) Other comprehensive income for the period - - (630) - 41 - (614) (1,203) Shares issued during the period 1,028 - - - - - - 1,028 Transaction costs - - - - - - - - Transactions with non-controlling interests - - - - - - 3,810 3,810 Options issued during the period - - - 5,136 - - - 5,136 Other finance costs - - - - - - - - Actuarial gains/(losses) on pension and retirement benefit schemes - - - - (1,917) - - (1,917) Share of other comprehensive income from equity accounted investees - - - - 119 - - 119 Transfers from option reserve 1,047 1,625 - (2,672) - - - - Transfer from equity convertible notes - - - - - - - - Balance at 31 December 2012 178,518 (153,132) (5,329) 27,093 (4,137) - 30,950 73,963

AMBRE ENERGY LIMITEDACN 114 812 074

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY FOR THE PERIOD ENDED 31 DECEMBER 2012

The accompanying notes form part of these financial statements24AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

AMBRE ENERGY LIMITED ACN 114 812 074

NOTES TO THE FINANCIAL STATEMENTS FOR THE PERIOD ENDED 31 DECEMBER 2012

Note 1: Statement of significant accounting policies

The consolidated financial statements of Ambre Energy Limited and its controlled entities for the six month financial period ended 31 December 2012 comprises Ambre Energy Limited and its controlled entities (together referred to as the “group”). Ambre Energy Limited (the “parent”) is an unlisted public company incorporated in and domiciled in Australia.

The financial year end of the group was changed from 30 June to 31 December during the period to better align the reporting period with Ambre’s global business cycles. The comparative figures for the Statement of Comprehensive Income, Statement of Cashflows and Statement of Changes in Equity and related notes are for the 12 months to 30 June 2012. The results for the financial period ended 31 December 2012 are therefore not directly comparable with the results for 30 June 2012.

Basis of preparation

The consolidated financial statements are general purpose financial statements that have been prepared in accordance with Australian Accounting Standards (including Australian Accounting Interpretations) of the Australian Accounting Standards Board (“AASB”) and the Corporations Act 2001. The group is a for profit entity for financial reporting purposes under Australian Accounting Standards.

Australian Accounting Standards set out accounting policies that the AASB has concluded would result in financial statements containing relevant and reliable information about transactions, events and conditions. Compliance with Australian Accounting Standards ensures that the financial statements and notes also comply with International Financial Reporting Standards.

The consolidated financial statements, except for cashflow information, have been prepared on an accruals basis and are based on historical costs modified by the revaluation of selected non-current assets, financial assets and financial liabilities for which the fair value basis of accounting has been applied.

The parent entity has applied the relief available to it under Australian Securities and Investment Commission Class Order CO 98/100 and presents all monetary amounts in thousands of Australian dollars.

The group has early adopted AASB 10 Consolidated Financial Statements, AASB 11 Joint Arrangements, AASB 12 Disclosure of Interests in Other Entities, AASB 128 Investments in Associates and Joint Ventures, AASB 127 Separate Financial Statements and AASB 2011-7 Amendments to Australian Accounting Standards arising from the Consolidated and Joint Arrangements Standards from July 2011, because the new accounting policies provide more reliable and relevant information for users to assess the composition of the group and the amounts, timing and uncertainty of future cash flows. In accordance with the transition provisions, comparative figures have been restated where applicable.

The following is a summary of the material accounting policies adopted by the group in preparation of the financial statements. The accounting policies have been consistently applied, unless otherwise stated.

Accounting policies

(a) Principles of consolidation

A controlled entity is any entity which Ambre Energy Limited has control over. Ambre Energy Limited has such control when it is exposed, or has rights, to variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity.

25AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORT

FOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

AMBRE ENERGY LIMITED ACN 114 812 074

NOTES TO THE FINANCIAL STATEMENTS FOR THE PERIOD ENDED 31 DECEMBER 2012

Note 1: Statement of significant accounting policies (cont’d)

(a) Principles of consolidation (cont’d)

A list of controlled entities is contained in Note 21 to the financial statements. All controlled entities now have a 31 December financial year end.

As at the reporting date, the assets and liabilities of all controlled entities have been incorporated into the consolidated financial statements as well as their results for the period then ended. Where controlled entities have entered (left) the group during the period, their operating results have been included (excluded) from the date control was obtained (ceased).

Non-controlling interests, being the equity in a subsidiary not attributable, directly or indirectly, to a parent, are shown separately within the Equity section of the Statement of Financial Position and the Statement of Comprehensive Income. The non-controlling interests in the net assets comprise their interests at the date of the original business combination and their share of changes in equity since that date.

All inter-company balances and transactions between entities in the group, including any unrealised profits and losses are eliminated in preparing the financial statements.

Accounting policies of subsidiaries have been changed where necessary to ensure consistencies with those policies applied by the parent entity.

(b) Business combinations

Business combinations occur where an acquirer obtains control over one or more businesses.

A business combination is accounted for by applying the acquisition method unless it is a combination involving entities or businesses under common control, when assets and liabilities are transferred at book value. The acquisition method requires that for each business combination one of the combining entities must be identified as the acquirer. The business combination will be accounted for as at the acquisition date, which is the date that control over the acquiree is obtained by the parent entity. At this date, the parent shall recognise in the accounts and subject to certain limited exceptions, the fair value of the identifiable assets acquired and liabilities assumed.

In addition, contingent liabilities of the acquiree will be recognised where a present obligation has been incurred and its fair value can be reliably measured. The acquisition may result in the recognition of goodwill or a gain from a bargain purchase. All transaction costs incurred in relation to the business combination are expensed to the Statement of Comprehensive Income.

(c) Income tax

The income tax expense (revenue) for the period comprises current income tax expense (income) and deferred tax expense (income).

Current income tax expense charged to the profit or loss is the tax payable on taxable income. Current tax liabilities (assets) are therefore measured at the amounts expected to be paid to (recovered from) the relevant taxation authority.

Deferred income tax expense reflects movements in deferred tax asset and deferred tax liability balances during the period as well unused tax losses.

26AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

AMBRE ENERGY LIMITED ACN 114 812 074

NOTES TO THE FINANCIAL STATEMENTS FOR THE PERIOD ENDED 31 DECEMBER 2012

Note 1: Statement of significant accounting policies (cont’d)

(c) Income tax (cont’d)

Current and deferred income tax expense (income) is charged or credited directly to equity instead of the profit or loss when the tax relates to items that are credited or charged directly to equity.

Deferred tax assets and liabilities are ascertained based on temporary differences arising between the tax bases of assets and liabilities and their carrying amounts in the financial statements. Deferred tax assets also result where amounts have been fully expensed but future tax deductions are available. No deferred income tax will be recognised from the initial recognition of an asset or liability, excluding a business combination, where there is no effect on accounting or taxable profit or loss.

Deferred tax assets and liabilities are calculated at the tax rates that are expected to apply to the period when the asset is realised or the liability is settled, based on tax rates enacted or substantively enacted at reporting date. Their measurement also reflects the manner in which management expects to recover or settle the carrying amount of the related asset or liability.

Deferred tax assets relating to temporary differences and unused tax losses are recognised only to the extent that it is probable that future taxable profit will be available against which the benefits of the deferred tax asset can be utilised.

Where temporary differences exist in relation to investments in subsidiaries, branches, associates, and joint ventures, deferred tax assets and liabilities are not recognised where the timing of the reversal of the temporary difference can be controlled and it is not probable that the reversal will occur in the foreseeable future.

Current tax assets and liabilities are offset where a legally enforceable right of set-off exists and it is intended that net settlement or simultaneous realisation and settlement of the respective asset and liability will occur. Deferred tax assets and liabilities are offset where a legally enforceable right of set-off exists, the deferred tax assets and liabilities relate to income taxes levied by the same taxation authority on either the same taxable entity or different taxable entities where it is intended that net settlement or simultaneous realisation and settlement of the respective asset and liability will occur in future periods in which significant amounts of deferred tax assets or liabilities are expected to be recovered or settled.

Tax consolidation

Ambre Energy Limited and its wholly-owned Australian subsidiaries have formed an income tax consolidated group under the tax consolidation regime. Each entity in the group recognises its own current and deferred tax liabilities, except for any deferred tax assets resulting from unused tax losses and tax credits, which are immediately assumed by the parent entity. The current tax liability of each group entity is then subsequently assumed by the parent entity. The group notified the Australian Taxation Office that it had formed an income tax consolidated group to apply from 20 October 2006.

There are no tax sharing arrangements in place between members of the income tax consolidated group at the date of this report.

(d) Property, plant and equipment

Each class of property, plant and equipment is carried at cost less, where applicable, accumulated depreciation and impairment losses.

27AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORT

FOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

AMBRE ENERGY LIMITED ACN 114 812 074

NOTES TO THE FINANCIAL STATEMENTS FOR THE PERIOD ENDED 31 DECEMBER 2012

Note 1: Statement of significant accounting policies (cont’d)

(d) Property, plant and equipment (cont’d)

Property

Freehold land and buildings are shown at their fair value (being the amount for which an asset could be exchanged between knowledgeable willing parties in an arm’s length transaction), based on periodic, but at least triennial, valuations by external independent valuers, less subsequent depreciation for buildings.

Increases in the carrying amount arising on revaluation of land and buildings are credited to a revaluation reserve in equity. Decreases that offset previous increases of the same asset are charged against fair value reserves directly in equity; all other decreases are charged to the Statement of Comprehensive Income. Each year the difference between depreciation based on the revalued carrying amount of the asset charged to the Statement of Comprehensive Income and depreciation based on the asset’s original cost is transferred from the revaluation reserve to retained earnings.

Any accumulated depreciation at the date of revaluation is eliminated against the gross carrying amount of the asset and the net amount is restated to the revalued amount of the asset.

Plant and equipment

Plant and equipment are measured on the cost basis less accumulated depreciation and any accumulated impairment losses.

The carrying amount of plant and equipment is reviewed annually by directors to ensure it is not in excess of the recoverable amount from these assets. The recoverable amount is assessed on the basis of the expected net cash flows that will be received from the asset’s employment and subsequent disposal. The expected net cash flows have been discounted to their present values in determining recoverable amounts. A formal assessment of recoverable amounts are made when impairment indicators are present (see Note 1(h)).

The cost of fixed assets constructed within the group includes the cost of materials, direct labour, borrowing costs and an appropriate proportion of fixed and variable overheads.

Subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, as appropriate, only when it is probable that future economic benefits associated with the item will flow to the group and the cost of the item can be measured reliably. All other repairs and maintenance are charged to the Statement of Comprehensive Income during the financial period in which they are incurred.

Depreciation

The depreciable amount of all fixed assets, including buildings and capitalised lease assets but excluding freehold land, is depreciated on a straight-line basis over their useful lives to the consolidated group commencing from the time the asset is held ready for use. Leasehold improvements are depreciated over the shorter of either the unexpired period of the lease or the estimated useful lives of the improvements.

The depreciation rates used for each class of depreciable assets are:

Class of fixed asset Depreciation rate Buildings 2-100% Plant and equipment 2-100% Leasehold improvements 5-20%

28AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORTFOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

AMBRE ENERGY LIMITED ACN 114 812 074

NOTES TO THE FINANCIAL STATEMENTS FOR THE PERIOD ENDED 31 DECEMBER 2012

Note 1: Statement of significant accounting policies (cont’d)

(d) Property, plant and equipment (cont’d)

The assets’ residual values and useful lives are reviewed, and adjusted if appropriate, at each balance date.

An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carrying amount is greater than its estimated recoverable amount.

Gains and losses on disposal are determined by comparing proceeds with the carrying amount. These gains and losses are included in the Statement of Comprehensive Income.

When revalued assets are sold, amounts included in the revaluation reserve relating to that asset are transferred to retained earnings.

(e) Exploration and development expenditure

Exploration, evaluation and development expenditure incurred is capitalised in respect of each identifiable area of interest. These costs are only capitalised to the extent that they are expected to be recouped through the successful development of the area or where activities in the area have not yet reached a stage that permits reasonable assessment of the existence of economically recoverable reserves.

Accumulated costs in relation to an abandoned area are written off in full against profit in the period in which the decision to abandon the area is made.

When production commences, the accumulated costs for the relevant area of interest are amortised over the life of the area according to the rate of depletion of the economically recoverable reserves.

A regular review is undertaken of each area of interest to determine the appropriateness of continuing to carry forward costs in relation to that area of interest.

Costs of site restoration are provided over the life of the facility from when exploration commences and are included in the costs of that stage. Site restoration costs include the dismantling and removal of mining plant, equipment and building structures, waste removal, and rehabilitation of the site in accordance with clauses of the mining permits. Such costs have been determined using estimates of future costs, current legal requirements and technology on an undiscounted basis.

Any changes in the estimates for the costs are accounted on a prospective basis. In determining the costs of site restoration, there is uncertainty regarding the nature and extent of the restoration due to community expectations and future legislation. Accordingly the costs have been determined on the basis that the restoration will be completed within one year of abandoning the site.

29AMBRE ENERGY LIMITED | DIRECTORS’ AND FINANCIAL REPORT

FOR THE PERIOD 1 JULY 2012 TO 31 DECEMBER 2012

AMBRE ENERGY LIMITED ACN 114 812 074

NOTES TO THE FINANCIAL STATEMENTS FOR THE PERIOD ENDED 31 DECEMBER 2012

Note 1: Statement of significant accounting policies (cont’d)

(f) Leases

Leases of fixed assets where substantially all the risks and benefits incidental to the ownership of the asset, but not the legal ownership that is transferred to entities in the group are classified as finance leases.

Finance leases are capitalised by recording an asset and liability at the lower of the amounts equal to the fair value of the leased property or the present value of the minimum lease payments, including any guaranteed residual values. Lease payments are allocated between the reduction of the lease liability and the lease interest expense for the period.

Leased assets are depreciated on a straight line basis over the shorter of their estimated useful lives or the lease term.

Lease payments for operating leases, where substantially all the risks and benefits remain with the lessor, are charged as expenses in the periods in which they are incurred. Lease incentives under operating leases are recognised as a liability and amortised on a straight line basis over the life of the lease term.

(g) Financial instruments

Initial recognition and measurement

Financial assets and financial liabilities are recognised when the entity becomes a party to the contractual provisions to the instrument. For financial assets, this is equivalent to the date that the company commits itself to either the purchase or sale of the asset (i.e. trade date accounting is adopted).

Financial instruments are initially measured at fair value plus transaction costs, except where the instrument is classified ‘at fair value through profit or loss’, in which case transaction costs are expensed to profit or loss immediately.

Classification and subsequent measurement