Digitalisation of financial supply chain some trends 2015 to 2016

30

“BACK TO THE FUTURE” DEFINITELY MOVED INTO THE PAST 2015-2016 WHAT IS GOING ON IN THE DIGITALISATION JOURNEY OF THE FINANCIAL SUPPLY CHAIN WITH HIS POWERFUL E-INVOICING ENGINE? SOME THOUGHTS, REFLECTIONS AND TRENDS 22 juni-2013 InCoPro D4M Design for Margin Tel :+32/473.38.16.13 [email protected]

-

Upload

jos-feyaerts -

Category

Business

-

view

1.236 -

download

0

Transcript of Digitalisation of financial supply chain some trends 2015 to 2016

1.

“BACK TO THE FUTURE” DEFINITELY

MOVED INTO THE PAST

2015-2016 WHAT IS GOING ON IN

THE DIGITALISATION JOURNEY OF THE FINANCIAL SUPPLY CHAIN WITH HIS

POWERFUL E-INVOICING ENGINE?

SOME THOUGHTS, REFLECTIONS AND TRENDS

22 juni-2013

InCoPro D4M

Design for Margin

Tel :+32/473.38.16.13

Copyright 2015 by Jos Feyaerts All Rights reserved. The readers may share the whole document for

free and reproduce selected parts of the document content for non-commercial use if referring to

the source. All other use is subject of prior written permission of the author.

Keep on focusing, registering and crystalizing your journey

Enjoy reading it and all exchange of thoughts, remarks are welcome.

Jos Feyaerts

Your digitalization guide InCoPro bvba, ‘Design for Margin’ (D4M)

3

Contents

1. In 2016 “Back to the Future” will definitely be something of the past .............................. 4

2. ERP are more and more becoming backbone systems of standardized process data far

from the front. ............................................................................................................................ 5

3. Cloud-based accounting platforms will play a major role in the digitalization of the

“small-b” segment. ..................................................................................................................... 7

4. E-commerce is much more adopted in BtoB than we think. .............................................. 9

5. Order to Cash (OtoC) and Purchase to Pay (PtoP) are out, one shared end-to-end

Sourcing to cash (StoC ) is a new platform paradigm. ............................................................. 11

6. Analytics:D2III data to information insights and impact .................................................. 12

7. Say goodbye to conventional banking .............................................................................. 13

7.1 Cashless society: ........................................................................................................ 13

7.2 The Blockchain technology: ....................................................................................... 14

7.3 Paradigm Switch of Working Capital and the growth of supply chain finance ......... 14

8. Governments going digital ................................................................................................ 15

9. VAT-compliance an increasing challenge ......................................................................... 18

10. An e-invoice is a strong communication channel with the customer .............................. 21

11. Maturity, specialization and concentration ...................................................................... 23

12. Portals aren’t the endpoint: “We need invoices to talk back” ......................................... 25

13. E-invoicing was driving far too long by technology due to the “e” in e-invoicing............ 27

14. Everything is relative, nothing is absolute ........................................................................ 29

15. 2016 the year to talk back ................................................................................................ 29

4

1. In 2016 “Back to the Future” will definitely be something of the

past

2015 was the year where “Back to the Future”

definitely moved into the past. A lot of women

and men of my age, most with grey hair (or even

lost or coloured) , saw this film when they were

an adolescent. October 21st 2015 was in the

movie a date that was that far away that it

seemed as unreachable. Now it is in the past.

The fax machine1, for which the film devoted a

lot of credentials, did expand fast but it in 2015

it is after all gone in the day-to-day life. In the

digitalization of the financial supply chain, the

fax did play an important historical transition roll. How many orders, order confirmations were

going faster due to the fax?

1 Fax machines and phone booths: This is one of the biggest predictions the movie got wrong. In the movie everywhere the protagonist went, there would be fax machines. Although they are still used, they are not as prominent as the movie depicted them to be. Phone booths are also seldom. Those two are definitely technology of the past. https://youtu.be/eVebChGtLlY

5

The fax had a huge impact on the order

administration, but it seems already a long time

ago. People are not good in judging time. The way

we experience time is strongly distorted by our

actual subjective perception and actual habits. But

that is the same with the smartphones and tablets

of which we have nowadays the feeling that they

have been in our lives all the time, knowing that the

iPAD is only from mid-2010 on the market. On the

other hand, it seems that tablets are already on

their decline curve compared to smartphones. At least two things we can learn, time is relative, and

times flies. So make the best out of it in 2016, as you are the pilot and you determine the destiny.

From our side, we will reflect below on some movement, waves we saw in 2015 and of which we

have the feeling that they will matter in 2016 and beyond, concerning the digitalisation of the

financial supply chain. When I use “we”, this is because this document is not only my own insights,

but they are the results from a full year of exchanging thoughts of all of you. The blames that they

are wrong on the impact, or not so important and the selection criteria to be mentioned need to be

completely addressed to my account and I apologize for it.

2. ERP are more and more becoming backbone systems of

standardized process data far from the front.

In the nighties, ERP was growing fast and the batch systems were send to the eternal hunting

grounds. Mainframes weren’t hip anymore.

The slogans of the new paradigm were at that

time; avoid data redundancy, one single truth,

real-time systems. The integrated ERP-

systems would bring it all to us... We are 20

years later and I see more data redundancy

than probably ever before, especially the last

3-5 years, due to the explosion of

“platformization” and our APP-culture. Master

data was never our favorite thing, isn’t it?

Master data is important but already 20 years,

I am attracted to companies struggling

(euphemism) with it. Or was it indeed a representative sample of companies? For a lot of them,

master data was more a kind of nightmare, definitely not a free lunch. Master data seems to be

subject of some very easy natural laws: “shit in, shit out”, “nothing in, nothing out”.

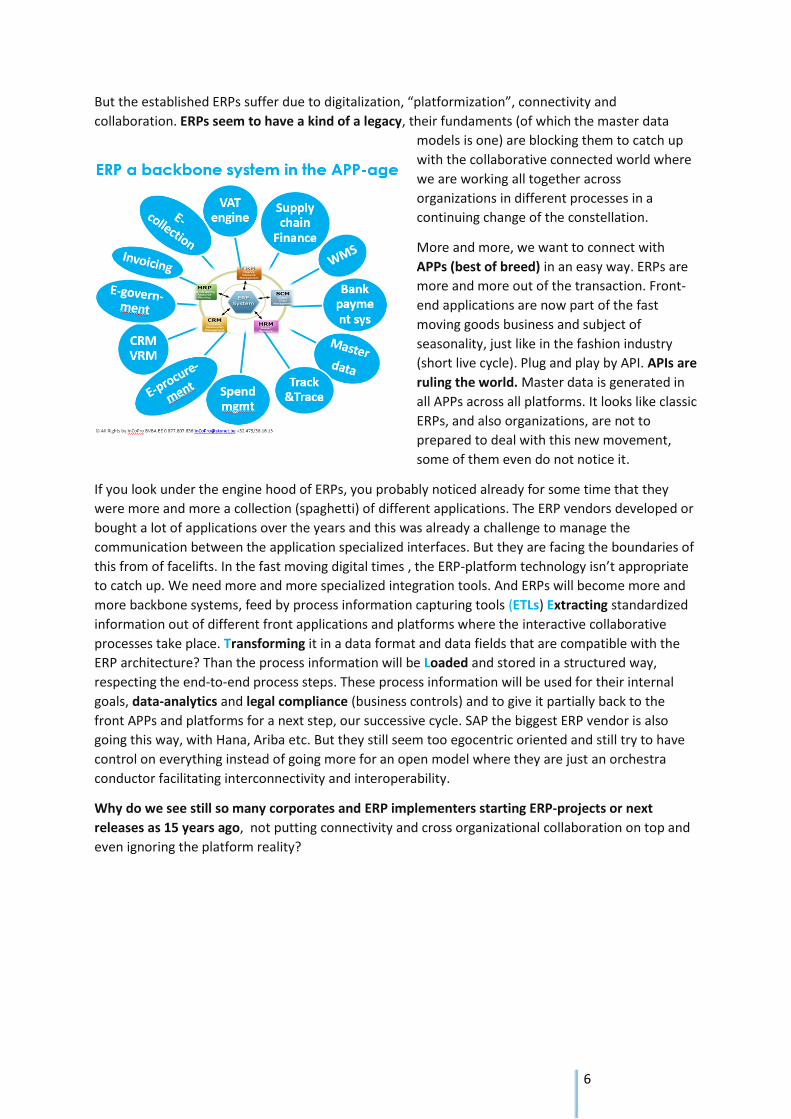

ERPs become backbone systems, gathering

standardised process data to fulfill the enterprise

needs on transactional process information, and

legal compliance.

6

But the established ERPs suffer due to digitalization, “platformization”, connectivity and

collaboration. ERPs seem to have a kind of a legacy, their fundaments (of which the master data

models is one) are blocking them to catch up

with the collaborative connected world where

we are working all together across

organizations in different processes in a

continuing change of the constellation.

More and more, we want to connect with

APPs (best of breed) in an easy way. ERPs are

more and more out of the transaction. Front-

end applications are now part of the fast

moving goods business and subject of

seasonality, just like in the fashion industry

(short live cycle). Plug and play by API. APIs are

ruling the world. Master data is generated in

all APPs across all platforms. It looks like classic

ERPs, and also organizations, are not to

prepared to deal with this new movement,

some of them even do not notice it.

If you look under the engine hood of ERPs, you probably noticed already for some time that they

were more and more a collection (spaghetti) of different applications. The ERP vendors developed or

bought a lot of applications over the years and this was already a challenge to manage the

communication between the application specialized interfaces. But they are facing the boundaries of

this from of facelifts. In the fast moving digital times , the ERP-platform technology isn’t appropriate

to catch up. We need more and more specialized integration tools. And ERPs will become more and

more backbone systems, feed by process information capturing tools (ETLs) Extracting standardized

information out of different front applications and platforms where the interactive collaborative

processes take place. Transforming it in a data format and data fields that are compatible with the

ERP architecture? Than the process information will be Loaded and stored in a structured way,

respecting the end-to-end process steps. These process information will be used for their internal

goals, data-analytics and legal compliance (business controls) and to give it partially back to the

front APPs and platforms for a next step, our successive cycle. SAP the biggest ERP vendor is also

going this way, with Hana, Ariba etc. But they still seem too egocentric oriented and still try to have

control on everything instead of going more for an open model where they are just an orchestra

conductor facilitating interconnectivity and interoperability.

Why do we see still so many corporates and ERP implementers starting ERP-projects or next

releases as 15 years ago, not putting connectivity and cross organizational collaboration on top and

even ignoring the platform reality?

7

For more info; slides Exchange Summit BCN October 5th 2015. The Impact of Platformization on P2P

and ERP-landscape: one of the presentations on http://www.vereon.ch/events/exc

3. Cloud-based accounting platforms will play a major role in

the digitalization of the “small-b” segment.

External bookkeepers were shared services centers long before corporates claimed the title for

their entities , often off-shored, centralizing large parts of the transactional processes of the financial

supply chain. The most external accounts still work on a batch principle with as a consequence a

mostly unbalanced cyclical workload without real collaboration and interaction with their client SME.

Onboarding the long tail of small companies is difficult and mostly without direct cost gains for the

SME. If you look more in detail to it, you will see that the processes are totally different from the

one’s of the corporates. Embarrassing is, that most law makers, lobbyists and political decision

makers are still reflecting on the processes as they are established by bigger organizations. Although

in mid-Europe the economy the SMEs(2) are by far the largest population.

2 More than 9 out of 10 (92.7 %) enterprises in the EU-28’s non-financial business economy were micro

enterprises (employing fewer than 10 persons) Eurostat Nov 2015.

8

By bringing small companies working on the same accounting platforms (not pure outbound

invoicing web-apps) in close real-time collaboration as their external accountants, we connect the

long tail segment automatically through the platforms in the digital business economy.

External accounts would not just offer Shared Service Centers but also a shared digital

collaboration platform to their customer base and interconnected them with the rest of the e-

business world. Incoming invoices would be brought to their SSC-platform (at the external

accountant) immediately

and not just the day before

the VAT-reporting deadline .

These platforms have to

deal with all existing

technologies to digitalize

documents (incl. scanning),

not only invoices but also

payroll, bank statements,

contracts, warranties, taxes

etc. It will increase the

visibility during the

accounting period and will

automate a lot of matching

work for the accountants

(ex.: payments done from

the platform and automated linked) and making the different manual follow-up-lists absolute at the

SME (ex. open standing customers and suppliers would be integrated), smoothing the workload

across the accounting period. The SMEs wouldn’t no longer have to deal with the different business

portals as their mutual platforms would offer them the opportunities (through interoperability) to

deliver the electronic business documents to the big buyers and suppliers, the governments but also

between their peers without doing anything special.

New accounting platforms are appearing as E-economic, Yuki using totally other basic concepts more

document oriented, but also the senior players transformed in 2015 and did more than just a catch

up as Exact online, who did a huge metamorphosis as well as Sage. But also Kluwer with EVA and

Winbooks are moving to real collaborative platforms, no way around.

If we can bring the SMEs working on the platform of their external accountants and if we can connect

these platforms with the corporates, we can gain access to the long tail easily and quickly and build

the fundaments for real digital business interactions without tremendous investments.

The everyday new appearing rather simple outbound invoice portals, often focused on the

segment of “small-Bs” should fear this evolution. The “Platformization” of accountants to the cloud

will expand fast, very fast. The outbound invoice portals should adopt their offerings and distribution

model. Otherwise they risk to be in the history books of digitalization, less relevant than the fax

machines, mentioned as valuable transition tools with a very short lifecycle and no ROI.

9

4. E-commerce is much more adopted in BtoB than we think.

It is impossible to imagine E-commerce out of our lives. One of the amazing confirmations we got

during the terror threat phases in Brussels, with the steep increase of 50% of the purchase through

the E-commerce channels at classic retailers as Carrefour and Delhaize. But E-commerce is not only

about BtoC , as you can see from the study below. E-commerce is also very famous for a lot of

companies, especially in indirect spends.

Amazing is that this evolution has some aspects of ”The Boiled Frog Syndrome”, slowly “E-

commerced” not noticing the process changes.

If you discuss this evolution with agents

from corporates they often stated in a first

reaction that their companies don’t use E-

commerce in indirect spends, until you start

asking how they order stationary, booking

business trips, books, office furniture,

standard maintenance spare-parts (screws),

ICT-appliances, security cloths , even coffee

and leasing cars are handled through

platforms.

We also see that spending on platforms, often gives a boost to the number of incoming invoices.

The hit of indirect invoice lines is nowadays often stationary and small maintenance parts, due to the

internet small amounts

ordered by all company

agents. It is my conviction

that this is an evolution that

is mostly unwanted and it

increases the AP-costs. It is

also often subject of extra

logistic charges for small

deliveries which can be

avoided by better

customizing the platforms

and processes.

10

The challenging opportunity for platforms is how to open the access to the long tail of e-shops for

our indirect spent without killing the flow of the business processes.

E-shops are often offering some price advantages compared to the classic indirect spend platforms

(ex the classic stationary companies). The problem is that we are in the long tail and the basic

principle of the long tail access is that the transaction cost should be nearly to zero.

11

This is a tremendous

opportunity for service

providers (iPAAS) offering

real end-to-end

collaborative process tool

and connectors with e-

marketplaces and e-

shops. (See also next

point).

Big players as Basware,

Tradeshift (acquires

Merchantry 08/2015) and

especially Coupa are

exploring this markets.

But also niche ERP players

as AXI surprised me in

2015 with their great

feature “E-Commerce –

Punch out catalogi” to

make the long tail

available into larger

organisations (in their case

a lot of public and

healthcare). Where I do

not judge whether this

specific approve is the

only way to reveal this long tail of E-commerce.

5. Order to Cash (OtoC) and Purchase to Pay (PtoP) are out,

one shared end-to-end Sourcing to cash (StoC ) is a new

platform paradigm.

With the actual configuration of our business processes based on the SoX and other models,

swearing by PO, GR, IR created in the own ERP, the transaction cost risks to exceed several times the

value of the bought on-line product or service. We can’t efficient and effective deal with continuous

changing relations in our classic master data management and business process models. Here the

BtoB providers can make some differences to explore the gains of indirect spend in the long tail of e-

shops. E-market places as Amazon, Bol.com, Aliexpress can also play a huge role in offering

appropriate API connectors. But what we need here is flexible end-to-end cross organizational

workflows in the cloud, settling the complete process, including payment (matching) and then

bringing the process data into our ERP as described above.

12

But this means that we have to be

open to more collaboration across

platforms and BtoB-service

providers and that we need more

interoperability and not just

exchange of documents but the

real-time transmission of events’

status. Let’s make the cake bigger.

(see also point 11: Portals aren’t

the endpoint: “We need invoices

to talk back, Portals are dead”)

6. Analytics:D2III data to information insights and impact

At InCoPro we executed most of our projects based on the D 2 iii methodology. We are gathering

Data and facts, structuring it to Information, crystalizing Insights from it and realizing Impact

defining concrete actions. Gathering data without impact is hallucination, costs money and is so

mostly a waste of cash.

Digitalization seems to generate an unavoidable by-

product that calls data and it seems to be more than we

can consume. The same is happening on BtoB-platforms

and at BtoB service providers, let’s cultivate it.

“Your digital shadow”(3)

3 Digital disrupt or die, Mark J. Barrenechea

13

And oooh yes service providers are working on it. Data Mining based products/services will

overwhelm us in the coming period as:

Payment habits will be monitored in BtoB but also BtoC

Credit rates will come available for BtoB based on data that is much easier to capture as the

classic rating agencies (as D&B, Graydon etc.) can with more relevance and less effort.

Spend analytics but also price comparison within sectors can be done, on product groups,

even product items.

VAT tax compliance audits

Creditworthiness based on social media acting, etc.

Risk management (financial, legal, procurement chain)

Fraud detection

Cash flow prediction

Automatic replenishment proposals of indirect spend

Automatic generated shopping lists proposals, also for BtoB

…

There are surely a lot of privacy issues to reflect but also a lot of social-economic gains. These must

be set-off against each other. For example fraud detection and insight in creditworthiness can avoid

bankruptcy, where there is mostly a substantial cost to bear by the remaining society, that is left with

unpaid invoices, taxes, unemployment and psychological traumas of involved people.

7. Say goodbye to conventional banking

7.1 Cashless society:

We have seen an increased move into a cashless

society and I believe this will continue in 2016, with a

further decline in conventional retail banking but not

necessarily without the banks (they are transforming

and can deliver the compliance and have the funds).

Sweden (4) is definitely in a leading position in going

to a cashless society, but in most EU countries you

notice this evolution.

Also mobile payment will increase and this will be

used in B-to-small-B and at E-commerce indirect

spend at corporates.

On the other side also corporate multi-bank payment platforms are transforming fast, as the Belgian

Isabel went mobile. This makes payment approval cycles much more flexible as a lot of payment

approvers (often CxO-level) are travelling.

4 KTH Royal Institute of Technology in Stockholm

14

7.2 The Blockchain technology

Whether or not you are a believer in Bitcoins, the technologic behind the crypto currencies which is

described as blockchain can and will be used in a lot of other financial processes. In the domain of

trade finance and documentary credit the block chain has been already explored.

We are convinced that there will follow more of cross industry financial supply chain processes as in

the recent presented car rent process of VISA, DocuSign and Hertz.

Visa and DocuSign (5) have

unveiled a new proof-of-

concept that uses bitcoin

blockchain technology to

revolutionise the car leasing

process, allowing people to

rent a car without having to

plough through reams of

paperwork. The project aims

to digitise the whole process,

from configuring the lease,

insurance and other expenses

like parking and tolls, to digitally signing and paying for the car itself. Everything is done on the

screen of the connected ar. https://www.youtube.com/embed/2rLNbd6MQXg

7.3 Paradigm Switch of Working Capital and the growth of supply chain finance

Supply chain finance aims to improve the financial efficiency of the supply chain and substantially

reduce the working

capital of both buyers

and suppliers. It allows

buyers to extend

payment terms while

providing suppliers access

to better financing rates.

It creates a true win-win

situation for the buyer as

well as for the supplier.

We clearly see a paradigm switch in BtoB where the suppliers are asking “to be paid NOW”. SME just

don’t have the means or access to working capital to finance their mostly bigger customers. As

especially for starters it is a hurdle on their growth.

Our working capital thinking has also something from a kind of schizophrenia. In private life we learn

our children to save first and then spend, we won’t transform the keys of our cars if it wasn't paid

before. But in professional life we act completely the opposite way.

5 https://youtu.be/2rLNbd6MQXg

15

At the other side there is in BtoC another

paradigm crystalizing: “I want to pay after

delivery”. A movement that might have negative

impact on cash. In The Nordics there are already

some platforms offering tools for it, as for

example Klarna (6). This paradigm will get more

impact once E-commerce of fresh food is

breaking through. The price of 5 bananas is only

known after they are picked. When I pay after

delivery for bananas, please also for the other

goods.

Supply chain finance is not reverse factoring, it’s much more. Reverse factoring is just a form of

supply chain finance, just like trade finance, consignation, cash-pooling, dynamic discounting

factoring etc. Please, dear marketers don’t misuse the word by making the reader myopic, what

stops him from process/system thinking.

“Inline (process) financing” is getting hot and is coming from the USA over the UK to central Europe.

The effective use nevertheless is still low but will grow. Some of the major problems I see for the low

expansion in central Europe are: member state compliance difference concerning VAT treatment of

cash discounts, regulation of financial institutes, but also the process complexity (invoice (supplier)

and approval process (buyer) capability dependency between the partners), a realistic rate-level,

more automated payment as USA (no checks, SEPA) etc.

8. Governments going digital Governments obligate to deliver e-invoices to their buyer platforms? More and more countries are

implementing obligations to deliver e-invoices to

governmental organisations. Austria, Italy, Spain

and Switzerland from 2016 on. In Belgium, the

Flemish region is explicit that they also will make it

obligatory by 2017.

Personally I’m not the great believer that an

obligation of the government is the best signal to

get traction on the digitalisation. The first

argument is that the impact of the governmental

organisation is not that big. Most retailers and

huge corporates are doing more invoices than

governments. As an example, the Belgian federal

government has 1.2 million incoming invoices, the

Flemish region nearly 0.7 million. To have a real

high impact on making the economy more digital,

6 Klarna: payments company lets customers try before they pay http://www.ft.com/cms/s/2/d881cb3c-f95e-11e4-ae65-00144feab7de.html#axzz3uatxnFzq; http://www.bloomberg.com/news/videos/b/c25a18a8-c4eb-4572-a97d-ab24e56fe85b

16

there is still missing focus on the added value for the counter partners, the collaborative aspects and

the automation of the related processes and documents.

If it comes to outgoing invoicing (they make a lot of invoices outside the tax notices ) than we see

that they are not so consequent, or not that far in the

digital journey. Will they send their invoices to the

different dedicated platforms of their customers (the

enterprises and private persons)? Wouldn’t it be a

logical consequence, walk the talk? Indeed, it will be

a challenge to deal with the complexity of these

millions of different connections, but isn’t it exactly

the same proportional complexity that all non-public

organisations and especially SME are confronted

with? Solving this would boost the digitalization, if it

is an open solution useful for the long tail inter-

relation and relations of BtoSmall-b and BtoC. In my

opinion, this is the challenge the governments need

to pick up. Also government suppliers could use it to deliver the invoices to them and it would

improve the adoption rate in their PtoP-process and the whole society.

Has anybody obliged you to use a mobile phone?

I encourage everyone to learn from the mobile phone

explosion. Has anybody obliged you to use a mobile phone?

I don’t think so. But due to the network coverage, the

interoperability across providers and nations, the use has

been spread. Being part of the network was important.

Everybody has his provider, I don’t have to go to a specific

portal (in the old days the booth), you don’t have to know

which provider your conversation partner is using,… You just

need his digital address (phone number), a network and

collaboration between the providers who deals with the

connection problems.

Stimulating investments in digitalisation of the financial supply chain:

Belgium granted to SMEs extra tax deduction for investments in E-invoicing, an example that could

be followed by other countries.

A Belgian Royal Decree of December 2, 2015 (Belgian Official Gazette December 8, 2015) extra tax

compensation for digital investments. It aims to support an increase in investments by SMEs in the

domains of digitization of commercial operations and cyber security. The Royal Decree defines the

different categories of investments eligible for the investment tax credit for digital investments.

With regard to digital assets that serve for the integration and exploitation of digital payment and

billing systems:

1 ° investments in systems (hardware or software) that facilitate electronic payment;

2 ° investments in systems (hardware or software) for electronic invoicing, signature or archiving.

17

The investment allowance is a tax advantage whereby 13.5% of the invested amount is deducted

from the taxable profit once.

A standard for the public sector risks to become just one (more ) of the standards.

A lot of people believe a general standard for E-invoicing

will make the adoption expand from itself, but I’m not

convinced that even 1.000 different standards would be

the biggest hurdle to overcome, as long as the mandatory

fields are present (which mostly is the case) and the

semantic and syntax documentation is available.

For me, the lack of connectivity and inter-collaboration is a

prior hurdle to overcome. Providers will do the mapping

and conversion where necessary. That is for a lot of them

one of their original core business.

If you stand on a bridge (as on the picture)

the type of car (the format) is not the

problem, the lack of connection taking you

from continuing your digital journey, seems

to me more important at that moment.

The standard semantic is from the

beginning mortgaged by the non-

harmonized national legal obligations in the

different EU-member states, to be used

outside the BtoG.

The lower attention to end-to-end VAT-obligations (record to report) and the process difference between corporates and SMEs often with external accountants. Although a lot of public organisations are more VAT-registered.

The new standard developed for BtoG seems not to deal with discount calculation which is subject of non-harmonized legislation, but is on the other hand intensively used in BtoB and BtoC.

The standard seems not to reflect self-billing, a technique that is more and more used to simplify the billing process in the long tail, also at governmental organization. Self-billing is also a great example of non-harmonized obligations in the different countries.

In paralleln there is also a standardization workshop going on about CENBII/3 used by Peppol.

18

The increased interest in hybrid formats (a syntax) in Central Europe.

Hybrids are indeed getting more and more attraction in Germany, France but also in Belgium. In Belgium there is the specific format e-fff (form for the future of accountants). E-fff is based on UBL and was at the start an XML with embedded XML and changes now to PDF with embedded XML. I’m very pleased with this change, although I’m not involved in the e-fff workgroups. The transition

phase we are in (still for a few years), seems to me a way to support interoperability, interconnectivity and legal compliance. The latter are huge challenges and create at least a feeling of an increased complexity (multi-way). To start, hybrids do not exclude the use of pure XML neither PDF and even paper. For me it all depends on the segment and the segment should be materialized enough for a specific approach. The same argument counts for the next hybrid discussion about the XML with embedded PDF or the PDF with embedded XML In environments where the focus is on highly automated processes, where the invoice is automatically approved based on previous events and documents, the PDF should indeed perhaps be not in the front. More interesting details can be found on iTEXT info search on ZugFeRD.7

9. VAT-compliance an increasing challenge

2015 is indeed a year where legal compliance got more attention. Uber was disrupting the taxi industry, quote by many people, but is Uber in 2015 not disrupted by his non-compliance?

I notice that they take back their development in most Central European countries. But it woke up the tax-administrations who are now realizing that there is not a real difference between digital platforms and the physical world. They realize that the sourcing industry is not new. What is the real difference between a tour operator and AirBnB and between an interim agency and Uber? Platforms

7 ZUGFeRD overview: http://www.slideshare.net/iTextPDF/zugferd-an-overview More about the technic of hybrids in “ZUGFeRD The new standard for invoicing” an E-book of iTEXT : http://pages.itextpdf.com/ZUGFeRD.html

19

will be in the focus of the taxman in 2016. All sharing and sourcing platforms need to be aware the times changed. Also marketplaces and BtoB platforms will have to do their reflections on their liability.

There is a huge understanding gap about VAT-compliance between “Form-compliance” and “Content-compliance”. Most platforms offer services for Form-compliance (mandatory files filled out and digital signature where necessary, etc.).

Content-compliance is about checking whether the invoices respect the rules of VAT (correct %, correct exemptions, correct reference to exemption rules etc.). As tax authorities are going more and more to line item control (SAF-T8; VAT-books, even in real time 2017 in Spain; Germany with GoBD and DaRT). Data mining isn’t just hot in BtoB also the tax administrations are more than exploring it, they are even experienced in the meantime.

VAT-Content compliance is getting more and more attention,

especially from large buying organizations who don’t want not content-compliant invoices entering their premises. They want to avoid dealing with the correction cycle (wrong invoice , credit note, correct invoice) and want a gatekeeper to avoid compliance issues with tax-administrations losing their deduction increase with interest and penalties.

VAT-compliance is a nightmare for E-commerce, but end to end automation (from VAT-registration in a country to declaration) can help. Buying organisations will have to put more control on VAT-content compliance of incoming invoices especially when exploring the long tail of changing supplier relationships (in indirect spend through e-market places).

8 SAF-T (Standard Audit File for Tax) is an international standard for electronic exchange of reliable accounting data from organizations to a national tax authority or external auditors. The standard is defined by the Organisation for Economic Co-operation and Development (OECD). The file format is based on XML.

20

Inline automated VAT-compliance monitoring within the PtoP process can bring protection in a world where tax-auditors are looking on a line item level. Spain announced that from 2017 the SII/IIS

(Immediate Information Sharing)9 will be in place, obligating companies issuing or receiving an invoice, they must send the information to the tax office within a maximum of 4 working days.

Why an iVAT Engine and content compliance?

• Data mining is hot • VAT returns to be filed in Spain electronically in real time 2017 • Periodical SAF-T files in PT 2014 • SAF-T capability in France and Luxembourg • DaRT capability in Germany GoBD 2015 • E-commerce is in focus of the taxman and is complex and important in BtoB

9 The so-called IIS (SII) is a VAT (Value Added Tax) management platform, based on the real-time reporting of company business transactions. Every time a company issues or receives an invoice, they must send the information to the Tax Office within a maximum of 4 working days. These invoice details will be provided in the form of VAT record books, which contain the essential information on the invoices and can be managed through the electronic systems and solutions linked to the Tax Agency platform.

21

10. An e-invoice is a strong communication channel with the

customer An invoice is also a communication tool. The essence of an invoice for a supplier is to inform his customer that he executed his part of the contractual agreement and that it is now to the customer to fulfill his part, the payment. A nice supplier specific lay-out can then be very supportive. Most customers in BtoC and BtoSmall-b who are also the decision makers are mostly looking to the invoice with more than an average attention rate. A lot of companies already used this

document to communicate about the next step in the customer journey. But also to give general information such as address changes, new products, holidays, special actions. That is also why we should not forget the importance of the lay-out of an invoice. I learned over the years that at each billing implementation a more than expected (even unreasonable) time went to the lay-out of the invoice where the marketing department and often the CxO level was involved. The invoice also plays a very important role in the dunning process, when copies of the invoice often must be resend. Readable form and proper

lay-out are also very important at that moment. But an invoice can also be used for gamification to get cash earlier or to collect Taxes (Corporates can learn from the Portuguese TAX-gamification) and naturally to payment facilities (Hyperlink, QR-codes etc). It can also bear a link to the next customer journey as: links to product warrantee, user guides and user groups. We see an increased number of players which are working around invoice communication in the OtoC cycle and the dunning and incasso process. An incasso process, even a digitalized one, is taking place out of the normal processes, a proper invoice lay-out is than very important, because in this stage it is definitely all about the communication. The invoice appearance should stay under the control of the sender in a lot of segments, because it has a more than average impact on a lot of related processes. That is why Hybride invoice models can play an important role in a lot of segments. Don’t forget that in the small-SMEs world there is mostly no PO system or related documents and the reader is also the decision maker. Even in corporate land we can see that people are more comfortable with approving original digital copies than with standardized representations of the digital content. Supplier specific invoice lay-out helps to increase the speed of solving the exemptions. Also in fraud detection a company specific layout helps.

22

“Only through mobile, merchants can be present in the pocket, the home and the heart of the customer, at all times !”10 It is all about the process and not just the automation for the automation. One can say that this is all not the goal of an invoice but it is a practical factual use of invoices which we cannot stop that easily. And why we should? I can recommend; do more with your invoice, use the attention the digital communication is even more with pictures than ever before.

10 Doccle at BeCommerce Summit 2015:” How big is your e-Commerce business ?”

23

11. Maturity, specialization and concentration

At the beginning of 2015 we made a post about the Consolidation and Concentration movement

that we felt in the market of e-financial supply chain providers. We asked you to fasten your safety

belts and yes there were a lot of announcements which are regularly added in the post and

comments.

www.linkedin.com/pulse/consolidation-digital-business-world-e-invoicing-e-fsc-jos-feyaerts It were mostly bigger players who were involved in the M&A. What with all those smaller often national or even regional players in the market? Can they survive? Will they be eaten by the established players? True questions but more difficult to observe. A lot of these smaller players come and go and even merge without being noticed because no official announcements are made. One thing is for sure, a lot of them will have difficult times to survive, due to the need of mammal scale to be fundable and long lasting. The digital financial supply chain is in expansion in crowd and users but also in technology. This latter makes feature lifecycles short and huge needs in investments of resources, compliance and market development. SAAS is fantastic but not for the provider as he is bootstrapped by the cash investments in market deployment (sales efforts) with future cash flows (no upfront license fees) and a lot of investments in R&D. But besides the M&A we also see more and more collaboration between the providers and specialization focus. This shows that the market is coming to maturity. Collaboration and specialization are a typical sign for it. Look at the car industry? What is the difference between an VW, BMW, Audi, Ford, Peugeot, FIAT etc? They are all developed by and in collaboration with the same OEM suppliers, they exchange and share spare parts, engines, platforms and models. Isn’t it a consortium of Audi, BMW and Daimler who bought in the summer months the HERE map service from Nokia for $3 Billion? The same trend to more specialization, collaboration and willingness to interoperability can be noticed in the service provider sector. And we are very pleased with it. More collaboration and interoperability will make the cake bigger. We should stop fighting about slogans as “Open” and start real collaboration. It is in the end the customer who will decide which platforms and technologies he wants to work together, and not the providers. The crowd is always right (often). Fighting for the angle of the piece of the cake is probably not that efficient as we can increase the radius of the digitalization cake to so many more aspects of the e-business by specialization, collaboration and interoperability. Decreasing the angle by ex. 10% in sharing the cake with more specialized partners, to increase the radius of the cake with 5% will give a fantastic boost to the market as the cake surface is R*R*π. So let’s focus on the radius from 2016 on.

Services providers will explore more and more services. Some of the areas where we see traction:

SCF: dynamic discounting, reverse factoring, trade finance (ex e-LC), etc.

Integration with invoice markets

Invoice clearing (ico payment factories, cross industry)

24

Multi bank payments

More and more payment remittance

E-commerce connections

Data Mining :

spend analytics

spend advice,

replacement of indirect spend

credit rating and payment experiences (BtoB and even BtoC)

fraud detection

spam indicators for fake invoices (ex. recognizing changed Bank Account or suspicious ones)

etc.

Risk management in the supply chain

Cloud scanning and cloud capturing (CAAS, capturing as a service)

VRM (vender relation management, master data exchange and control on use.

E-collection and E-incasso

Credit insurance

VAT Content Compliance; VAT Form Compliance and legal archive

Support to government clearing models (Spain 2017)

Services to support business controls and audit trails and SAF-t compliance in a platformized world

Blockchain technology to connect processes (example car rent end-to-end)

Invoice marketing and invoice communication

Extending the customer journey to product warranty, contracting, user guides, etc.

Exchange of track and trace of logistics for my indirect spend

More and more event and status exchange across platforms in state of pure document exchange and portal exploitation (real collaboration in my unique environment)

Etc.

By means of example, we list some of the specialists we see on the Belgian market who could collaborate and serve each other and other platforms in this area. Sorry to forget important tools and yes there is some support for my Belgian compatriots behind it. The same specialization could be seen for other players outside Belgium.

Arco with his CAAS (capturing as a service)

AXi: “E-Commerce – Punch out catalogi”

Nallian : for VRM and master data exchange and controle.

Sector specific platforms as e-Health asbl/vzw created on 2004, March 30th is an association grouping 31 suppliers from Pharma.be and Unamec.

Edbex an Invoice Markets:

VAT Applications: Comp. AAS (VAT content compliance as a service)

Graydon: company ratings

Data.be: official company records and financial info

Datastories: Data-analytics:

Datascouts: DATA analyses with GIS and MAP display

iController: Digital Collection

Doccle: with his document collaboration model for BtoC and BtoSmallb

Isabel: Payment platform

POM: Pay your invoices in one click.

CODA: dematerialize and process of the other documents Bank, Pay-roll etc

25

Atradius with his Cashfirst online credit insurance

ExArte: ERP focused solutions for Mircorsoft Dymanic integration tools

Babelway for his format mapping services as OEM

Lean Pricing: pricing consulting subscription economy and SAAS-providers

KBC with his click shop e-marketplace

Xpenditure with his out of pocket administration tools

Sign2Pay: authenticated with your signature for contracts, to sign in for a service , payments

Etc.

12. Portals aren’t the endpoint: “We need invoices to talk back”

Portals are walls with limited visibility and not the optimal collaboration in the supply chain.

The portal history was boosted in the accounts payable with the huge invoice senders

obligating the customer to come and get his invoice on the portal of the seller. The AR-

departments were

optimizing the

distribution cost but often

increasing the efforts for

the receivers. The buyers

learnt quickly and had

more power, and started

to oblige the supplier to

bring the invoice to their

buyer portal, optimizing

their AP process where

most corporates (often

the same) seem to be

convinced to win much

more. But still this isn’t an

optimal situation for the

end-to-end process across

the partners (buyer and seller). Buyer portals are often, in my opinion, an obligated puzzle piece

in the transition phase, but the possible gains for the eco-system seems to reach the boarders.

They are starting to suffer from and becoming the victim of their own popularity. Every large

corporate has his own portal.

For many medium players (suppliers), dealing with all those different buyer portals where they

have to communicate on, are faced with real bottlenecks, inefficiency and ineffectiveness in their

AR-process. Many of the mid-segment suppliers are confronted with up to more than 20

different portals to deal with all of their customers. This phenomenon is also killing the

deployment of the next services in the supply chain as SCF-tools. How will I manage my invoices

finance trough twenty different portals?

We need more information exchange across portals, platforms and providers and that is indeed

more than exchange of documents. It also means exchange of process event information and

status from the actions taking place in shared cloud-platform (for example E-commerce),

between interoperable platforms and the processes at the supplier eco-system and those at the

buyers ecosystem. This exchange of events will be explored more and more by the providers, as

26

this is a way they can let the cake (e-market) grow and, in combination with the previous

mentioned specialization, improve their future and remuneration (monetize) model.

A nice recent quote in this context from Douwe Lycklama “We need invoices to talk back”.

“Wouldn't it be great when outstanding invoices would communicate their status at the

debtors in real time back to the original sender (creditor)?”

More of my thoughts on this, you can learn from my slides of the exchange summit 2015 in BCN

October 5th,2015 about "The impact of platformization on P2P and ERP landscape" especially

slides 15-26): www.vereon.ch/events/exc

Peppol’s network is getting more attraction.

E-invoicing alone will not bring a lot of advantages to SMEs if we cannot automate the related documents and processes (payment, bank contracts, payslips, warranties, taxes, etc). Obligating delivery without network, is not a mutual

benefit. Governmental obligation to deliver invoices to portals is like obligating people to go with a taxi (paying for a service to convert a PDF invoice to a XML) or by feet (register it on the portal) to a phone booth in an age where cell phones are possible, because we don’t invest first in a network.

Last phone booth in Belgium was removed on 1st June 201511

Belgium government will put effort on deployment of Peppol in the first quarter of 2016, following the Nederland’s with Simplerinvoicing. I hope that if they obligate anything it is in the first stage the connectivity with Peppol of providers of platforms, ERP and larger accounting packages. Where from my point of view they can do it on their own or through a collaboration with an existing OEMs. I still hope that the Belgian and Dutch Peppol community becomes a single BENELUX Peppol community with unified forces joining forces and resources for further developments.

11 Last phone booth in Belgium removed on 1st June 2015

http://www.gva.be/cnt/dmf20150601_01708233/laatste-telefooncel-van-het-land-weggehaald

27

13. E-invoicing was driving far too long by technology due to the

“e” in e-invoicing

E-invoicing and digitalization of the financial supply chain was driven far too long by technology providers. No one should blame them. We should be happy they did it. But I’m convinced that we, on the business side, are now to bring or part into the play and take more than ever a leading role. The technology is a tool, a mean to reach the goal not the ultimate purpose of our digitalization journey.

It is all about the process, where people act in it and tools are facilitating the actions to be done. That is not new. But the awareness that the network is also part of the journey is still missing in a lot of ERP and business process automation projects. The network must be open, interconnected and interoperable across platforms, software versions and devices.

We are in a transition not in a revolution. In a transition it is all about segmentation and change management. The best technological technic will not always win, that’s how it was in the past and is

28

also now. We must reflect on the end-to-end process systems and the scaling possibilities. Far too much startups and technology partners are not aware of the habits and existing use of documents. I see that a lot of people even are not aware anymore of the most important essence of an invoice, communicating that I did my job and you have to pay me. The communication aspect of invoices is important in this fundamental role and a lot of people are ignoring this. As I mentioned before, it was used a lot for attracting people’s awareness on simple events such as holidays, products, and in some sectors as delivery confirmation by signing it off. Making the invoice in XML need to replace even this simple process. Denning these habits and perhaps at first look strange uses, makes that people do not understand why it is so difficult to change to perfect in the backyard XML exchange.

So please let 2016 be the year that the CFOs become CDOs and take back a leading role in the digitalization of the (financial) supply chain. Digitalization of the economy has tremendous impact on corporate finance, not only on Working Capital12. The change to service oriented economy where car makers aren’t selling cars, but offering mobility will have a huge impact on all financial aspects.

‘Design for Margin’ (D4M) should get back the focus as the margin is the fuel for your future cash flows.

12 For more reflection look at my presentation and blog text „Die Digitalisierung der Financial Supply Chain: Auswirkungen auf die Unternehmensfinanzierung und das Umlaufvermögen“ http://www.basware.de/blog/die-digitalisierung-der-financial-supply-chain-gastbeitrag-jos-feyaerts

Remember John Gall’s Law

“A complex system that works is invariably found to have evolved from a simple system that worked. A complex system designed from scratch never works and cannot be made to work. You have to start over beginning with a working simple system.”

29

14. Everything is relative, nothing is absolute It is indeed all about perception and perspective, don’t blame me for trying to find new trends with you. The 7 Worst Tech Predictions of All Time13

1. "I think there is a world market for maybe five computers." Thomas Watson, president

of IBM, 1943

2. "Television won't be able to hold on to any market it captures after the first six

months. People will soon get tired of staring at a plywood box every night." Darryl

Zanuck, executive at 20th Century Fox, 1946

3. "Nuclear-powered vacuum cleaners will probably be a reality within ten years." Alex Lewyt, president of Lewyt vacuum company, 1955

4. "There is no reason anyone would want a computer in their home." Ken Olsen, founder of Digital Equipment Corporation, 1977

5. "Almost all of the many predictions now being made about 1996 hinge on the Internet's continuing exponential growth. But I predict the Internet will soon go spectacularly supernova and in 1996 catastrophically collapse." Robert Metcalfe, founder of 3Com, 1995

6. "Apple is already dead." Nathan Myhrvold, former Microsoft CTO, 1997 7. "Two years from now, spam will be solved." Bill Gates, founder of Microsoft, 2004

15. 2016 the year to talk back

We wish you an inspiring year-end of 2015 and a successful 2016 where you can realize the impact

you want to achieve, but above all a lot of fun and a good health.

Keep on focusing, registering and crystalizing your journey

See you in 2016!

Jos Feyaerts

Your digitalization guide InCoPro bvba, ‘Design for Margin’ (D4M)

13 Source: http://www.pcworld.com/article/155984/worst_tech_predictions.html?page=2