Development of a Business Plan Malaria Bond of a Business Plan Malaria Bond Task Force on Innovative...

29

Development of a Business Plan Malaria Bond Task Force on Innovative Financing Resource Mobilization Sub‐Committee November 2011

-

Upload

hoangthuan -

Category

Documents

-

view

219 -

download

1

Transcript of Development of a Business Plan Malaria Bond of a Business Plan Malaria Bond Task Force on Innovative...

Development of a Business Plan Malaria Bond

Task Force on Innovative Financing Resource Mobilization Sub‐Committee

November 2011

2

Contents 1. Executive summary ............................................................................................................................... 3

1.1 Introduction ........................................................................................................................................ 3

1.2 Description .......................................................................................................................................... 4

1.3 Cost and benefits ................................................................................................................................ 4

1.4 Principles ............................................................................................................................................. 4

Pay‐for‐performance............................................................................................................................. 4

Securitization ........................................................................................................................................ 5

2. Set‐up options and budget ................................................................................................................... 7

2.1 Set up options ..................................................................................................................................... 7

2.1 Set‐up budget....................................................................................................................................13

3. Global Health Metrics .........................................................................................................................14

4. Governance and organization............................................................................................................. 15

5. Marketing and communication plan................................................................................................... 17

6. Key success factors and immediate next steps................................................................................... 17

Annex B – Estimation of set‐up and ongoing costs based on IFFIm benchmark ........................................ 21

Annex C – Possible indicators ..................................................................................................................... 24

Annex D – IFFIm’s governance structure .................................................................................................... 28

3

1. Executive summary

1.1 Introduction Malaria is a major global health burden for the developing world. The World Malaria Report 2010 estimates that around 255 million episodes of malaria occurred in 2009, resulting in more than 789,000 deaths. Children under the age of five account for the majority of malaria‐related deaths. The majority of this burden is shouldered by those living in Sub‐Saharan Africa, where 91% of global malaria mortality occurs. It is estimated that each year Africa loses USD 12 billion due to malaria in both direct and indirect costs.1

Progress has been made in addressing malaria in the last decade. Malaria programs have delivered remarkable improvements. For example, a total of 400 million insecticidal nets have been procured by 2010 (up from 5 million in 2004) and 490 million ACTs were procured in 2008‐2010, up from 2 million in 2003. As a result of these and similar engagements 43 countries have slashed malaria deaths by more than 50% since 2000, 11 of them in Africa. Successful malaria control requires bold, decisive steps to achieve widespread coverage within a short timeframe. This should be followed by a period of well‐supported public health services to maintain improvements.2

Increased funding is required to consolidate and enhance progress. The fight against malaria is far from won. There is a risk that funding will ebb away once malaria prevalence has decreased, thereby threatening recent progress. Traditional donor funds should be complemented by new sources, such as the private sector or financial investors, to maintain and expand programs.

New approaches should be pioneered to implement and manage malaria programs. Besides raising new funds, the malaria community should stretch existing scarce funds as far as possible. New interventions and approaches are required to create incentives for all parties to operate in the most effective and efficient manner.

A pay‐for‐performance malaria bond has the potential to enhance efficiency and tap into the private investor market to help to mobilize funds by 2015. A bond can attract new sources of funding thereby reducing reliance on traditional donors. It can also help redistribute risks amongst stakeholders. Moreover it can set new performance incentives for implementers. Overall, a pay‐for‐performance bond can attract more resources to the fight against malaria, and incentivise more effective spending. Ultimately, it can save lives.

The malaria bond is an innovative, first‐in‐its‐kind and unique mechanism that if successful will be a major leap for innovative financing in the malaria space.

1 World Health Organization, World Malaria Report 2010 2 Towards near zero deaths by 2015. Effective interventions and addressing challenges. UNITAID Consultative Forum, Geneva 4‐5 October 2011

4

1.2 Description The most promising option is a mechanism where a donor fully pays only if implementers deliver results. As the implementer requires additional funds to complete the interventions, the bond allows the implementer to borrow these funds from socially‐minded private sector investors. The bond creates value by realizing cost‐efficiencies in funds disbursement, funds allocation and/or program implementation. These cost efficiencies are realized by aligning the incentives of donors and implementing agencies through pay for performance. Monetary contribution and financial risk incentivize the implementer to increase efficiency, and may ultimately translate in reduced payments by the donor for the same intervention.

1.3 Cost and benefits The malaria bond’s possible benefits are the following:

Lowering costs of malaria interventions, by paying for performance and thus aligning incentives and stimulating cost efficiencies

Tapping into the private investor market, thus potentially freeing up donor resources

Strengthening the development and economic growth of endemic countries, as increased malaria interventions will have strong societal benefits, for example by lowering health care costs due to decreased hospitalization and by enhancing workers’ productivity in the long run

The bond aims to reach these objectives by measuring and compensating performance, and by dividing the risks and returns across a range of stakeholders, including private sector investors.

1.4 Principles

Payforperformance

Principles Description

The implementer should be financially accountable in case of failure

For pay‐for‐performance to succeed, the implementer should carry a financial risk. They need to contribute part of the upfront investment, which would only be reimbursed, with an additional compensation for the risk carried, in case of success. This is needed to set the right incentives, achieve cost efficiencies and build investor confidence

In theory, the implementer could be a non‐governmental organization (NGO), a private sector provider, or another implementing organization such as the Ministry of Health (MOH)

In practice, NGOs and MOHs can be denied bonuses or future disbursements, but most of them cannot be held truly financially accountable for failures, due to a lack of cash reserves

Private sector entities and international organizations can make upfront investments from their equity/cash reserves, and therefore can more easily share the financial risk

Runesb

Highlight

Runesb

Highlight

5

Performance indicators should focus on outcomes and outputs

The pilot study will be based on output and outcome measures, as they bring greater attribution, objectivity, reliability and cost‐efficiency

Changes in results of impact‐based indicators are harder to attribute to the specific interventions financed through the malaria bond.3 Furthermore, it may be more costly to collect and analyze the data needed to evaluate the results. It would be harder to have a bond with a shorter time to maturity (such as 2‐3 years) as impact takes time to manifest

While we should initially measure and reward based on outcomes ‐ the impact can still be articulated by e.g. the Lives Saved Tool (LiSTl). The LiST model allows users to set up and run multiple scenarios to estimate the impact of different interventions and to set expectations on potential results

Securitization

Principles Description

Private sector investor expects return of the principal

Donors prefer to place as much risk as possible with the private sector investor, and have them incur as much of the failure costs as possible

However, the private sector investor might be reluctant and risk‐averse to lose their principal investment. The feasibility and acceptance of the pilot bond will be higher if there is guaranteed return of at least the principal to investors

Investors might have more appetite for social impact investment when there is “no downside” but only potentially a “lower upside”

In addition, part of the cost of the malaria bond is linearly correlated with the risk to the investor, as higher interest needs to be paid to compensate his risk. However this higher interest should be seen in the context of greater cost‐efficiencies

o Investors will demand increased returns for increased risk (e.g. difference between pay‐off in terms of failure vs. pay‐off in terms of success)

o For example, in the case of a guaranteed return a private sector investor might demand only 2%. However – in the case where an investor can lose the principal upon failure, he may demand a 10% return upon success.

o The return that the donor has to pay to the investor in case of success is an additional cost to the mechanism, compared to the cost the donor would have carried by investing directly. This cost should be seen in the context of the additional benefits of greater cost‐efficiencies triggered by the pay‐for‐performance mechanism. Therefore the mechanism can work only if the benefit of greater

3 The results of impact‐based indicators are highly influenced by external events such as weather patterns, or by similar interventions of other implementers.

6

cost‐efficiencies is higher than the additional cost.

The malaria bond could potentially be structured with two kinds of bonds, one for investors who seek guaranteed principal, and one where the principal is at risk. More aggressive risk‐sharing setups with investors could furthermore be explored in later bond issues (after the pilot)

Donors will likely have to remain traditional bilateral donors

Additional opportunities will be explored

Bilateral donors will be interested in the pay‐for‐performance component

Private sector companies have in addition been suggested as potential donors. The Taskforce will further explore in a concept note the potential to engage companies by identifying specific opportunities.

The bond issue should likely have time to maturity of 2‐4 years

The timeline of the bond should be long enough to allow programming of interventions and results measurement. This would likely require a minimum of two to four years

The bond issue should likely have a minimum size of $50 million

The issuing agency will incur significant costs related to the set‐up and management of the malaria bond. These costs will include transaction costs, legal costs, marketing and sales expenses

The objective should be to keep the set‐up and ongoing costs at 2‐4% of the total bond value

Donors might accept a pilot with a smaller scale or at a higher relative cost percentage

The International Finance Facility for Immunisation’s (IFFim) operational management costs were USD 22 million over four years, or 0.6%4, 5

To compensate for transaction costs, the minimum scale of the bond issuance should take into account the implied size and scale of the interventions, as well as investors’ demand

4 HLSP, Evaluation of the International Finance Facility for Immunisation, June 2011. IFFIm has operational costs of 0.6% and borrowing costs of around 4%. 5 In comparison, the management fees for alternative investment vehicles are usually 2%.

7

2. Setup options and budget

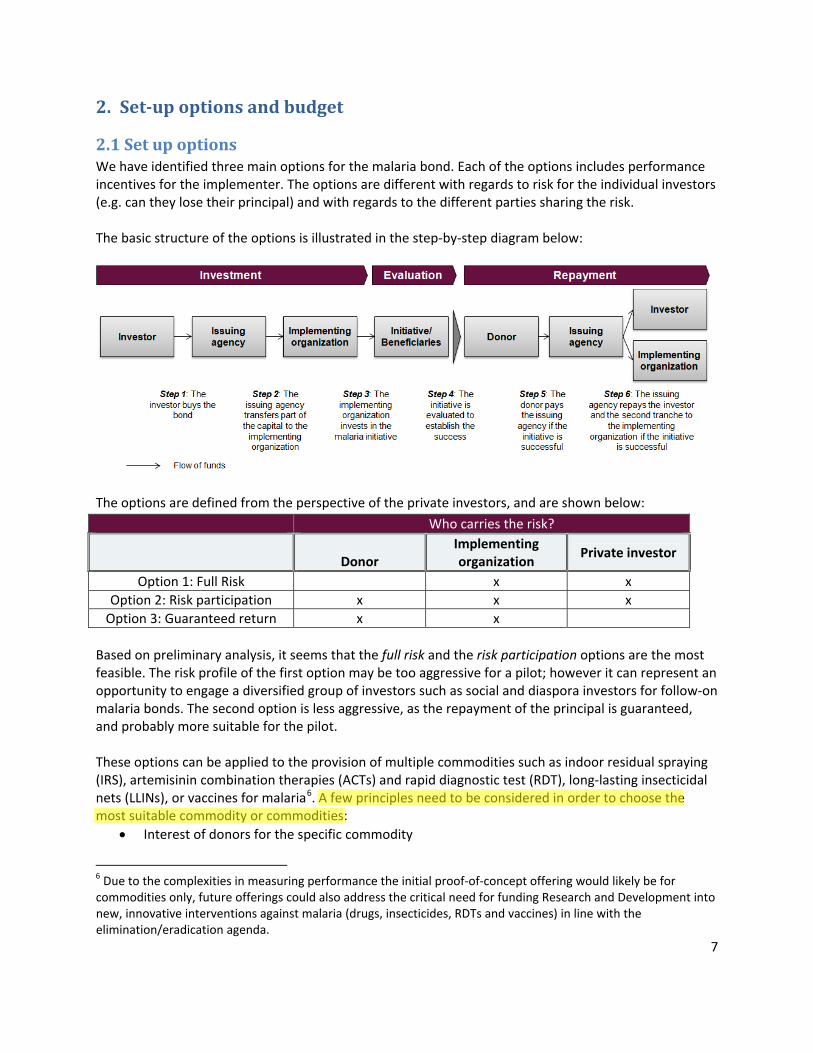

2.1 Set up options We have identified three main options for the malaria bond. Each of the options includes performance incentives for the implementer. The options are different with regards to risk for the individual investors (e.g. can they lose their principal) and with regards to the different parties sharing the risk. The basic structure of the options is illustrated in the step‐by‐step diagram below:

The options are defined from the perspective of the private investors, and are shown below:

Who carries the risk?

Donor

Implementing organization

Private investor

Option 1: Full Risk x x

Option 2: Risk participation x x x

Option 3: Guaranteed return x x

Based on preliminary analysis, it seems that the full risk and the risk participation options are the most feasible. The risk profile of the first option may be too aggressive for a pilot; however it can represent an opportunity to engage a diversified group of investors such as social and diaspora investors for follow‐on malaria bonds. The second option is less aggressive, as the repayment of the principal is guaranteed, and probably more suitable for the pilot. These options can be applied to the provision of multiple commodities such as indoor residual spraying (IRS), artemisinin combination therapies (ACTs) and rapid diagnostic test (RDT), long‐lasting insecticidal nets (LLINs), or vaccines for malaria6. A few principles need to be considered in order to choose the most suitable commodity or commodities:

Interest of donors for the specific commodity

6 Due to the complexities in measuring performance the initial proof‐of‐concept offering would likely be for commodities only, future offerings could also address the critical need for funding Research and Development into new, innovative interventions against malaria (drugs, insecticides, RDTs and vaccines) in line with the elimination/eradication agenda.

Runesb

Highlight

8

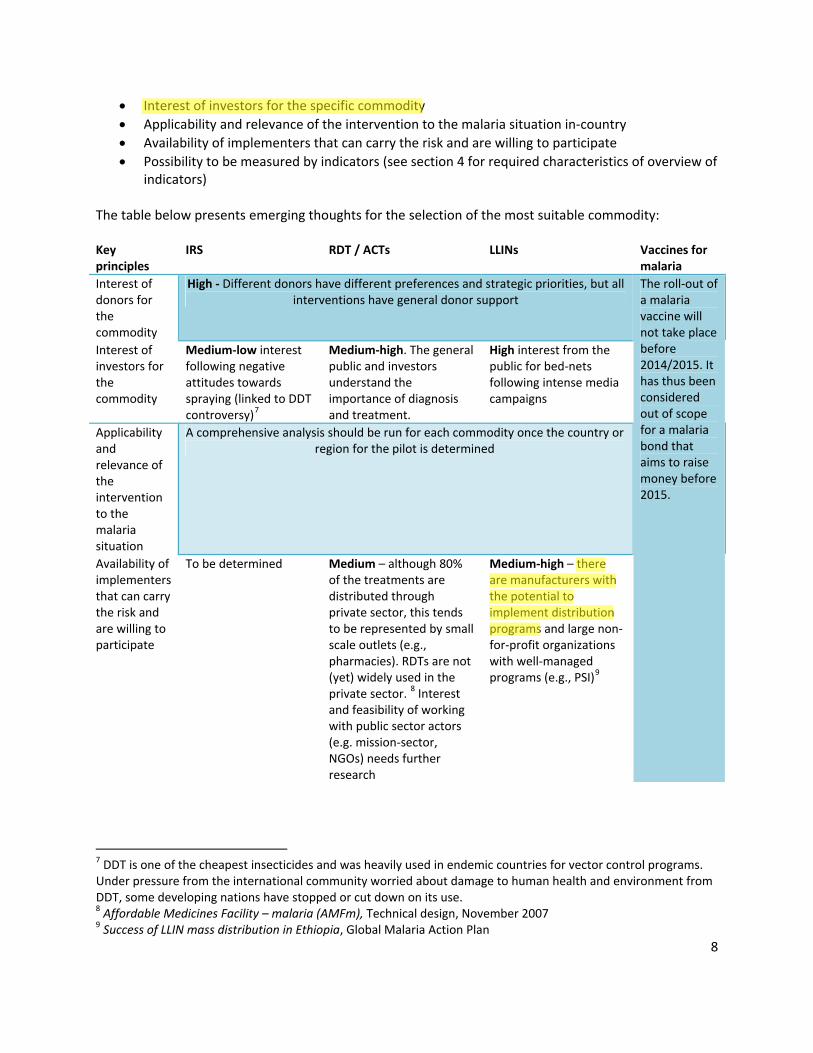

Interest of investors for the specific commodity

Applicability and relevance of the intervention to the malaria situation in‐country

Availability of implementers that can carry the risk and are willing to participate

Possibility to be measured by indicators (see section 4 for required characteristics of overview of indicators)

The table below presents emerging thoughts for the selection of the most suitable commodity: Key principles

IRS RDT / ACTs LLINs Vaccines for malaria

Interest of donors for the commodity

High ‐ Different donors have different preferences and strategic priorities, but all interventions have general donor support

Interest of investors for the commodity

Medium‐low interest following negative attitudes towards spraying (linked to DDT controversy)7

Medium‐high. The general public and investors understand the importance of diagnosis and treatment.

High interest from the public for bed‐nets following intense media campaigns

Applicability and relevance of the intervention to the malaria situation

A comprehensive analysis should be run for each commodity once the country or region for the pilot is determined

Availability of implementers that can carry the risk and are willing to participate

To be determined Medium – although 80% of the treatments are distributed through private sector, this tends to be represented by small scale outlets (e.g., pharmacies). RDTs are not (yet) widely used in the private sector.

8 Interest and feasibility of working with public sector actors (e.g. mission‐sector, NGOs) needs further research

Medium‐high – there are manufacturers with the potential to implement distribution programs and large non‐for‐profit organizations with well‐managed programs (e.g., PSI)

9

The roll‐out of a malaria vaccine will not take place before 2014/2015. It has thus been considered out of scope for a malaria bond that aims to raise money before 2015.

7 DDT is one of the cheapest insecticides and was heavily used in endemic countries for vector control programs. Under pressure from the international community worried about damage to human health and environment from DDT, some developing nations have stopped or cut down on its use. 8 Affordable Medicines Facility – malaria (AMFm), Technical design, November 2007 9 Success of LLIN mass distribution in Ethiopia, Global Malaria Action Plan

Runesb

Highlight

Runesb

Highlight

9

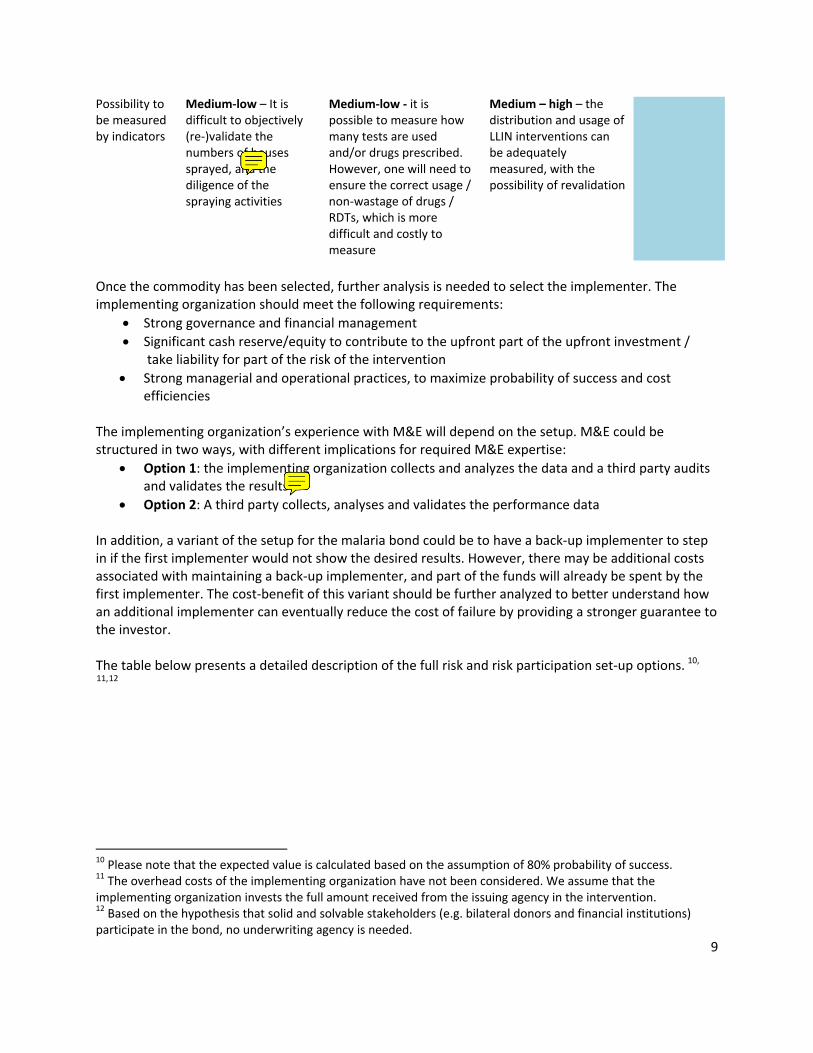

Possibility to be measured by indicators

Medium‐low – It is difficult to objectively (re‐)validate the numbers of houses sprayed, and the diligence of the spraying activities

Medium‐low ‐ it is possible to measure how many tests are used and/or drugs prescribed. However, one will need to ensure the correct usage / non‐wastage of drugs / RDTs, which is more difficult and costly to measure

Medium – high – the distribution and usage of LLIN interventions can be adequately measured, with the possibility of revalidation

Once the commodity has been selected, further analysis is needed to select the implementer. The implementing organization should meet the following requirements:

Strong governance and financial management

Significant cash reserve/equity to contribute to the upfront part of the upfront investment / take liability for part of the risk of the intervention

Strong managerial and operational practices, to maximize probability of success and cost efficiencies

The implementing organization’s experience with M&E will depend on the setup. M&E could be structured in two ways, with different implications for required M&E expertise:

Option 1: the implementing organization collects and analyzes the data and a third party audits and validates the results

Option 2: A third party collects, analyses and validates the performance data

In addition, a variant of the setup for the malaria bond could be to have a back‐up implementer to step in if the first implementer would not show the desired results. However, there may be additional costs associated with maintaining a back‐up implementer, and part of the funds will already be spent by the first implementer. The cost‐benefit of this variant should be further analyzed to better understand how an additional implementer can eventually reduce the cost of failure by providing a stronger guarantee to the investor. The table below presents a detailed description of the full risk and risk participation set‐up options. 10, 11,12

10 Please note that the expected value is calculated based on the assumption of 80% probability of success. 11 The overhead costs of the implementing organization have not been considered. We assume that the implementing organization invests the full amount received from the issuing agency in the intervention. 12 Based on the hypothesis that solid and solvable stakeholders (e.g. bilateral donors and financial institutions) participate in the bond, no underwriting agency is needed.

Runesb

Sticky Note

this is simply wrong. you can easily assess how well an IRS campaign has been implemented by sampling and chemical analysis.

Runesb

Sticky Note

where the implementer is identical to the manufacturer, this means that the manufacturer sells the product, distributes and then checks that distribution and the products are in order.

10

Option 1: FULL RISK

Description: Private investors invest $100 expecting a high return in case of success and the repayment of part of the principal in case of failure. The expected value of this set‐up for investors is $110 (expected return of 10%) The implementing organization receives a first tranche of the investment, the possible second tranche is conditional to the proven success of the intervention If the initiative is successful, donor pays principal + return to the investor and an additional contribution to the implementing organization If the initiative fails, the implementing organization does not receive the second tranche of investment which will be repaid to the investor

Illustration of mechanism:

Necessary conditions: Private investors have a high risk tolerance, and are willing to lose at least part of their principal Donors are risk‐averse, and are willing to pay significantly higher costs in case of success to be able to pay less in case of failure. These higher costs should be compensated by higher benefits due to increased cost‐efficiency.

Key risks/drawbacks: It might be difficult to find investors who are willing to accept such a high level of risk

Existing examples: The Social Impact Bond on Criminal Justice from Social Finance represents a good example of bond where the investor carries the full risk

Overall feasibility: Potentially investor risk profile is too aggressive for the pilot, and more feasible for follow‐on malaria bonds

11

The guaranteed return option is included in Annex A.

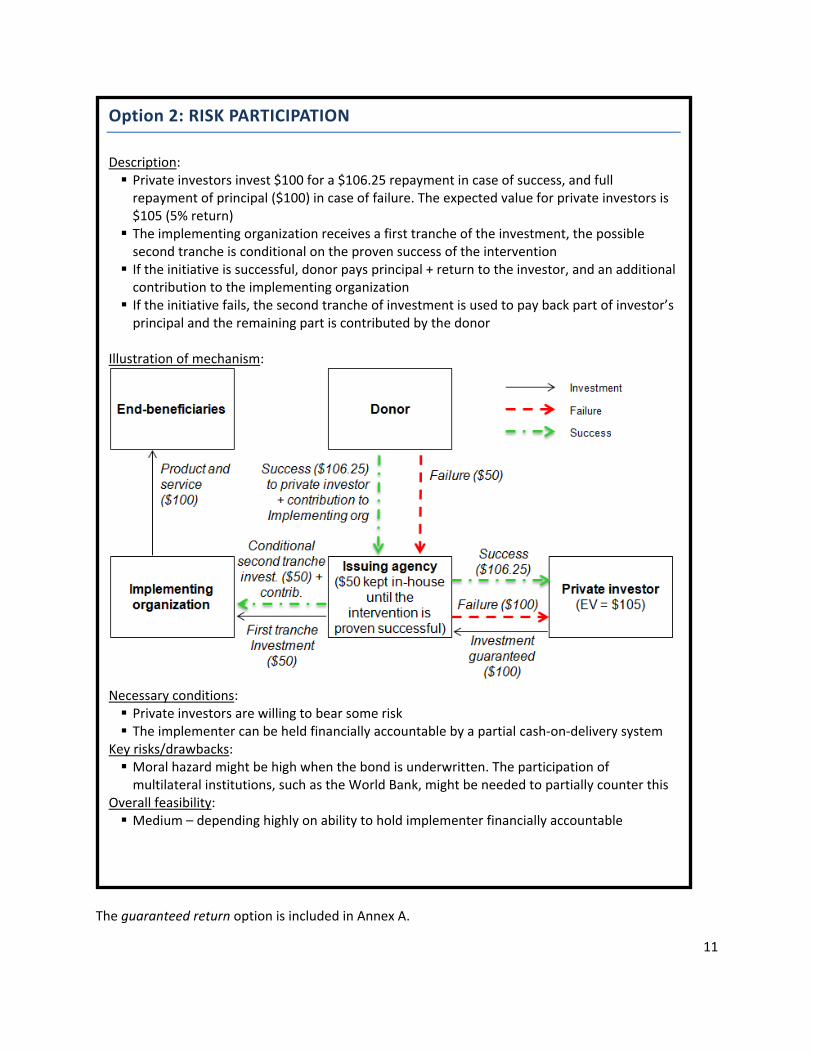

Option 2: RISK PARTICIPATION

Description: Private investors invest $100 for a $106.25 repayment in case of success, and full repayment of principal ($100) in case of failure. The expected value for private investors is $105 (5% return) The implementing organization receives a first tranche of the investment, the possible second tranche is conditional on the proven success of the intervention If the initiative is successful, donor pays principal + return to the investor, and an additional contribution to the implementing organization If the initiative fails, the second tranche of investment is used to pay back part of investor’s principal and the remaining part is contributed by the donor

Illustration of mechanism:

Necessary conditions: Private investors are willing to bear some risk The implementer can be held financially accountable by a partial cash‐on‐delivery system

Key risks/drawbacks: Moral hazard might be high when the bond is underwritten. The participation of multilateral institutions, such as the World Bank, might be needed to partially counter this

Overall feasibility: Medium – depending highly on ability to hold implementer financially accountable

12

The Taskforce agreed that a structure that aggregates the two options above is probably the most feasible solution. This will allow the malaria bond to consist of two individual financial products, one product for investors who seek guaranteed principal and one where the principal is at risk. In addition the Taskforce agreed that, independently from the option selected, the success of the intervention should be defined across a range of different levels. The donor’s repayment should be structured accordingly in line with the level of success. The table below simulates this principle by using the full risk option as an example. If we assume that the goal of the intervention is to achieve LLINs usage by 90% of the population and that less than 50% usage is a failure, donors repay investors based on a sliding scale. 13

Target goal of the intervention: LLINs used by 90% of the population in a specific area

% population using LLINs <50% 50% 60% 70% 80% 90%

% donor repayment 0% 56% 67% 78% 89% 100%

$ donor repayment $ 50 $ 69.4 $ 83.3 $ 97.2 $ 111.1 $ 125

In addition the Taskforce recognized that the practical implementation of this mechanism will engage multiple investors and implementing organizations. The selection of the latter will be based on specific drivers such as the commodity selected, the geographical presence, past performance and the type of organization (e.g., private sector, NGO). The management of these players, although critical to increase funds and probability of success, may generate additional costs and challenges for the instruments which will need to be clarified and addressed during the set‐up. In order to exemplify how an additional implementing organization and investor may affect the flow of funds, three scenarios have been developed below for the full risk options:

13 The calculation of the donor repayment is based on the assumption that 90% coverage equates to the full repayment of principal plus return as illustrated in option 1 (See page 8). If instead the coverage level is at 70% which equates to 78% of target coverage level, then the donor repayment will be $97.2 or 78% of $125.

13

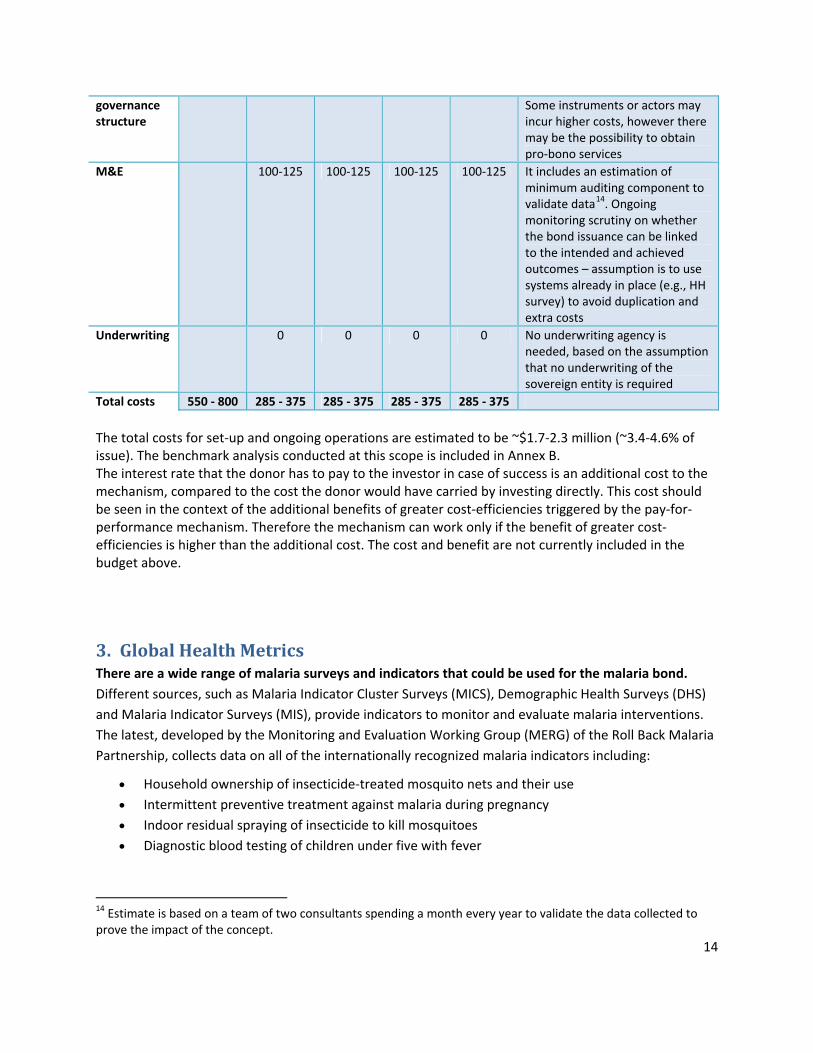

2.1 Setup budget Below is a preliminary budget for setting up and managing a four year malaria bond. This budget is based on a $50 million bond issue. $ thousand Set‐up Ongoing

Line of budget

Year 0 Year 1 Year 2 Year 3 Year 4 Comments

Structuring the mechanism

300 – 450 Estimate includes 2 people at 50% for 1 year and additional fixed costs

Marketing and issuing of the bond

250 ‐ 350 May contain pro‐bono element, requires further validation

Legal advice 60 ‐ 125 60 ‐125 60 ‐125 60 ‐ 125 The total legal cost can vary significantly based on the possibility to obtain pro‐bono services. Unexpected events such as legal disputes will affect the total cost

Treasury management and

125 125 125 125 ~1 % of issue – assuming a $50 million issue.

14

governance structure

Some instruments or actors may incur higher costs, however there may be the possibility to obtain pro‐bono services

M&E 100‐125 100‐125 100‐125 100‐125 It includes an estimation of minimum auditing component to validate data14. Ongoing monitoring scrutiny on whether the bond issuance can be linked to the intended and achieved outcomes – assumption is to use systems already in place (e.g., HH survey) to avoid duplication and extra costs

Underwriting 0 0 0 0 No underwriting agency is needed, based on the assumption that no underwriting of the sovereign entity is required

Total costs 550 ‐ 800 285 ‐ 375 285 ‐ 375 285 ‐ 375 285 ‐ 375

The total costs for set‐up and ongoing operations are estimated to be ~$1.7‐2.3 million (~3.4‐4.6% of issue). The benchmark analysis conducted at this scope is included in Annex B. The interest rate that the donor has to pay to the investor in case of success is an additional cost to the mechanism, compared to the cost the donor would have carried by investing directly. This cost should be seen in the context of the additional benefits of greater cost‐efficiencies triggered by the pay‐for‐performance mechanism. Therefore the mechanism can work only if the benefit of greater cost‐efficiencies is higher than the additional cost. The cost and benefit are not currently included in the budget above.

3. Global Health Metrics There are a wide range of malaria surveys and indicators that could be used for the malaria bond.

Different sources, such as Malaria Indicator Cluster Surveys (MICS), Demographic Health Surveys (DHS)

and Malaria Indicator Surveys (MIS), provide indicators to monitor and evaluate malaria interventions.

The latest, developed by the Monitoring and Evaluation Working Group (MERG) of the Roll Back Malaria

Partnership, collects data on all of the internationally recognized malaria indicators including:

Household ownership of insecticide‐treated mosquito nets and their use

Intermittent preventive treatment against malaria during pregnancy

Indoor residual spraying of insecticide to kill mosquitoes

Diagnostic blood testing of children under five with fever

14 Estimate is based on a team of two consultants spending a month every year to validate the data collected to prove the impact of the concept.

15

M&E costs will be minimized and acceptance increased if the bond uses existing monitoring systems and

metrics. This also aligns with best practices in using common monitoring frameworks rather than

duplicating systems.15

Indicators should have high scores on attribution, measurability, objectivity, and cost efficiency. The

indicator should be attributable to the intervention financed by the bond, and not be unduly influenced

by external events such as weather patterns, or by similar interventions of other implementers. The

indicator should not measure a result that is not part of the intended results of the intervention. The

data for the indicator should be collected by an external objective party that has no conflict of interest

vis‐à‐vis the outcomes of the indicator. Moreover, the data collection should be straightforward and

replicable, allowing all parties to validate the results. Finally, the collection of indicators should be cost

efficient by maintaining a balance between cost incurred and benefits provided.

A select group of output and outcome indicators seems the most useful instruments to measure

success of funded interventions. Impact indicators give maximum freedom to implementers to choose

the most effective interventions to reach their goals. However, impact indicators such as mortality and

morbidity take time to manifest, and may require more expensive data collection and analysis.

Furthermore, the attribution to a specific intervention is weak. Annex C provides a list of MIS outcome

metrics from the National Malaria Indicator Survey Mozambique 2007. The indicators for commodity

supply are promising, as they are easily measurable and verifiable, are less influenced by external

events, and are easily understood by the general public and investors.

Once the metrics are selected, donors and implementers need to define what differentiates success

from failure, in order to compare results with expectations and set possible performance compensation.

The LiST model used to estimate the impact of different interventions and to set expectations on

potential results, might also be used to evaluate programs and communicate results.

4. Governance and organization The governance structure of a malaria bond should demonstrate the following principles:

Simple transparent cash flows

Credible treasury manager

Oversight function to ensure achievement of financial sustainability and developmental goals

Independence of funding and performance decisions from parties with financial vested interests

Multi‐stakeholder Design Team ceases to exist after the launch of the mechanism

15 Donors, developing countries and UN agencies agreed to three core principles – known as the "Three Ones" ‐ to better coordinate the scale up of national AIDS responses. The "Three Ones" principles are: one agreed HIV/AIDS action framework that provides the basis for coordinating the work of all partners, one national AIDS coordinating authority, with a broad based multi‐sector mandate, and one agreed country‐level monitoring and evaluation system.

Runesb

Highlight

Runesb

Highlight

Runesb

Sticky Note

several times in the text and the innovative financing text, this role can be played by the implementer, which is it?

Runesb

Highlight

Runesb

Sticky Note

but are they strategically relevant to the campaign or fight against malaria at large?

16

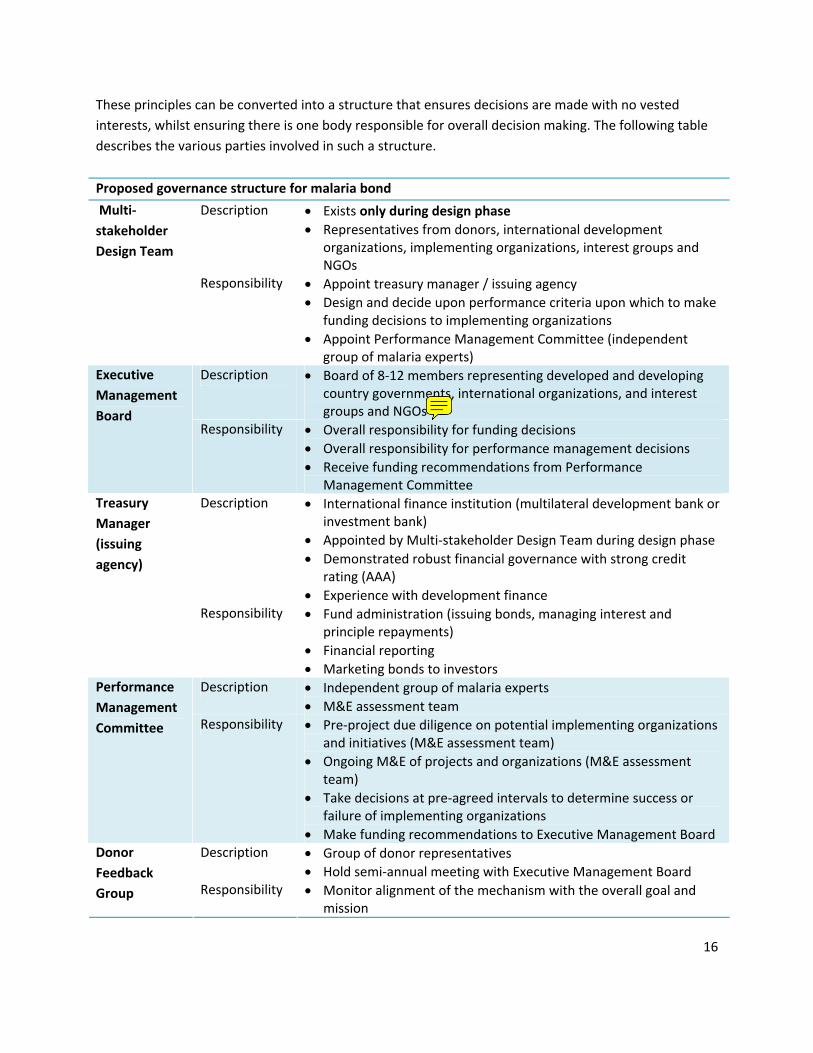

These principles can be converted into a structure that ensures decisions are made with no vested

interests, whilst ensuring there is one body responsible for overall decision making. The following table

describes the various parties involved in such a structure.

Proposed governance structure for malaria bond

Description Exists only during design phase

Representatives from donors, international development organizations, implementing organizations, interest groups and NGOs

Multi‐

stakeholder

Design Team

Responsibility Appoint treasury manager / issuing agency

Design and decide upon performance criteria upon which to make funding decisions to implementing organizations

Appoint Performance Management Committee (independent group of malaria experts)

Description Board of 8‐12 members representing developed and developing country governments, international organizations, and interest groups and NGOs

Executive

Management

Board Responsibility Overall responsibility for funding decisions

Overall responsibility for performance management decisions

Receive funding recommendations from Performance Management Committee

Description International finance institution (multilateral development bank or investment bank)

Appointed by Multi‐stakeholder Design Team during design phase

Demonstrated robust financial governance with strong credit rating (AAA)

Experience with development finance

Treasury

Manager

(issuing

agency)

Responsibility Fund administration (issuing bonds, managing interest and principle repayments)

Financial reporting

Marketing bonds to investors Description Independent group of malaria experts

M&E assessment team

Performance

Management

Committee Responsibility Pre‐project due diligence on potential implementing organizations and initiatives (M&E assessment team)

Ongoing M&E of projects and organizations (M&E assessment team)

Take decisions at pre‐agreed intervals to determine success or failure of implementing organizations

Make funding recommendations to Executive Management Board Description Group of donor representatives

Hold semi‐annual meeting with Executive Management Board

Donor

Feedback

Group Responsibility Monitor alignment of the mechanism with the overall goal and mission

Runesb

Sticky Note

what would an NGO do here when they have practically been excluded from participation

17

The Executive Manager Board, Treasury Manager and Performance Management Committee functions

should be kept separate and independent from each other to ensure transparency and oversight. The

Multi‐stakeholder Design Team should ensure that each entity has a clear mandate and that no

duplication occurs. In addition, the organization should be committed to use existing structures as much

as possible, while acknowledging the need for potential new structures due to legal and governance

requirements. The IFFIm governance structure represents a good example of this principle. Most of the

tax, accounting, regulatory, credit, rating, legal and market requirements that were required could be

built around GAVI, IFFIm and the World Bank. IFFIm’s governance structure is included in annex D.

5. Marketing and communication plan The success of the marketing and communication plan will be based on the capacity to reach out and engage the key players. This will be an iterative process and will include the following:

Donors: their interest and eventual financial commitment is fundamental for making the malaria bond a reality. They constitute also a smaller, more easily addressable group then the implementing organizations or the investor community. Finally, they can provide crucial resources for the development of a detailed technical design.

Implementing organizations and endemic country representatives: the focus is on explaining the concept of the malaria bond and the payment for performance setup, and identifying implementing organizations interested in risk sharing.

Investors and financial players: The marketing campaign and investor outreach should be undertaken by the issuing agency or a separate financial intermediary, responsible for the structuring and marketing of the bonds.

6. Key success factors and immediate next steps The key next steps to move towards the launch of this mechanism are outlined below. As mentioned

under the marketing and communication plan, a key success requirement for the next phase is obtaining

donor interest, both for the overall feasibility of the bond and for unlocking resources to further develop

the technical design.

Governance. Establish a new taskforce (Multi‐stakeholder Design Team) which will take responsibility for the next phase of the malaria bond, including outreach towards donors and development of the technical design.

Outreach. Implement the marketing and outreach towards key stakeholders: o Seek the feedback of the RBM Board o Engage other stakeholders in the malaria‐ and innovative financing community to test

the concepts and incorporate their perspectives. o Explain the concept to endemic countries/region and incorporate their feedback o Organize donor briefings to test the preliminary interest of donors o Test the preliminary interest of implementing organizations for a pay‐for‐performance

mechanism o Identify potential issuing agencies

18

Technical design. Refine the analysis on the structure of the bond, with special attention for: o The overall business case (benefits, investments and ongoing costs) o The commodity selection and criteria for selection of implementer organizations o The risk‐sharing / pay‐for‐performance mechanism for implementers o Finalized M&E metrics, with input from the MERG o The required risk premium for investors o Overall risks and their mitigation

A next natural milestone is the RBM board meeting in May 2012. The Task Force recommends that the

Multi stakeholder design team work actively on engaging in outreach activities and refining the technical

design in the next six months. We would recommend that a limited budget for support to outreach and

further refinement will be allocated to support the Task Force. This required budget is estimated to be

approximately USD 150K, which will come out of the overall setup budget (USD 550K‐800K).

After taking stock of the status at the board meeting, the following scenarios might emerge:

Scenarios (result after six months)

Status of Donors outreach

Status of Implementing organizations outreach

Status of Investors outreach

Implications/ Next steps/ Potential challenges

“Go”

Donors have committed to fund the mechanism

A short list of vetted organizations who have stated interest to participate

There is a credible market study showing investor interest in the mechanism

Next steps:

Formally engage with issuing agency to develop bonds

Move to contracting and implementation phase for all stakeholders (e.g. donor, investors, etc.)

Potential challenges:

Donor commitments usually take at least 1 year and often significantly longer, to become approved, however seeing that this is a pilot it may be possible for some donors to fast‐track the approval.

“Stand‐by”

Donors show interest in the mechanism (no commitment yet)

A long list of organizations who have showed interest in participating

There is no data‐driven market study of investor interest (yet)

Implications:

Further analysis is needed, and the outreach phase should be prolonged

No funds should yet be spent on the issuing agency (lack of

19

certainty of positive outcome). If at all, the only contracting should be on a no cure‐no‐pay basis.

Next steps: Prolong the outreach with the goal to receive especially a stronger donor commitment

“No go”: Stop any outreach activities

Donors do not show interest in the mechanism

Interest from implementing organizations and investors will not be sufficient to move toward the implementation phase

Next steps: Abandon / change / revisit the overall concept

20

Annex A Option 3: GUARANTEED RETURN Description: Private investors invest $100 with a guaranteed return of 2%. The expected value of this option for the private investor is $102 The implementing organization receives a first tranche of the investment, the possible second tranche is conditional to the proven success of the intervention If the initiative is successful, donor pays principal + return to the investor, and an additional contribution to the implementing organization If the initiative fails, the second tranche of investment is used to pay back part of investor’s principal and the remaining part is contributed by the donor

Illustration of mechanism:

Necessary conditions:

Key risks/drawbacks: Return may not be high enough to attract private investors

Existing examples: No example available

Overall feasibility: Potentially investor incentives are too small

21

Annex B – Estimation of setup and ongoing costs based on IFFIm benchmark Cost Description Estimation for the

malaria bond ($)16 Benchmark (IFFIm)17 from inception in late 2006 to the end of 2010

Structuring the mechanism

Design the mechanism

Select all parties (e.g. issuing agency, implementer)

Determine terms and conditions, roles & responsibilities for all parties

Determine financial value proposition and risks and returns for all parties

Set the M&E framework

Drafts the ordinance or resolution and other legal documents

~$300,000‐450,000 Estimate includes 2 people at 50% for 1 year and additional fixed costs

[The malaria bond is likely less complex than IFFIm18. Moreover part of the cost above may be absorbed by the host organization and same savings may realize]

Personnel: 4 people at 50% for 2 years ~$600,000

Part of the structuring was done pro‐bono: GAVI legal advisers have estimated that their costs were just over £1m but there was an element that was uncharged ‐ fees were charged at 75% of market rates~$5.5 million (~8% for 2004 to 2006)19

Set‐up

Marketing and issuing the bond

Registration: the legal documents are filed with regulatory authorities (e.g. SEC)

If the document contain the appropriate information the reg. authority approves the issue

After the approval the bond document is distributed to potential purchasers

The bond is sold

Bond issuance: ~$250,000‐350,000 (~0.5‐0.7% of issue)

[may contain pro‐bono element, requires further validation]

Bond issuance: $13,8 million to the end of 2009 ~0.4‐0.5% of issue (IFFIm has undertaken 18 bond issues on 10 occasions In 5 markets, raising to $3.2 billion to date)

16 The cost estimates are preliminary and further analysis may be needed to explore the risk of potential higher costs for the bond’s smaller scale compared to IFFIm’s. 17 HLSP, Evaluation of the International Finance Facility for Immunisation, June 2011. 18 There will be fewer donor countries then IFFIm, and the GAVI setup with additional new entities and legal structures was complex. However, the performance management and implementation side of the malaria bond will be more complex then IFFIm 19 Source: GAVI evaluation report by HLSP

22

After the closing, the legal adviser distributes a complete set of the closing documents to each participant

Legal advice Registration of ongoing bond issues

~$250,000 ‐ 500,000 [The total legal cost can vary significantly based on the possibility to obtain pro‐bono services. Unexpected events such as legal disputes will affect the total cost]

2 law firms for a total cost of $1‐2 million per year ~$6.5 million over 2006 to 2010 (~9% of total costs)

Treasury management

Custody duty Funds disbursement: on‐going accounting for the payment of return and principal

~1% of issue – assuming a $50 million issue ~$500,000

Governance and treasury management costs ~$30 million to the end of 2010 (~1% of issue).

[The total treasury and governance structure costs were higher as a part was provided pro‐bono]

Governance structure

Board operational costs [included in line above]

[see line above]

M&E Measurement of indicators

Auditing cost– to check data consistency, particularly during the pilot ~$400,000 ‐ 500,000

Ongoing monitoring scrutiny on whether the bond issuance can be linked to the intended and achieved outcomes – assumption is to use systems already in place (e.g., HH survey) to avoid duplication and extra costs

NA Ongoing

Underwriting Underwriting NA [No underwriting

~$14 million up to the end of 2009

23

agency is needed, based on the assumption that no underwriting of the sovereign entity is required]

Total costs (set‐up and ongoing)

~$1.7 ‐2.3 million ~$70 million

Share 3.4‐4.6% assuming a $50 million issue

~2.2% of $3.2 billion issue

24

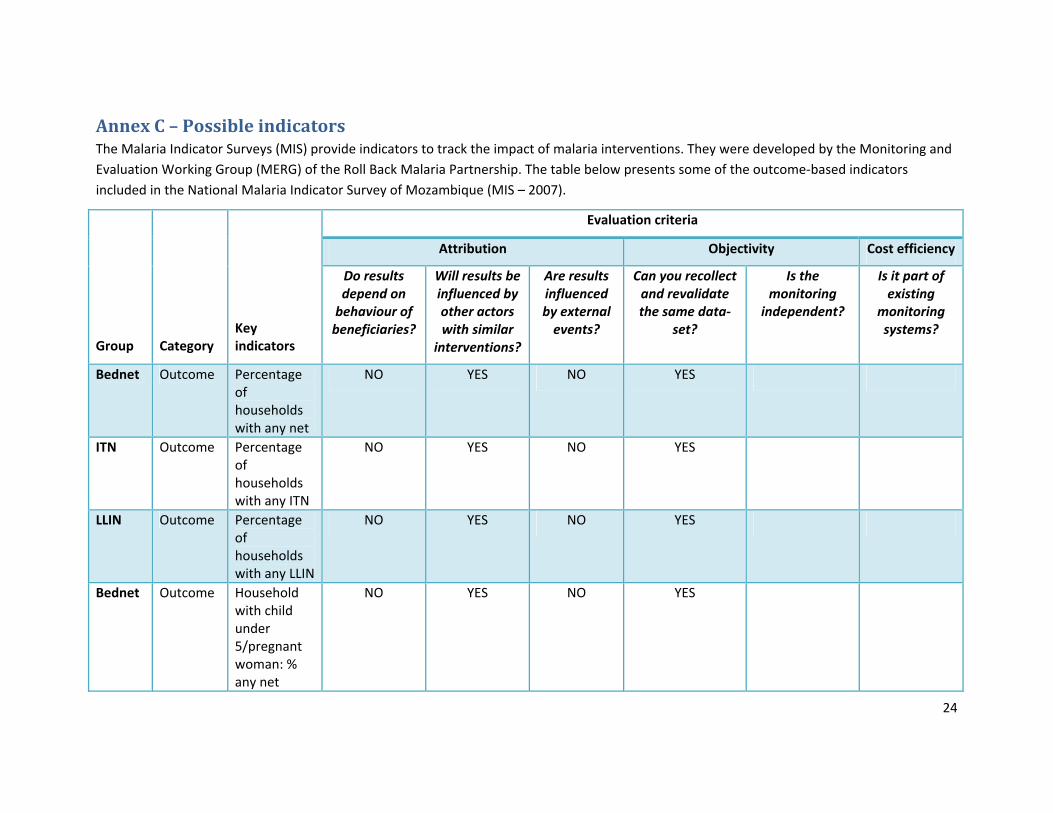

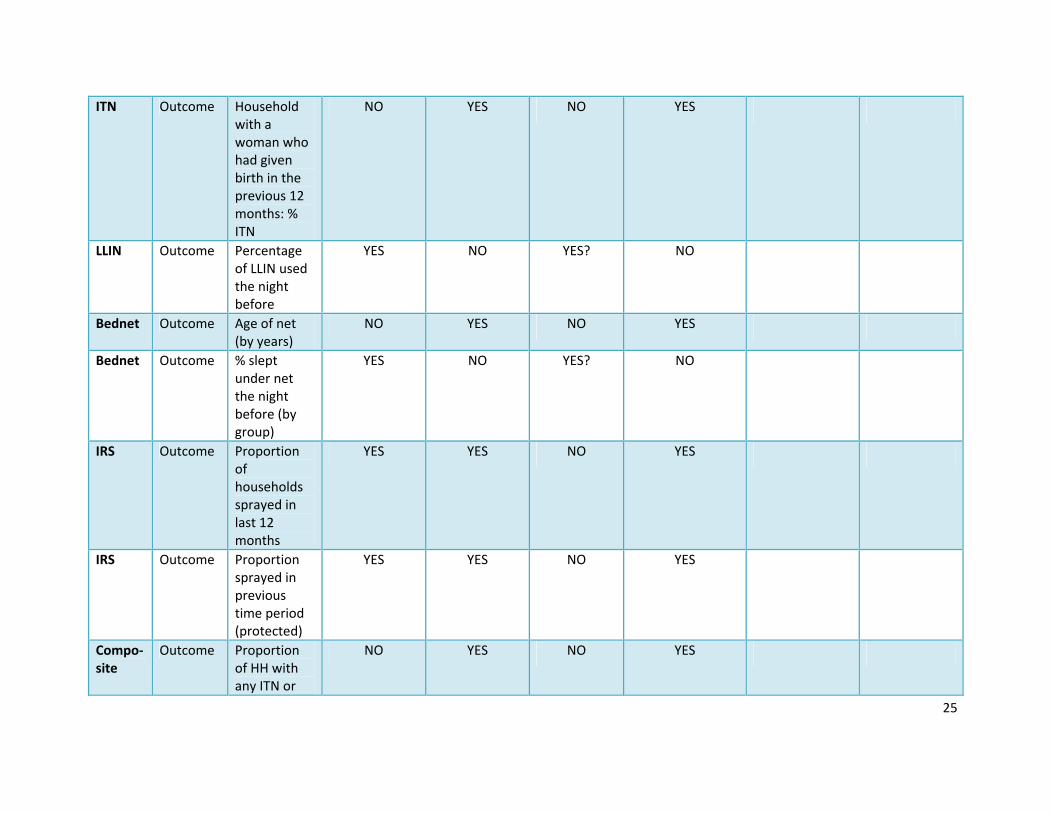

Annex C – Possible indicators The Malaria Indicator Surveys (MIS) provide indicators to track the impact of malaria interventions. They were developed by the Monitoring and

Evaluation Working Group (MERG) of the Roll Back Malaria Partnership. The table below presents some of the outcome‐based indicators

included in the National Malaria Indicator Survey of Mozambique (MIS – 2007).

Evaluation criteria

Attribution Objectivity Cost efficiency

Group Category Key indicators

Do results depend on behaviour of beneficiaries?

Will results be influenced by other actors with similar

interventions?

Are results influenced by external events?

Can you recollect and revalidate the same data‐

set?

Is the monitoring

independent?

Is it part of existing

monitoring systems?

Bednet Outcome Percentage of households with any net

NO YES NO YES

ITN Outcome Percentage of households with any ITN

NO YES NO YES

LLIN Outcome Percentage of households with any LLIN

NO YES NO YES

Bednet Outcome Household with child under 5/pregnant woman: % any net

NO YES NO YES

25

ITN Outcome Household with a woman who had given birth in the previous 12 months: % ITN

NO YES NO YES

LLIN Outcome Percentage of LLIN used the night before

YES NO YES? NO

Bednet Outcome Age of net (by years)

NO YES NO YES

Bednet Outcome % slept under net the night before (by group)

YES NO YES? NO

IRS Outcome Proportion of households sprayed in last 12 months

YES YES NO YES

IRS Outcome Proportion sprayed in previous time period (protected)

YES YES NO YES

Compo‐site

Outcome Proportion of HH with any ITN or

NO YES NO YES

26

sprayed in the previous 12 months

IPT Outcome Number of IPT doses received (by number), women who gave birth in previous 1 or 2 years

NO YES NO NO

Fever Outcome Fever in previous 2 weeks

YES NO YES NO

Fever Outcome (Febrile): received malaria medicine in 24h

YES YES YES NO

Fever Outcome Type of malaria treatment (by %)

NO YES YES YES

Anemia Outcome Anemia levels: children under 5

NO NO YES YES

Anemia Outcome Anemia levels: pregnant women

NO NO YES YES

Parase‐taemia

Outcome Children under 5:

NO NO YES YES

27

blood slide positive, RDT positive

Parase‐taemia

Outcome Pregnant women: blood slide positive, RDT positive

NO NO YES YES

Aware‐ness

Outcome Women’s knowledge of malaria (several indicators)

YES YES YES NO

28

Annex D – IFFIm’s governance structure The International Finance Facility for Immunisation (IFFIm) exists to rapidly accelerate the availability

and predictability of funds for immunisation. The resources raised by IFFIm are used by the GAVI

Alliance, a public‐private partnership, which provides funds to purchase and deliver life‐saving vaccines

and strengthen health services in the world's poorest countries.

IFFIm uses long‐term pledges from donor governments to sell 'vaccine bonds' in the capital markets,

making large volumes of funds immediately available for GAVI programmes. Launched in 2006,

IFFIm was the first aid‐financing entity in history to attract legally‐binding commitments of up to 20

years from donors and offers the "predictability" that developing countries need to make long‐term

budget and planning decisions about immunisation programmes.

The International Finance Facility for Immunisation Company is a UK Charity managed by its Board of

Directors. The Board's activities include:

Reviewing GAVI immunisation programme funding requests and ensuring proper disbursement

of funds;

Mandating the World Bank as Treasury Manager to arrange borrowing transactions to fund

immunisation programmes;

Monitoring IFFIm's investment portfolio and liquidity;

Reviewing and approving IFFIm's annual report of the trustees and financial statements;

Overseeing IFFIm's governance and policies;

Assessing IFFIm's efficacy as an innovative financing mechanism supporting international

development.

The World Bank is the Treasury Manager for IFFIm. In that capacity, the World Bank manages IFFIm's

finances according to prudent policies and standards agreed with the IFFIm Board. The World Bank's

work as Treasury Manager includes managing IFFIm's funding strategy and its implementation, rating

agency and investor outreach, hedging transactions, and investment management. The World Bank also

29

coordinates with IFFIm's donors and manages their pledges and payments as well as IFFIm's

disbursements for immunisation and health programmes through the GAVI Alliance.

GAVI is responsible for the operational activities related to the immunisation, health system

strengthening and vaccine procurement programmes for which IFFIm provides funding.